PRODUCTIVITY DECODING OF FINANCIAL SIGNALS

149

PRODUCTIVITY DECODING OF FINANCIAL SIGNALS: A PRIMER FOR MANAGERS ON DETERMINISTIC PRODUCTIVITY ACCOUNfiNG V The Library BAZILJ. VAN of tlic Witwaterstand Johannesburg by WtTMEA PUBLISHER Productivity Measurement Associates United Kingdom

-

Upload

fami4real2000 -

Category

Documents

-

view

0 -

download

0

Transcript of PRODUCTIVITY DECODING OF FINANCIAL SIGNALS

PRODUCTIVITY DECODING OFFINANCIAL SIGNALS:

A PRIMER FOR MANAGERS ONDETERMINISTIC PRODUCTIVITY ACCOUNfiNG

V

The Library BAZILJ. VAN

of tlic Witwaterstand

Johannesburg

by

WtTMEA

PUBLISHERProductivity Measurement AssociatesUnited Kingdom

This book is copyright under the Berne Convention. In termsof the Copyright Act, No 98 of 1978, no part of this book maybe reproduced or transmitted in any form or by any means,electronic or mechanical, including photocopying, recording orby information storage and retrieval system, without permissionin writing from the Publisher.

Key words:- ProductivityDecodeFinancialSignalsManagerDeterministicAccounting

Prior to publication of this book, I communicated the ofdeterministic productivity accounting to university students and tothrough lectures, articles and books which assume the reader hat anappreciation of advanced mathematics.

This book attempts to introduce another dimension to the literature thesubject. It aims at providing the non—mathematical reader an overview q theproductivity notion and relates.the "hard" (i.e., mathematicallynotion of productivity measurement to the "soft" objective of

in a manner conducive to raising productivity.

My principal business activity is training and providing consulting sqtjportto management of corporations who have decided to adoptproductivity accounting as part of the productivity management jqtjrneydescribed jn this book. In addition, I enjoy lecturing part—time inuniversities on the subject covered by this book to both andpostgraduate students in engineering and commerce faculties. Such teictingactivities revealed a need for an introductory text book which providflt anoverview of the productivity concept and the role of productivityin improving productivity.

The demand for such a book extends beyond universities into the pqlicyformation arena as governments increasingly acknowledge the need for contreteprograms to foster productivity growth. Government agencies theriforeacknowledge that they are also targets for the ideas expressed in this

To simplify the measurement component of the ideas set forth in this asimple notation is employed. A more quantitative audience is referred myother works for a rigurous algebraic specification of the axioms on thework rests.

Growing awareness of this work in academic circles is evident from theincreasing number of candidates for higher degrees who aspire to use this &jorkfor their research. It is interesting that some candidates intendthe mathematical structure while others intend taking it as given to moflitorprogress in the soft i:omponents of the productivity improvement process.

Growing awareness of this work in business circles flows from two roots, Itis stimulated in part by a management recognition thatimprovement is a good idea whose time has come. It is also stimulated injartby the activities of postgraduate university students who perceive the peedfor sound productivity measurement to underpin systematic efforts tooperations and raise productivity.

I hope that this bcok will therefore serve the needs of productivityconstituents in universities, business and government. Toupfront intellectual investment which users of the concept need to make, barehas been taken to include an expert system in the latest softwareknown as Financial Productivity Management (FPM). Hence the principal Ueascontained in this book can readily be accessed from the software inform to reinforce in the mind of the user what is stated more fullybook.

Bazil J. van.

To the Players, onsite and offsite

COPYRIGHT 1988 Basil James van Loggerenberg

PREFACE

"In their deep concerns men clever enough to dissimulate". C.P. Snow

Published by

Productivity Measurement AssociatesP.O. Box 201WITS 2050

301014429

ISBN 0 620 10540 2BDOZZO61

CONTENTS

PART A — BACKGROUND

Chapter Al TIlE PRODUCTIVITY CONCEPT

Chapter AZ PRODUCTIVITY MEASUREMENT AND PRODUCTIVITY IMPROVEMENT

Chapter A3 PRODUCTIVITY MANAGEMENT JOURNEY

Chapter A4 HOW MEASUREMENT ASSISTS PRODUCTIVITY MANAGEMENT

PART B — INPUT FUNCTIONS

Chapter Bl DATA REQUIREMENTS AND DEFAULT VALUES

PART C — AXIOMS FOR ALL REPORTS

Chapter Cl OVERVIEW OF ALL AXIOMS

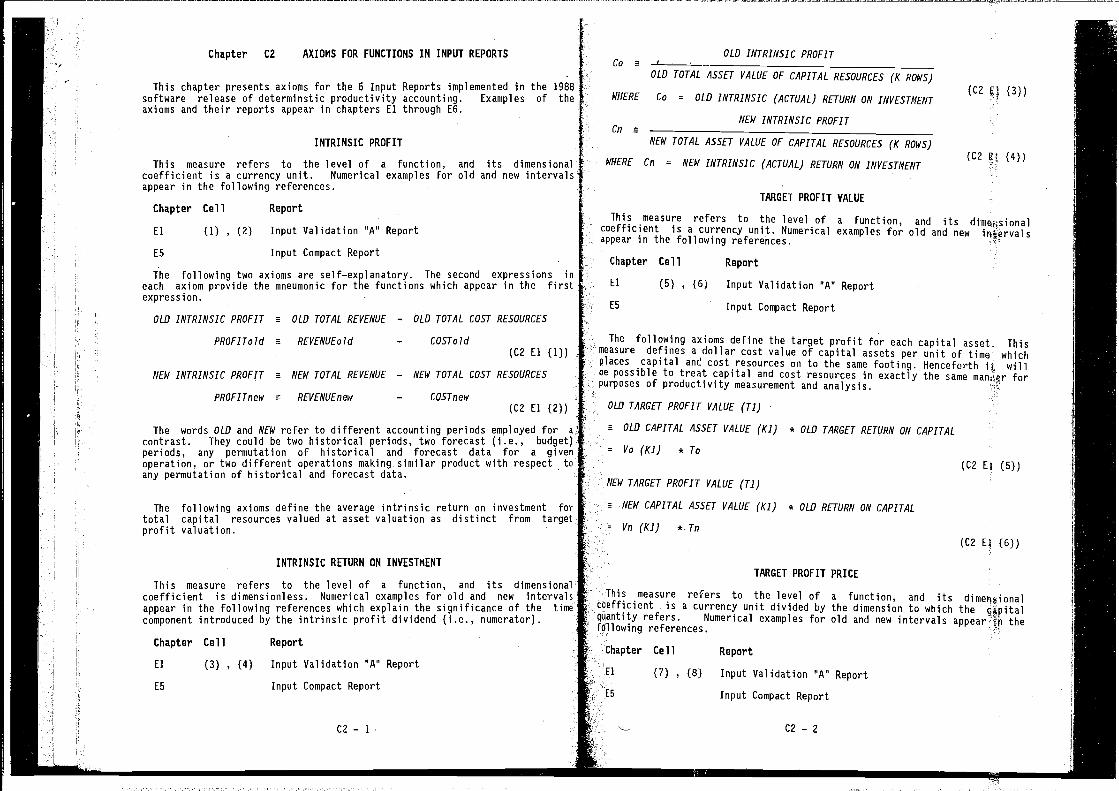

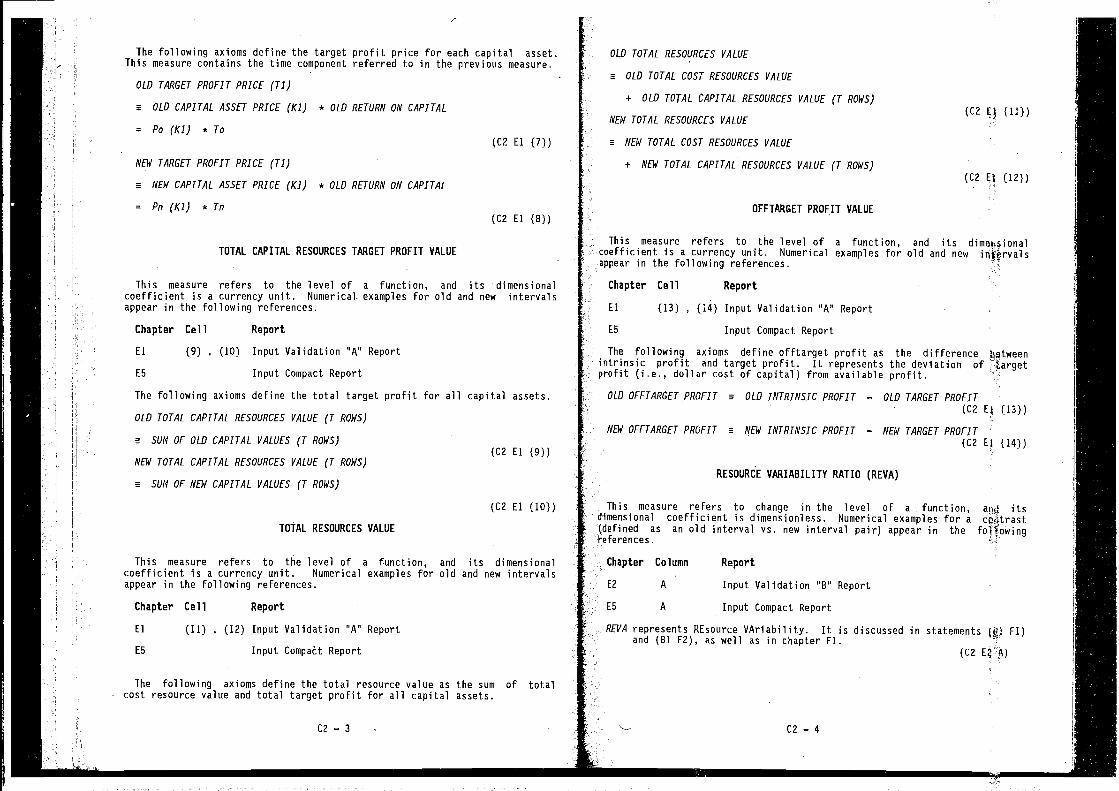

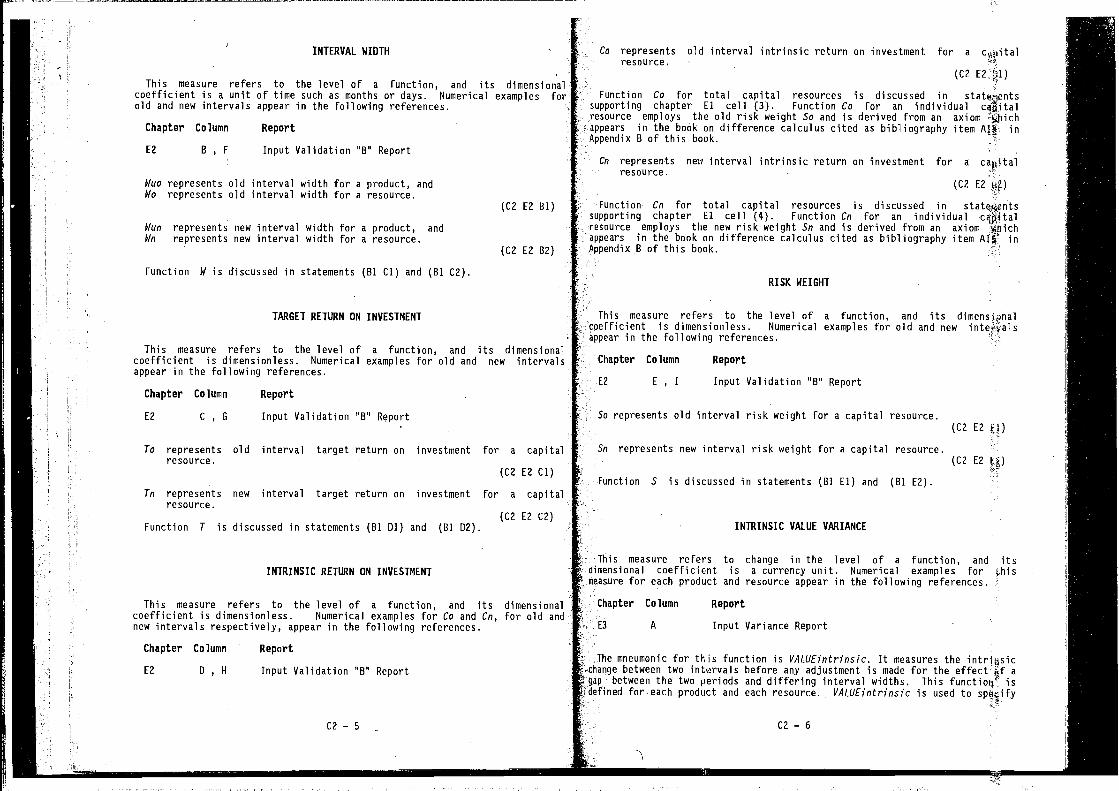

Chapter C2 AXIOMS FOR FUNCTIONS IN INPUT REPORTS

Chapter C3 AXIOMS TO GENERALIZE FUNCTIONS FORNEW RESOURCE QUANTITY AND NEW RESOURCE PRICE

Chapter C4 AXIOMS FOR FUNCTIONS TO MEASURE CHANGE IN PRODUCTIVITY,4CAPACITY UTILIZATION AND EFFICIENCY

Chapter C5 AXIOMS FOR FUNCTIONS TO MEASURE CHANGE IN LONG TERM SHORT

TERM PRODUCT PROFIT

Chapter C6 AXIOMS FOR FUNCTIONS TO MEASURE CHANGE IN LONG TERM ANQ SHORTTERM PRODUCT COST

Chapter C7 AXIOMS FOR FUNCTIONS IN PROFIT AND COST RECONCILIATIONRE PORTS

PART 0 — GRIDS FOR PERFORMANCE REPORTS AND RECONCILIATION

Chapter Dl QUANTITY GRID (LONG TERM)

Chapter D2 QUANTITY GRID (SHORT TERM)

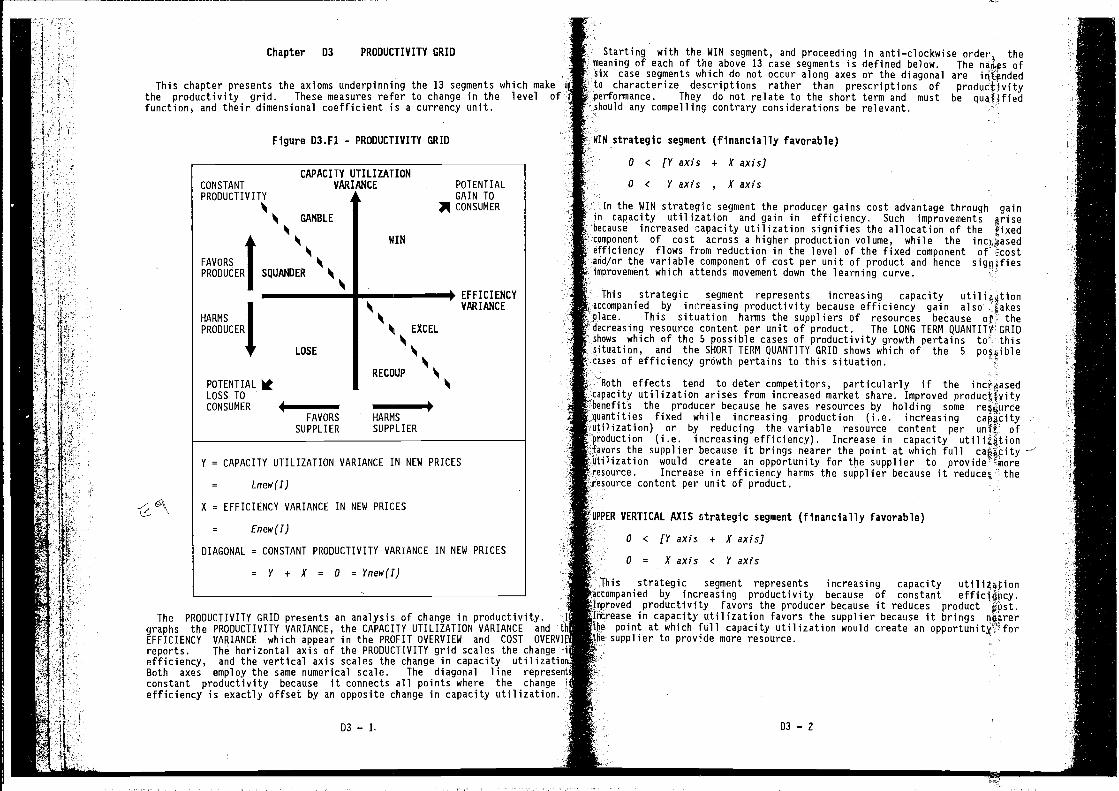

Chapter D3 PRODUCTIVITY GRID

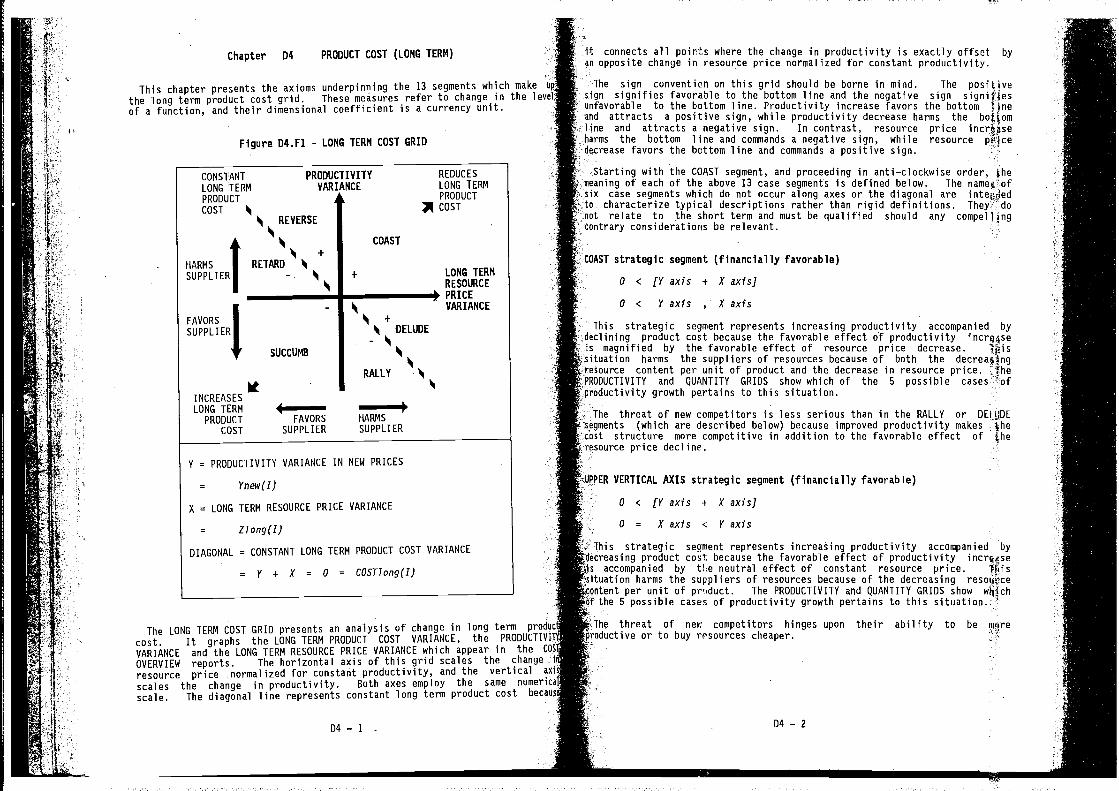

Chapter D4 PRODUCT COST GRID (LONG TERM)

Chapter D5 PRODUCT COST GRID (SHORT TERM)

Chapter D6 PRiCE GRID

Chapter 07 PRODUCT PROFIT GRID (LONG TERM)

CONTENTS — I

Chapter

Chapter

Chapter

Chapter

Chapter

Chapter

Chapter

D8

09

D10

011

012

D13

Dl 4

CONTENTS — 2

Chapter 12 DETERMINISTIC PRODUCTIVITY ACCOUNTING EXTENSIONTO BENEFIT TO COST RATIOS

APPENDIX B - BIBLIOGRAPHY

CONTENTS — 3

PRODUCT PROFIT GRID (SHORT TERM)

PRODUCT MIX COST GRID

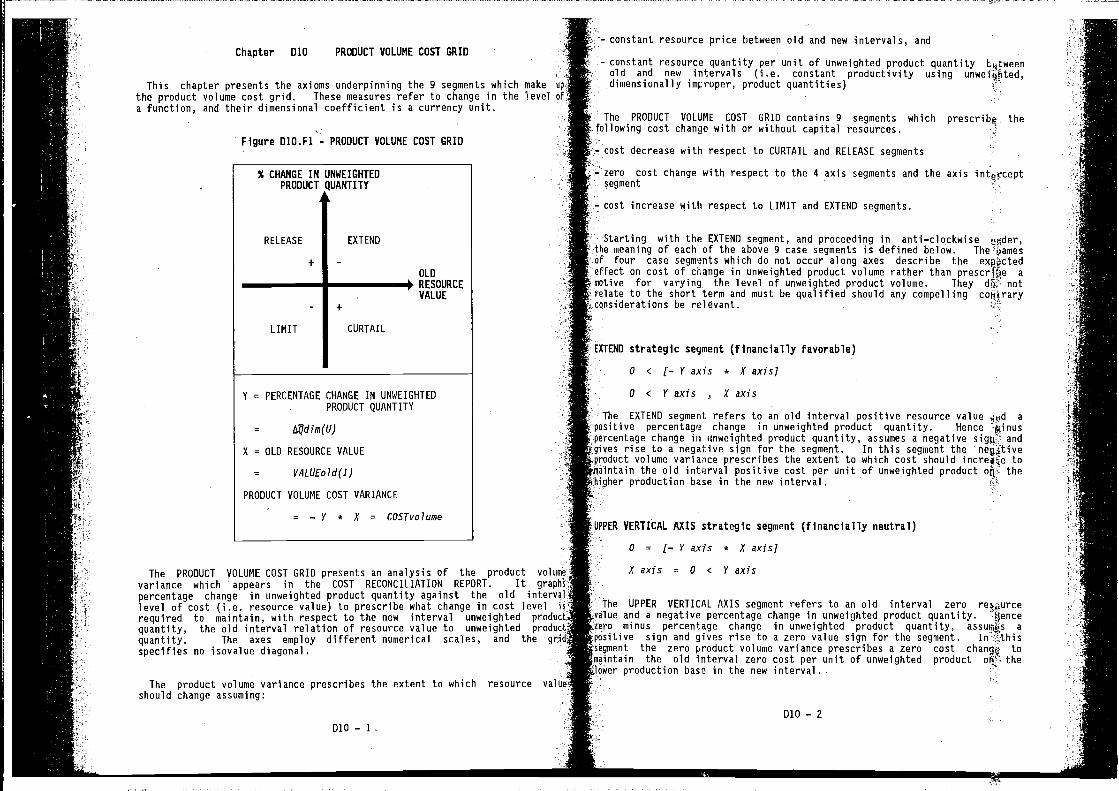

PRODUCT VOLUME COST GRID

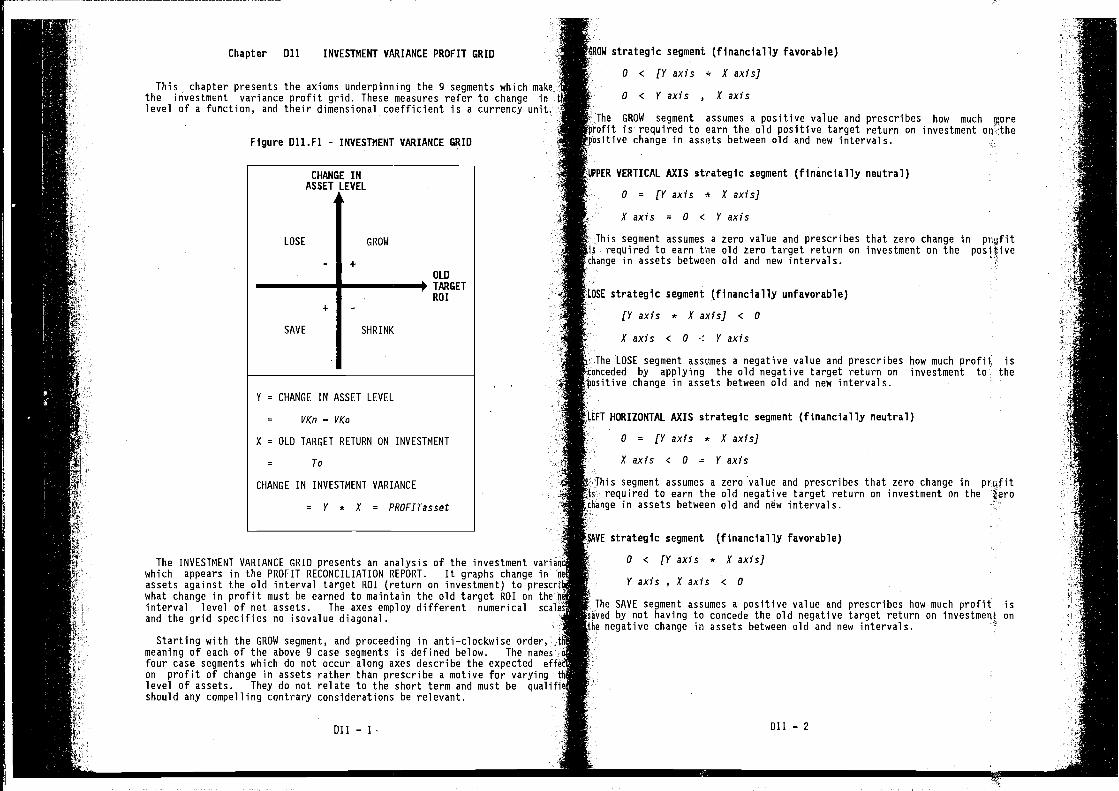

INVESTMENT VARIANCE PROFIT GRID

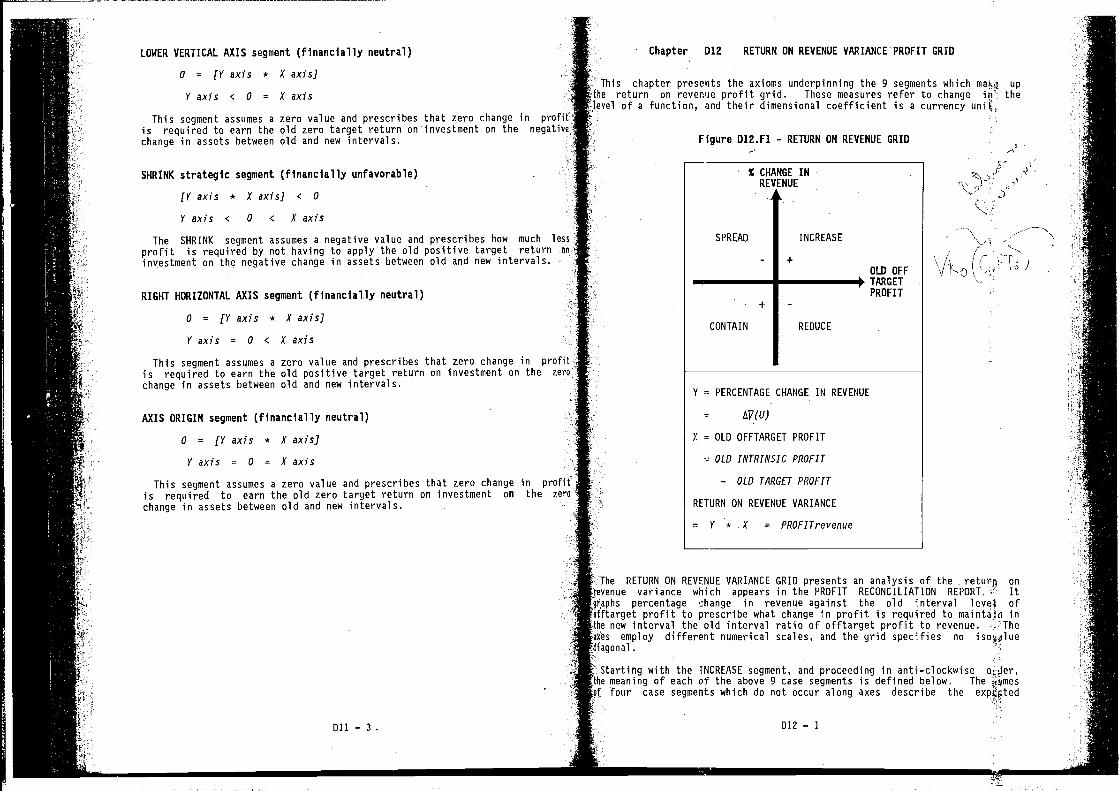

RETURN ON REVENUE VARIANCE PROFIT GRID

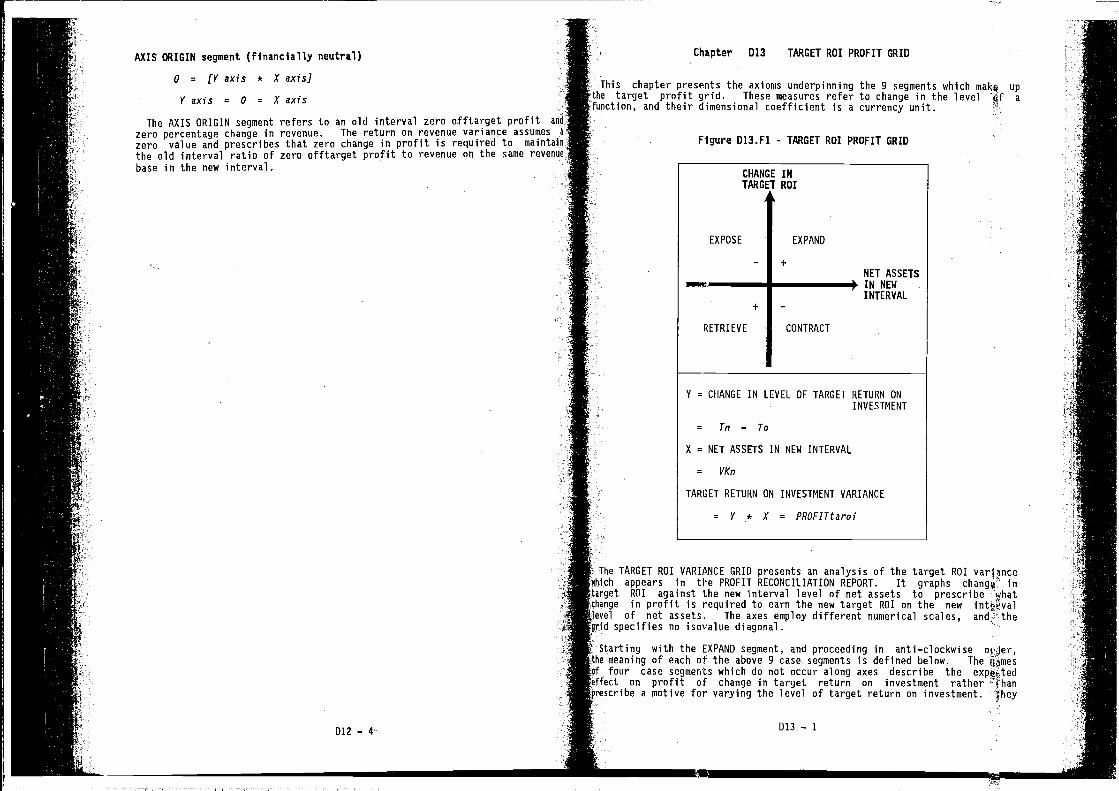

TARGET ROI PROFIT GRID

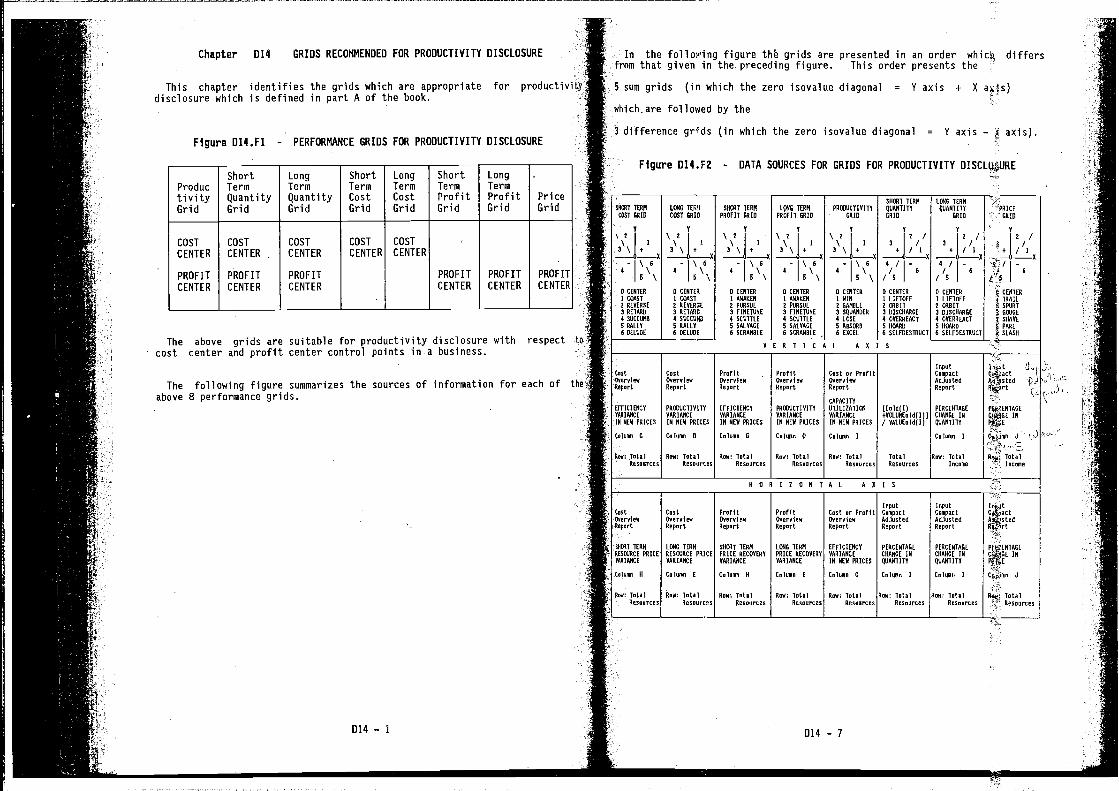

GRIDS RECOMMENDED FOR PRODUCTIVITY DISCLOSURE

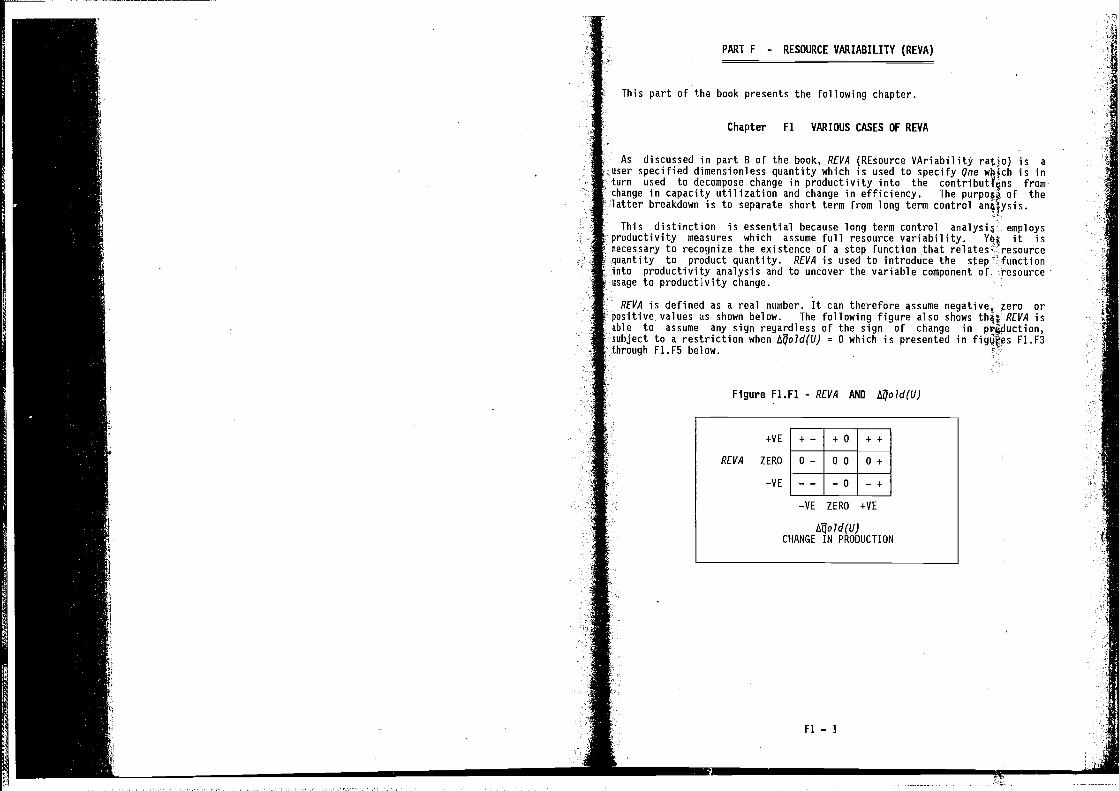

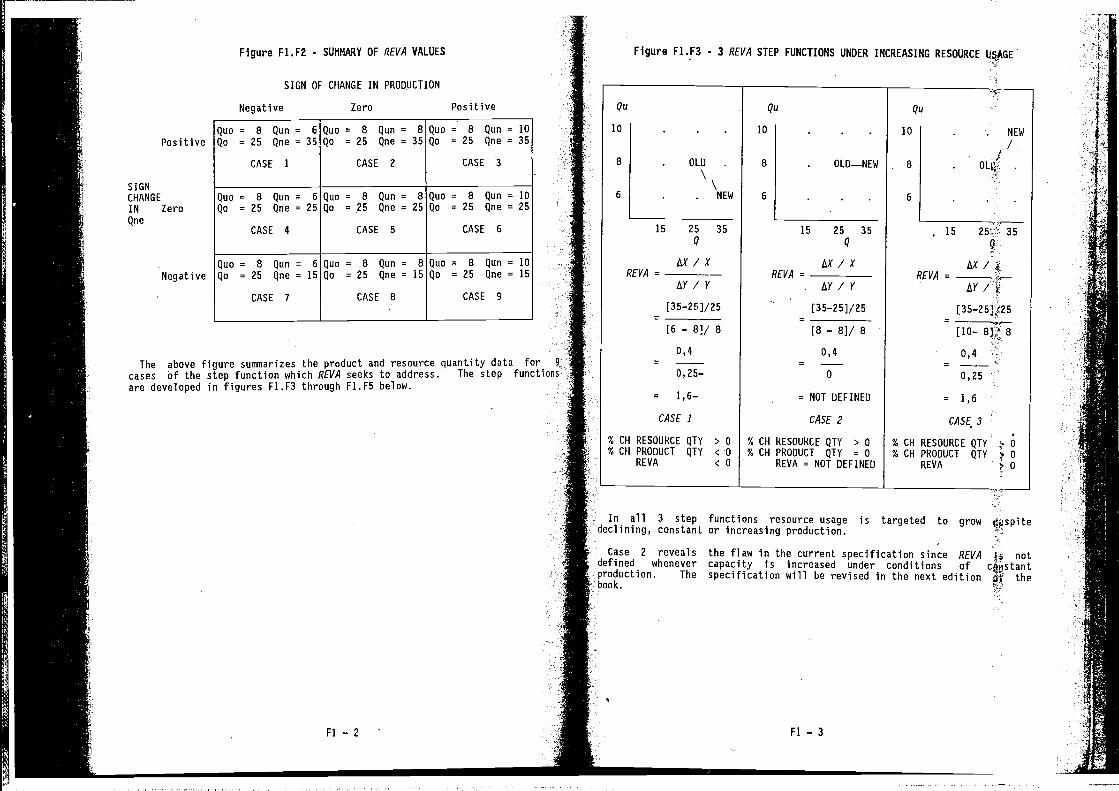

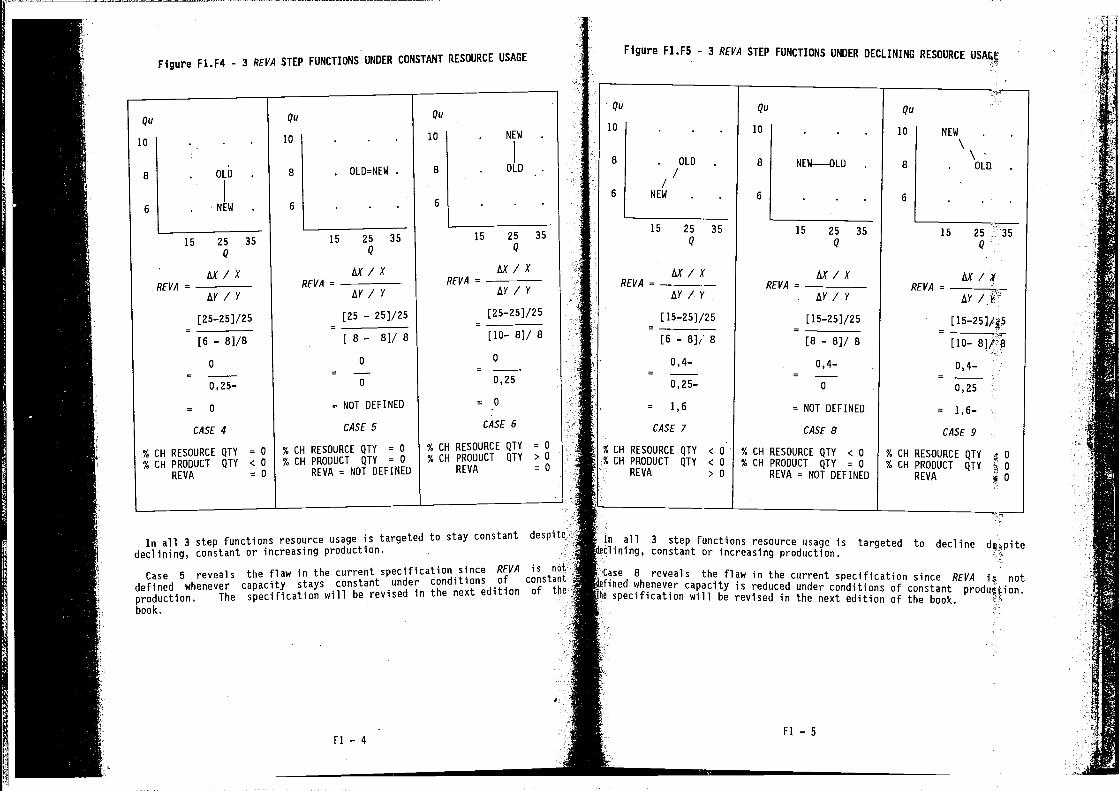

PART F — RESOURCE VARIABILITY (REVA

Chapter Fl 'VARIOUS CASES OF REVA

PART G — PROXY DATA

Chapter Gl PROXY PRICES AND PROXY QUANTITIES WHEN NONE ARE AVAILAWI

Chapter G2 SCORING MATRICES FOR PROXY PRODUCT QUANTITY

PART H — TRADEOFF ANALYSIS

Chapter Hl TRADITIONAL PRODUCTIVITY INDEX NUMBERS AND WORK STUDYAPPROACHES

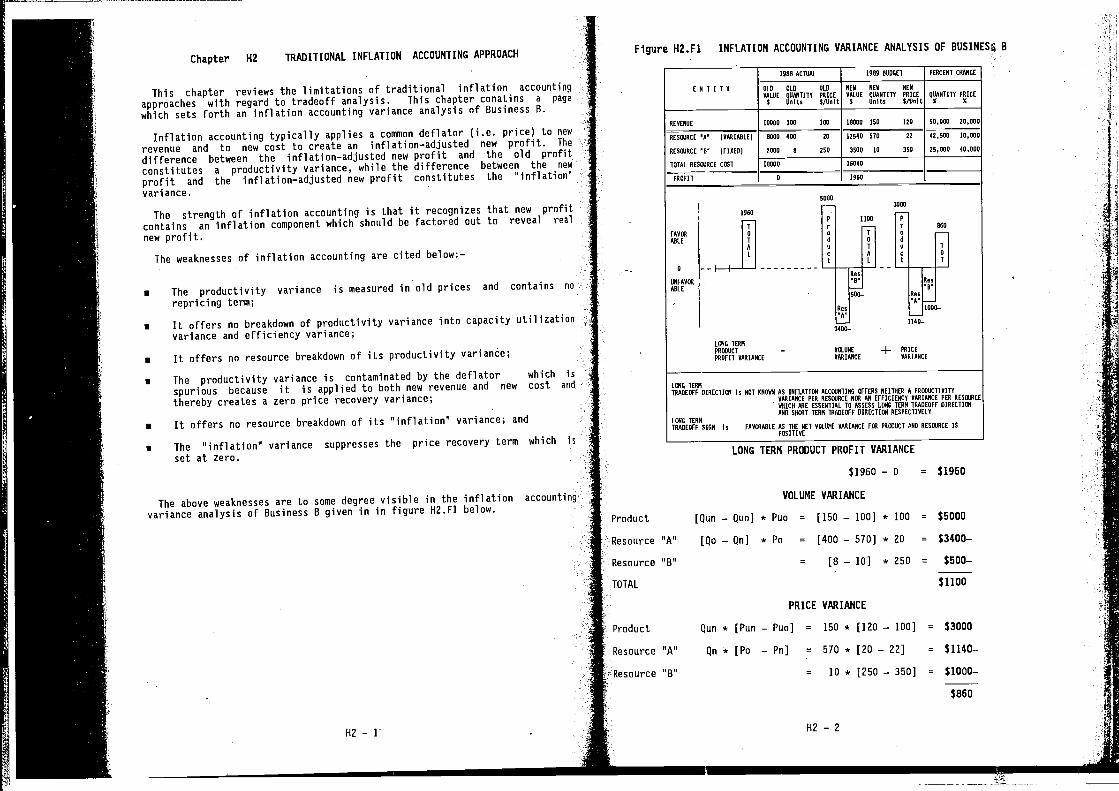

Chapter HZ TRADITIONAL INFLATION ACCOUNTING APPROACH

Chapter H3 1RADITIONAL STANDARD COST ACCOUNTING APPROACH ANDEXPENSE TO REVENUE RATIO APPROACH

Chapter H4 DETERMINISTIC PRODUCTIVITY ACCOUNTING APPROACH

Chapter H5 COMPARISON OF TRADITIONAL STANDARD COSTING ANDPRODUCTIVITY ACCOUNTING APPROACHES

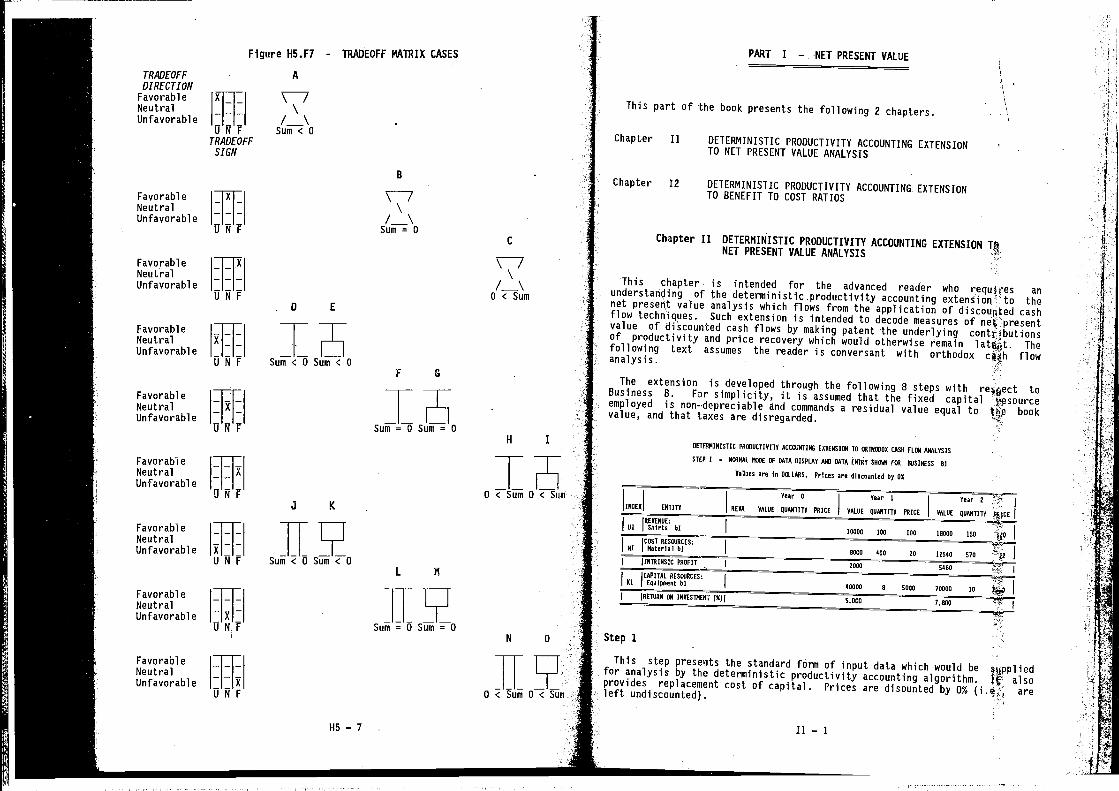

PART I — NET PRESENT VALUE

Chapter Ii DETERMINISTIC PRODUCTIVITY ACCOUNTING EXTENSIONTC NET PRESENT VALUE ANALYSIS

PART E — EXAMPLE

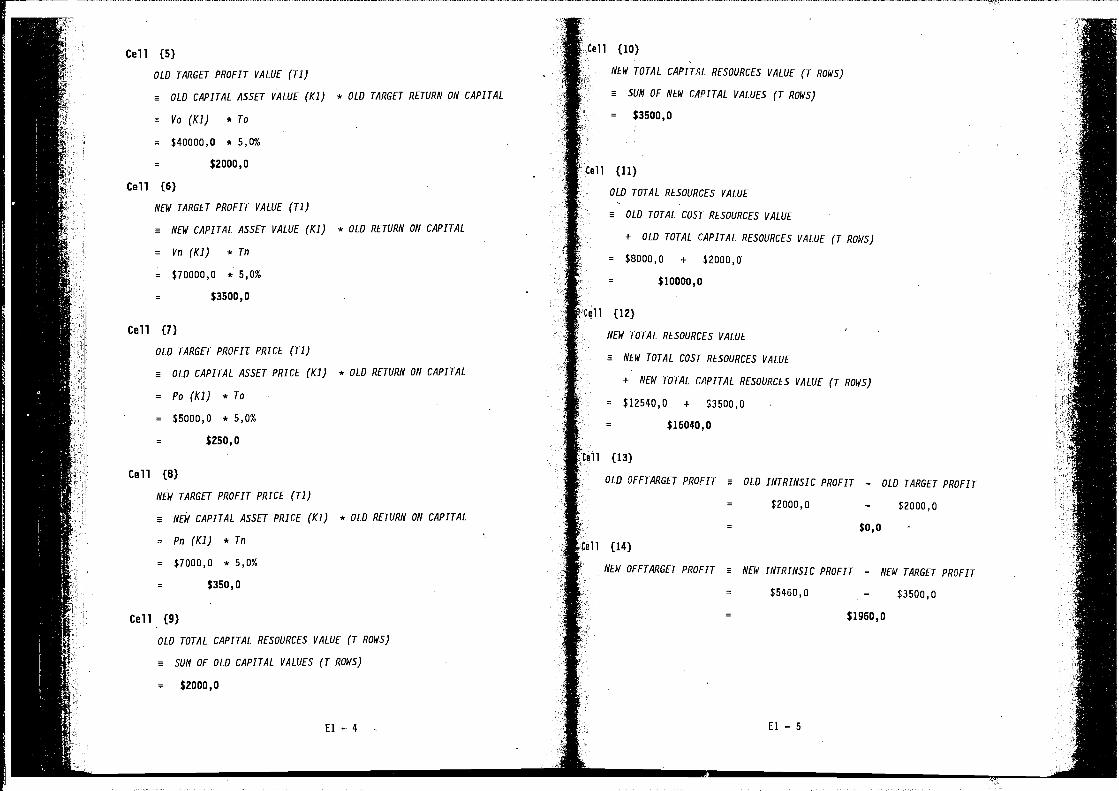

Chapter El EXAMPLE OF INPUT VALIDATION "A" REPORT

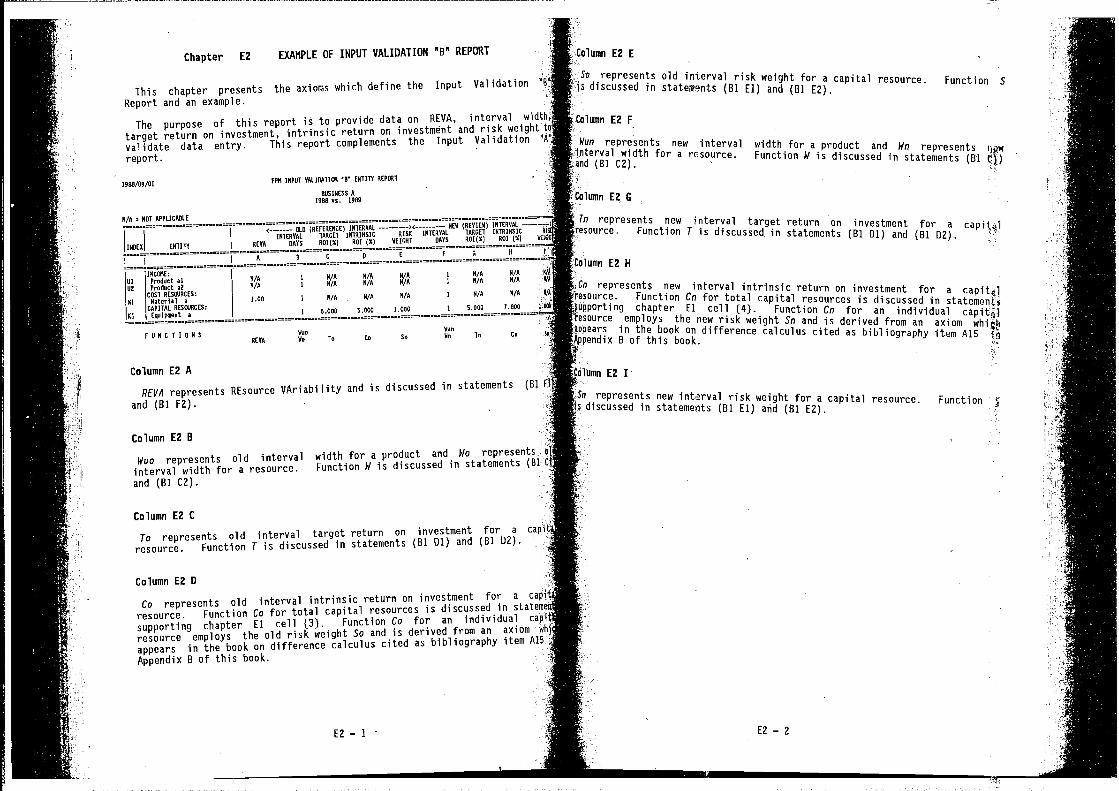

Chapter E2 EXAMPLE OF INPUT VALIDATION "B" REPORT

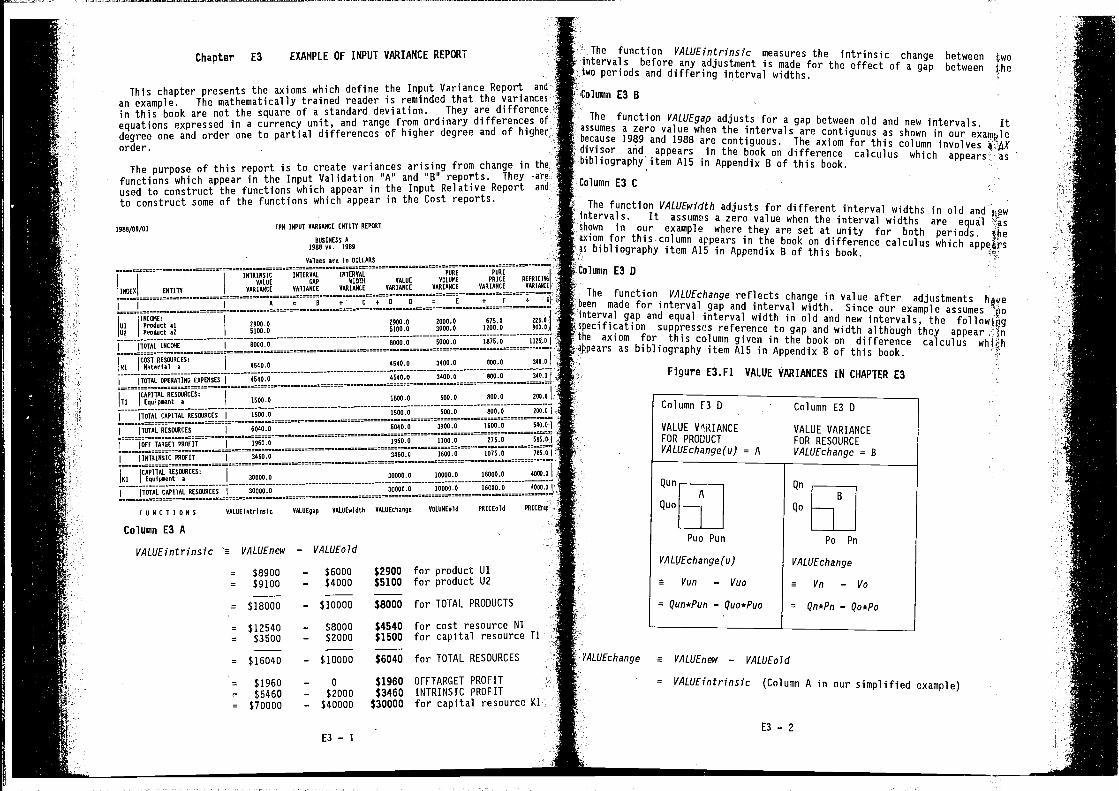

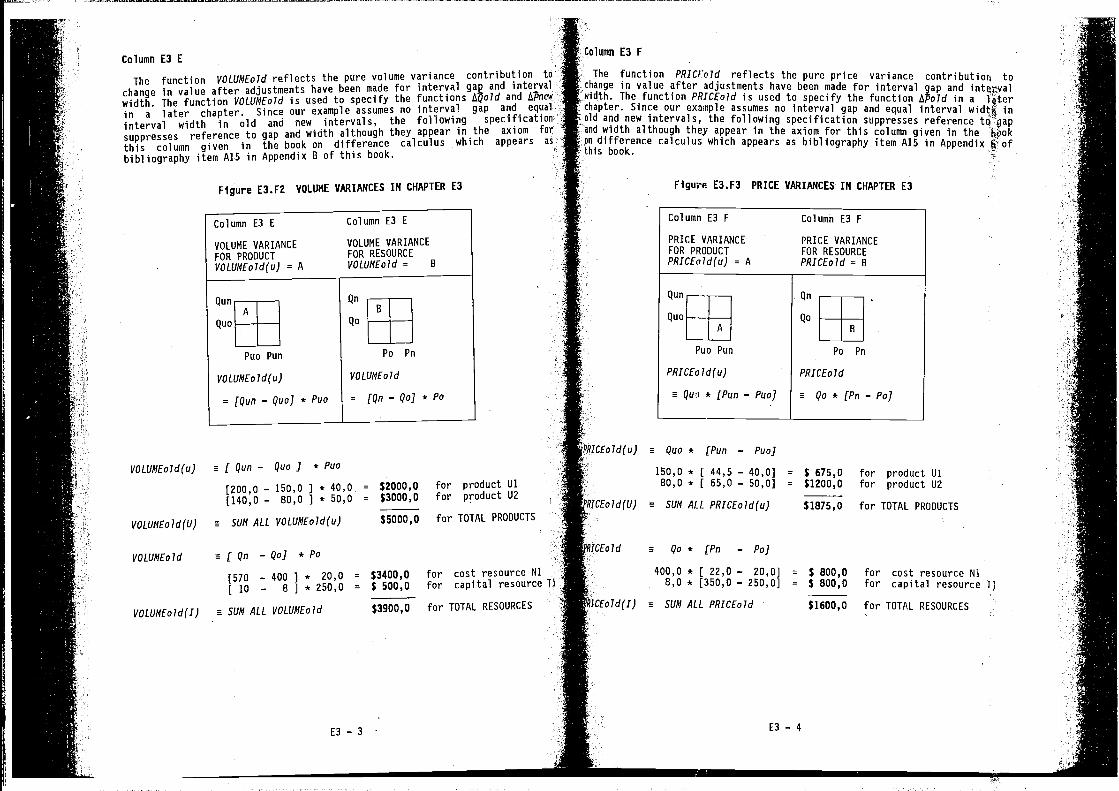

Chapter E3 EXAMPLE OF INPUT VARIANCE REPORT

Chapter E4 EXAMPLE OF INPUT RELATIVE REPORT

Chapter ES EXAMPLE OF INPUT COMPACT REPORT

Chapter E6 EXAMPLE OF INPUT NORMALIZED QUANTITY AND PRICE REPORT

Chapter E7 EXAMPLE OF PROFIT BACKGROUND REPORT

Chapter E8 EXAMPLE OF PROFIT RECONCILIATION REPORT

Chapter E9 EXAMPLE OF PROFIT OVERVIEW REPORT

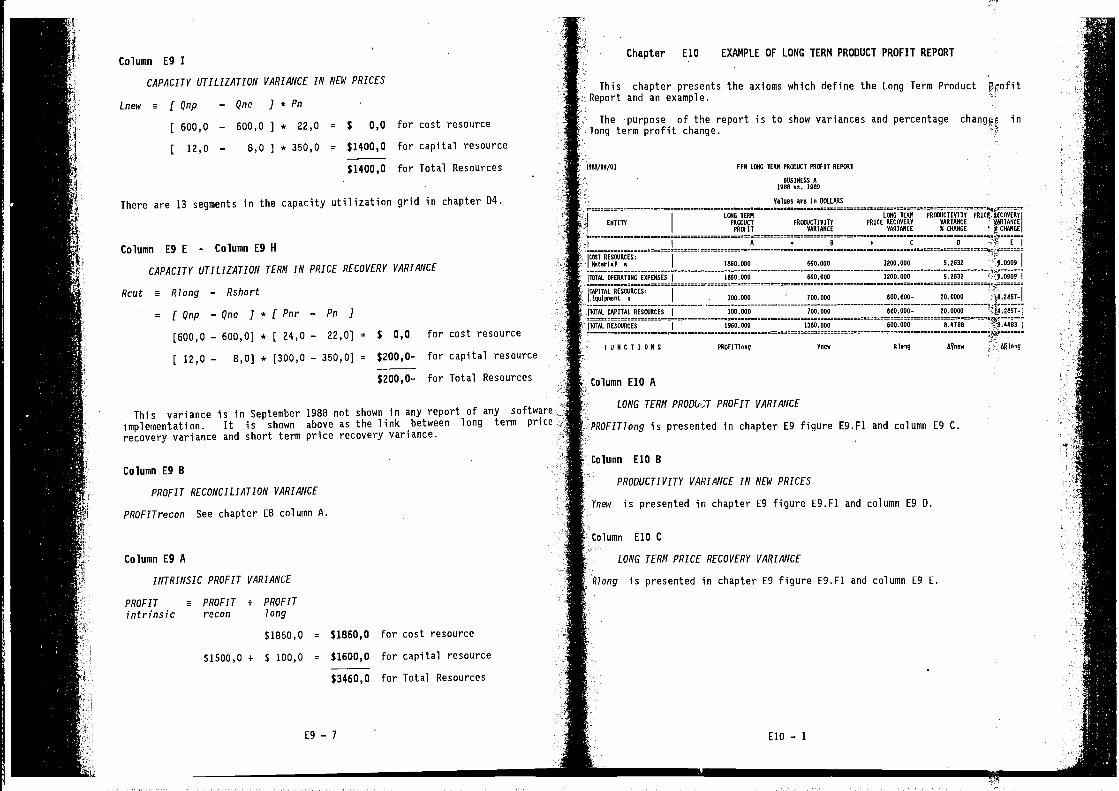

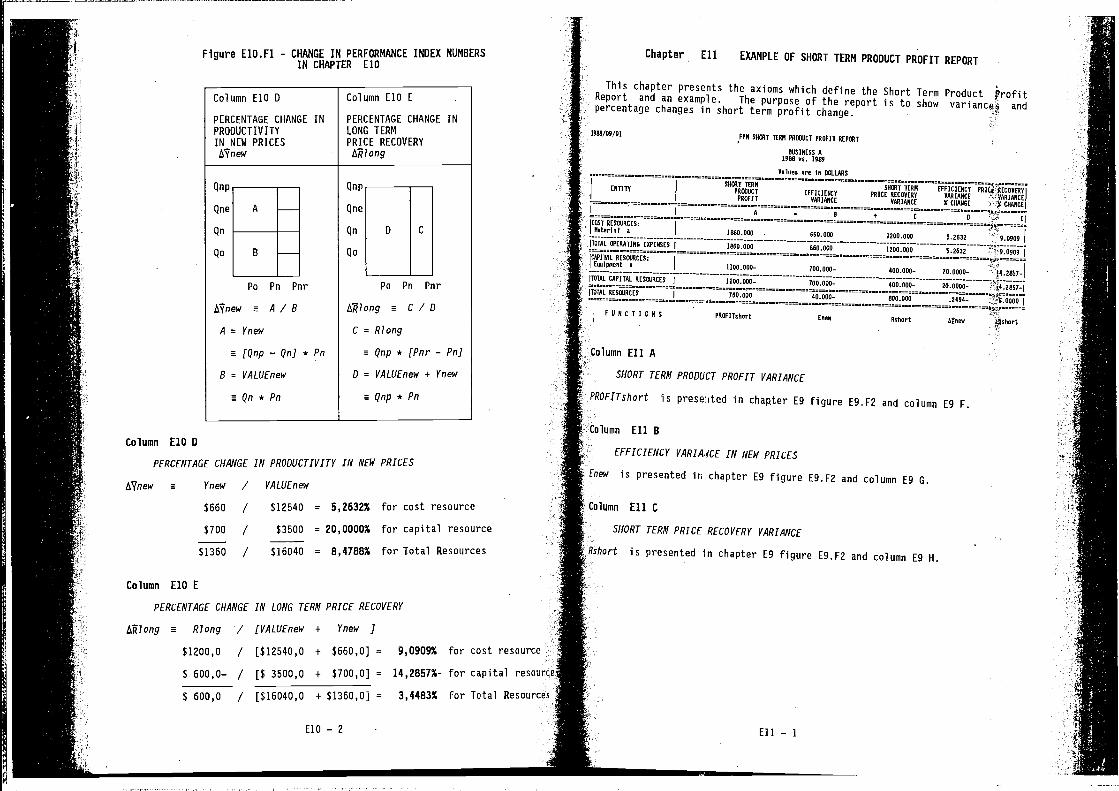

Chapter E1O EXAMPLE OF LONG TERM PRODUCT PROFIT REPORT

Chapter Eli EXAMPLE OF SHORT TERM PROOUCT PROFIT REPORT

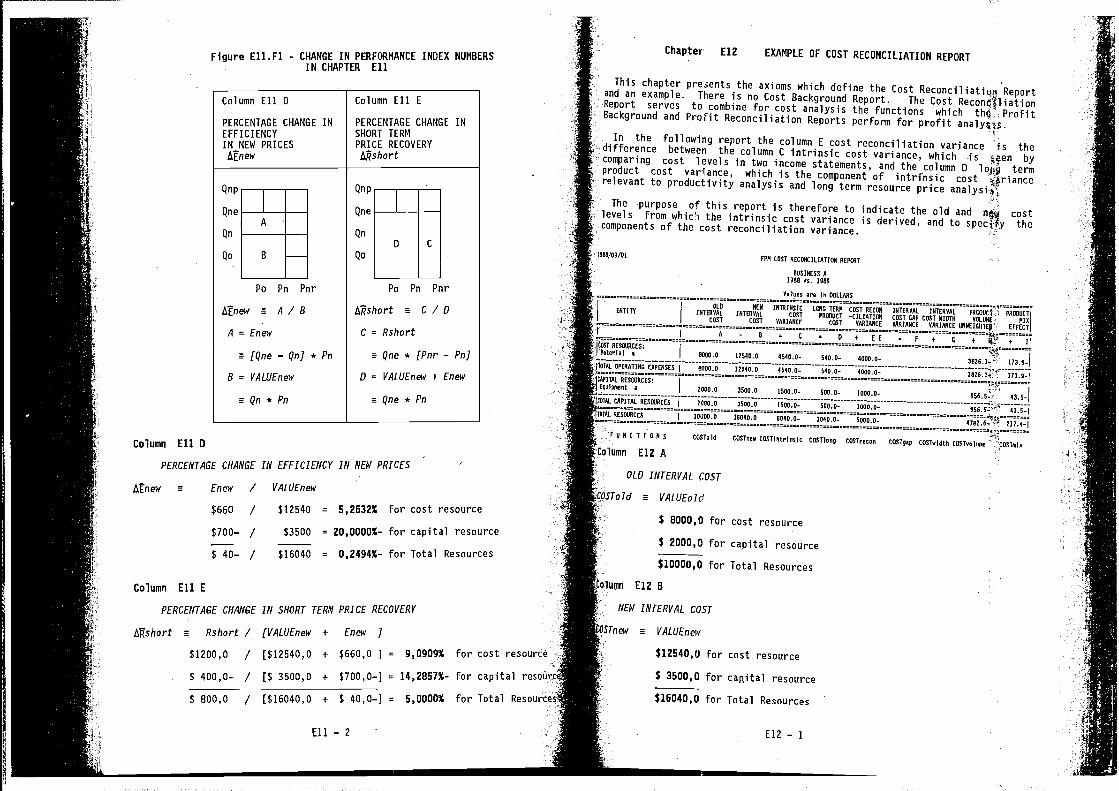

Chapter E12 EXAMPLE OF COST RECONCILIATION REPORT

Chapter E13 EXAMPLE OF COST OVERVIEW REPORT

Chapter

Chapter

EI4

ElS

EXAMPLE OF LONG TERM PRODUCT COST REPORT

EXAMPLE OF SHORT TERM PRODUCT COST REPORT

Chapter E16 EXAMPLE OF PRODUCTIVITY OLD AND NEW VARIANCE REPORT

Chapter E17 EXAMPLE OF PRODUCTIVITY COMPONENT VARIANCE REPORT

Chapter E18 EXAMPLE OF PRODUCTIVITY COMPONENT OLD & NEW REPORT

PART ,J — UNIT LIFE CYCLE COST

Chapter JI DETERMINISTIC PRODUCTIVITY ACCOUNTING EXTENSIONTO UNIT LIFE CYCLE COST ANALYSIS

PART K — PRODUCT NORMALIZATIONS

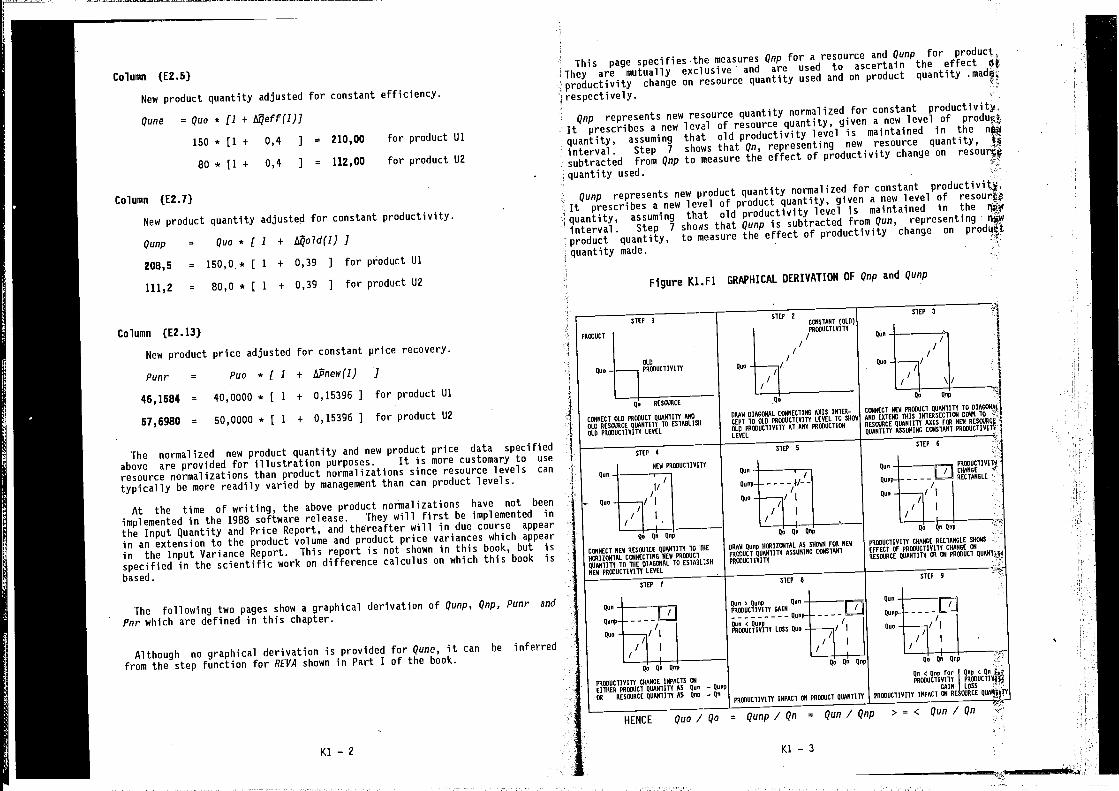

Chapter KI AXIOMS TO NORMALIZE NEW LEVELS OF PRODUCT QUANTITY AND PftICE

APPENDIX A - SPECIMEN EXPERT SYSTEM REPORTS

I

PART A — BACKGROUND

This part of the book presents the following 4 chapters.

Chapter Al THE PRODUCTIVITY CONCEPT

Chapter A2 PRODUCTIVITY NEASUREMENT AND PRODUCTIVITY IMPROVEMENT

Chapter A3 PRODUCTIVITY MANAGEMENT JOURNEY

Chapter A4 HOW MEASUREMENT ASSISTS PRODUCTIVITY MANAGEMENT

Chapter Al — THE PRODUCTIVITY CONCEPT

The purpose of this book is to bring to the attention of managers the notionof productivity and to expose them to a simplified form of a comprehensivemathematical structure (see Appendix B item A15 for the companionbook) which underpins proper productivity measurement. Simplyproductivity is the following quotient.

PRODUCT (i.e. OUTPUT) QUANTITYPRODUCTIVITY m (Al

RESOURCE (i.e. INPUT) QUANTITY

Whereas production refers to the conversion of resources comprising labor,material and capital (i.e. input) into goods and services of

a quotient which relates toa subset of resources used in the production process. Since usedin the production process extend beyond labor, the definition ofalso deals with resources other than labor. Yet labor plays a centrar rpl e,since capital and materials cannot produce anything unless labor theprocess. Although it is common to talk of productivity as output per oflabor input, it must be borne in mind that an increase in this canalso be driven by utilization of materials and capital

The author believes that managers should familiarise withproductivity and its proper measurement in view of the growing need fur thebenefits to be derived from productivity improvement. The relaflonshipbetween productivity measurement and productivity improvement is dftcussedin the ensuing chapter.

This chapter discusses the importance of promoting productivity growth,corrects common fallacies about the productivity concept, presents an q,jerviewof productivity measurement, identifies defects in conventionalmeasures and specifies characteristics for sound productivitywhich are satisfied by the approach defined in the companion techni4i bookcited above.

The Importance of Promoting Productivity Growth

Productivity is becoming a hot issue in the unpredictable,economic environment in which we live. It is increasingly recognized the

Al — 1

I11 productivity performance of private and public sector undertakings is theprincipal determinant of cost—effectiveness and hence viability. Leadingundertakings and government policy—makers in First, Second and Third Worldsare to varying degrees articulating a commitment to productivity improvementbecause of the rewards it brings.

C]\ The purpose of raising productivity is to increase the profitability of theJ private sector, the cost—effectiveness of thepublic sector and the realliving standard of consumers. A commitment to improve productivity createsaudiences interested in monitoring productivity trends (i.e. trackingproductivity). They range from the microcosm up to the macrocosm andinclude:

• the industrial engineer defining engineered standards (i.e productivitynorms) for labor and/or plant

• the accountant controlling a cost center within a profit center

i the product or group controller monitoring different profit centers withina business and/or different businesses

• the business economist and the financial/investment analyst monitoringlarge corporations or industries

• the rate—making officer adjudicating on a rate increase application

• the economist scrutinizing the performance of the national economy and itsunderlying sectors such as manufacturing, construction and services etc.

Productivity tracking is facilitated when measures of productivity changeare directly related to an operationally familiar measure, For example, afinancial officer would value a measure of the contribution of productivitychange to budgets for production, costs, net income or investment. Similarly,a rate—making (i.e., tariff—setting) tribunal would value a measure of the

• contribution of productivity change to the requested rate increase.

The improvement of productivity is of paramount importance where themajority of the population expects to achieve a higher standard of living thanit presently enjoys. Standard of living is measured as the consumption (ofgoods and services in the national economy) per person in the totalA\ population, and the standard of living cannot for long increase without

• increase in the production (of goods and services in the national economy) perperson employed in the total population.

The requirement that there should be increase in production per employeeshould not be construed to mean that productivity deals only with labor.

It is clear that a stable socio—political future of any country requires asound economy which will be sufficiently vigorous to provide job opportunityfor hundreds of thousands of people trying to enter the labor market. Thissituation signifies a growing economy. Economic growth will be largelydependent upon our competitiveness which, in turn, is a function ofproductivity.

The interesting aspect of productivity improvement is that it is not simplysomething for "the other party" to do, since everyone must contribute to it.The managerial cadre can play a key role in productivity improvement, sinceone of the prime reasons for a country's inadequate productivity performancemust be sought in the lack of highly skilled people together with an inability

Al — 2

to use technology to its fullest extent.

It is therefore to he expected that increasing pressure will be placed uponmanagers to focus their efforts more on the contributions they can make toincreasing productivity. The managerial cadre should be cognisant ofpressure and equip itself with knowledge related to productivity issues inorder to meet the challenge of the new situation.

Correcting Common Fallacies About Productivity

There is no commonly accepted intuitive definition of "productivity"there is, albeit imprecise, intuitive understanding of notions such as "bjm","unemployment", "inflation" and "profitability". It is thereforeto give cursory attention to the following examples of misleading rhetori&andhow they should be qualified:

• economic growth flows from a boom and not from productivity• productivity growth promotes unemployment• productivity change is irrelevant to inflation• profitability is niore important than productivity.

Informed opinion would typically correct the above ambiguities withpositions such as the following: -

• economic growth is derived from two potential sources, viz.,more resources into the production process and using such resources joreproductively. Both factors can give rise to an economic boom.

• productivity growth may cause short term retrenchments but will tocause long term increase in employment as a result of acompetitive position. The notion that productivity growth leads tounemployment flows from an incorrect perception that productivitydisplaces labor aione, specifically when capital is substituted forOn the contrary, it is clear that productivity growth can be derivedhigher materials and/or capital productivity. In this situation inthe materials and/or capital content per unit of output takes place.

• productivity growth tends to reduce inflation (defined here asprice increase) while productivity loss tends to increase inflation.

• productivity is the key, but not the sole, determinant of how sustainable agiven level of profitability (defined here as the ratio of tocapital assets) might be. High productivity tends to sustain sighprofitability while low productivity tends to erode high

To create perspective for a definition of productivity, one must ask whodetermines the level of productivity in the country. In a strict sense it istrue that anyone who works contributes to the productivity level thecountry as a whole. A comprehensive classification of the economy wguldreflect the following breakdown:

• formal sector, comprising all production of goods and services whichin the Sytem of National Accounts which is specified by internatiäpalconvention and which is subdivided into a private sector and asector.

• informal sector, comprising all production of goods and services notincluded in the System of National Accounts and which includes, inter alia,

Al — 3

the following:

• production of households

• production of small producers who evade detection by not reportingactivity to government's statistics gathering or tax collectingagencies. In the United States some estimate that exclusion of theinformal sector leads to an undercounting of up to 15% of thevalue of output in the national economy. This sector is alwaysimportant in a developing economy.

For reasons of' brevity the remainder of this book limits the followingdiscussion of productivity measurement to the formal sector.

Productivity Measurement Overview

This overview is intended to provide readers with an understanding of thepractical benefits which flow from productivity measurement. Peter Drucker,an American authority on management, makes the case for productivity'measurement as follows:—

"Without productivity objectives a business does not have direction.Without productivity measurement, it does not have control".

It is easy to appreciate why Drucker makes the above statement if one

considers the definition of productivity given above in statement (Al Al) tounderstand why leading businesses are generally preocuppied with "controlsystems" to ensure their solvency and viability.

The above definition of productivity is related first to a private sectorbusiness and then to the public sector teaching and research environments inthe ensuing discussion of productivity measurement.

Private Sector MeasuresIn the business environment final "product" refers to the goods and/or

services created for sale, while "resource" refers to the materials, labor andcapital inputs which are needed to make product. Examples of differentproductivity measures are given below for a hypothetical shirt manufacturer:—

Number of shirts producedCloth productivity = (Al Bl)

Labor productivity =

Capital productivity =

Number of shirts produced

Number of man—hours used

Number of shirts produced

Each of the above measures represents a "partial" productivity measurebecause it relates product quantity to less than all the resources needed tomake product. A "total resource" productivity measure would relate productquantity to a Rand measure which combines all the resource quantities needed

to make product. Both partial and total resource productivity measures beexpressed as an index number which would simply express in percetitage form theratio of a new (Le. current period) productivity measure to an old (j;e. baseperiod) productivity measure.

If one ignores the effect of changes in the selling price of product and inthe purchase price of resources used, the link between andsolvency becomes clear when one bears in mind that productgenerate revenue (i.e. cash inflow) for the business, whilequantities used generate expenses (i.e. cash outflow).

If, in the example of the shirt manufacturer cited above,productivity (also known as materials yield) declines from, say, 4 shk9s per10 square metres of textile used to 3 shirts per 10 square metres of7textileused because of either inferior material quality or shoddy workmanship whichdoes not withstand the scrutiny of final product quality control, willbe a decline in revenue with respect to expenses which will diluteIn this example of higher wastage rate at final product quality stage,the decline in materials productivity will be accompanied by inenergy productivity, labor productivity and capital productivitysignificantly dilute profits and perhaps jeopardise solvency.

Awareness of the connection between productivity loss and threats tq profitsis the prime driver which motivates management to institute "control"which cover both the production and financial areas. Examples of cqs',trolsin each area are discussed below.

materials yield (which is a materials productivity norm)energylaborplant

contentcontentthroughput

(which is anenergy(which is a labor(which is a capital

productivityproductivityproductivity

norm)norm)norm)

• Inventory control to ensure, consistent with the facts of lead time neededfor suppliers to supply raw material and the need for proper prcgJuctionscheduling, that quantities of raw material inventory do not morequickly than output. An acceptable deviation from this rule could ifmanagement builds raw material inventory through "hedge—buying" to floid anexpected increase in the purchase price of raw material. S4ilarly,management may decide to build finished product inventory in dSer tooptimize on production scheduling.

• Standard costing to ensure that the actual cost per unit of oqtput iscompared with he standard cost per unit of output which can be Uaed oneither a "hard' (i.e. engineered) standard or a "soft" (i.e. year)standard.

• Inflation accounting to ensure that profit is adjusted by theeffect of prce change on both revenue and expense parts of incomestatement.

• Linear programming which purports to achieve a least cost combinaL)on ofresources to product where more than one combination of tomake product is known.

Examples of control system in the production area include:

• Engineered star4ards for

(Al B2)

(Al B3)

Number of Metres of textile used

Al — 4Al — 5

Examples of control system in the financial area include:

i Credit control to ensure that goods are not supplied to prospective, new

customers whose inability, or unwillingness, to pay could lead to a baddebt which would constitute a capital productivity loss

_________________________________

• Debtors control to ensure that capital tied up in these short—term assetsdoes not, without express management intention, increase more rapidly thanoutput. Conclusion

On the positive side, management also recognizes that a well controlledbusiness achieves higher productivity and a resulting lower cost per unit of Given the case for productivity measurement, it does not follow th4t alloutput which confers a cost advantage over competitors. If the market is productivity measurement is sound or that measurement 'per willprice—sensitive, the well controlled business may use its cost advantage for automatically imprcve productivity. Productivity measurement is necessagy, butaggressive pricing which could generate more demand and thereby lead to even not sufficient, to improve productivity. Different types of measuremeht and

higher productivity, their relationship with productivity improvement are discussed next. --

Public Sector MeasuresIn the teaching and research environment final "product" refers to the

services produced, while "resource" refers to the materials, labor and capitalinputs which are needed to make product. The absence of readily identifiablespecifications of product in this environment constitutes such a datadeficiency that it is often argued that it is impossible to measureproductivity in such environment and that productivity measurement istherefore irrelevant. This "irrelevance" argument becomes an excuse for notmeasuring, and hence not managing, productivity performance.

Notwithstanding such "irrelevance" argument, it is possible to quantifyoutput measures for most areas in the teaching/research environment using a

scoring matrix based on objectives. This tool is versatile and has been usedsuccessfully for measuring output in service activities such as information,teaching, social planning and underground surveying. -

Use of the scoring matrix tool boils down to individuals involved inactivity identifying the outputs and objectives which they deem to be ofcritical importance to their activity. They then decide on the minimumachievable level of output, the current level of output and the objective(i.e. desired) level of output which they should strive to attain. Theselevels and linear (or other) interpolations are then assigned score valueswhich are combined, using a set of subjectively determined weights, into an

overall proxy measure of output. Any person interested in a more detailedexposition of the methodology can obtain additional information from theauthor.

Assuming that an acceptable definition of proxy final product could be

specified in the teaching and research environment, the following productivity.measures could be defined.

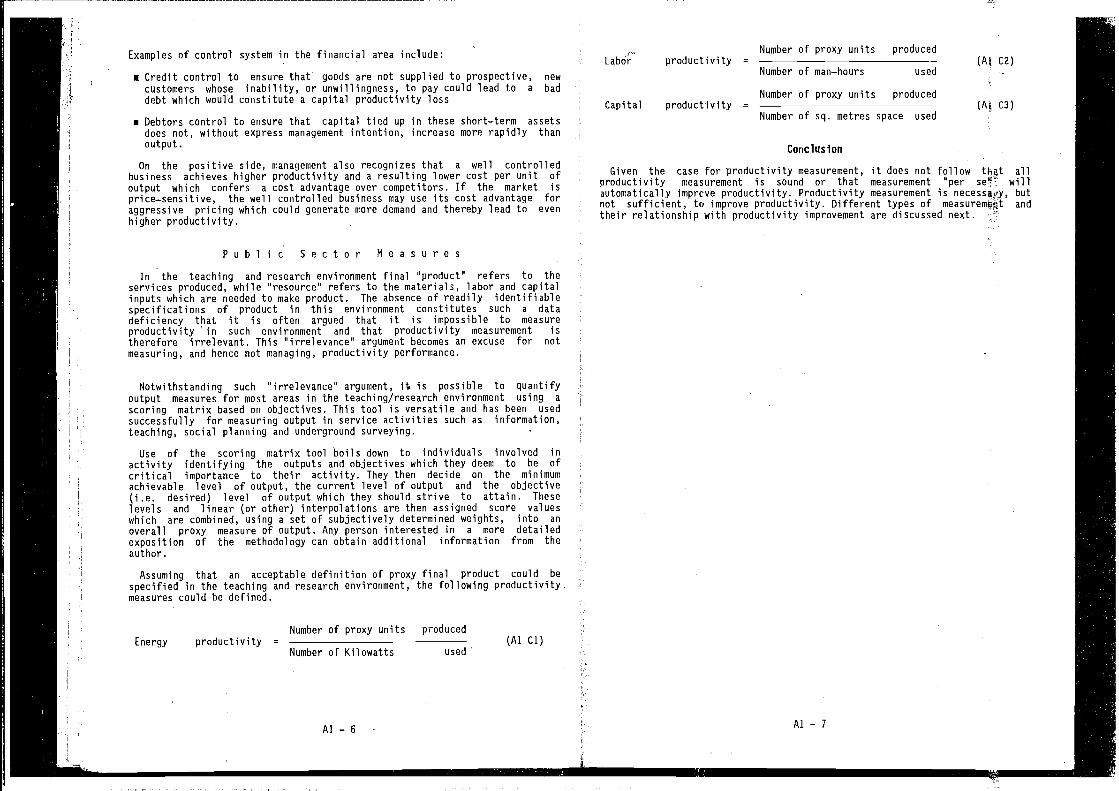

Number of proxy units producedEnergy productivity = (Al Cl)

Number of Kilowatts used

Al—6 Al—7

-t

Number of proxy units producedLabor productivity = C2)

Number of man—hours used

Number of proxy units producedCapital productivity = (A! C3)

Number of sq. metres space used

Chapter A2 - PRODUCTIVITY IMPROVEMENT AND PRODUCTIVITY MEASUREMENT

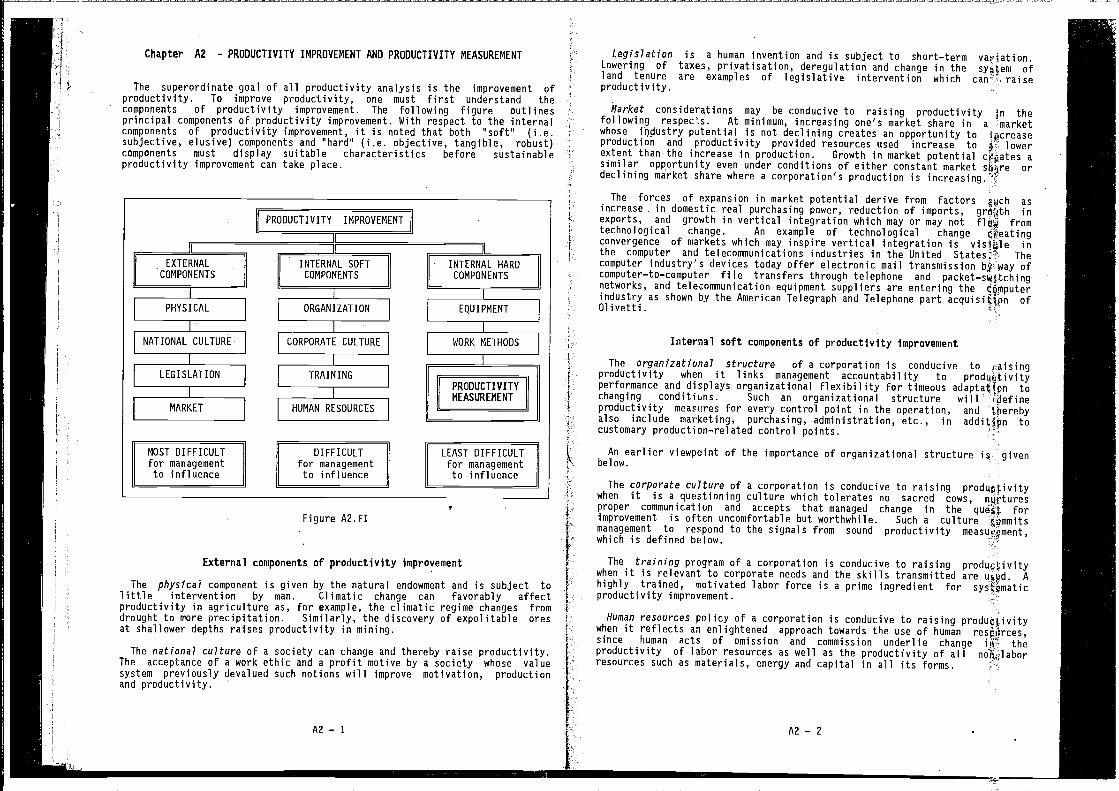

The superordinate goal of all productivity analysis is the improvement ofproductivity. To improve productivity, one must first understand thecomponents of productivity improvement. The following figure outlinesprincipal components of productivity improvement. With respect to the internalcomponents of productivity improvement, it is noted that both 'soft" (i.e.subjective, elusive) components and "hard" (i.e. objective, tangible, robust)components must display suitable characteristics before sustainableproductivity improvement can take place.

External components of productivity Improvement

The physical component is given by the natural endowment and is subject tolittle intervention by man. Climatic change can favorably affectproductivity in agriculture as, for example, the climatic regime changes fromdrought to more precipitation. Similarly, the discovery of expolitable oresat shallower depths raises productivity in mining.

The national culture of a society can change and thereby raise productivity.The acceptance of a work ethic and a profit motive by a society whose valuesystem previously devalued such notions will improve motivation, productionand productivity.

Legislation is a human invention and is subject to short—term variation.Lowering of taxes, privatisation, deregulation and change in the ofland tenure are examples of legislative intervention which raiseproductivity.

Market considerations may be conducive to raising productivity jn thefollowing respects. At minimum, increasing one's market share in a marketwhose industry potential is not declining creates an opportunity to Ipcreaseproduction and productivity provided resources used increase to lowerextent than the increase in production. Growth in market potential asimilar opportunity even under conditions of either constant market shire ordeclining market share where a corporation's production is increasing.

The forces of expansion in market potential derive from factors ;och asincrease in domestic real purchasing power, reduction of imports, inexports, and growth in vertical integration which may or may not fromtechnological change. An example of technological change

Fconvergence of markets which may inspire vertical integration is inthe computer and telecommunications industries in the United Thecomputer industry's devices today offer electronic mail transmission way ofcomputer—to—computer file transfers through telephone and packet—switching

• networks, and telecommunication equipment suppliers are entering the• industry as shown by the American Telegraph and Telephone part acquisitfon ofOlivetti.

Internal soft components of productivity Improvement

The organizational structure of a corporation is conducive to raisingproductivity when it links management accountability to prodqotivityperformance and displays organizational flexibility for timeous adaptat(pn tochanging conditions. Such an organizational structure will iiefineproductivity measures for every control point in the operation, andalso include marketing, purchasing, administration, etc., in additipn tocustomary production—related control points.

An earlier viewpoint of the importance of organizational structure is givenbelow.

The corporate culture of a corporation is conducive to raising productivitywhen it is a questioning culture which tolerates no sacred cows,proper communication and accepts that managed change in the quéi.j forimprovement is often uncomfortable but worthwhile. Such a culture {bmmitsmanagement to respond to the signals from sound productivitywhich is defined below.

The training program of a corporation is conducive to raisingwhen it is relevant to corporate needs and the skills transmitted are uud. Ahighly trained, motivated labor force is a prime ingredient forproductivity improvement.

Human resources policy of a corporation is conducive to raisingwhen it reflects an enlightened approach towards the use of humansince human acts of omission and commission underlie change i11 theproductivity of labor resources as well as the productivity of allresources such as materials, energy and capital in all its forms.

k

Figure A2.F1

A2—1 A2—2

Internal hard components of productivity improvement

The equipment (and supporting technology) used by a corporation are

conducive to raising productivity when they are the best available which can

be economically justified.

The work methods used by a corporation are conducive to raising productivitywhen they are the best available which can be economically justified. Work

methods include the following engineering ("hard system") approaches towards

improving operations: Value engineering, just—in—time, group technology, total

quality control, multiple resource planning, computer aided design, computer

aided manufacture, and so forth.

The productivity measurement system used by a corporation is conducive to

raising productivity when it is the best available which can be economically

justified. Deterministic and stochastic approaches to productivity

measurement are defined below as a prelude to a discussion of the strengths

and weaknesses of different types of productivity measurement.

Deterministic and stochastic approaches to measurement

Deterministic approaches to measurement start by defining certain equations

as axioms or identities (i.e. relationships which are always valid) and then

proceed to derive other relationships from transformations of the initialaxioms. A deterministic model permits total accuracy provided initial axioms

can be specified and the model can be populated with credible data.

Stochastic approaches to measurement start with the assumption that axioms

are not known to define the relationship in question. Stochastic approaches

therefore resort to probablistic equations which employ regressions (i.e.statistical inferences) to estimate a relationship which is not known with

certainty. A stochastic methodology is justified and plays an indispensable

role only when a deterministic one cannot be identified.

The approach presented in this volume is deterministic. The preference of

the engineering and accounting communities for rigor, precision and freedom

from ambiguity indicated at an early stage a need to develop, as far as

possible, a deterministic methodology in lieu of a stochastic one. Business

economists, industrial engineers and accountants have long used deterministic

models to appraise the performance of the individual producer establishment.

Yet the reader with econometrics training may be surprised to encounter in

this book some novel deterministic specifications in areas where stochasticspecifications are customarily found in econometric literature.

The author offers no apology for this fact, and points out that the adoption

of a stochastic methodology implies that a deterministic one cannot be

identified. On the contrary, the practitioners of stochastic methodology, for

those types of analysis for which a deterministic methodology has now been

identified, will be obliged to justify their stochastic practice.

General weakness and strength of all productivity measurement

A general weakness of all productivity measurement arises from the fact thatthe productivity quotient has no necessary causal significance. Changes in

productivity express effect and not cause. Causal insight can only be provided

by those familiar with a given operation. Ongoing productivity measurement,

known as productivity tracking, therefore poses rather than answers questions.

A2 — 3

A general strength of all productivity measurement with toproductivity improvement. efforts arises from its overall monitor as

attempts are made to change soft and hard components cited above. Ato improve productivity creates a need for productivity measurement.

productivity measurement there would be no score—card to ascertainsystematic efforts to raise productivity are bearing any fruit.

Productivity measurement is a hard component of productivity irlipregement

which can quantify the effect of productivity change on financialThe soft components must be activated to enable management to proceedeffect and thereby uncover cause so that remedial action to improvecan be formulated and implemented.

Specific weakness and strength of individual productivity measurement

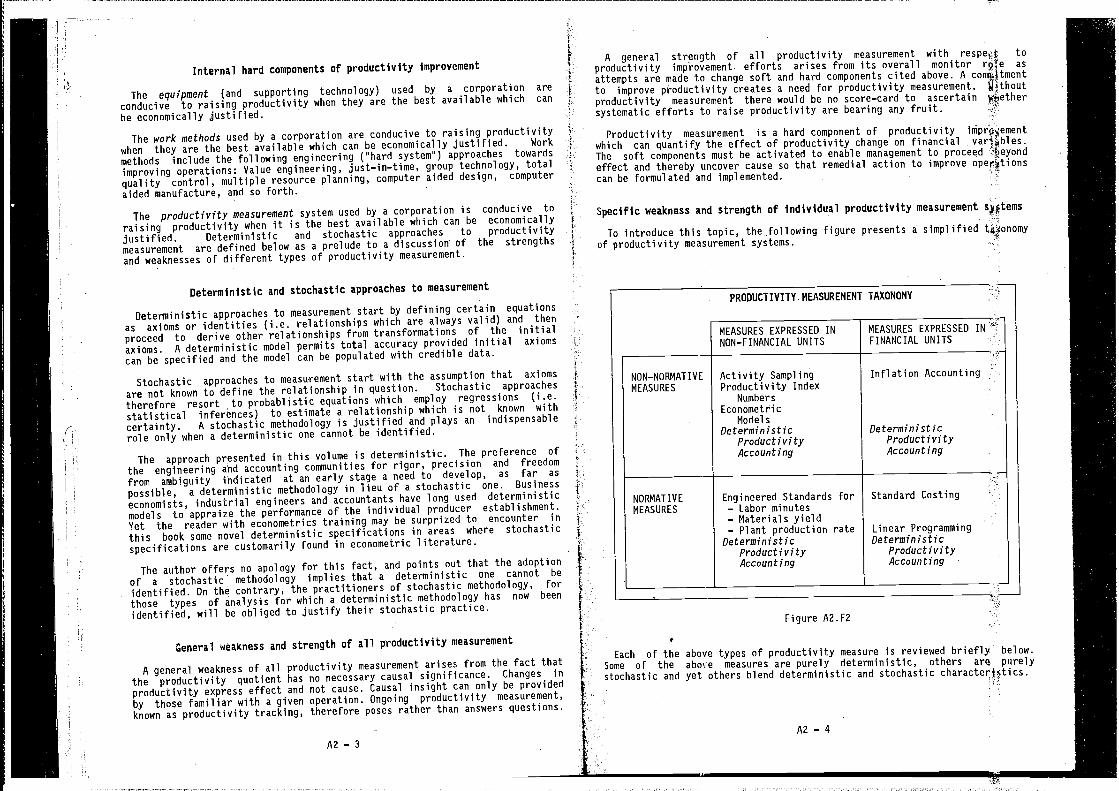

To introduce this topic, the following figure presents a simplified tgAonomyof productivity measurement systems.

I

PRODUCTIVITY. MEASUREMENT TAXONOMY

MEASURES EXPRESSED INNON—FINANCIAL UNITS

•1

- MEASURES EXPRESSED INFINANCIAL UNITS

NON—NORMATIVE

MEASURES

Activity SamplingProductivity Index

NumbersEconometPi c

ModelsDeterministic

ProductivityAccounting

Inflation Accounting

DeterministicProductivityAccounting

NORMATIVEMEASURES

Engineered Standards for— Labor minutes— Materials yield— Plant production rate

DeterministicProductivityAccounting

Standard Costing

Linear ProgrammingDeterministic

ProductivityAccounting

Each of theSome of thestochastic and

Figure A2.F2

above types of productivity measure is reviewed briefly below.above measures are purely deterministic, others are purelyyet others blend deterministic and stochastic characterbtics.

AZ — 4

Non-norñiatiVe, non-financial measures

These measures are termed non—normative and non—financial because they

typically compare actual productivity levels in two accounting periods and

express the result in percentage form rather than in a currency unit.

Activity Sampling is the most elementary form of productivity measurement.

It is expressed as a percentage which is constructed from division of the

number of observations in which work takes place by the total number of

observations. It can be done through human observation or mechanical

observation by way of a camera periodically photographing an operation.

Although the activity sampling quotient for a given accounting period isdeterministic, trend values can be derived using either a deterministic or a

stochastic approach.

Change in productivity index numbers indicate the percentage change in a

given productivity quotient between two accounting periods. Although the basic

quotient for a given accounting period is deterministic, trend values can be

derived using either a determinsitic or a stochastic approach.

Econometric models are used to estimate percentage change in productivity.

They are constrained by some deterministic axioms but make extensive use of

regression analysis (i.e. a stochastic approach).

Deterministic productivity accounting contains measures which belong to this

group. All measures in this approach are purely deterministic, as indicated

by the first word in the title of the approach. Within the group of non—

normative, non—financial measures, deterministic productivity accounting

measures comprise change in index numbers which refer to value, quantity,price, productivity and price recovery. The latter indicate percentage change

in a given price recovery quotient between two accounting periods. Price

recovery is defined below. It complements the notion of productivity and canalso be defined for a single resource or an aggregation of resources.

PRDDUCT (i.e. DUTPUT) PRICEPRICE RECDVERY a

(A2 Al)RESDURCE (i.e. INPUT) PRICE

Non-normative, financial measures

These measures are termed non—normative and financial because they typicallycompare actual productivity levels in two accounting periods and express the

result on profit or on cost in a currency unit.

A primary feature of these approaches is the specification of productivitymeasures which offer a "bottom line" linkage, i.e. linkage to the financial

accounting system of the producer. Experience shows that any measure of

productivity which exists as a discrete measure unconnected to the financial

system commands limited credibility since it sooner or later sends signals

which conflict with signals from the financial accounting system. A classical

example of sqch a conflict arises when the productivity measure signalsimprovement while the financial accounting system signals deterioration.

Inflation accounting is presented by way of a numerical example in a laterchapter. All measures in this approach are normally deterministic. Itinvolves the deflation of new period revenues and costs (expressing new

quantities in new prices) to adjusted values which purport to represent new

quantities in old prices. The resulting adjusted profit pqrports toeliminate price change and to represent the effect of productivity ihange on

profits. Questions of accuracy arise from the use of deflators (Uè. .priceindex numbers which express the ratio of a new price to an old pricej.

Deterministic productivity accounting contains measures which to thisgroup. They comprise accounting variances (which will be specifj4d later)for change in different variables expressed in a currency unit.which appear in this group would compare actual performance leveh in twoaccounting periods rather than a contrast in which one of the accountingperiods contains performance targets or performance norms.

Normative, non-financial measures

These measures are termed normative and non—financial because they typicallycompare normative (i.e. standard or target) productivity in oneaccounting period with actual productivity levels in another accoun%(ng periodand express the result not in a currency unit but as a percentage oWin unitsof resource. Hence the deviation of, say, actual minutes frop4 standardminutes can be expressed either in minutes or as a percentage.

Engineered standards for 7abor minutes prescribe the number minutesspecified tasks should take. Computation. of the time sta&ard was

historically drterministic but has in recent years become more

since use of regression analysis accelerates (and hence reduces of)quantifying the time standard. Deviation of actual from standard is expressedas a percentage or in labor minutes, i.e., labor resource units. I

Engineered standards for materials yield prescribe the resourcecontent per unit of product. Computation of the standard yield fiows fromspecified assumptions on product quality and materials It istypically deterministic but would be stochastic in the event of hiatisticalinference being used to quantify the relationship. Deviation of acçual fromstandard is uxpressed as a percentage or as a materials quantityj:i.e., inmaterials resource units.

Engineered standards for plant production rate prescribe a plant productionrate with respect to specified operating conditions. of theproduction rate standard is typically deterministic but would be inthe event of 5tatistical inference being used to quantify the re44ionship.Deviation of actual from standard is expressed as a percentage, machine—

hours, i.e., in capital resource units, or in units of production orlost.

Deterministic productivity accounting contains measures which to thisgroup. Although input data into this approach can be either determjoistic orstochastic in origin, deterministic productivity accounting datain a purely deterministic manner. Within the group of normative, non-financial measures, deterministic productivity accounting measuret comprisechange in index numbers which refer to value, quantity, price,and price recovery as defined above.

A2—6A2-5

I

Normative, financial measures

These measures are termed normative and financial because they typicallycompare normative (i.e. standard or target) productivity levels in oneaccounting period with actual productivity levels in another accounting periodand express the effect on cost or on profit in a currency unit.

Standard costing typically compares cost or profit based on standardproductivity levels and standard prices with cost or prodit based on actualproductivity levels and prices. The standards are defined using either a

deterministic approach or a stochastic approach, but the data are subsequentlymanipulated in a purely deterministic manner as explained by way of a

numerical example in a later chapter. -

Linear Programming is applied to situations where more than one combinationof resources to make product is known. This purely deterministic techniquewould compute total cost of production associated with each "recipe" toascertain which method of making product minimizes cost and hence maximizesprofit. It does not show a contribution per resource to explain changes inthe variables with which it deals.

Deterministic productivity accounting contains measures which belong to thisgroup. It typically compares cost or profit based on standard productivitylevels and standard prices with cost or prodit based on actual productivitylevels and prices. The standards are defined using either a deterministicapproach or a stochastic approach, but the data are subsequently manipulatedin a purely deterministic manner as explained by way of a numerical example ina later chapter. Although the deterministic productivity accounting approachapparently coincides with that of standard costing, it will later be shownthat its measures are significantly different and can contradict, withjustification, signals from standard costing.

Defects in conventional productivity measurement

Figure A2,F2 lists different approaches towards productivity measurement.They can be classified into conventional approaches (all of which are in someway flawed) and a new approach known as deterministic productivity accounting.The latter approach has been developed by the author to eliminate the flawscontained by conventional approaches which comprize all other approacheslisted in figure A2.F2 above.

This book does not provide a detailed demonstration of the defects inherentin the various conventional approaches to productivity measurement employed byeconomists, accountants and engineers. However, later chapters will providefor the non—mathematical reader numerical examples to expose the weaknesses ofproductivity index numbers, standard costing and inflation accounting. Forthe mathematical reader a list of defects in conventional productivitymeasurement would cite:

• unjustified use of a differential operator when a difference operator isrequi red

• failure to rationalize the attribution of higher ordered interactions whena difference operator is employed

• dimensionally improper arithmetic operations

• use of ordinary differences when partial differences are required

• use of a stochastic methodology when a deterministic one can be

The above list of defects signifies that none of themeasurement approaches provides systematic insight into productivityand itsassociated financial impacts. This limitation arises because ofthe conventional measurement approaches possesses thecan be prescribed for sound productivity measurement.

Characteristics of sound productivity measurement

Although the purpose of all productivity measurement is control, soundproductivity measurement has more demanding characteristics. It withrespect to a private sector business, employ full accounting rigor to:

• provide simple and unambiguous signals to improve profits;

• break down change in profit into the underlying contributions froip eachresource in production (i.e. materials, energy, labor, and

i break down the contributions to profit change from each resource iHto a

productivity term and a price recovery term to isolate the ofdisparate change in product price vis—a—vis resource price

• break down the productivity- term into a capacity utilization term qud anefficiency term (i.e. differentiate short—range fromshort—range potentially controll able factors);

• use the price recovery term to evaluate whether productivity lqs orproductivity gain for a given resource is appropriate;

• transform the above measures of change in profit intomeasures for cnange in profitability, change in cost per unit ofand change in performance index numbers (e.g. productivity indexand

• provide consistent signals for profit improvement regardless of the- unitsin which the measure is expressed.

Translation of the above features from a private sector businessto the the public sector environment entails substituting the notion costfor the notion of profit and the notion of resource price for the notldn ofprice recovery. -

Deterministic productivity accounting is a new approach towards productivitymeasurement which does possess the characteristics prescribed soundproductivity measurement and which is free of the defects cited above.

When is productivity measurement unnecessary ?

There is one situation in which productivity measurement is notfor proper control. It is the case of the small business in whichis responsible for the 5 business phases represented by

• production, marketing, credit control and planning. In such a situatthji, thefive human senses could be sufficient to gather the information forproper control and productivity measurement would therefore be

A2 — 8A2 — 7

•

•1.

Productivity measurement is merely a component of the productivityimprovement process which is holistic by nature. If isolated from other softcomponents discussed above, productivity measurement will fail to thrive and

in consequence not contribute to productivity improvement. The processwhereby managers could strive to pilot the migration of an organisation fromproductivity measurement to productivity improvement is described by theproductivity management journey in the next chapter.

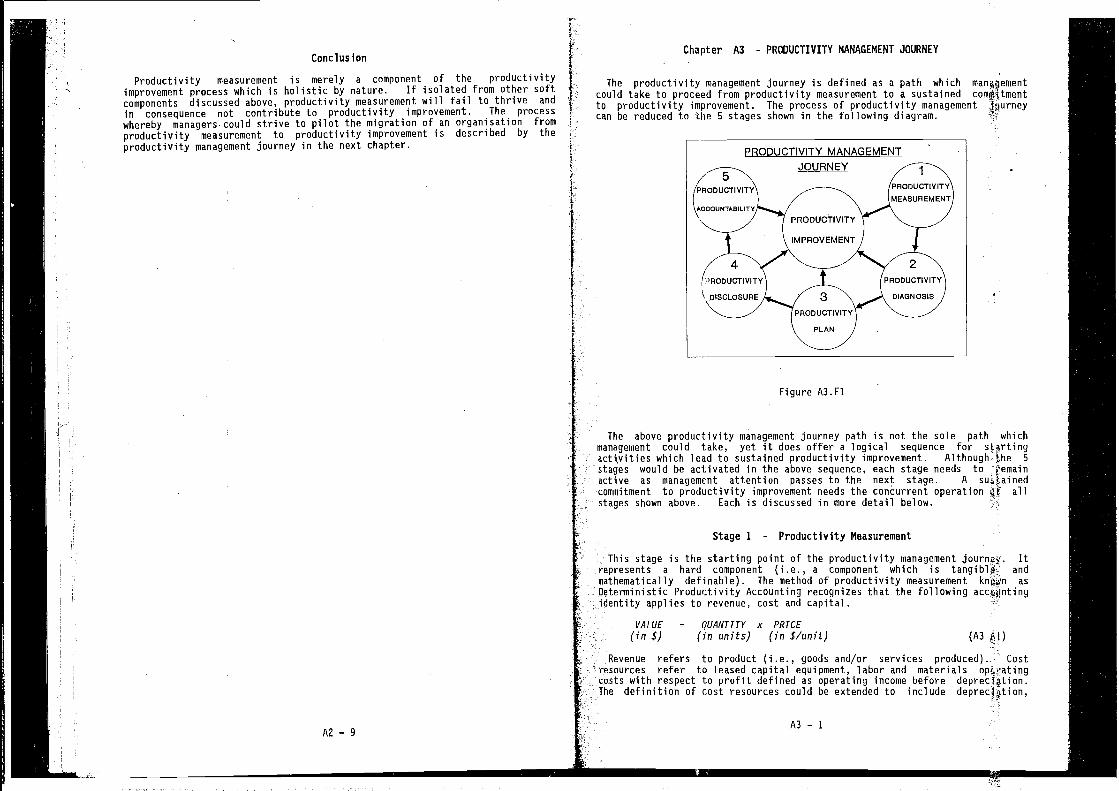

The productivity management journey is defined as a path whichcould take to proceed from productivity measurement to a sustainedto productivity improvement. The process of productivity managementcan be reduced to the 5 stages shown in the following diagram.

The above productivity management journey path is not the sole path whichmanagement could take, yet it does offer a logical sequence for startingactivities which lead to sustained productivity improvement. Although 5

stages would be activated in the above sequence, each stage needs toactive as management attention passes to the next stage. A

commitment to productivity improvement needs the concurrent operation allstages shown above. Each is discussed in more detail below.

Stage 1 - Productivity Measurement

This stage is the starting point of the productivity management journey. Itrepresents a hard component (i.e., a component which is andmathematically definable). The method of productivity measurement asDeterministic Productivity Accounting recognizes that the followingidentity applies to revenue, cost and capital.

VALUE = QUANTITY x PRICE(in 5) (in units) (in s/unit) (A3 fl)

Revenue refers to product (i.e., goods and/or services produced). Costresources refer to leased capital equipment, labor and materialscosts with respect to profit defined as operating income beforeThe definition of cost resources could be extended to include deprec4flion,

Chapter A3 - PRODUCTIVITY MANAGEMENT JOURNEYConclusion

PRODUCTIVITY MANAGEMENT

Figure A3.F1

A2—9A3—l

interest paid and other finance—related charges with respect to profit defined

as taxable income. Capital resources refer to fixed capital assets and to

working capital assets.

Deterministic Productivity Accounting employs the above value axiom to

derive various other axioms which include the following:

PRODUCT QUANTITY

PRODUCTIVITY a(A3 Bi)

RESOURCE QUANTITY

PRODUCT PRICE

PRICE RECOVERY a(A3 Cl)

RESOURCE PRICE

The above measures are then applied to uncover the financial effect of,

inter alia, productivity change and price recovery change of each cost

resource and capital resource used in a given operation.

The limitation of all productivity measurement is that it focusses on effect

rather than cause and is therefore a mechanism for posing rather than

answering questions. The strength of Deterministic Productivity Accounting is

that it provides an overall financial monitor of all systematic effort to

raise productivity.

Stage 2 - Productivity Diagnosis

This stage represents a soft component (i.e., a component which is

intangible and cannot be mathematically defined). It strives to proceed

beyond effect to uncover cause and hence to explain the reasons for

productivity change. Its strength is that it attempts to answer questions

posed by measurement, Yet it will fail whenever the corporate cultureresists ascertainment of cause.

Success in the productivity diagnosis stage depends upon management's

ability to create and nurture an open, questioning culture in which there are

no sacred cows to which the cause of productivity improvement can be held

hostage. Quality circles which are effective can be an example of such

desirable attributes in the corporate culture of an organization.

Stage 3 - Productivity Plan

This stage represents hard and soft components. Using the insights gained

by productivity diagnosis, this stage strives to formulate a productivity plan

which identifies what changes are needed to move the organization from itscurrent productivity levels to target productivity levels which are specified

in this stage and which are included in budgets.

A productivity plan typically contains hard components which includes

equipment, measures such as key performance ratios, productivity and price

recovery targets, as well as other engineering—based hard systems such as

value engineering, multiple resource planning and just—in—time control

systems. A productivity plan also contains soft components (i.e., changes in

organization, training and culture). This stage requires a clear specificationof objectives, strategy and tactics needed in the soft components to ensure

that the hard components of the plan will be achieved. It would also

A3 - 2

introduce productivity measurement as an overall financial monitor of effortto raise productivity.

Stage 4 Productivity Disclosure

This stage represents a hard component. It involves disclosing tg internaland external audiences the family of grids defined byProductivity Accounting as the profit grid, productivity grid, grid,price grid and cost grid. The grids preserve confidentiality of nuSric dataand simply show position with respect to defined segments in jach grid.Disclosure of the grids could start with internal audiences and ththteafter beextended to include external audiences.

Disclosure to internal audiences within the organization creates •awarenessof the productivity concept, assists its assimilation within the corporateculture and prepares the organization for the major step ofdisclosure to external audiences. External audiences are intended functionas a proxy for competition in markets where there are few In thecase of a private sector undertaking the external audience investorsand consumers, whereas in the case of a public sector a

central or local government body, the external audience comprizes :taxpayersand consumers.

Productivity disclosure to external audiences represents the acid test ofmanagement commitment to the notion of productivity Onceinitiated, this stage cannot easily be revoked and will inevitably to thefollowing stage.

Stage 5 - Productivity Accountability

This stage represents a soft component. It involvesaccountability for productivity performance disclosed by the grids specifiedabove.

Specifically, it relates to actual productivity performance well as

planned productivity performance. Actual productivity wouldrelate! actual productivity in a given accounting period to that indicated by

either a prior actual accounting period or a budget for theperiod. Planned productivity performance would relate planned ina given budget to that indicated by either a prior actual

a prior accounting period.

Irrespective of the signal from the grids at the time of initial disclosureto an external audience, management stands to gain credit from the action ofexternal disclosure. If the initial grids signal inproductivity, management is praised for candor in disclosing dfleriorationand, by inference, for committing itself to reverse the direction f$om one ofdeterioration to one of improvement in productivity. On the hand, ifthe initial gvids signal improvement in productivity, management :4p praisedfor good performance and, by inference, for committing itself sustainimprovement in productivity.

Management accountability for disclosed productivity willmotivate management to respond to signals from ongoing fl4ductivitymeasurement, productivity diagnosis and productivity planning. - In otherwords, productivity accountability will induce management to walkdown the path of productivity improvement. -

A3 — 3

C

The Outcome - Productivity Improvement

This stage represents hard and soft components. It will not be possible toattain and maintain productivity improvement unless hard and soft componentscited above are continually melded together. Productivity improvement wouldbe detected through productivity measurement and communicated to stakeholdersthrough productivity disclosure. Stakeholders are defined as suppliers,producers and consumers. Suppliers include the suppliers of labor, materialsand capital resources. In the case of the private sector investors supplyinvestment capital and are included in the definition of suppliers. In thecase of the public sector taxpayers supply investment capital and are includedin the definition of suppliers.

A disclosed, healthy productivity and price recovery track record would tendto reduce uninformed consumer resistance to increase in product price from a

private business, increase in utility rate from a rate—regulated utility orincrease in tax rate from central or local government. Instead it offersobjective facts which indicate the extent to which the producer achievesproductivity growth to finance the absorption of resource price increase whichhe does not recover from consumers by way of an increase in the product price,utility rate or tax rate. Hence the difference between the resource priceincrease and that which is recovered from the consumer would constitute priceunder—recovery and the transfer of a subsidy from the producer to theconsumer.

Conclusion

The productivity management journey contains hard and soft components. Itcan determine the extent of sustainable productivity improvement and hencecompetitive strength, the safety of the investment and the extent to which theproducer can afford to subsidise the consumer.

The productivity management journey can be usefully compared with themanagement of the flight path of an aircraft in the following manner. The

flight of an aircraft is managed by the pilot who is dependent upon bothdirect sensing devices, which provide data on fuel supply, speed etc., andremote sensing devices such as a radar altimeter which provides data on heightabove the earth, Throughout the flight altimetry provides ongoinginformation on the changing topographical features of the earth surface belowthe aircraft. The pilot can elect to disregard remotely sensed altimetricdata and thereby imperil the aircraft.

p

Similarly, the role of productivity measurement is to provide remote sensingof the financial consequences of the changing productivity terrain whicharises from movement of the organization through time and space. The managercan elect to disregard remotely sensed productivity data and thereby imperilthe organization.

Both altimetry and productivity measurement represent hard components withsoft objectives. They seek, respectively, to influence the decision behaviourpattern of the pilot managing the flight path of the aircraft and the managercharged with managing the productivity journey of the organization.

Success in the soft and hard components described in chapter A2 will impactupon productivity and hence financial performance as monitored bydeterministic productivity accounting. In the productivity management journeyproductivity measurement should therefore be seen as a background activity todetect productivity change and calibrate efforts to improve productivity.

A3—4

Chapter A4 - HOW MEASUREMENT ASSISTS PRODUCTIVITY MANAGEMENT

The purpose of this chapter is to define in practise how measurementprovides information to enable management to make better decisions,operations and progress along the productivity management journey.

Productivity Diagnosis for Management

The total resource productivity measurement approach described in this bookmeasures the profit contribution of each resource in terms of capacityutilization, efficiency, and price recovery. Using this information candiagnose which resources contribute significantly to higher profit potágtialwhich can be attained by better allocation of resources. k-

The price recovery term for each resource is used to determineproductivity gain or loss is appropriate for that resource. Subject t( anyappropriate constraints, resources making the less favorable toprice recovery should be targeted for productivity growth (i.e., reduced usageper unit of output) which must more than offset any trade—off productIvityloss (i.e., increased usage per unit of output) from resources making tha'morefavorable contributions to price recovery.

It is appropriate to contrast short term price recovery with efficiency (forshort—term control cycles). It is also appropriate to contrast long, termprice recovery with productivity (for long—term control cycles) since ip thelong term, all resources are variable and, hence, controllable. - Thiscomparison permits the systematic substitution of cheap resources forexpensive resources to optimize profit consistent with the length of thecontrol cycle. Since this approach provides bottom—line measures of chanfl incapacity utilization, efficiency, and price recovery for eachmanagement can pinpoint where productivity improvement efforts will thegreatest beneficial impact on the business.

Some corporations have attempted to analyze their productivity usingconventional approaches such as partial production measures, totalproductivity index numbers, inflation accounting, and/or standard Tcostaccounting. None of these conventional measurement approaches, howk.ver,provides systematic insight into productivity change and itsfinancial impacts. This limitation arises because none of the conventionalmeasurement approaches possesses the characteristics that can befor sound productivity measurement as specified in chapter A2 thediscussion of Characteristics of sound productvity measurement.

Management Control

The approach presented in this book shows that it is possible to thebottom—line impact of change in productivity and change in price recovery foreach resource used in the operation of a business. This fact hassignificance because it permits management to gauge the bottom—line dellareffect of change in the allocation of individual resources withincontrol points. This argument is explained below with respect to bgth alow level control print and a higher level control point.

Even if it is unable to influence price recovery because of itsto control product and resource prices, management at a low level cöwtrolpoint such as a production control point has some prospect of

A4 — 1

the efficiency term in the productivity change. Management at a low levelcontrol point which offers no control of price recovery can still use the

price recovery measure to validate its targets for productivity change.

Sound productivity targeting requires a net positive tradeoff from

changes in resource allocation which give rise to productivity gain

on resources which are used less intensively and to productivity loss on

resources which are used more intensively as a result of planned

substitutions. Business profit improves when relatively cheaper resources

are substituted for relatively dearer resources.

The price recovery variance per resource enables management to determine

whether resources making the least favorable contribution to price recoveryare targeted for productivity growth.- Productivity growth is achieved by

tolerating less than offsetting productivity loss in resources making a more

favorable contribution to price recovery. In this manner the price recovery

variance is used to validatE the direction of productivity change for each

resource.

The sign and magnitude of the bottom—line impact of the price recovery

variance for each resource can send different types of signals to various

levels of control points in a business. For example, negative pricerecovery for a given resource signifies that product price increase does notrecover the extent of price increase for that resource. From this signaldifferent control points may draw the following types of inference.

• A production control point may infer that it should strive throughresource reallocation to target that resource for productivitygrowth (i.e., reduced usage per unit of production).

• A purchasing control point may infer that it should strive, ifpossible, to lower the specification for that resource to achieve a

favorable purchasing variance.

• A production planning control point may infer that it should explore

a make—versus—buy option for that resource, and this analysis may

identify technological gaps that the research and development functioncould explore.

Existing control systems explore the above questions by way of discreteinitiatives which drive specific studies of these questions. The

proposed control system would expliciXly integrate the price recovery

signal, with its decomposition by resource, into the basic profit variance

analysis which is seen by management. This would help management focus

on what questions it should be asking on the setting of productivitytargets for selected individual resources or sets of resources.

At a higher level control point which makes decisions on both production

and product pricing, management may trade price recovery variance offagainst productivity variance in the following manner. If a product

experiences a price elasticity of demand greater than positive unity,management may decide to reduce product price (and hence opt for less

A4 — 2

favorable price recovery variance) to generate more—than—offsettjpg profitfrom production volume (and hence opt for more favorableproductivity variance which flows principally from improvqG capacityutilization).

This possibility of measuring for each resource the ofproductivity change and price recovery change to change in profit, suggeststhat their agjregation permits explaining the origin of in theincome statement as portrayed in the 9—box diagram on the cover book,

Summary

Profitability can be described as the result of the contribution of pricerecovery and productivity. Although management cannot always pricerecovery, it can always influence productivity. The first step influenceproductivity contributions of all resources used is to adopt a soun4 method bywhich they can be measured.

Sound productivity measurement possesses characteristics (a,j specifiedearlier) which should underpin all systematic efforts to raiseregardless of whether those efforts originate from high—level contSl pointssuch as the management committee or low—level control points such as costcenter expense budgets in a plant.

The model discussed above and the PM software implementation of the model

used in this book provide an analytical tool that can be used validateother studies focusing on improving productivity through such as

vertical integration, investment, technological change,incentive schemes, and training.

• A financialintegrationunattractiveprofitabilityquestion.

planningshould be

on costin the

control point may inferinvestigated if the make

grounds and there existsbusiness sector supplying the

that reverseoption is

acceptableresource in

L

A4 — 3

PART B — INPUT FUNCTIONS

part of the book presents the following chapter.

Chapter 81 DATA REQUIREMENTS AND DEFAULT VALUES

Chapter Bi DATA REQUIREMENTS AND DEFAULT VALUES

The 10 input functions (i.e. user specified functions) required by the modelare defined in this chapter. If the user fails to provide informationby the model, use is made of either default values (which are definedchapter) or proxy values (which are defined in Part G of the book).

The distinction between default values and proxy values is soajçwhatarbitrary, but is nonetheless clearly defined. With the exception of thefunction TARGET RETURN ON IN VESTMENT, whose default value is set at oldintrinsic return on investment, all default values of input functions setat 0 or at 1. In contrast, proxy values assume a wider range ofvalues as shown in Part 0.

The 10 input functions required from the user are specified in stateRents(81 Al) through (81 32).

Q (QUANTITY FUNCTION) is a user specified functibn.(81 Al)

dimension is typically given in physical units.(81

The above suite of statements refers to the level of a function. It dbtinesthe Quantity function which is specifed by the user on the basic partitthr ofaccounting data. This function is dimensioned and is typically expressed insome physical unit such as tons, work—hours etc. It is defined forand resource.

There is no default value for the quantity function, and its proxy valutc isdefined in Part.G of the book. 2

P (PRICE FUNCTION) is a user specified function.(81 hI)

P dimension is given in currency unit / physical units.(81

The above suite of statements refers to the level of a function. It detjnesthe Price function which is specifed by the user on the basic partitin ofaccounting data. This function is dimensioned and is typically insome currency unit divided by physical units. It is defined for product andresource.

There is no default value for the price function, and its proxy isdefined in Part 0 of the book.

81—1

W (INTERVAL WIDTH FUNCTION) is a user specified function.

W dimension is given in days or other unit of time.

(81 Cl)

(81 C2)

The above suite of statements refers to the level of a function. It definesthe user specified interval Width. This function is dimensioned and istypically expressed in some unit of time such as hours, shifts or days of a

given intensity. This feature of the model would, for example, allow a chainstore user to weight, say, a Saturday with a greater intensity than a Monday.This function is defined for product and resource.

Function W is important in the following two cases:

— high frequency control cycles (i.e., a month and shorter periods), sinceit is misleading to compare, say, an 18 workday month such as Februarywith a 22 workday month such as March.

— a change in th.e closing month for an accounting year could give rise todiffering numbers of months per year when the last of the old years andthe first of the new years are compared.

The following entity rule of function W is implemented in the axioms and isspecified below:

Function W is applied to function Q(U), i.e., product Quantity

Function W is applied to function Q(N), i.e., cost resource Quantity

Function W is applied to function T(K,), i.e., target rate of returnin turn applied toP(K) representingresource asset Price.

The value functions for revenue (i.e., product value), operating expense(i.e., cost resource value) and target profit (i.e., cost of capital) allcontain a time component in contrast with the value function for capitalassets (i.e., capital asset value) which is time free. In other wordsreve4lile, cost and target profit values are time bound since they refer to a

flow concept with respect to a time interval such as a month, quarter or yearwhereas asset value is time free since it refers to a point concept such as

the value at close of business on the last business day within such timeinterval

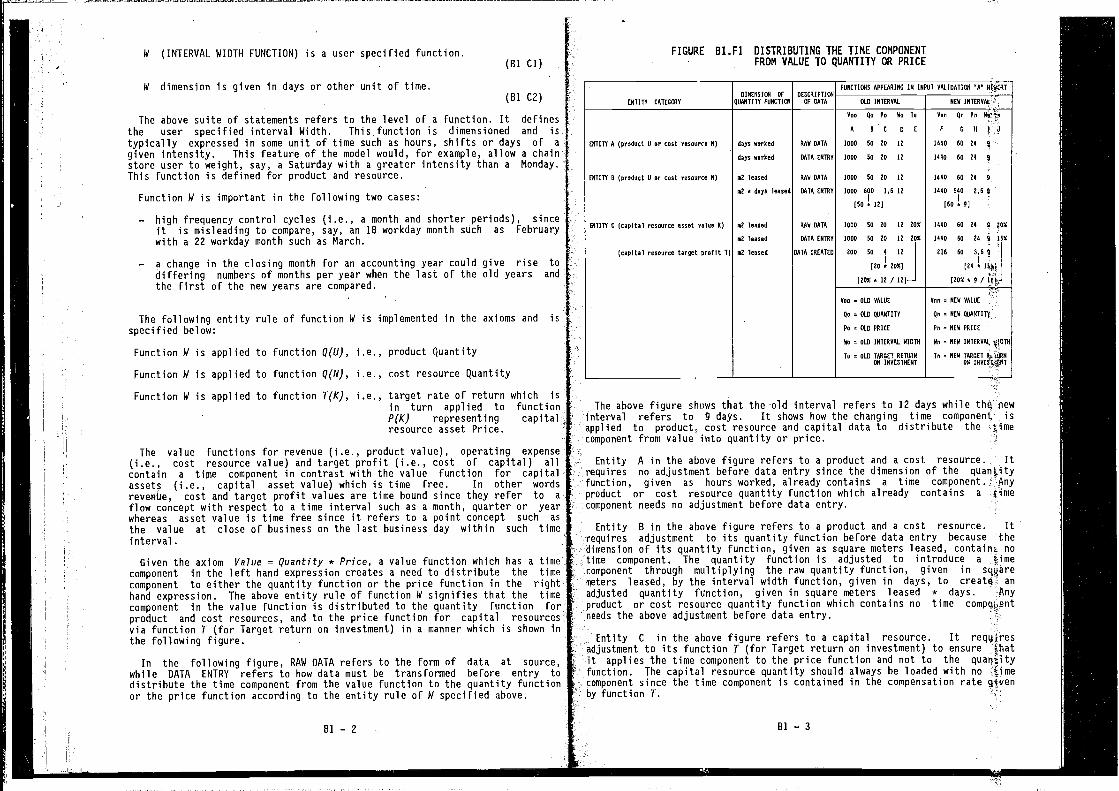

Given the axiom Value = Quantity * Price, a value function which has a timecomponent in the left hand expression creates a need to distribute the timecomponent to either the quantity function or the price function in the righthand expression. The above entity rule of function W signifies that the timecomponent in the value function is distributed to the quantity function forproduct and cost resources, and to the price function for capital resourcesvia function T (for Target return on investment) in a manner which is shown inthe following figure.

In the following figure, RAW DATA refers to the form of data at source,while DATA ENTRY refers to how data must be transformed before entry todistribute the time component from the value function to the quantity functionor the price function according to the entity rule of W specified above.

FIGURE B1.F1 DISTRIBUTING THE TIME COMPONENTFROM VALUE TO QUANTITY OR PRICE

ENTITY CAIEIONYDINENSION OF

QUANTITY FUNCTIONDESCRIPTIV4

OF DATA

FUNCTIONS APPEARING IN INPUT

OLD INTERAAL

VALIDATION NtAC41T

NEN

ENTITY 0 (product U or cost roosore, N) deys worked VAN DATA

Roe Qo Ps No To

A DC DC1000 DO 1D ID

Von Re Po

F OR1440 60 DO

days worked DOTA ENTVV DODD 10 DD ID 1440 NO D4

ENTDTT D (product U or coot rooource N) ml leased RAN DATA 1000 00 20 Il 1440 60 24 5

ml o doyo Teased DATA ENTRY 1000 ADO 16 Il[10 a Il]

1440 040 0,0

[60 0 4]

ENTITY C (capital reooorce wooeD 'jaDe, K)

(capital reoeerce taroet profit T)

ml leased

ml leased

ml loosed

RAN DATA

DATA ENTRY

DATA CREATED

1000 50 DO ID 20%

1000 10 20 Il 200

200 50 4 Il[20 o 00%)

[lOO0ll/lD)_J

1440 60 04 !INRO 00 24 ISO

216 00 3,0

[00 a

)lOTeD/l&I.

Poe = OLD VALUE One NEA VALUE

Re = OLD QUANTITY Qe = NEW QUANTITY

Po OLD PRICE Pn = NCA P01CC

Ne = OLD INTERVAL 01010

To = OLD TVROET VETOONON INVESTMENT

An NEW INTERVAL

Tn NEW TAOOET RAVURNON

The above figure shows that the old interval refers to 12 days while thg pewinterval refers to g days. It shows how the changing time component isapplied to productn cost resource and capital data to distribute the ttimecomponent from value into quantity or price.

Entity A in the above figure refers to a product and a cost resource. Itrequires no adjustment before data entry since the dimension of the quantityfunction, given as hours worked, already contains a time component.product or cost resource quantity function which already contains a fleeComponent needs no adjustment before data entry.

Entity B in the above figure refers to a product and a cost resource. Itrequires adjustment to its quantity function before data entry because thedimension of its quantity function, given as square meters leased, containt notime component. The quantity function is adjusted to introduce a timecomponent through multiplying the raw quantity function, given in sqparemeters leased, by the interval width function, given in days, to create. anadjusted quantity function, given in square meters leased * days. fryproduct or cost resource quantity function which contains no time compqt5entneeds the above adjustment before data entry.

Entity C in the above figure refers to a capital resource. It requiresadjustment to its function T (for Target return on investment) to ensure thatit applies the time component to the price function and not to thefunction. The capital resource quantity should always be loaded with no timecomponent since the time component is contained in the compensation rate givenby function T.

81—2 81—3

which iSfunctioncapital

The default value for the width function W is I unit of time. The modeluses the quotient of new interval width and old interval width and therebycreates a quotient of dimensionless unity when I unit of time is entered for,say, each of two years containing 365 days. A default value would bewhen the user specifies a quantity function but omits to specify a widthfunction. Proxy values for the width function arise when a proxy product or a

proxy cost resource is required, as specified in Part G of the book.

T is a dimensionless function.

(Cl DI)

(Cl D2)

The above suite of statements refers to the level of a function. It definesthe user specified Target return on investment which is used to define thetarget profit level by individual element of capital investment. It is definedonly for capital resources.

The default value for both old target return on investment and new targetreturn on investment is the function for old intrinsic return on investmentwith respect to a specified contrast. It is used when the user specifiescapital asset value but omits to specify a target return on investment. A

proxy value for target return on investment arises when proxy capital isrequired, as specified in Part G of the book.

S (RISK WEIGHT FOR INVESTMENT) is a user specified function.

S is a dimensionless function.

(Cl El)

(Cl E2)

The above suite of statements refers to the level of a function. It definesthe user specified risk weight on investment which is one of the functionsused to distribute the intrinsic profit level to the individual elements ofcapital investment.

The default value for risk weight for investment is dimensionless unity. Itis used when the user specifies capital quantity and price but omits tospecify a risk weight for investment. A proxy value for the risk weight forinvestment arises when proxy capital is required, as specified in Part G ofthe book.

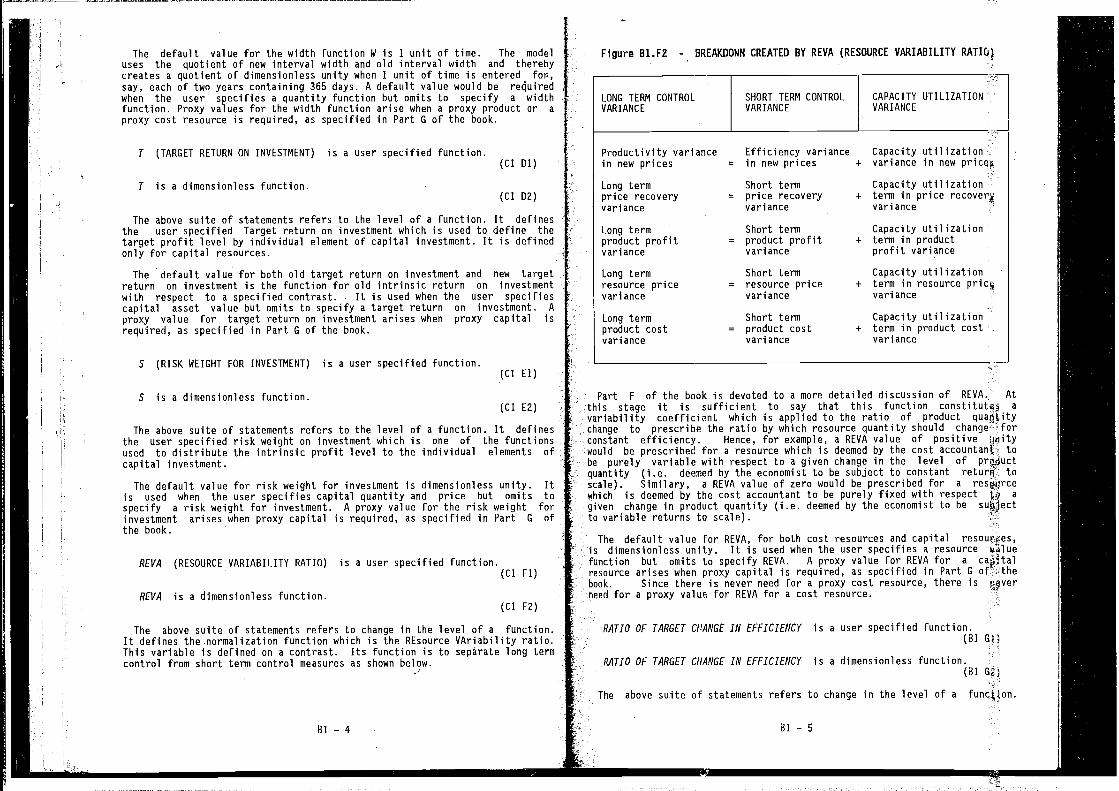

REM (RESOURCE VARIABILITY RATIO) is a user specified function.

REV/i is a dimensionless function.(Cl F2)

The above suite of statements refers to change in the level of a function.It defines thenormalization function which is the REsource VAriability ratio.This variable is defined on a contrast. Its function is to separate long termcontrol from short term control measures as shown

Part F of the book is devoted to a more detailed discussion of REVA. Atthis stage it is sufficient to say that this function constitutes a

variability coefficient which is applied to the ratio of product quafltitychange to prescribe the ratio by which resource quantity should change forconstant efficiency. Hence, for example, a REVA value of positive unitywould be prescribed for a resource which is deemed by the cost tobe purely variable with respect to a given change in the level ofquantity (i.e. deemed by the economist to be subject to constant returii toscale). Similary, a REVA value of zero would be prescribed for a resiurcewhich is deemed by the cost accountant to be purely fixed with respect a

given change in product quantity (i.e. deemed by the economist to be subjectto variable returns to scale).

The default value for REVA, for both cost resources and capitalis dimensionless unity. It is used when the user specifies a resourcefunction but omits to specify REVA. A proxy value for REVA for a caAitalresource arises when proxy capital is required, as specified in Part Gbook. Since there is never need for a proxy cost resource, there isheed for a proxy value for REVA for a cost resource.

B1—4 Bl—5

U

T (TARGET RETURN ON INVESTMENT) is a user specified function.

Figure B1.F2 -. BREAKDOWN CREATED BY REVA (RESOURCE VARIABILITY RATIQI

LONG TERM CONTROL SHORT TERM CONTROL CAPACITY UTILIZATIONVARIANCE VARIANCE VARIANCE

Efficiency variance Capacity utilization= in new prices + variance in new

Productivity variancein new prices

Long termprice recoveryvan ance

Long termproduct profitvan ance

Long termresource pricevariance

Long termproduct costvariance

Short term= price recovery

variance

Short term= product profit

variance

Short term= resource price

variance

Short term= product cost

variance

Capacity utilization+ term in price recovery

variance -

Capacity utilization+ term in product

profit variance

Capacity utilization+ term in resource

variance

Capacity utilization+ term in product cost

variance

(Cl Fl)

RATIO OF TARGET ClAP/GE IN EFFICIENCY is a user specified function.(BI Gi)

RATIO OF TARGET C/lANGE IN EFFICIENCY is a dimensionless function.(Bl Ga)

The above suite of statements refers to change in the level of a function.