Principles of Corporate Finance - e-Learning - UNIMIB

37

Principles of Corporate Finance Vittoria Cerasi 2020-21 Vittoria Cerasi Principles of Corporate Finance 2020-21 1 / 37

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Principles of Corporate Finance - e-Learning - UNIMIB

Principles of Corporate Finance

Vittoria Cerasi

2020-21

Vittoria Cerasi Principles of Corporate Finance 2020-21 1 / 37

Organization of the course

Instructor: Vittoria Cerasi.

Lectures: theory and empirics.

Online written exam at the end of the course: April 12, h.15.30.

One question can be skipped by presenting in class a report on ajournal article.

Exercises to be discussed in class will increase the final grade up to 2points.

Course material: Lecture notes and published articles, selectedchapters of books.

All material and news are posted in the e-learning site (Moodle).

Vittoria Cerasi Principles of Corporate Finance 2020-21 2 / 37

Organization of the course

Vittoria Cerasi Principles of Corporate Finance 2020-21 3 / 37

Topics

Financial structure of the firm (week 1 & 2)

The role of banks vs. bond-holders (week 2 & 3)

Initial public offering (end of week 3)

Venture capital (week 4)

Conglomerates (week 5)

Vittoria Cerasi Principles of Corporate Finance 2020-21 4 / 37

Introduction to corporate finance

Vittoria Cerasi Principles of Corporate Finance 2020-21 5 / 37

Introduction to corporate finance

Companies find it difficult to raise external finance. Why?

Agency costs and asymmetries of information between investors andinsiders.

Agency costs: conflict of interest between insiders (entrepreneur ormanager) and outsiders (investors).

Asymmetries of information: insiders know more than outsiders ofthe company true value and activities.

For these reasons the cost of external finance may increase or be toohigh, hence no external investor wants to fund the company.

Vittoria Cerasi Principles of Corporate Finance 2020-21 6 / 37

Introduction to corporate finance

Financial structure is the resulting combination of different financialcontracts.

Financial contracts (debt or equity) differ for:

Monetary reward they pay to investors in different contingencies;

Control rights they give to investors in different contingencies.

Stake-holders (holders of financial contracts) may act differently ifthey are institutions, single investors, insiders or outsiders of thecompany.

Vittoria Cerasi Principles of Corporate Finance 2020-21 7 / 37

Standard financial contracts

Assume that a firm can be fully described by its cash flow X ∈ (0, ∞)(random variable at date t = 0).

The cash flow captures the future revenues from all the current andpast productive projects of the firm.

The cash flow is observable by third parties and reflects the trueeconomic state of the firm (accounting manipulation is ruled out).

Standard financial contracts are then a specific transformation of thecash flow.

Vittoria Cerasi Principles of Corporate Finance 2020-21 8 / 37

The financial structure of the firm

Outline

Standard financial contracts (equity and debt)

Modigliani-Miller Theorem

Vittoria Cerasi Principles of Corporate Finance 2020-21 9 / 37

Standard financial contracts

A firm with debt

The firm at an initial date t = 0 has issued debt with ”face value” D.

This means that at a future date, T > 0 it promises to return D toits creditors.

If the firm does not repay its creditors at date T , i.e. it defaults on itspromises, bankruptcy occurs.

Creditors do not own the firm, but can seize the assets of thecompany in case of default.

The shareholders are owners of the firm and are protected by limitedliability.

Vittoria Cerasi Principles of Corporate Finance 2020-21 10 / 37

Standard financial contracts

Value of debt and equity

If X ≥ D then the creditors receive D and the shareholders areresidual claimant, thus earn (X −D).

If X < D the entrepreneur defaults: the firm is liquidated and all thecash flow, X , goes to creditors; shareholders earn 0 in case of default(because of limited liability).

The value of equity is given by the transformation of the cash flowmax{X −D, 0}.The value of debt is instead min{X ,D}.

Vittoria Cerasi Principles of Corporate Finance 2020-21 11 / 37

Standard financial contracts

Option Analogy

Equity pays: max{X −D, 0} = (X −D)+ which is equivalent to

- Call option on X with strike price D.

Risky debt with face value D pays: min{D,X} = D − (X −D)+

which is equivalent to:

- Risk-free bond with face value D plus- Written put on X with strike price D.

Equity gets the upside, but does not bear the full downside.

Like option value, the value of equity increases in risk, while the valueof debt decreases in risk.

Vittoria Cerasi Principles of Corporate Finance 2020-21 12 / 37

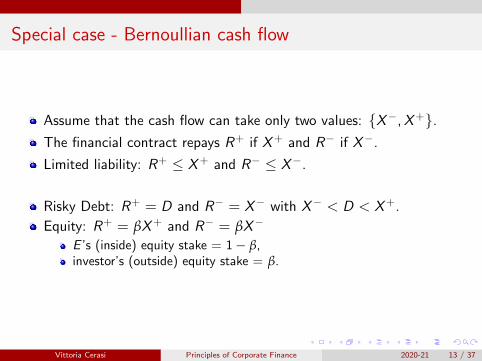

Special case - Bernoullian cash flow

Assume that the cash flow can take only two values: {X−,X+}.The financial contract repays R+ if X+ and R− if X−.

Limited liability: R+ ≤ X+ and R− ≤ X−.

Risky Debt: R+ = D and R− = X− with X− < D < X+.

Equity: R+ = βX+ and R− = βX−

E ’s (inside) equity stake = 1− β,investor’s (outside) equity stake = β.

Vittoria Cerasi Principles of Corporate Finance 2020-21 13 / 37

Standard financial contracts

Real-life complications

Junior (subordinated) vs. senior debt.

Debt with collateral.

Ordinary vs. preferred stocks.

Ibrid contracts: convertible debt (option).

Vittoria Cerasi Principles of Corporate Finance 2020-21 14 / 37

Modigliani-Miller Theorem

Irrelevance of the financial structure:

Assume firm’s cash flow X is distributed according to a continuousprobability function g(x) with support [0, ∞).

The firm’s expected value V is given by the expected value of debtplus the expected value of equity, that is

VE = E (max{X −D, 0}) =∫ ∞D (x −D)g(x)dx

VD = E (min{D,X}) =∫ ∞D Dg(x)dx +

∫ D0 xg(x)dx

VE + VD =∫ ∞0 xg(x)dx ≡ E (X )! → V does not depend upon D:

hence the financial structure of a firm (the mix of Debt and Equity)does not affect the value of the firm.

Vittoria Cerasi Principles of Corporate Finance 2020-21 15 / 37

Vittoria Cerasi Principles of Corporate Finance 2020-21 16 / 37

Debt and incentives

Two dates (t = 1, 2), no discounting (r = 0), everybody isrisk-neutral.

Pennyless entrepreneur E (borrower, insider) has a project thatrequires funding I .

Moral hazard:

If undertaken, the project generates at t = 2 a cash flowX ∈ {XL,XH}.The expected return (cash flow) depends on E ’s effort: e = {eL, eH}.The success probability with effort (eH) is pH .

The success probability without effort (eL) is pL where∆p = pH − pL > 0.

Shirking results in (non-transferable) private benefits B to theentrepreneur.

Vittoria Cerasi Principles of Corporate Finance 2020-21 17 / 37

Debt and incentives

Contract (Loan agreement): in exchange for contributing I at t = 1,investor is promised a repayment at t = 2

RL if X = XL and RH if X = XH

where ∆R = RH − RL denotes the “repayment spread”and Ri ≤ Xi

(limited liability)

Competitive capital markets: RL + pH∆R = I

Project has a positive NPV with effort: XL + (pL + ∆p)∆X − I > 0

Exerting effort is efficient: ∆p∆X > B

Vittoria Cerasi Principles of Corporate Finance 2020-21 18 / 37

Debt and incentives

First Best (Modigliani-Miller): Financing choices are irrelevant in theabsence of moral hazard (if B = 0, or eH is contractible)

Risky Debt: Suppose E chooses to raise I with risky debt with facevalue D:

RL = XL

RH = D

Equity: E sells a fraction β of existing shares:

RL = βXL RH = βXH

Vittoria Cerasi Principles of Corporate Finance 2020-21 19 / 37

Debt and incentives

Optimality of Debt

Irrelevance of financing choice breaks down, once effort is costly andnon-contractible.

At t = 1, the entrepreneur chooses e = eH if

pH (XH − RH ) + (1− pH )(XL − RL) ≥ pL(XH − RH ) + (1− pL)(XL − RL) + B

The incentive compatibility constraint (IC) can be rewritten as

∆p (∆X − ∆R ) > B or ∆R ≤ ∆maxR ≡ ∆X − B/∆p

We need to solve the following:

minRL,RH

∆R

RL ≤ XL RH ≤ XH

I = RL + pH∆R

Vittoria Cerasi Principles of Corporate Finance 2020-21 20 / 37

Debt and incentives

Debt financing is the best way to incentivate the entrepreneur toprovide effort.

- Debt: ∆R = I−XLpH

- Equity ∆R = I−βXL

pH

Irrespective of financing, E receives the investment’s entire NPV(because capital markets are competitive).

All projects that can be financed with equity can also bedebt-financed but the reverse is not true.

Intuition: The optimal contract maximizes the fraction of the returnfrom effort that accrues to the entrepreneur. Hence, debt maximizeshis incentive to exert effort.

Vittoria Cerasi Principles of Corporate Finance 2020-21 21 / 37

Debt and incentives

Remarks:

Jensen and Meckling (1976) show that debt dominates equity. Debtdominates all other possible contracts.

Debt as incentive contract has two specific features:

With debt the entrepreneur is residual claimant and bears substantialrisk. Risk-neutrality is required to avoid trade-off between incentivesand insurance.

Full incentives: Agent receives entire income at the margin, only forincomes above repayment level.

Vittoria Cerasi Principles of Corporate Finance 2020-21 22 / 37

Debt and incentives

Exercise 1Consider the following firm/project: I = 60 and

eL and B = 10 Cash flow

1− pL = 0.8 40

pL = 0.2 90

eH Cash flow

1− pH = 0.2 40

pH = 0.8 90

1 Check that the NPV when E chooses eH is positive.

2 Consider financing the project by issuing a stock which leaves aproportion β ∈ (0, 1) to investors: will E choose eH?

3 Consider financing the project with risky debt, i.e. a debt contractwith face value 40 < D < 90: will E choose eH?

Vittoria Cerasi Principles of Corporate Finance 2020-21 23 / 37

Vittoria Cerasi Principles of Corporate Finance 2020-21 24 / 37

Debt and risk-shifting

Two dates (t = 1, 2), no discounting (r = 0), everybody isrisk-neutral.

Penniless entrepreneur E (borrower, insider) requires funding I .

When funded, E chooses at t = 1 between two mutually exclusiveprojects, Project A and B:

Pr[X = 2X̂

]Pr

[X = X̂

]Pr [X = 0]

Project A: θ1 1− (θ1 + θ2) θ2

Project B: θ1 + ∆11− (θ1 + θ2)−(∆1 + ∆2)

θ2 + ∆2

Project cash flows realize at date t = 2.

Vittoria Cerasi Principles of Corporate Finance 2020-21 25 / 37

Debt and risk-shifting

Assumptions:

0 < ∆1 < ∆2, θ1 + ∆1 + θ2 + ∆2 < 1

Project B has a smaller NPV than Project A and it is riskier:

NPVA = θ1 × 2X̂ + (1− θ1 − θ2)× X̂ + 0 = (1 + θ1 − θ2)X̂ > I

NPVB = (1 + θ1 − θ2)X̂ − (∆2 − ∆1)X̂ − I

which is less than NPV of Project A, the difference being:

(∆2 − ∆1)X̂ > 0

Hence, I should be used for Project A (First Best).

Vittoria Cerasi Principles of Corporate Finance 2020-21 26 / 37

Debt and risk-shifting

Suppose that I is raised in debt with face value D paying min{X ,D}.Assume (for simplicity) that 2X̂ > D > X̂ .

Hence E gets a positive payoff only if X = 2X̂ .

With project A, E gets: θ1(2X̂ −D)

while with Project B, E gets: (θ1 + ∆1)(2X̂ −D)

Once I has been raised, E picks Project B, as it is more likely togenerate X = 2X̂ .

Because of limited liability, E does not internalize the losses in the lowstate, but maximizes returns in the state where is residual claimant.

If NPV of Project B < 0, no funding even though there is a project(Project A) with a positive NPV (market breaks down).

Vittoria Cerasi Principles of Corporate Finance 2020-21 27 / 37

Debt and risk-shifting

Suppose I has been raised in equity. The sold fraction β entitlesinvestors to βX .

Once I is raised and invested, E receives a fraction 1− β of the cashflow and maximizes the expected cash flow:

(1− β)(1 + θ1 − θ2)X̂ > (1− β)(1 + θ1 + ∆1 − θ2 − ∆2)X̂

Hence, she undertakes Project A.

Equity finance does not induce any distortion in the investmentdecisions.

The problem is that levered equity’s payoff is convex in cash flows: Eis willing to incur cost of lower mean in order to increase the varianceof the cash flow (Risk-shifting or asset substitution problem).

Vittoria Cerasi Principles of Corporate Finance 2020-21 28 / 37

Debt and risk-shifting

Exercise 2E needs I = 4.2 to undertake a productive project. Once financed, E canchoose between {A,B}, i.e. two risky projects with the followingstochastic structure:

2X̂ = 10 X̂ = 5 X = 0

A 0.2 0.6 0.2

B 0.3 0.2 0.5

1 Compute the NPV of the two projects and define in which of the twoit is profitable to invest.

2 Assume E issues risky debt with face value 5 < D < 10: which projectwill be selected? Compute the rational face value D for investors.

3 assume instead E issues equity by promising a proportion β of X toinvestors: which project will be selected? Compute the rationalproportion β for investors.

Vittoria Cerasi Principles of Corporate Finance 2020-21 29 / 37

Vittoria Cerasi Principles of Corporate Finance 2020-21 30 / 37

Debt overhang problem

Myers (1977) shows why firms (may) limit borrowing

(Too much) risky debt induces a suboptimal investment strategy.

That is, some positive NPV projects are forgone.

Basic insight: Because debt is senior and risky, it captures (a toolarge) part of the surplus generated by the investment.

This discourages junior claimants (equity) from contributing capital.

Too much debt reduces ex-ante value of firm.

Vittoria Cerasi Principles of Corporate Finance 2020-21 31 / 37

Debt overhang problem

Two dates (t = 1, 2), no discounting, everybody is risk neutral.

At t = 1, E is running a firm with:

Asset in place generates X ∈ {X−,X+} at t = 2

with ∆X = X+ − X− > 0 and p = Pr{X = X+}Existing investors hold claims on X with promised repayments att = 2

More precisely, they hold debt with face value D so that

R− = min{D,X−} and R+ = min{D,X+}

Vittoria Cerasi Principles of Corporate Finance 2020-21 32 / 37

Debt overhang problem

At t = 1, E considers undertaking a project: Investing I increases pto p + ∆p

This investment has a positive NPV:

∆p∆X − I > 0

The existing debt-holders’ payoff is: R− + p∆R

If I is invested, their payoff increases by

∆p∆R

and E ’s payoff increases by

(∆p∆X − I )︸ ︷︷ ︸project’s NPV

− ∆p∆R︸ ︷︷ ︸part accruing to

existing debt-holders

Vittoria Cerasi Principles of Corporate Finance 2020-21 33 / 37

Debt overhang problem

Existing debt acts as a tax on investment. Hence, E invests iff

∆p∆X − I > ∆p∆R

With risky debt (∆R > 0), the investment policy is distorted towardsunderinvestment. Indeed, projects such that ∆p∆R > ∆p∆X − I > 0should be undertaken, but are rejected.

E would incur the entire investment cost, but gets only part of thereturn.

Holders of existing risky claim do not contribute to the funding, buttheir claim becomes less risky: they get additional ∆p∆R and thismay prevent optimal investment policy.

Debt overhang is a problem only if debt is risky, not with risk-freedebt (∆R = 0).

Is conditional renegotiation the solution?

Vittoria Cerasi Principles of Corporate Finance 2020-21 34 / 37

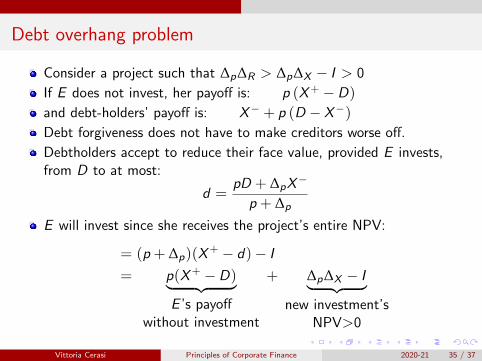

Debt overhang problem

Consider a project such that ∆p∆R > ∆p∆X − I > 0

If E does not invest, her payoff is: p (X+ −D)

and debt-holders’ payoff is: X− + p (D − X−)

Debt forgiveness does not have to make creditors worse off.

Debtholders accept to reduce their face value, provided E invests,from D to at most:

d =pD + ∆pX

−

p + ∆p

E will invest since she receives the project’s entire NPV:

= (p + ∆p)(X+ − d)− I

= p(X+ −D)︸ ︷︷ ︸E ’s payoff

without investment

+ ∆p∆X − I︸ ︷︷ ︸new investment’s

NPV>0

Vittoria Cerasi Principles of Corporate Finance 2020-21 35 / 37

Debt and risk-shifting

Exercise 3Consider a firm that in its past has issued debt with face value D = 50.This debt was issued to invest in a productive project that generates apayoff of 100 or 20 with equal probability. Firm has an investmentopportunity: Its costs are 10 and the additional payoff is 15 with certainty.Assume that E has enough liquidity to finance this new investmentopportunity.

1 Will E invest in this new opportunity?

2 What if the face value of the past debt was renegotiated down tod < D?

Vittoria Cerasi Principles of Corporate Finance 2020-21 36 / 37

Vittoria Cerasi Principles of Corporate Finance 2020-21 37 / 37