LEVEL 6 CORPORATE FINANCE

114

Your road to success LEVEL 6 CORPORATE FINANCE Your road to success • A B E • O F F I C I A L S T U D Y G U I D E abeuk.com

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of LEVEL 6 CORPORATE FINANCE

Y o u r r o a d t o s u c c e s s

LEVEL 6 CORPORATE FINANCE

Your road to success

• ABE • OF

FIC

IA

L S T U DY GU

IDE

abeuk.com

© ABEii

© ABE 2017

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying and recording, or held within any information storage and retrieval system, without permission in writing from the publisher or under licence from the Copyright Licensing Agency Limited. Further details of such licences (for reprographic reproduction) may be obtained from the Copyright Licensing Agency Limited, Barnard’s Inn, 86 Fetter Lane, London EC4A 1EN.

This study guide is supplied for study by the original purchaser only and must not be sold, lent, hired or given to anyone else.

Every attempt has been made to ensure the accuracy of this study guide; however, no liability can be accepted for any loss incurred in any way whatsoever by any person relying solely on the information contained within it. The study guide has been produced solely for the purpose of professional qualification study and should not be taken as definitive of the legal position. Specific advice should always be obtained before undertaking any investment.

ABE cannot be held responsible for the content of any website mentioned in this study guide.

ISBN: 978-1-911550-28-0

Copyright © ABE 2017 First published in 2017 by ABE 5th Floor, CI Tower, St. Georges Square, New Malden, Surrey, KT3 4TE, UK www.abeuk.com

All facts are correct at time of publication.

Author: Stuart Green MSc, MPhil, PGCE, PGCE (HE), FHEA, CPFAReviewer: Colin Linton MRes MBA PGCHE DipM DipFS FCIB FCIM FCIPS FCIEA FHEA FInstLM

Editorial and project management by Haremi Ltd.Typesetting by York Publishing Solutions Pvt. Ltd., INDIA

Every effort has been made to trace all copyright holders, but if any have been inadvertently overlooked, the Publishers will be pleased to make the necessary arrangements at the first opportunity.

The rights of Stuart Green to be identified as the author of this work have been asserted by him in accordance with the Copyright, Design and Patents Act 1998.

Acknowledgements

The publishers gratefully acknowledge permission to reproduce the followingcopyright material: p9 garagestock/ Shutterstock.com; p12 zaozaa19/ Shutterstock.com; p22 yanik88/ Shutterstock.com; p31 Stone36/ Shutterstock.com; p38 Idutko/ Shutterstock.com; p53 kan_chana/ Shutterstock.com; p54 allstars/ Shutterstock.com; p55 leungchopan/ Shutterstock.com; p56 ESB Professional/ Shutterstock.com; p60 Robert Kneschke/ Shutterstock.com; p63 Natee K Jindakum/ Shutterstock.com; p65 Rawpixel.com/ Shutterstock.com; p69 create jobs 51/ Shutterstock.com; p73 Pavel L Photo and Video/ Shutterstock.com; p75 one photo/ Shutterstock.com; p76 SFIO CRACHO/ Shutterstock.com; p78 Uber Images/ Shutterstock.com; p80 garagestock/ Shutterstock.com; p83 FedotovAnatoly/ Shutterstock.com; p87 ariadna de raadt/ Shutterstock.com; p90 Marina Pousheva/ Shutterstock.com; p92 ZeroThree/ Shutterstock.com; p97 Danny E Hooks/ Shutterstock.com; p98 Rawpixel.com/ Shutterstock.com; p107 Anton Violin/ Shutterstock.com

© ABE iii

Contents

Using your study guide iv

Chapter 1 The Importance of Capital Structure 2

1.1 Corporate finance and capital structure 3

1.2 The roles played by stakeholders, different types of risk and business strategy in capital structure 7

1.3 Alternative frameworks for the development of a capital structure 13

Chapter 2 Sources of Finance 18

2.1 Alternative approaches to sources of equity and debt 19

2.2 Sources of finance and how they relate to strategic objectives and strategic environment 24

2.3 Decision-making frameworks that could be applied to ensure that the business utilises sources of finance that are appropriate to its needs and strategic circumstances 39

Chapter 3 The Cost of Capital 44

3.1 Alternative approaches to the valuation of equity 45

3.2 Methods for the calculation of the cost of capital to provide a basis on which strategic financing and investment decisions can be made 52

3.3 The effects of risk on the cost of capital 59

Chapter 4 Advanced Investment Appraisal 68

4.1 Select and justify appropriate investment appraisal techniques 69

4.2 Application of investment appraisal techniques 73

4.3 A critical evaluation of investment appraisal techniques 86

Chapter 5 Contemporary Issues in Corporate Finance 94

5.1 Alternative perspectives on the role of ethics in corporate finance 95

5.2 Appraise approaches to corporate governance in the context of legal, regulatory and professional requirements 98

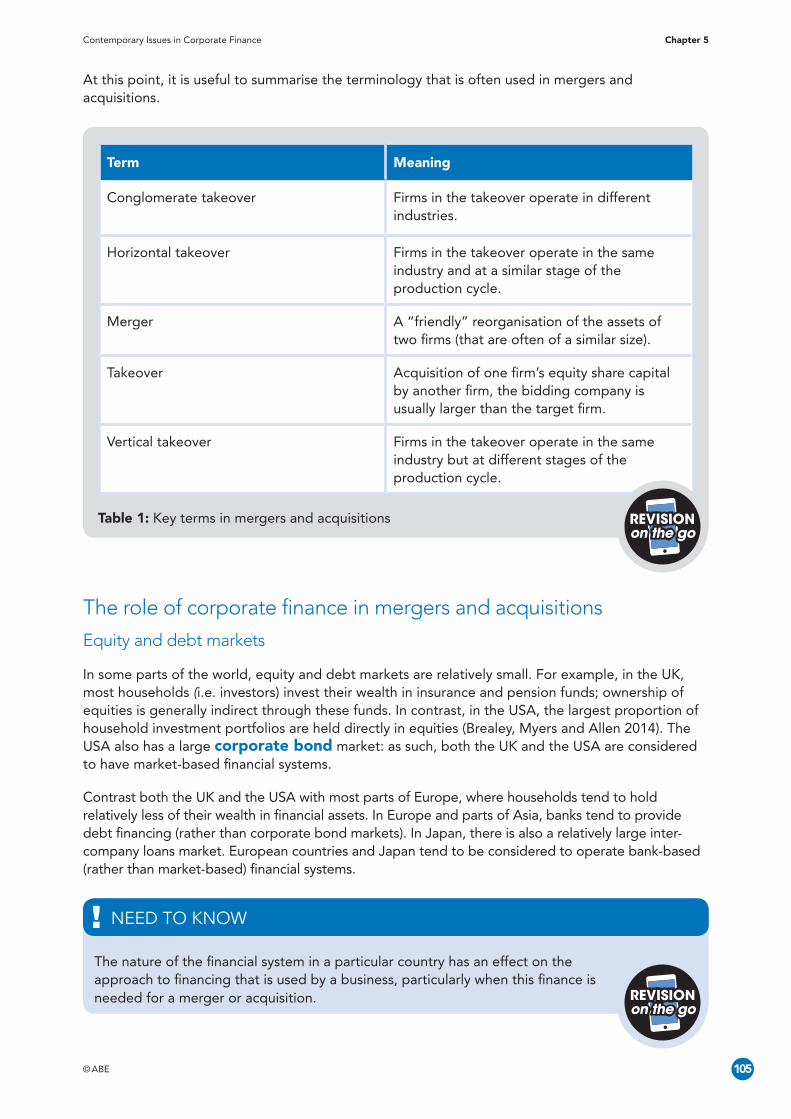

5.3 Critically evaluate the role of corporate finance in mergers and acquisitions 104

Glossary 109

© ABEiv

Using your study guideWelcome to the study guide for Level 6 Corporate Finance, designed to support those completing their ABE Level 6 Diploma.

Below is an overview of the elements of learning and related key capabilities (taken from the published syllabus).

Element of learning Key capabilities

Element 1: The importance of capital structure

• Ability to develop an approach to formulating the capital structure for a business based on sound conceptual and theoretical underpinning

• Ability to manage stakeholders and risks as part of selecting a financing structure, ensuring that the choice reflects the strategic objectives and existing and potential strategic pressures

Financial management, application of theoretical frameworks, appreciation of impact of strategic objectives of financial decision-making, communication, influence, stakeholder management, approaches to business strategy

Element 2: Equity and debt financing

• Ability to critically evaluate alternative sources of finance in order to ensure that financing decisions reflect the strategic objectives and strategic circumstances of the business

• Ability to apply criteria and decision-making frameworks in the context of equity and debt financing

Critical thinking, analysis, business acumen, commercial awareness, decision-making

Element 3: The cost of capital • Ability to critically evaluate different approaches to the calculation of the cost of capital in line with a business’s strategic direction

• Ability to apply techniques to calculate the cost of capital that take account of alternative approaches to the valuation of equity and different types of risk

Critical thinking, analysis, calculations, decision-making, risk assessment

Element 4: Advanced investment appraisal

• Ability to select and apply appropriate investment appraisal techniques that reflect the strategic objectives and environment in which the business operates

• Ability to apply investment appraisal techniques that take account of cash flows, taxation and inflation

Analysis, decision-making, influence and persuasion, investment appraisal techniques

Element 5: Contemporary issues in corporate finance

• Appreciation of contemporary issues in corporate finance and their impact on businesses

• Recognition of the importance of ethics, corporate governance and the role of corporate finance in ownership and control in a globalised economy

Critical thinking, contemporary issues, ownership and control, ethical issues

© ABE v

This study guide follows the order of the syllabus, which is the basis for your studies. Each chapter starts by listing the syllabus learning outcomes covered and the assessment criteria.

L6 descriptor

Knowledge descriptor (the holder…) Skills descriptor (the holder can…)

• Has advanced practical, conceptual or technological knowledge and understanding of a subject or field of work to create ways forward in contexts where there are many interacting factors

• Understands different perspectives, approaches or schools of thought and the theories that underpin them.

• Can critically analyse, interpret and evaluate complex information, concepts and ideas.

• Determine, refine, adapt and use appropriate methods and advanced cognitive and practical skills to address problems that have limited definition and involve many interacting factors.

• Use and, where appropriate, design relevant research and development to inform actions.

• Evaluate actions, methods and results and their implications

The study guide includes a number of features to enhance your studies:

’Over to you’: activities for you to complete, using the space provided.

Case studies: realistic business scenarios to reinforce and test your understanding of what you have read.

’Revision on the go’: use your phone camera to capture these key pieces of learning, then save them on your phone to use as revision notes.

’Need to know’: key pieces of information that are highlighted in the text.

Examples: illustrating points made in the text to show how it works in practice.

Tables, graphs and charts: to bring data to life.

Reading list: identifying resources for further study, including Emerald articles (which will be available in your online student resources).

Source/quotation information to cast further light on the subject from industry sources.

Highlighted words throughout denoting glossary terms located at the end of the study guide.

Note

Website addresses current as at August 2017.

on the goREVISION

© ABE

Introduction

In this chapter, you will consider the strategic role and purpose of corporate finance in a business. Capital structure, or the mix of long-term finance in a business that minimises the cost of capital, is a key aspect of corporate finance; decisions on capital structure can be critical to the success of a business.

You will examine how to formulate a capital structure that reflects the strategic objectives and strategic environment of the business. For businesses to survive and prosper, capital structure must be developed and maintained in a way that reflects both the existing and potential strategic pressures to which the business is exposed. You will also consider the key conceptual and contemporary ideas that underpin capital structures in modern business. While Modigliani and Miller (1958) argue that capital structure is unimportant, in practice it appears that decisions on the use of different methods of financing do have considerable consequences for many businesses.

Learning outcomes

On completing the chapter, you will be able to:

1 Critically analyse the factors that influence capital structure decisions and strategy

Assessment criteria

1 Critically analyse the factors that influence capital structure decisions and strategy

1.1 Appraise the alternative role and purpose of corporate finance in order to decide how best to formulate a capital structure for the business

1.2 Critically analyse the roles played by different stakeholders, different types of risk and alternative approaches to business strategy in order to select a capital structure that reflects the strategic objectives and strategic environment of the business

1.3 Critically evaluate the alternative frameworks for the development of a capital structure to ensure that it is based on a sound conceptual underpinning

The Importance of Capital Structure

Chapter 1

© ABE 3

1.1 Corporate finance and capital structure

The role and purpose of corporate finance

Corporate finance is concerned with the efficient and effective management of business finances in order to achieve business objectives (Watson and Head, 2016). Financial resources must be acquired (also known as “raised”). These financial resources must then be allocated (also known as “invested”) and their use must be controlled (or “managed”). Atrill (2014) suggests that the overarching aim of corporate finance is the optimal allocation of scarce resources in a business, the scarcest resource of which is money (or “finance”).

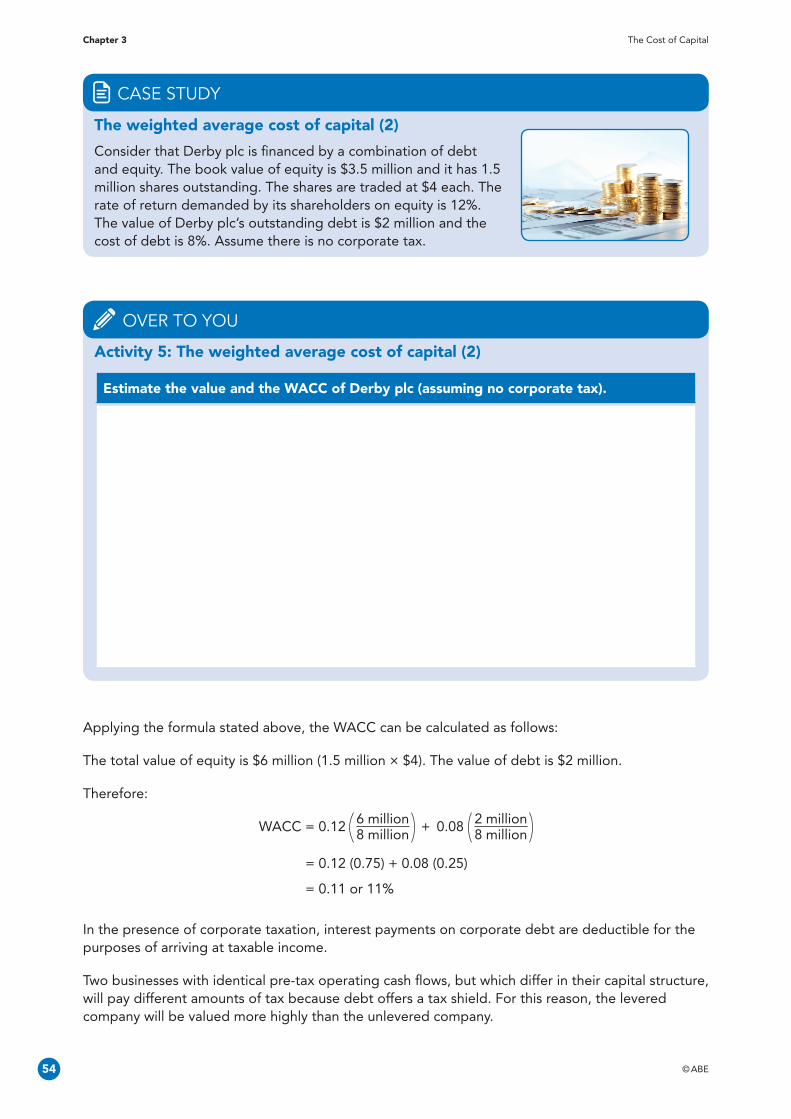

Capital structure is concerned with the particular mix of long-term finance that is used by a business. The cost of capital is the rate of return required by investors to supply finance to a business (and therefore the rate of return that is required of prospective investors). An optimal capital structure is one that minimises the cost of capital (Ogier, Rugman and Spicer, 2004). You will return to the cost of capital later in the module.

Capital structure is concerned with the mix of long-term finance that is used by a business. An optimal capital structure is one that minimises the cost of capital.

NEED TO KNOW

on the goRevision

In this module, we will view businesses as investment agencies: the role of business is to raise and invest finance in a way that generates profit. This profit could then be reinvested in the business in order to generate more profit. Some or all of the profit could be returned to shareholders in the form of dividends.

Businesses can be seen as investment agencies. Their role is to raise and invest finance in a way that generates profit. Profit can be reinvested in the business or returned to shareholders in the form of dividends.

NEED TO KNOW

on the goRevision

Level 6 Corporate Finance

© ABE4

Chapter 1 The Importance of Capital Structure

In a capitalist system, shareholders are considered to be of paramount importance. They provide funds to businesses in return for ownership rights. Shareholders invest in the expectation that they will receive the maximum possible increase in wealth in return for their investment. This key idea underpins modern corporate finance: the primary objective of a business is to maximise the wealth of its shareholders. Since shareholders receive their wealth through dividends and capital gains, shareholder wealth will therefore be maximised by optimising the value of the dividends and capital gains that shareholders receive over time.

The primary objective of a business is to maximise the wealth of its shareholders. Shareholders provide funds to businesses in the expectation that they will receive the maximum possible increase in wealth in return for their investment.

NEED TO KNOW

on the goRevision

Activity 1: Shareholder wealth maximisation

If we accept that the primary objective of a business is to maximise the wealth of its shareholders, then how will a business know that is has achieved this primary objective? Explain the problems that might exist when trying to determine if this objective has been achieved.

OvEr TO yOu

The Importance of Capital Structure Chapter 1

© ABE 5

Watson and Head (2016) identify three key problems with the concept of shareholder wealth maximisation. These problems are summarised in Table 1.

Problem Description

Measurement Maximisation of shareholder wealth requires that wealth is defined and measured accurately, and that all factors contributing to it are known and can be taken into account.

This is often problematic. Measures of wealth can vary markedly. The factors that contribute to wealth creation are not always observable.

Timescale Should wealth be maximised in the short term or the long term? Is short-term wealth maximisation consistent with long-term wealth maximisation?

Risk The processes of wealth generation and measurement do not always take account of risk. Wealth generation may be foregone in order to secure lower levels of risk.

Source: Watson and Head (2016, p. 11/12).

Table 1: Problems in the measurement of shareholder wealth on the goREVISION

The concept of shareholder wealth maximisation can be problematic. These problems include measurement, timescale and risk.

NEED TO KNOW

on the goREVISION

Atrill (2014) suggests that the concepts of a business as an investment agency and the primary objective of wealth maximisation are probably a little simplistic. Businesses do not exist in isolation from the environments in which they operate. Attempts to maximise the wealth of shareholders need to take account of a range of factors. As you will see later in this chapter, other stakeholders can have an effect on corporate finance decisions in a business. The strategic environment in which finance is raised and invested is of critical importance to a business. What “works” for one firm may be entirely inappropriate for another one.

Activity 2: Strategic environment and corporate finance

Search online for ‘’Indian companies facing wave of shareholder activism’’ and read the FT newspaper article featuring Diageo.

Consider the strategic environment in which businesses like Diageo operate in India. Identify the factors in the strategic environment that might have an effect on the corporate finance decisions that are made by these businesses.

OVER TO YOU

© ABE6

Chapter 1 The Importance of Capital Structure

The relationship between corporate finance and the formulation of a capital structure

As we have seen, businesses do not exist in isolation from the strategic environments in which they operate. While wealth maximisation remains the primary objective of business, it is also important to take account of a range of other factors, including risk, legal form and corporate governance. The aim of corporate finance includes the need to balance the primary objective of wealth maximisation with these factors.

Factor Context

Risk and return Decisions of any type relate to the future. An appropriate balance needs to be maintained between risk and return. In financial management, risk is considered to relate to circumstances in which all possible outcomes can be identified and quantified.

Legal form Many businesses operate under the legal form of a company, whether this is private limited or public limited. A key feature of a company is limited liability: shareholders cannot be held personally responsible for the company’s liabilities.

Corporate governance Corporate governance relates to the practice of board leadership and to effectiveness, remuneration, accountability and relations with shareholders. A business’ approach to corporate governance and the regulatory regime to which it is subjected will have a major effect on financial decision-making.

Table 2: Other factors that might affect capital structure on the goRevision

The Importance of Capital Structure Chapter 1

© ABE 7

Risk and return, legal form and corporate governance must also be considered when formulating the capital structure of the business. Remember that capital structure is concerned with the particular mix of long-term finance that is used by a business; an optimal capital structure is one that minimises the cost of capital. It may be that wealth maximisation (and the minimum cost of capital) could be achieved through the use of a particular capital structure. However, the need to consider factors other than wealth maximisation means that an alternative capital structure (and a higher cost of capital) might be necessary. We will return to this idea later in the module.

Capital structure is concerned with the particular mix of long-term finance that is used by a business. Wealth maximisation could be achieved through the use of a particular capital structure. However, the need to consider factors such as risk and return, legal form and corporate governance might mean that an alternative capital structure is required.

NEED TO KNOW

on the goRevision

1.2 The roles played by stakeholders, different types of risk and business strategy in capital structure

The stakeholder approach

Freeman and Reed (1983) define stakeholders as persons, groups or organisations that have an interest in a business, that can affect a business or that are affected by a business. The stakeholder theory of corporate finance reflects the idea that investment and financing decisions should be guided by the need to create and maintain positive working relationships with key stakeholders.

Stakeholders are persons, groups or organisations that have an interest in a business that can affect a business or that are affected by a business (Freeman and Reed, 1983). The stakeholder theory of corporate finance reflects the idea that investment and financing decisions should be guided by the need to create and maintain positive working relationships with key stakeholders.

NEED TO KNOW

on the goRevision

Stakeholders can be internal or external to the business. Examples of internal stakeholders include shareholders and employees. External stakeholders include suppliers and lenders. Some stakeholders are also more important than others, these key stakeholders will include shareholders, but other stakeholders might also be important due to the extent of their power to affect the business.

© ABE8

Chapter 1 The Importance of Capital Structure

Stakeholder analysis techniques: Mendelow’s (1991) Power–Interest Matrix

Mendelow’s (1991) power–interest matrix is a technique that can be used to analyse stakeholders in a way that reflects the emphasis that must be applied to their needs. This emphasis is determined using the extent of the impact (or “power”) and interest that the stakeholder may have on the activities of the business. If done correctly, this should allow the key stakeholders to be identified and managed appropriately. The four categories of stakeholders are shown in Figure 1 below, followed by a brief explanation of each.

Low level of interestLow level of power

High level of interestLow level of power

Low level of interestHigh level of power

High level of interestHigh level of power

Figure 1: Mendelow’s (1991) Power–Interest Matrixon the goRevision

Low level of interest and low level of power: This group will usually follow instructions and accept the plan.

High level of interest, low level of power: These stakeholders are interested in the organisation but have no power. If not convinced about plans for the organisation, they may join with those with high power.

Low level of interest, high level of power: By keeping this group satisfied and not involved, they will not affect or influence the business.

High level of interest, high level of power: This group needs to be fully communicated with and listened to as they have the power to alter the course of the organisation if it is not in line with their view.

Activity 3: Stakeholder mapping and the power–interest matrix

Develop a power–interest matrix for the stakeholders of Diageo. Focus your analysis on the business’ operations in India.

Identify each of the stakeholders then rank each in terms of their power (think about the influence that they might have on Diageo’s business) and the extent of their interest.

For tips on how to prepare a power–interest matrix, use the following link: http://www.brighthubpm.com/resource-management/80523-what-is-the-powerinterest-grid/

[Accessed on: 27 February 2017]

OvEr TO yOu

The Importance of Capital Structure Chapter 1

© ABE 9

Stakeholders and corporate finance

For most businesses (particularly companies), three groups of stakeholders are often key (Watson and Head, 2016): ordinary shareholders, lenders and managers. Shareholders provide equity finance to companies and expect a return in the form of dividends and in growth in the market price of the shares that they own. Lenders provide debt finance and expect this finance to be repaid on maturity. Returns are expected in the form of interest payments. Managers direct and control the business and are responsible for its financial performance.

Interactions between these three groups of stakeholders have to be managed effectively. Careful consideration needs to be given to the strategic objectives, the strategic environment in which it operates and the power/interest of key stakeholders. Shareholders, particularly large institutional investors, will often try to influence strategy. In addition to this, they may try to influence operational management structure and executive pay. Lenders may also try to influence strategy and operations by making loans contingent on covenants relating to financial structure and financial performance. Managers will have their own personal objectives that, sometimes, may conflict with those of shareholders and lenders.

Shareholders will often try to influence strategy. They may also try to influence operational management structure and executive pay. Lenders may try to influence strategy and operations by making loans contingent on covenants. Managers will have their own personal objectives that may conflict with those of shareholders and lenders.

NEED TO KNOW

on the goRevision

Aviva plc

Aviva plc is a multinational financial services company that provides insurance, savings and investment products. It has 31 million customers worldwide and is the UK’s largest insurer.

In May 2012 Aviva lost a vote on executive pay at its annual general meeting (AGM) when 54% of ordinary shareholders (excluding abstentions) voted against Aviva’s proposed policy for executive remuneration. This was seen as a major embarrassment for the directors of the company. Shareholders were angry about poor financial results and the amount that the new UK chief executive, Trevor Matthews, was paid when he joined the company. Following the vote, company chairman Colin Sharman apologised to investors for ignoring their views on executive pay.

CASE STuDy

© ABE10

Chapter 1 The Importance of Capital Structure

This shareholder revolt at Aviva was set in the context of a falling share price and reduced dividends. Within days of the vote, Aviva’s group chief executive, Andrew Moss, had left the company.

Source: Adapted from BBC (2012)

Activity 4: Analyse the impact of the conflicts between stakeholders in Aviva plc

Identify the stakeholders in the Aviva plc case. Consider the potential conflicts between each stakeholder. Explain how these conflicts might be reflected in terms of Aviva plc’s approach to corporate finance.

OvEr TO yOu

Conflicts between key stakeholders are reflected in different aspects of corporate finance. Examples are summarised in Table 3.

Conflict Corporate financial strategy

Governance The roles of chairperson and chief executive should be separate.

Executive remuneration Pay and other financial rewards should be set by remuneration committees. These committees should comprise independent non-executive directors. Recommendations on executive pay should be subject to a vote by ordinary shareholders at the business AGM.

Dividend policy Management needs to be mindful of the expectations of ordinary shareholders and of other key stakeholders such as lenders.

Capital structure Management must comply with loan covenants.

Table 3: Conflicts between key stakeholders and their effects on a business’s approach to corporate finance

on the goRevision

The Importance of Capital Structure Chapter 1

© ABE 11

Conflicts between key stakeholders can often be reflected in aspects of corporate finance such as governance, executive remuneration, dividend policy and capital structure.

NEED TO KNOW

on the goRevision

The international context and capital structure

Arrangements of capital structure vary greatly around the world (Brealey, Myers and Allen, 2014). For example, the United States is said to have a market-based financial system: capital structures are reflective of a large equity market and a large market in corporate bonds (a type of debt financing). In parts of Europe and in Japan, bank-based financial systems apply; bank loans are a more common form of debt financing than corporate bonds and equity markets are relatively small. Differences in financial systems have important implications for capital structure, particularly for businesses that operate on a multinational basis. An understanding of these differences can be crucial when formulating a capital structure.

Different systems of ownership and control also apply in different countries. A summary is provided in Table 4. Again, these differences will have an impact on capital structure. They also have important management implications for businesses that operate on a multinational basis.

Country Ownership and control

UK and USA Managers have a legal responsibility to act in the best interests of shareholders. Ownership is often dispersed and shares are actively traded, although ownership of many large businesses is often concentrated in financial institutions.

Japan Banks form a central “hub” for large, co-operative groups of businesses. Significant cross-ownership exists between the main bank in the group, other banks and the businesses within the group.

Germany and much of Europe Banks traditionally have long-standing relationships with businesses. Larger businesses have two boards of directors. Management boards are responsible for business operations, but report to supervisory boards. These supervisory boards represent all employees as well as shareholders. Business decisions are made in the interests of the business “as a whole” rather than shareholders.

Source: Brealey, Myers and Allen (2014, p. 851)

Table 4: Ownership and control in an international context on the goRevision

© ABE12

Chapter 1 The Importance of Capital Structure

The international context and capital structure

Let’s return to a case study that we considered earlier in the chapter. Aviva plc is a multinational financial services company that provides insurance, savings and investment products. It has 31 million customers worldwide and is the UK’s largest insurer.

Aviva plc has its origins in the UK. The original business was established almost 300 years ago. Aviva plc’s capital structure and system of ownership and control reflect that of a traditional UK company.

CASE STUDY

Activity 5: The international context and capital structure

Imagine that Aviva plc is thinking of setting up a subsidiary company in Japan. The new Japanese subsidiary will have a capital structure and system of ownership and control that reflects those of a “typical” Japanese business. Explain how the capital structure and system of ownership and control will differ from that of a “typical” UK company.

OvEr TO YOU

Irrespective of differences in capital structure, ownership and control, remember that the key principles of corporate finance still apply; businesses in all countries would recognise the concepts of capital structure and the cost of capital. All would be familiar with the idea of the maximisation of shareholder wealth as the primary objective of business.

Differences in financial systems, patterns of ownership and governance arrangements will have an effect on capital structure. Businesses that operate on a multinational basis must be aware of these differences when formulating their capital structure.

NEED TO KNOW

on the goRevision

The Importance of Capital Structure Chapter 1

© ABE 13

1.3 Alternative frameworks for the development of a capital structure The advantages and disadvantages of different types of capital structure

Sources of finance can be grouped into two broad categories: equity and debt. A range of potential sources of each of these two broad types of finance is available. The mix of these two broad types can be referred to as capital structure (also known as financing structure). Capital structure must be developed and maintained in a way that reflects both the existing and potential strategic pressures to which the business is exposed. As you have seen so far in this chapter, the formulation of a capital structure that reflects the strategic objectives and strategic environment of the business is not an easy task.

There is a need to take account of a range of factors: shareholders are considered to be of paramount importance, but the concept of maximising shareholder wealth is not clear. Risk and return, legal form and corporate governance all need to be considered when formulating capital structure. Conflicts between key stakeholders can also have an effect and, sometimes, can be difficult to reconcile. International differences in financial systems and systems of ownership and control can further complicate these problems.

So, how can businesses develop a capital structure that takes account of all of these issues? Thankfully, a number of frameworks exist that can be of help. You will return to these decision-making frameworks later in the module. For now, consider their key features, advantages and disadvantages of each. These are summarised in Table 5.

Framework Key features Advantages Disadvantages

Pecking order theory (Myers, 1984)

An “order of priority” for the financing of investments. Retained profit, debt and, finally, share capital should be used to finance investments.

Reflects asymmetries of information between businesses and capital markets

Some empirical support, e.g. Baskin (1999)

Does not take account of existing capital structure

Some empirical criticism, e.g. Frank and Goyal (2003)

Contradicts aspects of dividend theory

Matching principle of finance

Maturity of financing should be matched with the maturity of asset types

Reflects desired levels of risk and return

Can lead to reduced flexibility and higher costs

Table 5: Frameworks for the development of capital structureon the goRevision

© ABE14

Chapter 1 The Importance of Capital Structure

Pecking order theory suggests that there is an “order of priority” for the financing of investments. Retained profit, debt and, finally, share capital should be used to finance investments.

NEED TO KNOW

on the goRevision

Conceptual underpinning for capital structure

For Modigliani and Miller (1958) any capital structure is as good as another: the relative mix of debt and equity finance in a business’s capital structure is unimportant. Provided that markets are perfect, financing decisions and their effects on financial gearing do not matter. Modigliani and Miller (1958) suggest that this is because a business’s value is determined by its real assets, not by financing decisions.

Perfect markets are those that are perfectly competitive. In such markets, there are no barriers or even temporary delays to the formation of perfectly fair prices. Prices should instantaneously and universally reflect all available and relevant information. Certain conditions are needed to produce perfect markets. These conditions are summarised in Table 6.

Condition Description

Large number of buyers and sellers

A sufficiently large number of participants must exist such that no individual participant or group of participants can manipulate prices.

No barriers to entry or exit Entry to and exit from the market is free. For example, registration or listing fees do not exist.

Information All participants can gain all of the information that they need on which to base their decisions. This information is free and is available instantaneously.

No transaction costs There are no transaction costs such as stamp duties or brokers’ commissions. Tax regulations and accounting practices do not affect the relative attractiveness of different investment opportunities. Regulatory constraints do not prevent investors from participating in markets.

No effects on market prices Decisions by prominent investors do not have an impact on market prices.

Table 6: Conditions that need to be met in order for a perfect market to exist on the goRevision

Many of these conditions are unrealistic. Most empirical research suggests that it is unlikely that perfect markets do exist (Megginson, 1997). However, businesses do not need markets to be perfect. What they need is for markets to be efficient and to offer fair prices so that they can make sound financing and investment decisions (Watson and Head, 2016). A business should be able to make decisions on, for example, the use of debt finance, and understand the practical effects of changes in capital structure.

The Importance of Capital Structure Chapter 1

© ABE 15

In perfect markets, prices should instantaneously and universally reflect all available and relevant information. However, the conditions that are needed to produce perfect markets are unrealistic.

NEED TO KNOW

on the goRevision

Contemporary issues in the formulation of capital structure

Capital structure has been an issue of considerable importance for many businesses in recent years. In particular, the “Great Recession” that followed the financial crisis of 2008 meant that the use of debt relative to equity financing has been questioned in some businesses. The risks associated with debt financing in times of economic stress have meant that some businesses have had to change their capital structure.

You will return to this and other contemporary issues later in the module.

Brealey, Myers and Allen (2014) suggest that the mix of debt and equity finance in a business can be used as a “starting point” with which to evaluate potential investment opportunities via the calculation of a cost of capital. Investment opportunities that are funded using unusually risky financing methods can be reflected in adjustments to the cost of capital.

The cost of capital is the rate of return that is required by investors who supply financing to a business. Hence, it is also the minimum rate of return that is required on prospective investment projects. While Modigliani and Miller (1958) argue that the relative mix of debt and equity in a business’s financing structure is unimportant, in practice it appears that decisions on the use of different methods of financing do have considerable consequences for many businesses.

NEED TO KNOW

on the goRevision

Activity 6: Financing structure, financial gearing and entrepreneurs

Research online for the paper by Milana (2010) at http://onlinelibrary.wiley.com/doi/10.1002/jsc.860/abstract. If you don’t have access to this article, perform your own online research to answer the question that follows.

This article provides an account of an interview with an entrepreneur and offers a perspective on the relative balance of debt and equity finance in a business.

Identify and explain the key factors that might need to be considered in the achievement of an appropriate balance of debt and equity finance in a business. Outline the additional factors that might influence this choice for an entrepreneur.

OvEr TO yOu

© ABE16

Chapter 1 The Importance of Capital Structure

• Atrill, P. (2014) Financial management for decision makers, 7th edition, Harlow: Pearson.

• Baskin, J.B. (1989) “An empirical investigation of the pecking order hypothesis”, Financial Management, 18, pp. 26–35.

• BBC (2012) “Aviva loses vote on executive pay at its AGM”, Retrieved from: http://www.bbc.co.uk/news/business-17938865 [Accessed on: 30 December 2012].

• Brealey, R. A., Myers, S. C. & Allen, F. (2014) Principles of corporate finance, 11th edition, Maidenhead: McGraw-Hill.

• Financial Times (2014) “Indian companies facing a wave of shareholder activism”, Financial Times, December 2014.

• Frank, M. and Goyal, V. (2003) “Testing the pecking order theory of capital structure”, Journal of Financial Economics, 67, pp. 217–48.

• Freeman, R. and Reed, D. (1983) “Stockholders and stakeholders: a new perspective on corporate governance”, California Management Review, 59 (1), pp. 88–106.

• Kaptein, M. and Van Tulder, R. (2003) “Toward effective stakeholder dialogue”, Business and Society Review, 108 (2), pp. 203–224.

• Megginson, W. (1997) Corporate finance theory, Reading: Addison-Wesley.

• Modigliani, F. and Miller, M.H. (1958) “The Cost of Capital, Corporation Finance and the Theory of Investment”, The American Economic Review, 48(3), pp. 261–297.

• Myers, S. (1984) “The capital structure puzzle”, Journal of Finance, 39, pp. 575–592.

• Ogier T., Rugman, J. and Spicer, L. (2004) The real cost of capital: a business field guide to better financial decisions. Harlow: Pearson.

• Watson, A. and Head, A. (2016) Corporate finance: principles and practice. 7th edition, Harlow: Pearson.

rEADiNg LiST

The Importance of Capital Structure Chapter 1

© ABE 17

For tips on how to prepare a power–interest matrix, use the following link: http://www.brighthubpm.com/resource-management/80523-what-is-the-powerinterest-grid/

[Accessed on: 27 February 2017]

Milana, C. (2010) “Rebalancing the optimal financial structure: the entrepreneurs’ point of view”, Strategic Change, 19 (1), pp. 91–95. Retrieved from: http://onlinelibrary.wiley.com/doi/10.1002/jsc.860/abstract.

[Accessed on: 31 August 2017]

rESOurCES

© ABE

Introduction

Sources of finance can be grouped into two broad categories: equity and debt. In this chapter, you will consider the key features of different types of equity and debt financing. You will examine how to measure the market value of a business’s share capital and the different ways in which share capital can be issued. You will also consider how different types of finance relate to the strategic objectives of a business and its environment.

A key feature of this chapter is a critical evaluation of alternative sources of both equity and debt finance. Businesses must take care to select sources of finance that are appropriate. Failure to do so may result in an inefficient use of resources and a failure to take full advantage of investment opportunities. At worse, it could result in the destruction of value in the business. You will consider criteria and decision-making frameworks, including models of financial distress that could be applied to ensure that sources of finance are appropriate to the strategic objectives and environment of the business.

Learning outcomes

On completing the chapter, you will be able to:

2 Critically evaluate alternative sources of finance to ensure that financing decisions reflect the strategic objectives and strategic circumstances of the business

Assessment criteria

2 Critically evaluate alternative sources of finance to ensure that financing decisions reflect the strategic objectives and strategic circumstances of the business

2.1 Compare alternative approaches to sources of equity and debt in relation to the strategic objectives and strategic environment of the business

2.2 Critically evaluate the impact of the use of a range of equity and debt financing on business’s financing structure

2.3 Apply criteria and decision-making frameworks in equity and debt financing

Sources of Finance

Chapter 2

© ABE 19

2.1 Alternative approaches to sources of equity and debtThe matching principle of finance and its importance in the selection of source of equity or debt

The matching principle of finance states that short-term investment needs should be financed with short-term sources of finance. Long-term investment needs should be financed with long-term sources of finance. Atrill (2014) asserts that this concept of “matching” can be seen as, perhaps, a very simple idea but is, in fact, at the heart of corporate finance.

The matching principle of finance means that short-term investment needs should be financed with short-term sources of finance. Long-term investment needs should be financed with long-term sources of finance.

NEED TO KNOW

on the goRevision

So, there is a need to consider the purpose to which finance is to be applied: this should then be matched with a source of finance that “matches” with the duration of the investment. The investment of a business in non-current assets (e.g. property, machinery, vehicles) should be financed by long-term sources of finance. Current assets that fluctuate (e.g. inventories, trade receivables) should be financed using short-term sources of finance.

You will consider the distinctions between long-term and short-term sources of finance and between internal and external sources of finance later in the chapter. For now, firstly reflect on the two broad categories of finance: equity and debt. You have already considered the nature of equity and debt finance earlier in the chapter. Secondly, reflect on the distinction between internal and external sources of finance. The latter require the agreement of one or more third parties before they can be used. In contrast, internal sources of finance can be used without the agreement of third parties.

Level 6 Corporate Finance

© ABE20

Chapter 2 Sources of Finance

External sources of finance require the agreement of one or more third parties before they can be used by a business.

NEED TO KNOW

on the goRevision

As discussed in Chapter 1, a business can be viewed as an investment agency. Its role is to acquire (or “raise”) finance and then to spend (or “invest”) that finance to generate a profit. This profit could then be reinvested in the business in order to generate more profit. Some or all of the profit could be returned to shareholders in the form of dividends.

The way in which finance is raised can have huge implications for a business. Essentially, a business has two options: finance can be raised in the form of equity or in the form of debt. Definitions and examples of each are provided in Table 1.

Type of finance Description Examples

Equity The “ownership interest” in a business

Ordinary shares and some other types of shares, retained earnings, revaluation reserves, and other reserves

Debt Sometimes referred to as “borrowing”. A common feature of this type of finance is the finance charge or “interest” that is applied to each

Loans, debentures, lease arrangements and preference shares

Table 1: Types of financeon the goRevision

Essentially, a business can raise up two different types of finance: equity and debt.

NEED TO KNOW

on the goRevision

Activity 1: Equity and debt

The distinction between equity and debt as types of finance is usually clear. However, there are some sources of finance that have characteristics that make the distinction difficult.

OvEr TO yOu

Sources of Finance Chapter 2

© ABE 21

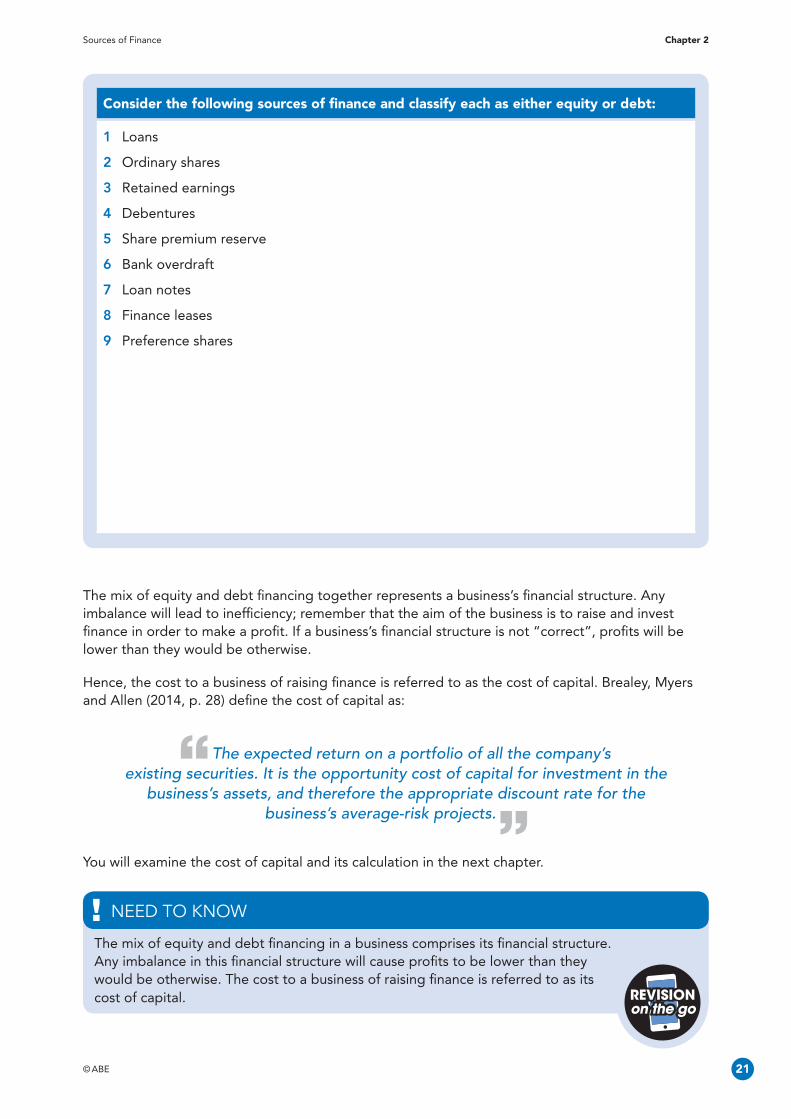

Consider the following sources of finance and classify each as either equity or debt:

1 Loans

2 Ordinary shares

3 Retained earnings

4 Debentures

5 Share premium reserve

6 Bank overdraft

7 Loan notes

8 Finance leases

9 Preference shares

The mix of equity and debt financing together represents a business’s financial structure. Any imbalance will lead to inefficiency; remember that the aim of the business is to raise and invest finance in order to make a profit. If a business’s financial structure is not “correct”, profits will be lower than they would be otherwise.

Hence, the cost to a business of raising finance is referred to as the cost of capital. Brealey, Myers and Allen (2014, p. 28) define the cost of capital as:

The expected return on a portfolio of all the company’s existing securities. It is the opportunity cost of capital for investment in the

business’s assets, and therefore the appropriate discount rate for the business’s average-risk projects.

You will examine the cost of capital and its calculation in the next chapter.

The mix of equity and debt financing in a business comprises its financial structure. Any imbalance in this financial structure will cause profits to be lower than they would be otherwise. The cost to a business of raising finance is referred to as its cost of capital.

NEED TO KNOW

on the goRevision

© ABE22

Chapter 2 Sources of Finance

Equity and debt finance

Edmonton plc is a multinational petrochemicals company that manufactures plastic drinks containers. The company’s net assets have a balance sheet value of $300 million: $250 million of these assets are financed by debt, with the rest financed by equity. Edmonton plc has revenues of $80 million, but has experienced a prolonged period of poor financial performance. Recently, the company has experienced a severe shortage of cash.

The company relies heavily on materials purchased from a number of key suppliers. Significant trade credit is in danger of becoming overdue to these key suppliers.

The company finance director has concerns. Finance charges (also known as interest payments) are due on the debt next month and the company will be unable to pay these charges. The company finance director also believes that Edmonton plc will not be able to refinance $100 million of its debt when it reaches maturity in six months’ time.

The board of directors have agreed that a restructuring of the company’s financial structure is required.

CASE STuDy

Activity 2: Equity and debt finance

Consider the actions that the board of directors of Edmonton plc might need to take in each of the short-term, the medium-term and the longer-term situations. Explain how the company’s finances might be restructured as a basis for longer-term stability.

OvEr TO yOu

Sources of Finance Chapter 2

© ABE 23

Other factors: legal, regulatory and market requirements

The matching principle is an important idea in financial management. Other factors that need to be considered when selecting a source of finance are outlined in Table 2.

Factor Description

Cost Different sources of finance have different cost implications for a business.

Flexibility Short-term sources of finance can offer greater flexibility than long-term sources.

Refinancing risk Short-term sources of finance have to be renewed more frequently than long-term sources. This can be problematic for businesses that are in financial difficulties or if there is a shortage of finance overall in the market.

Interest rates Fluctuating interest rates can cause problems when a business uses debt as a source of finance. This can be a particular problem when combined with the need to re-finance debt.

Table 2: Elements in the cost of debt financingon the goRevision

Activity 3: How best to meet the financing needs of the business

Read the paper by Dolar and Yang (2013) at https://aabri.com/manuscripts/121305.pdf.

This paper provides evidence that the consolidation of the banking sector has had a negative impact on the level of lending to small businesses.

Critically evaluate the effect of the financial crisis on the availability of debt finance to small businesses.

OvEr TO yOu

© ABE24

Chapter 2 Sources of Finance

2.2 Sources of finance and how they relate to strategic objectives and strategic environment Internal and external sources of finance

You have already considered the nature of equity and debt finance earlier in the chapter. Share capital is a form of equity and is an external source of finance: it requires the agreement of potential shareholders (who agree to purchase the shares) in order to raise finance. Debt is also an external source of finance: again, it requires the agreement of parties outside the business (one or more lenders) before it can be used. Internal sources of finance, in contrast, arise from decisions that do not require agreement from other parties beyond the directors of the business (Atrill, 2014).

External sources of finance require the agreement of parties outside of the business in order to raise the finance. Internal sources of finance arise from decisions that do not require agreement from other parties beyond the directors of the business.

NEED TO KNOW

on the goRevision

Internal: Retained profit

Retained profit is a type of equity finance. The retention of profit (rather than distribution in the form of dividends) is, in effect, a way to raise finance (Atrill and McLaney, 2014). Unlike share capital, retained profit is an internal source of finance, its use does not depend on agreement from parties other than the directors of the business. Typically, it is long term in nature.

Atrill and McLaney (2014) report that retained profit has represented about half of all the long-term finance raised by UK businesses in recent years. Despite the popularity of the use of retained profit, a number of important factors need to be considered before it is used. These issues are summarised in Table 3.

Factor Description

Dividend policy The retention of profit and the subsequent use as a source of equity finance will have an effect on the dividends paid. Some suggest that this will reduce the net wealth of investors.

Issue costs Other approaches to the raising of equity finance, such as Initial Public Offerings, have issue costs. Retained profit can be attractive for this reason.

Risk There is no guarantee that additional retained profits will be generated in the future.

Dilution of control The use of retained profits does not affect the voting strength of investors.

Table 3: Factors to consider in the use of retained profit as financeon the goRevision

Sources of Finance Chapter 2

© ABE 25

Activity 4: Retained profit

Are retained profits a “free” source of finance? How might shareholders feel if a business consistently uses retained profit as a source of finance, rather than distributing it to shareholders in the form of a dividend?

Source: Atrill, (2014, p. 254)

OvEr TO yOu

Internal: Working capital

This is another internal source of finance. Four principal elements comprise working capital: inventories, trade receivables, cash and trade payables. Effective management and control of these elements can provide opportunities to generate and “drive out” sources of finance that can be used to support a business’s activities.

Atrill and McLaney (2014) note that the effective management of working capital is linked to longer term financing decisions. The amount of working capital that needs to be held across time, the timing of cash flows and the level of risk involved all need to be considered when reflecting on the importance of working capital and financing.

Activity 5: Working capital

In some industries, current assets such as inventories, receivables and cash can constitute a significant proportion of the total asset base. The appropriate management of payables can also be critical, particularly for a business that purchases goods and services on a credit basis.

In which industries might working capital represent a significant proportion of a business’s asset base?

OvEr TO yOu

© ABE26

Chapter 2 Sources of Finance

Working capital comprises inventories, account receivables, cash and accounts payable. Effective management of working capital is linked to longer term financing decisions. Timing of cash flows and levels of risk are important when considering the amount of working capital that might be available as a source of finance.

NEED TO KNOW

on the goRevision

The level of inventories held by a business will vary according to a number of factors, including the industry in which the business operates. Businesses are not obliged to hold inventories. The level of inventories held will be informed by a number of factors. These factors are summarised in Table 4.

Factor Description

Trade-off Optimal inventory levels involve a trade-off between carrying costs and order costs.

Carrying costs Carrying costs include the cost of storing goods as well as the cost of capital tied up in inventor.

Frequency of orders A business can manage its inventories by waiting until they reach some minimum level and then replenish them by ordering a predetermined quantity. When carrying costs are high and order costs are low, it makes sense to place more frequent orders and maintain higher levels of inventory.

Non-linearity Inventory levels do not rise in direct proportion to sales. As sales increase, the optimal inventory level rises, but less than proportionately.

Table 4: Factors in the determination of inventory levels on the goRevision

Cash is another important element of working capital. The amount of cash held by a business needs to be considered with great care: the marginal value of holding such a liquid asset as a cash balance declines as the amount of cash held increases.

Sources of Finance Chapter 2

© ABE 27

Activity 6: Cash

Identify and discuss the costs of holding:

1 too little cash

2 too much cash.

OvEr TO yOu

The marginal value of holding cash declines as the amount of cash held increases. The costs of holding too little cash include a failure to meet payables and other obligations when they fall due. The costs of holding too much cash include the opportunity cost of failing to use cash to finance profitable investment opportunities.

NEED TO KNOW

on the goRevision

External: Share capital

You have seen that equity represents the “ownership interest” in a business. For businesses that are limited companies, examples of equity finance include share capital. This share capital comprises all of the funds raised by a business in exchange for shares in that business (Brealey, Myers and Allen, 2014). Usually, share capital is issued in exchange for cash although sometimes forms of non-cash consideration can be used.

There are a number of different methods by which share capital can be issued.

Initial public offering

The process of selling shares to the public for the first time is called an initial public offering (IPO). IPOs can take a number of different forms, including:

• primary offerings: new shares are sold to raise additional cash for the business;

• secondary offerings: often confined to small, less-established types of business.

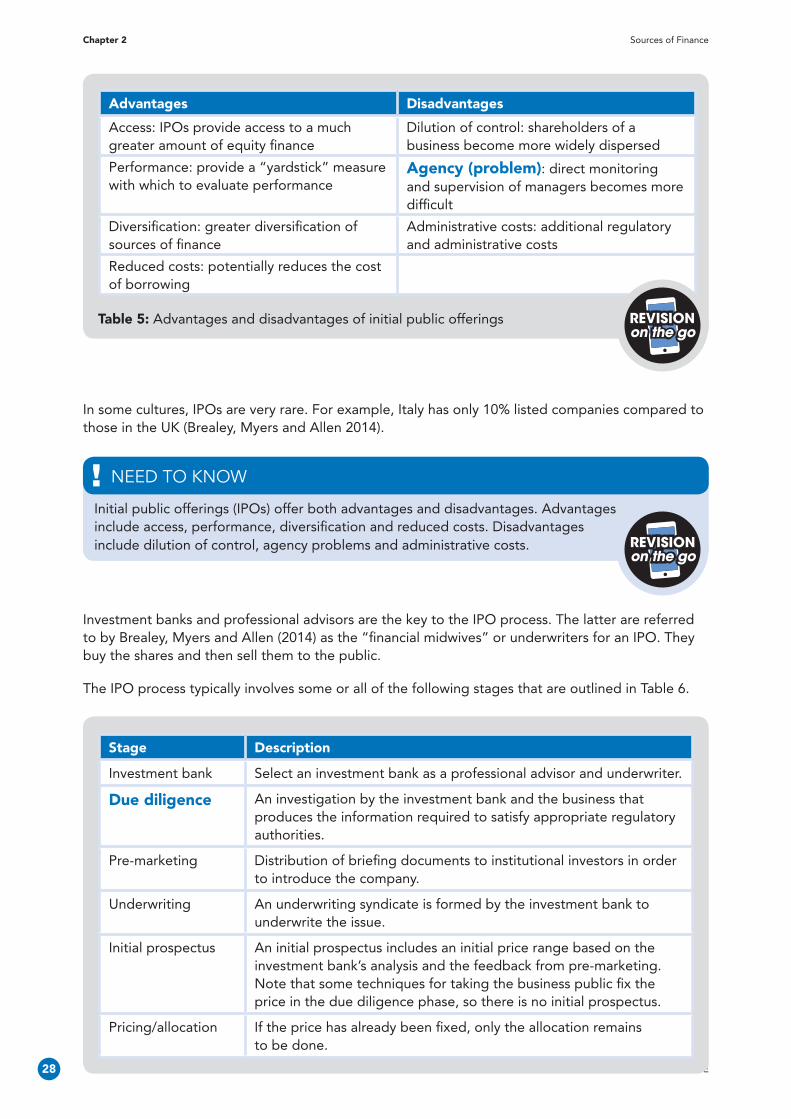

IPOs offer both advantages and disadvantages. A summary of each is provided in Table 5.

© ABE28

Chapter 2 Sources of Finance

Advantages Disadvantages

Access: IPOs provide access to a much greater amount of equity finance

Dilution of control: shareholders of a business become more widely dispersed

Performance: provide a “yardstick” measure with which to evaluate performance

Agency (problem): direct monitoring and supervision of managers becomes more difficult

Diversification: greater diversification of sources of finance

Administrative costs: additional regulatory and administrative costs

Reduced costs: potentially reduces the cost of borrowing

Table 5: Advantages and disadvantages of initial public offerings on the goRevision

In some cultures, IPOs are very rare. For example, Italy has only 10% listed companies compared to those in the UK (Brealey, Myers and Allen 2014).

Initial public offerings (IPOs) offer both advantages and disadvantages. Advantages include access, performance, diversification and reduced costs. Disadvantages include dilution of control, agency problems and administrative costs.

NEED TO KNOW

on the goRevision

Investment banks and professional advisors are the key to the IPO process. The latter are referred to by Brealey, Myers and Allen (2014) as the “financial midwives” or underwriters for an IPO. They buy the shares and then sell them to the public.

The IPO process typically involves some or all of the following stages that are outlined in Table 6.

Stage Description

Investment bank Select an investment bank as a professional advisor and underwriter.

Due diligence An investigation by the investment bank and the business that produces the information required to satisfy appropriate regulatory authorities.

Pre-marketing Distribution of briefing documents to institutional investors in order to introduce the company.

Underwriting An underwriting syndicate is formed by the investment bank to underwrite the issue.

Initial prospectus An initial prospectus includes an initial price range based on the investment bank’s analysis and the feedback from pre-marketing. Note that some techniques for taking the business public fix the price in the due diligence phase, so there is no initial prospectus.

Pricing/allocation If the price has already been fixed, only the allocation remains to be done.

Sources of Finance Chapter 2

© ABE 29

Activity 7: Initial public offerings

Read the paper by Smith (2013) You can access it at https://aabri.com/manuscripts/ 121367.pdf

This paper examines alternative methods of abnormal performance detection and applies the most powerful method to examine the price performance of IPOs. This application is used to determine if IPOs generate abnormal performance.

Critically evaluate the evidence that IPOs generate abnormal performance.

OvEr TO yOu

Seasoned equity offerings

A business’s need for equity rarely ends at the IPO. Profitable investment opportunities occur throughout the life of the business. In some cases, it will not be feasible for these investment opportunities to be financed using other sources of finance. As a result, businesses return to equity markets and offer new shares for sale; this is a type of offering called a seasoned equity offering (SEO), also known as a security sale.

There are two kinds of SEOs:

• cash offers: the business offers new shares to investors at large;

• rights offers: the business offers new shares only to existing shareholders.

When a business issues shares using an SEO, it follows many of the same steps as for an IPO. The main difference is that a market price for the shares already exists. This means that the price-setting process is not necessary.

A seasoned equity offering (SEO) can be used to raise additional equity finance following an initial public offering (IPO). The key difference between an SEO and an IPO is that, in an SEO, a market price for the shares already exists.

NEED TO KNOW

on the goRevision

Research has shown that, on average, the equity markets greet the news of an SEO with a decline in the market price of a business’s shares. Often, the value destroyed by the price decline can be a significant fraction of the new finance raised. A business that is concerned with protecting its existing shareholders will tend to sell new shares at a price that correctly values or overvalues the business, investors infer from the decision to sell that the company is likely to be overvalued, therefore, the market price drops with the SEO announcement.

© ABE30

Chapter 2 Sources of Finance

Seasoned equity offerings (SEOs) often lead to a reduction in the market price of a business’s shares. Equity markets tend to interpret SEOs as a sign that a business’s shares are overvalued and so the market price of those shares falls with the announcement of an SEO.

NEED TO KNOW

on the goRevision

Rights issues

This form of SEO involves the offer of new shares, for cash, to existing investors. To encourage existing investors to take up a rights offer, a price is set that is usually below the current market price. The number of shares that an existing investor has the “right” to take up will depend on the number of shares owned by that investor prior to the SEO.

Activity 8: Rights issues

Baker Holdings plc has 20 million ordinary shares of £0.50 in issue. These shares are currently valued on the London Stock Exchange at £1.60 per share. The directors of Baker Holdings plc believe that the business requires additional long-term capital and have decided to make a one-for-four rights issue (that is, one new share for every four shares held) at £1.30 per share. What is the value of the rights per new share?

OvEr TO yOu

Market forces will usually ensure that the actual price of rights and the theoretical price will be fairly close. Rights issues are a popular approach to the raising of equity finance. Atrill and McLaney (2014) report that, between 2001 and 2010, rights issues averaged 45% of total SEOs.

External: Debt

There are many other sources of debt finance. In this part of the chapter, we will consider some of the most popular types of debt financing.

Loans

Loans are a major source of debt finance for many businesses. This form of debt financing is an external source of finance. Loans can be both short-term and long-term in nature.

Sources of Finance Chapter 2

© ABE 31

Lenders invest in businesses via a contract that will typically specify interest rates, dates of interest payments, capital repayments and the security for the amount lent to the business. To protect themselves against the non-repayment of interest and capital amounts, lenders seek some form of security for their investment (Atrill, 2014).

The cost of this type of debt financing will typically be made up of the elements that are outlined in Table 7.

Element Description

Finance costs (interest charges) The cost of borrowing and a reflection of the level of risk that the lender perceives to arise as a result of their investment in the business

Security charges The means by which lenders establish some form of security on their investment. The charge may be fixed on particular assets of the business or “floating” on the whole asset base of the business

Fees Arrangement and administrative fees may also be incurred as a result of borrowing

Table 7: Elements in the cost of debt financingon the goRevision

There are many types of debt finance. The cost of debt includes finance costs (interest charges, security charges and fees).

NEED TO KNOW

on the goRevision

Long-term loans are available from banks and other financial institutions. Fixed and floating (also known as variable) rates of interest can be applied to these loans. These finance costs (interest charges) reflect the perceived risk of the borrowing business. The greater the risk that is perceived by a bank or financial institution, the higher the interest rate.

Payments on long-term loans will include both principal (also known as capital) and interest elements. The annual repayment amount on a loan can be found by dividing the amount of the loan by the cumulative present value (also known as the annuity) factor at the relevant rate of interest.

Annual repayment amounts on a long-term loan

Liqui manages a highly successful hairdressing business in Hong Kong. She started the business 10 years ago with her business partner, Meifing. Liqui and Meifing opened their first salon in Kowloon.

CASE STuDy

© ABE32

Chapter 2 Sources of Finance

The business now comprises five salons in various areas of Hong Kong. Each salon has approximately 3,000 customers per year, although the salon in Kowloon attracts 7,000 customers per year. Most of the supplies that are used by the business are purchased from a single supplier.

Liqui and Meifing’s business is a limited company. A local businessman owns 45% of the shares in the company. The rest of the shares are owned by 30 other investors, who include Liqui and Meifing.

Liqui plans to expand operations into mainland China. Liqui intends to finance this expansion using a loan from a local bank.

Consider that Liqui plans to use a $100,000 bank loan at an interest rate of 10% per year. The loan is repayable in equal annual instalments over five years.

Activity 9: Annual repayment amounts on a long-term loan

Carefully read through the information in the case study above and calculate the annual repayment amount on the loan.

Remember that this can be found by dividing the amount of the loan by the cumulative present value (also known as the annuity) factor at the relevant rate of interest.

Source: Watson and Head (2016, p. 147)

OvEr TO yOu

The annual repayment amount on a long-term loan can be found by dividing the amount of the loan by the cumulative present value (also known as the annuity) factor at the relevant rate of interest.

NEED TO KNOW

on the goRevision

Sources of Finance Chapter 2

© ABE 33

For many businesses, loans are a major source of debt finance. Loans are an external source of finance and can be both short-term and long-term in nature.

Providers of loan finance use contracts that will typically specify interest rates, dates of interest payments, capital repayments and the security for the amount lent to the business. To protect themselves against the non-repayment of interest and capital amounts, lenders seek some form of security for their investment.

Source: Atrill (2014) on the goRevision

Bonds

Many firms raise finance via issuing securities that bear a fixed interest rate that is payable on the face value of those securities (Atrill and McLaney, 2014). These securities include loan notes, debentures and bonds.

A bond is an evidence of debt issued by a business or a government body (government bonds are sometimes referred to as “gilts”). A bond represents a loan made by investors to the issuer. In return for this investment, the investor receives a legal claim on future cash flows of the borrower. The issuer promises to:

• make regular coupon payments (interest payments) every period until the bond matures

• pay the face/par/maturity value of the bond when it matures (i.e. when the bond becomes due for repayment.

The nominal yield or coupon rate is the rate of interest on the face value of the bond. This is not necessarily the same as the market rate of interest. The current yield is the nominal interest payment divided by the current market price.

Bonds are a form of debt finance and represent a loan made by investors to the issuer. The nominal rate of interest is the rate of interest on the face value of the bond. This is not necessarily the same as the market rate of interest. The current yield is the nominal interest payment divided by the current market price.

NEED TO KNOW

on the goRevision

Redeemable bonds (i.e. bonds for which the principal amount needs to be repaid when the bond matures) can be valued by discounting the future interest payments and the future redemption value by the debt holders’ required rate of return. Interest payments are usually made on an annual or semi-annual basis. The formula for the valuation of a redeemable bond is:

PO = I(1 + Kd ) + I

(1 + Kd )2 + I(1 + Kd )3 + … + I + RV

(1 + Kd )n

Where:

PO = ex-market rate of interest

I = interest paid ($)

© ABE34

Chapter 2 Sources of Finance

Kd = rate of return required by debt investors (%)

RV = redemption value ($)

n = time to maturity (years)

The formula for the calculation of the value of a redeemable bond is:

PO = I(1 + Kd ) + I

(1 + Kd )2 + I(1 + Kd )3 + … + I + RV

(1 + Kd )n

NEED TO KNOW

on the goRevision

Activity 10: Bond valuation

Consider a bond that pays an annual interest of 10% and that is redeemable at a nominal value of £100 in four years’ time. Assume that investors in this bond require an annual rate of return of 12%.

Calculate the value on the bond.

Source: Watson and Head (2016, p. 155)

OvEr TO yOu

The world’s debt markets provide the basis for the issue and trading of many types of bonds. Typically, these bonds have terms (also known as “maturities”) of up to 10 years but can have much shorter or longer terms.

The need to meet these finance costs can present a number of risks to a business. Assuming that the level of profit remains constant, then the need to meet these finance costs means that there will be less profit to distribute to shareholders in the form of dividends. Alternatively, if the debt finance is used to generate additional profit that exceeds the finance costs, then this will increase the amount of profit that is available to distribute to shareholders in the form of a dividend.

Sources of Finance Chapter 2

© ABE 35

Advantages and disadvantages of different sources of equity and debt financing

Equity: advantages and disadvantages

The use of equity can offer advantages to a business, not least the avoidance of the disadvantages that are associated with the use of debt. You will consider some of the theoretical underpinnings for the use of equity finance later in the chapter.

However, the use of equity can lead to problems. Brealey, Myers and Allen (2014) suggest that these problems arise most commonly due to conflict between shareholders and managers. Shareholders will often try to influence strategy. Conflicts of interest can exist between shareholders and managers, while the latter have a theoretical responsibility to act in the best interests of the former, this might not always be the case in reality.

Shareholders will often try to influence strategy. They may also try to influence operational management structure and executive pay. Lenders may try to influence strategy and operations by making loans contingent on covenants. Managers will have their own personal objectives that may conflict with those of shareholders and lenders.

NEED TO KNOW

on the goRevision

Activity 11: Shareholders and corporate finance

Re-read the case study on page 9 in Chapter 1, Section 1.2: Aviva plc.

Consider the potential conflicts between shareholders and management in Aviva plc. Explain how these conflicts might be reflected in terms of Aviva plc’s approach to corporate finance.

OvEr TO yOu

© ABE36

Chapter 2 Sources of Finance

Conflicts between key stakeholders can often be seen to be reflected in aspects of corporate finance such as governance, executive remuneration, dividend policy and capital structure.

NEED TO KNOW

on the goRevision

Debt: advantages and disadvantages

One of the key advantages of debt finance is the creation of a “tax shield”. These tax shields protect profits from corporate tax. You will consider tax shields and their effects later in the chapter. For now, consider the key features, advantages and disadvantages of the main types of debt finance which are summarised in Tables 8 and 9.

Type Key features Advantages Disadvantages

Subordinated loan

Ranked below other types of borrowing: interest payments and capital repayments on other borrowing are paid in priority to subordinated loans. Sometimes referred to as “junior debt”

Loan covenants on other types of loan often ignore subordinated loans, as they pose no threat to their claims: so, subordinated loans can be a source of borrowing when other sources are not available

Normally incur higher interest charges due to higher risks to lenders

Term loans Tailored to meet the specific needs of borrowers

Terms are open to negotiation and agreement. Flexible and often cheap

Restricted availability

Loan notes Divided into units and offered for sale to investors. Often traded on a stock exchange

Can be attractive to investors

Market value may fluctuate

Mortgages Secured on an asset Often long term Lack of flexibility

Source: Adapted from Atrill (2014)

Table 8: The key advantages and disadvantages of the main types of debton the goRevision

A commonly cited disadvantage of debt finance is the existence of loan covenants (Brealey, Myers and Allen, 2014). Many of the types of debt finance that are outlined in Table 8 will include these restrictions. Loan covenants are assurances or “promises” made by businesses that certain activities will or will not be carried out. Typically, loan covenants will be included in a contract between a borrower and a lender.

Sources of Finance Chapter 2

© ABE 37

Loan covenants offer protection to lenders against the risk of default (i.e. a failure to meet finance charges or repayment obligations) by borrowers. Table 9 provides an outline of the typical types of loan covenant:

Type Key features

Merger restrictions Restrict the business’s ability to develop mergers and other types of partnerships with other businesses.

Dividend or other payment restrictions

Restrict the ability of a business to pay dividends or other payments. Approval may be required by the lender.

Debt covenants Restrict the amount of additional borrowing by the business.

Default-related events Trigger specific actions as a result of the default on debt obligations.

Changes in control Restrict the business’s ability to make changes to its management team.

Source: Adapted from Brealey, Myers and Allen (2014)

Table 9: Types of loan covenanton the goRevision

Atrill and McLaney (2014) note that all lenders will worry, to some extent, about the risk of default. Loan covenants result in some providers of debt finance having greater security than others.

The effect of corporate taxes in the selection of different sources of finance

Debt, corporate taxes and tax shields

As we saw in the previous chapter, the use of debt as a source of finance is not without its risks. Nevertheless, if debt finance is used to generate additional profit that exceeds the cost of debt, then this will increase the amount of profit that is available to distribute to shareholders in the form of a dividend. Research by, for example, Dimson, Marsh and Staunton (2011) suggests that debt finance is cheaper than equity finance, at least in the short-term.

Debt is a very popular source of finance for many businesses. Research suggests that this is because it is cheaper than equity finance, at least in the short-term.

NEED TO KNOW

on the goRevision

Finance costs (also known as interest charges) create “tax shields”. These tax shields protect profits from corporate tax. This is one of the reasons why debt finance is often cheaper than equity finance. Tax shields are calculated as the present value of future tax savings arising from the use of debt finance (Watson and Head, 2016).

© ABE38

Chapter 2 Sources of Finance

Tax shields