Amorphous Solid Dispersions as Oral Delivery System ... - edoc

Price Dispersion in Monetary Unions: The Role of Fiscal Shocks ∗

Fabio Canova†and Evi Pappa‡

February 3, 2003

Abstract

We study the effect of regional expenditure and revenue shocks on regional price dispersionin a monetary union using 48 US states and 10 EU countries. We identify fiscal shocks usingsign restrictions on the dynamics of expenditures, revenues, deficits and output and constructtwo estimates for structural price dispersion dynamics which optimally weight the informationcontained in the data for all units. We find that, fiscal shocks explain between 10 and 20percent of the variability of price dispersion in the US and between 3 and 4 percent in the EU.On average, the predictions of standard theory are confirmed: expansionary fiscal disturbancesproduce positive price dispersion responses in both areas while distortionary balance budgetshocks produce negative price dispersion responses. In about one third of the units, negativeprice dispersion responses to expansionary shocks are observed. Further, heterogeneities inshapes and peak responses are observed. Explanations for the puzzling features are provided.

JEL classification numbers: E3,E5,H7

Key words: Price dispersion, Fiscal policy, Bayesian methods, Monetary unions

∗We thank Tim Basley and Marco Del Negro for allowing us the use of some of their data. We also thank A. Vredin,C. Favero, N. Kiyotaki, R. Perotti and D. Quah and the participants of seminars at the Riksbank, the University ofOslo, LSE and the conference ”Political, Institutional and Economic Determinants of Fiscal Policy” for commentsand suggestions.

†Universitat Pompeu Fabra and CEPR, Department of Economics, Ramon Trias Fargas 25-27, 08005 Barcelona,Spain, email: [email protected]

‡London School of Economics, Department of Economics, Houghton Street, WC2 2AE London, email:[email protected]

1

1 INTRODUCTION 2

1 Introduction

The creation of the European Monetary Union came together with a set of rules for membership,known as the ”Maastricht criteria”, which stressed the need for convergence in the nominal andreal side of economies of candidate countries. The presence of such rules signal the aversion ofEuropean leaders to regional dispersions. There is some logic behind this concern. For example,price dispersions in two otherwise similar regions makes monetary policy difficult to conduct. Boththe ECB and the Fed, in fact, are concerned with the average rate of inflation in the union but notwith its spread. While casual observation suggests that inflation differentials are relatively smallwithin the US - a result recently challenged by Cecchetti, Mark and Sonora (2000), - differences inthe price dynamics within the Euro area appear to be more a norm. For example, the maximuminflation differential in the area, was above two percent up to 2001 and exceeded three percent in2002.

Whether dispersion in price dynamics is a problem or not depends on its causes. A typicalexplanation, based on the Balassa-Samuelson effect, indicates that it is differential productivitylevels which may induce regional variations output and prices. The mechanism is simple: in thepresence of non-traded goods, an increase in regional productivity of traded goods leads to higherregional real wages. This in turn drives regional relative price of non-traded goods up and whenthere are common prices for traded goods, the price level in the region increases relative to the unionaverage (see e.g. Canzoneri, Valles and Vinals (1996)). If productivity differences are persistent,differential in output growth and inflation rates could be observed. Such differentials, however, donot necessarily call for restraining actions by Federal institutions.

Demand factors, combined with a large component of non-tradables in the locally consumedbasket of goods, may also be the reason for price dispersions. Persistent increases in demand fornon-traded goods may generate localized burst of inflation whenever the supply of these goods is notperfectly elastic with respect to demand conditions. One component of demand which is typicallytilted towards non-traded and local goods is government expenditure. If local government expen-diture is an important source of price dispersion, federal authorities who dislike regional differencesmay be justified in attempting to control regional fiscal policies - e.g., imposing limits to budgetdeficits as percentage of GDP (as the Maastricht criteria) or strict balance budget requirements (asthe Graam, Rudman and Hollings amendment does in the US).

A related but different issue has to do with whether fiscal policy can be used to affect regionalprice levels. For example, it may be the case that in maximizing a weighted average of the welfareof consumers, a union wide monetary authority selects an inflation rate which is ”undesirable” fora portion of the agents (e.g. too high or too volatile, given national preferences). Alternatively,demand may be stronger than average in one region. One may be therefore interested in knowingwhether and to what extent fiscal policy can affect regional price differentials.

This paper empirically studies the relationship between fiscal disturbances and regional pricedispersions in monetary unions using a sample of 10 European and 48 US states. Given the shortlife of the Euro area, the US experience may provide useful insights and crucial indications on howprice differences may evolve within the Euro area. Identifying economically meaningful shocks isalways a difficult enterprise and fiscal disturbances are not exceptions to this rule. Endogeneity of

1 INTRODUCTION 3

fiscal variables, interactions between fiscal and monetary policy decisions, delays between planning,approval and implementation of policies, and scarceness of reasonable zero restrictions makes fiscaldisturbances difficult to recover. Here we follow Canova and Nicoló ’s (2002) approach and achieveidentification using sign restrictions on the dynamics of output and deficits derived from a large classof dynamic general equilibrium models. Montfourd and Uhlig (2002) provide an earlier applicationof this methodology to extract fiscal shocks in aggregate US data. We differ in the implementationof the restrictions, in the specification of the VAR and in the estimators we consider.

Although our interest is examining responses to a broad class of expenditure and revenue shockswe make several important distinctions within each class using available theory. Following Baxterand King (1993) and Ludvigson (1996) we attempt to identify two types of expenditure shocks:those financed by bond creation, which produce positive comovements in both regional outputand deficits; and those financed by distorting taxation, which leave deficits unchanged and producenegative comovements in regional outputs. In the class of revenue shocks we also distinguish betweentextbook type shocks, i.e. tax cuts which increase budget deficits and output, and ”Reagan-Laffer”shocks, i.e. tax cuts that leave deficits unchanged (or even decrease them) and have positive effectson output. Since restrictions of this type are routinely used in applied analyses to informallycheck the reasonableness of the identification results, it makes sense to impose them directly whenextracting the informational content of a reduced form shock.

Given the panel nature of the data, our exercises are concerned in characterizing both averagetendencies and highlight idiosyncratic differences. Since the data sets are short and the modeldynamic, standard panel data techniques are likely to give unsatisfactory answers. The approachwe take is Bayesian: we model the cross section of experiments as repeated observations on thesame underlying unknown phenomena (the response of regional price dispersions to fiscal shocks).In this sense, information coming from, say, New York data may be useful in estimating the effectsof fiscal shocks in, say, New Jersey. We assume that the parameters of the structural model foreach unit are drawn from a common distribution and we construct posterior distributions for thestructural parameters which reflect our a-priori assumptions and the information contained in thedata.

Our results suggest that while fiscal policy is an important source of regional price dispersionin US states, it is less crucial in Euro area. The magnitude of the effects vary with the unit andthe type of shock. On average, fiscal shocks explain between 10 and 20 percent of the variabilityof regional price dispersion in US states and between 3 and 4 per cent in Euro countries. Pricedispersion dynamics conforms, on average, with the predictions of standard theory: expansionaryfiscal disturbance increase relative prices, while balance budget shocks (expansionary fiscal shocksfinanced by distortionary taxation) decrease relative prices. Substantial heterogeneities in thesign, the size and the shape of price dispersion responses across units are however evident. Forexample, in about one third of US states and of Euro nations expansionary fiscal disturbanceslead to significant decreases in local price dispersion. Puzzling as it might sound this outcome isconsistently reported in analyses conducted with aggregate US data (see Canzoneri, Cumby andDiba (2002) or Mountford and Uhlig (2002)). Contrary to CEPS (2002) we record this patternalso in a number of Euro countries. We find that there is a geographical dimension in the patternof responses but also that political, economic and social indicators do not help us to explain why

2 THE REDUCED FORM MODEL 4

prices dispersion responses are perverse.We investigate two other types of explanations for this phenomenon. One has to do with

geographical spillovers: if either the state is large in size or public (and private) expenditureis tilted toward non-locally produced goods, increases in local demand may also affect prices inneighbouring states. If these spillovers matter for union-wide prices, price dispersion may declinefollowing expansionary fiscal shocks. The second explanation has to do with movements in aggregatesupply. If expansionary fiscal shocks exercise an effect on the labour or capital supply of the localeconomy (as, for example, it is predicted in RBC models), it is possible for output expansions tocoexist with price dispersion declines. For the case of revenue shocks, the type of distorting taxesused to raise revenues may also explain both the heterogeneities across units and the magnitude ofthe effects - e.g. labour supply responses to sales tax shocks should differ substantially from thosefollowing labour income or capital tax shocks. In the majority of the cases, we find that one ofthese two explanations suffices to explain puzzling price dispersion responses.

The rest of the paper is organized as follows. The next section describes the reduced formmodel. Section 3 details the identification restrictions used. Section 4 discusses the econometricprocedure used to combine cross sectional information. Section 5 presents the results and section6 concludes.

2 The reduced form model

The data available for both monetary unions is short: we have annual data from 1969 to 1995 forUS states and quarterly data from 1999:1 to 2002:2 for the Euro nations. The shortness of the dataset prevents us not only to study issues connected with the transmission of shocks across states ornations but also to be able to analyse medium scale empirical models which include local, regionaland union wide variables. Given these limitations we are forced to make a number of choices.We initially neglect possible neighbourhood effects and model the VAR for each unit using fourendogenous variables, three exogenous variables and a constant. The endogenous variables are thesame for both US states and Euro countries: the log of the local price level relative to aggregateunion wide prices; the local real per-capita GDP, the log of local real government revenues andthe log of local real government expenditure both in per-capita terms. The exogenous variables weinclude are the area-wide nominal interest rate, the area-wide unemployment rate and the level ofoil prices. Oil prices are used to capture aggregate area-wide supply effects, while with the nominalinterest rate and the aggregate unemployment rate we attempt to capture aggregate demand driveneffects common to all units. The sources of the data and the transformation performed are describedin appendix A.

While theory indicates that these variables are crucial to understand the effects of fiscal policy onprice dispersion (see e.g. Duarte and Wollman (2002)), in practice it is not clear which indicatorsmight be most relevant. For this reason, we also examined several variants of the above model(e.g. a VAR with revenues and expenditures in percentage of GDP, a model where aggregateGDP level substitutes for the aggregate unemployment level, a model where local GDP per-capitais substituted by the local unemployment rate, a model where all variables are scaled by thecorresponding US or Euro averages and a model where variables are expressed in growth rates (but

3 THE IDENTIFICATION RESTRICTIONS 5

not per-capita terms)). The results we present are broadly invariant to all of these changes.Favero and Monacelli (2002) estimate fiscal policy rules for aggregate US data and find that

debt is an important determinant of taxes and expenditure. We cannot include debt in our exercisesfor two reasons. First, debt data is not available for US states on a consistent basis. Second, itexists at the annual frequency in Euro countries, but displays very little variations over the sample.Therefore, debt is unlikely to be important in capturing endogenous variations in the fiscal rulepresent in these nations.

To claim that the fiscal shocks we recover are economically meaningful a number of orthogonalityassumptions need also to be made. For example, one could envision the possibility that stategovernment expenditure is (positively) correlated with the expenditure of neighbouring states orthat it is (negatively) correlated with union wide expenditure. Therefore, omission of these variablesmay lead to misspecification of the shocks. To measure the extent of this problem we have run twoother VARs where in place of state expenditure we inserted the residual of a preliminary regressionof state expenditure on either union wide expenditure or the expenditure of the region where thestate (country) is located. The results obtained are unchanged suggesting that, if present, thesecorrelations are small.

Finally, given the small number of observations, we restrict the lag length of our VARs to onefor each unit. For robustness, we checked for US states whether the inclusion of a second lagmade a difference: it didn’t. After a short specification search we settled on making union wideunemployment and interest rates enter only contemporaneously in the system. Contemporaneousvalues and one lag of oil prices are also included.

3 The identification restrictions

While structural VARs have been extensively used to study the transmission of monetary policyshocks (see Christiano, Eichenbaum and Evans (1999) for references), little has been done to identifyfiscal disturbances and to examine their effects on macroeconomic variables. Relevant exceptionsare Ramey and Shapiro (1998), Edelberg, Eichenbaum and Fisher(1999), Fatas and Mihov (1999),Neri (2001), Mountford and Uhlig (2002), Blanchard and Perotti (2002), Burnside, Eichenbaumand Fisher (2002).

This apparent lack of interest is due, in part, to the fact that fiscal policy is rarely unpredictable.A fiscal change is usually subject to long discussions and political debates before it is implemented.These delays make standard innovation accounting problematic: agents adjust their behaviourto the new conditions when the old regime still prevails; macrovariables start moving before theshock occurs and no surprise is measurable at the time when the change in policy actually takesplace. This ”non-fundamentalness” problem plagues fiscal shocks more than e.g., monetary ones. Asecond conceptual problem has to do with the fact that, even when the policy stance is unchanged,expenditures and revenues move in response to the state of the economy. Hence, do variationsin fiscal variables represent exogenous policy shifts or endogenous reactions to the state of theeconomy? Third, as it is for example suggested in the recent fiscal theory of the price level (see e.g.Christiano and Fitzgerald (2001) for a survey), fiscal and monetary policy actions may be related.This was true in the past in many European countries were monetary authorities residually satisfied

3 THE IDENTIFICATION RESTRICTIONS 6

government budget constraints. Whenever this is the case, identifying fiscal shocks in isolation mayprovide misleading results (see e.g. Neri (2001)).

Our set up is designed to avoid, in principle, all these problems. First, because we considermonetary unions, we can take monetary policy actions as given when examining regional fiscalpolicy. We do this by imposing the exogeneity of the economy wide interest rate with respect toregional variables. Second, all VAR variables are, by construction, endogenous and we control forthe state of the aggregate business cycle by introducing a number of area wide variables. Thesecontrols should effectively eliminate sources of fluctuations which are unrelated to the phenomenonwe are considering, without any need to produce cyclically adjusted estimates of fiscal variables.Moreover, given the nature of the VAR, predictable and unpredictable movements can be clearlyseparated. Third, since we define the kind of fiscal disturbances we are looking for, there shouldbe no confusion about the sort of unpredictable events they represent. To be precise, we seek localexpenditure shocks with the following characteristics:

1. (G-1) They must produce contemporaneous positive comovements in regional output andregional deficit.

2. (G-2) They are contemporaneously perfectly and positively correlated with tax revenues andproduce contemporaneously negative comovements on output.

The first type of expenditure shocks is the one usually encountered in macroeconomic text-books and in dynamic RBC models (see e.g. Baxter and King (1993) or Aiyagari, Christiano andEichenbaum (1992)). An unexpected increase in government spending, financed either by lumpsum taxation or bond creation, increases by definition regional deficit, stimulates aggregate de-mand and boosts output. In identifying this type of shocks we are agnostic about the behaviour oftax revenues: they are allowed to stay unchanged or move together with expenditure as long as thecorrelation with the latter is not perfect. At the identification stage that we do not take any positionin the controversy between Keynesian and neoclassical expenditure shocks (see e.g. Giavazzi andPagano (1996)). Once shocks are identified, one can name a expenditure shock Keynesian whenthe magnitude of contemporaneous output responses exceeds that of the contemporaneous expen-diture disturbance, and neoclassical when the magnitude of output responses falls short of that ofgovernment spending shocks. Also, although we are not able to distinguish between productive andincome support expenditure because of data limitations, shocks to both types of spending shouldin principle lead to the same pattern of deficit and output responses.

The second type of shocks we consider are budget-balanced shocks: these disturbances leaveregional deficits almost unchanged and generate negative comovements in regional output. Theserestrictions are standard in general equilibrium models of fiscal policy. For example, Baxter andKing (1993) showed that an increase in government spending, financed through labour taxation,decreases consumption and investment in the short run and has protracted negative effects onoutput. In general, expenditure shocks financed by distorting taxation should lead to falls inoutput but the magnitude of the fall depends on the financing (income taxes vs. capital taxes), theelasticity of labour and capital supply to distortionary taxes and the details of the model used.

For revenue disturbances, we seek two types of shocks:

3 THE IDENTIFICATION RESTRICTIONS 7

1. (T-a) Those producing contemporaneous negative comovements in both local output anddeficits.

2. (T-b) Those which produce contemporaneous negative comovements in local output but leavelocal deficits either unchanged or make them contemporaneously and positively comove withthe disturbances.

The first type of revenue disturbance is again standard. A decrease in tax revenues decreasesdeficits and stimulates output by reducing the tax burden on the local economy. Here governmentexpenditure is NOT assumed to be unchanged: in fact, it could react to output movements inducedby revenues cut (for example, if the amount of unemployment compensation paid decreases). Whatis important for identification is that the comovements of expenditure and taxes are low so thatbudget deficit positively comove with revenue disturbances.

The second type of disturbance is a ”Reagan-Laffer” shock. Whenever a high level of currentdistortionary taxation is in place, a decrease in tax revenue (engineered though a decline in averageor marginal tax rates) may stimulate output to such an extent that the initial cut in revenue ismore than compensated by the larger tax base over which the lower tax applies. Hence, despite taxcuts, deficits may decrease. Once again, we place no restriction on the behaviour of expenditure:we only require that it is consistent with the sign restrictions we impose on deficits.

We summarize the identifying restrictions for the four types of shocks in table 1. Since thedynamic response of local to union wide prices is unrestricted, we are in the position to examinewhat the data has to tell us about their behaviour in response to these shocks.

Identification restrictions Expenditure Shocks Revenues Shocks

Standard G-1

Budget balanced G-2

Standard T-a

“Reagan-Laffer” T-b

Cor(G,Y)>0

Cor(G,DF)>0 Cor(G,T)>0

Cor(G,Y)<0

Cor(G,DF)=0 Cor(G,T)=1

Cor(T,Y)<0

Cor(T,DF)<0 Cor(G,T)=0

Cor(T,Y)<0

Cor(T,DF)≥0 Cor(G,T)=0

It is useful to compare our identification strategy to those employed in the literature. Theexisting literature typically uses case study approaches, zero restrictions on the contemporaneouscovariance matrix of shocks or extraneous information to disentangle fiscal shocks from reducedform innovations. One important distinction between our approach and the existing ones is thatour restrictions are theory based, while those employed by standard approaches are, most of thetimes, conventional. In the case of fiscal shocks and with low frequency data, these restrictionsare often hard to justify. For example, assuming that tax revenues do not respond to expenditureshocks within a period - an assumption which would allow to disentangle revenue and tax shocks - is

4 COMBINING THE INFORMATION FROM DIFFERENT UNITS 8

clearly problematic with annual data. Furthermore, the restrictions needed to identify expenditureshocks in quarterly data - e.g. output and prices do not respond to expenditure shocks within aquarter, or that it takes more than a quarter for discretionary changes in government spending torespond to changes in output (Blanchard and Perotti (2002)) - may be problematic in annual databecause of the presence of automatic stabilizers. With our methodology, all reduced form shockshave, in principle, information for structural shocks. In other words, our approach can solve theinherent underidentification problem which results from the general equilibrium nature of fiscalshocks. Since the restrictions we employ are theory based and fiscal shocks are allowed to affect allvariables contemporaneously, endogeneity is unlikely to be a problem in our exercises 1.

4 Combining the information from different units

Since both data sets are short structural responses are likely to be imprecisely estimated. One wayto improve their quality is to construct an estimate of price dispersion responses which efficientlycombines cross sectional information. In addition, if extra-sample information is available, onecould combine sample and extra-sample information to construct ”improved” estimates of thedynamics of interest. We use both ideas in this paper. For the US we use cross unit information toconstruct posterior estimators of the structural responses which endogenously weights unit specificand average cross sectional information. This estimator collapses to a standard OLS estimator ofthe structural impulse responses, unit by unit, when there is no information in the cross section,and to a pooled estimator, when the cross sectional information swamps the one present in a singleunit. For Euro area we use the posterior distribution for the average price dispersion responses inUS to calibrate a prior which attempts to extract information from the noisy unit specific impulseresponses.

Let the VAR for each unit i = 1, . . . N be written in a companion form as Zit = AiZit−1 +BiWt + Uit where Wt includes all the exogenous area-wide variables and Uit ∼ (0,Σi). Let thestructural moving average (MA) representation for the system be

Xit ≡ Zit −AtiZi0 = Bit−1Xj=0

AjiWt−j +Xj

CjiEit−j (1)

where Cji = AjiPi(θ), Eit = Pi(θ)

0DiUit, Pi(θ)Pi(θ)0 = I; θ ∈ (0,π) is a rotation angle, D0iDi = Σuiwhere Di = QR0.5 and Q is a matrix of eigenvectors and R the matrix of eigenvalues. Let αi =vec(C01i, C

11i, C

21i, . . . , C

p1i), where C1i is the first row of Ci. We assume that αi are related across i

1To recover shocks with the required characteristics we use the methodology of Canova and De Nicoló (2002). Theapproach requires an eigenvalues-eigenvector orthogonalization of the variance covariance matrix of the reduced formresiduals and the examination of the responses of the endogenous variables to each of the orthogonalized shocks. If noshock which produced the required co movements in the variables is found, the eigenvalue-eigenvector decompositionis rotated by an orthonormal matrix P (θ), which is parametrized to be a function of an angle θ, and the co movementsof variables to the new shocks are examined. This process continues until a shock with the required characteristicsis found. By varying θ in the range (0,π), we can thoroughly span the space of identification and examine whetherthe restrictions we impose are vacuous or not. Also, when more than one shock with the required characteristics isfound, we average the responses across candidates.

5 THE RESULTS 9

according to the following unit invariant specification:

αi = µ+ vi vi ∼ N(0, τ) (2)

where µ represents the vector of average structural MA for the cross section and τ its dispersion.Our interest is in estimating the average relative price response (i.e. the posterior distribution ofµ) and the relative price response in unit i (i.e. the posterior distribution of αi).

For US states we assume a vague prior on µ so that there is little information about thelocation of the structural MA coefficients for each unit. For Euro nations we assume that thea-priori distribution of µ is proportional to the posterior distribution of µ obtained for US states.In Appendix B we describe in details the structure of this prior and the form of the posteriordistributions for µ and αi for the two monetary unions.

Here it suffices to note that since both posterior distributions are normal, the posterior meancan be used as point estimate and the posterior standard error as a measure of the uncertaintysurrounding structural impulse responses.

5 The Results

Our identification of structural shocks was partially successful: while in most US states and Eurocountries we were able to identify (G-1) and (T-a) shocks, we were less or not at all successful inidentifying the other two types of shocks. For example, despite the presence of balance budgetrequirements, we are able to recover balance budget shocks only in 4 US states, Arizona, Iowa,Minnesota and Utah. Our inability to identify these shocks could be due to the fact that a largepart of the sample covers a period when a balanced budget was not yet required by law. However,this could only a part of the explanation since informal balance budget practices were used inseveral states. In fact, changing the end point of the sample or completely eliminating the last fiveyears of the sample makes little difference for the results. Furthermore, in all Euro countries wewere unable to identify any balance budget shocks. Reagan-Laffer shocks with the characteristicswe have described do not appear to be present either in the US states or the Euro countries. Weconjecture that the difficulties in identifying these shocks with Euro data are due to the shortsample and the limited number of these types of events in the data. In many cases, in fact, thecomovements across variables are imprecisely estimated and the signs of the responses are notclearly pinned down.

For US states we identify 45 G-1 shocks. However only in Alabama, Connecticut, Delaware,Idaho, Iowa, Montana, Nebraska, New Jersey and Virginia the instantaneous response in outputis larger than the expenditure impulse. That is to say, in the majority of the cases, unitarydisturbances to government expenditure crowd-out either consumption or investment (see alsoBlanchard and Perotti (2002) and Mountford and Uhlig (2002)). The maximum response to aunitary expenditure shock in these eight states is 6.9 and occurs in Iowa. For the other 36 shocks,local output responses are in the range [0,0.87].

Keynesian-type shocks are more numerous in the Euro. Out of the nine G-1 shocks we haveidentified, only those in Ireland produce an output multiplier which is smaller than one. Themaximal responses is 19 and it occurs in Italy. For Ireland, the multiplier is only 0.09.

5 THE RESULTS 10

5.1 Average Effects

We start by describing the dynamics of price dispersion on average. In all the figures we normalizeexpenditure shocks to be positive and revenue shocks to be negative.

5.1.1 The United States

The left panel of Figure 1 presents the results for the US. In each box we report the posteriormean and the 68 percent posterior range. Overall, the results are consistent with theoreticalexpectations. A G-1 type disturbance significantly increases the ratio of local to union wide priceson average, while a G-2 type disturbance significantly decreases it. Recall that our identificationscheme requires the first type of spending shocks to increase output and deficits. Standard textbookanalysis suggests that such a shock shifts local demand to the right. Whenever demand is biasedtoward locally produced goods or when the size of the state demand is small relative to union widedemand, local prices should increase more than union wide prices.

Figure 1: Average Price Dispersion Responses

US Euro Area G-1

years0 5 10 15

-0.025

0.000

0.025

0.050

0.075

quarters

0 2 4 6 8 10-0.012

0.000

0.012

0.024

G-2

years0 5 10 15

-0.36

-0.24

-0.12

0.00

0.12

T-a

years0 5 10 15

-0.025

0.000

0.025

0.050

0.075

quarters0 2 4 6 8 10

-0.009

0.000

0.009

0.018

0.027

0.036

The fall of relative prices in the case of balance budget disturbances can also be easily interpreted

5 THE RESULTS 11

by recalling the identification restrictions we have imposed. A balanced budget shock, in fact, isassumed to be financed with distortionary taxation and has a contractionary effect on output.Therefore, although the increase in government spending may shift local demand to the right, theincrease in distortionary taxation shifts the same curve to the left. As a result, both local output andprices may decrease whenever the distortions induced more than compensate the expansionary effectof the initial higher spending. For both G-1 and G-2 type shocks the initial effect is statisticallysignificant for about two years.

Surprise decreases in tax revenues have similar effects: they shifts local demand to the rightand increase local output. Relative prices then increase as a consequence of the increased demandfor local goods. For T-a shocks, price responses are contemporaneously significant but they becomeinsignificant immediately afterward. Quantitatively speaking, revenue cuts have larger impacteffects on price dispersion responses than expenditure increases, a result which squares well withthe findings of Mountford and Uhlig (2002) for aggregate data.

It is interesting to note that the maximum price response in the case of G-1 and G-2 shocksis instantaneous, suggesting little sluggishness in price dispersion adjustments beyond the one-yearhorizon. This is not the case for revenue shocks: the peak response occurs after one year. However,care must be exercised in this latter case since the timing of the peak response is not identifiedwith high precision.

5.1.2 The Euro area

Estimates of the structural responses in the Euro area are obtained under the assumption that,a-priori, the distribution of the vector of average structural impulse responses µ, is similar to theposterior distribution of average of US states. Clearly, this does not necessarily imply that the twoexperiences are the same: it simply suggests that, in principle, there is no reason to believe thatthe average US outcome should differ substantially from the expected average Euro outcome. Yet,if Euro data is different substantially from the US one and prior restrictions are sufficiently loose,the posterior distribution of structural parameters will reflect this difference.

The results presented in the right column of figure 1 confirm theoretical expectations. Both aG-1 and a T-a type disturbance increase, on average, price dispersion. However, while in the firstcase price dispersion responses are significant for three quarters and the peak response occur afterone quarter, in the second case responses are significantly different from zero only seven quartersafter the shock. Hence, while there are differences in the timing of the responses - confirming thatthere is enough information to pull Euro data away from the prior - it is comforting to see that thequalitative conclusions in the two unions are similar. In particular, the maximum response of pricedispersion to expenditure disturbances occurs within the first year while the maximum response torevenue disturbances occurs within the second year.

To summarize, price dispersion responses conform to the predictions of theory: on average, fiscaldisturbances which expand output and deficit increase price dispersion; disturbances which contractoutput (and leave deficit unchanged) are instead associated with decreases in price dispersions.

5 THE RESULTS 12

5.2 Individual unit pattern

Although average local to union wide price responses present little surprises, they turn out to beheterogeneous across units in terms of signs, shapes and magnitude in both monetary unions.

5.2.1 US States

Since the reader may not be aware of the consequences that our pooling procedure has on structuralimpulse responses for each unit, we start by discussing the differences obtained using single unitand cross sectional information. We only discuss G-1 disturbances since T-a disturbances presenta similar pattern. In Figure 2 we present estimates of price dispersion responses for the two mostextreme cases, Oregon (OR) and South Dakota (SD) and for two more normal ones, Maine (ME)and Alabama (AL).

Figure 2: Mean Posterior versus OLS Estimates

Oregon South Dakota

OR

0 50.00

0.05

0.10

0.15

SD

0 5-0.050

0.000

0.050

0.100

0.150

0.200

Maine Alabama

ME

0 5-0.09

0.00

0.09

0.18

0.27

0.36

AL

0 5-0.0050

0.0000

0.0050

0.0100

0.0150

0.0200

For OR relative prices appear to be exploding when structural responses reflect only unit specificinformation (dashed line) but they are well behaved when the information contained in the crosssection is used (straight line). For SD the response of relative prices is large (five times larger thanthe impact of the shock) and decays very slowly when only SD data is used. When the information

5 THE RESULTS 13

contained in the cross section is employed, responses are still persistent but the magnitude ofthe peak response is substantially reduced. For ME and AL, estimates are similar and magnitudedifferences are remarkably small. In general, the information contained in the cross section does notchange either the shape or the timing of the structural impulse responses but alters the magnitudeof the peak responses and the smoothness of the dynamics.

In figure 3 we present 68 percent posterior bands for price dispersion movements to G-1 shocks.To facilitate the interpretation, responses are organized according to the eight BLS regions: NewEngland, Mideast, Great Lakes, Plains, Southeast, Southwest, Rockies and Farwest. Here andin the following figures responses are non-normalized (they represent responses to one standarddeviation shock and standard deviations may be different across states).

Figure 3a: US Relative Price Responses to a G-1 shock

New England Mideast Great Lakes Plains Southwest

CT

0 5-0.030

0.000

0.030

0.060

0.090

0.120

DE

0 50.00

0.08

0.16

0.24

0.32

IL

0 5-0.018

-0.009

0.000

0.009

0.018

0.027

IA

0 5-0.01

0.00

0.01

0.02

0.03

AZ

0 5-0.075

-0.050

-0.025

0.000

0.025

MA

0 50.000

0.025

0.050

0.075

0.100

MD

0 50.000

0.025

0.050

0.075

0.100

0.125

IN

0 5-0.100

-0.075

-0.050

-0.025

-0.000KS

0 50.000

0.005

0.010

0.015

0.020

0.025

NM

0 50.00

0.01

0.02

0.03

0.04

ME

0 5-0.09

0.00

0.09

0.18

0.27

0.36

NJ

0 50.0

0.1

0.2

0.3

0.4

0.5

MI

0 5-0.18

-0.16

-0.14

-0.12

-0.10

-0.08

MO

0 5-0.075

-0.050

-0.025

0.000

TX

0 50.000

0.025

0.050

0.075

0.100

NH

0 50.009

0.018

0.027

0.036

0.045

NY

0 5-0.036

-0.027

-0.018

-0.009

0.000

0.009

OH

0 5-0.125

-0.100

-0.075

-0.050

-0.025

-0.000

NB

0 5-0.105

-0.070

-0.035

0.000

0.035

RI

0 5-0.016

0.000

0.016

0.032

0.048

PA

0 5-0.06

-0.04

-0.02

0.00

0.02

WI

0 5-0.018

0.000

0.018

0.036

0.054

0.072

SD

0 5-0.016

0.000

0.016

0.032

0.048

VT

0 50.000

0.025

0.050

0.075

0.100

Price dispersion responses to a G-1 expenditure shock conform to the average in 31 states but in

5 THE RESULTS 14

14 states relative price responses are negative. In all cases the standard error bands are small andresponses highly significant. In the majority of cases, and contrary to what happened in the average,the peak response of price dispersion occurs about a year after the shock. The shape of responsesdiffers dramatically across states, but one can notice the presence of some geographical pattern: forexample, in New England and the FarWest relative price responses are uniformly positive, they arehump-shaped (Maine being the exception) and the peak responses are approximately of the samemagnitude within each region. In the Great Lakes region, on the other hand, responses of relativeprices are all negatives except in Wisconsin. Here, however, the shape and the magnitude of thepeak responses varies significantly with the state.

Figure 3b: US Relative Price Responses to a G-1 shock

Southeast Southeast Rockies Farwest

AL

0 5-0.0050

0.0000

0.0050

0.0100

0.0150

0.0200

MS

0 50.000

0.009

0.018

0.027

0.036

0.045

CO

0 5-0.018

0.000

0.018

0.036

0.054

CA

0 5-0.018

0.000

0.018

0.036

0.054

AR

0 5-0.06

-0.04

-0.02

0.00

0.02

NC

0 5-0.1

0.0

0.1

0.2

0.3

0.4

ID

0 50.000

0.018

0.036

0.054

NV

0 5-0.02

-0.01

0.00

0.01

0.02

0.03

FL

0 5-0.08

-0.06

-0.04

-0.02

0.00

0.02

SC

0 5-0.018

0.000

0.018

0.036

0.054

0.072

MT

0 50.000

0.025

0.050

0.075

OR

0 50.000

0.008

0.016

0.024

0.032

GA

0 50.0

0.1

0.2

0.3

0.4

0.5

TN

0 50.00

0.08

0.16

0.24

0.32

UT

0 5-0.036

-0.027

-0.018

-0.009

0.000

0.009

WA

0 5-0.009

0.000

0.009

0.018

0.027

KY

0 5-0.120

-0.090

-0.060

-0.030

0.000

0.030

VA

0 50.00

0.08

0.16

0.24

0.32

WY

0 5-0.018

-0.009

0.000

0.009

0.018

LA

0 5-0.045

0.000

0.045

0.090

0.135

WV

0 5-0.02

0.00

0.02

0.04

0.06

5 THE RESULTS 15

Interestingly, positive price dispersion responses tend to be larger than negative ones: a 1percent increase in government spending instantaneously increases the gap between state and union-wide prices on average by 0.14 percent for states with positive price dispersion responses, while itdecreases the gap approximately by 0.03 percent for states with negative price dispersion responses.The most extreme cases are New Jersey (increase by 1.44 percent) and Michigan (fall by 0.06percent).

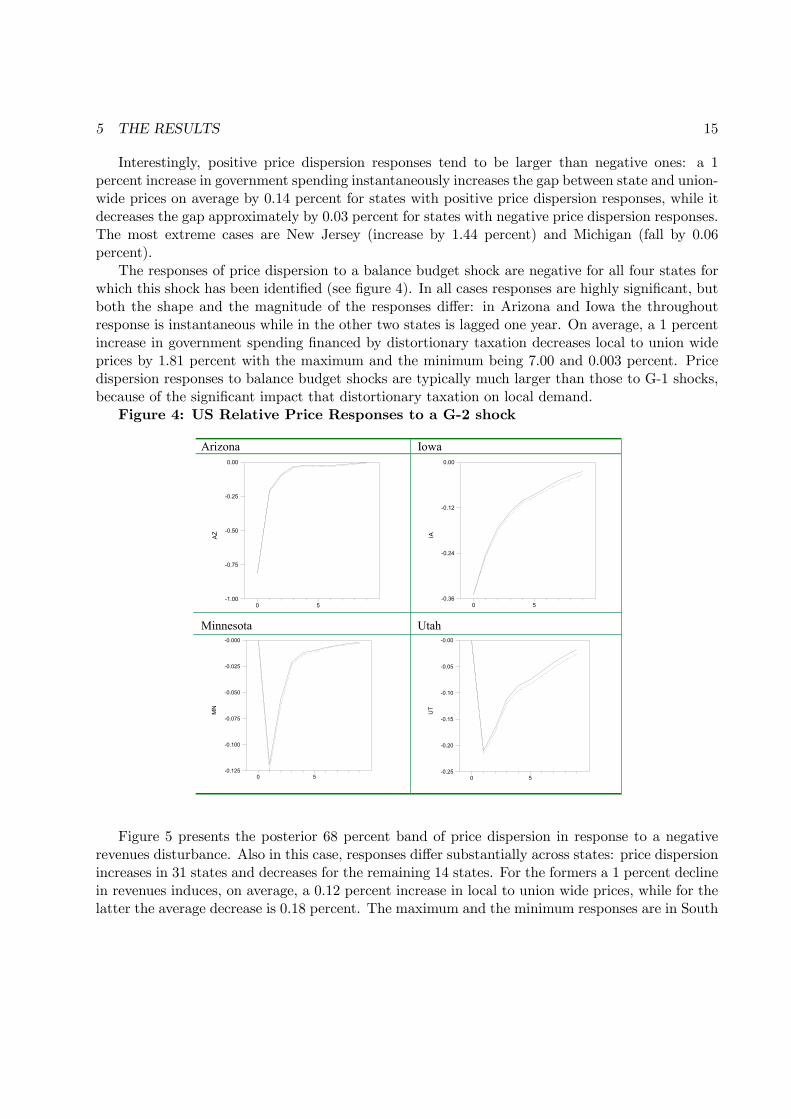

The responses of price dispersion to a balance budget shock are negative for all four states forwhich this shock has been identified (see figure 4). In all cases responses are highly significant, butboth the shape and the magnitude of the responses differ: in Arizona and Iowa the throughoutresponse is instantaneous while in the other two states is lagged one year. On average, a 1 percentincrease in government spending financed by distortionary taxation decreases local to union wideprices by 1.81 percent with the maximum and the minimum being 7.00 and 0.003 percent. Pricedispersion responses to balance budget shocks are typically much larger than those to G-1 shocks,because of the significant impact that distortionary taxation on local demand.

Figure 4: US Relative Price Responses to a G-2 shock

Arizona Iowa

AZ

0 5-1.00

-0.75

-0.50

-0.25

0.00

IA

0 5-0.36

-0.24

-0.12

0.00

Minnesota Utah

MN

0 5-0.125

-0.100

-0.075

-0.050

-0.025

-0.000

UT

0 5-0.25

-0.20

-0.15

-0.10

-0.05

-0.00

Figure 5 presents the posterior 68 percent band of price dispersion in response to a negativerevenues disturbance. Also in this case, responses differ substantially across states: price dispersionincreases in 31 states and decreases for the remaining 14 states. For the formers a 1 percent declinein revenues induces, on average, a 0.12 percent increase in local to union wide prices, while for thelatter the average decrease is 0.18 percent. The maximum and the minimum responses are in South

5 THE RESULTS 16

Carolina (0.6 percent increase) and West Virginia (0.7 percent decrease). There are differences inthe shapes of the responses. However, in the majority of the cases, price dispersion responses arehump-shaped, with the hump occurring after one-two years. There is some geographical patternalso in the responses to a T-a shock: for example, an unexpected decrease in government revenueincreases the gap between state and union-wide prices in New England and in the majority ofMidWest states, while it decreases it in the majority of SouthWest states.

Figure 5a: US Relative Price Responses to a T-a shock

New England Mideast Great Lakes Plains Southwest

CT

0 50.000

0.050

0.100

0.150

DE

0 5-0.05

0.00

0.05

0.10

IL

0 5-0.018

0.000

0.018

0.036

0.054

IA

0 5-0.02

0.00

0.02

0.04

0.06

AZ

0 5-0.024

-0.012

0.000

0.012

0.024

MA

0 50.0

0.1

0.2

0.3

0.4

MD

0 5-0.07

0.00

0.07

0.14

0.21

IN

0 50.00

0.05

0.10

0.15

KS0 5

-0.06

0.00

0.06

0.12

0.18

0.24

NM

0 5-0.15

-0.10

-0.05

0.00

0.05

ME

0 5-0.018

0.000

0.018

0.036

NJ

0 5-0.035

0.000

0.035

0.070

0.105

MI

0 5-0.024

-0.018

-0.012

-0.006

-0.000

0.006

MN

0 5-0.64

-0.48

-0.32

-0.16

0.00

OK

0 5-0.20

-0.15

-0.10

-0.05

-0.00

0.05

NH

0 5-0.016

0.000

0.016

0.032

0.048

0.064

NY

0 50.000

0.016

0.032

0.048

0.064

WI

0 5-0.012

-0.006

0.000

0.006

0.012

0.018

MO

0 5-0.018

0.000

0.018

0.036

TX

0 50.072

0.090

0.108

0.126

VT

0 5-0.02

0.00

0.02

0.04

0.06

0.08

PA

0 5-0.021

-0.014

-0.007

-0.000

0.007

OH

0 5-0.012

0.000

0.012

0.024

0.036

0.048

ND

0 5-0.008

0.000

0.008

0.016

0.024

0.032

NB

0 5-0.08

-0.06

-0.04

-0.02

0.00

0.02

Expenditure increase and revenue cuts tend to have asymmetric effects on price dispersion. In

5 THE RESULTS 17

fact, only in 26 states expenditure increases and revenue cuts move local to union wide prices inthe same direction (increases occur in 20 states and decreases in 6 states (AR,AZ,MI,NB,PA, UT)).Furthermore, an unexpected reduction in tax revenues produce larger price dispersions responsesthan an unexpected expenditure increase. For example, in New England, where both types ofdisturbances have a positive impact on the ratio of state to union-wide prices, a 1 percent increasein government spending produces a 0.03 percent average increase in prices while a decrease in taxrevenues increase prices by 0.17 percentage points on average.

Figure 5b: US Relative Price Responses to a T-a shock

S o u th e a s t S o u th e a s t R o c k ie s F a r w e s t

AL

0 5-0.005

0.000

0.005

0.010

0.015

0.020

MS

0 5-0.018

-0.009

0.000

0.009

CO

0 5-0.02

0.00

0.02

0.04

0.06

0.08

CA

0 5-0.02

0.00

0.02

0.04

0.06

AR

0 5-0.048

-0.032

-0.016

0.000

0.016

NC

0 50.00

0.02

0.04

0.06

0.08

ID

0 50.000

0.018

0.036

0.054

NV

0 5-0.2

0.0

0.2

0.4

0.6

0.8

FL

0 5-0.0045

0.0000

0.0045

0.0090

0.0135

SC

0 50.00

0.14

0.28

0.42

MT

0 5-0.050

0.000

0.050

0.100

OR

0 5-0.06

-0.04

-0.02

0.00

GA

0 5-0.040

-0.035

-0.030

-0.025

-0.020

TN

0 5-0.054

-0.036

-0.018

0.000

0.018

UT

0 5-0.36

-0.27

-0.18

-0.09

-0.00

0.09

KY

0 5-0.05

0.00

0.05

0.10

WV

0 5-0.42

-0.28

-0.14

0.00

0.14

WY

0 5-0.045

0.000

0.045

0.090

0.135

LA

0 5-0.040

0.000

0.040

0.080

In conclusion, price dispersion responses tend to be heterogeneous in sign, size and shape buthighly significant, at least initially. Central Banks worrying about regional inflation differentialsmay be interested in knowing how important are the fiscal shocks we have identified in quantitativelyexplaining movements in local to union wide prices. Table 2 presents this information: for eachdata set we report the mean, the 68 percent interval, the minimum and the maximum for theproportion of price dispersion movements explained by the three types of shocks we have identified.On average in the US, expenditure shocks explain 13 percent, balance budget shocks explain on

5 THE RESULTS 18

average 21 percent and tax shocks about 8 percent of price dispersion movements. The 68 percentbands are relatively large and the right tail of the distribution is long. For example, there arefive states (DE, FL, MO, NY, TN) in which expenditure shocks explain 50 percent or more of thevariability of local to union wide prices. However, it is hard to find common geographical, politicalor economic characteristics among these states which could justify this exceptional behaviour. Atentative conclusion is therefore that fiscal shocks explain a modest but significant portion of pricedispersion movements, but there are cases when their explanatory power is large.

Table 2: Variance decomposition

US 10 years horizon

average contribution

68% confidence bands min max

G-1 shocks

13%

0.16% -21.4%

0.014%

67.9%

G-2 shocks

21%

2.4%

53.0%

T-a shocks

8.1%

0.43% -11%

0.08%

64.2%

Euro area 20 quarters horizon

average contribution

min max

G-1 shocks

2.4%

0.10%

10%

T-a shocks

3.5%

0.03%

17.6%

5.2.2 Euro Countries

Price dispersion responses of Euro countries to fiscal shocks are similar: there are cross countrydifferences in the signs, in the shapes and in the location of the peak responses. The top panelof figure 6, which presents 68 percent band responses to a G-1 disturbance, demonstrates theseheterogeneities. In Germany and Italy price dispersion responses are positive at all horizons, inBelgium and France they start negative but become positive after one quarter while in Finland,Ireland and Portugal they are negative for 2 or 3 quarters and positive thereafter. Finally, inAustria, and the Netherlands price dispersion responses are generally insignificant

Excluding Belgium and France, responses display a hump-shaped pattern with the peak responseoccurring between 2 and 4 quarters after the shock but the magnitude of the peak response differsacross countries. A 1 percent increase in spending produces a maximum price dispersion responsein the range [-0.33,0.42].

The heterogeneity of price dispersion responses to revenue shocks is also clear from the lowerpanel of figure 6. In general, tax revenue shocks generate significantly negative effects either on

5 THE RESULTS 19

impact (Ireland) or with one period lag. Only in Austria tax cuts increase national to union wideprices within a year, but this effect is short lived. Consistent with the responses presented in figure1, in five of the six countries, price dispersion responses are significantly positive after about sevenquarters. The magnitude of the peak response is somewhat similar: a 1 per decrease in tax revenuesproduces a maximum response of national to union wide prices of about 1.6 percent.

Figure 6: Euro Relative Price Responses to shocks

G-1 shocks

Austria

0 5-0.012

0.000

0.012

0.024

France

0 5-0.12

-0.06

0.00

0.06

Italy

0 5-0.014

0.000

0.014

0.028

0.042

Belgium

0 5-0.135

-0.090

-0.045

-0.000

0.045

Germany

0 5-0.008

0.000

0.008

0.016

0.024

0.032

NL

0 5-0.01

0.00

0.01

0.02

Finland

0 5-0.050

-0.025

0.000

0.025

Ireland

0 5-0.036

-0.018

0.000

0.018

Portugal

0 5-0.024

-0.016

-0.008

0.000

0.008

0.016

T-1 shocks

Austria

0 2 4 6 8 10-0.016

0.000

0.016

0.032

0.048

Finland

0 2 4 6 8 10-0.028

-0.014

0.000

0.014

0.028

Ireland

0 2 4 6 8 10-0.018

-0.009

0.000

0.009

0.018

0.027

Belgium

0 2 4 6 8 10-0.060

-0.030

0.000

0.030

Germany

0 2 4 6 8 10-0.032

-0.016

0.000

0.016

0.032

NL

0 2 4 6 8 10-0.018

-0.009

0.000

0.009

0.018

0.027

Fiscal disturbances are less important in explaining price dispersion dynamics in the Euro than

5 THE RESULTS 20

in the US. In fact, the mean percentage of price dispersion variability explained by fiscal shocksis only 3-4 percent. However, in a couple of nations either expenditure or revenue shocks explainmore than 10 percent of the variability of price dispersion.

It is worth relating the dynamic of price dispersion responses to one particular episode which hasattracted attention in the policy circles. To induce foreign investments into the country, the Irishgovernment reduced taxes on capital income in the third quarter of 1999 and this led to a significantincrease in output in 2000 and the first quarter of 2001. In February 2001 the European Coun-cil issued a warning (Action against Ireland, Euro Official Journal, 9/3/2001, C077, pp.7) callingIrish authorities to restraint their attempts to reduce the cyclically adjusted surplus. In particular,the Council was concerned with the effects that such policy had on local inflation. Figure 6 sug-gests that these concerns were groundless: a one percent decrease in revenues has a negative impactof 0.50 percent on local to union wide prices. Furthermore, this effect dies out in about two quarters.

5.3 Some explanations

In some US states and European countries an unexpected increase in spending (or unexpectedreductions in revenues) bring about a significant and at times persistent reduction in local tounion wide prices. These responses are surprising from the point of view of conventional theory(both of Keynesian and neoclassical orientation) because in identifying shocks we have imposedthe restriction that output must increase in response to both of these shocks 2. This, for example,excludes explanations based on substantial crowding out of other components of aggregate demandor expectational effects of the type emphasized by e.g., Giavazzi and Pagano (1996). In this cases,in fact, both output and prices should move in the same direction. While this pattern of responsesis puzzling, it is by no means uncommon. In fact Mountford and Uhlig (2002), CEPS (2002) andCanzoneri, Cumby and Diba (2002) all find that, at aggregate level, US prices decline after eithera revenue cut or an expenditure increase.

In an attempt to characterize the units for which relative price movements have a perversepattern, we have looked at a number of indicators. Besides the geographical position of a unit, weexamined whether its size (measured by the population size), the size of its local government onaverage over the sample (measured by expenditure over GDP), the magnitude of local governmentdebt and at the state of government finances (as measured by the Average Moody rating over theperiod), the composition of output and, for US states, the political colour of the governors andof the state parliament and the average price of land could be used to interpret price dispersionresponses. In general, we found little similarities along these dimensions in both monetary unions.Take the US, for example. Among, the states with negative price responses, we have both smalland large states (e.g. Kentucky and Wyoming vs. Florida for expenditure shocks and Missouri andWest Virginia vs. again Michigan for revenue shocks), states where the expenditure to GDP ratiois both small and large relative to the average (Kentucky and Utah vs. Florida or Missouri) stateswith good and bad credit ratings or high and low average level of debt (e.g. Georgia and Kentucky

2In the estimation, we have not restricted the sum of relative price responses to be zero. Therefore, we should notexpect some price dispersion responses to be positive and others to be negative.

5 THE RESULTS 21

vs. Wyoming or Arizona), states where agricultural sector is large and small (e.g. Nebraska vs.Michigan) and states which were, on average, republican and democrat (e.g. Florida and NewMexico vs. Ohio) and states where land prices are higher or lower than average (e.g. New Yorkand Wyoming).

Theoretically, we can think of two sets explanations for why fiscal expansions may inducenegative price dispersion responses. The first has to do with spillover effects: if increases in localdemand are spread over a number of (neighbouring) units, union-wide demand may increase morethan local demand in response to the local fiscal expansion. The second has to do with movementsin the local aggregate supply curve: expansionary policies may in fact shift such a curve to theright as agents readjust their labour supply and investment decisions in response to the shocks.

Spillover effects may occur for many reasons. One is that the size of the state is large andthe multiplicative effects generated in the region are of an order of magnitude larger than thosegenerated locally. We have seen that for US states size does not matter. In Europe, it is smallcountries such as Belgium, Ireland and Finland that produce paradoxical price dispersion move-ments in response to expansionary shocks and neighbouring nations (e.g. the Netherlands in thecase of Belgium) do not seem to be affected by local fiscal shocks. A second reason for why pricedispersion may fall is that expansionary fiscal policy may induce increase in the demand of non-locally produced goods. This could occur, for example, when the industrial structure of a unit hasparticular features (e.g. value added is skewed toward a particular activity), when the productivestructure is such that local output is produced with intermediate inputs coming from neighbouringunits or when home bias in consumption is small. To effectively examine this hypothesis one needsintrastate and intracountry trade data or the industrial composition of value added in each state(nation). While we have managed to find such data for Euro countries, this data is not available forUS states. As shown in table 4, there is some evidence that spillover effects are important withinthe Euro: the size of the impact (one period lagged) coefficient of imports from the Euro coun-tries to expansionary expenditure shocks in Belgium, France and the Netherlands - the countrieswhere price dispersion react negatively to a government spending shock - is significantly positiveand larger than the Euro average and the average coefficient in the countries with positive pricedispersion responses.

Lacking trade data for US states, we check for spillover effects by directly examining BLSregional prices. Our working conjecture is that if these effects are present, they should be localizedwithin BLS geographical regions. Therefore, if the hypothesis is correct regional prices shouldincrease in response to expansionary local fiscal shocks or, at the very least, decrease less.

The results are overall supportive of the spillover hypothesis. In 7 of the 14 states where localexpenditure shocks reduced local to union wide prices, regional to union wide prices increase andin 12 of the 14 states where local revenue shocks reduced local to union wide prices, regional tounion wide prices increase (or decline less than local prices). We present two typical cases in figure7. Following an expenditure shock Florida relative price persistently fall, while SouthEast relativeprices increase for two years before tracking state to union wide prices. In New Mexico revenuecuts have an initially strong negative impact on local relative prices but they push regional pricessignificantly up. Contrary to the previous case, this differential is evident for the first seven years.After that, relative state and regional prices track each other quite closely.

5 THE RESULTS 22

Figure 7: Regional Price Effects

G-1 shock T-a shock

-0.09-0.08-0.07-0.06-0.05-0.04-0.03-0.02-0.010.000.010.02

1 2 3 4 5 6 7 8 9 1011 121314 151617 181920

FL

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20NM

Dynamic general equilibrium models of fiscal policy tell us that changes in the fiscal stancemay also have important repercussions on the aggregate supply of the economy. We can think oftwo different reasons for why the aggregate supply curve may move in response to expansionaryexpenditure shocks. The first is a direct one due, for example, to the fact that higher spending oninfrastructure increases the productivity of factors of production. Since the marginal product ofcapital and labour increases, the aggregate supply shifts. If relative movements in the aggregatedemand and the aggregate supply are ”right”, it is possible that local to union wide prices to coun-tercyclically respond to local fiscal shocks. The second effect is indirect: an increase in governmentspending might induce an increase in labour supply which, in turns, shifts the aggregate supplycurve to the right. This could happen, for example, if agents expect the increase in governmentspending to be financed by future taxation: because of an income effect, agents would be inducedto work harder in the current period and intertemporally substituting leisure. While intuitivelyplausible, calibrated analyses of general equilibrium models (e.g. King and Baxter (1993)) havehard time to make this effect non-negligible. In general, if either of these channels is operative weshould expect to see units for which local to union wide prices fall to display increases in employ-ment which are larger than average. Similarly, if these channels are operative we should expect tosee units where local to union wide prices fall to display output multipliers which are larger thanthose obtained in units where local to union wide prices increase.

We present evidence on this two conjectures in tables 3 and 4 where we report the fiscal multi-pliers and the instantaneous response of local employment to expansionary expenditure shocks forthe units where local to union wide prices fall. Consider first the US. In terms of output multi-pliers the evidence is mixed: in only one of the 14 states the expenditure multiplier is larger thanaverage and in only in four the revenue multiplier is larger than the average. However, employmentresponses seem to tell a different story. In about half of the states, in fact, employment rises muchmore than in the average with Ohio and Indiana being the most extreme cases. Also employment

5 THE RESULTS 23

increases, on average, in states where price dispersion declines and declines in states where pricedispersion increases.

Table 3: Fiscal Multipliers and employment effects, US

G -1 sh o c k s T -a sh o c k s S ta te s G -m u ltip lie r E m p lo y m e n t

c o e ffic ie n t S ta te s T -m u lt ip lie r

A Z 0 .0 2 -0 .2 2 A Z 0 .0 3 A R 0 .0 2 -0 .0 3 A R 0 .0 6 F L 0 .0 3 0 .0 1 G A 0 .0 7 IL 0 .0 3 -0 .1 1 M I 0 .5 9 IN 0 .0 0 1 .6 1 M N 0 .0 0 K Y 0 .0 6 0 .2 5 M S 0 .0 6 M I 0 .0 2 0 .0 5 N B 1 .4 6 M O 0 .0 3 -0 .0 3 N M 0 .1 4 N B 0 .2 5 0 .0 9 O K 0 .5 2 N Y 0 .0 2 -0 .0 8 O R 0 .5 5 O H 0 .0 2 1 .0 0 P A 0 .1 7 P A 0 .0 2 -0 .0 9 T N 0 .0 1 U T 0 .0 0 0 .2 7 U T 0 .1 4 W Y 0 .0 1 0 .0 2 W V 0 .0 2 S ta te s w ith (- ) r e sp o n se s

0 .0 5

0 .1 9

0 .2 7

S ta te s w ith (+ ) re sp o n se s

0 .1 0

-0 .2 1

0 .3 2

M ea n U S 0 .0 8 0 .0 6 M e a n U S 0 .3 1

Table 4: Fiscal Multipliers, import and employment effects, Euro area

G-1 shocks T-a shocks Countries G-

multiplier Employment coefficient

Imports Coefficient

Countries T-multiplier

AU 1.00 0.005 0.02 AU 14.9 BE 4.71 -0.001 0.04 BE 21.9 FIN 5.43 -0.014 0.01 FIN 2.73 FRA 1.11 -0.005 0.05 DEU 1.08 DEU 2.04 -0.026 0.02 IRL 0.17 IRL 0.09 0.019 -0.00 NL 0.18 IT 18.4 -0.015 -0.01 NL 7.01 0.194 0.02 POR 8.78 - -0.04 States with (-) responses

4.02 -0.00 0.02 States with (-) responses

5.22

States with (+) responses

7.25 0.04 0.01 States with (+) responses

14.9

M ean EM U 5.46 0.019 0.01 M ean EM U 6.83

5 THE RESULTS 24

In Europe, fiscal multipliers are larger than in the US but the evidence in favour of supply sideeffects is weak. For the nations with negative price dispersion responses, only in Portugal and inthe Netherlands the spending multiplier is higher than average, while only in Belgium the revenuemultiplier is larger than average. Employment responses are not very supportive of aggregatesupply effects either, except for the Netherlands.

The composition of tax revenues can also provide important information about the movementsin local aggregate supply. If a revenue cut is engineered via reduction of income taxation, pricedispersion may fall when the substitution effect is strong and dominates the income effect on agents’labour supply. A decrease on income taxation makes agents wealthier and, as a result, may reducetheir labour supply. On the other hand, a cut in income taxation increases the relative price ofleisure and may induce agents to work harder. This could be especially the case if agents viewsuch a decrease as temporary. If this second effect dominates, the aggregate supply shifts to theright and relative prices may fall. If the reduction in revenues is engineered via reduction of capitaltaxes, one should expect the marginal product of capital to increase, this will make investmentmore profitable and therefore reduce consumption. Therefore, cuts in capital taxation may alsoreduce relative prices in some scenario. It is however hard to conceive the existence of positivesupply effects when revenue reductions are engineered through cuts in indirect and sales taxes 3.

Table 5: Tax Decomposition for Selected US states

States Taxes on Income Corporation Taxes Sales Taxes Arkansas 0.27 0.08 0.65 Arizona 0.24 0.06 0.70 Georgia 0.34 0.09 0.57 Michigan 0.34 0.15 0.50 Minnesota 0.44 0.09 0.47 Montana 0.16 0.06 0.78 Nebraska 0.30 0.06 0.64 New Mexico 0.16 0.05 0.79 Oklahoma 0.32 0.06 0.62 Oregon 0.71 0.10 0.19 Pennsylvania 0.26 0.13 0.61 Tennessee 0.02 0.11 0.87 Utah 0.35 0.05 0.60 West Virginia 0.23 0.05 0.72 US average 0.28 0.08 0.64

For Euro countries sources of tax revenues are available but the short sample and the lack ofsignificant independent variations among the various components, do not allow us to verify thisconjecture 4. For US states, where the sample is larger and the variations more significant, we can

3Since sales taxes are included in the CPI one should expect to see relative price decrease as taxes decrease in thevery short run. However, this effect should dissipate within a year.

4For example, income tax revenues are approximately constant proportion of total revenues in the three years ofthe sample and the correlation between the two is perfect.

5 THE RESULTS 25

check whether the argument has some support. In Table 5 we present the average share of thedifferent types of taxes in local revenues in states where price dispersion decline after a tax cut.Interestingly, the bulk of tax revenues in these states are generated through sales taxes and only inMinnesota, Michigan and Oregon, income and corporation taxes account for about 50 percent ofrevenues.

When we substitute income, capital or sales taxes to total revenue in the VAR, price dispersionresponses are supportive of our conjectures. For example, in 8 of the 14 states we find that sub-stituting sales tax revenues to total tax revenue produces price dispersion increases while in onlythree states we find that substituting income or capital tax revenues to total revenues changes thenegative sign of price dispersion responses. To illustrate the point figure 8 presents these responsesfor two states. In Georgia, sales tax shocks increase price dispersion substantially, while income taxshocks have the opposite effect. Similarly, in Montana sales tax shocks increase price dispersionwhile corporate tax shocks decrease them. Overall, we find that price dispersion declines whenincome/capital taxes are cut while it increases when sales taxes are cut, confirming that fiscal ex-pansions may have important aggregate supply effects.

Figure 8: Relative price responses to income, capital and sale tax shocks

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

1 3 5 7 9 11 13 15 17 19

GA

: inc

ome

vs. s

ales

taxe

s

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

1 3 5 7 9 11 13 15 17 19

MT:

cap

ital v

s. s

ale

taxe

s

6 CONCLUSIONS 26

6 Conclusions

This paper studies the relationship between local fiscal policy and price dispersion in monetaryunions using a sample of 48 US states and 10 Euro countries. We identify fiscal shocks using signrestrictions on output and deficits produced by dynamic stochastic general equilibrium models offiscal policy. We attempt to identify two types of expenditure shocks: those financed by bondcreation, which produce positive comovements in local output and deficits; and those financed bydistorting taxation, which leave deficits unchanged and produce negative comovements in localoutputs. Within the class of revenue shocks, we distinguish between textbook type shocks, i.e. taxcuts which increase local budget deficits and output, and ”Reagan-Laffer” shocks, i.e. tax cuts thatleave deficits unchanged (or even decrease them) and have a positive effect on local output. Weconstruct estimates of the average and of the local price dispersion responses using an approachwhich efficiently combines cross sectional and/or extraneous information.

Our results suggest that fiscal policy is an important source of price dispersion. The magnitudeof effects varies with the unit but fiscal shocks explain, on average, between 10 and 20 percent ofprice dispersion fluctuations in US states. For Euro countries this average is smaller (3-4 percent),but there are at least two countries where the contribution exceeds 10 percent. Local to union wideprice movement conforms, on average, with the predictions of theory: expansionary fiscal shocks(expenditure increases financed by bond increase or revenue cuts) increase price dispersion, whilebalance budget shocks (expenditure increases financed by distortionary taxation) decrease local tounion wide prices and the peak response typically occur within one or two years. While the averageresponses conform to theoretical expectations, responses for individual units are heterogeneous andin about a third of US states and more than half of Euro nations expansionary fiscal disturbanceslead to significant decreases in local to union wide prices. We find that there is a geographicaldimension to the pattern of responses but little else, along those political, economic and socialconditions which could help us to understand why price dispersion responses are perverse.

We investigate two other types of explanations. One has to do with spillover effects: if either thestate is large in size or local expenditure is tilted toward non-locally produced goods, local increasesin demand may affect regional prices more than local ones. The second explanation has to do withmovements in aggregate supply. If local fiscal shocks exercise an effect on the labour (and capital)supply of the local economy, it is possible for output expansions to coexist with price declines.We find that a combination of both explanations goes a long way in accounting for perverse pricedispersion responses both in the US states and Euro countries.

We conclude by discussing the policy implications of our results. First, our exercises indicatethat local fiscal policy has non-negligible effect on local prices. Therefore, policymakers who careabout regional price dispersion may find in our work empirical justification for imposing limits toboth the size and the variability of local fiscal policy. Second, we find that revenue shocks induceprice movements which are typically larger than those induced by expenditure shocks. This isperhaps not surprising given that taxes are distortionary and that expenditure increases typicallyproduce smaller output multipliers than revenue cuts. What is important to note here is thatthe latter effect is of an order of magnitude larger than the former one. Therefore, keeping taxsmoothing motives aside, revenue cuts could be an important local stabilization instrument. Third,

6 CONCLUSIONS 27

local balance budget shocks have large effects on both local output and local prices: expenditureincreases financed by distortionary taxation are, by and large, the most important source of pricedispersion fluctuations. Since these shocks produce large swings in the endogenous variables, theyneed to be used with considerable care. Fourth, surprise declines in local income taxes, by exercisingan important effect on the aggregate supply, may reduce regional price therefore contributing tostabilize overheated economies. Fifth, there are important similarities in the responses of pricedispersion in the US and the Euro area, and these similarities help us to understand better thedevelopments of the newly created Euro area.

As mentioned in the introduction, this paper is concerned with the somewhat narrow questionof whether local fiscal policy has effects on local prices. Hence, we did not address the importantpolicy question of whether local fiscal policy should be used to affect local to union wide prices.This problem is examined in Pappa (2002). There it is shown that local fiscal policy can be used,in alternative to the exchange rate, to stabilize the local price level in economies where the centralmonetary authority is concerned only with union wide average price stability.

6 CONCLUSIONS 28

Appendix A• US data

Regional output, regional government expenditure and tax revenues are in real per capita termsand they have been constructed using information from the Statistical Abstract of the United Statespublished by the Bureau of the Census, the Compendium of State Government Finances, and fromthe Bureau of Economic Analysis (BEA). Data on state population are taken from the StatisticalAbstract of the United States. State and national unemployment rates come from BLS. Nationalvalues for the CPI and the interest rates and oil prices are from the FRED data base of the St. LouisFed. Regional prices have been constructed by Del Negro (1998). The definition of the variablesused are:

Output: State IncomeGovernment Spending: State Government expenditure.Tax revenues: State Revenues from Sales, Income and Corporate Taxes.Unemployment rate: Annual regional unemployment rates (end of the year or average values).Prices: The price level for state i is computed as:

Pit = wui P

uit + (1− wui )PRit (3)

where PRit denotes the price level in rural areas of state i and it is taken from the Monthly LabourReview data of the Bureau of Labour Statistics (after 1978) and the ”cost of living for intermediatelevel budget” from the same source (before 1978). wui measures the fraction of population living inrural areas of state i and comes from the Statistical Abstract on the percentage of rural populationby state. Puit is constructed as:

Puit =KXk=1

ωki Pkit + (1−

KXk=1

ωki )PBit (4)

where P kit is the CPI in metropolitan area k obtained from the ACCRA (American Chamber ofCommerce Realtors Association) and the Bureau of Labour Statistics data on CPI for UrbanConsumers (CPI-U) and CPI by Regions and by Urban Population and ωki is the percentage ofurban population living in metropolitan area k obtained from the Bureau of Economic Analysis siteat the University of Virginia. PBit is the CPI in other urban areas taken from the Monthly LabourReview data of the Bureau of Labour Statistics. State CPI is normalized so that in each year theirpopulation average coincides with the US CPI.

Union wide Interest Rate: Fed Funds rate (end of the year or average values)Union wide Unemployment Rate: Annual national unemployment rates (end of the year value).Union wide Price level: Annual national CPI (all goods) (end of the year value).Oil Prices: Crude Oil Domestic First Purchase Nominal Price.

• European Data

6 CONCLUSIONS 29

All European data except for Ireland are from the OECD Main economic Indicators. The datafor Ireland, are from the December 2002 issue of the International Financial Statistics (December2002). The European aggregates come from the Euro Area Statistics (EAS) database of the ECB.The definition of the variables used are as follows

Output: National GDP.Government Spending: Government final consumption expenditure.Tax revenues: Taxes on products less subsidies.Price level: National Harmonized CPIUnemployment rate: National unemployment rates.Union Wide Interest Rate: 3-month EuroRIBOR rateUnion Wide Unemployment Rate: quarterly Euro wide unemployment rateUnion Price level: Quarterly Euro wide Harmonized CPI.

Appendix BThe assumptions made to derive the posterior distribution are the following.For the US the prior on µ is uninformative, i.e. g(µ) = 1; τ fixed and known; uit are normally