PENSION REFORM AND CAPITAL MARKETS: ARE THERE ANY (HARD) LINKS

73

Revista ABANTE, Vol. 5, Nº 2, pp. 77-149 (octubre 2002) PENSION REFORM AND CAPITAL MARKETS: ARE THERE ANY (HARD) LINKS? * EDUARDO WALKER ** FERNANDO LEFORT ** ABSTRACT The creation of fully funded, privately managed pension systems may have significant positive direct effects on savings, growth and welfare. However, the indirect link, via capital market development, may be as important. This hypothesis is verified with evidence from emerging economies that have recently engaged in such reforms with a focus on Chile, Argentina and Peru. There is abundant qualitative and anecdotal evidence that relates pension reform with the accumulation of "institutional capital", with the existence of an adaptive legal framework, with increased specialization, transparency and integrity and even with better corporate governance. Evidence of increased financial innovation is also found while there is little evidence of bank disintermediation. In addition, time-series and panel data evidence is generally consistent with the following hypothetical effects: a reduction in the cost of capital; lower security-price volatility; and higher traded volumes. The evidence suggests that the indirect channel via capital market development may have important implications for economic growth and productivity. Keywords: Pensions, Reform, Capital markets, Emerging markets, Economic growth JEL classifications G23, O54, O16. * We appreciate partial financial support from the World Bank. We thank Robert Palacios, P.S. Srinivas, Salvador Valdés, Dimitri Vittas, Juan Yermo, EFMA 2000 conference participants, and especially an anonymous referee related to the World Bank’s Pension Group for excellent comments. We also appreciate the significant research assistance of Fabián Carrillo and Juan Ernesto Sepúlveda; and thank Andrea Perotto for part of the information from Argentina; Milagros Piaggio, for part of the information from Perú; and Primamerica Consultores and Cristián Ross for part of the information from Chile. Any errors are of our exclusive responsibility. ** School of Business Administration, Pontificia Universidad Católica de Chile. Email: [email protected]; [email protected]

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of PENSION REFORM AND CAPITAL MARKETS: ARE THERE ANY (HARD) LINKS

Revista ABANTE, Vol. 5, Nº 2, pp. 77-149 (octubre 2002)

PENSION REFORM AND CAPITAL MARKETS:ARE THERE ANY (HARD) LINKS?*

EDUARDO WALKER**

FERNANDO LEFORT**

ABSTRACT

The creation of fully funded, privately managed pension systems mayhave significant positive direct effects on savings, growth and welfare.However, the indirect link, via capital market development, may be asimportant. This hypothesis is verified with evidence from emergingeconomies that have recently engaged in such reforms with a focus onChile, Argentina and Peru. There is abundant qualitative andanecdotal evidence that relates pension reform with the accumulationof "institutional capital", with the existence of an adaptive legalframework, with increased specialization, transparency and integrityand even with better corporate governance. Evidence of increasedfinancial innovation is also found while there is little evidence of bankdisintermediation. In addition, time-series and panel data evidence isgenerally consistent with the following hypothetical effects: a reductionin the cost of capital; lower security-price volatility; and higher tradedvolumes. The evidence suggests that the indirect channel via capitalmarket development may have important implications for economicgrowth and productivity.

Keywords: Pensions, Reform, Capital markets, Emerging markets,Economic growthJEL classifications G23, O54, O16.

* We appreciate partial financial support from the World Bank. We thank RobertPalacios, P.S. Srinivas, Salvador Valdés, Dimitri Vittas, Juan Yermo, EFMA 2000conference participants, and especially an anonymous referee related to the World Bank’sPension Group for excellent comments. We also appreciate the significantresearch assistance of Fabián Carrillo and Juan Ernesto Sepúlveda; and thankAndrea Perotto for part of the information from Argentina; Milagros Piaggio, for partof the information from Perú; and Primamerica Consultores and Cristián Rossfor part of the information from Chile. Any errors are of our exclusive responsibility.

** School of Business Administration, Pontificia Universidad Católica de Chile. Email:[email protected]; [email protected]

78 REVISTA ABANTE, VOL. 5, Nº 2

RESUMEN

La reforma de los sistemas de pensiones basada en la acumulación deahorros en cuentas individuales y administración privada y competiti-va puede tener un impacto significativo directo sobre el ahorro, elcrecimiento y el bienestar. Pero habría además un impacto sobre eldesarrollo del mercado de capitales que puede ser igualmente impor-tante. Esta hipótesis se verifica con datos de países emergentes quehan implementado esta reforma recientemente, enfocándose principal-mente a Chile, Argentina y Perú. Hay abundante evidencia cualitativay anecdótica que relaciona la reforma con la acumulación de “capi-tal institucional”, con un ambiente regulatorio adaptativo, con cre-ciente especialización en administración de carteras, mayor transpa-rencia e integridad y mejor gobierno corporativo. Hay también evi-dencia de innovación financiera, mas no de desintermediación banca-ria. A esto se suma evidencia de series de tiempo y de datos de panelconsistente con las hipótesis de menor costo de capital, menorvolatilidad en los retornos de los activos y mayores volúmenestransados. Esto sugiere que el impacto indirecto de la reforma, víadesarrollo de los mercados de capitales, puede incidir de manera im-portante en el crecimiento económico y la productividad.

The interest in pursuing pension reform shown by multinationalorganizations, developing countries and economists around the world, assumesthat privatization of social security, and more specifically, the creation offully-funded privately-managed pension systems has important positive effectson welfare. In particular, it has been argued that pension reform improvesmacroeconomic stability by reducing the political and demographic pressuresof the standard pay-as-you-go systems, and by inducing fiscal reformduring the transition. In addition, funding requirements associated withpension reform may help increase savings, fueling economic growth andproductivity. Pension savings will increase total savings if there are liquidityconstraints that do not allow individuals to borrow against future pensions.Recent evidence suggests that this effect may be more important thanpreviously thought for developed countries1. However, other findings showthat the direct effects of pension reform on savings is ambiguous andsometimes empirically unimportant2.

1 See Poterba et al. (1996).2 See Coronado (1998), Morandé (1998), Hachette (1998).

PENSION REFORM AND CAPITAL MARKETS 79

An increasing number of studies looking at the impact of financialdevelopment on economic growth, productivity and savings, have cited thepossibility that pension reform may have an additional desirable through apositive impact on capital market development. The existence of a positiveeffect of capital market development on growth has its main theoreticalsupport in endogenous growth models, whereby more liquid and efficientstock markets provide the incentives for long-run investments, thus increasingeconomic growth. Empirical evidence by Levine and Zervos (1998),Rousseau and Wachtel (1998) and Arestis et al. (2001) support the validityof this channel, although the latter believe that the positive effect of stockmarkets on growth has been exaggerated.

Therefore, in addition to the direct effect that pension reform may haveon growth and savings, the creation of a fully-funded, privately-managedpension system may also accelerate the process of capital marketdevelopment, improving growth and welfare. The main question that weask in this paper is therefore the following: If pension funds simply happento substitute other sources of private savings, why would this reform haveany beneficial effect on economic growth and productivity? Furthermore,pension reform has been accompanied in most cases by other concurrentreforms, which have their own effects. The main purpose of this paper isto verify the hypothesis that pension fund reform significantly affects thefunctioning of capital markets after controlling for other reforms.

Many economists have asked similar questions3, so one of the contributionsof this paper is to synthesize the main hypotheses that relate capital marketdevelopment with pension reform, discuss their validity, and perhaps positnew ones. We also analyze the extent to which the qualitative evidence isconsistent with these hypotheses. Finally, when possible, we try to empiricallyassess the importance of such effects, something that has not been done sofar. We consider the evidence primarily from Chile, Peru and Argentina,since these countries have the longest experience with this type of pensionreform. However, even in the latter two cases this time period is relativelyshort, so the statistical evidence is scarce. We also analyze panel dataevidence using a sample of 33 emerging economies, and a subsample of

3 See for example, Valdés and Cifuentes, 1990; Arrau, 1994; Fontaine, 1996; the critiqueby Singh, 1996; Blommestein, 1997; Holzmann, 1997; Burtless, 1997; Uthoff, 1997;Blommestein, ed. 1998, particularly the chapters by himself, de Rick and Lannoo; Blakeand Orzag, 1998; Camus and Sánchez, 1998.

80 REVISTA ABANTE, VOL. 5, Nº 2

seven Latin American countries. Some of the conclusions we offer mustbe considered preliminary and will need to be verified again as a longerperiod of observation becomes available.

Overall, the evidence provided in this paper seems to be consistent withthe claims by advocates of reform. Pension reform facilitates theaccumulation of institutional capital through an adaptive legal framework,increased specialization in the investment decision-making process, moretransparency and integrity (particularly via the mandatory risk-rating process),and also through a new corporate governance balance, particularly evidentin the case of Chile.

We analyze the hypothesis that one of the main channels through whichpension fund reform affects economic performance is through a reductionin the effective cost of capital for firms. The econometric analyses, withboth time-series and panel data estimation techniques, indicate that dividendyields are lower (stock prices and price-to-book ratios larger) with reform.The evidence also favors the hypothesis of lower security-price volatilityafter reform.

We provide qualitative evidence regarding the creation of new financialinstruments. In this context, the institutional environment plays a centralrole. One interesting result however, is that there does not seem to be bankdisintermediation, although after reform the role of banks partly changes.Perhaps one of the most important effects could be an improvement in theallocation of invested funds, which should translate into better resourceallocation. This may have permanent positive effects on growth and welfare,even if total savings are not affected.

The paper is organized as follows: Section II discusses the main linksbetween pension reform and capital market development. Section III providesqualitative and selected time series evidence. Section IV analyzes paneldata, and section V concludes.

I. PENSION REFORM AND CAPITAL MARKET DEVELOPMENT

In this section, we intend to clarify the rationale behind the link frompension reform to capital market development, and from that to economicgrowth and development. We see these links through three sets of economicphenomena related to pension fund reform. Naturally, the extent of theeffect of pension fund reform on capital market development will depend

PENSION REFORM AND CAPITAL MARKETS 81

upon the specific characteristics of the reform. We take as a benchmarkfor a reformed pension fund system one that allows the competitive allocationof pension funds in the spirit of the Chilean-style pension reform4.

There are many channels through which pension reform may support thedevelopment of capital markets. Therefore, we first providea summary ofthe main ideas (hypotheses or claims) presented in the specialized literatureregarding this process, including a few new ones. There are many concurrentconditions to the process of pension reform that may reinforce or limit thepositive effect on capital market development. We thus also provide a listof these. Finally, the development of a capital market under some conditionsmay have consequences on economic growth, capital accumulation andother real effects on welfare. We also refer to them in this section.

II. PROCESSES, CONDITIONS AND CONSEQUENCES OFPENSION FUND-INDUCED CAPITAL MARKET DEVELOPMENT

Focusing on the final impact regarding the development of local capitalmarkets, here we organize our arguments in terms of the processes that areinduced by the accumulation of pension funds, what the concurrent conditionsmay have to be and finally what consequences are expected of the forcesenumerated above.

A. Processes

A.1. Accumulation of Institutional Capital

Valdés and Cifuentes (1990) develop this concept, which may be par-ticularly important in emerging markets and also in countries of Civil Lawtradition, since in the latter, laws are required before certain improvementscan be implemented. The accumulation of relatively large amounts ofinvestable wealth by pension funds induces the authorities to provide and

4 The idea behind this is that pension funds could allocate funds more efficiently only ifinvestment in securities issued by the private sector is allowed. Alternatively, if pensionreform requires fund managers to hold only government bonds one may expect verylittle effect of pension reform on capital market development. On the other hand, apension fund reform Canadian style, where funds are managed by the state does not complywith the competitive allocation of funds requirement.

82 REVISTA ABANTE, VOL. 5, Nº 2

private sector participants to develop financial instruments in which pensionfunds can invest. Institutions issuing such instruments will have to disclosethe required information. This process is also likely to improve transpar-ency in terms of financial market practices and fund management. There-fore, the push provided by pension fund growth requires a (dynamic) setof regulations, labeled Institutional Capital (p. 39). We generalize this ideaas “the regulatory and institutional environment in which investors, firms andauthorities interact with each other”. Institutional Capital is thus a publicgood that can contribute indefinitely in the process of modernizing capitalmarkets.

It can be argued that even without pension reform there may be a trendtoward modernization of laws and institutions, due to increasing financialmarket integration and technological developments. This is certainly true,but if the legal authorities can identify significant local institutional investorsacting on behalf of future pensioners as valid clients there will be additionalsupport to the required reforms. In what follows, we analyze specificcomponents of this institutional capital (also see Blommestein, 1997, 1998;Iglesias, 1998; and Vittas, 1998).

As explained, progress required in order to accommodate the growingneeds of institutional investors to securitize growing portions of a nation’scapital stock5. This also leads to taking advantage of foreign expertise,although in the case of Chile, for example, many of the legal changes,including the pension reform itself, originated at home6.

The enforcement of better regulations regarding disclosure, accountingand auditing standards should lead to greater capital market transparency.Also, because of practical considerations, increasing importance of pensionfunds may imply a trend toward self-regulation, which in turn may be amore efficient way to help the development of a capital market7. The cre-ation of risk-rating systems provides an additional way of providing trans-parency to capital markets. In fact, when public trust is at stake, particu-larly in the case of mandatory pension systems, it is expected that somekind of certification or independent opinion regarding the riskiness of the

5 See Pérez Mackenna (1988).6 Valdés and Cifuentes, op. cit., p. 41, claim that the some of the legal changes introduced

in the 1986 Chilean Bank Law took place even before the same happened in developedcountries.

7 Self-regulation is sometimes associated with the formation of cartels, however.

PENSION REFORM AND CAPITAL MARKETS 83

instruments that can be used by pension funds will be required by theauthorities. One such mechanism is a mandatory risk-rating requirement.

Pension fund managers are not expected to control companies but theymay become significant minority shareholders. If fund managers act in theinterest of future pensioners, they potentially become important representa-tives of minority shareholder interests (Vittas, 1996; Lanoo, 1998; Blake andOrszag, 1998). In addition, common interests among pension fund manag-ers may open the possibility of electing independent board members.Moreover, pension fund representatives are expected to have access to theregulatory authorities and to influence public opinion. Finally, since pensionfunds are relatively large investors for whom it is possible to co-ordinatecertain actions, they tend to overcome the free-rider problem that plaguesother minority shareholders. Thus, a positive effect on the corporate gov-ernance balance might be expected. However, it is also possible thatpension fund managers do not act in the interest of their investors but inthose of the manager’s related businesses. In addition, the relationshipbetween fund managers and their clients may itself be subject to differentkinds of agency problems. Naturally, regulations try to limit this. If prop-erly guided, it would seem likely that a new corporate governance balancethat favored the development of capital markets would arise.

A.2. Increased specialization in the investment decision-making process

In a pension reform that increases the degree of funding, assets typicallygrow during a long transitional period. Managing increasing volumes offunds justifies increasing levels of specialization and requires professionalmanagement. This effect is reinforced if the reform has a net positiveeffect on savings (for example, when the transition is tax-financed) and alsoif agents substitute individual investment management by pension fundinvestment management. However, there may also be a transfer frombanks and savings associations to pension fund managers. Since in no casedo we expect banks to be completely substituted, a different kind of expertisewill be developed in addition to the existing one. Levine and Zervos (1998)point out that banks and capital markets presumably play different roles interms of supporting growth and productivity.

This process of specialization of pension fund management also impliesa spillover effect affecting other related agents, such as investment-bankers,firm managers and regulatory authorities. It should imply the use of more

84 REVISTA ABANTE, VOL. 5, Nº 2

recent knowledge, as well as newer communications and informationtechnology. At the same time, professional investors have an interest inhelping authorities to determine the appropriate direction for improvementsin the legal framework.

A. 3. Financial innovation incentives

Bodie (1989) argues that the accumulation of funds has been an importantforce shaping the evolution of financial innovation. As capital markets grow,there are bigger gains to financial innovation. However, the industry analyzedin his study consists mostly of defined-benefit pension plans in the UnitedStates. This structure implies particular kinds of incentives. In the case ofChilean-style defined-contribution systems, there may be an emphasis onshorter-term performance, as in the case of mutual funds. On the otherhand, there is evidence of herd behavior among managers of defined benefitpension funds. In any event, if significant amounts of funds accumulate,there are natural incentives to creating new financial instruments, includinglong-term instruments, securities from new sectors of the economy, andalso to allow investments in foreign markets (Iglesias, 1998).

From a different perspective, Prowse (1998) argues that in the UnitedStates pension funds have been the major source of finance for limitedpartnerships and joint venture funds, which operate in the private equitymarket, and are a major financing source for start-ups and small firms. Asimilar argument is made by Catalán et al. (2000) for contractual savingsin general: portfolio managers assume liquidity risk in exchange of higherexpected returns. However, this argument might be stronger with regardto life insurance companies and defined benefit schemes. In the case ofcompetitive defined-contribution pension systems, as in the case of mutualfunds, portfolio managers face the incentives to show attractive returnsover relatively short periods of time. This may limit the desire of portfoliomanagers to favor more illiquid and harder to value investments.

B. Concurrent Conditions

Pension reform seldom takes place in isolation, and this has twoimplications. First, other reforms that take place simultaneously confoundthe possible incremental effects of pension reform. Second, it is possible

PENSION REFORM AND CAPITAL MARKETS 85

that without other concurrent conditions, pension reform turns out not to besuccessful in terms of supporting the development of a capital market.Thus, it is important to identify concurrent conditions, meaning the list ofinstitutional and economic reforms that may facilitate or condition the positiveeffect of pension reform on capital market development. However, inmany cases these concurrent conditions might not be truly exogenous, sinceother reforms are required to make pension reform successful (such as thelast points in this section). Here we take ideas from Fontaine (1996),Blommestein (1997) and Uthoff (1997), in addition to elaborating new onesand organizing them into a smaller number of broader categories.8

B.1. Macroeconomic stability in a market environment

Macroeconomic instability is likely to reduce the positive effects of pensionreform on capital market development. Since capital markets intermediatefunds from different sources, well functioning credit markets and non-distortedfundamental prices are required, such as price levels, real exchange ratesand real interest rates. Although not necessarily true for all economies,based on the Chilean experience with endemic inflation, we can argue thatthe availability of indexation (inflation-protection) helps the development offixed income markets9. It is also likely that pension reform will directlycontribute to macroeconomic stability, by alleviating the political anddemographic pressures imposed by pay-as-you-go systems, since it usuallyrequires significant fiscal reform. The reform requires explicit recognitionof the pension system’s debt levels and raises a discussion of how this isto be financed. In the end, whether or not pension reform helpsmacroeconomic stability will depend on the strength of the reform and thefinancing of the transition10. Later, we discuss the impact of pensionreform on savings.

8 For an analysis of the reforms and stabilization process of the Chilean economy, seeBosworth et al. (1994).

9 Diamond and Valdés (1994) also noted this. Walker (1998) in addition emphasizes theneed of a consistent legal environment.

10 However, pension reform may fail to reduce the fiscal profligacy if, for instance, fundmanagers are required to hold large blocks of government debt, avoiding hard fiscaldecisions altogether.

86 REVISTA ABANTE, VOL. 5, Nº 2

B.2. Adequate tax incentives

A well-known fact is that the development of specific financial instrumentsimportantly depends on tax-incentives. For example, other things equal, taxadvantages for debt will provide incentives to the development of a marketfor corporate debt. Taxes may also give advantages to using retainedearnings instead of issuing equity; or related-firm lending instead of issuingnew debt. Uthoff (1998) emphasizes for the case of Chile that due to tax-incentives earnings retention by firms has been one of the important sourcesof increased savings in Chile. Notice that earnings retention may be apolicy favored by long-term institutional investors, especially under a shortageof investment alternatives, which makes these facts interdependent. Also,Walker (1998) points out that inflation-neutrality in the tax code favors thedevelopment of an indexed debt market. Therefore, the kind of tax regimein place is an important variable to be controlled for when assessing theimpact of pension reform on capital markets.

B.3. Progressive capital control liberalization

It may be debatable whether the incremental impact of pension reformon capital markets depends or not on the extent there is freedom in capitalinflows and outflows, although it is likely that restrictions negatively affectthe overall development of the market. There may thus be a joint positiveeffect. However, if both reforms tend to happen simultaneously it may bedifficult to determine the impact of each.

B.4. Adequate regulation and competition in the financial servicesindustry

Overregulation or lack of competition in the financial services industrymay limit the development possibilities of capital markets. For example,competition among security traders and stock exchanges allows fortransaction costs that do not inhibit trading. Also, prudential bank regulationimplies fair competition among alternative fund suppliers, including pensionfunds.

PENSION REFORM AND CAPITAL MARKETS 87

B.5. Property rights, bankruptcy legislation and investor protection

In capital markets, contingent-claims on the value of firms are traded. Ifthese claims’ boundaries are not well delimited, security prices will besignificantly penalized, rendering the issuance of such claims unattractivefor firms seeking funds. It is thus obvious that a required condition for acapital market to develop, with or without pension reform, is that propertyrights are well established. La Porta et al. (1996, 1997) argue that legalprotection to investors has no good substitutes, especially in Civil Lawcountries. This has additional implications in the case of regulated industries.In any case, it is important to keep in mind that regulators that pursue asuccessful pension reform must adapt investor protection and bankruptcylegislation to the needs of the new institutional investor. Lack of protectionmay negatively affect public trust of the reform.

B.6. Privatization of state-owned companies

Privatization of state-owned firms is likely to have important effects onthe development of capital markets. Firms that relied before on centralizedcredit allocation may now opt for the bond and stock markets. Also, if theprivatization process purposely considers a vast dispersion of property, highertransaction volumes in stocks are expected. Pension fund participation mayenhance these effects. However, privatization can be implemented in manyways, such as assigning shares of the privatized firms directly into individualaccounts, with or without authorization to trade them. In addition, it couldbe implemented as a private transaction between the State and a singlecontrolling shareholder. In the later two cases, no impact on capital marketdevelopment is expected. Finally, reversals could take place. After the1998 Asian crisis, many of the previously privatized firms in Latin Americawere purchased by private investors that bought out minority shareholders,converting them into closely-held companies, and sometimes delisted themfrom the exchanges. Explanations for this may be related with a lack ofinvestor protection and rent seeking by controlling shareholders (Bebchuk1999).

88 REVISTA ABANTE, VOL. 5, Nº 2

C. Consequences of pension fund induced capital market development

Recent empirical evidence has established links between indicators offinancial market development, economic growth and productivity11. In thispaper, we are interested in the effect of pension reform on capital marketdevelopment. Thus, we only discuss the effects on economic activity thatpension reform is likely to have via capital markets. We do not analyzeother channels through which pension fund reform and economic growthmay be related.

From a theoretical point of view, the development of capital markets mayhave a positive effect on economic growth through two channels: (a)increased savings; and (b) more efficient allocation of savings.

C.1. Increased savings

The effect of pension fund reform on savings depends on manycharacteristics of the reform and the economy. To name a few: (a) thefinancing of the transition towards a new pension system; (b) the extent ofcrowding out of voluntary savings by mandatory savings; (c) the strengthof intergenerational transfer motives; and (d) redistribution effects betweengroups with different marginal saving rates and/or borrowing constraints12.In addition, pension reform is likely to accelerate the process of capitalmarket development. Through this channel, the reform helps improve theprocess of screening and monitoring of new projects and also helps with thediversification of systemic risk. This enables individuals to participate inmore investment projects, increasing the rate of investment of the economy.

At the empirical level, the effect of pension fund reform on savings isambiguous. On the one hand, some studies analyzing the Chilean case showa negligible effect on net of Social Security saving rates and others apositive effect on saving rates among higher income households because oftax benefits (Coronado, 1999). From a list of 19 econometric studiessurveyed by Schmidt-Hebbel (1998), on the response of voluntary privatesavings to social security contributions and benefits, 8 report lower savingrates, 3 report higher saving rates and 8 report no significant effect. The

11 See Levine and Zervos (1998), Levine et al. (1998), De Gregorio (1998), Rousseau(1998) and Arestis et al. (2001).

12 For an analysis and empirical evidence on the effect of pension fund reform on savingssee Coronado (1997), Schmidt-Hebbel (1998), Burtless (1997), and Mackenzie et al.(1997).

PENSION REFORM AND CAPITAL MARKETS 89

indirect impact on savings through capital market development does notseem to perform better. Levine and Zervos (1998) show that none of thefinancial indicators provided in their study is significantly correlated withprivate savings.

C.2. Cost of capital reduction for firms

Iglesias (1998) argues that the fully funded pension systems may implya reduction in the cost of funds for firms, and attributes this effect to theaccumulation of financial savings as opposed to other types of wealth. Ifprivate savings are not intermediated by financial markets they take theform of private equity, land, gold and others13. Vittas (1996) argues thatpension reform brings pooling of long-term financial savings, which canunderpin capital market development.

These arguments are incomplete because it is necessary to identify thekind of structural change that need to take place in order to justify that therequired rates of return may indeed decrease after the accumulationsignificant pension funds. This is particularly important given that, as wepointed out above, econometric studies show only small increases in savingsattributable to pension reform. In other words, if pension funds were simplyto substitute other sources of private savings, why would this imply a lowercost of capital? We can think of three possible answers to this: lower directcosts of issuing securities, lower term premia, and lower risk premia.These arguments resemble the effects that usually are attributed to capitalmarket integration (for example, see Bekaert and Harvey, 1998 and thereferences cited therein)14.

First, due to the overall development of the capital market, the directcosts of issuing securities are likely to be lower. This naturally implies areduction in the cost of capital. We analyze this channel in more detail laterin this section.

13 See also Pérez Mackenna (1988).14 In any case, studies such as that of Fama and French (2001) have found that there has

been a downward trend in the equity premium. In this context, pension reform mayhave an incremental impact, either by accelerating the premium reduction or by havingan additional independent effect. This is a potentially complex issue and we do notintend to dilucidate it in this paper.

90 REVISTA ABANTE, VOL. 5, Nº 2

Second, the time-horizon of pension funds is expected to be longer thanthat of individuals or firms that buy financial instruments. In the case ofindividuals, even if at aggregate levels total savings are stable over time, theaverage maturity of such savings (duration) is likely to be relatively short.This should indeed be the case, considering the precautionary nature ofsavings. In the case of firms, whose business is not financial, they transitorilyinvest in financial securities. Thus, by definition they are short-terminvestments. In contrast, and even though pension fund performance maybe measured in the short term, the certainty that a large fraction of thesefunds need not be liquidated until the distant future, at least in the aggregate,allows pension fund managers to chose longer investment maturity. Thismeans that even if total savings do not increase after a pension reform, theaverage maturity of the financial securities would be lengthened. In otherwords, the required term premium (also called liquidity premium) shouldbe lower15. The next argument reinforces this idea.

Third, given that pension funds manage other people’s money and thatabsolute volatility is not expected to have a direct effect on the welfare ofmanagers, it is likely that the average risk tolerance of the capital marketwill increase. This implies a lower equity risk premium, which also lowersthe average cost of capital for firms.

Thus, the above implies that the cost of capital should fall. Moreover,if such cost of capital is evaluated at the optimal mix of financing sourceswe may be able to conclude even more strongly that the risk-adjusted costof capital would decrease16. Here it is important to notice that the abilityto obtain the appropriate kind of longer-term funding may imply reductionsin the residual losses of issuing securities, because of more efficient risk-sharing mechanisms. For example, a higher degree of asset-liability duration-matching by industrial firms, lowers expected bankruptcy costs thus reducingfinancing costs.

This may also have implications for the costs associated with informationasymmetries. Even if such asymmetries were to remain the same, thesecosts may be reduced. For example, Myers’ (1982) pecking-order theoryestablishes that there will be a sequence of preferred financing sources,

15 Short-term performance evaluation may indeed shorten the investment horizons of pensionfund managers, but these are still expected to be longer than individual investors’.Applying the same argument to defined benefit systems it may be true that the reductionin the required premia would be larger in such a case.

16 It is not enough to just look at the average interest rate that would be charged to firms.

PENSION REFORM AND CAPITAL MARKETS 91

starting with short-term debt, ending with equity, depending on the degreeof information asymmetry, ceteris paribus. This argument takes as givena reasonable equilibrium among the costs of the different financingalternatives. The fact that firms could now get better-suited financingpackages would reduce the residual losses due to information asymmetry,because a lower number of projects would be left out due to inappropriatefinancing sources.

The above implies that even though pension reform may not increasetotal savings, it is likely to have a positive effect on growth and welfarecaused by a better allocation of investment funds. If the overall (risk-adjusted) cost of capital indeed falls, at every point in time there will be adifferent (not necessarily larger) set of attractive investment projects. Iflonger-term-higher-expected-return projects are now accepted (whichperhaps also are the riskier ones, from the perspective of a short-terminvestor) this implies higher expected economic growth17.

C.3. Financial market integration

Obstfeld (1994) argues that more integrated capital markets allow betterrisk sharing mechanisms tilting the market portfolio towards higher-returninvestments thus increasing economic growth. De Gregorio (1999) findsevidence that financial integration increases the depth of financial systeminducing higher economic growth.

An institutional environment that favors the development of the pensionfund industry is likely to give additional incentives to the international integrationof financial markets. Financial integration can be understood as an alignmentof the risk-return trade-off with the rest of the world’s. Increased liquidity,transparency and especially a better protection of minority shareholder rightsallow us to expect more foreign portfolio investment.

From a different perspective, since pension funds can become quite largewith respect to the size of the domestic capital market, the possibility ofallowing local funds to invest abroad becomes more likely. However, thisprocess may be slow. Perhaps because of incentives arising from competition

17 It may be argued that this need not be true if there is access to external capital markets.Nevertheless, as Chile’s 1982 experience indicates, external financing may entail significantrisks for projects in the non-tradable sector of the economy. Thus, given a lack ofcurrency matching, fewer projects would be considered attractive on a risk-adjusted basis.

92 REVISTA ABANTE, VOL. 5, Nº 2

among AFPs, but also because of regulatory restrictions, Chile began investingsignificant amounts abroad only after the Asian financial crisis.

Finally, information requirements, sound market practices and minorityshareholder protection may make it easier for local firms to issue securitiesabroad (such as bonds and ADRs). The three forces lead the capital marketstowards integration.

Here it is important to keep in mind that, independent of pension reform,financial integration per se may also lead to a reduction in the cost of capitalfor firms. Thus, it is necessary to control for this in order to verify empiricallyif indeed the implementation of a pension system reduces the cost of ca-pital. For instance, for Chile, Walker and Lefort (1999) report a permanentand significant fall in the dividend yield levels in 1990, which in turn reflectsa fall in the cost of equity capital that is probably due to higher integration.This coincides with a time-period in which pension funds were allowed toincrease their participation in local equity.

C.4. Reduction of transaction costs, increased liquidity and lower pricevolatility

Several authors have written about these issues (for example, seeBlommestein, 1997; Iglesias, 1998; Vittas, 1998). From a theoretical pointof view, more liquid (less expensive) stock markets increase incentives toinvest in long-duration projects, because investors can more easily sell theirstake before the project matures (Levine and Zervos, 1998). Therefore,good investment projects with long duration can be undertaken, increasingeconomic growth. Moreover, because of economies of scale, there may bea virtuous circle in the relationship between transaction costs, liquidity andvolatility, in that they can be presumed to reinforce each other. In addition,new institutions may be created to handle increased transaction volumes,such as new electronic security trading systems, more competition amongalternative markets, centralized custody deposits, and others alike. Shleiferand Vishny (1986) present a less optimistic view. They argue that moreliquidity in the market facilitates security selling, reducing incentives ofminority shareholders to monitor controlling shareholders. The empiricalevidence, however, shows that both more liquidity and less price volatilityare positively correlated with current and future economic growth18.

18 See Levine and Zervos (1998).

PENSION REFORM AND CAPITAL MARKETS 93

The expectations of lower security price volatility and higher volumescaused by pension funds can be justified using the same kind of argumentsregarding the effects of capital market integration (for example see Bekaertand Harvey, 1998): it happens due to a wider investor base jointly withaccess to more information and analysis. This implies that prices fluctuatemore closely with fundamental values and that small deviations from suchfundamentals cause large volumes of trades.

There is yet another perspective that may allow us to conclude thatsecurity price volatility could decrease because of pension reform – thetime dimension. Indeed, at least part of the correlation exhibited by securityreturns across different markets and regions can be attributed to variationin required risk premia. If local pension funds’ risk tolerance is assumedto remain relatively constant over time, then advantage should be taken ofvariations in risk premia (that perhaps are caused by variations in foreigninvestors’ risk tolerance). This is done by purchasing securities when therisk premia is high (at low prices) and vice versa. Thus, price variationsshould be less extreme when compared with a market that does not havethis class of investors. Notice that this is consistent with Caballero’s (2001)idea that local capital markets should help mitigate external shocks.

C.5. Secondary effects on the financial system’s structure and othermarkets

The development of a pension system may imply different forms ofdevelopment and organization of other competing/complementary industries.For example, Blommestein (1998) finds related development of the life anddisability insurance industry in OECD countries. Thus government financing,banks, life insurance companies, and even certain industries will be affected.For example, it may impact the housing industry if the mortgage bondmarket is successful.

Since significant long-term resources are accumulated, a redefinition ofthe market niches for banks and other fund providers is likely to take place.Banks will probably concentrate on shorter-term financing and/or onindividuals and smaller firms.

It is important to consider that, at the capital market level, funds aremelted together and it becomes impossible to relate specific sources offunds with specific uses. It would therefore be inappropriate to judge the

94 REVISTA ABANTE, VOL. 5, Nº 2

impact that pension funds have on aggregate investment without consideringthese indirect effects. For instance, it may be true that a significant fractionof the pension funds is invested in government securities, but this freesfunds from other potential sources, such as banks. That is why it may beincorrect to assert that a particular kind of financial investment by pensionfunds is “not productive” as suggested by Uthoff (1997).

III. QUALITATIVE AND TIME SERIES EVIDENCE

This section is organized as follows: We first analyze qualitative andtime series evidence regarding the effect of pension fund reform on capitalmarket development for three reformer countries, Argentina, Chile andPeru, and assess whether it supports or contradicts the hypotheses pre-sented in the previous section. We look both at the effect of pension fundreform on capital market development and at the consequences of thisdevelopment in terms of lower cost of capital and financial integration. Wealso consider other explanations (from the list of concurrent conditions) totest the robustness of this evidence.

We use several data sources. First, the most specific data regardingpension fund portfolio composition is obtained from the pension fund super-visory entity of each country. Specifically, for Chile, Peru and Argentina,we obtain data on portfolio composition and the number of bond and stockissuers present in the pension fund portfolios from the local supervisoryagencies, and Ramos (1999) for Peru. For these three countries, we alsoconsider several stock market indicators that are compared to the LatinAmerican average. These numbers come from the IFC databases andcomprise dividend yields, price-to-book ratios, traded volumes, stock marketreturns, and volatility measures. Other data sources are local stock ex-changes and central banks. Finally, country data on macroeconomic andother capital market indicators is obtained from Beck et al. (1999). Wealso measure the importance of pension fund investments in the corporatesector (stocks and bonds) relative to total market capitalization. Regardingtransaction costs we use information from Iglesias (1998) and De la Cuadraand Galetovic (1998) in the case of Chile, and from The Emerging MarketsFactbook (1998) for a list of 45 different countries.

PENSION REFORM AND CAPITAL MARKETS 95

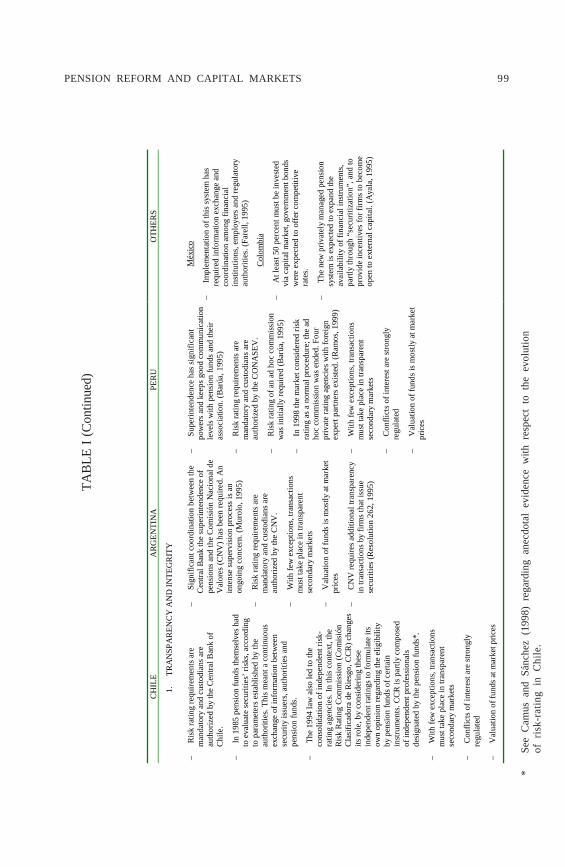

A. Institutional capital and increased specialization in asset management

The anecdotal evidence presented in Table I heuristically supports theidea of an environment that favors modernization and reform, and the notionof an adaptive legal framework. It is important to highlight the formal andinformal participation by pension funds in the legislative process, whichprobably becomes more important the larger pension funds are relative tothe local economy. This ensures that resulting laws effectively resolve theproblems faced by these investors. For example, allowing Chilean pensionfunds to hedge using currency forwards helps explain why as of December1998 a significant 5.6 percent of the total funds managed were alreadyinvested abroad19.

Competitive pension fund management in a global environment providesincentives for specialization in the fund management business. Moreover,with the internationalization of local pension funds, technology is transferredfrom foreign to local fund managers. This means using modern informationservices and technology, a learning process to understand and invest in newinstruments, and a permanent transfer of technology from the more advancedcountries. Frequent contact with authorities and security issuers requiresincreased professionalism on their part as well.

The role of pension funds regarding corporate governance is also illustratedin Table I, and the evidence seems to be supportive of an improved balanceamong market participants. The main channels are the participation ofindependent board members representing pension funds, and the changes incorporate legislation. Iglesias (2000) argues that partly because of pensionreform, in Chile the number of independent boards members increased,monitoring costs fell as a result of improved information quality, companieswhere pension funds have invested are under close public scrutiny, shareholdermeetings become more relevant, and bondholder protection also improves.

The evidence presented is also consistent with the claim that bothtransparency and integrity improve with reform. Risk rating procedures atthe very least promote information exchange and coordination among issuers,authorities and pension funds, which is expected to improve transparency.In addition, transactions have to take place in organized secondary marketsand securities have to be valued at market prices, which provides incentivesto monitor security prices.

19 Of course, liberal investment regulations and poor local market performance also explainwhy Chilean pension fund managers started to look abroad.

96 REVISTA ABANTE, VOL. 5, Nº 2TA

BLE

IIN

STIT

UTI

ON

AL

CAPI

TAL:

EV

IDEN

CE

CH

ILE

ARG

ENTI

NA

PE

RU

O

THER

S

1.

AD

APT

IVE

LEG

AL

ENV

IRO

NM

ENT

− V

aldé

s an

d C

ifuen

tes

(199

0, T

able

s 1

and

2)

pres

ent

a lis

t of

15

le

gal

mod

ifica

tions

re

late

d w

ith

pens

ion

refo

rm.

Arr

au

(199

4)

adds

th

ree

addi

tiona

l on

es.

Igle

sias

(1

999)

m

entio

ns t

hat

in a

ll, s

ome

25 s

uch

refo

rms

have

be

en

rela

ted

with

th

e in

vest

men

t an

d tra

nspa

renc

y re

quire

men

ts o

f pen

sion

fund

s.

− Th

e pr

oces

s of

re

form

s ha

s be

en

cont

inuo

us a

nd m

ostly

cau

sed

or a

t le

ast a

ccel

erat

ed b

y pe

nsio

n fu

nds.

− Pe

nsio

n fu

nds

dire

ctly

par

ticip

ate

in

the

form

ulat

ion

of (

or o

bser

vatio

ns to

) ne

w la

ws.

For e

xam

ple,

ther

e w

as jo

int

wor

k of

inde

pend

ent p

rofe

ssio

nals

with

th

e re

gula

tory

aut

horit

ies

to f

orm

ulat

e th

e C

apita

l M

arke

t R

efor

m o

f 19

94.

Pens

ion

fund

s ac

tivel

y pa

rtici

pate

d in

th

e fin

al st

age

of th

e pr

oces

s.

− A

dded

fle

xibi

lity

to

the

norm

s re

gard

ing

the

inve

stm

ent

of p

ensi

on

fund

s ab

road

, in

clud

ing

the

use

curre

ncy

forw

ard

cont

ract

s as

hed

ging

in

stru

men

ts

(this

w

as

not

initi

ally

co

nsid

ered

in th

e 19

94 la

w).

− Th

e m

ere

disc

ussi

on o

f th

e pe

nsio

n re

form

in

Arg

entin

a to

ok m

ore

than

tw

o ye

ars

to b

e pr

epar

ed im

plem

ente

d,

whi

ch

occu

rred

in

19

93.

(Mur

olo,

19

95)

− A

t le

ast

19 r

efor

ms

to c

apita

l mar

ket

law

s an

d 28

res

olut

ions

are

ass

ocia

ted

with

the

accu

mul

atio

n of

pen

sion

fund

s (A

SAP,

199

8, p

.157

-158

, p. 1

65-1

69).

− Th

e Pe

ruvi

an

pens

ion

refo

rm

of

Dec

embe

r 19

92

was

th

e m

ost

impo

rtant

refo

rm o

f the

rece

nt y

ears

. It

is e

xpec

ted

to h

ave

a si

gnifi

cant

impa

ct

on th

e ec

onom

y. (B

arúa

, 199

5)

− Th

e fin

anci

al

syst

ems

face

s tw

o im

puls

es: l

iber

aliz

atio

n of

the

econ

omy

and

new

ru

les

that

se

ek

the

mod

erni

zatio

n an

d de

velo

pmen

t of

the

capi

tal

mar

ket,

in

the

cont

ext

of

inst

itutio

nal

inve

stor

s th

at

requ

ire

incr

easi

ng

inve

stm

ent

oppo

rtuni

ties

(Ram

os, 1

999)

Méx

ico

− Th

e co

mpl

emen

tary

pen

sion

ref

orm

(S

iste

ma

de

Aho

rro

para

el

R

etiro

, SA

R)

requ

ired

signi

fican

t m

odifi

catio

ns to

the

soci

al s

ecur

ity a

nd

hous

ing

law

s. (F

arel

l, 19

95)

Col

ombi

a

− Pe

nsio

n re

form

w

as

appr

oved

in

D

ecem

ber 1

993

afte

r a

long

legi

slat

ive

deba

te.

The

new

sy

stem

st

arte

d to

op

erat

e in

Apr

il 19

94. (

Aya

la, 1

995)

PENSION REFORM AND CAPITAL MARKETS 97TA

BLE

I (C

ontin

ued)

CH

ILE

AR

GEN

TIN

A

PER

U

OTH

ERS

2 .IN

CREA

SED

SPE

CIA

LIZA

TIO

N IN

TH

E IN

VES

TMEN

T D

ECIS

ION

-MA

KIN

G P

ROCE

SS

− Th

e la

test

info

rmat

ion

serv

ices

and

te

chno

logi

es a

re u

sed

for m

anag

ing

pens

ion

fund

s, gi

ven

the

com

petit

ive

adva

ntag

e th

at th

ey p

rovi

de

− Se

curit

y iss

uers

hav

e ro

unds

of

“con

vers

atio

ns”

with

pen

sion

fund

s an

d lif

e in

sura

nce

com

pani

es (A

FPs

are

not a

llow

ed to

“ne

gotia

te”

and

dete

rmin

e pr

ices

in a

dvan

ce to

the

actu

al tr

adin

g). F

or e

xam

ple,

fees

and

in

vest

men

t pol

icie

s of l

ocal

inve

stm

ent

fund

s are

neg

otia

ted

with

AFP

s. Th

e re

quire

d cr

edib

ility

incr

ease

s the

co

unte

rpar

ts’ p

rofe

ssio

nalis

m.

− In

vest

ing

in “

new

” in

stru

men

ts (s

uch

as fo

rwar

d co

ntra

cts)

requ

ires a

co

ntin

uous

lear

ning

pro

cess

− W

ith th

e in

tern

atio

naliz

atio

n of

loca

l pe

nsio

n fu

nd in

vestm

ents

, tec

hnol

ogy

is tra

nsfe

rred

from

fore

ign

fund

m

anag

ers.

− In

itial

ly, t

echn

olog

y w

as tr

ansf

erre

d fro

m C

hile

an c

ount

erpa

rts a

t all

leve

ls (o

ffici

al a

nd p

rivat

e).

− U

se o

f lat

est i

nfor

mat

ion

serv

ices

and

te

chno

logy

− C

onta

ct w

ith se

curit

y is

suer

s

− In

itial

ly te

chno

logy

was

tran

sfer

red

from

Chi

lean

cou

nter

parts

at a

ll le

vels

(offi

cial

and

priv

ate)

.

− U

se o

f lat

est i

nfor

mat

ion

serv

ices

and

te

chno

logy

− A

utho

rizat

ion

of th

e in

vest

men

t in

Bra

dy b

onds

requ

ires a

spec

ific

lear

ning

pro

cess

in o

rder

to o

pera

te in

th

at m

arke

t

− Co

ntac

t with

secu

rity

issu

ers

98 REVISTA ABANTE, VOL. 5, Nº 2TA

BLE

I (C

ontin

ued)

CH

ILE

ARG

ENTI

NA

PE

RU

OTH

ERS

3.

CO

RPO

RA

TE G

OV

ERN

AN

CE

BA

LAN

CE

− In

vest

ors p

rete

ndin

g to

obt

ain

or

incr

ease

con

trol o

f firm

s usu

ally

ex

plai

n th

eir p

lans

to p

ensi

on fu

nds,

and

cons

ider

thei

r opi

nion

as

(som

etim

es sm

all b

ut) i

nflu

entia

l sh

areh

olde

rs.

− A

FPs a

re re

quire

d to

vot

e fo

r in

depe

nden

t can

dida

tes t

o be

mem

bers

of

the

boar

d of

dire

ctor

s whe

re fu

nds

are

inve

sted

− D

urin

g th

e bo

ard

mem

ber e

lect

ion

perio

d, n

egot

iatio

ns a

mon

g pe

nsio

n fu

nds t

ake

plac

e, in

ord

er to

det

erm

ine

the

nam

es o

f can

dida

tes t

hat p

ass t

he

inde

pend

ence

requ

irem

ents

est

ablis

hed

by la

w.

− Th

e A

ssoc

iatio

n of

Pen

sion

Fun

ds

(ASA

FP) i

nfor

ms a

utho

ritie

s and

the

publ

ic o

pini

on in

gen

eral

abo

ut

corp

orat

e go

vern

ance

situ

atio

ns th

at

are

nega

tive

for p

ensi

on fu

nds.

− A

FPs a

re ty

pica

lly re

quire

d by

the

Supe

rinte

nden

ce to

file

repo

rts

rega

rdin

g ev

ents

or t

rans

actio

ns b

y se

curit

y is

suer

s tha

t may

hav

e ne

gativ

e ef

fect

s on

pens

ion

fund

inve

stm

ents

.

− A

new

ban

krup

tcy

law

is im

plem

ente

d (L

aw 2

4.55

2 of

199

5).

− A

FPs a

ctiv

ely

prom

oted

that

larg

e fir

ms b

e el

igib

le (p

ayin

g th

emse

lves

th

e re

late

d ex

pens

es).

− B

eing

“A

FPab

le”

beca

me

a ne

w

stat

us, r

efle

ctin

g in

form

atio

n tra

nspa

renc

y (R

amos

, 199

9)

PENSION REFORM AND CAPITAL MARKETS 99

*Se

e C

amus

and

Sán

chez

(19

98)

rega

rdin

g an

ecdo

tal

evid

ence

with

res

pect

to

the

evol

utio

nof

ris

k-ra

ting

in C

hile

.

TAB

LE I

(Con

tinue

d)

CH

ILE

AR

GEN

TIN

A

PER

U

OTH

ERS

1.

TRA

NSP

AR

ENC

Y A

ND

INTE

GR

ITY

− R

isk

ratin

g re

quire

men

ts a

re

man

dato

ry a

nd c

usto

dian

s are

au

thor

ized

by

the

Cen

tral B

ank

of

Chi

le.

− In

198

5 pe

nsio

n fu

nds t

hem

selv

es h

ad

to e

valu

ate

secu

ritie

s’ ri

sks,

acco

rdin

g to

par

amet

ers e

stab

lishe

d by

the

auth

oriti

es. T

his m

eant

a c

ontin

uous

ex

chan

ge o

f inf

orm

atio

n be

twee

n se

curit

y is

suer

s, au

thor

ities

and

pe

nsio

n fu

nds.

− Th

e 19

94 la

w a

lso

led

to th

e co

nsol

idat

ion

of in

depe

nden

t ris

k-ra

ting

agen

cies

. In

this

con

text

, the

R

isk

Rat

ing

Com

mis

sion

(Com

isió

n C

lasi

ficad

ora

de R

iesg

o, C

CR

) cha

nges

its

role

, by

cons

ider

ing

thes

e in

depe

nden

t rat

ings

to fo

rmul

ate

its

own

opin

ion

rega

rdin

g th

e el

igib

ility

by

pen

sion

fund

s of c

erta

in

inst

rum

ents

. CC

R is

par

tly c

ompo

sed

of in

depe

nden

t pro

fess

iona

ls

desi

gnat

ed b

y th

e pe

nsio

n fu

nds*

.

− W

ith fe

w e

xcep

tions

, tra

nsac

tions

m

ust t

ake

plac

e in

tran

spar

ent

seco

ndar

y m

arke

ts

− C

onfli

cts o

f int

eres

t are

stro

ngly

re

gula

ted

− V

alua

tion

of fu

nds a

t mar

ket p

rices

− Si

gnifi

cant

coo

rdin

atio

n be

twee

n th

e C

entra

l Ban

k th

e su

perin

tend

ence

of

pens

ions

and

the

Com

isió

n N

acio

nal d

e V

alor

es (C

NV

) has

bee

n re

quire

d. A

n in

tens

e su

perv

isio

n pr

oces

s is a

n on

goin

g co

ncer

n. (M

urol

o, 1

995)

− R

isk

ratin

g re

quire

men

ts a

re

man

dato

ry a

nd c

usto

dian

s are

au

thor

ized

by

the

CN

V.

− W

ith fe

w e

xcep

tions

, tra

nsac

tions

m

ust t

ake

plac

e in

tran

spar

ent

seco

ndar

y m

arke

ts

− V

alua

tion

of fu

nds i

s mos

tly a

t mar

ket

pric

es

− C

NV

requ

ires a

dditi

onal

tran

spar

ency

in

tran

sact

ions

by

firm

s tha

t iss

ue

secu

ritie

s (R

esol

utio

n 26

2, 1

995)

− Su

perin

tend

ence

has

sign

ifica

nt

pow

ers a

nd k

eeps

goo

d co

mm

unic

atio

n le

vels

with

pen

sion

fund

s and

thei

r as

soci

atio

n. (B

arúa

, 199

5)

− R

isk

ratin

g re

quire

men

ts a

re

man

dato

ry a

nd c

usto

dian

s are

au

thor

ized

by

the

CO

NA

SEV

.

− R

isk

ratin

g of

an

ad h

oc c

omm

issi

on

was

initi

ally

requ

ired

(Bar

úa, 1

995)

− In

199

8 th

e m

arke

t con

side

red

risk

ratin

g as

a n

orm

al p

roce

dure

; the

ad

hoc

com

mis

sion

was

end

ed. F

our

priv

ate

ratin

g ag

enci

es w

ith fo

reig

n ex

pert

partn

ers e

xist

ed. (

Ram

os, 1

999)

− W

ith fe

w e

xcep

tions

, tra

nsac

tions

m

ust t

ake

plac

e in

tran

spar

ent

seco

ndar

y m

arke

ts

− C

onfli

cts o

f int

eres

t are

stro

ngly

re

gula

ted

− V

alua

tion

of fu

nds i

s mos

tly a

t mar

ket

pric

es

Méx

ico

− Im

plem

enta

tion

of th

is sy

stem

has

re

quire

d in

form

atio

n ex

chan

ge a

nd

coor

dina

tion

amon

g fin

anci

al

inst

itutio

ns, e

mpl

oyer

s and

regu

lato

ry

auth

oriti

es. (

Fare

ll, 1

995)

Col

ombi

a

− A

t lea

st 5

0 pe

rcen

t mus

t be

inve

sted

vi

a ca

pita

l mar

ket,

gove

rnm

ent b

onds

w

ere

expe

cted

to o

ffer c

ompe

titiv

e ra

tes.

− Th

e ne

w p

rivat

ely

man

aged

pen

sion

sy

stem

is e

xpec

ted

to e

xpan

d th

e av

aila

bilit

y of

fina

ncia

l ins

trum

ents

, pa

rtly

thro

ugh

“sec

uriti

zatio

n”, a

nd to

pr

ovid

e in

cent

ives

for f

irms t

o be

com

e op

en to

ext

erna

l cap

ital.

(Aya

la, 1

995)

100 REVISTA ABANTE, VOL. 5, Nº 2

Finally, the clear identification and penalization of inadequate resolutionof the conflicts of interest faced by pension fund managers helps identifysimilar situations in the case of other market participants. Bad marketpractices become more clearly recognized in terms of their negative effectson third parties, in this case on future pensioners. Thus, they may facemore severe social sanction, be it formal or informal.

In any case, for the three countries analyzed, other reforms tookplace at the same time, including macroeconomic stabilization plans. Naturally,these complementary reforms underpin the modernization process that isreflected in the accumulation of institutional capital.

B. Cost of capital reduction for firms

In general, it is difficult to estimate the impact that the competitiveallocation of pension funds towards private securities has had on the costof capital. A thorough analysis is needed, because many other variablesmay have evolved favorably or unfavorably during the same time period.But the analysis presented below provides a reference point.

B.1. The qualitative evidence

An indirect way to look at the effect that pension funds may have onfirms’ cost of capital is to consider their importance within the existing stockof securities. If pension funds buy a large fraction of a growing stock ofsecurities, it probably reflects a convenient required rate of return fromthe perspective of issuers; otherwise they would not issue such securities.Furthermore, the lack of investment alternatives frequently noted by pensionfund managers might even reflect disequilibrium rates of return, whichwould be too low for periods of time in which insufficient investmentalternatives are available.

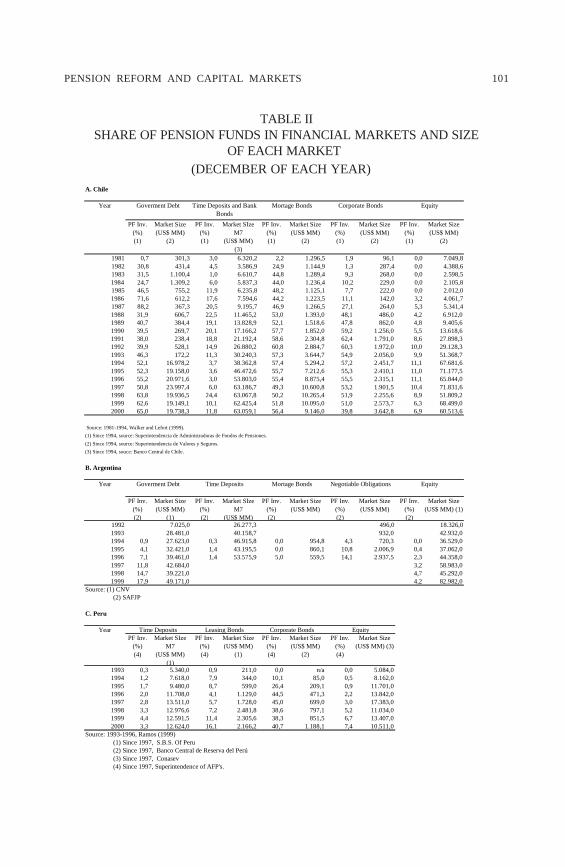

Table II shows that in December of 2000 Chilean pension funds heldabout 40 percent of the total amount outstanding of corporate bonds. Thisnumber has ranged between 40 and 62 percent since 1988. Also in Decemberof 2000 they held 7 percent of the total equity market cap (within the range4-11 percent). These percentages further increase if insurance companiesare also considered.

For Argentina, Table II shows that in 1997 pension funds held importantpercentages of the total amount outstanding of each kind of security. This

PENSION REFORM AND CAPITAL MARKETS 101

TABLE IISHARE OF PENSION FUNDS IN FINANCIAL MARKETS AND SIZE

OF EACH MARKET (DECEMBER OF EACH YEAR)

Year

PF Inv. (%) (1)

Market Size (US$ MM)

(2)

PF Inv. (%) (1)

Market SIze M7

(US$ MM) (3)

PF Inv. (%) (1)

Market Size (US$ MM)

(2)

PF Inv. (%) (1)

Market Size (US$ MM)

(2)

PF Inv. (%) (1)

Market Size (US$ MM)

(2)

1981 0,7 301,3 3,0 6.320,2 2,2 1.296,5 1,9 96,1 0,0 7.049,81982 30,8 431,4 4,5 3.586,9 24,9 1.144,9 1,3 287,4 0,0 4.388,61983 31,5 1.100,4 1,0 6.610,7 44,8 1.289,4 9,3 268,0 0,0 2.598,51984 24,7 1.309,2 6,0 5.837,3 44,0 1.236,4 10,2 229,0 0,0 2.105,81985 46,5 755,2 11,9 6.235,8 48,2 1.125,1 7,7 222,0 0,0 2.012,01986 71,6 612,2 17,6 7.594,6 44,2 1.223,5 11,1 142,0 3,2 4.061,71987 88,2 367,3 20,5 9.195,7 46,9 1.266,5 27,1 264,0 5,3 5.341,41988 31,9 606,7 22,5 11.465,2 53,0 1.393,0 48,1 486,0 4,2 6.912,01989 40,7 384,4 19,1 13.828,9 52,1 1.518,6 47,8 862,0 4,8 9.405,61990 39,5 269,7 20,1 17.166,2 57,7 1.852,0 59,2 1.256,0 5,5 13.618,61991 38,0 238,4 18,8 21.192,4 58,6 2.304,8 62,4 1.791,0 8,6 27.898,31992 39,9 528,1 14,9 26.880,2 60,8 2.884,7 60,3 1.972,0 10,0 29.128,31993 46,3 172,2 11,3 30.240,3 57,3 3.644,7 54,9 2.056,0 9,9 51.368,71994 52,1 16.978,2 3,7 38.362,8 57,4 5.294,2 57,2 2.451,7 11,1 67.681,61995 52,3 19.158,0 3,6 46.472,6 55,7 7.212,6 55,3 2.410,1 11,0 71.177,51996 55,2 20.971,6 3,0 53.803,0 55,4 8.875,4 55,5 2.315,1 11,1 65.844,01997 50,8 23.997,4 6,0 63.186,7 49,3 10.600,8 53,2 1.901,5 10,4 71.831,61998 63,8 19.936,5 24,4 63.067,8 50,2 10.265,4 51,9 2.255,6 8,9 51.809,21999 62,6 19.149,1 10,1 62.425,4 51,8 10.095,0 51,0 2.573,7 6,3 68.499,02000 65,0 19.738,3 11,8 63.059,1 56,4 9.146,0 39,8 3.642,8 6,9 60.513,6

Source: 1981-1994, Walker and Lefort (1999).(1) Since 1994, source: Superintendencia de Administradoras de Fondos de Pensiones.(2) Since 1994, source: Superintendencia de Valores y Seguros.(3) Since 1994, souce: Banco Central de Chile.

B. Argentina

Year

PF Inv. (%) (2)

Market Size (US$ MM)

(1)

PF Inv. (%) (2)

Market SIze M7

(US$ MM)

PF Inv. (%) (2)

Market Size (US$ MM)

PF Inv. (%) (2)

Market Size (US$ MM)

PF Inv. (%) (2)

Market Size (US$ MM) (1)

1992 7.025,0 26.277,3 496,0 18.326,01993 28.481,0 40.158,7 932,0 42.932,01994 0,9 27.623,0 0,3 46.915,8 0,0 954,8 4,3 720,3 0,0 36.529,01995 4,1 32.421,0 1,4 43.195,5 0,0 860,1 10,8 2.006,9 0,4 37.062,01996 7,1 39.461,0 1,4 53.575,9 5,0 559,5 14,1 2.937,5 2,3 44.358,01997 11,8 42.684,0 3,2 58.983,01998 14,7 39.221,0 4,7 45.292,01999 17,9 49.171,0 4,2 82.982,0

Source: (1) CNV (2) SAFJP

C. Peru

YearPF Inv.

(%) (4)

Market SIze M7

(US$ MM) (1)

PF Inv. (%) (4)

Market Size (US$ MM)

(1)

PF Inv. (%) (4)

Market Size (US$ MM)

(2)

PF Inv. (%) (4)

Market Size (US$ MM) (3)

1993 0,3 5.340,0 0,9 211,0 0,0 n/a 0,0 5.084,01994 1,2 7.618,0 7,9 344,0 10,1 85,0 0,5 8.162,01995 1,7 9.480,0 8,7 599,0 26,4 209,1 0,9 11.701,01996 2,0 11.708,0 4,1 1.129,0 44,5 471,3 2,2 13.842,01997 2,8 13.511,0 5,7 1.728,0 45,0 699,0 3,0 17.383,01998 3,3 12.976,6 7,2 2.481,8 38,6 797,1 5,2 11.034,01999 4,4 12.591,5 11,4 2.305,6 38,3 851,5 6,7 13.407,02000 3,3 12.624,0 16,1 2.166,2 40,7 1.188,1 7,4 10.511,0

Source: 1993-1996, Ramos (1999) (1) Since 1997, S.B.S. Of Peru (2) Since 1997, Banco Central de Reserva del Perú (3) Since 1997, Conasev (4) Since 1997, Superintendence of AFP's.

Negotiable Obligations

Time Deposits Leasing Bonds Corporate Bonds Equity

A. Chile

Equity

Goverment Debt Time Deposits and Bank Bonds

Mortage Bonds Corporate Bonds Equity

Goverment Debt Time Deposits Mortage Bonds

102 REVISTA ABANTE, VOL. 5, Nº 2

illustrates the significance of pension funds, despite their short history. Also(ASAP, 1998, p. 160) the percentage of total assets held by institutionalinvestors has increased from 2.5 percent to 20 percent. Finally, during the1995 crisis, institutional investors’ funds almost completely replaced thereduction in holdings by foreigners. This is indicative of the stabilizing roleof institutional investors.

In Perú, the fraction held by pension funds of the outstanding bond issueshas been in the range of 41-45 percent since 1996 (Table II). Also, pensionfunds held near 7 percent of the total equity market cap by 2000. All thishas happened in the context of growing markets. The corporate bondsoutstanding increased from 85 million US dollars in 1994, to nearly 1.2 billionin 2000. Ramos (1999) argues that investment limits have distorted interestrates, since pension funds cannot invest abroad and must take as given theconditions offered by local issuers.

In addition, Table II also indicates an important growth in the sizes of thecorporate bond markets toward the year 2000, which suggests an interestingsubstitution effect. In times of depressed stock prices firms may find itconvenient to change their source of financing to debt. This added flexibilitywill exist only if there are important local providers of funds denominatedin local currency. The flexibility in the financing sources may imply lowerfinancing costs, on average. Here we do not discuss the rationality of suchactions (e.g., market timing) by firms.

Table III shows the number of issuers present in pension fund portfolios.Upward trends in these numbers for all three countries indicate that theseissuers have found a convenient source of financing in pension funds. TableIV shows the importance of pension fund investments in the corporatesector (stocks and bonds) relative to total market capitalization. This weightindicates the importance that pension funds might have on the cost ofcapital for traded firms. In Chile, this weight became near 5 percent in1986, whereas in Argentina and Perú this happened in 1996. Nevertheless,for the latter countries the importance of pension funds has grown at afaster pace. By 2000, the relative importance of pension funds was largerfor Argentina and Perú than the maximum ever observed in Chile.

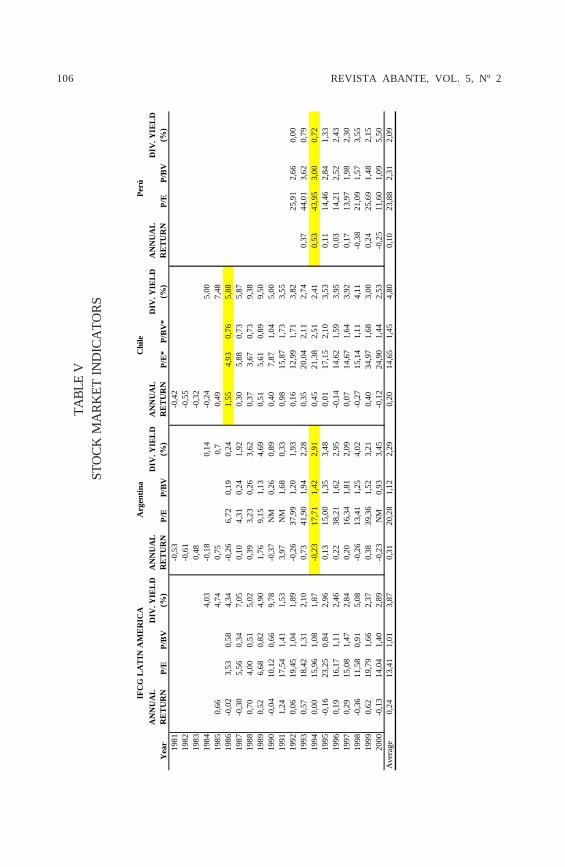

Any effect on the cost of capital should be reflected on the historicalevolution of price-to-book ratios, dividend yields and price-earnings ratios.Book values, dividends and earnings are different ways of scaling the equityprice level. These indicators reflect the cost of equity capital for firms and

PENSION REFORM AND CAPITAL MARKETS 103

TABLE IIINUMBER OF DIFFERENT ISSUERS IN PENSION FUND PORTFOLIOS

A . C hile

Y ear Sto ck Corp . Bon ds

M ortga ge Bon ds 1

Bo nd s b y fi nan cial

ins ti tu cio ns 2

In v es tm en t Fu n ds

Foreign In ves tm en t 3

D eriv ati ves 4

19 85 2 4 2 619 86 5 4 2 319 87 8 9 2 219 88 8 15 2 219 89 2 4 1519 90 3 2 2419 91 4 4 3219 92 5 3 33 2 1 1 319 93 7 7 34 2 6 1 5 7 1319 94 7 9 39 2 6 1 6 1 0 1819 95 10 2 40 2 8 1 4 1 9 1119 96 11 7 40 3 0 1 4 1 9 5219 97 11 9 38 2 8 1 4 2 3 8319 98 11 6 39 2 9 1 4 2 3 8419 99 12 3 46 2 9 8 2 3 2 17 1320 00 10 7 40 3 0 6 2 3 2 44 23