peco energy company

62

PECO ENERGY COMPANY STATEMENT NO. 5 BEFORE THE PENNSYLVANIA PUBLIC UTILITY COMMISSION PENNSYLVANIA PUBLIC UTILITY COMMISSION v. PECO ENERGY COMPANY – GAS DIVISION DOCKET NO. R-2022-3031113 ____________________________________________ DIRECT TESTIMONY ____________________________________________ WITNESS: PAUL R. MOUL SUBJECT: OVERALL RATE OF RETURN, INCLUDING CAPITAL STRUCTURE RATIOS, EMBEDDED COST OF DEBT AND THE COST OF EQUITY, FOR PECO ENERGY COMPANY’S GAS DIVISION DATED: MARCH 31, 2022

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of peco energy company

PECO ENERGY COMPANY

STATEMENT NO. 5

BEFORE THE

PENNSYLVANIA PUBLIC UTILITY COMMISSION

PENNSYLVANIA PUBLIC UTILITY COMMISSION

v.

PECO ENERGY COMPANY – GAS DIVISION

DOCKET NO. R-2022-3031113

____________________________________________

DIRECT TESTIMONY

____________________________________________

WITNESS: PAUL R. MOUL

SUBJECT: OVERALL RATE OF RETURN,

INCLUDING CAPITAL STRUCTURE

RATIOS, EMBEDDED COST OF DEBT

AND THE COST OF EQUITY, FOR PECO

ENERGY COMPANY’S GAS DIVISION

DATED: MARCH 31, 2022

TABLE OF CONTENTS

Page No.

I. INTRODUCTION AND SUMMARY OF RECOMMENDATIONS ............................. 1

II. NATURAL GAS RISK FACTORS ................................................................................. 9

III. FUNDAMENTAL RISK ANALYSIS ........................................................................... 13

IV. CAPITAL STRUCTURE RATIOS ................................................................................ 20

V. COST OF SENIOR CAPITAL ....................................................................................... 23

VI. COST OF EQUITY – GENERAL APPROACH ........................................................... 25

VII. DISCOUNTED CASH FLOW ....................................................................................... 26

VIII. RISK PREMIUM ANALYSIS ....................................................................................... 41

IX. CAPITAL ASSET PRICING MODEL .......................................................................... 46

X. COMPARABLE EARNINGS APPROACH .................................................................. 51

XI. CONCLUSION ON COST OF EQUITY ....................................................................... 55

APPENDIX A - EDUCATIONAL BACKGROUND, BUSINESS EXPERIENCE AND

QUALIFICATIONS

GLOSSARY OF ACRONYMS AND DEFINED TERMS

ACRONYM DEFINED TERM

AFUDC Allowance for Funds Used During Construction

β Beta

b Represents the retention rate that consists of the fraction of

earnings that are not paid out as dividends

b x r Represents internal growth

CAPM Capital Asset Pricing Model

CCR Corporate Credit Rating

CE Comparable Earnings

DCF Discounted Cash Flow

Exelon Exelon Corporation

FERC Federal Energy Regulatory Commission

FOMC Federal Open Market Committee

g Growth rate

IGF Internally Generated Funds

IRPA Interest Rate Protection Agreement

Lev Leverage modification

LT Long Term

Moody’s Moody’s Investors Service

OCI Other Comprehensive Income

P-E Price-earnings

Pandemic COVID-19 Pandemic

PECO PECO Energy Company

PUC Public Utility Commission

r represents the expected rate of return on common equity

Rf Risk-free rate of return

Rm Return on the market

RP Risk Premium

DIRECT TESTIMONY OF PAUL R. MOUL

2

s Represents the new common shares expected to be issued by a

firm

s x v Represents external growth

S&P Standard & Poor’s

V Represents the value that accrues to existing shareholders from

selling stock at a price different from value

ytm Yield to maturity

DIRECT TESTIMONY 1

OF 2

PAUL R. MOUL 3

I. INTRODUCTION AND SUMMARY OF RECOMMENDATIONS 4

1. Q. Please state your name, occupation and business address. 5

A. My name is Paul Ronald Moul. My business address is 251 Hopkins Road, 6

Haddonfield, New Jersey 08033-3062. I am Managing Consultant at the firm 7

P. Moul & Associates, an independent financial and regulatory consulting 8

firm. My educational background, business experience and qualifications are 9

provided in Appendix A, which follows my direct testimony. 10

2. Q. What is the purpose of your testimony? 11

A. My testimony presents evidence, analysis, and a recommendation concerning 12

the appropriate cost of common equity and overall rate of return that the 13

Pennsylvania Public Utility Commission (“PUC” or the “Commission”) 14

should recognize in determining the revenues PECO Energy Company 15

(“PECO Energy” or the “Company”) will be authorized to realize at the 16

conclusion of this proceeding for its Gas Division. My analysis and 17

recommendation are supported by the detailed financial data contained in 18

PECO Exhibit PRM-1, which is a multi-page document divided into fourteen 19

schedules. My testimony is based upon my first-hand knowledge of PECO 20

Energy, consisting of information obtained from meetings with the 21

2

Company’s management and Company-specific data that is widely 1

disseminated within the financial community. 2

3. Q. Based upon your analysis, what is your conclusion concerning the 3

appropriate rate of return for the Company? 4

A. My conclusion is that the Company should be afforded an opportunity to earn 5

a 7.68% overall rate of return, which includes a 10.95% rate of return on 6

common equity. My 10.95% rate of return on common equity includes 7

recognition of the exemplary performance of the Company’s management and 8

is established using capital market and financial data relied upon by investors 9

when assessing the relative risk, and hence the cost of capital for the 10

Company. The 10.95% rate of return on common equity is composed of a 11

10.85% cost of equity determined from the results of my proxy group analysis 12

and 0.10% in recognition of the exemplary performance of the Company’s 13

management. My analysis of the Company and its superior performance is 14

based upon the direct testimony of Mr. Ronald A. Bradley, the Company’s 15

Vice President of Gas Operations, and the testimony of Robert J. Stefani, the 16

Senior Vice President, Chief Financial Officer, and Treasurer of PECO 17

Energy. 18

My overall rate of return recommendation is determined by using the 19

weighted average cost of capital approach. This approach provides a means to 20

apportion the return to each class of investor. The calculation of the weighted 21

average cost of capital requires the selection of appropriate capital structure 22

ratios and a determination of the cost rate for each capital component. The 23

3

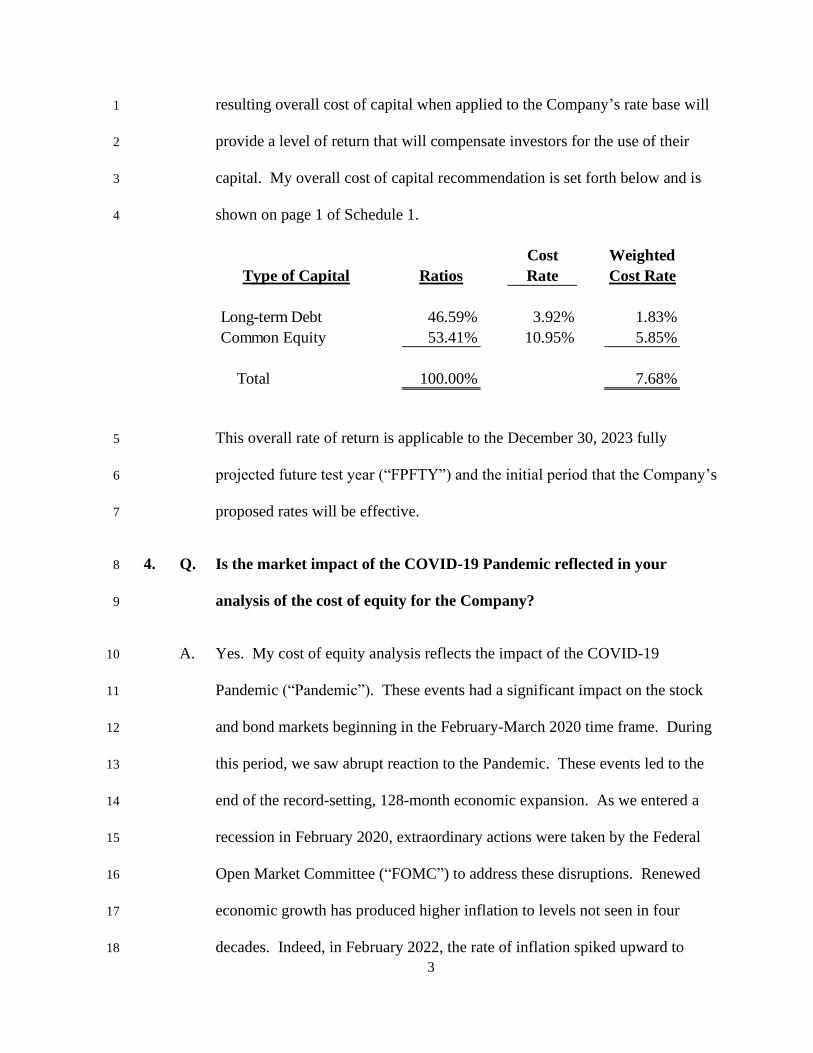

resulting overall cost of capital when applied to the Company’s rate base will 1

provide a level of return that will compensate investors for the use of their 2

capital. My overall cost of capital recommendation is set forth below and is 3

shown on page 1 of Schedule 1. 4

Cost Weighted

Type of Capital Ratios Rate Cost Rate

Long-term Debt 46.59% 3.92% 1.83%

Common Equity 53.41% 10.95% 5.85%

Total 100.00% 7.68%

This overall rate of return is applicable to the December 30, 2023 fully 5

projected future test year (“FPFTY”) and the initial period that the Company’s 6

proposed rates will be effective. 7

4. Q. Is the market impact of the COVID-19 Pandemic reflected in your 8

analysis of the cost of equity for the Company? 9

A. Yes. My cost of equity analysis reflects the impact of the COVID-19 10

Pandemic (“Pandemic”). These events had a significant impact on the stock 11

and bond markets beginning in the February-March 2020 time frame. During 12

this period, we saw abrupt reaction to the Pandemic. These events led to the 13

end of the record-setting, 128-month economic expansion. As we entered a 14

recession in February 2020, extraordinary actions were taken by the Federal 15

Open Market Committee (“FOMC”) to address these disruptions. Renewed 16

economic growth has produced higher inflation to levels not seen in four 17

decades. Indeed, in February 2022, the rate of inflation spiked upward to 18

4

7.9%, the highest in forty-years, due to pandemic-related supply side issues, 1

strong consumer demand, and tight labor markets. Supply shortages have also 2

significantly impacted the consumer sector of the economy. Energy prices 3

have increased as well, with the commodity cost of natural gas moving up. 4

While short-term interest rates remain at historically low levels, longer term 5

interest rates began to rise in February 2021. At this point, short-term interest 6

rates are poised to increase after the FOMC ends its bond buying program. 7

The FOMC has indicated that several increases in the Fed Funds rate will 8

likely occur in 2022 and 2023. The first of these increases occurred on March 9

16, 2022, when the Fed Funds rate was increased by 0.25%. Recently, the 10

yield on ten-year Treasury notes reached 2.00% for the first time since mid-11

2019. Over the course of the Pandemic, stock prices rebounded and reached 12

new highs in reaction to renewed economic growth. There has been a 13

pullback in overall market prices in early 2022, commonly known as a market 14

correction. It followed a stellar market performance in 2021 i.e., a 26.89% 15

annual price appreciation. I have considered these events as they impact the 16

inputs that I used in the various models of the cost of equity. 17

5. Q. What factors have you considered in the determination of the Company’s 18

cost of equity in this proceeding? 19

A. The Company is a wholly owned subsidiary of Exelon Corporation 20

(“Exelon”). The common stock of Exelon is traded on the Nasdaq Global 21

Select Market. Exelon is a component of the Standard & Poor’s (“S&P’s”) 22

500 Composite Index. The Company provides natural gas distribution service 23

5

to approximately 543,000 customers located in the suburban counties 1

surrounding the City of Philadelphia. PECO Energy also provides electric 2

delivery service to more than 1,600,000 electric customers in both the City of 3

Philadelphia and the surrounding counties. Throughput to the Company’s gas 4

customers in 2020 was composed of approximately 47% to residential 5

customers, approximately 26% to small commercial and industrial customers, 6

and 27% to large commercial and industrial customers. Approximately 30% 7

of throughput goes to transportation customers. With approximately 670 8

unique large commercial and industrial customers, the energy needs of a few 9

customers can have a significant impact on the Company’s operations. PECO 10

Energy obtains its gas supplies from producers and marketers with 11

transportation arrangements through interconnections with three interstate 12

pipelines. The Company has storage arrangements with pipeline service 13

providers and owns liquefied natural gas and propane facilities to supplement 14

flowing gas. Since the restructuring of the gas utility industry in 15

Pennsylvania, PECO Energy has been the supplier of last resort for customers 16

that do not obtain their own supply. 17

6. Q. How have you determined the cost of common equity in this case? 18

A. The cost of common equity is established using capital market and financial 19

data relied upon by investors to assess the relative risk, and hence the cost of 20

equity for a natural gas utility such as PECO Energy. In this regard, I have 21

considered four well-recognized models. These methods include the 22

Discounted Cash Flow (“DCF”) model, the Risk Premium (“RP”) analysis, 23

6

the Capital Asset Pricing Model (“CAPM”), and the Comparable Earnings 1

(“CE”) approach. The results of a variety of approaches indicate that the 2

Company’s rate of return on common equity is 10.95%, including 0.10% in 3

recognition of the Company’s exemplary management performance. 4

7. Q. In your opinion, what factors should the Commission consider when 5

determining the Company’s cost of capital in this proceeding? 6

A. The Commission’s rate of return allowance must be set to cover the 7

Company’s interest and dividend payments, provide a reasonable level of 8

earnings retention, produce an adequate level of internally generated funds to 9

meet capital requirements, be commensurate with the risk to which the 10

Company’s capital is exposed, assure confidence in the financial integrity of 11

the Company, support reasonable credit quality, and allow the Company to 12

raise capital on reasonable terms. The return that I propose fulfills these 13

established standards of a fair rate of return set forth by the landmark 14

Bluefield and Hope cases.1 That is to say, my proposed rate of return is 15

commensurate with returns available on investments having corresponding 16

risks. 17

8. Q. How have you measured the cost of equity in this case? 18

A. The models that I used to measure the cost of common equity for the 19

Company were applied with market and financial data developed from a 20

1 Bluefield Water Works & Improvement Co. v. P.S.C. of W. Va., 262 U.S. 679 (1923) and F.P.C.

v. Hope Nat. Gas Co., 320 U.S. 591 (1944).

7

group of companies engaged in the distribution of natural gas. I will refer to 1

these companies as the “Gas Group” throughout my testimony. I began with 2

all of the gas utilities contained in The Value Line Investment Survey, which 3

consists of ten companies. Value Line is an investment advisory service that 4

is a widely used source in public utility rate cases. I eliminated two 5

companies from the Value Line group. UGI Corporation was removed due to 6

its diversified businesses consisting of six reportable segments, including 7

propane, two international LPG segments, natural gas utility, energy services, 8

and electric generation. I also removed South Jersey Industries from the Gas 9

Group because it entered into an agreement to be acquired by a private equity 10

investor. The remaining eight companies in the Gas Group are identified on 11

page 2 of Schedule 3. Aside from South Jersey Industries, these are the same 12

companies that were used to apply the cost of equity models in the recent 13

Quarterly Earnings Report approved by the Commission on January 13, 2022 14

(Docket No. M-2021-3030045). 15

9. Q. How have you performed your cost of equity analysis with the market 16

data for the Gas Group? 17

A. I have applied the methods/models for estimating the cost of equity using the 18

average data for the Gas Group. I have not measured separately the cost of 19

equity for the individual companies within the Gas Group, because the 20

determination of the cost of equity for an individual company can be 21

problematic. The use of group average data will reduce the effect of 22

8

potentially anomalous results for an individual company if a company-by-1

company approach were utilized. 2

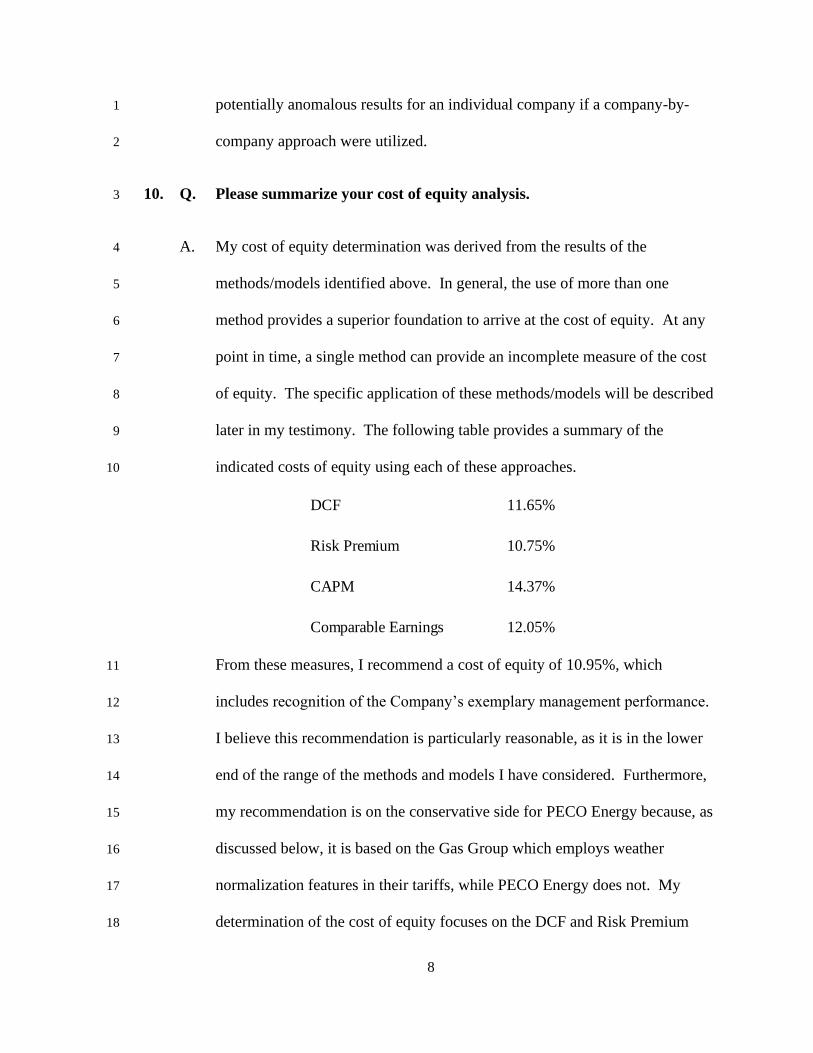

10. Q. Please summarize your cost of equity analysis. 3

A. My cost of equity determination was derived from the results of the 4

methods/models identified above. In general, the use of more than one 5

method provides a superior foundation to arrive at the cost of equity. At any 6

point in time, a single method can provide an incomplete measure of the cost 7

of equity. The specific application of these methods/models will be described 8

later in my testimony. The following table provides a summary of the 9

indicated costs of equity using each of these approaches. 10

DCF 11.65%

Risk Premium 10.75%

CAPM 14.37%

Comparable Earnings 12.05%

From these measures, I recommend a cost of equity of 10.95%, which 11

includes recognition of the Company’s exemplary management performance. 12

I believe this recommendation is particularly reasonable, as it is in the lower 13

end of the range of the methods and models I have considered. Furthermore, 14

my recommendation is on the conservative side for PECO Energy because, as 15

discussed below, it is based on the Gas Group which employs weather 16

normalization features in their tariffs, while PECO Energy does not. My 17

determination of the cost of equity focuses on the DCF and Risk Premium 18

9

approaches that, when averaged, indicate a return of 11.20% (10.75% + 1

11.65% = 22.40% ÷ 2). Averaging the results gives equal weight to the Risk 2

Premium and DCF results. My 10.95% cost of equity recommendation 3

includes 10 basis points or 0.10% recognition for the exemplary performance 4

of the Company’s management and falls within the range of 10.75% to 5

11.20% indicated above. Mr. Bradley’s testimony in PECO Energy Statement 6

No. 1 demonstrates that the Company’s superior customer service and 7

management effectiveness. To obtain new capital to support an expanded 8

construction program and retain existing capital, the rate of return on common 9

equity must be high enough to satisfy investors’ requirements. Along these 10

lines, the Company is spending considerable amounts of new capital, which 11

are large by historical standards, that will put a strain on financial 12

performance in the short run. In recognition of its performance, the Company 13

should be granted an opportunity to earn a 10.95% rate of return on common 14

equity. 15

II. NATURAL GAS RISK FACTORS 16

11. Q. What factors currently affect the business risk of natural gas utilities? 17

A. Gas utilities face risks arising from competition from other energy sources, the 18

purveyors of those sources and natural gas, economic regulation, the business 19

cycle, and customer usage patterns. Natural gas utilities have focused 20

increased attention on safety and reliability issues and on conservation. In 21

10

order to address these issues, natural gas companies are now allocating more 1

of their resources to addressing aging infrastructure issues. 2

12. Q. Are there other features of the Company’s business that should be 3

considered when assessing the Company’s risk? 4

A. Yes. Most of the Company’s residential customers use natural gas for space 5

heating purposes. Indeed, 89% of residential throughput is to customers with 6

natural gas space heating. This indicates that the energy requirements of a 7

large proportion of the Company’s residential customers are significantly 8

influenced by temperature conditions over which the Company has absolutely 9

no control. It is noteworthy that all of the companies that comprise the Gas 10

Group have some form of weather normalization feature in their tariffs. If 11

weather patterns in the future do not align with rate case test period data, a 12

weather normalization feature enables a company to adjust its revenue 13

collections to account for those variations. As PECO Energy has no such 14

provision in its gas tariff, the Company is exposed to more risk than the Gas 15

Group. With more risk, its return on equity should be higher than that 16

indicated for the Gas Group because investors’ return expectations for the Gas 17

Group companies reflect the risk mitigation attributes of weather 18

normalization. 19

In addition, PECO Energy’s ten largest volume customers, which account 20

for 10.9 million cubic feet of throughput, are engaged in the manufacturing, 21

pharmaceuticals, food processing, health care, and electric generation 22

(including cogeneration) businesses. Changes in the business environment 23

11

can negatively affect these companies, and, in that way, cause material 1

reductions in throughput on PECO Energy’s distribution system. This risk is 2

especially apparent in this time of economic uncertainty attributed to inflation, 3

supply-side issues, and global geopolitical situations. Additionally, large 4

volume users, which predominantly use transportation service, may be located 5

close enough to interstate pipelines to take gas directly from those sources and 6

bypass the local distribution company (“LDC”) entirely. The Company has 7

identified customers with combined annual throughput of approximately 8.4 8

million cubic feet (“MCF”) of gas that have the potential to bypass the 9

Company’s distribution system. Because a large part of PECO Energy’s 10

distribution revenue recovers fixed costs, which the Company continues to 11

bear even if a customer leaves the system, the loss of 8.4 million MCF of 12

throughput would impose a significant amount of uncompensated fixed costs 13

that PECO Energy would not have the opportunity to recover until it could 14

complete another base rate case. 15

13. Q. Can the Company’s construction program affect its risk profile? 16

A. Yes. The Company must undertake substantial investments to maintain and 17

upgrade existing facilities in its service territory to ensure safe and reliable 18

service to its customers. In particular, the rehabilitation of the Company’s 19

infrastructure requires it to invest capital without adding any new customers 20

and without increasing sales to existing customers. In short, infrastructure 21

rehabilitation increases fixed costs without an attendant increase in revenues. 22

Moreover, the Company is confronting significant levels of infrastructure 23

12

investment. For example, at year-end 2020, 879 miles (or approximately 1

13%) of the Company’s distribution system consisted of cast iron and ductile 2

iron pipe and steel pipe that is not cathodically protected and is, therefore, 3

susceptible to corrosion. These are all considered vulnerable materials that 4

will need to be replaced. Also, 16,731 (or approximately 4%) of the 5

Company’s services were constructed of unprotected steel. The Company 6

projects that its construction expenditures will approximate $7,457 million 7

during the period 2022-2026, which represents approximately 67% ($7,457 8

million ÷ $11,117 million) of its net utility plant as of December 31, 2021. Of 9

these amounts, construction expenditures for the gas division are expected to 10

be $1,757 million during the period 2022-2026. 11

14. Q. How should the Commission respond to the issues facing natural gas 12

utilities in general and PECO Energy in particular? 13

A. The Commission should recognize and take into account the high-risk profile 14

of PECO Energy’s Gas Division and its future capital requirements in 15

determining the cost of equity for the Company. A fair rate of return is key to 16

PECO Energy maintaining a financial profile that will provide it with the 17

ability to raise the capital necessary to meet its capital needs on reasonable 18

terms. 19

13

III. FUNDAMENTAL RISK ANALYSIS 1

15. Q. Is it necessary to conduct a fundamental risk analysis to provide a 2

framework for a determination of a utility’s cost of equity? 3

A. Yes, it is. It is necessary to establish a company’s relative risk position within 4

its industry through a fundamental analysis of various quantitative and 5

qualitative factors that bear upon investors’ assessment of overall risk. The 6

qualitative factors that bear upon Company risk have already been discussed. 7

The quantitative risk analysis follows. The items that influence investors’ 8

evaluation of risk and their required returns were described above. For this 9

purpose, I compared the Company to the S&P Public Utilities, an industry-10

wide proxy consisting of various regulated businesses, and to the Gas Group. 11

16. Q. What are the components of the S&P Public Utilities? 12

A. The S&P Public Utilities is a widely recognized index that is comprised of 13

electric power and natural gas companies. These companies are identified on 14

page 3 of Schedule 4. 15

17. Q. What companies comprise the Gas Group? 16

A. My Gas Group consists of the following companies: Atmos Energy Corp., 17

Chesapeake Utilities Corporation, New Jersey Resources Corp., NiSource, 18

Inc., Northwest Natural Holding Co., ONE Gas, Inc., Southwest Gas 19

Holdings, and Spire, Inc. 20

14

18. Q. Is knowledge of a utility’s bond rating an important factor in assessing its 1

risk and cost of capital? 2

A. Yes. Knowledge of a company’s credit quality rating is important because the 3

cost of each type of capital is directly related to the associated risk of the firm. 4

So, while a company’s credit quality risk is shown directly by the rating and 5

yield on its bonds, these relative risk assessments also bear upon the cost of 6

equity. This is because a firm’s cost of equity is represented by its borrowing 7

cost, plus compensation, to recognize the higher risk of an equity investment 8

compared to debt. 9

19. Q. How do the credit quality ratings compare for the Company, the Gas 10

Group, and the S&P Public Utilities? 11

A. Presently, the Company’s Long Term (“LT”) issuer credit quality rating is A2 12

from Moody’s Investors Service (“Moody’s”) and the corporate credit rating 13

(“CCR”) is BBB+ from S&P. The ratings represent the LT issuer rating by 14

Moody’s and CCR from S&P, which focuses upon the credit quality of the 15

issuer of the debt rather than upon the debt obligation itself. For the Gas 16

Group, the average LT issuer rating is A3 by Moody’s and A- by S&P, as 17

displayed on page 2 of Schedule 3. For the S&P Public Utilities, the average 18

credit quality rating is A3 by Moody’s and BBB+ by S&P, as displayed on 19

page 3 of Schedule 4. Many of the financial indicators that I will 20

subsequently discuss are considered during the rating process. 21

15

20. Q. How do the financial data compare for the Company, the Gas Group, and 1

the S&P Public Utilities? 2

A. The broad categories of financial data that I will discuss are shown on 3

Schedules 2, 3, and 4. The data cover the five-year period from 2016-2020. I 4

obtained financial data for PECO Energy from the S&P Utility Compustat 5

data base, which, in turn, was based on the financial statements in PECO 6

Energy’s SEC Forms 10-K. Those data include the results of operations of the 7

Company’s natural gas distribution, electric distribution and transmission 8

businesses. While it is possible to analyze the operations of the Gas Division 9

for items “above the line” (i.e., net operating income), most of the financial 10

data that I considered involved ratios that include interest expense, investor-11

provided capitalization, and cash-flow components that are not separately 12

reported for the Gas Division. Hence, my fundamental analysis is based on 13

PECO Energy’s combined operations. The important categories of relative 14

risk may be summarized as follows: 15

Size. In terms of capitalization, the Company is larger than the 16

average size of the Gas Group, and much smaller than the average size of the 17

S&P Public Utilities. All other things being equal, a smaller company is 18

riskier than a larger company because a given change in revenue and expense 19

has a proportionately greater impact on a small firm. As I will demonstrate 20

later, the size of a firm can impact its cost of equity. This is the case for 21

PECO Energy and the Gas Group as compared to the S&P Public Utilities. 22

16

Market Ratios. Market-based financial ratios, such as earnings/price 1

ratios and dividend yields, provide a partial measure of the investor-required 2

cost of equity. If all other factors are equal, investors will require a higher 3

rate of return for companies that exhibit greater risk. That is to say, a firm that 4

investors perceive to have higher risks will experience a lower price per share 5

in relation to expected earnings.2 6

There are no market ratios available for the Company because its 7

stock is owned by Exelon. The five-year average price-earnings (“P-E”) 8

multiple was somewhat higher for the Gas Group as compared to the S&P 9

Public Utilities. The five-year average dividend yield was lower for the Gas 10

Group as compared to the S&P Public Utilities. The five-year average 11

market-to-book ratio was fairly similar for the Gas Group and the S&P Public 12

Utilities. 13

Common Equity Ratio. The level of financial risk is measured by 14

the proportion of long-term debt and other senior capital that is contained in a 15

company’s capitalization. Financial risk is also analyzed by comparing 16

common equity ratios (the complement of the ratio of debt and other senior 17

capital). A firm with a higher common equity ratio has lower financial risk, 18

while a firm with a lower common equity ratio has higher financial risk. The 19

five-year average common equity ratios, based on permanent capital, were 20

54.0% for PECO Energy, 52.6% for the Gas Group, and 41.3% for the S&P 21

2 For example, two otherwise similarly situated firms each reporting $1.00 in earnings per share

would have different market prices at varying levels of risk (i.e., the firm with a higher level of risk will have

a lower share value, while the firm with a lower risk profile will have a higher share value).

17

Public Utilities. The Company’s common equity ratio was higher than the 1

Gas Group, thereby indicating somewhat lower financial risk. However, for 2

the purpose of this case, the Company’s common equity ratio is within the 3

range of other gas distribution utilities. 4

Return on Book Equity. Greater variability (i.e., uncertainty) of a 5

firm’s earned returns signifies relatively greater levels of risk, as shown by the 6

coefficient of variation (standard deviation ÷ mean) of the rate of return on 7

book common equity. The higher the coefficients of variation, the greater 8

degree of variability. For the five-year period, the coefficients of variation 9

were 0.098 (1.2% ÷ 12.3%) for the Company, 0.105 (1.0% ÷ 9.5%) for the 10

Gas Group, and 0.039 (0.4% ÷ 10.3%) for the S&P Public Utilities. The 11

variability of the Company’s rates of return was fairly similar to the Gas 12

Group and higher than the S&P Public Utilities. High variability signifies 13

higher risk. 14

Operating Ratios. I have also compared operating ratios (the 15

percentage of revenues consumed by operating expense, depreciation, and 16

taxes other than income).3 The five-year average operating ratios were 78.6% 17

for the Company, 83.2% for the Gas Group, and 78.8% for the S&P Public 18

Utilities. The Company’s operating ratios were somewhat lower than the Gas 19

Group, thereby indicating slightly lower risk. The operating ratios were 20

similar for PECO Energy and the S&P Public Utilities. 21

3 The complement of the operating ratio is the operating margin that provides a measure of

profitability. The higher the operating ratio, the lower the operating margin.

18

Coverage. The level of fixed charge coverage (i.e., the multiple by 1

which available earnings cover fixed charges, such as interest expense) 2

provides an indication of the earnings protection for creditors. Higher levels 3

of coverage, and hence earnings protection for fixed charges, are usually 4

associated with superior grades of creditworthiness. Excluding Allowance for 5

Funds Used During Construction (“AFUDC”), the five-year average pre-tax 6

interest coverage was 4.79 times for the Company, 4.28 times for the Gas 7

Group, and 3.02 times for the S&P Public Utilities. The interest coverages 8

were higher for the Company as compared to the Gas Group, thereby 9

indicating lower credit risk for lenders. 10

Quality of Earnings. Measures of earnings quality usually are 11

revealed by the percentage of AFUDC related to income available for 12

common equity, the effective income tax rate, and other cost deferrals. These 13

measures of earnings quality usually influence a firm’s internally generated 14

funds because poor quality of earnings would not generate high levels of cash 15

flow. During the Pandemic, there was further pressure on cash flows due to 16

the suspension of collection activities and the moratorium against shut off 17

service due to nonpayment. Quality of earnings has not been a significant 18

concern for the Company, the Gas Group, and the S&P Public Utilities. 19

Internally Generated Funds. Internally generated funds (“IGF”) 20

provide an important source of new investment capital for a utility and 21

represent a key measure of credit strength. Historically, the five-year average 22

percentage of IGF to capital expenditures was 62.2% for the Company, 59.2% 23

for the Gas Group, and 69.5% for the S&P Public Utilities. The Company’s 24

19

IGF to construction expenditures dropped in 2020 after the reduction in the 1

provision for deferred taxes due to the elimination of bonus depreciation. 2

Betas. The financial data that I have been discussing relate primarily 3

to company-specific risks. Market risk for firms with publicly-traded stock is 4

measured by beta coefficients. Beta coefficients attempt to identify 5

systematic risk, i.e., the risk associated with changes in the overall market for 6

common equities.4 Value Line publishes such a statistical measure of a 7

stock’s relative historical volatility to the rest of the market. A comparison of 8

market risk is shown by the Value Line beta of 0.86 as the average for the Gas 9

Group (see page 2 of Schedule 3) and 0.90 as the average for the S&P Public 10

Utilities (see page 3 of Schedule 4). The systematic risk for the Gas Group as 11

measured by the Value Line beta is fairly similar to the S&P Public Utilities. 12

21. Q. Please summarize your risk evaluation. 13

A. The investment risk of PECO Energy parallels that of the Gas Group in 14

certain respects. PECO Energy has lower risk as shown by its historic higher 15

common equity ratio, its lower operating ratio, and higher interest coverages. 16

Similar risk factors for PECO Energy and the Gas Group are the variability of 17

earnings, quality of earnings, and internally generated funds. 18

4 Beta is a relative measure of the historical sensitivity of the stock’s price to overall fluctuations in

the New York Stock Exchange Composite Index. The ‘‘Beta coefficient’’ is derived from a regression

analysis of the relationship between weekly percentage changes in the price of a stock and weekly percentage

changes in the NYSE Index over a period of five years. The betas are adjusted for their long-term tendency

to converge toward 1.00. A common stock that has a beta less than 1.0 is considered to have less systematic

risk than the market as a whole and would be expected to rise and fall more slowly than the rest of the market.

A stock with a beta above 1.0 would have more systematic risk.

20

22. Q. Based on your analysis, does the Gas Group provide a reasonable basis to 1

measure the Company’s cost of equity for this case? 2

A. Yes. On balance, the risk factors average out, indicating that the cost of 3

equity for the Gas Group provides a reasonable basis for measuring the 4

Company’s cost of equity. 5

IV. CAPITAL STRUCTURE RATIOS 6

23. Q. Please explain the selection of capital structure ratios for PECO Energy 7

in this case. 8

A. The capital structure ratios of PECO Energy should be employed for rate of 9

return purposes. If the operating public utility raises its own debt directly in 10

the capital markets, as PECO Energy does, the operating public utility’s own 11

capital structure ratios should be used to determine its overall rate of return. 12

Additionally, if the Company’s actual capital structure ratios are used, as they 13

should be, then consistency requires that the embedded cost rates associated 14

with the senior securities reflected in those capital structure ratios should also 15

be employed. 16

24. Q. Does Schedule 5 provide the Company’s capitalization and capital 17

structure ratios? 18

A. Yes. The capitalization and capital structure ratios at December 31, 2021, 19

2022 and 2023 correspond with the end of the historic test year (“HTY”), 20

future test year (“FTY”), and FPFTY in this case. The capitalization and 21

21

capital structure ratios for the FTY and FPFTY reflect the Company’s plan to 1

issue $725 million of new long-term debt in the third quarter of 2022 and 2

$475 million in the third quarter of 2023. A $350 million debt maturity will 3

occur in the third quarter of 2022 and a $50 million debt maturity will occur in 4

the second quarter of 2023. Future equity financings include $231.184 5

million in the FTY and $314.855 million in the FPFTY. The build-up of 6

retained earnings is also reflected. In presenting the Company’s capital 7

structure on Schedule 5, I have removed the call premiums on the early 8

redemption of high-cost long-term debt and preferred stock. 9

25. Q. Please describe the adjustment for the call premiums paid to redeem 10

high-cost debt and preferred stock. 11

A. I have adjusted the principal amounts of long-term debt to exclude the 12

amounts used to finance premiums paid for the early redemption of long-term 13

debt and preferred stock previously redeemed. To do otherwise would deny 14

PECO Energy the opportunity to recover the costs (i.e., a return on and of the 15

money used to fund the call premiums) that PECO incurred solely to redeem 16

high-cost capital. The additional debt that PECO issued to finance the call 17

premiums does not increase the Company’s rate base. That is to say, no 18

additional rate base was created as a consequence of issuing additional debt 19

and preferred stock to finance the redemptions. Therefore, an adjustment to 20

the capitalization is required to provide the return necessary to service the 21

additional capital PECO Energy issued to fund the call premiums. Thus, 22

while rate base does not change, the return component of the overall cost of 23

22

capital reflects an adjustment that, when applied to the rate base, furnishes the 1

return necessary to pay the cost of the incremental capitalization that 2

supported the call premiums paid by PECO Energy. 3

The adjustment for call premiums is appropriate because customers 4

receive all of the cost savings, in the form of a lower overall rate of return, 5

produced by refinancing higher-cost debt and preferred stock, while PECO 6

Energy is simply made whole by recovering the actual costs it incurred to 7

provide these benefits to its customers. In order to produce the savings that 8

resulted from redeeming higher-cost debt and preferred stock, the Company 9

paid to the holders of that debt and preferred stock a premium to surrender 10

their securities prior to maturity. Those premiums represented an investment 11

made by PECO Energy to reduce its overall cost of capital. Because the 12

reduced interest costs and preferred stock dividends are reflected in the lower 13

cost of capital to customers, it is proper that the Company recover the costs 14

incurred to produce these savings, which consist of a return of and a return on 15

the unamortized premiums. Adjusting the principal amounts in the capital 16

structure provides for the appropriate cost recovery by providing a return on 17

the funds used to pay the premiums, which is reflected as an increment 18

included in the embedded cost rates of PECO’s total capital. 19

26. Q. Should short-term debt be included in the capital structure for rate of 20

return purposes? 21

A. There is no need to consider short-term debt in the capital structure because 22

the amount of short-term debt is well below the construction work in progress 23

23

(“CWIP”) at the end of the FTY and the FPFTY. Exclusion of short-term 1

debt is required because it finances CWIP, and hence the cost of short-term 2

debt is reflected in the AFUDC rate. To avoid double-counting, short-term 3

debt must be excluded from the capital structure ratios when setting base 4

rates. 5

27. Q. What capital structure ratios do you recommend for determining PECO 6

Energy’s overall cost of capital in this proceeding? 7

A. Because rate-setting is prospective, the rate of return should, at a minimum, 8

reflect known or reasonably foreseeable changes that will occur during the 9

course of the test year. As a result, I will adopt the Company’s FPFTY capital-10

structure ratios of 46.59% long-term debt and 53.41% common equity. 11

V. COST OF SENIOR CAPITAL 12

28. Q. What cost rate have you assigned to the debt portion of PECO Energy’s 13

capital structure? 14

A. The determination of the long-term debt cost rate is essentially an arithmetic 15

exercise. This is because the Company has contracted for the use of this 16

capital for a specific period at a specified cost rate. As shown on Schedule 6, 17

pages 1, 2 and 3, I have computed the weighted average embedded cost rates 18

of long-term debt as of the end of the HTY, FTY and FPFTY, respectively. 19

For the planned new issues of debt, the Company has budgeted 3.45% as the 20

coupon rate for the debt issue in calendar 2022 and 3.45% for the debt issue in 21

24

2023. The development of the individual effective cost rates for each series of 1

long-term debt, using the cost rate to maturity technique, is shown on 2

Schedule 6, page 4. The cost rate, or yield to maturity (“ytm”), is the rate of 3

discount that equates the present value of all future interest and principal 4

payments with the net proceeds of the bond. In my calculation of the 5

embedded cost of long-term debt, I have recognized the costs associated with 6

the Company’s early redemption of high cost debt. As previously explained, 7

it is necessary to compensate PECO Energy for the costs incurred to lower the 8

embedded debt cost rate, which reduces the cost of capital charged to 9

customers. 10

29. Q. What cost rate have you determined for the Company’s long-term debt? 11

A. I will adopt the 3.92% embedded cost of long-term debt as of December 31, 12

2023, as shown on Schedule 6, page 3. This rate is related to the amount of 13

long-term debt shown in the last three columns of Schedule 5, which provides 14

the basis for the 46.59% long-term debt ratio. 15

25

VI. COST OF EQUITY – GENERAL APPROACH 1

30. Q. Please describe how you determined the cost of equity for the Company. 2

A. Although my fundamental financial analysis provides the required framework 3

to establish the risk relationships among PECO, the Gas Group, and the S&P 4

Public Utilities, the cost of equity must be measured by standard financial 5

models that I identified above. Differences in risk traits, such as size, business 6

diversification, geographical diversity, regulatory policy, financial leverage, 7

and bond ratings must be considered when analyzing the cost of equity. 8

It is also important to reiterate that no one method or model of the 9

cost of equity can be applied in an isolated manner. Rather, informed 10

judgment must be used to take into consideration the relative risk traits of the 11

firm. It is for this reason that I have used more than one method to measure 12

the Company’s cost of equity. As I describe below, each of the methods used 13

to measure the cost of equity contains certain incomplete and/or overly 14

restrictive assumptions and constraints that are not optimal. Therefore, I favor 15

considering the results from a variety of methods. In this regard, I applied 16

each of the methods with data taken from the Gas Group and arrived at a cost 17

of equity of 10.95% for PECO, which includes an increment for exemplary 18

management performance. 19

26

VII. DISCOUNTED CASH FLOW 1

31. Q. Please describe the DCF model. 2

A. The DCF model seeks to explain the value of an asset as the present value of 3

future expected cash flows discounted at the appropriate risk-adjusted rate of 4

return. In its simplest form, the DCF-determined return on common stock 5

consists of a current cash (dividend) yield and future price appreciation 6

(growth) of the investment. The dividend discount equation is the familiar 7

DCF valuation model, which assumes that future dividends are systematically 8

related to one another by a constant growth rate. The DCF formula is derived 9

from the standard valuation model: P = D/(k-g), where P = price, D = 10

dividend, k = the cost of equity, and g = growth in cash flows. By rearranging 11

the terms, we obtain the familiar DCF equation: k= D/P + g. All of the terms 12

in the DCF equation represent investors’ assessment of expected future cash 13

flows that they will receive in relation to the value that they set for a share of 14

stock (P). The DCF equation is sometimes referred to as the “Gordon” 15

model.5 My DCF results are provided on Schedule 1, page 2, for the Gas 16

Group. The DCF return is 11.65% with the leverage adjustment and 10.20% 17

without the leverage adjustment for the Gas Group. The leverage adjustment 18

is discussed more fully below. 19

5 Although the popular application of the DCF model is often attributed to the work of Myron J.

Gordon in the mid-1950s, J.B. Williams exposited the DCF model in its present form nearly two decades

earlier.

27

Among the limitations of the model, there is a certain element of 1

circularity in the DCF method when applied in rate cases. This is because 2

investors’ expectations for the future depend upon regulatory decisions. In 3

turn, when regulators depend upon the DCF model to set the cost of equity, 4

they rely upon investor expectations that include an assessment of how 5

regulators will decide rate cases. Due to this circularity, the DCF model may 6

not fully reflect the true risk of a utility. Other limitations of the DCF include 7

the constant P-E multiple assertion that does not conform with actual stock 8

market performance. And, indeed, the FERC has moved to using multiple 9

methods for measuring the cost of equity due to the limitations of the DCF. 10

32. Q. What is the dividend yield component of a DCF analysis? 11

A. The dividend yield reveals the portion of investors’ cash flow that is generated 12

by the return provided by the dividends an investor receives. It is measured 13

by the dividends per share relative to the price per share. The DCF 14

methodology requires the use of an expected dividend yield to establish the 15

investor-required cost of equity. For the twelve months ended February 2022, 16

the monthly dividend yields are shown on Schedule 7. The month-end prices 17

were adjusted to reflect the buildup of the dividend in the price that has 18

occurred since the last ex-dividend date (i.e., the date by which a shareholder 19

must own the shares to be entitled to the dividend payment – usually about 20

two to three weeks prior to the actual payment). 21

For the twelve months ended February 2022, the average dividend 22

yield was 3.22% for the Gas Group based upon a calculation using annualized 23

28

dividend payments and adjusted month-end stock prices. The dividend yields 1

for the more recent six-month and three-month periods were 3.33% and 2

3.16%, respectively. For applying the DCF model, I have used the six-month 3

average dividend yield of 3.33% for the Gas Group. The use of this dividend 4

yield will reflect current capital costs while avoiding spot yields. For the 5

purpose of a DCF calculation, the average dividend yield must be adjusted to 6

reflect the prospective nature of the dividend payments, i.e., the higher 7

expected dividends for the future. Recall that the DCF is an expectational 8

model that must reflect investors’ anticipated cash flows. I have adjusted the 9

six-month average dividend yield in three different but generally accepted 10

manners and used the average of the three adjusted values as calculated in the 11

lower panel of data presented on Schedule 7.6 This adjustment adds twelve 12

basis points to the six-month average historical yield, thus producing the 13

3.45% adjusted dividend yield for the Gas Group. 14

33. Q. What factors influence investors’ growth expectations? 15

A. As noted previously, investors are interested principally in the dividend yield 16

and future growth of their investment (i.e., the price per share of the stock). 17

6 These adjustments are the 1/2 growth approach, the discrete approach, and the quarterly

approach. Under the 1/2 approach, the procedure to adjust the average dividend yield for the expectation of

a dividend increase during the initial investment period will be at a rate of one-half the growth component,

which assumes that half of the dividend payments will be at the expected higher rate during the initial

investment period. Under the discrete approach, the “g” in the DCF model reflects the discrete growth in

the quarterly dividend, which is required for the periodic form of the DCF to properly recognize that

dividends are expected to grow on a discrete basis. The quarterly approach takes into account that

investors have the opportunity to reinvest quarterly dividend receipts. Recognizing the compounding of the

periodic quarterly dividend payments (D0) results in this third DCF formulation. This DCF equation

provides no further recognition of growth in the quarterly dividend. A compounding of the quarterly

dividend yield recognizes the necessity for an adjusted dividend yield.

29

Future growth in earnings per share is the DCF model’s primary focus 1

because, under the model’s assumption that the P-E multiple remains constant, 2

the price per share of stock will grow at the same rate as earnings per share. A 3

growth rate analysis considers a variety of variables to reach a consensus of 4

prospective growth, including historical data and widely available analysts’ 5

forecasts of earnings, dividends, book value, and cash flow (all stated on a 6

per-share basis). A fundamental growth rate analysis is frequently based upon 7

internal growth (“b x r”), where “r” is the expected rate of return on common 8

equity and “b” is the retention rate (a fraction representing the proportion of 9

earnings not paid out as dividends). To be complete, the internal growth rate 10

should be modified to account for sales of new common stock (external 11

growth), which is represented by the formula s x v, where “s” is the number of 12

new common shares that the firm expects to issue and “v” is the value that 13

accrues to existing shareholders from selling stock at a price above book 14

value. Fundamental growth, which combines internal and external growth, 15

encompasses the factors that cause book value per share to grow over time. 16

Growth also can be expressed in multiple stages. This expression of 17

growth consists of an initial “growth” stage during which a firm enjoys 18

rapidly expanding markets, high profit margins, and abnormally high growth 19

in earnings per share. Thereafter, a firm enters a “transition” stage during 20

which fewer technological advances and increased product saturation begin to 21

reduce the growth rate and profit margins come under pressure. During the 22

“transition” stage, investment opportunities begin to mature, capital 23

requirements decline, and a firm begins to pay out a larger percentage of 24

30

earnings to shareholders. Finally, the mature or “steady-state” stage is 1

reached when a firm’s earnings growth, payout ratio, and return on equity 2

stabilize at levels where they remain for the life of a firm. The three stages of 3

growth assume a step-down of high initial growth to lower sustainable growth. 4

Even if these three stages of growth can be envisioned for a firm, the third 5

“steady-state” growth stage, which is assumed to remain fixed in perpetuity, 6

represents an unrealistic expectation because the three stages of growth can be 7

repeated. That is to say, the stages can be repeated where growth for a firm 8

ramps up and ramps down in cycles over time. For these reasons, there is no 9

need to analyze growth rates individually for each cycle, but rather to rely 10

upon analysts’ growth forecasts that are used by investors when pricing 11

common stocks. 12

34. Q. How did you determine an appropriate growth rate? 13

A. The growth rate used in a DCF calculation should measure investor 14

expectations. Investors consider both company-specific variables and overall 15

market sentiment (i.e., level of inflation rates, interest rates, economic 16

conditions, etc.) when balancing their capital gains expectations with their 17

dividend yield requirements. Investors are not influenced solely by a single 18

set of company-specific variables weighted in a formulaic manner. Therefore, 19

all relevant growth rate indicators should be evaluated using a variety of 20

techniques when formulating a judgment of investor-expected growth. 21

31

35. Q. What data for the Gas Group have you considered in your growth rate 1

analysis? 2

A. I considered the growth in the financial variables shown on Schedules 8 and 9, 3

which reflect historical (Schedule 8) and projected (Schedule 9) rates of 4

growth in earnings per share, dividends per share, book value per share, and 5

cash flow per share for the Gas Group. While analysts will review all 6

measures of growth, as I have done, earnings per share growth directly 7

influences the expectations of investors for the future performance of utility 8

stocks. Forecasts of earnings growth are required because the DCF model is 9

forward-looking, and, with the constant P-E multiple and constant payout ratio 10

that the DCF model assumes, all other measures of growth will mirror 11

earnings growth. The historical growth rates were obtained from the Value 12

Line publication that provides this data. While historical data cannot be 13

ignored, they are much less significant when applying the DCF model than 14

projections of future growth. Investors cannot purchase the past earnings of a 15

utility. To the contrary they are only entitled to future earnings, which are the 16

focus of growth projections. Furthermore, if significant weight is assigned to 17

historical performance, the historical data are double-counted because they are 18

already factored into analysts’ forecasts of earnings growth. 19

36. Q. Is a five-year investment horizon associated with the analysts’ forecasts 20

consistent with the traditional DCF model? 21

A. Yes, it is. Although the constant form of the DCF model assumes an infinite 22

32

stream of cash flows, investors do not expect to hold an investment 1

indefinitely. Rather than viewing the DCF in the context of an endless stream 2

of growing dividends (e.g., a century of cash flows), the growth in the share 3

value (i.e., capital appreciation, or capital gains yield) is most relevant to 4

investors’ total return expectations. Hence, the sale price of a stock can be 5

viewed as a liquidating dividend that can be discounted along with the annual 6

dividend receipts during the investment-holding period to arrive at the 7

investors’ expected return. The growth in the price per share will equal the 8

growth in earnings per share if, as the DCF model assumes, there is no change 9

in the P-E multiple. As such, my company-specific growth analysis, which 10

focuses principally upon five-year forecasts of earnings per share growth, 11

conforms with the type of analysis that influences investors’ expectations of 12

their actual total return. Moreover, academic research also focuses on five-13

year growth rates specifically because market outcomes occurring over that 14

investment horizon are what influence stock prices. Indeed, if investors 15

required forecasts beyond five years in order to properly value common 16

stocks, then it would be reasonable to expect that some investment advisory 17

service would begin publishing that information for individual stocks in order 18

to meet the demands of the marketplace. The absence of such a publication 19

suggests that there is no market for this information because investors do not 20

require forecasts for an infinite series of future data points in order to make 21

informed decisions to purchase and sell stocks. 22

33

37. Q. What are the analysts’ forecasts of future growth that you considered? 1

A. Schedule 9 provides projected earnings per share growth rates taken from 2

analysts’ five-year forecasts compiled by IBES/First Call, Zacks, and Value 3

Line. These are all reliable authorities of projected growth that investors use 4

to make buy, sell, and hold decisions. The IBES/First Call and Zacks 5

estimates are obtained from the Internet and are widely available to investors. 6

The growth rates reported by IBES/First Call and Zacks are consensus 7

forecasts taken from a survey of analysts that make growth projections for 8

these companies. Notably, First Call’s earnings forecasts are frequently 9

quoted in the financial press. The Value Line forecasts also are widely 10

available to investors and can be obtained by subscription or free of charge at 11

most public and collegiate libraries. The IBES/First Call and Zacks forecasts 12

are limited to earnings per share growth, while Value Line makes projections 13

of other financial variables. The Value Line forecasts of dividends per share, 14

book value per share, and cash flow per share for the Gas Group are also 15

included on Schedule 9. 16

38. Q. What are the projected growth rates published by the sources you 17

discussed? 18

A. Schedule 9 shows the prospective five-year earnings per share growth rates 19

projected for the Gas Group by IBES/First Call (4.83%), Zacks (6.00%), and 20

Value Line (7.44%). 21

34

39. Q. Are certain growth rate forecasts entitled to greater weight in developing 1

a growth rate for use in the DCF model? 2

A. Yes. While a variety of factors should be examined to reach a reasonable 3

conclusion on the DCF growth rate, growth in earnings per share should 4

receive the greatest emphasis. Growth in earnings per share is the primary 5

determinant of investors’ expectations of the total returns they will obtain 6

from stocks because the capital gains yield (i.e., price appreciation) will track 7

earnings growth if the P-E multiple remains constant, as the DCF model 8

assumes. Moreover, earnings per share (derived from net income) are the 9

source of dividend payments and are the primary driver of retention growth 10

and its surrogate, i.e., book value per share growth. As such, under these 11

circumstances, greater emphasis must be placed upon projected earnings per 12

share growth. In fact, Professor Gordon, the foremost proponent of the use of 13

the DCF model in setting utility rates, concluded that the best measure of 14

growth for use in the DCF model is a forecast of earnings per-share growth.7 15

Consistent with Professor Gordon’s findings, projections of earnings per share 16

growth, such as those published by IBES/First Call, Zacks, and Value Line, 17

provide the best indication of investor expectations. 18

7 Gordon, Gordon & Gould, “Choice Among Methods of Estimating Share Yield,” The Journal of

Portfolio Management (Spring 1989).

35

40. Q. What growth rate do you use in your DCF model? 1

A. The forecasts shown on Schedule 9 for the Gas Group exhibit a range of 2

average earnings per share growth rates from 4.83% to 7.44%. DCF growth 3

rates should not be established by mathematical formulation, and I have not 4

done so. In my opinion, a growth rate of 6.75% is a reasonable estimate of 5

investor-expected growth for the Gas Group. This value is within the array of 6

analysts’ forecasts of five-year earnings per share growth rates. The 7

reasonableness of this growth rate is also supported by the expected 8

continuation of gas utility infrastructure spending. 9

41. Q. Are the dividend yield and growth components of the DCF adequate to 10

accurately depict the rate of return on common equity when it is used to 11

calculate a utility’s weighted average overall cost of capital? 12

A. The components of the DCF model are adequate for that purpose only if the 13

capital structure ratios are measured by the market value of debt and equity. 14

In the case of the Gas Group, average capital structure ratios are 40.89% long-15

term debt, 0.45% preferred stock, and 58.66% common equity, as shown on 16

Schedule 10. If book values are used to compute the capital structure ratios, 17

then a leverage adjustment is required. 18

42. Q. What is a leverage adjustment? 19

A. If a firm’s capitalization, as measured by its stock price, diverges from its 20

capitalization, measured at book value, the potential exists for a financial risk 21

36

difference. Such a risk difference arises because a market-valued 1

capitalization contains more equity and less debt than a book-value 2

capitalization and, therefore, has less risk than the book-value capitalization. 3

A leverage adjustment properly accounts for the risk differential between 4

market-value and book-value capital structures. 5

43. Q. Why is a leverage adjustment necessary? 6

A. In order to make the DCF results relevant to the capitalization measured at 7

book value (as is done for rate setting purposes), the market-derived cost rate 8

must be adjusted to account for this difference in financial risk. The only 9

perspective that is important to investors is the return that they can realize on 10

the market value of their investment. As I have measured the DCF, the simple 11

yield (D/P) plus growth (g) provides a return applicable strictly to the price 12

(P) that an investor is willing to pay for a share of stock. The need for the 13

leverage adjustment arises when the results of the DCF model (k) are to be 14

applied to a capital structure that is different from the capital structure 15

indicated by the market price (P). From the market perspective, the financial 16

risk of the Gas Group is accurately measured by the capital structure ratios 17

calculated from the market-valued capitalization of a firm. If the ratemaking 18

process utilized the market capitalization ratios, then no additional analysis or 19

adjustment would be required, and the simple yield (D/P) plus growth (g) 20

components of the DCF would satisfy the financial risk associated with the 21

market value of the equity capitalization. Because the ratemaking process 22

uses ratios calculated from a firm’s book value capitalization, further analysis 23

37

is required to synchronize the financial risk of the book capitalization with the 1

required return on the book value of the firm’s equity. This adjustment is 2

developed through precise mathematical calculations, using well-recognized 3

analytical procedures that are widely accepted in the financial literature. To 4

arrive at that return, the rate of return on common equity is the unleveraged 5

cost of capital (or equity return at 100% equity) plus one or more terms 6

reflecting the increase in financial risk resulting from the use of leverage in 7

the capital structure. The calculations presented in the lower panel of data 8

shown on Schedule 10, under the heading “M&M,”8 provide a return of 9

7.70% when applicable to a capital structure with 100% common equity. 10

44. Q. Are there specific factors that influence market-to-book ratios that 11

determine whether the leverage adjustment should be made? 12

A. No. The leverage adjustment is not intended, nor was it designed, to address 13

the reasons that stock prices vary from book value. Hence, any observations 14

concerning market prices relative to book value are not on point. The 15

leverage adjustment deals with the issue of financial risk and does not 16

transform the DCF result to a book value return through a market-to-book 17

adjustment. Again, the leverage adjustment that I propose is based on the 18

fundamental financial precept that the cost of equity is equal to the rate of 19

return for an unleveraged firm (i.e., where the overall rate of return equates to 20

8 Franco Modigliani and Merton H. Miller, “The Cost of Capital, Corporation Finance, and the

Theory of Investments,” American Economic Review, June 1958, at 261-97. Franco Modigliani and

Merton H. Miller, “Taxes and the Cost of Capital: A Correction,” American Economic Review, June 1963,

at 433-43.

38

the cost of equity with a capital structure that contains 100% equity) plus the 1

additional return required for introducing debt and/or preferred stock leverage 2

into the capital structure. 3

Further, as noted previously, the relatively high market prices of 4

utility stocks cannot be attributed solely to the notion that these companies are 5

expected to earn a return on the book value of equity that differs from their 6

cost of equity determined from stock market prices. Stock prices above book 7

value are common for utility stocks, and indeed the stock prices of non-8

regulated companies exceed book values by even greater margins. It is 9

difficult to accept that the vast majority of all firms operating in our economy 10

are generating returns far in excess of their cost of capital. Certainly, in our 11

free-market economy, competition should contain such “excesses” if they 12

actually exist. 13

Finally, the leverage adjustment adds stability to the final DCF cost 14

rate. That is to say, as the market capitalization increases relative to its book 15

value, the leverage adjustment increases while the simple yield (D/P) plus 16

growth (g) result declines. The reverse is also true: when the market 17

capitalization declines, the leverage adjustment also declines as the simple 18

yield (D/P) plus growth (g) result increases. 19

39

45. Q. Is the leverage adjustment that you propose designed to transform the 1

market return into one that is designed to produce a particular market-2

to-book ratio? 3

A. No, it is not. What I label a “leverage adjustment” is merely a convenient way 4

of showing the amount that must be added to (or subtracted from) the result of 5

the simple DCF model (i.e., D/P + g) when the DCF return applies to a capital 6

structure used for ratemaking that is computed with book-value weighting 7

rather than market-value weighting. Although I specify a separate factor, 8

which I call the leverage adjustment, there is no need to do so other than to 9

identify this factor. If I were to express my return solely in the context of the 10

book value weighting that we use to calculate the weighted average cost of 11

capital and ignore the familiar D/P + g expression entirely, then a separate 12

element in the DCF cost of equity determination would not be needed to 13

reflect the differential in financial leverage between a market-value and book-14

value capitalization. As shown in the bottom panel of data on Schedule 10, 15

the equity return applicable to the book value common equity ratio is equal to 16

7.70%, which is the return for the Gas Group appropriate for a capital 17

structure with no debt (i.e., a 100% equity ratio) plus 3.88% to compensate 18

investors for the risk of a 51.27% debt ratio and 0.07% for a 1.73% preferred 19

stock ratio. These are the book-value ratios that differ markedly from the 20

market-value based ratios I discussed previously. Under this approach, the 21

parts add up to 11.65% (7.70% + 3.88% + 0.07%), and there is no need to 22

even address the cost of equity in terms of D/P + g. To express this same 23

40

return in the context of the familiar DCF model, I added the 3.45% dividend 1

yield, the 6.75% growth rate, and 1.45% for the leverage adjustment in order 2

to arrive at the same 11.65% (3.45% + 6.75% + 1.45%) return. I know of no 3

means to mathematically solve for the 1.45% leverage adjustment by 4

expressing it in the terms of any particular relationship of market price to 5

book value. The 1.45% adjustment is merely a convenient way to compare 6

the 11.65% return computed using the Modigliani & Miller formulas to the 7

10.20% return generated by the DCF model (i.e., D1/P0 + g, or the traditional 8

form of the DCF shown on Schedule 1, page 2) based on a market-value 9

capital structure. A 10.20% return assigned to anything other than the market 10

value of equity cannot equate to a reasonable return on book value that has 11

higher financial risk. My point is that when we use a market-determined cost 12

of equity developed from the DCF model, it reflects a level of financial risk 13

that is different (in this case, lower) from the capital structure stated at book 14

value. This process has nothing to do with targeting any particular market-to-15

book ratio. 16

46. Q. Please provide the DCF return based upon your preceding discussion of 17

dividend yield, growth, and leverage. 18

A. As explained previously, I have utilized a six-month average dividend yield 19

(D1/P0) adjusted in a forward-looking manner for my DCF calculation. This 20

dividend yield is used in conjunction with the growth rate (g) previously 21

developed. The DCF also includes the leverage modification (Lev.) required 22

when the book value equity ratio is used in determining the weighted average 23

41

cost of capital in the ratemaking process rather than the market value equity 1

ratio related to the price of stock. The resulting DCF cost rate is 11.65%, 2

computed as follows: 3

D 1 /P 0 + g + lev. = k

Gas Group 3.45% + 6.75% + 1.45% = 11.65% 4

The DCF result shown above represents the simplified (i.e., Gordon) form of 5

the model that contains a constant-growth assumption. I should reiterate, 6

however, that the DCF-indicated cost rate provides an explanation of the rate 7

of return on common stock market prices without regard to the prospect of a 8

change in the P-E multiple. An assumption that there will be no change in the 9

P-E multiple is not supported by the realities of the equity market because P-E 10

multiples do not remain constant. This is one of the constraints of this model 11

that makes it important to consider the results of other models when 12

determining a company’s cost of equity. 13

VIII. RISK PREMIUM ANALYSIS 14

47. Q. Please describe your use of the Risk Premium approach to determine the 15

cost of equity. 16

A. With the Risk Premium approach, the cost of equity capital is determined by 17

corporate bond yields plus a premium to account for the fact that common 18

42

equity is exposed to greater investment risk than debt capital. The result of my 1

Risk Premium study is shown on Schedule 1, page 2. That result is 10.75%. 2

48. Q. What long-term public utility debt cost rate did you use in your Risk 3

Premium analysis? 4

A. In my opinion, and as I will explain in more detail further in my testimony, a 5

4.00% yield represents a reasonable estimate of the prospective yield on long-6

term, A-rated public utility bonds. 7

49. Q. What historical data are shown by the Moody’s data? 8

A. I have analyzed the historical yields on the Moody’s index of long-term public 9

utility debt as shown on Schedule 11, page 1. For the twelve months ended 10

February 2022, the average monthly yield on Moody’s index of A-rated public 11

utility bonds was 3.20%. For the six- and three-month periods ended 12

February 2022, the yields were 3.20% and 3.38%, respectively. During the 13

twelve months ended February 2022, the range of the yields on A-rated public 14

utility bonds was 2.95% to 3.68%. Page 2 of Schedule 11 shows the long-run 15

spread in yields between A-rated public utility bonds and long-term Treasury 16

bonds. As shown on page 3 of Schedule 11, the yields on A-rated public 17

utility bonds have exceeded those on Treasury bonds by 1.10% on a twelve-18

month average basis, 1.18% on a six-month average basis, and 1.31% on a 19

three-month average basis. With these data, 1.25% represents a reasonable 20

spread for the yield on A-rated public utility bonds over Treasury bonds. 21

43

50. Q. What forecasts of interest rates have you considered in your analysis? 1

A. I have determined the prospective yield on A-rated public utility debt by using 2

the Blue Chip Financial Forecasts (“Blue Chip”) along with the spread in the 3

yields that I describe below. Blue Chip is a reliable authority and contains 4

consensus forecasts of a variety of interest rates compiled from a panel of 5

banking, brokerage, and investment advisory services. In early 1999, Blue 6

Chip stopped publishing forecasts of yields on A-rated public utility bonds 7

because the Federal Reserve deleted these yields from its Statistical Release 8

H.15. To independently project a forecast of the yields on A-rated public 9

utility bonds, I have combined the forecast yields on long-term Treasury 10

bonds published on March 1, 2022 and a yield spread of 1.25%, derived from 11

historical data. 12

51. Q. How have you used these data to project the yield on A-rated public 13

utility bonds for the purpose of your Risk Premium analyses? 14

A. Shown below is my calculation of the prospective yield on A-rated public 15

utility bonds using the building blocks discussed above, i.e., the Blue Chip 16

forecast of Treasury bond yields and the public utility bond yield spread. For 17

comparative purposes, I also have shown the Blue Chip forecasts of Aaa-rated 18

and Baa-rated corporate bonds. These forecasts are: 19

44

30-Year

Year Quarter Aaa-rated Baa-rated Treasury Spread Yield

2022 First 3.2% 3.9% 2.2% 1.25% 3.45%

2022 Second 3.4% 4.2% 2.5% 1.25% 3.75%

2022 Third 3.7% 4.4% 2.6% 1.25% 3.85%

2022 Fourth 3.9% 4.6% 2.7% 1.25% 3.95%

2023 First 4.0% 4.8% 2.9% 1.25% 4.15%

2023 Second 4.1% 4.9% 3.0% 1.25% 4.25%

Corporate A-rated Public Utility

Blue Chip Financial Forecasts

52. Q. Are there additional forecasts of interest rates that extend beyond those 1

shown above? 2

A. Yes. Twice yearly, Blue Chip provides long-term forecasts of interest rates. 3

In its December 1, 2021 publication Blue Chip published longer-term 4

forecasts of interest rates, which were reported to be: 5

30-Year

Averages Aaa-rated Baa-rated Treasury

2023-2027 4.4% 5.2% 3.4%

2028-2032 4.9% 5.7% 3.8%

Blue Chip Financial Forecasts

Corporate

The longer-term forecasts by Blue Chip suggest that interest rates will move 6

up from the levels revealed by the near-term forecasts. A 4.00% yield on A-7

rated public utility bonds represents a reasonable benchmark for measuring 8

the cost of equity in this case. All the data I used to formulate my conclusion 9

as to a prospective yield on A-rated public utility debt are available to 10