Pakistan WT/TPR/S/95 Page 25 - WTO Documents Online

53

Pakistan WT/TPR/S/95 Page 25 III. TRADE POLICIES AND PRACTICES BY MEASURE (1) OVERVIEW 1. Since its previous Trade Policy Review in 1995, Pakistan has taken steps, often unilaterally, to liberalize its trade regime. These steps are aimed at fostering private sector activity, notably investment. Trade liberalization has been especially marked since January 1999 as a consequence of commitments made to the IMF and World Bank as well as efforts by Pakistan to integrate its economy into the international trading system. 2. The tariff remains Pakistan's main trade policy instrument; its importance increased as a result of the recent elimination of non-tariff barriers on several items. At the same time, it is a major, albeit declining, source of tax revenue. Pakistan's average applied tariff rate has fallen from 56% to 20.4% since its previous Review. Nevertheless, tariff protection is still high, especially for a few sensitive items, and although efforts are being made to reduce tariff peaks and dispersion, tariff rates vary widely. Consequently, the tariff remains a potentially important distortion to domestic competition and thus an obstacle to the efficient allocation of resources. The scope for improving efficiency through further substantial cuts in tariffs may be limited by their importance to the Government as a source of revenue and by the internal tax system's vulnerability to avoidance and evasion (see below). 3. Some one third of tariff lines are currently bound. Given the reduction in applied rates, there is a widening gap between bound and applied rates. This imparts a degree of uncertainty to the tariff, with the Government retaining freedom to raise applied rates within bindings; this uncertainty is somewhat compounded as applied tariff rates on 91 tariff lines (down from 241 in 2000/01) (mostly textiles and clothing) exceed the bound rates by as much as 17 percentage points; steps are to be taken to address this problem. 4. During the period under review, Pakistan's tariff has been simplified considerably. Some two fifths of all tariff lines are now concentrated in the 25% to 30% range, although there are no longer any duty-free lines. Nonetheless, the tariff remains relatively complex, involving 26 different rates (49 in 2000/01), 13 of which are ad valorem, 11 specific, and 2 compound. Widely different tariff rates provide considerable scope for misclassification of imports by customs officials. The complexity of the tariff is exacerbated by concessions, although their scope seems to have been reduced recently. While most tariffs involve relatively transparent ad valorem rates, some 1% of tariff lines are subject to either specific or compound duties, which are intrinsically more opaque than ad valorem rates, tending to conceal relatively high ad valorem equivalent (AVE) rates. The transparency of Pakistan's tariff regime has improved through submissions to the WTO Integrated Database as well as its availability on the Internet. 5. Further protection from imports is provided by several other border taxes and charges. "Regulatory" duties appear to have been reinstated (for imports of edible oil and oil seeds for crushing). Moreover, withholding taxes are levied on imports (and exports); these taxes, which may be deductible from income taxes, are apparently intended to combat income tax evasion. In addition, a capital-value tax is levied on imported motor vehicles. 6. Plans for the simplification of existing complicated registration requirements for importers are under consideration. In addition, customs clearance for specific items or importers has been accelerated by the introduction of an express lane facility and an electronic assessment system. In the context of the implementation of the WTO Agreement on Customs Valuation, Pakistan discontinued the use of the Brussels Definition of Value, but maintained provisions for setting minimum import

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Pakistan WT/TPR/S/95 Page 25 - WTO Documents Online

Pakistan WT/TPR/S/95Page 25

III. TRADE POLICIES AND PRACTICES BY MEASURE

(1) OVERVIEW

1. Since its previous Trade Policy Review in 1995, Pakistan has taken steps, often unilaterally,to liberalize its trade regime. These steps are aimed at fostering private sector activity, notablyinvestment. Trade liberalization has been especially marked since January 1999 as a consequence ofcommitments made to the IMF and World Bank as well as efforts by Pakistan to integrate its economyinto the international trading system.

2. The tariff remains Pakistan's main trade policy instrument; its importance increased as aresult of the recent elimination of non-tariff barriers on several items. At the same time, it is a major,albeit declining, source of tax revenue. Pakistan's average applied tariff rate has fallen from 56% to20.4% since its previous Review. Nevertheless, tariff protection is still high, especially for a fewsensitive items, and although efforts are being made to reduce tariff peaks and dispersion, tariff ratesvary widely. Consequently, the tariff remains a potentially important distortion to domesticcompetition and thus an obstacle to the efficient allocation of resources. The scope for improvingefficiency through further substantial cuts in tariffs may be limited by their importance to theGovernment as a source of revenue and by the internal tax system's vulnerability to avoidance andevasion (see below).

3. Some one third of tariff lines are currently bound. Given the reduction in applied rates, thereis a widening gap between bound and applied rates. This imparts a degree of uncertainty to the tariff,with the Government retaining freedom to raise applied rates within bindings; this uncertainty issomewhat compounded as applied tariff rates on 91 tariff lines (down from 241 in 2000/01) (mostlytextiles and clothing) exceed the bound rates by as much as 17 percentage points; steps are to betaken to address this problem.

4. During the period under review, Pakistan's tariff has been simplified considerably. Sometwo fifths of all tariff lines are now concentrated in the 25% to 30% range, although there are nolonger any duty-free lines. Nonetheless, the tariff remains relatively complex, involving 26 differentrates (49 in 2000/01), 13 of which are ad valorem, 11 specific, and 2 compound. Widely differenttariff rates provide considerable scope for misclassification of imports by customs officials. Thecomplexity of the tariff is exacerbated by concessions, although their scope seems to have beenreduced recently. While most tariffs involve relatively transparent ad valorem rates, some 1% oftariff lines are subject to either specific or compound duties, which are intrinsically more opaque thanad valorem rates, tending to conceal relatively high ad valorem equivalent (AVE) rates. Thetransparency of Pakistan's tariff regime has improved through submissions to the WTO IntegratedDatabase as well as its availability on the Internet.

5. Further protection from imports is provided by several other border taxes and charges."Regulatory" duties appear to have been reinstated (for imports of edible oil and oil seeds forcrushing). Moreover, withholding taxes are levied on imports (and exports); these taxes, which maybe deductible from income taxes, are apparently intended to combat income tax evasion. In addition,a capital-value tax is levied on imported motor vehicles.

6. Plans for the simplification of existing complicated registration requirements for importers areunder consideration. In addition, customs clearance for specific items or importers has beenaccelerated by the introduction of an express lane facility and an electronic assessment system. In thecontext of the implementation of the WTO Agreement on Customs Valuation, Pakistan discontinuedthe use of the Brussels Definition of Value, but maintained provisions for setting minimum import

WT/TPR/S/95 Trade Policy ReviewPage 26

values for a few items. Cash margin requirements on the opening of all import letters of credit wereimposed temporarily, but have now been abolished.

7. Import prohibitions and restrictions have been maintained on a number of grounds. However,virtually all those for balance-of-payments purposes (numerous textiles and clothing articles, chassisfor trucks) were phased out; the importation of certain items depends largely upon the status of theimporter, origin, prior approval or other conditions. The scope of restrictions on imports of useditems has been widened. Imports of a specific type of raw sugar have been prohibited (as of 2000),but seemingly are no longer in force. No contingency measures have been applied. In governmentprocurement, price preferences have been granted to domestic suppliers, particularly for engineeringgoods contracts. Having encountered difficulties in eliminating its local content scheme by the dateset under the WTO Agreement on Trade-Related Investment Measures, Pakistan obtained anextension of the transition period for implementing this commitment.

8. The scope of export prohibitions seems to have been reduced by, inter alia, placing greateremphasis on compliance with international commitments (including those aimed at protectingintellectual property rights). Nevertheless, several restraints (including prohibitions and export taxes)aimed at ensuring adequate domestic supplies and minimum value added for certain items have beenmaintained, although their scope was reduced; these restraints tend to reduce the prices of the goodscovered and therefore constitute an implicit subsidy to domestic users of these goods. Exports ofcertain textiles and clothing items remain subject to access-related restraints in several major markets.Preshipment registration of export contracts is required for certain sensitive items (cotton, rice, urea);preshipment inspection requirements have applied to rice (since 1999). Export subsidies, largelylinked to export-performance requirements, have been provided in various forms, including financialsupport (quality certification, software, sugar, freight costs), concessionary export finance, andexport-processing zones; support to software exports is a new element in this policy since theprevious Review.

9. Support to production and trade is provided through a variety of tax and non-tax incentives;priority areas are science and technology and small and medium-sized enterprises. During the periodunder review, state participation in production and trade has persisted mainly in agriculture,chemicals, transport equipment, fuels, machine tools, mining and energy, as well as in engineering,financial, telecommunication, transport, and tourism services. Financial support has also beenprovided to strengthen quality certification.

10. New legislation has been passed to strengthen the protection of intellectual property rights;however, limited adherence to international treaties in this area, and poor enforcement seem to havecontributed to persistent high levels of piracy and trade in counterfeit goods.

11. As regards competition policy, the elimination of business entry restrictions seems to havereduced industrial concentration.

(2) MEASURES DIRECTLY AFFECTING IMPORTS

(i) Registration and documentation requirements

12. Since the previous Review of Pakistan, there have been no major changes in the list of entitieseligible to import, except for the inclusion in the list of overseas Pakistanis.1 The entities comprise

1 Overseas Pakistanis are allowed to import or send freely importable goods up to an annual value of

US$10,000; these items must be paid with their own foreign exchange earnings and there is no need to open a

Pakistan WT/TPR/S/95Page 27

any firm holding a registration certificate, commercial importers, industrial consumers, and actualusers.2 Nearly all importers must register as importers with the Export Promotion Bureau (EPB)3;public sector departments are exempt from registration requirements. Only firms listed in publicnotices issued by the Ministry of Commerce may apply for import authorization; a person or familyowning more than one firm, may register one of its firms only. In the year 2000, there were plans toamend the regulatory framework with a view to simplifying registration procedures and introducingan automatic database upgrade.4

13. The EPB issues a so-called "Category Pass Book" to importers of items subject to certainimport conditions (other than freely importable goods), for purposes of opening letters of credit andcustoms clearance (section 2(vi), Table III.3).5

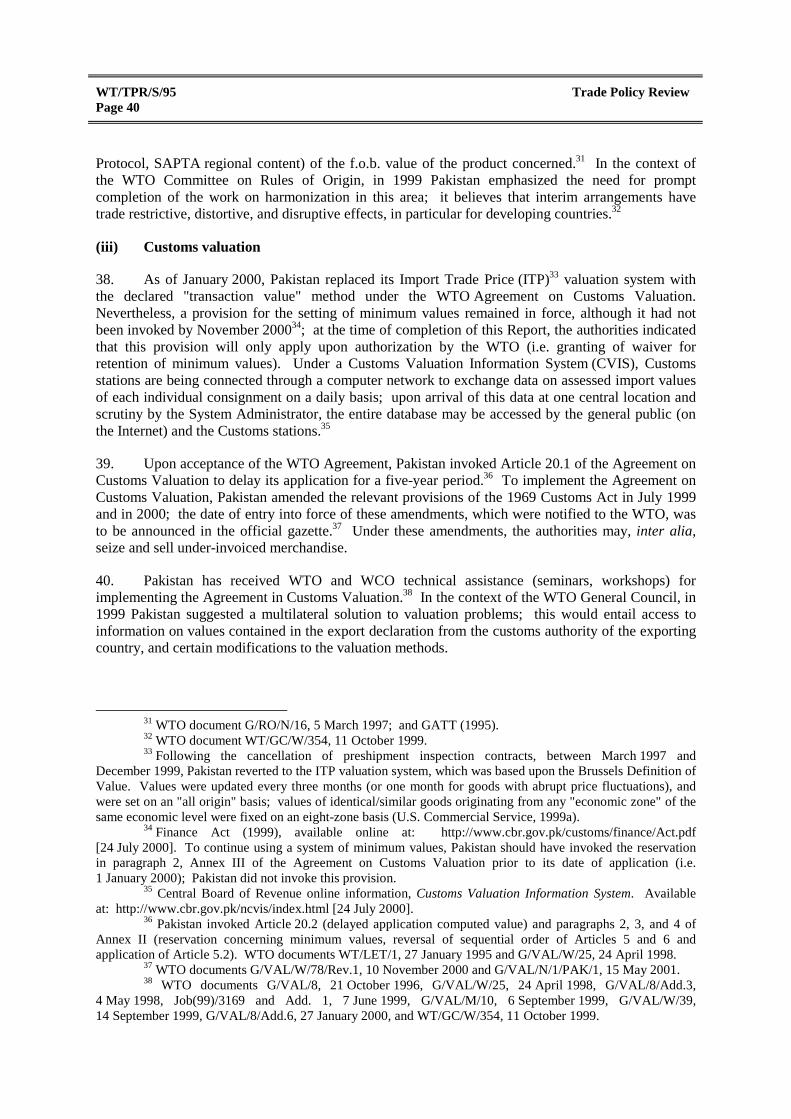

14. Basic documentation requirements remain unchanged (Import General Manifest, bill of entry,invoice, packing lists, copies of letters of credit6, and insurance certificates). In the case of itemssubject to certain conditions, a recommendation/clearance or prior approval from the competentgovernment agency, or certificates from the exporting country may be required (section 2(xi)(a),Table III.3).7 In most cases, in order to obtain the duty concessions for import of machinery and rawmaterials granted to various industrial establishments, importers need to furnish an indemnitybond/bank guarantee to the extent of duty exempted. A certificate of origin may be required for itemssubject to special import (e.g. preferential treatment), depending on the origin.

15. As of February 2000, an Electronic Assessment System (EASY) ensures more speedyassessment and customs clearance as well as reduced contact between taxpayers and the tax collectors(which leaves less scope for corruption).8 At a first stage, EASY has been available to multinationalsand local firms eligible for an "express lane facility" (operated since 1998). EASY covers: dutiableimports by public-sector entities (i.e. federal/provincial governments, state-owned corporations, localbodies); all items subject to specific rates of customs duty (excluding compound rates,section 2(ii)(d)); and, certain items subject to zero rates of customs duty and sales tax. EASY doesnot apply to old/used/second-hand/re-conditioned items, scrap, and items subject to restrictions orbans or duty exemptions (section 2(ii)(i)). A share of 5% of goods are randomly selected by computerfor clearance under "normal" (i.e. ordinary) procedure, which takes about one day.

16. No compulsory storage requirements seem to have been applied.

letter of credit, register as an importer or for sales tax registration by the consignee (Articles 2.2(d) and 2.5 ofImport Policy Order, 1999 and Articles 1.5 and 15.1(o) of Import Export Procedure Order (1999)).

2 GATT (1995).3 Since the previous Review, exemption from registration has been extended to imports of reading

material and goods for mountaineering and imported by some members of trekking expeditions for their ownuse, and to imports by overseas Pakistanis and to importers exempt under the terms of paragraph 9 ofRegistration (Importers and Exporters) Order (1993).

4 Export Promotion Bureau (2000).5 Article 1.1 of the Import Export Procedures Order (1999), and F.E Circular No. 54 of 1998 of the

State Bank of Pakistan [Online]. Available at: http://www.sbp.org.pk/femanual/FE%20Circulars/1998/c54.htmand http://www.sbp.org.pk/femanual/FE Circulars/1998/c54.htm [18 September 2000].

6 When opening the letter of credit the importer must, inter alia, ensure that the import is made at themost competitive price.

7 For example, food colouring material requires a certificate from the responsible agency in theexporting country indicating that it is in use in the country of origin at the time of shipment or registered in thatcountry (Import Policy Order (1999)).

8 Central Board of Revenue online information. Available at: http://www.cbr.gov.pk/customs/igm/easy.html [24 July 2000].

WT/TPR/S/95 Trade Policy ReviewPage 28

(ii) Tariffs

(a) General features

17. The customs tariff is Pakistan's main trade policy instrument. It is announced annuallythrough the Finance Act and published in the official gazette (Gazette of Pakistan ExtraordinaryPart II). In addition, at the start of each financial year the Central Board of Revenue (CBR) publishesthe Customs Tariff along with Notifications (SROs) containing various duty exemptions, rules, andchanges; the Customs Tariff and accompanying regulations are also available at the CBR onlineinformation. Although it has provided import data since 1997, Pakistan has submitted its customstariff to the Integrated Database of the WTO only as from 2000.9 The customs tariff is an important,albeit declining, source of tax revenues; its share of total tax revenues dropped from 30.1% in1994/95 to 13.7% in 2000/01 (section 4(i)).

18. As of 2001/02, the tariff structure has been simplified considerably. As an instrument of tradepolicy, the tariff accords varied levels of protection to domestic industry and is therefore a potentiallyimportant distortion to competition and thus an obstacle to the efficient allocation of domesticresources.10 The tariff is also a complex instrument; based on the 1996 nomenclature of theHarmonized System (HS), it currently (2001/02) contains 5,477 tariff lines (at the 8-digit HS), 13.6%less than in 1996/97, and involves 26 different rates (13 ad valorem rates levied at the c.i.f. value ofimports, 11 specific rates, and 2 compound rates).11 On the other hand more than 99% of tariff ratesare ad valorem, which are more transparent than other tariffs. As a result of subsequent cuts inapplied rates, bound MFN tariff rates are, by and large, considerably higher than applied MFN rates,thereby providing plenty of scope for the authorities to raise applied rates without breaching bindings.The summary indicators highlight these and several of the other main features of Pakistan's customstariff, together with the significant changes that it has undergone during the period under review(Table III.1).12

19. Duties (as well as all indirect taxes and other charges levied at the border) seem to be settledwith the Customs prior to the goods' release from custody.13 In cases of "urgent consignment",however, customs duties may be paid within ten days of clearance.14 Duty payment may also bedeferred for other items under certain conditions (section 2(ii)(j) and Table III.2). Under the1969 Customs Act, the Ministry of Finance, Economic Affairs, Statistics and Revenue and the CBRare empowered to exempt imports from duty and impose regulatory or special customs duties.15

9 WTO document G/MA/IDB/2/Rev.11, 7 June 2001.10 The authorities indicated that the tariff barely offsets high domestic costs of transport, infrastructure,

purchase of technology, and interest rates.11 In 1996/97 there were 60 different rates (22 ad valorem, 20 compound, 5 alternate, and 13 specific

rates).12 All tariff-related estimates in the charts and tables of this report reflect import duties contained in

Pakistan's Customs Tariff and its amendments; only the ad valorem component of compound and alternateduties is used as no ad valorem equivalents are available. No specific rates or occasional/temporary tariffincreases or reductions or other types of duties are taken into consideration in these calculations.

13 U.S. Commercial Service (1999a).14 Urgent consignments are: human body organs, perishable medicines, live animals and plants,

newspapers, journals, radioactive material, replacement parts of computers, machines and drilling components,fertilizer imported by Fertilizer Import Department, etc. (Prior Release of Urgent consignments (Import andExports) Rules (1994)).

15 Various Customs SROs; and GATT (1995).

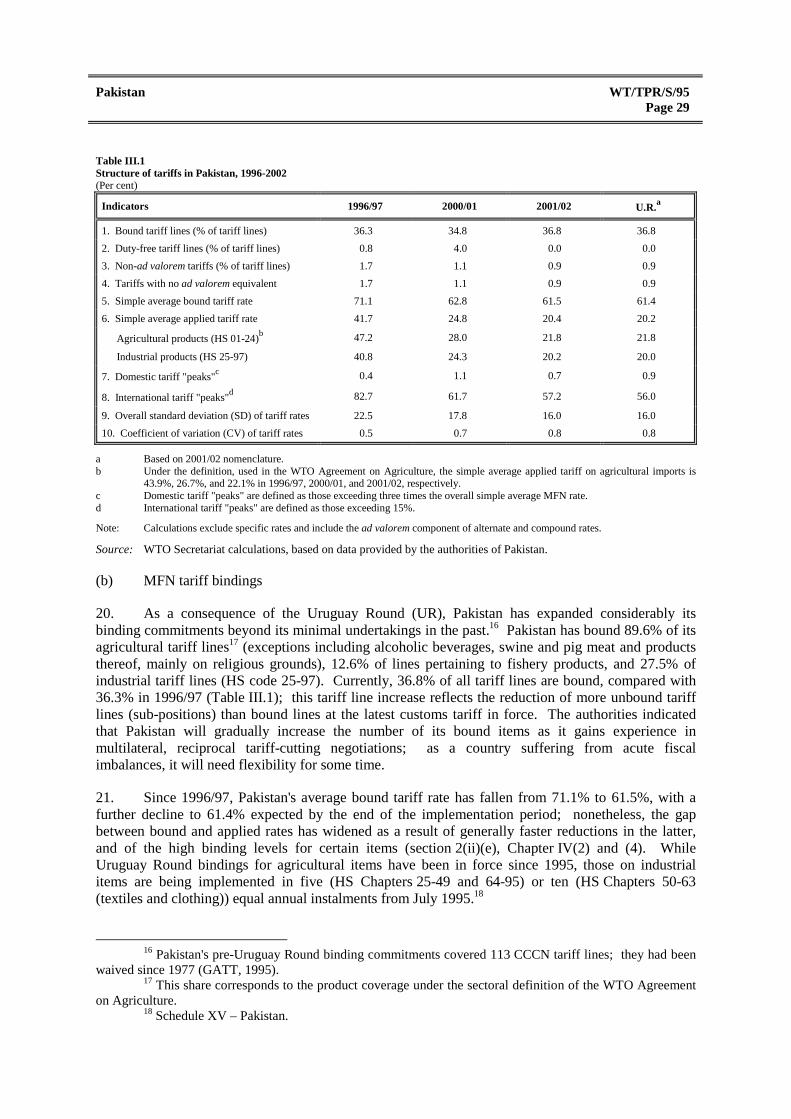

Pakistan WT/TPR/S/95Page 29

Table III.1Structure of tariffs in Pakistan, 1996-2002(Per cent)

Indicators 1996/97 2000/01 2001/02 U.R.a

1. Bound tariff lines (% of tariff lines) 36.3 34.8 36.8 36.8

2. Duty-free tariff lines (% of tariff lines) 0.8 4.0 0.0 0.0

3. Non-ad valorem tariffs (% of tariff lines) 1.7 1.1 0.9 0.9

4. Tariffs with no ad valorem equivalent 1.7 1.1 0.9 0.9

5. Simple average bound tariff rate 71.1 62.8 61.5 61.4

6. Simple average applied tariff rate 41.7 24.8 20.4 20.2

Agricultural products (HS 01-24)b 47.2 28.0 21.8 21.8

Industrial products (HS 25-97) 40.8 24.3 20.2 20.0

7. Domestic tariff "peaks"c 0.4 1.1 0.7 0.9

8. International tariff "peaks"d 82.7 61.7 57.2 56.0

9. Overall standard deviation (SD) of tariff rates 22.5 17.8 16.0 16.0

10. Coefficient of variation (CV) of tariff rates 0.5 0.7 0.8 0.8

a Based on 2001/02 nomenclature.b Under the definition, used in the WTO Agreement on Agriculture, the simple average applied tariff on agricultural imports is

43.9%, 26.7%, and 22.1% in 1996/97, 2000/01, and 2001/02, respectively.c Domestic tariff "peaks" are defined as those exceeding three times the overall simple average MFN rate.d International tariff "peaks" are defined as those exceeding 15%.

Note: Calculations exclude specific rates and include the ad valorem component of alternate and compound rates.

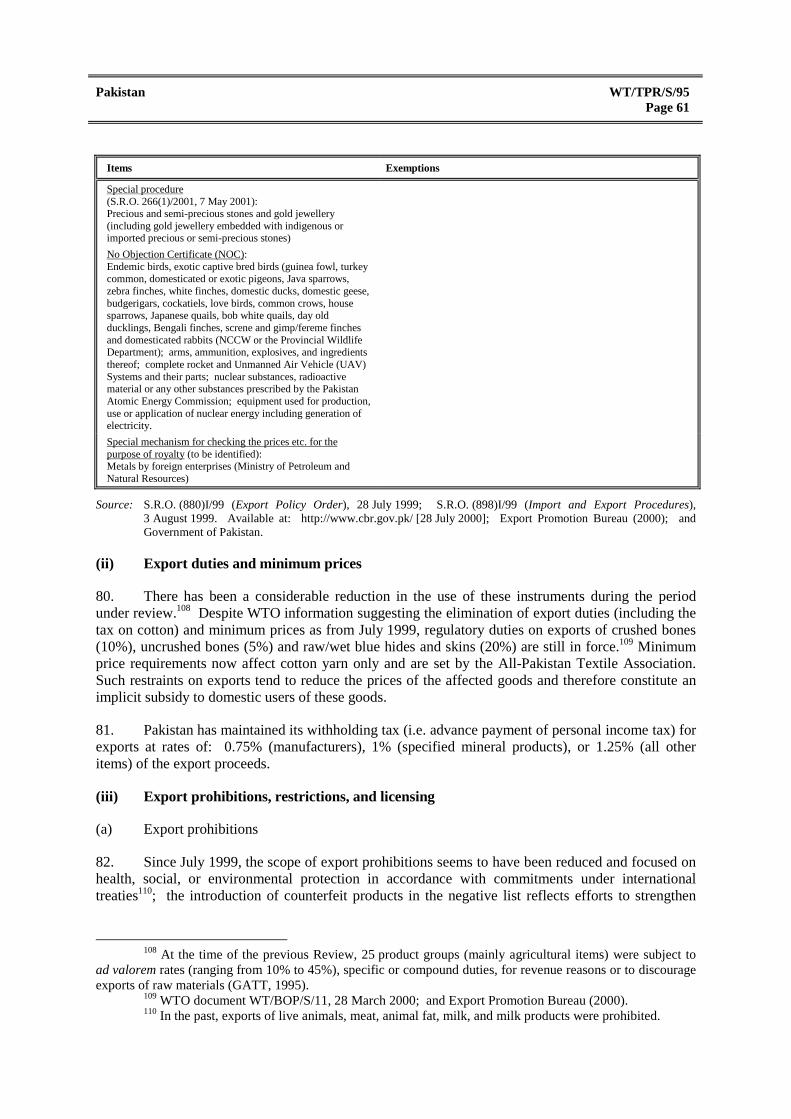

Source: WTO Secretariat calculations, based on data provided by the authorities of Pakistan.

(b) MFN tariff bindings

20. As a consequence of the Uruguay Round (UR), Pakistan has expanded considerably itsbinding commitments beyond its minimal undertakings in the past.16 Pakistan has bound 89.6% of itsagricultural tariff lines17 (exceptions including alcoholic beverages, swine and pig meat and productsthereof, mainly on religious grounds), 12.6% of lines pertaining to fishery products, and 27.5% ofindustrial tariff lines (HS code 25-97). Currently, 36.8% of all tariff lines are bound, compared with36.3% in 1996/97 (Table III.1); this tariff line increase reflects the reduction of more unbound tarifflines (sub-positions) than bound lines at the latest customs tariff in force. The authorities indicatedthat Pakistan will gradually increase the number of its bound items as it gains experience inmultilateral, reciprocal tariff-cutting negotiations; as a country suffering from acute fiscalimbalances, it will need flexibility for some time.

21. Since 1996/97, Pakistan's average bound tariff rate has fallen from 71.1% to 61.5%, with afurther decline to 61.4% expected by the end of the implementation period; nonetheless, the gapbetween bound and applied rates has widened as a result of generally faster reductions in the latter,and of the high binding levels for certain items (section 2(ii)(e), Chapter IV(2) and (4). WhileUruguay Round bindings for agricultural items have been in force since 1995, those on industrialitems are being implemented in five (HS Chapters 25-49 and 64-95) or ten (HS Chapters 50-63(textiles and clothing)) equal annual instalments from July 1995.18

16 Pakistan's pre-Uruguay Round binding commitments covered 113 CCCN tariff lines; they had been

waived since 1977 (GATT, 1995).17 This share corresponds to the product coverage under the sectoral definition of the WTO Agreement

on Agriculture.18 Schedule XV – Pakistan.

WT/TPR/S/95 Trade Policy ReviewPage 30

22. Between November 1977 and December 1995 Pakistan's pre-Uruguay Round commitmentswere waived to, inter alia, allow the introduction of the Harmonized System nomenclature19; in thiscontext, Pakistan notified improvements to its concessions on textiles and clothing products and thesewere approved.20 As of April 1997, its Uruguay Round commitments under Article II of GATT 1994have been waived to allow for the implementation of the recommended amendments to theHarmonized System nomenclature on 1 January 1996, and subsequently to undertake Article XXVIIInegotiations.21 In October 1998, Pakistan submitted documentation required for these negotiations22;reservations regarding Pakistan's proposed HS96 documentation were raised by three trading partners,of which one withdrew its reservation in September 2000, one was consulting with Pakistan byNovember 2000 and the third had to specify its concerns for its general reservation. In 1999, Pakistanmade a notification subsequent to its tariff commitments under Attachment II of the Memorandum ofUnderstanding on Market Access for Textile Products, signed between Pakistan and the EU on27 March 1996.23 The authorities indicated that Pakistan was transposing its customs tariff, at the timeof completion of this report, to HS 2000.

(c) Duty-free items

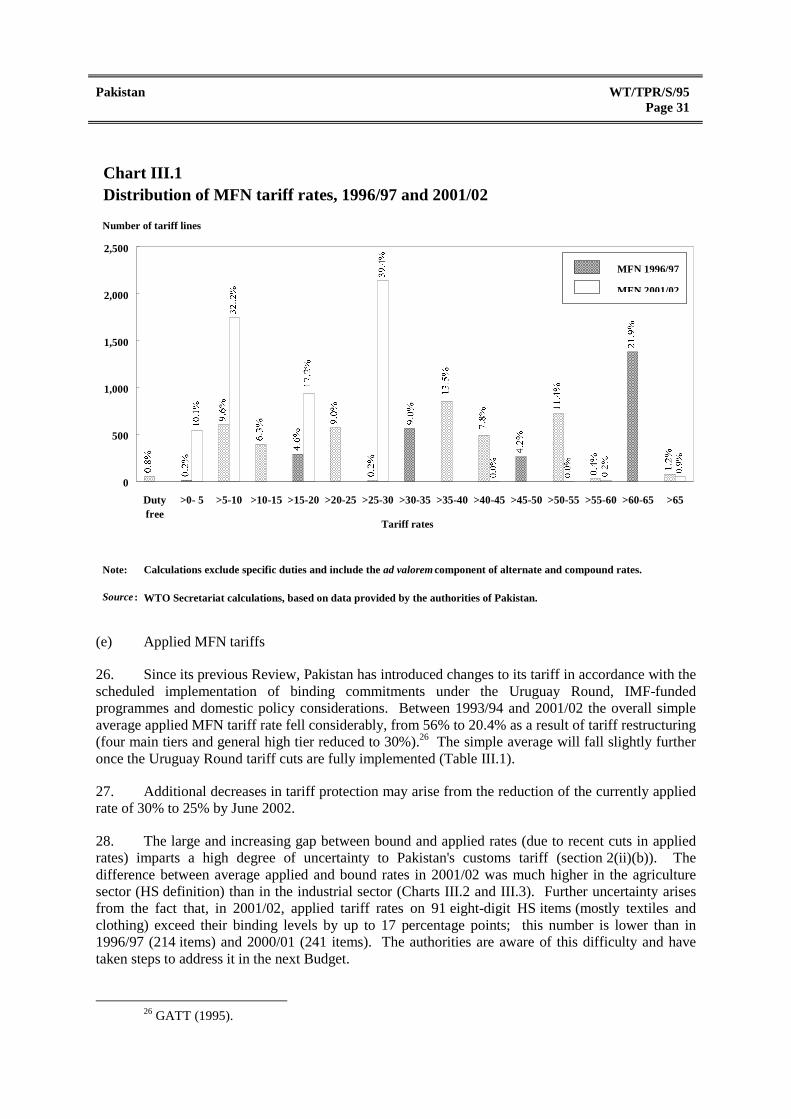

23. Following changes introduced in the customs tariff, as from 2001/02 no tariff lines are dutyfree as the lowest tariff rate has been raised to 5% (Chart III.1); duty-free entry is allowed on anexceptional basis. Prior to this change (i.e. 2000/01), 4% of the tariff lines were duty free (five timesas many as in 1996/97).

(d) Specific, compound, and alternate duties

24. Specific and compound duties currently account for only 0.9% of all tariff lines, and theirscope has been reduced since 1996/97 (Table III.1); alternate duties (29 items in 1996/97) are nolonger in force. Such duties tend to be more opaque than ad valorem duties and can therefore concealhigh rates. Whereas specific duties presently cover 44 (8-digit HS) tariff lines (e.g. certain oil seeds,vegetable plaiting materials, motor spirit, soya-bean and palm oil, liquid soda), compound duties areapplied to 3 lines (lubricating oil). Ad valorem equivalent (AVE) rates for these duties are notavailable.

25. Pakistan introduced specific duties (set and settled in foreign currency), in July 1999, rangingfrom US$5,000 to US$175,000 per unit on imports of passenger motor vehicles with an enginecapacity exceeding 800 cm3, for a period of one year.24 These duties favoured four-wheel-drivevehicles with an engine capacity exceeding 1,600 cm3.25 In the light of the prohibitively high rate(section 2(ii)(f)) that is regularly applied to automobiles of all types (250%), the only reason foradopting specific duties seems to have been to reduce the ad valorem customs duty burden for aspecific category of buyers (i.e. buyers of large engined four-wheel-drive vehicles).

19 WTO document WT/L/102, 24 November 1995. Pakistan renegotiated modifications of its

pre-Uruguay commitments with nine contracting parties.20 WTO documents G/SP/10, 13 January 1995 and G/MA/SP/2, 8 August 1995.21 WTO documents WT/L/216, 20 May 1997, G/C/W/200, 7 April 2000, and WT/L/400, 10 May 2001.22 WTO document G/SECRET/HS96/40, 10 December 1998.23 WTO documents G/MA/TAR/RS/61, 26 October 1999 and G/MA/TAR/RS/61 Corr.1, 5 May 2000.24 Section 18 of Finance Act (1999) available online at: http://www.cbr.gov.pk/customs/finance/

Act.pdf [24 July 2000].25 Duties on all vehicles up to 1,600 cm3 range from US$5,000 to US$20,000 and are similar for

four- and two-wheel-drive cars. For vehicles with higher engine capacity, the level of duties is significantlylower for four-wheel-drive cars; for example, the rate for a two-wheel-drive vehicle with an engine capacityexceeding 4,200 cm3 is US$175,000, against US$70,000 for a four-wheel-drive car with similar engine capacity.

Pakistan WT/TPR/S/95Page 31

0

500

1,000

1,500

2,000

2,500

Dutyfree

>0- 5 >5-10 >10-15 >15-20 >20-25 >25-30 >30-35 >35-40 >40-45 >45-50 >50-55 >55-60 >60-65 >65

Calculations exclude specific duties and include the ad valorem component of alternate and compound rates.

WTO Secretariat calculations, based on data provided by the authorities of Pakistan.

MFN 1996/97

MFN 2001/02

Number of tariff lines

Chart III.1 Distribution of MFN tariff rates, 1996/97 and 2001/02

Tariff rates

Note:

Source :

(e) Applied MFN tariffs

26. Since its previous Review, Pakistan has introduced changes to its tariff in accordance with thescheduled implementation of binding commitments under the Uruguay Round, IMF-fundedprogrammes and domestic policy considerations. Between 1993/94 and 2001/02 the overall simpleaverage applied MFN tariff rate fell considerably, from 56% to 20.4% as a result of tariff restructuring(four main tiers and general high tier reduced to 30%).26 The simple average will fall slightly furtheronce the Uruguay Round tariff cuts are fully implemented (Table III.1).

27. Additional decreases in tariff protection may arise from the reduction of the currently appliedrate of 30% to 25% by June 2002.

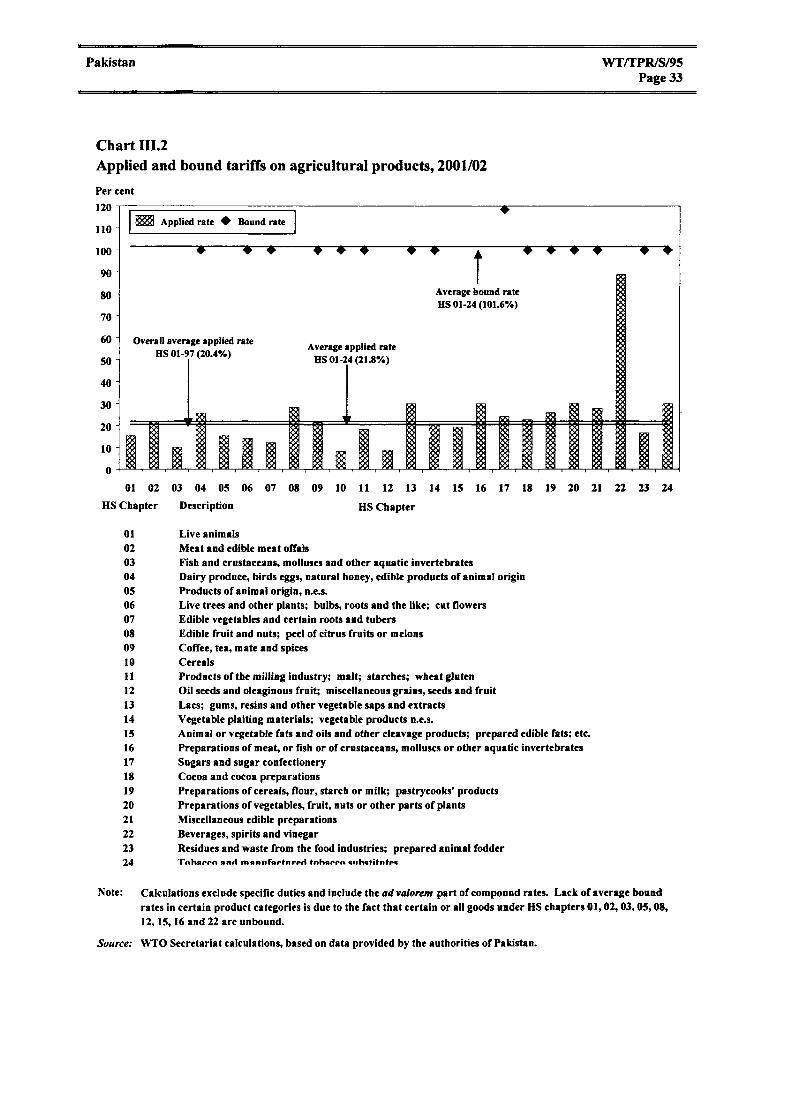

28. The large and increasing gap between bound and applied rates (due to recent cuts in appliedrates) imparts a high degree of uncertainty to Pakistan's customs tariff (section 2(ii)(b)). Thedifference between average applied and bound rates in 2001/02 was much higher in the agriculturesector (HS definition) than in the industrial sector (Charts III.2 and III.3). Further uncertainty arisesfrom the fact that, in 2001/02, applied tariff rates on 91 eight-digit HS items (mostly textiles andclothing) exceed their binding levels by up to 17 percentage points; this number is lower than in1996/97 (214 items) and 2000/01 (241 items). The authorities are aware of this difficulty and havetaken steps to address it in the next Budget.

26 GATT (1995).

WT/TPR/S/95 Trade Policy ReviewPage 32

29. In line with the downward trend in bound rates, and especially applied MFN tariff rates, theaverage rate of customs duty collected on total imports has also dropped, from 24.5% in 1994/95 to12.9% in 1999/00 (Chart III.4). This collected duty rate has been considerably lower than the averageapplied MFN rate. The large, albeit declining, gap between these two rates may be attributed,inter alia, to the duty concessions still available on a large number of products (section 2(ii)(j),Table III.2), the possibility that some tariff rates are prohibitive (i.e. automotive sector), andmisclassification of imports.

(f) MFN tariff dispersion

30. The potential efficiency losses associated with the customs tariff depend not just on theaverage applied MFN tariff rates, but also on the dispersion of those rates across products. Judgingfrom three of the four summary indicators (7-10) of tariff dispersion reported in Table III.1, thedispersion in applied tariff rates has declined as a consequence of the changes introduced into the2001/02 tariff; that is, domestic and international tariff "peaks" as well as the standard deviation ofapplied tariff rates have declined (the coefficient of variation has risen slightly). However, thesesummary indicators do not show the increasing concentration of tariff lines in rates ranging between10% and 30% (Chart III.1); at present, 62 eight-digit HS items are subject to duties exceeding 30%.In 2001/02, imports of 9 eight-digit HS items (automobiles) bear the highest ad valorem tariff of250%, while one item (certain fermented beverages) is subject to the second highest rate of 200%, andnine items (beer, other types of motor vehicles) to the third highest rate of 150%; about 24 items(wine, ethyl alcohol, spirits and spirituous beverages, certain types of automobiles, trucks,motorcycles) are subject to tariffs of 100% and 120%.

(g) MFN tariff escalation

31. Escalation remains an important feature of Pakistan's customs tariff in most sectors. It is mostpronounced for fully processed goods (Chart III.5 and Table AIII.1).

(h) Regulatory duties

32. Pakistan appears to have reinstated regulatory duties on imports of edible oil at a rate offive paisa (US$0.0042) per kg. (as from July 1999), and on oil seeds for crushing at a rate of 10% onthe amount of the customs duty collected (as from July 2000); at the time of the previous Review,regulatory duties were apparently merged into the tariffs.27 The stated purpose of this regulatory dutyis the development of a "Cess Fund" to finance the activities of the Pakistan Oilseed DevelopmentBoard. (Regulatory duties are not reflected in the tariff indicators found in Table III.1.)

33. In July 2001, regulatory duties on several other items were abolished.28 Remaining regulatoryduties are to lapse gradually, in line with outstanding agreements with certain industries.

27 SRO 816(I)/99, 1 July 1999; SRO 372(I)/2000, 17 June 2000; and GATT (1995).28 These duties affected: calcium chloride, urea fertilizer, steel bars, formic acid, urea formaldehyde,

moulding compound, BOPP film, medium density fibre board, craft paper, sacks, and jute bags.

WT/TPR/S/95 Trade Policy ReviewPage 34

0

10

20

30

40

50

60

70

80

25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73 75 78 80 82 84 86 88 90 92 94 96

Per cent

HS Chapter

Average applied rateHS 25-97 (20.2%)

HS DescriptionChapter 25 Salt; sulphur; earths and stone, etc.26 Ores, slag and ash27 Mineral fuels, mineral oils, etc.28 Inorganic chemicals; organic or inorganic compounds of precious metals, etc.29 Organic chemcials30 Pharmaceutical products31 Fertilizers 32 Tanning or dyeing extracts etc. 33 Essential oils and resinoids; perfumery, cosmetic or toilet preparations34 Soap, organic surface-active agents washing prep., etc. 35 Albuminoidal substances; modified starches; glues, etc.36 Explosives; pyrotechnic products; matches, etc37 Photographic or cinematographic goods38 Miscellaneous chemical products39 Plastics and articles thereof40 Rubber and articles thereof41 Raw hides and skins and leather42 Articles of leather, etc.43 Furskins and artifical fur; manufactures thereof44 Wood and articles of wood, etc.45 Cork and articles of cork46 Manuf. of straw, of esparto, etc. 47 Pulp of wood or of other fibrous cellulosic material

HS DescriptionChapter48 Paper and paper board, etc.49 Printed books, newspapers, etc.50 Silk51 Wool; fine or coarse animal hair, etc.52 Cotton53 Other vegetable textile fibres 54 Man-made filaments 55 Man-made staple fibres 56 Wadding, felt and non-wovens; special yarns; twine, cordage, etc.57 Carpets; other textile floor coverings58 Special woven fabrics; lace, etc.59 Impregnated, coated, covered or laminated textile fabrics, etc.60 Knitted or crocheted fabrics 61 Articles of apparel and clothing accessories, knitted or crocheted62 Articles of apparel and clothing accessories, not knitted, etc.63 Other made-up textile articles; sets, worn clothing, etc.64 Footwear, gaiters, etc.65 Headgear and parts thereof66 Umbrellas, walking-sticks, etc. 67 Prepared feathers and down, etc.68 Articles of stone, plaster, etc.69 Ceramic products70 Glass and glassware71 Natural or cultured pearls, precious or semi-precious stones, precious metals, etc.

HS DescriptionChapter72 Iron and steel73 Articles of iron and steel74 Copper and articles thereof75 Nickel and articles thereof76 Aluminium etc. 78 Lead and artilces thereof 79 Zinc and articles thereof 80 Tin and articles thereof81 Other base metals, etc.82 Tools, implements, cutler spoons and forks, etc.83 Misc. articles of base metals84 Nuclear reactors, boilers, machinery, etc.85 Electrical machinery and equipment, etc.86 Railway or tramway locomotives, etc.87 Vehicles other than railway or tramway rolling-stock; etc.88 Aircraft, spacecraft, etc.89 Ships, boats, etc.90 Optical, photographic, etc. apparatus91 Clocks and watches, etc.92 Musical instruments, etc.93 Arms and ammunition, etc.94 Furniture, bedding, etc.95 Toy, games, etc.96 Miscellaneous manuf. articles97 Works of art, antiques, etc.

Chart III.3Average tariff rates on manufactured products by HS chapter, 2001/02 and 2004/05

26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60 62 64 66 68 70 72 74 76 79 81 83 85 87 89 91 93 95 97

Average bound rate HS 25-97 (45.4%)

Overall average applied rate HS 01-97 (20.4%)

Applied rate (2001/02)

Bound rate (2001/02)

Average final bound rate HS 25-97 (43.9%)

Final bound rate (2004/05)

Calculations exclude specific duties and include ad valorem parts of compound rates. The absence of average bound rates for most chapters is due to these chapters remaining unbound.

WTO Secretariat calculations, based on data provided by the authorities of Pakistan.

Note:

Source:

Pakistan WT/TPR/S/95Page 35

0

5

10

15

20

25

30

35

40

45

1994/95 1995/96 1996/97 1997/98 1998/99 1999/00 2000/01

Chart III.4 Share of customs duties collection in total import value and indirect tax revenue, 1994-2001Per cent

Share of custom duties in total import value

Share of custom duties in total indirect tax revenue

Source : Ministry of Finance, Economic Survey 2000-2001, Appendix Tables 4.3 and 8.2 [Online]. Available at:http://www.finance.gov.pk/ [21 September 2001].

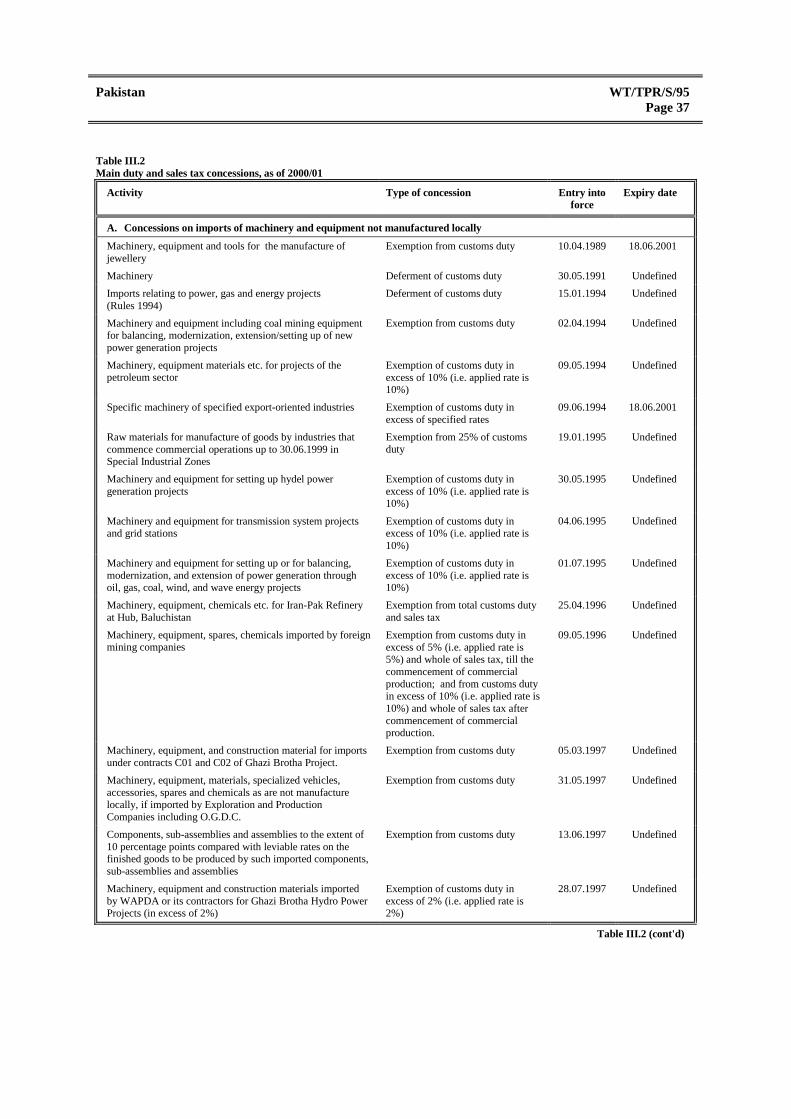

(i) Duty concessions/exemptions

34. In recent years, Pakistan has contained the expansion in the scope of duty (and related taxconcessions) in form of exemptions or deferred payment (Table III.2); at present, more than 60 legaltexts (SROs) provide for activity- or industry-specific concessions that exclude items produced locally(thus protecting local industry); no expiry date has been defined for these concessions. In June 2000,several duty (and related tax concessions) affecting machinery, equipment or parts for specialindustrial zones, sea ports, oil or gas projects, agri-based industries, hi-tech industries, pharmaceuticalindustries, were eliminated or replaced (i.e. hi-tech industries, export industries, pharmaceuticals).

35. Payment of half of customs duties on machinery and spare parts for any project may bedeferred for a period up to three years upon submission of a bank guarantee, undertaking/collateralguarantee and payment of surcharges at an annual rate of 14%, calculated on six monthly basis;deferred payment for whole or part of the duties on import of machinery and spare parts for power,gas, and energy projects is subject to an 18% annual surcharge (which is substantially more than theinflation rate and nominal interest rates).29

29 SRO 490(I), 30 May 1991 and SRO 36(I), 15 January 1994.

WT/TPR/S/95 Trade Policy ReviewPage 36

0

10

20

30

40

50

60

70

80

Food,beverages

and tobacco

Textiles andleather

Wood andfurniture

Paper,printing andpublishing

Chemicals Non-metallicmineral

products

Basic metal Fabricatedmetal

products andmachinery

Other

Chart III.5Tariff escalation by 2-digit ISIC industry, 1996/97 and 2001/02

Calculations exclude specific duties and include the ad valorem component of alternate and compound rates.

WTO Secretariat calculations, based on data provided by the authorities of Pakistan.

0

10

20

30

40

50

60

70

80

Food,beverages

and tobacco

Textiles andleather

Wood andfurniture

Paper,printing andpublishing

Chemicals Non-metallicmineral

products

Basic metal Fabricatedmetal

products andmachinery

Other

Average applied rate in manufacturing(42 1%)

Note:

Source :

Per cent

First stage of processing Fully processedSemi-processed

Per cent

Average applied rate in manufacturing(20.9%)

1996/97

2001/02

Pakistan WT/TPR/S/95Page 37

Table III.2Main duty and sales tax concessions, as of 2000/01

Activity Type of concession Entry intoforce

Expiry date

A. Concessions on imports of machinery and equipment not manufactured locally

Machinery, equipment and tools for the manufacture ofjewellery

Exemption from customs duty 10.04.1989 18.06.2001

Machinery Deferment of customs duty 30.05.1991 Undefined

Imports relating to power, gas and energy projects(Rules 1994)

Deferment of customs duty 15.01.1994 Undefined

Machinery and equipment including coal mining equipmentfor balancing, modernization, extension/setting up of newpower generation projects

Exemption from customs duty 02.04.1994 Undefined

Machinery, equipment materials etc. for projects of thepetroleum sector

Exemption of customs duty inexcess of 10% (i.e. applied rate is10%)

09.05.1994 Undefined

Specific machinery of specified export-oriented industries Exemption of customs duty inexcess of specified rates

09.06.1994 18.06.2001

Raw materials for manufacture of goods by industries thatcommence commercial operations up to 30.06.1999 inSpecial Industrial Zones

Exemption from 25% of customsduty

19.01.1995 Undefined

Machinery and equipment for setting up hydel powergeneration projects

Exemption of customs duty inexcess of 10% (i.e. applied rate is10%)

30.05.1995 Undefined

Machinery and equipment for transmission system projectsand grid stations

Exemption of customs duty inexcess of 10% (i.e. applied rate is10%)

04.06.1995 Undefined

Machinery and equipment for setting up or for balancing,modernization, and extension of power generation throughoil, gas, coal, wind, and wave energy projects

Exemption of customs duty inexcess of 10% (i.e. applied rate is10%)

01.07.1995 Undefined

Machinery, equipment, chemicals etc. for Iran-Pak Refineryat Hub, Baluchistan

Exemption from total customs dutyand sales tax

25.04.1996 Undefined

Machinery, equipment, spares, chemicals imported by foreignmining companies

Exemption from customs duty inexcess of 5% (i.e. applied rate is5%) and whole of sales tax, till thecommencement of commercialproduction; and from customs dutyin excess of 10% (i.e. applied rate is10%) and whole of sales tax aftercommencement of commercialproduction.

09.05.1996 Undefined

Machinery, equipment, and construction material for importsunder contracts C01 and C02 of Ghazi Brotha Project.

Exemption from customs duty 05.03.1997 Undefined

Machinery, equipment, materials, specialized vehicles,accessories, spares and chemicals as are not manufacturelocally, if imported by Exploration and ProductionCompanies including O.G.D.C.

Exemption from customs duty 31.05.1997 Undefined

Components, sub-assemblies and assemblies to the extent of10 percentage points compared with leviable rates on thefinished goods to be produced by such imported components,sub-assemblies and assemblies

Exemption from customs duty 13.06.1997 Undefined

Machinery, equipment and construction materials importedby WAPDA or its contractors for Ghazi Brotha Hydro PowerProjects (in excess of 2%)

Exemption of customs duty inexcess of 2% (i.e. applied rate is2%)

28.07.1997 Undefined

Table III.2 (cont'd)

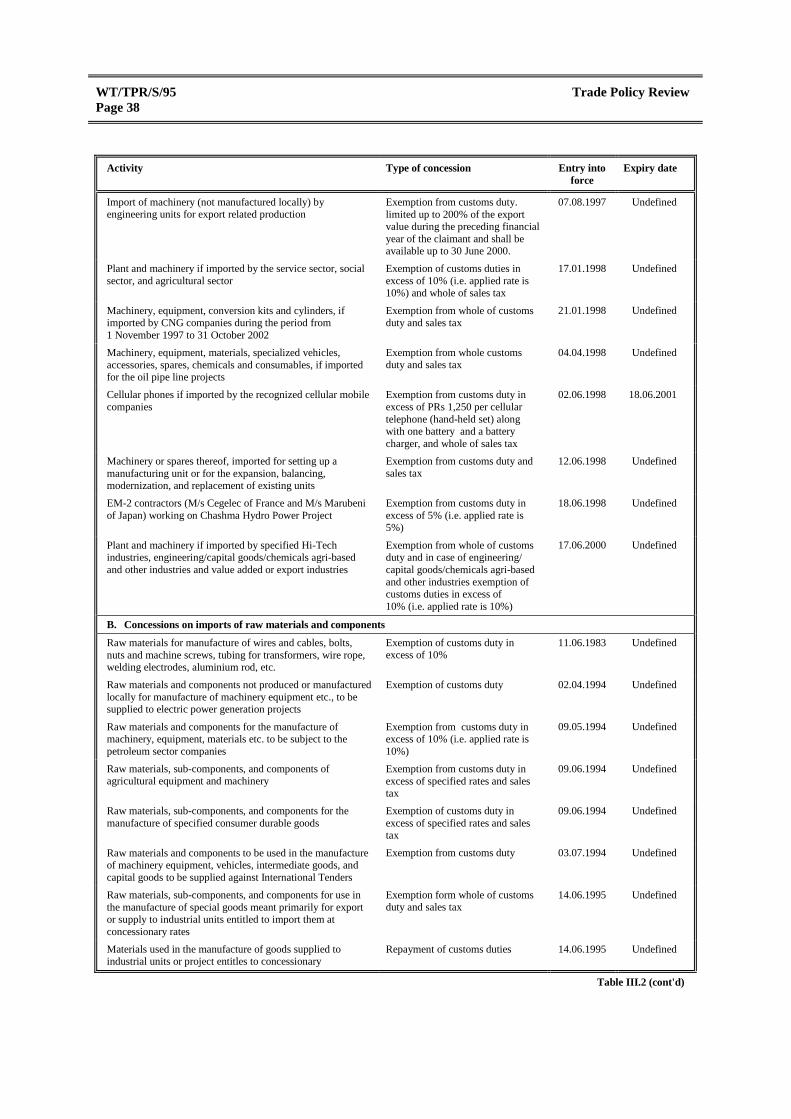

WT/TPR/S/95 Trade Policy ReviewPage 38

Activity Type of concession Entry intoforce

Expiry date

Import of machinery (not manufactured locally) byengineering units for export related production

Exemption from customs duty.limited up to 200% of the exportvalue during the preceding financialyear of the claimant and shall beavailable up to 30 June 2000.

07.08.1997 Undefined

Plant and machinery if imported by the service sector, socialsector, and agricultural sector

Exemption of customs duties inexcess of 10% (i.e. applied rate is10%) and whole of sales tax

17.01.1998 Undefined

Machinery, equipment, conversion kits and cylinders, ifimported by CNG companies during the period from1 November 1997 to 31 October 2002

Exemption from whole of customsduty and sales tax

21.01.1998 Undefined

Machinery, equipment, materials, specialized vehicles,accessories, spares, chemicals and consumables, if importedfor the oil pipe line projects

Exemption from whole customsduty and sales tax

04.04.1998 Undefined

Cellular phones if imported by the recognized cellular mobilecompanies

Exemption from customs duty inexcess of PRs 1,250 per cellulartelephone (hand-held set) alongwith one battery and a batterycharger, and whole of sales tax

02.06.1998 18.06.2001

Machinery or spares thereof, imported for setting up amanufacturing unit or for the expansion, balancing,modernization, and replacement of existing units

Exemption from customs duty andsales tax

12.06.1998 Undefined

EM-2 contractors (M/s Cegelec of France and M/s Marubeniof Japan) working on Chashma Hydro Power Project

Exemption from customs duty inexcess of 5% (i.e. applied rate is5%)

18.06.1998 Undefined

Plant and machinery if imported by specified Hi-Techindustries, engineering/capital goods/chemicals agri-basedand other industries and value added or export industries

Exemption from whole of customsduty and in case of engineering/capital goods/chemicals agri-basedand other industries exemption ofcustoms duties in excess of10% (i.e. applied rate is 10%)

17.06.2000 Undefined

B. Concessions on imports of raw materials and components

Raw materials for manufacture of wires and cables, bolts,nuts and machine screws, tubing for transformers, wire rope,welding electrodes, aluminium rod, etc.

Exemption of customs duty inexcess of 10%

11.06.1983 Undefined

Raw materials and components not produced or manufacturedlocally for manufacture of machinery equipment etc., to besupplied to electric power generation projects

Exemption of customs duty 02.04.1994 Undefined

Raw materials and components for the manufacture ofmachinery, equipment, materials etc. to be subject to thepetroleum sector companies

Exemption from customs duty inexcess of 10% (i.e. applied rate is10%)

09.05.1994 Undefined

Raw materials, sub-components, and components ofagricultural equipment and machinery

Exemption from customs duty inexcess of specified rates and salestax

09.06.1994 Undefined

Raw materials, sub-components, and components for themanufacture of specified consumer durable goods

Exemption of customs duty inexcess of specified rates and salestax

09.06.1994 Undefined

Raw materials and components to be used in the manufactureof machinery equipment, vehicles, intermediate goods, andcapital goods to be supplied against International Tenders

Exemption from customs duty 03.07.1994 Undefined

Raw materials, sub-components, and components for use inthe manufacture of special goods meant primarily for exportor supply to industrial units entitled to import them atconcessionary rates

Exemption form whole of customsduty and sales tax

14.06.1995 Undefined

Materials used in the manufacture of goods supplied toindustrial units or project entitles to concessionary

Repayment of customs duties 14.06.1995 Undefined

Table III.2 (cont'd)

Pakistan WT/TPR/S/95Page 39

Activity Type of concession Entry intoforce

Expiry date

Materials, components, modules, and sub-assemblies for themanufacture of electronic equipment and systems

Exemption from customs duties inexcess of specified rates and salestax

14.06.1995 Undefined

Raw material, sub-components, and components formanufacture of automotive vehicles and theircomponents/sub-assemblies

Exemption from customs duty inexcess of specified rates.

08.01.1996 Undefined

Karachi Shipyard and Engineering Works on raw materials,components, machinery etc. for use in building/repairingships, boats, etc.

Exemption from duty in excess of20% (i.e. applied rate is 20%) forlocal use and from whole ofcustoms duty for exports

13.06.1996 Undefined

Goods imported by manufacturers-cum-exporters of gemsand jewellery

Exemption from customs duty 07.08.1997 18.06.2001

Conditional exemption of import duties of raw materials andcomponents as are not manufactured locally

Exemption from customs duty 12.06.1998 Undefined

Raw materials and packing materials for manufacture ofpharmaceutical products, drugs, and pharmaceutical activeingredients

Exemption from customs duty inexcess of 10% (i.e. applied rate is10%)

17.06.2000 Undefined

C. Other

Goods for manufacture of leather made-ups Exemption of customs duty inexcess of 20% (i.e. applied rate is20%)

26.12.1990 Undefined

Ships for scrapping (Rules 1993) Deferment of customs duty 31.03.1993 Undefined

Ground handling equipment Exemption from customs duty 08.09.1998 Undefined

Hemodialysis machines, etc. Exemption from customs duty andsales tax

28.11.1998 Undefined

Source: Various SROs contained in Central Board of Revenue (1999a), Pakistan Customs Tariff, Volume II AlliedNotifications & Orders, 15th Edition, Islamabad; SROs contained in Central Board of Revenue of Pakistan onlineinformation. Available at: http://www.cbr.gov.pk/budget/sro.htm [24 July 2000]; and Government of Pakistan.

(j) Tariff preferences and rules of origin

Preferences

36. Pakistan continues to grant limited preferential tariff treatment on imports from: Iran andTurkey under the additional Protocol on Preferential Tariff of the Economic the Co-operationOrganization (16 items); signatories to the GATT Protocol relating to Trade Negotiations amongDeveloping Countries (12 items); the Global System of Trade Preferences; Iran, Afghanistan, China,and Nepal (17 product categories)30; and countries participating in the SAARC Preferential TradingArrangements (SAPTA) (677 products, mainly confined to items originating in least developedparticipants, as from July 2000) (Chapter II(6)(ii)(b)). Preferential treatment has taken the form oftariff cuts (between 10% and 30%) or a fixed customs duty (i.e. 25% lower than the rate otherwiseapplied) depending on the arrangement.

Rules of origin

37. Since its previous Review, Pakistan has not applied non-preferential rules of origin. Pakistanuses the rules of origin criteria set under each preferential scheme cited above; minimumlocal-content requirements range from 30% (SAPTA, least developed member) to 50% (GATT

30 These preferences affect only imports by land and include all manufactured articles, manufactured

tobacco, silk, motor vehicles and parts thereof, tea, apples, etc. (SRO 492(I)/88, 26 June 1988 and subsequentamendments)

WT/TPR/S/95 Trade Policy ReviewPage 40

Protocol, SAPTA regional content) of the f.o.b. value of the product concerned.31 In the context ofthe WTO Committee on Rules of Origin, in 1999 Pakistan emphasized the need for promptcompletion of the work on harmonization in this area; it believes that interim arrangements havetrade restrictive, distortive, and disruptive effects, in particular for developing countries.32

(iii) Customs valuation

38. As of January 2000, Pakistan replaced its Import Trade Price (ITP)33 valuation system withthe declared "transaction value" method under the WTO Agreement on Customs Valuation.Nevertheless, a provision for the setting of minimum values remained in force, although it had notbeen invoked by November 200034; at the time of completion of this Report, the authorities indicatedthat this provision will only apply upon authorization by the WTO (i.e. granting of waiver forretention of minimum values). Under a Customs Valuation Information System (CVIS), Customsstations are being connected through a computer network to exchange data on assessed import valuesof each individual consignment on a daily basis; upon arrival of this data at one central location andscrutiny by the System Administrator, the entire database may be accessed by the general public (onthe Internet) and the Customs stations.35

39. Upon acceptance of the WTO Agreement, Pakistan invoked Article 20.1 of the Agreement onCustoms Valuation to delay its application for a five-year period.36 To implement the Agreement onCustoms Valuation, Pakistan amended the relevant provisions of the 1969 Customs Act in July 1999and in 2000; the date of entry into force of these amendments, which were notified to the WTO, wasto be announced in the official gazette.37 Under these amendments, the authorities may, inter alia,seize and sell under-invoiced merchandise.

40. Pakistan has received WTO and WCO technical assistance (seminars, workshops) forimplementing the Agreement in Customs Valuation.38 In the context of the WTO General Council, in1999 Pakistan suggested a multilateral solution to valuation problems; this would entail access toinformation on values contained in the export declaration from the customs authority of the exportingcountry, and certain modifications to the valuation methods.

31 WTO document G/RO/N/16, 5 March 1997; and GATT (1995).32 WTO document WT/GC/W/354, 11 October 1999.33 Following the cancellation of preshipment inspection contracts, between March 1997 and

December 1999, Pakistan reverted to the ITP valuation system, which was based upon the Brussels Definition ofValue. Values were updated every three months (or one month for goods with abrupt price fluctuations), andwere set on an "all origin" basis; values of identical/similar goods originating from any "economic zone" of thesame economic level were fixed on an eight-zone basis (U.S. Commercial Service, 1999a).

34 Finance Act (1999), available online at: http://www.cbr.gov.pk/customs/finance/Act.pdf[24 July 2000]. To continue using a system of minimum values, Pakistan should have invoked the reservationin paragraph 2, Annex III of the Agreement on Customs Valuation prior to its date of application (i.e.1 January 2000); Pakistan did not invoke this provision.

35 Central Board of Revenue online information, Customs Valuation Information System. Availableat: http://www.cbr.gov.pk/ncvis/index.html [24 July 2000].

36 Pakistan invoked Article 20.2 (delayed application computed value) and paragraphs 2, 3, and 4 ofAnnex II (reservation concerning minimum values, reversal of sequential order of Articles 5 and 6 andapplication of Article 5.2). WTO documents WT/LET/1, 27 January 1995 and G/VAL/W/25, 24 April 1998.

37 WTO documents G/VAL/W/78/Rev.1, 10 November 2000 and G/VAL/N/1/PAK/1, 15 May 2001.38 WTO documents G/VAL/8, 21 October 1996, G/VAL/W/25, 24 April 1998, G/VAL/8/Add.3,

4 May 1998, Job(99)/3169 and Add. 1, 7 June 1999, G/VAL/M/10, 6 September 1999, G/VAL/W/39,14 September 1999, G/VAL/8/Add.6, 27 January 2000, and WT/GC/W/354, 11 October 1999.

Pakistan WT/TPR/S/95Page 41

(iv) Import deposits

41. Since its previous Review, Pakistan has imposed minimum cash-margin requirements on theopening of all import letters of credit at rates of 30% (from July 1998 to February 1999) and 35%(from October 1999 to July 2000)39; in both cases the requirement was withdrawn progressively. Theauthorities indicated that there is no intention to reintroduce such requirements.

(v) Other levies and charges

42. A few withholding-type taxes have also been levied on imports. As of July 2000, the rate ofthe withholding tax (section 4(i)(a)) was increased from 5% to 6% (edible oil at 3%) of the c.i.f. valueplus customs duties plus taxes and charges on virtually all imports.40 This tax is, in principle,deductible from income tax, which means that it does not constitute an additional levy on imports aslong as the income taxes payable are sufficient to be offset by the tax. If the importer is in anon-taxpaying position, however, (e.g. because the importer is operating at a loss for income taxpurposes, or enjoying a tax holiday), the levy is effectively an import surcharge. (The same applies tosimilar types of withholding taxes on exports (section (3)(ii).)

(vi) Import prohibitions, restrictions, and licensing

43. Import prohibitions or restrictions are operated for the protection of health, national security,environmental conservation, as well as on religious or commercial grounds in accordance withdomestic legislation or international commitments. Imports of any good from any source may betemporarily or permanently suspended to protect public interest. Imports from countries applyingdiscriminatory measures against Pakistan's exports may also be restricted.41 The terms and conditionsgoverning importation are set annually, and are currently found in three Orders.42

(a) Import prohibitions

44. Since its previous Review, Pakistan has continued to prohibit imports of several itemscontained in its negative list (Table III.3, Section A) on an MFN basis; the number of items in this listseems to have been reduced.43 The main prohibitions on commercial grounds affecting numeroustextiles and clothing articles and chassis for trucks were phased-out between July 2000 andJanuary 2001; these prohibitions were introduced for balance-of-payments reasons (GATT 1994Article XVIII:B) in 1997.44 As of September 2000, Pakistan prohibited imports of raw sugar below

39 Initially, cash-margin requirements were imposed at rates of 10% (industrial raw materials) and 20%

(machinery and parts) but were soon withdrawn. WTO documents WT/BOP/S/11, 28 March 2000 andWT/BOP/N/51, 7 July 2000; State Bank of Pakistan, BPRD Circulars Nos. 03, 05, 08, 33, 37, 38 of 1999 andCircular No. 15 and 19 of 2000. Available online at: http://www.sbp.org.pk/bprd/index.htm[18 September 2000].

40 The following importers are exempt: provincial and local authorities; foreign companies held by aforeign government; importers of machinery and equipment for setting up industry; importers entitled to taxholiday, etc. (Ministry of Finance (2000a)).

41 Article 1.4 of the Import Policy Order (1999), SRO 895(I)/99, 3 August 1999.42 The Import Policy Order, the Import Export Procedure Order, and the Import Trade Order, issued

from time to time (latest issue 6 July 1998).43 In September 2000, the list contained 71 items (excluding those of general nature) under around

121 HS headings, compared with 75 in 1994 (GATT, 1995).44 In October 1997, Pakistan submitted to the WTO a list of BOP-restricted items (textile and clothing

products, chassis), but a phase-out programme was announced only one year later; in July 2000, thisprogramme was temporarily suspended due to a worsening in the BOP situation (WTO documentsWT/BOP/N/31, 31 October 1997, WT/BOP/N/31/Add.1, 31 October 1997, WT/BOP/N/40, 12 November 1998,

WT/TPR/S/95 Trade Policy ReviewPage 42

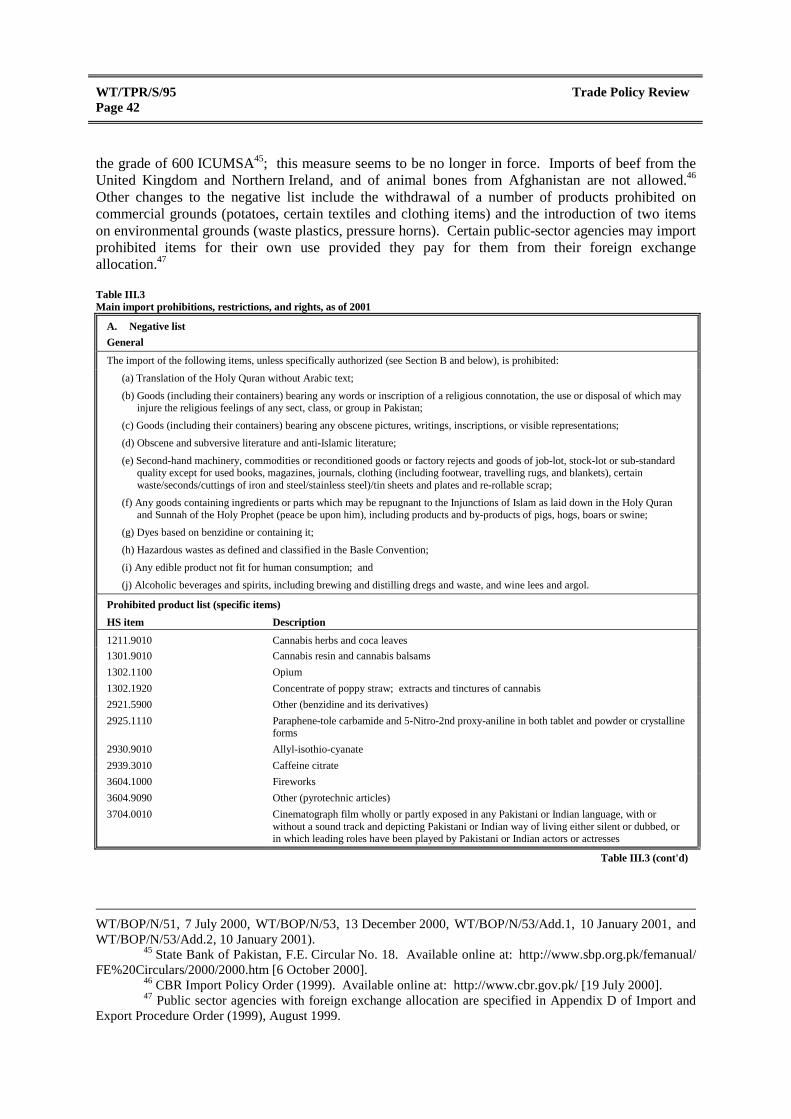

the grade of 600 ICUMSA45; this measure seems to be no longer in force. Imports of beef from theUnited Kingdom and Northern Ireland, and of animal bones from Afghanistan are not allowed.46

Other changes to the negative list include the withdrawal of a number of products prohibited oncommercial grounds (potatoes, certain textiles and clothing items) and the introduction of two itemson environmental grounds (waste plastics, pressure horns). Certain public-sector agencies may importprohibited items for their own use provided they pay for them from their foreign exchangeallocation.47

Table III.3Main import prohibitions, restrictions, and rights, as of 2001

A. Negative listGeneral

The import of the following items, unless specifically authorized (see Section B and below), is prohibited:

(a) Translation of the Holy Quran without Arabic text;

(b) Goods (including their containers) bearing any words or inscription of a religious connotation, the use or disposal of which mayinjure the religious feelings of any sect, class, or group in Pakistan;

(c) Goods (including their containers) bearing any obscene pictures, writings, inscriptions, or visible representations;

(d) Obscene and subversive literature and anti-Islamic literature;

(e) Second-hand machinery, commodities or reconditioned goods or factory rejects and goods of job-lot, stock-lot or sub-standardquality except for used books, magazines, journals, clothing (including footwear, travelling rugs, and blankets), certainwaste/seconds/cuttings of iron and steel/stainless steel)/tin sheets and plates and re-rollable scrap;

(f) Any goods containing ingredients or parts which may be repugnant to the Injunctions of Islam as laid down in the Holy Quranand Sunnah of the Holy Prophet (peace be upon him), including products and by-products of pigs, hogs, boars or swine;

(g) Dyes based on benzidine or containing it;

(h) Hazardous wastes as defined and classified in the Basle Convention;

(i) Any edible product not fit for human consumption; and

(j) Alcoholic beverages and spirits, including brewing and distilling dregs and waste, and wine lees and argol.

Prohibited product list (specific items)HS item Description

1211.9010 Cannabis herbs and coca leaves1301.9010 Cannabis resin and cannabis balsams1302.1100 Opium1302.1920 Concentrate of poppy straw; extracts and tinctures of cannabis2921.5900 Other (benzidine and its derivatives)2925.1110 Paraphene-tole carbamide and 5-Nitro-2nd proxy-aniline in both tablet and powder or crystalline

forms2930.9010 Allyl-isothio-cyanate2939.3010 Caffeine citrate3604.1000 Fireworks3604.9090 Other (pyrotechnic articles)3704.0010 Cinematograph film wholly or partly exposed in any Pakistani or Indian language, with or

without a sound track and depicting Pakistani or Indian way of living either silent or dubbed, orin which leading roles have been played by Pakistani or Indian actors or actresses

Table III.3 (cont'd)

WT/BOP/N/51, 7 July 2000, WT/BOP/N/53, 13 December 2000, WT/BOP/N/53/Add.1, 10 January 2001, andWT/BOP/N/53/Add.2, 10 January 2001).

45 State Bank of Pakistan, F.E. Circular No. 18. Available online at: http://www.sbp.org.pk/femanual/FE%20Circulars/2000/2000.htm [6 October 2000].

46 CBR Import Policy Order (1999). Available online at: http://www.cbr.gov.pk/ [19 July 2000].47 Public sector agencies with foreign exchange allocation are specified in Appendix D of Import and

Export Procedure Order (1999), August 1999.

Pakistan WT/TPR/S/95Page 43

3706.0000 Cinematograph film wholly or partly exposed and developed in any Pakistani or Indian language,with or without a sound track and depicting Pakistani or Indian way of living, either silent ordubbed, or in which leading roles have been played by Pakistani or Indian actors or actresses

3915.1000, 3915.9000 Waste, parings and scrap, of polyethylene and polypropylene plastics4012.1000 Retreaded tyres4012.2000 Used pneumatic tyres4301.0000 to 4303.0000 Furskins and manufactures thereof, other than raw furskins and tanned or dressed furskins of

sheep, lambs, rabbits, goats, kids thereof and calf6812.5010 Clothing (of asbestos)8438.4000 Brewery machinery8512.3000 Pressure horns8710.0000 Tanks and other armoured fighting vehicles, motorized, whether or not fitted with weapons and

parts of such vehicles, other than armoured security vans9301.0000 Artillery weapons, machine-guns, sub-machine-guns, automatic rifles of all calibre and other

military fire-arms and projectiles (other than revolvers and pistols)9302.0010 Revolvers and pistols of prohibited bores and of calibers higher than 0.46 inches bore9303.3020 Arms of prohibited bores including semi-automatic rifles of 7.62 mm and rifles of 8 mm to 9 mm

bores9303.3030 Arms of calibers higher than 0.22 bore rifles9303.9000 Other (fire arms and similar devices which operate by firing of an explosive charge)9304.0000 Other arms (for example, spring, air or gas guns and pistols truncheons), excluding those of

heading No. 93079305.1000 and 9305.2000 Parts and accessories of articles of heading No. 9301 to 9304, excluding parts and accessories of

heading No. 9305.2900 barrel blanks for recoilless rifles, guns, and mortars9306.1000, 9306.2110,9306.2900, 9306.3019,9306.3029, 9306.3090 and9306.9000

Parts of ammunition and ammunition, except ammunition for weapons of non-prohibited bores

9508.0010 Gambling equipment

B. Prior approval, recommendation and/or clearance requirements (compliance with health and safety requirements)Item Requirement/agencyAnimal semen Recommendation and clearance/Livestock DivisionAnimals and plants, dead or alive,including any recognizable part orderivatives thereof specified inAppendices I, II and III to theConvention on International Tradein Endangered Species of WildFauna and Flora.

Prior approval/Ministry of Food and Agriculture

Cotton seed Prior approval/Ministry of Food and AgricultureSugarcane seeds and bananasuckers

Prior approval/Department of Plant Protection

Vegetable seeds, seed potatoes,flower seeds and other field cropseeds including tubers, rhizomes,roots, cuttings, etc.

Drawing of seeds samples and testing of seed quality/Federal Seed CertificationAgency (Ministry of Food & Agriculture)

Radioactive material and radiationapparatus

Prior approval/Directorate of the Pakistan Nuclear Safety and Radiation Protection (PakistanAtomic Energy Commission)

Calcium carbide, whether or notchemically defined.

Prior approval/Department of Explosives

Explosives Prior approval/Department of ExplosivesSteam and vapour generatingboilers (other than central heatinghot water boilers capable also ofproducing low pressure steam) andsuper-heated waterboilers (HS 8402.0000)

Prior approval/Chief Inspector of Boilers

Table III.3 (cont'd)

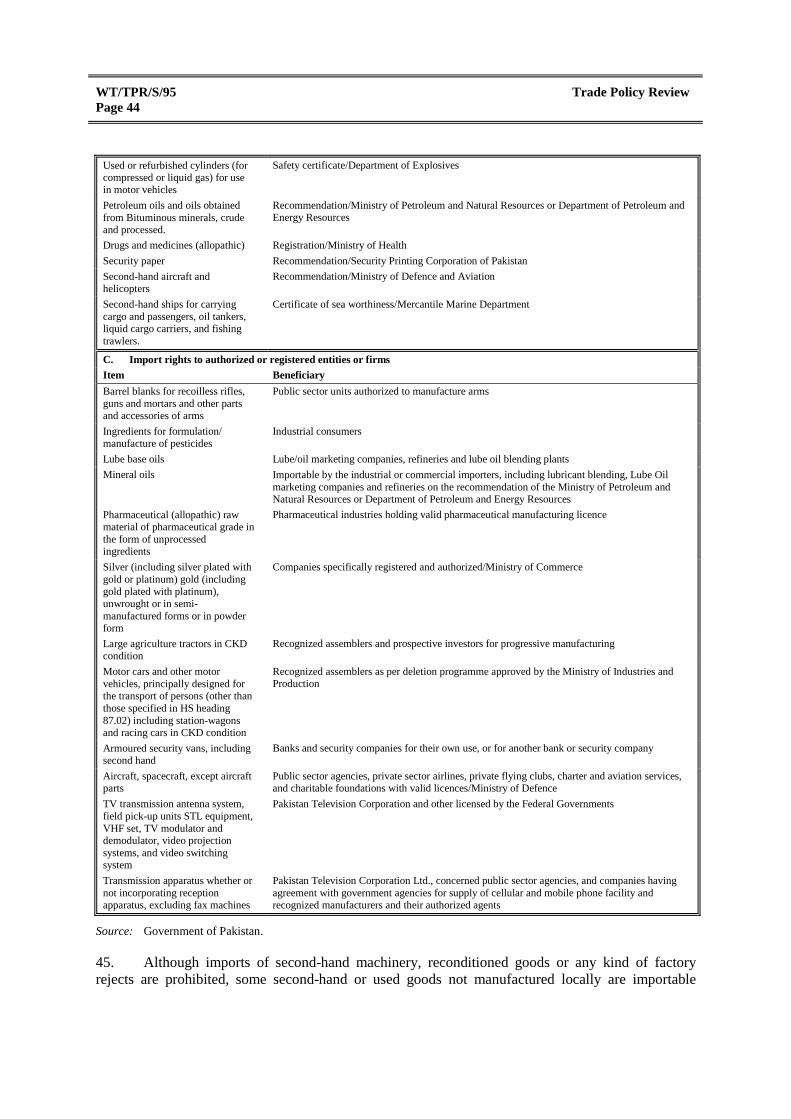

WT/TPR/S/95 Trade Policy ReviewPage 44

Used or refurbished cylinders (forcompressed or liquid gas) for usein motor vehicles

Safety certificate/Department of Explosives

Petroleum oils and oils obtainedfrom Bituminous minerals, crudeand processed.

Recommendation/Ministry of Petroleum and Natural Resources or Department of Petroleum andEnergy Resources

Drugs and medicines (allopathic) Registration/Ministry of HealthSecurity paper Recommendation/Security Printing Corporation of PakistanSecond-hand aircraft andhelicopters

Recommendation/Ministry of Defence and Aviation

Second-hand ships for carryingcargo and passengers, oil tankers,liquid cargo carriers, and fishingtrawlers.

Certificate of sea worthiness/Mercantile Marine Department

C. Import rights to authorized or registered entities or firmsItem BeneficiaryBarrel blanks for recoilless rifles,guns and mortars and other partsand accessories of arms

Public sector units authorized to manufacture arms

Ingredients for formulation/manufacture of pesticides

Industrial consumers

Lube base oils Lube/oil marketing companies, refineries and lube oil blending plantsMineral oils Importable by the industrial or commercial importers, including lubricant blending, Lube Oil

marketing companies and refineries on the recommendation of the Ministry of Petroleum andNatural Resources or Department of Petroleum and Energy Resources

Pharmaceutical (allopathic) rawmaterial of pharmaceutical grade inthe form of unprocessedingredients

Pharmaceutical industries holding valid pharmaceutical manufacturing licence

Silver (including silver plated withgold or platinum) gold (includinggold plated with platinum),unwrought or in semi-manufactured forms or in powderform

Companies specifically registered and authorized/Ministry of Commerce

Large agriculture tractors in CKDcondition

Recognized assemblers and prospective investors for progressive manufacturing

Motor cars and other motorvehicles, principally designed forthe transport of persons (other thanthose specified in HS heading87.02) including station-wagonsand racing cars in CKD condition

Recognized assemblers as per deletion programme approved by the Ministry of Industries andProduction

Armoured security vans, includingsecond hand

Banks and security companies for their own use, or for another bank or security company

Aircraft, spacecraft, except aircraftparts

Public sector agencies, private sector airlines, private flying clubs, charter and aviation services,and charitable foundations with valid licences/Ministry of Defence

TV transmission antenna system,field pick-up units STL equipment,VHF set, TV modulator anddemodulator, video projectionsystems, and video switchingsystem

Pakistan Television Corporation and other licensed by the Federal Governments

Transmission apparatus whether ornot incorporating receptionapparatus, excluding fax machines

Pakistan Television Corporation Ltd., concerned public sector agencies, and companies havingagreement with government agencies for supply of cellular and mobile phone facility andrecognized manufacturers and their authorized agents

Source: Government of Pakistan.

45. Although imports of second-hand machinery, reconditioned goods or any kind of factoryrejects are prohibited, some second-hand or used goods not manufactured locally are importable

Pakistan WT/TPR/S/95Page 45

subject to certain conditions (Table III.3, Sections A and B)48; imports of permissible second-handmachinery are subject to preshipment inspection, however, to ensure that the machinery hasreasonable useable life.

46. Pakistan prohibits all imports from Israel; it has increased progressively the number of(HS) items that may be imported from India from 571 (1993) to 603 (as of July 2000).49

(b) Import approval and restrictions

47. Pakistan maintains that it does not operate an import licensing system; nonetheless, priorapprovals/recommendations/clearance requirements implicitly entail import licensing.50 As ofSeptember 2000, Pakistan had notified its regulatory framework on import-licensing procedures; butit has not submitted any replies to annual questionnaires on its import licensing procedures.51

48. At present, imports of several products are subject to prior approval, recommendations, andclearance from different ministries/departments in accordance with safety and health requirements(Table III.3, Section B). Import authorization from the Ministry of Commerce is required mainly inthe case of the importation, by certain entities, of otherwise banned items: foreign airlines, oil and gascompanies, refineries and mining companies, foreign construction companies, and foreign contractingfirms engaged in various projects in Pakistan; and where no foreign exchange is involved.

49. Certain products may be imported only by the public sector or industrial consumers(Table III.3, Section C). Imports of 19 product categories are subject to various conditions, such asreceipt of certificates by suppliers, payment for imports from the importer's own foreign currencyaccount, etc. Although Pakistan does not maintain any quantitative restrictions, certain imports (e.g.ozone depleting substances, certain chemicals) are subject to quantitative limits determined on adomestic needs basis or by the Central Board of Revenue in consultation with competent governmentagencies.

(vii) State-trading

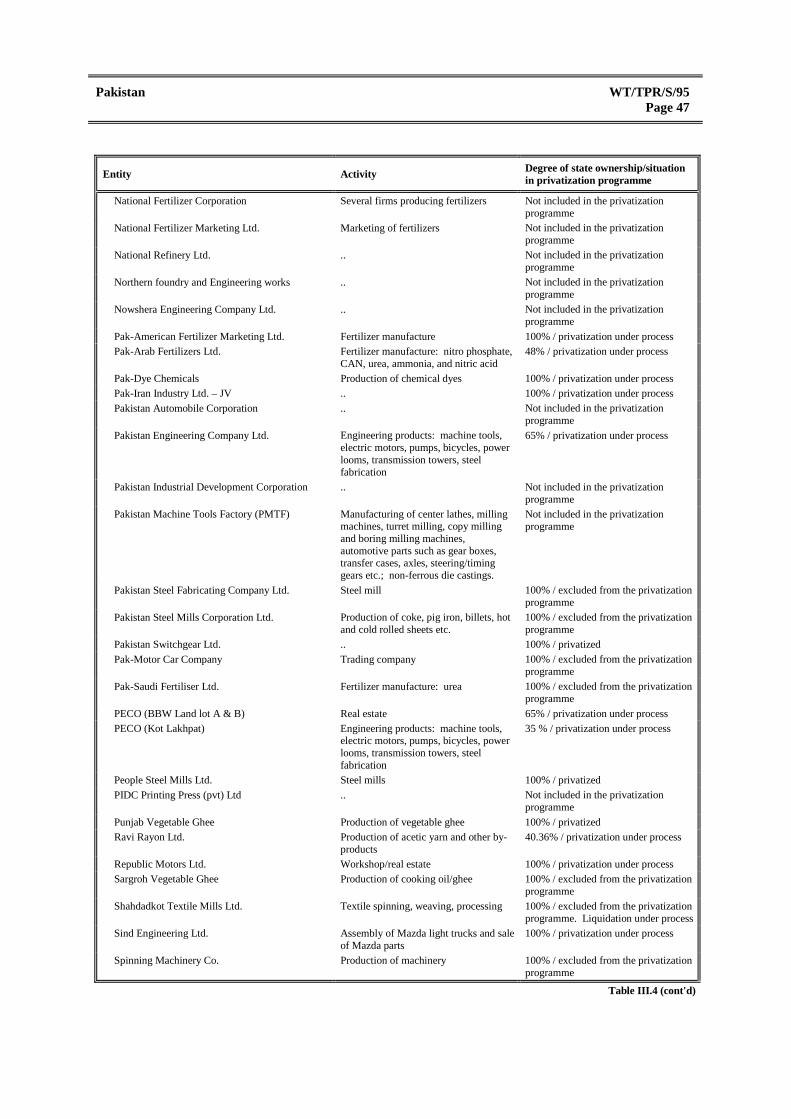

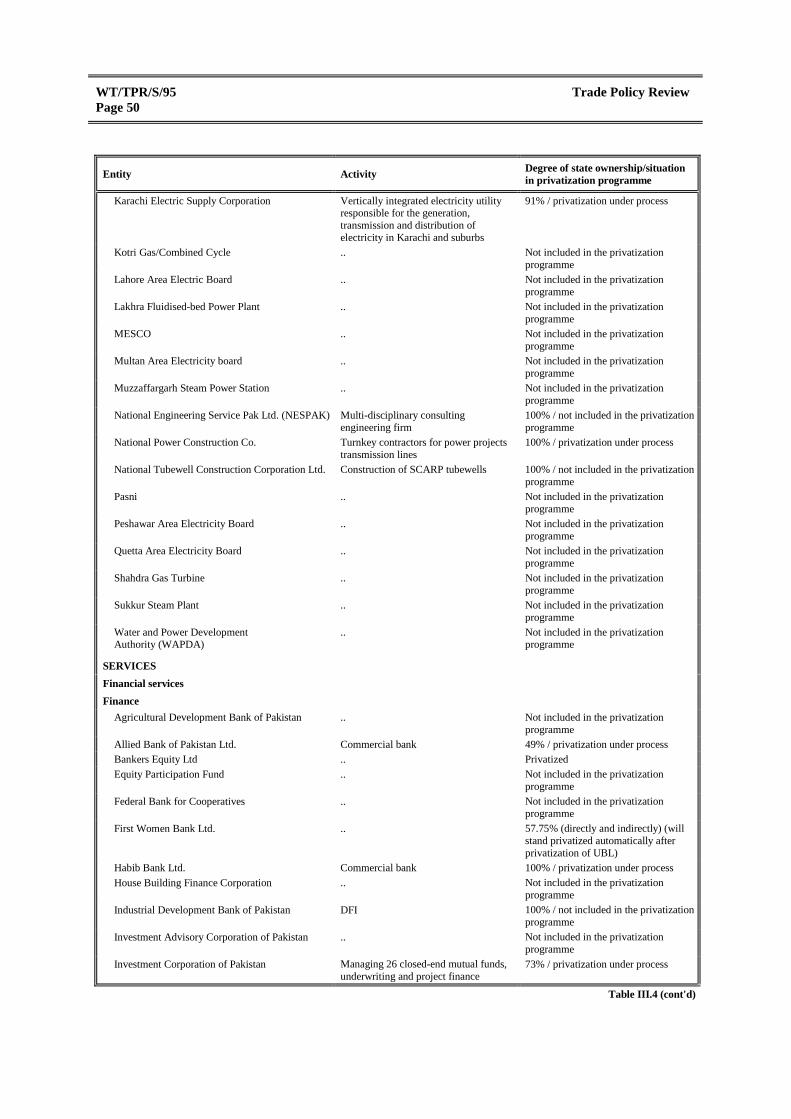

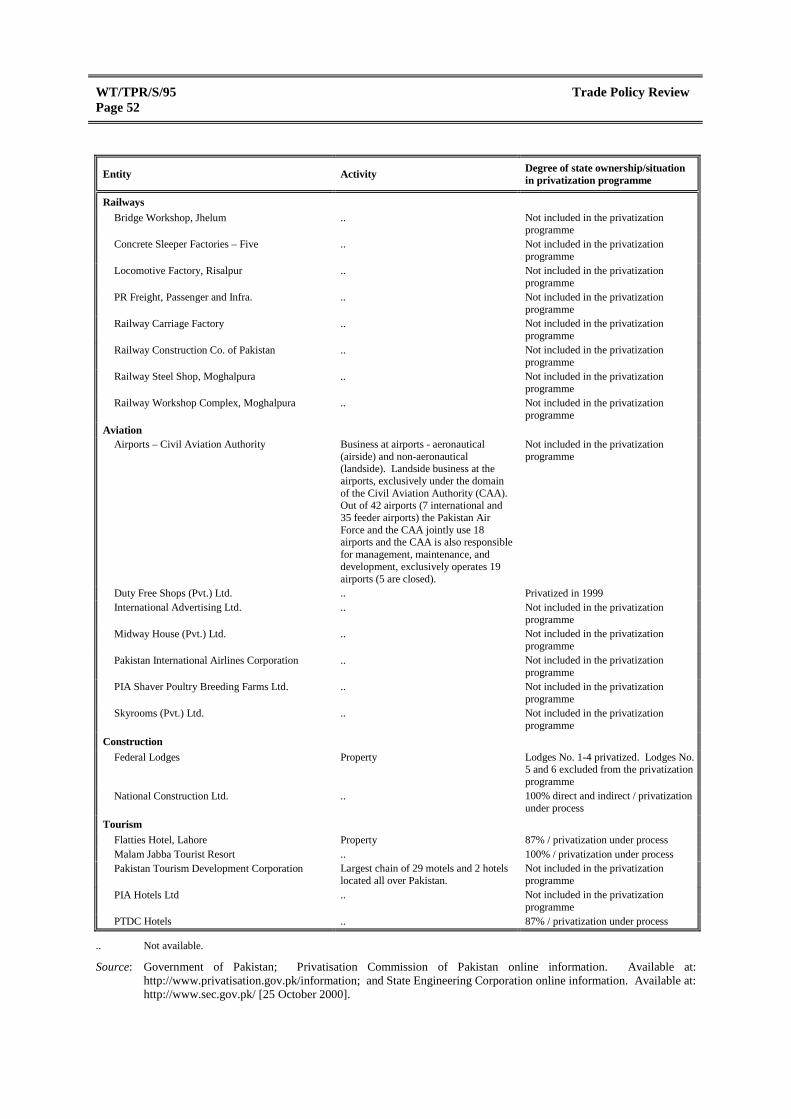

50. Despite efforts to reduce its involvement in the economy, the State participates in awide-range of trade and/or trade-related activities (Table III.4). Participation seems particularlypronounced in the following activities: trade in certain essential commodities; production/marketingof vegetable ghee, fertilizers, chemicals, cement, transport equipment, fuels, machine tools; oil andgas exploration and exploitation; power production and distribution; financial, telecommunication,transport, tourism, and engineering services. Government-owned industrial enterprises are thought toemploy almost 46,000 workers.52

48 Other exceptions include used books, magazines, journals, clothing (including footwear, travelling

rugs, and blankets), certain waste/seconds/cuttings of iron and steel/stainless steel/tin sheets and plates andre-rollable scrap.

49 Export Promotion Bureau (2000); and Appendix E of the Import & Export Procedure (1999),SRO(I), 898(I)/99, August 1999.

50 WTO document G/LIC/N/1/PAK/1, G/LIC/N/2/PAK/1, 29 May 1996.51 WTO document G/LIC/W/13, 21 September 2000.52 U.S. Commercial Service (1999a).

WT/TPR/S/95 Trade Policy ReviewPage 46

Table III.4State involvement in enterprises in Pakistan, 2001

Entity Activity Degree of state ownership/situationin privatization programme

GOODSAgriculture

Trading Corporation of Pakistan (merged withCotton Export Corporation of Pakistan and RiceExport Corporation of Pakistan)

Trading of essential commodities Not included in the privatizationprogramme

Manufacturing (including food processing)Industries and production

A&B Industries Gases Production of cooking oil/ghee 100% / excluded from privatizationprogramme. Liquidation under process

A&B Oil Industries .. 100% / privatizedAl-Abbas Ltd. (Rice) .. Not included in the privatization

programmeBela Engineering Ltd. Manufacture/assembly of diesel engines 100% / liquidatedBolan Textile Mills Qeutta Textile: spinning, weaving, processing 100% / privatization under processCivic Centres Corporation Not included in the privatization

programmeDir Forest Industry Complex Production of plywood 100% / excluded from privatization

programme and transferred toprovincial government

Domestic Appliances Ltd. - JV Production of domestic appliances Not included in the privatizationprogramme

E&M Oil Mills Production of cooking oil/ghee 100% / privatization under processENAR Petrotech Services (Pvt) Ltd. Technical consultancy; feasibility

studies; energy conservation studies;technology/process evaluation;conceptual/basic/process engineeringdesign; procurement services; projectmanagement services; supervision ofinstallation and commissioningoperations; installation services forinstrumentation systems.

Not included in the privatizationprogramme

Federal Ceramics and Chemical Corporation Production of ceramics and chemicals Not included in the privatizationprogramme

Ghee Corporation of Pakistan Several firms producing ghee andcooking oil

Not included in the privatizationprogramme

Harnai Woollen Mills Manufacture of woollen fabric andblankets

81.4% / liquidated

Hazara Phosphate Fertiliser Ltd. Production of phosphate fertilizer 100% / privatization under processHeavy Electrical Complex Production of power transformers. Not included in the privatization

programmeHeavy Mechanical Complex (HMC) Design, manufacture and supply of

industrial plants and machineryincluding complete sugar mills, portlandcement plants and white cement plant,etc.

Not included in the privatizationprogramme

Karachi Pipe Mills Ltd. Production of G.I. & M.S. pipes Not included in the privatizationprogramme

Koh-i-Noor Oil Mills Production of cooking oil/ghee 45.69% / excluded from privatizationprogramme

Larkana Sugar Mills Sugar manufacture 100% / liquidatedLasbella Textile Mills, Ulhal Textile spinning, weaving, processing 100% / privatization under processLyallpur Chemicals and Fertilizer Ltd. Fertilizer manufacture 75% / privatization under processMaqbool Oil Mills Production of cooking oil/ghee 61.85% / privatization under processMorafco Industries Production of cooking oil 53.10% / privatization under process

Table III.4 (cont'd)

Pakistan WT/TPR/S/95Page 47

Entity Activity Degree of state ownership/situationin privatization programme

National Fertilizer Corporation Several firms producing fertilizers Not included in the privatizationprogramme

National Fertilizer Marketing Ltd. Marketing of fertilizers Not included in the privatizationprogramme

National Refinery Ltd. .. Not included in the privatizationprogramme

Northern foundry and Engineering works .. Not included in the privatizationprogramme

Nowshera Engineering Company Ltd. .. Not included in the privatizationprogramme

Pak-American Fertilizer Marketing Ltd. Fertilizer manufacture 100% / privatization under processPak-Arab Fertilizers Ltd. Fertilizer manufacture: nitro phosphate,

CAN, urea, ammonia, and nitric acid48% / privatization under process

Pak-Dye Chemicals Production of chemical dyes 100% / privatization under processPak-Iran Industry Ltd. – JV .. 100% / privatization under processPakistan Automobile Corporation .. Not included in the privatization

programmePakistan Engineering Company Ltd. Engineering products: machine tools,

electric motors, pumps, bicycles, powerlooms, transmission towers, steelfabrication

65% / privatization under process

Pakistan Industrial Development Corporation .. Not included in the privatizationprogramme

Pakistan Machine Tools Factory (PMTF) Manufacturing of center lathes, millingmachines, turret milling, copy millingand boring milling machines,automotive parts such as gear boxes,transfer cases, axles, steering/timinggears etc.; non-ferrous die castings.

Not included in the privatizationprogramme

Pakistan Steel Fabricating Company Ltd. Steel mill 100% / excluded from the privatizationprogramme

Pakistan Steel Mills Corporation Ltd. Production of coke, pig iron, billets, hotand cold rolled sheets etc.

100% / excluded from the privatizationprogramme

Pakistan Switchgear Ltd. .. 100% / privatizedPak-Motor Car Company Trading company 100% / excluded from the privatization

programmePak-Saudi Fertiliser Ltd. Fertilizer manufacture: urea 100% / excluded from the privatization

programmePECO (BBW Land lot A & B) Real estate 65% / privatization under processPECO (Kot Lakhpat) Engineering products: machine tools,

electric motors, pumps, bicycles, powerlooms, transmission towers, steelfabrication

35 % / privatization under process

People Steel Mills Ltd. Steel mills 100% / privatizedPIDC Printing Press (pvt) Ltd .. Not included in the privatization

programmePunjab Vegetable Ghee Production of vegetable ghee 100% / privatizedRavi Rayon Ltd. Production of acetic yarn and other by-

products40.36% / privatization under process

Republic Motors Ltd. Workshop/real estate 100% / privatization under processSargroh Vegetable Ghee Production of cooking oil/ghee 100% / excluded from the privatization

programmeShahdadkot Textile Mills Ltd. Textile spinning, weaving, processing 100% / excluded from the privatization

programme. Liquidation under processSind Engineering Ltd. Assembly of Mazda light trucks and sale

of Mazda parts100% / privatization under process

Spinning Machinery Co. Production of machinery 100% / excluded from the privatizationprogramme

Table III.4 (cont'd)

WT/TPR/S/95 Trade Policy ReviewPage 48

Entity Activity Degree of state ownership/situationin privatization programme

State Cement Corporation of Pakistan Cement production Not included in the privatizationprogramme

State Engineering Corporation Manufacturing of power plantequipment; designing, engineering andmanufacturing know-how for industrialplants and machinery

Not included in the privatizationprogramme

State Engineering Project Co. .. Not included in the privatizationprogramme

Suzuki Motorcycles Pakistan Ltd. – JV Production assembly of motorcycles 4.18% / excluded from the privatizationprogramme

Talpur Textile Mills Textile mills 100% / privatization under processTarbela Cotton and Spinning Mills Spinning and mills Not included in the privatization