Oshkosh Corporation Analyst Day

189

2012 Oshkosh Corporation Analyst Day September 14, 2012 Oshkosh Corporation Analyst Day September 14, 2012

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Oshkosh Corporation Analyst Day

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

Pat DavidsonInvestor Relations

Oshkosh Corporation Analyst DaySeptember 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

Forward-Looking Statements

This presentation contains statements that the Company believes to be “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact, including, withoutlimitation, statements regarding the Company’s future financial position, business strategy, targets, projected sales, costs,earnings, capital expenditures, debt levels and cash flows, and plans and objectives of management for future operations, areforward-looking statements. When used in this presentation, words such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “should,” “project” or “plan” or the negative thereof or variations thereon or similar terminology are generally intended to identify forward-looking statements. These forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties, assumptions and other factors, some of which are beyond the Company’s control, which could cause actual results to differ materially from those expressed or implied by such forward-looking statements. These factors include the cyclical nature of the Company’s access equipment, commercial and fire & emergency markets, especially in the current environment where there are conflicting signs regarding the future global economic outlook; the expected level and timing of the U.S. Department of Defense (DoD) procurement of products and services and funding thereof; risks related to reductions in government expenditures in light of U.S. defense budget pressures and an uncertain DoDtactical wheeled vehicle strategy; risks that profit on the definitization of contracts with the DoD could differ from the Company’s estimates; increasing commodity and other raw material costs, particularly in a sustained economic recovery; the ability to increase prices to raise margins or offset higher input costs; risks related to the Company’s exit from its ambulanceand European mobile medical businesses, including the amounts of related costs and charges; risks related to facilities consolidation and alignment, including the amounts of related costs and charges and that anticipated cost savings may not be achieved; the Company’s ability to produce vehicles under the FMTV contract at targeted margins; the duration of the ongoing global economic weakness, which could lead to additional impairment charges related to many of the Company’s intangible assets and/or a slower recovery in the Company’s cyclical businesses than Company or equity market expectations; the potential for the U.S. government to competitively bid the Company’s Army and Marine Corps contracts; the consequences of financial leverage, which could limit the Company’s ability to pursue various opportunities; risks related to the collectability of receivables, particularly for those businesses with exposure to construction markets; the cost of any warranty campaigns related to the Company’s products; risks related to production or shipment delays arising from quality or production issues; risks associated with international operations and sales, including foreign currency fluctuations and compliance with the Foreign Corrupt Practices Act; risks related to actions of activist shareholders; and the Company’s ability to successfully execute on its strategic road map and meet its long-term financial goals. Additional information concerning these and other factors is contained in the Company’s filings with the Securities and Exchange Commission. The Company assumes no obligation, and disclaims any obligation, to update information contained in this presentation. Investors should be aware that the Company may not update such information until the Company’s next quarterly earnings conference call, if at all.

3

2012 Oshkosh Corporation Analyst Day September 14, 2012

Charlie SzewsCEO

Oshkosh Corporation Analyst DaySeptember 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

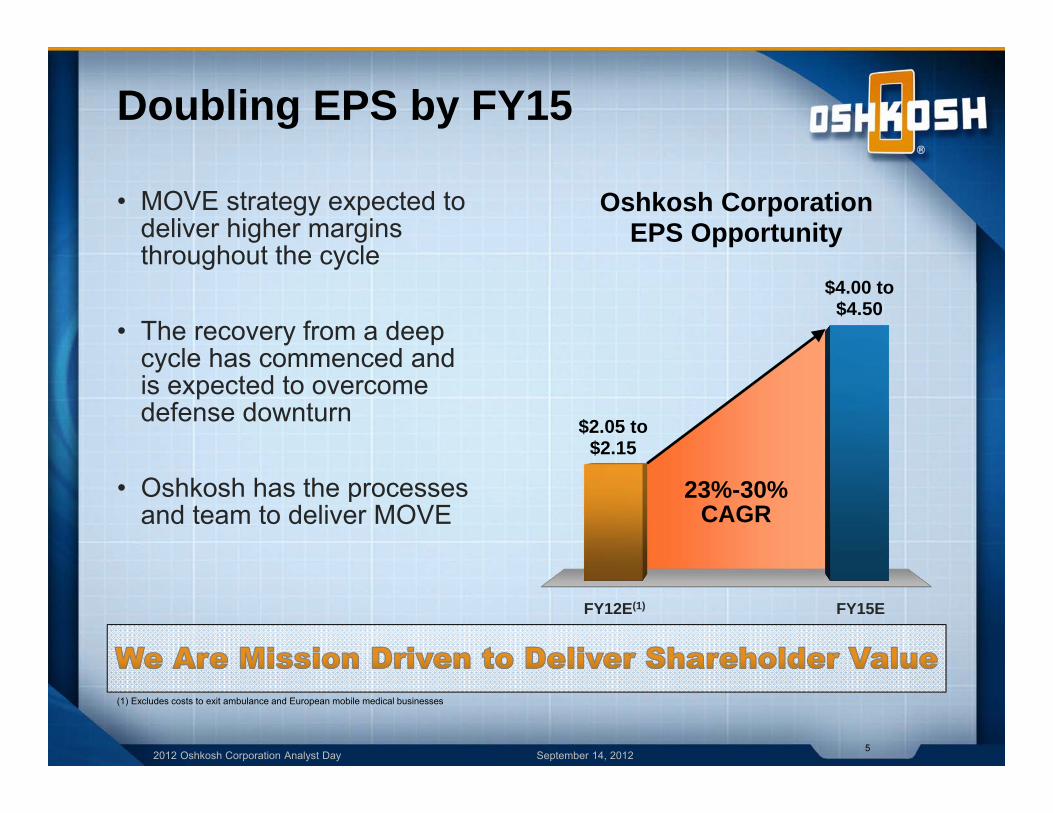

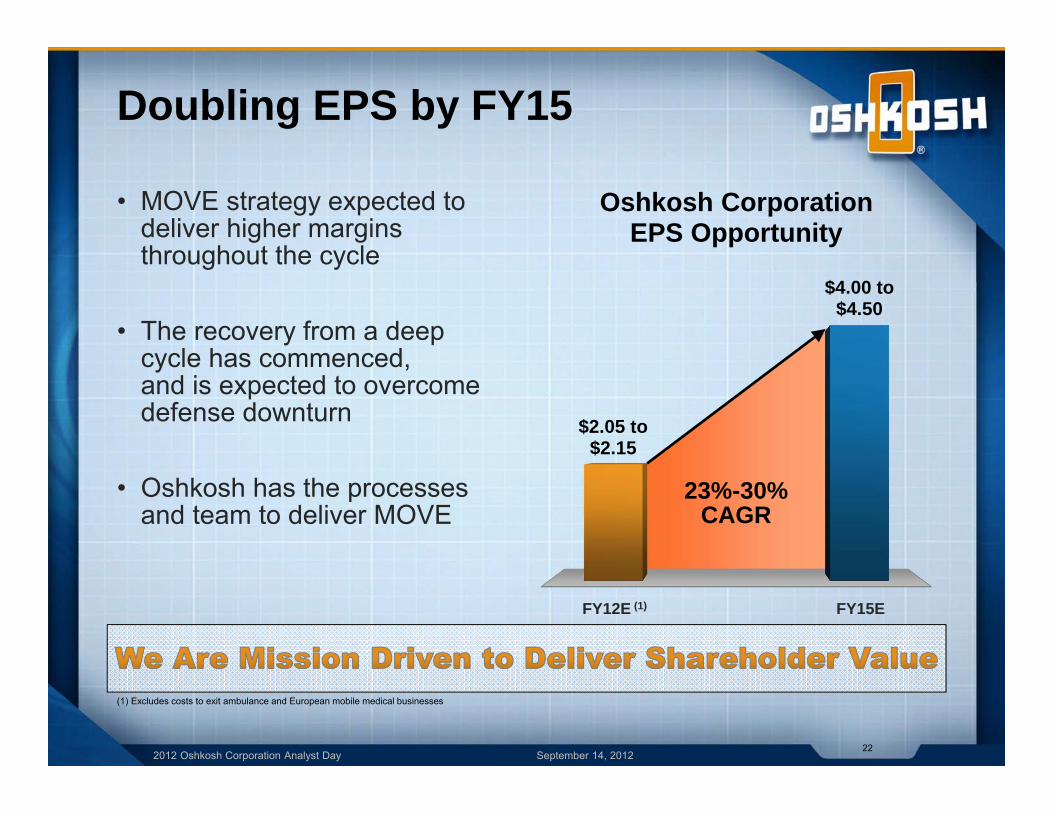

Doubling EPS by FY15

• MOVE strategy expected to deliver higher margins throughout the cycle

• The recovery from a deep cycle has commenced and is expected to overcome defense downturn

• Oshkosh has the processes and team to deliver MOVE

$2.05 to $2.15

$4.00 to $4.50

Oshkosh CorporationEPS Opportunity

23%-30% CAGR

FY12E(1) FY15E

5

(1) Excludes costs to exit ambulance and European mobile medical businesses

2012 Oshkosh Corporation Analyst Day September 14, 2012

Agenda

6

Welcome Pat Davidson

Doubling into a Global Industrial Charlie Szews

MOVE Delivers Wilson Jones

Supporting Our Recovery Outlook

Frank NerenhausenJohn UriasJim Johnson Todd Fierro

Processes and Team to Deliver MOVE:• Quality & Continuous Improvement• Global Procurement & Supply Chain• Innovation

Colleen MoynihanGreg FredericksenGary Schmiedel

Financial Summary Dave Sagehorn

Concluding Remarks Charlie Szews

Q & A Panel All Presenters

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh’s Rich History

2012 Oshkosh Corporation Analyst Day September 14, 2012

Mission Driven

• 95 years performing mission critical work• Innovative, high performance culture• 13,000 dedicated employees working for customers around the world• Board of Directors and management team committed to driving

shareholder value

8

2012 Oshkosh Corporation Analyst Day September 14, 2012

Moving the World at Work

• Our vehicles move people and materials at work– Most protect people or property– Many lift people or property– All do so safely and efficiently

• Often share common customers/ distribution channels– JLG, Jerr-Dan, IMT, McNeilus and Pierce sell

into rental channel– Every segment sells to the U.S.

federal government• Share common components/suppliers,

technologies and manufacturing processes

9

2012 Oshkosh Corporation Analyst Day September 14, 2012

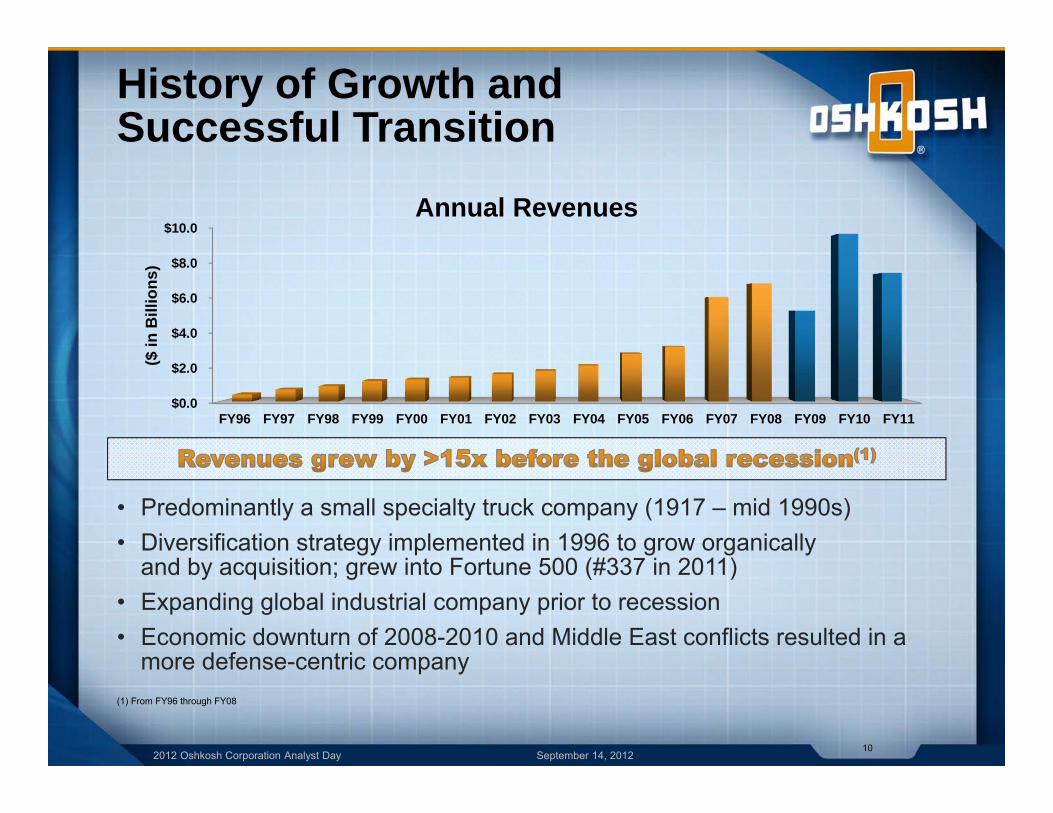

History of Growth and Successful Transition

• Predominantly a small specialty truck company (1917 – mid 1990s)• Diversification strategy implemented in 1996 to grow organically

and by acquisition; grew into Fortune 500 (#337 in 2011)• Expanding global industrial company prior to recession• Economic downturn of 2008-2010 and Middle East conflicts resulted in a

more defense-centric company

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

FY96 FY97 FY98 FY99 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

($ in

Bill

ions

)

Annual Revenues

10

(1) From FY96 through FY08

2012 Oshkosh Corporation Analyst Day September 14, 2012

Doubling into a Global Industrial

2012 Oshkosh Corporation Analyst Day September 14, 2012

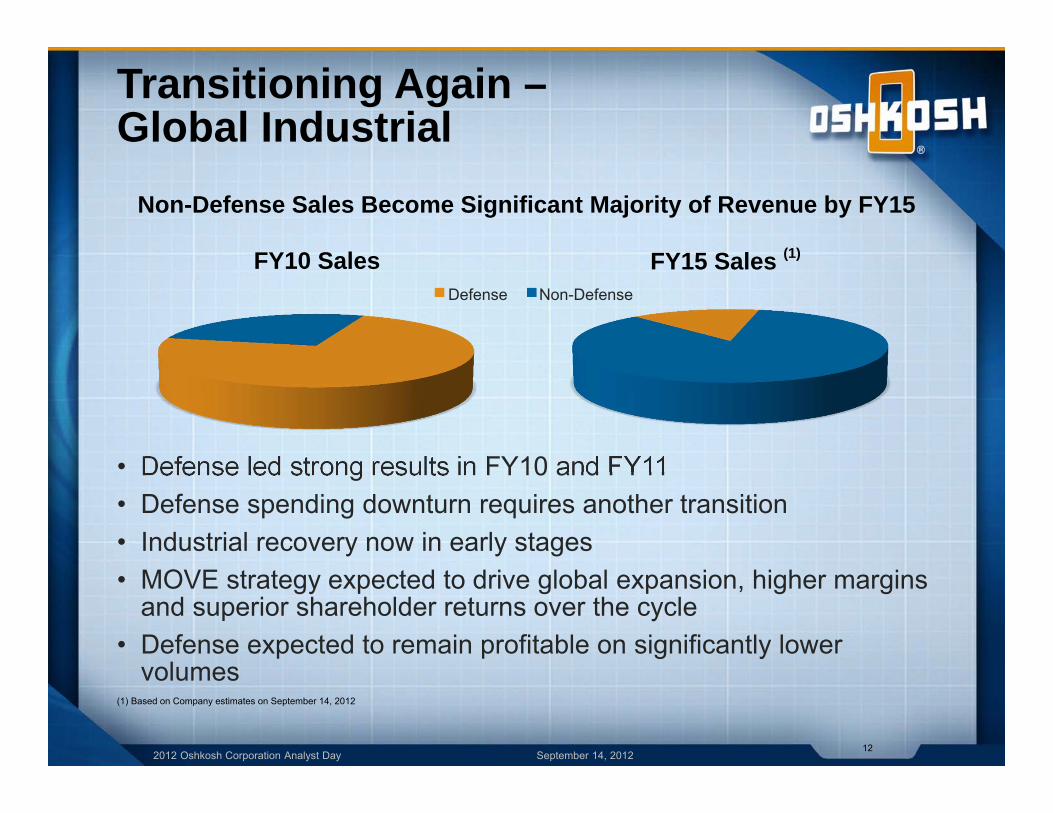

Transitioning Again –Global Industrial

• Defense led strong results in FY10 and FY11• Defense spending downturn requires another transition• Industrial recovery now in early stages• MOVE strategy expected to drive global expansion, higher margins

and superior shareholder returns over the cycle• Defense expected to remain profitable on significantly lower

volumes

12

FY15 Sales (1)FY10 SalesDefense Non-Defense

Non-Defense Sales Become Significant Majority of Revenue by FY15

(1) Based on Company estimates on September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Route to Doubling Earnings

2012 Oshkosh Corporation Analyst Day September 14, 2012

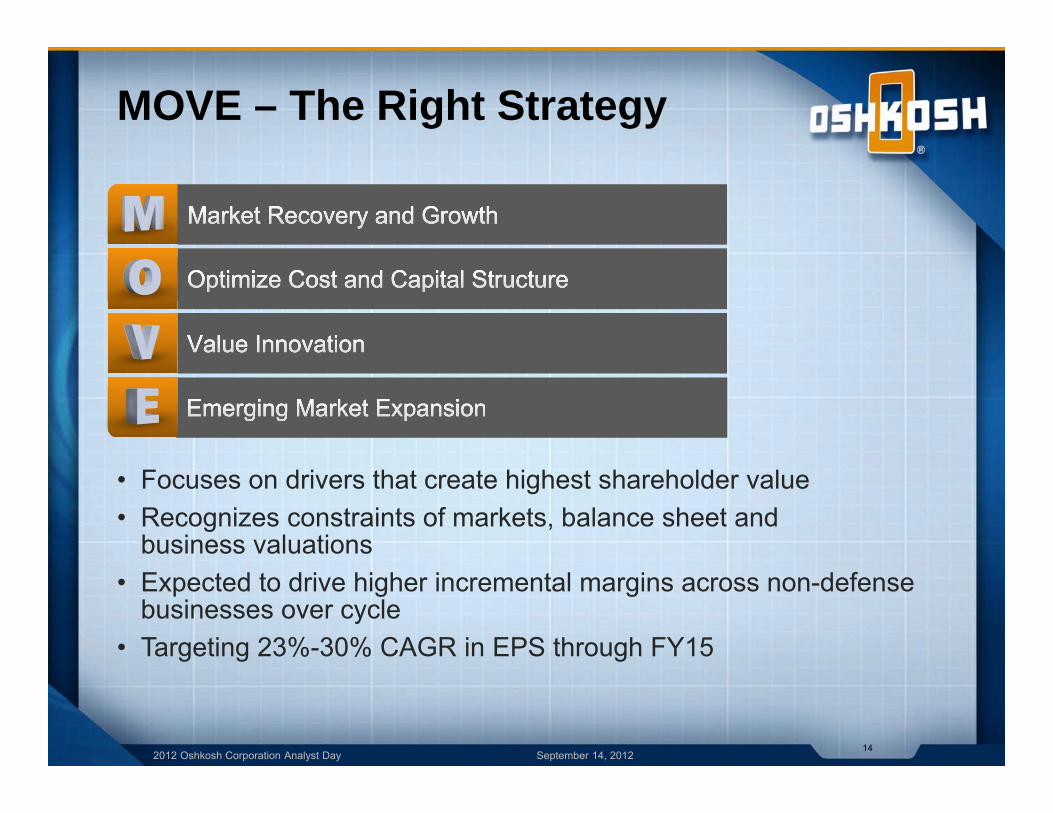

MOVE – The Right Strategy

• Focuses on drivers that create highest shareholder value• Recognizes constraints of markets, balance sheet and

business valuations• Expected to drive higher incremental margins across non-defense

businesses over cycle• Targeting 23%-30% CAGR in EPS through FY15

14

2012 Oshkosh Corporation Analyst Day September 14, 2012

Market Recovery Overcomes Defense Downturn• Key North American markets in slow recovery

– Old fleets need to be renewed– Construction recovery expected to strengthen in FY13 and beyond

• Mining, infrastructure and economic development aiding key Oshkosh markets in Latin America, Australia, Middle East & Asia

• European recovery delayed, but expected to extend AWP cycle• Green solutions, rising safety standards and productivity

requirements suggest stronger demand for Oshkosh products• Oshkosh will manage its defense business to remain profitable

15

2012 Oshkosh Corporation Analyst Day September 14, 2012

Leveraging a Common Structure: Oshkosh Operating System

• Customer-centric application of lean principles– Sets guiding principles for

relationships with customers

• Improves processes needed todeliver key elements of MOVE

• Supports drive to improve cash flow

• Implementation gaining momentum

• Company-wide foundation for building shareholder value

16

2012 Oshkosh Corporation Analyst Day September 14, 2012

Focused Board and Management Team

• Successfully navigated through unprecedented economic conditions• Diverse & complementary backgrounds

– Continually developing/acquiring talent• Incentive compensation objectives strongly aligned

with shareholder interests• Acting decisively for shareholders

17

2012 Oshkosh Corporation Analyst Day September 14, 2012

MOVE is Delivering in FY12• Raised outlook by one-third as year

progressed• Capturing access equipment recovery• Addressing challenges

– FMTV profitable; margins have continued to improve

– Exiting underperforming non-core businesses

• International sales up 31% YTD(1) FY12– 750 M-ATVs for U.A.E. for FY13

• Accelerating Oshkosh Operating System deployment

• Exercising prudent capital allocation strategy

Total Shareholder Return(CAGRs) Since 1996(2)

OSK 19.2%

All Peers 10.9%

S&P 500 6.6%

Total Shareholder ReturnCalendar YTD 2012(2)

OSK 24.8%

(1) Through June 30, 2012

(2) Through September 7, 2012

18

2012 Oshkosh Corporation Analyst Day September 14, 2012

Poised to Deliver Results

• MOVE strategy expected to deliver higher margins throughout cycle• Market recovery, from deep cycle, has commenced

– Is expected to overcome defense downturn • Oshkosh processes and team support execution of MOVE

$2.05 to $2.15

$4.00 to $4.50

Oshkosh CorporationEPS Opportunity

23%-30% CAGR

FY12E(1) FY15E

Industry Leading Brands

Access Equipment #1 Global

Fire Apparatus #1 Global

Airport Products #1 Global

Defense TWV #1 Global

Concrete Mixers #1 Americas

Refuse Collection #1 Americas

(1) Excludes costs to exit ambulance and European mobile medical businesses

19

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

Wilson JonesPresident and COO

Oshkosh Corporation Analyst DaySeptember 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

$2.05 to $2.15

$4.00 to $4.50

Oshkosh CorporationEPS Opportunity

23%-30% CAGR

FY12E (1) FY15E

Doubling EPS by FY15

• MOVE strategy expected to deliver higher margins throughout the cycle

• The recovery from a deep cycle has commenced, and is expected to overcome defense downturn

• Oshkosh has the processes and team to deliver MOVE

(1) Excludes costs to exit ambulance and European mobile medical businesses

22

2012 Oshkosh Corporation Analyst Day September 14, 2012

Our Commitment to Deliver

23

2012 Oshkosh Corporation Analyst Day September 14, 2012

0

50

100

150

200

250

300

350

400

0

2

4

6

Non-Defense Revenue (1)

($ in Billions)

Market Recovery and Growth

(1) Reflects estimated benefits of market recovery captured in financial estimates. Does not include benefits of other MOVE initiatives. Market recovery operating income growth opportunity from FY11 to prior peak sales levels for non-defense segments estimated at ~$500 million.

(2) Excludes costs to exit ambulance and European mobile medical businesses

24

~$220MOpportunity(FY12-FY15)

FY11 FY15EFY12E

~10% CAGR(FY12-FY15)

FY11 FY15EFY12E (2)

Non-Defense Operating Income (1) ($ in Millions)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Deliver with Strong Sales, Inventory and Operations Planning

25

Volume and Margin

Capture

• Disciplined demand planning– Correlate demand factors, voice of

customer and order pipeline– Weekly course corrections– Right inventory in right regions

globally

• Integrated teams focused on lead time reduction– Reducing WIP & inventory– Increasing flexibility to react

• Strong incremental revenue opportunities

2012 Oshkosh Corporation Analyst Day September 14, 2012

Optimize Cost andCapital StructureTargeting 250 bps incremental operating income margin by FY15 (1)

• Product, process and overhead improvements

• Dedicated cost reduction teams

• No compromises: reduce cost structure with no negative impact to customers or brand

• Incrementally improved margins in economic recovery

• Opportunity not dependent on volume increases

(1) Versus FY11

26

Mission Deployment Center

2012 Oshkosh Corporation Analyst Day September 14, 2012

Optimize Cost andCapital StructureMeasure Processes, Drive Results

• Common tools and KPIs

27

2012 Oshkosh Corporation Analyst Day September 14, 2012

Delivering Results - Product

28

New offering

Previous offering

Weight ReductionIndustry’s Lightest Unit

2012 Oshkosh Corporation Analyst Day September 14, 2012

New Platform++ Weight Reduction

New Frame+++ Weight Reduction

New Axles and Spindles

New CWT and Rear Hoods+++ Weight Reduction

New Turntable++ Weight Reduction

Breakdown of Major Sub-systems Redesign

29

Previous offering

2012 Oshkosh Corporation Analyst Day September 14, 2012

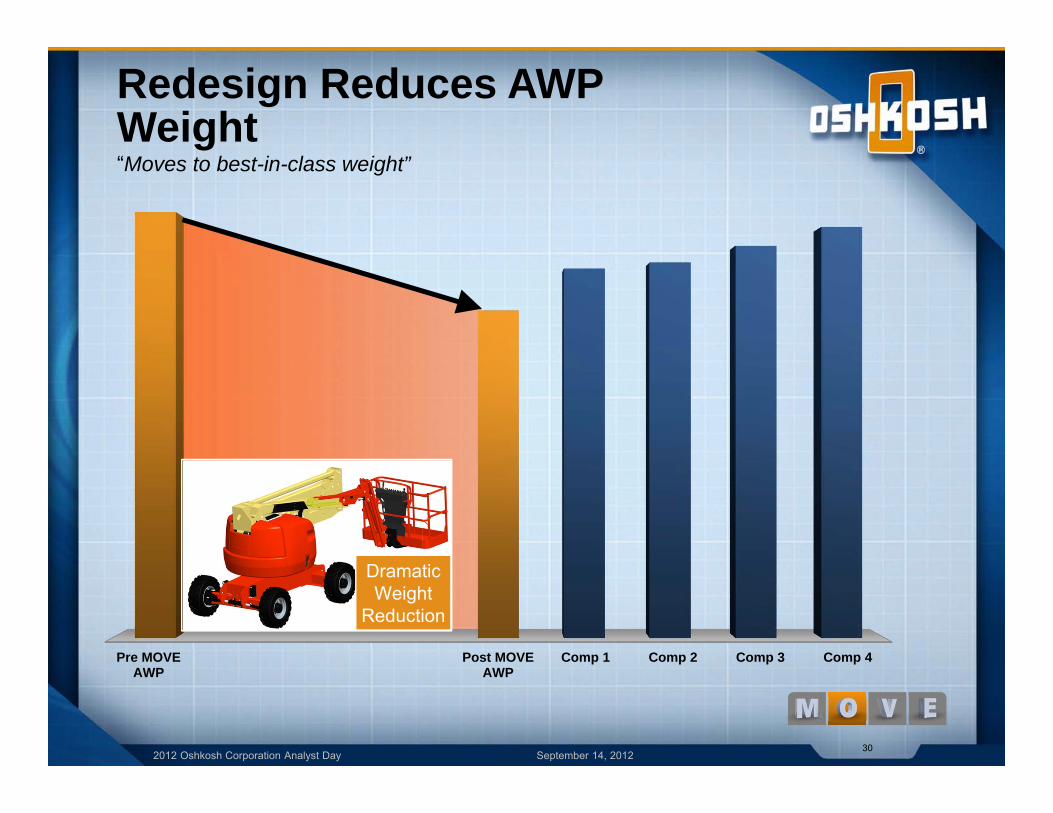

Redesign Reduces AWP Weight

30

“Moves to best-in-class weight”

Pre MOVEAWP

Post MOVEAWP

Comp 1 Comp 2 Comp 3 Comp 4

DramaticWeight

Reduction

2012 Oshkosh Corporation Analyst Day September 14, 2012

Delivering Results -Process Improvement

• Commercial Segment 4 in 1 line efficiency has improved by more than 20%

• Commonizedplatforms simplify fixturing

• Flexible fixturingenables multiple products to be produced on one line to free up space

31

Realizing strong efficiencies with 4 in 1 line

2012 Oshkosh Corporation Analyst Day September 14, 2012

Delivering Results -Overhead Reduction• Transferred 450/510 AWP

production from Belgium to Romania, permitting closure of 25,000 sq. ft. facility

• Achieving quality, delivery and cost targets– Defects per unit well below goal– Positive trend for on time

delivery– 109% of labor savings goal

attained

• Additional insourcingpossibilities

32

2012 Oshkosh Corporation Analyst Day September 14, 2012

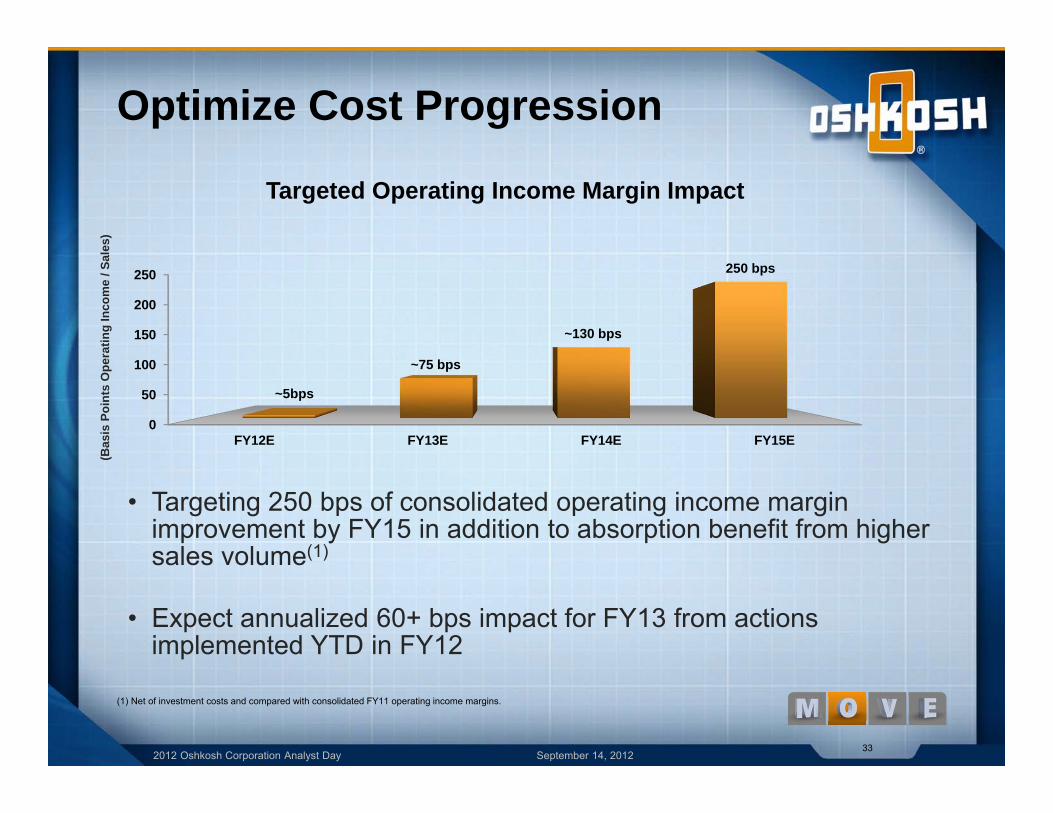

Optimize Cost Progression

(1) Net of investment costs and compared with consolidated FY11 operating income margins.

33

0

50

100

150

200

250

FY12E FY13E FY14E FY15E

~5bps

~75 bps

~130 bps

250 bps

Targeted Operating Income Margin Impact

• Targeting 250 bps of consolidated operating income margin improvement by FY15 in addition to absorption benefit from higher sales volume(1)

• Expect annualized 60+ bps impact for FY13 from actions implemented YTD in FY12

(Bas

is P

oint

s O

pera

ting

Inco

me

/ Sal

es)

2012 Oshkosh Corporation Analyst Day September 14, 2012

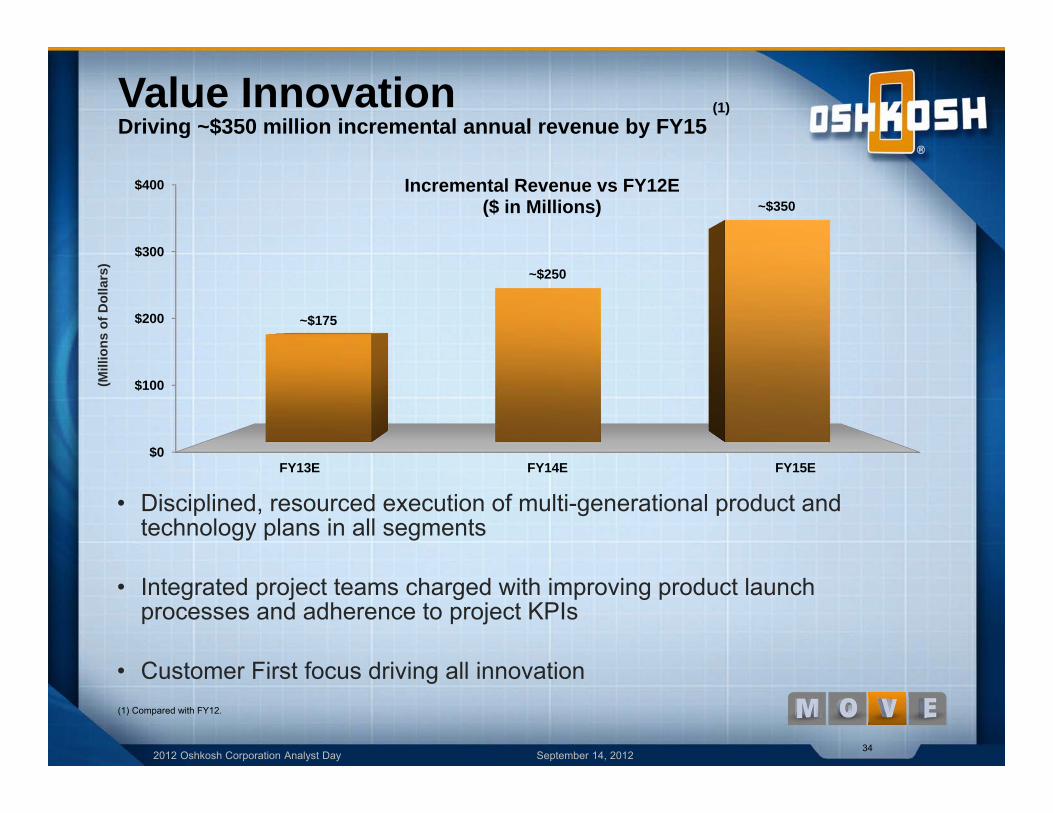

Value InnovationDriving ~$350 million incremental annual revenue by FY15

(1)

• Disciplined, resourced execution of multi-generational product and technology plans in all segments

• Integrated project teams charged with improving product launch processes and adherence to project KPIs

• Customer First focus driving all innovation(1) Compared with FY12.

34

$0

$100

$200

$300

$400

FY13E FY14E FY15E

~$175

~$250

~$350Incremental Revenue vs FY12E

($ in Millions)

(Mill

ions

of D

olla

rs)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Value Innovation -RS Scissor• Opens new markets for JLG

• Innovation targeting price-value segment

• Field validation underway

• Global customers pleased with RS quality and value

35

Tianjin Facility

New RSScissor

2012 Oshkosh Corporation Analyst Day September 14, 2012

Global Presence

36

Countries where Oshkosh has a presence

2012 Oshkosh Corporation Analyst Day September 14, 2012

Emerging Market Expansion> 25% of revenues by FY15 (30% by FY16)

• Expanding sales, service and manufacturing operations • Forward deploying business development professionals for defense• Developing products for global markets• Leveraging international facilities across segments

37

17%~20%

>25%Sales Outside the U.S.

~10%-15% CAGR (FY12-FY15)

FY11 FY15EFY12E

(Per

cent

of R

even

ue)

2012 Oshkosh Corporation Analyst Day September 14, 2012

MOVE-ing Forward

• Right Strategy

• Recovery has Begun

• Right Processes & Team

38

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 201240

Slide intentionally left blank

2012 Oshkosh Corporation Analyst Day September 14, 2012

Frank NerenhausenAccess Equipment

Oshkosh Corporation Analyst DaySeptember 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Access Equipment Advantage

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Access Equipment Advantage

43

JLG is positioned for sustained industry leading performance

Global Leader in Access Equipment

Industry Leading

Innovation

Superior Product Range

Full Spectrum Parts, Service, and Support

Flexible Manufacturing

and Supply Chain

Global Market Presence

2012 Oshkosh Corporation Analyst Day September 14, 2012

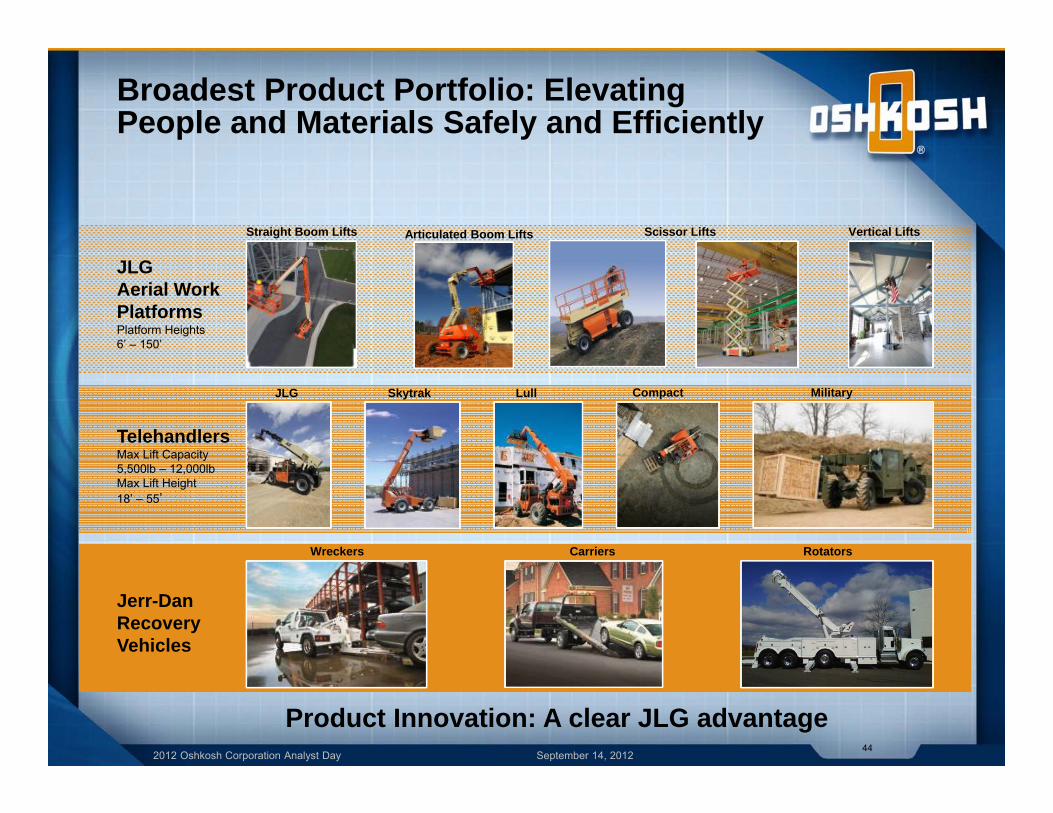

Broadest Product Portfolio: Elevating People and Materials Safely and Efficiently

44

Product Innovation: A clear JLG advantage

JLG Aerial Work PlatformsPlatform Heights 6’ – 150’

TelehandlersMax Lift Capacity5,500lb – 12,000lbMax Lift Height18’ – 55’

Jerr-Dan Recovery Vehicles

Straight Boom Lifts Scissor Lifts Vertical Lifts

CompactJLG Military

Wreckers Carriers

Articulated Boom Lifts

Skytrak Lull

Rotators

2012 Oshkosh Corporation Analyst Day September 14, 2012

Industry Leading Lifecycle Solutions: A Clear JLG Advantage

45

Leading Systems and ProcessesLeading Systems and Processes

Worldwide Parts and Service Network• Full range of JLG program

and competitive parts• Extended service network

Customer Support• Cutting edge training• Industry-leading call centers

Enabling Technology• Online Express• Mobile Apps• Telematics

Next Phase of Equipment Life• Pre-owned• Reconditioning

Deep installed base provides runway for growth

Deep Experience World Class Solutions

2012 Oshkosh Corporation Analyst Day September 14, 2012

Global Market Presence: A Clear JLG Advantage

46

3 Regional Headquarters9 Manufacturing Facilities19 Sales and Service Centers4 Parts Distribution Centers3 Engineering Centers

Customer Support in all Regions

Leveraged Global Supply Chain

Global Product

Platforms

Flexible Global

Operations

2012 Oshkosh Corporation Analyst Day September 14, 2012

Supporting the Outlook

2012 Oshkosh Corporation Analyst Day September 14, 2012

North American Rental Companies are Refreshing Their Fleets, Increasing Market Penetration

48

Total Construction Spending(Y-O-Y % Change)

NA Rental Equipment Access - Fleet Age(AWP and TMH)

NA Rental Equipment Company Fleet Utilization

50

55

60

65

70

75

1Q'10 2Q'10 3Q'10 4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12Ind. Avg.

40

45

50

55

60

2009 2010 2011 2012

(Age

in M

onth

s)

Age (months)

-20

-10

0

10

20

2006 2007 2008 2009 2010 2011 2012E 2013E 2014E 2015EUnited States Canada

NA Rental Equipment Company CapEx (Y-O-Y % Change)

Source: IHS Global data/projections Source: Rouse Rental Report

Based on International Rental News/Dan Kaplan sample of medium to large NA rental equipment companies (United Rental, RSC, HERC, Ameco, Neff).

‐90

‐60

‐30

0

30

60

90

120

150

2004 2005 2006 2007 2008 2009 2010 2011

CapEx

Based on International Rental News/Dan Kaplan sample of medium to large NA rental equipment companies (United Rental, RSC, H&E, HERC).

(% C

hang

e)(%

Util

izat

ion)

(% C

hang

e)

2012 Oshkosh Corporation Analyst Day September 14, 2012

FY07 FY08 FY09 FY10 FY11 FY12E FY13E FY14E FY15E

17 13 4 4 7 13 14 16 20

8067

13 1235

57 59 59 60

(Uni

ts in

Tho

usan

ds)

Telehandlers AWPs

North America – Strong Rental and Market Conditions, Sustained Growth Cycle• Favorable construction spending outlook• Rental industry robust

– Fleet age 55+ months (near peak)– Utilization near 70% (trending up)– Strong CapEx plans

• Rental penetration continues upward trajectory• Energy projects, industrial retooling driving demand

Source: AEM data and Company estimates

(1) Prior Telehandler peak volume of 23,000 units in FY06

49

97

80

17

42

70 73 75 80

FY15E still well short of

prior peak unit volume

16

(1)

2012 Oshkosh Corporation Analyst Day September 14, 2012

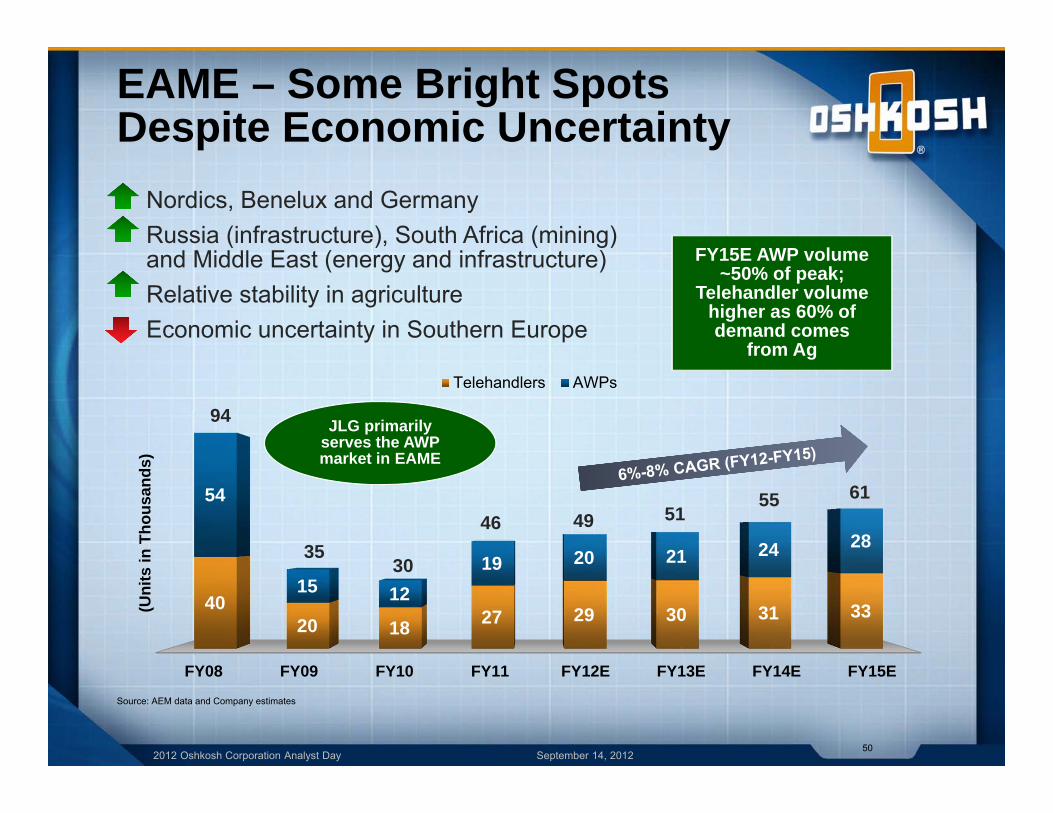

EAME – Some Bright Spots Despite Economic Uncertainty• Nordics, Benelux and Germany• Russia (infrastructure), South Africa (mining)

and Middle East (energy and infrastructure)• Relative stability in agriculture• Economic uncertainty in Southern Europe

Source: AEM data and Company estimates

50

FY08 FY09 FY10 FY11 FY12E FY13E FY14E FY15E

4020 18 27 29 30 31 33

54

15 1219 20 21 24 28

(Uni

ts in

Tho

usan

ds)

Telehandlers AWPs

94

3530

46 49 5155 61

FY15E AWP volume ~50% of peak;

Telehandler volume higher as 60% of demand comes

from Ag

JLG primarily serves the AWP market in EAME

2012 Oshkosh Corporation Analyst Day September 14, 2012

Latin America – Brazil Remains Attractive, Construction Strengthening Throughout

• Major projects with over $500 billion in investment expected in Brazil

• Rental concept strengthening• Product adoption increasing in Mexico, Chile and

Panama• Inconsistent supply of capital

Source: AEM data and Company estimates

51

FY08 FY09 FY10 FY11 FY12E FY13E FY14E FY15E1 0 1 2 2 2 2 23

23

5 68

911

(Uni

ts in

Tho

usan

ds)

Telehandlers AWPs

42

4

78

10

13

Demand driven by Olympics,

FIFA World Cup and mining

11

2012 Oshkosh Corporation Analyst Day September 14, 2012

Asia Pacific – Australia Steady, China in Early Phase of Adoption• Australia energy, mining and supporting infrastructure• Rental concept emerging in China• Vietnam, Indonesia and Malaysia showing potential• Singapore adoption growing• Slow recovery in Japan and South Korea

Source: AEM data and Company estimates

52

FY08 FY09 FY10 FY11 FY12E FY13E FY14E FY15E

3 1 2 1 1 1 1 2

14

5 6 8 9 11 13 13

(Uni

ts in

Tho

usan

ds)

Telehandlers AWPs

17

6 89

1012

14 15

Product adoption drives growth

faster than GDPincrease

JLG – Led Formation of

China Work Safety Committee (WSC)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Financial Outlook

2012 Oshkosh Corporation Analyst Day September 14, 2012

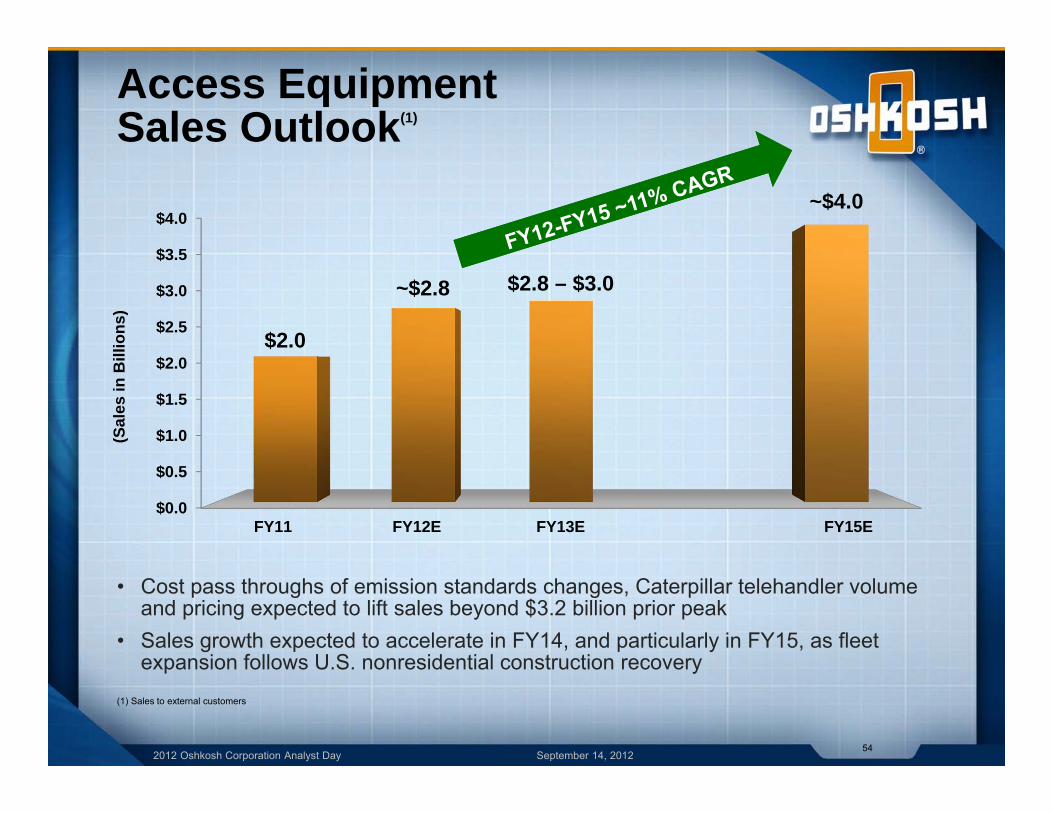

Access Equipment Sales Outlook(1)

(1) Sales to external customers

54

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

FY11 FY12E FY13E FY15E

$2.0

~$2.8 $2.8 – $3.0

~$4.0

(Sal

es in

Bill

ions

)

• Cost pass throughs of emission standards changes, Caterpillar telehandler volume and pricing expected to lift sales beyond $3.2 billion prior peak

• Sales growth expected to accelerate in FY14, and particularly in FY15, as fleet expansion follows U.S. nonresidential construction recovery

2012 Oshkosh Corporation Analyst Day September 14, 2012

Access Equipment Operating Income Margin Outlook

• Steady margin improvement expected over next three years• Operating income margin in the last cycle peaked at 11.3%• Operating income margins reduced by ~ $50 million of annual

intangible amortization

55

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

FY11 FY12E FY13E FY15E

3.2%

~7.7%9.5%-10.0%

~15.0%

(Ope

ratin

g In

com

e M

argi

n %

)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Access Equipment Operating Income Margin Drivers

• MOVE impact expected to accelerate in FY14 and FY15 as FY12 and FY13 investments provide returns

• Numerous “O” initiatives already providing benefits56

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Prior Peak(FY08)

FY12E "M"Initiatives

"O"Initiatives

"V"Initiatives

"E"Initiatives

FY15E

11.3%

~7.7%

~15.0%

(Ope

ratin

g In

com

e M

argi

n %

)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

John UriasDefense

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Oshkosh Defense Advantage

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Oshkosh Defense Advantage

60

Defense Engineering & Product

Development

Scalable Manufacturing & Operations

Vertical Integration of Specialized

Components

Defense Program

Management

Vehicle Fleet Modernization

Service, Lifecycle

Sustainment

Defense industry expertise that leverages the full capabilities of Oshkosh Corporation

2012 Oshkosh Corporation Analyst Day September 14, 2012

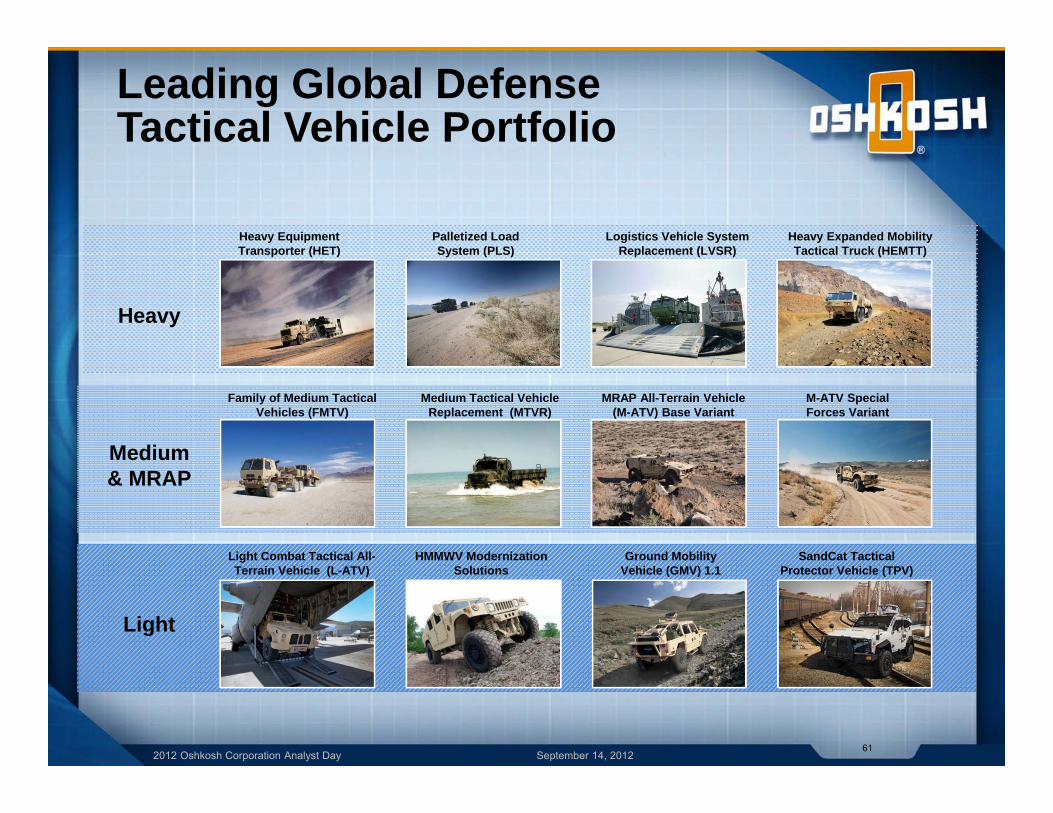

Leading Global Defense Tactical Vehicle Portfolio

61

Heavy Equipment Transporter (HET)

Heavy Expanded Mobility Tactical Truck (HEMTT)

Palletized Load System (PLS)

Logistics Vehicle System Replacement (LVSR)

Medium Tactical Vehicle Replacement (MTVR)

Family of Medium Tactical Vehicles (FMTV)

MRAP All-Terrain Vehicle (M-ATV) Base Variant

M-ATV Special Forces Variant

Light Combat Tactical All-Terrain Vehicle (L-ATV)

HMMWV Modernization Solutions

SandCat Tactical Protector Vehicle (TPV)

Ground Mobility Vehicle (GMV) 1.1

Heavy

Light

Medium& MRAP

2012 Oshkosh Corporation Analyst Day September 14, 2012

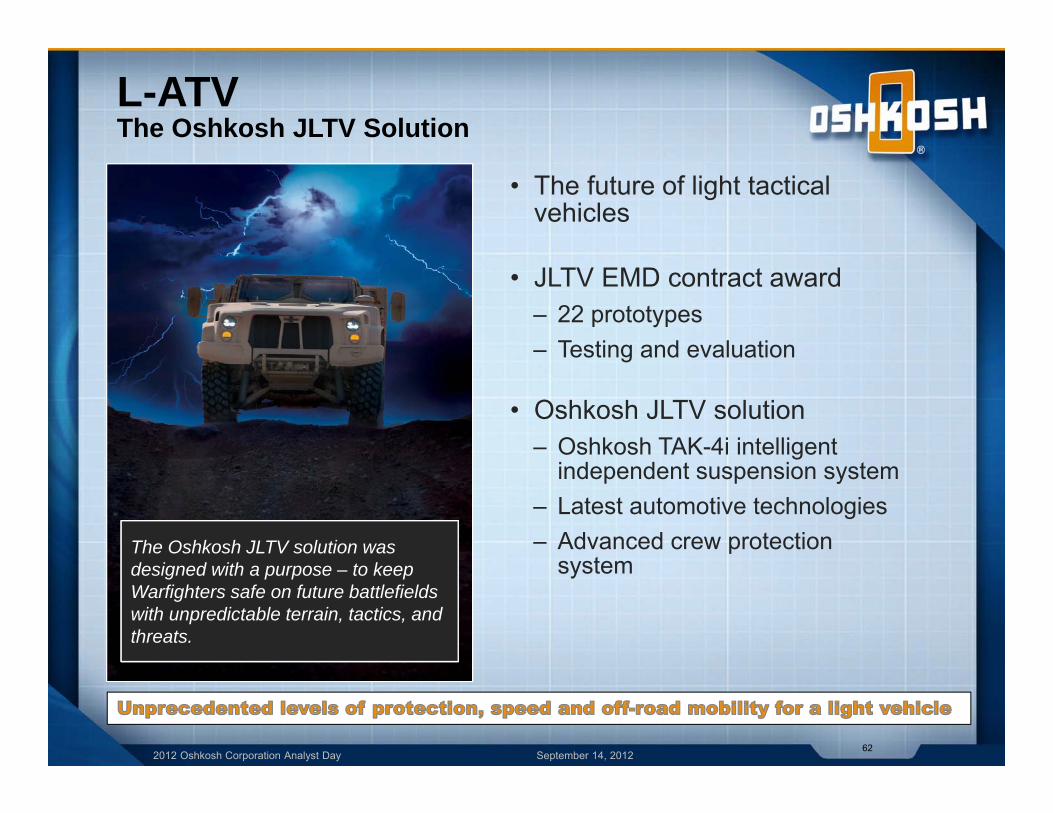

L-ATVThe Oshkosh JLTV Solution

• The future of light tactical vehicles

• JLTV EMD contract award– 22 prototypes– Testing and evaluation

• Oshkosh JLTV solution – Oshkosh TAK-4i intelligent

independent suspension system– Latest automotive technologies– Advanced crew protection

system

62

The Oshkosh JLTV solution was designed with a purpose – to keep Warfighters safe on future battlefields with unpredictable terrain, tactics, and threats.

2012 Oshkosh Corporation Analyst Day September 14, 2012

Defense Product Lifecycle Solutions

63

RecapitalizationIn-factory modernization to the latest configuration; returned with zero mile/hour warranty

ResetIn-theater or in-factory upgrade to restore capability

Tech Upgrades/KitsAdding new capability on an urgent needs basis

Field Maintenance and SupportField Service Reps provide technical support in-theater; full range of logistics and training solutions support operational readiness

Defense vehicle engineering, design and supply chain expertisecreates differentiation for our aftermarket solutions

Military Experience Quality Management SystemLean Processes

2012 Oshkosh Corporation Analyst Day September 14, 2012

Supporting the Outlook

2012 Oshkosh Corporation Analyst Day September 14, 2012

Global Defense Spending Forecast

65

East Asia2012a 23,7872017f 32,987CAGR 6.76%12‐17(f) 172,063

East Europe2012a 6,6252017f 6,994CAGR 1.09%12‐17(f) 40,232

Latin America2012a 14,9162017f 20,280CAGR 6.34%12‐17(f) 103,809

MENA2012a 37,9532017f 44,905CAGR 3.42%12‐17(f) 248,005

North America2012a 206,5912017f 198,135CAGR ‐0.83%12‐17(f) 1,224,340

Russia & CIS2012a 21,5672017f 28,108CAGR 5.44%12‐17(f) 150,570

South Asia2012a 17,9512017f 25,210CAGR 7.03%12‐17(f) 129,020

South East Asia2012a 8,7592017f 11,696CAGR 5.96%12‐17(f) 129,020

South Europe2012a 11,2052017f 12,360CAGR 1.98%12‐17(f) 68,893

West Europe2012a 63,8702017f 63,772CAGR ‐0.03%12‐17(f) 363,249

- U.S. Defense spending represents nearly 50% of global spend 2012-2017- Regional spending increases driven by air and sea- Ground vehicle opportunities exist

Source: Jane’s Defence Budgets, June 13, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

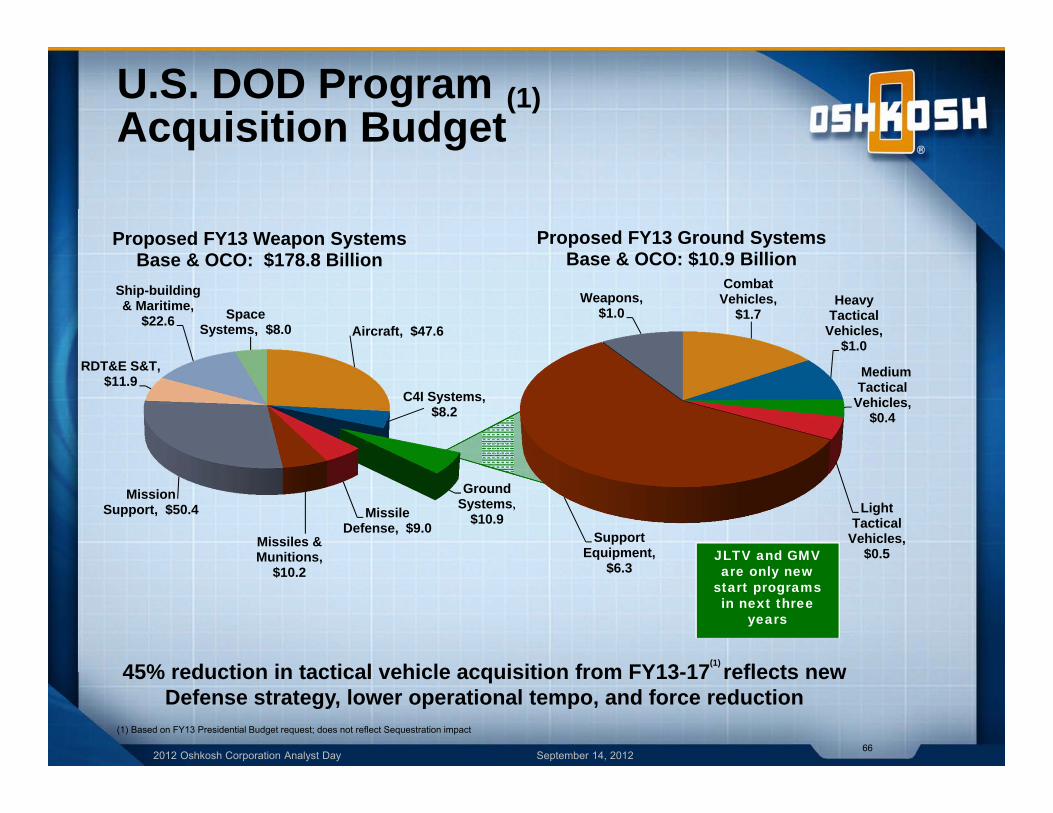

U.S. DOD ProgramAcquisition Budget

(1)

(1) Based on FY13 Presidential Budget request; does not reflect Sequestration impact

66

Aircraft, $47.6

C4I Systems, $8.2

Ground Systems,

$10.9 Missile Defense, $9.0

Missiles & Munitions,

$10.2

Mission Support, $50.4

RDT&E S&T, $11.9

Ship-building & Maritime,

$22.6 Space Systems, $8.0

Proposed FY13 Weapon Systems Base & OCO: $178.8 Billion

Combat Vehicles,

$1.7 Heavy

Tactical Vehicles,

$1.0

Medium Tactical

Vehicles, $0.4

Light Tactical

Vehicles, $0.5

Support Equipment,

$6.3

Weapons, $1.0

Proposed FY13 Ground Systems Base & OCO: $10.9 Billion

JLTV and GMV are only new

start programs in next three

years

45% reduction in tactical vehicle acquisition from FY13-17(1) reflects new Defense strategy, lower operational tempo, and force reduction

2012 Oshkosh Corporation Analyst Day September 14, 2012

Macro Defense Market Trends

67

Macro market trends will redefine the competitive landscape for vehicle contracts of all types and sizes

U.S. Defense

Spending

Vertical Integration

Export Policies to Support U.S. Industrial Base

U.S. Acquisition

Reform

International Business

Opportunities

Offset Req’t

Competitive Landscape

Reset

“I've made clear, and I'll continue to do so, that if sequestration is allowed to go into effect, it'll be a disaster for national defense and it would be a disaster, frankly, for defense communities as well.”

Leon PanettaU.S. Defense Secretary

2012 Oshkosh Corporation Analyst Day September 14, 2012

Adapting to the Domestic Defense Spending Downturn

68

Current Operations Profile

New Vehicle Production Aftermarket &

Modernization

Tech & Product Development

Future Operations Profile

New Vehicle Production

Aftermarket & Modernization

Tech & Product Development

HEAVY, MEDIUM & MRAP VEHICLES MEDIUM, MRAP & LIGHT VEHICLES

– Compete to win in the Light vehicle segment– Optimize our cost structure

2012 Oshkosh Corporation Analyst Day September 14, 2012

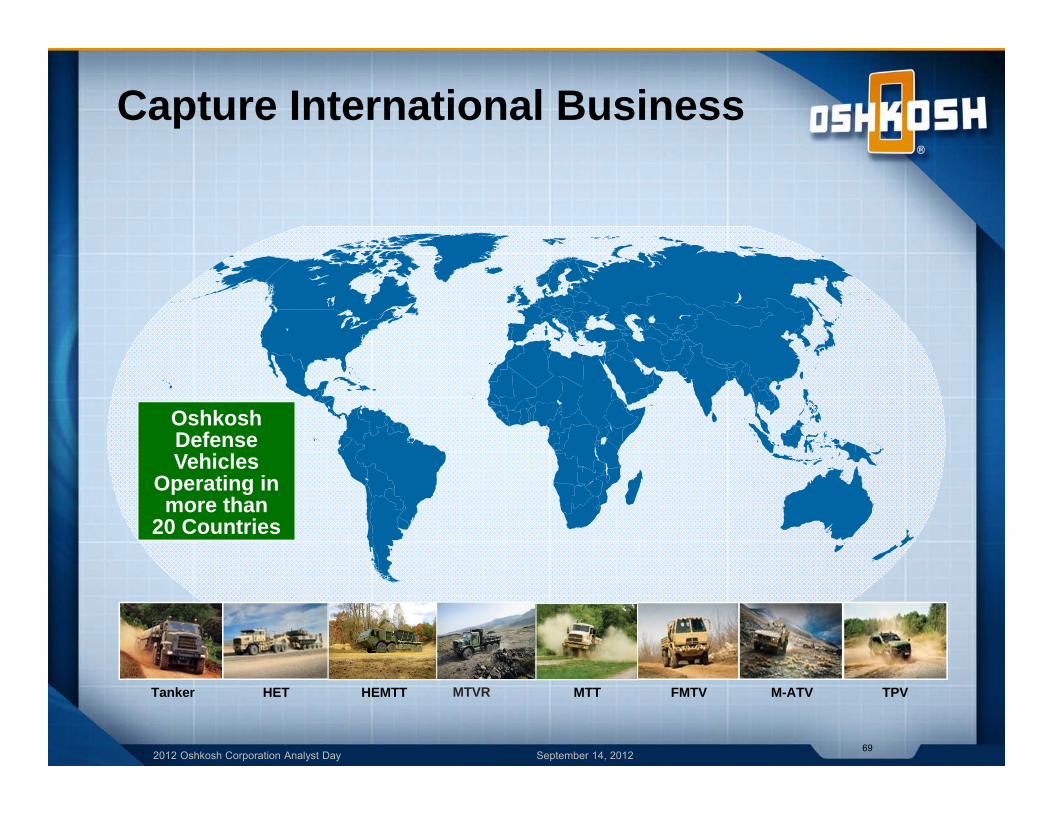

Capture International Business

69

Tanker HET HEMTT MTT FMTV M-ATV TPV

OshkoshDefense Vehicles

Operating in more than

20 Countries

MTVR

2012 Oshkosh Corporation Analyst Day September 14, 2012

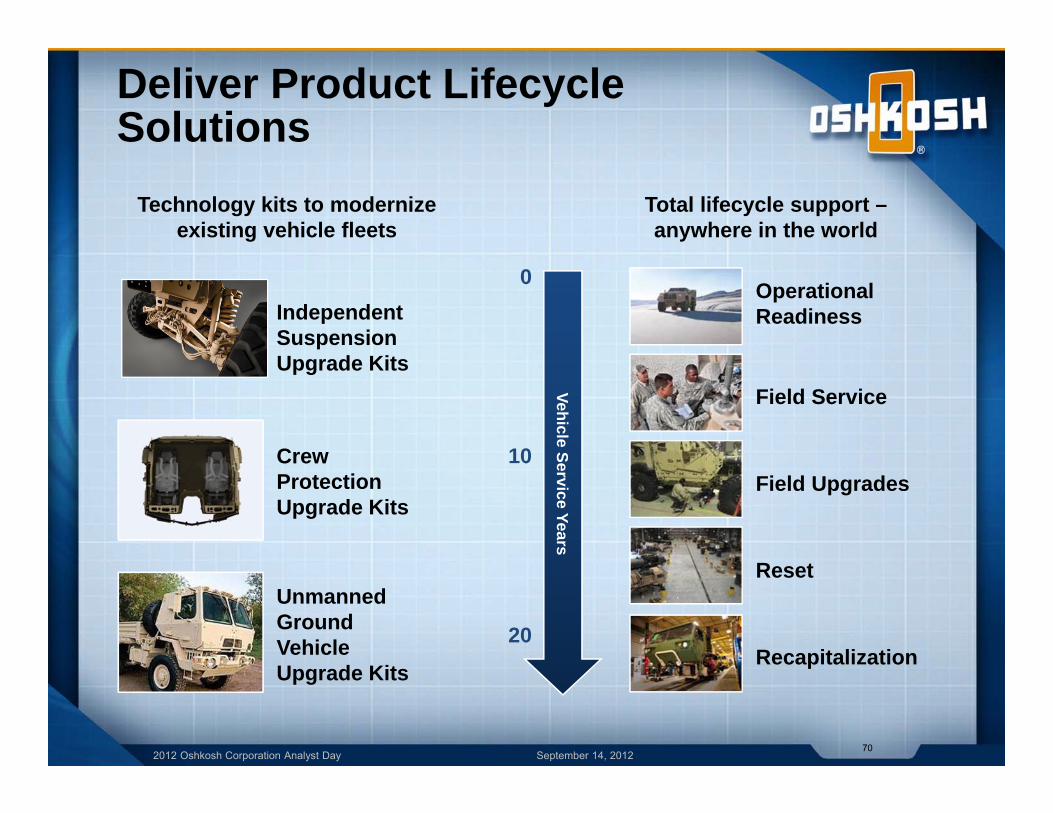

Deliver Product Lifecycle Solutions

70

Technology kits to modernize existing vehicle fleets

Total lifecycle support –anywhere in the world

Independent Suspension Upgrade Kits

Crew ProtectionUpgrade Kits

Unmanned Ground Vehicle Upgrade Kits

Operational Readiness

Field Service

Field Upgrades

Reset

Recapitalization

Vehicle Service Years

0

10

20

2012 Oshkosh Corporation Analyst Day September 14, 2012

Financial Outlook

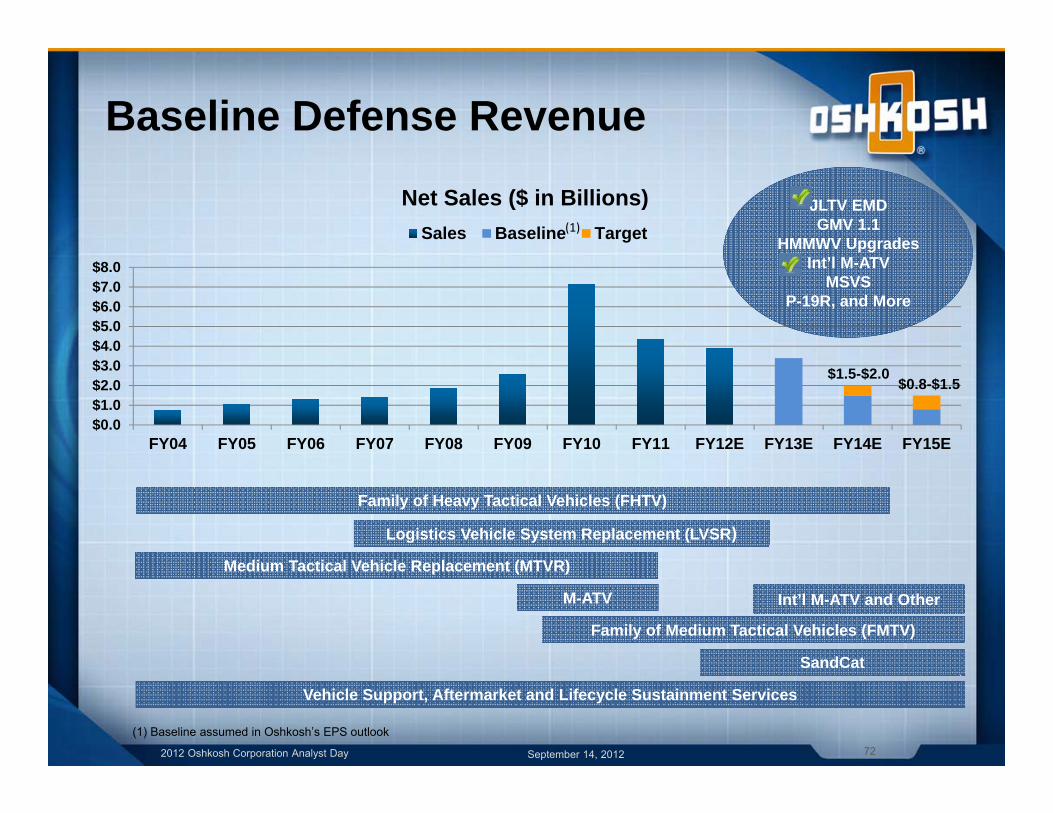

Baseline Defense Revenue

72September 14, 20122012 Oshkosh Corporation Analyst Day

$0.0$1.0$2.0$3.0$4.0$5.0$6.0$7.0$8.0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12E FY13E FY14E FY15E

Net Sales ($ in Billions)Sales Baseline Target

JLTV EMDGMV 1.1

HMMWV UpgradesInt’l M-ATV

MSVSP-19R, and More

Family of Heavy Tactical Vehicles (FHTV)

M-ATV

Family of Medium Tactical Vehicles (FMTV)

Medium Tactical Vehicle Replacement (MTVR)

Logistics Vehicle System Replacement (LVSR)

Vehicle Support, Aftermarket and Lifecycle Sustainment Services

SandCat

Int’l M-ATV and Other

(1) Baseline assumed in Oshkosh’s EPS outlook

(1)

$1.5-$2.0$0.8-$1.5

2012 Oshkosh Corporation Analyst Day September 14, 2012

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

FY11 FY12E FY13E FY14E FY15E

(Sal

es in

Bill

ions

)

Baseline (1)

Baseline(1)

$4.4

~ $3.9

$3.3 - $3.4

$2.0 Target

$1.5 Target

• Baseline sales in FY15E, assuming no contract wins, decline to $800 million

• Target sales for FY15E is $1.5 billion based on initiatives to drive global and aftermarket sales

Defense Sales Outlook

73

(1) Baseline assumed in Oshkosh’s EPS outlook

$1.5

$0.8

2012 Oshkosh Corporation Analyst Day September 14, 2012

Defense Operating Income Margin Outlook

• Company will adjust cost structure as needed to remain profitable• New contract wins present upside to Baseline

74

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

FY11 FY12E FY13E FY14E FY15E

12.4%

~5.5% 5.0%-5.5%Baseline

~3.0% Baseline~2.0%(O

pera

ting

Inco

me

Mar

gin

%)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 201276

Slide intentionally left blank

2012 Oshkosh Corporation Analyst Day September 14, 2012

September 14, 2012

Jim JohnsonFire & Emergency

Oshkosh Corporation Analyst Day

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Fire & Emergency Advantage

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Fire & Emergency Advantage

79

InnovationLeader

PremierDistribution and Service

Unrivaled Product

Performance

#1 Brands

Leading global provider of specialty vehicles that serve, protect and save lives

2012 Oshkosh Corporation Analyst Day September 14, 2012

Delivering Market Leading Products

80

Custom Pumpers Rescues Aerials Commercial Pumpers

Aircraft Rescue & Firefighting

Broadcast

Pierce Fire Apparatus

Oshkosh Airport Products

Frontline Communications Products

Diverse solutions for fire, emergency and broadcast professionals

Command Military Simulators

Airport Snow Removal

2012 Oshkosh Corporation Analyst Day September 14, 2012

Going Global to Offset Domestic Pressure

81

Fire & Emergency headquartersManufacturing facilitiesFire and ARFF dealersSnow Removal dealersFrontline dealersCompany owned sales/service Changi Airport Commissioning Ceremony, Singapore

Added 22 dealers in Asia in past 3 years

2012 Oshkosh Corporation Analyst Day September 14, 2012

Leveraging Premier Dealer Network• Pierce

– Domestic– 30 exclusive dealers with ~300

sales representatives– 60 service centers with more than

600 service technicians– Direct sales to Department of Defense– International dealer network

– Added 11 new dealers in FY12• Airport

– Domestic dealers and direct sales representatives

– 60 international sales representatives and dealers

• Oshkosh international offices– Dubai, United Arab Emirates– Beijing and Shanghai, China– Moscow, Russia– Singapore– New Delhi, India

82

Atlantic Emergency Solutions

Oshkosh Warehouse, Singapore

2012 Oshkosh Corporation Analyst Day September 14, 2012

Supporting the Outlook

2012 Oshkosh Corporation Analyst Day September 14, 2012

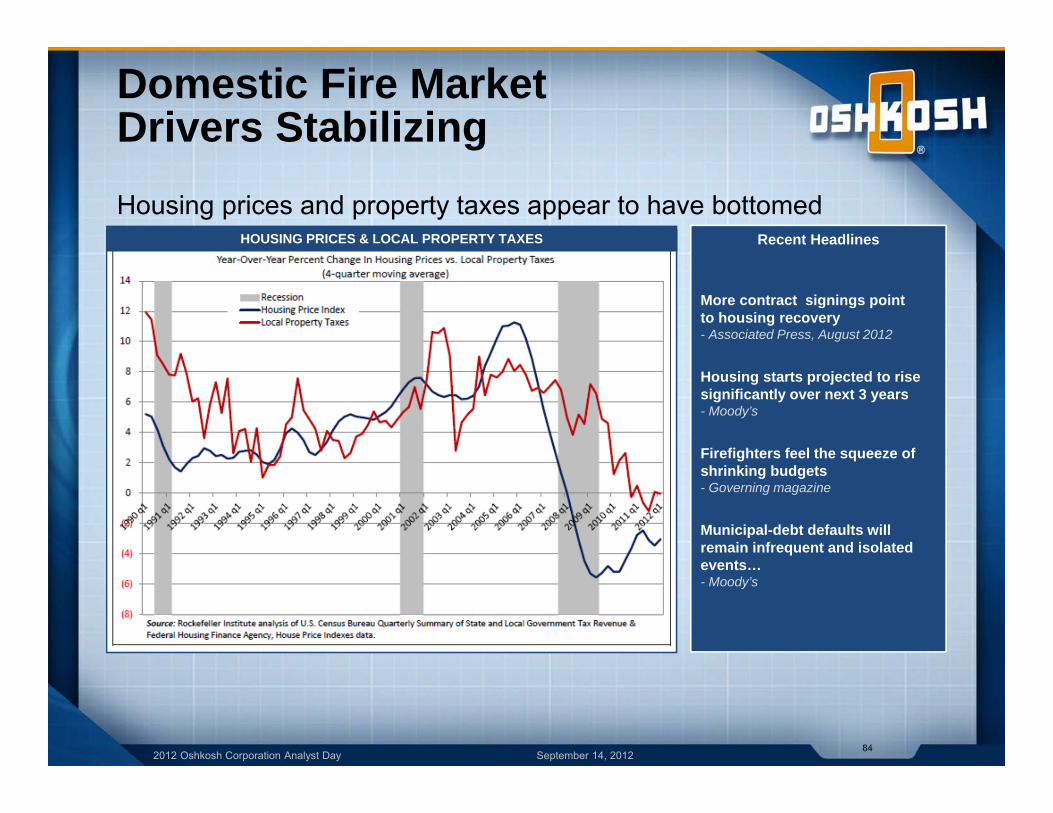

Domestic Fire Market Drivers Stabilizing

84

Housing prices and property taxes appear to have bottomedRecent Headlines

More contract signings pointto housing recovery- Associated Press, August 2012

Housing starts projected to rise significantly over next 3 years- Moody’s

Firefighters feel the squeeze of shrinking budgets- Governing magazine

Municipal-debt defaults will remain infrequent and isolated events…- Moody’s

HOUSING PRICES & LOCAL PROPERTY TAXES

2012 Oshkosh Corporation Analyst Day September 14, 2012

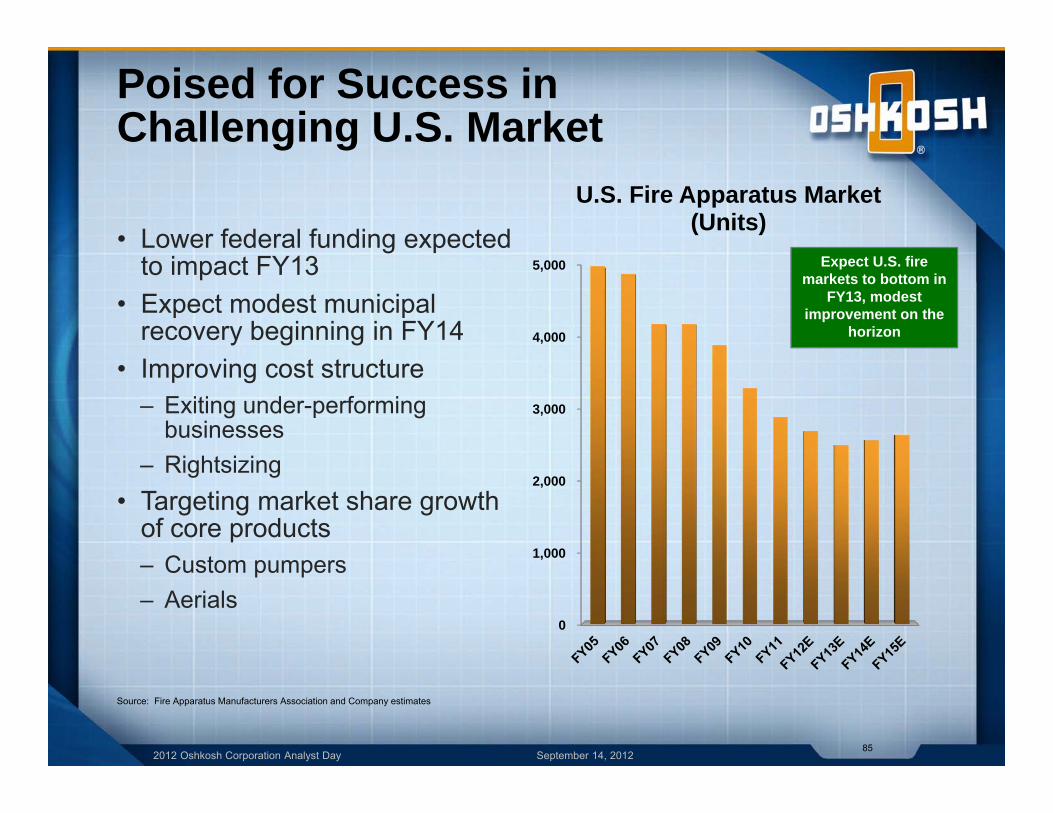

Poised for Success in Challenging U.S. Market

• Lower federal funding expected to impact FY13

• Expect modest municipal recovery beginning in FY14

• Improving cost structure– Exiting under-performing

businesses– Rightsizing

• Targeting market share growth of core products– Custom pumpers– Aerials

Source: Fire Apparatus Manufacturers Association and Company estimates

85

0

1,000

2,000

3,000

4,000

5,000

U.S. Fire Apparatus Market (Units)

Expect U.S. fire markets to bottom in

FY13, modest improvement on the

horizon

2012 Oshkosh Corporation Analyst Day September 14, 2012

International Market Growth Opportunities• Expect continued growth in

developing countries– Investing in safety and security– Expanding infrastructure

• World air traffic projected to continue growing– Middle East and Asia Pacific

expected to increase 8%-10% per year

– Driving increased demand for Oshkosh Airport Products

• International customers seeking technologically superior products

(1) Source: Air Traffic Growth (regional growth in passenger kilometers) per International Civil Aviation Organization

86

0%

2%

4%

6%

8%

10%

12%

World Air Traffic 2012 - 2014 Projected Average Annual Growth Rate

Pierce Industrial Pumper, Liaoning Province, China

(1)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Capitalizing on International Opportunities

87

Recent ordersPierceOshkosh Airport

Recent Headlines

Strategic Action Plan to Improve Aviation Safety in Africa-International Civil Aviation Organization

India Invests in Airport Development-Asian Aviation

Oshkosh Fire & Emergency Sales Surge in China-Fire Engineering

China to Build 70 Airports by 2015-The Telegraph

Airport conquest accounts in

Europe

Chongqing, China

17 high rise pumpers

Brasilia, Brazil30 custom pumpers

SingaporeChangi Airport

7 ARFF & Pierce

2012 Oshkosh Corporation Analyst Day September 14, 2012

Financial Outlook

2012 Oshkosh Corporation Analyst Day September 14, 2012

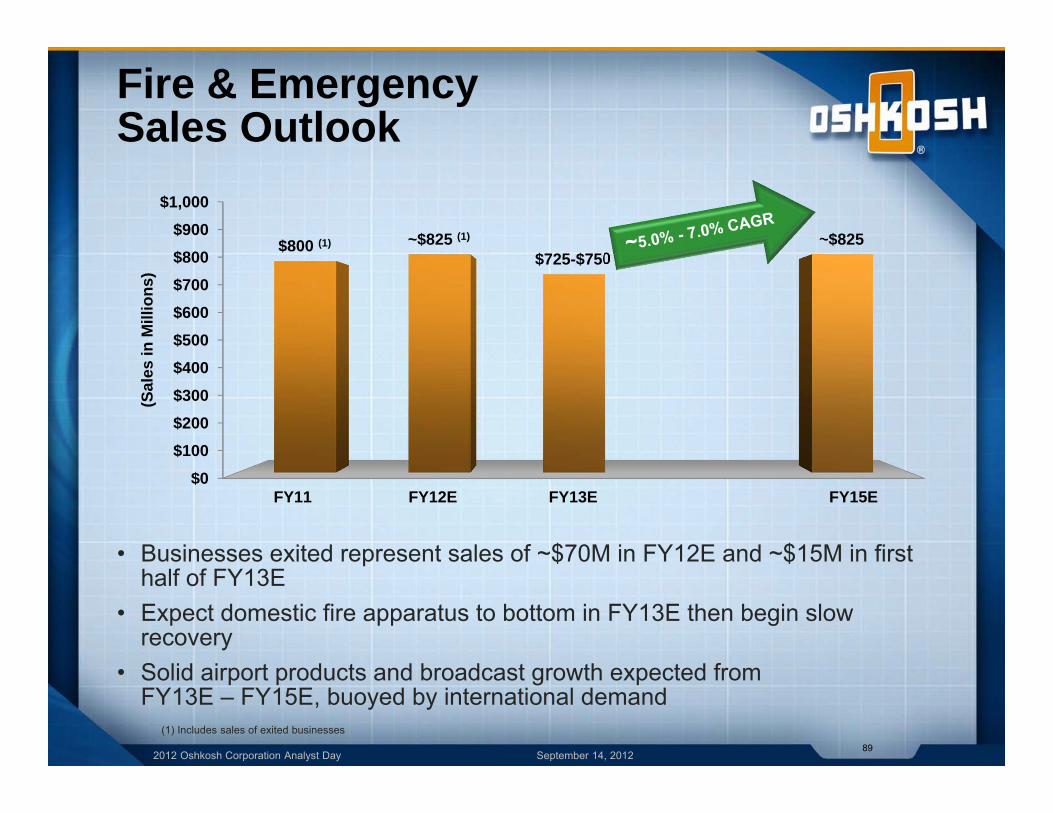

Fire & Emergency Sales Outlook

• Businesses exited represent sales of ~$70M in FY12E and ~$15M in first half of FY13E

• Expect domestic fire apparatus to bottom in FY13E then begin slow recovery

• Solid airport products and broadcast growth expected from FY13E – FY15E, buoyed by international demand

89

$0$100$200$300$400$500$600$700$800$900

$1,000

FY11 FY12E FY13E FY15E

$800 (1) ~$825 (1)

$725-$750~$825

(Sal

es in

Mill

ions

)

(1) Includes sales of exited businesses

2012 Oshkosh Corporation Analyst Day September 14, 2012

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

(0.4%) (0.8%)

2.0% - 2.5%

~6.0%

Fire & EmergencyOperating Income Margin Outlook

• Exit of under performing businesses lifts margins ~2% in FY13; when exit complete, Company will seek to accelerate margin improvement

• Operating income margin expected to recover to mid-single digits in FY14

90

(1) Excludes impact of non-cash impairment charges

(2) Excludes costs to exit ambulance and European mobile medical businesses

FY11 FY12E FY13E FY15E(2)(1)

(Ope

ratin

g In

com

e M

argi

n %

)

2012 Oshkosh Corporation Analyst Day September 14, 2012

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Prior Peak(FY08)

FY12E "M"Initiatives

"O"Initiatives

"V"Initiatives

"E"Initiatives

FY15E

9.3%

(0.8%)

~6.0%

Fire & Emergency Operating Income Margin Drivers

91

(1) Excludes costs to exit ambulance and European mobile medical businesses

(1)

• Margins impacted by emerging market investments

• Over time, Company will seek to accelerate margin recovery targets despite soft domestic markets

(Ope

ratin

g In

com

e M

argi

n %

)

2012 Oshkosh Corporation Analyst Day September 14, 2012

September 14, 2012

Oshkosh Corporation Analyst Day

2012 Oshkosh Corporation Analyst Day September 14, 2012

Todd FierroCommercial

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Commercial Advantage

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Commercial Advantage: Street Smart, Street Tough

95

Broadest Product Line

Direct Distribution,

Customer Intimacy

Scalable, Flexible

Manufacturing & Operations

Access to Technology, Alternative

Fuels Leadership

Innovation and New Product Development

Best in class Aftermarket Service and

Support

Integrated factory

Refuse collection vehicle product line

Alternative fuel technology

2012 Oshkosh Corporation Analyst Day September 14, 2012

Broadest Product Line

96

Standard

Front Loader Rear Loader

Bridgemaster Front Discharge

ConcreteMixers

Refuse Collection Vehicles

Articulating CranesDominator Batch Plants

Side Loader

Service Bodies, Cranes, Plants

2012 Oshkosh Corporation Analyst Day September 14, 2012

Distribution and Operations Advantages

• Operations Advantages– Scalable and flexible capacity– Lean manufacturing initiatives

97

• Distribution Advantages– 23 factory owned

branch locations– Customer intimacy

via direct sales force– Parts distribution managed

close to customers

2012 Oshkosh Corporation Analyst Day September 14, 2012

Supporting the Outlook

2012 Oshkosh Corporation Analyst Day September 14, 2012

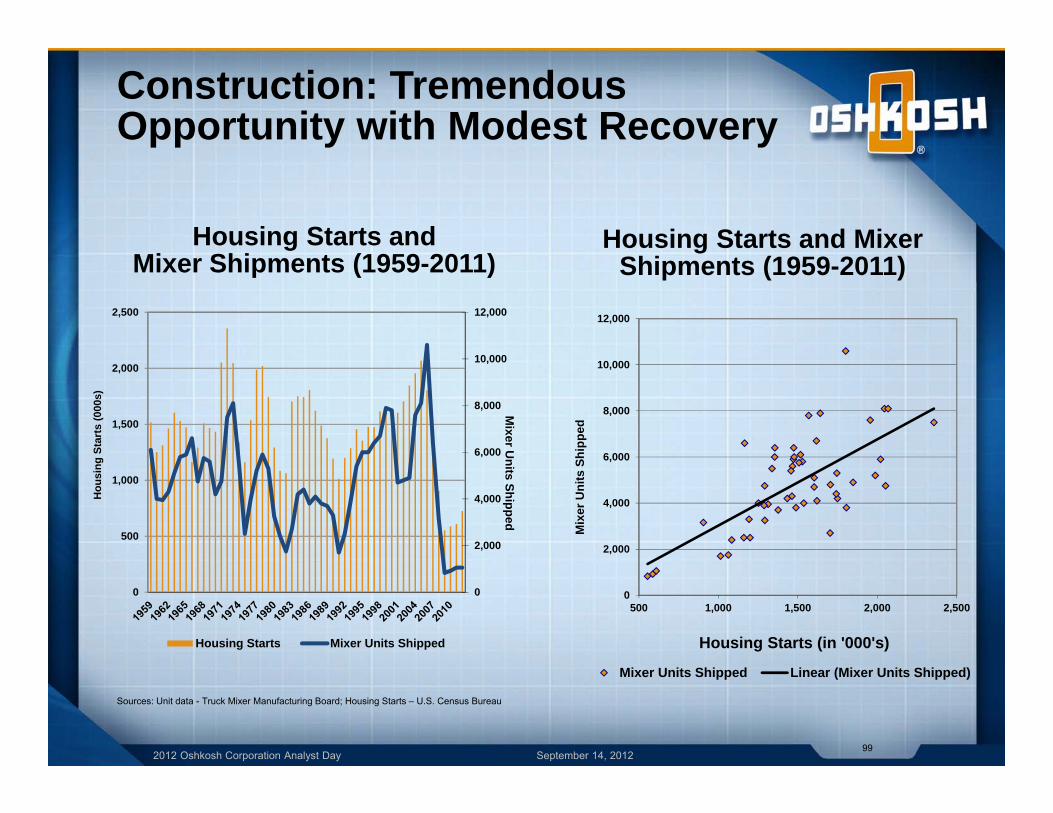

Construction: Tremendous Opportunity with Modest Recovery

Sources: Unit data - Truck Mixer Manufacturing Board; Housing Starts – U.S. Census Bureau

99

Housing Starts and Mixer Shipments (1959-2011)

Housing Starts and Mixer Shipments (1959-2011)

0

2,000

4,000

6,000

8,000

10,000

12,000

0

500

1,000

1,500

2,000

2,500

Mixer U

nits Shipped

Hou

sing

Sta

rts

(000

s)

Housing Starts Mixer Units Shipped

0

2,000

4,000

6,000

8,000

10,000

12,000

500 1,000 1,500 2,000 2,500

Mix

er U

nits

Shi

pped

Housing Starts (in '000's)

Mixer Units Shipped Linear (Mixer Units Shipped)

2012 Oshkosh Corporation Analyst Day September 14, 2012

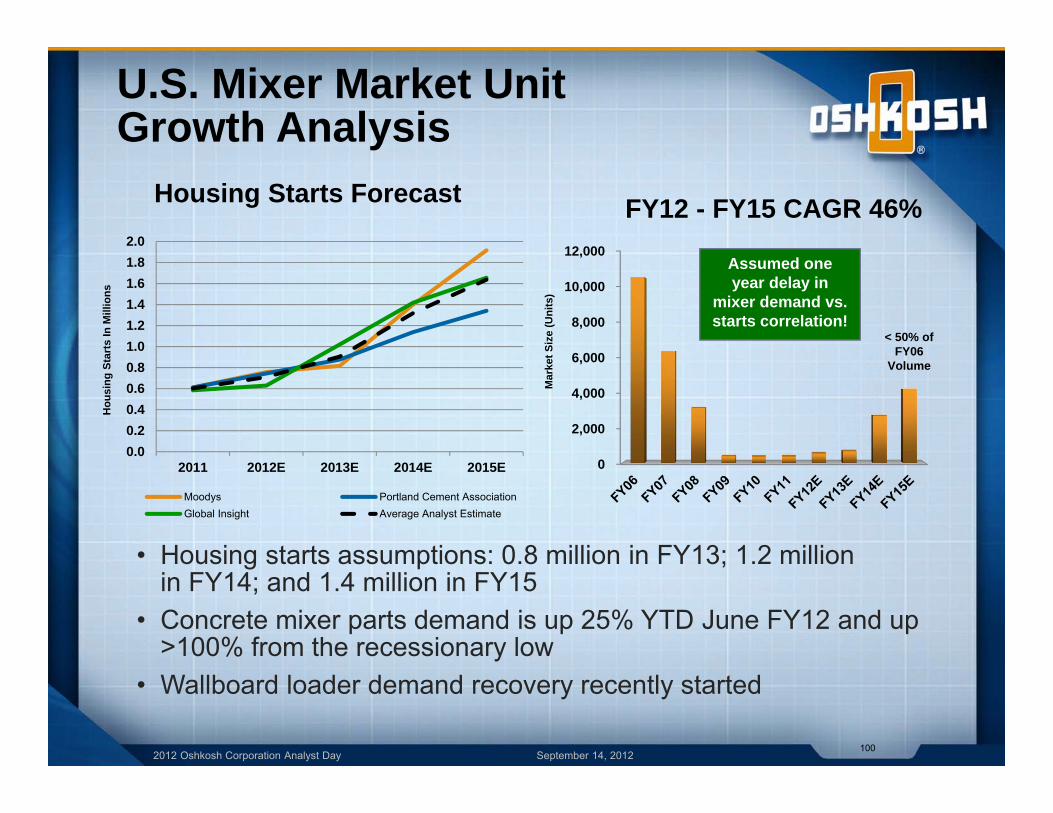

U.S. Mixer Market Unit Growth Analysis

• Housing starts assumptions: 0.8 million in FY13; 1.2 million in FY14; and 1.4 million in FY15

• Concrete mixer parts demand is up 25% YTD June FY12 and up >100% from the recessionary low

• Wallboard loader demand recovery recently started

100

0

2,000

4,000

6,000

8,000

10,000

12,000

Mar

ket S

ize

(Uni

ts)

FY12 - FY15 CAGR 46%

< 50% of FY06

Volume

0.00.20.40.60.81.01.21.41.61.82.0

2011 2012E 2013E 2014E 2015E

Hou

sing

Sta

rts

In M

illio

ns

Housing Starts Forecast

Moodys Portland Cement AssociationGlobal Insight Average Analyst Estimate

Assumed one year delay in

mixer demand vs. starts correlation!

2012 Oshkosh Corporation Analyst Day September 14, 2012

Significant Opportunity with Modest RCV Recovery• RCV market expected to be driven by:

– Population growth – CAGR 1%– Market recovery / fleet age – CAGR 1%– Construction and demolition – CAGR 1%

101

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12E FY13E FY14E FY15E

Mar

ket S

ize

(uni

ts)

Realistic projections based on

historical data

2012 Oshkosh Corporation Analyst Day September 14, 2012

Financial Outlook

2012 Oshkosh Corporation Analyst Day September 14, 2012

Commercial Sales Outlook

• Housing recovery expected to drive strong concrete mixer demand by FY15– > 40% concrete mixer FY12E - FY15E sales CAGR

• Modest refuse collection vehicle growth outlook103

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

FY11E FY12E FY13E FY15E

Mixer and Other Refuse

$565

~$680 $725 – $750

~$1,250

(Sal

es in

Mill

ions

)

2012 Oshkosh Corporation Analyst Day September 14, 2012

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

FY11 FY12E FY13E FY15E

0.7%

~4.0%4.5% - 5.0%

>10.0%

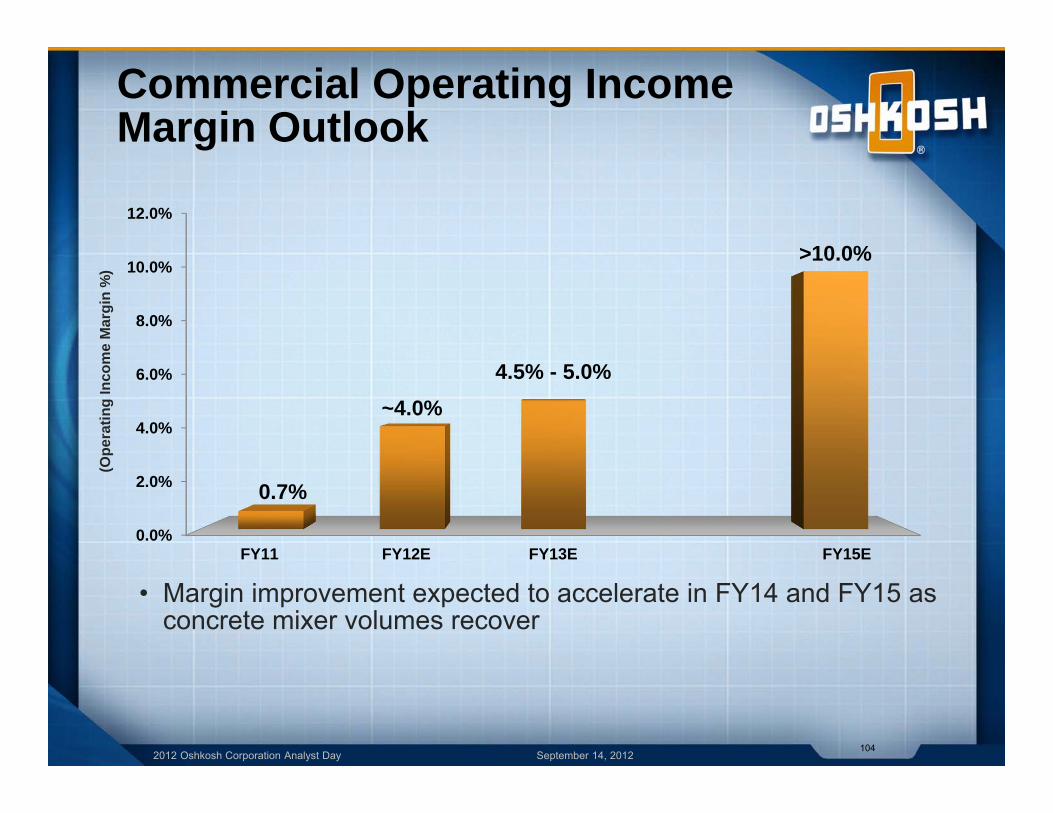

Commercial Operating Income Margin Outlook

• Margin improvement expected to accelerate in FY14 and FY15 as concrete mixer volumes recover

104

(Ope

ratin

g In

com

e M

argi

n %

)

2012 Oshkosh Corporation Analyst Day September 14, 2012

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Prior Peak(FY00)

FY12E "M"Initiatives

"O"Initiatives

"V"Initiatives

"E"Initiatives

FY15E

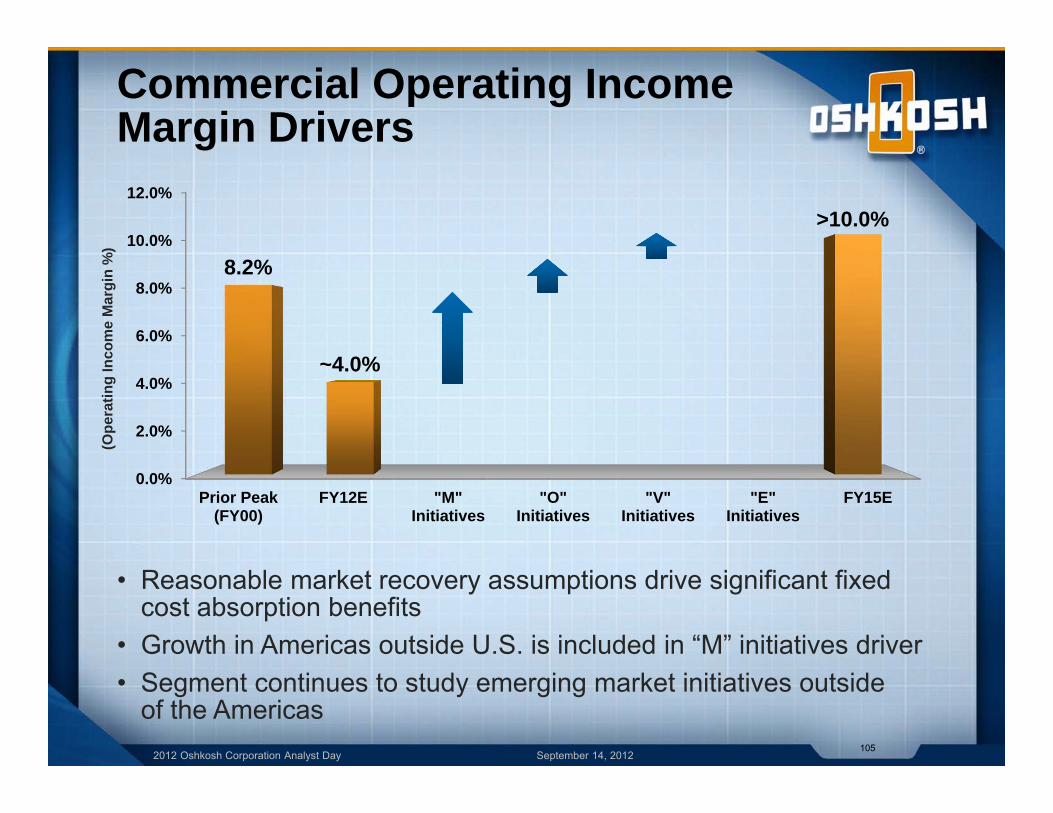

8.2%

~4.0%

>10.0%

Commercial Operating IncomeMargin Drivers

• Reasonable market recovery assumptions drive significant fixed cost absorption benefits

• Growth in Americas outside U.S. is included in “M” initiatives driver• Segment continues to study emerging market initiatives outside

of the Americas105

(Ope

ratin

g In

com

e M

argi

n %

)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012107

Slide intentionally left blank

2012 Oshkosh Corporation Analyst Day September 14, 2012108

Slide intentionally left blank

2012 Oshkosh Corporation Analyst Day September 14, 2012

September 14, 2012

Colleen MoynihanQuality & Continuous ImprovementOshkosh CorporationAnalyst Day

2012 Oshkosh Corporation Analyst Day September 14, 2012110

Provide Coaching and Training

Deploy SystemsAnd Standards

Measure Results And Delight

Q&CI Priorities Support MOVE

Customer First

Customer Supporting Systems

Customer Satisfaction

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Oshkosh Operating System and Our Deployment Journey

2012 Oshkosh Corporation Analyst Day September 14, 2012

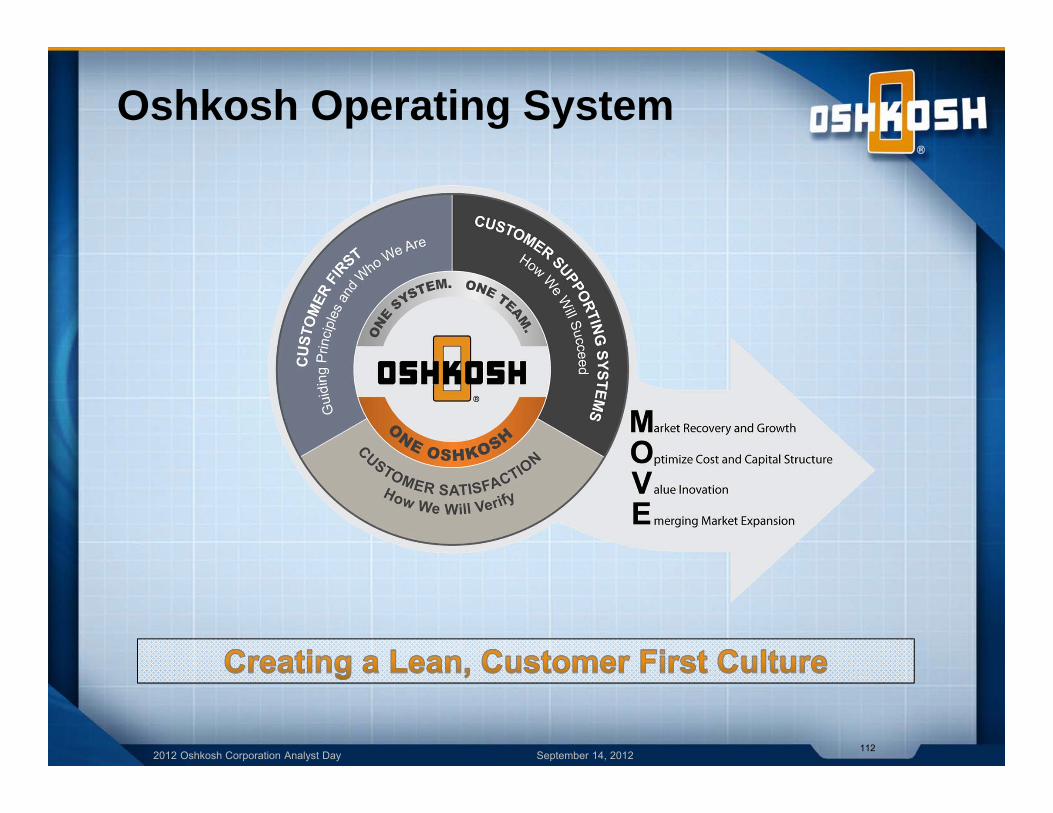

Oshkosh Operating System

112

2012 Oshkosh Corporation Analyst Day September 14, 2012

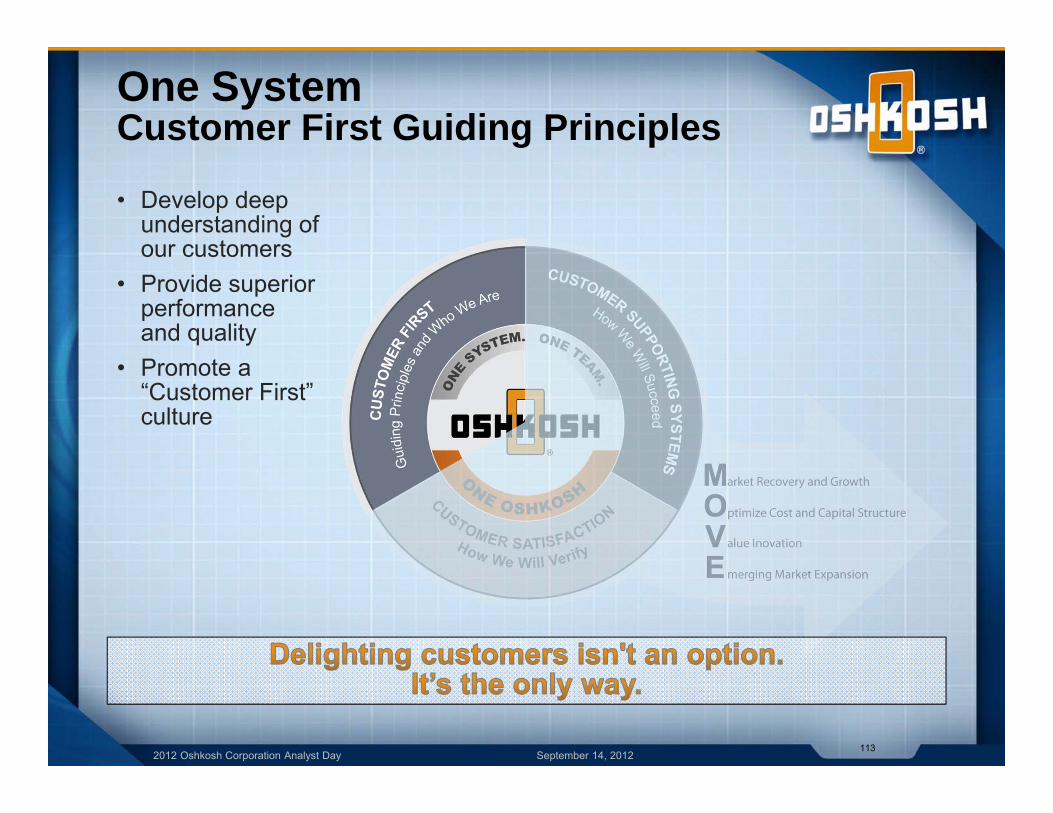

One SystemCustomer First Guiding Principles

• Develop deep understanding of our customers

• Provide superior performance and quality

• Promote a “Customer First” culture

113

2012 Oshkosh Corporation Analyst Day September 14, 2012

One Team Customer Supporting Systems

• Align our objectives and establish plans to deliver improvement

• Create processes that provide value to our customers

• Use lean tools to continually improve costs, performance and delight our customers

114

2012 Oshkosh Corporation Analyst Day September 14, 2012

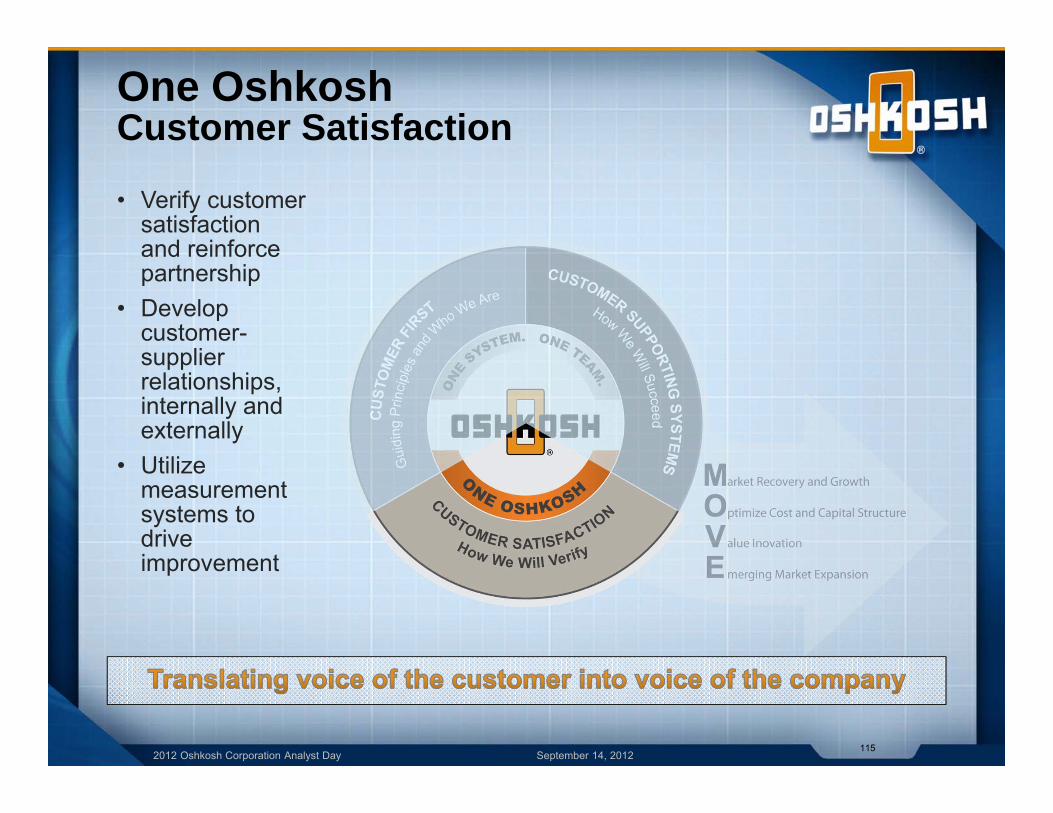

One OshkoshCustomer Satisfaction

• Verify customer satisfaction and reinforce partnership

• Develop customer-supplier relationships, internally and externally

• Utilize measurement systems to drive improvement

115

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Operating SystemAccelerates MOVE• Create

common way of thinking and operating

• Establish standard set of practices that will improve our business

• Engage all of our employees in delighting our customers

116

2012 Oshkosh Corporation Analyst Day September 14, 2012

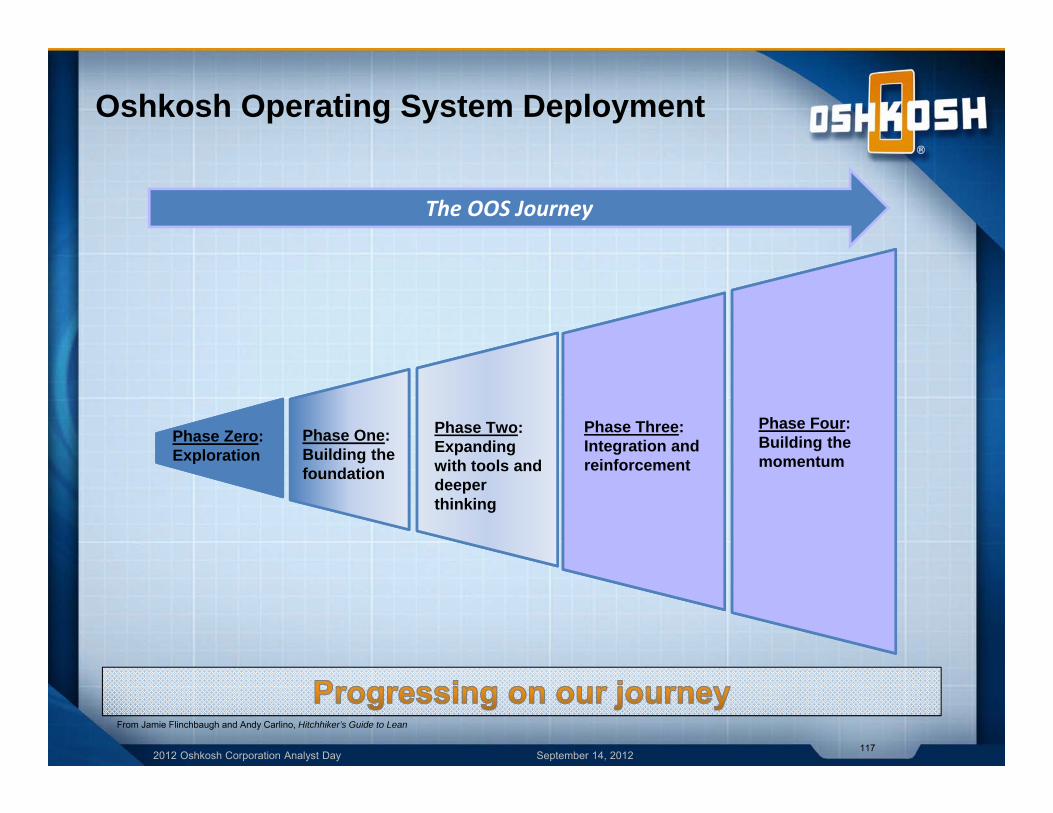

Oshkosh Operating System Deployment

117

From Jamie Flinchbaugh and Andy Carlino, Hitchhiker’s Guide to Lean

The OOS Journey

Phase Zero:Exploration

Phase One:Building the foundation

Phase Two:Expanding with tools and deeper thinking

Phase Three:Integration and reinforcement

Phase Four:Building the momentum

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Operating System Deployment Expanding with Tools and Deeper Thinking

118

Communication Deploy a top down communication strategy

EducationImplement an education program for OOS principles, systems and tools (Oshkosh University)

Tools and Methods Define, develop and deploy the OOS tools, methods, and measurement systems

Application Execute OOS projects to meet business performance targets

Infrastructure Implement organizational structure to deploy and sustain OOS across the enterprise

Leadership Engagement Strengthen leadership behaviors to reinforce OOS

2012 Oshkosh Corporation Analyst Day September 14, 2012

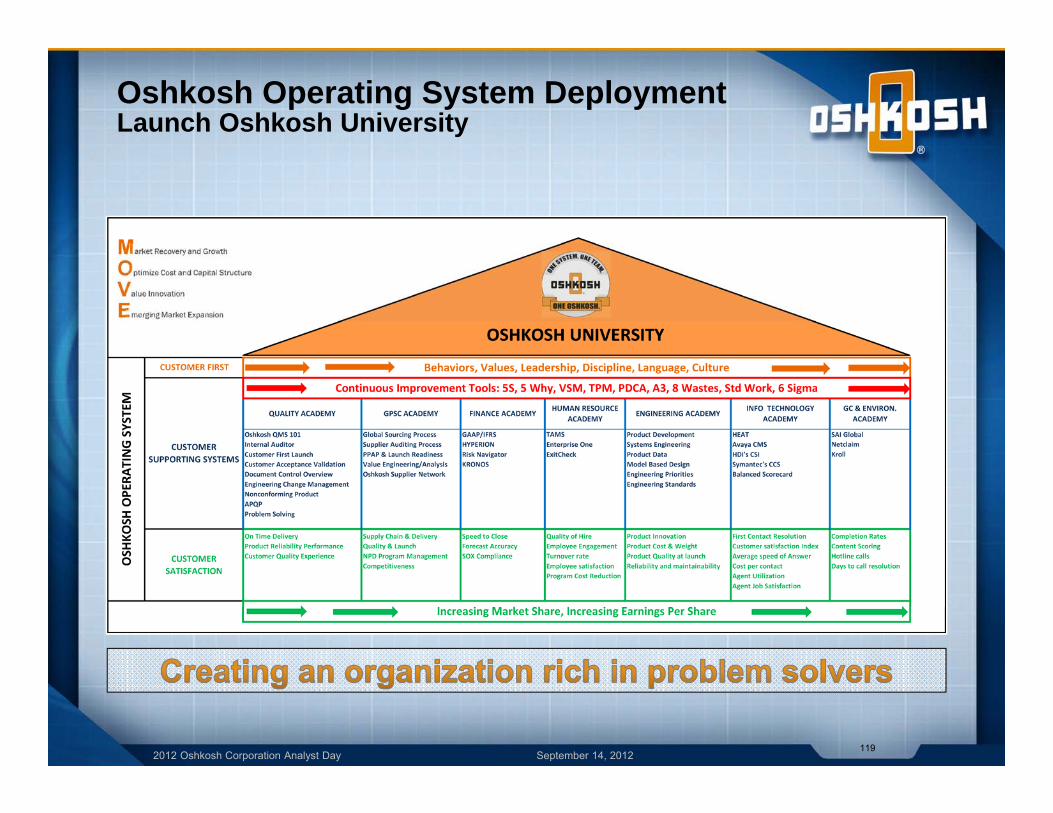

Oshkosh Operating System Deployment Launch Oshkosh University

119

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Operating SystemStandardize Tools and Methods

120

We’ve Got It… We’ve Found It…

We’re Developing It…

SixPilot

Projects

Business Unit

Procedures

External Best

Practices

OshkoshQuality ManagementSystem

Customer Acceptance Validation

Customer Quality

Experience

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Oshkosh Operating System and Execution of our MOVE Strategy

2012 Oshkosh Corporation Analyst Day September 14, 2012

Before: Excessive WIP, inefficient cell layout, wait time

After: Reduced WIP, improved labor utilization

OOS Project Results: • Reduced Work In Process by 50% - raw and finished

booms• Reduced floor space usage through consolidation of

800 boom upper fly and carrier tube build cells• Reduced wait time… New layout enabled use of 5th

overhead crane which reduced wait time

JLG - Boom Fab Cell Flow Improvement

Before: Masking tape and paper applied to all openings.

After: New primer surface eliminated need for taping and unmasking

OOS Project Results: • Reduced indirect supplies through changes in material

selection• Reduced direct labor involved in taping and

unmasking

Pierce Appleton – Cab Paint Improvement

Oshkosh Operating System ResultsIncreasing Manufacturing Efficiency

122

Before: Operator utilization at 73% of takt time

After: Operator utilization at 92% of takt time

OOS Project Results: • Redeployed assemblers to new business needs• Reduced overtime• Reduced floor space usage by 20,000 sq. ft.

Defense – Line Balance Improvement

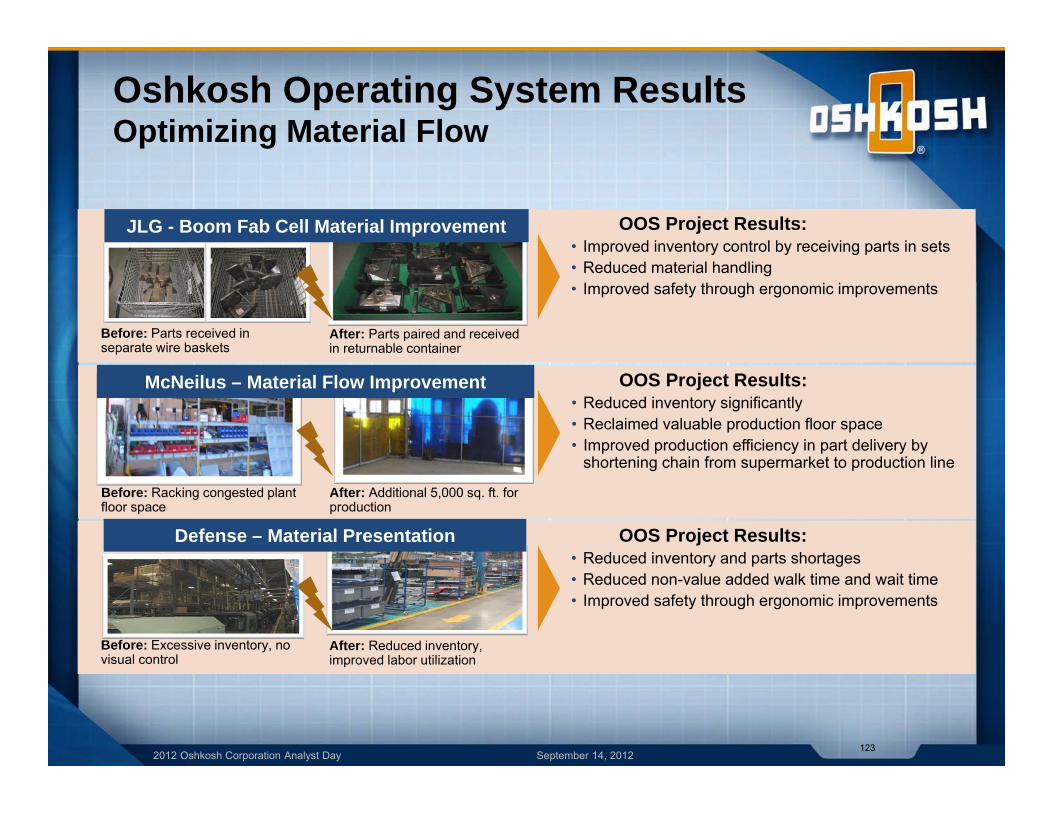

2012 Oshkosh Corporation Analyst Day September 14, 2012123

Before: Parts received in separate wire baskets

After: Parts paired and received in returnable container

OOS Project Results: • Improved inventory control by receiving parts in sets• Reduced material handling• Improved safety through ergonomic improvements

Before: Excessive inventory, no visual control

After: Reduced inventory, improved labor utilization

OOS Project Results: • Reduced inventory and parts shortages• Reduced non-value added walk time and wait time• Improved safety through ergonomic improvements

Defense – Material Presentation

JLG - Boom Fab Cell Material Improvement

Oshkosh Operating System ResultsOptimizing Material Flow

Before: Racking congested plant floor space

After: Additional 5,000 sq. ft. for production

OOS Project Results: • Reduced inventory significantly • Reclaimed valuable production floor space• Improved production efficiency in part delivery by

shortening chain from supermarket to production line

McNeilus – Material Flow Improvement

2012 Oshkosh Corporation Analyst Day September 14, 2012

Def

ects

per

Uni

t

FY12 Q3 ActualFY11 Baseline

FMTV Pre-Delivery Inspection Results

FMTV Internal Customer Inspection Results

FY12 Q3 ActualFY11 Baseline

FY12 Q3 ActualFY11 Baseline

FMTV External Customer Inspection Results

124

Oshkosh Operating System ResultsImproving Product Quality

81% Reduction

50% Reduction

Contract Goal

74% Reduction

2012 Oshkosh Corporation Analyst Day September 14, 2012125

Oshkosh Operating System ResultsExpanding Lean to Business Processes

Visual Management in Corporate Finance

Standard Work to Align and Execute our Objectives

Through Strategy DeploymentValue Stream Mapping

the Product Development Process

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Operating SystemHow We Will Succeed

126

2012 Oshkosh Corporation Analyst Day September 14, 2012

September 14, 2012

Oshkosh CorporationAnalyst Day

2012 Oshkosh Corporation Analyst Day September 14, 2012128

Slide intentionally left blank

2012 Oshkosh Corporation Analyst Day September 14, 2012

Greg FredericksenGPSC

Oshkosh CorporationAnalyst DaySeptember 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

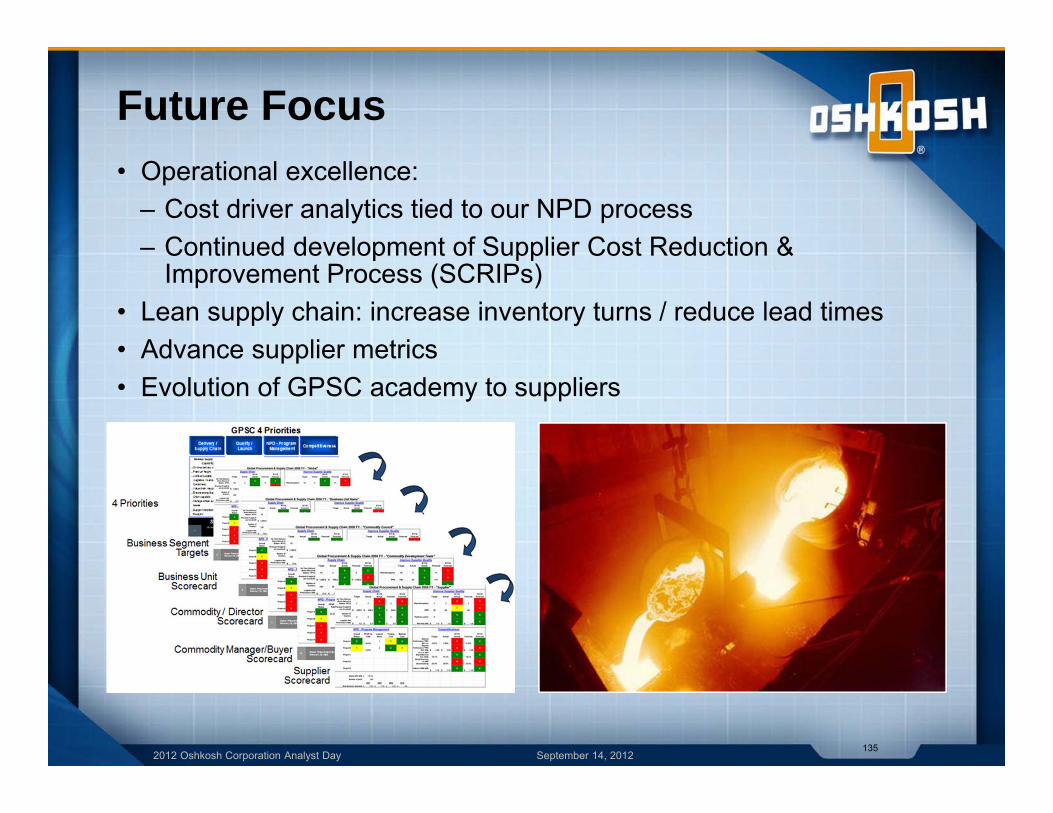

GPSC Four Priorities

130

Competitiveness

Delivery /Supply Chain

Quality / Launch

NPD - Program Management

Suppliers Must Perform To All Four Priorities

2012 Oshkosh Corporation Analyst Day September 14, 2012

Building a World Class Procurement Organization• Talent and expertise upgraded• Active participation in design process to drive cost & quality• Cost management leveraging size & scale across the segments• Forensic cost tool box to address all cost drivers

131

2012 Oshkosh Corporation Analyst Day September 14, 2012

High Impact Successes

• M-ATV supplier management

• Access Equipment Tianjin plant start up

• Access Equipment global capacity management

• FMTV

132

2012 Oshkosh Corporation Analyst Day September 14, 2012

Cross Segment Synergies

• Fabrications/commodities – weldments, steel, etc.• Powertrain – engines, transmissions and component

“dress” items• Driveline – axles, drive components and

suspension systems• Hydraulics – cylinders, valves, hoses and fittings• Chassis – configurations across multiple manufacturers• Wheels and tires – including components and the

assembly process to provide our plants a single subassembly to install

133

2012 Oshkosh Corporation Analyst Day September 14, 2012

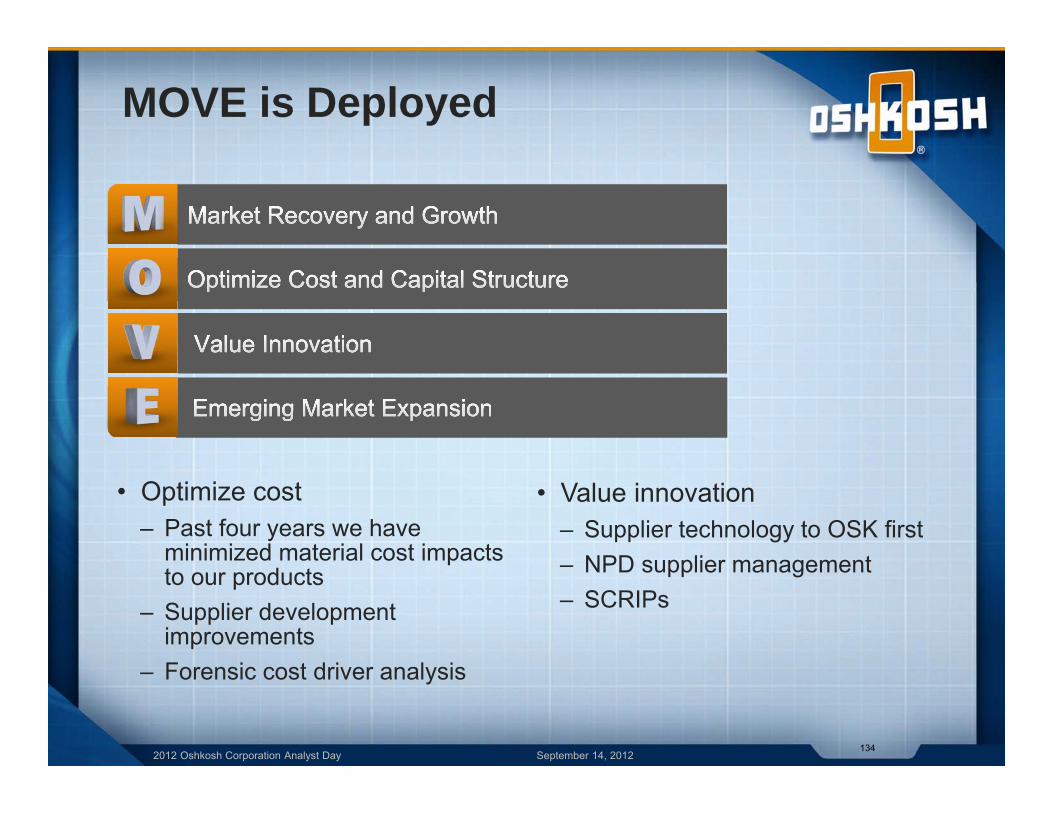

• Optimize cost– Past four years we have

minimized material cost impacts to our products

– Supplier development improvements

– Forensic cost driver analysis

134

MOVE is Deployed

• Value innovation– Supplier technology to OSK first– NPD supplier management– SCRIPs

2012 Oshkosh Corporation Analyst Day September 14, 2012

Future Focus• Operational excellence:‒ Cost driver analytics tied to our NPD process‒ Continued development of Supplier Cost Reduction &

Improvement Process (SCRIPs) • Lean supply chain: increase inventory turns / reduce lead times• Advance supplier metrics• Evolution of GPSC academy to suppliers

135

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh CorporationAnalyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

Gary SchmiedelTechnology

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

OSK Engineering Priorities

138

Innovation Leadership

NPD Program Management

CompetitivenessCost & Weight

Quality &Launch

2012 Oshkosh Corporation Analyst Day September 14, 2012 139

Innovation Leadership

NPD Program Management

Quality &Launch

Competitiveness Cost & Weight

“Improve our Customers’ Work”

“Flawlessly Launch to Customers”

“Provide Best Value for our Customers”

“Effectively Deliver What Customers

Want”

2012 Oshkosh Corporation Analyst Day September 14, 2012

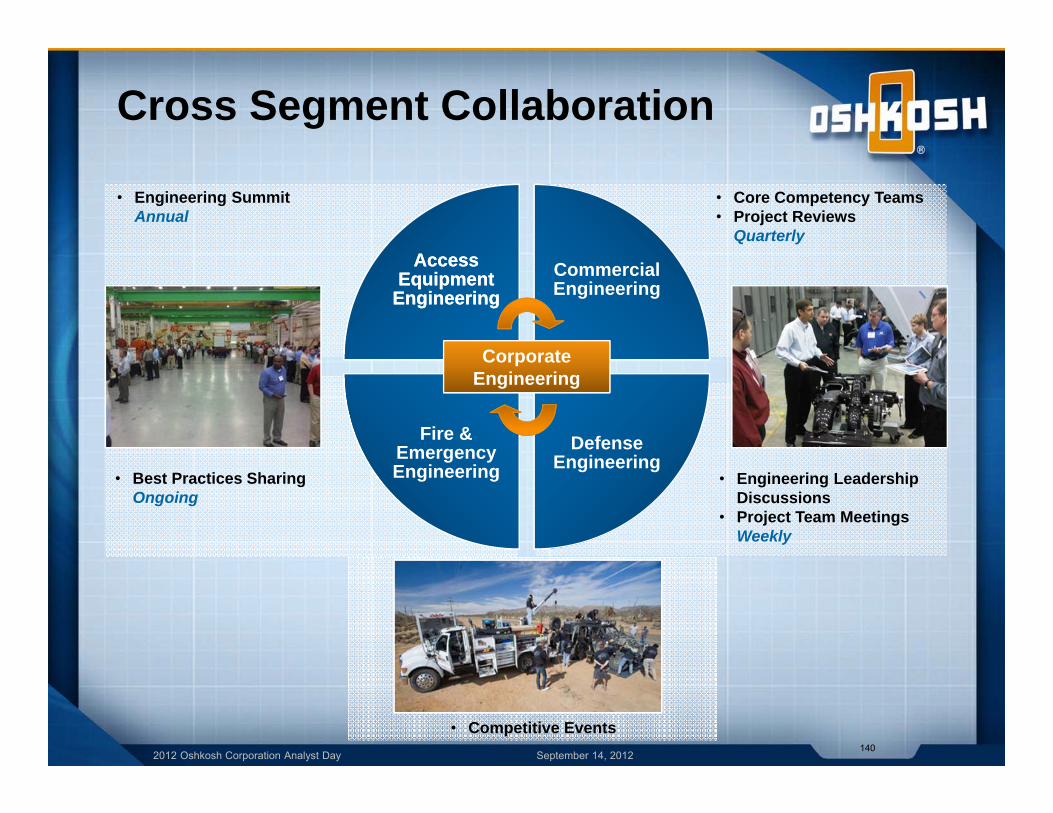

Cross Segment Collaboration

140

• Engineering Summit Annual

• Best Practices Sharing Ongoing

• Core Competency Teams• Project Reviews

Quarterly

• Engineering Leadership Discussions

• Project Team Meetings Weekly

Access Equipment

Engineering

Access Equipment

EngineeringCommercial Engineering

Fire & Emergency Engineering

Defense Engineering

Corporate Engineering

• Competitive Events

2012 Oshkosh Corporation Analyst Day September 14, 2012

Innovation Leadership

2012 Oshkosh Corporation Analyst Day September 14, 2012

Vehicle Mobility

142

Oshkosh continues as the gold standard for off road mobility

2012 Oshkosh Corporation Analyst Day September 14, 2012

Safety Systems

143

Cab Crush Resistance Frontal Impact Protection

SkyGuard™ Control Panel Protection

Unsurpassed Visibility and Cab Roominess

2012 Oshkosh Corporation Analyst Day September 14, 2012

Safety Systems

Electronic stability control

144

2012 Oshkosh Corporation Analyst Day September 14, 2012

Autonomy• Cargo Unmanned Ground Vehicle (Cargo-UGV)

– Customer evaluation completed August 2012– System suitable for a wide range of host vehicles– Vehicle remains human driveable– Full autonomy– Shadow mode– Remote control

145

Handheld tele-operation controller

Autonomous vehicles operating in dusty conditions

2012 Oshkosh Corporation Analyst Day September 14, 2012

New Product Introductions

2012 Oshkosh Corporation Analyst Day September 14, 2012

New Products – Access Equipment

147

• Telehandlers– Emissions updates: EU machines to

Stage IIIB, NA machines to Tier 4i– Improved visibility

• 1500SJ– 150 foot working height– Transportable without oversize height

or width permits

• RS Scissors – Manufactured in Tianjin, China– 6m and 10m configurations

• 340AJ– Named “Best Product of the Year” by

Hire and Rental Industry Association – 34 foot lift, 17 foot up and over

capability– Dual fuel (propane/gasoline) or diesel

engines available

New North American and European Telehandler Configurations

1500SJ RS Scissors 340AJ

2012 Oshkosh Corporation Analyst Day September 14, 2012

New Products – Defense

• Joint Light Tactical Vehicle (JLTV)• HMMWV upgrades and replacements• Ground Mobility Vehicle (GMV)• Multi Mission Recovery System (MMRS)

148

Joint Light Tactical Vehicle

(JLTV)

HMMWV Suspension

Upgrade

Ground Mobility Vehicle (GMV)

Multi-Mission Recovery System (MMRS)

2012 Oshkosh Corporation Analyst Day September 14, 2012

New Products –Fire & Emergency

149

Dash Cab Forward aerial

3000 gallon capacity Global Striker

H-Series with Oshkosh broom subsystem

Pierce Industrial Pumper – Chongqing, China

2012 Oshkosh Corporation Analyst Day September 14, 2012

New Products – Commercial

• Compressed natural gas continues to grow as an alternative fuel– CNG variants available in all primary product configurations

• Main stream products refined for cost and weight improvements• Niche products address specific markets

150

Extended reach Zero Radius side loader

Organics front loader

Ready mix market embracing CNG as a fuel

CNG Powered front and rear loadersContender front loader Split rear loader, 60/40

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

Dave Sagehorn CFO

Oshkosh CorporationAnalyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

Consolidated Sales Bridge

• Defense sales upside exists from baseline levels• Expect MOVE to significantly offset Defense segment sales decline• Assumes no acquisitions(1) Sales decline to baseline level, assuming no new sales capture beyond current Oshkosh programs

154

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

FY12E DefenseDecline

"M"Initiatives

"V"Initiatives

"E"Initiatives

FY15E

(Sal

es in

Bill

ions

)

~$8.1

$6.5-$6.9

(1)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Consolidated Operating IncomeMargin Bridge

• Expect MOVE to more than offset impact of lower Defense sales on operating income margins

• Potential for Defense operating income upside from sales above baseline level

(1) Excludes costs to exit ambulance and European mobile medical businesses

155

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

FY12E DefenseDecline

"M"Initiatives

"O"Initiatives

"V "Initiatives

"E"Initiatives

FY15E

(Ope

ratin

g In

com

e M

argi

n %

)

4.3%-4.4%

9.2%-9.8%

(1)

2012 Oshkosh Corporation Analyst Day September 14, 2012

Doubling EPS by FY15

• Other FY15 Assumptions– Interest expense and other ~$55 million– Tax rate ~34%– Share count ~ 90.5 million

$2.05 to $2.15

$4.00 to $4.50

Oshkosh CorporationEPS Opportunity

23%-30% CAGR

FY12E(1) FY15E

156

(1) Excludes costs to exit ambulance and European mobile medical businesses

2012 Oshkosh Corporation Analyst Day September 14, 2012

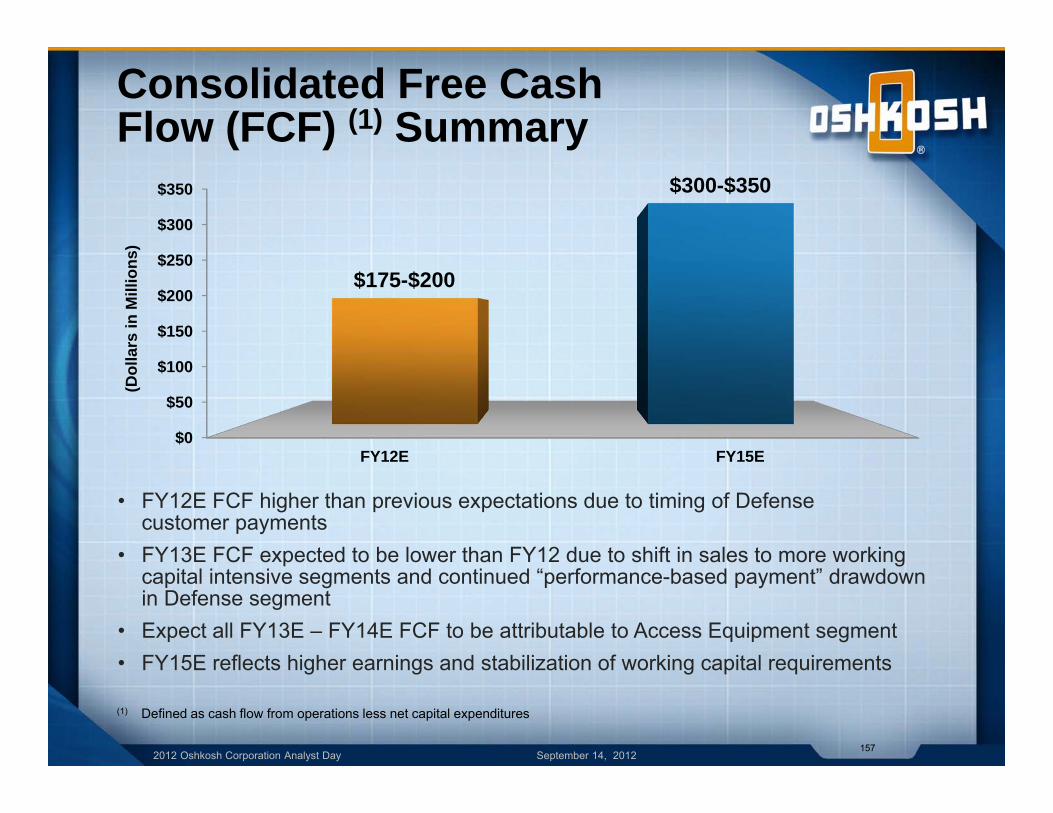

Consolidated Free CashFlow (FCF) (1) Summary

• FY12E FCF higher than previous expectations due to timing of Defense customer payments

• FY13E FCF expected to be lower than FY12 due to shift in sales to more working capital intensive segments and continued “performance-based payment” drawdown in Defense segment

• Expect all FY13E – FY14E FCF to be attributable to Access Equipment segment• FY15E reflects higher earnings and stabilization of working capital requirements

(1) Defined as cash flow from operations less net capital expenditures

157

$0

$50

$100

$150

$200

$250

$300

$350

FY12E FY15E

$175-$200

$300-$350

(Dol

lars

in M

illio

ns)

2012 Oshkosh Corporation Analyst Day September 14, 2012

FY13 Early View Estimates

158

Full Year Low High

Sales (billions) $7.5 $7.8

Operating Income (millions) $380 $420

Diluted EPS $2.35 $2.60

• Comments on First Quarter– Seasonally lowest sales and EPS quarter– International M-ATV sales begin in Q2– Potential customer pause pending outcome of November elections

2012 Oshkosh Corporation Analyst Day September 14, 2012

FY13 Early View Estimates (Continued)

159

• Corporate expenses up ~10% (higher IT investment)• Tax rate of ~33%• CapEx of ~$70 million• Free cash flow $75 - $100 million• Share count of ~91.5 million

Segment expectations

Measure Access Equipment Defense Fire &

Emergency Commercial

Sales(billions) $2.8-$3.0 $3.3-$3.4 $0.72-$0.75 $0.72-$0.75

Operating Income Margin 9.5%-10.0% 5.0%-5.5% 2.0%-2.5% 4.5%-5.0%

2012 Oshkosh Corporation Analyst Day September 14, 2012

Capital Allocation Strategy

2012 Oshkosh Corporation Analyst Day September 14, 2012

Disciplined Capital Allocation Framework

• Continually review capital structure• Apply free cash flow to uses that we believe provide highest returns• Expect to opportunistically use capital for share repurchases or acquisitions

161

Return capital to shareholders

Re-invest in core business

Invest in external growth

opportunities

Hold cash

Reduce debt

Long-term targeted capital

structure

2012 Oshkosh Corporation Analyst Day September 14, 2012

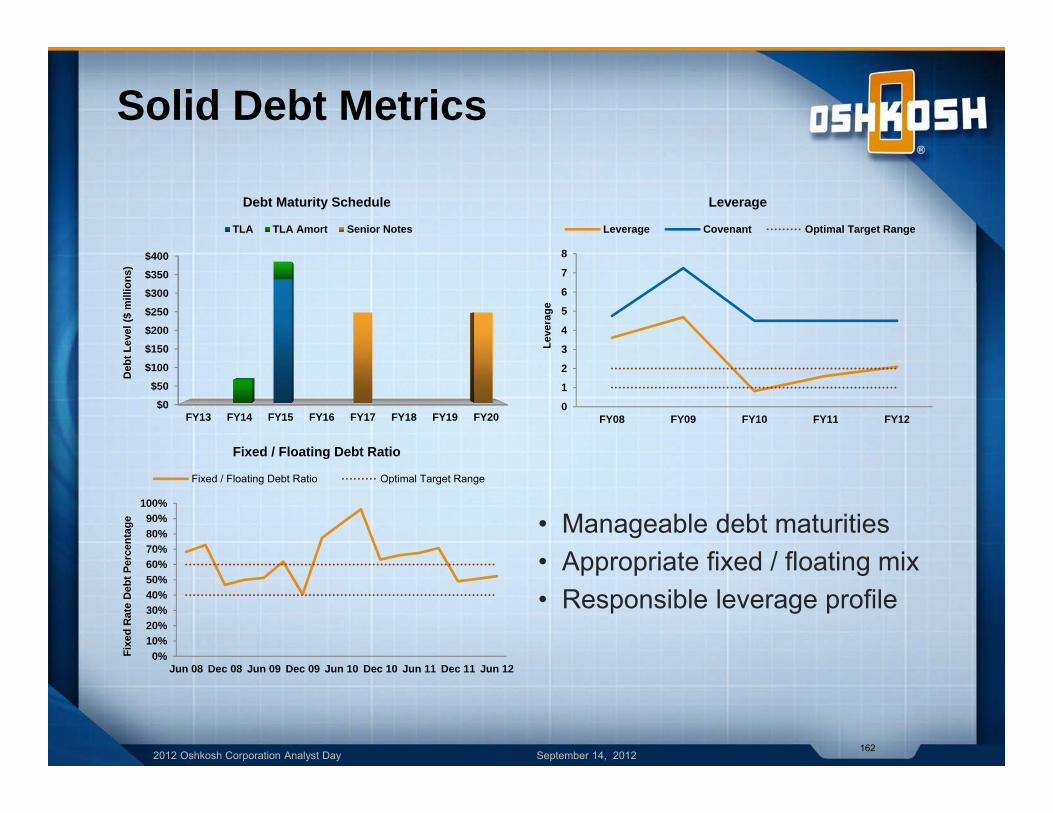

Solid Debt Metrics

• Manageable debt maturities• Appropriate fixed / floating mix• Responsible leverage profile

162

$0

$50

$100

$150

$200

$250

$300

$350

$400

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Deb

t Lev

el ($

mill

ions

)

Debt Maturity Schedule

TLA TLA Amort Senior Notes

0%10%20%30%40%50%60%70%80%90%

100%

Jun 08 Dec 08 Jun 09 Dec 09 Jun 10 Dec 10 Jun 11 Dec 11 Jun 12

Fixe

d R

ate

Deb

t Per

cent

age

Fixed / Floating Debt Ratio

Fixed / Floating Debt Ratio Optimal Target Range

0

1

2

3

4

5

6

7

8

FY08 FY09 FY10 FY11 FY12

Leve

rage

Leverage

Leverage Covenant Optimal Target Range

2012 Oshkosh Corporation Analyst Day September 14, 2012

Returning Capital to Shareholders

• Driving share price over the long-term• Share Repurchase Program

– Invest in attractive internal rate of return opportunities– Established 10b5-1 share repurchase program

• While maintaining a solid balance sheet

163

Enhancing long-term shareholder value

Shares repurchased since July 31(1)

~547,000

Average price per share $24.40

(1) As of September 7, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

External Growth Opportunities

• Opportunistic acquirer mindset– Right target– Right time– Right price

….No compelling need to make an acquisition at this time

• Potential deal characteristics– Target similar to existing products, but different end markets– Market leader– Large enough to make a difference, but not too big– Domestic or internationally located

• Focused on improving OSK valuation

164

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh CorporationAnalyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012166

Slide intentionally left blank

2012 Oshkosh Corporation Analyst Day September 14, 2012167

Slide intentionally left blank

2012 Oshkosh Corporation Analyst Day September 14, 2012168

Slide intentionally left blank

2012 Oshkosh Corporation Analyst Day September 14, 2012

The Road to Doubling to a Global Industrial

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012

Doubling EPS by FY15

• MOVE strategy expected to deliver higher margins throughout the cycle

• The recovery from a deep cycle has commenced and is expected to overcome defense downturn

• Oshkosh has the processes and team to deliver MOVE

$2.05 to $2.15

$4.00 to $4.50

Oshkosh CorporationEPS Opportunity

FY12E(1)

23%-30% CAGR

FY15E

170

(1) Excludes costs to exit ambulance and European mobile medical businesses

2012 Oshkosh Corporation Analyst Day September 14, 2012

Appendix

2012 Oshkosh Corporation Analyst Day September 14, 2012

Non-GAAP ReconciliationsThe table below presents a reconciliation of the Company’s presented non-GAAP measures to the most directly comparable GAAP measures ($ in millions, except per share amounts)

172

Fiscal 2012 EstimatesOperating income (loss):

As presented $ (6.6) $ (6.6) $ 345.0 $ 355.0Costs to exit ambulance and

European mobile medical businesses (18.0) (14.0) (18.0) (14.0)GAAP $ (24.6) $ (20.6) $ 327.0 $ 341.0

Operating income (loss) margin:As presented (0.8)% (0.8)% 4.3% 4.4% Impact of costs to exit ambulance and

European mobile medical businesses (2.2)% (1.7)% (0.2)% (0.2)%GAAP (3.0)% (2.5)% 4.1% 4.2%

EPS:As presented $ 2.05 $ 2.15 Impact of costs to exit ambulance and

European mobile medical businesses, net of tax (0.15) (0.12)GAAP $ 1.90 $ 2.03

Fiscal 2012E to 2015E EPS CAGR (1)

As presented 23% 30%Based on GAAP EPS 25% 33%

ConsolidatedLow High

Fire & EmergencySegment

Low High

(1) CAGR – compound annual growth rate

2012 Oshkosh Corporation Analyst Day September 14, 2012

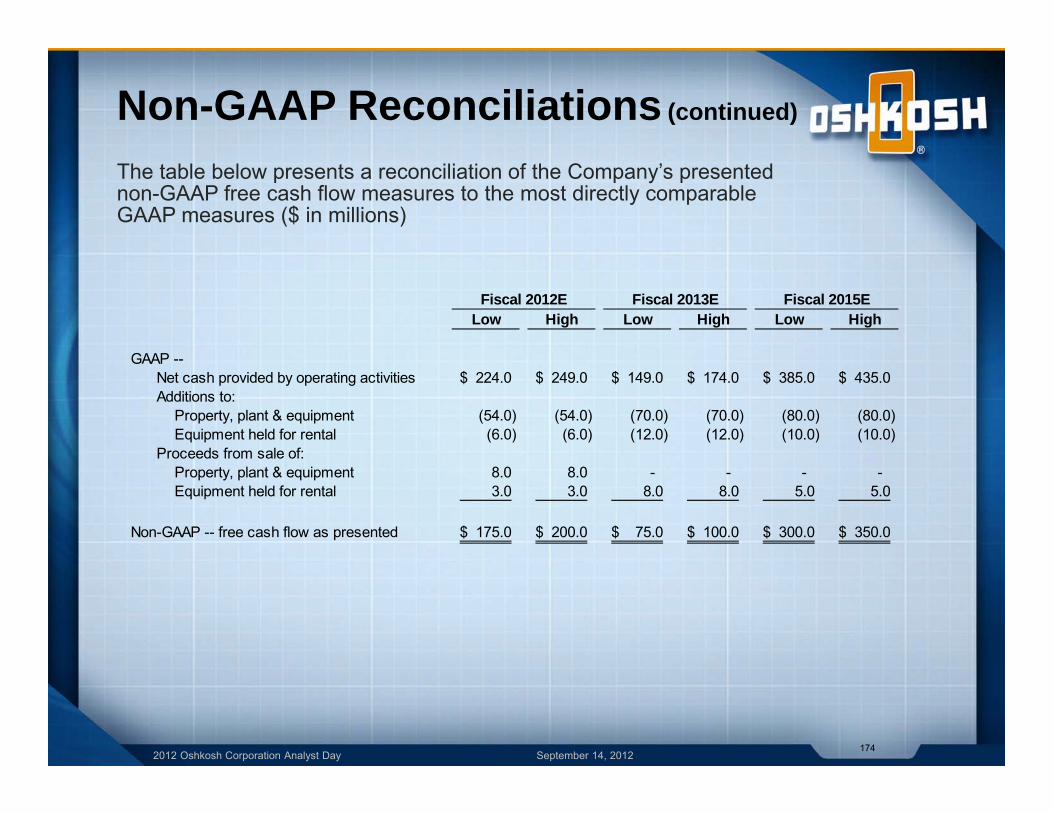

Non-GAAP Reconciliations (continued)The table below presents a reconciliation of the Company’s presented non-GAAP measures to the most directly comparable GAAP measures ($ in millions)

173

Non-DefenseAs reported:

Consolidated $ 7,584.7 $ 500.9 6.6%Less Defense segment (4,359.9) (543.0)Plus Corporate expense - 107.1

Non-Defense segments $ 3,224.8 $ 65.0 2.0%Plus goodwill and long-lived asset impairment charges - 4.8

Non-GAAP – non-Defense segments as presented $ 3,224.8 $ 69.8 2.2%

Fire & EmergencyAs reported $ 782.3 $ (8.2) (1.0)%Plus goodwill and long-lived asset impairment charges - 4.8Non-GAAP Fire & Emergency as presented $ 782.3 $ (3.4) (0.4)%

(1) To external customers

Operating Income (Loss)$ % of RevenueRevenue

(1)

Fiscal 2011

2012 Oshkosh Corporation Analyst Day September 14, 2012

Non-GAAP Reconciliations (continued)

The table below presents a reconciliation of the Company’s presented non-GAAP free cash flow measures to the most directly comparable GAAP measures ($ in millions)

174

Low High Low High Low High

GAAP --Net cash provided by operating activities 224.0$ 249.0$ 149.0$ 174.0$ 385.0$ 435.0$ Additions to:

Property, plant & equipment (54.0) (54.0) (70.0) (70.0) (80.0) (80.0) Equipment held for rental (6.0) (6.0) (12.0) (12.0) (10.0) (10.0)

Proceeds from sale of:Property, plant & equipment 8.0 8.0 - - - - Equipment held for rental 3.0 3.0 8.0 8.0 5.0 5.0

Non-GAAP -- free cash flow as presented 175.0$ 200.0$ 75.0$ 100.0$ 300.0$ 350.0$

Fiscal 2012E Fiscal 2013E Fiscal 2015E

2012 Oshkosh Corporation Analyst Day September 14, 2012

Oshkosh Corporation Analyst Day

September 14, 2012

2012 Oshkosh Corporation Analyst Day September 14, 2012176

Slide intentionally left blank

• Charles L. Szews• Charles L. Szews is Oshkosh Corporation Chief Executive Officer (CEO).

Most recently, Szews served as President and CEO, a position he was appointed to in January 2011. Szews joined the company in 1996 as Vice President and Chief Financial Officer (CFO), was appointed Executive Vice President in October 1997, and appointed President and Chief Operating Officer (COO) in October 2007. Szews was elected to the Oshkosh Board of Directors in 2007, a position he holds in addition to his other responsibilities.

• Prior to joining Oshkosh, Szews spent eight years with Fort Howard Corporation, holding a series of positions with increasing responsibility, most recently as vice president and controller.

• Szews holds a bachelor's degree summa cum laude in business administration from the University of Wisconsin - Eau Claire. He received his certified public accountant certification in 1980 and has 10 years of independent auditing experience with Ernst & Young.

• Szews currently also serves on the board of directors of Gardner Denver, Inc., a recognized leader in compressed air and gas, vacuum and fluid transfer technologies to industries throughout the world.

177September 2012Analyst Day Executive Biographies

Executive Biographies

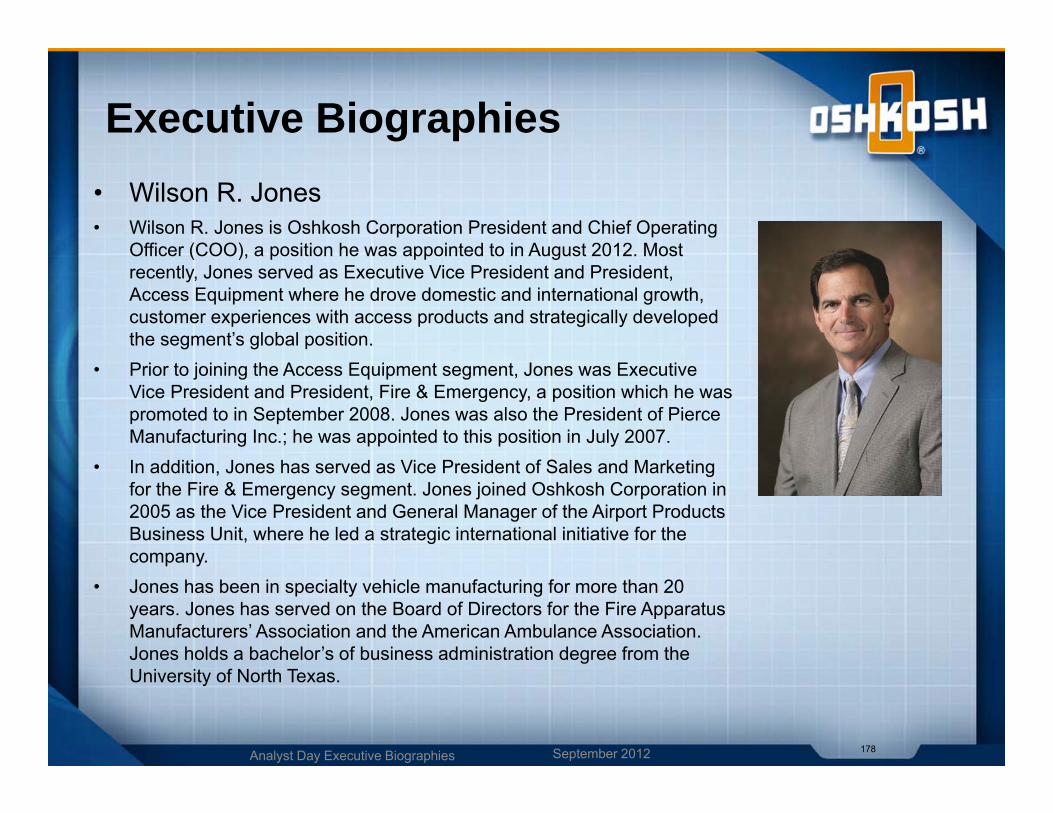

• Wilson R. Jones• Wilson R. Jones is Oshkosh Corporation President and Chief Operating

Officer (COO), a position he was appointed to in August 2012. Most recently, Jones served as Executive Vice President and President, Access Equipment where he drove domestic and international growth, customer experiences with access products and strategically developed the segment’s global position.

• Prior to joining the Access Equipment segment, Jones was Executive Vice President and President, Fire & Emergency, a position which he was promoted to in September 2008. Jones was also the President of Pierce Manufacturing Inc.; he was appointed to this position in July 2007.

• In addition, Jones has served as Vice President of Sales and Marketing for the Fire & Emergency segment. Jones joined Oshkosh Corporation in 2005 as the Vice President and General Manager of the Airport Products Business Unit, where he led a strategic international initiative for the company.

• Jones has been in specialty vehicle manufacturing for more than 20 years. Jones has served on the Board of Directors for the Fire Apparatus Manufacturers’ Association and the American Ambulance Association. Jones holds a bachelor’s of business administration degree from the University of North Texas.

178September 2012Analyst Day Executive Biographies

Executive Biographies

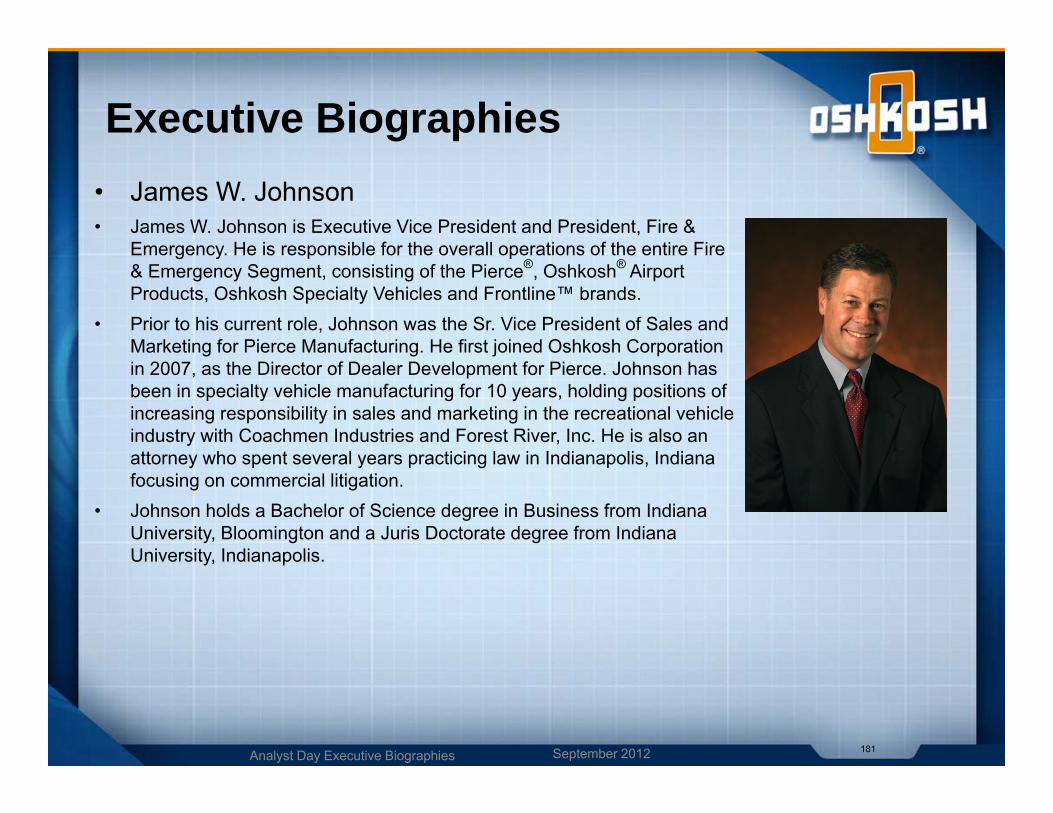

179September 2012Analyst Day Executive Biographies

Executive Biographies• Frank R. Nerenhausen• Frank R. Nerenhausen is Oshkosh Corporation Executive Vice President

and President, Access Equipment, a position he was appointed to in August 2012. Nerenhausen oversees all aspects of the company’s Access Equipment segment, which includes JLG Industries, Inc. and Jerr-Dan Corporation.

• Most recently, Nerenhausen served as Oshkosh Corporation’s Executive Vice President and President, Commercial, where he was responsible for all companies within the Commercial business segment including McNeilus, CON-E-CO, London Machinery and IMT.

• Nerenhausen has had positions of increasing responsibility in various functional areas since joining Oshkosh Corporation in 1986. Nerenhausenhas a bachelor’s of Business Administration degree in Finance and Management Information Systems and an MBA with a marketing emphasis from the University of Wisconsin-Oshkosh.

• John M. Urias• John M. Urias is Oshkosh Corporation Executive Vice President and

President, Defense. He was appointed to this position in October 2011. Urias is responsible for leading all aspects of the company’s global defense business, including vehicle programs, new product development, life-cycle sustainment and aftermarket services.