Optimal Network for BPD Regional Champion (BRC ... - USAID

65

Optimal Network for BPD Regional Champion (BRC) to Support Financial Inclusion SEADI DISCUSSION PAPER SERIES

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Optimal Network for BPD Regional Champion (BRC ... - USAID

Optimal Network for BPD Regional Champion (BRC) to Support Financial Inclusion

SEADI DISCUSSION PAPER SERIES

Optimal Network for BPD Regional Champion (BRC) to Support Financial Inclusion

July 2013

This publication was produced by DAI/Nathan Group for review by the United States Agency for International Development (USAID). It is made possible by the support of the American people. Its contents are the sole responsibility of the author or authors and do not necessarily reflect the views of USAID or the United States government.

SEADI Discussion Paper No. 5 This paper was written by Research and Training in Economics and Business (P2EB), Faculty of Economics and Business (FEB), Universitas Gadjah Mada (UGM) pursuant to a grant funded by the USAID Support for Economic Analysis Development in Indonesia Project.

Acknowledgements The authors listed below gratefully acknowledge the financial grant provided by SEADI-USAID. We express our gratitude to ASBANDA, who provided tremendous support for us in contacting all BPDs sampled. Constructive feedback and comments from James R. Hambric, Anwar Nasution, and Hery Kameswara are gratefully acknowledged. We thank Risky Raisa Putra, Haryo Saktioko and Pratiwi for excellent assistance during the project. All remaining errors are our responsibility.

Authors

Research and Training in Economics and Business (P2EB) Faculty of Economics and Business (FEB), Universitas Gadjah Mada (UGM) Rimawan Pradiptyo Catur Sugiyanto Sumiyana Inayati Nuraini Dwiputri Yudistira Hendra Permana Stephanus Eri Kusuma Wihana Kirana Jaya Fuad Rahman Andreas Kurniawan

Contents Glossary v

Abstract vii

Executive Summary ix

1. Background 1

2. Methodology 5

3. Banking Policies and Financial Inclusion 7

4. Network Formations of Sampled BPDs 9 Network Formation among BPDs 9

Network Formation in BPDs 11

Pattern of Networks and Transaction Costs 17

5. Interest Rates and Prudential Measures 21

6. Consumptive versus Productive Credits 23

7. Culture and Financial Inclusion 25

8. Local Government Policies 31

9. Other Support for Financial Inclusion 33

10. Conclusions and Policy Recommendations 35

References 37

Appendix A. Literature Review

Appendix B. Interprovince Network of Sampled BPDs

Figures Figure 1. Challenges in Financial Inclusion 2 Figure 2. Financial Network Formation of Bank Kalteng 13 Figure 3. Financial Networking of Bank DKI 15 Figure 4. Financial Network in BPD DIY 16 Figure 5. Financial Network of Bank Sulselbar 17 Figure 6. Relationship between Regional Economic and Financial Inclusion Process 18

Glossary Anakaraeng The past custom of patron-client relationship for Bugis and Makassar people AoRD Agent of Regional Development APEX Bank A bank supervised by another bank ASBANDA Asosiasi Bank Pembangunan Daerah (Association of Regional Bank

Development) Awigawig Custom rules in Bali Bappepam-LK Badan Pengawas Pasar Modal dan Lembaga Keuangan (Capital Market and

Financial Institutions Supervisory Agency); it is under supervisory of the Ministry of Finance

BI Bank Indonesia BKD Badan Kredit Desa (Village-owned Credit Agency) BMT Baitul Maal wat Tamwil; a sharia-based MFI BPD Bank Pembangunan Daerah (Regional Development Bank); classified into

general bank according to Act No. 7/1992 Bank Aceh BPD of Aceh Province Bank Nagari BPD of West Sumatera Province BPD DKI BPD of Jakarta Province BJB BPD of West Java and Banten Province Bank Jateng BPD of Central Java Province BPD DIY BPD of Yogyakarta Province Bank Jatim BPD of East Java Province BPD Bali BPD of Bali Province Bank Kalteng BPD of Central Kalimantan Province Bank Kalsel BPD of South Kalimantan Province Bank Kaltim BPD of East Kalimantan Province Bank Sulselbar BPD of South Sulawesi and West Sulawesi Province Bank Sultra BPD of South-East Sulawesi Province Bank Papua BPD of Papua and West Papua Province Bank plecit Informal moneylender in the traditional market Bendesa adat The head of a customary village in Bali BPR Bank Perkreditan Rakyat (People’s Credit Bank); a rural bank operating at

the same level as a general bank according to Act No. 7/1992 BPRS A sharia-based arm of BPR BPS Badan Pusat Statistik (National Statistic Agency) BRC BPD Regional Champion; program initiated by ASBANDA and BI to

improve role of BPD BUKP Badan Usaha Kredit Pedesaan (Village Credit Enterprise); an MFI

developed during the new order era and owned by local government Inkopdit Induk Koperasi Kredit (Credit Union Central)

V I

IPO Initial public offering JETS Jatim (East Java) Electronic Transfer System Korindo Credit insurance company KUR Kredit usaha rakyat (small loans); a program of Coordinating Ministry of

Economic Affairs KSP Koperasi Simpan Pinjam (Saving-Loan Cooperative) LDKP Lembaga Dana Kredit Pedesaan (Village-owned Credit Fund Enterprise);

another form of MFI that is similar to BUKP LKM Lembaga Keuangan Mikro (Micro Credit Institution) LPD Lembaga Perkreditan Desa (Village-owned Credit Institution); a village-

owned credit organization that is supervised by the local government of Bali LPH Lumbung Pitih Nagari (Local Saving-Loan Agency); a agency similar to

LPD, but from West Sumatera Mindring Credit provider for house appliance purchasing MFI Micro-finance Institution MSME Micro, small, and medium enterprise Nelulasi Common interest rate of Javanese people (about 30% on every maturity date) OJK Otoritas Jasa Keuangan (Financial Service Authority) p.a. per annum p.m. per month Pasaran Weekly days of Javanese people (five days in a week) Patron-client Relationship between lender (bank) and borrowers, in which the lender plays

a role as a supervisor for the customer PBI Peraturan Bank Indonesia (Bank Indonesia’s regulator) Perusda Perusahaan daerah (local-state owned enterprise) PINBUK Pusat Inkubasi Bisnis Usaha Kecil (Center for Micro Enterprise Incubation);

a private organization for micro enterprise development Punggawa-sawi Sharing system in a patron-client relationship for Bugis and Makassar people SOE State-owned Enterprise SME Small and medium enterprise Sparkassen National development bank in Germany

Abstract This study aims to investigate the networking of regional development banks (BPDs) to reach potential customers that are considered non-bankable. A market chain method is used to trace the pattern of networking starting from the BPD down to the final customers. The study involved 13 out of 26 BPDs across Indonesia. In each sampled BPD, interviews were conducted at the head office and two branch offices, one of which was situated in an agricultural area and the other in an industrialized area. Micro-finance institutions (MFIs), which are directly linked with BPDs, were also interviewed and snowballing random sampling has been used to select the sampled MFIs. The results suggest that the network formation between BPDs and MFIs depends on the structure and economic conditions of the area where the BPDs are situated. There is a strong tendency of networking to occur between bank-based MFIs. The cooperation between bank-based MFIs and non-bank-based MFIs tends to be limited since the transaction costs and the risks of establishing such cooperation are substantially high.

Keyword: networking, financial inclusion, microfinance institutions, transaction costs, consumptive credits, productive credits.

JEL Classification: G21, G28.

Executive Summary Financial inclusion is an ingenious way to reach non-bankable households and small and micro scale entrepreneurs (SMSEs) to help them gain access to the formal financial sector. Various studies have found that financial inclusion can aid poverty alleviation. Such programs help low-income households, who predominantly live in rural areas, access capital from the formal financial sector. The challenges of financial inclusion are not only limited to creating new financial institutions, or developing new financial products, which may reach non-bankable households, but also educating targeted groups about the advantages of existing financial institutions and their products. On the other hand, formal financial institutions ought to learn how to serve the targeted groups; particularly where the characteristics of non-bankable households and entrepreneurs may be significantly different from those of bankable customers using developed formal financial institutions.

This study aims to seek the optimum network formation among BPDs and between BPDs and other micro-finance institutions (MFIs). Our research will do the following: a) explore the existing network formations of BPDs, both the internal and external sides, with other small and micro-financial institutions; b) identify the factors that determine the pattern of BPDs with regard to other MFIs; c) estimate the optimum future role of BPDs as either development banks or commercial banks; and d) analyze the existing regulations that may support or need to be revised for the role of BPDs. In order to meet the requirements of a comprehensive study, thirteen out of twenty-six BPDs in Indonesia were involved in in-depth interviews. In addition, networks of BPDs in the financial inclusion process were also interviewed to explore the practices in the field in various places in Indonesia.

This report is organized so that readers may easily understand the implementation of the financial inclusion process of BPDs in Indonesia. Chapter 1 describes the background of this study and our position to explore the implementation of financial inclusion processes by BPDs in Indonesia. Chapter 2 discusses the methodology that was used in this study, including the reason for choosing the BPDs sampled in this study. Chapter 3 explains the role of banking policies and systems in the financial inclusion process, including banking regulations, in Indonesia. Chapters 4, 5, 6, and 7 feature the main analysis of the financial inclusion processes, in which BPDs provide the main point of view, and which includes cultural analysis. Chapters 8 and 9 show the potential role of government and other formal institutions in supporting BPDs and promoting the financial inclusion process. Finally, Chapter 10 offers our conclusions and policy recommendations.

We found that the network formations of BPDs with rural banks and also MFIs depend on the nature of economic conditions in each region. In areas where the structure and performance of the economy tend to be simple, the network formations of financial inclusion of BPDs tend to be short. Surprisingly, the networking of Bank DKI, which is in an economy with the most vibrant and complex structure, tends to be short and simple, similar to those of the areas with economies that have a simple structure. Between two extreme structures of the economy, the networking of BPDs with other financial institutions tends to be extensive and involves various types of financial institutions.

X O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

This creates a relationship between the economic structure and the networking of financial inclusion, which may be depicted as an inverse U-shaped curve.

Indeed, all BPDs are members of ASBANDA (the association of BPDs) and they all have a close relationship with each other. Nevertheless, there is a strong tendency for BPDs to expand their business in other provinces. If each BPD pursues this as its dominant strategy then ASBANDA members will find themselves in direct competition with each other in an attempt to capture market share. Complexities arise because all BPDs tend to embrace similar strategies, and the targeting of similar groups of customers. Thus, the intensification of this expansive strategy by each member of ASBANDA implies that, in the future, competition among ASBANDA members is inevitable.

A network between BPDs and rural banks can be easily established. From the perspective of BPDs, the transaction costs to establish a network of rural banks is much lower than that of establishing a network with other micro-finance institutions (MFIs). This is because the same authority, Bank Indonesia, supervises BPDs and rural banks. On the other hand, linkage programs between BPDs and MFIs are not easily established, yet we found that networking exists between rural banks and MFIs. This occurs because it is difficult for BPDs and rural banks to observe the performance and the credibility of MFIs. The discrepancy in the intensity and the quality of supervision between banking and non-banking institutions is largely due to the complexity of banking and non-banking financial institution networks.

This study found that all sampled BPDs have embraced a similar strategy for channeling their credits to micro-enterprises and low-income households. This channeling has occurred through a cultural approach, where the characteristics of customers or potential customers are the main consideration in making banking decisions. Rural banks and other MFIs have embraced similar strategies. Financial institutions, especially small scale MFIs, in many places in Indonesia are still formed through culturally based approaches. This is reflected in their products, which are easily understandable and accepted by their customers. For example, this cultural emphasis can be seen in the case of mindring in Central Java, LPDs in Bali, and minimizing risk approaches of BPDs and rural banks in West Sumatera.

This study proposes several recommendations to increase BPD’s performance in the financial inclusion process. Firstly, potential rivalry among BPDs may be reduced through good coordination and communication under the umbrella of ASBANDA. Limiting the opening of new branch offices in other provinces, and better cooperation among BPDs in generating funds (supply side), may provide more sustainable strategies than the current race to open branch offices in the other provinces.

Secondly, Bank Indonesia’s supervision of the banking sector has created low transaction costs among the sector’s agents to collaborate and to create networks. In 2014, all financial supervision is going to be conducted by the Financial Service Authority (OJK). OJK faces the challenge of whether it will be able to match the intensity and the quality of supervision across all financial institutions, as the Bank Indonesia has achieved with the banking sector. OJK should endeavor to use its resources to match, or even to improve, the level of supervision across various financial institutions, which may reduce the transaction costs of establishing collaboration across financial institutions.

Third, ideally the measures for BPDs should be distinguished from the measures for commercial banks. BPDs have two main objectives: maximizing profit while operating as corporations, while at the same time acting as agents of regional development (AoRD). These roles may not necessarily converge, and in some circumstances they may be in conflict. The majority of BPDs imposed

E X E C U T I V E S U M M A R Y X I

considerably high net interest margins (NIM) 5%-7%. This may not necessarily be suited to the BRC measure in which the targeted maximum NIM is 5.5%.

1. Background Indonesia is one of the most populated countries in the world after China, India and the USA, with a population of 237.56 million in 2010 (BPS, 2011). The country provides a tremendous potential supply of labor and capital; however, the World Bank (2007) reported that about 60% of Indonesia’s population has no access to the formal financial sector. From this, one may infer that about 60% of the Indonesian population has not been bankable. An un-bankable person includes the impoverished or people from low-income backgrounds. In 2010, about 13.33% of the population lived below the poverty line, and 64.25% of the population lived in rural areas (BPS, 2011). This implies that the source of domestic capital for the formal sector is from the top 40% of income earners in Indonesia, the majority of whom live in urban areas.

Those who do not have access to the formal sector, and/or live in rural areas, may not necessarily have capital. It is common for people in rural areas to have non-monetary capital, even though it is hard for this to be transformed into monetary capital. People in rural areas have suffered from limited access to formal financial institutions.1 Irrespective of whether people live in urban or in rural areas, individuals have a tendency to smooth their consumption over time (Morduch 1995; Kinsey et.al. 1998; Wik 1999; Zeller 2000; Skoufias 2003; Notten & Crombrugghede 2006; and Laczo 2007). Both factors above have encouraged households in rural areas to create informal financial institutions.

Financial inclusion is defined as any method to improve access of economically vulnerable groups to the formal financial system at affordable cost (see Dev 2006, Kamath 2007, Sarma 2010, inter alia). In India, for instance, Dev (2006) reported that there was a strong tendency for farmers to obtain loans more from informal sources than formal ones. The interest rate on credit from informal financial institutions may reach up to 50% or 60% per annum, and moneylenders have exploited many households. Given the fact that the households may bear the credit interest rate of 50% or 60%, a question should be raised as to whether the households are actually financially excluded (Dev 2006).

Zarazua and Copestake (2008) argued that access to financial services depends significantly on educational attainment, employment, and housing status. The main challenge for financial inclusion programs is how to go beyond creating new formal institutions or framing newer rules that call for a renewed thrust of the formal sector in rural areas (Kamath 2007). Formal financial institutions have to learn to serve the poor and vulnerable, which may require focusing on different characteristics than found in the formal banking sector.

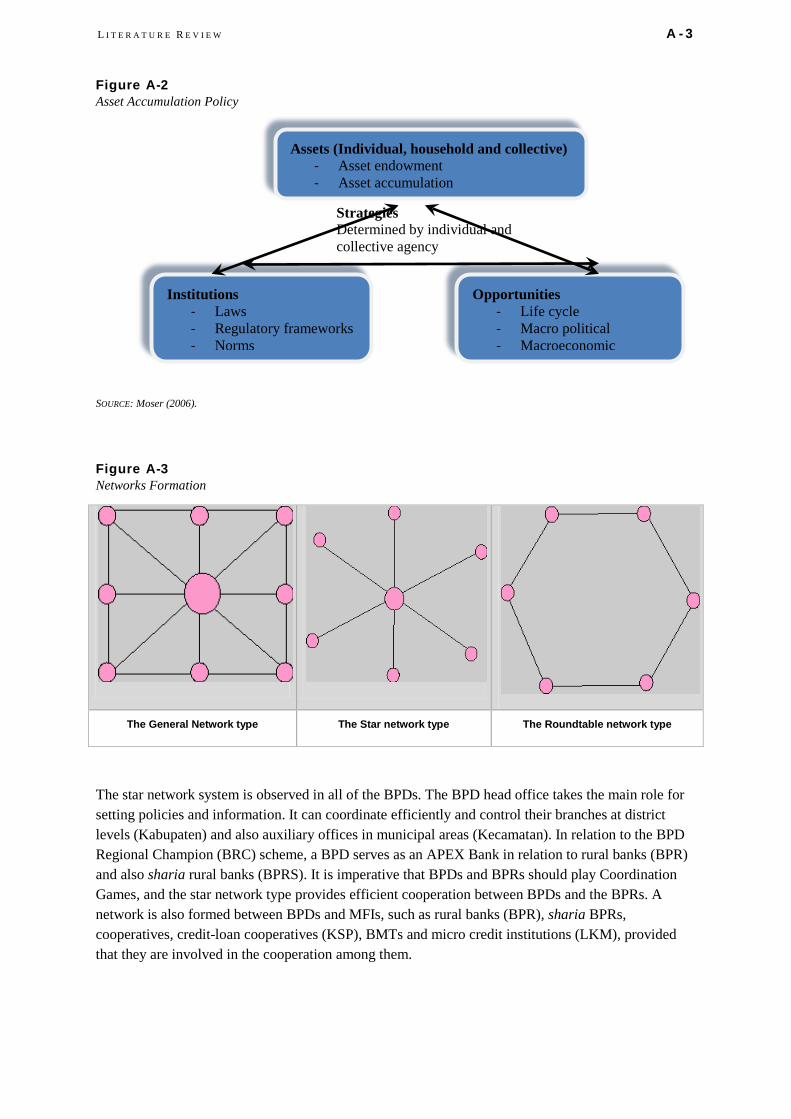

The ability of a financial institution to reach non-bankable households or small and micro enterprises depends on the type and the extent of its network with other financial institutions. In cooperative games, the types of networks determine the speed of coordination of all members within the network (Bala and Goyal, 2001). How extensive the network among financial institutions is may determine the

1Case (1995), Dercon (1996), Zeller et al (1997), Robinson (2002), CEPPS and Bank Indonesia (2004), and Roog (2006), among others.

2 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

ability to reach groups targeted for financial inclusion. There are at least three types of network formation: general relations, roundtable formation, and star-formation. The star-formation has the fastest cooperation rate, whereas the general formation has the slowest cooperation rate (Bala and Goyal 2000). Further discussion on the impact of networking on financial inclusion is found in Appendix A.

Figure 1 Challenges in Financial Inclusion

Figure 1 shows the structure of financial inclusion. The focus of the financial inclusion is how to attract non-bankable households and enterprises to formal financial institutions. There are two main challenges in financial inclusion. First, from the supply side, financial institutions need to obtain sources of funding, which may come from enterprises and households. In developing countries, including in Indonesia, it is not necessary for affluent households or small and medium enterprises to use formal financial institutions to save their money. There are various explanations put forward to describe this phenomenon, ranging from cultural and religious factors to educational factors. The complexity of financial products increases for low-income households and micro enterprises.

Second, from the demand side, financial institutions need to channel the funding that they obtain to enterprises and households that need money. The challenges on the demand side are similar to those on the supply side. Attempts to incorporate both poor households and small and micro scale enterprises to have a link to the formal financial sector are the main challenges of financial inclusion.

As part of its financial inclusion strategy, Bank Indonesia and ASBANDA (the association of state-own regional banks or BPDs) recently launched the BPD Regional Champion (BRC) program. The program aims to improve the role of BPDs at the province level, both as a financial intermediary institution and as agents of regional development (AoRD). In addition to this, the program aims to accommodate the advancement of economic activities and remittances in local areas.

Two strategies that have been pursued by BPDs include developing a network of cooperation among BPDs (horizontal integration) and BPDs serving as APEX banks in relation to micro-finance

I N T R O D U C T I O N 3

institutions (MFIs).2 As an APEX Bank, a BPD may work collaboratively with rural banks (BPRs) and serve as a “central bank” when rural banks require liquidity.

Thus far, the role of BPDs as APEX Banks is limited only to BPRs (rural banks) and it has not been extended to MFIs, such as Baitul Maal wat Tamwil or BMT, BKD, KSP, etc. The reason behind this policy is the fact that both BPDs and BPRs have been supervised by Bank Indonesia. Bank Indonesia has provided an online system that enables any commercial or rural bank to check the performance of the other commercial banks and rural banks instantly. This implies that the transaction costs and risks of collaboration between commercial banks and rural banks tend to be minimal, if not negligible.

The transaction costs and risks of establishing working collaboration between BPDs and non-banking institutions, such as multi-financers, venture capital, insurance, cooperatives, BMT, and other MFIs, tend to be higher, since those financial institutions have not been supervised by Bank Indonesia. The supervision of the financial institutions is more complex because there is no direct linkage among financial institution supervisory bodies by Bank Indonesia, The Ministry of Cooperative and Small Scale Enterprises, and Bappepam-LK. By 2015, all financial institutions will ideally be supervised by OJK (Indonesia’s financial service agency). Nevertheless there is no guarantee that the quality of supervision under OJK will be better, due to problems of coordination within the new supervisory system for financial institutions (Pradiptyo, et al, 2012).

This study aims to seek the optimum network formation among BPDs and between BPDs with other small and micro scale financial institutions. The purpose of the study, therefore, is to answer the following questions:

1. What are the existing network formations among BPDs and between BPDs with other small and micro scale financial institutions?

2. What are the factors attributable to the pattern of networking between BPDs with other small and micro finance institutions (MFIs)?

3. In terms of prudential rules and regulations, what is the optimum role of BPDs? Should they become development banks or commercial banks?

4. In order to optimize the role of BPDs, are the existing laws and regulations sufficient to support the new role of BPDs? If not, what kind of additional regulations should be prepared to support the new role of BPDs?

2 The APEX bank will enable BPDs to serve as the leader of a flying geese model, whereby BPDs act as a leader and the other micro financial institutions are followers.

2. Methodology There are two ways to trace the networking of a bank with MFIs for the purpose of financial inclusion. First, attempts may be made to trace the networking of a bank starting from the final customers. The end customers may consist of either households or small and micro enterprises that save and/or borrow money from financial institutions. This method may be compelling, however, it may be quite risky to pursue this since there is no guarantee that the financial institutions are willing to participate in the study.

Second, an attempt may be made to trace the networking of a bank starting from the bank itself followed by tracing its marketing chain up until the networking prior to the households/final consumers. There are several banks that focus on customers in rural areas, namely BRI, BTPN, Bank Danamon, and BPDs. In comparison to the other banks, BPDs are the easiest to involve in the study. This is because BPDs have formed an association called ASBANDA, which enables the research team to gain access to BPDs and MFIs within the network of the BPDs. Indeed, this approach may not be ideal, however considering the complexity of conducting the alternative method; the current approach is considered the most attainable method.

There are twenty-six BPDs around Indonesia, and these are situated in twenty-six out of the country’s thirty-three provinces. The BPDs that have been chosen as samples for this study cover 50% of the total (thirteen BPDs). They have been chosen by considering several factors: how representative they are of each region/island, their institutional status, either as a perusda (locally stated-owned enterprise) or as a limited company, and the uniqueness of the cultural factors that influence financial institutions in their particular region. In terms of regions, it is assumed that Indonesia consists of 7 major regions/islands, Sumatera, Java, Kalimantan, Sulawesi, Papua, Moluccas and Nusa Tenggara, for this study. Bank Nagari (West Sumatera) and Bank Aceh (Aceh) represent BPDs on the island of Sumatera. Bank Kaltim, Bank Kalsel and Bank Kalbar represent Kalimantan. Bank Jatim, Bank Jateng, BPD DIY and Bank DKI represent Java. Bank Sulselbar and Bank Sultra represent Sulawesi. Bank Papua represents Papua. BPD Bali represents Moluccas and Nusa Tenggara. The aim of choosing BPDs across various regions is to investigate the pattern of networking between BPDs, BPRs, and MFIs in each region.

Bank Aceh and Bank Papua were chosen because they represent the most westerly and the most easterly of the regions in Indonesia. Another three BPDs that have not yet changed their status from Perusda are BPD DIY, Bank Kalteng and Bank Sultra, and all of them were chosen to be part of the sample of BPDs. These BPDs were sampled in order to investigate whether the networking of a BPD is subject to its status, since the Perusda BPDs tend to have limited capital compared to the limited company BPDs. Bank Bali and Bank Nagari represent BPDs with a particular culture that supports financial operation of BPDs in their regions. In Bali, almost every village has a Lembaga Perkreditan Desa/LPD, and its operation has taken into consideration the culture in Bali. In a similar vein, Lumbung Pitih Nagari (LPH) in West Sumatera operates using a similar approach.

6 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

Initially, Bank Jabar and Banten (BJB) were chosen to represent BPDs with the most successful IPOs3. Unfortunately, BJB decided not to participate in the study, thus Bank Jateng was chosen to replace it. Bank DKI was chosen because it has been operating in the most vibrant and the biggest city in Indonesia. Bank Jatim was chosen because it is the most advanced APEX bank among the BPDs.

A survey was conducted on the sampled BPDs and their respective financial institutions, including rural banks and MFIs that have been working collaboratively with them. For every BPD, interviews were conducted in the headquarters, branch offices, industrial areas and agricultural areas to identify the heterogeneity of its operations. Snowball random sampling has been used to trace any financial institutions that are part of the BPDs’ network. In each branch office, a representative of small and micro financial institutions was interviewed to trace the networking of the BPD up through the lowest financial institutions before households/final customers. This survey aims to find the existing network formations among BPDs and between BPDs and other small and micro financial institutions.

3 BJB is the first BPD in Indonesia that underwent an IPO, in 2010, and soon its stock was part of LQ 45. Currently the BJB has opened branches in several countries, including in Singapore, Hong Kong and South Africa.

3. Banking Policies and Financial Inclusion The role of banking policy in promoting financial inclusion in the past was mostly focused on the provision of relatively small loans to clients with micro, small, and medium enterprises (MSMEs). It is generally hypothesized that these relatively small loan clients have difficulty accessing financial services from formal financial institutions.

Bank Indonesia has been providing support and assisting the development of MSMEs.4 Bank Indonesia’s policies toward MSME development aim to support the banking sector to reinforce MSME credit disbursement (supply side) and to strengthen MSME eligibility and capability to meet bank requirements (demand side). This policy has been pursued through three instruments: credit policy, institutional development, and technical assistance.5

During the period of 2009 – 2012, Bank Indonesia released two Bank Indonesia Regulations (PBIs) and two circulation letters aimed at promoting support for MSMEs. PBI No. 14/22/PBI/2012 recommended that each commercial bank should distribute a minimum of 20% of its total credit outstanding to MSMEs by 2018. In addition, PBI No. 14/26/PBI/2012 regulated a minimum proportion of total credit outstanding by a bank, which should be channeled through productive credits. For a bank whose main capital is less than IDR1 trillion, at least 55% of its credit outstanding should be channeled through productive loans. The threshold of 60% is applicable for the bank whose main capital is between IDR1 trillion to less than IDR5 trillion. The majority of BPDs lie within these classifications, and this goal will ideally be reached in 2018.

These regulations show a relentless commitment and effort by Bank Indonesia to promote the disbursement of credits to the real sector, especially to MSMEs. On the other hand, this policy may not be appropriate across the board due to heterogeneity within the banking sector in Indonesia. However, the policies provide support to MSMEs, create complexities for some banks, and force banks to embrace a homogeneous strategy to channel their credits.

In order to reach potential customers for financial inclusion, Bank Indonesia has promoted a linkage program. The program enables cooperation between financial institutions. This program has three schemes: a) executing scheme;6 b) channeling scheme;7 and c) joint-financing scheme8. The linkage

4 This role has been mandated in accordance with Act No. 23 of 1999 as amended by Act No. 3 of 2004 and Act No. 6 of 2009.

5Indonesian Banking Booklet, 2010 6 In this scheme, a larger scale financial institution lends money to MFIs, which tend to be smaller. The

smaller financial institution then provides additional loans to its clients.

8 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

programs may be implemented either among banking institutions or between banking and non-banking financial institutions. The program may help commercial banks that have not developed advanced micro credit to reach small and micro scale enterprises and low-income households. Through this program, commercial banks may provide small and micro-scale financial institutions with extra funds for their operations. This program also assists commercial banks, the majority of whom are based in urban areas, to reach potential clients in rural and remote areas through the help of non-banking financial institutions.

The linkage program also aims to promote division in target marketing between BPDs and MFIs. As a commercial bank, a BPD is more capable of handling larger scale clients, while MFIs are more capable of handling smaller scale clients. Thus, it will be more efficient if BPDs distribute relatively small loans through the help of MFIs. In reality, however, this division of labor may not necessarily occur as BPDs and MFIs may compete with each other. In some sampled areas, even rural banks may compete head to head against a BPD. This occurs because the scale of the rural banks may not be significantly different from the BPD. These are some of the complexities in promoting cooperation among financial institutions.

A network among banking institutions is much easier to form compared to a network between banking and non-banking institutions. Prior to initiating a linkage scheme with an MFI, a bank must analyze the performance and reputation of the potential MFI partners. Nevertheless, this may not be easy to perform since the MFIs have been supervised by other authorities, which use a different approach and quality of supervision.9 Indeed, this creates a transaction cost to establish a linkage between banking institutions that is much more economical than that of a linkage between banking and non-banking institutions. It should be noted that rural banks (BPRs) are a small portion of banks compared to the other types of MFIs, such as cooperatives, rural savings and credit institutions (LPDs, BKDs, BUKPs, and other LDKPs), and BMTs, which have more advantages in terms of the proximity to groups targeted for financial inclusion (e.g., non-bankable households, especially rural/remote areas, less educated, and low-income households).

In 2011, Bank Indonesia formulated a new strategy to increase public access to financial services. It is in line with the implementation of the “National Framework of Financial Inclusion.” There are five pillars of inclusive financial policy covered in the framework: a) financial education; b) financial eligibility; c) supporting financial regulation; d) intermediation facilities; and e) distribution.10 In addition, various measures have been implemented by Bank Indonesia to support financial inclusion, including Tabunganku (fee-based income saving), financial education development, implementation of the Financial Identity Number, and the implementation of a literacy survey. Bank Indonesia also developed a payment system that is more efficient, reliable, straightforward, and secure by emphasizing infrastructural development, system development, and the strengthening of the legal framework.

7 In this scheme a financial institution recommends potential clients to an MFI, then the former financial institution distributes their funds to the potential clients and gives some fees to the latter financial institution that recommends the potential clients.

8 In this scheme several financial institutions share their funds and work together in distributing the credits. 9 Bank Indonesia uses three measures to supervise the banking sector; these are micro prudential, macro

prudential and business conduct. Bappepam-LK supervises non-banking financial institutions using business conduct as the primary measure. Lastly, the Ministry for Cooperatives supervises cooperative-based financial institutions by using cooperative principle measures.

10 For the details of the pillars, see Indonesian Banking Booklet, 2010, 2011, 2012

4. Network Formations of Sampled BPDs NETWORK FORMATION AMONG BPDS Theoretically, all BPDs are members of ASBANDA (the association of BPDs). By the end of 2012, Bank BJB (West Java and Banten Province) decided to leave ASBANDA. Today, ASBANDA is comprised of 25 BPDs, and none of them have conducted an IPO (Initial Public Offering). Bank BJB was the first BPD to successfully conduct an IPO. Bank BJB has expanded its operations abroad by opening branch offices in Singapore, Hong Kong, and Johannesburg.

Of the 25 BPDs in ASBANDA, a majority have already transferred their status from perusda (local state-owned enterprise) to “limited company.” Thus far only three BPDs are still under perusda status, Bank Kalteng, Bank Sultra, and BPD DIY. Recently, DPRD-DIY (Regional House of Representative of DIY) has granted approval for BPD DIY to transfer its status to limited company after almost six years of convincing the DPRD DIY.

As a perusda, a BPD may not be able to generate capital easily since any decision regarding capital should be confirmed by all stockholders, which are all municipal governments and the Local House of Representatives (DPRDs). With BPD DIY for instance, they have maintained around IDR 250 billion in capital since 2005. In contrast, all BPDs with limited company status have more flexibility to generate capital because this decision relies on an annual general meeting of shareholders. This explains why the majority of BPDs with limited company status have capital of more than IDR1 trillion.

ASBANDA was founded on March 24th, 1999. The aim of ASBANDA is to drive BPDs to become leading banks in each region through BRC (BPD Regional Champion). The main goal of BRC is to create good corporate governance within all BPDs through three pillars: a) strong institutions; b) the ability to be an agent of regional development; and c) to serve community’s needs.

ASBANDA has made a strong commitment to support financial inclusion. ASBANDA has assisted BPDs to channel KUR (small loans) by working in cooperation with PT Korindo (credit insurance company) and Perum Jamkrindo (Perusahaan Umum Jaminan Kredit Indonesia).11 ASBANDA has played a key role in cooperating with government institutions in channeling the credit programs of BPDs. Through this cooperation, government activities and projects will be funded by BPDs. This strategy aims to help BPDs achieve BRC criteria that require a minimum of 40% of total outstanding credits to be allocated to productive credit by 2014.

11 Perum Jamkrindo is the state-owned enterprise that operates in each province.

10 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

ASBANDA provides a communication forum among BPDs to compare experiences, best practices, and also to discuss any problems that emerge in the banking industry with other associations and with Bank Indonesia. During the process of transformation from perusda to limited company in BPD DIY for instance, they received tremendous support and assistance from the other BPDs. At managerial and official levels, the members of ASBANDA have developed close personal communication among them.

At the business level, it is still not obvious what form of cooperation has been developed among ASBANDA members. Thus far, we found little evidence to suggest that the BPDs have limited liquidity cooperation. Recently, there has been a tendency for several BPDs to extend their operations by expanding their branch offices to other provinces. For example, Bank Jateng and Bank Kalsel have expanded their operations by opening branch-offices in Jakarta. Also, Bank Papua has opened its branch offices in Surabaya, Makassar, and Yogyakarta.

Indeed, for BPDs with excess liquidity, opening a branch office in other provinces is compelling since they can expand their business by getting potential customers there. For example, Bank Papua had benefited from this strategy in which the LDR raised was about 70% in 2012, compared to 40% in 2011, after opening branch-offices outside the province. By early 2013, Bank Papua had opened its branch-office in Yogyakarta, and this is expected to improve the LDR of Bank Papua (Appendix B).

The direction of BPD expansion to the other regions may indicate a financial drain of domestic funds. BPDs in Java are found to absorb more credit than savings and deposits, which are supplied by the outer islands. This means that financial inclusion in terms of channeling credit to domestic customers of their respective BPDs is not comparable to financial inclusion in terms of the savings-deposit funds from the BPDs. We should note that the opening of BPD branches in Jakarta indicates an outflow, where the BPDs channel credits to Jakarta, but not vice versa. Indeed, the reason Bank Papua opened a branch in Yogyakarta was not because there are many Papua people residing in Yogyakarta, but to facilitate credit disbursement in Yogyakarta. A similar reason may apply to Bank Jatim, Bank Jateng, BJB, Bank Bali, and other BPDs for opening branches in Jakarta, since the goal is definitely not for generating funds, but rather for lending. Therefore, a better infrastructure of BPDs tends to channel out funds from surplus areas, regardless of the economy’s structure and performance.

Although becoming members of ASBANDA could benefit BPDs tremendously, the future of this association seems to be in jeopardy because of the tendency of members to enter into direct competition with each other. If the competition to expand the business by opening new branches in other provinces escalates then it is inevitable that fierce competition will occur among BPDs. This competition may jeopardize the existence of ASBANDA in the future.

Will BPDs maintain their roles as agents of regional development in their own regions if they embrace opening branches in the other regions as a dominant strategy? A similar question should be raised about the tendency of BPDs to open branches in other countries once the BPDs have undergone an IPO. It seems there is a conflict between the role of BPD as a commercial bank and as an agent of regional development.

Attempts have been made by BPDs to learn the best practices of Sparkassen, a development bank, which has been operating successfully in Germany. It should be noted, however, that BPDs have fundamentally different business strategies to the Sparkassen. A member of Sparkassen, which is a regional bank similar to a BPD, is not allowed to open branches in other provinces when another Sparkasse has been operating in the region. In contrast, direct competition is permitted among BPDs, and each BPD tends to extend its business to other regions regardless of the existence of BPDs

N E T W O R K F O R M A T I O N S O F B P D S 11

operating there. The majority of BPDs tend to be homogeneous in terms of their size, captive market, and also their potential customers. The homogeneity of BPDs tends to escalate the complexity of direct competition among them, particularly if each BPD thinks that opening branches in the other regions is a route to attraction or a dominant strategy.

NETWORK FORMATION IN BPDS The banking sector operates under a specific type of activity, e.g. bank services. The production process would be under scrutiny if the provision of liquidity to end users (households or businesses) goes through the banking system. Therefore, funds collected from third parties can be redistributed among debtors, who may be overseas, utilizing the centralized banking system.

Under the current network, BPDs are trying to minimize the cost of financial network development and provide liquidity. In addition, there is a further advantage in protecting the networks from financial crisis, which arises from defaults and may also minimize the risk of unbalanced financial reports in the centralized banking system.

In all sampled BPDs, the cooperation between BPDs and BPRs within the APEX Bank has the form of a star network, whereby BPDs serve as the center of the network. This star network is also implemented in non-banking institutions, such as multi-finance, cooperatives, savings-loan cooperatives, BMT, venture capital, and other MFIs. Yet, the star network with non-BPRs was not developed through an APEX Bank system. It should be noted, however, that the likelihood of BPDs forming a network relation with MFIs tends to be lower than that between BPDs and rural banks.

The implementation of the star network was conducted in Aceh. Bank Aceh was forced to embrace a new method of operation in the aftermath of the civil war and tsunami. With the new development of the organization and new market, close control from the center was necessary. With respect to the more mature organizations and the more advanced financial markets, as in Bali, we anticipate the possibility of a more decentralized network being considered.

As an alternative network,12 different from the general network above, we consider a decentralized financial system where each branch is an independent bank, which exchanges liquidity with the other banks. Liquidity may now circulate much more effectively and always be promptly transmitted from agents in surplus (be they banks or depositors) to those in deficit. Moreover, an interbank network for exchanging liquidity represents a safety net for each bank, which may obtain the liquidity it needs from many channels, as well as for the system as a whole, because it warrants that, even in case of default of a single bank, liquidity would still continue to flow to and from every local area of the economy via alternative channels.

In Bali, Lembaga Perkreditan Desa (Village-owned Credit Institution/LPD) is an established financial institution, and each LPD has a close relationship with the other LPD. BPD located nearby LPDs in tourism areas may collect more funds and then transfer the funds to another BPD branch with high credits. It should be noted that not all branches of a BPD have a fully decentralized network because not all of the branches have potential extra funds. Otherwise, the system is very costly because each bank has to gather information about every other bank with which it exchanges liquidity, as well as about each of its partners’ partners (because financial troubles of any of the latter may impact the

12 Giocoli, Nicola, Network Efficiency, the Coase Question and the Banking System (January 13, 2011). Available at SSRN: http://ssrn.com/abstract=1739611 or http://dx.doi.org/10.2139/ssrn.1739611, downloaded on Dec 1, 2012.

12 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

bank’s direct partners’ ability to repay debts). Still, under a very strong central BPD and the very strong social and cultural punishment of mismanagement, the costs may be minimized.

BPD Bali may exercise a transition to operate under a decentralized network. In sum,13 should the BPD Bali consider operating under a decentralized network, there are four elements to take into account when evaluating the banking system case: 1) the cost of establishing a communication channel (say, a contract) between two agents; 2) the effectiveness in the transmission of the inputs/information among the agents; 3) the robustness of the entire system, or of parts of it, to the breakdown of an agent or a communication channel; and 4) the cost of providing each agent with the capacity to manage the inputs/information received. Comprehensive networks may improve the interbank deposit market so that the exchange of liquidity is efficient. The better the interbank transfer through the network, the more efficient their allocation of public funds. Therefore, a measure of the efficiency of the network is how far and how fast the funds can be transferred between banks/financial institutions.

The networking between BPDs and MFIs vary from one BPD to another. There are various candidates of factors that are attributable to the variation of the financial network, including the value of capital, the status of BPD either as perusda or as a limited company, and economic conditions in areas where the BPDs have been operating. The results show that the pattern of the network depends on the economic conditions in areas where the BPD has been operating as opposed to the other factors.

Box 1. BPD Bali and Its Linkages Bank BPD Bali is a closed liabilities company owned by the Local Government of Bali, and was established in 1962. By the end of 2011, it had 11 branch-offices, 30 auxiliary-offices, 44 cash payment points, and 79 ATMs. This network enables BPD Bali to reach clients in almost all sub-districts and most villages in Bali province. Through its wide channel of distribution, BPD Bali has been able to maintain their growth performance in the recent years. Their assets grew from 5 trillion to 10.5 trillion rupiahs during 2007–2011, while it revenues rose from 0.4 trillion to 0.7 trillion rupiahs in the same period.

Their third party funds and loans outstanding grew by almost 30 percent (on average) year after year. This has been supported by an increasing trend of operational efficiency and better asset quality performance. Although BPD Bali is a commercial institution, it also acts as a development agent who must contribute to regional economic growth and welfare. In reaching these goals, BPD Bali focuses on the promotion of financial inclusion, especially in serving micro, small, and medium enterprises in Bali province.

To achieve this objective, BPD Bali has developed into an APEX Bank, a group of rural banks and other viable microfinance institutions linked through a program mechanism. In the linkage program, BPD Bali not only gives credit to its linkage partners, but also gives them training and applies close monitoring to track the usage of the linkage funds. It is important to note that the collaboration between BPD Bali and microfinance institutions is still limited to rural banks and cooperatives. For example, BPD Bali wants to collaborate with Lembaga Perkreditan Desa (LPD), a sub-village level community-based microfinance institution. However, it is constrained by government rules, as LPD does not pay taxes. Beside the linkage program, BPD Bali has also adopted other strategies to support

N E T W O R K F O R M A T I O N S O F B P D S 13

their financial inclusion promotion efforts, such as product diversification, competitive interest rate promotion, network expansion, coordination with the government on MSMEs credit funding and guarantee, and human resource and cultural advantage utilization..

The variation of financial networking depends on the economic situation and its structure. In regions with less vibrant economic conditions, the pattern of financial networking tends to be less complicated and less extensive. On the other hand, in regions with a more vibrant economic situation, the pattern of financial networking tends to be complicated and extensive.

Financial networking in Bank Kalteng is considered a simple financial network. In order to reach final customers, Bank Kalteng does not need to have an extensive and complicated networking system. Figure 2 shows the financial network of Bank Kalteng; channeling from the bank to the end customer tends to be short.

Figure 2 Financial Network Formation of Bank Kalteng

Figure 2 shows that the bank may reach end customers from its branch offices and/or auxiliary offices. It should be noted that end customers comprise four groups:

1. Medium and large scale enterprises, 2. Small and micro enterprises, 3. Medium and high income households, and 4. Low-income households.

In the case of Bank Kalteng, the majority of credits are in the form of consumption credit channeled to civil servants, either directly from their branch or through collaboration with civil servant cooperatives. This occurs because the risk of providing credit to civil servants and channeling credit

14 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

through civil servant cooperatives is much lower than providing credit to customers from other occupations.

A similar pattern of networking has been found at Bank Sultra and Bank Papua- the structure and the economic conditions in those areas are similar to those of Bank Kalteng. In comparison with other provinces, the structure and the economic conditions in Papua, West Papua, South East Sulawesi and Central Kalimantan are less vibrant than those of other sampled provinces.

Indeed, there are simultaneous correlations between economic activities of an area and the performance of a bank. The economic activities of an area may be improved by the role of a bank, yet the performance of a bank depends on the economic activities of an area where the bank is situated. The development of BPDs in Papua, West Papua, Central Kalimantan, and Southeast Sulawesi has been hindered by the limited economic growth in these areas. For instance, prior to operation of their branches in Surabaya and Makassar, the LDR of Bank Papua was only 40%. This number has increased to nearly 70% after the operation of their branches in Surabaya and Makassar, since both cities provide more potential customers.

Although Bank Indonesia has promoted the linkage program between commercial banks and MFIs, the program may not be as easy as it seems. The main challenge faced by BPDs in establishing a linkage program with MFIs is the fact that it is quite difficult to access reliable information about the performance of non-banking financial institutions. BPD Sultra is a perfect example of this problem. There are many cooperatives spread across various areas in Southeast Sulawesi province. Nevertheless, BPD Southeast Sulawesi was skeptical about the performance and the prospects of these cooperatives. As a consequence, BPD Sultra was reluctant to give credit to these institutions. The existence of rural banks in this province is very limited. For this reason, it has been difficult for BPD Southeast Sulawesi to build a linkage relationship with other MFIs, at least in the short to medium term.

Bank DKI has a similar financial networking pattern to Bank Papua, Bank Kalteng, and Bank Sultra (see Figure 3). Indeed, the economic structure and performance in DKI Jakarta are the most vibrant and complex in Indonesia, even though Bank DKI has a simple pattern of financial networking. This is due to the fact that there are plenty of medium and large-scale enterprises and also affluent households in Greater Jakarta (Jabodetabek).

Bank DKI has distributed their credit through multifinance, which has flourished in Jabodetabek. When the transaction costs of providing micro scale credit are similar to medium and large-scale credit, any BPD that is operating in a more vibrant economy tends to focus their efforts on providing medium and large-scale credit. This was the case for Bank DKI, which is totally rational. As an intermediary institution, it is rational for Bank DKI to minimize transaction costs and also risks.

N E T W O R K F O R M A T I O N S O F B P D S 15

Figure 3 Financial Networking of Bank DKI

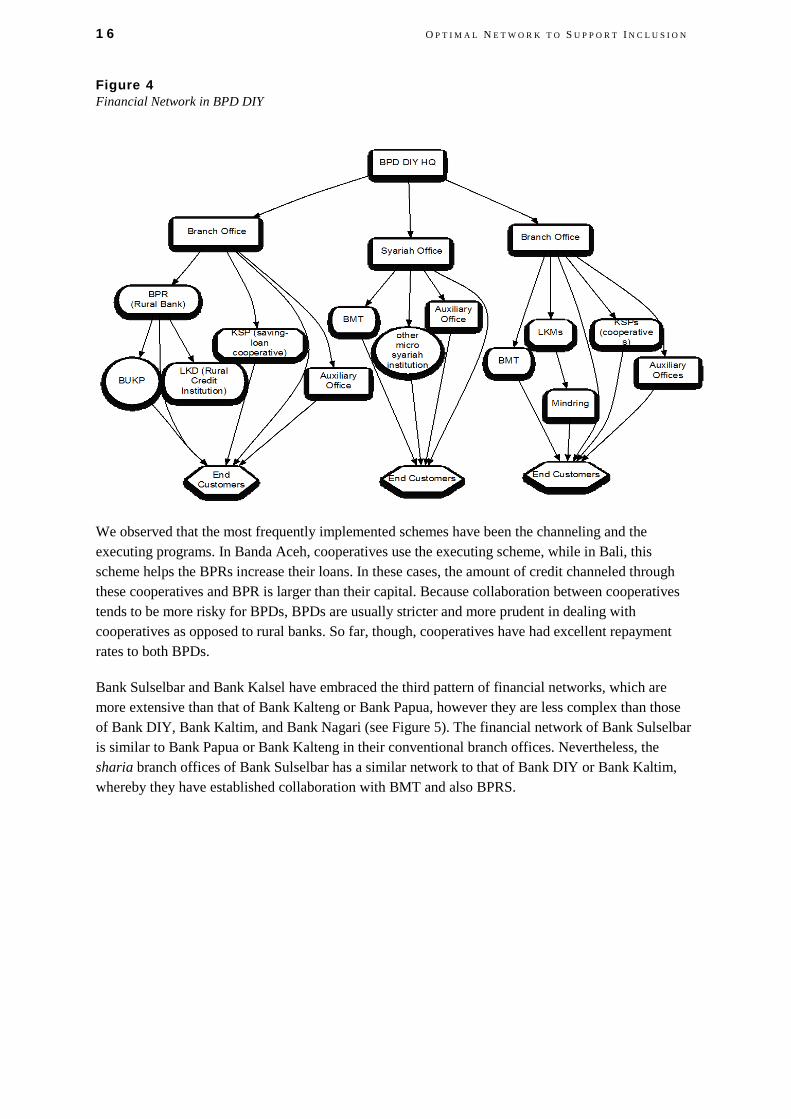

In contrast to the four banks above, the financial network of Bank DIY is much more complex, and involves MFIs channeling credit to small and medium enterprises and low-income households (see Figure 4). BPD DIY reaches their end customers through their branch offices and sharia branch offices. These branch offices have been supported by auxiliary offices, which are situated at Kecamatan (municipal) level.

The conventional branch offices have established cooperation with BPRs (rural banks), KSPs (saving-loan cooperatives), LKMs (micro=credit institutions) and also BMTs (sharia-based rural banks). At the next level, rural banks have cooperated with BUKPs and LKDs (rural credit institutions) before the BUKPs and LKDs reach their end customers. Similarly, mindring (informal commodity credit) may distribute credit that they obtained from LKM to their end customers. The typical mindring entrepreneur obtains capital from LKM, and buys some house appliances to sell to customers. The customers then will pay back the credit on a regular basis, either daily or weekly, to the mindring entrepreneur, who regularly visits the clients’ houses to collect the payment. A similar pattern can be found for the sharia branch offices, which have established cooperation with BMT and other sharia-based micro credit institutions.

16 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

Figure 4 Financial Network in BPD DIY

We observed that the most frequently implemented schemes have been the channeling and the executing programs. In Banda Aceh, cooperatives use the executing scheme, while in Bali, this scheme helps the BPRs increase their loans. In these cases, the amount of credit channeled through these cooperatives and BPR is larger than their capital. Because collaboration between cooperatives tends to be more risky for BPDs, BPDs are usually stricter and more prudent in dealing with cooperatives as opposed to rural banks. So far, though, cooperatives have had excellent repayment rates to both BPDs.

Bank Sulselbar and Bank Kalsel have embraced the third pattern of financial networks, which are more extensive than that of Bank Kalteng or Bank Papua, however they are less complex than those of Bank DIY, Bank Kaltim, and Bank Nagari (see Figure 5). The financial network of Bank Sulselbar is similar to Bank Papua or Bank Kalteng in their conventional branch offices. Nevertheless, the sharia branch offices of Bank Sulselbar has a similar network to that of Bank DIY or Bank Kaltim, whereby they have established collaboration with BMT and also BPRS.

N E T W O R K F O R M A T I O N S O F B P D S 17

Figure 5 Financial Network of Bank Sulselbar

Bank Kalsel shares a similar financial network to that of Bank Sulselbar, however, its conventional bank has a more complex financial network rather than the sharia bank side. Bank Kalsel has established cooperation with multifinances, sharia-based venture capital, cooperatives, and also rural banks in order to channel their credit to end customers.

The financial network of BPDs will depend on their economic performance and structure. As shown in the figures above, the lower performance and simpler structure of the regional economy, the shorter financial network chain of BPDs in financial inclusion process. Nevertheless, there is an extreme point of this phenomenon, since the most complex economic conditions (DKI Jakarta) take Bank DKI to the “simple financial network.” It resembles a “reversed U-shape curve” in its relationship between economic performance and structure and length of financial network of BPDs.

PATTERN OF NETWORKS AND TRANSACTION COSTS From the perspective of BPDs, establishing cooperation with rural banks (BPRs) and sharia rural banks (BPRSs) is simpler than with the other MFIs, such as BMTs, KSPs and LKMs. This is due to the fact that BPDs, BPRs, and BPRSs have been supervised by Bank Indonesia and the banking sector has been highly regulated. It is very easy for BPDs to learn about the performance and the reputation of any BPR and BPRS since all information may be accessed through Bank Indonesia’s website and monitoring reports. Bank Indonesia also provides a health rating for rural banks. This makes the assessment of a rural bank’s performance easier. The rural banks have received sufficient technical or management assistance from Bank Indonesia.

18 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

Figure 6 Relationship between Regional Economic and Financial Inclusion Process

In contrast, establishing cooperation with the other micro credit institutions requires higher transaction costs and risk. In Indonesia, the non-banking financial industry, such as venture capital, multi-finance, insurance, etc. had been monitored and regulated by Bappepam-LK, and since 2013 has been monitored and regulated by OJK (financial service authority). Cooperatives are regulated and supervised by the Ministry for Cooperatives, some portion of credit unions are supervised by Inkopdit, some part of Baitul Maal wat-Tamwil or BMTs are supervised by PINBUK, and Rural Credit and Saving Institutions are supervised by the regional government. In contrast to Bank Indonesia, which has provided information on the rating of all commercial banks, there is no rating system that ranks non-banking MFIs according to their health. In addition, there are also many non-banking MFIs that are not supervised by a legal institution, such as some village-based groups or various informal lenders.

As a central bank and the lender of last resort, Bank Indonesia has used three pillars in conducting banking supervision: micro-prudential, macro-prudential, and business conduct. In contrast, Bappepam-LK used only one pillar (business conduct) to supervise non-banking financial institutions. Kemenkop-UKM, on the other hand, has used cooperative principles to supervise all types of cooperatives, including cooperative-based financial institutions like BMT. Since BPDs are the part of the banking sector that has embraced prudential measures, it is less risky to establish cooperation with BPR and BPRS, which have been supervised by BI, instead of the MFIs.

Sometimes, MFIs implement a customized method in their operation that is considered too risky for a bank to do. For example, some non-banking MFIs do not ask for collateral and do not need a thorough screening analysis for loan clients that have a good track record of repaying the loan in the previous period. These facts make any commercial bank that wants to build a linkage relationship with non-bank MFIs uncertain and cautious about the real performance quality of non-bank MFIs. Thus, in order to ensure the quality of the non-bank MFIs, the bank tends to make a bigger effort and incur higher costs to analyze the performance of non-banking MFIs. In addition, for the banks that do not want the burden of this extra cost, they simply cancel their plan to make a linkage with non-banking

N E T W O R K F O R M A T I O N S O F B P D S 19

MFIs. Unfortunately, the group of MFIs that is avoided by banks is scattered in many areas and probably has a lot of potential to reach the unbankable population.

The implementation of MFI, especially for the non-banking MFIs, must carefully consider the costs borne by both the oversight body and for the MFIs in terms of compliance costs. These tend to be substantial for microfinance (more than the standard banking system) given the number and diversity of activities that compose the sector, the higher degree of decentralization, and the more labor-intensive nature of inspecting MFI portfolios (Christen, et al. in Pouchous, 2012).

Similar patterns of financial networks to BPD DIY are found in Bank Bali, Bank Jateng, Bank Jatim, Bank Nagari (West Sumatera), and Bank Kaltim. The variation of the financial networks among those banks arises from cultural factors. For instance, Bank Bali has established cooperation with LPDs that are situated at the village level. The driving force of the establishment of LPDs in Bali involves cultural factors that are only applicable in Bali.

It is interesting to see the similarities between the financial networks of BPD DIY and Bank Kaltim. In both cases, mindring (informal commodity credits) are part of their financial networks. In Bank Kaltim, bank plecit (informal money lenders) are part of the financial network, however this phenomenon cannot be found in BPD DIY. These similarities are due to the fact that the majority of financial institutions and the end costumers at both Banks are Javanese.

We know from surveys that most BPDs utilize the intermediation facilities and distribution pillar of the financial inclusion framework through the expansion of their own service units, whether they are branch-offices, auxiliary-offices, mobile cash, cash payments, or ATMs. Almost all BPDs surveyed are in a cooperation program with government institutions (in terms of various credit programs). The linkage strategy, especially with rural banks, also becomes one of the main strategies taken by most BPDs to support financial inclusion.

One unique case that needs to be mentioned is the development of the payment system in BPD East Java. Besides their success in becoming the APEX Bank of rural banks, they also have become the first BPD that is successful in building and implementing a real time payment system for their APEX BPR, called JETS (Jatim Electronic Transfer System). The implementation of the system enables more people to access more complete services from financial institutions.

Patterns of networking by BPDs may be different from those of commercial banks. Although commercial banks have similar micro-credit programs, the banks are used to minimizing transaction costs through financial networking. In this case, the risk of financial institutions being related becomes a focus for commercial banks. For this reason, most commercial banks tend not to have longer financial networks, especially in the micro-finance market. Additionally, commercial banks can divert funds for cooperation with MFIs to other areas.

5. Interest Rates and Prudential Measures The effectiveness of Bank Indonesia’s regulation and supervision may be seen in the interest rates that have been set by BPD, BPR, and BPRS. In general BPD and BPR may only take a 2-3% per annum interest rate margin from their credits, which is considered very conservative. Suppose BPD provides credit to BPR with an interest rate of 13%, and then BPR takes a margin of 2% - 3% and charges the end customer an interest rate of 15% - 16%. This happened to both BPD and BPR implementing the prudential measures imposed by Bank Indonesia. In order to obtain credit from BPDs or BPRs, a potential customer has to fulfill 5C principles, the conditions of economy, capacity, capital, collateral, and character. Any potential creditors that may fulfill these prudential measures, lowers the risk to lend money to him/her in comparison to those who cannot fulfill the measures.

The main difference between BPDs and any other financial institutions is in its interest rate system. All sampled BPDs have been implementing the effective rate system instead of a flat interest rate system, which has been used by the other financial institutions.14 The effective rate system allows debtors to have an amortization system during the payment period. It seems to be effective in capturing the customers in the micro-financial market because they consider the effective rate system to be more beneficial than the flat rate system. Also, this could be a strategy for BPDs in the competitive market by creating price competition through reducing the real interest rate.

This feature may not be found in the related MFIs and commercial banks. Although related MFIs may obtain a loan with the interest rate of 13% (effective rate system) from BPDs, they may lend their credit to either members or customers at an interest rate of 20% (flat rate system) or more.15 This occurred when MFIs do not necessarily need to implement comprehensive prudential measures at the same level as BPDs and BPRs. Furthermore, their existing regulatory and supervisory institutions might not impose prudential measures as strictly as Bank Indonesia. Indeed, this may occur from the difference in the nature of business across the financial institutions. For some cooperatives, for instance, they only lend money to active members. Nevertheless, some cooperatives may extend their business by offering credit to potential members, even though the individuals have not yet become active members.

Concerning the issue of the inadequacy of standard supervisory tools, Christen, et al. in Pouchous (2012) argued that traditional inspection and audit instruments are not appropriate for microfinance. This is because some management situations of bank MFIs (or MFI clients) are different from non-

14 The effective rate system is widely used by all BPDs in Indonesia. This system had implemented the amortization system, in which the real interest rate imposed to the customers was about 60% - 70% of the nominal interest rate.

15 The high interest rate imposed by MFIs is naturally accepted by either members or customers. Flexibility and ease of the MFIs is preferable compared to other formal financial institutions.

22 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

banking MFIs. For example, the documentation management of non-bank MFIs tends to be more poorly reported compared to banking MFIs. In addition, the complexity of policy and characteristics of MFIs ask for more specialized techniques and expertise in MFI supervision. Other examples include the recommendation of capital calls, top lending orders, and mergers that cannot be fulfilled by MFIs.16

Box 2. Prudential Measures of Bank Nagari Bank Nagari has been actively building relationships with other financial institutions in order to participate in the financial inclusion process. This includes rural banks, cooperatives, BMTs, and business units. Its relationship with cooperatives, BMTs, and business units has been problematic, since they are not under Bank Indonesia’s system. This is different for rural banks, yet still causes Bank Nagari to be more concerned about those financial institutions.

In this case, Bank Nagari develops a relationship with the related agencies of local government in monitoring cooperatives, BMTs, and business units. The local government’s agencies can supervise them or give a recommendation to access funds from Bank Nagari. Also, Bank Nagari utilizes the cultural approach, providing a fieldwork team to monitor the debtors.

The monitoring of Bank Nagari serves as an indirect assessment of rural banks. Most rural banks do not take risks in channeling funds to either new or un-recommended debtors according to their neighbors. Those approaches are needed by both Bank Nagari and rural banks in order to minimize the risk of micro-finance institutions.

A higher rate of interest, which has been imposed by the MFIs, also occurs due to social norms around borrowing money from private lenders. In Java, for instance, people are accustomed to using the term nelulasi (Javanese, meaning the rule of thirteen). Nelulasi is a common interest rate of Javanese people in which the lender takes about 30% on each maturity date. It should be noted that this rate is based on a flat rate, thus the variable rate may reach about 40%. The period of borrowing depends on private agreement between the borrower and the lender, thus given the rate of interest, the longer the period of borrowing agreed by both parties, the stronger the advantage for the borrower over the other party. The private moneylender, or bank plecit and also mindring, may use this interest rate as a reference.

In the future, all financial institutions will be supervised and regulated by OJK. The scope of OJK will cover all forms of financial institutions (in both the banking and non-banking systems). It will include cooperatives, BMTs, KSPs, and other MFIs as mandated in Act No. 21/2011 and Act No. 1/2013. BPDs, however, will feel the impact of this act, even though they are not under OJK supervision, since their financial networks are capturing those financial institutions’ forms. The challenge for OJK is whether it can match the performance of Bank Indonesia, which successfully managed the interest rate margin between BPDs and BPRs.17

16 For further information, see “A Guide to Regulation and Supervision of Microfinance” (CGAP, 2012) 17 As it is mandated in Act No 21/2011 and Act No. 1/2013, the OJK have not regulated the technical aspects

of running a micro-financial business. To some extent, this needs to be revised in order to strengthen the supervisory role of OJK to the MFIs.

6. Consumptive versus Productive Credits One of the indicators for BPDs is whether they achieve Bank of Regional Champion (BRC) status, which includes all BPDs with at least IDR 1 trillion of core capital by 2014. Furthermore, they are required to provide more productive credit, which has a consumptive credit ratio of 60%:40%. In December 2012, Bank Indonesia issued a decree, No.14/26/PBI/2012, which rules that banks with core capital less than IDR1 trillion have to provide 55% of their credit for the productive sector. In addition, any bank with core capital between IDR1 trillion to IDR5 trillion should lend 60% of total credit to the productive sector. These bank classifications seem to be suitable for the size of BPDs, but the question raised is: are these objectives achievable?

Based on interviews with the BPDs sampled, the ratio of productive credit against consumptive credit is 20%:80%. In relation to the BRC, regulators need to ask whether BPDs manage to fulfill the ratio of 40%:60% for their credit. Indeed, this is a very steep objective that may not be fulfilled, although we cannot say it is impossible.

There are several factors that are attributable to the complexity of BPDs in achieving some of the performance of BRC indicators. First, in all sampled BPD, the civil servants’ salary in the respective region was paid through BPDs. Second, civil servants are the most contestable customers since the risk to lend money to them is near zero. In Indonesia, civil servants have only a slim probability of losing their jobs, and, moreover, they are subjects of insurance and pension schemes. Consequently, for any BPD, giving consumptive credit to civil servants is a dominant strategy since the risk is low, the transaction costs are low, and the loans are safe because BPD distributes civil servants’ salary every month.

From the perspective of BPD, it is easier and safer to give consumptive credits to civil servants compared to providing productive credit to the other members of society. Although the interest rate of the consumptive credit is about 2% – 3% lower than the productive credits, providing consumptive credit to civil servants is more compelling to BPDs, since the risk and the transaction costs of the credit are low.

The average amount of the consumptive credit given to civil servants is about IDR100 million to IDR200 million.18 After BPD has approved a civil servant’s loan, the civil servant may allocate the money for consumptive purposes or for productive purposes. The problem is, up until now, even the BPDs themselves do not know what portion of the application for consumptive credit sought by civil servants has been allocated for productive activities. This unobserved heterogeneity can be estimated, which puts the expected proportion of productive to consumptive credit in excess of 20%:80%.

18 This micro-credit type is also provided for micro-scale enterprises to some extent.

24 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

All BPDs under ASBANDA must also satisfy the PBI No. 14/26/PBI/2012 in the same way as commercial banks.19 Yet, there is lenience for BPDs to satisfy the requirements of PBI No. 14/26/2012 by the end of 2017, while commercial banks are required to satisfy it by the end of 2015. The main problem for BPDs is the potential conflict of interest between BRC and the PBI on channeling funds to either the productive or consumptive sector. It is widely known that BRC requires a higher portion of productive credits than for PBI (60%:55%).

19 PBI No. 14/26/PBI/2012 will later regulate business plans and activities for all of the bank’s forms according to the core capital.

7. Culture and Financial Inclusion The availability of local and traditional financial institutions influences the development of BPDs. A BPD’s approach to both local culture and people could strengthen financial networks. Yet, the idea of financial inclusion may be defined differently between regions. For example, Bali shows that BPDs can have made a longer financial network, as long as MFIs are bounded with norms. BPD DIY, for example, shows that they are allocating funds for local culture and people in order to achieve customer loyalty. In this section, we introduce the role of related financial BPD businesses that have benefited from and taken a cultural approach.

Bank Plecit are private moneylenders that give loans to people at high interest rates (up to 20% - 50% per month). Such businesses are doing well because of friendships and because bank plecit are usually located far from formal financial institutions. Location is a key reason poor people choose bank plecit to borrow money, even though they impose very high interest rates.

Box 3. The Features of Bank Plecit (private money lender) Bank Plecit mostly operate in Java Island, and serves the customers twenty-four hours a day. Theoretically, customers should not prefer it because Bank Plecit charges a higher interest rate than any other financial institution. Nevertheless, most customers, especially in the traditional market, are accustomed to its service because no significant requirements are needed by Bank Plecit. It seems to be the main competitor for not only for micro-financial institutions, but also for commercial banks.

In some sense, the operation of bank plecit increases the number of poor people with access to financial resources. Indeed, bank plecit mirrors the micro-finance market, as its funds help smooth poor people’s consumption or income. As mentioned by BPD branch managers in Bantul and Kulonprogo, they have to compete against the bank plecit in the effort to include small-scale firms or households. Poor people generally prefer the convenience and easy access to financial sources, rather than preferential interest rates. Informality and ease could be the key for BPDs to attract the poor.

Beside bank plecit, there are mindring,20 a traditional commodity-based lending system. Mindring are conducted by selling goods (usually house appliances), with the clients paying credit on a regular basis, usually every pasaran (every five days according to Javanese lunar calendar) or weekly. The minding business provides commodities, instead of funds, to his/her customers or members whom the

20Mindring is a goods selling business conducted by an individual with other individuals using a credit system. The credit payment is conducted daily or weekly, depending on agreement between creditors and customers. Goods sold and credited include household appliances, electronic equipment, and clothes. The creditor (mindring provider) takes a profit rate between 50% up to100% in two months. So, the interest rate of mindring was about 25% up to 50% per month.

26 O P T I M A L N E T W O R K T O S U P P O R T I N C L U S I O N

entrepreneur knows well. Knowing the members/customers is paramount in this business since the system requires trust and kinship from both creditors and debtors, and because there are no provisions to the loans. The mindring providers usually visit the debtors daily to collect payments, and perform monitoring and evaluating debtor’s loan performance.