Nepalese Journal of Management - Uniglobe College

117

Nepalese Journal of Management A Publication of New Baneshwor, PO Box: 7953, Kathmandu, Nepal | Tel: 977-1-411 56 90 / 411 55 69 Email: [email protected] | URL: www.uniglobe.edu.np Pokhara University Affiliate JULY 2014 VOLUME 1 NUMBER 1 N M J

-

Upload

khangminh22 -

Category

Documents

-

view

6 -

download

0

Transcript of Nepalese Journal of Management - Uniglobe College

Nepalese Journal of Management

A Publication of

New Baneshwor, PO Box: 7953, Kathmandu, Nepal | Tel: 977-1-411 56 90 / 411 55 69

Email: [email protected] | URL: www.uniglobe.edu.np

Pokhara University Affiliate

JULY 2014 VOLUME 1 NUMBER 1

NMJ

Chief Editor Dr. Radhe S. Pradhan Academic Director, Uniglobe CollegeExecutive Editor Dr. Nar Bahadur Bista Principal, Uniglobe CollegeAdvisory Board Prof. Alojzy Z. Nowak Faculty of Management, University of Warsaw Prof. Muhammad Z. Mamun Unversity of Dhaka, Bangladesh Prof. Jayanta K. Parida Utkal University, Bhubaneshwor, India Prof. Voradej Chandarasorn President, Shinawatra University, Thailand Prof. Jawahar Lal Srivastav University of Delhi, India Dr. Khagendra P. Ojha Chairman, Uniglobe College Dr. Manish Thapa IR Director, Uniglobe College Mr. Gangadhar Dahal Executive Director, Uniglobe CollegeEditors Dr. Niraj Poudyal Research Director, Uniglobe College Dr. Ramji Poudyal Visiting Faculty, Uniglobe College Mr. Dipkar Thapa Program Director, Uniglobe College Mr. Keshav Acharya Faculty, Uniglobe College Mr. Shikhar Nepal Faculty, Uniglobe CollegeDesign and Layout Mohan Himamshu Dahal

Production Team Min Bahadur Bista Khima Dahal Madhav Subedi Bishnu ThapaPrinted in Nepal

Nepalese Journal of ManagementJULY 2014 VOLUME 1 NUMBER 1

NMJ

Editorial Policy

Nepalese Journal of Management (NJM) is the official publication of the Uniglobe College (Pokhara University affiliate). It is published on half-yearly basis. Annual subscription rates are Rs. 500 for libraries and organizations, and Rs. 300 for individuals. For availability of back issues, contact Executive Editor, NJM. Claims for missing copies must be made within three months of publication to Executive Editor, NJM, Uniglobe College 977-1-411 56 90/ 411 55 69, Fax: 411 55 69, E-mail: [email protected]. The subscribers are requested to add postage charges on subscription rates. Send address changes and correspondence related to dues and subscriptions to the Executive Editor NJM, Uniglobe College.

The basic objective of the publication is to promote research in the area of management especially in the context of Nepal. This publication also aims at bringing into light research reviews, analysis, theoretical comments, theoretical and empirical research on the various aspects of management with emphasis on the problems of developing countries especially Nepal. It contains articles and research notes related to major issues and the results of research carried out by the members of the College and other professional experts on management. Nepalese Journal of Management (NJM) welcomes contributions from national and international scholars and professionals concerned with Management.

NMJ

NotesArticles are subject to editorial review by referees from the community of Management experts. Comments or notes regarding articles are welcome and will be considered tor publication to the extent that space permits. The opinions and the interpretations expressed in the articles are the personal opinions of authors and reviewers and do not necessarily reflect the views of the publisher and editors, or of any institution with which the author may be associated. The Editorial Board does not guarantee the accuracy of data and the information included in the articles and accepts no responsibility, whatsoever, for any consequences of their use.

Subscription InformationNepalese Journal of Management (NJM) is a Journal published half yearly by the Uniglobe College. The publication is for the benefit of the management experts, economists, planners, professionals as well as those interested in management. Copies of the Journal may be subscribed/purchased from the Uniglobe College. The subscription rates are as follows:

Individuals Library and Institution Per Copy One Year Per Copy One Year Nepal Rs. 300 Rs. 500 Rs. 500 Rs. 900SAARC Countries US $6.0 US $ 10.0 US $8.0 US $ 15.0Other Countries US $8.0 US $ 15.0 US $12.0 US $ 22.0

Mailing charge to be paid extra.Claims for the missing numbers should be made within the month following the regular month of publication. The publisher will supply the missing numbers free of cost only when it is confirmed and when the reserve stock permits.

If you change your address, please notify us immediately, giving both your old and new addresses. Allow five weeks for the change. Back issues prior to last year's volume, if available, can be obtained from the college. Request for the subscriptions should be addressed to:

Nepalese Journal of Management (NJM) Uniglobe College, New Baneshwor

Kathmandu, Nepal.PO Box: 7953

Phone # 977-1-4115690, 4115569.Format for Subscription Request.......................................................................................................................................................................................

I would like to subscribe to Nepalese Journal of Management, a half yearly publication of theUniglobe College, New Baneshwar, Kathmandu, Nepal.

Subscription type: Personal Institutional Vol. ...................... Issue .....

For: 1 Year 2 Years ...................... Years .

Mode of payment: Cash/Cheque/Draft Total amount NRs. /US$ ...........................................

Name & Designation: ............................................................................................................................................

Institution: ...............................................................................................................................................................

Mailing Address: ....................................................................................................................................................

Telephone: ................................................. E-mail: ........................................................ Fax: .............................

.......................................................................................................................................................................................

Please transfer the amount to Nepalese Journal of Management,

- Citizens Bank International Ltd., New Road, Kathmandu

Account No: 0070000032CC, SWIFT: CTZNNPKT

- Please do not send cash by mail.

- Only cheques drawable in Kathmandu will be accepted.

ContentsThe cross-section of expected stock returns in Nepal .......... 1-9 Prof. Dr. Radhe S. Pradhan

Corporate culture and firm performance: A case of Nepalese commercial banks ....................................................................... 10-20Kavina Shrestha

Factors influencing customer adoption in internet banking: A study on Nepalese commercial banks ................ 21-29 Regina Shrestha

Disclosure practices in Nepalese insurance companies........ 30-42Prof. Dr. Prashant Kumar and Rabindra Ghimire

Factors influencing customer adoption in internet banking: A study on Nepalese commercial banks ................ 43-53Jyoti Kafle

CPFR practices in automobile industry in India ............. 54-66Dr. A.K. Verma

Impact of customer relationship management efforts on customer loyalty in Nepalese commercial banks ............. 67-75Neeta Joshi

A comparative study of organizational culture in public and private Banks .............................................. 76-86Shavina Goyal, Angadveer Singh Bhatti & Dr. Navjot Kaur

Employees’ job satisfaction and financial performance: A case of Nepalese commercial banks ........... 87-99Kushal Joshi

Service quality, customers’ satisfaction and customers’ loyalty in commercial banks of Nepal ............... 100-106Manju Maharjan

Nepalese Journal of ManagementJULY 2014 VOLUME 1 NUMBER 1

NMJ

The cross-section of expected stock returns in Nepal

- Prof. Dr. Radhe S. Pradhan*

AbstractThe CAPM asserts that market betas are sufficient to explain the cross section of expected stock returns. However, beta showed either no relationship or a weak relationship with the expected stock returns when other company specific variables affecting stock returns are used. This study aims at examining the ability of beta and other company specific factors such as firm size, book to market ratio, sales to price ratio, dividend yield and earning price ratio to explain cross section of stock returns in Nepal. The study reveals that the beta has a very weak relation with stock returns in Nepal. The coefficient of beta is not significant and hence there is no evidence that beta explains variation of stock returns. The study showed that size, dividend yield, and book to market ratio has been found to be significant factors affecting stock returns in Nepal while beta, earning price ratio, and sales to price ratio do not explain the variation in stock returns.

Keywords: beta, book to market ratio, dividend yield, earning price, firm size, sales to price ratio, stock returns.

*Dr. Pradhan was Professor, Central Department of Management, Tribhuvan University, and currently serving as Academic Director, Uniglobe College affiliated to Pokhara University..

1

Nepalese Journal of Management

1. Introduction

The pricing implication of common stocks has drawn considerable attention since the publication of seminal work of Markowitz (1952) - the mean-variance portfolio theory. Since then there is an ongoing debate on whether the market risk factors explain better or there are some other anomalies influencing common stock returns. Based on the mean-variance portfolio theory, Sharpe (1964), Linter (1965), and Black (1972) then proposed extensively argued asset pricing theory- the capital asset pricing model (CAPM). The central prediction of the CAPM is that the rate of return associated with common stocks investment is determined by the extent to which the common stock returns are correlated with market portfolio. CAPM asserts that the market risk factors proxied by beta can capture significant variation in common stock returns.

Asset pricing theories attempt to understand why some assets have higher returns than other assets. In early stages of the corporate finance, investors and researchers began attributing higher returns for higher risk. It is only with the development of the CAPM that economist

NEPALESE JOURNAL OF MANAGEMENT VOL.1, NO.1, JULY 2014

NMJ

were able to quantify risk and the reward for bearing it. The CAPM asserts that expected returns of assets are a positive linear function of their market betas and market betas are sufficient to describe the cross section of expected returns.

However, empirical work on asset pricing has identified a number of variables that help explain cross sectional variation in stock returns in addition to the market risk variable. Notably, firm size (Banz, 1981; Keim, 1983), leverage (Bhandari,1988), P/E ratio (Basu, 1983), ratio of cash flow to stock price (Rosenberg et al., 1985), book to market equity (Fama and French, 1992), and past sales growth (Lakonishok et al., 1994) are among those that are found to have significant explanatory power in asset pricing tests. In their seminal work, (Fama and French, 1992) found that book to market equity stands out as the most significant factor in explaining cross section of returns. Market risk measured by beta, on the other hand, has no explanatory power. The challenge posed by the (Fama and French, 1992) findings to traditional structural models has created a significant hurdle to the understanding of more complex and dynamic properties of the cross section of stock return.

The study by (Chan et al., 1991) related the cross sectional differences in stock returns on Japanese stocks to the underlying behavior of four fundamentals variables: earnings yield, size, book to market ratio and cash flow yield. Of the four variables considered, book to market value ratio and cash flow yield have been found to be most significant variables affecting expected returns.

The empirical studies pointed out many inconsistencies in the CAPM that prescribes that expected stock return is directly related to systematic risk. The most noteworthy is the size effect on expected stock return. The size, measured as the market value of equity (ME), has significant impact on the stock return, that is, smaller size of the firm, higher would be the returns (Banz and Reinganum, 1981). In Malaysia, size variable alone explains about one third of the expected stock returns (Pandey and Chee, 2001). The finding indicates the significance of B/M ratio disappears in multivariate regressions that also include E/P ratio. It is also indicated that market beta with or without other variables has a positive relation with stock return. The other significant variables include E/P ratio, dividend yield and leverage.The above shows that a number of studies have been conducted on the stock returns in developed and big capital markets but their relevance is yet to be seen in the context of emerging capital markets. Information on stock returns in such emerging capital markets would help development of realistic theoretical models and formulation of relevant hypotheses for empirical testing in finance.

In Nepal, the listing of shares in stock exchange and their trading in the stock market is still not very popular. The Nepalese stock market is still characterized by a low trading volume, absence of professional brokers, early stage of growth, limited movement of share prices, and limited information available to investors. Viewed in this way, this study devoted to stock returns in Nepal carries a lot of significance. There is a need to arouse investors’ interest in stock markets leading to pursuit of higher returns. Little is known about the nature of stock returns in Nepalese capital market.

A study on fundamentals of stock returns in Nepal revealed that dividend yield, capital gain yield and total yield are related to earnings yield, size book to market ratio and cash flow yield (Pradhan and Balampaki, 2006).

Nepalese Journal of Management 2

This study aims at examining the ability of beta and company specific factors like size, book to market ratio, sales to price ratio, dividend yield and earning price ratio to explain stock returns in context of Nepal. The remainder of this paper is organized as follows. Section two describes the sample, data, and methodology. Section three presents the empirical results and the final section draws conclusions and discusses the implications of the study findings.

2. Methodological aspectsThe study is based on the secondary data which were gathered for 23 banks in Nepal for the period 2006/07 to 2011/12, leading to the total of 138 observations. The secondary data have been obtained from data base maintained by office of the Security Board of Nepal (SEBON), NEPSE and other concerned banks.

The pooled cross-sectional data analysis has been undertaken in the study. The research design adopted in this study is causal comparative type as it deals with relationship of beta, size, book to market ratio, sales to price ratio, dividend yield, and earnings price ratio with stock returns. More specifically, the study examines the effect of beta, size, book to market ratio, sales to price ratio, dividend yield, and earnings price ratio on stock returns. These data were collected for the period 2006/07 to 2011/12. Table 1 shows the number of commercial banks selected for the study along with the study period and number of observations.

Table 1: Number of commercial banks selected for the studyS. No. Name of the commercial banks Study period Observations

1 Ratriya Banijya Bank Limited 2006/07-2011/12 6

2 Nepal SBI Bank Limited 2006/07-2011/12 6

3 Bank of Kathmandu Limited 2006/07-2011/12 6

4 Citizens’ Bank International Limited 2006/07-2011/12 6

5 Laxmi Bank Limited 2006/07-2011/12 6

6 DCBL 2006/07-2011/12 6

7 Agricultural Development Bank Limited 2006/07-2011/12 6

8 Bank of Asia Limited 2006/07-2011/12 6

9 Nepal Investment Bank Limited 2006/07-2011/12 6

10 Nepal Standard and Chartered Bank Limited 2006/07-2011/12 6

11 Himalayan Bank Limited 2006/07-2011/12 6

12 NMB Bank Limited 2006/07-2011/12 6

13 Lumbini Bank Limited 2006/07-2011/12 6

14 NABIL Bank Limited 2006/07-2011/12 6

15 NIC Bank Limited 2006/07-2011/12 6

16 Global Bank Limited 2006/07-2011/12 6

17 Kumari Bank Limited 2006/07-2011/12 6

18 Everest Bank Limited 2006/07-2011/12 6

19 Machhapuchhre Bank 2006/07-2011/12 6

20 Prime Bank Limited 2006/07-2011/12 6

21 Sidhartha Bank Limited 2006/07-2011/12 6

22 Sunrise Bank Limited 2006/07-2011/12 6

23 Nepal Bangladesh Bank Limited 2006/07-2011/12 6

Total number of observations 138

Pradhan 3

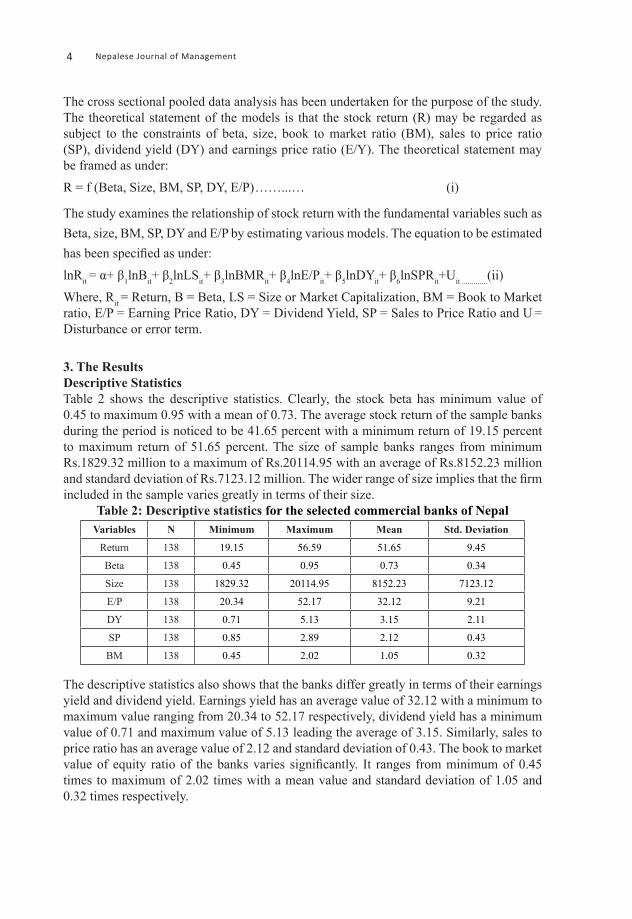

The cross sectional pooled data analysis has been undertaken for the purpose of the study. The theoretical statement of the models is that the stock return (R) may be regarded as subject to the constraints of beta, size, book to market ratio (BM), sales to price ratio (SP), dividend yield (DY) and earnings price ratio (E/Y). The theoretical statement may be framed as under:R = f (Beta, Size, BM, SP, DY, E/P) ……...… (i)

The study examines the relationship of stock return with the fundamental variables such as Beta, size, BM, SP, DY and E/P by estimating various models. The equation to be estimated has been specified as under:lnRit = α+ β1lnBit+ β2lnLSit+ β3lnBMRit+ β4lnE/Pit+ β5lnDYit+ β6lnSPRit+Uit .............(ii)Where, Rit = Return, B = Beta, LS = Size or Market Capitalization, BM = Book to Market ratio, E/P = Earning Price Ratio, DY = Dividend Yield, SP = Sales to Price Ratio and U = Disturbance or error term.

3. The ResultsDescriptive Statistics Table 2 shows the descriptive statistics. Clearly, the stock beta has minimum value of 0.45 to maximum 0.95 with a mean of 0.73. The average stock return of the sample banks during the period is noticed to be 41.65 percent with a minimum return of 19.15 percent to maximum return of 51.65 percent. The size of sample banks ranges from minimum Rs.1829.32 million to a maximum of Rs.20114.95 with an average of Rs.8152.23 million and standard deviation of Rs.7123.12 million. The wider range of size implies that the firm included in the sample varies greatly in terms of their size.

Table 2: Descriptive statistics for the selected commercial banks of NepalVariables N Minimum Maximum Mean Std. Deviation

Return 138 19.15 56.59 51.65 9.45

Beta 138 0.45 0.95 0.73 0.34

Size 138 1829.32 20114.95 8152.23 7123.12

E/P 138 20.34 52.17 32.12 9.21

DY 138 0.71 5.13 3.15 2.11

SP 138 0.85 2.89 2.12 0.43

BM 138 0.45 2.02 1.05 0.32

The descriptive statistics also shows that the banks differ greatly in terms of their earnings yield and dividend yield. Earnings yield has an average value of 32.12 with a minimum to maximum value ranging from 20.34 to 52.17 respectively, dividend yield has a minimum value of 0.71 and maximum value of 5.13 leading the average of 3.15. Similarly, sales to price ratio has an average value of 2.12 and standard deviation of 0.43. The book to market value of equity ratio of the banks varies significantly. It ranges from minimum of 0.45 times to maximum of 2.02 times with a mean value and standard deviation of 1.05 and 0.32 times respectively.

Nepalese Journal of Management 4

Correlation analysisHaving indicated the descriptive statisitics, the Pearson Correlation Coefficients have been computed and the results are presented in Table 3. All the correlations can be considered as low since the highest correlation has been observed to be 0.567 between ln Size and ln SP. The lowest correlation of -0.132 has been observed between stock return and DY. The stock return is negatively related to DY and BM and positively related to beta, size, E/P and SP. Beta has a positive correlation with Size, E/P, and SP.Table 3: Computation of correlation coefficients for the selected commercial banks of

NepallnReturn lnBeta lnSize lnE/P lnDY lnSP ln BM

lnReturn 1

lnBeta .295 (.192) 1

lnSize .253 (.162)

.521* (.012) 1

lnE/P .231 (.289)

.326 (.115)

.455 (.112) 1

lnDY -.132 (.389)

-.453* (.069)

-.552 (.023)

-.732 (.012) 1

lnSP .267 (.189)

.452* (.092)

.567* (.028)

.211* (.298)

-.512* (.039) 1

lnBM -.457* (.102)

-.221 (0.235)

-.239 (.198)

-.235 (.178)

.236 (.178)

-.283 (.281) 1

Notes: 1. Figures in parentheses are t-values.2. The sign * denotes that the results are significant at 5 percent level of significance.

Regressions resultsIn order to analyze the effect of beta, size, E/P, DY, SP and BM on stock returns, the regression equations specified earlier are estimated and the results are presented in Table 4. The regression coefficients for beta are positive in all the regression equations indicating that higher the beta, higher would be the stock returns though the results are not significant at 5 percent level of significance. Stock returns are better explained by size as beta coefficients are all positive and significant at 5 percent level of significance. It indicates that larger the size of the firm, higher would be the stock returns. Among others, this finding supports the findings of Banz (1981), Reinganum (1981), Keim (1983) and Fama and French (1992).

However, the earnings yield (E/P) could explain the variation on stock returns as beta coefficients for this variable are sometimes positive and sometimes negative and the results are also not significant at 5 percent level of significance. But the dividend yield (DY) has been found to be an important factor affecting stock returns as not only beta coefficients are positive but they are also significant at 5 percent level of significance. It indicates that higher dividend yield leads to higher stock returns. This finding on dividend yield, among others, support the findings of Lamont (1980) and Boudoukh et al. (2007). Like earnings yield, sales to price ratio could not explain the variation in stock returns as the signs of beta coefficient

Pradhan 5

are not consistent and the results are also not significant at 5 percent level of significance. However, book to market (BM) has been found to be an important factor affecting stock returns as beta coefficients are consistently negative and significant at 5 percent level of significance in all the equations. It indicates that higher the book to market, lower would be the stock returns. Among others, this finding is in consistency with the findings of Stattman (1980) and Chan et al. (1991).

Table 4: Results for the regression of beta, size, E/P, DY, SP and BM on stock returnsThe results are based on pooled data of 23 selected banks for the period of 2006/07 to 2011/12, leading to the total of 138 observations. The model is, lnRi = α+β1lnBetai+ β2lnSizei+ β3lnBMi+ β4lnE/Pi+ β5lnDYi+ β6lnSPi+Uit where, BM= book to market ratio, E/P = earning price ratio, DY = dividend yield, SP = sales to price ratio.

Models InterceptRegression Coefficients of

Adj. R-bar2 F DW

lnBeta lnSize lnE/P lnDY lnSP lnBM

(1)2.11

(8.21)0.41

(0.92)0.34 20.75 1.34

(2) 9.12(4.23)

1.32(2.32)*

0.43 19.84 1.57

(3) 7.21(2.23)

-0.65(1.32)

0.31 17.45 1.87

(4) 4.78(2.38)

1.98(2.87)*

0.45 30.65 1.35

(5)10.32(2.87)

-0.92(0.78)

0.31 32.72 1.74

(6)-0.92

(2.82)*0.48 29.21 1.60

(7)2.36

(2.23)0.28

(1.43)1.42

(2.91)*-1.85(1.13)

0.78 35.67 2.09

(8)3.21

(3.23)0.33

(0.62)0.28

(2.84)*-1.73

(3.27)*0.82 39.28 1.94

(9)6.21

(2.73)0.46

(0.83)0.86

(2.66)*0.54

(2.87)*-0.45(-3.24)*

0.75 43.31 1.96

(10)3.59

(3.86)0.392(1.34)

1.43

(3.13)*

0.45

(1.45)

2.21(4.14)*

-0.16(-.63)

-0.67(-4.65)*

0.82 47.95 2.04

Nepalese Journal of Management 6

4. Summary and conclusionAttempts were made by asset pricing theories to understand why some assets have higher returns than other assets. According to CAPM, the expected stock returns are a positive linear function of their market betas. The model asserts that market betas are sufficient to explain the cross section of expected stock returns. As a result, the CAPM has been widely used by portfolio mangers, institutional investors, financial mangers and individual investors to predict asset returns. Beta is a measure of systematic risk in CAPM and is assumed to be positively related to stock returns. However, several studies revealed that other variables could significantly explain the variation in stock returns and the beta showed either no relationship or a weak relationship with the expected stock returns.

The studies on cross-sectional variation in common stock returns provide an important insight into the understanding of pricing implication of common stock. This study aims at examining the ability of beta and company specific factors such as firm size, book to market ratio, sales to price ratio, dividend yield and earning price ratio to explain cross section of stock returns of Nepalese stock market.

This study reveals that the beta has a very weak relation with stock returns. The result of regressions show that the coefficient of beta is insignificant and it does not explain variation of stock returns. Firm size displays a positive and statistically significant coefficient in explaining stock returns. The study, therefore, reveals that size has a significant impact on stock returns and suggests larger stocks have higher returns. The relationship of E/P with stock return is uncertain and hence does not explain the variation in stock returns. The coefficients for sales to price ratio (SP) are negative in all the equations but they are not significant. The dividend yield (DY) coefficient is positive and significant indicating that higher dividend yield leads to higher stock returns. The book to market (BM) coefficients are all negative and significant also indicating that higher book to market leads to lower stock returns or vice versa.

To conclude, size, dividend yield, and book to market ratio has been found to be significant factors affecting stock returns in Nepal. Overall, beta, earning price ratio, and sales to price ratio have been observed to be poor predictors of stock returns.

References

Pradhan 7

Banz, R. W. (1981). The relationship between return and market value. Journal of Financial Economics, 3-18.

Banz, R. W., & D. Reinganum, (1981). Size related anomalies and stock return seasonality. The Journal of Financial Economics, 41(5), 54-67.

Barbee, W. C., S. Mukherji, & S., & G. A. Raines (1996). Do sales price and debt equity explain stock returns better than book market and firm size. Financial Analyst Jour-nal, 23(1), 56-60.

Barry, P., M. Blume, & K. Henry (2002). B/M and average stock returns. The Journal of Finance, 21(3), 201-233.

Basu, S. (1983). The relationship between earnings yield, market value and return for NYSE common stocks: Further evidence. Journal of Financial Economics, 41(12), 129-156.

Nepalese Journal of Management 8

Bhandari, L. C. (1988). Debt/equity ratio and expected common stock returns: Empirical evidence. The Journal of Finance, 43(2), 507-528.

Bhatta, G. (2010). Does Nepalese stock market follow random walk? SEBON Journal, 5, 18-58.

Black, F. (1972, June). Capital market equilibrium with restricted borrowing. The Journal of Business, 45(3), 444-455.

Boudoukh, J., R. Michaely, M. Richardson, & M. R. Roberts (2007). On the importance of measuring payout yield: Implications for emprical asset pricing. The Journal of Finance, 62(2), 21-45.

Chan, L. K., Y. Hamao, Y., & J. Lakonishok, (1991). Fundamentals and stock returns in Ja-pan. The Journal of Finance, 46(5), 1739–1764.

Chan, Y. (1991). The cross sectional relationship between stock returns and domestic and global factors in the Tokyo Stock Exchange. School of Economics and Finance, 51(5), 234-241.

Fama, E. F. (1990). Stock returns, expected returns, and real activity. The Journal of Fi-nance, 45(4), 121-137.

Fama, E. F., & K. R. French, (1992, June). The cross-section of expected stock returns. The Journal of Finance, 47(2), 427-465.

Fama, E. F., & K. R. French, (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(4), 3-56.

Fama, E. F., & K. R. French (1995). Size and book to market factors in earnings and returns. The Journal of Finance, 50(1), 213-245.

Fama, E. F., & K. R. French (1996). Multifactor explanation of asset pricing anomalies. Journal of Finance, 51(1), 55-84.

Fama, E. F., & K. R. Kenneth (2008). Dissecting anomalies. The Journal of Finance, 53(4), 1653-1675.

Fama, E. F., & J. D. MacBeth (1973). Risk, return, and equilibrium: Empirical tests. The Journal of Political Economy, 81(3), 607-636.

Fama, E. F., & W. Schwert (1977). Asset returns and inflation. The Journal of Financial Economics, 4(1), 115-146.

Keim, D. B. (1983, June). Size related anomalies and stock return seasonality. Journal of Financial Economics, 13-32.

Keim, D. B. (1990). A new look at the effect of firm size and E/P ratio on stock return. The Journal of Financial Analysts, 46(2), 56-68.

Lakonishok, J., A. Schleifer, & R. W. Vishny (1994). Contrarian investment, extrapolation and risk. The Journal of Finance, 49(5), 1541-1578.

Lamont, O. (1998, October). Earnings and expected returns. The Journal of Finance, 53(5), 1563-1587.

Lamont, O. A. (1980). Investment plans and stock returns. The Journal of Finance, 55(3), 213-246.

Pradhan 9

Lintner, J. (1965). The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. The Review of Economics and Statistics, 471(1), 13-37.

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77-91.Merton, R. C. (1973). An intertemporal capital asset pricing model. Econometrica, 41(5),

867-887.Pandey, I., & Chee, H. K. (2001). The expected stock returns of Malaysian firms: A panel

data analysis. The Journal of Financial Review, 51(2), 121-143.Porta, R. L. (1996, December). Expectations and the cross-section of stock returns. The Jour-

nal of Finance, 51(5), 1715-1742.Pradhan, R. S. (1993). Stock market behavior in a small capital market:A case of Nepal. The

Nepalese Management Review, 9(1), 23-49.Pradhan, R. S., & S. B. Balampaki (2006). Fundamentals of stock returns in Nepal. Research

in Nepalese Finance, 9(1).Reinganum, M. R. (1981). Misspecification of capital asset pricing empirical anomalies

based on earnings yields and market values. The Journal of Financial Economics, 9(1), 19-46.

Reinganum, M. R. (1990). Empirical tests of multi-factor pricing model. The Journal of Finance, 36(3), 313-321.

Roll, R., & S. A. Ross (1994). On the cross-sectional relation between expected return and betas. The Journal of Finance, 49(1), 101-121.

Rosenberg, B., K. Reid, & R. Lanstein (1985). Persuasive evidence of market inefficiency. The Journal of Portfolio Management, 11(3), 9-16.

Ross, S. A. (1976). The arbitrage theory of capital asset pricing. The Journal of Economic Theory, 13(1), 341-360.

Sharpe, W. F. (1964). Capital asset prices:A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425-442.

Sharpe, W. F. (1991). Capital asset pricing with and without negative holdings. The Journal of Finance, 42(2), 489-509.

Stattman, D. (1980). Book value and stock returns. The Journal of Finance, 32(1), 215-230.Wang, D., & D. Xu (2004). What determines Chinese stock returns? Journal of Financial

Analysts, 34(2), 221-235.Wong, K. A., R. K. Tan, & W. Liu (2006). The cross-section of stock returns on the Shanghai

Stock Exchange. Quantitative Finance and Accounting, 26(1), 23-39.

10

Corporate culture and firm performance: A case of Nepalese commercial banks

- Kavina Shrestha

Nepalese Journal of Management

Abstract

This paper examines the impact and importance of corporate culture on firm performance. The volume of loan, cost to income ratio and net interest margin are selected as Bank’s performance variables for this study and these three are the Dependent Variables. Cultural strength index is used as proxy for the linkage of corporate culture and firm performance. Credit risk, capital, age of the bank, operating income, cash reserve ratio, total assets and macroeconomic variables (inflation rate and growth rate of GDP) as independent variables. The result shows that culture of bank has no impact on performance of commercial banks because there is no sufficient evidence to prove that culture of bank does have impact on performance of commercial banks. The impact of credit risk and capital are negatively significant and positively significant with volume of loan. Likewise, operating income has negative and significant impact on cost to income ratio of Nepalese commercial banks. Similarly, the results showed that cash reserve ratio has positive and significant impact on net interest margin of commercial banks.

Keywords: corporate culture, cultural strength index, volume of loan, cost to income ratio, net interest margin

1. Introduction

The banking sector acts as the life blood of modern trade and commerce to provide them with a major source of finance. Commercial bank occupies quite an important place in the framework of every economy (Hussain, 2010). It provides capital for the development of industry, trade and business investing the saving collected as deposit. All economic activities of every country are greatly influenced by the commercial banking business of that country. Integrated and speedy development of the country is possible only when competitive banking services reach nooks and corners of the country. The success of banking sector depends upon various factors. Among those factors, organizational culture of the banks is also considered as one of the most important factors that improves the performance of commercial banks. Organizational culture is considered as a critical success factor for organizations because it enhances employee retention, increases productivity, reduces turnover, enhances customer satisfaction and loyalty, improves teamwork and ultimately increases the financial performance of commercial banks(Rashid, Sambasivan & Johari, 2003). The culture of an organization can be defined as the embodiment of its collective systems, beliefs, norms, ideologies, myths and rituals. They can motivate people and can become

NEPALESE JOURNAL OF MANAGEMENT VOL.1, NO.1, JULY 2014

NMJ

valuable source of efficiency and effectiveness (Sudarsanam, 2010). Organizational culture can be described as a combination and admixtures of rites, rituals, traditions, values, regulations, legends, customs, habits, habitats, symbols, cult and artifacts of an organization. Broadly speaking and keeping in view the rapid changes in the organizational dynamics all over the world, the modern day corporate culture revolves around the psychology, attitudes, experiences, beliefs, values, policies and procedures of any corporate body. Corporate culture energizes, empowers and strengthens the organization and gives it a new identity. It aims at the realization of organizational goals and deals with the stakeholders’ return (Kotler & Heskett, 1992) .Hansen & Wemerfelt (1989) have established that corporate culture has a significant effect on an organization’s long-term sustainability and economic performance. They found, over an 11-year period, that organizations with an embedded culture had greater revenue increases, larger workforce expansions, greater increases in share price and larger improvements in net income than their counterparts with weaker cultures. Peters & Waterman (1982) in the analysis of sustained superior financial performance of certain organizations have attributed their success to the specific culture of each of the respective organization. Culture is often conceived as intangible, difficult to understand and worthy of focus only if there is time. However, the ability to identify the cultural traits of an organization provides a platform for better understanding of the operations of the organization for a better performance. Unfortunately, most often organizational cultural issues are overlooked, while attention is directed towards activities that may have little or no positive effect on performance (Davidson, 2007).The powerful and pervasive role of culture plays in shaping organizational life lends plausibility to speculations that cultural factors like participation, consistency and adaptability may be linked with exceptional levels of organizational performance (Alvesson, 1993). A commonly hypothesized link suggests that if an organization’s culture is to contribute to or enhance performance, it must be both “strong” and possess distinctive “traits”: particular values, beliefs, and shared behavior patterns. Some scholars have claimed that positive cultural traits boost performance in proportion to the strength of their manifestation (Denison & Mishra, 1995).The superior financial performance can be either temporary or sustained. Temporary superior performance is the result of competitive dynamics widely described in microeconomics. Suppose a particular firm is able, for any of a variety of reasons, to obtained superior financial performance. Other firms, observing this, typically will seek to obtain this same level of performance by duplicating whatever makes a successful firm successful. Imitation increases the competition to initially successful firm, reduces margins, and decreases the level of financial performance(Ogbonna & Harris, 2000). The link between culture and performance depends on the ability to affect organizational learning in response to internal and external organizational changes. In fact, in stable environment firms with the strong culture has less variable performance (Sorensen, 2001).The major purpose of this study is to examine the relationship between corporate culture and firm performance in context of Nepalese banking sector. The other specific objectives of this study are: to identify the most important determinant of organization’s culture in Nepalese commercial banks, to examine the causal relationship between the organization culture and net interest margin of selected commercial banks of Nepal, to assess the impact of cash reserve ratio and total assets in net interest margin of selected commercial banks in Nepal, to measure the effect of bank’s age in volume of loan, cost to income ratio and

Shrestha 11

net interest margin of selected Nepalese commercial banks and to determine the impact of macroeconomic variables (inflation rate and growth rate of gross domestic product) on volume of loan, cost to income ratio and net interest margin of selected Nepalese commercial banks.

2. MethodologyThe study is based on the both primary and secondary data which were gathered for 17 commercial banks in Nepal. The primary source of data has been used to assess the opinion of bank’s employees regarding the corporate culture and performance of commercial banks in Nepal. The data for the bank specific including amount of loan balances, cost to income ratio and net interest margin have been collected from annual reports of concerned sample banks, supervision reports published by Nepal Rastra Bank (NRB) and official websites of concerned banks. From the each of the strata (joint ventures, non- joint ventures and public banks) essential data have been collected for each year from 2002/03 to 2011/12.This study has used panel data to analyze the relationship between banks’ performance and its determinants.The research design adopted in this study are descriptive and causal comparative type as it deals with relationship between banks specific (loan, net interest margin, cost to income ratio, credit risk, age of bank ,amount of capital balances in bank, cash reserve ratio at the bank, total assets and operating income) and macroeconomic variables (GDP growth rate and inflation rate). The study analyzes the relationship between corporate culture and bank performance using panel data of the selected commercial banks. Volume of loan, cost to income ratio and net interest margin have been used as the dependent variables and proxy for bank performance. Hence, the multiple regression models have been employed in this study to analyze the relationship between banks’ performances and its determinants. The multiple regression models used in this study are:LOANit = α+ β1CSIbnk+ β2LOANit-1+ β3CRit + β4CR it-1+ β5AGEit+ β6Kit+ β7K it-1+ β8INFt+ β9INF t-1 + β10 GDPGR t+ β11GDPGR t-1 + β12t+ β13D1+ β14D2+ εit…………………………………..(1)CIRit = α+ β1CSIbnk+ β2CIRit-1+ β3OIit + β4OI it-1+ β5AGEit+ β6 INF t+ β7INF t-1+ β8 GDPGR t+ β9 GDPGR t-1 + β10t+ β11D1+ β12D2+ uit……………………………………………………………………..(2)NIMit = α+ β1CSIbnk+ β2NIMit-1+ β3AGEit + β4CRR it + β5CRR it-1+ β6 TA it+ β7TA it-1+ β8 INF t+ β9 INF t-1 + β10GDPGR t + β11GDPGR t-1 + β12 t+ β13 D1+ β14D2+ vit …………………..…(3)

Where,i= 1, 2, 3, 4, 5, 6…………, 17, t= 1, 2, 3, 4, 5…………., 10, LOANit= Loan balances of bank i at time period t, α = Intercept of dependent variable, CSIbnk= Cultural strength indexof bank, CRit= Credit risk of bank i at time period t, AGEit = Age of bank i at time period t, Kit= Volume of capital of bank i at time period t, INFt= Inflation rate at time period t, GDPGR t = Growth rate of gross domestic product at time period t, LOANit-1= One year lagged loan balances of bank i at time period t, CR it-1= One year lagged credit risk of bank i at time period t, INFt-1= One year lagged inflation rate at time period t, GDPGR t-1= One year lagged growth rate of gross domestic product at time period t, CIRit= Cost to income ratio of bank i at time period t, OIit= Operating income of bank i at time period t, CIRit-1= One year lagged cost to income ratio of bank i at time period t, OI it-1=One year lagged operating income of bank i at time period t, NIMit= Net interest margin of bank i at time period t, CRRit= Cash reserve ratioof bank i at time period t, TA it=Total assets of bank i at time period t, NIMit-1= One year lagged net interest margin of bank i at time period t, CRR it-1= One year lagged cash reserve

Nepalese Journal of Management 12

ratioof bank i at time period t, TA it-1= One year lagged total assets of bank i at time period t, D1= 1 if joint ventured and 0 for others, D2= 1 if non joint ventured and 0 for others

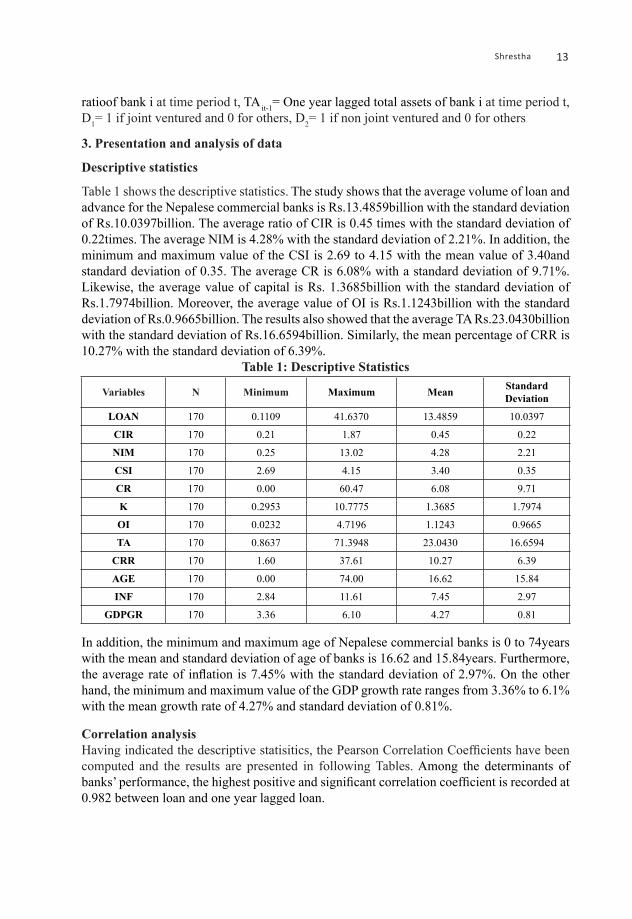

3. Presentation and analysis of data

Descriptive statistics

Table 1 shows the descriptive statistics. The study shows that the average volume of loan and advance for the Nepalese commercial banks is Rs.13.4859billion with the standard deviation of Rs.10.0397billion. The average ratio of CIR is 0.45 times with the standard deviation of 0.22times. The average NIM is 4.28% with the standard deviation of 2.21%. In addition, the minimum and maximum value of the CSI is 2.69 to 4.15 with the mean value of 3.40and standard deviation of 0.35. The average CR is 6.08% with a standard deviation of 9.71%. Likewise, the average value of capital is Rs. 1.3685billion with the standard deviation of Rs.1.7974billion. Moreover, the average value of OI is Rs.1.1243billion with the standard deviation of Rs.0.9665billion. The results also showed that the average TA Rs.23.0430billion with the standard deviation of Rs.16.6594billion. Similarly, the mean percentage of CRR is 10.27% with the standard deviation of 6.39%.

Table 1: Descriptive Statistics

Variables N Minimum Maximum Mean Standard Deviation

LOAN 170 0.1109 41.6370 13.4859 10.0397

CIR 170 0.21 1.87 0.45 0.22

NIM 170 0.25 13.02 4.28 2.21

CSI 170 2.69 4.15 3.40 0.35

CR 170 0.00 60.47 6.08 9.71

K 170 0.2953 10.7775 1.3685 1.7974

OI 170 0.0232 4.7196 1.1243 0.9665

TA 170 0.8637 71.3948 23.0430 16.6594

CRR 170 1.60 37.61 10.27 6.39

AGE 170 0.00 74.00 16.62 15.84

INF 170 2.84 11.61 7.45 2.97

GDPGR 170 3.36 6.10 4.27 0.81

In addition, the minimum and maximum age of Nepalese commercial banks is 0 to 74years with the mean and standard deviation of age of banks is 16.62 and 15.84years. Furthermore, the average rate of inflation is 7.45% with the standard deviation of 2.97%. On the other hand, the minimum and maximum value of the GDP growth rate ranges from 3.36% to 6.1% with the mean growth rate of 4.27% and standard deviation of 0.81%.

Correlation analysisHaving indicated the descriptive statisitics, the Pearson Correlation Coefficients have been computed and the results are presented in following Tables. Among the determinants of banks’ performance, the highest positive and significant correlation coefficient is recorded at 0.982 between loan and one year lagged loan.

Shrestha 13

Table 2: Correlations coefficient of loan and its determinants of commercial banks LOAN CSI LOANt-1 CR CR t-1 AGE K K t-1 INF INF t-1 GDPGR G D P G R

t-1

LOAN1

CSI0.005 1

LOAN t-10.982** -0.006 1

CR-0.149 -0.07 -0.098 1

CR t-1-0.181* -0.073 -0.128 0.881** 1

AGE0.453** -0.087 0.452** 0.392** 0.418** 1

K0.618** -0.022 0.633** 0.052 0.085 0.313** 1

K t-10.558** -0.017 0.606** 0.065 0.073 0.294** 0.941** 1

INF0.531** 0 0.473** -0.258** -0.206* 0.157* 0.320** 0.264** 1

INF t-10.517** 0 0.518** -0.244** -0.233** 0.143 0.287** 0.298** 0.629** 1

GDPGR0.194* 0 0.129 -0.127 -0.014 0.05 0.133 0.072 0.218** 0.224** 1

GDPGR t-10.183* 0 0.167* -0.14 -0.111 0.039 0.091 0.113 0.388** 0.187* -0.051 1

The results indicate that volume of loan amount is positively related with the cultural strength index and negatively related with credit risk. The negative correlation betweenone year lagged credit risk and volume of loan indicate that larger the volume of loan, lower would be the credit risk. It is also important to notethat age of the bank, capital, one year lagged capital amount, inflation, one year lagged inflation rate, GDPGR and one year lagged GDPGR is positively correlated with volume of loan. Among the observed correlations, the degree of correlation of one year lagged loan is most strong in order of their importance which means this variable better explain the banks’ performance in case of Nepalese commercial banks.

Table 3 shows that the highest positive and significant correlation coefficient is recorded at 0.836 between cost to income ratio and one year lagged cost to income ratio.Cultural Strength Index (CSI), inflation, GDP growth rate and one year lagged GDP growth rate is negatively correlated with cost to income ratio. This indicate that higher the volume of loan, lower would be CSI, inflation, GDP growth rate and GDP growth rate of previous year. Likewise, one year lagged operating income and age of bank is positively correlated with cost to income ratio. Among the observed correlations, the degree of correlation of one year lagged cost to income ratio is most strong in order of their importance which means this variable better explain the banks’ performance in terms of cost to income ratio of Nepalese commercial banks.

Nepalese Journal of Management 14

Table 3: Correlations coefficient of cost to income ratio and its determinants

CIR CSI CIR t-1 OI OI t-1 AGE INF INF t-1 GDPGR GDPGR t-1

CIR 1

CSI -0.117 1

CIR t-1 0.836** -0.107 1

OI 0.126 -0.027 0.159* 1

OI t-1 0.245** -0.047 0.151 0.982** 1

AGE 0.626** -0.087 0.639** 0.638** 0.656** 1

INF -0.086 0.000 -0.132 0.419** 0.357** \0.157* 1

INF t-1 0.002 0.000 -0.112 0.395** 0.411** 0.143 0.629** 1

GDPGR -0.027 0.000 -0.023 0.121 0.083 0.050 0.218** 0.224** 1

GDPGR t-1 -0.053 0.000 -0.038 0.146 0.096 0.039 0.388** 0.187* -0.051 1

The correlation analysis of net interest margin for the total sample bank of the study has been presented in Table 4 along with the test of significance. One year lagged net interest margin, cash reserve ratio, one year lagged cash reserve ratio, total assets, one year lagged total assets, age of the bank and one year lagged GDP growth rate are the positively correlated with net interest margin. Among the determinants of banks’ performance, the highest positive and significant correlation coefficient is recorded at 0.649 between one year lagged net interest margin and net interest margin. Other variables like cultural strength index, inflation, a year lagged inflation and GDP growth rate is negatively correlated with net interest margin of the Nepalese commercial banks.Table 4: Correlations coefficient of net interest margin and its determinants

NIM CSI NIM t-1 CRR CRR t-1 TA TA t-1 AGE INF INF t-1 GDPGR GDPGR

t-1

CSI -0.044 1

NIM t-1 0.649** -0.043 1

CRR 0.362** -0.132 0.267** 1

CRR t-1 0.420** -0.103 0.400** 0.710** 1

TA 0.102 -0.053 0.038 0.330** 0.247** 1

TA t-1 0.247** -0.071 0.084 0.347** 0.277** 0.981** 1

AGE 0.403** -0.087 0.370** 0.486** 0.507** 0.675** 0.701** 1

INF -0.121 0.000 -0.319** 0.288** 0.148 0.473** 0.414** 0.157* 1

INF t-1 -0.073 0.000 -0.125 0.291** 0.224** 0.460** 0.454** 0.143 0.629** 1

GDPGR t-1 -0.125 0.000 -0.214** 0.116 -0.028 0.167* 0.108 0.05 0.218** 0.224** 1

GDPGR t-1 0.199* 0.000 -0.128 0.106 0.072 0.164* 0.137 0.039 0.388** 0.187* -0.051 1

Regression analysisThe regression of bank performance and its determinants has been analysed by defining bank performance in terms of volume of loan, cost to income ratio and net interest margin. The regression of volume of loan and its determinants is explained in Table 6. The table indicates that beta coefficients are positive for one year lagged volume of loan, age of the bank, capital and growth rate of GDP. Thus higher the volume of loan for previous year,age of the bank and capital, larger would be the volume of loan of the year and beta coefficients is also significant at 1 percent level of significance. However, the beta coefficient of growth rate of GDP is

Shrestha 15

significant at 5 percent level of significance. The result also shows that beta coefficients are positive for cultural strength index,one year lagged credit risk and one year lagged growth rate of GDP but these beta coefficients are insignificant.

The table indicates that beta coefficients are negative for credit risk and one year lagged capital amount. Thus larger the credit risk, lower would be volume of loan and the beta coefficient is significant at 1 percent level of significance. The results also indicate that larger the capital amount of previous year, lower the volume of loan of th year and beta coefficient is also significant at 1 percent level of significance. Likewise, time is insignificant so there is no evidence that there is trend in volume of loan of commercial banks and it depends upon culture. Similarly, both dummies are significant at 1% level of significance. This indicates that there is difference in impact of independent variables on dependent variables among joint ventured, non joint ventured and public banks. The significant coefficients of dummy 1 show that joint ventured bank have better impact on volume of loan than other type of banks. Similarly, the significant coefficient of dummy 2 show that non joint ventured bank have better impact on volume of loan than other type of banks.

Table 5: Estimated regression results of loan and advances and its determinantsThis table shows regression results of variables based on panel data of 17 sample commercial banks with 170 observations from the year 2002/03 to 2011/12. The reported values are intercepts and slope coefficients of respective explanatory variables with t-statistics. Dependent variable is volume of loan denoted as LOAN and independent variables are cultural strength index, one year lagged loan, credit risk, one year lagged credit risk, age of the bank, capital, one year lagged capital, inflation rate, one year lagged inflation rate, growth rate of gross domestic product and one year lagged growth rate of gross domestic product, time, dummy 1 and dummy 2. The reported results also include the values of F-statistics (F), adjusted coefficient of determination (Adj. R2).LOANit = α+ β1CSI+ β2LOANit-1+ β3CRit + β4CR it-1+ β5AGEit+ β6Kit+ β7K it-1+ β8INFt+ β9INF t-1 + β10 GDPGR t+ β11GDPGR t-1 + β12t+ β13D1+ β14D2+ εit………(1)

Variables MODEL I

Coefficient t- value P- value

(Constant) -6.192 -2.756 0.007

CSI 0.273 0.752 0.454

LOAN t-1 1.011 39.945 0.000

CR -0.095 -3.028 0.003

CR t-1 0.009 0.293 0.770

AGE 0.099 3.586 0.000

K 0.923 4.133 0.000

K t-1 -0.757 -3.396 0.001

INF -0.016 -0.177 0.859

INF t-1 -0.155 -1.707 0.090

GDPGR 0.349 2.171 0.032

GDPGR t-1 0.177 1.063 0.290

t 0.089 0.597 0.552

D1 4.448 3.204 0.002

D2 4.480 2.933 0.004

Adjusted R-square 0.976

F-ratio 437.401

Sig. (p-value) 0.000Table 6 shows the concerned with the regression of cost to income ratio and its determinants.

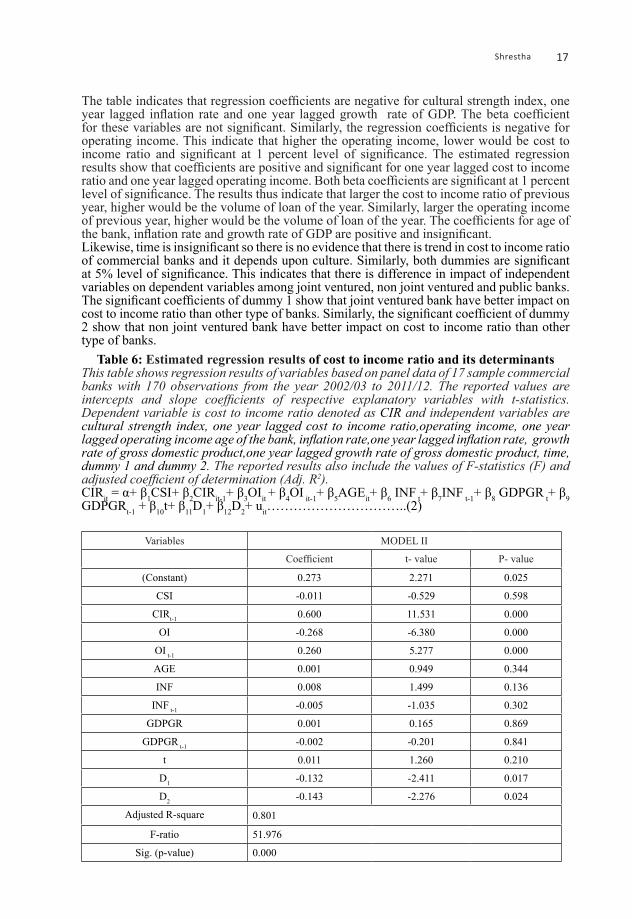

Nepalese Journal of Management 16

The table indicates that regression coefficients are negative for cultural strength index, one year lagged inflation rate and one year lagged growth rate of GDP. The beta coefficient for these variables are not significant. Similarly, the regression coefficients is negative for operating income. This indicate that higher the operating income, lower would be cost to income ratio and significant at 1 percent level of significance. The estimated regression results show that coefficients are positive and significant for one year lagged cost to income ratio and one year lagged operating income. Both beta coefficients are significant at 1 percent level of significance. The results thus indicate that larger the cost to income ratio of previous year, higher would be the volume of loan of the year. Similarly, larger the operating income of previous year, higher would be the volume of loan of the year. The coefficients for age of the bank, inflation rate and growth rate of GDP are positive and insignificant.Likewise, time is insignificant so there is no evidence that there is trend in cost to income ratio of commercial banks and it depends upon culture. Similarly, both dummies are significant at 5% level of significance. This indicates that there is difference in impact of independent variables on dependent variables among joint ventured, non joint ventured and public banks. The significant coefficients of dummy 1 show that joint ventured bank have better impact on cost to income ratio than other type of banks. Similarly, the significant coefficient of dummy 2 show that non joint ventured bank have better impact on cost to income ratio than other type of banks.

Table 6: Estimated regression results of cost to income ratio and its determinantsThis table shows regression results of variables based on panel data of 17 sample commercial banks with 170 observations from the year 2002/03 to 2011/12. The reported values are intercepts and slope coefficients of respective explanatory variables with t-statistics. Dependent variable is cost to income ratio denoted as CIR and independent variables are cultural strength index, one year lagged cost to income ratio,operating income, one year lagged operating income age of the bank, inflation rate,one year lagged inflation rate, growth rate of gross domestic product,one year lagged growth rate of gross domestic product, time, dummy 1 and dummy 2. The reported results also include the values of F-statistics (F) and adjusted coefficient of determination (Adj. R2).CIRit = α+ β1CSI+ β2CIRit-1+ β3OIit + β4OI it-1+ β5AGEit+ β6 INF t+ β7INF t-1+ β8 GDPGR t+ β9 GDPGRt-1 + β10t+ β11D1+ β12D2+ uit…………………………..(2)

Variables MODEL II

Coefficient t- value P- value

(Constant) 0.273 2.271 0.025

CSI -0.011 -0.529 0.598

CIRt-1 0.600 11.531 0.000

OI -0.268 -6.380 0.000

OI t-1 0.260 5.277 0.000

AGE 0.001 0.949 0.344

INF 0.008 1.499 0.136

INF t-1 -0.005 -1.035 0.302

GDPGR 0.001 0.165 0.869

GDPGR t-1 -0.002 -0.201 0.841

t 0.011 1.260 0.210

D1 -0.132 -2.411 0.017

D2 -0.143 -2.276 0.024

Adjusted R-square 0.801

F-ratio 51.976

Sig. (p-value) 0.000

Shrestha 17

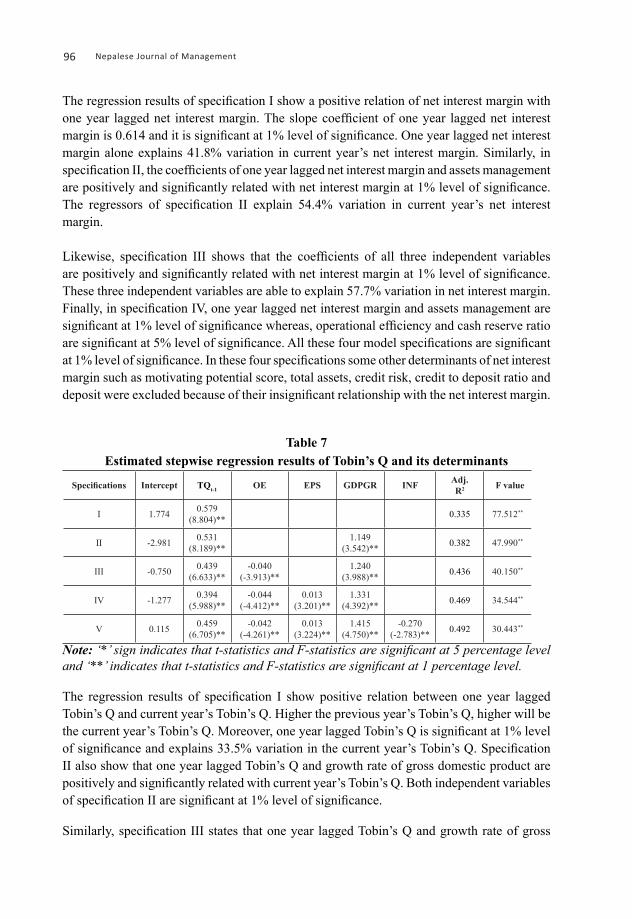

Table 7 shows the the concerned with the regression of net interest margin and its determinants. the table indicates that regression coefficients is negative for total asset indicating that higher the total asset, lower would be the net interest margin and beta coefficiant is significant at 1 percent level of significance. Similarly, the coefficients are also negative for age of the bank, one year lagged cash reserve ratio and one year lagged inflation rate and these cofficients are not significant.The estimated regression results show that coefficients are positive and significant for one year lagged net interest margin, cash reserve ratio, one year lagged total asset, inflation rate, growth rate of GDP and one year lagged growth rate of GDP at 1 percent, and 10 percent level of significance respectively. The results thus indicate that larger the net interest margin of previous year, higher would be the net interest margin of the year. Similarly, higher the cash reserve ratio, higher would be the net interest margin. The result also indicate that higher the total asset of previous year, larger would be net interest margin. Likewise, larger the inflation rate, larger would be the net interest margin. Similarly, higher the growth rate of GDP and one year lagged growth rate of GDP, higher would be the net interest margin of the year.

Table 7: Estimated regression results of net interest margin and its determinantsThis table shows regression results of variables based on panel data of 17 sample commercial banks with 170 observations from the year 2002/03 to 2011/12. The reported values are intercepts and slope coefficients of respective explanatory variables with t-statistics. Dependent variable is net interest margin denoted as NIM and independent variables are cultural strength index, one year lagged net interest margin , age of the bank, cash reserve ratio, one year lagged cash reserve ratio, total assets, one year lagged total assets, inflation rate, one year lagged inflation rate, growth rate of gross domestic product,one year lagged growth rate of gross domestic product, time, dummy 1 and dummy2.The reported results also include the values of F-statistics (F) and adjusted coefficient of determination (Adj. R2).

NIMit = α+ β1CSI+ β2NIMit-1+ β3AGEit + β4CRR it + β5CRR it-1+ β6 TA it+ β7TA it-1+ β8 INF t+ β9 INF t-1 + β10GDPGR t + β11GDPGR t-1+ β12 t+ β13 D1+ β14D2+ vit………….(3)

Variables MODEL VI

Coefficient t- value P- value

(Constant) -1.560 -0.933 0.353

CSI 0.218 0.730 0.467

NIMt-1 0.522 8.576 0.000

AGE -0.014 -0.868 0.387

CRR 0.048 1.855 0.066

CRR t-1 -0.004 -0.147 0.883

TA -0.178 -5.067 0.000

TA t-1 0.201 5.072 0.000

INF 0.238 3.243 0.001

INF t-1 -0.091 -1.143 0.255

GDPGR 0.225 1.715 0.089

GDPGR t-1 0.622 4.605 0.000

t -0.162 -1.259 0.210

D1 -1.368 -1.891 0.061

D2 -1.643 -2.027 0.045

Adjusted R-square 0.655

F-ratio 21.584

Sig. (p-value) 0.000

Nepalese Journal of Management 18

Likewise, time is insignificant so there is no evidence that there is trend in net interest margin of commercial banks and it depends upon culture. Similarly, dummy 1 and dummy 2 are significant at 10% and 5% level of significance. This indicates that there is difference in impact of independent variables on dependent variables among joint ventured, non joint ventured and public banks. The significant coefficients of dummy 1 show that joint ventured bank have better impact on net interest margin than other type of banks. Similarly, the significant coefficient of dummy 2 shows that non joint ventured bank have better impact on net interest margin than other type of banks.

4. Discussion and conclusion

From the past few years, it has been seen that Nepalese commercial banks are playing a significant role in the economic development of a country. There are numerous empirical evidences of developed countries that corporate culture has significant impact on the improving the performance of commercial banks. However, despite of several empirical evidences, corporate culture and bank performance issues are still unsolved in context of Nepalese banking industry. So, determining the strength of corporate culture as well as its impact on the performance of commercial banks has always been a crucial issue for every Nepalese commercial bank. Therefore, this study attempts to identify the determinants of corporate culture and its impact on the performance of Nepalese commercial banks.

The study reveals that one year lagged volume of loan, credit risk, age of the bank, capital and one year lagged capital are the most dominant variables that have significant impact on performance of commercial banks in Nepal as measured by volume of loan from growth perspective. Likewise, from the perspective of cost, one year lagged cost to income ratio, operating income and one year lagged operating income are the most dominant variables that have significant impact on performance of Nepalese commercial banks. Similarly, one year lagged net interest margin, cash reserve ratio, total assets, one year lagged total assets, inflation rate and one year lagged growth rate of gross domestic product are the most dominant variables that have significant impact on performance of commercial banks as measured by net interest margin from the perspective of profit.

The results indicate that culture of bank has no impact on performance of commercial banks because there is no sufficient evidence to prove that culture of bank does have impact on performance of commercial banks. The study also concludes that involvement is the most important factor for maintaining strong culture in the bank followed by consistency, adaptability and mission. Likewise, it can also be concluded that strong culture have more impact on performance level of the employees. The study also concluded that strong culture motivates the employees as well as enhances coordination and control.

Shrestha 19

ReferencesAlvesson, M. (1993). Cultural perspectives on organizations. New York: Cambridge University Press.

Davidson, G. (2007). Organizational culture and financial performance in a South African Investment Bank. SA Journal of Industrial Psychology, 33 (1), 38-48.

Denison, D. R., & A. K. Mishra (1995). Toward a theory of organizational culture and effectiveness. Organizational Science. 6, pp. 204 – 223.

Nepalese Journal of Management 20

Hansen, G., & B. Wernerfelt (1989). ‘Determinants of firm performance: The relative importance of economic and organizational factor. Strategic Management Journal, 10, 399 - 411.

Hussain, G. (2010). Evidencence on structure conduct performance hypothesis in Pakistani commercial banks. International Journal of Business and Management, 5(9), 174-187.

Kotler, J. P., & J. L. Heskett (1992). Corporate culture and performance. New York: Free Press.

Ogbonna, E., & L. Harris (2000). Leadership style, organizational culture and performance: Empirical evidence from UK companies. International Journal of Human Resources Management, 11(4), 766-788.

Peters, T., & R. Waterman (1982). In search of excellence: Lessons from America’s best-r run companies. (p. 75). New York: Harper & Row.

Sudarsanam, J. (2010). Creating value from mergers and acquisition. UK: Pearson Education Ltd.

21

Factors influencing customer adoption in internet banking: A study on Nepalese commercial banks

- Regina Shrestha

Nepalese Journal of Management

AbstractThis paper examines the impact and importance of factors influencing customer adoption in Internet banking. The factors influencing customer adoption considered in this study are Awareness, Perceived Cost, Perceived Usefulness, Perceived Risk, Perceived Ease of Use and Advantage of Internet. The data are collected from primary sources and is based on pre-specified questionnaires through the survey method. 200 questionnaires were distributed in Kathmandu valley through family, relatives and friends. The result shows that there is a positive significant impact of customer adoption on perceived usefulness, awareness, advantage of Internet, perceived risk, perceived ease of use whereas the perceived cost has negative and insignificant effect on customer adoption.

Keywords: customer adoption, Perceived cost, Perceived risk, Perceived usefulness, Perceived ease of use, Awareness, Advantage of Internet banking.

1. IntroductionBanking has recently become a highly information intensive activity that relies heavily on information technology (IT) to acquire, process, and deliver the information to all relevant users. Not only is IT critical in the processing of information, it provides a way for the banks to differentiate their products and services. Banks find that they have to constantly innovate and update to retain their demanding and discerning customers and to provide convenient, reliable, and expedient services. Driven by the challenge to expand and capture a larger share of the banking market, some banks invest in more bricks and mortar to enlarge their geographical and market coverage. Banks have been using the Internet as one of their distribution channels because Internet Banking services benefit both the banks and their customers (Karjaluoto, 2002). Banks are important in every country and have a significant effect in supporting economic development through efficient financial services. They provide a mechanical system to group saving and convert them into investment. For over a decade, banks have been affected by changes associated with globalization and financial liberalization. Reacting to these changes, banks expand the choice of services offered to the customers and increase their reliance on technology (Al-Smadi and Al-Wabel, 2011).

NEPALESE JOURNAL OF MANAGEMENT VOL.1, NO.1, JULY 2014

NMJ

Banks have used electronic channels to do banking operations with both domestic and international customers. Currently, banks are mostly using electronic channels to receive instructions and deliver their products and services to their customers. Although the range of services provided by banks over the electronic channel varies widely in content, this form of banking is generally referred to as electronic banking (Azouzi, 2009).

Sathye (1999) says that the Internet becomes more widely accessible households will conduct their financial transactions over the Internet. This means that, the more widespread the access to computer/Internet the greater the possibility of use of Electronic banking adoption. The terms Internet banking and online banking are often used in the literature to refer the same things. Nowadays the Internet is the main channel for electronic banking. Internet banking offers many benefits to banks and their customers (Karjaluoto, 2002). According to Sathye (1999), while the use of internet banking services is fairly new experience to many people, low awareness of internet banking is a major factor in causing people not to adopt internet banking. Consumers were unaware about the possibilities, advantages/disadvantages involved with internet banking. Furthermore, using electronic services can reduce the cost of resources needed for traditional banking services. The main benefits to banks are cost savings, reaching new segments of the population, efficiency, enhancement of the bank’s reputation and better customer service and satisfaction (Jayawardhena and Foley, 2000).

Internet banking also offers new value to the customers of the banks. With the help of the internet, banking is no longer bound to time or geography. Consumers all over the world have relatively easy access to their accounts 24 hours per day, seven days a week. It makes available to customers a full range of services including some services not offered at branches. Internet banking has the advantage that the customer avoids traveling to and from a bank branch. In this way, Internet banking saves time and money provides convenience and accessibility (Karjauloto, 2003). Davis et al. (1989) suggested that adding external variables to TAM can influence technology adoption indirectly through perceived ease of use and perceived usefulness. Perceived usefulness was defined as the degree to which individuals believe that using a particular system would enhance their job performance whereas perceived ease of use relates to the degree to which individuals believe that using a particular system would require no effort (Davis, 1989).

Many studies regarding factors influencing customer adoption in internet banking was conducted in developed countries and have similar findings. The study that banks will be better able to manage consumer experiences with moving to internet banking if they understand that such experiences involve a process of adjustment and learning over time, and not merely the adoption of a new technology (Sharman and Kirsty, 2006). Furthermore, the study found that perceived ease of use may actually be a causal antecedent to perceived usefulness, as opposed to a parallel, direct determinant of system usage. Implications are drawn for future research on user acceptance (Fred, 2008). A study found that in terms of e-banking, ATM services is adapted by most of the banks in Nepal, while mobile banking getting the popularity but internet (computer-based) banking is still not available (Banstola, 2007).

Chen and Barnes (2007) pointed out that perceived usefulness, perceived security, perceived privacy, perceived good reputation, and willingness to customize are the important antecedents

Nepalese Journal of Management 22

to online initial trust. It is also discovered that both online initial trust and familiarity with online purchasing have a positive impact on purchase intention. Riyadh et al. (2009) stated that “Seven variables affecting e-banking adoption by SMEs are identified. They are: organizational capabilities, perceived benefits, perceived credibility, perceived regulatory support, ICT industries readiness, lack of financial institutions readiness and institutional influence. Among ‘early adopters’, convenience was a more important indicator of intentions to adopt internet banking. Risk, security and prior internet knowledge is also an important factor influencing customers adopting internet banking after convenience (Nasri, 2011). The purpose of this study is to identify the factors that influence internet banking adoption in Nepalese banking sector. It determines the usefulness of internet banking system to the customers. It examines the customer awareness and trust of users on internet banking in Nepal. It evaluates ease of use and risk of internet banking in Nepal. It determines the quality and quantity of information the customers have on the internet banking system. It identifies the customers perceived risk towards internet banking system.

2. MethodologyThe study is based on the primary data which were gathered from 14 banks in Nepal. The primary sources of data is collected from the customer of different commercial banks and will be used to assess the opinion of respondents with respect to overall customer adoption towards internet banking and the importance of these practices in Nepalese commercial banks. The data has been collected through questionnaire from the joint venture banks, public banks and government owned banks. The sample product used for the research purpose was the users of internet banking services provided by commercial banks. The selection of the respondents was made on the basis of personal contact and in a random basis. The respondents have been approached personally and given a detailed explanation about the survey (including its purpose, the meaning of the items and what is expected of the respondents).The research design adopted in this study is descriptive and causal comparative type as it deals with the current level of customer adoption with dimensions of internet banking services. This design has also been employed to assess the opinions and perceptions of customers. The study includes survey method of all kinds, including comparative and correlation methods. The study used variables like customer adoption, perceived ease of use, perceived usefulness, awareness, perceived cost, perceived risk and advantage of internet banking for analysis. The following table 1 shows the number of commercials banks in Kathmandu where data was collected and the numbers of respondents who were taken for the study from each bank.

The model of this study shows the relationship between the awareness in internet banking and customer’s adoption. The independents variable awareness, perceived ease of use, perceived usefulness, perceived risk and perceived cost as impact on dependent variable customer adoption. The model given below shows the relationship between these variables.The equation for Customer Adoption in internet banking is tested as follows:

Equation: Y =α+β1X1+β2X2+β3X3 +β4X4 +β5X5 +β6X6+eWhere, Y= Customer Adoption, X1= Advantage of internet banking, X2= Perceived cost X3=Perceived risk, X4= Perceived ease of use, X5= Perceived usefulness, X6= Awarenessα = Intercept of dependent variable and, β1, β2, β3, β4, β5 and β6 are the beta coefficients of the explanatory variables to be estimated, e = random error term.

Shrestha 23

Table 1: Number of commercial bank selected for the studyStrata Name of bank No. of respondents

Public banks

Prime Commercial Bank Ltd 18

Kumari Bank Ltd 13

Citizen Bank Ltd 13

Laxmi Bank Ltd 29

Machhapuchhre Bank Ltd 12

Siddhartha Bank Ltd 21

Global IME Bank Ltd 18

Nepal Investment Bank Ltd 4

Joint venture banks

Nepal SBI Bank Ltd 9

Himalayan Bank Ltd 7

Nabil Bank Ltd 11

Everest Bank Ltd 10

Government owned banksNepal Bank Ltd 15

Rastriya Banijya Bank Ltd 11

Total 191

AwarenessConsumers’ level of awareness of internet banking influences the adoption of internet banking. The internet banking literature supports that individual factor like knowledge (Singhal and Padhmanabhan, 2008) has an impact on consumer’s adoption of internet banking. Sathye (1999) highlighted that many consumers were simply unaware of internet banking and its unique benefits. Here knowledge refers to the consumers’ awareness of internet banking and the benefits associated with internet banking, and their knowledge of how to use basic technology. Sathye (1999) found that the lack of awareness about electronic banking and its benefits contribute to the non-adoption of electronic banking. Therefore consumers who are more aware of internet banking are more likely to perceive internet banking as more useful, easy to use and more reliable, thereby influencing adoption of internet banking.

Perceived ease of use (PEOU)Perceived ease of use, refers to “the degree to which a person believes that using a particular system would be free of effort.”This follows from the definition of “ease”: “freedom from difficulty or great effort.”Effort is a finite resource that a person may allocate to the various activities for which he or she is responsible (Ramdhony and Ramjee,2010). All else being equal, we claim, an application perceived to be easier to use than another is more likely to be accepted by users.

Perceived usefulness (PU)Perceived usefulness is defined here as “the degree to which a person believes that using a particular system would enhance his or her job performance.”This follows from the definition

Nepalese Journal of Management 24

of the word useful:”capable of being used advantageously.”Within an organizational on-text, people are generally reinforced for good performance by raises, promotions, bonuses, and other rewards Howcroft, Hamilton and Hewer (2002). A system high in perceived usefulness, in turn, is one for which a user believes in the existence of a positive use-performance relationship.Perceived risk (PR)The implicit nature and uncertainty of using online environment for transaction have rendered risk as an inevitable element of online banking system. The main components of perceived risk are trust and security. Due to some planned action and user negative intention, trust and security over online banking system is on the heart of the users and has prevailed as one of the major concern. Trust can be defined as a user’s confident belief in a bank’s honesty toward the user. Perceived trust in online Banking system is consumers’ belief that e-payment transactions will be processed in accordance with their planned expectation and knowledge like: the security of the system; the service provider’s reputation; loss of privacy; and concerns about risks associated with the reliability of online banking. Previous research has found the risk associated with possible losses from the online banking transaction is greater than in traditional environments. Many studies showed PR as an important factor that influences online banking adoption; which is negatively related.

Advantages of internet bankingInternet banking has added an entirely new dimension of convenience to banking. Customers now have unprecedented access to their bank accounts at all times, and never have to wait for banking hours to perform simple banking transactions fees or to find out details about their accounts. There are some internet banking systems that have a slight lag time. Find out whether your bank uses real-time reporting before depending on it for time-sensitive balance and transaction information. Because each bank has its own system, it can be hard to get used to each system and to avoid making mistakes with transactions.