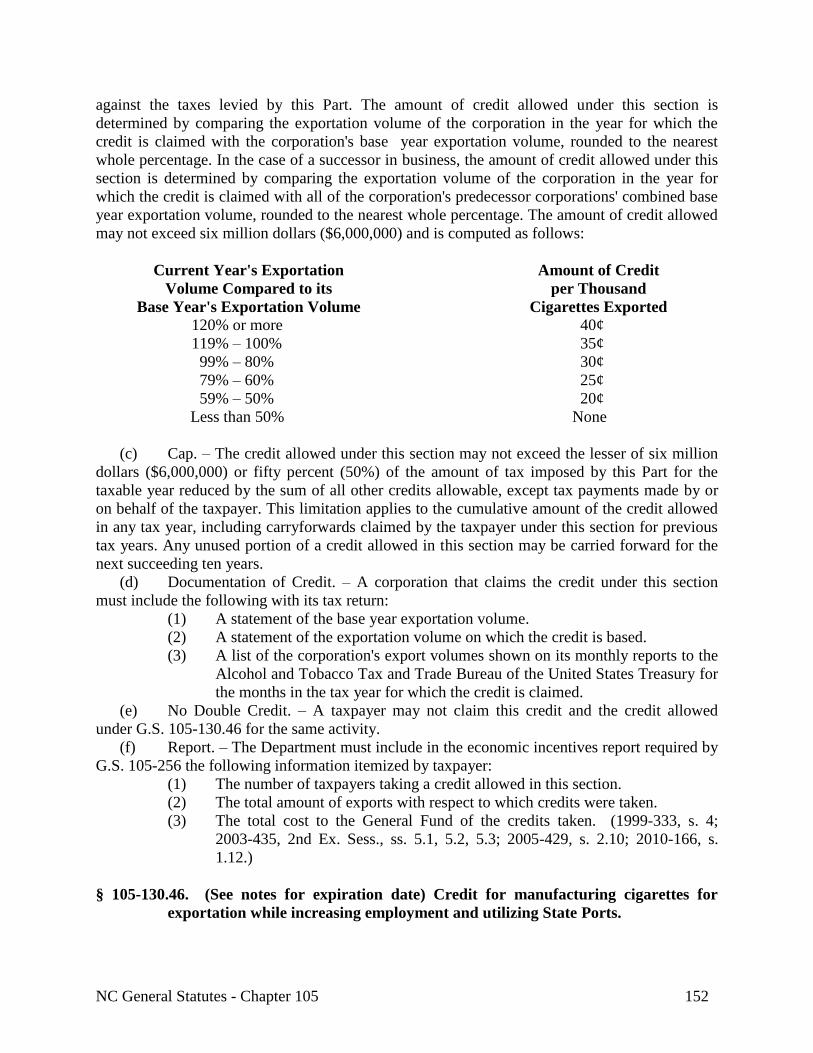

NC General Statutes - Chapter 105 1 ... - Onslow County

676

NC General Statutes - Chapter 105 1 Chapter 105. Taxation. SUBCHAPTER I. LEVY OF TAXES. § 105-1. Title and purpose of Subchapter. The title of this Subchapter shall be "The Revenue Act." The purpose of this Subchapter shall be to raise and provide revenue for the necessary uses and purposes of the government and State of North Carolina during the next biennium and each biennium thereafter, and the provisions of this Subchapter shall be and remain in full force and effect until changed by law. It is the policy of this State that as many State taxes as possible be structured so that they are deductible for federal income tax purposes under the Internal Revenue Code. (1939, c. 158, ss. A, B; 1941, c. 50, s. 1; 1983 (Reg. Sess., 1984), c. 1097, s. 1.) § 105-1.1. Supremacy of State Constitution. The State's power of taxation is vested in the General Assembly. Under Article V, Section 2(1), of the North Carolina Constitution, this power cannot be surrendered, suspended, or contracted away. In the exercise of this power, the General Assembly may amend or repeal any provision of this Subchapter in its discretion. No provision of this Subchapter constitutes a contract that the provision will remain in effect in future years, and any representation made to the contrary is of no effect. (2003-416, s. 12.) Article 1. Inheritance Tax. §§ 105-2 through 105-32: Repealed by Session Laws 1998-212, s. 29A.2(a), effective January 1, 1999, and applicable to the estates of decedents dying on or after that date. Article 1A. Estate Taxes. § 105-32.1: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and applicable to the estates of decedents dying on or after that date. § 105-32.2: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and applicable to the estates of decedents dying on or after that date. § 105-32.3: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and applicable to the estates of decedents dying on or after that date. § 105-32.4: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and applicable to the estates of decedents dying on or after that date.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of NC General Statutes - Chapter 105 1 ... - Onslow County

NC General Statutes - Chapter 105 1

Chapter 105.

Taxation.

SUBCHAPTER I. LEVY OF TAXES.

§ 105-1. Title and purpose of Subchapter.

The title of this Subchapter shall be "The Revenue Act." The purpose of this Subchapter shall

be to raise and provide revenue for the necessary uses and purposes of the government and State

of North Carolina during the next biennium and each biennium thereafter, and the provisions of

this Subchapter shall be and remain in full force and effect until changed by law. It is the policy

of this State that as many State taxes as possible be structured so that they are deductible for

federal income tax purposes under the Internal Revenue Code. (1939, c. 158, ss. A, B; 1941, c.

50, s. 1; 1983 (Reg. Sess., 1984), c. 1097, s. 1.)

§ 105-1.1. Supremacy of State Constitution.

The State's power of taxation is vested in the General Assembly. Under Article V, Section

2(1), of the North Carolina Constitution, this power cannot be surrendered, suspended, or

contracted away. In the exercise of this power, the General Assembly may amend or repeal any

provision of this Subchapter in its discretion. No provision of this Subchapter constitutes a

contract that the provision will remain in effect in future years, and any representation made to

the contrary is of no effect. (2003-416, s. 12.)

Article 1.

Inheritance Tax.

§§ 105-2 through 105-32: Repealed by Session Laws 1998-212, s. 29A.2(a), effective January

1, 1999, and applicable to the estates of decedents dying on or after that date.

Article 1A.

Estate Taxes.

§ 105-32.1: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and

applicable to the estates of decedents dying on or after that date.

§ 105-32.2: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and

applicable to the estates of decedents dying on or after that date.

§ 105-32.3: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and

applicable to the estates of decedents dying on or after that date.

§ 105-32.4: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and

applicable to the estates of decedents dying on or after that date.

NC General Statutes - Chapter 105 2

§ 105-32.5: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and

applicable to the estates of decedents dying on or after that date.

§ 105-32.6: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and

applicable to the estates of decedents dying on or after that date.

§ 105-32.7: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and

applicable to the estates of decedents dying on or after that date.

§ 105-32.8: Repealed by Session Laws 2013-316, s.7(a), effective January 1, 2013, and

applicable to the estates of decedents dying on or after that date.

Article 2.

Privilege Taxes.

§ 105-33. Taxes under this Article.

(a) General. – Taxes in this Article are imposed for the privilege of carrying on the

business, exercising the privilege, or doing the act named.

(b) License Taxes. – A license tax imposed by this Article is an annual tax. The tax is due

by July 1 of each year. The tax is imposed for the privilege of engaging in a specified activity

during the fiscal year that begins on the July 1 due date of the tax. The full amount of a license

tax applies to a person who, during a fiscal year, begins to engage in an activity for which this

Article requires a license. Before a person engages in an activity for which this Article requires a

license, the person must obtain the required license.

(c) Other Taxes. – The taxes imposed by this Article on a percentage basis or another

basis are due as specified in this Article.

(d) Repealed by Session Laws 1998-95, s. 2.

(e) Repealed by Session Laws 1989, c. 584, s. 1.

(f), (g) Repealed by Session Laws 1998-95, s. 2.

(h) Liability Upon Transfer. – A grantee, transferee, or purchaser of any business or

property subject to the State taxes imposed in this Article must make diligent inquiry as to

whether the State tax has been paid. If the business or property has been granted, sold,

transferred, or conveyed to an innocent purchaser for value and without notice that the vendor

owed or is liable for any of the State taxes imposed under this Article, the property, while in the

possession of the innocent purchaser, is not subject to any lien for the taxes.

(i), (j) Repealed by Session Laws 1998-95, s. 2.

(k) Repealed by Session Laws 1987, c. 190. (1939, c. 158, s. 100; 1943, c. 400, s. 2;

1951, c. 643, s. 2; 1953, c. 981, s. 1; 1963, c. 294, s. 3; 1973, c. 476, s. 193; 1977, c. 657, s. 1;

1981, c. 83, ss. 1, 2; 1985, c. 114, s. 10; 1985 (Reg. Sess., 1986), c. 826, ss. 1, 2; c. 934, s. 3;

1987, c. 190; 1989, c. 584, s. 1; 1989 (Reg. Sess., 1990), c. 814, s. 1; 1991 (Reg. Sess., 1992), c.

981, s. 1; 1993, c. 539, s. 688; 1994, Ex. Sess., c. 24, s. 14(c); 1996, 2nd Ex. Sess., c. 14, ss. 18,

19; 1998-95, ss. 1, 2.)

§ 105-33.1. Definitions.

The following definitions apply in this Article:

(1) City. – Defined in G.S. 105-228.90.

NC General Statutes - Chapter 105 3

(1a) Code. – Defined in G.S. 105-228.90.

(2) Repealed by Session Laws 1998-95, s. 3.

(3) Person. – Defined in G.S. 105-228.90.

(4) Secretary. – Defined in G.S. 105-228.90. (1991, c. 45, s. 1; 1991 (Reg. Sess.,

1992), c. 922, s. 2; 1993, c. 12, s. 3; c. 354, s. 6; 1998-95, s. 3.)

§ 105-34: Repealed by Session Laws 1979, c. 63.

§ 105-35: Repealed by Session Laws 1979, c. 72.

§§ 105-36 through 105-37: Repealed by Session Laws 1996, Second Extra Session, c. 14, s.

17.

§ 105-37.1: Repealed by Session Laws 2013-316, s. 5(a), effective January 1, 2014, and

applicable to gross receipts derived from an admission charge sold at retail on or after

that date.

§ 105-37.2: Repealed by Session Law 1998-96, s. 3.

§ 105-38: Repealed by Session Laws 1999-337, s. 14(b).

§ 105-38.1: Repealed by Session Laws 2013-316, s. 5(a), effective January 1, 2014, and

applicable to gross receipts derived from an admission charge sold at retail on or after

that date.

§ 105-39. Repealed by Session Laws 1987 (Reg. Sess., 1988), c. 1082, s. 1.)

§ 105-40: Repealed by Session Laws 2013-316, s. 5(a), effective January 1, 2014, and applicable

to gross receipts derived from an admission charge sold at retail on or after that date.

§ 105-41. Attorneys-at-law and other professionals.

(a) Every individual in this State who practices a profession or engages in a business and

is included in the list below must obtain from the Secretary a statewide license for the privilege

of practicing the profession or engaging in the business. A license required by this section is not

transferable to another person. The tax for each license is fifty dollars ($50.00).

(1) An attorney-at-law.

(2) A physician, a veterinarian, a surgeon, an osteopath, a chiropractor, a

chiropodist, a dentist, an ophthalmologist, an optician, an optometrist, or

another person who practices a professional art of healing.

(3) A professional engineer, as defined in G.S. 89C-3.

(4) A registered land surveyor, as defined in G.S. 89C-3.

(5) An architect.

(6) A landscape architect.

NC General Statutes - Chapter 105 4

(7) A photographer, a canvasser for any photographer, or an agent of a

photographer in transmitting photographs to be copied, enlarged, or colored.

(8) A real estate broker as defined in G.S. 93A-2. A real estate broker who is also

a real estate appraiser is required to obtain only one license under this section

to cover both activities.

(9) A real estate appraiser, as defined in G.S. 93E-1-4. A real estate appraiser who

is also a real estate broker is required to obtain only one license under this

section to cover both activities.

(10) A person who solicits or negotiates loans on real estate as agent for another

for a commission, brokerage, or other compensation.

(11) A mortician or embalmer licensed under G.S. 90-210.25.

(12) An individual licensed under Article 9F of Chapter 143 of the General

Statutes, the Home Inspector Licensure Act.

(b) The following persons are exempt from the tax:

(1) A person who is at least 75 years old.

(2) A person practicing the professional art of healing for a fee or reward, if the

person is an adherent of an established church or religious organization and

confines the healing practice to prayer or spiritual means.

(3) A blind person engaging in a trade or profession as a sole proprietor. A "blind

person" means any person who is totally blind or whose central visual acuity

does not exceed 20/200 in the better eye with correcting lenses, or where the

widest diameter of visual field subtends an angle no greater than 20 degrees.

This exemption shall not extend to any sole proprietor who permits more than

one person other than the proprietor to work regularly in connection with the

trade or profession for remuneration or recompense of any kind, unless the

other person in excess of one so remunerated is a blind person.

(c) Every person engaged in the public practice of accounting as a principal, or as a

manager of the business of public accountant, shall pay for such license fifty dollars ($50.00),

and in addition shall pay a license of twelve dollars and fifty cents ($12.50) for each person

employed who is engaged in the capacity of supervising or handling the work of auditing,

devising or installing systems of accounts.

(d) Repealed by Session Laws 1998-95, s. 7, effective July 1, 1999.

(e) Licenses issued under this section are issued as personal privilege licenses and shall

not be issued in the name of a firm or corporation. A licensed photographer having a located

place of business in this State is liable for a license tax on each agent or solicitor employed by

the photographer for soliciting business. If any person engages in more than one of the activities

for which a privilege tax is levied by this section, the person is liable for a privilege tax with

respect to each activity engaged in.

(f) Repealed by Session Laws 1981, c. 17.

(g) Repealed by Session Laws 1998-95, s. 7, effective July 1, 1999.

(h) Counties and cities may not levy any license tax on the business or professions taxed

under this section.

(i) Obtaining a license required by this Article does not of itself authorize the practice of

a profession, business, or trade for which a State qualification license is required. (1939, c. 158,

s. 109; 1941, c. 50, s. 3; 1943, c. 400, s. 2; 1949, c. 683; 1953, c. 1306; 1957, c. 1064; 1973, c.

476, s. 193; 1981, c. 17; c. 83, ss. 4, 5; 1989, c. 584, s. 7; 1991 (Reg. Sess., 1992), c. 974, s. 1;

NC General Statutes - Chapter 105 5

1993, c. 419, s. 13.2; 1998-95, s. 7; 2002-158, s. 3; 2005-276, s. 23A.1(b); 2008-206, s. 1;

2009-445, s. 1; 2011-330, s. 6.)

§ 105-41.1. Repealed by Session Laws 1975, c. 619, s. 2, effective October 1, 1975.

§ 105-42: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-43. Repealed by Session Laws 1973, c. 1195, s. 8.

§ 105-44: Repealed by Session Laws 1981 (Regular Session, 1982), c. 1228.

§§ 105-45 through 46: Repealed by Session Laws 1996, Second Extra Session, c.14, s. 17.

§ 105-47: Repealed by Session Laws 1979, c. 69.

§ 105-48: Repealed by Session Laws 1979, c. 67.

§ 105-48.1: Repealed by Session Laws 1981, c. 7.

§ 105-49: Repealed by Session Laws 1989, c. 584, s. 10.

§ 105-50: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-51: Repealed by Session Laws 1989, c. 584, s. 12.

§ 105-51.1: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-52: Repealed by Session Laws 1979, c. 16, s. 1.

§§ 105-53 through 105-55: Repealed by Session Laws 1996, Second Extra Session, c. 14, s.

17.

§ 105-56: Repealed by Session Laws 1981, c. 5.

§ 105-57: Repealed by Session Laws 1987 (Reg. Sess., 1988), c. 1081, s. 1.

§ 105-58: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-59: Repealed by Session Laws 1981 (Regular Session, 1982), c. 1282, s. 44.

§§ 105-60 through 105-61: Repealed by Session Laws 1996, Second Extra Session, c. 14, s.

17.

§ 105-61.1: Repealed by Session Laws 1989, c. 584, s. 17.

§ 105-62: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

NC General Statutes - Chapter 105 6

§ 105-63: Repealed by Session Laws 1979, c. 65.

§ 105-64: Repealed by Session Laws 1989, c. 584, s. 19.

§ 105-64.1: Repealed by Session Laws 1989, c. 584, s. 19.

§§ 105-65 through 105-65.1: Repealed by Session Laws 1996, Second Extra Session, c. 14,

s.17.

§ 105-65.2: Repealed by Session Laws 1989, c. 584, s. 19.

§ 105-66: Repealed by Session Laws 1989, c. 584, s. 19.

§ 105-66.1: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-67: Repealed by Session Laws 1991 (Regular Session, 1992), c. 965, s. 1.

§ 105-68: Repealed by Session Laws 1981 (Regular Session, 1982), c. 1229.

§ 105-69: Repealed by Session Laws 1973, c. 1200, s. 1.

§ 105-70: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-71: Repealed by Session Laws 1979, c. 70.

§ 105-72: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-73. Repealed by Session Laws 1957, c. 1340, ss. 2, 9.

§ 105-74: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-75: Repealed by Session Laws 1979, 2nd Session, c. 1304, s. 1.

§ 105-75.1: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-76: Repealed by Session Laws 1979, c. 62.

§ 105-77: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-78: Repealed by Session Laws 1979, c. 66.

§ 105-79: Repealed by Session Laws 1979, c. 150, s. 4.

§ 105-80: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

NC General Statutes - Chapter 105 7

§ 105-81. Repealed by Session Laws 1947, c. 501, s. 2.

§ 105-82: Repealed by Session Laws 1989, c. 584, s. 24.

§ 105-83. Installment paper dealers.

(a) Every person engaged in the business of dealing in, buying, or discounting

installment paper, notes, bonds, contracts, or evidences of debt for which, at the time of or in

connection with the execution of the instruments, a lien is reserved or taken upon personal

property located in this State to secure the payment of the obligations, shall submit to the

Secretary quarterly no later than the twentieth day of January, April, July, and October of each

year, upon forms prescribed by the Secretary, a full, accurate, and complete statement, verified

by the officer, agent, or person making the statement, of the total face value of the obligations

dealt in, bought, or discounted within the preceding three calendar months and, at the same time,

shall pay a tax of two hundred seventy-seven thousandths of one percent (.277%) of the face

value of these obligations.

(b) Repealed by Session Laws 1998-95, s. 9.

(c) If any person deals in, buys, or discounts any obligations described in this section

without paying a tax imposed by this section, the person may not bring an action in a State court

to enforce collection of an obligation dealt in, bought, or discounted during the period of

noncompliance with this section until the person pays the amount of tax, penalties, and interest

due.

(d) This section does not apply to corporations liable for the tax levied under G.S.

105-102.3 or to savings and loan associations.

(e) Counties and cities shall not levy any license tax on the business taxed under this

section. (1939, c. 158, s. 148; 1957, c. 1340, s. 2; 1973, c. 476, s. 193; 1981, c. 83, ss. 8, 9; 1991,

c. 45, s. 3; 1991 (Reg. Sess., 1992), c. 965, s. 3; 1998-95, s. 9; 1998-98, s. 1(f).)

§ 105-84: Repealed by Session Laws 1979, c. 150, s. 5.

§§ 105-85 through 105-86: Repealed by Session Laws 1996, Second Extra Session, c. 14, s.

17.

§ 105-87: Repealed by Session Laws 1981, c. 6.

§ 105-88. Loan agencies.

(a) Every person, firm, or corporation engaged in any of the following businesses must

pay for the privilege of engaging in that business an annual tax of two hundred fifty dollars

($250.00) for each location at which the business is conducted:

(1) The business of making loans or lending money, accepting liens on, or

contracts of assignments of, salaries or wages, or any part thereof, or other

security or evidence of debt for repayment of such loans in installment

payment or otherwise.

(2) The business of check cashing regulated under Article 22 of Chapter 53 of the

General Statutes.

(3) The business of pawnbroker regulated under Part 1 of Article 45 of Chapter

66 of the General Statutes.

NC General Statutes - Chapter 105 8

(b) This section does not apply to banks, industrial banks, trust companies, savings and

loan associations, cooperative credit unions, the business of negotiating loans on real estate as

described in G.S. 105-41, or insurance premium finance companies licensed under Article 35 of

Chapter 58 of the General Statutes. This section applies to those persons or concerns operating

what are commonly known as loan companies or finance companies and whose business is as

hereinbefore described, and those persons, firms, or corporations pursuing the business of

lending money and taking as security for the payment of the loan and interest an assignment of

wages or an assignment of wages with power of attorney to collect the amount due, or other

order or chattel mortgage or bill of sale upon household or kitchen furniture. No real estate

mortgage broker is required to obtain a privilege license under this section merely because the

broker advances the broker's own funds and takes a security interest in real estate to secure the

advances and when, at the time of the advance, the broker has already made arrangements with

others for the sale or discount of the obligation at a later date and does so sell or discount the

obligation within the period specified in the arrangement or extensions thereof; or when, at the

time of the advance the broker intends to sell the obligation to others at a later date and does,

within 12 months from date of initial advance, make arrangements with others for the sale of the

obligation and does sell the obligation within the period specified in the arrangement or

extensions thereof; or because the broker advances the broker's own funds in temporary

financing directly involved in the production of permanent-type loans for sale to others; and no

real estate mortgage broker whose mortgage lending operations are essentially as described

above is required to obtain a privilege license under this section.

(c) At the time of making any such loan, the person, or officer of the firm or corporation

making the loan, shall give to the borrower in writing in convenient form a statement showing

the amount received by the borrower, the amount to be paid back by the borrower, the time in

which the amount is to be paid, and the rate of interest and discount agreed upon.

(d) A loan made by a person who does not comply with this section is not collectible at

law under G.S. 105-269.13.

(e) (Repealed effective July 1, 2015) Counties, cities, and towns may levy a license tax

on the business taxed under this section. Except as provided in G.S. 160A-211 and G.S.

153A-152, the tax may not exceed one hundred dollars ($100.00). (1939, c. 158, s. 152; 1967, c.

1080; c. 1232, s. 2; 1973, c. 476, s. 193; 1991, c. 45, s. 4; 1993, c. 539, s. 695; 1994, Ex. Sess., c.

24, s. 14(c); 1998-98, s. 1(g); 1999-438, s. 2; 2000-120, s. 3; 2000-173, s. 2; 2012-46, s. 25;

2014-3, s. 12.3(b).)

§§ 105-89 through 105-90: Repealed by Session Laws 1996, Second Extra Session, c. 14, s.

17.

§ 105-90.1: Repealed by Session Laws 1989 (Regular Session, 1990), c. 814, s. 4.

§ 105-91: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-92: Repealed by Session Laws 1981 (Regular Session, 1982), c. 1227.

§ 105-93: Repealed by Session Laws 1979, c. 68.

§ 105-94. Repealed by Session Laws 1947, c. 501, s. 2.

NC General Statutes - Chapter 105 9

§ 105-95. Repealed by Session Laws 1947, c. 831, s. 2.

§ 105-96: Repealed by Session Laws 1981 (Regular Session, 1982), c. 1231.

§§ 105-97 through 105-99: Repealed by Session Laws 1996, Second Extra Session, c. 14, s.

17.

§ 105-100: Repealed by Session Laws 1979, c. 64.

§ 105-101: Repealed by Session Laws 1979, c. 85, s. 1.

§ 105-102: Repealed by Session Laws 1981 (Regular Session, 1982), c. 1230.

§ 105-102.1: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-102.2: Repealed by Session Laws 1981 (Regular Session, 1982), c. 1213.

§ 105-102.3. (Repealed effective June 30, 2016) Banks.

There is imposed upon every bank or banking association, including each national banking

association, that is operating in this State as a commercial bank, an industrial bank, a savings

bank created other than under Chapter 54B or 54C of the General Statutes or the Home Owners'

Loan Act of 1933 (12 U.S.C. §§ 1461-68), a trust company, or any combination of such facilities

or services, and whether such bank or banking association, hereinafter to be referred to as a bank

or banks, is organized, under the laws of the United States or the laws of North Carolina, in the

corporate form or in some other form of business organization, an annual privilege tax. A report

and the privilege tax are due by the first day of July of each year on forms provided by the

Secretary. The tax rate is thirty dollars ($30.00) for each one million dollars ($1,000,000) or

fractional part thereof of total assets held as provided in this section. The assets upon which the

tax is levied shall be determined by averaging the total assets shown in the four quarterly call

reports of condition (consolidating domestic subsidiaries) for the preceding calendar year as

required by bank regulatory authorities. If a bank has been in operation less than a calendar year,

then the assets upon which the tax is levied shall be determined by multiplying the average of the

total assets by a fraction, the denominator of which is 365 and the numerator of which is the

number of days of operation. If a bank operates an international banking facility, as defined in

G.S. 105-130.5(b)(13), the assets upon which the tax is levied shall be reduced by the average

amount for the taxable year of all assets of the international banking facility which are employed

outside the United States, as computed pursuant to G.S. 105-130.5(b)(13)c. For an out-of-state

bank with one or more branches in this State, or for an in-state bank with one or more branches

outside this State, the assets of the out-of-state bank or of the in-state bank upon which the tax is

levied shall be reduced by the average amount for the taxable year of all assets of the out-of-state

bank or of the in-state bank which are employed outside this State. The tax imposed in this

section shall be for the privilege of carrying on the businesses herein defined on a statewide basis

regardless of the number of places or locations of business within the State. Counties and cities

may not levy a license or privilege tax on the businesses taxed under this section, nor on the

business of an international banking facility as defined in subsection (b)(13) of G.S. 105-130.5.

NC General Statutes - Chapter 105 10

(1973, c. 1053, s. 7; 1981, c. 855, s. 2; 1985 (Reg. Sess., 1986), c. 985, s. 4; 1995, c. 322, s. 2;

1998-95, s. 10; 1998-98, s. 1(h); 2015-241, s. 32.13(g); 2015-268, s. 10.1(h).)

§ 105-102.4: Repealed by Session Laws 1989, c. 584, s. 35.

§ 105-102.5: Repealed by Session Laws 1996, Second Extra Session, c. 14, s. 17.

§ 105-102.6: Repealed by Session Laws 2015-286, s. 4.11(a), effective October 22, 2015.

§ 105-103. Unlawful to operate without license.

When a license tax is required by law, and whenever the General Assembly shall levy a

license tax on any business, trade, employment, or profession, or for doing any act, it shall be

unlawful for any person, firm, or corporation without a license to engage in such business, trade,

employment, profession, or do the act; and when such tax is imposed it shall be lawful to grant a

license for the business, trade, employment, or for doing the act; and no person, firm, or

corporation shall be allowed the privilege of exercising any business, trade, employment,

profession, or the doing of any act taxed in this schedule throughout the State under one license,

except under a statewide license. (1939, c. 158, s. 181; 1998-98, s. 41.)

§ 105-104: Repealed by Session Laws 2007-491, s. 2, effective January 1, 2008.

§ 105-105. Persons, firms, and corporations engaged in more than one business to pay tax

on each.

Where any person, firm, or corporation is engaged in more than one business, trade,

employment, or profession which is made under the provisions of this Article subject to State

license taxes, such persons, firms, or corporations shall pay the license tax prescribed in this

Article for each separate business, trade, employment, or profession. (1939, c. 158, s. 183.)

§ 105-106. Effect of change in name of firm.

No change in the name of a firm, partnership, or corporation, nor the taking in of a new

partner, nor the withdrawal of one or more of the firm, shall be considered as commencing

business; but if any one or more of the partners remain in the firm, or if there is change in

ownership of less than a majority of the stock, if a corporation, the business shall be regarded as

continuing. (1939, c. 158, s. 184.)

§ 105-107: Repealed by Session Laws 1998-95, s. 12, effective July 1, 1999.

§ 105-108. Property used in a licensed business not exempt from taxation.

A State license, issued under any of the provisions of this Article shall not be construed to

exempt from other forms of taxation the property employed in such licensed business, trade,

employment, or profession. (1939, c. 158, s. 186.)

§ 105-109. Obtaining license and paying tax.

(a) Repealed by Session Laws 1998-95, s. 13, effective July 1, 1999.

(b) License Required. – Before a person may engage in a business, trade, or profession

for which a license is required under this Article, the person must be licensed by the Department.

NC General Statutes - Chapter 105 11

To obtain a license, a person must submit an application to the Department for the license and

pay the required tax. An application for a license is considered a return.

The Department must issue a license to a person who files a completed application and pays

the required tax. A license must be displayed conspicuously at the location of the licensed

business, trade, or profession.

(c) Repealed by Session Laws 1998-212, s. 29A.14(a), effective January 1, 1999.

(d) Penalties. – The penalties in G.S. 105-236 apply to this Article. The Secretary may

collect a tax due under this Article in any manner allowed under Article 9 of this Chapter.

(e) (Repealed effective July 1, 2015) Local License Taxes. – The penalty and collection

provisions of this section apply to taxes levied by counties of the State under the authority of this

Article in the same manner and to the same extent as they apply to taxes levied by the State. The

provisions of this section for the collection of delinquent license taxes apply to license taxes

levied by the cities and towns of this State under authority of this Article, or any other provision

of law, in the same manner and to the same extent as they apply to taxes levied by the State.

(1939, c. 158, s. 187; 1957, c. 859; 1963, c. 294, s. 5; 1973, c. 108, s. 51; c. 476, s. 193; 1993, c.

539, ss. 698, 699; 1994, Ex. Sess., c. 24, s. 14(c); 1998-95, s. 13; 1998-212, s. 29A.14(a);

2007-491, s. 7; 2014-3, s. 12.3(b).)

§ 105-109.1. Repealed by Session Laws 1999-337, s. 16..

§ 105-110: Repealed by Session Laws 1998-212, s. 29A.14(b).

§ 105-111: Repealed by Session Laws 2001-414, s. 2.

§ 105-112: Repealed by Session Laws 1998-212, s. 29A.14(c).

§ 105-113. Repealed by Session Laws 1999-337, s. 17.

§ 105-113.1: Deleted.

Article 2A.

Tobacco Products Tax.

Part 1. General Provisions.

§ 105-113.2. Short title.

This Article may be cited as the "Tobacco Products Tax Act" or "Tobacco Products Tax

Article." (1969, c. 1075, s. 2; 1991, c. 689, s. 266; 1998-98, s. 56.)

§ 105-113.3. Scope of tax; administration.

(a) Scope. – The taxes imposed by this Article shall be collected only once on the same

tobacco product. Except as permitted by Article 2 of this Chapter, a city or county may not levy a

privilege license tax on the sale of tobacco products.

(b) Administration. – Article 9 of this Chapter applies to this Article. (1969, c. 1075, s. 2;

1991, c. 689, s. 268; 1998-212, s. 29A.14(d).)

§ 105-113.4. Definitions.

NC General Statutes - Chapter 105 12

The following definitions apply in this Article:

(1) Affiliate. – A person who directly or indirectly controls, is controlled by, or is

under common control with another person.

(1a) Affiliated manufacturer. – A manufacturer licensed under G.S. 105-113.12

who is an affiliate of a manufacturer licensed under G.S. 105-113.12.

(1b) Cigar. – A roll of tobacco wrapped in a substance that contains tobacco, other

than a cigarette.

(1c) Cigarette. – Any of the following:

a. A roll of tobacco wrapped in paper or in a substance that does not

contain tobacco.

b. A roll of tobacco wrapped in a substance that contains tobacco and

that, because of its appearance, the type of tobacco used in the filler, or

its packaging and labeling, is likely to be offered to or purchased by a

consumer as a cigarette described in subpart a. of this subdivision.

(1k) (Effective June 1, 2015) Consumable product. – Any nicotine liquid solution

or other material containing nicotine that is depleted as a vapor product is

used.

(2) Cost price. – The price a person liable for the tax on tobacco products

imposed by Part 3 of this Article paid for the products, before any discount,

rebate, or allowance or the tax imposed by that Part.

(3) Distributor. – Either of the following:

a. A person, wherever resident or located, who purchases non-tax-paid

cigarettes directly from the manufacturer of the cigarettes and stores,

sells, or otherwise disposes of the cigarettes.

b. A manufacturer of cigarettes.

(4) Repealed by Session Laws 1991, c. 689, s. 267.

(4a) Integrated wholesale dealer. – A wholesale dealer who is an affiliate of a

manufacturer of tobacco products, other than cigarettes, and is not a retail

dealer.

(5) Licensed distributor. – A distributor licensed under Part 2 of this Article.

(6) Manufacturer. – A person who produces tobacco products or a person who

contracts with another person to produce tobacco products and is the exclusive

purchaser of the products under the contract.

(7) Package. – The individual packet, can, box, or other container used to contain

and to convey tobacco products to the consumer.

(8) Person. – Defined in G.S. 105-228.90.

(9) Retail dealer. – A person who sells a tobacco product to the ultimate consumer

of the product.

(10) Sale. – A transfer, a trade, an exchange, or a barter, in any manner or by any

means, with or without consideration.

(10a) Secretary. – The Secretary of Revenue.

(11) Repealed by Session Laws 1993, c. 442, s. 1, effective January 1, 1994.

(11a) (Effective until June 1, 2015) Tobacco product. – A cigarette, a cigar, or any

other product that contains tobacco and is intended for inhalation or oral use.

NC General Statutes - Chapter 105 13

(11a) (Effective June 1, 2015) Tobacco product. – A cigarette, a cigar, or any other

product that contains tobacco and is intended for inhalation or oral use. The

term includes a vapor product.

(12) Repealed by Session Laws 1993, c. 442, s. 1, effective January 1, 1994.

(13) Use. – The exercise of any right or power over cigarettes, incident to the

ownership or possession thereof, other than the making of a sale thereof in the

course of engaging in a business of selling cigarettes. The term includes the

keeping or retention of cigarettes for use.

(13a) (Effective June 1, 2015) Vapor product. – Any nonlighted, noncombustible

product that employs a mechanical heating element, battery, or electronic

circuit regardless of shape or size and that can be used to produce vapor from

nicotine in a solution. The term includes any vapor cartridge or other

container of nicotine in a solution or other form that is intended to be used

with or in an electronic cigarette, electronic cigar, electronic cigarillo,

electronic pipe, or similar product or device. The term does not include any

product regulated by the United States Food and Drug Administration under

Chapter V of the federal Food, Drug, and Cosmetic Act.

(14) Wholesale dealer. – Either of the following:

a. A person who acquires tobacco products other than cigarettes for sale

to another wholesale dealer or to a retail dealer.

b. A manufacturer of tobacco products other than cigarettes. (1969, c.

1075, s. 2; 1973, c. 476, s. 193; 1991, c. 689, s. 267; 1993, c. 354, s. 7;

c. 442, s. 1; 2007-435, s. 2; 2009-559, s. 1; 2011-330, s. 2(a); 2014-3,

s. 15.1(a).)

§ 105-113.4A. Licenses.

(a) General. – To obtain a license required by this Article, an applicant must file an

application with the Secretary on a form provided by the Secretary and pay the tax due for the

license. An application must include the applicant's name, address, federal employer

identification number, and any other information required by the Secretary. A license is not

transferable or assignable and must be displayed at the place of business for which it is issued.

(b) Requirements. – An applicant for a license must meet the following requirements:

(1) If the applicant is a corporation, the applicant must either be incorporated in

this State or be authorized to transact business in this State.

(2) If the applicant for a license is a limited liability company, the applicant must

either be organized in this State or be authorized to transact business in this

State.

(3) If the applicant for a license is a limited partnership, the applicant must either

be formed in this State or be authorized to transact business in this State.

(4) If the applicant for a license is an individual or a general partnership, the

applicant must designate an agent for service of process and give the agent's

name and address.

(c) Denial. – The Secretary may investigate an applicant for a license required under this

Article to determine if the information the applicant submits with the application is accurate and

if the applicant is eligible to be licensed under this Article. The Secretary may refuse to issue a

license to an applicant that has done any of the following:

NC General Statutes - Chapter 105 14

(1) Submitted false or misleading information on its application.

(2) Had a license issued under this Article cancelled by the Secretary for cause.

(3) Had a tobacco products license or registration issued by another state

cancelled for cause.

(4) Been convicted of fraud or misrepresentation.

(5) Been convicted of any other offense that indicates the applicant may not

comply with this Article if issued a license.

(6) Failed to remit payment for a tax debt under this Chapter. The term "tax debt"

has the same meaning as defined in G.S. 105-243.1.

(7) Failed to file a return due under this Chapter.

(d) Refund. – A refund of a license tax is allowed only when the tax was collected or paid

in error. No refund is allowed when a license holder surrenders a license or the Secretary revokes

a license.

(e) Duplicate or Amended License. – Upon application to the Secretary, a license holder

may obtain without charge a duplicate or amended license as provided in this subsection. A

duplicate or amended license must state that it is a duplicate or amended license, as appropriate:

(1) A duplicate license, if the license holder establishes that the original license

has been lost, destroyed, or defaced.

(2) An amended license, if the license holder establishes that the location of the

place of business for which the license was issued has changed.

(f) Information on License. – The Secretary must include the following information on

each license required by this Article:

(1) The legal name of the license holder.

(2) The name under which the license holder conducts business.

(3) The physical address of the place of business of the license holder.

(4) The account number assigned to the license by the Department.

(g) Records. – The Secretary must keep a record of the following:

(1) Applicants for a license under this Article.

(2) Persons to whom a license has been issued under this Article.

(3) Persons that hold a current license issued under this Article, by license

category.

(h) Lists. – The Secretary must provide the list required under subsection (g) of this

section upon request of a manufacturer that is a license holder under this Article. The list must

state the name, account number, and business address of each license holder on the list. (1991

(Reg. Sess., 1992), c. 955, s. 3; 2013-414, s. 22(a).)

§ 105-113.4B. Reasons why the Secretary can cancel a license.

(a) Reasons. – The Secretary may cancel a license issued under this Article upon the

written request of the license holder. The Secretary may summarily cancel the license of a

license holder when the Secretary finds that the license holder is incurring liability for the tax

imposed under this Article after failing to pay a tax when due under this Article. In addition, the

Secretary may cancel the license of a license holder that commits one or more of the following

acts after holding a hearing on whether the license should be cancelled:

(1) Fails to obtain a license required by this Article.

(2) Willfully fails to file a return required by this Article.

(3) Willfully fails to pay a tax when due under this Article.

NC General Statutes - Chapter 105 15

(4) Makes a false statement in an application or return required under this Article.

(5) Fails to keep records as required by this Article.

(6) Refuses to allow the Secretary or a representative of the Secretary to examine

the person's books, accounts, and records concerning tobacco product.

(7) Fails to disclose the correct amount of tobacco product taxable in this State.

(8) Fails to file a replacement bond or an additional bond if required by the

Secretary under this Article.

(9) Violates G.S. 14-401.18.

(b) Procedure. – The Secretary must send a person whose license is summarily cancelled

a notice of the cancellation and must give the person an opportunity to have a hearing on the

cancellation within 10 days after the cancellation. The Secretary must give a person whose

license may be cancelled after a hearing at least 10 days' written notice of the date, time, and

place of the hearing. A notice of a summary license cancellation and a notice of hearing must be

sent by registered mail to the last known address of the license holder.

(c) Release of Bond. – When the Secretary cancels a license and the license holder has

paid all taxes and penalties due under this Article, the Secretary must take one of the following

actions concerning a bond or an irrevocable letter of credit filed by the license holder:

(1) Return an irrevocable letter of credit to the license holder.

(2) Return a bond to the license holder or notify the person liable on the bond and

the license holder that the person is released from liability on the bond.

(1999-333, s. 6; 2013-414, s. 22(b).)

§ 105-113.4C. Enforcement of Master Settlement Agreement Provisions.

The Master Settlement Agreement between the states and the tobacco product manufacturers,

incorporated by reference into the consent decree referred to in S.L. 1999-2, requires each state

to diligently enforce Article 37 of Chapter 66 of the General Statutes. The Office of the Attorney

General and the Secretary of Revenue shall perform the following responsibilities in enforcing

Article 37:

(1) The Office of the Attorney General must give to the Secretary of Revenue a

list of the nonparticipating manufacturers under the Master Settlement

Agreement and the brand names of the products of the nonparticipating

manufacturers.

(2) The Office of the Attorney General must update the list provided under

subdivision (1) of this section when a nonparticipating manufacturer becomes

a participating manufacturer, another nonparticipating manufacturer is

identified, or more brands or products of nonparticipating manufacturers are

identified.

(3) The Secretary of Revenue must require the taxpayers of the tobacco excise tax

to identify the amount of tobacco products of nonparticipating manufacturers

sold by the taxpayers, and may impose this requirement as provided in G.S.

66-290(10).

(4) The Secretary of Revenue must determine the amount of State tobacco excise

taxes attributable to the products of nonparticipating manufacturers, based on

the information provided by the taxpayers, and must report this information to

the Office of the Attorney General. (1999-311, s. 2.)

NC General Statutes - Chapter 105 16

§ 105-113.4D. Tax with respect to inventory on effective date of tax increase.

Every person subject to the taxes levied in this Article who, on the effective date of a tax

increase under this Article, has on hand any tobacco products must file a complete inventory of

the tobacco products within 20 days after the effective date of the increase, and must pay an

additional tax to the Secretary when filing the inventory. The amount of tax due is the amount

due based on the difference between the former tax rate and the increased tax rate. (1969, c.

1075, s. 2; 1973, c. 476, s. 193; 1991, c. 689, s. 263; 2009-451, s. 27A.5(b).)

Part 2. Cigarette Tax.

§ 105-113.5. Tax on cigarettes.

A tax is levied on the sale or possession for sale in this State, by a distributor, of all cigarettes

at the rate of two and one-fourth cents (2.25¢) per individual cigarette. (1969, c. 1075, s. 2; c.

1246, s. 1; 1991, c. 689, s. 262; 2004-170, s. 5; 2005-276, s. 34.1(a), (b); 2009-451, s. 27A.5(a).)

§ 105-113.6. Use tax levied.

A tax is levied upon the sale or possession for sale by a person other than a distributor, and

upon the use, consumption, and possession for use or consumption of cigarettes within this State

at the rate set in G.S. 105-113.5. This tax does not apply, however, to cigarettes upon which the

tax levied in G.S. 105-113.5 has been paid. (1969, c. 1075, s. 2; 1993, c. 442, s. 2.)

§ 105-113.7: Recodified as G.S. 105-113.4D by Session Laws 2009-451, s. 27A.5(b), effective

September 1, 2009.

§ 105-113.8. Federal Constitution and statutes.

Any activities which this Article may purport to tax in violation of the Constitution of the

United States or any federal statute are hereby expressly exempted from taxation under this

Article. (1969, c. 1075, s. 2.)

§ 105-113.9. Out-of-state shipments.

Any distributor engaged in interstate business shall be permitted to set aside part of the stock

as necessary to conduct interstate business without paying the tax otherwise required by this Part,

but only if the distributor complies with the requirements prescribed by the Secretary concerning

keeping of records, making of reports, posting of bond, and other matters for administration of

this Part.

"Interstate business" as used in this section means:

(1) The sale of cigarettes to a nonresident where the cigarettes are delivered by

the distributor to the business location of the nonresident purchaser in another

state; and

(2) The sale of cigarettes to a nonresident wholesaler or retailer registered through

the Secretary who has no place of business in North Carolina and who

purchases the cigarettes for the purposes of resale not within this State and

where the cigarettes are delivered to the purchaser at the business location in

North Carolina of the distributor who is also licensed as a distributor under the

laws of the state of the nonresident purchaser. (1969, c. 1075, s. 2; 1973, c.

476, s. 193; 1977, c. 874; 1993, c. 442, s. 3.)

NC General Statutes - Chapter 105 17

§ 105-113.10. Manufacturers exempt from paying tax.

(a) Shipping to Other Distributors. – Any manufacturer shipping cigarettes to other

distributors who are licensed under G.S. 105-113.12 may, upon application to the Secretary and

upon compliance with requirements prescribed by the Secretary, be relieved of paying the taxes

levied in this Part. No manufacturer may be relieved of the requirement to be licensed as a

distributor in order to make shipments, including drop shipments, to a retail dealer or ultimate

user.

(b) Shipping for Affiliated Manufacturer. – A manufacturer may, upon application to the

Secretary and upon compliance with requirements prescribed by the Secretary, be relieved of

paying the taxes levied in this Part on cigarettes that are manufactured by an affiliated

manufacturer and temporarily stored at and shipped from its facilities. (1969, c. 1075, s. 2; c.

1246, s. 2; 1973, c. 476, s. 193; 1975, c. 275, s. 2; 1993, c. 442, s. 4; 2011-330, s. 2(b).)

§ 105-113.11. Licenses required.

After the effective date of this Article, no person shall engage in business as a distributor in

this State, without having first obtained from the Secretary the appropriate license for that

purpose as prescribed herein. Any license required by this Article shall be in addition to any and

all other licenses which may be required by law. (1969, c. 1075, s. 2; 1973, c. 476, s. 193.)

§ 105-113.12. Distributor must obtain license.

(a) A distributor shall obtain for each place of business a continuing distributor's license

and shall pay a tax of twenty-five dollars ($25.00) for the license.

(b) For the purposes of this section, a "place of business" is a place where a distributor

receives or stores non-tax-paid cigarettes.

(c) An out-of-state distributor may obtain a distributor's license upon compliance with

the provisions of G.S. 105-113.24 and payment of a tax of twenty-five dollars ($25.00). (1969, c.

1075, s. 2; 1991 (Reg. Sess., 1992), c. 955, s. 4; 1993, c. 442, s. 5.)

§ 105-113.13. Secretary may require a bond or irrevocable letter of credit.

(a) Repealed by Session Laws 2013-414, s. 22(c), effective September 1, 2013.

(b) The Secretary may require a distributor to furnish a bond in an amount that

adequately protects the State from loss if the distributor fails to pay taxes due under this Part. A

bond must be conditioned on compliance with this Part, payable to the State, and in the form

required by the Secretary. The Secretary must set the bond amount based on the anticipated tax

liability of the distributor. The Secretary should periodically review the sufficiency of bonds

required of the distributor and increase the required bond amount if the amount no longer covers

the anticipated tax liability of the distributor and decrease the amount if the Secretary finds that a

lower bond amount will protect the State adequately from loss.

For purposes of this section, a distributor may substitute an irrevocable letter of credit for the

secured bond required by this section. The letter of credit must be issued by a commercial bank

acceptable to the Secretary and available to the State as a beneficiary. The letter of credit must be

in a form acceptable to the Secretary, conditioned upon compliance with this Article, and in the

amounts stipulated in this section. (1969, c. 1075, s. 2; 1973, c. 476, s. 193; 1991 (Reg. Sess.,

1992), c. 955, s. 5; 1993, c. 442, s. 6; 2013-414, s. 22(c); 2014-3, s. 9.1(a).)

NC General Statutes - Chapter 105 18

§§ 105-113.14 through 105-113.15: Repealed by Session Laws 1991 (Regular Session,

1992), c. 955, s. 6, effective July 15, 1992.

§ 105-113.16. Repealed by Session Laws 1999-333, s. 7.

§ 105-113.17. Identification of dispensers.

Each vending machine that dispenses cigarettes must be marked to identify its owner in the

manner required by the Secretary. (1969, c. 1075, s. 2; 1973, c. 476, s. 193; 1991 (Reg. Sess.,

1992), c. 955, s. 8.)

§ 105-113.18. Payment of tax; reports.

The taxes levied in this Part are payable when a report is required to be filed. The following

reports are required to be filed with the Secretary:

(1) Distributor's Report. – A distributor shall file a monthly report in the form

prescribed by the Secretary. The report covers sales and other activities

occurring in a calendar month and is due within 20 days after the end of the

month covered by the report. The report shall state the amount of tax due and

shall identify any transactions to which the tax does not apply.

(1a) Report of Free Cigarettes. – A manufacturer who distributes cigarettes without

charge shall file a monthly report in the form prescribed by the Secretary. The

report covers cigarettes distributed without charge in a calendar month and is

due within 20 days after the end of the month covered by the report. The

report shall state the number of cigarettes distributed without charge and the

amount of tax due.

(2) Use Tax Report. – Every other person who has acquired non-tax-paid

cigarettes for sale, use, or consumption subject to the tax imposed by this Part

shall, within 96 hours after receipt of the cigarettes, file a report in the form

prescribed by the Secretary showing the amount of cigarettes so received and

any other information required by the Secretary. The report shall be

accompanied by payment of the full amount of the tax.

(3) Shipping Report. – Any person, except a licensed distributor, who transports

cigarettes upon the public highways, roads, or streets of this State, upon notice

from the Secretary, shall file a report in the form prescribed by the Secretary

and containing the information required by the Secretary.

(4) Repealed by Session Laws 1981 (Regular Session, 1982), c. 1209, s. 1. (1969,

c. 1075, s. 2; 1973, c. 476, s. 193; 1981 (Reg. Sess., 1982), c. 1209, s. 1; 1993,

c. 442, s. 7; 1993 (Reg. Sess., 1994), c. 745, s. 2.)

§§ 105-113.19 through 105-113.20: Repealed by Session Laws 1993, c. 442, s. 8.

§ 105-113.21. Discount; refund.

(a) Repealed by Session Laws 2003-284, s. 45A.1(a), effective for reporting periods

beginning on or after August 1, 2003.

(a1) Discount. – A distributor who files a timely report under G.S. 105-113.18 and who

sends a timely payment may deduct from the amount due with the report a discount of two

NC General Statutes - Chapter 105 19

percent (2%). This discount covers expenses incurred in preparing the records and reports

required by this Part, and the expense of furnishing a bond.

(b) Refund. – A distributor in possession of packages of stale or otherwise unsalable

cigarettes upon which the tax has been paid may return the cigarettes to the manufacturer as

provided in this subsection and apply to the Secretary for refund of the tax. The application shall

be in the form prescribed by the Secretary and shall be accompanied by an affidavit from the

manufacturer stating the number of cigarettes returned to the manufacturer by the applicant. The

Secretary shall refund the tax paid, less the discount allowed, on the unsalable cigarettes. The

distributor must return the cigarettes to the manufacturer of the cigarettes or to the affiliated

manufacturer who is contracted by the manufacturer of the cigarettes to serve as the

manufacturer's agent for the purposes of validating quantities and disposing of unsalable

cigarettes. (1969, c. 1075, s. 2; cc. 1222, 1238; 1973, c. 476, s. 193; 1993, c. 442, s. 9; 2001-414,

s. 3; 2003-284, s. 45A.1(a); 2004-84, s. 2(a); 2011-330, s. 2(c).)

§§ 105-113.22 through 105-113.23: Repealed by Session Laws 1993, c. 442, s. 8.

§ 105-113.24. Out-of-State distributors to register and remit tax.

(a) The Secretary may authorize any distributor outside this State engaged in the business

of selling and shipping cigarettes into the State to obtain a license and report and pay taxes

required by this Part.

(b) A nonresident distributor must agree to submit the distributor's books, accounts, and

records to reasonable examination by the Secretary or the Secretary's duly authorized agents. The

Secretary may require a nonresident distributor to file a bond in accordance with G.S.

105-113.13.

(c) Each such nonresident distributor, other than a foreign corporation which has

qualified with the Secretary of State as doing business in this State shall, by a duly executed

instrument filed in the office of the Secretary of State, constitute and appoint the Secretary of

State his lawful attorney in fact upon whom any original process in any action or legal

proceeding against such nonresident distributor arising out of any matter relating to this Article

may be served, and therein agree that any original process against him so served shall be of the

same force and effect as if served on him within this State, and that the authority thereof shall

continue in force irrevocably so long as any such nonresident distributor shall remain liable for

any taxes, interest and penalties under this Article.

(d) Any nonresident distributor who shall comply with the provisions of this section may

be licensed as a distributor. (1969, c. 1075, s. 2; 1973, c. 476, s. 193; 1991 (Reg. Sess., 1992), c.

955, s. 9; 1993, c. 442, ss. 9.1(a), 9.1(b).)

§ 105-113.25: Repealed by Session Laws 1993, c. 442, s. 8.

§ 105-113.26. Records to be kept.

Every person required to be licensed under this Article and every person required to make

reports under this Article shall keep complete and accurate records of all sales and other

information as required under this Article. The records shall be in the form prescribed by the

Secretary.

These records shall be safely preserved for a period of three years in a manner to ensure their

security and accessibility for inspection by the Department. The Secretary may consent to the

NC General Statutes - Chapter 105 20

destruction of any records at any time within this three-year period. (1969, c. 1075, s. 2; 1973, c.

476, s. 193; 1993, c. 442, s. 10.)

§ 105-113.27. Non-tax-paid cigarettes.

(a) Except as otherwise provided in this Article, licensed distributors shall not sell,

borrow, loan, or exchange non-tax-paid cigarettes to, from, or with other licensed distributors.

(b) No person shall sell or offer for sale non-tax-paid cigarettes.

(c) The possession of more than six hundred cigarettes on which tax has been paid to

another state or country, by any person other than a licensed distributor, is prima facie evidence

that the cigarettes are possessed in violation of this Part. (1969, c. 1075, s. 2; 1993, c. 442, s. 11;

1999-337, s. 18.)

§ 105-113.28: Repealed by Session Laws 1993, c. 442, s. 8.

§ 105-113.29. Unlicensed place of business.

It shall be unlawful for any person to maintain a place of business within this State required

by this Article to be licensed to engaged in the business of selling or offering for sale cigarettes

without first obtaining such licenses. (1969, c. 1075, s. 2.)

§ 105-113.30. Records and reports.

It shall be unlawful for any person who is required under the provisions of this Article to

keep records or make reports, to fail to keep such records, refuse to keep such reports, make false

entries in such records, fail to produce such records for inspection by the Secretary or his duly

authorized agents, fail to file a report, or make a false or fraudulent report or statement. (1969, c.

1075, s. 2; 1973, c. 476, s. 193.)

§ 105-113.31. Possession and transportation of non-tax-paid cigarettes; seizure and

confiscation of vehicle or vessel.

(a) It shall be unlawful for any person to transport non-tax-paid cigarettes in violation of

this Part. The Secretary may adopt rules allowing quantities of non-tax-paid cigarettes, not

exceeding six hundred, to be brought into this State by a transient, a tourist, or a person returning

to this State after traveling outside this State, for their own use. The possession or transportation

of these cigarettes is not subject to the penalties imposed by this section.

(b) (1) Every person who transports non-tax-paid cigarettes on the public highways,

roads, streets, or waterways of this State must transport with the cigarettes

invoices or delivery tickets for the cigarettes showing the true name and

complete and exact address of the consignee or purchaser, the quantity and

brands of the cigarettes transported, and the true name and complete and exact

address of the person who has paid or who will pay the tax imposed by this

Part or the tax, if any, of the state or foreign country at the point of ultimate

destination.

(2) A common carrier that has issued a bill of lading for a shipment of cigarettes

and is without notice to itself or to any of its agents or employees that the

cigarettes are non-tax-paid in violation of this Part is considered to have

complied with this Part and the vehicle or vessel in which the cigarettes are

being transported is not subject to confiscation under this section. In the

NC General Statutes - Chapter 105 21

absence of the required invoices, delivery tickets, or bills of lading, the

cigarettes so transported, the vehicle or vessel in which the cigarettes are

being transported, and any paraphernalia or devices used in connection with

the non-tax-paid cigarettes are declared to be contraband goods and may be

seized by any officer of the law, who shall take possession of the vehicle or

vessel and cigarettes and shall arrest any person in charge of the vehicle or

vessel and cigarettes.

(3) The officer shall at once proceed against the person arrested, under the

provisions of this Part, in any court having competent jurisdiction; but the

vehicle or vessel shall be returned to the owner upon execution by the owner

of a good and valid bond, with sufficient sureties, in a sum double the value of

the property, which bond shall be approved by the officer and shall be

conditioned to return the property to the custody of the officer on the day of

trial to abide the judgment of the court. All non-tax-paid cigarettes seized

under this section shall be held and shall, upon the acquittal of the person so

charged, be returned to the established owner.

(4) Unless the claimant can show that the non-tax-paid cigarettes seized were not

transported in violation of this Part and that the property seized belongs to the

claimant or that in the case of property other than cigarettes, the property was

used in transporting non-tax-paid cigarettes in violation of this Part without

the claimant's knowledge or consent, with the right on the part of the claimant

to have a jury pass upon this claim, the court shall order a sale by public

auction of the property seized, and the officer making the sale, after deducting

the cost of the tax due, which the officer shall pay upon sale, expenses of

keeping the property, the fee for the seizure, and the costs of the sale, shall

pay all liens according to their priorities, which are established, by

intervention or otherwise, at the hearing or in another proceeding brought for

the purpose as being bona fide and as having been created without the lien or

having any notice that the vehicle or vessel was being used for the unlawful

transportation of non-tax-paid cigarettes, and shall pay the balance of the

proceeds to the State Treasurer for the General Fund.

(5) All liens against property sold under the provisions of this section shall be

transferred from the property to the proceeds of the sale of the property. If,

however, no one is found claiming the cigarettes, or the vehicle or vessel, then

the taking of the cigarettes, vehicle, or vessel, along with a description, shall

be advertised in a newspaper having circulation in the county where the items

were taken, once a week for two weeks and by notices posted in three public

places near the place of seizure, and if no claimant appears within ten days

after the last publication of the advertisement, the property shall be sold, and

the proceeds, after deducting the expenses and costs, shall be paid to the State

Treasurer for the General Fund.

(6) This section does not authorize an officer to search any vehicle or vessel or

baggage of any person without a search warrant duly issued, except where the

officer has knowledge that there are non-tax-paid cigarettes in the vehicle or

vessel. (1969, c. 1075, s. 2; 1973, c. 476, s. 193; 1993, c. 442, s. 12.)

NC General Statutes - Chapter 105 22

§ 105-113.32. Non-tax-paid cigarettes subject to confiscation.

All non-tax-paid cigarettes subject to the tax imposed by this Part, together with any

container in which they are stored or displayed for sale (including but not limited to vending

machines), are declared to be contraband goods and may be seized by any officer of the law.

The officer shall arrest any person in charge of the contraband goods and shall at once proceed

against the person arrested, under the provisions of this Part, in any court having competent

jurisdiction. The disposition of the seized cigarettes and container shall be governed by the

provisions of G.S. 105-113.31. (1969, c. 1075, s. 2; 1993, c. 442, s. 13.)

§ 105-113.33. Criminal penalties.

Any person who violates any of the provisions of this Article for which no other punishment

is specifically prescribed shall be guilty of a Class 1 misdemeanor. (1969, c. 1075, s. 2; 1993, c.

539, s. 700; 1994, Ex. Sess., c. 24, s. 14(c).)

§ 105-113.34: Repealed by Session Laws 1993, c. 442, s. 8.

Part 3. Tax on Other Tobacco Products.

§ 105-113.35. Tax on tobacco products other than cigarettes.

(a) Tax on Tobacco Products. – An excise tax is levied on tobacco products other than

cigarettes and vapor products at the rate of twelve and eight-tenths percent (12.8%) of the cost

price of the products.

(a1) Tax on Vapor Products. – An excise tax is levied on vapor products at the rate of five

cents (5¢) per fluid milliliter of consumable product. All invoices for vapor products issued by

manufacturers must state the amount of consumable product in milliliters.

(a2) Limitation. – The taxes imposed under this section do not apply to the following:

(1) A tobacco product sold outside the State.

(2) A tobacco product sold to the federal government.

(3) A sample tobacco product distributed without charge.

(b) Primary Liability. – The wholesale dealer or retail dealer who first acquires or

otherwise handles tobacco products subject to the tax imposed by this section is liable for the tax

imposed by this section. A wholesale dealer or retail dealer who brings into this State a tobacco

product made outside the State is the first person to handle the tobacco product in this State. A

wholesale dealer or retail dealer who is the original consignee of a tobacco product that is made

outside the State and is shipped into the State is the first person to handle the tobacco product in

this State.

(c) Secondary Liability. – A retail dealer who acquires non-tax-paid tobacco products

subject to the tax imposed by this section from a wholesale dealer is liable for any tax due on the

tobacco products. A retail dealer who is liable for tax under this subsection may not deduct a

discount from the amount of tax due when reporting the tax.

(d) Manufacturer's Option. – A manufacturer who is not a retail dealer and who ships

tobacco products other than cigarettes to either a wholesale dealer or retail dealer licensed under

this Part may apply to the Secretary to be relieved of paying the tax imposed by this section on

the tobacco products. A manufacturer who ships vapor products to either a wholesale dealer or

retail dealer licensed under this Part may apply to the Secretary to be relieved of paying the tax

imposed by this section on the vapor products shipped to either a wholesale dealer or retail

dealer. Once granted permission, a manufacturer may choose not to pay the tax until otherwise

NC General Statutes - Chapter 105 23

notified by the Secretary. To be relieved of payment of the tax imposed by this section, a

manufacturer must comply with the requirements set by the Secretary.

Permission granted under this subsection to a manufacturer to be relieved of paying the tax

imposed by this section applies to an integrated wholesale dealer with whom the manufacturer is

an affiliate. A manufacturer must notify the Secretary of any integrated wholesale dealer with

whom it is an affiliate when the manufacturer applies to the Secretary for permission to be

relieved of paying the tax and when an integrated wholesale dealer becomes an affiliate of the

manufacturer after the Secretary has given the manufacturer permission to be relieved of paying

the tax.

If a person is both a manufacturer of cigarettes and a wholesale dealer of tobacco products

other than cigarettes and the person is granted permission under G.S. 105-113.10 to be relieved

of paying the cigarette excise tax, the permission applies to the tax imposed by this section on

tobacco products other than cigarettes. A cigarette manufacturer who becomes a wholesale

dealer after receiving permission to be relieved of the cigarette excise tax must notify the

Secretary of the permission received under G.S. 105-113.10 when applying for a license as a

wholesale dealer.

(d1) Limitation. – Except as otherwise provided in this Article, integrated wholesale

dealers may not sell, borrow, loan, or exchange non-tax-paid tobacco products other than

cigarettes to, from, or with other integrated wholesale dealers.

(e) Repealed by Session Laws 2009-451, s. 27A.5(c), effective September 1, 2009.

(1969, c. 1075, s. 2; 1977, c. 1114, s. 4; 1991, c. 689, s. 269; 1991 (Reg. Sess., 1992), c. 955, s.

10; 2003-284, s. 45A.1(b); 2004-84, s. 2(b); 2005-276, s. 34.1(c); 2007-323, s. 6.23(a);

2007-435, s. 3; 2009-451, s. 27A.5(c); 2009-559, s. 2; 2014-3, s. 15.1(b); 2015-6, s. 2.5(a).)

§ 105-113.36. Wholesale dealer and retail dealer must obtain license.

A wholesale dealer shall obtain for each place of business a continuing tobacco products

license and shall pay a tax of twenty-five dollars ($25.00) for the license. A retail dealer shall

obtain for each place of business a continuing tobacco products license and shall pay a tax of ten

dollars ($10.00) for the license. A "place of business" is a place where a wholesale dealer or

where a retail dealer makes tobacco products other than cigarettes or a wholesale dealer or a

retail dealer receives or stores non-tax-paid tobacco products other than cigarettes. (1969, c.

1075, s. 2; 1973, c. 476, s. 193; 1991, c. 689, s. 270; 1991 (Reg. Sess., 1992), c. 955, s. 11.)

§ 105-113.37. Payment of tax.

(a) Monthly Report. – Except for tax on a designated sale under subsection (b), the taxes

levied by this Article are payable when a report is required to be filed. A report is due on a

monthly basis. A monthly report covers sales and other activities occurring in a calendar month

and is due within 20 days after the end of the month covered by the report. A report shall be filed

on a form provided by the Secretary and shall contain the information required by the Secretary.

(b) (Effective until June 1, 2015) Designation of Exempt Sale. – A wholesale dealer

who sells a tobacco product to a person who has notified the wholesale dealer in writing that the

person intends to resell the item in a transaction that is exempt from tax under G.S.

105-113.35(a)(1) or (2) may, when filing a monthly report under subsection (a), designate the

quantity of tobacco products sold to the person for resale. A wholesale dealer shall report a

designated sale on a form provided by the Secretary.

NC General Statutes - Chapter 105 24

A wholesale dealer is not required to pay tax on a designated sale when filing a monthly

report. The wholesale dealer shall pay the tax due on all other sales in accordance with this

section. A wholesale dealer or a customer of a wholesale dealer may not delay payment of the

tax due on a tobacco product by failing to pay tax on a sale that is not a designated sale or by

overstating the quantity of tobacco products that will be resold in a transaction exempt under

G.S. 105-113.35(a)(1) or (2).

A person who does not sell a tobacco product in a transaction exempt under G.S.

105-113.35(a)(1) or (2) after a wholesale dealer has failed to pay the tax due on the sale of the

item to the person in reliance on the person's written notification of intent is liable for the tax and

any penalties and interest due on the designated sale. If the Secretary determines that a tobacco

product reported as a designated sale is not sold as reported, the Secretary shall assess the person

who notified the wholesale dealer of an intention to resell the item in an exempt transaction for

the tax due on the sale and any applicable penalties and interest. A wholesale dealer who does

not pay tax on a tobacco product in reliance on a person's written notification of intent to resell

the item in an exempt transaction is not liable for any tax assessed on the item.

(b) (Effective June 1, 2015) Designation of Exempt Sale. – A wholesale dealer who sells

a tobacco product to a person who has notified the wholesale dealer in writing that the person

intends to resell the item in a transaction that is exempt from tax under G.S. 105-113.35(a2)(1) or

G.S. 105-113.35(a2)(2) may, when filing a monthly report under subsection (a), designate the

quantity of tobacco products sold to the person for resale. A wholesale dealer shall report a

designated sale on a form provided by the Secretary.

A wholesale dealer is not required to pay tax on a designated sale when filing a monthly

report. The wholesale dealer shall pay the tax due on all other sales in accordance with this

section. A wholesale dealer or a customer of a wholesale dealer may not delay payment of the

tax due on a tobacco product by failing to pay tax on a sale that is not a designated sale or by

overstating the quantity of tobacco products that will be resold in a transaction exempt under

G.S. 105-113.35(a2)(1) or G.S. 105-113.35(a2)(2).

A person who does not sell a tobacco product in a transaction exempt under G.S.

105-113.35(a2)(1) or G.S. 105-113.35(a2)(2) after a wholesale dealer has failed to pay the tax

due on the sale of the item to the person in reliance on the person's written notification of intent

is liable for the tax and any penalties and interest due on the designated sale. If the Secretary

determines that a tobacco product reported as a designated sale is not sold as reported, the

Secretary shall assess the person who notified the wholesale dealer of an intention to resell the

item in an exempt transaction for the tax due on the sale and any applicable penalties and

interest. A wholesale dealer who does not pay tax on a tobacco product in reliance on a person's

written notification of intent to resell the item in an exempt transaction is not liable for any tax

assessed on the item.

(c) Repealed by Session Laws 1991 (Regular Session, 1992), c. 955, s. 12.

(d) Shipping Report. – Any person who transports other tobacco products upon the public

highways, roads, or streets of this State must, upon notice from the Secretary, file a report in a

form prescribed by and containing the information required by the Secretary. (1969, c. 1075, s.

2; 1973, c. 476, s. 193; 1991, c. 689, s. 271; 1991 (Reg. Sess., 1992), c. 955, s. 12; 2009-559, s.

3; 2014-3, s. 15.1(c).)

§ 105-113.38. Bond or irrevocable letter of credit.

NC General Statutes - Chapter 105 25

The Secretary may require a wholesale dealer or a retail dealer to furnish a bond in an

amount that adequately protects the State from loss if the dealer fails to pay taxes due under this

Part. A bond must be conditioned on compliance with this Part, payable to the State, and in the

form required by the Secretary. The bond amount must be proportionate to the anticipated tax

liability of the wholesale dealer or retail dealer. The Secretary should periodically review the

sufficiency of bonds required of dealers, and increase the amount of a required bond when the

amount of the bond furnished no longer covers the anticipated tax liability of the wholesale