namibia senior secondary certificate - MINISTRY OF ...

54

REPUBLIC OF NAMIBIA MINISTRY OF EDUCATION NAMIBIA SENIOR SECONDARY CERTIFICATE THESE PAPERS AND MARK SCHEMES SERVE TO EXEMPLIFY THE SPECIFICATIONS IN THE LOCALISED NSSC ACCOUNTING HIGHER LEVEL SYLLABUS 2006 ACCOUNTING SPECIMEN PAPERS 1 - 2 AND MARK SCHEMES HIGHER LEVEL GRADES 11 – 12

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of namibia senior secondary certificate - MINISTRY OF ...

REPUBLIC OF NAMIBIA

MINISTRY OF EDUCATION

NAMIBIA SENIOR SECONDARY CERTIFICATE

THESE PAPERS AND MARK SCHEMES SERVE TO EXEMPLIFY THE SPECIFICATIONS IN THE LOCALISED

NSSC ACCOUNTING HIGHER LEVEL SYLLABUS

2006

ACCOUNTING SPECIMEN PAPERS 1 - 2 AND MARK

SCHEMES

HIGHER LEVEL

GRADES 11 – 12

Ministry of Education National Institute for Educational Development (NIED) Private Bag 2034 Okahandja Namibia © Copyright NIED, Ministry of Education, 2005 NSSCH Accounting Specimen Paper Booklet Grades 11 - 12 ISBN: 99916-69-76-0 Printed by NIED Publication date: 2005

TABLE OF CONTENTS Paper 1: Specimen Paper ..........................................................................................................1

Paper 1: Mark Scheme............................................................................................................19

Paper 2: Specimen Paper ........................................................................................................27

Paper 2: Mark Scheme............................................................................................................42

1

MINISTRY OF EDUCATION

Namibia Senior Secondary Certificate (NSSC)

ACCOUNTING: HIGHER LEVEL

PAPER 1 SPECIMEN PAPER

TIME: 2 hours 30 minutes INSTRUCTIONS TO CANDIDATES Write your name, centre number and candidate number in the spaces at the top of this page. Answer all questions. Write your answers in the spaces provided on the question paper. INFORMATION FOR CANDIDATES The number of marks is given in brackets [ ] at the end of each question or part question. You may use a calculator. Where layouts are to be completed, you may not need all the lines for your answer.

2

QUESTION 1 Muller Limited maintains control accounts, the balances of which are transferred to its Trial Balance at the end of its financial year. The company’s Trial Balance as at 30 June 2004 included:

Dr Cr N$ N$ Debtors Control account 36 840 1 300 Creditors Control account 1 600 33 100

The details below relate to the company’s transactions with its customers and suppliers for the financial year ended 30 June 2005. All transactions are on a credit basis.

N$ Sales Invoice value before trade discount 378 400 Invoice value after trade discount 357 100 Sales Returns Invoice value before trade discount 8 200 Invoice value after trade discount 6 900 Cheques received from customers 342 500 Cheques returned to customers as dishonoured 800 Discounts allowed to customers 7 300 Bad debts 1 400 Purchases Invoice value before trade discount 210 400 Invoice value after trade discount 193 300 Purchase Returns Invoice value before trade discount 2 200 Invoice value after trade discount 1 940 Cheques paid to suppliers 178 700 Discounts received from suppliers 5 800

At 30 June 2005 the Debtors Ledger included credit balances totaling N$1 900. At the same date the Creditors Ledger included debit balances totaling N$1 100.

3

Fountain Limited is both a supplier and a customer of Muller Limited. At 30 June 2005 the account balances of Fountain Limited in Muller Limited’s books were:

N$ Debtors Ledger 2 300 Creditors Ledger 2 650

It was decided to set off Fountain Limited’s balance in the Debtors Ledger against its balance in the Creditors Ledger. REQUIRED: (a) Prepare the Debtors Control account and the Creditors Control account for the year

ended 30 June 2005.

Debtors Control account

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

…………………………………………………………………………………… [11]

4

Creditors Control account

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

…………………………………………………………………………………… [9]

(b) State and explain three advantages of using control accounts.

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

…………………………………………………………………………....…… [9]

Total [29]

5

QUESTION 2 The following are the summarised Balance Sheets of Duneside Limited at 31 December.

2004 2005 N$ N$ N$ N$ Fixed Assets Premises at cost 800 000 850 000Machinery (net book value) 240 000 259 500Motor Vehicles (net book value) 79 000 71 000 1 119 000 1 180 500 Working Capital 32 800 44 500 Current Assets Stock 43 200 41 000 Debtors 28 500 26 200 Bank 18 200 34 600 89 900 101 800 Current Liabilities Creditors 27 100 32 300 Proposed Dividends 30 000 25 000 57 100 57 300 1 151 800 1 225 000 Capital and Reserves Ordinary Shares 1 000 000 1 070 000 General Reserve 100 000 110 000Profit and Loss 51 800 45 000 1 151 800 1 225 000

(i) Machinery costing N$68 000 had been purchased during 2005. There were no disposals of machinery.

(ii) A motor vehicle with a written down value of N$7 000 had been sold during 2005

for N$6 000. This had been replaced by a motor vehicle costing N$14 000.

(iii) Premises are not depreciated.

6

REQUIRED: (a) Calculate the net profit for the year ended 31 December 2005.

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

…………………………………………………………………………………. [5]

(b) Prepare the Cash Flow Statement for the year ended 31 December 2005.

Workings:……...…………………………………………………………………………

……………………………………………………………………………………………

…………………….………….……..……………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

…………………………………………………………………………………………

Cash Flow Statement for the year ended 31 December 2005

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

…………………………………………………………………..……………… [18]

7

(c) Briefly discuss two differences between a Cash Flow Statement and a Profit and Loss Account.

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………….………………………………………………………………..… [8]

Total [31]

8

QUESTION 3 Simon Alberts started in business on 1 June 2003. He purchased the following machinery and paid by cheque.

Machine number Date of purchase N$ Machine 1 1 June 2003 20 000 Machine 2 1 June 2004 40 000 Machine 3 1 March 2005 50 000

Machinery is depreciated at the rate of 25 % per annum using the straight-line method. On 31 May 2005 it was decided that Machine 1 had become obsolete and had no residual value. All remaining depreciation for this machine was charged at this date and the machinery disposed of. Depreciation on machinery is charged for each proportion of a year for which it is held. REQUIRED: (a) Prepare the following accounts for each of the years ended 31 May 2004 and

31 May 2005.

(i) Machinery account

…………………………………………………………………………………………

………………………………………………………………………………….………

………………………………………………………………………………….………

………………………………………………………………………………….………

………………………………………………………………………….………………

………………………………………………………………………………….………

………………………………………………………………………………… [4]

(ii) Provision for Depreciation of Machinery account

………………………………………………………………………………..…………

………………………………………………………………………………………..…

………………………………………………………………………………………..…

……………………………………………………………………………………..……

……………………………………………………………………………………..……

………………………………………………………………………………… [5]

9

(b) Comment on the statement ‘Provision for depreciation is made to provide for the replacement of a fixed asset’.

……………………………………………………………………………………..……

……………………………………………………………………………………..……

……………………………………………………………………………………..……

……………………………………………………………………………………..……

……………………………………………………………………………………..……

………………………………………………………………………………… [6]

Total [15]

10

QUESTION 4 Amy and Byron are in partnership. A Balance Sheet extract at 31 December 2004 showed the following balances.

N$ Capital Accounts

Amy 90 000 Byron 90 000

Current Accounts

Amy 14 600 credit Byron 22 000 credit

Fixed Assets (net book value) 240 000

The partnership agreement provided for: (i) interest on capital at 6 % per annum, (ii) no interest on drawings, (iii) Amy and Byron share profits and losses in the ratio 3:2 On 1 July 2005 Amy and Byron decided to admit Cynthia to the partnership. Cynthia would introduce capital of N$100 000 cash and the partnership borrowed a further N$50 000 from Amy. The new partnership agreement provided that: (i) interest on capital was to remain at 6 % per annum, (ii) there would be no interest on drawings, (iii) Cynthia was to be entitled to a salary of N$14 000 per annum, (iv) interest on loan will be calculated at 10 % p.a.,

(v) profits and losses were to be shared among Amy, Byron and Cynthia in the ratio

3:2:1. In addition, on 1 July 2005 fixed assets were to be revalued to N$250 000. No fixed assets were bought or sold during 2005. Depreciation on fixed assets is charged at 5 % per annum on the net book value and is charged for each proportion of the year for which the fixed assets are held. Goodwill was to be valued at N$30 000 on 1 July 2005. The Goodwill was to remain in the books of the firm.

11

The partners made the following drawings.

N$ Amy 21 000 Byron 17 000 Cynthia 8 000

The net profit before appropriation for the six months ended 30 June 2005 was N$44 600, and the net profit before appropriation for the six months ended 31 December 2005 was N$77 980. REQUIRED: (a) Prepare the Partnership Appropriation Accounts for:

(i) the six months ended 30 June 2005, (ii) the six months ended 31 December 2005.

(i) Partnership Appropriation account for the six months ended 30 June 2005

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

....................................................................................................................................

12

(ii) Partnership Appropriation account for the six months ended 31 December 2005

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

.....................................................................................................................................

..................................................................................................................... [12]

(b) Prepare the Current accounts for each of the partners for the year ended

31 December 2005

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

................................................................................................................... [12]

13

(c) Cynthia joined the partnership during the year and is entitled to a part of the goodwill. She did not pay extra for this benefit, but the bookkeeper credited her Capital account with the appropriate amount. Amy objected to this, but the bookkeeper argued that it was after all Cynthia’s money. Give your advice on how this transaction should be treated.

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

......................................................................................................................... [5]

(d) Explain why Goodwill may be brought into a partnership’s accounts when there is a

change in the partnership.

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

........................................................................................................................ [3]

Total [32]

14

QUESTION 5 Gobabis Limited has an authorized share Capital of N$6 100 000, divided into 600 000 N$10 ordinary shares and 100 000 5 % preference shares of N$1 each. On 1 March 2004, the company issued 400 000 N$10 ordinary shares at a premium of N$2 and all of the 5 % preference shares at par value. The issue was fully taken up on 1 March 2004 with the exact amount received. Additional information:

(i) The net profit for the year ended 28 February 2005 is N$805 000. (ii) The market price per share on 28 February 2005 was N$14.

(a) Prepare the following ledger accounts to fully record the share issue.

Ordinary Share Capital account

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

5 % Preference Share Capital account

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

Share Premium account

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

15

Bank account

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

[6]

(b) (i) Name four types of preference shares.

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

....................................................................................................................... [4]

(ii) Explain the difference between authorised and issued share capital. Refer to the information of Gobabis Limited.

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................... [4]

16

(c) Calculate the following ratios of Gobabis Limited:

(i) earnings per share

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

.................................................................................................................... [6]

(ii) Price/Earnings ratio

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

....................................................................................................................... [4]

Total [24]

17

QUESTION 6 Linda Mundee started a business on 1 June 2005 and used the LIFO method of stock valuation. At the end of her first three months trading on 31 August 2005 Linda decided that it would have been better to use the FIFO method of stock valuation. Linda’s purchases and sales for the three months ended 31 August 2005 were as follows.

Purchases 3 June 200 units at N$30 each 2 July 120 units at N$36 each 1 August 140 units at N$39 each Sales Total for June 160 units at N$40 each Total for July 80 units at N$45 each Total for August 150 units at N$49 each

(a) Calculate the value of the closing stock on 31 August 2005 using

(i) the FIFO method of stock valuation

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

............................................................................................................... [4]

(ii) the LIFO method of stock valuation

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

................................................................................................................. [7]

Show your workings.

18

(b) Calculate the gross profit using:

(i) the FIFO basis of stock valuation

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................... [5]

(ii) the LIFO basis of stock valuation

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

...................................................................................................................................

........................................................................................................................ [3]

Total [19]

19

MINISTRY OF EDUCATION

Namibia Senior Secondary Certificate (NSSC)

ACCOUNTING: HIGHER LEVEL

PAPER 1 MARK SCHEME

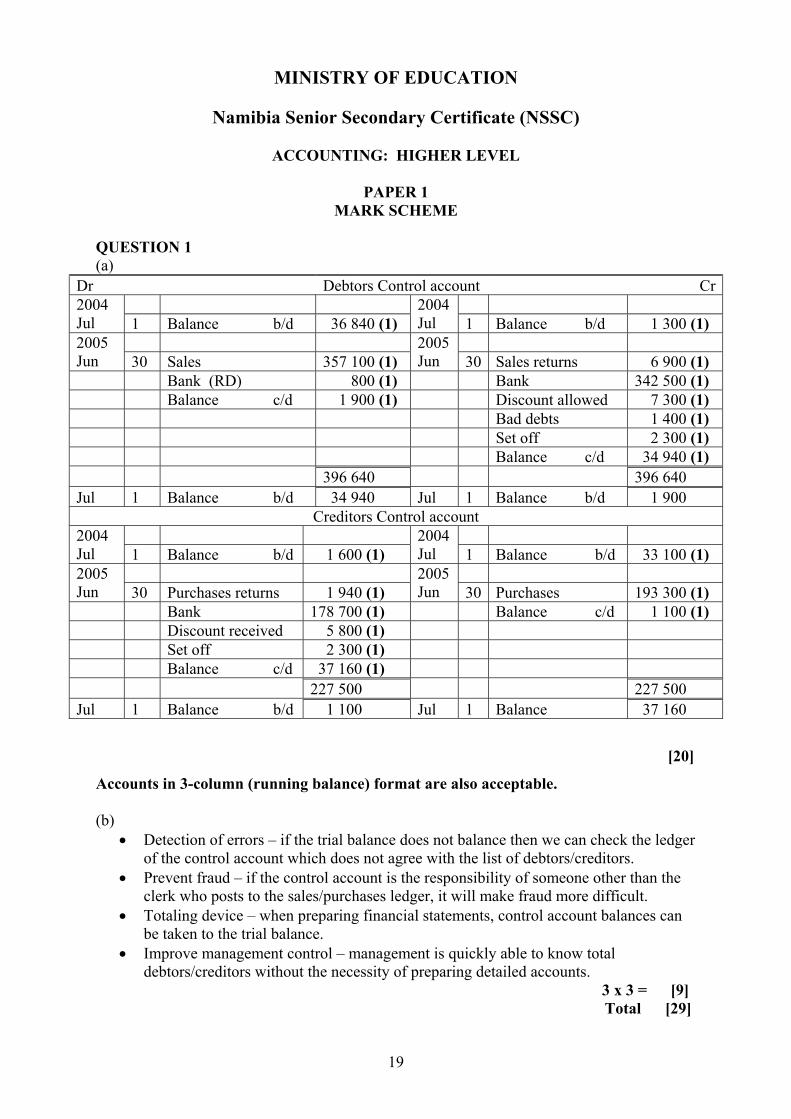

QUESTION 1 (a)

Dr Debtors Control account Cr 2004

Jul 1 Balance b/d 36 840 (1) 2004 Jul 1 Balance b/d 1 300 (1)

2005 Jun 30 Sales 357 100 (1)

2005 Jun 30 Sales returns 6 900 (1)

Bank (RD) 800 (1) Bank 342 500 (1) Balance c/d 1 900 (1) Discount allowed 7 300 (1) Bad debts 1 400 (1) Set off 2 300 (1) Balance c/d 34 940 (1) 396 640 396 640 Jul 1 Balance b/d 34 940 Jul 1 Balance b/d 1 900

Creditors Control account 2004

Jul 1 Balance b/d 1 600 (1) 2004 Jul 1 Balance b/d 33 100 (1)

2005 Jun 30 Purchases returns 1 940 (1)

2005 Jun 30 Purchases 193 300 (1)

Bank 178 700 (1) Balance c/d 1 100 (1) Discount received 5 800 (1) Set off 2 300 (1) Balance c/d 37 160 (1) 227 500 227 500 Jul 1 Balance b/d 1 100 Jul 1 Balance 37 160

[20]

Accounts in 3-column (running balance) format are also acceptable. (b)

• Detection of errors – if the trial balance does not balance then we can check the ledger of the control account which does not agree with the list of debtors/creditors.

• Prevent fraud – if the control account is the responsibility of someone other than the clerk who posts to the sales/purchases ledger, it will make fraud more difficult.

• Totaling device – when preparing financial statements, control account balances can be taken to the trial balance.

• Improve management control – management is quickly able to know total debtors/creditors without the necessity of preparing detailed accounts.

3 x 3 = [9] Total [29]

20

QUESTION 2 (a) Net profit 28 200 (1) Profit & Loss b/f 51 800 (1) 80 000 Dividends 25 000 (1) Transfer to General Reserve 10 000 (1) 35 000 Profit & Loss c/f 45 000 (1) [5]

(b) Operating profit 28 200 Depreciation 48 500 15 000 63 500 (4) Loss on sale 1 000 (1) Dec stock 2 200 (1) Dec debtors 2 300 (1) Inc creditors 5 200 (1) 102 400 Cash Flow Statement for the year ended 31 December 2005 Net cash inflow from operating activities 102 400 Dividend paid (30 000) (2) Inventing activities:

Purchase fixed assets (50 000) (1) (68 000) (1) (14 000) (1)

Sale fixed assets 6 000 (1) (126 000) Issue shares 70 000 (2) 16 400 Increase in cash 16 400 (2) [18]

(c) Cash Flow Profit

• Show all cash movements for the period, regardless of whether for another period

• Includes all types of expenditure, Capital and revenue. No separate treatment.

• Only includes actual cash movements. Cash inflows and cash outflows for the period.

• Free of subjective valuations. Entries are actual movements. Precise.

• Prepared on accruals basis, with value relevant to period only and adjustments made.

• Only includes revenue expenditure. Capital expenditure dealt with separately in Balance Sheet.

• Includes non-cash movements. Book-keeping entry only. Depreciation, provision for doubtful debts.

• Includes subjective valuations, e.g. rate of provision of doubtful debts. Some room for movement.

4 x 2 marks [8] Total [31]

21

QUESTION 3 (a)

Machinery account 2003 2004 Jun 1 Bank 20 000 (1) May 31 Balance c/d 20 000 2004 2005 Jun 1 Balance b/d 20 000 May 31 Disposal 20 000 (1) Bank 40 000 (1) Balance c/d 90 000 2005 Mar 1 Bank 50 000 (1) 110 000 110 000 Jun 1 Balance b/d 90 000

Provision for depreciation of machinery account 2004 2004 May 31 Balance c/d 5 000 May 31 Depreciation 5 000 (1) 2005 2004 May 31 Disposal 20 000 (1) Jun 1 Balance b/d 5 000 Balance c/d 13 125 2005 May 31 Depreciation

15 000 (1)

10 000 (1) 28 125 3 125 (1) 33 125 33 125 Jun 1 Balance b/d 13 125

[9]

Accounts in 3-column (running balance) format are also acceptable. (b)

• Provision made to ensure correct Balance Sheet valuation, to spread costs/matching.

• Depreciation reduces profit for dividend, could argue saving cash for replacement.

• Bookkeeping entry only, does not provide for replacement.

• If fund required for replacement, then would need setting up in addition to provision for depreciation.

3 x 2 = [6] Total [15]

22

QUESTION 4 (a)

Appropriation Accounts (i) 30 Jun 2005 (ii) 31 Dec 2005 Net Profit 44 600 77 980 Interest on Capital A 2 700 (1) 3 240 (1) B 2 700 (1) 3 240 (1) C - 3 000 (1) Salary C - 5 400 7 000 (2) 16 480 39 200 61 500 Share Profit A 23 520 (1) O/F 30 750 (1) O/F B 15 680 (1) O/F 20 500 (1) O/F C - 39 200 10 250 (1) O/F 61 500

[12]

(b)

Current accounts A B C A B C 2005

Dec 31 Drawings 21 000 17 000 8 000 (1)

2005 Jan 1 Balance b/d 14 600 (1) 22 000 (1) -

Balance c/d 42 140 51 040 22 500 Dec 31 Profit 54 270 (1) 36 180 (1) 10 250 (1) Interest on Capital

5 940 (1) 5 940 (1)

3 000 (1)

Salary - - 7 000 (1) Interest on loan

2 500 (2)

63 140 68 040 30 500 63 140 68 040 30 500 2006

Jan 1 Balance b/d 42 140 51 040 22 500 [12]

Separate accounts and accounts in 3-column (running balance) format are also acceptable. (c) Amy’s objection is correct. (1)

The money does not belong to Cynthia once it has been paid. (1) N$5 000 of the N$100 000 capital contributed has to compensate for the goodwill created by Amy and Byron. (1) Therefore the Capital accounts of Amy and Byron will increase with N$5 000 respectively (1) and the Capital account of Cynthia will decrease with N$5 000 (debit) (1) [5]

(d) To prevent a partner gaining from the goodwill created by the previous partners. Without paying anything for it or being charged in any way. [3]

Total [32]

23

QUESTION 5 (a) General Ledger of Gobabis Limited

Dr Ordinary Share Capital account Cr 2004

March 1 Bank 4 000 000 (1)

5 % Preference Share Capital account 2004

March 1 Bank 100 000 (1)

Share Premium account

2004 March 1 Bank 800 000 (1)

Bank account

2004 March 1 Ordinary Share Capital 4 000 000 (1)

5 % Preference Share Capital 100 000 (1) Share Premium 800 000 (1)

[6]

Accounts in 3-column (running balance) format are also acceptable. (b) (i) Cumulative

Non-cumulative Participating Redeemable

4 x 1 = [4]

(ii) Authorised share capital: It is the total of share capital, which the company is allowed to issue to share holders. N$ (1) Gobabis Limited: Ordinary share capital 6 000 000

5 % Preference Share Capital 100 000 (1) [2]

Issued share capital: Is the total of share capital actually issued to shareholders. N$ (1) Gobabis Limited: Ordinary Share Capital 4 000 000

5 % Preference Share Capital 100 000 (1) [4]

24

(c) (i) EPS = Net profit after tax – preference share dividend number of issued ordinary shares

= 805 000 (1) – 5 000 (2)

400 000 (1) = N$2,00 (2) C/F (1) O/F [6]

(ii) PER = Market price

EPS = 14 (1)

2 (1) O/F = 7 (2) C/F (1) O/F [4]

Total [24]

25

QUESTION 6 (a) (i) Value of closing stock using FIFO –

70 units (1) at N$39 each (2) N$2 730 (1) [4] (ii) Value of closing stock using LIFO –

40 units (1) at N$30 each (2) N$1 200 30 units (1) at N$36 each (2) N$1 080 N$2 280 (1) O/F [7]

(b) (i) Sales 17 350 (1)

Less: Cost of sales 13 050 Purchases 15 780 (1) - Closing stock 2 730 (1) O/F ______

Gross profit 4 .300 (1) O/F (2) C/F

(ii) Sales 17 350 Less: Cost of sales 13 500

Purchases 15 780 - Closing stock 2 280 (1) O/F _____

Gross profit 3 850 (1) O/F (2) C/F [8] Total [19]

26

ASSESSMENT OBJECTIVES GRID

NSSCH – PAPER 1

Marks Skill

Question Topic Syllabus Reference Total

A (40) B (60) C (35) D (15) 1 (a) (b)

Control accounts Theory on Control accounts

T1 U3 T1 U3

20

9

20

3

- -

-

6

- -

29 23 - 6 - 2 (a) (b) (c)

Calculation of net profit Cash Flow Statement Theory on Cash Flow Statement and Profit and Loss Account

T2 U1 T4 U1 T2 U1

5 18

8

- - -

-

18 -

5 - -

- -

8 31 18 5 8 3 (a) (b)

Ledger accounts for fixed asset and depreciation Theory on depreciation

T1 U1 T2 U2 T2 U2

9 6

4 -

5 -

- 6

- -

15 4 5 6 4 (a) (b) (c) (d)

Appropriation Accounts: Partnerships Current accounts: partnerships Theory on Goodwill Theory on Goodwill

T2 U3 T2 U3 T2 U3 T2 U3

12

12 5 3

-

3 - -

5

7 - -

7

2 - 3

- - 5 -

32 3 12 12 5 5 (a) (b) (c)

Ledger accounts: Companies’ issue of shares Theory on share capital Ratios: companies

T2 U5 T2 U5 T2 U5 T4 U1

6 8

10

6 4 -

- 4

10

- - -

- - -

24 10 14 - - 6 (a) (b)

Calculation of value of closing stock Calculation of gross profit

T5 U1 T5 U1

11

8

- -

11

-

-

8

- -

19 8 11 - - Total 150 40 60 37 13 ACKNOWLEDGEMENTS Question 1- - 1270/1 October 2002 (Question 2) Question 2 - 1270/1 October 2002 (Question 4) Question 3 - 1270/1 October 2002 (Question 6) Question 4 - 1270/2 October 2002 (Question 3) Question 5 - 1270/1 October 1999 (Question 3 - information part)

27

MINISTRY OF EDUCATION

Namibia Senior Secondary Certificate (NSSC)

ACCOUNTING: HIGHER LEVEL

PAPER 2 SPECIMEN PAPER

TIME: 2 hours 30 minutes INSTRUCTIONS TO CANDIDATES Write your name, centre number and candidate number in the spaces at the top of this page. Answer all questions. Write your answers in the spaces provided on the question paper. INFORMATION FOR CANDIDATES The number of marks is given in brackets [ ] at the end of each question or part question. You may use a calculator. Where layouts are to be completed, you may not need all the lines for your answer.

28

QUESTION 1 Naute Computer Systems CC trades as a close corporation. The following information for the year ended 31 December 2005 is provided. 1. Balances as on 1 January 2005

Cr N$ Members’ contribution 500 000 Retained income 25 000 Receiver of Revenue (Income tax) 12 000 Distribution payable to members 42 000

2. The interest of the two members in the corporation is J. de Waal 60 % and

K. Witbooi 40 % . 3. Transactions for 2005 were as follows.

January 5 Issued cheques to the members to pay the outstanding distribution as on 1 January 2005.

March 30 Paid the amount owing to the Receiver of Revenue (income tax).

April 25 J. de Waal rendered services for the amount of N$4 000 on behalf of the

business. This amount was added to his contribution in the business.

June 1 The following cheques were issued.

N$50 000 to the Receiver of Revenue for provisional tax. N$30 000 to members for an interim distribution of profit.

December 31 Issued a cheque of N$25 000 to the Receiver of Revenue for a second

provisional tax payment. 4. Additional information supplied.

(i) A final distribution of profit of N$40 000. (ii) The total income tax assessed by the Receiver of Revenue was N$80 000. (iii) The net income for the current accounting period was N$180 000.

29

REQUIRED: (a) Explain three features of a close corporation.

1. .…..……………………………………………………………………….………

.…..…………………………………………………………………………….…

……………………………………………………………………………………

2. ...……………………………………………………………………………….…

……………………………………………………………………………………

……………………………………………………………………………………

3. ……………………………………………………………………………………

……………………………………………………………………………………

………………………………………………………………………… [6]

Complete the following accounts in the General Ledger of Naute Computer Systems CC.

General Ledger of Naute Computer Systems CC

Members’ Contributions account

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

………………….…… [3]

Retained Income account ....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

................……............................................................................................................................................

................................................. [3]

30

Receiver of Revenue (Income Tax) account ....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

........ [6]

Distribution payable to members account ....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

..........................................................................................………………………………………………

………..….. [6]

Appropriation Account ....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................…..…………………………

……………………………………............................................................................................................

................................... [6]

Total [30]

31

QUESTION 2 The following information for the year ended 28 February 2005, was extracted from the books of Swakop Leather Works. N$ Stock on 1 March 2004: Raw materials 15 000 Finished goods 18 300 Work in progress 12 700 Stock on 28 February 2005: Raw materials 13 850 Finished goods 11 500 Work in progress 12 300 Purchases of raw materials 125 500 Sales 200 000 Carriage outwards 1 200 Carriage inwards on raw materials 1 500 Purchases Returns of raw materials 5 000 Provision for depreciation: Machinery 66 500 Office furniture and fittings 24 000 Water and electricity 12 000 Factory insurance 6 000 Sundry office expenses 26 500 Cash discounts allowed 8 320 Trade debtors 18 460 Machinery 350 000 Direct wages 28 350 Indirect wages 68 000 Rates: Factory 18 000 Office 6 000 Office fixtures and fittings 60 000 Additional information: 1. The expense for water and electricity is to be apportioned.

Factory 75 % Office 25 %

2. Included in the amount for factory insurance is an annual premium of N$3 000 for the period 1

June 2004 to 31 May 2005. 3. Rates due on 28 February 2005 amounted to

Factory N$3 000 Office N$1 000

4. Assets are to be depreciated as follow. Machinery at 10 % on book value

Office fixtures and fittings at 20 % on cost

32

REQUIRED: Prepare the Manufacturing Account of Swakop Leather Works for the year ended 28 February 2005. Indicate prime cost and production cost of finished goods.

Swakop Leather Works Manufacturing Account for the year ended 28 February 2005

N$ N$

…………………………………………………………………..................…………................

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

……………………………………………………………………………………………………………

………………………………………………………………………

Total [18]

33

QUESTION 3 The Hot Shot Snooker Club was formed some years ago. The Club has a total of 250 members. The annual membership subscription is N$70. During December 2004 five members paid their subscriptions for 2005. On 1 January 2005 twenty members still owed their subscription for 2004. In addition to the subscriptions the Club had the following assets and liabilities on 1 January 2005.

N$ Equipment at valuation 14 000 Bank balance 40 000 (Dr) Insurance prepaid 136 Rent expense accrued 100

The Club’s receipts and payments for the year ended 31 December 2005 were as follows: N$ N$ Subscriptions Purchase of clubhouse 32 000

For 2004 1 400 Purchase of equipment 1 500 For 2005 10 150 Expenses of tournament 1 250

Income from tournament 2 060 Rent expenses 5 100 Insurance (for 12 months to end of February 2005) 840 On 31 December 2005. 1. A total of one hundred members had not paid their subscription for 2005. 2. The equipment was valued at N$13 500 3. Rent for two months still outstanding. (a) Prepare the subscriptions account of the Hot Shot Snooker Club for the year ended

31 December 2005.

General Ledger of Hot Shot Snooker Club Subscriptions account

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

................................................................................. [6]

34

(b) Prepare the Income and Expenditure Account of the Hot Shot Snooker Club for the year ended 31 December 2005.

Hot Shot Snooker Club

Income and Expenditure Account for the year ended 31 December 2005

N$ N$

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

....................................................................................................................................................................

.........................................……………………………………….. [10]

(c) (i) Calculate the difference in the bank balance as at 31 December 2004 and

31 December 2005. Suggest two possible reasons for this change.

............................................................................................................................

............................................................................................................................

............................................................................................................................

............................................................................................................................

............................................................................................................................

............................................................................................................................

............................................................................................................................

.....................................................................................................................……

[4]

35

(ii) Explain why the bank balance on 31 December 2005 is different to the balancing figure on the Income and Expenditure Account for the year ended 31 December 2005.

............................................................................................................................

............................................................................................................................

............................................................................................................................

............................................................................................................................

............................................................................................................................

......................................................................................................…… [4]

(iii) Explain what actions you would recommend the club to take in relation to those

members who have not paid their subscriptions for 2005. ............................................................................................................................

............................................................................................................................

............................................................................................................................

............................................................................................................................

............................................................................................................................

..................................................……….............................................. [4]

Total [28]

36

QUESTION 4 Anja Runnaways runs a retail clothing business and makes up her accounts on 31 October each year. On 31 October 2005 her accountant had difficulty balancing the books, but eventually the following list of balances was produced. N$ Capital (1 November 2004) 150 000 Debtors 127 300 Creditors 75 400 Fixed assets at cost (1 November 2004) 200 000 Provision for depreciation on fixed assets (1 November 2004) 35 000 Sales 607 500 Purchases 473 200 Purchases returns 3 000 Wages 59 000 Other operating expenses 33 000 Loan from J. Roodt 30 000 Discounts received 6 000 Provision for doubtful debts (1 November 2004) 5 900 Drawings 38 000 Bank overdraft 107 700 Stock (1 November 2004) 89 100 Suspense account To be calculated The following errors were then discovered.

1. The Purchases returns account had been overcast by N$250. 2. A Sales invoice for N$4 000 had been entered as N$400 in the debtor’s account. 3. A contra entry between a supplier and a customer of N$1 200 had been entered only in the

creditors’ ledger. 4. Goods costing N$1 500 was taken by Anja for her own use. No entries had been made. 5. Discount received of N$875 was incorrectly entered on the debit side of the discount

received account. 6. On 31 October 2005 it was decided to adjust the provision for doubtful debts to N$6 115.

37

REQUIRED: (a) Record the above items in the General Journal. Narrations are not required.

General Journal of Anja Runnaway – October 2005

Dr Cr N$ N$

1. ..........................................................................................................................................

........................................................................................................................................................

............................................................................................................................

2. ..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

3. ..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

4. ..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

5. ..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

6. ..........................................................................................................................................

..........................................................................................................................................

..........................................................................................................................................

[16]

38

(b) Prepare the Suspense Account on 31 October 2005. Calculate the opening balance of this account, using the list of balances.

Calculation:........................................................................................................................................

...........................................................................................................................................................

................................................................................................................

.............................................................................................................................................

.............................................................................................................................................

Suspense account

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

[8]

(c) Prepare a statement of corrected net profit for the year ended 31 October 2005. Before the

corrections were made, the net profit was N$62 200.

Statement of corrected net Profit N$

Net profit before corrections 62 200

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

......................................................................................................................................................

[6]

39

(d) The current ratio before any corrections of errors were made on 31 October 2005, was 2:1. Use all relevant information and determine the value of closing stock. Do not take errors and additional information into account.

.............................................................................................................................................

.............................................................................................................................................

.............................................................................................................................................

.............................................................................................................................................

.............................................................................................................................................

.............................................................................................................................................

[6] Total [36]

QUESTION 5 (a) Terrace Limited produces a single product. Its sales and costs for the year ended

30 September 2005 were as follows.

Sales in units 40 000 Selling price N$80 per unit

Variable costs per unit

Wages N$24 Material N$36

Fixed costs N$320 000 per annum.

For the year ended 30 September 2005

(i) calculate the break-even point in units and sales value

............................................................................................................................................

............................................................................................................................................

............................................................................................................................................

............................................................................................................................................

............................................................................................................................................

....................................... [3]

40

(ii) calculate the profit.

…………………………………………………………………………………

…………………………………………………………………………………

…..………………………………………………………………………………………..

………………………………………………………………………………………..……

…………………………………………………………………………………..…………

……………………………………………………………………………..…..…………

……………………………………………

[5]

(b) The marketing division suggests that sales could be increased to 60 000 units per annum. This would involve the following changes to cost and revenue. Wages will be increased by N$2 per unit. Material costs will be reduced by 5 %, by arranging a long-term contract with one supplier. Fixed costs will increase by N$32 440 per annum The selling price will be N$80 per unit. For the year commencing 1 October 2005

(i) Calculate the forecast break-even point in units and sales value;

……………………………………………………………………………………………

………...…………………………………………………………………....………………

…...………………………………………………………………………………………...

……………………………………………………………………………………………

……………………………………………………...………………………………………

……………………………………..………………………………………………………

……………………………….…...………………………………………………………

……………………….

[6]

41

(ii) Calculate the forecast profit. ……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

……………………………………………………………………………………………

…...….................................................................................................................................

............................................................................................................................................

.............................................………………………………….…………………………

…..

[8]

(c) Using the results of your calculations in (a) and (b), advise the management of Terrace Limited

whether to continue with the present policy or to implement the suggestions made by the marketing division.

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

[12]

(d) Before final decisions are made, it is important to management to have accurate and sufficient

information. Suggest two situations in which marginal costing can assist management in the decision-making process.

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

………………………………………………………………………………………

[4]

Total [38]

42

MINISTRY OF EDUCATION

Namibia Senior Secondary Certificate (NSSC)

ACCOUNTING: HIGHER LEVEL

PAPER 2 MARK SCHEME

QUESTION 1 (a) Features:

- Members have limited liability - Specific legal requirements to establish and run the business - Simpler way for smaller businesses to do business, because fewer members

(1 – 10) are actively involved in running the business - The Registrar of Close Corporations controls the administration of a Close Corporation - Any other relevant features

Any 3 x 2 = [6] (b)

General Ledger of Naute Computer Systems CC

Dr Members’ Contribution account Cr 2005 Dec 31

Balance c/d

504 000

2005 Jan 1

Balance b/d

500 000 (1)

April 25 Services rendered 4 000 (1) 504 000 504 000 2006

Jan 1 Balance b/d

504 000 (1)

[3]

Retained Income account

2005 Dec 31

Appropriation account

25 000 (1)

2005 Jan 1

Balance b/d

25 000 (1)

2006 Jan 1

Appropriation account

55 000 (1)

[3]

43

Receiver of Revenue (Income Tax) account

2005 March 30 Bank 12 000 (1)

2005 Jan 1 Balance b/d 12 000 (1)

June 1 Bank 50 000 (1) Dec 31 Appropriation (Income Tax) 80 000 (1) Dec 31 Bank 25 000 (1) Dec 31 Balance c/d 5 000 92 000 92 000

2006 Jan 1 Balance b/d 5 000 (1)

[6]

Distribution payable to members account 2005

Jan 5 Bank 42 000 (1) 2005 Jan 1 Balance b/d 42 000 (1)

June 1 Bank 30 000 (1) June 1 Distribution to members 30 000 (1) Dec 31 Balance c/d 40 000 Dec 31 Distribution to members 40 000 (1) 112 000 112 000

2006 Jan 1 Balance b/d 40 000 (1)

[6]

Appropriation Account 2005

Dec 31 Receiver of Revenue (Income Tax) 80 000 (1)

2005 Dec 31 Profit and Loss 180 000 (1)

Distribution to members 70 000 (2) Retained Income 25 000 (1) Retained Income 55 000 (1) 205 000 205 000

[6]

Alternative form

Appropriation Account 2005

Dec 31 Receiver of Revenue (Income Tax) 80 000 (1)

2005 Dec 31 Profit and Loss 180 000 (1)

Distribution Payable 30 000 (1) Retained Profit 25 000 (1) Distribution Payable 40 000 (1) Retained Profit 55 000 (1) 205 000 205 000

[6]

3-column (running balance) format also acceptable. [24] Total [30]

44

QUESTION 2

Swakop Leather Works Manufacturing Account for the year ended 28 February 2005

N$ N$ Raw materials: Stock (1 March 2004) 15 000 (1) Purchases 125 500 (1) Less Purchases Returns 5 000 (1) 120 500 Carriage Inwards 1 500 (1) 137 000 Less Stock (28 February 2005) 13 850 (1) Cost of raw materials consumed 123 150 Direct Wages 28 350 (1) Prime cost 151 500 (1) Overheads Water and Electricity (12 000 x 25 %) 9 000 (2) Factory insurance (6 000 – 750) 5 250 (2) Rates (18 000 + 3 000) 21 000 (1) Provision for depreciation: Machinery [(350 000–66 500) x 10/100] 28 350 (2) Indirect wages 68 000 (1) 131 600 Production cost 283 100 Add Work in progress (1 March 2004) 12 700 (1) 295 800 Less Work in progress (28 February 2005) 12 300 (1) Production cost of finished goods 283 500 (1) O/F Total [18]

45

QUESTION 3

General Ledger of Hot Shot Snooker Club (a) Subscriptions Account

N$ N$ 2005 Jan 1 Balance/Accrued b/d 1 400 (1)

2005 Jan 1 Balance/Received in advance

b/d 350 (1)

Dec 31

Income & Expenditure (1)

17 500 (1) Dec 31 Bank/Cash (10150 + 1400)

11 550 (1)

Balance/Accrued b/d 7 000 18 900 18 900 2004 7 000 (1)O/F Jan 1 Balance/Accrued b/d

[6]

Alternative presentation

Subscriptions Account Dr Cr Balance 2005 N$ N$ N$ Jan 1 Balance 1 400 (1) 350 (1) 1 050 Dr Dec 31 Bank/Cash 11 550 (1) 10 500 Cr

Income & Expenditure (1) 17 500 (1) 7 000 Dr (1) O/F

[6]

(b) Hot Shot Snooker Club

Income and Expenditure Account for the year ended 31 December 2005 N$ N$ Income Subscriptions 17 500 (1) O/F Tournament – Income 2 060

Less Expenses 1 250 810 (2) 18 310

Expenditure Rent expense [5100 + 1000 (1) – 100 (1)] 6 000 Insurance [840 + 136 (1) – 140 (1)] 836 Depreciation of equipment [14000 + 1500 (1) – 13500 (1)] 2 000 8 836 Surplus 9 474 (1) O/F

Horizontal presentation acceptable [10]

46

(c) (i) N$12 020 (2) Bank balance has fallen because

$33 600 spent on fixed assets Rest of payments only just covered by the receipts Large amount of unpaid subscriptions

Or other acceptable point Any 2 points (1) each [4]

(ii) Bank balance differs from surplus (O/F Deficit) because

Bank account includes all monies spent and received: I & E Account only includes revenue income and expenditure Bank account does not include non-monetary items: I & E Account includes non-monetary items such as depreciation Bank account does not include any year end accruals: I & E Account includes adjustments for accruals and prepayments

Or other acceptable points Any 2 points up to (2) each [4]

(iii) Action regarding unpaid subscriptions

Send written reminders to the members concerned Ban the members concerned from the Club until arrears are paid Cancel the membership of the members concerned Or other acceptable points Any 2 points (2) each [4]

Total [28]

47

QUESTION 4 (a)

General Journal of Anja Runnaway – October 2005

Dr Cr N$ N$ 1. Purchases returns 250 Suspense (2) 250 2. Debtors 3 600 Suspense (2) 3 600 (1) 3. Suspense 1 200 Debtor (2) 1 200 4. Drawings 1 500 Purchases (2) 1 500 5. Suspense 1 750 Discount Received (2) 1 750 (1) 6. Profit and Loss 215 Provision for Bad Debts (2) 215 (2)

[16]

(b) N$900

Suspense Account 2005 2005 Oct 31 Balance b/d 900 (4) Oct. 31 Purchases returns 250 (1) Debtors 1 200 (1) Debtors 3 600 (1) O/F Discount Received 1 750 (1) 3 850 3 850

[8]

Running balance format acceptable (c) Net Profit before corrections N$62 200 (1) Provision for Bad Debts (215) (1) (2) Purchases Returns (250) (1) (3) - (4) - (5) Purchases 1 500 (1) (6) Discount Received 1 750 (1) 64 985 (2) C/F (1) O/F [6]

48

(d) Current Assets Current Liabilities Debtors 121 400 (1) O/F Creditors 75 400 (1) Suspense 900 (1) O/F Bank 107 700 (1) Closing Stock 243 900 (2)

[6]

Total [36]

49

QUESTION 5 (a) (i) N$320 000 = 16 000 units (2)

20 x N$80 = N$1 280 000 (1) [3]

(ii) Selling price 80

- Variable Cost 60 Contribution 20 (1) x units 40 000 (1)

800 000 - Fixed costs 320 000 (1) Profit 480 000 (2) [5]

(b) (i) Wages 26,00

Material cost 34,20 Total Variable cost 60,20 (1) (320 000 + 32 440) = 17 800 units (1) (80 (1) – 60,20 (1)) x N$80 = N$1 424 000 (2) [6]

(ii) Selling price 80,00

Variable cost 60,20 Contribution 19,80 (2) x Unit 60 000,00 (2)

1 188 000,00 - Fixed Cost 352 440,00 (2) Profit 835 560,00 (2) [8]

(c) Extra production increases profit by N$355 560 in total.

Profit per unit as at 30-09-05 = N$12,00 Profit per unit new contract = N$13,93 % Increase (N$13,93 – N$12) = 1,93 (2) x 100 (1) = 16,08 % (2)

12 (1) 1 Option B would be preferred, although the extra costs involved in marketing should be taken into account. (2) It is also a risk to rely only on one supplier for materials. If he can’t comply with contract agreements, the supply of raw materials may delay production. Or other acceptable points Any 2 points up to (2) each = (4) [12] (d) Pricing a product

Accept or reject special orders “Make or buy” decisions Continue or close down (Any two x 2 each) [4]

Total [38]

50

ASSESSMENT OBJECTIVES GRID

NSSCH – PAPER 2

Marks Skill

Question Topic Syllabus Reference Total

A (35) B (60) C (35) D (20) 1 (a) (b)

Theory on close corporations Ledger accounts of close corporations

T2 U6 T2 U6

6

24

6

18

-

6

- -

- -