MY IIP REPORT

76

1.PROFILE OF THE COMPANY 1.1 Corporate History: SNEHA CONSULTANCY SERVICES is a firm set-up in the year 2001 by retired officers of ANDHRA BANK with considerable service in credit department. Sneha Consultancy Services is presently engaged in providing support services in the area of project appraisal, financial analysis and viability study of the projects that approach banks for financial assistance which include term loans and working capital limits. The firm is engaged in preparation of Bank credit appraisal of various borrowers. The firm prepares project report consisting of project details and financials of various borrowers according to their credit requirements. The project report would be prepared in such a way that it helps the banks for preparation of appraisal of credit requirements of their borrower very easily in their structured formats. 1.2 Vision and Mission: There is no Vision and Mission for this organization. This organization is listed in “Financial Planning Personal” page. 1.3 Products and Services offered by company: 1. Company engaged in project appraisal & Techno Economic Viability Study (TEV) of Industrial Manufacturing units, assessment of finance requirement and capacity to service 1

Transcript of MY IIP REPORT

1.PROFILE OF THE COMPANY1.1 Corporate History:

SNEHA CONSULTANCY SERVICES is a firm set-up in the year

2001 by retired officers of ANDHRA BANK with considerable

service in credit department. Sneha Consultancy Services is

presently engaged in providing support services in the area of

project appraisal, financial analysis and viability study of the

projects that approach banks for financial assistance which

include term loans and working capital limits. The firm is

engaged in preparation of Bank credit appraisal of various

borrowers. The firm prepares project report consisting of project

details and financials of various borrowers according to their

credit requirements. The project report would be prepared in such

a way that it helps the banks for preparation of appraisal of

credit requirements of their borrower very easily in their

structured formats.

1.2 Vision and Mission:

There is no Vision and Mission for this organization.

This organization is listed in “Financial Planning Personal”

page.

1.3 Products and Services offered by company:

1. Company engaged in project appraisal & Techno Economic

Viability Study (TEV) of Industrial Manufacturing units,

assessment of finance requirement and capacity to service

1

debt, market study/research, assessment of potential

viability in sick units and their rehabilitation.

2. Preparation of Detailed Project Reports: Company prepares

detailed project reports for some of the following

industries. The report covers EIC Analysis for the specific

unit - Economic environment, Industry analysis and company

analysis. EIC analysis encompasses macro-economic factors of

the economy and how these factors influence industry in

particular. Then covers the particular activity and provides

SWOT analysis of the company; financial analysis covering

the justification of the project cost and capex requirement;

and does thorough check of the capital expenditure

requirement and evaluate the cost of project. Profitability

analysis; DSCR; IRR; Cost Benefit Analysis; and Sensitivity

Analysis.

3. Company prepares loan applications along with financial

statements for customers of various banks which include both

public sector and private sector banks.

4. CDR Proposals: Company worked on corporate debt

restructuring proposal of many units for customers of

different banks.

1.4 About Company:

The prime activity of Sneha Consultancy Services is preparation

of project reports, financial appraisals and viability studies

for financial analysis for customers of various Banks.

2

The areas include:

Automobile Ancillary Industry

Agriculture & Related Industries

Horticulture

Poultry

Hatcheries Broilers Layers Poultry Feed

manufacturing Warehouses(Rural Godowns)

Sheep units

Dairy

Farming Milk chilling plants

Cold storages

Integrated Rice Mills

Ginning Mills

Godowns (Rural)

Granite Industry

Hospitality Industry

Star Hotels Bar Restaurants Resorts

Healthcare – Multi -Specialty Hospitals

Educational Institutions

Engineering Colleges Medical Colleges

Fertilizer & Pesticide units

Foundry units

Infrastructure

Civil&Electrical Contractors

BOT operators Manufacturing industry

Pharmaceutical units

Bulk Drugs Formulations 100% EOUs

Power Plants

Solar Power units Thermal units Bio Diesel units Hydro power units Wind Mills

Readymade Garment units

Retail Trade

Textile Units

Quarry units

The client base covers very big ticket loan facilities. Some of

the focused areas are Hospitality, Shopping Malls, Poultry Farms&

3

Hatcheries, Plastic Industries, and Power Generation Units up to

20 MW, Solvent Extraction Plants, Steel Mills, Rice Mills, Real

estate development and plantation advances. The core team

consists of three people who have more than two decades of rich

experience in the Credit Management in Banking Industry.

1.5 Infrastructure:

Office is located at RTC Cross Roads - Hyderabad, is fully

furnished in a spacious office with 6 work stations and 24x7

power supply. Wi-Fi facility is also available at office.

1.6 Customers: Customers of Sneha Consultancy services are all the typesof business firm members who approaches the various banks forsecuring loan applications along with financial statements.

1.7 Competition: Competitive company for the products and servicesprovided by Sneha Consultancy services is Zubeda consultancyservices.

1.8 SWOT analysis of the company: Strengths:

14 years of experience

Listed in “Financial Planning Personnel” page

Helps Banks in preparation of proposal forms

Preparation of many proposals than any other consultancy

does

Preparation of a proposal of any business firm.

4

Weakness:

More Competition

Less Infrastructure

Few Consultants

Opportunities:

Business expansion

Significant Opportunity in platform segment

Threats:

Increase the workforce

Emerging Technology

1.9 Organizational structure:

Sneha Consultancy is a partnership firm. It consists of total

6members i.e., 3 employees, 2 partners and supporting staff.

Managing Director is Mr.M.Venkateswarlu

Mr. T.Krishna Prasad and Mr. M.Venkateshwarlu are Partners

Mr. K.Seethapathi is supporting consultant with more than

two decades experience in credit and FOREX in Andhra Bank.

Mr. A. Ramakrishna Rao is Company Secretary with MBA and is

a support consultant.

Mr. Harinarayana Sharma and ,Mr. P.Venkat Rao are the

employees

5

Key Persons Profile:

Mr. M. Venkateswarlu (B. Tech, MBA; CAIIB; PGDCMP)

Mr. Venkateswarlu is an engineer by profession. After spending 7

years in the telecom industry he moved to Banking Industry in the

year 1980 as Technical Officer and worked in key positions in

Credit Department of Andhra Bank Central Office for 20 years. He

handled big ticket Loan accounts during his stay in Andhra Bank.

He worked as Manger in two very large branches and handled big

ticket loan accounts. He took VRS in the year 2001 March and

started Consultancy Services along with his colleagues. He is

providing consultancy services in the areas of credit management,

financial services and Project finance and Restructuring of

loans.

Mr. T. Krishna Prasad (M.Com; CAIIB)

Mr. Krishna Prasad joined Andhra Bank as Probationary Officer in

the Year 1978. Having worked as manager in many branches for

about 22 years, he took VRS in the year 2001 January and started

consultancy services along with his other senior colleagues. He

is providing consultancy services in the areas of Credit

management and general management.

Mr. K. Seethapathi (MSc, CAIIB; CTM)

Mr. Seethapathi joined the Andhra Bank in the year 1976 and

worked till 1998. He worked at International Division Bombay as

6

Forex Dealer and also manager, was exposed to foreign exchange

management including credit management of export & import

accounts. He also worked in Export Import Credit Department in

the Head office of Andhra Bank and handled very big ticket loan

accounts. Having been exposed to ALM in the Banks he moved to

Academics and contributed to research related work in Credit

Management, Foreign Exchange Management and Risk management in a

leading Academic Institute at Hyderabad. He is extending

consultancy services in the area of Foreign Exchange, Credit

Management and Risk management.

Sri N.Harinarayana Sarma

Sri N.Harinarayana Sarma who worked in Andhra Bank for more than

two and a half decades and held different positions including

Managerial -provide support services in credit appraisal and

reports preparation and Mr. A. Ramakrishna Rao, a qualified

Company Secretary who had worked in the industry for more than

two decades provide support services related to company law and

statutory compliance for our detailed project reports

respectively.

Mr. P.Venkat Rao

Mr. P.Venkat Rao who worked in the industry provides support

services in credit analysis and report preparation. Mr. N.

Harinarayana Sarma and Mr. Venkat Rao who has rich experience in

the areas of credit and analysis provide support services for

various analytical assignments.

7

Mr. A Ramakrishna Rao (M.Com; MBA; ACS)

Mr. A. Ramakrishna Rao started his career in the year 1976 as

Accounts assistant in VST Industries Hyderabad and worked in

accounts / exports department till 1998. He moved to manage

secretarial administrative work of a Hyderabad based Software

Industry. Having worked for 4 years since 1999 in the software

industry he moved to academics and consulting in the year 2002

and has been pursuing the same since then. He is extending

consultancy services in the area of Foreign Exchange, statutory

compliance and company affairs related work.

8

2. OBJECTIVES OF THE STUDY

To learn the theoretical aspects of Project Appraisal and

Project Financing.

To understand the role of financial statements in Project

Appraisal.

To analyze the importance of various financial tools in

preparing a project report.

To prepare a project report for an Industry Unit.

9

3. AN OVERVIEW OF IIP

The IIP was spread over a period of 45-60 days. During this

period I was involved in processing project reports relating to

various segments of the industry on the job Training mainly in

respect of FINANCIAL ANALYSIS. With the knowledge I have gained

in 45 days I have prepared a PROJECT REPORT for WOOD PECKER PVT

LTD. This report was appreciated by the officials of the company.

10

4. PROJECT APPRAISAL OVERVIEW

4.1 Project Appraisal Definition:

11

The assessment of the viability of proposed long-term investments

in terms of shareholder’s wealth.

1. WHEN it is done: After preparation and design of the

project.

2. WHAT is Project Appraisal: Provides a comprehensive review

of all aspects of the project.

3. WHY does the Bank appraise projects:

As a development institution: significant impact on

economic and social.

As a borrowing institution: maintain WB standing in

financial markets.

The first step in Project Appraisal is to find out whether the

project is prima facie acceptable by examining salient features

such as:

The background and experience of the applicants,

particularly in the proposed line of activity

The potential demand for the product

The availability of the required inputs, utilities and other

infrastructural facilities

Whether the project is in keeping with the priorities, if

any, laid down by the Government.

Project Appraisal should contain the following essential

information, such as:

12

Particulars of the project along with a copy of the Project

Feasibility Report furnishing details of the technology,

manufacturing process, availability of construction /

production facilities, etc.

Estimates of Cost of the project detailing the itemized

assets acquired / to be acquired, inclusive of Preliminary /

Pre-operative Expenses and WC margin requirements.

Details of the proposed means of financing indicating the

extent of promoters’ contribution, the quantum of Share

Capital to be raised by public issue, the composition of the

borrowed capital portion with particulars of Term Loans,

Foreign Currency Loans, etc.

WC requirements at the peak level (i.e., when the level of

Gross Current Assets is at the peak) during the first year

of operations after the commencement of commercial

production and the banking arrangements to be made for

financing the WC requirements.

Project Implementation Schedule review in the light of

actual implementation; Main stages in the project

implementation and whether the time schedule for

construction, erection/installation of P&M, start-up/trial

run, commencement of commercial production is reasonable

&acceptable

Organizational set up along with a list of Board of

Directors and indicating the qualifications, experience and

competence of

13

i) The key personnel to be in charge of implementation of

the project during the construction period and

ii) The executives to be in charge of the functional areas

of purchase, production, marketing and finance after commencement

of commercial production.

– Demand projection based on the overall market prospects

together with a copy of the market survey report.

– Details of the nature and value of the securities

offered.

– Regulatory Consents from the Government / other

authorities and any other relevant information.

– Interactive Financial Model Containing detailed

Projections with assumptions including following at a

minimum

• Estimates of sales, CoP and profitability.

• Projected P&L Account and Balance Sheet for the

operating years during the currency of the Bank’s

term assistance.

• Proposed amortization schedule, i.e., repayment

program.

• Projected Funds Flow Statement covering both the

construction period and the subsequent operating

years during the currency of the Term Loan.

14

4.2 Credit Appraisal:

Credit Appraisal means an investigation/assessment done by

the banks before providing any Loans & advances/project finance &

also checks the commercial, financial & technical viability of

the project proposed, its funding pattern & further checks the

primary & collateral security cover available for recovery of

such funds.

Credit Appraisal is a process to ascertain the risks

associated with the extension of the credit facility. It is

generally carried by the financial institutions, which are

involved in providing financial funding to its customers. Credit

risk is a risk related to non-repayment of the credit obtained by

the customer of a bank. Thus it is necessary to appraise the

credibility of the customer in order to mitigate the credit risk.

Proper evaluation of the customer is performed this measures the

financial condition and the ability of the customer to repay back

the Loan in future. Generally the credits facilities are extended

against the security know as collateral. But even though the

Loans are backed by the collateral, banks are normally interested

in the actual Loan amount to be repaid along with the interest.

15

Thus, the customer's cash flows are ascertained to ensure the

timely payment of principal and the interest.

It is the process of appraising the credit worthiness of a

Loan applicant. Factors like age, income, number of dependents,

nature of employment, continuity of employment, repayment

capacity, previous Loans, credit cards, etc. are taken into

account while appraising the credit worthiness of a person. Every

bank or lending institution has its own panel of officials for

this purpose.

4.3 Credit Appraisal Standards

Qualitative:

At the outset, the proposition is examined from the angle of

viability & also from the Bank's prudential levels of exposure to

the borrower, Group & Industry. Thereafter, a view is taken about

our past experience with the promoters, if there is a track

record to go by. Where it is a new connection for the bank but

the entrepreneurs are already in business, opinion reports from

existing bankers & published data if available are carefully

pursued. In case of a maiden venture, in addition to the drill

mentioned heretofore, an element of subjectively has to be

perforce introduced as scant historical data weightage to be

placed on impressions gained out of the serious dialogues with

the promoter & his business contacts.

16

Liquidity:

Current Ratio (CR) of 1.33 will generally be considered as a

benchmark level of liquidity. However the approach has to be

flexible. CR of 1.33 is only indicative & may not be deemed

mandatory. In cases where the CR is projected at a lower than the

benchmark or a slippage in the CR is proposed, it alone will not

be a reason for rejection for the loan proposal or for the

sanction of the loan at a lower level. In such cases, the reason

for low CR or slippage should be carefully examined & in

deserving cases the CR as projected may be accepted. In cases

where projected CR is found acceptable, working capital finance

as requested may be sanctioned. In specific cases where

warranted, such sanction can be with the condition that the

borrower should bring in additional long-term funds to a specific

extent by a given future date. Where it is felt that the

projected CR is not acceptable but the borrower deserves

assistance subject to certain conditions, suitable written

commitment should be obtained from the borrower to the effect

that he would be bringing in required amounts within a mutually

agreed time frame.

Net Working Capital:

Although this is a corollary of current ratio, the movements

in Net Working Capital are watched to ascertain whether there is

a mismatch of long term sources vis-à-vis long term uses for

17

purposes which may not be readily acceptable to the Bank so that

corrective measures can be suggested.

Financial Soundness:

This will be dependent upon the owner's stake or the

leverage. Here again the benchmark will be different for

manufacturing, trading, hire-purchase & leasing concerns. For

industrial ventures a Total Outside Liability/ Tangible Net worth

ratio of 3.0 is reasonable but deviations in selective cases for

understandable reasons may be accepted by the sanctioning

authority.

Turn-Over:

The trend in turnover is carefully gone into both in terms

of quantity & valve as also market share wherever such data are

available. What is more important to establish a steady output if

not a rising trend in quantitative terms because sales

realization may be varying on account of price fluctuations.

Profits:

While net profit is ultimate yardstick, cash accruals, i.e.,

profit before depreciation & taxation conveys the more comparable

picture in view of changes in rate of depreciation & taxation,

which have taken place in the intervening years. However, for the

sake of proper assessment, the non-operating income is excluded,

18

as these are usually one time or extraordinary income. Companies

incurring net losses consistently over 2 or more years will be

given special attention, their accounts closely monitored, and if

necessary, exit options explored.

Credit Rating:

Wherever the company has been rated by a Credit Rating

Agency for any instrument such as CP / FD this will be taken into

account while arriving at the final decision. However as the

credit rating involves additional expenditure, we would not

normally insist on this and only use this tool if such an agency

had already looked into the company finances.

Credit Appraisal Techniques:

Credit Appraisal Techniques act as a tool for credit

portfolio managers to take right decisions. It is a first and

prime most function performed by the Credit Appraisal cell before

providing any sort loans and advances. The appraisal technique

for each type of loan is separate from each other. Each type of

loan whether secured or unsecured has to be analyzed in a

different way. The different techniques of credit analysis or

credit appraisal are discussed below:

19

4.4 Process of Credit Appraisal for Term Loans:

Term loans are repayable in not less than 36months are

referred as Term Loan. In the interest of sound risk management

practices, banks monitor the percentage of Term Loans in their

credit portfolio with a view to keeping the term loan component

within a predetermined stage.

Requirements to obtain with a proposal:

Copies of project report

Where loan is on participation basis, a copy of the

appraisal note of the lead institution/ bank should be

obtained.

Scrutiny of Proposals.

Scope of the project

Background of the promoters

Government consents

The Technical appraisal

Cost of the project

Sources of Finance

The schedule of Implementation

The financial projections and profitability

Cash flow statements

Calculation of debt service coverage ratio(DSCR)

Breakeven analysis

20

Disbursement

Follow up(post sanction)

Assessment:

Term loan is provided for medium & long term (3 to 15 years)

periods for new / existing projects for expansion /

diversification. Its repayment is for specific period with

initial holiday period and secured by fixed assets such as land/

building/ plant / machinery/ other fixed assets. Basic aspect in

Term loan is that the borrower should repay the amount with

interest from the anticipated income earned from the assets

acquired. Technical & economic viability of the project is a must

for considering the term loan. In India, the commercial banks

extend term loan along with other banks & F I’s in the Consortium

/ multiple banking modes.

For assessment purposes, the forms prescribed are used and

debt-equity ratio and average DSCR, BEP payback period, etc. are

taken into consideration. The following minimum financial

parameters are required to be satisfied for a Term loan proposal

to merit consideration:

Debt Equity Ratio Not more than 2.33:1(1.71:1

may be accepted in the case of

real estate sector and

generally for different type

of industry different level of

21

DER is acceptable)Average DSCR Not less than 1.5 to 2 (ratio

lower than this is to be

looked into)

4.4.1 Ratios for appraising term loans:

Debt Equity Ratio: long term debt

Tangible Net

worth

Average DSCR: PAT + Depreciation + Interest on Term

Loans

Interest on term

Loan + Term Loan installments

Breakeven point: Fixed cost

Sales-Variable

cost (Contribution)

It should be noted that the banks generally consider only term

loans repayable within 5 to 7 years.

Term loans with maturity beyond 7yeras are normally not

experienced except infrastructure loans.

22

Debt-equity ratio:

A measure of a company’s financial leverage calculated by

dividing it’s to liabilities by stockholders’ equity. It

indicates what proportion of equity and debt the company is using

to finance its assets. Also known as the Personal Debt/Equity

Ratio, this ratio can be applied to personal financial statements

as well as companies.

A high debt/equity ratio generally means that a company has

been aggressive in financing its growth with debt. This can

result in volatile earnings as a result of the additional

interest expense. If a lot of debt is used to finance increased

operations (high debt to equity), the company could potentially

generate more earnings than it would have without this outside

financing. If this were to increase earnings than it would have

without this outside financing. If this were to increase earnings

by a greater amount than the debt cost (interest), then the

shareholders benefit as more earnings are being spread among the

same amount of shareholders. However, the cost of this debt

financing may overweigh the return that the company generates on

the debt through investment and business activities and become

too much for the company to handle. This can lead to bankruptcy,

which would leave shareholders with nothing.

Debt-Service coverage Ratio (DSCR):

23

The ultimate purpose of project appraisal is to ascertain

the viability of a project which has a direct bearing on the

repayment of the installments under the proposed term loan /

deferred payment guarantee. While the repayment program will

depend upon the profitability of a project, the quantum of annual

instalments has to be related to the size of the annual each

servicing by the debt service coverage ratio.

The debt service coverage ratio is the core test ratio in

project financing. This ratio indicates the degree of viability

of a project and influences in fixing the repayment period, and

quantum of annual installments. For the purpose of this ratio,

“debt” means maturing obligations viz., installments payable

during a year under all the term loans/deferred payment

guarantees and ‘service’ means cash accruals (service) available

to cover the maturity obligation (debt) during each year.

The debt service coverage ratio indicates the ability of the

firm to generate car accruals for repayment of instalment and

interest. For example, a DSCR of 3:1 indicates that for each

Re.1/- long term debt including interest to be paid the business

generates cash accrual of Rs.3/- to be utilized for repayment of

debt. The difference accrual and debt is known as margin of

safety (Rs.2/- in this case).

The ratio of 1.5 to 2 is considered reasonable. Ratio lower

than this should be further looked into. A very high ratio may

24

indicate the need for lower moratorium period/repayment of loan

in shorter schedule. This ratio provides a measure of the ability

of an enterprise to service its debts i.e. ‘interest’ and

‘principal’ repayment besides indicating the margin of safety.

The ratio may vary from industry from to industry but has to be

viewed with circumspection when it is less than 1.5.

4.4.2 Term loan Appraisal consists of:

No item to be ignored in project financing.

Costs shown should be true & not overstated.

Three sets of quotation from various suppliers to be

obtained.

Supplier’s details and credibility need to be verified.

Building construction estimates to be properly vetted.

Funds to be released based on progress of the work.

Security coverage is to be assessed.

4.4.3 Techniques of Term Loan Appraisal are:The purpose of Project Appraisal is to ascertain whether the

project will be sound – technically, economically, financially

and managerially – and ultimately viable as a commercial

proposition. The ultimate objective of the appraisal exercise is

to ascertain the viability of a project with a view to ensuring

the repayment of the borrower’s obligations.

1. Technical feasibility

2. Commercial viability

25

3. Managerial competence

4. Financial feasibility

Technical Feasibility

Its objective is to determine the suitability of the

technology selected and the adequacy of the technical

investigation, and design.

It consists of:

Technology / process

Indian/ foreign/Collaboration

Back up arrangement

Infrastructure

Availability of land /R M / transport/ power / water

Pollution/ Project implementation

Commercial viability

Its objective is to ascertain the extent of profitability of

the project and its sufficiency in relation to the repayment

obligations pertaining to term finance.

It consists of:

E I C analysis

Demand/ supply of the product

Competition/ market

Marketing abilities

Product / service differentiation

Managerial competence

26

Its objective is to ascertain that competent men are behind

the project to ensure its successful implementation and efficient

management after commencement of commercial production.

It consists of:

Organization set up

CCC of the borrower

finance

management

Operations

H R

Qualified technical persons

Financial feasibility

Its objective is to determine the accuracy of cost

estimates, suitability of the envisaged pattern of financing and

general soundness of the capital structure.

It consists of:

Cost of the project & means of finance

Production/Profitability

Cash flow/ funds flow

Projected balance sheet

profitability statements

B E P / CMA

4.4.4 Written Down Value Method of Depreciation (WDV) Under the Written Down Value Method, depreciation according

to a fixed percentage calculated upon the original cost (in the

first year) and written down value, (in subsequent years) of an

27

asset, is written off during each accounting period over the

expected useful life of the asset. Under this method, the rate of

depreciation remains constant year after year whereas the amount

goes on decreasing.

Calculation of Rate of Depreciation under WDV Method:

R= (1 - n s/c) x 100 (or)

WDV=Cost of assets -Depreciation

Where R = Rate of Depreciation (in %),

n = Useful life of the asset (in years)

s = Scrap value at the end of useful life of the asset

4.4.5 Cost of Project and Means of Finance:

Project financing is an innovative and timely financing

technique that has been used on many high-profile corporate

projects, including Euro Disneyland and the Eurotunnel. Employing

a carefully engineered financing mix, it has long been used to

fund large-scale natural resource projects, from pipelines and

refineries to electric-generating facilities and hydro-electric

projects. Increasingly, project financing is emerging as the

preferred alternative to conventional methods of financing

infrastructure and other large-scale projects worldwide.

Project Financing discipline includes understanding the

rationale for project financing, how to prepare the financial

plan, assess the risks, design the financing mix, and raise the

funds. In addition, one must understand the cogent analyses of

why some project financing plans have succeeded while others have

28

failed. A knowledge-base is required regarding the design of

contractual arrangements to support project financing; issues for

the host government legislative provisions, public/private

infrastructure partnerships, public/private financing structures;

credit requirements of lenders, and how to determine the

project's borrowing capacity; how to analyze cash flow

projections and use them to measure expected rates of return; tax

and accounting considerations; and analytical techniques to

validate the project's feasibility

Project finance is different from traditional forms of

finance because the credit risk associated with the borrower is

not as important as in an ordinary loan transaction; what is most

important is the identification, analysis, allocation and

management of every risk associated with the project. The purpose

of this project is to explain, in a brief and general way, the

manner in which risks are approached by financiers in a project

finance transaction. Such risk minimization lies at the heart of

project finance.

In a no recourse or limited recourse project financing, the

risks for a financier are great. Since the loan can only be

repaid when the project is operational, if a major part of the

project fails, the financiers are likely to lose a substantial

amount of money. The assets that remain are usually highly

specialized and possibly in a remote location. If saleable, they

may have little value outside the project. Therefore, it is not

29

surprising that financiers, and their advisers, go to substantial

efforts to ensure that the risks associated with the project are

reduced or eliminated as far as possible. It is also not

surprising that because of the risks involved, the cost of such

finance is generally higher and it is more time consuming for

such finance to be provided.

Project finance is the financing of long-term infrastructure

and industrial projects based upon a complex financial structure

where project debt and equity are used to finance the project.

Usually, a project financing scheme involves a number of equity

investors, known as sponsors, as well as a syndicate of banks

which provide loans to the operation. The loans are most commonly

non-recourse loans, which are secured by the project itself and

paid entirely from its cash flow, rather than from the general

assets or creditworthiness of the project sponsors. The financing

is typically secured by all of the project assets, including the

revenue-producing contracts. Project lenders are given a lien on

all of these assets, and are able to assume control of a project

if the project company has difficulties complying with the loan

terms.

Generally, a special purpose entity is created for each

project, thereby shielding other assets owned by a project

sponsor from the detrimental effects of a project failure. As a

special purpose entity, the project company has no assets other

than the project. Capital contribution commitments by the owners

30

of the project company are sometimes necessary to ensure that the

project is financially sound. Project finance is often more

complicated than alternative financing methods. It is most

commonly used in the mining, transportation, telecommunication

and public utility industries.

Cost of project

Land (Inc dev charges)

Building / Machinery

(Inc fright / transp. erection charges)

Other fixed assets

Technical Know- how

Consultancy charges

Preliminary expenses

Contingent expenses

Working capital margin

Means of Finance

Total Capital (equity)

USL from others

Term loan from bank/s

Term loan from F I’s

Subsidy from Government (if any)

Total

4.4.6 Financial Evaluation Techniques:

31

Some common techniques of evaluating viability of projects are

given below:

• Pay-Back Period Method

• Accounting Rate of Return Method

• NPV (Net Present Value) Method

• Profitability Index Method

• IRR (Internal Rate of Return) Method

Pay-Back Period Method:

The Pay-Back Period is the length of time required to

recover the initial outlay on the project Or It is the time

required to recover the original investment through income

generated from the project.

Pay-Back Period =OriginalCostofInvestmentAnnualCashInflows∨Savings

Pros: - a) It is easy to operate and simple to understand.

b) It is best suited where the project has shorter gestation

period and project cost is also less.

c) It is best suited for high risk category projects. Which

are prone to rapid technological changes.

d) It enables entrepreneur to select an investment which

yields quick return of funds.

32

Cons: - a) It emphasizes more on liquidity rather than

profitability.

b) It does not cover the earnings beyond the payback

period, which may result in wrong selection of investment

projects.

c) It is suitable for only small projects requiring

less investment and time

d) This method ignores the cost of capital which is

very important factor in making sound investment decision.

Decision Rule: - A project which gives the shortest pay-back

period, is considered to be the most ACCEPTABLE

Accounting Rate of Return (ARR):

This method is considered better than pay-back period method

because it considers earnings of the project during its full

economic life. This method is also known as Return on Investment

(ROI). It is mainly expressed in terms of percentage.

ARR or ROI = Average Annual Earnings after Tax_____

* 100

Average Book Investment after Depreciation

Here, Average Investment = (Initial Cost –

Salvage Value) * 1 / 2

Decision Rule

In the ARR, A project is to be ACCEPTED when (If Actual ARR

is higher or greater than the rate of return) otherwise it is

33

rejected and In case of alternate projects, one with the highest

ARR is to be selected.

Pros: - a) It is simple to calculate and easy to understand.

b) It considers earning of the project during the entire

operative life.

c) It helps in comparing the projects which differ

widely.

d) This method considers net earnings after depreciation and

taxes.

Cons: - a) It ignores time value of money.

b) It lays more emphasis on profit and less on cash flows.

c) It does not consider re-investment of profit over years.

d) It does not differentiate between the size of

investments required for different projects.

Net Present Value (NPV):

This method mainly considers the time value of money. It is

the sum of the aggregate present values of all the cash flows –

positive as well as negative – that are expected to occur over

the operating life of the project.

NPV = PV of Net Cash Inflows – Initial Outlay (Cash outflows)

Decision Rule: -

• If NPV is positive, ACCEPT

• If NPV is negative, REJECT

• If NPV is 0, then apply Payback Period Method

34

The standard NPV method is based on the assumption that the

intermediate cash flows are reinvested at a rate of return equal

to the cost of capital. When this assumption is not valid, the

investment rates applicable to the intermediate cash flows need

to be defined for calculating the modified NPV.

Pros: - a) This method introduces the element of time value of

money and as such is a scientific method of evaluating the

project.

b) It covers the whole project from start to finish

and gives more accurate figures

c) It indicates all future flows in today’s value.

This makes possible comparisons between two mutually

exclusive projects.

d) It takes into account the objective of maximum

profitability

Cons: -a) It is difficult method to calculate and use.

b) It is biased towards shot run projects.

c) In this method profitability is not linked to capital

employed.

d) It does not consider Non-Financial data like the

marketability of a product.

Profitability Index Method:

Profitability Index is the ratio of present value of

expected future cash inflows and Initial cash outflows or cash

outlay. It is also used for ranking the projects in order of

35

their profitability. It is also helpful in selecting projects in

a situation of capital rationing. It is also known as Benefit /

Cost Ratio (BCR).

PI = PresentvalueofFuturecashInflowInitialCashOutlay

Decision Rule: - In Case of Independent Investments, ACCEPT a

Project If a PI is greater (> 1) and Reject it otherwise.

In Case of Alternative Investments, ACCEPT

the project with the largest PI, provided it is greater than (>

1) and Reject others.

Internal Rate of Return Method (IRR):

This method is known by various other names like Yield on

Investment or Rate of Return Method. It is used when the cost of

investment and the annual cash inflows are known and rate of

return is to be calculated. It takes into account time value of

Money by discounting inflows and cash flows. This is the most

alternative to NPV. It is the Discount rate that makes it NPV

equal to zero.

36

In this Method, the IRR can be ascertained by the Trial & Error

Yield Method, Whose the objective is to find out the expected

yield from the investment.

IRR= Smaller discount rate +NPV@Smallerrate

∑ oftheabsolutevaluesoftheNPV@smaller∧thebiggerdiscountrates

Pros: - a) It is conceptually sound.

b) It considers time value of money.

c) It Facilitates ranking of projects which help in the

selection of projects.

Cons: - a) It is vulnerable to different interpretations.

b) Its computation Process is complex

4.5 Process of Credit Appraisal for providing Cash

Credit/Working Capital:Working Capital for any unit means the total amount of

circulating funds required for meeting day to day requirements of

the unit. For proper working a manufacturing unit needs a

specific level of current assets such as Raw Material, Stock in

process, Finished Goods, Receivables and Other current assets

such as Cash in Hand/Bank and advances etc. So the working

capital means the funds invested in current assets. The trading

units need the working capital for storing the goods and allowing

the credit to its customers.

37

Types of working capital provided by Indian Banks are cash

credit (Open/ Key) / overdraft / Bills discounting or purchase

and STL .Cash credit / bills limits are assessed based on the

production/ projected sales/inventory holdings/ past credit

limits. Customer allowed to draw the amount from the cash credit

account as per his requirement & also deposit the amount based on

the surplus funds available. Cash credit / overdrafts are running

accounts & the credits in the account should reflect the sales of

the company.

There are three methods of working capital assessment.

The turn over method (Nayak committee),

The inventory method &

II method of lending (Chore committee)

4.5.1 Working Capital Cycle for Manufacturing and Non-

Manufacturing firm:

38

4.5.2 Factors affecting the Requirement of Working

Capital: Nature of business

Size of the business

Production cycle process

Production policy

Terms of purchase & sales(policies)

Business cycle ( Upward/ downward)

Growth & expansion

Availability of R M

Profit level

Operating efficiency

Availability of credit

Nature of Activity: Manufacturing units need more working capital

as compared to trading and service units.

39

The length of operating cycle: More the length of operating

cycle, more the requirement of working capital. Lengthy the

process of manufacture, more the need of working capital due to

increase of length of working capital cycle.

Market trend: The market trend of allowing credit to customers

also varies from industry to industry and city to city. More the

credit allowed to customers, more the need of working capital.

Availability of Raw Materials: When the availability of raw

materials is assured and comfortable, lower the stock maintenance

is required .when there is expectation of shortage or expectation

of rise prices, more amounts is blocked in raw materials.

Location of unit: When the unit is located near the source of raw

material, lower stock maintenance is required.

Type of customers: When there are regular customers, low stock of

finished products is needed. When there are sales are to be made

walk-in customers more level of stock of finished products is

required.

Seasonality factor: When the raw material required is available

in a particular season, the stock for the whole of year is to be

purchased in the particular season. E.g., Sugarcane, Cotton,

Paddy, etc. Similarly the woolen products and products required

in a particular season such as ACs for keeping the production

running, higher level of finished stocks have to be kept.

4.5.3 Parameters for various stages in computation of

Working Capital:

40

S.No Stage Time ValueI Raw Material Holding period Value of RM

consumed during

the periodIi SIP Time taken in

converting the

RM into FG

RM+Mfg Exp.

during the

period (Cost of

production)Iii FG Holding period

of FG before

being sold

RM+Mfg.Exp+Adm

Overheads for

the period (Cost

of sales)Iv Receivables Credit allowed

to Buyer

RM+Mfg.Exp+Adm.E

xp

+Profit for the

period (sales)

4.5.4 Methods of Working Capital Assessment:

1. Turn Over Method:

It is also known as Nayak Committee. Its operating cycle is

less than or equal to three months.

Assessment is:

25% of the projected turn over

41

Minimum working capital margin ( NWC) - 5% of the

projected sales

Borrower has to bring additional margin if it is less

than the prescribed limit

Working capital eligibility = (25 % of projected

turn over – min NWC or actual NWC ) whichever is less

NWC = Current assets - current liability

2. Inventory Method:

Its operating cycle is more than three months. The minimum

stipulated margins can vary from banks to banks based on the

credit policy guidelines.

Assessment is:

1 Build up of current assets

2 Buildup of current liabilities

(other than Bank borrowings for W C)

3 Working capital gap ( 1-2)

4 Actual NWC

5 Required NWC ( min 15% of current

assets )

6 Maximum permissible bank borrowings ( 3-4

) or

42

( 3-5) whichever is less

7 Margin to be brought in ( 5-4)

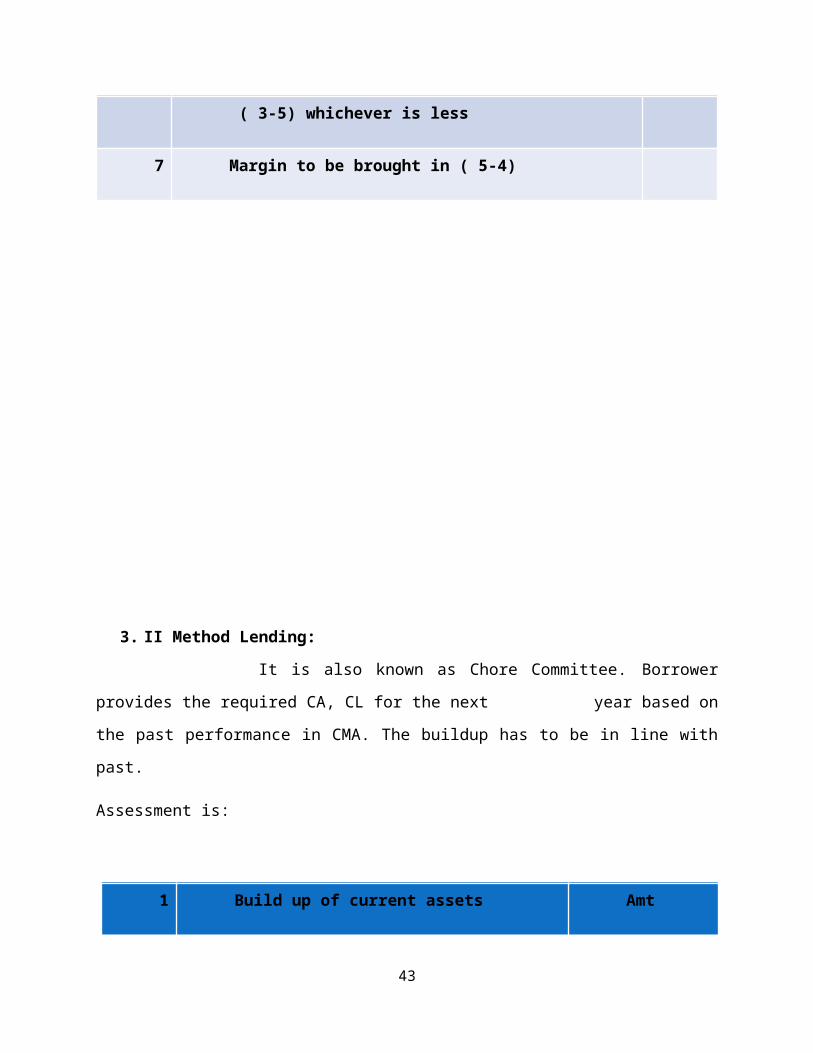

3. II Method Lending:

It is also known as Chore Committee. Borrower

provides the required CA, CL for the next year based on

the past performance in CMA. The buildup has to be in line with

past.

Assessment is:

1 Build up of current assets Amt

43

2 Buildup of current liabilities

(other than Bank borrowings for

W C)

3 Working capital gap ( 1-2)

4 Actual NWC

5 Required NWC ( min 25% of

current assets )(excluding export

receivables)

6 Maximum permissible bank

borrowings ( 3-4 ) or ( 3-5)

whichever is less

7 Margin to be brought in ( 5-4)

44

5.0 LEARNINGS FROM THE IIP

1. Preparation of financial statements.

2. An overview and understanding of financial analysis process.

3. Understanding the Loan Processing in a bank

4. Estimates & Projections.

45

6.0 STRUCTURE OF THE REPORT

1) Overview of PHARMACEUTICAL INDUSTRY

2) Project at a glance

3) Executive summary

4) Infrastructure

5) Cost of the project & Means of Finance

6) Assumptions

7) Implementation Schedule

8) SWOT analysis

9) Conclusion

46

7.0 OVERVIEW OF PHARMACEUTICAL INDUSTRY

The Indian pharmaceutical industry currently tops the chart

amongst India’s science-based industries with wide ranging

capabilities in the complex field of drug manufacture and

technology. A highly organized sector, the Indian pharmaceutical

industry is estimated to be worth $ 4.5 billion, growing at about

8 to 9 percent annually. It ranks very high amongst all the third

world countries, in terms of technology, quality and the vast

range of medicines that are manufactured. It ranges from simple

headache pills to sophisticated antibiotics and complex cardiac

compounds, almost every type of medicine is now made in the

Indian pharmaceutical industry.

The Indian pharmaceutical sector is highly fragmented with

more than 20,000 registered units. It has expanded drastically in

the last two decades. The Pharmaceutical and Chemical industry in

India is an extremely fragmented market with severe price

47

competition and government price control. The Pharmaceutical

industry in India meets around 70% of the country’s demand for

bulk drugs, drug intermediates, pharmaceutical formulations,

chemicals, tablets, capsules, orals and injectable. There are

approximately 250 large units and about 8000 Small Scale Units,

which form the core of the pharmaceutical industry in India

(including 5 Central Public Sector Units).

The Government has also played a vital role in the

development of the India Software Industry. In 1986, the Indian

government announced a new software policy which was designed to

serve as a catalyst for the software industry. This was followed

in 1988 with the World Market Policy and the establishment of the

Software Technology Parks of India (STP) scheme. In addition, to

attract foreign direct investment, the Indian Government

permitted foreign equity of up to 100 percent and duty free

import on all inputs and products.1.2 Current Scenario India’s

pharmaceutical industry is now the third largest in the world in

terms of volume and stands 14th in terms of value.

According to data published by the Department of

Pharmaceuticals, Ministry of Chemicals and Fertilizers, the total

turnover of India’s pharmaceuticals industry between September

2008 and September 2009 was US$ 21.04 billion. Of this the

domestic market was worth US$ 12.26 billion. The Indian

pharmaceuticals market is expected to reach US$ 55 billion in

2020 from US$ 12.6 billion in 2009.

48

The market has the further potential to reach US$ 70 billion

by 2020 in an aggressive growth scenario. Moreover, the

increasing population of the higher-income group in the country,

will open a potential US$ 8 billion market for multinational

companies selling costly drugs by 2015. Besides, the domestic

pharma market is estimated to touch US$ 20 billion by 2015,

making India a lucrative destination for clinical trials for

global giants. Further estimates the healthcare market in India

to reach US$ 31.59 billion by 2020.

About the firm project & Promoters

Vision: To be a leading active pharmaceutical company by

providing high quality, affordable and innovative solutions

through continuous research.

Mission: ABC Pharmaceuticals goal is to create world class

facilities for manufacturing of complex active pharmaceuticals

for generic industry. The company is committed to innovative

research to develop active pharmaceutical ingredients. The

company will strive for continuous in everything that they do,

through active involvement of their employees, promoters,

customers and to the society.

Goal: Ability to develop products for complex active

pharmaceuticals.

Excellent team of skilled professional in all areas

related to research, production and business development.

49

A strong commitment towards society on safety and

environment.

Transparency and open communications.

Excellent quality system to produce active

pharmaceuticals to meet customer specifications.

PROJECT

M/s ABC Pharma Limited was constituted on 03.07.2012 with an

objective to set up a manufacturing industry to manufacture

bulk drugs and intermediaries.

The company purchased land measuring 5.09 acres at Plot

No.23 D, APIIC Achtapuram, APSEZ, and Visakhapatnam

The present proposal of the company is to set up industry to

manufacture bulk drugs and intermediates with a total

capacity of 204 tons per annum.

The proposed industry will have the plant and machinery to

manufacture the following products.

Famotidine

Itraconazole

Ketoconazole

Lopinavir

Emtricitabine

Acelovir/Acyclovir

The company is in the process of obtaining necessary approvals

and permissions from various authorities for the proposed

50

industry. Some of important approvals are already obtained. The

industry is expected to commence production 01.01.2016.

PROJECT OUT LAY

The project cost is estimated at Rs.2737.04 lakhs which is

inclusive of working capital margin.

The land cost is estimated at Rs.244.57 lakhs which include

cost of land, registration charges and land development cost

inclusive of internal roads and land scaping.

Total volume of the civil works in the finished structure

stands at Rs 619.79 lacs and is arrived based on estimates

made by engineers.

The estimates for the civil works are as per the approved

plan of the factory.

The main plant and machinery is estimated to cost Rs.990.76

lakhs which will be utilized for processing.

Auxiliary equipment is provided at Rs. 574.36 lacs. This

includes provision made for Quality Control Equipment &

Glassware, Power, Safety, AHU, Maintenance and Ware House

Deposits are provided at Rs 22.00 lacs for making deposits

with the Government Departments

The preliminary expenses are estimated at Rs.217.04 lakhs

which include interest during construction period amounting

to Rs.201.60 lakhs

The working capital margin is estimated at Rs.68.52 lakhs

8.0 PROJECT AT A GLANCE

51

Name of the Company

M/s ABC Pharma Limited

Constitution Limited Company

Date of Incorporation

03.07.2012

Registered Office H.No.8-372/F1/1/3, Subhash Nagar

Yellareddyguda, Ameerpet, Hyderabad - 500073

Directors Sri A.Hari Babu Director

Sri M.Koteswara Rao Director

Unit Location (Proposed)

Plot No.23 D, APIIC, Achtapuram, APSEZ, Visakhapatnam

Line of activity Manufacturing of bulk drugs & intermediaries

End User Segment Pharmaceutical industries

Project Cost Particulars Cost (Rs in lakhs)

Land 244.57

Buildings 619.79

Plant & Machinery 990.76

Other machinery 574.36

Deposits 22.00

Preliminary expenses 217.04

Margin for working capital

68.52

Total 2737.04

Means of Finance Particulars Cost (Rs in lakhs)

Promoters 900.00

Term Loan 1800.00

Unsecured loans 37.04

52

Total 2737.04

Working capital CC Rs.200.00 lakhs

ILC/FLC Rs.100.00 lakhs

9.0 EXECUTIVE SUMMARY

THE GLOBAL PHARMACEUTICAL INDUSTRY The pharmaceutical industry, which includes the development,

production and marketing of pharmaceutical products, is

characterized by its large size, growth, globalization and

significant investment in research and development (“R&D”). The

global pharmaceutical industry is driven by a continuing need for

medicines for the treatment of disease, demographic shifts that

strengthen this underlying demand and improved healthcare

infrastructures that are providing people with greater access to

medicines.

According to IMS, sales in the global pharmaceutical

industry exceeded U.S.$845 billion in 2011 with a 7% positive

growth rate. The global pharmaceutical industry has historically

been dominated by the United States, European and Japanese

markets. In 2011, the United States market was the largest market

accounting for sales of U.S. $320 billion. However, it is now

believed that China, India, Brazil and Russia are very attractive

nations for growth in the pharmaceutical industry. These markets

offer a high growth potential due to their rising GDPs, expanding

53

access to healthcare, improving intellectual property and

regulatory environments.

The Chart set forth below gives a breakdown of the

contribution to sales of various major markets to the global

pharmaceuticals industry in 2011.

THE INDIAN PHARMACEUTICAL INDUSTRY The size of the Indian pharmaceutical industry was estimated

at U.S.$29.1 billion (including exports) in 2011-2012. Of this,

the domestic formulations market was valued at U.S.$11.6 billion

(or ` 556.6 billion). Exports to semi-regulated markets, which

have grown at 16% over the same period, also supported growth in

overall exports. Over the next few years, formulations exports

are expected to continue to grow at a CAGR of 14-16%, driven by

54

the growing opportunity from off-patent drugs in regulated

markets and a favorable growth in semi-regulated markets.

Bulk Drugs

Bulk drug exports too are expected to grow at a similar pace

of 14-16% CAGR, as the growing generics market and rising cost

pressures faced by innovators provide a significant opportunity.

Additionally, India's key strengths such as low-cost

manufacturing, high process chemistry skills, manufacturing

facilities and increasing number of drug master filings (“DMFs”)

are expected to drive growth in bulk drug exports.

THE INDIAN BIOTECHNOLOGY SECTOR

The biotechnology industry in India, comprising

approximately 380 companies, has grown threefold in the last five

years, to reach U.S. $4 billion in fiscal 2011. India’s

biotechnology sector is benefitting from several advantages such

as cost effectiveness, R&D, expertise and personnel skills. India

is widely recognized as an ideal location for manufacturing

biotechnology products and for conducting high-level research

programs in the field. The Indian biotechnology industry has seen

good growth with a CAGR in excess of 20%. Of all the sectors, the

Indian biotechnology industry is primarily dominated by

biopharma, which includes vaccines and biosimilars.

India is also making major strides in agri-bio, which is

the fastest growing sub-sector in the biotechnology industry.

With up to U.S. $25 billion worth of innovator biologics losing

patent protection by 2016, companies from the developed markets

55

of the United States and Europe are looking to diversify into

generics and biosimilars by partnering with Indian companies,

given their industry’s well-developed leadership in this segment.

Further, increased focus on disease prevention, rising incomes

and government participation are key drivers of the sector’s

domestic growth. Indian biotechnology companies are gaining large

orders for vaccines from the Governments under various health

care initiatives for immunization. All these factors have poised

the industry for doubling in size in five years’ time to reach a

size of U.S. $8 billion by 2015. Financial indicators:

Parameter 31.03.16

31.03.17

31.03.18

31.03.19

Net Sales 852.92 5228.02

5687.19

7159.46PBDITA 134.71 705.21 776.02 908.01

Operating Profit (before interest)

108.87 601.87 672.68 804.67PBT 40.93 419.09 471.70 649.50PAT 34.19 343.59 372.12 481.11Cash Accruals 60.02 446.93 475.45 584.45Paid up Capital 900.00 900.00 900.00 900.00NW 934.19 1,277.

781,649.

892,131.

00TNW 934.19 1,277.78

1,649.89

2,131.00NWC 133.97 275.33 445.21 724.10

Total Current Liabilities 364.81 394.35 402.01 430.70Total Funded Debt 1837.0

41509.7

71182.5

0855.23

Other Current Liabilities 64.81 94.35 102.01 130.70Total Outside Liabilities (TOL) 2201.8

61904.1

21584.5

11285.9

3Total long term sources 2771.23

2787.55

2832.39

2986.23Total Current Assets (TCA) 498.78 669.67 847.22 1154.79

56

Fixed Assets (Net Block) 2403.65

2300.31

2196.97

2093.63Total Tangible Assets 2924.4

22991.9

83066.1

93270.4

2Total Assets 3136.04

3181.90

3234.40

3416.93Depreciation 25.83 103.34 103.34 103.34

Interest 67.94 182.78 200.98 155.16RM (incl.stores etc.) 208.50 325.68 353.03 460.23Stock-in-process 0.00 0.00 0.00 0.00Finished goods 56.08 87.07 93.88 119.42Inventory 264.58 412.74 446.91 579.65Receivables (domestic + export) 199.01 217.83 355.45 536.96Receivables over 6 months 0.00 0.00 0.00 0.00RM+stores & spares consumed 441.36 2751.0

62982.0

33883.8

0Cost of production 771.72 4543.05

4900.16

6239.34

BASE DATA 31.03.16

31.03.17

31.03.18

31.03.19

Cost of sales 715.64 4512.07 4893.34 6213.80

Power & Fuel 63.92 273.99 292.30 310.61

Direct Labour 36.43 142.45 143.94 145.45

Other Mfg. Expenses 20.03 115.17 124.22 157.25

Selling, Gen. and Admin. Exp. 22.98 92.37 99.46 119.28

Bank Finance 300.00 300.00 300.00 300.00

Sundry Creditors 51.15 80.35 87.11 113.81

Gross Sales 895.09 5486.49 5968.36 7513.42

Raw Material Purchases (Indigen.) 547.56 2809.84 2995.87 3937.58

Opening Stock 0.00 106.20 164.98 178.82

Consumption 441.36 2751.06 2982.03 3883.80

Closing Stock 106.20 164.98 178.82 232.60

57

Raw Material Purchases (Import.) 286.44 1215.44 1267.84 1692.31

Opening Stock 0.00 102.30 160.70 174.21

Consumption 184.14 1157.04 1254.33 1638.90

Closing Stock 102.30 160.70 174.21 227.63

Total (Imp.+Indig.) R.M Purch. 834.00 4025.28 4263.72 5629.90

RATIOSYear --> 31.03.1

631.03.17

31.03.18

31.03.19Current Ratio 1.37 1.70 2.11 2.68

TOL/TNW 2.36 1.49 0.96 0.60D/E 1.97 1.18 0.72 0.40OP/Net Sales % 12.76 11.51 11.83 11.24PBT/Net Sales % 4.80 8.02 8.29 9.07PBDITA/Net Sales % 15.79 13.49 13.65 12.68OP/TTA % 3.72 20.12 21.94 24.60PBT/TTA % 1.40 14.01 15.38 19.86PBDITA/TTA % 4.61 23.57 25.31 27.76NetProfit/NW (ROE) 3.66 26.89 22.55 22.58PBDITA/Interest 1.98 3.86 3.86 5.85TTA/NWC 21.83 10.87 6.89 4.52Net Sales/Current Assets 1.71 7.81 6.71 6.20Net Sales/FA 0.35 2.27 2.59 3.42

58

Net Sales / Total Tangible Assets

0.29 1.75 1.85 2.19Net Sales/TNW 0.91 4.09 3.45 3.36NWC to TCA (%) 26.86 41.11 52.55 62.70Bk.Finance to TCA(%) 60.15 44.80 35.41 25.98Sundry Cred.to TCA (%) 10.26 12.00 10.28 9.86Other CL (exc.sund.cred) to TCA (%)

12.99 14.09 12.04 11.32Fixed Assets/Long Term Sources % 86.74 82.52 77.57 70.11RM & Stores,Spares/ RM & Stores,spares consumed

172 43 43 43S-I-P/Cost of Production 0 0 0 0Finished Goods/Cost of Sales 29 7 7 7Inventories to Net Sales(days) 113 29 29 30Receivables to Gross Sales (days) 81 14 22 26Sundry Creditors to Purchases (days)

22 7 7 7RM+Stores & Spares consumed/Net Sales %

51.75 52.62 52.43 54.25Power & Fuel/Net Sales % 7.49 5.24 5.14 4.34Direct Labour/Net Sales % 4.27 2.72 2.53 2.03OME/Net Sales % 2.35 2.20 2.18 2.20Selling, General & Adm. Expenses/Net Sales %

2.69 1.77 1.75 1.67Interest/Net Sales % 7.97 3.50 3.53 2.17PBT/Net Sales % 4.80 8.02 8.29 9.07

10.0 INFRASTRUCTURE

Management:

The company will be managed by the board of directors comprising

eminent persons in the field of production and marketing of bulk

drugs and intermediates. They shall be assisted by competent and

experienced staff in all the areas of production, marketing,

finance, quality control, research and development.

Location:

The unit is located at Visakhapatnam which has several

59

advantages.

- There are no civic restrictions for establishing

pharmaceutical manufacturing industries

- The Government is providing incentives in the form of income

tax rebate

- The place has manpower pool and there is no problem of drawing

people of all disciplines.

- The power supply position is satisfactory

- The place has industrial atmosphere and no labour problems are

envisaged

- There is enormous growth in pharma industry in the area and

the fortunes are expected high

- Supplies treated water

- Common effluent treatment plant

- Road network connecting the NH-5

- Hazardous waste management facility

- Common security & surveillance

60

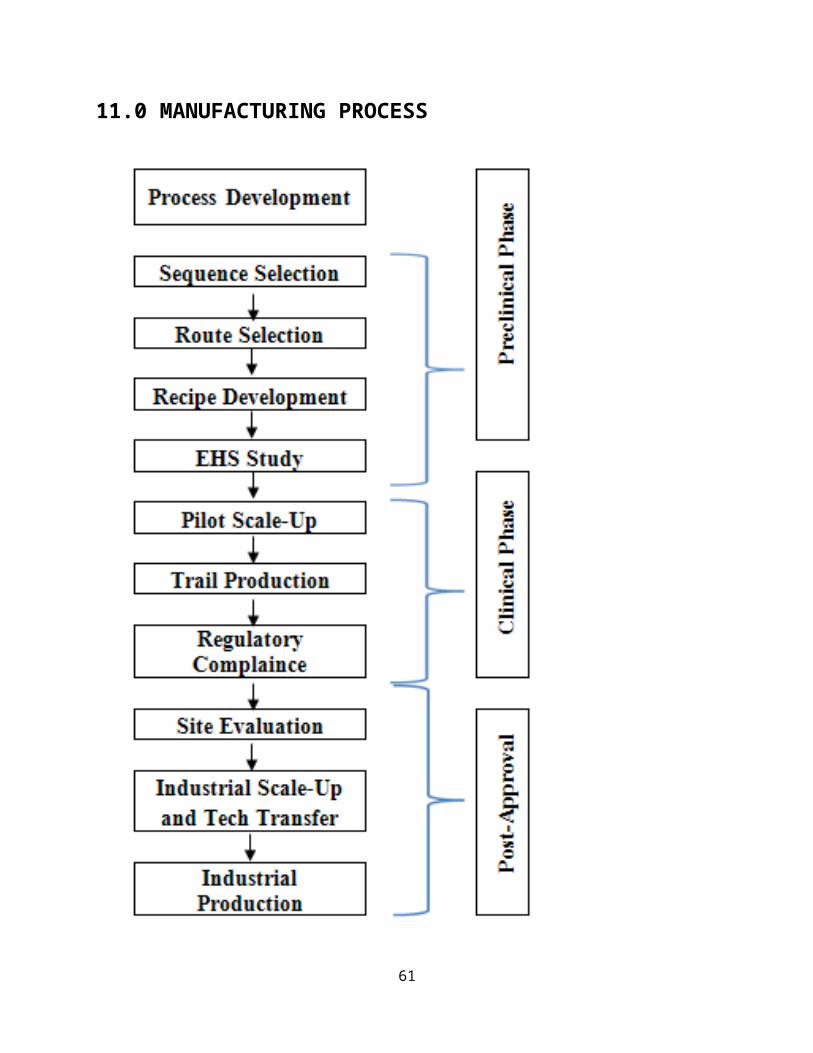

11.0 MANUFACTURING PROCESS

61

12.0 COST OF THE PROJECT & MEANS OF FINANCE

PROJECT COST

Land & Land Development 244.57

Building 619.79

Plant & Machinery (Indigenous) 990.76

Other machinery/equipment 574.36

Deposits 22.00

Preliminary & Pre-operative Expenses 217.04

Working Capital Margin 68.52

TOTAL 2737.04

MEANS OF FINANCE

Rs. Lacs

Item Amount

Equity Capital 900.00

Term loan 1800.00

Unsecured Loans 37.04

Total 2737.04

62

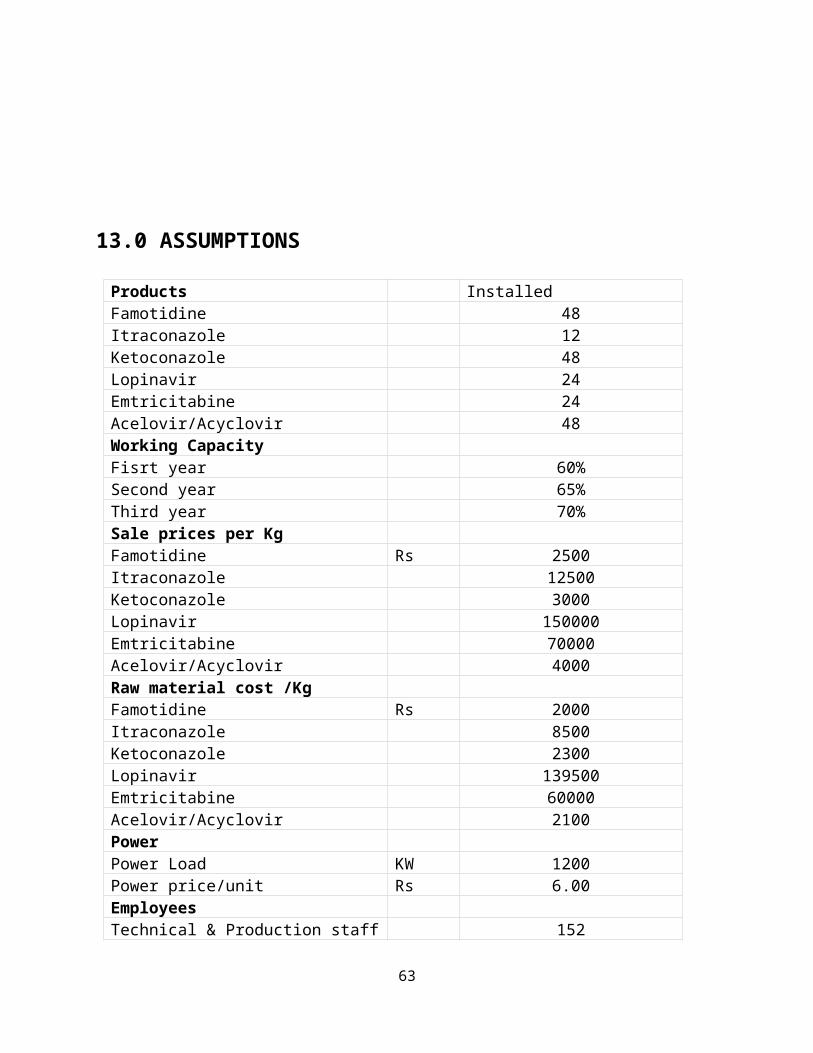

13.0 ASSUMPTIONS

Products Installed Famotidine 48Itraconazole 12Ketoconazole 48Lopinavir 24Emtricitabine 24Acelovir/Acyclovir 48Working CapacityFisrt year 60%Second year 65%Third year 70%Sale prices per KgFamotidine Rs 2500Itraconazole 12500Ketoconazole 3000Lopinavir 150000Emtricitabine 70000Acelovir/Acyclovir 4000Raw material cost /KgFamotidine Rs 2000Itraconazole 8500Ketoconazole 2300Lopinavir 139500Emtricitabine 60000Acelovir/Acyclovir 2100PowerPower Load KW 1200Power price/unit Rs 6.00EmployeesTechnical & Production staff 152

63

Administrative staff 24Repairs & Maintenance to talBuildings 0.50%Plant & Machinery 1.00%Annual increase 5%

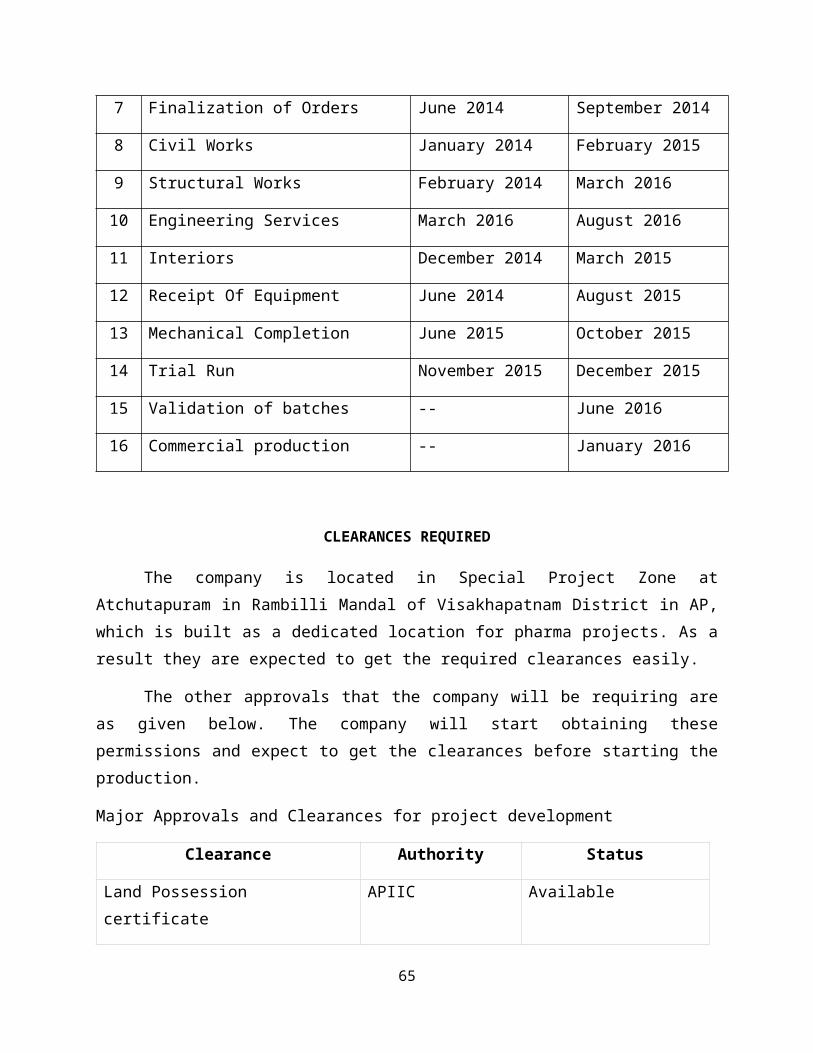

14.0 IMPLEMENTATION SCHEDULE

Total construction period for the project is proposed to be 18 months from 1st January, 2014 thereafter 6 months exclusively fortrial run and validation of products.

The schedule of implementation of the project is summarized below:

Sr.No.

ActivityDate of Commencement

Expected Date of Completion

Land & Land Development

1 Land Acquired --

2 Preliminary Studies/Surveys

Completed --

3 Land leveling Completed June 2014

4 Statutory Approvals All Critical Approvals already Obtained

June 2014

Facilities

5 Architectural Drawings December 2013 April 2014

6 Detailed Engineering December 2013 April 2014

64

7 Finalization of Orders June 2014 September 2014

8 Civil Works January 2014 February 2015

9 Structural Works February 2014 March 2016

10 Engineering Services March 2016 August 2016

11 Interiors December 2014 March 2015

12 Receipt Of Equipment June 2014 August 2015

13 Mechanical Completion June 2015 October 2015

14 Trial Run November 2015 December 2015

15 Validation of batches -- June 2016

16 Commercial production -- January 2016

CLEARANCES REQUIRED

The company is located in Special Project Zone atAtchutapuram in Rambilli Mandal of Visakhapatnam District in AP,which is built as a dedicated location for pharma projects. As aresult they are expected to get the required clearances easily.

The other approvals that the company will be requiring areas given below. The company will start obtaining thesepermissions and expect to get the clearances before starting theproduction.

Major Approvals and Clearances for project development

Clearance Authority Status

Land Possession certificate

APIIC Available

65

Land Registration APIIC Completed

Plan Approval IDA Approved

Electricity Eastern Power Distribution

Company of A.P.Ltd

Approved

Environment Clearance Ministry of Forest &

Environment

Pollution control board

clearance – Consent for

Establishment

APPCB

Permission for EOU’s status

DC, VSEZ Approved

Other Permissions & Clearances for operation

Administration level

S.No Details Name of Department

1 TDS Account Income Tax Department

2 VAT & CST Commercial Tax Dept.

66

3 Shops and Establishments Registration

Labour Department

4 Professional Tax Regn. Commercial Tax Department

5 Service Tax Registration Central Excise

6 Provident Fund PF dept.

Operational level

1 Pollution Control Board Clearance - Consent for Operation

The company has completed the formalities and obtained consent to set up industrial unit

2 Registration with inspector of Boilers

Dept for factories and boilers and will be obtained

3 Registration with labor inspector

Labor Department – will be registered

4 Registration with Electrical department

Electrical Dept- In principle letter is being obtained. The feasibility certificate will be obtained shortly

5 Explosive license Dy./ Asst. Director of explosives

6 License from the inspector of weights and measurements

Dept of weights and measurements – will be obtained

7 Registration with state excise dept.

State Excise Dept.

8 Registration with Central Central Excise Dept.

67

excise dept.

9 ESIC Registration Regional Director, ECIC

10 PF Register Inspector of PF

11 Registration with district Industries Centre

GM, DIC- IND. Dept.

12 Drug manufacturing/ Test License

Drug Control Administration

Quality:

Company will be following the international quality norms: In

the first phase of operations company will develop ISO 9002

Quality systems, also having plans to implement the Safety, Health

& Environment (SHE) policy. In Coming Future company will

implement the Occupational Safety & Health Administration (OSHA)

as well as ISO14000 Systems. All these standards are applicable

for the company products. From the beginning of operations,

Company will also follow 21 CFR regulations. Title 21 is the

portion of the Code of Federal Regulations that governs food and

drugs within the United States for the Food and Drug

Administration (FDA), the Drug Enforcement Administration (DEA),

and the Office of National Drug Control Policy (ONDCP).

Company will develop QC standards & systems that suit the

requirements of International standards & regulatory markets. The

main focus will be in the regulatory markets; mainly USA & EUROPE.

68

The company is planning to get the approvals of US FDA and the

European drug authorities before the commercial operations.

15.0 SWOT ANALYSIS

Strengths

Experience of the promoters for about three decades in the

same industry/activity.

High value of expected orders on hand from domestic and

export market

69

Tie up arrangements for job work with companies having

production facilities

Structured organization to meet challenges consisting of

experience and expertise

Reputation of the company’s promoters in the industry at

Hyderabad.

Largest facility with state of art technology bulk drug

manufacturing

Availability of Manpower (both skilled & unskilled) at

cheaper cost.

Inbuilt safety and housekeeping practices ensure better

productivity.

The value of Pharma Industry is growing from strength to

strength and India occupies the fourth position in the world

in manufacture of bulk drugs.

India has a large pool of skilled technical manpower.

Increasing liberalization of Government Policies.

Indian Pharmaceuticals Industry possesses excellent

chemistry and process reengineering skills. This adds to

the competitive advantage of the Indian companies.

Weaknesses

Sudden infrastructure breakdown.

Labour intensive industry.

Number of supplying units at different locations

Distance and logistic problems

70

Even after 55 years of our nation’s independence, pharmacy

has not been able to get proper recognition on par with the

profession of medicine, engineering, veterinary, agriculture

and science.

Non-availability of major intermediaries for bulk drugs.

Lack of experience to exploit efficiency of the new patent

regime.

Very low key Research & Development.

Very low level of Biotechnology in India and also for New

Drug Discovery Systems.

Low level of strategic planning for future and also for

technology forecasting.

Opportunities

Huge opportunities in this industry and scope for promotion

of industries in a big way.

Subsidies, Incentives from State & Central Governments for

Export sales

Ageing of the world population.

Growing Incomes.

Growing attention for health.

New diagnoses and new social diseases.

Spreading prophylactic approaches.

New therapy approaches.

Spreading attitude for soft medication (OTC drugs).

Spreading use of Generic Drugs.

Threats

71

Natural calamities like floods, drought, economic recession

and earthquake affect any business/industry.

Change in government policies.

Price and exchange fluctuations.

The profession of pharmacy is around six-decade old in the

country but it is very unfortunate that it could not have a

University of its own in many states of the country.

Containment of rising health-care cost.

High cost of discovering new products and fewer discoveries.

High entry cost into new markets.

High cost of sales and marketing.

Competition, particularly from generic products.

16.0 CONCLUSION

The project is viewed technically feasible and economically

viable subject to our observations mentioned in the overview and

the effect of the adverse factors as indicated under sensitivity

analysis.

72

17.0 REFERENCES

[1] “Indian Pharmaceutical Industry Vision 2015” A report by

73

Organization of Pharmaceutical Producers of India,

[2] Bell, M and K.Pavitt (1993) “Technological accumulation and

industrial growth: contrasts between developed world and

developing countries”, Industrial and corporate change,

Vol.2, no.2, pp157-210

[3] Chadda, A. (2006) “Destination India - the right choice

for the pharmaceutical industry”, Delhi Business Review Vol.

7, No. 1 (January - June 2006) pp 1-8

[4] Chaturvedi, K. and Chataway, J., (2006) , “ Innovation In

The Post-Trips Regime In Indian Pharmaceutical Firms:

Implications For Pharmaceutical Innovation Model”,

International Journal of Business Innovation and Research,

Volume 1, Number 1-2 , pp 27-50.

[5] Gupta, Desh Bandhu, (2007), “Exciting Opportunities for

the Indian Pharmaceutical Industry”, Indian Chemical Engineer,

Vol. 49 No. 2 April-June 2007, pp. 154-157

[6] Lanjouw, J.O., and Cockburn, I.M. (2001) “New pills for

poor people? Empirical evidence after GATT”, World

Development, 29(2) February, 265-289.

[7] Neeraj Dixit “A study of change in marketing strategies

of Indian Pharmaceutical Companies under the WTO regime”.

[8]http://www.freepatentsonline.com/article/International-

Journal-Business-Research/190616992.html.

[9] Demosthenes Lorandos, P.C, “Changes in India's Patent Law

and its Repercussions on the Global Drug Industry”

[10]

74

http://www.lorandoslaw.com/Publications/Changes

-in-Indias-atent-Law.shtml

[11] M. Qaiser, and P. Mohan Chandran, “What is Indian

Pharma's Next Move?”

http://www.ipfrontline.com/depts/article.aspx?id=6775&deptid=6

[12] Sahana Ghosh, “Outsourcing

Clinical Research”

[13]http://www.hindu.com/biz/

2004/01/19/stories/2004011900261500.htm

[16] Mishra P., and Chandra T. (2010) “Mergers, Acquisitions

and Firm’s Performance: Experience of Indian Pharmaceutical

Industry”, Eurasian Journal of Business and Economics 3(5),

111-126.

[17] Ravi Kiran and Mishra, Sunita (2010) “New IPR Regime and

Challenges of the Small Pharma Industry”, Interdisciplinary

journal of Contemporary Research in Business, Vol.1, No 10.

pp 42-60.

75

76