Multistep value-at-risk and expected shortfall forecasting using copula-GARCH models

23

Multistep value-at-risk and expected shortfall forecasting using copula-GARCH models Eugene Levin October 12, 2012 Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH models October 12, 2012 1 / 23

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Multistep value-at-risk and expected shortfall forecasting using copula-GARCH models

Multistep value-at-risk and expected shortfallforecasting using copula-GARCH models

Eugene Levin

October 12, 2012

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 1 / 23

Presentation Structure

1. Motivation

2. Models

3. Model evaluation

4. Data and results

5. Conclusion

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 2 / 23

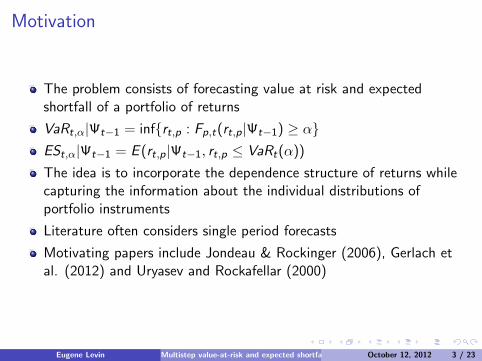

Motivation

The problem consists of forecasting value at risk and expectedshortfall of a portfolio of returns

VaRt,α|Ψt−1 = inf{rt,p : Fp,t(rt,p|Ψt−1) ≥ α}ESt,α|Ψt−1 = E (rt,p|Ψt−1, rt,p ≤ VaRt(α))

The idea is to incorporate the dependence structure of returns whilecapturing the information about the individual distributions ofportfolio instruments

Literature often considers single period forecasts

Motivating papers include Jondeau & Rockinger (2006), Gerlach etal. (2012) and Uryasev and Rockafellar (2000)

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 3 / 23

Motivation

Value at risk vs Expected shortfall

Figure : VaR vs ES

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 4 / 23

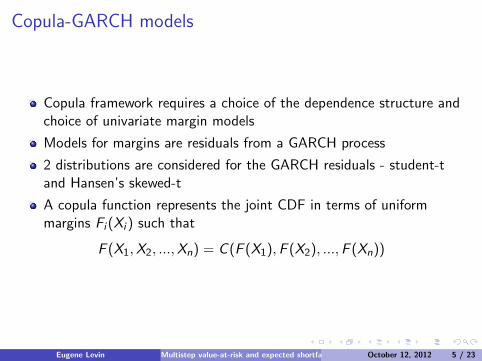

Copula-GARCH models

Copula framework requires a choice of the dependence structure andchoice of univariate margin models

Models for margins are residuals from a GARCH process

2 distributions are considered for the GARCH residuals - student-tand Hansen’s skewed-t

A copula function represents the joint CDF in terms of uniformmargins Fi (Xi ) such that

F (X1,X2, ...,Xn) = C (F (X1),F (X2), ...,F (Xn))

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 5 / 23

Copula-GARCH models

Two copula models are considered - Gaussian copula and t-copula

Why no asymmetric dependence?

Time-varying correlations are examined using the dynamic of aDCC(1, 1) model (Engle (2002))

Rt is the correlation matrix that is being forecasted

Rt−1 is estimated using IFM method - either from a Gaussian copulaor a t-copula

Qt = (1−M∑

m=1

αm −N∑

n=1

βn)Q̄ +M∑

m=1

αm(εt−mε′t−m) +

N∑n=1

βnQt−n

Rt = Q ∗−1t QtQ∗−1t

where Q∗t contains diagonal elements of Q where the typical element isqij = σij

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 6 / 23

Models summary

Table : Models’ summary

(G-t-c) Gaussian copula with student-t margins (constant)(G-sk-t-c) Gaussian copula with Hansen’ skewed-t margins (constant)(T-t-c) t-copula with student-t margins (constant)(T-sk-t-c) t-copula with Hansen’s skewed-t margins (constant)(G-t-DCC) Gaussian copula with student-t margins (DCC)(G-sk-t-DCC) Gaussian copula with Hansen’ skewed-t margins (DCC)(T-t-DCC) t-copula with student-t margins (DCC)(T-sk-t-DCC) t-copula with Hansen’s skewed-t margins (DCC)

Estimation of copula parameters is done using the IFM methodproposed by Joe & Xu (1996)

Estimation of DCC and GARCH parameters is done using QMLE

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 7 / 23

Model evaluation

Model evaluation is done in terms of how often the value at risk isgreater than the actual portfolio return or rp,t < VaRt,α - in this caseIt = 1, otherwise It = 0

Proportion of violations (vRate) should be close to α in a model thataccurately forecasts VaR

For each step ahead forecasts we get a vector I consisting of 0’s and1’s - now we can test for statistical validity of the unconditional andconditional coverage - Christoffersen (1998)

An alternative test is used as well - out-sample dynamic quantile testproposed by Engle and Manganelli (2004) - to test for no correlationin lagged values of I and the VaR forecasts themselves

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 8 / 23

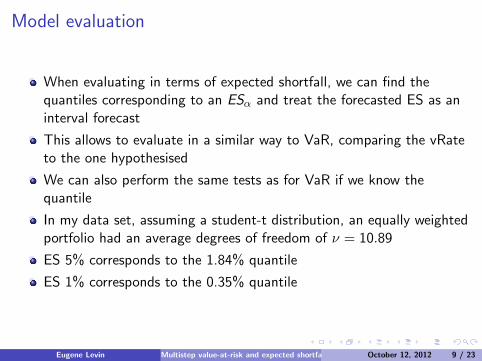

Model evaluation

When evaluating in terms of expected shortfall, we can find thequantiles corresponding to an ESα and treat the forecasted ES as aninterval forecast

This allows to evaluate in a similar way to VaR, comparing the vRateto the one hypothesised

We can also perform the same tests as for VaR if we know thequantile

In my data set, assuming a student-t distribution, an equally weightedportfolio had an average degrees of freedom of ν = 10.89

ES 5% corresponds to the 1.84% quantile

ES 1% corresponds to the 0.35% quantile

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 9 / 23

Data and results

Data consists of returns for international stock indices - ASX200,HSI, DAX, FTSE 100, NASDAQ, NEIKEI 225

The total data time frame used → from 17/10/2001 to 27/08/2012 -total of 2777 observations (adjusted for public holidays)

In sample estimation was done using a rolling window of 1765observations

Total out of sample forecasts = 1012

Why this data set? Potential problems?

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 10 / 23

Data and results

NASDAQ prices

0 500 1000 1500 2000 2500 3000800

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800NASDAQ in and out−of−sample periods

NASDAQ in−sample periodNASDAQ out−of−sample period

Figure : NASDAQ prices

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 11 / 23

Table : 1 step ahead vRate under equal weights

Equal weights, 5% VaR Equal weights 1% VaR

G-t-c 0.0731 0.0208G-sk-t-c 0.0692 0.0148

T-t-c 0.0652 0.0158T-sk-t-c 0.0692 0.0138

G-t-DCC 0.0731 0.0198G-sk-t-DCC 0.0692 0.0158

T-t-DCC 0.0741 0.0168T-sk-t-DCC 0.0648 0.0158

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 12 / 23

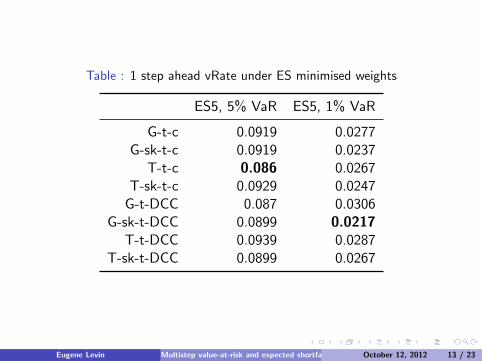

Table : 1 step ahead vRate under ES minimised weights

ES5, 5% VaR ES5, 1% VaR

G-t-c 0.0919 0.0277G-sk-t-c 0.0919 0.0237

T-t-c 0.086 0.0267T-sk-t-c 0.0929 0.0247

G-t-DCC 0.087 0.0306G-sk-t-DCC 0.0899 0.0217

T-t-DCC 0.0939 0.0287T-sk-t-DCC 0.0899 0.0267

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 13 / 23

Table : 1 step ahead vRate under MVP weights

MVP 5% VaR MVP, 1% VaR

G-t-c 0.087 0.0287G-sk-t-c 0.084 0.0237

T-t-c 0.0899 0.0287T-sk-t-c 0.087 0.0237

G-t-DCC 0.086 0.0277G-sk-t-DCC 0.0879 0.0237

T-t-DCC 0.0879 0.0267T-sk-t-DCC 0.0868 0.0237

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 14 / 23

Equal weights, 5% VaR vRate

1 2 3 4 5 6 7 8 9 100.04

0.05

0.06

0.07

0.08

0.09

0.1

0.11

0.12

Steps ahead forecast

vR

ate

5% vRate − Equal weights

G−t−cG−sk−t−cT−t−cT−sk−t−cG−t−DCCG−sk−t−DCCT−t−DCCT−sk−t−DCCExpected vRate

Figure : VaR vs ESEugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 15 / 23

Equal weights, 1% VaR vRate

1 2 3 4 5 6 7 8 9 100

0.01

0.02

0.03

0.04

0.05

0.06

Steps ahead forecast

vR

ate

1% vRate − Equal weights

G−t−c

G−sk−t−c

T−t−c

T−sk−t−c

G−t−DCC

G−sk−t−DCC

T−t−DCC

T−sk−t−DCC

Expected vRate

Figure : VaR vs ESEugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 16 / 23

ES minimised weights, 5% VaR vRate

1 2 3 4 5 6 7 8 9 100

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

Steps

vR

ate

5% vRate − ES minimised weights

G−t−c

G−sk−t−c

T−t−c

T−sk−t−c

G−t−DCC

G−sk−t−DCC

T−t−DCC

T−sk−t−DCC

Expected vRate

Figure : VaR vs ESEugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 17 / 23

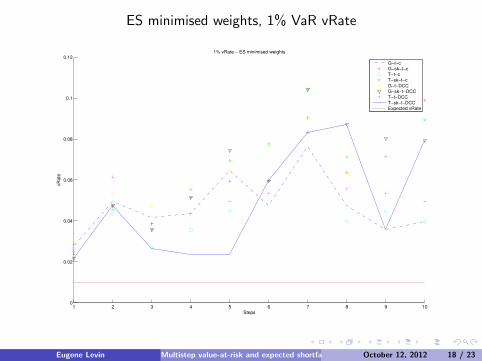

ES minimised weights, 1% VaR vRate

1 2 3 4 5 6 7 8 9 100

0.02

0.04

0.06

0.08

0.1

0.12

Steps

vR

ate

1% vRate − ES minimised weights

G−t−c

G−sk−t−c

T−t−c

T−sk−t−c

G−t−DCC

G−sk−t−DCC

T−t−DCC

T−sk−t−DCC

Expected vRate

Figure : VaR vs ESEugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 18 / 23

MVP weights, 5% VaR vRate

1 2 3 4 5 6 7 8 9 100.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

Steps

vR

ate

5% vRate − MVP minimised weights

G−t−c

G−sk−t−c

T−t−c

T−sk−t−c

G−t−DCC

G−sk−t−DCC

T−t−DCC

T−sk−t−DCC

Expected vRate

Figure : VaR vs ESEugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 19 / 23

Table : ES forecast evaluation

EQ weights 5% ES quantile level 1% ES quantile level

G-t-c 0.0326 0.0069G-sk-t-c 0.0237 0.003

T-t-c 0.0247 0.003T-sk-t-c 0.0217 0.001

G-t-DCC 0.0346 0.0079G-sk-t-DCC 0.0247 0.004

T-t-DCC 0.0336 0.0044T-sk-t-DCC 0.033 0.0043

Correct level 0.0184 0.0035

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 20 / 23

Table : ES evaluation - ES minimised weights

ES weights 5% ES quantile level 1% ES quantile level

G-t-c 0.0435 0.0158G-sk-t-c 0.0385 0.0089

T-t-c 0.0415 0.0119T-sk-t-c 0.0415 0.0089

G-t-DCC 0.0435 0.0168G-sk-t-DCC 0.0425 0.0109

T-t-DCC 0.0415 0.0099T-sk-t-DCC 0.0405 0.0089

Correct level 0.0184 0.0035

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 21 / 23

Table : MVP weights - ES forecast evaluation

MVP weights 5% ES quantile level 1% ES quantile level

G-t-c 0.0425 0.0158G-sk-t-c 0.0385 0.0099

T-t-c 0.0405 0.0109T-sk-t-c 0.0375 0.0079

G-t-DCC 0.0435 0.0188G-sk-t-DCC 0.0385 0.0109

T-t-DCC 0.0415 0.0099T-sk-t-DCC 0.0405 0.089

Correct level 0.0184 0.0035

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 22 / 23

Conclusion

In this presentation I did not include:

Risk-vs-return properties of the portfolio

Whether or not the ES forecasts correspond to the realised ES

How the models performed in the non-crisis period

Eugene Levin Multistep value-at-risk and expected shortfall forecasting using copula-GARCH modelsOctober 12, 2012 23 / 23