Mrs. Bectors Food Specialities

36

Please refer to important disclosures at the end of this report Market Cap Rs22bn/US$302mn Year to March FY20 FY21E FY22E FY23E Bloomberg BECTORS IN Net Revenue (Rs mn) 7,621 8,655 10,492 12,209 Shares Outstanding (mn) 58.7 Net Profit (Rs mn) 304 635 716 869 52-week Range (Rs) 594/288 Dil. EPS (Rs) 5.3 10.8 12.2 14.8 Free Float (%) 32.1 % Chg YoY (8.3) 103.9 12.7 21.4 FII (%) 16.9 P/E (x) 70.6 34.6 30.7 25.3 Daily Volume (US$'000) NA CEPS (Rs) 12.6 18.4 22.0 25.5 Absolute Return 3m (%) NA EV/EBITDA (x) 23.8 16.8 14.6 12.6 Absolute Return 12m (%) NA Dividend Yield (%) 0.2 0.3 0.4 0.5 Sensex Return 3m (%) 16.9 RoCE (%) 10.7 15.4 16.0 18.2 Sensex Return 12m (%) 15.0 RoE (%) 9.5 14.9 14.6 15.4 Equity Research January 31, 2021 BSE Sensex: 46286 ICICI Securities Limited is the author and distributor of this report Initiating coverage Consumer Staples & Discretionary Target price: Rs400 Shareholding pattern Dec ‘20 Promoters 51.1 Institutional investors 10.5 MFs and other 5.3 Banks/FIs 0.1 Insurance 1.7 FIIs 3.4 Others 38.4 Source: BSE Price chart 300 350 400 450 500 550 600 650 24-Dec 29-Dec 3-Jan 8-Jan 13-Jan 18-Jan 23-Jan 28-Jan (Rs) Mrs. Bectors Food Specialities ADD Multiple drivers of growth; initiate at ADD Rs375 Research Analysts: Manoj Menon [email protected] +91 22 6637 7209 Vismaya Agarwal, CFA [email protected] +91 22 2277 7632 Karan Bhuwania [email protected] +91 22 6637 7351 INDIA We believe the expansion of domestic biscuits and branded breads business into new regions driven by sales initiatives will be a key driver for growth. Further, focus on premiumisation within existing product segments with focus on increasing sales realisations, volume and provide differential offerings to customers will drive margin expansion. Strong relationships with institutional customers (QSRs, Mondelez, exports) augurs well for adopting innovations faster to drive penetration and customer acquisitions. We initiate coverage with an ADD rating and DCF-based target price of Rs400 (implied P/E of 27xFY23E). Sales driven initiatives to accelerate growth: We expect Mrs. Bectors growth to be driven by (1) Expansion of domestic biscuit business in NCR and Uttar Pradesh, (2) Distribution reach expansion in existing markets and (3) Expansion of branded bakery business into metros – Mumbai and Bengaluru. Focus on premiumisation to drive margin expansion in domestic branded business: We expect margin expansion to be driven by (1) expand product offering to niche biscuits and bakery products, (2) reducing the contribution of lower margin glucose biscuits, (3) targeting developed and emerging export markets and (4) premium products in bakery segment such as sub-breads, frozen doughs, pizzas, garlic breads, cheese garlic bun fills and frozen cookies. Growth in Chain Food Service market to drive growth in institutional bakery segment: The chain food service market in India is projected to grow at a CAGR of 19% to Rs966bn by FY25. We believe that strong relationships with these large QSR players will help the institutional bakery division to mirror the strong growth expected in the QSR industry in India. New product development and innovations to improve penetration and help recruit new customers: We believe that Mrs. Bectors Food is well positioned to capitalise its relationships with large institutions to accelerate new product launches and innovation. In biscuits, it can benefit from its relationship with Mondelez (the largest global biscuit manufacturer) and its experience in biscuits exports business. Similarly, in branded breads segment, the company is likely to benefit from its relationship with reputed QSRs. Valuations and risks: We model revenue / EBITDA / PAT CAGR of 17% / 24% / 42% over FY20-23E. Initiate at ADD with a DCF-based target price of Rs400. At our target price, the stock will trade at 27x P/E multiple March-23E. Key downside risks are delays or failures distribution expansion or steep rise in competitive intensity and raw material prices.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Mrs. Bectors Food Specialities

Please refer to important disclosures at the end of this report

Market Cap Rs22bn/US$302mn Year to March FY20 FY21E FY22E FY23E

Bloomberg BECTORS IN Net Revenue (Rs mn) 7,621 8,655 10,492 12,209

Shares Outstanding (mn) 58.7 Net Profit (Rs mn) 304 635 716 869

52-week Range (Rs) 594/288 Dil. EPS (Rs) 5.3 10.8 12.2 14.8

Free Float (%) 32.1 % Chg YoY (8.3) 103.9 12.7 21.4

FII (%) 16.9 P/E (x) 70.6 34.6 30.7 25.3

Daily Volume (US$'000) NA CEPS (Rs) 12.6 18.4 22.0 25.5

Absolute Return 3m (%) NA EV/EBITDA (x) 23.8 16.8 14.6 12.6

Absolute Return 12m (%) NA Dividend Yield (%) 0.2 0.3 0.4 0.5

Sensex Return 3m (%) 16.9 RoCE (%) 10.7 15.4 16.0 18.2

Sensex Return 12m (%) 15.0 RoE (%) 9.5 14.9 14.6 15.4

Equity Research January 31, 2021

BSE Sensex: 46286

ICICI Securities Limited is the author and distributor of this report

Initiating coverage

Consumer Staples & Discretionary

Target price: Rs400

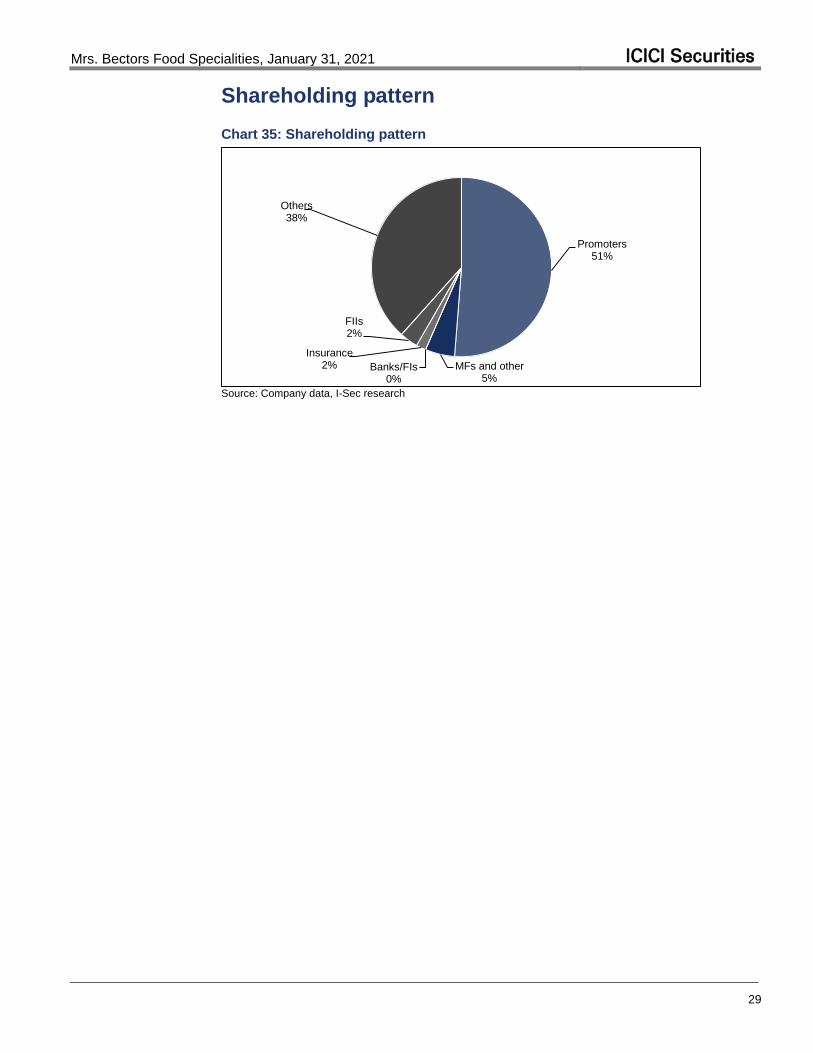

Shareholding pattern

Dec ‘20

Promoters 51.1 Institutional investors 10.5 MFs and other 5.3 Banks/FIs 0.1 Insurance 1.7 FIIs 3.4 Others 38.4

Source: BSE

Price chart

300

350

400

450

500

550

600

650

24

-Dec

29

-Dec

3-J

an

8-J

an

13

-Jan

18

-Jan

23

-Jan

28

-Jan

(Rs)

Mrs. Bectors Food Specialities ADD

Multiple drivers of growth; initiate at ADD Rs375

Research Analysts:

Manoj Menon [email protected]

+91 22 6637 7209

Vismaya Agarwal, CFA [email protected]

+91 22 2277 7632

Karan Bhuwania [email protected]

+91 22 6637 7351

INDIA

We believe the expansion of domestic biscuits and branded breads business into

new regions driven by sales initiatives will be a key driver for growth. Further,

focus on premiumisation within existing product segments with focus on

increasing sales realisations, volume and provide differential offerings to

customers will drive margin expansion. Strong relationships with institutional

customers (QSRs, Mondelez, exports) augurs well for adopting innovations faster

to drive penetration and customer acquisitions. We initiate coverage with an ADD

rating and DCF-based target price of Rs400 (implied P/E of 27xFY23E).

Sales driven initiatives to accelerate growth: We expect Mrs. Bectors growth to

be driven by (1) Expansion of domestic biscuit business in NCR and Uttar Pradesh,

(2) Distribution reach expansion in existing markets and (3) Expansion of branded

bakery business into metros – Mumbai and Bengaluru.

Focus on premiumisation to drive margin expansion in domestic branded

business: We expect margin expansion to be driven by (1) expand product offering

to niche biscuits and bakery products, (2) reducing the contribution of lower margin

glucose biscuits, (3) targeting developed and emerging export markets and (4)

premium products in bakery segment such as sub-breads, frozen doughs, pizzas,

garlic breads, cheese garlic bun fills and frozen cookies.

Growth in Chain Food Service market to drive growth in institutional bakery

segment: The chain food service market in India is projected to grow at a CAGR of

19% to Rs966bn by FY25. We believe that strong relationships with these large

QSR players will help the institutional bakery division to mirror the strong growth

expected in the QSR industry in India.

New product development and innovations to improve penetration and help

recruit new customers: We believe that Mrs. Bectors Food is well positioned to

capitalise its relationships with large institutions to accelerate new product launches

and innovation. In biscuits, it can benefit from its relationship with Mondelez (the

largest global biscuit manufacturer) and its experience in biscuits exports business.

Similarly, in branded breads segment, the company is likely to benefit from its

relationship with reputed QSRs.

Valuations and risks: We model revenue / EBITDA / PAT CAGR of 17% / 24% /

42% over FY20-23E. Initiate at ADD with a DCF-based target price of Rs400. At our

target price, the stock will trade at 27x P/E multiple March-23E. Key downside risks

are delays or failures distribution expansion or steep rise in competitive intensity and

raw material prices.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

2

TABLE OF CONTENT

Investment thesis ............................................................................................................. 3

#1 Sales driven initiatives to accelerate growth .............................................................. 3

#2 Focus on premiumisation to drive margin expansion in domestic branded business 7

#3 Growth in Chain Food Service market to drive growth in institutional bakery segment

........................................................................................................................................ 9

#4 New product development and innovations to improve penetration and help recruit

new customers .............................................................................................................. 10

Financial performance, assumptions, estimates........................................................ 11

Valuations and risks ...................................................................................................... 15

DCF assumptions .......................................................................................................... 15

Relative valuation .......................................................................................................... 17

Risks ................................................................................................................................ 18

Company description .................................................................................................... 19

Operations ..................................................................................................................... 19

Industry – Category Size ............................................................................................... 22

Domestic biscuits market .............................................................................................. 22

Global Biscuits Export Market ....................................................................................... 25

Indian Breads and Buns Retail Market ......................................................................... 25

Promoters and management profile ............................................................................ 27

Shareholding pattern ..................................................................................................... 29

Financials ........................................................................................................................ 30

Index of tables and charts ............................................................................................. 35

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

3

Investment thesis

#1 Sales driven initiatives to accelerate growth

Expansion of domestic biscuit business in NCR and Uttar Pradesh

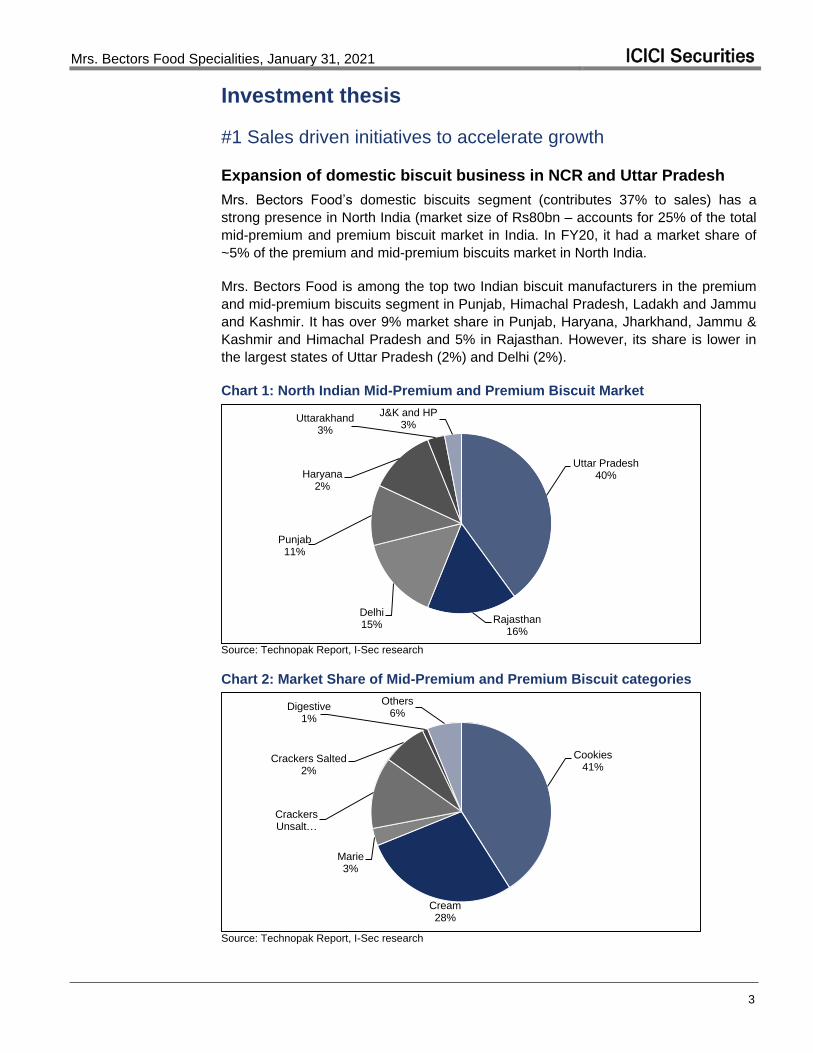

Mrs. Bectors Food’s domestic biscuits segment (contributes 37% to sales) has a

strong presence in North India (market size of Rs80bn – accounts for 25% of the total

mid-premium and premium biscuit market in India. In FY20, it had a market share of

~5% of the premium and mid-premium biscuits market in North India.

Mrs. Bectors Food is among the top two Indian biscuit manufacturers in the premium

and mid-premium biscuits segment in Punjab, Himachal Pradesh, Ladakh and Jammu

and Kashmir. It has over 9% market share in Punjab, Haryana, Jharkhand, Jammu &

Kashmir and Himachal Pradesh and 5% in Rajasthan. However, its share is lower in

the largest states of Uttar Pradesh (2%) and Delhi (2%).

Chart 1: North Indian Mid-Premium and Premium Biscuit Market

Uttar Pradesh40%

Rajasthan16%

Delhi15%

Punjab 11%

Haryana 2%

Uttarakhand3%

J&K and HP3%

Source: Technopak Report, I-Sec research

Chart 2: Market Share of Mid-Premium and Premium Biscuit categories

Cookies41%

Cream28%

Marie3%

Crackers Unsalt…

Crackers Salted2%

Digestive1%

Others6%

Source: Technopak Report, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

4

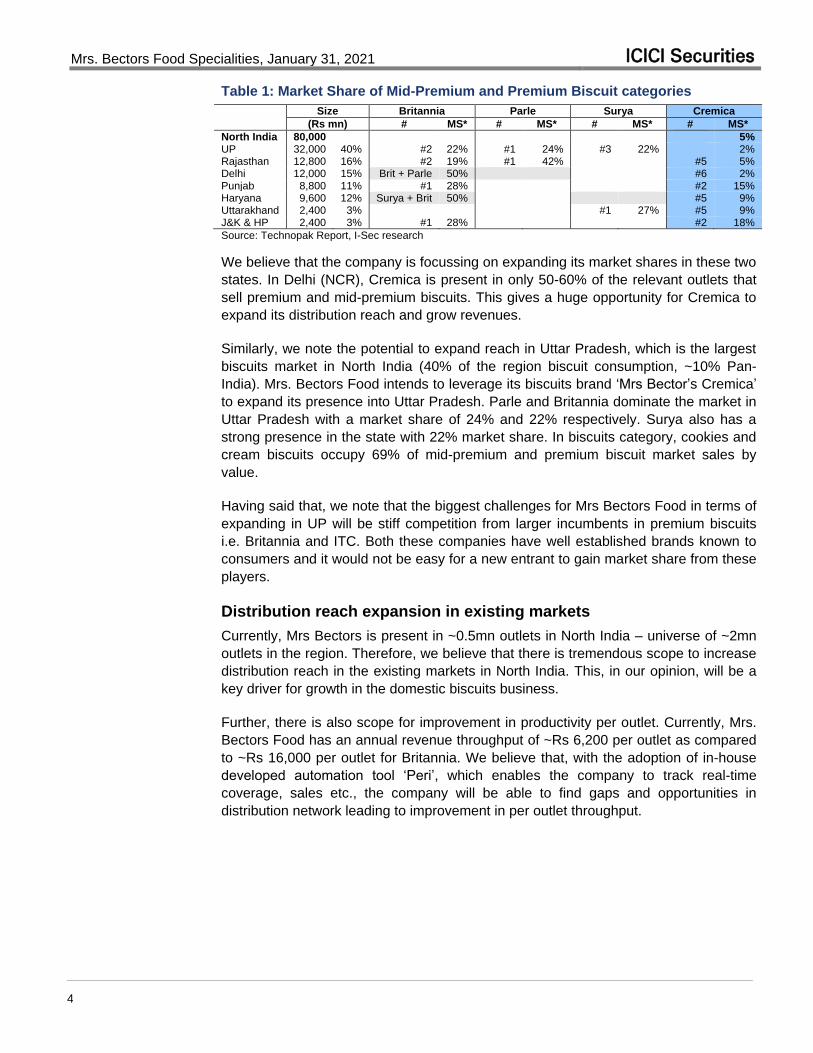

Table 1: Market Share of Mid-Premium and Premium Biscuit categories

Size Britannia Parle Surya Cremica

(Rs mn) # MS* # MS* # MS* # MS*

North India 80,000 5% UP 32,000 40% #2 22% #1 24% #3 22% 2% Rajasthan 12,800 16% #2 19% #1 42% #5 5% Delhi 12,000 15% Brit + Parle 50% #6 2% Punjab 8,800 11% #1 28% #2 15% Haryana 9,600 12% Surya + Brit 50% #5 9% Uttarakhand 2,400 3% #1 27% #5 9% J&K & HP 2,400 3% #1 28% #2 18%

Source: Technopak Report, I-Sec research

We believe that the company is focussing on expanding its market shares in these two

states. In Delhi (NCR), Cremica is present in only 50-60% of the relevant outlets that

sell premium and mid-premium biscuits. This gives a huge opportunity for Cremica to

expand its distribution reach and grow revenues.

Similarly, we note the potential to expand reach in Uttar Pradesh, which is the largest

biscuits market in North India (40% of the region biscuit consumption, ~10% Pan-

India). Mrs. Bectors Food intends to leverage its biscuits brand ‘Mrs Bector’s Cremica’

to expand its presence into Uttar Pradesh. Parle and Britannia dominate the market in

Uttar Pradesh with a market share of 24% and 22% respectively. Surya also has a

strong presence in the state with 22% market share. In biscuits category, cookies and

cream biscuits occupy 69% of mid-premium and premium biscuit market sales by

value.

Having said that, we note that the biggest challenges for Mrs Bectors Food in terms of

expanding in UP will be stiff competition from larger incumbents in premium biscuits

i.e. Britannia and ITC. Both these companies have well established brands known to

consumers and it would not be easy for a new entrant to gain market share from these

players.

Distribution reach expansion in existing markets

Currently, Mrs Bectors is present in ~0.5mn outlets in North India – universe of ~2mn

outlets in the region. Therefore, we believe that there is tremendous scope to increase

distribution reach in the existing markets in North India. This, in our opinion, will be a

key driver for growth in the domestic biscuits business.

Further, there is also scope for improvement in productivity per outlet. Currently, Mrs.

Bectors Food has an annual revenue throughput of ~Rs 6,200 per outlet as compared

to ~Rs 16,000 per outlet for Britannia. We believe that, with the adoption of in-house

developed automation tool ‘Peri’, which enables the company to track real-time

coverage, sales etc., the company will be able to find gaps and opportunities in

distribution network leading to improvement in per outlet throughput.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

5

Chart 3: Revenue and growth rates – Domestic Biscuits

(10)

(5)

-

5

10

15

20

25

30

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

(Rs m

n)

Value (Rs mn) - Domestic Growth YoY - RHS

Source: Company data, I-Sec research

Chart 4: Volume and growth rates – Domestic Biscuits

(10)

(5)

-

5

10

15

20

25

-

10,000

20,000

30,000

40,000

50,000

60,000

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

(MT

)

Volumes (MT) - Domestic Growth YoY - RHS

Source: Company data, I-Sec research

Expansion of branded bakery business into metros – Mumbai and

Bengaluru

Similar to the domestic biscuits business, Mrs. Bectors Food’s presence in branded

breads business is largely in North India and within that primarily in NCR. Mrs Bectors

Food sells it branded breads under the brand ‘English Oven’. It is currently one of the

fastest growing largescale bakery brands in India and is one of the largest selling

brands in the premium bakery segment in Delhi / NCR.

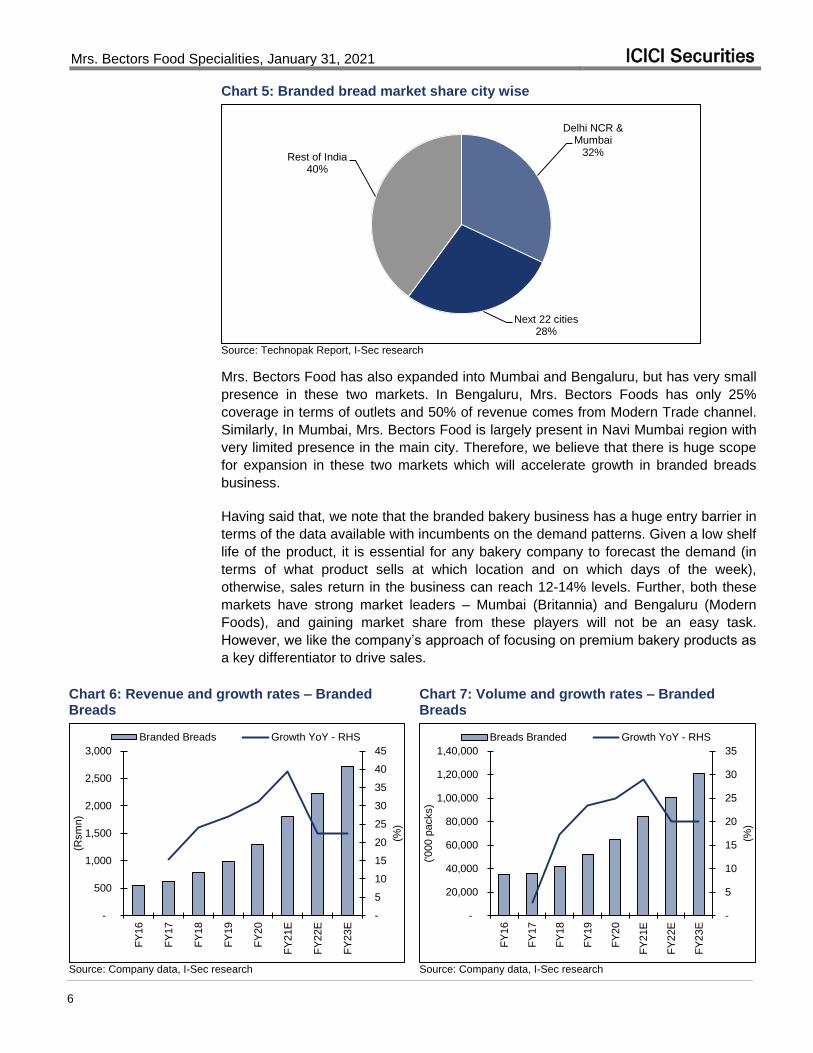

The demand for breads in India is concentrated mainly around metros, tier I and larger

tier II cities due to higher disposable incomes and changing meal preferences. Delhi

NCR and Mumbai amount for about 32% of overall branded breads market.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

6

Chart 5: Branded bread market share city wise

Delhi NCR & Mumbai

32%

Next 22 cities 28%

Rest of India 40%

Source: Technopak Report, I-Sec research

Mrs. Bectors Food has also expanded into Mumbai and Bengaluru, but has very small

presence in these two markets. In Bengaluru, Mrs. Bectors Foods has only 25%

coverage in terms of outlets and 50% of revenue comes from Modern Trade channel.

Similarly, In Mumbai, Mrs. Bectors Food is largely present in Navi Mumbai region with

very limited presence in the main city. Therefore, we believe that there is huge scope

for expansion in these two markets which will accelerate growth in branded breads

business.

Having said that, we note that the branded bakery business has a huge entry barrier in

terms of the data available with incumbents on the demand patterns. Given a low shelf

life of the product, it is essential for any bakery company to forecast the demand (in

terms of what product sells at which location and on which days of the week),

otherwise, sales return in the business can reach 12-14% levels. Further, both these

markets have strong market leaders – Mumbai (Britannia) and Bengaluru (Modern

Foods), and gaining market share from these players will not be an easy task.

However, we like the company’s approach of focusing on premium bakery products as

a key differentiator to drive sales.

Chart 6: Revenue and growth rates – Branded Breads

Chart 7: Volume and growth rates – Branded Breads

-

5

10

15

20

25

30

35

40

45

-

500

1,000

1,500

2,000

2,500

3,000

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

(Rsm

n)

Branded Breads Growth YoY - RHS

-

5

10

15

20

25

30

35

-

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

('000 p

acks)

Breads Branded Growth YoY - RHS

Source: Company data, I-Sec research Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

7

#2 Focus on premiumisation to drive margin expansion in domestic branded business

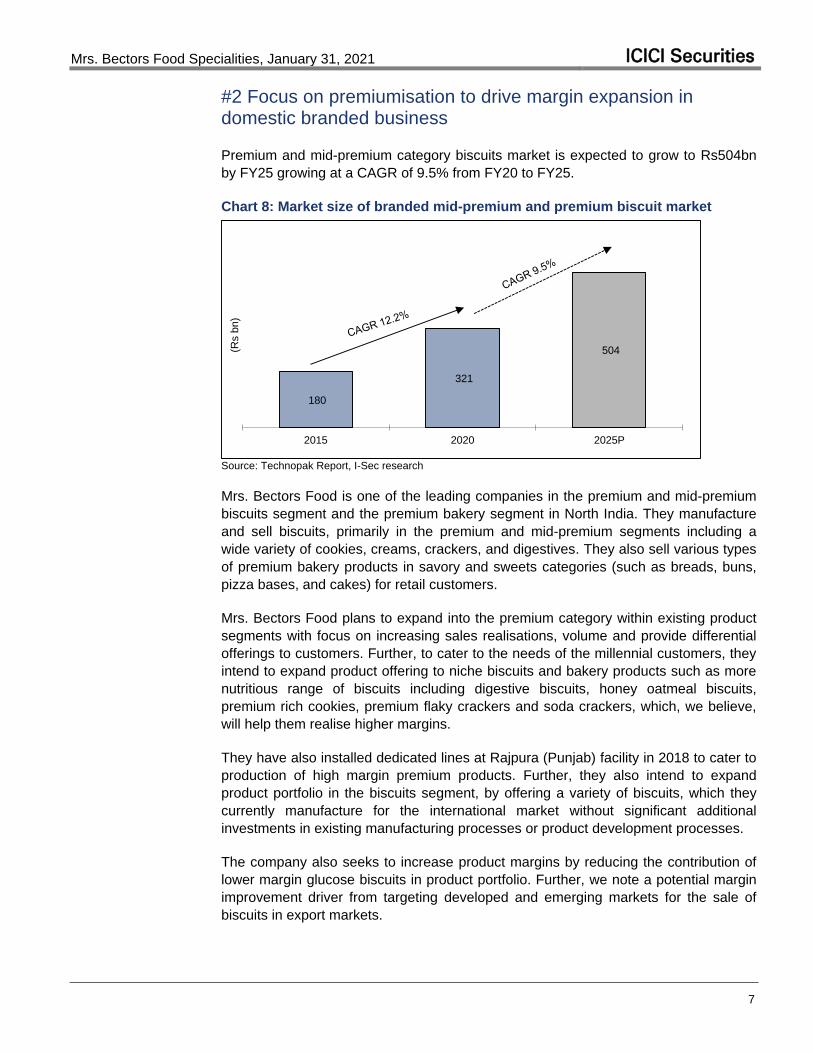

Premium and mid-premium category biscuits market is expected to grow to Rs504bn

by FY25 growing at a CAGR of 9.5% from FY20 to FY25.

Chart 8: Market size of branded mid-premium and premium biscuit market

180

321

504

2015 2020 2025P

(Rs b

n)

Source: Technopak Report, I-Sec research Mrs. Bectors Food is one of the leading companies in the premium and mid-premium

biscuits segment and the premium bakery segment in North India. They manufacture

and sell biscuits, primarily in the premium and mid-premium segments including a

wide variety of cookies, creams, crackers, and digestives. They also sell various types

of premium bakery products in savory and sweets categories (such as breads, buns,

pizza bases, and cakes) for retail customers.

Mrs. Bectors Food plans to expand into the premium category within existing product

segments with focus on increasing sales realisations, volume and provide differential

offerings to customers. Further, to cater to the needs of the millennial customers, they

intend to expand product offering to niche biscuits and bakery products such as more

nutritious range of biscuits including digestive biscuits, honey oatmeal biscuits,

premium rich cookies, premium flaky crackers and soda crackers, which, we believe,

will help them realise higher margins.

They have also installed dedicated lines at Rajpura (Punjab) facility in 2018 to cater to

production of high margin premium products. Further, they also intend to expand

product portfolio in the biscuits segment, by offering a variety of biscuits, which they

currently manufacture for the international market without significant additional

investments in existing manufacturing processes or product development processes.

The company also seeks to increase product margins by reducing the contribution of

lower margin glucose biscuits in product portfolio. Further, we note a potential margin

improvement driver from targeting developed and emerging markets for the sale of

biscuits in export markets.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

8

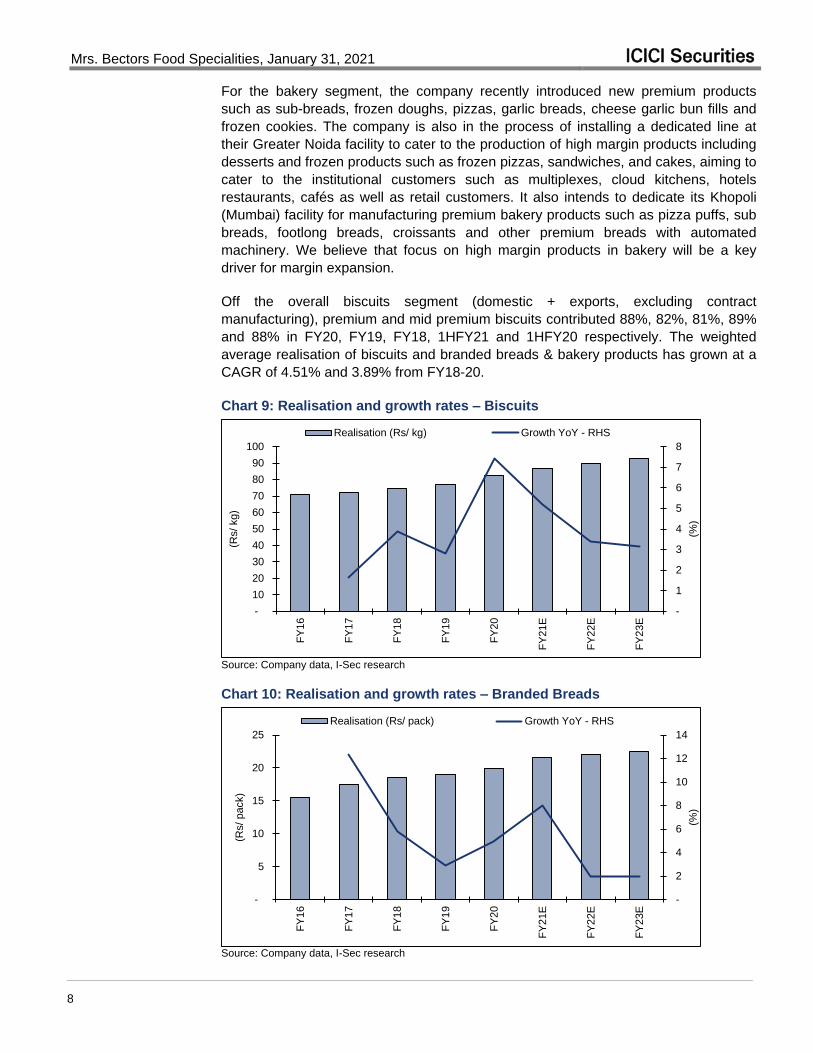

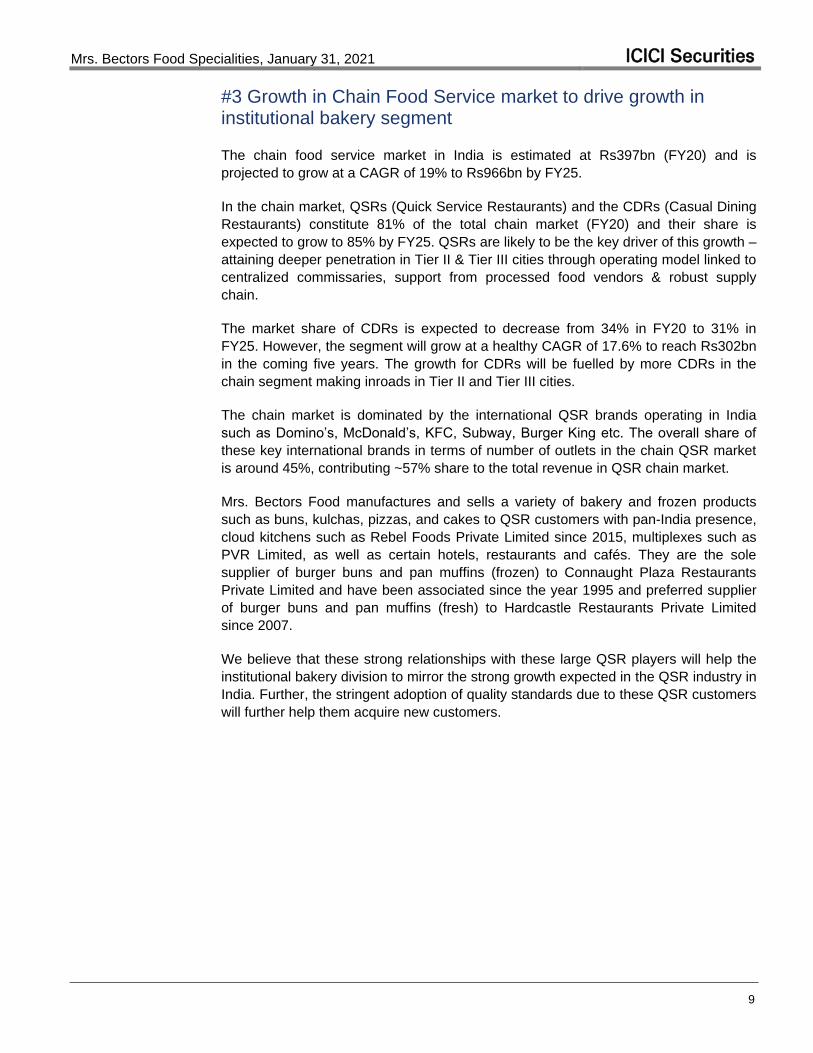

For the bakery segment, the company recently introduced new premium products

such as sub-breads, frozen doughs, pizzas, garlic breads, cheese garlic bun fills and

frozen cookies. The company is also in the process of installing a dedicated line at

their Greater Noida facility to cater to the production of high margin products including

desserts and frozen products such as frozen pizzas, sandwiches, and cakes, aiming to

cater to the institutional customers such as multiplexes, cloud kitchens, hotels

restaurants, cafés as well as retail customers. It also intends to dedicate its Khopoli

(Mumbai) facility for manufacturing premium bakery products such as pizza puffs, sub

breads, footlong breads, croissants and other premium breads with automated

machinery. We believe that focus on high margin products in bakery will be a key

driver for margin expansion.

Off the overall biscuits segment (domestic + exports, excluding contract

manufacturing), premium and mid premium biscuits contributed 88%, 82%, 81%, 89%

and 88% in FY20, FY19, FY18, 1HFY21 and 1HFY20 respectively. The weighted

average realisation of biscuits and branded breads & bakery products has grown at a

CAGR of 4.51% and 3.89% from FY18-20.

Chart 9: Realisation and growth rates – Biscuits

-

1

2

3

4

5

6

7

8

-

10

20

30

40

50

60

70

80

90

100

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

(Rs/ kg)

Realisation (Rs/ kg) Growth YoY - RHS

Source: Company data, I-Sec research

Chart 10: Realisation and growth rates – Branded Breads

-

2

4

6

8

10

12

14

-

5

10

15

20

25

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

(Rs/ pack)

Realisation (Rs/ pack) Growth YoY - RHS

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

9

#3 Growth in Chain Food Service market to drive growth in institutional bakery segment

The chain food service market in India is estimated at Rs397bn (FY20) and is

projected to grow at a CAGR of 19% to Rs966bn by FY25.

In the chain market, QSRs (Quick Service Restaurants) and the CDRs (Casual Dining

Restaurants) constitute 81% of the total chain market (FY20) and their share is

expected to grow to 85% by FY25. QSRs are likely to be the key driver of this growth –

attaining deeper penetration in Tier II & Tier III cities through operating model linked to

centralized commissaries, support from processed food vendors & robust supply

chain.

The market share of CDRs is expected to decrease from 34% in FY20 to 31% in

FY25. However, the segment will grow at a healthy CAGR of 17.6% to reach Rs302bn

in the coming five years. The growth for CDRs will be fuelled by more CDRs in the

chain segment making inroads in Tier II and Tier III cities.

The chain market is dominated by the international QSR brands operating in India

such as Domino’s, McDonald’s, KFC, Subway, Burger King etc. The overall share of

these key international brands in terms of number of outlets in the chain QSR market

is around 45%, contributing ~57% share to the total revenue in QSR chain market.

Mrs. Bectors Food manufactures and sells a variety of bakery and frozen products

such as buns, kulchas, pizzas, and cakes to QSR customers with pan-India presence,

cloud kitchens such as Rebel Foods Private Limited since 2015, multiplexes such as

PVR Limited, as well as certain hotels, restaurants and cafés. They are the sole

supplier of burger buns and pan muffins (frozen) to Connaught Plaza Restaurants

Private Limited and have been associated since the year 1995 and preferred supplier

of burger buns and pan muffins (fresh) to Hardcastle Restaurants Private Limited

since 2007.

We believe that these strong relationships with these large QSR players will help the

institutional bakery division to mirror the strong growth expected in the QSR industry in

India. Further, the stringent adoption of quality standards due to these QSR customers

will further help them acquire new customers.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

10

#4 New product development and innovations to improve penetration and help recruit new customers

We like Mrs. Bectors Food’s focus on new product development as a key growth driver

across its portfolio.

In the recent past, within biscuits segments, the company has launched new products

such as ‘Trufills’, ‘Premium Sugar and Classic Crackers’, ‘Pista Almond Cookies’,

‘Choco Chip Cookies’, ‘Honey Oatmeal Cookies’. In bakery, it introduced new

premium products such as sub breads, frozen doughs, pizzas, garlic breads, cheese

garlic bun fills and frozen cookies.

We believe that Mrs Bectors Food is well positioned to capitalise its relationships with

large institutions to accelerate new product launches and innovation. In biscuits, it can

benefit from its relationship with Mondelez (the largest global biscuit manufacturer –

Mrs. Bectors Food does contract manufacturing for Oreos and Chocobakes for

Mondelez) and its experience in biscuits exports business. Similarly, in branded

breads segment, the company is likely to benefit from its relationship with reputed

QSRs and introduce products which are supplied to them to retail consumers. For

example, they have recently introduced ‘sub breads’ branded as ‘English Oven Sub’,

which helps customers create varied ranges of ‘DIY sandwiches’ at home.

Further, the company tends to benefit by working closely with these institutions, as

they are able to incorporate stringent quality standards and industry best practices

required by these customers in overall manufacturing process, thereby further

improving operational standards and quality of products.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

11

Financial performance, assumptions, estimates

Estimate 17% & 24% revenue & EBITDA CAGR over FY20-23E

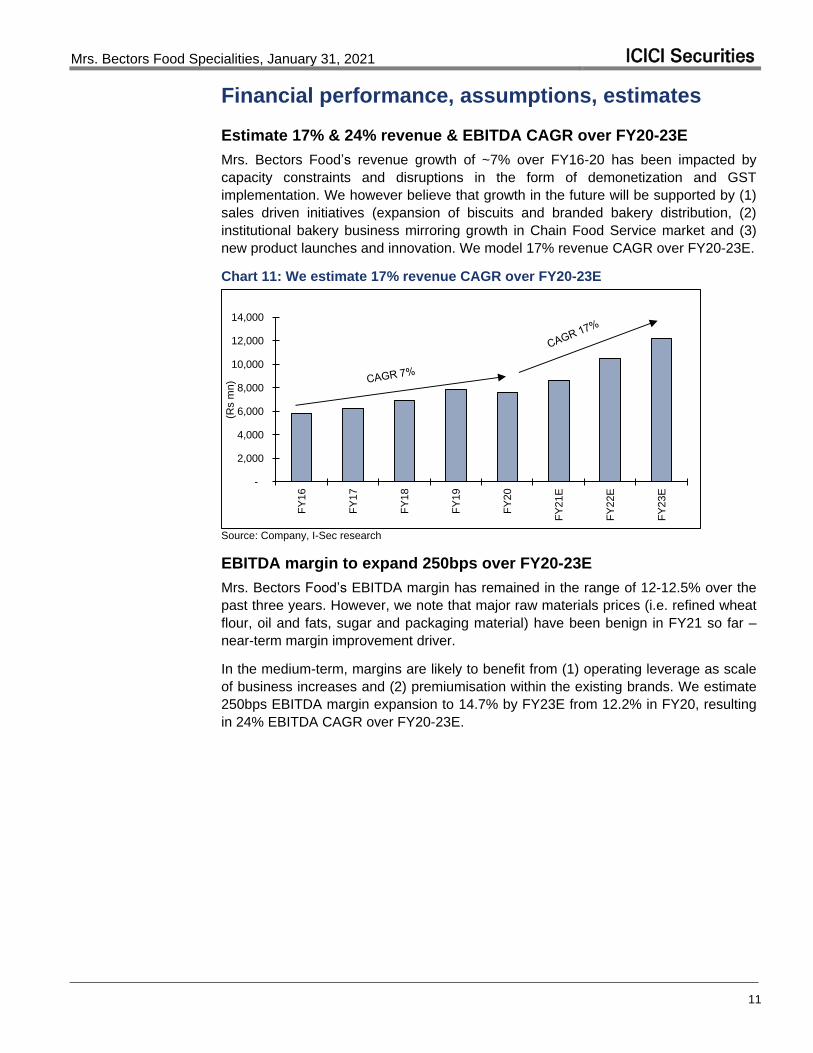

Mrs. Bectors Food’s revenue growth of ~7% over FY16-20 has been impacted by

capacity constraints and disruptions in the form of demonetization and GST

implementation. We however believe that growth in the future will be supported by (1)

sales driven initiatives (expansion of biscuits and branded bakery distribution, (2)

institutional bakery business mirroring growth in Chain Food Service market and (3)

new product launches and innovation. We model 17% revenue CAGR over FY20-23E.

Chart 11: We estimate 17% revenue CAGR over FY20-23E

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(Rs m

n)

Source: Company, I-Sec research

EBITDA margin to expand 250bps over FY20-23E

Mrs. Bectors Food’s EBITDA margin has remained in the range of 12-12.5% over the

past three years. However, we note that major raw materials prices (i.e. refined wheat

flour, oil and fats, sugar and packaging material) have been benign in FY21 so far –

near-term margin improvement driver.

In the medium-term, margins are likely to benefit from (1) operating leverage as scale

of business increases and (2) premiumisation within the existing brands. We estimate

250bps EBITDA margin expansion to 14.7% by FY23E from 12.2% in FY20, resulting

in 24% EBITDA CAGR over FY20-23E.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

12

Chart 12: EBITDA margin to expand 250bps over FY20-23E

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

(70bps)

Source: Company, I-Sec research

Chart 13: Gross margin Chart 14: Staff costs (as a % of sales)

39

40

41

42

43

44

45

46

47

48

49

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.5

16.0

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

Source: Company, I-Sec research

Source: Company, I-Sec research

Chart 15: Other opex (as a % of sales)

-

5.0

10.0

15.0

20.0

25.0

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

13

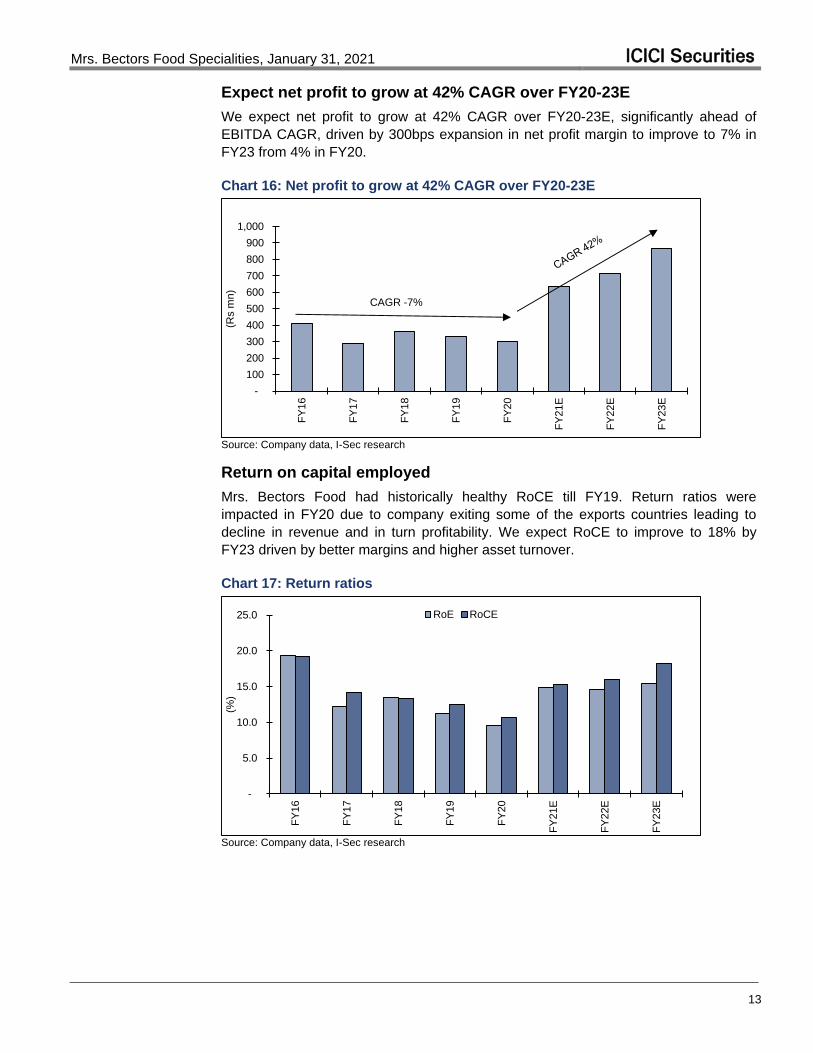

Expect net profit to grow at 42% CAGR over FY20-23E

We expect net profit to grow at 42% CAGR over FY20-23E, significantly ahead of

EBITDA CAGR, driven by 300bps expansion in net profit margin to improve to 7% in

FY23 from 4% in FY20.

Chart 16: Net profit to grow at 42% CAGR over FY20-23E

-

100

200

300

400

500

600

700

800

900

1,000

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(Rs m

n)

CAGR -7%

Source: Company data, I-Sec research

Return on capital employed

Mrs. Bectors Food had historically healthy RoCE till FY19. Return ratios were

impacted in FY20 due to company exiting some of the exports countries leading to

decline in revenue and in turn profitability. We expect RoCE to improve to 18% by

FY23 driven by better margins and higher asset turnover.

Chart 17: Return ratios

-

5.0

10.0

15.0

20.0

25.0

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

RoE RoCE

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

14

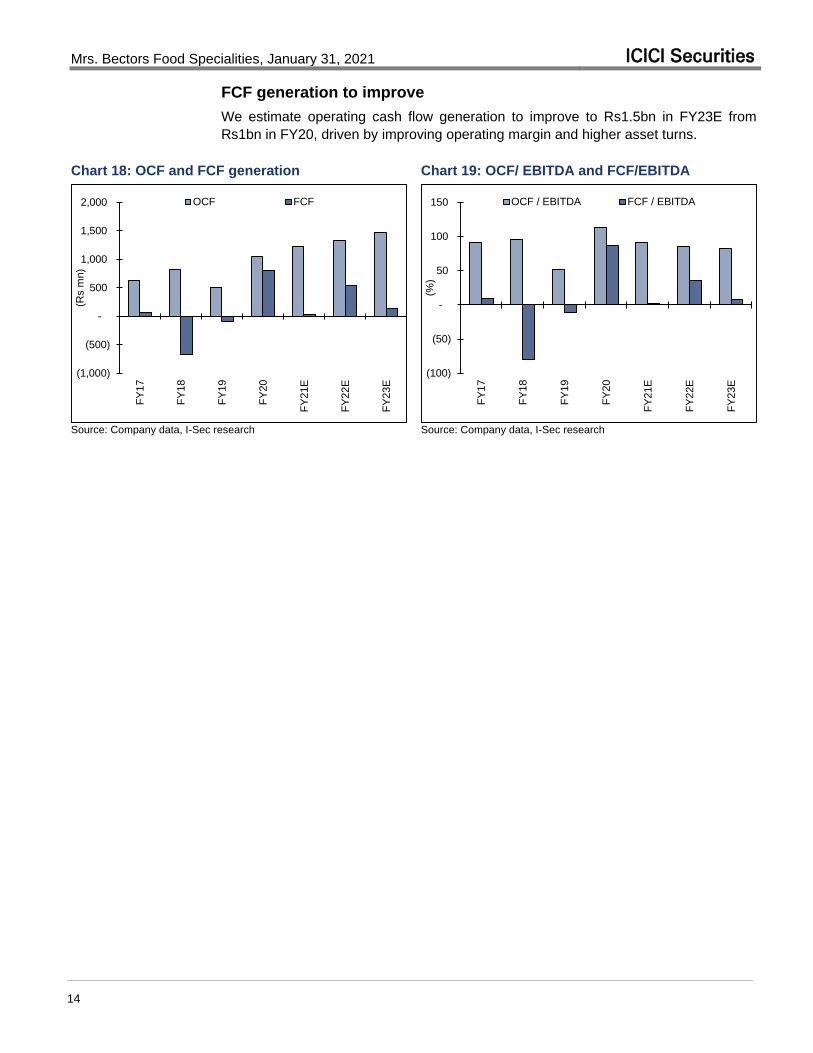

FCF generation to improve

We estimate operating cash flow generation to improve to Rs1.5bn in FY23E from

Rs1bn in FY20, driven by improving operating margin and higher asset turns.

Chart 18: OCF and FCF generation Chart 19: OCF/ EBITDA and FCF/EBITDA

(1,000)

(500)

-

500

1,000

1,500

2,000

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(Rs m

n)

OCF FCF

(100)

(50)

-

50

100

150

FY

17

FY

18

FY

19

FY

20

FY

21E

FY

22E

FY

23E

(%)

OCF / EBITDA FCF / EBITDA

Source: Company data, I-Sec research Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

15

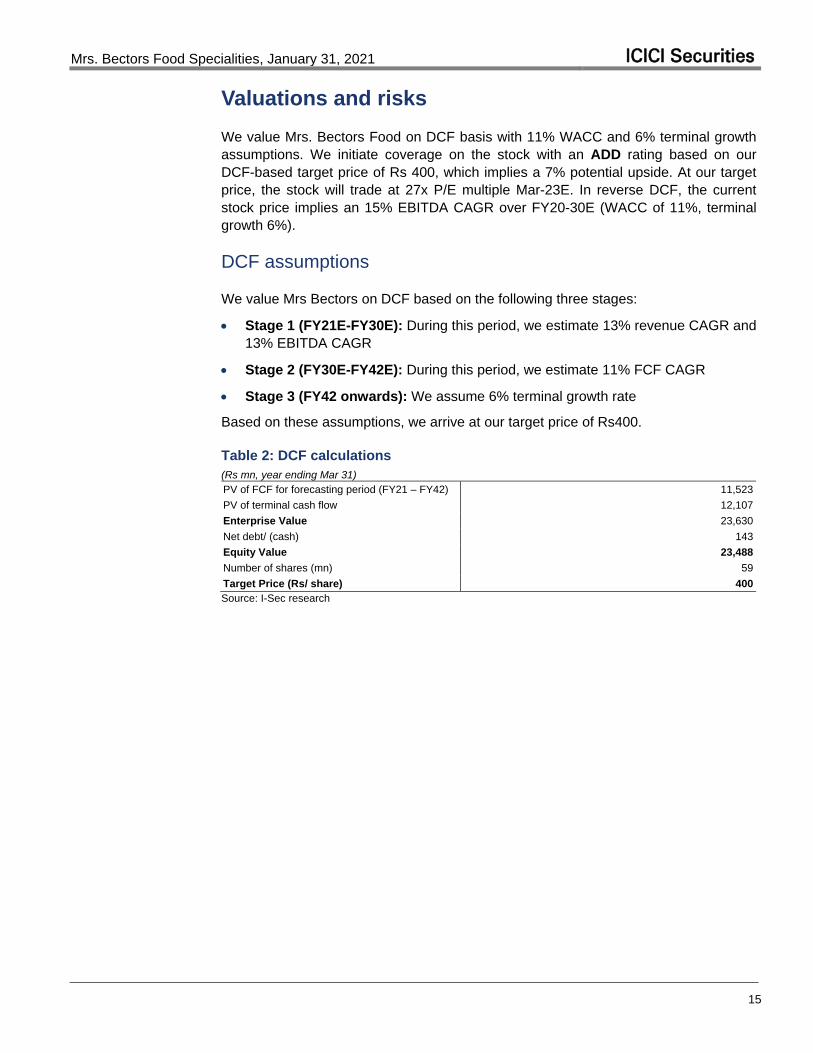

Valuations and risks

We value Mrs. Bectors Food on DCF basis with 11% WACC and 6% terminal growth

assumptions. We initiate coverage on the stock with an ADD rating based on our

DCF-based target price of Rs 400, which implies a 7% potential upside. At our target

price, the stock will trade at 27x P/E multiple Mar-23E. In reverse DCF, the current

stock price implies an 15% EBITDA CAGR over FY20-30E (WACC of 11%, terminal

growth 6%).

DCF assumptions

We value Mrs Bectors on DCF based on the following three stages:

Stage 1 (FY21E-FY30E): During this period, we estimate 13% revenue CAGR and

13% EBITDA CAGR

Stage 2 (FY30E-FY42E): During this period, we estimate 11% FCF CAGR

Stage 3 (FY42 onwards): We assume 6% terminal growth rate

Based on these assumptions, we arrive at our target price of Rs400.

Table 2: DCF calculations

(Rs mn, year ending Mar 31)

PV of FCF for forecasting period (FY21 – FY42) 11,523

PV of terminal cash flow 12,107

Enterprise Value 23,630

Net debt/ (cash) 143

Equity Value 23,488

Number of shares (mn) 59

Target Price (Rs/ share) 400

Source: I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

16

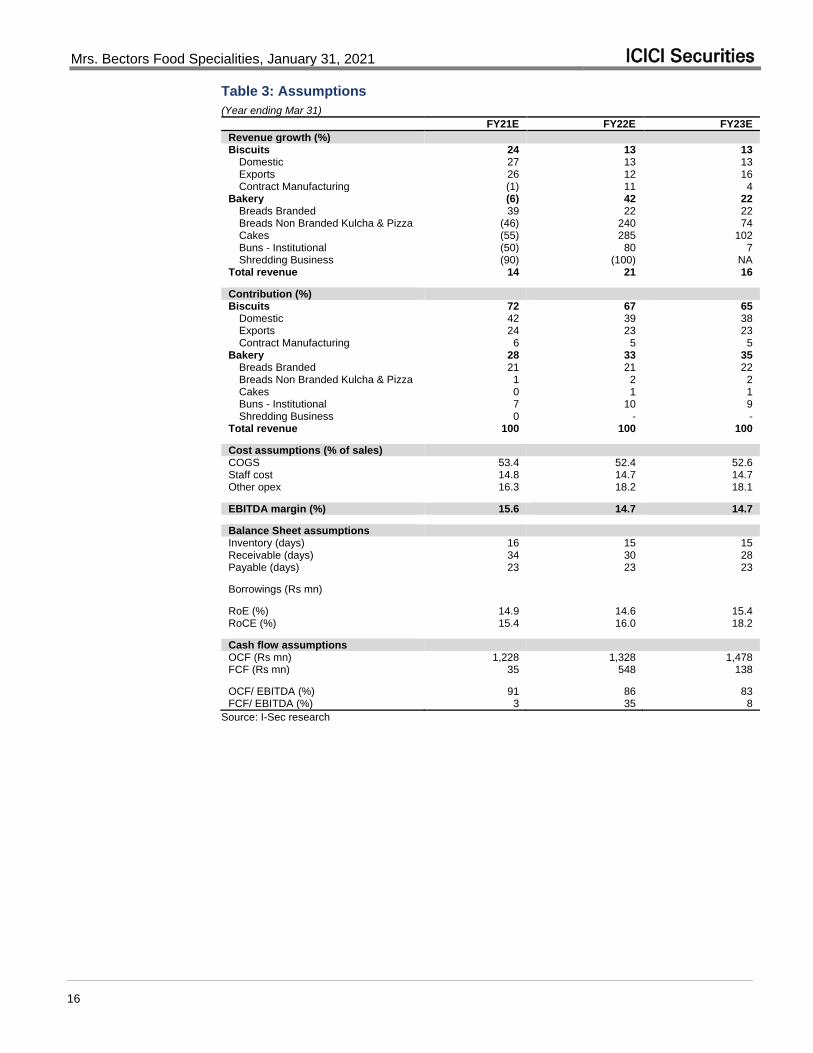

Table 3: Assumptions

(Year ending Mar 31)

FY21E FY22E FY23E

Revenue growth (%) Biscuits 24 13 13

Domestic 27 13 13 Exports 26 12 16 Contract Manufacturing (1) 11 4

Bakery (6) 42 22 Breads Branded 39 22 22 Breads Non Branded Kulcha & Pizza (46) 240 74 Cakes (55) 285 102 Buns - Institutional (50) 80 7 Shredding Business (90) (100) NA

Total revenue 14 21 16

Contribution (%) Biscuits 72 67 65

Domestic 42 39 38 Exports 24 23 23 Contract Manufacturing 6 5 5

Bakery 28 33 35 Breads Branded 21 21 22 Breads Non Branded Kulcha & Pizza 1 2 2 Cakes 0 1 1 Buns - Institutional 7 10 9 Shredding Business 0 - -

Total revenue 100 100 100

Cost assumptions (% of sales) COGS 53.4 52.4 52.6

Staff cost 14.8 14.7 14.7 Other opex 16.3 18.2 18.1

EBITDA margin (%) 15.6 14.7 14.7

Balance Sheet assumptions Inventory (days) 16 15 15

Receivable (days) 34 30 28 Payable (days) 23 23 23

Borrowings (Rs mn)

RoE (%) 14.9 14.6 15.4 RoCE (%) 15.4 16.0 18.2

Cash flow assumptions OCF (Rs mn) 1,228 1,328 1,478

FCF (Rs mn) 35 548 138

OCF/ EBITDA (%) 91 86 83 FCF/ EBITDA (%) 3 35 8

Source: I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

17

Relative valuation

Table 4: Valuation summary

Company CMP

(Rs) TP

(Rs) Upside

(%) Rating

PE (x) EV/EBITDA (x) ADTV Market Cap

FY22E FY23E FY22E FY23E (US$ mn) (Rs bn) (US$ bn)

Staples

Bajaj Consumer 209 250 19 ADD 14 14 12 11 1.6 33 0.4 Britannia 3,501 3,200 (9) REDUCE 44 39 33 29 41.2 870 11.8 Colgate 1,603 1,700 6 ADD 43 38 28 25 17.1 415 5.6 Dabur 515 580 13 ADD 49 42 42 36 28.5 941 12.8 Emami 483 540 12 ADD 29 25 25 23 4.9 216 2.9 GCPL 745 850 14 ADD 39 33 29 25 17.4 797 10.8 HUL 2,264 2,600 15 ADD 59 51 41 35 71.6 5,638 76.4 ITC 203 240 18 ADD 17 16 13 12 93.2 2,557 34.7 Jyothy Labs 162 190 17 BUY 23 19 17 15 1.4 58 0.8 Marico 416 470 13 ADD 41 36 29 25 16.5 530 7.2 Mrs. Bectors Food 375 400 7 ADD 31 25 15 13 34.0 23 0.3 Nestle 17,060 17,500 3 HOLD 63 52 42 35 38.5 1,679 22.8 Tata Consumer 560 720 29 BUY 45 37 28 24 33.4 529 7.2 Varun Beverages 899 1,015 13 ADD 39 30 17 15 4.6 258 3.5 Zydus Wellness 1,933 2,500 29 BUY 34 27 28 24 1.4 124 1.7 Discretionary Avenue Supermarts 2,652 2,600 (2) REDUCE 74 58 52 41 24.6 1,838 24.9 Bata 1,501 1,400 (7) REDUCE 50 43 22 19 17.2 200 2.7 Jubilant Foodworks 2,590 3,000 16 ADD 59 51 26 24 39.8 359 4.9 Page Industries 27,176 31,000 14 ADD 61 49 40 34 19.0 327 4.4 Sheela Foam 1,954 2,300 18 BUY 32 25 21 18 0.7 98 1.3 Titan 1,420 1,600 13 ADD 56 45 35 28 51.6 1,332 18.1 United Spirits 579 700 21 ADD 41 34 26 22 19.7 461 6.3 Westlife Development 465 500 8 ADD 64 52 23 19 1.9 71 1.0 Paints Akzo Nobel 2,228 3,000 35 BUY 37 32 24 20 0.6 109 1.5 Asian Paints 2,407 2,950 23 ADD 61 53 40 35 83.7 2,411 32.7 Berger Paints 707 770 9 HOLD 97 84 61 53 11.5 727 9.9 Kansai Nerolac 549 650 18 HOLD 48 42 30 26 2.6 330 4.5

Source: Bloomberg, I-Sec research

EV/ sales (x) P/B (x) P/CEPS (x) RoE (%) RoCE (%) CAGR (FY20-22E) (%)

Company FY22E FY23E FY22E FY23E FY22E FY23E FY22E FY23E FY22E FY23E Revenues EBITDA PAT

Staples Bajaj Consumer 3.2 3.0 3 3 14 14 24 21 25 24 4 7 8 Britannia 6.2 5.5 16 13 40 35 36 32 25 24 9 17 16 Colgate 8.4 7.6 22 20 36 32 57 61 68 72 7 12 14 Dabur 8.6 7.6 11 9 43 37 23 24 18 19 11 13 10 Emami 7.2 6.6 10 8 28 23 36 36 35 34 8 13 21 GCPL 6.8 6.1 8 7 35 30 22 23 18 19 8 12 12 HUL 10.3 9.1 12 11 52 45 20 23 19 21 15 16 14 ITC 4.7 4.3 4 4 15 14 25 26 27 27 5 3 (1) Jyothy Labs 2.9 2.6 4 4 19 16 19 20 18 19 11 18 21 Marico 6.1 5.4 15 13 37 32 37 39 33 36 9 11 11 Mrs. Bectors Food 2.2 1.9 4 4 17 15 15 15 16 18 17 29 53 Nestle 10.4 8.9 64 47 54 45 120 104 46 44 12 17 15 Tata Consumer 4.0 3.6 3 3 36 31 8 9 9 10 14 19 29 Varun Beverages 3.3 2.9 6 5 21 18 16 18 16 19 12 8 19 Zydus Wellness 5.7 5.2 3 2 31 26 8 9 8 9 6 12 40 Discretionary

Avenue Supermarts 4.7 3.8 12 10 63 50 17 18 22 23 22 26 31 Bata 5.9 5.2 9 8 28 24 19 19 26 26 2 1 9 Jubilant Foodworks 7.1 6.2 19 15 35 31 37 33 28 27 10 21 39 Page Industries 8.6 7.4 26 21 53 43 47 47 38 38 10 19 20 Sheela Foam 3.0 2.7 7 5 25 20 24 24 23 24 18 21 20 Titan 4.2 3.4 14 12 47 38 29 29 33 35 19 20 23 United Spirits 4.5 4.0 8 7 33 27 21 22 23 24 2 3 14 Westlife Development 4.2 3.6 12 10 28 24 20 21 26 33 6 21 221 Paints

Akzo Nobel 3.4 3.0 7 6 28 24 19 19 19 19 2 3 6 Asian Paints 9.0 7.9 17 14 49 43 30 29 27 26 12 18 18 Berger Paints 10.2 9.0 20 18 74 64 22 23 19 19 4 4 4 Kansai Nerolac 4.9 4.4 7 6 37 33 15 15 14 14 6 10 10

Source: Bloomberg, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

18

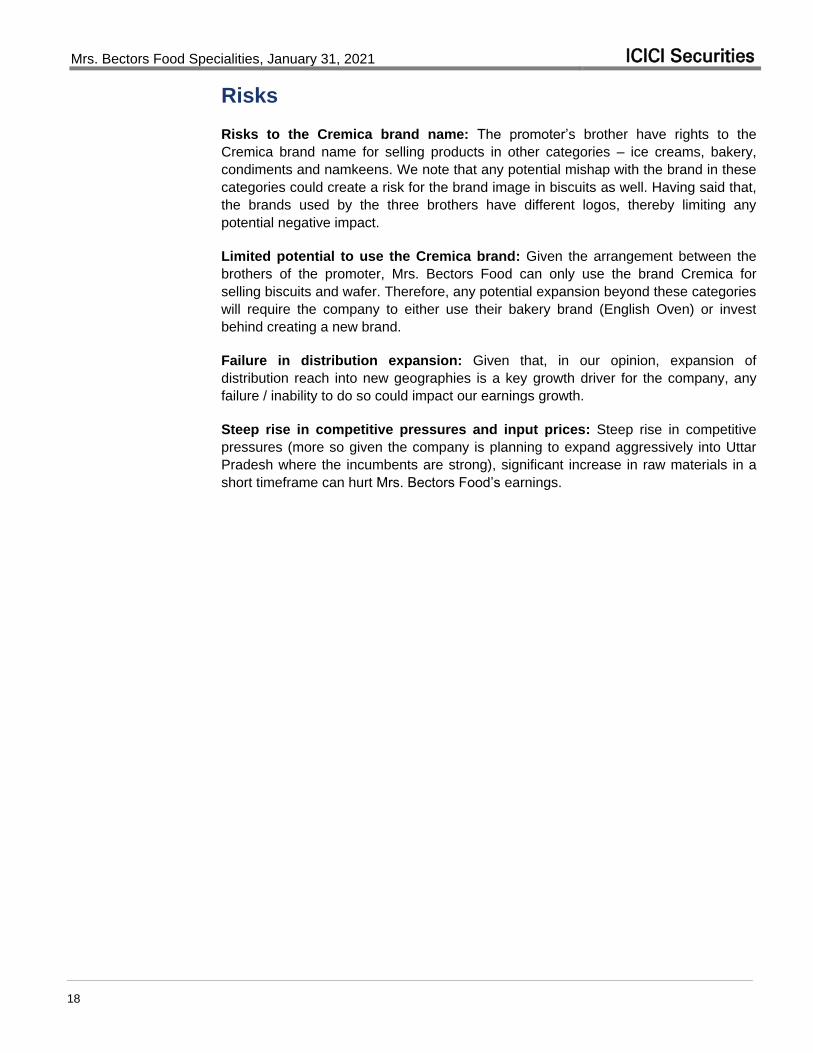

Risks

Risks to the Cremica brand name: The promoter’s brother have rights to the

Cremica brand name for selling products in other categories – ice creams, bakery,

condiments and namkeens. We note that any potential mishap with the brand in these

categories could create a risk for the brand image in biscuits as well. Having said that,

the brands used by the three brothers have different logos, thereby limiting any

potential negative impact.

Limited potential to use the Cremica brand: Given the arrangement between the

brothers of the promoter, Mrs. Bectors Food can only use the brand Cremica for

selling biscuits and wafer. Therefore, any potential expansion beyond these categories

will require the company to either use their bakery brand (English Oven) or invest

behind creating a new brand.

Failure in distribution expansion: Given that, in our opinion, expansion of

distribution reach into new geographies is a key growth driver for the company, any

failure / inability to do so could impact our earnings growth.

Steep rise in competitive pressures and input prices: Steep rise in competitive

pressures (more so given the company is planning to expand aggressively into Uttar

Pradesh where the incumbents are strong), significant increase in raw materials in a

short timeframe can hurt Mrs. Bectors Food’s earnings.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

19

Company description

Operations

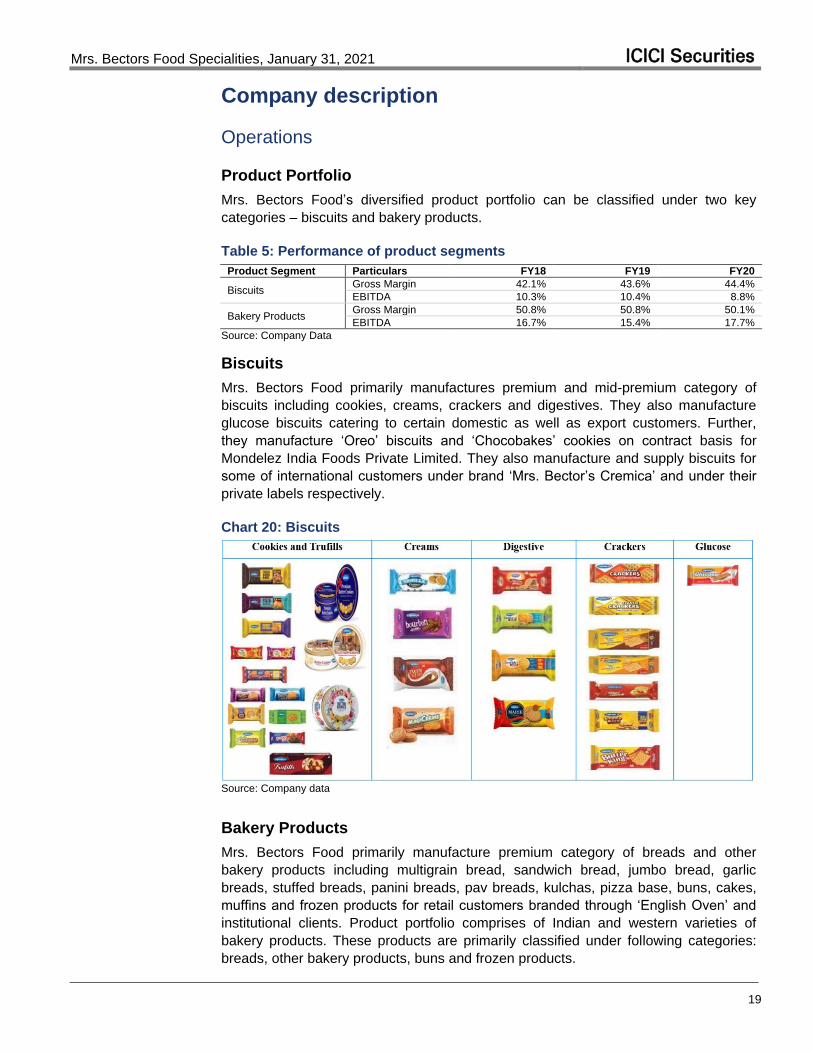

Product Portfolio

Mrs. Bectors Food’s diversified product portfolio can be classified under two key

categories – biscuits and bakery products.

Table 5: Performance of product segments

Product Segment Particulars FY18 FY19 FY20

Biscuits Gross Margin 42.1% 43.6% 44.4%

EBITDA 10.3% 10.4% 8.8%

Bakery Products Gross Margin 50.8% 50.8% 50.1%

EBITDA 16.7% 15.4% 17.7%

Source: Company Data

Biscuits

Mrs. Bectors Food primarily manufactures premium and mid-premium category of

biscuits including cookies, creams, crackers and digestives. They also manufacture

glucose biscuits catering to certain domestic as well as export customers. Further,

they manufacture ‘Oreo’ biscuits and ‘Chocobakes’ cookies on contract basis for

Mondelez India Foods Private Limited. They also manufacture and supply biscuits for

some of international customers under brand ‘Mrs. Bector’s Cremica’ and under their

private labels respectively.

Chart 20: Biscuits

Source: Company data

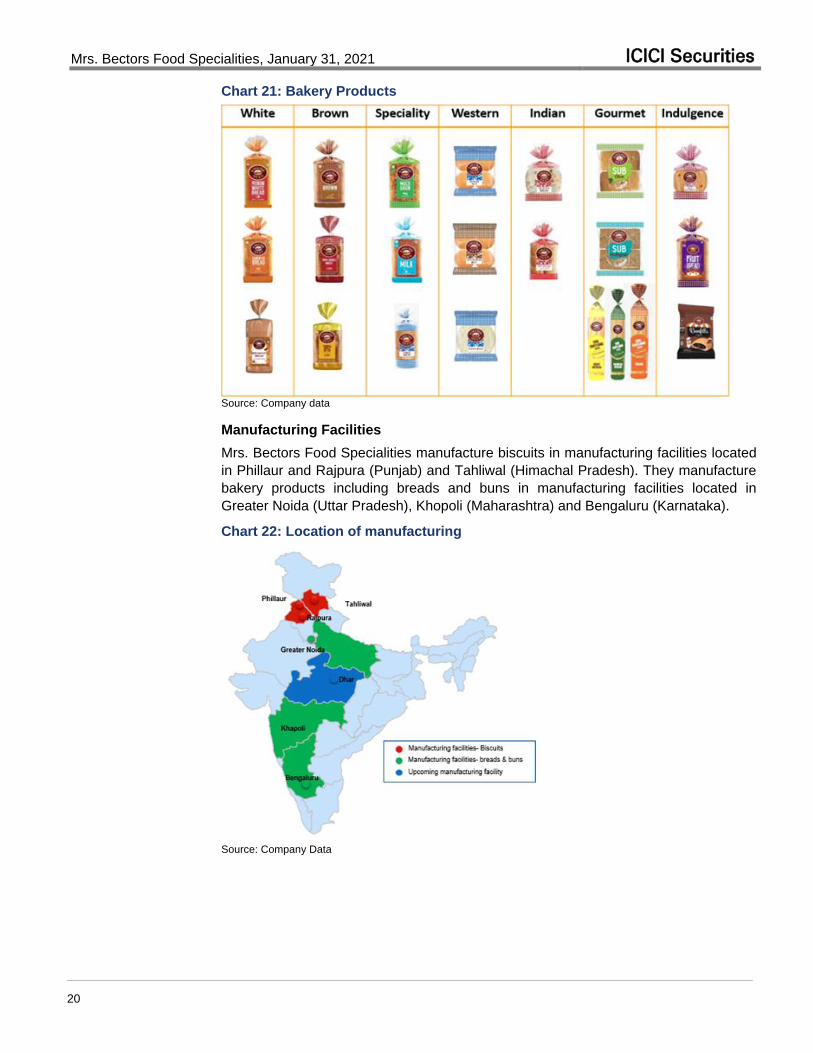

Bakery Products

Mrs. Bectors Food primarily manufacture premium category of breads and other

bakery products including multigrain bread, sandwich bread, jumbo bread, garlic

breads, stuffed breads, panini breads, pav breads, kulchas, pizza base, buns, cakes,

muffins and frozen products for retail customers branded through ‘English Oven’ and

institutional clients. Product portfolio comprises of Indian and western varieties of

bakery products. These products are primarily classified under following categories:

breads, other bakery products, buns and frozen products.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

20

Chart 21: Bakery Products

Source: Company data

Manufacturing Facilities

Mrs. Bectors Food Specialities manufacture biscuits in manufacturing facilities located

in Phillaur and Rajpura (Punjab) and Tahliwal (Himachal Pradesh). They manufacture

bakery products including breads and buns in manufacturing facilities located in

Greater Noida (Uttar Pradesh), Khopoli (Maharashtra) and Bengaluru (Karnataka).

Chart 22: Location of manufacturing

Source: Company Data

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

21

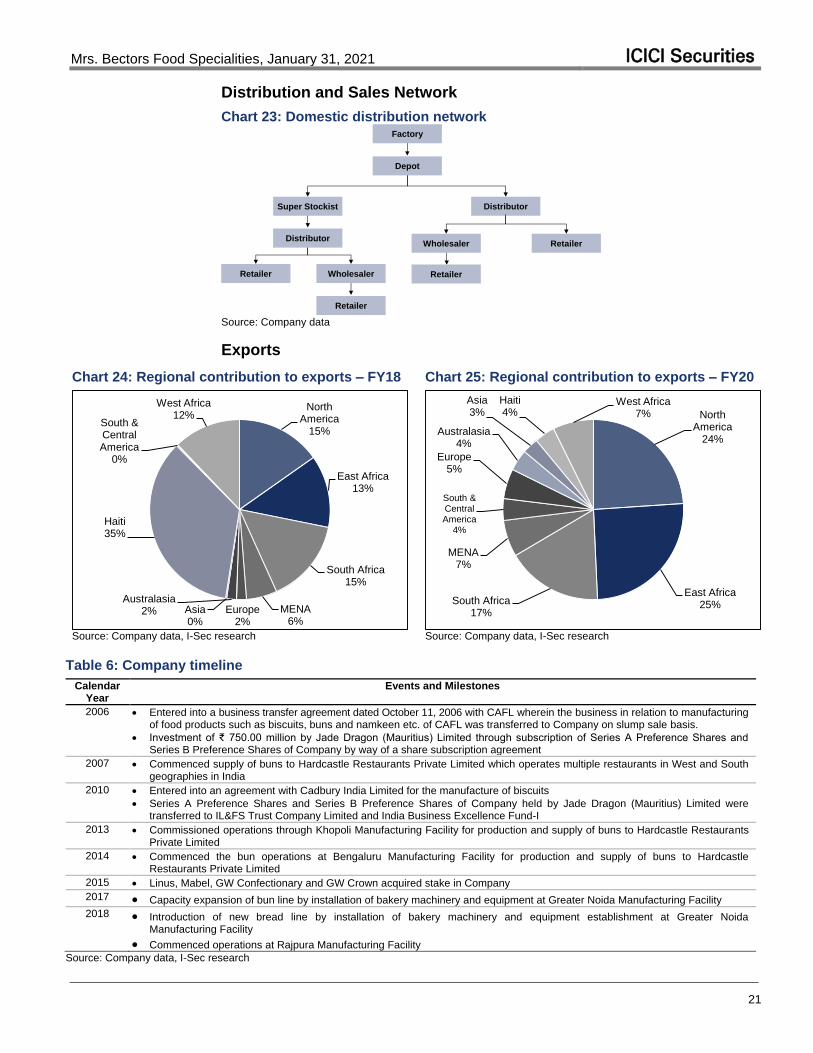

Distribution and Sales Network

Chart 23: Domestic distribution network Factory

Depot

Super Stockist Distributor

Retailer Wholesaler

Retailer

Wholesaler Retailer

Retailer

Distributor

Source: Company data

Exports

Chart 24: Regional contribution to exports – FY18 Chart 25: Regional contribution to exports – FY20

North America

15%

East Africa13%

South Africa15%

MENA6%

Europe2%

Australasia2% Asia

0%

Haiti35%

South & Central America

0%

West Africa12%

North America

24%

East Africa25%South Africa

17%

MENA7%

South & Central America

4%

Europe5%

Australasia4%

Asia3%

Haiti4%

West Africa7%

Source: Company data, I-Sec research

Source: Company data, I-Sec research

Table 6: Company timeline

Calendar Year

Events and Milestones

2006 Entered into a business transfer agreement dated October 11, 2006 with CAFL wherein the business in relation to manufacturing of food products such as biscuits, buns and namkeen etc. of CAFL was transferred to Company on slump sale basis.

Investment of ₹ 750.00 million by Jade Dragon (Mauritius) Limited through subscription of Series A Preference Shares and Series B Preference Shares of Company by way of a share subscription agreement

2007 Commenced supply of buns to Hardcastle Restaurants Private Limited which operates multiple restaurants in West and South geographies in India

2010 Entered into an agreement with Cadbury India Limited for the manufacture of biscuits

Series A Preference Shares and Series B Preference Shares of Company held by Jade Dragon (Mauritius) Limited were transferred to IL&FS Trust Company Limited and India Business Excellence Fund-I

2013 Commissioned operations through Khopoli Manufacturing Facility for production and supply of buns to Hardcastle Restaurants Private Limited

2014 Commenced the bun operations at Bengaluru Manufacturing Facility for production and supply of buns to Hardcastle Restaurants Private Limited

2015 Linus, Mabel, GW Confectionary and GW Crown acquired stake in Company

2017 Capacity expansion of bun line by installation of bakery machinery and equipment at Greater Noida Manufacturing Facility

2018 Introduction of new bread line by installation of bakery machinery and equipment establishment at Greater Noida Manufacturing Facility

Commenced operations at Rajpura Manufacturing Facility

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

22

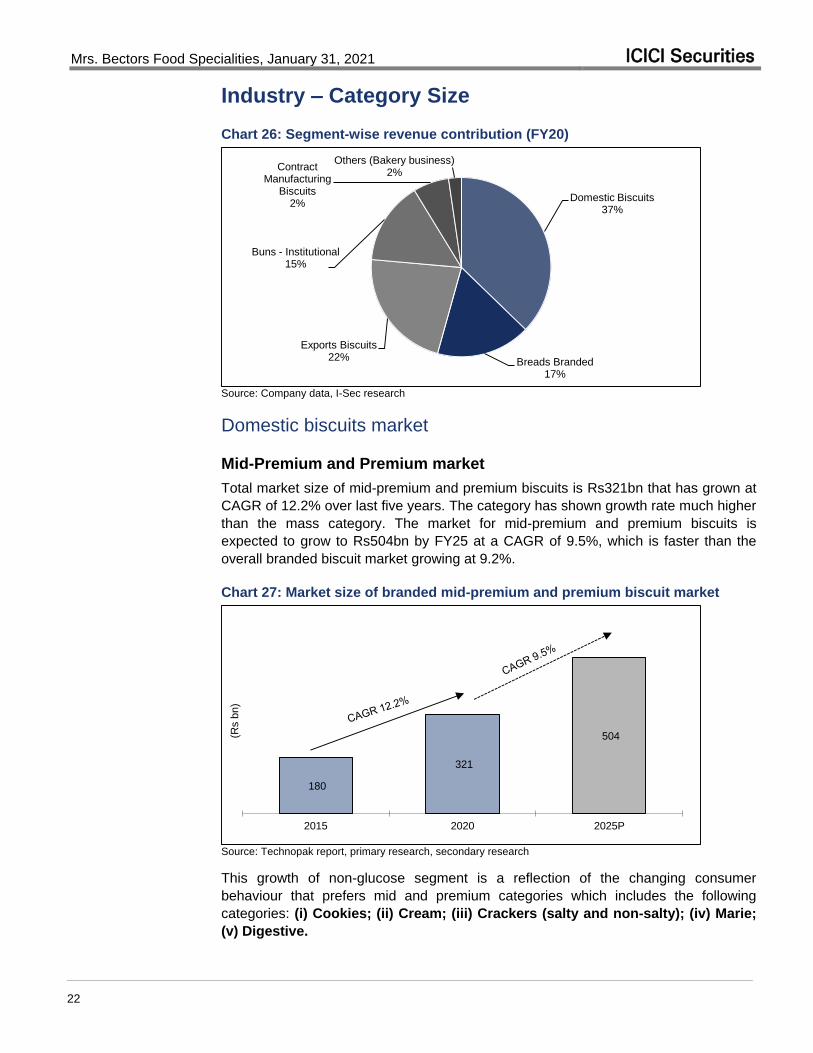

Industry – Category Size

Chart 26: Segment-wise revenue contribution (FY20)

Domestic Biscuits37%

Breads Branded17%

Exports Biscuits22%

Buns - Institutional15%

Contract Manufacturing

Biscuits2%

Others (Bakery business)2%

Source: Company data, I-Sec research

Domestic biscuits market

Mid-Premium and Premium market

Total market size of mid-premium and premium biscuits is Rs321bn that has grown at

CAGR of 12.2% over last five years. The category has shown growth rate much higher

than the mass category. The market for mid-premium and premium biscuits is

expected to grow to Rs504bn by FY25 at a CAGR of 9.5%, which is faster than the

overall branded biscuit market growing at 9.2%.

Chart 27: Market size of branded mid-premium and premium biscuit market

180

321

504

2015 2020 2025P

(Rs b

n)

Source: Technopak report, primary research, secondary research

This growth of non-glucose segment is a reflection of the changing consumer

behaviour that prefers mid and premium categories which includes the following

categories: (i) Cookies; (ii) Cream; (iii) Crackers (salty and non-salty); (iv) Marie;

(v) Digestive.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

23

Cookies: Cookies are the largest category of biscuits occupying 29% of the market

share by value. The category is estimated to be Rs106bn in FY20. It is dominated by

national players such as Britannia, Parle and ITC. The segment offers high

contribution margin of upwards of 10% to brands. Good Day (Britannia) brand is the

market leader with more than one third of the market by value. Britannia and Parle

account for more than one third of the market by value. Regional brands like Surya,

Anmol, and Unibic have combined market share of close to 10% by value. Cremica

has a market share of 2% by value. Cremica has a large portfolio of cookies that

includes Golden Bytes, Choco Bico and many other variants.

Cream: Cream is the second largest category of biscuits occupying 19% of market

share by value. The category is estimated to be Rs72bn in FY20. It is dominated by

national players such as Britannia, Parle and ITC which accounts for a combined

~65% of the total value of the cream biscuits market. Players like Surya, Cremica and

Anmol have combined market share of ~10% by value. Britannia’s Bourbon is the

most popular brand in this segment. Cremica’s portfolio in cream biscuits includes

Cremica Crèmes, Bourbon, Magicrème and TwinCrème.

Marie: The category is estimated to be Rs45bn in FY20. It is dominated by Britannia

with 60% market share by value owing to its Marie Gold range of biscuits. Parle and

ITC have a combined market share of 16% by value.

Cracker (Salty): The category is estimated to be Rs22bn in FY20. Parle leads the

market with a value share of 28% due to its famous brand Krackjack. Players like

Anmol and Surya have a significant market share in this category, close to 18% each.

Cremica’s portfolio in this category includes Butter King and Jeera Lite.

Cracker (Non-Salty): The category is estimated to be Rs44bn in FY20. National

players dominate the market. Parle and Britannia have a combined market share of

close to 52% by value. Parle-Monaco is the most notable brand in this sub-segment.

Cremica’s portfolio in this category includes Crisp ‘n’ Lite, Party Crackers, Sugar

Crackers and Classic crackers.

Digestive: The category is estimated to be Rs6.5bn in FY20. Britannia dominates the

market with a market share of close to 72% by value. Britannia offers the biscuit by

name Nutri Choice, the most famous brand in the category. Cremica’s portfolio in this

category includes Cremica Digestive, Cornflakes and Oatmeal Digestive.

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

24

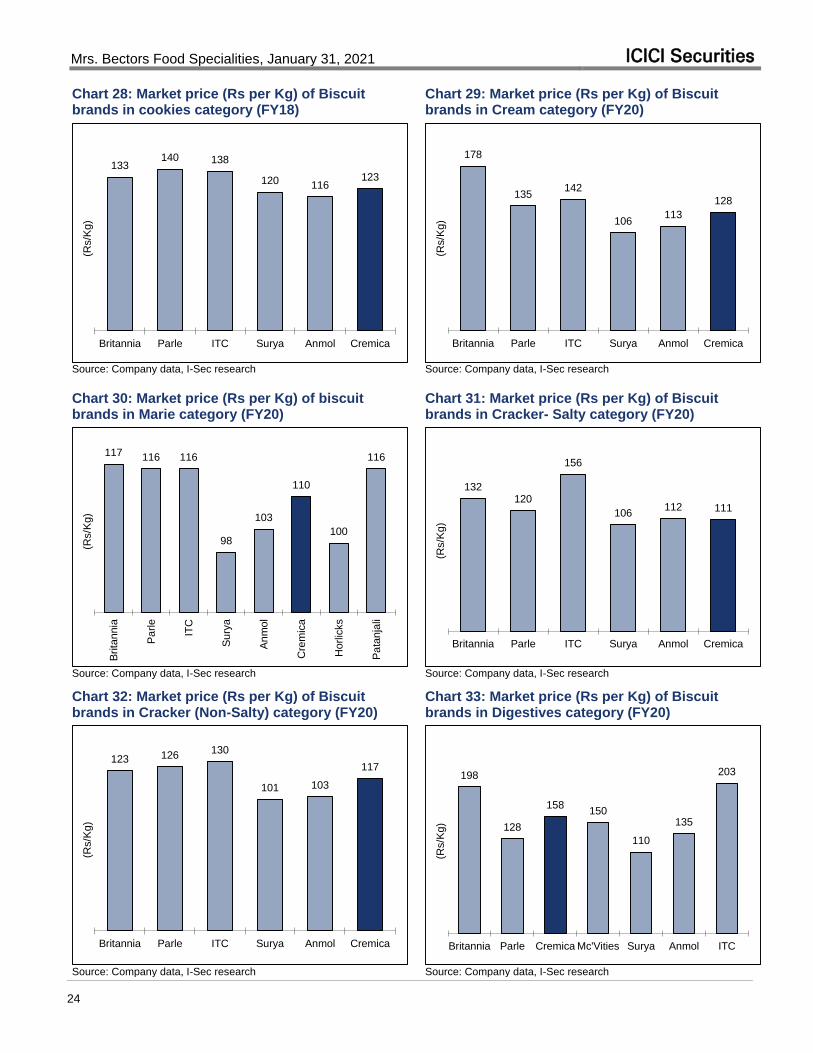

Chart 28: Market price (Rs per Kg) of Biscuit brands in cookies category (FY18)

Chart 29: Market price (Rs per Kg) of Biscuit brands in Cream category (FY20)

133140 138

120 116123

Britannia Parle ITC Surya Anmol Cremica

(Rs/K

g)

178

135142

106113

128

Britannia Parle ITC Surya Anmol Cremica

(Rs/K

g)

Source: Company data, I-Sec research Source: Company data, I-Sec research

Chart 30: Market price (Rs per Kg) of biscuit brands in Marie category (FY20)

Chart 31: Market price (Rs per Kg) of Biscuit brands in Cracker- Salty category (FY20)

117 116 116

98

103

110

100

116

Brita

nnia

Pa

rle

ITC

Su

rya

An

mol

Cre

mic

a

Horlic

ks

Pa

tanja

li

(Rs/K

g)

132120

156

106112 111

Britannia Parle ITC Surya Anmol Cremica

(Rs/K

g)

Source: Company data, I-Sec research

Source: Company data, I-Sec research

Chart 32: Market price (Rs per Kg) of Biscuit brands in Cracker (Non-Salty) category (FY20)

Chart 33: Market price (Rs per Kg) of Biscuit brands in Digestives category (FY20)

123 126130

101 103

117

Britannia Parle ITC Surya Anmol Cremica

(Rs/K

g)

198

128

158150

110

135

203

Britannia Parle Cremica Mc'Vities Surya Anmol ITC

(Rs/K

g)

Source: Company data, I-Sec research Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

25

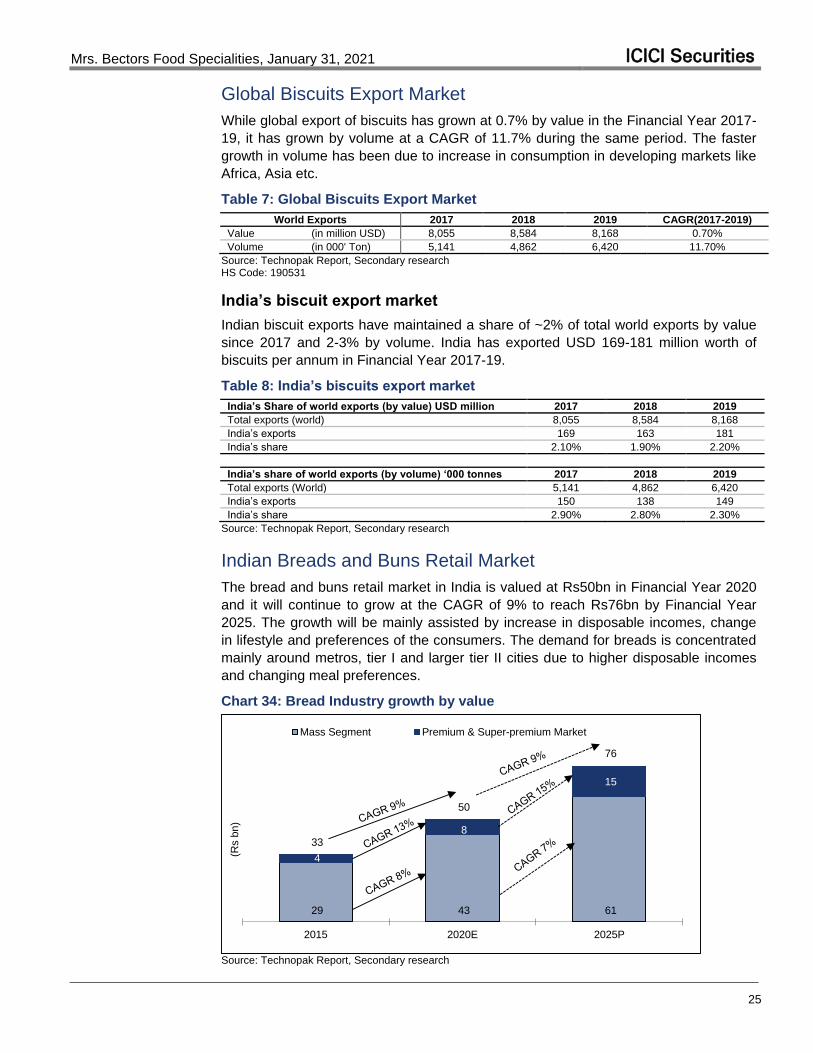

Global Biscuits Export Market

While global export of biscuits has grown at 0.7% by value in the Financial Year 2017-

19, it has grown by volume at a CAGR of 11.7% during the same period. The faster

growth in volume has been due to increase in consumption in developing markets like

Africa, Asia etc.

Table 7: Global Biscuits Export Market

World Exports 2017 2018 2019 CAGR(2017-2019)

Value (in million USD) 8,055 8,584 8,168 0.70%

Volume (in 000' Ton) 5,141 4,862 6,420 11.70%

Source: Technopak Report, Secondary research HS Code: 190531

India’s biscuit export market

Indian biscuit exports have maintained a share of ~2% of total world exports by value

since 2017 and 2-3% by volume. India has exported USD 169-181 million worth of

biscuits per annum in Financial Year 2017-19.

Table 8: India’s biscuits export market

India’s Share of world exports (by value) USD million 2017 2018 2019

Total exports (world) 8,055 8,584 8,168

India’s exports 169 163 181

India’s share 2.10% 1.90% 2.20%

India’s share of world exports (by volume) ‘000 tonnes 2017 2018 2019

Total exports (World) 5,141 4,862 6,420

India’s exports 150 138 149

India’s share 2.90% 2.80% 2.30%

Source: Technopak Report, Secondary research

Indian Breads and Buns Retail Market

The bread and buns retail market in India is valued at Rs50bn in Financial Year 2020

and it will continue to grow at the CAGR of 9% to reach Rs76bn by Financial Year

2025. The growth will be mainly assisted by increase in disposable incomes, change

in lifestyle and preferences of the consumers. The demand for breads is concentrated

mainly around metros, tier I and larger tier II cities due to higher disposable incomes

and changing meal preferences.

Chart 34: Bread Industry growth by value

29 43 61

4

8

15

33

50

76

2015 2020E 2025P

(Rs b

n)

Mass Segment Premium & Super-premium Market

Source: Technopak Report, Secondary research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

26

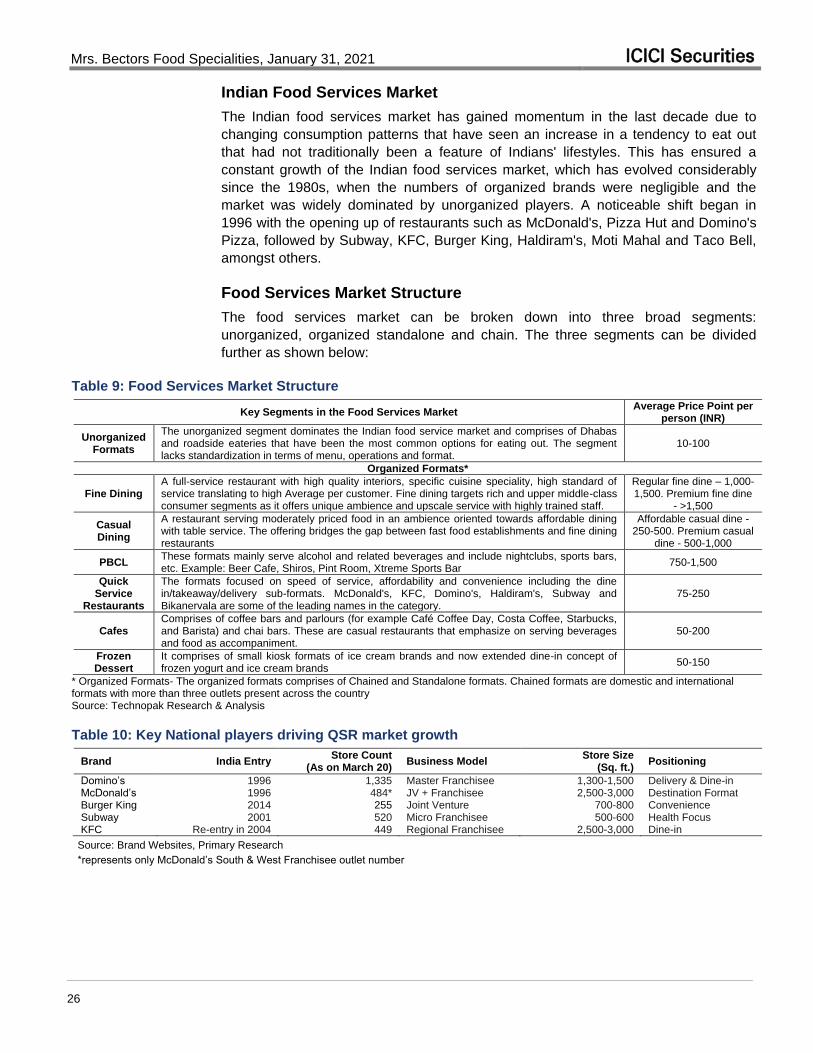

Indian Food Services Market

The Indian food services market has gained momentum in the last decade due to

changing consumption patterns that have seen an increase in a tendency to eat out

that had not traditionally been a feature of Indians' lifestyles. This has ensured a

constant growth of the Indian food services market, which has evolved considerably

since the 1980s, when the numbers of organized brands were negligible and the

market was widely dominated by unorganized players. A noticeable shift began in

1996 with the opening up of restaurants such as McDonald's, Pizza Hut and Domino's

Pizza, followed by Subway, KFC, Burger King, Haldiram's, Moti Mahal and Taco Bell,

amongst others.

Food Services Market Structure

The food services market can be broken down into three broad segments:

unorganized, organized standalone and chain. The three segments can be divided

further as shown below:

Table 9: Food Services Market Structure

Key Segments in the Food Services Market Average Price Point per

person (INR)

Unorganized Formats

The unorganized segment dominates the Indian food service market and comprises of Dhabas and roadside eateries that have been the most common options for eating out. The segment lacks standardization in terms of menu, operations and format.

10-100

Organized Formats*

Fine Dining A full-service restaurant with high quality interiors, specific cuisine speciality, high standard of service translating to high Average per customer. Fine dining targets rich and upper middle-class consumer segments as it offers unique ambience and upscale service with highly trained staff.

Regular fine dine – 1,000-1,500. Premium fine dine

- >1,500

Casual Dining

A restaurant serving moderately priced food in an ambience oriented towards affordable dining with table service. The offering bridges the gap between fast food establishments and fine dining restaurants

Affordable casual dine - 250-500. Premium casual

dine - 500-1,000

PBCL These formats mainly serve alcohol and related beverages and include nightclubs, sports bars, etc. Example: Beer Cafe, Shiros, Pint Room, Xtreme Sports Bar

750-1,500

Quick Service

Restaurants

The formats focused on speed of service, affordability and convenience including the dine in/takeaway/delivery sub-formats. McDonald's, KFC, Domino's, Haldiram's, Subway and Bikanervala are some of the leading names in the category.

75-250

Cafes Comprises of coffee bars and parlours (for example Café Coffee Day, Costa Coffee, Starbucks, and Barista) and chai bars. These are casual restaurants that emphasize on serving beverages and food as accompaniment.

50-200

Frozen Dessert

It comprises of small kiosk formats of ice cream brands and now extended dine-in concept of frozen yogurt and ice cream brands

50-150

* Organized Formats- The organized formats comprises of Chained and Standalone formats. Chained formats are domestic and international formats with more than three outlets present across the country Source: Technopak Research & Analysis

Table 10: Key National players driving QSR market growth

Brand India Entry Store Count

(As on March 20) Business Model

Store Size (Sq. ft.)

Positioning

Domino’s 1996 1,335 Master Franchisee 1,300-1,500 Delivery & Dine-in McDonald’s 1996 484* JV + Franchisee 2,500-3,000 Destination Format Burger King 2014 255 Joint Venture 700-800 Convenience Subway 2001 520 Micro Franchisee 500-600 Health Focus KFC Re-entry in 2004 449 Regional Franchisee 2,500-3,000 Dine-in

Source: Brand Websites, Primary Research

*represents only McDonald’s South & West Franchisee outlet number

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

27

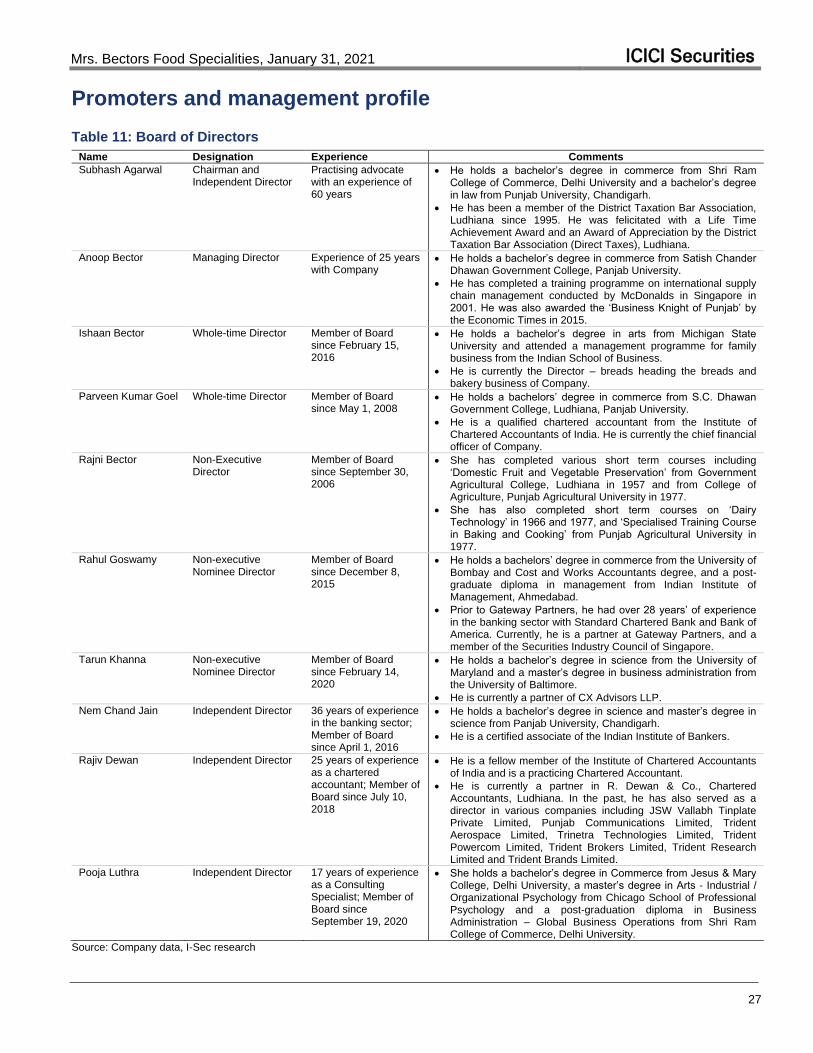

Promoters and management profile

Table 11: Board of Directors

Name Designation Experience Comments

Subhash Agarwal Chairman and Independent Director

Practising advocate with an experience of 60 years

He holds a bachelor’s degree in commerce from Shri Ram College of Commerce, Delhi University and a bachelor’s degree in law from Punjab University, Chandigarh.

He has been a member of the District Taxation Bar Association, Ludhiana since 1995. He was felicitated with a Life Time Achievement Award and an Award of Appreciation by the District Taxation Bar Association (Direct Taxes), Ludhiana.

Anoop Bector Managing Director Experience of 25 years with Company

He holds a bachelor’s degree in commerce from Satish Chander Dhawan Government College, Panjab University.

He has completed a training programme on international supply chain management conducted by McDonalds in Singapore in 2001. He was also awarded the ‘Business Knight of Punjab’ by the Economic Times in 2015.

Ishaan Bector Whole-time Director Member of Board since February 15, 2016

He holds a bachelor’s degree in arts from Michigan State University and attended a management programme for family business from the Indian School of Business.

He is currently the Director – breads heading the breads and bakery business of Company.

Parveen Kumar Goel Whole-time Director Member of Board since May 1, 2008

He holds a bachelors’ degree in commerce from S.C. Dhawan Government College, Ludhiana, Panjab University.

He is a qualified chartered accountant from the Institute of Chartered Accountants of India. He is currently the chief financial officer of Company.

Rajni Bector Non-Executive Director

Member of Board since September 30, 2006

She has completed various short term courses including ‘Domestic Fruit and Vegetable Preservation’ from Government Agricultural College, Ludhiana in 1957 and from College of Agriculture, Punjab Agricultural University in 1977.

She has also completed short term courses on ‘Dairy Technology’ in 1966 and 1977, and ‘Specialised Training Course in Baking and Cooking’ from Punjab Agricultural University in 1977.

Rahul Goswamy Non-executive Nominee Director

Member of Board since December 8, 2015

He holds a bachelors’ degree in commerce from the University of Bombay and Cost and Works Accountants degree, and a post-graduate diploma in management from Indian Institute of Management, Ahmedabad.

Prior to Gateway Partners, he had over 28 years’ of experience in the banking sector with Standard Chartered Bank and Bank of America. Currently, he is a partner at Gateway Partners, and a member of the Securities Industry Council of Singapore.

Tarun Khanna Non-executive Nominee Director

Member of Board since February 14, 2020

He holds a bachelor’s degree in science from the University of Maryland and a master’s degree in business administration from the University of Baltimore.

He is currently a partner of CX Advisors LLP.

Nem Chand Jain Independent Director 36 years of experience in the banking sector; Member of Board since April 1, 2016

He holds a bachelor’s degree in science and master’s degree in science from Panjab University, Chandigarh.

He is a certified associate of the Indian Institute of Bankers.

Rajiv Dewan Independent Director 25 years of experience as a chartered accountant; Member of Board since July 10, 2018

He is a fellow member of the Institute of Chartered Accountants of India and is a practicing Chartered Accountant.

He is currently a partner in R. Dewan & Co., Chartered Accountants, Ludhiana. In the past, he has also served as a director in various companies including JSW Vallabh Tinplate Private Limited, Punjab Communications Limited, Trident Aerospace Limited, Trinetra Technologies Limited, Trident Powercom Limited, Trident Brokers Limited, Trident Research Limited and Trident Brands Limited.

Pooja Luthra Independent Director 17 years of experience as a Consulting Specialist; Member of Board since September 19, 2020

She holds a bachelor’s degree in Commerce from Jesus & Mary College, Delhi University, a master’s degree in Arts - Industrial / Organizational Psychology from Chicago School of Professional Psychology and a post-graduation diploma in Business Administration – Global Business Operations from Shri Ram College of Commerce, Delhi University.

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

28

Table 12: Management profile

Name Designation Experience Comments

Manoj Verma National Sales Director (Domestic sales)

26 years of experience in sales and marketing

He holds a bachelor’s degree in arts from Agra University and a diploma in marketing management from the National Institute of Sales in New Delhi.

He has previously worked with Colgate Palmolive (India) Limited, Aditya Birla Retail Limited and Mondelez India Foods Private Limited (erstwhile Cadbury India Limited) while holding various positions.

Neeraj Aggarwal Vice President (Biscuits and Projects operations)

He holds a bachelor’s degree in electrical engineering from Thapar Institute of Engineering and Technology in Patiala, Punjab.

He has previously worked with Britannia Industries Limited as unit head.

Romel Kumar National Sales Manager

15 years of experience in the FMCG sector

He holds a bachelor’s degree in arts from Magadh University and a post graduate degree in business management from Birla Institute of Management Technology, New Delhi.

He has previously worked with Pepsico India and UNIBIC Foods.

Rajeev Dubey Director-Bread sales 26 years of experience in sales

He holds a bachelor’s degree in Commerce from University of Delhi.

He has previously worked with Ready Roti India Pvt Limited (Harvest Gold) as general manager (sales and marketing).

Asim Bhaumik Group Head of Quality, Technical, Research and Development

23 years of experience in production and operations

He holds a bachelor’s degree in science (chemistry) from the University of Calcutta and a master’s degree in chemistry from University of Calcutta.

He has previously worked with Dabur India Limited as an additional general manager (operations) and Britannia Industries Limited as unit head.

Shantilal Sukalal Chaudhari

General Manager -Operations

24 years of experience in production

He holds a degree of master of science in food technology from Central Food Technological Research Institute in Mysore.

He has previously worked with Al Rashed Food Limited as production-manager, Mini Bakeries (Nairobi) Limited as operations manager.

Gurpreet Singh Amrit

Chief Marketing Officer

19 years of experience in the consumer goods industry

He holds a post graduate diploma in management from Symbiosis, Pune.

He has previously worked with Dabur India Limited, Wrigley India (P) Limited, Bajaj Corp Limited, and Emami Limited.

Deep M.S Bajaj Group Senior Corporate Chef

14 years of experience in the hotel industry.

He has completed a three year diploma course in hotel management and catering technology and a diploma in a two year kitchen management programme from the Oberoi Centre of Learning and Development.

He has previously worked with Kilimanjaro Hotel, Kempinski, Djibouti Palace Kempinski, Oberoi Group of Hotels & Resorts, Trident Hotel and The Ritz Carlton Hotel Company.

Deepak Kumar Jain

Head of Finance and Corporate Strategy

10 years in finance and business planning

He is a qualified chartered accountant from the Institute of Chartered Accountants of India and Company Secretary from the Indian Institute of Company Secretaries of India. He holds a bachelor’s degree of commerce from the Maharshi Dayanand Saraswati University of Ajmer.

He has previously worked with Parag Milk Foods Limited, JSW Steel Limited and ICICI Prudential Life Insurance Limited.

Suvir Bector Vice president - Exports

He has graduated with bachelor’s degree in arts with honours in management with marketing from University of Exeter and has a master’s in global supply chain management from Cass Business School, City University in London.

Neha Bector Assistant General Manager

8 years of experience in management

She holds a bachelor’s degree in commerce from Lady Shri Ram College of Women, University of Delhi and a master of science in finance with a specialism in corporate finance from Cass Business School, City University in London.

She has previously worked with Lotus Integrated Texpark Limited as the chief executive officer and Trident Limited as a front line entrepreneur in the corporate division.

Mayank Arora Vice President (Human resources)

10 years of experience in human resources

He holds a bachelor’s degree in law from Bharati Vidyapeeth in Pune, a degree in MBA-LLM from the National Law University in Jodhpur and also a master’s degree in business laws from National Law School of India University in Bengaluru.

He has previously worked with Cargill India Private Limited as head- sales HR.

Atul Sud Company Secretary He holds a bachelor’s degree in arts from Kurukshetra University. He also completed a bachelor’s degree in law from Kurukshetra University in 2008 and a post graduate diploma in business administration from Symbiosis Centre for Distance Learning in 2011.

He has previously worked with Nahar Poly Films Limited as a company secretary July 2011 until August 12, 2016.

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

29

Shareholding pattern

Chart 35: Shareholding pattern

Promoters51%

MFs and other5%

Banks/FIs0%

Insurance2%

FIIs2%

Others38%

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

30

Financials

Table 13: Profit and loss statement

(Rs mn, year ending Mar 31)

FY18 FY19 FY20 FY21E FY22E FY23E

Net Revenue 6,906 7,837 7,621 8,655 10,492 12,209

Less:

Cost of goods sold 3,828 4,240 4,075 4,622 5,497 6,417 Employee cost 913 1,097 1,179 1,278 1,544 1,791 Other expenses 1,311 1,538 1,440 1,407 1,907 2,211

Total operating expenses 6,051 6,876 6,693 7,307 8,948 10,419

EBITDA 855 961 928 1,347 1,544 1,790

Less: D&A 283 352 415 442 575 628

EBIT 571 609 513 905 970 1,162

Less: Gross Interest 61 127 150 118 96 51 Add: Other Income 18 24 29 61 83 51

Recurring PBT 528 506 391 849 957 1,162

Less: Taxes 169 175 88 214 241 292 Less: Minority Interest 0 1 0 - - -

Net Income (Reported) 359 331 304 635 716 869

Extraordinary items - - - - - -

Recurring Net Income 359 331 304 635 716 869

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

31

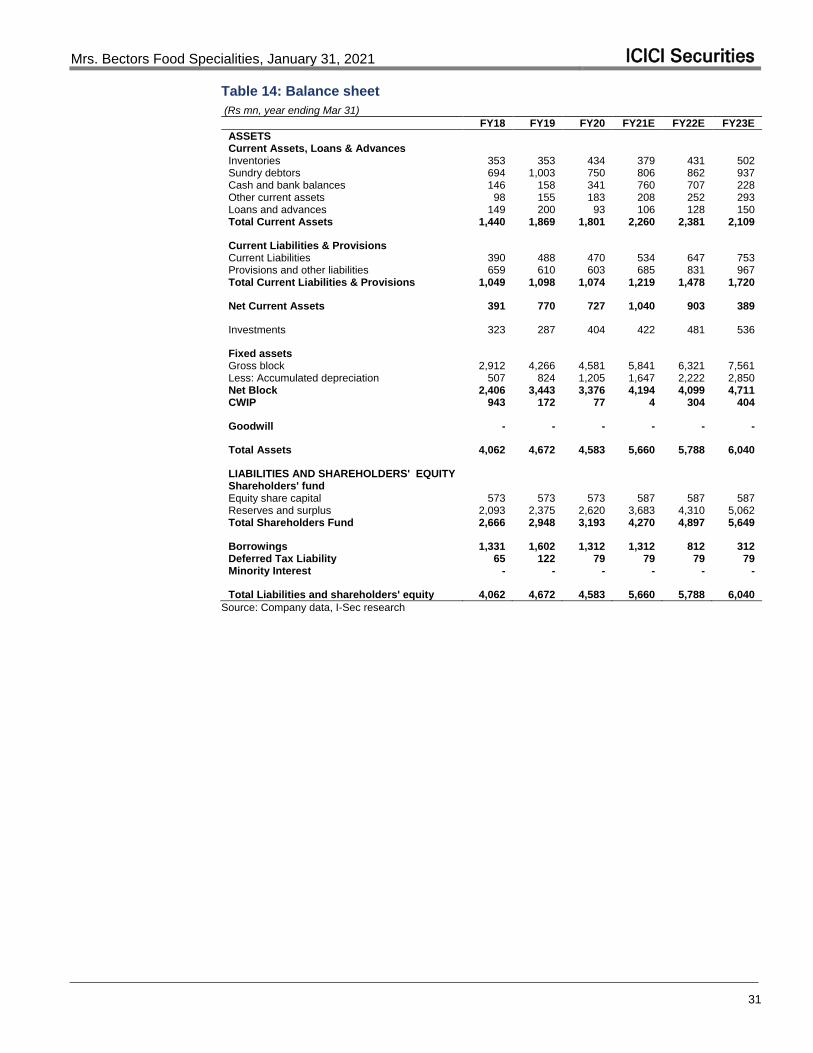

Table 14: Balance sheet

(Rs mn, year ending Mar 31)

FY18 FY19 FY20 FY21E FY22E FY23E

ASSETS Current Assets, Loans & Advances Inventories 353 353 434 379 431 502

Sundry debtors 694 1,003 750 806 862 937 Cash and bank balances 146 158 341 760 707 228 Other current assets 98 155 183 208 252 293 Loans and advances 149 200 93 106 128 150 Total Current Assets 1,440 1,869 1,801 2,260 2,381 2,109

Current Liabilities & Provisions Current Liabilities 390 488 470 534 647 753

Provisions and other liabilities 659 610 603 685 831 967 Total Current Liabilities & Provisions 1,049 1,098 1,074 1,219 1,478 1,720

Net Current Assets 391 770 727 1,040 903 389

Investments 323 287 404 422 481 536

Fixed assets Gross block 2,912 4,266 4,581 5,841 6,321 7,561

Less: Accumulated depreciation 507 824 1,205 1,647 2,222 2,850 Net Block 2,406 3,443 3,376 4,194 4,099 4,711 CWIP 943 172 77 4 304 404

Goodwill - - - - - -

Total Assets 4,062 4,672 4,583 5,660 5,788 6,040

LIABILITIES AND SHAREHOLDERS' EQUITY Shareholders' fund Equity share capital 573 573 573 587 587 587

Reserves and surplus 2,093 2,375 2,620 3,683 4,310 5,062 Total Shareholders Fund 2,666 2,948 3,193 4,270 4,897 5,649

Borrowings 1,331 1,602 1,312 1,312 812 312 Deferred Tax Liability 65 122 79 79 79 79 Minority Interest - - - - - -

Total Liabilities and shareholders' equity 4,062 4,672 4,583 5,660 5,788 6,040

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

32

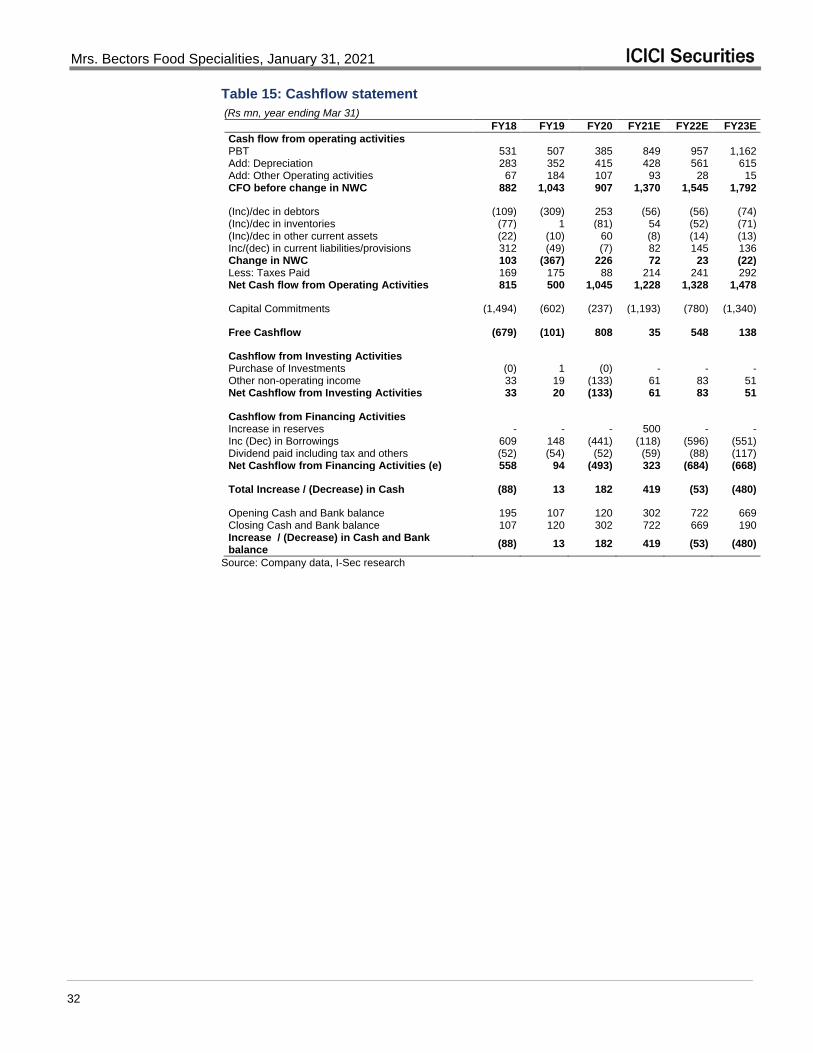

Table 15: Cashflow statement

(Rs mn, year ending Mar 31)

FY18 FY19 FY20 FY21E FY22E FY23E

Cash flow from operating activities

PBT 531 507 385 849 957 1,162 Add: Depreciation 283 352 415 428 561 615 Add: Other Operating activities 67 184 107 93 28 15 CFO before change in NWC 882 1,043 907 1,370 1,545 1,792

(Inc)/dec in debtors (109) (309) 253 (56) (56) (74) (Inc)/dec in inventories (77) 1 (81) 54 (52) (71) (Inc)/dec in other current assets (22) (10) 60 (8) (14) (13) Inc/(dec) in current liabilities/provisions 312 (49) (7) 82 145 136 Change in NWC 103 (367) 226 72 23 (22) Less: Taxes Paid 169 175 88 214 241 292 Net Cash flow from Operating Activities 815 500 1,045 1,228 1,328 1,478

Capital Commitments (1,494) (602) (237) (1,193) (780) (1,340)

Free Cashflow (679) (101) 808 35 548 138

Cashflow from Investing Activities

Purchase of Investments (0) 1 (0) - - - Other non-operating income 33 19 (133) 61 83 51 Net Cashflow from Investing Activities 33 20 (133) 61 83 51

Cashflow from Financing Activities

Increase in reserves - - - 500 - - Inc (Dec) in Borrowings 609 148 (441) (118) (596) (551) Dividend paid including tax and others (52) (54) (52) (59) (88) (117) Net Cashflow from Financing Activities (e) 558 94 (493) 323 (684) (668)

Total Increase / (Decrease) in Cash (88) 13 182 419 (53) (480)

Opening Cash and Bank balance 195 107 120 302 722 669 Closing Cash and Bank balance 107 120 302 722 669 190 Increase / (Decrease) in Cash and Bank balance

(88) 13 182 419 (53) (480)

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

33

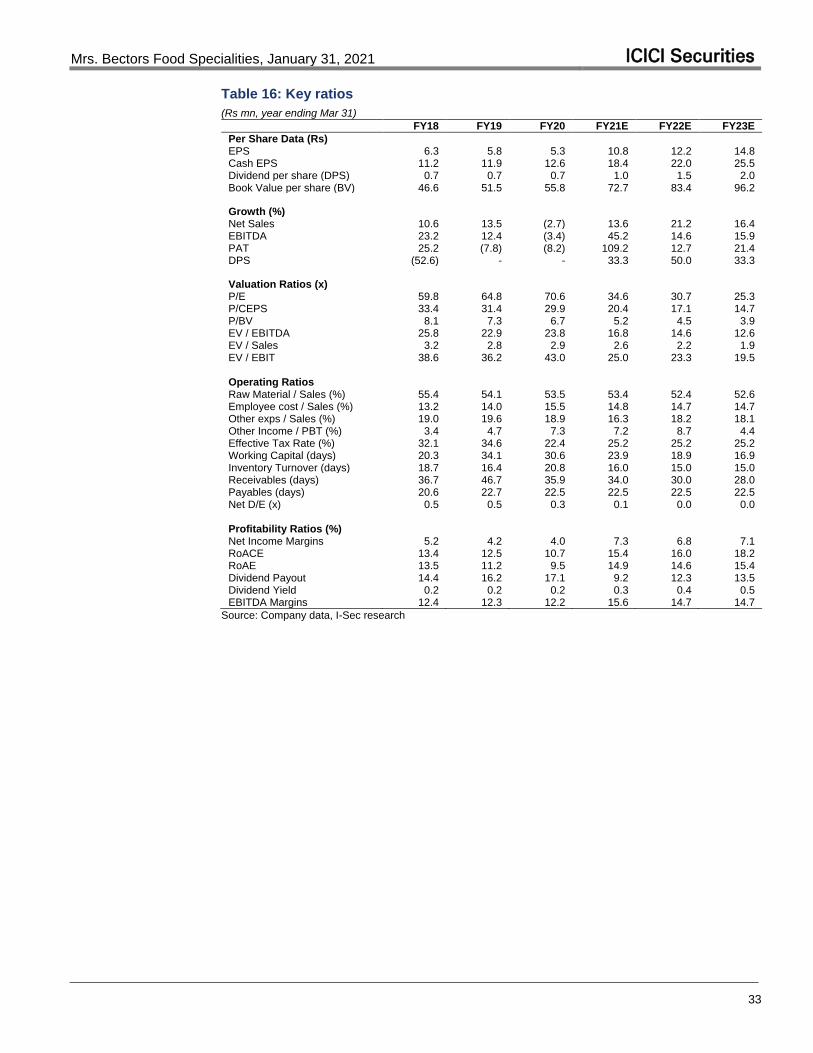

Table 16: Key ratios

(Rs mn, year ending Mar 31)

FY18 FY19 FY20 FY21E FY22E FY23E

Per Share Data (Rs)

EPS 6.3 5.8 5.3 10.8 12.2 14.8 Cash EPS 11.2 11.9 12.6 18.4 22.0 25.5 Dividend per share (DPS) 0.7 0.7 0.7 1.0 1.5 2.0 Book Value per share (BV) 46.6 51.5 55.8 72.7 83.4 96.2

Growth (%)

Net Sales 10.6 13.5 (2.7) 13.6 21.2 16.4 EBITDA 23.2 12.4 (3.4) 45.2 14.6 15.9 PAT 25.2 (7.8) (8.2) 109.2 12.7 21.4 DPS (52.6) - - 33.3 50.0 33.3

Valuation Ratios (x)

P/E 59.8 64.8 70.6 34.6 30.7 25.3 P/CEPS 33.4 31.4 29.9 20.4 17.1 14.7 P/BV 8.1 7.3 6.7 5.2 4.5 3.9 EV / EBITDA 25.8 22.9 23.8 16.8 14.6 12.6 EV / Sales 3.2 2.8 2.9 2.6 2.2 1.9 EV / EBIT 38.6 36.2 43.0 25.0 23.3 19.5

Operating Ratios

Raw Material / Sales (%) 55.4 54.1 53.5 53.4 52.4 52.6 Employee cost / Sales (%) 13.2 14.0 15.5 14.8 14.7 14.7 Other exps / Sales (%) 19.0 19.6 18.9 16.3 18.2 18.1 Other Income / PBT (%) 3.4 4.7 7.3 7.2 8.7 4.4 Effective Tax Rate (%) 32.1 34.6 22.4 25.2 25.2 25.2 Working Capital (days) 20.3 34.1 30.6 23.9 18.9 16.9 Inventory Turnover (days) 18.7 16.4 20.8 16.0 15.0 15.0 Receivables (days) 36.7 46.7 35.9 34.0 30.0 28.0 Payables (days) 20.6 22.7 22.5 22.5 22.5 22.5 Net D/E (x) 0.5 0.5 0.3 0.1 0.0 0.0

Profitability Ratios (%)

Net Income Margins 5.2 4.2 4.0 7.3 6.8 7.1 RoACE 13.4 12.5 10.7 15.4 16.0 18.2 RoAE 13.5 11.2 9.5 14.9 14.6 15.4 Dividend Payout 14.4 16.2 17.1 9.2 12.3 13.5 Dividend Yield 0.2 0.2 0.2 0.3 0.4 0.5 EBITDA Margins 12.4 12.3 12.2 15.6 14.7 14.7

Source: Company data, I-Sec research

Mrs. Bectors Food Specialities, January 31, 2021 ICICI Securities

34

Price charts

Akzo Nobel Asian Paints Avenue Supermarts Bajaj Consumer Bata India

1,300

1,500

1,700

1,900

2,100

2,300

2,500

2,700

Jan

-18

Jul-1

8

Jan

-19

Jul-1

9

Jan

-20

Jul-2

0

Jan

-21

(Rs)

600

1,100

1,600

2,100

2,600

3,100

Jan

-18

Jul-1

8

Jan

-19

Jul-1

9

Jan

-20

Jul-2

0

Jan

-21

(Rs)

400

800

1,200

1,600

2,000

2,400

2,800

3,200

Jan

-18

Ju

l-1

8

Jan

-19

Ju

l-1

9

Jan

-20

Ju

l-2

0

Jan

-21

(Rs)

100

175

250

325

400

475

550

Jan

-18

Jul-1

8

Jan

-19

Jul-1

9

Jan

-20

Jul-2

0

Jan

-21

(Rs)

0

500

1,000

1,500

2,000

Jan

-18

Ju

l-1

8

Jan

-19

Ju

l-1

9

Jan

-20

Ju

l-2

0

Jan

-21

(Rs)

Berger Paints Britannia Colgate Dabur Emami

100

200

300

400

500

600

700

800

900

Jan

-18

Jul-1

8

Jan

-19

Jul-1

9

Jan

-20

Jul-2

0

Jan

-21

(Rs)

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Jan

-18

Ju

l-1

8

Jan

-19

Ju

l-1

9

Jan

-20

Ju

l-2

0

Jan

-21

(Rs)

600

800

1,000

1,200

1,400

1,600

1,800

Jan

-18

Ju

l-1

8

Jan

-19

Ju

l-1

9

Jan

-20

Ju

l-2

0

Jan

-21

(Rs)

200

250

300

350

400

450

500

550

600

Jan

-18

Jul-1

8

Jan

-19

Jul-1

9

Jan

-20

Jul-2

0

Jan

-21

(Rs)

0

100

200

300

400

500

600

700

Jan

-18

Ju

l-1

8

Jan

-19

Ju

l-1

9

Jan

-20

Ju

l-2

0

Jan

-21

(Rs)

GCPL HUL ITC Jubilant Foodworks Jyothy Labs

320

420

520

620

720

820

920

1,020

Ja

n-1

8

Jul-1

8

Ja

n-1

9

Jul-1

9

Ja

n-2

0

Jul-2

0

Ja

n-2

1

(Rs)

800

1100

1400

1700

2000

2300

2600

Ja

n-1

8

Ju

l-18

Ja

n-1

9

Ju

l-19

Ja

n-2

0

Ju

l-20

Ja

n-2

1

(Rs)

125

175

225

275

325

375

Jan

-18

Jul-1

8

Jan

-19

Jul-1

9

Jan

-20

Jul-2

0

Jan

-21

(Rs)

200

700

1,200

1,700

2,200

2,700

3,200

Jan

-18

Jul-1

8

Jan

-19

Jul-1

9

Jan

-20

Jul-2

0

Jan

-21

(Rs)

0