Moving People - Bus Industry Confederation

133

Moving People Australian Bus and Coach Industry: a snapshot BUS INDUSTRY CONFEDERATION PO Box 6171, KINGSTON ACT 2604 Tel: +61 2 6247 5990 Fax: +61 2 6273 1035 Email: [email protected] Web: www.movingpeople.com.au

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Moving People - Bus Industry Confederation

Moving People

MOVING PEOPLE

> A

ustralian Bus and C

oach Industry: a snapshot

ISBN: 978-0-6485585-1-4

Copyright 2021 Bus Industry Confederation Inc.

First Published September 2021.

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission from the Bus Industry Confederation. Requests and enquiries concerning reproduction and rights should be addressed to the BIC National Secretariat, PO Box 6171, KINGSTON ACT 2604.

Email: [email protected].

Australian Bus and Coach Industry: a snapshot

BUS INDUSTRY CONFEDERATIONPO Box 6171, KINGSTON ACT 2604

Tel: +61 2 6247 5990Fax: +61 2 6273 1035

Email: [email protected]: www.movingpeople.com.au

Moving People

MOVING PEOPLE

> A

ustralian Bus and C

oach Industry: a snapshot

ISBN: 978-0-6485585-1-4

Copyright 2021 Bus Industry Confederation Inc.

First Published September 2021.

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission from the Bus Industry Confederation. Requests and enquiries concerning reproduction and rights should be addressed to the BIC National Secretariat, PO Box 6171, KINGSTON ACT 2604.

Email: [email protected].

Australian Bus and Coach Industry: a snapshot

BUS INDUSTRY CONFEDERATIONPO Box 6171, KINGSTON ACT 2604

Tel: +61 2 6247 5990Fax: +61 2 6273 1035

Email: [email protected]: www.movingpeople.com.au

11Moving People > Australian Bus and Coach Industry: a snapshot

MOVING PEOPLE Australian Bus and Coach Industry:

a snapshot

BUSW

A

22 Moving People > Australian Bus and Coach Industry: a snapshot

ForewordIn June 2018, the Bus Industry Confederation (BIC) commissioned the Institute of Transport and Logistics Studies to research, collate and report on various data and statistics relating to the bus and coach industry in Australia. The research component of this report was completed in June 2019 with the BIC taking it further to include analysis of data from the latest motor vehicle survey (2018) and census (2019) conducted by the Australian Bureau of Statistics and industry surveys (2020) undertaken by the BIC.

The information included in this report is based on data and information sources available during the period 2016 to 2020. Where there is information and data gaps in some sections of this report, the conclusions are reliably based on anecdotal advice and industry assumptions. The BIC believes the information provided in this report not only provides an accurate picture of the Australian bus and coach industry in 2020 but also serves as a guide as to where future information and data collection improvements are required.

33Moving People > Australian Bus and Coach Industry: a snapshot

AcknowledgementsThe Bus Industry Confederation wishes to acknowledge the below individuals for their valued contribution in the research, data analysis, writing and editing of this industry report.

Bus Industry Confederation

> Michael Apps, Executive Director

> Madonna Woodhead, National Operations & Marketing Manager

> Luke Hardy, National Technical Manager

Institute of Transport and Logistics Studies, The Business School, The University of Sydney

> Professor David A Hensher, Founding Director ITLS

> Dr Yale Z Wong, Honorary Associate

44 Moving People > Australian Bus and Coach Industry: a snapshot

M

OVING PEOPLE

THEPEOPLE

Executive Overview of the bus and coach industryThis report provides a 2020 update to its predecessor Fact Sheet: Passenger Transport Activity in Australia, last released in 2003 and prior to that in 1999. This report compiles the latest statistics on the bus and coach industry in Australia including its contribution to:

• the passenger transport task

• the changing fleet profile

• government expenditure in each state and territory

• current and emerging industry issues

• the social and environmental contribution to the Australian economy.

The task of the bus and coach industryBuses and coaches represent the most important mode of public transport. Every day, far more Australians are transported by bus and coach on the nation’s road network than are moved by rail, even in our largest capital cities. Buses provide an alternative travel choice to the car for people’s daily commute and other travel purposes which in turn addresses the challenges of congestion and its economic impacts in our urban and regional centres. Buses also provide a vital lifeline for individuals and communities, promoting social inclusion and access to education, healthcare, employment and social opportunities.

Based on various industry surveys undertaken by the Bus Industry Confederation (BIC) in 2018 and 2020, the bus and coach industry in Australia directly employs more than 85,000 people in a range of jobs including drivers, mechanics, engineers, skilled production workers and transport professionals in various specialised fields such as planning and service delivery.

The bus and coach industry is predominantly based around the provision of school bus and public transport (route) services that are provided under state and territory government contractual arrangements. These contracted services are primarily provided by privately owned bus and coach businesses, with a small percentage of bus fleets being government owned and operated. The industry also provides contracted government services such as special school transport for children with disabilities and coach services to support the rail network. The bus industry is also becoming involved in other emerging markets such as aged care, health and para-transit.

The bus and coach industry also provide services, in what might be termed, the ‘deregulated’ market providing charter, tourism, long distance, mining, correctional services, airline and airport services and specialised services that support other industries. The last few years has seen a period of transition and disruption of traditional transport service provision generally, such as Uber. The bus and coach industry has not been isolated from this disruption and has been active in exploring new areas of transport service connectivity and delivery with a range of vehicle types, modes and providers.

This report touches upon these service delivery issues as does the BIC’s policy paper series of publications (listed in Appendix 1).

The broader transport policy issues related to the bus and coach industry are reviewed in this report, highlighting the changing and increasing role of the federal government in cities – their functionality and sustainability, regional development and connectivity, the importance of transport and how we move people as a nation. There can be no doubt as to the increasing and important role for the federal government in public transport with bus service provision forming a critical part of the solutions to the challenges for growing Australian cities, regional centres and remote areas. The BIC has produced a comprehensive series of policy discussion papers (listed in Appendix 1) which provide a more detailed investigation into these issues and the role of the bus and coach industry in working with all levels of government to deliver positive transport and mobility outcomes for Australia.

The Australian bus and coach manufacturing and supply sectorThe manufacturing, supplies and services sector of the bus and coach industry is an important contributor to the Australian economy. It is also an important contributor to a heavy vehicle automotive manufacturing labour skill set that goes beyond just building buses and coaches. It continues to meet the many challenges of a global vehicle market place that remains competitive in the Australian market, including some small export opportunities.

The BIC estimates that in the manufacturing of the completed bus, $5 billion is contributed to the Australian economy each year and close to $1.5 billion in supplies and services to keep the bus operational and delivering services. The 2019 and 2020 industry reported deliveries of buses and coaches were 1,449 and 1,226 respectively. The economic impact of Covid-19 on the manufacturing sector was most evident in the delivery of long distance coaches seeing a down-turn of 74% from 2019. Route bus deliveries were also down by 20% whilst Charter and School bus deliveries remained consistent throughout 2020. The BIC estimates that the manufacturing sector employs more than 10,000 people in Australia including a strong network of Australian and global component manufacturers (eg. public transport seats) and suppliers that support the build of a bus (eg. air conditioning units) most of whom have setup businesses in Australia.

Over the past 15 years greater competition has appeared in the Australian bus and coach market place with fully built vehicles mainly from Asia, Europe and South America being imported. In 2020, 88.9% of public transport passenger route service buses and 59.6% of school buses are manufactured in Australia, the majority built by Australian body manufacturers on a European or Asian chassis; the remainder being fully imported buses and coaches primarily from Asia, with some from Europe and South America.

The Australian bus and coach manufacturing market has in some ways been protected by Australian Design Rules (ADR) and unique state-based vehicle standards. These “best practice” requirements, combined with the Australian markets practice of early adoption of new safety technologies, have resulted in Australian manufactured and compliant imported

55Moving People > Australian Bus and Coach Industry: a snapshot

66 Moving People > Australian Bus and Coach Industry: a snapshot

buses and coaches being among the safest in the world. This has not stopped, it must be noted, competition from international markets.

The market is also protected by its size in terms of total sales and deliveries in a global sense which requires re-engineering of international factory requirements to meet the vehicle Australian safety and regulatory requirements of ADR.

The bus and coach manufacturing sector can also be seasonal in nature with sales and deliveries sometimes significantly reliant on the public transport and school bus procurement of state and territory governments. The procurement process can often be based on short term sharp increases in demand for bus passenger services caused by increases in fuel and living costs; the long term impact of congestion in an ever increasing urban Australia; electoral cycle priorities; regulated vehicle replacement programs; average age of fleet and maximum age regulations; and the rise and fall of the Australian dollar.

These are just a few of the factors in the external environment that make the task of bus manufacturing challenging when planning for the needs of the market. The statistics supplied in this report are reflective of market procurement trends.

Future mobility and emerging marketsAustrade (2019) summarises the future of the transport and mobility sector from ownership to usership, transportation to mobility and internal combustion to electric propulsion. As a generalisation this is probably correct though issues of ownership and usership will take some time as this “disruption” will involve complex business models, different types of ownership developed across and between modes and mobility choices offered that will require much greater partnership and collaboration between transport fleet and vehicle owners, mobility technology owners and government authorities.

Austrade has identified three key sectors for future transport and mobility:

• Intelligent Transport Systems (ITS)

• Connected Automated Vehicles (CAV’s)

• Mobility as a Service (MaaS).

These transportation and personal mobility policy issues are addressed in Sections 10 and 11 of this report and in the BIC’s comprehensive policy discussion papers (listed in Appendix 1).

The future transport market was valued a $212.5 million in 2016 and is expected to grow to more than $16.6 Billion in revenue by 2025 (Frost and Sullivan, 2017).

Australian governments, with the urging of organisations such as the BIC, have been encouraged to take a nationally consistent approach to regulatory reform and the safety of automated vehicle technologies. There also needs to be a hands on approach by governments to ownership and the operations of mobility services including open access and the sharing of data so that these technologies can be assessed and delivered in an efficient and timely manner.

In 2018 the federal government established the Office of Future Transport Technology to prepare Australia for the imminent arrival of autonomous vehicles and other transport innovations. The transformation of transport mobility will need to be inventive to address the challenges of Australia’s growing and ageing population; the challenges of congestion on the economy and future land use; the planning and development of our growing cities and regions with innovative and better connected public transit networks, systems and personal mobility choices. This has been a priority focus of the Australian bus and coach industry and of the BIC in 2020 and will continue to be over the next 30 years.

About the Bus Industry Confederation The Bus Industry Confederation (BIC) is the national peak body, representing the interests of bus and coach operators, manufacturers and parts and service suppliers in the industry. The BIC represents the interests of its members (listed in Appendix 4) to governments and the community on a range of issues including technical, vehicle and parts-based issues to the broader challenge of meeting the growing passenger transport task and providing Australian travellers with a genuine alternative to the private car. The BIC and its members are dedicated to the moving people task and the promotion of safe, efficient and effective bus and coach transport in Australia.

The BIC was established as an incorporated Association in 1994 with the secretariat being formed in April 2002 in Canberra. A list of councillors who have served the BIC since 1994 to 2020 are included in Appendix 3.

In 2014, the BIC established and became the National member of the Bus Australia Network which also includes state association members: BusNSW, BusVic, BusSA, BusWA, TasBus and QBIC.

Policy Direction of the BIC and present-day industry issuesAt the beginning of each calendar year, the BIC undertakes a review of its 3-year strategic work program to provide a ‘working paper’ for the year that details the present-day issues and policy work to be undertaken. This working paper is presented as part of ‘BIC on the road’ meetings with federal, state and territory Ministers and senior officials involved in the transport, infrastructure, planning, cities/regions and tourism portfolios.

The 2020 BIC working paper is provided in Appendix 2 as a useful present-day reference document relating to:

• BIC Research Program 2020-2022

• BIC/Roads Australia Workshop with Infrastructure Australia on Future Mobility

• fleet and infrastructure innovation

• future mobility design

• energy transition to low/zero emissions

77Moving People > Australian Bus and Coach Industry: a snapshot

• review of:

- National Heavy Vehicle Law

- Australian Design Rules

- Road Vehicle Standards

- Performance Based Standards

- Accessible Transport Standards

• national framework for bus service procurement and contracts

• controlled access bus network

• road user charging

• industrial relations agenda

• travel to learn agenda

• long distance, charter, express and tourism agenda.

Our Moving People Vision

Our vision is to enhance the sustainability and liveability of Australia’s cities and regions by moving people using bus and coach transportation. We aim to do this by representing the collective interests of our members and to assist them in promoting the safety, efficiency and effectiveness of bus and coach transport in Australia.

Our Moving People Objectives

> Encourage investment in public transport infrastructure and services.

> Promote policies and actions that are environmentally responsible.

> Promote the development of a viable and improved bus and coach industry in Australia.

> Foster and promote a viable Australian bus and coach manufacturing industry.

> Protect the business interests of operators, manufacturers and suppliers.

> Promote public understanding of the contribution made by the bus and coach industry to Australia’s economy, society and environment.

> Ensure the accessibility and mobility needs of Australians are met, regardless of where they live or their circumstances.

> Promote the use of public transport as a viable alternative to the car.

> Coordinate and make more effective existing federal, state and local government policies and programs that relate to passenger transport.

> Ensure that buses and coaches operate safely and effectively.

WO

RKPL

ACE RELATIONS

MOVING PEOPLE REDU

CIN

G C

ON

GE

STIO

N

LIVE

AB

LE C

ITIES SOCIAL INCLUSION

CONNECTI

VITY

One Message Many Voices

88 Moving People > Australian Bus and Coach Industry: a snapshot

Bus Manufacturing

Fleet on the

road

Bus Operations

The Bus Passenger

Long Distance and Tourism Sector

Industry Areas of Policy and Program Focus

99Moving People > Australian Bus and Coach Industry: a snapshot

ContentsForeword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3Executive Overview of the bus and coach industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5Bus Manufacturing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131. What is a bus? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

1.1 Profile of the bus manufacture and supply sector. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .131.2 Number of buses delivered based on bus task . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .231.3 Number of buses delivered based on Emission Standards. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24

Fleet on the road . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 272. The Bus Fleet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27

2.1 Number of registered buses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .272.2 Number of registered buses based on fuel type and emissions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .312.3 Average Age of the bus fleet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

Bus Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 393. Who operates the buses on the roads . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39

3.1 The service provided by the bus operator . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .413.2 Road use by the bus . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .433.3 The costs of operating a bus or coach business. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .463.4 Operating cost efficiencies and effectiveness of a bus operation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .483.5 Safety in bus and coach operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .513.6 Who drives the bus . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .56

The Bus Passenger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 614 Who is the passenger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61

4.1 Mode choice . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .614.2 The commute for the passenger . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .654.3 Bus and coach patronage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .674.4 The value of mobility for the passenger. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .69

Long Distance and Tourism Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 715 About the Coach Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .71

5.1 The coach sector and the tourism dollar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .715.2 Coaches driving land transport tourism to regional Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79

Industry Areas of Policy and Program Focus . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 816 Federal Election Primer – 2019 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .81

6.1 Moving People, Cities, Regions and the Federal Government . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .816.2 ‘Fair Go’ Guarantee for Public Transport Users, Drivers and Manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .826.3 The ‘Fair Go’ Guarantee 10 Point Action Plan. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .82

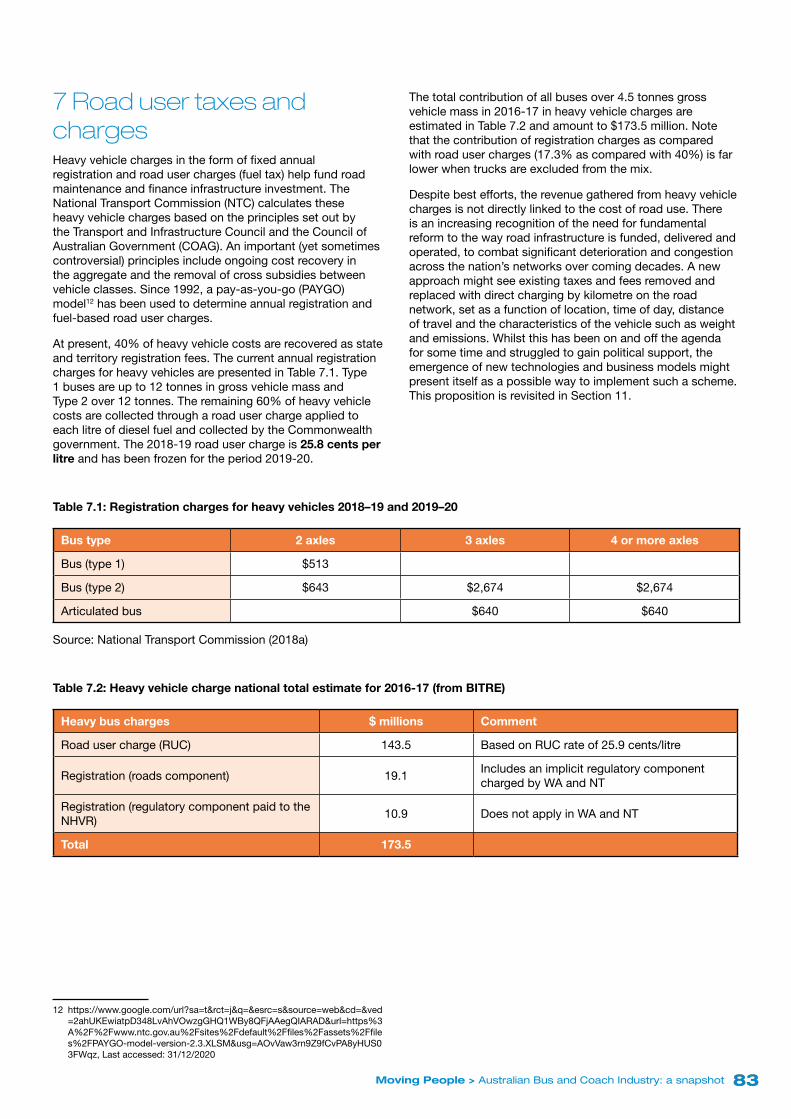

7 Road user taxes and charges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .838 Perceptions and realities of car costs on society . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .849 Contractual developments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .86

9.1 Recent developments in Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .869.2 Best practice in bus contracting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .879.3 Future competition and regulation issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .899.4 Case study Singapore bus contracting model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .89

10 New technologies, business models and trends. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9110.1 New entrants in the passenger mobility market . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .91

11 Mobility as a service (MaaS) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9412 Bus rapid transit and branded bus services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .97

12.1 Review of BRT and BBS - a study of 27 systems in Australia. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9712.2 Key recommendations for governments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .98

Appendix 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100Solutions for Policy Thinkers Series. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .100Appendix 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Bus and coach industry briefing paper on policy and advocacy directions and current issues [May 2020] . . . . . . . . . . . . . . . . .105Appendix 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120Honour Roll of Councillors 1995-2020. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .120Appendix 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126BIC National Members . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .126References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

1010 Moving People > Australian Bus and Coach Industry: a snapshot

FiguresFigure 1.1: Total bus and coach deliveries January 2008 to December 2019 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14Figure 1.2: Market share of chassis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15Figure 1.3: Chassis manufacturer market share by year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15Figure 1.4: Chassis market share for top 5 manufacturers by state/territory. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16Figure 1.5: Market share of body manufacturers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17Figure 1.6: Body manufacturer market share by year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18Figure 1.7: Body market share for top 5 manufacturers by state/territory. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18Figure 1.8: Top ten air conditioning manufacturers by total sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20Figure 1.9: Top ten seating manufacturers by total sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20Figure 1.10: Chinese chassis manufacturers market share . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22Figure 1.11: Chinese body manufacturers market share . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22Figure 1.12: Deliveries and their applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23Figure 1.13: Deliveries by emissions standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24Figure 1.14: Deliveries by emissions standards by state/territory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Figure 2.1: Registered buses ABS 2019 – small, medium and large . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28Figure 2.2: ‘Commercial-use’ registered buses – under and over 12 tonne . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28Figure 2.3: Number of registered ‘commercial-use’ buses by state/territory. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30Figure 2.4: Percentage of buses on register by state/territory. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30Figure 2.6: Emissions in the transport sector by mode . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32Figure 2.7: Carbon dioxide emissions per passenger kilometre by private car and public transport modes (ITLS

estimate from 2009-10 BITRE data) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33Figure 2.8 Comparison of modal emission totals for Australian bus use and rail transport, in gigagrams of full fuel cycle CO2 equivalent for 2015 Mulley et al., 2017—includes urban and non-urban bus . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .34Figure 2.9: Buses on register by age . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35Figure 2.10: Buses on register by age and state/territory of registration. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36Figure 2.11: Average age of bus/coach fleet by state/territory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37Figure 3.1: Average kilometres travelled bus/coach in a 12 month period by service type (30 June 2018) . . . . . . . . . . . . . . . . . .42Figure 3.2: Total bus/coach kilometres travelled in a 12 month period by service type (30 June 2018) . . . . . . . . . . . . . . . . . . . . .42Figure 3.3: Total kilometres travelled in a 12 month period by service and vehicle type (30 June 2018) . . . . . . . . . . . . . . . . . . . .43Figure 3.4: Total kilometres travelled by road vehicle type in a 12 month period (end June 2018) . . . . . . . . . . . . . . . . . . . . . . . . .44Figure 3.5: Total bus/coach kilometres travelled in a 12 month period by area of operation (end June 2018) . . . . . . . . . . . . . . . .44Figure 3.6: Average bus/coach kms in a 12 month period by area of operation (end June 2018) . . . . . . . . . . . . . . . . . . . . . . . . .45Figure 3.7: Gross and net cost per service kilometre compared across Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49Figure 3.8: Heavy vehicle fatalities grouped by vehicle type, against total number of road fatalities 2008-2017 . . . . . . . . . . . . . .52Figure 3.9: Fatalities with bus involvement, segmented by road user type (1989-2019) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .52Figure 3.10: Fatalities with bus involvement, segmented by speed environment (1989-2019) . . . . . . . . . . . . . . . . . . . . . . . . . . . .53Figure 3.11: Fatalities with bus involvement, segmented by age and gender (1989-2019). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .53Figure 3.12: Number of bus and coach drivers historical trend and projection 2007-2022. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .57Figure 3.13: Bus and coach drivers employed by state/territory 2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .57Figure 3.14: Bus and coach drivers employed by age profile 2017. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58Figure 3.15: Bus and coach drivers employed by education level 2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58Figure 4.1: National mode share by passenger kilometres, of a total 433.1 billion passenger kilometres travelled in 2015-2016 62Figure 4.2: Historical trend of bus/coach contribution to the national land passenger transport task, overlayed on national

passenger kilometres travelled on land modes 1974-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .62Figure 4.3: Capital city mode share by passenger kilometres, out of a total 197.26 billion passenger kilometres travelled

in 2014-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .63Figure 4.4: Historical trend of bus/coach contribution to the capital city passenger transport task, overlayed on capital city

passenger kilometres travelled 1976-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64Figure 4.5: Historical trend of bus/coach passenger kilometres by capital city 1976-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64Figure 4.6: Journey-to-work by mode (2016), out of a total working population of 8.92 million . . . . . . . . . . . . . . . . . . . . . . . . . . .66Figure 4.7: Historical trend of public transport and public transport plus other method in the journey-to-work mode share

1986-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .66Figure 4.8: Passenger boardings by government operator in 2016-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .67Figure 5.1: Top 10 countries from which visitors hailed by number of visitors and expenditure in the year ending March 2018 . .73Figure 5.2: Visitors and expenditure by state/territory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .73Figure 5.3: Total number of nights spent and the average length of each stay for those who travelled on each particular mode 74Figure 5.4: International visitor nights spent by mode and state/territory of travel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .74Figure 5.5: International visitor nights spent by mode and travel purpose . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .75

1111Moving People > Australian Bus and Coach Industry: a snapshot

Figure 5.6: International visitor nights spent by mode and life cycle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .75Figure 5.7: Mode share of domestic visitors as measured by total nights stayed. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .76Figure 5.8: Domestic visitor nights spent by mode and state/territory of travel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .77Figure 5.9: Domestic visitor nights spent by mode and travel purpose. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .77Figure 5.10: Domestic visitor nights spent by mode and life cycle . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .78Figure 8.1: Perceived and actual costs of private car and public transport (ITLS estimate from 2009-10 BITRE

data/ABS/RACV) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .85Figure 9.1: The original STO (strategic/tactical/operational) framework from van de Velde (1997: 6),

which has grown to become a Thredbo centrepiece. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .88Figure 10.1: Shared mobility providers in Australia—the vast majority of which have entered over the past three years . . . . . . .92Figure 11.1: ITLS proposed framework for the MaaS ecosystem, comprising the new function for a mobility broker

aggregating different suppliers and delivering integrated service to demanders . . . . . . . . . . . . . . . . . . . . . . . . . . . . .95Figure 11.2: Individually tailored mobility packages tested in our ITLS research (Ho et al., 2018). . . . . . . . . . . . . . . . . . . . . . . . .95

Tables

Table 1.1: Top ten chassis plus body combinations and sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19Table 2.1: Registered ‘commercial-use’ buses as at 31 January 2019 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29Table 2.2: Bus and coach fuel consumption by fuel type . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31Table 2.3: Average and maximum age requirements for buses by state/territory and service type . . . . . . . . . . . . . . . . . . . . . . . .37Table 3.1: Estimate of bus operators by state/territory and service type . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39Table 3.3: Typical capacities and capital costs by mode and vehicle type based on mid-2014 prices . . . . . . . . . . . . . . . . . . . . .47Table 3.4: Operating costs of each mode by category, based on mid-2014 prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .48Table 3.5: The concepts of efficiency and effectiveness as it relates to bus and coach operations . . . . . . . . . . . . . . . . . . . . . . . .48Table 3.6: Productivity comparison by passenger kilometre intensity for 2016-17 (ITLS estimate from BITRE/ABS data). . . . . . .50Table 3.7: Productivity comparison by state/territory by passenger trip intensity for 2016-17

(ITLS estimate from BITRE/ABS and state/territory-provided data). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .50Table 3.8: Key statistics on the bus and coach driving profession . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .56Table 4.1: Total passengers carried by the bus and coach industry in each state/territory

(data collated by ITLS correspondence with state/territory authorities and associations) . . . . . . . . . . . . . . . . . . . . . . .68Table 4.2: Dimensions and definitions of social exclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .69Table 5.1 Key strategic areas for coach travel to disperse tourists to regional Australia. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .79Table 6.1: ‘Turn Up and Go’ Minimum Service Levels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .82Table 7.1: Registration charges for heavy vehicles 2018–19 and 2019–20 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .83Table 7.2: Heavy vehicle charge national total estimate for 2016-17 (from BITRE) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .83Table 8.1: Estimate of corrective fuel excise (tax) for Australian passenger cars—2015 price estimate . . . . . . . . . . . . . . . . . . . .85Table 9.1: Organising the tactical environment, adapted from Stanley and Longva (2010: 82) . . . . . . . . . . . . . . . . . . . . . . . . . . . .88Table 9.2: Various cost/revenue sharing contractual arrangements, adapted from Stanley and van de Velde (2008: 24) . . . . . . .88Table 9.3: Singapore bus contracting rounds and winners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .90Table 9.4: Remaining contract rounds and offerings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .90Table 10.1: On demand trials in NSW (as at mid-2018) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .93

1212 Moving People > Australian Bus and Coach Industry: a snapshot

M

OVING PEOPLE

THEMANUFACTURERS

& SUPPLIERS

1313Moving People > Australian Bus and Coach Industry: a snapshot

Bus Manufacturing 1. What is a bus? The Australian Bureau of Statistics (ABS) defines a bus [or coach], based on the current definition (1989) under Australian Design Rules (ADR) as a motor vehicle constructed for the carriage of passengers, with 9 or more seats, including the driver’s seat. When not specified, the term ‘bus’ in this report applies to a bus or a coach type motor vehicle.

The bus and coach industry defines the construct of a bus as:

• a buggy type chassis (2, 3 or 4 axle) and associated mechanical components (engine, steering, axle, etc.) and the body (panels, floors, seating, etc.)

• a composite bus (also called monocoque) which does not have a traditional buggy chassis, is a composite of all mechanical and body components as an integral unit.

The bus and coach industry generally defines the size of a bus as:

• large – a bus that has a GVM of 10 tonne or more, a body length of 12.5 to 18 metres with a seat capacity (including driver) of 26 or more

• medium – a (midi) bus that has a GVM of less than 10 tonne, a body length of 8 to 10 metres with a seat capacity (including driver) of 16 to 25

• small – a (mini) bus that has a GVM of less than 4.5 tonne, a body length of less than 8 metres with a seat capacity (including driver) of 9 to 15.

Buses can also vary in style based on its primary area of operations (urban or regional) and/or primary duties (route, school, charter, long distance) and can be:

• single deck or double deck

• articulated or rigid

• high floor or low floor accessible.

1 .1 Profile of the bus manufacture and supply sectorThe data presented in this Section is compiled from bus data published by Australasian Bus and Coach (ABC), an industry magazine that publishes monthly delivery data supplied by chassis manufacturers. Data from quarterly survey information provided by BIC Members has also been used to assist in differentiating buggy-type chassis buses and monocoque (composite) constructs.

Most Australian buses are of a body-on-frame construct method usually with separate chassis and body manufacturers. Splitting body and chassis construction allows businesses to specialise in different fields and also offers customers greater choice in chassis/body combinations. The majority of buses are built in Australia on a European chassis (and increasingly Asian chassis). In recent years, there has been a growth in monocoque buses, manufactured locally and abroad.

In a recent BIC analysis of available ABC delivery data (ie. all large bus types delivered to a bus operator) from Jan 2017 to Feb 2020, 36.3% were fully imported buses and 63.7% were built locally on either imported chassis or as a monocoque.

In this 3-year period, the market can be further broken down.

City type public transport/route buses:

• 11.1% – fully imported

• 88.9 % – locally built (on either imported chassis or as a monocoque).

School Buses:

• 40.4 % – fully imported

• 59.6% – locally built (on either imported chassis or as a monocoque).

The Australian bus market has seen significant change over the past decade from 100% Australian manufactured, with the school bus market most effected through imports from Asia.

Based on various industry surveys undertaken by the BIC in 2010, 2018 and 2020, the BIC estimates that:

• $5 billion is contributed to the Australian economy each year in the manufacture of buses

• there can be up to 40 manufacturing and parts supply companies (local and abroad) that contribute to the final assembly of a single bus

• the sector employs more than 10,000 Australians

• close to $1.5 billion is contributed to the Australian economy each year in supplies and services to keep the buses operational and in service.

1414 Moving People > Australian Bus and Coach Industry: a snapshot

Number of buses supplied in Australia

A total of 17,969 buses were delivered into the Australian marketplace for the calendar years 2008 to 2019.

The 2019 and 2020 industry reported deliveries of buses and coaches were 1,449 and 1,226 respectively. The economic impact of Covid-19 on the manufacturing sector was most evident in the delivery of long distance coaches seeing a down-turn of 74% from 2019. Route bus deliveries were also down by 20% whilst Charter and School bus deliveries remained consistent throughout 2020.

Reported bus deliveries average around 1,500 per year but the annual total deliveries vary based on a number of external factors including:

• government procurement of buses for route and school services

• increases in demand for bus passenger services caused by increases in fuel and living costs

• the long term impact of congestion in an ever increasing urban Australia

• electoral cycle priorities

• regulated vehicle replacement programs

• average age of fleet and maximum age regulations

• rise and fall of the Australian dollar.

Figure 1.1 highlights the annual variation in total deliveries recorded which can significantly impact on the capacity of some businesses to deal with the peaks and troughs.

Figure 1.1: Total bus and coach deliveries January 2008 to December 2019

16901843 1903

14781580

14811398 1369

1223 12061349

1449

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Bus deliveries by year (2008-2019)

Source: Australasian Bus and Coach (January 2008 to December 2019)

1515Moving People > Australian Bus and Coach Industry: a snapshot

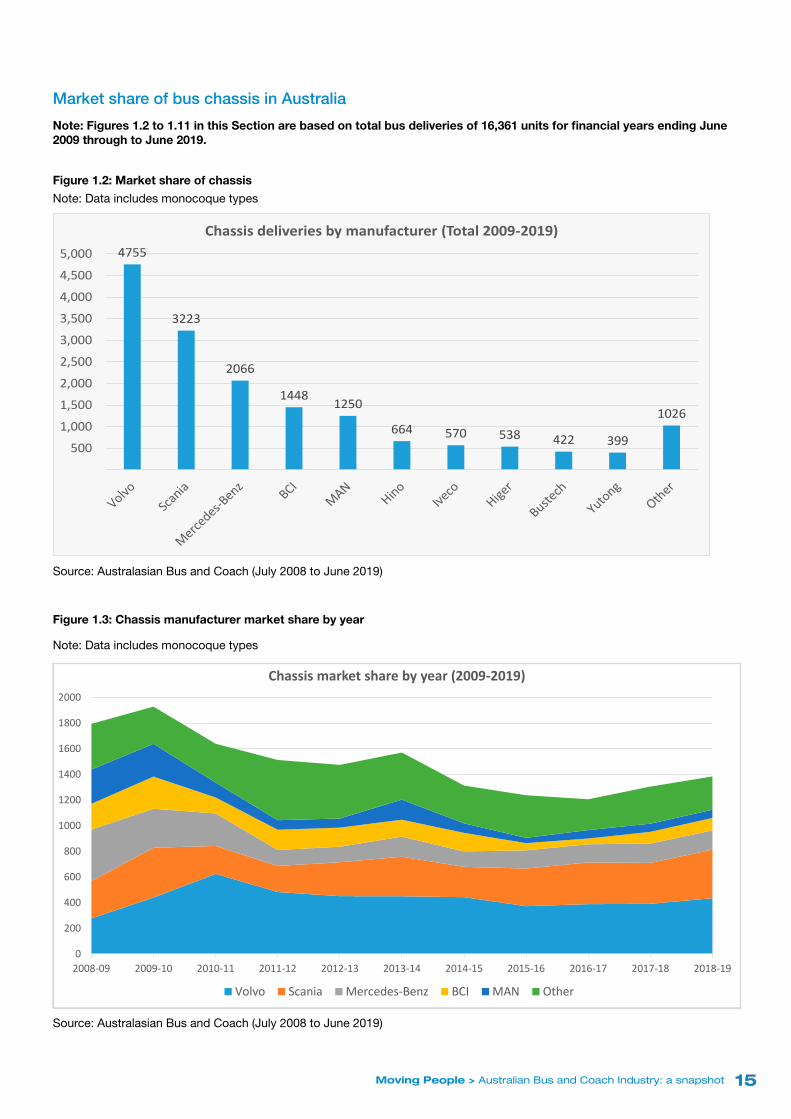

Market share of bus chassis in Australia

Note: Figures 1.2 to 1.11 in this Section are based on total bus deliveries of 16,361 units for financial years ending June 2009 through to June 2019.

Figure 1.2: Market share of chassis

Note: Data includes monocoque types

4755

3223

2066

1448 1250

664 570 538 422 399

1026

5001,0001,5002,0002,5003,0003,5004,0004,5005,000

Chassis deliveries by manufacturer (Total 2009-2019)

Source: Australasian Bus and Coach (July 2008 to June 2019)

Figure 1.3: Chassis manufacturer market share by year

Note: Data includes monocoque types

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Chassis market share by year (2009-2019)

Volvo Scania Mercedes-Benz BCI MAN Other

Source: Australasian Bus and Coach (July 2008 to June 2019)

1616 Moving People > Australian Bus and Coach Industry: a snapshot

Figure 1.4: Chassis market share for top 5 manufacturers by state/territory

Note: Data includes monocoque types

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

NSW VIC QLD WA SA TAS ACT NT

Chassis market share by state (Total 2009-2019)

Volvo Scania Mercedes-Benz BCI MAN Other

Source: Australasian Bus and Coach (July 2008 to June 2019)

1717Moving People > Australian Bus and Coach Industry: a snapshot

Market share of bus body in Australia

The bus body market sees greater market diversity compared with the chassis market in terms of the number of bodybuilders active, but also more concentrated market share amongst the largest players.

Based on total deliveries for the financial years 2009 to 2019, the top ten manufacturers accounted for 84.4%

of all bodies delivered (Figure 1.5). The top five body manufacturers accounted for 72.0% of deliveries in 2008-09 and 61.7% in the 2018-2019 financial year (Figure 1.6). Similar to the chassis market share, the market share of each body manufacturer varies significantly between states and territories (Figure 1.7).

Figure 1.5: Market share of body manufacturers

Note: Data includes monocoque types

4999

2417

1508 1403

676 673 532 431 418 399

2480

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000Body deliveries by manufacturer (Total 2009-2019)

Source: Australasian Bus and Coach (July 2008 to June 2019) Note (*) UBC/Chiron are no longer partnered

1818 Moving People > Australian Bus and Coach Industry: a snapshot

Figure 1.6: Body manufacturer market share by year

Note: Data includes monocoque types

200400600800

1,0001,2001,4001,6001,8002,000

Body market share by year (2009-2019)

Volgren Custom BCI Bustech Higer Other

Source: Australasian Bus and Coach (July 2008 to June 2019)

Figure 1.7: Body market share for top 5 manufacturers by state/territory

Note: Data includes monocoque types

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

NSW VIC QLD WA SA TAS ACT NT

Body market share by state (Total 2009-2019)

Volgren Custom BCI Bustech Higer Other

Source: Australasian Bus and Coach (July 2008 to June 2019)

1919Moving People > Australian Bus and Coach Industry: a snapshot

Table 1.1 outlines the top ten chassis plus body combinations ordered by total deliveries for the financial years 2009 to 2019.There is a wide variety of combinations but also heavy concentration in terms of the market share for the most popular combinations. A number of monocoque buses also appeared in the top ten.

Table 1.1: Top ten chassis plus body combinations and sales

Chassis Body Deliveries

Volvo Volgren 3,140

BCI BCI 1,441

Scania Custom 896

Scania Volgren 809

Mercedes-Benz Volgren 653

Volvo Custom 552

Higer Higer 538

Bustech Bustech 422

Volvo Bustech 359

Mercedes-Benz Custom 353

Source: Australasian Bus and Coach (July 2008 to June 2019)

Market share of other suppliers

Air conditioning and seating constitute important inputs into the bus manufacturing supply chain. Whilst some chassis and body manufacturers also make air conditioning and seating components, most of these products are made by specialty third party manufacturers or importers.

Figures 1.8 and 1.9 provide an analysis of the market shares for the financial years 2009 to 2019.

There are a number of other major suppliers (and industries) supported by the bus manufacturing sector. As noted at the start of this Section, the BIC estimates up to 40 companies can be involved in the final assembled bus supplying various components and services.

Parts and Services

• Engine

• Transmission

• Suspension

• Axles

• Dynamic safety systems

• Wheels and tyres

• Steel materials and manufactured structure

• Sheet metal fabrication

• Fibreglass and plastic panel components

• Electrical harnesses

• Flooring materials

• Glazing

• Bonding materials

• Multiplexing systems

• Seating

• Door and associated controls & safety systems

• Fire suppressions systems

• 2-way radio

• Decals

• Reverse camera

• Insulation

• Various electrical components

• Lighting

• Textiles/coverings

• Windscreen blinds

• Destination sign

On-board monitoring devices

• Driver assistance systems

• CCTV

• Vehicle telematic systems

• GPS and vehicle tracking systems

• Child safety systems

2020 Moving People > Australian Bus and Coach Industry: a snapshot

Figure 1.8: Top ten air conditioning manufacturers by total sales

6350

18731594

1085708 676 641 559 405 389

1657

1,000

2,000

3,000

4,000

5,000

6,000

7,000

ThermoKing

Coachair Denso Hispacold Carrier Cooltek Spheros Tracs Kingtec Yutong Other

Air conditioning manufacturers by sales (Total 2009-2019)

Source: Australasian Bus and Coach (July 2008 to June 2019)

Figure 1.9: Top ten seating manufacturers by total sales

6634

3423

1600

940 832

403 336 211 178 136

1244

1,000

2,000

3,000

4,000

5,000

6,000

7,000Seating manufacturers by market share (Total 2009-2019)

Source: Australasian Bus and Coach (July 2008 to June 2019)

2121Moving People > Australian Bus and Coach Industry: a snapshot

Market share case study of Chinese manufacturers (and electric buses)

Chinese companies are entering the international stage in the transportation and infrastructure sectors.

Chinese chassis manufacturers have become active in Australia over the past decade (Figure 1.10), although the total market share of Chinese bus and coach deliveries has remained steady since 2011-12. BCI is included in this analysis which although Australian-owned, moved its production to China in 2006. In the body manufacturing sector (Figure 1.11), market shares have been remarkably similar due to the high proportion of composite (monocoque) buses sold. A major exception is King Long which has been active since before 2008-09 and uses any chassis including MAN, Hino and Daewoo; only 55% of King Long bodied buses sold were of monocoque construction.

Other Chinese manufacturers are expected to expand their presence in Australia and include Ankai, Youngman, Zhongtong, BYD and CRRC. CRRC is the world’s largest rail manufacturer (formed after the merger of CNR and CSR) which has recently ventured into road transport through what is marketed as autonomous rail rapid transit (or trackless trams) which is essentially an optically-guided bus (other examples operate in Rouen, France and Castellón, Spain).1 Already in operation in Zhuzhou, China, this technology has recently attracted interest as a cost effective alternative to light rail investment. Shanghai Electric also produces magnetic guidance bus technology and has seen interest expressed to supply their products in Australia and New Zealand.

BYD is a major manufacturer of electric buses and in their production city of Shenzhen has an all-electric bus fleet 16,400 strong—greater than the rest of the world combined. Their success hinges on China’s New Energy Vehicle policy initiated in 2009 to prioritise the electrification of the road transport system, through establishing national mandates, subsidising manufacturers and nurturing policy competition amongst cities. These policies have helped propel the industry and allow the manufacturing sector to reap economies of scale, as well as propel China to become the home of 99% of the world’s electric buses. In March 2019, it was announced that local level subsidies would be abolished, and overall subsidies reduced by more than 50%. Chinese manufacturers are therefore likely to pursue international markets to offset lower domestic demand.

A major operator in Shenzhen is Shenzhen Bus Group,2 a joint venture between Hong Kong-based Transport International and the Shenzhen Municipality.3 In 2017, they submitted a bid in the Bukit Merah (tranche 4) round in Singapore (see Section 9.4) where electrification featured as a large part of their offering, showing Chinese bus operators’ interest in entering the international stage. Shenzhen Group is also at the forefront of exporting electric bus operation know-how to the world through their partnership with the International Association of Public Transport (UITP) Academy.

1 For more discussion, see https://theconversation.com/looking-past-the-hype-about-trackless-trams-107092

2 As of September 2018, the group is also the world’s largest pure electric taxi operator with a fleet of 4,700

3 Shenzhen has been designated a Special Economic Zone since 1980

There are a number of hybrid and electric bus trials underway in Australia. Vehicles in these trials tend to be dominated by Chinese manufacturers. Points of contention that arise include asset allocation issues (especially around capital and maintenance costs since electric buses tend to be more expensive to acquire but have lower ongoing costs), as well as the merits of hybrid fleets (which require two concurrent systems), opportunity charging and type of charging infrastructure (e.g., bus mounted pantographs versus inverted pantographs).

Overseas companies are also actively entering China in the urban passenger transport operations space. MTR Corporation (HK company) is operating in the Chinese mainland under build-operate-transfer and public-private partnerships arrangements in Beijing, Shenzhen and Hangzhou. RATP Dev Transdev Asia is active in Hong Kong, Macau, Jiangsu and Anhui provinces as well as Shenyang, and Shanghai Keolis (Shanghai Shentong Metro Group and Keolis joint-venture) in Shanghai. Regulatory and competition reforms in the future will further open up opportunities for foreign involvement.

2222 Moving People > Australian Bus and Coach Industry: a snapshot

Figure 1.10: Chinese chassis manufacturers market share

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

350

400

450Chinese chassis manufacturers market share (2009-2019)

BCI Bonluck Higer King Long Yutong Percentage Chinese

Source: Australasian Bus and Coach (July 2008 to June 2019)

Figure 1.11: Chinese body manufacturers market share

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

350

400

450

500Chinese body manufacturers market share (2009-2019)

BCI Bonluck Higer King Long Yutong Percentage Chinese

Source: Australasian Bus and Coach (July 2008 to June 2019)

2323Moving People > Australian Bus and Coach Industry: a snapshot

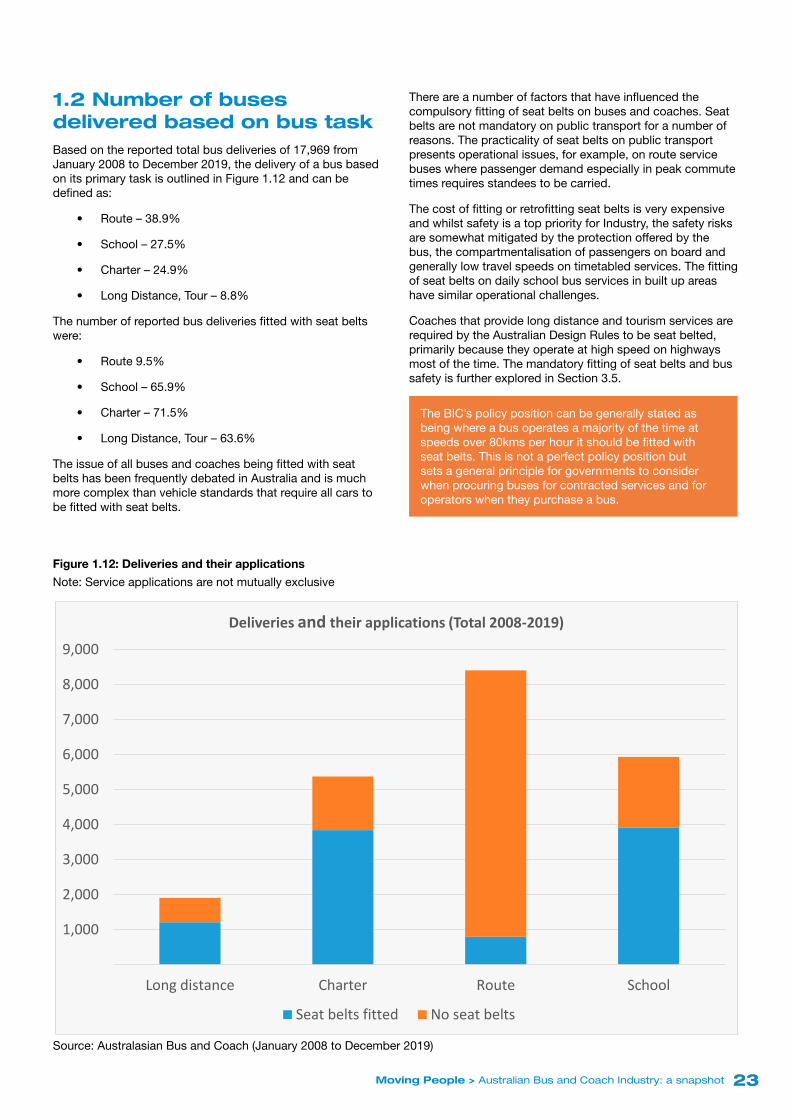

1 .2 Number of buses delivered based on bus taskBased on the reported total bus deliveries of 17,969 from January 2008 to December 2019, the delivery of a bus based on its primary task is outlined in Figure 1.12 and can be defined as:

• Route – 38.9%

• School – 27.5%

• Charter – 24.9%

• Long Distance, Tour – 8.8%

The number of reported bus deliveries fitted with seat belts were:

• Route 9.5%

• School – 65.9%

• Charter – 71.5%

• Long Distance, Tour – 63.6%

The issue of all buses and coaches being fitted with seat belts has been frequently debated in Australia and is much more complex than vehicle standards that require all cars to be fitted with seat belts.

There are a number of factors that have influenced the compulsory fitting of seat belts on buses and coaches. Seat belts are not mandatory on public transport for a number of reasons. The practicality of seat belts on public transport presents operational issues, for example, on route service buses where passenger demand especially in peak commute times requires standees to be carried.

The cost of fitting or retrofitting seat belts is very expensive and whilst safety is a top priority for Industry, the safety risks are somewhat mitigated by the protection offered by the bus, the compartmentalisation of passengers on board and generally low travel speeds on timetabled services. The fitting of seat belts on daily school bus services in built up areas have similar operational challenges.

Coaches that provide long distance and tourism services are required by the Australian Design Rules to be seat belted, primarily because they operate at high speed on highways most of the time. The mandatory fitting of seat belts and bus safety is further explored in Section 3.5.

The BIC’s policy position can be generally stated as being where a bus operates a majority of the time at speeds over 80kms per hour it should be fitted with seat belts. This is not a perfect policy position but sets a general principle for governments to consider when procuring buses for contracted services and for operators when they purchase a bus.

Figure 1.12: Deliveries and their applications

Note: Service applications are not mutually exclusive

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Long distance Charter Route School

Deliveries and their applications (Total 2008-2019)

Seat belts fitted No seat belts

Source: Australasian Bus and Coach (January 2008 to December 2019)

2424 Moving People > Australian Bus and Coach Industry: a snapshot

1 .3 Number of buses delivered based on Emission StandardsAn important government-mandated consideration is the environmental performance of new buses and coaches. Buses and coaches are subject to standards based on the international harmonisation with European Union (EU) vehicle standards, with US and Japanese equivalent standards accepted. This applies to heavy vehicle emissions standards and are commonly recognised as Euro Emission Standards.

The Euro Emission Standards for heavy vehicles has been mandated for all new buses and coaches in chronological order as follows:

• Euro I (1992)

• Euro II (1998)

• Euro III (2000)

• Euro IV (2005)

• Euro V (2010)

• Euro VI – expected to be mandated in 2027, though Euro VI buses and coaches are already operating in Australia.

Newer vehicles are fitted with technologies such as particulate traps which have very low emission rates of (carcinogenic) fine particulate matter. Figure 1.13 shows the reported emissions standards of buses delivered over the past decade. In 2008-09, 59.8% of deliveries were of Euro IV standard. By 2012-13, Euro IV had all being phased out, comprising instead of EEV (37.0%) and Euro V (61.7%) deliveries; EEV (Enhanced environmentally friendly) refers to an emissions standard between the levels Euro IV and Euro V. In 2018-2019, Euro V comprised of 72.70% of deliveries and Euro VI, 20.02%. A small number of electric buses have also been delivered in the past 5 years.

23% of Australia’s bus fleet is over 17 years old (Figure 2.10) meaning they are meeting Euro III or less emission standards. Data on Australia’s ageing bus and coach fleet and its renewal is further discussed in Section 2.

Figure 1.13: Deliveries by emissions standards

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000Deliveries by emissions standards (2009-2019)

Euro 3 Euro 4 EEV Euro 5 Euro 6

Source: Australasian Bus and Coach July 2018 to June 2019

2525Moving People > Australian Bus and Coach Industry: a snapshot

Figure 1.14: Deliveries by emissions standards by state/territory

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

NSW VIC QLD WA SA TAS ACT NT

Deliveries by emisssions standards by state/territory (Total 2009-2019)

Euro 3 Euro 4 EEV Euro 5 Euro 6

Source: Australasian Bus and Coach (July 2008 to June 2019)

2626 Moving People > Australian Bus and Coach Industry: a snapshot

M

OVING PEOPLE

THEFLEET

2727Moving People > Australian Bus and Coach Industry: a snapshot

Fleet on the road2. The Bus FleetThe Australian bus fleet (route/school) is old and of good quality. The reasons for this vary but in general it relates to state and territory government budgets for procurement of buses and the number and frequency of services provided for public transport (route) and school bus services, which make up the majority of the Australian fleet on the road. Coaches for example operating in the long distance and tourism market tend to be newer to provide superior levels of passenger comfort and attract customers and are a small percentage of the overall passenger task and fleet on the road.

Route and school bus services procured by or operated by state and territory governments have operated at service levels that result in very low vehicle kilometres travelled each year by a bus and therefore the vehicles full life cycle, if maintained to specification, can be up to 25 years. This has over many decades seen buses, as a generalisation, providing route and school services proceed through a service life cycle that begins with a new bus providing high patronage urban passenger services and ends with lower patronage services in regional and rural areas. Many vehicles over 15 years also act as replacement service vehicles and used for charter purposes. This approach has maximised the return on investment in the vehicle out to 25 years of age.

Some states and territories have average age of fleet and maximum age requirements as outlined in this Section of the report (see Table 2.3). The reality is, 23% of the Australian bus fleet is 17 years or older and operate with Euro III or less emission standards. More detail on this follows in Section 2.3. This reflects a large percentage of the fleet performing the passenger task in vehicles that have poor emission performance and offer very little in the way of modern comfort features for passengers compared with new buses. This is hardly conducive to attracting passengers to use public transport or school bus services or addressing greenhouse and other emissions from transport.

2 .1 Number of registered buses Fleet size and composition data in this Section is compiled from the ABS Motor Vehicle Census (2019) and the ABS Motor Vehicle Use Survey (2018). The census publication (2019) presents statistics relating to vehicles which were registered with a motor vehicle registration authority by the 31st January of each year. In 2019, the number of registered buses was 105,331 (Figure 2.1).

It is important to note that the ABS in undertaking motor vehicle surveys, uses the following definitions from Australian Design Rules (ADR):

• Omnibus – a passenger vehicle having more than 9 seating positions, including that of the driver; and

• C Class vehicle – a passenger vehicle equipped to seat no more than 12 adults (including driver) with a gross vehicle mass (GVM) of up to 4.5 tonne.

The ABS also categorises registered buses as:

• 2 axle with a GVM of less than 4.5 tonne

• 2 axle with a GVM of 4.5 to 12 tonne

• 2 axle with a GVM of over 12 tonne

• 3 axle with a GVM of over 12 tonne

• 3 axle articulated with a GVM of over 4.5 tonne.

In February 2020, the BIC undertook a significant analysis of the data from the ABS 2018 survey and 2019 census. Through this analysis, the BIC has been able to identify the number and types of buses being utilised by Industry to accurately reflect the current fleet on the road.

When extrapolating data from the ABS survey and census, the BIC has included registered ‘commercial-use’ buses, defined as a bus that:

• has a seat capacity (including the driver) of 12 seats or more (ie., not a C Class vehicle)

• is less than 26 years of age (eligibility criterion for government contracted services)

• is 4.5 GVM tonne and above.

The BIC analysis identifies 43,684 ‘commercial-use’ buses (Figure 2.2) operating in the bus and coach industry delivering public transport, school and other government contracted services, tour, charter, long distance and other commercial services.

2828 Moving People > Australian Bus and Coach Industry: a snapshot

Figure 2.1: Registered buses ABS 2019 – small, medium and large

59541

15189

30601

010000200003000040000500006000070000

Small Omnibus Medium Omnibus Large Omnibus

Num

ber o

f Bus

es

Small Bus: 9 to 15 seats including driverMeduim Bus: 16 to 25 including driverLarge Bus: 26 including driver and over

Registered buses - ABS Total - 105,331

Source: Australian Bureau of Statistics, 2019

Figure 2.2: ‘Commercial-use’ registered buses – under and over 12 tonne

Note: Based on BIC analysis of ABS 2019 not including small (mini) buses under 4.5 tonne GVM or buses 26 years of age or older.

NSW VIC QLD SA WA TAS NT ACT Total ByType

Medium Buses (under 12T GVM) 4640 3074 3818 1085 3463 578 586 148 17392Large Buses (over 12T GVM) 9042 5940 5043 1786 2911 684 427 459 26292

0

5000

10000

15000

20000

25000

30000

'Commercial-use' registered buses - total 43,684

2929Moving People > Australian Bus and Coach Industry: a snapshot

Market share of registered buses by state/territory

Close to three quarters (31,557) of the total number (43,684) of ‘commercial-use’ buses are registered in the eastern states NSW, Vic and Qld. Table 2.1 provides a break-down of these buses in 2019 by axle-type and GVM for all states/territories. 2 axle buses (41,004) accounted for the bulk of registered

buses on Australia’s road network. Of these 2 axle buses, 60% have a GVM of 12 tonne or more. The distribution of buses amongst states/territories in Australia is broadly proportional to the population split in the country (Figures 2.3 and 2.4). All states and territories (except NT) lie between 1.4 and 2.4 buses per 1,000 capita; the NT has 4 buses per 1,000 capita.

Table 2.1: Registered ‘commercial-use’ buses as at 31 January 2019

Note: Based on BIC analysis of ABS 2019 not including small (mini) buses under 4.5 tonne GVM or buses 26 years of age or older.

NSW VIC QLD SA WA TAS NT ACTTotal By

TypeBuses – 2 axle – over 4.5 to 12t GVM

4640 3074 3818 1085 3463 578 586 148 17392

Buses – 2 axle – over 12t GVM 8042 5483 4515 1500 2702 640 359 371 23612

Buses – 3 axle – over 12t GVM 747 418 463 113 104 18 68 47 1978

Buses/artic – 3 axle – over 4.5t GVM 253 39 65 173 105 26 0 41 702

Total 13682 9014 8861 2871 6374 1262 1013 607 43684

Less than 12t GVM 4640 3074 3818 1085 3463 578 586 148 17392

Over 12t GVM 9042 5940 5043 1786 2911 684 427 459 26292

3030 Moving People > Australian Bus and Coach Industry: a snapshot

Figure 2.3: Number of registered ‘commercial-use’ buses by state/territory

Note: Based on BIC analysis of ABS 2019 not including small (mini) buses under 4.5 tonne

13,682

9,014 8,861

2,871

6,374

1,262 1,013 6070

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

NSW VIC QLD SA WA TAS NT ACT

Registered 'commercial-use' buses less than 26 years of age

NSW has the largest fleet with approx. 4,500 more buses than either Qld and Vic.

Figure 2.4: Percentage of buses on register by state/territory

Note: Based on BIC analysis of ABS 2019 not including buses 26 years of age or more.

31%

21%20%

7%

15%

3% 2% 1%

Percentage of buses/coaches over 4.5 t on register by state/territory

NSW

VIC

QLD

SA

WA

TAS

NT

ACT

3131Moving People > Australian Bus and Coach Industry: a snapshot

2 .2 Number of registered buses based on fuel type and emissionsThe running of buses and coaches on Australia’s roads relies heavily on diesel with over 90% of the current fleet using that fuel (Table 2.2). The Other category in Table 2.2 (1.7%) includes natural gas buses which although originally hailed as an environmental alternative, suffered from reliability issues and higher maintenance costs. Hybrid and electric buses are also a new category which is quickly garnering interest around Australia.

Euro III emission standards were introduced in Australia for New Heavy Vehicles operating on diesel, LPG and compressed natural gas (CNG) in 2000 as part of Australian Design Rules (ADR) 80/00 (Emissions Control for heavy vehicles). There are at least 9,981 registered ‘commercial-use’ buses or coaches that are operating at Euro III or lower emissions standards. More commentary on emissions standards are provided as part of bus chassis deliveries in Section 1.3. 23% of Australia’s bus fleet is over 17 years old meaning they are meeting Euro III or less emission standards (Figure 2.10). Data on Australia’s ageing bus and coach fleet and its renewal is further discussed in Section 2.3.

Market share of fuel type and emissions compared across all transport

The average rate of fuel consumption varies widely between road transport modes (Figure 2.5). Across all sectors (excluding trucks), fuel consumption has reduced significantly. In the bus sector, fuel efficiency has improved

14% over the past decade to an average of 25.4 L/100km travelled for buses built after 2012. This figure varies between 18.4 L/100km for petrol buses, 25.7 L/100km for diesel buses and 24.6 L/100km for LPG/CNG/dual fuel/hybrid and other fuel types. For post-2000 vehicle models, diesel vehicles tend to be more fuel efficient than their petrol counterparts. It is worth noting that petrol efficiency is greater in the bus sector probably because the petrol fleet is geared towards smaller buses, whilst diesel powers full-size buses (including doubledeckers and articulated buses) and coaches.

In terms of greenhouse gas emissions, the transport sector contributes 97 million tonnes per annum of carbon dioxide equivalent (Figure 2.6). The majority (45%) of this is emitted by cars, followed by trucks (22%), light commercial vehicles (14%) then domestic aviation (9%). Buses emit just 2 million tons (or 2%) of enhanced greenhouse gases per annum. Railways emit double this amount at 4 million tonnes.

The emissions intensity of different passenger transport modes is considered in Figure 2.7. Public transport emits less than half that of private car by passenger kilometre transported, demonstrating the sustainable value of mode shifts. The bus figure presented is biased relatively downwards by long distance coaches, which have considerably better average efficiencies than most urban route buses. This is because coaches operate primarily in an economically deregulated market and they see higher passenger loadings per trip. City buses also face extra congestion and stop-start conditions which lead to substantially higher average fuel consumption rates than for non-urban use. The national rail level presented is biased upwards by the heavy use of lignite for electricity generation in Victoria. Across public transport modes, buses perform better on environmental emission terms than rail.

Table 2.2: Bus and coach fuel consumption by fuel type

Note: ABS (2019) data does not account for age of bus (a BIC analysis would normally exclude buses 26 years or older).

National heavy vehicle code Diesel Electric PetrolLPG/Dual

fuelOther

Buses – 2 axle – over 4.5 to 12t GVM 17629 3 494 40 5

Buses – 2 axle – over 12t GVM 22696 24 279 1683 13

Buses – 3 axle – over 12t GVM 2167 0 29 3 3

Buses – 4 axle – over 12t GVM 3 0 3 0 0

Buses/artic – 3 axle – over 4.5t GVM 727 0 8 34 767

Total 43222 27 813 1760 788

Source: Australian Bureau of Statistics (2019)

3232 Moving People > Australian Bus and Coach Industry: a snapshot

Figure 2.5: Road transport average rate of diesel fuel consumption (L/100km)

Note: ABS (2018) data includes all vehicles that have seated capacity of 9 or more including the driver.

0.0 10.0 20.0 30.0 40.0 50.0 60.0

Passenger vehicles

Light commercial vehicles

Rigid trucks

Articulated trucks

Non-freight carrying trucks

Buses

Passenger vehicles Light commercial vehicles Rigid trucks Articulated trucks Non-freight carrying trucks Buses2013 and after 11.4 12.1 28.3 55.4 17.3 25.72003 to 2012 11.3 12.5 28.9 55.5 27.9 29.92002 and earlier 14.8 12.1 28.9 52.7 25.3 35.0

Road transport average rate of diesel fuel consumption (L/100km)

2013 and after 2003 to 2012 2002 and earlier

Figure 2.6: Emissions in the transport sector by mode

0

5

10

15

20

25

30

35

40

45

50

Emissions by sector Mt CO2-e (2017)

Source: Department of the Environment and Energy, 2017

3333Moving People > Australian Bus and Coach Industry: a snapshot