Microcredit: Empowerment and Disempowerment of Rural Women in Ghana

64

Microcredit: Empowerment and Disempowerment of Rural Women in Ghana ABSTRACT Microcredit for women is a commonly used strategy for women empowerment. Based on longitudinal qualitative research with rural women who are involved in an NGO-run micro-lending scheme in Ghana, this paper examines the empowerment effects of rural women’s access to microcredit. We found that some women are empowered as a result of their access to credit; some have little control over the use of loans and are no better off; and some are subjected to harassment and are worse off due to their inability to repay loans in time. The implications of these findings for policy and practice are discussed. 1

Transcript of Microcredit: Empowerment and Disempowerment of Rural Women in Ghana

Microcredit: Empowerment and Disempowerment of RuralWomen in Ghana

ABSTRACT

Microcredit for women is a commonly used strategy for

women empowerment. Based on longitudinal qualitative

research with rural women who are involved in an NGO-run

micro-lending scheme in Ghana, this paper examines the

empowerment effects of rural women’s access to

microcredit.

We found that some women are empowered as a result of

their access to credit; some have little control over the

use of loans and are no better off; and some are

subjected to harassment and are worse off due to their

inability to repay loans in time. The implications of

these findings for policy and practice are discussed.

1

Keywords: Microfinance; Women; Empowerment;

Disempowerment; Ghana.

1. INTRODUCTION

Limited savings and lack of access to credit make it

difficult for many poor people, particularly women in

low-income countries, to become self-employed and to

undertake productive employment and income-generating

ventures (Khandker, 1998). Microcredit programmes for

women have thus emerged and are currently being promoted

as both a solution to women’s limited access to credit

and a strategy for poverty reduction and women

empowerment (Hashemi, Schuler & Riley, 1996).

2

Based on data generated from original longitudinal

qualitative research we conducted in 5 rural communities

in Ghana with women who are involved in a popular local

microenterprise development programme run by a big

international non-governmental organization (NGO), this

paper investigates how rural women’s access to

microcredit empowers them or otherwise. Findings show

that some women have become more empowered, while others

have also become disempowered as a result of accessing

the loan.

2. BACKGROUND OF RESEARCH

This paper forms part of a larger, original research that

sought to explore the relationship between microcredit

and the socio-economic empowerment of women in rural

Ghana. Microcredit or microfinance (these terms are often

used interchangeably) is simply the extension of small

amount of collateral–free institutional loans to jointly

liable poor group members for their self-employment and

income-generation (Rahman, 1999). The strategy is based

on a creative grassroots alternative to reliance on

3

informal lenders as the source of credit in situations

where people, especially the poor, cannot get access to

formal credit such as loans from banks (McDermott, 2001).

In low-income countries worldwide, microcredit for women

is increasingly used as a strategy for poverty

alleviation and women empowerment. Currently, there are

arguments that micro-lending to poor women holds the key

to 21st century’s sustainable economic and social

development (Norwood, 2005; UN, 2011). The argument is

that the biggest promises of microfinance are to reduce

poverty and empower women (Norword, 2005). Indeed,

Mohammed Yunus, founder of the Grameen Bank’s

microfinance programme in Bangladesh, has concluded that

he can eradicate global poverty among women by means of

one simple idea – microcredit (Hulme and Mosley, 1996).

It is within this context that the micro-lending

activities of World Vision Ghana in the Nadowli District

are to be understood. World Vision Ghana is an

international Christian relief and development NGO

4

dedicated to helping children and their communities

worldwide to reach their full potential by tackling the

causes of poverty. In Ghana, World Vision began operation

in 1980, and started the Nadowli Area Development

Programme in October 1993. The extension of microcredit

to women for micro-enterprise development is one of World

Vision’s strategies for women empowerment.

World Vision Ghana’s microcredit scheme is modelled on

the approach of the Grameen Bank. It lends to very poor

individuals, all of whom are women. At the time of this

research, 3,042 women were benefitting from the scheme.

Lending was based on groups rather than individuals,

although loan sizes vary from one group member to the

other, usually depending on loan managers’ evaluation of

the capacity of each group member to effectively manager

the loan. A typical group consisted of 10 - 20 borrowers,

and lending to individuals within the group occurs in

sequence. The average loan size was 15 Ghana cedi (then

approximately US$15 and now approximately US$ 7.50). No

collateral was required, and a flat interest rate of 20

5

per cent per month was charged on loans. Loans to groups

were usually for a period of 6months, with potential for

increasing loan amounts each cycle. In principle, the

size of loan should steadily increase with regular and

timely monthly interests payment by all group members. In

practice however, delays in payment of interests often

make it difficult for group members to receive additional

funds at the end of each loan cycle. Borrowers are

expected to start making their monthly interest payment

after a grace period of one month. The central feature of

the programme is the joint-liability condition. That is in the

event of any group member defaulting, no group member is

allowed to borrow again, and group members are also

collectively responsible for paying up the debt of any

single group member in case of default.

In view of the fact that World Vision Ghana’s microcredit

scheme, has women empowerment objective, it is important

to know the extent to which women have been empowered as

a result of their access to these loans. Strikingly, 30

years into the microfinance movement there is little

6

solid evidence of how microcredit affects the lives of

clients in measureable ways (Roodman & Morduch, 2009).

Some studies from Asia suggest that participation in

Grameen Bank and the Bangladesh Rural Advancement

Committee micro-lending schemes is positively associated

with a woman’s level of empowerment (Hashemi et al, 1996;

Sinha, 1998). Beyond the context of Bangladesh however,

few detailed studies have been undertaken (Roodman &

Morduch, 2009; UN, 2011). In Ghana, although there are

few studies that have examined different aspects of

microfinance (Afrane, 2002; Arku & Arku, 2009;

Schnindler, 2010), to the authors’ knowledge, none of the

existing studies focused on women empowerment. Yet, it is

unclear whether empowerment is an automatic outcome for

all women everywhere, particularly in Africa where

economic, political and socio-cultural circumstances may

differ. It is from the void of solid evidence to explain

how microcredit affects the lives of women in Africa that

this paper becomes relevant. As the UN Office of the

Special Adviser on Africa recently argued, now is a good

7

time to reassess the role of microfinance in Africa’s

development (UN, 2011).

3. DEFINING EMPOWERMENT AND INDICATORS OF WOMEN’S

EMPOWERMENT

For various reasons, the concept of empowerment is

elusive to define (Mason, 1987). Common to most

conceptualizations, however, is that empowerment is about

change, choice and power. In this paper, we defined

empowerment as a process of change by which individuals

or groups (in this case rural women) with limited choice,

freedom and power are enabled to gain and leverage power

that enhances their ability to exercise choice and

freedom in ways that positively contribute to their well-

being.

That conceptualizations of empowerment are diverse makes

the identification and delineation of measureable

indicators to assess women’s empowerment very difficult

(Mayoux, 1998). Particularly problematic is the possible

disjunction that may arise between women’s own aims and

notions of empowerment and externally derived empowerment

criteria established apriori. Similarly, behaviours and

attitudes that might be used to measure women’s

empowerment in one society may have no relevance in

another (Hashemi et al, 1996). Moreover, women are not a

homogeneous group, so that it might not be possible to

8

identify one or two sets of criteria for women’s

empowerment that are equally relevant for all women.

Therefore, we agree with Mayoux (1998) that women’s own

aspirations and strategies are a central element in

explaining programme outcomes, and must therefore be

included in any empowerment analysis

To explore the level of women’s empowerment as a result

of their involvement in World Vision’s micro-credit

scheme, three main pathway matrixes of women empowerment

were used: Material, Relational, and Perceptual. Under

these matrixes are a total of 7 indicators and specific

actions that characterize women empowerment. These

indicators were arrived at through extensive preliminary

discussions with women and loan managers using

participatory learning and action approaches (Mayoux,

1998) and pre-testing.

(a) Material pathway matrix

The material pathway matrix to women empowerment

encapsulates both measureable and non-measureable

material elements, possession and/ or ownership of which

are deemed necessary in the determination of whether a

woman is empowered or otherwise. In the study

communities, the following specific indicators were

identified.

9

- Engagement in income-generating activity: A woman was asked

whether before and after she was given the credit, she

engaged in any economic activity or employment that

generated income.

- Having disposable income - to make small purchases, pay

children’s school fees, buy food and medicine, and give

ko kuo (small amount of money given to support community

members when they are bereaved). A respondent was asked

whether before and after she got involved with the credit

scheme, she had any cash savings or disposable income

that she could use to make small purchases on her own,

buy food and medicine as well as give ko kuo.

(b) Relational pathway matrix

The relational pathway matrix describes the relationship

and interaction between women and other members of their

household and community. Indicators here include:

- Control over loan use and income from loans: Once a respondent was

established to have received credit from World Vision, we

asked to know who controlled the loans, funded

enterprises, and any incomes or assets that may accrue

from the loan investment. A respondent was specifically

asked whether she exercised full, significant, partial or

no control over any profits or income that accrued from

investment made with the loan. A woman was also

specifically asked whether her husband or any other

10

member of her family has ever forcefully taken away

income from her loan investment. This was particularly

important because our preliminary engagement with both

loan officials and women to determine what counts as

empowerment for women revealed that having control over

funded enterprises is a very important first-step towards

empowerment.

- Involvement in major family decision-making: We also asked women

whether before and after they received the loan, they

participated in decision-making (individually or jointly

with husband or other kinsmen) within the family on such

issues as sale of family land or livestock, sending

children to school or the clinic and marrying out of

their daughters.

- Relative freedom from domination and abuse: A woman was asked

whether before and after she had access to the loan,

money, jewellery, or livestock had been taken away from

her against her will. The respondent was also asked

whether before and after she received the loan, she had

suffered any physical, emotional or verbal abuse from her

husband or any member of her family.

(c) Perceptual pathway matrix

The perceptual pathway matrix of women empowerment is

based on a woman’s own rough assessment of her status in

the household, family and community. In other words, this

11

aspect of empowerment seeks to shed light on women

perception of well-being and the changes that they have

experienced since their involvement in the micro-credit

scheme. Specific indicators that were identified include:

- Reduced economic dependence on husband: Women were asked to

compare their level of economic dependence on their

husbands or other family members before and after

receiving the loan. Specifically, respondents were asked

whether before or after receiving credit, they depended

more on the earnings of their husbands or other family

members to make small purchases (e.g. food and clothing)

for themselves or for other family members such as

children.

- Mobility and self-confidence/assertiveness: A respondent was

presented with a list of places and events – market,

clinic, and naming, wedding and funeral ceremonies in or

outside the community – and asked whether before and

after she received the loan, she had gone to any of these

places and events, whether she needed the permission of

her husband or another person, and whether she went there

alone. A respondent was further asked whether she felt

her self-confidence or level of assertiveness had

increased or decreased before or after she accessed the

loan.

12

We acknowledge that although these empowerment indicators

resulted from discussions with women and loan managers,

they might not fully capture the phenomenon of women

empowerment. This is all the more so in the context of

Ghana where women’s disempowerment is rooted in a number

of factors including: limited political participation;

low levels of female education; poor health including

high maternal morbidity and mortality, and female

genital mutilation; less supportive legal environment

that promotes gender equality and women’s right;

patriarchal and hegemonic masculinity norms that view

women as inferior to men; limited economic

opportunities; and cultural practices such as forced

marriage (Anyidoho & Manuh, 2010). Indeed, as the

indicators we identified above are only paths out, it is

possible that women empowerment might be rooted in

something that microfinance is unable to adjust for.

Nevertheless, our research with women suggests that these

indicators fairly approximate the concept of women

empowerment in the study communities.

13

4. METHODS

(a) Research design

This study was designed as a longitudinal qualitative

research, involving an initial research phase and two

additional phases of follow-up research. The first phase

of the research (December 2006 – January 2007) was a

baseline survey to identify loan recipients and to enrol

them in the qualitative study. This phase also aimed to

work with women and loan managers to identify and

delineate relevant indicators of women empowerment. The

second research phase (December 2009- January 2010) was

used to gather data on the income generating activities

of loan recipients and the effect of the loans on their

empowerment. The last research phase took place in

December 2011, a period during which World Vision was

preparing to fold-up its operations in the Nadowli

district. The aim of this last research phase was to

evaluate changes in women empowerment overtime. The data

reported in this paper however focuses on and compares

findings from the first research phase to the final round

of research. This is because no significant differences

14

were observed between the results of our mid-term

research and those of final round.

The choice of a qualitative study design was informed by

the fact that the inherently limited potential for

structured surveys to contribute to understandings of

women empowerment has been widely acknowledged in the

literature (Mayoux, 1998; Sinha, 1998; Roodman & Morduch,

2009). Mayoux (1998) and Sinha (1998) believe it is

unlikely that existing quantitative methods can

realistically assess the impact of women’s access to

credit on their empowerment. Thus although a quantitative

design such as a survey with a large sample could have

been used in this research, such a design offers limited

space for an in-depth exploration of local narrative

accounts on the effects of microcredit on women

empowerment. Qualitative research, however, attempted to

provide access to the opinions, aspirations and power

relationships that helped to explain how people, places,

and events (e.g. women empowerment) arose in identifiable

local contexts which privileged individual’s lived

15

experiences (Karnieli-Miller, Strier & Pessach, 2009).

The qualitative methods used in this research generated

rich, contextually detailed, and valid process data that

left the participants’ perspectives minimally altered and

enabled in-depth exploration of the topic. Because

majority of the women in this study could not read and

write to answer written questions, qualitative research

using interviews was indeed a better option.

(b) Study setting and research participants

Field research was conducted in five rural communities in

the Nadowli District of the Upper West Region of Ghana.

Participants were women drawn from the 3,042 rural women-

loan recipients and workers from the Nadowli Area

Development Programme of World Vision Ghana. In all,

there were 232 participants. Of this number, 230 were

women-loan recipients, and this represented 8 per cent of

all women borrowers at the time. The remaining two (2)

were local staff of World Vision. The ages of the women

varied between 18 and 46 years. Majority of the women had

no formal education. Several of the women were married or

16

living with a partner. Majority of the women also had

between 1 and 5 surviving children. In comparison with

Ghana’s 2010 Population and Housing Census data for the

Upper West Region, the socio-demographic characteristics

of our study participants were generally very typical of

the women population in the region (see Ghana Statistical

Service, 2012).

We chose World Vision Ghana’s microcredit scheme mainly

because of its emphasis on women empowerment. We also

chose Nadowli District because it is the first district

in the region where World Vision Ghana started its micro-

lending scheme. The five communities were also chosen

because they were among the oldest programme areas of

World Vision Ghana in the district.

(c) Sampling procedures

The strategy for recruiting participants involved both

probability and non-probability sampling procedures. For

the women, a simple random sampling procedure was used to

select participants. This involved a three-stage

procedure. First, we obtained the individual files

17

containing names and personal records of each of the

women-loan recipient from the five study communities from

a central registry. Taking cognizance of the fact that

our total sample represented 8 per cent of the entire

women borrowers population, we determined that for each

of the five communities, 8 per cent of the borrowers

population was also to be sampled. In the second stage of

the sampling, we made a blindfolded person to randomly

select the required number of participants from the pool

of files for each community. Third, we then contacted

each of the randomly selected persons in their various

communities to discuss the study as well as conduct

interviews. Where any of the randomly selected

participants was not available or declined to participate

in the study (and there were only two such cases), we

repeated the process to get replacements.

A purposive sampling technique was however used to select

staff of World Vision Ghana. This was a judgmental

selection based on the participant’s perceived role or

knowledge of the subject of study.

18

(d) Data collection methods

To reproduce rural women’s experiences about their

participation in World Vision’s micro-lending programme,

focus group discussions and in-depth interviews were

employed to collect data. This was however complemented

with the development of a structured instrument to

collect detailed demographic and socio-economic

organizational information about the participants. Five

focus groups (involving a total of 80 women borrowers)

and 150 in-depth interviews were conducted. In each study

community, 1 focus group was conducted in addition to

completing at least 25 individual in-depth interviews.

Focus groups consisted of 12 to 20 women and all

discussions were held in the communities, usually at

venues chosen by the women and were organized on non-

working days. All focus groups were conducted in the

local dialect (Dagaare) of the study communities. Each

focus group lasted for 90 minutes. In all groups,

participants’ verbal consents were gained and the

discussions were audio taped. This consent was attained

19

in addition to ethical clearance obtained from management

of World Vision, traditional and opinion leaders of the

study communities, and women group leaders.

(e) Research instruments

Two main instruments were used. For the focus groups and

in-depth interviews, an open-ended thematic topic guide

and question guide respectively were designed to ensure

that the same themes were covered in each interview. The

instrument allowed questioning to flow naturally while

permitting us to probe more in-depth on certain pertinent

issues. These instruments focused primarily on

documenting use of credit in household economy,

interactions between women–loan recipients, and

borrowers’ interaction with members of their household.

Some of the questions explored include: how did you

become a member of world vision’s micro-lending scheme –

did you make the decision by yourself; before you

received the credit, were you engaged in any economic

activity or employment that generated income; did you

have any cash savings or disposable income that you could

20

use to make small purchases on you own; presently, do you

have any cash savings or disposable income on your own;

what did you do with the loan you received; are you

making profit from any investments that you made with the

loan; before you received the loan, did you participate

in decision-making in your family/household, and on what

kind of issues; currently do you take part in household

decision-making; who controls the profit or income that

you generate from your loan investment; and has your

husband ever forcefully taken away income from your loan

investment? In addition, a more structured instrument or

what Hashemi et al (1996) called the ‘household survival

matrix’ was developed and administered to all 230 women.

This instrument sought to collect detailed information at

several points in time about economic activities and

earnings of members and processes of change in women’s

role and status within and outside the household.

To ensure that the final research instruments were

reliable, a pre-test was done in the study communities

21

prior to actual data collection. The pre-test enabled us

to refine questions and use appropriate concepts.

(f) Analysis

Following the completion of interviews, we analysed the

data using the Attride-Stirling’s (2001) thematic network

qualitative data analysis framework. This involved

several steps. The first step involved transcription and

reading of transcripts and field notes for overall

understanding. The first author and an independent

language (Dagaare) specialist transcribed all tape-

recorded interviews from Dagaare to English. All the

authors then reviewed the transcript for overall

understanding and comprehension of meaning. This first

step was completed with a separate summary of each

transcript outlining the key points participants made.

Second, the interview transcripts were exported to NVivo

9 qualitative data analysis software, where the data was

both deductively and inductively coded. Codes are labels,

which are assigned to whole or segments of transcripts

and interview notes to help catalogue key concepts (Miles

22

and Huberman (1994). We continued coding the data until

theoretical saturation was reached (i.e. when no new

concepts emerged from successive coding of data). Third,

we applied the code structure to develop and report

themes. Themes simply represented some level of patterned

response or meaning within the data set (Boyatzis 1998).

Finally, all the themes identified were collated into a

thematic chart to reflect basic themes, organizing

themes, and global themes. To ensure that the thematic

chart reflected the data, we went through the data

segments related to each theme. Where necessary,

refinements were made. Where appropriate, we used

verbatim quotations from interview transcripts to

illustrate relevant themes. In few instances too,

qualitative responses are aggregated and presented in a

quantitative fashion to facilitate easy understanding.

5. FINDINGS AND DISCUSSION

(a) Targeting women

We begin the presentation of our findings by briefly

reflecting on why women are the targets of World Vision

23

Ghana’s microcredit scheme. The official policy position

of World Vision Ghana for targeting women with credit is

that empowering rural women through the provision of

microcredit would enhance their productive capacity, and

increase their economic security and their confidence in

demanding continued and expanded opportunities for

themselves (Sam, 2005). Targeting women is further

founded on the assumption of women’s greater contribution

to family welfare. The argument here is that the priority

of women is always to first invest their earnings in

their children, then subsequently, accompanied by

spending on their household necessities. The organization

therefore believes providing women with credit in order

to increase their earnings would generate more

qualitative and quantitative direct transformational

benefits to family welfare.

However, interviews with loan managers suggest other

reasons that directly raise questions about the sincerity

of the programme’s commitment to women empowerment. One

loan manager said:

24

Why we give the loan to only women? Well, you know[that] in the communities we work in, the men arenot correct. When you give them loan they will spendit or they will refuse to pay back. It is very hardto work with them…you know most of them are verymobile and so can easily disappear with the loan.The other thing is that I am a woman…and with themen if I call a meeting they will be reluctant tocome. Even if they come, they will argue with you…some are very arrogant. But with the women, they areok, they are always around the community and theyare reliable. If I call a meeting today, they willall come and they are also ok when it comes topaying back the interests on their instalment. Thatis why we work with them. (Loan Manager (Woman),IDI, Nadowli ADP).

In this way, the idea of targeting women, apart from it

being seen as the ‘rational thing to do’, is also a

strategic one, meant to facilitate easy recovery of loans.

But World Vision’s approach also highlights an important

lesson about how poorly adapted microfinance

methodologies applied without sufficient understanding of

the socio-cultural context can have some unexpected,

adverse consequences, even while achieving some good

outcomes. Thus having an understanding of the nature of

potential loan recipients and the socio-cultural context

within which they live could be vital for the survival,

effectiveness and long-term success of any microfinance

programme.

25

(b) Volume, adequacy, and timing of loan

Table 1 shows the length of time respondents have

benefited from the scheme and the amount of loan

received. Most of the women (70 per cent) we interviewed

have been in the scheme from 6-10 years. In an earlier

study in Bangladesh, Hashemi et al (1996) suggested that

the longer a woman stayed as a member of either BRAC or

Grameen Bank, the greater the likelihood that she will be

empowered. Our focus group discussions and in-depth

interviews with women revealed no such relationship. Thus

the fact that one has benefited from the scheme for long

does not mean that one would be empowered socially and

economically. This, the women reported, was because the

ability to be empowered depended on other more important

factors such as the type of investment the loan was put

into and whether a woman even had control over the loan

use and the income accruing thereof.

TABLE 1 HERE

Table 1: Years of Involvement in Scheme and Loan Amount Received

26

From the time they joined the scheme till the time of

this research, most women have received a cumulative loan

amount of between GH¢11 and GH¢30. While World Vision

considered the various amounts it loaned to women

appropriate for rural women empowerment at the time, our

interviews with women regarding the adequacy of the loan

amount they received showed that most (92 per cent)

believed the amount was woefully inadequate to engage in

any meaningful income-generating activity. Participants

noted that the small size of the loan did not allow for

investment in different ventures or investments in

business ventures that are high profit-yielding but

requiring larger capital investment. Although some women

managed to improve their incomes nevertheless, as we show

below, the small sizes of the loan that most women

27

complained about is part of the reason why some women

failed to invest their loans in economically rewarding

ventures, faced considerable difficulty repaying their

loans, and have even become more vulnerable and

disempowered.

One other related problem our study documented was the

timing of the loan. Usually, loans are disbursed to women

annually in the month of June. About 56 per cent of the

women interviewed said this timing was inappropriate

mainly for two reasons. First, the time coincided with

what the women described as the ‘‘hunger gap’’ in the

district, during which time food is difficult to come by.

One widow illustrates the point:

…Ah, time? This was a time I had nothing to feed mychildren with. So when World Vision gave me theloan, I used it to buy food! Should I invest thismoney in selling salt or pepper while my familystarve to death? (Woman, FGD).

Second, respondents noted that during this time of the

year, there is usually shortage of agricultural produce

such as guinea corn – commodities women either trade-in

directly or used as raw materials for the production of

28

other goods such as pito (local beer brewed using maize or

guinea corn). As a result, many loans are either

mismanaged or channelled into direct consumption. By

showing how disbursing loans for business start-ups in

the hungry season leads to non-investment, non-repayment,

and disempowerment, the findings here not only raise

questions about the specific methodology of World Vision

Ghana, but they also suggest that lack of appreciation of

the local economic context within which a microcredit

scheme is implemented could easily contribute to

ineffectiveness.

(c) The impact of World Vision Ghana’s microcredit Scheme

(i) Women’s involvement in Income-generating Activities

As a first step towards empowerment, World Vision

provides credit to women so that they might engage in

income-generating activities and thus bring about

meaningful socio-economic changes in their lives. Once

loans are granted, borrowers must invest their loans in

productive activities and start paying their instalments

every month using the profit earned from the loan

29

investment. Data was elicited to evaluate whether women

are actually involved in income-generating activities,

the proportion of loan recipients who already had income-

generating activities before receiving the loan, and how

many of those who did not have a business activity at the

beginning succeeded in starting one after receiving the

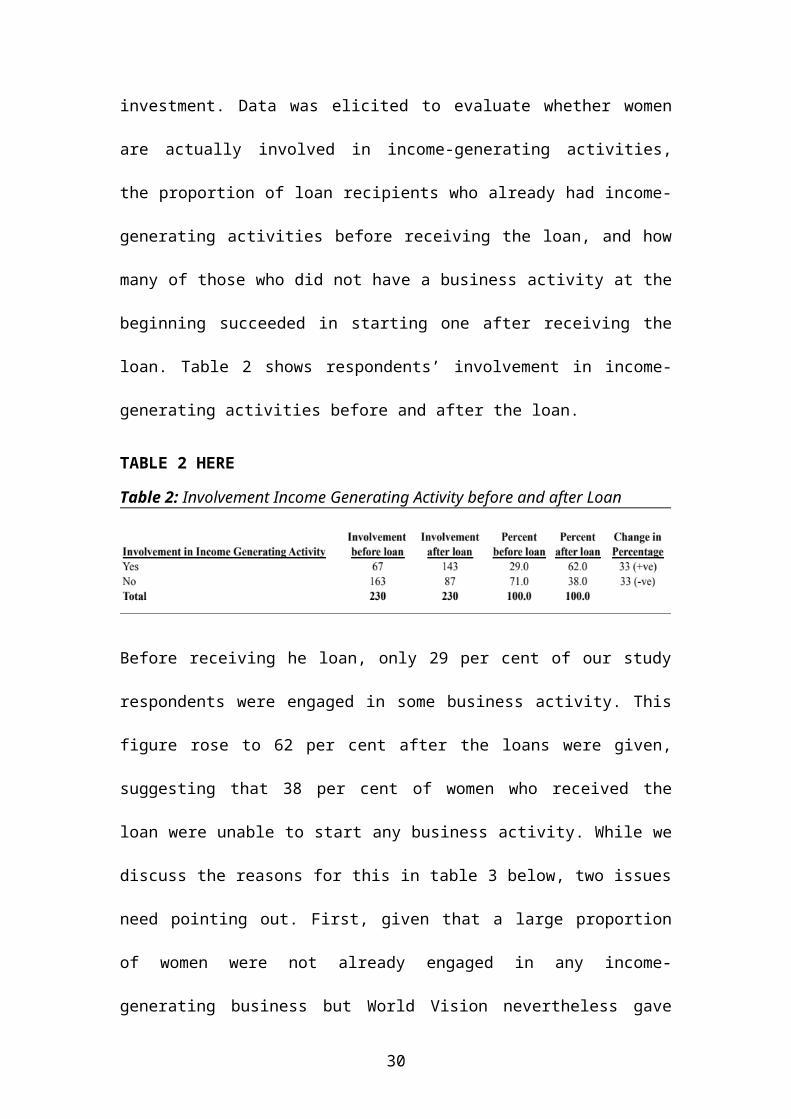

loan. Table 2 shows respondents’ involvement in income-

generating activities before and after the loan.

TABLE 2 HERE

Table 2: Involvement Income Generating Activity before and after Loan

Before receiving he loan, only 29 per cent of our study

respondents were engaged in some business activity. This

figure rose to 62 per cent after the loans were given,

suggesting that 38 per cent of women who received the

loan were unable to start any business activity. While we

discuss the reasons for this in table 3 below, two issues

need pointing out. First, given that a large proportion

of women were not already engaged in any income-

generating business but World Vision nevertheless gave

30

them loans for the purpose of starting up one, one could

applaud the organization for enhancing these women’s

access to finance. However, that majority of these women

failed to start-up any business suggests that World

Vision’s approach did not adequately appreciate what

women’s access to microcredit can do or not do in a

context where economic opportunities for women are

limited and where women faced other economic necessities

such as poverty and hunger. Second, our interviews with

loan recipients revealed that most of the women who

hitherto were not engaged in any business activity but

managed to start one after receiving the loan were

actually doing so for the first time. Although exposure

to income-earning activities in a single generation might

not be sufficient to wipe away long periods of cultural

conditioning, for these women, the fact that their

involvement in the NGO’s micro-lending programme has

enabled them to be involved in economic activities that

might generate income was itself empowering.

It is very good that I got this loan. I used to stayat home and do nothing. Things were very hard, butnow, at least I feel better because at the end of

31

the day I will get something [money] from my pitobusiness to support my family (Woman, IDI).

Table 3 shows the patterns of loan utilization among the

62 per cent of the women who were engaged in some form of

business activity after they received the loan. Most

women invested their loans in one of ten different

economic activities including pito brewing and food crop

farming. Our research however revealed two problematic

issues as regards women’s loan investment decisions. The

first is that most women invested their loans in

activities that yielded little profit. In our discussions

with loan staff, it was clear that World Vision simply

assumed that there are profitable income-earning ventures

out there that rural women could engage in if only these

women have access to finance. However, our interviews

with women found that male dominance in the local

economic sphere tends to push most women into less

profitable economic activities such as those described in

table 3. But some women also reported that they invested

their loans in these types of activities because of the

small size of the loan they received. That women are

investing their loans in low-profit businesses suggests

32

that the prospects of paying the 20 per cent monthly

interest on loans could be unrealistic. Indeed, as we

show below, this is one primary reason why many women are

unable to pay the monthly 20 per cent interest on their

loans, which then leads to several undesirable outcomes

including verbal abuse from other group members.

TABLE 3 HERE

Table 3: Loan Investment Patterns

The second issue is that a significant number of women

(38 per cent) have even failed to invest their loans in

any venture that could generate income. Two main reasons

accounted for this. First, the initial loan capital went

into direct consumption. Several accounts were given

about loans being used to meet immediate household needs

such as purchase of food and medicine. Second, the loan

33

was forcefully seized or in some instances women

themselves voluntarily handed over the loan to their

husbands or another family member. For all these women,

losing the initial loan capital often calibrate a process

of dispossession and indebtedness that culminates in a

gradual but profound socio-economic privation and

disempowerment. But that a substantial number of the loans

are used for purposes other than investment in income-

generating activities could be related to the fact that

World Vision’s loan operation policy does not focus on

women who already have an income-generating activity

neither does it emphasize a strong supervisory role for

loan mangers. Rather it relies on mutual trust and the

joint liability clause to ensure that borrowers use their

loans for income-earning activities and to pay monthly

interest from the income earned. Unfortunately, these

management mechanisms are not always effective as loans

are rarely monitored. Thus lack of focus on women who

are already engaged in viable economic activities,

breakdown of the monitoring mechanism within the

household economy, low level of loan investment

34

supervision, and limited household resources, often

intermingle to force borrowers - who are usually faced

with other economic necessities – into diverting loans

into uses other than those sanctioned by the

organization. Of course the exact use of the loan should

not be so relevant if the purpose of World Vision’s

microfinance scheme was only to enhance women’s access to

finance. However, given that many loan recipients do not

usually have any form of business activity before

receiving the loan, and the fact that the scheme

emphasizes the investment of loans in income-generating

activities, an outright use of loan funds for such

activities as school fees or food clearly raises

questions about the appropriateness of extending loans to

women to start-up new businesses. Our interviews with

women suggest that in a context such as the Nadowli

district where economic opportunities are limited and

huger and poverty very rife, a focus on women who are

already involved in income-generating activities has a

better chance of succeeding due to the high potential for

35

small business start-ups to fail, and the fungibility of

loans among starters.

(ii) Impact on women’s income and contribution to

household welfare

Figure 1 is a representation of women’s own valuation of

their income status since accessing the credit, while

table 4 shows the distribution of changes in income

between women who already had an income-generating

activity before receiving the loan and those who did not.

These results are the outcome of a question that asked

women to describe their income after they had accessed

the loan.

FIGURE 1 HERE

36

Figure 1: Credit Impact on Women’s Income

Table 4: Distribution of Changes in Income after Loan

Figure 4 indicates that 41 per cent (94), 43 per cent

(99) and 16 per cent (37) of the women sampled,

respectively, reported that their income levels have

improved, worsen and not changed. Table 4 however shows

that majority of the women who had income-earning

activities before receiving the loan reported increases

(49) or no change (16) in income. On the contrary,

majority of our respondents who reported decreases in

incomes (97) were women who did not have any income-

37

earning business before accessing the loan. Our

interviews found that most women who reported

improvements in their income had invested their loans in

one productive activity or the other or had expanded

their existing businesses and were making monthly profits

of between GH¢1 and GH¢10. Although these women admitted

that the income they were earning were rather meagre due

in part to the low profit-yielding nature of their

investments, most were particularly proud of the

financial contribution they now make to their family

welfare and children’s education. A few of these women

reported how they are using their loans and the incomes

accruing from their loan investment to provide better

quality and quantity food, pay expenses of their

children’s education and clothing needs.

However, for the majority of women whose incomes worsened

or remained stagnant, the situation is opposite. Such

women were found not either to be making any profits from

their investments or to have lost the initial loan

capital to non-productive ventures such as direct

38

consumption. For majority of this category of

respondents, not only are they not able to contribute to

their family welfare but also they find it extremely

difficult paying the monthly interest on their loans.

These women painfully tell of how they often have to

borrow from friends and other moneylenders to pay the

monthly interest on their loan in order to avoid

defaulting and escape the social pressures and shame that

comes with defaulting.

…Right now I really don’t know what to tell you…Idon’t know because this loan has made thingsdifficult for me. My business is not doing very wellbut you know…every month I have to pay interest. Idon’t have the money to always do that. But I don’twant to default in paying the loan…they will say Iam bad. So in the past I have had to take part ofthe initial loan capital to go and pay the interest.I have even borrowed from two of my friends to paythe interest. Now I am in big debt. I am really introuble (Woman, IDI).

Clearly, our findings here suggest that microfinance

schemes for women are likely to have more positive impact

on household incomes if such schemes are targeted at

women already engaged in some business venture.

39

(iii) Control over loan and income from funded

enterprises

World Vision Ghana provides credit to women on the

assumption that women will - individually or collectively

- exercise full control over both the loan and the

investments that they make. However, in reality, this

assumption usually does not apply. Findings show that in

more than half of the cases women had no control over

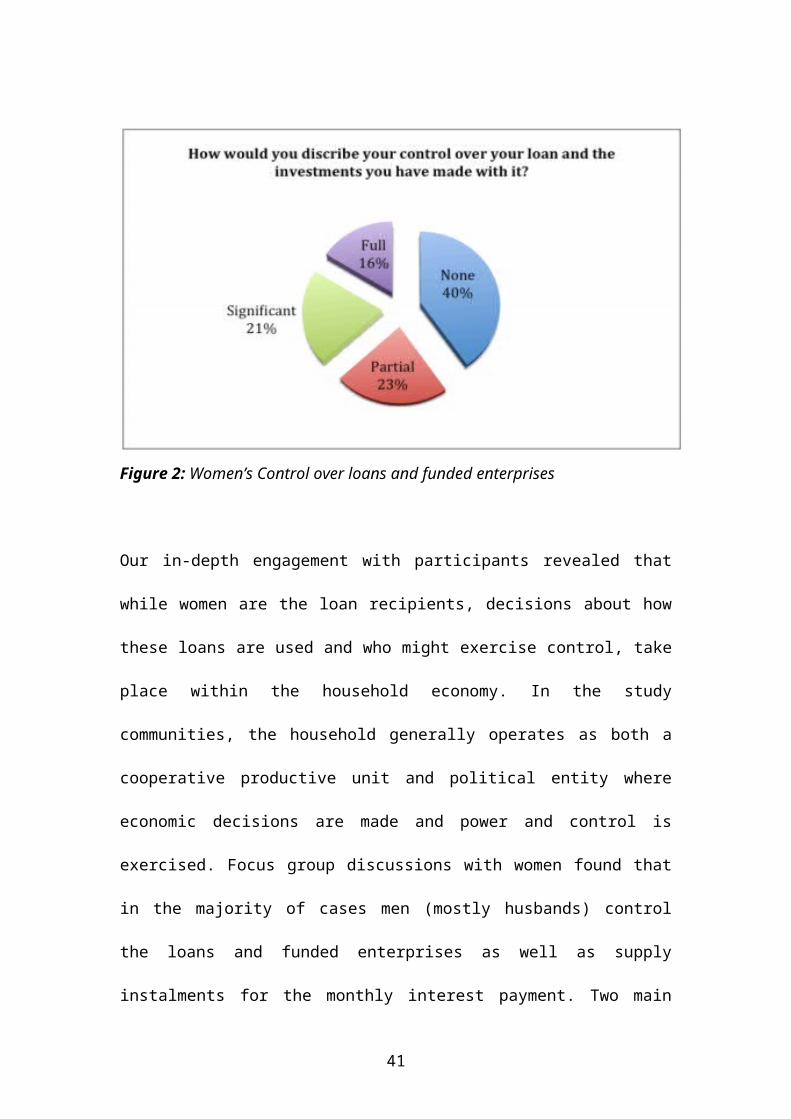

funded enterprises. Figure 2 illustrates this. Forty per

cent of the women sampled indicated that they exercised

no control over the loan they received, including funded

enterprises as well as incomes and assets that may

accrue. Only 16 per cent are able to fully control their

loans and enterprises while some 21 per cent and 23 per

cent exercised significant and partial control

respectively.

FIGURE 2 HERE

40

Figure 2: Women’s Control over loans and funded enterprises

Our in-depth engagement with participants revealed that

while women are the loan recipients, decisions about how

these loans are used and who might exercise control, take

place within the household economy. In the study

communities, the household generally operates as both a

cooperative productive unit and political entity where

economic decisions are made and power and control is

exercised. Focus group discussions with women found that

in the majority of cases men (mostly husbands) control

the loans and funded enterprises as well as supply

instalments for the monthly interest payment. Two main

41

reasons explain this. The first is related to the fact

that in more than half of the cases, husbands and other

male relations in the household made the initial decision

for a woman to join the credit programme by either

sending or influencing her to become a member of World

vision Ghana’s micro-lending programme. In a few cases,

women gave graphic accounts of how their husbands not

only asked them to join but also literally forced them to

join in order to acquire funds for their (husbands)

usage. In part, this explains why husbands will either

completely seize the loan or exercise total control over

the loan and funded enterprises. Indeed, there were

several accounts of husbands forcefully taking away

income or selling out assets acquired by women from their

loan investment. The second reason why very few women are

able to exercise control over the loans and funded

enterprises is that existing patriarchal and socio-

cultural norms restrict women’s ability to own or

exercise control over assets. In the existing socio-

cultural milieu of the Nadowli district, women may own

assets through inheritance or self-purchase. However,

42

fewer women are able to claim ownership and control over

these assets because men usually exercise management and

use rights even if it is the woman who acquires the

assets legally. One participant makes the point:

…Control assets in the house? Don’t you know ourtradition? When a man marries a woman, he owns andcontrols her, her children, and everything the womanhas! How will a woman own and control anything in aman’s house? (Woman, IDI).

In focus groups, some participants related personal

accounts about how they willingly handed over their

loans, assets and resources to their male counterparts

thinking that men are better in handling and managing

monetary transactions. Todd (1995) suggests that since

men’s enterprises are often more profitable than women’s,

investing loans in men’s activities may be a rational

strategy. While this may be true, women tell of how men

often misappropriate these resources or utilize them in a

manner that greatly disfavours them (women).

In our interviews, women’s qualitative accounts suggested

that lending to women who have full or significant

control over proceeds from their loans was more likely to

43

enhance their incomes and empowerment, while lending to

those who have no control over the loan and income from

their investments only make things worse.

I think the loan is only good for those women whotake care of themselves…I mean women who are in-charge of their businesses and can determine whatthey want to use the loan for. For others likemyself who do not control how the loan should beused, and our husbands determine everything, thingsare really not good…for me things are very bad…Ican’t pay the monthly interest on time and all that(Woman, IDI).

(iv) Credit and women’s involvement in major family

decision-making

Access to credit and participation in income-generating

activities are assumed to strengthen women’s bargaining

position within the household, thereby allowing them to

influence a greater number of strategic decisions

(Hashemi et al, 1996). In poor Ghanaian communities in

particular, men’s domination over women is strongest

within the household. Women’s ability to participate and

influence decisions that affect their lives at the

household level is therefore considered one of the

principal components of empowerment. While it is less

clear exactly what types of decisions and what degree of

44

participation and influence should be classified as

empowerment, this study records marginal increase in

women’s levels of participation in making important

household decisions after access to credit. Table 5

compares respondents’ participation in household decision

making before and after their access to the loan.

Of particular significance is the general drop in the

percentage of women who were hitherto non-participants in

household decision-making from 50.4 to 23. Of course

correlation here does not mean causality. However, based

on women’s own accounts, their involvement in World

Vision Ghana’s micro-lending scheme appears to have

contributed to an increase in the number who now

participated in making various household decisions. One

woman recounted:

Ah World Vision! World Vision has made it possiblefor me to have a say in whatever happens in thehouse. Before then, I had no say. My husband neverrespected my opinions (Woman, IDI).

45

Accordingly, if for nothing at all, and even if they

(women) ceded control over their loans and funded

enterprises to their husbands – voluntarily or forcefully

- the fact that they (women) have become means through

which new resources (loan funds) could be pulled into the

household has greatly increased their status and

bargaining power within the household.

TABLE 5 HERE

Table 5: Women’s Participation in Household Decision-making before and after Access to Loan

(v) Credit and women’s relative freedom from domination

and abuse

While World Vision Ghana’s credit programme might have

had marginal empowerment benefits in terms of women’s

participation in household decision-making, domination

46

and abuse against women borrowers have escalated in all

study villages. Our in-depth interviews with women

revealed that the increase in abuse comes from two main

sources: group members and husbands.

Abuse from group members emanates from the scheme’s

reliance on the joint-liability condition. Because of the

joint-liability condition, the credibility of a

particular women-borrower-group to World Vision Ghana and

the potential for new loans for its members is often

greatly jeopardized when even one member in the group

fails to maintain regular monthly payment of interests.

Indeed, in the event that one member delays payments or

totally defaults, all the other group members who paid

their interests in a timely manner must wait until such a

time that every member in the group pays up. This often

generates enormous conflict among group members as

pressure is often exerted on defaulting members to pay.

Several women borrowers in our study lamented over how

other group members used moral coercion, verbal

47

aggression and physical assault to compel them to pay

their monthly interest.

Have I had any problems? Yes…Yes. Recently, I wasalmost wounded at the borehole! Why?...because whenit was time to pay the interest on my loan, I didn’thave money. So on the day of interest payment, allmy group members went to pay except me. In fact Iwas busy going from one market to the other at thattime hoping that I would get the money. But when Ireturned to the village, the group leader and othermembers confronted me to pay the interest. I toldthem I didn’t have the money yet, but they would notlisten to me. They used very bad words on me … veryabusive language and hurled insults on me. Some saidI was lazy; others said I was very irresponsible;and some even threatened to beat me if I failed topay…and there are several others like me in thisvillage who also feel this pressure and suffer thisabuse because they are unable to pay. This is a bigproblem we face…it is a problem that our own selveshave created (Woman, IDI).

Others tell of how their peers violently confiscated

their saleable household items and personal assets

including cooking pots and sold them out in order to

collect monthly instalment. What makes the situation

worse according to most accounts is the fact that very

often, the confiscation and abuse take place in the

public sphere such as in the market. This brings shame,

embarrassment and emotional trauma to victims and their

household. Clearly, these are the hidden costs of the

48

Grameen-style group liability approach; but perhaps

without such enforcements too the group methodology would

not work and women would not have access to the loans

because the scheme would not be sustainable if clients

did not repay. In this regard, it is worth pointing out

that the ways in which the groups enforce the joint

liability makes the loans not entirely as collateral-free

as they appear. Given that the groups are largely able to

enforce the joint liability condition among themselves –

loan repayment performance rate was estimated to be above

65 per cent - we would argue that the NGO does not even

have to impose any collateral on loans.

But it is not only women borrowers who perpetrate abuse

on defaulting group members. Within the household too,

majority of the loan recipients interviewed said they

experience both physical and verbal assaults of some kind

from their husbands and other male guardians, albeit for

different reasons. Findings here suggest that abuse

against women borrowers results mainly from disagreement

over loan use or control. As argued earlier, men control

49

the management and use of most loans that women bring

into the household. But before men are able to establish

full management or use control, abuse is often involved.

The incidence of domestic abuse against women loan

borrowers arises as a result of some women challenging

the legitimacy and/ or propriety of men’s attempt to

exercise management and use rights over loans and funded

enterprises. In majority of the cases, respondents

reported that women questioned their husbands’ management

or use of the loan or funded enterprise, incurring in the

process, the wrath of angry husbands who feel their

authority is being threatened by their wife’s behaviour.

Are you asking whether we have had any problems withour husbands since we were given the loan? That one…I can personally say I have had a lot. Every now andthen my husband would fight me. This happenedanytime I asked him to pay me back monies he hastaken from my business. I really don’t know, but anytime I asked, he would just be angry…he would insultme and if I asked further questions he would justbeat me up. In fact I wanted to stop taking theloan, but he is the one who insisted I stay in theprogramme. Yet, every now and then he would fightme. I am just tired of the whole thing (Woman, FGD).

In this way, our findings here sharply contradict one

study on the Grameen Bank which found that credit

50

programmes reduced domestic violence by channelling

resources to families through women (Schuler, Hashemi &

Riley (1997). They are however consistent with those of

Rahman’s (1999) study in the Tangail region of Bangladesh

where abuse against women borrowers was found to have

escalated following their access to credit. For most of

the women surveyed in this paper, abuse against them

within the household furthers their disempowerment - a

development that is complete anathema to the original

intent and purpose of World Vision’s micro-lending

scheme.

(vi) Credit and women’s economic dependence on husband

Women’s economic independence is another major factor

that can enhance their empowerment. Traditionally, women

in the study area are engaged in household activities

that are non-wage earning such as working in their

husbands’ farms and caring for children. This renders

them economically dependent on their husbands and other

male kin. World Vision Ghana is of the opinion that if

women had opportunities for gainful employment outside

51

the household through their access to credit, their

contribution to household wellbeing would help reduce

household poverty as well as reduce women’s overall

economic dependence on their husbands.

In this research, women’s economic independence was

evaluated both before and after their involvement with

the loan scheme. The results are presented in table 6.

TABLE 6 HERE

Table 6: Women’s Economic Dependence on Husband’s/ Kin’s before andafter Loan

Generally, women’s access to credit appears to have a

very limited effect on their dependence on the earnings

of their husbands or other relatives. Apart from food

purchases and expenditures from payment of children

52

school fees, which experience marginal decline in terms

of the number of women depending on their husbands or

other kinsmen earnings, women’s economic dependence has

increased for the rest of the evaluated variables.

Qualitative analysis identified two main reasons why this

is the case. First is the limited control women have over

their loan and funded enterprises. Generally, husbands

control women’s loans and funded enterprises.

Consequently, not only do women depend on their husbands

for the supply of instalments to pay their monthly

interests, but they have also become chronically

dependent on the same husbands for procuring certain

basic necessities and personal effects.

I think things have gone from bad to worse. I usedto ask him [referring to husband] for money to buyingredients for making soup, clothing and otherthings. But now, I have to even ask for more…moneyto pay the interest on the loan. You know he was theone who used the loan, but I am the one who went forit…I am therefore responsible for paying all theinterests. If I don’t pay, I would be in trouble,but if he doesn’t also give me the money what can Ido? (Woman, IDI).

The second reason is that the income-generating

activities that are primarily controlled by women such as

pito brewing typically yield modest income compared with

53

the earnings of men in wage labour. In this vein, most

women are not self-sufficient in terms of personal income

and therefore still have to depend on the earnings of

their male counterparts to make various purchases and

meet different household expenditures.

(vii) Credit and women’s mobility and

self-confidence/assertiveness

Fernardo and Porter (2002) have argued that increasing

women’s mobility can empower them to exercise greater

control over their lives by increasing their access to

markets, education and information. We therefore

evaluated the effects of microcredit on women’s social

and economic mobility and how they promote women’s self-

confidence or assertiveness in the Nadowli district.

Findings from qualitative interviews with women suggest

that prior to their involvement with the loan scheme,

most women were consigned to the private sphere and the

affairs of the home. This heavily restricted women’s

mobility and self confidence to be actively involved in

market transactions, thereby providing them with limited

54

opportunity and ability to meet different people and gain

new experiences for their empowerment. However, many of

the women-loan-recipients reported several important

changes after they joined the scheme. One participant

recalled:

Me…before I had this loan to start my pito brewingbusiness I was the home type, poor and very timid. Icould not even afford the twenty (20) Ghana Pesewascharged as lorry fare from Serekpere to Sombomarket! I could not attend funerals because I couldnot pay the kuor kuo (funeral levies). Anytime Iwanted to go anywhere, I needed to ask my husbandfor money, and anytime he said he didn’t have money,it means I couldn’t go. But now that I am doing thisbusiness and I am making small money, I feel veryconfident, I don’t fear…I can go to Nadowli market,Sankana market, Tangasie market, Bussie market, andeven Wa (the regional Capital) without depending onhim to give me lorry fare (Woman, FGD).

Also, few women noted that through their travel to do

business or participate in weekly group meetings, not

only is their mobility greatly enhanced, but also these

movements do ‘open their eyes and ears to the outside

world’. They therefore gain exposure to new ideas as well

as opportunities for their empowerment. Furthermore, by

participating in weekly meetings, these women are able to

acquire a degree of self-confidence.

55

At the same time however, a substantial number of

borrowers noted that sometimes the shame and

embarrassment associated with defaulting and having to be

confronted by other borrowers, prevented some women from

moving into the public sphere. For such women, access to

credit has actually profoundly limited their mobility

beyond the home.

6. CONCLUSION AND POLICY IMPLICATIONS

The extension of microfinance to women has the potential

to impact powerfully on women’s empowerment. Our aim in

this paper was to examine the empowerment effects of the

micro-lending operation of an NGO-managed microcredit

scheme to poor women in a rural district of Ghana.

Findings show that some women are empowered along several

dimensions as a result of their access to loans; several

other women have little control over the use of loan

funds and are therefore no better off due to receiving

credit; while some women are subjected to harassment and

abuse due to their indebtedness and inability to repay

56

loans, and are therefore worse off. Our findings suggest

that those women who became more empowered as a result of

their access to credit were women who either were already

engaged in some business venture before receiving the

loan or they exercised full or significant control over

proceeds from their loans. On the contrary, women

borrowers who became vulnerable and even disempowered

were those who either received loans to start-up new

businesses but who actually failed to do so due to loss

of loans to other unapproved loan uses such as direct

consumption, or those who had no control over investments

and earnings from their loans.

Of course, these results must be interpreted with the

understanding that identifying credit impact on women

empowerment is a rather problematic enterprise due to the

fungibility of credit, non-randomness in programme

participation (selection bias), and non-randomness of

programme placement (Khandker, 1998). Moreover, it might

be too ambitious to expect that years of male domination

over women will be removed by a few years of women

57

involvement in a microcredit programme. Nevertheless,

the evidence presented in this paper clearly exposes the

gulf that can exist between the vision for promoting

women’s access to microcredit and its actual operation

and impact on women empowerment, and called into question

some of the specific methodology used by World Vision

Ghana as well as the general notion that microcredit

empowers women.

Our findings show that the impact of any microfinance

scheme depends on the socio-economic and cultural

contexts in which it is implemented, and that women might

experience both great advantages and disadvantages from

accessing credit, depending on their situations and

whether they are able to service their debt or not. In

some cases, access to credit might be the only input

needed on the road to women empowerment. At the same

time, our findings also suggest that in a culture in

which women have little control over their loans and

income from their investments, it is a singularly poor

environment to give out credit to women to start-up new

58

businesses. This would suggests that World Vision’s and

other similar microcredit schemes need to revise their

micro-lending approach to focus on a number of things.

First, it might be better to focus on clients already

having an income-generating activity that generates

sufficient income to repay the loan. This would not only

help loan recipients to grow their existing businesses

and generate more income, but it would also ensure the

sustainability of the schemes themselves. Second, it

might also be useful to first screen and determine which

clients have adequate control to be able to use a loan

productively. This might require moving beyond individual

women to focusing also on families and communities to

redress powerlessness and gender-based discrimination

against women.

But in addition to the above recommendations, the loan

size, timing of initial disbursement, and monitoring, are

issues that must be relooked at. Our study indicates that

small loan sizes, inappropriate timing of loan

disbursement, and general laxity in the supervision of

59

how disbursed loans are managed within the household

economy led not only to the use of credit for untended

purposes, but also to an increase in the debt-liability

of borrowers. Also the low profit-yielding nature of

women’s investment activities contributed to undermining

the spaces for women empowerment, while struggles over

loan use and control over loan-funded enterprises within

the household as well as increasing debt-liability of

individual borrowers created new forms abuse, dominance

and control over borrowers. These findings from our

research clearly support the need to increase the sizes

of loans to levels that are sufficient enough to be

invested in high profit-yielding income-generating

ventures. Similarly, we recommend that the timing of

initial loan disbursement should be changed to be in a

season where economic opportunities and food are abundant

rather than scarce, while effective loan monitoring

mechanisms should be put in place to address the high

potential for loan fungibility.

60

Finally, and with regards to how the joint liability

condition is enforced when one group member is unable to

pay the interest in time, we recommend that groups should

be encouraged to build-up their own emergency

savings/funds through small contributions at their

regular meetings. Such funds could be loaned out (and to

be replaced later) to group members who might have

legitimate reasons for being unable to repay at the time

of collection. This could reduce the harassment, abuse

and seizure of assets that insolvent borrowers often

experience due to other group members having to cover for

them out of their own pocket.

In conclusion, empowerment cannot always be assumed to

be an automatic outcome of women’s access to microfinance

particularly in contexts such as Ghana where women still

face considerable socio-economic disadvantages relative

to men. Therefore, it is unlikely that just giving a loan

to a woman by itself is going to overturn these social

and cultural conditions that deprive women of control

over their economic activities and the proceeds thereof.

61

However with adequate loan size, appropriate timing,

effective monitoring, and better screening methods that

avoid giving loans to those who are not likely to be in a

position to repay through the determination of which

women have inadequate control to be able to use a loan

productively, women’s access to microcredit can enhance

their empowerment.

REFERENCES

Afrane S (2002), Impact assessment of microfinanceinterventions in Ghana and South Africa: A synthesis ofmajor impacts and lessons. African Journal of Microfinance, 4(1):37-58.

Anyidoho NA & Manuh T (2010), Discourses on Women's Empowerment in Ghana. Development, 53(2): 267–273.

Arku C and Arku FS (2009), More money, new householdcultural dynamics: women in micro-finance in Ghana.Development in Practice, 19(2): 200-213

Attride-Stirling J (2001), Thematic networks: an analytictool for qualitative research. Qualitative Research, 1(3): 385-405.

Boyatzis R (1998), Transforming Qualitative Information: Thematic and Code Development. Thousand Oaks, CA: Sage.

Fernando P and Porter G (2002), Bridging the gap betweengender and transport. In P. Fernandon & G. Porter (eds.),Balancing the Load: Women, Gender and Transport, London, UnitedKingdom: Zed Books.

62

Green, J. (2007), The Use of Focus Groups in Researchinto Health. In M. Saks and J. Allsop (eds.), ResearchingHealth: Qualitative, Quantitative and Mixed Methods. London: SagePublications.

Hashemi SM, Schuler RS and Riley A (1996), Rural creditand women’s empowerment in Bangladesh. World Development,24(4):635-653.

Hulme, D. and Mosley, P. (1996), Finance Against Poverty.London & New York: Routledge.

Karnieli-Miller O, Strier R and Pessach L (2009), Powerrelations in qualitative Research. Qualitative Health Research,19:279-289.

Khandker, SR (1998), ‘Microcredit programme evaluation: acritical review’, IDS Bulletin, 29(4): 11- 20.

Mason KO (1987), The impact of women’s social position onfertility in developing countries. Journal of Eastern sociologicalSociety, 2(4): 718-745.

Mayoux L (1998), Participatory learning for women’sempowerment in microfinance programmes: negotiatingcomplexity, conflict and change. IDS Bulletin, 29(4): 39 -50.

McDermott P (2001), Globalization, women and development:microfinance and factory work in perspective. Journal ofPublic Affairs, XIII: 65-79.

Miles MB & Huberman M (1994), Qualitative Data Analysis: A Sourcebook of New Methods (2nd Edition). Beverly Hills, CA: Sage.

Norwood C (2005), Macro promises of micro-credit: a caseof a local eSusu in rural Ghana. Journal of International Women’sStudies, 7:1.

Rahman A (1999), Micro-credit initiatives for equitableand sustainable development: who pays? World Development,27(1): 67-82.

63

Roodman D and Morduch J (2009), The impact of microcrediton the poor in Bangladesh: revisiting the evidence.Centre for Global Development Working Paper, No. 174. Sam A (2005), Partners: A Magazine of World Vision Ghana. Accra:World Vision Ghana

Schindler K (2010), Credit for What? Informal Credit as aCoping Strategy of Market Women in Northern Ghana.Development in Practice, 46(2): 234-253.

Schuler SR, Hashemi, S and Riley AP (1997), Men’sviolence against women in rural Bangladesh; undermined orexacerbated by microcredit programmes? Paper presented atthe 1997 population Association of America annualMeetings, Washington, DC, March, 1997. Sinha S (1998), Introduction and overview. IDS Bulletin,29(4): 1- 10.

Todd H (1995), Women at the Centre: Grameen Bank Borrowers tenYears On. Malaysia: CASHPOR.

United Nations (2011), Microfinance in Africa: Overview andSuggestions for Action by Stakeholders. United Nations Office of theSpecial Adviser on Africa, New York.

64