the impact of microcredit on poverty and women's

275

THE IMPACT OF MICROCREDIT ON POVERTY AND WOMEN’S EMPOWERMENT: A CASE STUDY OF BANGLADESH By SAYMA RAHMAN A Thesis Submitted in Fulfilment of the Requirements For the Award of the Degree of Doctor of Philosophy School of Economics and Finance College of Law and Business University of Western Sydney Sydney Australia March 2007

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of the impact of microcredit on poverty and women's

THE IMPACT OF MICROCREDIT ON POVERTY AND WOMEN’S

EMPOWERMENT:

A CASE STUDY OF BANGLADESH

By

SAYMA RAHMAN

A Thesis Submitted in Fulfilment of the Requirements

For the Award of the Degree

of

Doctor of Philosophy

School of Economics and Finance

College of Law and Business

University of Western Sydney

Sydney Australia

March 2007

ii

THE IMPACT OF MICROCREDIT ON POVERTY AND WOMEN’S

EMPOWERMENT: A CASE STUDY OF BANGLADESH

Abstract

The microcredit program in Bangladesh is a unique innovation of credit delivery

designed to enhance the income generating activities of the poor. Its uniqueness is

reflected in its collateral-free group-based lending strategy. The program extends

small loans to poor people, mainly women, for self-employment activities thus

allowing clients to achieve a better quality of life. This program is regarded as a very

exciting anti-poverty tool for the poorest, especially for women.

This study investigates the impact of microcredit on economic indicators as well as

consumption behaviour of the borrowers. It further analyses the impact of

microcredit on women’s empowerment. Primary data has been collected from the

borrowers of two major microcredit institutions in Bangladesh. Alongside the

borrowers, data have also been collected from non-borrowers of the same village to

compare the impact between borrowers and control group. The empirical work has

used sophisticated econometric techniques. Five different econometric methods -

OLS, 2SLS, Probit, Tobit and SURE estimators - have been applied to the sample

data of this study.

The most important finding indicates that microcredit programs are effective in

increasing borrowers’ income, assets and consumption but it is more pronounced

towards high income borrowers than low income borrowers. It further finds that

microcredit programs are empowering for women.

iii

STATEMENT OF AUTHENTICATION

I, Sayma Rahman, declare that this thesis has not been submitted, either in whole or

in part, for a degree at this university or any other academic institution. I also certify

that the work presented in this thesis is, to the best of my knowledge and belief, my

own work and original except as acknowledged in the text.

Sayma Rahman

------------------------------

Signature of Candidate

iv

DEDICATION

TO MY MOTHER, SISTERS AND BROTHERS

FOR YOUR FAITH IN ME

TO AWAB

FOR ENCOURAGING AND SUPPORTING ME

WITH MY LOVE…

v

ACKNOWLEDGEMENTS

Thank you, to the following people who assisted me and made it possible for me to

complete this thesis by offering their support, encouragement and professional

consultation in different ways:

First of all, to Professor P N (Raja) Junankar, my principal supervisor, thank you so

much for all the valuable advice and encouragement that I have received from you

for your professional support and for entrusting me with this work. Thank you for all

the confidence and generosity you showed me during my PhD study, especially in

the last few months.

To my co-supervisor, Dr Girijasankar Mallik, thank you for your supervision and

discussions, and for your interest and comments throughout this study. I would like

to express my gratitude to you for your time and encouragement that you have

provided me throughout this study. Thank you for helping me with data entry and

compilation.

I also express my sincere gratitude to Professor Anis Chowdhury for providing me

with updates on the issue of my research whenever he found any. My appreciation

goes to Dr Sudhir Lodh for his comments at different stages of my thesis. Special

thanks and appreciation go to Muhammad Arifur Rahman for providing me

comments and support. Many thanks to all my friends and colleagues for their

friendly assistance and encouragement in many matters during my PhD study. I also

wish to thank Angela Damis for proof reading my thesis and all the academic and

vi

administrative staff in the School of Economics and Finance at the University of

Western Sydney for necessary support and help.

Thank you all; without your support, this study would have not been possible.

Sayma Rahman

vii

TABLE OF CONTENTS

-----------------------------------------------------------------------------------------------------

Abstract ii

Statement of Authentication iii

Dedication iv

Acknowledgements v

List of Tables and Figures xi

Chapter One: Scope and Framework of the Study………………………….…....1

1.1 Introduction………………………….…….…………………............1

1.2 How Far the Grameen Bank Differs from BRAC……………………3

1.3 Research Problem and Question……….….………..…………….......4

1.4 Why is the Problem Worthy of Research?...........................................6

1.5 Data and the Econometric Approach…………………………………8

1.6 Thesis Outline…………………………………………...……………9

Chapter Two: Survey of Literature: Rural Credit Market and the Bangladesh

Economy …………………………………………………………………………...12

2.1 Relevant Theories on Rural Credit Market (Part A)………………..12

2.1.1 The Rural Credit Market……………………………………14

2.1.2 The Monopolistic Nature of the Rural Credit Market………15

2.1.3 Interlinked Factor Markets………………………………….19

2.1.4 Potential Risk………………………………………………..22

2.1.5 Significance of Credit Policy in the Rural Areas…………...23

2.1.6 Conclusion of Part A………………………………………….24

2.2 The Bangladesh Economy: Pre-Microcredit (Part B)……..……......25

2.2.1 Inception of Microcredit Institutions……………………….27

2.2.2 Background of the Grameen Bank……………...………….28

2.2.3 Growth and Expansion of the Grameen Bank.......................29

2.2.4 Savings Mobilisation by the Grameen Bank……………….32

2.2.5 Background of BRAC………….…………………………..33

2.2.6 Growth and Development of BRAC………….……………35

2.2.7 Savings Mobilisation by BRAC………...…….……...…….37

viii

2.3 The Bangladesh Economy and Recent Development………………39

2.3.1 Conclusion of Part B………………………………………..42

2.4 Introduction to Review of Literature (Part C)………………………43

2.4.1 Impact of Microcredit on Poverty ………………………….45

2.4.2 Women’s Empowerment……………………………………54

2.4.3 Household Consumption …………………………………...58

2.4.4 Conclusion of Part C………………………………………….61

Chapter Three: Assessment of Income and Asset Accumulation of Microcredit

Borrowers…………….………………………………………….………....63

3.1 Introduction…………………………………………………………63

3.2 Previous Studies on Impact Assessment…………………………....65

3.2.1 Data …………………………………………………….…..…66

3.2.2 The Selectivity Problem……………………………………....67

3.2.3 Research Questions…………………………………….……..69

3.2.4 Hypotheses……………………………………………………69

3.3 Model Specification…………………………………………………70

3.3.1 Endogeneity of Credit Program……………………………..72

3.3.2 Methodology………………………………………………...72

3.4 Specification of the Instruments and Variables……………………..73

3.4.1 Description of the Variables…………………………...……...74

3.4. 2 Specification of the Variables…………………………..……75

3.5 Estimation Results and Discussion………………………………….78

3.5.1 Descriptive Statistics of the Variables………………… ……78

3.5.2 Impact of Microcredit on Household Outcomes…………...…80

3.5.3 Impact of Microcredit based on Different Income Levels……85

3.5.4 Estimating Censored Regression Problem …………………...89

3.5.5 Censored Problem on different Income levels………………..93

3.6 Conclusion…………………………………………………………..95

ix

Chapter Four: Assessment of Consumption of Microcredit Borrowers

Compared to Non-borrowers………………………………………………….…97

4.1 Introduction……………………………………………………………..97

4.2 Literature Review on Expenditure Elasticity………………………….100

4.3 Introduction to Relevant Theories…………………………..…………104

4.3.1 Theory of Mixed Demand…………………………………...105

4.3.2 An Almost Ideal Demand System…………………………...107

4.3.3 Specification of the AIDS model……………………………108

4.4 Model Specification……………………………………………………112

4.5 Empirical Results……………………………………………………....118

4.5.1 Percentage and Mean Consumption ……………………….118

4.5.2 Preliminary Findings of the Descriptive Table…………...…121

4.5.3 Estimation Results and Discussion…………………………..125

4.5.4 Test of Significant Difference……………………………….134

4.5.5 Testing for Uncorrelated Error Terms…………………….....138

4.6 Conclusion……………………………………………………………..143

Chapter Five: Factors Affecting Women’s Empowerment in Microcredit

Programs...………………………………………………………..148

5.1 Introduction………………...………………………………………….148

5.2 Defining Women’s Empowerment……………………………….……154

5.3 Towards Development of Empowerment Index……………….………156

5.4 Calculation of Empowerment Index…………………………………...159

5.4.1 Economic Security Index……………………………………159

5.4.2 Purchase Decision Index…………………………………….160

5.4.3 Control over Asset Index…………………………………….161

5.4.4 Mobility Index……………………………………………….161

5.4.5 Awareness Index…………………………………………….162

5.4.6 Empowerment Index……………………………………..….163

5.5 Summary Table of the Indices…………………………………………164

5.6 What Causes Women to be Empowered?..............................................170

5.6.1 Research Questions...………………………………… ……171

5.6.2 Hypotheses…………………………………………………..171

5.6.3 Specification of the Variables…………………………….....172

x

5.7 Model Specification…………………….………………..……………172

5.7.1 Model of the Study………………………………………….173

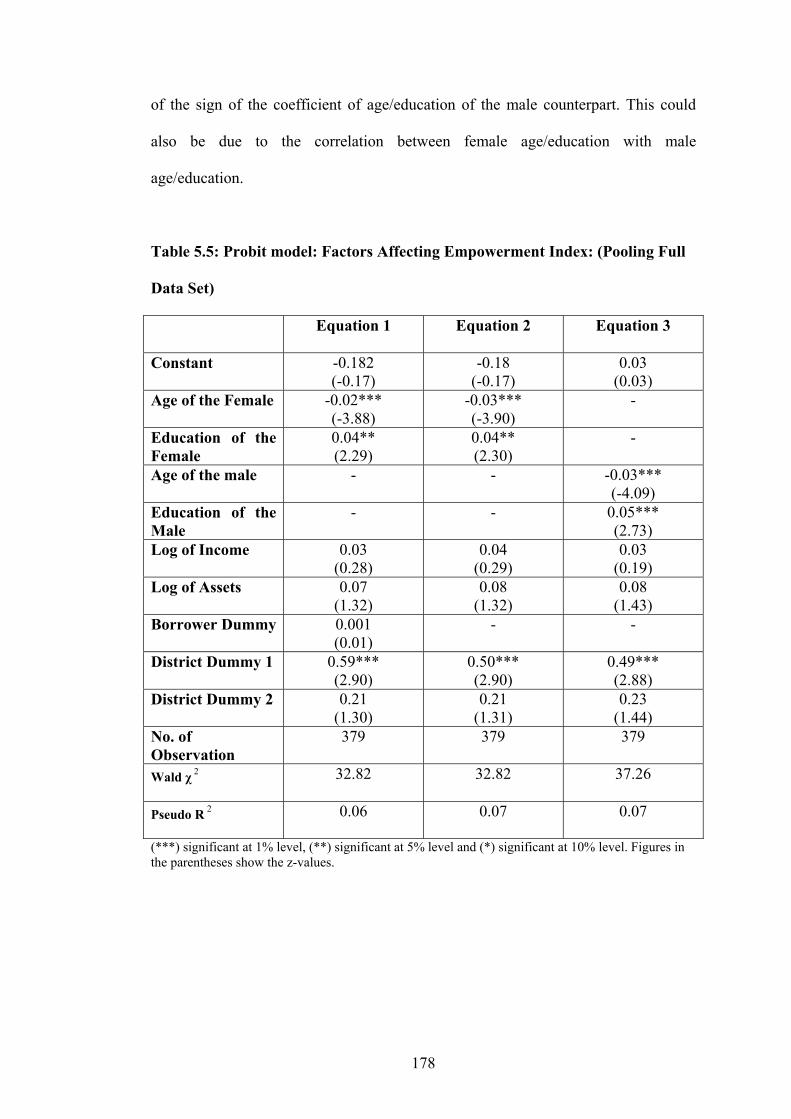

5.8 Estimation Results and Discussion……………………………..……..173

5.8.1 Factors Affecting Empowerment…................................... ....174

5.8.2 Factors Affecting Empowerment for both Groups………..…176

5.8.3 Factors Affecting Empowerment: Different Groups…...…....179

5.8.4 Do Microcredit Programs Empower Women?.........…..…….181

5.9 Conclusion…………………………………………………………......185

Chapter Six: Conclusion and Future Research….……….…………………….188

6.1 Introduction…………………………………………….……………...188

6.2 Summary of the Study………………………………….……………...189

6.3 Key Findings of the Study……………………………………………..192

6.4 Policy Implications………………………………………..…………...200

6.5 Study Limitations………………………………………………..…….201

6.6 Avenues for Future Research………………………………….…..…..202

6.7 Concluding Notes……………………………………………………...203

APPENDICES……………………………………………………………………205

7.1 Appendix A: Global Poverty Figure…………………………….…….205

7.2 Appendix B: The Sixteen Decisions of the Grameen Bank……...……206

7.3 Appendix C: Household Survey Questionnaire………………….……208

7.4 Appendix D: Map of Bangladesh……………………………………..225

7.5 Appendix E: List of the Village……………………………………….226

7.6 Appendix F: Descriptive Tables of Consumption Patterns…………....227

7.7 Appendix G: Experiences from Field Trip…………………………….236

7.8 Appendix H: Abstract of the Paper Published in the FIBR Conference

Proceedings……………………………………………………...…249

7.9 Appendix I: Abstract of the Paper accepted for publication in a

forthcoming issue in the Journal of Development Areas……….…250

7.10 Appendix J: Abstract of the Paper published in the Conference

Proceedings……………………………………………………….251

REFERENCES…………………………………………………………………..252

xi

List of Tables and Figures

List of Tables:

Table 2.1 Number of Schools, Students and Graduates from BRAC 36

Table 2.2 Job Creation by BRAC 36

Table 2.3 Comparing BRAC with the Grameen Bank 38

Table 2.4 Major Socio-Economic Conditions: 1975-2005 40

Table 2.5 Sectoral GDP Growth Rates: 1979/80-1999/00 41

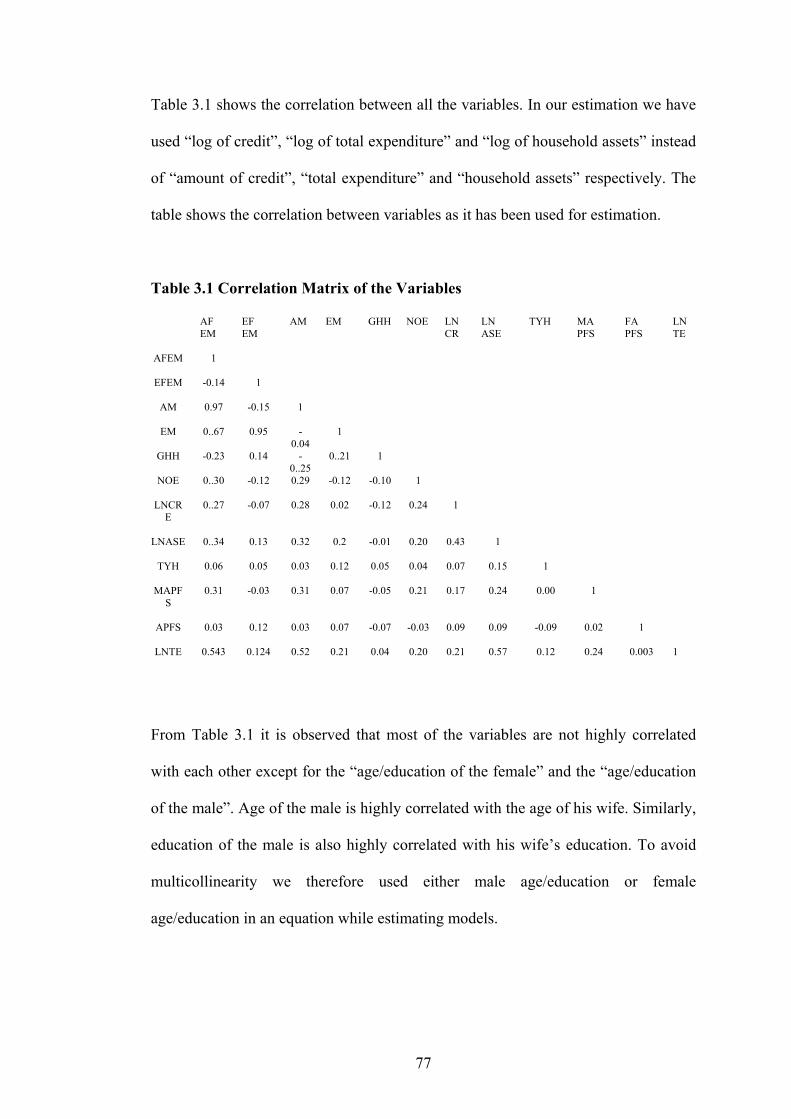

Table 3.1 Correlation Matrix of the Variables 77

Table 3.2 Descriptive Statistics of Dependent and Independent Variables 79

Table 3.3 2SLS Estimation of Amount of Borrowing on

Household Outcome: Log of Total Expenditure 81

Table 3.4 2SLS Estimation of Amount of Borrowing on

Household Outcome: Log of Assets 82

Table 3.5 2SLS Estimation of Amount of Borrowing on

Different Income Level: Log of Total Expenditure 86

Table 3.6 2SLS Estimation of Amount of Borrowing on

Different Income Level: Log of Assets 87

Table 3.7 Tobit Estimation of Amount of Credit Using Censored Data 90

Table 3.8 OLS Estimation of Household Outcomes Using Estimated Value

Of Amount of Credit from Tobit Estimation 92

Table 3.9 OLS Estimation of Household Outcomes Based on Different Income

Level Borrowers: Expenditure (Income) 93

Table 3.10 OLS Estimation of Household Outcomes Based on Different Income

Level Borrowers: Assets 94

Table 4.1 Average Consumption of Borrowers and Non-Borrowers

Of three Districts 120

Table 4.1a T-test Results of Mean Expenditure and Budget Share of Different

items Consumed by Borrowers and Non-Borrowers 121

Table 4.2 OLS Estimation of the AIDS Model 127

Table 4.3 Testing for Differential Slope Coefficient 136

Table 4.4 Seemingly Unrelated Regression Estimates 140

xii

Table 4.5 Testing for Different Slope Coefficients Using SURE 141

Table 4.5a Estimation of Income Elasticity for Borrowers and non-borrowers141

Table 4.6 Comparing and Contrasting OLS and SURE 142

Table 5.1 Defining Women’s Empowerment 151

Table 5.2 Borrowers’ and Non-Borrowers all indices according to Districts 165

Table 5.3 Empowerment Index of Borrowers and Non-Borrowers

According to Districts 166

Table 5.4 Probit Model: Factors Affecting Empowerment Index

Borrowers and Non-Borrowers Separately 175

Table 5.5 Probit Model: Factors Affecting Empowerment Index

Pooling Full Data Set 178

Table 5.6 Probit Model: Factors Affecting Empowerment Index

Based on Different Data Set 181

Table 5.7 OLS Estimation of the Equations 183

Table 5.8 Probit Estimation: Using the Estimated Value of the

Amount of Credit 184

List of Figures:

Figure 2.1 Monopoly Market 17

Figure 2.2 Number of Branches 31

Figure 2.3 Number of Borrowers 31

Figure 4.1 Consumption Tree . 99

1

Chapter One

SCOPE AND FRAMEWORK OF THE STUDY

1.1 Introduction

This research explores the impact of microcredit organisations in the Bangladesh

economy. It is one of the first comprehensive studies that analyses the impact of

microcredit in a broader spectrum. This is an original study not only in terms of use

of a new data set but also in terms of use of econometric techniques1 that have not

been used by other researchers in this area. The academic discourse in this research

is quite relevant and goes a long way to contributing to the existing literature. This

study touches on wide-ranging theoretical issues related to this field and highlights

the developments in the literature on the subject area. Microcredit is not only a very

topical issue the founder of the Grameen Bank has just been awarded the 2006 Nobel

Peace Prize but it has also been a topic of interest to researchers since its inception in

early 1970s. In this research we have analysed the impact of microcredit programs

on the borrowers of two large microcredit institutions in Bangladesh − the Grameen

Bank and the Bangladesh Rural Advancement Committee (BRAC).

The Grameen Bank is the largest moneylending institution in the world, measured in

terms of numbers of borrowers. In 2005 alone, Grameen Bank’s borrower count rose

from 4 to 5 million. Microcredit programs have created a revolution not only in

Bangladesh but also through out the world for their novelty. Microcredit is a unique

1 This is the first study that uses An Almost Ideal Demand System (AIDS) model to analyse the consumption behaviour of the microcredit borrowers, Tobit estimations to analyse the impact of microcredit on household outcomes and Two Stage Least Square estimation to analyse the impact of microcredit on women’s empowerment.

2

innovation in credit delivery techniques that enhances income generating activities.

Its uniqueness is reflected in its collateral-free group-based lending strategies, high

repayment rates and also a special focus on women. A microcredit program2 extends

small loans to poor people, mainly women, for self-employment activities thus

allowing clients an opportunity to achieve a better quality of life. It is the most

sensational anti-poverty tool for the poor people, especially women (Microcredit

Summit 1997, World Bank). For these reasons, microcredit programs in Bangladesh

have drawn the attention of academics, researchers, international agencies and policy

makers throughout the world. The Grameen Bank the largest microcredit institution

and BRAC the largest non-governmental organisation (NGO) – have been the

pioneers of microcredit in Bangladesh for almost three decades.

There are more than a thousand microcredit institutions providing financial and

social development services in Bangladesh (Khalily, Imam and Khan, 2000 p. 105).

The Grameen Bank and BRAC are the major contributors to this credit market.

About 94 % of the borrowers in this market are female. Bangladesh’s microcredit

program is widely known as a ‘lending program to the poor without any collateral’.

The main focus of this endeavour is to eliminate poverty and empower women in

rural country areas in Bangladesh (Khandker, 2003).

2 According to Khalily, Imam and Khan (2000), “program” is synonymously used with “institution.” Program encompasses those microcredit or micro-finance institutions that are providing micro-financial services.

3

1.2 How Far the Grameen Bank Differs from BRAC

In order to achieve the main objective of delivering credit the Grameen Bank and

BRAC both provide various support programs including social services3 and social

development programs along with financial discipline. As part of such initiatives the

Grameen Bank sets out guidelines and codes of conduct for the borrowers promoting

social and financial discipline (see Appendix B). To develop social awareness among

borrowers, BRAC provides skills training, adult literacy and primary health care etc.

BRAC’s social development approach is more extensive (integrated program)

compared to the Grameen Bank’s minimalist (credit only) approach.

One of the central concerns of both the Grameen Bank and BRAC is to support the

poor - making productive use of their credit and income. It should be mentioned that

although there are differences between the Grameen Bank and BRAC in their

approaches to loan provision, both institutions adopt a credit based poverty

alleviation approach in rural Bangladesh.

The credit delivery model developed by the Grameen Bank does not require tangible

collateral. The “group liability” may be interpreted as intangible collateral in the

sense that, in case of default, a member loses its opportunity for future loans. The

model developed by the Grameen Bank has been replicated in many parts of the

world (Khandker et al., 1995, p. 2). Malaysia, Guinea, Malawi, Colombia, the

Philippines and Nigeria are some less developed countries (LDCs) that have

replicated the Grameen model. In developed countries, the Women’s Self-

3 These include providing free education, awareness development for using proper sanitation, pure drinking water, plantation and birth control measures.

4

employment Project of Chicago, Illinois, the Good Faith Fund in Pine Bluff

Arkansas, in the United States and the Native Self-employment Loan Fund of

Toronto, Ontario in Canada are noteworthy (Wahid, 1993).

1.3 Research Problem and Questions

The founder of the Grameen Bank, Professor Muhammad Yunus, won the Nobel

Peace Prize in 2006 for waging a war against poverty with a revolutionary

microcredit system. He was praised by the Nobel Committee as “a leader who has

managed to translate visions into practical action for the benefit of millions of

people, not only in Bangladesh, but also in many other countries”. This signifies the

importance of a critical examination of the microcredit program.

Although there have been quite a number of studies on various aspects of

microcredit4, none of those studies has comprehensively analysed whether programs

are successful in bringing about an improvement in the quality of life of the

borrowers. On the other hand, the impact assessment studies often show

contradictory results. This study, therefore, analyses the impact of microcredit on

various household outcomes. It examines the consumption patterns of borrowers

compared to non-borrowers and assesses the impact of microcredit on women’s

empowerment.

4 Stiglitz (1993) and Varian (1990) in their theoretical paper have used the principal-agent framework to explain group-based lending. Hossain’s study (1988) is one of the authoritative studies on the impact of credit programs. Gonzalez-Vega and Chavez (1993) and Yaron (1992) have examined the subsidy issue in the context of financial viability of credit programs.

5

This study raises a number of critical questions that need to be addressed by

economists.

Question One: Do microcredit programs in Bangladesh improve various household

outcomes such as income and asset accumulation?

Question Two: Do microcredit programs in Bangladesh provide improved

consumption for borrowers compared to that of the non-borrowers?

Question Three: Do microcredit programs in Bangladesh empower women?

In the existing literature there are two general hypotheses about the impact of

microcredit programs.

First Hypothesis: Microcredit programs are successful in improving the standard of

living of the rural people5 and improving their consumption behaviour.

Second Hypothesis: Microcredit programs are successful for empowering women.

This study answers these questions and examines the hypotheses by using

econometric techniques such as the Ordinary Least Square estimation (OLS), Two-

stage Least Square estimation (2SLS), Tobit, Probit and Seemingly Unrelated

Regression Estimates (SURE). It compares the performance of borrowers with a

control group, non-borrowers to find out if borrowers are better off compared to non-

borrowers.

5 Khandker et al. (1998) showed credit programs have a positive impact on income, production and employment particularly in non-farm sector. Mustafa et al. (1996) showed that not all money borrowed is invested but some portions are used for consumption. Hashemi et al. (1996) and Zaman, (1998) showed that credit programs are empowering for women.

6

The existing literature does not provide a comprehensive study, that is, one covering

all the goals that the credit programs claim to achieve. This study incorporates the

major issues such as impact assessment and conducts a thorough analysis of the

impact of credit on consumption and on women’s empowerment. It uses a new

approach to measure consumption and integrates some new explanatory variables in

the general model specification. In particular this study does not look at the impact

of microcredit on poverty reduction in Bangladesh overall.

1.4 Why is the Problem Worthy of Research?

The success stories of microcredit are fading nowadays as the programs are drawing

increasing amount of attention as well as inevitable criticism. The evidence from the

literature shows that the impact of microcredit on poverty in Bangladesh is

contradictory. There is research to suggest that the access to credit has the potential

to reduce poverty significantly (Hossain, 1988; Khandker, 1998a; Wahid, 1994); on

the other hand, there are studies, that argue that microcredit has a minimal impact on

poverty reduction (Morduch, 1999 and 2000; Weiss and Montgomery, 2005). In

spite of their recent fame, microcredit programs are facing criticism, on the grounds

that they charge very high rates of interest and the poor have not benefited from the

programs. As micro finance transactions are very small in volume, they are unlikely

to have a sustained aggregate impact on poverty reduction. Also, there is concern

that funding for microcredit programs could have been used for other much needed

programs such as health, water, and education. Credit programs may enable poor

people to improve their conditions, but they do not eliminate the need for other basic

social and infrastructure services. Some studies even claim that the benefits from

microcredit are so small that borrowers often borrow from other informal sources to

7

repay loans (Matin, 1999). The very purpose of the micro-finance movement as a

lending instrument for the poor is thus questioned.

In spite of rigorous involvement of world development organisations to reduce

poverty, world poverty has been increasing over the last decade6. This implies that in

many countries the existing policies may not be effective in reducing poverty.

Professor Yunus’ Nobel Peace award reinforces the fact that the world’s

development planners are considering microcredit as one of the key anti-poverty

tools for poorest people. World development organisations such as the World Bank

are planning to replicate the model widely to eradicate poverty from the world.

Since, on the one hand, the impact of microcredit programs on poverty eradication is

still a controversial issue and on the other, world development organisations are

considering microcredit as a key solution to eradicate world’s poverty, it is

extremely important to conduct a thorough analysis of the impact of microcredit

programs in a LDC such as Bangladesh. It is also important to find an answer to the

controversy as well as to find out the extent of the poverty reduction effect of

microcredit programs.

Even though there is a broad consensus about credit objectives, program outreach

and high repayment rates, it is not clear how far credit programs benefit the poor and

whether the poor are utilising the loans in a proper way. It is necessary to investigate

how far microcredit programs are successful in (1) increasing income and asset

accumulation (alleviating poverty) via increasing the standard of living of the poor,

6 Even though the Global Poverty figures between 1990 to 1999 shows an overall reduction in poverty in the world, but in some part such as Europe and Central Asia, Latin America and the Caribbean, Sub-Saharan Africa and in China poverty has increased. Please refer to Appendix A.

8

(2) increasing the consumption of borrowers, and (3) empowering rural women to

whom they are delivering loans. It is imperative to investigate the programs with

first-hand information collected from the beneficiaries to find out the actual benefit

received by the microcredit clients, the extent of clients’ awareness and the extent of

poverty reduction as a result of the intervention of the microcredit programs.

This study analyses the impact of microcredit in terms of poverty reduction and

women’s empowerment using primary data. A detailed questionnaire7 with a series

of questions has been administered to 571 usable respondents out of which 387 are

borrowers and 184 are non-borrowers. Appropriate econometric methods are used to

analyse the responses. Some existing models that have been used by other

researchers are also used after modifying the model specification and/or the

estimation methods.

1.5 Data and the Econometric Approach

Primary data have advantages over secondary data as there is less possibility of

biased estimation caused by omitted variables. On the other hand, the World Bank

and other international agencies have already used secondary data extensively.

Therefore, we have collected primary data during July-August 2004 for the purpose

of our analysis. A well-organised questionnaire is prepared for data collection. Our

study draws the sample from three major districts in Bangladesh, viz., Gazipur,

Dinajpur and Chokoria. The districts have been chosen on the basis of different agro-

7 Please refer to Appendix C

9

climatic and economic conditions. From each district, five villages8 have been

selected in a cluster. Forty households has been selected using multistage stratified

random sampling from each of these five villages. The samples of the households’

have been randomly selected without replacement from the list of households

available from the program’s local office of each village. The non-borrowers data

has been collected from the same cohort to make a proper comparison. Finally the

total sample size eventually was approximately 600.

These cross-section data are estimated firstly, using the basic methods of Ordinary

Least Squares (OLS), secondly, the instrumental variable method Two Stage Least

Square (2SLS), thirdly, censored Tobit estimation, binary Probit estimation and

Seemingly Unrelated Regression Estimates (SURE) to estimate multiple equation

models.

1.6 Thesis Outline

This study provides a comprehensive body of theoretical and empirical work on

microcredit. It outlines theoretical considerations of the monopolistic nature of the

rural credit market on the basis of which microcredit programs have been developed.

The study presents an extensive analysis of the theory of rural credit as well as an

empirical examination. It is organised in six chapters which are as follows:

8 The map of Bangladesh showing the areas from which data has been collected and the list of the villages are provided in Appendix D and E respectively.

10

Chapter Two outlines the relevant theories on the rural credit market. It then

discusses the inception of microcredit institutions in Bangladesh, provides an overall

picture of the Bangladesh economy before and after the introduction of the

microcredit movement. Finally the chapter provides review of a wide range of

literature on microcredit.

Chapter Three provides an empirical analysis of the impact of microcredit on

various household aspects such as income and asset accumulation. This chapter

closely follows the model of Pitt and Khandker (1996) but extends the analysis by

introducing new variables. It examines the impact of microcredit on various

household outcomes using Two-Stage Least Squares estimation. It further analyses

the impact on household outcomes for different income level borrowers. Finally,

after pooling the data for both borrowers and non-borrowers, Tobit estimation is

undertaken for the censored data.

Chapter Four presents an empirical analysis of the consumption patterns of

borrowers compared to non-borrowers using the AIDS model. Ordinary Least

Squares (OLS) estimation as well as Seemingly Unrelated Regression Estimate

(SURE) is used for the model and results are compared. We allow for differences

between borrowers and non-borrowers in their consumption patterns in this chapter.

Chapter Five provides an empirical analysis of women’s empowerment. Firstly, the

chapter considers alternative definitions of empowerment that has appeared in the

literature. Secondly, the chapter defines empowerment from a new perspective and

develops an empowerment index based on this definition. Thirdly, it finds out the

11

difference between borrowers and non-borrowers in terms of various empowerment

correlates. Fourthly, it studies the factors that affect women’s empowerment. Finally,

the chapter shows whether credit programs are effective in empowering women.

Finally, Chapter Six summarises the results of the study together with policy

implications and provides some suggestions for further research.

12

Chapter Two

SURVEY OF LITERATURE: RURAL CREDIT MARKET AND

THE BANGLADESH ECONOMY

This chapter is organised in three parts. Part A outlines relevant theories on rural

credit market. Part B discusses the historical perspective leading to the inception of

microcredit institutions in Bangladesh. It also examines the scope of the activities

undertaken by these credit institutions. Further, it makes an informal attempt to

understand the ways in which microcredit programs may have contributed towards

the development of the Bangladesh economy. The chapter further examines the

broad trends in socio-economic developments that have taken place over recent

decades in Bangladesh and endeavours to relate these to the activities of the

microcredit institutions. Finally, Part C provides a review of literature on

microcredit.

Part A

2.1 Relevant Theories on the Rural Credit Market

Prior to the introduction of microcredit institutions, the debate in development

economics literature centred on the availability of rural financing in developing

countries (Reserve Bank of India, 1977). Several previous studies on rural financing

show the existence of large interest rate differentials between rural and urban regions

in developing countries (Wharton, 1962; Bailey, 1964; Rahman, 1979). However,

these studies suggest that such interest rate differentials may be of existence for a

temporary period. Basu (1997) suggests that arbitrage across regions on such

13

financing may take place because it is possible to borrow from low interest regions

and then lend the sum to high interest regions (p. 268). Basu further states that

according to standard comparative static analysis this process will continue until

market forces eliminate interest rate differentials between urban and rural regions.

Saleem (1987) argues that the existence of high interest rate differentials can only be

explained by the segmentation of regional funds through risk or monopolistic

barriers.

As well, the existence of such relatively high interest rates in rural regions may be

caused by an inherent and known higher risk default factor to recover the principal

from the borrowers (Tun Wai, 1958; Raj, 1979). While this is an attractive

proposition, research evidence suggests that it may only be a partial explanation of

rural-urban interest rate differentials (Bottomley, 1975). Another explanation for

such differentials may be caused by high transaction costs in channelling finance

from urban to rural areas. These high transaction costs ultimately act as a barrier for

formal commercial banking institutions entering the rural funds market. One of main

foci of rural financing is that the size of rural loans is generally smaller than urban

loans. Rural loans are more disparate requiring relatively higher administrative and

overhead costs when undertaken by established commercial banks (Lipton, 1976). In

contrast, local lenders have a cost advantage with local knowledge leading to lower

information search costs in providing loans. Bottomley (1964) argues that the

administrative costs of collecting a large number of local small loans are less for

local lenders specialising in specific rural regions. Thus, cost differentials based on

this asymmetric information leads to high entry barriers and local monopolies in

rural fund markets.

14

It should be noted that in the past (that is, prior to the introduction of microcredit

institutions in Bangladesh) small informal lenders (mostly local merchants, large

landowners and moneylenders) dominated rural funds markets in many developing

countries (Bhaduri, 1977). In general, these informal lenders find it profitable to

invest their surplus capital (funds) in local small loans that have higher returns,

instead of depositing the surplus with formal commercial banks. According to

standard market theory (as has been stated earlier), such high entry barriers leading

to local monopolies will result in an under-allocation of funds to rural regions.

2.1.1 The Rural Credit Market

Prior to the introduction of microcredit in Bangladesh, credit was not widely

available in the rural economy. Informal lenders (as in most developing countries),

were the sole providers of rural credit (Adams and Fitchett, 1992; Ghate, 1992).

These informal lenders (who are commonly known as “moneylenders”) had an

information advantage about their clients, which helped them to monitor their

activities in an easier and cheaper way. These moneylenders used to charge high

interest rates. For example, Hossain (1988 p. 23) argues that in the case of

Bangladesh interest rate charged by these moneylenders were about 10% per month.

These moneylenders basically provide loans only to the people who worked for them

or over whom they have some sort of control. The nature of operation of these

moneylenders may be described in terms of a monopolist or duopolistic market. The

following section provides the relevant theoretical explanation of the monopolist

market.

15

2.1.2 The Monopolistic Nature of the Rural Credit Market

It is a common practice in rural areas that moneylenders lend to people over whom

they have some control. For example, a merchant lends only to those who buy/sell

regularly from their shop or business. The rural credit market is defined as

“fragmented”9 (Basu, 1997). This credit market is further characterised by a whole

array of interest rates differentials. The theoretical relevance of this fragmented rural

economy is demonstrated here in terms of a monopolistic market.

The personalised relationship between the borrower and the lender determines most

often the terms and conditions of rural lending. In general, it is observed that each

lender lends to the person in whom they have greater personal confidence. That is,

according to Bottomley (1964), the monopoly power of the rural moneylender is

dependent on the intimate knowledge of the borrower’s circumstances.

The monopolistic rural credit market as analysed by Basu (1997) is discussed below.

Following Basu’s (1997) model the demand function is derived, assuming the

borrower can get loans only from one moneylender and the borrower is a price taker,

as follows:

)1.2(0)(),( ' <= iLiLL

where L is the amount of credit and i the interest rate.

The inverse function of Equation (2.1), according to Basu, is just another way of

looking at the same relation, as follows:

9 A fragmented rural credit market means that each moneylender with a potential client becomes a small “Credit Island” and the credit market effectively becomes broken up into small fragments (Basu 1997).

16

)2.2(0)(),( ' <= LiLii

This relationship is shown in Figure 2.1, where the line AD shows the demand

function and AM represents the marginal revenue curve. The personalised relation

ensuring there is no default, the moneylender chooses L amount of loan with i

interest to maximise his/her interest earnings.

Now assuming that the lender has the option of investing money elsewhere and

earning an interest r on the lending, the lender’s objective function, according to

Basu, is derived, as follows:

LrLLiL

−)(max}{

The first-order condition of this problem is shown as follows:

)3.2()()( ' LLiLir +=

The left-hand side of this equation represents the marginal cost of giving loans and

the right-hand side is the marginal revenue. Hence, Equation 2.3 depicts the standard

equilibrium in a monopolistic market where MC=MR. This relationship is shown in

Figure 2.1, as having equilibrium level of amount of loan and interest rate which is

indicated by *L and *i respectively.

17

A

i

*i

r C E

O *L M F D L

B

Figure 2.1 Monopoly Market

According to Basu, “the rural financial market is fragmented into little monopolistic

islands … the rural economy itself will be characterised by a whole array of interest

rates” (p. 270). Basu also states that this model is not without limitations. Firstly,

Basu argues, “The analysis presumes that the borrower always has enough money to

repay a loan”. In reality, given the widespread poverty of rural borrowers, this is

unrealistic (p. 271). The second criticism, according to Basu, is that “monopoly

analysis is general” (p. 271).

In Figure 2.1, it is shown that the urban interest rate r is lower than i* (rural interest

rate) when the moneylender has access to the urban market. Here it is presumed that

the borrower always has enough money to repay the loan. In reality, however,

18

according to Basu, the borrowers often face a liquidity crisis and, therefore,

sometimes use alternative mode of repayments including personal labour; mortgage

land and personal belongings.

According to Basu (1997, p. 271), the demand function of the borrower (Equation

2.2) is treated as “primitive” It is derived assuming that the borrower takes loans

only in order to invest. Let R denote the total earnings from investment and L denote

the amount of loan; the function is derived, as follows (p. 272):

0)0(,0)(,0)(),( "' =<>= RLRLRLRR

Basu (1997) advocates that in the case of a producer who employs workers up to the

point where wage equals marginal product of labour, given i, the borrower chooses L

so that 1+i equals marginal earnings from L. Thus, according to Basu,

“The marginal earnings curve represents the demand curve for loans and the area

under this curve is equal to the total earnings of the borrower” (p. 272). Therefore,

the demand curve for loans put forward by Basu is as follows:

)(1 ' LRi =+

This is the equation of the curve AD in Figure 2.1.

If the moneylender-monopolist considers lending a certain amount *OL , according to

Basu the maximum amount the borrower is willing to pay for this is *OABL . Basu

shows that, according to Figure 2.1, the lender has the option of earning an interest

of r elsewhere; the lender’s net income will be ABCr.

19

If the lender adopts this strategy of extracting the maximum the borrower is willing

to pay, according to Basu the lender does best by giving loans equal to OF, for a net

income of AEr. Since AEr> *BCri Basu argues that, “by this strategy the monopolist

earns a larger profit than he would by behaving like a textbook monopolist” (p. 272).

This finding of Basu (1997) is consistent with that of Bardhan (1976 and 977) where

he uses a model that shows the equilibrium percentage of revenue is higher, other

things remaining the same for the monopolistic landlord.

2.1.3 Interlinked Factor Markets

The rural credit market is not only dominated by moneylenders who are

monopolistic in nature as discussed above. The landlord-tenant relationship is also

an important characteristic of the rural market. The relationship described in the

literature is master-serf in nature. A widely noted theoretical paper on the interlinked

factor markets in an agrarian economy is by Bhaduri (1973) where he shows that the

landlord who is a provider of consumption loans to a tenant may have no incentive to

adopt yield increasing innovations, if the landlord’s interest income from their loans

to the tenant goes down (because the tenant will borrow less as they shares the

increase in yield) sufficiently to offset his share of the increased yield. Bhaduri’s

(1973) four prominent features of the agricultural economy make it easy to

understand the theory on rural credit market. Bhaduri portrays the agricultural

market as “semi-feudal” because the existing relations of production have more in

common with classical feudalism of the master-serf type than with industrial

capitalism. The features are as follows:

20

(1) Sharecropping: Sharecropping is a common form of land tenure used in the

agricultural sector. According to Bhaduri (1973) “The landlord leases out his land

for at least one full production cycle and the net harvest10 is shared between tenant

and the landlord on some legally stipulated basis” (p. 121). He further mentioned

that this tenancy system may have enormous complications as the tenant may have

some land of his own or working on fixed capital or the entire amount is supplied by

the landlord.

(2) Perpetual Indebtedness: “The tenant is always heavily indebted. A substantial

portion of the tenant’s legal share of the harvest is taken away immediately after the

harvest as repayment of past debt with interest, thus reducing his actual availability

balance of the harvest well below his legal share of the harvest” (Bhaduri 1973, p.

122). According to Bhaduri (1973) this does not leave enough food for the tenant to

survive from this harvest to the next harvest. The only way of survival is to borrow

for consumption. This actually perpetuates the indebtedness of the tenant.

(3) Landowner as the Lender of Consumption-loans: “This perpetual indebtedness of

the tenant is combined with another important factor which lends the whole system

the definite character of semi-feudalism the lender of the consumption-loan is also

typically the tenant’s landlord” (Bhaduri, 1973 p. 122). Thus the tenant leases their

land from the same man to whom they are perpetually indebted and this reduces

them virtually to the state of a traditional serf. The tenant is more or less tied to their

landlord. According to Bhaduri (1973), this semi-feudal landlord exploits the tenant

both through their traditional property rights in land and through usury and both

10 Net harvest as defined by Bhaduri (1973) is the gross harvest minus seed required for the next harvest.

21

these modes of exploitation are important features of the agricultural market in

LDCs.

(4) Inaccessibility to the Market: “The semi-feudal economic relationship between

the tenant and his landlord works with full severity when the rate of interest on

consumption-loans is extraordinarily high. The tenant is usually not credit-worthy in

any commercial banking sense because he has no asset to borrow against. His only

lender is usually his landlord, who lends against the future harvest and the tenant has

to borrow on terms which the latter dictates” (Bhaduri, 1973, p. 122).

These four types of landlord-tenant relationship appeared in the theory of

agricultural economy in different ways. Bardhan (1980) shows that a monopolistic

landlord does land rationing at a fixed rental share. Bardhan (1980) argues that “the

tenant is dependent on the landlord for credit to finance a given subsistence

consumption in the lean season11 and he pays back the loan along with interest at the

end of the harvest” (p. 89). According to Bardhan (1980), “since the interest rates are

high, it matters a great deal as to how long one has to wait until income comes. The

tenant knows that as a wage labourer he can get some wage income immediately in

lean season, whereas as a tenant he has to wait until the crop is harvested in peak

season” (p. 89).

In the model developed by Bardhan (1976 and 1977) the landlord has three sources

of income, rental income from leased-out land, income from self-operated land net of

wages paid in lean and peak seasons, and interest income. They maximise their total

11 In agricultural production there are two seasons lean and peak. Lean is the preparation season and peak is the harvest season.

22

income with respect to their two decision variables, the amount of land to lease out

and the amount of labour to use on their self-operated farm. According to Bardhan

1980, “the tenant considers his income from cultivating the leased-in area and from

wage income net of interest payment on lean-season consumption credit and

maximises it with respect to his only decision variable, labour-intensity per acre on

his leased-in area.” Bardhan (1980) shows in his comparative static parametric

variations model that the equilibrium percentage of area under tenancy will be higher

for the monopolistic landlord.

2.1.4 Potential Risk

The Interlinked rural credit market characterised by Basu (1997) is when the

landlord agrees to take on a tenant at a fixed rent and also agrees to provide the

tenant with credit at a certain interest rate. According to Basu (1997) there is some

risk associated with a loan on part of the landlord. There is always a probability that

certain portion of loans will not be repaid. According to Basu (1997), “if a debtor is

the lender’s tenant or has some historical ties with the lender, it is very unlikely that

the debtor will get away with defaulting. If, on the other hand, a debtor has no

dealings, nor any prior ties, with the lender, it is likely that the debtor will not repay,

there being hardly any legal machinery in backward regions to enforce repayment”.

It is not unrealistic that for every moneylender among all potential borrowers there is

a set of people from whom the lender can recover money and there is another set

over whom the landlord has no control. Therefore, according to Basu (1997) if a

landlord does not discriminate between potential borrowers, he will attract all

“lemons” and eventually become bankrupt. The landlord in general provides loans to

23

those over whom they have some control and where there is no ‘potential risk’ of

default.

2.1.5 Significance of Credit Policy in the Rural Areas

The monopolistic nature of the rural credit market has become a concern for policy

makers in understanding the nature and depth of the market. In the case of LDCs,

credit policy is a great worry for policy makers because the moneylenders are the

only credit providers and they charge exorbitant interest rates.

For over a century official policy has been directed at replacing traditional

moneylenders with formal institutions such as cooperatives, rural development bank,

and commercial bank branches. However, these institutions may not cater for the

needs of rural borrowers due to the lack of securities, which is a pre-requisite for

formal borrowing. The government of LDC and the relevant global institutions such

as the World Bank and IMF are always concerned to improve the condition of poor

people in the rural areas. Since there is always an unsatiated demand for rural

finance in rural areas, the governments of LDCs take various initiatives. The major

concern for rural people is how to survive. If they (rural people) could obtain

affordable long-term credit for investment as well as for consumption, then they

could improve their living conditions.

Since 1976 in Bangladesh the microcredit institutions such as the Grameen Bank

have made a remarkable achievement in rural lending. They have set their objective

to reduce poverty by mobilising resources and targeting credit and non-lending

services to poor rural households for the purpose of setting up new enterprises

24

(Yunus, 1984; Hossain, 1984; Getubig, 1992; and Khandker, 1996). Much has been

written about this new class of “banks for the poor”, and there have been enthusiastic

replications in a number of countries including the United States (Ravallion and

Wodon, 2000). Several nations are now trying to emulate the Grameen Bank model.

2.1.6 Conclusion of Part A

Earlier theoretical discussion shows that the landlords can prevent a tenant from

renting other land or from working for wages. Landlords can include these

restrictions in the contract or they can enforce them. The landlord also has an extra

control instrument by means of contract terms that limit the tenant to their wage

rate12 (reservation utility) (Binswanger and Rosenzweig, 1984, p 17).

Some interesting observations may be derived about the microcredit programs of

Bangladesh based on the above mentioned theoretical discussion of interlinked rural

factor markets. The microcredit movement that has been initiated in Bangladesh is a

breakthrough in the history of rural financing in developing countries. Its operating

style is in many ways different from the traditional moneylenders, who lend to rural

borrowers, as well as landlords, who make tenants work for them. It has already been

mentioned earlier that the traditional moneylenders are monopolistic in nature. Thus,

microcredit programs do not reveal such characteristics. Unlike traditional

moneylenders that make their tenants work for them, the borrowers of microcredit

are allowed to choose the activities in which they are willing to invest. The credit

delivery mechanism is very different from traditional lending systems. This does not

12 Bardhan and Srinivasan (1971) developed a similar model where the landlord is not allowed to control tenancy size.

25

allow a master-serf relationship as portrayed by Bhaduri between the loan providers

(microcredit institutions) and their borrowers. It is exciting to see that the programs

are now trying to change the traditional rural lending system and trying to make rural

financing available and affordable for everyone. One very interesting observation

about the microcredit programs are that they do not distinguish between clients’

“potential risk”, rather they provide loans to everyone. It has removed the

moneylenders to some extent and is trying to save the rural economy from very high

interest rates. The popularity of the programs is demonstrated by their outreach and

high recovery rate. The features that attracted most attention are their use of “peer

monitoring” which has substituted the need for collateral. Although lending is

provided to individuals, borrowers are formed into groups of four or five. According

to the Grameen Bank model, each of these groups is held jointly accountable for the

behaviour of its members. If one member is in default to repay the credit then the

likelihood of obtaining credit by the other members becomes remote. That is, one

member’s non-repayment can cause all other members to be denied future credit.

This collective microcredit model creates peer pressure and also encourages the

development of mutual help within groups.

Part B

2.2 The Bangladesh Economy: Pre-Microcredit

Bangladesh became an independent nation in 1971 after a brutal civil war with

Pakistan that lasted about nine months. The government of Bangladesh has faced the

difficult task of reconstructing and rehabilitating the fragile economy since then.

Bangladesh’s economy was forced through a very vulnerable period followed by

26

several natural calamities including the devastating flood of 1974. The War and

natural calamities combined took a heavy toll on mainly the agriculture-based

economy of Bangladesh. Consequently, the production of rice, which is the staple

food, faced a major setback (Hossain, 1988). Soon after independence the economy

had to rely quite heavily on imported food. For example, Bangladesh’s imported

food was worth13 Tk14 500, Tk 870 and Tk 1,310 million at constant prices in the

years 1973-74, 1974-75 and 1975-76 respectively.

In the face of a growing population, the agricultural sector of the economy could not

expand sufficiently. This sector also failed to create more jobs and absorb additional

people joining the labour force every year due to the high population growth (Wahid,

1993). In contrast, the manufacturing sector had an even a bleaker image with poor

structure as well as small size during the 1970s. The major manufacturing industries

were nationalised by the government soon after liberation but they proved to be

liabilities rather than assets due to widespread mismanagement and corruption.

Overall, the economy was characterised by low economic growth, high population

growth and inequality in distribution of resources during 1970s. Khandker (1998a)

identified landlessness15 in rural areas as a major contributor to poverty in the

country at that time. Along with landlessness, lack of human and physical capital

among the poorer population in the rural areas prevented the economy from

productive investment. Coleman (1999) rightly argues that the poor often find

13 Bangladesh Bank Economic Trends, vol. XV (5), (1990), p. 18. 14 Tk. stands for taka, the currency of Bangladesh. 15 In Bangladesh, households with less than 0.5 acre are considered functionally landless, since the amount of land they own cannot be a significant source of income (Hossain, 1988, p.15).

27

themselves in a vicious circle: they are producing at a subsistence level, which in

turn makes it harder for them either to invest in productive resources or to gain

access to formal credit market.

2.2.1 Inception of Microcredit Institutions

In the post-independence period, state owned commercial banks and specialised

agricultural banks such as the Bangladesh Krishi Bank (BKB) could not cater to the

needs of the rural people in the country for several reasons. Firstly, these banks

required collateral for providing loans, which rural poor people found difficult to

arrange. Secondly, the loan sanctioning procedures and other related formalities were

too cumbersome for mainly less educated rural people. Thirdly, these financial

institutions preferred handling large loans rather than small loans. Finally, another

problem was the high transaction costs for the banks that include cost of obtaining

information about the rural borrowers to access their creditworthiness, monitoring

the use of loans and ensuring repayments.

For the reasons outlined above the commercial and other formal banks could not

operate successfully in the rural financial market of Bangladesh. Due to non

availability of credit from the formal sources the rural people had to rely heavily on

informal money lenders who used to charge exorbitant interest rates. All these

factors taken together effectively opened up an opportunity for a new type of

financial institution to come into existence which is called the “microcredit

28

institution”16 (most recently these microcredit institutions are also often called

microfinance institutions).

Nobel laureate Professor Muhammad Yunus, the founder of the largest microcredit

institution in Bangladesh – Grameen Bank was convinced that the poor people were

more capable of taking care of themselves than what was and currently is portrayed

in traditional literature (Yunus, 1999, p. 69). He observed that poor villagers with

virtually no assets worked hard at a variety of crafts and service jobs and in the

absence of any major shocks could somehow manage to survive (Yunus 1999, p.

71). Unfortunately, they could not accumulate any capital because firstly, their

income was quite low and secondly, out of this income, after deducting for

sustenance, whatever insignificant surplus they gathered was going to the local

moneylenders from whom they had to borrow (a small amount of ) capital. Thus, if

the poor villagers were to succeed, according to Yunus, (1999) “credit” was the key.

2.2.2 Background of the Grameen Bank

The Grameen Bank of Bangladesh is one of the largest microcredit institutions in

Bangladesh. In 1976, Professor Yunus tried an experimental research project in a

village near Chittagong University. In his experimental project, he started

lending the equivalent of $26 to a group of 42 workers. Borrowers invested this

16 Microcredit is defined as a credit provided to “poor” free of collateral through institutionalised

mechanism (the only collateral is the “peer” collateral). This credit is made available as and when needed, at the doorstep of the client (Bajwa, 2001). On the other hand, microfinance is inclusive of savings and other services. As a matter of fact, this concept has been used and applied in variety of contexts and used interchangeably with microfinancing - such examples include Badan Kredit Kecamatan (BKK) Indonesia, Agriculture Cooperation, and Banks Rakyat Indo Unit Desa.

29

small amount in craft making and repaid the loan on time. From this small

experiment, he realised lending to the poor had a future.

In March 1978, the project developed an appropriate mechanism for delivering

credit to the poor. In June 1979, the Grameen Bank project was launched in a

wider area with assistance from the Bangladesh Bank (Central Bank of

Bangladesh). Within a year 24 branches were set up. It ensured 98 % recovery of

loans by the due date. With assistance from ‘International Funds for Agricultural

Development (IFAD)’ the project expanded its activities to other districts besides

Dhaka. In 1982-83, 50 branches were set up in five districts. A government

ordinance in September 1983 transformed the project into a “bank”, a specialised

financial institution for the rural poor.

2.2.3 Growth and Expansion of the Grameen Bank

The Grameen Bank has reversed conventional banking practice by removing the

need for collateral and created a banking system based on mutual trust,

accountability, participation and creativity (a group-base lending strategy). The bank

focused its market mainly on the rural areas where population density is very high.

Prior to the introduction of microcredit institutions, a large number of rural people

could not get access to formal credit. Microcredit institutions have taken the risk of

lending to mainly rural people who had been neglected in the past. In the past these

borrowers were classified as high risk borrowers. Most interestingly, through the

introduction of microcredit these so-called “high-risk” borrowers were allowed to

30

borrow collateral-free loans17 and the recovery rate of these loans is considered to be

very high, that is about 95%18 (Yunus 1999, p. 114).

The Grameen Bank is not only the largest rural finance institution in Bangladesh; it

is also the largest moneylending institution in the world in terms of number of

clients. In 2005, the bank’s borrower count rose from 4 to 5 million. 94% of

borrowers are women. With 2,345 branches, the Grameen Bank provides services in

75,359 villages, covering 90% of the total number of villages in Bangladesh. At

present the bank disburses general, seasonal, housing and other types of loan under

the categories of Processing and Manufacturing, Agriculture and Forestry, Livestock

and Fisheries, Service, Trading, and Peddling and Shopkeeping. Since its inception,

the Grameen Bank has sanctioned 290.03 billion taka19 (The Grameen Bank, Annual

Report, 2006).

Figures 2.2 and Figure 2.3 shows the expansion of Grameen Bank membership and

branches over 12 years. It is observed from the figure that the membership has

increased by approximately 150% and the number of branches have grown by more

than 50% in 12 years.

17 Although the Grameen Bank does not require any tangible collateral in giving loans, but the “group liability” may be interpreted as intangible collateral in the sense that, in case of default, a member loses its opportunity for future loans. 18 In 1999, the recovery rate was 95 %which has gone up to 98 % in 2006. 19 One taka is $US 0.017 (approximately).

31

Figure 2.2 Number of Branches

Number of Branches

0

500

1000

1500

2000

2500

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Years

Branches

Source: The Grameen Bank, Annual Report (2006).

Figure 2.3 Number of Borrowers

Number of Borrowers

0

100000

200000

300000

400000

500000

600000

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Years

Borrowers

Source: The Grameen Bank, Annual Report (2006).

32

In addition to its financial services, the Grameen Bank implements diverse programs

to promote social development. It encourages members to open nursery schools at its

centres, distribute seeds and seedlings to encourage gardening and plantation, and it

helps members and their families to improve their health and nutrition. The bank has

opened 14,804 schools by 2003. The total number of children enrolled in these

schools grew from 71,467 in 1985 to 396,289 by 1994 which is a remarkable

increase of 454.5% from 1985 to 1994. Children’s enrolment at schools is still

increasing at a reasonable rate with the expansion of the banks branches (The

Grameen Bank Annual Report, 2003).

2.2.4 Savings Mobilisation by the Grameen Bank

The Grameen Bank mobilises savings by requiring members to make deposits of

different types. The objectives in doing so are to overcome market imperfections and

promote financial security for members/borrowers. These savings are alternative

sources of credit for borrowers and help to gradually minimise the bank’s

dependence on outside borrowing.

The Grameen Bank’s members are required to contribute one taka weekly to the

group fund as savings. These contributions are held as individual savings that are

refundable when members drop out. Individual members are also required to

contribute 5% of the principal amount borrowed to the group fund. Unlike their

individual savings, group members cannot reclaim this group fund contribution, but

they are allowed to borrow from this fund with the approval of other members.

33

There are two other types of loan, from the “emergency fund” and “welfare fund”.

The emergency fund offers protection against debt or liability when a member dies,

or when theft, loss and damage to property (including livestock and crops) of

members/borrowers occurs. The children’s welfare fund was designed to provide

education for members’ children in schools managed and run by the Grameen Bank

members, and to support children’s involvement in small-scale income earning-

projects.

Although the Grameen Bank initiated microcredit programs, subsequently several

other institutions have started providing microcredit in Bangladesh. At this stage, the

major microcredit institutions in Bangladesh include the Grameen Bank, Bangladesh

Rural Advancement Committee (BRAC), which is the biggest non-government

organisation (NGO),20 Rural Development Project-12 (RD-12), Bangladesh Rural

Development Board (BRDB), Association of Social Advancement (ASA) and

Proshika Manobik Unnayan Kendra (PROSHIKA).

Since we have confined our analysis in the study to the Grameen Bank and BRAC,

the following section discusses BRAC.

2.2.5 Background of BRAC

The Bangladesh Rural Advancement Committee (BRAC), the largest non-

governmental organisation in Bangladesh, was formed in 1972 as a relief

20 Non-government organisations provide help to those who fail to accumulate sufficient resources to survive. In its most ambitious form, an NGO is a private, not for profit institution dedicated to influencing the working structure of government and ensuring the greater welfare of all citizens (Mustafa et al. 2000)

34

organisation for the post-war period. The founder of BRAC, Mr Fazle Hasan Abed

realised that pervasive poverty could not be addressed with short-term relief

measures. Thus in 1973, BRAC shifted its focus from relief to long-term community

development. It started its operation with the objective of improving the economic

and social status of the rural poor. Since then BRAC has operated as an NGO, but its

journey has not always been very smooth. It faced many challenges from different

corners of society including the rural communities and the village elites who

controlled many of the social and economic opportunities of the poor, but these

could not stop the activities of BRAC.

BRAC realised that rural people lack the skills and opportunities to derive benefit

from their own labour. The organisation presently delivers both social services and

credit to its members through its two major programs, the rural development

program (RDP) and the rural credit program (RCP). The RDP was started in 1986,

the RCP in 1990. Both programs have evolved over time through the process of

learning by doing with the objective of poverty reduction and empowering women.

Women in the rural areas of Bangladesh play a vital and unacknowledged role in

production both within and outside the household. Women are often the sole

providers for their households due to the death of a spouse, divorce, desertion or the

migration of men looking for paid labour. Recognising these factors and the low

status of women in Bangladeshi society, BRAC targeted women in its programs and

made women’s empowerment a pillar of its programming. The RDP addresses the

socio-economic development of underprivileged rural women through access to

35

credit, capacity development, savings mobilisation, institution building and

awareness raising.

2.2.6 Growth and Development of BRAC

BRAC’s social development programs are aimed partly at alleviating poverty and

partly at supporting government organisations. BRAC also emphasises the role of

women in development by mobilising more women than men. It has helped improve

women’s social status by increasing their economic role in the family. BRAC

intervenes in education, health care, legal activities, vulnerable group development,

and skill development. Its non-formal primary education program and its oral

dehydration therapy are widely known.

BRAC has developed two primary school models the non-formal primary education

program and the primary education program for older children. In addition, BRAC

assists the government in expanding primary education throughout the country.

BRAC’s primary education models aim to reduce mass illiteracy, ensure women’s

education and involve communities in their own socio-economic development.

The non-primary education program, begun in 1985, is a three-year program for 8 to

10 year-old boys and girls. These children, who have never attended school, are

enrolled in the fifth grade of the formal primary school system after graduating from

this program. The primary education for older children program, begun in 1988 is a

three-year program for 11 to 16 year-olds who have never attended school. Books

and other materials are provided free for the students.

36

Table 2.1 Number of BRAC Schools, Students and Graduates

Bangladesh Rural Advancement Committee (BRAC) (as at June 2006

Number of Primary Schools 3,200

Number of Students 1 million

Number of Graduates 3.49 million

Number of Pre-Primary School 20,168

Number of Students 0.54 million

Source: Bangladesh Rural Advancement Committee, Annual Report (2006).

Table 2.2 Job Creation21

by BRAC

Job Creation by BRAC (as at June 2006)

Poultry 1,708,145

Livestock 570,266

Agriculture 853,390

Forestry 79,062

Fisheries 2,772,330

Sericulture 25,549

Horticulture 184,031

Handicraft Product 15,223

Small Enterprise 136,159

Small Trade 2,635,212

TOTAL 63,53,482

Source: Bangladesh Rural Advancement Committee, Annual Report (2006).

21 Job creation here does not refer to traditional textbook definition. Rather it refers to the number of people who have invested in different sectors.

37

Table 2.1 shows, recent figures for the number of students who have graduated from

BRAC schools since BRAC’s inception. It also shows the number of schools and

pre-primary schools established by BRAC and the number of students enrolled.

Table 2.2 shows job creation by BRAC at the sectoral level since BRAC’s inception

until June 2006.

2.2.7 Savings Mobilisation by BRAC

Savings mobilisation is an integral part of BRAC’s lending process. In addition to

depositing two taka per week as individual savings, borrowers must pay 10% of the

principal loan amount. Out of this, 5% is transformed into individual savings, 1% is

kept for a group insurance fund, and 4% is given to a group fund. The basic objective

of the group insurance scheme is to provide financial support, a maximum of Tk

5,000 to the family of the deceased member so that the family is not displaced and

does not suffer financial hardship. BRAC pays 9% interest on both individual

savings and group funds. This rate is higher than that offered by commercial banks

(BRAC Annual Report, 2004).

Table 2.3 provides some basic statistics in respect of the Grameen Bank and BRAC.

Though we do not directly compare these two institutions in this study, as is evident

from the table both the institutions are quite comparable (similar) in terms of many

indicators.

38

Table 2.3 Comparing BRAC with the Grameen Bank

Items BRAC Grameen Bank

Number of Borrowers 4.51million 6.61million

Number of Branches 1172 2226

Villages Covered 65,000 71,371

Loan Disbursement Tk. 185,580 million

(US$ 3385million)

Tk. 290.03 billion

(US$ 5.72 billion)

Repayment Rate 98.85% 98.85%

Interest Rate Charged 15% 20%

Source: 2006 Annual Reports of the Grameen Bank and BRAC.

39

2.3 The Bangladesh Economy and Recent Developments

Even though the Bangladesh economy went through a very difficult time in the

period following independence, it has recovered substantially in the last two decades

and has shown its potential for becoming an example of success. The UNDP Human

Development Report (2000) referred Bangladesh as “a case that stood out as a

potential instructive story of development”. Philip Browning, the former editor of the

Far Eastern Economic Review, wrote in a very recent article in the International

Herald Tribune on 7th May 2005:

“Bangladesh is a paradox. It lacks good governance and is beset by natural calamities, corruption and self-destructive political infighting. Yet its gross national product persistently maintains a growth rate of 6%, well above average for developing countries. It has overtaken India on several social indicators. Its aid dependence has fallen from 6% to 1.8% of gross domestic product…...Of course this is still a desperately poor, overpopulated country, where 50% of children are underweight. But India is no better on that score. Bangladesh has made much more progress than its neighbours over the past 10 years, becoming self-sufficient in food. Social progress has been even more marked. Educational standards may be poor, but primary school education is even more striking. There are now more girls than boys at secondary level. Gender equality also seems reflected in the fall in fertility rate, which has halved from 6.0 to 3.0 in two decades the steepest fall almost anywhere other than China. It is now below India’s and far below Pakistan’s. The lowest birth rate is linked to a steep fall in child mortality, and to the enhanced economic role of women as small-scale village entrepreneurs and as garment workers. Economic advancement has been underpinned by the individual initiative of hundreds and thousands of Bangladeshis working overseas. Their remittances exceed the net earnings of the garment industry, amounting to more than $3.5 billion a year, mostly from Britain, the United States and Middle East…..”

Despite many obstacles some man-made and some natural Bangladesh experienced

moderately accelerated growth in the 1990s, compared to the previous decades. Its

economic growth rate has increased from 2% in 1975 to 6% in 2005. Bangladesh has

become successful in reducing population growth which has decreased from 3% to

1.48% in last 30 years. The life expectancy of both males and females has increased

40