Megaprojects - IBR 2013

14

This article appeared in a journal published by Elsevier. The attached copy is furnished to the author for internal non-commercial research and education use, including for instruction at the authors institution and sharing with colleagues. Other uses, including reproduction and distribution, or selling or licensing copies, or posting to personal, institutional or third party websites are prohibited. In most cases authors are permitted to post their version of the article (e.g. in Word or Tex form) to their personal website or institutional repository. Authors requiring further information regarding Elsevier’s archiving and manuscript policies are encouraged to visit: http://www.elsevier.com/authorsrights

Transcript of Megaprojects - IBR 2013

This article appeared in a journal published by Elsevier. The attachedcopy is furnished to the author for internal non-commercial researchand education use, including for instruction at the authors institution

and sharing with colleagues.

Other uses, including reproduction and distribution, or selling orlicensing copies, or posting to personal, institutional or third party

websites are prohibited.

In most cases authors are permitted to post their version of thearticle (e.g. in Word or Tex form) to their personal website orinstitutional repository. Authors requiring further information

regarding Elsevier’s archiving and manuscript policies areencouraged to visit:

http://www.elsevier.com/authorsrights

Author's personal copy

Managing global megaprojects: Complexity and risk management

Ilke Kardes a, Ayse Ozturk b, S. Tamer Cavusgil b,*, Erin Cavusgil c

a University of Applied Sciences, Dusseldorf, Germanyb Georgia State University, United Statesc University of Michigan-Flint, United States

1. Introduction

In 2009, five countries agreed to cooperatively construct a gas pipeline between the Eastern border of Turkey and Austriain Europe, running through Bulgaria, Romania and Hungary. This international megaproject, called ‘‘Nabucco,’’ consists ofthe construction of a 3900 km pipeline beginning in 2013 with the initial gas flow scheduled for 2017.1

A closer examination of Nabucco project, detailed in Appendix A, serves to illustrate the complexity of megaprojects. Anambitious and large-scale project, Nabucco carries with it a degree of technological sophistication, funding concerns, as wellas the political uncertainty brought upon changing political winds among the participating countries. Complexity is aninherent and indispensable part of megaprojects. As globalization trends intensify, the importance of managing complexitycannot be overemphasized for the success of megaprojects. For instance, supply chain structures get more complicated thanever with countless international suppliers, or a partnership may include private and public investors from multiplecountries with very diverse cultures. Consequently, such large-scale projects bear high risks that require systematic riskmanagement approaches. Without appropriate risk management strategies in place, megaprojects are bound to fail due tomultiple, risk-prone events.

International Business Review 22 (2013) 905–917

A R T I C L E I N F O

Article history:

Received 29 July 2011

Received in revised form 1 December 2012

Accepted 17 January 2013

Keywords:

Megaprojects

Global collaborative projects

Complexity

Illusion of control

Sunk cost effect

Prospect theory

Risk management

A B S T R A C T

‘‘Megaproject,’’ a concept of growing importance in today’s globally connected business

environment, requires a closer examination as a result of the expansion of global networks,

increasing collaborations among numerous partners, and the complexity of managing

such projects. Yet, given their high rate of failure, it is critical to examine the factors that

contribute to success of megaprojects. In such a high-pressure, competitive, and complex

environment, it is inevitable that companies will engage in complex, global, collaborative

projects in order to reap the rewards of these significant, large-scale initiatives and

ultimately become major players in the game. Despite the considerable scale of

megaprojects, the international business literature has largely neglected to examine this

topic. This paper takes an exploratory approach to identify key characteristics of global

megaprojects, factors contributing to disappointing outcomes, and offers a risk manage-

ment framework and managerial prescriptions for enhancing success. Building on the

prospect theory, self-justification theory, and sunk cost effect, we examine the behavior of

decision making under risk in megaprojects. We conclude that by adopting a successful

risk management approach and following best practice, success rate and the productivity

of global collaborative projects can be enhanced.

Published by Elsevier Ltd.

* Corresponding author at: CIBER, J. Mack Robinson College of Business, Georgia State University, Suite 1424, 35 Broad Street, NW, Atlanta, GA 30303,

United States.

E-mail address: [email protected] (S.T. Cavusgil).1 For detailed information: For detailed information: http://www.nabucco-pipeline.com.

Contents lists available at SciVerse ScienceDirect

International Business Review

jo ur n al ho mep ag e: www .e lsev ier . c om / lo cate / ib u s rev

0969-5931/$ – see front matter . Published by Elsevier Ltd.

http://dx.doi.org/10.1016/j.ibusrev.2013.01.003

Author's personal copy

Megaprojects are large-scale manufacturing or infrastructure undertakings which transform landscapes rapidly andprofoundly in very visible ways. They involve coordinated applications of capital, sophisticated technology, intense planning,and political influence (Gellert & Lynch, 2003). They require the engagement of numerous contractors, often from variouscountries, and take years for completion. Gellert and Lynch (2003) categorize megaprojects into four types: infrastructure(e.g., dams, ports, and railroads); extraction (e.g., minerals, oil, and gas); production (e.g., massive military hardware such asfighter aircraft, chemical plants, and manufacturing parks); and consumption (e.g., tourist installations, malls, and themeparks). There are abundant examples of megaprojects currently in progress around the world. In Table 1 we highlight a widevariety of recent and current megaprojects around the world.

Worldwide population growth, urbanization, technological developments, enrichment and increased desires formaintaining a comfortable and modern life have stimulated the demand for new physical infrastructure. Companies havediscovered a lack of appropriate infrastructure in developing countries and emerging markets. Thus, the number of large-scale projects has exploded in the past two decades. Spending on infrastructure in emerging markets is estimated by MerrillLynch to be $2.25 trillion annually between 2009 and 2012. As an example, Table 2 shows that the highest spending amongthe emerging markets is expected to be in China – estimated at $725 billion (Businessweek, 2008). Moreover, spending forupdating current infrastructure in developed countries and building new infrastructure in emerging markets is estimated byOECD at $53 trillion between 2007 and 2030 (Gil & Beckman, 2009; OECD, 2007).

In the present study, we examine multi-country collaborations. Megaprojects are often of international scope as theyinvolve the participation of sponsors, funding agencies, and contractors from multiple countries. Long-term nature of theseprojects, participation of numerous partners and contractors with divergent interests, fluid nature of technologies deployed,and dynamism in the external environments are just some of the factors that contribute to monumental complexity ofmegaprojects.

Yet this topic has received little attention in the academic literature. Megaprojects have mostly been a topic in the projectmanagement literature. Even those few studies in the international business literature that explored this topic have mainlyexamined it from the perspective of project management (Lam, 1999; Miller & Lessard, 2007; van Marrewijk et al., 2008).Although the present study also discusses project management views, the perspective we adopt is of international business.As an exploratory study in an area yet to be fully developed, this investigation highlights international megaprojects forinternational business scholars, and leads the way for further theoretical and empirical studies in the field.

Given the paucity of relevant academic studies, and the rise in the number of megaprojects worldwide, this article offersinsights into the structure of megaprojects, explores challenges encountered in management of megaprojects, andsuggests risk management approaches to leverage the benefits of these huge undertakings. We also offer a riskmanagement framework for megaprojects which should serve as a guide to address the complexity of the projects and yieldhigher project performance. Since our goal is to develop an overarching framework for megaprojects, our discussion isbased on a careful integration of industry practice, pertinent literature, and theoretical contributions, The remainder of thisarticle is organized as follows: first, the features of the international megaprojects are discussed followed by a detailedexamination of the major challenges of complexity. We introduce the concept of ‘‘illusion of control’’ as a major factorcontributing to complexity. Next, we describe why ‘‘sunk cost effect’’ contribute to ill-fated outcomes of megaprojects.Further, we explain the decision making processes in managing megaprojects based on the prospect theory and the self-justification theory. We then elaborate on effective risk management approaches and offer a conceptual framework foreffective management of megaprojects, followed by managerial prescriptions. We conclude with a review of futureresearch questions.

2. Key features of global megaprojects

Large-scale investment projects or major infrastructure projects are usually commissioned by governments anddelivered by private contractors who specialize in design, architectural, and manufacturing/construction services. Oftenthere are multiple tiers of contractors and subcontractors. High levels of public attention and/or political interest areattracted due to the substantial cost, and direct and indirect impact these projects have on the community, environment, andbudgets (Capka, 2004; van Marrewijk et al., 2008).

Megaprojects are characterized by complexity, uncertainty, ambiguity, dynamic interfaces, significant political orexternal influences, and time periods reaching a decade or more (Floricel & Miller, 2001). They also involve internationalparticipants with a variety of cultural differences, backgrounds, political systems, and languages (Shore & Cross, 2005).Table 3 highlights some of the differences between megaprojects and other project types (Hass, 2009).

At least three features associated with megaprojects are notable: large sum of resources; high human, social andenvironmental impact; and extreme complexity (Capka, 2004; Flyvbjerg, Bruzelius, & Rothengatter, 2003).

Large deployment of resources: Megaprojects require high amounts of costs, labor, physical and financial resources. Thetotal amount of funding varies depending on the context, but multibillion-dollar mega-infrastructure projects are notuncommon (van Marrewijk et al., 2008).

High human, social and environmental impact: Megaprojects affect various communities differently; one project mayrevive or weaken regional economies. The impact may be transnational, occurring over a long-term period, affectingmultiple generations, and impacting the economy, civil society and the natural environment (Flyvbjerg et al., 2003; Kipp,Riemer, & Wiemann, 2008; Warrack, 1993). Moreover, these projects are often an issue of public interest because public

I. Kardes et al. / International Business Review 22 (2013) 905–917906

Author's personal copy

Table 1

Some examples of the megaprojects worldwide.

Project name Project details

Lockheed Martin F-35

Joint Strike Fighter, USA

The F-35 Lightening II is designed to meet the bulk of the needs of the US military throughout the first half of the

21st century. It is being designed and built by prime-contractor Lockheed Martin and partners Northrop

Grumman and BAE Systems, the Pratt & Whitney and the GE Rolls-Royce, assisted by innumerable

subcontractors. The global supply network includes over 1000 companies worldwide. Funding is primarily

provided by the USA, followed by the United Kingdom and seven other countries: Italy, Netherlands, Turkey,

Australia, Norway, Denmark, and Canada.a The contract was awarded to Lockheed-Martin in 2001. The initial

cost estimates were about $200 billion and the delivery was scheduled for 2016.b However, costs have

skyrocketed in the past few years and delays are expected for the introduction date.c The cost of each next-

generation F-35 Lightning II Joint Strike Fighter (JSF) aircraft has ballooned from $50 million per craft in 2001 to

more than $113 million in 2010.d

Dubai World Central, UAE Dubai World Central, one of the most ambitious projects of the government of Dubai, is a planned residential,

commercial and logistics complex scheme. It comprises Free Zones (Dubai Logistics City, DWC Aviation City);

Real Estates (Residential, Commercial and Golf Cities, and Staff Village); and most importantly the $8.1 billion

Dubai World Central International Airport which is planned as the world’s largest passenger and cargo hub,

even with a higher capacity (up to 150 million passengers annually) than the world’s currently busiest airport,

Hartsfield-Jackson Atlanta International Airport (90 million passengers).e

Three Gorges Dam, China The Three Gorges Dam is the world’s largest hydroelectric plant with an expected generating capacity of more

than 22,000 MWe. The project sets records for number of people displaced (1.4 million), number of cities and

towns flooded (13 cities, 140 towns, 1350 villages), and length of reservoir (640 km).f The construction began in

1994 and was mostly completed in 2006 with a budget of $26.3 billion.g,h

The Snowy Mountains Scheme, AustraliaThe Snowy Mountains Hydro-Electric Scheme is the largest engineering project ever undertaken in Australia. It

consists of sixteen major dams, seven power stations, a pumping station and 225 km of tunnels, pipelines and

aqueducts. The project was completed on time and to budget, taking 25 years (1949–1974) and costing A$820

million.i

Gautrain, South Africa The Gautrain is a state-of-the-art rapid rail network in Gauteng, South Africa. Its construction started in 2006

and is planned to be completed in 2011, costing nearly $4 billion.j

Galileo (satellite navigation), EU Galileo is Europe’s own global navigation satellite system, as a substitute for US GPS and Russian GLONASS

systems. The system is expected to be operational by 2014 with a total budget estimate of less than s3.4 billion

($4.76 billion).k

Eurofighter Typhoon, EU The aircraft ‘‘Eurofighter Typhoon’’ is Europe’s largest military collaborative program in cooperation with six

nations (Germany, Italy, Spain, United Kingdom, Austria and Saudi Arabia).l Billions more have already been

spent on developing the fighter plane than was originally anticipated, it is still not ready for ground attacks until

2018. Development and production costs have risen by a fifth to £20.2 billion.m The aircraft is $58 million price.

Boeing 787 Dreamliner The Boeing 787 is a super-efficient airplane. It will use 20 percent less fuel for comparable missions than today’s

similarly sized airplane.n Because of several technical problems during the test phase, first delivery of the

airplane delayed and the company was more than three years behind schedule when the product was

introduced in 2011.o

Marmaray Tunnel, Turkey The project consists of the construction of an undersea rail tunnel, high-speed railway under the Bosphorus

strait creating a network between Europe and Asia. Total length is 76.3 km.p The construction contract has been

assigned to a Japanese-Turkish consortium in 1999. The project is being financed by the Japan Bank for

International Cooperation (JBIC) and the European Investment Bank (EIB). The total project cost was estimated

at $4.1billion. Construction work of the project was scheduled to be completed in April 2009 and opened in

October 2011.q The tunnel has been postponed to October 2013.r The cost increase is estimated over $500

million. The reasons of the cost overrun is explained through the postpone because of exacavation and legal

causes, cost increase in raw material and labor, and instabile exchange rate.s

a http://www.lockheedmartin.com/data/assets/aeronautics/mediacenter/mediakits/f35/F-35FastFacts01142010.pdf.b http://www.defense.gov/news/newsarticle.aspx?id=62829.c http://www.pbs.org/newshour/bb/military/jan-june10/defense_04-21.html.d http://www.dailytech.com/F35+Lightning+II+Cost+has+Doubled+F136+Engine+Completes+Afterburner+Test/article17944.htm.e http://www.dwc.ae/web/index.html.f http://www.internationalrivers.org/china/three-gorges-dam.g http://www.worldwater.org/data20082009/WB03.pdf.h http://www.bjreview.com.cn/eye/txt/2008-12/06/content_168792.htm.i http://australia.gov.au/about-australia/australian-story/snowy-mountains-scheme.j http://www.gautrain.co.za/.k http://www.reuters.com/article/2011/05/23/us-eu-satellites-galileo-idUSTRE74M4EA20110523.l http://www.eurofighter.com/.m http://www.channel4.com/news/multibillion-eurofighter-typhoon-overspend-revealed.n http://www.boeing.com/commercial/787family/background.html.o http://www.nytimes.com/2011/01/19/business/19boeing.html?_r=1.p http://www.marmaray.com.q http://www.railway-technology.com/projects/marmaray/.r http://www.sondakika.com/haber-basbakan-erdogan-marmaray-tuneli-ni-inceledi-2560283/.s http://www.ekoayrinti.com/news_detail.php?id=36774.

I. Kardes et al. / International Business Review 22 (2013) 905–917 907

Author's personal copy

entities and public spending is involved in the process. As a result, the reputation of project participants, including publicofficials and government, depends on the project outcome (Kipp et al., 2008).

Complexity: Technically speaking, these super-large projects are complex undertakings requiring cutting-edgeengineering and construction techniques. Difficulty resulting from the lack of cooperation between stakeholders withconflicting interests and the changes occurring during the duration of the projects, such as changes in laws and regulations,increase the complexity (Capka, 2004). Complexity also implies risk and uncertainty in terms of funding and construction(Frick, 2008).

Of these features, complexity emerges as a major challenge for managers of megaprojects. Accordingly, it deserves specialattention from scholars. We next elaborate on the complexity challenge of megaprojects.

3. Complexity challenge

The complexity of megaprojects is brought about by a number of contributing factors such as tasks, components,personnel, and funding, as well as numerous sources of uncertainty and their interactions (Mihm, Loch, & Huchzermeier,2003; Sommer & Loch, 2004). Research evidence suggests that the principal factors leading to complexity include: the largescale, long time span, multiplicity of technological disciplines, the number of participants, multi-nationality, the interests ofstakeholders, sponsor interest, escalating costs over time, country risk, uncertainty, and high levels of public attention orpolitical interest (van Marrewijk et al., 2008).

We can examine complexity of megaprojects under both technical and social complexity. While technical complexity isrelated to the size of the project, social complexity includes the interactions among the people involved in the project(Baccarini, 1996; Bruijn & Leijten, 2008; Cleland & King, 1983). As an example, the Channel Tunnel, which was opened in1994 as an undersea rail tunnel linking England to northern France, presented both technical and social complexities.Technical complexities were encountered because the project entailed building the longest undersea portion of any tunnelsworldwide. The considerations for geology, design, engineering, and power supply all aggravated the technical complexities.However, social complexities were mostly due to coordination among the large number of contractors and employees thatonce amounted to 15,000 people with daily expenditure over £3 million (Anderson & Roskrow, 1994). These complexities aresimilar to many other megaprojects across the world such as the ‘‘Big Dig’’ Central Artery/Tunnel Project in the U.S.A., KualaLumpur International Airport in Malaysia, Ultra Mega Power Plants in India, GLONASS, a satellite navigation system, inRussia; Port of Shanghai, the world’s busiest container port, in China, and Burj Khalifa, the world’s tallest building, in Dubai.These examples illustrate the widespread nature of the dilemmas encountered by project management.

The first and foremost reason for complexity is the large scale and scope of international megaprojects. Infrastructureprojects such as tunnels, bridges, airports or rail systems are enormous, highly visible, and monumental endeavors (Frick,2008). It can take several decades from project initiation to final completion. During this period, changes occur in theeconomy, political landscape, and within the laws and regulations (Capka, 2004). Further contributing to complexity is theexistence of significant numbers of different, ambiguous, and interconnected tasks and activities to complete the project. Inaddition, since the technology used in megaprojects is often new, developmental or cutting-edge, its behavior andfunctionality are often hard to predict. In the case of an already complex product as the F-35 Joint Strike Fighter – asophisticated fighter aircraft – the design phase (which took almost an entire decade) witnessed countless adjustments asthe underlying technologies constantly evolved. Evidence shows that new developments and changes in technology increaseuncertainty (Shenhar, 2001).

Finally, the substantial number of project participants including contractors, sub-contractors, sponsors/governments,suppliers, investors, funding agencies, etc., lead to further increase in complexity. Aligning a significant number ofstakeholders is thorny if each stakeholder’s interests are to be maintained. Sponsors and stakeholders often have competingcharacteristics and goals. In addition to the difficulty of finding common ground for a large number of people, conflicts andmisinterpretations can arise during the long life of project implementation. Undertakings with large amounts of resourcesmay create controversy among stakeholders and over the management of resources. Moreover, the visibility of megaprojectsand public attention increase the complexity (Capka, 2004; Kolltveit & Grønhaug, 2004; Vaaland & Hakansson, 2003).

Table 2

Estimated infrastructure spending in emerging countries between 2009 and 2012 by Merrill Lynch.

Emerging economies Estimated spending for infrastructure investment

China $725 billion

Gulf Region $400 billion

Russia $325 billion

India $240 billion

Brazil $225 billion

Mexico $120 billion

Turkey $65 billion

South Africa $60 billion

Central and Eastern Europe (CEE) $45 billion

Source: Businessweek (2008).

I. Kardes et al. / International Business Review 22 (2013) 905–917908

Author's personal copy

The scale of megaprojects can be so large that sponsoring governments or countries may be significantly affected by thesuccess or failure of a single project. Failure of megaprojects often results in inefficient use of resources, cost overruns, lower-than-predicted revenues, delays in delivery, loss of business, technical failures – sometimes with devastating consequences,such as the bankruptcy of companies or government upheaval (Flyvbjerg et al., 2003).

According to the World Bank, investment commitments of 46 canceled projects recently amounted to $21 billion. Thissum of money does not include the larger renegotiation costs, the time and money cost to the citizens, communities andbusinesses in the countries affected from the failed services – water, power, sewer, telecom, etc. – interrupted services, andthe misallocated resources of delayed or canceled projects (Orr & Metzger, 2005).

Table 3

Characteristics of megaprojects.

Complexity dimensions Independent project Moderately complex

project

Highly complex project Highly complex

program

‘‘megaproject’’

Size 3–4 team members 5–10 team members >10 team members Multiple diverse teams

Time <3 months 3–6 months 6–12 months Multi-year

Cost <$250 K $250–$1 M >$1 M Multiple millions

Schedule/budget Flexible Minor variations Inflexible Aggressive

Team composition Internal, worked

together before

Internal and external,

worked together before

Internal and external,

have not worked together

before

Complex structure of

varying competencies

and performance

records

Contracts Straightforward Straightforward Complex Highly complex

Customer support Strong Adequate Unknown Inadequate

Requirements Understood,

straightforward

Understood, unstable Poorly understood,

volatile

Uncertain, evolving

Political implications None Minor Major, impact core

mission

Impact core mission of

multiple

organizations, states,

countries

Communications Straightforward Challenging Complex Arduous

Stakeholder management Straightforward 2–3 stakeholder groups Multiple stakeholder

groups with conflicting

expectations

Multiple

organizations, states,

countries, regulatory

groups

Organizational

change-impacts on

A single business unit,

one familiar business

process, and one IT

system

2–3 familiar business

units, processes, and IT

systems

Enterprise, shifts or

transforms many business

processes and IT systems

Multiple

organizations, states,

countries;

transformative new

venture

Commercial change No changes to existing

commercial practices

Enhancements to existing

commercial practices

New commercial and

cultural practices

Ground-breaking

commercial and

cultural practices

Risk level Low Moderate High Very high

External constraints No external influences Some external factors Key objectives depend on

external factors

Project success

depends largely on

external organizations,

states, countries,

regulators

Integration No integration issues Challenging integration

effort

Significant integration

required

Unprecedented

integration effort

Technology Proven and well-

understood

Proven but new to the

organization

Immature, complex, and

provided by outside

vendors

Groundbreaking

innovation and

unprecedented

engineering

IT complexity Application

development and

legacy integration

easily understood

Application development

and legacy integration

largely understood

Application development

and legacy integration

poorly understood

Multiple ‘‘systems of

systems’’ to be

developed and

integrated

Adapted from Haas (2009).

I. Kardes et al. / International Business Review 22 (2013) 905–917 909

Author's personal copy

Poor performance of megaprojects results primarily from the underestimation of project related features such as costs,delays, contingencies and changes in quality, price, project specifications, designs, exchange rates, and externalenvironmental factors (Jaafari, 2001). Costs are underestimated in 9 out of 10 transport infrastructure projects, resultingin cost overruns. For example, the Big Dig, Boston’s Central Artery/Tunnel Project, suffered from a substantial cost escalation.Although the initial estimated cost was $2.56 billion, the project cost escalated to $14.8 billion in 2007. The overrun projectbudget resulted from the unrealistic initial cost estimation (Greiman, 2010).

In addition to inaccurate estimation of costs, there are also demand prediction failures. Reasons for demand predictionfailures can be attributed to methodology weaknesses, poor databases, unexpected changes in exogenous factors, and theeffects of appraisal bias by consultants or by promoters (Flyvbjerg et al., 2003). For example, the Norwegian governmentbuilt a fish processing plant in Kenya in 1971 to provide jobs to the natives. A few years after the completion of the $22million project, the plant shut down. The lack of experience of the local people with fishing or eating fish directly led to thefailure of the project.2

Even in case of failures in estimating costs, demand or time, it is uncommon to cancel a megaproject. In a recentconference on complex cross-border collaborative projects, Hillary Sillitto, the UK director of system engineering in Thalesgroup, states that ‘‘. . .international collaborative projects tie stakeholders into an interdependent web and it means that noone stakeholder can kill the project. For example, the Eurofighter, every government has wanted to pull out at some point,but none of them have been able to. So although the project has probably taken longer and cost more than originallyintended, the air forces now have their airplane. Whereas if it had been a national program, the probability of it beingcanceled would have been much higher’’ (Cavusgil & Mahnke, 2012).

3.1. A managerial trap: illusion of control

The tendency to underestimate complexity does not always result from a lack of experience or management skills. Insome cases, the negative outcome may be a result of the ‘illusion of control’ bias. Project leaders often mistakenly believe thatthey have the ability to influence the outcome, when the outcomes are obviously chance determined (Langer, 1975). Indeed,forecasting fails under conditions of high uncertainty, leading to project failures. This bias is a result of overconfidence. Amanager’s misperception of his management ability or his power to influence the outcomes of the project leads to theunderestimation of the risk and overvaluation of the positive information (Durand, 2003; Simon, Houghton, & Aquino, 2000).The ‘‘Illusion of control’’ pitfall arises often due to the high degree of uncertainty which leads to an inherent difficulty inforecasting. Thus, the greater the uncertainty, the greater the perception of control and level of overconfidence which leadsto a higher probability of underestimating the risks (Durand, 2003; Titus Jr., Covin, & Slevin, 2011).

Furthermore, assumptions underlying forecasts may cause deception by various actors with conflicting interests. In orderto sell projects that have an economic gain or political leverage, project sponsors can exaggerate the benefits whileunderestimating costs (Flyvbjerg, Garbuio, & Lovall, 2009). Therefore, the decision maker, knowingly or unintentionally,optimistically misinterprets project facts and figures. This behavior leads to the failure of a megaproject in terms of costoverruns or benefit shortfalls.

3.2. The curse of megaprojects: the sunk cost effect, prospect theory, and self-justification theory

Underestimating of the cost or the duration of the project, unrealistic and overconfident decisions, conflicting interestsamong partners during the lapse of time, and opportunistic behavior of one or more partners can bring megaprojects to adead end. This is the point where the project faces deviation from the planned schedule encountering problems such as costoverruns, excessive project delay, and technological failures. Left unresolved, these issues can force collaborative partnersinto situations where they have to cancel the project.

As partners get deeper into a megaproject, investing more money and time, they eventually reach a point of no return. Atthis point, sponsors and partners do not dare to take such a drastic measure as canceling the project all together, since somuch has been invested and their reputation is on the line. Also, the project’s high visibility to the public creates a situationwhere its failure can lead to the loss of trust and a tarred reputation. Therefore, risk is not only associated with the loss of theinvested money but also with the overall development of business or investment for the future.

Three perspectives from behavioral economics help us understand the decision making under risk in megaprojects. First,the sunk cost effect or the ‘‘Concorde’’ fallacy explains the behavior of reinvestment despite losses (Arkes & Ayton, 1999).Sunk cost effect is the tendency to keep alive an endeavor once a substantial investment has been made and cannot berecovered (Arkes & Hutzel, 2000). A possible trigger of the sunk cost effect may occur on a psychological level. Cancelation ofa project after a huge investment, along with the acknowledgment of the flop, results in a psychological risk for decisionmakers – risk of being viewed as an unsuccessful and wasteful person. Moreover, it jeopardizes the credibility and positionsof the decision makers within the organization. Thus, decision makers often sustain investment in a failing project, andactually escalate their commitment in order to avoid criticism or loss of reputation (Boulding, Morgan, & Staelin, 1997; Sharp& Salter, 1997; Tan & Yates, 1995) For instance, although the aerospace project neither was profitable nor had the potential

2 http://www.msnbc.msn.com/id/22380448/ns/world_news-africa/t/examples-failed-aid-funded-projects-africa/.

I. Kardes et al. / International Business Review 22 (2013) 905–917910

Author's personal copy

future gains, the British and French governments continued to fund the faster transatlantic Concorde flights, investing $1.5million, (Court, 2006). To illustrate the psychological behavior underlying sunk cost syndrome, consider the followingcomment: ‘‘When 85% of your project for a radar-blank plane is completed to be $15 million, another firm begins marketing a plane

which is much faster and far more economical than the plane your company is building. The question is: should you invest the last

15% of the research funds to finish your radar-blank plane?’’ (Arkes & Blumer, 1985).A second perspective for explaining decision making under risk comes from the prospect theory. The prospect theory

provides a logical framework for explaining deviations from rational behavior as predicted by expected utility theory(Kahneman & Tversky, 1979; Thaler, 1980). Prospect theory explains decision making behavior under a risky situationwhere choices are evaluated in relation to a reference point. If the assumptive future seems to be under the reference point,losses will be greater than gains, concluding that the individual shows a tendency toward risk seeking behavior. Otherwise,they are risk-averse (Kahneman & Tversky, 1979). In the context of the sunk cost effect, prior investment is seen as a loss.Because the point of departure is loss of the investment so far, further losses do not cause large decreases in perceived value.Therefore, risk seeking behavior arises, and to continue to invest in the failed project in hope of future gain is more likely tohappen than total withdrawal (Schaubroeck & Davis, 1994; Zeelenberg & van Dijk, 1997). For example, once $100 millionhas already been spent in an unsuccessful project, an additional $10 million is not perceived a big loss to complete it(Roxburgh, 2003).

If a project is failing to a certain degree, then it would be wise to stop the investment and terminate the project. However,megaprojects are rarely canceled. Apart from reference points, prospect theory provides another explanation for this.Kahneman and Tversky (1979) argue that people underweight outcomes that are probable compared to outcomes that arecertain. This is called the certainty effect, which again ends up with risk-seeking behavior in situations with sure lossesversus probable losses. In megaprojects, deviations in the decision weights and underweighting probable losses can be thereason why managers fail to evaluate risks rationally, and why they behave more emotionally. Likewise, Thaler argues thatpeople often underweight opportunity costs compared to out-of-pocket costs (Thaler, 1985). Overall, based on the prospecttheory, the bias in the weighting of losses and gains, combined with reference points, make economic agents behavedifferently than the optimal behavior predicted by the expected utility theory. In the context of megaprojects, thisphenomenon is observed in such cases as prolonging a failing project, underestimating the costs and risks, andoverestimating expected favorable outcomes.

Finally, the third perspective of decision making can be linked to the self-justification theory. This theory provides anexplanation for escalating commitment of managers – the tendency of decision makers to stick with a failing course of action.Self-justification posits that decision makers are unwilling to admit that their prior decisions and resource allocations werenot on the mark (Brockner, 1992; Whyte, 1986). Instead, managers tend to justify their behavior and deny negative feedback.In megaprojects, self-justification can be a major driver of escalating commitments to a failing megaproject.

In sum, many factors can contribute to biases in decision making processes surrounding megaprojects. Sunk cost effect,reference points, underweighting probable losses or self-justification of decision makers can lead to suboptimal decisions.Although many factors may prevent decision makers from making prudent and realistic choices, risk management canaddress these issues. Challenges of complexity of these huge undertakings bring about the question of how to manage theenormous risks in megaprojects. The next section examines this issue in detail.

4. Risk management in megaprojects

Control of risk is an overarching goal of project managers. Risk control can be secured through the identification of the risktype and by using the appropriate risk management strategy (El-Sayegh, 2008; Lam, 1999). The discussion below amplifiesthe concept of risk, elaborates on risk management strategies, and proposes an integrative conceptualization for managingmegaproject risk.

4.1. Conceptualizing of risk

Miller and Lessard (2007) define risk as the possibility that events will turn out differently than anticipated. While riskcan be described in statistical terms, uncertainty represents situations which are not fully understood in terms of causalforces and potential outcomes. So, odds are known for risks but not for uncertainty. Megaprojects involve both high risk anduncertainty; so we refer to all such cases as risk. Risk categorizations differ largely in the literature. Most commonclassification of risks is done at the macro and micro levels (Bing, Akintoye, Edwards, & Hardcastle, 2005). On the macro level,the project suffers from exogenous factors. These external factors are not project related and have an indirect impact on thesuccess of the project. The risk on this level is associated with development and changes in the political, economic, natural,industrial, and social environment (Bing et al., 2005). For example, in the context of political risk, government control of thelocal coal created a risk in building the Karachi Power Plant in Pakistan associated with the quantity and quality of the coal(Lam, 1999). On the other hand, risk on the micro level is endogenous and associated with the project related factors such asrelationship among stakeholders as well as the technical and operational side of the project (Bing et al., 2005; Miller &Lessard, 2007). The project of the Second-Stage Expressway in Thailand included risk on a micro level in the context of theresponsibilities of each party. It was unclear who would pay the VAT (value added taxes) or who should take what percent ofthe revenue (Lam, 1999).

I. Kardes et al. / International Business Review 22 (2013) 905–917 911

Author's personal copy

Another basis for conceptualizing risk is causal factors: (i) technical and operational risks emanating from the project itself;(ii) market risks associated with demand, supply and financial markets; and (iii) institutional/social risks related to thepolitical, social, and economic setting of the project (Miller & Lessard, 2007).

As a major source of risks in megaprojects, Cavusgil and Deligonul (2011) examine the supply chain. Due to multi-countryand multi-layered nature of global supply networks, megaprojects suffer from low visibility and misalignment. Visibility

refers to the partner’s transparency to proactively reveal and share the strategically relevant intent, information andprocesses, and alignment refers to the fit among partners so that benefits are assured without clashes (Nguyen, 2011).Alignment comprises these four dimensions: goal and strategic congruence, process congruence, cultural congruence, andstructural congruence. If a partnership has incongruence in these dimensions or poor visibility in the supply network, thenthe project becomes vulnerable to risks. This situation can even generate a systemic risk, which refers to a hazard at one pointpropagating to other players in a chain reaction in the supply network. The high interconnectedness and complicatedinteractions in megaprojects allow for adverse shocks to propagate. If a shock occurs in one stage of the supply chain, ittransfers quickly to the other stages through both backward and forward linkages (Cavusgil & Deligonul, 2011). Thus,visibility and alignment in the supply chain represent crucial factors in risk management of megaprojects.

Miller and Lessard (2007) investigate risks over the project life cycle. They argue that risks emerge and evolve over time.Risks in consideration during the initial phases of the project are usually very different from the ones at the completion phaseof the project. New risks and opportunities arise over time and require changes in project execution plans. Therefore, riskmanagement calls for continuous monitoring by project executives.

4.2. Overall strategies for managing risks

Once the type and possibility of the risk is identified, an appropriate strategy to combat risk should be formulated. Ingeneral, literature identifies four risk response strategies: elimination or avoidance, reduction, transfer, and retention(Akintoye & MacLeod, 1997; Lyons & Skitmore, 2004). The strategy of risk elimination or avoidance is used under thecircumstances of an unacceptable risk level. In this case, the investment is intentionally delayed until the situation issafe or the uncertainties decrease to an acceptable level (Wernerfelt & Karnani, 1987). In the risk reduction strategy,financial hedging and defining pre-specified project content such as fixed price, time, quantity, etc. are the mostcommon techniques to prevent possible risk (Miller, 1992). Moreover, companies try to dominate environmental factors.For example, lobbying against a regulation and gaining political and market power are strategies used to set your ownrules in business and minimize risk (Allaire & Firsirotu, 1989; Ring, Lenway, & Govekar, 1990). Risk transfer can besecured through long-term contractual agreements and collaboration (Akintoye & MacLeod, 1997). Becausemegaprojects are huge investments realized through considerable financial and non-financial resources, formingalliances spreads the risk. Finally, risk retention is preferred if the other risk management strategies are not applicable,and the financial impact and the other negative consequences are tolerable or small (Kallman, 2009; Williams & Heims,1989).

A study on a large engineering project identifies more detailed six risk-management strategies based on the level ofcontrol over risk and the degree to which they are specific to the project (Miller & Lessard, 2007): (i) decisioneering to assessand mitigate risks (e.g., quantitative sensitivity analyses, probabilistic models); (ii) building robust strategic systems (e.g.,creating systems for information gathering, maintaining core competency, allocation of resources, using laws andregulations); (iii) instilling governability (e.g., balancing cohesion and flexibility); (iv) shaping institutions (e.g.,transformation of laws and regulations); (v) hedging and diversifying risks through portfolios (e.g. partnering, investingin different countries); and (vi) embracing residual risks.

In recent years, new approaches for risk management have emerged, such as the enterprise risk management (ERM). ERMis a new paradigm for managing the risk portfolio of an organization taking a company-wide approach in identifying,assessing and managing risks. The Committee of Sponsoring Organizations of the Treadway Commission (COSO) defines ERMas ‘‘. . .a process, affected by an entity’s board of directors, management and other personnel, applied in strategy setting andacross the enterprise, designed to identify potential events that may affect the entity, and manage risk to be within its riskappetite, to provide reasonable assurance regarding the achievement of entity objectives’’.3 The volatility in internationalmarkets, interactions among different risk types, and need for holistic risk management systems have led to wide acceptanceof ERM globally (Kleffner, Lee, & McGannon, 2003). The ERM framework provided by COSO represents the base of the riskmanagement framework we propose for megaprojects in the next session.

4.3. A proposed conceptual framework for managing risks in megaprojects

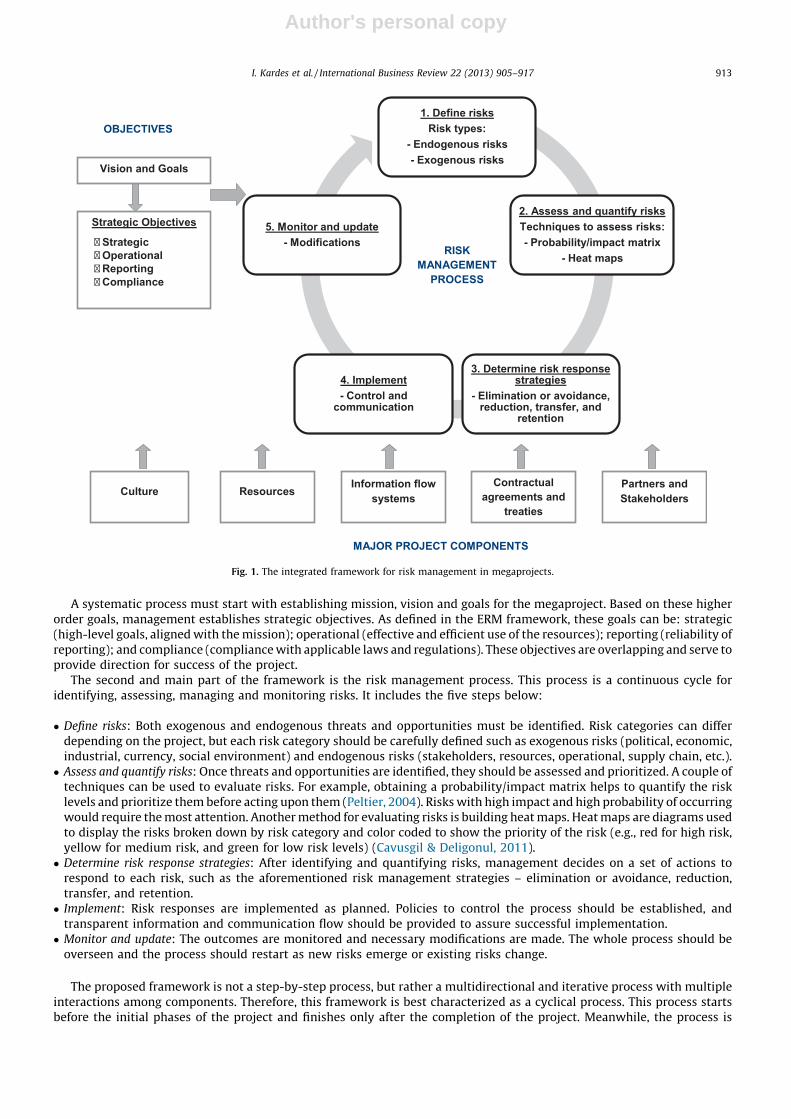

Previous studies have tackled risk from various angles, but there is a lack of an integrative framework which helps usunderstand the range of interrelated risks in megaprojects. Accordingly, we propose such an integrated risk managementframework for megaprojects below and illustrate in Fig. 1.

3 For detailed information, see COSO’s Enterprise Risk Management – Integrated Framework (2004) at http://www.coso.org/Publications/ERM/

COSO_ERM_ExecutiveSummary.pdf.

I. Kardes et al. / International Business Review 22 (2013) 905–917912

Author's personal copy

A systematic process must start with establishing mission, vision and goals for the megaproject. Based on these higherorder goals, management establishes strategic objectives. As defined in the ERM framework, these goals can be: strategic(high-level goals, aligned with the mission); operational (effective and efficient use of the resources); reporting (reliability ofreporting); and compliance (compliance with applicable laws and regulations). These objectives are overlapping and serve toprovide direction for success of the project.

The second and main part of the framework is the risk management process. This process is a continuous cycle foridentifying, assessing, managing and monitoring risks. It includes the five steps below:

� Define risks: Both exogenous and endogenous threats and opportunities must be identified. Risk categories can differdepending on the project, but each risk category should be carefully defined such as exogenous risks (political, economic,industrial, currency, social environment) and endogenous risks (stakeholders, resources, operational, supply chain, etc.).� Assess and quantify risks: Once threats and opportunities are identified, they should be assessed and prioritized. A couple of

techniques can be used to evaluate risks. For example, obtaining a probability/impact matrix helps to quantify the risklevels and prioritize them before acting upon them (Peltier, 2004). Risks with high impact and high probability of occurringwould require the most attention. Another method for evaluating risks is building heat maps. Heat maps are diagrams usedto display the risks broken down by risk category and color coded to show the priority of the risk (e.g., red for high risk,yellow for medium risk, and green for low risk levels) (Cavusgil & Deligonul, 2011).� Determine risk response strategies: After identifying and quantifying risks, management decides on a set of actions to

respond to each risk, such as the aforementioned risk management strategies – elimination or avoidance, reduction,transfer, and retention.� Implement: Risk responses are implemented as planned. Policies to control the process should be established, and

transparent information and communication flow should be provided to assure successful implementation.� Monitor and update: The outcomes are monitored and necessary modifications are made. The whole process should be

overseen and the process should restart as new risks emerge or existing risks change.

The proposed framework is not a step-by-step process, but rather a multidirectional and iterative process with multipleinteractions among components. Therefore, this framework is best characterized as a cyclical process. This process startsbefore the initial phases of the project and finishes only after the completion of the project. Meanwhile, the process is

1. De fine ris ks

Risk types:

- Endogenous risks

- Exo gen ous ris ks

2. Assess an d q uan tify ris ks

Techniq ues to a ssess ris ks:

- Probabili ty/im pact ma trix

- Heat ma ps

3. De termi ne ris k respon se strategies

- Elimi nati on or avoida nce, red ucti on, trans fer, an d

rete ntion

4. Im plement

- Cont rol and communic ation

5. Mon itor an d upd ate

- Mod ific atio nsRISK

MANAGEMENT

PROCESS

OBJ ECTIVES

Vis ion an d Goals

Strate gic Obje ctives

� Strate gic

� Operational

� Reporting

� Compli ance

Cont ractual

agreemen ts and

treaties

Partn ers an d

Stakeh olders

Informa tio n flo w

systemsResourcesCulture

MAJOR PROJECT C OMPONENTS

Fig. 1. The integrated framework for risk management in megaprojects.

I. Kardes et al. / International Business Review 22 (2013) 905–917 913

Author's personal copy

affected considerably by the major components of the project such as culture, resources, information flow systems,contractual agreements and treaties, and partners and stakeholders. The successful implementation of the risk managementprocess highly depends on these underlying components of the megaproject. Organizations with effective systems foraligning cultures, allocating resources efficiently, providing transparent information flow systems, establishing clearcontractual agreements and building trust with partners will be relatively more successful in managing risk and uncertainty.Well thought-out institutional arrangements and managing risks appropriately are prerequisites for creating such systems.

5. Managerial prescriptions

Beyond adopting a risk management framework proposed above, managers can use some specific guidelines to cope withthe challenges of megaprojects. These guidelines relate in essence to the major project components in our proposed riskmanagement framework. As a starting point, to cope with complexity, both managers and employees should possess theskills and knowledge to use the necessary technology. In this context, training plays an important role in ensuring that thenew technology is used effectively and resistance to change is reduced (Marler, Liang, & Dulebohn, 2006).

Second, because disagreements among people may cause deviations from the project goals, the management shouldallocate adequate time to the clarification of goals and interpretations, and revelation of hidden agendas by making atransparent information flow on each organizational level (Remington & Pollack, 2007).

The third prescription relates to the role of contracts. Contractual agreements and treaties should clearly define goals, rightsand obligations for all partners and sponsors. Contracts are preventive mechanisms against the possible deception which canarise from the conflict of interests during the long duration of the project life such as moral hazard. In a moral hazard relatedissue, one partner changes his behavior on the basis of the signed agreement to maximize his own interest rather than thebenefit of the collaboration, and reduces or stops resource flow or efforts in investment (Elitzur & Gavious, 2003; Frenzen &Nakamoto, 1993; Macho-Stadler & Perez-Castrillo, 1993). As a backup plan and precaution against moral hazard, somecompanies second source or have alternatives for the more critical elements in the supply chain (Cavusgil & Mahnke, 2012).

Fourth, ‘‘illusion of control’’, can be overcome through greater transparency, independent project appraisals, and scrutiny.Using reference class forecasting, which compares the current project to projects of a similar class and scale, enables betterproject estimations regarding cost, duration, and potential problems. For example, costs and duration of 46 comparable railprojects were investigated before the start of the Edinburgh tram system in UK in 2004 and the budget was revised (WorldFinance, 2009).

Fifth, a healthy spirit of collaboration is a prerequisite for the success of megaprojects. It is important to not only focus onhard criteria (e.g., market position, technical skills, financial capability) but also pay attention to soft criteria such as partnerselection and people selection. In this context, detailed knowledge of potential partner’s management culture, strongrelationships, effective communication, trust and confidence, cross-cultural communication, evaluation and monitoring ofthe relationship quality, and creating a cooperative environment are necessary to ensure success (Hitt, Dacin, Levitas,Arregle, & Borza, 2000; Kelly, Schaan, & Joncas, 2002; Wuyts & Geyskens, 2005).

Sixth, maintaining lasting mutual interests for the parties concerned can go a long way toward contributing tomegaproject success. Some practitioners argue that successful collaborations are based on gain-sharing and risk-sharingarrangements – a structure of ‘‘sink or swim together’’ (Cavusgil & Mahnke, 2012). For example, London Heathrow Terminal5 was completed on time in 2008 and within the estimated budget of £4.2 billion. The reason for this success is attributed tothe risk and profit sharing structure of the consortium. All partners and contractors were paid for their work, a risk budgetwas maintained, problems were dealt quickly and in the most cost efficient manner, and remaining profits were shared.Single equivalent management structure and contractual agreements assured the success of this project.

Seventh, beyond a structural contract, trust, prior cooperative experience between partners and the reputation of thecompanies before partnership are among the key determinants of relationship quality (Arino, de la Torre, & Ring, 2001).Increasing the relationship quality between companies can create a ‘‘moral contract’’ and decrease the risk of moral hazardor other potential troubles (Cavusgil, 1998).

Eight, control and commitment are also crucial elements of megaprojects. However, their balance is very critical.Excessive control can cause distrust and increase the possibility of self-serving behavior, shifting focus away from thepartnership’s interests. If partners lose their commitment, needed contributions will not be forthcoming (Sundaramurthy &Lewis, 2003; van Marrewijk, 2005). Hence, it is important to balance the power.

Finally, another prescription for success would be starting out with viable project ideas and thoroughly shaping projectsduring the early stages since most projects have little flexibility after initiation (Miller & Lessard, 2007). Investments in theearly stages of the project can help alleviate problems and improve quality. Therefore, cost reduction is secured and betteroutcomes are achieved (Magnussen & Samset, 2005). Similarly, according to a study of more than 1000 projects by the WorldBank (World Bank, 1996), projects with better initial design processes showed a success rate of 80%, whereas projects withinsufficient front-end phases showed a success rate of 35%.

6. Conclusion

With this study, we aimed to bring many issues into light regarding megaprojects – a relatively neglected topic in thescholarly literature. First, we define global megaprojects and emphasize the challenges they pose in today’s global

I. Kardes et al. / International Business Review 22 (2013) 905–917914

Author's personal copy

marketplace. Complexity, illusion of control, and sunk cost effect emerge as the major issues of megaprojects that requirefurther attention in the international business literature. Prospect theory and self-justification theory help explain whydecision making processes in megaprojects can be biased and emotionally charged. Although the risk management literatureis extensive, there is a dearth of studies presenting an integrated framework in risk management approaches. This studyintegrates extant literature, and, building on it, proposes an integrated framework for the risk management, specificallydesigned for megaprojects.

There are multiple benefits of using this framework for practitioners. First of all, an integrated approach to megaprojectswill ensure a better control over the whole process. Also, by following the steps in this framework, managers will be able toproactively respond to risks. Proactive responses of managers will significantly enhance efficiency and reduce overall costs.Furthermore, continuous monitoring of this process will ensure that the problems during the execution of the megaprojectare also proactively identified and could be solved before they pose a significant threat.

High visibility, monetary costs, and complexity of today’s global megaprojects are so overwhelming that entire nationsmay be affected by the fate of a single project. Yet, despite the significant cost overruns, revenue shortfalls and remarkablypoor performance records in terms of economic, environmental and public domains, megaprojects continue to be initiatedin large numbers around the world – which is referred as ‘‘megaproject paradox’’ (Flyvbjerg, Bruzelius, & Rothengatter,2003). A deeper understanding of the underlying problems to achieve better outcomes for megaprojects is absolutelyimperative.

The opportunity for cost reduction, revenue growth, risk sharing or reduction, gaining knowledge and experience,or political motives arouses the desire for investors to undertake megaprojects. For example, Boeing partnered withUnited Airlines as its ‘‘launch customer’’ in developing its new line of 777 jets, and therefore reduced its own riskssince United Airlines will purchase a large number of the new planes. Other reasons for partnering in megaprojectsinclude offering lower prices or encouraging healthier and more profitable industry conduct (Dull, Mohn, & Noren,1995).

Additionally, globalization encourages the development of megaprojects. First, globalization of financial capital and lawfacilitates cross-national partnerships. Second, technological innovations secure big, complex constructions. Finally, despitethe high numbers of former failures, difficulty in forecasting or risk analysis encourages the project partners to develop highsuccess expectations (Douglass, 2010; Flyvbjerg et al., 2003).

This study presented a comprehensive view of the issue while addressing possible solutions for the problemsencountered. Where do we go from here? A number of specific issues need further examination.

First, the number of megaprojects has skyrocketed in recent years due to increasing infrastructure needs in emergingmarkets. The fact that emerging markets are relatively inexperienced in megaprojects compared to their developedcounterparts complicates the projects even more in these geographies. Therefore, it is worthy to examine megaprojectsdeeper for emerging markets; i.e., how they differ from developed countries in terms of megaproject risks, requirements ormanagement styles; or what the unique characteristics or specific challenges are due to infrastructure, culture, language ortrade barriers.

Second, a key element for the success of a megaproject is a robust collaboration among partners. Thus, partner selection ismaybe the most crucial subject for companies engaging in megaprojects. Some previous studies have addressed the issue ofpartner selection in the context of international partnering (Cavusgil, 1998) or partnering in emerging versus developedmarkets (Hitt et al., 2000). However, further research is needed to develop new insights for partner selection in the context ofmegaprojects, taking into account their unique characteristics and needs.

Finally, the failure or success of megaprojects is an ambiguous matter and begs scholarly attention. Some practitionerseven dispute that cost overruns or time delays should be considered a failure. If a project is completed much later thananticipated, then it should be called a ‘delayed success,’ they argue, not a failure. For example, some say that the Dreamlinerproject, even after falling behind predetermined delivery date and experiencing at least $6 billion overruns, is not a failure aslong as there are thousands of Dreamliners offering good customer service at some point in time (Cavusgil & Mahnke, 2012).This may be one explanation for why very few megaprojects are terminated before completion despite many signals forfailing outcomes. Failure might also be defined in terms of project, system or product failure. Accordingly, scholars ought toclarify what exactly constitutes failure or success in megaprojects. This will help practitioners be more focused on successand avoid any chances of failure.

Limitations of the present investigation include the difficulty of data collection due to limited number of previous workin the literature, and the difficulty of studying the subject in depth due to the long-term nature of megaprojects.Consequently, we utilized a multidisciplinary literature and used numerous field observations and case studies in thepresent research.

This study contributes to the advancement of knowledge in megaprojects in multiple ways. First, we raise awareness in asubject that has been largely neglected in the international business literature, in spite of the huge significance and impact ofmegaprojects on world economies. Second, we provide a less ambiguous characterization of their features and challenges.Third, we incorporate such conceptual contributions as the moral hazard theory, the prospect theory, the self-justificationtheory, and the illusion of control literature. Moreover, based on conceptual foundations, we develop an integratedframework for risk management in megaprojects. This framework, along with the managerial prescriptions offered, wouldcontribute to the knowledge and practice of megaproject management. We hope that this research will stimulate others forfurther in depth-analyses.

I. Kardes et al. / International Business Review 22 (2013) 905–917 915

Author's personal copy

Appendix A. Nabucco project

The Nabucco is a proposed project for building a natural gas pipeline which starts at the Georgian/Turkish and the Iraqi/Turkish border, and finishes in Vienna, crossing Bulgaria, Romania and Hungary. The project’s goal is to open a new gas supplycorridor into Europe. A consortium formed by six companies manages the project, and the intergovernmental agreement wassigned on 13 July 2009 by participating countries: Turkey, Romania, Bulgaria, Hungary and Austria. The initial discussions for theproject have started in 2002, construction has been planned to start in 2013, and the project has been expected to finish by 2017.Below are some facts signaling the complexity of the project:4

Shareholders Bulgarian Energy Holding (Bulgaria), Botas (Turkey), FGSZ1 (Hungary), OMV (Austria),

RWE (Germany), and Transgaz (Romania). Each shareholder has an equal share of 16.67%.

Length of pipeline 3900 km

Total investment EUR 7.9 billion (Currently under review)

Financing 30% equity and 70% debt financing

Social and economic effects The largest European infrastructure project in terms of countries involved. The project

has been expected to create thousands of new jobs, thus boost the European economy.

Control centers Sofia, Bulgaria; Medias, Romania; Budapest, Hungary; Baumgarten, Austria

Legal obligations The Law of each transit country; EU Directives and relevant International Agreements;

ISO 14001, 9000 and 18000 Standards for Environmental, Quality and Safety Management

Systems, respectively, etc.

Some sources have been claiming that the project is likely to be terminated due to some changing landscape over time (e.g., political concerns, European

financial crises, cost and financing concerns, etc.; http://www.upi.com/Business_News/Energy-Resources/2012/02/13/Nabucco-is-over-analyst-says/UPI-

85071329140348/). Indeed, a modified concept for the pipeline project has been recently submitted and approved in June 2012. The new project, called

‘‘Nabucco West’’ cuts the length of the pipeline to from 3900 km to 1300 km. The Nabucco West pipeline will bring Caspian gas from the Bulgarian-Turkish

border to Austria.

References

Akintoye, A. S., & MacLeod, M. J. (1997). Risk analysis and management in construction. International Journal of Project Management, 15, 31–38.Allaire, Y., & Firsirotu, M. E. (1989). Coping with strategic uncertainty. Sloan Management Review, 30, 7–16.Anderson, G., & Roskrow, B. (1994). The channel tunnel story. London, UK: E & F N Spon.Arino, A., de la Torre, J., & Ring, P. S. (2001). Relational quality: Managing trust in corporate alliances. California Management Review, 44, 109–131.Arkes, H. R., & Ayton, P. (1999). The sunk cost and concorde effects: Are humans less rational than lower animals? Psychological Bulletin, 125, 591–600.Arkes, H. R., & Blumer, C. (1985). The psychology of sunk cost. Organizational Behavior and Human Decision Processes, 35, 124–140.Arkes, H. R., & Hutzel, L. (2000). The role of probability of success estimates in the sunk cost effect. Journal of Behavioral Decision Making, 13, 295–306.Baccarini, D. (1996). The concept of project complexity – A review. International Journal of Project Management, 14, 201–204.Bing, L., Akintoye, A., Edwards, P. J., & Hardcastle, C. (2005). The allocation of risk in PPP/PFI construction projects in the UK. International Journal of Project

Management, 23, 25–35.Boulding, W., Morgan, R., & Staelin, R. (1997). Pulling the plug to stop the new product drain. Journal of Marketing Research, 34, 164–176.Brockner, J. (1992). The escalation of commitment to a failing course of action: Toward theoretical progress. Academy of Management Review, 39–61.Bruijn, J. A., & Leijten, d. M. (2008). Management characteristics of mega-projects. In H. Priemus, B. Flyvbjer, & G. P. van Wee (Eds.), Decision-making on mega-

projects. Cost–benefit analysis, planning and innovation (pp. 23–39). Cheltenham, UK/Northhampton, MA, USA: Edward Elgar Publishing Limited.Businessweek. (2008). Infrastructure spending to surge in emerging markets Retrieved from http://www.businessweek.com/globalbiz/content/jun2008/

gb20080625_321091.htm.Capka, J. R., (2004). Megaprojects – They are a different breed. Public Roads Magazine, 68, http://www.fhwa.dot.gov/publications/publicroads/04jul/01.cfm

(accessed on 24.05.11).Cavusgil, S. T. (1998). International partnering: A systematic framework for collaborating with foreign business partners. Journal of International Marketing, 6, 91–

100.Cavusgil, S. T., & Deligonul, S. (2011). Exogenous risk analysis in global supplier networks: Conceptualization and field research findings. Information Knowledge

Systems Management, 10, 1–19.Cavusgil, S. T., & Mahnke, V. (2012). Managing complex cross-border collaborative projects: Tamer Cavusgil interviews four managers experienced in doing it. In S.

Harris, O. Kuivalainen, & V. Stoyanova (Eds.), International business – New challenges, new forms, new perspectives (pp. 191–217). Houndmills, Basingstoke, UK:Palgrave MacMillan.

Cleland, D. I., & King, W. R. (1983). Systems analysis and project management (3rd ed.). Singapore: McGraw-Hill.Court, R. (2006). Integrated management. Financial Management, June, 41–42.Douglass, M. (2010). Globalization, mega-projects and the environment: Urban form and water in Jakarta. Environment and Urbanization Asia, 1, 45–65.Dull, S. F., Mohn, W. A., & Noren, T. (1995). Partners. McKinsey Quarterly, 4, 63–72.Durand, R. (2003). Predicting a firm’s forecasting ability: The roles of organizational illusion of control and organizational attention. Strategic Management Journal,

24, 821–838.El-Sayegh, S. M. (2008). Risk assessment and allocation in the UAE construction industry. International Journal of Project Management, 26, 431–438.Elitzur, R., & Gavious, A. (2003). Contracting, signaling, and moral hazard: A model of entreprenerus, ‘angels,’ and venture capitalists. Journal of Business Venturing,

18, 709–725.Floricel, S., & Miller, R. (2001). Strategizing for anticipated risks and turbulence in large-scale engineering projects. International Journal of Project Management, 19,

445–455.Flyvbjerg, B., Bruzelius, N., & Rothengatter, W. (2003). Megaprojects and risk: An anatomy of ambition. Cambridge, UK: Cambridge University Press.Flyvbjerg, B., Garbuio, M., & Lovall, D. (2009). Delusion and deception in large infrastructure projects: Two models for explaining and preventing executive

disaster. California Management Review, 51, 170–193.Frenzen, J., & Nakamoto, K. (1993). Structure, cooperation and the flow of market information. Journal of Consumer Research, 20, 360–375.Frick, K. T. (2008). The cost of the technological sublime: Daring ingenuity and the new San Francisco–Oakland Bay Bridge. In H. Priemus, B. Flyvbjerg, & B. v. Wee

(Eds.), Decision-making on mega-projects: Cost–benefit analysis, planning and innovation (pp. 239–262). Cheltenham, UK: Edward Elgar Publishing.Gellert, P. K., & Lynch, B. D. (2003). Mega-projects as displacements. International Social Science Journal, 55, 15–25.

4 http://www.nabucco-pipeline.com.

I. Kardes et al. / International Business Review 22 (2013) 905–917916

Author's personal copy

Gil, N., & Beckman, S. (2009). Infrastructure meets business: Building new bridges mending old ones. Introduction. California Management Review, 51, 6–29(2009)).

Greiman, V. (2010). The big DIG: Learning from a mega project. Ask Magazine NASA, 39, 47–52.Hass, K. (2009). Planting the seeds to grow a complex project management practice Retrieved from http://www.kathleenhass.com/WhitePapers.htm.Hitt, M. A., Dacin, M. T., Levitas, E., Arregle, J.-L., & Borza, A. (2000). Partner selection in emerging and developed market contexts: Resource-based and

organizational learning perspectives. Academy of Management Journal, 43, 449–467.Jaafari, A. (2001). Management of risks uncertainties and opportunities on projects: Time for a fundamental shift. International Journal of Project Management, 19,

89–101.Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47, 263–292.Kallman, J. (2009). Risk financing transfer tools. Risk Management, 56, 58–59.Kelly, M. J., Schaan, J. L., & Joncas, H. (2002). Managing alliance relationships: Key challenges in the early stages of collaboration. R&D Management, 32, 11–22.Kipp, A., Riemer, K., & Wiemann, S. (2008). IT mega projects: What they are and why they are special. ECIS 2008 Proceedings (Paper 152).Kleffner, A. E., Lee, R. B., & McGannon, B. (2003). The effect of corporate governance on the use of enterprise risk management: Evidence from Canada. Risk

Management and Insurance Review, 6(1), 53–73.Kolltveit, B. J., & Grønhaug, K. (2004). The importance of the early phase: The case of construction and building projects. International Journal of Project

Management, 22, 545–551.Lam, P. T. I. (1999). A sectoral review of risks associated with major infrastructure projects. International Journal of Project Management, 17, 77–87.Langer, E. J. (1975). The illusion of control. Journal of Personality and Social Psychology, 32, 311–328.Lyons, T., & Skitmore, M. (2004). Project risk management in the Queensland engineering construction industry: A survey. International Journal of Project

Management, 22, 51–61.Macho-Stadler, I., & Perez-Castrillo, J. D. (1993). Moral hazard with several agents: The gains from cooperation. International Journal of Industrial Organization, 11,

73–100.Magnussen, O. M., & Samset, K. (2005). Successful megaprojects: Ensuring quality at entry. In Proceedings of the EURAM.Marler, J. H., Liang, X., & Dulebohn, J. H. (2006). Training and effective employee information technology use. Journal of Management, 32, 721–742.Mihm, J., Loch, C., & Huchzermeier, A. (2003). Problem-solving oscillations in complex engineering projects. Management Science, 49, 733–750.Miller, K. D. (1992). A framework for integrated risk management in international business. Journal of International Business Studies, 23, 311–331.Miller, R., & Lessard, D., (January 2007). Evolving strategy: Risk management and the shaping of large engineering projects. MIT Sloan School of Management. Working

Paper, 4639–4607.Nguyen, H. V., (2011). Risk and Visibility in Global Supply Chains: An Empirical Study. Unpublished Ph. D. Dissertation, Georgia State University.OECD. (2007). Infrastructure to 2030: Mapping policy for electricity, water and transport (vol. 2, pp. ). ). Paris: OECD.Orr, R. J., & Metzger, B. (2005). The legacy of global projects: A review and reconceptualization of the legal paradigm. In Proceedings of the 1st General Counsels’

Roundtable (pp. 1–51) From http://crgp.stanford.edu/publications/working_papers/proceedings1.pdf.Peltier, T. (2004). Risk analysis and risk management. EDPACS, 32(3), 1–17.Remington, K., & Pollack, J. (2007). Tools for complex projects. Hampshire, England: Gower Publishing Ltd.Ring, P. S., Lenway, S. A., & Govekar, M. (1990). Management of the political imperative in international business. Strategic Management Journal, 11, 141–151.Roxburgh, C. (2003). Hidden flaws in strategy. The McKinsey Quarterly, 2, 26–39.Schaubroeck, J., & Davis, E. (1994). Prospect theory predictions when escalation is not the only chance to recover sunk costs. Organizational Behavior and Human

Decision Processes, 57, 59–82.Sharp, D. J., & Salter, S. B. (1997). Project escalation and sunk costs: A test of the international generalizability of agency and prospect theories. Journal of

International Business Studies, 28, 101–121.Shenhar, A. J. (2001). One size does not fit all projects: Exploring classical contingency domains. Management Science, 47, 394–414.Shore, B., & Cross, B. J. (2005). Exploring the role of national culture in the management of large-scale international science projects. International Journal of Project

Management, 23, 55–64.Simon, M., Houghton, S. M., & Aquino, K. (2000). Cognitive biases, risk perception and venture formation: How individuals decide to start companies. Journal of

Business Venturing, 15, 113–134.Sommer, S. C., & Loch, C. H. (2004). Selectionism and learning in projects with complexity and unforeseeable uncertainty. Management Science, 50, 1334–1347.Sundaramurthy, C., & Lewis, M. (2003). Control and collaboration: Paradoxes of governance. The Academy of Management Review, 28, 397–415.Tan, H.-T., & Yates, J. F. (1995). Sunk cost effects: The influences of instruction and future return estimates. Organizational Behavior and Human Decision Processes,

63, 311–319.Thaler, R. (1980). Toward a positive theory of consumer choice. Journal of Economic Behavior and Organization, 1, 39–60.Thaler, R. (1985). Mental accounting and consumer choice. Marketing Science, 4(3), 199–214.Titus, V., Jr., Covin, J. G., & Slevin, D. P. (2011). Aligning strategic processes in pursuit of firm growth. Journal of Business Research, 64, 446–453.Vaaland, T. I., & Hakansson, H. (2003). Exploring interorganizational conflict in complex projects. Industrial Marketing Management, 32, 127–138.van Marrewijk, A. (2005). Strategies of cooperation: Control and commitment in mega-projects. Management, 8, 89–104.van Marrewijk, A., Clegg, S. R., Pitsis, T. S., & Veenswijk, M. (2008). Managing public–private megaprojects: Paradoxes, complexity and project design. International

Journal of Project Management, 26, 591–600.Warrack, A., (May 1993). Megaproject decision making: Lessons and strategies. Western Centre for Economic Research, Faculty of Business, University of Alberta,

Number 16.Wernerfelt, B., & Karnani, A. (1987). Competitives strategy under uncertainty. Strategic Management Journal, 8, 187–194.Whyte, G. (1986). Escalating commitment to a course of action: A reinterpretation. Academy of Management Review, 311–321.Williams, C. A., & Heims, R. M. (1989). Risk management and insurance. New York, USA: McGraw Hill.World Bank. (1996). Evaluation results 1994 Retrieved from http://www.wds.worldbank.org.World Finance. (2009). Managing mega projects Retrieved from http://www.worldfinance.com/magazinearticles/article958.html.Wuyts, S., & Geyskens, I. (2005). The formation of buyer–supplier relationships: Detailed contract drafting and close partner selection. Journal of Marketing, 69,

103–111.Zeelenberg, M., & van Dijk, E. (1997). A reverse sunk cost effect in risky decision making: Sometimes we have too much invested to gamble. Journal of Economic

Psychology, 18, 677–691.

I. Kardes et al. / International Business Review 22 (2013) 905–917 917