MBA ESSAY AND ACCOUNTING TERM PAPER - THE RELEVANCE OF ACCOUNTING INFORMATION TO INVESTMENT...

61

ESSAY AND ACCOUNTING TERM PAPER TOPIC: THE RELEVANCE OF ACCOUNTING INFORMATION TO INVESTMENT DECISIONS IN NIGERIA

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of MBA ESSAY AND ACCOUNTING TERM PAPER - THE RELEVANCE OF ACCOUNTING INFORMATION TO INVESTMENT...

ESSAY AND ACCOUNTING TERM PAPER

TOPIC: THE RELEVANCE OF ACCOUNTING INFORMATION TO

INVESTMENT DECISIONS IN NIGERIA

ABSTRACT

This research paper investigates the relevance of accounting informationto investment decisions in Nigeria. The paper became imperative in thelight of some studies that explored the proposition that accountinginformation in published financial statements lost its relevance over theperiod of time, as well as the instances of presentation of financialinformation by some corporate bodies as regards their networth andexistence which is a far cry from the true picture of their actualfinancial position (of not being credit worthy, for instance). Thesekinds of happening have provoked thoughts and opinions from theintellectual world over the role of ethics and reliability of accountinginformation as a decision background for investment purposes. It is as afallout of this background that this research is carried out. Themethodology adopted is descriptive using a qualitative method i.e.purposive sampling method in getting responses to carefully framedquestionnaires on the subject matter. In total, two hundred and fifty(250) respondents were sampled through purposive sampling method and twohundred (200) questionnaires were collected back, thus achieving aresponse rate of eighty percent (80%). Findings from responses receivedrevealed accounting information as relevant and essential for investmentdecision-making.

The afore-mentioned measures are anticipated to increase investors’confidence in accounting numbers and by extension the economic growth inNigeria.

It was therefore recommended that there is need for a more ethical re-orientation of members of the industry in their ethical responsibility tothe public and increase in punitive measures as well as solid policyframework readjustment for the industry.

Accounting Information in published financial statements lost their relevance over the period of time. (Ball and Brown 1968, Oyerinde D.T., 2009). In United Kingdom, it has found that the financial statement was considered as the least effective means of communicating information. (Guthrie J., 2007).

There is need to increase the ethical knowledge, discipline and its

practice into the profession of accounting most especially as it concerns

the public through consistent and practical education

There is need for punitive measures where unethical practices such as

poor accounting information or presentation are made to the public.

There is need to give public access to other corporate information in

order to minimize these corporate fraud.

There is need for a stringent policy readjustment to regulating the

affairs of these corporate bodies in accounting presentation.

There is also need for whistle blowing philosophy by the public when

these issues are noticed.

SECTION 1: INTRODUCTION

1.1 BACKGROUND TO THE STUDY.

Listed companies in Nigeria use financial statements as one of the major

medium of communication with their stakeholders. Therefore, stock market

regulators and accounting standards setters are trying to improve the

quality of financial statements in order to increase the transparency

level in financial reporting. (Vishnani S., Shah B.K., 2008). Financial

Statements may consist different types of information which can be named

as Financial Information/Accounting Information and Non Financial

Information/Non Accounting Information. Accounting Information are

information which describes an account for a utility. It processes

financial transactions to provide external reporting to outside parties

such as to stockholders, investors, creditors, and government agencies

etc. and non accounting information are information which cannot be

measured in monetary terms to make investment decisions by the investors.

This type of investment is called as ethical investment.

Financial information is essential in making sound investment decisions

and it will reduce the informational asymmetry problem between the firm’s

managers and the investors (Hossain, D. M., Khan, A., Yasmin, I. 2004).

Though the investors use non financial information in order to make

investment decisions, still conventional investors give more weight to

financial information. Akintoye (2008) discovered that the quality of

accounting information in terms of its accuracy, adequacy, reliability

and mode of disclosure is a major determinant of the level of efficiency

of the capital market and other decision tasks.

Recent happenings in the global world however and various empirical

studies explored that Accounting Information in published financial

statements lost their relevance over the period of time. (Ball and Brown

1968, Oyerinde D.T., 2009). In United Kingdom, it has found that the

financial statement was considered as the least effective means of

communicating information. (Guthrie J., 2007). Having discovered that

studies into the relevance of accounting information are existent in

other countries (Ball and brown 1968, Francis & Scghipper, 1999, Vishnani

S., Shah B.K., 2008, and Ronen J.), the gap is still yet to be filled in

Nigeria. Hence, this research work intends to fill this gap by

investigating on The Relevance of accounting information to investments

decisions in Nigeria.

1.2 STATEMENT OF THE PROBLEM

The mobilization and allocation of both domestic and foreign savings are

critical in the national growth process (Aregbeyen, 2011). It is

therefore, obvious that the investment markets have a significant role to

play in economic development. Growth occurs when savings are channeledinto productive investments which in turn enhance the capacity of the

economy to produce goods and services which have bearing on standard of

living. Alile (2007) indicates that the capital market which is the main

investment market for listed companies publishing financial or accounting

information play a crucial role in stimulating industrial growth as well as

economic growth and development.

This means that a capital market will succeed in facilitating economic

growth and development if it can encourage the flow of savings / investment

through the purchase of securities issued by government or private

enterprise and others with the aim of financing the implementation of

capital projects. However, instead of the potential of this industry to be

harnessed we are having a big abuse of financial and accounting information

presentation to the general public. Inaccurate financial and accounting

statement disclosures and falsification is now the other of the day.

Traditionally, investors within the public rely on this accounting and

financial information and general information from enquiries as a basis

for their investment decisions but this is not the case any more, with

the level of corruption and incompetence that has bedvilled the sector.

This has large implications for ethical practices within the sector,

growth of the sector, investment direction and growth and development of

the country.

1.3 AIMS AND OBJECIVES OF THE STUDY

The aim of the research is to investigate the relevance of accounting

information to investment decisions in Nigeria.

OBJECTIVES

The aim of the research is intended to be achieved through the following

objectives:

Examine the current state of accounting information as an aid

to investment decisions in Nigeria

Examine if accounting information in Nigeria meet regulatory

criteria and standards.

Examine the contribution of accounting information to

investors decision among other factors

Proffer recommendations in helping to solve the inherent

problems in accounting information and presentation in Nigeria

1.4 SIGNIFICANCE OF STUDY

The quality of accounting information in terms of its accuracy, adequacy,

reliability and mode of disclosure is a major determinant of the level of

efficiency of the capital market and other decision tasks. The relevance

of accounting information to day-to-day running of the organization and

the general public, especially for investors cannot be over-emphasized.

Investments are normally undertaken under condition of uncertainty.

Hence, one of the incentives required is a mechanism to help reduce the

level of uncertainty to which a potential investor could be exposed

(Ariyo, 2007). A careful execution of this research work which is

tended to reveal problematic areas and investors concern would if

implemented well would position the mechanism of accounting and financial

information in performing its primary role vis-à-vis information and

reduction of risk. A good accounting information presentation and

mechanism if so achieved determines the nature and extent of moral hazard

to which existing and potential investors could be exposed, thereby

influencing the level of optimality of allocation of societal resources.

The research will also tend to inform and educate the illiterate public

on the dangers involved in decisions based on paper data alone without

corroboration from objective financial experts. Furthermore, the research

paper would be advisory to government and financial regulatory policies

in formulating procedures and more stringent policies in combating these

professional gaps within the industry. As well this research is intended

to fuel further researches in this field of study.

1.5 RESEARCH QUESTION

In carrying out this research the following research questions are set:

Does accounting information in Nigeria follow laid down

professional standards and procedures?

Is accounting information in Nigeria a true reflection of the

financial state of listed companies?

Is accounting information significantly reliable for

investment purposes?

Does accounting information affect the rate of investment in

Nigeria?

What is the public perception relating to accounting

information and financial presentation in Nigeria?

1.6 RESEARCH HYPOTHESIS

In this research, three (3) hypotheses were set, namely:

Ho: Accounting information does not significantly represent a true

reflection of financial situation of listed companies in Nigeria

Hi: Accounting information significantly represents a true

reflection of financial situation of listed companies in Nigeria.

Ho: Accounting information in Nigeria is not significantly reliable

for investment purposes in Nigeria.

Hi: Accounting information in Nigeria is significantly reliable for

investment purposes in Nigeria.

Ho: Accounting information does not significantly affect the rate

of investments in Nigeria

Ho: Accounting information significantly affects the rate of

investments in Nigeria

1.7 SCOPE AND LIMITATIONS OF STUDY

This research work is primarily on accounting information relevant to

investors in Nigeria and this would involve only accounting and financial

indexes computed and published to the public by listed companies alone

and does not involve any other type of accounting information or

management accounting information not published or obtained or used

within the organization or not published. Furthermore, this research

would as well be a reflection of the experiences of investors or

respondents quite recent to the research likely a period of 5 years back

from now since the research work is a qualitative one.

In terms of limitation, the research work is a qualitative one and thus

will be based on respondents’ judgment which has its weaknesses but

effort will be tailored at using ranked options (ordinal attitudinal

scales) in order to capture the scale of their perceptions. Furthermore,

ability to get respondents that are finally literate enough who is an

investor, aware and uses financial information is seen also as very

important to the research. In other to lessen the effect of this

limitation, the sampling methodology was purposive.

The question of motivation to fill a research instrument nowadays by

business seem to them as time wasting, consequently much time wasting was

involved in lobbying respondents into helping in completing the

questionnaire. Conclusively, all instruments were to every extent

retrieved back to ensure further work.

1.8 TERMINOLOGIES IN THE RESEARCH

Accounting: The systematic recording, reporting, and analysis of

financial transactions of a business

Financial: related to finance which is the science of the management of

money and other assets

Investment: the purchase of a financial product or other item of value

with an expectation of favorable future returns

Monetary: of or relating to money or to the mechanisms by which it is

supplied to and circulates in the economy

Regulatory: To control or direct according to rule, principle, or law or

to adjust to a particular specification

Standard: A level of quality or attainment, universally or widely

accepted, agreed upon, or established means of determining what something

should be

SECTION TWO: LITERATURE REVIEW

2.1 GENERAL REVIEW OF LITERATURE

According to Meyer (2007) accounting plays a significant role within the

concept of generating and communicating wealth of companies. Financial

statements remain the most important source of externally feasible

information on companies. In spite of their widespread use and continuing

advance, there is some concern that accounting practice has not kept

faith with ethics and pace with rapid economic and high technology

changes which in invariably affects the value relevance of accounting

information.

Before the nature of Accounting can be addressed, this field of study

must first be delineated. This entails an identification of the area of

interest and of the borders of the discipline in relation to neighbouring

disciplines or mediating concepts. Thus a successful definition of

Accounting should clearly delineate the boundaries of the discipline at a

point in time, give a precise statement of its essential nature, and be

flexible so that innovation and growth in the discipline can be

accommodated.

A number of definitions of Accounting have appeared in the literature,

each attempting to demarcate its field of study. Developing a single

definition of Accounting is however beset with difficulties. The first

difficulty stems from the dynamic nature of Accounting. Glautier and

Underdown (1986) point out that the changing environment continually

extends the boundaries of Accounting, which makes defining the scope of

the subject problematical. A second difficulty, which stems from the

first, is the question of boundaries. Accounting can be described as

being simultaneously eclectic and pervasive, consequently definitions of

Accounting tend to have fuzzy and changing boundaries (Glautier and

Underdown (1986). A third difficulty stems from the often debated

question of whether Accounting is an art or science. According to the

AICPA (1953) Accounting is an art.

The Committee on Terminology of the AICPA (1953, par.5) defined

Accounting as follows:

“Accounting is the art of recording, classifying and summarising in a

significant manner and in terms of money, transactions and events which

are, in part at least, of a financial character and interpreting the

results thereof.”

An example of definitions in accounting textbooks is supplied by Kieso

and Weygaardt (1992) who identify the three essential aspects of

Accounting as - the identification, measurement and communication of

financial information on economic entities to interested parties, being

the users of financial information. This definition does not take into

consideration the use of such information to users, and limits the

information to financial data. A more comprehensive definition of

Accounting is provided by Ansari, Bell, Klammer & Lawrence (1997) who

state that it consists of four key ideas:

• It is by nature a measurement process;

• Its scope includes financial and operational information;

• Its purpose is to assist the organisation in reaching its strategic

objectives;

and

• Its attributes are to enhance the understanding of the measured

phenomena, and provide information for decision making, and therefore

encourages actions and supports and creates shared values, beliefs and

mind sets.

This definition has a number of strengths. It identifies that accounting

information should include both financial and operational information. It

stresses the increasing importance of supporting strategic decision

making in the organisation as a result of a volatile and competitive

business environment. It views Accounting as more than the technique of

processing and measuring data. Behavioural and social responsibility

aspects are recognised in the definition as attributes. This view is,

however, restricted as it defines Accounting from a Management Accounting

perspective and overlooks the financial reporting aspects. Another

limitation is that it does not state specifically that in Accounting

change and continuous improvement are measured, although it is implied.

By facilitating change, the implication is that

accounting information should include aspects such as flexibility and

companies’ ability to adapt to change.

The construct of flexibility does not appear in any of the definitions on

Accounting, because the definitions were developed during stable periods.

The environment however has changed – uncertainty has increased and

predictability has declined. In view of the fact that flexibility is a

function of uncertainty, greater value will be attached to flexibility in

organisations as uncertainty escalates. It is therefore appropriate to

include the construct of flexibility in the definition especially during

periods of uncertainty.

Although the term flexibility has appeared in the accounting literature

if not in the definitions on Accounting, it is often referred to in a

negative context. Flexibility in Accounting is viewed by some authors in

a negative light. Wolk, Francis & Tearney (1984) for example, define

flexibility as the choice between different accounting policies. The aim

of Accounting is to reduce the number of acceptable accounting policies

so that a transaction is treated consistently by different reporting

entities. This implies in turn, that “flexibility” should be eliminated,

too. This endless pursuit of consistency and to a lesser extent

comparability, contributes to the inflexibility of Accounting and to the

negative perceptions of flexibility in the accounting community.

From a functionalist perspective, Accounting is viewed not as an end in

itself, but rather as a commodity or language that is useful in decision

making. This implies as mentioned before, that the continued existence of

Accounting is dependent on its usefulness to society, and in a narrower

context, its usefulness to the users of accounting information (see

Puxty, 1993). Several of the above definitions are in line with a

functionalist approach in that they emphasise the need to provide

information useful in the decision-making process of users. These users

of financial information can be divided into two main categories, namely

internal and external users. Internal users of information include

management and employees who require information for

strategic, operational and administrative decisions. This type of

information is

communicated in internal and management reports and is the domain of

Management Accounting. External users include investors, lenders,

suppliers,

customers, government and the public who require information for various

purposes. Information to external users is communicated by means of the

annual and special purpose financial reports and is the domain of

Financial Accounting.

FINANCIAL ACCOUNTING AND MANAGEMENT ACCOUNTING

The apparently divergent needs of internal and external users of

accounting

information have resulted in the development of two subdisciplines within

the discipline, namely Management Accounting and Financial Accounting.

Drury (1996) states that Management Accounting is concerned with the

provision of information to people within the organisation to help them

make better decisions, whereas Financial Accounting is concerned with the

provision of information to stakeholders outside the organisation.

The divergent development of Management Accounting and Financial

Accounting has resulted in, effectively, two information systems within

organisations. Johnson and Kaplan (1991) suggest that Management

Accounting has developed faster in recent times than Financial

Accounting. They argue that in the past, Financial Accounting was the

foremost factor that inhibited development in Management Accounting. Once

the legislative and standardised approach ascribed to in Financial

Accounting was abandoned, Management Accounting became more flexible and

management and accountants more willing to experiment in meeting the

demands of management. As a result management has come to view financial

statements as a costly but necessary exercise in order to comply with

legislation and GAAP. The information contained in the financial

statements is rarely useful to management and often far removed from the

information needed to run the business.

The external users receive information in the financial reports which is

not necessarily relevant for assessing the particular business and the

performance of management. Thus it is not surprising that recommendations

of the Jenkins Report (AICPA, 1994a, p.5) included the following on

external business reporting:

• External business reporting must provide more information with

forward-

looking perspective, including with regard to management’s plans;

• It should focus more on the factors that create long-term value and

on non-financial measures which indicate how sectors of the business are

performing; and

• It must provide greater alignment between the information reported

externally and the information reported to senior management.

The independent development of Financial Accounting and Management

Accounting has widened the gap between information needed by management

and the information reported to other users and is inefficient and costly

in a competitive environment. As has already been mentioned, the

effective use of technology can be used to develop one flexible

information system in an enterprise that meets the different needs of

both internal and external users. The Institute of Chartered Accountants

of Nigeria (1998) made proposals on how one accounting information

system, by means of a set of corporate reports coupled with computer

technology, could satisfy the needs of both internal and external users

of information. For the purpose of this paper, the assumption is made

that there is only one accounting information system and only one

discipline, namely Accounting, which encompasses the fields of study of

Financial Accounting as well as Management Accounting.

The purpose of accounting information

The product of Accounting is accounting information. Accounting

information is used in deciding between different courses of action and

results in informed decision making. It serves to reduce the uncertainty

inherent in the business environment where decisions are made about the

future. It further reduces entropy based on the assumption that chaos

exists where there is no information. Littlejohn (1989) views information

as a measure of uncertainty or entropy in a situation. This implies that

the greater the uncertainty or entropy, the more accounting and other

information are required.

The role of the accountant in producing accounting information is to

observe, screen and recognise events and transactions, to measure and

process them and to compile corporate reports with accounting information

that are communicated to users. These are then interpreted, decoded and

used by management and other user groups. The main requirement for such

corporate reports is that they should be useful to users. The provision

of information that is useful to the decision-making process is currently

recognised as the main purpose of accounting information. This holds for

theoretical frameworks on financial reporting as well as accounting

literature. Gray (1994, p.9) confirms that accounting literature is

currently dominated by the notion of decision usefulness. This implies

that corporate reporting should continuously meet the changing needs of

all users of accounting information.

The robustness and meaning of “decision usefulness” as the main objective

of

accounting information has, however, been criticised in the literature

(Williams, 1987; Pallot, 1991). Gray (1994) calls decision usefulness a

flaccid term without any element of degree. Although accounting

information may be used, it does not necessarily imply that it is

decision useful. In fact, very little concern seems to be given to

defining what exactly decision usefulness is supposed to connote

(Williams, 1987, p.179).

In Canada, the Stamp Report (CICA, 1980) on corporate reporting

identified four major objectives of financial reporting:

• To provide useful information to all the potential users of such

information in a form and time frame that is relevant to their needs;

• To provide information to minimise uncertainty about the validity of

information and to enable the user to make his or her own assessment of

risks associated with the enterprise;

• To develop standards governing financial reporting which allow ample

scope for innovation and evolution as improvements become feasible; and

• To be directed towards the needs of users who are capable of

comprehending a complete set of financial statements.

The theme of decision usefulness as the main purpose of accounting

information is also apparent in Management Accounting. Drury (1996)

suggests that management requires information that will assist them in

their decision-making and control activities and Ansari et al . (1997)

identify as an attribute of Accounting the provision of information for

decision making. Decision usefulness as the main objective of Accounting

information cannot remain static, however, but will evolve and change

over time. It will be influenced by political, social, economic and

technological changes in the environment. Changes in the environment may

influence not only the nature and objectives of accounting information,

but also the needs of its users. This requires the accounting information

system to be flexible so that it can adapt to the changing demands of its

users.

Accordingly, standards governing financial reporting should furthermore

also be flexible. A flexible information system and flexible reporting

standards will not inhibit innovation, experimentation and evolution in

adapting to the changing demands of users, but rather promote it.

2.2 THEORECTICAL FRAMEWORK

Accounting plays a significant role within the concept of generating and

communicating wealth of the companies. Financial statements still remain

the most important source of externally feasible information on

companies. Regardless of their extensive use and enduring advance, there

is some concern that accounting theory and practice have not kept pace

with rapid economic changes and high technology changes. (Meyer C., 2007)

This situation affects the relevance of accounting information. Number of

previous studies explored that accounting information decreased their,

relevance over the period of time. (Francis J., and Schipper K., 1999) In

the same time a number of researchers claim that accounting information

has not lost its relevance. (Oyerinde D.T.,2009, Vieru, Perttunen and

Schadewitz, 2005, Collins, Maydew and Weiss, 1997: cited by Oyerinde

D.T.,2009)

For financial reporting to be effective, accounting information to be

relevant, complete and reliable. (Hendricks, 1976) The primary purpose of

the financial statements is to provide information about a company in

order to make better decisions for users particularly the investors.

( Germon and Meek 2001). It should also increase the knowledge of the

users and give a decision maker the capacity to predict future actions.

Therefore, relevance accounting information can be described as an

essential pre requisite for stock market growth. ( Oyerinde D.T., 2009)

According to the previous studies many researchers used relationship

between Market price per share as the dependent variable and a set of

independent variables. Ball and Brown in 1968, highlighted the

relationship between stock prices and the accounting information

disclosed in the financial statements.( Ball and Brown 1968). Ohlson in

1995 explained that the value of a firm can be expressed as a linear

function of book value, earnings and other relevant information. The

Ohlson model stands among the most important developments in capital

market research. (Dung N.V., 2010) Francis and Schipper in 1999 had

different approaches in this regard. The predictive view of value

relevance ( the accounting numbers are relevant if it can be used to

predict future earnings, dividends or future cash flows),the information

view of value relevance(the value relevance is measured in terms of

market reactions to new information), fundamental analysis view of value

relevance( the accounting information is relevance in valuation if

portfolios formed on the basis of accounting information are associated

with abnormal returns) and the measurement view of value relevance( the

financial statementis measured by its ability to capture or summaries

information that affects equity value.

(Francis J., and Schipper K., 1999). Oyerinde D.T in 2009 explained the

correlation between accounting information such as Earning Per Share

(EPS), Return On Equity (ROE) , Earning Yield (EY)and Market Price per

Share.(MPS)

According to Keynes (1936) investment is often equated with real

investment that adds to existing stock of capital. Ariyo (2007) further

stressed the classification of investment into two groups-financial and

Non-financial. The former refers to interest bearing or dividend yielding

assets such as stocks, bends, shares and other forms of securities,

traded in the stock market. The latter group refers to what is generally

described as real investments usually in physical forms e.g. buildings,

equipment and machinery.

Developments within the industrial world have, overtime made accounting

information arguably the most important decision making tool relied upon

by investors. In view of the following, Porter (1980) opines that

accounting records provide evidence that elaborates cost accounting

records maintained to support management’s estimation of product costs

during a given period. Tyson (1992)

argues that cost accounting systems, in conjunction with a managerial

component, supported a broad scope of decisions in the textile and

manufacturing industries.

Fleishman and Tyson (1998) identify managerial decision-making and

control as the primary use of accounting information during the

industrial revolution in the US and UK. Thus accounting is concerned with

the provision of financial and other relevant information for making

informed decisions about allocation and management of resources and for

appraising corporate performance.

At this juncture, it is essential to review the concept “forecasting” as

it is an empowerment tool for decision makers. It is an exercise designed

to enhance the quality and appropriateness of decision making and to

foster purposeful and realistic planning. Forecasting involves the use of

cognitive and mathematical models (Ariyo and Tomassini 1985).

2.3 CONCEPTUAL MODEL

The theory of rational expectation propounded by Mush (1961) serves as a

basis for earnings forecasting. It presumes that economic agents optimize

available information efficiently when forming expectations about the

future values of economic variables, such as prices and income/earning.

However, empirical evidence has shown that financial analysts’ earning

forecasts are not always consistent with rational expectation theory.

Basu and Markov (2003) argue that financial analysts do not efficiently

use information in prior earnings levels (extreme), earnings changes,

forecast revisions, forecast errors and stock returns. Furthermore, a lot

of empirical studies have been carried out on the accuracy of financial

analysts’ forecasts or predictions of corporate earnings, equity returns

and even stock market rational expectations. Prayag and Van Rensburg

(2004) note that most research work on the accuracy of security analysts

earnings forecasts have produced conflicting findings. This was in

consonance with the findings reported by Elton and Cruber (1972) in

respect of analysts earnings for a large pension fund, an investment

advisory service. Brown and Rozeff (1978) evaluated two sets of quarterly

earnings forecasts for 50 firms over the period 1971 to 1975. Some

theories have been propounded to enhance the understanding of the

characteristics of investment behaviour and performance. Briefly, one of

these theories which emphasizes the influence of financial factors is in

two dimensions – the first if the theory of profit developed by Sharpiro

(1978). This theory takes profit (especially undistributed refrained

earnings) as a source of internal funds for financing investment. It

defines investment as a function of profits, which depends on level of

corporate income or earnings.

Another variant of the ongoing discussion is the cashflow theory of

investment propounded by Duesenberry (1958) which integrates the profit

theory with that of acceleration theory of investment. It stressed that

the aggregate cashflow is the main determinant of investment. He regards

investment as a function of national income (Y) capital stock (K) profit

(P) and capital consumption allowances.

These are independent variables and can be expressed as:

I = f(Yt-1, Kt-1, P,R)

where t refers to the current period and (t-1) to the previous period.

P = aY – bK

where a and b are coefficients. Putting lag into consideration it

becomes,

Pt = aYt-1 – bKt-1

where p refers to current profits, capital consumption allowances are

expressed as:

Rt = K (Kt-1)

In another vein, Keynes (1936) concerns internal rate of returns as a

better guide to informed decisions, than the interest rate. Elaborating

further, Keyres (1936) notes that MEI (Marginal efficiency of investment)

can be equated with the rate of discount at which the present value of

the stream of returns expected from the capital assess over its lifespan

is just equal to the supply price of that capital.

Finally, a brief review of Q theory of investment is provided, developed

and widely applied by various scholars, including Keynes (1936). Brain

hard and Tobin (1968, 1977), Hayoshi (1982). A distinguishing feature of

the theory is that it shifts attention from bond and money markets

towards equity markets, explaining investment behaviour in real assets.

It is recalled that conventional theory relies on interest rates for

explaining investment behaviour as follows:

I = (r,m)

Where I = Investment, r is real interest rate, and m is marginal

efficiency of capital. In contrast, the Q theory explains investment

behaviour as:

I – I (q)

For which Iq > 0 and I (I) = dk while

q = Pc/Pk and (2.7)

Pc = PeE/Pk (2.8)

Where Pc is the shadow equity market price of a unit of capital k, Pk is

the current cost of k, Pe is the market price of one unit of equity

share. E is the number of equity issued and fully paid for, d is the rate

of depreciation.

This can be further simplified in the derivation of q by substituting

equation (2-7) into (2.6) such that:

q = PeK/PKK

further rearranged thus;

K = PeE

qPk

Hence, if q, Pk are held constant, or the rate of increase in Pk is less

than the rate of increase in Pe, then an increase in PeE leads to an

increase in stock of (that is, additional investment in capital, k.

Some implications of this review could be summarized as follows. First

the ultimate aim of any investment is profitability. Hence, must of the

theories of investment reviewed herewith anchor their arguments on issues

relating to the relationship between returns on an investment and the

applicable “cost” of such investment. All the relevant information

identified by these theories is essentially accounting based, and should

be disclosed as much as possible in proposals to potential investors. The

first set was derived from the application of Box-Jenkins (1970) models

to each firm’s previous earnings forecasts of security analysts as

reported in the Value Line Investment Survey (VLIS).

Gwoly and Lakonishok (1984) observe that financial analysts earnings

forecasts do incorporate the past history of realizations and predictions

in an unbiased manner and as such, can be classified as being rational.

O’Brien (1988) compared the accuracy of three composite analysts’ EPS

forecasts: the mean, the median and the most current forecast. The result

shows that the most current forecast available was the most accurate

among the three forecasts. Another study by HSU (2001) measured the

earnings surprises of international firms in 40 countries from the

Asia/Pacific and Europe regions. He found out that financial analysts

were not accurate in forecasting, and that they tend to overestimate the

firm’s future earnings. Black and Carnes (2002) studied the determinants

of accuracy of analysts’ earnings

forecasts in the larger economics of the Asian/Pacific region (Ariyo,

2007).

Literature seems to have provided certain research evidence in support of

the overestimation bias in analysts’ performance forecasts. Debondt and

Taler (1985) and Capstaff et al (1995) report that analysts exhibited

optimistic overreaction in the forecast of corporate performance of

selected corporate firms in the continental Europe, United Kingdom (UK)

and the United States of America (USA).

From the foregoing we discover that forecasts based on economy wide and

firm specific fundamentals are more reliable than those based on

accounting information derived from previous annual reports of a firm

(Ariyo, 2007). Given the review above, Perdicoulis (2001) states that

forecasts should be subjected to credibility and resemblance tests before

they can be accepted or relied upon as a guide to investment decisions.

SECTION 3: METHODOLOGY

This section presents the methods and procedures for this study. The

chapter will be discussed under the following sub-headings:

1. Research design

2. Population

3. Sample and sampling technique

4. Research instruments

5. Pilot study

6. Validity and reliability of instrument

7. Method of data collection

8. Method of data analysis

3.1 Research Design

The descriptive research design will be adopted for this research study.

Gay (1976) asserted that the design is appropriate for collection of data

from members of a community or target population with respect to one or

more variables. Osuala (2000) observed that the design permits the

description of situations as they exist at a particular point in time.

3.2 Population

The population for this study will comprise all individuals within the

Lagos metropolis found to have the requisite education and investment

knowledge and made interactions with Lagos State.

3.3 Sample and Sampling Technique

The sample will comprise of 250 participants selected using purposive

sampling method from the residents of Lagos metropolis. Since purposive

sampling method is intended efforts will be made to sample the relevant

individuals with required educational background and various dealings

with the Nigerian Stock exchange.

3.4 COLLECTION OF DATA

The source of data of this study is through the primary source which

involves a field survey of the involved respondents within Lagos

metropolis obtained through purposive sampling method.

After ascertain the readiness of the respondents, a questionnaire was

issued and this totaled 250 and retrieval was right there and then.

This is to allow questions to be asked in areas that looked

confusing. Collected questionnaires are checked for missing items and

inappropriate responses. The responses were coded appropriately in

coding sheets before analysis.

Secondary data will also be used where applicable. This will be sourced

from textbooks, internet, journals, magazines and past researches as

deem fit.

3.5 RESEARCH INSTRUMENTS, STATISTICAL TOOLS AND ANALYTICAL PROCEDURE

The research instrument will comprise of a self developed, structured,

and validated questionnaire of five point Likert attitudinal scale of

(1) Strongly Agree, (2) Agree and (3) Undecided, (4) Disagree and (5)

Strongly Disagree. The instrument consist of two sections; Section A

measuring respondents social-economic characteristics and section B

measuring the relevant questions (items) designed for the research.

There were administered and retrieved back.

STATISTICAL TOOLS AND ANALYTICAL PROCEDURE

The analysis of data involved the use of descriptive analytical

techniques i.e Frequency distributions and percentages, measures of

central tendency, mean particularly will also be used. Results would

be fully interpreted.

Inferential statistics was also used in the tests of hypothesis carried

out using Chi-Square tests at 0.05 level of significance. This was

carried out using the Statistical Package for Social Scientist (SPSS

Version 17)

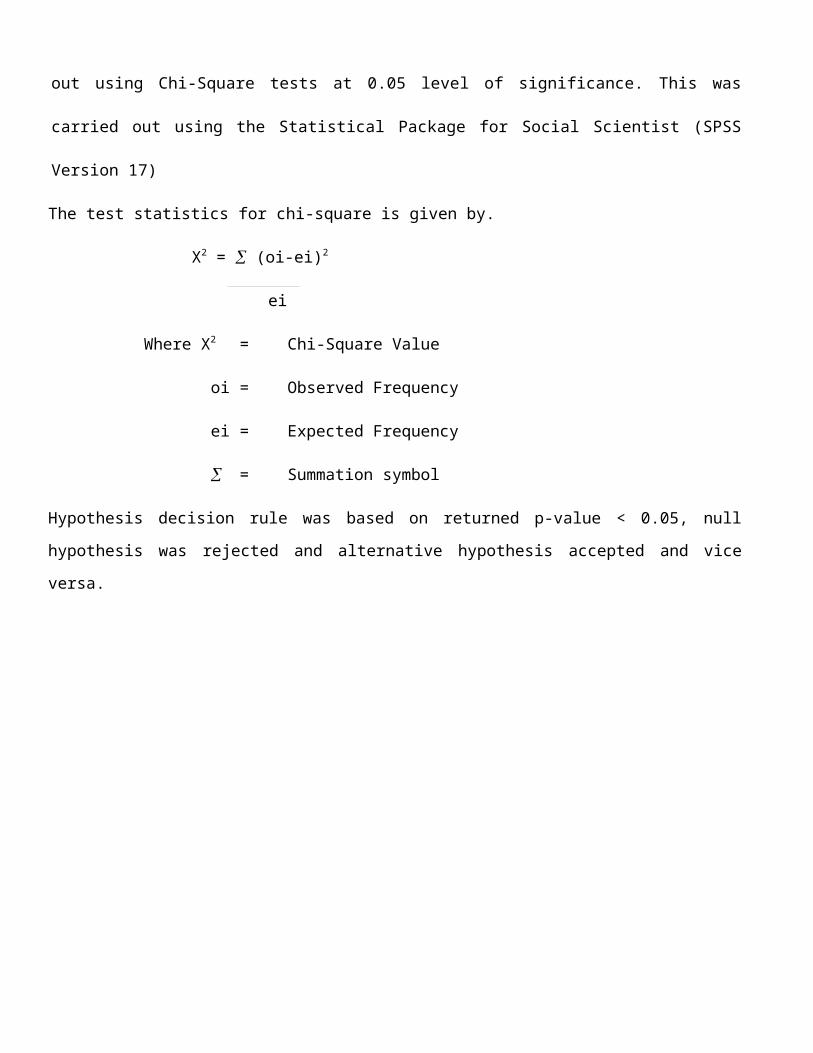

The test statistics for chi-square is given by.

X2 = (oi-ei)2

ei

Where X2 = Chi-Square Value

oi = Observed Frequency

ei = Expected Frequency

= Summation symbol

Hypothesis decision rule was based on returned p-value < 0.05, null

hypothesis was rejected and alternative hypothesis accepted and vice

versa.

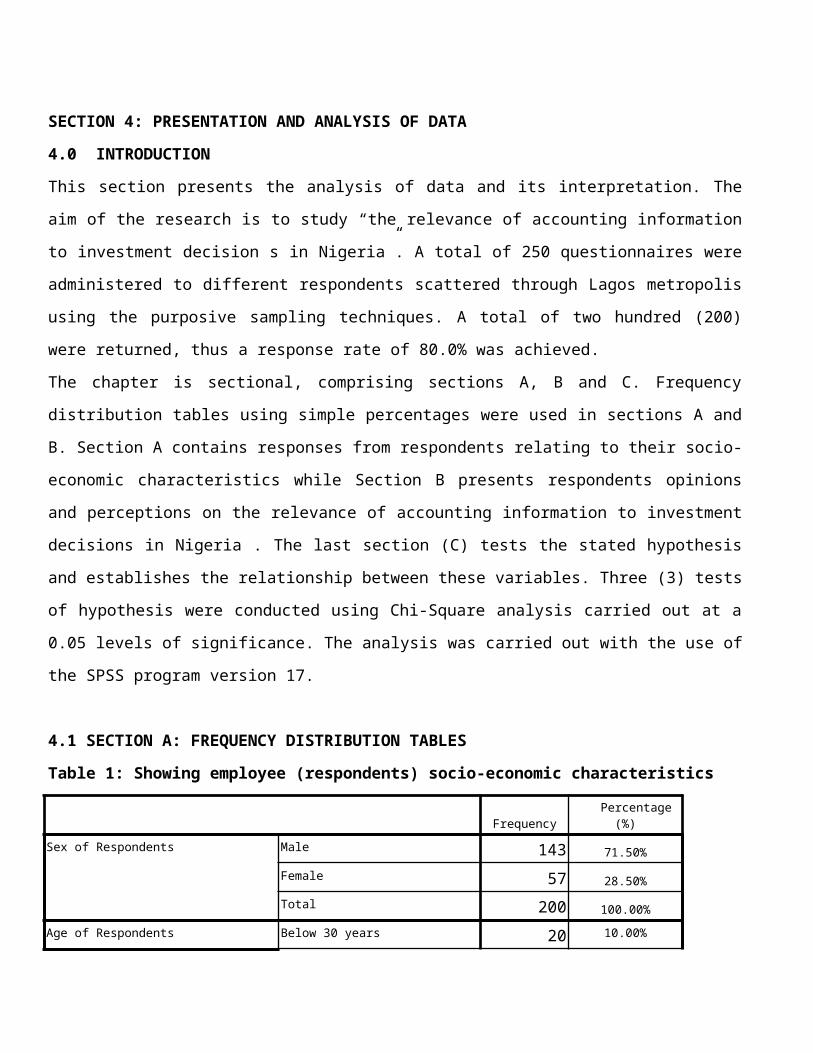

SECTION 4: PRESENTATION AND ANALYSIS OF DATA

4.0 INTRODUCTION

This section presents the analysis of data and its interpretation. The

aim of the research is to study “the relevance of accounting information

to investment decision s in Nigeria”. A total of 250 questionnaires were

administered to different respondents scattered through Lagos metropolis

using the purposive sampling techniques. A total of two hundred (200)

were returned, thus a response rate of 80.0% was achieved.

The chapter is sectional, comprising sections A, B and C. Frequency

distribution tables using simple percentages were used in sections A and

B. Section A contains responses from respondents relating to their socio-

economic characteristics while Section B presents respondents opinions

and perceptions on the relevance of accounting information to investment

decisions in Nigeria . The last section (C) tests the stated hypothesis

and establishes the relationship between these variables. Three (3) tests

of hypothesis were conducted using Chi-Square analysis carried out at a

0.05 levels of significance. The analysis was carried out with the use of

the SPSS program version 17.

4.1 SECTION A: FREQUENCY DISTRIBUTION TABLES

Table 1: Showing employee (respondents) socio-economic characteristics

Frequency Percentage

(%)Sex of Respondents Male 143 71.50%

Female 57 28.50%Total 200 100.00%

Age of Respondents Below 30 years 20 10.00%

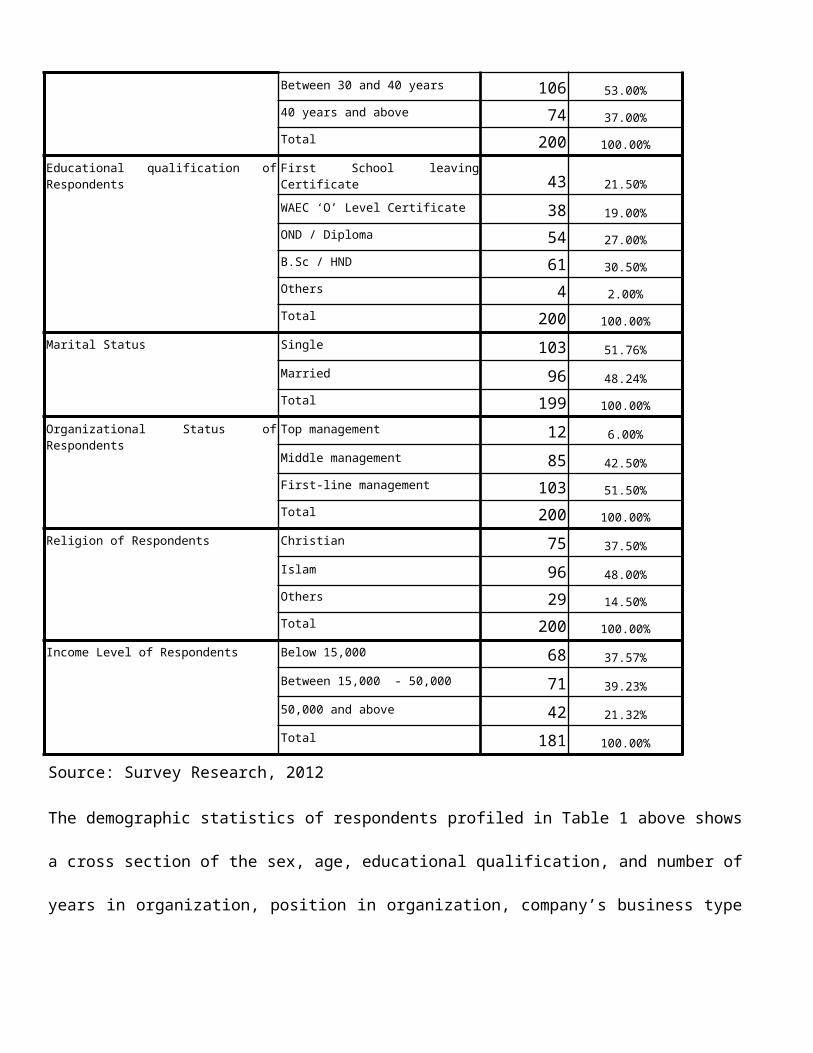

Between 30 and 40 years 106 53.00%40 years and above 74 37.00%Total 200 100.00%

Educational qualification ofRespondents

First School leavingCertificate 43 21.50%WAEC ‘O’ Level Certificate 38 19.00%OND / Diploma 54 27.00%B.Sc / HND 61 30.50%Others 4 2.00%Total 200 100.00%

Marital Status Single 103 51.76%Married 96 48.24%Total 199 100.00%

Organizational Status ofRespondents

Top management 12 6.00%Middle management 85 42.50%First-line management 103 51.50%Total 200 100.00%

Religion of Respondents Christian 75 37.50%Islam 96 48.00%Others 29 14.50%Total 200 100.00%

Income Level of Respondents Below 15,000 68 37.57%Between 15,000 - 50,000 71 39.23%50,000 and above 42 21.32%Total 181 100.00%

Source: Survey Research, 2012

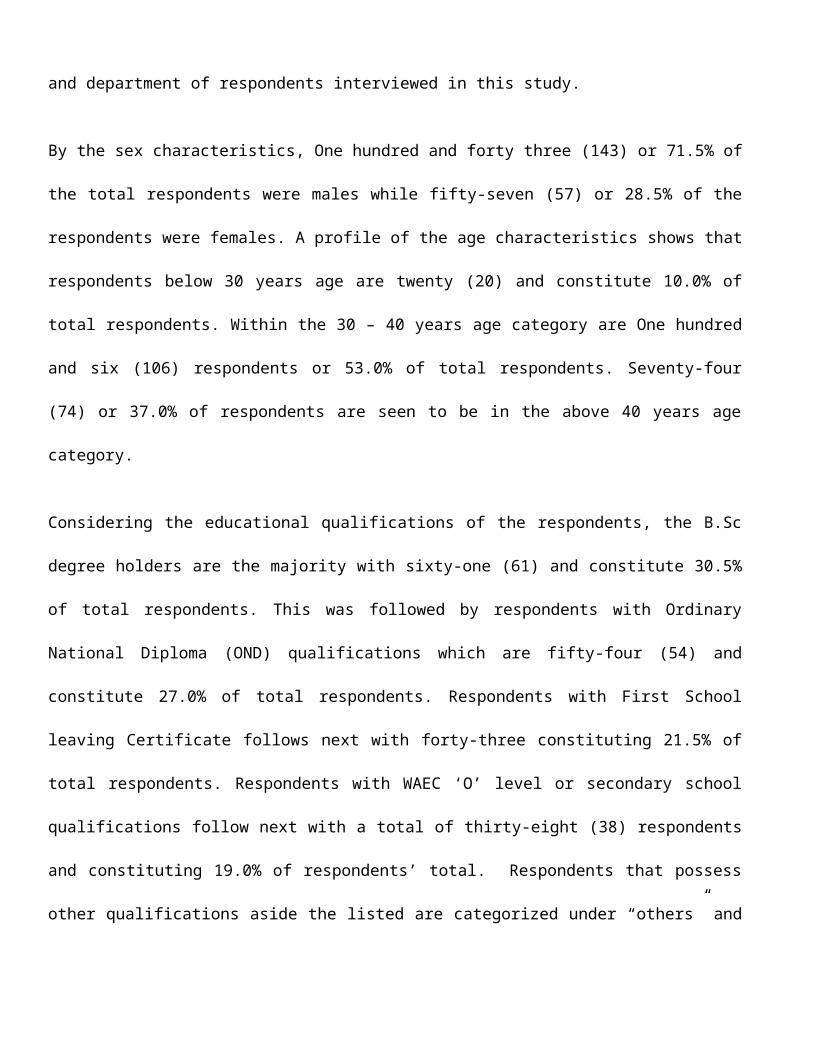

The demographic statistics of respondents profiled in Table 1 above shows

a cross section of the sex, age, educational qualification, and number of

years in organization, position in organization, company’s business type

and department of respondents interviewed in this study.

By the sex characteristics, One hundred and forty three (143) or 71.5% of

the total respondents were males while fifty-seven (57) or 28.5% of the

respondents were females. A profile of the age characteristics shows that

respondents below 30 years age are twenty (20) and constitute 10.0% of

total respondents. Within the 30 – 40 years age category are One hundred

and six (106) respondents or 53.0% of total respondents. Seventy-four

(74) or 37.0% of respondents are seen to be in the above 40 years age

category.

Considering the educational qualifications of the respondents, the B.Sc

degree holders are the majority with sixty-one (61) and constitute 30.5%

of total respondents. This was followed by respondents with Ordinary

National Diploma (OND) qualifications which are fifty-four (54) and

constitute 27.0% of total respondents. Respondents with First School

leaving Certificate follows next with forty-three constituting 21.5% of

total respondents. Respondents with WAEC ‘O’ level or secondary school

qualifications follow next with a total of thirty-eight (38) respondents

and constituting 19.0% of respondents’ total. Respondents that possess

other qualifications aside the listed are categorized under “others” and

are 4 constituting the least, 2.0% of respondents’ total.

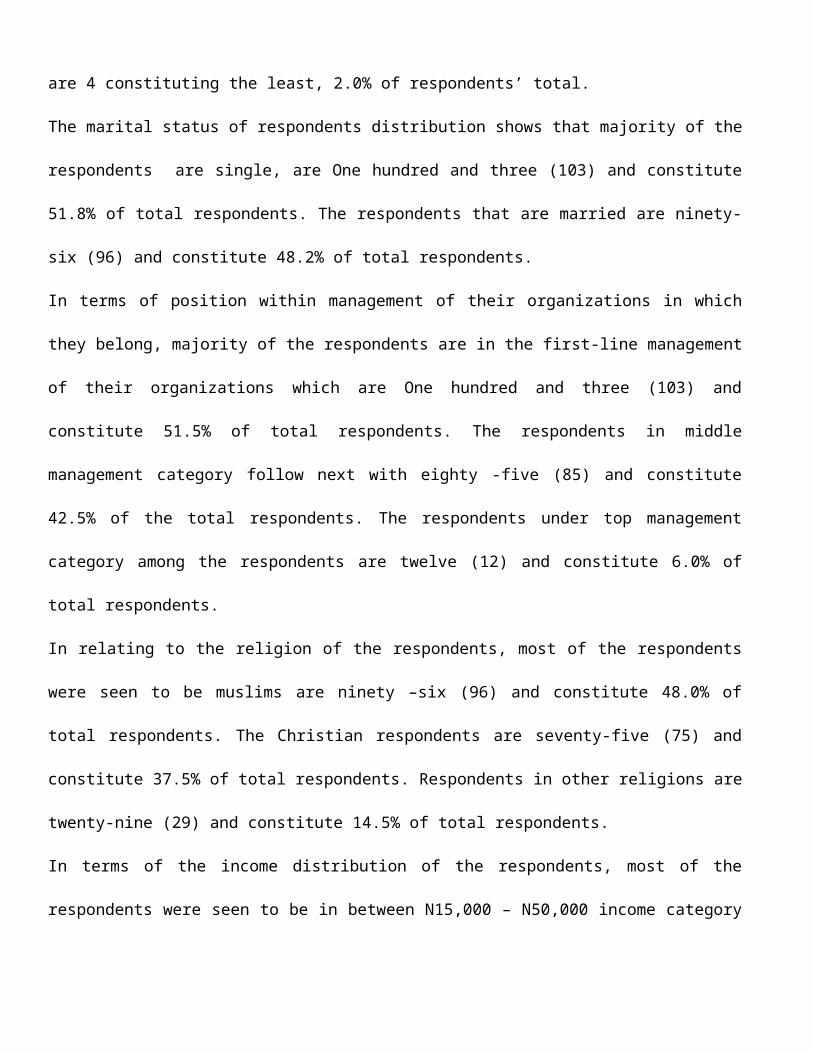

The marital status of respondents distribution shows that majority of the

respondents are single, are One hundred and three (103) and constitute

51.8% of total respondents. The respondents that are married are ninety-

six (96) and constitute 48.2% of total respondents.

In terms of position within management of their organizations in which

they belong, majority of the respondents are in the first-line management

of their organizations which are One hundred and three (103) and

constitute 51.5% of total respondents. The respondents in middle

management category follow next with eighty -five (85) and constitute

42.5% of the total respondents. The respondents under top management

category among the respondents are twelve (12) and constitute 6.0% of

total respondents.

In relating to the religion of the respondents, most of the respondents

were seen to be muslims are ninety –six (96) and constitute 48.0% of

total respondents. The Christian respondents are seventy-five (75) and

constitute 37.5% of total respondents. Respondents in other religions are

twenty-nine (29) and constitute 14.5% of total respondents.

In terms of the income distribution of the respondents, most of the

respondents were seen to be in between N15,000 – N50,000 income category

are seventy-one (71) and constitute 39.23% of respondents’ total.

Respondents earning below N15, 000 follows next are sixty-eight (68) and

constitute 37.6% of respondents’ total. Respondents earning above N50,

000 are the least among the respondents are forty-two (42) and

constitutes 21.3% of respondents total.

4.2 SECTION B: FREQUENCY DISTRIBUTION TABLES

Table 2: Opinion of Respondents Concerning the Relevance of Accounting

Information to Investment Decisions in Nigeria.

SA(5)

A(4)

U(3)

D(2)

SD(1)

Total

%Agreement

8. I am aware of accounting

information been reported by

listed companies as relevant to

investment decisions

72 81 3 20 23 199 77%

9. The current state of companiesfinancial reporting andaccounting information isprofessional and satisfactory

31 42 6 53 68 200 37%

10.

Corporate accountinginformation follow regulatorystandards and manners ofpresentation such as laid downby CBN and other regulatorybodies

41 57 11 40 45 194 51%

11 Accounting information is a

true indication and reflection

26 38 20 52 64 200 32%

of the financial and market

status of the listed company

12.

Accounting information guides

majorly most of your investment

in the stock exchange.

20 16 31 88 45 200 18%

13 I place heavy reliance of

accounting and financial

information published by listed

companies before taking any

investment decision.

17 41 23 63 56 200 29%

14.

Lack of professionals and

structures have been affecting

Nigerian corporate

organizations financial

reporting

31 36 0 63 68 198 34%

15 Issues of ethical conduct and

criminal conduct has been the

bane of transparent financial

reporting

51 118 4 16 10 199 85%

16.

The state of financial

reporting among listed

companies has divested

investments to other sectors of

the economy.

56 64 5 31 44 200 60%

17.

The investing public is

ignorant of this corporate ill

and thus patronage is still

17 34 14 81 54 200 26%

significant

18.

The general public perceivesthis corporate behavoir hasnormal for survival

19 32 17 49 81 198 26%

19.

The regulatory bodies areperforming to ensuring a saferand healthy accountinginformation reporting forinvestors and the public ingeneral

51 59 11 42 37 200 55%

20.

The rate of investment inNigeria can be said to benegatively affected by thestate of accounting informationpublished by listed companies.

43 62 9 45 41 200 53%

Source: Survey research 2012

From table 4.2 above, Item 8 showed respondents’ opinion on I am aware of

accounting information been reported by listed companies as aid to

investment decisions. The responses revealed that 77% of the respondents

agreed that they are aware of accounting information been reported by

listed companies as aid to investment decisions. This arose from 36

percent of the total respondents who strongly agreed with the statement

and 41 percent of respondents who ordinarily agreed. On the other hand, a

total of 23% of respondents disagree. This was from 10 percent of

respondents who ordinarily disagreed and 13 percent who strongly

disagreed to the statement. Also 10 percent of the respondents are seen

to be undecided. This implies that respondents agreed that they are aware

of accounting information been reported by listed companies as aid to

investment decisions.

Item 9 showed respondents’ opinion on the current state of companies

financial reporting and accounting information is professional and

satisfactory. The responses revealed that 37% of the respondents agreed

that the current state of companies financial reporting and accounting

information is professional and satisfactory. This arose from 16 percent

of the total respondents who strongly agreed with the statement and 21

percent of respondents who ordinarily agreed. On the other hand, a total

of 60% of respondents disagree. This was from 26 percent of respondents

who ordinarily disagreed and 34 percent who strongly disagreed to the

statement. Also 3 percent of the respondents are seen to be undecided.

This implies that respondents disagreed that the current state of

companies financial reporting and accounting information is professional

and satisfactory.

Item 10 showed respondents’ opinion on corporate accounting information

follow regulatory standards and manners of presentation such as laid down

by CBN and other regulatory bodies. The responses revealed that 51% of

the respondents agreed that Corporate accounting information follow

regulatory standards and manners of presentation such as laid down by CBN

and other regulatory bodies. This arose from 21 percent of the total

respondents who strongly agreed with the statement and 29 percent of

respondents who ordinarily agreed. On the other hand, a total of 43

percent of respondents disagree. This was from 21 percent of respondents

who ordinarily disagreed and 22 percent who strongly disagreed to the

statement. Also 6 percent of the respondents are seen to be undecided.

This implies that respondents agreed that Corporate accounting

information follow regulatory standards and manners of presentation such

as laid down by CBN and other regulatory bodies.

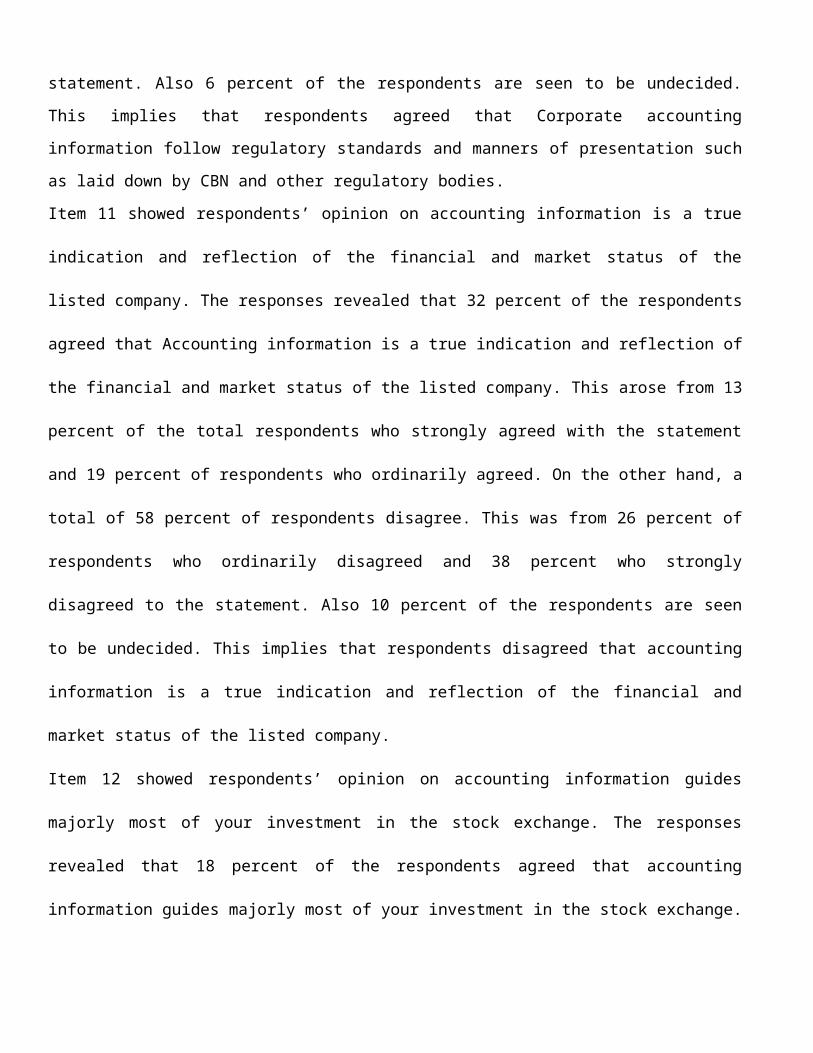

Item 11 showed respondents’ opinion on accounting information is a true

indication and reflection of the financial and market status of the

listed company. The responses revealed that 32 percent of the respondents

agreed that Accounting information is a true indication and reflection of

the financial and market status of the listed company. This arose from 13

percent of the total respondents who strongly agreed with the statement

and 19 percent of respondents who ordinarily agreed. On the other hand, a

total of 58 percent of respondents disagree. This was from 26 percent of

respondents who ordinarily disagreed and 38 percent who strongly

disagreed to the statement. Also 10 percent of the respondents are seen

to be undecided. This implies that respondents disagreed that accounting

information is a true indication and reflection of the financial and

market status of the listed company.

Item 12 showed respondents’ opinion on accounting information guides

majorly most of your investment in the stock exchange. The responses

revealed that 18 percent of the respondents agreed that accounting

information guides majorly most of your investment in the stock exchange.

This arose from 10 percent of the total respondents who strongly agreed

with the statement and 8 percent of respondents who ordinarily agreed. On

the other hand, a total of 66percent of respondents disagree. This was

from 44 percent of respondents who ordinarily disagreed and 22 percent

who strongly disagreed to the statement. Also 16 percent of the

respondents are seen to be undecided. This implies that respondents

disagreed that Accounting information guides majorly most of your

investment in the stock exchange.

Item 13 showed respondents’ opinion on I place heavy reliance of

accounting and financial information published by listed companies before

taking any investment decision. The responses revealed that 29 percent of

the respondents agreed that they place heavy reliance of accounting and

financial information published by listed companies before taking any

investment decision. This arose from 9 percent of the total respondents

who strongly agreed with the statement and 20 percent of respondents who

ordinarily agreed. On the other hand, a total of 60 percent of

respondents disagree. This was from 32 percent of respondents who

ordinarily disagreed and 28 percent who strongly disagreed to the

statement. Also 12 percent of the respondents are seen to be undecided.

This implies that respondents disagreed that on they or individuals place

heavy reliance of accounting and financial information published by

listed companies before taking any investment decision.

Item 14 showed respondents’ opinion on lack of professionals and

structures have been affecting Nigerian corporate organizations financial

reporting. The responses revealed that 34 percent of the respondents

agreed that lack of professionals and structures have been affecting

Nigerian corporate organizations financial reporting. This arose from 16

percent of the total respondents who strongly agreed with the item and 18

percent of respondents who ordinarily agreed. On the other hand, a total

of 66 percent of respondents disagree. This was from 32 percent of

respondents who ordinarily disagreed and 34 percent who strongly

disagreed to the statement. None of the respondents are seen to be

undecided on this item. This implies that respondents disagreed that the

lack of professionals and structures have been affecting Nigerian

corporate organizations financial reporting.

Item 15 showed respondents’ opinion on Issues of ethical conduct and

criminal conduct has been the bane of transparent financial reporting.

The responses revealed that 85 percent of the respondents agreed that

issues of ethical conduct and criminal conduct has been the bane of

transparent financial reporting. This arose from 26 percent of the total

respondents who strongly agreed with the item and 59 percent of

respondents who ordinarily agreed. On the other hand, a total of 13

percent of respondents disagree. This was from 8 percent of respondents

who ordinarily disagreed and 5 percent who strongly disagreed to the

statement. It was seen that 2 percent of the respondents are seen to be

undecided on this item. This implies that respondents agreed that issues

of ethical conduct and criminal conduct has been the bane of transparent

financial reporting.

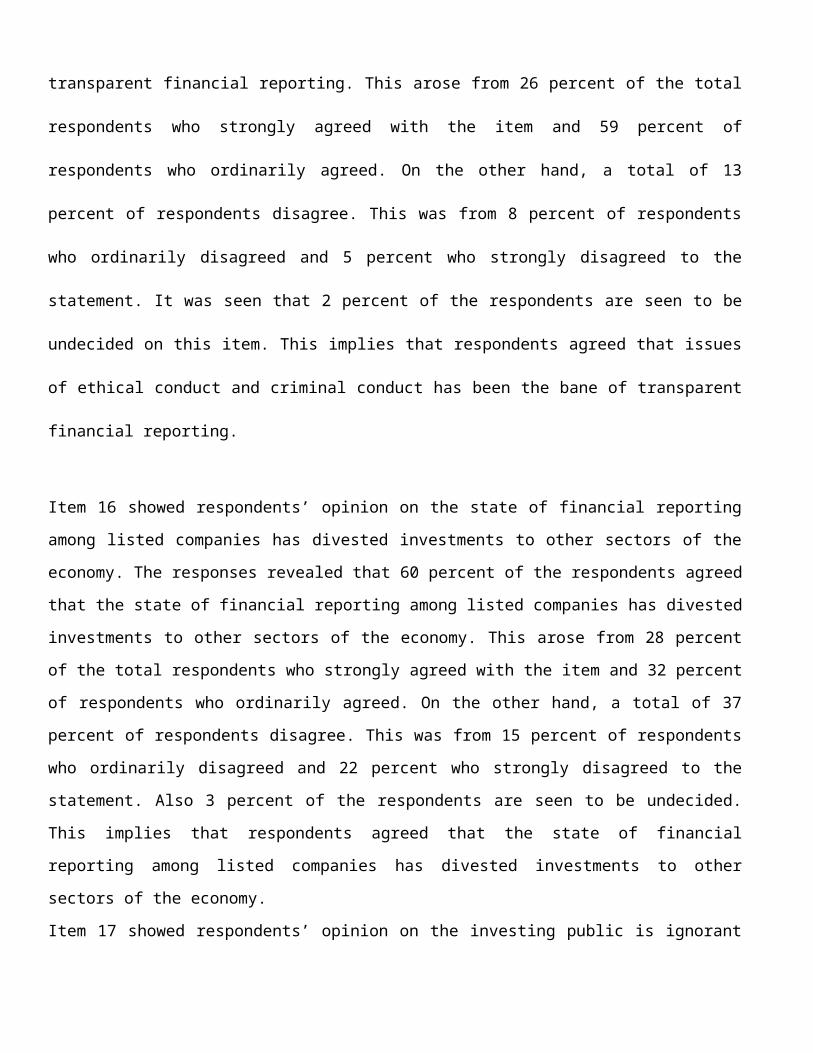

Item 16 showed respondents’ opinion on the state of financial reporting

among listed companies has divested investments to other sectors of the

economy. The responses revealed that 60 percent of the respondents agreed

that the state of financial reporting among listed companies has divested

investments to other sectors of the economy. This arose from 28 percent

of the total respondents who strongly agreed with the item and 32 percent

of respondents who ordinarily agreed. On the other hand, a total of 37

percent of respondents disagree. This was from 15 percent of respondents

who ordinarily disagreed and 22 percent who strongly disagreed to the

statement. Also 3 percent of the respondents are seen to be undecided.

This implies that respondents agreed that the state of financial

reporting among listed companies has divested investments to other

sectors of the economy.

Item 17 showed respondents’ opinion on the investing public is ignorant

of this corporate ill and thus patronage is still significant. The

responses revealed that 26 percent of the respondents agreed that the

investing public is ignorant of this corporate ill and thus patronage is

still significant. This arose from 9 percent of the total respondents who

strongly agreed with the item and 17 percent of respondents who

ordinarily agreed. On the other hand, a total of 67 percent of

respondents disagree. This was from 40 percent of respondents who

ordinarily disagreed and 27 percent who strongly disagreed to the

statement. Also 7 percent of the respondents are seen to be undecided.

This implies that respondents disagreed that the investing public is

ignorant of this corporate ill and thus patronage is still significant.

Item 18 showed respondents’ opinion on the general public perceives this

corporate behavoir has normal for survival. The responses revealed that

26 percent of the respondents agreed that the general public perceives

this corporate behavoir has normal for survival. This arose from 10

percent of the total respondents who strongly agreed with the item and 16

percent of respondents who ordinarily agreed. On the other hand, a total

of 65 percent of respondents disagree. This was from 24 percent of

respondents who ordinarily disagreed and 41 percent who strongly

disagreed to the statement. Also 9 percent of the respondents are seen to

be undecided. This implies that respondents disagreed that the general

public perceives this corporate behavoir has normal for survival.

Item 19 showed respondents’ opinion on the regulatory bodies are

performing to ensuring a safer and healthy accounting information

reporting for investors and the public in general. The responses revealed

that 55 percent of the respondents agreed that the regulatory bodies are

performing to ensuring a safer and healthy accounting information

reporting for investors and the public in general. This arose from 25

percent of the total respondents who strongly agreed with the item and 30

percent of respondents who ordinarily agreed. On the other hand, a total

of 49 percent of respondents disagree. This was from 21 percent of

respondents who ordinarily disagreed and 18 percent who strongly

disagreed to the statement. Also 6 percent of the respondents are seen to

be undecided. This implies that respondents agreed that the regulatory

bodies are performing to ensuring a safer and healthy accounting

information reporting for investors and the public in general. .

Item 20 showed respondents’ opinion on the rate of investment in Nigeria

can be said to be negatively affected by the state of accounting

information published by listed companies. The responses revealed that 53

percent of the respondents agreed that the rate of investment in Nigeria

can be said to be negatively affected by the state of accounting

information published by listed companies. This arose from 22 percent of

the total respondents who strongly agreed with the item and 31 percent of

respondents who ordinarily agreed. On the other hand, a total of 43

percent of respondents disagree. This was from 22 percent of respondents

who ordinarily disagreed and 21 percent who strongly disagreed to the

statement. Also 4 percent of the respondents are seen to be undecided.

This implies that respondents agreed that the rate of investment in

Nigeria can be said to be negatively affected by the state of accounting

information published by listed companies.

4.3 SECTION C: ANALYSIS OF DATA

In this research work, three hypotheses were formulated. The hypotheses

were tested statistically using the Chi Square test.

1. Ho: Accounting information does not significantly represent a

true reflection of financial situation of listed companies in

Nigeria

Hi: Accounting information significantly represents a true

reflection of financial situation of listed companies in Nigeria.

2. Ho: Accounting information in Nigeria is not significant reliable

for investment purposes in Nigeria.

Hi: Accounting information in Nigeria is significant reliable for

investment purposes in Nigeria

3. Ho: Accounting information does not significantly affect the rate

of investments in Nigeria

Ho: Accounting information significantly affect the rate of

investments in Nigeria

(i) In testing the first hypothesis which states that ‘Accounting

information does not significantly represent a true reflection of

financial situation of listed companies in Nigeria, a Chi Square test was

carried out using the responses from item 11 (see table 4.3 below).

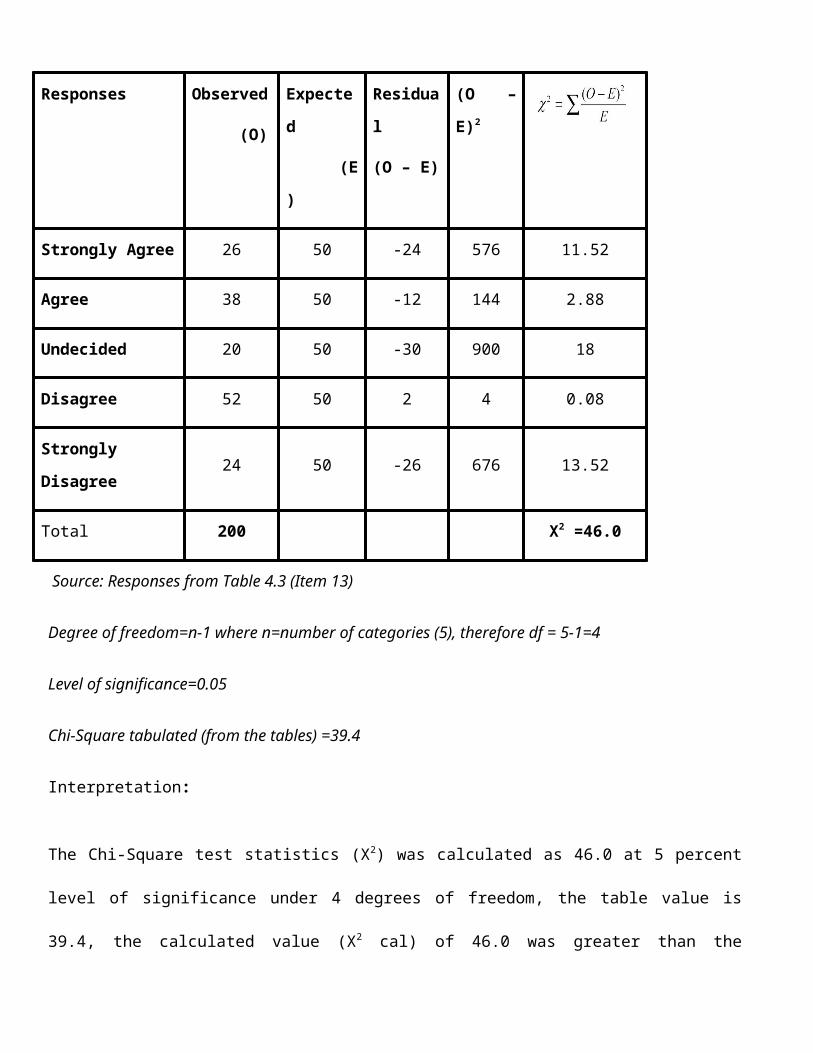

Table 4.3: Chi Square Analysis of hypothesis one

Responses Observed

(O)

Expecte

d

(E

)

Residua

l

(O – E)

(O –

E)2

Strongly Agree 26 50 -24 576 11.52

Agree 38 50 -12 144 2.88

Undecided 20 50 -30 900 18

Disagree 52 50 2 4 0.08

Strongly

Disagree24 50 -26 676 13.52

Total 200 X2 =46.0

Source: Responses from Table 4.3 (Item 13)

Degree of freedom=n-1 where n=number of categories (5), therefore df = 5-1=4

Level of significance=0.05

Chi-Square tabulated (from the tables) =39.4

Interpretation:

The Chi-Square test statistics (X2) was calculated as 46.0 at 5 percent

level of significance under 4 degrees of freedom, the table value is

39.4, the calculated value (X2 cal) of 46.0 was greater than the

tabulated value (X2 tab) of 39.4, thus the null hypothesis was accepted.

Therefore, Accounting information does not significantly represents a

true reflection of financial situation of listed companies in Nigeria.

Hypothesis two:

2. In testing the second hypothesis which states that ‘Ho: Accounting

information in Nigeria is not significant reliable for investment

purposes in Nigeria.’, a Chi Square test was carried out using the

responses from item 13 (see table 4.4 below).

Table 4.4: Chi Square Analysis of hypothesis two

Responses Observe

d

(O

)

Expected

(E)

Residua

l

(O-E)

(O –

E)2

Strongly

agree 17 50 -33 1089 21.78

agree 41 50 -9 81 1.62

Undecided 23 50 -27 729 14.58

Disagree 63 50 13 169 3.38

Strongly

disagree56 50 6 36 0.72

200 42.08

Source: Responses from Table 4.2 (Item 13)

Degree of freedom=n-1 where n=number of categories (5), therefore df=5-1=4

Level of significance=0.05

Chi-Square tabulated (from the tables) = 39.4

Interpretation: The test statistics (X2) is calculated as 42.08. At 5

percent level of significance with degree of freedom 4, the table value

is 39.4, the calculated value (X2 cal) of 61.79 was greater than the

tabulated value (X2 tab) of 39.4, thus the null hypothesis is accepted.

Hence, Accounting information in Nigeria is not significant reliable for

investment purposes in Nigeria

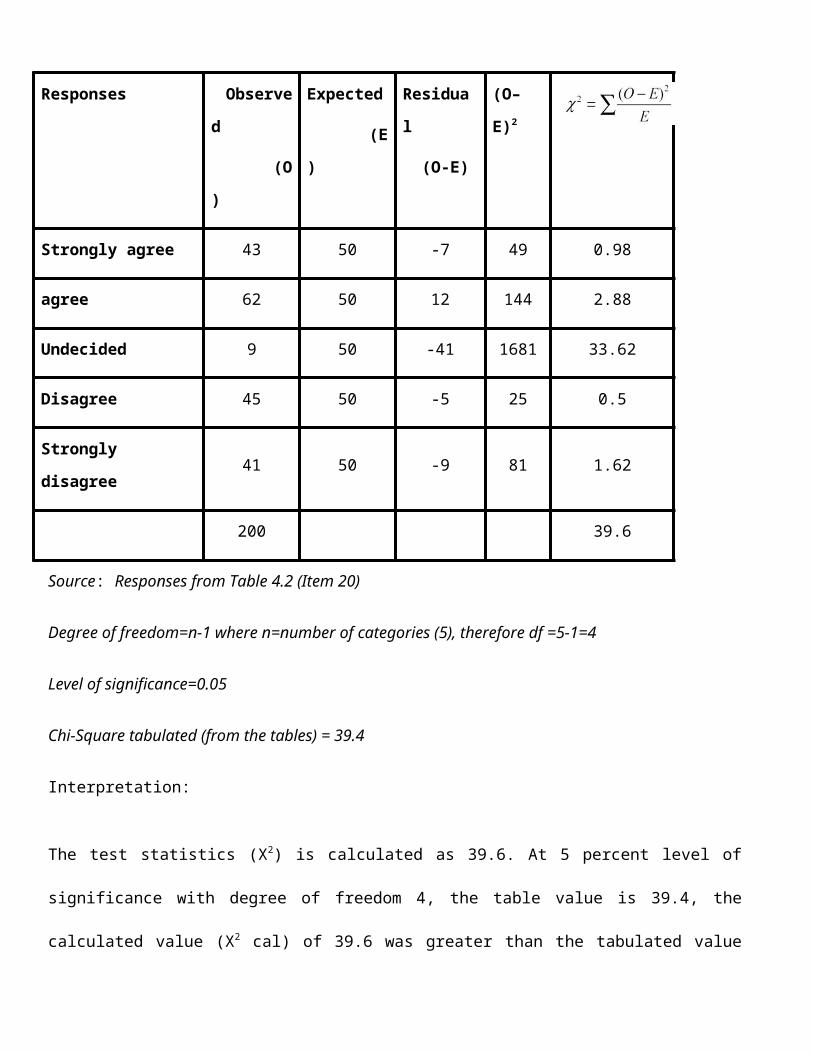

Hypothesis three: In testing the third hypothesis which states that ‘Ho:

Accounting information does not significantly affect the rate of

investments in Nigeria.’, a Chi Square test was carried out using the

responses from item 20 (see table 4.5 below).

Table 4.5: Chi Square Analysis of hypothesis two

Responses Observe

d

(O

)

Expected

(E

)

Residua

l

(O-E)

(O–

E)2

Strongly agree 43 50 -7 49 0.98

agree 62 50 12 144 2.88

Undecided 9 50 -41 1681 33.62

Disagree 45 50 -5 25 0.5

Strongly

disagree41 50 -9 81 1.62

200 39.6

Source: Responses from Table 4.2 (Item 20)

Degree of freedom=n-1 where n=number of categories (5), therefore df =5-1=4

Level of significance=0.05

Chi-Square tabulated (from the tables) = 39.4

Interpretation:

The test statistics (X2) is calculated as 39.6. At 5 percent level of

significance with degree of freedom 4, the table value is 39.4, the

calculated value (X2 cal) of 39.6 was greater than the tabulated value

(X2 tab) of 39.4, thus the null hypothesis is accepted. Hence, Accounting

information does not significantly affect the rate of investments in

Nigeria

SECTION 5: DISCUSSION OF FINDINGS

This section discusses the findings of the research aimed at

investigating the relevance of accounting information to investment

decision in Nigeria. Accounting information does not significantly

represents a true reflection of financial situation of listed companies

in Nigeria.

Three (3) hypotheses were tested for inference and the prior hypothesis

was confirmed. Thus, the three main empirical inferences from the

research hypothesis were that firstly; accounting information in Nigeria

is not significantly reliable for investment purposes in Nigeria for

hypothesis 1. Secondly, accounting information in Nigeria is not

significantly reliable for investment purposes in Nigeria, deducted from

hypothesis 2 and thirdly; Accounting information does not significantly

affect the rate of investments in Nigeria deducted from hypothesis 3.

Other findings include: and the general public respondents agreed are

aware of accounting information been reported by listed companies as aid

to investment decisions. Respondents disagreed that the current state of

companies financial reporting and accounting information is professional

and satisfactory. Respondents agreed that Corporate accounting

information follow regulatory standards and manners of presentation such

as laid down by CBN and other regulatory bodies. Respondents disagreed

that accounting information is a true indication and reflection of the

financial and market status of the listed company. Respondents disagreed

that Accounting information guides majorly most of your investment in the

stock exchange. Respondents disagreed that on they or individuals place

heavy reliance of accounting and financial information published by

listed companies before taking any investment decision. Respondents

disagreed that the lack of professionals and structures have been

affecting Nigerian corporate organizations financial reporting.

Respondents agreed that issues of ethical conduct and criminal conduct

has been the bane of transparent financial reporting. Respondents agreed

that the state of financial reporting among listed companies has divested

investments to other sectors of the economy. Respondents disagreed that

the investing public is ignorant of this corporate ill and thus patronage

is still significant. Respondents disagreed that the general public

perceives this corporate behavoir has normal for survival. Respondents

agreed that the regulatory bodies are performing to ensuring safer and

healthy accounting information reporting for investors and the public in

general. Respondents agreed that the rate of investment in Nigeria can

be said to be negatively affected by the state of accounting information

published by listed companies.

The findings in this studysuggested among other things, that the current level of adequacy of accounting informationmade available to potential and existing investors requires significant improvement.We therefore recommend:•Strict compliance with prescribed accounting information disclosurerequirements. This could be achieved if the relevant regulatory agencieseffectively pursue the disclosure requirements recognized by...

SECTION 6: SUMMARY / CONCLUSIONS AND RECOMMENDATIONS

6.1 SUMMARY/ CONCLUSION

The state of accounting information in present day Nigeria under these

prevailing conditions is generally poor, though they follow regulatory

standards as cited by regulatory bodies such as CBN. This accounting

information in most cases is not a true reflection of the state of the

corporate bodies they represent as such individuals do not rely on these

information for their investment decisions.

6.2 RECOMMENDATIONS

There is need to increase the ethical knowledge, discipline and its

practice into the profession of accounting most especially as it concerns

the public through consistent and practical education

There is need for punitive measures where unethical practices such as

poor accounting information or presentation are made to the public.

There is need to give public access to other corporate information in

order to minimize these corporate fraud.

There is need for a stringent policy readjustment to regulating the

affairs of these corporate bodies in accounting presentation.

There is also need for whistle blowing philosophy by the public when

these issues are noticed.

REFERENCES

Adhikari A. and R.h. Tondkar (1992). Environmental Factors Influencing

Accounting Disclosure Requirements of Global Stock Exchanges. Journal of

International Financial Management and Accounting. Vol 4(2): 75-105.

Akintoye, I.R. (2006), Optimising Management Financial Decision in

Tertiary Educational Institutions in Nigeria. A Ph.D Dissertation, Delta

State university, Abraka Nigeria.

Anao, R.A (1978). The information content of published accounts of

Nigerian Public Limited Companies: A note on the publication forecasts.

Niegrian Journal of Economic and Social studies, 20, 125-140

Ariyo A and Soyode A. (1985) – A framework for measuring information

adequacy and redundancies in annual financial reports. In Inanga, E.L.

(Ed.) Managing Nigeria Economic System, A book of readings, Lagos.

Heinemann Books.

Ariyo, A (1985) Relevant accounting information for investment

decisions: An empirical investigation. NASMET: Journal of Management

Education and Training 2, 59-68.

Balalrishnan, H., T. Harris, and P.K. Sen. 91990). “The Predictive

Ability of Geographic Segment Disclosures.” Journal of Accounting

Research.

Ball R., Brown P., (1968), “ An empirical evaluation of accounting

numbers” , Journal of Accounting Research, Vol 6, pp 159-177.

Bearer, W. Lambert R. and Morse D. 91980), The Information content of

security prices- Journal of Accounting and Economics, Vol 2(16)

Brown, L.D. (1993) Earnings forecasting research: Its implications for

capital markets research. International journal of forecasting, vol 9(2)

Capstaff, J. Pandyal, K. and Rees, W. (1995). The accuracy and

rationality of earnings forecasts. Journal of Business Finance and

Accounting, January, Vol. 22(1)

Central Bank of Sri Lanka, Annual Report 2008.

Chow, C.W. and A. Wong-Boren. (1987) “Voluntary Financial Disclosure by

Mexican Corporations.” Accounting Review (July) Vol. 62, No 3:533-541.

Cooke, T.E. (1991) “An Assessment of Voluntary Financial Disclosure in

the Annual Reports of Japanese Corporations.” International Journal of

Accounting.. Vol.26(3); 174-189.

Cragg, J.G. and malkiel B.G (1968). The consensus and accuracy of some

predictions of corporate earnings. Journal of Fiannce, March: Vol 4(19)

De Grort, M.H (1970) Optimal Statistical decisions (New York, Mcgraw

Hill).

Dontoh, A., Radhakrishnan S. and Ronen J.,(2000),The declining value

relevance of accounting information and non information based trading:

An empirical analysis, Working paper(University of New York )

Dung N.V.(2010), Value-Relevance of Financial Statement Information: A

Flexible Application of Modern Theories to the Vietnamese Stock Market,

Working paper (Foreign Trade University) Dept. of Census and statistics,

Statistical Abstract, 2008

Foster G. (1978). Financial Statement Analysis. New Jersey: Pretice

Hall.

Francis J., Schipper K.,(1999), “Have financial statements lost their

relevance.” Journal of Accounting Research, Vol 37, pp 319-352 .

Germon, H., Meek, G..,( 2001), Accounting: An international perspective.

McGraw Hill.

Gray S.J. and C.B. Roberts (1989). “Voluntary Information Disclosure and

the British Multinationals: Corporate Perceptions of Costs and

Benefits.” In International Pressures for Accounting Change, A.G.

Hopwood, Ed. Englewood Cliffs, NJ: Prentice-Hall.

Guthrie J., (2007), “The death of the annual report” Working paper.

University of Sydney.

Hadi M.M., (2004), “The importance of accounting information to the