CHARLES KYEYUNE MBA(1)

67

THE CONTRIBUTION OF MICROFINANCE INSTITUTIONS (MFIS) TO THE ECONOMIC ACTIVITIES OF THE YOUTH AND WOMEN IN LUWERO DISTRICT. A CASE OF FINCA UGANDA by KYEYUNE CHARLES 2003/HDI0/1911 U A Dissertation Submitted in Partial Fulfillment of the Requirements for the Award of the Master of Business Administration (MBA) Of Makerere University

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of CHARLES KYEYUNE MBA(1)

THE CONTRIBUTION OF MICROFINANCE

INSTITUTIONS (MFIS)

TO THE ECONOMIC ACTIVITIES OF THE YOUTH AND

WOMEN IN

LUWERO DISTRICT. A CASE OF FINCA UGANDA

by

KYEYUNE CHARLES

2003/HDI0/1911 U

A Dissertation Submitted in Partial Fulfillment of the

Requirements for the Award of the Master of Business Administration (MBA) Of Makerere University

DEDICATION

I dedicate this book to my dear parents, Mr. and Mrs. Bernard C. Mbaziira of Kabalagala who

sewed the first seed of civilization into me, along with formal education, and who, by God's grace,

have seen it grow to this level of Education. I also dedicate it to my dear brothers and sisters, Peter,

Theresa, Joseph, Ann Mary and Margaret, who have kept my morale up in pursuit of this course.

Iii

ACKNOWLEDGEMENT

I would like to thank my dear parents, brothers and sisters plus the entire family ofMr and Mrs

Edward Kiggundu of Kansanga as well as uncle Joe, for their never ending support to me; they

consistently covered all the gaps in my life which had been created by the pressures of the course.

Special thanks go to my supervisor, Dr. Nkote Nabeta, for the patience, encouragement, criticism

and constant guidance to me all through the course. All my future lay in his hands and here he is

giving it back to me.

Many thanks go to the management ofFINCA Uganda for their help in my search for knowledge

and information. A special token of appreciation to the CEO, Fabian and Evelyn, the officer in

charge of Wobulenzi branch.

To my supervisor at my workplace, Ernest and to MTN Uganda as a whole, I say thank you for the

facilitation.

Finally and most important, I would like to thank the Almighty for the divine intervention that saw

me through the many ups and downs since I started my life and particularly during this course.

Thank you all once again

IV

ABSTRACT

Following the several services and products offered by MFIs to rural women and youth in

rural areas, a study was conducted to investigate the contribution of FINCA on the Economic

activities of rural youth and women in Wobulenzi. The study was guided by the following research

objectives: to examine the nature of financial services offered by micro finance institutions to the

rural youth and women in Wobulenzi, Luwero; identify the indicators of growth in economic

activities of micro finance beneficiaries in Wobulenzi, Luwero; establish the contribution of micro

finance funding to the economic activities of the youth and women in Luwero. And to design

appropriate strategies that will increase the outreach of micro finance institutions so as to enhance

economic development.

The researcher used both primary and secondary data. The primary data was got from FINCA clients

(past, present and non beneficiaries) and from management. The information was obtained by use of

self-administered questionnaires and interviews. Secondary data was obtained from published

materials, which included journals, textbooks magazines, internal reports and newspapers. The study

came up with the several conclusions, notable among them is that FINCA offers several services to

clients; there are several indicators of growth in economic activities; FINCA has positive

contribution on economic growth of rural youth and women to cite a few. The study yielded the

following recommendations; lower interest rates, lengthen the repayment period, sensitization of

client, expanding the product portfolios, emphasizing village banking, evaluation of project proposals

to cite a few.

VII

CHAPTER ONE

1.0 BACKGROUND

Micro credit and micro finance are relatively new terms in the field of development, first coming to

prominence in the 1970s, according to Robinson (2001) and Otero (1999). Prior to then, from the

1950s through to the 1970s, the provision of financial services by donors or governments was mainly

in the form of subsidized rural credit programmes. These often resulted in high loan defaults, high

losses and an inability to reach poor rural households (Robinson, 2001).

Robinson states that the 1980s represented a turning point in the history of microfinance in that MFls

such as Grameen Bank and BRI began to show that they could provide small loans and savings

services profitably on a large-scale outreach. They received no continuing subsidies, were

commercially funded and fully sustainable, and could attain wide outreach to clients (Robinson,

2001). It was also at this time that the term "microcredit" came to prominence in development

(Micro finance Information Exchange, 2005).

The difference between microcredit and the subsidized rural credit programmes of the 1950s and

1960s was that micro credit insisted on repayment, charging interest rates that covered the cost of

credit delivery and by focusing on clients who were dependent on the informal sector for credit

(ibid.). It was now clear for the first time that micro credit could provide large-scale outreach

profitably. The 1990s "saw accelerated growth in the number of micro finance institutions created

and an increased emphasis on reaching scale" (Robinson, 2001). Microfinance had now turned into

an industry according to Robinson (2001).

1

Along with the growth in microcredit institutions, attention changed from just the provision of credit

to the poor (microcredit), to the provision of other financial services such as savings and pensions

(micro finance) when it became clear that the poor had a demand for these other services (Micro

finance Information Exchange, 2005).

Currently close to 500,000 (Five hundred thousands) clients have access to micro financing in

Uganda with a total loan bill of 100 billion Uganda shillings. The average loan size ranges between

Uganda shillings 50,000 and 20 million and the majority of the clients are the low-income earners

and salary earners. MFIs have a deep outreach of over fifty major branches country wide including

Wobulenzi and this is expected to grow further.

Data extracted from FINCA Uganda Internal Management Report (2004), revealed that of the total

number of groups operating in Wobulenzi, eight (8) client loan groups exhibited a 33% drop out rate

and these were: Tukolebukozi, Balikyewunya, Bamunanika, Nezikokolima, Tusaba Katonda,

Mazima, Tusitukirewamu, and Kamukamu. They had received a total loan disbursement of

Ugshs48,587,000 from FINCA Uganda Microfinance.

Despite the fact that FINCA disburses a loan portfolio of nearly Ugshs150,000,000 (one hundred and

fifty million) to beneficiaries in Wobulenzi, its impact still remains low. The challenge therefore is to

evaluate and ascertain whether these MFIs have created a positive or negative impact to the

economic activities of the population through the creation of accessible sources of funding to the

small scale businesses as well as individuals at less stringent conditions. The above background sets

the basis of the study.

2

1.1 STATEMENT OF THE PROBLEM

Although micro finance services have endeavored to offer financial services to the vulnerable

groups, (youth and women), their impact on the economic activities of the beneficiaries still remains

low. For instance the percentage drop out rate of the FINCA Wobulenzi beneficiaries stands at 33%

on average (FINCA Internal Annual Management Report 2004). Some drop outs may be due to

improvement in welfare of the people while in other cases some have lost even the little they used to

own (Nakawesi, 2003). This therefore sets the basis for the study.

1.2 PURPOSE OF THE STUDY

The purpose of the study was to assess whether micro finance institutions have had an impact on the

economic activities of the rural youth and women of Wobulenzi, Luwero.

1.3 OBJECTIVES OF THE STUDY

The study was guided by the following objectives

i) To examine the nature of financial services offered by micro finance institutions to the rural

Youth and women in Wobulenzi, Luwero.

ii.) To identify the indicators of growth in economic activities of macro finance beneficiaries in

Wobulenzi, Luwero.

iii.) To establish the contribution of micro finance funding to the economic activities of the Youth

and Women in Luwero.

iv.) To design appropriate strategies that will increase the outreach of micro finance institutions so

as to enhance economic development

3

1.4 RESEARCH QUESTIONS

The study was guided by the following research questions

i.) What is the nature of financial services offered by micro finance institutions to the rural youth

and women in Wobulenzi, Luwero?

ii.) What are the indicators of growth in economic activities of micro finance beneficiaries in

Wobulenzi, Luwero?

iii.) What is the contribution of micro finance funding on the economic activities of the rural Youth

and Women of Luwero?

(iv) What are the appropriate strategies put In place to Increase the outreach of micro finance

institutions so as to increase on their contribution to economic development?

1.5 SCOPE OF THE STUDY

Subject Scope

The study focused on the contribution of micro finance institutions (MFIs) to the Household Income

and Asset Development of the rural youth and women In Wobulenzi, Luwero.

Geographical Scope.

The study covered the youth and women in Wobulenzi, Luwero.

4

1. 1.6 SIGNIFICANCE

The information will enable financial managers of small-scale industries / businesses to assess and

evaluate potential viable development projects and also give them an insight into the likely problems.

It will also assist the credit officers of MFIs to advise the potential borrowers of how and where to

invest in order to benefit from the loans and also reduce on the failure rate that creates bad debts to

MFIs.

The individuals who are seeking projects to invest in can also use this information to assess their

potential in investing in priority areas. It can also help them in their investment appraisals. The

information will reveal other factors that are responsible for the successes or failures of

organizations.

The information can also be used by various stakeholders to avoid re occurrence of past mistakes

thus ensuring continuity and sustainability of economic activities in low developing countries.

5

CHAPTER TWO

2.0 LITERATURE REVIEW

This chapter reviews the existing literature on key micro finance concepts, looks at the nature of

services offered by MFIs, identifies the indicators of economic activities growth and evaluates the

contribution of MFIs to the economic activities of the rural youth and women in Wobulenzi, Luwero.

2.1 Micro Finance Services

Sinha (1998) states, "Micro credit refers to small loans, whereas micro finance is appropriate where

NGOs and MFIs supplement the loans with other financial services (savings, insurance)"; therefore

micro credit is a component of micro finance in that it involves providing credit to the poor, but

micro finance involves additional non-credit financial services such as savings, insurance, pensions

and payment services (Okiocredit, 2005). The provision of micro finance services focuses on three

core dimensions of poverty alleviation. These are centred on the terms "Promotion" (promotion of

individuals and households out of poverty) and "Protection" (protection of people from vulnerability

because of fluctuations of income) Rogaly (1999).

The MFIs offer Enterprise Development facilities by assisting people, individually and in groups, to

access financial services to start and grow enterprises which can sustain them and their families

above the poverty line. This is mainly done through the provision of access to Microcredit services,

for building up self-employment, in form of loans at interest free, low interest and market rates (

Rogaly 1999). Making inexpensive credit available to the rural poor has been key to breaking the

vicious circle of low capital, low productivity, low savings thus overcoming poverty.

6

They also offer loans for Consumption and Asset Development which help beneficiaries to build up

asset bases for their families or consume certain products that they would not consume if they were

earning low incomes (transport, meals, and weddings). This may be enhanced through encouraging

of Savings especially using low or no fee small deposit savings accounts. Saving is at least as

important, if not more so, than loans in the effort to help households to accumulate resources

(Shreiner and Morduch, 2001). Savings are financial assets that the poor can accumulate against

emergencies and long term needs.

Insurance and Income Protection services are also offered such that people protect themselves from

income fluctuations and become financially protected from life misfortunes (illnesses, death,

accidents) Through Insurance, that is by raising of distress funds and forming of small scale

insurance cooperatives, MFIs can assist individuals and groups to become more financially secure.

Savings can also act as guarantee against outstanding loans and are mandated payments especially

for emergencies.

Other Micro finance services that are offered by MFIs include provision of:- Financial Literature by

training people to develop basic financial competencies which can be used to guard their assets from

being eroded by misusing the already available resources. Counseling and Financial Management

which help people develop debt management skills to avoid loan defaulting which can lead to loss of

the securing assets or collateral security.

7 2.

2.2 Indicators of Growth in Economic Activities of Households and Groups

Economic activities require commitment, cooperation, and cohesion at all levels of development -

individual, household, community, and national. While micro finance alone does not improve roads,

housing, water supply, education and health services, it can play an important role in making these

and other sustainable contributions to the community. The following are some of the indicators of

growth in economic activities that can be enjoyed by beneficiaries of MFIs: - Consumption and Asset

Development can used as a measure of growth in economic activity. As the incomes of beneficiaries

increase, there is likely to be an improvement in the consumption patterns of the people as well as in

the asset bases for their families. Beneficiaries can now afford some of the expenditure and assets

that were out of their reach originally.

Growth in profitability is also one of the indicators of improvement in economic activity. Such

growth should be reflected in profitable enterprises, growing enterprises, and conversion into

medium or large enterprises. In addition, small-scale businesses' growth can be measured in terms of

profits. Profit making organizations look at the rate of return on the resources of the firm (Pandey,

1996).

According to section 5(5) of the income Tax Act, payment of income tax by enterprises is sign of

growth since they are seen as engines of development, employing 90% of the non-farm economically

active poor people (Ministry of Finance and economic activities Report, 2000). The growth in

business can make it possible for firms to train its employees. Naisbitt (1985), growing businesses

have human resource objectives such as helping employees improve their career opportunities or

improving performance through job skill training.

8

Increase in the Market Share is also a sure way of measuring growth. According to Kotler (2000), the

company's growth will be determined by the increase in rate of growth of its market share. The

increase in the market share will be reflected in the increased volume of sales and establishment of

distributional channels for the goods and services to target market segment.

Growth in economic activities is measured by strong management. Owners of businesses usually

have previous managerial experience. In fact the competitive strength of the firm is often based upon

the founder's unique skills on cost control, sales and so on. The managers of the business must be

able to take risks. Management must be willing to work hard to overcome the challenges associated

with growth possibilities.

Customer care also stands out as a signal of growth in enterprises. Donald (1987) stated that growth

of economic activities could be viewed in the level of customer service offered to customers. The

customer service is offered in form of product quality, diversification or innovation.

Technological advancement in enterprises can also be viewed as a sign of development. Enterprises

will say move from the use of typewriters to the use computers or even where they have computers,

to continuously upgrade their equipment. This may not be the case in the developed countries where,

because of market opportunity and likely success due to environmental enabling factors, it is easier to

secure new technology. Besides, this technology originates from the developed countries and unlike

in the developing countries where it must be imported, it is relatively cheap (Coleman, et al, 2005).

9

Improved savings and economic assurance: MFIs can help people become more economically

secure. Savings serve as reserves for important household expenditures (such as school fees, feeding

and other emergencies), and as insurance against sudden crises (such as illness, natural disasters, or

accidents) that can otherwise result in destitution for people already living at the poverty line

(Cheston et al 1999). MFIs can build upon Africa's traditional savings ethics to enhance outreach and

quality of services. It is important to keep in mind that for any financial service to have a lasting

impact on poverty eradication, it must be flexible and innovative to adapt to the needs of its clients

(Joanna, 1999)

The greater the rate of increase in number of employees, the greater the likelihood of growth. MFIs

help people start or improve their own small businesses, providing income generation and

employment for themselves and their families (Okiocredit, 2005). Studies on CERUDEB, an MFI in

Uganda, show that loans given to small farmers have resulted in substantial increases in part-time

and permanent wage labor of non-clients. Expansion in scale of production leads to the development

of departments and consequently increase in number of employees (Afrane, 2002).

Credit can be used as working capital so that clients' efforts become more productive; for example,

clients can buy produce in bulk at discounted or wholesale prices and resell at retail prices for more

profitability (Brau, et al, 2005). As clients become more productive, their incomes increase and they

are able to accumulate savings for other investments as well as improvements in welfare (nutrition,

hygiene, housing) and emergencies (Hashemi, 2003). Improvement in economic activities of the

beneficiaries of MFIs will mean substantial improvements in their clothing, sanitation, feeding,

housing, medical care, household property/equipment owned and ability to cover costs related to

school fees, transportation and other physiological needs (Armendariz et al, 2005).

10

2.3 Contributions of Micro Finance Funding to Economic Activities

When properly harnessed and supported, micro finance can scale-up beyond the micro-level as a

sustainable part of the process of economic empowerment by which the poor can lift themselves.

Considerable debate remains about the effectiveness of micro finance as a tool for directly improving

on the economic activities and about the characteristics of the people it benefits (Chowdhury, Mosley

and Simanowitz, 2004). Sinha (1998) argues that it is notoriously difficult to measure the impact of

micro finance programmes on social economic activities.

2.4 Designation of Appropriate Strategies

Objective four sought to find out appropriate strategies that would make FINCA services readily

accessible to its potential and actual targeted groups. The strategies include among others; lower

interest rates, lengthen the loan repayment periods, Scrap off collateral security, rural outreach,

expansion product portfolios and Project appraisal

Ryne et al, (2002), argued that lowering the interest rates is a strategy geared at making MFIs

services more accessible to them. This would go a long way in enticing users to become users as well

as ensuring increased use of the services by the current clients. It will also enable MFIs clients to

benefit more as interest rates are lowered since it will favorably impact on their profitability.

11

Gyasi (2002) argued that the management of MFIs should revisit the loan repayment period

offered to clients. This is due to the fact that majority of the F CA clients in Luwero depend on

agriculture and trade which needs a long period to reap from the operation. Lengthening the

repayment period would enable them meet their financial obligations in time. The respondents also

wanted FINCA to give them a grace period before start of the payment period to enable them start

the payment schedules after a reasonable degree of business stability.

Jerik, (2005) argued that one of the hindering factors limiting accessibility to MFIs services is

collateral security. He suggested that it should be scrapped off so as to enable those without it to

access the services freely. This may however not be practical since security is a requirement by all

banks.

Palakow (2003) argued that most MFIs branches are in urban and peri-urban areas. He suggested that

FINCA should endeavor to open up more branches in rural areas so as to make its services more

accessible to all target groups. Currently most of the clients are supposed to travel to head office or to

district headquarters for meetings and remitting of their weekly loan installments. This however,

increases their operational costs and is time consuming as well (Walter, 2002).

Sebstard et al, (1996) argued that MFIs need to expand or increase on the product portfolio offered.

The products currently offered are very few compared to the clients' demands. This in a way has

fueled the misappropriation of funds received by the clients to other purposes not prescribed in the

loan contract which increases high default rate (Hoque, 2004).

12

Coleman et al, (2005), argued that management of MFIs should endeavor to appraise and recommend

projects to be funded. Their experience over time should assist them to realize the types of businesses

with the least failure rate and be able to advise their clients accordingly. The management should go

an extra mile to periodically monitor the operations of the projects funded so as to reduce on the

default rate.

13

CHAPTER THREE

3.0 RESEARCH METHODOLOGY

This chapter outlines in detail the manner in which the study was executed. It highlights the areas of

study, the research design, the sampling design and procedure. It also states the data collection

methods, the data processing and analysis, which the researcher used.

3.1 Research Design

The study was cross-sectional; both descriptive and analytical methods were used. The data was

collected from both primary and secondary data sources, from FINCA in Wobulenzi region, and the

study focused on the contribution of MFIs to the economic activities of the rural youth and women

for the period 2004-2006.

3.2 Study Population

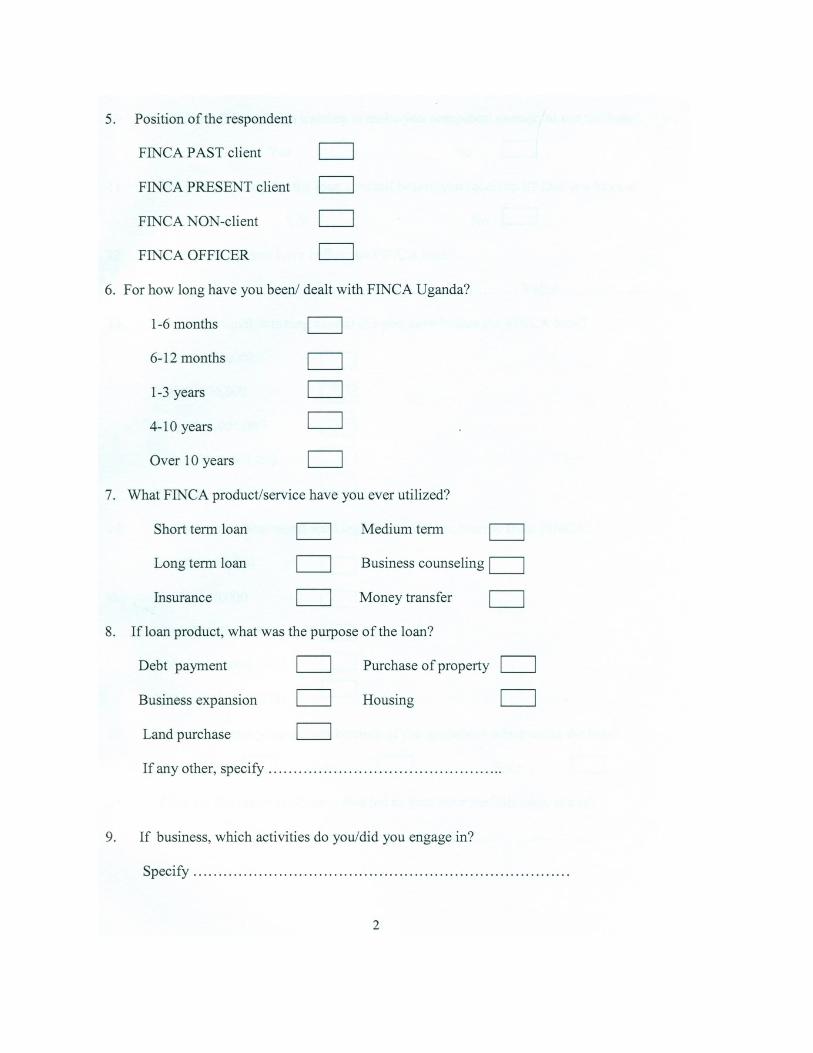

The study covered a total population of 400 people, namely, 100 past and 200 present FINCA clients,

50 non-beneficiaries and 50 management staff. Since the type of information required was qualitative

in nature, judgment sampling! purposive was the most appropriate to use.

3.3 Sample Procedure and Size

The study population was selected using purposive sampling technique basing on the fact that the

researcher was well knowledgeable about the economic activities parameters and that the

respondents were believed to have appropriate information pertaining to the study. For purposes of

obtaining the relevant information, the researcher targeted 140 FINCA clients (past and present and

non beneficiaries) and 10 FINCA management officials (credit officers) as shown in table 3.1.

Stratified random sampling was used to obtain the clients.

14

3. Table 3.1 Population & Sample size structures Nature of the respondents Population Expected Sample

Past FINCA clients 100 40

Present FINCA clients 200 80

Non- beneficiaries 50 20

Management 50 10

Total 400 150

Source: Primary data

3.4 Sources of Data

The researcher used both primary and secondary sources of data.

Primary Data

The data was obtained from FINCA clients (past, present and non beneficiaries) and from

management. The information was obtained by use of self-administered questionnaires and

interviews.

Secondary Data

This data was obtained from published materials, which included journals, textbooks magazines,

internal reports and newspapers. They included among others, minutes, internal and credit officers'

reports of FINCA, which talked about the control and utilization of loanable funds and customer

business operations.

15

3. 5 Instruments of data collection

The researcher used a number of data collection instruments namely, questionnaires, interview

schedule and observation.

Questionnaire.

The researcher designed self administered questionnaires which were distributed to FINCA

management staff, past and present clients as well as non beneficiaries of FINCA services. The

completed questionnaires were then picked from respondents for analysis.

Interview schedule

The researcher designed appropriate questions relating to the topic of discussion and then presented

the questions to FINCA respondents noting the responses thereof. The collected responses were then

be analyzed.

Observation

The researcher employed the observation method to note whatever was taking place in the

organization and its clients. For instance, the general appearance of the FINCA premises, staff attire,

interior and exterior design, equipment in use, staff attitudes (disgruntlement, receptive faces and

others), the dressing code of clients, their health plus other attributes.

3. 6 Data Analysis

The researcher used both descriptive and statistical approaches in processing and analyzing the data.

Mostly qualitative data was obtained from the questionnaires and analyzed using statistical methods

to give it a broader and more meaningful picture of the sample.

16

CHAPTER FOUR

4.0 PRESENTATION, ANALYSIS AND INTERPRETATION OF FINDINGS

4.1 Introduction

This chapter presents the findings of the study. The findings relate to the discussion, analysis and

presentation as revealed by the field survey conducted by the researcher. Both primary and secondary

data was used. The findings are presented in percentage tables, bar graphs, pie charts and line graphs.

The presentation is guided by the following objectives; to examine the nature of financial services

offered by micro finance institutions to the rural youth and women in Wobulenzi, Luwero; to identify

the indicators of growth in economic activities of micro finance beneficiaries in Wobulenzi, Luwero;

establish the contribution of micro finance funding to the economic activities of the youth and

women in Luwero and to design appropriate strategies to enable the organization achieve its vision

and mission.

4.2 General Background Information

This section presents the general characteristics of the respondents. These include the response rate,

sex, marital status, age brackets, educational level and position of the respondents. These are

presented in the subsequent sections.

4.2.1 Response Rate

Out of the expected sample of 150 respondents, only 118 accepted to be interviewed and answered

the questionnaires, thus giving a response rate of 79%. The results of the study are presented in table

4.2 below.

17

Table 4.2: Showing the Composition of the Respondents

Particulars Frequency Percentage

Past FINCA clients 28 24

Present FINCA clients 58 49

Non beneficiaries 22 19

Management 10 8

Total 118 100 Source: Primary Data

According to table 4.2 , a total of 118 people accepted to be interviewed and answered the self

administered questionnaires thus giving a response rate of 118%. Those that accepted constituted

about 50% present FINCA clients, 25% past FINCA clients, 20% non beneficiaries and almost 10%

were from the management.

This means that close to 75% of the respondents are or have been actual beneficiaries of micro

financing through FINCA and this implies a good target group for the study. 4.3 Gender Distribution of the Respondents

The study examined the extent to which women used the services offered by micro finance

institutions using FINCA as example. Figure 1 shows the findings

18

From figure 3 above, nearly 48% represented the age bracket of (26-35); 29% represented the age bracket

of (36-45); 17% represented the age bracket of 45 an above and lastly 6% represented the age bracket of

(18-25). This implies that majority of the respondents were in the Youthful category (54%). That is, the

dynamic, enterprising, risk taking and working class age. They have the potential to grow their savings

and investment and consequently support themselves, the company and the economy at large. The future

of any bank lies in this age and this is why FINCA strategically targets such group.

4.2.5 Educational Background of the Respondents

The study wanted to examine if there was a link between the level of education attained by the clients and

the use of micro finance services. The respondents had different educational levels namely; primary,

secondary, certificate, diploma, degree and others as shown in the figure 4.

22

4.3 Nature of Micro Finance Products/Services Offered

The first objective of the study was to examine the nature of micro financial services offered to the youth and

women in Wobulenzi Luwero District.

4.3.1 Nature of Microfinance Products/Services

The study identified the types of services offered by FINCA micro finance institution and included among

others; insurance, money transfers and loans. The findings pertaining to this were extracted from a sample of

past and present FINCA clients and these are shown in Table 4.3

Table 4.3: The Ranking of Micro Finance Products/Services

Services /products Rank

Money Transfer 4

Insurance 5

Loan for Education and Others 2

Loan for Small Business Enterprise 1

Loan for Housing 3

Source: Primary Data

24

According to the table 4.3 above, loans for small business was ranked number 1, loans for education

and others was ranked number 2, loans for housing was ranked number 3, money transfer was ranked

number 4, and insurance was ranked number 5. The above ranking from one to five shows the level

of importance attached to each particular service, the most important being ranked number 1 while

the least important being ranked number 5. The implication is that most of the client in MFis mostly

go for loans purposely to expand or open up business ventures as is one of the pillars for offering a

loan and other services are coincidental.

4.3.2 Time Taken Using FINCA Services

A study was also carried out to asses the time taken by the clients as customers of FINCA before

leaving for any reason. This was done on the past and present clients. The finding are recorded in

figure 5

25

4.4 Indicators of Growth in Economic Activities among Beneficiaries.

The second objective of the study was to identify the indicators of growth in economic activities

basing on the beneficiaries. Notable among these were business expansion, infrastructures, increment

in assets, prompt payment of financial obligations, increase in FINCA clients incomes and increase in

the purchasing power.

4.4.1 Economic Indicators for Business Growth

The clients were asked to choose and rank from the selected criteria, what they feel should be the

best measure of economic growth or their performance as they use the services of FINCA. The

findings relating to indicators of growth in economic activities are as summarized in Table 4.4.

Table 4.4: The Different Economic Indicators for Business Growth Economic Indicators Frequency Percentage

Business Expansion 19 16

Prompt Payment of Loans 24 20

Increase in Assets 17 14

Ability to Pay Expenses 7 6

General Increase in Purchasing Power 17 12

Increase in FINCA Clients' Incomes 28 24

Improvement of Infrastructures 9 8

Total 118 100

Source: Primary Data

29

From the table 4.4 above, 24% of the respondents said that increase in people's incomes was the

major measure of business success, 20% said prompt payment of loans, 16 % said business

expansion, and 14% said meeting expenses in time, 12% said improvement in the standard of living.

The majority of respondents therefore prefer increase in income as the best measure of growth in

business and individual welfare, closely followed by the ability to pay back the loans.

4.4.2 Problems Encountered in Using FINCA Services

Several problems encountered in using FINCA services were enumerated as follows; high interest

rates, short repayment periods, lack of collateral security and inaccessibility of FINCA services to

mention a few. The respondent were asked to rank problems according to their individual feelings

and the results came out as in table 4.5

Table 4.5: Showing Problems Encountered in Using FINCA Services

Problems Frequency Percentage

High interest rates 26 22

Short payment periods 21 18

Lack of collateral security 28 24

Inaccessibility of FINCA services 35 30

Other 7 6

Total 118 100

Source: Primary Data.

30

4.4.3 Reasons for Poor Performance

The respondents were required to give account of the reasons as to why they perform/performed

poorly in any of the cycles they had or were going through. The outcomes of this question arose

from the work places of the clients and were centered around the reasons as highlighted in the Table

4.6.

Table 4.6: Reasons for Poor Performance

Reasons Frequency Percentage

Misappropriation of Funds 35 30

Bad Seasons 24 20

Shifting Business Premises 7 6

Destruction of Property /Goods 12 10

Electricity Shortages 24 20

Sickness and Other 17 14

Total 118 100

Source: Primary Source

From table 4.6 , it's clear that nearly 30% of the respondents said that the major problem facing

FINCA clients is misappropriation of funds, 20% said bad trading season, 20% electricity shortages,

6% said shifting of business premise and 14% said sickness and other reasons.

It is important that prior to acquisition of loans, training should be done to assist the clients acquire

some financial discipline tips thus avoiding misappropriation of funds. The rest of the problems are a

result of poor feasibility study or reasons beyond the control of the clients; Electricity shortages,

sickness are some of the examples.

32

4.4.4 Reasons for Excellent Performance

The respondents were asked to give factors that led to their excellent performance in any of the

cycles they had gone through or were going through at that time. Several reasons responsible for the

excellent performance were given namely group pressure, good clientele base, personal discipline,

good season, good monitoring and supervision. The results are merged and recorded in table 4.7

below

Table 4.7: Reasons for Excellent Performance

Reasons Frequency Percentage

Group pressure 35 32

Personal discipline 23 20

Monitoring 21 18

Good seasons 19 16

Good clientele base 17 14

Total 118 100

Source: Primary Data From Table 4.7, it is clear that about 32% of the respondents gave 'group pressure' as the reason for

their excellent performance, 20% gave 'personal discipline' , good monitoring and supervision was

given by 18%, good season was given by 16 %, and good clientele base was cited by 14 % of the

respondents .The implication behind this is that most of the respondents had good reasons for

performing better and in order for FINCA to achieve its mission and vision, its important that such

attributes are incorporated in their strategy or policy. Group pressure, training and supervision should

be given priority in its strategic planning.

33

4.5 To Establish the Contribution of Micro Finance Funding on the Economic Activities of

the Youth and Women in Luwero.

The third objective was to establish the contribution of micro finance funding to the economic

activities of the concerned groups. The major contributors were the increment in working capital and

proper record keeping leading to a variety of outcomes. The findings pertaining to these were

extracted from primary data records and summarized in the subsequent sections.

4.5.1 Present Working Capital

The respondents were asked to reveal the amounts of cash they have received from FINCA so that

the amounts received are related to the kinds of businesses they have undertaken in order to asses the

effect of such advances on the their economic activities. The quantity of working capital in relation to

the kind of business undertaken greatly affects the economic activities. Table 4.8 contains records

about the working capital that the respondents received from FINCA.

Table 4.8: Present working capital

Working capital Frequency Percentage

50,000 - 500,000 76 64

500,000 - 1,000,000 24 20 •

1,000,000 - 5,000,000 14 12

5,000,000 - 20,000,000 5 4

Total 118 100

Source: Primary Data

34

From figure 9 above, it's evident that 50% of the respondents have good record keeping skills, 30% had

poor record keeping and 20% had fair record keeping. The implication is that majority of the respondents

were good record keepers though it also brings out the 30% poor record keepers. There is need for

improvement of this kind of status through training, supervision and politicization. It is possible that the

respondents in this category have made losses or profits but they are not recorded anywhere and this may

bring out an untrue picture of the growth of their activities.

4.5.4 Contribution of Micro Finance Institutions in Wobulenzi

Respondents were asked to rank how they feel about the contribution of micro financing in Wobulenzi.

Various criteria were used to determine the extent to which FINCA has helped in uplifting the standards

of living of the women and the youth plus their development ventures. Almost every body admitted that

there is an effect that FINCA has made in Wobulenzi and the respondents were required to identify the

areas where they feel the impact is more and then rank them accordingly.

36

Table 4.9 Showing the Economic Contribution of Micro Finance Institutions in

Wobulenzi.

Economic Contributions Rank Percentage

Business Expansion 30 25

Ability to Pay Taxes in Time 24 20

Improvement in Farming Practices 27 23

Increase in Peoples' Incomes 12 10

Improvement in Infrastructure 5 4

Meeting Customer Demands in Time 5 4

Meeting Financial Obligations in Time 13 11

Others 4 3

Total 118 100

Source: Primary Data From table 4.9, its evident that 25% of the respondents said that the major economic contribution of

microfinance is business expansion, 23% said improvement in farming practices, and 20% said it's the

ability to pay taxes, 11 % said its meeting financial obligations, 10% said increase in people's incomes,

and 4% said improvement in infrastructures and meeting customers' demands in time and 3% for other

reasons respectively. Whereas there are various ways that can assist in gauging the performance, as

indicated by the 'other' category, it is clear from most respondents that once there is 'expansion of

business premises', there is obviously an improvement in the performance of the business due to a boost

in working capital.

37

4.6 Designation of Appropriate Strategies

Objective four sought to find out appropriate strategies that would make FINCA services readily

accessible to its potential- and actual targeted groups. The findings after the study satisfactorily

answered it. The strategies revealed included among others; lower interest rates, lengthen the loan

repayment periods, reconsider collateral security requirement policy, rural outreach, expansion

product portfolios and Project appraisal

The findings after the study revealed that most respondents suggested lowering the interest rates as a

strategy geared at making FINCA services more accessible to them. This would go a long way in

enticing non FINCA users to become users as well as ensuring increased use of the services by the

current clients. It will also enable FINCA clients to benefit more as interest rates are lowered since it

will favorably impact on their profitability.

The findings also revealed that FINCA clients have always complained about the short repayment

period. This is due to the fact that majority of the FINCA clients in Luwero depend on agriculture

and trade which needs a long period to reap from the operation. Lengthening the repayment period

would enable them meet their financial obligations in time. The respondents also wanted FINCA to

give them a grace period before start of the payment period to enable them start the payment

schedules after a reasonable degree of business stability.

38

One of the hindering factors limiting accessibility to FINCA services is collateral security

requirement policy. The respondents suggested that it should be scrapped off or reconsidered so as to

enable those without it to access the services freely. It will also assist users to access larger loans.

This may however not be practical since security is a requirement by all banks. The idea of group

pressure as security does not seem to be good enough for the respondents as it limits the advances

required by them to certain limits which are seemingly peanuts to people with big ventures.

The findings revealed that most FINCA branches are in urban and peri-urban areas. They therefore

suggested that FINCA should endeavor to open up more branches in rural areas so as to make its

services more accessible to all target groups. Currently most of the clients are supposed to travel to

head office or to district headquarters for meetings and remitting of their weekly loan installments.

This increases their operational costs and is time consuming as well.

The study further disclosed that the respondents wanted FINCA to expand or increase on the product

portfolio offered. The products currently offered are very few compared to the clients' demands. This

in a way has fueled the misappropriation of funds received by the clients to other purposes not

prescribed in the loan contract which increases high default rate.

FINCA for example is not interested in directly supporting the agricultural sector due to the long

gestation period of most crops. FINCA is also not keen at assisting 'starters' of whatever business

however good a client's feasibility study may be, because of the high risk involved in the initial

stages of business ventures.

39

The study further discovered that FINCA management should endeavor to appraise and recommend

projects to be funded. Their experience over time should assist them to realize the types of businesses

with the least failure rate and be able to advise their clients accordingly. The management should go

an extra mile to periodically monitor the operations of the projects funded so as to reduce on the

default rate.

40

CHAPTER FIVE

5.0 ANALYSIS OF FINDINGS, CONCLUSIONS AND RECOMMENDATIONS

5.1 Introduction

This chapter discusses the findings of the study, the conclusions and recommendations in relation to

the study objectives. The discussion explains the findings of the study in support or in contrast to the

literature after which conclusions and recommendations are drawn

5.2 Nature of Financial Services Offered by MFIs

The findings after the study revealed that loans for small businesses was ranked number one, loans

for 'education and others' was ranked number two and loans for housing was ranked number three.

Over 75% of the services offered by FINCA are loans, though for different needs. The loan service is

the most used by FINCA clients in Wobulenzi though they offer a number of other services which

include money transfer, insurance, and others at large. The study findings further revealed that there

is both minimal knowledge and at the same time little need for the insurance services. Money transfer

service is also not so commonly used in Wobulenzi despite the fact that it's a high income earner for

MFIs. Urban clients have more dealings in such a service than rural ones.

This is in agreement with Sinha, (1998) who provided the composition of Micro finance services as

stated above. The findings are also supported by (Rogery, 1999), who suggested that Micro Finance

services are for promotion of individuals and households out of poverty, and protection/insurance of

people from vulnerability of fluctuations of income. The argument is at the same time in line with

Afrane, (2002), who argued that the importance attached to money transfers is of limited use among

rural communities.

41

5.3 Indicators of Growth in Economic Activities

The findings revealed that 24% of the respondents suggested 'increase in people's incomes' as their

measure of growth in economic activities, while 20% gave prompt payment of loans, 16% said business

expansion, and 14% said meeting expenses in time, and 12% said improvement in the standard of living

as the indicators of growth in economic activities. The majority of respondents therefore prefer increase in

income as the best measure of growth in business and individual welfare, closely followed by the ability

to pay back the loans.

Most authors contend that there are several indicators of growth in economic activities, the above

indicators inclusive, notable among these are; Dyck, Alexander (1997); Hoque, Serajul (2004); and

Daley, Harris, Snodgrass, Sebstad (2002) just to cite a few. However, Ledgerwood, (1999), noted from

the clients that there are no particularly outlined ways of measuring growth in economic activities.

5.4 Contribution of Micro Finance Institutions Funding to Rural Women and Youth

The study findings deduced that out of selected attributes for the contribution of MFIs funding to the rural

women and youth, business expansion was ranked number one, followed by improvement in the farming

practices, prompt tax payment turned out to be number three, 'meeting financial obligations in time' was

ranked number four, increase in peoples' incomes became number five, others included improvement in

infrastructures and meeting customer demands on time. This therefore implies that MFIs playa vital role

in boosting up the incomes of their clients.

42

This is supported by (Brau, James Gary, Woller, 2005), who conceded that growth was also reflected

by the increase in the different business ventures, prompt tax payment and meeting financial

obligations among others. However a few clients harbor a different view about MFI funding. They

argue that MFIs charge high interest rates coupled with the very short repayment period which

culminates into confiscation of property, imprisonment and general impoverishment and hence they

see no positive contribution at all. This argument is supported by Otero and Halt (1993).

5.5 Appropriate Strategies

The findings after the study revealed that certain strategies need to be adopted in order to make MFIs

work better. These include lowering the interest rates, lengthening the loan payment period,

reconsidering of the collateral security policy, and expansion of product portfolio, constant project

appraisal and increase in the rural outreach. Barry, (2000); Cheston, Susy and Larry Reed (1999)

also support the above strategies. Much as the strategies have to be put in place, there is need of

considering the investors motives of targeting a particular rate of return on investment. This therefore

places the implementation of the above strategies of MFIs into jeopardy leaving would be

beneficiaries into a take it or leave it situation (Gyasi 2002).

43 4.

5.6 CONCLUSION

Micro Financing is becoming increasingly important to poor countries like Uganda as an engine of

growth and development and it is therefore important that policy makers accord more attention to it than

ever before in order that the current and potential 'beneficiaries' can actually stand to improve on their

welfare.

On the MFIs services, the reason behind the massive use of the loan service as compared to the rest of the

services is that most small scale entrepreneurs require funds for starting up ventures, reinvesting in the

existing businesses or overcoming various financial obligations. Insurance services are not easily

adaptable to even people of a recognized degree of literacy due to their complexity and to make it worse,

the rural women and youth do not have the asset base that can warrant the need for such services. Money

transfer services are also rare in rural set ups and are therefore not attractive to Wobulenzi people. The

general poverty level coupled with the illiteracy rate in Wobulenzi are the major causes of the higher rate

in the use of loans as compared to the rest of the services. MFIs should for that matter concentrate more

on the improvement of this service than any other service.

Evidence from clients reveals that it is up to the clients to gauge from their individual situations and come

up with a way of accounting for their performance. The parameters for the measure of performance are

therefore bound to change from person to person, period to period and circumstances of the time.

Management of MFIs should therefore set up individual appraisal parameters for each client basing on

already drawn policies. Such policies should be flexible.

44

There is no single rule to use as the correct measure of the contribution of MFIs funding to the clients'

business growth. Loan officers can at the same time not dictate any parameters to measure this because

different clients will use different approaches. It is also not good to leave important information untapped

lest it is required in the future. Management should therefore device 'middle ground' parameter to use

especially where the client is undecided as to what parameter to use

Since micro finance institutions are proving important to the less developed societies, it is paramount that

various strategies be formulated to pave a way forward for them thus propelling the people from the

current status to greater heights.

45

5.7 RECOMMENDATIONS

The study findings yielded the following recommendations in view of the contribution of MFIs funding

on the Economic Growth of the rural youth and women of Wobulenzi.

Management of MFIs should emphasize village banking in order to overcome or reduce on the default

rate. Such a method creates psychological coercion amongst the clients to pay back the borrowed money.

Individual borrowers tend to default a lot which poses a big risk to the organization.

MFIs should provide conducive organizational environment where by their staff are provided with the

relevant tools, facilities, and incentives that enable them work comfortably. This will alleviate the

likelihood of officers working' for the sake' and will ensure proper planning and appraisal of the clients

dealings with in situation.

The management of MFIs should stretch further to rural areas so as to be able to serve the needs and

wants of the rural business men. Cost benefit analysis should be considered when such a decision is being

embarked on so that both parties can equally benefit from the venture.

The management of MFIs should increase on the product portfolios offered to the rural people. The

existing product portfolios do not cater for all the needs and wants of the rural people. The marketing

department should endeavor to research on the clients' desired options and be able to include the probable

and realistic ones onto the list.

46

The management of MFIs should endeavor to sensitize their clients about the need to secure loans from

one source other than multiple sources so as to encourage them to acquire loans they can afford to pay.

This calls prior training and briefing of clients

MFIs should be duty bound to lower the interest rates charged on the loans secured. The current interest

rates ranging from 24% to 36% per annum are too high. This can not easily be afforded by the low

income earners who are engaged in low profitability ventures. MFIs have the biggest percentage of their

income earners centered on interest on loans but it is advisable that the product portfolio be increased and

interest lowered in turn in order to achieve the goal. Management of MFIs should also endeavor to

lengthen the loan payment period. The current loan payment period is too short to pay the loan.

The management of MFIs should endeavor to evaluate project proposals for clients wanting to secure

loans. A department responsible for evaluating project proposals should be instituted. Past experience

together with secondary data sources should now be in position to assist the department to compile

dependable information that can be used to recommend a portfolio of viable ventures to clients in various

areas for investment.

External internal interference should be eliminated, donors should not impose their ideas on micro

finance institutions rather they should work together to achieve tangible results.

47

AREAS FOR FURTHER RESEARCH

The researcher recommends further research in the following areas.

The effect of MFIs funding on profitability of small scale businesses

The effect of information technology on MFIs funding

The effect of MFIs on the social, economic and political set up of Uganda.

48

REFERENCES

Barry, N. (2000), Similarities in Micro Finance World Wide, IDB , Micro enterprises

David, H. and Mosley, P. (1996), Micro Finance Against Poverty Vol 1.

Graham, A. Wright,(1999), The Impact of Micro Finance Services on increasing incomes or reducing

poverty.

Holt, L.S. (1993), Village banking, a cross study of a community based lending methodology,

USA1D Bureau for Asia and private enterprises, GEMENI Washington.

Joana Ledgerwood. (1999), micro finance hand book

Kibeer Micheal (1996) interest rates; why less may really be more, Kampala.

Montigomery, B. (1999), The experience of MFIs in eradication of hunger and poverty in

Uganda. The case of PAP Kampala.

Nakawesi, (2003), Why New Businesses Fail, New Vision 9th September 2003 the New Publishing

Press.

Afrane, S. (2002). "Impact Assessment of Microfinance Interventions in Ghana and South

Africa: A Synthesis of Major Impacts and Lessons." Journal of Microfinance, Spring, pp. 37- 58.

Armendariz de Aghion, Beatriz and Jonathan Morduch. (2005). The Economics of Microfinance.

The MIT Press.

Brau, James & Gary Woller. (2005). "Microfinance: A Comprehensive Review of the Existing

Literature and an Outline for Future Financial Research." Journal of Entrepreneurial Finance and

Business Ventures.

Cheston, Susy and Larry Reed. (1999). "Measuring Transformation: Assessing and Improving

the Impact of Microcredit." Microcredit Summit Meeting of Councils in Abidjan, Cote d'Ivoire, 24-

26 June.

49

Cheston, Susy and Lisa Kuhn. (2002). "Empowering Women through Microfinance." United Nations

Fund for Women.

Coleman, Isobel. (2005). "Defending Microfinance." (Winter), Fletcher Forum of World Affairs.

Copestake, James, Helen Gosnell, David Musona, Gibson Masumbu, and Welenge Mlotshwa. (2001).

"Impact Monitoring and Assessment of Microfinance Services Provided by CETZAM on the Zambian

Copperbelt 1999-200l." University of Bath, U.K.

Daley-Harris, Sam. (2002). Pathways out of Poverty: Innovations in Microfinance for the Poorest

Families. Kumarian Press, Inc., Bloomfield, CT.

Drake, Deborah and Elisabeth Rhyne. (2002). The Commercialization of Microfinance

Balancing Business and Development. Kumarian Press, Inc., Bloomfield, CT.

Dunn, Elizabeth & 1. Cordon Arbuckle, Jr. (2001). "The Impacts of Microcredit: A Case Study from

Peru:'

Dyck, I. 1. Alexander. (1997). "Country Analysis: A Framework to Identify and Evaluate the ational

Business Environment." Harvard Business School Note 9-797-092.

Fraioli, Lisa Kuhn. (2003). "In Search of a 'Recipe' for Empowerment and Transformation: An In-depth

Look at Microcredit and Training at Work in the Lives of Ghanian Women." Opportunity International.

Gyasi-Fosu, Anthony. (2002). "Socio-Economic Impact Assessment of Microfinance

Programmes: A Case Study, Sinapi Aba Trust." Post Graduate Diploma Project, Ghana Institute of

Management & Public Administration.

Hishigsuren, Gaamaa. (2004). "Impact Assessment Findings Using the SEEP-AIMS Tools at

Sinapi Aba Trust, Ghana." The Institute for Development Studies (IDS) Imp-Act Programme.

Hishigsuren, Gaarnaa, Brian Beard, and Lydia Opoku. (2004). "Client Impact Monitoring

50

Finding from Sinapi Aba Trust, Ghana." The Institute for Development Studies (IDS)Imp-Act

Programme.

Hoque, Serajul. (2004). "Micro-credit and the Reduction of Poverty in Bangladesh." Journal of

Contemporary Asia, Vol. 34 0.1, pp 21-32.

Kabeer, aila and Helzi oponen. (2005). "Social and Economic Impacts of PRADAN's Self

Help Group Microfinance and Livelihoods Promotion Program: Analysis from Jharkhand, India."

Imp-Act Working Paper No. 11.

Jurik, Nancy C. (2005). Bootstrap Dreams: U.S. Microenterprise Development in an Era of Welfare

Reform. Cornell University Press.

Morduch, Jonathan. (2000). "The Microfinance Schism." World Development, Vol. 28, No.4, pp

617-629.

Polakow-Suransky. Sasha. (2003). "Giving the Poor Some Credit: Microloans are in vogue.

Are they a sound idea?". The American Prospect (Summer) A 19-A21.

Sebstad, Jennefer and Gregory Chen. (1996). "Overview of Studies on the Impact of Microenterprise

Credit." Assessing the Impact of Microenterprise Services (AIMS), Washington D.C.

Simanowitz, Anton and Alice Walter. (2002). "Ensuring Impact: Researching the Poorest while

Building Financially Self-Sufficient Institutions, and Showing Improvement in the Lives of the

Poorest Women and Their Families." In Sam Daley-Harris Pathways out of Poverty. Kumarian

Press,Inc., Bloomfield, CT.

Snodgrass, Donald R. and Jennefer Sebstad. (2002). "Clients in Context: The Impacts of

Microfinance in Three Countries: Synthesis Report." Assessing the Impact of Microenterprise

Services ( IMS), Washington D.C.

51

SOME ABBREVIATIONS

FI CA - a leading Micro Finance Institutions in Uganda

MFIs - Micro Finance Institutions

CERUDEB - Centenary Rural Development Bank

GO - on Governmental Organization

I

![[5365]-11 MBA 101](https://static.fdokumen.com/doc/165x107/6322631aae0f5e819105deed/5365-11-mba-101.jpg)