Maximizing Your Social Security Benefits

15

Diane Owens, Speaker & Consultant “Step Up Your Social Security”

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Maximizing Your Social Security Benefits

Diane Owens, Speaker & Consultant “Step Up Your Social Security”

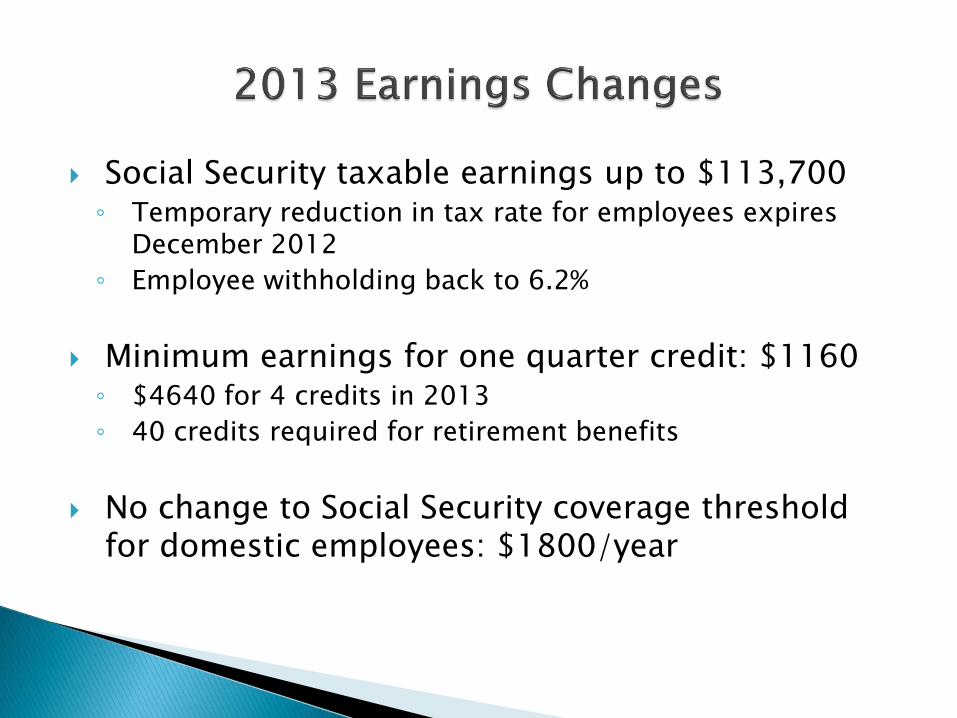

Social Security taxable earnings up to $113,700 ◦ Temporary reduction in tax rate for employees expires

December 2012

◦ Employee withholding back to 6.2%

Minimum earnings for one quarter credit: $1160 ◦ $4640 for 4 credits in 2013

◦ 40 credits required for retirement benefits

No change to Social Security coverage threshold for domestic employees: $1800/year

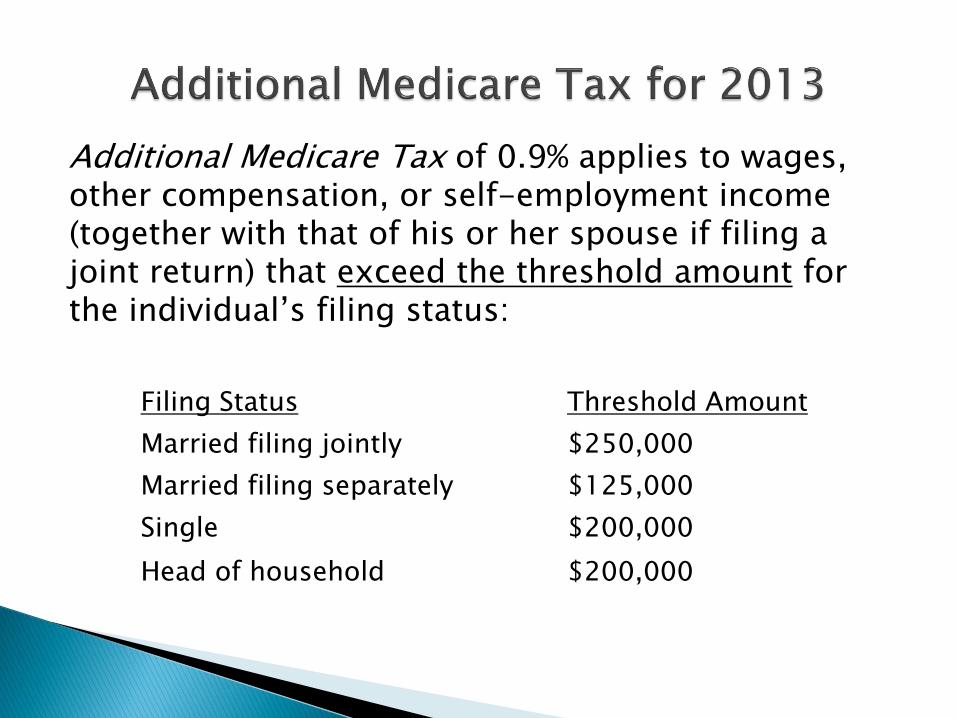

Additional Medicare Tax of 0.9% applies to wages, other compensation, or self-employment income (together with that of his or her spouse if filing a joint return) that exceed the threshold amount for the individual’s filing status:

Filing Status Threshold Amount

Married filing jointly $250,000

Married filing separately $125,000

Single $200,000

Head of household $200,000

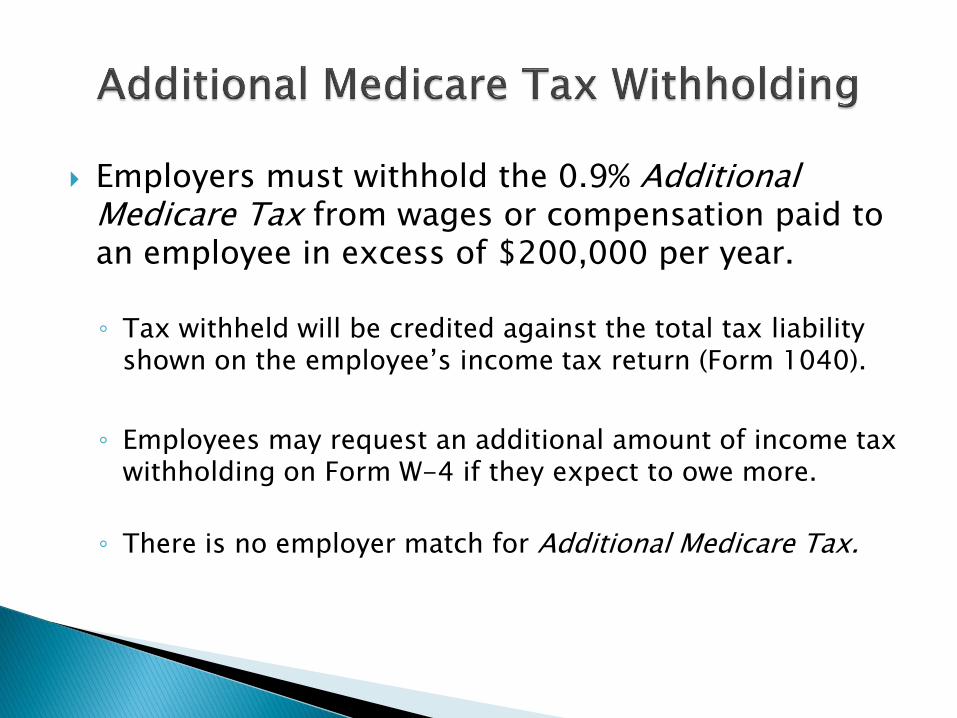

Employers must withhold the 0.9% Additional Medicare Tax from wages or compensation paid to an employee in excess of $200,000 per year.

◦ Tax withheld will be credited against the total tax liability shown on the employee’s income tax return (Form 1040).

◦ Employees may request an additional amount of income tax

withholding on Form W-4 if they expect to owe more.

◦ There is no employer match for Additional Medicare Tax.

Beginning 2013, a 3.8% Medicare tax will apply to: ◦ Net investment income of single taxpayers with AGI above

$200,000 and joint filers with AGI over $250,000 or $125,000 if filing separately.

Net investment income is: ◦ Interest, dividends, royalties, rents, gross income from a

trade or business involving passive activities, and net gain from disposition of property (other than property held in a trade or business).

◦ Reduced by deductions that are allocable to that income. Tax won't apply to income in tax-deferred retirement accounts.

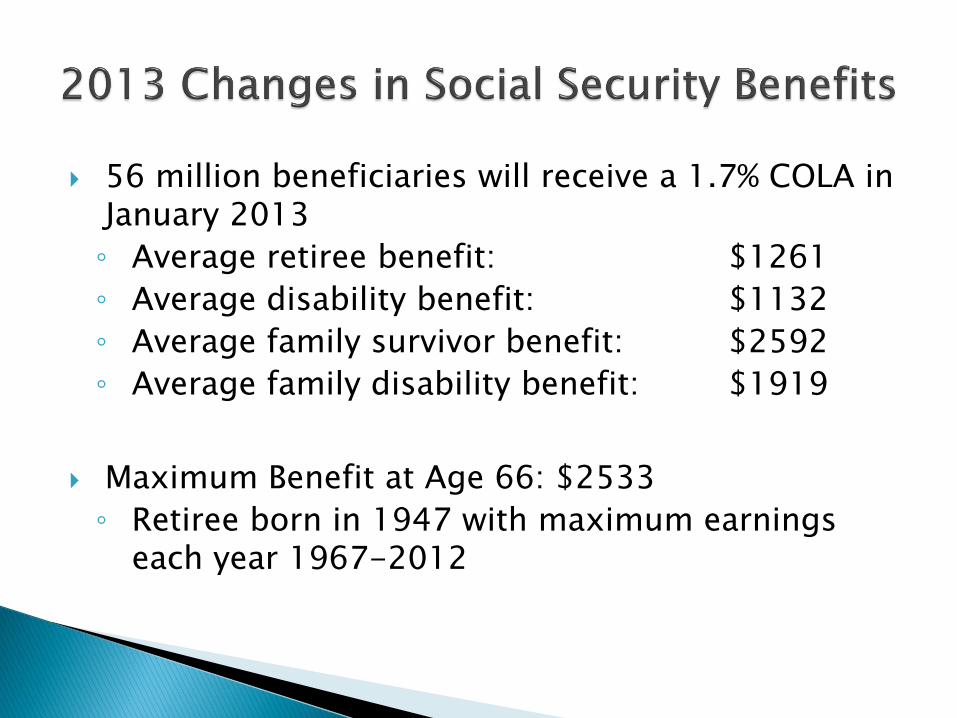

56 million beneficiaries will receive a 1.7% COLA in January 2013

◦ Average retiree benefit: $1261

◦ Average disability benefit: $1132

◦ Average family survivor benefit: $2592

◦ Average family disability benefit: $1919

Maximum Benefit at Age 66: $2533

◦ Retiree born in 1947 with maximum earnings each year 1967-2012

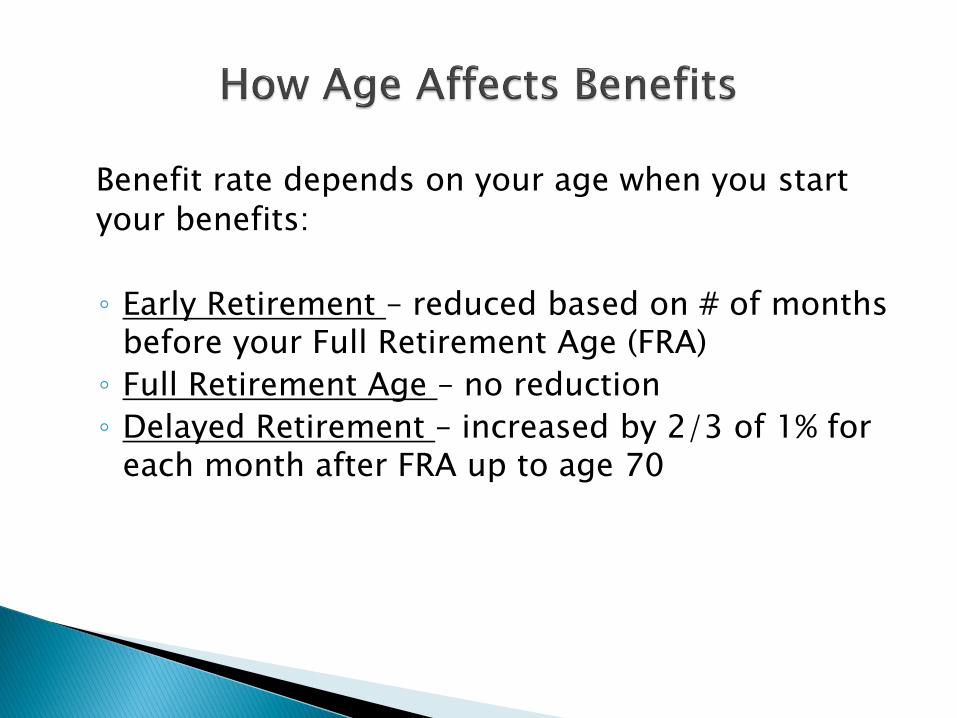

Benefit rate depends on your age when you start

your benefits:

◦ Early Retirement – reduced based on # of months before your Full Retirement Age (FRA)

◦ Full Retirement Age – no reduction

◦ Delayed Retirement – increased by 2/3 of 1% for each month after FRA up to age 70

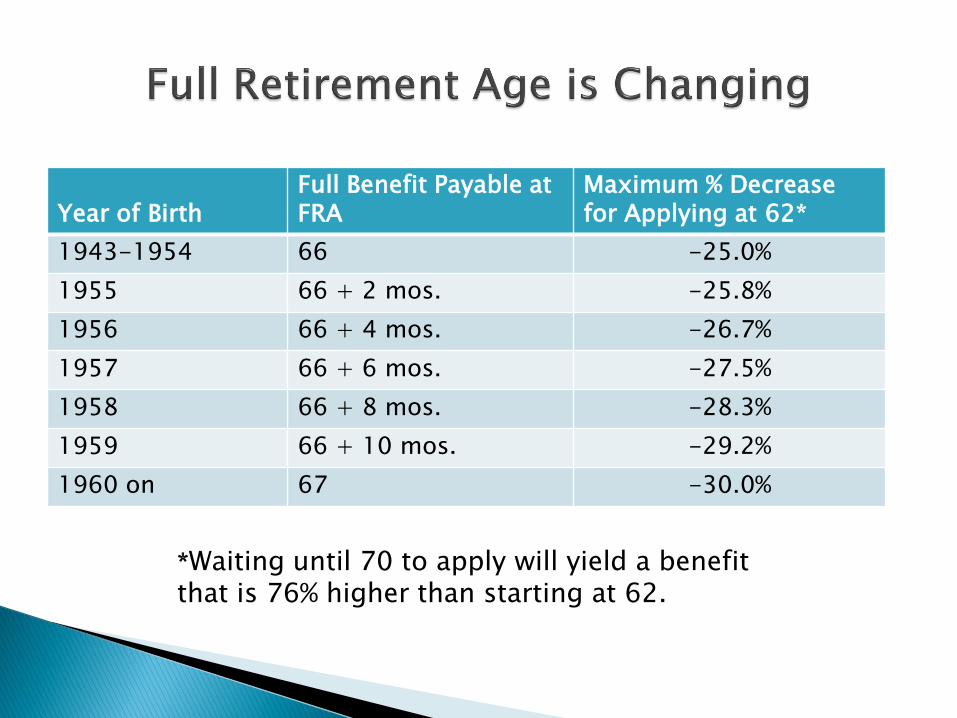

Year of Birth

Full Benefit Payable at FRA

Maximum % Decrease for Applying at 62*

1943-1954 66 -25.0%

1955 66 + 2 mos. -25.8%

1956 66 + 4 mos. -26.7%

1957 66 + 6 mos. -27.5%

1958 66 + 8 mos. -28.3%

1959 66 + 10 mos. -29.2%

1960 on 67 -30.0%

*Waiting until 70 to apply will yield a benefit that is 76% higher than starting at 62.

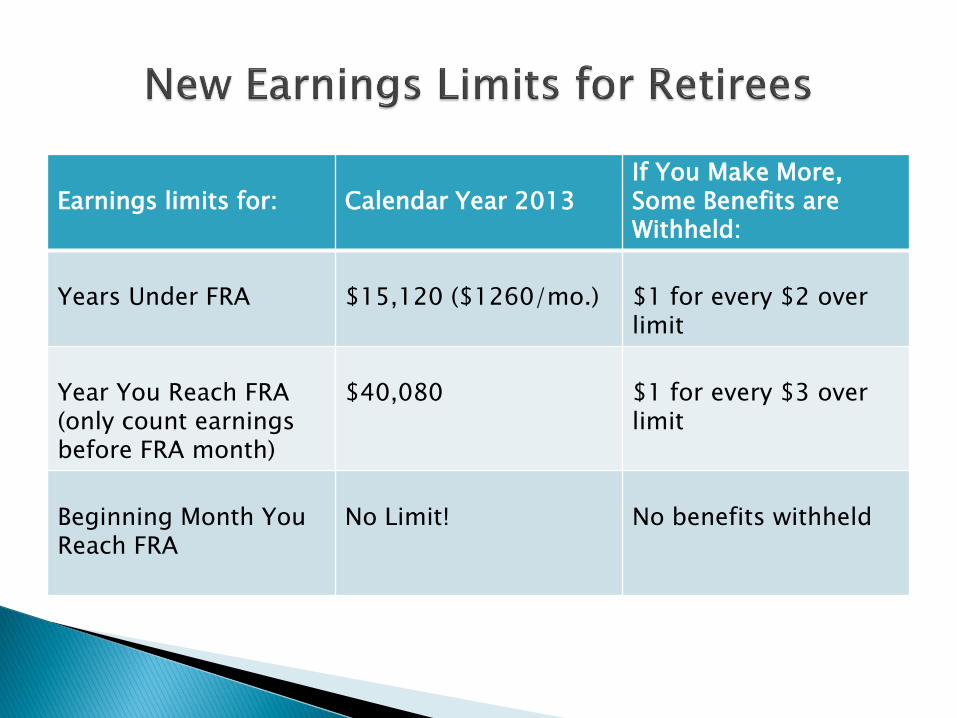

Earnings limits for:

Calendar Year 2013

If You Make More, Some Benefits are Withheld:

Years Under FRA

$15,120 ($1260/mo.)

$1 for every $2 over limit

Year You Reach FRA (only count earnings before FRA month)

$40,080

$1 for every $3 over limit

Beginning Month You Reach FRA

No Limit!

No benefits withheld

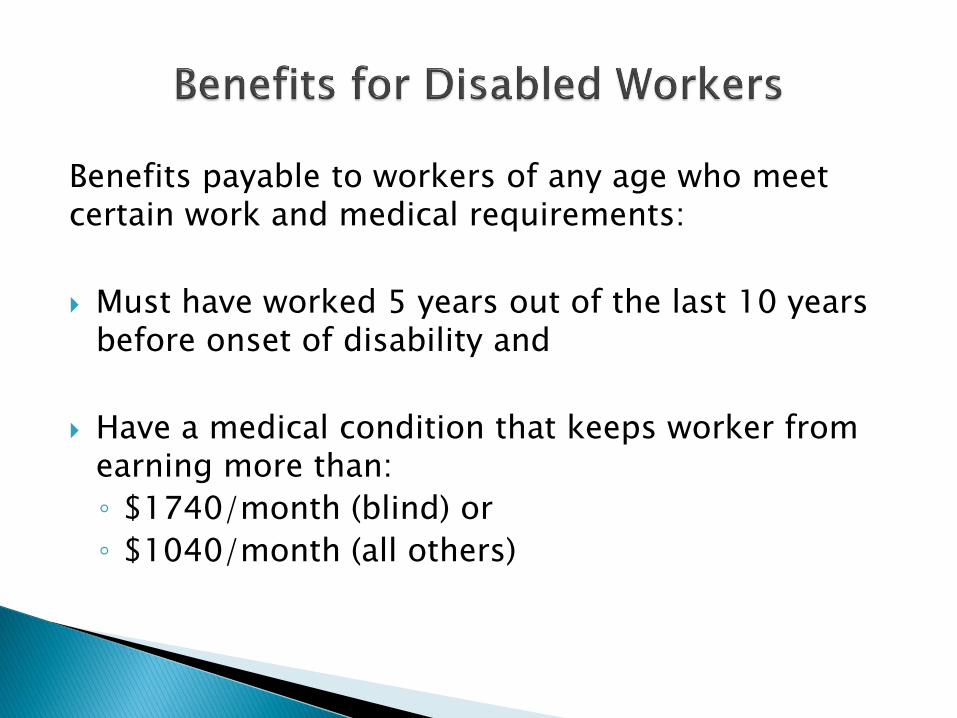

Benefits payable to workers of any age who meet certain work and medical requirements:

Must have worked 5 years out of the last 10 years before onset of disability and

Have a medical condition that keeps worker from earning more than:

◦ $1740/month (blind) or

◦ $1040/month (all others)

To qualify a husband or wife must be: ◦ At least age 62 (benefits reduced based on age)

◦ If divorced, must be unmarried and have been married at least 10 years to worker.

Worker must apply for and be entitled to retirement or disability benefits. ◦ Exception: divorced spouse may qualify earlier.

Spouse can receive between 35% (at 62) to 50% (at FRA) of worker’s full retirement benefit rate.

Average couple will receive $2048/month in 2013

To qualify a widow or widower must be: ◦ At least age 60

◦ If divorced, marriage must have lasted at least 10 years.

Reduced benefit at age 60 is 71.5% of deceased worker’s FRA benefit rate

Maximum payable at widow(er)’s FRA is 100% of worker’s benefit at time of death. ◦ The longer the worker waits to apply for retirement (up to

age 70), the higher the potential survivor’s benefit will be.

Average widow(er) will receive $1214/month in 2013

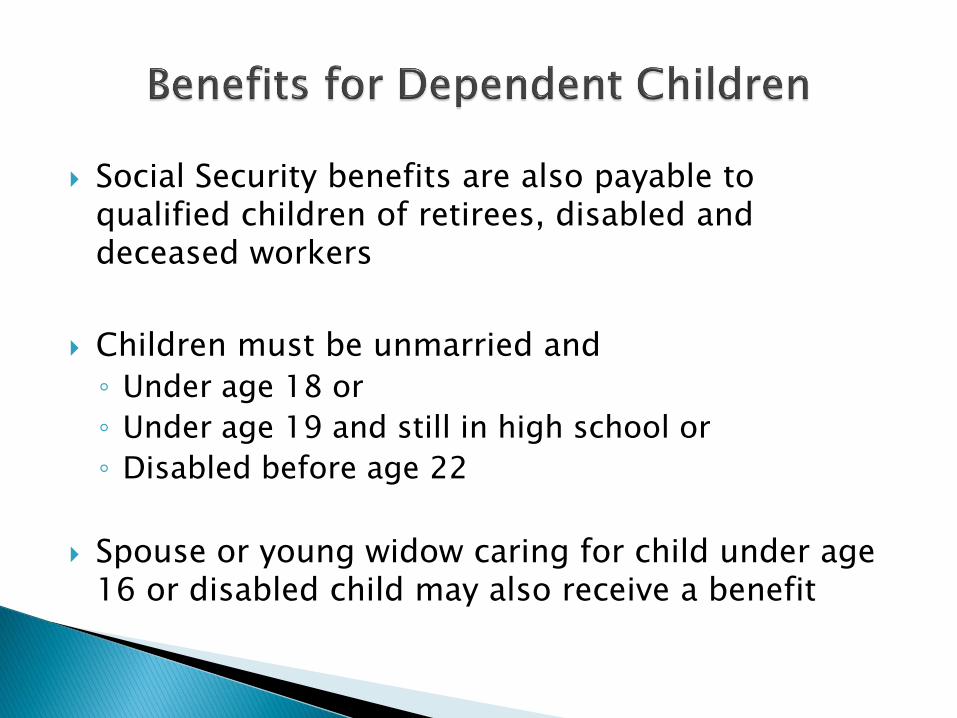

Social Security benefits are also payable to qualified children of retirees, disabled and deceased workers

Children must be unmarried and

◦ Under age 18 or

◦ Under age 19 and still in high school or

◦ Disabled before age 22

Spouse or young widow caring for child under age 16 or disabled child may also receive a benefit

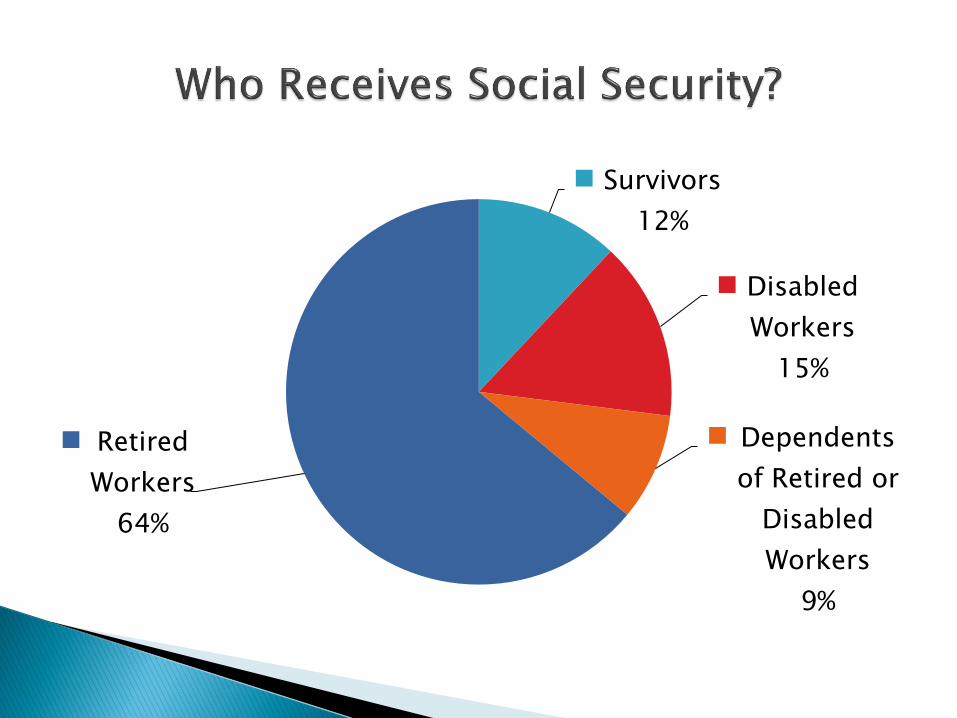

Survivors

12%

Disabled

Workers

15%

Dependents

of Retired or

Disabled

Workers

9%

Retired

Workers

64%

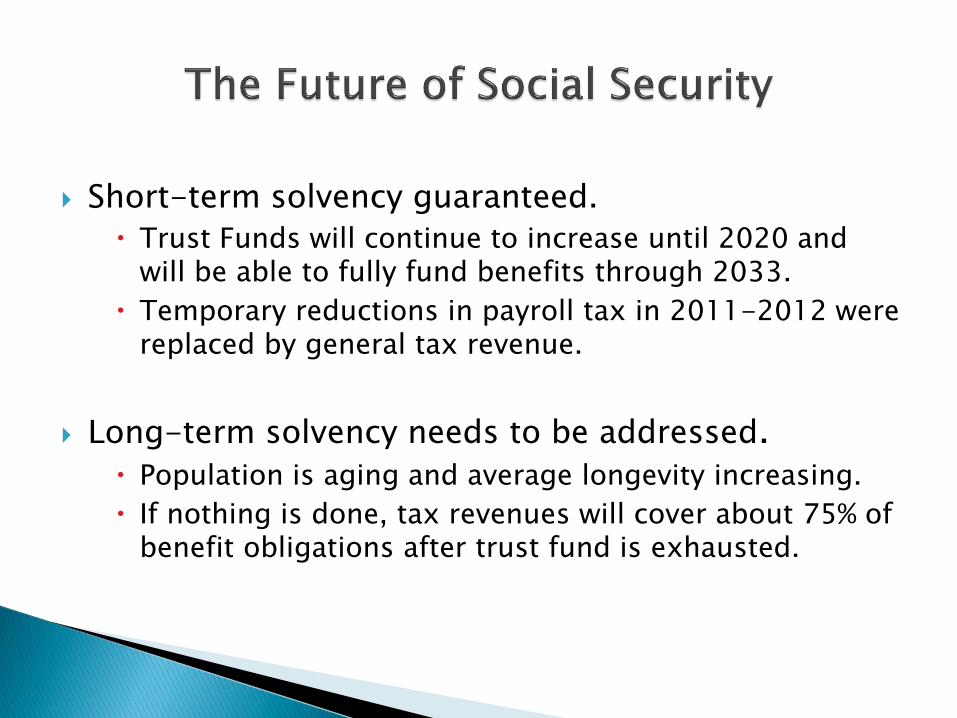

Short-term solvency guaranteed.

Trust Funds will continue to increase until 2020 and will be able to fully fund benefits through 2033.

Temporary reductions in payroll tax in 2011-2012 were replaced by general tax revenue.

Long-term solvency needs to be addressed. Population is aging and average longevity increasing.

If nothing is done, tax revenues will cover about 75% of benefit obligations after trust fund is exhausted.