Mathematics and Statistics - Horizon Research Publishing

72

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

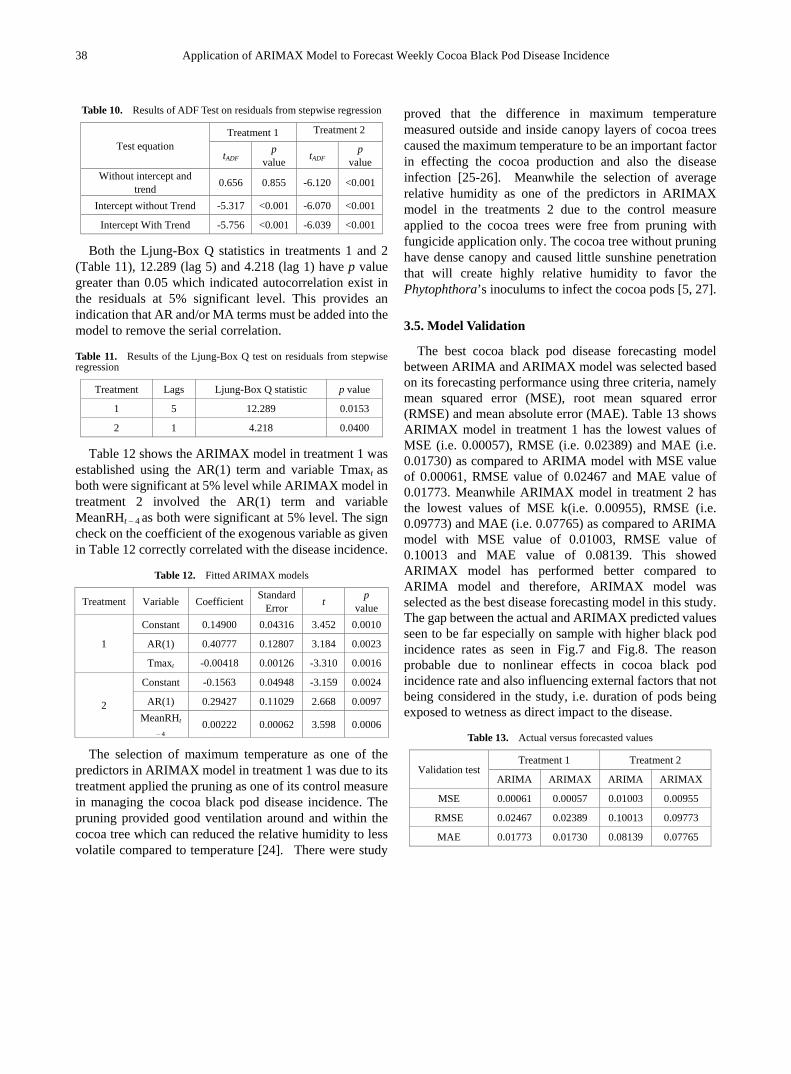

download

0

Transcript of Mathematics and Statistics - Horizon Research Publishing

Horizon Research Publishing, USA

Mathematics and Statisticshttp://www.hrpub.org

ISSN: 2332-2071Volume 7 Number 4A 2019Special Edition on Discovering New Knowledge through Research

Editors: Assoc. Prof. Dr. Sharidan Shafie (Universiti Teknologi Malaysia) Dr. Mohd Rijal Ilias (Universiti Teknologi MARA, Malaysia) Fazillah Bosli (Universiti Teknologi MARA, Malaysia)

http://www.hrpub.org

Mathematics and Statistics Mathematics and Statistics is an international peer-reviewed journal that publishes original and high-quality research papers in all areas of mathematics and statistics. As an important academic exchange platform, scientists and researchers can know the most up-to-date academic trends and seek valuable primary sources for reference. The subject areas include, but are not limited to the following fields: Algebra, Analysis, Applied mathematics, Approximation theory, Combinatorics, Computational statistics, Computing in Mathematics, Design of experiments, Discrete mathematics, Dynamical systems, Geometry and Topology, Logic and Foundations of mathematics, Number theory, Numerical analysis, Probability theory, Quantity, Recreational mathematics, Sample Survey, Statistical modelling, Statistical theory.

General Inquires Publish with HRPUB, learn about our policies, submission guidelines etc. Email: [email protected] Tel: +1-626-626-7940

Subscriptions Journal Title: Mathematics and Statistics Journal’s Homepage: http://www.hrpub.org/journals/jour_info.php?id=34 Publisher: Horizon Research Publishing Co.,Ltd Address: 2880 ZANKER RD STE 203 SAN JOSE, CA 95134 USA Publication Frequency: bimonthly Electronic Version: freely online available at http://www.hrpub.org/journals/jour_info.php?id=34

Online Submission Manuscripts should be submitted by Online Manuscript Tracking System (http://www.hrpub.org/submission.php). If you are experiencing difficulties during the submission process, please feel free to contact the editor at [email protected].

Copyright Authors retains all copyright interest or it is retained by other copyright holder, as appropriate and agrees that the manuscript remains permanently open access in HRPUB 's site under the terms of the Creative Commons Attribution International License (CC BY). HRPUB shall have the right to use and archive the content for the purpose of creating a record and may reformat or paraphrase to benefit the display of the record.

Creative Commons Attribution License (CC-BY) All articles published by HRPUB will be distributed under the terms and conditions of the Creative Commons Attribution License(CC-BY). So anyone is allowed to copy, distribute, and transmit the article on condition that the original article and source is correctly cited.

Open Access Open access is the practice of providing unrestricted access to peer-reviewed academic journal articles via the internet. It is also increasingly being provided to scholarly monographs and book chapters. All original research papers published by HRPUB are available freely and permanently accessible online immediately after publication. Readers are free to copy and distribute the contribution under creative commons attribution-non commercial licence. Authors can benefit from the open access publication model a lot from the following aspects: • High Availability and High Visibility-free and unlimited accessibility of the publication over the internet without any

restrictions; • Rigorous peer review of research papers----Fast, high-quality double blind peer review; • Faster publication with less cost----Papers published on the internet without any subscription charge; • Higher Citation----open access publications are more frequently cited.

Mathematics and Statistics Editor-in-Chief

Prof. Dshalalow Jewgeni Florida Inst. of Technology, USA

Members of Editorial Board

Jiafeng Lu

Nadeem-ur Rehman

Debaraj Sen

Mauro Spreafico

Veli Shakhmurov

Antonio Maria Scarfone

Liang-yun Zhang

Ilgar Jabbarov

Mohammad Syed Pukhta

Vadim Kryakvin

Rakhshanda Dzhabarzadeh

Sergey Sudoplatov

Birol Altın

Araz Aliev

Francisco Gallego Lupianez

Hui Zhang

Yusif Abilov

Evgeny Maleko

İmdat İşcan

Emanuele Galligani

Mahammad Nurmammadov

Zhejiang Normal University, China

Aligarh Muslim University, India

Concordia University, Canada

University of São Paulo, Brazil

Okan University, Turkey

Institute of Complex Systems - National Research Council, Italy

Nanjing Agricultural University, China

Ganja state university, Azerbaijan

Sher-e-Kashmir University of Agricultural Sciences and Technology, India

Southern Federal University, Russia

National Academy of Science of Azerbaijan, Azerbaijan

Sobolev Institute of Mathematics, Russia

Gazi University, Turkey

Baku State University, Azerbaijan

Universidad Complutense de Madrid, Spain

St. Jude Children's Research Hospital, USA

Odlar Yurdu University, Azerbaijan

Magnitogorsk State Technical University, Russia

Giresun University, Turkey

University of Modena and Reggio Emillia, Italy

Baku State University, Azerbaijan

Horizon Research Publishing http://www.hrpub.org

Special Issue Scientific Committee

Prof. Dr. Goh Kim Leng, University Malaya, Malaysia

Assoc. Prof. Dr. Mohd Bakri Adam, Universiti Putra Malaysia

Assoc. Prof. Dr. Nazirah Ramli, Universiti Teknologi MARA, Malaysia

Assoc. Prof. Dr. Nicoleta Caragea, Ecological University of Bucharest, Romania

Dr. Agus Maman Abadi, Universitas Negeri Yogyakarta, Indonesia

Dr. Dharini A/p Pathmanathan, Universiti Malaya, Malaysia

Dr. Hartono, Universitas Negeri Yogyakarta, Indonesia

Dr. Kismiantini, Universitas Negeri Yogyakarta, Indonesia

Dr. Nur Haizum Abd Rahman, Universiti Putra Malaysia, Malaysia

Dr. Nurul Sima Mohamad Shariff, Universiti Sains Islam Malaysia, Malaysia

Dr. Rohayu Binti Mohd Salleh, Universiti Tun Hussein Onn Malaysia, Malaysia

Dr. Shazlyn Milleana Shaharudin, Universiti Pendidikan Sultan Idris, Malaysia

Dr. Siti Marponga Tolos, International Islamic University Malaysia, Malaysia

Dr. Syafrina Abdul Halim, Universiti Putra Malaysia, Malaysia

Dr. Zeina Mueen, University of Baghdad, Iraq

Mofeng Yang, University of Maryland, USA

ISSN: 2332-2071 Table of Contents Mathematics and Statistics

Volume 7 Number 4A 2019

The Investigation on the Impact of Financial Crisis on Bursa Malaysia Using Minimal Spanning Tree (https://www.doi.org/10.13189/ms.2019.070701) Hafizah Bahaludin, Mimi Hafizah Abdullah, Lam Weng Siew, Lam Weng Hoe ............................................................ 1

A 2-Component Laplace Mixture Model: Properties and Parametric Estimations (https://www.doi.org/10.13189/ms.2019.070702) Zakiah I. Kalantan, Faten Alrewely ................................................................................................................................. 9

Comparison of Queuing Performance Using Queuing Theory Model and Fuzzy Queuing Model at Check-in Counter in Airport (https://www.doi.org/10.13189/ms.2019.070703) Noor Hidayah Mohd Zaki, Aqilah Nadirah Saliman, Nur Atikah Abdullah, Nur Su Ain Abu Hussain, Norani Amit .. 17

Performance of Classification Analysis: A Comparative Study between PLS-DA and Integrating PCA+LDA (https://www.doi.org/10.13189/ms.2019.070704) Nurazlina Abdul Rashid, Wan Siti Esah Che Hussain, Abd Razak Ahmad, Fatihah Norazami Abdullah ..................... 24

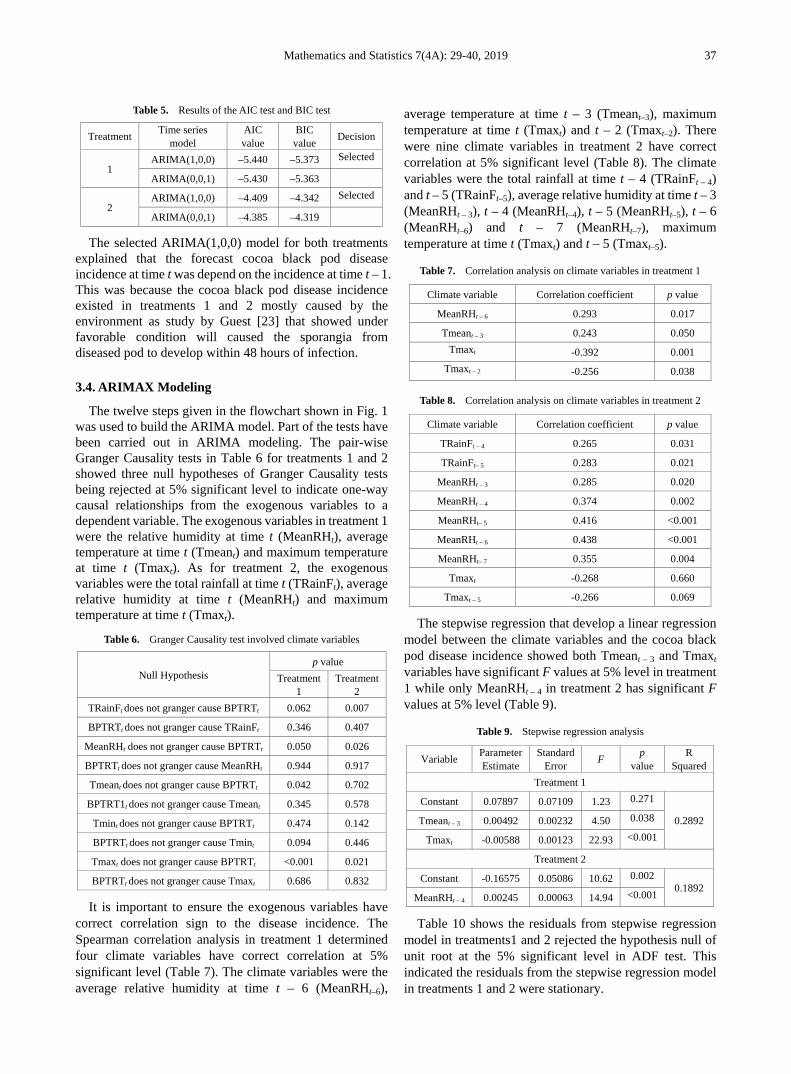

Application of ARIMAX Model to Forecast Weekly Cocoa Black Pod Disease Incidence (https://www.doi.org/10.13189/ms.2019.070705) Ling, A. S. C., Darmesah, G., Chong, K. P., Ho, C. M. ................................................................................................. 29

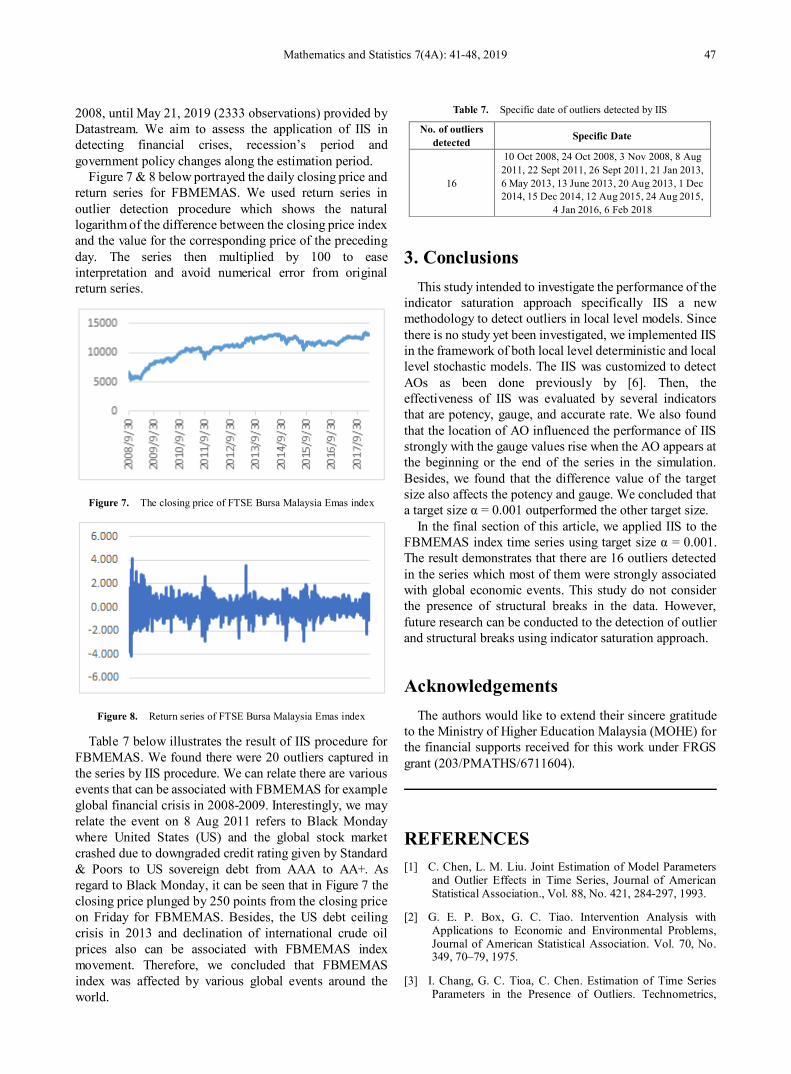

Outlier Detection in Local Level Model: Impulse Indicator Saturation Approach (https://www.doi.org/10.13189/ms.2019.070706) F. Z. Che Rose, M. T. Ismail, N. A. K. Rosili ................................................................................................................ 41

Investigation on the Clusterability of Heterogeneous Dataset by Retaining the Scale of Variables (https://www.doi.org/10.13189/ms.2019.070707) Norin Rahayu Shamsuddin, Nor Idayu Mahat ............................................................................................................... 49

Tree-based Threshold Model for Non-stationary Extremes with Application to the Air Pollution Index Data (https://www.doi.org/10.13189/ms.2019.070708) Afif Shihabuddin, Norhaslinda Ali, Mohd Bakri Adam ................................................................................................ 58

Mathematics and Statistics 7(4A): 1-8, 2019 http://www.hrpub.org DOI: 10.13189/ms.2019.070701

The Investigation on the Impact of Financial Crisis on Bursa Malaysia Using Minimal Spanning Tree

Hafizah Bahaludin1, Mimi Hafizah Abdullah1,*, Lam Weng Siew2,3, Lam Weng Hoe2,3

1Department of Computational and Theoretical Sciences, International Islamic University Malaysia, Malaysia 2Department of Physical and Mathematical Science, Universiti Tunku Abdul Rahman, Malaysia

3Centre for Mathematical Sciences, Universiti Tunku Abdul Rahman, Kampar Campus, Jalan Universiti, Malaysia

Received July 11, 2019; Revised September 5, 2019; Accepted September 19, 2019

Copyright©2019 by authors, all rights reserved. Authors agree that this article remains permanently open access under the terms of the Creative Commons Attribution License 4.0 International License

Abstract In recent years, there has been a growing interest in financial network. The financial network helps to visualize the complex relationship between stocks traded in the market. This paper investigates the stock market network in Bursa Malaysia during the 2008 global financial crisis. The financial network is based on the top hundred companies listed on Bursa Malaysia. Minimal spanning tree (MST) is employed to construct the financial network and uses cross-correlation as an input. The impact of the global financial crisis on the companies is evaluated using centrality measurements such as degree, betweenness, closeness and eigenvector centrality . The results indicate that there are some changes on the linkages between securities after the financial crisis, that can have some significant effect in investment decision making.

Keywords Financial Network, Minimal Spanning Tree, Centrality Measures

1. IntroductionRelationship between two stocks can be measured using

a cross-correlation coefficient that uses series of log return as an input. Cross-correlation coefficients play a major role in many areas such as portfolio optimization theory and risk management model. However, if the number of stocks is large, the correlations between stocks cannot be visualised clearly. Thus, building a financial network is necessary so that the interactions between stocks can be displayed clearly. Financial network helps market participants get an overview of the connections between stocks traded in the market.

Minimal spanning tree (MST) is one of the approaches to construct a financial network as suggested by Mantegna [1]. This approach is widely used specifically in analysing

the emerging market networks such as the Indian stock market [2], United States stock market [3], Chinese stock market[4], Hong Kong stock market [5],Brazilian stock market [6,7], and Malaysian stock market [8]. Further, researchers are motivated to examine the impact of financial crisis in stock market network. For instance, [9] investigated the structural changes in the minimal spanning tree of the Korean stock market around the global financial crisis. The result showed that there were changes in terms of the topological structure and the central hub of the network for the period before, during and after crisis. [10] showed that the global financial crisis has an impact towards South African stock market in which the network clustered differently in terms of degree centrality, sectorial betweenness centrality and domination strength sub-metric. There are several papers stated that the global financial crisis has different impacts on MST structure such as [3,9,11,12].

Although previous literature applied MST in examining the financial network of various stock markets, to the best of our knowledge, no studies have been found in investigating the impact of global financial crisis on Bursa Malaysia. Thus, this paper aims to examine the effect of a global financial crisis towards Bursa Malaysia by using MST.

This paper is structured as follows. Section 2 presents the data set. Section 3 elaborates the methods to construct the financial network. Section 4 reports the result on how the network changes during pre-, during and post-crises. Section 5 presents the conclusion.

2. DataThis paper utilises the adjusted closing price in which

adjusted for dividends and split of hundred companies based on top hundreds of market capitalisation listed on

2 The Investigation on the Impact of Financial Crisis on Bursa Malaysia Using Minimal Spanning Tree

Bursa Malaysia. The data is obtained from Thomson Reuters Data stream database. The period of the data is from June 2, 2006, to December 30, 2010. The period of the data is divided into three parts; pre-, during and post-crises by referring to the seminal works of Lee and Nobi [9]. This paper considers the period of pre-crisis from June 2, 2006, until November 30, 2007. The duration of crisis period is from December 3, 2007, until June 30, 2009, due to the high mean volatility in all indices[13]. This period is based on the global financial crisis which was started from the bankruptcy of Lehman Brothers [14]. The post-crisis period is from July 1, 2007, until November 30, 2010, in which the mean volatility of some developed markets return to normal state [9]. The number of stocks for each period varies due to the availability of the data in which pre-crisis has 69 companies, during crisis has 70 companies, and post-crisis has 74 companies. The stocks are divided into twelve sectors: industrial, products and services, energy, property, transportation and logistics, health care, consumer products and services, plantation, financial services, real estate investment trusts, telecommunications and media, utilities, technology and construction. The details of the corresponding symbols, and the sectors of companies are listed in Appendix.

3. Methodology This section presents the procedure to construct a

financial network by using minimal spanning tree. The first subsection explains the procedure to construct the network using minimal spanning tree and the second subsection shows the calculation of centrality measures.

3.1. Minimal Spanning Tree

L Firstly, cross-correlation matrices based on the log return of adjusted closing prices are calculated. The correlation coefficient, ijC , between stocks i and j is given by

( ) ( )222 2

i j i jij

i i j j

r r r rC

r r r r

−=

− − − (1)

where ir is the vector of the log-returns. The log-returns can be compute as ( ) ( ) ( )ln lni i ir t P t P tτ= + − and ( )iP t is the price of

stock i on date t . The symbol ... represents an average over time. Correlation coefficients obtained within the range of 1 1ijC− ≤ ≤ , indicate that -1 means inversely correlated and 1 means completely correlated between stocks. The value of 0 means the stocks are uncorrelated. The correlation coefficient between stocks i and j will form the symmetric N N× matrix.

Secondly, correlation coefficients are transformed into a distance matrix as suggested by [1] and [15]However, correlation coefficients cannot be considered as a distance between two stocks because they do not satisfy the properties of Euclidean metric which are

0ij

ij ji

ij ik kj

dd d

d d d

≥ = ≤ +

(2)

Thus, the distance between stock and stock can be calculated as follows:

( )2 1ij ijD C= − (3)

Thirdly, financial network is constructed using the minimum spanning tree based on the distance matrix via a Kruskal algorithm[16].There are several steps listed in Kruskal algorithm which are, 1) sort the distance between two stocks in ascending order, 2) choose a pair of stocks with the smallest distance and connect them with an edge, 3) choose a second small distance, 4)connect the nearest pair and ignore the pair if it forms a cycle in the network, and 5) repeat the steps until all the stocks are connected in a unique network.

3.2. Centrality Measures

Centrality measures are employed for further analyses of the financial network. This study uses four types of centrality measures, namely, degree, betweenness, closeness and eigenvector centrality.

Degree centrality represents the total number of stocks that are connected to a stock i . The calculation of degree centrality is as follows:

( )1

Nijj

Degree

AC i

N=

−∑ (4)

where 1ijA = if the stock i and stock j is connected and 0 otherwise.

Closeness centrality for one node can be calculated as the average distance of all distances from this node to all other nodes in the network [17] as in equation (5).A stock that has the highest value of closeness centrality is considered important when studying the effect of crisis situation in the network. Further, a stock with a high closeness centrality shows that the overall impact of the connectivity and distance in the network is severe.

( ) ( )1

1,

N

closenessj

C i d i j−

=

= ∑ (5)

where ( ),d i j is the shortest path from stock i and stock

j .

Betweenness centrality evaluates whether a stock plays a

i j

Mathematics and Statistics 7(4A): 1-8, 2019 3

role as an intermediate between many stocks. It means that the stock lies between other stocks with respect to their shortest paths. The higher the value of betweenness centrality, the more important is the stock, since it controls the flow of information between many nodes [17]. The betweenness centrality can be evaluated using the following equation (6)

( ) ( )jkBetweenness

j k jk

g iC i i k j

g<

= ≠ ≠∑ (6)

where jkg is the total number of shortest path from node

j to k and ( )jkg i is the number of paths that pass through i .

The importance of stocks i within the financial network can be measured with eigenvector centrality. The value of this measure relies on a number of other crucial stocks that are linked to stock i. Eigenvector centrality is based on an adjacency matrix of the network and can be calculated as in equation (7)

( )1

1 N

eigen ij jj

C i A xλ =

= ∑ (7)

where jx is the eigenvector of stock j and ijA is an element of the adjacency matrix.

Since each centrality represents different measurements, this paper uses principal component analysis to summarize the performances of stocks in the financial network. The score of stock based on the overall centrality measure can be evaluated as

( ) ( ) ( ) ( )1 2 3 4i Degree Betweenness Closeness EigenvectorU e C i e C i e C i e C i= + + +

(8)

where ( )1 2 3 4, , , te e e e e= is the eigenvector of a covariance matrix S from the vector matrix of size N p×

and p is the first until the fourth column representing the score of degree, betweenness, closeness and eigenvector centrality. This eigenvector is associated with the largest eigenvalue.

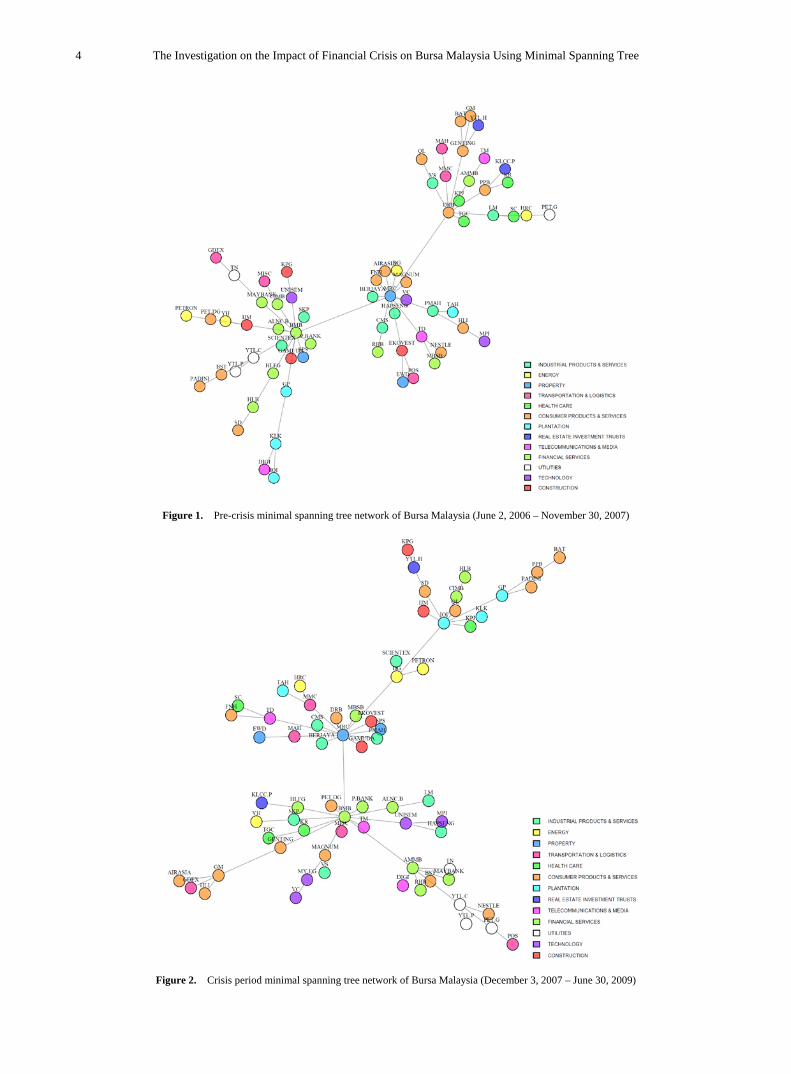

4. Results and Discussion Figure 1 shows the pre-crisis minimal spanning tree

network of Bursa Malaysia. From the figure, there are three clustered groups in the network, led by Bursa Malaysia Berhad (BMB), Malaysian Resources Corporation (MRC) and DRB-Hicom (DRB). BMB is considered as the centre of the network and is connected with other 14 companies, MRC is connected with other 13 companies, and DRB is connected with other nine companies. In addition, it shows that before the global financial crisis, Malaysian market has a strong reliance on financial services, property, consumer products and service sectors.

However, there are some changes in the network during the crisis period as depicted in Figure 2. BMB and MRC maintained as the centres of the network with additional companies included such as IOI Corporation (IOI) and AMMB Holdings (AMMB). However, DRB was no longer considered as a hub of the network. MST shows that the companies were clustered into four groups during crisis period instead of three groups as before the crisis.

Contrary, after the crisis, the hub of the network disappeared as shown in Figure 3. This changes was similar to the German stock exchange [18] and the Korean stock market [19]. BMB sustained its position as the hub of the network which was connected with 10 companies. Meanwhile, 7 companies were connected to Maybank and MRC, UEM and MPI were connected to 5 companies. The empirical evidence shows that after the global financial crisis, the number of nodes that have links with a hub decreased.

i

4 The Investigation on the Impact of Financial Crisis on Bursa Malaysia Using Minimal Spanning Tree

Figure 1. Pre-crisis minimal spanning tree network of Bursa Malaysia (June 2, 2006 – November 30, 2007)

Figure 2. Crisis period minimal spanning tree network of Bursa Malaysia (December 3, 2007 – June 30, 2009)

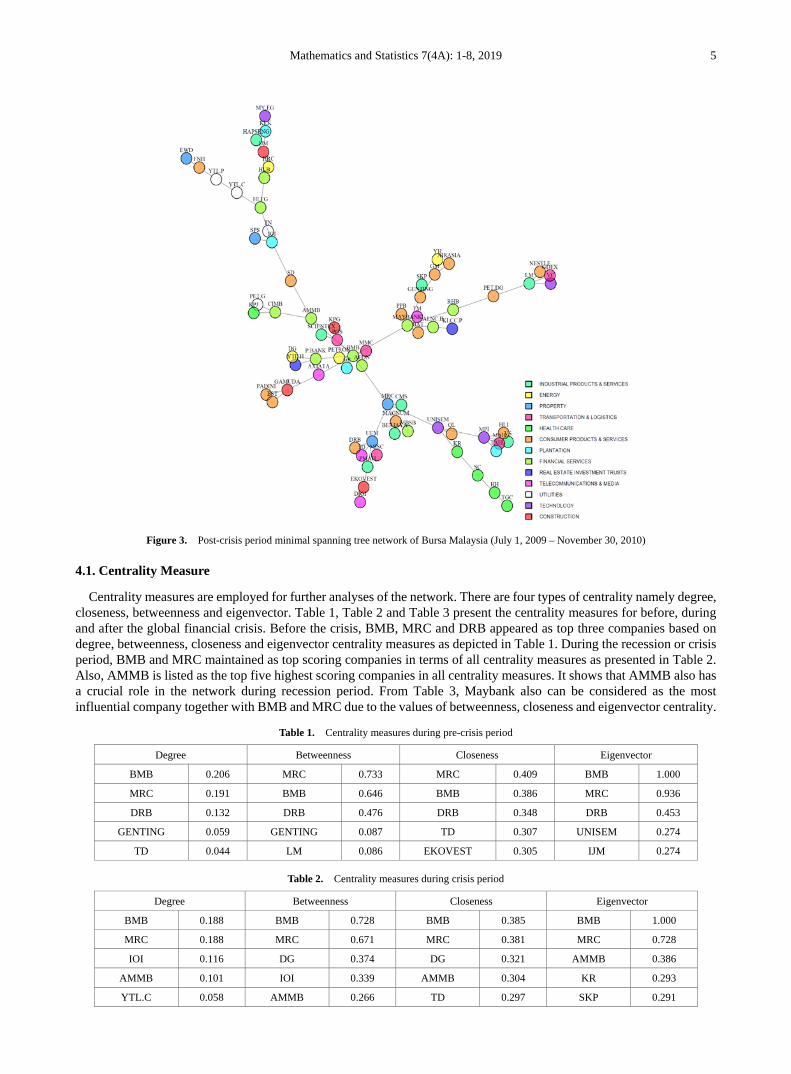

Mathematics and Statistics 7(4A): 1-8, 2019 5

Figure 3. Post-crisis period minimal spanning tree network of Bursa Malaysia (July 1, 2009 – November 30, 2010)

4.1. Centrality Measure

Centrality measures are employed for further analyses of the network. There are four types of centrality namely degree, closeness, betweenness and eigenvector. Table 1, Table 2 and Table 3 present the centrality measures for before, during and after the global financial crisis. Before the crisis, BMB, MRC and DRB appeared as top three companies based on degree, betweenness, closeness and eigenvector centrality measures as depicted in Table 1. During the recession or crisis period, BMB and MRC maintained as top scoring companies in terms of all centrality measures as presented in Table 2. Also, AMMB is listed as the top five highest scoring companies in all centrality measures. It shows that AMMB also has a crucial role in the network during recession period. From Table 3, Maybank also can be considered as the most influential company together with BMB and MRC due to the values of betweenness, closeness and eigenvector centrality.

Table 1. Centrality measures during pre-crisis period

Degree Betweenness Closeness Eigenvector

BMB 0.206 MRC 0.733 MRC 0.409 BMB 1.000

MRC 0.191 BMB 0.646 BMB 0.386 MRC 0.936

DRB 0.132 DRB 0.476 DRB 0.348 DRB 0.453

GENTING 0.059 GENTING 0.087 TD 0.307 UNISEM 0.274

TD 0.044 LM 0.086 EKOVEST 0.305 IJM 0.274

Table 2. Centrality measures during crisis period

Degree Betweenness Closeness Eigenvector

BMB 0.188 BMB 0.728 BMB 0.385 BMB 1.000

MRC 0.188 MRC 0.671 MRC 0.381 MRC 0.728

IOI 0.116 DG 0.374 DG 0.321 AMMB 0.386

AMMB 0.101 IOI 0.339 AMMB 0.304 KR 0.293

YTL.C 0.058 AMMB 0.266 TD 0.297 SKP 0.291

6 The Investigation on the Impact of Financial Crisis on Bursa Malaysia Using Minimal Spanning Tree

Table 3. Centrality measures during post-crisis period

Degree Betweenness Closeness Eigenvector

BMB 0.188 BMB 0.728 BMB 0.267 BMB 1.000

MRC 0.188 MRC 0.671 MRC 0.239 MAYBANK 0.565

IOI 0.116 DG 0.374 AMMB 0.233 MRC 0.448

AMMB 0.101 IOI 0.339 MAYBANK 0.230 POS 0.359

YTL.C 0.058 AMMB 0.266 AXIATA 0.209 P.BANK 0.337

Principal component analysis is used to determine the most influential stock in the network for each period. Before the crisis, the most prominent stocks belong to MRC, BMB and DRB. MRC and BMB are still selected as the companies with the highest scores in overall centrality measures together with AMMB during crisis. After the global financial crisis, MRC, BMB and MAYBANK are the most crucial stocks in Bursa Malaysia.

The dominated stock for each period give the influence in the market in terms of comovement of stock price relatively towards the connected stocks. Besides, the most influential stock has effect on stock returns and the more vital within the network of stock market typically had higher revenue for compensation since they endured greater exposure to correlation risk.

5. Conclusions This paper aims to investigate the effects of global financial crisis on the correlation of stocks traded on Bursa

Malaysia using a minimal spanning tree. The Period of data used is divided into three parts: before, during and after the global financial crisis. In general, minimal spanning tree topology changes for each period. Before the crisis, the stocks clustered clearly into three groups and during the crisis, the stocks are dispersed into four groups. However, the stocks are scattered throughout the map after the financial crisis. The results were further assessed using degree, betweeness, closeness and eigenvector centrality. The empirical evidence shows that MRC and BMB are the most crucial stocks before, during and after the crisis.

Acknowledgements The authors thank the Ministry of Higher Education Malaysia (MOHE) under Fundamental Research Grant Scheme

(FRGS15-191-0432) and International Islamic University Malaysia under Research Initiative Grant Scheme (P-RIGS18-031-0031) for the financial support provided.

Appendix Table 4. Companies, sectors and their corresponding symbols

Symbol Company Sector Symbol Company Sector

VS VS INDUSTRY Industrial Products & Services GDEX GD EXPRESS CARRIER Transportation &

Logistics

PETRON PETRON MAL.REFN.& MKTG. Energy BERJAYA BERJAYA CORPORATION Industrial Products &

Services SPS SP SETIA Property HH HARTALEGA HOLDINGS Health Care

SKP SKP RESOURCES BERHAD

Industrial Products & Services HLI HONG LEONG INDUSTRIES Consumer Products &

Services

MMC MMC CORPORATION Transportation & Logistics TN TENAGA NASIONAL Utilities

HRC HENGYUAN REFINING COMPANY Energy SC SUPERMAX CORPORATION Health Care

KR KOSSAN RUBBER Health Care UNISEM UNISEM (M) Technology

SD SIME DARBY Consumer Products & Services AIRASIA AIRASIA GROUP Consumer Products &

Services

PET.DG PETRONAS DAGANGAN

Consumer Products & Services PADINI PADINI HOLDINGS Consumer Products &

Services

Mathematics and Statistics 7(4A): 1-8, 2019 7

MAGNUM MAGNUM Consumer Products & Services KLK KUALA LUMPUR KEPONG Plantation

CMS CAHYA MATA SARAWAK

Industrial Products & Services HAPSENG HAP SENG CONSOLIDATED Industrial Products &

Services

IOI IOI CORPORATION Plantation DIGI DIGI.COM Telecommunications & Media

AEON AEON CREDIT SERVICE Financial Services PET.G PETRONAS GAS Utilities

GENTING GENTING Consumer Products & Services BST BERJAYA SPORTS TOTO Consumer Products &

Services

KLCC.P KLCC PROPERTY

HOLDINGS STAPLED UNITS

Real Estate Investment Trusts MISC MISC BHD. Transportation &

Logistics

DRB DRB-HICOM Consumer Products & Services CIMB CIMB GROUP HOLDINGS Financial Services

TD TIME DOTCOM Telecommunications & Media QL QL RESOURCES Consumer Products &

Services

LM LAFARGE MALAYSIA

Industrial Products & Services KPG KERJAYA PROSPEK GROUP Construction

PPB PPB GROUP Consumer Products & Services ALNC.B ALLIANCE BANK MALAYSIA Financial Services

MAH MALAYSIA AIRPORTS HDG.

Transportation & Logistics TAH TA ANN HOLDINGS Plantation

TGC TOP GLOVE CORPORATION Health Care EWD ECO WORLD DEV.GROUP Property

GP GENTING PLANTATIONS Plantation GM GENTING MALAYSIA Consumer Products &

Services

FNH FRASER & NEAVE HOLDINGS

Consumer Products & Services YTL.H YTL HOSPITALITY REIT Real Estate

Investment Trusts

MAYBANK MALAYAN BANKING Financial Services POS POS MALAYSIA Transportation & Logistics

NESTLE NESTLE (MALAYSIA) Consumer Products & Services BAT BRIT.AMER.TOB.(MALAYSIA) Consumer Products &

Services P.BANK PUBLIC BANK Financial Services HLFG HONG LEONG FINL.GP. Financial Services

HLB HONG LEONG BANK Financial Services KPJ KPJ HEALTHCARE Health Care

RHB RHB BANK BHD Financial Services AMMB AMMB HOLDINGS Financial Services

YTL.C YTL CORPORATION Utilities PMAH PRESS METAL ALUMINIUM HOLDINGS

Industrial Products & Services

YTL.P YTL POWER INTERNATIONAL Utilities IJM IJM CORPORATION Construction

MBSB MALAYSIA BUILDING SOC. Financial Services MPI MALAYSIAN PACIFIC INDS. Technology

MY.EG MY EG SERVICES Technology DG DIALOG GROUP Energy

BMB BURSA MALAYSIA Financial Services TM TELEKOM MALAYSIA Telecommunications & Media

YH YINSON HOLDINGS Energy EKOVEST EKOVEST Construction

UEM UEM SUNRISE Property SCIENTEX SCIENTEX Industrial Products & Services

VC VITROX CORPORATION Technology GAMUDA GAMUDA Construction

MRC MALAYSIAN RESOURCES

CORPORATION Property AXIATA AXIATA GROUP Telecommunications

& Media

8 The Investigation on the Impact of Financial Crisis on Bursa Malaysia Using Minimal Spanning Tree

REFERENCES R. N. Mantegna. Hierarchical structure in financial markets. [1]

The European Physical Journal B, Vol.11, No.1, 193-197, 1999.

S. Sinha, R. K. Pan. Uncovering the internal structure of the [2]Indian financial market: large ross-correlation behavior in the NSE. Econophysics of Markets and Business Networks, Vol. 66, 3-19, 2007.

Y. Tang, J. J. Xiong, Z. Jia, Y. Zhang. Complexities in [3]financial network topological dynamics: modeling of emerging and developed stock markets. Complexity, 1-31, 2018.

W-Q. Hunag, X-T. Zhuang, S. Yao. A network analysis of [4]the Chiense stock market. Physica A: Statistical Mechanics and its Applications, Vol.388, No.14, 2956-2964, 2009.

W. Zhang, J. Wen, Y. Zhu. Minimal spanning tree analysis [5]of topological structures: the case of Hang Seng Index. Iberian Journal of Information System and Technologies, Vol.7, 145-155, 2016.

B. M. Tabak, T. R. Serra, D. O. Cajueiro. Topological [6]properties of stock market networks: The case of Brazil. Physica A, Vol.389, 3240-3249, 2010.

L. Sandoval. A map of the Brazilian stock market. Advances [7]in Complex Systems 2, Vol.15, No.4, 2012.

L. S. Yee, R. M. Salleh, N. M. Asrah. Multidimensional [8]minimal spanning tree: The Bursa Malaysia. Journal of Science and Technology, Vol.10, 136-143, 2018.

J. W. Lee, A. Nobi. State and network structures of stock [9]markets around the global financial crisis. Computational Economics. Vol.51, No.2, 195-210, 2017.

M. Majapa, S. J. Gossel. Topology of the South African [10]stock market network across the 2008 financial crisis. Physica A, Vol.445, 35-47, 2016.

E. Kantar, M. Keskin, B. Deviren. Analysis of the effects of [11]the global financial crisis on the Turkish economy, using hierarchical methods. Physica A, Vol.391, 2342-2352, 2012.

L. Xia, D. You, X Jiang, Q. Guo. Comparison between [12]global financial crisis and local stock disaster on top of Chinese stock network. Physica A: Statistical Mechanics and its Applications, Vol.490, 222-230, 2018.

A. Nobi, S. E. Maeng, G. G. Ha, J. W. Lee. Random matrix [13]theory and cross-correlations in global financial indices and local stock market indices. Journal-Korean Physical Society, Vol.62, No.4, 569-574, 2013.

N. Baba, F. Packer. From turnoil to crisis: Dislocations in the [14]FX swap market before and after the failure of Lehman Brothers. Journal of International Money and Finance, Vol.28, No.8, 1350-1374, 2009.

G. Bonanno, G. Caldarelli, F. Lillo, S. Miccich. Networks of [15]equities in financial markets. Physics of Condensed Matter, Vol.38, No.2, 363-371, 2004.

J. Kruskal. On the shortest spanning subtree of a graph and [16]the traveling salesman problem. Proceedings of the American Mathematical Society, Vol.7, No.1, 48-50, 1956.

M. E. J. Newman. A measure of betweenness centrality [17]based on random walks. Social Networks, Vol.27, No.1, 39-54, 2005.

M. Wiliński, A. Sienkiewicz, T. Gubiec, R. Kutner, Z. R. [18]Struzik. Structural and topological phase transitions on the German Stock Exchange. Physica A: Statistical Mechanics and its Applications, Vol.392, 5963-5973, 2013.

A. Nobi, S. E. Maeng, G. G. Ha, J. W. Lee. Structural [19]changes in the minimal spanning tree and the hierarchical network in the Korean stock market around the global financial crisis G. Journal of the Korean Physical Society, Vol.66, No.8, 1153-1159, 2015.

Mathematics and Statistics 7(4A): 9-16, 2019 http://www.hrpub.org DOI: 10.13189/ms.2019.070702

A 2-Component Laplace Mixture Model: Properties and Parametric Estimationsi

Zakiah I. Kalantan1,*, Faten Alrewely2

1Faculyu of Science, King Abdulaziz University, Jeddah, Saudi Arabia 2Faculty of Science, Al Jouf University, Sakaka, Saudi Arabia

Received July 1, 2019; Revised August 28, 2019; Accepted September 20, 2019

Copyright©2019 by authors, all rights reserved. Authors agree that this article remains permanently open access under the terms of the Creative Commons Attribution License 4.0 International License

Abstract Mixture distributions have received considerable attention in life applications. This paper presents a finite Laplace mixture model with two components. We discuss the model properties and derive the parameters estimations using the method of moments and maximum likelihood estimation. We study the relationship between the parameters and the shape of the proposed distribution. The simulation study discusses the effectiveness of parameters estimations of Laplace mixture distribution.

Keywords Laplace Distribution, Mixture Distribution, Method of Moments, Maximum Likelihood Estimation

1. IntroductionLaplace distribution has wide applications in various

fields such as engineering, business, medicine, and others. It is also known as a double exponential distribution because it is considered as two exponential distributions with additional location parameter. It considers as a member of lifetime distributions.

Mixture distributions and the problem of mixture decomposition about the identification of the constituent components and parameters dates back to 1846, but most of the reference is made due to the work of Karl Pearson in 1894 [7]. The approach taken by Pearson was to fit a univariate mixture of two normal to data through the choice of five parameters of the mixture in a way that empirical moments matched the model. The work by Pearson was successful in identifying two distinct sub-populations and also showing the flexibility of mixtures as a moment matching tool. Other later works focused on addressing the problems, but the invention of the modern computer and the popularization of the maximum likelihood parameterization techniques caused a stir in research work on mixture models [6]. In 2002, Figueiredo and Jain

applied the finite mixture to unsupervised learning models and gave important insights into mixture models [3]. Bhowmick et al introduced the Laplace mixture model instead of the Gaussian mixture model due to the tail length and a weight of the Laplace distribution, then applied the mixture micro-experiments [2]. Ali and Nadarajah found the information matrices for the Gaussian distribution mixture and the Laplace distribution mixture [5]. A mixture of asymmetric Laplace and Gaussian distributions was estimated using the EM algorithm by Shenoy and Gorinevsky [11]. Amini-Seresht and Zhang provided random comparisons of two finite-mixture models with different mixing ratios and independent variables [1].

Most of the references presented comprehensive studies and applications of finite mixture models which is based on the work of McLachlan, and Peel [6]. Ramana et al., introduced the two-component mixture of Laplace and Laplace type bimodal distributions, and they find the properties and estimation for the common parameters between the two-component mixture [9]. The previous studies are based on equal mixing parameters or constant scale parameters. The aim of this paper is to study the two components Laplace mixture model and estimate its parameters in the case of unknown all model parameters using parametric estimation methods.

The paper is organized as follows: Section 2 presents the definition of Laplace mixture distribution. Section 3 discusses the distribution function. The properties of the proposed distribution are studied in Section 4. The estimation methods are presented in Section 5. The simulation studies are presented in Section 6. Finally, conclusions are drawn in Section 7.

2. Laplace Mixture Distribution

2.1. Definition of Mixture Distribution

The Consider dataset 𝑋𝑋 = (𝑥1, 𝑥2, . . . , 𝑥𝑛) be

10 A 2-Component Laplace Mixture Model: Properties and Parametric Estimations

N-dimensional random variable, then 𝑋𝑋 follows 𝑘 components Laplace mixture distribution if its probability density function can be written as:

𝑓�𝑥; 𝜃� = ∑ 𝛼𝑖𝑘𝑖=1 𝑓𝑖�𝑥; 𝜃𝑖� (1)

where 𝛼𝑖 , 𝑖 = 1,2, … , 𝑘 are the mixing probabilities that satisfy 𝛼𝑖 ≥ 0 and ∑ 𝛼𝑖𝑘

𝑖=1 = 1.

2.2. Mixture of a Two Laplace Distribution

Let 𝑋𝑋 a random variable, the overall formula of the distribution of Laplace is

𝑓(𝑥; 𝜃) = 12𝜆

𝑒𝑥𝑝 �−│𝑥−𝜇│𝜆

�, (2)

where −∞ < 𝑥 < ∞,−∞ < 𝜇𝜇 < ∞, and 𝜆 > 0. In this paper, we will consider two components (k=2) for

Laplace mixture (A2-CLPM) distribution, where the first component provides the proportion α1 and density parameters 𝜇𝜇1, 𝜆1. The second one provides the proportion 𝛼2 = (1 − 𝛼1) and the second density parameters 𝜇𝜇2, 𝜆2, then the A2-CLPM distribution can be written as:

𝑓�𝑥; 𝜃� = 𝛼1 𝐿𝑎𝑝𝑙𝑎𝑐𝑒(𝜇𝜇1, 𝜆1) + (1 − 𝛼1) 𝐿𝑎𝑝𝑙𝑎𝑐𝑒(𝜇𝜇2, 𝜆2) (3)

Then, the probability density function (pdf) for A2-CLPM distribution is

𝑓�𝑥; 𝜃� = 𝛼12𝜆1

𝑒𝑥𝑝 �−│𝑥−𝜇1│𝜆1

� + (1−𝛼1)2𝜆2

𝑒𝑥𝑝 �−│𝑥−𝜇2│𝜆2

�, (4)

where −∞ < 𝑥 < ∞,−∞ < 𝜇𝜇1,𝜇𝜇2 < ∞, 𝜆1, 𝜆2 > 0 , and 𝛼1 + (1 − 𝛼1) = 1.

Figure 1 presents the curve of A2-CLPM distribution with parameters equal 𝜃 = (𝛼1, 𝜇𝜇1,𝜇𝜇2, 𝜆1, 𝜆2).

Figure 1. The frequency curves of the mixture Laplace distribution.

3. The Cumulative Density Function (CDF)

We state that the given pdf is a density function by computing the integral of the mixture distribution over its range, then we have

∫ 𝑓�𝑥; 𝜃�+∞−∞ 𝑑𝑥 = ∫ � 𝛼1

2𝜆1 𝑒𝑥𝑝 �−│𝑥−𝜇1│

𝜆1� +∞

−∞(1−𝛼1)2𝜆2

𝑒𝑥𝑝 �−│𝑥−𝜇2│𝜆2

�� 𝑑𝑥 = 1. (5)

The cumulative distribution function (CDF) of 𝑋𝑋 defines as:

𝐹(𝑥) = � 𝑓�𝑤; 𝜃�𝑑𝑤𝑥

−∞

𝐹(𝑥) = � �𝛼1

2𝜆1 𝑒𝑥𝑝 �−

│𝑤 − 𝜇𝜇1│𝜆1

�𝑥

−∞

+(1 − 𝛼1)

2𝜆2 𝑒𝑥𝑝 �−

│𝑤 − 𝜇𝜇2│𝜆2

�� 𝑑𝑤

then we have

𝐹(𝑥) =12

�𝛼1 𝑒𝑥𝑝 �𝑥 − 𝜇𝜇1𝜆1

� + (1 − 𝛼1) 𝑒𝑥𝑝 � 𝑥 − 𝜇𝜇2𝜆2

��,

for 𝑥 ≤ 𝜇𝜇1,𝜇𝜇2 and

𝐹(𝑥) = 𝛼1 �1 −12𝑒𝑥𝑝 �−

(𝑥 − 𝜇𝜇1)𝜆1

��

+ (1 − 𝛼1) �1 −12𝑒𝑥𝑝 �−

(𝑥 − 𝜇𝜇2)𝜆2

��,

for 𝑥 > 𝜇𝜇1,𝜇𝜇2 (6)

4. The Properties of Laplace Mixture Distribution

In what follows, the distribution properties are studied by obtaining the mean, the mode, the median, and the variance of A2-CLPM distribution. The mean of the random variable 𝑋𝑋 is

𝜇𝜇 = 𝐸(𝑥) = � 𝑥𝑓�𝑥; 𝜃� +∞

−∞𝑑𝑥

𝜇𝜇 =𝛼1

2𝜆1∫ 𝑥𝑒𝑥𝑝 �− │𝑥−𝜇𝜇1│

𝜆1�+∞

−∞ 𝑑𝑥 +

(1− 𝛼1)2𝜆2

∫ 𝑥 𝑒𝑥𝑝 �− │𝑥−𝜇𝜇2│

𝜆2�+∞

−∞ 𝑑𝑥 = 𝛼1𝜇𝜇1 + (1 − 𝛼1)𝜇𝜇2.

(7)

The mode of the random variable 𝑋𝑋 given from 𝑑𝑑𝑥𝑓�𝑥; 𝜃� = 0. (8)

when derived the equation (4) were 𝑥 ≥ 𝜇𝜇 or 𝑥 < 𝜇𝜇, we get the same mode for both of them, the formula are following as:

𝑥 = 𝜆2𝜇1+𝜆1𝜇2𝜆1+𝜆2

. (9)

The median of this distribution can be obtained as 𝑝(𝑥 ≤ 𝑐 ) = 1

2 , (10)

Mathematics and Statistics 7(4A): 9-16, 2019 11

because of symmetry, we can suppose that

𝑐 ≤ 𝜆2𝜇1+𝜆1𝜇2𝜆1+𝜆2

. (11)

The variance and standard deviation of the mixture distribution.

The variance is defined as:

𝜎2 = 𝑣𝑎𝑟(𝑥) = 𝐸(𝑥2) − �𝐸(𝑥)�2. (12)

Then, we find 𝐸(𝑥2), as following as:

𝐸(𝑥2) = ∫ 𝑥2 𝑓�𝑥; 𝜃�+∞−∞ 𝑑𝑥.

𝐸(𝑥2) =𝛼1

2𝜆1� 𝑥2 exp�−

│𝑥 − 𝜇𝜇│𝜆1

�+∞

−∞𝑑𝑥 +

(1 − 𝛼1)

2𝜆2� 𝑥2 𝑒𝑥𝑝 �−

│𝑥 − 𝜇𝜇│𝜆2

�+∞

−∞𝑑𝑥

𝐸(𝑥2) = 𝛼1�𝜇𝜇12 + 2𝜆12� + (1 − 𝛼1)�𝜇𝜇22 + 2𝜆2

2�. (13)

Then, substitute Eq (7) and Eq (13) in Eq (12), we get

𝜎2 = 𝑣𝑎𝑟(𝑥)

𝜎2 = 𝛼1�𝜇𝜇12 + 2𝜆12� + (1 − 𝛼1)�𝜇𝜇22 + 2𝜆2

2� − [𝛼1𝜇𝜇1 + (1 − 𝛼1)𝜇𝜇2]2. (14)

The stander deviation of the random variable 𝑋𝑋 is the square root of the variance.

𝜎 = �𝑣𝑎𝑟(𝑥)

𝜎 = �𝛼1�𝜇𝜇12 + 2𝜆12� + (1 − 𝛼1)�𝜇𝜇22 + 2𝜆2

2� − 𝛼1𝜇𝜇1 +(1 − 𝛼1)𝜇𝜇2. (15)

Tables (1-5) present the properties of three samples of size 1000 taken from Laplace mixture distribution, we compute the mean, mode, median, variance, skewness and

kurtosis with different parameters values for Laplace mixture distribution. For simplicity, we take special cases of mixture distribution in order to study the performance of the Laplace mixture distribution.

In Table 2, we state the performance of scale parameters by assuming that location parameters 𝜇𝜇1 = 0,𝜇𝜇2 = 2 ,α1 = 0.3 and λ2 = 2. As expected, the simulation results illustrate that the Laplace mixture distribution has a positive skewness and a heavy tail which provides a good fitted model for life applications where outliers have located in the right tail of the mixture curve. As also as, the Laplace mixture distribution has a positive kurtosis equals 3.317 which indicates that the curve approximately has normal curve. For Table 2, we compute the distribution properties with different values of second scale parameter λ2 by setting other parameters by 𝜇𝜇1 = 3,𝜇𝜇2 = 5,α1 = 0.4 and λ1= 0.5.

The third case studies the properties of the proposed mixture model with different values of mixing parameter α1 = 0.2, 0.5 and 0.9 , we assume 𝜇𝜇1 = 0, 𝜇𝜇2 = 5 , λ1 =1, and λ2 = 2. The results are presented in Table 3, which illustrates equal values of mean and median. At α1 = 0.2, we observe that kurtosis equals 3.25 which indicates that the curve approximately has normal curve. In contrast, when α1 = 0.5 and 0.9 the curve has heavy tail. Table 4 displays the results of studying three samples from Laplace mixture distribution with parameters values α1 = 0.6, 𝜇𝜇2 = 3, λ1 = 4, and λ2 = 6. In this case we use different values of first location parameter 𝜇𝜇1 = (1, 2, 4). We observe that the three distributions have skewness = 0.5 or 0.6, and kurtosis ≅ 2.1 which means that the curves are close to the normal distribution curve. The results of final case is presented in Table 5, it also draws the same conclusions that when 𝜇𝜇1 = 5, λ1 = 1, λ2 = 5 andα1 = 0.2 , while the vector of second location number equals to 𝜇𝜇2= (1, 2, 3).

Table 1. The results of three samples of Laplace mixture distribution when λ1 = (0.5, 1, 3)

(𝛂𝟏,𝛍𝟏,𝛍𝟐,𝛌𝟏,𝛌𝟐) Mean Median Variance Skew. Kurt.

(𝟎.𝟑,𝟎,𝟐,𝟎.𝟓,𝟐) 0.0495 0.0144 0.0049 1.865 3.317

(𝟎.𝟑,𝟎,𝟐,𝟏,𝟐) 0.0494 0.0169 0.0038 1.212 0.005

(𝟎.𝟑,𝟎,𝟐,𝟑,𝟐) 0.0489 0.0253 0.0027 1.202 0.310

Table 2. The results of three samples of Laplace mixture distribution when λ2 = (1, 2, 3)

(𝛂𝟏,𝛍𝟏,𝛍𝟐,𝛌𝟏,𝛌𝟐) Mean Median Variance Skew. Kurt.

(𝟎.𝟒,𝟑,𝟓,𝟎.𝟓,𝟏) 0.0497 0.0023 0.0081 1.986 6.233

(𝟎.𝟒,𝟑,𝟓,𝟎.𝟓,𝟐) 0.0486 0.0125 0.0062 2.442 0.733

(𝟎.𝟒,𝟑,𝟓,𝟎.𝟓,𝟑) 0.0469 0.0191 0.0054 2.849 12.34

Table 3. The results of three samples of Laplace mixture distribution when α1 = (0.2, 0.5, 0.9)

(𝛂𝟏,𝛍𝟏,𝛍𝟐,𝛌𝟏,𝛌𝟐) Mean Median Variance Skew. Kurt.

(𝟎.𝟐,𝟎,𝟓,𝟏,𝟐) 0.0328 0.0328 0.0026 1.0183 3.259

(𝟎.𝟓,𝟎,𝟓,𝟏,𝟐) 0.0309 0.0309 0.0029 1.4448 5.078

(𝟎.𝟗,𝟎,𝟓,𝟏,𝟐) 0.0126 0.0126 0.0080 2.555 9.144

12 A 2-Component Laplace Mixture Model: Properties and Parametric Estimations

Table 4. The results of three samples of Laplace mixture distribution when 𝜇𝜇1 = (1, 2, 4)

(𝛂𝟏,𝛍𝟏,𝛍𝟐,𝛌𝟏,𝛌𝟐) Mean Median Variance Skew. Kurt.

(𝟎.𝟔,𝟏,𝟑,𝟒,𝟔) 0.0430 0.0364 0.0007 0.5553 2.082

(𝟎.𝟔,𝟐,𝟑,𝟒,𝟔) 0.0428 0.0360 0.0007 0.622 2.294

(𝟎.𝟔,𝟒,𝟑,𝟒,𝟔) 0.0418 0.0360 0.0008 0.5604 2.170

Table 5. The results of three samples of Laplace mixture distribution when 𝜇𝜇2 = (1, 2, 3)

(𝛂𝟏,𝛍𝟏,𝛍𝟐,𝛌𝟏,𝛌𝟐) Mean Median Variance Skew. Kurt.

(𝟎.𝟕,𝟓,𝟏,𝟑,𝟏.𝟓) 0.0464 0.0346 0.002 0.4193 1.693

(𝟎.𝟕,𝟓,𝟐,𝟑,𝟏.𝟓) 0.0464 0.0306 0.002 0.6367 1.912

(𝟎.𝟕,𝟓,𝟑,𝟑,𝟏.𝟓) 0.0463 0.0273 0.002 0.9090 2.433

5. Parametric Estimation Methods In this section, we obtain the parameter estimates of Laplace mixture distribution using two parametric estimation

methods: method of moments (MME) and maximum likelihood estimation (MLE) method. The illustrations are presented in the following subsections.

5.1. The Method of Moments (MME)

Let 𝑋𝑋 be a random variable with A2-CLPM (α1,µ1, µ2, λ1, λ2) distribution. The 𝑟 𝑡ℎ moments are defined as:

𝐸(𝑥𝑟) = � 𝑥𝑟 𝑓�𝑥; 𝜃�𝑑𝑥+∞

−∞

= ∫ 𝒙𝒓 � 𝜶𝟏𝟐𝝀𝟏

𝒆𝒙𝒑 �−│𝒙−𝛍𝟏│𝝀𝟏

� + (𝟏−𝜶𝟏)𝟐𝝀𝟐

𝒆𝒙𝒑 �−│𝒙−𝛍𝟐│𝝀𝟐

��𝒅𝒙 ∞−∞ . (16)

For simplicity, we use the Taylor series instead of integration, because, we need to find eight moments, and solve these integrations are very hard, see [8], as following as:

𝜇𝜇�� = 𝐸(𝑥𝑟)

= �𝛂𝟏𝟐���

𝒓!(𝒓 − 𝒌)!

𝛌𝟏𝒌𝛍𝟏(𝒓−𝒌)�𝟏 + (−𝟏)𝒌�� + �

(𝟏 − 𝛂𝟏)𝟐

���𝒓!

(𝒓 − 𝒌)! 𝛌𝟐

𝒌𝛍𝟐(𝒓−𝒌)�𝟏+ (−𝟏)𝒌��𝒓

𝒌=𝟎

𝒓

𝒌=𝟎

.

𝜇𝜇𝑟 = �0 , 𝑖𝑓 𝑟 𝑖𝑠 𝑜𝑑𝑑,

2α1 λ1𝑟 𝑟! + 2(1 − α1) λ2

𝑟 𝑟! , 𝑖𝑓 𝑟 𝑖𝑠 𝑒𝑣𝑒𝑛. (17)

The 𝑟𝑡ℎ means of the population are equal to

𝑀/𝑟 = 𝑃1

∑ 𝑥𝑖1𝑟𝑛

𝑖=1𝑛1

+ (1 − 𝑃1) ∑ 𝑥𝑖2

𝑟𝑛𝑖=1𝑛2

, (18)

where 𝑟 = 1,2,3, … ,𝑛 and 𝑃1 + (1 − 𝑃1) = 1 they are population mixing parameters. Then, by solve equations, as following as:

𝜇𝜇�� = 𝑀/𝑟. (19)

The estimations are made for the five parameters 𝜃 = (𝛼1,𝜇𝜇1, 𝜇𝜇2, 𝜆1, 𝜆2). For this mixture distribution, we compute the first eight raw moments in order to obtain the moment estimations of distribution parameters. It is noted that, we find parameter estimation 𝛼�2 from compute 1 − 𝛼�1. Also, it is noted that 𝐸(𝑥𝑟) = 0, for odd values > 1 𝑜𝑓 𝑟 therefore, we base our estimation on the first moment and the even moments. Now, from Eq (17) we get the first moment, as following as: when 𝑟 = 1

𝜇𝜇1 = 𝐸(𝑥) = 𝛼1𝜇𝜇1 + (1 − 𝛼1)𝜇𝜇2. (20)

when 𝑟 = 2

Mathematics and Statistics 7(4A): 9-16, 2019 13

��𝜇2 = 𝐸(𝑥2) = 𝛼1 �𝜇𝜇12+2𝜆1

2�+ (1−𝛼1 ) �𝜇𝜇22+2 𝜆2

2�. (21)

when 𝑟 = 4

��𝜇4 = 𝐸(𝑥4) = 𝛼1 �𝜇𝜇14 + 12 𝜆12 𝜇𝜇12 + 24 𝜆1

4� + (1 − 𝛼1 )�𝜇𝜇24 + 12 𝜆22 𝜇𝜇22 + 24 𝜆2

4�. (22)

when 𝑟 = 6

��𝜇6 = 𝐸(𝑥6) = 𝛼1 �𝜇𝜇16 + 30 𝜆1

2 𝜇𝜇14 + 360 𝜆1

4 𝜇𝜇12 + 720 𝜆1

6�+ (1−𝛼1 )

�𝜇𝜇26 + 30 𝜆22 𝜇𝜇24 + 360 𝜆2

4 𝜇𝜇22 + 720 𝜆26�. (23)

when 𝑟 = 8 ��𝜇8 = 𝐸(𝑥8) = 𝛼1 �µ18 + 56 𝜆1

2 µ16 + 1680 𝜆14 µ14 + 20160 𝜆1

6 µ12 + 40320 𝜆18�

+(1 − 𝛼1 )�µ28 + 56 𝜆22 µ26 + 1680 𝜆2

4 µ24 + 20160 𝜆26 µ22 + 40320 𝜆2

8�. (24)

To obtain estimates of the distribution parameters, equate the five equations above with Eq (18) for 𝑟 = 1,2,4,6,8 and then solving them. As following as:

𝜇𝜇/1 = 𝑀/

1

𝛼1𝜇𝜇1 + (1 − 𝛼1)𝜇𝜇2 = 𝑃1 ∑ 𝑥𝑖1𝑛𝑖=1𝑛1

+ (1 − 𝑃1) ∑ 𝑥𝑖2𝑛𝑖=1𝑛2

. (25)

𝜇𝜇/2 = 𝑀/

2

𝛼1 �𝜇𝜇12+2𝜆12� + (1 − 𝛼1 )�𝜇𝜇22+2 𝜆2

2�

= 𝑃1 ∑ 𝑥𝑖1

2𝑛𝑖=1𝑛1

+ (1 − 𝑃1) ∑ 𝑥𝑖22𝑛

𝑖=1𝑛2

. (26)

𝜇𝜇/4 = 𝑀/

4

𝛼1 �𝜇𝜇14 + 12 𝜆12 𝜇𝜇12 + 24 𝜆1

4� + (1 − 𝛼1 )

�𝜇𝜇24 + 12 𝜆22 𝜇𝜇22 + 24 𝜆2

4� = 𝑃1 ∑ 𝑥𝑖1

4𝑛𝑖=1𝑛1

+ (1 − 𝑃1) ∑ 𝑥𝑖24𝑛

𝑖=1𝑛2

. (27)

𝜇𝜇/6 = 𝑀/

6

𝛼1 �𝜇𝜇16 + 30 𝜆12 𝜇𝜇14 + 360 𝜆1

4 𝜇𝜇12 + 720 𝜆16�

+(1 − 𝛼1 )�𝜇𝜇26 + 30 𝜆22 𝜇𝜇24 + 360 𝜆2

4 𝜇𝜇22 + 720 𝜆26�

= 𝑃1 ∑ 𝑥𝑖1

6𝑛𝑖=1𝑛1

+ (1 − 𝑃1) ∑ 𝑥𝑖26𝑛

𝑖=1𝑛2

. (28)

𝜇𝜇/8 = 𝑀/

8

𝛼1 �µ18 + 56 𝜆12 µ16 + 1680 𝜆1

4 µ14 + 20160 𝜆16 µ12 + 40320 𝜆1

8� +

(1 − 𝛼1 )�µ28 + 56 𝜆22 µ26 + 1680 𝜆2

4 µ24 + 20160 𝜆26 µ22 + 40320 𝜆2

8� = P1 ∑ 𝑥𝑖1

8𝑛𝑖=1n1

+ (1 − P1) ∑ 𝑥𝑖28𝑛

𝑖=1n2

. (29)

Hence, the parameter estimates using method of moments can be obtained by solving the above equations numerically via R software.

2. The Maximum Likelihood Estimation (MLE)

The maximum likelihood estimation method (MLE) is used to estimate the parameters of the distribution. Now, let 𝑋𝑋 = (𝑥1 , 𝑥2, . . . . , 𝑥𝑛) is a random sample then the likelihood function of a given distribution is defined as:

𝐿 (𝜃) = ∏ 𝑓 � 𝑥𝑖 ; 𝜃�𝑛𝑖=1 . (30)

The maximum likelihood estimates for θ is calculated by finding a value of θ that maximizes log-likelihood function. i.e.

𝜃 = arg𝑚𝑎𝑥∑ 𝑙𝑜𝑔𝑓�𝑥𝑖 ; 𝜃�𝑛𝑖=1 . (31)

For Laplace mixture distribution, define 𝐿(𝜃) = 𝐿(𝛼1, 𝜆1, 𝜆2| 𝑥), where the location parameters are known, and equals 𝜇𝜇1 = 0,𝜇𝜇1 = 2. Then

14 A 2-Component Laplace Mixture Model: Properties and Parametric Estimations

𝐿(𝜃) = ∏ 𝑓(𝑥𝑖;𝛼1, 𝜆1, 𝜆2) =𝑛𝑖=1 ∏ � 𝛼1

2𝜆1 𝑒𝑥𝑝 �−│𝑥𝑖│

𝜆1� + (1−𝛼1)

2𝜆2 𝑒𝑥𝑝 �−│𝑥𝑖−2│

𝜆2��𝑛

𝑖=1 . (32)

log 𝐿(𝜃) = ∑ 𝑙𝑜𝑔 � 𝛼12𝜆1

𝑒𝑥𝑝 �−│𝑥𝑖│𝜆1� + 𝛼2

2𝜆2 𝑒𝑥𝑝 �−│𝑥𝑖−2│

𝜆2��𝑛

𝑖=1 . (33)

Next, to find the maximization of log-Likelihood we need to find the derivatives of log-likelihood function with respect to distribution parameters see [10], then we have

𝜕𝑙𝜕𝛼1

= ∑1

2𝜆1 𝑒𝑥𝑝�−

│𝑥𝑖│𝜆1

�− 12𝜆2

𝑒𝑥𝑝�−│𝑥𝑖−2│𝜆2

�

� 𝛼12𝜆1 𝑒𝑥𝑝�−

│𝑥𝑖│𝜆1

�+ 𝛼22𝜆2

𝑒𝑥𝑝�−│𝑥𝑖−2│𝜆2

�� 𝑛

𝑖=1 . (34)

𝜕𝑙𝜕𝜆1

= ∑𝑒𝑥𝑝�−

│𝑥𝑖│𝜆1

��𝛼1│𝑥𝑖│−𝛼1 𝜆1�

2𝜆13� 𝛼12𝜆1

𝑒𝑥𝑝�−│𝑥𝑖│𝜆1

�+ 𝛼22𝜆2

𝑒𝑥𝑝�−│𝑥𝑖−2│𝜆2

�� 𝑛

𝑖=1 . (35)

𝜕𝑙𝜕𝜆2

= ∑𝑒𝑥𝑝�−

│𝑥𝑖−2│𝜆2

��𝛼2│𝑥𝑖│−𝛼2 𝜆2�

2𝜆23� 𝛼12𝜆1

𝑒𝑥𝑝�−│𝑥𝑖│𝜆1

�+ 𝛼22𝜆2

𝑒𝑥𝑝�−│𝑥𝑖−2│𝜆2

��

𝑛𝑖=1 . (36)

The next step is to set the equation (34), equation (35), and equation (36) to zero. Then, solve the system for the three parameters α1, 𝜆1 and 𝜆2, this step obtains the MLE of α1, 𝜆1 and 𝜆2. In practical, the parameter estimations via MLE method are obtained numerically using Newton-Raphson method by providing initial values for parameters. This is done through the implementation of method using R software

6. Simulation Study We study the effectiveness of Laplace mixture model by providing two scenarios. Firstly, we obtain the MLE

estimations for a two components Laplace mixture distribution, and for simplicity, we assume that the location parameters 𝜇𝜇1 = 0 and 𝜇𝜇2 = 2. We study two case studies as illustrated in what follows:

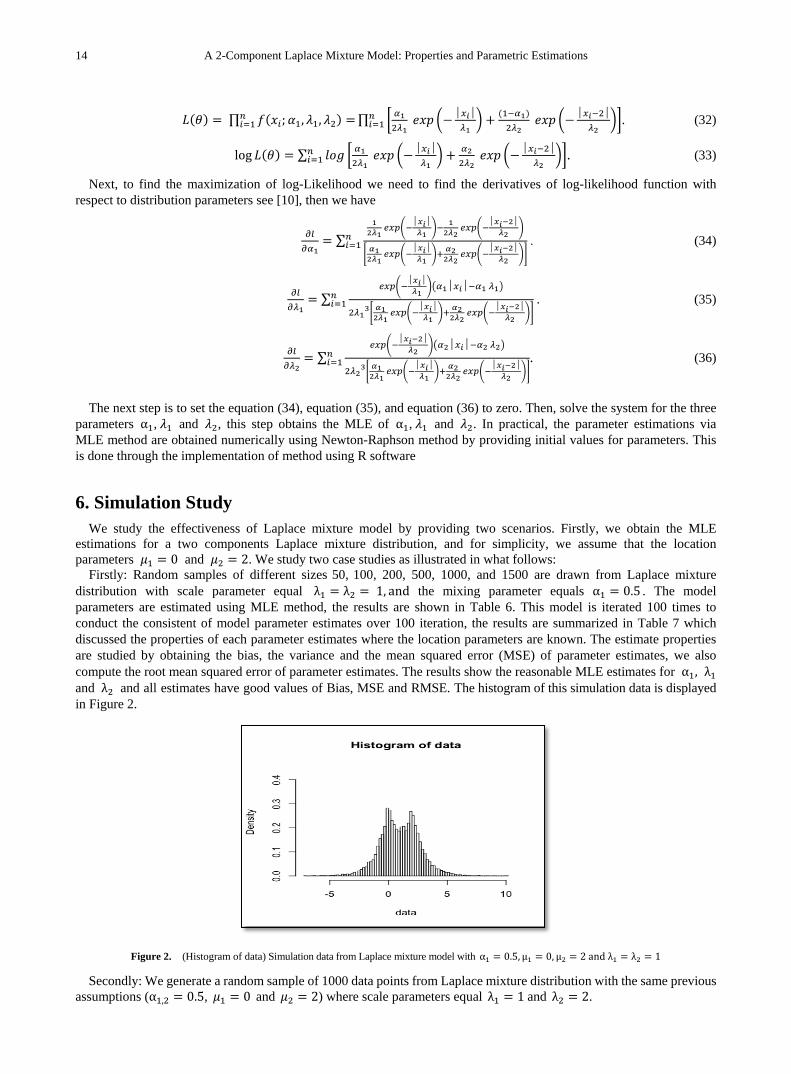

Firstly: Random samples of different sizes 50, 100, 200, 500, 1000, and 1500 are drawn from Laplace mixture distribution with scale parameter equal λ1 = λ2 = 1, and the mixing parameter equals α1 = 0.5 . The model parameters are estimated using MLE method, the results are shown in Table 6. This model is iterated 100 times to conduct the consistent of model parameter estimates over 100 iteration, the results are summarized in Table 7 which discussed the properties of each parameter estimates where the location parameters are known. The estimate properties are studied by obtaining the bias, the variance and the mean squared error (MSE) of parameter estimates, we also compute the root mean squared error of parameter estimates. The results show the reasonable MLE estimates for α1, λ1 and λ2 and all estimates have good values of Bias, MSE and RMSE. The histogram of this simulation data is displayed in Figure 2.

Figure 2. (Histogram of data) Simulation data from Laplace mixture model with α1 = 0.5,µ1 = 0, µ2 = 2 and λ1 = λ2 = 1

Secondly: We generate a random sample of 1000 data points from Laplace mixture distribution with the same previous assumptions (α1,2 = 0.5, 𝜇𝜇1 = 0 and 𝜇𝜇2 = 2) where scale parameters equal λ1 = 1 and λ2 = 2.

Mathematics and Statistics 7(4A): 9-16, 2019 15

Table 6. Simulation study: Estimated parameters for Laplace mixture model using MLE method, where α1 = α2 = 0.5,µ1 = 0, µ2 = 2 and λ1 =λ2 = 1

𝛂�𝟏 𝛂�𝟐 𝛌�𝟏 𝛌�𝟐

Sample size

50 0.5008221 0.4991779 0.9535337 0.9781209

100 0.4764069 0.5235931 0.9286988 0.9959736

200 0.5055666 0.4944334 1.015432 0.9848837

500 0.5055416 0.4944584 1.007108 0.9894546

1000 0.4993363 0.5006637 1.000324 0.9988492

Table 7. The properties of MLE estimated Laplace mixture parameters for the simulated, where α1 = α2 = 0.5,µ1 = 0, µ2 = 2 and λ1 = λ2 = 1

Model parameters

𝛂𝟏 𝛂𝟐 𝛌𝟏 𝛌𝟐 Initial values 0.5 0.5 1 1

estimate 0.501317 0.49868 0.9989 0.99651 Bias 0.0013168 0.001317 0.00107 0.003490

Variance 5.47×10-6 5.47×10-6 5.52×10-6 3.70×10-5 MSE 7.21×10-6 7.21 ×10-6 6.67×10-6 4.92×10-6

RMSE 1.44×10-5 1.44×10-5 6.67×10-6 4.92×10-5

Table 8. Simulation study Estimated parameters for Laplace mixture model using MLE method, where α1 = α2 = 0.5,µ1 = 0, µ2 = 2, λ1 =1 and λ2 = 2

Model parameters

𝛂𝟏 𝛂𝟐 𝛌𝟏 𝛌𝟐

Initial values 0.5 0.5 1 2

estimate 0.541058 0.458942 1.090983 2.059199

Bias 0.041057 0.041057 0.090983 0.059199

Variance 0.001050 0.001050 0.067408 0.183973

MSE 0.001686 0.001686 0.008278 0.003504

RMSE 0.003371 0.003371 0.008278 0.001752

7. Conclusions This paper proposed Laplace mixture distribution with

two components. The properties of the proposed mixture model are discussed theoretically. Moreover, the parameters are estimated using method of moments and maximum likelihood estimations method. The simulation study has been indicated that the model parameter estimates provide reasonable results and close to true values of model parameters. For future work, one can apply semi-parametric methods to derive parameter estimations for Laplace mixture distribution with 𝑘 components.

Acknowledgements The second author is grateful to King Abdulaziz

University and Al-Jouf University for the constructive cooperation between them. This article is also a part of the master's thesis of the second author, supervised by Dr. Zakiah Kalantan.

REFERENCES E. Amini-Seresht, Y. Zhang. Stochastic comparisons on two [1]

finite mixture models. Operations Research Letters, 45(5), 475-480, 2017.

D. Bhowmick, A. Davison, D. R. Goldstein, Y. Ruffieux. A [2]Laplace mixture model for identification of differential expression in microarray experiments: Biostatistics, 7(4), 630-641, 2006.

M. A. Figueiredo, A. K. Jain. Unsupervised learning of finite [3]mixture models: IEEE Transactions on pattern analysis and machine intelligence, 24(3), 381-396, 2002.

S. Kotz, T. Kozubowski, K. Podgorski. The Laplace [4]distribution and generalizations: a revisit with applications to communications, economics, engineering, and finance, Springer Science & Business Media, 2012.

M. Ali, S. Nadarajah. Information matrices for normal and [5]Laplace mixtures: Information Sciences, 177(3), 947-955, 2007.

G. McLachlan, D. Peel. Finite Mixture Models. John Wiley [6]and Sons, Inc., New York. MR17894, 2000.

K. Pearson. Contribution to the mathematical theory of [7]

16 A 2-Component Laplace Mixture Model: Properties and Parametric Estimations

evolution. Philosophical Transactions of the Royal Society, 185, 71–110, 1894.

J. Philip, Davis & R. Philip. Methods of numerical [8]integration. Courier Corporation, 0486453391, 2007.

DV Ramana Murty, G. Arti, M, Vivekananda Murty. Two [9]component mixture of Laplace and Laplace type distributions with applications to manpower planning models. International Journal of Statistics and Applied Mathematics, 3(4), 01-11, 2018.

R. M. Norton. The Double Exponential Distribution: Using [10]Calculus to Find a Maximum Likelihood Estimator. The American Statistician, 38 (2), 135–136, 1984.

S. Shenoy, D. Gorinevsky. Gaussian-Laplace mixture model [11]for electricity market. Paper presented at the Decision and Control (CDC), 2014 IEEE 53rd Annual Conference on, 2014.

i Conference Papers Zakiah Kalantan, Faten Alrewely, A 2-Components Laplace Mixture Model: Properties and Parametric Estimations, Conference: The 4 International Conference on Computing, Mathematics and Statistics 2019 (iCMS2019). At: Ombak Villa, Langkawi Island, Malaysia.

Mathematics and Statistics 7(4A): 17-23, 2019 http://www.hrpub.org DOI: 10.13189/ms.2019.070703

Comparison of Queuing Performance Using Queuing Theory Model and Fuzzy Queuing Model at

Check-in Counter in Airport

Noor Hidayah Mohd Zaki*, Aqilah Nadirah Saliman, Nur Atikah Abdullah, Nur Su Ain Abu Hussain, Norani Amit

Faculty Computer and Mathematical Sciences, Universiti Teknologi MARA Negeri Sembilan, Malaysia

Received July 1, 2019; Revised August 28, 2019; Accepted September 20, 2019

Copyright©2019 by authors, all rights reserved. Authors agree that this article remains permanently open access under the terms of the Creative Commons Attribution License 4.0 International License

Abstract A queuing system is a process to measure the efficiency of a model by underlying the concepts of queue models: arrival and service time distributions, queue disciplines and queue behaviour. The main aim of this study is to compare the behaviour of a queuing system at check-in counters using the Queuing Theory Model and Fuzzy Queuing Model. The Queuing Theory Model gives performance measures of a single value while the Fuzzy Queuing Model has a range of values. The Dong, Shah and Wong (DSW) algorithm is used to define the membership function of performance measures in the Fuzzy Queuing Model. Based on the observation, the problem often occurs when customers are required to wait in the queue for a long time, thus indicating that the service systems are inefficient. Data including the variables were collected, such as arrival time in the queue (server) and service time. Results show that the performance measures of the Queuing Theory Model lie in the range of the computed performance measures of the Fuzzy Queuing Model. Hence, the results obtained from the Fuzzy Queuing Model are consistent to measure the queuing performance of an airline company in order to solve the problem in waiting line and will improve the quality of services provided by airline company.

Keywords Queuing Theory Model, Fuzzy Queuing Model, Dong, Shah and Wong (DSW) Algorithm

1. IntroductionQueues happen at any place such as airport terminal,

hospital, grocery store and even petrol station. Customers queue while getting service either at counters or machines before they are served. Long queuing lines can be seen at an airport check-in counter especially during the arrival

and departure of planes. The long queues may happen due to an insufficient service system and low service quality, thus increasing the waiting time. Reducing waiting time and providing quick service are very important in service-related operations [1]. Service-related companies place importance on reducing the waiting time of customers in order to increase customer satisfaction through improving their service quality. The queuing theory can be measured using the quantitative analysis technique to predict the characteristics of a waiting line [2]. The queuing theory is used to translate the customer’s arrival time as well as analyze the queuing behaviour mathematically from the amount of time that a customer needs to wait in the system based on a real queuing situation [3].

Fuzzy queuing can be defined as a new technique which is often seen in a real world situation. According to [4], the existence of fuzzy numbers can help the manager to facilitate the service time with uncertainty and at the same time maximize the profit. In addition, fuzzy queuing also can be applied into the fuzzy possibilistic-queuing model where the main objectives are to minimize total cost and cost for transportation [5]. Furthermore, the fuzzy set theory is easily adaptable compared to other theories [6]. The fuzzy set theory is also done as an assessment for sensitive stochastic delay of flights [7]. In relation to the airport system, the fuzzy theory is also used to define the arrival and service times in airports [8] [9].

This study focuses on the queuing line system at passenger check-in counters in an airport terminal. The aim of this paper is to compare the queuing theory model and fuzzy queuing theory model on queuing performance measures. Queuing theory model has provided the limited capability in explaining some situation in real life while fuzzy queuing theory has a capability of making decision from multiple inputs or criteria. The Dong, Shah and Wong

18 Comparison of Queuing Performance Using Queuing Theory Model and Fuzzy Queuing Model at Check-in Counter in Airport

(DSW) algorithm is used for the fuzzy queuing model for an α-cut method. The DSW algorithm is used to define a membership function of the performance measures in a multi-server fuzzy queuing model [10]. Both models are compared based on the results of the average number of customers in the queue (Lq), average number of customers in the system (L), average waiting time of a customer in the queue (Wq), and average waiting time of a customer in the system (W).

2. Methods

2.1. Queuing Theory Model

The queuing theory was first introduced by A.K. Erlang in 1909. In this study, Lq, Ls, Wq and Ws are computed for the multi-server channel single phase (M/M/s) [11].

The average server utilization,

(1)

Probability of zero customers in the system,

(2)

The average number of customers in the waiting line,

(3)

The average number of customers waiting in the system,

(4)

The average time a customer waits for service,

(5)

The average time a customer is in the system,

(6)

2.2. Fuzzy Queuing Theory Model

Zadeh [12] invented the idea of a fuzzy set in the queuing theory and transformed the idea into fuzzy queue models, as implemented by [13], [14] and others. Shanmugasundaram [15] also stated that the fuzzy queuing theory seems to be more practical to be implemented in a real queuing situation rather than the queuing theory model.

2.2.1. Preliminaries The following are preliminaries to compute the

performance measures of the fuzzy queuing theory.

Interval Analysis Arithmetic Thamotharan [16] has provided the interval analysis

arithmetic to constitute the output interval for membership functions for the - cut levels that are selected.

Consider the interval and where and

Addition

(7)

Subtraction

(8)

Multiplication

(9)

Division

[ ] [ ] [ ]

[ ]provided that

,

,

÷ ×

∉

1 1

0

e, f x, y = e, f ,y x

x y (10)

From max and min, the range values will be computed as below:

[ ] [ ][ ]

for for < 0

,α = α α α > α α α

0

e fe, ff, e

(11)

Strong and Weak - cut According to [17], for a fuzzy set of A, it is defined on x

for any . The - cut will be shown according to the following crisp set.

Strong - cut, Aα

( ){ }A∈ µ > αx X | x (12)

ρ

=sλρµ

0P

01

0

1

1 1 1! ! 1

−

=

= + − ∑

n ss

n

P

n sλ λµ µ ρ

Lq

( )2! 1

=−

s

qLs

λρµ

ρ

sL

= +s qL L λµ

Wq

LW

λ

Ws

= ss

LW

λ

α

[ ]e, f [ ]x, y ≤e f≤x y

[ ] [ ] [ ]e, f + x, y = e + x, f + y

[ ] [ ] [ ]− − −e, f x, y = e x , f y

[ ] [ ] ( ) ( )min max, × e, f x, y = ex,ey, fx, fy ef,ey, fx, fy

α

[ ]α = 0,1 α

α

Mathematics and Statistics 7(4A): 17-23, 2019 19

Weak α-cut, Aα

( ){ }A∈ µ α≥x X | x (13)

Trapezoidal Fuzzy Number [18]

(14)

(15)

(16)

Let be the family of h-trapezoidal fuzzy numbers, that is;

( ) ( ), , ; ,

< ≤

= ≤ ≤ ≤ =

1 2

0 1

:

TN3, 4 1 2 3 4F h

h

A a a a a h a a a a

(17)

The - cut interval for Trapezoidal Fuzzy Number [18]

(18)

(19)

By using equation (18) and (19), equation (20) is obtained

( ) ( )4 4 3 2 1 1,for 0 1

− − ≤ ≤ − +

≤ ≤

ha a a hx a a hah

α α (20)

Therefore, the equation (21) for the range of Trapezoidal Fuzzy Number is obtained

(21)

2.2.2. DSW Algorithm The fuzzy queuing theory model is more realistic and

produces a more refined result [19]. In this study, the DSW algorithm is used to describe a membership function of the multi-server fuzzy queuing model’s performance measures [10]. The α-cut shows the possibility of the fuzzy queuing

performance measure in the related range. At the range of α = 0, it shows that the performance measures could appear, while α = 1 shows the performance measures that are likely to be [20]. There are four steps to follow [21]:

Step 1 Select α cut value where 0 ≤ α ≤ 1. Step 2 Find the intervals in the arrival rate and service

rate membership functions that correspond to this α. Step 3 Using standard binary interval operations,

compute the interval for membership function for the selected α-cut levels.

Step 4 Repeat steps 1 to 3 for different values of α to complete an α-cut representation of the solution.

2.2.3. Lq, Ls, Wq and Ws

After completing the calculations in the DSW algorithm, we need to compute the performance measures for the fuzzy queuing theory model. The different values of α will be substituted into the following formula of performance measures. Below are the lists of formulas derived from [16] to form the trapezoidal fuzzy queuing model.

The utilization factor, ρ

(22)

The probability that there are zero customers in the system, :

(23)

The average number of customers in the system (waiting in queue and being served), Lq :

(24)

The average number of customers in the system,

(25)

The average time a customer waits for service,

(26)

The average time a customer is in the system,

(27)

Where

[ ] [ ][ ] [ ]

, : Arrival rate, , , ,

, : Service rate, , , ,

= + − =

= + − =

x b e b c d e

y f i f g h i

α α λ

α α µ (28)

( )

( )( )

( )( )

≤ ≤

≤ ≤

≤ ≤

x - a1h ,a x a1 2a - a2 1h ,a x a 1 2A x =

a - x4h ,a x a43a - a4 30 ,otherwise

( )TNF h

α

( ) ( )( )( ) for

≥

≥ α

≥ α

≥ α + ≤ ≤

1

0 1

1

2 1

1 2 1

1 2 1

2 1 1

x - ah

a - ah x - a a - a

hx - ha a - a

hx a - a ha h

( ) ( )( )( )

( ) for

4

4 3

4 4 3

4 4 3

4 3 4

4 4 3

a - xh

a - ah a - x a - a

ha hx a - a

-hx a - a ha

hx ha a - a h

≥

≥ α

− ≥ α

≥ α −

≤ − α ≤ ≤

1

0 1

( ) ( ) ( ){ }4 4 3 2 1 1, TNF h ha a a a a ha= − − − +α α

=xsy

ρ

0P

01

0

1

1 1 1! ! 1

−

=

= + − ∑

n ss

n

Px x

n y s y ρ

( )

0

2! 1

=−

s

q

x Py

Ls

ρ

ρ

sL

= +s qxL Ly

Wq

LW

x

Ws

= ss

LW

x

20 Comparison of Queuing Performance Using Queuing Theory Model and Fuzzy Queuing Model at Check-in Counter in Airport

Both arrival and service rates are represented as trapezoidal fuzzy numbers. The trapezoidal fuzzy numbers are represented as and respectively. The minimum and maximum for arrival rate,

are represented by [b,e], whereas for service rate the minimum and maximum are represented by [f,i].

3. Results The data were collected from the check-in counter of a

local airline in Malaysia. As decided, these data were collected manually every Saturday in a month for two hours from 2 p.m. until 4 p.m. Below is the summary of our data collection for four weeks.

Table 1. Data collection at check-in counter

Week Number of customers

Average number of customers

Service rate

Week 1 (11/8/2018) 111 23 0.74

minutes Week 2

(18/08/2018) 100 20 0.99 minutes

Week 3 (25/08/2018) 100 20 0.85

minutes Week 4

(8/09/2018) 118 23.6 0.85 minutes

Total 429 86.60 3.43 minutes

The data obtained are analyzed to get the input parameters, which are the arrival rate and service rate. These parameters are used to measure the multi-servers performance using the queuing theory model and fuzzy queuing model.

The result of this study is divided into three sections. The first is the queuing theory model’s performance measure. Second, the DSW algorithm fuzzy queuing model’s performance measure and the third is the comparison of both fuzzy queuing models.

Table 2. Performance measures of Queuing Theory Model

Performance Measures Result

Average number of customers waiting in the queue, Lq 0.000061

Average number of customers in the system, Ls 0.6111 Average time a customer spends waiting in the queue,

Wq 0.000006

Average time a customer spends in the system, Ws 0.0555

The performance measures for the queuing theory model are computed using QM for Windows version 3.1. The Lq, the average number of customers waiting in the queue in an hour is 0.000061, which is less than 1 person per hour as shown in Table 2. For Ls, the average number of customers in the system is 0.6111, which is less than 1 customer every hour. For Wq, the average time a customer spends waiting in the queue is 0.000006 hour, which equals to 0.00036 minutes taken for each customer to wait in line. Lastly for Ws, the average time a customer spends in the system is 0.0555 hour or 3.33 minutes per person. This means that it takes about 3 minutes for a customer to complete the process in the system.

Microsoft Excel is used to compute the α-cut of λ and µ at multiple α-cut levels. The levels are 0, 0.1, 0.2, 0.3, 0.4, 0.5, 0.6, 0.7, 0.8, 0.9 and 1. The performance measures for

, , and are as tabulated in Table 3. If α=0,

it has the possibility of the performance measures to be shown. But if α=1, it is sure for the performance measures to be shown. α=1 is the core of the fuzzy system for the performance measures, while α=0 is the support of the fuzzy system for the performance measures to appear. The calculations for level α=0.1 until α=0.9 show that the value of the performance is in the range [0,1]. In the study, the average mean of the performance measures lies between the range of α=1 to α=0, which means it never falls outside of the range α=0.

Table 3. Performance measures for Fuzzy Queuing Theory Model

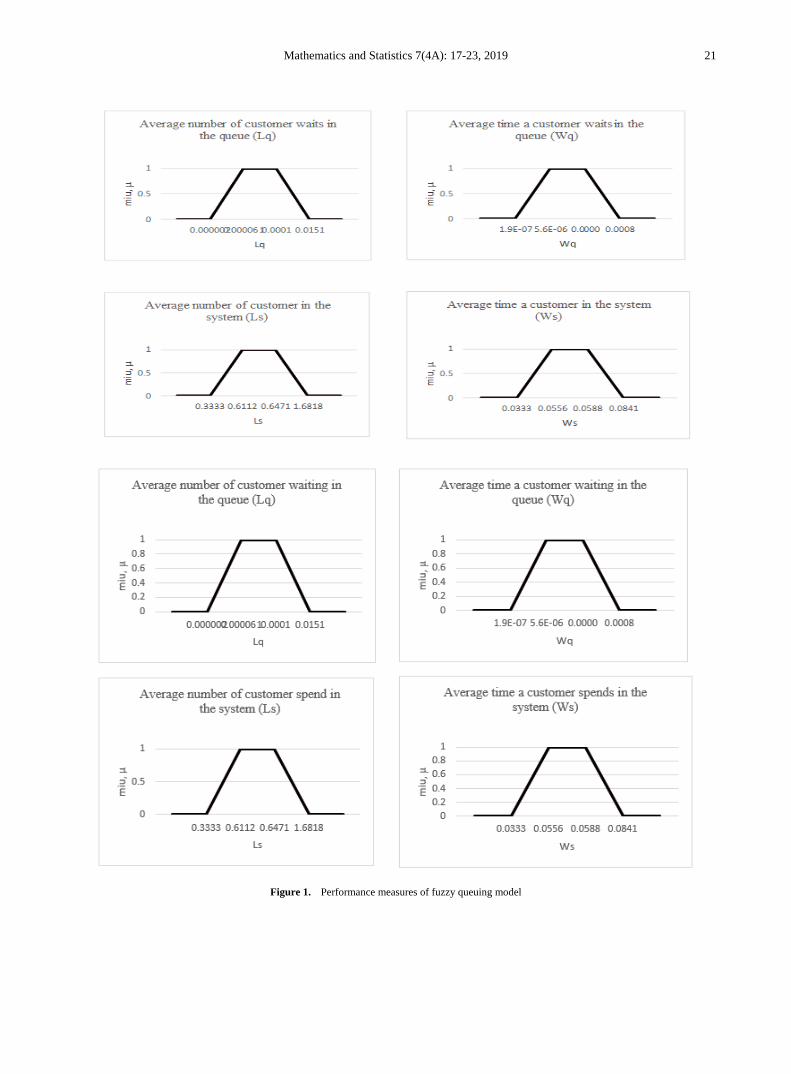

α (customer) (customer) (hour) (hour)

0 [0.0000019,0.01514] [0.3333,1.6818] [0.00000019,0.00076] [0.0333,0.0841]

0.1 [0.0000025,0.00953] [0.3507,1.5375] [0.00000025,0.00050] [0.0347,0.0805]

0.2 [0.0000034,0.00596] [0.3696,1.4060] [0.00000034,0.00033] [0.0362,0.0773]

0.3 [0.0000047,0.00370] [0.3902,1.2852] [0.00000045,0.00021] [0.0379,0.0743]

0.4 [0.0000065,0.00228] [0.4127,1.1737] [0.00000062,0.00014] [0.0397,0.0716]

0.5 [0.0000091,0.00138] [0.4375,1.0703] [0.00000086,0.00009] [0.0417,0.0691]

0.6 [0.0000129,0.00083] [0.4649,0.9742] [0.00000012,0.00006] [0.0439,0.0667]

0.7 [0.0000185,0.00048] [0.4954,0.8844] [0.00000017,0.00004] [0.0463,0.0646]

0.8 [0.0000270,0.00028] [0.5294,0.8003] [0.00000025,0.00002] [0.0490,0.0625]

0.9 [0.0000402,0.00016] [0.5677,0.7214] [0.00000037,0.00001] [0.0521,0.0606]

1 [0.0000611,0.00008] [0.6112,0.6471] [0.00000056,0.00001] [0.0556,0.0588]

qL sL qW sW

qL sL qW sW

Mathematics and Statistics 7(4A): 17-23, 2019 21

Figure 1. Performance measures of fuzzy queuing model

22 Comparison of Queuing Performance Using Queuing Theory Model and Fuzzy Queuing Model at Check-in Counter in Airport

The graphs of membership function of , ,

and for the fuzzy queuing model with trapezoidal fuzzy number is shown in Figure 1. The performance measures fall between range of α=1 and never falls outside the range of α=0. The range for the average number of customers waiting in the queue is between 0.000002 and 0.0151. At α=0, it will lie between 0.0000002 and 0.0151 while for α=1, the range is between 0.000061 and 0.0001. Hence, it shows that the number of customers waiting in the queue is less than 1 per hour. The range for the average number of customers in the system is between 0.3333 and 1.6818. At α=0, it will lie between 0.3333 and 1.6818 while for α=1, the range is between 0.6112 and 0.6471. Hence, the value of α-cut values is less than 1 which shows that the number of customers in the system is more than 1 customer per hour. The range for the average time a customer waits in the system is between 0.00000019 and 0.00076 hour. At α=0, it will lie between 0.00000019 and 0.00076 while for α=1, the range is between 0.00000056 and 0.00001. Hence, it shows that the time a customer waits in the queue is less than 1 minute per customer. The range for the average time a customer spends in the system is between 0.3333 and 0.0841 hour. At α=0, it will lie between 0.3333 and 0.0841 while for α=1, the range is between 0.0556 and 0.0588. Hence, it shows that the time a customer spends in the system is more than 1 minute per customer.

4. Discussion Table 4. Comparison performance measures between the Queuing Theory Model and Fuzzy Queuing Model

Performance Measures Queuing Theory Model Fuzzy Queuing, α = 1

0.000061 [0.0000611,0.00008]

0.6111 [0.6112,06471]

0.000006 hour (0.00036 minutes) [0.00000056,0.00001]

0.0555 hour (3.33 minutes) [0.0556,0.0588]

Based on the table above, the performance measures for the queuing theory model is compatible with the fuzzy queuing model. The queuing theory model and fuzzy queuing model show that Lq is approximately less than 1 customer queuing in the waiting line, Ls is approximately less than 1 customer queuing in the system, Wq is the customer waiting less than 1 minute in the waiting line, and Ws is the customer waiting more than 1 minute in the system. The values of Lq, Ls, Wq and Ws for the queuing theory model lie in the fuzzy queuing model range value for α=1. Hence, the results of performance measures for the queuing theory model and fuzzy queuing model show both

models are equivalent. Since the value of queuing theory model obtained are lay in the range of performance measures of fuzzy queuing model. Therefore, it shows the result obtained is consistent.

5. Conclusions In this study, the result shows that the performance

measures Lq, Ls, Wq and Ws for both Queuing Theory Model and Fuzzy Queuing Model were computed and compared. Based on the result, the Fuzzy Queuing Model is much more effective and efficient to measure the performance of multi-server in a queuing system since the Fuzzy set theory is more easily adaptable compared to other theories [6]. Garai and Garg (2019) stated that the vagueness or uncertainty situation can be solve using fuzzy model [22]. Applying the Fuzzy queuing model provides broader information, which will be very useful in defining a queuing system. Thus, this study concludes that fuzzy queuing is one of the alternative ways to compute the performance measures since the information obtained from the application is much easier to understand and interpret. Therefore, the Fuzzy Queuing Model is an alternative way to measure the performance of multi-server in a queuing system.

REFERENCES B. T. Taylor. Introduction To Management Science, [1]

England : Pearson Education Limited, 2016.

N. Amit, N. A. Ghazali. Using simulation model queuing [2]problem at a fast-food restaurant, In: Regional Conference on Science Technology and Social Sciences (RCSTSS), 1055-1062, Singapore:Springer , 2018.

A. B. N. Yakubu, U. Najim. An application of queuing [3]theory to ATM service optimization: A case study, Mathematical Theory and Modelling, 11-23, 2014.

M. J. Pardo, D. Fuenta. Optimizing a priority-discipline [4]queuing model using fuzzy set theory. Computers and Mathematics with Applications, Vol.54, 267-281, 2007.

B. Vahdani, R. Tavakkoli-Moghaddam, F. Jolai. Reliable [5]design of a logistics network under uncertainty: A fuzzy possibilistic-queuing model, Applied Mathematical Modelling, Vol.37, No.5, 3254-3268, 2013.

T. Ebrahim, M. Ali, G. Iman, A. Hadi, F. Mehdi. Optimizing [6]multi supplier systems with fuzzy queuing approach: Case study of SAPCO, International MultiConference of Engineers and Computer Scientists, 1-7, 2011.

S. Meng, D. Wu, Z. Huimin, L. Bo, W. Chunxiao. Study on [7]an airport gate assignment method based on improved ACO algorithm. Emerald Insight, 20-43, 2018.

Aydin, Ozlem, A. Apaydin. Multi-channel fuzzy queuing [8]systems and membership functions of related fuzzy services

qL sL qW

sW

qL

sL

qW

sW

qL

sL

qW

sW

Mathematics and Statistics 7(4A): 17-23, 2019 23

and fuzzy inter-arrival times, Asia-Pacific Journal of Operational Research, Vol.25, No.5, 697–713, 2008.

N. Sujatha, V. S. Murthy Akella, G. V. S. Deekshitulu. [9]Analysis of multiple server fuzzy queueing model using α – cuts. International Journal of Mechanical Engineering and Technology (IJMET), Vol.8, No.10, 35–41, 2017.

S. Thamotharan. A study on multi server fuzzy queuing [10]model in triangular and trapezoidal fuzzy numbers using cuts, Vol.5, No.1, 226–230, 2016.

J. Kingman. The first Erlang century—and the next. [11]Queueing Systems, 63(1-4), 3, 2009.

L. A. Zadeh. A note on prototype theory and fuzzy sets. [12]587-593, 1965.

J. J. Buckley. Elementary queueing theory based on [13]possibility theory, Journal Fuzzy Sets and Systems, Vol.37, No.1, 43 – 52, 1990

M. Meenu, T. P. Singh, G. Deepak. Threshold effect on a [14]fuzzy queue model with batch arrival, Arya Bhatta Journal of Mathematics and Informatics,Vol.7, No.1, 109- 118, 2015.

S. Shanmugasundaram, S. Thamotharan, M. Ragapriya. A [15]study on single server fuzzy queuing model using DSW algorithm, International Journal of Latest Trends in Engineering and Technology (IJLTET), Vol.6, No.1, 162–169, 2015.