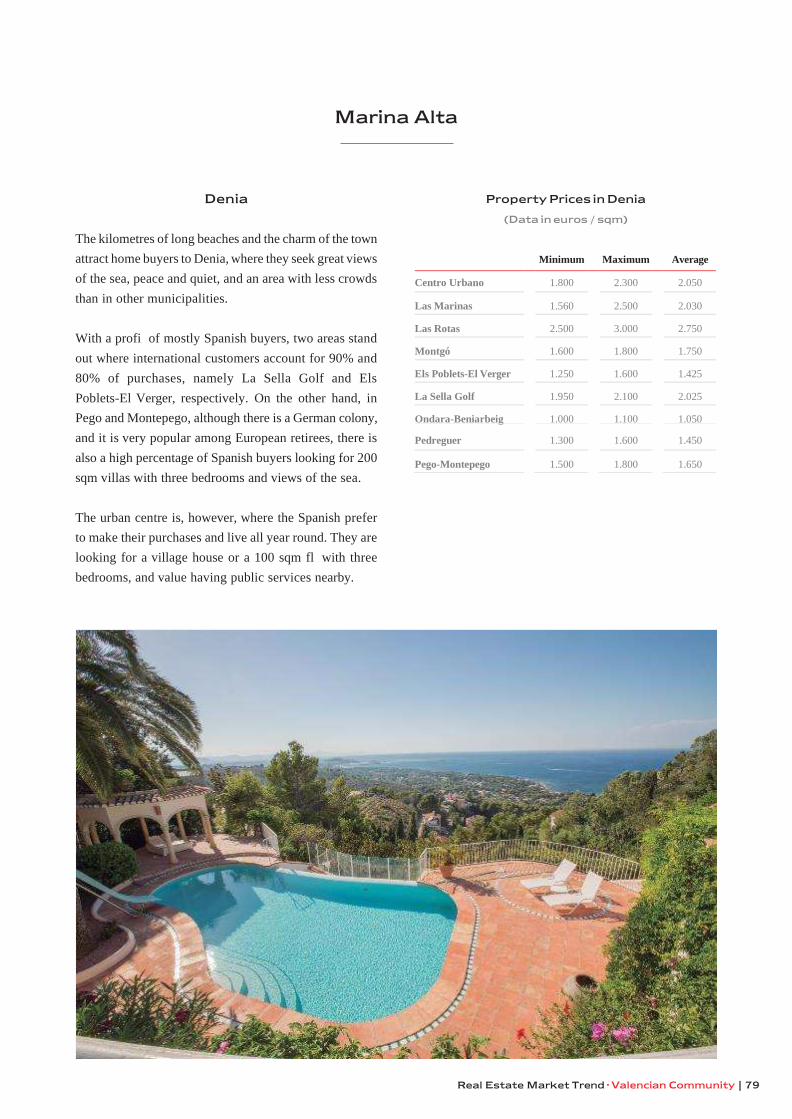

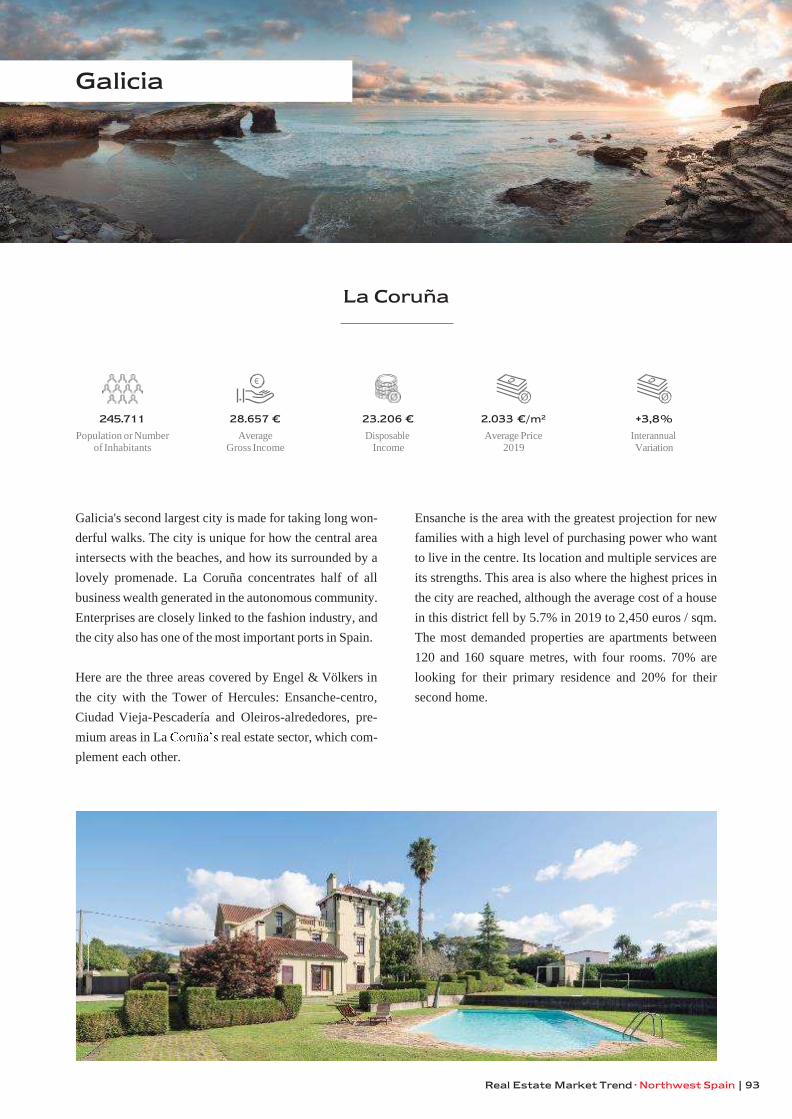

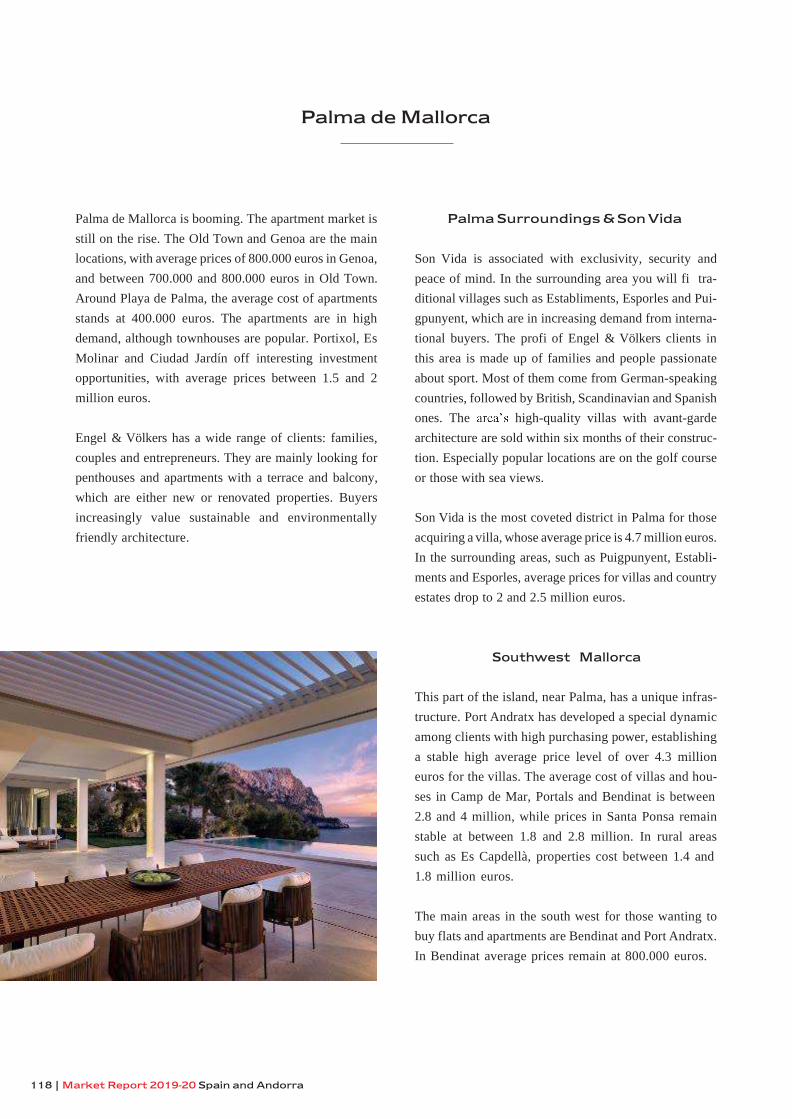

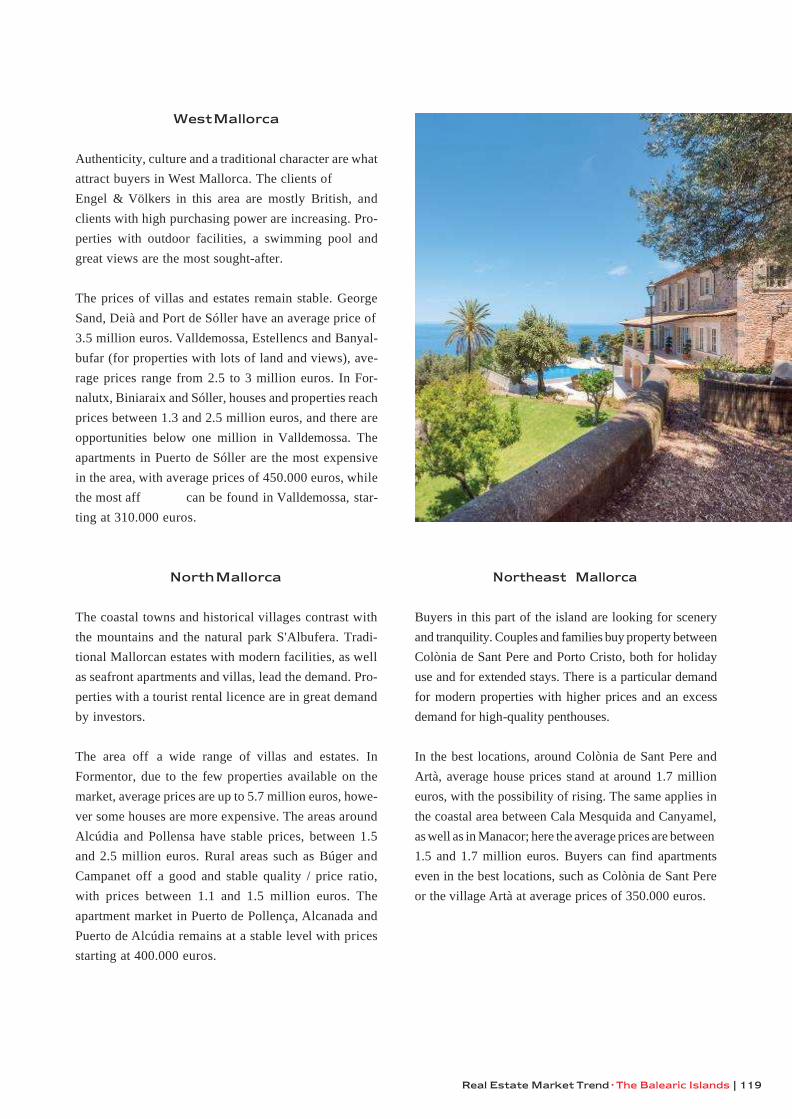

Market Report 2019-20 Spain and Andorra - Engel & Völkers

146

Market Report 2019-20 Spain and Andorra

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Market Report 2019-20 Spain and Andorra - Engel & Völkers

Market Report 2019-20

Spain and Andorra

MARKET REPORT 2019-20 · SPAIN AND ANDORRA

INDEX

05 Editor’s Note

16 Real Estate Market Trend in Spain

132 Andorra

06 World Economic

Outlook

Real Estate in Spain

4 | Market Report 2019-20 Spain and Andorra

Editor’s Note | 5

EDITOR’S NOTE

Juan-Galo Macià

The balance sheet of the real estate sector in 2019 did

not meet expectations. Although it was not a bad year,

political and economic uncertainty aff the housing

market, causing a drop in home sales in June and July,

when a new mortgage law came into full eff

Housing prices rose by 4% while sales dropped by 3,3%.

The belief among many Spanish households that

economy would soon undergo a recession, strongly

contributed to this decrease in sales. However, no such

recession took place in 2019 and no international organi-

zation believes one will aff our country before the

conclusion of this report.

Generally speaking, my current view is no diff than

the one I held last year. It is my opinion that the

housing market in Spain is still in its expansionary phase.

Nevertheless, within a phase of expansion there are some

fl with periods that are excellent, others that

are good, and some that are simply stable, the latter

of which would apply to 2019, and, according to our

forecast, to 2020. I disagree with the analysts who think

we are now approaching the transition from expansion

Juan-Galo Macià

CEO of Engel & Völkers in Spain, Portugal and Andorra

to recession. Interest rates are lower than at any period

in modern history, while banks are especially

willing to grant credit. a great formula for a strong

preventative medicine.

That being said, in 2020 the behavior will be

diff than in previous years. It is possible that big

capital, which was the driving force behind the market's

improvement, will no longer be so and that economic

uncertainty will cause investment to be withdrawn. The

demand for investment will therefore be lower than in

previous years.

At Engel & Völkers, we are ready to face the future of

real estate with confi and strength. As a well-or-

ganized company, we are more than capable of adapting

to the shifting tides. Whereas before we enjoyed smooth

sailing, this year we will be pushing forward of our own

accord. Our dedication to ensuring client satisfaction is

what will continue to achieve the excellent results we

value. The demand for housing has not disappeared, it

has simply changed. Fortunately, we possess the expertise

required to accomodate the needs of our potential clients.

6 | Market Report 2019-20 Spain and Andorra

Current Situation

Global Economy

In 2020, the world economy will maintain its moderate

growth rate of 2-3%, against 2.9% from last year. Its

development will be heavily conditioned by the impact

from the coronavirus, counteracting positive factors such

as the easing of commercial tensions between the United

States and China, an orderly Brexit, and an accommoda-

tive monetary policy.

International organizations warn that the situation is fra-

gile, and advocate extreme caution with regards to the

full extent of the epidemic which started in China. Both

the International Monetary Fund (IMF) and the Organi-

sation for Economic Cooperation and Development

(OECD) have assessed the downward trends in their eco-

nomic forecasts for 2020. The IMF has announced that

the economic growth could decrease by 0.1%

and 0.2% as a result of the extent. The OECD

has warned that the growth of the world economy could

be reduced by 1.5% in 2020, which is half of what was

forecast last November, if the epidemic is not stopped.

The impact caused by the coronavirus will aff all

regions. The United States is the only developed country

that will reach a growth of 1.9% to 2%, whereas the euro

zone will not reach 1%, and Japan will see no growth at

all, and might even enter a recession. Regarding China,

a decrease from around 6% to less than 5% is predicted.

In any case, the world economy will be capable of a swift

recovery and see its growth increase by more than 3% in

2021. This will happen if the virus is successfully con-

tained and if tax or monetary measures are implemented.

Although monetary policy remains expansionary, extraor-

dinary measures by the central banks, such as

maintaining fi costs at a minimum and injecting

liquidity, are not ruled out.

GDP Growth

4,5

4

3.5

3

Percentage Variation %

2.5 2011 12 13 14

15 16 17

18 19

20 21

22 23 24

Grupo de Cuatro World

Source: IMF Footnote. Grupo de Cuatro = China, eurozone, Japan and US

World Economic Outlook | 7

Spain’s Economy

A low growth profi marked by global economic uncer-

tainties for the better part of 2020, will condition the

development of economy. According to forecasts,

it will grow from around 1.5%-1.6%, against 2% in 2019.

The external sector will stop contributing to

growth due to deteriorating world trade. Export will be

weakened while imports will increase at a rate consistent

with the demand, but not lesser than the demand, which

is what happened in 2019.

The lower growth rate will also be conditioned by dete-

rioration in the internal sector. We are expecting to see a

decline in investment and public consumption. While we

can count on an upturn in some areas of private consump-

tion, it will not be sufficient to compensate for the degree

of moderation expected with regards to the domestic

demand.

The impact of the coronavirus on the economy could

result in the downturn hitting its lowest point by the

middle of the year. In the second half of the year, we will

see a rebound in activity as a consequence of the impro-

vement expected in the exterior sector, which will entail

greater growth in the Growth Domestic Product (GDP),

ranging between 1.7% and 1.9% in 2021.

The Evolution of the GDP in Spain

Inter-annual variation %

5

0

-5

Source: INE (National Statistics Institute)

National and External Demand

Contribution to annual growth in terms of GDP volume

6

4

2

0

-2

-4

-6

-8

-10

-8,2

4,0

0,4

-0,1

2,2

-5,3

1,9

-0,9

4,3

-0,1

1,5

1,0

3,1

-0,9

1,8 1,2

0,6 0,1

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

2007

T3

2007

T4

2008

T1

2008

T2

2008

T3

2008

T4

2009

T1

2009

T2

2009

T3

2009

T4

2010

T1

2010

T2

2010

T3

2010

T4

2011

T1

2011

T2

2011

T3

2011

T4

2012

T1

2012

T2

2012

T3

2012

T4

2013

T1

2013

T2

2013

T3

2013

T4

2014

T1

2014

T2

2014

T3

2014

T4

2015

T1

2015

T2

2015

T3

2015

T4

2016

T1

2016

T2

2016

T3

2016

T4

2017

T1

2017

T2

2017

T3

2017

T4

2018

T1

2018

T2

2018

T3

2018

T4

2019

T1

2019

T2

2019

T3

2019

T4

8 | Market Report 2019-20 Spain and Andorra

Domestic Demand Foreign Demand Source: INE (National Statistics Institute)

World Economic Outlook | 9

Infl could recover this year at an inter-annual rate

of around 1.3% by December. However the impact of the

coronavirus on the economy and on the price of petrol,

will be stronger in the fi part of the year, giving an

average annual rate of 0.8%.

The lower dynamics of the economy will also be refl -

ted in the labor market. The creation of employment will

slow down, even though more than 800,000 net jobs will

be generated in the next three years. This year the rate

of unemployment will decrease to around 13.5% and in

2021 to 12.3%.

The main problem for the Spanish economy continues

to be the public defi whose reduction will be minimal

during this period, remaining well above the target. The

public debt is also concerning, as it is above 95% of the

GDP, causing the price of financing to rise should interest

rates become normalized.

Rate of Inflation in Spain

Year-on-year change %

1,5

0

1,5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan 2020

Source: INE (National Statistics Institute)

Unemployment Rate in Spain

%

28

7

Source: INE (National Statistics Institute)

1,3

1,1 1,0

1,1

0,8 0,5 0,8 0,4

0,3 0,4

0,1 0,1

2007

T3

2007

T4

2008

T1

2008

T2

2008

T3

2008

T4

2009

T1

2009

T2

2009

T3

2009

T4

2010

T1

2010

T2

2010

T3

2010

T4

2011

T1

2011

T2

2011

T3

2011

T4

2012

T1

2012

T2

2012

T3

2012

T4

2013

T1

2013

T2

2013

T3

2013

T4

2014

T1

2014

T2

2014

T3

2014

T4

2015

T1

2015

T2

2015

T3

2015

T4

2016

T1

2016

T2

2016

T3

2016

T4

2017

T1

2017

T2

2017

T3

2017

T4

2018

T1

2018

T2

2018

T3

2018

T4

2019

T1

2019

T2

2019

T3

2019

T4

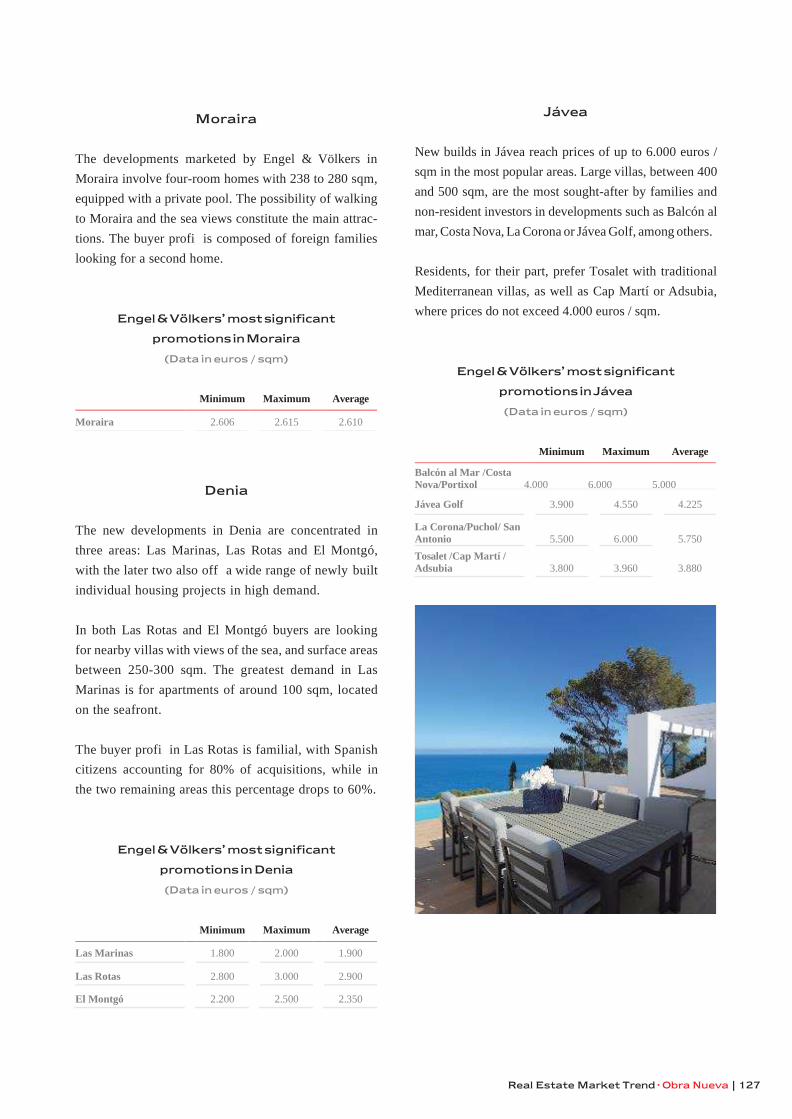

Seal Estate in Spain | 9

Current Situation

In the context of an economic slowdown after 5 years of

consecutive growth, the real estate market showed the

first signs of decline in 2019. Data from the National

Statistics Institute (INE) register a drop in sales by 3.3%

compared to last year, with a total of 501,085 operations

completed. Prices have maintained an upward trend,

although at lesser intervals than in the last three years.

Along with the economic and political uncertainty, the

real estate sector was aff last year by the changes

implemented to regulate rent and enforce the Real Estate

Credit Law. Experts think these factors will cease to have

further repercussions in the market once agents become

accustomed to the new environment.

Therefore the real estate market foresees a favorable evo-

lution this year, but with regards to prices and sales, the

pace of progress will be moderate, and we will also see

a progressive adjustment.

Historically, the development of the real estate sector

paralleled the economic cycle. In the current deceleration

phase, we can expect moderate growth in the following

years. In any case, analysts see the risk of a real estate

bubble given that current prices are still below those rea-

ched during the crisis by 20%.

Number of Registered Home Sales

In the thousands

2015 2016 2017 2018 2019

New Used

501,1

467,6

405,4

355,6

426,3 408,2 384,4

330,3 278,6

77,0 75,1 83,2 91,7 92,9

Real Estate Sector in Spain

10 | Market Report 2019-20 Spain and Andorra

DIC

-18

EN

E-1

9

FE

B-1

9

MA

R-1

9

AB

R-1

9

MA

Y-1

9

JUN

-19

JUL

-19

AG

O-1

9

SE

P-1

9

OC

T-1

9

NO

V-1

9

DIC

-19

Financing

The interest rates and fi conditions will continue

to be favorable for a prolonged period due to policies set

forth by the European Central Bank. Experts predict

a rise in interest rates during the second half of 2021. In

fact, the market is awaiting a revision of the mone-

tary policy strategy, predicted to be fi during the

aforementioned period.

2019 was the fourth consecutive year of nega-

tive growth, which is not forecasted to rise above 0%

within the next two years. Its lowest point was recorded

last August to have an average of -0.356%, after which

it rose by the end of the year to an average of -0.261%.

Taking the last 12 months as a reference, the index regis-

tered a drop of -0.132 points. This meant that 30-year

mortgages of 150,000 euros, with a Euribor differential of

+0.99%, which will need a revision, undersold by 104.64

euros for its annual payment compared to the same month

last year, or, in other words, by 8.72 euros a month.

By midyear, the slow upward trend could cause

mortgages to become more expensive if they are revised,

as the rates in 2020 will not be as negative as in 2019.

Last Year’s Euribor

0,00%

-0,05%

-0,10%

-0,15%

-0,20%

-0,25% -0,261% -0,30% -0,35% -0,40% -0,45% -0,50%

Source: Bank of Spain

Seal Estate in Spain | 11

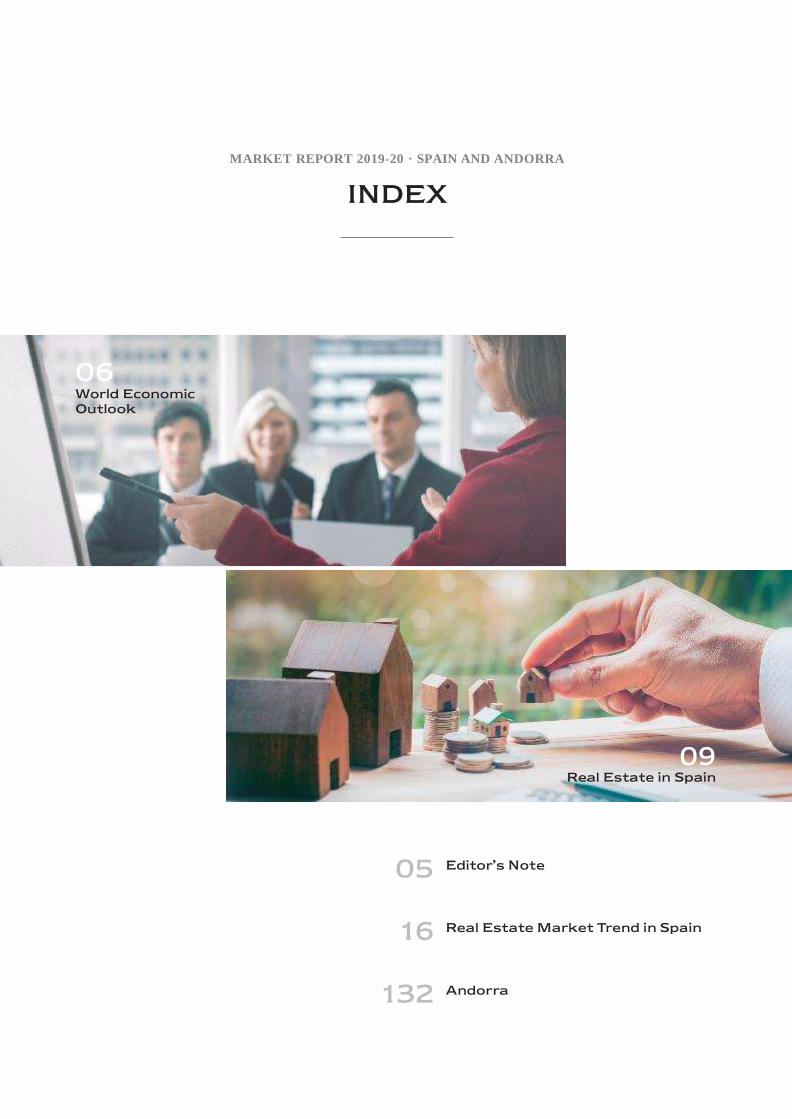

Financial Position of Spanish Households

Spanish families currently enjoy a healthy economic stan-

ding. The net wealth of households, obtained by deducting

fi liabilities from total assets, was at 1.57 trillion

euros in the third quarter of last year. This fi marks

a historical high point, representing a 7.1% increase com-

pared to the same period from the year before. It is equal

to 127.4% of gross domestic product. The ratio

between the two amounts shows an increase of 4.1 per-

centage points against the previous year.

According to data from the Bank of Spain, the balance of

financial assets from Spanish homes reached 2.33 trillion

euros, which is 4.7% more than the previous year. This

increase was the result of a net acquisition of 53 billion

in fi assets, due primarily to a rise in the price of

equity assets. Regarding the GDP, financial assets of Spa-

nish households constituted 189.4% at the end of the third

quarter in 2019, an increase of 1.8 points compared to the

Furthermore, in the third quarter of 2019, according to the

National Statistics Institute (INE), the household savings

rate was at 6.4%, removing seasonal and calendar effects.

This figure is 1.4 points less than in the previous quarter.

Spanish households spent more than they earned, and, not

including seasonal effects, families in Spain registered

savings at -1.3% of their disposable income. Between July

and September, household disposable income amounted

to 176,055 million euros, a 3.1% increase, while expendi-

tures rose by 2.5% up to 177,132 million.

Household Savings

Percentage of Quarterly Gross Disposable Income

Corrections of Seasonal and Calendar Effects

15

12,1

year before. The bulk of household fi assets was 10

in cash and deposits (39% of the total), followed by equity

holdings (27%), pension funds and insurance (17%), and 5

mutual fund shares (14%).

0

On the other hand, household debt stood at 708,499

million between July and September 2019, in line with -5

10,7

5,3

8,9

4,3

6,2 7,0

5,4

6,4

what was recorded in the same period in 2018. This level

of debt accounts for 57.4% of the GDP, a long way from

the 85% registered in 2010.

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: INE (National Statistics Institute)

Property Ownership of Spanish Families

(Data in a million of millions of euros)

8

7

4

3

2 1,57

1

0 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

6

5

5,463

12 | Market Report 2019-20 Spain and Andorra

Net Financial Wealth Real Estate Wealth

Source: Engel & Völkers with information from the Bank of Spain and Inverco

Seal Estate in Spain | 13

Price Development

In line with a curbed demand, last prices saw a

moderated growth. The appraised price of free housing in

2019 amounted to 1,653 euros/sqm, constituting a 2.1%

increase, the slowest growth rate registered in the last three

years, according to data from the Ministry of Transport,

Mobility and Urban Agenda. This amount is the highest

seen since the last quarter of 2011, but it is also slightly

more than 20% lower than the maximum reached in 2008,

when the real estate boom was in full swing.

The regions which registered the greatest increase in pri-

ces were the Balearic Islands (6.7%), Navarre (6.1%) and

Madrid (4.9%), whereas the largest decrease took place

in Cantabria (-2.2%), La Rioja (-1.9%), Extremadura

(-1.2%), Asturias (-0.5%), Murcia (-0.3%), and Castilla

La Mancha (-0.2%).

By province, again the Balearic Islands, Navarre and

Madrid showed the most growth, along with Valencia

(4.1%), Las Palmas (3.8%) and Biscay (3.5%). The lar-

The 10 most expensive

municipalities in Spain

(euros/sqm)

gest decrease by province took place in Soria (-8.7%),

Palencia (-7.8%), Lleida and Cáceres (both by -2.8%)

and Albacete (-2.6%).

Regarding municipalities with more than 25,000 inhabi-

tants, the highest prices were seen in San Sebastián, Ibiza

and Santa Eulalia del Río (Ibiza), all of which were above

3,700 euros/sqm.

In turn, the latest available data from the INE's Housing

Price Index (HPI) (which refers to house purchases)

corresponding to the third quarter of 2019 showed an

annual increase of 4.7%, six tenths less than in the pre-

vious quarter and the lowest annual percentage in the last

three years. By type of housing, both the annual rates for

new and second-hand housing decreased six tenths as

compared with the previous quarter, standing at 6.6%

and 4.4%, respectively.

Source: Ministry of Development

San Sebastián 3.811,1

Ibiza 3.809,9

Santa Eulalia del Río 3.711,5

Sant Cugat del Vallès 3.474,6

Barcelona 3.387,4

Madrid 3.332,9

Pozuelo de Alarcón 3.322,1

Castelldefels 3.191,7

Calvià 3.126,4

Majadahonda 3.033,3

14 | Market Report 2019-20 Spain and Andorra

IPV Annual Rate

General index, new and second-hand property. Percentage

10,4

6,3

7,0

6,8

7,2

8,0

6,6

6,8

7,2

6,6

5,7 5,7 6,1 6,4 6,2 5,3

5,0

4,7

4,4

General Index New-builds Second-hand

Source: INE (National Statistics Institute)

Experts point out that both prices and sales should see a

decline in the following years, but without dropping by a

significant amount except in certain urban centres with

overvalued housing markets. One forecast is based on the

fact that price levels, indebtedness, and the financial effort

of Spanish families, are still moderate.

Average property price per square metre (€/sqm)

2.200

2.000

1.800

1.600

1.400

1.200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: The Ministry of Development

T1 T2 T3 T4 T1 T2

2019

T3

2018

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

T1

T2

T3

T4

Seal Estate in Spain | 15

Mortgages and Purchases

The new Mortgage Law that came into force last June

marked an important development in mortgages in 2019.

The eff of the law were felt in August and September

even as the market returned to normal. In fact, the num-

ber of home mortgages transacted shot up by 43%, rea-

ching 30,285 in the last month of the year, according to

the provisional fi from the National Statistics Ins- titute

(INE). This means that a total of 357,720 home

mortgages were secured during the last period, a 2.7%

increase compared to 2018. The increase was the lowest

seen since 2014, although this is the sixth consecutive

year of growth and the best annual turnout since 2011.

The average value of signed mortgages amounted to

125,007 euros, 0.6% more than in 2018, while capital

loans from fi institutions reached 44,717 million

euros, a 3.3% increase. The communities with the highest

number of home mortgages in 2019 were in the Commu-

nity of Madrid (69,616), Andalusia (67,845) and Cata-

lonia (57,787). The most amount of loans were given in

these communities for mortgages.

Fixed-term mortgages are gaining ground. In December

they constituted 44% of all mortgages compared to 41.4%

in the same period of the year before. The average rate

of interest for mortgages at the end of last year was 2.20%

for variable rates (a 9.1% decrease), and 3.06% for fi ed

rates (a 2.6% increase).

For their part, the Association of Property Registrars

shows that the average contract period of mortgages is

279 months (23 years and three months), a decrease of

about 2.11%. The average monthly mortgage payment

in the fourth quarter of 2019 was 604.09 euros. The effort

made by Spanish households to pay off their mortgages

and interest rates reached around 31% of their disposable

income, which is lower than what was seen in 2008, when

it amounted to over 50%.

The highest average of monthly mortgage payments were

registered in the Balearic Islands (924.04 euros), the

Community of Madrid (876.69 euros) and the Basque

Country (636.24 euros).

1.600.000

1.400.000

1.200.000

1.000.000

800.000

600.000

400.000

200.000

0

Registered Home Mortgages

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: INE (National Statistics Institute)

16 | Market Report 2019-20 Spain and Andorra

-2,4 %

-4,9 %

-7,5 %

-14 %

0,5 %

7,5 %

-3,3 %

2,5 %

1,2 %

-10,9 %

-0,3 %

After five years of growth, the buying and selling of homes

declined last period by 3.3% to 501,085 purchases, accor-

ding to the INE. This decline is due to the contracting of

second-hand flats, which fell by 4.2%, while sales of new

homes increased by 1.2% to a total of 92,844, thus accu-

mulating three consecutive years of growth. All in all, the

2019 sales figure is the fourth best in the last 13 years.

Here are the percentages by autonomous community: Cas-

tilla La Mancha (7.5%), Extremadura (5.7 %) and La Rioja

(3,1 %) registered the highest increase in buying and

selling, whereas the most pronounced decline was seen in

the Canary Islands (-14 %), the Balearic Islands (-10,9 %),

and Navarre Navarra (-9,7 %). Andalucía was the region

with the highest number of homes bought and sold

(100.339 transactions), followed by Catalonia (79,751),

the Valencian Community (74,910) and Madrid (70,835).

The latest figures for the third quarter of 2019, taken from

the Ministry of Development, show a drop in buying and

selling by 4% to a total of 411,234 homes sold.

Registered property sales based

on the buyer’s nationality

Year 2019

Source: Spanish Association of Registrar

Property Purchase by Autonomous Communities

Andalusia

Cataonia

Valencian Community

Community of Madrid

Canary Islands

Castile and León

Castilla-La Mancha

Basque Country

Galicia

Region of Murcia

Balearic Islands

Aragon

Principality ofAsturias

Extremadura

Cantabria Chartered Community

of Navarre La Rioja

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

-1,1 %

National Total

2014 347.170 2015 383.107 2016 436.574 2017 509.847 2018 410.883 2019 501.085

100.000

Source: INE (National Statistics Institute)

Nationalities % % Foreigners

United Kingdom 1,74 13,94

France 0,98 7,85

Germany 0,89 7,12

Morocco 0,77 6,17

Belgium 0,73 5,83

Romania 0,73 5,87

Italy 0,64 5,13

Sweden 0,56 4,48

China 0,49 3,97

Russia 0,40 3,20

Holand 0,34 2,74

Norway 0,23 1,87

Polond 0,20 1,63

Ukraine 0,19 1,56

Algeria 0,18 1,43

Ireland 0,16 1,30

Bulgaria 0,14 1,12

Denmark 0,12 0,96

Switzerland 0,11 0,87

Other 2,86 22,96

Foreigners 12,45% 100,00%

Nationalities 87,55% TOTAL 100,00%

Seal Estate in Spain | 17

16 1 Market Report 2019-20 Spain and Andorra

Real Estate Market Trend Residencial Español | 17

Spanish

Residential Market

18 COMMUNITY OF MADRID

Madrid

Surroundings

34

CATALONIA

Barcelona

Surroundings

Costa Brava

Tarragona

Cerdanya

66

VALENCIAN COMMUNITY

Valencia

Castellón

Alicante - Costa Blanca

84

ANDALUSIA

Costa del Sol

92

NORTHEAST REGION IN SPAIN

Galicia

Asturias

Castile and León

102

NORTHERN REGION IN SPAIN

Basque Country

Navarre

112

CANARY ISLANDS

Tenerife

116

BALEARIC ISLANDS

Mallorca

Menorca

Ibiza

122

NEW BUILDS

18 | Market Report 2019-20 Spain and Andorra

Community of Madrid

Madrid

3.226.126

38.224 €

30.094 €

3.732 €/m²

+1,3 %

Population or Number of Inhabitants

Average Gross Income

Disposable Income

Average Price 2019

Interannual Variation

The Spanish capital is the leader in attracting foreign

investments in the country. Madrid ranks as the fourth

most attractive destination in Europe for investing in

real estate, according to Emerging Trends in Real

Estate Europe in 2019 by ULI and PwC. One of every

five companies created in Spain has their offi in

Madrid, and 72% of the 2,000 main Spanish compa-

nies have their head offi in the city.

The entry into force of the new mortgage law along

with the moderation of economic growth have altered

the demand for homes in the whole country. In Madrid,

while the real estate market remains strong with pen-

ding urban developments such as Madrid Nuevo Norte

(The New North Madrid), or the Programa de Actua-

ción Urbanística (Urban Action Program) in southeast

Madrid. In the third quarter of 2019, housing sales in

the Community of Madrid reached 17,427 units, a

decrease by 3.57% compared to the same quarter the

year before, according to data from the Spanish pro-

perty registry.

Prices maintained some stability over the past year,

with increases of less than 5%. Forecasts from Engel

& Völkers point to sustainable growth throughout 2020

with similar spikes in areas where there is still room

for improvement and a correction in those that have

experienced strong increases. Despite their upward

trend, prices are still far from the highest point recor-

ded in 2007, about 33% below.

The Community of Madrid registers the highest bank

debt per square metre in the country. According to the

Spanish Association of Property Registrars, the debt

reached 1,985 euros / sqm in the third quarter of 2019.

Madrid also holds the greatest amount of home mort-

gage debt, reaching a sum of 202,426 euros / sqm. Its

longest average for periods of new mortgage contracts

was 307 months, 25 years and 7 months. The region

also holds the highest monthly mortgage rates, with an

average of 873.90 euros in the middle of last year.

With regards to the average time to sell a property, the

fi has fallen over the last four years from an ave- rage

of 6.4 months required to sell a property to 3.6

months at present. This fi is well below the 8.2

months that Tinsa has on average in Spain.

According to Tinsa, the average gross return on a home

for rent in the capital stands at 4.4%, although this

percentage varies considerably depending on the

district.

Real Estate Market Trend · Community of Madrid | 19

Districts in the City of Madrid

Fuencarral - El Pardo

Hortaleza

Barajas

Moncloa - Aravaca

Tetuán

Chamberí

Centro

Chamartín

Salamanca

Retiro

Ciudad Lineal

Moratalaz

San Blas

Latina

Carabanchel

Arganzuela

Usera

Puente

de Vallecas

Vicálvaro

Villa de Vallecas

Villaverde

Prices in euros / sqm

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

5.500

6.000 - - - - - - - - - - -

1.500 2.000 2.500 3.000 3.500 4.000 4.500 5.000 5.500 6.000 6.500

Salamanca 6.370 Hortaleza 3.800 Carabanchel 2.825

Retiro 5.150 Moncloa - Aravaca 3.660 Villa de Vallecas 2.430

Centro 5.105 Arganzuela 3.585 Usera 2.170

Chamberí 5.095 Barajas 3.350 Moratalaz 2.040

Chamartín 4.725 San Blas 3.095 Puente de Vallecas 1.895

Ciudad Lineal 3.905 Latina 3.035 Vicálvaro 1.645

Tetuán 3.895 Fuencarral - El Pardo 2.960

20 | Market Report 2019-20 Spain and Andorra

Centro and Arganzuela

The urban planning modifi carried out in the cen-

tral district were decisive for the signifi increase in

prices recorded in previous years. The expectation crea-

ted by the Canalejas complex and the pedestrianization

of the Gran Vía boosted the average price of the district

to 5,170 euros / sqm at the close of 2018. Since then the

price fell by 1.3% in 2019 to around 5,100 euros / sqm.

The neighborhoods closest to these projects-----Sol and

Universidad-----is where a small decline was seen in the

last year, whereas in other areas, such as Palacio and

Justicia, we saw a slight increase in prices of second-

hand homes.

The housing typology in highest demand are apartments

with more than two rooms, and a surface area between

80 and 150 sqm. Spanish clients constitute 68% of pur-

chases compared to 32% of foreigners, among which the

majority are from Venezuela, France, Italy, the US,

England and China. Looking at purchases according to

the nationality helps determine their motives.

50% of them seek a primary residence, 40% are making

an investment, and only 10% of the purchases are for a

second residence.

In Arganzuela, buyers tend to be Spanish families, cons-

tituting 90% of all transactions. Among the 10% of

foreign clients, it is worth pointing out that the Chinese

clients comprise the majority.

Palos de Moguer and Acacias are the neighborhoods in

highest demand, along with the residential area known

as Metales, where most fl complexes are new gated

housing projects offering community spaces such as pools

and gardens. Younger clients still prefer the area closest

to the Matadero because it is well connected and off

a variety of services.

Property Prices inCentro and Arganzuela

(Data in euros / sqm)

District by district

Minimum Maximum Average

Justicia 4.496 7.826 5.524

Cortes 4.324 6.915 5.261

Embajadores 3.089 5.123 4.082

Universidad 3.825 5.783 4.529

Palacio 4.102 6.520 4.901

Sol 4.493 4.500 4.400

Acacias 4.100 5.090 4.595

Palos de Moguer 3.125 4.529 4.017

Latina 2.938 3.692 3.034

Carabanchel 2.400 2.934 2.826

Real Estate Market Trend · Community of Madrid | 21

Retiro Salamanca

In 2019, the average price of the six neighborhoods com-

prising the Retiro district, surpassed 4,000 euros / sqm.

The top two were Jerónimos and Ibiza, both of them in

high demand due to their excellent location in front of

the most iconic park.

The buyer profi in 2019 became more international. If

in 2018, the ratio of clients was 90% Spanish and 10%

foreign, in 2019, we found that 70% of the buyers to be

Spanish, and 30% international, the majority of which

came from Mexico.

The stately street known as Alfonso XII is the main artery

of the Jerónimos neighborhood, and it continues to be

preferred by foreigners with a high purchasing power,

who seek houses with an area larger than 200 sqm, in

classical buildings. Meanwhile, wealthy Spanish families

opt for the neighborhoods Ibiza and Niño Jesús.

The 20.000 euros / sqm reached in the most exclusive

areas of the district highlight both the buyer profi and

the desired housing typology, in two of the most charac-

teristic neighborhoods in Salamanca: Recoletos and Cas-

tellana. Capacious and luxurious homes whose operations

are carried out by Spanish families and foreigners, both

with high purchasing power, in a ratio of 60% to 40%,

respectively.

However, other neighborhoods in the district, such as

Guindalera, offer more affordable prices, with an average

of about 4.440 euros / sqm. These neighborhoods join

the revival which Fuente del Berro already experienced

in previous periods.

After the surge of Venezuelans buying property in the dis-

trict for the past few years, in 2019 we saw that

now the main people doing the selling. Mexicans continue

to purchase homes with a surface area of around 120 sqm.

Property Prices in Retiro

(Data in euros / sqm)

Property Prices in Salamanca

(Data in euros / sqm)

Minimum Maximum Average

Jerónimos 4.750 9.580 7.520

Ibiza 5.470 6.521 5.890

Pacífico 3.900 4.280 4.120

Niño Jesús 4.543 4.831 4.687

Adelfas 3.909 4.347 4.189

Estrella 3.697 4.472 4.136

Minimum Maximum Average

Goya 3.740 8.155 6.300

Lista 3.378 7.745 6.299

Castellana 4.360 21.420 7.664

Recoletos 4.575 23.850 8.959

Guindalera 2.480 6.580 4.441

Fuente del Berro 2.170 9.400 4.545

22 | Market Report 2019-20 Spain and Andorra

Chamartín Chamberí

Homes of around 145 square metres distributed among

three bedrooms are typically in high demand in the

fi district. 80% of all purchases are carried out by

Spanish clients compared to the 20% by foreigners. Of

the latter, last year we saw a notable rise in transactions

involving Mexicans and North Americans.

Buyers mainly look for a main residence 84% of the time,

which they acquire using their own resources and through

fi Then a meager 8% of the purchases are for

investment purposes, and another 8% of buyers seek a

second residence.

Due to the excellent ratio of quality to price found in the

properties, this district boasts some of the most coveted

residential areas in the city centre, such as El Viso, Nueva

España, and Hispanoamérica.

In 2019 we saw a drop in prices by around 2% with a

volume of operations similar to the previous period. It

is worth pointing out that most sales were made for

properties under a million euros. 85% of the purchases

were carried out by Spaniards looking for 145 sqm

homes, with three bedrooms, preferably penthouses.

60% of the buyers fi their homes with mortgages

compared to 40% using their own resources. 15% of

the international clients, made up of primarily Venezue-

lans, French, Belgians, and Mexicans, sought remode-

led properties in classical buildings at prime locations

like Almagro, Trafalgar and Ríos Rosas.

Of these three aforementioned neighborhoods, the

second and third have become the most highly deman-

ded due to their slightly greater degree of aff

in comparison to the fi Therefore, the average price

in Almagro surpasses 5,500 euros / sqm, while Trafalgar

and Ríos Rosas remain beneath this fi re, with a diffe-

rence of little more than the 4,000 euros / sqm charged

in Vallehermoso.

Property Prices in Chamberí

(Data in euros / sqm)

Property Prices in Chamartín

(Data in euros / sqm)

Minimum Maximum Average

Viso 2.889 7.417 5.273

Nueva España 2.941 5.548 4.652

Hispanoamérica 3.596 6.898 4.694

Castilla 2.800 5.618 4.711

Prosperidad 1.335 5.309 4.452

Ciudad Jardín 3.800 5.206 4.591

Minimum Maximum Average

Almagro 4.095 7.100 5.598

Trafalgar 3.352 5.120 4.236

Ríos Rosas 3.215 5.210 4.213

Arapiles 3.021 5.500 4.261

Gaztambide 3.410 5.212 4.311

Vallehermoso 3.220 5.115 4.168

Argüelles /Moncloa 2.825 5.520 4.173

Real Estate Market Trend · Community of Madrid | 23

Tetuán Fuencarral

In the adjacent district known as Tetuan, Cuatro Caminos

is the area claiming the highest demand. It is in fact quite

similar to Castillejos in both the type of properties off

and the price range.

Then you have Valdeacederas, Almenara and Berruguete

undergoing a rising trend due to their proximity to the

Caleido Tower, fifth skyscraper. Their average

price stands below 3,300-3,500 euros / sqm.

The housing typology in highest demand is a fl with three

bedrooms distributed over an area of 180 sqm. These fl

are usually fi with a mortgage and purchased to be

used as primary residences.

The residential neighborhoods comprising nor-

theast region, are in great demand by families interested

in spacious homes with an area greater than 120 sqm

distributed among at least three bedrooms. However, the

type of property varies according to the nationality of the

client. While Spaniards prefer flats, foreigners seek either

terraced or single-family homes.

Property Prices in Tetuán

(Data in euros / sqm)

We have seen a lot of foreigners joining the common

buyer purchasing in Mirasierra, most of whom are Ger-

mans moved to Madrid since the German

College was established in Montecarmelo. Fuencarral

is a young district which, aside from its German com-

munity, attracts families with children that are younger

than in areas such as Mirasierra, Fuentelarreina or the

neighborhood known as El Pilar.

Peñagrande is also a good option for the young buyer,

especially after the major renovation carried out, so that

it now off terraced and single-family units at aff -

dable prices.

Property Prices in Fuencarral

(Data in euros / sqm)

Minimum Maximum Average

Mirasierra 2.650 4.259 2.960

Montecarmelo 3.351 4.606 4.192

Peñagrande 2.261 4.500 3.380

Fuentelarreina 2.727 3.292 3.000

La Paz 2.600 4.600 3.600

El Pilar 2.200 4.200 3.200

Minimum Maximum Average

Cuatro Caminos 5.800 3.200 4.500

Castillejos 5.800 3.200 4.500

Bellas Vistas 4.100 2.900 3.500

Valdeacederas 4.400 2.700 3.550

Almenara 4.500 2.100 3.300

Berruguete 4.300 2.300 3.300

24 | Market Report 2019-20 Spain and Andorra

Moncloa - Aravaca

Even though Spaniard comprise 85% of all purchases,

more and more clients buying in this district are interna-

tional. Of the remaining 15% who are international

buyers, the main nationalities we fi are Venezuelans,

Mexicans, and a growing presence of French and Bel-

gians in Moncloa-Arguelles, along with some Chinese.

The kind of property preferred by all of them are ample

homes with four bedrooms, in fl with more than 150 sqm

of surface area, or detached houses of around 300 sqm.

Specifi in the prestigious area known as Puerta de Hie- rro,

Spanish families tend to prefer fl whereas foreigners opt for

semi-detached, terraced, and single-family units.

Argüelles holds its status as the most premium area in

Moncloa, with prices reaching 6,000 euros / sqm. It is

located by the emblematic places like Parque del Oeste

and Temple of Debod.

In Aravaca and in the housing project called El Plantío,

maximum prices have remained at around 7,800 euros /

sqm, although a slight decline in the average price has

been registered in purchases.

Property Prices in Moncloa - Aravaca

(Data in euros / sqm)

Minimum Maximum Average

Argüelles 3.532 6.109 4.815

Ciudad Universitaria 2.856 3.225 3.041

Valdemarín 2.091 7.375 4.465

Aravaca 1.803 7.754 3.790

El Plantío --- La Florida 1.250 7.800 2.693

Puerta de Hierro 1.751 3.785 2.900

Real Estate Market Trend · Community of Madrid | 25

Ciudad Lineal Hortaleza

Although It is one of the largest in Madrid, a unique

feature is that the entire district is structured around one

street: Arturo Soria, the main artery running through

several highly diff areas.

In the northern area you can find neighborhoods resisting

depreciation, such as Costillares, Atalaya, Colina and San

Pascual, where the average price stands at around 4,000

euros / sqm. While during the crisis in the previous decade,

these areas took the longest to suffer from lowering prices,

they were also the first to go up during the recovery.

Quintana, Ventas and Pueblo Nuevo are located in the

southern area, where average prices approach around

2,000 euros / sqm, with the neighborhood Concepción

representing the intermediate area with regards to both

price and the type of property.

In 2019 Ciudad Lineal experienced a large volume of

sales whose average prices have stayed the same in an

environment of light decline. The properties built are of

high quality and the abundance of trees and

green spaces make Ciudad Lineal one of the most inte-

resting areas in Madrid for investment.

Property Prices in Ciudad Lineal

(Data in euros / sqm)

Hortaleza is a very extensive district to the west of

Madrid, in which you can see numerous contrasts

between the types of homes and the profiles of inves-

tors. With prime areas like Piovera, where you find

extremely high-quality buildings and excellent services,

you also get affordable prices in neighborhoods like

Santiago Apóstol.

Palomas represents one of the most valued areas in the

district. Its prices are more moderate than in Piovera, but

with high quality homes. For their part, Canillas, Pinar

del Rey and Santiago Apóstol are attractive neighbor-

hoods to investors. You can fi excellent well-connec-

ted fl to rent out, which allow high returns within the

surrounding M-40 freeway.

Property Prices in Hortaleza

(Data in euros / sqm)

Minimum Maximum Average

Palomas 2.894 4.211 3.553

Piovera 4.125 5.003 4.564

Canillas 2.895 3.189 3.042

Pinar del Rey 2.256 2.784 2.520

Santiago Apóstol 2.199 2.687 2.443

Minimum Maximum Average

Costillares 2.575 5.200 3.888

Atalaya 3.557 4.700 4.129

Colina 2.200 5.417 3.809

San Juan Bautista 3.302 4.117 3.710

San Pascual 2.300 5.123 3.712

Concepción 2.412 4.720 3.566

Quintana 1.923 3.321 2.622

Ventas 1.258 3.050 2.154

Pueblo Nuevo 1.850 2.520 2.185

26 | Market Report 2019-20 Spain and Andorra

Sanchinarro,

Las Tablas and Valdebebas

Barajas - San Blas

Located in the north of Madrid, these districts are largely

comprised of family residential neighborhoods. The constant

growth and high demand kept prices on the rise in 2019, with

Sanchinarro at the top, where the average cost has climbed

by 8% compared to 2018, surpassing 4,000 euros / sqm.

The most sought-after areas in Sanchinarro are closest to

El Corte Inglés mall and to the Sanitas Hospital in La Mora-

leja. The preferred neighborhoods in Las Tablas are closest

to the BBVA and Telefónica offi The demand is not as

high in Valdebebas since it is still undergoing development.

Since these residential neighborhoods are primarily inha-

bited by young Spanish families, the properties in highest

demand have three bedrooms. In Sanchinarro and Las

Tablas, properties are distributed throughout a surface

area ranging between 100 and 130 sqm, and up to 120-

150 sqm in Valdebebas.

About 90% of purchased homes are used as main resi-

dences, while the remaining 10% is for investors. Most

clients require financing, although that has seen a decline

throughout this year, and 10% of the buyers made their

purchase using their own funds, as opposed to the 5%

who did the same in 2018.

Located near airport, these districts off ave-

rage prices at around 3,000 euros, although the costs

can range considerably due to the wide variety of pro-

perties off

Alameda-Barajas are not neighborhoods well-known by

the general public. However, the average price is relati-

vely high compared to similar areas. This is due to their

high demand by people who already reside there, who

value their tranquility, the ample green spaces and superb

public transport.

San Blas is a relatively popular district, whose interesting

development has future prospects. Despite its location

outside of the M-30 freeway, the fact that it is right on

the border makes it attractive, especially with regards to

neighborhoods like El Salvador, where you can find some

outstanding properties, mainly in Rosas and Simancas.

From an investment point of view, Rejas off a great oppor-

tunity in east Madrid. Improvements planned for public

transport in the area promise an upcoming revaluation.

Property Prices in Barajas - San Blas

(Data in euros / sqm)

Property Prices in

Sanchinarro - Las Tablas - Valdebebas

(Data in euros / sqm)

Minimum Maximum Average

Sanchinarro 3.495 4.419 4.110

Las Tablas 3.360 4.270 4.027

Valdebebas 3.560 4.530 4.320

Minimum Maximum Average

Aeropuerto 1.586 1.854 1.720

Alameda de Osuna 3.340 3.485 3.413

Corralejos 1.420 5.000 3.210

Casco Antiguo Barajas 1.827 3.729 2.778

Timón 2.027 3.756 2.892

Rejas 2.260 3.286 2.773

Salvador 3.041 3.272 3.157

Simancas 2.090 2.373 2.232

Real Estate Market Trend · Community of Madrid | 27

Rentals

What makes rent attractive as a vehicle for investment,

mainly in the context of alternative assets with reduced

profi , is the remarkable dynamism of

market. This situation caused an upward trend in prices

in the last few years, but in 2019, the trend came to a halt

in districts with the highest demand.

In the city as a whole, the average price has risen by 5%

to 16.4 euros / sqm, even though in the most popular

districts such as Centro, Salamanca, and Chamberí, a

slight decline was registered, whereas in areas like Mon-

cloa or Chamartín, the increase reached around 6%.

In 2019, the most in-demand home was an apartment

with a surface area of 80-100 sqm, with two bedrooms,

two bathrooms, and a good location.

Engel & Völkers increased its leasing transactions by

20% in the city of Madrid in 2019, a trend they hope to

continue for the rest of the year.

Price of rent in Madrid by districts

(Data in euros / sqm)

Minimum Maximum Average

Centro 9 35 18,7

Salamanca 8,5 38 19,4

Chamartin 8,9 37,5 16,5

Chamberi 8 35 18,2

Moncloa 6,87 24,8 15

Hortaleza 5,5 23,1 12,4

Tetuán 9,25 26,7 16

Retiro 9,1 30 16,6

Noroeste 3,6 24,37 10,38

Norte 3,4 28 12,09

28 | Market Report 2019-20 Spain and Andorra

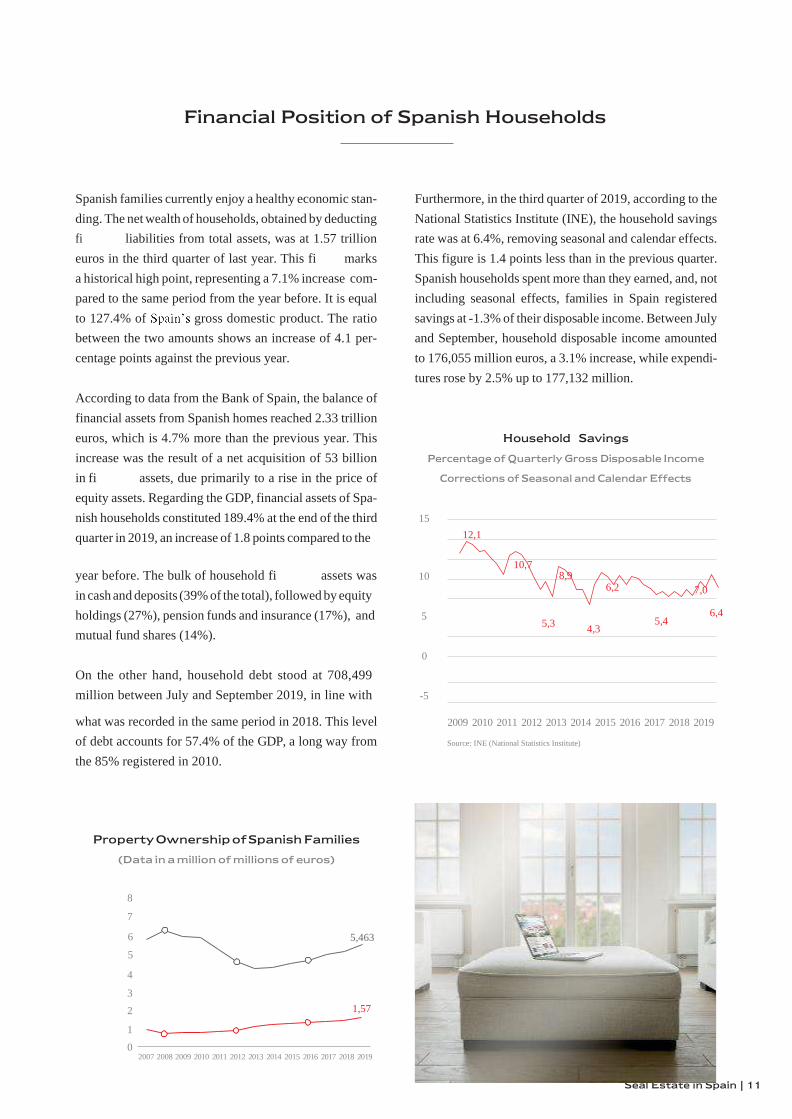

Madrid’s Surroundings

Pozuelo - Boadilla del Monte

Las Rozas - Majadahonda

La Moraleja

Zona Norte

Algete (Zona Norte)

San Sebastián de los Reyes (Zona Norte)

Cobeña (Zona Norte)

Las Rozas La Moraleja

Paracuellos (Zona Norte)

Majadahonda

Madrid

Boadilla del Monte Pozuelo

Real Estate Market Trend · Community of Madrid | 29

Pozuelo - Boadilla del Monte

Pozuelo de Alarcón and Boadilla del Monte remain the

municipalities with over 20,000 inhabitants and the

highest average of annual income per capita in Spain.

The first of the two, with an income of 25,957 euros per

inhabitant, is divided in two well-differentiated parts: La

Estación and Pueblo, two areas holding the bulk of the

district's services, and both surrounded by exclusive hou-

sing communities. Some of these communities, such as

Somosaguas, Montealina, Monte Gancedo, or Monteclaro,

are in high demand by Spanish families, who constitute

85% of the purchases compared to 15% of foreigners.

Throughout 2019, prices in the municipal centre

showed a notable increase, while the northern area and

the Estación maintained their maximum rates at 7,000

and 8,500 euros / sqm.

Property Prices in Pozuelo de Alarcón

(Data in euros / sqm)

Madrid’s Surroundings

Minimum Maximum Average

Pozuelo Pueblo 1.786 4.853 3.320

Pozuelo Norte 1.800 7.353 3.033

Pozuelo Estacion 2.250 3.800 3.025

Avenida de Europa 1.971 5.611 3.790

Montealina 1.629 4.000 2.531

Prado Largo 1.267 5.000 2.636

Monteclaro 1.513 4.250 3.121

Somosaguas 1.257 12.667 3.196

Prado de Somosaguas 2.130 5.236 3.295

La Finca 1.708 8.264 3.672

30 | Market Report 2019-20 Spain and Andorra

In 2019, the average housing price in Pozuelo de Alar-

cón stood at 3,155 euros / sqm, while in Boadilla del

Monte it stood at 2.416 euros / sqm, and in Villaviciosa

de Odón, at 1.977 euros / sqm, with an increase between

5% and 10%.

The housing typology in Pozuelo can be divided into

two categories: fl between 150 and 200 sqm distribu- ted

among four bedrooms, and spacious detached hou- ses

in green areas. The fi one you fi in Boadilla del Monte

and Villaviciosa de Odón, where you have in-de- mand

housing projects such as Valdecabañas and Mon-

tepríncipe. The second category you have in El Bosque,

where houses have surface areas between 400 and 500

sqm distributed throughout more than 5 bedrooms.

Property Prices in Boadilla del Monte

(Data in euros / sqm)

Property Prices in Villaviciosa de Odón

(Data in euros / sqm)

Minimum Maximum Average

El Bosque 877 3.780 1.821

Centro 566 4.980 2.477

Castillo - Campodon 1.014 3.798 1.781

Minimum Maximum Average

Monteprincipe 1.220 4.087 2.278

Valdepastores - Las Encinas 1.013 6.977 2.391

Bonanza 1.100 3.246 2.015

El Olivar 1.301 3.160 2.043

Las Lomas 781 4.200 2.154

Sector S 1.730 3.400 2.568

Sector B 1.800 3.990 2.965

Centro 1.925 3.681 2.508

Parque Boadilla 903 3.385 1.881

Real Estate Market Trend · Community of Madrid | 31

Las Rozas - Majadahonda

Las Rozas de Madrid is the third municipality in Spain

whose population of over 20,000 people has the highest

income per inhabitant, according to the Urban Indicators,

published by the INE in 2019. It presents a pro-

fi similar to Majadahonda, Villafranca del Castillo and

Villanueva del Pardillo.

In Las Rozas and Majadahonda, Spanish families prima-

rily demand penthouse flats and apartments in the central

area, with a surface area of around 120 sqm, and three

or four bedrooms. Regarding foreigners, buyers from

South America comprise 20% of all purchases in the area,

with a clear preference for capacious stand alone houses.

Property Prices in Las Rozas

(Data in euros / sqm)

The rising prices observed in all of the areas in Maja-

dahonda, is proof that the municipality is one of the most

desirable locations in the northeast of the capital.

Property Prices in Majadahonda - Villafranca

del Castillo - Villanueva del Pardillo

(Data in euros / sqm)

Minimum Maximum Average

Monte del Pilar 1.550 5.200 3.350

Centro 1.500 4.200 3.000

Golf - Carralero 2.300 5.400 3.500

Norte 1.450 4.800 2.900

Carretra del Plantío 1.200 4.800 2.760

Villafranca del Castillo 700 3.200 1.800

Villanueva del Pardillo 765 3.350 2.065

Minimum Maximum Average

Centro 1.200 4.300 2.750

Molino de la Hoz 940 3.700 1.800

Pinar - Punta Galea 900 3.500 1.870

Club de Golf 750 3.500 1.850

La Marazuela 960 4.000 2.450

El Burgo - Abajón 1.650 4.800 2.650

El Cantizal 1.700 4.100 2.900

Monte Rozas 750 3.300 1.950

Las Matas - Peñascales 750 3.500 1.900

32 | Market Report 2019-20 Spain and Andorra

La Moraleja

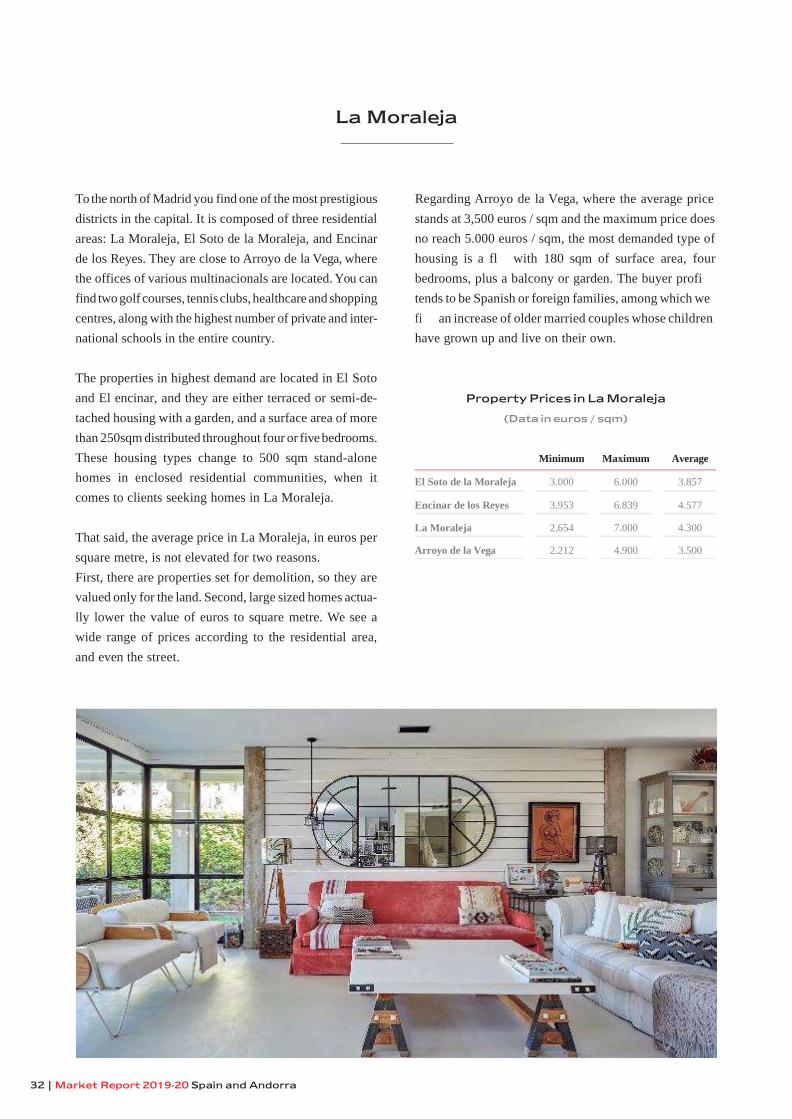

To the north of Madrid you find one of the most prestigious

districts in the capital. It is composed of three residential

areas: La Moraleja, El Soto de la Moraleja, and Encinar

de los Reyes. They are close to Arroyo de la Vega, where

the offices of various multinacionals are located. You can

find two golf courses, tennis clubs, healthcare and shopping

centres, along with the highest number of private and inter-

national schools in the entire country.

The properties in highest demand are located in El Soto

and El encinar, and they are either terraced or semi-de-

tached housing with a garden, and a surface area of more

than 250sqm distributed throughout four or five bedrooms.

These housing types change to 500 sqm stand-alone

homes in enclosed residential communities, when it

comes to clients seeking homes in La Moraleja.

That said, the average price in La Moraleja, in euros per

square metre, is not elevated for two reasons.

First, there are properties set for demolition, so they are

valued only for the land. Second, large sized homes actua-

lly lower the value of euros to square metre. We see a

wide range of prices according to the residential area,

and even the street.

Regarding Arroyo de la Vega, where the average price

stands at 3,500 euros / sqm and the maximum price does

no reach 5.000 euros / sqm, the most demanded type of

housing is a fl with 180 sqm of surface area, four

bedrooms, plus a balcony or garden. The buyer profi

tends to be Spanish or foreign families, among which we

fi an increase of older married couples whose children

have grown up and live on their own.

Property Prices in La Moraleja

(Data in euros / sqm)

Minimum Maximum Average

El Soto de la Moraleja 3.000 6.000 3.857

Encinar de los Reyes 3.953 6.839 4.577

La Moraleja 2.654 7.000 4.300

Arroyo de la Vega 2.212 4.900 3.500

Real Estate Market Trend · Community of Madrid | 33

Northern Region

In the region furthest to the north of the capital, you can

fi a variety of residential areas. Going beyond the La

Moraleja, we come across attractive modern municipa-

lities like San Sebastián de los Reyes, which is in full

expansion. It is well-connected, and increasingly desired

by young families, due to more aff ble prices when

compared to its neighbor, Alcobendas.

San Agustín de Guadalix has become a favorite desti-

nation for Madrileños wanting to purchase a second

home. Aside from the excellent stock of single-fa-

mily detached homes, and its proximity to the nearby

mountain range, the fl off aff prices, making

the properties an attractive investment to accommodate

the large number of people who work at companies in

the region.

Tres Cantos is a young, 35 year old modern city offering

a wide variety of flats, terraced housing and single-family

units, where Soto de Viñuelas claims the highest stan-

dards. The fact that it is so well-connected to Madrid

makes it desirable for many families, although its rising

prices are directing the interest of potential buyers

towards Colmenar Viejo.

Around the National I freeway, we can fi characteris-

tic residential areas such as Fuente del Fresno, Ciudal-

campo and Santo Domingo. Its single-family houses of

high standing, built in the 70s and 80s on large plots of

land, offer an excellent choice because of their affordable

prices, as opposed to the more modern homes in the area.

Lastly, we have the area known as Paracuellos del

Jarama. At the beginning of the century it saw significant

growth, making it a modern town that is well-organized

and equipped with high-quality properties, popular

among those who work at the airport and at industrial

companies nearby.

Housing price

in the northern region of Madrid

(Data in euros / sqm)

Minimum Maximum Average

San Sebastián de los Reyes 1.250 4.125 2.688

San Agustín de Guadalix 1.589 2.075 1.832

Fuente del Fresno, Ciudalcampo, Santo Domingo 1.798 2.595 2.197

Paracuellos del Jarama 720 3.197 1.959

Tres Cantos 2.150 2.895 2.523

Colmenar Viejo 1.351 1.846 1.599

34 | Market Report 2019-20 Spain and Andorra

Barcelona

1.636.762

37.124 €

29.199 €

4.390 €/m²

-4 %

Population or Number of Inhabitants

Average Gross Income

Disposable Income

Average Price 2019

Interannual Variation

In 2019, the housing market in Barcelona underwent

two diff stages. The fi one, which took place between

January and May, saw a slight increase in pri- ces and

transactions. The second, between June and

December, saw both variables drop considerably. The

outcome at the end of the year was negative, with a

decline in sales volume of new homes by 7% and 4% in

second-hand homes.

Economic, legal and political factors marked the diff -

rence between both stages. On the one hand, the demand

shrank. Many families saw the economic slowdown as a

sign that another crisis was underway. They decided to

postpone acquiring a new home and save their money

instead. On the other hand, the new mortgage laws in

Spain came into full eff in June and July, causing a

large decline in real estate transactions, although the

decrease was temporary.

In Barcelona, an analysis by district allows us to sepa-

rate them according to price changes. The following

districts registered an increase in costs: Nou Barris,

Sant Andreu, Gràcia, Sant Martí y Horta-Guinardó.

Then you have districts that registered a decline: Sarrià-

Sant Gervasi, Les Corts, Eixample, Ciutat Vella and

Sants-Montjuïc.

The trend in the outskirts was quite diff Despite its

unattractive setting, prices and transactions saw a good

increase. Sales costs climbed by 8%, standing at 2,170

euros / sqm.

The rental market in Barcelona remained stable, with

prices staying at 17.7 euros / sqm. This amount does not

include renewed contracts, only new rental agreements.

Diff trends unfolded. Expensive fl saw their pri- ces

get lower, as a consequence of all the tenants with more

purchasing power choosing to stop renting and start

buying. Meanwhile, cheaper fl became a bit more

expensive because of their growing demand. In the

outer area, rent rates rose by 2% to an average price of

10.8 euros / sqm.

In 2020, the price for both new and second-hand homes

will continue its decline in Barcelona, whereas in the rental

market, we will see a changing trend. Prices will undergo a

slight decrease in both the capital and the surrounding nei-

ghborhoods. The main reason will be that young families

switch from renting to buying. This change is owed to the

signifi raise in salaries seen in 2019 and 2020, along with

a greater willingness on behalf of banks willing to

concede loans and lower monthly costs, setting the mort-

gage rate at a similar amount as rent.

Catalonia

Real Estate Market Trend · Catalonia | 35

Districts of Barcelona

Prices in euros / sqm

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

5.500

6.000 - - - - - - - - - - -

1.500 2.000 2.500 3.000 3.500 4.000 4.500 5.000 5.500 6.000 6.500

Sarrià-Sant Gervasi 5.010 Sant Martí 4.170 Horta-Guinardó 3.020

Les Corts 4.890 Ciutat Vella 4.085 Sant Andreu 2.900

Eixample 4.750 Sants-Montjuïc 3.790 Nou Barris 2.620

Gràcia 4.300

Sarrià-Sant Gervasi

Les Corts

Sant Andreu

EixEaimxapmleple

Ciutat Vella

36 | Market Report 2019-20 Spain and Andorra

Barcelona by district

Ciutat Vella

old city , encompasses the historical centre

of the city, which includes neighborhoods such as Raval,

the Gothic Quarter, Born and the seaside area, the Bar-

celoneta. The unique character of the Ciutat Vella has

maintained the demand for homes in the area, primarily

by international clients, whose presence has grown.

In 2019, 62% of clients buying through Engel & Völkers,

were foreign. That is four points more than in 2018. Of

this percentage, 28.3% are French, 15% are Italian, and

9.4% are German. The common denominator among all

of them is their preference for old historical buildings that

conserve some of their original elements, with hydraulic

flooring and traditional Catalan volta ceilings.

The most highly demanded property in the district has

between 60 and 80 sqm of surface area, with two rooms.

A special preference is given to flats with an elevator and

outdoor access. 54% of all purchases are for primary

residences, 20% for secondary residences, and the 26%

for investment purposes make the city centre the most

prized location in Barcelona for this type of purchase.

Furthermore, many clients turn their secondary residen-

ces into profi assets by renting them out.

In 2019, the average price for properties in Ciutat Vella

was held at 4.085 euros / sqm, which is an 8% decline

compared to 2018, the most popular neighborhoods being

Born, the Gothic Quarter, Raval and Barceloneta.

Property Prices in Ciutat Vella

(Data in euros / sqm)

Minimum Maximum Average

Barri Gòtic 2.800 6.355 4.350

Raval 1.585 6.110 3.360

Barceloneta 1.760 7.930 5.030

Sant Pere, Santa Caterina i la Ribera 2.330 6.155 4.405

Real Estate Market Trend · Catalonia | 37

Eixample

Located in the centre of Barcelona, Eixample is the quin-

tessential modernist district, where the average price of a

home stood at 4,750 euros / sqm last year, which is a 7%

decrease compared to the previous period. Aside from the

decline in price, in 2019 the area saw a drop in foreign

clients and investors at the same time as a growing number

of national buyers sought to purchase their first residence.

The number of foreigners purchasing homes in Eixample

last year was 43%, compared to 52% in 2018. Chinese

buyers constituted most of the buyers, although a notable

rise in Italian and French clients was also observed. In

2019, Eixample claimed the most amount of expedited

Golden Visas transactions in Ciudad Condal (Barcelona).

Penthouse apartments and fl with balconies ranging

from 90 to 130 sqm, along with three rooms, represent

the most sought-after homes in Eixample. The most in-de-

mand areas are la Dreta de l'Eixample and l'Antiga Esque-

rra de l'Eixample, due to their proximity to major streets

like Passeig de Gràcia, the Rambla de Catalunya, and

Enric Granados.

That being said, Sant Antoni stands out as an increasin-

gly popular neighborhood to live in, with great restau-

rants, entertainment, and services, propelled by the remo-

deling of the market and the creation of new pedestrian

spaces such as Superilla.

Property Prices in Eixample

(Data in euros / sqm)

Minimum Maximum Average

La Dreta de l'Eixample 3.470 8.400 5.290

La Nova Esquerra de l'Eixample 3.110 7.320 4.410

La Sagrada Família, Fort Pienc 2.490 6.660 4.125

L'Antiga Esquerra de l'Eixample 3.140 8.080 4.810

Sant Antoni 2.690 5.730 4.260

38 | Market Report 2019-20 Spain and Andorra

Sants-Montjuïc Les Corts

Located in the south of Barcelona, about 10 minutes away

by subway from the centre, Sants-Montjuïc is one of the

most iconic districts in the city, as it combines the moun-

tains, the sea, and an excellent array of cultural activities.

It is also next to the most important train station in Cata-

lonia and the second in Spain.

The value of the properties dropped by 2.8% last year in

this district till it stood at 3,790 euros / sqm. Sales closed

by Engel & Völkers dropped by 5% in this area to a total

of 35 units.

The most in-demand properties offer 50 to 90 sqm of sur-

face area, with two or three rooms, and all buyers show a

special preference for penthouse apartments. Sants and El

Poble Sec-Parc de Montjuïc, which share part of the

demand for property in Sant Antoni, represent the most

coveted areas. Hostafrancs holds the highest average price

at 4,280 euros / sqm. The largest portion of the demand

comes from national buyers, comprising 65% of interested

parties. With regards to the international buyers, the majo-

rity come from France. 71% of all clients purchase homes

intended as their primary residence.

Three neighborhoods comprise this middle-class district:

Les Corts, Pedralbes and la Maternitat. Les Corts, Pedral-

bes and la Maternitat i San Ramon. It has a number of

advantages granted by its location, known as a fi

centre hosting Universidad Politécnica.

The average price of housing last year stood at 4.890

euros / sqm, which represents a decrease by 4% from

2018. The housing in the highest demand are fl and

penthouses with three rooms, and a surface area of 70

to 90sqm.

The neighborhoods Pedralbes and Les Corts claim the

highest demand, with the former known for the most

exclusive residential areas in Barcelona, where interna-

tional buyers seek houses with gardens. Regarding Les

Corts, it is one of the most consolidated areas with the

best services in the city. It is a familial neighborhood

off excellent transport and lots of tranquility.

75% of buyers are Spanish, but although the presence

of foreigners is not as great as in other districts, last

year two Golden Visa operations. Most purchases are

for primary residences, with only 8% constituting an

investment.

Property Prices in Les Corts

(Data in euros / sqm)

Property Prices in Sants-Montjuïc

(Data in euros / sqm)

Minimum Maximum Average

Poble Sec - Parc Montjuïc 3.100 5.225 3.950

Hostafrancs 4.120 4.340 4.280

Sants 2.215 4.565 3.530

Sants - Badal 3.270 3.800 3.625

Minimum Maximum Average

La Maternitat i Sant Ramon 3.310 4.885 4.000

Les Corts 3.230 5.060 4.150

Pedralbes 4.015 6.970 5.445

Real Estate Market Trend · Catalonia | 39

Sarrià-Sant Gervasi

The area with the highest income per capita in Barcelona

holds the most distinguished neighborhoods in the city.

This comfortable residential district brings together

numerous parks, prestigious schools and health centres.

The average price of the area fell by 3% last year to 5,010

euros/m2, and will remain more or less at this amount,

as this year expects to see some stability after the read-

justments from recent months.

Houses, penthouses and fl with a communal area and

parking are the most demanded properties. Sought-after

homes have three or more rooms from 130 to 200 sqm.

Galvany is one of the neighbourhoods with the highest

demand and where requests are centred on royal estates,

while in Sarrià and Bonanova there is a high demand for

houses with gardens.

87% of buyers are domestic, an increase of percentage

points compared to the previous year. The local client

has entered the market more strongly and is causing

downward closing price adjustments. Even so, the pro-

perties of more than four million euros continue to be in

demand by the international client.

85% of the purchases are made to acquire a main resi-

dence, and only 6% as an investment. 53% of the opera-

tions are done with a mortgage, a percentage that is

growing due to the increase in Spanish clients and low

interest rates.

Property Prices in Sarrià-Sant Gervasi

(Data in euros / sqm)

Minimum Maximum Average

El Putxet i el Farró 3.620 6.260 4.140

Sant Gervasi - Galvany 4.030 6.200 4.980

Sant Gervasi - La Bonanova 3.180 7.190 5.280

Les Tres Torres 4.530 6.070 5.440

Sarrià 3.160 7.000 5.075

Vallvidrera, el Tibidabo i les Planes

2.840

4.810

4.385

40 | Market Report 2019-20 Spain and Andorra

Gràcia

One of the oldest districts is also the smallest, but

that does not prevent it from registering the second

highest fi in terms of population density.

The price of properties reached 4,300 euros / sqm last

year, which is 7% more than the previous year. This

increase is due to a price adjustment for the type of pro-

perties sold by Engel & Völkers. More operations were

therefore carried out on refurbished properties in 2019,

whereas in 2018, they were done on unrefurbished pro-

perties.

Looking at 2020, an adjustment of current prices is expec-

ted considering the increase in foreign customers com-

pared to the previous year.

Property Prices in Gràcia

(Data in euros / sqm)

The area has stood out among international clients, who

are attracted by the charm of the neighbourhood's Cata-

lan-style atmosphere. Foreigners accounted for 37% of

the total purchases in 2019, compared to 15% in 2018.

Among them are a majority of French buyers, followed

by Chinese, Americans and British.

Flats and apartments from 70 to 90 sqm with two or three

rooms are the most requested in Gràcia. The four-be-

droom properties, although not frequently off in the

area, do have a high demand and are the ones that sell

the fastest. 80% of the buyers are looking for a main

residence, 10% for a second home and another 10% are

buying to invest.

The Vila de Gràcia, Camp d'en Grassot and Gràcia Nova

are the most sought-after neighbourhoods. All three are

characterized by having all kinds of services (hospitals,

schools, shops...), being located near the city centre, and

being well-connected.

Minimum Maximum Average

El Camp d'en Grassot i Gràcia Nova 3.230 6.160 4.690

La Salut 1.035 4.320 2.210

La Vila de Gràcia 2.270 7.170 4.480

Vallcarca i els Penitents 2.995 5.545 3.750

Real Estate Market Trend · Catalonia | 41

Horta - Guinardó Nou Barris

Located in the northeast of the city in a large valley, Hor-

ta-Guinardó is the third largest district of Barcelona after

Sants-Montjuïc and Sarrià-Sant Gervasi. It has a very

differentiated and heterogeneous urban structure due to

the varied topography, which includes the Collserola

mountain range, the Hebron valley or the Horta stream.

Horta-Guinardó is in increasing demand because, like its

neighbour Gràcia, it is both very well-connected and

equipped with all the necessary services. A great off of

green spaces makes it complete. The average price of a

property reached 3,020 euros / sqm in 2019, which is an

increase of 2% compared to the previous year.

Houses and fl from 110 to 150 sqm with three to four

rooms claim the main demand in this district. Among

them, the most sought-after properties are single-family

homes with gardens. The neighborhoods Can Baró and

La Font d'en Fargues receive the highest number of appli-

cations, the latter due to the fact that it is a residential

garden area. Spanish buyers comprise 75% of the demand,

the majority of whom are also among the sellers. Prac-

tically all purchases are for a primary residence, while

only 3% are made as an investment.

Property Prices in Horta - Guinardó

(Data in euros / sqm)

The youngest district of the city is located in the north

of the city. Composed of13 districts, Nou Barris off

green spaces next to historical buildings such as the Cas-

tell de Torre Baró. This brick castle with a medieval feel

is located at the top of the Collserola mountain range and

is one of the city's most privileged viewpoints.

The average price of a home in this district reached 2,620

euros / sqm in 2019. Apartments between 75 and 90

square metres constitute the most popular housing type.

The neighbourhoods attracting the largest number of

purchase requests, all of which come from Spanish citi-

zens, are Vilapicina i Torre Llobeta and Porta, known as

economic hubs off excellent transport to the centre.

Property Prices in Nou Barris

(Data in euros / sqm)

Minimum Maximum Average

La Guineueta 2.350 2.730 2.500

la Prosperitat 2.320 2.790 2.490

La Trinitat Nova 1.700 2.570 2.200

Porta 2.840 3.475 3.150

Vilapicina i la Torre Llobeta 1.245 3.000 1.850

Minimum Maximum Average

Can Baró 2.550 4.640 3.245

El Baix Guinardó - - 4.120

El Guinardó 3.250 3.970 3.710

Horta 1.980 3.730 2.670

La Font d'en Fargues 2.280 5.000 3.015

Montbau 2.050 3.330 2.880

42 | Market Report 2019-20 Spain and Andorra

Sant Andreu Sant Martí

The urban transformation of Sant Andreu is closely linked

to the arrival of the AVE (high-speed train) in the district

and the creation of the new La Sagrera station. This new

infrastructure and its railway accesses will give a more

innovative character to the neighborhoods of La Sagrera

and Sant Andreu. Therefore, while the average cost of

housing stood at 2,900 euros / sqm in 2019, the new

developments will drive increased demand and rising

prices in 2020.

Apartments between 90 and 110 square metres with three

or four bedrooms attract the highest demand in a district

where 89% of the buyers are Spanish people looking for

their main residence. On the other hand, 7% of the clients

carry out their purchases as an investment strategy, since

rent off more profi than in other areas.

Property Prices in Sant Andreu

(Data in euros / sqm)

With a privileged coastal location within the city, excellent

transport, and a wide range of services, Sant Martí offers

opportunities to renovate large three to four bedroom apart-

ments. The area received a boost in opportunities generated

from the Glòries Tower, where relevant companies in the

technology sector established their headquarters, attracting

their workers to the area.