Islamic Development Bank Development through South-South ...

Making development accountableA critical analysis of the systems of accounting

and accountability for the ConstituencyDevelopment Fund in Kenya

Robert Ochoki NyamoriSchool of Accounting, La Trobe University, Melbourne, Australia

Abstract

Purpose – The purpose of this paper is to describe and critically evaluate the systems of accountingand accountability for the Constituency Development Fund (CDF) in Kenya. It suggests a newframework of accounting and accountability that places the goals and aspirations expressed in publicdiscourse at the centre of accountability.

Design/methodology/approach – The theoretical insights of Bourdieu and Foucault are mobilizedso as to tease out the nature of power relations between the various fields associated with the CDF inKenya. The study analyses newspaper commentaries as text for identifying the main themesassociated with the management of the CDF in Kenya.

Findings – The paper finds that the CDF’s systems of accounting and accountability are skewedtowards the needs of centralized national planning and development, contrary to its expressed aim ofbringing about citizens’ participation in development.

Research limitations/implications – Use of newspaper commentaries and reports does notnecessarily represent the views of the majority of the people of Kenya.

Practical implications – A new framework is suggested which places the goals and aspirations ofpublic discourse at the centre of accounting with the various capitals suggested by these goals andaspirations forming the dimensions on which the CDF can be accounted for. Novel forms of accountingand accountability are suggested which include presentation of CDF implementation and results atpublic forums where the managers of CDF can be interrogated on the basis of the goals and aspirationsexpressed in public discourse.

Originality/value – Study of the CDF systems of accounting and accountability is a uniquecontribution to accounting for development in developing countries.

Keywords Accounting, Accounting systems, Kenya

Paper type Research paper

Introduction

I think the objective of getting resources down to the community level allowing them to own,monitor, hold the government accountable for use of resources [. . .] that is an objective weshare (Colin Bruce, World Bank Representative to Kenya, quoted in Daily Nation, 2006f).

Studies have remarked on how recent transformations of the public sector have beenaccompanied by shifts in conceptions of accountability from democratic forms tomanagerial ones (Broadbent et al., 1996; Humphrey et al., 1993) and from professionalto market accountability (Fowles, 1993). There has been a marked shift fromaccountability for processes, equity and access to inputs, outputs and results (Parkerand Gould, 1999). The main mechanism of public accountability is increasinglybecoming the annual report, accounting the dominant language and ends means the

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1832-5912.htm

Systems ofaccounting and

accountability

197

Received 28 April 2008Revised 12 January 2009

Accepted 6 February 2009

Journal of Accounting &Organizational Change

Vol. 5 No. 2, 2009pp. 197-227

q Emerald Group Publishing Limited1832-5912

DOI 10.1108/18325910910963436

rationality (Humphrey et al., 1993; Sinclair, 1995; Andrews, 2003). While researchershave remarked about the potential asymmetrical effects of systems of accounting andaccountability (Christensen and Skaebaek, 2007; Shenkin and Coulson, 2007), there hasbeen little empirical study of this phenomenon especially in developing countries. Theemphasis has tended to be the shifts from public to private enterprise in the context ofnew public management ignoring other equally important transformations thatinvolve forms of decentralization within the public sector. The studies have also tendedto privilege the state and its programmes of reform, while the targets of suchaccountability shifts (the public) rarely register on the radar of research. While Sinclair(1995) studied what managers of public entities thought about accountability, no studyI am aware of has been conducted on how public discourse, represented in newspaperreports could be implicated in the design systems of accounting and accountability inthe public sector. This is surprising because the expressed aim of public sector reformhas been, inter alia, to improve accountability to the public.

This paper analyses one form of public sector reconfiguration, the attempt by theKenyan Government to decentralize development by establishing the ConstituencyDevelopment Fund (CDF) through an Act of Parliament (Kenya Government, 2003).The CDF Act requires the Government of Kenya to allocate 2.5 per cent of the grossannual revenue collection to the CDF. Three quarters of this amount is allocatedequally to each constituency[1] and the rest distributed to each constituency on thebasis of its perceived level of poverty (Kenya Government, 2003)[2]. Under CDF,Ksh1.26 billion (US$ ¼ Ksh 65) was allocated in 2003/2004, Ksh 7.25 billion in2004/2005 and Ksh 21.8 billion in 2006/2007. The Act requires the Member ofParliament (MP) to firstly, constitute a constituency development committee (CDC)(made of constituents) to manage the CDF at constituency level and secondly, convenea constituency meeting where the constituents can articulate their needs. It is on thebasis of this articulation that the CDC is expected to select the projects to be funded andthe amount of funding for each project. Since the money is availed to each constituencydirectly, the CDF is a welcome break from the previous systems of bureaucratic centralcontrol where priorities and disbursement of funds were decided in Nairobi, the capitalcity of Kenya. The CDF marks a shift in development thinking towards the need forcitizens to be empowered so as to be active agents in their own development followingfailure of the post-independence centralized big project development models (Mansuriand Rao, 2003; Triantafillou and Nielsen, 2001; Drydyk, 2005).

The launch of the CDF has therefore been hailed as one of the most positive andremarkable developments in post-independence Kenya (Kimenyi, 2005; Oyugi, 2007).While the CDF has been lauded as a home-grown innovation (The East AfricanStandard, 2006h)[3] the programme contains elements of some of the programmeswhich have been championed by international development institutions such as theWorld Bank (Narayan, 2002). These programmes have the explicit objective ofreversing existing power relations in a manner that creates agency and voice for thepoor, allowing them to have more control over development programmes (Mansuri andRao, 2003; Narayan, 2002)[4]. While initially dominated by international developmentagencies, this approach is becoming embraced by national governments as in the caseof the CDF in Kenya[5]. The benefits of this approach however hinge on the existenceof mechanisms that ensure accountability to citizens, yet the nature of thesemechanisms or the form this accountability should take are contested (Mansuri and

JAOC5,2

198

Rao, 2003; Ribot, 1999). While there has been marked research interest on the nature ofsystems of accountability for organizations involved in development (Dixon et al., 2006;Gray et al., 2006; Drydyk, 2005), these efforts have been largely confined toaccountability in the context of NGOs to funders. The forms that accountability shouldtake where the state delegates development to citizens has however, not merited muchrecent attention. The question is how can development be made accountable to thepeople who are expected to be beneficiaries of development? I raise this question in thecontext of the CDF in Kenya.

The objectives of this paper are threefold. First, I aim to analyse the systems ofaccounting and accountability for the CDF in Kenya. Second, employing Foucault’s(1991) concept of governmentality, Bourdieu’s concept of field and capital (Bourdieu,1989; Oakes et al., 1998) and the literature on accountability (Roberts, 1991; Lehman,2001; Shenkin and Coulson, 2007), I evaluate whether prevailing CDF systems couldpossibly be in harmony with the articulated aim of decentralizing development andbringing about active citizen participation in their development. This evaluation is alsoundertaken against the various perspectives held by commentators and reporters onthe CDF as reported in Kenya’s two largest newspapers, the Daily Nation and the EastAfrican Standard. Third, I analyse these newspaper reports and commentaries toilluminate how these public discourses might influence the systems of accounting andaccountability for the CDF in Kenya and propose a new framework of accountability.

The paper is organized into eight sections as follows. In the second section, I discussthe context of CDF in Kenya. In the third section, I discuss the theory and methodologyemployed in this paper. In the fourth section, I delineate Kenya’s fields of developmentemploying Bourdieu’s theory of social practice and then describe the systems ofaccounting and accountability for CDF in fifth section. I discuss the limits of thesesystems in light of the articulated aims of CDF in sixth section while in seventh section,I suggest a new system of accounting and accountability that places the goals andaspirations of citizens at the centre and emphasizes accountability from the governor tothe governed. I conclude the paper in eighth section.

Context of CDF: development in KenyaSoon after Kenya attained political independence from Britain, the governmentasserted that development could not be achieved without active and overt governmentinvolvement (Kenya Government, 1965). This position became associated with theemergence of a large bureaucracy with a dominant role in decision making regardingnational planning and development (Cohen, 1993). The way decisions regardingdevelopment have been made and implemented in Kenya has therefore been largelycentralized in Nairobi, the capital city (Mapesa and Kibua, 2006; Chweya, 2006) withlittle systematic input by Kenya’s citizens into what objectives should be pursued andhow these objectives should be implemented. The only formal system of citizenparticipation has been through five year election cycles, during which Kenyans electlegislators, but over whom they have little or no control. This state of affairs has beenassociated with the lopsided development of the country with some regions moredeveloped than others, a reflection of the regional origin of the country’s presidents,ministers and top civil servants. This state of affairs continues to pose a seriouschallenge to Kenya’s political and economic stability[6]. There have been a number ofefforts to change this development model in a way that takes development closer to the

Systems ofaccounting and

accountability

199

people through decentralization[7], but these efforts have not drawn on lessons fromthe failures of previous decentralization efforts (Hans Seidel Foundation – HSF, 2006).It is therefore unsurprising that in spite of all these efforts, inequality and povertycontinue to afflict the majority of Kenya’s people (Mapesa and Kibua, 2006; Oyugi,2007).

It is against these earlier failed efforts that the CDF (Kenya Government, 2003) wasintroduced[8]. This fund was motivated by the need to redress the imbalances causedby prior development models. Specifically, it was aimed at addressing the corruptionthat had become associated with a system where individuals bought political powerusing money stolen from public coffers. This situation had created a spiral wherecitizens expected to be bribed and where to bribe it was deemed normal to steal fromthat very public. The fund was also hoped to redirect public expenditure fromrecurrent to development expenditure. Before then, the recurrent expenditureconsumed 80 per cent of the budget (Mapesa and Kibua, 2006). Whatever hadpreviously been allocated to development expenditure was also allocated and used inan opaque manner, but CDF aimed to create a transparent process for the allocationand use of these funds. Over the years, some of the development funds were also notutilized, with a lot of the money returned to Treasury, while the problems they weremeant to address lingered or got worse. The CDF was also aimed at continuing supportfor community initiatives, which hitherto had been at the beck and call of the local areaMP (Mapesa and Kibua, 2006). The wider objective was to decentre development sothat the local people would have a say in the decisions that affect their daily lives(Kenya Government, 2003). While the novelty and importance of CDF has been widelyacknowledged (Okungu, 2008), not much empirical study has been undertaken on itssystems of accounting and accountability[9].

Theoretical frameworkThis paper draws on aspects of governmentality (Foucault, 1991, 1988)[10], field(Bourdieu, 1985, 1989; Oakes et al., 1998) and communal and socializing forms ofaccountability (Roberts, 1991; Lehman, 2001; Shenkin and Coulson, 2007) to makesense of the regime of accounting and accountability associated with the CDF in Kenyaand to propose an alternative framework. Governmentality is concerned to explain thementality within advanced liberal democracies to govern every aspect of human life,and to illuminate the mechanisms deployed for this purpose. While the traditional viewof government privileged the state as the centre of political power, governmentalityurges us to consider the myriad centres through which government is achieved whichinclude supranational organizations such as the World Bank (Rahman et al., 2007),NGOs, community organizations, professional organizations, to name just a few. Theaim of government is to influence the conduct of people, but not through repression orcoercion, but through aligning the interests of the targets of power with those of thecentre. Once people’s interests are aligned with those of a centre, they can governthemselves, which makes governing easier and more efficient. Government in thisapproach is achieved at a distance through inscriptions such as accounting (Robson,1992, 1991). CDF promises to change long held centralized top-down approaches topower, so Foucault’s governmentality is useful in trying to make sense of therationalities and myriad centres involved in this initiative (Dean, 1999). The advantageof a governmentality analysis is that it enables attention to be directed to the way a

JAOC5,2

200

programme like CDF can be achieved while being vigilant to the dangers[11] of such aprogramme (Triantafillou and Nielsen, 2001).

The concept of field on the other hand enables us to theorise on the way social spaceis organized and the nature of relationships between social organizations or agents inthese organizations (Shenkin and Coulson, 2007). Bourdieu viewed social space asdivisible into loosely coupled and dynamic groups called fields. Membership of a fieldis determined by the volumes of capital that each field possesses and the proportion inwhich this capital is held. Bourdieu (1989) categorized these capitals into economic,social, cultural and symbolic. Economic capital refers to financial assets; culturalcapital refers to acquired dispositions and habits, and the accumulation of culturallyvalued objects such as training and education; social capital refers to the ties andnetworks that an individual or group possesses which enables him or her to acquireresources; symbolic capital on the other hand refers to the ability to “define andlegitimize cultural, moral, artistic values, standards, and styles” (Anheier et al., 1995,p. 862). Bourdieu conceived each field as competing with one another over limitedresources, with fields possessing certain defined capitals being associated withdifferent forms of advantage. Accountability is implicated in this struggle as amechanism through which each field seeks to augment its capital through exercisingcontrol over what is accounted for, to whom and even who is the audience, with thedominant fields having the tendency to control how information is produced anddefined (Christensen and Skaebaek, 2007). For example, there have been suggestionsthat annual reports serve the interests, not of citizens, but public sector elites (Taylorand Rosair, 2000) and in the context of privatized public entities, questions continue tobe raised regarding the implications of this singular focus on democracy (Andrews,2003). Bringing the two concepts of governmentality and field together,governmentality enables us visualize how different fields can mobilizeaccountability to exercise power over other fields and the contests associated withthis exercise.

The accountability literature enables us question the meaning and formaccountability can take, and combined with Bourdieu and Foucault enables us toproblematise the singular view of accounting as equivalent to accountability (Roberts,1991; Lehman, 2001). This equation propagates a certain view of society as manageablethrough calculative forms of disclosure. Such a view, it is suggested, is consistent withthe promotion of economic forms of capital to the detriment of cultural and other formsof capital (Oakes et al., 1998) since accounting does not enable comprehension of whatis happening at the community level (Dixon et al., 2006). A new framework would haveto emerge from the subjugated knowledge (Foucault, 1980) of various communitieswhich would reflect the way agents communicate and act on cultural objects andprovide alternatives through which social change could be brought about (Shenkin andCoulson, 2007). This framework is based on community or social forms ofaccountability (Roberts, 1991) where transparency and closeness and othersocializing forms of accountability might be appropriate alternatives to proceduraland accounting forms of accountability (Gray et al., 2006).

The need for this radical framework is especially important for CDF becauseevidence abounds that citizens hardly use annual reports (Coy et al., 2001; Alijarde,1997; Steccolini, 2004; Hay, 1994). There are questions about the capacity of recipientsof information with suggestions that the cognitive capacities of the receivers of

Systems ofaccounting and

accountability

201

accounting information is limited in terms of digesting the mass of accounting datathat are provided on a regular basis (Hopwood, 1974). This lack of capacity isespecially pertinent in a developing country like Kenya where:

If social accountability is to do an effective job, it needs to get its message across [. . .]to Kenyans who do not read newspapers, have no access to the internet, and who own notelevision (Gichuki, 2005, quoted in IEA, 2006).

This quote underscores the fact that in developing countries, as in the developed,providing accounting information is not enough to meet the accountabilityrequirements for a participatory development since participation is premised onagents being able to make decisions and influence decisions that affect their lives. Thecase for new forms of accountability is powerfully made by Shenkin and Coulson (2007,p. 300):

The idea that we have to challenge the very meaning of accountability to enhance its formgestures towards not only a political but also a methodological challenge. We argue thatimplicit to this challenge is one core idea: that effective reactions to growing demands foraccountability are unlikely to be produced through refining existing procedures for reporting.In response, we argue that for a constructive element to emerge from the existing critique, itmust be constituted by practices that challenge the very meaning of information.

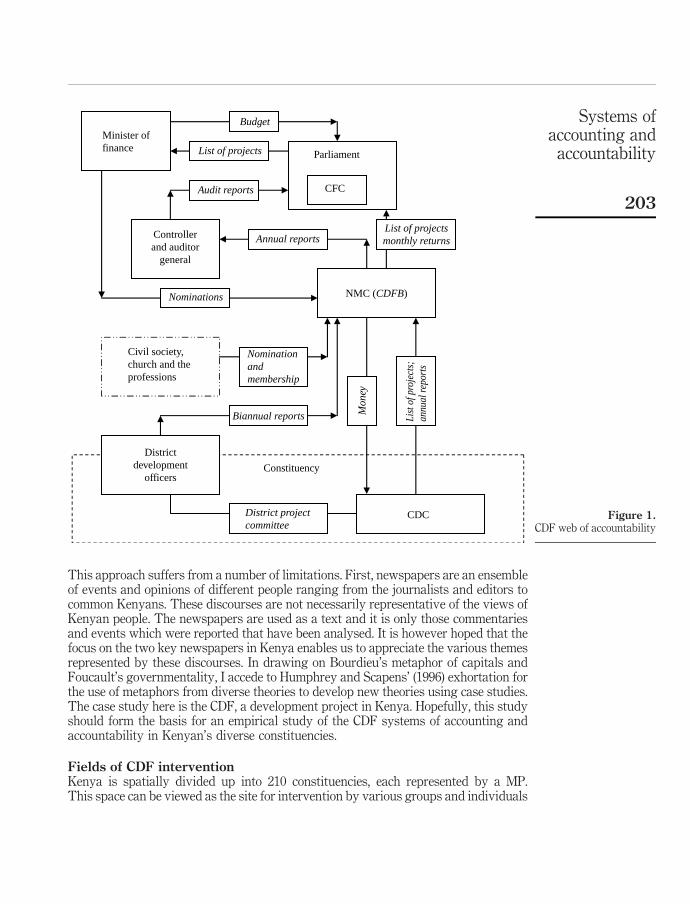

MethodThe first phase of the analysis involved a study of the accountability, governmentalityand field and capital literatures. The second phase involved a reading of the legislationand official documents regarding CDF. In this phase, I sought to understand theprevailing framework of accounting and accountability through attention to the CDFAct 2003, the CDF Amendment Act 2007 and other official publications. This analysisenabled me to come up with a diagram of the extant framework of accounting andaccountability for CDF (Figure 1).

The third phase involved the collection of newspaper articles on the CDF fromKenya’s two main newspapers, Daily Nation and the East African Standard for theperiod 2004-2008. I also accessed a range of commentaries on the CDF in Kenya. I readthese texts line by line and identified and summarized broad themes or categories fromeach article. The categories from each article were then compared with those from theother articles so that common themes were identified. These themes were thenclassified further into overarching theoretical constructs based on study of theliterature and prior experience. The approach aimed to pay attention to what has beensaid by various commentators regarding CDF and then trying to deduce the system ofaccounting and accountability[12].

I evaluated the CDF systems of accounting and accountability on the basis of thesepublic discourses and the literature. I was able to ask myself: to what extent were the CDFsystems of accounting and accountability addressing the CDF aims and the goals andaspirations represented in the Kenyan press? I drew on the work of Foucault (1991) andBourdieu to analyze the power relations inherent in the prevailing CDF accountingand accountability systems. On the basis of these analyses, I suggest a radical frameworkthat shifts accountability from the governor to the governed and places the goals andaspirations expressed in public discourse at the centre of accountability.

JAOC5,2

202

This approach suffers from a number of limitations. First, newspapers are an ensembleof events and opinions of different people ranging from the journalists and editors tocommon Kenyans. These discourses are not necessarily representative of the views ofKenyan people. The newspapers are used as a text and it is only those commentariesand events which were reported that have been analysed. It is however hoped that thefocus on the two key newspapers in Kenya enables us to appreciate the various themesrepresented by these discourses. In drawing on Bourdieu’s metaphor of capitals andFoucault’s governmentality, I accede to Humphrey and Scapens’ (1996) exhortation forthe use of metaphors from diverse theories to develop new theories using case studies.The case study here is the CDF, a development project in Kenya. Hopefully, this studyshould form the basis for an empirical study of the CDF systems of accounting andaccountability in Kenyan’s diverse constituencies.

Fields of CDF interventionKenya is spatially divided up into 210 constituencies, each represented by a MP.This space can be viewed as the site for intervention by various groups and individuals

Figure 1.CDF web of accountability

Parliament

NMC (CDFB)

CDC

Constituency

Minister offinance

Controllerand auditor

general

CFC

CDC

Districtdevelopment

officers

Mon

ey

List

of p

roje

cts;

annu

al re

port

s

Annual reports

Audit reports

List of projectsmonthly returns

List of projects

Budget

Nominations

Civil society,church and theprofessions

Nominationandmembership

Biannual reports

District projectcommittee

Systems ofaccounting and

accountability

203

in the name of bringing about development. The dominant group involved in thisintervention is the Government of Kenya, which consists of the three branches, namely,the judiciary, executive and legislature. The other is external but important groups andindividuals, key of which are bilateral and multilateral organizations such as the WorldBank and NGOs. The focus of all these agents is the Kenyan people whose lot they seekto improve. It is therefore possible to recast the Kenyan space into a development spaceand to then categorize this space on the basis of the volumes and relative amounts ofcapitals held by members in each category (Bourdieu, 1989). Following this schema,Kenya can loosely be categorized into three fields, namely, the national planning anddevelopment field, the community field and the wider field.

The national planning and development field may be viewed as made up of themembers that have traditionally been seen as responsible for national development andwho have traditionally formulated and implemented national development policy. Themembers of the national planning and development field are defined by the CDF Act2003 and include the National Management Committee (NMC), Parliament, ministersand civil servants. A defining characteristic of this field is that it possesses largevolumes of economic capital be it through tax revenue collection or through borrowing.The individuals within this group, who include ministers and civil servants tend tohave more of this resource through entry requirements and the capital accumulationthat comes with being in the top of the civil service or politics. These members havetraditionally played a central role in reform and implementation of the public sector(Therkildsen, 2001). Branch and Cheeseman (2006, p. 12) argue that an alliance betweenthe bureaucracy and the executive “has dominated governance for the past century”and extends to every part of the country. Branch and Cheeseman (2006, p. 25) furtherargue that members of this field have been “able to present a political platform tailoredto their own vested interests as a set of policies intended to benefit all” and have beenable to reproduce themselves and demobilize popular forces. Since the targets ofdevelopment have traditionally had little say, I exclude them from this field unlikeRahman et al. (2007).

The bulk of Kenya’s national space can be viewed as occupied by the communityfield which is a lot harder to define but can be considered to include the 210constituencies in Kenya and the various communities who reside within theseconstituencies. The members of this field are those who are targets of thesedevelopment efforts and who have not benefited from decades of misguideddevelopment policies. These members are now being repositioned as active citizens(Triantafillou and Nielsen, 2001). This field is deficient in economic capital as definedby their scores on the poverty index, the basis for CDF allocations. While possessingsocial capital emanating from historical, geographical and community networks ofliving within the same constituency, it is their ability to leverage this capital to accessnational resources, hence translate it to economic capital that is at issue here. Thesecommunities underscore the multidimensionality of discursive fields because theyhave different cultures and ways of life and are at different stages of meeting variousdevelopment needs (Oyugi, 2007).

The widespread field, similar to Rahman et al. (2007) includes diverse agencies suchas bilateral and multilateral donors, civil society groups, academia and NGOs.The widespread field possesses large volumes of economic capital and is oftenin partnership or competition with the government in defining development,

JAOC5,2

204

the mechanisms for achieving it and ways of evaluating it. The role of civil society forexample, in African development has been on the ascendance and is coalescingthrough networks of research, conferences and civic education programmes. Some ofthese organizations have been especially vocal regarding the need for participatorydevelopment because of their traditional involvement at the community level(Economic Commission for Africa (ECA), 2003). Members of this field drive manypublic sector reforms through technical and financial inputs and through social andpolitical networks. These fields are not definitive, but hopefully this delineation wouldenables us examine the vexing question of accounting and accountability for the CDF.

CDF systems of accounting and accountabilityThe nature of accountability between these fields is defined by the CDF Act 2003 andits subsequent CDF Amendment Act 2006 and is shown in Figure 1. The AmendmentAct came about after a period of highly sustained criticisms of CDF (the East AfricanStandard, 2005), so in analyzing these systems, I attempt to draw out how thisamendment changed or retained the extant systems of accounting and accountability.I however contend that the Amendment Act did not change the power relationsbetween the governed and the governor as envisaged when the CDF was introduced.

CDF Act 2003The CDF Act 2003 constituted the NMC headed by a chief executive and made up ofthe minister of finance and the permanent secretaries of the ministries of finance,economic planning, regional development and agriculture. The NMC also includes theclerk to the national assembly and eight persons appointed by the minister of financefrom a list of two nominees (one of each gender) submitted by each of the following:Kenya Farmers Union, The Institute of Engineers of Kenya, The Kenya NationalChamber of Commerce, the Catholic Church, the Kenya National Union of Teachers,the NGO Council of Kenya, the National Council of Churches of Kenya and the SupremeCouncil of Kenyan Muslims. The 2003 Act assigned the NMC responsibility for theapproval, allocation and disbursement of funds to every constituency for specificprojects (Daily Nation, 2006m). This body is required to ensure compilation of properrecords, returns and reports from the constituencies and their timely submission toparliament.

The NMC is accountable to parliament, which places the latter at the centre of CDFgovernance. Parliament participates in the governance of CDF in diverse ways. First,the minister of finance, who is also a member of NMC is a MP. It is parliament whichformulates and enacts the laws and the policy governing CDF. The CDF Actestablishes the Constituency Fund Committee (CFC), which is made up of MPs, inproportion to the strength of the political parties. The CFC scrutinizes the list ofprojects submitted by the NMC from each constituency and then recommends the finallist to be submitted to the minister of finance for inclusion in the budgetary estimates.The CFC oversees the implementation of the Act, considers any issues arising andsuggests policy directions. Once the minister has included the projects in the budgetaryestimates, they are presented to parliament for approval. Parliament also receivesannual reports from the NMC on each constituency and also audit reports on CDF fromthe auditor general.

Systems ofaccounting and

accountability

205

The influence of parliament is extended to the constituency where the MP is thesupervisor of the CDF. The MP as indicated is involved in making laws, yet they areexpected to supervise the choice and implementation of projects at the constituencylevel. Since the MP is potentially a member of the executive through appointment to thecabinet and through their membership of CFC, I include them in the national planningand development field although they are supposed to represent a constituency. Thisway, I consider the MP as extending the influence of the national planning anddevelopment field to the constituency. This influence is pervasive because the MP isrequired to constitute the CDC with himself or herself as chairperson, decide on theneeds of constituents and implement projects to meet these needs.

The MP is not the only agent of the national planning and development field at theconstituency level. The line ministries have offices at the local level headed by districtofficers. These officers are non-voting members of the CDC who share the monitoringand implementation of projects. Payments for any projects are effected and processedaccording to government regulations which require that, all tenders and quotations aretabled and approved at a meeting of the District Projects Committee (DPC). Thedepartments are required to keep and maintain records of disbursement of funds andprovide progress reports of projects. The district development officer is required tocompile and maintain a record of all receipts and disbursements every month andsubmit returns to the NMC.

The CDC is meant to serve a very important function: accountability to constituentsthrough ensuring that they participate in their development; and through the NMC,accountability to parliament, and hence the wider public for the use of funds entrustedto each constituency. The Act requires the CDCs to form tender committees whichwould supervise the tendering for all projects. The aim of this requirement is to ensurecompliance with public finance regulations that seek to foster public accountabilitythrough transparency of the process of awarding tenders. The CDC may designate acommittee to oversee such implementation from which it can demand for an account.

The interaction between the national development field and the community fieldoccurs through procedures defined in the Act. While Section 21(1) of the CDF Act 2003requires that projects should be community based and ensure benefits to as manypeople as possible, there are no defined mechanisms for holding the nationaldevelopment field accountable to the community field. The direction of accountabilityis mainly from the community field to the national planning and development field.There are three main ways the community field members are involved in CDF, besidesbeing mere objects of this programme. First, members of the CDC are drawn from theconstituency. The CDC includes two councilors in the constituency, one district officerand two religious men. It also includes two men and two women, one youth and oneperson from a local NGO. Just like the NMC, the composition of the CDC is aimed atachieving as wide a representation as possible. It is also aimed at ensuring that the keyplayers in the constituency are included in the CDCs. The CDC once again underscoresthe reach of the national planning and development field since the Act does not specifyhow the MP should constitute this committee. This lacuna places the MP in a verypowerful position to influence the projects chosen, their distribution and the amount offunding allocated[13] hence continuing the marginalization of the community field.

Second, the community field members could have their needs dictate which projectsare selected and how much funding they should be awarded. However, again the MP is

JAOC5,2

206

accorded a lot of influence regarding how these needs are captured, interpreted andultimately implemented. The MP is required to convene locational[14] meetings withinthe first year of parliament and at least once every two years in the constituency todeliberate on development matters in the location[15] and the constituency. It is fromthese meetings that constituents are expected to come up with a list of priority projectswhich are submitted to the CDC. The Act also provides for the community to originateand submit its own projects to the CDC. Where a community submits such a project itmay elect two people to represent its interests during and after implementation of theproject. The CDC then deliberates and prepares the priority list to be submitted to theNMC and ultimately to the Clerk of the National Assembly. The CDC is accountable forthe keeping of accounts and the submission of the same to the NMC. It is required tomaintain its own bank account showing receipts and payments. There is however, littleaccountability from the national development field to the community field.

The wider field is implicated in the CDF systems of accounting directly throughmembership of the NMC and the CDCs and more indirectly through political activism.The CDF Act 2003 requires various organizations to nominate members to the NMC asalready indicated. The Act further reserves a slot for NGOs in the CDCs. Since theaccountability framework provided for in the CDF Act does not provide ways in whichthe needed shift in power relations from the government to citizen can be achieved,civil society organizations are increasingly taking on the role of seeking to constitutecitizens not as subjects but as active participants in their own development. The mainmechanisms employed by these groups include civic education, knowledgedissemination, media campaigns and participatory research (Triantafillou andNielsen, 2001). The HSF for example recently organized direct awareness workshopsand a media campaign to enable views of citizens to be aired on national radio and astakeholders’ conference for government, academia and the private sector (EastAfrican Standard, 2006g). The potential role of citizens in the governance of CDF wassummed up by one civil society activist:

The problem is not that the laws we have are inadequate; it is the people who do not have thecapacity to pursue the common good; to make responsible and effective civic participationpossible. The best way to ensure accountability is to encourage the kind of scrutiny andquestioning that gives people the final say (Daily Nation, 2006l).

In sum, the systems of accounting and accountability for the CDF under the 2003 Actwere based on upward accountability from the constituencies ultimately to parliament,employing the mechanisms of accounting. Thus, starting from the minister of financeto the district development officers, a web of accountability is constituted based onclearly defined procedures and information. The policy is decided at the national levelwith little input from the constituencies. The only local inputs are the inscriptions inthe form of annual returns. This framework was the subject of much criticism leadingto the CDF Amendment Act 2007.

CDF Amendment Act 2007The CDF Amendment Act 2007 introduced forms of managerialism into thegovernance of CDF and also delineated the boundaries between parliament and thenational management of the CDF. The CDF Amendment Act 2007 replaced the NMCwith the Constituencies Development Fund Board (CDFB). The CDFB is a bodycorporate, which is to be headed by a chief executive officer. The board retained its

Systems ofaccounting and

accountability

207

membership of civil servants but required that persons nominated to this board bequalified in finance, accounting, law, engineering, economics or communitydevelopment. The minister of finance was required to nominate an additional fourpeople with similar qualifications to achieve regional balance. Parliament would alsoapprove the names of all nominees to the board. The CEO is to be appointed on acompetitive basis and approved by parliament. The Amendment Act sought tointroduce forms of private sector management to the government of the CDF withemphasis being placed on managerialism and professionalism. The CDF AmendmentAct requires the CDFB to appoint managers and post them to the 210 constituencies.The managers are required to be graduates with a background in accounting,economics or business. The managers’ role is to coordinate CDF projects within aconstituency, keep proper records, prepare books of accounts and submit financial andother annual returns to the board.

The Amendment Act delineated the functions to be performed by the board andthose to be performed by parliament. The CDFB board is to formulate all policy andwhere the board comes across any policy situation, to refer the matter to the CFC. Theboard is to consider all proposals from the constituencies, but where it does notapprove a proposal from a constituency, it is to refer the matter to the CFC givingreasons for declining the proposal. The Amendment Act requires the CDFB to receiveand address complaints and disputes regarding the CDF. The CFC is to make the finaldecision on the proposal. The board is to submit a report to the CFC on a monthly basisdetailing project proposals received from the constituency and their approval status;the disbursement of funds to the constituencies for that preceding month; the status ofthe disbursements of funds from the treasury to the national account; and a statementshowing the balance or shortfall, if any, arising out of its approved annual budget forthat year. This way, the Amendment Act sought to resolve the conflict between theMPs and the NMC.

The effect of the amendment is that the board has greater leeway to act, but stillremains under the control of MPs. The chief executive is appointed by parliamentwhich further extends the power of parliament over CDF. The control of MPs, ratherthan being watered down has actually been extended. The controversial role of the MPin the management of the CDC was not resolved. The MP will constitute theConstituency Development Fund Committee (CDFC) for each constituency, whichreplaces the CDC. Each CDFC would serve for a term of three years, with a new MPconstituting a new committee. The accountability rather than shifting to a morecommunitarian one has largely remained inured to procedural periodical norms whichemploy the mechanisms of accounting within a Westminster system.

The Amendment Act required the DPC (part of the line ministry) to furnish theCDFC in each district with a list of other government allocations for various projects inthe district. The CDFC was assigned responsibility for the allocation of funds to allprojects in the constituency. Each CDFC is to file a return with the CDFB at the end ofthe year specifying the projects undertaken and for each project, the amount allocated,disbursed, and unspent on the projects. To seal loopholes for theft, the Amendment Actrequires every payment from the CDF account to be on the basis of a written resolutionof the CDFC. In sum, the Amendment Act vested responsibility for project selection,allocation and implementation including the management of funds in the constituencyon the CDFC and not the district officers, who are civil servants, and whom as

JAOC5,2

208

indicated, are assigned to the planning and national development field. Thesemeasures, it was hoped, would eliminate the confusion and duplication associated withboth the CDFC and the district development officers being vested with theimplementation of projects and the central government undertaking projects thatoverlapped CDF ones. I undertake a critical evaluation of these systems in thefollowing section.

Evaluation of the CDF Systems of Accounting and AccountabilityThe CDF was established to ensure citizen participation in their own development andthe equitable distribution of national resources. I contend that the achievement of theseobjectives required a major change in power relations between the national planningand development field and the community field. In this section, I evaluate the systemsof accounting and accountability for CDF described in the previous section, with a viewto establishing whether these systems could enable this envisaged shift in powerrelations. I argue that the prevailing systems do not alter extant power relations in anysignificant way and instead perpetuate the control of Kenya’s national development bythe centralized national planning and development field to the continued disadvantageof the community field.

Dominance of the national planning and development fieldThe NMC as already indicated, is constituted of members from the national planningand development field. The Amendment Act sought to achieve greater regionalbalance in the composition of the CDFB by including four extra members. Thecomposition of the NMC reflects a concern to represent as wide a cross-section ofagencies as possible and to achieve gender and religious parity. The fact itsmembership does not include members from the community field suggests its affinityto the national planning and development field. These members are far removed fromthe constituencies which is the foci of the CDF. The permanent secretaries included inthis committee have been at the apex of the centralized national development model.Their inclusion suggests a concern to ensure CDF is aligned with national economicplans, but more tellingly, their position at the apex of CDF underscores the continuedpropagation of control by central government and political elites. The perpetuation ofcontrol by the national planning and development field is further evidenced by thecentralized location of the NMC in Nairobi, the traditional centre of developmentplanning and implementation. This location removes it from events at the communityfield. The NMC tries to influence events in the constituencies through inscriptions suchas annual reports, but such reports provide only a partial view of events at the local.For example, using these distance originating reports, it was reported that Tharaka,Wajir West, Ndhiwa, Kisauni, Githunguri, Galole and Mandera East constituencieswere denied their allocations of funding for 200-2007 because either they had notaccounted for the money previously received, had not submitted fresh proposals or hadtheir accounts frozen due to irregularities (Daily Nation, 2006o). The influence of thesenational elite was pronounced in the way funds were allocated, but more so in theinfluence exerted by MPs on CDF[16].

The national planning and development field controlled the formula for allocation offunds to the constituencies. Citizens were not consulted regarding the criteria forallocation of CDF funds. The CDF funds were required to be allocated to constituencies

Systems ofaccounting and

accountability

209

on the basis of a formula informed by the constituency’s poverty index, as alreadyexplained. Empirical research into the way funds have been allocated has led tosuggestions that the allocation of funds to CDF was perpetuating the very equities itwas designed to help fight by ignoring the size and stage of development alreadyachieved (Oyugi, 2007). Questions were raised as to how Embakasi with a populationof 400,000 had been allocated Ksh43.5 million while Lamu East with 17,000 people wasallocated Ksh26 million (Daily Nation, 2006f).

This control was further exhibited in the way the national planning anddevelopment field continued to duplicate roles that could be left to the constituencies.Heads of department of line ministries are held accountable for CDF funds as dothe CDCs and both are assigned responsibility for implementation of CDF projects.The Public Finance Act governed the way CDF managed its funds and dischargedits accountability. This duplication of roles between ministries and CDF createdwaste (East African Standard, 2006b, 2007d) hence there were calls for harmonizationof CDF with central government plans especially the poverty reduction strategy (EastAfrican Standard, 2006i; HSF, 2006). The adoption of a constitution with devolvedgovernment was offered as the solution to this anomaly (East African Standard,2006b). The financial rules governing CDF are in line, not with accountability toconstituents, but to parliament. This control by one field was, however more pervasivein regard to MPs.

The CDF Act placed MPs in the unique position where they make the law and thenimplement it. These MPs are required to monitor these laws to ensure they are meetingtheir objectives (Daily Nation, 2006f, l; East African Standard, 2007e, 2006a, c, j).Regarding implementation, MPs allocate the CDF funds to the constituencies and alsohold the constituencies accountable for the use of these funds (Daily Nation, 2006f). Atthe constituency level, MPs allocate these funds to projects and supervise the use ofthese funds since the 2003 Act required MPs to appoint members of the CDCs and at thesame time supervise their work. This arrangement contradicts the separation of thethree branches of government, which is a basis for accountability in a liberaldemocracy. This arrangement has been associated with unfortunate but ratherpredictable consequences.

Parliament has sought to exercise control over all the other bodies associated withthe management of the CDF. The NMC is a case in point. While some commentatorsare of the view that the NMC is conducting a fiduciary and oversight duty byconstituting committees for finance and administration, publicity, complaints andaudit (East African Standard, 2006i), MPs vowed to amend the CDF Act to do awaywith it. Some MPs were reported as suggesting that the NMC be whittled down to amere secretariat with the CFC enjoying more control and executive management ofCDF (East African Standard, 2006i). There were fears however, that such anamendment would give MPs leeway to do what they want (Daily Nation, 2006l; EastAfrican Standard, 2006i). In the end, MPs had their way. The CDF Amendment Actabolished the NMC and put in its place the CDFB, with a more clearly defined role, butunder greater influence by parliament. Since the CDFB is a body corporate, it would beconstrued to be more independent from the influence of MPs. The reality is likely to befar from the truth since CDFB would retain many of the members of the previousbody, the NMC. The CEO of the CDFB has to be approved by parliament, suggestingthat one who is too independent is unlikely to be approved for the position.

JAOC5,2

210

Furthermore, Parliament could make the life of this body difficult if it proved tooindependent since it has to account to it.

Parliament has also sought greater control over the amounts allocated to the CDF.The CDF Act set the amounts to be allocated to the CDF at 2.5 per cent of GDP.Parliament has sought to increase the amount allocated to CDF, but has met resistancefrom the treasury. This move has been associated with conflicts between MPs andtreasury over the amount of allocations. The government’s refusal to increase the CDFbudget from 2.5 to 7.5 per cent was given as the reason MPs refused to endorse thesupplementary budget (East African Standard, 2006k). If parliament represented thewishes of the people of Kenya, trying to take control over the amounts allocated to theCDF would be a welcome development since the failures CDF promises to address canpartly be attributed to the treasury. There have however, been questions as to theintent of parliament in increasing these amounts. These questions have grown louderwith the passage of time as the abuses associated with the CDF and MPs culpabilityhave come to light.

The control of MPs over other bodies and the associated claims of abuse of CDFhave been more evident in the constituencies where they have leeway over who shouldbecome a member of the CDC. There have been claims that the process of selectingthese members is not transparent (Daily Nation, 2006f). Lack of transparency wasblamed on MPs who packed the CDC with their own relatives and political supporters(Daily Nation, 2006e, j, 2007; East African Standard, 2006d). The Minister for Justiceand Constitutional Affairs, Ms Martha Karua, was reported conceding that in herconstituency, members of CDCs were chosen by her and did what she wanted (EastAfrican Standard, 2006j). The problem of selection was exacerbated by the capacity ofthe members of CDCs with claims that they were not educated and had no appreciationof the need for strategic plans, procurement and financial prudence (East AfricanStandard, 2006i; Daily Nation, 2006a, j). Though MP’s influence was watered downsomewhat with the appointment of managers by the CDFB to manage CDCs, MPs stillretain inordinate influence over the running of the CDCs through their supervisory role.Furthermore, MPs play a significant role in decisions regarding what the needs of theconstituents are and what projects can address these needs.

The control of the membership of the CDC and its management has been associatedwith concerns that MPs are using the CDF for their personal aggrandizement (EastAfrican Standard, 2006b; Okungu, 2008). There have been worries that MPs could useCDF to campaign to be elected by funding only their pet projects and areas where theydrew their support from (Daily Nation, 2006c, e, h, i, j, 2007). One MP was criticized forallocating a large proportion of CDF to students in a school he owns (East AfricanStandard, 2006b, c) and another of allocating a large fraction of the funds to theequipping of local school laboratories with the schools required to buy the equipmentfrom his company (East African Standard, 2006b, c). There were concerns that the CDFwas perpetuating intra-constituency inequities, defeating its very aims. The CDFappears to have opened new doors for the perpetuation of corruption in Kenya withTransparency International listing the CDF as among the most corrupt institutions(East African Standard, 2006b).

This inordinate influence of MPs in CDF comes amidst concerns about theirsuitability for managing the CDF. First, MPs serve five-year re-electable terms, hencemight not be able to (or want to) focus on the long-term interests of their constituencies

Systems ofaccounting and

accountability

211

(Daily Nation, 2006a). Second, Kenyan MPs are considered to be inherently selfish(Daily Nation, 2006l; Okungu, 2008). This selfishness has been more marked in the lasttwo parliamentary terms where they have voted themselves astounding perks andrefused to have them taxed. Third, MPs might not be able to write proposals that couldrelease funding for their constituencies partly because of the limited education of someof them (Okungu, 2008). The control of CDF by the national planning and developmentfield is aggravated by citizen apathy and ignorance.

Citizen apathy and non-involvementThe inordinate control of MPs over most aspects of CDF challenges one of its centraltenets, which is, ensuring citizen involvement in decisions affecting their lives. Therewere concerns that many Kenyans were unaware of CDF and therefore did notparticipate in it (KHRC survey referred to by the East African Standard (2006i); DailyNation, 2006b, f). This lack of participation arose out of ignorance of CDF or apathy asfor example, in Machakos where constituents had shown little interest in how the CDFmoney was being used (Allafrica.com, 2006). Even where constituents were aware ofthe CDF, they did not understand that this was a tax payer funded programme, and notthe MP’s money (Oyugi, 2007).

This apathy and ignorance was however, not universal. For example, residents ofKwanza Constituency reportedly demanded that their MP, Dr Noah Wekesa, addressthem about CDF, not politics: “Don’t tell us about coalitions [. . .] Tell us about CDF [. . .]We don’t eat politics. We are tired” (East African Standard, 2007a). Furthermore,some constituents sometimes found it difficult to get in touch with their MP, e.g.residents of Riruta reportedly communicated to their MP through a newspaper articlebecause she was inaccessible (East African Standard, 2004). These differences lead usto suggest the need for empirical work to find out why members of some constituencieswere more aware than those of others. This is especially necessary because there havebeen claims that people may not be aware of their problems (Daily Nation, 2006d). Thisapathy was exacerbated by the weak capacity of the CDC, especially that of itsmembers and its formal financial management and control systems which, it issuggested, are largely orientated towards the needs of the national planning anddevelopment field.

Capacity of CDCMPs’ control of CDCs weakened accountability to constituents, which was exacerbatedby their choice of members to CDCs, who did not have sufficient knowledge andexperience to manage such an entity and owed their position to MPs. The CDF wasoperated haphazardly and lacked planning and proper management structures (DailyNation, 2006e, f, j, 2007). The budgeting systems were weak with little linkage betweenthe budget and project implementation. There was little information about whichprojects were implemented, how much they cost and their status (East AfricanStandard, 2006f). There was no transparency in the way CDF was operated (DailyNation, 2006f), and there were no proper mechanisms to monitor and audit CDF fundsand evaluate projects (East African Standard, 2006f). This weak capacity wasassociated with theft and pilferage. One such a case was the theft of KSh17.6 million forthe Eldoret East CDF (Daily Nation, 2006i, 2007). Therefore, there were many

JAOC5,2

212

suggestions that CDF establish proper mechanisms of accountability, projectmanagement and quality control (Daily Nation, 2006d; East African Standard, 2006d).

The CDF Amendment Act sought to address some of these ills by hiring newmanagers with knowledge of accounting (Daily Nation, 2007). The appointments wereexpected to weaken MPs hold over the CDF (East African Standard, 2007b) and allayfears over possible election-related abuse of CDF (East African Standard, 2007f;Mwalulu and Irungu, 2004). The managers were expected to exercise independentjudgment though there were fears that these managers would be manipulated by theMPs. These managers were therefore posted away from their constituencies wherethey could be under pressure from their local MP (East African Standard, 2007b; DailyNation, 2007). The employment of professional managers to run CDCs sought tointroduce professional accountability in the governance of CDF, but it raisesinteresting questions. These managers were appointed, not by the CDC, but by theCDFB board. The question is where is the community input into these appointments?(East African Standard, 2007c). There is also a danger that the establishment of a localbureaucracy to manage CDF might lead to the privatization of accountability withthese managers dismissing the right of citizens to hold them accountable (Patton,1992). Such managers might feel they owe accountability to the national and planningfield which hires them and with whom they share common capitals. These limitationslead me to suggest a new system of accounting and accountability where control by thenational planning and development field is transferred to the constituency and wherethe capacity of constituents is enhanced so as to enable them control their owndevelopment.

Towards a new framework of accounting and accountability for the CDFThe evaluation of the CDF systems of accounting and accountability above hasilluminated many of the weaknesses which have been echoed in public discourse inKenya. First, the laws regarding the CDF are made by the same people who implementthese laws and who are guardians over the ensuing systems of accounting andaccountability. Second, and related to this first point, the systems of accounting andaccountability are oriented towards providing information to parliament with littlecare for members of the community field. The systems portray members of thecommunity field as being objects to be reported upon and not agents in thedevelopment process. This way, I contend that age-old asymmetrical power relationsbetween the centre and the periphery are perpetuated. Thus, third, the system does notenable an evaluation of the performance of the CDF against its core goals of achievingcitizen involvement and equitable development. It is also questionable whether thesereports are measuring the main objective of CDF, which is poverty eradication throughcommunity-based decision making. Since accountability is mainly framed in the formof accounting reports, which are aimed for NMC and ultimately to parliament both ofwhich are based in Nairobi where many rural constituents cannot access them, itserves more to alienate them than include them in their development. In sum, membersof the national development field decide what information the community field shouldprovide. The extant system of CDF emphasizes accounting and accountability from theconstituency upwards to the national institutions of parliament and the executive andnot downwards to the citizens. I propose a framework of accounting and accountabilitywhich places the goals and aspirations of CDF at the core of accounting

Systems ofaccounting and

accountability

213

and accountability. These goals and aspirations reflect the sort of capitals (Bourdieu,1989) that these discourses suggest should be augmented. The system of accountingand accountability should mirror these capitals and should enable an account of howthese capitals are being augmented[17]. The components of this framework arediscussed next.

Putting citizens hopes and aspirations at the centre of accountabilityThe aim of CDF as officially articulated was to bring about equitable nationaldevelopment and involve people in decisions which affect them (CDF Act 2003). Theseaims were articulated and sometimes extended in public discourse with CDF viewedwith great optimism. Some commentators opined that CDF is the best approach toemerge in Kenya in the last 40 years during which the government had failed todevelop rural areas (East African Standard, 2006c, Daily Nation, 2006a, b, c, d). Thissense of optimism and renewed hope extended beyond Kenya’s borders: PresidentsThabo Mbeki (South Africa) and Olusegun Obasanjo (Nigeria) are reported to havelauded CDF as an example that Africans could achieve something for themselves(Okungu, 2008). Such was the popularity of this innovation that one MP asserted that ifthe president of Kenya tampered with the CDF, he will be voted out of office the sameafternoon (Daily Nation, 2006f). The commentators expected that CDF would eradicatepoverty (Daily Nation, 2006l; East African Standard, 2007c), distribute resourcesequitably (East African Standard, 2006c; Daily Nation, 2006a, b, e) and reach every partof the country (East African Standard, 2007e). There was great expectation that CDFwould reverse decades of lopsided development planning and execution by opening anew chapter of development but at the same time be a more efficient system (EastAfrican Standard, 2006b; Daily Nation, 2006c, b, f, g). These aspirations are associatedwith the improvement of the well-being of constituents, and may be considered asfalling in the realm of economic capital.

These aspirations were associated with hopes for the improvement of constituents’rights and empowerment. Some commentators expected CDF to enable citizendemocratic decision making by offering avenues through which people got engagedregarding what they wanted and how they wanted it (East African Standard, 2006c,2007e; Daily Nation, 2006b, d, e). This democratic engagement was expected to enhancetheir human rights and invigorate the fight against corruption from below (EastAfrican Standard, 2006i). This way, CDF was presented as, not merely a process forachieving certain outputs, but also one through which peoples’ lives could betransformed in a way that they would be more actively involved in development(Triantafillou and Nielsen, 2001). The social engagement with matters affecting theirlives might be expected to strengthen the ability of members of the community field toforge ties and bargain with members of the national planning and development fieldfor the sharing of national resources. It might also create trust and coordination leadingto projects that address their needs hence social capital.

The desire for the augmentation of these broad categories of capitals would suggestthat the system of accounting and accountability discussed in the previous section isdeficient, since it emphasized accountability for only those capitals which are amenableto measurement and reporting using technical devices like accounting. Instead,I propose a tentative system of accounting and accountability where for each broad

JAOC5,2

214

category of capital, there are loosely defined accountable mechanisms that wouldaugment that capital. I start with economic capital.

Accountability for economic capitalThe premise here is that CDF should enhance the economic capital of the constituents.Any meaningful system of accounting and accountability should therefore enable anaccount and evaluation of the achievement of the goals and aspirations associated witheconomic capital. The public discourse did not disclose a singular view of what anachievement of economic capital would entail, but it seemed to be encapsulated in theterm development with some reports opining that CDF had achieved tremendousdevelopment (Daily Nation, 2006g). Development was associated with a diverse rangeof things, with some reports indicating that CDF projects were the only visible signs ofdevelopment in some areas of the country (Daily Nation, 2006d; Kimenyi, 2005). CDFwas associated with improvements in security, e.g. in Gutunduti in Mathira District anew police station has been credited for reduced crime (Daily Nation, 2006d). A student(Abdi Noor) narrated how through CDF, he was able to pursue further education unlikemany of his peers (InequalityKenya, 2006). There were contradictory claims that CDFhas not been successful in alleviating poverty (East African Standard, 2006d) orachieving equitable development, for example in Kisumu Rural Constituency (KisumuRural Constituency Fund, 2005).

Many of these indices of development are amenable to measurement, e.g. it ispossible to calculate how many schools or hospitals or kilometers of road were builtusing CDF monies. It is also possible to measure changes in defined developmentattributes such as levels of income, school attendance, and contraction of certaindiseases against the resources expended on each constituency. A spatial analysis ofeach constituency can be undertaken to establish how equitably CDF projects arespread in each constituency. Constituents can be contacted to determine to what extentthey have access to resources and services provided by CDF. Accountability for theseoutputs can be undertaken employing the Westminster system where eachconstituency can prepare a periodic report indicating how it has performed withCDF funding. These measures can be subjected to audit by the Auditor General whocan then report to parliament. These forms of accountability are necessary for financialdiscipline over government budgets and ensure that it is spent according toprogramme design and intent and for fiscal and managerial accountability (Sevilla,2005).

Generally, though development outcomes are more challenging to define, they aresomewhat amenable to Westminster systems of accountability which enablesconstituency and national debate and informs the direction of future development. Thisform of accountability is however limited where many constituents are illiterate andare far removed from where these debates take place. The annual reports and auditreports suggested above should therefore, not be produced for consumption only by thenational planning and development field, since such a situation would perpetuate theasymmetry that CDF seeks to remove. There were suggestions that the CDF Act beamended to provide auditing mechanisms that would be made public (East AfricanStandard, 2006b) during consultative reviews and public forums (East AfricanStandard, 2006e). The NMC for example hired professionals to carry out an audit of the210 constituencies (Daily Nation, 2006n) and promised to make these audit reports

Systems ofaccounting and

accountability

215

public to enable Kenyans know how their CDF funds were used (East AfricanStandard, 2007f quoting Mr Nduati Kariuki, NMC Vice Chairman, CDF). Along withthe public presentation of the audit reports should be a presentation of periodic reportson the performance of CDF so that constituents can engage in a discussion of theefficacy of CDF. During each forum, the politicians and other leaders would appraisethe public on development projects financed by CDF (East African Standard, 2006g)and field questions.

This suggestion implies availability of information to constituents and that is achallenge when looking at vast constituencies with populations poorly linked tocommunication lines, many of whom are illiterate. There were suggestions for therevival of the Rural Press Programme[18] to publish periodic reports on the work of theCDF so as to spur debate (Daily Nation, 2006c). The NMC has provided a number ofavenues for obtaining information, e.g. it now requires each CDC to put up anotice-board detailing CDF expenditure, names of projects, the amount committed, theexpected cost of completion, location and completion date and name of contractor.Regarding bursaries, the notice-boards display name of beneficiary, institution andamount given (East African Standard, 2007f). The teething problems facing CDF hadcompelled NMC to organize nationwide training workshops for CDC members andlaunched a web site to allow the public to monitor how funds were being used in theirconstituencies (Daily Nation, 2006p). A number of constituencies, e.g. Kisumu Ruralalso have established web sites, which provide breakdowns of how its CDF funds willbe used (Kisumu Rural Constituency Development Fund, 2005). The wider field hasalso contributed to providing information with some NGOs being involved in attemptsto rank constituencies on the basis of CDF use (East African Standard, 2007d).

The programmes associated with improving the economic well-being of residentsare amenable to accountability through mere visibility or access or use. Whether it is aroad or a school, constituents seeing it can be happy that CDF has broughtdevelopment to their constituency. For example, there were reports that CDF projectswere the only visible sign of development in some constituencies (Daily Nation, 2006i).This visibility has however, to be complemented by a record of expectations againstwhich constituents can decide whether the project they are seeing is what they saidthey wanted. In some cases, the implemented projects did not address the expressedneeds of constituents, as in the case of Nyakach Constituency where a chief’s office wasrenovated while appeals for repairs to Sondu-Nyabondo-Bodi and Sondu-Sigoti-Bodiroads went unheeded (Daily Nation, 2006k). Such a record should enable constituents tomake judgment on whether the projects are of acceptable quality or not. Regarding thelatter, there were concerns that in some constituencies, CDF concentrated on quantity,not quality (Daily Nation, 2006f).

The focus of accountability for economic capital should be on whether constituentsare better-off materially with CDF. This dimension is fairly amenable to theWestminster systems of accounting and accountability, but this accountability islargely from the bottom to the top and not easily accessible to constituents. Thesuggestion here is that the annual reports and the audits should be explained toconstituents during public forums. Cases of CDF intervention should be narrated inpublic. The CDCs could buy time on vernacular radio and explain what they are doingwith CDF, since this medium is likely to reach most constituents. Constituents shouldbe encouraged to go and see the cases of intervention but should be armed with a

JAOC5,2

216

record of their expectations to enable them pass judgment on the extent to which CDFhas improved their material lot. The constituents should be encouraged, again throughpublic forum, to share their evaluations of CDF, which should form a basis forimproving the CDF. Such a public discussion should enhance the symbolic capital ofresidents who would feel empowered to contribute to decisions affecting their lives.

Accountability for social capitalThe forms of accountability suggested above, namely, narration and publicpresentations should augment the ties between the constituents which they candraw on for personal and community improvement. The premise here is that CDFshould enhance constituencies’ social capital. The goals and aspirations of CDF do notdirectly root for the enhancement of social capital, but the need to foster citizeninvolvement in the choice and implementation of projects gestures towards a new orderthat would enhance this capital by creating collective and individual engagement.Public discourse emphasized the need to break the control MPs over the CDF througha separation of MPs’ legislative role from implementation (East African Standard,2006b, c), as key to bringing about this participation. There were calls for themanagement of CDF funds to be removed from the hands of MPs (East AfricanStandard, 2006a, d) and the CDF Act amended to make it more explicit on how CDFmoney is used to benefit communities by compelling MPs to produce financial reportson projects (East African Standard, 2007c). There have also been suggestions for theinvolvement of external non-governmental agencies and civil society in CDF so as toimprove its performance and accountability. One professional body, the Instituteof Chartered Accountants of Kenya was for example concerned that three yearsdown the line and billions of shillings of CDF disbursed, the government had notinvited its members to audit the books or be part of the management committee(Daily Nation, 2006o). The involvement of civil society was presented as necessary inguiding citizens towards identifying their problems (Daily Nation, 2006d; East AfricanStandard, 2006i).

The greater weight of the suggestions has however fallen on improvingrepresentation of the constituents, with MPs viewed as removed from theirconstituents and the people they select serving, not the constituents’ interest, butthose of the MP. The question of representation is particularly pertinent because of theprevailing constituent apathy to CDF and also because it would be naı̈ve to expect thatall citizens would be involved in this process. The issue of representation has facedthose promoting participatory approaches where:

[. . .] locally accountable representative alternatives are difficult to construct beyond thetemporary legitimating presence of outside development agents [. . .] where rural authoritiesare upwardly accountable to the central state rather than downwardly accountable to thelocal population (Ribot, 1999, p. 23).

Ribot argues that if equity is to be achieved, then structures of community decisionmaking must be representative and accountable. Many commentators have suggestedthat CDC members be elected in a democratic manner with public involvement inthe establishment of CDC (East African Standard, 2006d, e). Some commentatorssuggested that selection of members to the CDC be done on a competitive basis, withthe best candidate being selected (Daily Nation, 2006j).

Systems ofaccounting and

accountability

217

These suggestions emphasize the character of those selected to the committees andtheir training and education. These persons should represent diverse groups in theconstituencies, who should be credible and respectable (East African Standard, 2006d).There were also suggestions that members of CDCs should have a minimum educationand that CDC committees should have some professionals in the committees (DailyNation, 2006o; East African Standard, 2006a). Some reports proposed that personsinvolved with CDF projects should be under the spotlight of Public Officer EthicsAct, Procurement Act and Kenya Anti-Corruption and Economic Crimes Act (EastAfrican Standard, 2006f), essentially to ensure they conduct themselves in line with thepublic interest.

Beside representation, a major concern has been how to involve constituents in CDF,with the president of Kenya calling for citizens to “actively participate in prioritizingcommunity projects financed by CDF” (East African Standard, 2006g). Citizens wereurged to demand for accountability (Daily Nation, 2006l) regarding the way the CDF isspent (Daily Nation, 2006i; East African Standard, 2006a; Allafrica.com, 2006; HSF,2006), projects selected and the work carried out (Daily Nation, 2006i; East AfricanStandard, 2006e). There were calls to Kenyans to ensure that formulation andimplementation of CDF funded projects is directly done with constituents’participation and approval (East African Standard, 2006f). Citizens were asked toaudit their MPs and their use of the CDF, especially whether it had enabledconstituents to benefit from the funds or whether they had used it to pursue selfishinterests. The citizens were urged to vote out those who had not used CDF to thebenefit of their people (Daily Nation, 2006o; East African Standard, 2007d).

The concern to involve the citizen has been accompanied by the realization thatsuch an active citizen has to be constructed. Specifically, commentators from the widerfield suggested that civic education and nationwide capacity building for publicofficials and citizens should be intensified to improve management of funds(HSF, 2006). The President of Kenya called for citizens to be educated on their civicduties (East African Standard, 2006g; Daily Nation, 2006l). There have also beensuggestions for fostering a sense of ownership, not through fiscal decentralization, butthrough assigning part of the revenue constituencies raise to be used for theirdevelopment. That way, constituents might feel a sense of ownership instead of theway it is now where the money is viewed as “mheshimiwa’s money” (Mapesa andKibua, 2006).

ConclusionThis paper has analysed public discourses on CDF in Kenya’s two leading newspapers,CDF legislation and other commentaries and reports to identify the major weaknessesassociated with the programme and to propose a new framework of accounting andaccountability. These discourses were analysed as text and an interpretation made ofthe major themes that should guide a new system of accounting and accountability.A limitation of this approach is that newspaper reports and commentaries do notnecessarily represent the wishes of the people of Kenya. Nevertheless, it is hoped thatfuture researchers would undertake empirical studies of the systems of accountabilityin the various communities in Kenya and how these systems can be mobilized into theCDF. Central to such research might be an examination of why some constituents are

JAOC5,2

218

more willing to participate than others and why CDF seems to have been moresuccessful there than elsewhere.