Maine Health and Higher Educational Facilities Authority

260

This Preliminary Official Statement and any information contained herein are subject to completion and amendment. Under no circumstances may this Preliminary Official Statement constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the Series 2016A Bonds in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such jurisdiction. PRELIMINARY OFFICIAL STATEMENT DATED JUNE 16, 2016 NEW ISSUE Ratings: Moody’s: Baa3 S&P: BBB See “RATINGS” herein In the opinion of Hawkins Delafield & Wood LLP, Bond Counsel to the Authority, under existing statutes and court decisions and assuming continuing compliance with certain tax covenants described herein, (i) interest on the Series 2016A Bonds is excluded from gross income for Federal income tax purposes pursuant to Section 103 of the Internal Revenue Code of 1986, as amended (the “Code”), and (ii) interest on the Series 2016A Bonds is not treated as a preference item in calculating the alternative minimum tax imposed on individuals and corporations under the Code; such interest, however, is included in the adjusted current earnings of certain corporations for purposes of calculating the alternative minimum tax imposed on such corporations. In addition, in the opinion of Bond Counsel to the Authority, under existing statutes, interest on the Series 2016A Bonds is exempt from the State of Maine income tax imposed on individuals. See “TAX MATTERS” herein. $174,035,000* Maine Health and Higher Educational Facilities Authority Revenue Bonds, Eastern Maine Healthcare Systems Obligated Group Issue, Series 2016A Dated: Date of Delivery Due: July 1, as shown on the inside cover The above-referenced bonds (the “Series 2016A Bonds”) are issuable only as fully registered bonds and, when issued, will be registered in the name of Cede & Co., as nominee for The Depository Trust Company (“DTC”), New York, New York. DTC will act as securities depository for the Series 2016A Bonds. Purchases of the Series 2016A Bonds will be made in book-entry form, in the denomination of $5,000 or any integral multiple thereof. Purchasers will not receive certificates representing their interest in Series 2016A Bonds purchased. So long as Cede & Co. is the Bondholder, as nominee for DTC, references herein to the Bondholders or registered owners shall mean Cede & Co., as aforesaid, and shall not mean the Beneficial Owners of the Series 2016A Bonds. Principal and semiannual interest on the Series 2016A Bonds will be paid by U.S. Bank National Association, Boston, Massachusetts, as Paying Agent. So long as DTC or its nominee, Cede & Co., is the Bondholder, such payments will be made directly to such Bondholder. Interest will be payable on January 1, 2017 and semiannually thereafter on January 1 and July 1. The Series 2016A Bonds are subject to redemption prior to maturity, including redemption at par under certain circumstances, as described herein under “THE SERIES 2016A BONDS - REDEMPTION.” The Series 2016A Bonds are special, limited obligations of the Maine Health and Higher Educational Facilities Authority (the “Authority”) payable solely out of the revenues or other receipts, funds or moneys of the Authority pledged therefor or otherwise available to U.S. Bank National Association (the “Bond Trustee”) under the Bond Indenture, dated as of July 1, 2016, between the Authority and the Bond Trustee (the “Bond Indenture”), consisting solely of payments made by the Institutions (as hereinafter defined) pursuant to the Loan Agreement, dated as of July 1, 2016 (the “Agreement”), among the Authority, Eastern Maine Medical Center (“EMMC”), Charles A. Dean Memorial Hospital (“CA Dean”), Inland Hospital (“Inland”), Maine Coast Regional Health Facilities (“Maine Coast”), The Aroostook Medical Center (“TAMC”), and The Blue Hill Memorial Hospital (“Blue Hill” and, together with EMMC, CA Dean, Maine Coast, Inland and TAMC, the “Institutions”), all as more fully described herein. To secure the payments under the Agreement, EMMC, Acadia Hospital, Corp. (“Acadia”), Eastern Maine Healthcare Systems (“EMHS” or the “Obligated Group Agent”), Mercy Health System of Maine (“MHSM”), Mercy Hospital (“Mercy”), VNA Home Health & Hospice (“VNA”), Blue Hill, Inland, Lakewood (“Lakewood”), Sebasticook Valley Health (“SVH”), TAMC, Maine Coast and, prior to or concurrently with the issuance of the Series 2016A Bonds, CA Dean (collectively, the “Obligated Group”) will issue a note (the “Series 2016A Note”) to the Authority, which will be assigned to the Bond Trustee, secured by a pledge of Gross Receipts (as defined herein) of the Obligated Group pursuant to a Master Trust Indenture, dated as of April 1, 2010, as amended and supplemented, among the members of the Obligated Group and U.S. Bank National Association, as Master Trustee (the “Master Trustee”). The Series 2016A Bonds will also be secured by mortgages granted to the Master Trustee on certain real and personal property of EMMC, Mercy, SVH and Maine Coast. THE SERIES 2016A BONDS ARE NOT AND SHALL NOT BE DEEMED TO CONSTITUTE A DEBT OR LIABILITY OR A PLEDGE OF THE FAITH AND CREDIT OF THE STATE OF MAINE OR ANY POLITICAL SUBDIVISION THEREOF BUT SHALL BE PAYABLE SOLELY FROM PLEDGED REVENUES UNDER THE BOND INDENTURE. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE STATE OF MAINE OR OF ANY POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OF THE PRINCIPAL OF OR INTEREST ON THE SERIES 2016A BONDS. THE AUTHORITY HAS NO TAXING POWER. The Series 2016A Bonds are being offered when, as and if issued by the Authority and accepted by the Underwriters, subject to prior sale or to withdrawal or modification of the offer without notice and subject to the approval of legality by Hawkins Delafield & Wood LLP, New York, New York, Bond Counsel to the Authority. Certain legal matters will be passed upon for the Obligated Group by Eaton Peabody, PA, Bangor, Maine, and for the Underwriters by McCarter & English, LLP, Newark, New Jersey. Certain legal matters will be passed upon for the Authority by Verrill Dana, LLP, Portland, Maine. It is expected that the Series 2016A Bonds will be available for delivery to DTC in New York, New York, on or about July __, 2016. Raymond James BofA Merrill Lynch Goldman, Sachs & Co. Morgan Stanley Wells Fargo Securities Dated: July __, 2016 * Preliminary, subject to change.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Maine Health and Higher Educational Facilities Authority

This

Pre

limin

ary

Offi

cial

Sta

tem

ent a

nd a

ny in

form

atio

n co

ntai

ned

here

in a

re s

ubje

ct to

com

plet

ion

and

amen

dmen

t. U

nder

no

circ

umst

ance

s m

ay th

is P

relim

inar

y O

ffici

al S

tate

men

t con

stitu

te a

n of

fer t

o se

ll or

the

solic

itatio

n of

an

offe

r to

buy,

nor s

hall

ther

e be

any

sal

e of

the

Serie

s 20

16A

Bond

s in

any

juris

dict

ion

in w

hich

suc

h of

fer,

solic

itatio

n or

sal

e w

ould

be

unla

wfu

l prio

r to

regi

stra

tion

or q

ualifi

catio

n un

der t

he s

ecur

ities

law

s of

suc

h ju

risdi

ctio

n.PRELIMINARY OFFICIAL STATEMENT DATED JUNE 16, 2016

NEW ISSUE Ratings: Moody’s: Baa3S&P: BBB

See “RATINGS” herein

In the opinion of Hawkins Delafield & Wood LLP, Bond Counsel to the Authority, under existing statutes and court decisions and assuming continuing compliance with certain tax covenants described herein, (i) interest on the Series 2016A Bonds is excluded from gross income for Federal income tax purposes pursuant to Section 103 of the Internal Revenue Code of 1986, as amended (the “Code”), and (ii) interest on the Series 2016A Bonds is not treated as a preference item in calculating the alternative minimum tax imposed on individuals and corporations under the Code; such interest, however, is included in the adjusted current earnings of certain corporations for purposes of calculating the alternative minimum tax imposed on such corporations. In addition, in the opinion of Bond Counsel to the Authority, under existing statutes, interest on the Series 2016A Bonds is exempt from the State of Maine income tax imposed on individuals. See “TAX MATTERS” herein.

$174,035,000*Maine Health and Higher Educational Facilities Authority

Revenue Bonds, Eastern Maine Healthcare Systems Obligated Group Issue, Series 2016A

Dated: Date of Delivery Due: July 1, as shown on the inside cover

The above-referenced bonds (the “Series 2016A Bonds”) are issuable only as fully registered bonds and, when issued, will be registered in the name of Cede & Co., as nominee for The Depository Trust Company (“DTC”), New York, New York. DTC will act as securities depository for the Series 2016A Bonds. Purchases of the Series 2016A Bonds will be made in book-entry form, in the denomination of $5,000 or any integral multiple thereof. Purchasers will not receive certificates representing their interest in Series 2016A Bonds purchased. So long as Cede & Co. is the Bondholder, as nominee for DTC, references herein to the Bondholders or registered owners shall mean Cede & Co., as aforesaid, and shall not mean the Beneficial Owners of the Series 2016A Bonds.

Principal and semiannual interest on the Series 2016A Bonds will be paid by U.S. Bank National Association, Boston, Massachusetts, as Paying Agent. So long as DTC or its nominee, Cede & Co., is the Bondholder, such payments will be made directly to such Bondholder. Interest will be payable on January 1, 2017 and semiannually thereafter on January 1 and July 1. The Series 2016A Bonds are subject to redemption prior to maturity, including redemption at par under certain circumstances, as described herein under “THE SERIES 2016A BONDS - REDEMPTION.”

The Series 2016A Bonds are special, limited obligations of the Maine Health and Higher Educational Facilities Authority (the “Authority”) payable solely out of the revenues or other receipts, funds or moneys of the Authority pledged therefor or otherwise available to U.S. Bank National Association (the “Bond Trustee”) under the Bond Indenture, dated as of July 1, 2016, between the Authority and the Bond Trustee (the “Bond Indenture”), consisting solely of payments made by the Institutions (as hereinafter defined) pursuant to the Loan Agreement, dated as of July 1, 2016 (the “Agreement”), among the Authority, Eastern Maine Medical Center (“EMMC”), Charles A. Dean Memorial Hospital (“CA Dean”), Inland Hospital (“Inland”), Maine Coast Regional Health Facilities (“Maine Coast”), The Aroostook Medical Center (“TAMC”), and The Blue Hill Memorial Hospital (“Blue Hill” and, together with EMMC, CA Dean, Maine Coast, Inland and TAMC, the “Institutions”), all as more fully described herein. To secure the payments under the Agreement, EMMC, Acadia Hospital, Corp. (“Acadia”), Eastern Maine Healthcare Systems (“EMHS” or the “Obligated Group Agent”), Mercy Health System of Maine (“MHSM”), Mercy Hospital (“Mercy”), VNA Home Health & Hospice (“VNA”), Blue Hill, Inland, Lakewood (“Lakewood”), Sebasticook Valley Health (“SVH”), TAMC, Maine Coast and, prior to or concurrently with the issuance of the Series 2016A Bonds, CA Dean (collectively, the “Obligated Group”) will issue a note (the “Series 2016A Note”) to the Authority, which will be assigned to the Bond Trustee, secured by a pledge of Gross Receipts (as defined herein) of the Obligated Group pursuant to a Master Trust Indenture, dated as of April 1, 2010, as amended and supplemented, among the members of the Obligated Group and U.S. Bank National Association, as Master Trustee (the “Master Trustee”). The Series 2016A Bonds will also be secured by mortgages granted to the Master Trustee on certain real and personal property of EMMC, Mercy, SVH and Maine Coast.

THE SERIES 2016A BONDS ARE NOT AND SHALL NOT BE DEEMED TO CONSTITUTE A DEBT OR LIABILITY OR A PLEDGE OF THE FAITH AND CREDIT OF THE STATE OF MAINE OR ANY POLITICAL SUBDIVISION THEREOF BUT SHALL BE PAYABLE SOLELY FROM PLEDGED REVENUES UNDER THE BOND INDENTURE. NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE STATE OF MAINE OR OF ANY POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OF THE PRINCIPAL OF OR INTEREST ON THE SERIES 2016A BONDS. THE AUTHORITY HAS NO TAXING POWER.

The Series 2016A Bonds are being offered when, as and if issued by the Authority and accepted by the Underwriters, subject to prior sale or to withdrawal or modification of the offer without notice and subject to the approval of legality by Hawkins Delafield & Wood LLP, New York, New York, Bond Counsel to the Authority. Certain legal matters will be passed upon for the Obligated Group by Eaton Peabody, PA, Bangor, Maine, and for the Underwriters by McCarter & English, LLP, Newark, New Jersey. Certain legal matters will be passed upon for the Authority by Verrill Dana, LLP, Portland, Maine. It is expected that the Series 2016A Bonds will be available for delivery to DTC in New York, New York, on or about July __, 2016.

Raymond James BofA Merrill Lynch

Goldman, Sachs & Co. Morgan Stanley Wells Fargo Securities

Dated: July __, 2016

* Preliminary, subject to change.

$174,035,000* MAINE HEALTH AND HIGHER EDUCATIONAL FACILITIES AUTHORITY

Revenue Bonds, Eastern Maine Healthcare Systems Obligated Group Issue, Series 2016A

MATURITIES, AMOUNTS, INTEREST RATES, YIELDS AND CUSIPS

$57,500,000* ____% Term Bonds Due July 1, 2041, Yield ____%, CUSIP Number 560427_____∗∗

$116,535,000* ____% Term Bonds Due July 1, 2046, Yield ____%, CUSIP Number 560427_____∗∗

* Preliminary, subject to change.

∗∗ “CUSIP” is a copyright of American Bankers Association. The CUSIP numbers listed above are being provided solely for the convenience of Bondholders only at the time of issuance of the Series 2016A Bonds and none of the Authority, the Obligated Group or the Underwriters makes any representation with respect to such numbers or undertakes any responsibility for their accuracy now or at any time in the future.

i

IN CONNECTION WITH THIS OFFERING, THE UNDERWRITERS LISTED ON THE COVER PAGE HERETO (“THE UNDERWRITERS”) MAY OVERALLOT OR EFFECT TRANSACTIONS THAT STABILIZE OR MAINTAIN THE MARKET PRICE OF THE SERIES 2016A BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME.

No dealer, broker, salesman or other person has been authorized by the Maine Health and Higher Educational Facilities Authority, the Obligated Group or the Underwriters to give any information or to make any representations with respect to the Series 2016A Bonds, other than those contained in this Official Statement, and, if given or made, such other information or representations must not be relied upon as having been authorized by any of the foregoing. The information contained herein under the heading “The Authority” has been furnished by the Maine Health and Higher Educational Facilities Authority. All other information contained herein has been obtained from other sources which are believed to be reliable, but it is not guaranteed as to accuracy or completeness by, and is not to be construed to be the representation of, the Maine Health and Higher Educational Facilities Authority or the Underwriters. Neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the parties referred to above since the date hereof. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy, and there shall not be any sale of, the Series 2016A Bonds in any state in which it is unlawful to make such offer, solicitation or sale.

THE SERIES 2016A BONDS HAVE NOT BEEN REGISTERED WITH THE SECURITIES AND EXCHANGE COMMISSION UNDER THE SECURITIES ACT OF 1933, AS AMENDED, NOR HAS THE INDENTURE BEEN QUALIFIED UNDER THE TRUST INDENTURE ACT OF 1939, AS AMENDED, IN RELIANCE UPON EXEMPTIONS CONTAINED IN SUCH ACTS. THE REGISTRATION OR QUALIFICATION OF THE SERIES 2016A BONDS IN ACCORDANCE WITH APPLICABLE PROVISIONS OF THE SECURITIES LAWS OF THE STATES, IF ANY, IN WHICH THE SERIES 2016A BONDS HAVE BEEN REGISTERED OR QUALIFIED AND THE EXEMPTION FROM REGISTRATION OR QUALIFICATION IN CERTAIN OTHER STATES CANNOT BE REGARDED AS A RECOMMENDATION THEREOF. NEITHER THESE STATES NOR ANY OF THEIR AGENCIES HAVE PASSED UPON THE MERITS OF THE SERIES 2016A BONDS OR THE ACCURACY OR COMPLETENESS OF THIS OFFICIAL STATEMENT. ANY REPRESENTATION TO THE CONTRARY MAY BE A CRIMINAL OFFENSE.

The order and placement of materials in this Official Statement, including the Appendices, are not to be deemed to be a determination of relevance, materiality or importance, and this Official Statement, including the Appendices, must be considered in its entirety.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Official Statement contains forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 that are not limited to historical facts, but reflect current beliefs, expectations or intentions regarding future events. These statements include in general forward-looking statements.

Statements that are not historical facts, including statements that use terms such as “anticipates,” “believes,” “expects,” “intends,” “plans,” “projects,” “seeks” and “will” and that relate to plans and objectives of the Obligated Group for future operations, are forward-looking statements. In light of the risks and uncertainties inherent in all forward-looking statements, the inclusion of such statements in this Official Statement should not be considered as a representation by any person that the objectives or plans of the Obligated Group will be achieved. These forward-looking statements include, without limitation, expectations with respect to the synergies, future financial and operating results of the Obligated Group, and the Obligated Group’s plans, objectives, expectations and intentions with respect to future operations and services.

All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those in the forward-looking statements, many of which are generally outside the control of the Obligated Group and are difficult to predict. These risks and uncertainties also include those set forth under “BONDHOLDERS’ RISKS” herein.

ii

TABLE OF CONTENTS Page

INTRODUCTORY STATEMENT ............................................................................................................................................. 1 THE AUTHORITY ..................................................................................................................................................................... 6 THE SERIES 2016A BONDS ..................................................................................................................................................... 9 SECURITY FOR THE SERIES 2016A BONDS ...................................................................................................................... 15 CERTAIN FINANCIAL COVENANTS .................................................................................................................................. 19 EASTERN MAINE HEALTHCARE SYSTEMS ..................................................................................................................... 19 PLAN OF FINANCE ................................................................................................................................................................ 20 ESTIMATED SOURCES AND USES OF FUNDS ................................................................................................................. 21 DEBT SERVICE REQUIREMENTS ........................................................................................................................................ 22 BONDHOLDERS’ RISKS ........................................................................................................................................................ 23 UNDERWRITING .................................................................................................................................................................... 48 RATINGS .................................................................................................................................................................................. 49 FINANCIAL ADVISOR ........................................................................................................................................................... 49 LITIGATION ............................................................................................................................................................................ 49 LEGALITY OF SERIES 2016A BONDS FOR INVESTMENT AND DEPOSIT ................................................................... 50 SERIES 2016A BONDS NOT LIABILITY OF THE STATE OF MAINE .............................................................................. 50 AGREEMENT OF THE STATE............................................................................................................................................... 50 LEGAL MATTERS ................................................................................................................................................................... 50 TAX MATTERS ....................................................................................................................................................................... 51 INDEPENDENT ACCOUNTANTS ......................................................................................................................................... 53 CONTINUING DISCLOSURE ................................................................................................................................................. 54 MISCELLANEOUS .................................................................................................................................................................. 55 Appendix A – Information Concerning Eastern Maine Healthcare Systems and the Obligated Group .................................. A-1 Appendix B – Consolidated Financial Statements of Eastern Maine Healthcare Systems ...................................................... B-1 Appendix C – Certain Provisions of Principal Documents ...................................................................................................... C-1 Appendix D – Form of Opinion of Bond Counsel ................................................................................................................... D-1 Appendix E – Form of Continuing Disclosure Agreement ...................................................................................................... E-1

1

MAINE HEALTH AND HIGHER EDUCATIONAL FACILITIES AUTHORITY

_________________________

OFFICIAL STATEMENT

Relating to

$174,035,000*

Maine Health and Higher Educational Facilities Authority Revenue Bonds, Eastern Maine Healthcare Systems Obligated Group Issue, Series 2016A

INTRODUCTORY STATEMENT

The descriptions and summaries of various documents set forth herein do not purport to be comprehensive or definitive, and reference is made to each document for the complete details of all terms and conditions. All statements herein are qualified in their entirety by reference to each document. See Appendix C for certain provisions of the principal documents and for definitions of certain capitalized words and terms used but not defined elsewhere in this Official Statement.

Purpose

The purpose of this Official Statement, including the cover page, inside cover and appendices hereto, is to set forth certain information concerning the Maine Health and Higher Educational Facilities Authority (the “Authority”) and its $174,035,000* Revenue Bonds, Eastern Maine Healthcare Systems Obligated Group Issue, Series 2016A (the “Series 2016A Bonds”), issued pursuant to a Bond Indenture, dated as of July 1, 2016 (the “Bond Indenture”), between the Authority and U.S. Bank National Association, Boston, Massachusetts, as Bond Trustee (the “Bond Trustee”), and authorized by the Authority’s Bond Resolution adopted June 15, 2016 (the “Bond Resolution”). The Series 2016A Bonds are issued and secured under the Bond Indenture and the Bond Resolution in accordance with the Maine Health and Higher Educational Facilities Authority Act, being Chapter 413 of Title 22, Sections 2051 to 2077, inclusive, of the Maine Revised Statutes Annotated, as it may be amended from time to time (the “Act”). The Series 2016A Bonds and any additional bonds that may be issued pursuant to the Bond Indenture are referred to collectively as the “Bonds.”

Use of Proceeds

The proceeds of the Series 2016A Bonds will be loaned by the Authority to EMMC, CA Dean, Inland, Maine Coast, TAMC and Blue Hill (collectively, the “Institutions”) pursuant to a Loan Agreement (the “Agreement”), dated as of July 1, 2016, by and among the Institutions and the Authority. The Institutions will agree to make payments sufficient to repay the Authority’s loan and make certain other payments pursuant to the terms of the Loan Agreement. See Appendix C – “CERTAIN PROVISIONS OF PRINCIPAL DOCUMENTS – CERTAIN PROVISIONS OF THE AGREEMENT.”

* Preliminary, subject to change.

2

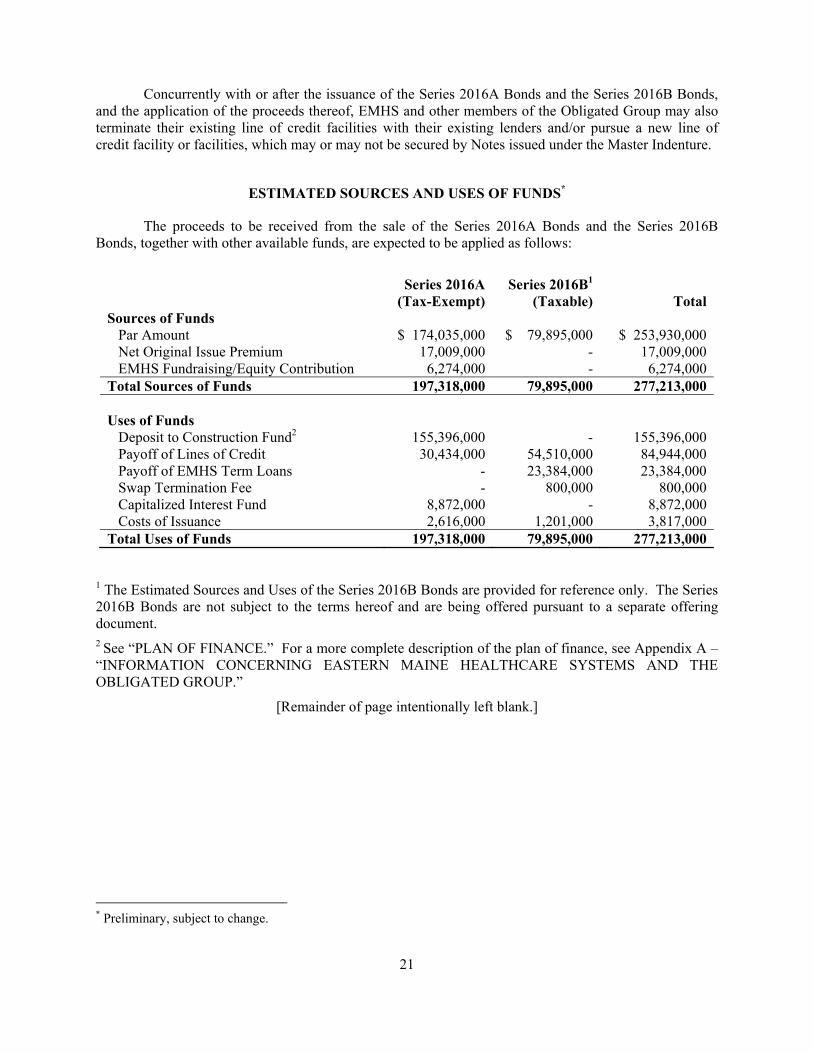

The proceeds of the Series 2016A Bonds, together with other available funds, will be used by the Institutions to (a) finance or refinance capital improvements and acquisition costs of the Institutions; (b) reimburse prior expenditures and refinance bank debt of certain of the Institutions; (c) fund capitalized interest, if any, on a portion of the Series 2016A Bonds; and (d) fund costs of issuing the Series 2016A Bonds. See “PLAN OF FINANCE” and “ESTIMATED SOURCES AND USES OF FUNDS” herein and Appendix A hereto.

Security

The Series 2016A Bonds are special obligations of the Authority, equally and ratably secured by and payable from amounts received by the Bond Trustee from the Institutions pursuant to the Agreement. Simultaneously with the issuance of the Series 2016A Bonds and in consideration of the Authority’s loan to the Institutions of proceeds of the Series 2016A Bonds under the Agreement, the Obligated Group will issue a note dated as of July 1, 2016 (the “the Series 2016A Note”) to the Authority, which will be assigned to the Bond Trustee. The Series 2016A Note will be issued under and pursuant to the Master Trust Indenture, dated as of April 1, 2010, as amended and supplemented (the “Master Indenture”), by and among the Obligated Group (as defined below) and U.S. Bank National Association, as Master Trustee (the “Master Trustee”). The Series 2016A Note will be pledged and assigned by the Authority to the Bond Trustee under the Bond Indenture for the sole benefit of the Holders of the Series 2016A Bonds and the holders of any Additional Bonds issued pursuant to the Bond Indenture. The Series 2016A Note will have terms and conditions to provide payments thereon sufficient to pay all amounts to become due on the Series 2016A Bonds. To further secure the Obligated Group’s obligations under the Series 2016A Note, the members of the Obligated Group have granted a security interest in all of their Gross Receipts under the Master Indenture. See Appendix C – “CERTAIN PROVISIONS OF PRINCIPAL DOCUMENTS.”

As further security for its obligations under the Agreement, certain members of the Obligated Group have granted security interests and/or mortgage liens in favor of the Master Trustee as follows: (a) a mortgage lien on the main campus of EMMC; (b) a mortgage lien on both hospitals of Mercy and its Westbrook campus and gastroenterology clinic; (c) a security interest in certain equipment of SVH and a mortgage lien on the hospital of SVH; and (d) a mortgage lien on the hospital and a medical office building and housing facility of Maine Coast (collectively, the “Mortgages”). See “SECURITY FOR THE SERIES 2016A BONDS – MORTGAGED PROPERTY” herein.

The Series 2016A Bonds will be secured by the Mortgages and the Series 2016A Note on a parity basis with all outstanding Notes and obligations issued and to be issued under the Master Indenture. See “SECURITY FOR THE SERIES 2016A BONDS – MASTER INDENTURE” herein.

Eastern Maine Healthcare Systems

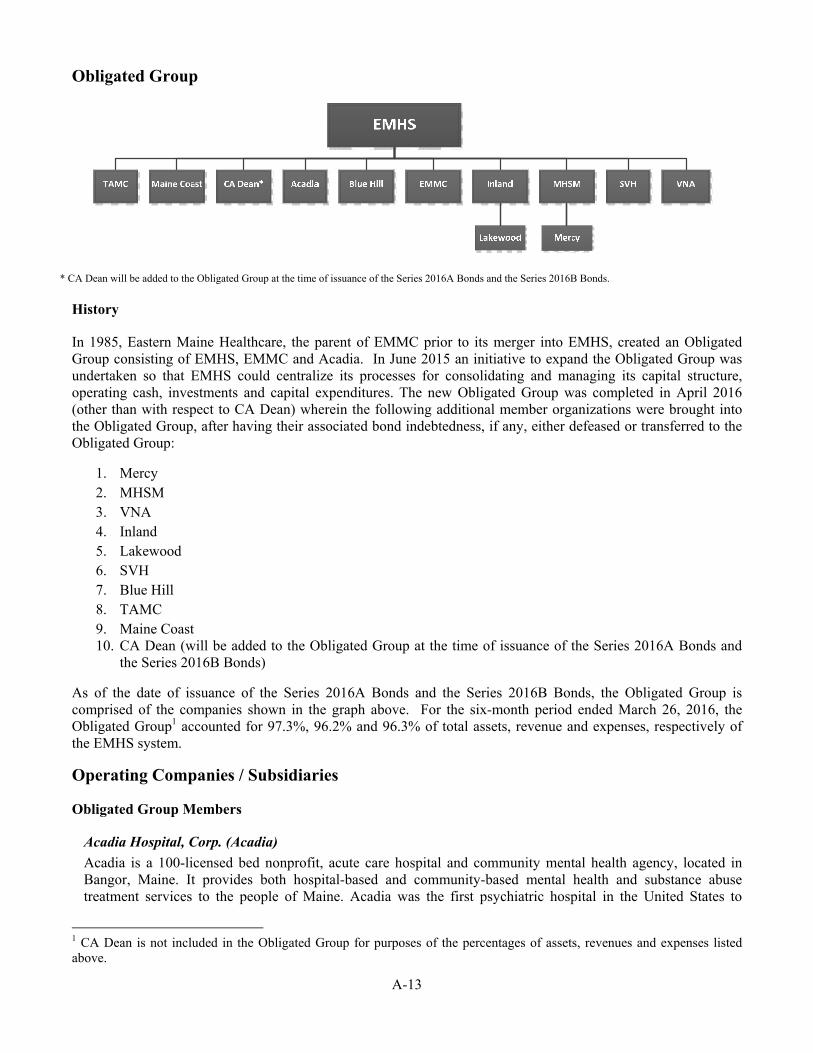

Eastern Maine Healthcare Systems (“EMHS” or the “Obligated Group Agent”) is a Maine nonprofit corporation, which controls a group of affiliated health care organizations constituting an integrated health delivery system serving the state of Maine. EMHS, through its affiliates, offers a broad range of health delivery services and providers, including acute care, medical-surgical hospitals, a free-standing acute psychiatric hospital, primary care and specialty physician practices, long-term care and home health agencies, and ground and air emergency transport services. EMHS is a member of the Obligated Group and is the sole member of, or controls the sole member of, each other member of the Obligated Group. EMHS provides management and support services to its subsidiaries. For the six-

3

month period ended March 26, 2016, the Obligated Group1 comprised 97.3%, 96.2% and 96.3% of total consolidated assets, revenue and expenses, respectively, for the EMHS system.

The Obligated Group

In addition to EMHS, the members of the Obligated Group, each of which is a Maine nonprofit corporation and an organization described in Section 501(c)(3) of the Code, currently consist of the following:

Acadia Hospital, Corp. (“Acadia”). Acadia owns and operates an acute care, regional, psychiatric hospital located in Bangor, Maine, with 100-licensed beds. Acadia provides both hospital-based and community-based mental health and substance abuse treatment services to the people of Maine.

The Aroostook Medical Center (“TAMC”). TAMC owns and operates a community hospital located in Presque Isle in northern Maine with 89-licensed beds. TAMC also owns and operates Aroostook Health Center (“AHC”), a long term care and rehabilitation facility with 72-licensed beds. TAMC provides a full range of hospital, primary and specialty services.

The Blue Hill Memorial Hospital (“Blue Hill”). Blue Hill owns and operates a critical access hospital located in Blue Hill, Maine with 25-licensed beds. Blue Hill offers primary and selected specialty healthcare services.

Eastern Maine Medical Center (“EMMC”). EMMC owns and operates a regional acute care medical center located in Bangor, Maine with 411-licensed beds. EMMC is the largest EMHS hospital, serving communities throughout central, eastern, and northern Maine.

Inland Hospital (“Inland”). Inland owns and operates a community hospital in Waterville, Maine with 48-licensed beds.

Lakewood (“Lakewood”). Lakewood owns and operates a long term care facility with 105-licensed beds. Inland is also the sole corporate member of Lakewood, which is also located on the Inland campus. Lakewood provides a continuum of skilled nursing and rehabilitation services, secure dementia care and long term care services.

Maine Coast Regional Health Facilities d/b/a Maine Coast Memorial Hospital (“Maine Coast”). Maine Coast is a community hospital located in Ellsworth, Maine with 64-licensed beds. Maine Coast provides emergency, primary and specialty inpatient, surgical and diagnostic services.

Mercy Health System of Maine (“MHSM”). MHSM is a community health care system sponsored by the Sisters of Mercy of the Americas. MHSM is the Class A corporate member of Mercy and VNA. EMHS is the sole corporate member of MHSM, and the Class B corporate member of Mercy and VNA.

Mercy Hospital (“Mercy”). Mercy owns and operates an acute care hospital with two campuses located in Portland, Maine with a total of 230-licensed beds. Mercy provides inpatient and outpatient medical and surgical care as well as obstetrics and gynecological services.

1 CA Dean is not included in the Obligated Group for purposes of the percentages of assets, revenues and expenses listed above.

4

Sebasticook Valley Health (“SVH”). SVH owns and operates a critical access hospital located in Pittsfield, Maine with a total of 25-licensed beds.

VNA Home Health & Hospice (“VNA”). VNA is a provider of home health and hospice services to clients in Cumberland County, Maine and York County, Maine.

Prior to or concurrently with the issuance of the Series 2016A Bonds, Charles A. Dean Memorial Hospital (“CA Dean”), also a Maine nonprofit corporation and an organization described in Section 501(c)(3) of the Code, will become a member of the Obligated Group pursuant to the terms of the Master Indenture. CA Dean is a critical access hospital located in the Moosehead Lake region of Maine with 25-licensed beds, that provides acute, skilled, and nursing facility beds, as well as 24-hour emergency medical services and a ground ambulance program.

In the future, other entities may become members of the Obligated Group in accordance with the provisions of the Master Indenture and members of the Obligated Group may withdraw from the Obligated Group and be released from their respective obligations under the Master Indenture upon compliance with conditions prescribed therein. For more information related to additions to and withdrawals from the Obligated Group, see “CERTAIN PROVISIONS OF PRINCIPAL DOCUMENTS – CERTAIN PROVISIONS OF THE MASTER INDENTURE” in Appendix C hereto.

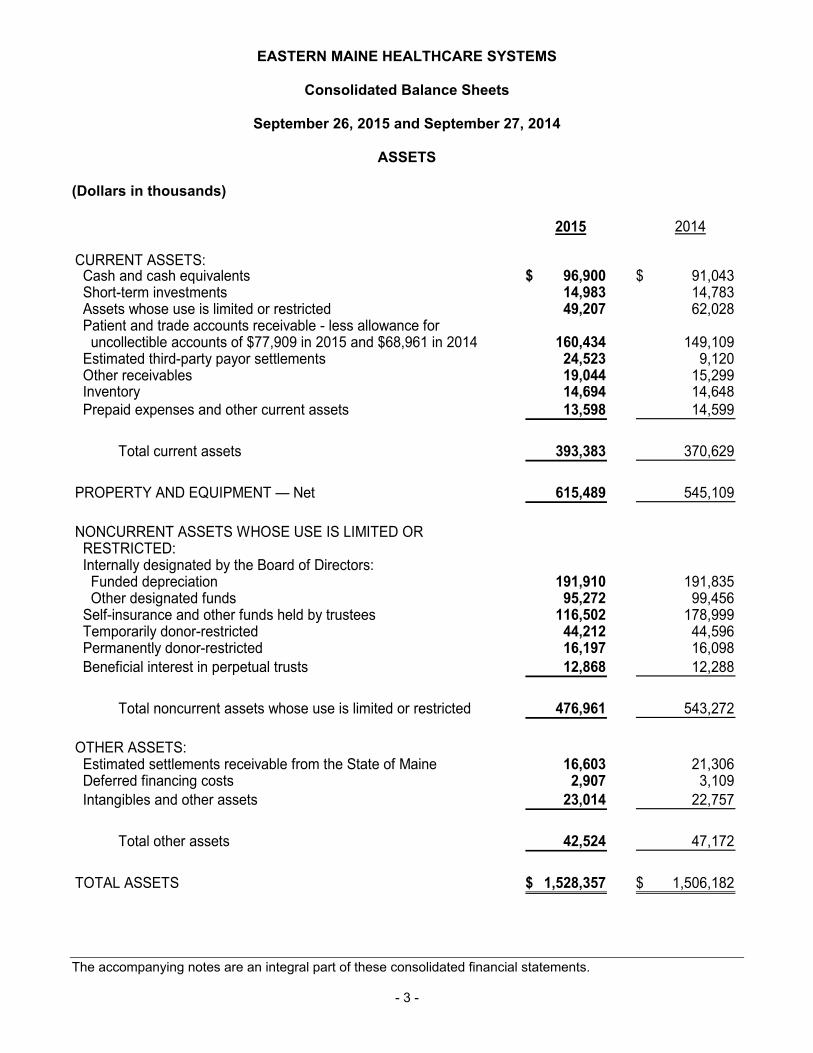

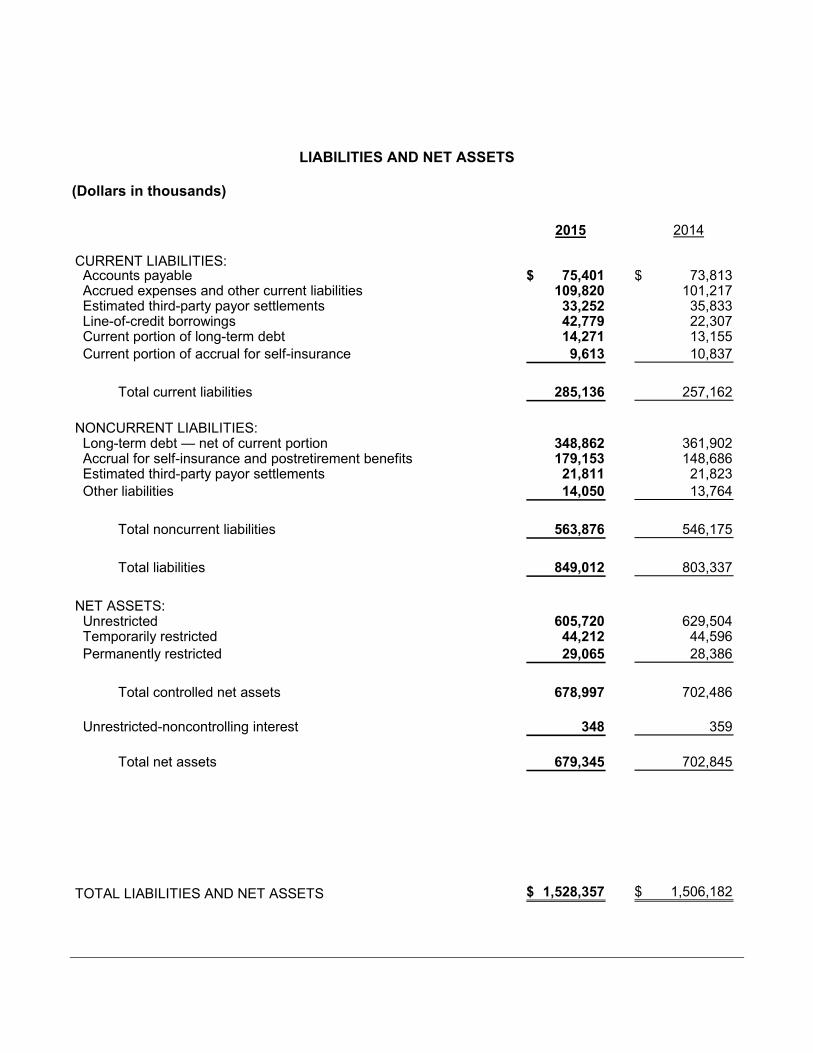

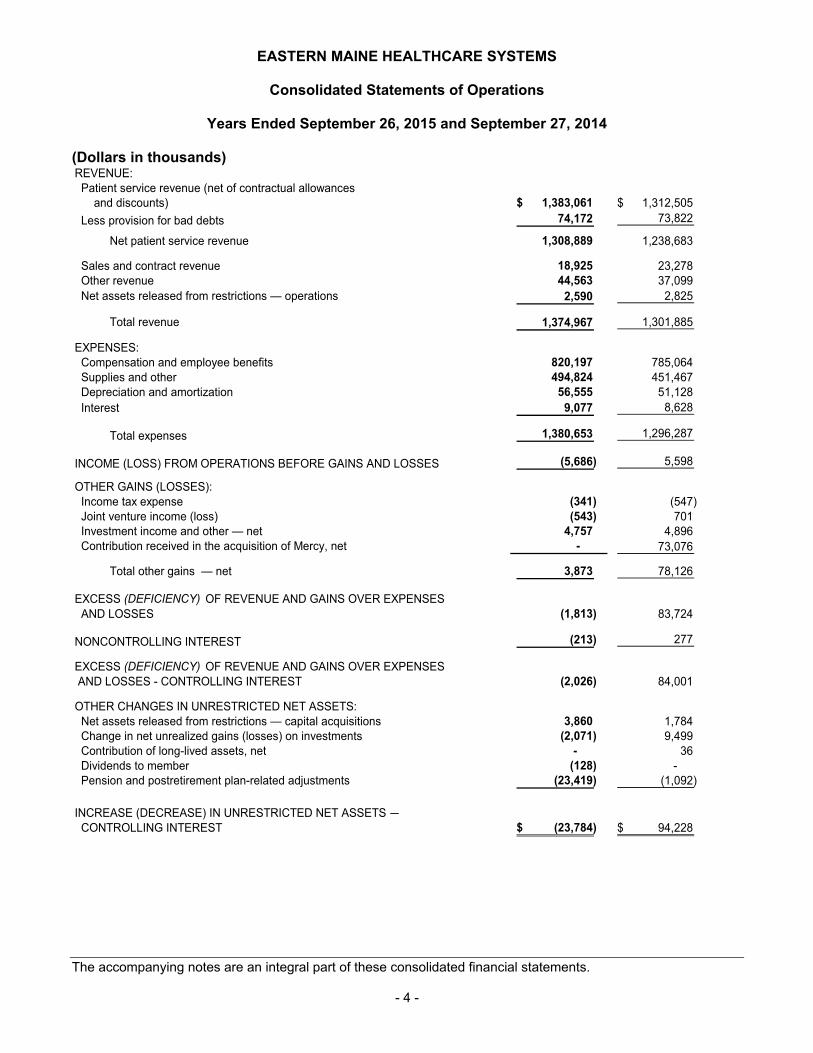

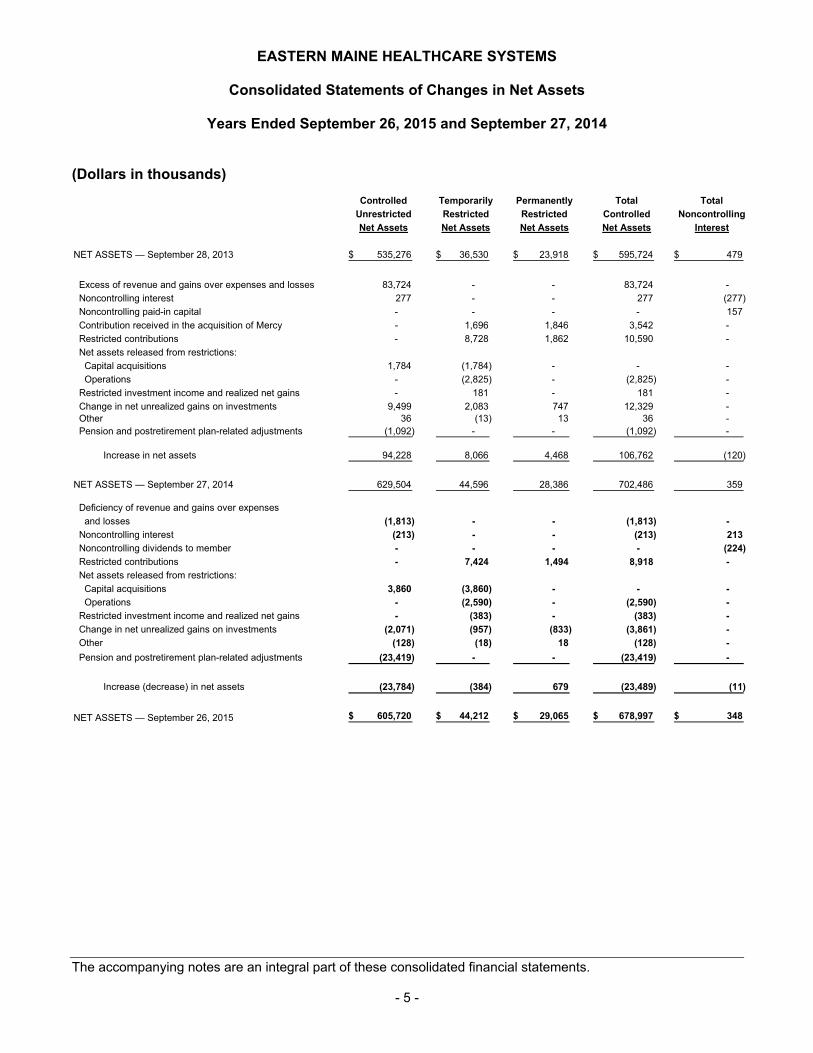

See Appendix A – “INFORMATION CONCERNING EASTERN MAINE HEALTHCARE SYSTEMS AND THE OBLIGATED GROUP” and Appendix B – “CONSOLIDATED FINANCIAL STATEMENTS OF EASTERN MAINE HEALTHCARE SYSTEMS” for more information on EMHS and the other members of the Obligated Group.

Special Obligations

The Series 2016A Bonds are special obligations of the Authority. Neither the State nor any political subdivision thereof shall be obligated to pay the principal of or interest on the Series 2016A Bonds, except from the Pledged Revenues, and neither the faith and credit nor the taxing power of the State or of any political subdivision thereof is pledged to the payment of the principal of or interest on the Series 2016A Bonds. The Authority does not have taxing power.

Other Financing Plans

Concurrently with the issuance of the Series 2016A Bonds, EMHS is expected to issue its Taxable Bonds, Series 2016B in the aggregate principal amount of $79,895,000* (the “Series 2016B Bonds”). The Series 2016B Bonds are being offered pursuant to a separate offering document and will be secured by the Series 2016B Note issued under the Master Indenture, which note will be secured by the lien on Gross Receipts, and by the Mortgages (as defined herein), in each case on a parity with the lien securing the Series 2016A Note.

Bondholders’ Risks

For information concerning certain risks relating to future revenues and expenses of the members of the Obligated Group, health care legislation which might affect the operations of the members of the Obligated Group, and other considerations, see the information included under the caption

* Preliminary, subject to change.

5

“BONDHOLDERS’ RISKS” herein and in Appendix A hereto, which information should be read in its entirety.

HOLDERS OF SERIES 2016A BONDS ARE ADVISED TO READ CAREFULLY THE SECTIONS ENTITLED “SECURITY FOR THE SERIES 2016A BONDS” AND “BONDHOLDERS’ RISKS” HEREIN AND APPENDIX A HERETO FOR A DISCUSSION OF CERTAIN RISK FACTORS WHICH SHOULD BE CONSIDERED IN CONNECTION WITH AN INVESTMENT IN THE SERIES 2016A BONDS. Careful consideration should be given to these risks and other risks described elsewhere in this Official Statement.

6

THE AUTHORITY

General

The Authority was created and established by the Act as a public body corporate and politic and an instrumentality of the State of Maine (the “State”). The purpose of the Authority, among others, is to assist health care institutions, social service institutions and institutions for higher education in the undertaking of projects involving the acquisition, construction, improvement, reconstruction and equipping of health care, social service and educational facilities and the refinancing of existing indebtedness.

The Act provides that the Authority members shall be the State Superintendent of Financial Institutions, ex-officio, the Commissioner of the Department of Human Services, ex-officio, the Commissioner of the Department of Education, ex-officio, the Treasurer of the State, ex-officio, and eight other members appointed by the Governor of the State who are required to be residents of the State and not more than four of whom shall be members of the same political party. Three of the appointed members shall be trustees, directors, officers or employees of health care facilities, two shall be trustees, members of a corporation or board of governors, officers or employees of institutions for higher education and one shall be a person having a favorable reputation for skill, knowledge and experience in state and municipal finance, either as a partner, officer or employee of an investment banking firm which originates and purchases state and municipal securities or as an officer or employee of an insurance company or bank whose duties relate to the purchase of state and municipal securities as an investment and to the management and control of a state and municipal securities portfolio. The members of the Authority are entitled to be paid necessary expenses incurred while engaged in the performance of their duties. The Authority elects from its members a Chairman and a Vice Chairman and appoints an Executive Director who is not a member.

[Remainder of page intentionally left blank.]

7

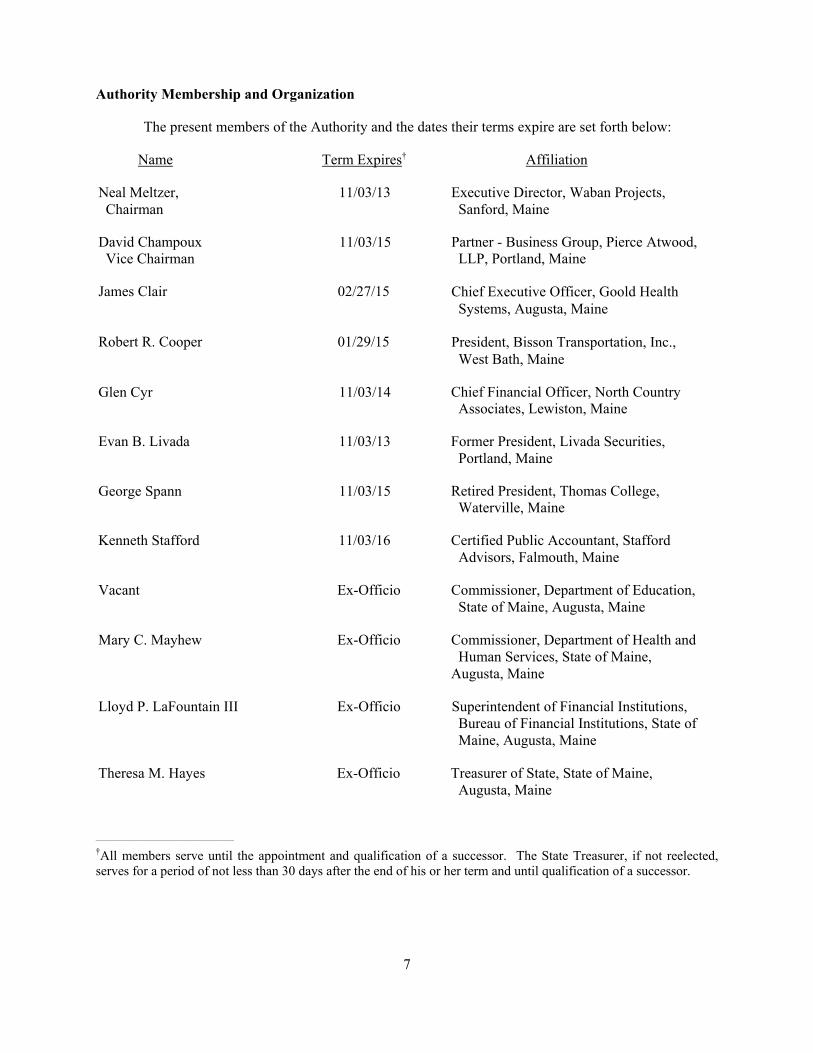

Authority Membership and Organization

The present members of the Authority and the dates their terms expire are set forth below:

Name Term Expires† Affiliation

Neal Meltzer, Chairman

11/03/13 Executive Director, Waban Projects, Sanford, Maine

David Champoux Vice Chairman

11/03/15 Partner - Business Group, Pierce Atwood, LLP, Portland, Maine

James Clair 02/27/15 Chief Executive Officer, Goold Health Systems, Augusta, Maine

Robert R. Cooper 01/29/15 President, Bisson Transportation, Inc., West Bath, Maine

Glen Cyr 11/03/14 Chief Financial Officer, North Country Associates, Lewiston, Maine

Evan B. Livada 11/03/13 Former President, Livada Securities, Portland, Maine

George Spann 11/03/15 Retired President, Thomas College, Waterville, Maine

Kenneth Stafford 11/03/16 Certified Public Accountant, Stafford Advisors, Falmouth, Maine

Vacant Ex-Officio Commissioner, Department of Education, State of Maine, Augusta, Maine

Mary C. Mayhew Ex-Officio Commissioner, Department of Health and Human Services, State of Maine,

Augusta, Maine

Lloyd P. LaFountain III Ex-Officio Superintendent of Financial Institutions, Bureau of Financial Institutions, State of Maine, Augusta, Maine

Theresa M. Hayes Ex-Officio Treasurer of State, State of Maine, Augusta, Maine

________________________________

†All members serve until the appointment and qualification of a successor. The State Treasurer, if not reelected, serves for a period of not less than 30 days after the end of his or her term and until qualification of a successor.

8

Michael R. Goodwin is Executive Director of the Authority and is responsible for the general management of the Authority’s affairs. Mr. Goodwin also serves as Executive Director of the Maine Municipal Bond Bank, the Maine Governmental Facilities Authority and the Maine Public Utility Financing Bank.

Verrill Dana, LLP, Portland, Maine, is serving as counsel to the Authority. Hawkins Delafield & Wood LLP, New York, New York, is serving as Bond Counsel to the Authority and will submit its approving opinion with regard to the legality of the Series 2016A Bonds substantially in the form attached hereto as Appendix D.

The Act provides that the Authority may employ such other consulting engineers, architects, attorneys, accountants, construction and financial experts, superintendents, managers and such other employees and agents as are necessary in its judgment.

Powers of the Authority

Under the Act, the Authority is authorized and empowered, among other things: to issue bonds and notes and to refund the same; to make loans to participating hospitals, nursing homes, licensed residential care facilities, licensed continuing care retirement communities, assisted living facilities, community mental health facilities, a licensed scene response air ambulance, community health centers and community health or social services facilities (“participating health care facilities”) or institutions for higher education or eligible institutions providing an educational program to its members or the general public for the cost of projects; to refinance existing indebtedness incurred by participating health care facilities or institutions for higher education to finance facilities; to charge and collect rates, rents, fees and charges for the use of and for the services furnished by a project; to acquire, construct, reconstruct, renovate, improve, replace, maintain, repair, extend, enlarge, operate, lease as lessee or lessor and regulate any project financed under the Act; to enter into contracts for any and all such purposes, including contracts for the management and operation of a project, and to designate a participating health care facility or a participating institution for higher education as its agent in connection with a project; to mortgage any project and the site thereof; to acquire directly or through a participating health care facility or a participating institution for higher education, as its agent, by purchase or by gift or devise such lands, structures, property, real or personal, rights, rights of way, franchises and easements as the Authority deems necessary; to sue and be sued; to receive and accept grants from the federal government, the State, or any other public agency; and to do all things necessary or convenient to carry out the purposes of the Act.

Financing Programs of the Authority

Pursuant to its powers under the Act, the Authority has adopted five resolutions establishing separate financing programs with respect to which the Authority issues bonds and makes loans to participating institutions. The five resolutions are (1) the General Bond Resolution adopted June 5, 1973 (which for presentation purposes in the Authority’s financial statements includes all transactions completed under separate bond indentures not secured by a common reserve fund, such as the Series 2016A Bonds), (2) the Reserve Fund Resolution adopted December 6, 1991, (3) the Medium Term Financing Reserve Fund Resolution adopted March 5, 1992, (4) the Taxable Finance Reserve Fund Resolution adopted December 15, 1992 (the “First Taxable Resolution”) and (5) the Taxable Finance Reserve Fund Resolution adopted July 11, 2003 (the “Second Taxable Resolution”). None of the common reserve funds or the funds and accounts established under the Authority’s various programs are pledged to the security of the Series 2016A Bonds.

9

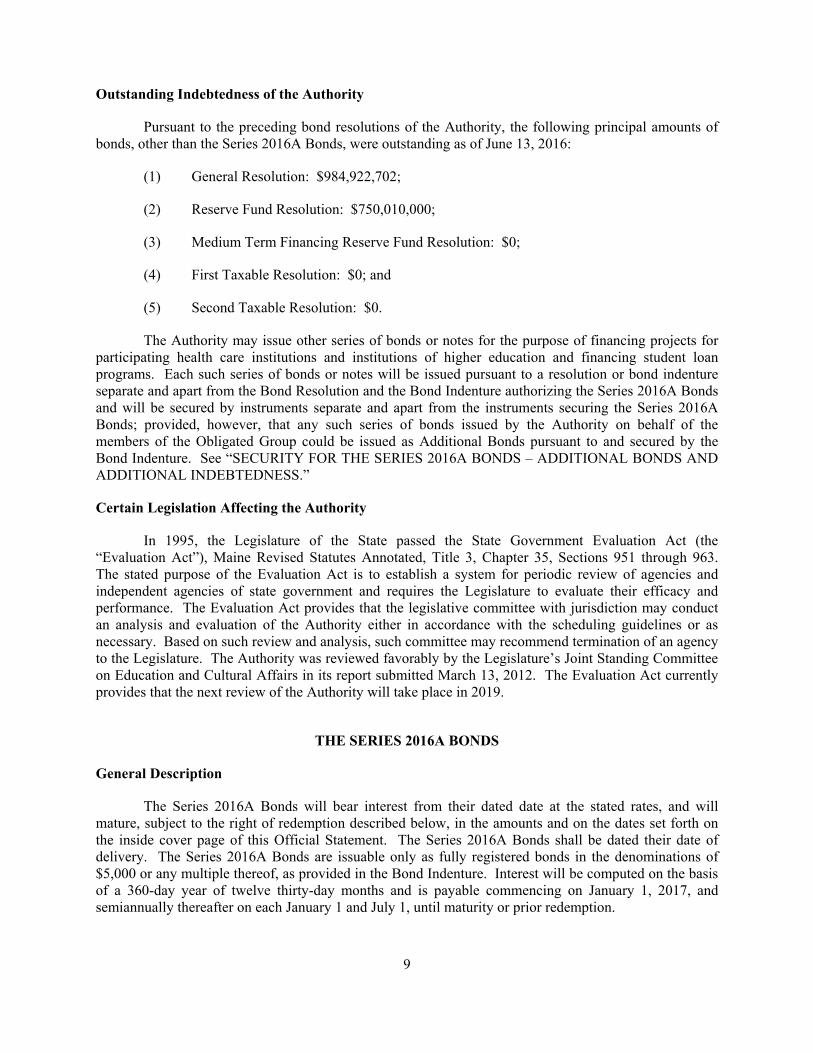

Outstanding Indebtedness of the Authority

Pursuant to the preceding bond resolutions of the Authority, the following principal amounts of bonds, other than the Series 2016A Bonds, were outstanding as of June 13, 2016:

(1) General Resolution: $984,922,702;

(2) Reserve Fund Resolution: $750,010,000;

(3) Medium Term Financing Reserve Fund Resolution: $0;

(4) First Taxable Resolution: $0; and

(5) Second Taxable Resolution: $0.

The Authority may issue other series of bonds or notes for the purpose of financing projects for participating health care institutions and institutions of higher education and financing student loan programs. Each such series of bonds or notes will be issued pursuant to a resolution or bond indenture separate and apart from the Bond Resolution and the Bond Indenture authorizing the Series 2016A Bonds and will be secured by instruments separate and apart from the instruments securing the Series 2016A Bonds; provided, however, that any such series of bonds issued by the Authority on behalf of the members of the Obligated Group could be issued as Additional Bonds pursuant to and secured by the Bond Indenture. See “SECURITY FOR THE SERIES 2016A BONDS – ADDITIONAL BONDS AND ADDITIONAL INDEBTEDNESS.”

Certain Legislation Affecting the Authority

In 1995, the Legislature of the State passed the State Government Evaluation Act (the “Evaluation Act”), Maine Revised Statutes Annotated, Title 3, Chapter 35, Sections 951 through 963. The stated purpose of the Evaluation Act is to establish a system for periodic review of agencies and independent agencies of state government and requires the Legislature to evaluate their efficacy and performance. The Evaluation Act provides that the legislative committee with jurisdiction may conduct an analysis and evaluation of the Authority either in accordance with the scheduling guidelines or as necessary. Based on such review and analysis, such committee may recommend termination of an agency to the Legislature. The Authority was reviewed favorably by the Legislature’s Joint Standing Committee on Education and Cultural Affairs in its report submitted March 13, 2012. The Evaluation Act currently provides that the next review of the Authority will take place in 2019.

THE SERIES 2016A BONDS

General Description

The Series 2016A Bonds will bear interest from their dated date at the stated rates, and will mature, subject to the right of redemption described below, in the amounts and on the dates set forth on the inside cover page of this Official Statement. The Series 2016A Bonds shall be dated their date of delivery. The Series 2016A Bonds are issuable only as fully registered bonds in the denominations of $5,000 or any multiple thereof, as provided in the Bond Indenture. Interest will be computed on the basis of a 360-day year of twelve thirty-day months and is payable commencing on January 1, 2017, and semiannually thereafter on each January 1 and July 1, until maturity or prior redemption.

10

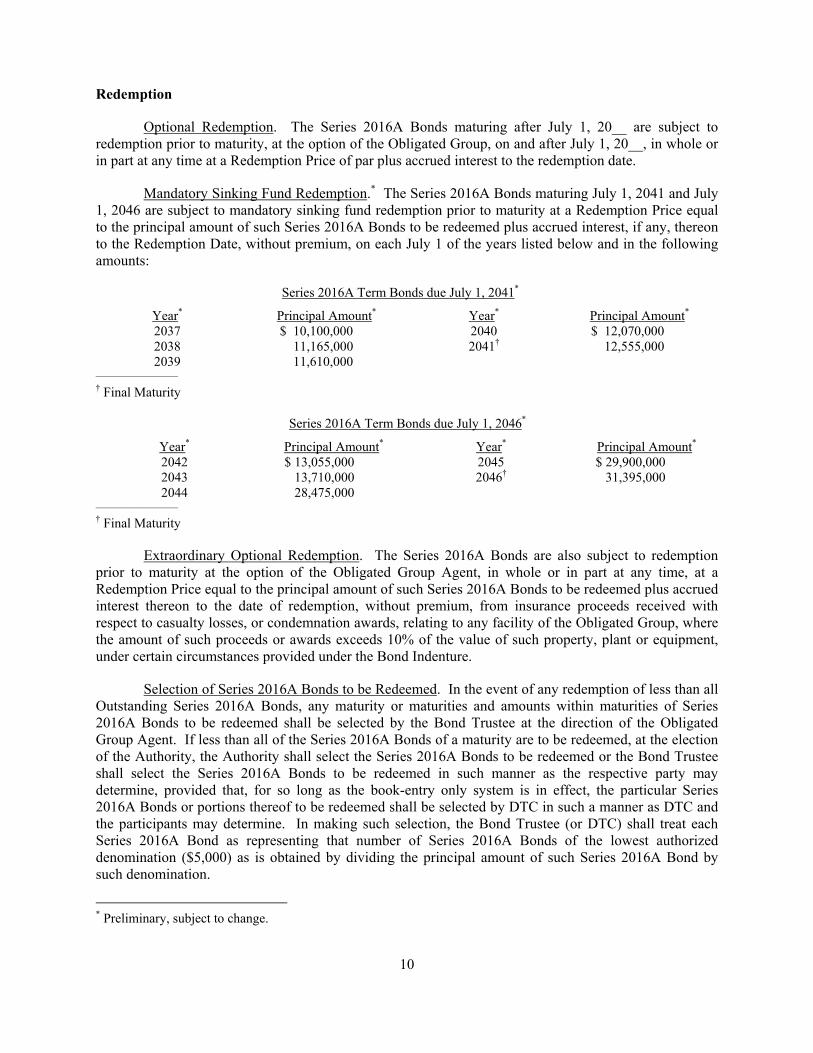

Redemption

Optional Redemption. The Series 2016A Bonds maturing after July 1, 20__ are subject to redemption prior to maturity, at the option of the Obligated Group, on and after July 1, 20__, in whole or in part at any time at a Redemption Price of par plus accrued interest to the redemption date.

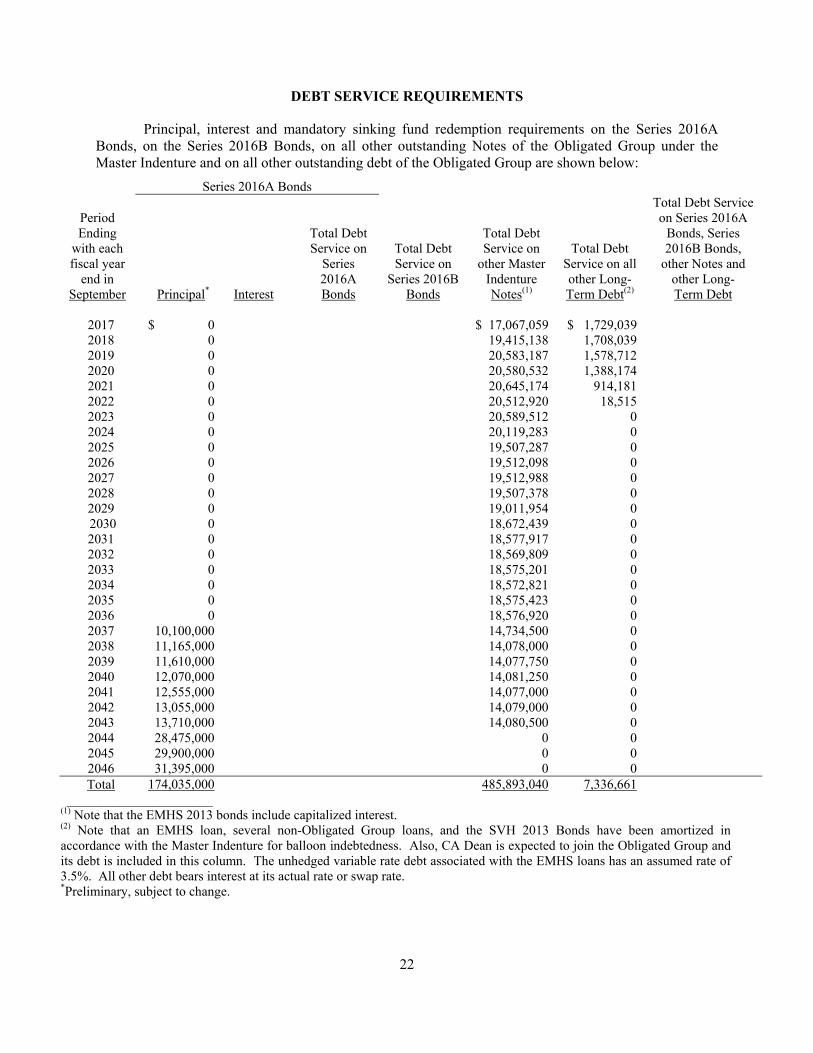

Mandatory Sinking Fund Redemption.* The Series 2016A Bonds maturing July 1, 2041 and July 1, 2046 are subject to mandatory sinking fund redemption prior to maturity at a Redemption Price equal to the principal amount of such Series 2016A Bonds to be redeemed plus accrued interest, if any, thereon to the Redemption Date, without premium, on each July 1 of the years listed below and in the following amounts:

Series 2016A Term Bonds due July 1, 2041*

Year* Principal Amount* Year* Principal Amount* 2037 $ 10,100,000 2040 $ 12,070,000 2038 11,165,000 2041† 12,555,000 2039 11,610,000

___________________

† Final Maturity

Series 2016A Term Bonds due July 1, 2046*

Year* Principal Amount* Year* Principal Amount* 2042 $ 13,055,000 2045 $ 29,900,000 2043 13,710,000 2046† 31,395,000 2044 28,475,000

___________________

† Final Maturity

Extraordinary Optional Redemption. The Series 2016A Bonds are also subject to redemption prior to maturity at the option of the Obligated Group Agent, in whole or in part at any time, at a Redemption Price equal to the principal amount of such Series 2016A Bonds to be redeemed plus accrued interest thereon to the date of redemption, without premium, from insurance proceeds received with respect to casualty losses, or condemnation awards, relating to any facility of the Obligated Group, where the amount of such proceeds or awards exceeds 10% of the value of such property, plant or equipment, under certain circumstances provided under the Bond Indenture.

Selection of Series 2016A Bonds to be Redeemed. In the event of any redemption of less than all Outstanding Series 2016A Bonds, any maturity or maturities and amounts within maturities of Series 2016A Bonds to be redeemed shall be selected by the Bond Trustee at the direction of the Obligated Group Agent. If less than all of the Series 2016A Bonds of a maturity are to be redeemed, at the election of the Authority, the Authority shall select the Series 2016A Bonds to be redeemed or the Bond Trustee shall select the Series 2016A Bonds to be redeemed in such manner as the respective party may determine, provided that, for so long as the book-entry only system is in effect, the particular Series 2016A Bonds or portions thereof to be redeemed shall be selected by DTC in such a manner as DTC and the participants may determine. In making such selection, the Bond Trustee (or DTC) shall treat each Series 2016A Bond as representing that number of Series 2016A Bonds of the lowest authorized denomination ($5,000) as is obtained by dividing the principal amount of such Series 2016A Bond by such denomination.

* Preliminary, subject to change.

11

Partial Redemption of Series 2016A Bonds. Upon the selection and call for redemption of, and the surrender of, any Series 2016A Bond for redemption in part only, the Authority shall cause to be executed and the Bond Trustee shall authenticate and deliver to or upon the written order of the Holder thereof, at the expense of the Institutions, a new Series 2016A Bond or Series 2016A Bonds of authorized denominations in an aggregate face amount equal to the unredeemed portion of the Series 2016A Bond surrendered, which new Series 2016A Bond or Series 2016A Bonds shall be a fully registered Series 2016A Bond or Series 2016A Bonds without coupons, in authorized denominations.

The Authority and the Bond Trustee may agree with any Holder of any Series 2016A Bond that such Holder may, in lieu of surrendering the same for a new Series 2016A Bond, endorse on such Series 2016A Bond a notice of such partial redemption, which notice shall set forth, over the signature of such Holder, the redemption date, the principal amount redeemed and the principal amount remaining unpaid. Such partial redemption shall be valid upon payment of the amount thereof to the registered owner of any such Series 2016A Bond and the Authority and the Bond Trustee shall be fully released and discharged from all liability to the extent of such payment irrespective of whether such endorsement shall or shall not have been made upon the reverse of such Series 2016A Bond by the owner thereof and irrespective of any error or omission in such endorsement.

Effect of Call for Redemption. On the date designated for redemption by notice given as provided in the Bond Indenture, the Series 2016A Bonds so called for redemption shall become and be due and payable at the Redemption Price provided for redemption of such Series 2016A Bonds on such date. If on the date fixed for redemption moneys for payment of the Redemption Price and accrued interest are held by the Bond Trustee or paying agents as provided in the Bond Indenture, interest on such Series 2016A Bonds so called for redemption shall cease to accrue, such Series 2016A Bonds shall cease to be entitled to any benefit or security under the Bond Indenture except the right to receive payment from the moneys held by the Bond Trustee or the paying agents and the amount of such Series 2016A Bonds so called for redemption shall be deemed paid and no longer Outstanding.

Any optional redemption of the Series 2016A Bonds shall be credited against mandatory sinking fund redemption requirements, if applicable, in such manner and order as may be directed by the Obligated Group Agent.

Notice of Redemption. If less than all the Series 2016A Bonds are to be redeemed, the Series 2016A Bonds to be redeemed shall be identified by reference to the issue and series designation, date of issue, serial numbers and maturity date. Notice of redemption of any Series 2016A Bonds shall be mailed by the Bond Trustee, provided the Bond Trustee has received seven (7) days prior written instructions from the Authority or the Obligated Group Agent (unless a shorter period is agreed to by the Bond Trustee), and the Holders will receive the notice not less than thirty (30) nor more than forty-five (45) days prior to the date set for redemption, to each registered Holder of a Series 2016A Bond to be so redeemed at the address shown on the books of the Registrar but failure to so mail or any defect in any such notice with respect to any Bond shall not affect the validity of the proceedings for the redemption of any other Series 2016A Bond with respect to which notice was so mailed or with respect to which no such defect occurred, respectively. Such notice shall state that any optional redemption or extraordinary optional redemption is conditional and shall be made only from and to the extent that funds shall be on deposit with the Bond Trustee and available for such purpose on the redemption date.

Purchase in Lieu of Redemption. Any Series 2016A Bonds called for optional redemption pursuant to the Bond Indenture, at the option of the Obligated Group Agent may, in lieu of redemption, be purchased by the Obligated Group Agent or by a Person designated by the Obligated Group Agent on the redemption date at a price equal to the principal amount thereof plus interest accrued to the redemption date, and if so purchased and not submitted for cancellation, shall continue to be Outstanding under the

12

Bond Indenture for all purposes and shall continue to be subject to optional redemption as provided in the Bond Indenture.

Acceleration

If a Bond Indenture Event of Default occurs, including a Bond Indenture Event of Default resulting from a payment default on the part of the Institutions under the Agreement, the principal of the Series 2016A Bonds may be accelerated and become immediately due and payable, at par, with interest payable thereon to the accelerated payment date. For a description of the Bond Indenture Events of Default, see Appendix C – “CERTAIN PROVISIONS OF PRINCIPAL DOCUMENTS – CERTAIN PROVISIONS OF THE AGREEMENT – DEFAULTS AND REMEDIES” and “CERTAIN PROVISIONS OF THE INDENTURE – DEFAULTS AND REMEDIES” and “SUMMARY OF THE SUPPLEMENTAL INDENTURE – DEFAULTS AND REMEDIES.”

Transfer and Exchange

Except while the book-entry only system is in effect as described above, Series 2016A Bonds may be exchanged upon presentation and surrender thereof to the Registrar for an equal aggregate principal amount of Series 2016A Bonds with the same interest rate and maturity. See “THE SERIES 2016A BONDS – BOOK-ENTRY ONLY SYSTEM.”

Book-Entry Only System

The Depository Trust Company (“DTC”), New York, New York, will act as securities depository for the Series 2016A Bonds. The Series 2016A Bonds will be issued as fully-registered securities registered in the name of Cede & Co. (DTC’s partnership nominee) or such other name as may be requested by an authorized representative of DTC. One fully-registered Series 2016A Bond certificate will be issued for each maturity of the Series 2016A Bonds in the aggregate principal amount of such maturity, and will be deposited with DTC.

DTC, the world’s largest securities depository, is a limited-purpose trust company organized under the New York Banking Law, a “banking organization” within the meaning of the New York Banking Law, a member of the Federal Reserve System, a “clearing corporation” within the meaning of the New York Uniform Commercial Code, and a “clearing agency” registered pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934. DTC holds and provides asset servicing for over 3.5 million issues of U.S. and non-U.S. equity issues, corporate and municipal debt issues, and money market instruments (from over 100 countries) that DTC’s participants (“Direct Participants”) deposit with DTC. DTC also facilitates the post-trade settlement among Direct Participants of sales and other securities transactions in deposited securities, through electronic computerized book-entry transfers and pledges between Direct Participants’ accounts. This eliminates the need for physical movement of securities certificates. Direct Participants include both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation (“DTCC”). DTCC is the holding company for DTC, National Securities Clearing Corporation, and Fixed Income Clearing Corporation, all of which are registered clearing agencies. DTCC is owned by the users of its regulated subsidiaries. Access to the DTC system is also available to others such as both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, and clearing corporations that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly (“Indirect Participants”). DTC has a Standard & Poor’s rating of AA+. The DTC Rules applicable to its Participants are on file with the Securities and Exchange Commission. More information about DTC can be found at www.dtcc.com.

13

Purchases of the Series 2016A Bonds under the DTC system must be made by or through Direct Participants, which will receive a credit for the Series 2016A Bonds on DTC’s records. The ownership interest of each actual purchaser of each Series 2016A Bond (“Beneficial Owner”) is in turn to be recorded on the Direct and Indirect Participants’ records. Beneficial Owners will not receive written confirmation from DTC of their purchase. Beneficial Owners are, however, expected to receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Series 2016A Bonds are to be accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in Series 2016A Bonds, except in the event that use of the book-entry system for the Series 2016A Bonds is discontinued.

To facilitate subsequent transfers, all Series 2016A Bonds deposited by Direct Participants with DTC are registered in the name of DTC’s partnership nominee, Cede & Co., or such other name as may be requested by an authorized representative of DTC. The deposit of Series 2016A Bonds with DTC and their registration in the name of Cede & Co., or such other DTC nominee do not effect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Series 2016A Bonds. DTC’s records reflect only the identity of the Direct Participants to whose accounts such Series 2016A Bonds are credited, which may or may not be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account of their holdings on behalf of their customers.

Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangements among them, subject to any statutory or regulatory requirements as may be in effect from time to time. Beneficial Owners of the Series 2016A Bonds may wish to take certain steps to augment the transmission to them of notices of significant events with respect to the Series 2016A Bonds, such as redemptions, tenders, defaults, and proposed amendments to the security documents. For example, Beneficial Owners of the Series 2016A Bonds may wish to ascertain that the nominee holding the Series 2016A Bonds for their benefit has agreed to obtain and transmit notices to Beneficial Owners. In the alternative, Beneficial Owners may wish to provide their names and addresses to the registrar and request that copies of the notices be provided directly to them.

Redemption notices shall be sent to DTC. If less than all of the Series 2016A Bonds within a single maturity are being redeemed, DTC’s practice is to determine by lot the amount of the interest of each Direct Participant in such maturity to be redeemed.

Neither DTC nor Cede & Co. (nor any other DTC nominee) will consent or vote with respect to the Series 2016A Bonds unless authorized by a Direct Participant in accordance with DTC’s MMI procedures. Under its usual procedures, DTC mails an Omnibus Proxy to the Authority as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co.’s consenting or voting rights to those Direct Participants to whose accounts the Series 2016A Bonds are credited on the record date (identified in a listing attached to the Omnibus Proxy).

Principal (including sinking fund installments, if any), redemption premium, if any, and interest payments on the Series 2016A Bonds will be made to Cede & Co., or such other nominee as may be requested by an authorized representative of DTC. DTC’s practice is to credit Direct Participants’ accounts upon DTC’s receipt of funds and corresponding detail information from the Authority or the Paying Agent on the payable date in accordance with their respective holdings shown on DTC’s records. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary practices, as is the case with securities held for the accounts of customers in bearer form or registered in “street name,” and will be the responsibility of such Participant and not of DTC, the Paying Agent, the

14

Obligated Group, the Bond Trustee, or the Authority, subject to any statutory or regulatory requirements as may be in effect from time to time. Payment of principal and interest to Cede & Co. (or such other nominee as may be requested by an authorized representative of DTC) is the responsibility of the Authority or the Paying Agent, disbursement of such payments to Direct Participants will be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners will be the responsibility of Direct and Indirect Participants.

DTC may discontinue providing its services as depository with respect to the Series 2016A Bonds at any time by giving reasonable notice to the Authority or the Bond Trustee. Under such circumstances, in the event that a successor depository is not obtained, Series 2016A Bond certificates are required to be printed and delivered.

The Authority may decide to discontinue use of the system of book-entry transfers through DTC (or a successor securities depository). In that event, Series 2016A Bond certificates will be printed and delivered to DTC.

The information in this section concerning DTC and DTC’s book-entry system has been obtained from sources that the Authority believes to be reliable, but none of the Authority, the Obligated Group or the Underwriters takes any responsibility for the accuracy thereof.

NEITHER THE BOND TRUSTEE NOR THE AUTHORITY SHALL HAVE ANY RESPONSIBILITY OR OBLIGATION TO ANY PARTICIPANT, ANY PERSON CLAIMING A BENEFICIAL OWNERSHIP INTEREST IN THE SERIES 2016A BONDS UNDER OR THROUGH DTC OR ANY PARTICIPANT, OR ANY OTHER PERSON WHO IS NOT SHOWN IN THE REGISTRATION BOOKS OF THE BOND TRUSTEE AS BEING A BONDHOLDER, WITH RESPECT TO: THE ACCURACY OF ANY RECORDS MAINTAINED BY DTC OR ANY PARTICIPANT; THE PAYMENT BY DTC OR ANY PARTICIPANT OF ANY AMOUNT IN RESPECT OF THE PRINCIPAL OF OR REDEMPTION PRICE, IF ANY, OR INTEREST ON THE SERIES 2016A BONDS; ANY NOTICE WHICH IS PERMITTED OR REQUIRED TO BE GIVEN TO BONDHOLDERS UNDER THE BOND INDENTURE; THE SELECTION BY DTC OR ANY PARTICIPANT OF ANY PERSON TO RECEIVE PAYMENT IN THE EVENT OF A PARTIAL REDEMPTION OF THE SERIES 2016A BONDS; OR ANY CONSENT GIVEN OR OTHER ACTION TAKEN BY DTC OR ITS NOMINEE, CEDE & CO., AS BONDHOLDER.

In the event that the book-entry only system is discontinued, principal and redemption price will be payable upon surrender of the Series 2016A Bonds at the corporate trust office of the Paying Agent and interest will be payable on each Interest Payment Date, by check or draft mailed or, at the option of the Holder of at least $500,000 aggregate principal amount of Series 2016A Bonds, by wire transfer, to the Bondholders as of the close of business on the Record Date.

If the book-entry only system is discontinued and Series 2016A Bond certificates have been delivered as described in the Bond Indenture, the Beneficial Owner, upon registration of certificates held in the Beneficial Owner’s name, will become the Bondholder. Thereafter, Series 2016A Bonds may be exchanged for an equal aggregate principal amount of Series 2016A Bonds in other authorized denominations and of the same maturity, upon surrender thereof at the principal corporate trust office of the Bond Trustee, as Registrar. The transfer of any Series 2016A Bond may be registered on the books maintained by the Bond Trustee, as Registrar, for such purpose only upon the surrender thereof to the Bond Trustee with a duly executed assignment in form satisfactory to the Bond Trustee. For every exchange or registration of transfer of Series 2016A Bonds, the Bond Trustee, as Registrar, may make a charge sufficient to reimburse it for any tax or other governmental charge required to be paid with respect to such exchange or registration of transfer, but no other charge may be made to the Bondholder for any exchange or registration of transfer of the Series 2016A Bonds. The Bond Trustee will not be required to

15

register the transfer of or exchange any Series 2016A Bond during the period from the Record Date to the Bond Payment Date or if such Series 2016A Bond (or any part thereof) has been or is being called for redemption.

SECURITY FOR THE SERIES 2016A BONDS

General

The Series 2016A Bonds constitute special obligations of the Authority payable solely from, and secured by a pledge of, the revenues of the Authority received from or on account of the Institutions and amounts on deposit from time to time in the funds and accounts established under the Bond Indenture (except the Rebate Fund), including the earnings thereon, subject to the application thereof for the purposes and on the terms and conditions set forth in the Bond Indenture. The Series 2016A Bonds will be secured on a parity with any Additional Bonds that may be issued under the Bond Indenture.

Bond Indenture

The Series 2016A Bonds will be issued by the Authority pursuant to the Bond Indenture. The Bond Indenture constitutes a contract among the Authority, the Bond Trustee and the Holders of the Series 2016A Bonds and the pledges and covenants made therein are for the equal and ratable benefit and security of the Holders of the Series 2016A Bonds. The Bond Indenture provides that the Series 2016A Bonds shall be special obligations of the Authority, payable solely from and secured solely by the payments made by the Institutions under the Agreement, and the funds available in the Bond Fund established under the Bond Indenture. As security for its obligations under the Bond Indenture with respect to the Series 2016A Bonds, the Authority has pledged to the Bond Trustee the payments of the Institutions received or receivable by the Authority pursuant to the Agreement, all funds held by the Bond Trustee under the Bond Indenture (except the Rebate Fund) and all income derived from the investment of such funds, and will assign to the Bond Trustee all such pledged funds, all of the Authority’s right, title and interest in the Agreement (except the right of the Authority to grant approvals, consents or waivers, to receive notices, or for indemnification or reimbursement of costs and expenses) and the Series 2016A Note.

The Bond Indenture provides that the security interest granted by the Authority to the Bond Trustee therein is for the equal and proportionate benefit and security of the Holders from time to time of the Series 2016A Bonds issued, authenticated, delivered and outstanding under the Bond Indenture, without preference, priority or distinction as to lien or otherwise of any Bonds over any other Bonds to the end that each Holder of any Bonds has the same rights, privileges and lien under and by virtue of the Bond Indenture.

Agreement

The Agreement is the full faith and credit general obligation of each of the Institutions, by which each is required, on a joint and several basis, to make payments to the Authority which will meet all debt service payment requirements on the Series 2016A Bonds. The Agreement is to remain in full force and effect until all Series 2016A Bonds have been fully paid, defeased or otherwise discharged.

Master Indenture

The obligations of the Institutions to make repayments of the loan to the Institutions by the Authority of the proceeds of the Series 2016A Bonds under the Agreement are evidenced by the Series 2016A Note issued by EMHS, as Obligated Group Agent, on behalf of itself and all other members of the Obligated Group. The Series 2016A Note will be issued under and pursuant to the Master Indenture and

16

Supplemental Master Trust Indenture No. 16, dated as of July 1, 2016 (the “Supplemental Master Trust Indenture No. 16”), by and among EMHS (on behalf of itself and the other members of the Obligated Group) and the Master Trustee.

As of the date of issuance of the Series 2016A Note, the Obligated Group has outstanding notes (the “Notes”) under the Master Indenture as follows:

1. The Series 2010 Notes securing loans by the Authority to each of EMMC and Acadia of the proceeds of the Authority’s Revenue Bonds, Series 2010A, outstanding in the aggregate principal amount of $57,947,325.00.

2. The Series 2013 Note securing a loan by the Authority to EMMC of the proceeds of the Authority’s Revenue Bonds, Eastern Maine Medical Center Obligated Group Issue, Series 2013, outstanding in the aggregate principal amount of $142,595,000.00.

3. The Series 2015 Taxable Note (Bangor Savings Bank Loan) securing loans by Bangor Savings Bank to MHSM, Mercy and VNA, outstanding in the aggregate principal amount of $7,008,521.00.

4. The Series 2015 Note (Mercy Hospital – Authority Series 2014 Bonds) securing loans by the Authority to MHSM, Mercy and VNA of the proceeds of the Authority’s Revenue Bonds, Mercy Hospital Issue, Series 2014, outstanding in the aggregate principal amount of $56,610,000.00.

5. The Series 2015 Note (Inland Series 2007B Loan Agreement Amendment) and the Series 2015 Note (Lakewood Series 2007B Loan Agreement Amendment) securing loans by the Authority to Inland and Lakewood of the proceeds of the Authority’s Revenue Bonds, Series 2007B, outstanding in the aggregate principal amount of $7,761,901.00.

6. The Series 2015 Note (Inland Series 2015A Loan Agreement Amendment) securing a loan by the Authority to Inland of the proceeds of the Authority’s Revenue Bonds, Series 2015A, outstanding in the aggregate principal amount of $837,580.00.

7. The Series 2015 Note (SVH Series 2013 (FAME) Loan Agreement Amendment) securing a loan by the Finance Authority of Maine (“FAME”) to SVH of the proceeds of FAME’s Revenue Obligation Securities Sebasticook Valley Health - Series 2013, currently outstanding in the aggregate principal amount of $8,563,282.00.

8. The Series 2015 Note securing a $140,000,000 non-revolving line of credit arrangement of EMHS, with borrowings outstanding in the aggregate principal amount of $80,115,673.62. Proceeds of the Series 2016A Bonds are expected to be used, among other uses, to partially pay down outstanding borrowings under this line of credit facility.

Concurrently with the issuance of the Series 2016A Bonds, EMHS, on behalf of the Obligated Group, is expected to issue the Series 2016B Note under the Master Indenture in the aggregate principal amount of $79,895,000* in order to secure the Series 2016B Bonds. Proceeds of the Series 2016B Bonds are expected to be used, among other uses, to partially pay down outstanding borrowings under the EMHS line of credit arrangement described above. Thereafter, EMHS may also terminate the existing

* Preliminary, subject to change.

17

line of credit facilities described above with the existing lenders and/or pursue a new line of credit facility, which may or may not be secured by Notes issued under the Master Indenture.

The Mortgages secure on a parity basis all Notes issued under the Master Indenture, including the Series 2016A Note and the Series 2016B Note. The Master Indenture provides that members of the Obligated Group, in addition to indebtedness secured by a Note, may incur additional indebtedness whether or not secured by a Note. See “CERTAIN FINANCIAL COVENANTS” and Appendix C – “CERTAIN PROVISIONS OF PRINCIPAL DOCUMENTS – CERTAIN PROVISIONS OF THE MASTER INDENTURE.”

Pledge of Gross Receipts

Under the Master Indenture, the members of the Obligated Group have granted, for the equal and ratable benefit of the holders of all Notes (including the Series 2016A Note and the Series 2016B Note) and other obligations previously issued and to be issued under the Master Indenture, a first lien on and security interest in their Gross Receipts.

Mortgaged Property

To secure all Notes and other obligations under the Master Indenture, the following members of the Obligated Group have granted to the Master Trustee a first mortgage lien on and security interest in certain real and/or personal property for the equal and ratable benefit of the holders of the Notes and any other obligations issued from time to time under the Master Indenture:

1. EMMC has granted to the Master Trustee a first mortgage lien on and security interest in the real property comprising EMMC’s main medical center campus consisting of approximately 25 acres in Bangor, Maine pursuant to a Mortgage and Security Agreement dated April 1, 2010.

2. Mercy has granted to the Master Trustee (as assignee of the master trustee for the Mercy obligated group pursuant to an Assignment of Mortgage dated September 25, 2015) a mortgage lien on the real property comprising its acute care hospital on State Street in Portland, Maine, its acute care hospital on Fore River Parkway in Portland, Maine, its gastroenterology clinic on Long Creek Drive in South Portland, Maine, and its radiology clinic in Westbrook, Maine pursuant to a Mortgage dated March 28, 2014, as amended on April 4, 2014.

3. SVH has granted to the Master Trustee (as assignee of Bangor Savings Bank pursuant to an Assignment of Mortgage dated as of November 2, 2015) a first mortgage lien on and security interest in the real and personal property comprising its hospital consisting of approximately 9.32 acres in Pittsfield, Maine pursuant to a Commercial Mortgage and Security Agreement with Financing Statement dated January 17, 2013.

4. Maine Coast has granted to the Master Trustee a mortgage lien on the real property comprising its main hospital, medical office building and housing facility on Union Street in Ellsworth, Maine pursuant to a Mortgage dated March 24, 2016.

The foregoing Mortgages are collectively referred to herein as the “Mortgages” and all real and personal property subject to the grant of the first Mortgage lien and security interest created by the Mortgages are collectively referred to as the “Mortgaged Property.”

In addition to the above, Inland and Lakewood have granted to the Authority a mortgage lien on and security interest in certain of their real and personal in order to secure their obligations related to the following tax-exempt bonds issued by the Authority as follows:

18

1. Inland has granted to the Authority a mortgage lien on and security interest in the real and personal property comprising Inland’s hospital facility located in Waterville, Maine pursuant to (a) a Loan Agreement and Mortgage, dated as of July 1, 2015, as amended and supplemented, securing Inland’s obligations related to the Authority’s Revenue Bonds, Series 2015A; and (b) a Loan Agreement and Mortgage, dated as of October 1, 2007, as amended and supplemented by a First Amendment to Loan Agreement and Mortgage, dated November 2, 2015, securing Inland’s obligations related to the Authority’s Revenue Bonds, Series 2007B.

2. Lakewood has granted to the Authority a leasehold mortgage lien on and security interest in the real and personal property comprising Lakewood’s long term care facility located in Waterville, Maine pursuant to a Loan Agreement and Mortgage, dated as of October 1, 2007, as amended and supplemented, securing Lakewood’s obligations related to the Authority’s Revenue Bonds, Series 2007B.

In addition, CA Dean has granted to an existing lender a mortgage lien on and security interest in the real and personal property comprising CA Dean’s hospital facility located in Greenville, Maine securing a $775,000 line of credit facility.

Note that the Inland, Lakewood and CA Dean mortgages described above are not part of the Mortgaged Property and, as such, do not secure on a parity basis the Notes issued under the Master Indenture.

Other properties of the Obligated Group, including but not limited to other property of EMMC, Mercy Hospital and Maine Coast, the hospital campus of Acadia in Bangor, Maine, the property of EMHS, the property of TAMC in Presque Isle, Maine and the property of Blue Hill in Blue Hill, Maine, are not mortgaged or encumbered, and thus are not included in the Mortgaged Property and are not subject to a Mortgage.