Madagascar Export Crops Sub-sector Review

184

Report No. S097-MAG Madagascar Export Crops Sub-sector Review Decemir 28, 1984 EastAfiica Prjects Dcpartmnent Central Agriculture Division FOR OFFICIAL USE ONLY 1::_ -bidlosued oAf tht World: Bank'atoiain MS ,. . -hi doumn ha a ret-ce ditibto an ma be use by .re-. ;. .. e.s. 1nl -nth per_orancef terffca du-s -t cotet ma no othewis be di,sclosed w_hu Wol Ban authorization Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Madagascar Export Crops Sub-sector Review

Report No. S097-MAG

MadagascarExport Crops Sub-sector ReviewDecemir 28, 1984

East Afiica Prjects DcpartmnentCentral Agriculture Division

FOR OFFICIAL USE ONLY

1::_

-bidlosued oAf tht World: Bank'atoiain

MS ,. .

-hi doumn ha a ret-ce ditibto an ma be use by .re-. ;. ..e.s.1nl -n th per_orancef terffca du-s -t cotet ma no othewis

be di,sclosed w_hu Wol Ban authorization

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

currency Unit tialsy Francs (FMG)USS1.00 - FMG 550 1/FMG 100 - US$0.18

WEIGHTS AND MEASURESmetric System

metric

1 hectare (ha) 2.47 acres1 kilometer (ka) - 0.62 mileI square kilometer (km2) , 0.39 square mile1 kilogram (kg) - 2.20 poundsI liter (1) 0.26 US gallon

0.22 Imperial gallon1 metric tonne (t) 2,204 pounds

GOVERNMENT ADNINISTRATIONFokonolona Institutions

Fokantany - villageFiraisam-pokontany - group of Fokontany

(or Firaisana) (former canton)Fivondronan-pokonolona - group of Firaisana

(or Fivondronana) (former sub-prefecture)Faricany - group of Fivondronana

(former province)

FISCAL YEAR

Government of Madagascar January 1-December 31Parastatals Vary by institutions but most

commonly january 1-December 31

11 The exchange rate between the US dollar and the Malagasy franc used inthis report is based on an average of the rates obtained during thesecond half of 19b3.

FOR OMCIAL USE ONLY

Abbreviations and Glossary

BCRDH Central Bank of Madagascar (Banque Centrale de la RepubliqueDemocratique de Madagascar)

BCSPG Clove Marketing Board and Price StabilIzatiou Fund (Bureau deCommercialisation et de Stabilisation des prix du Girofle)

BCSPP Pepper Marketing Board and Price Stabilization Fund (Bureau deCommercialisation et de Stabilisation des Prix du Poivre)

BFV National Commercial. Bank (Banky Fampandrosoana Ny Varotra)BNI National Industrial Development Bank (Bankin' Ny Indostria)BTH Rural Development Bank of Madagascar (Bankin' Ny Tantsaha

Mpamokatra)CAVAGI Coffee Vanilla and Cloves Stabilization FundsCCCE French Development Fund (Caisse Ceutrale de Cooperation

Econouique)-CMN Malagasy navigation company (Compagnie ialgache de Navigation)COROI State marketing company (Comptoir de Commerce et de

Representation de L'Oc-an ludien)CSPC Coffee Price Stabilization Fund (Caisse de Srabilisation des Prix

du Cafe)CSPV Vanilla Price Stabilization Fund (Caisse de Stabilisation des

Prix de la Vanille)DGP Directorate General of Planning (Direction Generale de la

Planification)EXA txport Assistance InternationalFAC Prench Technical Assistance Agency (Fonds d'Aide et de

Cooperation) -

FAO Food and Agiculture Organization of the United NationsFED European Development Fund (Fonds Europeen de D&vEloppement)FNUP Natioual Consolidated Equalization Fund (Fonds National Unique de

Pfir6quation)FOB Free on boardFOFIFA National Center for Applied Research on Rural Development (Foibe

Fikorahana Mombnon ny Fampandrosanan ny eny Ambarivohitra)GATT General Agreement on Tariffs and TradeGNIV National Vanilla Association (Groupement National

Interprofessionel de la Vanille)ICA International Coffee AgreementICCO International Cocoa OrganizationICO International Coffee OrganizationINSRE National Institute of Statistics and Economic Research (Institut

National des Statistiques er de la Recherche Economique)IPC International Pepper CommunityISNAR International Service for National Agricultural ResearchITC International Trade CenterMIEM Ministry of Industry, Energy and Mines (Ministare de l'Indust_ie,

de l'Energie et des Mines)MPAEF Ministry of Animal Production, Water and Forests (Ministere de la

Production Animale, des Eaux et Forets)

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

MPARA Ministry of Agricultural Production and Agrarian Reform(MinistAre de la Produciton Agricole et de la Reforme Agraire)

MPFE Ministry of Finance and Economy (Ministtre auprAs de laPrgsidence charge des Finance et de 1'Economie)

KRSTD Ministry of Scientific and Techaological Research (MinistAre dela Recherche Scientifique et Tecnnologique pour le d6vRloppement)

MTP Ministry of Public Works (Ministare des Travaux Publics)MTRT Ministry of Transport, Supply and Tourism (Ministare des

Transports, du Ravitaillement et du Tourisme)OAMCAF African and Malagasy Coffee Organization (Organisation Africaine

et Malgache du CafE)OCPGC Coffee, Pepper, Cloves and Cocoa Operation (Operation

Cafe-Poivre-Girofle-Cacao)ODR Rice Development Operation (Op6ration de Developpement Rizicole)RINDRA State audit company (Foibe Mpanaramaso Ny Fanjarianasa)RNCFM National railway network (REseau National des Chemins de Fer

Malagasy)

ROSO State marketing company (Tranombarotra Roso)SICE State marketiug company (SociEte Industrielle et Commrciale de

L'Emyrne)SMTM National maritime transport company (SocietE Malgache des

Transports Maritimes)SOMACODIS State marketing company (SociEte Malgache pour la Collecte et La

Distribution)UNCTAD United Nations Conference on Trade and Development

Executive Summary

Ci) Objectives and Focus. Export crops are the main means oflivelihood for almost one-third of Madagascar's population, and thecountry's principal source of foreign exchange. Coffee alone contributesan average 40-50X of annual export revenue. Cloves and vanilla are alsocritically important to the economy. Together these three account forabout 80% of export revenues. This report examines Madagascar'sperformance, policies and prospec.s with regard to development of these andother export crops, in order to provide a framework for Government/Bankdialogue and subsequent action in this important sub-seccor of agriculture(Chapter I).

(ii) External Market Constraints and Prospects. Over the past decadeMadagascar's export earnings have been sustained mainly by the 1976-77 boomin world market prices for coffee, and by the subsequent sharp rise inexport prices for cloves and vanilla. Simultaneously the export volume formost other crops has been in steep decline. Increases in export revenueswill be difficult to sustain in view of unpromising prospects for rapidgrowth in world markets for Madagascar's key export commoditites. Externalmarket constraints (including slow consumption growth, international quotaagreements and quality standards, and increasingly intense competition frommore enterprising trading countries) limit export growth potential.However internal policies and constraints (including declining volume,reliability and quality of production, lack of price incentives for exportcrop production, Government monopolies and excessive controls on exporttrading, and neglect of export services and promotion) have also seriouslyweakened Madagascar's ability to expand agricultural exports. Marketopportunities are identified for renewed growth in exports of coffee,vanilla, cocoa, green pepper, sisal and a diversified range of lesser,inadequately exploited crops (Chapter II).

(iii) Crop Production Constraints and Prospects. Despite favorablelands, soiLs and climatic conditions for tropical agriculture, productionof export crops (with the exception of cloves and, to a lesser extent,vanilla) has become increasingly unprofitable for small farmers as a resultof prevailing pricing policies. Yields are well below potential.Production is severely constrained by labor shortages at times of peakdemand, low standards of farming technology, inadequate input supplyservices, weak extension services, neglect of crop research, and lack offarmer access to wage goods and to protection against climatic risks.Faced with these problems, many cash crop farmers have reverted to asemi-subsistence system of cultivation. To reverse this situation, majoradjustments in agricultural policy and services are required, most urgentlyfor coffee. Cocoa, sisal and cassava also warrant attention forrehabilitation, and longer-term opportunities are identified for increasedproduction of coconut, cashew, maize, various fruit crops and spices. Toprovide an adequate foundation for future production growth, early actionis needed to overhaul extension services and techniques, to re-establishessential infrastructure and input supply services, to create a viablesystem for crop monitoring and forecasting, and to reformulate export croppricing policies to provide production incentives (Chapter III).

Cii)

(iv) Internal Marketing Constraints and Prospects. Policy changes andlegislative measures introduced during the 1970s greatly increasedGovernment involvement in the marketing system for export crops. Coffee,cloves, black pepper and certain lesser crops became subject to statetrading monopolies, and the activities of private sector marketing andprocessing enterprises were severely circumscribed. In general, theregulated marketing system has functioned poorly, and operationaLdifficulties are widespread. Lack of strategic planning, inadequatefaciliti-s at the primary marketing level, deteriorating transportinfrastructure, inefficiencies in port handling, severe weaknesses inquality control of export commodities, complex export administrationprocedures, inadequate market-research and promotion services, andstructural distortions in the marketing and pricing system are among themost serious constraints. Reduction of marketing costs offers possibly thegreatest scope for early improvement in the profitability of agriculturalexport production and trade. Initial action in this direction calls mainlyfor organizational and policy adjustments (Chapter IV).

(v) Pricing Policy Constraints and Prospects. For the main exportcrops a system of administered pricing, providing guaranteed minimum pricesto producers and exporters, has been maintained since Madagascar becameindependent in 1960. A separate price stabilization scheme is operated foreach commodity, and official price structures are issued annually. Thesystem has provided a degree of protection to growers under volatilecommodity trading conditions, but it has become arbitrary, inflexible andinefficient. Price setting procedures are bureaucratic, are not based oneconomic criteria, and have been unresponsive to farm production costs andconstraints. The structures and operations of the Price StabilizaitonFunds have not evolved in line with changing production and tradeconiditious, and have been weakened by poor financial management, seriousaccounting flaws and organizational weaknesses. Pricing policies aredictated mainly by the short-term needs of the Government Treasury. Thedecline of coffee production, for example, is mainly attributed toarbitrary pricing, heavy taxation, diversion of Stabilization Fund revenuesto non-productive sectors of the economy and inadequate re-investment ofresources in coffee development. Major changes in pricing policies andprocedures are called for, including reexamination of the level oftaxation, liberalisation or abolition of the set differentiels, andfixation of producer floor prices, based on improved knowledge of actualproduction and marketing costs and the criterion of border pricing (ChapterV).

(vi) Institutional Constraints and Prospects. Government policychanges since 1972 have vastly expanded the role and numbers of publicinstitutions in foreign and domestic trade. Export crop developmentdirectly or indirectly involves no fewer than eight ministries, of whichMPARA (and its dependent agency OCPGC) and MC (which overseas theStabilization Funds and parastatal trading agencies) are the mostimportant. Since 1982 an extensive realignment and internal reorganizationof these institutions has been underway, but the process is not yetcomplete. In the private sector, Government policies since the early 1970s

Ciii)

actively discouraged investment and severely curtailed export operations.Howerer, a well-established residual nucleus of private enterprises existswhich handles the vanilla trade and could rapidly expand exports of otheragricultural products under more favorable production and tradingconditions. A review of institutional structures and resources shows theneed to address a range of organizational issues facing the public sector(fragmented responsibilities, ill-defined objectives, weak planning andcoordination, poor information services, procedural and managementconstraints) and to re-activate private sector investment in order toaccelerate export growth (Chapter VI).

(vii) Action Undertaken. Since 1981 the Government has sought ways toinitiate a strong recovery in export crop production and trade. Variousstabilization measures and policy adjustments have been implemented to dealwith the broader economic and agricultural sector issues affecting exportgrowth. Specific steps taken recently to alleviate the identified externaltrading, production, marketing, pricing and institutional constraints areitemized (Chapter VII, 7.02-7.03). Outstanding issues for early attentionare identified (7.04-7.05). Conclusions and recommendations for follow-upaction arising from this review are both commodity-specific and applicableto the export crops sub-sector as a whole (7.06).

CViii) Coffee. The problems for coffee development are the mosteconomically important and complex among the major crops, and the leastamenable to rapid solutions. Long-term strategy should aim to strengthenMadagascar's competitive position in the world market through crop researchand technological diversification. A medium-term plan (1986-1990) shouldseek to revitalize the coffee sector through rehabilitation of robustacoffee production, exploitation of arabica coffee potential, and upgradingof coffee quality. Short-term action (1984-85) should focus on improvedcultivation, marketing and trading efficiency. Immediate prioritiesinclude action on: (a) pricing policy and incentives (including an increasein real producer prices of 502 over teLree years, and an initial increase in1984/85 of 15-20% over the 1983/84 guaranteed producer price); (b) thestructure and mechanisms for price setting and.administration (includingestablishment of economic criteria for price determination, and an improvedmethodology and procedure for annual price reviews); (c) improvement ofinput supply and distribution; (d) reduction of transport and shippingbottlenecks to coffee exporting, (e) upgrading of processing and qualitycontrol, and (f) improvements in organization and administration(7.07-?7.08).

(ix) Cloves. The prospects for development of clove exports are notpromising, since Madagascar's existing production capacity far exceeds theexpected growth rate of world market demand. A dual strategy isrecommended which calls for production and price restraint and vigorousexploitation of available markets for clove products. Medium-term planning(1986-1990) should aim to promote broader growth of the country's spicetrade based on established markets for cloves. Short-term action (1984-85)should focus on reduction of accumulated stocks. Immediate prioritiesinclude: (a) active market promotion in target countries; (b) more flexible

(iv)

export pricing to secure entry into new markets; (c) maintenance ofunchanged producer prices; (d) utilization of Stabilization Fund Resourcesto finance export market development; (e) basic improvements to cropquality and storage; and (f) formulation of a program of industrial andtechnological research to identify the scope for diversified product formsand industrial uses for subsidiary clove products (7.09-7.10).

(x) Vanilla. Demand growth prospects are relatively stable.Nadagascar's position as leading world supplier has made possibleapplication of monopolistic pricing policies; however, the high pricescharged are threatening Madagascar's revenue prospects as they haveencouraged consumers to switch to cheap synthetic flavorings. In order tosustain long-term demand, early action is recommended to raise yieldsthrough improved crop husbandry and extension services, to strengthenongoing agronomic research, and to explore new consumer uses for naturalvanilla. Short-term plans (1984-85) should focus on re-investment ofStabilization Fund resources in crop and market development under amedium-term (1986-1990) plan. Priorities for investment include: (a)development of vanilla research and extension services; (b) diversificationof production areas and cropping systems; (C) technological, productdevelopment and market research; and (d) providing institutional supportfor GNIV (the National Vanilla Association), a private sector institution(7.11-7.12).

(xi) Pepper. The outlook is favorable for continued growth in worldmarkets for both black and green pepper, but Madagascar's export growthprospects differ between the two. A pepper development strategy shouldfavor expanded production and promotion of green pepper (a Malagasyspeciality) by improving extension, input supply and crop collectionservices and by encouraging additional private sector investment in thisproduct. For black pepper, fundamental policy changes are needed quicklyto restore production and trade on a profitable basis. In the area oftrade policy, (a) removal of marketing and pricing controls and (b)abolition of the price stabilization scheme for black pepper arerecommended. Priorities from an agricultural policy standpoint shouldfocus on (c) raising crop yields through supply of improved plant material,reduction of plant material, reduction of plant disease, improved use offertilizer, and husbandry techniques, and (d) linkage of production andtrading operations within a coherent strategy and action plan torestructure and expand pepper exports with effect from 1985 (7.13-7.14).

(xii) Cocoa. Despite generally unpromising world market and pricetrends, cocoa offers some scope for increased production and exportearnings. Production by small farmers is expanding, yields are moderateand capable of further increases, and apparent demand exists for Malagasycocoa varieties. Short-term action (1984-85) should focus on: (a) carryingout a detailed study on cocoa development potential and (b) maintaining andincreasing support for varietal and yield improvement through OCPGC.Experience gained in this period would guide the formulation of a moreprecise medium-term (1986-1990) strategy for expansion of cocoa exports(7.15-7.16).

(v)

(xiii) Lesser Crops. In addition to the five principal export crops,eight other commodities are suggested for further research and developmentin the immediate future (7.17). An in-depth study is needed on sisal, awell-established crop in Madagascar and traditional foreign-exchange earner(7.18). Recent liberalization of trade in butter beans ('pois du cap')should assist a revival of production and renewed export growth of thiscrop (7.19). Production and long-term export possibilities for coconuthave not been sufficiently exploited (7.20). Another versatile crop,well-established in certain areas, is cashew, for which Madagascar has asmall export market capable of further development (7.21). Production ofcassava is second only to rice among the food crops, and provides the rawmaterial for processing and export of tapioca in increased quantities(7.22). High priority should be given to detailed study of maize exportpotential in the light of apparent adaptability of this crop to variousregions and unfulfilled export demand (7.23). The export prospects forvarious spices, such as cinnamon, nutmeg and ginger, have so far beenpoorly exploited and should be examined, in conjunction with vanilla andcloves, by a proposed National Spice Promotion Board (7.24). Madagascar'sdiversified climate and land resources also offer considerable long-termscope for increasing exports of tropical fruits, for which rehabilitationof transport infrastructure and an investment code to attract privatecapital would be essential pre-conditions for trade expansion (7.25).

(xiv) Export Crop Development Strategy. Development planning forspecific crops should be reviewed in the broader context of economic andsector development plans. Preparation of a long-term inter-sectoralstrategy and action plan for the export crops sub-sector is recommended andshould follow Government/Bank review of the present report (7.26).

Cxv) Components of an Export Crop Strategy. The principal policychoices lie between expansion, rehabilitaiton and diversification, or acombination of these three options. Crop diversification policy shouldalso weigh options for crop, product, market and production areadiversification. An overall strategy for Madagascar should seek to: (a)reconcile crop resource potential with external market opportunities, (b)establish policy linkages between production, internal marketing,agro-industrial processing and pricing policies for specific crops, and (c)ensure coordination of information, research, extension, input supply andpromotion services. Relationships between external and domestic marketsand prices, and between cash crop and food crop policies, should becarefully evaluated (7.27).

(xvi) Recommended Strategy. The three main export crops (coffee,cloves and vanilla) offer limited prospects for long-term economic growth.It is therefore recommended that Government's long term goals should focuson regional crop and product diversification. In the medium-term, however,Madagascar will remain heavily dependent on the existing major crops; forthe 1986-1990 period emphasis should be on expansion of established cropexports and progressive diversification of production. In the short term(1984-85), Government efforts should focus on (a) measures forrehabilitation of production and diversification of markets for the major

(vi)

export crops, (b) expansion of the existing export trade among lessercrops, and (c) preparation of a strategy and action plan for long-termdiversification and development (7.28).

(xviL) Priorities for Action. Follow-up action in response to thisreview will require Government/Bank dialogue on a range of issues whichcall for early attention. These issues include information management,manpower training, price policy formulation, institutional reform,marketing infrastructure, control of quality standards, and the role inexport crop development assigned to the private sector (7.29). The mainelements of an action plan and schedule to address these issues is annexedto this report (7.30). It is suggested that within this framework foraction, the agenda for discussions should focus on five key topics:

(a) coffee development(b) marketing policy issues(c) pricing policy issuesCd) institutional reforms(e) export diversification

MADAGASCAR

EXPORT CROPS

SUB-SECTOR REVIEW

Table of Contents

Page

I. INTRODUCTION .............................. ...... ........ .......... I

I1. EXPORT MARKETS: STATUS AND TRENDS

A. Structure of External Trade ............. ..... ............... 4B. The Market for Coffee . 4C. The Market for Cloves ......................................... 13D. The Market for Vauilla .. .... .. ... ..... .. . .. .. . * * * * * * * * * * * * * * * 17E. Markets for Lesser Crops ..... ............... .... .................... 22F. Conclusions ......... ........ ............ ................... ... 29

III. EXPORT CROP PRODUCTION

A. Ecological Conditions for Crop Production .............. ...... 31B. Production and Post-Harvest Practices ........................ 31C. Production Volumes and Yields ................................ 35D. Farming Systems and Constraints .............................. 40E. Economics of Crop Production ..... .... ........................ 44F. Scope for Crop Diversification ...... *..*................ .... 49G. Conclusions ................................................ . 52

IV. EXPORT CROP MARKETING

A. Crop Marketing Systems ........ ...................................... 54B. Status of Marketing Operations ............................... 58C. Conclusions ....... ........................................ .. 66

V. PRICING AND PRICE STABILIZATION

A. Price Administration System ............ . ................. 68B. PLices and Margins .......................................... 70C. Role and Operations of the Stabilization Funds ............ ... 73D. Utilization of Export Revenues ............................... 75E. Conclusions ....... ......... ....................... 78

VI, ORGANIZATION FOR EXPORT

A. Institutional Framework .. . .... .. . .. .. . ... . ... .. . ... . ... . .. .. 80B. *Private Sector Operations *.*... ... . .......... .87

C. Organization of Export Services ............................. 88

VII. PROSPECTS FOR DEVELOPM4ENT

A. General Situation Summary ....... **** ****. ................... . 92B. Commodity Prospects and Scope for Development ............... 98C. Towards an Export Crop Development Strategy ........... 105

Annex: Main Elements of an Action Plan

Tables (separate listing)

Graphs and Charts (separate listing)

map: IBRD 28282

List of Tables

TableNo. Title

1. Structure of Merchandise Imports (c.i.f_) 1978-19822. Structure of Merchandise Exports (f.o.b_) 1978-19823. Value and Volume of Total Exports, 1960-19824. Crop Production, 1973-19825. Major Merchandise Exports (Volume m/t), 1973-19826. Major Merchandise Exports (Value f.o.b., FMg mill.) 1973-19827_ World Net Imports of Coffee by Major Regions/Countries8. Coffee Prices, 1973-82 and 1983-95 (Projected)9. Price Differences between Centrals and Other Kinds of Coffee

10. Coffee Year 1983/84: Exporting Members Entitled to a basic Quota11. Coffee Year 1983/84: Exporting Members Initial Annual and Quarterly

Quotas12. Madagascar: Coffee Production and Exports 1973-198413. Coffee Exports by ICO Exporting Members to Non-Members14. Madagascar: Cloves Production and Exports 1973-198215. Indonesian Imports of Cloves, 1973-198116. Imports of Cloves (Excluding Indonesia), 1976-198017. New York Spot Prices for Cloves and Madagascar Producer Prices,

1973-1983

18. Madagascar: VaniUa Production and Exports, 1973-198419. Imports of Vanilla, 1976-198020. New York Spot Prices for Vanilla and Madagascar Producer Prices21. Madagascar: Pepper Production and Exports 1973-198422. World Imports of Pepper, 1976-198023. New York Spot Prices for Pepper and Madagascar Producer Prices24. Production and Export Volumes of Principal Export Crops, 1978-198325. Distribution of Farm Types (October 1983)26. Number of Producers and Farm Size (1983)27. Participation of Women in Agricultural Activities28. Crop Establishment Data for Export Crops29. Estimated Yields of Principal Export Crops30. Producer Prices for Export and Other Crops (October 1983)31. Returns per Laborday on Farm Production from Operation of Existing

Farms, 1982-8332. Prices of Farm Inputs (October 1983)33. Imports of Agricultural Chemicals (Tons), 1979-198334. Price Structure for Coffee, 1975-198335. Price Structure for Clove Buds, 1975-198436. Price Structure for Vanilla, 1975-198337. Price Structure for Black Pepper, 1974-198338. Changes in Coffee Price Components, 1978-198339. Changes iu Clove Price Components, 1978-198340. Changes in Vanilla Price Components, 1978-198341. Changes in Black Pepper Price Components, 1978-198342. Stabilization Fund Receipts and Expenditures, FY 1979/80-1982/8343. FNUP - Annual Receipts and Expenditures, 1979-8244. FNUP - Revenues, Expenses and Investments by Commodity

List of Graphs and Charts

Graphs

Figure 1 World and Brazil's Coffee Production

Figure 2 Real World Coffee Prices and World Stocks

Figure 3 Coffee prices, Actual and Projected

Figure 4 Ratio of Robusta to Arabica Prices

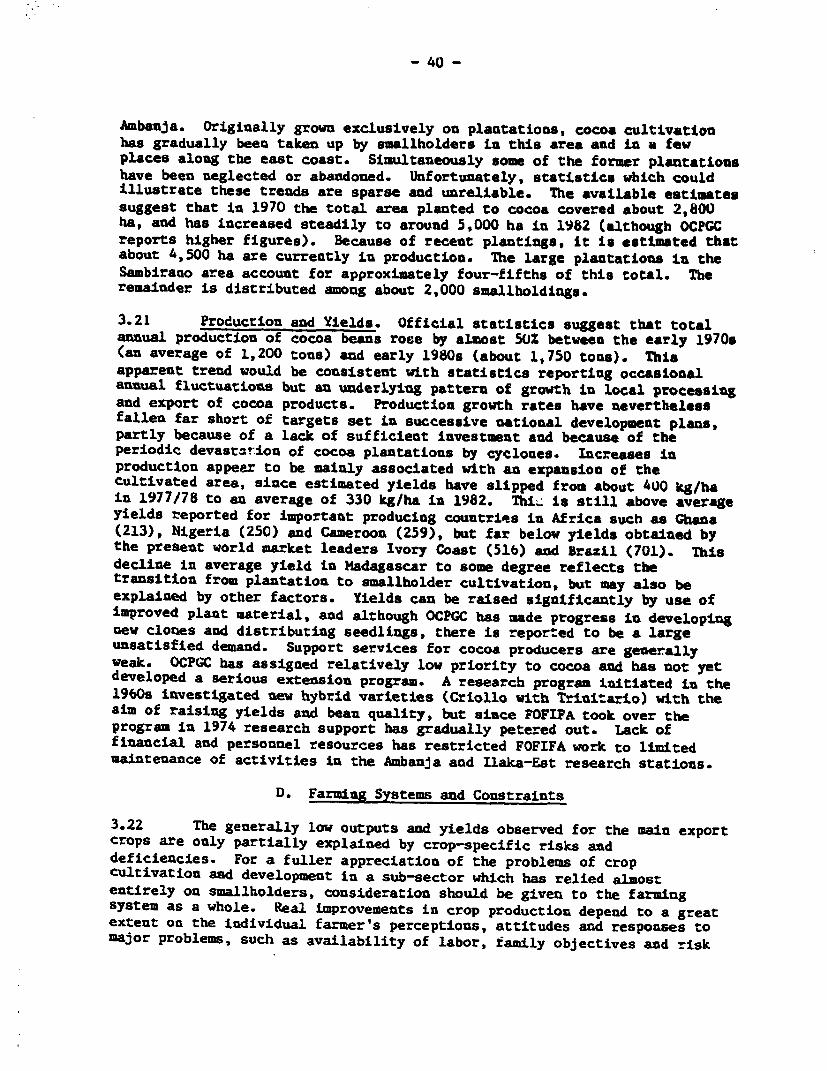

Figure 5 Producer Price as X of Coffee Guaranteed Export Price andActual Export Price

Figure 6 Producer Price as Z of Cloves Guaranteed Export Price andActual Export Price

Figure 7 Producer Price as Z of Vanilla Guaranteed Export Price andActual Export Price

Figure 8 Producer Price as Z of Pepper Guaranteed Export Price andActual Export Price

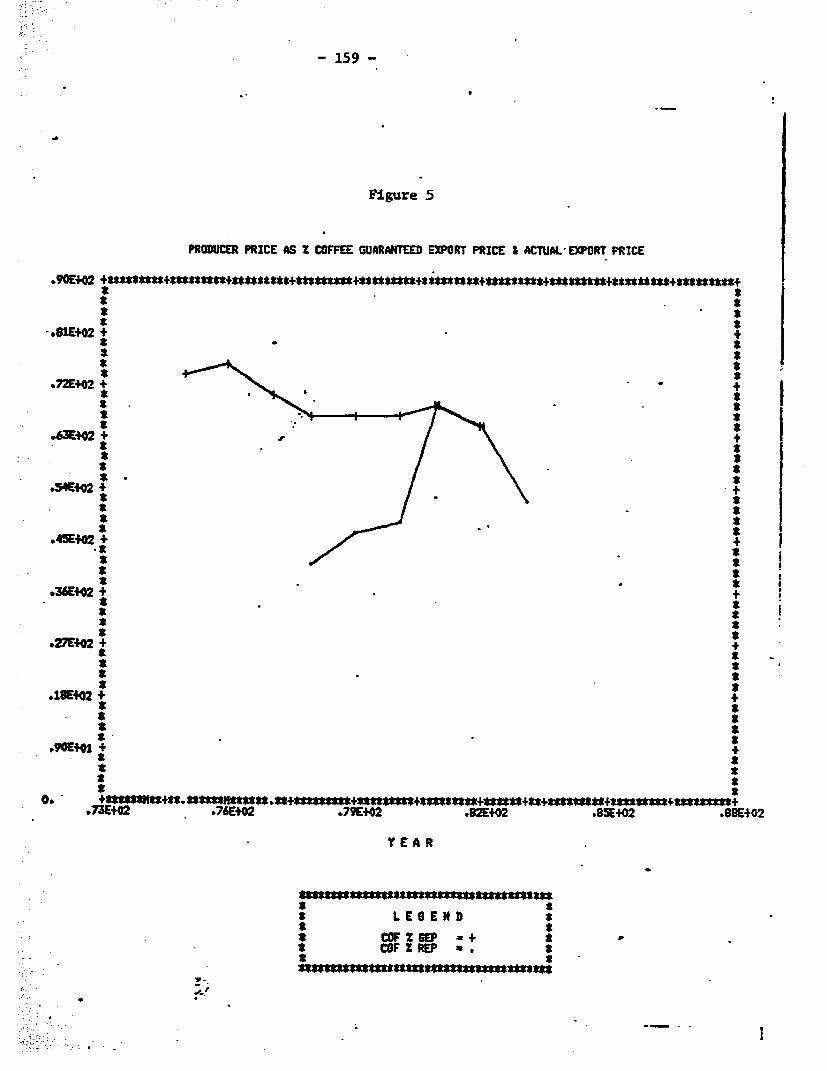

Figure 9 Producer Prices of Selected Crops as Z of Guaranteed ExportPrice

Figure 10 Producer Prices of Selected Crops as Z of Actual Export Prices

Charts

Chart 1 Export Crop Marketing Circuit

Chart 2 Export Crop Marketing Calendar

Chart 3 List of Participants in Decision-Making

Map: Principal Export Crops of Madagacsar

MADAGASCAR

EXPORT CROPS SUB-SECTOR REVIEW

I. INTRODUCTION

1.01 Objective. Export crops are the main means of livelihood formore than 500,000 farm families, almost one-third of the population ofladagascar. They are also the country's principal source of foreignexchange and important for the future expansion of employment opportunitiesin agriculture. Growth in this sector is therefore critical for social andeconomic development. How to improve Madagascar's competitive standing inworld markets, sustain and expand crop production, increase marketingefficiency, and ensure optimal use of export crop revenues are the mainissues addressed in this review. It is intended that the information,analysis and conclusions presented in the report should provide a frameworkfor Government/Bank dialogue on export policy in the agriculture sector andfor subsequent action.

1.02 Background. The present economic crisis in Madagascar hasprompted renewed interest in export crops after a prolonged period ofrelative neglect. When independence was achieved in 1960, production andtrade in agricultural commodities dominated the national economy. Duringthe 1960s the Government and the private sector sought to build on thiscolonial inheritance. Political changes in the early 1970s, however, ledto new approaches. By the mid-1970s agricultural policy had shiftedexplicitly towards achieving self-sufficiency in food production as apriority goal. Public sector investment increased, and many production andtrading enterprises were nationalised. While the value of crop exportscoutinued to rise, the volume of exports failed to keep pace. Growth inthe agriculture sector as a whole was slow. Another Government policyinitiative in 1978 sought to diversify the economy through rapid expansionof the manufacturing sector. An ambitious public investment programfollowed in 1979, financed in part by a sudden large increase in externalborrowings. As the worldwide recession approached, Madagascar found itsfinancial resources over-extended and the economy plunged quickly intosevere crisis. Since 1980 this crisis has dominated the national scene.Faced now with acute balance of payments difficulties, continued productionstagnation and widespread economic dislocation, the Government has begun tolook more deeply into its export crop performance and prospects.

1.03 Commodity Focus. The range of agricultural exports is broad. Itextends from tropical beverages and spices to livestock, fish, and variousprocessed products, such as tapioca, vegetable fibers and essential oils.Collectively these exports account for about 90% of foreign exchangeearnings. However, a few commodities account for a disproportionatelylarge share of the export trade. Coffee alone contributes an average40-50% of annual export revenue. Cloves and vanilla are also of criticaleconomic importance. In the 1981-82 period the combined value of thesethree crop exports amounted to 80% of foreign exchange earnings froi

-2-

agriculture. Of necessity, this report assigns priority to this group oftraditional exports.. Lesser crops, including pepper, sisal, cocoa, butterbeans (pois du cap), various other spices and essential oils play asignificant supporting role in the export trade and are also examined inthis review. The prospects for crop diversification are also given someconsideration. However, other important sub-sectors of agriculture -livestock, fisheries, and industrial crops such as sugar and cotton - areaddressed more appropriately either in separate studies or in the contextof ongoing Bank-assisted projects. They are therefore considered onlyperipherally in this report.

1.04 Multi-sectoral Implications. The problem of export cropdevelopment is not exclusively agricultural. The production process mustperforce be geared to the final goal of sale in international markets, andtrading performance may be affected by structural, organizational oreconomic weaknesses at any point in the farr-to-market chain. ForMadagascar, given the thousands of miles which separate rural producersfrom their major ultimate markets, this chain is exceptionally long. It isalso internally complex, involving both the public and private sector and alarge number of intermediaries and institutions. Within the Government,export crop development currently involves no fewer than eight ministries,those of Agricultural Production and Agrarian Reform (MPARA), Commerce(MC), Transport, Supply and Tourism (MTRT), Public Works (MTP), IndustryEnergy and Mines (MIEM), Scientific and Technological Research (MBSTD),Finance and Economy (MPFE), and Planning (DGP). The formulation of acoherent development policy in this sector must therefore engage all keyparticipants in the process. Accordingly, the approach adopted for thisreview is inter-sectoral. It recognises that constraints and theirremedies should be identified throughout the export crop production andtrading system.

1.05 Report Structure. The structure of the report is designed toassist sequential study of the system's component parts. Chapter IIexamines trends and prospects in the international commodity markets whichwill influence the progress of Madagascar's exports for the foreseeablefuture. It analyses both past and present constraints and seeks todifferentiate between short-term (19b4/85) and longer-term (1986-1990)opportunities. Chapter III reviews the production of export crops in thislight. It examines the ecological conditions and local environments forcrop production, farming practices, constraints and achievements, and thescope for expanding production in the context of prevailing prices andavailable services. Chapter IV looks into the internal workings of themarketing system on which the farmer depends and which must supply theproducts to the port of exit for international trade. Marketing channels,infrastructure, procedures and services are reviewed, and an assessment ismade of the scope for improving crop processing and marketing efficiency.Chapter V focusses on prices, pricing mechanisms and the issue of pricestabilization. It explores the role and operations of the PriceStabilization Funds, and the use made of export crop revenues controlled bythe Government. Desirable changes in pricing policies and procedures arealso identified. Chapter VI reviews the relationships between various

-3-

participants in the export crop trade, the institutions concerned, and therespective roles which are or should be played by the public and privatesectors. The organization and management of export operations is the mainissue addressed in this chapter. Finally, in Chapter VII, the prospectsfor development are summarized. For each of the commodities considered, aprofile is provided of the opportunities for growth and the measures neededto achieve that growth. The outlines of a coherent inter-sectoral exportcrop development policy are suggested, and alternative strategies andaction plans are reviewed. Relevant tables, charts, and matrices and mapsupporting the body of the report are grouped together in the Annexes.

1.06 Acknowledgements. The report is a product of Government/Bankconsultations on export crop issues over the past three years. It draws onmany sources, and benefits from considerable information assembled for apreliminary Bank working paper on export crops issued in June 1982. Thiscontributed to a first overview of agricultural export issues in the SectorMemorandum on Agriculture and Rural Development issued in March 1983.Following further discussions on these issues, a mission comprisingMessrs. N. Wilkie, E. Los (EAPCA) and M. Couillaud (consultant) visitedMadagascar in September 1983 to carry out a more extensive study of theexport crop sub-sector. The present report mainly reflects the work ofthis mission and its close collaboration with many Government officials inconcerned ministries and agencies. A follow-up mission in March 1984 byMr. N. Wilkie, the study coordinator, assisted in updating the analysis ofproduction and trade statistics and in reviewing institutional changesresulting from Government reorganization during the latter half of 1983.Outstanding information gaps and statistical inconsistencies, where theseare especially important, are discussed in relevant sections of thereport. EAPCA staff responsible for the present report recognize thevaluable contributions made by Malagasy officials, by the studies of otherorganizations cited in the text, and by colleagues in various quarterswithin the Bank during its preparation.

1.07 Note. The statistical data and commentary contained in thisreport were updated in April 1984. The report therefore does not takeaccount of either subsequent developments or action subsequently undertakenby the Government of Madagascar. Following review of the findings andconclusions of this report, additional economic analysis of export croppricing and taxation issues will be carried out by the Bank. The resultsof this work will be incorporated in follow-up discussions with theGovernment on its action plan for export crop development.

-4-

II. EXPORT MABRXETS: STATUS AND TRENDS

A. Structure of External Trade

2.01 As a large island situated in the Indian Ocean and adjacent tomainland Africa, Madagascar Is uniquely positioned for internationaltrade. Nevertheless the country's trading structure shows many featurescommon to other developing nations in the tropics. Exports consist mainlyof primary commodities. Imports consist mainly of capital goods, rawmaterials and energy supplies. Although independence in 1960 inspiredhopes for broader and more rapid economic growth, Madagascar, like otherdeveloping countries, has been profoundly affected both by the changingeconomic climate in world markets and by internal shifts in nationaldevelopment policy. In general progress has been slow. In recent yearseconomic difficulties have prompted significant changes in the import tradestructure, marked by rapid increases in rice and fuel imports.Simultaneously lack of progress in the never industry and energy sectorshas led to even greater dependence on primary agricultural commodities asthe foundation of export trade. (Tables 1 and 2).

Export Trends

_.02 Export revenues show a continuous upward tread. Sinceindependence, the value of total exports measured at current prices hasmultiplied sixfold, from FMG 18.4 billion in 1960 to FMG 109.0 billion in1982. With the excreptiou of 1977, when export revenue jumped by 25% overthe previous year (largely in response to the sudden boom in world marketprices for coffee), earnings from exports show a pattern of relativelysteady growth over more than two decades. Throughout the 1960s the volumeof exports grew even faster than export income, rising from 235,000 tons in1960 to 782,000 tons in 1970, an increase of 333%. (Export value, bycomparison, rose by only 218% over the same period.) In the 1970s,however, this promising trend was reversed. While in current termsearuings more than doubled from FMG 40.2 billion in 1970 to FMG 84.7billion in 1980 and in real terms export income continued to show modestgrowth, the actual volume of goods exported declined sharply. From thepeak of 782,000 tons in 1970 export volume dropped by 10% in 1971,recovered slightly In 1972-74, then declined steadily for the remainder ofthe decade. By 1980 export volume was only 372,000 tons, the lowest levelof achievement in 15 years (Table 3). While these officially reportedtrade figures are at best approximate and are subject to manyinconsistencies (deriving from the use of multiple sources, occasional datagaps, weaknesses in collection methods and - more recently - diffusion ofresponsibility for data collection), the general decline in exportperformance since 1970 is indisputable.

2.03 The export pattern for agricultural products generally reflectsthat of Madagascar's total export trade, demonstrating both the importanceof agricultural commodities in the export portfolio and also the almostuniversally poor performance across all sectors of the economy since theearly 1970s. In 1973, excluding agro-industrial products, agriculture's

-5-

share of exports amounted to 77% in value and 23Z in volume terms; in 1981the comparable proportion of primary agricultural commodity exports tototal exports amounted to 82% in value, 25% in volume. The addition ofagro-industrial exports (processed foods and other processed products,textiles, shoes, wood and paper products) shows that agriculture's totalshare amounted to 90% of the FMG 109.0 billion in export revenues earned byMadagascar in 1982. Stagnation in other sectors has meant that over the 10years from 1973 to 1982, despite declining output, the agriculture sectoras a whole has enjoyed a rising share of total export earnings. Of thisshare, the primary commodities have consistently accounted for at leasttwo-thirds in terms of both the value and the volume of agriculturaltrade. In the present period of crisis, the national economy is thereforeespecially dependent on export crops for earning foreign exchange.

Agricultural Commodity Trends

2.04 With its large land area (about 592,000 Im2), varied climate,topography and soils, and a total population of about 10 million,Madagascar has a diversified agricultural economy to support exportdevelopment. At present this potential is poorly exploited. Rice, thedominant crop and staple food of almost all Malagasy, was formerly also anexport crop. As recently as 1970 rice exports amounted to 66,000 tons.Stagnating production over the subsequent decade, however, has transformedMadagascar's trading status in rice to that of a major importer. In 1982imports of rice reached a peak of 352,000 tons while exports, a mere 170tons, virtually ceased. Bananas, likewise once included among the range ofexport crops (an average of 7,000 tons were exported annually between 1971and 1974), have also almost disappeared from the export balance sheet.Only 423 tons were exported in 1982, although production (281,000 tons in1982) remains close to the levels achieved a decade previously. Certainexport commodities, including sugar and cassava, show a pattern ofsustained or expanded production growth which contrasts with a sharpdecline in the actual export performance of these crops in world marketsover the past decade. Other formerly importaut export items, includinglivestock products, butter beans, sisal, raffia, and oilseed cake,demonstrate a steady decline in the volume of both exports and production.

2.05 While the agriculture sector as a whole has failed during thel97Us to keep pace wi:h domestic market demand and volatile conditions inglobal markets, several key export crops have proved more resilient.Coffee, the leading export revenue earner since the pre-independence era,is still the most important export crop. Although over the past decadecoffee export volume has declined by almost one-fifth from an annualaverage of 65,000 tons in the early 1970s to 53,000 tons in 1982, foreignexchange earnings from coffee, expressed in current prices, have more thandoubled over the same period. Exports of cloves have increasedsubstantially over the past decade and in the 1981-82 period werecontributing 27% of agricultural export earnings. Madagascar remains theleading world producer of vanilla, another high value crop, from whichexport earnings at current prices have multiplied ninefold since 1973.Other traditional crop exports such as pepper (black and green) retain some

-6-

importance in the export accounts. Production and exports of cocoa, apotentially high value but relatively new crop in Madagascar, have shownslight growth in the 1978-82 period over the previous five years. Effortsto halt the prolonged decline in the volume of agricultural exports and tosustain foreign exchange earnings in the short term will depend veryconsiderably on the performance of this key group of commodities. (Tables4, 5, and 6).

2.06 The position of each of these key commodities is being eroded inworld markets by factors only partially under Madagascar's control. Globalconsumption of coffee has shown little growth in recent years andinternational prices remain low. I: this tight and highly competitivemarket, for various reasons Madagascar is poorly placed to strengthen itsalready small (1.5:) world marKet share. As a member of the OAMCAF groupof Francophone African partners within the International Coffee Agreement(ICA), Madagascar has little influence on global decision-making.Competition in the (mainly Eastern European) markets not covered by the ICAis intense. Furthermore as an exporter of the robusta (canephora) varietyof coffee, and of only average quality, Madagascar's access to the premiummarkets for arabica and high-quality robusta coffees is extremely limited.The market for Madagascar's cloves is also fragile, being highly dependenton Indonesia's capacity to replace clove imports by local production forthe clove cigarette industry. Even Madagascar's near-monopoly domination(with an approximately 80% share) of world markets for natural vanilla isbeing progressively undermined by successful competition from the cheapsynthetic, vanillin, and other substitutes. These market situations, andpossible strategies to deal with them, are examined in detail later in thisreport. It suffices here to stress the extreme vulnerability ofMadagascar's entire export crops sub-sector in the light of recent worldmarket trends.

Trading Partners

2.07 In value terms, 96% of Madagascar's export trade is shared amongabout 30 importing countries. In 1979, the last year for which detaileddata are available almost half of export revenues derived from sales toWestern Europe: EEC member countries accounted for 42.2%. Trade withFrance, the former colonial power, accounted for more than half the EECshare and about a quarter of all exports. Western Germany is the secondmost important trading partner in the EEC. Exports to North America (14.8%of total in 1979) were almost exclusively to the USA, a major consumer ofboth coffee and vanilla from Madagascar. Asian countries took 20.2% ofexports in 1979, dominated by Indonesian imports of cloves and, to a lesserextent, Japanese imports of fish products and minerals. Trade with Africancountries (b.2Z, mainly Algeria), Eastern Europe (5.4%) and neighbouringcountries of the Indian Ocean (4.1%) accounted for almost all residualexports in 1979. Over the past ten years, Madagascar has managed todiversify its market outlets for export crops (especially coffee) byentering new markets in Western and Eastern European countries, NorthAfrica and elsewhere. however, these openings resulted mainly fromshort-term opportunities and have not provided stability. In the absence

-7-

of renewed and sustained vigor in export market development, the EEC, theUSA and (for cloves) Indonesia will continue to be the main outlets forMadagascar's agricultural export trade. Subsequent sections of thischapter explore trends in each of the world commodity markets affecting thegrowth of this trade.

B. The Market for Coffee

World Trade

2.08 The coffee plant, originally native to Africa, is now cultivatedin about 60 tropical countries around the world. Most of these producingcountries export virtually all of the coffee they grow. World productionfor the 1983/84 season is expected to be around 5.5 million tons (92million bags), of which approximately three-quarters will enter worldtrade.1/ In terms of export revenues for developing coutries, coffee isthe most important non-fuel commodity.

2.09 World Supply. Since 1950 the world coffee market has beencharacterized by slow growth and periodic adjustment to sharp fluctuationSin production and prices. On the supply side, market trends have beenmainly affected by events in Brazil, the largest producer country, whichpresently accounts for about one-third of world exports. Erratic swings inBrazilian coffee production, caused mainly by sudden frosts (severe in1975, less so in 1981), have intermittently destabilised prices andstrongly influenced movements in world trade. Shortfalls in Brazilianoutput have uevertheless been fully made up by other producers in LatinAmerica, Africa and Asia, and over a 30-year period the increase in globalproduction has averaged 2.1Z per annum (Figure 1).

2.10 World Demand. Growth of consumption has uot kept pace withoutput over the past two decades. Whereas total world net importsincreased by an average 2.0% in the period from 1961 to 1970, consumptiongrowth declined in the 1970-79 period to a mere 0.6Z per annum (Table 7).Although world import demand grew fairly steadily until 1976, rapid priceincreases that year in the wake of the Brazilian frost accentuated otherfactors depressing market growth in the main consuming regions. Theindustrialized countries of Western Europe, the U.S.A. and Japan, whichtogether account for about 90% of global coffee imports, experienced slowerincome growth. Competition from other beverages (especially soft drinksand fruit juices), conceru over health side-effects from coffee drinking,and technological developments increasing liquid coffee yields fromprocessed coffee beans have contributed to a fall-off in world demand.Although consumption trends vary markedly among the major consumingcountries, with above average growth in some countries of Western Europe,Japan aud certain newer markets in Eastern Europe, North Africa and the

1/ See World Bank "Prospects of World Coffee Economy and theirImplications on Producing Countries,' Revised Draft, 10/24/1983.

8-

Middle East, consumption in the United States, the single most importantcoffee-drinking country, shows a long-term decline in imports of 1.9% perannum. Global demand overall is currently rising by only about 1% perannum, and coffee stocks in producer countries, estimated at 50 million60-kg bags (3 million tons) in January 1984 were already at a post-1975record level and still rising at a rate of between 4 and 6 million bags perannum (Figure 2).

Prices

2.11 In most countries demand for coffee is highly inelastic withrespect to incomes and pr'ces. In the USA and EEC, which together accountfor about two-thirds of imports, the market response to the tripling ofprices which occurred in 1976-77 as a result of the Brazilian crop crisiswas a 12-15% drop in consumption levels. Price movements over the pastdecade therefore closely reflect the changing equilibrium between supplyand demand. The trends in prices are shown in Table 8 and Figures 2 and3. Low prices in the early 197 0s reflected the vastly increased plantingswhich took place during the 1960s and more moderate consumption growth.The unprecedented price boom of 1976-77 dramatically increased the coffeeearnings of Brazil's smaller competitors, but led quickly to a situation ofrenewed global over-production and steadily declining prices and a wave ofeconomic problems in producer countries. By 1981 prices had dropped byabout 55Z against 1977 levels, and in constant terms had again reverted tothe low levels of 1973-75. The generally depressed prices over the pastseveral years oblige producers to exploit more deliberately the specialized-arkets for particular coffee types and qualities.

Types and Qualities of Coffee

2.12 Although there are over a hundred known coffee plant varieties,world trade is conducted on the basis of two types: arabica and robusta.The arabicas thrive at higher altitudes and are most widely grown in LatinAmerica and East African highlands. Robustas, which are normally grown inlowland plantations and on hill slopes below 800 metres, are exportedmainly from Brazil, African and Asian countries. Arabica coffees areconsidered to have a milder flavor, higher acidity and lower caffeinecontent than robustas. Arabicas are generally regarded as superior forregular (ground roasted) coffee, and command a premium price about 5-15%above robusta prices on the world market. Nevertheless, robustas havetraditionally been favored in some major markets (e.g. France, Italy), andhave the advantage that they produce a higher yield of soluble coffee perpound of beans. Consumption of soluble C"instant) coffees has expandedsteadily since the early 1950s to a point where this form now dominatesconsumer sales in the U.K. and Japan and accounts for almost a quarter ofthe coffee sold in the U.S.A. Although arabicas and robustas areinterchangeable and most coffees reaching consumers are blends of severalvarieties of different origins, relative demand for robusta has increasedwhile robusta's share of world production has remained basically unchangedfor the past 20 years. The price discount of robusta against arabica hastherefore tended to decline over time (Figure 4).

-9-

2.13 Price differentials exist not ouly between arabica and robustabut among various coffees from different origins (Table 9). Coffee tradedon world markets through the New York and London commodity exchanges isalso subject to different premiums and discounts applicable to spotpurchases and deliveries against future coutracts. Differences in prices,however, are an inadequate gauge of product quality as perceived by coffeeimport -rs, roasters, blenders and ultimate consumers. Exportable 'green"coffee (i.e. hulled coffee beans), graded in accordance with internationalstandards, may further vary in color, taste and flavor characteristics andother properties important to the buyer. These variables are complex andcan occur not only between coffees of different types and country originsbut between different production areas within countries and withindifferent consignments (even within the same grade) for export. Trends inthe quality of coffee traded in the world market are therefore extremelydifficult to measure. Recent studies nevertheless suggest that worldquality standards, at least as perceived by major importers, are droppingcontinuously for all coffees in general. A Bank-financed study carried outin 1983 suggests that 'top quality' coffees are produced mainly by Kenya,Central America, Ethiopia, Tanzania, Papua New Guinea and Zimbabwe.2 /Annual availability of such top quality coffee is estimated at between100,000 and 150,000 tons or about 2Z of current world production.

Harket Regulation

2.14 For the past twenty years, regulation of the world coffee markethas been carried out under the International Coffee Agreement (ICA), towhich Nrdagascar is a signatory. Since tbe first agreement was signed in1962 by a large group of consuming and producing countries, the ICA hasbeen iatermittently successful in sustaiuing prices for producer countriesand regulating trade flows. It main instrument has been an export quotasystem. At the height of turbulence in the world coffee market in themid-1970s, quotas were in abeyance (1973-76) due to a breakdown inagreements between producer and consumer countries on price and quotalevels. In 1976 the ICA was renewed, with specific provisions to basemember country quotas not only on the basis of past export performance, ashitherto, but also on the basis of the stocks held by each producercountry. However, quota provisions under the ICA 1976 came into force onlyin October 1980 in response to the sharp fall in prices over the 1978-8Wperiod, ending a seven-year period of intense free market competition inthe world coffee trade. Since then the global market has again stabilised,and a new agreement, ICA 1983, which came into force in October 1983 isscheduled to last until September l189. The provisions of this agreementgovern curreat short-term and medium-term prospects for Madagascar's coffeetrade.

2/ "World Availability of Top Quality Arabica Coffee." Report to theWorld Bank (RMEA) by H.J. von Rilten, Coffee Consultant. August 1983.

- 10 -

2.15 Quota and Price Controls. Producer member countries of the ICAaccount for over 99% of world net exports; importing country membersaccount for about 88% of world net imports. The main non-member importingcountries include most Eastern European countries, the USSR, and somecountries in North Africa and the Middle East. Quotas are assigned to ICAproducer member countries only for their exports to ICA importing members,and no limits are placed on their sales to the non-quota countries whoabsorb 12% of global coffee exports. For ICA member countries, the Councilof the International Coffee Organization (ICO), its administrativeauthority, sets a global annual quota for each coffee year (October toSeptember), taking into account annual world consumption and estimatedchanges in inventory level among importing members. The mechanism by whichannual country quotas are set is complex but offers some scope fornegotiation by individual producer country members in the light of theirexport performance and production and stock levels. Initial global quotasare adjustable during the coffee year, increases or decreases in quotasbeing triggered at pre-determined price levels in response to market andprice fluctuations. From 1980 to 1983, however, initial and final annualquotas have stagnated around 56 million bags (equivalent to 3,360,000tons), which represents only about 77% of exportable production, or 59% oftotal world production at estimated current (1983/84) levels (Tables10,11). While this quota mechanism aud the relatively low levels set bythe ICO in recent years have effectively stabilized prices since 1980, thestagnant market has kept prices at generally depressed levels until the1983/84 season. The initial quota of 56.2 milliou bags agreed by ICAmembers in October 1983 for 1983/84 was increased by 1 million bags inDecember and subsequently by three further increments of I million bagsbetween February and June 1984, the first indicators of an upturn in marketand revenue prospects for producer countries for over four years.

Madagascar 's Export Performance

2.16 Notwithstanding the above-mentioned multiple constraints imposedby conditions and movements in the world coffee market, Madagascar'scompetitive performance in this market has been weak. Historical data showthat following the introduction of coffee cultivation during the nineteenthcentury, by 1930 Madagascar was the leading coffee producer in francophoneAfrica with an 83% share of exports to France from its African colonies.By 1956, annual global exports had reached over 50,000 tons. A new peak inproduction was reached in the 1970/71 season with an estimated output ofover 90,000 tons. Exports subsequently reached an all-time high of 72,960tons in 1976, since when they have only twice (in 1979 and 1980) exceeded60,000 tons. Since 1980 annual exports have retreated to the averagelevels, around 55,000 tons, which prevailed over a decade previously.(Table 12). Growth of the country's coffee exports has not kept pace withthe slow upward trend in the world market, of which Madagascar's currentshare is about 1.5%. Among francophone African exporting countries,Madagascar's once dominant position has been progressively eroded overtime. Whereas the OAMCAF group as a whole accounts for 12.3% of ICO'sglobal quota, Madagascar's present share of the OAMCAF quota is only11.0%. Since the early 1970s her export performance has been faroutstripped by Ivory Coast and, more recently, by Cameroon both in ICAquota markets and more recently in non-quota markets (Table 13).

- 11 -

2.17 Causes of Declining Market Share. Aspects of Madagascar'sperformance in the coffee sub-sector have been the subject of severalrecent studies and a National Coffee Symposium sponsored by Governmentagencies (OCPGC/BTM) at Toamasina in May 1983. A study of export prospectsundertaken in 1981 by the International Trade Center (ITC)3/ briefly citednumerous difficulties: (a) inadequate production (due to ageingplantations, dispersed and poorly maintalned smallholdings, shortage ofland, insufficient supplies of fertilizer, declining product quality, lowproducer prices, and competition with other crops), (b) inadequatetransportation (lack of feeder roads, deteriorating road surfaces, decayingharbour facilities, infrequent shipping services), and tc) various problemsin pricing and marketing (fluctuating world market prices, disincentiveeffects of internal pricing controls, and related factors). however, noattempt was made in this ITC study to analyse these factors and theirrelationship to export market performance, or to review more fundamentalissues of national policy and objectives, organization and structure of thecoffee trade, and priorities for sub-sector development. A simultaueousstudy carried out by an UNCTAD consultant4 / focussed primarily onmicroeconomic trends and prospects for coffee and other key commodities inMadagascar's export trade. Other studies have reviewed organizational andfinancial aspects of coffee marketing.5 / At the National Coffee Symposiumheld in May 1983, participants sought to trace the causes of deterioratingcoffee production and trading performance, identified various weaknesses incurrent marketing and pricing policies, and proposed a number of measuresto improve short-term and long-term production and exports.6/ Theseproposals are considered later in this report. It nevertheress appearsthat there has been no systematic effort to diagnose Maui.gascar'scompetitive position in the world coffee market from the standpoint ofcomparative advantage or to assess the root causes of declining exportvolumes in recent years.

31 "Etude du potentiel a l'exportation de la Republique Democratique deMadagascar et de la situation de l'offre des entreprises industrielleset commerciales exportatrices." Rapport de mission du M. Jean Muller,9 July - 22 October 191l. International Trade Centre, UNCTAD/GATT,June 1982.

4/ "Madagascar: Microeconomic Analysis of Commodity Production and Trade."Walter C. Labys, Consultant, UNCTAD - Geneva. September 1981.

5/ See "Development des Exportations Malgaches: Diagnostic des Caisses deStabilisation," Export Assistance International, Paris. March 1980;and 'Caisses et Bureau de Commercialisation et de Stabilisation desPrix du Cafe, de la Vanille et du Girofle (CA.VA.GI): Revue des comptesdes exercices 1978-1979 et 1979-1980 et du Dispositif de ControleInterne," RINDRA. May 1982.

61 Rapport du Colloque sur le Cafe:, 16-20 May 1983, Toamasina. OCP/BTM.

- 12 -

World Market Prospects

2.18 Recent Bank studies have assessed the prospects for coffee marketgrowth and expected price trends into the 1990s.7/ World import demand isprojected to grow at a very slow pace, about 1.0 - 1.5X per annum, up to1990. The adoption of the new ICA in 1983 and the willingness of producercountries in recent years to maintaln tight quotas to preserve pricessuggest that a period of relatively stable conditions accompanied by slowincreases in quotas may be expected for the remainder of the 1980s.Non-quota markets offer additional scope for producer countries, butintense competition as a result of excess world production and high stocklevels is likely to stimulate further downward pressure on prices in thesemarkets. While lower prices could encourage some importing countries tofollow the recent withdrawals of Hong Kong, Hungary and Israel from the ICAprior to the new 1983 agreement, this is not to be expected. Per capitaconsumption levels are thought to be already relatively high in some of theEastern European markets, and newer consumer countries in the Middle Eastand Africa are unlikely to expand rapidly given the still depressedeconomic conditions affecting these regions. Strong action is promisedunder the new ICA to clamp down on the hitherto profitable so-called-'tourist' coffee trade from non-quota into quota importing countries. Thiswould further curtail growth of market opportunities in the non-quotacountries.

2.19 The increases in ICA quotas since December 1983 and currentlyimproving prices are likely to strengthen the confidence of producercountries in the ICO and its quota system as the safest mechanism forcontinued expansion. However, given that their present stocks amountglobally to one year's world market supply and that Brazil has takenelaborate measures (by transferring production into more northerlyfrost-free areas) to combat previous disruptions of output, the scope forexpanding exports is extremely limited. The Bank's econometric projectionssupport the conclusion that for the remaining 1980s producing countrieswill need to adjust their production growth to the combined growth rate ofdomestic consumption and world export demand. For countries with smalldomestic markets this implies production increases of only about 1.32 perannum up to 1990. In the absence of unpredictable occurrences, such associo-political turmoil in a major producer country, stock accumulations ateven this modest rate of production growth are likely to postpone anysignificant increases in coffee prices until at least the early 1990s.

Implications for Madagascar

2.20 The above scenario implies that for Madagascar, as for othercoffee producing countries in Africa, world market prospects shoulddiscourage reliance on rising coffee prices as a source of Increasedforeign exchange earnings to fuel economic growth. UnLess economic

- 13 -

recovery in the industrialized countries stimulates abnormal growth ofdemand in major expanding coffee markets such as Japan, quotas and priceswill grow only very slowly. Competition from other beverages, greatercoucentration within the international coffee roasting and blendingindustry and narrowing profit margius are likely to further encouragetechnological innovations and stret.gthen existing trends to improve coffeeextraction rates and reduce coffee bean demand. (The recent introductionof -extended-yield- coffee, which uses about 20Z less coffee to produce anormal brew, is already making inroads on markets in the U.S.A_ and WestGermany; its effect is to decrease coffee bean demand even when demand forliquid coffee is stable.)

2.21 In the foreseen global market situation of slow consumptiongrowth, high stock levels and intense international competitioa betweenproducer countries, Madagascar cannot afford to permit any further declinein its steadily weakening position. Current prospects would suggest athree-pronged strategy: (a) for the short term (1984/85), to improveproduction, marketing and trading efficiency, (b) for the medium-term1986-1990), to revitalize the coffee sub-sector with a view to increasing

Madagascar 's share of world markets in the 1990s; and (c) to acceleratedevelopment planning for long-term crop and market diversification. Thedesirability and feasibility of achieving these goals are explored in moredetail in later chapters of this report.

C. The Market for Cloves

World Trade

2.22 The clove tree provides three products entering world trade.Dried clove buds, marketed wtole or iL ground form, are by far the mostimportant of these. They have two distinct markets. One use is as aspice, widely consumed by households and the food industries inindustrialized countries, for baked products, desserts and (by industry) inspice blends for seasonings, sauces and pickles. Their second, highlyspecialized, use is for blending with tobacco in the manufacture of'kretek' cigarettes in Indonesia, in which proportions of clove contentvary between 25-40%, according to brand. Approximately 40,000 tons ofcloves are absorbed internationally in these markets, of which about halfenters world trade. In normal years the Indonesian cigarette marketaccounts for up to 80% of this trade. Other cLove products are clove budoil, distilled from the buds, stalks and leaves of the tree for sale to theperfumery, pharmaceutical and flavoring industries, and clove oleoresin,which is used in extract form by the food processing industry as areplacement for the whole or ground spice. Madagascar has alternated withTanzania as the world's leading exporter of dried cloves and is the leadingexporter of clove bud oil.

2.23 World Supply. The clove trade is highly irregular from year toyear. Oa the production side, harvests are cyclical, with peaks in yieldreached every 3-4 years. In all three major producing countries -Indonesia, Tanzania (on the islands of Zanzibar and Pembal and Madagascar -

crop productiou patterns are also vulnerable to cyclones and plant

- 14 -

diseases. Annual output in Indonesia, the world's largest producer, rangesfrom 25,000 tons in an average season to 45,000 tons in a good year.ALthough production hectarage more than doubled between 1976 and 1981 in adrive towards staf-sufficiency in supplies for Indonesia's expanding clovecigarette industry, domestic output still meets only two-thirds ofrequirements. Imports from Tanzania and Madagascar have normally made upthis deficit. In Tanania, however, clove production has experienced asteady declifne over the past decade. Madagascar's production hasfluctuated sharply over the same period (between 4,200 tons in the low yearof 1979 and 17,800 tons in the bumper year of 1974). (Table 14). Theextremely uneven production patterns within the three largest clove tradingcountries have opened up market opportunities for the smaller producers,including Sri Lanka and Comoros, and for the start-up of new productionschemes in Brazil, India and Malaysia.

2.24 World Demand. Indonesia's kretek cigarette industry has been themain factor behind a slow but steady increase in world demand for clovesover the past decade. From an annual output of 22 billion kretekcigarettes in 1972, production had risen to over 40 billion by 1977 andapproximately 50 billion by the early 1980s. Despite a marked growth inIndonesia's production of cloves over this period, domestic output has notkept pace with demand. As a consequence, average annual imports have risenfrom around 10,000 tons in the early 1970s to about 15,000 tons in1980-1982 (Table 15). Global consumption of cloves as a culinary spice hasbeen stable over this period, with signs of a low level of growth inimports from around 4,000 tons in the early 1970s to around 4,600 tons inthe period 1976-1980 (Table 16). Among these markets, the U.S.A. has onaverage absorbed about 25% of exports and appears to have stabilizedcurrent imports around 1,000 tons per annum. Consumption in EEC countries,the second most important market grouping, has been increasing at around4.5Z per annum since the mid-1970s to a current annual level of around1,5U0 tons. Demand in other markets, including Japan, Scandinavia, EasternEurope, Saudi Arabia and Singapore, shows continued slow growth. Theentrepot trade in cloves through Singapore to Indonesia and other countriesnevertheless remains clauded by the uncertainties affecting Indonesianproduction. Demand for clove bud oil and oleoresins in industrializedcountries, the main markets, has been relatively stable.

Prices

2.25 Cloves are a high-value spice. In 1982 world market pricesreached an average of US$5.30 per lb, an all-time high. Despite theyear-to-year fluctuation in supplies within the major producing countries,clove prices remained relatively stable in the early 1970s. Later in thedecade, and particularly since 1980, there has been a strong upward trendin prices, although prices slipped to an average of US$4.70/lb in 1983.High prices reflect both the continued inadequacy of Indonesian supplies tofeed the domestic market and a slowly strengthening demand for cloveselsewhere. Prices show considerable competition between the exportingcountries, reflected in annual price movements. Until the late 1970sprices from Madagascar tended to be around 10% lower than prices fromTanzania and 5-1OZ lower than those from Sri Lanka. However, Brazilianprices in the U.S. market are presently 5% lower below those of Madagascar(Table 17).

- 15 -

Quality Factors

2.26 Demand for cloves, both for kretek cigarettes in Indonesia and asa spice ingredient for food preparations elsewhere, is sensitive to avariety of factors associated with product quality. Indonesia's clovesupply problem is partly affected by the high oil content of locallyproduced cloves, which are both less suitable for cigarette manufacture andless pungent than the Zanzibar and Malagasy varieties. The major qualitycriteria in the food industry are flavor and oil content, appearance, andfreedom from humidity and foreign matter. In these respects, cloves fromSri Lanka, Indonesia and Brazil appear to have acquired a competitive edgein major markets over the less selective suppliers, Madagascar andTanzania. Strict standards in the food industry, particularly thoseexerted by the Food and Drug Administration in the U.S.A., place a premiumon quality grading and dependability. Quality variables also have someinfluence on prices.

Market Regulation

2.27 The clove trade is virtually free from international regulation.Historically, standards and prices were mainly determined by traders inSingapore. During the 1970s Indonesia introduced regulations restrictingimport purchases to those coutracted directly with Tanzanian and Malagasysuppliers under letters of credit. These regulations, still in force, havesharply reduced but not eliminated the entrepot trade. On the exportsupply side, a Tanzanian/Malagasy Clove Marketing Organization (TAMCO) wasestablished in April 1977 toz increase sales, strengthen prices and improvethe quality of cloves. Through a marketing branch of TAMCO known asUni-Cloves, import orders were to be allocated between Tanzanian andMalagasy exporters. However, this organization never functionedeffectively and has been allowed to lapse.

Madagascar's Export Performance

2.28 Cloves have accounted for a rising share of Madagascar's exporttrade over the past decade. The volume of exports has grown from an annualaverage of 8,300 tons in the 1973-77 period to an average of 10,700 tons in1978-82 (see Table 5). This progress appears to have been roughly in linewith import demand growth in Indonesia and other markets. Over the decadethe value of clove exports has risen significantly faster than volume, froman average of FMg 7 billion at current prices in 1973-77 to FMg 17.5billion in 1978-82 (see Table 6). This impressive growth reflectsiacreases in both export volume and particularly prices. During the same10-year period Madagascar has also increased its world market share at theexpense of Tanzaiia. While Madagascar's export volume increased annuallyby an average of about 6% per arnum between 1973-77 and 1978-82, Tanzanianexports in 1980 (5,300 tons) had slumped to less than half the volumeachieved in 1973 (10,800 tons). By 1980 Madagascar had become theprincipal supplier of cloves to virtually all the major importingcountries. By these criteria the country's clove export performance over

i -~ ~ ~~~~~~~~~~~i

- 16 -

the past decade has been a notable success. In 1982, however, exportvolume and foreign exchange earnings from cloves dropped precipitously to1,972 tons and FMg 7 billion, representing respective declines of 81% and75Z over 1982 figures. These disappointing results stemed mainly fromfailure to negotiate a new trade contract with Indonesia, and expose thebasic vulnerability of Madagascar's clove export trade.

2.29 Underlying Trends. Various reviews by Government services andITC and UNCTAD consultants have charted the trend of Madagascar's cloveexports but offer little explasatory analysis. Among external factors,steadily rising demand and a continuing shortfall of domestic supplies ofcloves in Indonesia have driven up prices and provided the main spur toMadagascar's overall growth in export volume and earnings. The decline inTanzania's production and export capability has undoubtedly also worked toMadagascar's advantage. Internal policies have also influenced exportgrowth. Exceptionally high exports (22,300 tons) iz 1975 following a poorharvest in Indonesia in 1974 prompted the Malagasy Government to launch a5-year production expansion program from 1975 to 1980. Although this fellfar short of planting targets, comparatively favorable producer pricesstimulated sufficient production growth to sustain Madagascar's emergingposition as the primary source of large volume supplies available toIndonesia in poor harvest years (e.g. in 1982). This progress has not beenachieved without cost. The high world market prices prevailing over thepast few years have restrained consumption growth in other importingcountries and encouraged price competition from newer producers. Since1977 the emergence of Brazil and Malaysia as new clove exporters hasalready affected the level of Madagascar's exports to the U.S.A. andJapan. Recent ITC studies suggest that clove prices quoted by Madag2scarare now too high, that product quality has deteriorated, that deliveriesare unreliable, and that trading practices are unsatisfactory. These andother internal factors affecting the country's competitive position arereviewed in more detail later in this report. The latest market indicatorssuggest that Madagascar's clove export trade has now reached a crossroad.

World Market Prospects