Liberalised finance and economic stability: square pegs in round holes

20

26 th Annual Conference of The European Association for Evolutionary Political Economy Unemployment and Austerity in Mediterranean European Countries, University of Cyprus, Nicosia, Cyprus, 6-8 November 2014 Liberalised finance and economic stability: square pegs in round holes Faruk ÜLGEN Centre de Recherche en Economie de Grenoble (CREG) Grenoble Faculty of Economics – University of Grenoble Alpes – France 1

-

Upload

univ-grenoble-alpes -

Category

Documents

-

view

3 -

download

0

Transcript of Liberalised finance and economic stability: square pegs in round holes

26th Annual Conference of The European Association for Evolutionary Political Economy

Unemployment and Austerity in Mediterranean European Countries,

University of Cyprus, Nicosia, Cyprus, 6-8 November 2014

Liberalised finance and economic stability:

square pegs in round holes

Faruk ÜLGEN

Centre de Recherche en Economie de Grenoble (CREG)

Grenoble Faculty of Economics – University of Grenoble Alpes – France

1

What is at stake? Irrelevance of financial liberalization with regard to the characteristics of money and monetary relations in capitalist economies.

Reference: Institutionalist (Allan Gruchy) – Hyman Minsky (FIH and -more than- necessary tight state intervention).

Position: SOCIETAL CONSISTENCY: preventing speculative banking and finance. Main implication: Tough macro-prudential regulation to tame short-sighted finance.

Then we must abandon the ongoing market-friendly regulatory reforms which rest on the belief that self-interest based self-regulation would lead to system-consistent behaviour.

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014

2

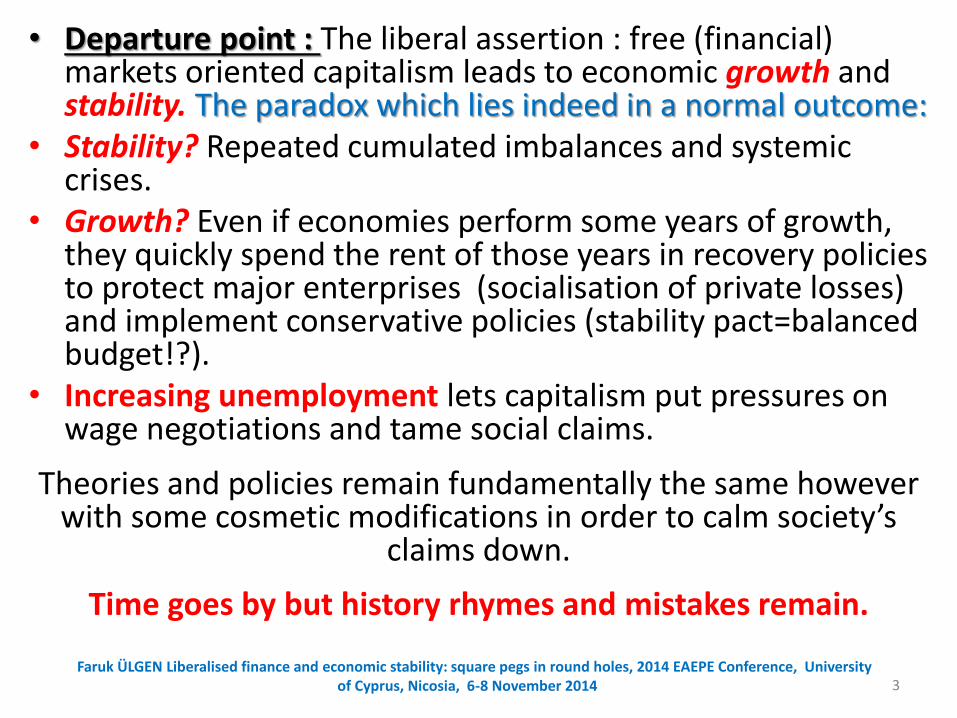

• Departure point : The liberal assertion : free (financial) markets oriented capitalism leads to economic growth and stability. The paradox which lies indeed in a normal outcome:

• Stability? Repeated cumulated imbalances and systemic crises.

• Growth? Even if economies perform some years of growth, they quickly spend the rent of those years in recovery policies to protect major enterprises (socialisation of private losses) and implement conservative policies (stability pact=balanced budget!?).

• Increasing unemployment lets capitalism put pressures on wage negotiations and tame social claims.

Theories and policies remain fundamentally the same however with some cosmetic modifications in order to calm society’s

claims down.

Time goes by but history rhymes and mistakes remain.

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014 3

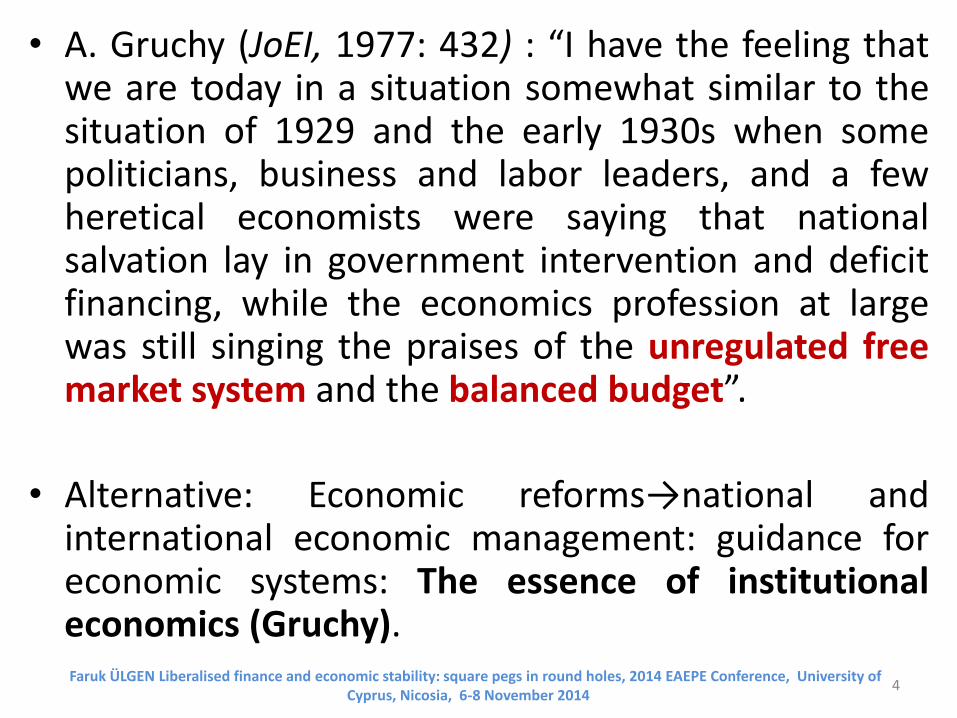

• A. Gruchy (JoEI, 1977: 432) : “I have the feeling that we are today in a situation somewhat similar to the situation of 1929 and the early 1930s when some politicians, business and labor leaders, and a few heretical economists were saying that national salvation lay in government intervention and deficit financing, while the economics profession at large was still singing the praises of the unregulated free market system and the balanced budget”.

• Alternative: Economic reforms→national and international economic management: guidance for economic systems: The essence of institutional economics (Gruchy).

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014

4

1. Consensual free market efficiency (FME) versus endogenous financial instability

1. 1. Scientific mantra - political motto

Mainstream wisdom: price-oriented free market mechanisms lead to economic efficiency (=efficient (optimal) social outcome). New Consensual Theory (NCT): opportunistic agglomeration of NeoC, NC, RBC, NK with FME.

2 assertions: - Ability of markets to self-adjust in case of disequilibria and - Efficiency of private/decentralised self-regulation compared with any collective/restrictive regulation.

Limited role to State (market-friendly incentives policies).

No room for specific analysis of insolvency/illiquidity concerns in a capitalist economy (shocks and crises come from the outside).

Inconsistent with the characteristics of capitalist (MONETARY/FINANCIALIZED) economies

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014

5

1. 2. Characteristics of Monetary capitalism Monetary economy: private/decentralised decisions ⇒ debt relations (bank credit and fin. intermediation) ⇒ eco. activity The debt-financing process depends on private units’ expectations about the future (but uncertain) profits: non-ergodic economy.

In such a process: Money is transversal: all economic transactions rely on monetary relations. Money/financial changes affect the whole economy irrespective of units which are/not involved in debt relations; Money is ambivalent: lies both in private decisions (banks/ entrepreneurs/profit expectations) and public rules (its general use and validity as a means of payment and general settlement depends on non-individual, public rules).

⇒ A social institution, a set of social rules Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University

of Cyprus, Nicosia, 6-8 November 2014 6

3 major systemic features of capitalism:

1) Monetary economy: financial relations (rules, mechanisms and markets): central/crucial role to let private agents take decentralised decisions;

2) Complex society: its evolution relies on the consistency of institutional patterns that shape private/public behaviour and systemic (in)stability;

3) Systemic viability: a macro-concern and cannot rest on micro-regulatory mechanisms that relate on private objectives.

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014 7

1.3.Endogenous instability of liberalised finance

1) Confusion between two (must-be) separated activities: to rate and to be rated (to judge and to be judged; to advise and to rate) (The liberal regulation abetted the decline of fin stability: IRB&rating agencies to assess the soundness/stability of banks and financial intermediaries=CONFLICT OF INTEREST).

2) Macular degeneration in decentralised markets: Agents/regulators try to make short-term speculative positions endure (they are unable to regard the evolution beyond the peripheral opportunities they can immediately perceive. They become blind to disaster, prisoners of cognitive dissonance; have faith in their belief in spite of the quite near truth).

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014

8

3) Fallacy of composition: confusion between micro-rationality and macro-consistency (individual econ. efficiency≠optimal society (Minsky, 1991: fragile posture of micro-rationality/subjective probabilistic risk calculations ignore the true nature of the world. Keynes, 1936: mass psychology allows individuals to enter into heroic but fragile and absurd positions).

4) Strong interconnectedness among actors/markets: macro concern while the self-regulation is only based on individual evaluation and capacity. However, micro behaviour may generate multilateral and multi-level effects, chain reactions in numerous market → Decentralised individual decisions contribute to the accumulation of systemic fragilities; they are also pyromaniac in face of distress.

THEREFORE: (Gruchy, 1952-74): Markets call for continuous public vigilance; Instead of spontaneous market equilibrium, institutionalist concept of balanced equilibrium under governmental direction in the tradition of Common’s social/public control in economic affairs → Minskyian analysis.

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014 9

2. Consistent institutional framework-relevant regulation

2.1. Institutional foundations of social consistency

The nature of the social process (≠equilibrium): focus on public institutions in the functioning of capitalism: search for social

consistency since institutions are rules that intend to:

- structure social interactions (Hodgson, 2006);

- make relations among people sustainable in order to allow society to evolve in a coherent way;

- make ordered decision and action possible by framing human activities in a consistent way.

To improve systemic performance: search for innovative/alternative institutional forms to frame and to

guide the economy in socially desirable directions: REDESIGNING FINANCE

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus,

Nicosia, 6-8 November 2014 10

One of the main policy issues in the Institutionalist agenda:

An alternative institutional macro-framework for more rational (=consistent) system-wide regulation that contains systemic fragilities and dampens instability.

All the ingredients/principles of a relevant analysis are HERE: crucial importance of monetary/financial relations (Mitchell, 1916; Veblen, 1919); central role of institutions and institutional change in shaping economic evolution (Hamilton, 1919; Commons, 1931); issues related to systemic stability/viability through collective action (Clark, 1919).

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014 11

2.2. A Minsky-institutional analysis of liberal evolution

• Minsky (1982/86/92) The Institutionalist (and The Schumpeterian): Economic evolution depends upon institutions, usages, and policies and closely related to the impact of alternative institutional specifications.

Evidence: From the 1970s-80s, specific institutional environment (financial deregulation-liberalisation): actors/markets new strategies, banks short-term speculative activities, transactional banking and securitisation products and processes.

• This evolution feeds a new regime of accumulation, based on speculative financial gains and transforms financing relations into Ponzi schemes à la Minsky.

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014

12

• From 2003 (after the dotcom burst) till 2007/08 crisis, the economy turns out to be a bubble environment, based on real-estate-related debt leveraging in search of K gains.

• The rise of land/home prices: driving force of wealth creation (Hudson, 2010). Thanks to fin. innovations and to loose regulation, the new regime moves towards more speculative opportunities: main helm of econ. decisions.

• Money manager capitalism dominates society’s economic horizon (Minsky, 1991; Wray, 2009).

• Economic development is then entrusted to a non-job-creating but short-term financial gains producing speculation industry.

No Future in Markets (there is no market anymore)! Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference,

University of Cyprus, Nicosia, 6-8 November 2014 13

2.3. For an alternative and system-consistent regulation

Even in the aftermath of the worldwide catastrophe, “new” regulations aim at patching up the malfunctioning of existing rules rather than to deal with structural issues. The alternative: Minsky’s financial instability approach and institutionalist social control theory. Those appr. rest on the key role of public institutions in economic development and advocate that policies must aim at supporting sustainable economic activity.

The redesign of financial regulation is a sine qua non condition in order to give markets a positive role in economic evolution.

(The ultimate challenge for regulatory policies is to make decentralised actions socially consistent according to

collective objectives.)

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014

14

Such orientation is related to two arguments:

1.Characteristics of capitalism: monetary/financial stability is a specific collective matter (it concerns the whole society and its viability*).

2.Monetary/financial stability cannot be produced or consumed according to decentralised/private market mechanisms.

⇒ Matter of logic: Systemic instability concerns must be addressed towards collective rules and principles.

Call for public intervention that must stand outside of private market relations in order to

organise, supervise and regulate capitalist monetary and financial system. It must then

play the role of societal referee.

(* Viability is the capacity of a system to endure and sail against stark and cold winds without being forced to call into question its fundamental values).

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014 15

Detail of arguments and causality chain

→ Systemic problems are the cumulative results of individual actions that imply collective actions (individuals’ capacities are limited to their own interests and micro knowledge).

→ Reduction of system-wide threats requires an enforceable system-wide regulation because:

• Systemic problems resolution generates social advantages superior to private advantages;

• Every private unit would benefit from the resolution of such problems even if she/he does not contribute to any effort by her/himself.

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014 16

Therefore, macro-prudential regulation principles must be substituted to micro-regulation schemas.

→ To modify the institutional structure of financial markets for tighter macro supervision and control.

→ CB/gov. must act as social organisers of financial markets.

→ Aiming at organising monetary/financial systems in an alternative way and leave the liberal ideological blindness to disaster (such a role goes beyond the role of LoLR in case of systemic distress and information provider through interest rates).

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of

Cyprus, Nicosia, 6-8 November 2014 17

• Minsky (1982) wisely argues that the central bank should use its monetary powers to guide the evolution of financial markets in directions that are compatible with financial stability in the longer run rather than improvise controls that put out fires but which allow the underlying market situation to remain unchanged.

(Kregel, 2009; Wray, 2012: the 2007-08 crisis is seen as a temporary liquidity crisis and central banks intervened through quantitative easing programs without regarding the structural weaknesses of liberalised speculation-oriented financial systems. Several years after, capitalist finance still remains highly fragile and crisis-prone.)

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus,

Nicosia, 6-8 November 2014 18

Different facets to the process of regulation to tame short-sighted finance:

→ Structural/economic regulation (about the financial market’s structure and competition); → Conduct regulation (private actors’ behaviour); → Social regulation (consumer and labour protection); → Societal regulation (collective objectives, development issues), etc. Gruchy (1974: 242): “In the open forum of the national planning program, whatever economic power was possessed by special interest groups would be exposed to view, and no interest group could operate in a manner that was contrary to the community welfare. “Business efficiency” would be subordinated to what Clark described as “social efficiency” ”.

Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of Cyprus, Nicosia, 6-8 November 2014

19

A little bit of incentives, a whole lot of prudential supervision

“Finance to finance” and “finance to produce” must be distinguished and the objective of realisation of societal long-term targets replace private-interest based incentives through two principles: - Constrained preventive financial structure: preventing systemic interconnectedness among individuals/institutions able to lead to instability degeneration (separating securitization and industry financing activities; tougher capital and liquidity requirements and severely limited speculative engagements) - Preventive funding: involving directly banks and speculators into crisis losses financing (increasing charges and commitments for banks’ activities as zero or punishment bonus-minus system and unlimited liability partnership)

Those regulatory measures must be accompanied by regular public evaluation of banks’ activities. Faruk ÜLGEN Liberalised finance and economic stability: square pegs in round holes, 2014 EAEPE Conference, University of

Cyprus, Nicosia, 6-8 November 2014 20