LEGISLATIVE PREVIEW - Maryland REALTORS®

48

2019 mdrealtor.org / marylandhomeownership.com MARYLAND REALTORS ® The Voice For Real Estate ® In Maryland LEGISLATIVE PREVIEW 8 Economic Recovery May Be In Late Stages 15 Meet the Staff 21 Member Benefits

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of LEGISLATIVE PREVIEW - Maryland REALTORS®

2019mdrealtor.org / marylandhomeownership.com

MARYLAND REALTORS® The Voice For Real Estate® In Maryland

VOLUME LIII NUMBER 1 / DECEMBER 2018 / JANUARY 2019

L E G I S L A T I V E P R E V I E W

8

Economic Recovery May Be In Late Stages

15 Meet the Staff

21 Member Benefits

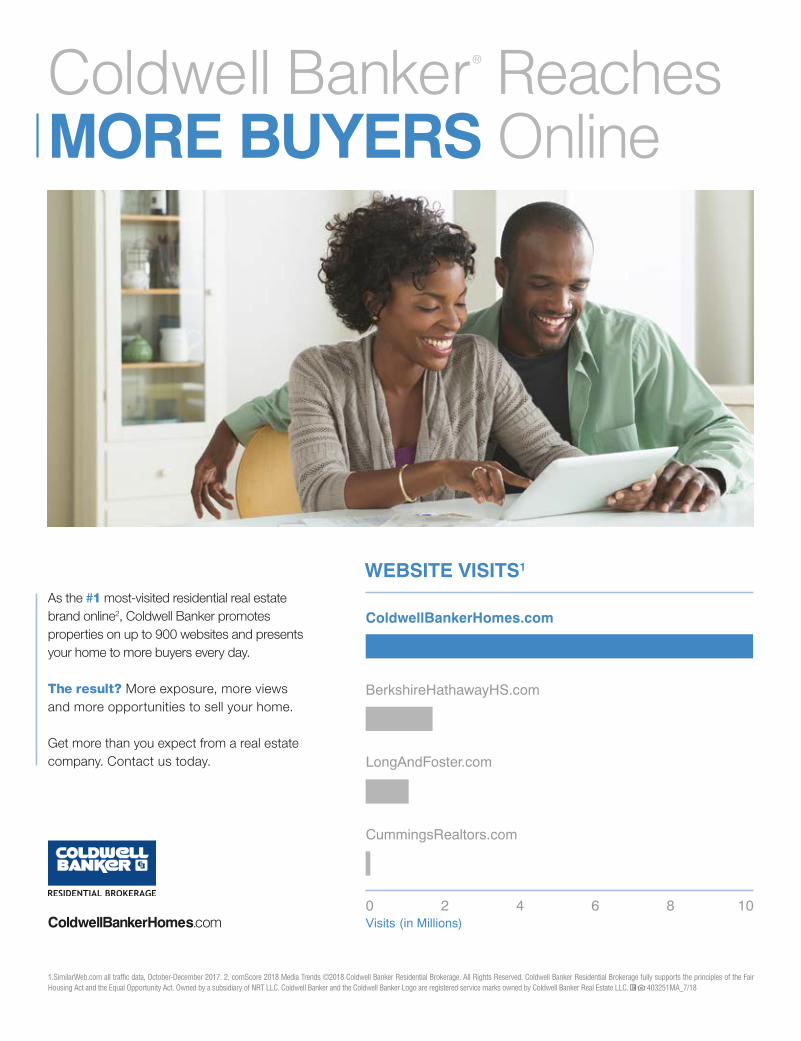

ColdwellBankerHomes.com

Coldwell Banker® Reaches MORE BUYERS Online

1.SimilarWeb.com all traffic data, October-December 2017. 2. comScore 2018 Media Trends ©2018 Coldwell Banker Residential Brokerage. All Rights Reserved. Coldwell Banker Residential Brokerage fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Owned by a subsidiary of NRT LLC. Coldwell Banker and the Coldwell Banker Logo are registered service marks owned by Coldwell Banker Real Estate LLC. 403251MA_7/18

WEBSITE VISITS1

ColdwellBankerHomes.com

BerkshireHathawayHS.com

LongAndFoster.com

CummingsRealtors.com

Visits (in Millions)6420 108

As the #1 most-visited residential real estate brand online2, Coldwell Banker promotes properties on up to 900 websites and presents your home to more buyers every day.

The result? More exposure, more views and more opportunities to sell your home.

Get more than you expect from a real estate company. Contact us today.

T A B L E O F C O N T E N T S

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 1

FEATURES2019 LEGISLATIVE PREVIEW REALTORS® Step Up 4

ECONOMIC RECOVERY MAY BE IN LATE STAGES 8

MEET THE STAFF 15

MEMBER BENEFITS 21

JANUARY IS RADON AWARENESS MONTH 25

HELPING VETERANS WITH HOUSING 26

ASSISTANCE ANIMALS– AGAIN 28

SELL MORE WITH MARYLAND! 38

DEPARTMENTSPRESIDENT’S PERSPECTIVE 3

RESIDENTIAL SALES 40

BRIGHT MLS 44

ASSISTANCE ANIMALS—AGAIN

288ECONOMIC RECOVERY MAY BE IN LATE STAGES

HELPING VETERANS WITH HOUSING

26

2019 LEGISLATIVE PREVIEW4

2019 Maryland REALTORS®

Leadership Team

Merry TobinPresidentRE/MAX Executive1919 Main StreetChester, MD [email protected]

John A. HarrisonPresident-ElectRE/MAX Executive8432 Veterans Hwy., Suite AMillersville, MD [email protected]

Craig WolfTreasurerAmerican Home Shield907 Autumn View Ct.Bel Air, MD [email protected]

Boyd CampbellImmediate Past PresidentCentury 21 New Millennium4201 Northview Drive #103ABowie, MD [email protected]

Charles Kasky, RCEChief Executive OfficerMaryland REALTORS®

200 Harry S Truman Parkway, Suite 200Annapolis, MD [email protected]

Maryland REALTORS®

200 Harry S Truman Parkway | Suite 200Annapolis, MD 21401-7348

800.638.6425 | www.mdrealtor.org

Leadership TeamMerry Tobin | President

John A. Harrison | President-ElectCraig Wolf | Treasurer

Dee Dee Miller | SecretaryBoyd Campbell | Immediate Past PresidentCharles Kasky, RCE | Chief Executive Officer

EditorMelissa Lutz | [email protected]

Advisory CommitteeStuart Schmidt | Chair

AdvertisingArlene Braithwaite | 410.772.0820

Publication DesignHBP, Inc., 952 Frederick Street, Hagerstown, MD 21741

800.638.3508 | www.hbp.com

Mission StatementThe Maryland REALTORS® exists to support all segments of its membership and their specialties. Maryland REALTORS®, through collective efforts with local boards/associations and the National Association of REALTORS®:■ Develops and delivers programs, services and related products

that maintain and elevate the high standards of the real estate business and the professional conduct of its practitioners;

■ Assists members in ethically and professionally serving the public;■ Promotes and preserves the right to own, transfer and use real

property; and■ Protects the right of members to conduct business within a

framework of fair and reasonable laws and government regulations.

In principle and in practice, Maryland REALTORS® values and seeks diversity and inclusive participation within the field of real estate and recognizes each member as a unique individual.

Maryland REALTOR® (USPS 0016-017) is published bimonthly by Maryland REALTORS®, Suite 200, 200 Harry S Truman Parkway, Annapolis, MD 21401-7348. Periodical postage paid at Annapolis and additional mailing offices. Postmaster send address changes to: Maryland REALTOR®, Suite 200, 200 Harry S Truman Parkway, Annapolis, MD 21401-7348.Member subscriptions of $3.81 are paid with annual dues.This publication is designed to provide accurate and authoritative information regarding the subject matter covered. It is offered with the understanding that the publisher is not engaged in rendering professional advice. If legal advice or other expert assistance is required, the services of a competent professional should be sought. Articles that appear in Maryland REALTOR® are an informational service to members. Their contents are the opinions of the authors alone and do not necessarily represent those of Maryland REALTORS®.Permission to reprint articles appearing in Maryland REALTOR® magazine must be requested in writing. Also include purpose for request.While this magazine makes a reasonable effort to establish the integrity of its advertisers, it does not endorse advertised products or services unless specifically stated. ©2018 Maryland REALTORS®, Inc.

®REALTORS

Dee Dee MillerSecretaryLong & Foster Real Estate568 A-Ritchie Hwy. Severna Park, MD [email protected]

2 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

Maryland Real Estate Commission News K A T H E R I N E C O N N E L L Y

Happy Holidays!

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 3

President’s Perspective M E R R Y T O B I N

I hope this finds you well & enjoying the holiday season with your loved ones. Also, I hope you take some time to recharge and get ready for the new year.

We are gearing up for the 2019 Legislative Session in Annapolis that begins on January 9th. The article on the bills that we expect to be supporting begins on page 4. Please make sure that your local board/association has your most current email address so that you can take part in any Calls For Action that are likely to come out of this legislative session.

On page 28, we discuss Assistance Animals and some of the nuances of the Fair Housing Act, to help understand how best to serve our clients and customers.

We have the annual review of the state of the Maryland economy with economist, Anirban Basu on page 40. Our economy is strong and healthy, but it remains to be seen whether that will continue in 2019. Turn to page 8 to learn more.

I encourage you to take a moment to read the “Meet the Staff” article on page 15. The professional staff at Maryland REALTORS® is second to none. They provide us with outstanding customer service, deliver the products and services we rely on, and can answer any real estate related question you might have.

The Leadership Team and I have spent the last 2 months traveling around the state participating in the installations of all of our 16 local boards and associations. It has been our privilege to be present when the new leaders have taken office. We look forward to working with the 2019 local leaders to move the Association forward.

Have the happiest holiday season!

4 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

2019L E G I S L A T I V E P R E V I E W

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 5

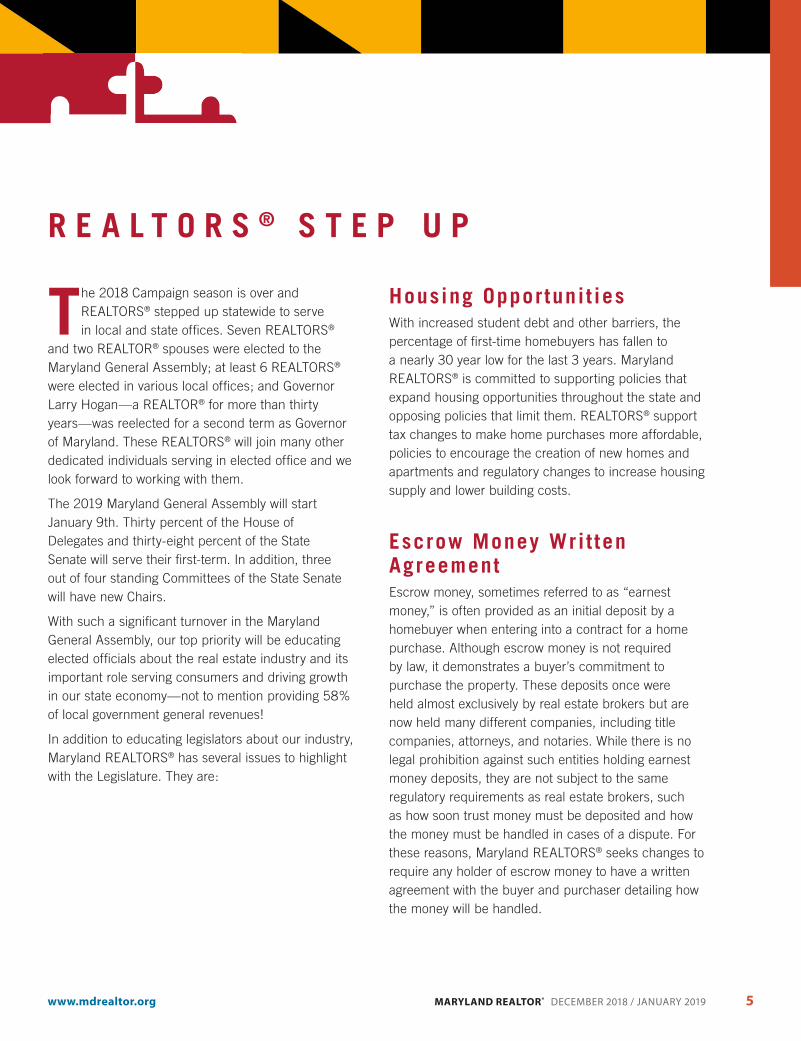

The 2018 Campaign season is over and REALTORS® stepped up statewide to serve in local and state offices. Seven REALTORS®

and two REALTOR® spouses were elected to the Maryland General Assembly; at least 6 REALTORS® were elected in various local offices; and Governor Larry Hogan—a REALTOR® for more than thirty years—was reelected for a second term as Governor of Maryland. These REALTORS® will join many other dedicated individuals serving in elected office and we look forward to working with them.

The 2019 Maryland General Assembly will start January 9th. Thirty percent of the House of Delegates and thirty-eight percent of the State Senate will serve their first-term. In addition, three out of four standing Committees of the State Senate will have new Chairs.

With such a significant turnover in the Maryland General Assembly, our top priority will be educating elected officials about the real estate industry and its important role serving consumers and driving growth in our state economy—not to mention providing 58% of local government general revenues!

In addition to educating legislators about our industry, Maryland REALTORS® has several issues to highlight with the Legislature. They are:

Housing Opportuni t iesWith increased student debt and other barriers, the percentage of first-time homebuyers has fallen to a nearly 30 year low for the last 3 years. Maryland REALTORS® is committed to supporting policies that expand housing opportunities throughout the state and opposing policies that limit them. REALTORS® support tax changes to make home purchases more affordable, policies to encourage the creation of new homes and apartments and regulatory changes to increase housing supply and lower building costs.

Escrow Money Wri t ten AgreementEscrow money, sometimes referred to as “earnest money,” is often provided as an initial deposit by a homebuyer when entering into a contract for a home purchase. Although escrow money is not required by law, it demonstrates a buyer’s commitment to purchase the property. These deposits once were held almost exclusively by real estate brokers but are now held many different companies, including title companies, attorneys, and notaries. While there is no legal prohibition against such entities holding earnest money deposits, they are not subject to the same regulatory requirements as real estate brokers, such as how soon trust money must be deposited and how the money must be handled in cases of a dispute. For these reasons, Maryland REALTORS® seeks changes to require any holder of escrow money to have a written agreement with the buyer and purchaser detailing how the money will be handled.

R E A L T O R S ® S T E P U P

6 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

Client Conf ident ial i tyConfidentiality is a key fiduciary duty of all real estate agents. This duty applies to different types of information that could undermine a client’s position if known by the other party. In fact, the duty of confidentiality is so important, it lasts even after the agent-client relationship has terminated. However, this duty does not apply when an agent is being interviewed for hire by a potential client. Regularly, the potential client discloses information that would be considered confidential. Maryland REALTORS® recommends changes to clarify that an agent has a duty to protect confidential information learned during a meeting held in anticipation of forming an agency relationship, even if the agent is not hired.

Ground Rents EscrowGround rents are payments made by a homeowner to a person or entity who owns the land on which the home was built. Ground rents are most common in Baltimore, but exist throughout Maryland. Under current law, the ground rent holder (the person that owns the land) is entitled to collect up to three years’ unpaid rent. If a ground rent holder fails to register the ground rent and a property is sold, title companies will escrow up to the maximum three years rent that can be collected. This escrow payment is a cash requirement that homebuyers must pay during settlement. In addition, title companies must hold and return the escrow money after three years.

Maryland REALTORS® recommends a change to law exempting a property subject to a sale from the collection of the past due ground rent unless it is actually registered with the state. Such a change would negate the tracking of the escrow money and save buyers cash at closing.

Short Term RentalsProperty rights are often described as a bundle of rights that include the right to: sell; own; occupy; and lease. However, as online, short-term rental platforms increase in popularity, some governments place severe restrictions on the right to lease property. Maryland REALTORS® recognizes that communities have an interest in reasonable regulation of short-term rentals but believe high barriers eliminate a fundamental right of property ownership.

Mortgage Debt Foregiveness Tax Credi tFinally, Maryland REALTORS® supports extending the Mortgage Debt Tax Foregiveness law at both the state and federal level.

2019 will bring many changes to Annapolis, and we look forward to working with you in support of policies that advance housing opportunities for all throughout Maryland.

When choosing a Brokerage, there really is no comparison.

Join Douglas Realty and keep 100% of your commission on every real estate deal!Visit JoinDouglasRealty.com or call 866-987-3937 to schedule your confidential interview!

GET MORE, KEEP MORE!

No B/SCommission splits Agent keeps 100% Agent keeps only 50-70%Technology fee No technology fee $60-$125 monthly technology feeFranchise fee No franchise fee 6% franchise feeRoyalty fee No royalty fee 1-3% royalty feeDesk duty/on-call No desk duty Required desk dutyListing leads Listing leads go to the listing agent Listing leads go to the agent on dutyCommission payments Paid at settlement Wait 7-10 daysBusiness model Work from anywhere in the world Brick and mortar dependentBranding Brand yourself or your team Brand the companyFreedom Freedom to run your own business Must work within company modelCommission rates Set your own rates Must comply with company set rates

Marketing and LeadsLead gen platform Free kvCORE platform No lead gen platformLead gen commission splits Agent keeps 100% Broker takes an additional 30%

Website and CRMConsumer-facing website Free website Agent pays for web siteConsumer-facing app Free app Agent pays for appCRM system Free CRM Agent pays for CRM

Transaction ManagementBusiness management system Free BackAgent cloud based platform Agent pays for management system

Business DevelopmentCoaching and training Free business development classes Agent pays up to $800 for a single class

Douglas Realty Other Brokerages

100% Commission Better TechnologyKeep all of your earned commission

on every transaction.Providing the best real estate lead

generation and CRM platform.

MORE MONEY MORE LEADSPersonal Development

Grow your business with professional training, seminars and CE classes.

MORE SUPPORT

*Individual brokerage offerings, splits, and fees may vary.

When choosing a Brokerage, there really is no comparison.

Join Douglas Realty and keep 100% of your commission on every real estate deal!Visit JoinDouglasRealty.com or call 866-987-3937 to schedule your confidential interview!

GET MORE, KEEP MORE!

No B/SCommission splits Agent keeps 100% Agent keeps only 50-70%Technology fee No technology fee $60-$125 monthly technology feeFranchise fee No franchise fee 6% franchise feeRoyalty fee No royalty fee 1-3% royalty feeDesk duty/on-call No desk duty Required desk dutyListing leads Listing leads go to the listing agent Listing leads go to the agent on dutyCommission payments Paid at settlement Wait 7-10 daysBusiness model Work from anywhere in the world Brick and mortar dependentBranding Brand yourself or your team Brand the companyFreedom Freedom to run your own business Must work within company modelCommission rates Set your own rates Must comply with company set rates

Marketing and LeadsLead gen platform Free kvCORE platform No lead gen platformLead gen commission splits Agent keeps 100% Broker takes an additional 30%

Website and CRMConsumer-facing website Free website Agent pays for web siteConsumer-facing app Free app Agent pays for appCRM system Free CRM Agent pays for CRM

Transaction ManagementBusiness management system Free BackAgent cloud based platform Agent pays for management system

Business DevelopmentCoaching and training Free business development classes Agent pays up to $800 for a single class

Douglas Realty Other Brokerages

100% Commission Better TechnologyKeep all of your earned commission

on every transaction.Providing the best real estate lead

generation and CRM platform.

MORE MONEY MORE LEADSPersonal Development

Grow your business with professional training, seminars and CE classes.

MORE SUPPORT

*Individual brokerage offerings, splits, and fees may vary.

8 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

Economic Recovery May be in Late Stages

In 2018, U.S. economic performance was better than it has been for at least

13 years. While there has been abundant negativity regarding the propriety of tariffs, trade skirmishes, abandonment of various treaties, shifting immigration policy, and rapidly expanding national debt, there can be little debate that near-term performance has been solid.

During 2018’s third quarter, the U.S. economy expanded 3.5 percent on an annualized basis. Industrial production has been surging, as has capacity utilization. Both white-collar and blue-collar segments have been adding jobs rapidly. As of September, there were 7.01 million available, unfilled jobs in America—an all-time high. According to the most recently available data, there are fewer than 6.1 million unemployed people in America, which means that there are approximately 7 job openings for every 6 jobseekers.

At least theoretically, there is a job for everyone, though job growth has been far more rapid in the American west and south than elsewhere.

2018 Was Fine, 2019 Might be Too, but Beyond That …

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 9

Among the 25 largest metropolitan areas, the fastest year-over-year job growth (September 2017–September 2018) was recorded in Orlando (5.9%). Other communities registering profound rates of employment expansion include Houston (4.3%), Miami (4.2%), Phoenix (3.8%), Tampa (3.8%), Seattle (3.7%), Dallas (3.0%), Riverside, CA (2.9%), Denver (2.7%), and Charlotte (2.4%). The slowest growing major metropolitan areas are Detroit (0.7%), Chicago (0.7%), and St. Louis (0.8%). The point is that employment growth is apparent in virtually all significant communities.

In October 2018, the nation added another 250,000 net new

jobs, surpassing the consensus expectation of 190,000 collectively predicted by market analysts. The official rate of unemployment remained at 3.7 percent for the month, effectively the lowest rate since December 1969 when the U.S. was just entering a recession that would last for 11 months.

So far this year, the Federal Reserve has raised interest rates three times, with one more rate hike planned in December. These rate hikes have worked their way down into mortgage rates. At the start of 2017, average rates on 15- and 30-year mortgages were 3.39 and 4.15 percent, respectively. At the start of 2018, they were 3.48 and 4.03 percent, evidence of low volatility

over the year. At the time of this writing, however, they are 4.31 and 4.90 percent, respectively. These dynamics can be observed in Exhibit 2.

With the unemployment rate at a level not seen in 49 years, and more job openings than there are people looking for employment, employers are being forced to increase wages and compensation to find the workers they need. This is especially relevant for contractors who have been dealing with a shortage in skilled workers in recent years. The increase in interest rates will make borrowing more expensive, slowing down the economy, which could also lead to a decrease in construction activity. The nature

-1000

-800

-600

-400

-200

0

200

400

600

Oct-03

Oct-04

Oct-05

Oct-06

Oct-07

Oct-08

Oct-09

Oct-10

Oct-11

Oct-12

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Net C

hang

e (0

00's

)

Exhibit 1. National Monthly Job Growth, October 2003–October 2018, SA

Source: Bureau of Labor Statistics

10 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

4.31%

4.90%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%Ja

n-95

Oct-

95Ju

l-96

Apr-

97Ja

n-98

Oct-

98Ju

l-99

Apr-

00Ja

n-01

Oct-

01Ju

l-02

Apr-

03Ja

n-04

Oct-

04Ju

l-05

Apr-

06Ja

n-07

Oct-

07Ju

l-08

Apr-

09Ja

n-10

Oct-

10Ju

l-11

Apr-

12Ja

n-13

Oct-

13Ju

l-14

Apr-

15Ja

n-16

Oct-

16Ju

l-17

Apr-

18

15-yr

30-yr

Exhibit 2. 15-Year & 30-Year Fixed Mortgage Rates, January 1995-November 2018

Source: Freddie Mac

of the industry, however, is such that there are already months of construction projects already planned and funded, so the impact of the slowdown shouldn’t be felt in the near future.

Despite an uncomfortable level of stock market volatility beginning in October 2018 and continuing into November, the U.S. economic outlook for early-2019 looks benign. Growth in gross domestic product has picked up relative to the earlier years of the recovery, the result of both upbeat consumers and

business operators. Additionally, leading indicators remain upbeat, including those related directly to construction spending such as the Architecture Billings Index and Associated Builders & Contractors’ Construction Backlog Indicator.

The tax reform that came into effect in 2018 remains in place and will presumably produce additional positive business investment impacts in 2019. Consumer and business confidence remain elevated and the global economy continues to expand. State and local government finances are much improved in much of the country, which should continue to fuel spending on school construction,

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 11

2.8 3.9

10.6

-

2.0

4.0

6.0

8.0

10.0

12.0

Howard

Princ

e Geor

ge's

Carroll

Montgo

mery

Baltim

ore Cou

nty

Charle

s

Harford

Anne

Arun

del

Frede

rick

MARYLA

ND

St. M

ary's

Wicomico

Washin

gton

Calvert

Cecil

Baltim

ore City

Queen

Anne

's

Carolin

e

Worcest

er

Alleg

any

Dorche

ster

Kent

Garrett

Somers

etTa

lbot

Exhibit 3. Months of Inventory by Maryland County, September 2018

Source: Maryland REALTORS®

roads, bridges, and other elements of the shared built environment.

Arguably, the most worrisome aspect of the economy takes the form of inflationary pressures. Economists deploy a term called the natural rate of unemployment. When unemployment falls below that natural rate, inflation has a tendency to spike, leading to sharp increases in borrowing costs and softer investment. At 3.7 percent, the official rate of U.S. unemployment is now meaningfully below that natural rate of unemployment. This situation prevailed just prior to the 1980-81 recession, the 90-91 recession, the 2001 recession, the 2007-09 recession, and now.

Similarly, the economy was humming in 2005 thanks largely to a red-hot housing market. That year, the U.S. economy expanded 3.5 percent, the last time the U.S. economy achieved the 3 percent threshold. Then the housing bubble burst in earnest during 2006’s first half, and by late-2007, the nation found itself in another recession—this time a very deep one.

Maryland Home Sales Fall while Prices RiseThree factors have conspired to suppress home sales in Maryland during recent quarters—higher prices, higher mortgage rates, and

limited inventory. Indeed, despite the presence of Fort Meade and many other federal installations and their contractors, home sales in Maryland fell sharply in September 2018 compared to the same time a year prior. According to data released by Maryland REALTORS®, home sales statewide were down 10.8 percent on a year over year basis. Some counties fared better than others, however. Howard County, for example, experienced a 1.4 percent decrease in year-over-year sales totals, one of the smaller declines among larger Maryland jurisdictions.

Only three counties experienced an increase in home sales on a

12 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

September 2017 to September 2018 basis: Somerset (+38.5%), Allegany County (+32.6%), and Wicomico County (+5.7%). The biggest losses among counties with at least 100 home sales were recorded in Frederick County (-16.3%), Baltimore City (-15.2%), Baltimore County (-14.9%), Harford County (-14.1%), Calvert County (-13.0%), St. Mary’s County (-12.0%), Washington County (-11.7%), Montgomery County (10.9%), and Prince George’s County (-9.9%).

Consistent with scarce housing inventory and decent regional economic performance, average and median home sales prices have continued to trend higher.

In September, the average home sale price in Maryland stood at $332,532, representing a 4.9 percent increase from the same month one-year prior. Median home price was $287,700, a 3.6 percent increase on a year-ago basis. Anne Arundel County experienced the largest increase in sales prices among jurisdictions with at least 100 monthly home sales, with rising average price rising 12.5 percent on a 12-month basis and median price up 10.9 percent.

The average months of inventory across Maryland was 3.9 months in September. Howard County (2.8 months) and Talbot County (10.6 months) bracketed the state, as seen in Exhibit 3.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Jan-

07

Jun-

07

Nov-

07

Apr-

08

Sep-

08

Feb-

09

Jul-0

9

Dec-

09

May

-10

Oct-

10

Mar

-11

Aug-

11

Jan-

12

Jun-

12

Nov-

12

Apr-

13

Sep-

13

Feb-

14

Jul-1

4

Dec-

14

May

-15

Oct-

15

Mar

-16

Aug-

16

Jan-

17

Jun-

17

Nov-

17

Apr-

18

Sep-

18

National UR Maryland UR

Exhibit 4: Maryland & National Unemployment Rates, seasonally adjusted, October 2007 to October 2018

Source: U.S. Bureau of Labor Statistics

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 13

Exhibit 5. Maryland Unemployment Rates by County (Not Seasonally Adjusted), September 2018

Source: U.S. Bureau of Labor Statistics

Maryland’s Numbers Didn’t Add UpFor months, the Bureau of Labor Statistics was suggesting that Maryland was barely adding jobs. For a period, government data indicated that the Baltimore region added more jobs than the entire state, implying that some parts of the state were struggling through an employment recession. Those data were not to be believed. More recent data appear more reasonable, and suggest that between October 2017 and October 2018, Maryland added 38,500 net new jobs, a perfectly respectable tally. During that same period, the Baltimore metropolitan area, responsible for

almost precisely half of Maryland’s output, added 25,400 net new jobs, also respectable performance. As of October 2018, the state’s unemployment rate stood at 4.1 percent and the Baltimore metropolitan area’s at 4.0 percent. As of September, 13 of Maryland’s 24 major jurisdictions was able to boast an unemployment rate of 4 percent or lower (Exhibit 5).

No segment of Maryland’s economy has added jobs as reliably as professional and business services. Over the past year, that sector has added nearly half of Maryland’s net new jobs (18,600). This is a sector that includes many white-collar professionals, including government contractors, many of which are

benefitting from stepped-up federal government outlays. Other segments adding jobs in large numbers are education/health services (+9,300), leisure/hospitality (+7,400), and distribution (+4,000). A handful of sectors has lost jobs over the past year, including financial services.

Looking AheadIt is expected that the national economy will enter 2019 with a healthy amount of economic momentum, which should bode well for Maryland. Though financial market volatility has been elevated of late, business and consumer confidence remain elevated. Many consumers have been emboldened by recent pay increases and

Rank CountyUnemployment

Rate (%)Rank County

Unemployment Rate (%)

1 Howard County 3.1 13 Baltimore County 4.0

2 Montgomery County 3.2 14 Kent County 4.1

2 Queen Anne's County 3.2 14 Prince George's County 4.1

4 Anne Arundel County 3.3 16 Cecil County 4.2

4 Carroll County 3.3 16 Garrett County 4.2

6 Calvert County 3.5 16 Washington County 4.2

6 Frederick County 3.5 19 Wicomico County 4.9

8 Caroline County 3.6 20 Dorchester County 5.0

8 Harford County 3.6 21 Allegany County 5.1

8 Talbot County 3.6 22 Worcester County 5.3

11 St. Mary's County 3.7 23 Baltimore City 5.6

12 Charles County 3.9 24 Somerset County 6.5

14 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

ongoing reports of large-scale worker shortfalls. Maryland also benefits from the presence of a number of large, developable sites able to accommodate large-scale investment, including Tradepoint Atlantic, Port Covington, National Harbor, downtown Columbia, downtown Towson, Bethesda, Hanover, Principio Business Park, and elsewhere.

Still, even as economic momentum persists, headwinds have become more apparent. The global economy appears to be faltering, with weakness recently observed in emerging markets like Argentina and Turkey and in advanced ones like Italy and Japan. China’s economic growth has also slowed recently as has Germany’s. These are the second and fourth largest economies on the planet, respectively. The Baltic Dry Index, our favorite global economic leading indicator, has been trending lower recently. The emerging weakness in global activity helps explain why oil prices in North America have recently drifted well below $60/barrel.

Weakness in a growing number of economies around the world has helped to strengthen the U.S. dollar. The U.S. dollar has also been solidified by tightening monetary policy and rising interest rates, which create more demand for U.S. dollar-denominated fixed-income assets. While a strong U.S. dollar is viewed with pride by some stakeholders, it also has a negative impact on America’s trade deficit

with the balance of the world. Though much has changed over the course of 2018, REALTORS® and others should remain wary of the impact of ongoing trade disputes, including the trade skirmish between America and China, the world’s two largest economies.

Softer export growth coupled with rising input costs are impacting corporate earnings. Moreover, a growing number of investors has become concerned by the significant amount of risky corporate debt presently outstanding. Recent increases in consumer indebtedness also represent cause for concern, since any evidence of economic slowing may cause many households to drastically reduce outlays in an effort to prevent additional debt accumulation.

Given this backdrop, it’s little wonder that financial markets have become more volatile. With the Federal Reserve likely to persist in monetary tightening in the context of massive human capital shortfalls and rising wages, asset price volatility is a likely theme for 2019. That said, consumer and business spending should hold up over the near-term. The large number of available job openings should keep job growth in pace during the early months of 2019 and beyond. Business spending, though softer recently, should continue to be positively impacted by the tax reform passed in late-2017.

However, the economic outlook for the latter half of 2019 and beyond is now shrouded in mystery. With interest rates so low for so long, there was a natural tendency for economic actors to leverage their balance sheets. The expansion of money supply by central banks around the world also helped to prop up asset prices, which helped generate positive wealth effects. But higher asset prices also signify greater downside risk, and those risks have become more evident recently.

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 15

Meet the Staff

Chief Executive Officer Chuck Kasky was elevated to CEO in October 2015, after having served as Maryland REALTORS® top in-house legal officer for 10 years. In addition to

overseeing the Association’s operations, he works closely with volunteer leadership to develop and implement policies and initiatives to promote the real estate industry and private property rights. Chuck is continuing the Association’s primary focus on representing member interests before the legislature and advocating REALTOR® professionalism with members and the public.

Prior to joining the Maryland REALTORS®, Chuck was engaged in the private practice of law, served as Counsel to several Committees of the Maryland General Assembly, and was Deputy Chief Administrative Officer for Howard County, Maryland.

Tracy Powelson is the Executive Assistant to the CEO. Tracy joined Maryland REALTORS® in September 2015 and is responsible for the administrative functions of the Association. Tracy staffs the Governance committees—Executive, Nominating, and Strategic Planning. She also supports the Board of Directors and General Membership meetings as well as the Presidents’ Council, made up of local board/association Presidents who meet to exchange information, develop ideas and share experiences. Her department organizes the Maryland REALTORS® Former Presidents meeting and other events during the year. She also oversees the prestigious Life Achievement Award.

Brenda Royce joined us this year as Administrative Assistant for the Administration and Housing Programs Departments. Brenda was previously a membership manager and event coordinator at the National Society of Histotechnology and also previously a REALTOR®. Brenda assists with Maryland REALTORS® meetings, events, volunteer coordination, and programs such as the Housing Opportunity Certification (HOC) program.

Brenda Royce

Tracy Powelson and Rebecca Baker

Chuck Kasky

16 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

Receptionist Rebecca Baker greets and talks to more members as the first point of contact at the Association office, than any other staffer. She answers hundreds of questions every week from members and the public, referring them to the appropriate staff person or other resources. Rebecca assists with meeting logistics, mailings, and other tasks requested by other departments.

Government AffairsThe Government Affairs Lobbying Team includes Senior Vice President, Bill Castelli and Director of Government Affairs, Susan Mitchell. Bill, an attorney and former aide to Rep. Steny Hoyer, develops and directs the Association’s legislative strategy in representing Maryland REALTORS® at the State House. In addition to Susan’s lobbying responsibilities, she also works with local boards/associations to assist in providing Maryland REALTORS® and NAR expertise on local issues such as land use and zoning. Susan oversees Maryland REALTORS® Local Government Affairs Director (GAD) Program, supervising the local GADs that Maryland REALTORS® provides to all local boards/associations who do not employ local lobbyists. This local program is designed to strengthen REALTOR® voices in those local jurisdictions. Additionally, she also directs Maryland REALTORS® grassroots advocacy efforts, including Calls for Action, and our advocacy outreach, customizing mobilization efforts on key issues.

Prior to joining Maryland REALTORS®, Susan was the Government Affairs Manager/ Washington Representative for Bristol-Myers Squibb pharmaceutical company in their Washington DC office, with responsibilities for both the federal and state grassroots lobbying program & PAC and also served as the industry Washington Representative to the pharmaceutical trade association.

Both lobbyists represent Maryland REALTORS® on various industry and other coalition groups and coordinate state efforts with NAR in representing REALTOR® interests before Maryland’s Congressional delegation. The team also includes contract lobbyists and attorneys Joel Rozner and Frank Boston. Government Affairs committees include Public Policy, Legislative, Issues Mobilization, and Legal Action.

Legal AffairsMaryland REALTORS® Legal Department, headed by Director of Legal Affairs Kathleen Dartez, includes Staff Attorneys Colette Massengale and Jeff Bernstein, along with Don Martin, Director of Board and Member Services; Mark Feinroth, Director of Political Advocacy, and Nicole Mack, Professional Standards Administrator and Legal Affairs Assistant. As a service to member boards, associations and firms,

Nicole Mack, Don Martin, Kathleen Dartez, and Colette Massengale

Susan Mitchell, and Bill Castelli

Jeff Bernstein

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 17

Maryland REALTORS® Legal Department visits offices and provides instructors for continuing education classes on risk reduction, agency law, real estate contracts, Code of Ethics, fair housing, legislative and legal updates and broker supervision. Legal Affairs also has responsibility for member services.

Kathleen staffs the Global Business and Real Property Operations Committees. Prior to joining the Maryland REALTORS®, Kathleen served as General Counsel for a regional real estate brokerage where she performed the full array of in-house functions, including legal analysis, form development, professional standards representation, human resources compliance and taught continuing education classes.

Colette staffs the Statewide Forms Committee. Prior to joining Maryland REALTORS® she worked at several law firms in the Metropolitan area and was a law clerk for Washington, D.C. Superior Court Judge Rhonda Reid Winston.

Jeff Bernstein joined Maryland REALTORS® earlier this year and staffs the Commercial Alliance Committee. In addition to answering the Legal Hotline and teaching CE classes, Jeff also assists in planning the annual Commercial Symposium for commercial practitioners. Prior to joining Maryland REALTORS®, Jeff staffed the Judicial College of Maryland where he developed a varied curriculum for Maryland’s judges and magistrates to complete their continuing education requirements. Jeff also volunteers his time to teach students in the University of Baltimore School of Law’s Moot Court Program about the intricacies of brief writing and oral argument in appellate courts.

Nicole serves as the Maryland REALTORS® Professional Standards Administrator. Through this program, Maryland REALTORS® provides resources and support to local boards/associations, members and the public regarding ethics cases, arbitration proceedings and alternative dispute resolution processes. Nicole manages the Dispute Resolution area of the Maryland REALTORS® website, which addresses dispute resolution issues and alternatives.

Kathleen, Colette, Jeff, and Nicole staff the Maryland REALTORS® Legal Hotline, the service REALTORS® routinely identify as one of the most valuable Maryland REALTORS® membership benefits. Members call or submit questions via an online form, available on the Legal tab of the Maryland REALTORS® website. Department attorneys also provide in-house legal and compliance assistance to the other Departments within Maryland REALTORS®.

Mark Feinroth staffs the RPAC Trustees, Legal Action Fund Committee, Lockbox Consortium and the Maryland REALTORS® Political Fund. Mark also teaches continuing education classes and is a frequent

Mark Feinroth

www.mdrealtor.org

Lisa Kinsman

speaker at brokerage and branch office meetings. He helps on the Legal Hotline and contributes occasional articles for the Maryland REALTOR® magazine.

Don Martin staffs the Grievance and Professional Standards Committees. Nicole provides support for all the Committees. Don is Maryland REALTORS® principal outreach to firms and local boards/associations, spending most of his time traveling around the state speaking at sales meetings and teaching continuing education classes. Don is the primary resource on Professional Standards issues and oversees local board/association compliance with NAR requirements regarding governance and services. To assist in compliance with the NAR Professional Standards program, the Department provides annual training to local Grievance and Professional Standards Committees.

EducationDirector Lisa Kinsman has been a Maryland REALTORS® staff member since 1981. She supervises the

activities and staffing for the REALTOR® Institute (GRI) and Leadership Academy committees and programs. The department coordinates the education programs for the Annual Conference, provides administrative services for professional standards training; and, oversees the recording of all continuing education credits earned for all CE programs provided by Maryland REALTORS® and contracted providers.

Education Assistant Lisa Haynes provides all Department administrative support and is the “point person” responsible for CE monitoring, CE recording at the Maryland Real Estate Commission, handling replacement certificate requests for any Maryland REALTORS® program; and any other general education question members may have. She provides additional support services to other departments as needed.

Maryland REALTORS® maintains an extensive educational database whereby attendee records (member and non-member) are updated for every CE or non-CE program Maryland REALTORS® offers. This system verifies attendance and confirms classes taken to track designation courses, mandatory state licensing renewal courses and any association training required sessions.

Lisa Haynes

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 19

Communications & Public AffairsThe Communications and Public Affairs Department is the public voice of Maryland REALTORS® charged with overseeing our communication with members and the public.

Department Director Melissa Lutz (pronounced Loots) oversees all the Departments activities, including publications, all communications with members and the public, and media relations. Melissa spearheads

the Maryland REALTORS® public and media relations efforts, which include promoting Maryland REALTORS® and the real estate profession. Melissa has primary responsibility for the Annual Conference held each fall, managing its large trade show and overseeing all onsite logistics. She also assists other departments with event planning. Melissa is chair of the National Association of REALTORS® Communications Directors Committee and sits on the Consumer Advocacy Outreach Board for 2019.

The Department staffs the Annual Conference, Communications/ PR, Community Action and REALTOR® Excellence (CARE), and REALTOR® of the Year committees. It also publishes the bi-monthly Maryland REALTOR® magazine and HotSheet and develops brochures and pamphlets.

Communications manages the affinity partnerships program to provide member benefits and non-dues revenue. The Department oversees the content and enhancements to the Maryland REALTORS® website www.mdrealtor.org and manages the Maryland REALTORS® social media channels, including Facebook, Twitter, YouTube, Instagram, Flickr and LinkedIn.

Housing ProgramsThe Housing Programs Department, headed by Director Laurie Benner, researches and identifies programs benefiting first-time homebuyers and low-to-moderate income buyers offered by federal, state and local government agencies as well as community-based, nonprofit housing organizations. Laurie is Maryland REALTORS® liaison with NAR on its housing related public policy programs, and with other statewide and national housing coalitions. The Department administers Maryland REALTORS® consumer website www.marylandhomeownership.com, manages consumer-focused communications, and oversees the Housing Opportunity Certification (HOC) education program. It also staffs the Housing Affordability and Equal Opportunity committee, which develops efforts to encourage Maryland REALTORS® to learn about financial literacy, housing finance programs, fair housing,

Melissa Lutz

Laurie Benner

20 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

homebuyer education, foreclosure prevention, and housing policy initiatives in their communities.

Laurie has extensive experience in residential real estate and affordable housing including legal work, finance, housing redevelopment, grant administration and nonprofit management. She recently earned her RCE certification from NAR.

Finance and TechnologyPatti Schmitt is Maryland REALTORS® Vice President of Finance. Her primary responsibility for developing and tracking Maryland REALTORS® annual budget, managing Maryland REALTORS® and affiliate organizations financial operations and working with its auditors and financial advisors. She provides economic and financial information to the CEO, Board of Directors and officers, Finance Committee and staff. Patti also oversees the operations and staff of the Technology Department.

Prior to joining Maryland REALTORS®, Patti was Assistant Controller for HRi, ASO & PEO Outsourcing, serving more than 150 employers with over 1,700 employees across 17 states. Patti also successfully started and operated a contracting business for fourteen years before selling her interest to her partner.

As Assistant Controller, Kim Knopp administers Maryland REALTORS® accounts payable and assists with daily financial transactions. Kim also maintains financial records for RPAC. Kim joined Maryland REALTORS® in 2001, first in the Legislative Department and then moving to the Finance Department in 2005.

Janelle Shannon is the Accounting Specialist. She administers Maryland REALTORS® accounts receivable and assists with daily financial transactions. Janelle also administers RPAC raffle sales, requests for state candidate campaign contributions and maintains major investor contributions.

IT Director, Michael Cunningham worked with Maryland REALTORS® for almost ten years as a consultant before joining the staff in 2005. Michael provides IT support and management, custom software development and programming and website design and management for the Association, staff, and affiliate organizations.

Membership Manager Cindy Sellers, a staff member since 1995, maintains member databases for Maryland REALTORS® and assists in helping staff with computer hardware and software systems. Cindy is also responsible for maintaining office supplies and other office equipment.

Janelle Shannon, Michael Cunningham, Kim Knopp, Cindy Sellers, and Patti Schmitt

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 21

M E M B E R B E N E F I T S

®REALTORS

22 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

Annual Conference & EXPOStay up-to-date with your license requirements and have fun! We offer a fast online registration that features an instant confirmation to your email address. Visit the EXPO Hall—one of the largest anywhere! The Annual Conference, one of our most popular member services, will be held on September 10–13, 2019

Maryland REALTORS® Legal Hotline- 1-800-888-1272Free authoritative legal advice is available by calling the Maryland REALTORS® Legal Hotline or by submitting a WebQuestion Form. Questions on all aspects of real estate law are answered. A written response is sent to all callers and their brokers.

http://www.mdrealtor.org/Legal/Legal-Hotline/Submit-Question-Online

AVISMaryland REALTORS® save up to 25% off Avis base rates when making a reservation with Avis Worldwide Discount (AWD) number D423529. Complete your reservation and receive instant online and email confirmation of your travel plans.

https://www.avis.com/en/home?dclid=COWRjeuXrdcCFQJaDAodSyAP6g

BudgetMaryland REALTORS® always save up to 25% off Budget base rates with offer code (BCD) D836629, plus get other great offers like dollars off, a complimentary upgrade, or a free weekend day.

https://www.budget.com/budgetWeb/html/bridge/assoc/index.html?D836629

REALTOR® License PlateShow everyone that you’re a REALTOR®. This special plate will set you apart from everyone else as a Maryland REALTOR®. For information or an application please contact Cindy Sellers at 800-638-6425 or [email protected]. (Vanity plates are not available with this offer.)

Nationwide InsuranceNationwide is a proud partner of the Maryland REALTORS®. Receive members-only discounts on auto insurance and much more. We offer a lot more than just car insurance. And through your affiliation with one of Nationwide’s preferred partners, you may be eligible for special discounts. To learn more call 1-866-238-1426 or click here.

https://www.nationwide.com/mdrealtors.jsp

FASTPARKEnroll in our Free Relax for Rewards Program using the company name Maryland REALTORS®. Once enrolled using your company code (B56354), MD REALTOR® and email address, a Fast Park card will be issued. Guaranteed daily flat rates, earn points towards free parking, print receipts, review parking history, and request free parking. Visit www.thefastpark.com to complete the application process.

Benefits by ChoiceWe offer Maryland REALTORS® a new way to shop for the insurance benefits they need. With our service, you will get comparison quotes from multiple insurance providers. Shop the most affordable Health, Dental, Vision and Life insurance available. For more information call Stuart Jackson 888-424-4842 x 101 or by visiting www.benefitsbychoice.com

Nationwideis on your side

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 23

Eco Ink BenefitsMaryland REALTORS® is pleased to announce in conjunction with Eco Ink Benefits the relaunching of the Ink & Toner program. The Eco Benefits Ink & Toner program has a new look and feel with higher-quality products, guarantees, coupons and free shipping on orders over $49!

https://mar.ecoinkbenefits.com/

EnergyPlusEnroll today to receive your electricity and natural gas for your home or business from Energy Plus, an energy supply company. To be eligible, you simply need an address within the Energy Plus service area, which currently covers areas serviced by BGE, Delmarva Power, and Pepco for electricity and BGE for natural gas.

http://www.energypluscompany.com/combined/mdrealtor/md/?apptype=EM&cellcode=02campaign+6134&pcb

TransUnion SmartMoveTransUnion SmartMove gives Maryland REALTORS® independent landlords all the screening tools they need, with none of the hassle. Visit us now to get started and create an account in minutes. Receive credit & criminal reports, and a leasing recommendation. No approval processes. No minimums.

https://mar.mysmartmove.com/

TaxBotTaxbot is an expense tracking system designed to save thousands every year. Did you know there are HUGE tax advantages for your business? Regardless of how much money you make, Taxbot teaches you how to keep more of what you earn! Guaranteed to save at least 20 times your investment in your first 30 days or your money back.

https://taxbot.com/

Office Depot/Office MaxMaryland REALTORS® have access to exclusive members only discounts at Office Depot and OfficeMax. Save up to 80% off preferred products, receive FREE next day delivery on orders over $50, exclusive low printing costs and much more.

http://officediscounts.org/mdrealtors/

Errors & Omissions InsuranceAs a leader in the insurance industry for 60 years and a longtime partner of the Maryland REALTORS®, Pearl Insurance is proud to share with you our quality Errors & Omissions Insurance, which offers valuable coverage that’s better and more affordable than ever before. Call us at 800-447-4982.

http://pearlinsurance.com/

24 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

REALTORS® Insurance MarketplaceREALTORS® Insurance Marketplace is an easy to use comparative shopping site designed to help NAR members obtain insurance by offering a wide roster of insurance plans and products. Offered under the REALTOR Benefits® Program, the Marketplace Health Insurance Exchange, featuring insurance plans from top-rated carriers nationwide that meet the mandates of the Affordable Care Act. Call us at any time 1-877-267-3752.

http://www.realtorsinsurancemarketplace.com/

Benefits of NAR MembershipParticipating in a membership of over 1,000,000 members gives you Real Strength. Real Advantages. NAR serves the diverse interests of all our members who specialize in residential or commercial real estate, including established and new agents, brokers/owners, association executives or board presidents.

https://www.nar.realtor/realtor-benefits-program

360 Coverage Pros Cyber Insurance360 Coverage Pros is an industry leader providing innovative insurance and benefit solutions. 360 Coverage Pros provides a comprehensive suite of products and services designed to help your business manage and insure today’s cyber security and data breach risks.

https://www.360coveragepros.com/mdrealtor

Constant Contact Email MarketingConstant Contact®, Inc.’s email marketing and online survey tools help small businesses and organizations connect to customers quickly, easily, and affordably and build stronger relationships. Maryland REALTORS® receive an additional 10% off the standard prepay discounts. That is 20% off six months, or 25% off the full year. Pre-payment is required for these member exclusive savings.

https://marylandrealtors.constantcontact.com/account-home

UPSMake the most of your Maryland REALTORS® membership and save up to 34%* on UPS® shipping services, plus 50%* off select services for up to four weeks after you enroll. To sign up and start saving today, click below or call 1-800-MEMBERS (1-800-636-2377) M–F 8 a.m.–6 p.m. EST.

https://www.ups.com/mrd/promodiscount?loc=en_US&promoCd=CCE04ASG6

Maryland REALTORS® RX ProgramThis program is being provided to you and your family to help lower your prescription drug costs. Simply create and print your FREE Prescription Drug Card below and receive savings of up to 75% (discounts average roughly 30%) at more than 68,000 national and regional pharmacies. This card can be used as your primary plan and/or it can be used on prescriptions not covered by your insurance plan. This program also includes other value added programs which will be listed on the card. This card is pre-activated and can be used immediately.

https://bit.ly/2UpzYYw

®REALTORS

®REALTORS

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 25

The Maryland Department of the Environment, in partnership with the Maryland Department of Health and local county health departments

are promoting January as Radon Awareness Month. Radon is an odorless, colorless, naturally occurring radioactive gas that easily migrates through the soil. It can accumulate within homes, initially in areas where floors and external walls are in contact with the ground, and is often a concern during property transfers. Radon is the second leading cause of lung cancer after tobacco smoke. People who smoke and are also exposed to elevated radon levels where they live are at a greater risk for lung cancer. Thus, it is important that all homes be tested for radon and corrective measures taken when necessary.

All homes, regardless of location, can have elevated radon levels. Historical data shows that radon levels are elevated in Northern Maryland (counties ranging from Cecil to Garrett) and Central Maryland (Howard, Montgomery, Baltimore, Anne Arundel, and Prince George’s counties). Because it is colorless and has no warning sign, the only way to know if dangerous levels of radon are present is to test the home. This can be done with a simple testing device. Radon levels are often higher in the basement, so it best to conduct the test in that area. Radon can also be high on the ground level in homes without basements. If radon levels are higher than 4 picocuries per liter (pCi/L) it can be remediated by contacting a certified radon service provider. https://mde.maryland.gov/programs/Air/RadiologicalHealth/Pages/radon.aspx

Although radon testing and mitigation methods are not complex, they are not foolproof. Certain procedures must be followed to help ensure desired outcomes. During Radon Awareness Month, the Maryland Department of the Environment, and its partners, will work closely with Maryland REALTORS® to provide information to help buyers, sellers and their agents better understand the nature of radon hazards, how to evaluate exposures, and how to resolve problems if elevated levels are found.

Save a life by testing and fixing your home today.

AWARENESS

Radon, Average pCi/L

0.2–2

2.1–4

4.1–61

26 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

Maryland REALTORS® 2019 President, Merry Tobin, is making it a priority to focus on veterans and military service members.

Mortgage loans and incentives are among the benefits for men and women who sacrifice so much serving this country. However, home buying can be challenging because of modest incomes and the possibility of being transferred to a new duty station. Despite this, homeownership among military members surpasses that of civilians. According to the National Association of REALTORS®’ (NAR) annual Veterans & Active Military Home Buyers Profile, active-duty service members tend to buy at a younger age and purchase larger homes with a higher median price than non-military. This spells opportunity for REALTORS® and lenders interested in working with this group.

The most well-known loan program is through the Department of Veterans Affairs (VA). These loans available to veterans and active-duty military members feature no down payment requirements, no mortgage insurance, lower than average interest rates, limit on closing costs, and more lenient credit requirements. Those who qualify include people who: served 90 consecutive days during wartime, 181 consecutive days on active duty during peacetime, 6 or more years

in the National Guard or Reserves, and some spouses of military members who died in the line of duty or in a service-connected disability. Loans are targeted to buyers who intend to live in the property full-time, although there are exceptions for spouses and families of deployed military members. To further assist active-duty members, the Servicemembers Civil Relief Act (SCRA) provides financial protection involving interest rates, income tax payments, eviction, and foreclosure. It is important to remember that VA loans are available for repeat use—they aren’t strictly for first-time buyers.

Lenders may have special programs or incentives targeted to veterans or current military service members. Although the State of Maryland Department of Housing and Community Development’s (DHCD) Maryland Mortgage Program Homefront program has been discontinued, DHCD does offer VA loans which can be coupled with the department’s down payment and closing cost assistance programs. USAA Bank waives a borrower’s appraisal, title, and VA funding fee for VA refinances. PenFed Credit Union offers a promotional credit of up to 1% of the loan amount. Other banks and organizations offer rebates to military personnel—most of which are tied to the use of an

Helping Veterans with Housing

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 27

affiliate real estate agent or realty group. No matter what lender a buyer uses, it can’t hurt to inquire about discounts or fee waivers.

REALTORS® interested in working with current and former military members can enhance their education through NARs Military Relocation Professional (MRP) certification—this program is designed to help identify housing solutions and available benefits and support. This one-day class outlines the process of military relocation, how to identify resources to help a military buyer, details about VA financing, and offers access to marketing tools. It can be taken online or in a classroom. With almost 23 million active and former military members in the U.S. (Maryland has the 12th highest population in the country), they are an important part of our home buying and selling market. For more information, visit the NAR website at www.nar.realtor.

Almost every county in Maryland has an organization or several whose mission it is to assist active-duty, retired, disabled, and homeless veterans. In Baltimore County, the Homefront Veterans Services Work Group targets strategies and delivers services including housing, legal services, health care, mental health services, education, and employment assistance. In

Baltimore City, nonprofit organizations MCVET and The Baltimore Station offer housing, substance abuse, and mental health services to veterans. The Mid-Shore Recovering Veterans Group looks to serve the needs of veterans in Talbot County and the surrounding areas. In St. Mary’s County, the Charlotte Hall Veterans Home provides nursing and assisted living care for veterans. The Maryland Department of Veterans Affairs (www.veterans.maryland.gov) has a comprehensive list of support services and resources for military veterans and their families. Most of these organizations welcome volunteer efforts and would be ideal for a team or office community involvement project.

Finally, Maryland veterans with a permanent and service-connected 100% disability rating from the VA can apply for an exemption from annual property taxes by visiting the State Department of Assessment & Taxation (SDAT) website.

Maryland REALTORS® will be concentrating on veteran’s housing issues in the coming year. For more information, please contact Laurie Benner at [email protected].

Assistance Animals–

Again

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 29

It is now 2018, fifty years after passage of the Fair Housing Act (“FHA”) and thirty years after passage of the Fair Housing Amendments Act (“FHAA”), which

added disability and familial status as protected classes. In 1988, persons with a disability were given the right to seek reasonable accommodations and modifications to ensure the opportunity to enjoy equal access to housing. In 2016, almost 60 percent of the Complaints filed with HUD alleged discrimination based on disability. As REALTORS®, we are required to understand the nuances of fair housing laws, to be able to identify fair housing issues and challenges, and to be able to provide information (not legal advice) to our clients. This article will provide a brief review of the applicable fair housing laws, plus more detailed information about some of the more nuanced areas of the law.

One of the most important concepts to master is the difference between requirements under the Americans with Disabilities Act (“ADA”) and requirements under the FHA and FHAA (referred to collectively as the “Act”). The ADA governs the rights of a person with a disability to use a service animal. The ADA applies to places of public accommodation, meaning places that are open to the public, like restaurants, shopping centers, movie theaters, real estate brokerage offices, title companies, etc.

Under the ADA, a place of public accommodation cannot prohibit “service animals” or prevent someone with a disability from entering with their “service animal.” Within the scope of the ADA, the definition of a “service animal” is narrow: Service animal means a dog (or a miniature horse) that has been individually trained to do work or perform tasks for the benefit of an individual with a disability. The most common example would be a guide dog or seeing eye dog for someone who is visually impaired or blind.

People with disabilities, however, don’t always require an animal to perform a specific task. Increasingly, people with disabilities require other types of assistance, such as emotional support for someone with a mental disability or being alerted to the onset of an anxiety attack. In many of these cases, the animal hasn’t had any official training, hasn’t passed any tests or obtained any certifications. While these animals would not be “service animals” under the ADA, they are considered “assistance animals” under

the fair housing laws, which term is much more broadly construed than “service animal.”

The most important points to remember are: (1) service animals, therapy pets, emotional support animals or animal aides (“Assistance Animals”) are all treated the same under applicable Fair Housing laws, (2) Assistance Animals do not require any specific training or certification; (3) any type of animal can be an Assistance Animal (not just dogs and miniature horses); (4) Assistance Animals are not pets, therefore, any policies that the landlord has regarding pets are not enforceable with respect to an Assistance Animal.

Courts have applied the Act to individuals, corporations, associations and others involved in the provision of housing and residential lending, including property owners, housing managers, homeowners and condominium associations, lenders, real estate agents, and brokerage services. So, how does your client determine whether someone legitimately has a disability and needs an assistance animal or whether someone just wants to circumvent the landlord’s “No Pets” policy? Equally important, how do you handle these requests without getting your client, your self and your brokerage into trouble? Keep reading!

A person is considered to have a disability under the Act when the person:

(1) has a physical or mental impairment that substantially limits one or more of their major life activities;

(2) has a record of having such an impairment; or

(3) is regarded as having such an impairment.

A physical impairment is defined by the ADA to include: any physiological disorder or condition, cosmetic disfigurement, or anatomical loss affecting one or more of the following body systems: neurological, musculoskeletal, special sense organs, respiratory (including speech organs), cardiovascular, reproductive, digestive, skin, and endocrine.

A mental impairment is defined by the ADA as including, but not limited to: any mental or psychological disorder, such as intellectual disability, organic brain syndrome, emotional or mental illness, autism, specific learning

30 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

disabilities, drug addiction and alcoholism. We’re going to focus on mental impairment, since that is the type of disability most associated with requests involving Assistance Animals.

Let’s suppose you’re the listing agent on a rental and the landlord has received an application from a tenant who has asked the landlord to allow her Assistance Animal, a cat, to occupy the property. The landlord has a No Pets policy, but you’ve taken enough Fair Housing classes to know that the landlord can’t simply deny the application because of the cat. You also know that if the applicant is a person with a disability, the landlord may have to provide a reasonable accommodation, which may mean allowing the applicant to rent the property and to waive the “No Pets” policy.

First things first – how does the landlord verify that the applicant is a person with a disability? Depending on the applicant’s circumstances, information verifying that she meets the Act’s definition of disability can be provided by the applicant herself (e.g., proof that an individual under 65 years of age receives Supplemental Security Income or Social Security Disability Insurance benefits or a credible statement by the individual). A doctor or other medical professional, a peer support group, a non-medical service agency, or a reliable third party who is in a position to know about the individual’s disability may also provide verification of a disability. In most cases, an individual’s medical records or detailed information about the nature of a person’s disability is not necessary for this inquiry.

Once the landlord has established that a person meets the Act’s definition of disability, any request for documentation should seek only the information that is necessary to evaluate if the reasonable accommodation is needed because of a disability. Such information must be kept confidential and must not be shared with other persons unless they need the information to make or assess a decision to grant or deny a reasonable accommodation request or unless disclosure is required by law (e.g., a court-issued subpoena requiring disclosure).

After the landlord or housing provider has verified that the applicant has a disability, the next step is to

consider the accommodation or modification that was requested. What is a “reasonable accommodation” for purposes of the Act? A “reasonable accommodation” is a change, exception, or adjustment to a rule, policy, practice, or service that may be necessary for a person with a disability to have an equal opportunity to use and enjoy a dwelling, including public and common use spaces. Since rules, policies, practices, and services may have a different effect on persons with disabilities than on other persons, treating persons with disabilities exactly the same as others will sometimes deny them an equal opportunity to use and enjoy a dwelling. The Act makes it unlawful to refuse to make reasonable accommodations to rules, policies, practices, or services when such accommodations may be necessary to afford persons with disabilities an equal opportunity to use and enjoy a dwelling.1

To show that a requested accommodation may be necessary, there must be an identifiable relationship, or nexus, between the requested accommodation and the individual’s disability. The following examples, from joint guidance issued by the Department of Housing and Urban Development (HUD) and the Department of Justice, may be useful:

Example 1: A housing provider has a policy of providing unassigned parking spaces to residents. A resident with a mobility impairment, who is substantially limited in her ability to walk, requests an assigned accessible parking space close to the entrance to her unit as a reasonable accommodation. There are available parking spaces near the entrance to her unit that are accessible, but those spaces are available to all residents on a first come, first served basis. The provider must make an exception to its policy of not providing assigned parking spaces to accommodate this resident.

1 See, JOINT STATEMENT OF U.S. DEP’T OF HOUS. AND URBAN DEVEL. AND DEP’T OF JUSTICE, “Reasonable Accommodations under the Fair Housing Act,” May 17, 2004, p. 6 (Response to question 6) (link: https://www.hud.gov/sites/documents/huddojstatement.pdf)

www.mdrealtor.org MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 31

there is a relationship between the tenant’s disability and the requested modification and the modification is reasonable, the housing provider must allow her to make the modification at the tenant’s expense.

Example 2: A homeowner with a mobility disability asks the condo association to permit him to change his roofing from shaker shingles to clay tiles and fiberglass shingles because he alleges that the shingles are less fireproof and put him at greater risk during a fire. There is no evidence that the shingles permitted by the homeowner’s association provide inadequate fire protection and the person with the disability has not identified a nexus between his disability and the need for clay tiles and fiberglass shingles. The homeowner’s association is not required to permit the homeowner’s modification because the homeowner’s request is not reasonable and there is no nexus between the request and the disability.

We’ve discussed disability, physical/mental impairment, verification of disability, reasonable accommodations and reasonable modifications. Let’s move on to some of the more nuanced questions that come up.

Q: What if the applicant doesn’t want to submit documentation from her

healthcare provider to keep an Assistance Animal? Can the landlord reject the applicant?

A: It’s important to know the rules about when and how you can ask for documentation. If the

applicant has an obvious disability-related need for an assistance animal, the landlord cannot ask for additional documentation and must make an exception to any pet policies so that the applicant can keep an Assistance Animal. If, on the other hand, the applicant doesn’t have an obvious disability-related need for an Assistance Animal, then the landlord can ask for documentation to verify that she has a disability and has a disability-related need for the Assistance Animal.

Example 2: A housing provider has a “no pets” policy. A tenant who is deaf requests that the provider allow him to keep a dog in his unit as a reasonable accommodation. The tenant explains that the dog is an assistance animal that will alert him to several sounds, including knocks at the door, sounding of the smoke detector, the telephone ringing, and cars coming into the driveway. The housing provider must make an exception to its “no pets” policy to accommodate this tenant.

In addition to a “reasonable accommodation,” persons who meet the Act’s definition of “person with a disability” may be entitled to a reasonable modification under the Act. Under the Act, a reasonable modification is a structural change made to the premises whereas a reasonable accommodation is a change, exception, or adjustment to a rule, policy, practice, or service. A person with a disability may need either a reasonable accommodation or a reasonable modification, or both, in order to have an equal opportunity to use and enjoy a dwelling, including public and common use spaces. Generally, under the Act, the housing provider is responsible for the costs associated with a reasonable accommodation unless it is an undue financial and administrative burden, while the tenant or someone acting on the tenant’s behalf, is responsible for costs associated with a reasonable modification.

As with a reasonable accommodation, there must be an identifiable relationship, or nexus, between the requested modification and the individual’s disability. If no such nexus exists, then the housing provider may refuse to allow the requested modification. 2

Example 1: A tenant, whose arthritis impairs the use of her hands and causes her substantial difficulty in using the doorknobs in her apartment, wishes to replace the doorknobs with levers. Since

2 See, JOINT STATEMENT OF U.S. DEP’T OF HOUS. AND URBAN DEVEL. AND DEP’T OF JUSTICE, “Reasonable Modifications under the Fair Housing Act,” March 5, 2008, p. 4 (Response to question 5) (link: https://www.hud.gov/sites/documents/reasonable_modifications_mar08.pdf)

32 MARYLAND REALTOR® DECEMBER 2018 / JANUARY 2019 www.mdrealtor.org

If an applicant refuses the request, you should explain that the landlord complies with all fair housing laws and that it’s the landlord’s policy that she can’t live there with the Assistance Animal without providing the necessary documentation. The applicant is asking for an exception to the pet policy—and she’s not entitled to a reasonable accommodation unless she can show that she has a disability-related need to keep an Assistance Animal. These communications should be documented.

Q: Can the landlord charge a pet deposit? What happens if the Assistance Animal

damages the property?

A: The landlord cannot charge a pet deposit to a person with a disability requiring a reasonable

accommodation, such as an Assistance Animal. A housing provider may require a tenant to cover the costs of repairs for damage caused by the Assistance Animal, reasonable wear and tear excepted, if it is the provider’s practice to assess tenants for any damage they cause to the premises.

Q: The current tenant has become disabled, and the landlord properly

allowed him to have an Assistance Animal. The tenant, however, cannot control the Assistance Animal. The dog growls and barks at other residents of the community and exhibits aggressive behavior. Can the landlord order the tenant to remove the dog? The landlord has received numerous complaints from the neighbors.

A: The landlord wouldn’t violate fair housing laws by refusing to allow the tenant to keep his dog as

an assistance animal. The landlord would be justified in sending notice to remove the dog or face eviction. The landlord should use her reasonable judgment to ascertain the nature, duration, and severity of the risk the dog created; the probability that potential injury will occur; and whether reasonable modifications of policies,

practices, or procedures will mitigate the risk prior to sending the notice.

Q: The applicant indicated that they had a disability and a disability-related need for

an Assistance Animal. The applicant provided sufficient and appropriate documentation from a medical provider to verify both the disability and the need for an Assistance Animal. The applicant’s Assistance Animal is a Pit Bull and the County where the property is located has a law prohibiting residents from owning or keeping Pit Bulls. Does the landlord have to reject the applicant because of the County law?

A: As established by the Supremacy Clause of the U.S. Constitution, federal laws such as the Fair