Archaeosomes can efficiently deliver different types of cargo into epithelial cells grown in vitro

RSM M.Sc. in Strategic Management

Master thesis Learning from M&A: the impact of the different

types of distance

Dr. Yang Fan (Supervisor)

Dr. Jatinder Sidhu (Co-reader)

Alexandre Favre ID 402770

Completed the 14th of June 2014

1

Preface:

The copyright of the Master thesis rests with the author. The author is responsible for its contents. RSM is only responsible for the educational coaching and cannot be held liable for the content

2

Contenu 1. Introduction .................................................................................................................................................... 5

2. Literature review ........................................................................................................................................... 9

2.1 International mergers and acquisitions ................................................................................................. 9

2.2 Mergers and acquisitions’ experience and performance implications .......................................... 10

2.3 The impact of the type of distance on the merger and acquisition’s learning process ............................. 12

2.3.1 Cultural distance ............................................................................................................................... 12

2.3.2 Administrative distance ................................................................................................................... 13

2.3.3 Geographic distance ......................................................................................................................... 14

2.3.4 Economic distance ........................................................................................................................... 15

2.4 The impact of distance on international M&A ............................................................................................ 17

3. Hypothesis ...................................................................................................................................................... 19

3.1 Hypothesis 1 ............................................................................................................................................... 19

3.2 Hypothesis 2 ............................................................................................................................................... 20

4. Methodology .................................................................................................................................................. 24

4.1 Sample ........................................................................................................................................................ 24

4.2 Method ....................................................................................................................................................... 25

4.3 Dependent variables ................................................................................................................................... 25

4.4 Independent variables ................................................................................................................................ 27

4.4.1 M&A Experience ............................................................................................................................. 27

4.4.2 Geographic distance ......................................................................................................................... 27

4.4.3 Cultural distance ............................................................................................................................... 27

4.4.4 Administrative distance ................................................................................................................... 28

4.4.5 Economic distance ........................................................................................................................... 28

4.5 Control variables ..................................................................................................................................... 28

4.5.1 Industry and year variable ............................................................................................................... 29

4.5.2 Firm’s characteristic variable ....................................................................................................... 29

4.5.3 M&A’s characteristic variable ...................................................................................................... 29

4.6 Estimation technique ............................................................................................................................... 29

5. Results ............................................................................................................................................................ 31

5.1 Descriptive statistics .................................................................................................................................. 31

5.2 Regression’s analysis ........................................................................................................................... 33

3

5.2.1 Experience ........................................................................................................................................ 35

5.2.2 Interaction and moderating effect ................................................................................................... 35

6. Discussion and Conclusion ........................................................................................................................... 37

6.1 Contribution and Implication ..................................................................................................................... 37

6.2 Limitations ................................................................................................................................................. 39

6.3 Conclusion ............................................................................................................................................... 40

References .......................................................................................................................................................... 41

4

1. Introduction

Companies through the world find it more and more difficult to achieve their objectives

and cope with the demand of their stakeholders. A popular answer to overcome these challenges

is the use of merger and acquisition either by acquiring related or unrelated business. The

importance of merger and acquisition in international business keeps on growing, with

worldwide acquisition reached $3.3 trillion in 1999, almost $3.5 trillion in 2000 and hits a

record of $4.5 trillion in 2007. It’s not only the value of the mergers and acquisitions that

increase it’s also their numbers. In the Figure 1.1, which shows the number of cross-border

mergers and acquisitions, involving publicly traded companies, in the period 1985-2007, we can

see that the number of merger and acquisition increase until the 2000 crisis. But after a few

years, the number increase again, reflecting the renewed confidence of investors and managers

in the growth of the economy. So we can expect that in the coming years the number of merger

and acquisition will increase again since the economy is recovering from the 2008 crisis.

Figure 1: Number of cross-border mergers and acquisitions (1985-2007)

Source: Securities Data Corporation Mergers and Acquisition Database

And we can imagine that this trend will continue since a lot of companies are searching

to consolidate their business and take advantage of the recovering international business health.

5

The paper starts by exploring the current situation concerning the explanation of

acquisitions and mergers’ performance. This is followed by a literature review on the divergent

findings of past research on the effect of prior experience on acquisitions and mergers’

performance, on the barriers raised by distance on the learning from previous experience and on

the impact of each type of distance on the learning process. Subsequently a problem definition is

formulated, including the hypothesis and research design. In the end, the limitations and the

conclusions will be presented.

Even if there is a growing number of acquisitions and mergers in the world, only a few of

them manage to produce a positive return in term of profitability or synergy for the new

company. An important number of studies tried to explain which factors can influence the

success of an acquisition or merger. For Haleblian and Finkelstein (1999), it is the prior

experience which explains the performance, for Kale and Singh (2007) it is the efficacy of the

learning process and for Hambrick, Cho and Chen (1996) it is the composition of the top

management team. This research will evaluate the moderating effect of geographical, cultural,

administrative and economic distance on the relation between previous acquisitions and

mergers’ experience and the performance of these ones. Distance can be classified in 4

dimensions, and the influence of some of them is yet to be examined.

Empirical and theoretical research on international acquisitions and merger has

highlighted the importance of the 4 dimensions of distance. Di Guardo, Marruco and Paci (2013)

found that the distance is a critical factor in the probability of one firm doing a merger or

acquisition with a foreign company. Ghemawat (2001) who discussed the 4 dimensions of

distance focused on another topic in his research. He tried to link the distance with the

performance of an internalization of a company. For him, the more distant the country you try to

enter is from your head quarter’s country, the more trouble and difficulty you will encounter to

achieve your objectives. Vestring, Rouse and Reinert (2005) also worked on the relationship

between distance and performance. But for them, distance is an opportunity for a firm especially

if you try to lower your cost by outsourcing or acquiring firm in country with low labor cost.

Furthermore, by doing business with other country you diversify your risk. However no research

6

has been conduct yet to link all the different types of distance with the use of prior experiences. It

is critical to research these gaps in order to improve the knowledge of M&A, which is central to

insure the successful growth of firms.

At the current time most of the research had been focusing on the cultural aspect of

distance (Reus&Lamont, 2009; Stahl&Voigt, 2003; Morosini et al., 1998), while there is a

consensus that the cultural aspect of distance is relevant and important, the other factors of

distance have been neglected and should be analyze to understand what kind of influence they

have on the acquisition and merger. This observation leads to the following main research

question:

What are the moderating effects of the different type of distances on the relationship

between prior international experience in M&A and the subsequent acquisition and merger’s

performance?

In order to contribute to the literature on mergers and acquisitions, we will analyze the

relation between M&A performance and experience and the moderating effect of distance.

Actually most of the research focus on the direct link between experience and performance but

little is known on possible moderating variables. This study hence aims to improve knowledge on

how distance can moderate the relationship between M&A experience and performance. This

study will also aim to inform manager of the possible dangers of distance preventing the future

prosperity of M&A. Practitioners usually choose the potential company to acquire just based on

the relatedness of the industry or the possible synergy but forget to take into account other

criteria. This study aims to provide them with additional hindsight and concrete criteria to

evaluate potential companies.

The most appropriate way to answer our question is to use quantitative method on a

multiple industries panel data. Hypothesis testing is especially suitable since the performance of a

M&A is usually measured in financial term and since we will use objective criteria to measure

distance and experience.

7

Our study will only focus on the moderating effect of distance, but we should keep in

mind that there are surely other variables moderating the effect between M&A experience and

performance. Furthermore we will limit our analysis to only four different industries during the

period from 2000 to 2009, which can bias our results and conclusions. The use of only US based

company publicly traded can introduce a bias regarding the size of the company since our

research will only focus on companies will relatively important financial and human capital.

8

2. Literature review

This chapter aims at taking a look at the relevant literature on the subject of international

M&A, M&A performance and experience, different types of distance, the learning process in

M&A, and the relationships between these factors. More specifically, this review will focus on

how the learning process through experience impact the learning process and how the types of

distance impact the learning process, both in the context of M&A.

We will start with a section (2.1) that introduces international M&A. Section 2.2 will dig

into the relationship between experience and performance in the context of M&A. Section 2.3

will link the type of distance with possible barriers in learning. The final section of this chapter

(2.4) will combine the international M&A learning and the four types of distance.

2.1 International mergers and acquisitions

International mergers and acquisitions are common and popular things, especially these

last few years. So when a company decides to acquire or merge, it faces two options:

international merger or acquisition or domestic merger or acquisition. Usually international

transactions involve more opportunities and challenges than domestic ones.

One of the main reasons for an international merger or acquisition is linked to growth

problems. To answer such challenges, firms can deploy different strategy related to the

international aspect of the transaction. For example, a firm can search to acquire new resources to

enter a new market (Amburgey and Miner, 1992).

A number of surveys have been conducted regarding the performance of the resulting

company, and they show mitigated results. According to PWC (2011), 62% of companies is

reporting a significant strategic success, 38% a financial one, and 30% an operational one. To

explain such variance in the successes we can look at exogenous parameters such as international

economic growth, inflation rates, but we can also look at endogenous factors such as the quality

of integration process routines. Prior experience in merger and acquisition has been identified by

different authors as one of the factors influencing the success of the transaction.

9

2.2 Mergers and acquisitions’ experience and performance implications

The learning process and thus the use of prior experience can be studied at different level.

Firstly we can look at experience at the individual level. For Simon “All learning takes place

inside individual human heads; an organization learns in only two ways: (1) by the learning of its

members, or (2) by ingesting new members who have knowledge the organization didn’t

previously have” (1991: 176). One challenge organizations should overcome if they want to learn

is to know where and how the previous knowledge is stored and who possess this information

(Simon, 1991).

This view is linked to the learning curve theory. Levitt and March stated that “… direct

labor costs in producing airframes declined with the cumulated number of airframes produce”

(1988: 4). This theory states the more employees produce an item, the more costs will decrease. It

relies on the assumption that when a new job, process, or activity begins it is likely that the

workforce involved will not achieve maximum efficiency immediately since this workforce has

no prior experience with the task they’re supposed to complete. So repetition of the task will

make the people more confident, knowledgeable, they will learn the process and thus realize the

operation more efficiently. So we can suppose that if employees in a company are assigned to

deal with merger and acquisition, they will be able to learn and merger or acquire more

efficiently.

Secondly, we can look at experience at the organizational level. For Nelson and Winter

“the possession of technical "knowledge" is an attribute of the firm as a whole, as an organized

entity, and is not reducible to what any single individual knows, or even to any simple

aggregation of the various competencies and capabilities of all the various individuals, equipment

and installations of the firm” (1982: 63). This view is more concerned about how an organization

as a whole will be able to learn and capitalize on this new knowledge. It tries to understand how

the organization learning process will adapt to internal and external change.

Some companies tried to take into account these two points of view and found a solution

by creating a merger and acquisition function. According to Kale and Singh (2007), to be

10

effective the specific function need to implement 4 processes which are articulation, codification,

knowledge sharing routines and internalization.

Articulation helps externalizing the individual tacit knowledge especially management

learning and making it more explicit. Articulation is defined by the creation of learning object

and tools such as templates, frameworks and guidelines to help people taking the right decision

regarding merger and acquisition. Sharing helps people to spread the tacit and explicit knowledge

through the firm. And finally internalization helps individual employee to absorb and retain the

knowledge from previous acquisition and merger. As we can see, organizing the learning in a

company can be a complex task, that’s why creating a focal point helps to initiate and coordinate

organizational and individual learning. But creating these four learning processes is only the first

step to be able to reap the benefits of prior experience.

The second step is to make sure that you acquire valuable and not useless or hurtful

experiences. Hayward (2002) explains which type of experience and what type of acquisition

firms should focus on. First of all, acquisition or merger shouldn’t be too similar (because in that

case you can miss valuable opportunities outside the field of expertise you created) or too

dissimilar (because the firm will lack some expertise and won’t be able to evaluate the real value

of one specific deal). Then managers will, most of the time, learn more from a small failure than

from an important one or from a success. If the acquisition and merger is a total failure, managers

will try to blame someone else and won’t try to figure out what went wrong. In the case of

success, the managers will not try to find a better way of doing things because they already

achieve their objectives, so they think there is no better way. Finally, companies shouldn’t let too

much time pass between acquisitions or merger because knowledge can become obsolete and

managers can forget what they learn before. But they should let a small period between

transactions, so that managers will be able to understand the problems and success of prior

experience.

If a firm fails to implement these best practices, it can fall into a “competency trap”

(Levitt and March, 1988). By doing a specific task, a company will develop a specialization in

this particular task. With specialization comes better efficiency and efficacy. But when an

11

environmental change occurs, specialized organizations have troubles to overcome the

competences they have developed in favor of competences needed in the new environment

(Whetten, 1987).

2.3 The impact of the type of distance on the merger and acquisition’s learning process

In 2001, Ghemawat, one of the most influential management gurus, started a study to

identify dimension of distance. In other words, Ghemawat tried to understand how distance

influences the success of international firms. To reach his goal, he conducted a thorough analysis

of 70 industries’ economic data concerning international trade. And to demonstrate how his

framework can help manager making better decision, he provided a case study of US-based

Tricon Restaurants International. From the data collected, Ghemawat found 4 types of distance,

each related to macroeconomic determinants. They were further discussed by Verbeke (2013).

Kale & Singh define the learning process as such “We see the alliance learning process as

a process that is directed toward helping a firm (and its managers) learn, accumulate, and

leverage alliance management know-how and best practices” (2007: 4). One way to look at the

learning process is through interactive learning and novelty generation. Relatively small distance

between firm’s countries is currently perceived as having a positive effect on learning. For

example, some dimensions of distance when they are considered low can create an important

learning and innovative potential (Boschma, 2005a, b). The use of prior experience is tightly

linked with the learning process because if you don’t learn from what you did, then your

experience is useless.

2.3.1 Cultural distance The first dimension, “cultural distance” refers to the distance resulting from

national cultural attributes easily spotted such as languages, religious beliefs and race. But there

are also attributes which are more difficult to identify and overcome like social norms or food

taste’s preferences. Researches show that the cultural distance prevents employees to learn

because of three mains reasons.

12

The first one is the type of culture. For example in Japan the context of a message

(gestures and body languages) influences greatly the meaning of this one. In the contrary, in

Norway or Finland, which are considered low context countries, the message doesn’t need a

specific context to convey its meaning. So if you’re use to work with one type of culture you can

misinterpret a learning message because of the influence you give to the context.

The second one is the languages. Sometimes, you can pass a particular meaning in a

language but you lose it if you try to translate it (Rolf, 2004). The difference in language between

firms can amplify the difficulties to communicate and enhance the complexity to express tacit

knowledge. We could think that nowadays since English is the main business language use in

most of the international companies the communication problems would decrease. But the degree

of mastery tends to differ between countries leading employees to misinterpret and

misunderstand the real meanings of the exchange.

The third one is categorization. Usually people tend to form group on the basis of their

similarities and differences. The culture can be used to assess these similarities and differences in

order to categorize people in a specific group leading to potential conflicts between these groups

or teams (Tajfel, 1982). The possibility of emotional conflict might increase with cultural

differences threatening the functioning of inter-organizational team because it favours group

thinking which leads to exclusions mechanisms (Harting, 2011).

We can say that the more cultural distance between countries, the higher the possibility to

misinterpret or lose the meaning of learning. If people can’t communicate properly, they can’t

pass their knowledge to other people, preventing the use of prior experience to improve

performance.

2.3.2 Administrative distance The second dimension, “administrative distance” refers to the distance resulting from

differences in societal institutions. This dimension is influenced by the existence of a common

history (colonial relationship, trade relationship), shared political family, economic and monetary

trade agreement and common government policies.

13

One if the main purpose of administrations and institutions is to implement a set of

sanctioning mechanisms ranging from formal to informal in order to set standards for economic

and social interaction (Talbot, 2007). These set of mechanisms moderate the inclination towards

opportunistic behaviors as well as their consequences (Zylbersztajn, 2006; Williamson, 1991).

Thus if companies have the same set of rules and mechanisms, they will be able to predict the

behavior of their partner increasing the mutual trust. In the contrary when they don’t share the

same rules and mechanisms these differences cause insecurity and relational risks and also

difficulty to enforce proprietary.

So we can say that the higher the administrative distance, the less the companies will be

able to predict their partners’ behavior, the higher the insecurity and relational risks will be. This

might lead to overly protective knowledge sharing process.

2.3.3 Geographic distance The third dimension, “geographic distance” represents not only the physical

distance but also the infrastructure allowing the transportation and communication between

different countries. It is also affected by the presence of a common border between two countries

or the presence of port and fluvial infrastructure to enhance transportation and communication.

The geographic distance between partners will enhance the difficulty to share tacit and

contextual knowledge because of two consequences. Firstly, geographic distance will reduce the

frequency of interaction. And secondly, it will change the means and hence the quality of

interaction (Hartig, 2011). And if a company can’t share its knowledge, it won’t be able to use its

prior experience to improve its performance.

The frequency of interaction is an important factor influencing the learning process. Allen

(1977), through empirical research observed that when distance grows between companies, there

is a logarithmic decline in communication frequency. Hough (1972) already found this

relationship between geographic distance and frequency of interaction in an analysis of

communication patterns between R&D sites in the home country of a firm and its sales

subsidiaries in foreign locations. This relationship is worsened by the difference between time

14

zones because it prevents people to exchange easily (Olson et al., 2009; Sapsed & Salter, 2004).

However, we can think that nowadays with the improvement in telecommunication and computer

technology, this relationship could, if not disappear, at least weakened. Boutellier and al. (2000)

think that the relationship is still correct even if not as powerful as before.

The quality of the interaction will change the value of the learning process. As we stated

before, we saw an incredible improvement in the media for information and communication.

They become more sophisticated and allow a deeper exchange. But unfortunately, even with

these new means of communication it is still nearly impossible to share tacit knowledge and

especially ‘know-how’ (Johnson et al., 2002). Johnson et al. (2002) argue that ‘it is very seldom

that a body of knowledge can be completely transformed into codified form without losing some

of its original characteristics’ (p. 246). And apart from losing some meanings during the

exchange, the information you try to diffuse can be misinterpreted or incomplete from the

beginning (D’Agata & Santangelo, 2003; Johnson et al., 2002). Thus, if you use Information and

communications technology as the main tool for knowledge sharing, your company takes the risk

of losing key elements in the learning of tacit knowledge such as body language and gestures,

feelings, intuition and context, (Jyrama et al., 2009; Morgan, 2004; Hinds, 1999). Harting added

regarding the use of ICT that “As central parts of knowledge are potentially dismissed, the

probability for misunderstandings, false interpretation, reduced learning and finally frustration

rise” (2011: 75).

To conclude, the more distance between multiple countries, the more you will use the ICT

in your learning process. The use of ICT is not as efficient as face-to-face meeting, so it decreases

the potential to learn from past experience and increase your performance.

2.3.4 Economic distance The fourth and final dimension, “economic distance” represents the differences in income

level and distribution, consumer habit of consumption, level of inequality, consumer wealth and

the cost and quality of natural, financial, human resources.

15

Tsang and Yip stated that “The technological level of a country is generally related to its

economic development” (2007: 2). So we can imagine that with a more important economic

distance, two countries will also have a more important technological distance.

The technological level reflects the knowledge bases and expertise level of one country.

So the more differences between the technological level of two countries the more challenging it

will be for the partners to enhance their ability to share knowledge. This idea is based on the

learning and cognitive theory in which it’s believed that the learning of new knowledge is

bounded by the actual knowledge and way of thinking of the learner (Amin & Cohendet, 2004;

Inkpen, 1998). To be able to learn something new, one will use existing knowledge to build,

interpret and attach meaning to what he is provided; learning can be described as a cumulative

process (Cohen & Levinthal, 1990; Inkpen, 1998).

For Cohen and Levinthal (1990) the absorptive capacity is tightly linked with the

existence of prior knowledge. Thus, if the knowledge to be acquired is close to the actual

knowledge, it will be easier to understand and absorb it.

Hinds and Pfeffer (2003) were interested in the difficulties to share expert knowledge.

They tried to explain which problems can arise when an expert teach some new knowledge to a

novice. The first step the expert made is to recall his own experience as a novice learning from an

expert. However, the process of recalling is usually incomplete, biased and often inexact. Hence,

when a company from a richer country try to share its knowledge with a company from a poorer

country, it’s most likely that the meaning gets altered and that the key message gets lost in the

sharing process.

In conclusion, the possible misrepresentation by each company can lead to friction,

recrimination, frustration or delays especially in M&A since there are so many changes. We can

summarize by saying that the more important the economic distant, the less probable the learning

of new knowledge.

16

2.4 The impact of distance on international M&A

The Scandinavian process model is based on behavioral theory of the firm and focus on

learning. It states that internationalization is driven by the familiarization with national culture

(Barkema and al., 1996). The model predicts that when a company encounters a new culture,

learning to understand this different culture is made through small steps, using the previous

knowledge acquired from similar experience (Johanson and Vahlne, 1977; Johanson and

Wiedersheim-Paul, 1975).

Using this model we can assume that if a company wants to do a new merger or

acquisitions, the previous experience will be more useful if it expands in the same country it did

in the past and still useful but to a lesser extent if the company expands to country with similar

cultures. The idea that a company can use its prior experience in the same country is

in line with the concept of 'experiential' knowledge (Johanson and Vahlne, 1977; Penrose,

1959) and thus supposed that the success in merging and acquiring a firm in the same country

will be more likely. When a firm enters a new country, it allows this firm to create new

links to other countries through its network. There is a stronger probability that the

links the company creates will be stronger with culturally similar countries since it’s

easier to communicate (Johanson and Vahlne, 1990). This fact or maybe the learning about

common cultural characteristics can explain the benefits a company reaps from prior experience

with dissimilar countries but with similar cultural specificity. Thus, i f a company wants to

merge or acqui re, its previous experience will be more useful if the partners come from the

same country as your previous partners, or a similar one.

Barkema and al. studied data from 225 foreign entries that 13 Dutch firms initiated from

1966 onwards. They found that “Firms face cultural barriers when expanding internationally,

tha t firm learn from their previous experience when gradually expanding into cultural space,

and tha t centrifugal expansion patterns are more successful than a random strategy” (1996:

12-13).

17

So we can say that cultural distance prevent the use of prior experience when a company

invests in countries with different culture. And we can assume that the same result will apply to

the other dimensions of distance.

As we saw during this literature review, we can conclude that the learning process

is one of the most difficult one to implement correctly. Ii is really complicated to reap the

benefits from previous experience. But if a company manages to use its prior experience to better

acquire or merger, it can develop a sustainable competitive advantage. To achieve this result,

even if the company implements these best practices, it should not overlook other barriers. Some

of those barriers are created by distance. Ghemawat considers that the more important the

distance is between two firms, the more difficult it will be for those two firms to benefit from

their interaction. And in the contrary, the less important the distance between two firms, the

easier it will be to take advantage of the transaction. In our study we can translate his view by:

the more distant the actual acquired firm’s country is compared to previous acquisitions, the less

you will be able to use the inference you draw from these previous experiences to improve the

probability of success. Another way to look at the impact of distance is through the learning

process a firm implement to reap the benefits of the ongoing flow of mergers and acquisitions.

18

3. Hypothesis

In the previous chapter, existing literature on the relationship between the learning

process, international M&A, cultural distance, geographic distance, economic distance and

administrative was reviewed. Special attention was paid to the framework developed by

Ghemawat (2001) and we adapted it so that the learning process could be included.

In this section, we argue that the previous experience in M&A will influence the

subsequent performance of this one and that the different types of distance have a moderating

effect on this relationship. We developed a framework (figure 2) which summarizes the different

relationship between our variables. In the following subsections we develop hypotheses based on

the literature. One hypothesis will test whether the previous experience influence the subsequent

performance of international M&A. And four hypotheses will test whether the four different

types of distance have a moderating effect on the relationship stated earlier.

3.1 Hypothesis 1

Through the literature review learning appears to be particularly important regarding the

success of a firm. The use of prior experience is tightly linked to learning. It’s not because you

did something before that you’re going to be better if you do the same thing. According to

Haleblian and Finkelstein (1999) acquisition experience is not sufficient to improve acquisition

performance. There are a lot of parameters you need to take into account if you want to learn and

turn your prior experience into knowledge. For example, Hayward (2002) highlighted the

similarity of the business acquired, the performance of these acquisitions and the time between

acquisitions as parameters that influence the performance.

Prior experience gives you the possibility to learn from your mistakes or successes. So by

doing merger or acquisition, a company gives itself the possibility to perform better in the

following one (Hayward, 2002). It allows the firm to successfully manage M&A by learning and

accumulating know-how about the obstacles and the practices you need to implement in order to

19

overcome them. Kale and Singh (2007) think that this process happens through 4 sub-processes,

articulation, codification, knowledge sharing and internalization. The company acquires

information which can overlapped or be redundant allowing the employees to better understand

the process and how to successfully implement it (Glynn, Lant, and Milliken, 1994). The

employees get a better sense of what to do first, of how to behave and treat new employees. By

knowing what to do and how to do it, the company will be able to finish the process faster. It will

allow the company to reap the benefits of the cost reduction and the value creation more rapidly,

improving the overall performance of the merger or acquisition.

Prior experience also helps the company to better assess potential partners and targets. By

being confronted to a specific culture or industry one time, the next time the firm will be able to

know what need to be done in order to increase its chance of success or it will be able to know if

something is wrong with the potential firm more easily (Bruton, Oviatt and White, 1994). In his

article, Wright (1936) stated that the repetition of one particular task by an employee reduce the

time and therefore the cost of performing this task. So thanks to previous acquisitions or mergers,

the due diligence will be simplified and faster, allowing the firm to reduce the cost and the

number of employees required. The company will better assess the cultural, strategic and

organizational fit between the firms, better assess the financial state of the partner, the difficulty

raised by the difference in the IT, tax and legal system.

Hypothesis 1: The greater the prior experience in international M&A, the better a firm’s

performance on subsequent international transactions.

3.2 Hypothesis 2

The learning process and thus the ability to use correctly the experience

accumulated in the past is a relatively complex and fragile process. A lot of variables can affect

this process and hence eliminate its benefits.

According to Nahapiet & Ghoshal (1998) the existence of shared language will improve

the willingness of people to exchange, their anticipation of the value creation and the

combination capability since it’s easier for them to immediately communicate, and to share their

experience through the same lens. So if you first acquire or merge with a company which has the

20

same language as your own, you can’t use this experience to assess the complementarity of

resource and the benefit the creation of new product or best practices if you acquire or merge

with a company which doesn’t share your language. It will be more difficult for people to

communicate and interact with your own firm. The same arguments can be raised regarding the

type of national culture a firm evolves in.

Hypothesis 2.a: Cultural distance is negatively moderating the relationship between the

prior experience on international M&A and the firm’s performance on subsequent international

deals.

Governments can implement different environmental or labor laws which are extremely

important if you want to restructure your process or your workforce (Crafts, 2006; Griffith and

Harrison and Simpson, 2006). If you did an acquisition or merger in a permissive labor law

country and then you want to do another one in a very strict country, you can’t count on your

experience to improve the performance of the transaction since the cost and the difficulty of

laying off employees will not be the same. The same goes for environmental measures, if you

merge or acquire a company in China you won’t have any trouble to modify the production

process even if it means a lot of pollution. If after this M&A you acquire or merger with a

German company you won’t be able to use the experience you acquire in China because German

environmental policies are way stricter.

Hypothesis 2.b: Administrative distance is negatively moderating the relationship

between the prior experience on international M&A and the firm’s performance on subsequent

international transactions.

When you conduct a merger or an acquisition you aim to delete or exchange resources

with the acquired firm either to lower your cost or to develop new capacity (Houston, James and

Ryngaert, 2001). So if you acquire or merger with a company in a country with a high quality of

transportation and communication infrastructure, you will be able to exchange financial, human

and physical resources quiet easily and with no over costs. This experience will be of no use in a

country with no proper infrastructure to allow you to communicate or exchange.

21

Hypothesis 2.c: Geographic distance is negatively moderating the relationship between

the prior experience on international M&A and the firm’s performance on subsequent

international purchases.

One of the reason companies merge or acquire is to enter new market and thus to have

access to new customers (Hamel and Prahalad, 1993; Amburgey and Miner, 1992). Developed

countries don’t have the same needs and potential buying power as developing countries where

the majority of people focus on more basic needs. So if you first acquire a company in a

developed country where people have a high buying power and then merge or acquire with a firm

in a developing country where you maybe need to change your product price or face lower

buying power, we will not be able to use the knowledge from the first acquisition or merger to

help you succeed in the second one.

Hypothesis 2.d: Economic distance is negatively moderating the relationship between the

prior experience on international M&A and the firm’s performance on subsequent international

investments.

Prior research (Santoz-Vijande, Lopez-Sanchez, Trespalacios, 2012) shows that

learning is one of the most critical factors in the success of the firm since it affects the firm

flexibility, innovation and performance. It’s especially true nowadays since the main differences

between firms are their employees, the knowledge they carry and their absorptive capacity. In

this paper we extend that work by looking at the effect of distance on the relation between prior

experience and thus the use of learning and the M&A’s performance (Figue 2).

22

Figure 2: The moderating effect of distance on the relation between prior experience and M&A’s performance.

In conclusion, as our framework show, we expect the prior M&A experience to have a

positive impact on the M&A performance since if you respect some best practices highlighted in

the literature review you are able to learn and not repeat the same mistake. Furthermore we

expect the different types of distance to weaken the impact of experience on performance since

the inference you make based on your prior knowledge will be less relevant in another

circumstances.

Prior M&A experience Merger and Acquisition’s performance

Administrative distance

Cultural distance

Economic distance

Geographic distance

23

4. Methodology

Ghemawat (2001) argued that the distance will influence the intensity of trade between

countries. We are going one step further and we will try to prove that distance influence the

success of an M&A through its impact on the learning process. For this thesis we will use panel

data in order to test our different hypothesis.

Section 4.1 will cover the sample that we will be using in this research. Section 4.2 will

explain the type of variables. Section 4.3 will define and explain the choice of our dependent

variable. Section 4.4 will describe the independent variables as well as point out where we will

find our data. Finally section 4.5 will define the control variables that can influence the

performance of an M&A.

4.1 Sample

The sample consists only of publicly traded US based company engaging in international

and domestic M&A for the ten years, 2000 through 2009. We will focus on the US based firm

because it is one of the most prolific markets in the world in term of M&A and since the firms are

publicly traded it allows us to ensure information accuracy and reliability as all publically traded

companies are obliged to report their financial and M&A relevant information. The time frame of

ten years was chosen firstly because it ensures that the M&A impact is fully integrated in the firm

performance and secondly because it gives us a sufficient variation in our sample to run our

analysis with the minimum probability of statistical problems. We focus on the period between

2000 and 2009 because there is an important variation in the number of M&A in this timeframe,

there is also a decreasing part and an increasing one, giving us more diversity in our sample. The

companies have been chosen randomly from seven industries classified by primary SIC code

where M&As are considered as an usual event: Pharmaceutical preparations (sic code: 2834),

Radio & Tv Broadcasting & Communications Equipment (sic code: 3663), Semiconductors &

Related Devices (sic code: 3674), Surgical & Medical Instruments & Apparatus (sic code: 3841),

Services-Prepackaged Software (sic code: 7372), Information Retrieval Services (sic code: 7375),

24

Services-Business Services, NEC (sic code: 7389). The choice of using different industries

allows us to test whether the findings were generalizable across industries. The focal M&As

include only US based firm’s international deals in which the acquirer’s stake is more than 50%

after the transaction. The source of the M&As data is the ThomsonOne and SDC databases.

These databases provide a lot of information concerning M&A histories, including the

announcement date of the bid, its value, the advisors used and other material terms and conditions

of the deal. In regard of the financial information we will use the annual report downloaded from

the official companies’ website and the WRDS database.

This approach netted a sample of 2068 domestic and international M&As.. Non-focal

acquisitions, those undertaken from 2000 to 2004, are important since we used them for the

experience variable. Our research looks into the performance of focal acquisitions, those

undertaken from 2005 to 2009. For this period the sample is reduced to 500. Of these 501

transactions, 50 were in Pharmaceutical preparations, 35 were in Radio & Tv Broadcasting &

Communications Equipment, 84 were in Semiconductors & Related Devices, 46 were in Surgical

& Medical Instruments & Apparatus, 199 were in Services-Prepackaged Software, 55 were in

Information Retrieval Services, 31 were in Services-Business Services, NEC.

4.2 Method

Firm M&As’ experience can be observed directly and so we test whether the

accumulation of experience increase acquisition performance. But the different dimension of

distance cannot be directly observed, so we will use diverse proxies to estimate them. The data

estimation draws on a pooled cross sectional sample of a firm’s acquisitions.

4.3 Dependent variables

M&As performance, which is the dependent variable in our research, is sometimes

defines as the level of wealth created by the acquirer’s company thank to this transaction. Our

25

approach is to explain the role of the M&A experience in the performance variation and then look

at the effect of distance on this relationship. A significant and positive relationship between

accumulated experience and the performance of these M&As suggests that the firm has

understood the mechanisms to improve subsequent M&A performance. As well, a negative and

significant impact between this relationship and the distance suggests that the distance weakens

the benefits of experience. Since the market is supposed to reflect all the information available or

at least an important proportion of it (Malkiel and Fama, 1970), it is appropriate to use investors’

opinions of whether the acquisition creates shareholder wealth

We will use the event study methodology to measures cumulative abnormal returns cause

by the M&A compared to the expected return without this event happening. This method was

also use by Haleblian and Finkelstein (1999) in their research about the accumulation of

experiences and the impact on learning. This measure reflects whether investors believe that the

M&A will bring some benefits to the acquirers or not. Healey, Palepu and Ruback (1992) found

in their study that the event study methodology can be uses as a predictor of the actual

performance of an M&A. Following this method, we will use a market value weighted model,

and not a constant mean return model because it is less precise, to estimate the expected return of

the firm’s stock price if the M&A didn’t happen. We’re looking at the date of announcement and

not the actual date of the M&A because the market will take into consideration the implication

and add the abnormal expected return of the transaction as soon as it knows that this transaction

will happen. The market model adopted for our research estimates the relationship between

companies’ returns and stock market returns for the 250 trading days preceding the 30th days

prior to the announcement of the acquisition. We use this 30 days interval to remove the

uncertainty regarding the possible rumors of M&A that could be incorporated in the stock price

of the acquiring company. The abnormal returns of the acquiring firms correspond to the

immediate returns observed over an 11 days interval (including the day of the acquisition

announcement, the day immediately prior such announcement). We will also check our results by

using a 5 days, 3 days interval. Then we will calculate the average of cumulative abnormal return

for every company of our sample to assess the real performance of the deals. CRSP and Eventus

are the source of the firm and market returns data.

26

4.4 Independent variables

4.4.1 M&A Experience Firm M&A experience is defined as the sum of recent acquisitions undertaken by the

firm, from 2000 to 2009 (Hayward, 2002). Companies that made only one M&A during time

frame of our research (2000-2009) will receive an experience equal to 0. This variable is

particularly important since the other variables will affect the relationship between M&A

experience and our explained variable.

4.4.2 Geographic distance The geographic distance between the acquirer company and the acquired company is

defined in absolute term. We will use the infrastructure difference between the two countries

because it reflects the easiness of interaction between them. The proxy for difference of the

infrastructure in the two firms’ countries is defined as the difference between numbers of internet

user in each country (Hartig, 2011). To assess this variable we will use the database from the

World Bank and Google map.

4.4.3 Cultural distance For the cultural distance we will use the definition of Hofstede. It will be defined

using the absolute value of the difference between the two companies’ country in regard of each

one of the 5 dimension found by Hofstede (2010). The power distance corresponds to the

acceptance and expectation of difference of power and inequalities inside a population. The

individualism versus the collectivism is whether a society is looking for each other and expects

help from other members of the community or not. The masculinity versus femininity is looking

at whether the society is competition and achievement oriented or cooperation and consensus-

oriented. The uncertainty avoidance is linked to the risk tolerance and the discomfort the risk

brings. Finally, the long-term versus short-term orientation is whether a society is focus on the

immediate results or more concerned about its future. We will take the sum of the average of all

27

the sub distance to calculate the overall cultural distance. To find these values we will use the

Hofstede website database.

4.4.4 Administrative distance The administrative distance will be calculated by using the absolute value of the

difference between the two companies’ country world governance indicators (Heuchemer,

Kleimeier and Sander, 2008). There are six different indicators. Voice accountability refers to the

degree of freedom given to a citizen (choice of his government, freedom of expression,

association…). Political stability and absence of violence look at to the probability of an

overthrow of a government by violent means. Government effectiveness is linked to the quality

of the public service and the quality of the government. Regulatory quality refers to the extent to

which the government is helping the private sector with the legislation. Rule of law correspond to

the degree of confidence citizens have in the law, the police and the application of the law.

Control of corruption captures the level of corruption in the government and the public sector.

We will take the sum of the average of each indicator to calculate the overall administrative

distance. To find these values we will use the World Bank database.

4.4.5 Economic distance To look at the economic distance, we will use the absolute value of the difference

between the GDP per capita of the two companies’ country (Heuchemer, Kleimeier and Sander,

2008). It seems to be the best estimator since it takes into account the relative cost of living and

the inflation rates of the countries of interest, rather than just looking at the exchange rates which

may not reveal the real differences in economic power between the countries.

4.5 Control variables

Numerous factors explain the M&A performance including the year of the M&A, the

firm’s industry, its financial condition, its endogenous characteristic and the nature of the M&A.

28

4.5.1 Industry and year variable Industry is also a series of dummy variables standing for the different industries present in our

sample. Both of them will be part of the estimation equation.

4.5.2 Firm’s characteristic variable Firm size is measured by the log of the total of assets in the year in which the M&A took place.

For the same deal, a bigger firm will be less influence by a merger or an acquisition than a

smaller one since the potential impact on its performance will be lower.

Firm performance is calculated by the return on assets of the acquiring firm the year of the

announced date of the deal. We are going to use the ratio of EBITDA to its total assets, because it

allows us to suppress the effect of the accounting, financial decisions of one firm as well as the

level of taxes the company should pay in its state.

Firm leverage is the ratio of the firm’s long term debt to its total assets. It allows us to control for

the financial decision of the firm.

Industry similarity is a dummy variable equal to 1 when the acquirer and the target companies

share the same 4 digit SIC code and 0 otherwise. It measures the similarity of the business

conducted by the two companies (Rumelt, 1974).

4.5.3 M&A’s characteristic variable Use of advisor is also a dummy variable equal to 1 when an advisor was used during the deal and

0 otherwise. An advisor can bring the competences a firm lacks in regard to M&A and thus assist

the firm in achieving a better performance (Hayward, 2002).

4.6 Estimation technique

In order to test our two hypotheses, the relationship between prior international M&A

experience and the performance measured by the event study method and the moderating effect

of the type of distance, we will use the ordinary least square estimation technique since our

variable is a continuous one. In the same time, we will control for many internal factors that may

influence the firm’s performance. We will use this technique because it’s supposed to be the best

29

linear unbiased estimator if our sample respects a few assumptions. To be sure that the

assumptions will be respected we will use a clustered estimator in order to suppress the potential

problems linked with heteroskedasticity and autocorrelation. The sample will be clustered by the

year in which the acquisition took place and by the companies’ CUSIP. We will prefer this model

to the random effect model because it gives us a mean to control for omitted variables. In a fixed

effects model, subjects serve as their own controls variables. Since we got an important

variability in our sample, we can apply the fixed effect model without fearing for too large

standard errors which can biased the estimation. Furthermore, Wooldrige (2013) says that if we

got more than two periods in our sample, the fixed effect model is the best one to produce a

correct estimation. In regard of external factors, economic trends over time may simultaneously

affect the firm’s performance and thus the M&A performance as well as the propensity of firms

to take the risk to merge or acquire. Again, we use the nature of the panel data to control for these

trends by including year fixed effects in our estimations.

To conclude we can say that we have a rather diverse sample with companies coming

from four industries, as well as a number of observation that allow us to draw conclusion from

our hypothesis. We will use the most common variable to measure performance in the case of

M&A and use different proxies for each dependent variable in order to have a better

understanding of the whole picture as well as control for a number of factors that could have

influence our results.

30

5. Results

We have now all the tools we need in order to run our analysis. We will finally be able to

test and check if our model can be of any help to managers and practitioners on the field. The

chapter will be divided in two sections.

The section 5.1 will describe different statistics about our sample. And the section 5.2 will

look at the results of our regression.

5.1 Descriptive statistics

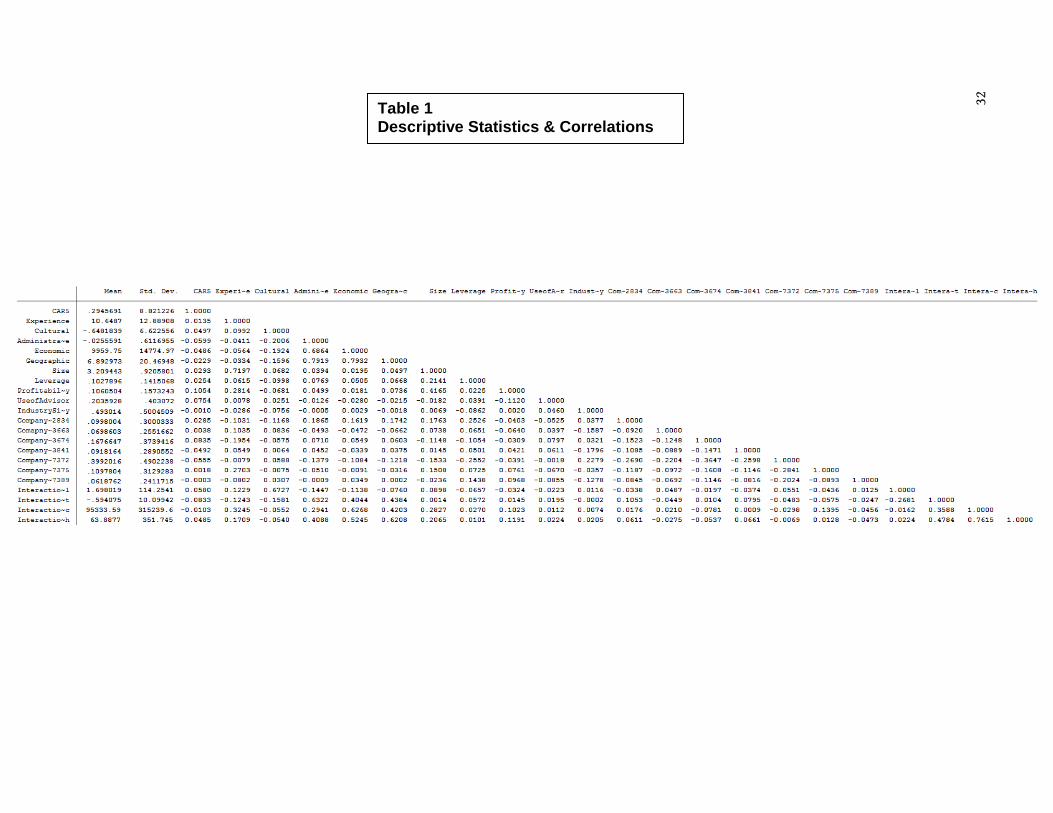

Table 1 provides descriptive statistics for the variables used in the study (means and

standard deviation), as well as their correlations. The positive and high mean for the cumulative

abnormal return represents the belief of the actors and the inclination of the market to see M&A

as a process which will create and bring value to the new entity. But the important standard

deviation value means that there are some important differences between each operation. We can

see that the average experience for a firm in our sample was around 10 M&A which indicate that

this kind of transaction is not an unusual one at all. The companies were doing around 1 M&A a

year. Again the standard deviation is important, so there is a lot of disparities in our observations.

Although most of the correlations are relatively small in magnitude, Administrative distance does

have a correlation of 0.6864 with the Economic distance and a correlation of 0.7919 with

Geographic Distance. Logically the interaction between Administrative distance and Experience

does also have a high correlation with the interaction of Economic distance and Experience and

Geographic Distance and Experience. But these results can be expected since usually the

countries with an important level of economic development are the one with the best network of

infrastructures and the best mode of governance. In the contrary, poor countries usually don’t

have an important infrastructure in place and usually suffer from corruption and other deviances

from the government. So it’s normal that the distance between countries reflects the reality of this

situation.

31

Table 1 Descriptive Statistics & Correlations

32

5.2 Regression’s analysis

Model 1 of these Tables includes only the control variables. For cumulative abnormal

return, this model yielded an R² of 0.0313 (see Table 2). When the model includes the direct

effect of cultural, administrative, economic and geographic distance, the R² increases to 0.0438

(model 2). Finally when we add the interaction between the types of distance and the experience

the R² attains 0.0626 (model 3).

Table 2: OLS Regression Results Cumulative Abnormal Return on a 5 days interval

Model 1 Model 2 Model 3

Coefficient P-Value Coefficient P-Value Coefficient P-Value

Size -0,3017103 0,302 -0,6663014 0,184 -1,891481 0,046 Leverage 1,154941 0,692 1,784288 0,557 -2,766163 0,415 Profitability 7,338762 0,096 7,907841 0,082 1,205356 0,079 Use of Advisor 1,870856 0,015 1,816077 0,02 -0,0037435 0,005 Industry Similarity -0,1796237 0,846 -0,0669927 0,946 0,0618635 0,894 Company Sic Code 2834 1,376768 0,522 2,083461 0,302 -5,200196 0,326 Company Sic Code 3663 0,6206005 0,797 0,4182298 0,859 -6,571764 0,836 Company Sic Code 3674 1,85116 0,272 2,08377 0,21 -5,771764 0,194 Company Sic Code 3841 -1,292742 0,446 -1,340088 0,419 -12,8584 0,453 Company Sic Code 7372 -0,1477541 0,936 -0,3314433 0,848 -5,323556 0,854 Company Sic Code 7375 0,375405 0,834 0,1811823 0,916 -9,091792 0,763 Company Sic Code 7389 0 Omitted 0 Omitted 0 Omitted Constante -0,4765309 0,817 0,3325438 0,881 0,6026397 0,794 Experience

0,0237617 0,464 0,0123235 0,617

Cultural Ditance

0,0750768 0,218 0,0832596 0,289 Administrative Distance

-1,460069 0,007 0,4891881 0,768

Economic Distance

-0,0000305 0,379 0,0000137 0,779 Geographic Distance

0,0366025 0,233 -0,0582853 0,282

Cultural distance x Experience

-0,0012811 0,741 Administrative Distance x Experience

-0,1180074 0,01

Economic Distance x Experience

-0,00000357 0,009 Geographic Distance x Experience

0,6026397 0

R² 0,0313 0,0438 0,0626

But unfortunately, our models don’t respect each and every assumption you need to make

in order to be sure that the OLS regression gives us the best linear unbiased estimators.

33

As we can see, the heteroskedasticity assumption is not respected since the variance of the

observations is not the same across our sample. But it’s not a major problem for our analysis

since we used the cluster option.

Table 2, Model 1 reports the results of the OLS regression of cumulative abnormal return

on the control variables. All the controls are non-significant except for the use of advisor.

Leverage, Profitability and Use of advisor are positively related to cumulative abnormal return. In

the contrary, Industry similarity, some of the industries variables are negatively related to the

performance variable. The negative coefficient for the industries means that being in a different

industry than the one with 7389 as a sic code will have lower your acquisition performance and

the positive coefficient that you will have a higher performance (we use the industry which has

the sic code 7389 as the industry of reference).

-40

-20

020

4060

CA

R5

0 20 40 60 80Experience

Table 3: Scatter plot Performance/Experience

34

5.2.1 Experience Hypothesis 1 predicts that firms with more experience in M&A will enjoy superior

performance. Table 2, model 2 tests this proposition by adding experience and the direct effect of

distance to the regression in model 1. The coefficient on Experience is positive but none

statistically significant at the 5% level. This result doesn’t provide indicative and important

support for Hypothesis 1.

5.2.2 Interaction and moderating effect Hypothesis 2.a predicts that cultural distance will negatively moderate the relationship

between prior experience and firm performance in M&A. To test this, model 3 adds the

interaction between Experience and cultural distance to the regression in model 2. In Column 3,

the coefficient on Experience represents the ‘simple’ effect of prior acquisition experience on

firm performance; this coefficient is not statistically different from zero. In addition, the

coefficient on the interaction term is positive but not statistically significant; thus, we cannot

conclude regarding the moderating effect of cultural distance.

Hypothesis 2.b predicts that administrative distance will negatively moderate the

relationship between prior experience and firm performance in M&A. To test this, model 3 adds

the interaction between Experience and Administrative distance to the regression in model 2. The

coefficient on the interaction term is negative and statistically significant (p-value= 0.01), thus

the more important the administrative distance between the two companies the less the

experience will influence the consequent acquisition performance.

Hypothesis 2.c predicts that economic distance will negatively moderate the relationship

between prior experience and firm performance in M&A. To test this, model 3 adds the

interaction between Experience and Economic distance to the regression in model 2. The

coefficient on the interaction term is negative and statistically significant (p-value= 0.009), thus

the more important the economic distance between the two companies the less the experience

will influence the consequent acquisition performance.

35

Hypothesis 2.d predicts that geographic distance will negatively moderate the relationship

between prior experience and firm performance in M&A. To test this, model 3 adds the

interaction between Experience and Geographic distance to the regression in model 2. The

coefficient on the interaction term is positive and statistically significant (p-value= 0) which

contradict our hypothesis, thus the more important the geographic distance between the two

companies the more the experience will influence the consequent acquisition performance.

Table 3: Summary of results

Expected relation

Effect on performance P-value

H1: Experience + 0,6026397 0,794 H2a: Interaction Experience Cultural - -0,0012811 0,356

H2b: Interaction Experience Administrative

- -0,1180074 0,01

H2c: Interaction Experience Economic - -3,57E-06 0,009

H2d: Interaction Experience Geographic + 0,6026397 0

To conclude, we used the most common regression model to test hypothesis (ordinary

least squared), as well as the clustered option to take care of the multiple observations within one

year. We can say that our analysis allow us to have a better understanding of the theoretical

framework and revealed some interesting and unexpected results.

36

6. Discussion and Conclusion In this paper, we developed a theoretical framework to explain how and under what

circumstances prior experience in acquisition is likely to improve firm performance’s. We tested

our theory over 10 years of data on a large sample of public U.S. corporations belonging to 7

different industries and found that more experience leads to better firm performance. We also

found that only the administrative and economic distance negatively impact the relationship

between experience and consequent performance while the geographic distance has a positive

impact.

We will divide this chapter in three sections. The first one will look at the implications

and contributions of our paper. The second one will point out the limitations and potential gaps.

And finally we will reach the overarching conclusion of our work.

6.1 Contribution and Implication

Prior acquisition experience has been identified as representing an important factor in the

outcome of the consequent performance for M&A (Hayward, 2002; Meschi and Metais, 2013).

It’s because it can help you grab some benefits such as building on technical knowledge (Ahuja

and Katila, 2001), or gaining market power (Baker and Bresnehan, 1985; Barton and Sherman,

1984). Our research doesn’t look at the mechanisms behind the impact of learning but it makes

another contribution to the literature supporting a positive link between prior experience and

performance in M&A.

The direct impact of cultural distance on acquisition was researched a lot and its

significance was proven multiple times (Barkema et al, 1996; Reus and Lamont, 2009). But its

impact on learning was a bit overlooked and apparently for a good reason since it didn’t seem to

have any impact on the learning process during the M&A. It might be linked to our performance

variable which look at the market reaction and the short term benefits of the M&A and thus might

not take into consideration long term problems. We can imagine that the market might overlooks

37

the potential pitfalls that arise when two companies with different culture try to exchange

knowledge and learn from each other.

The impact of our 3 other types of distance namely, Administrative, economic and

geographic was mostly researched for their influence on trade and learning (Ghemawat, 2001;

Hartig 2011) but not on their possible link with M&A. Surprisingly the geographic distance is

supposed to enhance the effect of learning on acquisition performance. It can be explained by the

fact that when you acquire geographic distant companies you also acquire their network. You are

thus able to create extra-national ties which allow you to access new and different knowledge

(Boschma, 2005a). By creating ties the company is also enhancing its social capital and thus is

able to increase its information volume and diversity (Koka & Prescott, 2002). The firm

potential’s for synergy improves thank to the geographic distance.

In the contrary as expected, the administrative and the economic distance decrease the

effect of learning on acquisition performance. These evidences support the view of Cohen and

Levinthal (1990) that the more different the knowledge acquired is, the more difficult it will be to

integrate and use it.

By elaborating on the theoretical backgrounds of prior experience and the factors

amplifying or diminishing the associated benefits, this paper not only contributes to our

understanding of experience in acquisition, but also extends the literature on M&A and the types

of distance beyond the well-established fact that learning, impact the long term health of the firm.

The paper’s results also have important implications for practice, in which the

ramifications of learning during, and especially after the acquisition phase have received

significant attention. In our sample, firms generate a greater ability to learn from the acquisition

experience alone. Acquisitions are a complex practice but lessons from one acquisition can be

extrapolated to another, or at least some best practices can be derived from that. In the present

logic, serial acquirers should be able to have a competitive advantage over their competitions

since they’re supposed to better conduct the subsequent M&A. But it’s not a sustainable

competitive advantage since it can be easily replicated. However, while many scholars have

38

explained which the benefits of learning are, rigorous systematic evidence regarding how others

variables can moderate the relationship between experience and firm performance has been

lacking.

We address this gap in the literature using a rich panel dataset containing seven different

industries, which allows us to control for a wide range of observable and unobservable factors

that influence firm performance as well as extending our interpretations to a bigger range of

corporations. We find that, ceteris paribus, a given firm has less chance to learn from its mistakes

when the administrative and economic distance between the acquirer and acquired are high and

thus also suffers from an inferior acquisition performance. And in the contrary, the firm profits

more from the learning benefits when the geographic distance between the two firms is high and

thus enjoys a better performance. Thus, our results suggest that CEOs when assessing the

potential candidate for a merger or an acquisition should ensure to minimize the administrative

and economic distance and try to maximize the geographic distance in order to achieve the best

performance possible.

6.2 Limitations

This study is not without limitations, many of which may indicate possible paths for

future research. While the quantitative and secondary data approach in this study has clear

strengths, we nonetheless acknowledge that the small sample field studies and qualitative

methods employed in other research domains may offer a richer and more precise understanding

of context than our large sample methods can. In particular, such studies may provide supporting

anecdotal evidence and a different point of view regarding the mechanisms that we theorize are

behind the benefits of learning for acquisition performance. We regard the different methods as

mutually complementary. It is only through a thorough investigation using multiple analyses that

we will gain the best appreciation of how learning and distance interact in M&A and can make

firm performance optimal.

The choice of our performance and control variables also had an impact on our analysis.

The event study method is a usual and logical measure in M&A but it’s focusing only on the

39

market reaction and the short term impact on the firm. In order to have a more complete view of

the phenomena, some long term measure of performance, such as the increase of Tobin’ Q or

return on assets over two year, can add another dimension to our findings. Furthermore, even if

we were able to control for a wide range of variables, there are certainly others factors that

impact the performance of an M&A, such as the size of the deal, and thus including them in an

analysis can enhance the quality of it.

Finally our sample consists only of US based company listed on the stock market

belonging to 7 different industries. It’s unfortunately linked with the scarcity of data for other

market and countries but it can bias our results. What is true for the US is not necessarily true in

Japan. As well as the size of the company can have a big impact on an acquisition results, if a

small firm acquire another firm it will have a bigger impact than if a multi-billion dollars

company acquires the same firm. The increase of geographic areas and type of corporations can

be two paths to follow in order to complete the puzzle.

6.3 Conclusion

This article began with the fact that learning from acquisition is a complex process but

can be improve by experience. Findings here suggest that experience is not only necessary but

also a sufficient condition for acquirer learning. But the learning process is not evolving inside a

bubble; a lot of factors can influence the easiness of reaping benefits from it and the impact it can

have on a corporation. The strategy of acquiring by doing usual due diligence may work, but will

not bring the best of the purchase. Instead, by looking at other factors such as the administrative,

economic and geographic distance between the two companies, you will have a better overview