Latin America Securitization: 2013 Outlook

25

STRUCTURED FINANCE Table of Contents: EXECUTIVE SUMMARY 1 ARGENTINA 2 BRAZIL 7 MEXICO 13 PANAMA 17 APPENDIX 1: 2012 REVIEW 18 Argentina 18 Brazil 19 Mexico 20 RATING LIST 22 Moody’s-Rated Argentine ABS Transactions 22 Moody’s-Rated Brazilian ABS Transactions 23 Moody’s-Rated Mexican ABS Transactions 23 MOODY’S RELATED RESEARCH 24 Analyst Contacts: SAO PAULO +55.11.3043.7300 Johann Grieneisen +55.11.3043.7305 Vice President - Senior Analyst [email protected] Sara Tonello +55.11.3043.7331 Associate Analyst [email protected] » contacts continued on the last page MOODY'S CLIENT SERVICES: New York: +1.212.553.1653 Tokyo: +81.3.5408.4100 London: +44.20.7772.5454 Hong Kong: +852.3551.3077 Sydney: +612.9270.8100 Singapore: +65.6398.8308 ADDITIONAL CONTACTS: Website: www.moodys.com DECEMBER 11, 2012 Latin America Securitization: 2013 Outlook Executive Summary The credit quality of new transactions in Argentina, Brazil and Mexico, the three most important markets, will be strong. In Argentina, new transactions in 2013 will have a high degree of total credit enhancement, consisting of substantial excess spread and significant subordination levels. In Brazil, new transactions will be stronger than transactions brought to market over the past two years because of more selective underwriting on the part of sponsors. Also in Brazil, the role-out of new Brazilian regulations will require new transactions to have structures that eliminate commingling risk entirely, which will further de-link the credit risk of the transaction from the corporate credit risk of the sponsor. In Mexico, the credit quality of new transactions will be strong, particularly RMBS issuance from the government-related issuers such as INFONAVIT and FOVISSTE, which dominate the market. In Argentina and Brazil, performance in 2013 of existing outstanding transactions will remain stable. Although delinquency levels rose in 2012 in both countries, the deterioration in asset performance remains within our original expectations. In both jurisdictions, high levels of credit enhancement in transactions have protected investors well. In Argentina delinquencies will improve modestly in 2013, to the 7%-9% range. In Brazil the high delinquency rates will remain at their current 6%-8% levels, given higher household indebtedness, a domestic phenomenon that will continue in 2013. Performance of existing transactions in Mexico, however, will be sponsor- specific. The credit quality of existing securitizations other than RMBS issued by the non-bank Sofol 1 sector will remain strong. However, the performance of Sofol RMBS of mortgages to low- income borrowers will continue to face serious challenges. Issuance volumes in 2013 in Argentina will remain steady for the most part, because sponsors rely on securitization as a funding source. Brazil will see a rebound after an anemic 2012. New regulatory requirements have been clarified, and sponsors side-lined in 2012 will re-enter the market. In addition, historically low interest rates are making securitization transaction more attractive to investors. Mexican issuance will also hold steady in 2013, driven by recurring RMBS issuance. 1 Sofols (Sociedad Financiera de Objeto Limitado) and Sofoms (Sociedad Financiera de Objeto Múltiple) are non-bank financial institutions operating in Mexico and engaged in mortgage and construction lending.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Latin America Securitization: 2013 Outlook

SPECIAL COMMENT

STRUCTURED FINANCE

Table of Contents:

EXECUTIVE SUMMARY 1 ARGENTINA 2 BRAZIL 7 MEXICO 13 PANAMA 17 APPENDIX 1: 2012 REVIEW 18

Argentina 18 Brazil 19 Mexico 20

RATING LIST 22 Moody’s-Rated Argentine ABS Transactions 22 Moody’s-Rated Brazilian ABS Transactions 23 Moody’s-Rated Mexican ABS Transactions 23

MOODY’S RELATED RESEARCH 24

Analyst Contacts:

SAO PAULO +55.11.3043.7300

Johann Grieneisen +55.11.3043.7305 Vice President - Senior Analyst [email protected]

Sara Tonello +55.11.3043.7331 Associate Analyst [email protected]

» contacts continued on the last page

MOODY'S CLIENT SERVICES: New York: +1.212.553.1653 Tokyo: +81.3.5408.4100 London: +44.20.7772.5454 Hong Kong: +852.3551.3077 Sydney: +612.9270.8100 Singapore: +65.6398.8308

ADDITIONAL CONTACTS: Website: www.moodys.com

DECEMBER 11, 2012

Latin America Securitization: 2013 Outlook

Executive Summary

The credit quality of new transactions in Argentina, Brazil and Mexico, the three most important markets, will be strong. In Argentina, new transactions in 2013 will have a high degree of total credit enhancement, consisting of substantial excess spread and significant subordination levels. In Brazil, new transactions will be stronger than transactions brought to market over the past two years because of more selective underwriting on the part of sponsors. Also in Brazil, the role-out of new Brazilian regulations will require new transactions to have structures that eliminate commingling risk entirely, which will further de-link the credit risk of the transaction from the corporate credit risk of the sponsor. In Mexico, the credit quality of new transactions will be strong, particularly RMBS issuance from the government-related issuers such as INFONAVIT and FOVISSTE, which dominate the market.

In Argentina and Brazil, performance in 2013 of existing outstanding transactions will remain stable. Although delinquency levels rose in 2012 in both countries, the deterioration in asset performance remains within our original expectations. In both jurisdictions, high levels of credit enhancement in transactions have protected investors well. In Argentina delinquencies will improve modestly in 2013, to the 7%-9% range. In Brazil the high delinquency rates will remain at their current 6%-8% levels, given higher household indebtedness, a domestic phenomenon that will continue in 2013.

Performance of existing transactions in Mexico, however, will be sponsor- specific. The credit quality of existing securitizations other than RMBS issued by the non-bank Sofol1 sector will remain strong. However, the performance of Sofol RMBS of mortgages to low-income borrowers will continue to face serious challenges.

Issuance volumes in 2013 in Argentina will remain steady for the most part, because sponsors rely on securitization as a funding source. Brazil will see a rebound after an anemic 2012. New regulatory requirements have been clarified, and sponsors side-lined in 2012 will re-enter the market. In addition, historically low interest rates are making securitization transaction more attractive to investors. Mexican issuance will also hold steady in 2013, driven by recurring RMBS issuance.

1 Sofols (Sociedad Financiera de Objeto Limitado) and Sofoms (Sociedad Financiera de Objeto Múltiple) are non-bank financial institutions operating in Mexico and

engaged in mortgage and construction lending.

STRUCTURED FINANCE

2 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

Argentina

Credit Quality of New Transactions Will Be Slightly Better in 2013

New Loans Will Be Slightly Stronger We believe that future deals will be slightly stronger than 2012’s, as a result of the better credit quality of new loans. Because the low level of economic activity in 2012 has hurt the performance of securitized consumer loan portfolios, most originators of consumer loans are aiming to lower the likelihood of borrower defaults and losses on new loans. To this end, the originators, primarily banks, consumer finance companies and home appliances stores, are reducing the average term of the loans and decreasing the exposure to riskier lines of business. These actions will continue in 2013, which will likely improve the performance of new transactions.

New Structures Will Continue to Be Very Strong

New structures in the Argentine securitization market will continue to be very strong. Since Argentina’s 2002 economic crisis, most securitizations have benefitted from high initial credit enhancement levels, turbo-sequential payment structures and high excess spread levels.

The Argentine market will continue to have no or limited exposure to global banks’ risks. The originators of the underlying loans in Argentine securitizations are primarily local financial institutions, consumer finance companies and home-appliances stores.

Servicer disruption risk continues to be the main risk in Argentine securitizations, particularly for transactions with in-store payments. Delinquencies will likely increase during a servicing transfer if borrowers keep paying the original servicer even after the new trustee has directed them to make payments to other parties such as the backup servicer. In addition, the handling of cash heightens commingling risk if the original servicer does not remit the cash to the trust account.

Performance in 2013 Will Improve Only Slightly

After having risen in 2012, delinquencies levels will decline slightly in 2013, reflecting the benefit of a stronger economic activity than in 2012. Yet while delinquency levels will fall, they will do so only slightly, because inflation-related factors, such as the deterioration of real salaries, will continue to negatively affect performance Our central scenario for Argentina is for an annual growth rate of 3.0%-4.0% in 2013. However, if macro-economic conditions deteriorate again in 2013 as in 2012, delinquency levels will increase significantly.

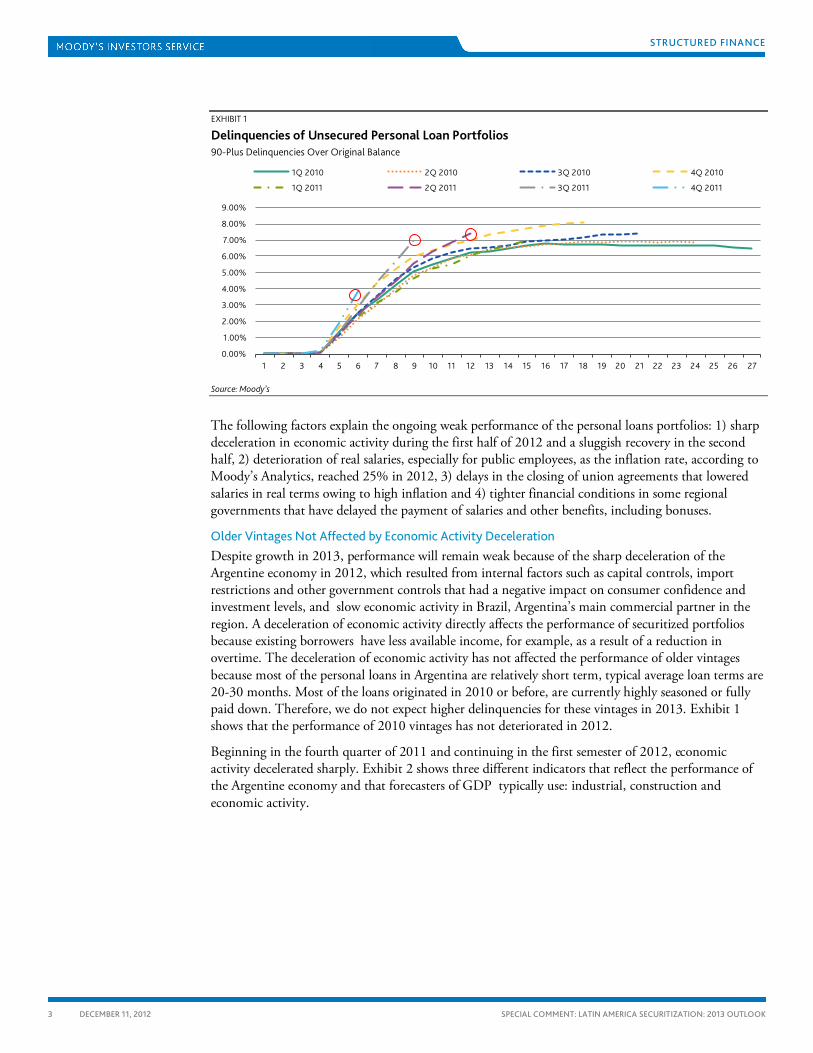

The poor delinquency performance applies to most vintages of loans, in particular loans from late 2011 and early 2012. Exhibit 1 shows the performance of static pools of personal loans from frequent issuers in the Argentine securitization market.

The indices do not include loans with automatic deduction of installments from the borrower’s paycheck. The performance of loans with automatic deduction features has not deteriorated, because these features decrease significantly the probability of default of the borrowers. Delinquencies levels are lower than 1.5%-2.0% for this asset type.

STRUCTURED FINANCE

3 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

EXHIBIT 1

Delinquencies of Unsecured Personal Loan Portfolios 90-Plus Delinquencies Over Original Balance

Source: Moody’s

The following factors explain the ongoing weak performance of the personal loans portfolios: 1) sharp deceleration in economic activity during the first half of 2012 and a sluggish recovery in the second half, 2) deterioration of real salaries, especially for public employees, as the inflation rate, according to Moody’s Analytics, reached 25% in 2012, 3) delays in the closing of union agreements that lowered salaries in real terms owing to high inflation and 4) tighter financial conditions in some regional governments that have delayed the payment of salaries and other benefits, including bonuses.

Older Vintages Not Affected by Economic Activity Deceleration Despite growth in 2013, performance will remain weak because of the sharp deceleration of the Argentine economy in 2012, which resulted from internal factors such as capital controls, import restrictions and other government controls that had a negative impact on consumer confidence and investment levels, and slow economic activity in Brazil, Argentina’s main commercial partner in the region. A deceleration of economic activity directly affects the performance of securitized portfolios because existing borrowers have less available income, for example, as a result of a reduction in overtime. The deceleration of economic activity has not affected the performance of older vintages because most of the personal loans in Argentina are relatively short term, typical average loan terms are 20-30 months. Most of the loans originated in 2010 or before, are currently highly seasoned or fully paid down. Therefore, we do not expect higher delinquencies for these vintages in 2013. Exhibit 1 shows that the performance of 2010 vintages has not deteriorated in 2012.

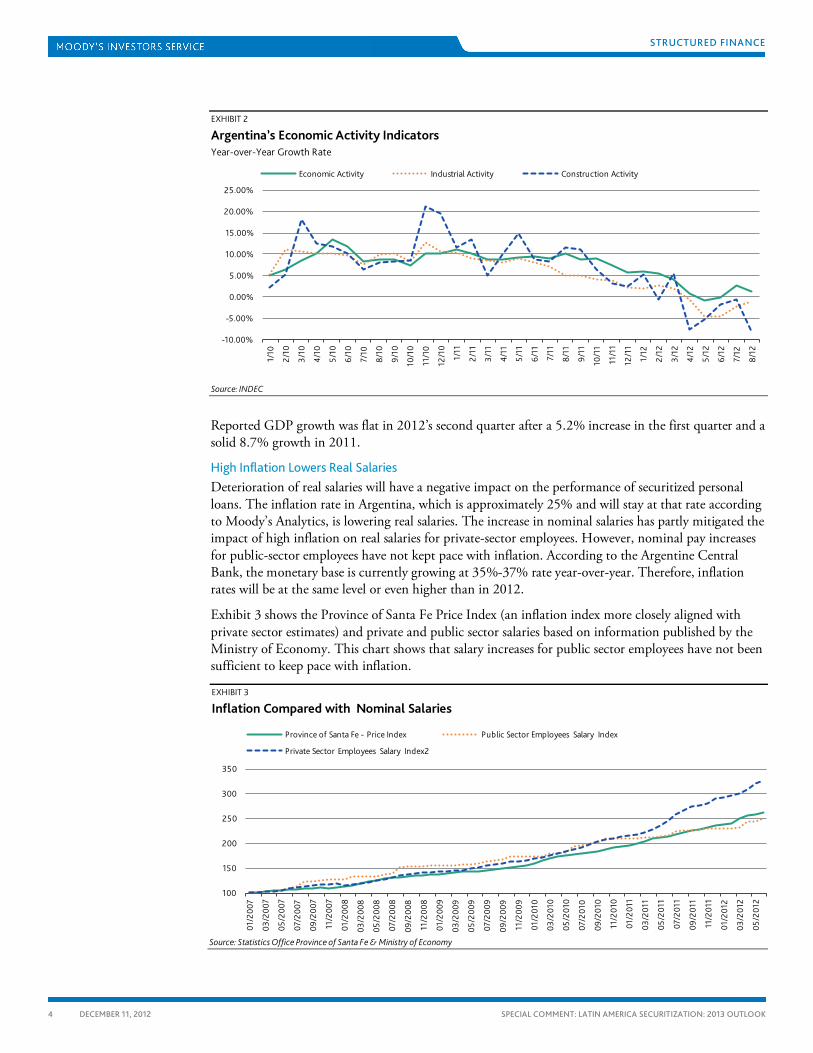

Beginning in the fourth quarter of 2011 and continuing in the first semester of 2012, economic activity decelerated sharply. Exhibit 2 shows three different indicators that reflect the performance of the Argentine economy and that forecasters of GDP typically use: industrial, construction and economic activity.

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

1Q 2010 2Q 2010 3Q 2010 4Q 2010

1Q 2011 2Q 2011 3Q 2011 4Q 2011

STRUCTURED FINANCE

4 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

EXHIBIT 2

Argentina’s Economic Activity Indicators Year-over-Year Growth Rate

Source: INDEC

Reported GDP growth was flat in 2012’s second quarter after a 5.2% increase in the first quarter and a solid 8.7% growth in 2011.

High Inflation Lowers Real Salaries Deterioration of real salaries will have a negative impact on the performance of securitized personal loans. The inflation rate in Argentina, which is approximately 25% and will stay at that rate according to Moody’s Analytics, is lowering real salaries. The increase in nominal salaries has partly mitigated the impact of high inflation on real salaries for private-sector employees. However, nominal pay increases for public-sector employees have not kept pace with inflation. According to the Argentine Central Bank, the monetary base is currently growing at 35%-37% rate year-over-year. Therefore, inflation rates will be at the same level or even higher than in 2012.

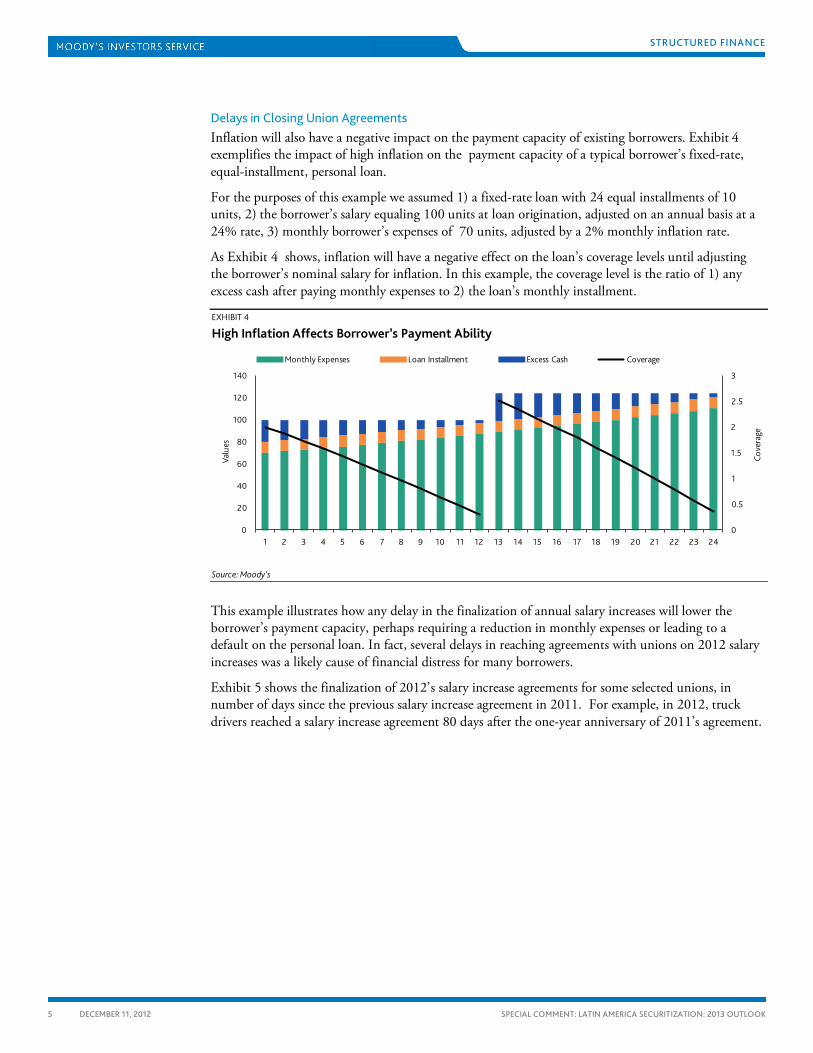

Exhibit 3 shows the Province of Santa Fe Price Index (an inflation index more closely aligned with private sector estimates) and private and public sector salaries based on information published by the Ministry of Economy. This chart shows that salary increases for public sector employees have not been sufficient to keep pace with inflation.

EXHIBIT 3

Inflation Compared with Nominal Salaries

Source: Statistics Office Province of Santa Fe & Ministry of Economy

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

1/10

2/10

3/10

4/10

5/10

6/10

7/10

8/10

9/10

10/1

0

11/1

0

12/1

0

1/11

2/11

3/11

4/11

5/11

6/11

7/11

8/11

9/11

10/1

1

11/1

1

12/1

1

1/12

2/12

3/12

4/12

5/12

6/12

7/12

8/12

Economic Activity Industrial Activity Construction Activity

100

150

200

250

300

350

01/2

007

03/2

007

05/2

007

07/2

007

09/2

007

11/2

007

01/2

008

03/2

008

05/2

008

07/2

008

09/2

008

11/2

008

01/2

009

03/2

009

05/2

009

07/2

009

09/2

009

11/2

009

01/2

010

03/2

010

05/2

010

07/2

010

09/2

010

11/2

010

01/2

011

03/2

011

05/2

011

07/2

011

09/2

011

11/2

011

01/2

012

03/2

012

05/2

012

Province of Santa Fe - Price Index Public Sector Employees Salary Index

Private Sector Employees Salary Index2

STRUCTURED FINANCE

5 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

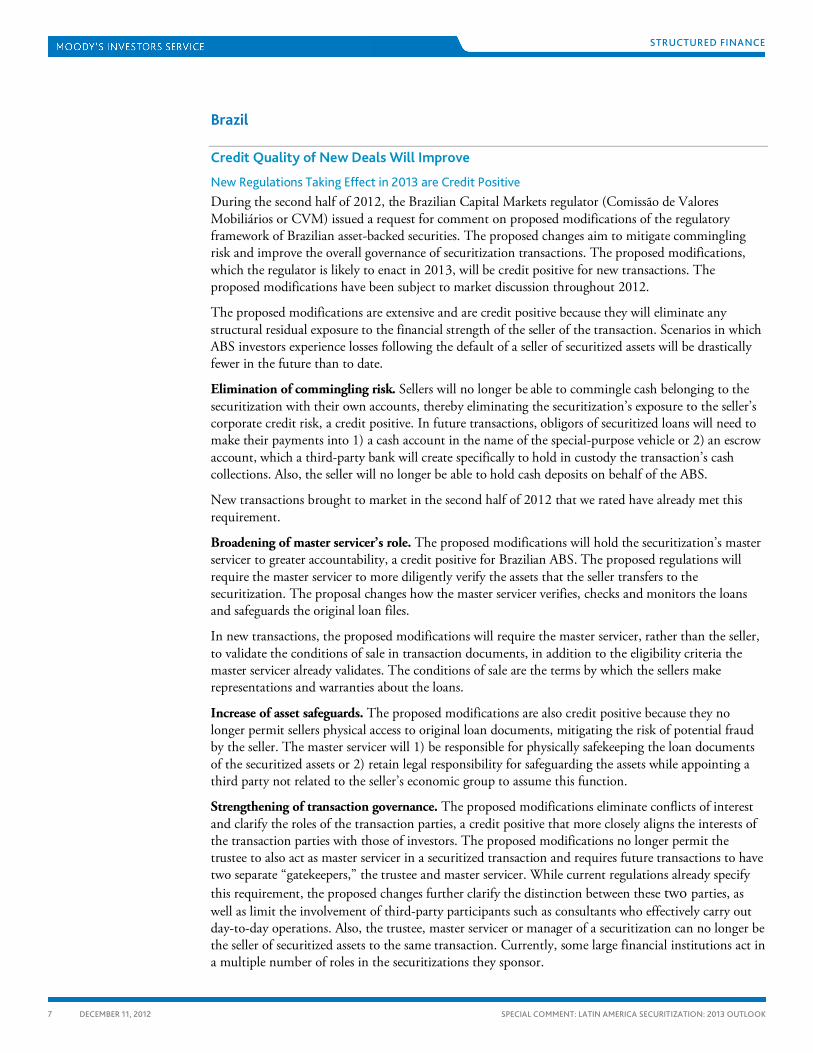

Delays in Closing Union Agreements Inflation will also have a negative impact on the payment capacity of existing borrowers. Exhibit 4 exemplifies the impact of high inflation on the payment capacity of a typical borrower’s fixed-rate, equal-installment, personal loan.

For the purposes of this example we assumed 1) a fixed-rate loan with 24 equal installments of 10 units, 2) the borrower’s salary equaling 100 units at loan origination, adjusted on an annual basis at a 24% rate, 3) monthly borrower’s expenses of 70 units, adjusted by a 2% monthly inflation rate.

As Exhibit 4 shows, inflation will have a negative effect on the loan’s coverage levels until adjusting the borrower’s nominal salary for inflation. In this example, the coverage level is the ratio of 1) any excess cash after paying monthly expenses to 2) the loan’s monthly installment.

EXHIBIT 4

High Inflation Affects Borrower’s Payment Ability

Source: Moody’s

This example illustrates how any delay in the finalization of annual salary increases will lower the borrower’s payment capacity, perhaps requiring a reduction in monthly expenses or leading to a default on the personal loan. In fact, several delays in reaching agreements with unions on 2012 salary increases was a likely cause of financial distress for many borrowers.

Exhibit 5 shows the finalization of 2012’s salary increase agreements for some selected unions, in number of days since the previous salary increase agreement in 2011. For example, in 2012, truck drivers reached a salary increase agreement 80 days after the one-year anniversary of 2011’s agreement.

0

0.5

1

1.5

2

2.5

3

0

20

40

60

80

100

120

140

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Cove

rage

Valu

es

Monthly Expenses Loan Installment Excess Cash Coverage

STRUCTURED FINANCE

6 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

EXHIBIT 5

Delays in Union Agreements Number of Days Since 2011’s Agreement Anniversary

Source: Moody’s

Tighter Financial Conditions Affect Some Regional Governments As in the first half of 2012, in 2013 some regional governments, municipalities and provinces will suffer from tighter financial conditions that cause delays in the payment of salaries and other benefits, such as year-end bonuses. These localities included the Province of Buenos Aires, which has a large base of public employees. These tighter conditions will continue in 2013 because of high inflation increases the salary expenditures of local and regional governments.

Credit Enhancement Will Mitigate Higher Delinquency Levels in 2013 Higher delinquency levels are within our expectations and will not materially weaken rated securitizations, because most deals in Argentina benefit from high credit enhancement levels. Senior tranches, generally rated Aaa.ar (or Ba3 on the Global Scale), have an initial subordination of 15-20%. This subordination level will increase over time because of a turbo sequential payment structure that captures all of the excess spread available in the transaction.

These transactions also benefit from high excess spread levels. Excess spread is the difference between the interest rate yield on the securitized assets and the coupon on the different securities, minus trust expenses and taxes. This spread will typically be in the 25% to 45% range on an annual basis depending on the characteristics of the assets and prevailing interest rates.

Issuance Will Remain Strong in 2013

Issuance Levels Will Rise Mainly Owing to High Inflation We expect higher issuance levels in Argentina in 2013, primarily owing to high inflation levels. Inflation has a direct impact on the average loan balances.

Also, several originators in the market rely on securitizations as a continuing source of funding and will continue to do so through 2013.

On November 9, the Central Bank of Argentina published a new regulation regarding minimal capital requirements for securitization originated by financial institutions. The purpose is to align current local regulations to Basel II. This new regulation will have a negative impact on the issuance level of securitizations backed by loans originated by financial institutions, because it increases the capital requirements for residual tranches.

0 10 20 30 40 50 60 70 80 90

Teachers

Commerce

Railroad

Construction

Truck Drivers

STRUCTURED FINANCE

7 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

Brazil

Credit Quality of New Deals Will Improve

New Regulations Taking Effect in 2013 are Credit Positive During the second half of 2012, the Brazilian Capital Markets regulator (Comissão de Valores Mobiliários or CVM) issued a request for comment on proposed modifications of the regulatory framework of Brazilian asset-backed securities. The proposed changes aim to mitigate commingling risk and improve the overall governance of securitization transactions. The proposed modifications, which the regulator is likely to enact in 2013, will be credit positive for new transactions. The proposed modifications have been subject to market discussion throughout 2012.

The proposed modifications are extensive and are credit positive because they will eliminate any structural residual exposure to the financial strength of the seller of the transaction. Scenarios in which ABS investors experience losses following the default of a seller of securitized assets will be drastically fewer in the future than to date.

Elimination of commingling risk. Sellers will no longer be able to commingle cash belonging to the securitization with their own accounts, thereby eliminating the securitization’s exposure to the seller’s corporate credit risk, a credit positive. In future transactions, obligors of securitized loans will need to make their payments into 1) a cash account in the name of the special-purpose vehicle or 2) an escrow account, which a third-party bank will create specifically to hold in custody the transaction’s cash collections. Also, the seller will no longer be able to hold cash deposits on behalf of the ABS.

New transactions brought to market in the second half of 2012 that we rated have already met this requirement.

Broadening of master servicer’s role. The proposed modifications will hold the securitization’s master servicer to greater accountability, a credit positive for Brazilian ABS. The proposed regulations will require the master servicer to more diligently verify the assets that the seller transfers to the securitization. The proposal changes how the master servicer verifies, checks and monitors the loans and safeguards the original loan files.

In new transactions, the proposed modifications will require the master servicer, rather than the seller, to validate the conditions of sale in transaction documents, in addition to the eligibility criteria the master servicer already validates. The conditions of sale are the terms by which the sellers make representations and warranties about the loans.

Increase of asset safeguards. The proposed modifications are also credit positive because they no longer permit sellers physical access to original loan documents, mitigating the risk of potential fraud by the seller. The master servicer will 1) be responsible for physically safekeeping the loan documents of the securitized assets or 2) retain legal responsibility for safeguarding the assets while appointing a third party not related to the seller’s economic group to assume this function.

Strengthening of transaction governance. The proposed modifications eliminate conflicts of interest and clarify the roles of the transaction parties, a credit positive that more closely aligns the interests of the transaction parties with those of investors. The proposed modifications no longer permit the trustee to also act as master servicer in a securitized transaction and requires future transactions to have two separate “gatekeepers,” the trustee and master servicer. While current regulations already specify this requirement, the proposed changes further clarify the distinction between these two parties, as well as limit the involvement of third-party participants such as consultants who effectively carry out day-to-day operations. Also, the trustee, master servicer or manager of a securitization can no longer be the seller of securitized assets to the same transaction. Currently, some large financial institutions act in a multiple number of roles in the securitizations they sponsor.

STRUCTURED FINANCE

8 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

The liquidation in 2012 by the Brazilian Central Bank of Banco Cruzeiro do Sul and the central bank’s intervention in Banco BVA have raised market awareness of risks relating to commingling and governance of securitizations that the proposed new regulations address. The securitizations of both sponsors allowed for commingling of cash flows, which disrupted cash flows to investors in both instances.

In the case of Banco Cruzeiro do Sul, the sponsor stopped transferring cash flows belonging to one of its securitizations (FIDC BC Sul Verax II) to the transaction master servicer following the bank’s liquidation on 14 September 2012. Transaction participants face operational challenges in separating the cash flows belonging to the securitization from cash flows belonging to the insolvent bank. The first lump-sum of partially recovered cash flows was not transferred to the securitization until 59 days after the liquidation. Re-establishment of ongoing periodic transfers of cash flows had yet to occur as of the writing of this report, or 74 days following liquidation of Banco Cruzeiro do Sul.

In the case of Banco BVA, according to media reports, the sponsor, a distressed bank, diverted cash flows belonging to the securitization to repay maturing bank debt because the bank faced deposit withdrawals in the weeks up to the Central Bank’s final intervention on19 October 2012.

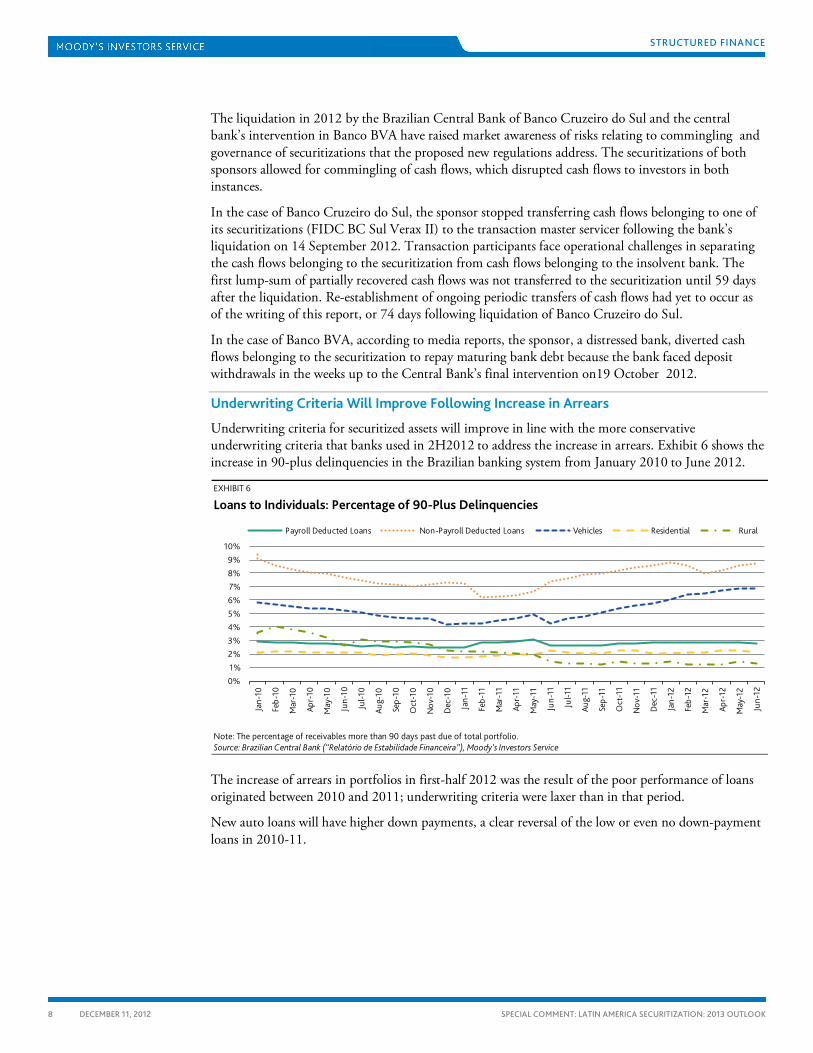

Underwriting Criteria Will Improve Following Increase in Arrears

Underwriting criteria for securitized assets will improve in line with the more conservative underwriting criteria that banks used in 2H2012 to address the increase in arrears. Exhibit 6 shows the increase in 90-plus delinquencies in the Brazilian banking system from January 2010 to June 2012.

EXHIBIT 6

Loans to Individuals: Percentage of 90-Plus Delinquencies

Note: The percentage of receivables more than 90 days past due of total portfolio. Source: Brazilian Central Bank (“Relatório de Estabilidade Financeira”), Moody’s Investors Service

The increase of arrears in portfolios in first-half 2012 was the result of the poor performance of loans originated between 2010 and 2011; underwriting criteria were laxer than in that period.

New auto loans will have higher down payments, a clear reversal of the low or even no down-payment loans in 2010-11.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr-

12

May

-12

Jun-

12

Payroll Deducted Loans Non-Payroll Deducted Loans Vehicles Residential Rural

STRUCTURED FINANCE

9 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

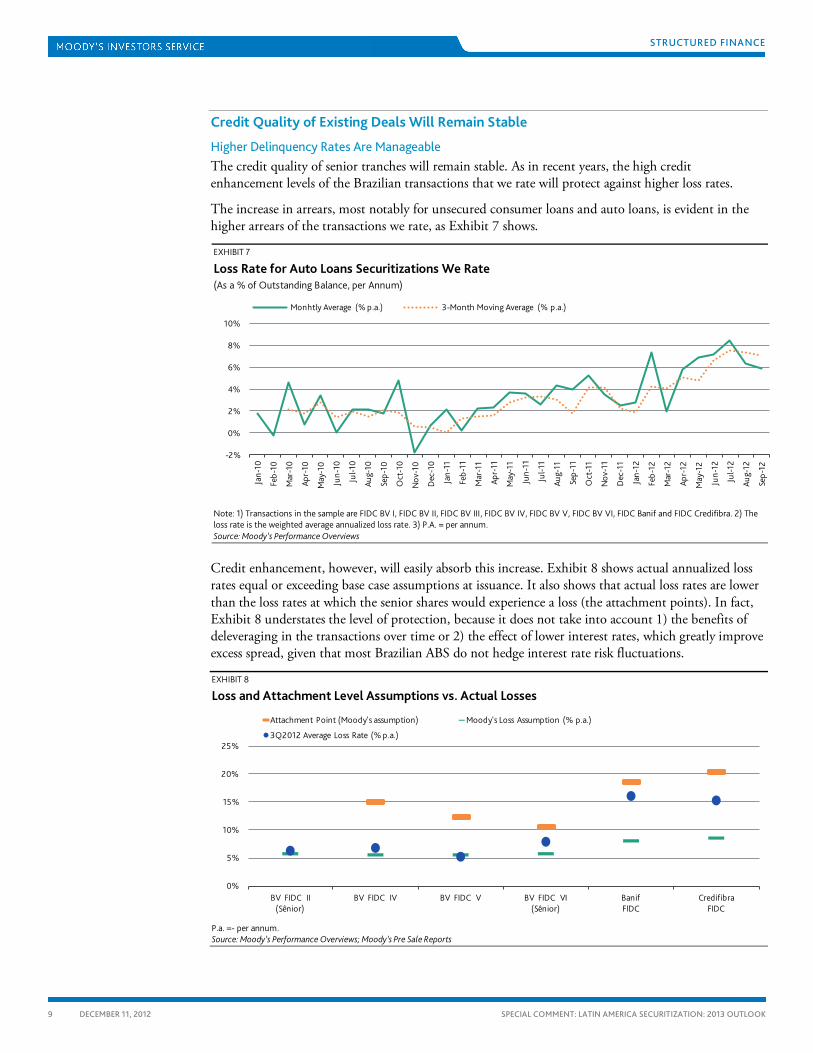

Credit Quality of Existing Deals Will Remain Stable

Higher Delinquency Rates Are Manageable The credit quality of senior tranches will remain stable. As in recent years, the high credit enhancement levels of the Brazilian transactions that we rate will protect against higher loss rates.

The increase in arrears, most notably for unsecured consumer loans and auto loans, is evident in the higher arrears of the transactions we rate, as Exhibit 7 shows.

EXHIBIT 7

Loss Rate for Auto Loans Securitizations We Rate (As a % of Outstanding Balance, per Annum)

Note: 1) Transactions in the sample are FIDC BV I, FIDC BV II, FIDC BV III, FIDC BV IV, FIDC BV V, FIDC BV VI, FIDC Banif and FIDC Credifibra. 2) The loss rate is the weighted average annualized loss rate. 3) P.A. = per annum. Source: Moody’s Performance Overviews

Credit enhancement, however, will easily absorb this increase. Exhibit 8 shows actual annualized loss rates equal or exceeding base case assumptions at issuance. It also shows that actual loss rates are lower than the loss rates at which the senior shares would experience a loss (the attachment points). In fact, Exhibit 8 understates the level of protection, because it does not take into account 1) the benefits of deleveraging in the transactions over time or 2) the effect of lower interest rates, which greatly improve excess spread, given that most Brazilian ABS do not hedge interest rate risk fluctuations.

EXHIBIT 8

Loss and Attachment Level Assumptions vs. Actual Losses

P.a. =- per annum. Source: Moody’s Performance Overviews; Moody’s Pre Sale Reports

-2%

0%

2%

4%

6%

8%

10%

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

- 10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr-

12

May

-12

Jun-

12

Jul-1

2

Aug-

12

Sep-

12

Monhtly Average (% p.a.) 3-Month Moving Average (% p.a.)

0%

5%

10%

15%

20%

25%

BV FIDC II(Sênior)

BV FIDC IV BV FIDC V BV FIDC VI(Sênior)

BanifFIDC

Credifibra FIDC

Attachment Point (Moody's assumption) Moody's Loss Assumption (% p.a.)

3Q2012 Average Loss Rate (% p.a.)

STRUCTURED FINANCE

10 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

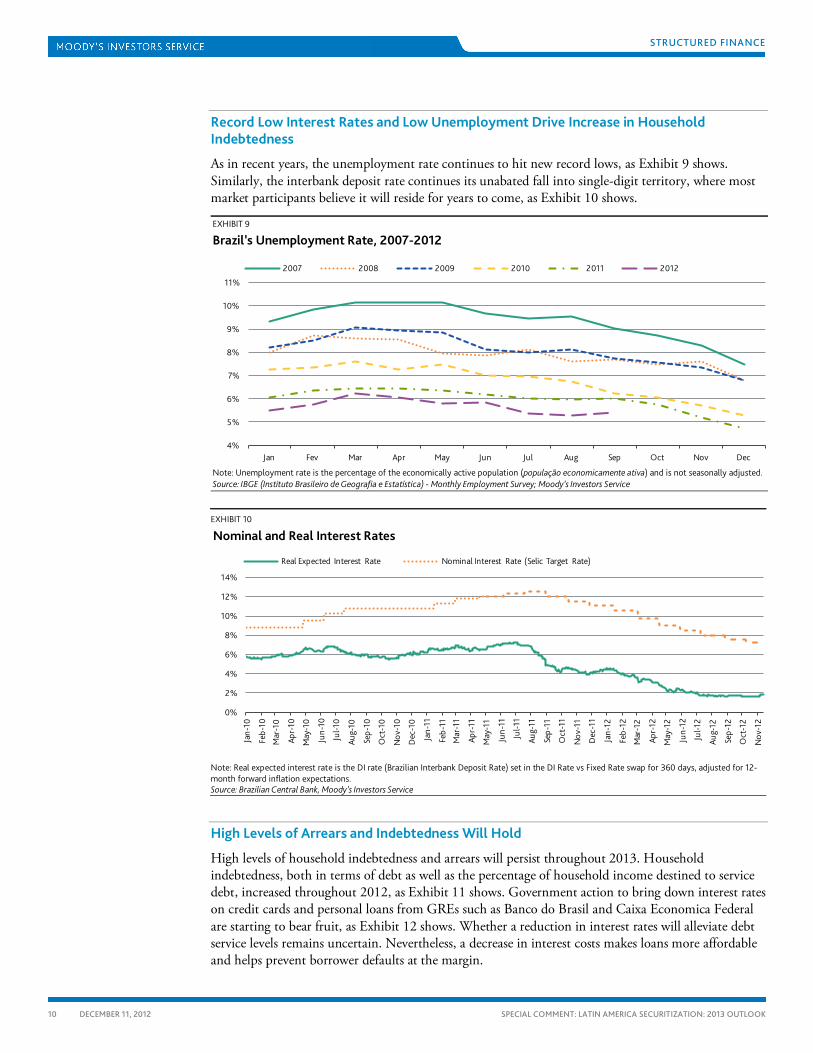

Record Low Interest Rates and Low Unemployment Drive Increase in Household Indebtedness

As in recent years, the unemployment rate continues to hit new record lows, as Exhibit 9 shows. Similarly, the interbank deposit rate continues its unabated fall into single-digit territory, where most market participants believe it will reside for years to come, as Exhibit 10 shows.

EXHIBIT 9

Brazil’s Unemployment Rate, 2007-2012

Note: Unemployment rate is the percentage of the economically active population (população economicamente ativa) and is not seasonally adjusted. Source: IBGE (Instituto Brasileiro de Geografia e Estatística) - Monthly Employment Survey; Moody’s Investors Service

EXHIBIT 10

Nominal and Real Interest Rates

Note: Real expected interest rate is the DI rate (Brazilian Interbank Deposit Rate) set in the DI Rate vs Fixed Rate swap for 360 days, adjusted for 12-month forward inflation expectations. Source: Brazilian Central Bank, Moody’s Investors Service

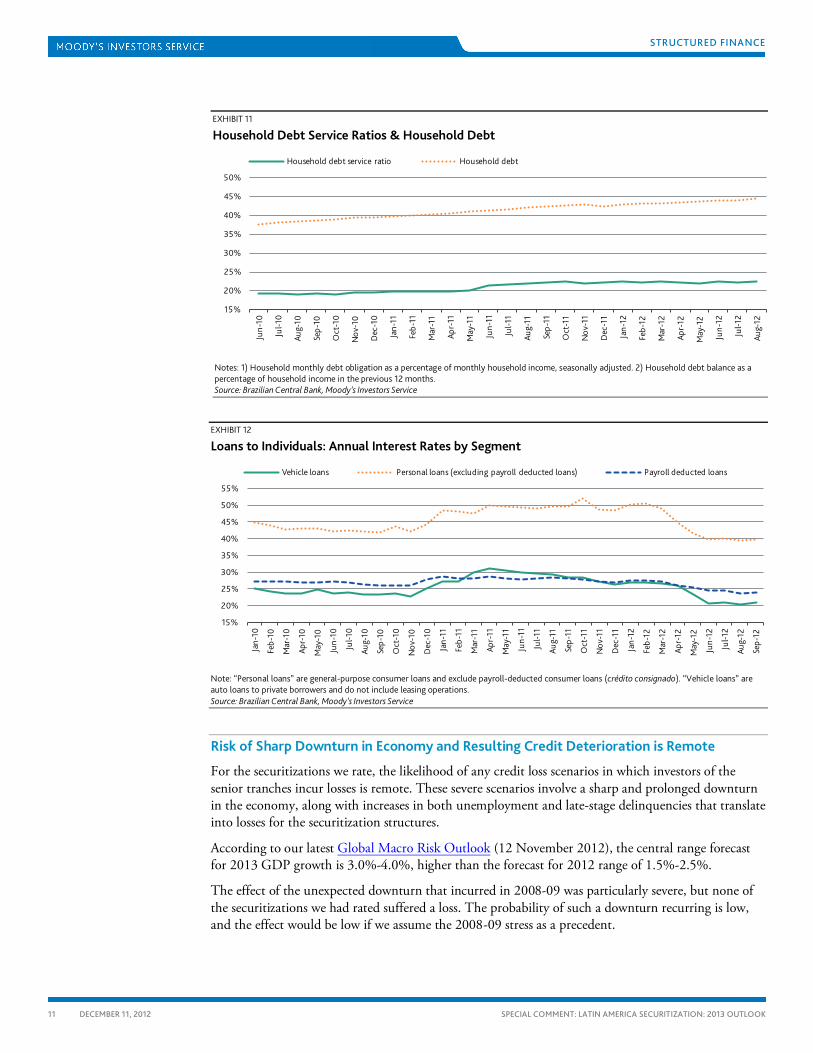

High Levels of Arrears and Indebtedness Will Hold

High levels of household indebtedness and arrears will persist throughout 2013. Household indebtedness, both in terms of debt as well as the percentage of household income destined to service debt, increased throughout 2012, as Exhibit 11 shows. Government action to bring down interest rates on credit cards and personal loans from GREs such as Banco do Brasil and Caixa Economica Federal are starting to bear fruit, as Exhibit 12 shows. Whether a reduction in interest rates will alleviate debt service levels remains uncertain. Nevertheless, a decrease in interest costs makes loans more affordable and helps prevent borrower defaults at the margin.

4%

5%

6%

7%

8%

9%

10%

11%

Jan Fev Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2007 2008 2009 2010 2011 2012

0%

2%

4%

6%

8%

10%

12%

14%

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr-

12

May

-12

Jun-

12

Jul-1

2

Aug-

12

Sep-

12

Oct

-12

Nov

-12

Real Expected Interest Rate Nominal Interest Rate (Selic Target Rate)

STRUCTURED FINANCE

11 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

EXHIBIT 11

Household Debt Service Ratios & Household Debt

Notes: 1) Household monthly debt obligation as a percentage of monthly household income, seasonally adjusted. 2) Household debt balance as a percentage of household income in the previous 12 months. Source: Brazilian Central Bank, Moody’s Investors Service

EXHIBIT 12

Loans to Individuals: Annual Interest Rates by Segment

Note: “Personal loans” are general-purpose consumer loans and exclude payroll-deducted consumer loans (crédito consignado). “Vehicle loans” are auto loans to private borrowers and do not include leasing operations. Source: Brazilian Central Bank, Moody’s Investors Service

Risk of Sharp Downturn in Economy and Resulting Credit Deterioration is Remote

For the securitizations we rate, the likelihood of any credit loss scenarios in which investors of the senior tranches incur losses is remote. These severe scenarios involve a sharp and prolonged downturn in the economy, along with increases in both unemployment and late-stage delinquencies that translate into losses for the securitization structures.

According to our latest Global Macro Risk Outlook (12 November 2012), the central range forecast for 2013 GDP growth is 3.0%-4.0%, higher than the forecast for 2012 range of 1.5%-2.5%.

The effect of the unexpected downturn that incurred in 2008-09 was particularly severe, but none of the securitizations we had rated suffered a loss. The probability of such a downturn recurring is low, and the effect would be low if we assume the 2008-09 stress as a precedent.

15%

20%

25%

30%

35%

40%

45%

50%

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul -1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr-

12

May

-12

Jun-

12

Jul-1

2

Aug-

12

Household debt service ratio Household debt

15%

20%

25%

30%

35%

40%

45%

50%

55%

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr-

11

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr -

12

May

-12

Jun-

12

Jul -1

2

Aug-

12

Sep-

12

Vehicle loans Personal loans (excluding payroll deducted loans) Payroll deducted loans

STRUCTURED FINANCE

12 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

Issuance Will Pick Up in 2013

Record Low Interest Rates and New Regulations Will Drive Rebound Brazilian securitization will pick up strongly from depressed issuance rates in 2012, because interest rates remain low and regulatory requirements will become clear.

Low interest rates will continue to make securitizations attractive to investors. Throughout 2012, interest rates continued to fall, a trend that commenced in 2H2011 and that we believe has bottomed. As real interest rates fall because of lower nominal interest rates coupled with higher inflation, investors will seek higher-yielding assets as their legacy investments in publicly placed securities mature.

As new regulations announced in 2012 roll out in 2013, sponsors of securitizations will re-enter the market once they understand how to structure new transactions to receive regulatory approval.

STRUCTURED FINANCE

13 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

Mexico

Credit Quality of New Transactions Will Remain Strong in 2013

Future Deals Will Be Strong, because INFONAVIT and FOVISSSTE Continue to Dominate RMBS Issuance Government-related entities INFONAVIT and FOVISSSTE, the issuers who will continue to dominate Mexican securitization in 2013 as they have since 2009, will securitize strong collateral. As government-related entities, they both have stable servicing platforms, reflecting their financial stability and their ability to collect payments using automatic payroll deduction.

Although INFONAVIT and FOVISSSTE securitize mortgages to primarily low-income or otherwise risky borrowers, their transactions performed well throughout the crisis and continue to do so, because the borrowers pay via automatic payroll deduction. This feature reduces the risk associated with the low-income borrowers that the two entities primarily target. Because INFONAVIT and FOVISSSTE can automatically deduct mortgage payments from their borrowers’ paychecks, their RMBS are subject to less credit risk, as long as borrowers remain employed in the formal economy. The formal economy accounts for approximately two thirds of employment in Mexico and includes tax-paying, salaried employees who work for private- or public-sector employers offering social security retirement benefits. INFONAVIT’s RMBS performance did weaken, however, mirroring the weakening in labor market conditions that started in 2008; however, performance has since improved, because layoffs and unemployment in the formal economy have subsided.

INFONAVIT’s new product offerings, including peso-denominated mortgages and mortgages to more creditworthy borrowers with higher incomes, will result in stronger securitization performance. This year, INFONAVIT began originating peso-denominated mortgages, which will be credit positive for INFONAVIT’s future securitizations because peso-denominated loans outperform traditional minimum wage-indexed loans, which up until recently accounted for 100% of INFONAVIT’s originations. INFONAVIT’s indexed loans pay principal in minimum wage units that adjust annually according to movements in national minimum wages. The certainty a peso-denominated loan provides is that the loan’s outstanding balance and payments do not automatically increase each year, as is the case with an indexed loan. This certainty is a powerful feature that improves a borrower’s willingness to pay, especially when an unemployed borrower takes a new job with a lower wage or if INFONAVIT cannot process automatic payroll deductions because the borrower is no longer employed in the private sector. INFONAVIT’s increased focus on borrowers outside the low-income sector will also result in stronger performance, because higher income borrowers typically have greater financial resources, resulting in a greater ability to pay following a job loss.

Proven Historical Performance is Necessary for Sponsors of Securitizations Backed by Other Asset Types

Barring abrupt downturns in the global and Mexican economies in 2013, investors will consider investing in securitizations backed by other asset types, to obtain higher yields in today’s low interest-rate environment. However, investors will focus on financially stable sponsors with a track record of strong collateral performance. Possible new securitization offerings include a mix of ABS backed by commercial properties and rent roll cash flows, collateralized loan obligations and accounts receivables.

Credit Quality of Existing Non-Sofol Sector Deals Will Remain Strong

Performance of bank, INFONAVIT, and FOVISSSTE RMBS will be strong The performance of RMBS issued by banks, INFONAVIT and FOVISSSTE will remain strong and stable in 2013, as Mexico continues its gradual recovery from the global recession, despite significant downside risks to the global economic outlooks. These transactions fared well during Mexico’s

STRUCTURED FINANCE

14 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

economic recession, but have not been immune to rises in delinquencies. However, even though delinquencies will continue to increase as the securitized mortgage pools age, the rate of increase will abate.

In November, we raised our 2012 growth rate forecast for Mexico to 3.5%-4.5% from 3.0%-4.0% as of August; this new growth rate is similar to Mexico’s 2011 growth rate of 3.9%. Our 2012 growth forecast for Mexico exceeds our 2012 growth forecast of 2.0%-3.0% for all G-20 economies and our 1.0% growth forecast for advanced G-20 economies. Of great importance to RMBS performance is that employment will continue to recover gradually, barring a sudden downturn in the US business cycle or a US fiscal cliff, given recent political gridlock. Mexico began to emerge from recession in the third quarter of 2009 after a severe year-long contraction, although the employment recovery has lagged because of the depth of the economic contraction. However, signs of improvement in the labor market have since emerged. As employment rises, RMBS performance will continue to stabilize.

The recent drop in unemployment has already had a particularly pronounced and positive effect on INFONAVIT, because it grants mortgages to primarily low-income borrowers employed in the private sector. These borrowers usually have minimal to non-existent savings; therefore, any reduction in income if they become un- or under-employed will hurt their ability and willingness to make their loan payments. As long as the borrowers remain employed, however, the automatic payroll deduction will limit the extent of defaults. The deterioration in the performance of INFONAVIT RMBS mirrored the weakening of labor market conditions that started in 2008, but performance has since improved as layoffs and unemployment have subsided.

Continued growth in the Mexican economy will continue to stabilize the performance of bank-issued RMBS as well. Obligors whose mortgages back these RMBS typically have higher incomes and savings, although the sector does not benefit from servicing via automatic payroll deduction. However, the more financially savvy, delinquent borrowers in this sector are more likely to resume their mortgage payments as soon as they find employment because they fully understand the repercussions of defaulting on a mortgage, including damage to their credit profiles.

Sofol RMBS Performance and Recovery Metrics Face Significant Challenges

Loan defaults remain high

In contrast to the performance of the INFANOVIT and FOVISSSTE sector, the performance of non-bank Sofol RMBS will continue to face serious challenges in 2013. Sofol RMBS performance will deteriorate at a somewhat slower pace than it did last year, but performance in this sector has not for certain stabilized.

The absence of automatic payroll deductions will result in very low cure rates for defaulted loans, even as the Mexican economy continues to improve. Unlike INFONAVIT and FOVISSSTE, which can resume automatic payroll deductions as soon as an unemployed borrower re-enters the workforce in the formal economy, Sofoles are at the mercy of the borrower’s decision whether or not to resume mortgage payments. Sofol RMBS performance has suffered as a result of not only rising unemployment, but also rising underemployment during the economic downturn. Unlike INFONAVIT, FOVISSSTE, and bank RMBS, many Sofol RMBS have a significant share of borrowers working in the informal economy and who lack a steady source of income.

Although low-income borrowers’ reduced capacity to pay following the crisis triggered the majority of loan defaults in Sofol RMBS, a large number of borrowers have also stopped making their payments owing to a reduced willingness to pay. These borrowers are increasingly abandoning their homes for a variety of reasons, including the contagion of neighboring foreclosures, which has led to a decline in property values and upkeep in many low-income housing developments nation-wide, a rise in crime and vandalism, and subpar sanitation services and school systems. Also plaguing the Sofol RMBS

STRUCTURED FINANCE

15 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

sector and driving borrowers to abandon their homes are the negative amortization associated with the once-popular inflation-linked mortgages known as Unidades de Inversión (UDI) mortgages and the remoteness of homes from borrowers’ place of employment. Although some of these challenges also affect low-income housing financed by Infonavit and Fovissste, “willingness to pay” is not a key driver of performance in these segments because as long as the borrower remains employed, Infonavit and Fovissste will continue to automatically deduct borrowers’ mortgage payments from payroll.

Recovery Lag Growing, Recovery Prospects Diminishing

In 2013, the ability of servicers to improve efficiency in foreclosure proceedings and real-estate-owned (REO) property sales will be critical to reducing recovery lags and maximizing recoveries. Despite the large pipeline of 90-plus delinquencies and foreclosures that has built up since 2008, REO activity and sales have yet to pick up significantly. A failure of recoveries on defaulted mortgages to accelerate in 2013 will signal that the lag between initial default and final liquidation has lengthened beyond the three- to four-year timeline we previously assumed in our ratings of Mexican RMBS. Absent positive developments in this area, we will consider using more stressful recovery lag and severity assumptions when rating and monitoring Mexican RMBS.

Several factors are contributing to the longer recovery lag for defaulted mortgages. First, the judicial system, which varies from state to state, prolongs servicers’ efforts to repossess properties. Second, the large number of loan defaults has made it difficult for servicers to keep up with volumes. Third, servicers are increasingly finding properties in the low-income sector in a severe state of disrepair, sometimes even uninhabitable, following years of neglect or vandalism and arson at the hands of discontented borrowers. Fourth, recently appointed substitute servicers have experienced delays in actively pursuing recoveries because they have had to take time to familiarize themselves with their new portfolios, gather the legal documentation necessary to foreclose and hire additional personnel to tackle the added volume. Fifth, some servicers often choose to exhaust other loss mitigation options, such as loan modifications, in an attempt to keep borrowers cashflowing immediately before pursuing foreclosure, but whether this strategy is yielding positive results is not apparent at this point.

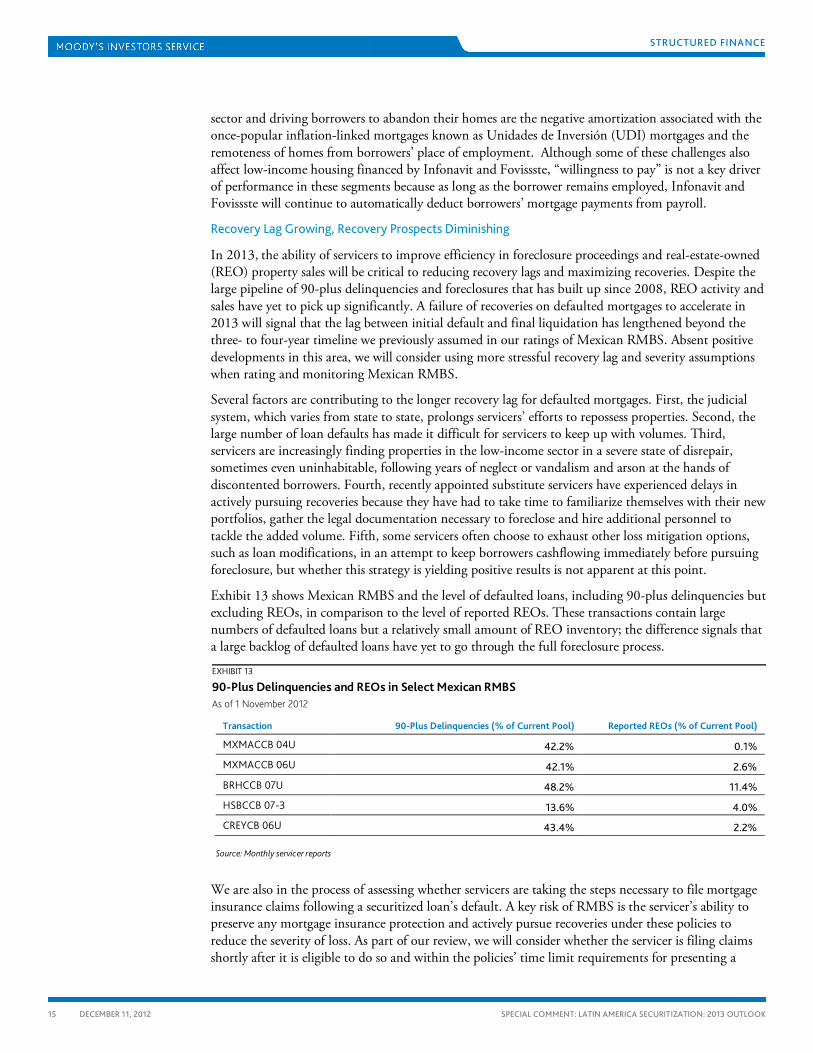

Exhibit 13 shows Mexican RMBS and the level of defaulted loans, including 90-plus delinquencies but excluding REOs, in comparison to the level of reported REOs. These transactions contain large numbers of defaulted loans but a relatively small amount of REO inventory; the difference signals that a large backlog of defaulted loans have yet to go through the full foreclosure process.

EXHIBIT 13

90-Plus Delinquencies and REOs in Select Mexican RMBS As of 1 November 2012

Transaction 90-Plus Delinquencies (% of Current Pool) Reported REOs (% of Current Pool)

MXMACCB 04U 42.2% 0.1%

MXMACCB 06U 42.1% 2.6%

BRHCCB 07U 48.2% 11.4%

HSBCCB 07-3 13.6% 4.0%

CREYCB 06U 43.4% 2.2%

Source: Monthly servicer reports

We are also in the process of assessing whether servicers are taking the steps necessary to file mortgage insurance claims following a securitized loan’s default. A key risk of RMBS is the servicer’s ability to preserve any mortgage insurance protection and actively pursue recoveries under these policies to reduce the severity of loss. As part of our review, we will consider whether the servicer is filing claims shortly after it is eligible to do so and within the policies’ time limit requirements for presenting a

STRUCTURED FINANCE

16 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

claim. We will also ask servicers to confirm whether mortgage insurance providers have terminated any policies or denied claims. Depending on the results of this review, we will consider using more stressful severity assumptions when rating and monitoring Mexican RMBS benefiting from mortgage insurance.

Greater Use of Loan Modifications Is Unlikely to Significantly Improve RMBS Performance

The new loan modification programs that some servicers introduced this year are unlikely to significantly improve Mexican RMBS performance.

Since 2009, some RMBS servicers have turned to loan modifications as a tool to contain the unprecedented level of loan defaults. Initially, they introduced programs that deferred past-due payments, forgave a portion of past-due interest payments and temporarily reduced mortgage payments. Following their implementation, the performance of Mexican RMBS did not noticeably improve. More recently, some servicers have turned to more aggressive loan modifications that grant principal reductions or reduce mortgage payments by lengthening loan terms or lowering interest rates. In the case of loans that have been in default for over a year, which represents the vast majority of the delinquency pipeline in Mexican RMBS, such products are likely too late to make defaulted borrowers cash-flowing again.

Large Pipeline of Loan Defaults Will Continue to Test Smaller Servicers’ Operations

The large pipeline of Mexican RMBS loan defaults and the exceedingly laborious foreclosure and REO workload will continue to test the operations of Sofoles, which service approximately 25% of Mexican RMBS. Of the key Sofol sponsors of Mexican RMBS, only two entities remain in operation: Patrimonio, S. A. de C. V. (NR) and Metrofinanciera, S. A. de C. V. (NR). Both face the challenge of servicing portfolios hurt by high delinquencies while also struggling to turn a profit in today’s less competitive environment for the Sofol sector. As a result, these servicers may not have the resources required to optimally service their portfolios. The servicer’s role is especially crucial in managing the delinquency levels of low-income borrowers, who require more frequent and intensive contact; any attempt to shortchange servicing levels will likely translate into increased borrower defaults.

In the case of Sofoles acting as substitute servicers of Mexican RMBS, such as Patrimonio, Pendulum and Tertius, not all these substitute servicers have the incentive to grow and improve their servicing platforms as necessary to control the transferred deals’ high delinquency levels and maximize recoveries on defaulted loans. The current servicing fee structure, in which most servicers receive a monthly fee equal to a fixed percentage of the pool balance, is not always profitable enough to motivate substitute servicers to expedite pending foreclosures and REO inventory sales. A variable and performance-based servicing fee would better motivate substitute servicers to maximize recoveries.

STRUCTURED FINANCE

17 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

Panama

First covered bond in Panama uses contractual law in absence of legislative framework

In 2012, Panama’s Global Bank issued the first cross-border covered bond in Latin America. Because Panama has no covered bond legislation, the bank structured the transaction using the contractual law that typical securitizations use. Transaction documents ring-fence the mortgage loans legally from the issuer´s balance sheet in order to form the cover pool, thereby protecting investors’ interests in the event of an issuer insolvency.

The rating of the program’s bonds is investment grade at Baa3 given the program’s credit strengths, which included a high level of committed over-collateralization, at 18.5%.

We limited the rating to one notch above the issuer’s Ba1 rating, however, because we believe that there remains a high likelihood of a timely payment default to covered bondholders if the sponsor defaults. The likelihood is high because of 1) the lack of a secondary wholesale market for mortgages in Panama and 2) the infrequency of servicing transfers in Panama. These factors apply to most jurisdictions in Latin America, and will likely limit the maximum rating for covered bonds in the region.

This particular issuance will not necessarily trigger other Latin American jurisdictions to issue covered bonds using contractual law, because most Latin American investors look to the covered bond legislation in their respective markets for deriving legal comfort. In Mexico, lawmakers recently introduced covered bond legislation but they have not as yet enacted it. In Brazil, the association of mortgage lenders has been the key advocacy group engaging in discussions with the government towards a Brazilian covered bond framework.

STRUCTURED FINANCE

18 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

Appendix 1: 2012 Review

Argentina

As Exhibit 14 shows, securitization issuance totaled the equivalent of ARS 14,716 million as of November 2012, which represents a decrease of 25.32% relative to the same period last year. In terms of the number of issuances, 167 transactions took place as of November 2012, compared with 234 in 2011.

During 2012, four large infrastructure-related transactions entered the market. The Argentine government typically sponsors or structures these deals for purchase mainly by ANSES and government-owned banks. The amounts issued under this category totaled the equivalent of ARS 2,505 million as of November 2012, compared with ARS 8,586 million for eleven transactions during the same period in 2011.

EXHIBIT 14

Amount of New Securitizations in Argentina

Source: Moody’s, Buenos Aires Stock Exchange, Rosario Stock Exchange.

EXHIBIT 15

Number of New Securitizations in Argentina

Source: Moody’s, Buenos Aires Stock Exchange, Rosario Stock Exchange.

0.00

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Nov-12

ARS

Mill

ions

Other Infrastructure

0.00

50.00

100.00

150.00

200.00

250.00

300.00

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Nov-12

Other Infrastructure

STRUCTURED FINANCE

19 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

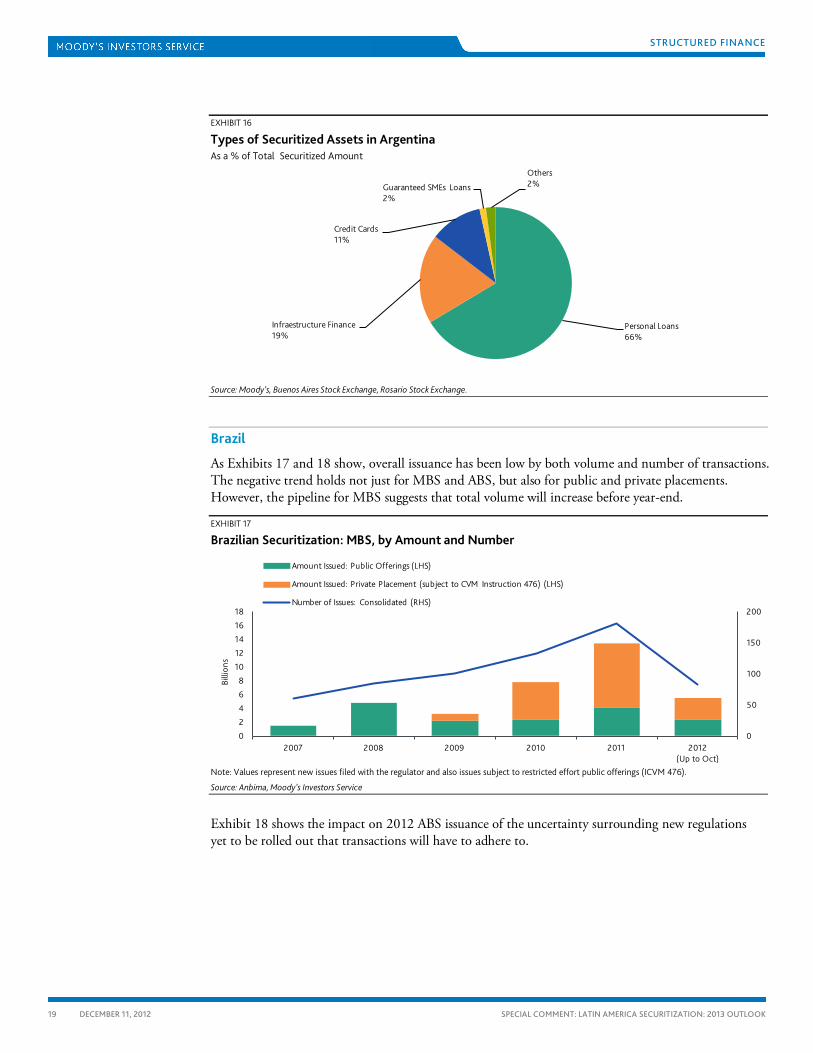

EXHIBIT 16

Types of Securitized Assets in Argentina As a % of Total Securitized Amount

Source: Moody’s, Buenos Aires Stock Exchange, Rosario Stock Exchange.

Brazil

As Exhibits 17 and 18 show, overall issuance has been low by both volume and number of transactions. The negative trend holds not just for MBS and ABS, but also for public and private placements. However, the pipeline for MBS suggests that total volume will increase before year-end.

EXHIBIT 17

Brazilian Securitization: MBS, by Amount and Number

Note: Values represent new issues filed with the regulator and also issues subject to restricted effort public offerings (ICVM 476).

Source: Anbima, Moody’s Investors Service

Exhibit 18 shows the impact on 2012 ABS issuance of the uncertainty surrounding new regulations yet to be rolled out that transactions will have to adhere to.

Personal Loans66%

Infraestructure Finance19%

Credit Cards11%

Guaranteed SMEs Loans2%

Others2%

0

50

100

150

200

0

2

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012 (Up to Oct)

Billi

ons

Amount Issued: Public Offerings (LHS)

Amount Issued: Private Placement (subject to CVM Instruction 476) (LHS)

Number of Issues: Consolidated (RHS)

STRUCTURED FINANCE

20 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

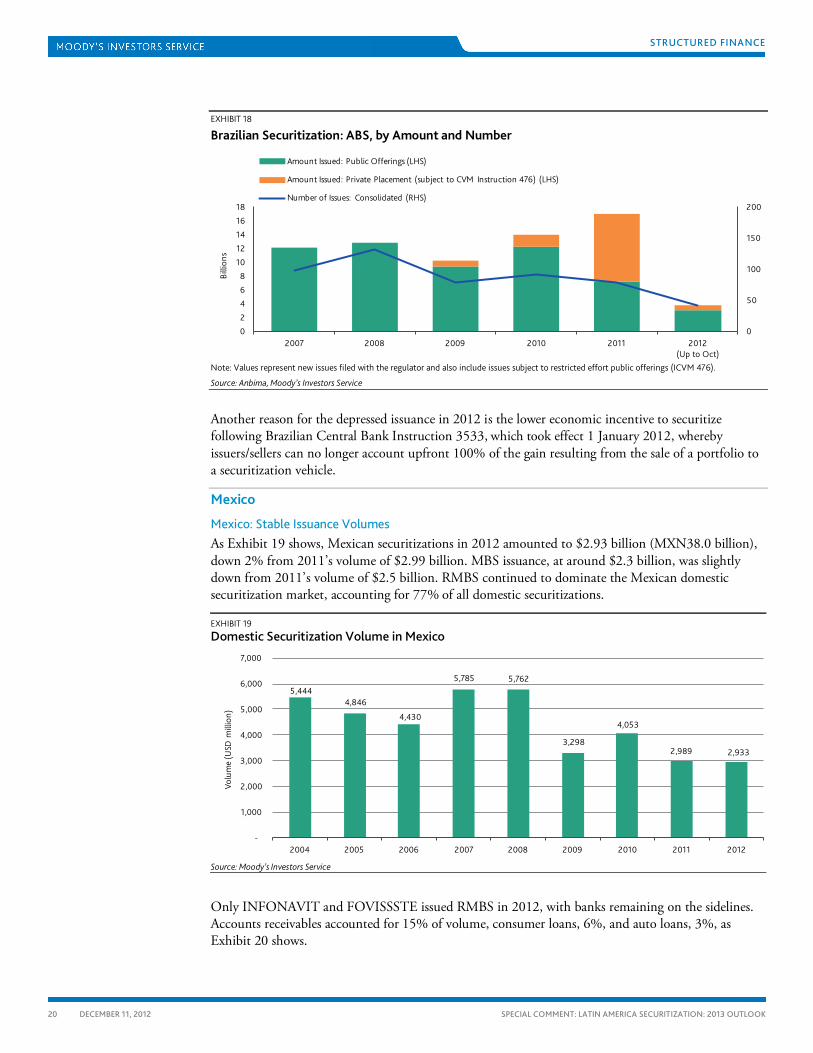

EXHIBIT 18

Brazilian Securitization: ABS, by Amount and Number

Note: Values represent new issues filed with the regulator and also include issues subject to restricted effort public offerings (ICVM 476).

Source: Anbima, Moody’s Investors Service

Another reason for the depressed issuance in 2012 is the lower economic incentive to securitize following Brazilian Central Bank Instruction 3533, which took effect 1 January 2012, whereby issuers/sellers can no longer account upfront 100% of the gain resulting from the sale of a portfolio to a securitization vehicle.

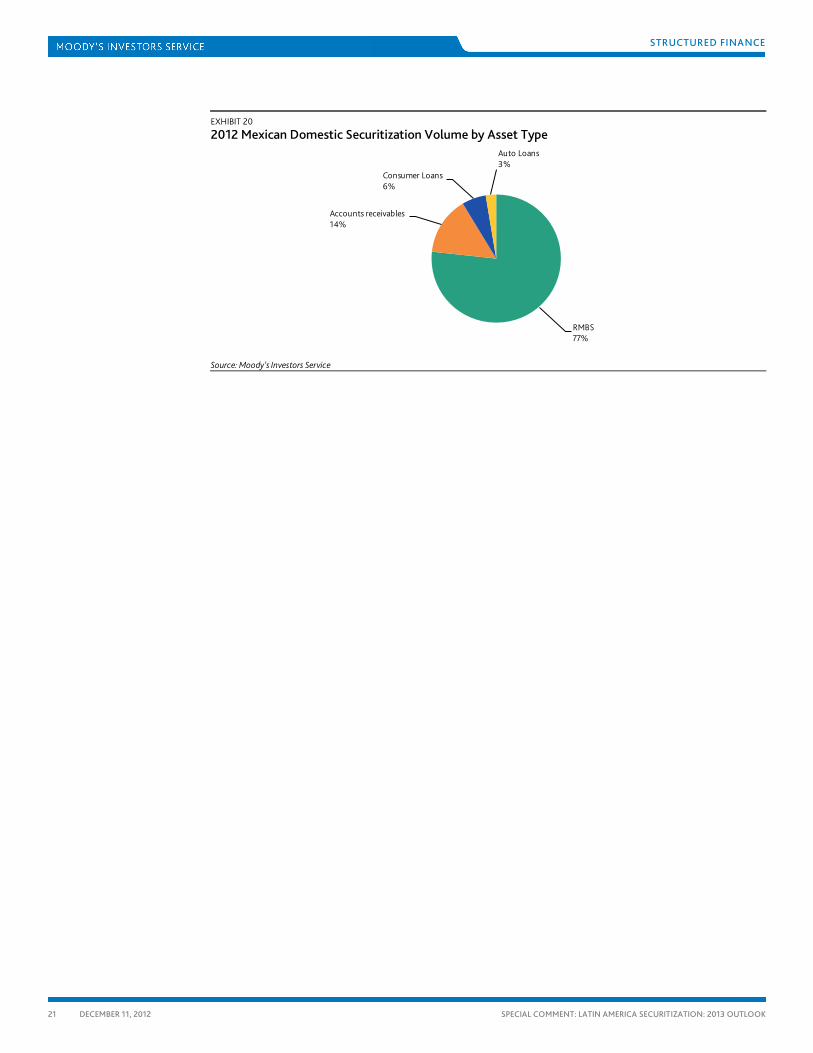

Mexico

Mexico: Stable Issuance Volumes As Exhibit 19 shows, Mexican securitizations in 2012 amounted to $2.93 billion (MXN38.0 billion), down 2% from 2011’s volume of $2.99 billion. MBS issuance, at around $2.3 billion, was slightly down from 2011’s volume of $2.5 billion. RMBS continued to dominate the Mexican domestic securitization market, accounting for 77% of all domestic securitizations.

EXHIBIT 19

Domestic Securitization Volume in Mexico

Source: Moody’s Investors Service

Only INFONAVIT and FOVISSSTE issued RMBS in 2012, with banks remaining on the sidelines. Accounts receivables accounted for 15% of volume, consumer loans, 6%, and auto loans, 3%, as Exhibit 20 shows.

0

50

100

150

200

0

2

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012 (Up to Oct)

Billi

ons

Amount Issued: Public Offerings (LHS)

Amount Issued: Private Placement (subject to CVM Instruction 476) (LHS)

Number of Issues: Consolidated (RHS)

5,444 4,846

4,430

5,785 5,762

3,298

4,053

2,989 2,933

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2004 2005 2006 2007 2008 2009 2010 2011 2012

Volu

me

(USD

mill

ion)

STRUCTURED FINANCE

21 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

EXHIBIT 20

2012 Mexican Domestic Securitization Volume by Asset Type

Source: Moody’s Investors Service

RMBS77%

Accounts receivables14%

Consumer Loans6%

Auto Loans3%

STRUCTURED FINANCE

22 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

Rating List

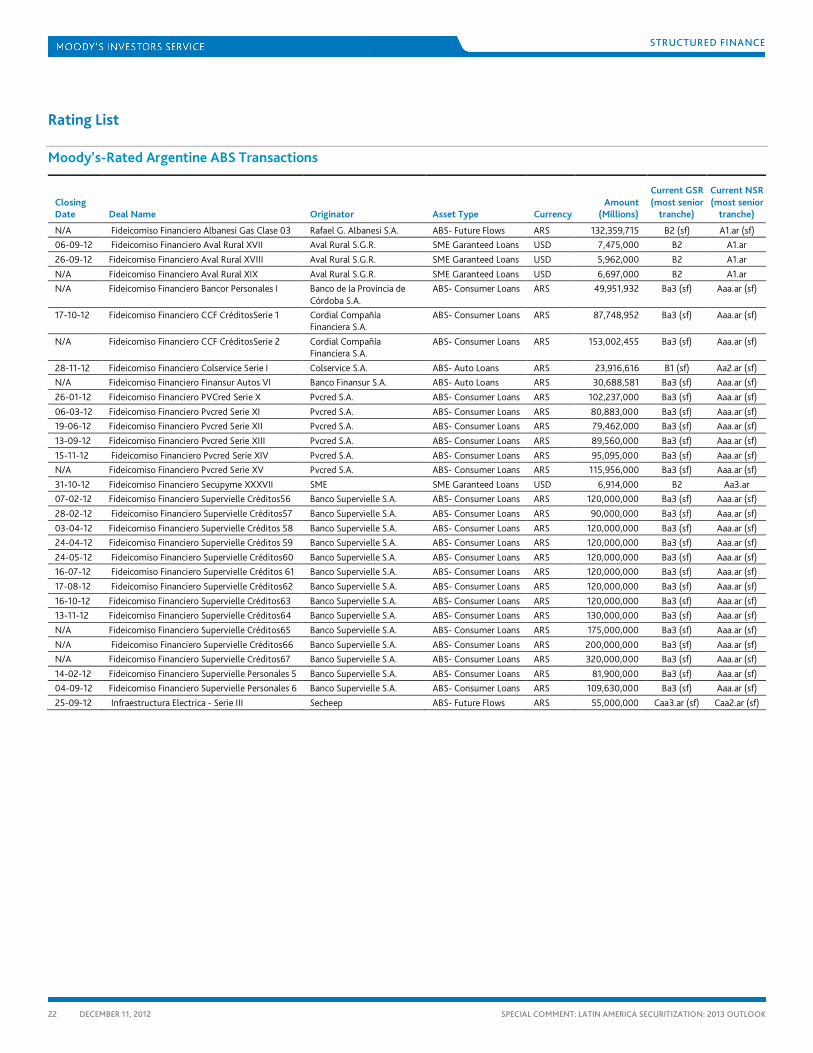

Moody’s-Rated Argentine ABS Transactions

Closing Date Deal Name Originator Asset Type Currency

Amount (Millions)

Current GSR (most senior

tranche)

Current NSR (most senior

tranche)

N/A Fideicomiso Financiero Albanesi Gas Clase 03 Rafael G. Albanesi S.A. ABS- Future Flows ARS 132,359,715 B2 (sf) A1.ar (sf) 06-09-12 Fideicomiso Financiero Aval Rural XVII Aval Rural S.G.R. SME Garanteed Loans USD 7,475,000 B2 A1.ar 26-09-12 Fideicomiso Financiero Aval Rural XVIII Aval Rural S.G.R. SME Garanteed Loans USD 5,962,000 B2 A1.ar N/A Fideicomiso Financiero Aval Rural XIX Aval Rural S.G.R. SME Garanteed Loans USD 6,697,000 B2 A1.ar N/A Fideicomiso Financiero Bancor Personales I Banco de la Provincia de

Córdoba S.A. ABS- Consumer Loans ARS 49,951,932 Ba3 (sf) Aaa.ar (sf)

17-10-12 Fideicomiso Financiero CCF CréditosSerie 1 Cordial Compañía Financiera S.A.

ABS- Consumer Loans ARS 87,748,952 Ba3 (sf) Aaa.ar (sf)

N/A Fideicomiso Financiero CCF CréditosSerie 2 Cordial Compañía Financiera S.A.

ABS- Consumer Loans ARS 153,002,455 Ba3 (sf) Aaa.ar (sf)

28-11-12 Fideicomiso Financiero Colservice Serie I Colservice S.A. ABS- Auto Loans ARS 23,916,616 B1 (sf) Aa2.ar (sf) N/A Fideicomiso Financiero Finansur Autos VI Banco Finansur S.A. ABS- Auto Loans ARS 30,688,581 Ba3 (sf) Aaa.ar (sf) 26-01-12 Fideicomiso Financiero PVCred Serie X Pvcred S.A. ABS- Consumer Loans ARS 102,237,000 Ba3 (sf) Aaa.ar (sf) 06-03-12 Fideicomiso Financiero Pvcred Serie XI Pvcred S.A. ABS- Consumer Loans ARS 80,883,000 Ba3 (sf) Aaa.ar (sf) 19-06-12 Fideicomiso Financiero Pvcred Serie XII Pvcred S.A. ABS- Consumer Loans ARS 79,462,000 Ba3 (sf) Aaa.ar (sf) 13-09-12 Fideicomiso Financiero Pvcred Serie XIII Pvcred S.A. ABS- Consumer Loans ARS 89,560,000 Ba3 (sf) Aaa.ar (sf) 15-11-12 Fideicomiso Financiero Pvcred Serie XIV Pvcred S.A. ABS- Consumer Loans ARS 95,095,000 Ba3 (sf) Aaa.ar (sf) N/A Fideicomiso Financiero Pvcred Serie XV Pvcred S.A. ABS- Consumer Loans ARS 115,956,000 Ba3 (sf) Aaa.ar (sf) 31-10-12 Fideicomiso Financiero Secupyme XXXVII SME SME Garanteed Loans USD 6,914,000 B2 Aa3.ar 07-02-12 Fideicomiso Financiero Supervielle Créditos56 Banco Supervielle S.A. ABS- Consumer Loans ARS 120,000,000 Ba3 (sf) Aaa.ar (sf) 28-02-12 Fideicomiso Financiero Supervielle Créditos57 Banco Supervielle S.A. ABS- Consumer Loans ARS 90,000,000 Ba3 (sf) Aaa.ar (sf) 03-04-12 Fideicomiso Financiero Supervielle Créditos 58 Banco Supervielle S.A. ABS- Consumer Loans ARS 120,000,000 Ba3 (sf) Aaa.ar (sf) 24-04-12 Fideicomiso Financiero Supervielle Créditos 59 Banco Supervielle S.A. ABS- Consumer Loans ARS 120,000,000 Ba3 (sf) Aaa.ar (sf) 24-05-12 Fideicomiso Financiero Supervielle Créditos60 Banco Supervielle S.A. ABS- Consumer Loans ARS 120,000,000 Ba3 (sf) Aaa.ar (sf) 16-07-12 Fideicomiso Financiero Supervielle Créditos 61 Banco Supervielle S.A. ABS- Consumer Loans ARS 120,000,000 Ba3 (sf) Aaa.ar (sf) 17-08-12 Fideicomiso Financiero Supervielle Créditos62 Banco Supervielle S.A. ABS- Consumer Loans ARS 120,000,000 Ba3 (sf) Aaa.ar (sf) 16-10-12 Fideicomiso Financiero Supervielle Créditos63 Banco Supervielle S.A. ABS- Consumer Loans ARS 120,000,000 Ba3 (sf) Aaa.ar (sf) 13-11-12 Fideicomiso Financiero Supervielle Créditos64 Banco Supervielle S.A. ABS- Consumer Loans ARS 130,000,000 Ba3 (sf) Aaa.ar (sf) N/A Fideicomiso Financiero Supervielle Créditos65 Banco Supervielle S.A. ABS- Consumer Loans ARS 175,000,000 Ba3 (sf) Aaa.ar (sf) N/A Fideicomiso Financiero Supervielle Créditos66 Banco Supervielle S.A. ABS- Consumer Loans ARS 200,000,000 Ba3 (sf) Aaa.ar (sf) N/A Fideicomiso Financiero Supervielle Créditos67 Banco Supervielle S.A. ABS- Consumer Loans ARS 320,000,000 Ba3 (sf) Aaa.ar (sf) 14-02-12 Fideicomiso Financiero Supervielle Personales 5 Banco Supervielle S.A. ABS- Consumer Loans ARS 81,900,000 Ba3 (sf) Aaa.ar (sf) 04-09-12 Fideicomiso Financiero Supervielle Personales 6 Banco Supervielle S.A. ABS- Consumer Loans ARS 109,630,000 Ba3 (sf) Aaa.ar (sf) 25-09-12 Infraestructura Electrica - Serie III Secheep ABS- Future Flows ARS 55,000,000 Caa3.ar (sf) Caa2.ar (sf)

STRUCTURED FINANCE

23 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

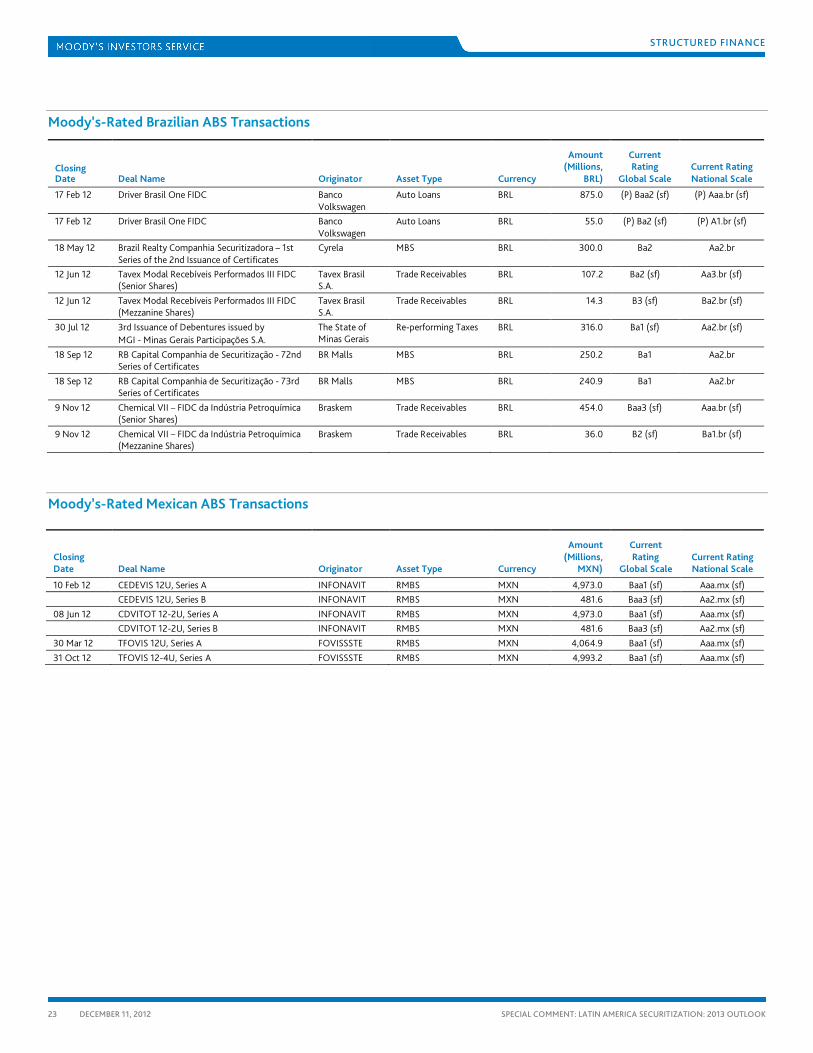

Moody’s-Rated Brazilian ABS Transactions

Closing Date Deal Name Originator Asset Type Currency

Amount (Millions,

BRL)

Current Rating

Global Scale Current Rating National Scale

17 Feb 12 Driver Brasil One FIDC Banco Volkswagen

Auto Loans BRL 875.0 (P) Baa2 (sf) (P) Aaa.br (sf)

17 Feb 12 Driver Brasil One FIDC Banco Volkswagen

Auto Loans BRL 55.0 (P) Ba2 (sf) (P) A1.br (sf)

18 May 12 Brazil Realty Companhia Securitizadora – 1st Series of the 2nd Issuance of Certificates

Cyrela MBS BRL 300.0 Ba2 Aa2.br

12 Jun 12 Tavex Modal Recebíveis Performados III FIDC (Senior Shares)

Tavex Brasil S.A.

Trade Receivables BRL 107.2 Ba2 (sf) Aa3.br (sf)

12 Jun 12 Tavex Modal Recebíveis Performados III FIDC (Mezzanine Shares)

Tavex Brasil S.A.

Trade Receivables BRL 14.3 B3 (sf) Ba2.br (sf)

30 Jul 12 3rd Issuance of Debentures issued by MGI - Minas Gerais Participações S.A.

The State of Minas Gerais

Re-performing Taxes BRL 316.0 Ba1 (sf) Aa2.br (sf)

18 Sep 12 RB Capital Companhia de Securitização - 72nd Series of Certificates

BR Malls MBS BRL 250.2 Ba1 Aa2.br

18 Sep 12 RB Capital Companhia de Securitização - 73rd Series of Certificates

BR Malls MBS BRL 240.9 Ba1 Aa2.br

9 Nov 12 Chemical VII – FIDC da Indústria Petroquímica (Senior Shares)

Braskem Trade Receivables BRL 454.0 Baa3 (sf) Aaa.br (sf)

9 Nov 12 Chemical VII – FIDC da Indústria Petroquímica (Mezzanine Shares)

Braskem Trade Receivables BRL 36.0 B2 (sf) Ba1.br (sf)

Moody’s-Rated Mexican ABS Transactions

Closing Date Deal Name Originator Asset Type Currency

Amount (Millions,

MXN)

Current Rating

Global Scale Current Rating National Scale

10 Feb 12 CEDEVIS 12U, Series A INFONAVIT RMBS MXN 4,973.0 Baa1 (sf) Aaa.mx (sf) CEDEVIS 12U, Series B INFONAVIT RMBS MXN 481.6 Baa3 (sf) Aa2.mx (sf) 08 Jun 12 CDVITOT 12-2U, Series A INFONAVIT RMBS MXN 4,973.0 Baa1 (sf) Aaa.mx (sf) CDVITOT 12-2U, Series B INFONAVIT RMBS MXN 481.6 Baa3 (sf) Aa2.mx (sf) 30 Mar 12 TFOVIS 12U, Series A FOVISSSTE RMBS MXN 4,064.9 Baa1 (sf) Aaa.mx (sf) 31 Oct 12 TFOVIS 12-4U, Series A FOVISSSTE RMBS MXN 4,993.2 Baa1 (sf) Aaa.mx (sf)

STRUCTURED FINANCE

24 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

Moody’s Related Research

For a more detailed explanation of our approach to this type of transaction as well as similar transactions please refer to the following reports:

Brazil »

»

Moody´s Approach to Rating Securities Backed by Brazilian Consumer Assets, November 2012 (SF294535)

»

Brazilian Factoring Securitizations: Undue Credit Risk and High Loss Severities, April 2011 (SF242050)

»

Brazil Securitization Regulations Will Increase the Likelihood of Mezzanine Defaults, August 2011 (SF256887)

Mexico:

Post Crisis, Brazilian Securitization Is Business as Usual, Subject to Increased Regulatory Oversight, September 2011 (SF261590)

» Moody's Structured Finance Rating Scale, August 2010 (SF214286)

» Moody’s Approach to Rating Mexican RMBS, August 2012 (SF287681)

» Moody's Approach to Monitoring Residential Mortgage-Backed Securitizations in Mexico, August 2009 (SF175820)

» Moody's Comments on Su Casita Mexican RMBS Interest Payment Defaults, May 2012 (SF285505)

» Reform of INFONAVIT Law and Scrutiny of Credit Bureau are Credit Positive for Mexico

Housing Industry, January 2012 (SF272834)

» Servicer Report: Instituto del Fondo Nacional de la Vivienda para los Trabajadores (INFONAVIT), April 2012 (SF281206)

» Originator Assessment: Instituto del Fondo Nacional de la Vivienda para los Trabajadores (INFONAVIT),February 2012 (SF276482)

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of this report and that more recent reports may be available. All research may not be available to all clients. Moody’s publishes a weekly summary of structured finance credit, ratings and methodologies, available to all registered users of our website, at www.moodys.com/SFQuickCheck.

STRUCTURED FINANCE

25 DECEMBER 11, 2012

SPECIAL COMMENT: LATIN AMERICA SECURITIZATION: 2013 OUTLOOK

» contacts continued from page 1

Analyst Contacts:

BUENOS AIRES +54.11.3752.2000

Martin Fernandez Romero

+54.11.5129.2621

Vice President - Senior Analyst [email protected]

Rodrigo Conde +54.11.5129.2630 Associate Analyst [email protected]

Sofia Ordonez + 54.11.3752.2642 Associate Analyst [email protected]

MEXICO CITY +52.55.1253.5700

Joel Sanchez +52.55.1253.5726 Analyst [email protected]

Gustavo Salaiz +52.55.1253.5747 Associate Analyst [email protected]

NEW YORK +1.212.553.1653

Karen Ramallo +1.212.553.0370 Vice President - Senior Analyst [email protected]

Linda Stesney +1.212.553.3691 Managing Director - Structured Finance [email protected]

Maria Muller +1.212.553.4309 Senior Vice President [email protected]

Report Number: SF309651

© 2012 Moody’s Investors Service, Inc. and/or its licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. (“MIS”) AND ITS AFFILIATES ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Each user of the information contained herein must make its own study and evaluation of each security it may consider purchasing, holding or selling.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MIS have, prior to assignment of any rating, agreed to pay to MIS for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Any publication into Australia of this document is by MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657, which holds Australian Financial Services License no. 336969. This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001.

Notwithstanding the foregoing, credit ratings assigned on and after October 1, 2010 by Moody’s Japan K.K. (“MJKK”) are MJKK’s current opinions of the relative future credit risk of entities, credit commitments, or debt or debt-like securities. In such a case, “MIS” in the foregoing statements shall be deemed to be replaced with “MJKK”. MJKK is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO.

This credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be dangerous for retail investors to make any investment decision based on this credit rating. If in doubt you should contact your financial or other professional adviser.