Large mining enterprises and regional development

28

AUTHOR/EDITOR QUERIES ARTICLE ID: JEG-LBT007 Please respond to all queries and send any additional proof corrections. Failure to do so could result in delayed publication Query No Section Paragraph Query Q1 Author names Please check that all names have been spelled correctly and appear in the correct order. Please also check that all initials are present. Please check that the author surnames (family name) have been correctly identified by a pink background. If this is incorrect, please identify the full surname of the relevant authors. Occasionally, the distinction between surnames and forenames can be ambiguous, and this is to ensure that the authors’ full surnames and forenames are tagged correctly, for accurate indexing online. Please also check all author affiliations. Q2 Abbreviation Please spell out “SME” and “EMN.” Q3 Funding Please provide a Funding statement, detailing any funding received. Remember that any funding used while completing this work should be highlighted in a separate Funding section. Please ensure that you use the full official name of the funding body, and if your paper has received funding from any institution, such as NIH, please inform us of the grant number to go into the funding section. We use the institution names to tag NIH-funded articles so they are deposited at PMC. If we already have this information, we will have tagged it and it will appear as coloured text in the funding paragraph. Please check the information is correct. Q4 Figures Figures have been placed as close as possible to their first citation. Please check that they have no missing sections and that the correct figure legend is present. Q5 Tables Table 1 seems to be a figure. Please suggest whether Table 1 could be displayed as figure and subsequent tables and figures be renumbered.

Transcript of Large mining enterprises and regional development

AUTHOR/EDITOR QUERIES

ARTICLE ID: JEG-LBT007

Please respond to all queries and send any additional proof corrections. Failure to do so could result in delayed publication

Query No

Section Paragraph Query

Q1 Author names

Please check that all names have been spelled correctly and appear in the correct order. Please also check that all initials are present. Please check that the author surnames (family name) have been correctly identified by a pink background. If this is incorrect, please identify the full surname of the relevant authors. Occasionally, the distinction between surnames and forenames can be ambiguous, and this is to ensure that the authors’ full surnames and forenames are tagged correctly, for accurate indexing online. Please also check all author affiliations.

Q2 Abbreviation Please spell out “SME” and “EMN.”

Q3 Funding

Please provide a Funding statement, detailing any funding received. Remember that any funding used while completing this work should be highlighted in a separate Funding section. Please ensure that you use the full official name of the funding body, and if your paper has received funding from any institution, such as NIH, please inform us of the grant number to go into the funding section. We use the institution names to tag NIH-funded articles so they are deposited at PMC. If we already have this information, we will have tagged it and it will appear as coloured text in the funding paragraph. Please check the information is correct.

Q4 Figures

Figures have been placed as close as possible to their first citation. Please check that they have no missing sections and that the correct figure legend is present.

Q5 Tables

Table 1 seems to be a figure. Please suggest whether Table 1 could be displayed as figure and subsequent tables and figures be renumbered.

Q6 References

Please note that following references have been listed but not cited in text: Barbour and Markusen (2007), Gobierno Regional de Antofagasta (2001), Martin and Sunley (2011), Nooteboom and Woolthuis (2005), Press (2006), Sariego (1992). Please provide their text citations or delete from the list.

Q7 References

Please note that Ref. CASEN (2009) is cited in text but not given in the list. Please provide its details in list or delete the text citation.

Q8 References Please provide the location of publisher for Ref. Kerr and Siegel (1954).

Q9 References Please provide name of the publisher for Ref. Press (2006).

Q10 Running Head Please confirm whether the short title is OK as given.

Making corrections to your proofs

• Please use the tools in the Annotation and Drawing Markups toolbars to

correct your proofs. To access these, press ‘Comment’ in the top right hand

corner.

• If you would like to save your comments and return at a later time, click

Publish Comments.

• If applicable, to see new comments from other contributors, press Check

for New Comments

• Once you have finished correcting your article, click Finalize/Finalize PDF

Comments.

• The Publish Comments and Finalize/Finalize PDF Comments options are

available either as:

1. A pop up JavaScript Window, shown right, or

2. By clicking ‘Tools’ in the top right hand corner, then clicking

‘JavaScript Window’, shown right.

3. Do not close the Javascript window.

Annotation tools

Insert text at cursor: click to set the

cursor location in the text and start typing to

add text. You may cut and paste text from

another file into the commenting box

Replace (Insert): click and drag the

cursor over the text then type in the

replacement text. You may cut and paste text

from another file into the commenting box

Strikethrough (Delete): click and drag

over the text to be deleted then press the

delete button on your keyboard for text to be

struck through

Underline: click to indicate text that

requires underlining

Add sticky note: click to add a comment

to the page. Useful for layout changes

Add note to text: click to add a note.

Useful for layout changes

Highlight text: click to highlight specific

text and make a comment. Useful for

indicating font problems, bad breaks, and

other textual inconsistences

Comments list This provides a list of all

comments and corrections made to the

article. It can be sorted by date or person.

Drawing tools There is the ability to draw

shapes and lines, if required.

Attach file, Record audio, and Add stamp are not in use.

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

Large mining enterprises and regional developmentin Chile: between the enclave and clusterMartın Arias*,y, Miguel Atienza** and Jan Cademartori***

5 *Bartlett, School of Planning, University College London, London, UK.**Departamento de Economıa, Universidad Catolica del Norte, Antofagasta, Chile.***Departamento de Economıa, Universidad Catolica del Norte, Antofagasta, Chile.yCorresponding author: Martın Arias, Bartlett, School of Planning, University College London,London, UK. email:[email protected]

10

AbstractVarious regions have recently proposed the creation of clusters around large-scalemining. However, until the 1980s, mining regions were predominantly consideredproductive enclaves. This article analyzes the case of the Antofagasta Region, the main

15 mining region in Chile. A descriptive analysis is put forward that addresses the idealtypes of the mining cluster and enclave, establishing as criteria of comparison themechanisms proposed by Marshall as sources of agglomeration economies. Despitestrong growth, the Antofagasta Region approximates more a mining enclave than acluster. This implies the need to revise and adapt the concept of enclave to the current

20 reality.

Keywords: enclave, cluster, multi-national corporations, mining regions

JEL classifications: O13, O19, Q32, R5Date submitted: 28 February 2012 Date accepted: 13 March 2013

1. Introduction

25 Over the last decades, a controversy has persisted on the role of multinationalcorporations (MNCs) in regional development. In the 1990s, MNCs were seenpredominantly as drivers of regional development (Dunning, 1997; Ramos 1998).However, since the end of the 20th century, several studies have emphasized thatForeign Direct Investment (FDI) can be counterproductive for host regions (Martin

30 and Sunley, 2003; Phelps, 2008). In this debate, research on mining regions indeveloping countries has been scarce. Nevertheless, the evolution of this type of regionhas been predominantly linked to the presence of MNCs. Traditionally, mining regionswere productive enclaves dominated by MNCs that do not contribute to a sustainableform of development (Cardoso and Faletto, 1969; Girvan, 1970; Weisskoff and Wolff,

35 1977; Auty, 1979; Emerson, 1982). Recently, however, several regions have proposeddevelopment strategies based on promoting mining clusters where MNCs would be themain actors.

Both the mining enclave and cluster are specialized agglomerations that have highgrowth rates and a strong export orientation. However, they have contrary impacts on

40 the host region. The mining enclave leads to unsustainable development (Cademartori,2008; Phelps, 2008), whereas a cluster generates a process of endogenous developmentand diversification of the industrial mix that is beneficial for the region (Markusen,

� The Author (2013). Published by Oxford University Press. All rights reserved. For Permissions, please email: [email protected]

Journal of Economic Geography (2013) pp. 1–24 doi:10.1093/jeg/lbt007

manu.s

Text Box

Q1

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

1996; Ramos, 1998; Cruz and Teixeira, 2010). Several works have contrasted theenclave and cluster models (Barrow and Hall, 1995; Rodrıguez-Clare, 1996; Cademar-tori, 2008; Phelps, 2008; Lagos and Blanco, 2010; Melese and Helmsing, 2010), but fewhave studied this difference in concrete cases. This is the main contribution of this

5 article as applied to mining regions with a major presence of MNCs.During the last decade, there has been a shift in the cluster literature from an ideal

type and essentially static perspective (Gordon and McCann, 2000; Markusen, 1996)toward evolutionary and knowledge-based explanations (Pinch et al., 2003; Phelps,2004; Cruz and Teixeira, 2010; Potter and Watts, 2011; Boschma and Frenken, 2011; Li

10 et al., 2012). However, there is no parallel development in the literature about enclaves.For this reason, we have used ideal type cluster literature as a starting point,recognizing that further studies could develop the evolutionary perspective of enclaves.Research on clusters has some elements that could be useful to understand the enclaveeconomy, in particular the inductive typology proposed by Markusen (1996), that

15 provides a wide range of categories that can help us to evaluate Porterian cluster policylabels that have been applied to the mining industry.

The objective of this article is to provide an analytical framework to investigatewhether a mining region approximates more a mining cluster or an enclave. To do this,the ideal types of the mining enclave and cluster are contrasted. The principal

20 dimensions of analysis are the three basic mechanisms that, according to Marshall(1890/1920), lead to increasing returns to scale in a specialized region as a result oflocalization economies: the division of labor, the existence of a thick labor market andthe existence of knowledge transference channels. This analytical framework is applied,through a descriptive analysis, to one of the main mining regions in Latin America,

25 Antofagasta in northern Chile, based on a variety of primary (a survey of 597 localSMEs) and secondary sources. Since 2001, this region has attempted to promote amining cluster and has been considered by CEPAL (2009) and the OECD (2009) as aleading region and example of economic growth and development in Latin America.

The results show that despite a strong growth rate, the Antofagasta Region maintains30 many of the characteristics of enclaves. This evidences the need to review and update

the concept of mining enclave as a useful analytical category to study miningagglomerations with a major presence of MNCs. It also shows the risk of implementinguniversal cluster policies without considering the regional context (Martin and Sunley,2003) and the need to design regional development policies that counteract the logic of

35 internalization of the MNCs (Phelps, 2000, 2008).The article is divided into five parts. The first part presents the mining cluster and

enclave ideal types. Following this, we describe the case study of the AntofagastaRegion and then explain the methodology of the study and the main results. Finally, weprovide conclusions, highlighting implications for regional development policies.

402. Between the enclave and the cluster

2.1. Mining and MNCs: what type of cluster?

Since the beginning of the 1990s, the promotion of clusters has been proposed in severalmining regions around the world, such as Yanacocha and Tamboraque in Peru(Kuramoto, 2001a, 2001b); Sudbury in Canada (Ritter, 2000; Warrian and Mulhern,

45 2009); Gauteng Province in South Africa (Economic Commission for Africa, 2004;

2 of 24 . Arias et al.

manu.s

Text Box

Q2

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

Walker and. Minnitt, 2006; Lydall, 2009); Western Australia mining cluster (Enrightand Roberts, 2001; Upstill and Hall, 2006) and Antofagasta in Chile (Buitelaar, 2001;Lagos and Blanco, 2010). All these cases present remarkable differences, and it isdifficult to state to what extent these regions are developing mining clusters. The most

5 successful experience of a well-established mining cluster is probably the Bothnian Gulfin the frontier between Sweden and Finland (Blomstrom and Kokko, 2007; Ejdemo andSoderholm, 2011). This area was specialized in mining activity since the 16th century,and during the past decades, the mines gave birth to metal processing, manufacturing ofchemical and mineral products, machinery, consulting and research and education

10 centers with the participation of both national and foreign MNCs. Currently, theindustrial mix of this area is diversified, and some local firms are specializedinternational suppliers of mining services and manufacturing and just a small fractionof extractive industry’s products is exported unprocessed (Geological Survey of Finland(GTK), 2011).

15 The analysis of mining clusters has received scant attention in the literature that hasbeen predominantly based on the experience of manufacturing regions. The formationof clusters was first studied by Marshall (1890/1920), in his analysis of industrialdistricts in Britain in the 19th century, where he identified three mechanisms thatexplain the productive advantages derived from physical proximity among businesses

20 with similar activities: the existence of a thick labor market, the division of labor andknowledge spillovers. This idea was revived a century later owing to the influence ofauthors such as Porter (1990), and the ‘cluster’ concept became a panacea of publicpolicies, thanks to the promise of producing more competitive regions (Martin andSunley, 2003). From a policy perspective, however, cluster policies based on Porter’s

25 ideas have been adopted in several developing countries, like Chile, in a rather uncriticaland decontextualized manner (Martin and Sunley, 2003). First, these policies have beenusually based on a singular concept, as if all clusters are essentially the same. Second,these policies have not always distinguished differences between the national andsubnational scale. Furthermore, differences in structural and historical contexts of

30 clusters have not been taken into account. This is particularly true in the case ofeconomies that are dependent on natural resources, where the enclave economy hasdominated in the past. As a result, there may well be a mismatch between theory andpolicy in the case of extractive countries and regions.

Mining operations are not organized as a network of small and medium enterprises35 specialized in the same activity, as is the case for Marshallian industrial districts

(Markusen, 1996). On the contrary, mining regions are characterized by the presence oflarge companies, normally MNCs that dominate the local economy. Consequently,the first question to be answered is: What kind of cluster can emerge aroundmining operations? A useful typology in answering this question is that proposed by

40 Markusen (1996)1, based on an inductive analysis drawing on the experience of severalcountries. Markusen noted that industrial districts could have distinct productivestructures. From this perspective, the ideal type that is best adapted to thecharacteristics of mining is that termed as hub-and-spoke district, characterized bythe presence of one or more large companies, normally MNCs, which form the ‘hubs’ of

45 the productive system. These companies have a high degree of vertical integration

1 For a more complete view of this typology, see Markusen (1996).

Large mining enterprises and regional development . 3 of 24

manu.s

Text Box

Q10

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

and dominate regional production. They are export oriented and have around them aset of local suppliers of goods and services that are organized as the spokes, with a highlevel of subcontracting.

To explain how agglomeration economies allow for the productive diversification5 and economic sustainability of this type of cluster, Markusen (1996) used two analogies,

productive system with ‘wide shoulders’ and ‘long arms’. The ‘wide shoulders’ refers tostimulus on the part of the hubs to consolidate a set of small and medium supplierfirms, which in the long term should allow for the creation of new hubs or clusters. The‘long arms’ refers to the access MNCs have to advanced technologies from their

10 headquarters and the vertical transfer of knowledge toward the spokes of local firms(Gray et al., 1996). Both characteristics activate the classic mechanisms of theMarshallian triad, generating a competitive and sustainable form of development.

This model emerged in a context of industrial regions but can be extended to miningregions where large mining MNCs can be found surrounded by small supplier firms and

15 can generate a virtuous process similar to that described by Markusen (1996).Therefore, this work adopts the hub-and-spoke industrial district model as the bestapproximation to a mining cluster available from the clusters literature.

2.2. The mining enclave

Traditionally, mining regions in underdeveloped countries have shown an economic20 enclave structure, characterized by the presence of MNCs in the area of mineral

extraction. Several works in economic and local development describe this structure asone with weak productive linkages to the local firms, foreign ownership of capital andexporter of goods with low or no value added, all of which led to a vicious circle forlocal development (Cardoso and Faletto, 1969; Girvan, 1970; Weisskoff and Wolff,

25 1977; Auty, 1979; Emerson, 1982; Phelps, 2008; Cademartori, 2008; Conning andRobinson, 2009). Despite this, the enclave was adopted as a development strategy byunderdeveloped countries rich in natural resources, especially in Latin America,between the end of the 19th century and the beginning of the 20th century. During thatperiod, the strong growth in output and exports in the mining enclaves created an image

30 of local development that proved to be illusionary. This illusion ended when mostenclaves experienced profound social, political and economic crisis, causing their abruptdisappearance during the first half of the 20th century (Cardoso and Faletto, 1969;Girvan, 1970; Conning and Robinson, 2009).

Furthermore, the mining enclave has important implications in geographical terms. It35 presents a hub-and-spoke structure, where the big mining MNCs act as hubs and the

supplier SMEs like spokes, but has specific characteristics that differentiate it fromvirtuous forms of regional organization. Some of these particular features are the lackof linkages to the local firms (Rodriguez Clare, 1996), the high concentration of foreigncapital, the mono-producer and mono-exporter character of the enclave and the

40 dependence on overseas (Cardoso and Faletto, 1969). This dependency of the localeconomy on enclaves is more pronounced in environments that historically have had nolocal export economies (Ackah-Baidoo, 2012) and is evidenced in the imports oftechnology to supply the mining sector, the asymmetry of negotiating power betweenthe MNCs and the government and local firms and the sensitivity to the demand shocks

45 of international markets.

4 of 24 . Arias et al.

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

Moreover, the enclave has a high level of labor productivity because of capital-intensive operations, which implies that aggregate demand is below the thresholdrequired to stimulate the local production of manufactured goods (Auty, 1979), leadingto an hyperspecialization in the primary sector. Also, in general, salaries in the enclave

5 are higher than in the agricultural or industrial regions; consequently, they receive aconsiderable amount of migrants and commuters from other regions with lower wages.One of the most important features of the mining enclave, compared with otherindustries, is that the barriers to exit are high, due to the fixed character of naturalresources. This obliges MNCs to interact with the region given that the negotiating

10 power of the social actors in this type of enclave, although weak, is greater than in anyother type (Zapata, 1977; Ramırez, 2005). However, this does not prevent EMNsexporting profits to international headquarters and the capture of public goods, leadingto a non-sustainable form of development (Phelps, 2008; Cademartori, 2008; Ackah-Baidoo, 2012).

15 The concept of enclave was progressively abandoned during the 1970s. As theconcept was broadened out from its original geographic and economic scope, it lostprecision (Hojman, 1983). However, some works have recently revived the concept withthe original economic focus owing to the limited benefits obtained by local economieswith a strong presence of MNCs (Ramırez, 2005; Phelps, 2008; Conning and Robinson,

20 2009; Heller and Rueschemeyer, 2009; Melese and Helmsing, 2010). The scarcity ofliterature about the enclave economy since the 1970s implies a significant theoreticalgap regarding the role of MNCs in the development of mining regions. At the sametime, cluster studies have significantly advanced in the past three decades (Cruz andTeixeira, 2010), revealing the variety of forms that specialized agglomerations can take

25 (Markusen, 1996; Gordon and McCann, 2000). It is noticeable, in this respect, thatsome of these forms of clustering are rather close to what has been historicallyconsidered as an enclave. This gives us a way to understand to what extent miningregions, particularly in Chile, have advanced toward more sustainable forms ofdevelopment.

30 2.3. Ideal types of the mining cluster and enclave

The enclave and the cluster have opposite long-term results but can occur in regionswith similar characteristics. Consequently, several works have compared them (Barrowand Hall, 1995; Rodrıguez-Clare, 1996; Cademartori, 2008; Phelps, 2008; Lagos andBlanco, 2010; Melese and Helmsing, 2010), and some regions have been considered as

35 mining clusters while they may still maintain several traits of the enclave.The dimensions used by Markusen (1996) to construct her typology of industrial

districts confirm that the mining enclave and cluster share many characteristics. Amongthese are the hub-and-spoke structure, the high rates of growth and export orientation,the presence of internal economies of scale, the specialization of local firms in services,

40 the low level of cooperation between suppliers and clients and the cooperation of thehubs with companies outside the agglomeration. At the same time, there are importantdifferences between the two models, given that in the enclave, the key investments aredecided upon in the headquarters of the MNCs, contracts are short term and there is ahigh proportion of workers from other regions, whereas in the cluster model, key

45 investments are decided locally, contracts are long term and large companies aresupplied by the local labor market.

Large mining enterprises and regional development . 5 of 24

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

In this article, we adopt as a starting point for the comparison of mining clusters and

enclaves an ideal type approach focused on the classical mechanisms that Marshall

described as sources of localization economies. Our choice here is a result of the fact

that past research on extractive industry enclaves has followed fundamentally a5 structural perspective that has traditionally focused on the productive linkages and the

characteristics of the labor market—both of which are aspects of the Marshallian triad.

The comparison between the two types is also based on the fact that they are currently

the main strategies proposed for the development of mining regions. Furthermore,

the ideal type approach can be used to infer change over time from one cluster form10 to another. It should also be kept in mind that in dealing with ideal types, the

particular cases observed in reality present mixed characteristics. As well, although both

ideal types develop dialectically (Sanchez de Puerta, 2006), this does not imply that

mining regions do not present other forms of organization. In this respect, it is

important to distinguish between the concepts of enclave and ‘hollow cluster’ proposed15 by Bathelt et al. (2004) and Bathelt (2009). In both types of industrial organization,

linkages to external markets are strong but do not guarantee local sustainability. These

ideal types have, however, different characteristics. In the ‘hollow clusters’, local firms

systematically search for strategic partnerships of interregional and international

reach (‘pipelines’) to create knowledge and produce local growth. This requires pre-20 existent complex capabilities and a shared institutional context to favor knowledge

transfer. The sustainability of ‘hollow clusters’ is threatened because the knowledge

acquired by the local firms connected to the ‘pipelines’ does not spill over to the rest of

local firms due to the lack of internal linkages (‘buzz’). In contrast, in the enclave, large

firms, often EMNs, search for locations where they can avoid knowledge transfer and25 even absorb local knowledge (McCann and Mudambi, 2004). In this case, pre-existent

local capabilities are scarce and cognitive, and organizational and institutional distance

between EMNs and local firms is wide (Boschma, 2005).Based on the previously established dimensions of analysis, a mining cluster is

understood as a specialized agglomeration in the production of minerals, with a strong30 presence of MNCs and the following characteristics:

1. Division of labor: As a result of specialization, mining has strong forward and

backward linkages with local firms that lead to significant multiplier effects and

reduce the costs of inputs and final outputs. This stimulates the creation of new

businesses and strengthens clusters of new activities. This is related to what35 Markusen (1996) called ‘wide shoulders’.

2. Thick labor market: Local qualified workers can find employment in the region, and

companies can find the workers they require within the region without drawing

upon the labor markets from other regions. This supposes the presence of a market

for trained labor and a relatively high level of turnover of workers among40 companies that facilitates the transference of knowledge (Scott, 2006).

3. Knowledge spillovers: Supposes the existence of knowledge transfers outside of

market relations, based on the interactions among workers, employers and

members of other public and private organizations. Knowledge transfer would be

fundamentally exogenous (originating from MNC headquarters) and vertical in45 character, related to what Markusen (1996) called ‘long arms’, which promotes the

innovative capacity and competitiveness of local firms.

6 of 24 . Arias et al.

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

In contrast, a mining enclave is understood as an agglomeration specialized in miningwith a high level of participation of foreign capital and the following characteristics:

1. Lack of a division of labor and weak productive linkages: The MNCs maintain weaklinkages with the local economy given that such linkages are mainly established

5 with the outside world. This limits the development of industrial activities (‘wideshoulders’) and productive diversification. Linkages with the local firms are usuallyrelated to activities with low added value and high levels of subcontracting.

2. Non-thick labor market: MNCs look to other regions to meet a significant part oftheir labor requirements through commuting and shift work systems. As well, the

10 occupations conducted within the enclave are fundamentally manual, physical androutine, while the managerial and more professional functions are largely locatedoutside the region (Buckley and Ghauri, 2004).

3. Limited knowledge spillovers: Knowledge spillovers from MNCs to local firms arelimited. R&D activities in the region are marginal, and the productive process

15 undertaken locally is routine, which leaves little space for innovation (Crone andRoper, 2001). Patents are normally internalized by the MNCs. Activities focused ongenerating knowledge transference to local supplier firms are not attractive tomining MNCs. These would only occur where the MNC perceives some benefit,such as improving quality or lowering costs (Dunning, 1993, p. 456). All of this

20 limits the competitiveness of local firms and their export capacity.

These characteristics result in the lack of an ‘industrial atmosphere’, whichcompromises regional sustainability in the context of a possible flight of FDI.

Comparing the two ideal types, Table 1 provides an analytical framework that helpsresolve the problem of observational equivalence between the mining cluster and

25 enclave that can occur in some mining regions because the two phenomena share severaldimensions, among them the hub-and-spoke structure and high rates of growth andexporting.

3. The case of Antofagasta

The Antofagasta Region is located in the Atacama Desert in northern Chile. It has a30 population of 569,634 inhabitants, which represents 3.4% of the country’s population

(CASEN, 2009). Mining is the main economic activity, and the Region has the largestdeposits of copper, iodine and lithium in the world, as well as major reserves of silverand molybdenum (USGS, 2011).

Historically the Antofagasta Region has had a high presence of mining MNCs.35 Between the 1880s and 1930s, Chile was the world’s largest producer of nitrates, which

meant a significant level of dependence of the national economy on this sector2, andconsiderable remittances of profits overseas (mostly to the United Kingdom) by theBritish nitrate MNCs. In Antofagasta, these companies formed the traditional miningenclaves organized as company towns (Kerr and Siegel, 1954) where the company

40 provided all the goods and services to the workers, such as housing, police and evenmoney. However, the employment conditions were extremely precarious, favored by

2 Nitrate production accounted for more than 70% of Chilean exports and around 30% of GDP (Meller,2007).

Large mining enterprises and regional development . 7 of 24

manu.s

Text Box

Q7

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

flexible labor legislation. This period ended abruptly at the beginning of the 1930s dueto the invention of synthetic nitrates, which led to one of the most serious economic andsocial crises in the history of Chile and to the progressive disappearance of companytowns (Salazar and Pinto, 2002; Meller, 2007).

5 Since the 1940s, and thanks to the incorporation of US investment, copper becamethe driver of regional and national growth. Following the nationalization of the coppersector in 1971, the National Copper Corporation of Chile (Corporation Nacional delCobre de Chile [CODELCO]) was created and became the main copper producernationally and globally (COCHILCO, 2010). This public enterprise is still active, but

10 since the beginning of the 1990s and thanks to tax, labor and environmental legislationextremely favorable to FDI, the Antofagasta Region has become the focus for a largenumber of international mining projects. Between 1990 and 2008, the region receivedbetween 15% and 30% of all FDI in Chile, for a total of US $9.228 billion dollars(Comite Inversiones Extranjeras), representing the second highest level of FDI to a

15 single region of the country after investment in the Metropolitan Region.Among the most important multinational mining projects in Antofagasta are the

mines Escondida, Zaldıvar, Mantos Blancos, Spence, Lomas Bayas and El Abra(Figure 1), all property of large MNCs, such as BHP Billiton, Anglo American, Xstrataand Barrick Gold. The copper production of these MNCs grew from 24% of the

20 national output in 1990 to 65% in 2010 (COCHILCO, 2010) as a result of the highcopper prices in the last decade and growing FDI in mining (Table 2). Output has alsobeen stimulated by recent free trade treaties signed with China, the United States, SouthKorea and Canada, which together account for around 50% of the world copperimports (COCHILCO, 2010).

25 This situation has generated a new form of dependence of the Antofagasta Region onlarge copper mining MNCs, with important differences with respect to the nitrate

Table 1. Comparison between the ideal types of mining cluster and enclave

Clusters Enclaves

Division of the labour

‘Wide shoulders’ ‘Narrow shoulders’

Labour market

Thick Thin

Knowledge spillovers

High‘Long arms’

Low‘Short arms’

8 of 24 . Arias et al.

manu.s

Text Box

Q5

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

Figure 1. Antofagasta region: main cities and mining companies, based on data in Lagos andBlanco (2010).

Table 2. Antofagasta copper production by mine and company 2010, based on data in COCHILCO

(2010)

Mines Company Copper

production

(thousand tons)

%

CODELCO – State of Chile 1020.8 35

Chuquicamata and

Radomiro Tomic

Division CODELCO Norte 903.7 31

Gaby CODELCO 117.1 4

Multinationals 1921.4 65

Escondida BHP BILLITON (57.5%), RTZ (30%);

Japanese Consortium (JECO,

lead by Mitsubishi 10%); World Bank (2.5%)

1086.7 37

Spence BHP BILLITON (100%) 178.1 6

Zaldıvar Barrick Gold (100%) 144.4 5

El Abra Freeport McMoran (51%); CODELCO (49%) 145.2 5

Mantos Blancos Anglo American (100%) 87.7 3

El Tesoro Antofagasta Minerals (70%); Marubeni Corp (30%) 95.3 3

Michilla Antofagasta Minerals (71%); others 41.2 1

Lomas Bayas Xstrata (100%) 71.8 2

Others Others 71.0 2

Total 2942.2 100

Large mining enterprises and regional development . 9 of 24

manu.s

Text Box

Q4

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

epoch. The most evident transformation is the abandonment of the company townmodel, replaced by a roster system in which the workers live at the mine for a certainnumber of days and then return to their homes. This has favored commuting from otherregions (Aroca and Atienza, 2008, 2011).

5 Three cities stand out in the urban system of the region (Figure 1): Antofagasta,regional capital, the center of economic activity and the main port for mineral exports,with a population of approximately 300,000 inhabitants (60% of the region); Calama,the neighboring community of the Chuquicamata open pit mine of CODELCO, with130,000 inhabitants (28% of the region); and Tocopilla, which benefits from

10 thermoelectricity and has port facilities, with around 25,000 inhabitants (5% of theregion).

Currently, 55% of the product of the Antofagasta Region comes from mining sector,which represents 50% of Chilean mining production (Banco Central de Chile). Thispercentage is relevant if we consider that Chile is the largest producer of copper

15 worldwide, with 35% of total production and 40% of exports (COCHILCO, 2010).Some 96% of exports from the Antofagasta Region are minerals, notably copper, whichalso represents 30% of the national exports (COCHILCO, 2010).

During the last two decades, the Antofagasta Region has had an average annualoutput growth rate of 6% (Banco Central del Chile), because of which different

20 international organizations have considered Antofagasta to be an example of a winnerregion in South America (CEPAL, 2009; OECD, 2009). At the same time, these resultshave led to the promulgation of a development strategy around mining operations inthe region. According to this strategy, since 2001, efforts have been made to promote amining cluster that in turn would encourage the development of a goods and services

25 supplier industry able to compete internationally and to maintain the high growth rateof the region.

4. Methodology

The concepts of cluster and enclave present analytical difficulties because they refer tocomplex and multidimensional phenomena. The study of their development in a

30 territory raises problems of observational equivalence and obstacles to empiricalcomparison. The concept of cluster has been considered ‘confusing’, ‘ambiguous’ and‘chaotic’ (Gordon and McCann, 2000; Martin and Sunley, 2003; Markusen, 2003;Phelps, 2008) due to the loss of conceptual clarity, the large number of cases it describesand its arbitrary use to explain any type of agglomeration of economic activity. The

35 same occurred with the concept of enclave, which was progressively abandoned duringthe 1970s because it had lost its original geographic and economic character and wasbeing used to address any manifestation of unbalanced growth (Hojman, 1983). Bothare ‘fuzzy concepts’ characterized by the lack of clarity in their content and by theadaptation of their definitions to the objectives of researchers or politicians, with the

40 consequent difficulty to identify them empirically (Markusen, 2003).One way to solve some of the problems presented by ‘fuzzy concepts’ is to establish

typologies that clarify the diversity of phenomena being addressed (Martin and Sunley,2003). In this study, we elaborate ideal types of the mining cluster and enclave, with theaim of clarifying the characteristics of each and to determine to which ideal type the

45 Antofagasta case is closest to. Although the two ideal types have common

10 of 24 . Arias et al.

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

characteristics, they differ in the mechanisms that determine their economic sustain-ability. In a mining cluster, the local economy becomes independent of MNCs,promoting sustainable growth in the region. In contrast, in the enclave model, the localeconomy is incapable of surviving if the MNCs abandon the region, which implies

5 unsustainable growth. As previously mentioned, the Marshallian triad brings togetherthe mechanisms used as operational criteria to compare the two proposed ideal types.The use of Marshallian sources of externalities as operational criteria is related to thetraditional definition of enclaves based on productive linkages and characteristics of thelabor market.

10 A descriptive analysis is made of each of the Marshallian mechanisms based onprimary data from a survey of 597 local SMEs in 20093, as well as a variety of secondaryinformation from public agencies and prior research in Chile detailed in Table 3. Theobjective of the analysis is not to estimate the agglomeration economies, given thatthere is not sufficient information to do this with all the components of the Marshallian

15 triad, particularly data on plants’ labor productivity and value added and on entry andexit of firms. Rather, the objective is to determine whether the conditions that theliterature has traditionally considered favorable to agglomeration economies throughMarshallian mechanisms exist. This approach, imposed by data availability, haslimitations. First, time series available at the firm level in Chile is too short for an

20 historical approach. Second, the number of variables used to describe each Marshallianmechanism is reduced, despite being consistent with measures used in other works(Potter and Watts, 2011). Furthermore, some of these variables, such as patents, haveattracted considerable debate within economic geography as an approximation for localknowledge spillovers. For this reason, indirect proxies of knowledge spillovers, such as

25 inter-firm cooperation and export capacity, have been included in the analysis. In anycase, further research, both quantitative and qualitative, would be needed to obtain acomplete picture of the ‘industrial atmosphere’ of the Antofagasta Region, especially inaspects related to unintentional spillovers of knowledge.

5. Results

30 5.1. Division of labor: ‘wide shoulders’

In a mining cluster, a broad range of local supplier firms have strong linkages withregional hubs that, over time, allow for the development of new local industries and amore diversified growth. In contrast, mining enclaves are characterized by weaklinkages and the lack of diversification. To evaluate the degree to which the

35 Antofagasta Region has an economy with ‘wide shoulders’, we first estimated thelinkages of the mining sector with the other local economic activities. We then evaluatedthe characteristics of the productive relationships between mining hubs and their local

3 According to the Servicio de Impuestos Internos (SII), the public organism responsible for collecting taxesin Chile, the universe of SMEs in the Region of Antofagasta was 4.744 firms in 2008. Primary data wereobtained by means of a field survey to a random stratified sample of 597 firms. Three strata were definedaccording to the county where the firms were located: Antofagasta, the administrative capital of theregion; Calama, the mining capital of the region; and the rest of smaller counties. The sample estimationerror was 6% and the confidence level was 95%. The questionnaire of the survey was personallyadministered within firms between July 2009 and January 2010 and comprises 92 questions grouped into 9modules that include both closed and open-ended questions.

Large mining enterprises and regional development . 11 of 24

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

suppliers, with special emphasis on the increasing reliance on subcontracting and,

finally, we analyzed the evolution of productive diversification.Backward and forward linkages measure the level of integration of an industry with

the rest of the local economy. According to Learmonth et al. (2007), the backward5 linkages associated with a cluster sector can be identified as the domestic production of

other commodities that are used as intermediate inputs in the production process of the

cluster. The forward linkages, on the other hand, track the amount of a particular

sector’s value added that is used, directly or indirectly, as intermediate inputs in other

regional output. We refined this method using the ‘key sector analysis’ proposed by10 Sonis and Hewings (2009), where those sectors whose forward and backward linkages

are higher than one are considered ‘key sectors’. This means that a change in final

demand of the key sector will create an above average increase in the economy and that

a change in all sector’s final demand would create an above average in the key sector.To estimate the forward and backward linkages of mining in Chile, we followed the

15 methodology proposed by Sonis and Hewings (2009), based on the regional input–

output matrices for 19964 from the Banco Central de Chile. These results were

contrasted to those of Aroca (2001) and Cademartori (2008). The major forward and

backward linkages in copper mining in Chile are found in the Antofagasta Region,

which turns mining into a ‘key sector’ for this region. This result was expected, given the20 high degree of specialization of Antofagasta on mining. However, these linkages are

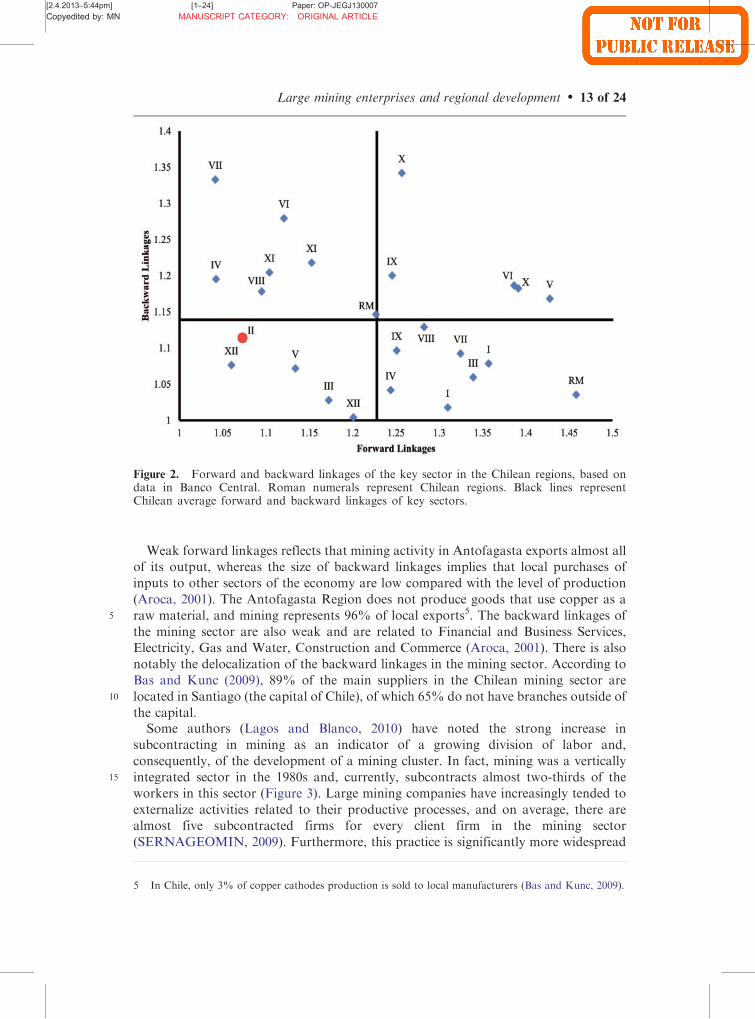

weak compared with the ‘key sectors’ of the other Chilean regions. Figure 2 presents the

first two ‘key sectors’ of each of the Chilean regions (depicted with Roman numerals),

compared with the mining sector of the Antofagasta Region, represented by the circle

and the Roman numeral II. Both the forward and backward linkages of copper mining25 in the Antofagasta Region are below the average of the ‘key sectors’ of other regions of

the country, indicated with thick black lines in Figure 2.

Table 3. Summary of the methodology

Marshallian triad Mechanisms Source

Division of labor 1. Linkages. 1. Input output matrices. Source: INE (1996)

2. Industrial structure 2. Location quotients and Hirschman

Herfindahl index. Source: Banco Central

(1985–2006), INE (1986–2006)

3. Subcontracting. 3. SME survey (2007, 2009), COCHILCO

Thick labor market 1. Commuting rate among regions 1. Census (2002), CASEN (2009) and Aroca

and Atienza (2008, 2011)

2. Spatial division of labor 2. 2002 Census and Atienza et al. (2010)

Knowledge spillovers 1. Collaboration between

SMEs and MNCs

1. SME survey (2007, 2009)

2. Local Patents 2. Bas and Kunc (2009)

3. SME export rate 3. SME survey (2007, 2009)

4 The Banco Central de Chile calculates the national input–output matrices every 10 years. Those availablecorrespond to the years 1977, 1986, 1996 and 2003, although the latter has not been regionalized yet.

12 of 24 . Arias et al.

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

Weak forward linkages reflects that mining activity in Antofagasta exports almost allof its output, whereas the size of backward linkages implies that local purchases of

inputs to other sectors of the economy are low compared with the level of production

(Aroca, 2001). The Antofagasta Region does not produce goods that use copper as a5 raw material, and mining represents 96% of local exports5. The backward linkages of

the mining sector are also weak and are related to Financial and Business Services,Electricity, Gas and Water, Construction and Commerce (Aroca, 2001). There is also

notably the delocalization of the backward linkages in the mining sector. According to

Bas and Kunc (2009), 89% of the main suppliers in the Chilean mining sector are10 located in Santiago (the capital of Chile), of which 65% do not have branches outside of

the capital.Some authors (Lagos and Blanco, 2010) have noted the strong increase in

subcontracting in mining as an indicator of a growing division of labor and,

consequently, of the development of a mining cluster. In fact, mining was a vertically15 integrated sector in the 1980s and, currently, subcontracts almost two-thirds of the

workers in this sector (Figure 3). Large mining companies have increasingly tended to

externalize activities related to their productive processes, and on average, there arealmost five subcontracted firms for every client firm in the mining sector

(SERNAGEOMIN, 2009). Furthermore, this practice is significantly more widespread

Figure 2. Forward and backward linkages of the key sector in the Chilean regions, based ondata in Banco Central. Roman numerals represent Chilean regions. Black lines representChilean average forward and backward linkages of key sectors.

5 In Chile, only 3% of copper cathodes production is sold to local manufacturers (Bas and Kunc, 2009).

Large mining enterprises and regional development . 13 of 24

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

in Chile than in countries such as Australia, Canada and South Africa, where mining

clusters have been promoted and where the percentage of subcontracted workers does

not exceed 26% of the total (Perez and Villalobos, 2009).Although the development of subcontracting contributes to a greater division of

5 labor, it is doubtful that in the case of the Antofagasta Region it has resulted in the

improved competitiveness of local companies. According to the survey of a sample of

597 regional SMEs in 2007 and 2009, subcontracted firms in the mining sector maintain

traditional forms of management, make little effort to modernize and have higher rates

of failure than other firms (Atienza, 2009). Almost 90% of these firms lack any form of10 international certification and only 1% declare having exports overseas. In particular,

differences with respect to direct mining suppliers are remarkable in terms of the

incorporation of workers with university degree and in the use of new technologies6.The lack of ‘wide shoulders’ in the Antofagasta Region is confirmed when we

consider the evolution of industrial diversification. Between 1986 and 2006, the degree15 of sectorial concentration of output, estimated with the Hirschman-Herfindahl

coefficient7, has been the highest in the country, using the International Standard

Industrial Classification (ISIC) at one digit level (Table 4). Output from the

Antofagasta Region continues to be highly dependent on the mining sector, which

Figure 3. Share of subcontracted workers in the mining industry—1975–2004, based on datain COCHILCO.

6 To identify subcontracted firms, the survey asks about the percentage of total sales to mining companiesmade through another firm. Subcontracted firms were considered those SMEs that sell 20% or more oftheir total sales to mining companies and whose indirect sales are bigger than their direct sales. Questionsabout management practices include certification, performance evaluation, quality control, planification,investment in innovation, age of equipments and machinery and customer services. The survey also allowsus to know the percentage of university graduates and technitians in the staff. A special section wasdedicated to the use of IT, with special focus on internet, web pages and e-commerce, widely used in thesupply chain of mining companies.

7 This coefficient is calculated as the sum of the squares of the share of each industry within totalemployment.

14 of 24 . Arias et al.

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

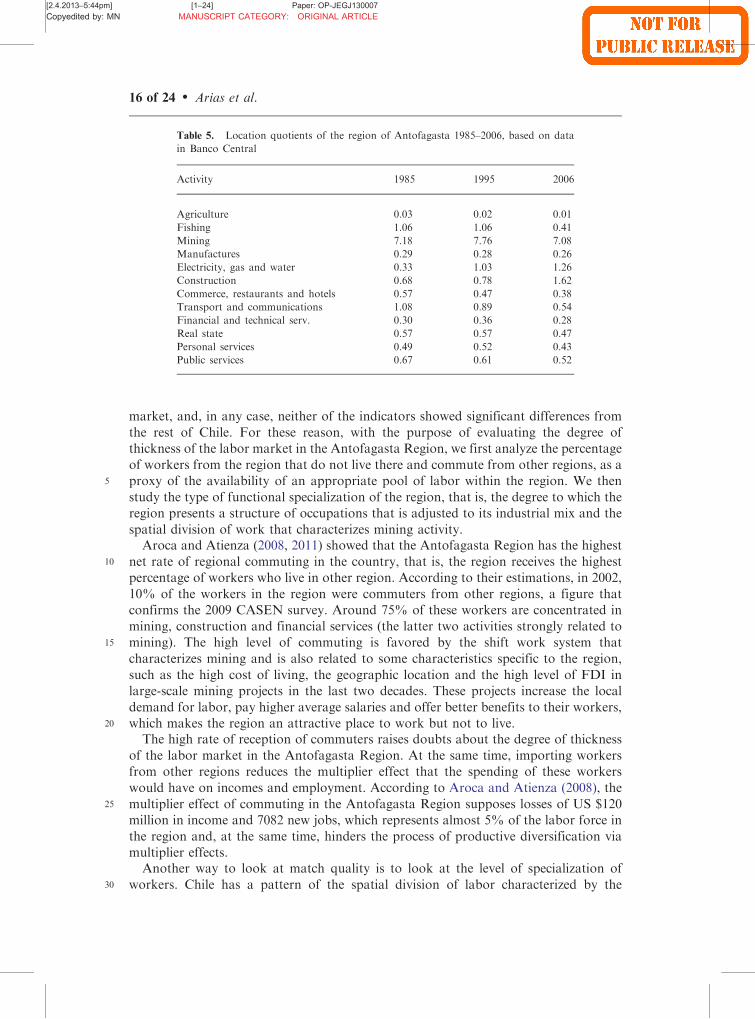

represented 56% of regional GDP between 1985 and 2006. Likewise, the locationquotients8, also calculated at one-digit ISIC (Table 5), show that during the last 20years, the region has maintained a productive structure that is seven times morespecialized in mining than the rest of country and that has developed new

5 specializations in construction and in utilities like electricity, gas and water.Between 1992 and 2002, location quotients calculated using employment at two-digit

ISIC show only three areas where specialization increased above a value of 1.3(Chemical Products, Fabrication of Metals and Metal Products), while the degree ofspecialization in Machinery and the majority of services related to mining decreased.

10 These results show the lack of expansion of the local ‘productive shoulders’ and raisedoubts about the sustainability of the region in the case of a crisis in the mining sector.

The results show the lack of ‘wide shoulders’ in the Antofagasta Region. The linkageswith the mining sector are weak, and productive diversification has been very limited inthe last 20 years, whereas the increase in subcontracting does not appear to contribute

15 to encouraging the competitiveness of local firms.

5.2. Labor market

The existence of a thick labor market is related to the quality of matching betweenworkers and employers. Some indicators that have been traditionally used to estimatethe thickness of a local labor market are the rate of turnover and the average time

20 employed to find a new job. According to the 2009 CASEN survey, the labor market inthe Antofagasta Region has the highest turnover rate of workers and the shortest timeto find a job in Chile. In accordance with Rosenthal and Strange (2004), however, theinterpretation of these indicators is ambiguous as a proxy of thickness of the labor

Table 4. Regional Hirschman—Herfindahl index 1985–2006 (based on GDP), based

on data in Banco Central

Region 1985 1995 2006

Tarapaca 0.11 0.11 0.18

Antofagasta 0.33 0.31 0.33

Atacama 0.19 0.21 0.20

Coquimbo 0.11 0.09 0.10

Valparaıso 0.17 0.14 0.13

M. R. 0.14 0.14 0.15

O’Higgins 0.10 0.08 0.07

Maule 0.11 0.09 0.10

Bıo Bıo 0.17 0.16 0.17

Araucanıa 0.13 0.11 0.10

Los Lagos 0.10 0.09 0.10

Aisen 0.19 0.13 0.11

Magallanes 0.21 0.15 0.19

Chile 0.11 0.11 0.11

8 This quotient measures the relative specialization of a region in an industry, as the ratio of the share of anindustry in a region and the share in the country.

Large mining enterprises and regional development . 15 of 24

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

market, and, in any case, neither of the indicators showed significant differences from

the rest of Chile. For these reason, with the purpose of evaluating the degree ofthickness of the labor market in the Antofagasta Region, we first analyze the percentage

of workers from the region that do not live there and commute from other regions, as a5 proxy of the availability of an appropriate pool of labor within the region. We then

study the type of functional specialization of the region, that is, the degree to which theregion presents a structure of occupations that is adjusted to its industrial mix and the

spatial division of work that characterizes mining activity.Aroca and Atienza (2008, 2011) showed that the Antofagasta Region has the highest

10 net rate of regional commuting in the country, that is, the region receives the highestpercentage of workers who live in other region. According to their estimations, in 2002,

10% of the workers in the region were commuters from other regions, a figure thatconfirms the 2009 CASEN survey. Around 75% of these workers are concentrated in

mining, construction and financial services (the latter two activities strongly related to15 mining). The high level of commuting is favored by the shift work system that

characterizes mining and is also related to some characteristics specific to the region,

such as the high cost of living, the geographic location and the high level of FDI inlarge-scale mining projects in the last two decades. These projects increase the local

demand for labor, pay higher average salaries and offer better benefits to their workers,20 which makes the region an attractive place to work but not to live.

The high rate of reception of commuters raises doubts about the degree of thickness

of the labor market in the Antofagasta Region. At the same time, importing workersfrom other regions reduces the multiplier effect that the spending of these workers

would have on incomes and employment. According to Aroca and Atienza (2008), the25 multiplier effect of commuting in the Antofagasta Region supposes losses of US $120

million in income and 7082 new jobs, which represents almost 5% of the labor force in

the region and, at the same time, hinders the process of productive diversification viamultiplier effects.

Another way to look at match quality is to look at the level of specialization of30 workers. Chile has a pattern of the spatial division of labor characterized by the

Table 5. Location quotients of the region of Antofagasta 1985–2006, based on data

in Banco Central

Activity 1985 1995 2006

Agriculture 0.03 0.02 0.01

Fishing 1.06 1.06 0.41

Mining 7.18 7.76 7.08

Manufactures 0.29 0.28 0.26

Electricity, gas and water 0.33 1.03 1.26

Construction 0.68 0.78 1.62

Commerce, restaurants and hotels 0.57 0.47 0.38

Transport and communications 1.08 0.89 0.54

Financial and technical serv. 0.30 0.36 0.28

Real state 0.57 0.57 0.47

Personal services 0.49 0.52 0.43

Public services 0.67 0.61 0.52

16 of 24 . Arias et al.

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

functional specialization9 of the Metropolitan Region in occupations that require ahigher level of human capital, such as managers, professionals and technicians, whereasthe other regions of the country, such as Antofagasta, are functionally specialized inoccupations of a routine and physical type that require a medium or low level of

5 qualification (Atienza et al., 2010). The functional specialization of the MetropolitanRegion is accentuated in the mining sector, with a higher presence than expected of65% in ‘managers’, 43% in ‘professionals’ and more than 15% in ‘technicians’ in 2002.In this sector, Antofagasta was notable for presenting a lower than expected presence of‘managers’ of 45%, and a slightly higher than expected percentage of ‘professionals’

10 and ‘technicians’ (Atienza et al., 2010).This pattern of the spatial division of labor raises doubts about the thickness of the

labor market of the Antofagasta region in relation to more qualified occupations and isrelated to the strong concentration of the headquarters of large mining MNCs in themetropolitan region, where they can benefit from the technological externalities of large

15 agglomerations and better access to international markets and suppliers. At the sametime, the branches and production centers of these large companies are located at thepoints of mineral extraction where they undertake logistical, operative and moreroutine functions. This form of organizing production limits the arrival to theAntofagasta Region of more qualified workers with decision-making power and adds to

20 the high rate of commuting to the Antofagasta Region, resulting in a labor market thatlacks thickness.

5.3. Knowledge spillovers: ‘long arms’

In a survey to SMEs of the Antofagasta region, Lufin and Garrido (2011) asked thefirms to identify their four main clients and suppliers and found that the network of

25 productive relationships in the region had a hub-and-spoke structure similar to thatdescribed by Markusen (1996) and Gray et al. (1996). The central nodes of this networkare the two main mining companies in the region—CODELCO and Minera EscondidaLimitada—around which emerged extensive spokes of local supplier firms with highlevels of subcontracting. Eleven of the 30 central nodes in the Antofagasta region are

30 mining MNCs, the supply chains of which are formed, on average, by 16 firms. Inaddition to the core of the network linked to the large MNCs, there are smallerperipheral networks that maintain very weak relationships with the mining sector.

In this type of network, increasing subcontracting by MNCs could become amechanism for long-term cooperation that facilitates the vertical transfer of informa-

35 tion and knowledge from the productive hubs to local enterprises (Kimura, 2002; Ramaet al., 2003). However, the existence of knowledge spillovers is not evident in regionsdominated by MNCs, especially when cognitive distance to local SMEs is too large(Boschma, 2005). Furthermore, McCann and Mudambi (2004, 2005) have indicatedthat the organization strategy of MNCs leads them to locate in regions that take the

40 form of ‘industrial complexes’ where the exchange of knowledge takes place throughformal long-term agreements managed in the framework of a bilateral monopoly. Inthis sense, given that a monopsonistic structure predominates in mining regions, it is notprobable that this type of exchange occurs, giving rise to a situation closer to that of an

9 This functional specialization is estimated using the index proposed by Barbour and Markusen (2007).

Large mining enterprises and regional development . 17 of 24

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

enclave where vertical knowledge spillovers are weak. To evaluate the existence ofchannels for knowledge transference between mining MNCs and their suppliers in theAntofagasta Region, we first analyzed cooperation agreements between the both groupsof firms, then the evolution of mining patents in Chile and, finally, the export capacity

5 of regional SMEs as an indirect indicator of their innovative and competitive capacity.According to the survey10 of a sample of SMEs in the Antofagasta Region in 2009,

36% of the companies that supply the mining industry have made some type ofcollaboration agreement with other organizations in the last 2 years. The SME miningsuppliers prioritize their relationships with large mining companies, and 20% of the

10 local suppliers have made agreements with their clients. However, the majority of theseagreements seek the commercialization of products, focusing on establishing alliancesto access new markets, while there are few agreements oriented to developing newproducts and processes. On the other hand, and as could be expected in a hub-and-spoke structure, the SME mining suppliers have weak horizontal cooperation

15 relationships with other suppliers, as well as with other companies and universities.Atienza et al. (2012) use a structural equation model survey with data collected in 2007from a sample of 351 SMEs mining suppliers located in the Antofagasta region toanalyze the best practices of local SMEs differentiating between first and second tiersuppliers of mining companies. These authors find that collaboration with clients does

20 not significantly affect investment in innovation and has no impact on SMEsperformance, independently on the position in the supply chain.

The scarcity of agreements between SMEs and MNCs, the orientation of existingagreements to commercialization and the lack of impact of collaboration with miningcompanies on investment in innovation and on local firms performance manifest limited

25 transference of knowledge from overseas to the local economy, putting into questionthe existence of ‘long arms’ in the region. It appears there are no incentives for MNCsto transfer the knowledge and technological innovations developed in their headquar-ters to the local firms. In fact, mining MNCs generally externalize services with lowadded value to local firms, such as transport, food and cleaning services. Goods and

30 services that require a higher level of human or technological capital are acquired inforeign markets, above all in developed countries with high levels of research anddevelopment, which limits the possibility of local suppliers offering these types ofservices given the high barriers to entry.

The previous result is also confirmed by the scarcity of domestic patents in the35 Chilean mining industry. Bas and Kunc (2009) measured the results of innovation in

copper mining in Chile in terms of the number of patents within what they called themining ‘cluster’, considered at a national level. Between 1976 and 2006, 9% of thecompanies belonging to the ‘cluster’ have patents registered with the USPTO11, ofwhich 99.74% are attributed to MNCs and only 0.26% to Chilean companies (Table 6).

40 According to the authors, this is because MNCs undertake research in theirheadquarters, leaving research centers located in Chile with the task of adaptingproducts, technologies and organizational strategies created in more developed

10 SMEs were asked about the existence of collaboration agreements in the past 2 years; whether theseagreement were with clients, suppliers, other firms, public organizations or universities; the objective ofthe agreements and their degree of formality.

11 United States Patent and Trademark Office, considered the most important market for knowledge-basedinnovations.

18 of 24 . Arias et al.

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

countries, hence impeding the emergence of what Markusen termed ‘long arms’ in thelocal economy.

This situation also reflects the lack of a culture of patenting innovations. Despite aspecific tax on mining established in Chile with the aim of contributing funds for

5 research and development projects in 2005, it is considered insufficient by experts inpatenting because the existing funds do not cover even half the costs implied inpatenting an innovation, which added to the length of time that the patenting processrequires and the costs of taking out patents, discourages local companies fromfollowing this path as a business strategy. To this is added the absence of professionals

10 trained on intellectual property in the region and the country, as well as the existence ofclauses in mining MNCs contracts stipulating that innovations made by any of theirworkers is the property of the company.

Finally, the local mining suppliers in the Region of Antofagasta are characterized bytheir limited export capacity and their high level of imports, demonstrating a lack of

15 competitiveness and dependence on foreign technological advances. According to thesurvey of 597 SMEs in the Antofagasta Region, only 10% of suppliers to the miningsector stated having exported overseas12. On the other hand, 66% of the suppliersimport solely to meet the needs of large mining companies (Bas and Kunc, 2009). Thisimplies that the mining industry is a net importer of knowledge, owing to the incapacity

20 of suppliers to produce goods and services that the large mining companies need.However, despite the low levels of exports among the local SMEs, when these arecompared with what was reported by the Longitudinal Business Survey for all of Chile(Centro de Microdatos, 2010), the Antofagasta’s SMEs has a greater level of exportorientation than the rest of the country, which could be considered a characteristic

25 specific to a mining cluster (Atienza, 2011).

6. Conclusions

Research on extractive industries has received scant attention in economic geographydespite the critical relevance of this activity for developing continents such as LatinAmerica, Africa and Asia, as well as its strategic significance for industrial economies.

30 The recent experience of the Antofagasta Region shows there is a need for a broaderdebate about the dynamics of mining regions, the role played by MNCs and to whatextent traditional enclaves are evolving toward either competitive clusters or new formsof enclave, which will determine the sustainability of the host region’s growth and its

Table 6. USPTO patents in the copper mining—1976–2006, based on Bas and Kunc (2009)

Total number of actors in the mining industry 501 100%

Total number of firms and suppliers with patents 46 9%

Total number of patents 1519 100%

Number of patents assigned to Chilean companies 4 0.26%

Number of patents assigned to foreign firms with operations in Chile 1515 99.74%

12 According to Bas and Kunc (2009), the total amount of exports from Chilean firms supplying the miningsector reached only 0.35% of total copper exports.

Large mining enterprises and regional development . 19 of 24

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

development possibilities. The strong economic growth experienced by the AntofagastaRegion in the last two decades does not appear to be related to the formation of amining cluster. On the contrary, the mechanisms pointed out by Marshall as generatorsof increasing returns to scale in a specialized agglomeration show scarce levels of

5 development in the region. Local companies have weak linkages to mining activities andhave not diversified in a manner to generating ‘wide shoulders’ around mining hubs. Aswell, the thickness of the regional labor market is weak as far as it is functionallyspecialized in routine physical tasks with limited decision-making capacity and dependsto a significant degree on outside workers. Finally, the indirect indicators used to

10 evaluate knowledge spillovers show a limited vertical transference of knowledge fromthe headquarters of the mining MNCs to the local firms. All these results situate theAntofagasta Region closer to the ideal type of a mining enclave and, consequently, raiseserious doubts about the sustainability of its regional growth and developmentpossibilities in the long term.

15 These results have both theoretical and policy implications. From a theoreticalperspective, the persistence of the structural features of a mining enclave raises the needto review and update this concept, considering the economic transformations caused bythe process of globalization. The results obtained in this article support the idea that theconcept of enclave is still useful as a category of analysis of mining regions with a major

20 presence of MNCs. It is challenging, in this respect, to understand the precise forms thatthe mining enclaves are taking and how recent changes in the organization and locationlogic of MNCs’ influence the observed results, considering the asymmetric bargainingpower that these firms have over the regional institutions, which facilitate the capture ofvalue and the exports of rents. It could also be useful in the understanding of mining

25 enclaves to complement the ideal type perspective proposed in this article with recentcluster research on social networks analysis, knowledge transfer and industry life cycle.

From a policy perspective, the persistence of some of the main features of enclaveseven in mining region that have been considered successful, such as Antofagasta, alsoraises the need to review the development strategies recently followed by several mining

30 regions where the promotion of clusters has been adopted without taking into accounttheir particular circumstances. It is evident that the development of these regionsstrongly depends on the economic activity of MNCs. For these reasons, it is importantto understand how these MNCs could engage in a process of collaboration andknowledge transfer to the network of local suppliers, in a context where, apparently,

35 there are not enough incentives for such type of behavior. In this respect, a key aspect inrelation to the development policies for mining regions relates to the role of the state.The direct intervention of the state can counteract the internalization logic and thecapture of public goods by MNCs with the aim of promoting the agglomerationeconomies of a cluster (Phelps, 2008). Furthermore, in the case of extractive industries,

40 public intervention presents fewer problems of delocalization of MNCs due to the fixedcharacter of the raw material and the high sunk costs related to this industry, because ofwhich the actions of the state can be more effective than in other type of regions. Aswell, there are large public enterprises in the Antofagasta region, such as CODELCO,that until now, have had a very narrow regional focus and can become a driver of

45 development for the local firms. An example of the potential role of the state in thisfield is the Bothnian mining cluster, where governments actively participate in theoverall development and coordination of natural resource policy to ensure its benefitsfor the regional development and growth.

20 of 24 . Arias et al.

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

Acknowledgements

This work was supported by Companıa Minera Zaldivar and Barrick and the Project NS 100046of the Iniciativa Cientıfica Milenio of the Ministry of Economics, Public Works and Tourism,Antofagasta, Chile.

5

References

Ackah-Baidoo, A. (2012) Enclave development and ‘offshore corporate social responsibility’:implications for oil-rich sub-Saharan Africa. Resources Policy, 37: 152–159.

Aroca, P. (2001) Impacts and development in local economies base on mining: the case of theChilean II region. Resources Policy, 27: 119–134.

10 Aroca, P., Atienza, M. (2008) La Conmutacion Regional en Chile y su Impacto en la Region deAntofagasta. Eure, 34: 97–120.

Aroca, P., Atienza, M. (2011) Economic implications of long distance commuting in the Chileanmining industry. Resources Policy, 36: 196–203.

Atienza, M. (2009) La Evolucion de la Pyme de la Region de Antofagasta: Hacia una Demografıa15 del Tejido Productivo Local. Antofagasta: Ediciones Universidad Catolica del Norte.

Atienza, M. (2011) La Pyme de la Region de Antofagasta: 2005–2009. Antofagasta: EdicionesUniversidad Catolica del Norte.

Atienza, M., Aroca, P., Stimson, R., Stough, R. (2012) A structural equation model approach toinvestigate best practices in small and medium enterprise mining suppliers in the Antofagasta

20 Region of Chile. WP2012-16, Departamento de Economıa, Universidad Catolica del Norte.Atienza, M., Lufin, M., Sarrias, M. (2010) Division Espacial del Trabajo en Chile 1992-2002,informe Anual 2009 ORDHUM. Antofagasta: Ediciones Universidad Catolica del Norte.

Auty, R. M. (1979) Transforming mineral enclaves: Caribbean Bauxite in the nineteen – seventies.Tijdschrift voor Econ. En Soc. Geografie, 71: 169–179.

25 Barbour, E., Markusen, A. (2007) Regional occupational and industrial structure: does one implythe other? International Regional Science Review, 30: 72–90.

Barrow, M., Hall, M. (1995) The impact of a large multinational organization on a small localeconomy. Regional Studies, 29: 635–653.

Bas, T., Kunc, M. (2009) National systems of innovations and natural resources clusters: evidence30 from copper mining industry patents. European Planning Studies, 17: 1861–1879.

Bathelt, H. (2009) Re-bundling and the development of hollow clusters in the East Germanchemical industry. European Urban and Regional Studies, 16: 363–381.

Bathelt, H., Malmberg, A., Maskell, P. (2004) Clusters and knowledge: local buzz, globalpipelines and the process of knowledge creation. Progress in Human Geography, 28: 31–56.

35 Blomstrom, M., Kokko, A. (2007) From natural resources to high-tech production: the evolutionof industrial competitiveness in Sweden and Finland. In D. Lederman, W. Maloney (eds)Natural Resources. Neither Curse Nor Destiny, pp. 213–258. Washington: World Bank.

Boschma, R. A. (2005) Proximity and innovation. A critical assessment. Regional Studies, 39:61–74.

40 Boschma, R., Frenken, K. (2011) The emerging empirics of evolutionary economic geography.Journal of Economic Geography, 11: 295–307.

Buitelaar, R. (2001) Aglomeraciones Mineras y Desarrollo Local en America Latina. Colombia:Cepal and Alfaomega Grupo Editor S.A.

Buckley, P., Ghauri, P. (2004) Globalisation, Economic geography and the strategy of45 multinational enterprises. Journal of Business Studies, 35: 81–98.

Cademartori, J. (2008) El Desarrollo Economico y Social de la Region de Antofagasta (Chile)Historia y Perspectiva. Antofagasta: Ediciones Universidad Catolica del Norte.

Cardoso, F., Faletto, E. (1969) Dependencia y Desarrollo en America Latina. Mexico: Siglo XXI.Centro de Microdatos (2010) Primera encuesta longitudinal de empresas. Presentacion general y

50 principales resultados. Santiago: Departamento de Economıa, Universidad de Chile.CEPAL (2009) Economıa y Territorio en America Latina y el Caribe: Desigualdades y Polıticas.Chile: Naciones Unidas.

Large mining enterprises and regional development . 21 of 24

manu.s

Text Box

Q3

[2.4.2013–5:44pm] [1–24] Paper: OP-JEGJ130007

Copyedited by: MN MANUSCRIPT CATEGORY: ORIGINAL ARTICLE

COCHILCO (2010) Yearbook: Copper and Other Mineral Statistics. Santiago: Comision Chilenadel Cobre, Gobierno de Chile.

Conning, J., Robinson, J. (2009) Enclaves and development: an empirical assessment. Studies inComparative International Development, 44: 359–385.

5 Crone, M., Roper, S. (2001) Local learning from multinational plants: knowledge transfers in thesupply chain. Regional Studies, 35: 535–548.

Cruz, S., Teixeira, A. (2010) The evolution of the cluster literature: shedding light on the regionalstudies—regional science debate. Regional Studies, 44: 1263–1288.

Dunning, J. (1997) Alliance Capitalism. London: Routledge.10 Dunning, J. H. (1993) Multinational Enterprises and the Global Economy. Wokingham: Addison –

Wesley.Economic Comission for Africa (2004) Minerals Cluster Policy Study in Africa: Pilot Studies ofSouth Africa and Mozambique. Addis Ababa: Publications Economic Comission for Africa.

Ejdemo, T., Soderholm, P. (2011) Mining investment and regional development: a scenario-based15 assessment for Northern Sweden. Resources Policy, 36: 14–21.