Lao PDR: Sustainable Natural Resources Management and ...

219

Documents Produced under Grant Project Number: 37579-032 October 2014 Lao PDR: Sustainable Natural Resources Management and Productivity Enhancement Project Banana, Sweet Potato and Peanut Value Chain Development in Champasak, Salavanh, and Savannakhet Provinces Prepared by the Ministry of Agriculture and Forestry for the Asian Development Bank. This is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. Your attention is directed to the “terms of use” section of this website. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Lao PDR: Sustainable Natural Resources Management and ...

Documents Produced under Grant

Project Number: 37579-032 October 2014

Lao PDR: Sustainable Natural Resources

Management and Productivity Enhancement Project

Banana, Sweet Potato and Peanut Value Chain Development

in Champasak, Salavanh, and Savannakhet Provinces

Prepared by the Ministry of Agriculture and Forestry for the Asian Development Bank.

This is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. Your attention is directed to the “terms of use” section of this website. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

Banana, Sweet Potato, and Peanut Value Chain Study

Page 1

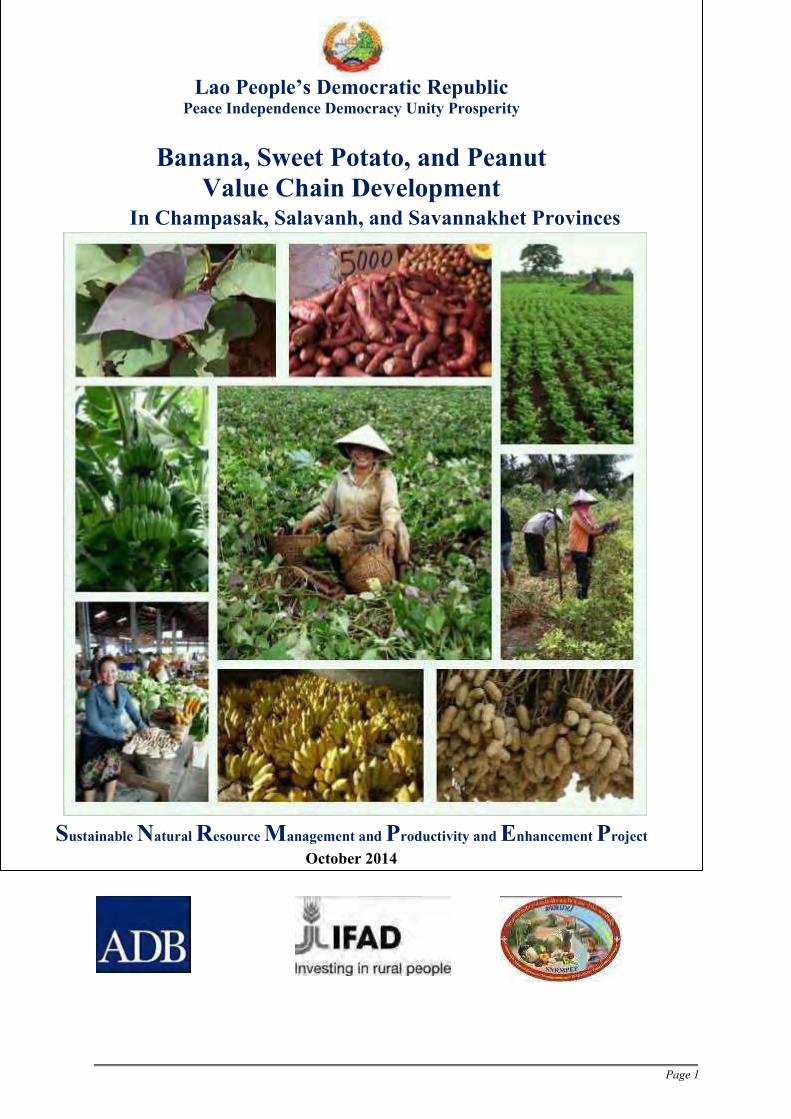

Lao People’s Democratic Republic Peace Independence Democracy Unity Prosperity

Banana, Sweet Potato, and Peanut Value Chain Development

In Champasak, Salavanh, and Savannakhet Provinces

Sustainable Natural Resource Management and Productivity and Enhancement Project

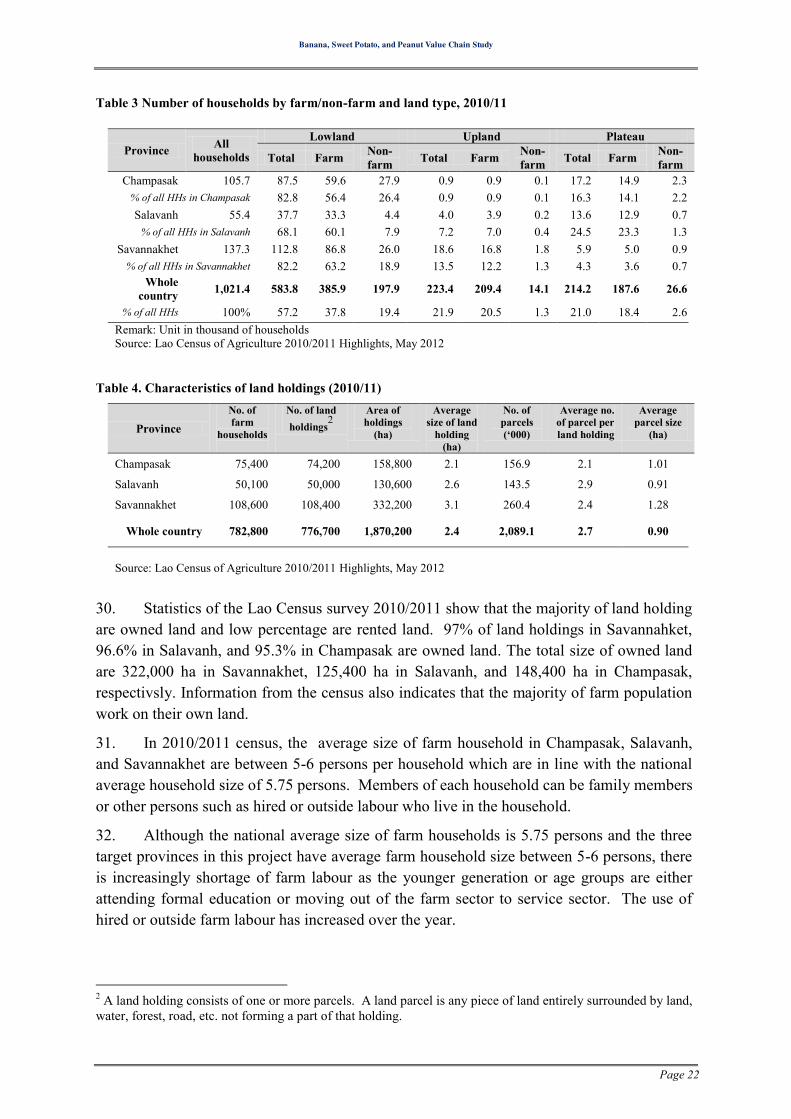

October 2014

Lao People’s Democratic Republic Peace Independence Democracy Unity Prosperity

Champasak Province Champasak Provincial Agriculture and Forestry Office (PAFO)

FEASIBILITY STUDY REPORT

Subproject: Integrated Cattle Raising for Commercialization of Cattle in Pathoumphone, Sukhuma, Khong, and Mounlapamoune Districts of Champasak Province

Category: Poverty Reduction

Banana, Sweet Potato, and Peanut Value Chain Study

Page 2

ACRONYMS AND ABBREVIATIONS

ADB – Asian Development Bank

ANR – agriculture and natural resources

CD & G – Community Development and Gender

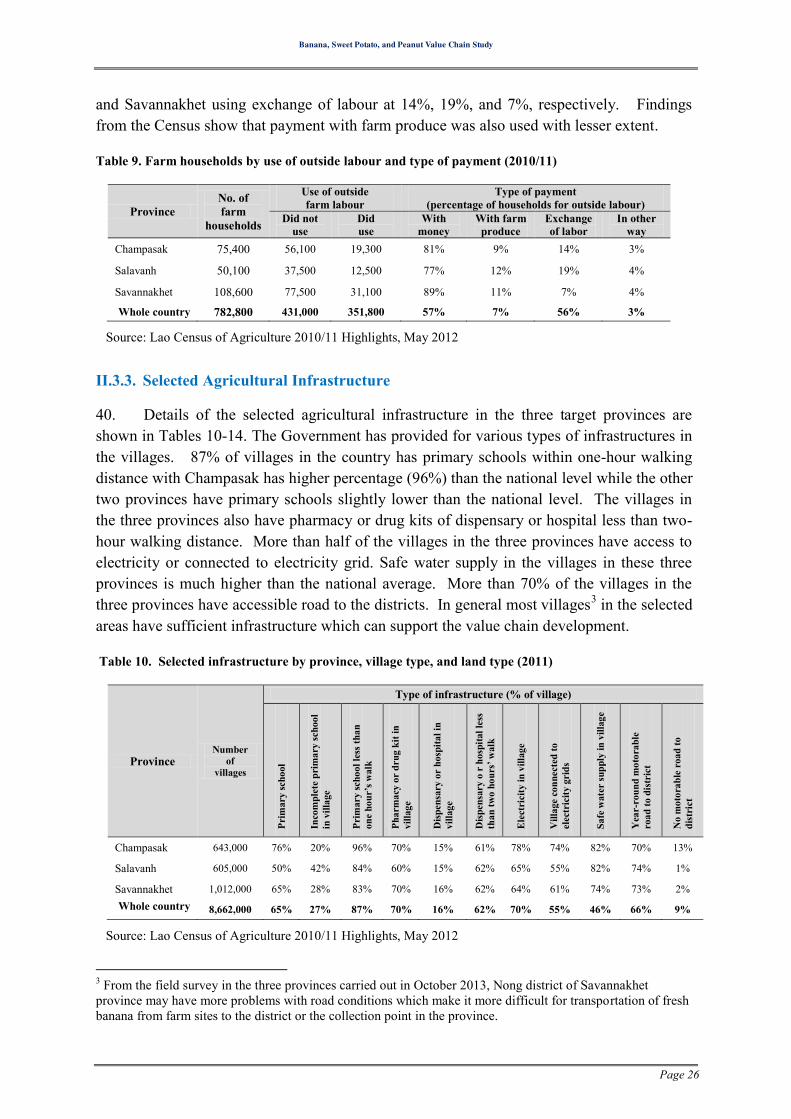

DAFO – District Agriculture and Forestry Office

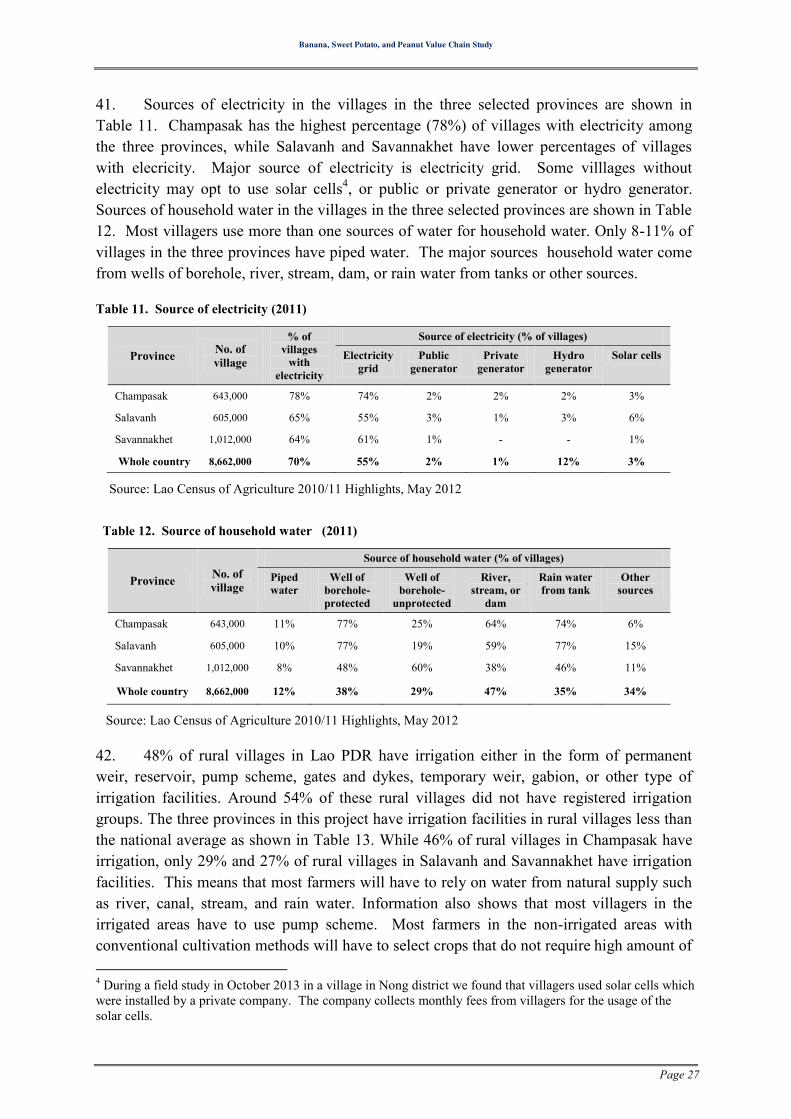

GIS – Geographic information system

GoL – Government of Lao People’s Democratic Republic

IFAD – International Fund for Agricultural Development

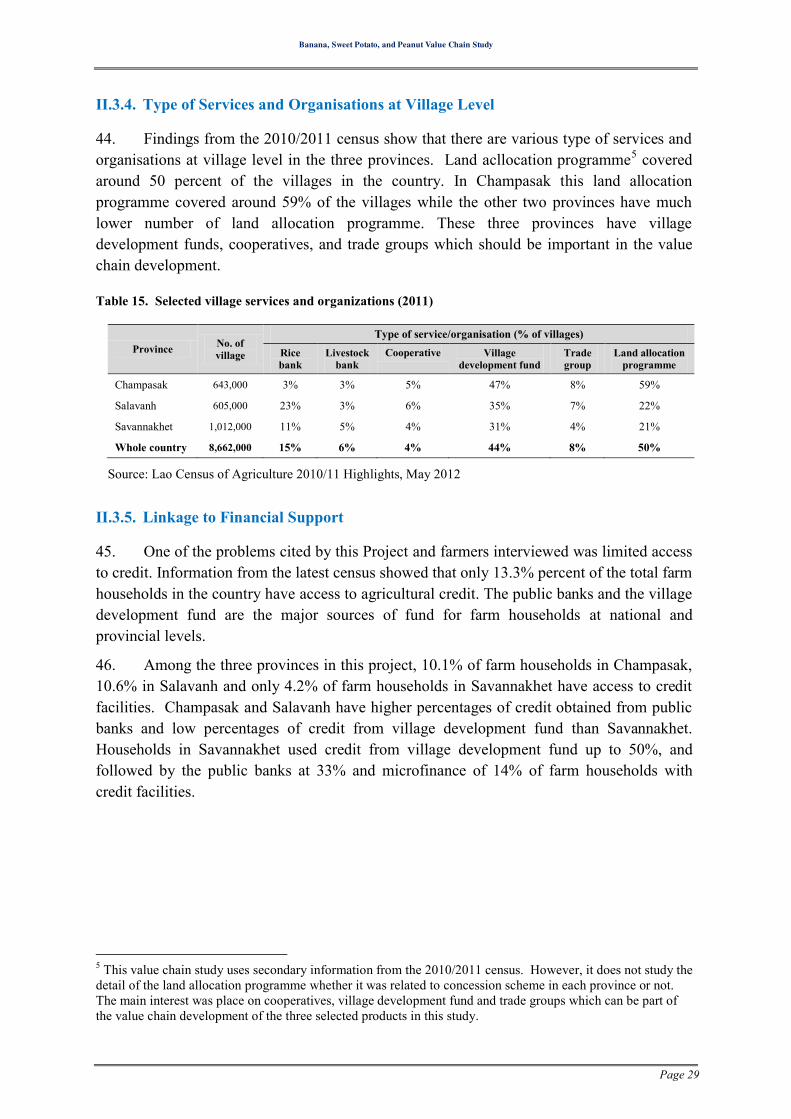

Lao PDR – Lao People’s Democratic Republic

MAF – Ministry of Agriculture and Forestry

PAFO – Provincial Agriculture and Forestry Office

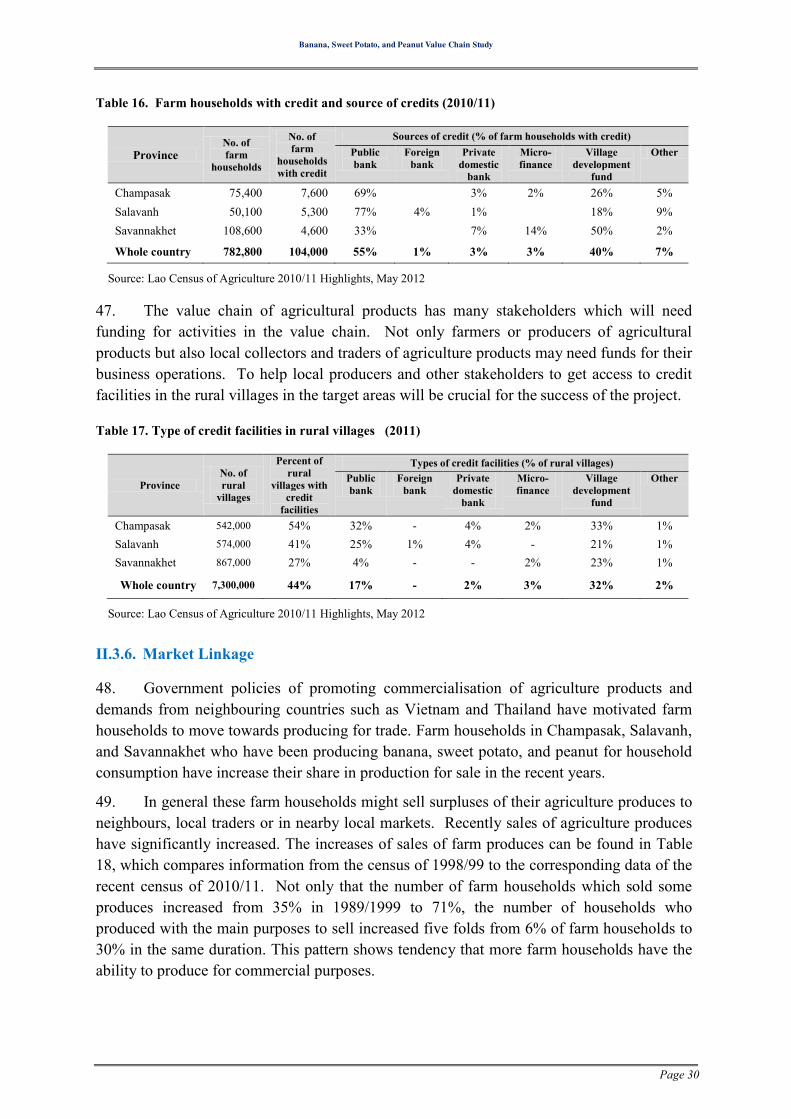

PAM – Project Administration Manual

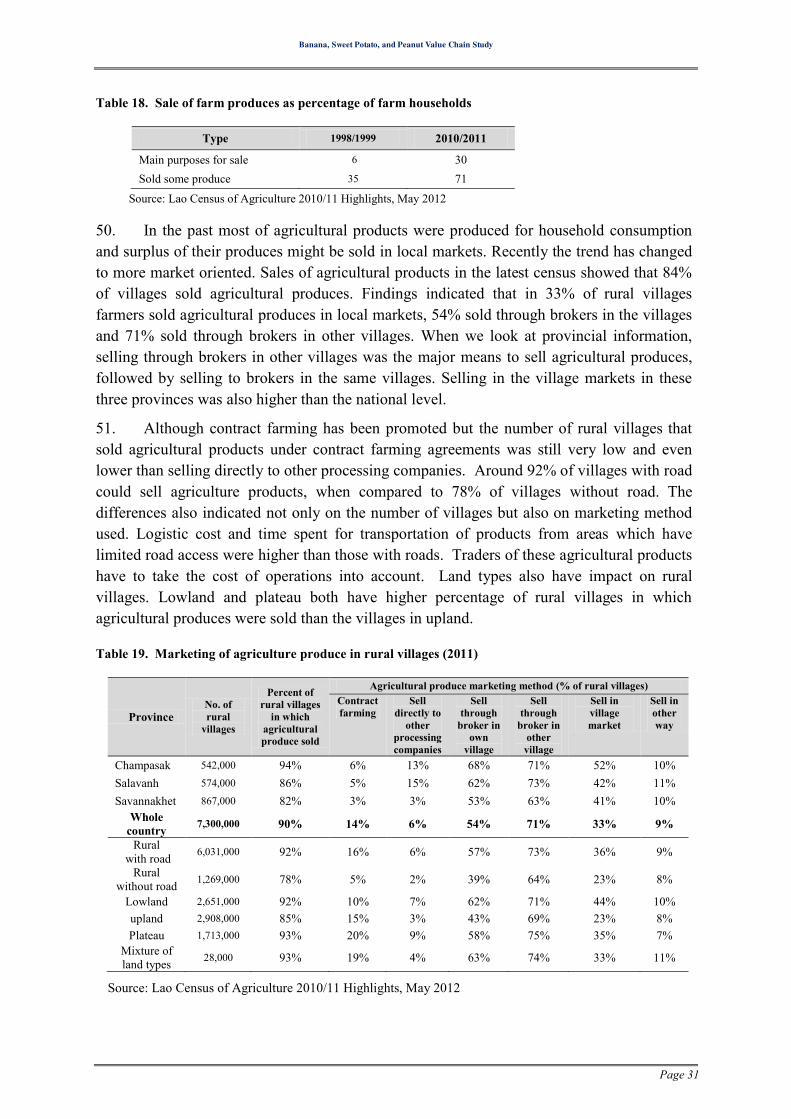

PPMES – Project performance monitoring and evaluation system

PPO – Provincial Project Office

SNRMPEP – Sustainable Natural Resource Management and Productivity Enhancement Project

TA – Technical assistance

THB – Thai Baht

US$ – United State Dollar

Banana, Sweet Potato, and Peanut Value Chain Study

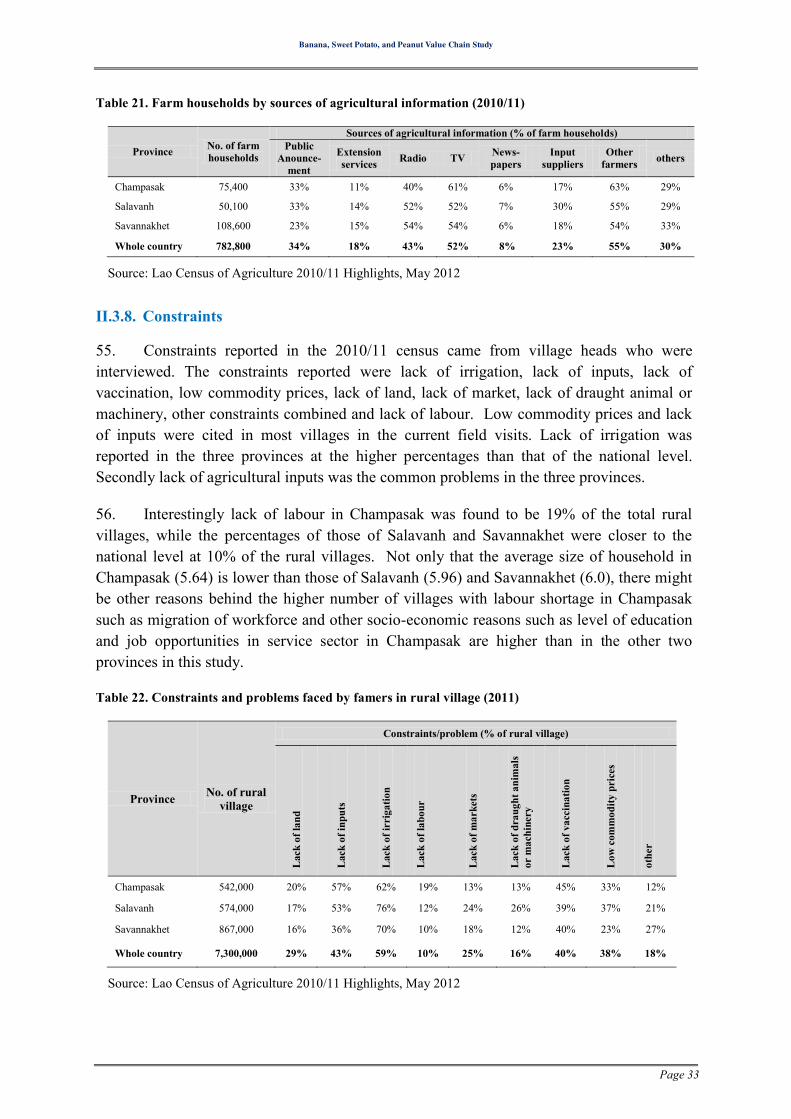

Page 3

ACKNOWLEDGEMENT I would like to express my special thanks to SNRMPEP and PPDs and consultants and local line government agencies that had kindly assited in the arrangement of the field visits and the secondary information of their selected project sites.

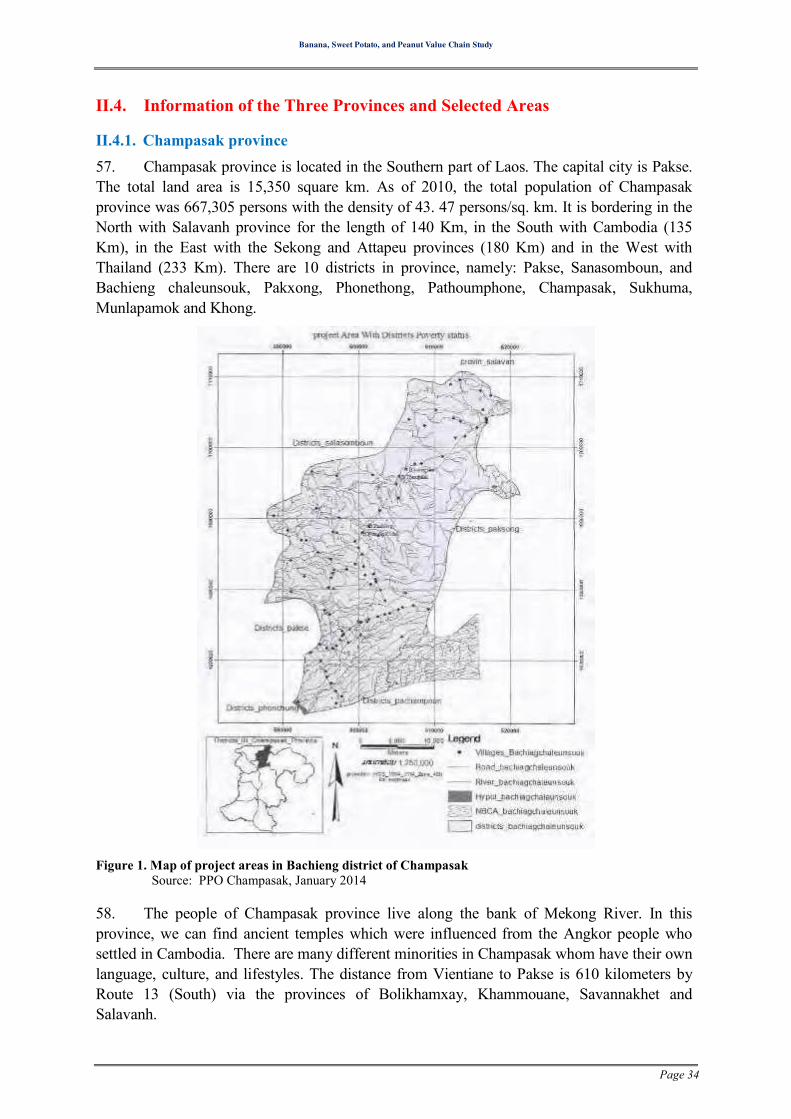

Although I could not mention the names of all people who helped to make this field study possible, I am in debt for their help with arrangements for the meetings and to all farmer groups, agricultural product collectors, traders and buyers who have given their valuable time and information to me.

This field study was carried out in a limited time and there are errors in this report. I would take the full responsibility for these errors.

Orawan Ananvoranich, Ph.D.

Banana, Sweet Potato, and Peanut Value Chain Study

Page 4

TABLE OF CONTENTS

ACRONYMS AND ABBREVIATIONS ........................................................... 2

ACKNOWLEDGEMENT .................................................................................. 3

CHAPTER I. SUMMARY DESCRIPTION ............................................. 15

I.1. SUBPROJECT NAME & LOCATION ................................................................................ 15

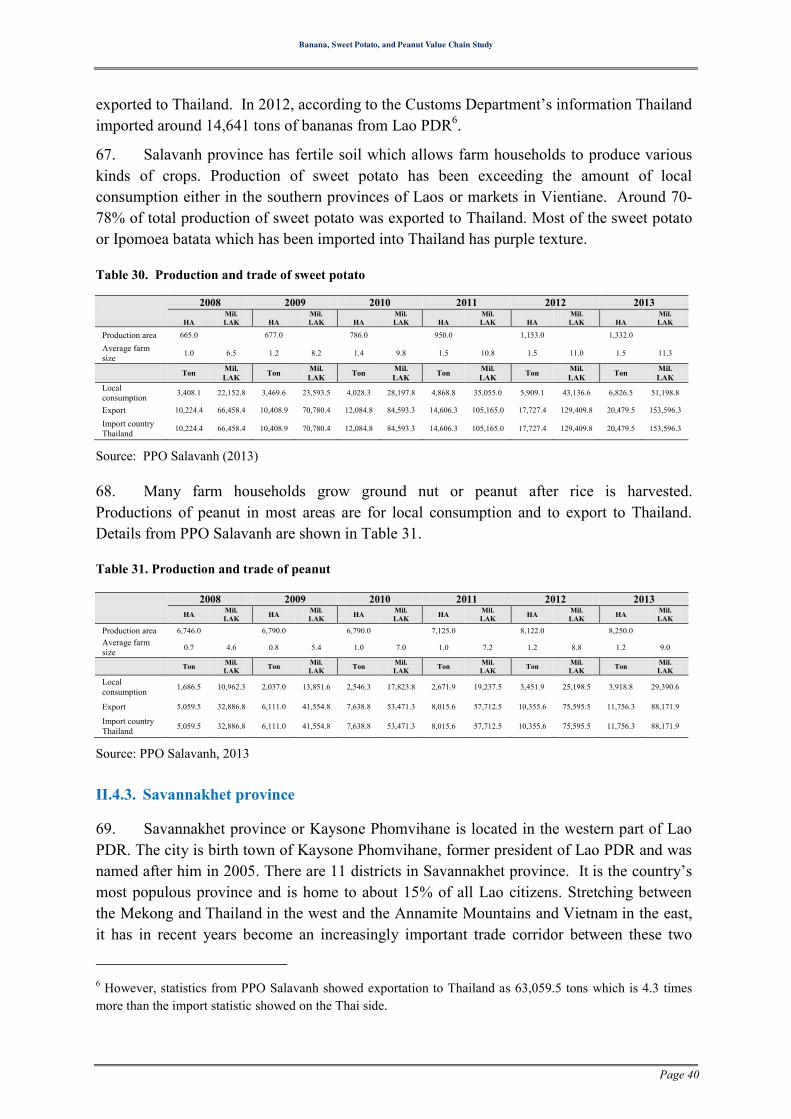

I.2. OBJECTIVES OF THE STUDY ........................................................................................ 15

I.3. COMPONENTS OF THE STUDY ..................................................................................... 16

I.4. OWNER/ INVESTOR/ FUNCTIONAL MANAGERS ........................................................... 16

I.5. PROJECT MANAGEMENT ............................................................................................. 17

I.6. SUBPROJECT IMPLEMENTATION PERIOD ..................................................................... 17

I.7. O&M AGENCY ........................................................................................................... 18

I.8. TARGET BENEFICIARIES ............................................................................................. 18

I.9. REPORT OF THE VALUE CHAIN STUDY ......................................................................... 19

CHAPTER II. BACKGROUND INFORMATION ................................... 20

II.1. DATA COLLECTION .................................................................................................... 20

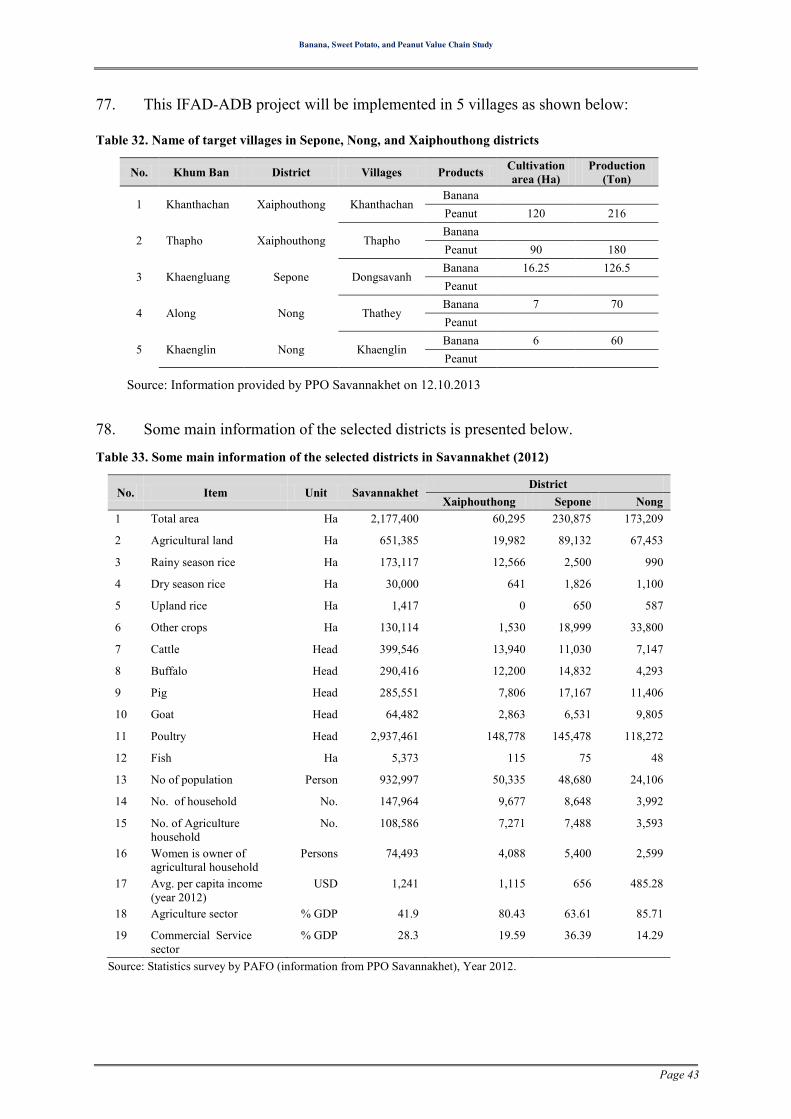

II.2. DEMOGRAPHIC INFORMATION .................................................................................... 20

II.3. LINKAGE TO EXISTING INFRASTRUCTURE IN THE SELECTED PROVINCES ..................... 23

II.3.1. Summary ....................................................................................................................... 23

II.3.2. Production of Temporary and Permanent Crops ........................................................... 23

II.3.3. Selected Agricultural Infrastructure .............................................................................. 26

II.3.4. Type of Services and Organisations at Village Level ................................................... 29

II.3.5. Linkage to Financial Support ........................................................................................ 29

II.3.6. Market Linkage ............................................................................................................. 30

II.3.7. Linkage to Information ................................................................................................. 32

II.3.8. Constraints .................................................................................................................... 33

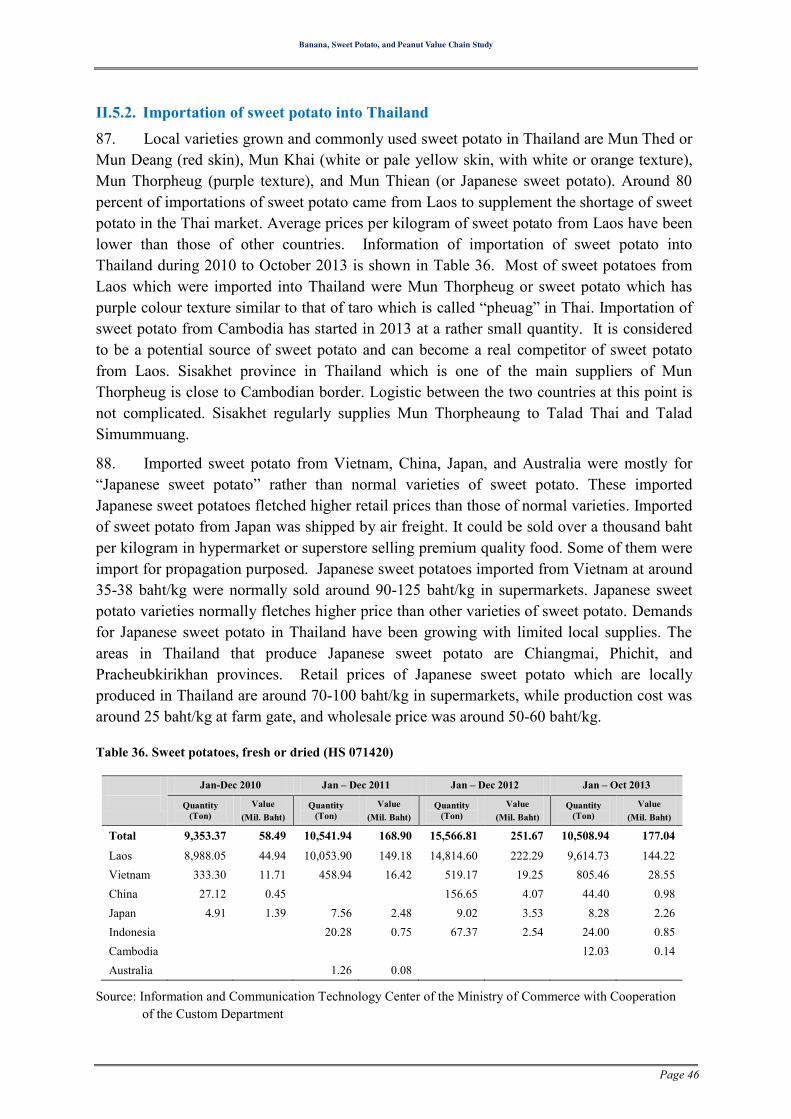

II.4. INFORMATION OF THE THREE PROVINCES AND SELECTED AREAS .............................. 34

II.4.1. Champasak province ..................................................................................................... 34

II.4.2. Salavanh province ......................................................................................................... 36

II.4.3. Savannakhet province ................................................................................................... 40

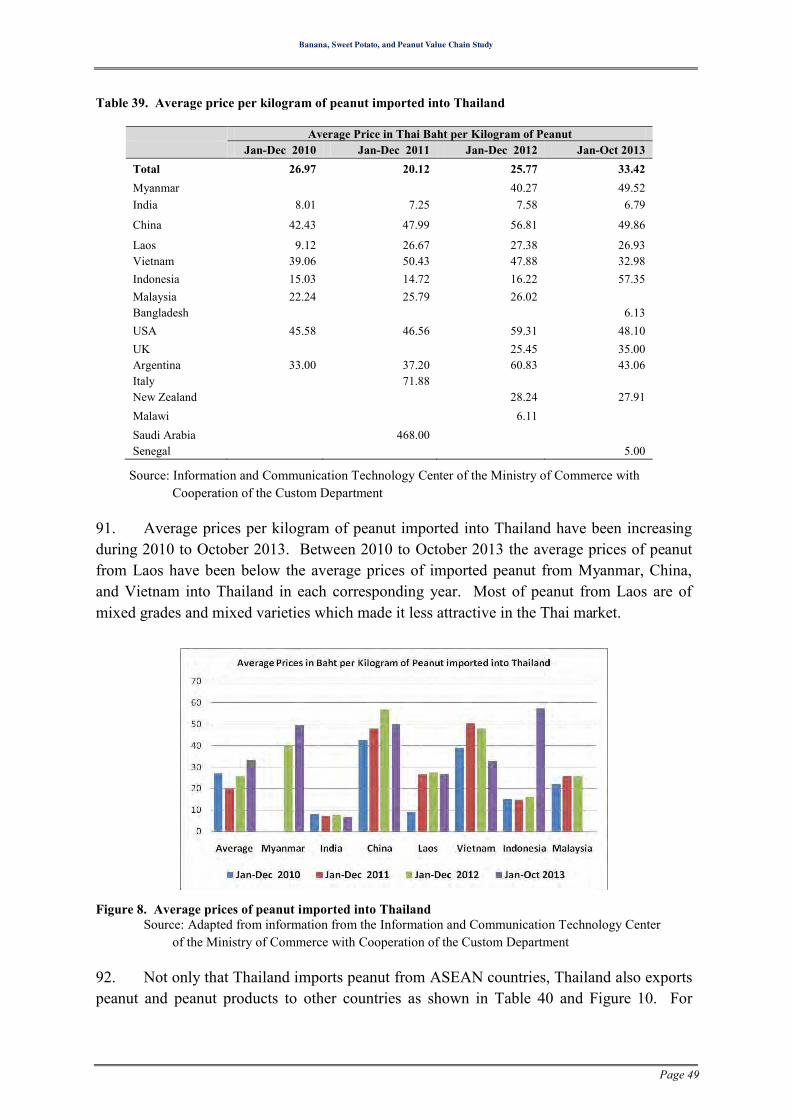

II.5. THAILAND IMPORT STATISTICS OF BANANA, SWEET POTATO, AND PEANUT ............. 44

II.5.1. Importation of banana into Thailand ............................................................................. 44

II.5.2. Importation of sweet potato into Thailand .................................................................... 46

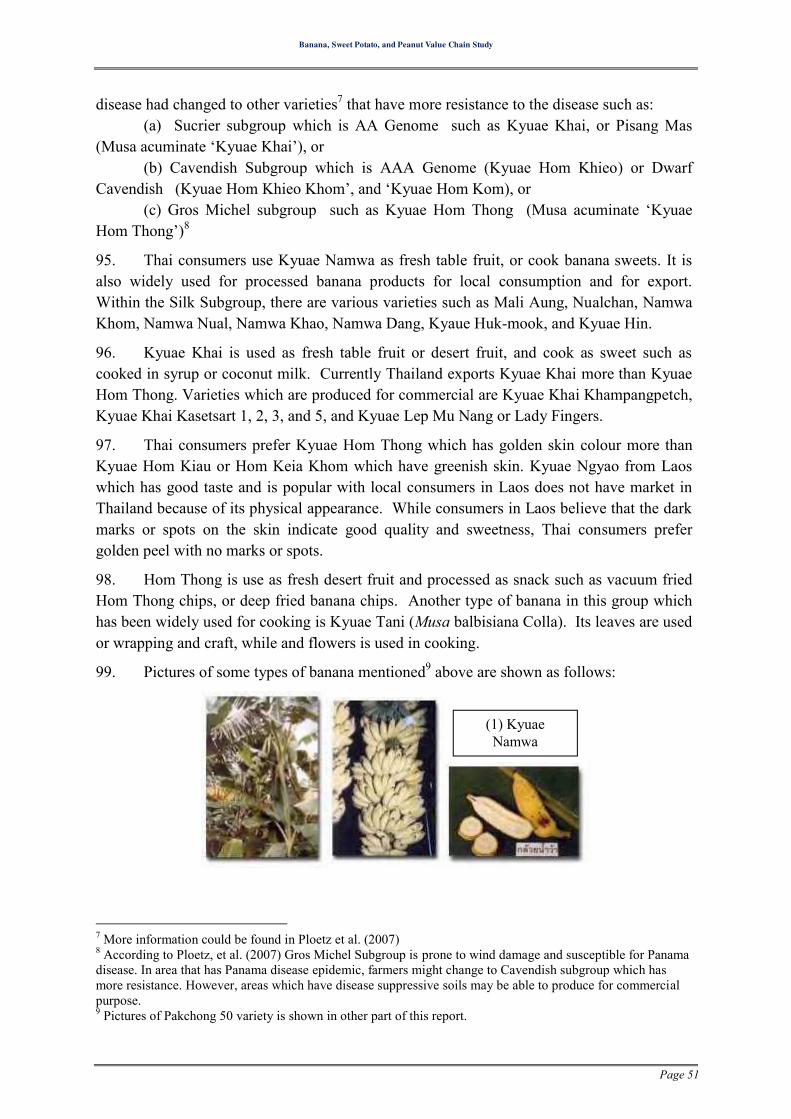

II.5.3. Importation of Peanut into Thailand ............................................................................. 47

II.6. VARIETIES OF BANANA, SWEET POTATO, AND PEANUT IN THAILAND ....................... 50

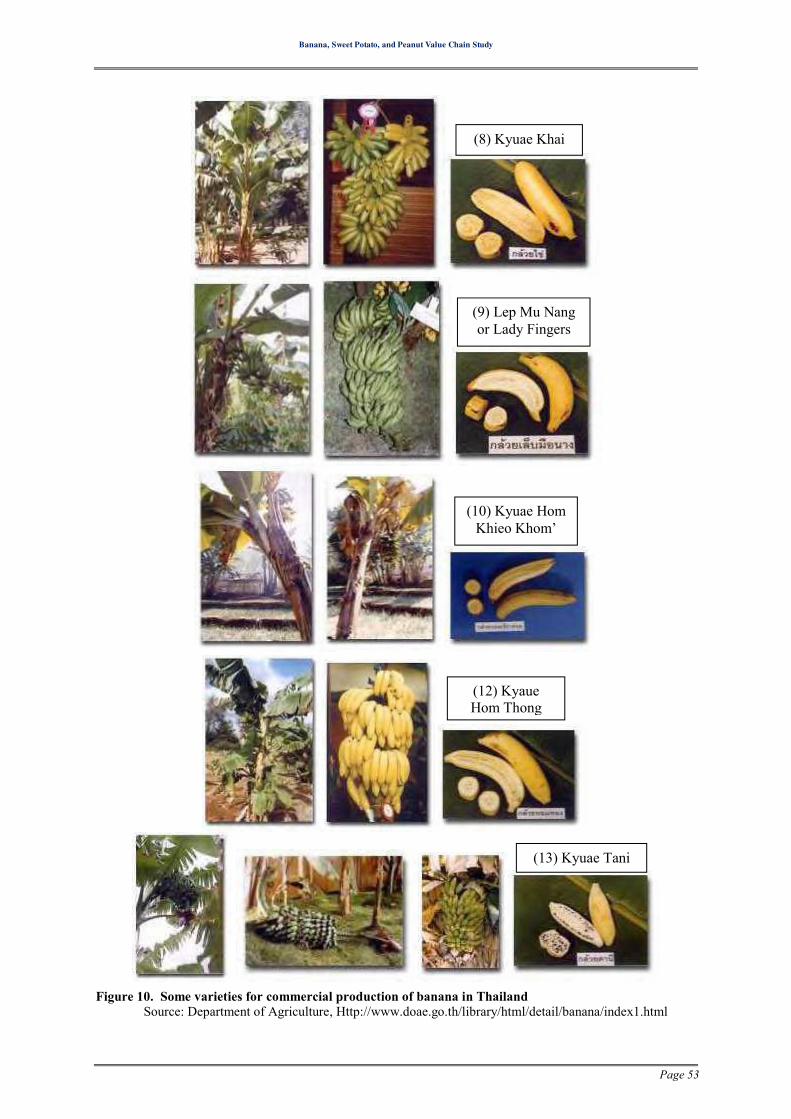

Banana, Sweet Potato, and Peanut Value Chain Study

Page 5

II.6.1. Varieties of Banana Available for Commercial in Thailand ......................................... 50

II.6.2. Varieties of Sweet Potato available in Thailand ........................................................... 54

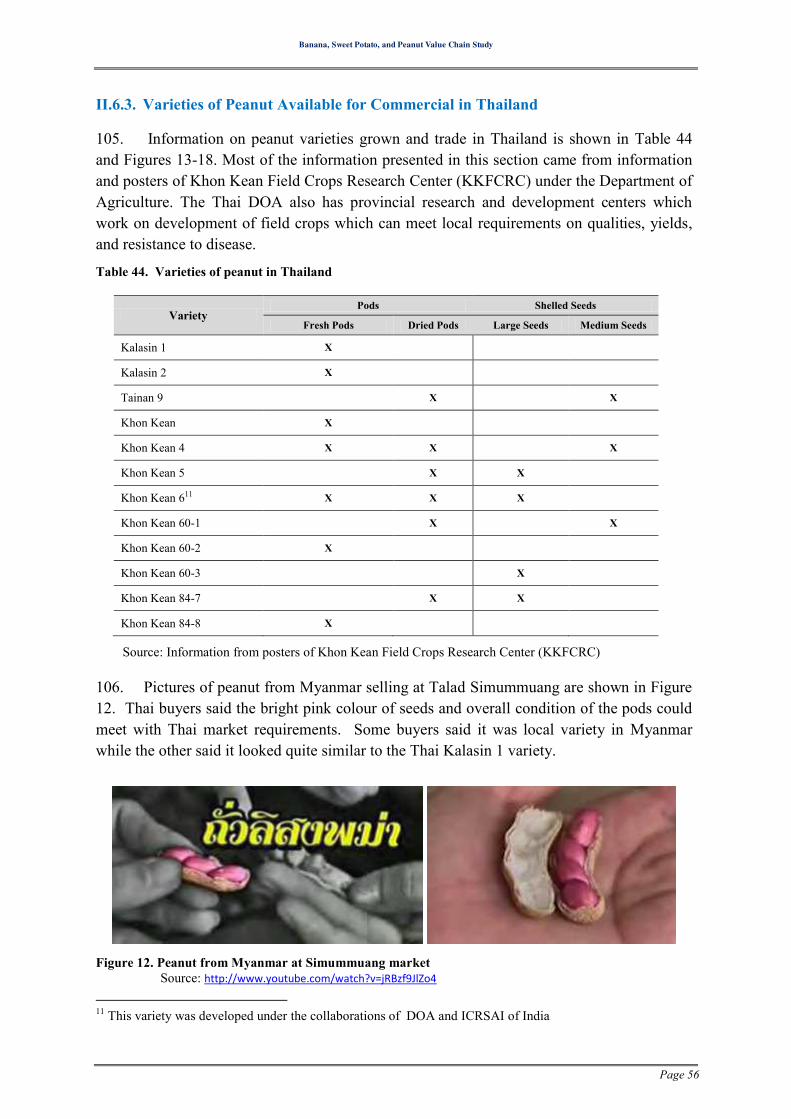

II.6.3. Varieties of Peanut Available for Commercial in Thailand .......................................... 56

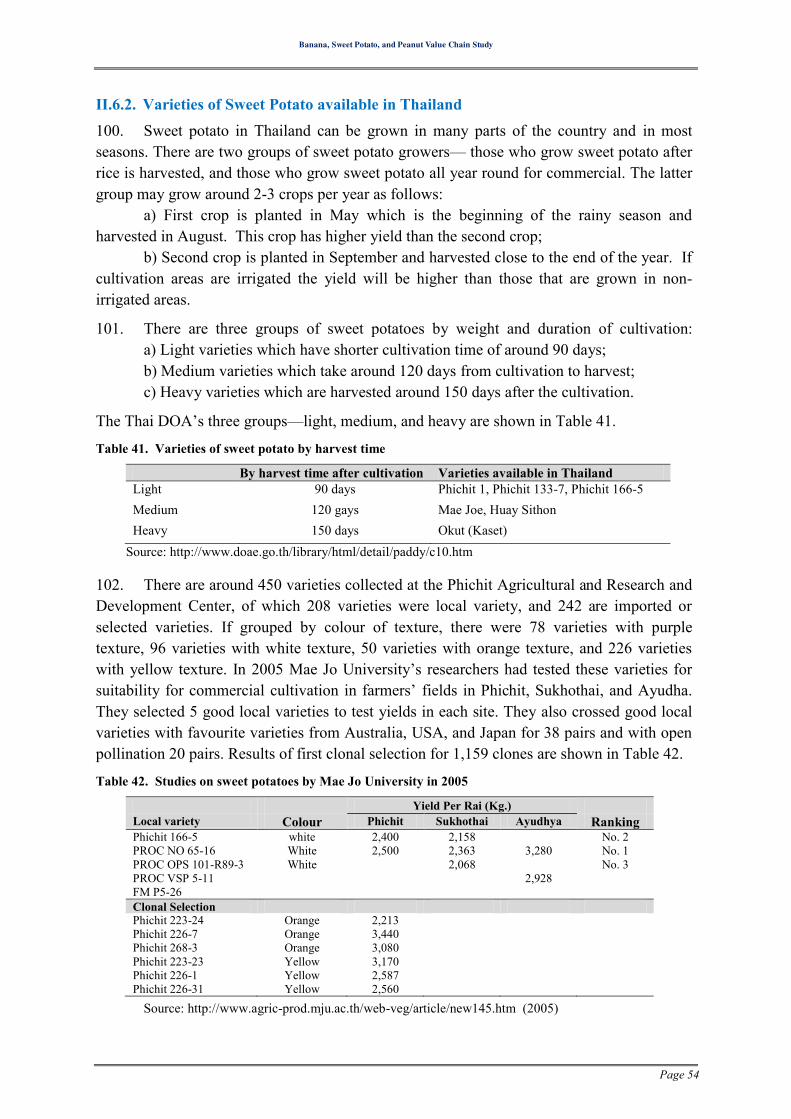

CHAPTER III. FIELD SURVEY ................................................................. 61

III.1. FIELD VISITS IN THAILAND ..................................................................................... 61

III.1.1. Banana at Talad Thai Agricultural Wholesale Market.................................................. 63

III.1.2. Sweet Potato at Talad Thai Agricultural Wholesale Market......................................... 67

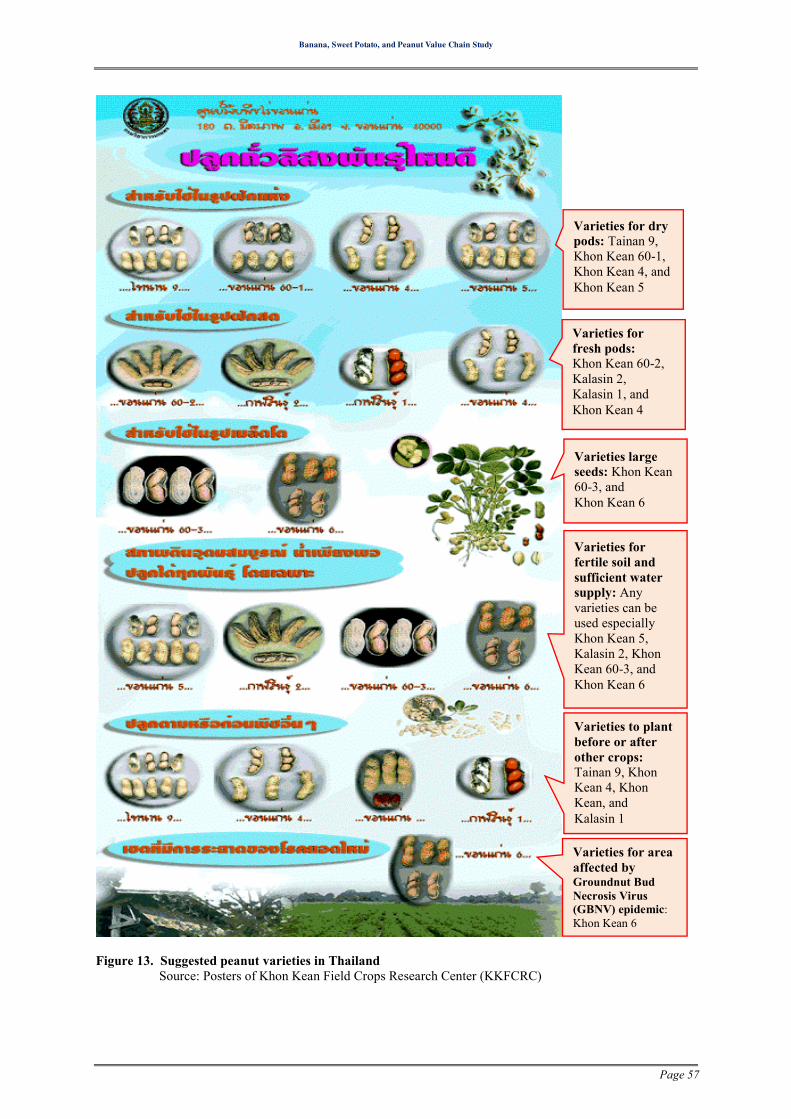

III.1.3. Peanut at Talad Thai Agricultural Wholesale Market ................................................... 70

III.1.4. Supermarkets, Trade Fairs, and Shops at Don Muang Airport ..................................... 73

III.1.5. Local markets in Thailand ............................................................................................. 79

III.1.6. Charoensri Wholesale Market in Ubonrachthani .......................................................... 83

III.1.7. Ban Kha Khome Women Group in Ubonrachthani ...................................................... 90

III.1.8. Khangsapeu Market in Ubonrachthani.......................................................................... 91

III.1.9. Warinchumrarp Market in Ubonrachthani .................................................................... 93

III.1.10. Kanthoraluk Market in Sisakhet ............................................................................... 95

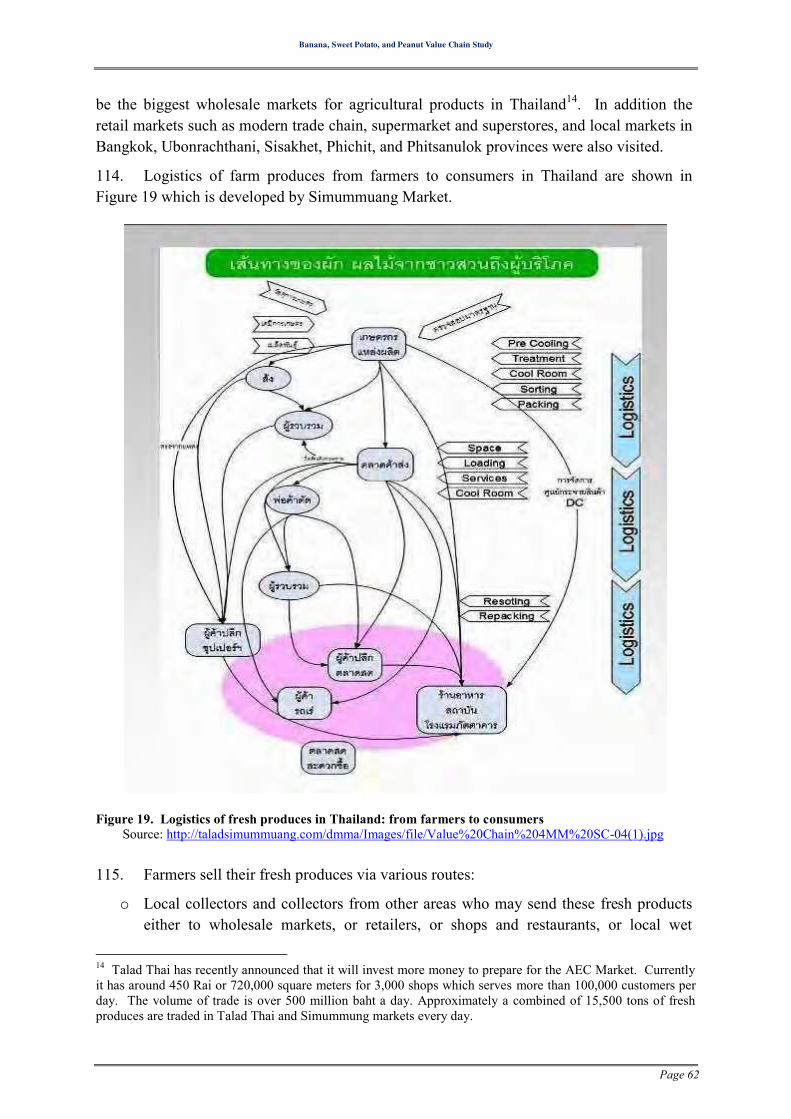

III.1.11. Field Visit to Phichit on Japanese Sweet Potato ....................................................... 97

III.1.12. Bangkrathum District of Phitsanulok province ......................................................... 98

III.1.13. Wat Phra Sri Rattanamahathat Market in Phitsanulok ............................................ 105

III.1.14. Pakchong Research Station, Nakornrachasima ....................................................... 108

III.1.15. Department of Physics, Silpakorn University, Nakornpathom ............................... 111

III.1.16. Institute of Nutrition, Mahidol University, Nakornpathom .................................... 116

III.2. FIELD VISITS IN LAO PDR .................................................................................... 117

III.2.1. Markets in Vientiane ................................................................................................... 117

III.2.2. Vientiane: Khua Din Market ....................................................................................... 118

III.2.3. Champasak Province: Banana ..................................................................................... 120

III.2.4. Champasak Province, Bachieng District: Peanut ........................................................ 123

III.2.5. Champasak: Pakse New Market................................................................................. 123

III.2.6. Salavanh Province: Banana ......................................................................................... 129

III.2.7. Salavanh Province: Sweet Potato ................................................................................ 131

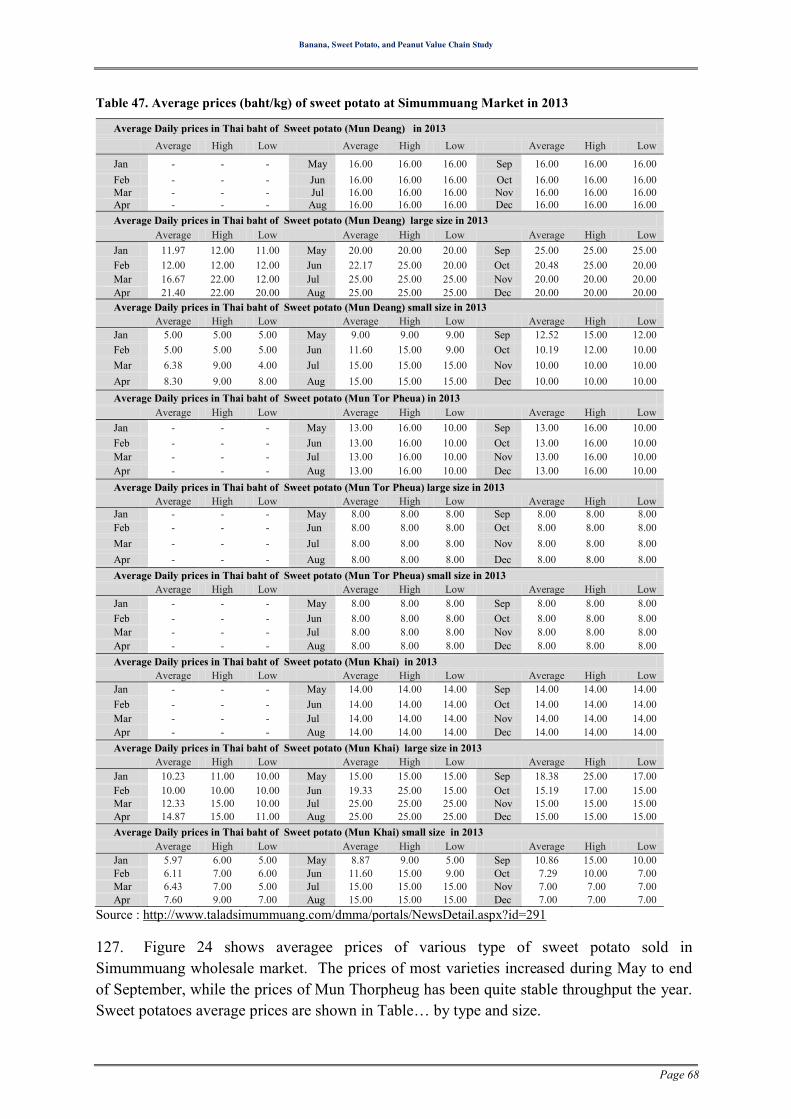

III.2.8. Salavanh Province: Peanut .......................................................................................... 133

III.2.9. Savannakhet Province, Nong District: Banana ........................................................... 137

III.2.10. Savannakhet Province, Sepone District: Banana .................................................... 140

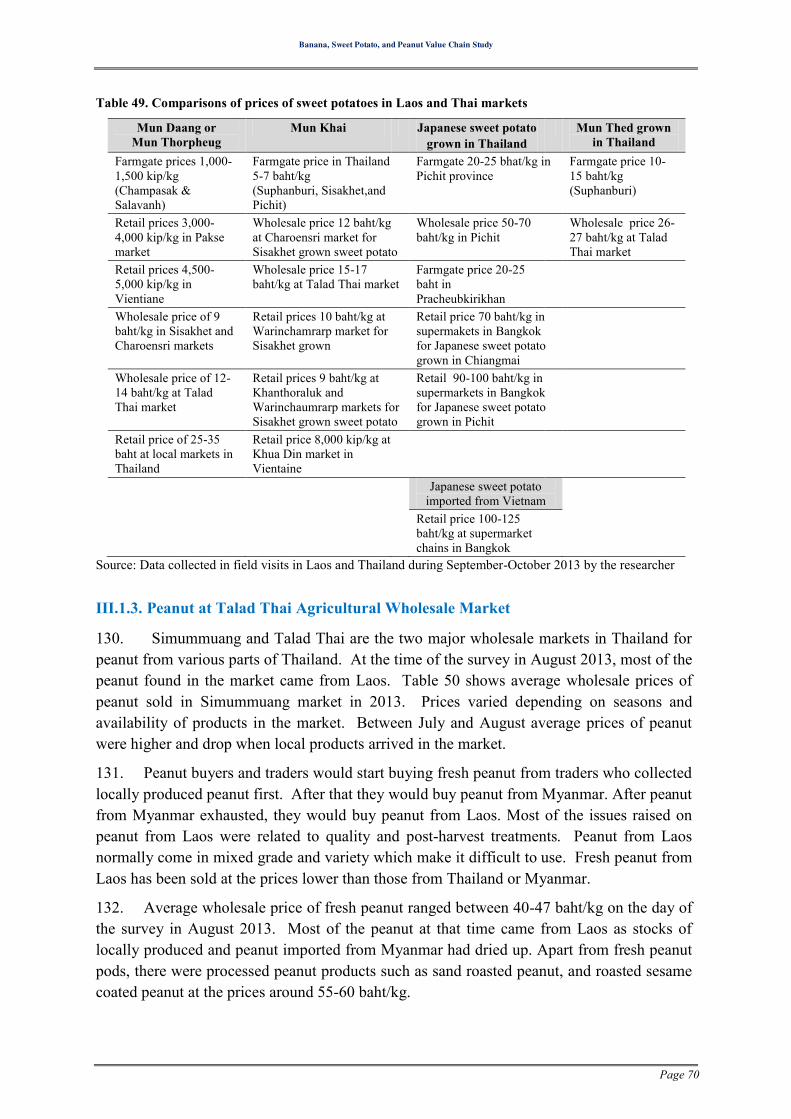

III.2.11. Savannakhet Province, Xaiphouthong District: Peanut .......................................... 144

III.2.12. Snack Market in the Three Target Provinces .......................................................... 148

CHAPTER IV. VALUE CHAIN ANALYSES .......................................... 151

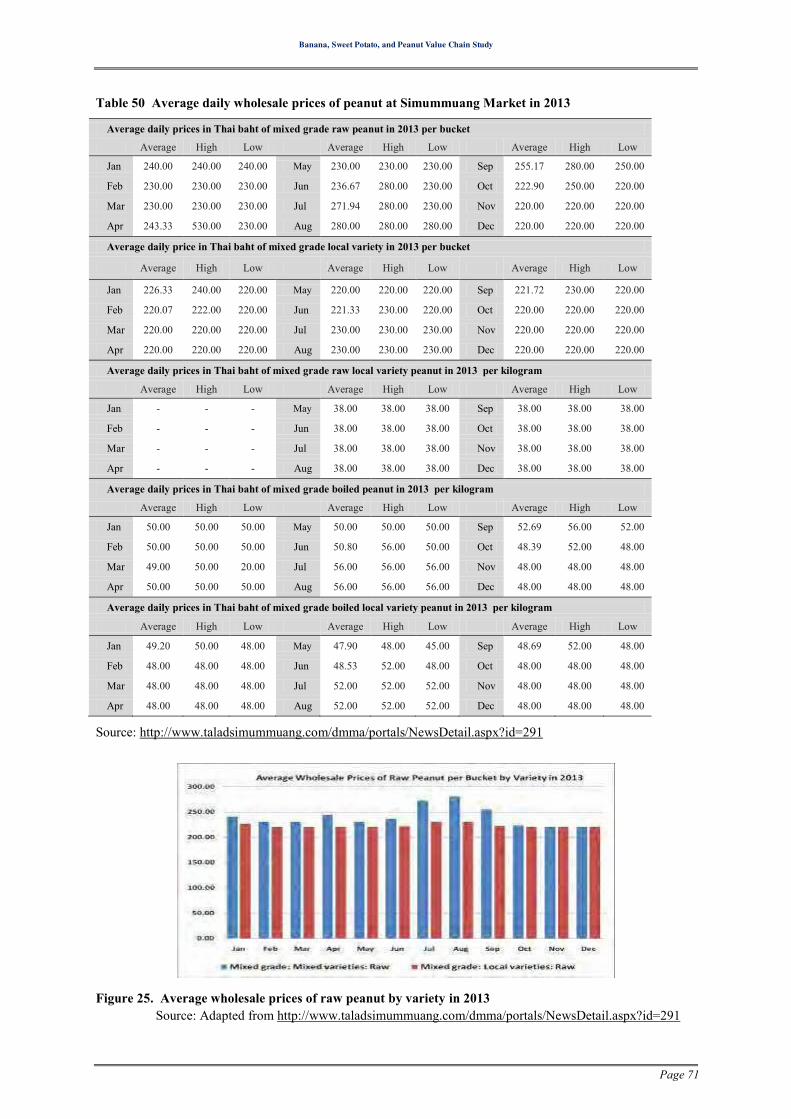

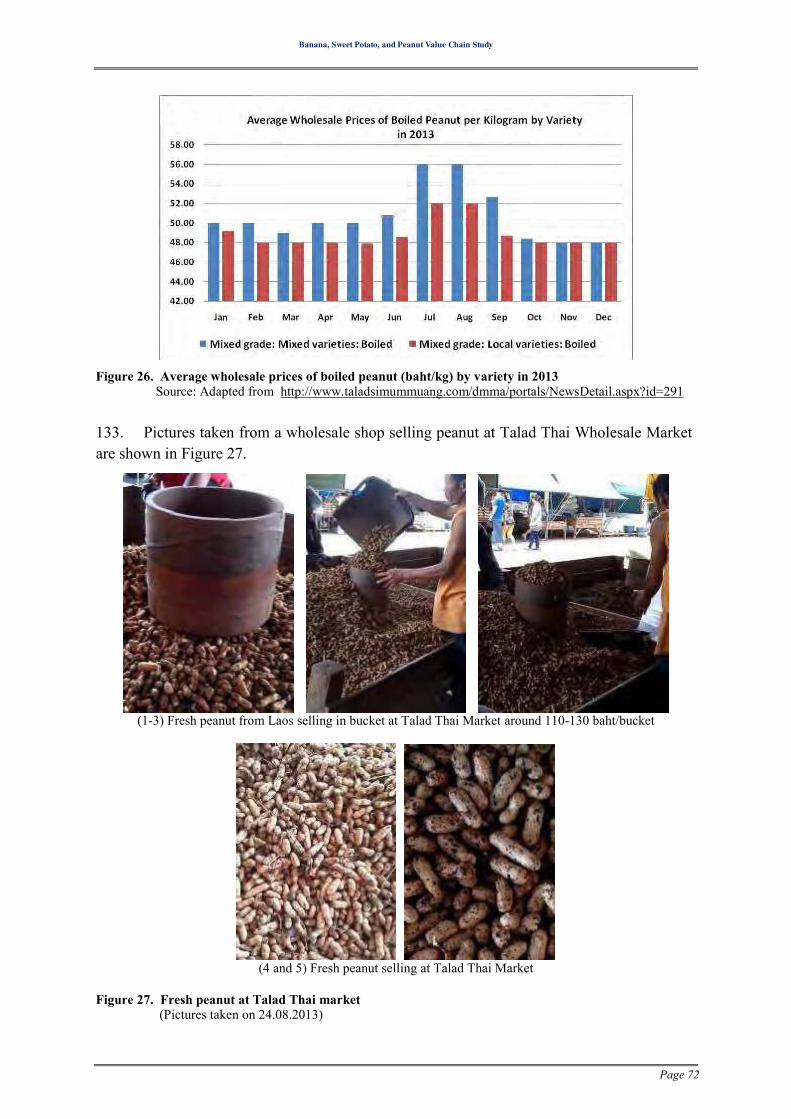

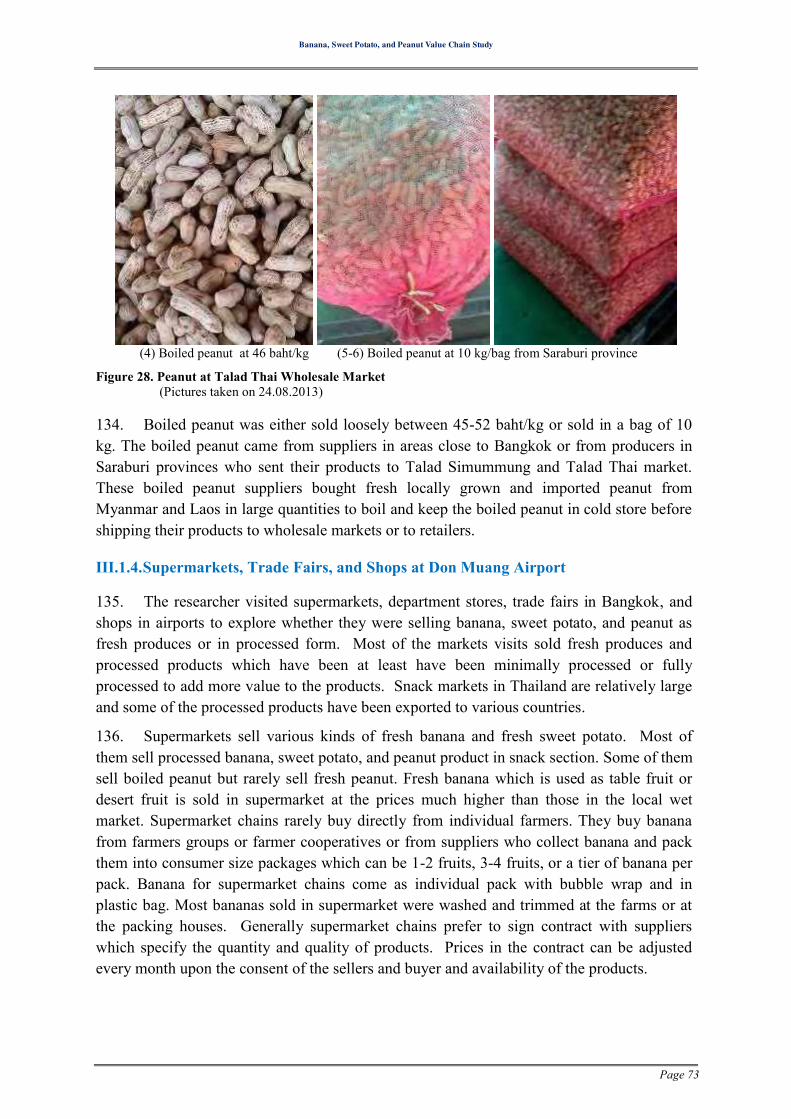

IV.1. VALUE CHAIN OF AGRICULTURAL PRODUCTS ...................................................... 151

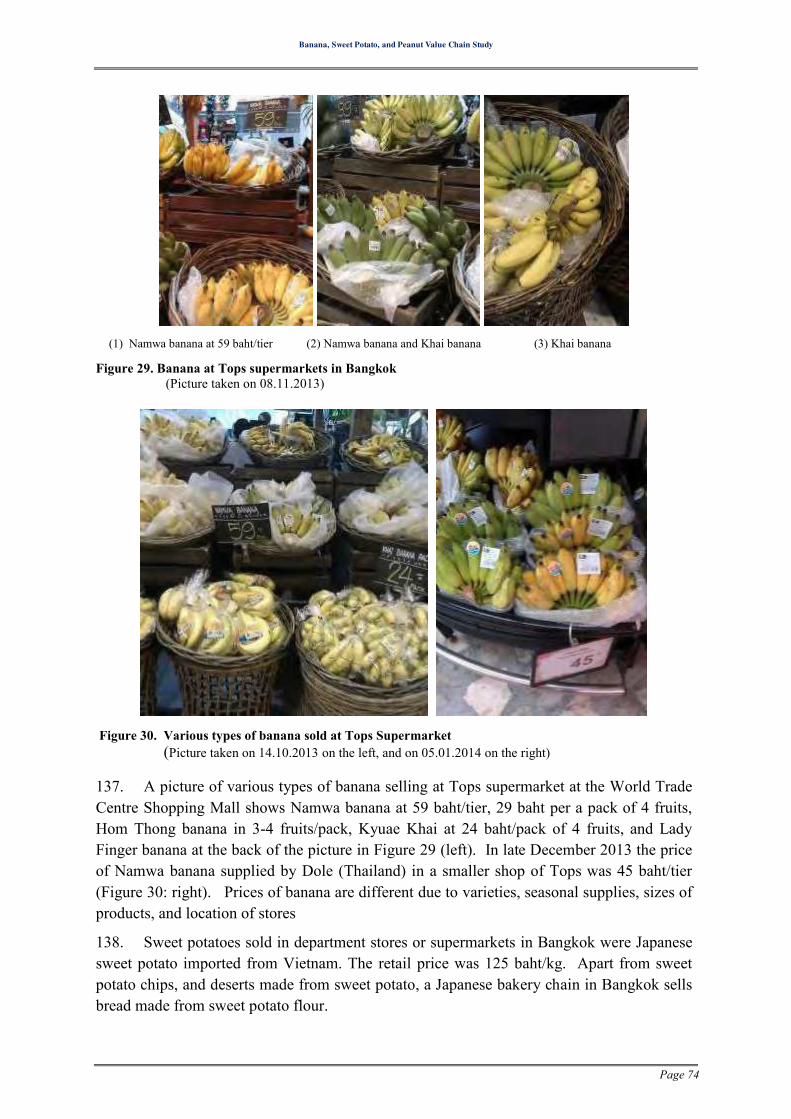

IV.1.1. SWOT Analysis .......................................................................................................... 155

Banana, Sweet Potato, and Peanut Value Chain Study

Page 6

IV.2. STAKEHOLDERS’ ROLES AND RESPONSIBILITIES .................................................. 158

IV.2.1. Agricultural input suppliers ........................................................................................ 158

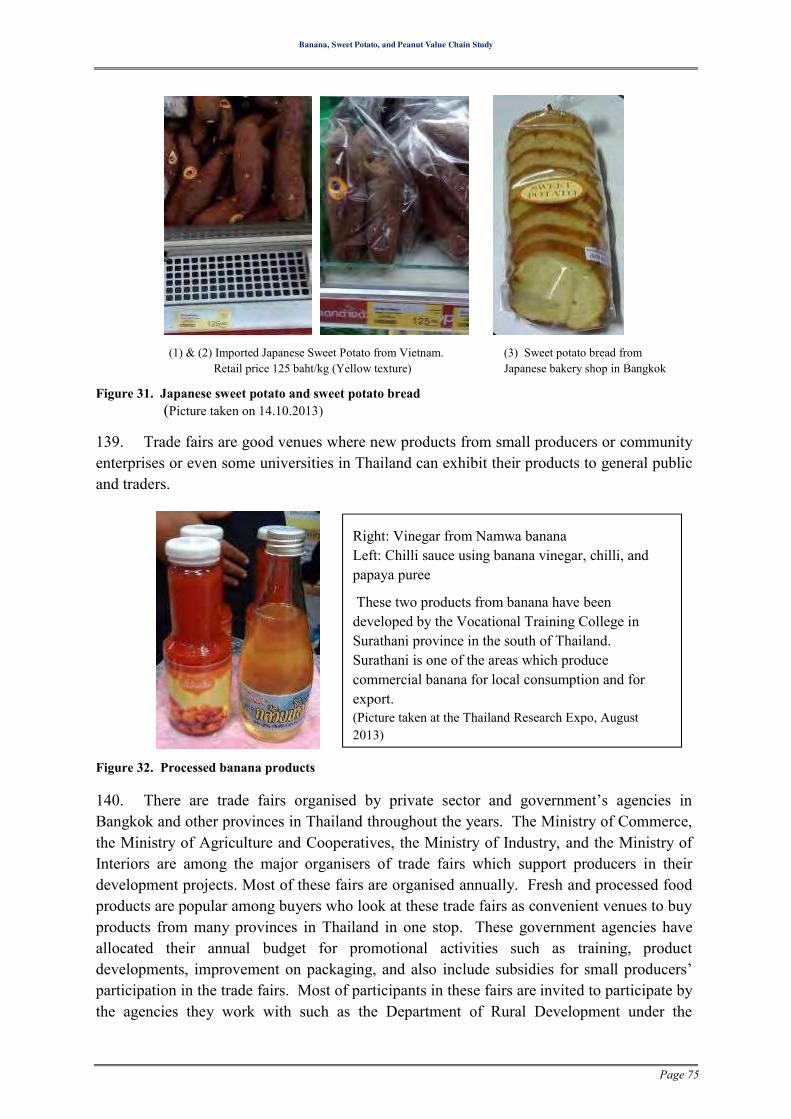

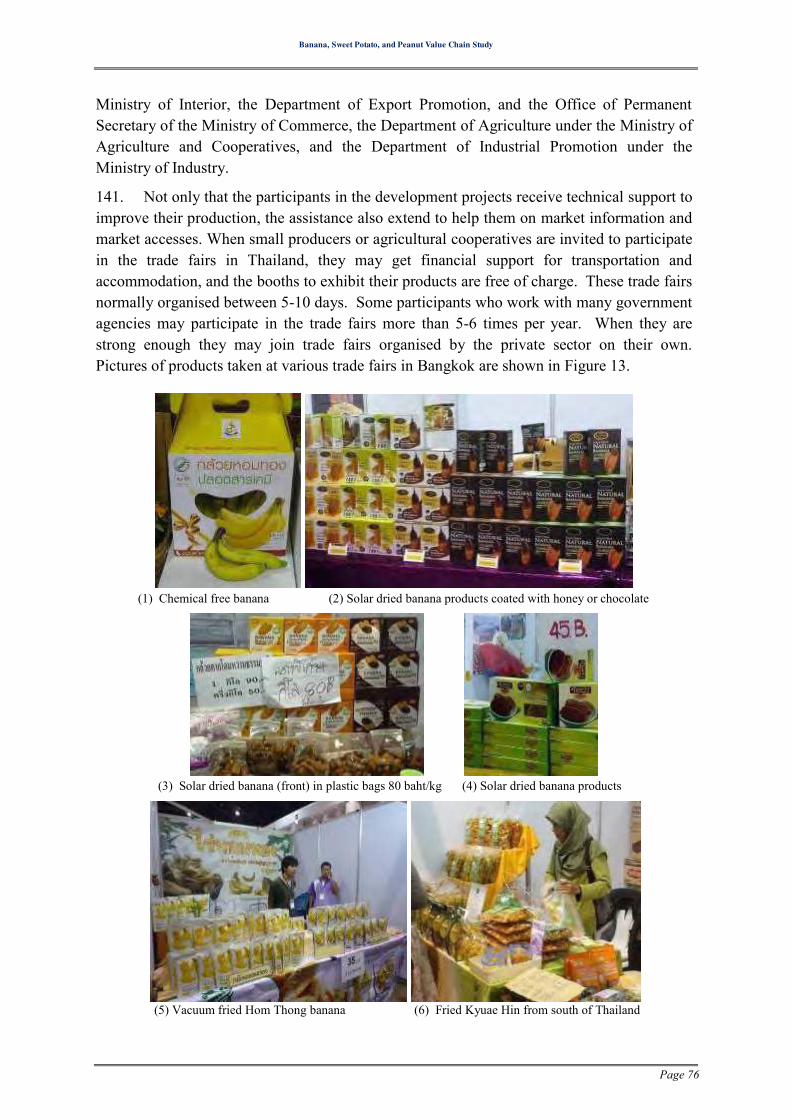

IV.2.2. Producers of Agricultural Products ............................................................................. 159

IV.2.3. Agricultural Product Collectors/Brokers ..................................................................... 159

IV.2.4. Buyers and Brokers of Agricultural Products ............................................................. 160

IV.2.5. Wholesalers and Traders ............................................................................................. 160

IV.2.6. Retailers ...................................................................................................................... 161

IV.2.7. Other Service Providers in the Value Chain ............................................................... 162

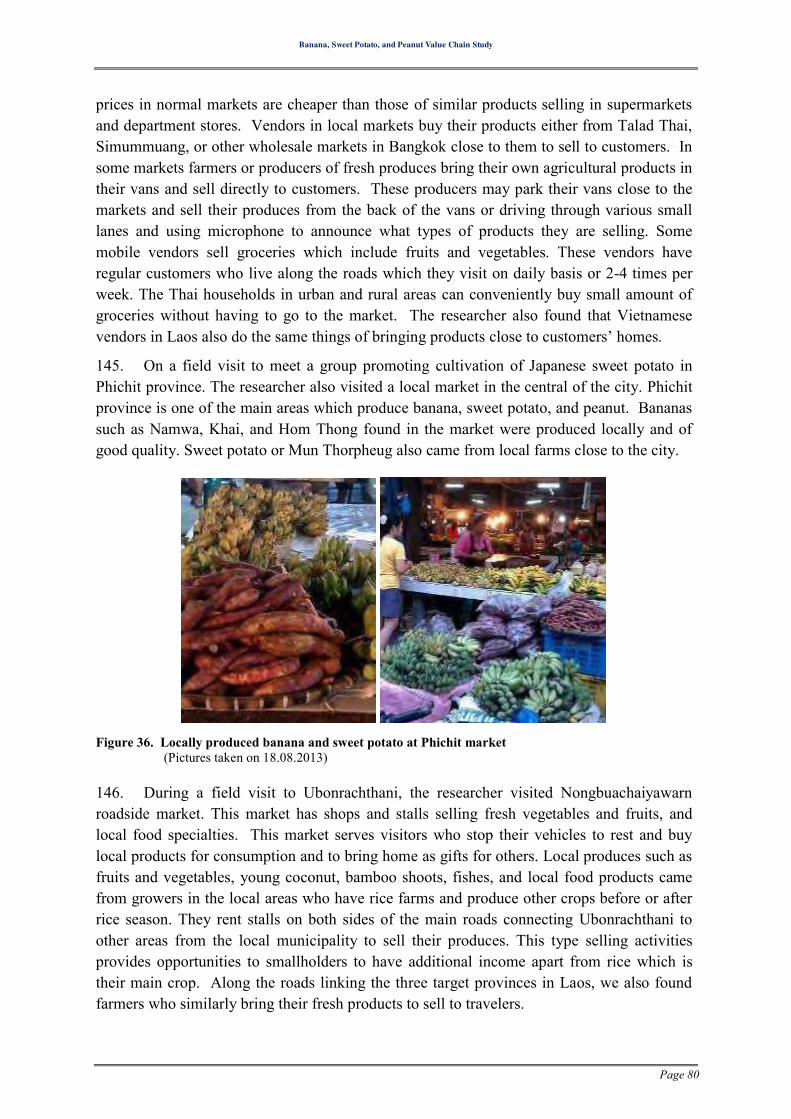

IV.2.8. Local Line Government Agencies .............................................................................. 162

IV.3. FLOWS OF AGRICULTURAL PRODUCTS ................................................................. 163

IV.4. BORDER TRADE BETWEEN LAO PDR AND THAILAND .......................................... 164

IV.4.1. Border Crossing Points ............................................................................................... 164

IV.5. COSTS AND EXPENSES RELATED TO SELECTED PRODUCTS ................................... 166

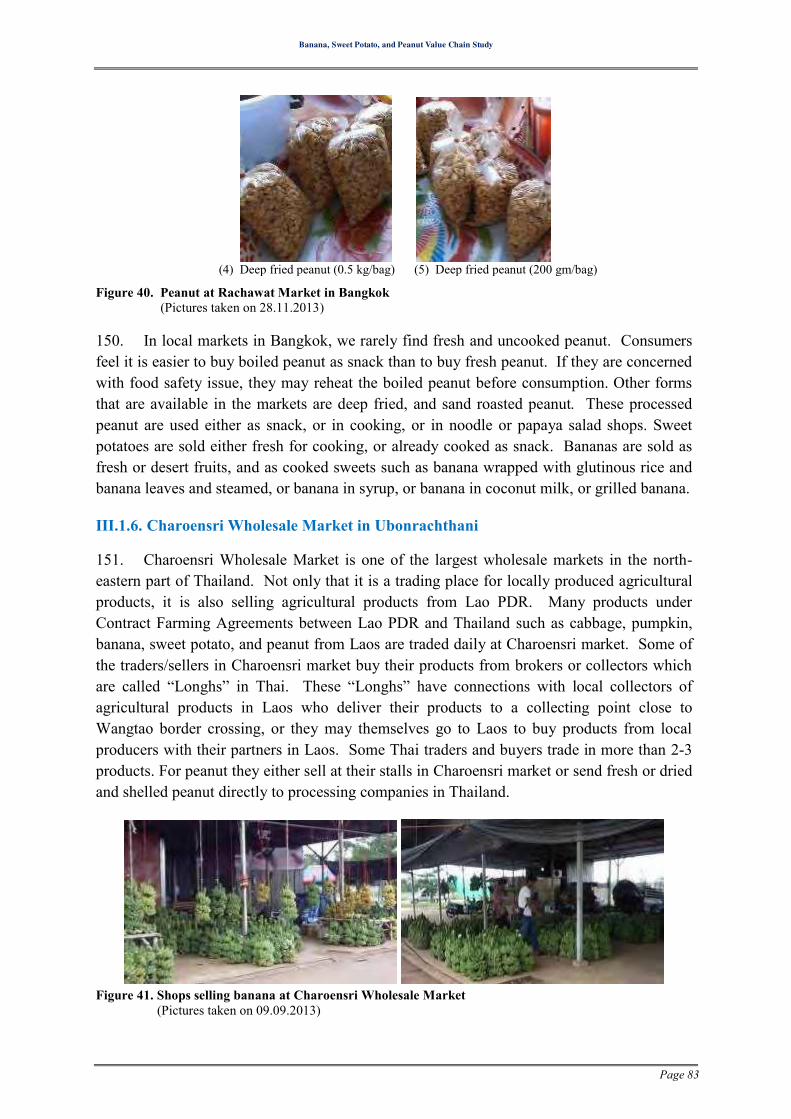

IV.5.1. Cost of Products in the Value Chain ........................................................................... 166

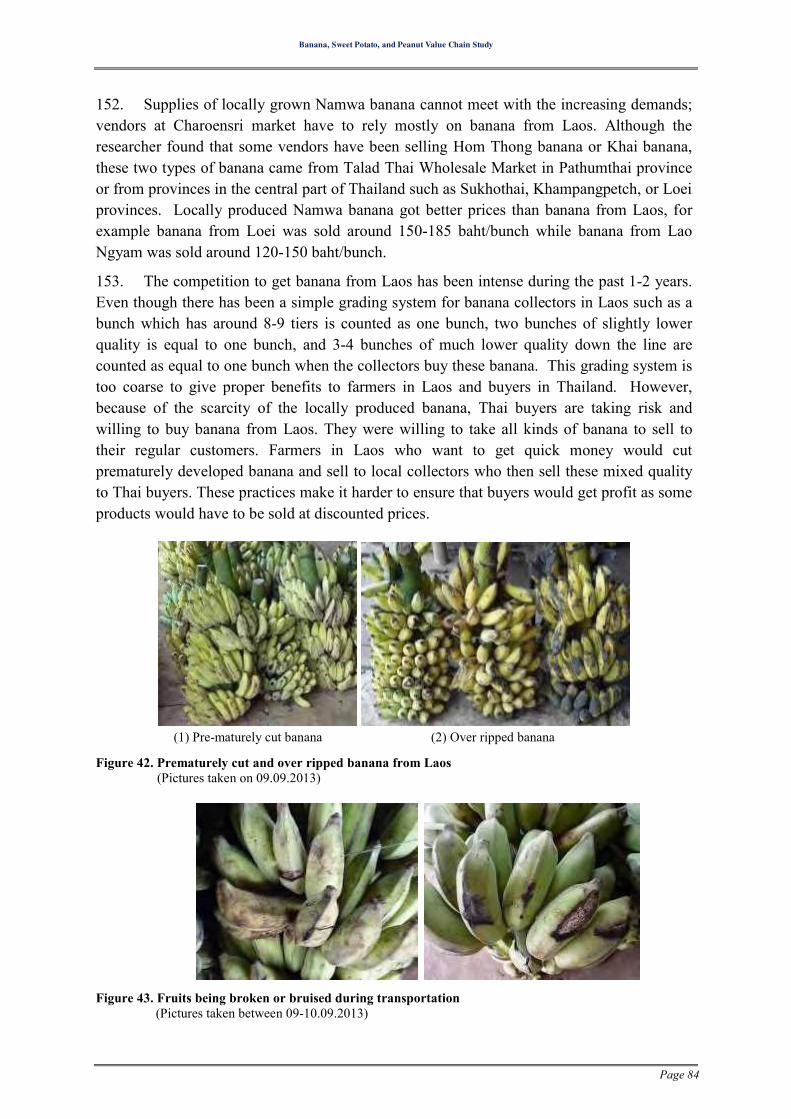

IV.5.2. Expense involved in Exporting Products to Thailand ................................................. 168

IV.5.3. Import duties ............................................................................................................... 169

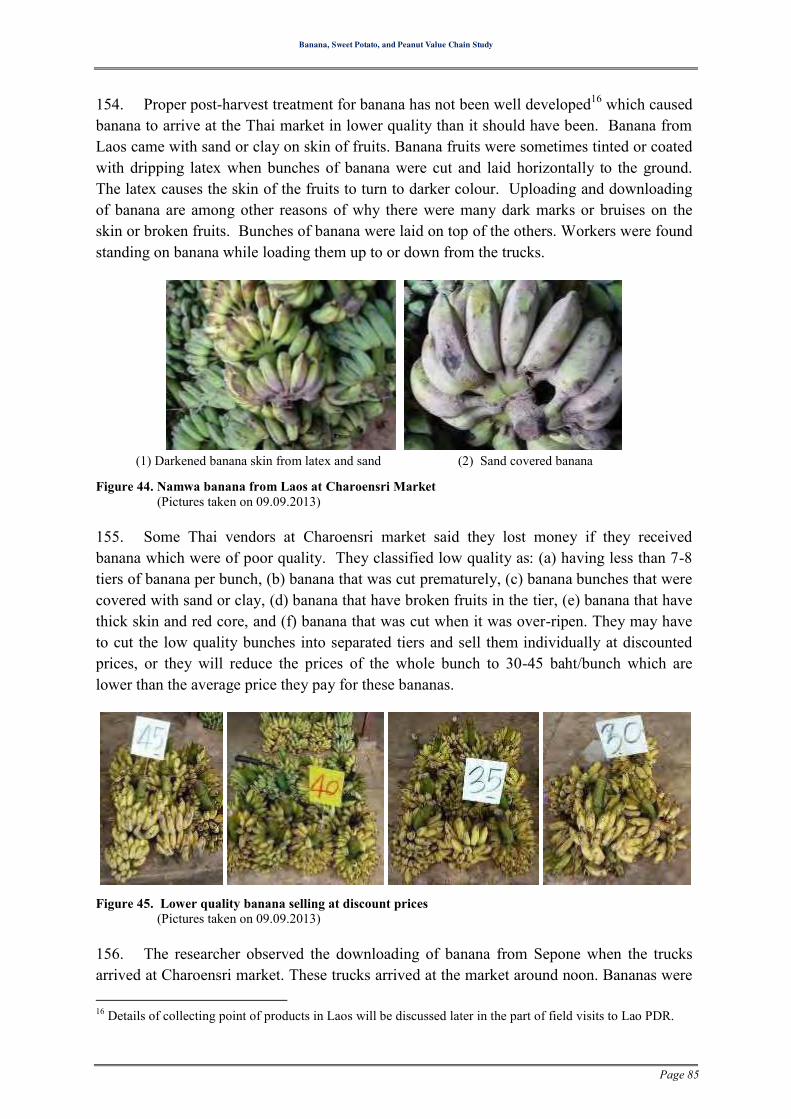

IV.6. TRADE OF BANANA, SWEET POTATO, AND PEANUT ............................................. 169

IV.6.1. Banana ......................................................................................................................... 169

IV.6.2. Sweet Potato ................................................................................................................ 173

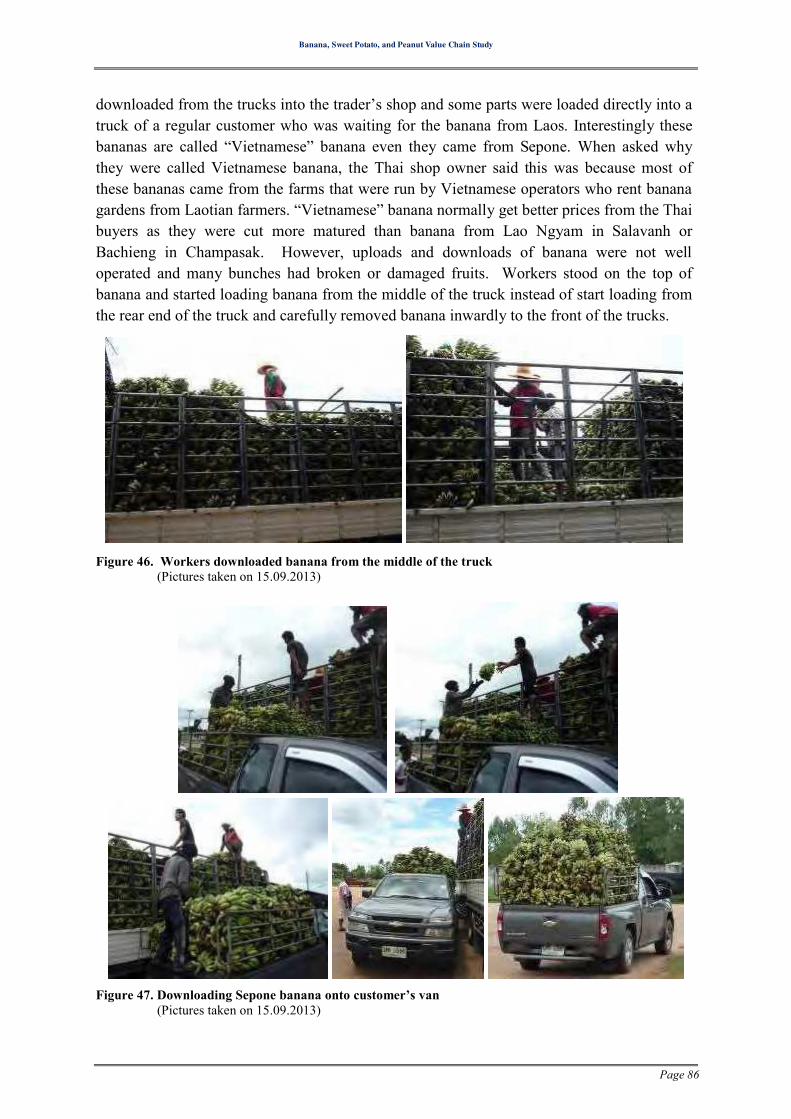

IV.6.3. Peanut .......................................................................................................................... 173

IV.7. OTHER FINDINGS FROM THE FIELD VISITS ............................................................ 175

IV.7.1. Limited Market Linkage ............................................................................................. 175

IV.7.2. Market Information ..................................................................................................... 176

IV.7.3. Post-harvest Management and Quality Issue .............................................................. 176

IV.7.4. Images of Agricultural Products from Lao PDR ......................................................... 176

IV.7.5. Technical Cooperation with Other Institutes .............................................................. 177

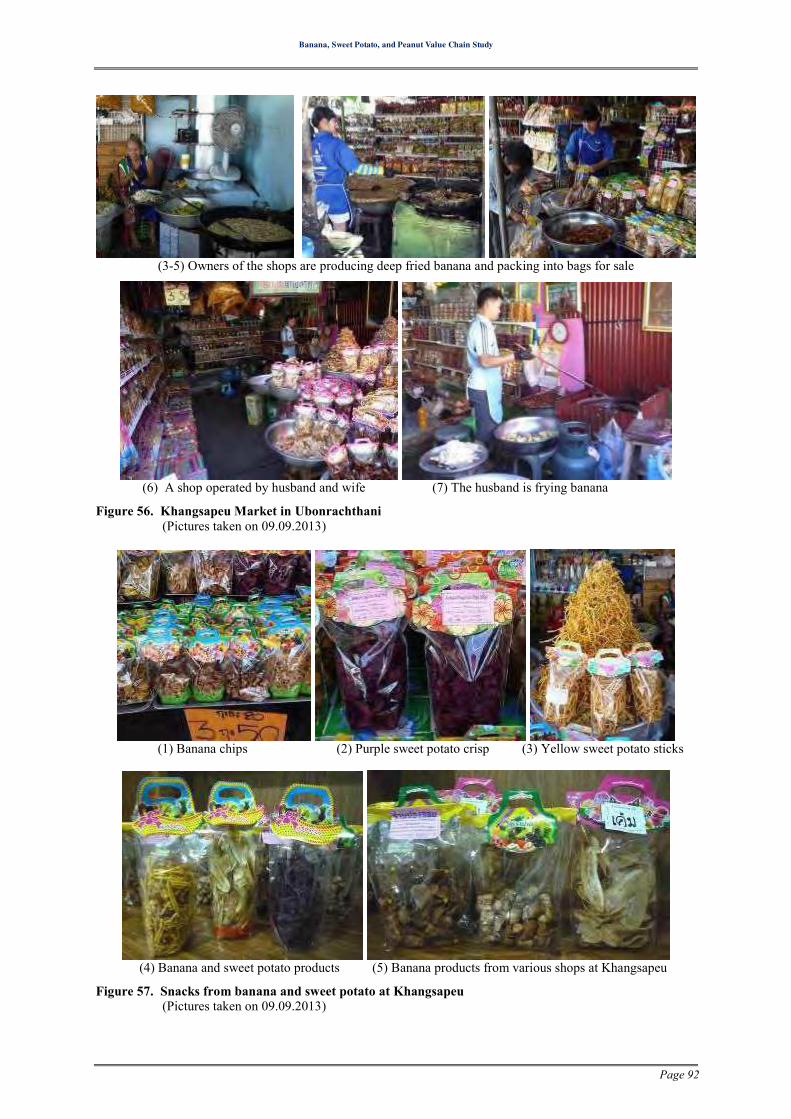

IV.7.6. Public Private Partnerships ......................................................................................... 177

IV.7.7. Capacity Building for Stakeholders in the Value Chain ............................................. 178

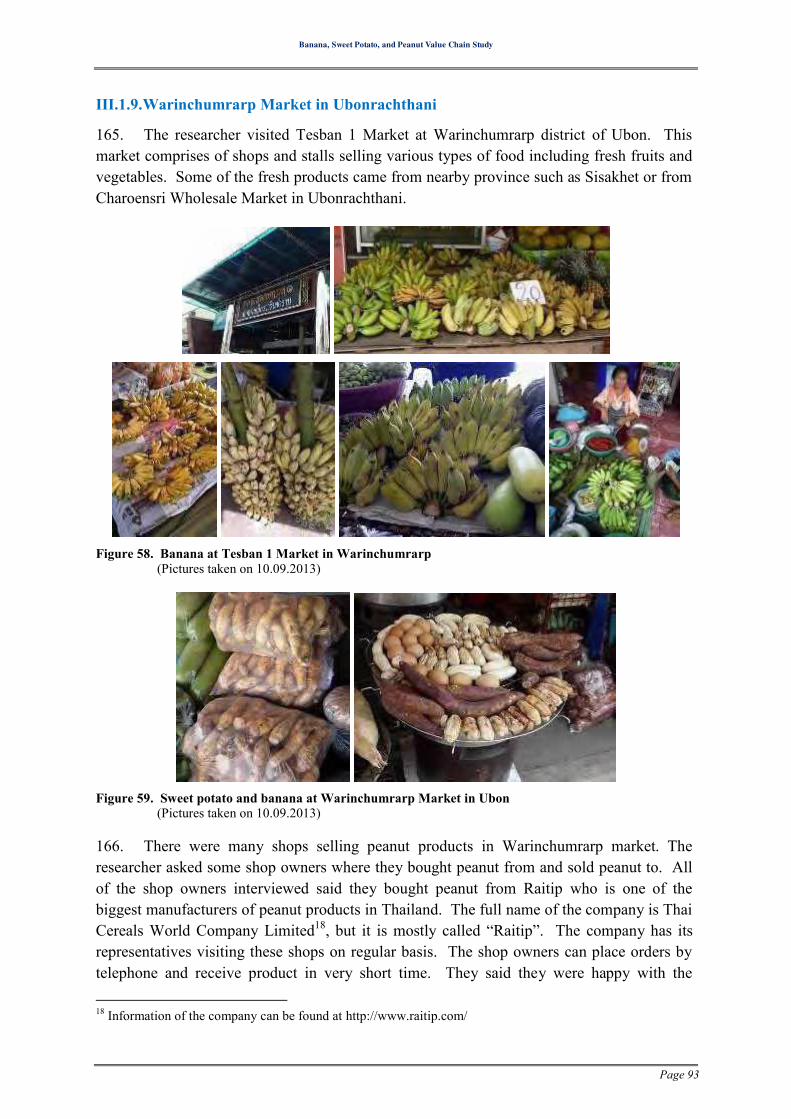

IV.7.8. Contract Farming Agreements .................................................................................... 178

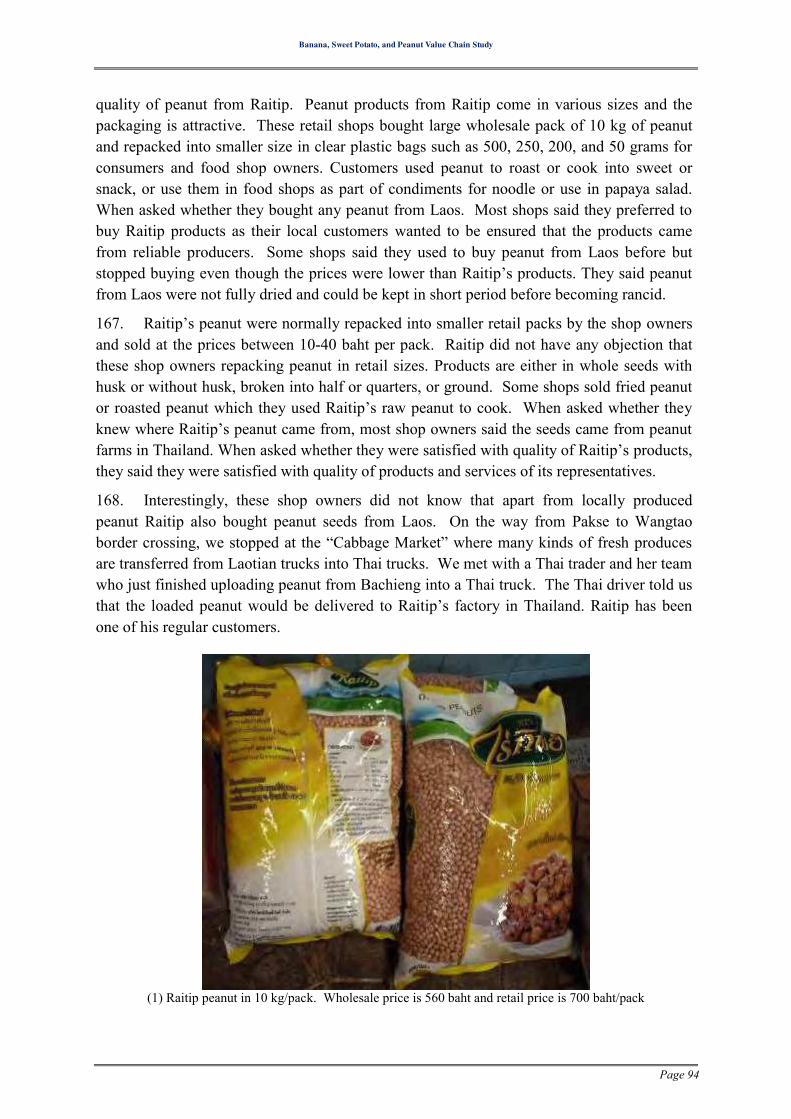

IV.7.9. Farmer Group Formation ............................................................................................ 180

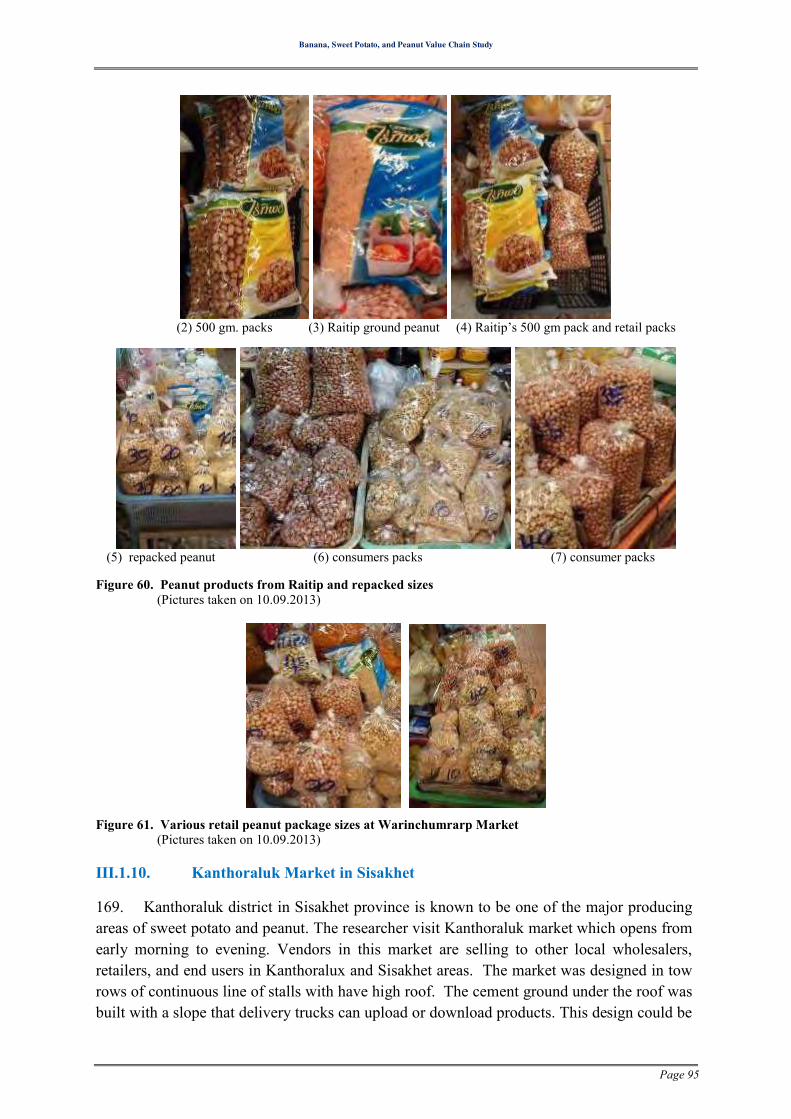

CHAPTER V. CONCLUSION AND RECOMMENDATIONS ............ 181

V.1. CONCLUSION ............................................................................................................ 181

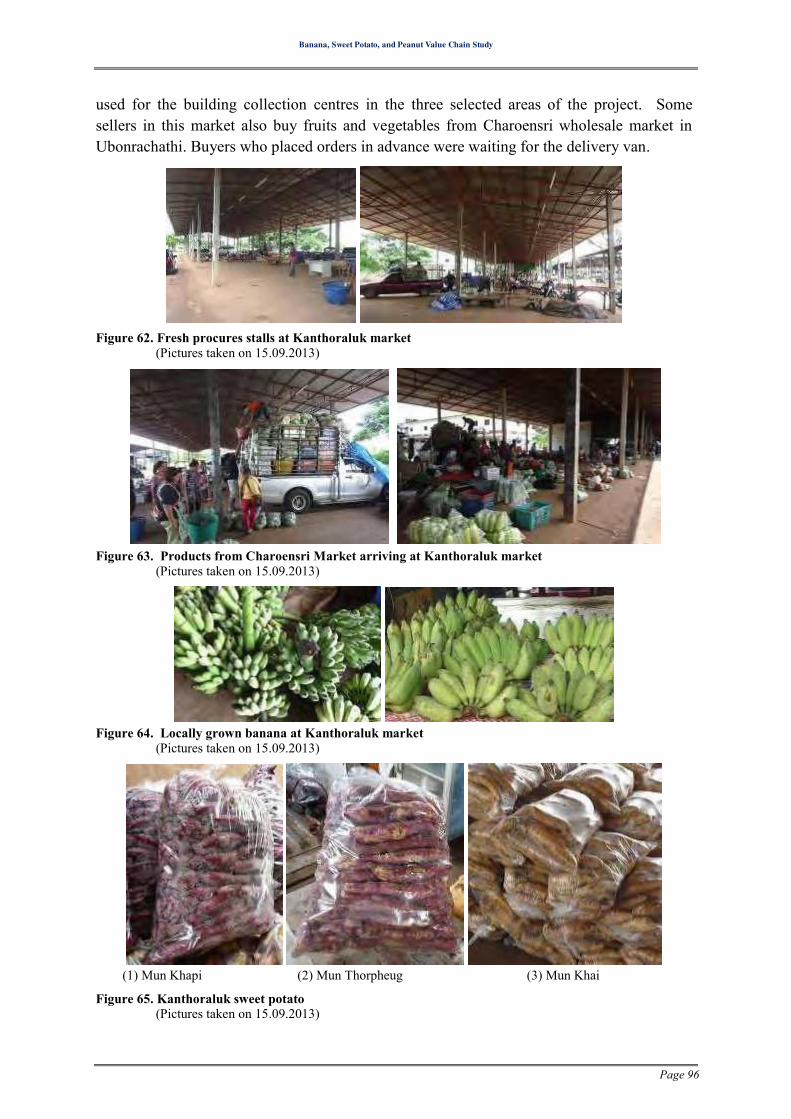

V.2. RECOMMENDATIONS ................................................................................................ 185

V.2.1. Value Chain Development of Banana ......................................................................... 185

V.2.2. Value Chain Development for Sweet Potato .............................................................. 190

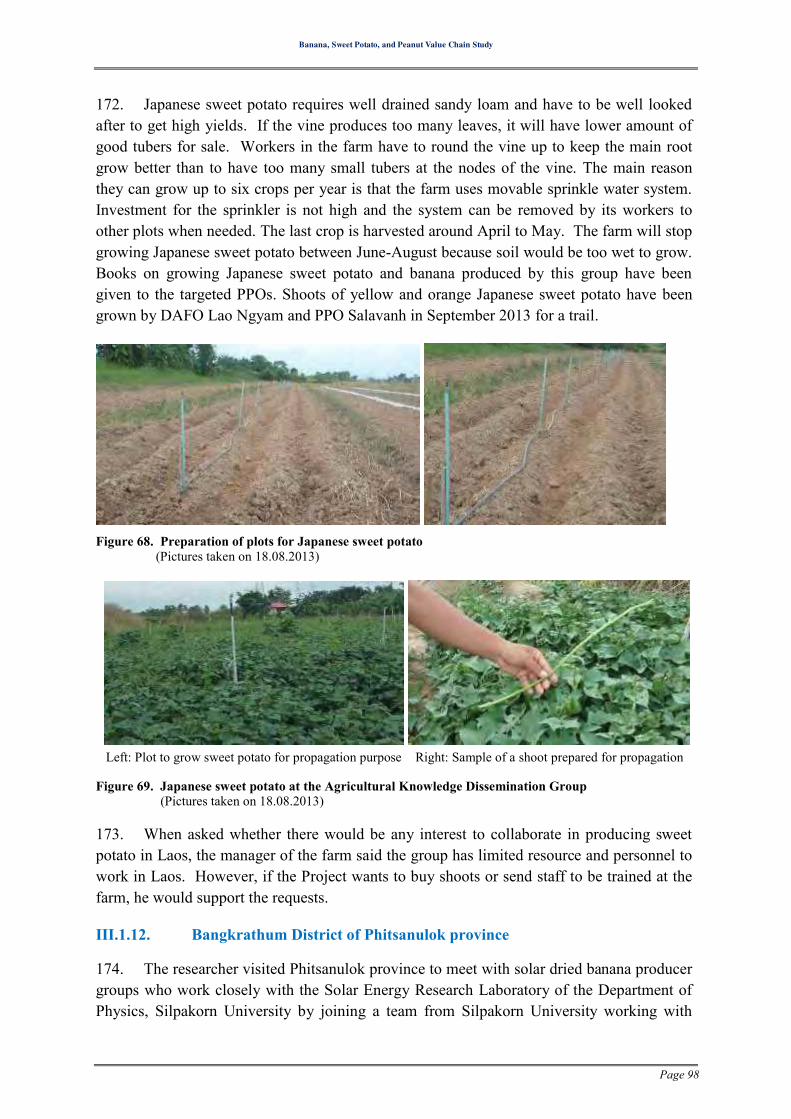

V.2.3. Value Chain Development of Peanut .......................................................................... 193

V.3. FINANCIAL AND NON FINANCIAL BENEFITS ............................................................... 197

Banana, Sweet Potato, and Peanut Value Chain Study

Page 7

V.3.1. Financial benefits ........................................................................................................ 197

V.3.2. Other non-quantified benefit of the Project: ............................................................... 198

V.4. ENVIRONMENTAL IMPACTS ...................................................................................... 199

V.5. VULNERABLE GROUPS .............................................................................................. 199

V.6. ETHNIC MINORITY GROUP ......................................................................................... 199

V.7. FINANCING PLAN ...................................................................................................... 200

V.8. IMPLEMENTATION ARRANGEMENTS ......................................................................... 202

V.8.1. Government agencies .................................................................................................. 202

V.8.2. Private Partners ........................................................................................................... 203

V.8.3. Smallholder Farmers/Producer Groups ....................................................................... 204

V.9. CONSULTANT REQUIREMENTS .................................................................................. 204

ANNEXES ......................................................................................................................... 206

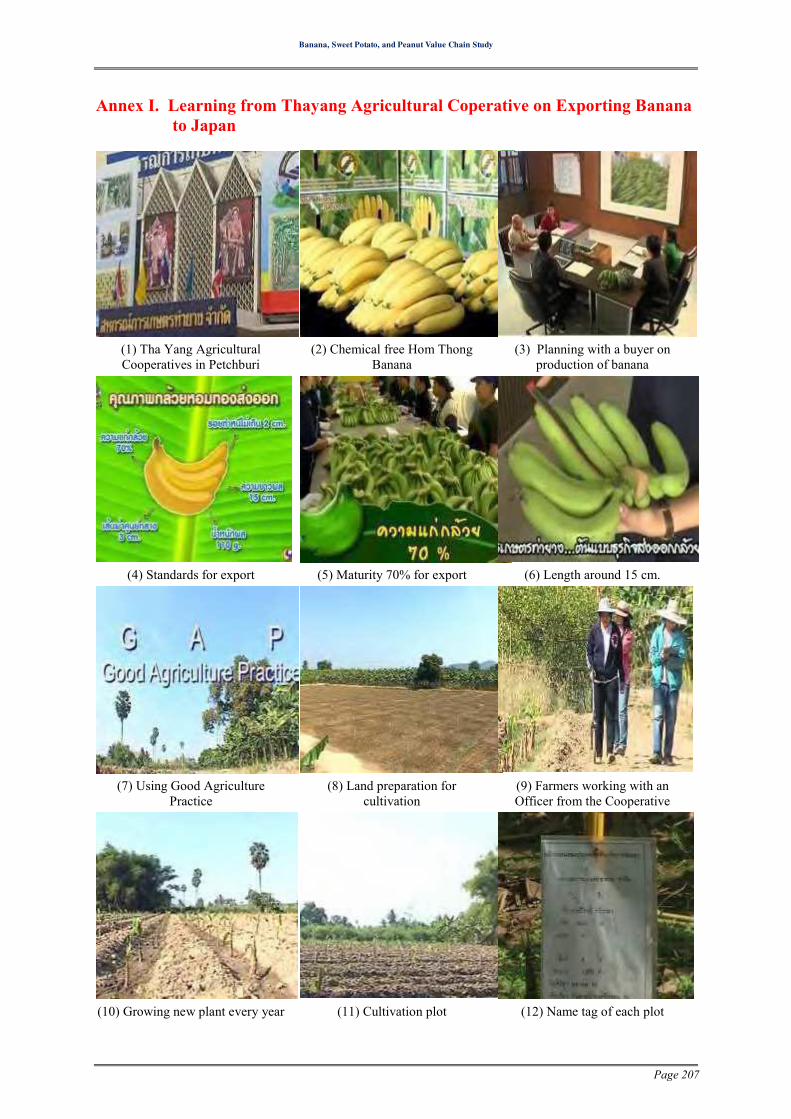

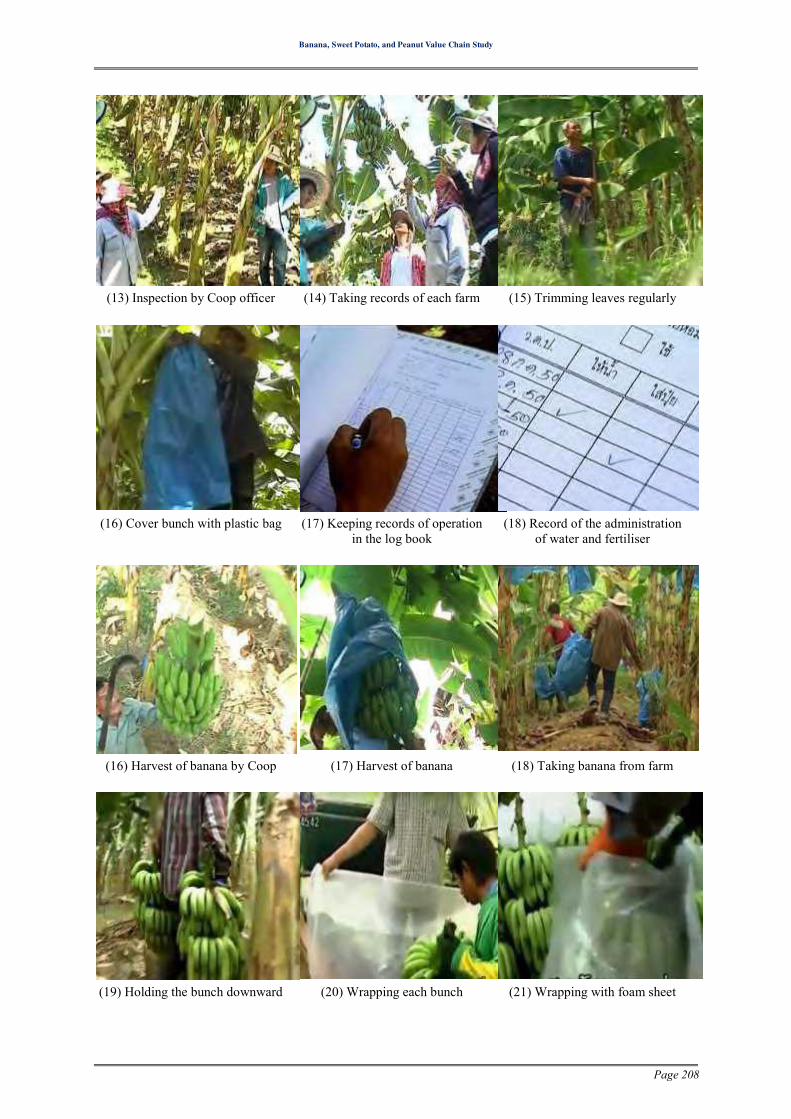

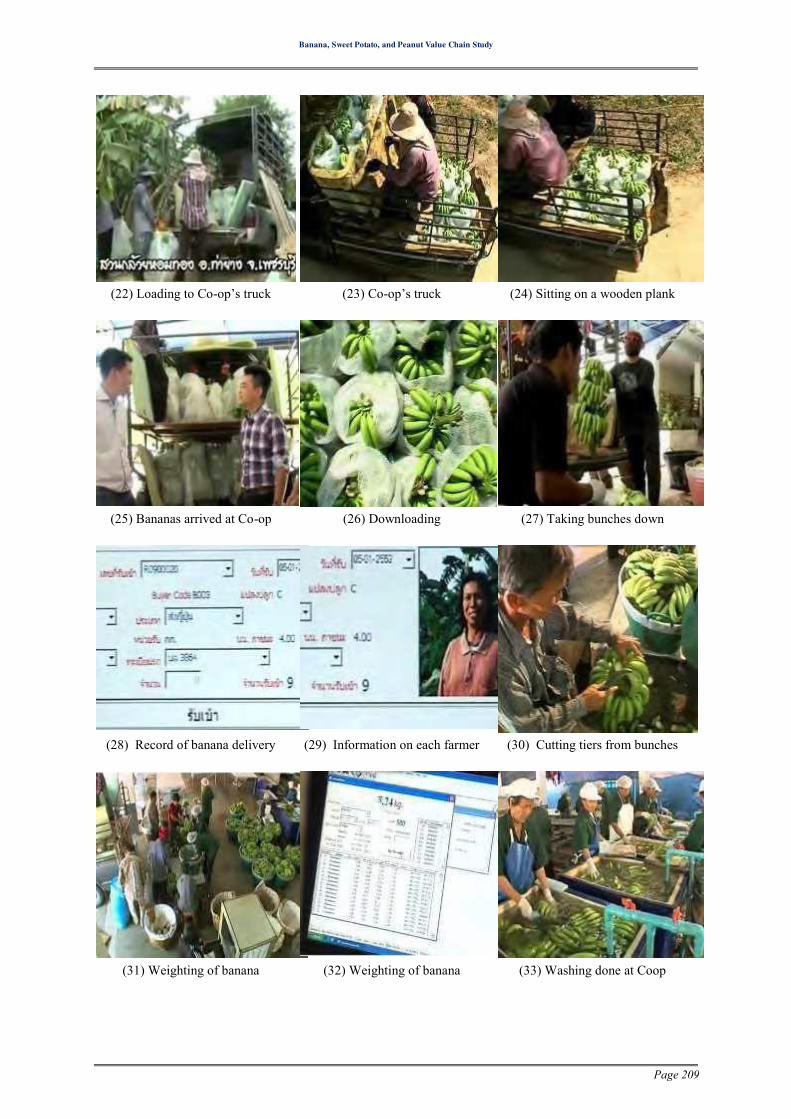

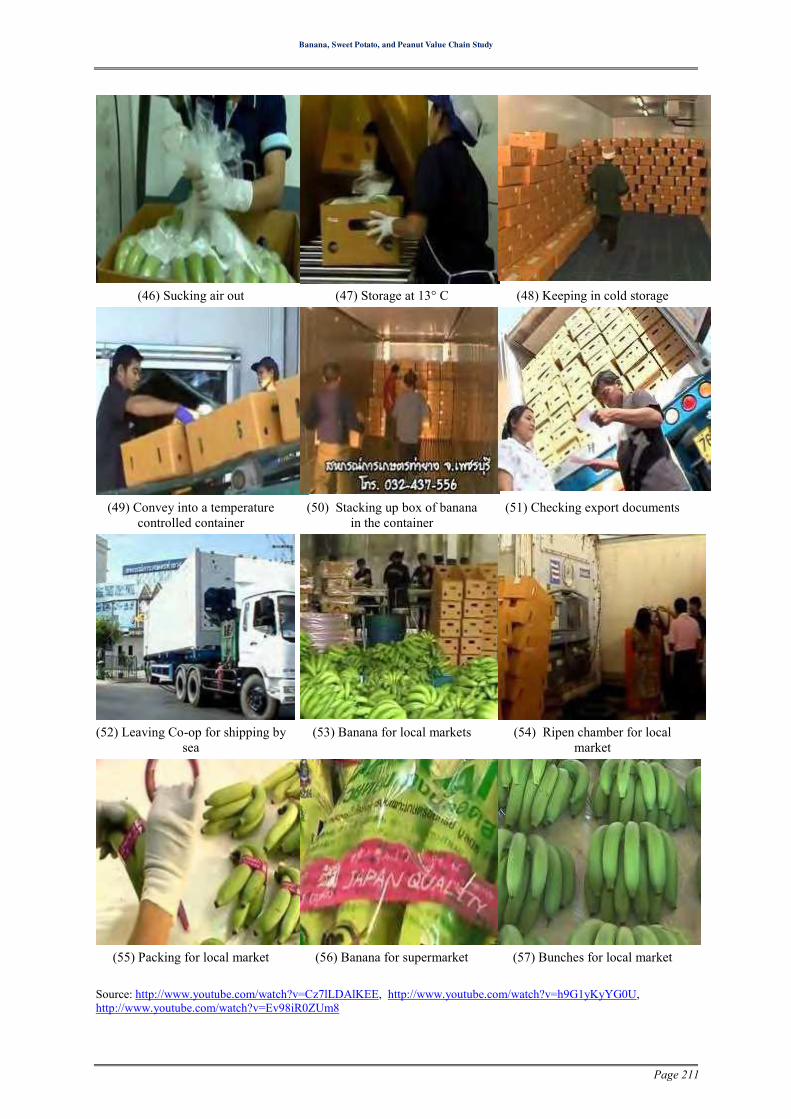

ANNEX I. LEARNING FROM THAYANG AGRICULTURAL COPERATIVE ON EXPORTING BANANA TO JAPAN ............................................................................................................................ 207

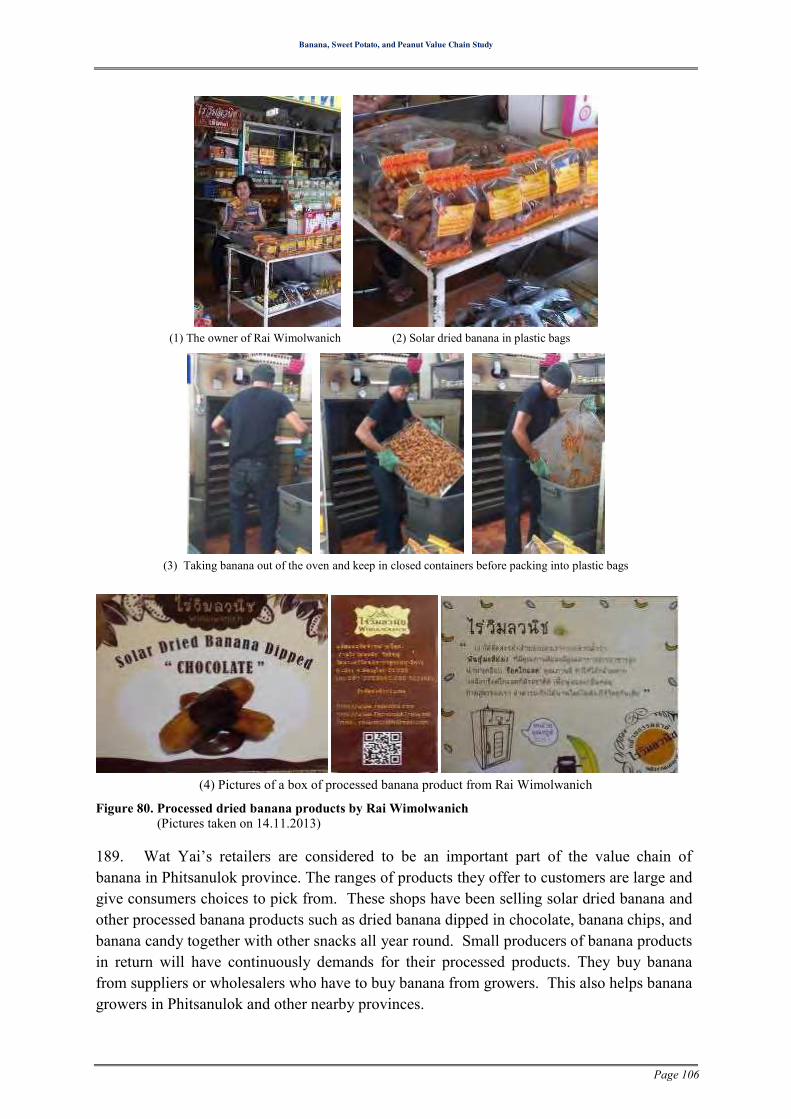

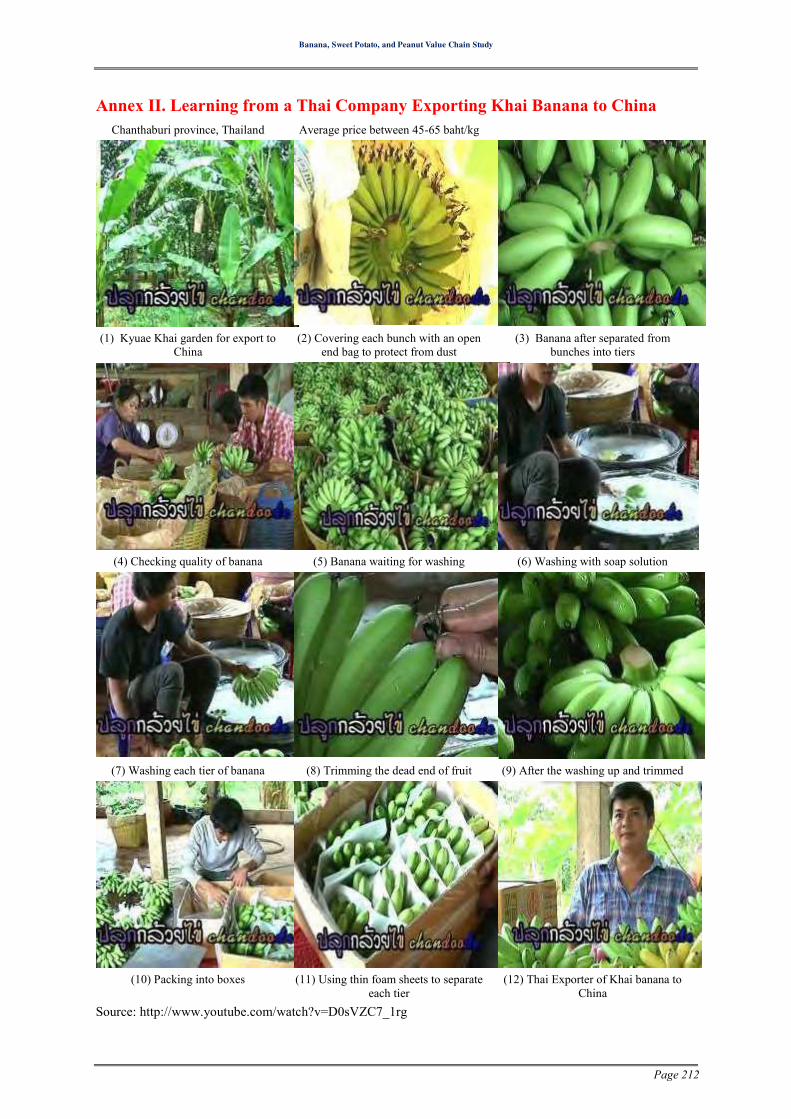

ANNEX II. LEARNING FROM A THAI COMPANY EXPORTING KHAI BANANA TO CHINA ....... 212

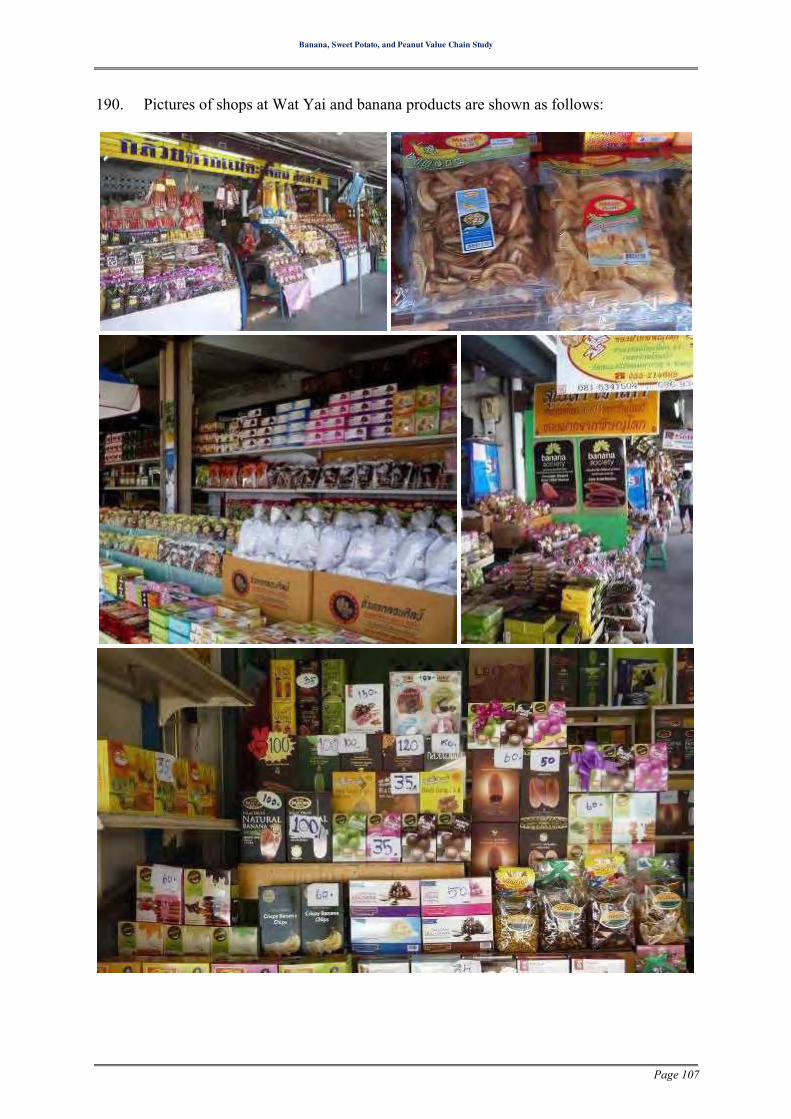

ANNEX III. USEFUL INFORMATION ..................................................................................... 213

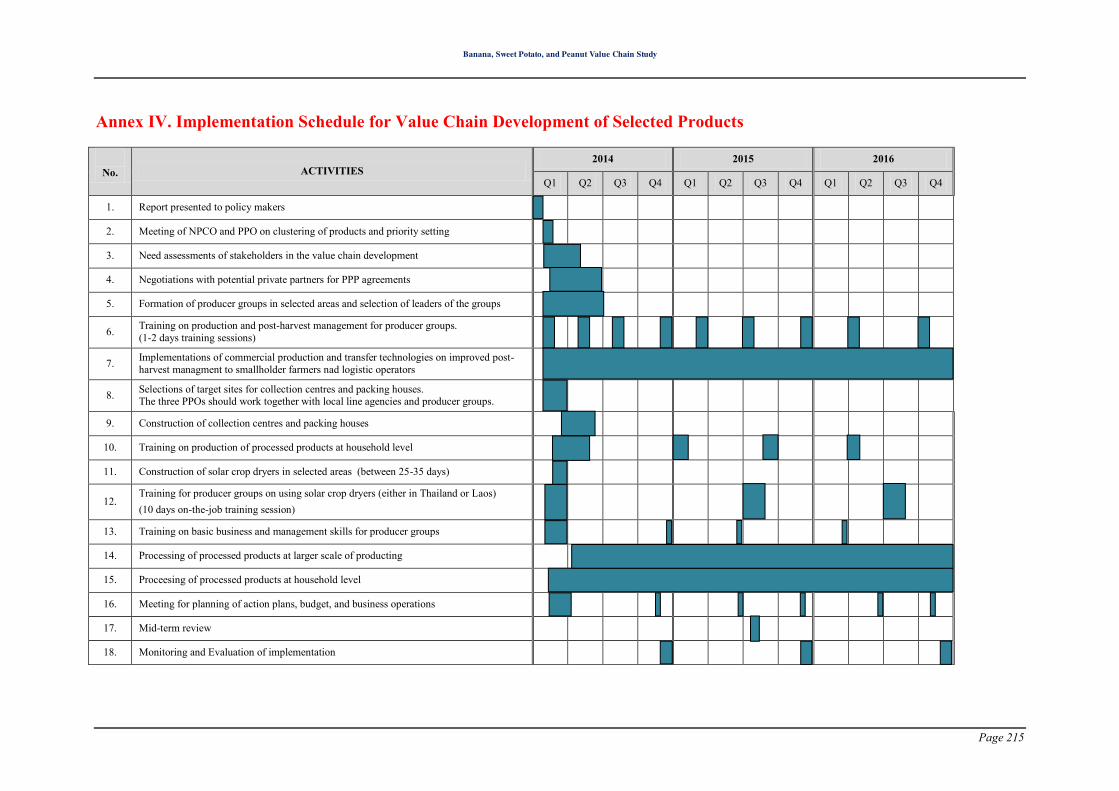

ANNEX IV. IMPLEMENTATION SCHEDULE FOR VALUE CHAIN DEVELOPMENT OF SELECTED PRODUCTS ........................................................................................................................... 215

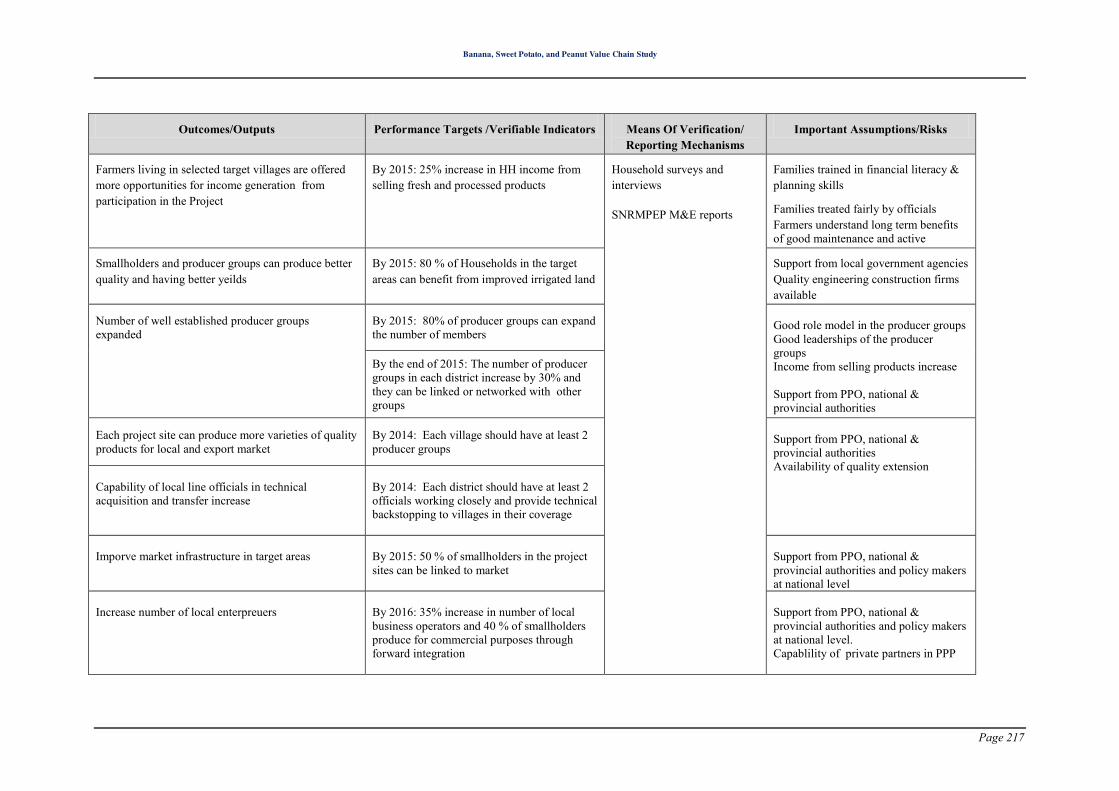

ANNEX V. MONITORING FRAMEWORK ............................................................................... 216

REFERENCE…. ............................................................................................. 218

Banana, Sweet Potato, and Peanut Value Chain Study

Page 8

LIST OF TABLES Table 1.Number of households by village type and province, 2010/11 .................................. 20

Table 2. Farm population by sex and age (2010/2011) .......................................................... 21

Table 3 Number of households by farm/non-farm and land type, 2010/11 ............................. 22

Table 4. Characteristics of land holdings (2010/11) ................................................................ 22

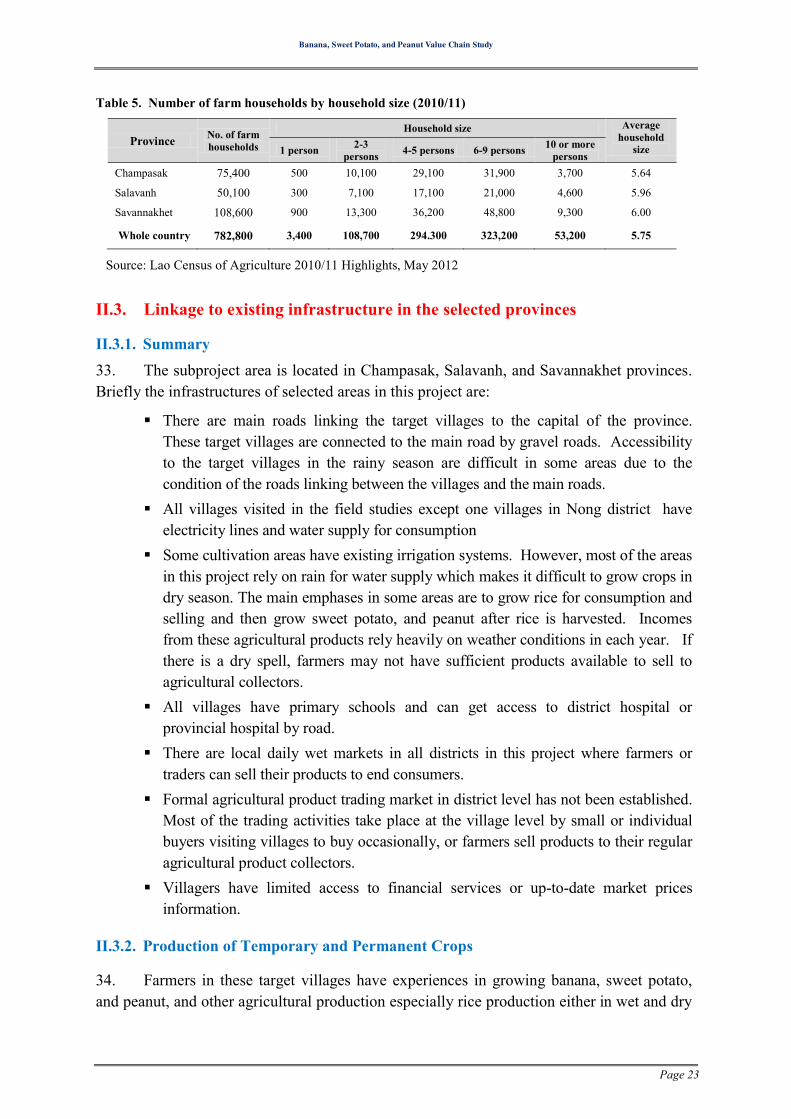

Table 5. Number of farm households by household size (2010/11) ....................................... 23

Table 6 Total areas of cultivation and number of growers of selected crops .......................... 24

Table 7. Production areas and numbers of growers of peanut and banana (2010/11) ............. 25

Table 8. Farm households using farm machinery by type of machine ................................... 25

Table 9. Farm households by use of outside labour and type of payment (2010/11) .............. 26

Table 10. Selected infrastructure by province, village type, and land type (2011) ................ 26

Table 11. Source of electricity (2011) .................................................................................... 27

Table 12. Source of household water (2011) ........................................................................ 27

Table 13. Type of Irrigation facilities in rural villages by irrigation type (2011) ................... 28

Table 14. Selected agricultural characteristics of rural villages (2011) ................................... 28

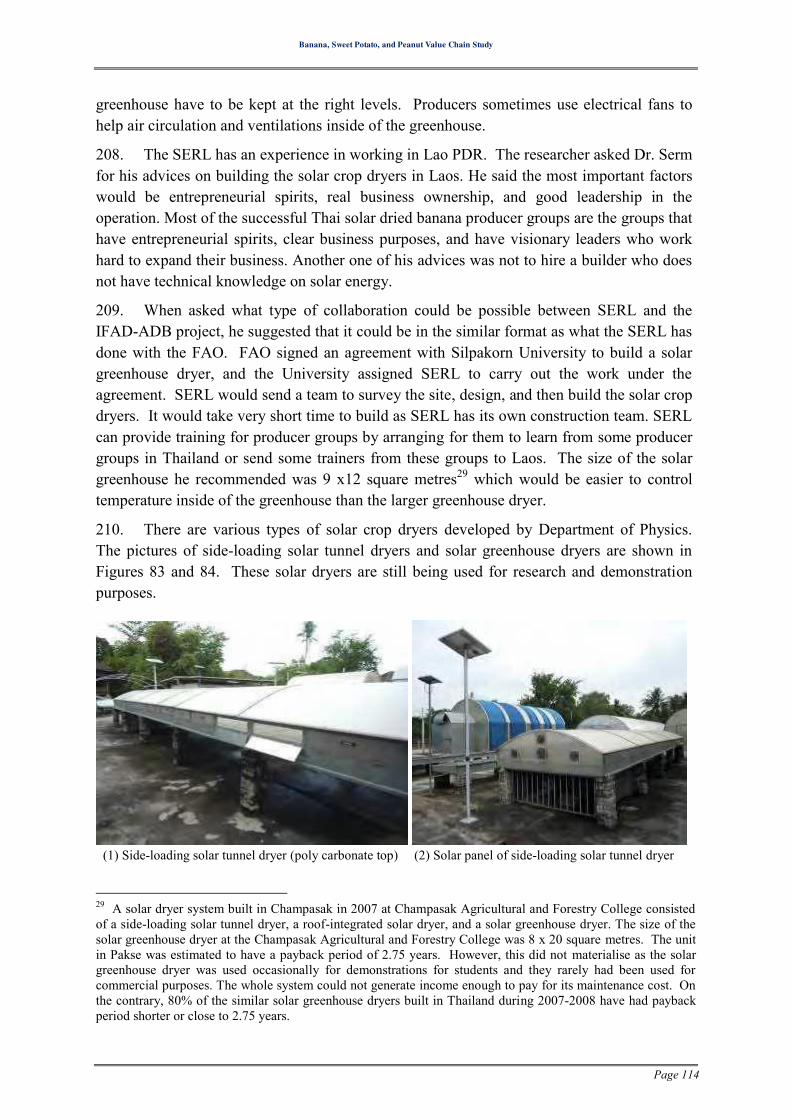

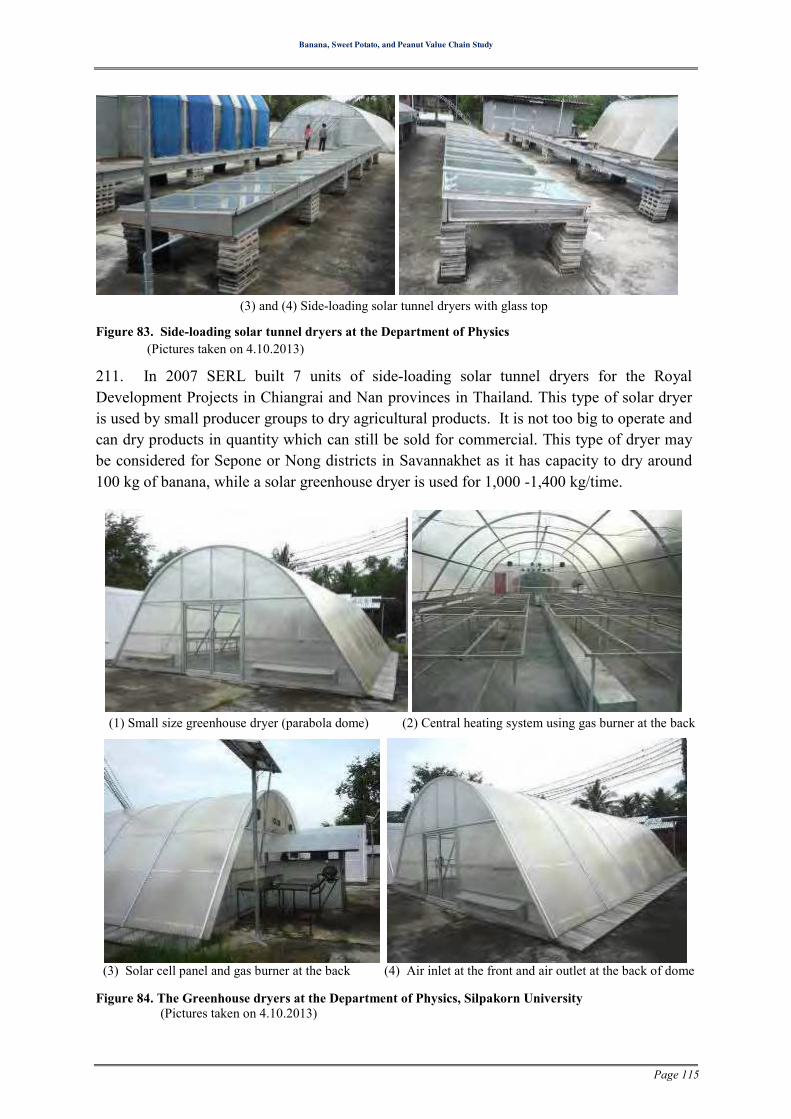

Table 15. Selected village services and organizations (2011) ................................................ 29

Table 16. Farm households with credit and source of credits (2010/11) ................................ 30

Table 17. Type of credit facilities in rural villages (2011) .................................................... 30

Table 18. Sale of farm produces as percentage of farm households ....................................... 31

Table 19. Marketing of agriculture produce in rural villages (2011) ..................................... 31

Table 20. Agricultural infrastructure in rural villages by type of infrastructure (2011) .......... 32

Table 21. Farm households by sources of agricultural information (2010/11)........................ 33

Table 22. Constraints and problems faced by famers in rural village (2011) .......................... 33

Table 23. Production areas of target villages in Bachieng Chaleunsouk ................................. 35

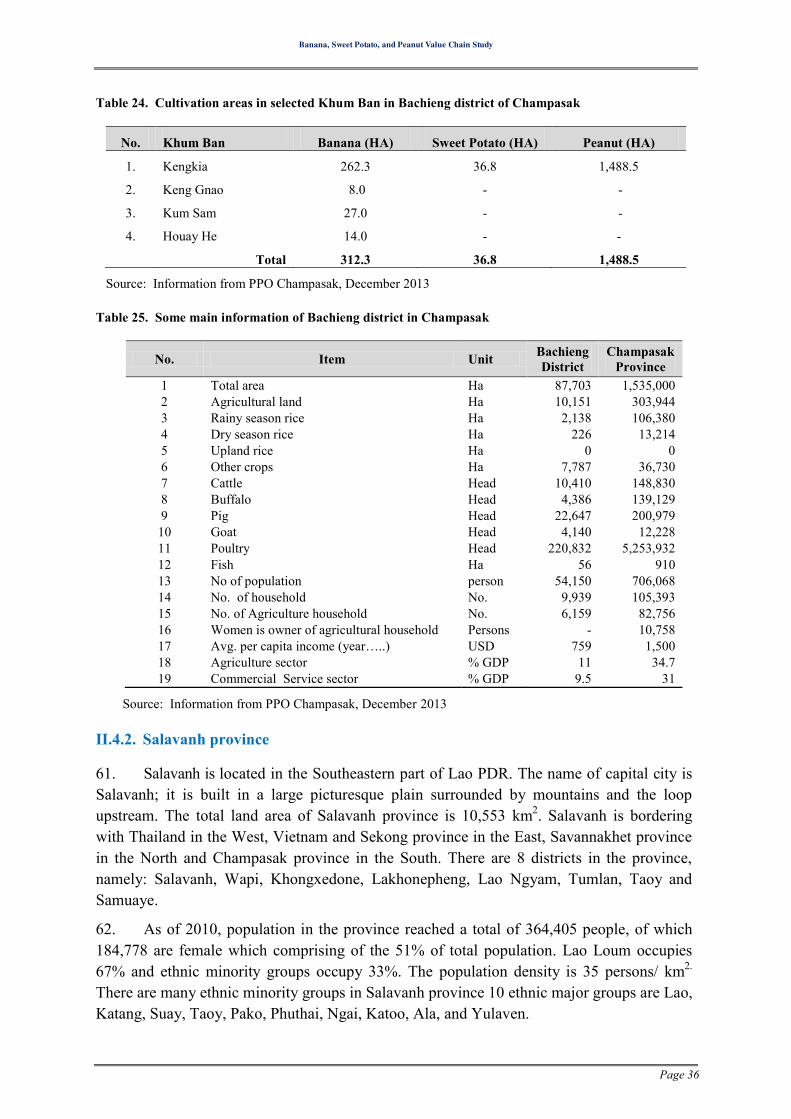

Table 24. Cultivation areas in selected Khum Ban in Bachieng district of Champasak ........ 36

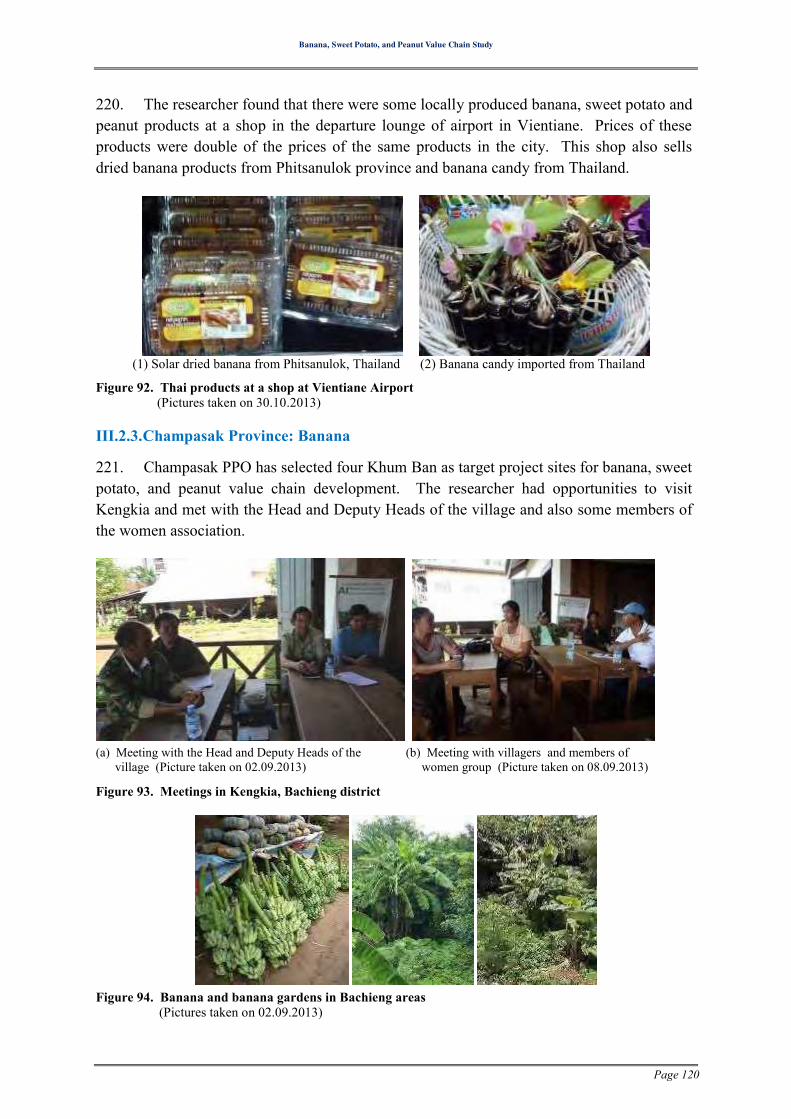

Table 25. Some main information of Bachieng district in Champasak .................................. 36

Table 26. Target villages in Lao Ngyam district of Salavanh province .................................. 38

Table 27. General information of Lao Ngyam district in Salavanh province ........................ 38

Table 28. Production of banana in Salavanh province ........................................................... 39

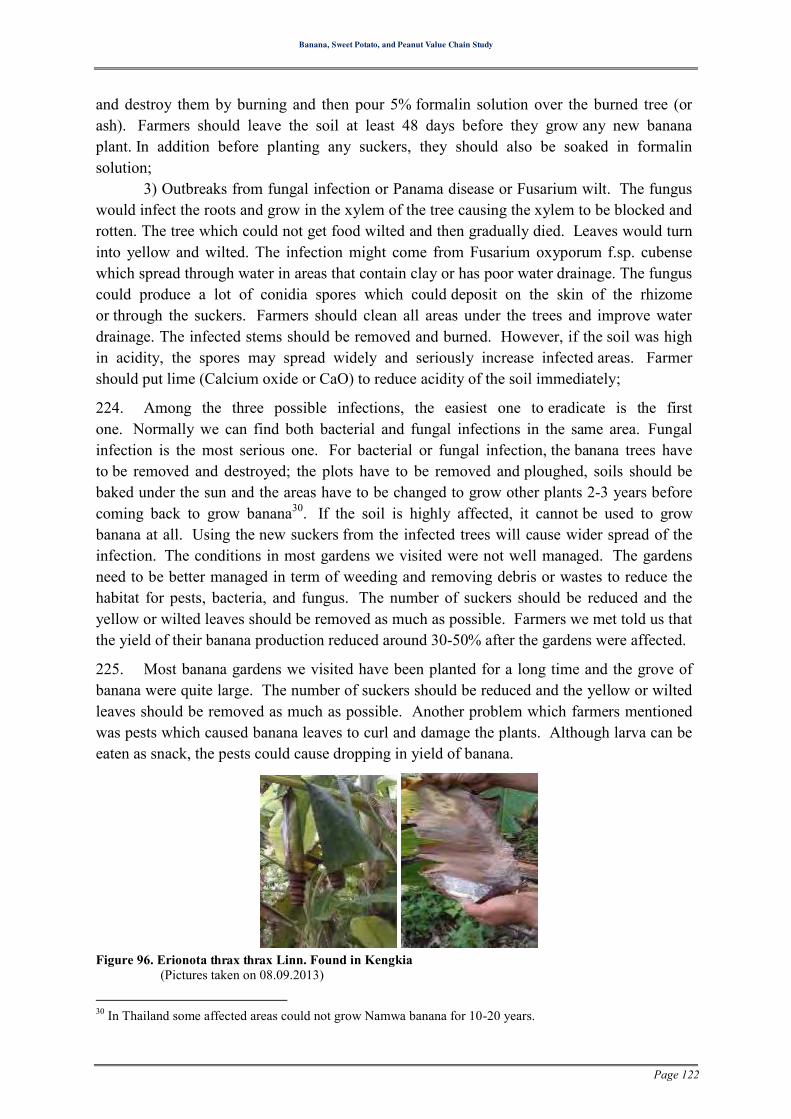

Table 29. Production and trade of banana of Salavanh ........................................................... 39

Table 30. Production and trade of sweet potato ...................................................................... 40

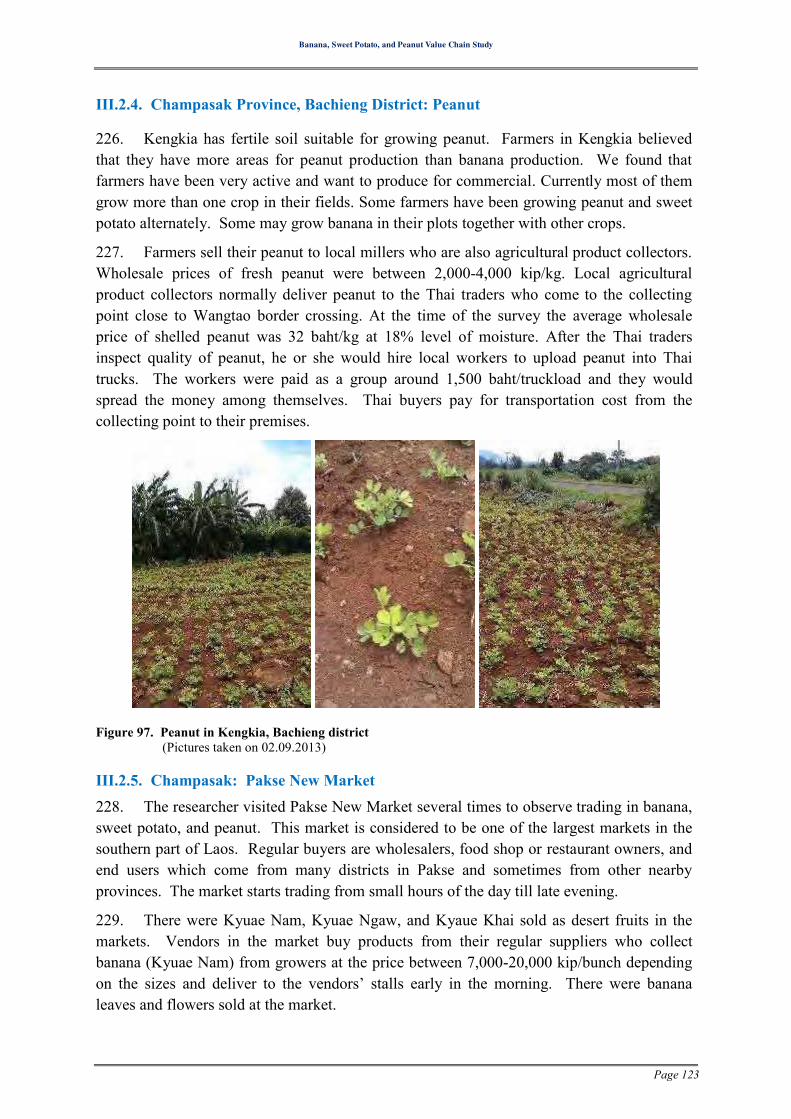

Table 31. Production and trade of peanut ................................................................................ 40

Table 32. Name of target villages in Sepone, Nong, and Xaiphouthong districts ................... 43

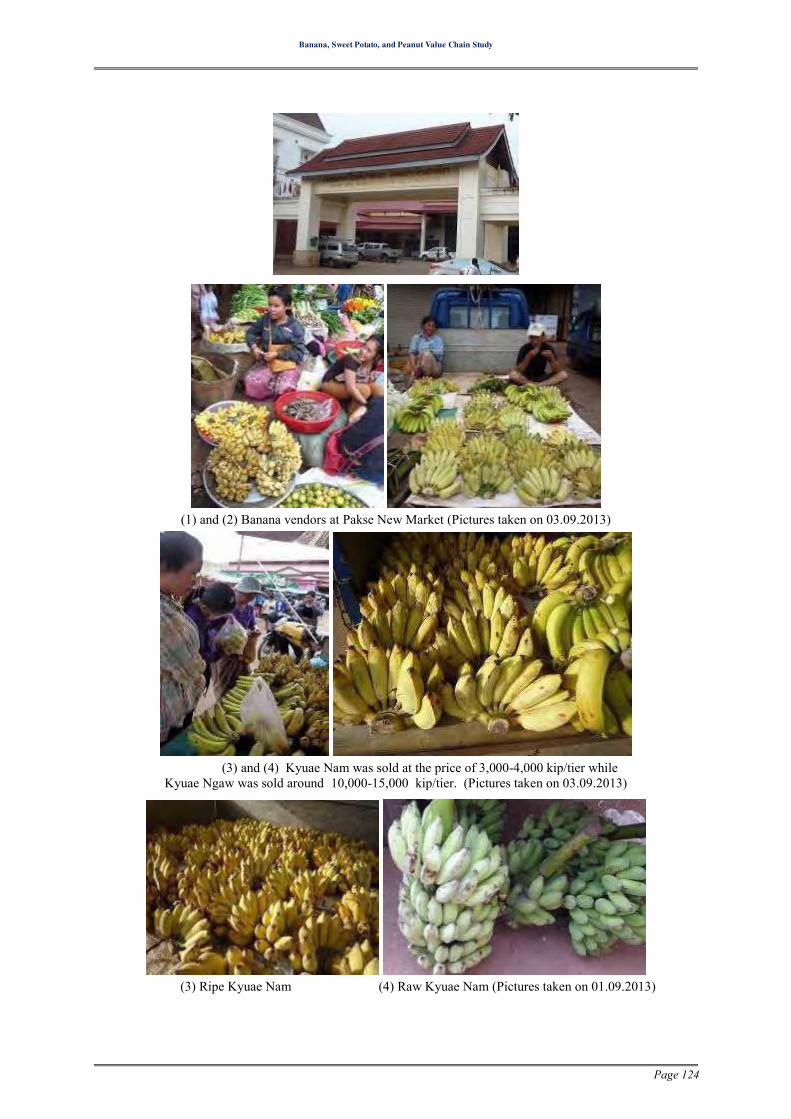

Table 33. Some main information of the selected districts in Savannakhet (2012) ................ 43

Banana, Sweet Potato, and Peanut Value Chain Study

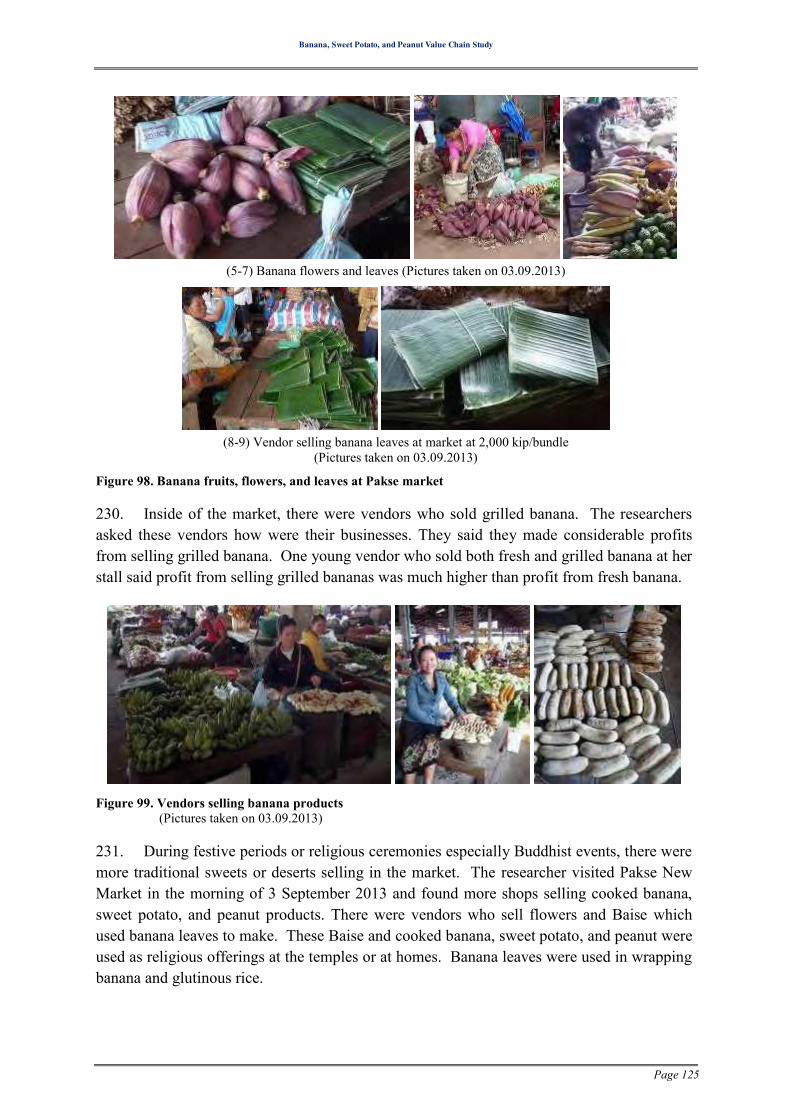

Page 9

Table 34. Import of bananas, including plantains, fresh or dried (HS 0803) into Thailand .... 45

Table 35. Average Price of Banana Imported into Thailand ................................................... 45

Table 36. Sweet potatoes, fresh or dried (HS 071420) ............................................................ 46

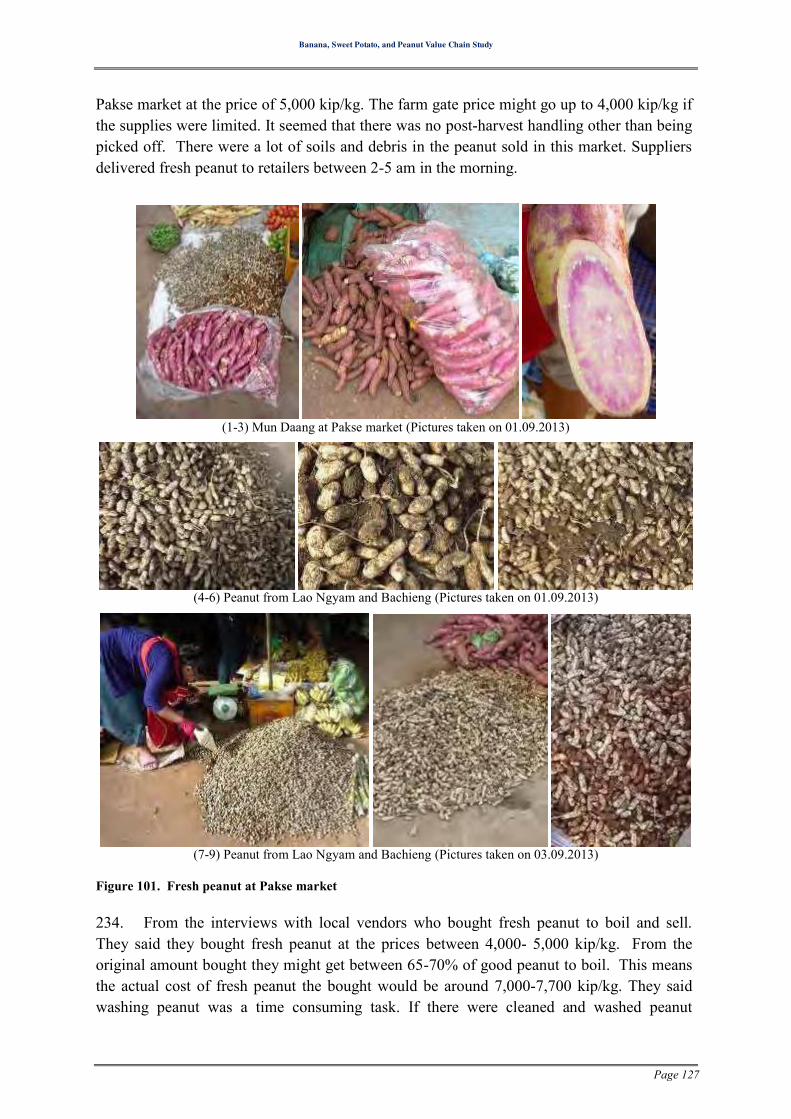

Table 37. Average price per kilogram of sweet potato imported into Thailand ...................... 47

Table 38. Peanut, not roasted or otherwise cooked, whether or not shelled or broken .......... 48

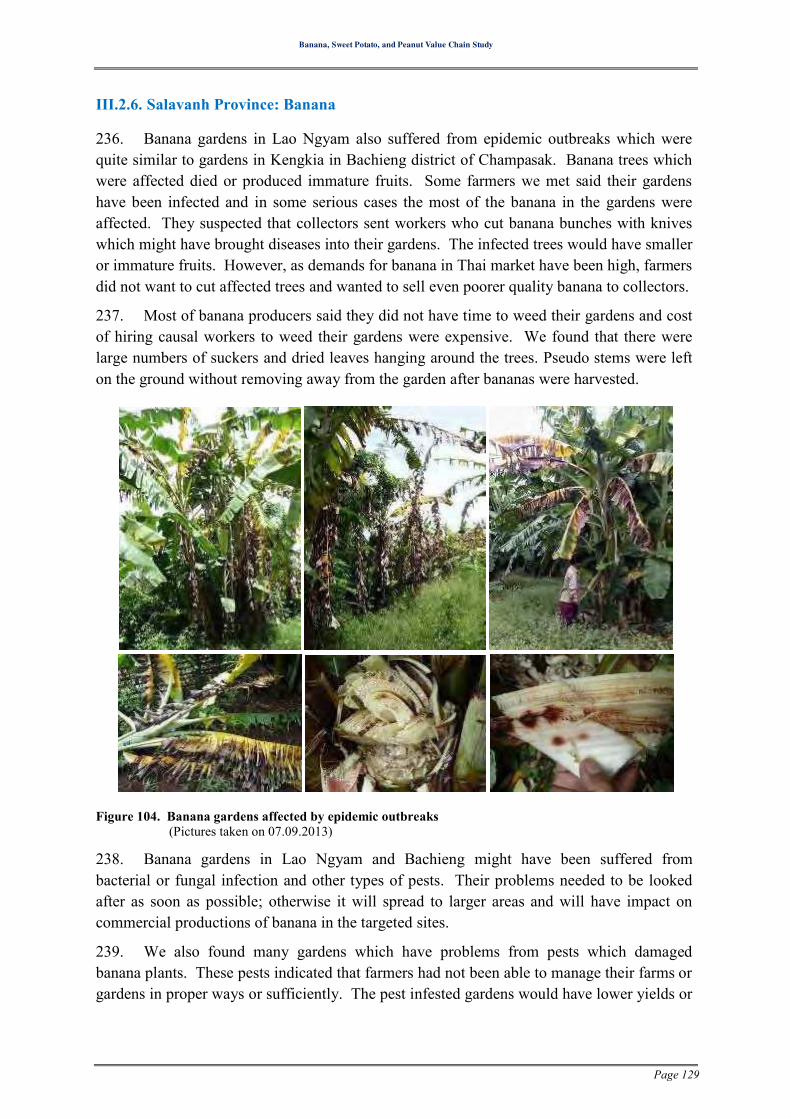

Table 39. Average price per kilogram of peanut imported into Thailand .............................. 49

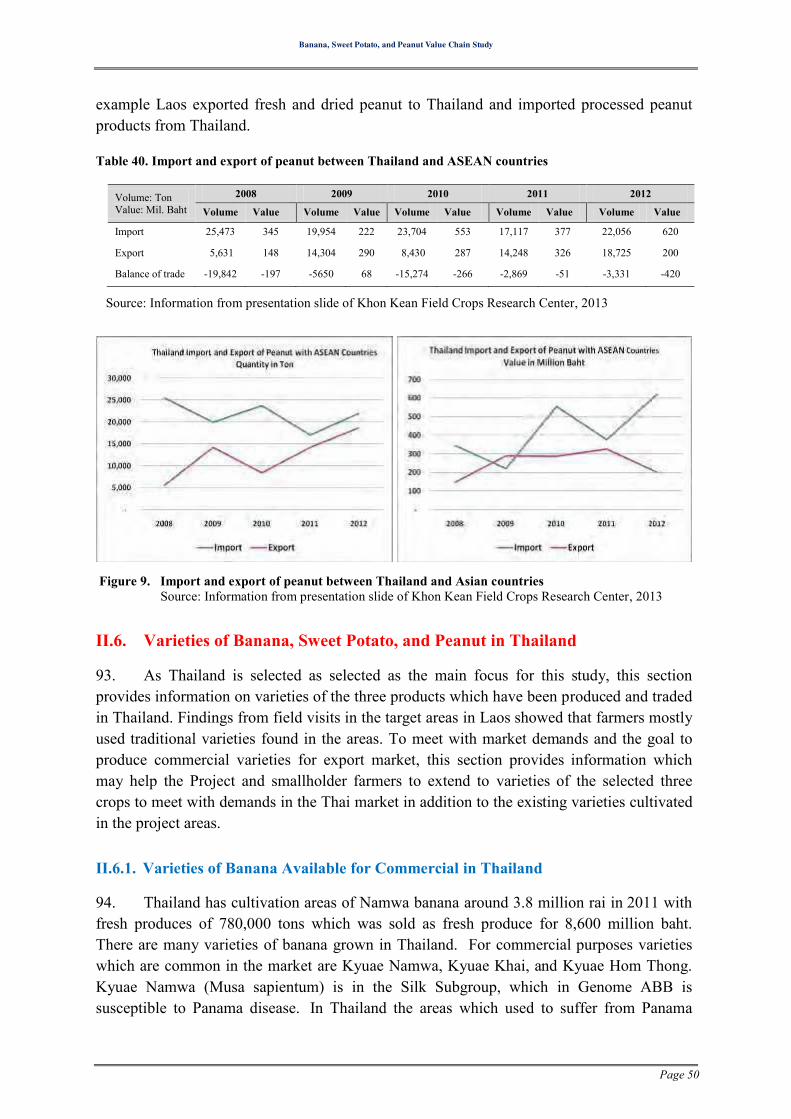

Table 40. Import and export of peanut between Thailand and ASEAN countries .................. 50

Table 41. Varieties of sweet potato by harvest time ............................................................... 54

Table 42. Studies on sweet potatoes by Mae Jo University in 2005....................................... 54

Table 43. Varieties of sweet potato and their characteristics .................................................. 55

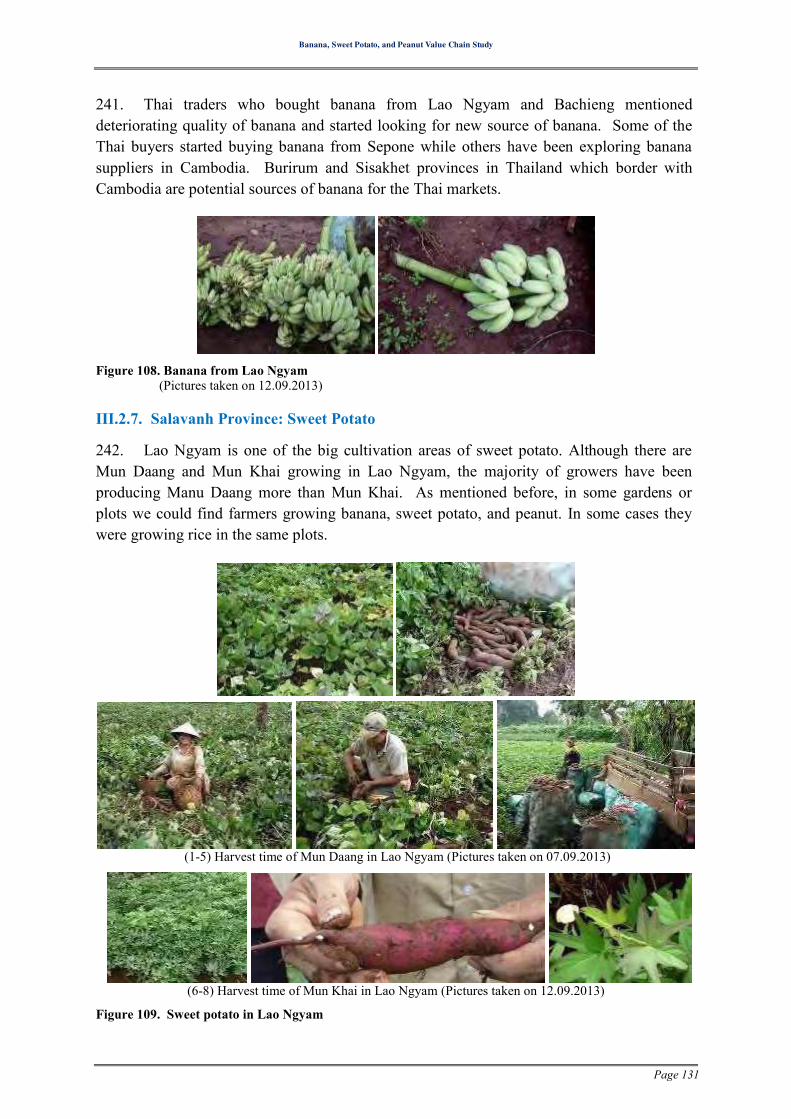

Table 44. Varieties of peanut in Thailand ............................................................................... 56

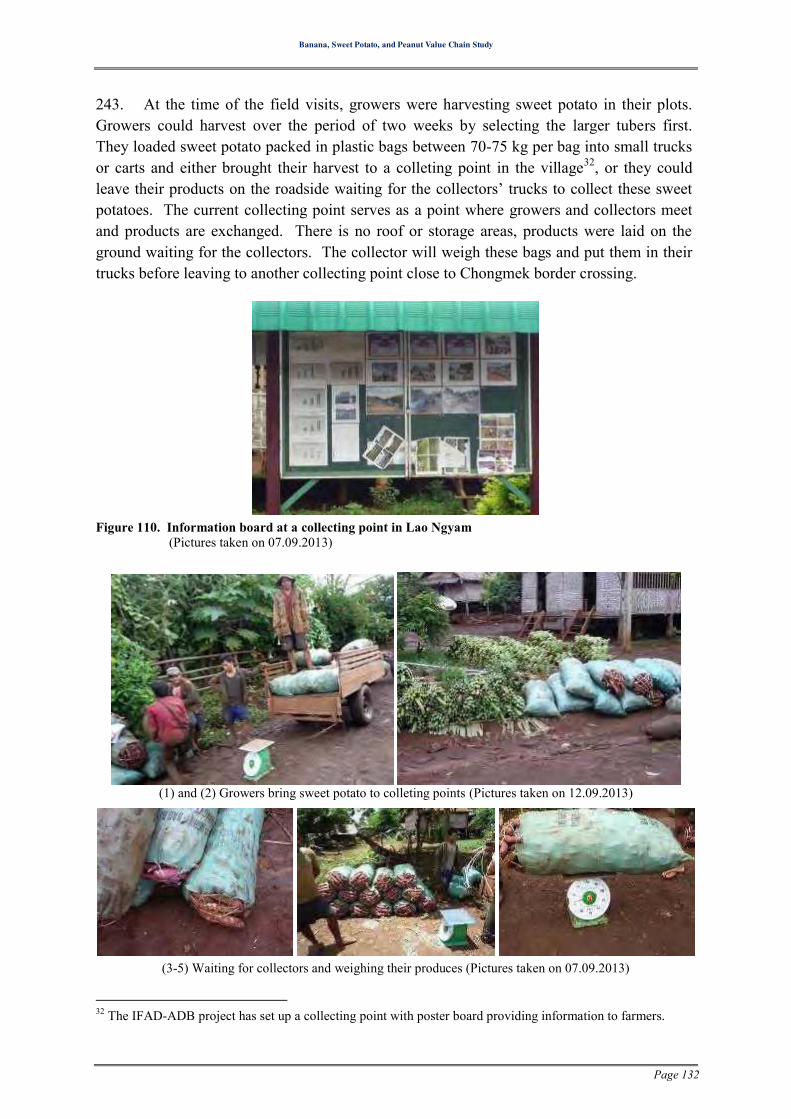

Table 45. Wholesale prices of banana by type and size at Talad Thai Market ....................... 63

Table 46. Average wholesale prices of banana at Talad Simummuang in 2013 .................... 65

Table 47. Average prices (baht/kg) of sweet potato at Simummuang Market in 2013 ........... 68

Table 48. Average prices of sweet potato at Talad Thai Market in 2013 ................................ 69

Table 49. Comparisons of prices of sweet potatoes in Laos and Thai markets ....................... 70

Table 50 Average daily wholesale prices of peanut at Simummuang Market in 2013 .......... 71

Table 51. Level of subsidy and economic indicators by size of dried banana producers ..... 113

Table 52. Comparison of economic indicators before and after using solar greenhouse dryer................................................................................................................................................ 113

Table 53. SWOT Analysis for value chain development ..................................................... 156

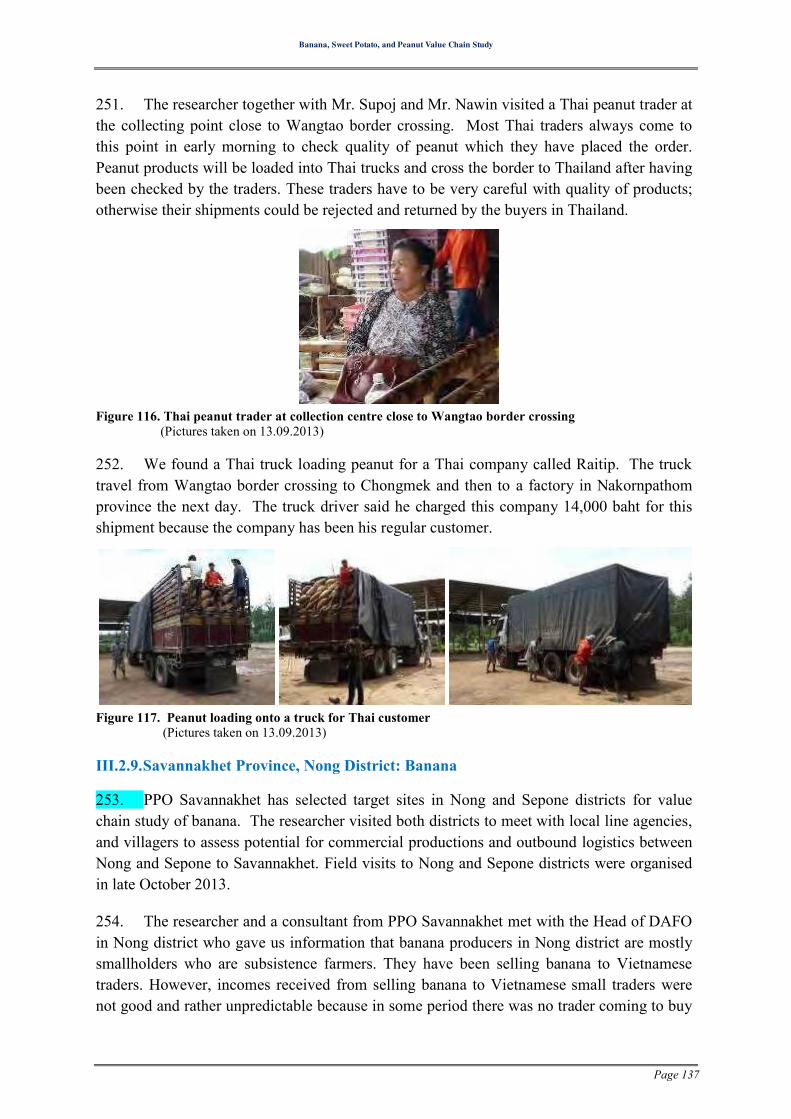

Table 54. Selling and buying prices of the three selected produces ..................................... 167

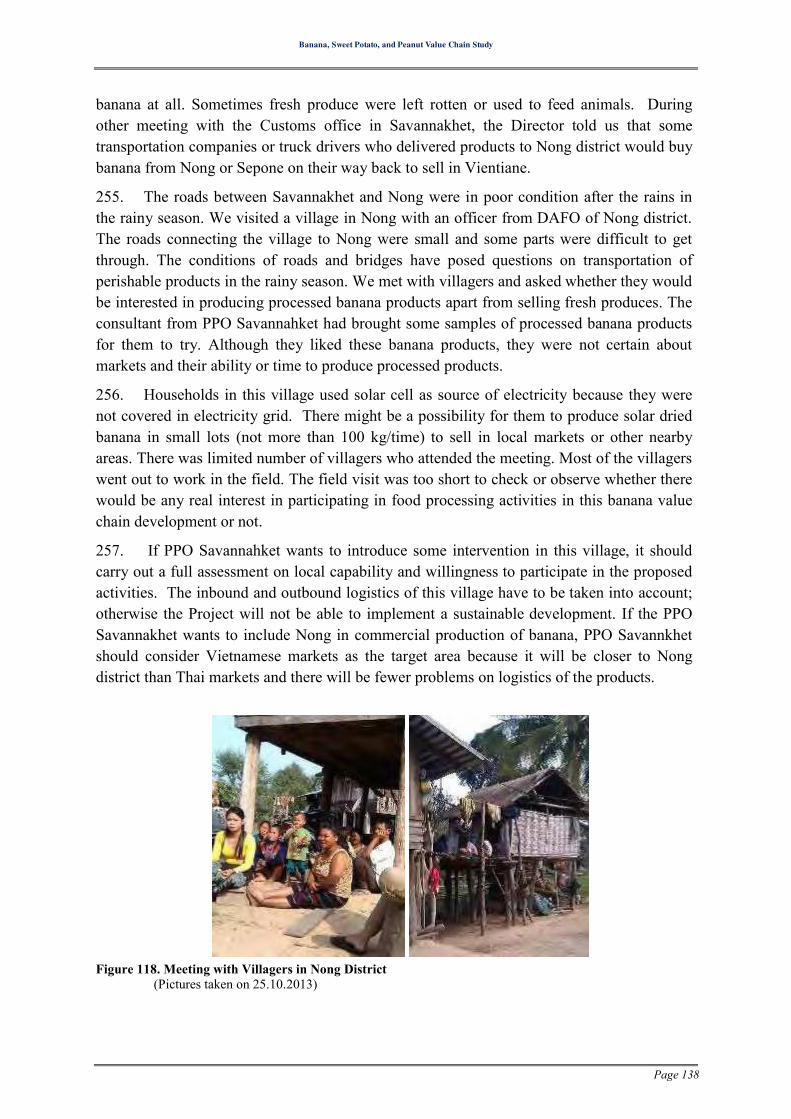

Table 55. Expenses in exporting agricultural products to Thailand (2013) .......................... 169

Table 56. Contract farming models and defining characteristics .......................................... 179

Table 57. Total cultivation areas in the targeted villages ..................................................... 182

Table 58. Proposals to move toward more value added banana products ............................ 188

Table 59. Proposals to move toward more value added sweet potato products .................... 192

Table 60. Proposals to move toward more value added sweet potato products .................. 196

Banana, Sweet Potato, and Peanut Value Chain Study

Page 10

LIST OF FIGURES Figure 1. Map of project areas in Bachieng district of Champasak ......................................... 34

Figure 2. Map of project areas in Lao Ngyam district of Salavanh Province .......................... 37

Figure 3. Project area in Nong district of Salavanh province .................................................. 41

Figure 4. Project area in Sepone district of Savannakhet province ......................................... 42

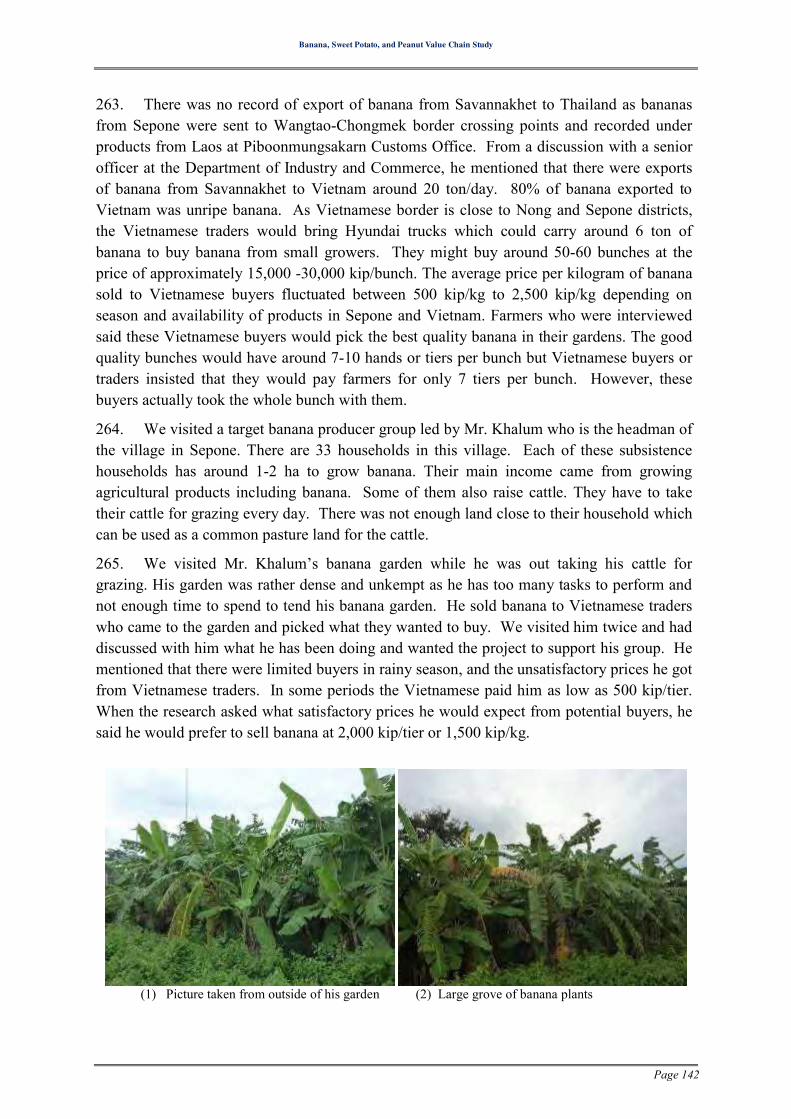

Figure 5. Project area in Xaiphouthong district of Savannakhet ............................................. 42

Figure 6. Average prices (baht/kg) of sweet potato imported into Thailand ........................... 47

Figure 7. Importation of peanut into Thailand by quantity ..................................................... 48

Figure 8. Average prices of peanut imported into Thailand ................................................... 49

Figure 9. Import and export of peanut between Thailand and Asian countries ..................... 50

Figure 10. Some varieties for commercial production of banana in Thailand........................ 53

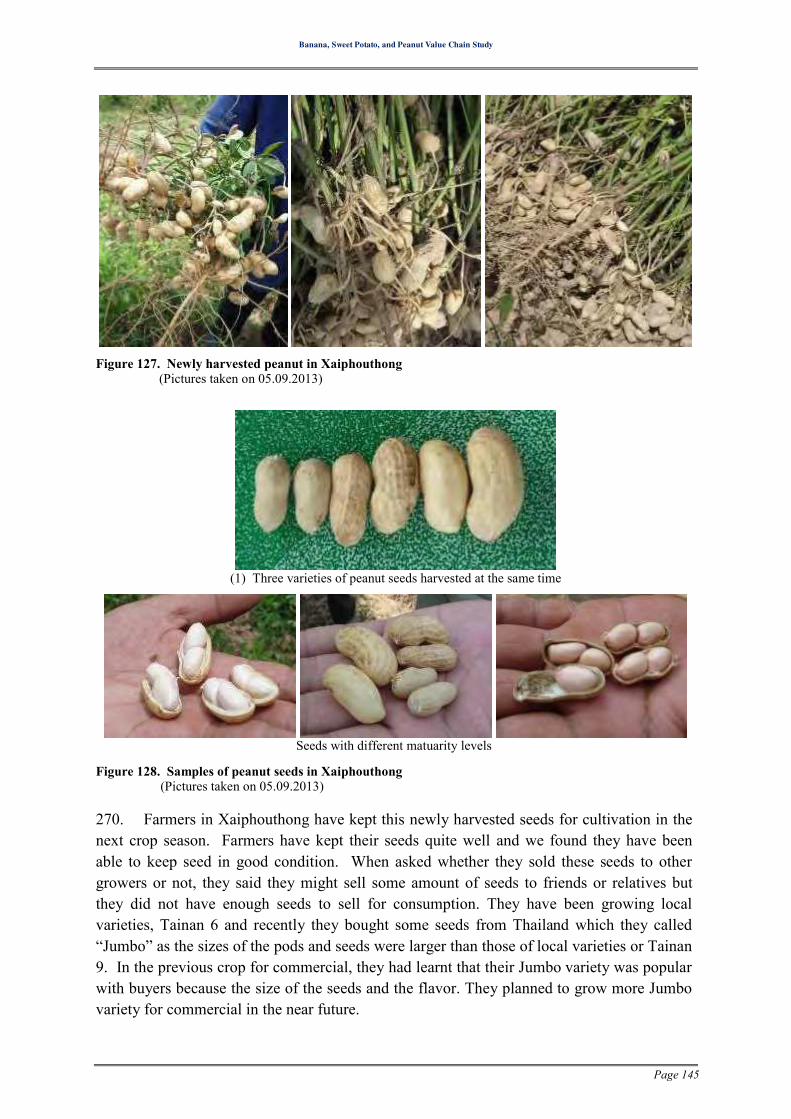

Figure 11. Samples of sweet potato available in Thai market ................................................. 55

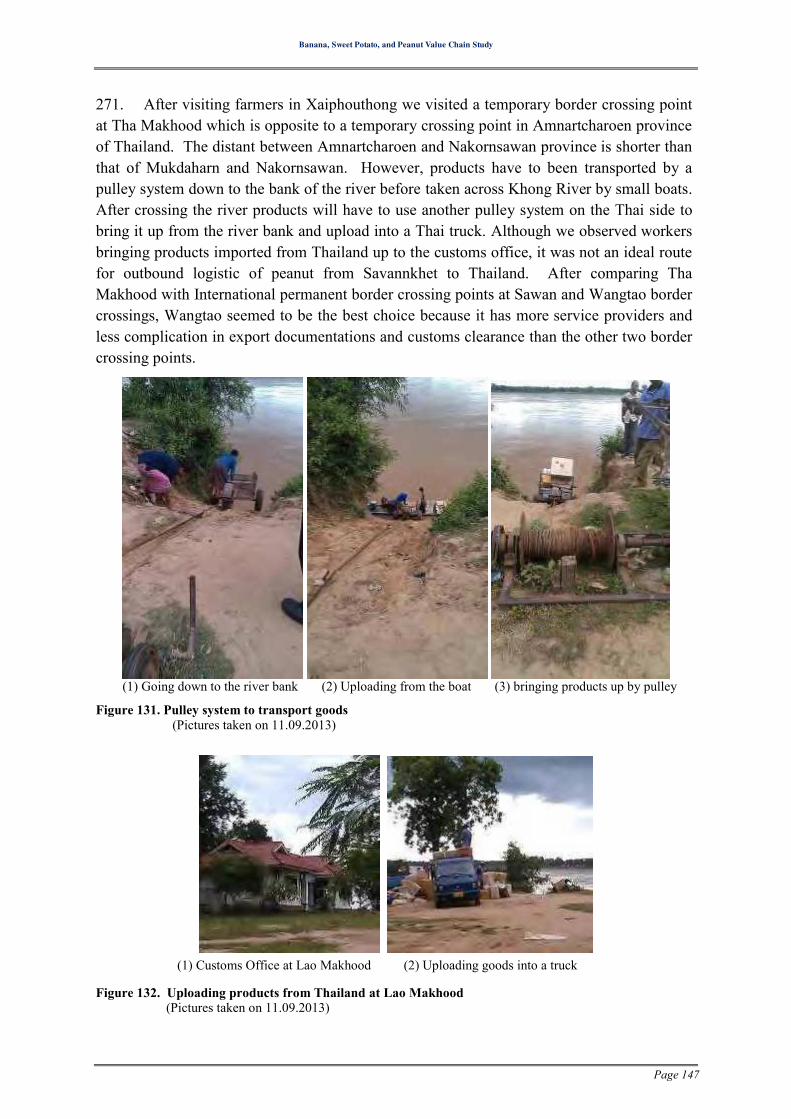

Figure 12. Peanut from Myanmar at Simummuang market .................................................... 56

Figure 13. Suggested peanut varieties in Thailand ................................................................. 57

Figure 14. Varieties for fresh peanut ...................................................................................... 58

Figure 15. Seeds of peanut varieties ........................................................................................ 58

Figure 16. Varieties for medium size seeds ............................................................................ 59

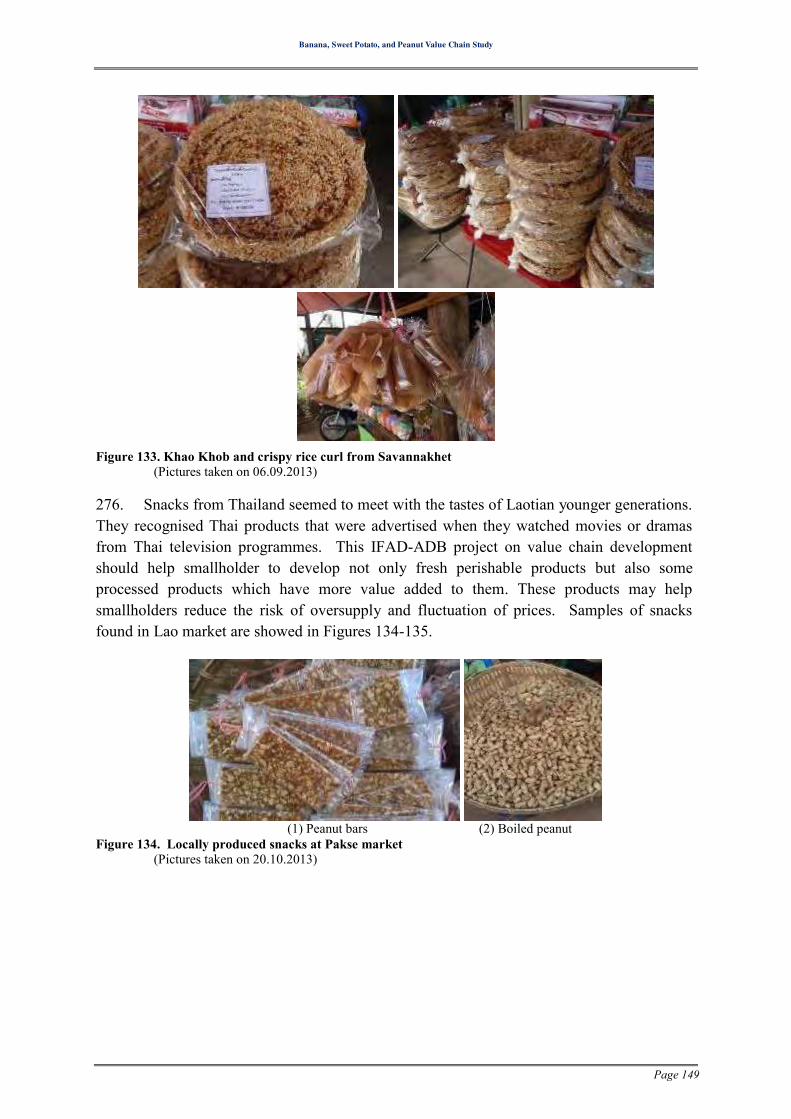

Figure 17. Details of selected peanut varieties ........................................................................ 60

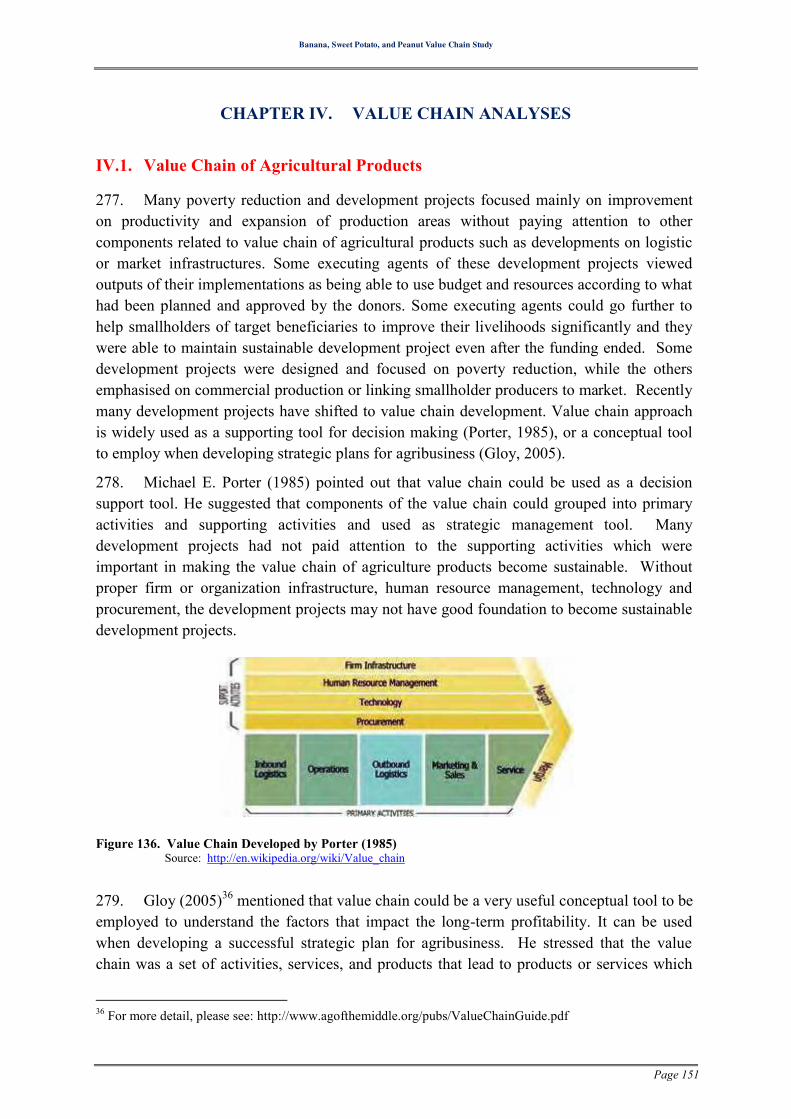

Figure 18. Samples of Peanut from Khon Kean Field Crops Research Centre ...................... 60

Figure 19. Logistics of fresh produces in Thailand: from farmers to consumers ................... 62

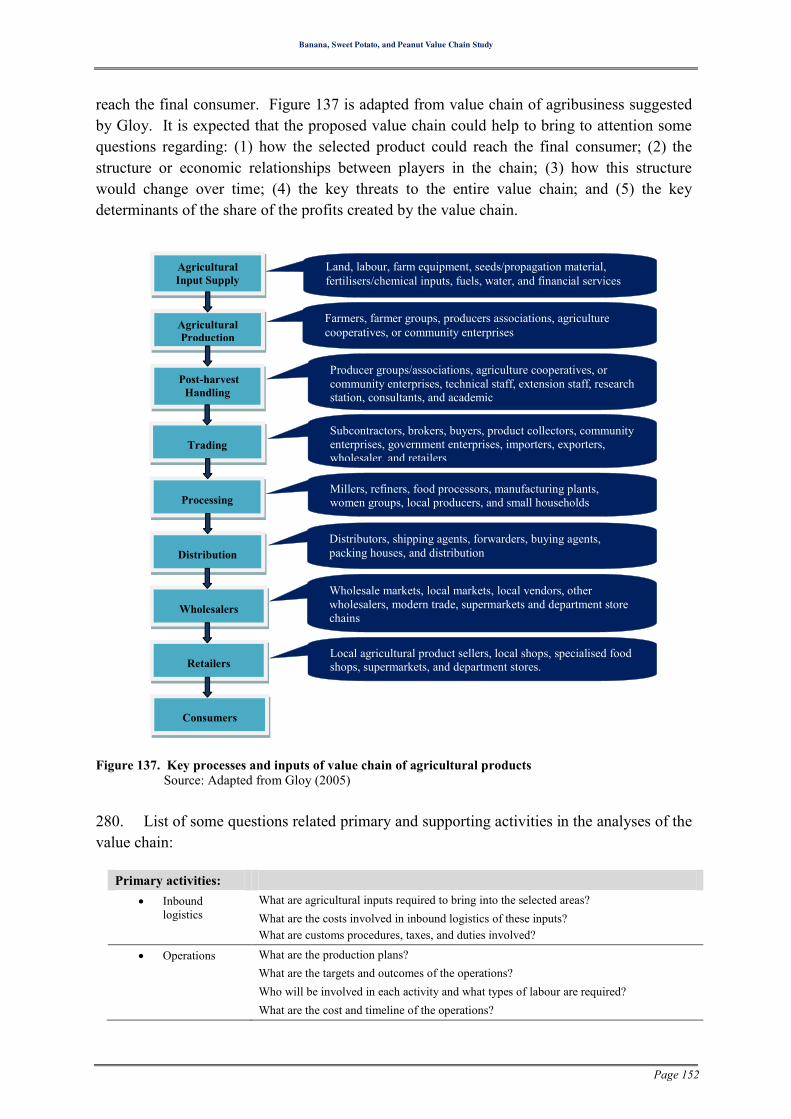

Figure 20. Talad Thai’s Wholesale prices of banana by type and size in 2013 ....................... 64

Figure 21. Average wholesale prices of banana in Thai market in 2013 ................................ 66

Figure 22. Banana at Talad Thai Wholesale Market, Pathumthani ........................................ 67

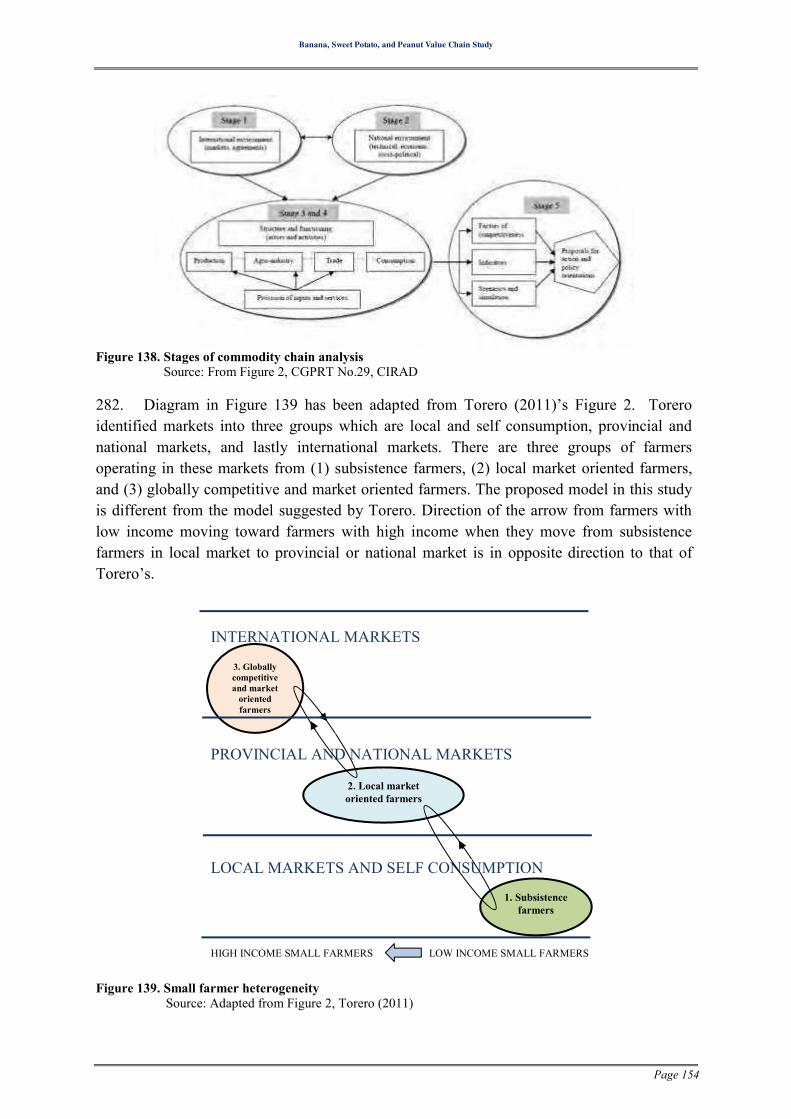

Figure 23. Sweet potato sold at Talad Thai Market ................................................................ 67

Figure 24. Average prices of sweet potato at Simummuang Market in 2013......................... 69

Figure 25. Average wholesale prices of raw peanut by variety in 2013 ................................. 71

Figure 26. Average wholesale prices of boiled peanut (baht/kg) by variety in 2013 ............. 72

Figure 27. Fresh peanut at Talad Thai market ........................................................................ 72

Figure 28. Peanut at Talad Thai Wholesale Market ................................................................ 73

Figure 29. Banana at Tops supermarkets in Bangkok ............................................................. 74

Figure 30. Various types of banana sold at Tops Supermarket .............................................. 74

Figure 31. Japanese sweet potato and sweet potato bread ...................................................... 75

Figure 32. Processed banana products .................................................................................... 75

Figure 33. Thai products available at trade fairs organised in Thailand ................................. 78

Banana, Sweet Potato, and Peanut Value Chain Study

Page 11

Figure 34. Processed banana products selling at Don Muang Airport ................................... 79

Figure 35. Locally produced Japanese sweet potato selling at the Royal Project shop .......... 79

Figure 36. Locally produced banana and sweet potato at Phichit market .............................. 80

Figure 37. Peanut and Khai banana at Nongbuachaiyawarn market ...................................... 81

Figure 38. Bananas at Rachawat Market in Bangkok .............................................................. 82

Figure 39. Sweet Potatoes at Rachawat Market in Bangkok ................................................... 82

Figure 40. Peanut at Rachawat Market in Bangkok ............................................................... 83

Figure 41. Shops selling banana at Charoensri Wholesale Market ......................................... 83

Figure 42. Prematurely cut and over ripped banana from Laos ............................................... 84

Figure 43. Fruits being broken or bruised during transportation ............................................. 84

Figure 44. Namwa banana from Laos at Charoensri Market ................................................... 85

Figure 45. Lower quality banana selling at discount prices.................................................... 85

Figure 46. Workers downloaded banana from the middle of the truck .................................. 86

Figure 47. Downloading Sepone banana onto customer’s van ................................................ 86

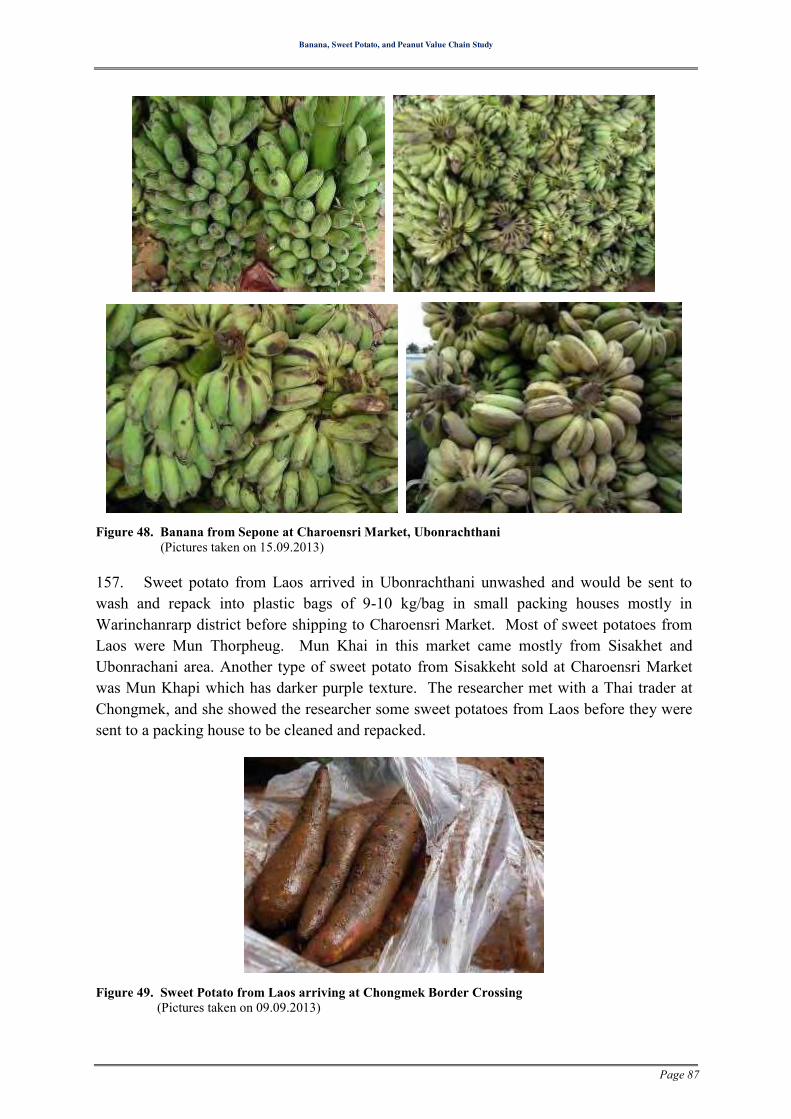

Figure 48. Banana from Sepone at Charoensri Market, Ubonrachthani ................................. 87

Figure 49. Sweet Potato from Laos arriving at Chongmek Border Crossing ......................... 87

Figure 50. Washed and repacked sweet potato arrived at Charoensri Market ........................ 88

Figure 51. Shops selling sweet potato at Charoensri market .................................................. 88

Figure 52. Shops at Charoensri Market selling fresh peanut .................................................. 89

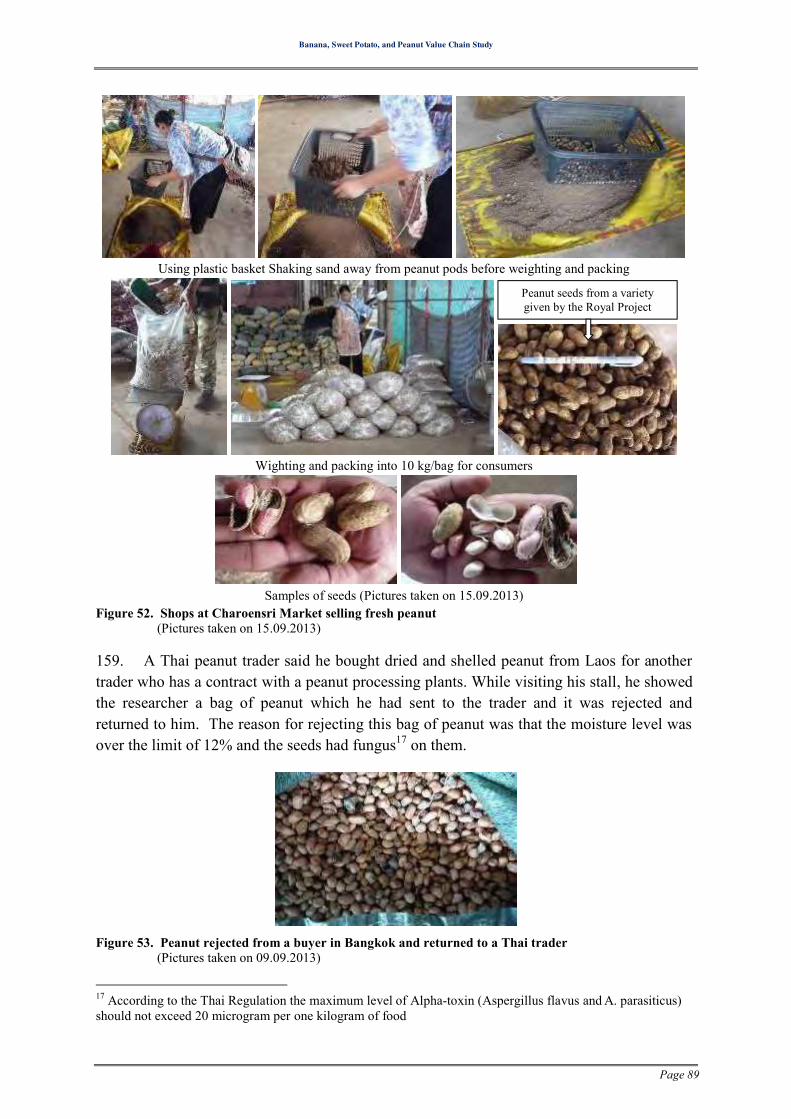

Figure 53. Peanut rejected from a buyer in Bangkok and returned to a Thai trader ............... 89

Figure 54. Kha Khome women group produces sand roasted peanut..................................... 90

Figure 55. Sand roasted peanut of Kha Khome Women Group .............................................. 91

Figure 56. Khangsapeu Market in Ubonrachthani .................................................................. 92

Figure 57. Snacks from banana and sweet potato at Khangsapeu .......................................... 92

Figure 58. Banana at Tesban 1 Market in Warinchumrarp ..................................................... 93

Figure 59. Sweet potato and banana at Warinchumrarp Market in Ubon .............................. 93

Figure 60. Peanut products from Raitip and repacked sizes ................................................... 95

Figure 61. Various retail peanut package sizes at Warinchumrarp Market ............................ 95

Figure 62. Fresh procures stalls at Kanthoraluk market .......................................................... 96

Figure 63. Products from Charoensri Market arriving at Kanthoraluk market ....................... 96

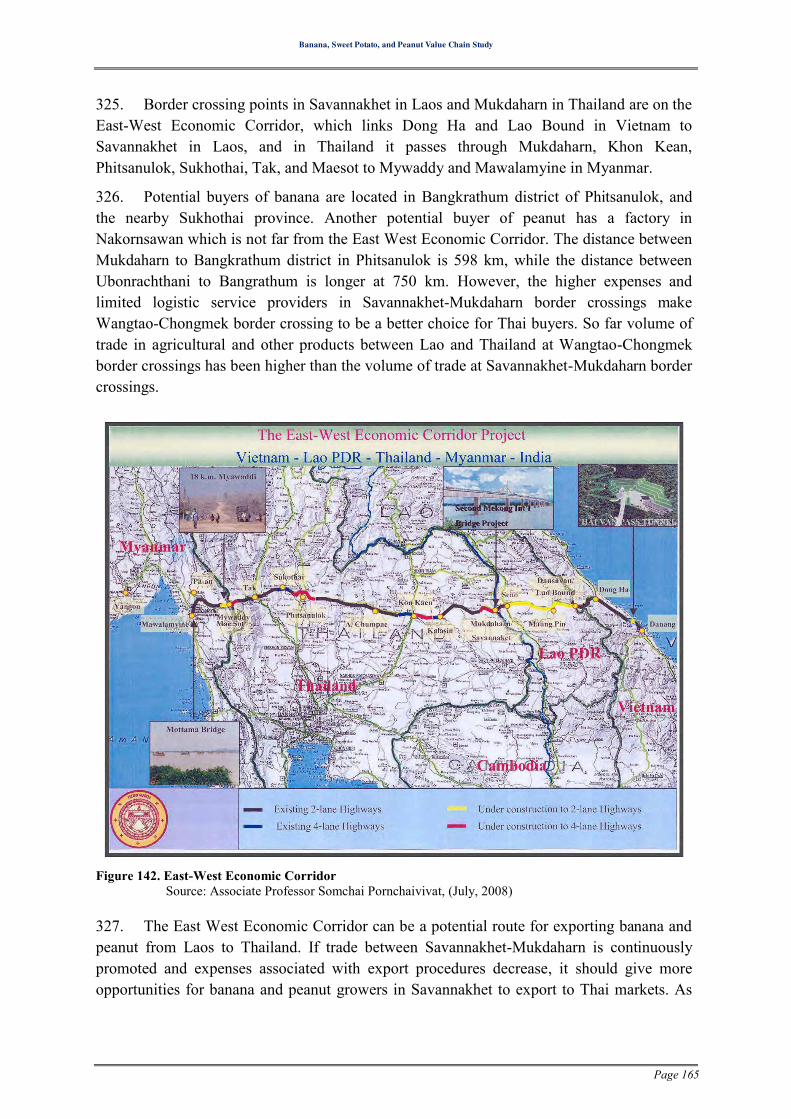

Figure 64. Locally grown banana at Kanthoraluk market ...................................................... 96

Figure 65. Kanthoraluk sweet potato ....................................................................................... 96

Figure 66. Locally produced peanut at Kanthoraluk market ................................................... 97

Figure 67. Peanut rejected and returned by buyers ................................................................. 97

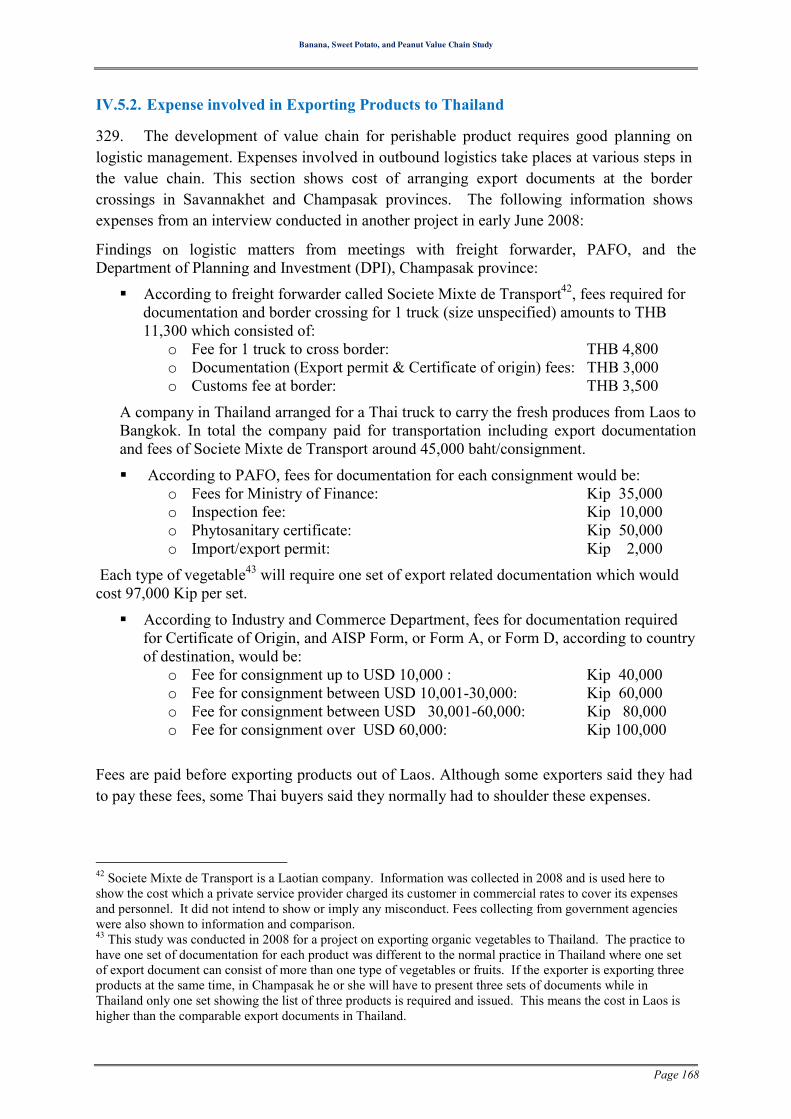

Figure 68. Preparation of plots for Japanese sweet potato...................................................... 98

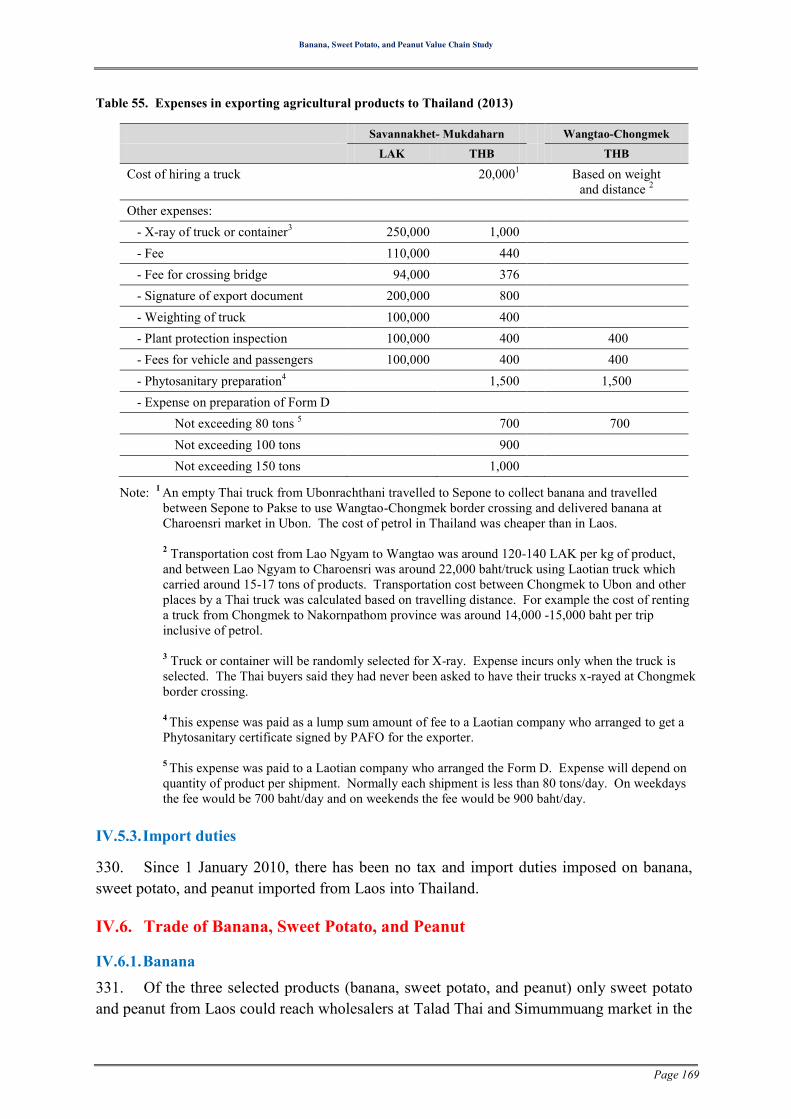

Banana, Sweet Potato, and Peanut Value Chain Study

Page 12

Figure 69. Japanese sweet potato at the Agricultural Knowledge Dissemination Group ....... 98

Figure 70. Bangkrathum Solar Dried Banana Women Group ................................................. 99

Figure 71. Members working for the group ............................................................................ 99

Figure 72. Mrs. Tuenta’s solar greenhouse dryer ................................................................. 101

Figure 73. Drying banana inside the solar greenhouse ......................................................... 101

Figure 74. Banana inside of the solar greenhouse dryer ....................................................... 102

Figure 75. Solar dried banana before packing ...................................................................... 102

Figure 76. Flattened dried banana are packed in .................................................................. 102

Figure 77. Leader of Community Learning Centre of Ban Klongkalon ................................ 103

Figure 78. Bananas bought from a supplier in Phitsanulok .................................................. 103

Figure 79. Solar greenhouse dryer and dried bananas .......................................................... 104

Figure 80. Processed dried banana products by Rai Wimolwanich....................................... 106

Figure 81. Banana products selling at shops at Wat Yai ....................................................... 108

Figure 82. Packchong 50 developed by Pakchong Research Station ................................... 109

Figure 83. Side-loading solar tunnel dryers at the Department of Physics ........................... 115

Figure 84. The Greenhouse dryers at the Department of Physics, Silpakorn University ...... 115

Figure 85. Books on Solar Crop Dryers by the Department of Physics ............................... 116

Figure 86. Cooked banana, sweet potato, and peanut in Vientiane ....................................... 117

Figure 87. Process products by street food vendors in Vientiane ......................................... 117

Figure 88. Processed banana and sweet potato at Phimphone supermarket .......................... 118

Figure 89. Banana at Khua Din Market ................................................................................ 119

Figure 90. Sweet potato at Khua Din Market ........................................................................ 119

Figure 91. Locally made processed products at Vientiane airport ......................................... 119

Figure 92. Thai products at a shop at Vientiane Airport ....................................................... 120

Figure 93. Meetings in Kengkia, Bachieng district .............................................................. 120

Figure 94. Banana and banana gardens in Bachieng areas ................................................... 120

Figure 95. Banana garden in Kangkia which has been infected ............................................ 121

Figure 96. Erionota thrax thrax Linn. Found in Kengkia ...................................................... 122

Figure 97. Peanut in Kengkia, Bachieng district .................................................................. 123

Figure 98. Banana fruits, flowers, and leaves at Pakse market .............................................. 125

Figure 99. Vendors selling banana products .......................................................................... 125

Figure 100. Cooked banana, sweet potato, and peanut at Pakse market ............................... 126

Figure 101. Fresh peanut at Pakse market ............................................................................ 127

Figure 102. Vendors of boiled peanut at Pakse market ........................................................ 128

Figure 103. Peanut products at Pakse market ....................................................................... 128

Banana, Sweet Potato, and Peanut Value Chain Study

Page 13

Figure 104. Banana gardens affected by epidemic outbreaks............................................... 129

Figure 105. Erionota thrax thrax Linn. Found in Lao Ngyam............................................... 130

Figure 106. Odoiporous logicollis Marshall found in Lao Ngyam banana gardens .............. 130

Figure 107. Pheaoseptoria leaf spot in Lao Ngyam .............................................................. 130

Figure 108. Banana from Lao Ngyam ................................................................................... 131

Figure 109. Sweet potato in Lao Ngyam .............................................................................. 131

Figure 110. Information board at a collecting point in Lao Ngyam ..................................... 132

Figure 111. Transfer of sweet potato from growers to collectors ......................................... 133

Figure 112. Cultivation plots of peanut and sweet potato in Lao Ngyam ............................. 134

Figure 113. Mr.Supoj and Mr. Nawin visiting Lao Ngyam ................................................... 134

Figure 114. Peanut growers in Lao Ngyam ........................................................................... 135

Figure 115. Milled peanut and sorting process at Lao Ngyam ............................................. 136

Figure 116. Thai peanut trader at collection centre close to Wangtao border crossing ......... 137

Figure 117. Peanut loading onto a truck for Thai customer ................................................. 137

Figure 118. Meeting with Villagers in Nong District ............................................................ 138

Figure 119. Banana gardens in Nong district......................................................................... 139

Figure 120. Roads connecting a selected village to Nong district ......................................... 139

Figure 121. Uploading of banana from Sepone for Thai market .......................................... 141

Figure 122. Another producer waiting for a trader to collect banana ................................... 141

Figure 123. Mr. Khalum’s banana garden ............................................................................. 143

Figure 124. Banana at Mr. Khalum’s house ......................................................................... 143

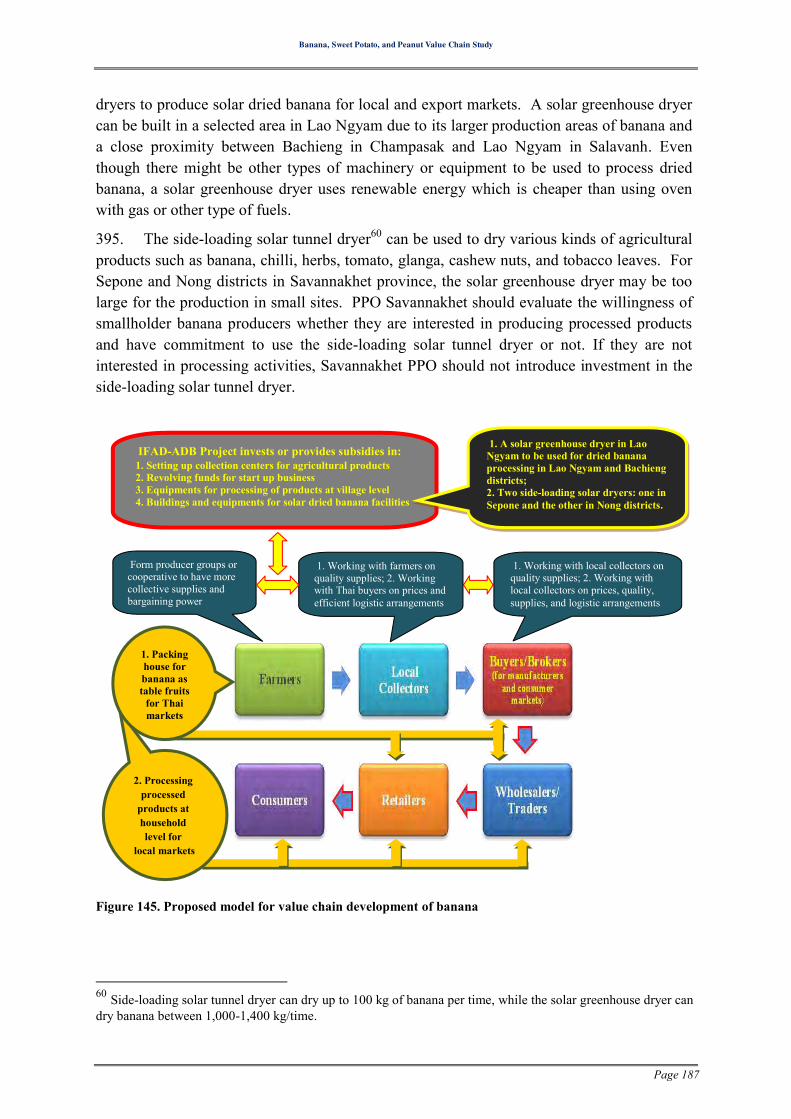

Figure 125. A meeting with banana producers in Sepone .................................................... 143

Figure 126. Peanut in Xiaphouthong district ......................................................................... 144

Figure 127. Newly harvested peanut in Xaiphouthong ........................................................ 145

Figure 128. Samples of peanut seeds in Xaiphouthong ........................................................ 145

Figure 129. Storage and drying space for peanut in Khanthachan, Xaiphouthong .............. 146

Figure 130. Peanut cultivation area in Xaiphouthong .......................................................... 146

Figure 131. Pulley system to transport goods ........................................................................ 147

Figure 132. Uploading products from Thailand at Lao Makhood ........................................ 147

Figure 133. Khao Khob and crispy rice curl from Savannakhet ............................................ 149

Figure 134. Locally produced snacks at Pakse market ......................................................... 149

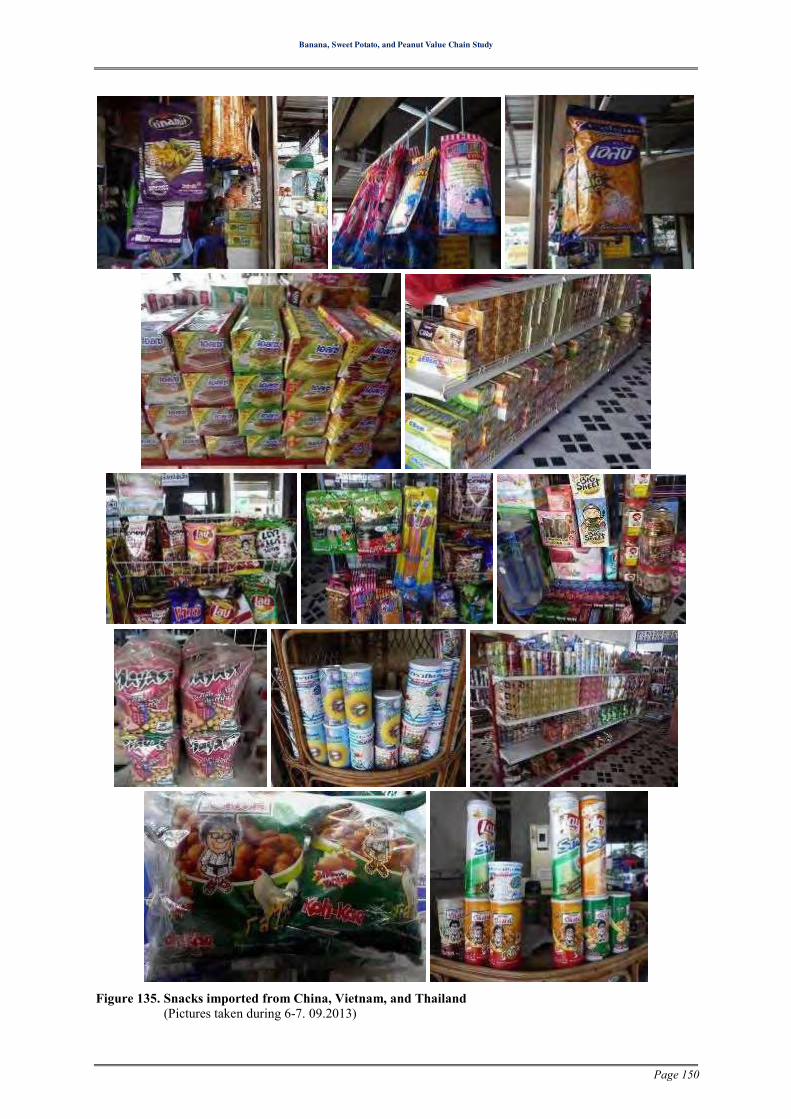

Figure 135. Snacks imported from China, Vietnam, and Thailand ....................................... 150

Figure 136. Value Chain Developed by Porter (1985) ......................................................... 151

Figure 137. Key processes and inputs of value chain of agricultural products .................... 152

Figure 138. Stages of commodity chain analysis................................................................... 154

Banana, Sweet Potato, and Peanut Value Chain Study

Page 14

Figure 139. Small farmer heterogeneity ................................................................................ 154

Figure 140. Main players in the flow of agricultural products ............................................. 163

Figure 141. Concerns of key players in the value chain ........................................................ 164

Figure 142. East-West Economic Corridor ............................................................................ 165

Figure 143. Border crossing points and locations of potential Thai buyers .......................... 166

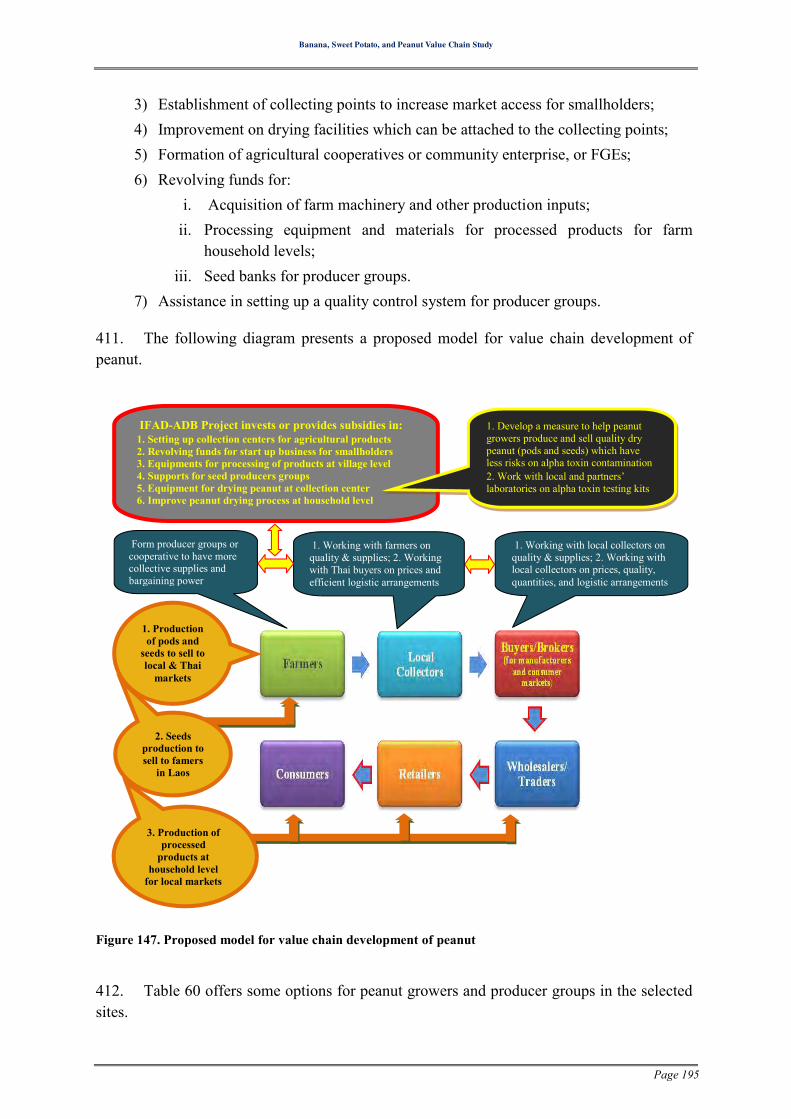

Figure 144. Number of loadings in transporting fresh produces to Thai market .................. 171

Figure 145. Proposed model for value chain development of banana ................................... 187

Figure 146. Proposed model for value chain development of sweet potato ......................... 191

Figure 147. Proposed model for value chain development of peanut.................................... 195

Banana, Sweet Potato, and Peanut Value Chain Study

Page 15

Banana, Sweet Potato, and Peanut Value Chain Development

CHAPTER I. SUMMARY DESCRIPTION

I.1. Subproject name & location

Subproject: Banana, Sweet Potato and Peanut Value Chain Development

Location: Bachieng district of Champasak province, Lao Ngyam District of Salavanh province, and Xaiphouthong and Sepone districts of Savannakhet province of Lao PDR.

I.2. Objectives of the Study

1. The objective of the smallholder banana, sweet potato and peanut value chain study is to present a clear, concise analysis of the smallholder banana, sweet potato and peanut sector. This analysis will be based on thorough research and will be the basis for presentation of a set of practical recommendations to government policy makers and industry players on development of joint strategies to improve the performance and profitability of the smallholder banana, sweet potato and peanut sector at all points on the value chain.

2. Banana, sweet potato and peanut are not new crops and farmers of Lao PDR grow them for the self-consumption and at some scale to supply local market to a limited extent. A special type of banana called as “Kyuae Nam” or “Kyuae Namwa” in Thai has been exported to Thailand and Vietnam for processing and consumer consumption. Salavanh and Champasak including Sepone, and Nong in Savannakhet provinces are major producers of banana. While the studies in Salavanh and Champasak provinces were carried out on the three products, the studies in Savannakhet were focused only on banana and peanut.

3. Smallholders who produce banana, sweet potato and peanut obtain a marginally profit from their crops. There are various factors identified by the Project such as:

o Lack of availability of quality varieties of banana, sweet potato and peanut; o Out-dated agronomic practices or poor quality production practices; o Lack of knowledge to improve quality of banana, sweet potato and peanut; o Poor technical back-up from extension services; o Lack of access to credit to improve production; o Lack of quality control measure; o Limited access to market information and market requirements; o Lack of processing facilities to create more value added products; o Lack of market linkages; o Dominant position of buyers in farm gate price setting; o Limited understanding of the roles of various players in a value chain flow model

and profit margins of various players in the value chain – such as collectors, brokers, buyers, wholesalers, processors, and retailers;

Banana, Sweet Potato, and Peanut Value Chain Study

Page 16

o Constraints in opportunities to: - improve competitiveness of Lao smallholders; - increase market share of Lao smallholder in both domestic and export

markets; - develop public-private partnerships between smallholder growers, private

sector, industry players and Government; - increase employment in the smallholder sector; - understand general market information on:

(i) consumer tastes and market opportunities; (ii) opportunities for niche markets for smallholders; and (iii) development of new more value added products.

I.3. Components of the Study

4. The components in the value chain study are:

Component 1: Value chain study of banana in Champasak, Salavanh, and Savannakhet provinces

Component 2: Value chain study of sweet potato in Champasak and Salavanh provinces

Component 3: Value chain study of peanut in Champasak, Salavanh, and Savannakhet provinces

5. Information from the three components should provide details on current data and information related to the three products in the selected areas and in Thailand which has been selected as the main market in the current analyses, value chain analysis for value chain development, and recommendations.

6. PPOs and local line government agencies selected districts and villages in this study in line with the IFAD-ADB Project and national policies. There are 31 selected villages in 14 Khum Bans in the three provinces.

I.4. Owner/ Investor/ Functional Managers

7. The project involves various stakeholders: Owner: District Agriculture and Forestry Offices (DAFOs) of the selected districts of the three provinces in this project. Other local agencies who may jointly be the owner of the project on processing and exportation parts are the Department of Industry and Commerce and (DIC) the Women Association. Investor for project and facilities for the operation: SNRMPEP and the Provincial Agriculture and Forestry Office (PAFO) of Champasak, Salavanh, and Savannakhet. Provincial PAFOs are the functional executing agency, the District DAFOs are the state management agency and the O&M responsibility is delegated to the cooperation of line agencies of the selected districts in the three provinces. Functional Manager: The business components and implementations of various stages of the operations in the value chain should involve relevant stakeholders such as

Banana, Sweet Potato, and Peanut Value Chain Study

Page 17

producer groups, agricultural product collectors, traders, brokers, business agents, processors, and service providers such as shipping companies, and forwarding agents, and buyers, if possible. Business operation: Business operation should be run by private partners or consortium of investor of the project who are interested to invest in the production, logistic, processing, and distribution of the fresh and processed products to potential markets. These private partners should work closely with producer groups in the selected areas with the aims of running on-going business operations with sufficient profits for long term and with fair treatments to all stakeholders in the value chain.

I.5. Project Management

8. Provincial PAFOs/PPOs of Champasak, Salavanh and Savannakhet provinces who are the investors have the responsibilities for implementations of the project.

9. The selected villages’ DAFOs: are the direct management agencies of the subproject under the overall management of the DAFOs. The coordinator of DAFOs and DIC will be responsible for daily inspection and management of all project activities. The DAFOs will also liaise with Departments/Management Companies/district and Kumb Ban authorities and producer groups responsible for post-handover management – on project design, pre-handover design inspections, and preparation of the O&M plan.

10. The components and activities in the value chain may exceed the scope of work of DAFO and PAFO. Some considerations should be placed on mutual involvements of the Department of Industry and Commerce (DIC) and also the Department of Transportation, and the Customs Department.

11. This value chain development should focus on the public private partnership as most of business activities should be carried out by participants in the private sector such as smallholder farmers, producer cooperatives, brokers, agricultural product collectors, traders and other service providers in the target areas. The government agencies should provide promotional, advisory, supporting, and facilitating roles rather than running business operations by themselves.

I.6. Subproject implementation period

12. The subproject will be started from January 2014 to the end of December, 2015. In which, the introduction of new production technologies, and the rehabilitation of the collecting points or collection centers, semi-processing plants take place in the first 10 months of the implementation period. It is estimated that the construction is started in March 2014 and completed by July, 2014; the supporting for revolving fund for the input arrangement and for demonstrations will start from January, 2014 to September, 2015. Implementation schedule of subproject is present in Annex IV. It is likely that this development project will be supported and funded beyond the end of 2015 by funding from another development project or loan.

Banana, Sweet Potato, and Peanut Value Chain Study

Page 18

I.7. O&M agency

13. The DAFOs of the selected districts will be responsible for operation and maintenance of the completed facilities. PAFOs of Champasak, Salavanh, and Savannakhet will be responsible for the operation and maintenance of the collecting points or collection centers and the regularly monitoring of processing facilities in their responsible areas.

14. Committee of beneficiary Khum Bans and the private sector will be responsible for the participatory supervisory board to take part in monitoring of the construction from design stage to completion, and O&M activities.

15. Roles of beneficiaries: Farmer groups in selected areas will participate and improve the quality and productivity of the chosen products—banana, sweet potato, and peanut for commercialisation production for local and regional markets; adopt new practices of production and post-harvest management development from using proper seeds and other propagation material introduced by the subprojects, soil preparation, compost making, and crop rotation etc.

16. Community enterprises setting up by the Project and the Supervisory Board will take responsibility to manage the revolving funds for various activities and also establish the linkages with the commercial banks for the financial activities for the commercialization of fresh banana, sweet potato, and peanut, processed products, and by-productions, and overall outputs with supports from designated line agencies in the selected areas. Community enterprises or cooperatives in the target areas and private partners will take part in the value addition and marketing of the agricultural products.

17. The private sector will work closely with farmer groups and collectors of agricultural products on trade and processing of their selected crops. Their investment which may be partially subsidised by the project should provide fair and mutual benefits to all stakeholders in the value chain. The private companies who become partners in the Project should support producer groups in market access and provide information on specification, market information, food safety measures, market linkages and the collaboration is based on sustainable development and for self-financed business operations in the long run.

I.8. Target Beneficiaries

18. Smallholder farmers of the selected agriculture products in targeted villages are expected to get direct benefits from the subproject; moreover, there are thousands of people in the neighbor villages who will be getting indirect benefits through transactions, exchanges, integration of production and processing activities. The subproject beneficiaries will earn more income from the value chain development and should hence be able to get good health and good education to improve their livelihoods.

19. It is expected that the value chain development will create more local employments especially for women in the food processing facilities in which this IFAD-ADB Development Project supports.

Banana, Sweet Potato, and Peanut Value Chain Study

Page 19

20. Local traders/brokers, agricultural product collectors, other services providers such as shipping agents, transportation service providers will also benefit from their participation in the value chain.

21. Apart from revolving funds for agricultural inputs, people in the target villages and neighbouring villages and districts can benefit from increasing demands for agricultural products as raw materials in the processing plants and obtain spillover effects on improvements in new technologies introduced by this Project in production, post-harvest and processing methods, storage management, logistic management, product processing, as well as access to market and information.

I.9. Report of the value chain study

22. Chapter I presents a summary description of the IFAD-ADB project. Chapter II provides background information on the three provinces in this projects as well as statistics which are related to the selected products in the three provinces and in Thailand. Chapter III presents information from the field surveys in Thailand and in the selected areas in Lao PDR at various points in the value chain. Findings from interviews with stakeholders and players in Lao PDR and in Thailand provide information on current states of the three products, and trade of these three products to Thailand which has been selected as the main market. Chapter IV provides details on value chain analysis of the three products which would lead to conclusion and recommendations in Chapter V.

23. This report covers the three selected products as they many similar characteristics and commons problems in the value chain development. It does not give details on cost of machinery or equipment. If the public and private sectors have agreed on what interventions or measures they want to employ in the Project, estimated cost of investment can be calculated and arranged accordingly.

24. The three PPOs should work collaborately in setting priorites and cluster of activites or implementations which could be shared in order that resources in the Project can be used efficiently.

Banana, Sweet Potato, and Peanut Value Chain Study

Page 20

CHAPTER II. BACKGROUND INFORMATION

II.1. Data Collection

25. The target areas for the IFAD-ADB Project for the value chain study of banana, sweet potato, and peanut are in Champasak, Salavanh, and Savannakhet provinces. Most of the statistical information of the three province used in this study came from secondary information and the Agricultural Statistics Year Books by the Department of Planning of the Ministry of Agriculture and Forestry, the Annual Statistics 2012 of the Lao Statistic Bureau of the Ministry of Planning and Investment, the Lao Census of Agriculture 2010/2011 Highlights of the Steering Committee for the Agricultural Census, the Agricultural Census Office, Department of Planning of the Ministry of Agriculture and Forestry. Information on selected districts comes from the Provincial Project Offices in the three selected provinces. It should be noted that by using various sources of secondary information there might be some discrepancies of information due to different methods of data collection and criteria used in these data analyses.

26. Information from the field studies in the three selected provinces, Vientiane in Lao PDR, and information in Thailand came from the field surveys carried out between the middle of August 2013 to the first half of November 2013 by the researcher. Field information was collected through interviews, and meetings with target groups. Other supporting information comes from public media such as newspapers, pressed released by relevant agencies, information from internet and media produced by public and private agencies relating to banana, sweet potato and peanut.

II.2. Demographic Information

According to the Lao Census of Agriculture 2010/11Highlights (May 2012), the numbers of farm households by farm/non farm, village type and provice, 2010/2011 in the three provinces in this IFAD-ABD Project shown in Table 1 indicate that the majority of housholds in the selected areas of Champasak, Salavanh, and Savannakhet are still in rual areas and are in farm sector.

Table 1.Number of households by village type and province, 2010/11

Province All households

Urban households Rural households with road Rural households without road

Total Total Farm Non-farm Total Farm Non-farm Champasak 105.7 30.1 57.2 46.1 11.2 18.4 15.3 3.1 Salavanh 55.4 5.1 48.8 45.8 3.0 1.6 1.5 0.1 Savannakhet 137.3 34.8 93.0 81.5 11.5 9.5 9.0 0.6

Whole country 1,021.4 313.9 622.3 556.3 66.0 85.2 78.8 6.5

Remark: Unit in thousand of households Source: Lao Census of Agriculture 2010/2011 Highlights, May 2012

27. Farm households have increased from 789,000 during the 1989/99 Census to 1,021,400 households in the 2010/11 Census. Information on farm poupulation of the three

Banana, Sweet Potato, and Peanut Value Chain Study

Page 21

provinces by sex and age is shown in Table 2 below. If we consider farm workforce of the popolation as those of the age of 15 years old and over, Champasak, Salavanh, and Savannakhet will have the farm population of 286,900, 186,3000, and 444,300 persons, respectively.

Table 2. Farm population by sex and age (2010/2011)

Province Total (‘000)

Age group (in ‘000 persons) 0-9

years 10-14 years

15-24 years

25-34 years

35-44 years

45-54 years

55-64 years

65 years & over

Champasak 425.1 83.0 55.3 92.4 59.2 50.7 41.0 24.9 18.7 Male 210.9 42.6 27.3 45.6 28.9 24.7 20.3 12.6 9.0

Female 214.3 40.4 28.0 46.8 30.3 26.0 20.8 12.3 9.7 Salavanh 298.5 72.4 39.8 59.4 42.0 31.7 26.3 15.8 11.2

Male 146.9 36.1 20.8 28.6 20.0 14.8 13.1 8.1 5.3 Female 151.6 26.3 18.9 30.7 22.0 16.9 13.3 7.6 5.9

Savannakhet 651.7 121.8 85.6 147.2 98.8 80.9 60.1 33.9 23.5 Male 324.3 60.5 45.1 72.7 47.2 39.6 30.1 17.0 12.2

Female 327.4 61.2 40.6 74.5 51.5 41.3 30.0 16.8 11.4 Whole

country 4,501.0 931.5 579.7 978.9 672.4 517.6 408.7 235.9 176.4

Male 2,262.4 473.0 298.7 484.9 331.5 257.3 204.4 123.9 88.6 Female 2,238.6 458.5 281.0 494.0 340.8 260.2 204.3 112.0 87.7

Source: Lao Census of Agriculture 2010/11 Highlights, May 2012

28. The number of households in rural area by farm1 and non-farm, and land type is shown in Table 3 below and information on farmhouseholds’ characteristic is in Table 4. Numbers of farm households in the lowland in champasak, Salavanh, and Savanakhet as percentages of total households in that province are 56.4%, 60.1%, and 63.2%, respectively. Numbers of farm households in the upland in champasak, Salavanh, and Savanakhet as percentages of total households in that province are 0.9%, 7.0%, and 12.2%, respectively. Numbers of farm households in the plateau in champasak, Salavanh, and Savanakhet as percentages of total households in that province are 14.1%, 23.3%, and 3.6%, respectively. The futile lowland and plauteau areas are the major areas for banana, and peanut productions.

29. Fragmentation of land by province in 2010/2011 shows that the national average size of land holding is 2.4 ha and average number of parcels per land holding is 2.7 parcels. Among the three provinces, Savannakhet has the largest average size of land holdings at 3.1 ha, while Champasak has the average size of farm holding at 2.1 ha which is lower than that of the national average size of land holding.

1 According to the definition of the 2010/11 census, “farm household” is a household that operated 0.02 ha or more of agricultural land in the 2010 wet season or 2010/11 dry season; or was raising 2 or more cattle or buffaloes, 5 or more pigs or goats, or 20 or more poultry at the time of the census; or was raising any other livestock at the time of the census; or had aquaculture facilities at the time of the census.

Banana, Sweet Potato, and Peanut Value Chain Study

Page 22

Table 3 Number of households by farm/non-farm and land type, 2010/11

Province All households

Lowland Upland Plateau

Total Farm Non-farm Total Farm Non-

farm Total Farm Non-farm

Champasak 105.7 87.5 59.6 27.9 0.9 0.9 0.1 17.2 14.9 2.3 % of all HHs in Champasak 82.8 56.4 26.4 0.9 0.9 0.1 16.3 14.1 2.2 Salavanh 55.4 37.7 33.3 4.4 4.0 3.9 0.2 13.6 12.9 0.7

% of all HHs in Salavanh 68.1 60.1 7.9 7.2 7.0 0.4 24.5 23.3 1.3 Savannakhet 137.3 112.8 86.8 26.0 18.6 16.8 1.8 5.9 5.0 0.9

% of all HHs in Savannakhet 82.2 63.2 18.9 13.5 12.2 1.3 4.3 3.6 0.7 Whole

country 1,021.4 583.8 385.9 197.9 223.4 209.4 14.1 214.2 187.6 26.6

% of all HHs 100% 57.2 37.8 19.4 21.9 20.5 1.3 21.0 18.4 2.6 Remark: Unit in thousand of households Source: Lao Census of Agriculture 2010/2011 Highlights, May 2012

Table 4. Characteristics of land holdings (2010/11)

Province No. of farm

households

No. of land holdings2

Area of holdings

(ha)

Average size of land

holding (ha)

No. of parcels (‘000)

Average no. of parcel per land holding

Average parcel size

(ha)

Champasak 75,400 74,200 158,800 2.1 156.9 2.1 1.01

Salavanh 50,100 50,000 130,600 2.6 143.5 2.9 0.91

Savannakhet 108,600 108,400 332,200 3.1 260.4 2.4 1.28

Whole country 782,800 776,700 1,870,200 2.4 2,089.1 2.7 0.90

Source: Lao Census of Agriculture 2010/2011 Highlights, May 2012

30. Statistics of the Lao Census survey 2010/2011 show that the majority of land holding are owned land and low percentage are rented land. 97% of land holdings in Savannahket, 96.6% in Salavanh, and 95.3% in Champasak are owned land. The total size of owned land are 322,000 ha in Savannakhet, 125,400 ha in Salavanh, and 148,400 ha in Champasak, respectivsly. Information from the census also indicates that the majority of farm population work on their own land.

31. In 2010/2011 census, the average size of farm household in Champasak, Salavanh, and Savannakhet are between 5-6 persons per household which are in line with the national average household size of 5.75 persons. Members of each household can be family members or other persons such as hired or outside labour who live in the household.

32. Although the national average size of farm households is 5.75 persons and the three target provinces in this project have average farm household size between 5-6 persons, there is increasingly shortage of farm labour as the younger generation or age groups are either attending formal education or moving out of the farm sector to service sector. The use of hired or outside farm labour has increased over the year.

2 A land holding consists of one or more parcels. A land parcel is any piece of land entirely surrounded by land, water, forest, road, etc. not forming a part of that holding.

Banana, Sweet Potato, and Peanut Value Chain Study

Page 23

Table 5. Number of farm households by household size (2010/11)

Province No. of farm households

Household size Average household

size 1 person 2-3 persons 4-5 persons 6-9 persons 10 or more

persons Champasak 75,400 500 10,100 29,100 31,900 3,700 5.64

Salavanh 50,100 300 7,100 17,100 21,000 4,600 5.96

Savannakhet 108,600 900 13,300 36,200 48,800 9,300 6.00

Whole country 782,800 3,400 108,700 294.300 323,200 53,200 5.75

Source: Lao Census of Agriculture 2010/11 Highlights, May 2012

II.3. Linkage to existing infrastructure in the selected provinces

II.3.1. Summary 33. The subproject area is located in Champasak, Salavanh, and Savannakhet provinces. Briefly the infrastructures of selected areas in this project are:

There are main roads linking the target villages to the capital of the province. These target villages are connected to the main road by gravel roads. Accessibility to the target villages in the rainy season are difficult in some areas due to the condition of the roads linking between the villages and the main roads.

All villages visited in the field studies except one villages in Nong district have electricity lines and water supply for consumption

Some cultivation areas have existing irrigation systems. However, most of the areas in this project rely on rain for water supply which makes it difficult to grow crops in dry season. The main emphases in some areas are to grow rice for consumption and selling and then grow sweet potato, and peanut after rice is harvested. Incomes from these agricultural products rely heavily on weather conditions in each year. If there is a dry spell, farmers may not have sufficient products available to sell to agricultural collectors.

All villages have primary schools and can get access to district hospital or provincial hospital by road.

There are local daily wet markets in all districts in this project where farmers or traders can sell their products to end consumers.

Formal agricultural product trading market in district level has not been established. Most of the trading activities take place at the village level by small or individual buyers visiting villages to buy occasionally, or farmers sell products to their regular agricultural product collectors.

Villagers have limited access to financial services or up-to-date market prices information.

II.3.2. Production of Temporary and Permanent Crops

34. Farmers in these target villages have experiences in growing banana, sweet potato, and peanut, and other agricultural production especially rice production either in wet and dry

Banana, Sweet Potato, and Peanut Value Chain Study

Page 24

seasons. However, the traditional cultivation techniques used, limited quality seeds or saplings, and poor post-harvest handling resulted in low productivities and quality.

35. The definition of permanent crops and temporary crops in the Lao Census of Agriculture 2010/11 Highlights are as follows:

“Permanent crops are with a greater than one year growing cycle…… Many permanent crops are not grown in a compact plantation bust scattered around the holdings. Scattered permanent crops or crops not planted in a systematic manner or sufficiently densely to permit the area to be measured are not included in crop area figures but are included in the number of grower figures.” (p.19, Lao Census of Agriculture 2010/2011 Highlights)

“Temporary crops are crops with less than one year growing cycle. Land used for temporary crops refers to land on which temporary crops were grown during the reference year, whereas area of temporary crops planted refers to the total area of all crops planted during the reference year. The area of temporary crops planted may be greater than the areas under temporary crops because of double copping….. Temporary crops that are not planted in a systematic manner or sufficiently densely to permit the area to be measured are not included in crop area figures but are included in the number of grower figures.” (p.19, Lao Census of Agriculture 2010/2011 Highlights)

Banana, sweet potato, and peanut have been widely grown in many areas in Lao PDR. Information from Table 6 shows that in the census of 2010/2011 the total areas of banana cultivation has decressed around 30.6% from the areas surveyed in 1989/1999 as weel as the number of banana growers reduced from 109,000 persons in 1989/1999 to 70,400 persons in the census in 2010/2011. Total area of peanut and banana production can be found in Table 7. Information from these Tables indicates that among the three target provinces Salavanh has the largest areas and number of growers of peanut while Savannakhet has the largest number of banana growers. The total area that planted banana in Savannakhet is close to the size of that of Salavanh while Champasak has the smallest size of area planted banana.

36. For temporary crops, sweet potato shows increasion in area of cultivation and decresion in the number of growers. Peanut cultivation area and number of growers were both increased during the two periods of the census. One of the explanations was that many farmers had changed from traditional crops to other cash crops such as tapioca, maize, sugar cane, or permanent crops such as rubber which were introduced in the period between the two censuses.

Table 6 Total areas of cultivation and number of growers of selected crops

Area1 (ha) Number of growers 1998/1999 2010/2011 % change 1998/1999 2010/2011 % change Permanent crop - Banana 13,400 9,300 -30.6% 109,000 70,400 -35.4% Temporary crops - Sweet potato 200 700 +250.0% 19,600 10,200 -48.0% - Peanut 4,900 8,300 +69.4% 21,400 28,500 +33.2%

Remark: 1 Area exclude crops planted in plots less than 100 sq.m. Source: Lao Census of Agriculture 2010/11 Highlights, May 2012

Banana, Sweet Potato, and Peanut Value Chain Study

Page 25

37. It should be noted that the figures appear in the planted area of Table 7 below do not include crops that were planted in the areas that were difficult to be measured. Findings from the field visits in this current study showed that many farmers planted banana, rice, peanut, and sweet potato in the same plots of land or planted them alternately. These patterns of cultivation might result in their production were not included in the results of the census. Therefore the figures in the latest census may be different from statistics from other sources of information.

Table 7. Production areas and numbers of growers of peanut and banana (2010/11)

Province Total area

for temporary

crops (ha)

Area planted peanut (ha)

No. of peanut growers

Total area for permanent

crops (ha)

Area planted banana (ha)

No. of banana growers

Champasak 107,100 1,900 2,600 33,800 500 5,200 Salavanh 88,400 2,800 5,500 13,900 2,200 7,000 Savannakhet 224,900 200 900 3,800 2,100 10,700 Whole country 1,231,000 8,300 28,500 149,200 9,300 70,400

Source: Lao Census of Agriculture 2010/2011 Highlights, May 2012

38. According to Table 8 on the usages of various types of farm machinery, the percentage of farm households using tractors increased three folds between 1989/1999 and 2010/2011. The mechanisation of farm activities has been limited in some rural areas. Information shows drastic increase in using two-wheel tractor from 20% in the previous census to 61% in the 2010/11 census. Increased income made it possible for farmer to buy the two-wheel tractor to use in their farms.

Table 8. Farm households using farm machinery by type of machine

Type of machinery 1989/1999 2010/2011 Truck n.a. 14% Generator 1% 2% Four-wheel tractor 2% 9% Two-wheel tractor 20% 61% Water pump 4% 4%

Source: Lao Census of Agriculture 2010/11 Highlights, May 2012

39. The use of outside family labour is another way to cope with shortage of labour in rural areas. The use of outside labour in the latest census shows an increase from the national average of 26% in 1989/1999 to 45% in 2010/2011 as shown in Table 9. The southern part of the country only 25% of farm households used outside labour which was lower percentage than the northern part of the country. In terms of payment for outside labour, cash payment in the southern provinces was used between 77-89% of total type of payment which were much higher than the national average use of cash payment of 50% in 1989/1999 and 57% in 2010/2011. Exchange of labour at national level is 56% which is much higher than the rates in the three selected provinces as shown in the Table below which Champasak, Salavanh,

Banana, Sweet Potato, and Peanut Value Chain Study

Page 26

and Savannakhet using exchange of labour at 14%, 19%, and 7%, respectively. Findings from the Census show that payment with farm produce was also used with lesser extent.

Table 9. Farm households by use of outside labour and type of payment (2010/11)

Province No. of farm

households

Use of outside farm labour

Type of payment (percentage of households for outside labour)

Did not use

Did use

With money

With farm produce

Exchange of labor

In other way

Champasak 75,400 56,100 19,300 81% 9% 14% 3%

Salavanh 50,100 37,500 12,500 77% 12% 19% 4%

Savannakhet 108,600 77,500 31,100 89% 11% 7% 4%

Whole country 782,800 431,000 351,800 57% 7% 56% 3%

Source: Lao Census of Agriculture 2010/11 Highlights, May 2012

II.3.3. Selected Agricultural Infrastructure

40. Details of the selected agricultural infrastructure in the three target provinces are shown in Tables 10-14. The Government has provided for various types of infrastructures in the villages. 87% of villages in the country has primary schools within one-hour walking distance with Champasak has higher percentage (96%) than the national level while the other two provinces have primary schools slightly lower than the national level. The villages in the three provinces also have pharmacy or drug kits of dispensary or hospital less than two-hour walking distance. More than half of the villages in the three provinces have access to electricity or connected to electricity grid. Safe water supply in the villages in these three provinces is much higher than the national average. More than 70% of the villages in the three provinces have accessible road to the districts. In general most villages3 in the selected areas have sufficient infrastructure which can support the value chain development.

Table 10. Selected infrastructure by province, village type, and land type (2011)

Province Number

of villages

Type of infrastructure (% of village)

Prim

ary

scho

ol

Inco

mpl

ete p

rim

ary

scho

ol

in v

illag

e

Prim

ary

scho

ol le

ss th

an

one h

our’

s wal

k

Phar

mac

y or

dru

g ki

t in

villa

ge

Disp

ensa

ry o

r ho

spita

l in

villa

ge

Disp

ensa

ry o

r h

ospi

tal l

ess

than

two

hour

s’ w

alk

Elec

tric

ity in

vill

age

Vill

age

conn

ecte

d to

el

ectr

icity

gri

ds

Safe

wat

er su

pply

in v

illag

e

Yea

r-ro

und

mot

orab

le

road

to d

istri

ct

No

mot

orab

le ro

ad to

di

stri

ct

Champasak 643,000 76% 20% 96% 70% 15% 61% 78% 74% 82% 70% 13%

Salavanh 605,000 50% 42% 84% 60% 15% 62% 65% 55% 82% 74% 1%

Savannakhet 1,012,000 65% 28% 83% 70% 16% 62% 64% 61% 74% 73% 2% Whole country 8,662,000 65% 27% 87% 70% 16% 62% 70% 55% 46% 66% 9%

Source: Lao Census of Agriculture 2010/11 Highlights, May 2012

3 From the field survey in the three provinces carried out in October 2013, Nong district of Savannakhet province may have more problems with road conditions which make it more difficult for transportation of fresh banana from farm sites to the district or the collection point in the province.

Banana, Sweet Potato, and Peanut Value Chain Study

Page 27