Kuwait Finance House Example of a Leader Islamic Bank

47

Kuwait Finance House Example of a Leader Islamic Bank By: Elhadi Habbani Doha April 2011 Page 1 of 47

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Kuwait Finance House Example of a Leader Islamic Bank

Kuwait Finance HouseExample of a Leader Islamic Bank

By: Elhadi HabbaniDoha April 2011

Page 1 of 47

Subject PageIntroduction 3Vision 3Mission 3Corporate values 3Globalizing the Islamic financial Services Industry

3

Subsidiaries and Associate Companies

4

Credit Rating 4Islamic Services 5- Retail Banking 5- Private Banking 5Commercial 5Real estate 6Credit 6Investment services 6

Page 2 of 47

Murabahah & Musawama & other Islamic Products

8

Direct investment 15Risk management 18Financial Analysis & Capital Adequacy

24

Depositors Accounts 30The most innovative products 31

Introduction: Kuwait Finance House (KFH) is the first Islamic bankestablished in the State of Kuwait and today it is one of theforemost Islamic Financial Institutions in the world.Since KFH started in 1977, it has grown into a robust bankingand financial institution, as well as a leader in the Islamicfinancial industry. KFH is now one of the market leaders notonly in the Islamic banking industry, but also in the bankingsector as whole. It provides a wide range of Shari’a compliantproducts and services covering banking, real estate, tradefinance, investment portfolios and corporate, commercial andretail financial markets.KFH has strong affiliations with leading internationalinstitutions, and in the past has successfully launched anumber of products in alliance with major global banks. In the Islamic banking arena, KFH holds a leadership positionin both profitability and total assets. The values arecontinually reinforced and adhered to in all aspects of itsoperations. Its integrity and sincerity has maintained qualityservice at all times. The employees of Kuwait Finance House are constantlyencouraged to be efficient, creative and above all successful.

Page 3 of 47

Career enhancement is actively promoted with an ever-changingfinancial world, creating a healthy professional environment.KFH provide services that exemplify fairness and mutuallybeneficial relationships between all stakeholders ascornerstone values of Islamic banking and finance.A number of services have been modernized and standardized tomeet the various needs of customers, while maintaining theethical boundaries embodied in the tenets of the Islamicfaith. Among these services are: Murabaha – trade with markup or cost plus sale Mudaraba – profit sharing agreement Musharaka – equity participation Leasing (Ijara Wa Iqtina) – renting for beneficial use Salam and Parallel Salam – deferred sale contracts Istisna’a and Parallel Istisna’a – project finance Sukuk – Islamic bondsVision: To lead the international development of Islamic financialservices and become the most trusted and sustainably mostprofitable Shariah-compliant bank in the world.Mission:To deliver superior innovation and customer service excellencewhile protecting and enhancing the interests of all ourstakeholders.Corporate Values: Upholding Islamic principles and values among all

activities of the organization. Supporting ongoing initiatives of the global Islamic

financing industry. Participating in and assisting the socio-economic endeavors

of local communities as a responsible corporate citizen.

As demand for Shari’a compliant services continues to grow atan astonishing pace KFH extends its services in retail,commercial and corporate banking sectors as well as realestate.Globalizing the Islamic Financial Services Industry: Islamic banking and finance is no longer a novelty. Islamicbanking and finance services are estimated to manage assets ofmore than US$1 Trillion globally and is one of the mostinfluential trends to transform the banking industry. Sincethe 1980’s, KFH has been riding this wave of opportunity toexpand internationally through joint ventures, acquisitionsPage 4 of 47

and subsidiaries. KFH is positioned at the forefront of theIslamic Finance Industry in terms of international presence,strategic alliances, networking, innovation and spectrum ofactivities. KFH’s spectrum of activities have grown to includeretail banking, corporate finance, Islamic capital markets,real estate finance, structured finance, and investmentportfolio management.KFH has established fully owned, independently functioningbanks in Turkey, Bahrain, and Malaysia while establishingsignificant stakes in dozens of other Islamic banks bothregional and worldwide.In collaboration with leading institutions; such as Citibank,Deutsche Bank, JP Morgan, Chase, BNP Paribas, ABN Amro, HSBC,and Islamic Development Bank, KFH successfully expandedinvestment activities into US, Europe and South East Asia.Through KFH’s regular conduction and sponsoring of seminarsand training related to Islamic finance, contemporaries haveaffectionately dubbed KFH the “Harvard of Islamic Banking.”Its commitment to education and development of the IslamicFinance Industry will continue to support the growth of theindustry as a whole, and encourage others of all cultures tochoose Shari’a compliant means as a way to meet banking andfinancing needs through a spirit of partnership. Subsidiaries and Associate Companies:

Company Name Principal ActivitiesNational Bank of Shariah Banking ServicesFirst Takaful Insurance Company K.S.C InsuranceLiquidity Management Centre B.S.C Banking & Financial

ServicesLiquidity Management House Investment Co.

Financial Services

Aref Investment Group K.S.C Investment BankAl-Muthana Investment Company Investment BankALAFCO – Aviation Leasing and Finance Company K.S.C

Aircraft Leasing & Finance

Human Investment Corporation EducationPublic Services Company K.S.C Administrative

ServicesAl-Nakheel United Real Estate Company K.S.C

Real Estate

Al-Enma’a Real Estate Services K.S.C Real EstateDevelopment Enterprises Holding Company K.S.C

Industrial

Islamic Trading Co. TradingInternational Turnkey Systems Company K.S.C

Technology

YIACO Medical Company K.S.C Health Care

Page 5 of 47

Al Salaam Hospital Company K.S.C Health CareSource: KFH website

Credit Rating:

KFH has successfully introduced Islamic financial transactionsas a daily reality in many communities and desirableinstruments in most of the major world markets. Within a shortperiod, KFH managed to lay down the foundations for an economycompliant with Islamic Sharia principles. This was realized bysetting the cornerstones of legislation and organization aswell as developing qualified human resources, thus renderingKFH a universal authority in Islamic banking. In this regard,KFH maintained the levels of credit rating granted byinternational rating agencies. According to the accreditationof the international rating agencies, the KFH credit rating asfollows in 2011:Rating Agency Long Term Short Term

KFH Credit Ratings during 2011Rating Agency Long -

TermShort -Term

Capital Intelligence

A+ A-1

Fitch A+ F-1Moody’s Aa3 P-1Standard & Poor’s

A- A-2

Source: 2011 annual report

Islamic ServicesKFH has introduced a variety of methods for its customers toconveniently satisfy their banking needs. These services canbe classified as follows:Retail Banking:Retail banking services represent the cornerstone of KFH’sperformance given KFH’s reputation in attracting investmentdeposits and offering multiple services which meet the needsof its different clients. KFH ranked as the first in thebanking deposit market segment in Kuwait, thus reflectingcustomer confidence and professionalism. Its market share,through such services, has reached 30% of the retail bankingmarket in Kuwait (the biggest share in the country).Page 6 of 47

KFH continued strategy aims at expanding the customer base,both quantitatively and qualitatively, by increasing itsbranches, developing communication channels with customers,innovating new products to meet increasing requirements, andstriving to improve services continuously in order to achievethe best banking efficiency and quality levels benchmarkedagainst international standards. During 2011, four new branches were inaugurated in Kuwaitbringing the total number of branches to 54 including 39female dedicated sections. It also renovated and refurbishedthe head office banking hall which had given the name of thelate Sheikh Ahmed Bazi Al Yasin in honor of his pioneeringrole in establishing KFH. An extensive network of branches in each locality to provideface to face customer care, As such, the number of KFH Groupbranches now total to 255; Kuwait Finance House-Turkey with181 branches, Kuwait Finance House-Bahrain with 9 branches,Kuwait Finance House-Malaysia with 11 branches in addition to54 local branches in Kuwait. To improve customer servicehandiness regardless their whereabouts. The bank has ATMs that over-arch the State of Kuwait,strategically located for easy access.And they increased to a proximately 250 covering all regionsof the State of Kuwait. Mobile Banking Vehicles also have been increased to cover allthe governorates and suburbs of the State of Kuwait.KFH has a secure online website that allows for 140 differentbanking services that can be conducted with ease from home oroffice.The bank also has a voice recognition call center called“SAWTAK” that operates 24/7. In this context, KFH reinforced its electronic services andonline channels and upgraded and equipped its Call Center withstate-of-theart technology, resources, and competencies.Customer calls which were handled and answered throughout theyear exceeded 2 million interactive calls. KFH also upgraded its Round-the-Clock customer friendlytelephone services to promote services, conduct surveys andresearch, investigate customer satisfaction levels and toidentify customer feedback by means of communication teamstargeting continuous interaction.19

Private Banking:KFH caters to clients through an experienced team of portfoliomanagers, who privately manage the banking and investment

Page 7 of 47

accounts of clients, in addition to supervising all theirpersonal transactions and affairs at KFH.Commercial:Through a wide network of KFH branches expanding all overKuwait and KFH showrooms, the bank enables clients to acquireShari’a compliant commodities and services in the consumerfinance market. It services include buying and selling of newand used cars, furniture and home appliances, constructionmaterials, yachts and marine equipment, commercial andindustrial deals.

Real Estate:Having extensive experience in the real estate business, thisdepartment is concerned with providing real estate financingto clients, trading and investing in real estate in Kuwait andabroad; in addition to exchanging and developing properties,and managing real estate portfolios.KFH also offers services to include: Lease to own Property evaluation Refinancing

Ekar call service Customers can keep in touch through its callservice. Inquiries about installment calculations, requireddocuments for successful transactions or any other relatedinquiries will be handled by its capable staff.Credit:KFH assists with granting new credit facilities for commercialclients, whether corporate or institutional, as well asrenewing and increasing the credit facilities given to currentcustomers. In addition, it studies Shari’a compliant creditand finance ideas in a way that suits the present and futurerequirements of the marketplace.Investment Services (PSIAs):KFH has been a leader in the Shari’a compliant approach as asolution to the issues faced by clients requesting a sociallyresponsible investment in line with their ideals and values.Its investment services include such functions as tradefinance, securitization, project finance, Istisna’a, and afurther focus on international real estate investments inselected markets.

Page 8 of 47

Such real estate investments include commercial, industrial,residential and multiusage properties forming a diversifiedportfolio. The Treasury Department provides the needed liquidity whilemanaging the best returns on its surpluses through such toolsas foreign currency trading, Murabaha, and KFH productfinance. Direct investments are managed with a focus on strategicinvestments that support its long term expansion strategy, inaddition to balancing medium and short term investmentportfolios with the aim of realizing appropriate returns andcapital profit upon maturity. Investments are all Shari’acompliant and in a variety of sectors with both geographic andsectoral diversification: e.g. Medical, Technology, Shipping,Aircraft and Real Estate. It also manages equity portfolios on behalf of customers.The main investment innovated products can be identified asfollows:

1-Wakala Investment Contract:1.1. Definition:

It is a contract between the customer as an investor and KFHas an agent for the investor. According to this Wakalacontract KFH is authorized to manage the investor'sinvestments according to agreed conditions. It is agreedbetween the investor (customer) and KFH (agent) on theinvestment period, investment currency, and automatic renewalof investment term unless non-renewal is requested. Theinvestor (customer) is not entitled to cancel the Wakalacontract prior to the expiry of the agreed period. Thisproduct is presented through all KFH branches.Investment periods include (1 week – 2 weeks – 1 month – 2months – 3 months) in main currencies (Kuwaiti Dinar –Sterling Pound – Euro – US$) with minimum investment amount KD25,000/- or equivalent in foreign currencies.

1.2. Profit rates: Expected Rate of Return on Investment

Period Less than KWD250,000

USD Foreign CurrenciesEuro

GBP

1 Week 0.3750 % 0.1000%

0.0500 % 0.3500%

2 Weeks 0.3750 % 0.1000%

0.0500 % 0.4000%

Page 9 of 47

1 Month 0.6250 % 0.1500%

0.1000 % 0.4500%

2 Months

0.7500 % 0.2000%

0.1100 % 0.5000%

3 Months

0.8750 % 0.3000%

0.1500 % 0.5500%

Source: KFH website Rates as of 06/01/2013 Rates are indicative Rates for KWD 250,000 and above/or equivalent in other

currencies contact VIP Dept.2-Al-Kawthar Investment deposit:2-1 Benefits: The deposit returns will be credited to customer's account

on a monthly basis. Investment and profit distribution are carried out in line

with the Islamic Sharia principles. Investors can easily get credit facilities from various KFH

sectors in lieu of the amount of the investment deposit.

2-2 Eligibility: The deposit lasts for one year and is automatically renewed

for a similar period unless the client requests the contrary prior to the maturity date.

The minimum amount of deposit is KD 10,000. Open bank account at any of KFH's branches to credit

allocated revenues in due dates. The invested amount should be kept in the account as a

minimum balance.2-3 Profit rates:

Rate of profit returns on Al-Kawthar deposits2013 Rate

January 1.0000 % February 1.1000 % March 1.1500 %

Source: KFH website

3-Continuous Investment Deposit3-1 Benefits: Substantial profits will be distributed on annual basis. Investment and profit distribution are carried out in line

with the Islamic Sharia principles. Investors can easily get credit facilities from various KFH

sectors in lieu of the amount of the investment deposit.3-2 Eligibility:

Page 10 of 47

The deposit lasts for one year and is automatically renewedfor a similar period unless the client requests thecontrary prior to the maturity date.

The minimum amount of deposit is KD 5,000. Open a banking account at any of KFH's branches to credit

the allocated revenues in due dates. The invested amount should be kept in the account as a

minimum balance.4-Thulathiya Investment Deposit4-1 Benefits: Profits will be distributed every 3 months. Investment and profit distribution are carried out in line

with the Islamic Sharia principles. Investor can easily get credit facilities from KFH against

the deposited amount.

4-2 Eligibility: The deposit lasts for 3 months and is automatically renewed

for a similar period unless the client requests thecontrary at least 6 working days before the maturity date.

The minimum amount of deposit is KD 10,000. Open a banking account at any of KFH's branches to credit

the allocated revenues in due dates. The invested amount should be kept in the account as a

minimum balance.

5-Al-Sedra Investment Deposit5-1 Benefits: Substantial profits will be distributed on annual basis. Investment and profit distribution are carried out in line

with the Islamic Sharia principles. Investor can easily get credit facilities from KFH against

the deposit amount.

5-2 Eligibility: The deposit lasts for one year and is automatically renewed

for a similar period unless the client requests thecontrary at least 6 working days before the maturity date.

The minimum amount of deposit is KD 1,000. Open a bank account at any of KFH's branches to credit

allocated revenues in due dates. The invested amount should be kept in the account as a

minimum balance.

Page 11 of 47

6-Investment Deposits in foreign currencies6-1 Benefits: Substantial profit to be distributed depending on the

investment period. Investment and profit distribution are carried out in line

with the Islamic Shari'a principles. Investor can easily get credit facilities from various KFH

sectors in lieu of the amount of the investment deposit.

6-2 Eligibility: Deposit validity period is optional (3 months, 6 months, 9

months, 1 year) and is automatically renewed for a similarperiod unless the client requests the contrary at least 2weeks before the maturity date. The minimum amount ofdeposit is USD 10,000 or GBP 5,000 or Euro 5,000.

Open a banking account at any of KFH's branches to creditthe allocated revenues in due dates. The invested amountshould be kept in the account as a minimum balance.

Murabaha & Musawama and other Islamic products:Murabaha and Musawama have got the lion share among allfinancing operations.

2011 2010Receivables per products Amount % Amount % Averag

eInternational commodity Murabaha

1,934,619

30% 1,503,381

25%28%

Local Murabaha and Wakala

4,283,598

67% 4,343,583

72%70%

Leased Assets1,422,4

42 18%1,272,7

03 17% 18%Istisna and other receivables

153,632 2% 184,806 3%3%

Total 7,794,291 100%

7,304,473 100% 100%

Source: Calculating from 2011 annual report

From the above table we can notice that:1-Local Murabaha & Wakala on 2011 represents 67% and in 2010

72% which is averaging 70%.2- International commodity Murabaha in 2011 was 30% and in

2010 25% which gives an average of 28%. This kind ofMurabaha actually short-term maturity and most of whichrepresents Tawaruq transactions.

3-Leased assets which are Ijarah transactions represents 18%on average.

Page 12 of 47

4-Istisna and the others receivables represents only 3% onaverage.

Comparing to other well known Islamic banks in GCC countriesKFH comes number three in terms of diversification of Islamicproducts following DIB and EIB and followed by QIB as numberfour as can be seen from the following chart.

DIB

EIB

Al Rajhi Bank

Bank Al Bilad

Bahrain Islamic Bank

Shamil Bank

KFH

QIB

0%

40%

80%

WakalahMusharakahMudharabahIjaraIstisna'Murabahah/Musawama

Source: Lectures 5 & 6 Dr. Tariqullah Khan – lecture 5 and 6 change - Theme-3 Islamic BankingPractices

KFH uses Murabaha to finance the following innovative activities and fields:1- Maintenance and Spare Parts:This activity offers maintenance service for vehicles &equipments with easy installments in case of accidents orbreak down, which may result in expensive repair cost. In addition, Murabaha department satisfies customers' needs toobtain all kinds of spare parts required for reparation. 1-1 Activity fields: Repairing the break-down of cars, equipments and boats. Repairing and maintaining the break-down of engine, gear or

other works. Renovation of car, equipment or boat. All kinds of spare parts. Other works related to maintenance and renovation.2- New and used boats:This activity satisfies customers' needs and finances allkinds of fishing and picnic boats, new or used, and eitherfrom individuals or companies. Besides, this activity servesall clients' categories, individuals and companies, whetherboats are for personal or commercial use. Murabaha departmentdoes not exclude specific model since boats are in goodcondition and can be used.2-1 Activity fields: Page 13 of 47

All kinds of boats with different types and shapes (fishing, picnic new or used and either from individuals orcompanies).

All kinds of new and used machines and marine equipments. High flexibility in boats model.

Machine & Marine Equipments:

This activity satisfies customers' needs and finances allkinds of machine and marine equipment, new or used, and eitherfrom individuals or companies. Besides, this activity servesall clients' categories, individuals and companies, whethermachine are for personal or commercial use.Activity fields:

All kinds of machines and marine equipments with different types and shapes.

All kinds of new and used machines and marine equipments. All electronic and electrical appliances as well as safety

and security devices for boats. Fishing equipments, radar device, navigation system and

wireless devices.

Commercial and Industrial Projects and Deals:

1- Trading Deals"

This service satisfies firms’ needs of financing for all kindof goods according to their commercial activity, from localand international markets. Settlement is conducted by monthlyinstallments or consecutive payments depending on the clients'request. Fields covered by this activity:

Car dealers. All kinds of factories. Construction materials. Heavy equipments. Industrial equipment and tools. Appliances, apparel and fabric showrooms. Equipment and devices for health clubs and institutes. Stationary supplies. Food. Medical tools and supplies for clinics. Any other commodity for other sectors in market.

Page 14 of 47

2- Heavy Equipments

Heavy equipments service is considered as one of the majorservices offered by Murabaha to all KFH clients, individualsor companies, where it satisfies their needs to get all kindsof heavy equipments, new or used and either from individualsor companies.

2-1 Heavy equipments fields: New and used heavy equipments, with different types, sizes

and shapes. Maintenance service, renovation and spare parts. No specific source is required, where all kinds of Heavy

equipments are accepted, from individuals or companies. High flexibility in accepting all models of Heavy

equipments.2-2 Service Facilities: Competitive profit margin. Profits are not collected in advance. Salary transfer is not prerequisite. Various settlement methods. High flexibility in transactions' acceptance for all

clients’ categories and guarantor is not always required. Immediate approval of transaction that fulfill all the

credit terms. Credit acceptance is granted within 15 minutes via fax.2-3 Transaction procedures:The client submits a quotation including the price andspecifications of the desired goods from the establishment orthe company (the principal seller). Hence, the quotationshould be directed to any of KFH Murabaha Department branches,where a special form has to be filled by the client. KFH purchases and possesses the desired goods. The desired goods will be sold to the client, who will be

given a delivery order to receive them from the principal seller (company, establishment, individual).

2-4 Required Documents2-4-1 Individuals:

From the client A quotation including the price and specifications of

goods. Civil ID.

Page 15 of 47

Recent salary certificate Bank statement of accountFrom the Guarantor (if required); Civil ID. Recent salary certificate. Bank statement of account.

2-4-2 2- Companies and establishments

Identification documents for companies and establishments; Letter specifying the facilities requested. Foundation contract and alterations. Trade license. Signature authorization. Rent contract. Civil number.Financial documents for companies and establishments; Financial documents for companies and establishments. Last two years financial audit. Financial status. Debit statement (balances). Statement of current account for the last 6 months. Facilities offered from banks

Legitimacy of Murabaha:To abide by Sharia requirements, the customer is required notto make a down payment to the merchant selling the goods orservice, or sign any receipts or sale contracts. As well asrefrain from asking the merchant to write the customer's nameon the shipping documents. The customer may not complete thetransaction with the merchant before opening an LC along witha Pro forma invoice.

Overseas Cars’ and other Object Delivery:This service is one of the recent services offered by KFH toits clients to satisfy their needs with all kinds of new andused cars as well as furniture. The buying and paymenttransactions are finalized in Kuwait, while car’s or furnituredelivery is affected abroad.1- Who benefits from the service? Tourists and residents abroad. Students in countries of delivery. Investors and businessmen. Diplomatic corps. Expatriates residents in Kuwait.

Page 16 of 47

2- Procedures to obtain the service:2-1 Car chosen inside Kuwait: The customer chooses the desired car from a list of carsdisplayed in the dealers’ showrooms accredited by KFH. Then,the following procedures of inquiry and booking are followed: The front desk employee identifies the car chosen by the

customer, fills a confirmation form for car’s booking, andsends the form to the Suppliers Service by Fax.

The Suppliers Service Unit approaches the car’s dealer toinquire about the car, and execute the booking procedures,and notifies the branch accordingly.

The branch issues a purchase order in accordance with theprice approved by the Suppliers Service Unit, and sends acopy of the purchase order to this Unit, which executesthe purchasing procedures with the car’s supplier.

The Suppliers Service Unit sends a copy of the purchaseorder by fax to the car’s supplier. The supplier initialsthe purchase order with his approval to sell the car, andsends back the initialed order to KFH. The concernedbranch is notified in order to finalize the purchasingprocedures and the selling procedures as well.

A delivery order of the car is issued in the name of thecustomer or his agent, and a copy thereof is sent by faxto the Suppliers Service Unit in order to send it to thecar’s supplier.

The company delivers the car to the customer or his agentand executes the required procedures to this effect.

The company sends the delivery documents to the SuppliersService Unit in KFH by courier service in order to effectpayment.

2-2 Car chosen outside Kuwait. The customer chooses the desired car either from thecompanies’ showrooms accredited by KFH in the respectivecountry of delivery, or from the local market of that countryupon consultation with the companies accredited by KFH. Whenthese companies endorse the price offered, the MurabahaDepartment and the endorsed companies can conclude the dealwith following procedures: The customer submits the desired car’s price offer, which

he obtained from the one of the accredited companies byKFH, in order to open a Murabaha transaction form.Alternatively, the customer may assign an agent tofinalize a transaction on his behalf inside Kuwait.

Page 17 of 47

The Suppliers Service Unit approaches the car’s dealer toinquire about the car, and execute the booking procedures,and notifies the branch accordingly.

The branch issues a purchase order in accordance with theprice approved by the Suppliers Service Unit, and sends acopy of the purchase order to this Unit, which executesthe purchasing procedures with the car’s supplier.

The Suppliers Service Unit sends a copy of the purchaseorder by fax to the car’s supplier. The supplier initialsthe purchase order with his approval to sell the car, andsends back the initialed order to KFH. The concernedbranch is notified in order to finalize the purchasingprocedures and the selling procedures as well.

A delivery order of the car is issued in the name of thecustomer or his agent, and a copy thereof is sent by faxto the Suppliers Service Unit in order to send it to thecar’s supplier.

The company delivers the car to the customer or his agentand executes the required procedures to this effect.

The company sends the delivery documents to the SuppliersService Unit in KFH by courier service in order to effectpayment.

3- Countries covered by the service: United Arab Emirates. Egypt. Lebanon. Germany. U.S.A.

Furniture, Electrical Appliances and Kitchen:

1- Furniture, Electrical Appliances and Kitchen:Through this activity we satisfy all customers needs andfinance all kinds of home appliances ,electronic devices andaccessories with special offers and lots of benefits .Thisservice covers the following fields:

1-1 Facilities and service controls: Competitive profit margin. Profits are not discounted in advance-. No salary transfer is required. Great flexibility in accepting the categories of

transactions for the collection of customers (citizens and residents).

Does not always require a sponsor.Page 18 of 47

The Transaction is immediately processed if it meets the conditions for granting credit.

1-2 The legitimacy of our finance deals:The sale of (Finance service) was approved by the Conferenceof the Islamic Research Academy. It is a particular kind ofsale, compliant with Sharia and one of Bayou Al Amanah(fiduciary), which requires the seller (KFH) to mention thecapital or the cost incurred on the commodities for sale andsells it to the buyer (Client) , adding to the agreed profit.Both parties can agree to pay in cash or in installments ordeferred. Based on this, our finance service is a commercialapplicable transaction in Kuwait Finance House Commercialbased on two pillars: first: Kuwait Finance House to buy theproduct from the source (the original seller) with fullownership and then sell it to the customer (prospectivebuyer) based on the profit rate agreed on. It is also a salesoperation ((Allah Almighty said " but Allah hath permittedtrade and forbidden usury.Second: the selling price is fixed after it has been set bymutual consent and doesn’t change; there is no increase incase of delay or decrease by acceleration. The financeservice in the context of its Sharia is a formula to fund allkinds of commodities and goods.

1-3 Sharia restrictions:While committing to the legitimacy of the transaction andwhereas Kuwait Finance House is the buyer of the goods anddeal with the original seller (the supplier) or the companyexecuting the work. Customers and suppliers are kindlyrequested to consider the following: The prospective clientis not allowed to pay a deposit to the original seller or tosign a contract of sales, nor taking a sales invoice orreceiving goods or part thereof from the seller. Nor shouldthe client ask the original seller of the goods to deliver itto a desired location. The Customer shall not deal with thecompany - the institution (executing the work) to startworking before the goods purchasing by Kuwait Finance Houseor before reaching an agreement first with (from theexecuting party) the supplier, followed by Kuwait FinanceHouse selling to the client (prospective client) and clientis being handed a written permission hereby authorizes thesupplier to deliver the goods to the customer or theexecution of istisna contract concluded by a "KFH" of thecompany executing the work.

Page 19 of 47

1-4 steps for completing transaction: The prospective client presents a quotation from

institution or company or individuals( Original Seller) that includes the specifications of the goods he wishes to receive addressed to any finance services branch Kuwait Finance House.

Kuwait Finance House buy and owns the goods. The sale of the goods to the client (prospective client )

and he receives a delivery order to receive goods from the original seller (Company, Institution or Individual).

1-5 Required Documents:From the Client From the

GuarantorQuotation including price and specifications of goods

Original Civil ID

Original Civil ID Net new salary certificate

Net new salary certificate Statement of account

Statement of accountSource: KFH website

1-6 Fields covered by this activity:This activity covers different fields like: Ready & custom made furniture. Handmade furniture. Readymade Kitchen & accessories. Computers, computer sets, printers, scanners, other

computer accessories and supplies, and Electronic and Electrical Appliances.

2- Construction Materials and Works:This activity finances all the materials that customers needfor construction works with easy installments ad flexiblesettlement methods. Moreover, this activity offers thefollowing services:

Providing the appropriate counseling prior and after the construction.

Engineering advice through competent engineers. Offering advice concerning the best material prices in the

local market from different suppliers.

Page 20 of 47

Activity fields:1- Financing all materials involved in constructionprocess.

2- Financing all the supply and installation works suchas;

Carpentry works. Concrete structure works. Swimming pools, waterfalls and fountains works. Central air conditioners. Interior and exterior paintings. Exterior coating. Ready-made houses and chalet works. Woodworks. Renovation works. Electric, intercom and telephone works. Aluminum works. Elevator works. Sanitary works.3- Credit:3-1Murabaha L/C:It suits the local commercial activities, it mostly concernsthe traders as it spares serenity and tranquility as itincludes many advantages and characteristics; like: No extra commission or fees added to the cost value. The profit is known and it does not include any non-

agreeable increase regarding the delay of payment. The customer is granted a suitable grace period to pay the

first installment. Presenting the needed consultation and technical advice.

3-2Other services presented by L/C Department:Kuwait Finance House presents services, which support Importand Export operation with high standard with accuracy andspeed through expanded network for international bankingcorrespondence with large experience in this field and itsproducts. Letter of Credit by Sight. Letter of Credit on Acceptance basis. Export L/C. Letter of Guarantees. Bills for Collection.

3-3Ijarah Leasing Contract:

Page 21 of 47

This type of contracts is characterized for lightening theoperational costs paid by the owners to purchase neededequipments and heavy machinery for the large projects thatrepresents a great burdening on the current capital. KFH leasethe equipments and machinery for monthly installments, and atthe end of the project, the customer either returns the leasedequipment and machinery to KFH, Or, buys them from KFH. Therange of equipment and machinery list expanded to includecomputers, cars, heavy machinery and the needs of bigprojects.

3-4Istisna Contracts:This product serves and suits the huge industrial and realestate constructional projects and others. Kuwait FinanceHouse performs the role of the owner in administrating andexecuting the project till the end. Kuwait Finance House willfinance, supervise, and undertakes the best technicalspecification. By this, the customer could execute his specialprojects then pays according to flexible schedule whilesparing a typical grace period to pay the first installment. 3-5Co-operative Marketing:It is one of the most innovative product being created andpracticed by KFH. The product specialized for financing thelocal trade and to encourage the national products. KFH buysthe high demand goods by the consumers from the originalsource (factory - supplier) and sells it to the co-operativesand pay to suppliers in cash and immediately the value ofthese purchases, so the supplier is not obliged to wait morethan 90 days to collect the values. The supplier, himselftransports and delivers the goods to the co-operatives onbehalf of KFH in a Wakala based contract.The co-operative marketing product fully supports and helpsthe suppliers to get back their capital in a very fast waythat paves the way freely to produce, develop and prevents thestumbles of capital resulted from the long term collection andthe non-sufficiency of the working capital.3-6Prohibited Import Goods: Tobacco products and Cigarettes. Goods which includes pictures of human beings or animals. Beer free from Alcohol. Videotapes and Musical equipment’s and all other related

items against Sharia.Goods needspermission

authority

All kinds of The Public Authority for Agricultural Affairs and Fish Resources.

Page 22 of 47

livestock. Animal Husbandry Department.Tools and HeavyEquipment’s.

Ministry of Commerce & Industry, Industrial Licenses Section.

Drugs and Medicines. Ministry of Health.Insect Killer andsimilar items.

Ministry of Health.

Weapons andAmmunition.

Ministry of Interior.

Telephone & Wireless. Ministry of Tele-Communications.Source:2010 and 2011 annual report

Direct Investment:Direct Investment Department is viewed as the arm of KuwaitFinance House in the field of capital investment. Thedepartment is entrusted with the direct investment activitieswhich are rated as per KFH general strategy. It invests incompanies, non-real estate funds and investment portfoliosusing KFH finance resources. Direct Investment Department doesnot serve KFH customers directly but invests their availablefunds through total funds portfolio available for KFH.1-Types of Direct Investment:1-1 Strategic Investments: These investments aim to reinforce the bank’s long termexpansion policies. This type of investment performed by ahighly professional and skilled team through investmentanalysis and due diligence, management of investment sale andpurchase transactions, , subsequent registration and controlover the investment portfolio. The investment portfolio bookvalue exceeded KD 1.5 billion as at the end of 2008.1-2 Mid-term investments:

These investments aim to realize adequate profit and liquidateand achieve capital gains on maturity.1-3 Short term investments: Asset management tools giving KFH customers the opportunity toinvest jointly with the bank.Direct investment department oversees subsidiaries, affiliatesand other KFH owned funds and portfolios. Investments arespread globally in 12 countries, centered initially in Kuwait,followed by GCC countries, Malaysia and the rest of the world.The department’s portfolio is diversified among variouseconomic sectors including banking, investment, commercial,real estate, healthcare, asset management services and otherinvestments.1-4 International Real Estate Department:

Page 23 of 47

Kuwait Finance House fixed policies comprise its continuousdedication to open investment channels with the global market.Based on this concept, the Senior Management has resolved toestablish an international real estate department that aims toreinforce “KFH” position in the investment sector in generaland to avail any potential opportunities in the internationalreal estate market in particular.International Real Estate Department undertakes the followingactivities: Establish and Manage Investment Funds:

This product incorporates to establish and managestructured real estate portfolios/funds to provide stablereturns to investors.

Project Financing: This service is provided to finance the purchase ofproperties outside Kuwait to institutions through Islamicfinancing tools.

Direct Investment: Investment on ownership basis in real estate directly orthrough real estate companies outside Kuwait oninternational level to benefit from cash returns andcapital gains.

KFH’s strategy targets investment in all real estate sectors(residential, commercial, and industrial/logistic) with highoccupancy rates and achieving sustainable cash flow incomestreams and potential capital gains at exit, as well as, toacquire lands and make the infrastructure development processsell them at capital gains. These investments are undertakenjointly with best global real estate operators who join asjoint investors/ asset managers in the purchase of assetsuntil property disposal.Real estate is forming the major part of “KFH” investmentportfolio. “KFH” successful record in real estate investmentsplays an active role to maintain “KFH” reputation globally.1-5 Treasury Department: Treasury Department provides the bank with direct and highlysignificant communication channels with local andinternational finance markets. Its role has developedremarkably over time simultaneously with KFH growth. The mainfunctions and responsibilities of the department includeprovision of liquidity to the bank, increase returns on thebank surplus and local and international market analysis. Italso recruits highly qualified and efficient employees and

Page 24 of 47

comprises highly developed and sensitive equipments to provideinstant response to market requirements. Liquidity Management department comprises the followingsections: Corporate Desk:

This section is responsible for ongoing communication withbank branches to provide FX sale and purchase services andrespond to their inquiries.

FX Desk: This section covers all foreign currency transactions onNOSTRO accounts (KFH accounts with foreign banks) to covercustomers' needs.MM Desk:This section is responsible for International MurabahahManagement and exchange of KD or FX deposits for customersor KFH.

1-6 Asset Management & Follow up Department: This function is conducted in accordance with the highestbanking practices applied by international banking society.The department is entrusted with the management and follow upof assets throughout various operational and functionaldivisions in the investment sector. Following are the mostsignificant functions of this department: Prepare performance reports on all investment sector

investments. Evaluate various KFH funds performance. Management of subscriptions and distributions and

maintenance of various investment funds of KFH customers. Cooperation and coordination with various KFH departments

and investment product customers and increase specialcommunication channels with VIP Department and branchesdepartment to communicate with KFH customers.

Communicate with the KCB and official authorities throughthe preparation of reports and studies.

1-7 International Relations and Financial Institutions: Main significant functions of this Department are: Maintain and develop relations with global international

institutions. Management of current correspondent banking services and

develop relations with local and foreign financial andbanking institutions and negotiation of terms andconditions with them.

Page 25 of 47

Management of NOSTRO and VOSTRO interest free accounts toachieve mutual benefit to participating banks andfacilitate inter-settlement transactions.

Discuss the exchange of business with correspondent banks(cash, commercial and Reverse Murabaha transactions).

Maintain very close ties and relations and communicationswith several major international banks and institutions toachieve efficient services and strengthen businessrelations.

Coordinate with all internal departments to overcome anybusiness problems related to correspondent bankingservices.

Prepare financial reports of financial institutions andbanks to allocate credit limits.

Management of Agency Functions related to Islamic financetransactions where KFH is mandated as an agent.

1-8 Major International Projects Finance: KFH has entrusted “Liquidity Management House Company” "KSC"with this major responsibility to execute major internationalprojects finance strategy and careful selection of suchprojects. LMH is managed by highly qualified, experienced andefficient team in the field of project finance. The companyworks within an accurate framework to manage risks. Thecompany endeavors to continuously cope with the bestapplicable practices in the banking field through its abilityto structure innovative, competitive and Sharia compliantinvestment and finance products i.e. Istisna, Murabahah,Musharakah and other Islamic finance instruments, issuance ofSukuk inside and outside Kuwait, development of Sukuk marketin cooperation with global financial institutions where thecompany purchases or securitizes assets e.g. (Murabahahreceivables, Musawamah receivables, Ijarah receivables) andissue the same in the form of financial instruments (Sukuk)to fulfill institutions and investors needs of financialinstruments with remarkable returns and Sharia compliant cashflows.The increased demand on Islamic finance instruments tofinance major global projects has provided several newopportunities which may be availed by KFH to reinforce itsleading role in Islamic investment and finance world.

Risk Management:

1- Credit Risk Credit Risk Weighted Exposure and Required Capital

Year Total Net Risk Weighted Required

Page 26 of 47

Exposure Exposure assets Capital2011 14,248,927 12,083,205 8,899,405 1,067,9292010 13,078,284 11,356,893 8,646,040 1,037,5252009 11,940,129 10,319,505 7,893,584 947,230

Source:2010 and 2011 annual report

From the table above we can notice the following:Credit Risk Weighted Exposure during the financial year2009 was amounted as KD 7,893,584 and the minimumrequired capital for credit risk is KD 947,230.

Credit Risk Weighted Exposure significantly increasedduring the financial year 2010 to reach KD 8,646,040and the minimum required capital for credit risk to KD1,037,525.

Credit Risk Weighted Exposure also increased during thefinancial year 2010 amounted to reach KD 8,899,040 andthe minimum required capital for credit risk to KD1,067,929.

2- Concentration of Assets and Liabilities:Concentrations arise when a number of counterparties areengaged in similar business activities, or activities in thesame geographic region, or have similar economic features thatwould cause their ability to meet contractual obligations tobe similarly affected by changes in economic, political orother conditions. Concentrations indicate the relativesensitivity of the Group’s performance to developmentsaffecting a particular industry or geographic location.2-1The distribution of assets by industry sector:

0%15%30%

Concentration by sector

Source:2010 and 2011 annual report

Page 27 of 47

It is quite obvious from the chart above that the bankconcentrate on banks and financial institution sectors as wellas construction and real estate.Both of banks and financial institution sectors as well asconstruction and real estate represents together 56% and 28%in the two years respectively.2-2The distribution of assets by region:

Geographic region 2011 2010

Banking Nonbanking

Total Banking Nonbanking

Total

The Middle East 8,218,084 201,758 8,419,842 7,618,05

2129,806 7,747,858

North America 2,296 76,690 78,986 112 36,845 36,957North America 70,846 340,401 411,247 60,381 361,109 421,490Other 2,420,439 51,640 2,472,079 2,145,08

5111,407 2,256,492

Total 10,711,665

670,489 11,382,154

9,823,630

639,167 10,462,797

Source:2010 and 2011 annual report

ehT elddiM

tsaE

htroNaciremA

htroNaciremA

rehtO

%0%02%04%06%08

noiger yb noitartnecnoC

01021102

It is quite obvious from the table and the chart above thatmore than 60% of the banks operation concentrated in theMiddle East.2-3The distribution of assets by products:

Receivables per products 2010 2011International Murabaha 1,832,130 1,397,9

45

Page 28 of 47

Local Murabaha & Wakala 3,899,458 3,990,7

94Istisna & other receivables 133,233 157,176Leased Assets (Ijarah) 1,422,442 1.272,70

3Sukuk 463,899 381,344Total 7,751,162 7,199,9

62Source:2010 and 2011 annual report

%0%02%04%06

stcudorp yb noitartnecnoC

From the table and the chart above local Murabaha and Wakalaplus international Murabaha represents approximately 74%.Although it is considered as a concentration but risk alliedto Murabaha instrument is normally acceptable and better thanthe risk of other instrument.2-4Asset risk classification:

Receivables 2011 2010HighGrade

Standard

Impairment

Total HighGrade

Standard

Impairment

Total

International Murabaha 209,570 1,552,4

5370,107 1,832,130 158,448 991,087 248,410 1,397,9

45Local Murabaha & Wakala 0 3,346,3

02553,156 3,899,458 0 3,377,1

74613,620 3,990,7

94Istisna & other receivables 248 111,434 21,551 133,233 248 101,606 55,322 157,176Leased Assets (Ijarah) 0 1,124,7 297,707 1,422,442 0 1,172,6 100,028 1.272,70

Page 29 of 47

35 75 3Sukuk 150,426 271,376 42,097 463,899 131,857 249,487 0 381,344Total 360,244 6,406,3

00984,618 7,751,162 290,553 5,892,0

291,017,380 7,199,9

62Source:2010 and 2011 annual report

High

Gra

de

Stan

dard

Impa

irme

nt

High

Gra

de

Stan

dard

Impa

irme

nt

20112010

0500,0001,000,0001,500,0002,000,0002,500,0003,000,0003,500,000

International MurabahaLocal Murabaha & WakalaIstisna & other receivablesLeased Assets (Ijarah)Sukuk

From the table and the chart above we notice the following: High grade in the two years is very minimal which is a bad

indication. The majority of the assets grading laying within standard

category which is normally including customers with pastdue up to 90 days.

The highest impairment laying within Local Murabaha andleased assets (Ijara) in the two years.

2-5Provisions: Although KFH's provisions in 2010 slightly declined from KD203,885 to KD 198,633 but the general trend is increasing ascan be seen from the table and chart below, and in 2011increased sharply from KD 198,633 to KD321,297 which indicatesa serious increment in NPLs.

Provisions to total & net exposures2011 2010 2009

Total Exposure 14,248,927

13,078,284

11,940,129

Net Exposure 12,083,205

11,356,893

10,319,505

Provisions 321,297 198,633 203,885 Provisions to Receivables

2.3% 1.5% 1.7%

Provisions to Net exposure 2.7% 1.7% 2.0%

Page 30 of 47

Source: calculated from 2010 and 2011 annual report

2011 2010 2009

0100,000200,000300,000400,000

Provisions

Although provisions to total receivables and provisions to netexposures ratios are both within the international acceptablepercentages but they have sharply increased in 2011 as can beseen in the following chart which indicates sharp increment inNPLs in 2011.

2011 2010 20090.00%2.00%4.00%

Provision Ratios

Provisions / Receivables Provisions / Net exposure

3- Liquidity Risk:Liquidity risk is the risk that the Bank will be unable tomeet its payment obligations when they fall due under normaland stress circumstances. To limit this risk, management hasarranged diversified funding sources in addition to its coredeposit base, manages assets with liquidity in mind, andmonitors future cash flows and liquidity on a daily basis.This incorporates an assessment of expected cash flows and theavailability of high grade collateral which could be used tosecure additional funding if required.The Bank maintains a portfolio of highly marketable anddiverse assets that can be easily liquidated in the event ofan unforeseen interruption of cash flow. The Bank also hascommitted lines of credit that it can access to meet liquidityneeds. The liquidity position is assessed and managed under avariety of scenarios, giving due consideration to stressfactors relating to both the market in general andspecifically to the Bank. The most important of these is tomaintain limits on the ratio of net liquid assets to customer

Page 31 of 47

liabilities, set to reflect market conditions. Net liquidassets consist of cash and short term Murabaha. The ratioduring the year was as follows:

Net Liquid Asset 2011 2010

31 December 22% 23%Average duringthe year

22% 22%

Highest 25% 24%Lowest 20% 20%

Source:2010 and 2011 annual report

The table below summarizes the maturity profile of the Groupassets and undiscounted liabilities at 31 December 2011 are asfollows:

3 month 3-6month

6-12month

> oneyear

Total

AssetsCash & banks 619,554 0 0 0 619,554Short-term Murabaha 1,478,05

20 0 0 1,478,05

2Receivables 1,132,62

3881,645 1,043,86

12,806,69

25,864,82

1Trading properties 1,328 173,534 2,655 96,169 273,686leased assets 384,939 285,050 305,186 447,267 1,422,44

2Financial assets available for sale

72,484 10,109 62,018 1,157,566

1,302,177

Investments in associates

0 0 0 490,062 490,062

Investments in properties

0 0 0 536,358 536,358

Other assets 274,983 32,558 78,377 319,633 705,551Property and equipment 0 0 0 767,130 767,130Total 3,963,96

31,382,89

61,492,09

76,620,87

713,459,8

33LiabilitiesDue to banks & financialinstitutes

976,204 138,416 216,901 487,115 1,818,636

Depositors accounts 4,949,100

650,509 284,987 2,997,249

8,881,845

Other liabilities 75,524 93,962 217,718 294,469 681,673Total 6,000,82

8882,887 719,606 3,778,83

311,382,1

54Surplus/Deficit - 500,009 772,491 2,842,04 2,077,67

Page 32 of 47

2,036,865

4 9

Source:2010 and 2011 annual report

As can be seen from the table the bank faces a mismatch riskbetween total assets and liabilities in category (3 month) byKD(2,036,865) which means that the bank could have not meethis 3 month liabilities bearing in mind that total assetsinclude some assets which might not be liquidated within theshort run like properly and equipment and other assets.4- Market risk:Market risk is the risk that the value of an asset willfluctuate as a result of changes in market prices. It isnormally managed on the basis of pre-determined assetallocations across various asset categories, a continuousappraisal of market conditions and trends and management’sestimate of long and short term changes in fair value.The Group is not exposed to any risk in terms of the re-pricing of its liabilities since the Group does not providecontractual rates of return to its depositors in accordancewith Islamic Sharia which is based on Mudarabah contract.3-1 Interest rate risk:Interest rate risk arises from the possibility that changes ininterest rates will affect future cash flows or the fairvalues of financial instruments. The Group is not exposed tointerest rate risk as the Bank does not charge or payinterest. Changes in interest rates may, however, affect thefair value of financial assets available for sale.3-2 Currency risk:Currency risk is the risk that the value of a financialinstrument will fluctuate due to changes in foreign exchangerates.Currency risk is managed on the basis of limits determined bythe Bank’s Board of Directors and a continuous assessment ofthe Group open positions, and current and expected exchangerate movements. The Group matches currency exposures inherentin certain assets with liabilities in the same or a correlatedcurrency. The Group also uses Islamic Derivatives such likecurrency swap and forward foreign exchange contracts tomitigate foreign currency risk.The tables below indicate the currencies to which the Bank hadsignificant exposure at 31 December 2011 on its non-tradingmonetary assets and liabilities and its forecast cash flows.The analysis calculates the effect of a reasonably possiblemovement of the currency rate against the Kuwaiti Dinar, withPage 33 of 47

all other variables held constant on the profit and the fairvalue reserve (due to the change in fair value of financialassets available for sale).

Effect of change in currencies on profit and fare value reserves2011

Currency

Δ in currencyrate

Effect onprofit

Effect on fair valuereserve

USD 1+ 2165 3566GBD 1+ 167 236

2010Δ in currency

rateEffect onprofit

Effect on fair valuereserve

USD 1+ 3015 2622GBD 1+ 104 62

Source:2010 and 2011 annual reportAs can be seen from the table above changes in USD & GBD werepositive and in turn have positive effects on the incomestatement and fair value reserve in 2011 as well as in 2010. Market Risk Weighted Exposure during the financial year 2011amounted as KD 722,492 thousand (2010: KD 600,642 thousand),based on the standardized approach. The minimum requiredcapital for market risk exposures amounts to KD 86,699thousand (2010: KD72,077 thousand).3-3 Equity price risk:Equity price risk is the risk that the fair values of equitiesdecrease as the result of changes in the levels of equityindices and the value of individual stocks. The non-tradingequity price risk exposure arises from the Group’s investmentportfolio. The Group manages this risk through diversificationof investments in terms of geographical distribution andindustry concentration.The effect on fair value reserve (as a result of a change inthe fair value of financial assets available for sale at 31December) due to a reasonably possible change in equityindices, with all other variables held constant is as follows:

Effect of change in equity price on fare value reserves2011

Market indices

Δ in equityprice

Effect on fair valuereserve

KSE 1+ 2920Other GCC indices

1+ 502

2010Δ in equity

priceEffect on fair value

reserveKSE 1+ 2740

Page 34 of 47

Other GCC indices

1+ 575

Source:2010 and 2011 annual reportAs can be seen also from the table above changes in KSE andother GCC indices were positive and in turn have a positiveeffects on the equity fare value reserves in 2011 as well asin 2010. 5- Operational risk:Operational risk is the risk of loss arising from systemsfailure, human error, fraud or external events. When controlsfail to perform, operational risks can cause damage toreputation, have legal or regulatory implications, or lead tofinancial loss. The Bank cannot expect to eliminate alloperational risks, but through a control framework and bymonitoring and responding to potential risks, the Bank is ableto manage the risks. Controls include effective segregation ofduties, access, authorization and reconciliation procedures,staff education and assessment processes, including the use ofinternal audit.The Bank has a set of policies and procedures, which isapproved by its Board of Directors and applied to identify,assess and supervise operational risk in addition to othertypes of risks relating to the banking and financialactivities of the Bank. Operational risk is managed by theoperational risk function, which ensures compliance withpolicies and procedures and monitors operational risk as partof overall Bank-wide risk management.The operational risk function of the Bank is in line with theCBK instructions concerning the general guidelines forinternal controls and the sound practices for managing andsupervising operational risks in Banks.Operational risk weighted exposures calculated during the year2011 amounted to KD 777,844 thousand (2010: KD 756,470thousand) as per the Basic Indicator Approach. The amountcalculated for operational risk weighted exposures is adequateto cover any projected risks to maintain a reasonable profitratio for shareholders and investment account owners. Theminimum required capital for operational risk exposuresamounted to KD 93,341 thousand (2010: KD 90,776 thousand).

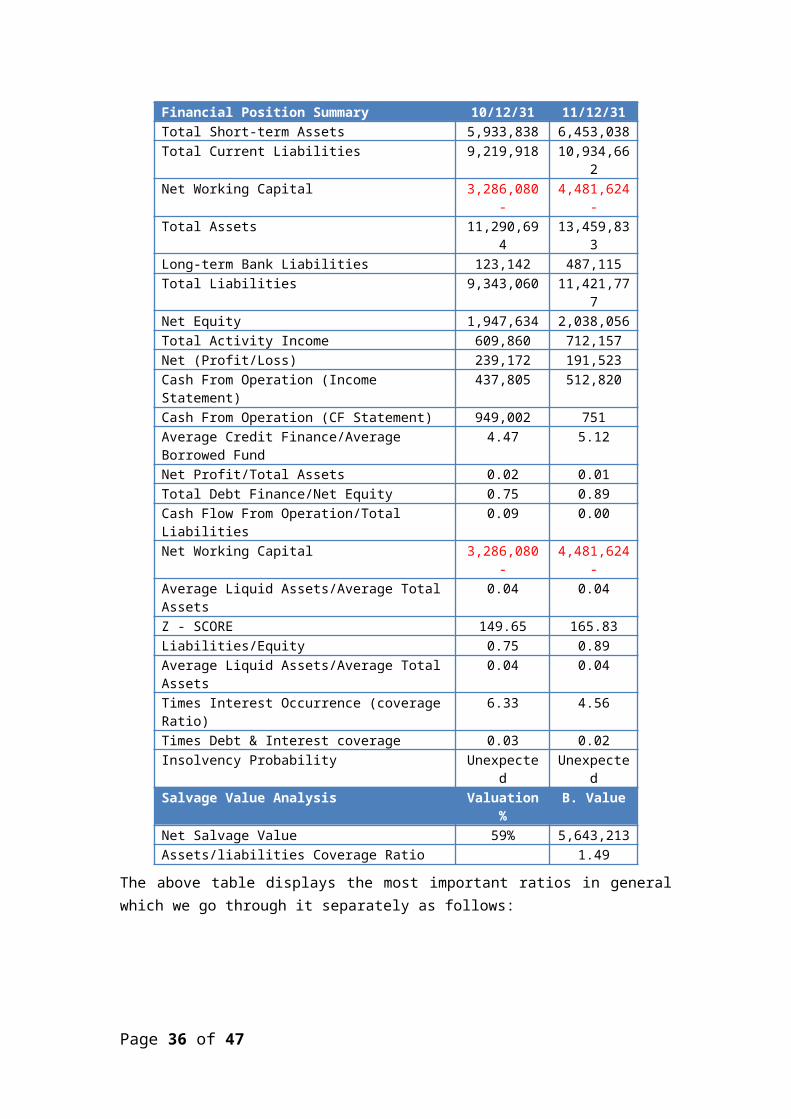

Financial Risks Assessment:-Here is a summary of the comparison financial ratio analysisand assessment to the financial statements as of 31/12/2009,31/12/2010, and 31/12/2011which highlights the most strengthand weakness points of KFH;

Page 35 of 47

Financial Position Summary 10/12/31 11/12/31Total Short-term Assets 5,933,838 6,453,038Total Current Liabilities 9,219,918 10,934,66

2Net Working Capital 3,286,080

-4,481,624

-Total Assets 11,290,69

413,459,83

3Long-term Bank Liabilities 123,142 487,115Total Liabilities 9,343,060 11,421,77

7Net Equity 1,947,634 2,038,056Total Activity Income 609,860 712,157Net (Profit/Loss) 239,172 191,523Cash From Operation (Income Statement)

437,805 512,820

Cash From Operation (CF Statement) 949,002 751 Average Credit Finance/Average Borrowed Fund

4.47 5.12

Net Profit/Total Assets 0.02 0.01Total Debt Finance/Net Equity 0.75 0.89Cash Flow From Operation/Total Liabilities

0.09 0.00

Net Working Capital 3,286,080-

4,481,624-

Average Liquid Assets/Average Total Assets

0.04 0.04

Z - SCORE 149.65 165.83Liabilities/Equity 0.75 0.89Average Liquid Assets/Average Total Assets

0.04 0.04

Times Interest Occurrence (coverage Ratio)

6.33 4.56

Times Debt & Interest coverage 0.03 0.02Insolvency Probability Unexpecte

d Unexpecte

d Salvage Value Analysis Valuation

%B. Value

Net Salvage Value 59% 5,643,213Assets/liabilities Coverage Ratio 1.49

The above table displays the most important ratios in generalwhich we go through it separately as follows:

Page 36 of 47

1-Growth Ratios: Growth Ratios 10/12/3

111/12/3

1Activity Income Growth Ratio -4.71% 16.77%

Net Recurring Earnings Growth Ratio -3.50% 16.53%

Cost Of Fund -17.73% 19.85%Operational Earning GrowthRatio -0.19% 26.48%

Total Earnings Growth Ratio -2.91% 18.35%

Total Liabilities Growth Ratio 12.56% 4.34%

Net Equity Growth Ratio 2.32% -2.83%Total Assets Growth Ratio 11.14% 3.43%

-From the above table we can note the following:1-1Strength Points:

Activity income growth ratio has increased sharply from(4.71%) in 2010 to 16.77% in 2011.

Net recurring earnings growth ratio has increased sharplyfrom (3.5%) in 2010 to 16.53% in 2011.

Operational earning growth ratio has increased sharply from(0.19%) in 2010 to 26.48% in 2011.

Total earnings growth ratio has increased from (2.91%) in2010 to 18.35% in 2011.

Total liabilities growth ratio decreased sharply from 12.56%in 2010 to 4.34% in 2011.

1-2Weakness Points:Cost of fund has increased sharply from (17.73%) in 2010 to19.85% in 2011.

Net equity growth ratio has decreased steadily from 2.32% in2010 to (2.83%) in 2011.

Total assets growth ratio decreased sharply from 11.14% in2010 to 3.43% in 2011.

2-Liquidity Ratios:

Liquidity Ratio 10/12/31

11/12/31

Average Liquid Assets/Average Total Assets 3.7% 4.3%

Net Working Capital -3,286,0

-4,481,6

Page 37 of 47

80 24Shrinkage rate of current assets -55% -69%

Cash From Operation (Income Statement) 273,674 359,010

Cash From Operation (CF Statement) 781,610 -

153,667Working Investment 6,170,3

896,578,2

65Working Investment/Sales 1011.77

% 923.71%

-From the above table we can note the following:2-1Strength Points:

Cash from operation based on the income statements increasedfrom KD273,674 in 2010 to KD359,010 in 2011.

Average liquid assets to average total assets ratio slightlyincreased from 3.7% in 2010 to 4.3% in 2011.

2-2Weakness Points:Net working Capital is minus in the two financial periodswhich indicates that the bank might face some difficultiesin facing its short-term liabilities. And for this reasonthe shrinkage rate of current assets is minus also in thetwo years.

Cash from operations based on the cash flow statementsdeclined from KD781,610 in 2010 to minus KD(153,667) whichindicates lack of efficiency in making cash flow from itsmain operations.

Working investment was slightly increased and its ratio tosales is also increase which indicates another prove forinefficiency to generate cash flow from the core normaloperations.

3-Allocations Ratios:

Allocations Ratios 2010/12/31

2011/10/31

Average Credit Finance/Average Available Fund 2.14 2.31

Average Total Allocations/Average Borrowed Fund 5.87 6.79

Average Total Allocations/Average Available Fund 2.81 3.07

Long-term Allocations/Average Available Fund 1.49 1.58

Investments/Average Available Fund 0.57 0.54

Page 38 of 47

3-1Strength Points:Average credit finance to Average Available Fund Ratioslightly increased from 2.14 to 2,31 in the two yearsrespectively.

Average Total Allocations/Average Borrowed Fund ratiorecorded a stable increment in the two years.

Average Total Allocations/Average Available Fund Ratio hasslightly grown from 2.81, to 3.07, in the two yearsrespectively.

3-2Weakness Points:Long-term Allocations/Average Available Fund Ratio hasslightly increased from 1.49 in 2010, to 1.58 in 2011 whichis negative indication specially within the weaknesses ofthe bank in creating sufficient fund to meets its short-termliabilities.

Investment/Average Available Fund ratio is the worst amongall other ratios.

4-Profitability Ratios:

Profitability Ratios 10/12/31

11/12/31

Net Profit/Net Earnings from recurring Activities

12.70% 5.64%

Net Profit/Total Assets (ROA) 0.6% 0.3%Net Profit/Net Equity (ROE) 4.5% 2.4%Interest Paid/Total Loans 2% 3%

31/12/200931/12/2010

31/12/20110.00%2.00%4.00%6.00%8.00%

ROA & ROE

ROA ROE

4-1Strength Points:Interest paid to total borrowed fund slightly increase from2% to 3%.

4-2Weakness Points:

Page 39 of 47

ROA is below the industry benchmark and also slightlydecreased from 0.6% to 0.3% in the two years respectively.

ROE is also below the industry bench mark and slightlydecreased from 4.5% in 2010 to 2.4% in 2011 despite the highleverage in 2011.

Net Profit/Net Earnings from recurring Activities hasdeceased sharply from 12.70% in 2010 to 5.64% in 2011.

If we can use the average performance of Islamic andconventional Banks in Qatar as a bench mark we which is ≥12% as can be shown from the table;

Bank/Company

NetIncome

NetEquity

NI/NE

QNB 6,260,164 46,209,659

14%

QCB 1,755,664 14,501,282

12%

QIB 1,130,812 11,344,700

10%

Rayan 1,083,409 9,213,633

12%

DB 1,060,529 7,359,038

14%

KCB 378,475 5,537,492

7%

QIIB 708,826 4,881,458

15%

AHLI 366,946 2,903,745

13%

NL 424,535 3,608,565

12%

Average 12% Source: Qatar Exchange www.qe.com.qa – Quarter 3 financial

reports

Achieving 4.5%, and 2.4% by KFH in the two periodsrespectively is quite low and need to be considered andrectified in the near future using one or more of thefollowing approaches; 1-Reduce Equity Multiplier by increasing Bank debts in

order to increase the leverage by maximum (2:1).2-Increase profits by a growth rate higher than equity

growth rate.

2009 2010 2011Dividends 56,85

749,304

39,623

Dividends Ratio 79% 69% 107%Retention Ratio 21% 31% -7%(Internal Growth Rate) 0.1% 0.1% 0.0%

Page 40 of 47

IGR(Sustainable Growth Rate) SGR

0.9% 0.7% -0.2%

2009 2010 2011-0.50%

0.00%

0.50%

1.00%IGR and SGR

IGR SGR

Due to the decrement trend of ROA and ROE in the three years,as can be seen from the above chart, IGR and SGR havedecreased steadily in 2010 and sharply in 2011.

5- Capital Adequacy Ratios:

Capital Adequacy Ratios 10/12/31

11/12/31

Total Debt Finance/Net Equity 0.75 0.89Average Net Equity/Average Total Assets 0.17 0.16

Total Risky Assets/Net Equity 5.32 6.01Net Equity/Total Allocations (Earning Assets) 0.19 0.17

Free Capital/Total Allocations 0.13 0.11Free Capital/Risky Assets 0.13 0.13

5-1Strength Points:Although Total debt/Net Equity has recorded a very lowpercentages but it increased from 75% in 2010 to 89% in2011.

Although free assets to risky assets have recorded a very lowpercentages but it remain stable in the two years.

5-2Weakness Points:Total Risky Assets to Equity is also high bearing in mindthere is a severe lack of risk diversity in KFH credit andinvestment portfolios in terms of products, sectors …etc.

Average net equity to average total assets slightly declinedin 2011.

Page 41 of 47

Total risky assets to net equity have also increased slightlyin 2011.

5-1Capital Adequacy Disclosures: Qualitative and quantitative disclosures related to CapitalAdequacy Standard under Basel II have been prepared inaccordance with KCB instructions and regulations issued as pertheir circular No.2/RBA/44/2009 dated 15 June 2009. General disclosures related to Capital Adequacy Standard underBasel II rely on calculating the minimum capital required tocover credit and market risks using the Standardized Approach.And the minimum capital required to cover operational riskusing the Basic Indicator Approach.The group does not have structure or complex equityinstruments which prohibited with Islamic Shari’a principle.As at 31 December 2011, Tier (1) “Core Capital” amounted KD1,404,493 thousand (2010: KD 1,415,691 thousand), Tier (2)“Supplementary Capital” amounted KD 23,206 thousand (2010: KD6,772 thousand) as detailed below:

Item 2011 2010Capital Structure:

Tier (1) Core Capital;Share Capital 268,904 248,985Disclosed reserves 1,030,6

391,018,7

63Minority interest inconsolidated subsidiaries

264,659 311,999

Total (1) 1,564,202

1,579,747

Deduction from Tier (1) – Core Capital;Treasury shares 46,813 26,722Goodwill 46,291 44,163Unconsolidated institutions 1,556 27,451Significant minorityinvestments

62,674 63,595

Investment in insuranceentities

2,375 2,125

Total (2) 159,709 164,056Total Tier (1) Capital 1,404,4

931,415,6

91Tier (2) Supplementary Capital;Asset revaluation reserves (20,197

)2,834

Faire value reserves (3,511) (11,610)

General provisions 113,519 108,719Total (3) 89,811 99,943

Page 42 of 47

Deduction from Tier (2) Supplementary Capital;Unconsolidated financialinstitutions

1,556 27,451

Significant minorityinvestments

62,674 63,595

Investment in insuranceentities

2,375 2,125

Total (4) 66,605 93,171Total Tier (2) Capital 23,206 6,772Total Available Capital 1,427,6

991,422,4

63Source:2010 and 2011 annual report

5-2Capital Adequacy Ratio:

Capital Adequacy 2011 2010RWA 10,399,7

4210,003,1

52Capital required 1,247,96

81,200,37

8Capital Available:Tier 1 capital 1,404,49

31,415,69

1Tier 2 capital 23,206 6,772Total Capital 1,427,69

91,422,46

3Tier 1 capital adequacyratio

13.51% 14.15%

Total capital adequacy ratio

13.73% 14.22%

Source:2010 and 2011 annual report

As can be seen from the above table KDH has achieved 13.51%& 14.15% as tier 1 CAR and 13.73%, 14.22% as total CAR inthe two years respectively which were above the minimumrequired capital adequacy ratio for tier 1 as well as fortotal capital as per Basel 11 which is 4% for tier 1 CAR and8% for total CAR and also as per & Basel 111 requirementswhich is 6% for tier 1 CAR and 8% for total CAR.

6- Debt Service Ratios: Debt Service Ratios 10/12/

3111/12/31

Cash Flow From Operation/TotalLiabilities 0.03 0.03

Times Interest Occurrence (Coverage Ratio) 2.67 1.70

Times Debt & Interest coverage 0.01 0.004

Page 43 of 47

6-1 Strength Points:Although cash from operation to total liabilities hasrecorded a very low percentages but it remains stable at 3%in the two years.

6-2 Weakness Points:Coverage ratio has slightly declined from 2.67 to 1.7 in thetwo years respectively.

7- Cash Flow Ratios: Cash Flow Ratios 10/12/

3111/12/31

Cash Flow From Operation/TotalSales 134% -32%

Cash Flow From Operation/TotalAssets 7% -2%

Cash Flow From Operation/TotalLiabilities 9% -2%

7-1 Strength Points:No strength points in the above three ratios.

7-2 Weakness Points:Obvious sharply decrement of Cash Flow from Operation toTotal sales from 134% in 2010, to (32%) in 2011 indicatingthat the bank has a serious disability to meet its short-term liabilities.

Also cash from operation to total assets and to totalliabilities has declined sharply.

8- Market Ratios: Market Ratios 10/12/

3111/12/31

EPS 0.03 0.01DPS 0.02 0.01DPR 0.69 1.07Shares Market Value/Total Liabilities 235.89 249.56

MVS 1120.00

1060.00

P/E (Share Price Multiplier) 35971.99

76819.39

DY (Dividends Yield or Share Proceeds) (%) 0.00 0.00

8-1 Strength Points: DPR increased steadily from 0.69 in 2010 to 1.07 in 2011.

Page 44 of 47

Share market value to total liabilities has increasedsteadily.

Share price multiplier has also increased sharply8-2 Weakness Points: MVS declined.DY is approximately zero.EPS and DPS were slightly decreased.

Depositors’ Accounts:The depositors’ accounts of the Bank comprise the following:1-Non-investment deposits in the form of current accounts.

These deposits are not entitled to any profits nor do theybear any risk of loss as the Bank guarantees to pay therelated balances on demand. Accordingly, these deposits areconsidered Qard Hasan from depositors to the Bank underIslamic Sharia.

2-Investment deposits comprise Khumasia, Mustamera, and Sedradeposits for unlimited periods and Tawfeer savings accounts.Unlimited investment deposits are initially valid for oneyear and are automatically renewable for the same periodunless notified to the contrary in writing by the depositor.Investment savings accounts are valid for an unlimitedperiod. In all cases, the investment deposits receive aproportion of the profit as the board of directors of theBank determines, or bear a share of loss based on theresults of the financial year.

The Bank generally invests approximately 100% of investmentdeposits for unlimited period (“Khumasia”), 90% of investmentdeposits for an unlimited period (“Mustamera”), 70% ofinvestment deposits for an unlimited period (“Sedra”) and 60%of investment saving accounts (“Tawfeer”). The Bank guaranteesto pay the remaining uninvested portion of these investmentdeposits. Accordingly, this portion is considered Qard Hasan fromdepositors to the Bank, under Islamic Sharia. Investing such Qard Hasan is made at the discretion of theBoard of Directors of the Bank, the results of which areattributable to the equity holders of the Bank.

The most innovated productsIslamic Derivatives:KFH is one of the first Islamic Banks customized and adaptedIslamic Derivatives in the ordinary course of business in

Page 45 of 47

forms of currency swaps, profit rate swaps, forward foreignexchange and forward commodity contracts to mitigate foreigncurrency and profit rate risk. Currency swaps and forwardcommodity contracts are based on Waad (promise) structurebetween two parties to buy a specified Sharia compliantcommodity at an agreed price on the relevant date in future.It is a conditional promise to purchase a commodity throughunilateral purchase undertaking. Currency swap structure comprises profit rate swap andcurrency swap. For profit rate swaps, counterparties generallyexchange fixed and floating rate profit payments based on anotional value in a single currency. For currency swaps, fixed or floating payments as well asnotional amounts are exchanged in different currencies.The currency swaps, forward foreign exchange and forwardcommodity contracts are being used to hedge the foreigncurrency risk of the firm commitments.Embedded swaps and profit rate contracts are balances withbanks and financial institutions with rates of return tied tochanges in value of precious metals.At 31 December 2011, the Group held currency swaps, profitrate swaps, forward foreign exchange and forward commoditycontracts designated as hedges of expected future collectionsfrom hedged items in foreign currency and variability inprofit rate.The table below shows the positive and negative fair values ofthese instruments, which are equivalent to the market values,together with the notional amounts. The notional amount is theamount of currency swap instruments’ underlying asset,reference rate or index and is the basis upon which changes inthe value of these instruments are measured. The notionalamounts indicate the volume of transactions outstanding at theyear end and are not indicative of the credit risk.

Item (+) Fairvalue

(-) fairvalue

Amount National amount by term tomaturity

3month

3-12month

> 12month

Cash flow hedges:Forward contracts 20 441 62,290 36,177 26,113 0Profit rates swap 215 90 10,237 0 0 10,237Currency swap 786 115 28,005 0 0 28,005Total 1,021 646 100,53

236,177 26,113 38,242

Not designated as hedges:Forward contracts 11,108 8,599 468,10

2373,95

694,146 0

Page 46 of 47

Profit rates swap 2,123 1,586 28,122 0 0 28,122Currency swap 1,485 1,533 26,287 0 0 26,287Embedded preciousmetals

0 1.338 174,600

166,188

8,389 23

Total 14,716 13,056 697,111

540,144

102,535 54,432

Grand Total 15,737 13,702 797,643

576,321

128,648 92,674

Source: 2011 annual report

Co-operative Marketing:It is one of the most innovative product being created andpracticed by KFH. The product specialized for financing thelocal trade and to encourage the national products. KFH buysthe high demand goods by the consumers from the originalsource (factory - supplier) and sells it to the co-operativesand pay to suppliers in cash and immediately the value ofthese purchases, so the supplier is not obliged to wait morethan 90 days to collect the values. The supplier, himselftransports and delivers the goods to the co-operatives onbehalf of KFH in a Wakala based contract.The co-operative marketing product fully supports and helpsthe suppliers to get back their capital in a very fast waythat paves the way freely to produce, develop and prevents thestumbles of capital resulted from the long term collection andthe non-sufficiency of the working capital.

Page 47 of 47