Lezaun& Calvillo. In the Political Laboratory: Kurt Lewin's Atmospheres

Upload

khangminh22Category

view

3download

0

Greater OKC Chamber

One of the nation’s largest chambers!

More than 5,000 Members

American Chamber of Commerce Executives

Best of Show in 2012

Consistently rated Top 10 Chamber

A Look Ahead At 2014 And Lessons From 2013

CREC February 20, 2014

ECONOMIC FORECAST & DATA TOOLS

GREATER OKLAHOMA CITY

2.4% 2.6% 2.3%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

0

100

200

300

400

500

600

700

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ann

ual P

erce

nt C

hang

e

MSA

Employ

men

t, Tho

usan

ds

OKC MSA Nonfarm and Private Employment

Percent Change, YOY OKC Nonfarm OKC Private

0.5% 2.2%

4.1%

6.7

21.0

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

0

5

10

15

20

25

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Anu

ual P

erce

nt Cha

nge

Mining Em

ploy

men

t, Tho

usan

ds

OKC MSA Mining Employment

Percent Change, YOY OKC Mining Employment

-‐12.1%

-‐4.6%

2.5% 1.8% 2.6%

-15%

-10%

-5%

0%

5%

10%

0

10

20

30

40

50

60

Ann

ual P

erce

nt Cha

nge

Man

ufac

turing

Employ

men

t, Tho

usan

ds

OKC MSA Manufacturing Employment

Percent Change, YOY OKC Manufacturing Employment

1.1%

3.6% 3.1%

-‐8.0%

-‐6.0%

-‐4.0%

-‐2.0%

0.0%

2.0%

4.0%

6.0%

0

10

20

30

40

50

60

70

80

90

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ann

ual P

erce

nt Cha

nge

PBS Em

ploy

men

t, Tho

usan

ds

OKC MSA Professional and Business Employment

Percent Change, YOY OKC Professional and Business Employment

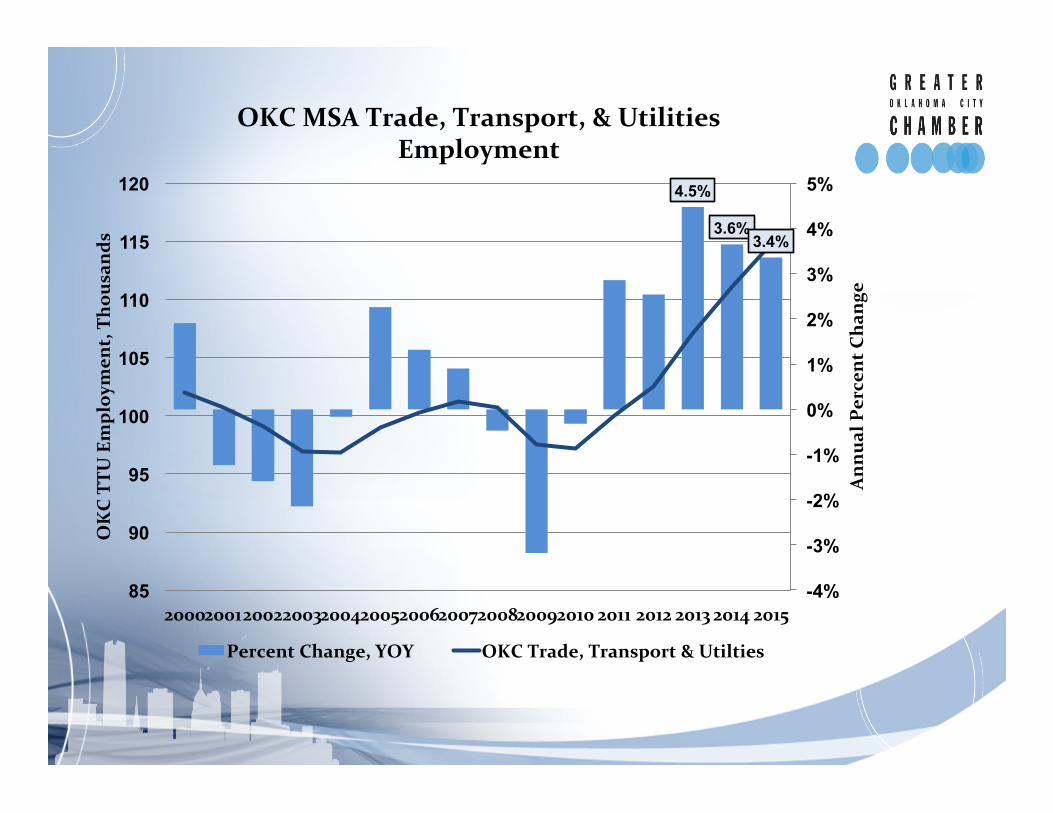

4.5%

3.6% 3.4%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

85

90

95

100

105

110

115

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Ann

ual P

erce

nt Cha

nge

OKC TTU

Employ

men

t, Tho

usan

ds

OKC MSA Trade, Transport, & Utilities Employment

Percent Change, YOY OKC Trade, Transport & Utilties

4.0%

4.6%

-10%

-5%

0%

5%

10%

15%

0

10,000

20,000

30,000

40,000

50,000

60,000

1990

19

91

1992

19

93

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

20

15

Ann

ual G

rowth

, %

Per Cap

ita Perso

nal Inc

ome ($)

OKC MSA Per Capita Personal Income

Annual Growth OKC Per Capita Personal Income

1.7% 1.6%

-2%

-1%

0%

1%

2%

3%

4%

5%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1970

19

72

1974

19

76

1978

19

80

1982

19

84

1986

19

88

1990

19

92

1994

19

96

1998

20

00

2002

20

04

2006

20

08

2010

20

12

2014

Ann

ual G

rowth

, %

MSA

Pop

ulation

OKC MSA Population

Annual Growth OKC MSA Population

-‐6%

-‐4%

-‐2%

0%

2%

4%

6%

8%

10%

0

100

200

300

400

500

600

700

800

900

Jan-

91

Sep-

91

May

-92

Jan-

93

Sep-

93

May

-94

Jan-

95

Sep-

95

May

-96

Jan-

97

Sep-

97

May

-98

Jan-

99

Sep-

99

May

-00

Jan-

01

Sep-

01

May

-02

Jan-

03

Sep-

03

May

-04

Jan-

05

Sep-

05

May

-06

Jan-

07

Sep-

07

May

-08

Jan-

09

Sep-

09

May

-10

Jan-

11

Sep-

11

NF Em

ploy

men

t, Tho

usan

ds

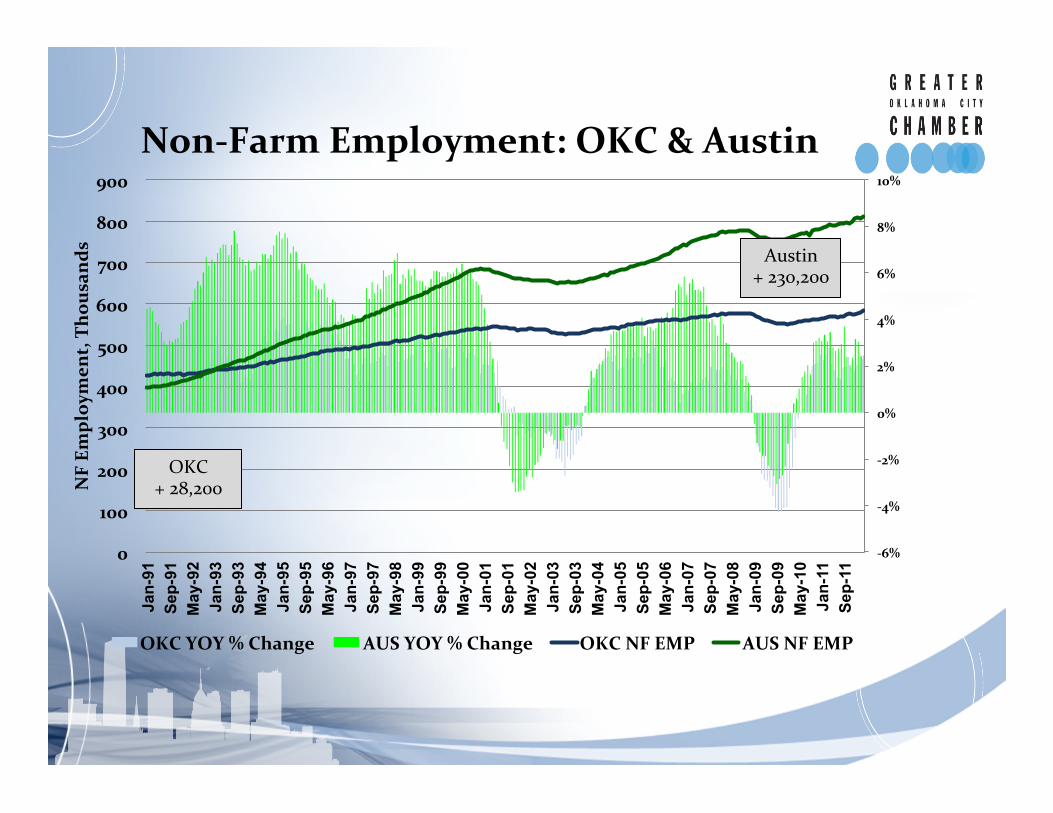

Non-‐Farm Employment: OKC & Austin

OKC YOY % Change AUS YOY % Change OKC NF EMP AUS NF EMP

OKC + 28,200

Austin + 230,200

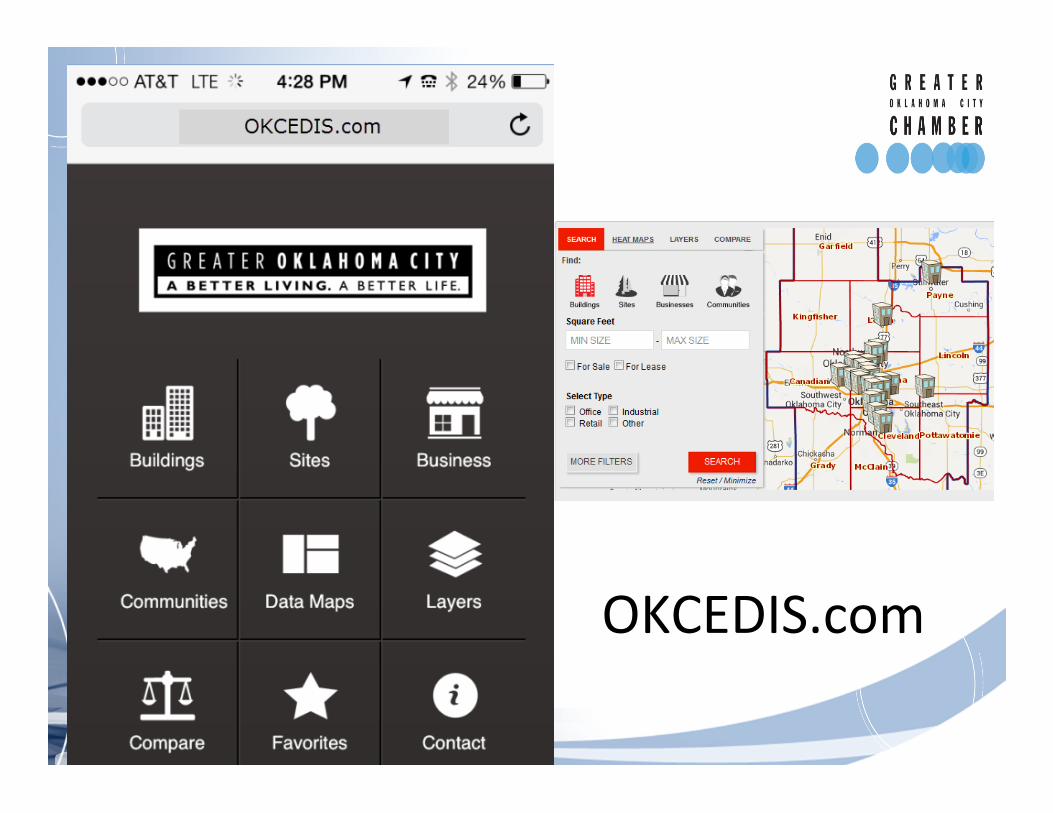

OESC Employer Locator 193,000 business records with contact info for Oklahoma companies

OKCEDIS.com

www.greateroklahomacity.com/OKCLBI

OKC Local Business Intelligence Tool

Compare your business to the compe??on • By industry, city, county, metro, state and na?on

Research Tools 2014 Economic Forecast available at: • www.greateroklahomacity.com/forecast

OESC Employer Locator (business list) • hUp://www.oesc.state.ok.us/lmi/EmployerLocator/ Commercial Property Locator • www.OKCEDIS.com

Local Business Intelligence Tool • www.greateroklahomacity.com/OKCLBI

2013 RESULTS AND PIPELINE ACTIVITY

GREATER OKLAHOMA CITY

2013 Actuals 2013 Goals Campaign

Actuals 5-‐Year Goals**

Jobs 6,561 4,000 – 5,000 15,110 20,000 – 25,000

Average Salary*** $43,533 $45,453 -‐-‐

$47,430 $54,736 $45,453 -‐ $47,430

Capital Investment $501,709,800 $180M -‐

$200M $1,297,219,330 $900M -‐ $1Billion

Local Tax Revenue* $13,058,477 $10M -‐ $11M $33,736,788 $50M -‐ $55M

Forward OKC IV Results

January 2014 Project Pipeline

*Note: Not all projects provide the key pieces of information listed above.

13,625 jobs $399 million payroll

$555 million capital investment

3.6 million Sq. Ft.

28 Ac?ve Projects

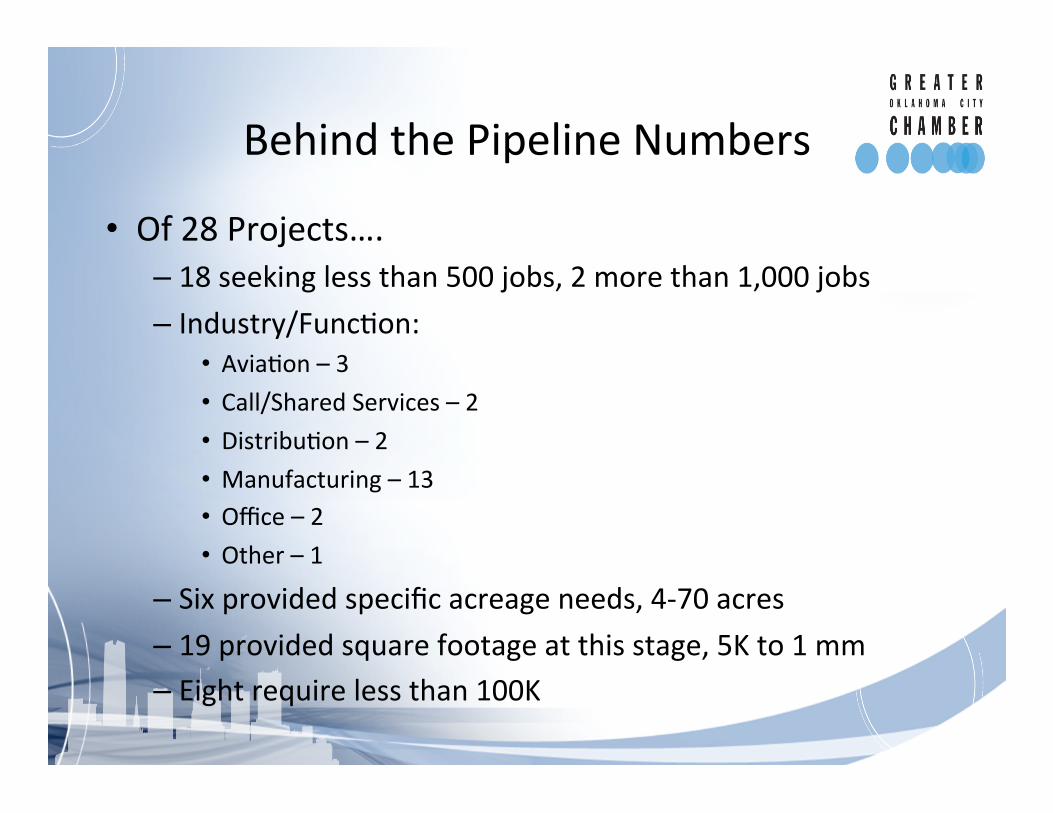

Behind the Pipeline Numbers

• Of 28 Projects…. – 18 seeking less than 500 jobs, 2 more than 1,000 jobs – Industry/Func^on:

• Avia^on – 3 • Call/Shared Services – 2 • Distribu^on – 2 • Manufacturing – 13 • Office – 2 • Other – 1

– Six provided specific acreage needs, 4-‐70 acres – 19 provided square footage at this stage, 5K to 1 mm – Eight require less than 100K

2013 Projects

10

15

20

25

30

35

40

Total Projetcs

2013 Jobs

0

4,000

8,000

12,000

16,000

20,000

*Note: Not all projects provide the key pieces of information listed above.

2013 Total Annual Payroll

$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

$300,000,000

$350,000,000

$400,000,000

$450,000,000

*Note: Not all projects provide the key pieces of information listed above.

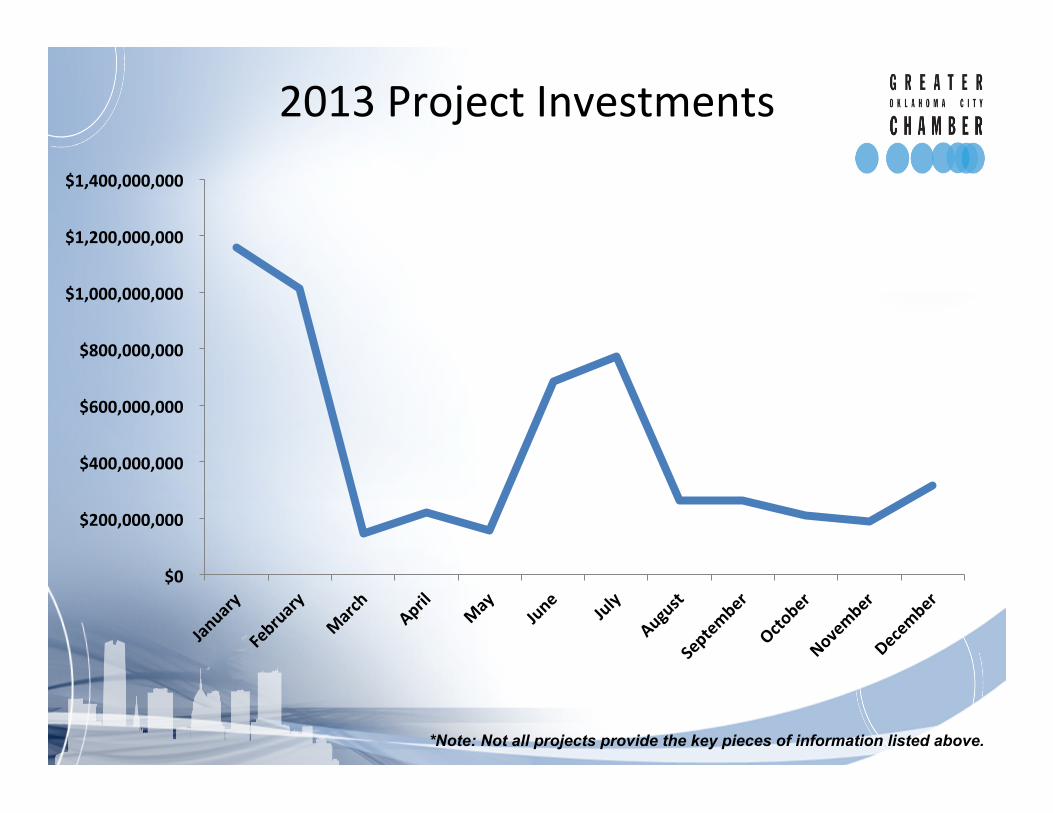

2013 Project Investments

$0

$200,000,000

$400,000,000

$600,000,000

$800,000,000

$1,000,000,000

$1,200,000,000

$1,400,000,000

*Note: Not all projects provide the key pieces of information listed above.

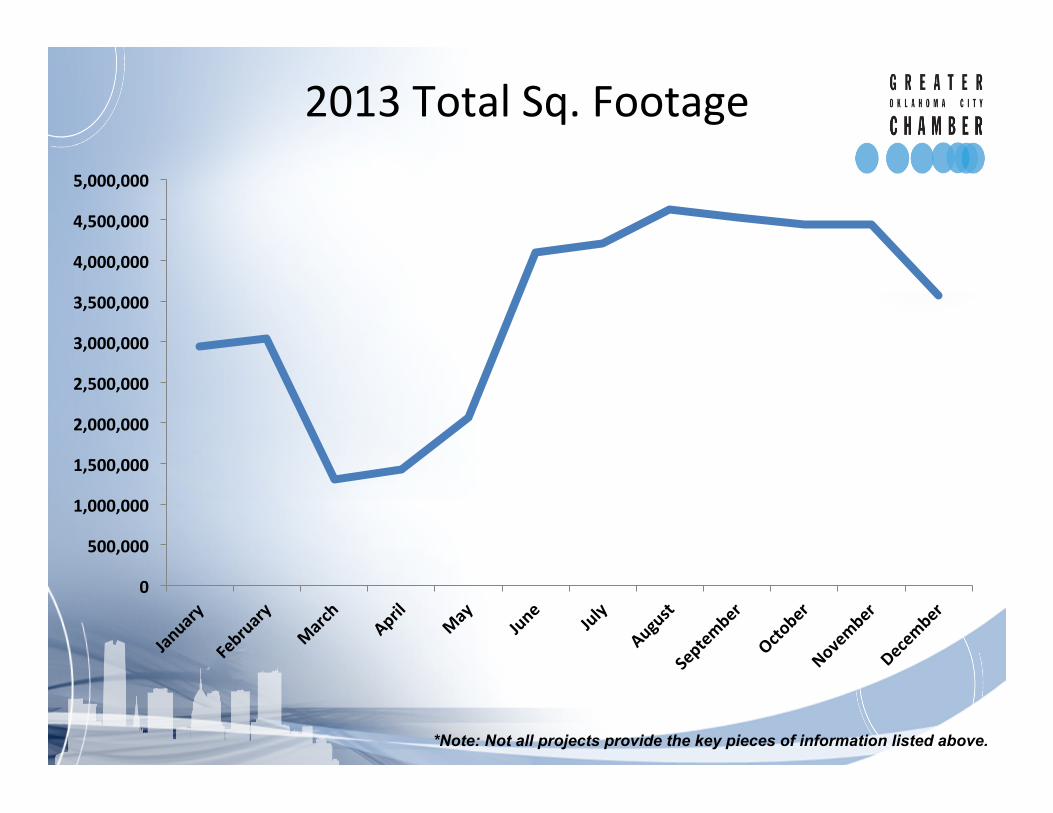

2013 Total Sq. Footage

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

*Note: Not all projects provide the key pieces of information listed above.

Retail Efforts: Results and Impacts • More than 40 site visits in OKC in 2013

– OKC con^nues to be on the radar of retailers recognizing OKC’s poten^al

• Moving from “Top of Low Priority List” to “Top of List” for 2014-‐15.

• Snapshot of Announcements in 2013 (All First Oklahoma Loca^ons) – Nordstrom Rack – Top Golf – Von Maur – Microsok

• Development and Redevelopment Opportuni^es Underway

Key Opportunity: Underserved Markets

• Why focus on these areas? – Tradi^onal market data and analysis may be inaccurate or misrepresent the economic poten^al and purchasing power

– Seeking to establish a healthier retail presence through public-‐private partnerships in underes^mated, primarily urban inner city markets

– Bring OKC prosperity to more por^ons of the City over ^me

Highligh^ng Underserved Markets • Held Program on Poten^al of Underserved Markets

– Partnered with Interna^onal Council of Shopping Centers (ICSC), City of OKC, Alliance for Economic Development, Urban Land Ins^tute (ULI) & Black Chamber

• Follow-‐up Underway with key interest groups • Community (residents, community based organiza^ons) • Government (elected officials and professional staff) • Developers • Retailers

• Working with exis^ng retailer, Alliance and City on a site in NE OKC to increase store footprint size and add further development

• Con^nue dialogue with retailers and developers about various underserved sites in OKC

Project Golden Fox

• Interna^onal company seeking new North American manufacturing loca^on

• Investment: $800 MM, 750 employees (avg. wage $53K+) • Need: 160 acre site • Outcome: OKC region dropped • Challenge: had only one site that was poten^ally a fit really.

School Lands site, requiring public bid process and had challenges on site too (easements, etc.)

Project Domino

• Petro Chemical plant • Investment: $550 MM, 80 employees (avg. wage $76K+) • Need: 60 acre site, rail served and 2 million gallons of water/

day plus lots of natural gas (60,000 MMBtu/day) • Outcome: OKC region dropped • Challenge: water requirement just not workable AND would

have been largest natural gas user in state

Project Lewis & Clark

• Fulfillment Center/distribu^on • Investment: 400-‐600 employees • Need: 300-‐500,000 sf building with 32 foot clear height and

very ^ght ^meframe (needed opera^onal in 12 months) • Outcome: OKC region dropped • Challenge: no exis^ng buildings; only built to suit op^ons.

Company was too nervous to have it work in their ^meframe

Project Delta

• Shared Service center (HR/IT/Finance) • Investment: 1,100 employees (avg. wage $39K+) • Need: Exis^ng 100,000 sf building • Outcome: OKC region dropped in finals, Nashville chosen • Challenge: two poten^al buildings. one was downtown,

second refiUed industrial building. Parking issues downtown and other challenges at second facility. Nashville, more op^ons for real estate, same ^me zone as HQ

Poten^al Take-‐Aways

• Challenges of Success are evident across most of MSA/region • Lack of product straining ability to capture some opportuni^es

– Lease rate expecta^ons and reali^es geung closer but not completely there yet

• Pressure by other uses on “good places” for employment opportuni^es con^nues to create challenges

• Need to determine ways to balance lessons learned in 1980s with expecta^ons/ interests of today’s prospects – Staying financially wise while crea^ng enough product

THANK YOU Eric Long Research Economist [email protected] 405-‐297-‐8976

Kurt Foreman EVP Economic Development [email protected] (405) 297-‐8945

Copyright © 2022 FDOKUMEN