DELIVERING BETTER OUTCOMES IN EDUCATION: THE WORLD BANK'S EXPERIENCE

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page I

KHADIM ALI SHAH BUKHARI INSTITUTE OF TECHNOLOGY (KASBIT)

INTERNAL AUDIT EFFECTIVENESS AND ITS IMPACTS ON THE BANK’S CREDITABILITY

A CASE STUDY OF HABIB BANK LTD

A Thesis By:

M Shahid Siddiqui

ID # 1183

Supervised By:

Muhammad Sarfraz Munir

Submitted to Faculty of Management Sciences of

Khadim Ali Shah Bukhari Institute of Technology (KASBIT)

In partial fulfillment of the requirements for the degree of

Masters of Business Administration (MBA) with distinction

June 2012

Copyright 2012 NAGHMA NAZ

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page II

All Rights Reserves

CERTIFICATE

I am pleased to certify that Mr. Muhammad Shahid Siddiqui S/o M Ishaque has satisfactorily

carried out a research work, under my supervision on the topic of “INTERNAL AUDIT

EFFECTIVENESS AND ITS IMPACTS ON THE BANK’S CREDITABILITY. A CASE STUDY OF HABIB BANK

LTD”.

I further certify that this distinctive original research and his thesis is worthy of presentation to the

Department of Finance, Faculty of Management Sciences, Khadim Ali Shah Bukhari Institute of

Technology (KASBIT) for the degree of Master of Business Administration (MBA).

______________________ Muhammad Sarfraz Munir

Project Supervisor

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page III

DECLARATION I declare that the thesis submitted for the degree of Master of Business Administration at the

Khadim Ali Shah Institute of Technology is my own work and effort. It has not been previously

submitted by me at another university for any degree. I cede copy right of this thesis in favor of

the Khadim Ali Shah Institute of Technology.

This thesis is a presentation of my original research. The work was done under the guidance of Mr.

Muhammad Sarfraz Munir.

I further declare that it is free of plagiarism is checked by online software.

MR MUHAMMAD SHAHID SIDDIQUI

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page IV

DEDICATION

This project is dedicated to my beloved Parents who have never failed to give me financial and

moral support throughout my academic career and also for their love, patience, encouragement

and prayers, for giving all my need during the time I developed my system and for teaching me

that even the largest task can be accomplished if it is done one step at a time.

I owe my deepest gratitude to my parents whose steadfast support of this project was greatly

needed and deeply appreciated.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page V

LETTER OF TRANSMITTAL

Respected Sir/Madam,

This research study submitted for the fulfillment of MBA by considering area of study “INTERNAL

AUDIT EFFECTIVENESS AND ITS IMPACTS ON THE BANK’S CREDITABILITY. A CASE STUDY OF HABIB

BANK LTD”.

This study based on statistical descriptions by considering the variables for the internal audit

effectiveness and its impact on the bank’s credibility. The researcher has considered the some

variables internal audit staff education, quality audit work, audit program, etc.

Analysis and Discussion section of this study supports that in future the importance of audit

department will be on peak as the managements are intended to have the high quality of internal

working without having any fraud risk. The respondents also acknowledge the importance of the

internal audit with respect to the external factors which includes the changing polices of central

bank, new technological changes etc.

Thank you,

Muhammad Shahid Siddiqui Reg. No. 1183 MBA Finance KASBIT

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page VI

ACKNOWLEDGEMENT

I am gratified to ALLAH, the most beneficial, who gave me the strength and will to overcome the

obstacles surfaced during the completion of this thesis.

Making a report of this stature could not be possible without the grace of ALLAH and continuous

support of my supervisor.

I feel exceptional warmth and gratitude in extending my appreciation for sincere and benevolent

guidance and patronage of the report to my Supervisor Muhammad Sarfraz Munir. It was a

privilege to have an advisor who gave me the freedom to explore on my own. His guidance at

every step of writing could not let my steps faltered. I am thankful to him for holding me to a high

research standard writing and for analyzing and rectifying my mistakes countless times. Also for

encouraging me too high when I considered myself to be in vain.

Last but not the least; I would render great thanks to all respondents and others who in one way

or other co-operated with me over the course of my research.

BY

Muhammad Shahid Siddiqui

Reg. No. 1183 Department of Finance, Faculty of Management Sciences, Khadim Ali Shah Bukhari Institute of Technology (KASBIT) Dated: 30th June 2012

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page VII

ABSTRACT

Purpose: The purpose of this project is to conduct the research on the internal audit effectiveness and its impacts on the bank’s credibility. The researcher has selected the Habib Bank Limited as Target Company for this research. Literature Review: The literature review reveals that internal audit department is playing vital role in the development of credibility of the bank in the external financial market. The literature review also acknowledges the importance of the internal audit with respect to internal control on fraud & forgeries. Target Group: The target group is the audit managers of the banking sector.

Design/Methodology/Approach: Primary data for the project was collected through the questionnaire duly filled by 50 (Fifty in Numbers) of respondents from Internal Audit Department of banking sector. Different statistical tools have been applied to analyze the responses from the respondents to prove the objective and purpose of the project. Limitations: The study is limited to banking sector only. Findings: It is observed that respondent acknowledges the importance of the internal audit department in the banking sector. The respondents also acknowledge the key role of the internal audit department in creating the credibility in the external financial market. The respondents also

of the opinion that quality of the internal audit, quality of education internal auditors, audit program effectiveness etc. are playing vital role in developing the credibility of the internal audit

department in any financial institution.

Results & Conclusion: After implementation of international guidelines by the central bank, the internal audit department standards have been improved. The impact of this adoption is not only on the working style and coverage of the financial workings. The credibility of the financial entity based on the internal audit workings and true and fair view of the management workings. Therefore the internal audit department is playing vital role in creating the credibility of the

financial institution in the financial market.

Originality/Value: Project finding and result concluded from personnel of Banking Sector, audit managers of banking sector.

Keywords: Banking Sector, Internal Audit, Internal Auditors, Internal Audit Department,

Credibility, Financial Market etc.

Project Type: Research Project

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page VIII

Table of Contents

Certificate II Declaration III Dedication IV Letter of Transmittal V Acknowledgement VI Abstract VII List of Tables XIV List of Graphs XV

CHAPTER 01 Introduction 1

1. Introduction 1

1.1 Researcher Objectives 1

1.2 Scope of the Study 1

1.3 Problem Definition 1

1.4 Problem Statement 1

1.5 Introduction 2

1.5.1 Definition of Internal audit 2

1.5.2 Internal Auditors? 2

1.5.3 Internal Audit Function 3

1.6 Audit Process 3

1.6.1 Planning 3

1.6.2 Announcement Letter 3

1.6.3 Initial Meeting 4

1.6.4 Preliminary Survey 4

1.6.5 Internal Control Review 4

1.6.6 Audit Program 4

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page IX

1.6.7 Fieldwork 4

1.6.8 Transaction Testing 5

1.6.9 Advice & Informal Communications 5

1.6.10 Audit Summary 5

1.6.11 Working Papers 5

1.6.12 Audit Report 5

1.6.13 Discussion Draft 6

1.6.14 Exit Conference 6

1.6.15 Formal Draft 6

1.6.16 Final Report 6

1.6.17 Client Response 7

1.6.18 Client Comments 7

1.6.19 Audit Follow-Up 7

1.6.20 Follow-up Review 7

1.6.21 Follow-up Report 8

1.6.22 Internal Audit Annual Report to the Board 8

1.6.23 The Process: A Collaborative Effort 8

1.7 Code of Ethics for Internal Auditors 9

1.8 Limitations 10

CHAPTER 02 Literature Review 11

2.1 Literature Review 11

2.2 Theoretical Framework 14

2.2.1 Policy and Procedure 14

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page X

2.2.2 Delegation of Authorities 14

2.2.3 Audit Program 14

2.2.4 Sampling 15

2.2.5 Staff Trainings 15

2.2.6 Quality of Work 15

2.2.7 Internal Audit Standard 16

2.2.8 Central Bank Guidelines 16

2.2.9 Bank’s Credibility and Internal Audit 17

2.2.10 Characteristics of the Individual Internal Auditor 17

2.2.11 Technical Skills 17

2.2.12 Behavioral Skills 18

2.2.13 Broader Organizational Enviorment 18

CHAPTER 03 Company Profile 19

3 Company Profile 19

3.1 Brand of HBL 19

3.2 Vision 19

3.3 Mission 19

3.4 Values 19

3.5 Excellence 19

3.6 Integrity 19

3.7 Customer Focus 19

3.8 Meritocracy 20

3.9 Progressive 20

3.10 Board of Directors 20

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XI

3.11 Management 21

3.12 Awards 22

3.13 Introduction 23

3.14 Ratings 23

3.15 History 24

3.16 Financial Performance of Habib Bank Ltd 25

3.16.1 Balance Sheet 25

3.16.2 Profit and Loss Statement 27

3.16.3 Valuation Statistics 29

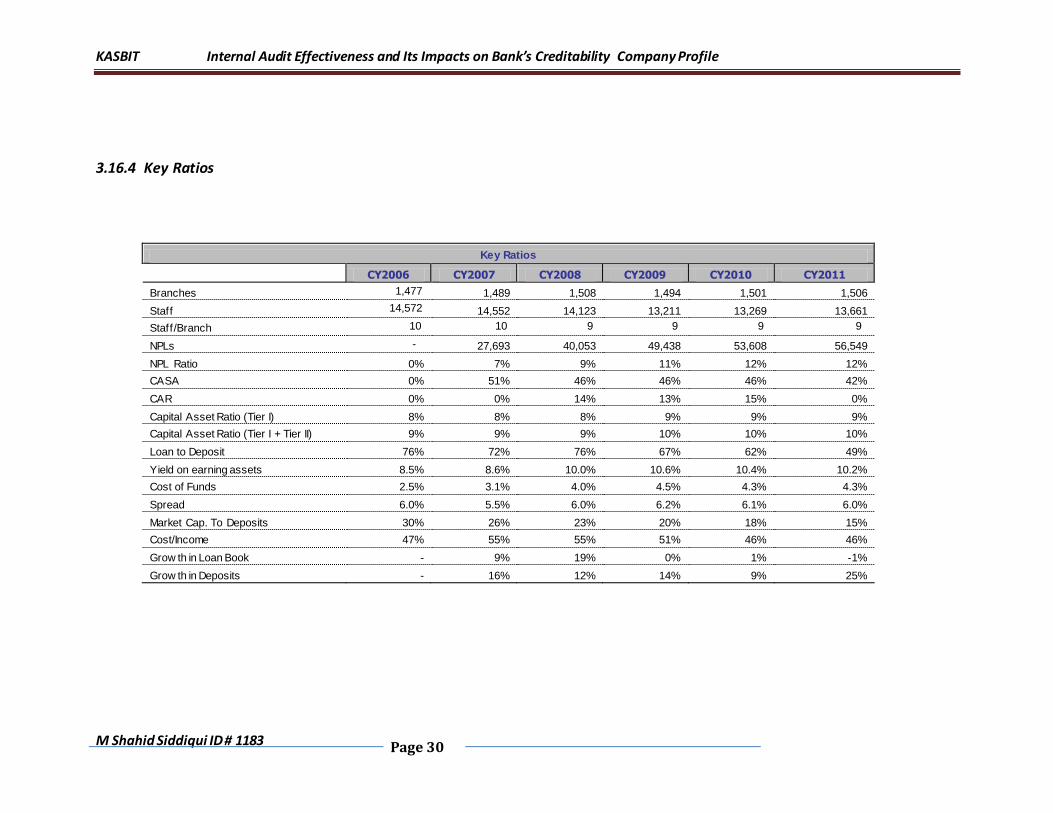

3.16.4 Key Ratios 30

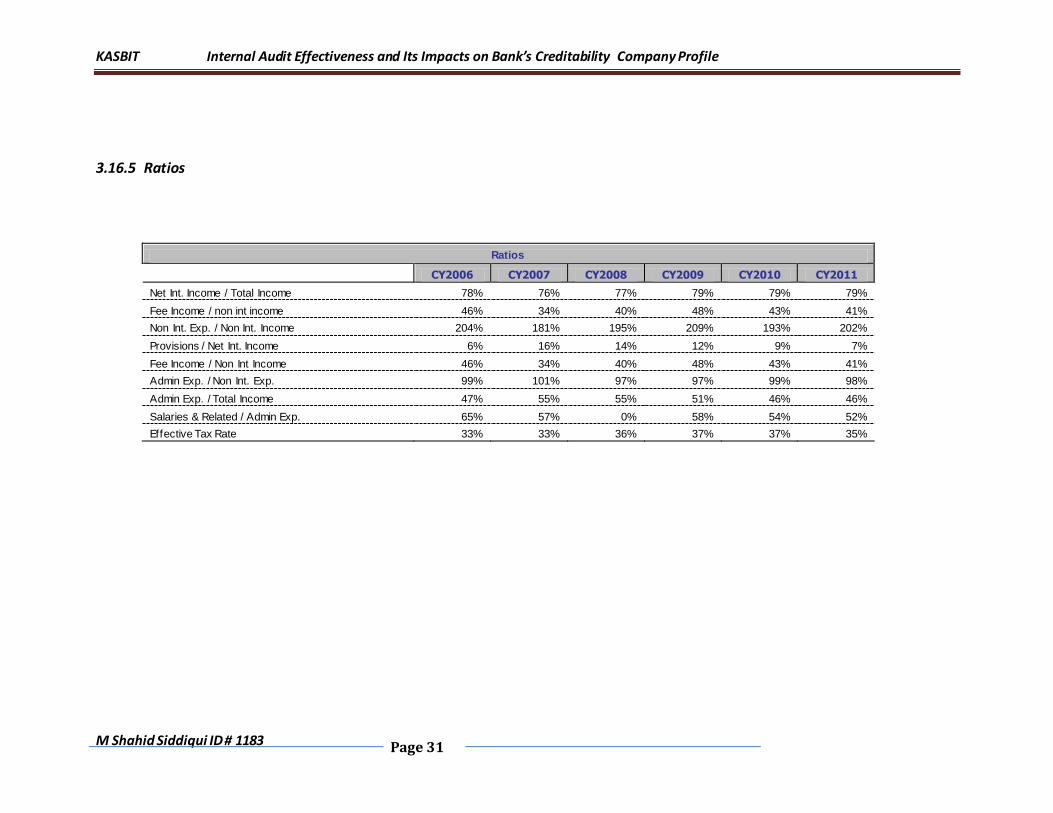

3.16.5 Ratios 31

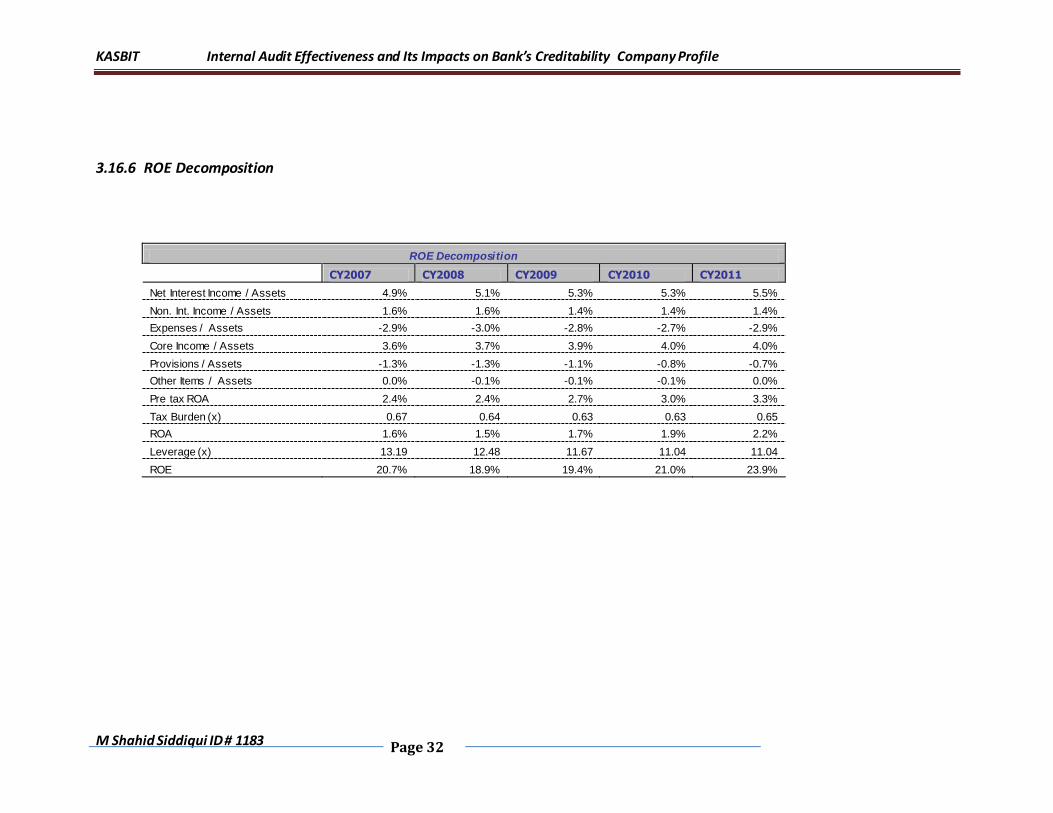

3.16.6 ROE Decomposition 32

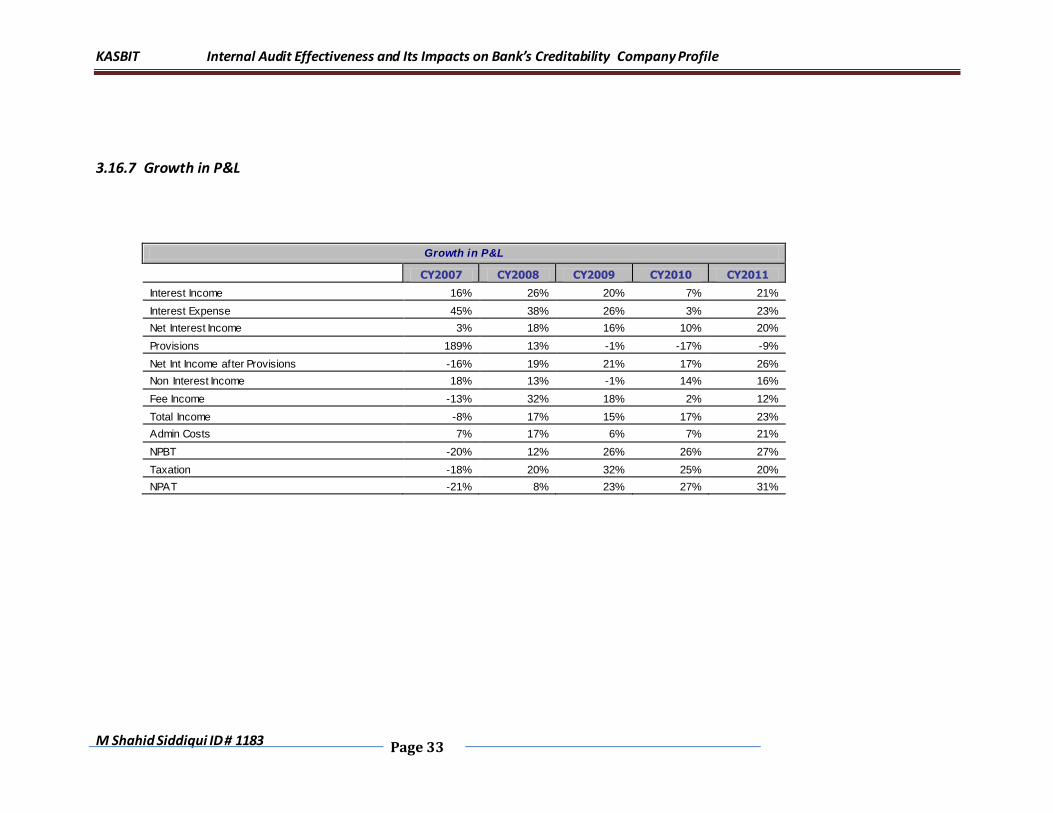

3.16.7 Growth in P&L 33

3.16.8 Graphical Representation 34

CHAPTER 04 Methodology 47

4.1 Problem Definition 47

4.2 Problem Statement 47

4.3 Research Design 48

4.3.1 The Purpose of the Study 48

4.3.2 The Type of Investigation 48

4.3.3 Extent of Research Interference 48

4.3.4 The Study Setting 48

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XII

4.3.5 The Unit of Analysis 48

4.3.6 The Time Horizon 48

4.4 Sample Design 49

4.4.1 Population 49

4.4.2 Sampling Frame 49

4.4.3 Sampling Unit 49

4.4.4 Sampling Type 49

4.4.5 Sampling Size 49

4.4.6 Sampling Plan 49

4.4.7 Select a Sample 50

CHAPTER 05 Data Analysis 51

05 Data Analysis 51

CHAPTER 06 Hypothesis Testing 56

6.1 Hypothesis Testing 56

6.1.1 Hypothesis No. 1 56

6.1.2 Hypothesis No. 2 57

6.1.3 Hypothesis No. 3 58

6.1.4 Hypothesis No. 4 59

6.1.5 Hypothesis No. 5 60

CHAPTER 07 Conclusion 61

7 Conclusion 61

7.1 Chapter wise Conclusion 61

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XIII

7.1.1 Chapter 1 61

7.1.2 Chapter 2 61

7.1.3 Chapter 3 61

7.1.4 Chapter 4 62

7.1.5 Chapter 5 62

7.1.6 Chapter 6 62

7.1.7 Chapter 7 62

7.2 General Conclusion 63

CHAPTER 08 Recommendations 66

8 Recommendations 66

8.1 Objective of Internal Audit Department 66

8.2 Independent Function of Audit Department 66

8.3 Professional Competencies 66

8.4 Internal Audit Integrity 66

8.5 Internal Audit Department Charter 66

8.6 Scope of the Internal Audit Department 67

8.7 Regulatory Requirements Audit 67

8.8 Permanent Status of Internal Audit Department 67

8.9 Responsibility of Board of Directors 67

8.10 Audit Committee 67

8.11 Responsibilities of Head of Internal Audit Department 67

8.12 Reporting to Internal Audit Department 68

8.13 Assessment of Risk Management 68

8.14 Transformation of Internal Audit Requirements 68

8.15 General Requirements 69

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XIV

CHAPTER 09 References 70

9 References 70

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XV

List of Table

Table 1: Balance Sheet

Table 2: Profit & Loss Statement

Table 3: Valuation Statistics

Table 4: Key Ratio Analysis

Table 5: Ratio Analysis

Table 6: ROE Decomposition

Table 7: Growth in P&L

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XVI

List of Graphs

Graph No. 1 Branches

Graph No. 2 Staff

Graph No. 3 Staff per Branch

Graph No. 4 Non-Performing Loans

Graph No. 5 NPL Ratio

Graph No. 6 CASA

Graph No. 7 Capital Assets Ratio (TIER I + TIER II)

Graph No. 8 Capital Assets Ratio (TIER I)

Graph No. 9 Loan to Deposits

Graph No. 10 Yield on Earning Assets

Graph No. 11 Cost of Fund

Graph No. 12 Spread

Graph No. 13 Market Capitalizations to Deposits

Graph No. 14 Cost / Income

Graph No. 15 Growths in Loan Books

Graph No. 16 Growths in Deposits

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XVII

1.1 Researcher Objectives

The researcher objective is to performance the analysis of audit techniques and its impacts on the

bank’s creditability. The researcher will have to perform the complete analysis of different audit

techniques, its methods, its sampling methods, and financial cost as well. The research will also

have to analysis of impacts of the effectiveness of the internal audit on the bank’s credibility.

1.2 Scope of the Study

The scope of the study is not limited to the one bank only however the same concept can be

applied to all banks. This study will be beneficial for finance as well as other students to analyze the

future of the market and job opportunities. This will help those who have interest in the internal

audit effectiveness. This research will serve as plat form for those students who want to work on

the inter audit management as well as new comers who want to excel their career in the same. The

students will also cater who want to conduct more research on the same topic with new aspects.

1.3 Problem Definition

What are the financial impacts of the internal audit effectiveness on the bank’s credibility?

1.4 Problem Statement

Internal audit is the main component of the any bank. The audit department established

with the idea of the establishment of bank. The Central Bank has the clear policy on the

internal audit department as well. Therefore the effectiveness of the internal audit

department will have the impacts on the credibility as well as on the financial performance

as well.

1.5 Introduction

1.5.1 Definition of Internal audit

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XVIII

Internal auditing is an independent appraisal function established within an organization

which examines and evaluates its activities as a service to the organization. The objective

of internal auditing is to assist the organization, in particular managers and members of the

board of directors, to discharge of their responsibilities effectively. To this end, internal

auditing furnishes them with analyses, appraisals, recommendations, advice and

information concerning the activities reviewed. The audit objective includes promoting

effective control at reasonable cost. This is how the Institute of Internal Auditors defines

internal auditing. It can also be regarded as the means by which management learns if its

internal control systems are appropriately designed and in fact working.

1.5.2 Internal Auditors?

As defined by the Institute of Internal Auditors (IIA), "Internal auditing is an independent,

objective assurance and consulting activity designed to add value and improve an

organization's operations. It helps an organization accomplish its objectives by bringing a

systematic, disciplined approach to evaluate and improve the effectiveness of risk

management, control, and governance processes.

Internal Auditors' roles include monitoring, assessing, and analyzing organizational risk and

controls; and reviewing and confirming information and compliance with policies,

procedures, and laws. Working in partnership with management, internal auditors provide

the board, the audit committee, and executive management assurance that risks are

mitigated and that the organization's corporate governance is strong and effective. And,

when there is room for improvement, internal auditors make recommendations for

enhancing processes, policies, and procedures."

1.5.3 Internal Audit Function

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XIX

The financial sector audit department exists by by-law to assist the Audit Committee of the

Board of Directors in effectively fulfilling their responsibilities. Internal Auditors are

charged with examining and evaluating the policies , procedures, and systems which are in

place to ensure: the reliability and integrity of information; compliance with policies, plans,

laws, and regulations; the safeguarding of assets; and, the economical and efficient use of

resources.

1.6 Audit Process

Although every audit project is unique, the audit process is similar for most engagements

and normally consists of four stages: Planning (sometimes called Survey or Preliminary

Review), Fieldwork, Audit Report, and Follow-up Review. Client involvement is critical at

each stage of the audit process. As in any special project, an audit results in a certain

amount of time being diverted from your department's usual routine. One of the key

objectives is to minimize this time and avoid disrupting ongoing activities. Following are

some sample flowcharts of the process from other organizations that you may find helpful:

1.6.1 Planning

During the planning portion of the audit, the auditor notifies the client of the audit,

discusses the scope and objectives of the examination in a formal meeting with

organization management, gathers information on important processes, evaluates existing

controls, and plans the remaining audit steps.

1.6.2 Announcement Letter

The client is informed of the audit through an announcement or engagement letter from

the Internal Audit Director. This letter communicates the scope and objectives of the audit,

the auditors assigned to the project and other relevant information.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XX

1.6.3 Initial Meeting

During this opening conference meeting, the client describes the unit or system to be

reviewed, the organization, available resources (personnel, facilities, equipment, funds),

and other relevant information. The internal auditor meets with the senior officer directly

responsible for the unit under review and any staff members s/he wishes to include. It is

important that the client identify issues or areas of special concern that should be

addressed.

1.6.4 Preliminary Survey

In this phase the auditor gathers relevant information about the unit in order to obtain a

general overview of operations. S/He talks with key personnel and reviews reports, files,

and other sources of information.

1.6.5 Internal Control Review

The auditor will review the unit's internal control structure, a process which is usually time-

consuming. In doing this, the auditor uses a variety of tools and techniques to gather and

analyze information about the operation. The review of internal controls helps the auditor

determine the areas of highest risk and design tests to be performed in the fieldwork

section.

1.6.6 Audit Program

Preparation of the audit program concludes the preliminary review phase. This program

outlines the fieldwork necessary to achieve the audit objectives.

1.6.7 Fieldwork

The fieldwork concentrates on transaction testing and informal communications. It is

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXI

during this phase that the auditor determines whether the controls identified during the

preliminary review are operating properly and in the manner described by the client. The

fieldwork stage concludes with a list of significant findings from which the auditor will

prepare a draft of the audit report.

1.6.8 Transaction Testing

After completing the preliminary review, the auditor performs the procedures in the audit

program. These procedures usually test the major internal controls and the accuracy and

propriety of the transactions. Various techniques including sampling are used during the

fieldwork phase.

1.6.9 Advice & Informal Communications

As the fieldwork progresses, the auditor discusses any significant findings with the client.

Hopefully, the client can offer insights and work with the auditor to determine the best

method of resolving the finding. Usually these communications are oral. However, in more

complex situations, memos and/or e-mails are written in order to ensure full

understanding by the client and the auditor. Our goal: No surprises.

1.6.10 Audit Summary

Upon completion of the fieldwork, the auditor summarizes the audit findings, conclusions,

and recommendations necessary for the audit report discussion draft.

1.6.11 Working Papers

Working papers are a vital tool of the audit profession. They are the support of the audit

opinion. They connect the client’s accounting records and financials to the auditor’s

opinion. They are comprehensive and serve many functions.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXII

1.6.12 Audit Report

Our principal product is the final report in which we express our opinions, present the

audit findings, and discuss recommendations for improvements. To facilitate

communication and ensure that the recommendations presented in the final report are

practical, Internal Audit discusses the rough draft with the client prior to issuing the final

report. For an audit report template including an executive summary click here.

1.6.13 Discussion Draft

At the conclusion of fieldwork, the auditor drafts the report. Audit management

thoroughly reviews the audit working papers and the discussion draft before it is presented

to the client for comment. This discussion draft is prepared for the unit's operating

management and is submitted for the client's review before the exit conference.

1.6.14 Exit Conference

When audit management has approved the discussion draft, Internal Audit meets with the

unit's management team to discuss the findings, recommendations, and text of the draft.

At this meeting, the client comments on the draft and the group works to reach an

agreement on the audit findings.

1.6.15 Formal Draft

The auditor then prepares a formal draft, taking into account any revisions resulting from

the exit conference and other discussions. When the changes have been reviewed by audit

management and the client, the final report is issued.

1.6.16 Final Report

Internal Audit prints and distributes the final report to the unit's operating management,

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXIII

the unit's reporting supervisor, the Vice President for Administration, the University Chief

Accountant, and other appropriate members of senior University management. This report

is primarily for internal University management use. The approval of the Internal Audit

Director is required for release of the report outside of the University.

1.6.17 Client Response

The client has the opportunity to respond to the audit findings prior to issuance of the final

report which can be included or attached to our final report. However, if the client decides

to respond after we issue the report, the first page of the final report is a letter requesting

the client's written response to the report recommendations.

In the response, the client should explain how report findings will be resolved and include

an implementation timetable. In some cases, managers may choose to respond with a

decision not to implement an audit recommendation and to accept the risks associated

with an audit finding. The client should copy the response to all recipients of the final

report if s/he decides not to have their response included/attached to Internal Audit's final

report.

1.6.18 Client Comments

Finally, as part of Internal Audit's self-evaluation program, we ask clients to comment on

Internal Audit's performance. This feedback has proven to be very beneficial to us, and we

have made changes in our procedures as a result of clients' suggestions.

1.6.19 Audit Follow-Up

Within approximately one year of the final report, Internal Audit will perform a follow-up

review to verify the resolution of the report findings.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXIV

1.6.20 Follow-up Review

The client response letter is reviewed and the actions taken to resolve the audit report

findings may be tested to ensure that the desired results were achieved. All unresolved

findings will be discussed in the follow-up report.

1.6.21 Follow-up Report

The review will conclude with a follow-up report which lists the actions taken by the client

to resolve the original report findings. Unresolved findings will also appear in the follow-up

report and will include a brief description of the finding, the original audit

recommendation, the client response, the current condition, and the continued exposure

to Indiana University. A discussion draft of each report with unresolved findings is

circulated to the client before the report is issued. The follow-up review results will be

circulated to the original report recipients and other University officials as deemed

appropriate.

1.6.22 Internal Audit Annual Report to the Board

In addition to the distribution discussed earlier, the contents of the audit report, client

response, and follow-up report may also communicated to the Audit Committee of the

Board as part of the Internal Audit Annual Report.

1.6.23 The Process: A Collaborative Effort

As pointed out, during each stage in the audit process--preliminary review, field work,

audit reports, and follow-up--clients have the opportunity to participate. There is no doubt

that the process works best when client management and Internal Audit have a solid

working relationship based on clear and continuing communication.

Many clients extend this working relationship beyond the particular audit. Once the audit

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXV

department has worked with management on a project, we have an understanding of the

unique characteristics of your unit's operations. As a result, we can help evaluate the

feasibility of making further changes or modifications in your operations.

1.7 Code of Ethics for Internal Auditors

Internal auditors shall:

Exercise honesty, objectivity and diligence in the performance of their duties

and responsibilities

Exhibit loyalty to the affairs of the organization which employs them and to

government. They shall not be a party to any illegal or improper activity

Not knowingly engage in acts or activities which are discreditable to the

profession of internal auditing, to the organization which employs them or to

government

Refrain from entering into any activity which may conflict with the interests of

government and the organization which employs them, or which would

prejudice their ability to carry out their duties and responsibilities objectively

Not accept anything of value from an employer, client, customer, supplier or

business associate of the organization which employs them, which would

impair, or be presumed to impair, their professional judgment

Undertake only those services which they can reasonably expect to complete

with professional competence

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXVI

Be prudent in the use of information acquired in the course of their duties.

They shall not use confidential information for any personal gain nor in any

manner which would be contrary to law or detrimental to the welfare of

government

When reporting on the results of their work, reveal all material facts known to

them, which if not revealed, could either distort reports of operations or

conceal unlawful practices

Continually strive for improvement in the proficiency, effectiveness and quality

of the services which they supply

Be ever mindful as professionals of their obligation to maintain high standards

of competence, morality and dignity

1.8 Limitations

Limitations are everywhere in the world. As like of every researcher I have also faced the

so many limitations while conducting the research. The main limitation is the data

limitations in this regard. There are so many researches available on the international level

but as far as concerned to Pakistan there is lacking of authenticated researches. As far as

concerned to the education in the respondents there is lacking of education people

working in credit risk department. We also faced lot of difficulties to get the right response

from the respondents.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXVII

2.1 Literature Review

In recent years, researchers and practitioners have widely discussed the need for internal

auditors of adding more value to their companies’ operations, and contributing to the

achievement of corporate objectives. This new perspective has focused increasing

attention on issues such as performance evaluation and effectiveness of internal auditing

(for instance Dittenhofer, 2001; Bou-Raad, 2000; IIA, 1999). Several parties advocated the

need to assess internal auditing (IA) effectiveness, though, at present, there is not a shared

framework of reference to this scope (for instance Ridley & D’Silva, 2008; Mihret &

Yismaw, 2007; Van Gansberghe, 2005; KPMG, 2004; Dittenhofer, 2001; Sawyer, 1995;

Barrett, 1986). Recently, Sarens (2009) have raised the question “when can we talk about

an effective IA function?” in his editorial about future perspectives of IA research. Looking

at the existing literature, there are many possible answers to this question. Different

authors have related IA effectiveness to different issues, focusing on IA processes, outputs

and outcomes.

Certain authors related IA effectiveness with the quality of IA procedures, such as the level

of compliance with IIA standards or the ability to plan, execute and communicate audit

findings (for instance Fadzil et al., 2005; Xiangdong, 1997; Spraakman, 1997). However, this

approach suffers from a major limitation as it is based on the hypothesis that IA activity is

effective if IA procedures are carried out properly, without considering the needs of the

main stakeholders in each individual audit (Lampe & Sutton, 1994). This is in contrast with

the current trend that stresses the relevance of value-added activities and indicates

stakeholders’ satisfaction as one of the critical performance categories for IA activities

(see, for instance, the Practice Advisory 1311-2).

A second stream of research relates IA effectiveness to the output of IA activities (Frigo,

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXVIII

2002), looking for instance at the ability of IA to respond to auditees’ needs (see, for

instance, Frigo, 2002; Ziegenfuss, 2000; Barrett, 1986). In this context, a recent work by

Ziegenfuss (2000) has highlighted that the survey results of auditee satisfaction and the

percent of recommendations that are implemented are the performance measures

considered by the CAE to be most suitable to evaluate IA effectiveness.

Finally, a few authors went further, relating IA effectiveness to the outcome of the audit

activities (i.e. the impact of a certain output of the audit process). According to Dittenhofer

(2001), “when evaluating the effectiveness of the internal auditing operation, a positive

response would be given when the internal auditor: (1) audits the achievement of the

auditees’ objectives and finds no problems, and no problems surface following the audit;

or (2) audits and finds problems; and (3) recommends solutions to the problems; and the

solutions resolve the problems”. From this statement it is clear that outcomes address a

wide range of aspects, i.e. all the elements on which audit activities have an impact. These

include both efficiency and effectiveness of the audited processes, and corporate

performances. At a process level, for example, the impact of IA activities has been related

to cost savings generated by the implementation of suggested recommendations (see, for

instance, Cashell and Aldhizer III, 2002). At a corporate level, outcome can address the IA

contribution to corporate performance, such as profit, growth, or share price; or its role in

the avoidance of corporate failures by ensuring sound corporate governance. This last

issue has been given particular attention in the most recent literature. Sarens (2009),

based on Gramling et al. (2004), suggested that IA can be considered effective when the

quality of IA function “has a positive impact on the quality of corporate governance”. He

also goes on linking IA quality to the “capacity to monitor and improve risk management

and internal control processes”.

In our opinion, this is a key point. In fact, to improve risk management and internal control

processes, the internal auditors have to convince the auditees about the quality of their

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXIX

work, persuading managers to implement their recommendations. The internal auditors, in

most of cases, do not act on the internal control-risk management system “directly”. They

can identify a criticism or an area of potential improvement and provide managers,

responsible of business processes, with an evaluation of the internal control–risk

management system. Then, managers and officers have to decide whether and how

enacting internal auditors’ recommendations. As highlighted by Mihret and Yismaw (2007),

audit findings and recommendations would not serve much purpose unless management is

committed to implement them. Implementation of audit recommendations is therefore

highly relevant to audit effectiveness (Van Gansberghe, 2005; Sawyer, 1995). The effect

that internal auditors have on the achievement of corporate objectives (i.e. their

effectiveness) is influenced by the extent to which managers consider internal auditors’

work valuable and decide to exploit it. In such view, the effectiveness of IA depends on the

quality perceived by the auditees.

Given the central role of auditees’ perceptions in relation to IA effectiveness, this paper

aims at analyzing which factors can influence the quality perceived by managers and can

enhance auditees’ satisfaction over internal auditors’ contribution.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXX

2.2 Theoretical Framework

2.2.1 Policy and Procedures

Policy and procedures are the back bone of any organization. The organization policy and

procedures are the sum of the all departments’ policy and procedures. In the same manner

the internal audit department will have its own policy and procedure which the internal

auditor has to follow and check the implementation of the other departments’ policy and

procedures as well. Therefore the definitions of the policies are the main and critical area

which has the significant impacts on the audit authentication and credibility.

2.2.2 Delegation of Authorities

The delegation of the authorities means the allocation of power to the subordinates. Its

means all powers should not be centric in the one point but other subordinates should

have powers so that they can take decisions. If the auditor have the authority to conduct

the audit but does not have the authority to find it either it is wrong or correct, its audit

objection or not then the audit will not be effective and decision making will required

sufficient time. This also have the positive impression on the outsiders that the

organization have the confidence on their auditors and give them enough room to prove

that what is wrong and what is right.

2.2.3 Audit Program

The audit program is the main course of action according to which the audit being

conducted during the year. Normally it is designed for the period of one year in which audit

department trying to cover all the aspects of the organization functional departments. This

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXXI

audit program is the clear indicator of the audit department performance whether they are

enough sufficient to utilized their abilities in the best interest of the bank that they can

cover the bank in the limited time period of year or not. Therefore the audit program is

designed in such a way that they can cover all the departments with effective audit

techniques and tools.

2.2.4 Sampling

Sampling is one of the tools which internal auditors used for the sampling of the

transactions for their checking and conducting audit. Sampling can be done based on the

amount, repetition of transactions, by nature of transaction, etc. Therefore the audit

checking is based on the sampling and the sampling criteria can be varied from department

to department according to nature of workings. Sampling needs to be effective as if the

sampling fails the purpose might be fraud transaction left and other will be conducts.

2.2.5 Staff Trainings

The training plays the vital role in the professional development of the employees. It’s

become vital when a trainer trains the internal audit staff. In this case the knowledge of

the trainer plays the vital role for the success of that auditor, as the auditor has the

deployed the same in its mind when conducting the audit. The training department should

be self-sufficient to conduct any type of training as and when required basis.

2.2.6 Quality of Work

The quality of work plays the vital role to create the credibility of the work and

organization. Quality means, do the less work but do the right things. Internal auditors are

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXXII

playing the vital role in maintaining and improvement of the quality of work in the

organization. As they are playing the supervisory role in the implementation of policy and

procedures the internal auditors are going to conduct the audit based on these guidelines.

There are also other guidelines which are also in considerations for the internal auditor to

conduct the quality audit which have the positive impact on their performance and

organizational credibility.

2.2.7 Internal Audit Standards

Internal audit standards are international guidelines for the conducting of audit in the

financial as well as manufacturing concerns. These guidelines are being followed by all the

organization to meet the international standards and meet the requirements of the world.

After successful implementation of these standards the organization are eligible for the

registration in the international stock and trade markets.

The implementation of these standards also checked the by external auditors as they have

to issue the report on the same. This brings the positive impact on the organizational

credibility in the market.

2.2.8 Central Bank Guidelines

The Central Bank also provides the guidelines on the internal auditors. These are the

comprehensive guidelines which include the complete set of the guidelines which includes

the establishment of the internal audit department, appointment of department head,

staff, policy and procedure for the internal audit department. The implementation of these

policy guidelines is required to avoid any penalization from the central bank as well as to

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXXIII

establish the credibility in the financial market.

2.2.9 Bank’s Credibility and Internal Audit

Banks credibility is the main factor which they have to keep maintains and improves with

the passage of time so that they can remain alive in the market. The maintenance of the

credulity is the vital factor to keep alive the organization in the market. Credibility means

that financial practices are crystal clear and financials are given the true and fair view of

the organization matters. This crystal clear view can only be obtained by having the strong

and professional internal audit department.

2.2.10 Characteristics of the Individual Internal Auditor

The second set of elements refers to the characteristics of individual internal auditors, with

specific reference to their skills. At a general extent, internal auditor’s skills can be

distinguished into two classes: cognitive and behavioral skills (Pickett, 2000). Cognitive

skills include technical competences. Behavioral skills include communication and

interpersonal ability. Both these skills can influence the quality perceived by the auditees

significantly.

2.2.11 Technical Skills

Technical skills ensure that the auditors are more able to provide advice to improve the

internal control system (mat Zain et al., 2006; Brody et al., 1998), to complete audits, to

find consistent solutions based on previous experiences and to deal with complex and

conflicting situations (mat Zain et al., 2006; Flesher & Zanzig, 2000). Previous studies

underlined that line managers often believe that internal auditors do not have enough

knowledge to provide useful help (Griffiths, 1999; Van Peursem 2004; 2005) and, if this is

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXXIV

the case, they do not take into account their advice, hence reducing the effectiveness of IA

(Van Peursem 2004; 2005).

2.2.12 Behavioral Skills

Behavioral skills are required by auditors to establish a sound relation with their auditees;

interpersonal and communication skills facilitate the understanding of audit findings and

the ability to accomplish their responsibilities effectively (for a review, see Smith, 2005).

Furthermore, auditors’ competencies, both behavioural and cognitive can increase the

effectiveness of the IA team by improving the recognition of their role within the

organization.

2.2.13 Broader Organizational Environment

The final set of elements influencing IA effectiveness deal with the broader organizational

environment: (1) regulatory context and (2) level of risk of the company.

The role of laws and regulations in relation to IA effectiveness is twofold: first laws and

regulations shape internal audit activities. In particular in those settings where the

attention to both internal controls and internal audit is recent organizations’ approaches

are not based on consolidated routines and their (re)action can be more strongly

influenced by external pressures in a process of external conformance (DiMaggio and

Powell, 1983; Meyer, 1994).

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXXV

3.1 Brand of HBL

Our brand identity is the outward expression of what we stand for as an organization. This is

summarized in our vision, mission and is supported by our values.

3.2 Vision

“Enabling people to advance with confidence and success”

3.3 Mission

“To make our customers prosper, our staff excel and create value for shareholders”

3.4 Values

Our values are the fundamental principles that define our culture and are

brought to life in our attitudes and behavior. It is our values that make

us unique and unmistakable. Our values are defined below:

3.5 Excellence

This is at the core of everything we do. The markets in which we operate are becoming

increasingly competitive, giving our customers an abundance of choice. Only through being the

very best - in terms of the service we offer, our products and premises - can we hope to be

successful and grow.

3.6 Integrity

We are the leading bank in Pakistan and our success depends upon trust. Our customers - and

society in general - expect us to possess and steadfastly adhere to high moral principles and

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXXVI

professional standards.

3.7 Customer Focus

We understand fully the needs of our customers and adapt our products and services to meet

these. We always strive to put the satisfaction of our customers first.

3.8 Meritocracy

We believe in giving opportunities and advantages to our employees on the basis of their ability.

We believe in rewarding achievement and in providing first-class career opportunities for all.

3.9 Progressive

We believe in the advancement of society through the adoption of enlightened working practices,

innovative new products and processes, and a spirit of enterprise.

3.10 Board of Directors

Sultan Ali Allana Chairman

R Zakir Mahmood President & CEO

Ahmed Jamal Director

Sajid Zahid Director

Mushtaq Malik Director

Sikandar Mustafa Khan Director

Moez Jamal Director

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXXVII

3.11 Management

R Zakir Mahmood President & CEO

Sohail Malik Chief Risk Officer

Nauman K Dar Head of Corporate & Investment

Banking &

International Banking

Sima Khalil Head of Retail Banking

Abid Sattar Head of Global Operations and Learning &

Development

Ayaz Ahmed Chief Financial Officer

Jamil Iqbal Chief Compliance Officer

Muddasir Khan Chief Information Officer

Salim Amlani Chief Internal Audit

Nausheen Ahmed Company Secretary

Aslam Gadit Remedial Assets

Aly Mustansir Head of Marketing

M Salah Uddin Manzoor Head of Global Treasury

Dr Razi Ahmed Head of Human Resource

Mubshir Maqbool Head of Commercial & Retail Lending

Mirza Saleem Baig Head of Islamic Banking

Faiq Sadiq Head of Payment Services

Tulu Islam General Manager Branch & Trade Operations

Abrar Rashid Awan Business Head of Semi Urban Area

Shahid Fakhur-ud-din General Manager International Market & Risk

Management

Aman Aziz Siddiqui Regional Gulf (UAE and Oman)

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXXVIII

Mohammad Ali Chief Representative

Rizwan Haidar Deputy Global Risk Management

3.12 Awards

2010

'HBL wins Best Emerging Market Banks award in Pakistan 2010'

2009

'The Best Emerging Market Bank in Pakistan'

HBL among Top 500 Global Financial Brands

2008

'Best Bank In Pakistan'

'Most Innovative Global Trade Finance'

'Buzziest Brands'

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XXXIX

3.13 Introduction

HBL was the first commercial bank to be established in Pakistan in 1947. Over the years, HBL has

grown its branch network and become the largest private sector bank with over 1,450 branches

across the country and a customer base exceeding five million relationships.

The Government of Pakistan privatized HBL in 2004 through which AKFED acquired 51% of the

Bank's shareholding and management control. HBL is majority owned (51%) by the Aga Khan

Fund for Economic Development, 42.5% of the shareholding is retained by the Government of

Pakistan (GOP), whilst 7.5% is owned by the general public i.e. over 170,000 shareholders

following the public listing that took place in July 2007.

With a presence in 25 countries, subsidiaries in Hong Kong and the UK, affiliates in Nepal,

Nigeria, Kenya and Kyrgyzstan and rep offices in Iran and China, HBL is also the largest domestic

multinational. The Bank is expanding its presence in principal international markets including the

UK, UAE, South and Central Asia, Africa and the Far East.

Key areas of operations encompass product offerings and services in Retail and Consumer

Banking. HBL has the largest Corporate Banking portfolio in the country with an active

Investment Banking arm. SME and Agriculture lending programs and banking services are

offered in urban and rural centers.

3.14 Rating

HBL is currently rated AA (Long term) and A-1+ (Short term) and has a balance sheet size of USD

10.2 billion. It is the first Pakistani bank to raise Tier II Capital from external sources.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XL

3.15 History

HBL established operations in Pakistan in 1947 and moved its head office to Karachi. Our first

international branch was established in Colombo, Sri Lanka in 1951 and Habib Bank Plaza was built

in 1972 to commemorate the bank’s 25th Anniversary.

With a domestic market share of over 40%, HBL was nationalized in 1974 and it continued to

dominate the commercial banking sector with a major market share in inward foreign remittances

(55%) and loans to small industries, traders and farmers. International operations were expanded

to include the USA, Singapore, Oman, Belgium, Seychelles and Maldives and the Netherlands.

On December 29, 2003 Pakistan's Privatization Commission announced that the Government of

Pakistan had formally granted the Aga Khan Fund for Economic Development (AKFED) rights to

51% of the shareholding in HBL, against an investment of PKR 22.409 billion (USD 389 million). On

February 26, 2004, management control was handed over to AKFED. The Board of Directors was

reconstituted to have four AKFED nominees, including the Chairman and the President/CEO and

three Government of Pakistan nominees

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page XLI

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page 25

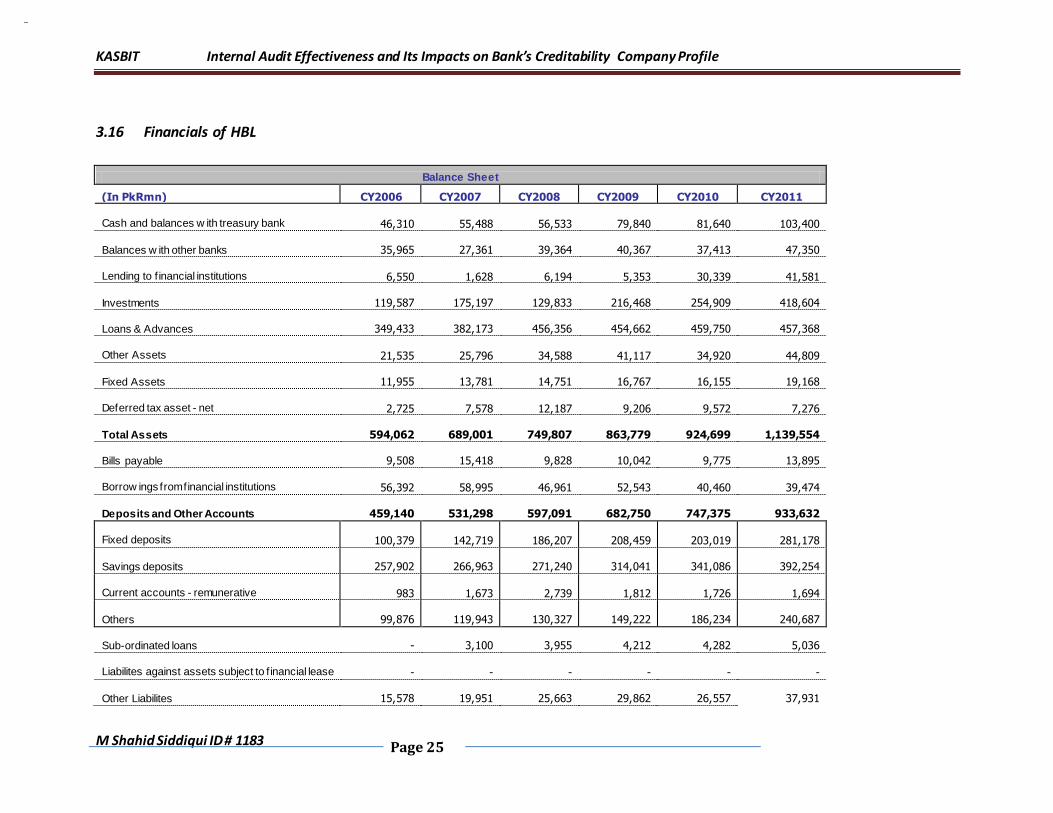

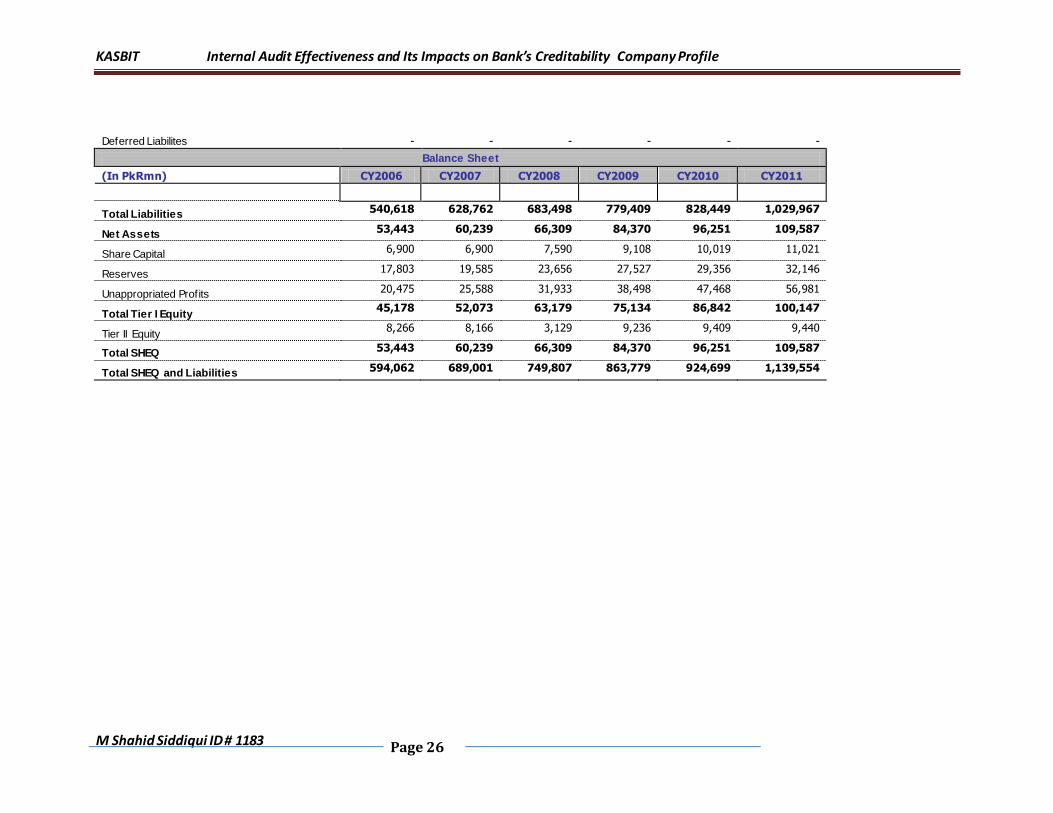

3.16 Financials of HBL

Balance Sheet

(In PkRmn) CY2006 CY2007 CY2008 CY2009 CY2010 CY2011

Cash and balances w ith treasury bank

46,310

55,488

56,533

79,840

81,640

103,400

Balances w ith other banks

35,965

27,361

39,364

40,367

37,413

47,350

Lending to f inancial institutions

6,550

1,628

6,194

5,353

30,339

41,581

Investments

119,587

175,197

129,833

216,468

254,909

418,604

Loans & Advances

349,433

382,173

456,356

454,662

459,750

457,368

Other Assets

21,535

25,796

34,588

41,117

34,920

44,809

Fixed Assets

11,955

13,781

14,751

16,767

16,155

19,168

Deferred tax asset - net

2,725

7,578

12,187

9,206

9,572

7,276

Total Assets

594,062

689,001

749,807

863,779

924,699

1,139,554

Bills payable

9,508

15,418

9,828

10,042

9,775

13,895

Borrow ings from financial institutions

56,392

58,995

46,961

52,543

40,460

39,474

Deposits and Other Accounts

459,140

531,298

597,091

682,750

747,375

933,632

Fixed deposits

100,379

142,719

186,207

208,459

203,019

281,178

Savings deposits

257,902

266,963

271,240

314,041

341,086

392,254

Current accounts - remunerative

983

1,673

2,739

1,812

1,726

1,694

Others

99,876

119,943

130,327

149,222

186,234

240,687

Sub-ordinated loans

-

3,100

3,955

4,212

4,282

5,036

Liabilites against assets subject to f inancial lease

-

-

-

-

-

-

Other Liabilites

15,578

19,951

25,663

29,862

26,557

37,931

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page 26

Deferred Liabilites

-

-

-

-

-

-

Balance Sheet

(In PkRmn) CY2006 CY2007 CY2008 CY2009 CY2010 CY2011

Total Liabilities 540,618 628,762 683,498 779,409 828,449 1,029,967

Net Assets 53,443 60,239 66,309 84,370 96,251 109,587

Share Capital 6,900 6,900 7,590 9,108 10,019 11,021

Reserves 17,803 19,585 23,656 27,527 29,356 32,146

Unappropriated Profits 20,475 25,588 31,933 38,498 47,468 56,981

Total Tier I Equity 45,178 52,073 63,179 75,134 86,842 100,147

Tier II Equity 8,266 8,166 3,129 9,236 9,409 9,440

Total SHEQ 53,443 60,239 66,309 84,370 96,251 109,587

Total SHEQ and Liabilities 594,062 689,001 749,807 863,779 924,699 1,139,554

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page 27

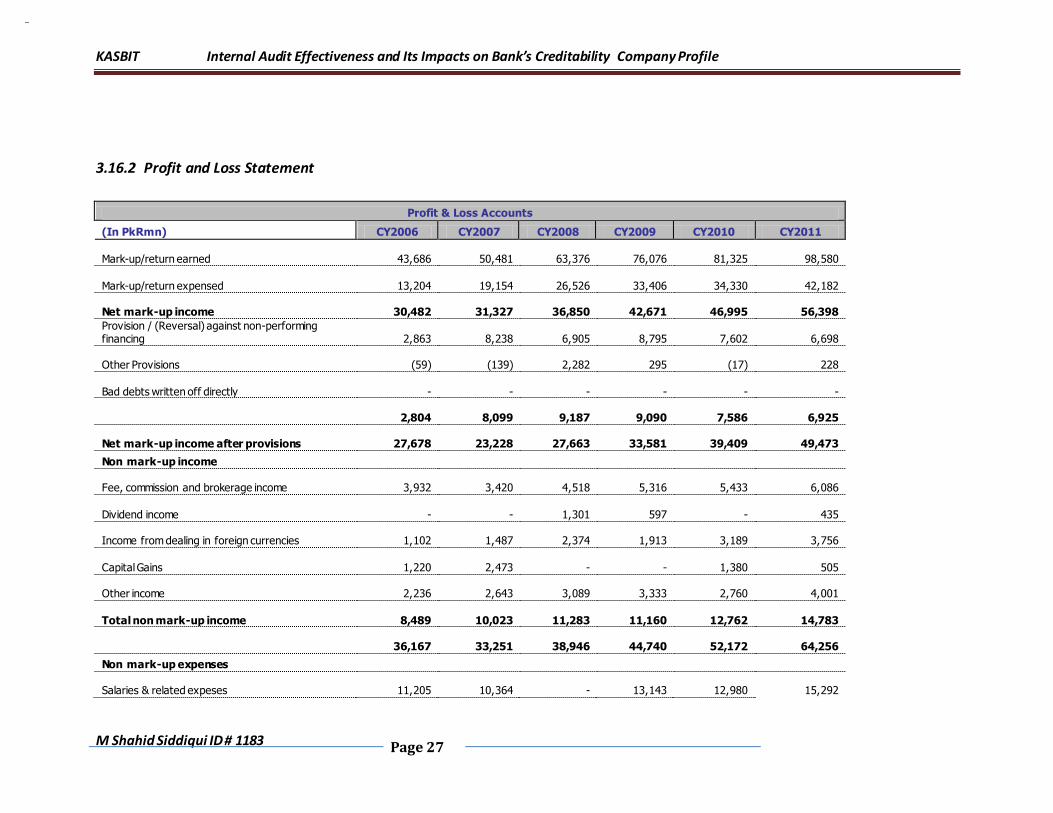

3.16.2 Profit and Loss Statement

Profit & Loss Accounts

(In PkRmn) CY2006 CY2007 CY2008 CY2009 CY2010 CY2011

Mark-up/return earned

43,686

50,481

63,376

76,076

81,325

98,580

Mark-up/return expensed

13,204

19,154

26,526

33,406

34,330

42,182

Net mark-up income

30,482

31,327

36,850

42,671

46,995

56,398

Provision / (Reversal) against non-performing financing

2,863

8,238

6,905

8,795

7,602

6,698

Other Provisions

(59)

(139)

2,282

295

(17)

228

Bad debts written off directly

-

-

-

-

-

-

2,804

8,099

9,187

9,090

7,586

6,925

Net mark-up income after provisions

27,678

23,228

27,663

33,581

39,409

49,473

Non mark-up income

Fee, commission and brokerage income

3,932

3,420

4,518

5,316

5,433

6,086

Dividend income

-

-

1,301

597

-

435

Income from dealing in foreign currencies

1,102

1,487

2,374

1,913

3,189

3,756

Capital Gains

1,220

2,473

-

-

1,380

505

Other income

2,236

2,643

3,089

3,333

2,760

4,001

Total non mark-up income

8,489

10,023

11,283

11,160

12,762

14,783

36,167

33,251

38,946

44,740

52,172

64,256

Non mark-up expenses

Salaries & related expeses

11,205

10,364

-

13,143

12,980

15,292

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page 28

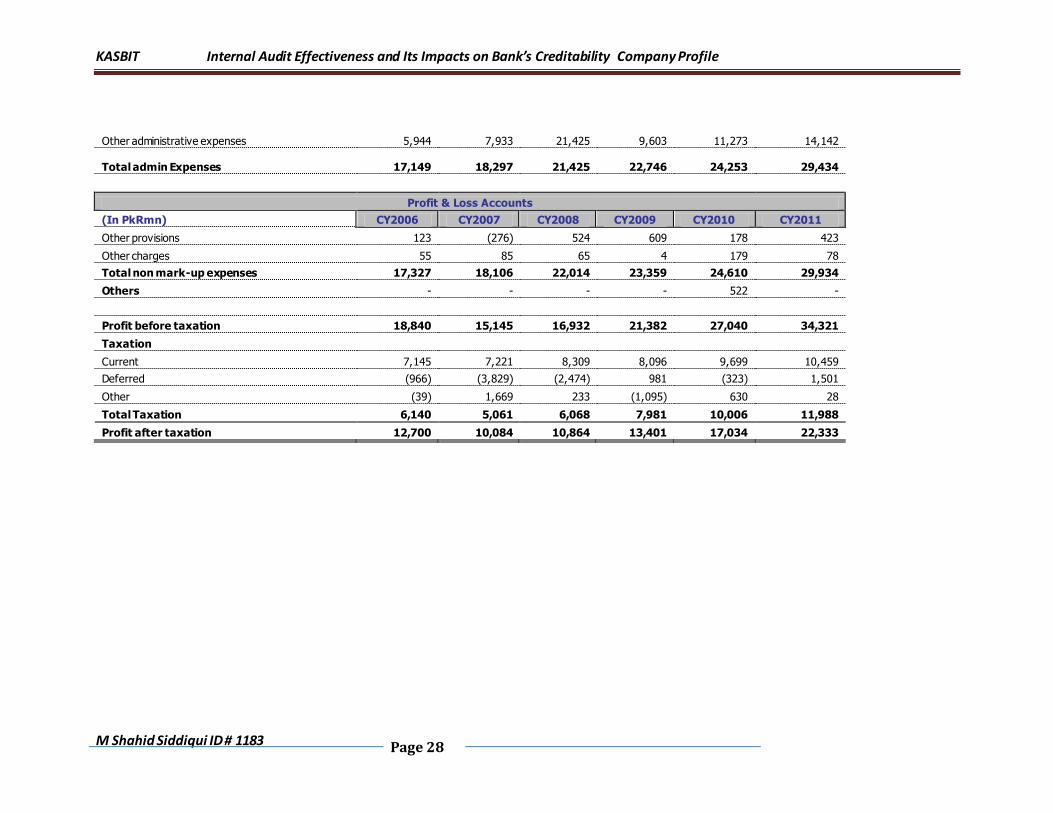

Other administrative expenses

5,944

7,933

21,425

9,603

11,273

14,142

Total admin Expenses

17,149

18,297

21,425

22,746

24,253

29,434

Profit & Loss Accounts

(In PkRmn) CY2006 CY2007 CY2008 CY2009 CY2010 CY2011

Other provisions 123 (276) 524 609 178 423

Other charges 55 85 65 4 179 78

Total non mark-up expenses 17,327 18,106 22,014 23,359 24,610 29,934

Others - - - - 522 -

17,327 18,106 22,014 23,359 25,132 29,934

Profit before taxation 18,840 15,145 16,932 21,382 27,040 34,321

Taxation Current 7,145 7,221 8,309 8,096 9,699 10,459

Deferred (966) (3,829) (2,474) 981 (323) 1,501

Other (39) 1,669 233 (1,095) 630 28

Total Taxation 6,140 5,061 6,068 7,981 10,006 11,988

Profit after taxation 12,700 10,084 10,864 13,401 17,034 22,333

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page 29

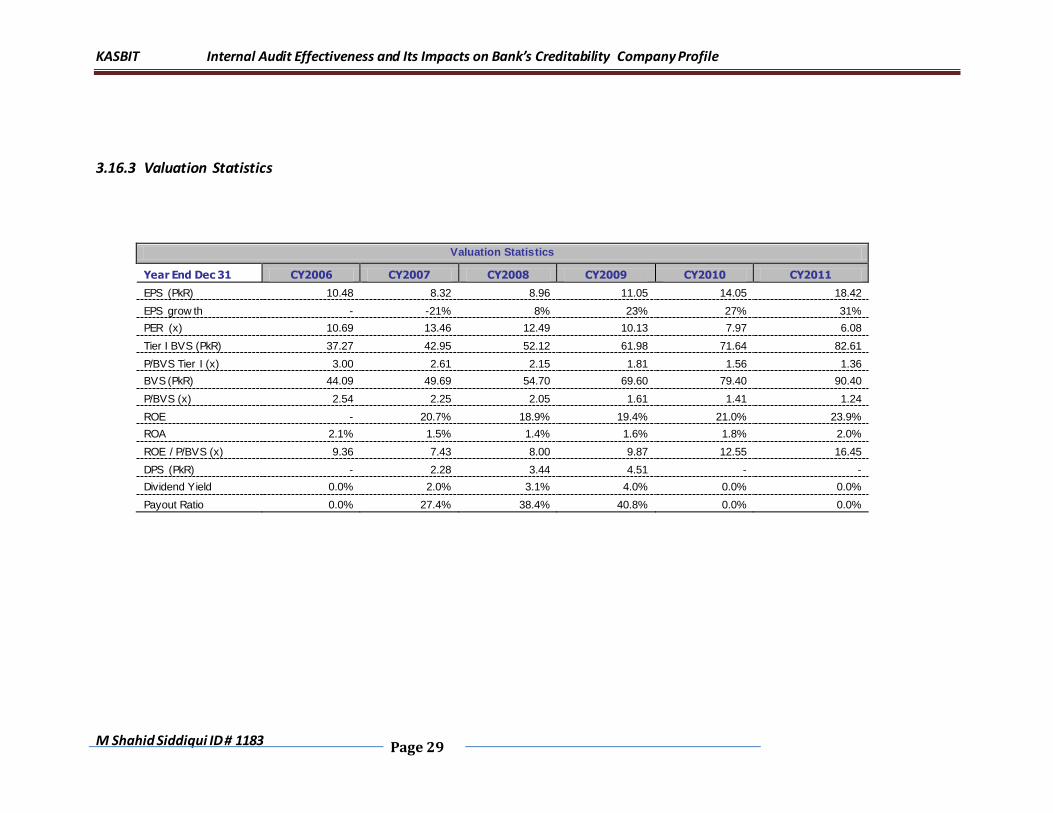

3.16.3 Valuation Statistics

Valuation Statistics

Year End Dec 31 CY2006 CY2007 CY2008 CY2009 CY2010 CY2011

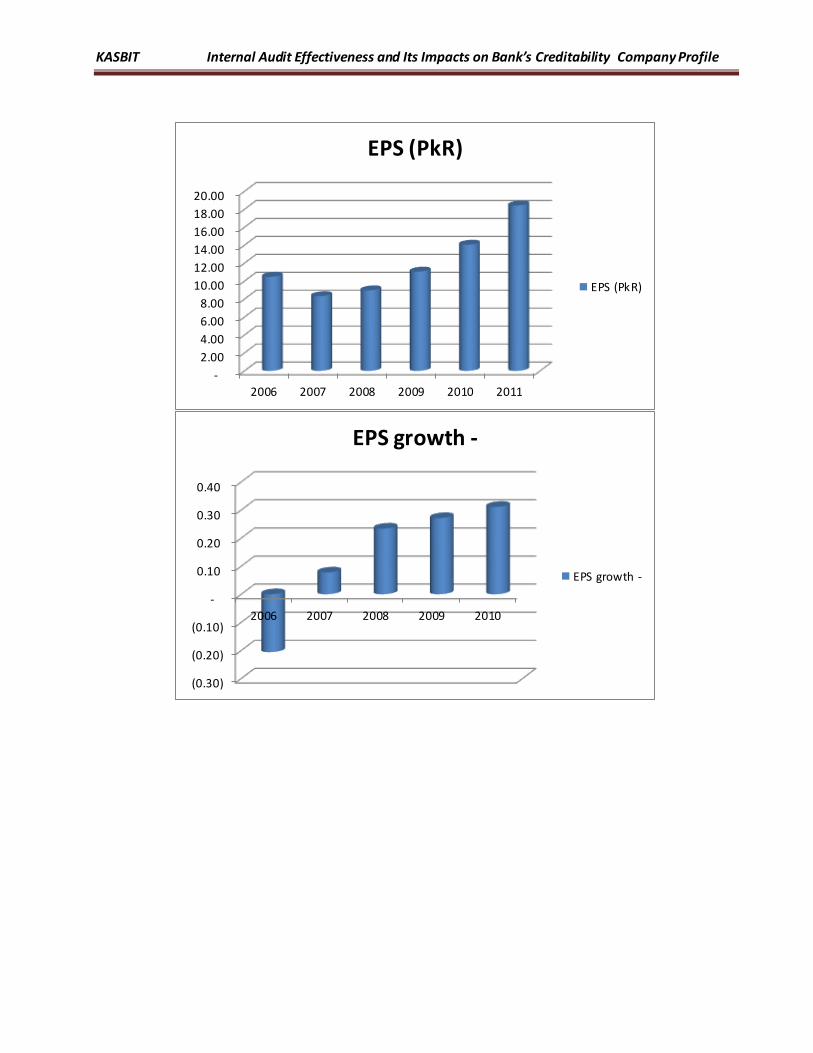

EPS (PkR) 10.48 8.32 8.96 11.05 14.05 18.42

EPS grow th - -21% 8% 23% 27% 31%

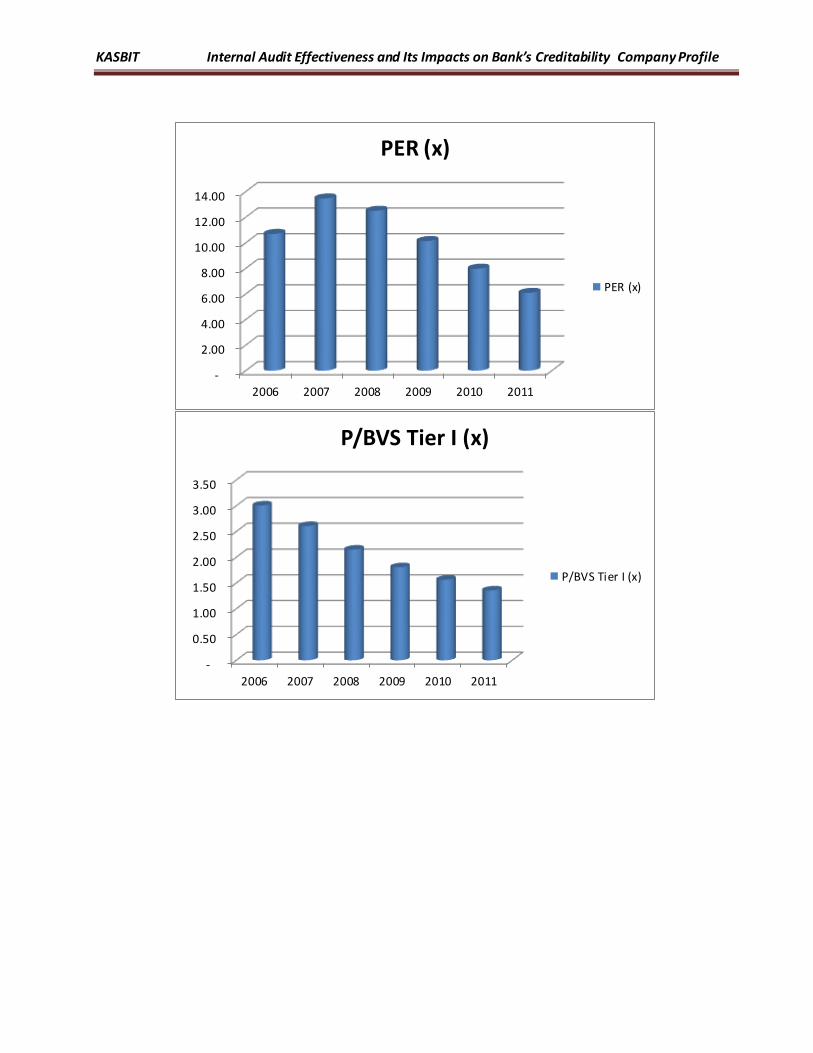

PER (x) 10.69 13.46 12.49 10.13 7.97 6.08

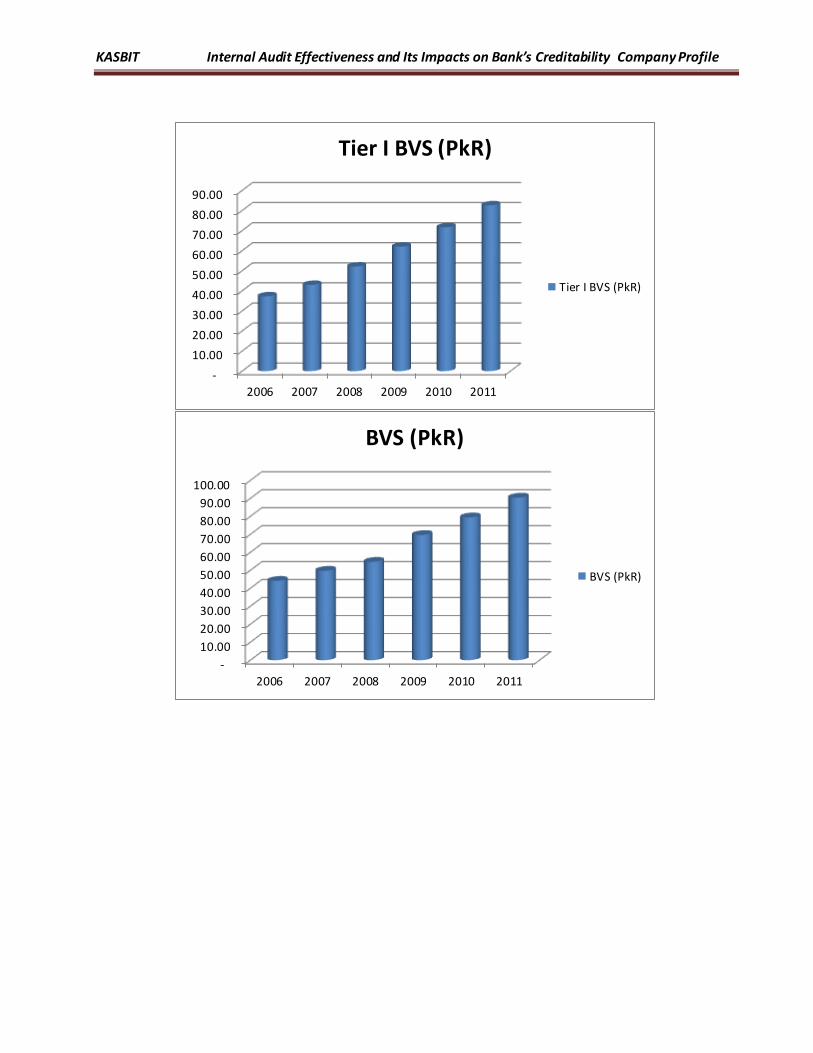

Tier I BVS (PkR) 37.27 42.95 52.12 61.98 71.64 82.61

P/BVS Tier I (x) 3.00 2.61 2.15 1.81 1.56 1.36

BVS (PkR) 44.09 49.69 54.70 69.60 79.40 90.40

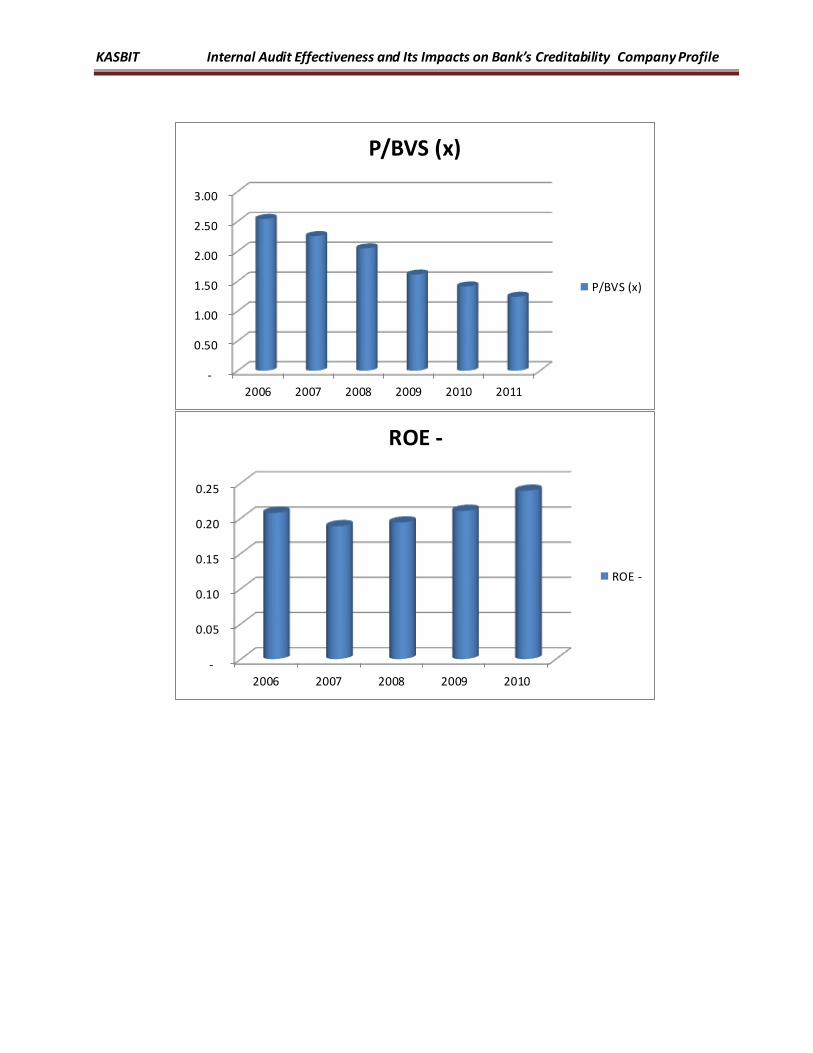

P/BVS (x) 2.54 2.25 2.05 1.61 1.41 1.24

ROE - 20.7% 18.9% 19.4% 21.0% 23.9%

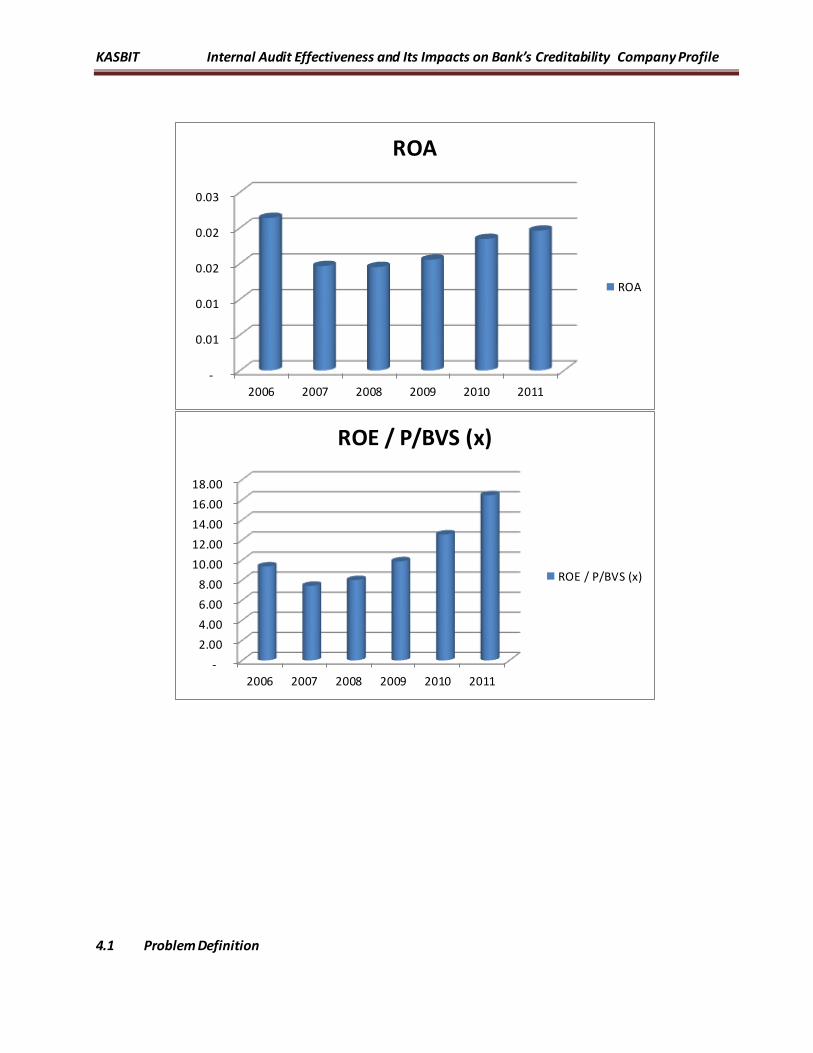

ROA 2.1% 1.5% 1.4% 1.6% 1.8% 2.0%

ROE / P/BVS (x) 9.36 7.43 8.00 9.87 12.55 16.45

DPS (PkR) - 2.28 3.44 4.51 - -

Dividend Yield 0.0% 2.0% 3.1% 4.0% 0.0% 0.0%

Payout Ratio 0.0% 27.4% 38.4% 40.8% 0.0% 0.0%

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page 30

3.16.4 Key Ratios

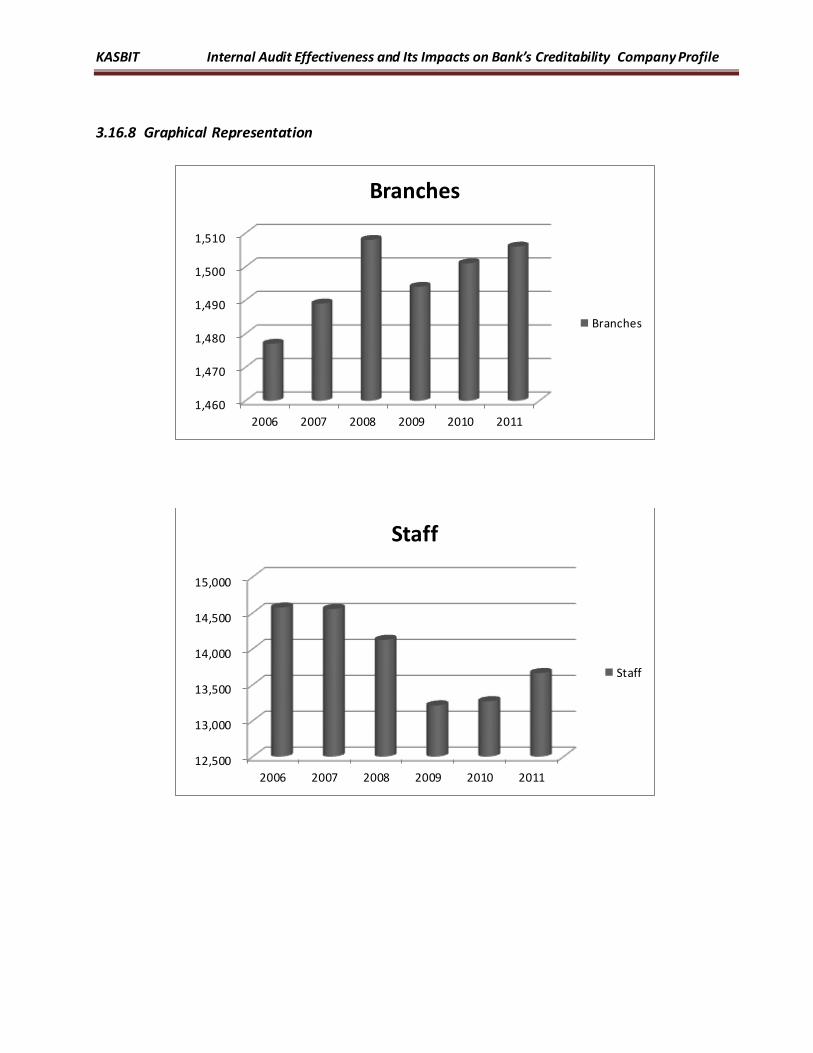

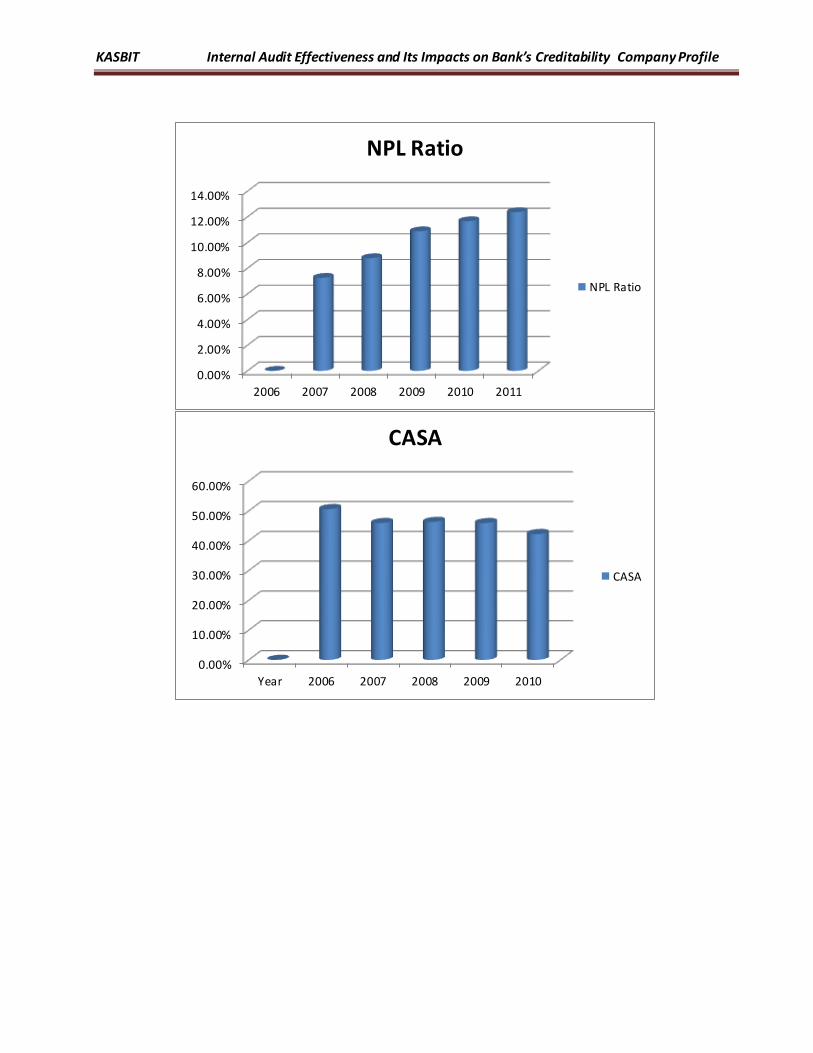

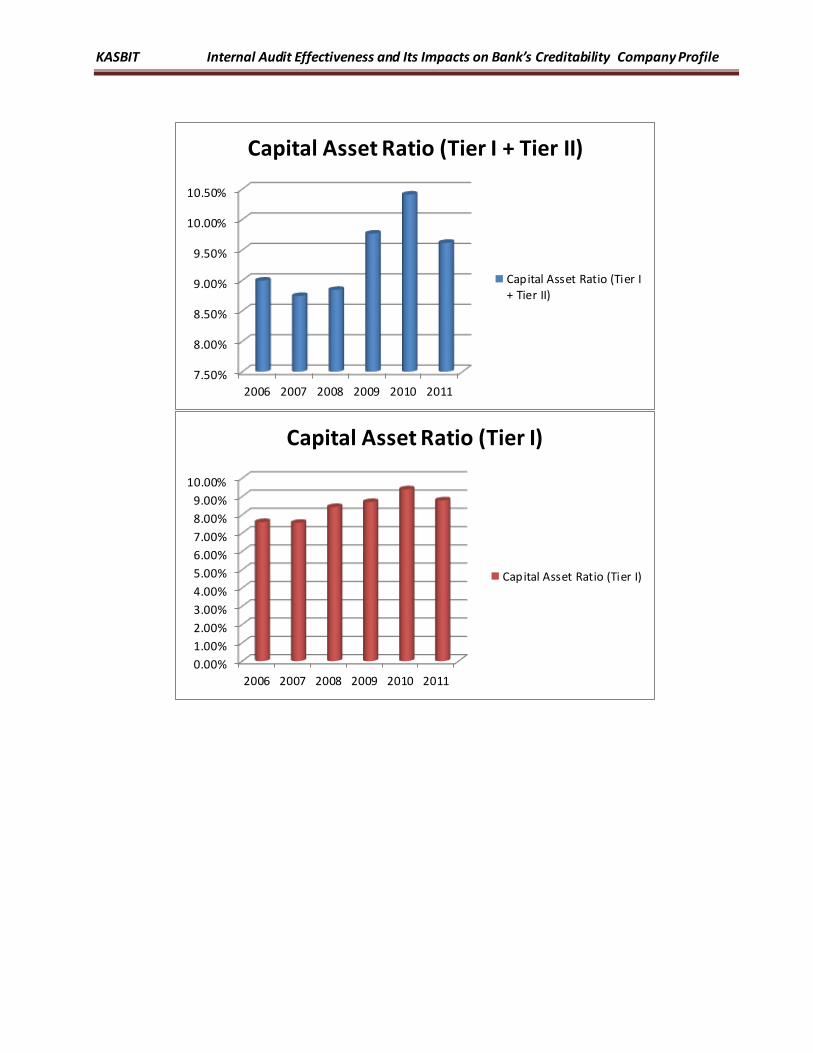

Key Ratios

CY2006 CY2007 CY2008 CY2009 CY2010 CY2011

Branches 1,477 1,489 1,508 1,494 1,501 1,506

Staff 14,572 14,552 14,123 13,211 13,269 13,661

Staff/Branch 10 10 9 9 9 9

NPLs - 27,693 40,053 49,438 53,608 56,549

NPL Ratio 0% 7% 9% 11% 12% 12%

CASA 0% 51% 46% 46% 46% 42%

CAR 0% 0% 14% 13% 15% 0%

Capital Asset Ratio (Tier I) 8% 8% 8% 9% 9% 9%

Capital Asset Ratio (Tier I + Tier II) 9% 9% 9% 10% 10% 10%

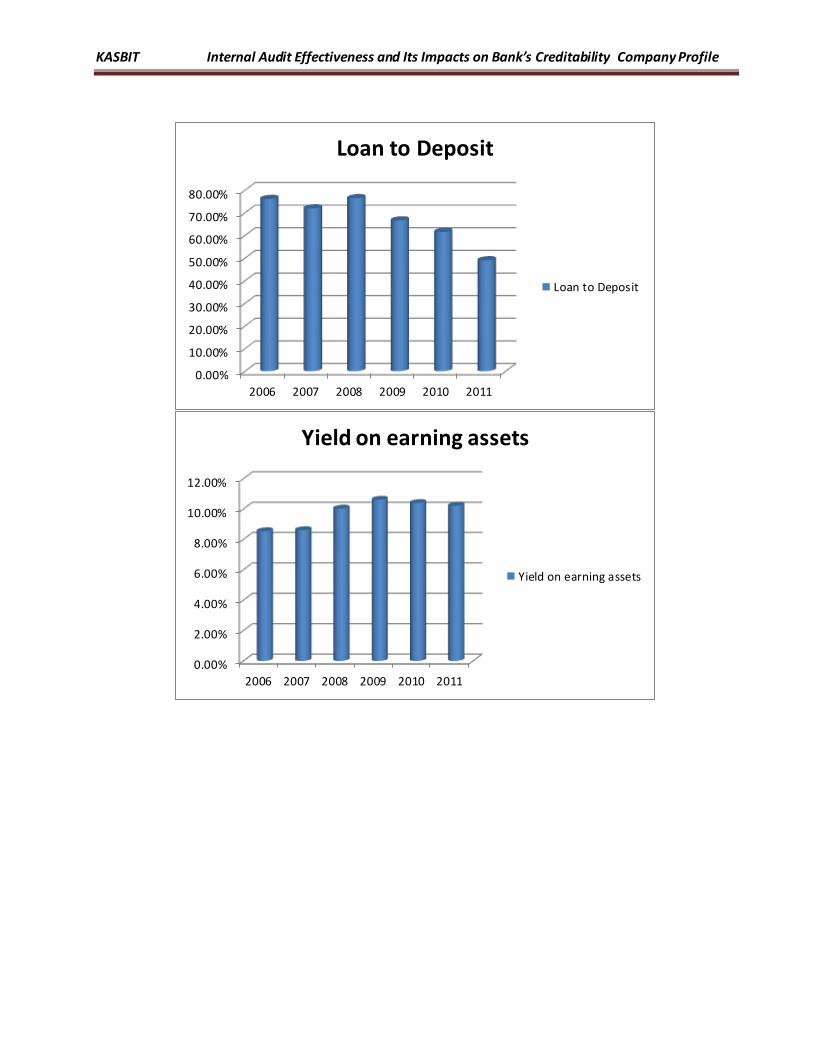

Loan to Deposit 76% 72% 76% 67% 62% 49%

Yield on earning assets 8.5% 8.6% 10.0% 10.6% 10.4% 10.2%

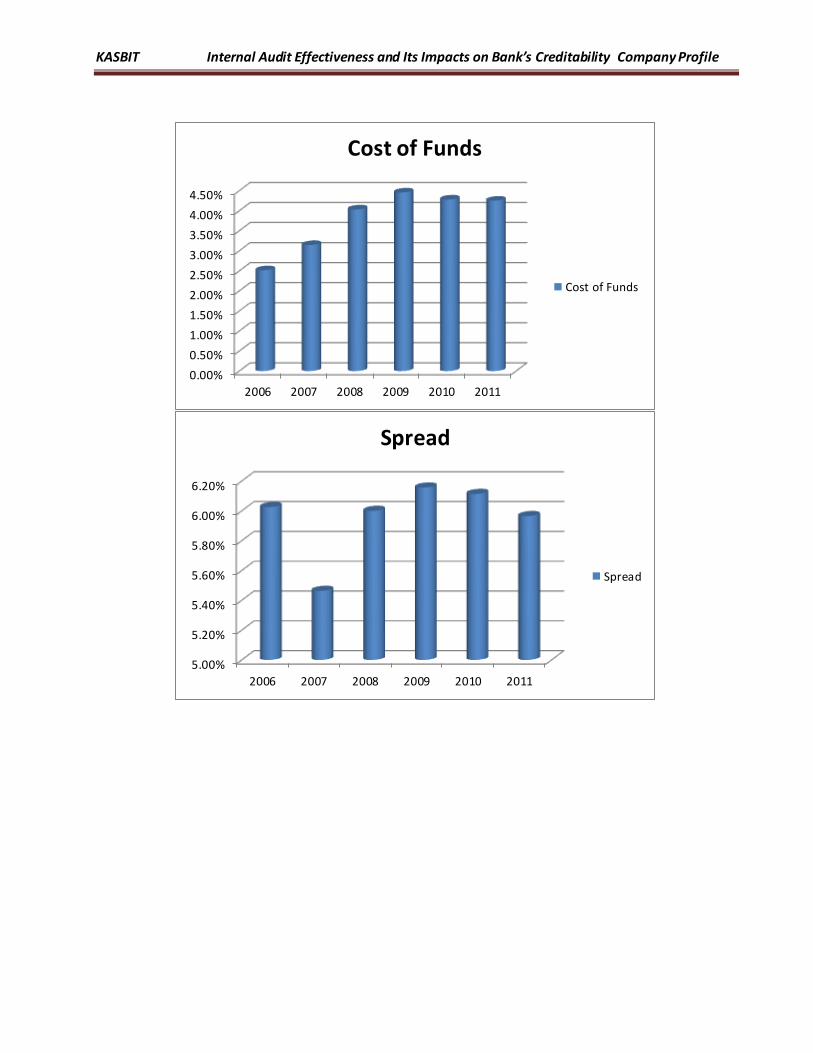

Cost of Funds 2.5% 3.1% 4.0% 4.5% 4.3% 4.3%

Spread 6.0% 5.5% 6.0% 6.2% 6.1% 6.0%

Market Cap. To Deposits 30% 26% 23% 20% 18% 15%

Cost/Income 47% 55% 55% 51% 46% 46%

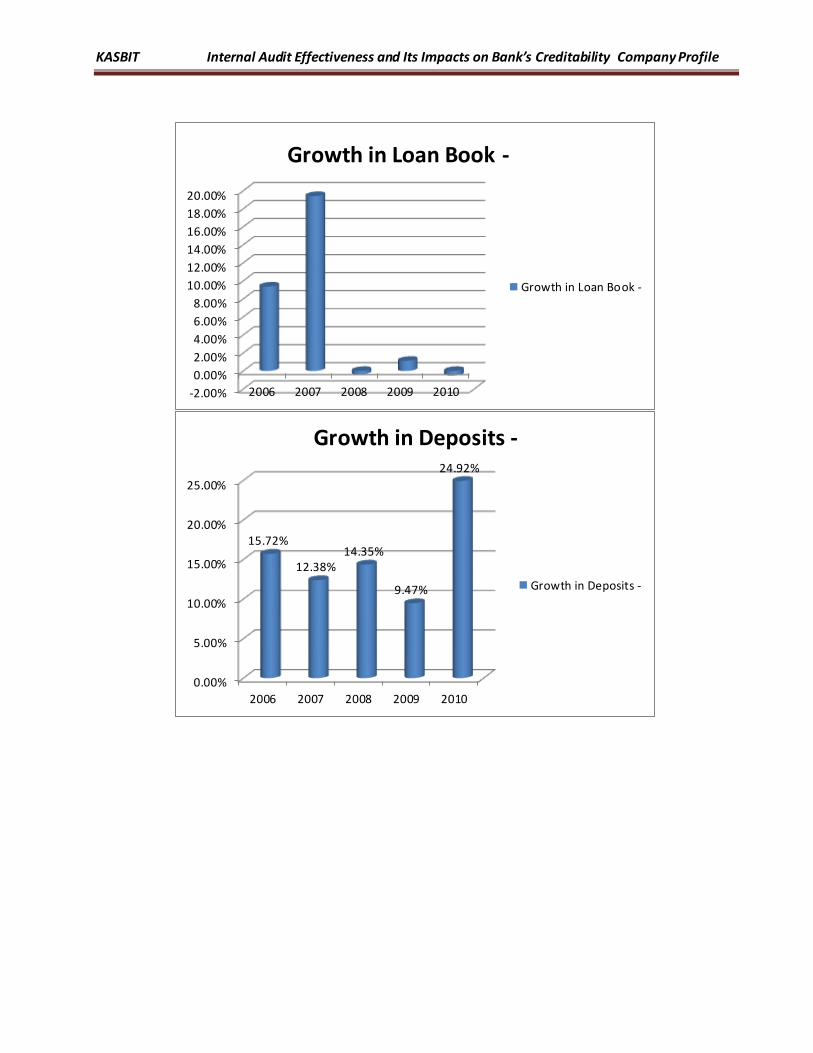

Grow th in Loan Book - 9% 19% 0% 1% -1%

Grow th in Deposits - 16% 12% 14% 9% 25%

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page 31

3.16.5 Ratios

Ratios

CY2006 CY2007 CY2008 CY2009 CY2010 CY2011

Net Int. Income / Total Income 78% 76% 77% 79% 79% 79%

Fee Income / non int income 46% 34% 40% 48% 43% 41%

Non Int. Exp. / Non Int. Income 204% 181% 195% 209% 193% 202%

Provisions / Net Int. Income 6% 16% 14% 12% 9% 7%

Fee Income / Non Int Income 46% 34% 40% 48% 43% 41%

Admin Exp. / Non Int. Exp. 99% 101% 97% 97% 99% 98%

Admin Exp. / Total Income 47% 55% 55% 51% 46% 46%

Salaries & Related / Admin Exp. 65% 57% 0% 58% 54% 52%

Effective Tax Rate 33% 33% 36% 37% 37% 35%

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page 32

3.16.6 ROE Decomposition

ROE Decomposition

CY2007 CY2008 CY2009 CY2010 CY2011

Net Interest Income / Assets 4.9% 5.1% 5.3% 5.3% 5.5%

Non. Int. Income / Assets 1.6% 1.6% 1.4% 1.4% 1.4%

Expenses / Assets -2.9% -3.0% -2.8% -2.7% -2.9%

Core Income / Assets 3.6% 3.7% 3.9% 4.0% 4.0%

Provisions / Assets -1.3% -1.3% -1.1% -0.8% -0.7%

Other Items / Assets 0.0% -0.1% -0.1% -0.1% 0.0%

Pre tax ROA 2.4% 2.4% 2.7% 3.0% 3.3%

Tax Burden (x) 0.67 0.64 0.63 0.63 0.65

ROA 1.6% 1.5% 1.7% 1.9% 2.2%

Leverage (x) 13.19 12.48 11.67 11.04 11.04

ROE 20.7% 18.9% 19.4% 21.0% 23.9%

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

M Shahid Siddiqui ID # 1183

Page 33

3.16.7 Growth in P&L

Growth in P&L

CY2007 CY2008 CY2009 CY2010 CY2011

Interest Income 16% 26% 20% 7% 21%

Interest Expense 45% 38% 26% 3% 23%

Net Interest Income 3% 18% 16% 10% 20%

Provisions 189% 13% -1% -17% -9%

Net Int Income after Provisions -16% 19% 21% 17% 26%

Non Interest Income 18% 13% -1% 14% 16%

Fee Income -13% 32% 18% 2% 12%

Total Income -8% 17% 15% 17% 23%

Admin Costs 7% 17% 6% 7% 21%

NPBT -20% 12% 26% 26% 27%

Taxation -18% 20% 32% 25% 20%

NPAT -21% 8% 23% 27% 31%

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

3.16.8 Graphical Representation

1,460

1,470

1,480

1,490

1,500

1,510

2006 2007 2008 2009 2010 2011

Branches

Branches

12,500

13,000

13,500

14,000

14,500

15,000

2006 2007 2008 2009 2010 2011

Staff

Staff

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

8

8

9

9

9

9

9

10

10

10

Year 2006 2007 2008 2009 2010

Staff/Branch

Staff/Branch

-

10,000

20,000

30,000

40,000

50,000

60,000

2006 2007 2008 2009 2010 2011

NPLs

NPLs

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

2006 2007 2008 2009 2010 2011

NPL Ratio

NPL Ratio

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Year 2006 2007 2008 2009 2010

CASA

CASA

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

7.50%

8.00%

8.50%

9.00%

9.50%

10.00%

10.50%

2006 2007 2008 2009 2010 2011

Capital Asset Ratio (Tier I + Tier II)

Capital Asset Ratio (Tier I+ Tier II)

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

2006 2007 2008 2009 2010 2011

Capital Asset Ratio (Tier I)

Capital Asset Ratio (Tier I)

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

2006 2007 2008 2009 2010 2011

Loan to Deposit

Loan to Deposit

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

2006 2007 2008 2009 2010 2011

Yield on earning assets

Yield on earning assets

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

2006 2007 2008 2009 2010 2011

Cost of Funds

Cost of Funds

5.00%

5.20%

5.40%

5.60%

5.80%

6.00%

6.20%

2006 2007 2008 2009 2010 2011

Spread

Spread

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

2006 2007 2008 2009 2010 2011

Market Cap. To Deposits

Market Cap. To Deposits

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

2006 2007 2008 2009 2010 2011

Cost/Income

Cost/Income

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

2006 2007 2008 2009 2010

Growth in Loan Book -

Growth in Loan Book -

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2006 2007 2008 2009 2010

15.72%

12.38% 14.35%

9.47%

24.92%

Growth in Deposits -

Growth in Deposits -

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

2006 2007 2008 2009 2010 2011

EPS (PkR)

EPS (PkR)

(0.30)

(0.20)

(0.10)

-

0.10

0.20

0.30

0.40

2006 2007 2008 2009 2010

EPS growth -

EPS growth -

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

2006 2007 2008 2009 2010 2011

PER (x)

PER (x)

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2006 2007 2008 2009 2010 2011

P/BVS Tier I (x)

P/BVS Tier I (x)

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

2006 2007 2008 2009 2010 2011

Tier I BVS (PkR)

Tier I BVS (PkR)

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

2006 2007 2008 2009 2010 2011

BVS (PkR)

BVS (PkR)

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

-

0.50

1.00

1.50

2.00

2.50

3.00

2006 2007 2008 2009 2010 2011

P/BVS (x)

P/BVS (x)

-

0.05

0.10

0.15

0.20

0.25

2006 2007 2008 2009 2010

ROE -

ROE -

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

4.1 Problem Definition

-

0.01

0.01

0.02

0.02

0.03

2006 2007 2008 2009 2010 2011

ROA

ROA

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

2006 2007 2008 2009 2010 2011

ROE / P/BVS (x)

ROE / P/BVS (x)

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

What are the financial impacts of the internal audit effectiveness on the bank’s credibility?

4.2 Problem Statement

Internal audit is the main component of the any bank. The audit department established

with the idea of the establishment of bank. The Central Bank has the clear policy on the

internal audit department as well. Therefore the effectiveness of the internal audit

department will have the impacts on the credibility as well as on the financial performance

as well.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

4.3. Research Methodology

The methodology for the study of this project is briefly discussed below:

4.3.1 Research Design:

4.3.1.1 The Purpose of Research:

The purpose of research is Descriptive in nature.

4.3.1.2 The Type of Investigation:

The type of investigation is Correlation.

4.3.1.3 Extent of Research Interference:

The research interference is Moderate in nature.

4.3.1.4 The Study Setting:

The type of study is Field Study. The researcher will perform Field

Experiment to identify cause and effect relationship.

4.3.1.6 The Unit of Analysis:

The unit of analysis is Banking Sector.

4.3.1.7 The Time Horizon:

The time horizon is Cross Sectional.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

4.3.2 Research Sample Design

4.3.2.1 Population

Banking sector consists of more than 45 companies.

4.3.2.2 Sampling Frame

Habib Bank Limited

4.3.2.3 Sampling Unit

Sampling unit Internal Audit Department.

4.3.2.4 Sampling Type

Sampling type is Proportionate Sampling

4.3.2.5 Sampling Size

Internal Audit Department of:

Selected 50

4.3.2.6 Sampling Plan

Researcher selects Audit managers and audit officers to conduct

interview / questionnaire to verify the Hypothesis.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

4.3.2.7 Select a Sample

We will select the Audit managers and Audit Staff for literature,

working since last 3 years in Audit Department.

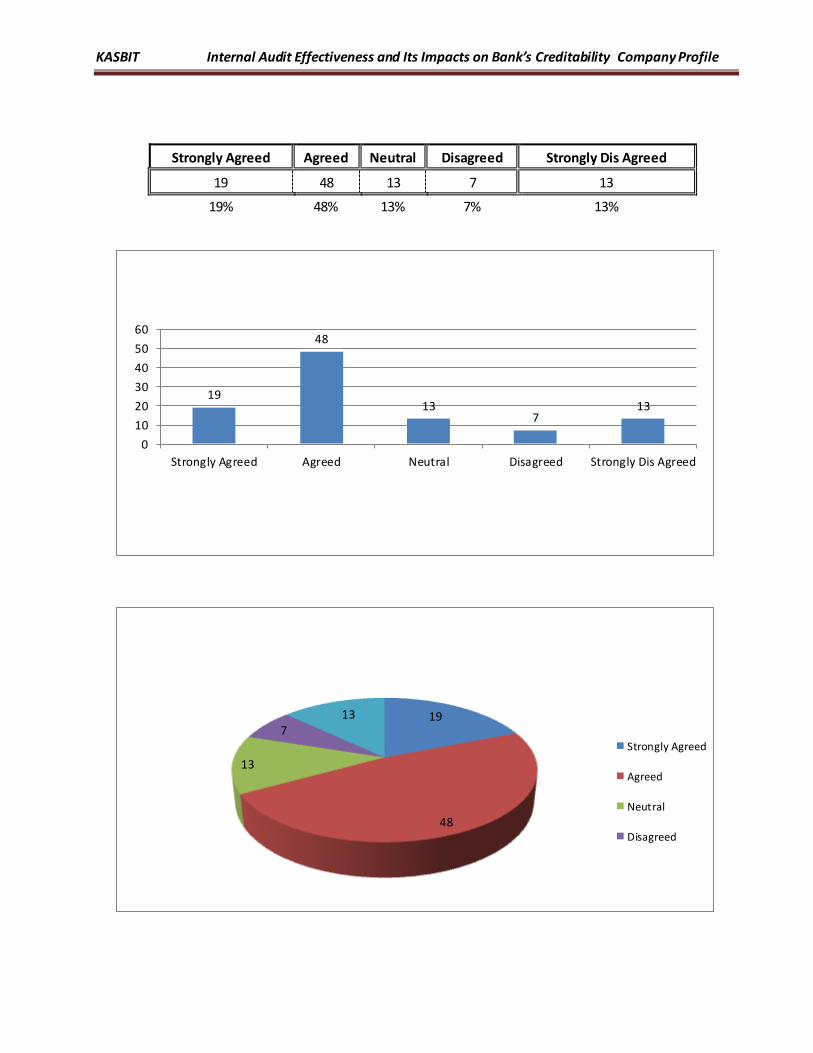

Q13 Do you Agree that Internal Audit Department plays the vital role in detection of fraud?

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

Strongly Agreed Agreed Neutral Disagreed Strongly Dis Agreed

19 48 13 7 13

19% 48% 13% 7% 13%

19

48

13 7

13

0

10

20

30

40

50

60

Strongly Agreed Agreed Neutral Disagreed Strongly Dis Agreed

19

48

13

7 13

Strongly Agreed

Agreed

Neutral

Disagreed

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

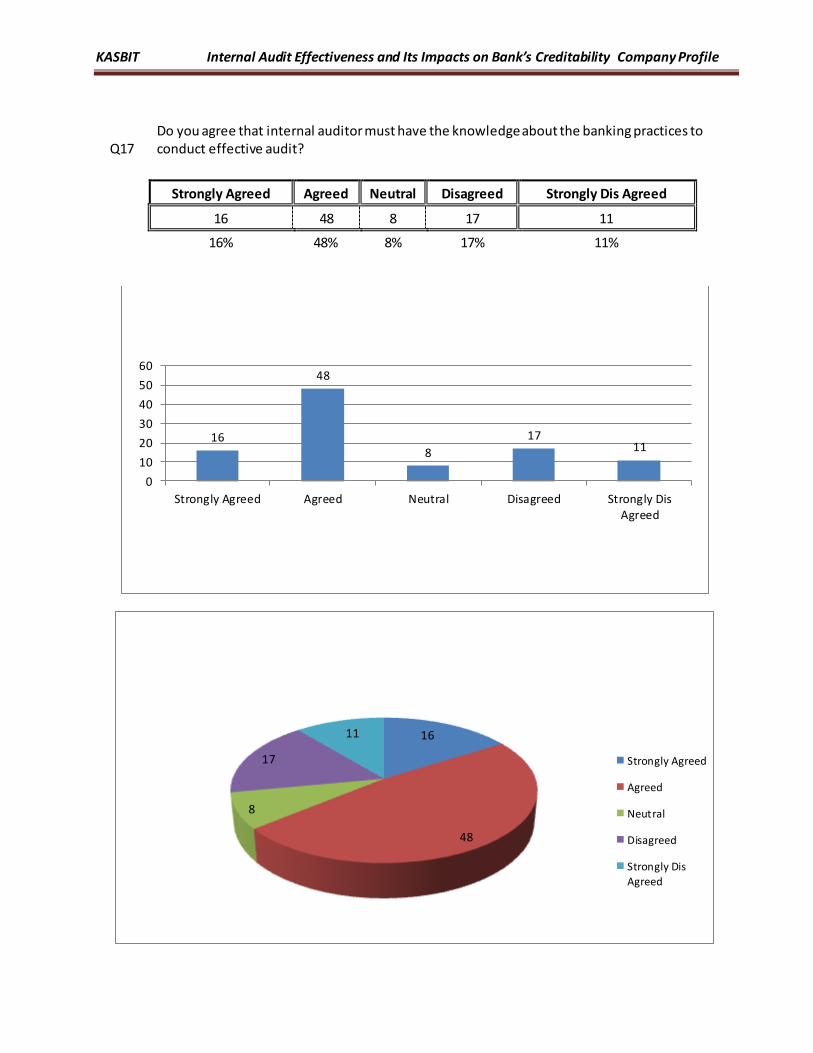

Q17 Do you agree that internal auditor must have the knowledge about the banking practices to conduct effective audit?

Strongly Agreed Agreed Neutral Disagreed Strongly Dis Agreed

16 48 8 17 11

16% 48% 8% 17% 11%

16

48

8

17 11

0

10

20

30

40

50

60

Strongly Agreed Agreed Neutral Disagreed Strongly DisAgreed

16

48

8

17

11

Strongly Agreed

Agreed

Neutral

Disagreed

Strongly Dis

Agreed

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

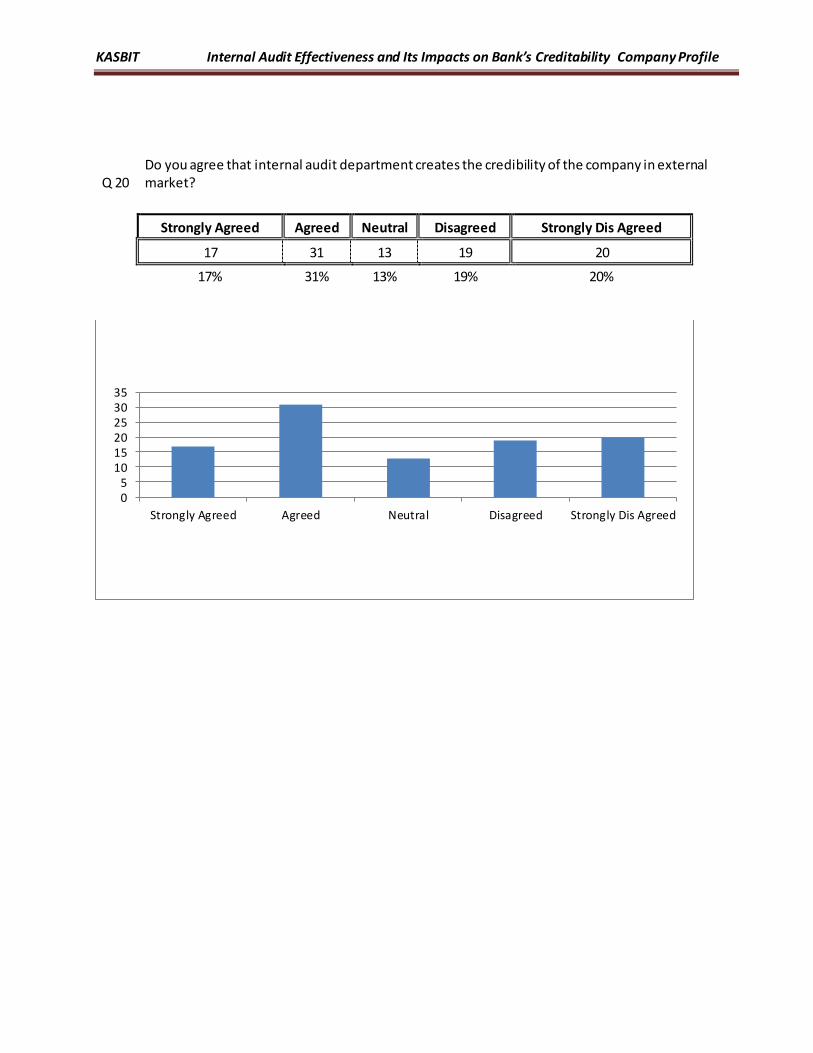

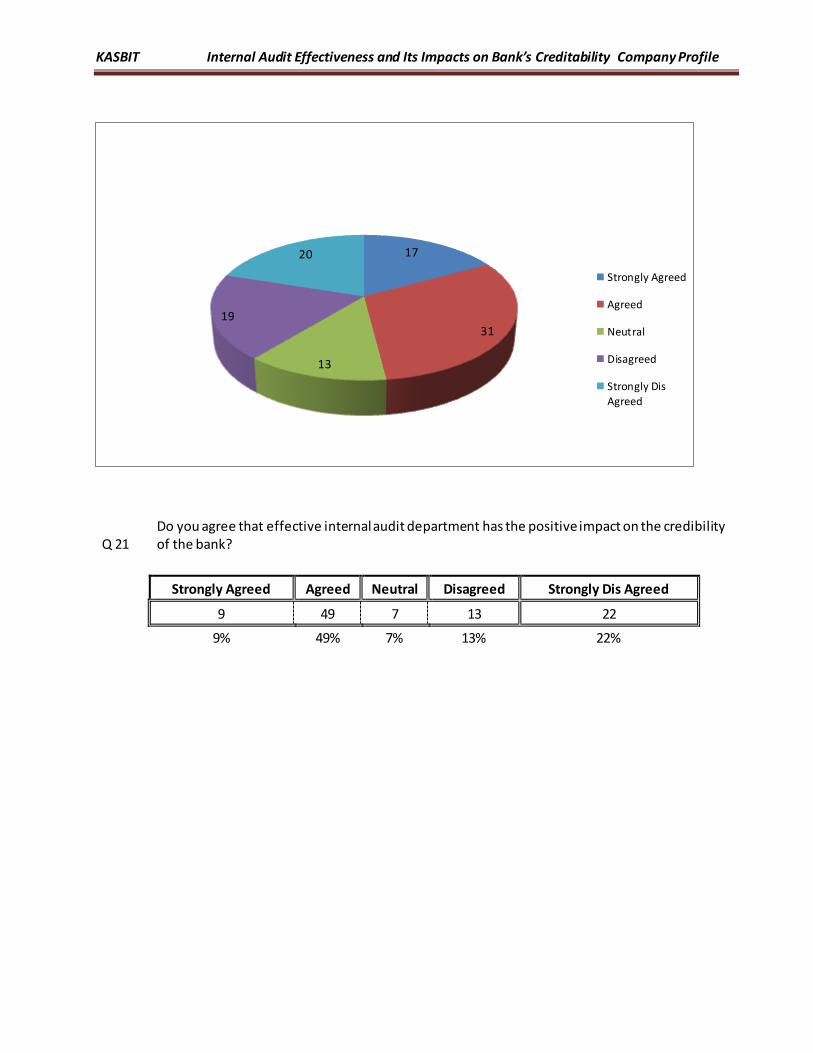

Q 20 Do you agree that internal audit department creates the credibility of the company in external market?

Strongly Agreed Agreed Neutral Disagreed Strongly Dis Agreed

17 31 13 19 20

17% 31% 13% 19% 20%

05

101520253035

Strongly Agreed Agreed Neutral Disagreed Strongly Dis Agreed

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

Q 21 Do you agree that effective internal audit department has the positive impact on the credibility of the bank?

Strongly Agreed Agreed Neutral Disagreed Strongly Dis Agreed

9 49 7 13 22

9% 49% 7% 13% 22%

17

31

13

19

20

Strongly Agreed

Agreed

Neutral

Disagreed

Strongly Dis

Agreed

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

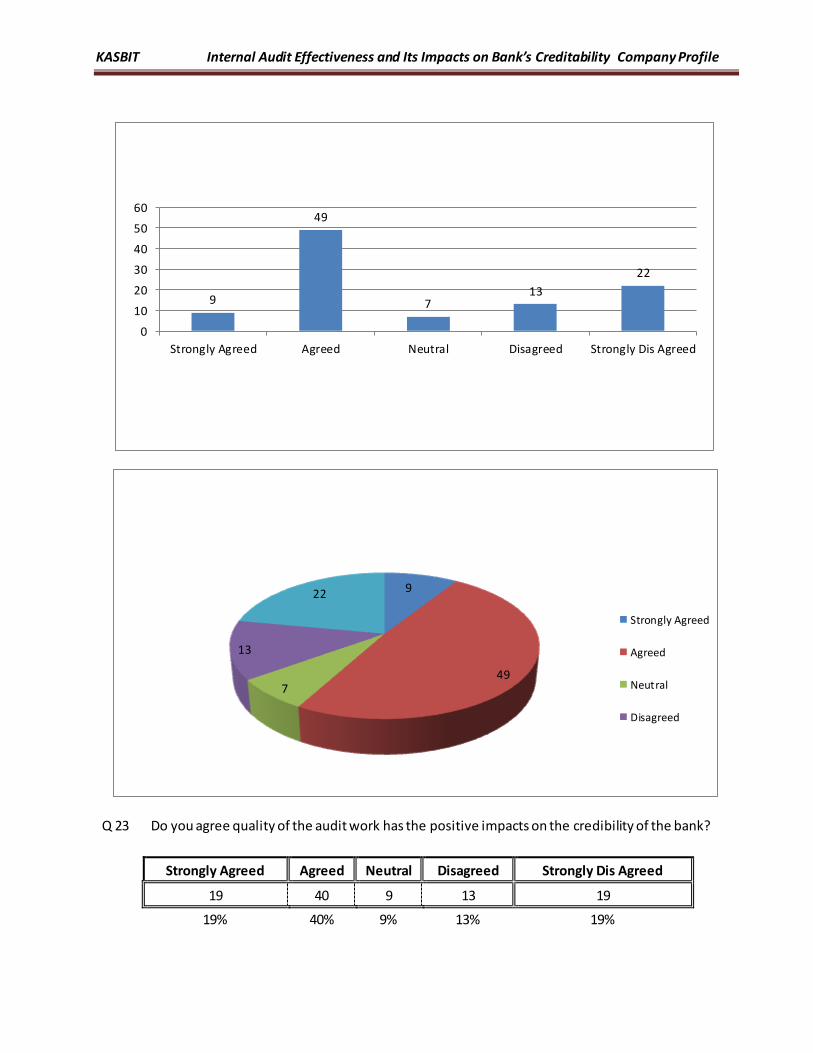

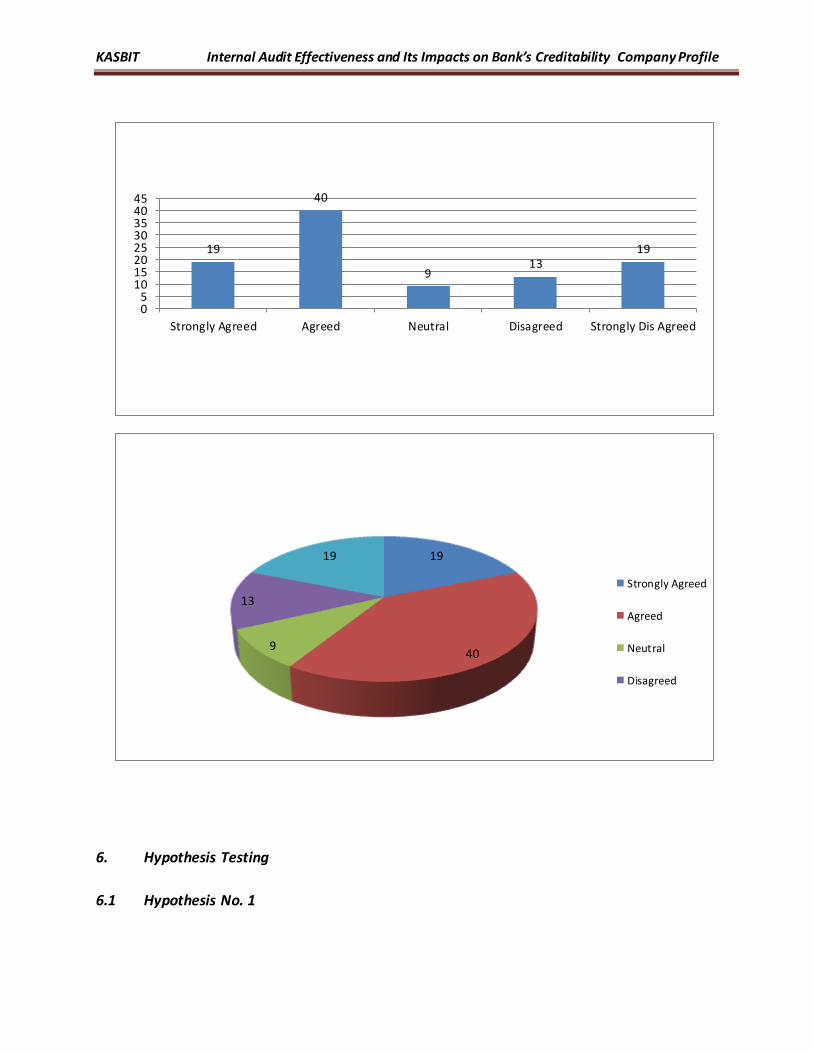

Q 23 Do you agree quality of the audit work has the positive impacts on the credibility of the bank?

Strongly Agreed Agreed Neutral Disagreed Strongly Dis Agreed

19 40 9 13 19

19% 40% 9% 13% 19%

9

49

7 13

22

0

10

20

30

40

50

60

Strongly Agreed Agreed Neutral Disagreed Strongly Dis Agreed

9

49 7

13

22

Strongly Agreed

Agreed

Neutral

Disagreed

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

6. Hypothesis Testing

6.1 Hypothesis No. 1

19

40

9 13

19

05

1015202530354045

Strongly Agreed Agreed Neutral Disagreed Strongly Dis Agreed

19

40 9

13

19

Strongly Agreed

Agreed

Neutral

Disagreed

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

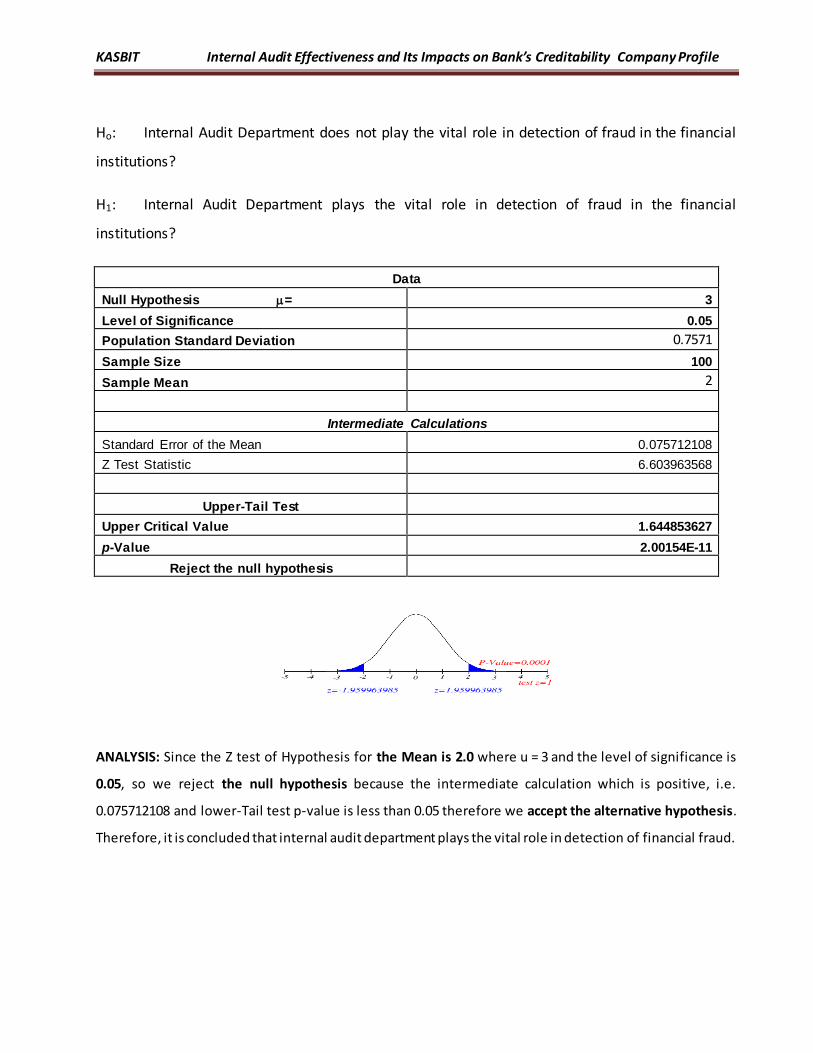

Ho: Internal Audit Department does not play the vital role in detection of fraud in the financial

institutions?

H1: Internal Audit Department plays the vital role in detection of fraud in the financial

institutions?

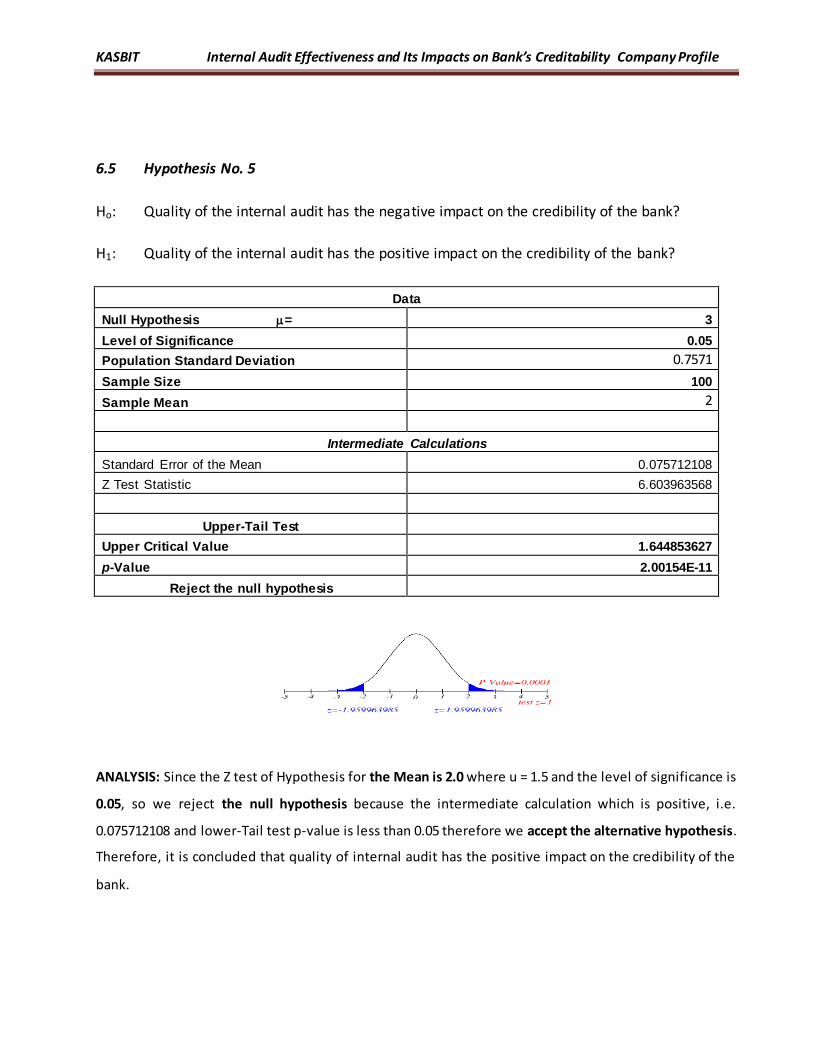

Data

Null Hypothesis = 3

Level of Significance 0.05

Population Standard Deviation 0.7571

Sample Size 100

Sample Mean 2

Intermediate Calculations

Standard Error of the Mean 0.075712108

Z Test Statistic 6.603963568

Upper-Tail Test

Upper Critical Value 1.644853627

p-Value 2.00154E-11

Reject the null hypothesis

ANALYSIS: Since the Z test of Hypothesis for the Mean is 2.0 where u = 3 and the level of significance is

0.05, so we reject the null hypothesis because the intermediate calculation which is positive, i.e.

0.075712108 and lower-Tail test p-value is less than 0.05 therefore we accept the alternative hypothesis.

Therefore, it is concluded that internal audit department plays the vital role in detection of financial fraud.

KASBIT Internal Audit Effectiveness and Its Impacts on Bank’s Creditability Company Profile

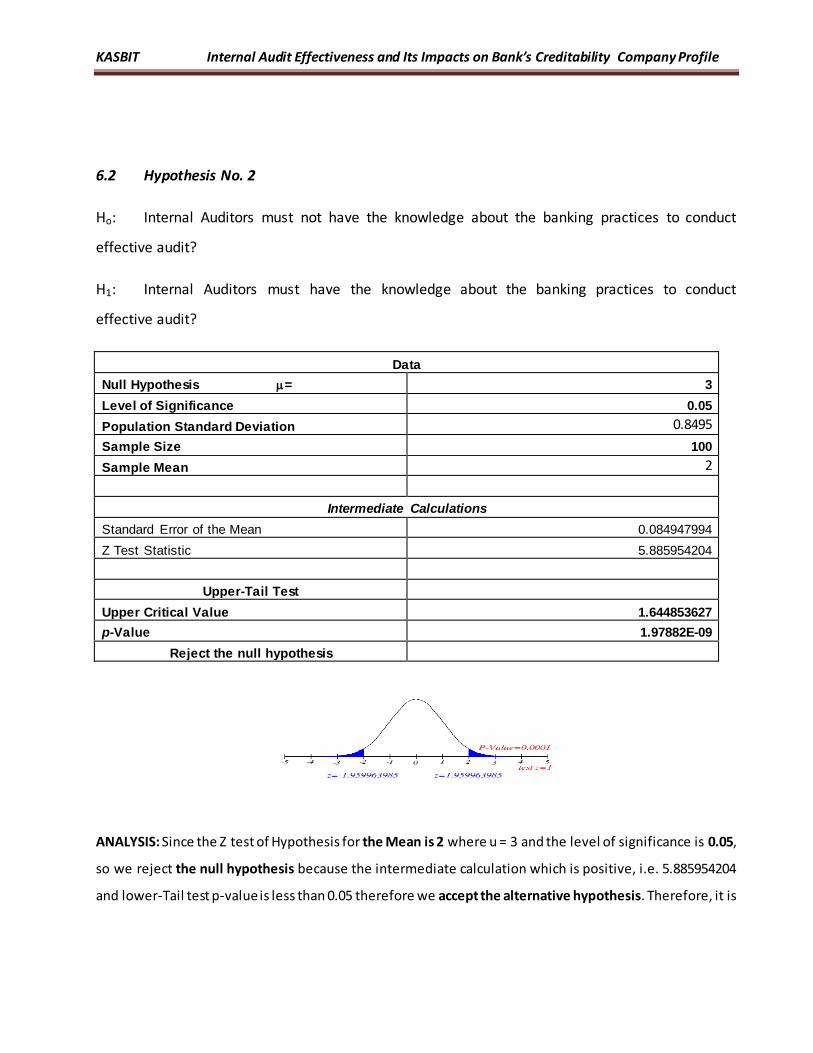

6.2 Hypothesis No. 2

Ho: Internal Auditors must not have the knowledge about the banking practices to conduct

effective audit?

H1: Internal Auditors must have the knowledge about the banking practices to conduct

effective audit?

Data

Null Hypothesis = 3

Level of Significance 0.05