Journal of Forensic and Investigative Accounting Volume 12

20

Journal of Forensic and Investigative Accounting Volume 12: Issue 2, July–December 2020 241 *The authors are, respectively, Professor at Texas A&M University – Corpus Christi and Professor at Kennesaw State University. A Different Approach to Detecting Fraud and Corruption: A Venn Diagram Fraud Model D. Larry Crumbley Donald L. Ariail* Introduction Ernst and Young’s (EY) 15 th Global Fraud survey in 2018 found that fraud and corruption have not declined globally in the past two years (EY, 2018). In fact, the PricewaterhouseCoopers’ (PwC) 2018 Global Economic Crime survey suggests that economic crime has moved from 41 percent in North America in 2016 to 54 percent in 2018. Other than economic damages from fraud, their surveys (2011, 2014, 2018) suggest that fraud affects employee morale, business relations, organization reputation/brand, relations with regulators, and share price. EY (2018) asserts that younger respondents are more likely to justify fraud or corruption to meet financial targets to help a business survive an economic downturn. Time will tell whether the coronavirus pandemic will cause a spike in fraud in the private sector, but certainly there will be massive fraud with the hastily passed $2 plus trillion government stimulus packages. Some models of white-collar fraud have been proposed, starting with Cressey’s (1953) embezzlement triangle (commonly called the fraud triangle) which includes the elements of motive, opportunity, and rationalization. Other major models include the AICPA’s SAS 99 (AU 316; AS 2401, n.d.) triangle with the elements of incentives/pressures, opportunity, and attitude/rationalization; the Wolfe and Hermanson (2004) model includes the four elements of incentive, opportunity, capacity, and rationalization; the Goldman (2010) model includes the five elements of pressure, opportunity, rationalization, employee disenfranchisement, and personal greed; the Dorminey et al. ( 2012) MICE (money, ideology, coercion, ego/entitlement) approach; the Kelly (2017) model including values, culture, and controls factors inside the fraud triangle; and the more recent complicated discourse fraud analysis providing a two page, 40 macro- and micro-level indicators of social, cultural, political, and power relationships (Harte and McHone, 2019). Also, Richard Baker et al. (2016) suggests these four factors beyond the fraud triangle: 1) certain cultural and ideological differences specific to France which may have led to a weakening of internal controls; 2) the possibility of collusive behavior; 3) willful blindness on the part of bank management even though there were well-designed controls in place; and 4) certain capabilities of the fraud perpetuator related to knowledge about how internal controls might be overridden. These models focus more on greed/self-interest and do not seem to cover frauds in the areas of social, altruistic, and non- financial frauds. After reviewing a plethora of past and current frauds, we propose a different approach to viewing fraud and corruption—one that focuses on the motivations/incentives of perpetuators of white-collar fraud and corruption. Our Venn Diagram Model of Fraud (Model) includes four motivations/incentives: greed/self-interest, social, altruism, and non- financial, which we conceive as often bleeding together. A second iteration of our model includes the focus of the four motivations as included in a context the three elements of the AICPA’s SAS 99 (cf. AS 2401) fraud triangle. That is, our four-component model includes motivation, pressure, rationalization, and opportunity. Examples of each type of motivation are provided. In addition, suggestions are made for ways that our fraud motivation types may be considered in external audits, including forensic accounting audits. We suggest that our model, which focuses on fraud motivations, will aid auditors in making better risk assessments related to both the internal and external environments of companies and thus help auditors in better detecting various types of fraud. This study proceeds as follows. First, there is a discussion of the four major types of fraud, and the second section provides two Venn diagrams of fraud motivation. The third section provides examples of the four types of fraud motivations, and the fourth section provides audit implications. The fifth section concludes the study.

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Journal of Forensic and Investigative Accounting Volume 12

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

241

*The authors are, respectively, Professor at Texas A&M University – Corpus Christi and Professor at Kennesaw State University.

A Different Approach to Detecting Fraud and Corruption: A Venn Diagram Fraud Model

D. Larry Crumbley

Donald L. Ariail*

Introduction

Ernst and Young’s (EY) 15th Global Fraud survey in 2018 found that fraud and corruption have not declined

globally in the past two years (EY, 2018). In fact, the PricewaterhouseCoopers’ (PwC) 2018 Global Economic Crime

survey suggests that economic crime has moved from 41 percent in North America in 2016 to 54 percent in 2018. Other than economic damages from fraud, their surveys (2011, 2014, 2018) suggest that fraud affects employee morale, business

relations, organization reputation/brand, relations with regulators, and share price. EY (2018) asserts that younger

respondents are more likely to justify fraud or corruption to meet financial targets to help a business survive an economic downturn. Time will tell whether the coronavirus pandemic will cause a spike in fraud in the private sector, but certainly

there will be massive fraud with the hastily passed $2 plus trillion government stimulus packages.

Some models of white-collar fraud have been proposed, starting with Cressey’s (1953) embezzlement triangle (commonly called the fraud triangle) which includes the elements of motive, opportunity, and rationalization. Other major

models include the AICPA’s SAS 99 (AU 316; AS 2401, n.d.) triangle with the elements of incentives/pressures,

opportunity, and attitude/rationalization; the Wolfe and Hermanson (2004) model includes the four elements of incentive,

opportunity, capacity, and rationalization; the Goldman (2010) model includes the five elements of pressure, opportunity, rationalization, employee disenfranchisement, and personal greed; the Dorminey et al. ( 2012) MICE (money, ideology,

coercion, ego/entitlement) approach; the Kelly (2017) model including values, culture, and controls factors inside the

fraud triangle; and the more recent complicated discourse fraud analysis providing a two page, 40 macro- and micro-level indicators of social, cultural, political, and power relationships (Harte and McHone, 2019). Also, Richard Baker et al.

(2016) suggests these four factors beyond the fraud triangle: 1) certain cultural and ideological differences specific to

France which may have led to a weakening of internal controls; 2) the possibility of collusive behavior; 3) willful blindness on the part of bank management even though there were well-designed controls in place; and 4) certain

capabilities of the fraud perpetuator related to knowledge about how internal controls might be overridden. These models

focus more on greed/self-interest and do not seem to cover frauds in the areas of social, altruistic, and non- financial

frauds.

After reviewing a plethora of past and current frauds, we propose a different approach to viewing fraud and

corruption—one that focuses on the motivations/incentives of perpetuators of white-collar fraud and corruption. Our Venn

Diagram Model of Fraud (Model) includes four motivations/incentives: greed/self-interest, social, altruism, and non-financial, which we conceive as often bleeding together. A second iteration of our model includes the focus of the four

motivations as included in a context the three elements of the AICPA’s SAS 99 (cf. AS 2401) fraud triangle. That is, our

four-component model includes motivation, pressure, rationalization, and opportunity. Examples of each type of

motivation are provided. In addition, suggestions are made for ways that our fraud motivation types may be considered in external audits, including forensic accounting audits. We suggest that our model, which focuses on fraud motivations, will

aid auditors in making better risk assessments related to both the internal and external environments of companies and

thus help auditors in better detecting various types of fraud.

This study proceeds as follows. First, there is a discussion of the four major types of fraud, and the second section

provides two Venn diagrams of fraud motivation. The third section provides examples of the four types of fraud

motivations, and the fourth section provides audit implications. The fifth section concludes the study.

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

242

Four Major Types of Fraud Motivations

A 2018 PwC survey (PwC, 2018) points out that fraud does not have to be a malicious or selfish act. The present

authors suggest that there are at least four major types of fraud motivations which can be understood as a four-circle interlocking Venn diagram. First, fraud may be committed for a personal gain, such as embezzlement, misappropriation of

assets, or false reporting to increase compensation (e.g., self-interest or greed). Second, fraud may be committed for social

reasons such as helping society in general or helping as a specific element of society. Third, fraudsters may behave altruistically for example in attempting to save the existence of the company. Fourth, fraud may be non-financial in

nature—frauds that may not have an initial impact or only an indirect impact on the financial statements—for example

improving the image of the company. While separately conceived, each fraud motivation type may possess elements of

one or more other fraud type. That is, they often bleed together. Nevertheless, the authors posit that separately identifying these types of fraud motivations can assist auditors in their fraud risk assessments and aid forensic accountants in focusing

on motivations to commit fraud.

Venn Diagrams of Fraud Motivations

In criminal investigations, investigators generally try to establish means, motive, and opportunity to prove one’s

guilt in a criminal trial. For white-collar crimes, the commonly called fraud triangle (but really an embezzlement triangle),

the Public Company Accounting Oversight Board’s (PCAOB) Auditing Standard (AS) 2401 (cf. SAS No. 99) fraud triangle, the fraud diamond, and the fraud pentagon (Crumbley et al. 2019, have been developed to describe white-collar

fraud, but these schemes have been criticized (especially the fraud triangle) as not covering other elements or motivations

for fraudsters (Lokanan, 2015).

Holderness et al. (2018) suggest that opportunity is a better predictor than motivation. But the 2016 PwC Global Economic Crime survey indicated that incentives/pressures are 20 percent of the contributing factors for economic crime,

11 percent rationalization, and 57 percent opportunity or ability by internal actors. Yet, PwC’s 2009 Global Economic

Crime survey found 18 percent of the contributing factors were opportunity, 68 percent incentive/ pressures, and 14

percent attitude/ rationalization.

The three elements of the Cressey embezzlement triangle (1953) are motive, opportunity, and rationalization, and

the three elements of AU 2401’s fraud triangle are incentives/pressures, opportunity, and attitude/ rationalization. The four elements of the fraud diamond (Wolfe and Hermanson, 2004) are incentive, opportunity, capacity, and

rationalization. The five elements of the fraud pentagon (Goldman, 2010) are pressure, opportunity, rationalization,

employee disenfranchisement, and personal greed.

Unlike the Cressey triangle and the fraud pentagon, the element of motivation is missing in the AS 2401 fraud triangle and in the fraud diamond. Thus, the authors posit that the Venn Diagrams of Fraud (Figures 1 and 2), which focus

on fraud motivations, can better explain the four major types of fraud motivations: greed or self-interest, social motive,

altruistic fraud, and non-financial fraud. These models consider behavioral aspects and motivation and should help companies and auditors prevent and detect fraud. As previously noted, the four types of fraud are not necessarily separate

and distinct—they often bleed together.

The first conception of our fraud model (Figure 1) focuses on the author’s posited four types of fraud motivations.

Each fraud motivation type is illustrated as a circle. Since distinctions between these fraud motivations are often not distinct, the four circles overlap. The circles of this Venn diagram do not represent the amount or number of such frauds.

However, there may be differences in the “red flags” associated with these frauds and in the ways these frauds are

detected.

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

243

Figure 1: Venn Diagram Fraud Model—First Iteration

The second iteration of our fraud model (Figure 2) depicts the four overlapping circles of motivation surrounded by

the elements of SAS 99 (AS 2401; AU 316) fraud triangle. That is, while our model of fraud and corruption is focused on

motivations, we posit that fraud detection also may benefit from considering the pressures, opportunity, and

rationalization elements conceived by Cressey. Thus, Figure 2, presents a four-element model of fraud and corruption—motivation (the four overlapping types of motivations) as the primary focus with the three elements of SAS 99 (AS 2401;

AU 316) fraud triangle having a secondary focus.

Figure 2: Venn Diagram Fraud Model—Second Iteration

The following examples of the four types of fraud motivations are illustrative of both their distinctions and

interrelationships.

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

244

Greed/Self-Interest

Hayes et al. (2015) indicates that managerial greed leads to a focus on short-term decisions and short-term

company performance. Chi and Ziebart (2019) found that firms with irregularities tend to issue more precise forecasts in the period where earnings are restated in order to capture a larger market reaction, enhance a stronger firm-investor trust

relationship, and lower investors’ perceived risk and uncertainty about future prospects. They also found that managers

may knowingly plan to employ more aggressive earnings management or know that they have the option to do so at the

time they issued their forecast and hence the company can be more precise in their earnings forecast.

Most fraud and/or forensics textbooks deal with greed or self-interest fraud such as embezzlement or stealing

assets or inventory. For example, a high school graduate, Controller and Treasurer Rita Crundwell stole more than $53

million from the city of Dixon, Illinois with an annual budget of $8–$9 million over 22 years to support her lifestyle, a $2.1 million-dollar motorhome, $259,000 horse trailer, and one of the best-known quarter horse breeding operations on an

$80,000 yearly salary. She was the only signatory to a secret municipal bank account, and a city commissioner praised

her: “She looked after every tax dollar as if it were her own” (U.S. v. Rita A. Crundwell, 2013). Of course, she did just

that.

Vernon Beck, an ex-pilot, embezzled $13.5 million over seven years from Texas Petrochemical using an

imaginary company to bill for invoices for work never done. His first fake invoice was for only $275. By the year he was arrested he and his co-fraudster were averaging $163,000 per week. Beck said, “it was nothing more than greed. I wish I

could blame it on a drug or alcohol problem (Fottrell, 2014).

An example of corporate greed (which also has aspects of altruistic behavior) would be Toshiba management who

over years created a technique called carryover (c/o) to overstate earnings by “. . . deferring operating expenses until they could be reported without causing a loss” (Stoyas v. Toshiba Corporation, 2015 ). These fictitious carryovers were used to

cover the gaps not covered by other sales initiatives. As Alan Oliphant said, “I don’t see many ways to eliminate greed; it

is an inherent part of human nature” (Banks, 2004, 36–37).

An example of non-corporate fraud would be attorney Michael Avenatti who was accused of embezzling $1.5

million from Miami Heat’s basketball player Hassan Whiteside. The seven-foot center for Miami, with a 2016 salary of

$22.12 million, wired Avenatti $2.75 million in January 2017 to cover most of the $3 million settlement with his ex-girlfriend. Allegedly, Avenatti was entitled to a legal fee of $1 million, but he kept $2.5 million to purchase a private jet.

How could someone believe they could get away with such obvious fraud? Even the one million fee sounds high. On

April 11, 2019, federal prosecutors accused the celebrity lawyer of embezzling $12 million from his clients (including the

Whiteside amount).

A fraud that was driven by greed involved two contract Amazon drivers who would travel to Seattle-Tacoma

International Airport, pick up items returned by customers, and routinely steal them. They also stole items they were

delivering to post offices. The stolen items were sold to several pawnshops, that in turn shipped the same items to Amazon warehouses until they were sold online. From 2013 until the fraud was discovered, the stolen merchandise was

sold for at least $10 million (Johnson, 2019). Surely, internal and external auditors could have caught this fraud with some

simple ratio analysis, comparing the state of Washington with other states.

Greed does not necessarily involve only a monetary reward. Jerome Kerviel worked for Société Générale, a French securities firm, as a junior level derivatives trader. During 2006 through 2008, he evaded all the French bank’s internal

controls to bet €73.5 billion on European markets—more than the bank’s market value, causing a loss of €4.9 billion loss.

Kerviel reported to work early, stayed late, and took only four days off in 2007. In France, six weeks of vacation is fashionable. Starting in early 2005, he made small unauthorized trades, and the bank missed the illicit trades and the red

flags.

Kerviel grew increasingly daring after no one at the bank detected a series of his small unauthorized trades. He entered fictitious and offsetting trades to minimize the odds of big losses. He stole other people’s computer access codes,

falsified documents, and employed other methods to cover his tracks.

He had an excellent understanding of the bank’s processing and control procedures so he could circumvent all the

controls (Blanch, n.d.). His motives were a quest for glory and a bonus (greed). Thus, he was looking for both psychic and monetary rewards. Although almost unbelievable, in 2016 Kerviel persuaded a French labor tribunal that his 50 billion

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

245

euros worth of unauthorized trades, committing forgery, and fraud to cover up his activities were not “real and serious

cause” for the bank to fire him. The tribunal ordered the bank to pay Kerviel 450,000 euros. He was supposed to serve

three years in prison for his activities (Clark, 2016), but he was released from jail with an electronic monitoring bracelet. After winning his wrongful dismissal suit, in September 2016, he had his 4.9 billion euros fine reduced by 99.98 percent

to one million euros (Jolly and Clark, 2016).

Social Motive Fraud

A fraud could be committed for a social motive such as the survival of a company or protection of the workforce

(sometimes called managerial altruism). Hayes et al. (2015) suggest that managerial altruism helps a company focus on

longer term decisions and long-term firm performance. These authors believe that extremes of either greed or altruism

likely will harm a company’s performance.

There is a small line between self-interest fraud (greed), earnings management, impression management, and

abusive earnings management. Katharine Schipper (1989) defined earnings management as the “purposeful intervention

in the external financial reporting process, with the intent of obtaining some financial gain.” Robinson and Lokanan (2017) pose the question, when does earnings management cross over to abusive earnings management? Or when does a

company cross the line between criminal behavior and merely conduct that is beneficial to the company, and why? Or

when does impression management cross over to fraud? The concept of impressions management revolves around individuals and companies attempting to influence the perceptions of others. For a discussion of impression management,

see Robinson and Lokanan (2017). The difference between earnings management and fraud is often less than the

thickness of the wall of a prison cell.

A 2014 CFO survey found that one-fifth of companies were distorting earnings. Companies followed the letter of GAAP but not necessary the spirit. Few CFOs felt that the auditors would catch them. If they did, the auditors would

probably not bring it up to management (Dichev, Graham, Harvey, and Rajgopal, 2014).

This social motive category is facilitated by either the executives (leaders) or by the employees (or a combination of both). A Milgram Experiment in 1962 found that morals are often influenced by situational forces rather than by

character or personal traits such as values (Milgram, 1974). Further studies about this “obedience to authority” position

found

• Women were about the same in obedience as men.

• Distance to the victim affects obedience.

• Distance to the person giving the orders affects the obedience.

• The appearance of the authority person and his/her rank can increase or decrease the obedience (Explorable.com,

2008).

When combined with a leader or executive high on the dark triad (narcissism, Machiavellianism, and psychopathy),

especially narcissism, may be a facilitator of a social motive fraud (massive collusion). In fact, Duchon and Drake (2009,

301) suggest that extreme narcissism is associated with unethical conduct. Further Amernic and Craig (2010) suggest that special features of financial accounting facilitate narcissism in susceptible CEOs. Relying on Duchon and Drake (2009),

they believe that the use of accounting language and measures lead to unethical behavior by extreme narcissistic

executives.

The extreme of the dark triad is psychopathic personality traits of lack of empathy, guilt, and remorse. A meta-

analytic review of psychopathy and leadership from 92 independent samples showed a weak positive correlation for

psychopathic tendencies and leadership emergence (Landay et al., 2019). These authors did find a weak negative

association with psychopathic tendencies and leadership effectiveness and a moderate negative correlation for psychopathic tendencies and transformation leaderships. These Landay et al. analytics differ from the popular belief that

approximately one out of five CEOs have psychopathic tendencies (Agerholm, 2016). So, if there is any truth in the fact

that CEOs are number one on the list of the 10 professions with the most psychopaths (Dodgson, 2018), this executive personality factor coupled with the “obedience to authority” theory could explain many of the major frauds caused by

collusion (e.g., Enron; WorldCom; HealthSouth; Taylor, Bean and Whitaker; VW; and Libor).

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

246

An example of a social motive fraud is the Wells Fargo fraud which started out as a sales or performance strategy to

increase the company’s market share or survival during the last financial crisis. From 2011 to 2015, Wells Fargo

employees in order to game the compensation system opened more than 1.5 million in unauthorized bank accounts and applied for at least 500,000 credit cards in their customers’ names without the customers’ knowledge (Levine, 2017). The

number of unauthorized bank accounts opened during a wider window (from 2009 to 2016) may have been as high as 3.5

million (Thomas, 2017). Thus, a strategy that was meant to help the company survive (a social motivation) ended up

incentivizing employees to fraudulently increase their compensation (greed/self-interest).

Another example might be the Taylor, Bean, and Whitaker (TBW) and Colonial Bank fraud where some bank

employees initially covered-up TBW’s over drafting of their operating account which reached at least $600 million.

Clearly, the Chairman of TBW, Lee Farkas was a self-interest, greedy fraudster in the multi-faceted, multi-billion-dollar fraud. On the TBW bankruptcy date there were around 1,473 fake mortgages. To avoid discovery of the fraudulent

behavior by executives at Colonial headquarters, Teresa Kelly testified that she was instructed to use Blackberry PIN

messaging which was untraceable on the company’s e-mail servers, and to use a private e-mail address to discuss transactions with Catherine Kissick, TBW’s chairman Lee Farkas, and TBW’s treasurer Desiree Brown (Ariail and

Crumbley, 2019).

But how do we classify Colonial Bank’s Catherine Kissick’s motivation, since she discovered the TBW fraud at the $10 million stage but continued the sweeping until the hole reached $120 million? At trial Ms. Kissick testified that “. . .

[her] biggest fears were my whole staff imploding and my customers losing their bank” (District Court of the U.S., 2017,

69). Did she fit into the social motive category, the altruistic category, or was she trying to protect her job (greed)?

Colonial Bank appeared to have a war mentality that caused employees to feel they had to help the company survive. She received no extra economic gain (Ariail and Crumbley, 2019). Internal auditor Sherron Watkins had the following to say

about Enron’s Jeff Skilling and Andy Fastow: “But there is not a defining point where they became corrupt. It was one

small step after another, with more and more rationalizations. There was a slow erosion of values over time” (Colloff,

2003). Was their behavior social fraud or greed (self-interest)?

Betty Vinson, the accountant in WorldCom, said she was pressured to make the massive entries to reduce expense.

At trial Judge Barbara S. Jones said Ms. Vinson was “among the least culpable member of the $11 billion conspiracy. Yet, had Ms. Vinson refused to make the entries, the “conspiracy might have been nipped in the bud” (as quoted in Associated

Press, 2005). She received five-month months in prison. Another accountant, Troy Normand merely made sure the books

and records were changed. He received a three-year suspended sentence (Associated Press, 2005). Would these

accountants fall under the greed (self-interest) or social motive category?

The Takata scandal could be a type of social motive fraud (and non-financial fraud) along with the obedience

theory, whereby employees took improper and illegal actions to protect the company (and their jobs). Takata was a maker

of 70 million automobile airbags with approximately 20 percent of the market (19 companies). There were around 42 million vehicles in the U.S. alone. At least 24 people were killed by exploding air bags, with 17 in the U.S. and 240

injured (Timeline, 2017; Newsome and Melton, 2019).

In the late 1990, Takata changed from stable sodium azide used as the propellant to the cheaper but less stable

ammonium nitrate. The company in January 2017, pleaded guilty and agreed to a $1 billion settlement with the Department of Justice, and three former executives were indicted. Takata’s scheme was to falsify test data (after changing

the propellant) about their airbag inflators which could explode and spray sharp metal pieces into the car onto passengers.

They found the problem in 2004, but apparently, technicians were ordered to destroy results of tests showing cracks in

some inflators (Riley, 2014; Tabuchi, 2016).

In March 2013, Takata took a $307 million expense and posted a $21.1 billion-year net loss because automakers

recalled more than four million vehicles. In 2014, the company took another special loss of $440 million. The first class-action lawsuit was filed in Florida and their stock price continued downward. On February 20, 2015, U.S. regulators

began imposing a $14,000 daily fine on them for failing to cooperate. At least 37 million cars have been recalled

(Timeline, 2017)

In May 2015, Takata admitted that they had discovered leaks in some of the inflators that could allow moisture to seep in and break down the chemical propellant, making the propellant explode more violently. On June 25, 2017, Takata

filed for Chapter 11 bankruptcy in the U.S., and filed for bankruptcy in Japan (Mullen, 2017; Plungis, et al. 2016).

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

247

Tokusai (or special adoption) is a Japanese word that refers to shipping of products and inventory that does not

meet the standards of the customer (e.g., do not meet safety standards) Often the customers are aware of the data

manipulation, but not always (e.g., Kobe Steel). This Japanese term could be considered social fraud. An example would be Kobe Steel where the practice of voluntary acceptance by customers occurred over 40 to 50 years. Products would be

shipped without inspection or with fake certificates (Obayashi, 2018). Other similar examples would be Mitsubishi

Materials and Toray Industries.

Whether the collusion is for greed or social motivation, when speaking about the fraud at HealthSouth, a

spokesperson for EY emphasized the difficulty of detecting accounting fraud during a conspiracy of senior executives and

false documentation (Mollenkamp, 2003). In the WorldCom fraud at least 40 people knew about the fraud, but they were

afraid to talk. Scott Sullivan handed out $10,000 checks to seven involved people (Blumenstein and Pullian, 2003).

Robert Tillman and Michael Indergaard (2007) found that of 834 companies that issued restatements between

January 1, 1997 and June 30, 2002, 374 (45 percent) were accused of securities fraud. An average of seven people was

normally involved—CEOs, CFOs, COOs, general counsel, directors, and internal and external auditors. In the Bernard Madoff Ponzi scheme, five employees were found guilty, including the accountant Paul Konigsberg. He pleaded guilty to

falsifying records of a broker-dealer and an investor advisor to help Madoff’s clients backdate trades.

Altruistic Fraud

A third category of fraud motivation would be a clearly altruistic fraud, such as Robin Hood or the imaginary $100

million anonymous gift to Minnesota in the 2016 movie Interrogation. Here two bad guys steal $400 million from the

Federal Reserve and give $100 million of the loot for scholarships for homeless children in and around Minneapolis. In

English folklore, outlaw Robin Hood stole from the rich and gave to the poor. But according to the Heroic Stoic (2012),

even Robin Hood was not altruistic.

John Friedrick, who was the Head of the Victorian Division of the National Safety Council of Australia

(NSCAVD), engaged in one of the largest frauds in Australia, that can be considered altruistically motivated. Between 1977 and 1989, Friedrich expanded the NSCAVD from a non-profit organization promoting safety awareness to a hi-tech

search and rescue operation. He hid a shady past from everyone until NSCAVD collapsed with debts of almost $300

million. The debt went undetected for a decade under the noses of investors and auditors. He did not use the ill-gotten gains for himself and family, but he put the funds into an organization that saved thousands of peoples’ lives. His lack of

conspicuous consumption helps explain why the massive fraud went undetected.

The PwC’s 2016 Global Economic Crime Survey devoted some discussion to the litigation aspects that

rationalization and altruistic motives have on proving willful deception (e.g., scienter). This PwC survey stated the

following:

For businesses, there’s a big difference between fraud committed for personal gain (such as embezzlement, or false

reporting intended to boost compensation) and fraud committed for “corporate motives” (such as company survival, protection of the workforce or even of the community). In our experience, material financial reporting fraud is

typically driven by corporate motives. This [altruistic fraud] presents a dilemma for prosecutors, investigators, and

plaintiffs, who, when faced with evidence of financial misrepresentation, generally look for the smoking gun of

financial gain.

PwC’s bottom-line, however, is that knowing financial misrepresentation is unacceptable—no matter what the

intent—even though the lack of scienter makes it difficult to prove fraud under some legal standards (PwC, 2016).

But Adelphia founder John Rigas rationalized at his trial saying, “in my heart and in my conscience, I’ll go to my grave really and truly believing I did nothing but to try to improve the conditions of my employees.” Prosecutors said

Rigas used a complicated cash management system to give money to various self-owned entities as a cover to steal $100

million for him and his family members (AP, 2005).

In the area of cryptocurrency, a hacker operating under the pseudonym “Bnatov Platon” talked to some CoinDesk

reporters in 2019. What appears to be a person- hacking- hackers, the individual threatened and demanded 300 bitcoins in

exchange for withholding 10,000 photos that supposedly showed the Binance exchange’s KYC data. In the individual’s

discussion with the CoinDesk reporters, the hacker maintained he was a “white hat hacker” and claimed to be altruistic.

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

248

He merely wanted to reveal how he allegedly hacked individuals behind an earlier hack in which 7,000 bitcoins were

stolen from the world’s largest exchange (Bigg and Kuhn, 2019).

There is probably little altruistic fraud, but some of the social and non-financial fraud may bleed somewhat into altruistic reasons. Tsai and Xie (2017) suggest that a person experiencing low confidence (e.g., passed over for a

promotion) can lead to attempts to boost confidence or status by engaging in fraud. If the person is seeking financial

status, they may behave more selfishly and cheat or commit fraud. According to Tsai and Xie, this state of confidence can fluctuate easily when a person’s situation changes, and confidence can increase selfish, money-making behaviors or

altruistic acts depend on whether money or altruism is perceived as the major source for increased status that can restore

low confidence. These authors found that one-third of low confidence people cheated compared to 10 percent for high

confidence people.

The Robin Hood defense has been used in both criminal and civil trials in the U.S. and Canada. In December 2014

in Naples, Florida Joyce M. Crain was found guilty on 10 of 11 felony, drug, fraud, and forgery counts. She was president

and founder of a nonprofit which worked as a prescription assistance program, an intermediary between drug companies and low-income patients who could not afford prescriptions. She schemed to illegally obtain a stockpile of free

medications worth more than $500,000 so she could give the medication to anyone she wanted. She forged doctors’

signatures, altered zoning documents, and made her own prescription labels. Prosecutors indicated she did not profit greatly from the operation, but she disregarded laws to get the medications to patients faster (Carpenter, 2014). She

received a 30-months prison sentence.

Jeffrey Gonsiewski was Vice-President of the loan department at First Security Trust and Savings in suburban

Chicago. Between September 2004 and February 209, he altered at least 100 loan documents to make it appear that 50 customers’ loan payments were current which bought time for loan customers but prevented the bank from taking timely

actions to collect delinquent loans and protect its assets. This modern-day Robin Hood received a 63-months prison

sentence and a $5.1 million mandatory restitution order (Bank vice president sentenced, 2010).

The former Quebec Lieutenant Governor Lise Thibault tried to use the Robin Hood defense in her criminal trial in

May 2015. She pleaded guilty to a criminal charge of fraud, and her defense attorney said she should be given a lenient

sentence for her Robin Hood fraud because she was an advocate for the disabled. Thibault cheated the Canadian and Quebec governments out of more than $429,000 by claiming improper expenses for gifts, trips, parties, meals, skiing and

golf lessons, earthworms, and fishing rods. Her large charitable deductions of $1.5 million to help establish 31 resorts for

para-alpine skiing could not save her at age 76 from an 18 months prison sentence and orders to pay $300,000 (Cherry,

2016). She served only six months, however. She also was ordered to pay almost $1.5 million of unpaid taxes on

unreported income.

The defense of stealing money to help the poor could not help Lorraine Reid in her scheme to send checks from

Bell Canada to family members and friends who she felt were experiencing financial troubles. Reid worked in the accounting department at Bell and was responsible for sending refunds to Bell’s clients who overpaid their bills. Rather

than sending the $145,000 of refunds to the proper customers, Reid would change the name of the payee to one of her

family members or friends. Police arrested Reid, her family members, and friends who received the fraudulent money

(Burghard, n.d.).

Detroit principals engaged in a scheme with a school supplies vendor Norman Shy by signing off on invoices for

supplies and services which he never intended to deliver. Nearly $2.7 million bogus invoices were paid by the district, and

Shy rewarded principals with approximately $1 million of kickbacks.

Josette Buendia was the principal at Bennett Elementary School who received around $45,775 in bribes between

2011 and 2015. Her attorney depicted the divorced, single mother of an 8-year old daughter and 15-year old son as a

benevolent Robin Hood who committed fraud but had the best intentions of her students in mine. She supposedly spent $65,000 on expenditures for her students. She was found guilty by the jurors, and the judge sentenced her to prison for

about nine months longer than the average 15-months other principals received because she showed no remorse. Vendor

Norman Shy received a five-year prison sentence (Burns, 2019).

Non-Financial Fraud

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

249

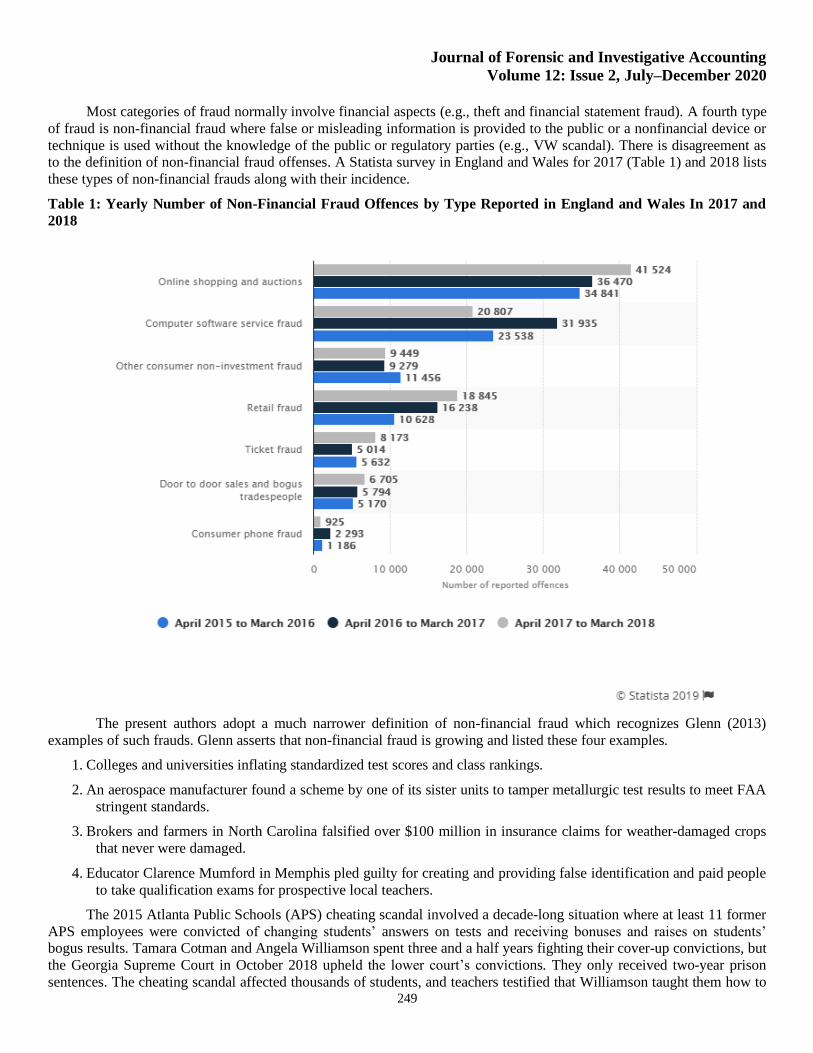

Most categories of fraud normally involve financial aspects (e.g., theft and financial statement fraud). A fourth type

of fraud is non-financial fraud where false or misleading information is provided to the public or a nonfinancial device or

technique is used without the knowledge of the public or regulatory parties (e.g., VW scandal). There is disagreement as to the definition of non-financial fraud offenses. A Statista survey in England and Wales for 2017 (Table 1) and 2018 lists

these types of non-financial frauds along with their incidence.

Table 1: Yearly Number of Non-Financial Fraud Offences by Type Reported in England and Wales In 2017 and

2018

The present authors adopt a much narrower definition of non-financial fraud which recognizes Glenn (2013)

examples of such frauds. Glenn asserts that non-financial fraud is growing and listed these four examples.

1. Colleges and universities inflating standardized test scores and class rankings.

2. An aerospace manufacturer found a scheme by one of its sister units to tamper metallurgic test results to meet FAA

stringent standards.

3. Brokers and farmers in North Carolina falsified over $100 million in insurance claims for weather-damaged crops

that never were damaged.

4. Educator Clarence Mumford in Memphis pled guilty for creating and providing false identification and paid people

to take qualification exams for prospective local teachers.

The 2015 Atlanta Public Schools (APS) cheating scandal involved a decade-long situation where at least 11 former

APS employees were convicted of changing students’ answers on tests and receiving bonuses and raises on students’ bogus results. Tamara Cotman and Angela Williamson spent three and a half years fighting their cover-up convictions, but

the Georgia Supreme Court in October 2018 upheld the lower court’s convictions. They only received two-year prison

sentences. The cheating scandal affected thousands of students, and teachers testified that Williamson taught them how to

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

250

cheat. At least 44 schools and 178 educators were participants and more than 80 confessed (McCray, 2018; Downey,

2018).

Tammy Whitehouse (n.d.) provides three major examples of non-financial fraud. BP ignored or pushed limits on pipeline maintenance which led to a 270,000-gallon oil spill in Alaska which sent oil prices upward in 2006. State Farm

settled hundreds of lawsuits after claims that they pressured engineers to alter reports and change their conclusions on

whether wind or water was responsible for damages. Also, Shell had to pay a fine in 2004 for overstating oil and gas

reserves to boost their valuations. Are these types of fraudulent behavior covered by Sarbanes-Oxley (SOX)?

Non-financial frauds can have significant impact on stakeholders. One health care example is the $9 billion

Theranos and CEO Elizabeth Holmes blood testing scandal. After dropping out of Stanford in 2003, she used an

educational trust from her parents to establish a company to devise a machine that could perform diagnostic tests with a small amount of blood. In October 2015, John Carreyrou suggested that Theranos was using traditional blood-testing

machines to test blood rather than their Edison devices. By September 2018, Theranos ceased operations (Carreyrou,

2018). Essentially, the Edison device was a hoax. Her trial is scheduled to begin July 28, 2020, and she faces 20 years in

prison.

Known as Dieselgate (c.f. Ariail, Cobb, and Crumbley, 2019), in 2015 Volkswagen (VW) was caught using illegal

software to cheat U.S. pollution control tests. The SEC said VW issued more than $13 billion in bonds and asset-backed securities at attractive rates when the company knew that more than 500,000 U.S. diesel vehicles grossly exceeded the

legal vehicle emissions standards. So far, this fraud has cost VW at least $30 billion (in September 2017). The scandal

caused one of the costliest recalls in history.

VW was known as a company with excellent engineers, tight-lipped management, and a culture of opacity (Collins, 2015). Emission testing is done by regulators in laboratories with the cars sitting on dynamometers with the front wheels

not turning. Real-world driving tests generally do not meet the laboratory test results. VW was not caught by the EPA, but

by third-party researchers affiliated with West Virginia University (WVU) who actually drove the cars. (Collins, 2015). Assistant Professor Arvind Thiruvengadam won a $70,000 grant from the International Council on Clean Transportation

to test and experiment on cars, and the VW scandal is history. The Council thought the VW cars were an example of how

diesel could be a clean fuel (Glinton, 2015).

There was no “defeat device,” nothing soldered to the tailpipe, or rigged software on the cars to commit the fraud.

The VW engineers put some extra lines of code in the algorithmic software to make the diesel engine perform better while

the front wheels were not turning on the dynamometer. The sensors could recognize when the auto was running on the

dynamometer or on the road (Collins, 2015). If the sensors indicated that the car was being driven on the open road, the car switched off the exhaust control (Moshinsky, 2015). So, if the EPA could not catch the non-financial fraud, how could

the external auditor PwC (Aktiengesesellschaft) catch the fraud? The five WVU researchers fit three portable emission

control devices on two VWs and a BMW on a run from San Diego to Seattle and caught the fraud (Nieuwenhuis, 2015).

Other auto companies also were caught with defective pollution control devices: Opel, Daimler (Mercedes), Fiat,

Chrysler, Mitsubishi, and possibly Groupe PSA (French automotive manufacturing corporation), and Renault.

Chevrolets/GMCs/Buicks were sold with window stickers two miles per gallon (MPG) above EPA numbers (Sorokanich,

2016). Mitsubishi Motors Corporation manipulated (falsified) MPG by as much as 10 percent over 25 years on as many as

625,000 cars. Their stock dropped 15 percent, wiping $1.2 billion off market share.

Should an external auditor be responsible for the non-financial fraud that occurred in McDonalds’ Monopoly game?

An ordinary customer between 1985–2001 did not have a chance to win a large prize from the Monopoly game. Jerome Jacobson, an ex-cop, scammed McDonalds for more than $24 million. He oversaw the print process and had access to the

winning pieces. He and his associates were eventually arrested. He was ordered to pay back $12.5 million and served just

over three years in prison (Bartiromo, 2018).

A more recent type of non-financial fraud involves organic farming. Grain sales of $142 million have netted guilty

pleas from a grain farmer and a broker in Missouri. This type of scam involves marketing grain (or other products) as

organic (which can be sold for higher prices) when in fact the grain (or products) are not organic. Unapproved substances

were used on the fields that were certified as organic. Three other farmers in Nebraska also have pled guilty to selling

fraudulently marketed organic grains (Bechtel 2019).

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

251

A non-financial/social motive fraud was the discovery in 2019, that the Houston Astros used technology to steal

catchers’ pitching signs during the 2017 regular season and post-season and part of the 2018 season during home games.

Using a camera-based system in centerfield, the pitching signs were relayed to a screen in their dugout, and a trashcan would be banged to alert the batter as to the type of incoming pitch. Under a “Codebreaking Scheme,” second baseman

Jose Altuve (5’6”) and Alex Bregman (and possibly others) wore a buzzer underneath their jerseys that would inform

them of the upcoming pitch. Especially for change-up pitches, this information gave the batter a huge advantage (Armour,

2020; Butler, 2020).

L.A. Dodger outfielder Cody Bellinger (among other Dodgers) said the Astros stole the World Series title from

them, and Astros’ Jose Altuve’s 2017 American League MVP Award was stolen from N.Y. Yankees’ Aaron Judge in

2017. Altuve hit a game-winning home run off Aroldis Chapman in the 2019 American League Championship Series (Butler, 2020). Former Blue Jays pitcher Mike Bolsinger sued the Astros for changing the course of his career. He was the

pitcher who was hit for four runs, four hits, and three walks in a third of an inning—29 pitches—August 4, 2017, in a

game in Houston (Armour), 2020).

Even a major CPA firm can be involved in a non-financial fraud. In fact, KPMG agreed to pay a $6.2 million

penalty, interest, and disgorgement fee for valuing oil and gas reserves at $489 million when the penny stock Mitchell

Energy Resources had only paid $4.5 million for these same reserves. They then issued an unqualified opinion. The KPMG engagement partner, who had no oil and gas experience, was disbarred from practice for two years because

KPMG’s audit departed from PCAOB auditing standards in several ways (In the Matter of KPMG, 2017).

In 2019, KPMG was ordered to pay a $50 million penalty to the SEC for illegally obtaining PCAOB plans to

review their audit working papers. Job offers were made to PCAOB employees for the illegal information (e.g., bribes).

KPMG then altered (e.g., scrubbed) past audit work to help pass the PCAOB’s audit of their work (SEC v. KPMG, 2019).

Likewise, numerous KPMG audit professionals cheated on internal training examinations by improperly sharing

answers and manipulating test results. These test results were intended to ascertain whether the employees understood a variety of accounting principles and related topics. Audit partners gave exam answers to other partners, and they solicited

answers from their subordinates. Passing grades were lowered so that one could pass the exam without answering 25

percent of the questions. Ironically, these exams were required by the SEC because of the botched audit of Mitchell

Energy Resources (KPMG LLP v. John Riordan, CPA, 2017; SEC v. KPMG, 2019).

Although the penalty may seem high at $50 million, the amount is only about 0.0053 percent of $9.4 billion of their

revenues. With approximately 2,213 partners, the cost per partner would be around $22,594. The average audit partner

salary is around $451,000. Will such a small penalty cause other CPA firms to misbehave?

In May 2017, UPS was fined $247 million in damages and penalties by New York State and New York City for

illegally shipping 683,000 cartons of untaxed cigarettes from Indian reservations to unlicensed dealers and individuals

(about $18 per cigarette). This non-financial fraud violated a 2005 agreement between the New York State and UPS not to ship cigarettes to unlicensed dealers. Judge Katherine B. Forrest said that a modest penalty would not send a message to

UPS. She criticized the UPS culture, indicating that the company executives had shown a lack of acceptance of

responsibility for their actions (Haag, 2017). With the prior 2005 agreement, there is the possibility that their external

auditor, Deloitte and Touché, should have discovered the non-financial fraud.

Three similar types of lawsuits were brought against FedEx for allegedly shipping millions of untaxed cigarettes

to residents of New York. FedEx agreed to a $35.4 million settlement on January 15, 2019, for these lawsuits

(Zubizarreta, 2019).

Audit Implications

The Venn Diagram Model of Fraud (Model) has numerous implications for auditors that include fraud risk

assessments related to tone-at-the-top and the environment in which the company operates. From a forensic audit viewpoint, the four types of fraud motivations suggest the need to expand audits to include forensic investigations of

randomly selected accounts or the use of complete forensic audits, at least on a periodic basis. Importantly, the present

authors suggest that the discovering of fraud motivations can best be accomplished through scrutiny of a company’s

internal and external environments.

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

252

Environmental auditing guidance. The Committee of Sponsoring Organizations’ (COSO) 2013 Framework for

Fraud Risk Assessment (COSO, 2019) includes guidance for obtaining an understanding of fraud by focusing on types of

frauds (which the present authors specify as types of fraud motivations) along with the AS 2401 (SAS 99; AU 316) elements of the fraud triangle. We suggest that the elements of the fraud triangle are most applicable to frauds involving

embezzlement, while types of fraud motivations are applicable to most, if not all, financial and non-financial statement

frauds. Thus, we posit that our model of fraud motivations can better aid auditors in detecting frauds by recognizing the limited applicability of the elements of the fraud triangle while giving a greater emphasis—a focus—to the assessment of

a company’s internal and external environments. The importance of a company’s environment in assessing enterprise risk

has been emphasized by COSO, while the Public Company Accounting Oversight Board’s (PCAOB) Auditing Standards

(AS) include the consideration of audit risks as an integral part of audit planning and performance.

In Enterprise Risk Management—Integrated Framework COSO (2004) included the internal environment as the

first of eight enterprise risk management components:

The internal environment encompasses the tone of an organization and sets the basis for how risk is viewed and addressed by an entity’s people, including risk management philosophy and risk appetite, integrity and ethical

values, and the environment in which they operate [emphasis added]. (COSO, 2004, p. 3)

The 2013 COSO Framework, which is included in COSO’s 2019 guidance for the health industry titled An Implementation Guide for the Healthcare Provider Industry, indicates that the control environment should ensure the

company’s compliance with applicable laws. Moreover, “risk assessment requires management to consider the impact of

possible changes in the internal and external environment and to potentially take action to manage the impact” [emphasis

added] (COSO, 2019, p. 5). The demonstration of a commitment to integrity and ethical values is the first of 17 internal

control principles.

Audit risks related to the material misstatement of financial statements are delineated in PCAOB AS 1101 as

having the two components of inherent risk and control risk. The auditor is required to access both risks, which are related to a company’s environment and internal controls. The assessment of inherent risk requires the use of risk assessment

procedures while the assessment of control risk involves collecting evidence and testing of controls (AS 1101).

PCAOB Auditing Standard 2201 (AS 2201) provides auditors with guidance in performing integrated audits. Sections of this standard particularly applicable to the present work include guidance regarding planning the audit (AS

2201.09) and guidance regarding identifying entity-level controls (AS 2201.25). AS 2201.09 relates to assessing risks

associated with a company’s external environment: Auditors should evaluate “matters affecting the industry in which the

company operates, such as financial reporting practices, economic conditions, laws and regulations, and technological changes. . . .” AS 2201.25 addresses the need for auditors to evaluate a company’s control environment, which

importantly includes assessing “whether sound integrity and ethical values, particularly of top management, are

developed and understood…” [emphasis added]. That is, an assessment of the tone-at-the-top, as communicated by

management, is an important part of identifying entity-level controls.

PCAOB Auditing Standard 2401 (AS 2401) titled Consideration of Fraud in a Financial Statement Audit includes

risk factors related to a company’s internal and external environments. This Standard identifies an external environmental

risk factor related to the fraud triangle element of incentive/pressures as when a company’s “financial stability is threatened by economic, industry, or entity operating conditions.” Further, a “high degree of competition,” . . .

vulnerability to rapid changes, such as in technology…” and “significant declines in customer demands. . .” are specified.

Under Attitudes/Rationalization, AS 2401.A.2 addresses several fraud risk factors related to a company’s internal environment. A company’s ethical tone-at-the-top is included in this list: “ineffective communication, implementation,

support, or enforcement of the entity’s values or ethical standards by management or the communication of inappropriate

values or ethical standards.”

The above auditing guidance and standards describe environmental factors as being composed of both internal and

external factors: internal risks which include the tone-at-the-top which drives the ethical cultures within companies and

external risks which include the company’s economic pressures. The present authors posit that audit risk assessments,

especially in considering the potential for fraud (cf. AS 2401) should emphasize a scrutiny of the company’s environments. Using the lens of our Model (Figure 2) would focus such a scrutiny on not only the three elements of the

fraud triangle (outer circle of the Model) while also looking for potential fraud motivations: non-financial, altruistic,

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

253

greed/self-interest, and social. We have previously indicated examples of the applicability of our Model to various past

frauds. The following two examples are illustrative of the Model’s applicability to audit risk assessments and to fraud

detection.

The Volkswagen fraud. The VW fraud is included as an example of a non-financial motivation and the Milgram

obedience to authority theory. This fraud involved the intentional violation of the Clean Air Act (CAA) of 1970—an

illegal act that, once discovered, materially impacted the financial statements that included a 78-year high net loss in 2015 (McGee and Campbell, 2016). As of 2019, this fraud has cost the company an estimated $30 billion (Taylor and Russell,

2019). PCAOB Auditing Standard 2405 (AS 2405) mandates that auditors detect and report on such material illegal acts.

As indicated by Ariail, Cobb, and Crumbley (2019), this fraud involved all three elements of the AS 2401 (SAS 99;

AU 316) fraud triangle (the outer circle in Figure 2). The tone-at-the-top, driven by chairman of the board, Martin Winterkorn, pressured the engineers to meet the strict air quality standards of the CAA (Krisher and McHugh, 2018). The

engineers had the opportunity to manipulate the computer algorithm that measured diesel engine emissions (Coutag et al.,

2016), and the executives and engineers involved could rationalize the fraud as helping the company be competitive in the

U.S. market.

In addition, the VW fraud can be viewed from the aspects of the elements of the Venn Diagram Model of Fraud—

non-financial motivations along with motivations related to greed (self-interest) and social concerns. Non-financial in that the fraud was not directly related to the financial accounting process while being mainly related to the company’s internal

and external environments. Greed in that the fraud resulted in industry accolades and awards (Loveday, 2014) and

increased sales, which affected the company’s market price and possibly provided executives and engineers with a

financial incentive. From a social viewpoint, the fraud had a “help the company prosper and succeed” aspect.

The VW fraud had both internal and external environmental aspects that could have served as audit red flags (cf.

Ariail et al., 2019). An internal factor was its unethical tone-at-the-top. The SEC’s investigation traced the fraud to the

company’s top executives that included Martin Wintercom, the chairman of the management board. U.S. Attorney Mathew Schneider stated that “the fact that this criminal conduct was allegedly blessed at Volkswagen’s highest levels . . .

[was] appalling” (Krisher and McHugh, 2018). An assessment of the ethical culture at VW should have helped the

auditors discover this fraud.

Volkswagen’s external environment in the U.S. was highly regulated and competitive. Nevertheless, the company

was selling supposedly clean diesel cars at competitive prices while claiming unusually high efficiency (53 miles per

gallon compared to competitor’s at around 46 miles per gallon). This seven per gallon difference gave VW a competitive

advantage—a better quality product sold at relatively the same price as the products of competitors—which resulted in increased sales. An audit assessment of VW’s external environment also could have provided audit red flags resulting in

earlier detection of the fraudulent deceptions (Ariail et al., 2019)?

Colonial Bank. The Colonial Bank fraud certainly presented all three elements of the SAS 99 fraud triangle (AS 2401). For example, Ms. Kissick was pressured by senior vice president Art Barksdale, her superior, to “just fix” the

problem; due to collusion with TBW the Colonial employees had the opportunity to perpetuate and cover up the fraud;

and Catherine Kissick and others rationalized that their actions would help the company survive. Nevertheless, Colonial’s

collusion lessened the fraud triangle as a useful tool for detecting this fraud (Ariail and Crumbley, 2019).

The Colonial Bank fraud is presented as an example of a social motivation and the obedience principle in that one

driver of the fraud was to “save the company” from failure and protect customers from “losing their bank” (District Court

of the U.S., 2017, p. 69). Using a lens focused on motivations, in addition to the elements of the fraud triangle, might have aided the external auditors in detecting this fraud. A careful review of Colonial Bank’s internal and external environments

might have found evidence of a fraud waiting to happen.

Apparently, Colonial had an unethical tone-at-the-top. At trial, Ms. Kissick indicated that Colonial’s “. . . culture was not receptive to ‘bad news’ and discouraged reporting the same” (District Court of the U.S., 2017, pp. 67-68). Ariail

and Crumbley (2019) suggest that the tone-at-the-top exhibited a war mentality where the company is in a survival mode

where the ends justify the means. Barksdale appears to have been mostly concerned with making the TBW problem go

away, whatever it took. Researchers (e.g., Americ and Craig, 2013; Campbell and Goritz, 2014) have suggested that managements at corrupt organizations communicate a war mentality. In addition, TBW being Colonial’s biggest mortgage

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

254

lending customer posed an important internal environment risk factor. In their audit risk assessment, PwC noted a large

amount of loans to a single mortgage originator as being the biggest risk of Colonial’s Mortgage Warehouse Lending

Division. Inexplicably, the auditors failed to inspect any supporting documentation for the TBW loans (Ariail and

Crumbley, 2019).

Scrutiny of Colonial’s external environment might have provided further insights regarding fraud motivations.

Chairman Lee Farkas led the fraud at TBW. He communicated an unethical tone-at-the-top that resulted in key employees at TBW colluding with employees at Colonial. This collusion included falsifying data and documents (Ariail and

Crumbley, 2019). Due to a dispute with Fannie Mae, Farkas was supposed to be taking a decreased role at TBW.

Nevertheless, Farkas signed PwC’s audit confirmations and pressured Ms. Kissick to cover up TBW’s overdrafts (District

Court of the U. S., 2017). Shouldn’t these external environmental factors have caused the auditors to have had a high degree of professional skepticism as required by PCAOB AS 1015.07? Could the potential for Farkas to pressure Colonial

Bank employees into aiding and abetting in the fraud have been foreseen?

Conclusion

Was managerial self-interest or managerial altruism the reason VW and other auto companies engaged in non-

financial fraud by programming software in millions of cars worldwide? Their programmed turbocharged direct injection

diesel engines would activate their emission control devices only during laboratory emission testing to allow their vehicles to meet U.S. emission standards (when the wheels were not turning). At normal driving by owners the vehicles were

polluting the environment. From 2009 through 2015, how were auditors going to find this non-financial fraud? Should

external auditors be responsible for finding this type of fraud? If so, auditors must scrutinize both a company’s internal

and external environments.

Or how could Deloitte and Touché determine that electrical transmission lines owned by Pacific Gas and Electric

(PG&E) would cause the wildfires that would burn 150,000 acres and kill 85 people? PG&E knew for years that dozens

of their aging power lines were a wildfire threat. But hindsight is always better than trying to guess the future. Well, after the fires, independent auditors AzP Consulting (regulatory consultants) found that PG&E did not track unspent money

meant to put power lines underground (Nguyen,2019). Was it the regulators fault for not finding the problems? Could a

detailed assessment of PG&E’s external environment have possibly aided auditors in evaluating this risk—a risk that

subsequently had a material impact on the company’s financial statements?

Currently, rather than using chemistry, test tubes, and physics, forensic accountant and auditors must use data

analytics to catch fraudsters. Also, auditors need to become proficient in many more non-financial areas and consider the

various economic, industry, and entity operating conditions if they want to catch the non-financial fraudsters. If they do

not detect non-financial fraud they may be sued, because the perception is that the external auditor is the watchdog.

To understand the importance of just one environmental “red flag” to an auditor, consider that you are alone on a

camping trip in the middle of a warm and muggy night in a small pup tent in the middle of the wilderness. You discover there is a mosquito flying around the pup tent. Just as the mosquito can be a serious problem, an environmental “red flag”

is not something to ignore. Materiality is not an accountant’s consideration when faced with a serious indication of fraud,

but a focus on the company’s environmental situations are critical in todays’ litigious society.

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

255

References

January 19. Retrieved from https://www.jurist.org/news/2019/01/fedex-agrees-to-35-4-million-settlement-over-untaxed-

cigarettes/ Agerholm, H. 2016. One in five CEOs are psychopaths, New study finds, Independent, September 13. Retrieved from https://www.independent.co.uk/news/world/australasia/psychopaths-ceos-study-statistics-one-in-

five-psychopathic-traits-a7251251.html

Amernic, J., and Craig, R. 2010. Accounting as a Facilitator of Extreme Narcissism, J. of Business Ethics, 96, February,

79-93. Retrieved from https://link.springer.com/article/10.1007/s10551-010-0450-0

Amernic, J., and Craig, R. (2013). Leadership discourse, culture, and corporate ethics: CEO-speak at News Corporation.

Journal of Business Ethics, 118(2), 379–394.

Ariail, D. L., Cobb, D., and Crumbley, D. L. (2019). Anatomy of a non-financial fraud: VW’s dieselgate. September

2019. Oil, Gas and Energy Quarterly, 69(2).

Ariail, D. L. and Crumbley, D. L. (2019). PwC and the Colonial Bank fraud: A perfect storm. Journal of Forensic and

Investigative Accounting, Vol. 11: Issue 3, July – December. Retrieved from https://www.nacva.com/jfia

Armour, Nancy. 2020. Pitcher Mike Bolinger says cheating Houston Astros changed the course of his career, USA Today,

February 10. Retrieved from https://www.usatoday.com/story/sports/columnist/nancy-armour/2020/02/10/mike-

bolsinger-sues-houston-astros-says-cheating-changed-his-career/4712164002/

Associated Press (2005). Ex-WorldCom accountant gets prison term, New York Times, August 6. Retrieved from

https://www.nytimes.com/2005/08/06/business/exworldcom-accountant-gets-prison-term.html

Associated Press (2005). Adelphia founder gets 15-years term; son gets 20. NBCNews.com, June 20. Retrieved from

http://www.nbcnews.com/id/8291040/ns/business-corporate_scandals/t/adelphia-founder-gets--year-term-son-

gets/

AS 1101 (n.d.). Audit Risk. Retrieved from https://pcaobus.org/Standards/Auditing/Pages/default.aspx

AS 1015 (n.d.). Due Professional Care in The Performance of Work. Retrieved from

https://pcaobus.org/Standards/Auditing/Pages/AS1015.aspx

AS 2110 (n.d.). Identifying and Assessing Risks of Material Misstatement. Retrieved from

https://pcaobus.org/Standards/Auditing/Pages/AS2110.aspx

AS 2201 (n.d.). An Audit of Internal Control Over Financial Reporting That Is Integrated with An Audit of Financial

Statements. Retrieved from https://pcaobus.org/Standards/Auditing/Pages/AS2201.aspx

AS 2401(n.d.). Consideration of Fraud in a Financial Statement Audit. Retrieved from

https://pcaobus.org/Standards/Auditing/Pages/AS2401.aspx

AU 316 (2002, December 15). Consideration of Fraud in A Financial Statement Audit. Retrieved

fromhttps://www.aicpa.org/Research/Standards/AuditAttest/DownloadableDocuments/AU-00316.pdf

Baker, C.R., Cohanier, B., and Leo, N.J. 2016. Consideration Beyond the Fraud Triangle in the Fraud at Société Générale, J. of Forensic and Investigative Accounting, July – December, Retrieved from

https://s3.amazonaws.com/web.nacva.com/JFIA/Issues/JFIA-2016-No3-5.pdf

Bartiromo, M. (2018). McScam: Report details how McDonalds’ Monopoly Game was fixed by ex-cop, Foxnews.com.

Retrieved from https://www.foxnews.com/food-drink/mcscam-report-details-how-mcdonalds-monopoly-game-

was-fixed-by-ex-cop

Bank vice president sentenced for loan fraud. Mortgage Blog, December 10. Retrieved from

https://www.mortgagefraudblog.com/bank_vice_president_sentenced_for_loan_fraud/

Banks, D.G. (2004). The fight against fraud, Internal Auditor, April, pp. 34–39.

Bechtel, W. (2019). Another farmer pleads guilty in $142 million organic grain fraud. Farm Journal’s AGPRO, May 17.

https://www.agprofessional.com/article/another-farmer-pleads-guilty-142-million-organic-grain-fraud

https://www.jurist.org/news/2019/01/fedex-agrees-to-35-4-million-settlement-over-untaxed-cigarettes/

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

256

Berfield, S., Trudell, C., Fisk, M.C., and Plungis, J. (2016). Sixty million car bombs: Inside Takata’s airbag crisis.

Bloomberg Businessweek, June 2. Retrieved from https://www.bloomberg.com/news/features/2016-06-02/sixty-

million-car-bombs-inside-takata-s-air-bag-crisis

Biggs, J. and Kuhn, D. (2019). An extortion gone bad: Inside Binance’s negotiations with the “KYC leaker,” CoinDesk,

August 7. Retrieved from https://www.coindesk.com/a-bitcoin-extortion-gone-wrong-inside-binances-

negotiations-with-its-kyc-hacker

Blanch, R. (n.d.). Jerome Kerviel – Société Générale Case, HG.org Legal Resources. Retrieved from

https://www.hg.org/legal-articles/jerome-kiervel-societe-generale-case-6028

Blumenstein, R. and Pulliam, S. (2003). WorldCom Fraud was Widespread, Wall Street J. June 10, p. 3.

Burgharad, M. (n.d.). Ex-lieutenant-governor Thibault and the Robin Hood-defense in fraud, Canadian Fraud News.

Burns, G. (2019). Ex-Detroit principal uses Robin Hood defense at corruption sentencing, postedJune 1, 1017 and updated

January 19, 2019. Retrieved from https://www.mlive.com/news/detroit/2017/06/ex-

detroit_principal_uses_robi.html

Butler, Alex. 2020. Dodgers’ Bellinger: Astros stole World Series, MVP from Yankees’ Judge, UPI, February 14.

Retrieved from https://www.upi.com/Sports_News/MLB/2020/02/14/Dodgers-Bellinger-Astros-stole-World-

Series-MVP-from-Yankees-Judge/7841581704686/

Campbell, J., and Goritz, A. S. (2014). Culture corrupts! A qualitative study of organizational culture in corrupt

organizations. Journal of Business Ethics, 120 (3), 291–311.

Carpenter, J. (2014). Marco Island nonprofit founder Joyce Crain guilty of 10 felonies, Naples Daily News, December 17.

Retrieved from http://archive.naplesnews.com/news/marco-island-nonprofit-founder-joyce-crain-guilty-of-10-

felonies-ep-829581532-332495132.html

Carreyrou, J. (2018). Bad blood: Secrets and lies in a Silicon Valley startup, Alfred A. Knopf.

Caterson, S. (2017). John Friedrich: Australia’s most altruistic fraudster, Daily Review, September 2. Retrieved from

https://dailyreview.com.au/john-friedrich-one-australias-notorious-enigmatic-imposters/64910/

Cherepanova, V. (2019). Yes, ethical culture can be measured, The FCPA Blog, July 22. Retrieved from

http://www.fcpablog.com/blog/2019/7/22/yes-ethical-culture-can-be-measured.html

Cherry, P. (2016). Former Quebec Lt-governor Lise Thibault to spend at least a few more days in jail, Montreal Gazette,

May 28. Retrieved from https://montrealgazette.com/news/local-news/former-quebec-lt-governor-lise-thibault-to-

spend-at-least-a-few-more-days-in-jail

Chi, Y. and Ziebart, D. A. (2019). Evidence regarding management’s choice of forensic precision and financial statement irregularities, Journal of Forensic and Investigative Accounting, Vol. 11: Issue 2, Special Edition.

https://www.nacva.com/jfia-current#3

Clark, N. (2016). Société Générale is ordered to pay trader who almost ruined it, The New York Times, June 7. Retrieved form https://www.nytimes.com/2016/06/08/business/dealbook/french-bank-is-ordered-to-pay-trader-who-almost-

ruined-it.html

Clean Air Act of 1970, 42 USC §206(a). Retrieved from https://www.law.cornell.edu/uscode/text/42/7521

COSO (2004, September). Enterprise Risk Management—Integrated Framework, Executive Summary. Retrieved from

https://www.coso.org/Documents/COSO-ERM-Executive-Summary.pdf

COSO (2019, January). COSO Internal Control—Integrated Framework: An Implementation Guide for the Healthcare

Provider Industry. Retrieved from https://www.coso.org/Documents/COSO-CROWE-COSO-Internal-Control-

Integrated-Framework.pdf

Collins, J. (2015). The facts behind Volkswagen’s diesel gate nightmare, Forbes, Sept. 22. Retrieved from

https://www.forbes.com/sites/greatspeculations/2015/09/22/the-facts-behind-volkswagens-diesel-gate-

nightmare/#24a18d7151ee

Journal of Forensic and Investigative Accounting

Volume 12: Issue 2, July–December 2020

257

Colloff, P. (2003). The whistle-blower, Texas Monthly, April. Retrieved from https://www.texasmonthly.com/articles/the-

whistle-blower/

Coutag, M., Li, G., Pawlowski, A., Domke, F., Levchenko, K., Holz, T., and Savage, S. (2016) How They Did It: An

Analysis of Emission Defeat Devices in Modern Automobiles. San Diego, CA: University of California.

Cressey, D. R. (1953). Other People’s Money, Montclair, N.J.: Patterson Smith.

Crumbley, D. L., Fenton Jr., E. and Smith, S., (2019). Forensic and Investigative Accounting, Chicago: Wolters Kluwer.

Dichev, Il, Graham, J., Harvey, C. and Rajgopal, S. (2016). The misrepresentation of earnings, Financial Analysts J., Vol.

72, No. 1.

District of the United States for the Middle District of Alabama Northern Division. (2017). Case 2:11-cv-00746-BJR-

TFM, Document 798, Filed 12/28/17. Order of the liability phase of the PWC Bench Trial.

https://static.reuters.com/resources/media/editorial/20180102/fdicvpwc.pdf

Dodgson, Lindsay. 2018. The 10 professions with the most psychopaths, Business Insider, Australia, May 16. Retrieved

from https://www.businessinsider.com.au/professions-with-the-most-psychopaths-2018-5

Dorminey, J.W., Fleming, A., Kranacher, M., and Riley, Jr., R.A. (2010). Beyond the Fraud Triangle, CPA Journal,

80(7), 16-23.

Downey, M. (2018). As co-defendants enter prison, Atlanta teacher criticizes trial. Get Schooled Blog. AJC, October 9. Retrieved from https://www.ajc.com/blog/get-schooled/defendants-enter-prison-atlanta-teacher-criticizes-

trial/9ojqKhFwcDEmqyTD625SuM/

Duchon, D. and Drake, B. 2009. 2009. Organizational Narcissism and Virtuous Behavior, J. of Business Ethics, 85, 301-

308. Retrieved from https://link.springer.com/article/10.1007%2Fs10551-008-9771-7

Explorable.com. 2008. Milgram Experiment—Obedience to Authority, February 6, Retrieved from

https://explorable.com/stanley-milgram-experiment

Fottrell, Q. (2014). Vernon Beck: The ex-pilot who embezzled $13.5 million, MarketWatch. Retrieved from

https://www.marketwatch.com/story/vernon-beck-the-ex-pilot-who-embezzled-135-million-2014-07-29

Glinton, S. (2015). How a little lab in West Virginia caught Volkswagen’s big cheat, NPR, September 24. Retrieved from

https://www.npr.org/2015/09/24/443053672/how-a-little-lab-in-west-virginia-caught-volkswagens-big-cheat

Goldmann, P.D. (2010). Fraud in the Markets, John Wiley, pp. 24–25.

Haag, M. (2017). Judge orders UPS to pay $247 million for illegally shipping cigarettes. New York Times, May 25.