![k jk;iqj MsOgyiesaV vFkkWfjVh] u](https://static.fdokumen.com/doc/165x107/6322d92d117b4414ec0c1209/k-jkiqj-msogyiesav-vfkkwfjvh-u.jpg)

JK Cement Ltd - Axis Direct

26

O JK Cement Ltd

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of JK Cement Ltd - Axis Direct

O

ACC Limited

JK Cement Ltd

Axis Annual Analysis

20th Sept, 2021

HOLD

Target Price

3330

JK Cement Ltd Cement

1

New Capacity Ramp-Up Delivers Impressive Growth; Maintain HOLD

Summary

JK Cement completed expansion of grey cement capacity of 4.2 mtpa at various locations in the last couple of years. It also completed wall putty expansion at its Katni plant, taking total Grey and White cement capacity to 17.2 million tonnes per annum (mtpa) (As of 31st March 2021)

The company witnessed encouraging market share growth in its premium products, especially in Superstrong and Weathershield.

The company announced a greenfield capacity expansion of 4 mtpa. This includes a 2 mtpa grinding unit at Panna, MP and a 2 mtpa split grinding unit at Hamirpur, UP along with 8000 TPD clinker capacity with a 22 MW WHRS plant. The total Capex for these projects would be ~Rs 2,950 Cr. This facility is expected to get operational by March,2023. Furthermore, its line 3 upgradation at the Nimbahera plant is expected to be completed in FY22.

Key Highlights

In FY21, JK Cement registered cement sales volume of 12.04 mtpa, up 18% over FY20 levels of 10.24 mtpa. The growth was driven by a superior demand environment in both trade as well as non-trade segments in H2FY21 and the new capacity ramp-up during the year.

The company’s EBITDA Margins stood at 23.3% in FY21 against 20.9% in FY20, registering a growth of 240bps. The expansion was driven by product mix optimization, prudent market mix, and cost-efficiency initiatives undertaken by the company during the year.

The company implemented several measures to improve efficiencies and leverage input cost levers across the value chain.

The company generated a healthy cash flow of Rs 1590 Cr during the year, enabling it to reduce its net Debt/EBITDA to 1.4x in FY21 from 2.2x in FY20.

Key competitive strengths

a) Capacity to produce both Grey and White cement as well as Wall Putty, enabling it to capture changing customer preferences; b) Robust sales & distribution network facilitating extensive customer reach; c) Strengthening financial position, d) Experienced and competent management bandwidth, and e) Improving traction in the Premium and value-added products, aiding margin profile of the company.

Strategies implemented

a) Focused on growth while maintaining margins; b) Improved efficiency through technological upgradation, process optimization, and productivity enhancements; c) Strengthened market reach through capacity building; d) Diversified revenue stream further by launching new products as per prevailing market needs; e) Broad-based ESG commitments to enhance operating sustainability. These initiatives enabled the company to record superior performance during an otherwise challenging year led by the Covid-19 disruptions.

Growth drivers

a) Housing for All, b) Real Estate Growth, c) The government’s keen focus on infrastructure development including roads, highways, metros, airports, and irrigation and water projects, d) Increasing rural Income, and e) The government’s supporting policies.

Key focus areas going ahead

a) Capacity expansion to further strengthen market reach, b) Improving operational efficiency at all levels, c) Consolidating market position, d) Widen visibility by augmenting distribution network while optimizing distribution cost, e) Launching value-added products to improve margin profile, and f) Strengthening business stickiness through customer-centricity.

Outlook & Recommendation

We expect the company to deliver Volume/Revenue/EBITDA/APAT growth of 10%/13%/16%/22% CAGR over FY21-23. This will be led by higher cement demand in its operating regions, superior product mix supporting higher realizations, the introduction of margin accretive value-added products, and efficiency gains. The stock is currently trading at 17x and 14x FY22E and FY23E EV/EBITDA. We value JKCL at 13.5x FY23E EV/EBITDA and assign a HOLD rating to the company.

Key Financials

(Rs Cr) FY21 FY22E FY23E

Net Sales 6606 7496 8413

EBITDA 1539 1669 2079

Net Profit 710 819 1051

EPS (Rs) 91 105 135

PER (x) 31 33 25

EV/EBITDA (x) 16 17 14

P/BV (x) 5.87 5.98 4.92

ROE (%) 21 20 21

Source: Company, Axis Research

(CMP as of 17th Sep, 2021)

CMP (Rs) 3379 146

Upside /(Downside (%)) (-1%) 23%

High/Low (Rs) 3700/1460 153/56

Market cap (Cr) 26234 3012

Avg. daily vol. (6m) Shrs. 45,877 1152304

No. of shares (Cr) 7.73 20.5

Shareholding (%)

Dec-20 Mar-21 June-21

Promoter 57.74 57.65 57.63

FIIs 15.44 16.86 16.9

MFs / UTI 19.94 18.86 18.93

Banks / FIs 0.01 0.01 0.01

Others 6.87 6.62 6.53

Financial & Valuations

Y/E Mar (Rs. Cr) FY21 FY22E FY23E

Net Sales 6606 7496 8413

EBITDA 1539 1669 2079

Net Profit 710 819 1051

EPS (Rs.) 91 105 135

PER (x) 31 33 25

EV/EBITDA (x) 16 17 14

P/BV (x) 5.87 5.98 4.92

ROE (%) 21 20 21

Change in Estimates (%)

Y/E Mar FY22E FY23E

Sales -1 2 EBITDA -4 2

PAT -2 3

ESG disclosure Score**

Environmental Disclosure Score 34

Social Disclosure Score 28

Governance Disclosure Score 64

Total ESG Disclosure Score 40

Source: Bloomberg, Scale: 0.1-100 **Note: This score measures the amount of ESG data a company reports publicly and does not measure the company's performance on any data point. All scores are based on 2020 disclosures

Relative performance

Source: Capitaline, Axis Securities

25

75

125

175

225

275

325

Jan-20 Jun-20 Nov-20 Apr-21 Sep-21

J K Cements BSE Sensex

Uttam K Srimal Research Analyst

Email: [email protected]

Shikha Doshi Research Analyst

Email: [email protected]

2

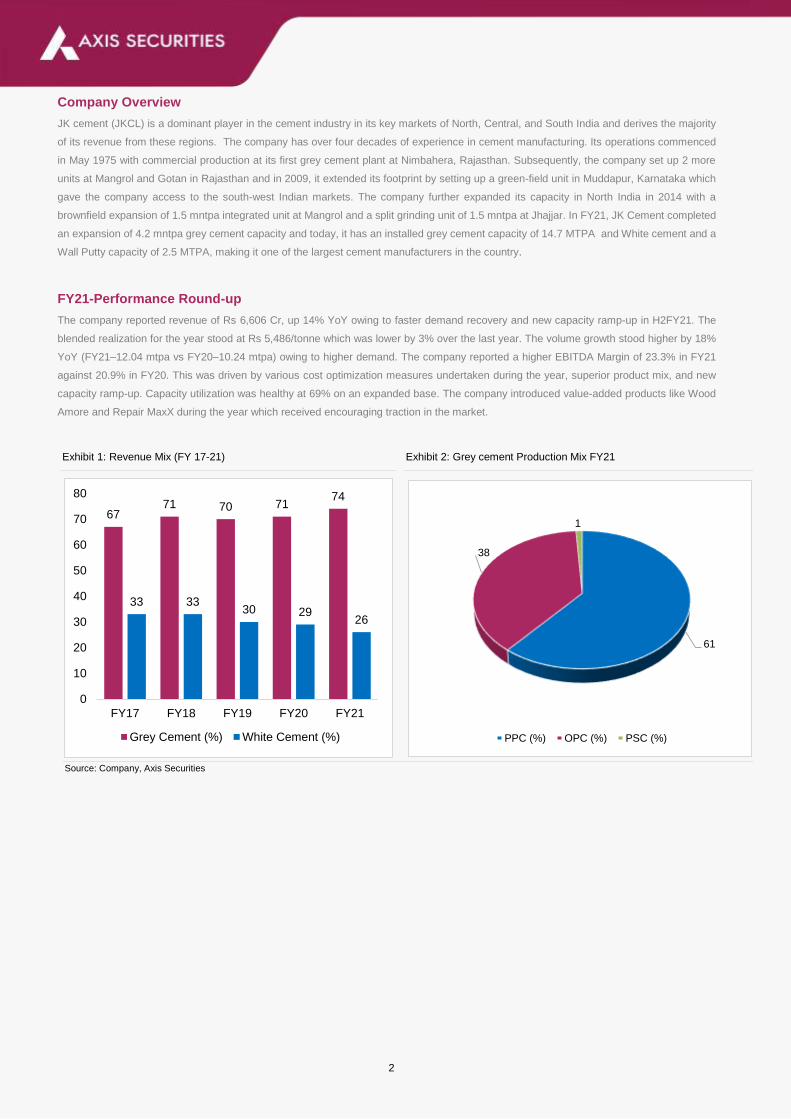

Company Overview

JK cement (JKCL) is a dominant player in the cement industry in its key markets of North, Central, and South India and derives the majority

of its revenue from these regions. The company has over four decades of experience in cement manufacturing. Its operations commenced

in May 1975 with commercial production at its first grey cement plant at Nimbahera, Rajasthan. Subsequently, the company set up 2 more

units at Mangrol and Gotan in Rajasthan and in 2009, it extended its footprint by setting up a green-field unit in Muddapur, Karnataka which

gave the company access to the south-west Indian markets. The company further expanded its capacity in North India in 2014 with a

brownfield expansion of 1.5 mntpa integrated unit at Mangrol and a split grinding unit of 1.5 mntpa at Jhajjar. In FY21, JK Cement completed

an expansion of 4.2 mntpa grey cement capacity and today, it has an installed grey cement capacity of 14.7 MTPA and White cement and a

Wall Putty capacity of 2.5 MTPA, making it one of the largest cement manufacturers in the country.

FY21-Performance Round-up

The company reported revenue of Rs 6,606 Cr, up 14% YoY owing to faster demand recovery and new capacity ramp-up in H2FY21. The

blended realization for the year stood at Rs 5,486/tonne which was lower by 3% over the last year. The volume growth stood higher by 18%

YoY (FY21–12.04 mtpa vs FY20–10.24 mtpa) owing to higher demand. The company reported a higher EBITDA Margin of 23.3% in FY21

against 20.9% in FY20. This was driven by various cost optimization measures undertaken during the year, superior product mix, and new

capacity ramp-up. Capacity utilization was healthy at 69% on an expanded base. The company introduced value-added products like Wood

Amore and Repair MaxX during the year which received encouraging traction in the market.

Exhibit 1: Revenue Mix (FY 17-21) Exhibit 2: Grey cement Production Mix FY21

Source: Company, Axis Securities

6771 70 71

74

33 3330 29

26

0

10

20

30

40

50

60

70

80

FY17 FY18 FY19 FY20 FY21

Grey Cement (%) White Cement (%)

61

38

1

PPC (%) OPC (%) PSC (%)

3

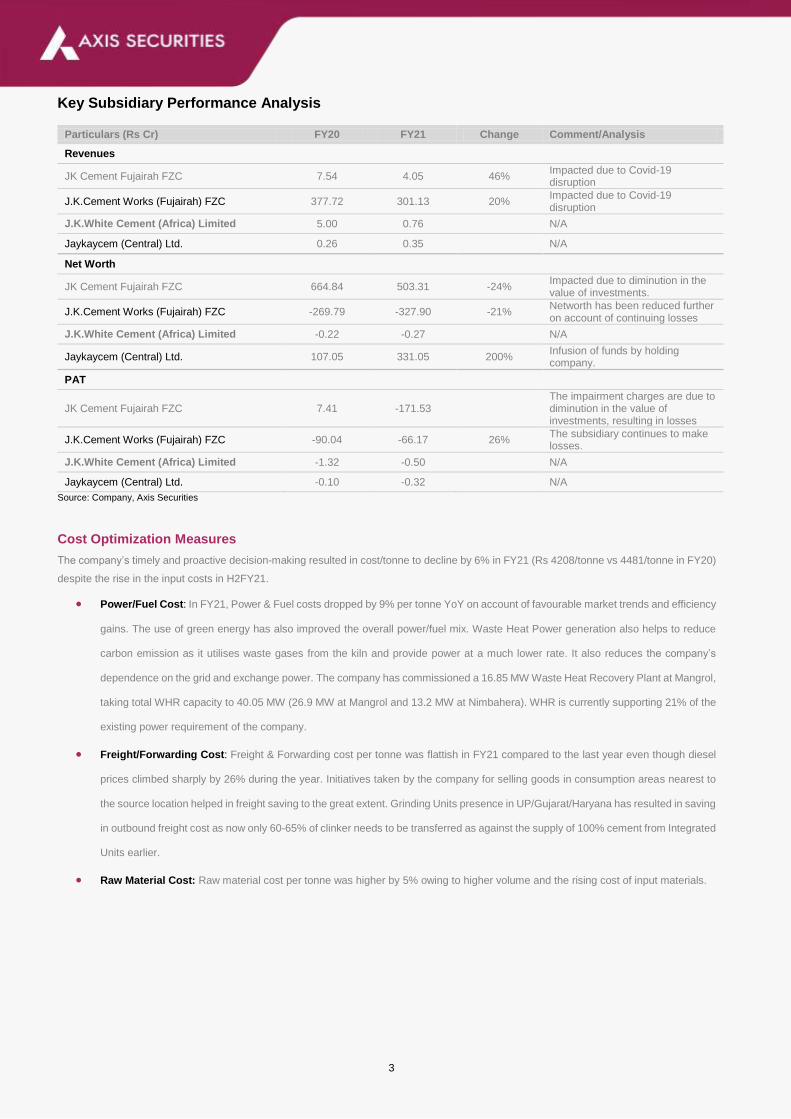

Key Subsidiary Performance Analysis

Particulars (Rs Cr) FY20 FY21 Change Comment/Analysis

Revenues

JK Cement Fujairah FZC 7.54 4.05 46% Impacted due to Covid-19 disruption

J.K.Cement Works (Fujairah) FZC 377.72 301.13 20% Impacted due to Covid-19 disruption

J.K.White Cement (Africa) Limited 5.00 0.76 N/A

Jaykaycem (Central) Ltd. 0.26 0.35 N/A

Net Worth

JK Cement Fujairah FZC 664.84 503.31 -24% Impacted due to diminution in the value of investments.

J.K.Cement Works (Fujairah) FZC -269.79 -327.90 -21% Networth has been reduced further on account of continuing losses

J.K.White Cement (Africa) Limited -0.22 -0.27 N/A

Jaykaycem (Central) Ltd. 107.05 331.05 200% Infusion of funds by holding company.

PAT

JK Cement Fujairah FZC 7.41 -171.53 The impairment charges are due to diminution in the value of investments, resulting in losses

J.K.Cement Works (Fujairah) FZC -90.04 -66.17 26% The subsidiary continues to make losses.

J.K.White Cement (Africa) Limited -1.32 -0.50 N/A

Jaykaycem (Central) Ltd. -0.10 -0.32 N/A

Source: Company, Axis Securities

Cost Optimization Measures

The company’s timely and proactive decision-making resulted in cost/tonne to decline by 6% in FY21 (Rs 4208/tonne vs 4481/tonne in FY20)

despite the rise in the input costs in H2FY21.

Power/Fuel Cost: In FY21, Power & Fuel costs dropped by 9% per tonne YoY on account of favourable market trends and efficiency

gains. The use of green energy has also improved the overall power/fuel mix. Waste Heat Power generation also helps to reduce

carbon emission as it utilises waste gases from the kiln and provide power at a much lower rate. It also reduces the company’s

dependence on the grid and exchange power. The company has commissioned a 16.85 MW Waste Heat Recovery Plant at Mangrol,

taking total WHR capacity to 40.05 MW (26.9 MW at Mangrol and 13.2 MW at Nimbahera). WHR is currently supporting 21% of the

existing power requirement of the company.

Freight/Forwarding Cost: Freight & Forwarding cost per tonne was flattish in FY21 compared to the last year even though diesel

prices climbed sharply by 26% during the year. Initiatives taken by the company for selling goods in consumption areas nearest to

the source location helped in freight saving to the great extent. Grinding Units presence in UP/Gujarat/Haryana has resulted in saving

in outbound freight cost as now only 60-65% of clinker needs to be transferred as against the supply of 100% cement from Integrated

Units earlier.

Raw Material Cost: Raw material cost per tonne was higher by 5% owing to higher volume and the rising cost of input materials.

4

Key growth drivers

Housing for all: The Pradhan Mantri Awas Yojana (PMAY) was launched in 2015 to provide ‘Housing for All’ by 2022. Under the

scheme, 10 Mn urban houses have been sanctioned, out of which, construction of 4.2 Mn houses has already been completed (as

of January 25, 2021). India continues to be the second-largest cement market in the world, both in terms of production and

consumption. However, the country’s per-capita cement consumption stands significantly lower at 235 kg vis-à-vis the global average

of over Rs 500 kg, indicating significant growth headroom available for the industry.

Real-Estate: The Indian real estate market is projected to reach $1 Tn by 2023 and attracted a massive estimated investment of Rs

46,000 Cr ($6.5 Bn) in FY20. Furthermore, lower home loan interest rates have considerably improved the affordability of urban

housing. This coupled with the increasing work-from-home trend, the real estate market in the Tier-1 cities is likely to gain

encouraging traction moving ahead. Rural and affordable housing, too, is expected to continue supporting the demand and boost

the cement industry going forward.

Infrastructure: The infrastructure sector is a pivotal contributor to the construction sector’s order book and an ambitious National

Infrastructure Project (NIP) launched by the government is expected to provide a significant boost to the construction industry.

Projects such as Bharatmala Pipeline, Metro and Railway projects in key cities such as Mumbai, Bangalore, Chennai, and

Ahmedabad, and National Airport projects are expected to aid in construction activities. These activities have resumed in recent

months, providing further thrust to the cement demand.

National Infrastructure Pipeline: The government’s focus on developing infra and housing has gained momentum in the last few

years which can be manifested in the capital outlay earmarked for the infrastructure sector in the Union Budget 2021-22. The National

Infrastructure Pipeline aims to invest 111 Lc Cr by 2025 in multiple projects comprising Transport, Energy, Social and Commercial

infrastructure, Communication, and Water & Sanitation, among others. This, in turn, is expected to provide a significant boost to the

cement demand over the medium to long term.

Rural Income: Higher Minimum Support Price (MSP) and the government’s increasing allocation to various agricultural projects are

improving farming income and thereby the rural economy. Moreover, higher fund allocation to the Mahatma Gandhi National Rural

Employment Guarantee Act (MGNREGA) is supporting enhanced rural income. This will boost construction activities in the rural

area and thereby provide growth impetus to the cement demand.

Exhibit 3: Cement consumption trend segment-wise: Housing remains the largest cement consumer

Source: Company, Axis Securities

55%

10%

22%

13%

0%

10%

20%

30%

40%

50%

60%

Housing Industrial & Commercial Infrastructure Low Cost Housing

5

Key operational activities during the year

Completed expansion projects: The company commissioned a grey cement grinding unit at Balasinor, Gujarat with an

installed capacity of 0.7 mtpa. It also completed 0.3 mtpa wall putty capacity expansion at the Katni plant to meet the growing

demand. With these completed projects, the company’s total plant capacity stands at 0.7 mtpa.

Ongoing Expansion Projects: The company is upgrading its Nimbahera kiln capacity by 1000 tpd which will enhance its

efficiency, reduce power and fuel consumption, and increase waste heat recovery generation. As volumes increase, EBITDA/tonne

for the grey segment will increase as well. The project is expected to complete in Q2FY22.

The company has also embarked on greenfield expansion projects of 4 mtpa capacity at Panna Madhya Pradesh, with a split

grinding unit at Hamirpur, Uttar Pradesh and WHR power generation of 22 MW. Civil work for the project has already started at the

site and orders have been placed for main equipment.

Capital Allocation: The company has completed 4.2 mtpa expansion incurring a Capex of Rs 1,739 Cr till 31 March 2021. The

Nimbahera Line 3 upgradation is also on track and has incurred ~Rs 357 Cr by 31 March 2021. Going forward, the remaining

expenditure of ~Rs 100 Cr will be incurred on these projects during FY22.

Greenfield expansion of 4 mtpa at Panna, Madhya Pradesh with a split grinding unit at Hamirpur, Uttar Pradesh would have a total

Capex of Rs 2,971 Cr and Rs 270 Cr has already been spent till 31st March 2021. Project expenditure would be Rs 800 Cr in FY22,

Rs 1,600 Cr in FY23, and a balance of Rs 300 Cr in FY24. Additional to these capital expenditures, it will incur a sustenance Capex

of ~Rs 250 Cr per annum.

Debt Profile: As of 31st March 2021, the company’s standalone gross debt stood at ~Rs 2,865 Cr and consolidated gross debt at

Rs 3252 Cr. The proposed borrowing for 4 mtpa expansion in the wholly-owned subsidiary would be around Rs 1,700 Cr, out of

which Rs 400 Cr would be drawn in FY22, Rs 1,000 Cr in FY23, and the balance Rs 300 Cr in FY24. The company’s Net

debt/EBITDA declined to 1.4x from 2.2 x in FY20 on the back of healthy cash generation during the year.

Capacity Utilization: Capacity utilization stood 69% during the year on an expanded base against 85% in FY20.

6

Sales and Distribution

Strong distribution network: The company has a strong channel network of over 17,000 plus dealers and retailers for marketing

grey cement products and around 67,000 plus dealers and retailers for marketing White cement products, who promptly and

efficiently serve customers across its markets. It also has a good presence overseas for its White cement business. The company

has established a strong sales & marketing team as well as a technical support team that drives the overall sales. It uses various

digital platforms including a hybrid approach to leverage the online media to generate awareness, leads, and enquiries from

prospective customers.

Strengthening relationships with channel partners: The company has undertaken various initiatives to effectively manage dealer

channel networks to drive growth in its key relevant markets. It has implemented several innovative measures to strengthen

relationships with its channel partners as well. It regularly rewards its top-performing dealers for their excellent performance. In F21,

it conducted virtual meets where channel partners and dealers were felicitated with trophies, certificates and cash prizes.

Improving digital presence: The company embarked upon a Digital Journey a few years back, starting with the automation of

functions such as paperless operations and fine-tuning of processes. In FY21, it stepped up the digital quotient by using the latest

and best technology including robotic process automation, artificial intelligence, smart procurement, and data science tools, among

others. These were suitably supplemented with the use of social media in branding and marketing which is apparent from the

customer coverage through digital channels.

7

Supply Chain & Logistics

The company follows stringent procurement practices to meet the business needs while ensuring a responsible supply chain. It

encourages procurement through vendors who adopt sustainable practices.

The customer-centric business model allows the company to be in tune with the changing needs of customers which enables it to

meet and surpass customer expectations.

The company optimizes logistics through effective and efficient Route planning. It also achieves optimized In-plant operations using

RFID. The company Track and Trace on a real-time basis through GPS enabled application which gives visibility to the customer

as well.

The company has shifted to real-time integration between SAP and third-party Apps through a Digital Access mechanism from

batch data updates previously. This has significantly enhanced customer engagement and cementing the company’s reputation as

a reliable supplier.

The company’s other initiatives include Artificially Intelligent processes including visual and data-based Intelligence training to the

system and Dynamic Dashboards with real-time visibility to decision-makers.

Research & Development

The company believes that R&D is key to consistently provide world-class products to its customers, leveraging which it launches

innovative products to the market. Its R&D drive also helps it exemplify quality and drive sustainability journey forward.

The company’s plants in Nimbahera, Mangrol, and Gotan are equipped with state-of-the-art labs with process control

instrumentations and quality control systems. Its Muddapur facility is equipped with the latest technologies, process control as well

as quality control with Robo lab and Automatic Blain Analyser. The entire plant operations are controlled from a Central Control

Room (CCR) with sophisticated systems including Fuzzy Operations.

The company is investing in R&D initiatives to reduce the use of natural resources in grey cement manufacturing and increase the

share of additives like fly ash and slag in the production process. Additionally, it aims to increase the production of blended cement

in the near future.

8

Key strategies moving forward

Capacity expansion: a) Undergoing capacity expansion of Line No. 3 at Nimbahera, Rajasthan. b) New greenfield expansion at

Panna is on track

Operational efficiency: a) Optimism efficiency as all plants are proximate to raw materials and growth markets. b) Manage

resources through product and technology innovations.

Consolidate market position: a) Fortify the Grey cement segment and enter into unexplored markets. b) Reinforce leadership

position in the White cement business by improving utilization

Widen visibility: a) Enhance brand visibility further through print and online media and consumer promotions. b) Expand and

improve distribution network and engage with key influencer and channel partners.

Launch of value-added products: a) Launch value-added products including Wood paint to be sold on one platform. b) Grow

proposition of value-added products across existing and new markets.

Customer Centricity: a) Meet customers’ rapidly changing expectations and strive to provide a rich customer experience. Supply

quality products at the right price and resolve customer grievances.

Business Outlook

The cement demand in FY21 was almost flat at 328 mntpa and declined further in the Q2CY21, which is the peak construction time, on

account of the nationwide lockdowns. However, post lockdown easing in H2CY21, the cement sector witnessed an uptick in demand, led by

robust rural consumption.

Going forward, the cement industry is expected to rebound with volume growth led by a revival in demand from the housing and infrastructure

sectors along with the timely release of funds as announced in the Union Budget 2021-22. However, the likelihood of COVID 3.0 advent and

rate of vaccination rollout would be key monitorable moving forward.

9

Risks and Mitigation

Key risks identified, assessed, and mitigated during the year under review include:

Market demand/Supply dynamics: Economic growth drives the demand for construction and adverse changes in demand may

impact sales, prices, and eventually industry performance. Furthermore, any behavioural changes in consumer patterns may lead

to an increase in product substitution and thereby affect the company’s revenue growth and profitability.

Mitigation: ~25% of revenues come from the White cement business which mitigates the risk of change in the Grey cement market

scenario and changes in consumer preference as the company is present in both cement types.

Business competition risk: The cement industry is passing through a consolidation phase where big players are acquiring small

and medium players in the industry. Against this backdrop, the Indian cement industry is likely to be dominated by large players

leading to an oligopolistic market. This may hurt competitive intensity among the consolidated players, affecting the company’s

profitability.

Mitigation: The company expanded the business to more regions including central India and increased its grey cement capacity

by establishing split grinding units in Uttar Pradesh and Gujarat. The company has also developed new techniques for efficient

utilization of natural resources such as energy, and water, among others.

Political risk: Economic, social and political instability can influence the cement industry and result in direct and indirect

consequences leading to operational uncertainty. Non-compliance with the regulations may lead to a serious impact on the financial

performance of the company.

Mitigation: The company proactively adheres to directives and state-specific action plans to enhance crisis management. The

company well-diversified product portfolio enables it to reduce the consequences of political risks.

Sustainability risk: Failure to meet the ESG goals may lead to fines and business disruptions. Moreover, controversies may get

escalated leading to damage to the company’s brand reputation.

Mitigation: The company conducts performance assessments and monitoring against the set targets and reporting it regularly,

develops new techniques for efficient utilization of natural resources to maintain a balance between ESG and business performance.

Additionally, it ensures resource efficiency by reducing freshwater withdrawal, rainwater harvesting, and energy efficiency

measures.

Energy Prices risk: Energy price hikes may lead to an increase in production costs and adversely impact the industry.

Consequently, this may affect the pricing of the product and future cash flows of the company.

Mitigation: Driving optimization of fuel mix, energy efficiency, and use of alternative fuel is a key focus area for the company.

Raw materials including minerals risk: Scarcity of natural resources such as limestone, unavailability of fuels for production,

stricter government regulations on consumption of fossil fuel, etc. may hamper normal business processes and affect the whole

supply chain of the company.

Mitigation: The company is undertaking various initiatives such as continually expanding the blended cement portfolio and

utilization of low-grade limestone, Driving the use of alternative materials to conserve natural resources, Utilizing low-quality fuels

as additives to high-quality fuels at the plant to reduce RM risk.

Legal and Compliance Risk: Risk associated with non-compliance to regulations can pose the challenge of lawsuits, monetary

claims, investigations and proceedings. It impacts growth, revenue, employee growth, and the business cycle.

Mitigation: The company is involved in a compliance program that aids in guiding and maintaining the regulations.

Cyber security risk: In the wake of the COVID crisis, the transition to remote location working has exposed the company to a

range of technical and human-centred vulnerabilities, increased risk from cyber-attacks, and operational errors.

Mitigation: The company put policies and procedures in place to protect itself from IT risks. These policies contain corrective

measures to be taken to mitigate any kind of incidents in a time-bound manner.

10

Progress on sustainability

Climate: Key focus areas are energy efficiency and use of clean energy, low-carbon transportation and logistics, resilient and

sustainable built environment.

Environment: Increase use of low-grade limestone while reducing dependency on high-grade limestone in the process and extend

quarry life. Increase green belt of the entire occupied area, Scale-up rainwater harvesting efforts, and Reduce dependency on

groundwater by increasing mine water utilization.

Waste as resources: Increase use of AFR, Increase replacement of virgin raw materials and fuels with alternative raw materials/

other substitutes, Reduce clinker ratio, Increase production of blended cement and fuel.

People & Communities: Key focus areas are skills enhancement, Enhance diversity and inclusiveness, Health & Safety,

Communities, Transport safety.

Profitability Analysis (Rs Cr)

Particulars FY20 FY21 Change Comments/Analysis

Sales 5801 6606 14% Revenue growth was driven by higher volume supported by the new capacity ramp-up during the year.

Raw Materials 871 1070 23% Raw materials costs were higher owing to higher volumes during the year.

Gross Profits 2733 3068 12% Gross Profits were higher due to higher volumes during the year.

Operating Expenses 1520 1529 -0.18% Operating expenses were flat due to savings in fixed costs and efficiency gains.

Interest 276 252 -9% The interest cost was lower owing to the lower interest rate YoY.

EBIT 1010 1345 33% EBIT was higher owing to higher sales and savings in the fixed costs during the year.

PAT 496 708 43% PAT was higher due to the combined impact of the above-mentioned attributes, lower interest costs, and higher other income.

EPS 64.26 92.1 43% EPS increased in line with PAT growth

Source: Company; Axis Securities

Exhibit 5: Volume and Growth trend

Source: Company, Axis Securities

Exhibit 6: Realization/tonne and Growth Trend

Source: Company, Axis Securities

8.219.40 9.99 10.24

12.04

1%

14%

6%

3%

18%

0%

5%

10%

15%

20%

0.00

5.00

10.00

15.00

FY17 FY18 FY19 FY20 FY21

Volume & Volume Growth

Volume(mntpa) Volume growth

4898 5156 5264 5666 5486

5.4% 5%

2.1%

7.6%

-3.2%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

4400

4800

5200

5600

6000

2017 2018 2019 2020 2021

Blended Realization/tonne (Rs.) Growth (%)

11

Exhibit 7: Cost/tonne Trend

Source: Company, Axis Securities

Growth Indicators (Rs Cr)

Particulars FY20 FY21 Change Comments/Analysis

Revenue 5801 6606 14% Revenue growth was driven by higher volumes supported by the new capacity ramp-up during the year.

EBITDA 1213 1538 27% EBITDA improved on account of volume and savings in the variable as well as fixed costs as various cost-containment measures paid off well.

PAT 496 708 43% PAT was higher due to the combined impact of the above-mentioned attributes, lower interest costs, and higher other income.

EPS 64.26 92.1 55% EPS increased in line with PAT growth

Volume (mtpa)

10.24 12.04 6% Volumes growth was driven by higher demand in its operating region both from trade and non-trade segments.

Source: Company; Axis Securities

Profitability Margins

Particulars FY20 FY21 Change Comments/Analysis

GPM 47.1% 46.4% -70 bps GPM was marginally lower as input cost escalated in H2FY21.

EBITDAM 20.9% 23.3% 240 bps EBITDAM improved due to higher volume and savings in fixed and variable costs.

PATM 8.3% 10.6% 230bps PATM was higher owing to superior operating performance and lower interest costs and higher Other Income during the year.

Source: Company; Axis Securities

Exhibit 8: Revenue & Revenue Growth Trend

Source: Company, Axis Securities

4014 4318 4429 4481 4208

0.9%

7.6%2.6% 1.2%

-6.1%

-10.0%

0.0%

10.0%

3500

4000

4500

5000

2017 2018 2019 2020 2021

Cost/tonne (Rs.) Trend

4021 4846 5259 5802 6606

6%

21%

9%

10%

14%

0%

5%

10%

15%

20%

25%

0

2000

4000

6000

8000

FY17 FY18 FY19 FY20 FY21

Revenue & Revenue Growth

Revenue (in cr) Revenue growth

12

Exhibit 9: Blended EBITDA/tonne Trend

Source: Company, Axis Securities

Exhibit 10: Net Profit & NPM Trend

Source: Company, Axis Securities

884 838 835 1185 1278

32%

-5% 0%

42%

8%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

500

1000

1500

FY17 FY18 FY19 FY20 FY21

Blended Ebitda & Ebitda Growth

Blended Ebitda/ton (Rs.) Blended Ebitda/ton growth

178 290 270 496 710

4.3%

5.9%5.0%

8.3%

10.6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

200

400

600

800

FY17 FY18 FY19 FY20 FY21

Net Profit NPM

13

Financial Ratios

Particulars FY20 FY21 Change Comments/Analysis

ROE 17% 21% 400bps ROE improved due to superior profitability, stringent cost control measures, lower interest costs, and higher other income.

ROCE 16.0% 18.5% 250bps ROCE was higher on account of superior operating performance leading to an EBIT margin improvement to 20% from 17% YoY.

Asset Turn 0.80x 0.84x Asset-turn was higher as revenue increased by 14% during the year.

Net Debt/Equity 0.9x 0.6x -30bps Net-debt was further reduced owing to higher cash generation during the year.

EV/EBITDA 11x 15.6x EV/EBITDA was higher as the market cap increased owing to the strong performance of the company.

Source: Company; Axis Securities

Exhibit 11: EV/EBITDA, ROE, & ROCE Trend

Source: Company, Axis Securities

Exhibit 12: Book Value (Rs)

Source: Company, Axis Securities

Exhibit 13: Leverage Ratio

Source: Company, Axis Securities

12.6 11.7 10.1 11.0 15.6

9.614.8

11.617.4

21.112.1

13.312.3

16.118.4

0.0

10.0

20.0

30.0

40.0

50.0

0.0

5.0

10.0

15.0

20.0

2017 2018 2019 2020 2021

ROE (%) ROCE(%)

245282

349389

480

0

100

200

300

400

500

600

FY17 FY18 FY19 FY20 FY21

Book Value (In Rs)

1.91.5

1.1 1.1 1.0

1.51.1

0.70.9

0.6

3.6

2.62.1 2.2

1.4

0.00

1.00

2.00

3.00

4.00

FY17 FY18 FY19 FY20 FY21

Total debt/Equity (x) Net debt/Equity (x) Net debt/EBITDA (x)

14

Key Balance Sheet Takeaways

Working Capital Management

Working capital intensity decreased in FY21 as the cash conversion cycle improved to 36 days in FY21 from 40 days in FY20. This

was on account of lower inventory and higher payable days. During the year, OCF to EBITDA conversion was 103% vs. 112% in

FY20.

From FY17-FY21, the company generated a total OCF of Rs 5,311 Cr and 61% of total OCF (Rs 3,238 Cr) was utilized towards the

company’s Capex program, indicating higher Capex intensity. While CFO remained the major source of funding for the company, it

generated an FCF of Rs 2,073 Cr during FY17-FY21.

Cash Conversion Cycle

Particulars FY20 FY21 Change Comments/Analysis

Inventory Days 82 78 -4 Inventory days decreased due to strict control on procurement.

Trade Receivables 17 20 3 Receivable days increased owing to higher sales during the year

Trade Payables 59 62 3 Trade payable days increased on account of relatively lenient credit terms.

Cash Conversion Cycle 40 36 Overall CCC decreased by 4 days to 36 as the company improved its WC management during the year.

Source: Company; Axis Securities

Exhibit 14: Cash Conversion Cycle

Source: Company, Axis Securities

18 18 18 17 20

94

75 7582 78

72

85 85

59 62

41

8 8

40 36

0

20

40

60

80

100

FY17 FY18 FY19 FY20 FY21

Cash Conversion Cycle

Trade Receivable Days Inventory Days Trade Payable Days Cas Coversion Cycle

15

Key Balance Sheet Takeaways (Cont...)

Debt Levels: The company’s long-term debt increased by Rs 553 Cr during the year while short-term debt decreased by Rs 125 Cr.

Fixed capital formation: Gross Fixed Capital Formation improved to Rs 7,825 Cr in FY21 from Rs 7,231 Cr in FY20, an improvement

of 8.25% as the company incurred Capex on expansion projects.

Capex plans: The company is expanding its capacity by setting up a 4 mtpa greenfield facility at Panna, MP at a capital

cost of Rs 2970 Cr. Besides line 3 upgradtion at Nimbahera is progressing well.

Cash and liquidity position: The company’s liquidity position has improved due to its superior profitability and efficient working

capital management in FY21. The Cash & Equivalent stood at Rs 1,323 Cr in FY21 against Rs 636 Cr in FY20, an increase of 108%

YoY.

Exhibit 15: Cash & Cash Equivalent (Rs Cr)

Source: Company, Axis Securities

Exhibit 16: Gross & Net Block

Source: Company, Axis Securities

501

650

906

636

1323

0

200

400

600

800

1000

1200

1400

FY17 FY18 FY19 FY20 FY21

Cash/ Cash Equivalent (Rs.Cr)

5,904 6,2317,232

7,826

4,5245,069

5,750 6,018

0

2000

4000

6000

8000

10000

FY18 FY19 FY20 FY21

Gross Block (Rs.Cr) Net Block (Rs. Cr)

16

Forex Analysis

The Foreign currency risk is the risk that the fair value or future cash flows of exposure will fluctuate with changes in the foreign

exchange rates. The company’s exposure to the risk of changes in foreign exchange rates relates primarily to the company's

operating activities (when revenue or expense is denominated in a foreign currency). The company manages its foreign currency

risk by taking foreign currency forward contracts if required.

Particulars FY20 FY21 Change Comments/Analysis*

USD 0.00 185155 100% Trade receivable

USD 4201498 4722146 12% Trade payable

euro 720545 332632 -54% Trade payable

GBP 0.00 360000 100% Trade payable

Yen 0.00 4750 100% Trade payable

Source: Company; Axis Securities;

Contingent Liability Analysis

Particulars (Rs Cr) FY20 FY21 Change Comments/Analysis

Excise Duty 251.68 69.41 -72%

Excise duty 22.77 23.51 3% no provision has been considered necessary by the management

Sales tax/Entry tax 66.95 13.80 -79% no provision has been considered necessary by the management

Service Tax 2.77 0.48 -82% no provision has been considered necessary by the management

Income tax 81.34 10.87 -86% no provision has been considered necessary by the management

Others 88.04 79.13 -12% no provision has been considered necessary by the management

Total 513.55 197.2 -61% Any adverse decision in the above cases may impact the operational performance of the company.

Source: Company; Axis Securities

17

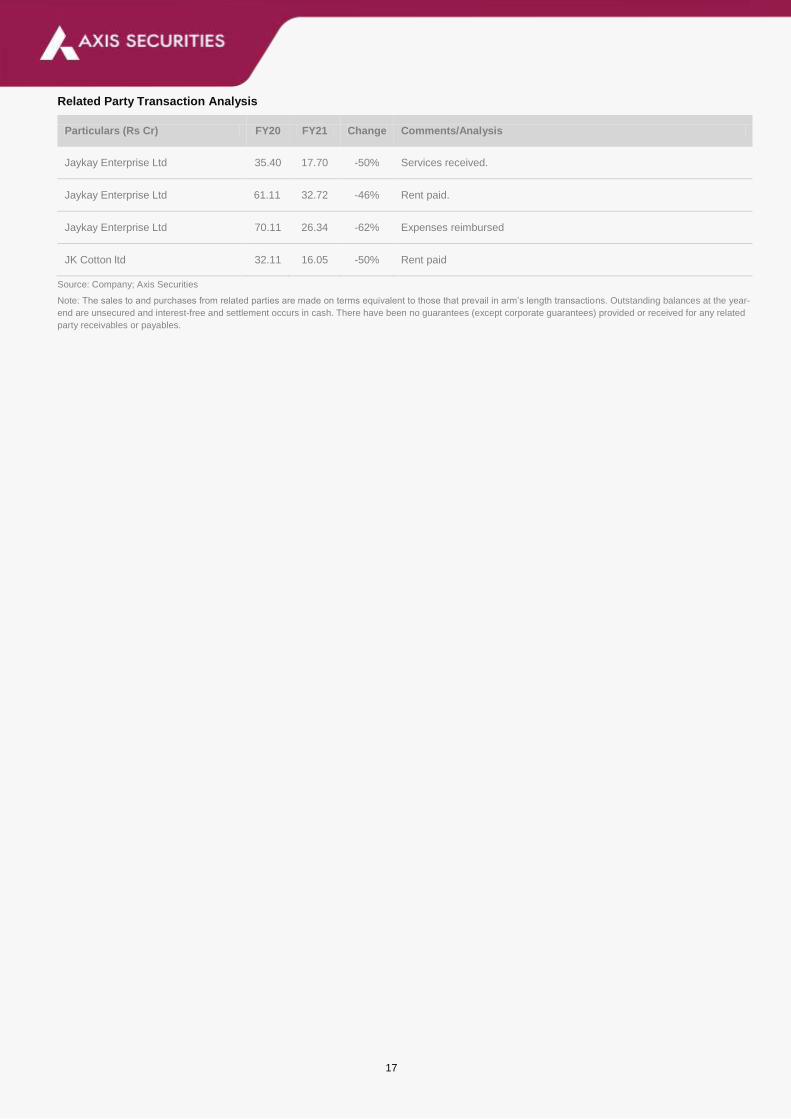

Related Party Transaction Analysis

Particulars (Rs Cr) FY20 FY21 Change Comments/Analysis

Jaykay Enterprise Ltd 35.40 17.70 -50% Services received.

Jaykay Enterprise Ltd 61.11 32.72 -46% Rent paid.

Jaykay Enterprise Ltd 70.11 26.34 -62% Expenses reimbursed

JK Cotton ltd 32.11 16.05 -50% Rent paid

Source: Company; Axis Securities

Note: The sales to and purchases from related parties are made on terms equivalent to those that prevail in arm’s length transactions. Outstanding balances at the year-

end are unsecured and interest-free and settlement occurs in cash. There have been no guarantees (except corporate guarantees) provided or received for any related

party receivables or payables.

18

Key Cash Flow Takeaways

Particulars (Rs Cr) FY20 FY21 Change Comments/Analysis

PBT 734 1092 49% PBT was higher due to superior operating performance during the year.

Non-cash expenses

Depreciation 288 306 6% Depreciation is as per the depreciation policy of the company.

Finance Cost 254 249 -13% Finance cost was lower owing to lower interest costs.

Others -38 -33 13% Due to higher interest income and other adjustments.

Working Capital Adjustments 282 171 -39% Stringent working capital management improved capital flow during the year.

CFO 1366 1590 16% Higher CFO YoY owing to superior operating performance and efficient WC management.

CFI -1483 -1343 -9% CFI declined owing to lower investments in PPE during the year.

CFF -108 -138 27% Higher due to the debt repayment.

Capex -1242 -768 -38% Lower as an existing expansion is on completion.

Free Cash Flow Generation 124 822 562% Higher YoY owing to superior operating performance and WC management.

Source: Company; Axis Securities

Exhibit 17: OCF, Capex, FCF Trend (in Cr)

Source: Company, Axis Securities

Exhibit 18: OCF, EBITDA, and Conversion ratio trend (Cr)

Source: Company, Axis Securities

772 883700

13671590

-404-202

-623

-1243

-768

368681

77 124

822

-1500

-1000

-500

0

500

1000

1500

2000

FY17 FY18 FY19 FY20 FY21

OCF, CAPEX, FCF (Rs Cr)

OCF Capex FCF

772 883 700 1367 1590726 787 834 1213 1539

106% 112%

84%

113%103%

0%

20%

40%

60%

80%

100%

120%

0

400

800

1200

1600

2000

FY17 FY18 FY19 FY20 FY21

OCF EBITDA Conversion Ratio

19

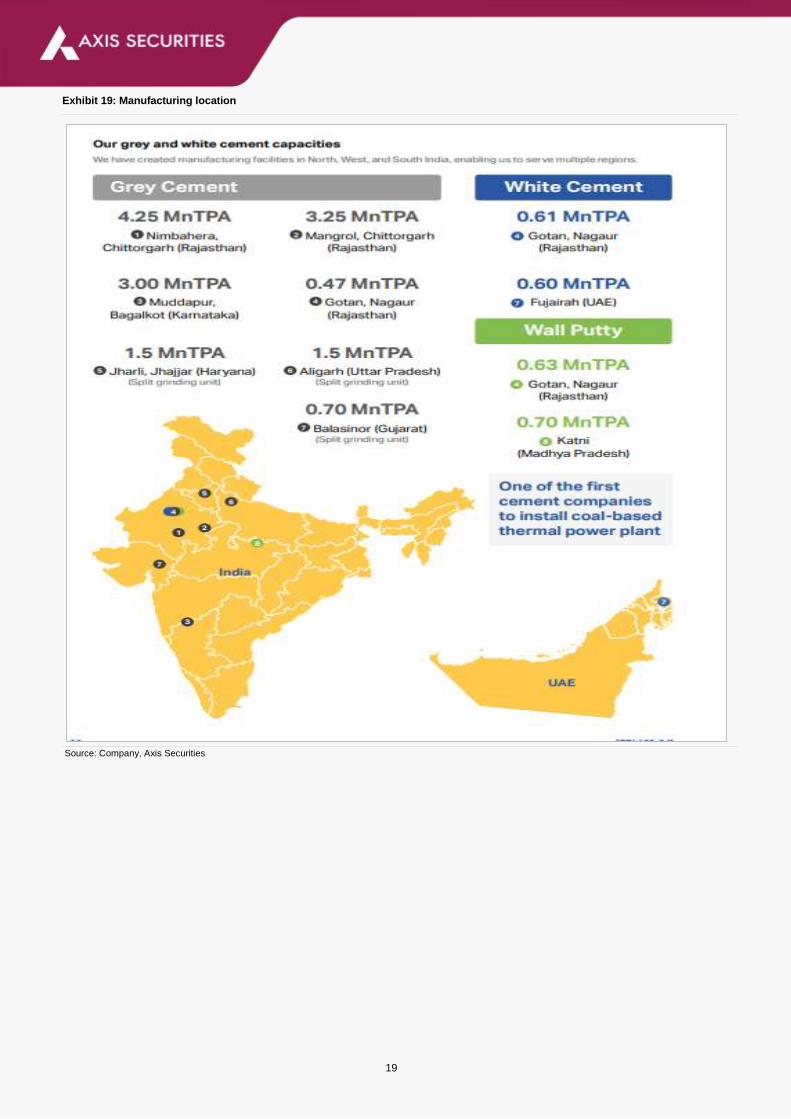

Exhibit 19: Manufacturing location

Source: Company, Axis Securities

20

Financials (Consolidated)

Profit & Loss (Rs Cr)

Y/E Mar, Rs Cr FY21 FY22E FY23E

Net sales 6606 7496 8413

Other operating income 0 0 0

Total income 6606 7496 8413

Raw Material 1071 1122 1200

Power & Fuel 1165 1444 1574

Freight & Forwarding 1302 1564 1705

Employee benefit expenses 462 524 576

Other Expenses 1067 1173 1279

EBITDA 1539 1669 2079

Other income 113 131 144

0 0 0

PBIDT 1652 1800 2223

Depreciation 306 323 361

Interest & Fin Chg. 253 250 255

E/o income / (Expense) 0 0 0

Pre-tax profit 1093 1228 1606

Tax provision 389 415 562

Minority Interests 7 7 7

Associates 0 0 0

RPAT 710 819 1051

Other Comprehensive Income 0 0 0

APAT after Comprehensive Income 710 819 1051

Source: Company, Axis Securities

Balance Sheet (Rs Cr)

Y/E Mar, Rs Cr FY21 FY22E FY23E

Total assets 9872 10720 11746

Net Block 6018 6821 7722

CWIP 510 400 400

Investments 142 142 142

Wkg. cap. (excl cash) 518 551 611

Cash / Bank balance 1225 1126 1132

Misc. Assets 146 168 174

Capital employed 9872 10720 11746

Equity capital 77 77 77

Reserves 3659 4402 5375

Minority Interests -26 -22 -29

Borrowings 3142 3142 3142

Def tax Liabilities 593 593 593

Other Liabilities and Provision 2426 2527 2587

Source: Company, Axis Securities

21

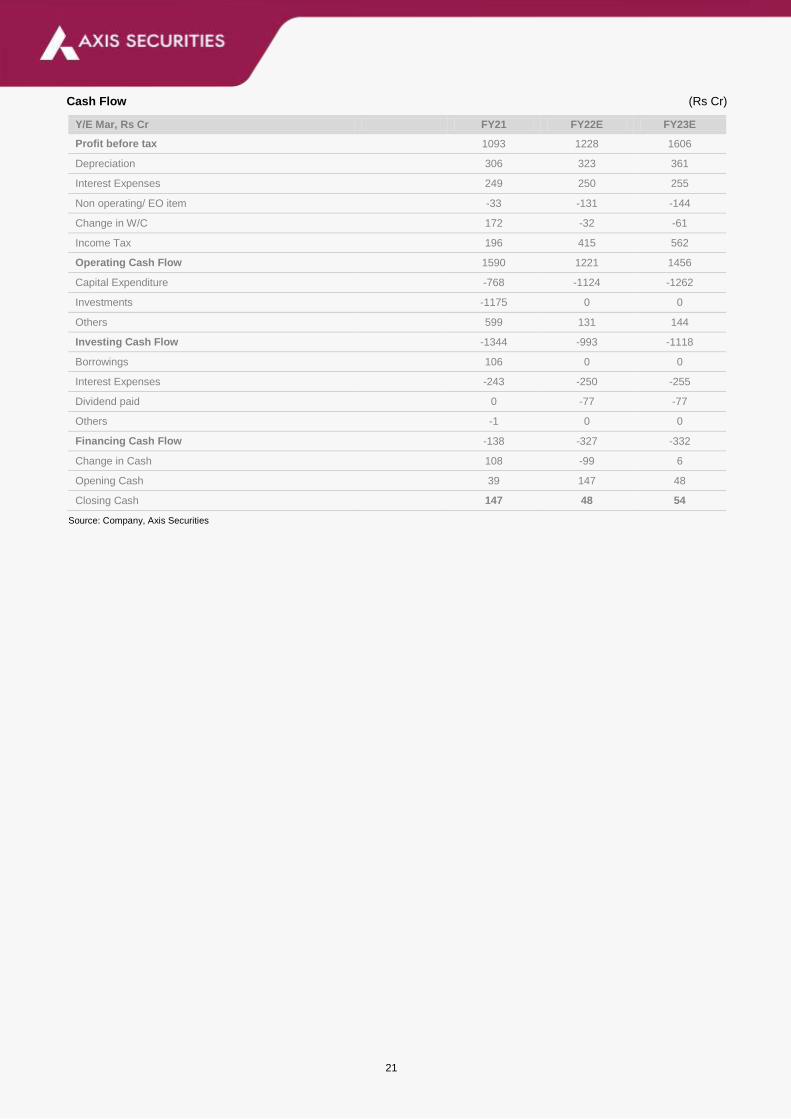

Cash Flow (Rs Cr)

Y/E Mar, Rs Cr FY21 FY22E FY23E

Profit before tax 1093 1228 1606

Depreciation 306 323 361

Interest Expenses 249 250 255

Non operating/ EO item -33 -131 -144

Change in W/C 172 -32 -61

Income Tax 196 415 562

Operating Cash Flow 1590 1221 1456

Capital Expenditure -768 -1124 -1262

Investments -1175 0 0

Others 599 131 144

Investing Cash Flow -1344 -993 -1118

Borrowings 106 0 0

Interest Expenses -243 -250 -255

Dividend paid 0 -77 -77

Others -1 0 0

Financing Cash Flow -138 -327 -332

Change in Cash 108 -99 6

Opening Cash 39 147 48

Closing Cash 147 48 54

Source: Company, Axis Securities

22

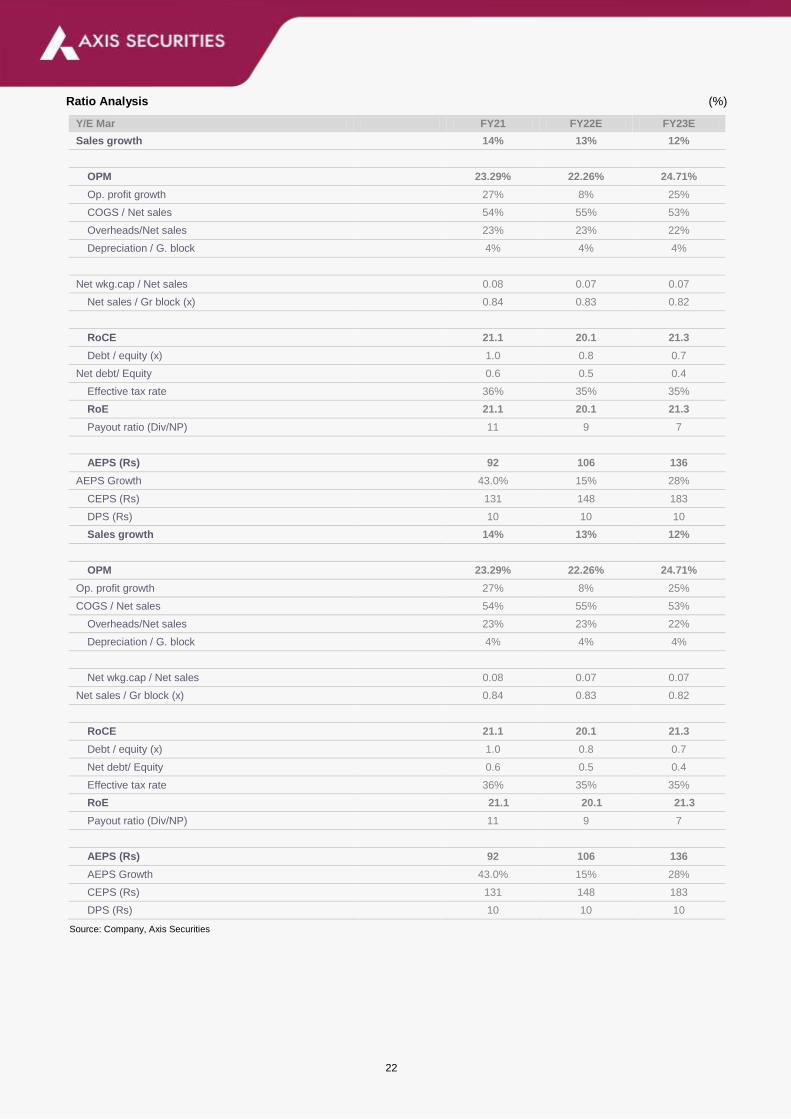

Ratio Analysis (%)

Y/E Mar FY21 FY22E FY23E

Sales growth 14% 13% 12%

OPM 23.29% 22.26% 24.71%

Op. profit growth 27% 8% 25%

COGS / Net sales 54% 55% 53%

Overheads/Net sales 23% 23% 22%

Depreciation / G. block 4% 4% 4%

Net wkg.cap / Net sales 0.08 0.07 0.07

Net sales / Gr block (x) 0.84 0.83 0.82

RoCE 21.1 20.1 21.3

Debt / equity (x) 1.0 0.8 0.7

Net debt/ Equity 0.6 0.5 0.4

Effective tax rate 36% 35% 35%

RoE 21.1 20.1 21.3

Payout ratio (Div/NP) 11 9 7

AEPS (Rs) 92 106 136

AEPS Growth 43.0% 15% 28%

CEPS (Rs) 131 148 183

DPS (Rs) 10 10 10

Sales growth 14% 13% 12%

OPM 23.29% 22.26% 24.71%

Op. profit growth 27% 8% 25%

COGS / Net sales 54% 55% 53%

Overheads/Net sales 23% 23% 22%

Depreciation / G. block 4% 4% 4%

Net wkg.cap / Net sales 0.08 0.07 0.07

Net sales / Gr block (x) 0.84 0.83 0.82

RoCE 21.1 20.1 21.3

Debt / equity (x) 1.0 0.8 0.7

Net debt/ Equity 0.6 0.5 0.4

Effective tax rate 36% 35% 35%

RoE 21.1 20.1 21.3

Payout ratio (Div/NP) 11 9 7

AEPS (Rs) 92 106 136

AEPS Growth 43.0% 15% 28%

CEPS (Rs) 131 148 183

DPS (Rs) 10 10 10

Source: Company, Axis Securities

23

JK Cement Price Chart and Recommendation History

Date Reco TP Research

21-Jul-20 BUY 1,697 Initiating Coverage

03-Aug-20 BUY 1,697 Pick of the week

03-Sep-20 BUY 1,691 Result Update

06-Oct-20 BUY 1,705 Company Update

11-Nov-20 BUY 2,150 Result Update

21-Dec-20 BUY 2,150 Result Update

10-Feb-21 BUY 2,520 Result Update

15-Jun-21 BUY 3,130 Result Update

17-Aug-21 HOLD 3,100 Result Update

17-Sep-21 HOLD 3,330 AAA

Source: Axis Securities

(Rs)

24

About the analyst

Analyst: Uttam Kumar Srimal

Email: [email protected]

Sector: cement/Infra

Analyst Bio: Uttam K Srimal is PGDBF from NMIMS with 20 years of experience in Equity

Market/Research.

About the analyst

Analyst: Shikha Doshi

Email: [email protected]

Sector: cement/Infra

Analyst Bio: Shikha Doshi is Master of Science in Finance from Illinois Institute of Technology, Chicago,

currently handling cement/infra sector.

Disclosures:

The following Disclosures are being made in compliance with the SEBI Research Analyst Regulations 2014 (herein after referred to as the Regulations).

1. Axis Securities Ltd. (ASL) is a SEBI Registered Research Analyst having registration no. INH000000297. ASL, the Research Entity (RE) as defined in

the Regulations, is engaged in the business of providing Stock broking services, Depository participant services & distribution of various financial products.

ASL is a subsidiary company of Axis Bank Ltd. Axis Bank Ltd. is a listed public company and one of India’s largest private sector bank and has its various

subsidiaries engaged in businesses of Asset management, NBFC, Merchant Banking, Trusteeship, Venture Capital, Stock Broking, the details in respect

of which are available on www.axisbank.com.

2. ASL is registered with the Securities & Exchange Board of India (SEBI) for its stock broking & Depository participant business activities and with the

Association of Mutual Funds of India (AMFI) for distribution of financial products and also registered with IRDA as a corporate agent for insurance business

activity.

3. ASL has no material adverse disciplinary history as on the date of publication of this report.

4. I/We, Uttam Srimal, (MBA-Finance) and Shikha Doshi (Master of Science in Finance), author/s and the name/s subscribed to this report, hereby

certify that all of the views expressed in this research report accurately reflect my/our views about the subject issuer(s) or securities. I/We (Research

Analyst) also certify that no part of my/our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this

report. I/we or my/our relative or ASL does not have any financial interest in the subject company. Also I/we or my/our relative or ASL or its Associates

may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the

Research Report. Since associates of ASL are engaged in various financial service businesses, they might have financial interests or beneficial ownership

in various companies including the subject company/companies mentioned in this report. I/we or my/our relative or ASL or its associate does not have

any material conflict of interest. I/we have not served as director / officer, etc. in the subject company in the last 12-month period.Any holding in stock –

No

5. 5. ASL has not received any compensation from the subject company in the past twelve months. ASL has not been engaged in market making activity for

the subject company.

6. In the last 12-month period ending on the last day of the month immediately preceding the date of publication of this research report, ASL or any of its

associates may have:

Received compensation for investment banking, merchant banking or stock broking services or for any other services from the subject company of this research

report and / or;

Managed or co-managed public offering of the securities from the subject company of this research report and / or;

Received compensation for products or services other than investment banking, merchant banking or stock broking services from the subject company of this

research report;

ASL or any of its associates have not received compensation or other benefits from the subject company of this research report or any other third-party in

connection with this report.

Term& Conditions:

This report has been prepared by ASL and is meant for sole use by the recipient and not for circulation. The report and information contained herein is strictly confidential and may not

be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or the media or reproduced in any form, without prior written consent of ASL. The report

is based on the facts, figures and information that are considered true, correct, reliable and accurate. The intent of this report is not recommendatory in nature. The information is obtained

from publicly available media or other sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or

implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. The report is prepared solely for informational

purpose and does not constitute an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments for the clients. Though disseminated to all

the customers simultaneously, not all customers may receive this report at the same time. ASL will not treat recipients as customers by their receiving this report.

25

Disclaimer:

Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to the recipient’s

specific circumstances. The securities and strategies discussed and opinions expressed, if any, in this report may not be suitable for all investors, who must make their

own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient.

This report may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this report should make such investigations as it

deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this report (including the merits and risks involved),

and should consult its own advisors to determine the merits and risks of such an investment. Certain transactions, including those involving futures, options and other

derivatives as well as non-investment grade securities involve substantial risk and are not suitable for all investors. ASL, its directors, analysts or employees do not take

any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but

not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. Past

performance is not necessarily a guide to future performance. Investors are advice necessarily a guide to future performance. Investors are advised to see Risk Disclosure

Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-

looking statements are not predictions and may be subject to change without notice.

ASL and its affiliated companies, their directors and employees may; (a) from time to time, have long or short position(s) in, and buy or sell the securities of the

company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities or earn brokerage or other compensation or act as a market maker

in the financial instruments of the company(ies) discussed herein or act as an advisor or investment banker, lender/borrower to such company(ies) or may have any other

potential conflict of interests with respect to any recommendation and other related information and opinions. Each of these entities functions as a separate, distinct and

independent of each other. The recipient should take this into account before interpreting this document.

ASL and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, the recipients of this report

should be aware that ASL may have a potential conflict of interest that may affect the objectivity of this report. Compensation of Research Analysts is not based on any

specific merchant banking, investment banking or brokerage service transactions. ASL may have issued other reports that are inconsistent with and reach different

conclusion from the information presented in this report. The Research reports are also available & published on AxisDirect website.

Neither this report nor any copy of it may be taken or transmitted into the United State (to U.S. Persons), Canada, or Japan or distributed, directly or indirectly, in the

United States or Canada or distributed or redistributed in Japan or to any resident thereof. If this report is inadvertently sent or has reached any individual in such country,

especially, USA, the same may be ignored and brought to the attention of the sender. This report is not directed or intended for distribution to, or use by, any person or

entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary

to law, regulation or which would subject ASL to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be

eligible for sale in all jurisdictions or to certain category of investors.

The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the

views expressed in the report. The company reserves the right to make modifications and alternations to this document as may be required from time to time without any

prior notice. The views expressed are those of the analyst(s) and the Company may or may not subscribe to all the views expressed therein.

Copyright in this document vests with Axis Securities Limited.

Axis Securities Limited, Corporate office: Unit No. 2, Phoenix Market City, 15, LBS Road, Near Kamani Junction, Kurla (west), Mumbai-400070, Tel No. – 022-40508080/

022-61480808, Regd. off.- Axis House, 8th Floor, Wadia International Centre, PandurangBudhkar Marg, Worli, Mumbai – 400 025. Compliance Officer: AnandShaha,

Email: [email protected], Tel No: 022-42671582.SEBI-Portfolio Manager Reg. No. INP000000654

DEFINITION OF RATINGS

Ratings Expected absolute returns over 12-18 months

BUY More than 10%

HOLD Between 10% and -10%

SELL Less than -10%

NOT RATED We have forward looking estimates for the stock but we refrain from assigning valuation and recommendation

UNDER REVIEW We will revisit our recommendation, valuation and estimates on the stock following recent events

NO STANCE We do not have any forward looking estimates, valuation or recommendation for the stock