Issue 01 | February 2014

20

Issue 01 | February 2014 IN PERSPECTIVE

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Issue 01 | February 2014

Issue 01 | February 2014

IN PERS

PECTIV

E

Table of Contents1. Foreword .............................................................................................................1

2. SMERA Crosses the Milestone of 25,000 MSME Ratings ...................................... 2

3. Economic Overview .............................................................................................3

4. Experts Views and Opinions .................................................................................6

5. Prudent Financial Management Practices .............................................................8

6. MSME News Highlights ......................................................................................10

7. Profile of SMERA Ratings ...................................................................................12

8. SMERA Activities ................................................................................................14

IN PERSPECTIVE

SMERA Ratings is pleased to announce the launch of its quarterly publication named 'MSME In Perspective'. The publication aims to share SMERA's perspective on the economy and evolving business environment that could impact MSME sector, opinions and views of the industry leaders/experts on issues that would be relevant to the MSMEs. Also, the publication will cover SMERA's views on the relevant issues and a glimpse of SMERA's activities in the MSME space. The first edition of the publication was timed to coincide with SMERA crossing the milestone of 25,000 MSME ratings.

The Indian economy continued to grow slowly during April 2013 to December 2013. Though some economic data is yet to flow, indicators available till now, combined with the expectations of the government and Reserve Bank of India (RBI), rule out early economic recovery. With most of the large corporate entities reporting lower performance in the current year, the cascading effect of this performance with respect to growth, profitability and working capital stretch is most acutely felt by the MSMEs.

While GDP growth in Q2 FY 14 was a tad better at 4.8% vis-à-vis 4.4% in Q1 FY14 the H1 FY14 was still lower at 4.6% compared to 5.3% in H1 FY13. Supply constraints and inflation continued to weigh on the growth trend, while domestic demand remained muted. Current account deficit (CAD) showed improvement from 4.9% as a percentage of GDP in Q1 FY14 to 1.2% as a percentage of GDP in Q2 FY14, with government taking steps to curb gold imports by hiking import duty. Fall in production and ban on exports from mining locations led to decline in average eight months IIP (which stood at -0.2%) vis-à-vis IIP in FY13 (which stood at 1.12%). On the policy front, the government initiated actions on clearing projects, especially in the infrastructure sector; however, these measures may take time to translate into the action at the ground level. Persistent high inflation, high fiscal deficit, high interest rates and uncertain global environment are some factors that pose risks to domestic growth. However with normal

Forewordmonsoon, the country is expected to see higher agricultural output, which in turn may boost rural income and help promote growth of manufacturing and service sector.

The rupee, which was in turmoil a few months ago, is now stable (after recovering by 9% from its all-time low) with the government taking remedial measures to arrest its precipitous drop. However, the US Fed's plan to taper its stimulus program by March 2014 may again hamper recovery of the rupee and impact the Indian market sentiments. A cautious approach needs to be maintained with focus on both, growth and inflation, considering weak macroeconomic indicators.

The economic slowdown has adversely affected recovery of dues of Medium Enterprises (MEs) dealing with large corporates from various sectors. The limited bargaining power of MEs has affected their collection of dues thus affecting their liquidity position.

The RBI measure of extending priority sector lending (PSL) benefits to ME loans, even for a temporary duration, is an important step in increasing and deepening credit flow to the MSME sector as a whole. PSL status will probably lead to increasing willingness of banks to lend to MEs. This is important because credit growth to MEs has not grown over the past few years. Extending PSL status to incremental loans to MEs may lead to higher willingness among banks to lend to the sector. Moreover, the enhancement of the exposure limit is also likely to incentivize banks to extend credit flow to Micro and Small Enterprises (MSEs). However, these measures also pose some challenges for banks, which may witness deterioration in asset quality of PSL assets and adverse impact on credit growth to other asset classes under PSL.

1

IN PERSPECTIVE

SMERA Ratings completes 25,000 Micro Small and

Medium enterprise (MSMEs) ratings and this

milestone was achieved by SMERA in just eight years

of its existence. Being a pioneer in the MSME

ratings, SMERA has established its credibility in

providing in-depth and unbiased analysis by taking

into consideration the required information to

indicate the units' ability and intention to honour its

commercial as well as financial commitments.

SMERA ratings are, therefore, highly respected by

financial institutions (including banks), industry

members, enterprises and their business associates.

The trust earned by SMERA from investor

community has enabled its MSME rated clients gain

access to bank finance, avail better borrowing

terms, inspire confidence in their employees,

customers, and suppliers and, most importantly,

embark on self-correction process to improve

subsequent ratings.

Mr. Parag Patki, CEO, SMERA Ratings, feels

that credit rating agencies (CRAs) play an

important role in fostering better credit

culture and discipline within the fraternity of

rated units to strengthen their capacity and

sustainability so that the entire economy

benefits. Through the process of credit

rating, discerning MSME units are able to

appreciate the benefits of creating

information symmetry within the financial

and commercial eco system and leverage

improvement in their ratings to gain

commercial as well financial benefits from

their bankers/ customers/ suppliers. Given

the importance of the MSME sector for the

Indian economy, SMERA is glad to be part of

this interesting journey in facilitating

financial inclusion with orderly growth of the

MSME sector in the country.

SMERA Crosses the Milestone of 25,000 MSME Ratings

SMERA rating portfolio is geographically-diversified

with the Western Region contributing the most

(37%) to the total rated universe of SMERA,

followed by the Northern Region, which contributes

28%. Contribution from the Southern Region and

Eastern Region stands at 26% and 9%, respectively.

SMERA has rated MSMEs across all sectors;

however, the highest share is of Metal and Metal

Products which stands at 24%, followed by

Electrical and Engineering Goods, Capital Goods,

Textile, Plastic, Food & Agro, Manufacturing

Sundry, Chemical, Services, Traders and Auto

Ancillary contributing in the range of 4% to 8%.

2

IN PERSPECTIVE

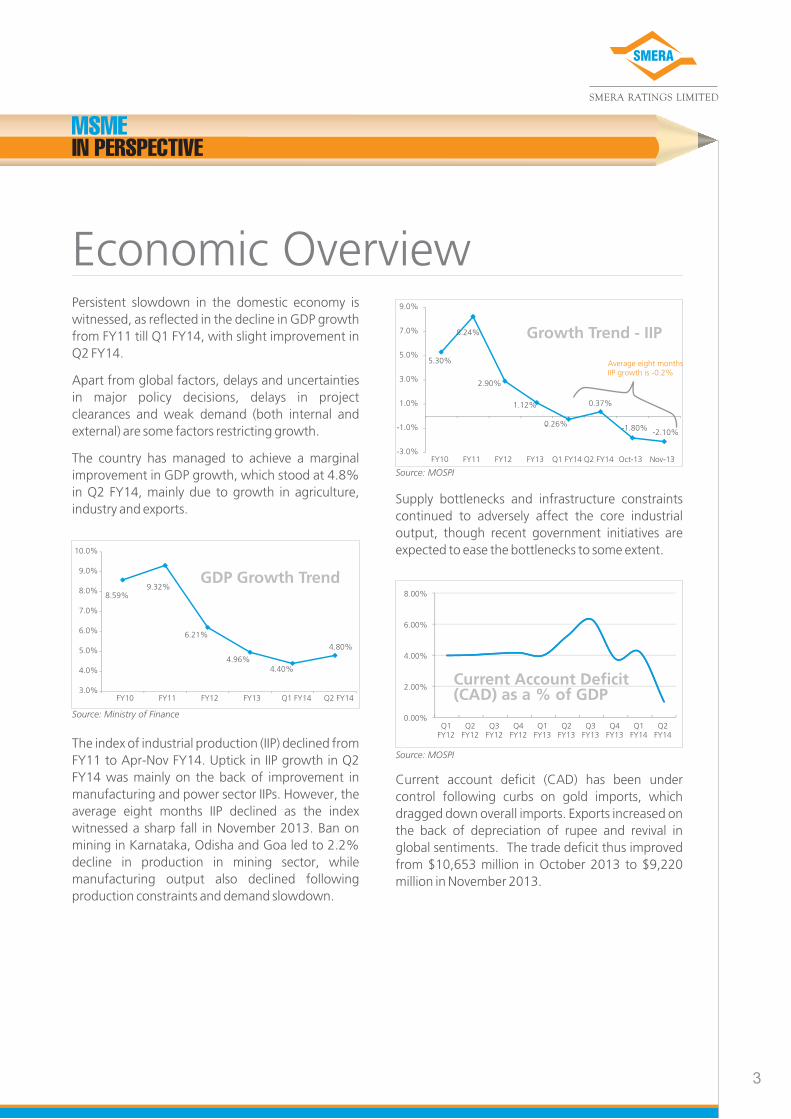

Economic Overview Persistent slowdown in the domestic economy is

witnessed, as reflected in the decline in GDP growth

from FY11 till Q1 FY14, with slight improvement in

Q2 FY14.

Apart from global factors, delays and uncertainties

in major policy decisions, delays in project

clearances and weak demand (both internal and

external) are some factors restricting growth.

The country has managed to achieve a marginal

improvement in GDP growth, which stood at 4.8%

in Q2 FY14, mainly due to growth in agriculture,

industry and exports.Supply bottlenecks and infrastructure constraints

continued to adversely affect the core industrial

output, though recent government initiatives are

expected to ease the bottlenecks to some extent.

The index of industrial production (IIP) declined from

FY11 to Apr-Nov FY14. Uptick in IIP growth in Q2

FY14 was mainly on the back of improvement in

manufacturing and power sector IIPs. However, the

average eight months IIP declined as the index

witnessed a sharp fall in November 2013. Ban on

mining in Karnataka, Odisha and Goa led to 2.2%

decline in production in mining sector, while

manufacturing output also declined following

production constraints and demand slowdown.

Current account deficit (CAD) has been under

control following curbs on gold imports, which

dragged down overall imports. Exports increased on

the back of depreciation of rupee and revival in

global sentiments. The trade deficit thus improved

from $10,653 million in October 2013 to $9,220

million in November 2013.

3

8.59%9.32%

6.21%

4.96%4.40%

4.80%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

FY10 FY11 FY12 FY13 Q1 FY14 Q2 FY14

GDP Growth Trend

5.30%

8.24%

2.90%

1.12%

-0.26%

0.37%

-1.80%-2.10%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

FY10 FY11 FY12 FY13 Q1 FY14 Q2 FY14 Oct-13 Nov-13

Growth Trend - IIP

Average eight months IIP growth is -0.2%

8.00%

6.00%

4.00%

2.00%

0.00%Q1

FY12Q2

FY12Q3

FY12Q4

FY12Q1

FY13Q2

FY13Q3

FY13Q4

FY13Q1

FY14Q2

FY14

Current Account Deficit (CAD) as a % of GDP

Source: Ministry of Finance

Source: MOSPI

Source: MOSPI

IN PERSPECTIVE

4

Continued high inflation remains to be a major

cause of concern in the current economic scenario.

Wholesale price index (WPI), which remained above

7% since August 2013, abated to 6.2% in

December 2013.

Constant high inflation has left little room for the

RBI to ease interest rates, which in turn has not only

impacted consumption but also overall credit

growth.

MSME Perspective

Economic Overview

0

4

8

12

16

20

FY 2009 FY 2010 FY 2011 FY 2012

MSME Output (Rs lakhs crore)

15.2416.19

17.2218.34

Fiscal deficit, which was 5.8% of the GDP in 2011-

12, reduced to 4.9% in 2012-13. The government

of India proposes to restrict fiscal deficit (as a

percentage of GDP for 2013-14) to 4.8%. However,

the target seems tough in view of poor revenue

realization and tepid progress of the disinvestment

programme (through which the Government of

India received Rs.3,000 crore during April 2013 to

November 2013, as against the budgeted target of

Rs.40,000 crore)..

Both demand and supply side factors need to be

corrected to ease inflation and help improve overall

market conditions. Improvement in fuel and power

availability, supply chain management and storage

and transport infrastructure would help improve

supply side situation.

However, slow economic growth, exchange rate

depreciation and increase in global commodity

prices would lead to subdued domestic demand.

Persistently high levels of inflation also pose risk to

exchange rate stability.

Total Exports (Rs in lakhs crore) - LHS

Average Exchange Rate ($ per rupee) - RHS

9.18 10.67

54.5

59.47

52

54

56

58

60

8

10

12

Apr -Oct 2012 Apr -Oct 2013

Exports vis-a-vis exchange rate

Source: RBI

Interest Rates (LHS) Inflation (WPI) (RHS)

Interest Rates vis-a vis Inflation (WPI)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

9.00%

Jan-1

1

Mar

-11

May

-11

Jul-11

Sep-1

1

Nov-

11

Jan-1

2

Mar

-12

May

-12

Jul-12

Sep-1

2

Nov-

12

Jan-1

3

Mar

-13

May

-13

Jul-13

Sep-1

3

Nov-

13

Source: RBI; MOSPI

Source: Ministry of MSME

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

9.00%

Jan-1

1

Mar

-11

May

-11

Jul-11

Sep-1

1

Nov-

11

Jan-1

2

Mar

-12

May

-12

Jul-12

Sep-1

2

Nov-

12

Jan-1

3

Mar

-13

May

-13

Jul-13

Sep-1

3

Nov-

13

Interest rates (LHS) MSME credit growth (RHS)

Interest Rates vis-a vis MSME credit growth

Source: RBI; Ministry of MSME

7.00%

6.50%

6.00%

5.50%

5.00%

4.50%

4.00%2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

Fiscal Deficit as a % of GDP

Source: MOSPI

IN PERSPECTIVE

5

MSMEs contribute around 45% of the total

manufacturing output in the country, though their

contribution to GDP is still low at 8-10%. However,

the sector provides employment to 40% of the

country's work force. The MSME sector is also a

major contributor to the total exports (around

40%).

Economic Overview

Economic slowdown, high input costs and high

interest rates have affected MSEs' repayment

ability, leading to increase in NPA levels.

-25.0%

-15.0%

-5.0%

5.0%

15.0%

25.0%

35.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Jan-1

1

Mar

-11

May

-11

Jul-11

Sep-1

1

Nov-

11

Jan-1

2

Mar

-12

May

-12

Jul-12

Sep-1

2

Nov-

12

Jan-1

3

Mar

-13

May

-13

Jul-13

Sep-1

3

MSE (LHS) Medium enterprises (RHS)

MSE vis-a-vis Medium enterprises - Credit growth

Source: Ministry of MSME

Source: RBI

MSE Gross NPA Ratio (%)

2.48%

3.40% 3.52%3.86%

5.41%

0%

1%

2%

3%

4%

5%

6%

FY09 FY10 FY11 FY12 FY13

The role of MSEs in Indian economy is becoming

vital. MSMEs thus require higher credit facility to

operate efficiently. The credit to MSE sector

witnessed an upward trend since the beginning of

the current financial year. However, medium

enterprises credit growth has been lower in

comparison with the credit growth in the MSE

sector.

RBI, in November 2013, announced three special

policy measures in order to extend liquidity support

to MSMEs. A Re.50 billion refinance fund

specifically for micro & small enterprises (MSEs),

enhancing the exposure limit for MSMEs to Rs.10 Cr

from Rs.5 Cr and extension of the priority sector

status (PSL) to incremental loans made out to

medium enterprises (MEs) till March 2014. Giving

PSL status to incremental loans extended to MEs

may to lead to higher willingness among banks to

lend to the sector. Moreover, the enhancement of

the exposure limit is also likely to incentivize banks

to extend credit flow to the MSME sector.

IN PERSPECTIVE

Experts Views and Opinions

Q. Considering lackluster macroeconomic indicators in FY14 and the following quarters, what is the expected trajectory for these indicators? Are there any signs of revival post government taking steps to boost growth, curtail fiscal deficit, restrict current account deficit and clear supply bottlenecks? What is the overall economic outlook?

Opinion: The overall economic outlook looks positive. Various green shoots are visible now. Exports are showing signs of pick-up and trade deficit has narrowed. The current account deficit for 2013-14 is expected to be below 2.5% of GDP, which is significantly lower than that of the previous year. Govt. is committed to maintain fiscal deficit target for FY 2014 which will also help in controlling

by Mr. N. K. Maini, Deputy Managing Director, SIDBI

*Extension of liquidity support to MSME's will improve the credit penetration

*Incremental credit to Medium Enterprises to qualify as Priority Sector

The liquidity support comes in the wake of slowdown in the economy, which has resulted in liquidity tightness in a large number of Micro and Small Enterprises (MSEs) in the manufacturing and services sector, particularly due to delayed settlement of receivables from large corporate entities, public sector undertakings and government departments.

In view of the need to ease the liquidity stress to Micro and Small Enterprises (MSE) sector, which is employment intensive and a significant contributor to exports, it has been decided to provide refinance of Rs.5,000 crore to the Small Industries Development Bank of India (SIDBI).

In order to enhance credit delivery to the MSE sector, it has been decided to include, as eligible priority sector lending, incremental credit (including export credit) extended to medium enterprises.

6

inflationary pressure. However, though CPI has declined significantly, it remains high at close to double digits. The silver lining is the robust agricultural performance, coupled with strong pick-up in the sowing of the rabi crop. Further, with the Cabinet Committee on Investment clearing a number of large projects, investments are going to pick up. Reserve Bank of India has also indicated that the GDP growth in 2014-15 is likely to be in the range of 5% - 6%, with likelihood of touching the upper range, as global outlook improves and inflation stabilizes.

The optimism is also corroborated by different business confidence surveys indicating better investment prospects, improving sales, new orders and export performance. For example, CII Business Confidence Index (CIIBCI) for Oct- Dec 2013 quarter increased sharply to 54.9 from 45.7 in the previous survey, revealing that 58 per cent of the respondents expect increase in their sales, new orders and value of production in the third quarter of 2013-14. Similarly, the 17TH Annual Global CEO Survey by PWC in January 2014 indicates that Indian CEOs are more upbeat and very confident of growth prospects in the next 12 months. The latest HSBC Manufacturing Purchasing Managers' Index (PMI) bounced to 51.4 in January 2014, its highest since March 2013, indicating that manufacturing activity moved into higher gear led by faster growth in new orders.

Q. Which are the sectors where credit growth is foreseen?

Opinion: I am happy to note that credit to MSME sector has increased. In the industry groups as per RBI data, credit growth is seen in industries like food processing, leather and leather products, paper and paper products, rubber and plastics, cement, etc.

Opinion on

IN PERSPECTIVE

7

Experts Views and Opinions

Credit is also flowing to the services sector. Facilitating availability of credit to knowledge – based enterprises is expected to have a salutary effect on the growth of the sector.

Q. To what extent will the RBI grant of Rs.5,000 crore help ease liquidity stress in MSME sector and would that support be adequate?

Opinion: We are indeed thankful to the Reserve Bank of India for having extended a refinance facility of ` 5000 crore through SIDBI to address the liquidity problem of MSEs. This fund has already been utilized fully, benefitting more than 12,000 MSEs by way of liquidity support to finance their receivables, including export receivables, both directly by SIDBI and also through banks. Since this facility is to be rolled over in 90 days and the fund is available with SIDBI till November 2014, we estimate that this gesture of RBI will enable credit availment of more than ` 20,000 crore by MSEs during the validity period. The number of MSEs will also increase with the rollover.

While on the subject of receivable financing, we would like refer to a 2008 Committee on Financial Sector Reforms, headed by the present RBI Governor, Shri Raghuram Rajan, which recommended facilitation of Electronic Bill Factoring Exchanges, whereby MSME bills against large companies can be accepted electronically and

“Since this facility is to be

rolled over in 90 days and

the fund is available with

SIDBI till November 2014, we

estimate that this gesture of

RBI will enable credit

availment of more than Rs.

20,000 crore by MSEs during

the validity period. The

number of MSEs will also

increase with the rollover”.

auctioned, to ensure prompt realisation of rece i vab les . Based on the Commit tee recommendations, SIDBI, in collaboration with National Stock Exchange, set up an E-discounting platform of MSME receivables, called 'NTREES'. This e-platform is being operated presently, in Phase I with single financier [SIDBI] model. Going forward, it is planned to graduate to next Phase involving multiple financiers [banks], so that MSMEs bills are discounted at the most competitive rates in a transparent manner. SIDBI is also in discussions with RBI / NSE to bring in further advanced features in the system.

Q. With inclusion of medium enterprises in priority sector lending, what would be the impact on the credit growth of Micro and Small Enterprises?

Opinion: This step may not have much impact on credit to Micro and Small Enterprises [MSEs] in the long run because the Reserve Bank of India's circular specifies inclusion of medium scale manufacturing sector only for a limited period from November 2013 to November 2014, that too, on incremental credit flow to that medium enterprise category. On the whole, the policy thrust will continue to remain on credit augmentation to MSEs. As per RBI's instructions, banks have been advised to achieve a 20 per cent year-on-year growth in credit to MSEs, a 10 per cent annual growth in the number of micro enterprise accounts and 60% of total lending to MSE sector to be earmarked for micro enterprises. Further, public sector banks have been advised to open at least one specialized MSME branch in each district. The banks have been permitted to categorize their MSME general banking branches having 60% or more of their advances to MSME sector, as specialized MSME branches for providing better service to this sector as a whole. More importantly, the credit flow to MSE sector is constantly monitored by Ministry of Finance, Government of India and RBI. As a result of these measures, credit flow to MSE sector has increased by 23.6 % as at end on December 2013 over the corresponding period of previous year. Considering these positive factors and the enabling environment already in place, we are confident that the credit flow to MSE sector will continue to increase in future.

IN PERSPECTIVE

Introduction

Instances of Imprudent Financial practices

Prudent financial management practices refers to

adequate financial planning with respect to

sourcing of funds and application of funds, timely

repayment of dues to financial institutions and

vendors, managing liquidity, proper maintenance of

books of accounts, etc. As per SMERA's experience

of having rated more than 25,000 entities, it is

observed that Micro and Small units require

improving their financial management practices as

compared to the medium and large sized corporate

entities. It is generally observed that micro and small

units enjoy lesser confidence from their potential as

well as existing, lenders, investors and other

stakeholder. It is believed that the financial

management practices prevailing at the micro and

small enterprises emanate due to inadequate

awareness on the importance of financial discipline

and its potential adverse impact on the firm's

prospects. Further, orderly maintenance of books

of accounts, optimum allocation of resources, lack

of consistency in payment track record, prudent

working capital management, etc. are few other

inhibiting factors discouraging potential investors

and lenders from investing in MSEs. Inadequate

capital support from lenders and low capital

infusion by the promoters affects the growth of

MSME businesses and expose them to severe stress

during the business downturns.

Hence it is important to lay emphasis and pay

greater focus on the prudent financial management

practices within MSEs.

*Improper utilisation of funds.

*Withdrawal of capital from business.

*Non-adherence to the credit terms of lenders

*Withdrawal of unsecured loans.

*Lack of tax planning.

*Maintaining inadequate capital in the business.

*Non-retention of profits in the business.

*Imprudent investments in other businesses,

investments in property, advances to related

parties by diverting capital.

Prudent Financial Management Practices

*Utilisation of short term funds to acquire long

term assets, leading to stressed liquidity position.

*Mismatch of quantum of working capital with

business requirements.

*Delays in repayment of interest and principal to

the lending institutions.

*Frequent inward cheque returns.

*Delays in making statutory payments.

*Overdrawing of working capital limits.

*Improper book keeping and maintenance of

accounts.

*Lack of professional financial planning during

the project execution adversely impacting

estimation of revenue, expenses, cash flows and

working capital requirements.

*Non-availability of contingency funds.

*Improper booking of revenue and expenses in

the profit and loss account.

*Low awareness on the importance of proper

financial discipline and its overall impact on the

health of the company.

*High technical capability but low commercial as

well as financial skills.

*Non engagement of professionals to manage

the commercial and financial aspects of the

business.

*Under reporting revenues and profits to

minimise tax liability.

*Fear of regulatory environment and related

stringent disclosures leading to sub-optimal

business scale.

Reasons for Imprudent Financial

Management

8

IN PERSPECTIVE

Benefits of Prudent Financial Management

Steps to Instil Prudent Financial

Management

*Increased confidence of financial institutions

and stakeholders.

*Ensure consistency in cash flow.

*Alternate avenues of capital sourcing such as:

private equity, angel investors, capital markets,

etc.

*Improvement in credit terms from suppliers.

*Increase in scale of operations and resultant

economies of scale.

*Adequate capital should be maintained in the

business either by way of infusion or by retention

of profits.

*Proper maintenance of books of accounts.

*Timely repayment of loans and effective

utilisation of working capital limits.

*Proper estimation of working capital needs.

*Efficient working capital management.

*Proper allocation of funds i.e. short-term sources

should be utilised for short-term uses..

*Proper financial planning with respect to project

cost, sourcing of funds and allocation of funds.

*Transparency with respect to inter-group

transaction and diversion of funds to related

parties.

*Timely payment to suppliers

*Hiring of professionals to manage finance.

Conclusion

SMERA believes that adoption of practices that instil

prudent financial management within the MSME

units would ensure better financial health leading to

growth, scalability and sustainability of the business

unit.

SMERA's Credit Ratings takes a comprehensive view

of the company's overall performance, financial

position, strengths and weakness and other related

factors.

9

Prudent Financial Management Practices

IN PERSPECTIVE

RBI decides to include medium enterprises

under priority sector

Slow pace of rice procurement to hit

Punjab millers

Due to the ongoing slowdown many medium-sized

units dealing with larger corporates are facing

delayed payments. Further, the limited bargaining

power of these medium-sized units has led to piled

up dues and stretched liquidity.

In view of this, Reserve Bank of India (RBI) has

recently announced to consider funding to medium

manufacturing enterprises as priority sector

lending, which is extended after November 2013 up

to March 2014.

SMERA believes that this new RBI initiative would

lead to enhanced liquidity and financial support to

medium enterprises; however, it could also lead to

deterioration of asset quality under priority sector

lending assets for banks. While banks would be

more amenable to lending to medium-sized units

for meeting their priority sector lending targets,

they would be careful about whom they lend to,

and would have to keep their screening standards

very stringent. Lastly, there is a need for taking

stronger measures to ensure that MSMEs get

adequate credit and have ample liquidity over the

long-term.

Punjab contributes a large share to the central pool

of the public distribution system (PDS) and has a

total of about 3,050 small rice processing mills.

These mills process non-basmati rice procured by

the central and state government agencies meant

for the PDS and are paid processing charges.

Further, they retain the by-products (such as paddy

husk and bran) with them.

However, this year Punjab's rice mills, mostly

MSMEs, are running far below their full capacity,

with entrepreneurs attributing this slowdown to

government's policies. Drop in levels of

procurement by the central and state government

agencies are forcing millers to operate at low

capacity.

Various millers met with government officials to

explain that due to the rise in the moisture content

after February, the grain would start deteriorating

and that is a loss to the millers. Some affluent millers

have installed sortex machines (machines that can

segregate damaged and coloured grain from

healthy grain), but very few can afford the sortex

machines.

Millers hope it is only a phase and that business will

revive soon. The implementation of the Food

Security Act, recently passed by parliament, would

trigger higher demand for food grain and increase

paddy processing in Punjab.

Over the past four years, many MSMEs in

Coimbatore have shut their businesses partially or

completely. It is estimated approximately 7,000

units have closed, causing job losses of 80,000-

100,000. Power cuts (four to six hours during

daytime and one hour in the evenings) are back in

the town after a gap of four months.

Coimbatore is known for its engineering goods

industry and pump sets manufacturing (mainly

agricultural pump sets). Over the past four to five

years, Coimbatore's share of India's output of pump

sets has fallen from 75% to 50%, while 40% of the

factories have shut their doors with orders now

flowing to other states, particularly to Gujarat.

The power outages are on account of power deficit

to the extent of about 2,500 MW. Coimbatore's

industries have sought the support of the central

and state governments.

Coimbatore MSME's facing crisis due to

power cuts

MSME News Highlights

10

IN PERSPECTIVE

MSME News Highlights

11

Government approves continuation of

Mill Gate Price Scheme (MGPS)

The Cabinet Committee on Economic Affairs has

approved the continuation of the Mill Gate Price

Scheme (which has been renamed as Yarn Supply

Scheme) for an outlay of Rs.443 crore during the

12th plan, along with 10 per cent subsidy

component with modifications.

The scheme provides subsidized yarn to

underprivileged weavers and vulnerable groups,

thereby enabling them to compete with

modernized units using power looms and mills. The

target under the 12th Plan would be to supply 3,506

lakh kg yarn worth Rs.4,364 crore to the

underprivileged weavers and vulnerable groups.

The National Handloom Development Corporation

(NHDC) has also proposed to open distribution

centres/warehouses in various parts of the country

in order to increase the coverage of primary weavers

societies and individual weavers. The proposed

move is also aimed towards introduction of cash

sale of yarn ( especially to small weavers) instead of

advance payments to precede indenting and supply

of yarn with a gap of about 15 to 45 days. For a

start, 10 such distribution centres are to be set up

by NHDC.

IN PERSPECTIVE

Geographical presence of SMERA

SMERA rating portfolio is geographically-diversified

with the Western Region contributing the most

(37%) to the total rated universe of SMERA,

followed by the Northern Region, which contributes

28%. Contribution from the Southern Region and

Eastern Region stands at 26% and 9%, respectively.

Below graph depicts the number of presence of

SMERA across states and region in India and their

percentage contribution to the total rated portfolio.

Profile of SMERA Ratings

Distribution of entities based on industry

SMERA has rated MSMEs across all sectors;

however, the highest share is of Metal and Metal

products which stands at 24%, followed by

Electrical and Engineering Goods, Capital Goods,

Textile, etc. contributing in the range of 4% to 8%.

12Number of Ratings Percentage

Industrywise Distribution

0

1,200

2,400

3,600

4,800

6,000

Met

al &

Met

al

Product

s

Elec

tric

al &

En

gin

eering G

oods

Cap

ital

Goods

Text

ile

Plas

tic

Food &

Agro

Trad

ers

Chem

ical

Man

ufa

cturing

- Su

ndry

Serv

ices

Auto

Anci

llary

Oth

ers

24

87 6 6

5 4 4 4 4 4

23

Ratings Percentage

Geographical Presence 20%

18%

14%

8% 7% 7% 7%5% 5%

11%

0

1,000

2,000

3,000

4,000

5,000

Mah

aras

htr

a

Gu

jara

t

Tam

il N

adu

Kar

nat

aka

Har

yan

a

Utt

ar P

rad

esh

Wes

t B

engal

Pun

jab

Del

hi

Oth

ers

`('

000

)

NSIC – D&B – SMERA Rating Scale

SMERA provides an opinion on the entity's

performance capability and financial strength

through the rating scale shown in the table.

Ratings from 1–5 indicate performance capability

with '1' being the highest rating and '5' being the

lowest.

'A, B and C' indicate Financial Strength of the

enterprise with 'A' being High and 'C' being Low.

For example, an entity with Highest Performance

Capability and High Financial Strength will be rated

as 'SE 1A' and the entity with Poor Performance

Capability and Low Financial Strength will be rated

as 'SE 5C'.

Financial Strength

High Moderate Low

PerformanceCapability

Highest

High

Moderate

Weak

Poor

SE 1A SE 1B SE 1C

SE 2A SE 2B SE 2C

SE 3A SE 3B SE 3C

SE 4A SE 4B SE 4C

SE 5A SE 5B SE 5C

Rating Indicators

Zonewise Distribution9%

28%

26%

37%

East North South West

IN PERSPECTIVE

13

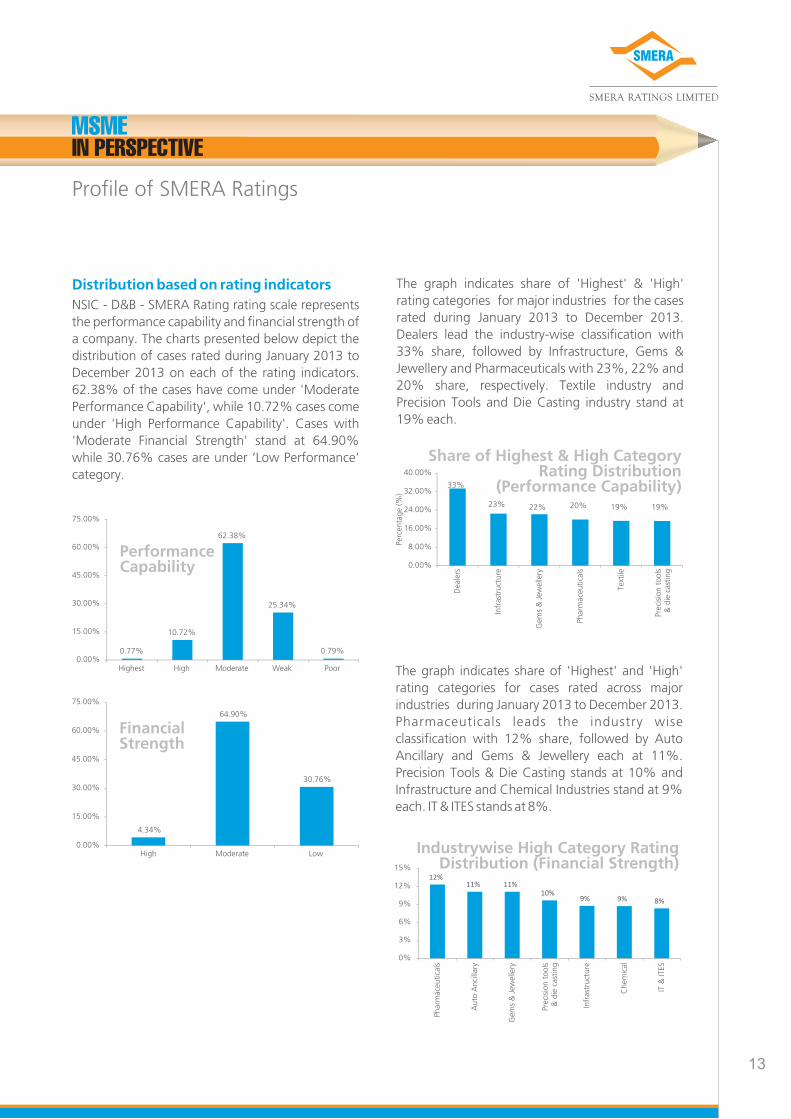

Distribution based on rating indicators

NSIC - D&B - SMERA Rating rating scale represents

the performance capability and financial strength of

a company. The charts presented below depict the

distribution of cases rated during January 2013 to

December 2013 on each of the rating indicators.

62.38% of the cases have come under 'Moderate

Performance Capability', while 10.72% cases come

under 'High Performance Capability'. Cases with

'Moderate Financial Strength' stand at 64.90%

while 30.76% cases are under ‘Low Performance'

category.

The graph indicates share of 'Highest' and 'High'

rating categories for cases rated across major

industries during January 2013 to December 2013.

Pharmaceuticals leads the industry wise

classification with 12% share, followed by Auto

Ancillary and Gems & Jewellery each at 11%.

Precision Tools & Die Casting stands at 10% and

Infrastructure and Chemical Industries stand at 9%

each. IT & ITES stands at 8%.

Profile of SMERA Ratings

0.77%

10.72%

62.38%

25.34%

0.79%0.00%

15.00%

30.00%

45.00%

60.00%

75.00%

Highest High Moderate Weak Poor

Performance Capability

4.34%

64.90%

30.76%

0.00%

15.00%

30.00%

45.00%

60.00%

75.00%

High Moderate Low

Financial Strength

The graph indicates share of 'Highest' & 'High'

rating categories for major industries for the cases

rated during January 2013 to December 2013.

Dealers lead the industry-wise classification with

33% share, followed by Infrastructure, Gems &

Jewellery and Pharmaceuticals with 23%, 22% and

20% share, respectively. Textile industry and

Precision Tools and Die Casting industry stand at

19% each.

33%

23% 22% 20% 19% 19%

0.00%

8.00%

16.00%

24.00%

32.00%

40.00%

Dea

lers

Infr

astr

uct

ure

Gem

s &

Jew

elle

ry

Phar

mac

eutica

ls

Text

ile

Prec

isio

n t

oo

ls

& d

ie c

astin

g

Perc

enta

ge

(%)

Share of Highest & High Category Rating Distribution

(Performance Capability)

12%11% 11%

10%9% 9% 8%

0%

3%

6%

9%

12%

15%

Phar

mac

eutica

ls

Au

to A

nci

llary

Gem

s &

Jew

elle

ry

Prec

isio

n t

ools

&

die

cas

ting

Infr

astr

uct

ure

Chem

ical

IT &

ITES

Industrywise High Category Rating Distribution (Financial Strength)

IN PERSPECTIVE

Date of Event: 07th June, 2013

Audience: Bankers / MSMEs

Guests: Mr. M. Narendra, CMD – IOB;

Mr. Naval Gupta, GM (SME) – IOB;

Mr. C.H. Radhakrishnan Prasad,

GM Chennai - I, IOB

Speaker: Mr. M. Narendra, CMD – IOB;

Mr. Parag Patki, CEO - SMERA

thDate of Event: 06 Aug, 2013

Audience: Branch Heads, Advance / Credit Managers

Guests: Shri Padmanabhan, GM - Andhra Bank

Shri Seshagiri Rao, Dy. GM –Andhra Bank

Speaker: Shri Padmanabhan, GM - Andhra Bank

Shri Seshagiri Rao, Dy. GM –Andhra Bank

Shri Virendra Goyal, VP Sales (SME) – SMERA

Shri P.R. Chaganti, Manager - NSIC

Date of Event: 26th Sept, 2013

Audience: Branch Heads, Advance / Credit Managers,

Officers and Entrepreneurs

Guests: Mr. Dhanesh Chander, GM-NBG IOB;

Mr. Balkishan T., CRM, KOL-I IOB;

Mr. Gopinath Bhattacharya, SBM NSIC;

Mr.Param Singh Chauhan, CRG, KOL-II IOB

Speakers: Mr. Dhanesh Chander, GM-NBG IOB;

Mr. Virendra Goyal, VP Sales (SME) – SMERA;

Mr. T R Jain, IOB;

Mr. Param Singh Chauhan, CRG, KOL-II IOB;

Mr. Balkishan T., CRM, KOL-I IOB;

Mr. Gopinath Bhattacharya, SBM – NSIC;

Mr. Shantanu Gangly, CRG, KOL-II IOB

SMERA ActivitiesFinancing Options for MSME's and Benefit 0f External Credit Rating (Joint Seminar Indian Overseas Bank and Smera), Chennai

Financing Options for MSME's and Benefit of External Credit Rating (Joint Seminar Andhra Bank and Smera), Hyderabad

Financing Options for MSME’s and role of Credit Rating, Kolkata

14

IN PERSPECTIVE

SMERA Ratings Limited (formerly SME Rating

Agency of India Ltd.) is a joint initiative of Small

Industries Development Bank of India (SIDBI), Dun &

Bradstreet Information Services India Private Limited

(D&B) and leading public and private sector banks in

India. SMERA Ratings commenced its operations in

2005 as an exclusive credit rating agency for Micro,

Small and Medium Enterprises (MSME) sector in the

country. Within a span of eight years, the company

has assigned ratings to over 25,000 MSMEs across

India.

SMERA Ratings is registered with the Securities and

Exchange Board of India (SEBI) as a Credit Rating

Agency. More recently, the company has received

accreditation from the Reserve Bank of India (RBI) as

an External Credit Assessment Institution (ECAI)

under BASEL - II norms for undertaking bank loan

ratings. SMERA Ratings is also empanelled as an

approved rating agency by the National Small

Industries Corporation Ltd. (NSIC) under the

'Performance & Credit Rating Scheme for Small

Industries"', approved by the Ministry of Small Scale

Industries, Government of India.

Today, SMERA Ratings has achieved the reputation

of providing comprehensive, transparent and

reliable ratings, thus providing comfort and

confidence to lenders and investors alike in decision

making. SMERA's ratings have gained wide

acceptability and are now an integral part of the risk

assessment process within the lending and investing

community.

SMERA Offerings

*

*

*

*

*

*

*

*

*

SME Ratings

NSIC D&B SMERA Rating

Corporate & Infrastructure Ratings

Bank Loan Ratings

Microfinance Institutions Grading (MFI)

Maritime Institutes Grading (MTI Grading)

Green Ratings

Project Grading / Greenfield / Brownfield

RESCO / Solar Grading

SMERA Ratings Limited

Corporate Office102, 1st floor, Sumer Plaza, Marol Maroshi Road, Marol, Andheri (East), Mumbai - 400 059T: +91 22 6714 1111 | F: +91 22 6714 1142 | E: [email protected] Rating HelpdeskT: +91 22 6714 1177

Ahmedabad 807, 8th floor, Abhijeet I, Navrangpura, Ahmedabad - 380 006 T: +91 79 3043 0432 / 33 / 34E: [email protected]

Bangalore 303, Trade Centre, Dickenson Road, Bangalore - 560 042 T: 080 2558 5561-64 / 2211 7743E: [email protected]

Chennai Eldorado Building, No. 112, 6th floor, Nungambakkam High Road, Chennai - 600 034 T: +91 44 4907 4545 / 2823 2122 / 4848F: +91 44 2821 1414E: [email protected]

Coimbatore No. 85, Poonka Plaza, 2nd floor, Avarampalayam Road, Siddhapudhur, Coimbatore - 641 044 T: +91 422 224 4622 / 33E: [email protected]

Hyderabad 21, Sanali Mall, 3rd floor, Opp. Chermas, Abids Road, Abids, Hyderabad - 500 001 T: +91 40 4027 4589 / 90E: [email protected]

Jaipur 307, 3rd Floor, Trimurty Luhadia TowerK-11, Ashok Marg, C-Scheme,Jaipur – 302 001T: 0141 4039347 – 50E: [email protected]

Kolkata 3A, Annapurna Apartment, 68, Ballygunge Circular Road, Kolkata - 700 019 T: +91 33 3028 8299 / 96F: +91 33 4006 0790E: [email protected]

Ludhiana Birson Complex 7, 1st floor, R K Road,Textile Colony Industrial Area, Ludhiana - 141 001 T: +91 161 463 0745 / 461 0745E: [email protected]

Mumbai 304, Dheeraj Kawal, LBS Marg, Vikhroli (West), Mumbai - 400 079 T: +91 22 4227 4747F: +91 22 4227 4749E: [email protected]

Navi Mumbai 402/405/406, 4th floor, Bldg No. 2, Sector - I, Millenium Business Park, Mahape,Navi Mumbai - 400 710 T: +91 22 6740 1111F: +91 22 6740 1199E: [email protected]

New Delhi 807, 8th floor, DLF Tower - A, Jasola District Centre, New Delhi - 110 029 T: +91 11 4180 6650F: +91 11 4180 6666E: [email protected]

New Delhi FB-03, NSIC - STP Extension, NSIC Bhavan, Okhla Industrial Estate, Phase 3, New Delhi - 110 020 T: +91 11 4618 4031 - 36F: +91 11 2644 5571E: [email protected]

Pune 12, 1st floor, Sukhwani Fortunes, Morwadi Court Road, Pimpri, Pune - 411 018 T: +91 20 6510 4701 - 08E: [email protected]

Surat 83 & 102, 1st floor, Sardar Complex, Gujarat Gas Circle, Adajan, Surat - 395 009 T: +91 261 401 6111 / 6002E: [email protected]