Do Customs Trade Facilitation Programmes Help Reduce Customs-Related Corruption?

Upload

khangminh22Category

view

1download

0

sITt'I I{:ID[JGOVERNMENT OF INDIA

rflar.1e-o uura orrgm or oraico (fuaraura o aor€ aro rftrrr )

OFFICE OF THE PRINCIPAL COMMISSIONER OF CUSTOMS (AIRPORT & A.C.C):flat oleo urcar, l5/l etrs is, oldor.n- 700001

CUSTOM HOUSE, 15/1 STRAND ROAD, KOLKATA- TOOOOI

?ffia / TELEPHONE : 031-22,13-5372

: 533-23 /2017 Adjn IAP & ACC]

: DRI/KZUlCFllNT-75 /2077 /Enq-so/ zOU /PI.-Sri Ram/4640

:04.L2.201.7

: KoL/CUS/Pr. CoMMIssloNER/APIADMN/oe / 2022

Wtq 6168, Date of order: 37.03.2022frrfq-{ fr1 ftft /Date of Dispat ch: o1.o4.2o22

iqfi/ Passed by Deep Shekhar

fiq1 gqo xen< Gxg-ffi GqTila{ a 6or{ ql,6 qfus-qy

Pr. Commissioner of Customs [Airport & ACC)

Sqr {(fi sfi,1 s/1, * t-s, o-td-o-rdr 70000 1-Custom House, L5/L, Strand Road, Kolkata-700001

{d 3{Cql / oRDER - rN - oRTGTNAL

1. T6qfr d€ ilqRdB!frrTfuE:Eqoonl fuqrqrarBmsA frC{6ft.|d fuqTqldrelThis copy is granted free of charge For the private use of the person to whom it is issued.

2. as 3rrari * sfiiqqa at{ tft qR, frqT g.rfi rtlqFqq, ls6zei ERI 12e [q dr{fi{ {s ctTasT A E-c$ o1scr {-d-6, dfrq B-flTE Eq6 cs +dr 6r qfidqsrfYmrur,qdA*qsrRar.iEBsr,zsi a.f,,1se,qT-dT{qrr&qriiqfrq.t-s,atf,fldr14-iqfioorvoarttAny person aggrieved by this order may, Under Section 1-29(A] of the Customs Act,1962, file an Appeal against the order to [a) The Customs, Central Exercise and ServiceTax Appellate Tribunal, East Regional Branch, Bamboo Villa, 7th Floor, 159, A. ). C. BoseRoad, Kolkata-14.

QS eifid {s en}sl m qrt 6 6t fr.fU e fi I-Si d eiet ed of slsfr t

(b) Such appeal shall be filed within three (3) months from the date of communicationof the order.

I)t\-t0ltot76\ I.0(xnl555Lr I c

81.{il.r. no.qESg{ti/.scN No.

qvSWftfll scN Daresflt{t € /order tto.

r . . i_, \,..-.,,,1.,J-* /;_ \

. -i-..: '.; ,- r* tlr ./. 'A .1,":FE ..i JE":L?r 1;-e) .i..'r.:''cjal+.

,.,,.*.$.,:1,' ,'- i

3 q6 qfidSqrq6f,qd qd-dqm d eTq Ed .rTq

qtd$C - 3

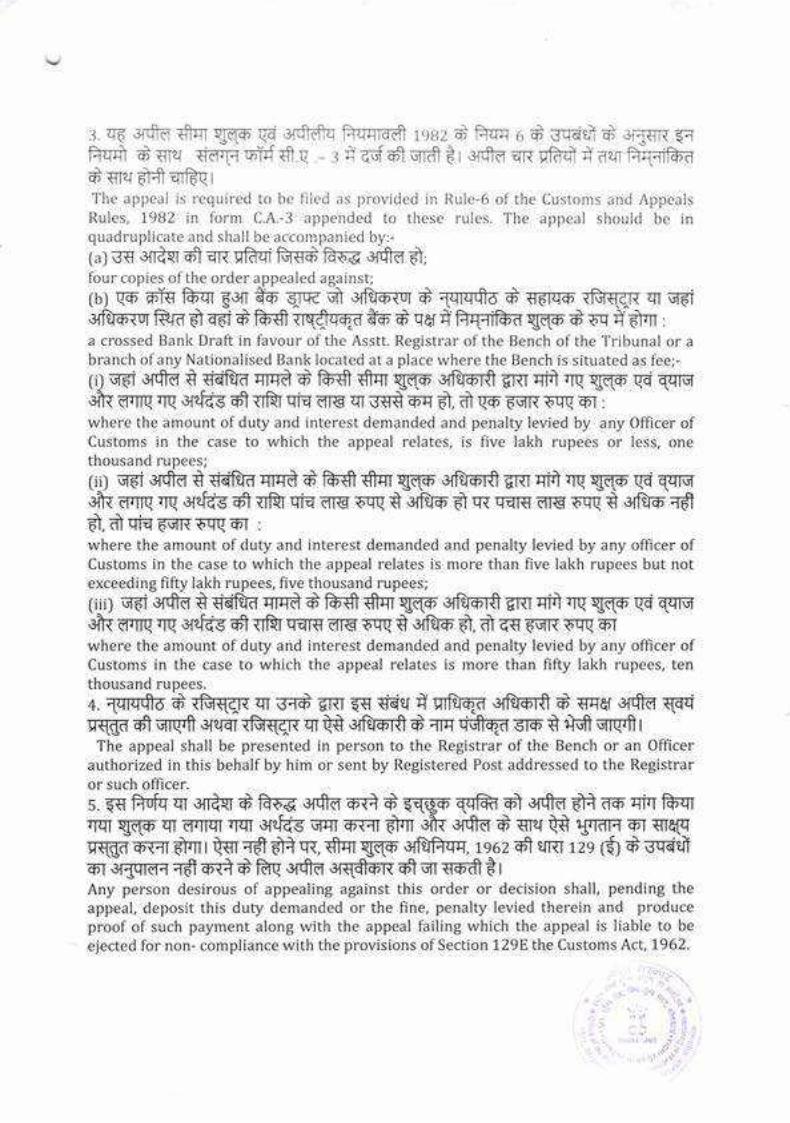

leBZ d Fw 6 ;; B!-qEl d 3l1sR gaorfr B r qfio qn qR.til fr au Fqnfudfredo1

deiq+fralGcrThe appeal is required to be liled as provided in Rule-6 of the Custonts and AppealsRules, 1982 in form C.A.-3 appended to these rules. The appeal should be inquadruplicate and shall be accompanred by:-(al ss BrasT o1 ER qfrqi ffi Et-g qfid E];four copies of the order appealed against;

O) \16 mis fust gGfi fu qt* q] qlqm-rlr A flsfrofr q6qo rBq^al qr qoirrlqo-iur Rrd d qEi S fum {q{qEa ilo d qqr C Nfr-d Eo-o d w i drn :

a crossed Bank Draft in favour of the Asstt. Registrar of the Bench of the Tribunal or a

branch ofany Nationalised Bank located at a place where the Bench is situated as fee;-(i) qdi crfi-d e .s.dfld qIq-d d Gffi Scr Ee-o +tfM ERT qit rr( {qo qE Wrqefu e.nq.rq i{dqs +t {rRr qia orc qr s€'-Q 6q d, A q-fi 6-qR sw 6-r :

where the amount of duty and interest demanded and penalty levied by any Officer ofCustoms in the case to which the appeal relates, is five lakh rupees or less, onethousand rupees;(ii) q6r qfr-d t rftifta qrrd d frffi frqT {-ffi qlq-+.r$ ERT cit rrq E-d-o. q?i {qMert{ drnq q vdes ol nRi qis drq FW € Gflsfi d trr qErnT 6pgr sw € orRr6 Tfrd Aqiq6qT{dw6r :

where the amount of duty and interest demanded and penalry levied by any officer ofCustoms in the case to which the appeal relates is more than five lakh rupees but notexceeding fifty lakh rupees, five thousand rupees;(iii) qdr Btfl-d t SdfYd qrrra A E S SrTr Eqo vf}s.rt em uit qq {q6 qd qqTqerh errs qs i{{6s o1 {rRr qqm f,rs sw e Brfu6 d, d eq EqR Tw o.rwhere the amount of duty and interest demanded and penalty levied by any officer ofCustoms in the case to which the appeal relates is more than fifty lakh rupees, tenthousand rupees.4 flqfi-d d {fu{^cR qr tsTS 6Rr qq €.iE fr qTf}-ed B+lffi d qcer qfid q+qq'rcd 01 qrqfr o{tror {Bqq{ qT qS €tfffi d rrq dtrEd sro € 0-fr qrsrfr

t

The appeal shall be presented in person to the Registrar of the Bench or an Officerauthorized in this behalf by him or sent by Registered Post addressed to the Registraror such officer.s. {fl.ftufq qr srecr d fr-s-e Grfi-d o-{i $ qqq6 WR o1 rltrd d+ ilfi qirT fuqrrErr wf, qT drTl.iII lql s{d(s qrrT 6-t;rr drn 3i{ q{-d a erq ts uftTH 6r sTetq

u-q{do-.rTdnt Qsrrfrd+qi, fiqr{-@ B{fuftqq :.s6zeir ERI12e dl dwdfior eEqrm-{ rd 6.-G S ftS oifi-d cf{fim.R' oi qr v+-fr t r

Any person desirous of appealing against this order or decision shall, pending theappeal, deposit this duty demanded or the fine, penalry levied therein and produceproof of such payment along with the appeal failing which the appeal is liable to beejected for non- compliance with the provisions of Section 129E the Customs Act,1962.

',.,.,/N-t'i;)EYr

3;'".+" ,"t.f ,

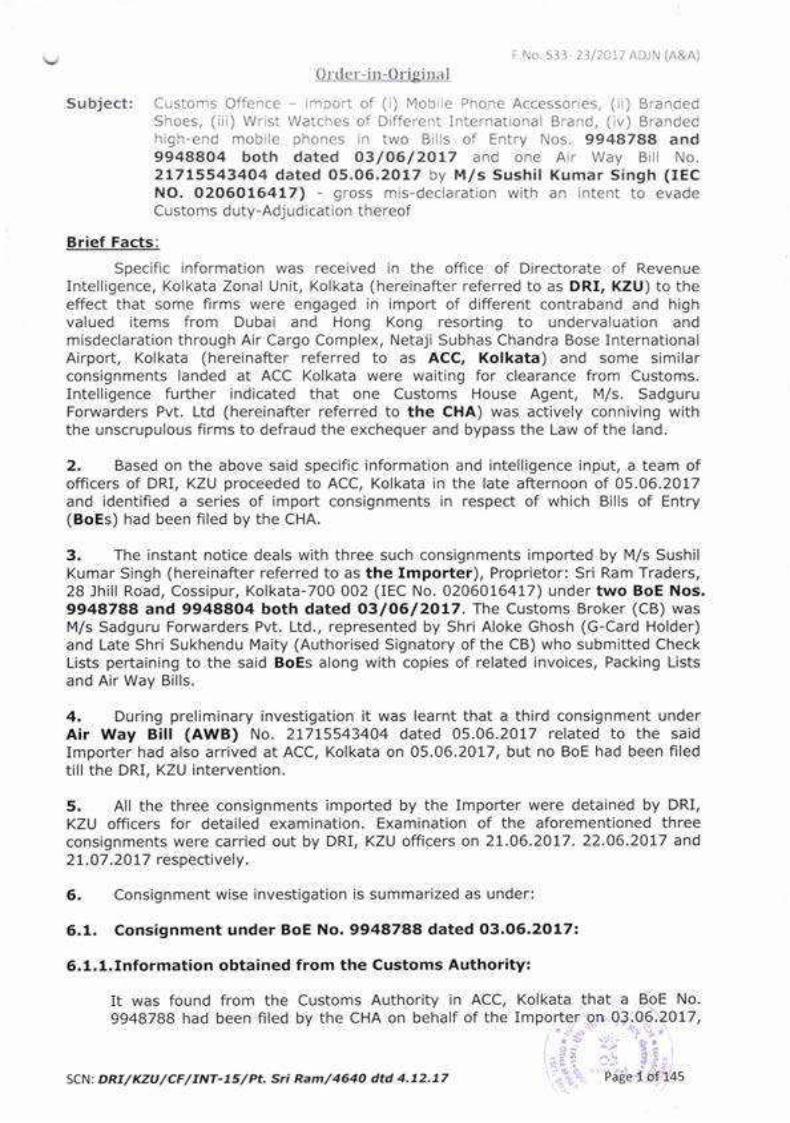

2. Based on the above said specific information and intelligence input, a team ofofficers of DRI, KZU proceeded to ACC, Kolkata in the late afternoon of 05.06.2017and identified a series of import consignments in respect of which Bills of Entry(BoEs) had been filed by the CHA.

3. The instant notice deals with three such consignments imported by M/s SushilKumar Singh (hereinafter referred to as the Importer), Proprietor: Sri Ram Traders,28 Jhill Road, Cossipur, Kolkata-700 002 (IEC No. 0206016417) under two BoE Nos.9948788 and 9948804 both dated O3|O6/2OL7. The Customs Broker (CB) wasM/s Sadguru Forwarders Pvt. Ltd., represented by Shri Aloke Ghosh (G-Card Holder)and Late Shri Sukhendu Maity (Authorised Signatory of the CB) who submitted CheckLists pertaining to the said BoEs along with copies of related invoices, Packing Listsand Air Way Bills.

4. During preliminary investigation it was learnt that a third consignment underAir Way Bill (AWB) No. 21715543404 dated 05.06.2017 related to the saidImporter had also arrived at ACC, Kolkata on 05.06.2017, but no BoE had been filedtill the DRI, KZU intervention.

5. All the three consignments imported by the Importer were detained by DRI,KZU officers for detailed examination. Examination of the aforementioned threeconsignments were carried out by DRI, KZU officers on 21.06.2017. 22.06.2077 and21.07.2017 respectively.

Consignment wise investigation is summarized as under:

1. Consignment under BoE No. 994878a dated 03,06.2017r

6.1.1.Information obtained from the Customs Authority:

It was found from the Customs Authority in ACC, Kolkata that a BoE No.9948788 had been filed by the CHA on behalf of the Importer on 03.06.2017,

6

6

gEI !"-

*"d=;"-.qSCN: DRI/ KzU /CF/INT-7,/ Pt. Sri Ram/464O dtd 4.72.77 Page 1 bf145

F.No.533 2 3/2Cl / ADrN (A&A)

Orcler-in-Origirr:rl

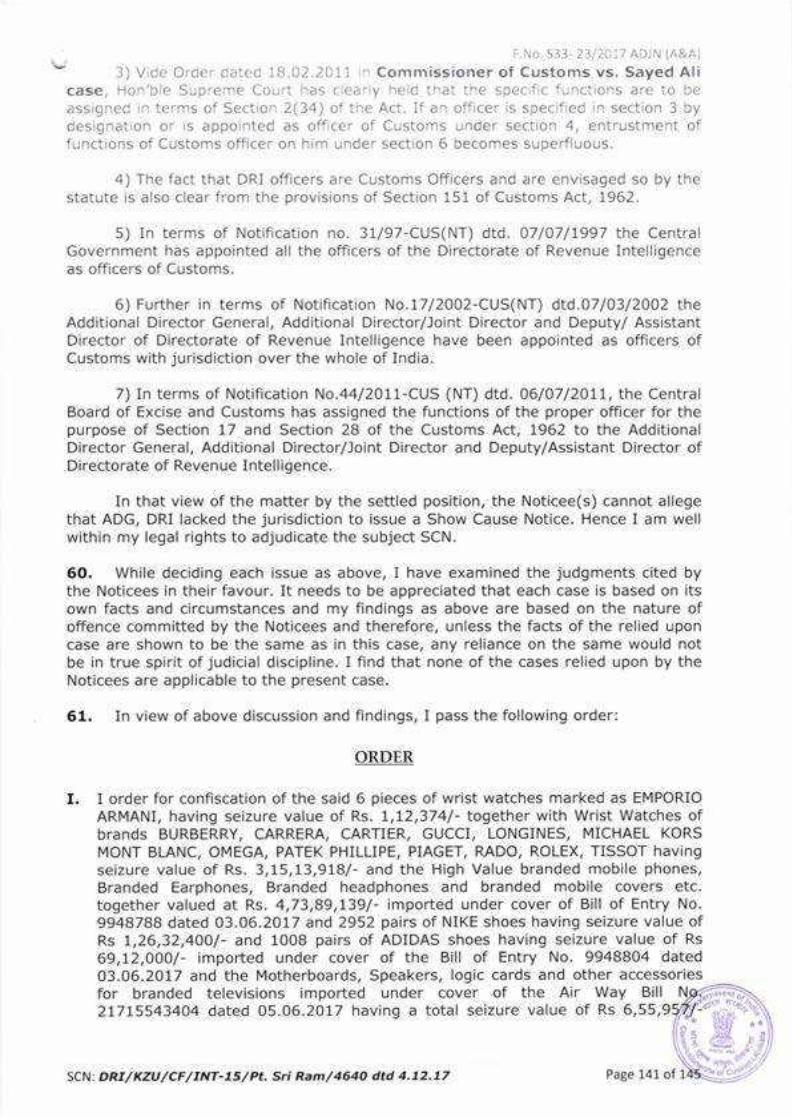

Subject: Customs Offence imDort of (i) Mobr e Phone Accessories, (ii) BrandedShoes, (iii) Wrlst Watches of Different lnternational Brand, (iv) Brandedhigh-end moblle phones in two Bills of Entry Nos. 9948788 and9948804 both dated 03l06/2017 and one Air Way Bill No.2L7155434O4 dated 05.06.2017 by M/s Sushil Kumar Singh (IECNO. 02060164t7) - gross mis-declaration with an intent to evadeCustoms duty-Adjudication thereof

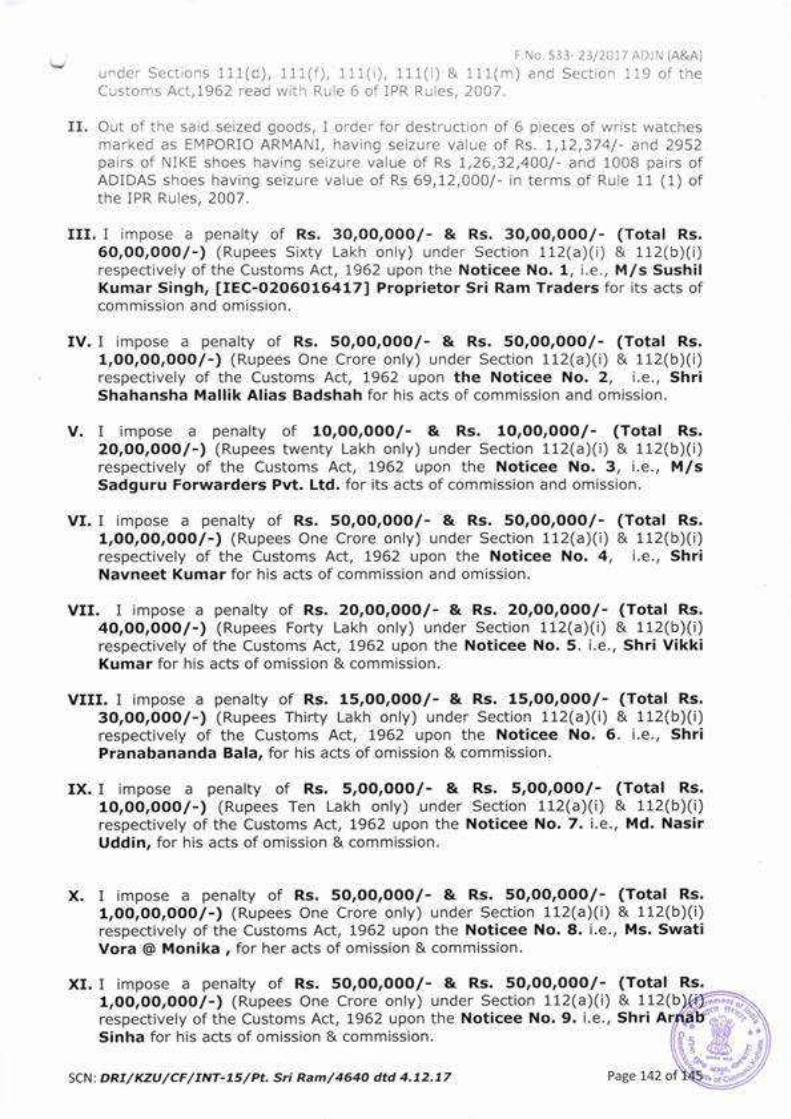

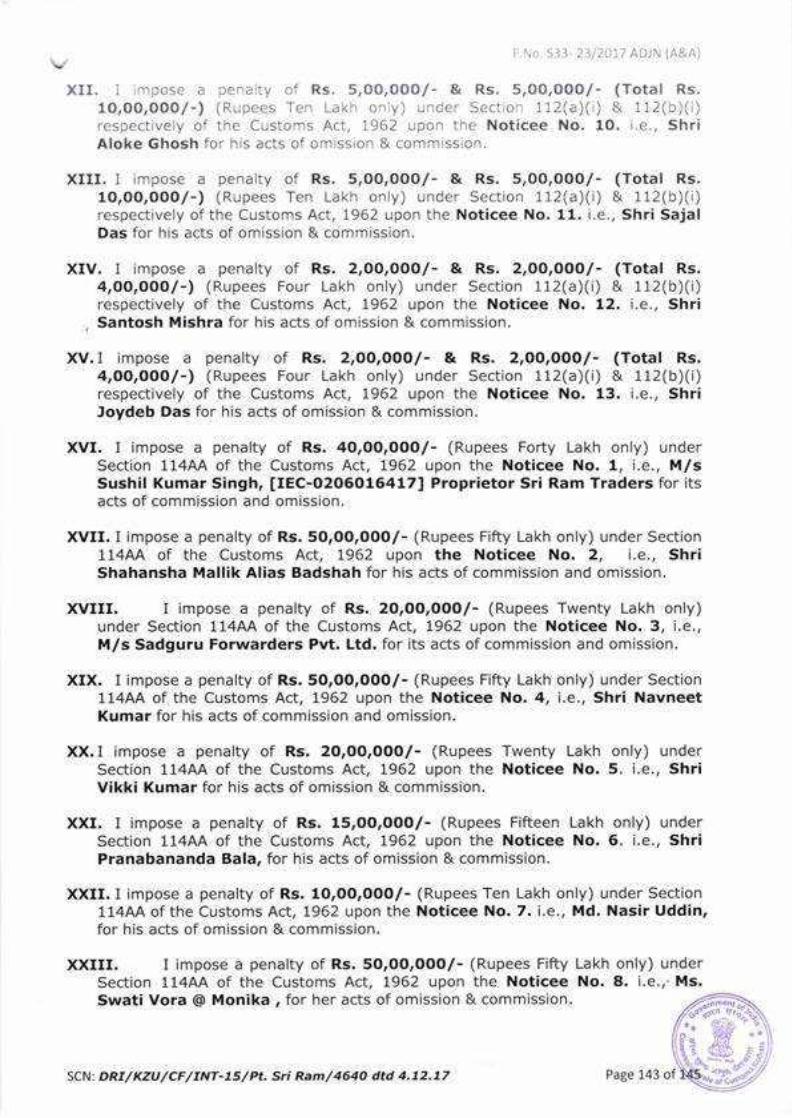

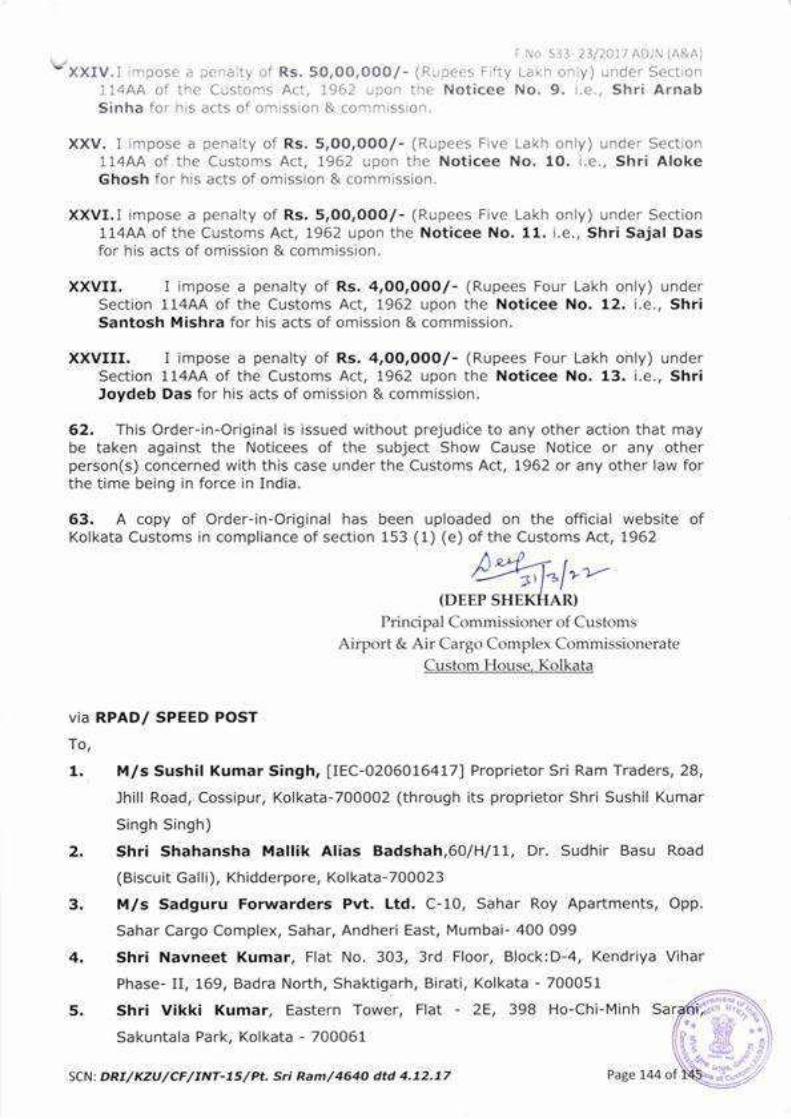

Brief Facts:

Specific information was received in the office of Directorate of RevenueIntelligence, Kolkata Zonal Unit, Kolkata (hereinafter referred to as DRI, KZU) to theeffect that some firms were engaged in import of different contraband and highvalued items from Dubai and Hong Kong resorting to undervaluation andmisdeclaration through Air Cargo Complex, Netaji Subhas Chandra Bose InternationalAlrport, Kolkata (hereinafter referred to as ACC, Kolkata) and some similarconsignments landed at ACC Kolkata were waiting for clearance from Customs.Intelligence further indicated that one Customs House Agent. M/s. SadguruForwarders Pvt. Ltd (hereinafter referred to the CHA) was actively conniving withthe unscrupulous firms to defraud the exchequer and bypass the Law of the land.

F-No- 533- 2312017 ADIN (A&A)

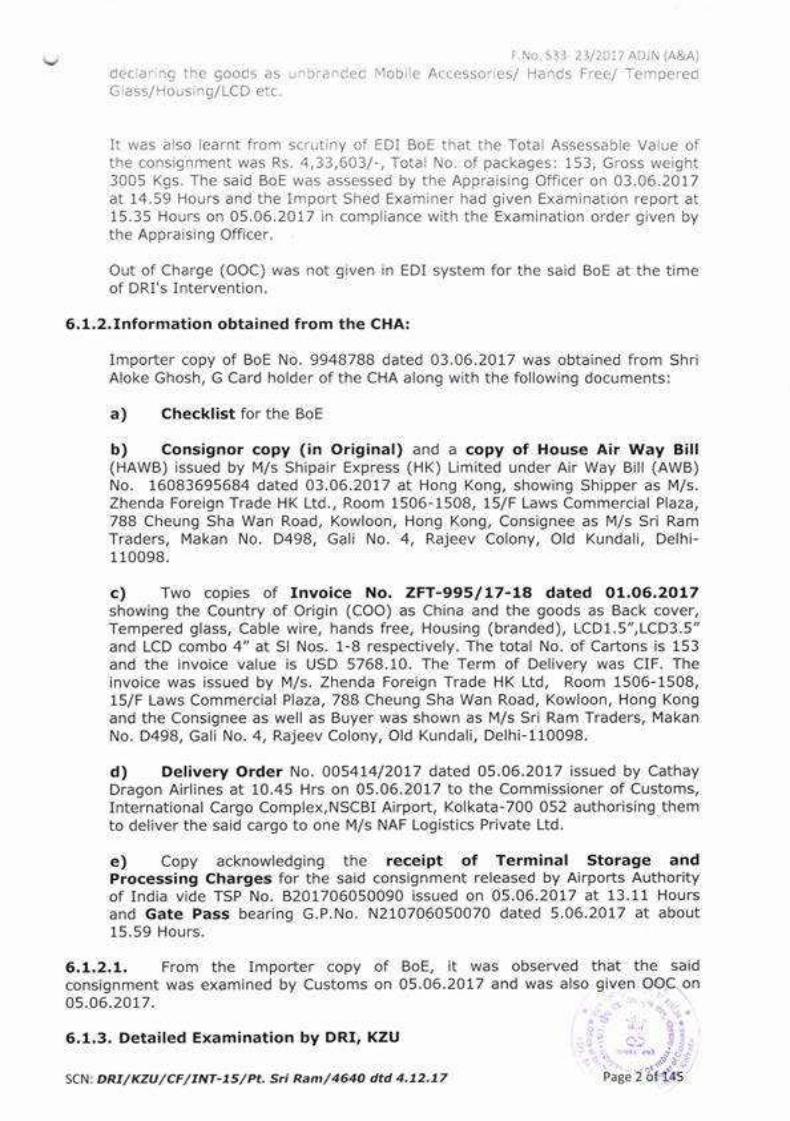

declaring the goods as unbranded Mobile Accessories/ Hands Free/ TemperedGlass/Housing/LCD etc.

It was also learnt from scrutiny of EDI BoE that the Total Assessable Value ofthe consignment was Rs. 4,33,603/-, Total No. of packages: 153. Gross weight3005 Kgs. The said BoE was assessed by the Appraising Officer on 03.06.2017at 14.59 Hours and the Import Shed Examiner had given Examination report at15.35 Hours on 05.06.2017 in compliance with the Examination order given bythe Appra ising Officer.

Importer copy of BoE No. 9948788 dated 03.06.2017 was obtained from ShriAloke Ghosh, G Card holder of the CHA along with the following documents:

a) Checklist for the BoE

c) Two copies of Invoice No. ZFT-995 I L7-La dated O1.06.2017showing the Country of Origin (COO) as China and the goods as Back cover,Tempered glass, Cable wire, hands free, Housing (branded), LCD1.5",LCD3.5"and LCD combo 4" at Sl Nos. 1-B respectively. The total No. of Cartons is 153and the invoice value is USD 5768.10. The Term of Delivery was CIF. Theinvoice was issued by M/s. Zhenda Foreign Trade HK Ltd, Room 1506-1508,15/F Laws Commercial Plaza, 788 Cheung Sha Wan Road, Kowloon, Hong Kongand the Consignee as well as Buyer was shown as M/s Sri Ram Traders. MakanNo. D498, Gali No. 4, Rajeev Colony, Old Kundali, Delhi-110098.

d) Delivery Order No. 0O5474/2Ot7 dated 05.06.2017 issued by CathayDragon Airlines at 10.45 Hrs on 05.06.2017 to the Commissioner of Customs,International Cargo Complex,NSCBI Airpoft, Kolkata-700 052 authorising themto deliver the said cargo to one M/s NAF Logistics Private Ltd.

e) Copy acknowledging the receipt of Terminal Storage andProcessing Charges for the said consignment released by Airports Authorityof India vide TSP No. 8201706050090 issued on 05.06.2017 at 13.11 Hoursand Gate Pass bearing G.P.No. N210706050070 dated 5.06.2077 at about15.59 Hours.

05.06.2017

6.1.3. Detailed Examination by DRI, KZU

ti.)"P!rr3E

rt%i1lPage 2 oSCN: DRI/ KzU /CF/INT-75/ Pt. Sri Ram/4640 dtd 4.72.77

Out of Charge (OOC) was not given in EDI system for the said BoE at the timeof DRI's Intervention.

6.1.2.Information obtained from the CHA:

b) Consignor copy (in Original) and a copy of House Air Way Bill(HAWB) issued by M/s Shipair Express (HK) Limited under Air Way Bill (AWB)No. 16083695684 dated 03.06.2017 at Hong Kong, showing Shipper as M/s.Zhenda Foreign Trade HK Ltd., Room 1506-1508, 15/F Laws Commercial Plaza,788 Cheung Sha Wan Road, Kowloon, Hong Kong, Consignee as M/s Sri RamTraders, Makan No. D498, Gali No.4, Rajeev Colony, Old Kundali, Delhi-110098.

6.L.2.L, From the Impofter copy of BoE, it was observed that the saldconsignment was examined by Customs on 05.06.2017 and was also given OOC on

F. No. 533'23/2017 ADIN (A&A)

6.1,3.1, 100o/o examination of the consignment by DRI, KZU was recorded videPanchanama proceedings dated 21.06.2017 and brlef inventory of the goods found inthe consignment is as below:

Sl. No. Good sDescript

Brandton

Qtv Seizure Value (inRs.

1 Wrist Watch Ca rtie r 1 1199554940

CarreraBurberryWrist Watch

Wrist Watch1

1

2

3

4 Wrist watch Emporio Armani 6 t123745 1 590706

Wrist WatchWrist Watch

GucciMichael Kors 363 t799295

7 Wrist watch Longines 3 4020001B Wrist Watch 6999

Wrist Watch Mont Bla nc a utomatic 1 27t7349

wrist Watch Omega11. Wrist Watch Patek Phlllppe 2 30000012. Wrist Watch Piaget 5 1309285

8 52000013. Wrist Watch RadoRolex14. Wrist Watch

wrist watch Tissot 3 5848015iPh one Apple BO 4139920

20 11980Battery Charger Sa msu ngSa msu ng,Lenovo,

HTC, MI3290 8905 5018 Data Ca ble

Lenovo, Oppo, Vivo,Samsung, Apple,Sony, HTC

46tO 342074019. Ear Phone

920 254284020. StereoHead FM

PhoneSony, lBL, Samsung

HTC, OPPO 820 1935402t. Charger AdapterHfC/ Samsung/ Ml/LG/ Nokia with/without battery

1862528822 lYobile Phone

552r6Apple B423. iPad flip cover2333 3631000I\40bile Phone LCD24.120 41880LeTV cha rg er LETV25.9t423 1235805026 Mobile Phone Back

15000060027. oTG cutting Ferule28. Power Bank

125000USB Charger29119970030 Other M isc Goods

Total

l

6.1,3.2. From the Panchanama proceedings as above, Import Documentsobtained from the CHA and information retrieved from Customs EDI system, it wasseen that the said BoE was found assessed, examined as per examination instructionto examine 57o packages and given "OOC" by Customs on 05.06'2017 beforeintervention by DRI, KZU. During the 100o/o examination by DRI, KZU it wasrecorded in the Panchanama proceeding that only two packages were found to havebeen opened earlier.

' t-'

,', .:. :SCN: DRI/ KzU /CF/INT-L,/ Pt. Sri Ram/464O dtd 4.72.77 Page 3 o[{{5

317550

I\4 ont Bla nc

78 2034230010.

27 6120870

16.T7,

11089

5 3995500

790t5431

F.No. S33 2312017 AD]N (A&A)

6.1.3.3. During the 100o/o examination by DRI, KZU, it was found that a numberof items like branded watches, branded mobile phones, branded head phones werenot declared in the said BoE. Against the declared value of Rs. 4,29,310.29, theascertained value of the goods actually found in the said consignment was found tobe Rs. 7.90 Crores as detailed in the Panchanama proceedings, making theattempted undervaluation in the said consignment to the tune of 1/200th of theascertained va lue.

6,1.3.4. After examination, as the goods in the consignment of 153 packageswere found to have been mis-declared, the consignment under the BoE No. 994B7BBdated 03.06.2017 had been seized u/s 110 of the Customs Act, 1962 by DRI, KZU onthe reasons to believe that the same were liable to confiscation u/s 111 of theCustoms Act, 1962 and copy of Seizure list and Inventory of the seized goods werehanded over to Shri Aloke Ghosh, G Card holder of the CHA.

6.2, Consignment under BoE No. 99488O4 dated 03.06.2017:

5,2.1.Information obtained from the Customs Authorityr

It was found from the Customs Authority in ACC, Kolkata that a BoE No.9948804 had been filed by the CHA on behalf of the Importer on 03.06.2017,declaring the goods as shoes without the mention of any brand.

It was also learnt from scrutiny of EDI BoE that the Total Assessable Value ofthe consignment was Rs. 5,53,O43/-, Total No. of packages: 110, Gross weight1861 Kgs. The said BoE was assessed by the Appraising Officer on 03.06.2017at 15.01 Hours and Examination order for 5Yo of the consignment was given.However, no entry regarding examination for the said BoE was observed.

Out of Charge (OOC) was not given in EDI system for the said BoE at the tlmeof DRI's Intervention.

Importer copy of BoE No. 9948804 dated 03.06.2017 was obtained from ShriAloke Ghosh, G Card holder of the CHA along with the following documents:

a) Checklist for the BoE

b) Consignor copy (in Original), Cargo manifest filed by M/s Shipairexpress (HK) Ltd under Master AWB No. 17654035881 & a copy of HAWB No.SE 96537 for 110 packages consigned to M/s. NAF Logistics showing thedescription of the goods as Shoes and showing the Shipper's name as M/s'Zhenda Foreign Trade HK Ltd., Room 1506-1508, 15/F Laws Commercial Plaza,788 Cheung Sha Wan Road, Kowloon, Hong Kong, Consignee as M/s Sri RamTraders, Makan No. D498, Gali No.4, Rajeev Colony, Old Kundali, Delhi-110098.

c) Two copies of Invoice No, ZFT-998 /17-La dated 3O.O5.2O17showing the Country of Origin (COO) as China and the goods as Shoes(footwear). The total No. of Cartons is 110 and the invoice value is USD 5586.The Term of Delivery was CIF. The invoice was issued by M/s. Zhenda ForeignTrade HK Ltd, Room 1506-1508, 15/F Laws Commercial Plaza, 788 CheungSha Wan Road, Kowloon, Hong Kong and the Conslgnee as well as Buyer wa5

SCN: DRI/ KzU /oF/INT-7|/ Pt. sri Ram/464O dtd 4.72.77 Page 4 of145

tt,"::$

5.2.2.Information obtained from the CHA:

F.No. 533 2312017 ADJN (A&A)

D498, Gali No. 4, Rajeev Colony,shown as M/s Sri Ram Traders, Makan NoOld Ku ndali, Derhi- 1 10098,

6.2.3. Detailed Examination by DRI, KZU

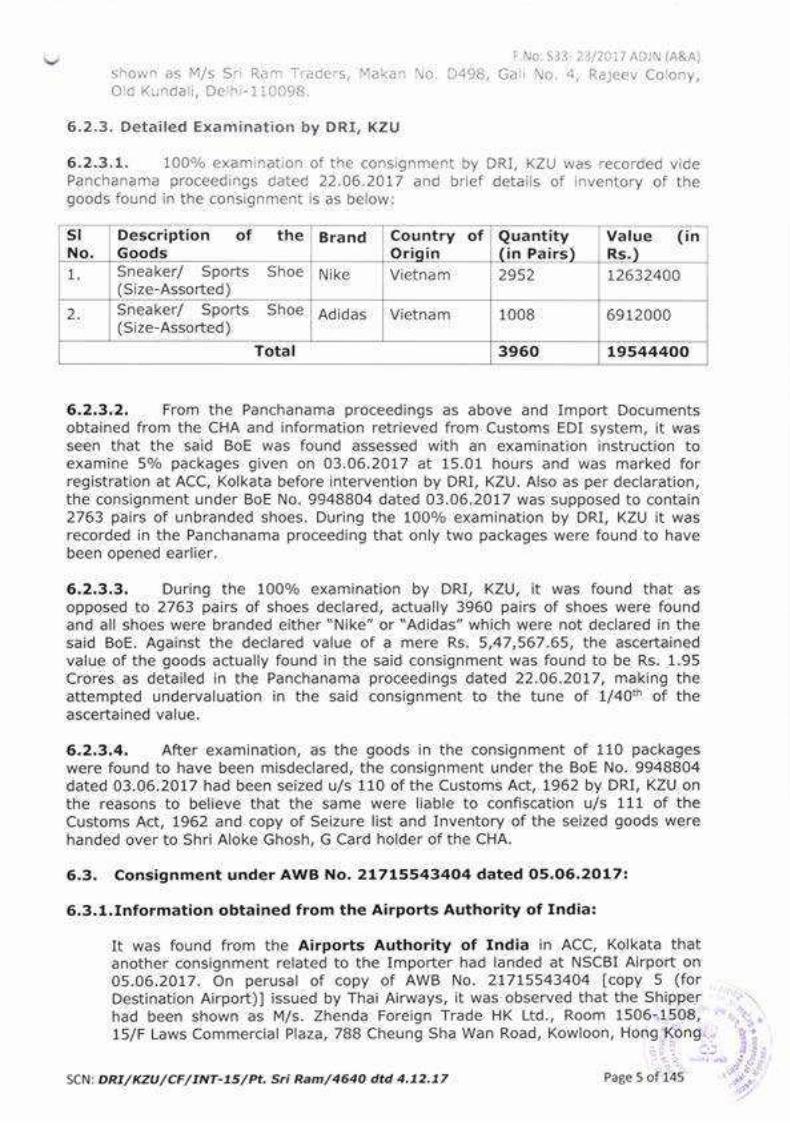

6.2.3.1. 100o/o examination of the consignment by DRI, KZU was recorded videPanchanama proceedings dated 22.06.2017 and brief details of inventory of thegoods found in the consignment is as below:

Description ofGood s

the Brand Country of Value (inOri tn Rs,

2952 72632400Sneaker/ Sports(Size-Assorted)

Shoe I Nlkg

Sneaker/ Sports Shoe(Size-Assorted)

6.2.3,2. From the Panchanama proceedings as above and Import Documentsobtained from the CHA and information retrieved from Customs EDI system, it wasseen that the said BoE was found assessed with an examination instruction toexamine 5olo packages given on 03.06.201,7 at 15.01 hours and was marked forregistration at ACC, Kolkata before intervention by DRI, KZU. Also as per declaration,the consignment under BoE No. 9948804 dated 03.06.2017 was supposed to contain2763 pairs of unbranded shoes. During the 100% examination by DRI, KZU it wasrecorded in the Panchanama proceeding that only two packages were found to havebeen opened earlier.

6,2.3.3. During the 1007o examination by DRI, KZU, it was found that asopposed to 2763 pairs of shoes declared, actually 3960 pairs of shoes were foundand all shoes were branded either "Nike" or "Adidas" which were not declared In thesaid BoE. Against the declared value of a mere Rs. 5,47 ,567 .65. the ascertainedvalue of the goods actually found in the said consignment was found to be Rs. 1.95Crores as detailed in the Panchanama proceedings dated 22.06.20t7, making theattempted undervaluation in the said consignment to the tune of 1/40th of theascertained value.

It was found from the Airports Authority of India in ACC, Kolkata thatanother consignment related to the Importer had landed at NSCBI Airport on05.06.2017. On perusal of copy of AWB No. 21715543404 lcopy 5 (forDestination Airport)l issued by Thai Airways, it was observed that the Shipperhad been shown as M/s. Zhenda Foreign Trade HK Ltd., Room 1506-1508,15/F Laws Commercial Plaza, 788 Cheung Sha Wan Road, Kowloon, Hong Kong

1 Vietna m

2 Vietnam 1008

Total 3960 L95444()()

SCN: DRI/ KzU /CF/INT-75/PI. Sri Ram/464O dtd 4.72.77 Page 5 of 145

6,2.3.4. After examination, as the goods in the consignment of 110 packageswere found to have been misdeclared, the consignment under the BoE No. 9948804dated 03.06.2017 had been seized u/s 110 of the Customs Act, 1962 by DRI, KZU onthe reasons to belleve that the same were liable to confiscation u/s 111 of theCustoms Act, 1962 and copy of Seizure list and Inventory of the seized goods werehanded over to Shri Aloke Ghosh, G Card holder of the CHA.

6.3. Consignment under AWB No. 21715543404 dated O5,O6.2O17:

6.3.1.Information obtained from the Airports Authority of India:

'$t',

J9!

*ul*sv

slNo.

Q ua ntity(in Pairs)

Adidas 6912000

F.No. S33 2312017 ADJN (A&A)

and the Consignee as well as Buyer had been shown as M/s Sri Ram Traders,lv'lakan No. D498, cali No.4, Rajeev Colony, Old Kundali, Delhi-110098.

It was also learnt from scrutiny of AWB that the concerned AWB was issued atBangkok, Thailand on freight prepaid basis and showed the description of thegoods as Electronic Parts in 9 packages.

6.3.2. Information obtained from the Customs Authoritiesl

No BoE had been flled for the subject consignment prior to the intervention of DRI,KZU on 05.06.2017.

6,3.3. Detailed Examination by DRI, KZU

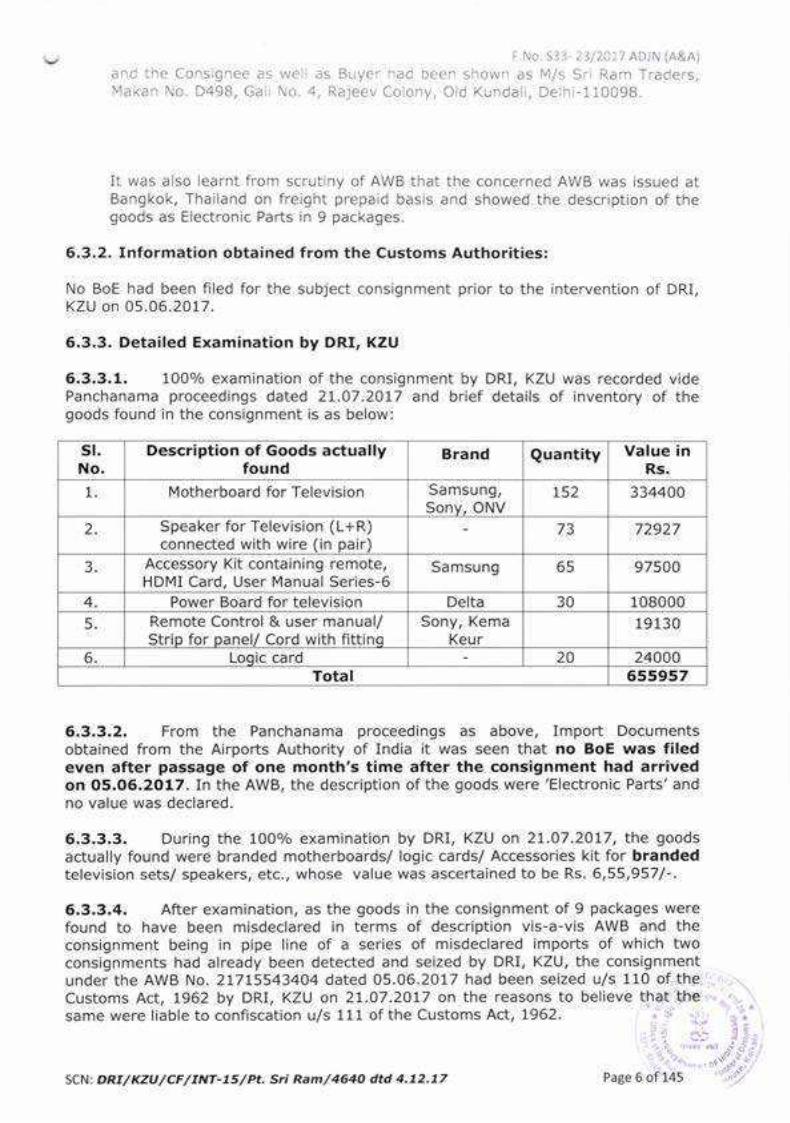

6.3,3.1, 100%o examination of the consignment by DRI, KZU was recorded videPanchanama proceedings dated 21.07.2017 and brief details of inventory of thegoods found in the consignment is as below:

6.3.3.2. From the Panchanama proceedings as above, Import Documentsobtained from the Airports Authority of India it was seen that no BoE was filedeven after passage of one month's time after the consignment had arrivedon O5.O6.2O17. In the AWB, the description of the goods were 'Electronic Parts'andno va lue was declared.

6,3.3.3. During the 1009o examination by DRI, KZU on 21.07.2017, the goodsactually found were branded motherboards/ logic cards/ Accessories kit for brandedtelevision sets/ speakers, etc., whose value was ascertained to be Rs. 6,55,957/-.

6,3.3.4. After examination, as the goods in the conslgnment of 9 packages werefound to have been misdeclared in terms oF description vis-a-vis AWB and theconsignment being in pipe line of a series of mlsdeclared imports of which twoconsignments had already been detected and seized by DRI, KZU, the conslgnmentunder the AWB No. 27715543404 dated 05.06.2017 had been seized u/s 110 of theCustoms Act, 1962 by DRI, KZU on 21.07 .2017 on the reasons to believe that thesame were liable to confiscation u/s 111 of the Customs Act, 1962.

sl.No.

Description of Goods actuallyfou nd

Bra nd Quantity Value inRs.

1 Motherboard for Television Sa msu ng,Sony, ONV

752 334400

2 Spea ker for Television (L+R)connected with wire (in pair)

72927

Accessory Kit containing remote,HDMI Card, User Manual Series-6

Sa msu ng

4 Power Board for television Delta 30 108000Remote Control & user manual/Strip for panel/ Cord with fittinq

Sony, KemaKeu r

6 Logic card 20 24000Tota I 655957

SCN: DRI/ KzU /cF/INT-7s/ Pt. Sri Ram/464O dtd 4.72.77 Page 6 of 145

\ "-o .'

-+ .?'.',s'.+i')*:'/

3 65 97500

5 19130

7, AKolkata

F.No- 533- 23l2017 ADJN (A&A)the seized goods were kept with the Airports Authority of India, ACC,

8.1. The IEC details of the Importer had been issued in 2006 in the name of oneShri Sushil Kumar Singh residing at 28, Jhill Road, Kolkata-700 002. There are threebranches of the IEC holder, having addresses as:i. Sri Ram Traders, 1/26, Ghosh Bagan Lane. Kolkata-700 002ii. Sri Ram Traders, Makan No. D498, Gali No.4, Rajeev Colony, Old Kundali, Delhi-

1 10098iii. Sri Ram Traders, 9 Old China Bazar Street, 3'd Floor Room No. 43, Kolkata-700 001.

8.2. Two phone numbers associated with the IEC were 03365122090 and9883653618.

8.3, The details083150050802120Kolkata-700 001.

of the bank account were mentioned as Current A/c No.held with Tamilnad Mercantile Bank Ltd. at 5BD, N.S.Road,

8.5. From the Customs EDI system it was observed that the IEC was extensivelyused during the period January,2015 to June,2017 through various ports and airportsof India. The IEC holder had expressed complete ignorance about the imports and hestated on record that he had lent out his IEC to one Customs Broker.

9. Search and Seizure

9.1. When a team of officers visited declared premises of Sushil Kumar Singh on27.06.2017, it observed that the premises is actually an address of a single roomapartment in a dilapidated condition. Only the wife of Shri Sushil Kumar Singh alongwith their sons were present. A summons was issued to Shri Sushil Kumar Singh toappear before the DRI officer on 28.06.2017.

9.2. From the supplier details for such misdeclared imports of cargo, it was foundthat in the case of Sri Ram Traders, all the three consignments were supplled by oneM/s Zhenda Foreign Trade HK Limited. Investigations conducted as well asIntelligence indicated that the Directors of the said company were Shri Arnab Sinhaand Smt Mohua Sinha, both of who were also listed as directors of M/s NAF LogisticsPrivate Limited who worked as freight forwarders for these consignments. Theresidential and Office premises of Shri Arnab Sinha and Smt Mohua Sinha weresearched on 23.10.2017. Although nothing incriminating was recovered from theresidence, some documents, two mobile phones of Shri Arnab Sinha and a Disk Drivewhich were reasonably believed to be useful in the investigation were recovered fromthe Office of M/s. NAF Logistics Pvt. Ltd. and subsequently seized.

9.3. The residence of Shri Navneet Kumar, Deputy Commissioner was searched on10.06.2077 and some incriminating documents and articles were recovered 'which

SCN: DRI/ KzU/cF/INT-7s/ Pt. Sri Ram/4640 dtd 4.72.77 Page 7 of 145

8. Import Export Code (IEC) Details

8.4. Shri Aloke Ghosh (G-Card holder of the CHA) submitted the Know YourCustomer (KYC) documents on 07.09.2017 comprising IEC printout from DirectorateGeneral of Foreign Trade (DGFT) website, photocopies of Voter Card No.WB/2U740/072382 and PAN Card No. BALPS4932D of said Sushil Kumar Singh.

F.No. 533 23l2017 AD.IN (A&A)lnclude four pages print-outs marked as "Wish Sales 59 Ctn" and "Whish Sales 117Ctn", in which package nos. with mark, items and weight were mentioned andagainst some packages "TO OPEN FOR INNSPECTION" is mentioned. These fourpages printouts appear to indicate details of two import consignment of M/s. WishSales Corporation of Delhi and which contained references of certainpa ckets/pa ckages which were not to be opened during examination by Customs atACC Kolkata. Md. Nasir Uddin identified these documents and also stated in hisstatement dated 09.06.2017 that these inspection instruction of M/s. Wish SalesCorporation of Delhi was sent to his e-mail by Monika Vora (Noticee No.O8) andafter he took out the print copies, he handed it over to Navneet Kumar.

10. Voluntary Statements u/s 1O8 of the Customs Act, 1962

1O,1. Importer, Supplier and the Middlemen

10.1.1. Shri Sushil Kumar Singh, Proprietor of M/s Sri Ram Traders, in hisvoluntary statements on 28.06.2017, 25.O7.20t7 and 11.09.2017 stated, inter-alia,that-

10.1.1.2. He never had nor presently has any officeat 28, Jhill Road, Cossipur, Kolkata-700002. Allmentioned in his IEC were false.

He had only one address i.e.the other addresses as

10.1.1,4. Badshah imported mobile parts and accessories under his IEC.Badshah met him (Sushil) and asked for his IEC. Initially, when he (Sushil) refused,Badshah told him that he (Badshah) was having setting with DC, Navneet Kumar atAirport Customs and Badshah took him to DC Shri Navneet Kumar sometime in l4ay2077. He met the DC at his olfice at Kolkata Airport and the DC asked him to give hisIEC to Badshah and also assured him that there would be no problem. Then he gavehis IEC to Badshah. Badshah proposed him a sum of Rs. 15OOO/- for eachconsig nment.

10.1.1.5. The consignment under the Bill of Entry 9948788 dated 03.06.2017 wasimported using his IEC and these goods were actually imported by Badshah andin the case of consignments imported under BoE No. 9948804 dated 03.06.2017,the goods were actually brought by Navneet Kumar,DC. If there is any dutyliabllity on these consignments, the duty is to be paid by the actual importers.

10.1.1.7. He did not know what were the goods brought under Airway Bill No.21715543404 in the name of his firm Sri Ram Traders.

SCN: DRI/ KZU /CF/INT-7'/ Pt. Sri Ram/464O dtd 4.72.77

10,1.1.1. He obtained the IEC - 0206076417 to lend the same to differentimporters and to earn money out of that lending.

10.1,1.3. Earlier on, he lent his IEC and KYC to one Bidhan who used to work inthe capacity of Customs Broker at Kolkata Airport and he (Sushil) used to get Rs.1OOO0 per consignment. Later in May 2077, he had given his IEC to oneShahansha Mallik alias Badshah who is having a shop in Fancy Market,Khidderpore, Kolkata. He also lent out his IEC to Arnab Sinha having office atN.S.Road in the name of Modern Freight and electronic goods like motherboard,TV, LED panels were brought by Arnab Sinha under his IEC.

10.1,1.6. He lent his IEC to Badshah and Navneet Kumar for easy money.

=;?,"",

Page 8 of 145

F.No. S33 2312017 ADJN (A&A)10.1,1.8, Being shown the Panchanama and inventory of the goods brought underthe Bill of Entry No. 9948788 and 9948804 and also under the airway bill no.277L55434O4, he stated that Badshah told him that he would be bringing mobileparts and other accessories under these consignments.

10,1.1.9. From 2006, he used to lend his IEC to different importers and under hisiEC, various importers imported various goods through Delhi, Chennai and KoikataPort and Airport. He did not know who the importers were and what the goods werebrought under his IEC. He gave his IEC to Bidhan of Indo Foreign Agency who usedto reside in Belur. The consignments imported under his IEC were handled by M/sK,R.Express in Delhi, M/s Dabke Clearing & Forwarding Pvt Ltd in Mumbaiand M/s Guru Shipping and Clearing Services in Chennai as told to him byBidhan. He did not know what were the goods actually imported in thoseconsignments and who paid the duty.

10.1.1.10. Sri Ram Traders has only one bank account at Tamil Nad MercantileBank Limited, Kolkata which has been closed in lanuary/ February 2017

10.1.1.11. His bank accounts are maintained by one Shri Rajendra Jain and oneShri Vedpra kash Agarwal.

10.1.1.13. Arrest u/s 1O4 of the Customs Act, t962: In view of activeabatement in huge evasion of Customs Duty, Shri Sushil Kumar Slngh was arrestedon 25.07.2017.

10.1.2. Shri Shahansha Mallik alias Badshah was summoned and in hisvoluntary statements recorded on 28.O6.2Ot7, 29.O6.2OL7 and 18.09.2017 stated,inter alia, that-

10.1.2.1, During his course of business in Fancy Market, Khidderpore in about2015, he used to bring Chinese mobile handsets, mobile accessories from localcouriers, which were, at times, intercepted by the CC(P) officers. In that connectionhe used to visit CC(P) office and there he met Navneet Kumar, DC.

10.1.2.3. In January 2017 , he met one Arnab Sinha of NAF logistics, who used towork as a forwarder and asked him for an IEC lender. He met Sushil Singh throughArnab Sinha and asked Sushil to lend his IEC on commission basis and the ratenegotiated was Rs, 1OOOO/- per consignment.

LO,L.2,4. Later, as the rate of Bappa was very high, he contacted Sajal Das ofIndo-Foreign Agency, who introduced him with Nasir Uddin who would be doing hisjob at a cheaper rate and he imported one consignment of Mobile back cover andscreen guards, where Nasir Uddin worked as CHA on behalf of Sadguru and NAF

logistics worked as a freight forwarder for the goods.

1O.1.2.5. Later during March 2017, when he was about to staft importing goods,he came to know that Navneet Kumar was the DC at Airport Cargo and then he '.

SCN: DRI/ KzU/ CF/INT-I,/ Pt. Sri Ram/464O dtd 4.72.77 Page 9 of 145

10.1.1.12. He did not know how many imports were done under his IEC sinceJanuary 2077 and how the payments were made for the imports. He had given hisIEC to Badshah and Nasir Uddin and they could explain the same.

LO.L.2.2. In December 2016, he brought three consignments of mobile covers,Screen Guards etc. through one Bappa, CHA, working at Kolkata Airport but he didnot know which company's IEC was used for those consignments.

:\1'Ddr&*3;#

N ."' r-".v'

1O,1.2.6. Navneet Kumar told them that there would be no problem if they wantto import goods through Air cargo. Then he enquired about the CHA, and afterlearning that Nasir was working as CHA, he directed to bring goods like mobilephones, watches, cigarettes by concealment and he also directed that an amount ofRs. 50000 per consignment would be paid to him.

10.1.2,8, He knew one Karan of Mumbai who deals in high end watches andmobiles and asked him whether he could load watches and mobiles in hisconsignment from Hong Kong and for that Karan would be required to pay him Rs100 per watch and Rs 200/- per mobile set. Karan agreed to load about 450 piecesof watches in one carton and 620 mobile phones in two caftons. He gave the addressof godown of NAF logistics at Hong Kong as was known to him from Arnab Sinha.

1O.1.2.9. One of his friend Nasir stays in Bungee Street, Shenzing (Shenzhen),China. He contacted the suppliers and paid them in advance on behalf of Badshah. Inturn Badshah payed the money in cash to Nasir's mother in Kolkata,

1O.1.2.1O, The imports were misdeclared so as to make some profit after makingpayments to the Customs Officers and the DC. If the goods were not misdeclaredand the full duty were to be paid on the goods, there would be no profit atall. That was why the consignments were arranged to be cleared withoutexamination as far as possible and was misdeclared not to reveal the contentslike watches and high-mobile phones.

10.1.2.11. He paid Rs l lakh in cash to DC Shri Navneet Kumar. NavneetKumar used to give him a phone number, some one used to contact him and collectthe money near Airport No. 1 gate.

LO.1.2.L2. Arrest u/s 1O4 of the Customs Act, 1962: In view of activeabatement in huge evasion of Customs Duty, Shri Shahansha Mallik alias Badsha wasarrested on 25.07.2017.

1O.1.3. Shri Arnab Sinha, Director of M/s Zhenda Foreign Trade HK Limited andM/s NAF Logistics Private Limited in his voluntary statements dated 23.10.2017 and24.70.2077, stated, inter-alia, that-

10.1.3,1. He alongwith his mother Mohua Sinha are Directors In Modern FreightConsolidator(P) Ltd and NAF Logistics Pvt Ltd.

10.1.3.2. M/s TH Mason Logistics in Hong Kong is a counterpart of M/s ModernFreight Consolidators as they both are involved in Freight forwarding business. He

took up a job in Hong Kong with TH Mason as Sales & Marketing Manager in the year2010.

F. No. S33- 2312017 AD.JN (A&A)

called him (Navneet) in his mobile no 98300150950 and met him ln his office alongwith Sushil Kumar Singh.

1O.L.2,7. In May 2017, he imported another two consignments where Nasir Uddinworked as CHA on behalf of Sadguru and NAF logistics worked as a freight forwarderfor the goods.

10.1.3.3. The controlling person of TH Mason was one Mr. Joseph Lee and at hisinsistance, Arnab Sinha al6ngwith his mother acquired the shares of a company inHong Kong named as M/s Zhenda Foreign Trade HK Limited as one of the DirectorandhismotherMohuaSinhaaSco-Director.Bothofthempurchasedthesharesof.

SCN: DRI/ KZU/ CF/INT-7L/ Pt, Sri Ram/464O dtd 4.72.77 Page 10 of 145

F.No. S33- 2312017 ADIN (A&A)

the new company on fifty-fifty basis from Mr. loseph Lee. A total of HKD 8000 wasspent on the formation of the said company which Arnab Sinha paid from hisearnings at Hong Kong.

1O.1.3.4. M/s Zhenda Foreign Trade HK Limited was acquired with an idea to getbetter business exposure for they would be supplying the goods to India. In all thecases NAF Logistics can act as freight forwarders.

1O.1.3.5. lY/s Zhenda Foreign Trade rented a godown in Hong Kong. The shippersfrom China were asked to deposit the goods at the said godown prior to shipment. TH lvlason would be issuing the Bill of Lading with M/s NAF Logistics as the consigneein India, and then, in turn, NAF Logistics would be issuing the delivery order to theactual importer or his clearing Agent.

1O.1,3.6. Presently, in place of M/ s TH lv'lason, another company managed by Mr.Lee, M/s Shipair Express is working as freight forwarder in Hong Kong. NAF Logisticsused to remit money to TH Mason earlier and presently the money is remitted toShipair Express to pay off the business dues.

LO.L.3.7. Since inception, NAF Logistics handled 17 shipments in 2011,68shipments in 2012, 11 shipments in 2013, 1 shipment in 2074, 18 shipments in 2015,41 in 2016 and 40 in 2017 expofted by M/s Zhenda Foreign Trade HK Limited.

10.1,3.8. M/s Zhenda Foreign Trade HK Limited did not have any bank account inHong Kong

10.1.3.9. He knew Sushil Kumar Singh as both of them were in transport business.Sushil Kumar Singh once approached him and said that he has an IEC in his nameand he wanted to import. Arnab quoted their rate and condition that M/s ZhendaForeign Trade HK Limited would be the supplier and M/ s Shipair Express would bethe carrler and the goods would be consigned to NAF Logistics and Sri Ram Traderswould be having the delivery order from NAF Logistics. Sushil Kumar Singh agreed tothe proposal and the rate. Arnab asked Sushil Kumar Singh whether he would importpersonally or somebody else would be importing on his behalf. Sushil Kumar Singhstated that he would lend his IEC but did not disclose the person to whom he wouldbe lending the IEC.

10.1.3.10. Sometime in lanuary/February of 2017 one person called him on hismobile No. 9899203809 and introduced himself as Badshah of Khidderpore. Heasked for some fEC lender and in response to this he(Arnab) gave him the nameand contact number of Sushil Kumar Singh.

10.1.3.11. Zhenda Foreign Trade HK Limited is actually the supplier of the 47consignments imported through Kolkata Airport during the period 2Ot5-2017.

10.1.3.12. The invoices and the packing lists of the three current consignmentsbear the signature of Hertman Wong signing as authorized signatory of ZhendaForeign Trade HK Limited. The actual name is Hertman Kong. This person is knownto him as working in TH Mason. Neither he nor his mother as Director of ZhendaForeign Trade HK Limited authorised any such person.

10.1.3.13. Arnab Sinha agreed that though Zhenda Foreign Trade HK Limited is thesupplier, the firm cannot receive any remittance from the importers of total 196consignments as no bank account has been opened by either of the Directors in HongKong in the name of that company. He admitted that the only alternative route for ..

': ". :

SCN DRI / KzU /CF/INT- 75/ Pt. sri Ram/464O dtd 4.72.77 Page 11 of145

F.No.533- 2 3/2017 ADJN (A&A)

Zhenda Foreign Trade HK limited to realize the remittance was through the iilegaltransaction channel, and that was also violative of the Foreign Trade (Development &Regulation) Act, 1992.

10.1.3.14, 1"1/s Zhenda Foreign Trade is basically a name lending firm. Thepurchasers purchased the goods and dispatched the same to the storage godown ofM/s Zhenda Foreign Trade HK Limited in packed condition. Zhenda issued theinvoices and the packing lists etc. without knowing about the goods based on thedictated description of the goods and value by the importers,

10.1,3.15, He admitted to have knowingly abetted the misdeclaration andundervaluation of the imports handled by Zhenda Foreign Trade HK Limited and M/sNAF Logistics

10.1,3.16, Arrest u/s 1O4 of the Customs Act, 1962: In view of the actions ofShri Arnab Sinha towards abetting the import of misdeclared goods in the case of SriRam Traders and other companies, he was arrested on 25.O7.2017.

1O.2, Customs Brokers, Employees and Contractors

1O.2.1. Voluntary statement of said Shri Aloke Ghosh, G-Card holder of the CHA,was recorded on 08.06.2017 wherein he stated, inter-alia, that;

1O.2.1.1. He was working under M/ s Sadguru Forwarders Pvt. Ltd. for the pastone and half year. He used to do different jobs like noting, location tracking etc. atACC Kolkata. Previously, he used to work under another Customs Broker namely M/sS. Murugan and Company.

LO.2.L.2, M/s Sadguru Forwarders Pvt. Ltd mainly handled the consignments ofMobile Accessories, LED TV, spares, LED Panel, Garments accessories, Shoes,Chinese unbra nded watches;

10.2.1.3. He did not know the owner of M/s Sadguru Forwarders Pvt. Ltd. So farhe knew they lived at Mumbai. He was answerable to Shri Sukhendu Maity,authorized signatory of the Customs Broking firm;

LO.2.L,4, He was present at ACC Kolkata on 05.06.2017. However, after he hadgot the news that DRI wanted to examine their consignment he fled away as perinstruction of his associate Md. Nasir Uddin;

1O.2.1,6. Nasir Uddin procured some clearance jobs and asked him to clear in thename of M/s Sadguru Forwarders Pvt. Ltd for which Nasir Uddin used to give him Rs.

15OO/- to Rs. 2000/- per consignment. Everyday, he would get Rs. 7000/- to Rs.

8000/- per day for the previous three months over and above his salary of .Rs. ..'

SCN DRI/ KZU/CF/INT-7,/ Pt. Sri Ram/464O dtd 4.72.77 Page 12 of 145

Bill of Entry for the instant consignment was filed by the Customs Broker M/ sSadguru Forwarders Pvt. Ltd and it was gathered that clearance of the importconsignments through ACC, Kolkata handled by the said Customs Broker was lookedafter by their G-Card license holder Shri Aloke Ghosh. However, preliminaryinvestigation also suggested that Shri Aloke Ghosh along with one Md. Nasir Uddinhandled such mis-declared consignments.

1O.2.1.5. Md. Nasir Uddin was a staff of Indo-Foreign Agents Pvt. Ltd. He knewNasir Uddin since 1998. Nasir Uddin used to help him in all his works like noting,location, examination, etc. ;

F.No. 533 2312017 ADIN (A&A)

He altogether received about Rs.10000/ got from M/ s Sadguru Forwarders Pvt. Ltd2,O0,O0A/- from Nasir Uddin.

1O.2.L.7, [4d, Nasir Uddin used to be present at the time of examination of theconsignment, the job of which were procured by him (Nasir); He (Aloke) was neverpresent at the tlme of examination, therefore he (Aloke) was not aware of the mis-declaration;

1O.2.1,8. Shri Pranabananda Bala, Examiner used to examine the goods clearedby M/s Sadguru Forwarders Pvt. Ltd.;

10.2.1.10, He identified the short signature of DC Navneet Kumar at the bottom ofthe first page of the Bill of Entry No. 9940859 dated 02.06.2017 mentioning thewords 'Pl Release'. The instant consignment was released as per manual outof charge order of DC Import Shed.

1O.2,1.11. He also identified the short signature of DC Navneet Kumar on the othertwo Bill of Entry under DRI's investigation where manual out of charge order wasgiven by him.

LO,2.2.L. From 2006, he used to work as freelancer at Air Cargo Complex, NSCBIAirport. Kolkata when he prepared Sales Tax Way Bill for different CHAs,

LO.2,2.3. He was once (one and half month back from then) called by ShriNavneet Kumar, DC, in his chamber at 2nd floor, Air Cargo Complex Building, NSCBIAirport, Kolkata. Navneet Kumar introduced him with one Shri Ansari (who is relatedto a different consignment cigarette seized by DRI Kolkata at ACC, Kolkata) as animporter and directed him (Nasir) to assist him(Ansari). When he informed NavneetKumar that he did not have any Customs license to clear import cargo, NavneetKumar told him to arrange a reliable Customs Broker to clear importconsignments of Mr. Ansari as he (Navneet Kumar) himself would befacilitating those imports. Navneet Kumar also assured that payment would notbe a problem as he (Navneet Kumar) would be supervising the entire process. Hewas further assured that he would get Rs. 4OOO/- to Rs. SOOO/ perconsignment. As he was in need for money, he agreed to the proposal of NavneetKumar. After that he approached Aloke Ghosh, G-card holder of M/s SadguruForwardes Pvt. Ltd and he told Aloke Ghosh that there would be no problem as DC

Navneet Kumar has given him this work. He offered Aloke Ghosh to pay Rs.2OOOI- per consignment. After a few days Navneet Kumar took his e-mailaddress ([email protected]) and informed him that the importer wouldbe sending the documents like invoice, packing list, Airway bill etc. in his e-mail. Thus, he was engaged in these impoft jobs.

SCN: DRI/ KZU/CF/ INT-75/ Pt. Sri Ram/464O dtd 4.72.77

1O.2.1.9. He heard from Naslr Uddin that all those parties work which was doneby him (Nasir) was actually done as per direction of DC Shri Navneet Kumar.

10.2.2, The above statement of Shri Aloke Ghosh and investigation suggestedthat Md. Nasir Uddin played a major role in the said smuggling. Accordingly,voluntary statements of Md. Nasir Uddin were recorded on 09.06.2017 and10.06.2017 wherein he, stated, inter-alia, that:

LO.2.2.2. He used to clear cargo for different importers in the name of theCustoms Broker, namely lvl/s Sadguru Forwarders Pvt. Ltd.

Page 13 of 145

1: \o.533 2ll2C17 ADIN (A&A)LO,2.2.4, So far he remen-ber-ed tr"e frrst im3ort cons gnment he nandled wase:her of M/s Wish Sales Corporation or Raghav International. But these two werenot the companies of Ansari. Navneet Kumar lnformed him that work of lvlr. Ansariitould be done later. These companies like M/s Wish Sales Corporation orRaghav International were of one Ms. Monika of Delhi and Shri NavneetKumar told him that he (Navneet Kumar) would be giving all support like Mr.Ansari's import. Navneet Kumar also told him that these consignments would beexamined by EO Pranabananda Bala and either Biplab Das or Vikki Kumar asAppraiser. Navneet Kumar further informed him that payment in respect ofimports of Monika would be gaven to him by the transporter Mr. Santosh.

1O.2.2.5. Accordingly, he filed Bills of Entry. The Annexure was signed bySukhendu Maity of Sadguru Forwarders Pvt. Ltd. The Check Lists were signed by himor Aloke Ghosh.

LO,2.2.6. He used to receive mails from Ms. Monika informing whlch cartons areto be opened for examination.

LO,2.2.7. The consignments were examined by EO Pranabananda Bala andAppraiser Vikki Kumar;

10.2.2.8. After examination, Mr. Santosh gave him the money in cash and thegoods were handed over to him (Santosh);

LO,2.2,9. After receiving the mails of Monika about the cartons to be opened, asper instruction of DC Navneet Kumar he handed over the print outs of the mails toNavneet Kumar who would inform him that Mr. Pranabananda Bala and Mr. VikkiKumar would be given instruction not to open any carton other than those arementioned in the list. Accordingly, no other cartons were opened by the EO andAppraiser during examination.

LO.2.2.LO. Soon after clearance of the consignments of Monika as stated above,Navneet Kumar had informed him that Ansari would import one consignment in thename of Sharma Sales Corporation and he (Ansari) would send import documents bye-mail. Accordingly, he received documents through e-mall along with a list ofcartons to be opened for examination. This consignment was also cleared in similarfashion. Regarding the consignments cleared by him, Nasir Uddin gave the names ofthe company under control of Ansari as M/s Sharma Sales Corporation and M/sBiswas Enterprise.

10.2.2.11. He stated the names of the company under control of Monika as M/ sS.R. Solutions, M/s Wish Sales Corporation, M/s Raghav International, M/s S. S.Overseas, M/s Yash International, M/s Pasiflc Enterprise, M/s Surya International,M/s Tapas Halder and M/s Sri Ram Traders. He stated that there may be some morecompanies of Smt. Monika which he did not remember.

LO.2.2,12. He had cleared almost 100 consignments in the past in this fashion; Inall the cases, the consignments were mis-declared. The consignments imported fromDubai contained Clgarettes whereas they were declared to contain Men's Chappal,Baby Pampers, Jugs, Flask. The consignments imported from Hong Kong actuallycontained branded sports shoes, mobile phones, moblle phone parts, watchesagainst declared as mobile accessories, unbranded shoes, mobile LCD. Theconsignments were examined by Pranabananda Bala, EO and either by Vikki Kumaror B. Das, Appraiser as instructed by Navneet Kumar;

,t.r)'4'&*33

SCN: DRI/ KZU/CF/INT-7,/ Pt. Sri Ram/464O dtd 4.72.77 Page 14 of 145

LO,2.2.L4, Navneet Kumar used to enquire about the status of work regularly fromhim. He regularly inform Navneet Kumar about the position of import consignmentsby WhatsApp messages. Navneet Kumar used to give order for manual out of chargeof the consignments for speedy clearance and also to avoid complications.

10,2.2.15. He used to send WhatsApp messages from his Samsung Galaxy J7Mobile phone set having connection No. 9830810095 to Navneet Kumar's mobilephone No. 9830050950.

tO.2.2,16. On 05.06.2017, when officers of DRI were searching for him in the ACC,NSCBI Airport, he contacted Navneet Kumar who directed him to flee from the spotand also to delete the WhatsApp Messages between him and Navneet Kumar and hedid accordingly;

LO.2,2.L7. Navneet Kumar, Pranabananda Bala and Vikki Kumar directed him notto appear before DRI, that is why he appeared late after 4 days of the incident.

to.2,z.La, In course of givlng statement, on being requested he accessed his e-mail account and took out printouts of the available mails regarding theconsignments handled by him and submitted the same after signing on each of thepages. The printouts contained the documents and secret information (examinationinstruction sheets) related to the consignments cleared in the past as well as someuncleared consignments which had been imported in the name of Tapash Halder(consignment of 132 Packages), Biswas Enterprise (consignment of 40 packages)Surya International (2 consignments of 200 pkgs and 169 pkgs) and S. R. Solutlons(consignment of 62 packages).

LO.2.2.L9. Shri Navneet Kumar informed him that all the 5 uncleared consignmentsas above were containing goods which would not match with the description anddeclaration in the Air Way Bill and the Invoice. Further the consignment of 62 Pkgsunder the Air Way Bill No.17636016164 imported in the name of S. R. Solutions wasto be processed and cleared on 05.06.2017 as per instructions of Navneet Kumar, DC,

but that could not be done because of DRI's Intervention.

LO.2.2.21, He earned about Rs. 5 Lakh for 100 consignments. Out of which hegave Rs. 2 Lakh to Aloke Ghosh who in turn gave Rs. 50000/- to Sukhendu Maity.

LO.2.2.22. On being confronted with the four pages print-outs marked as "WhishSales 59 Ctn"and "Whish Sales 117 Ctn", in which package nos. with mark, itemsand weight were mentioned and against some packages 'TO OPEN FOR

INNSPECTION"is mentioned, recovered from the house of Shri Navneet Kumar duringthe search on 10.06.2017 and where Navneet Kumar put his dated signature onlO.O6.2Ot7 and in respect of which Navneet Kumar commented that those wereprovided to him by an informer, Nasir Uddin stated that these were the copies ofdocuments received by him (Nasir) in his e-mail from Monika (e-mail ,, Ou'n9,, ,. '.'

SCN: DRI/ KzU /CF/INT-7|/ Pt. Sri Ram/464o dtd 4.72.77 Page 15 of 145 '""''i".'

F. No. s33'23/20i7 AD]N (A&A)

1O.2.2,13, In most of the cases he used to receive e-mails rncorporating the cartonnos. to be placed for examination and he would give the same to Navneet Kumarwho in turn gave it to the officers. In a few cases where he did not receive such e-mails, Navneet Kumar would give the carton nos. directly to the officers and him byway of writing in a piece of paper;

1O,2.2.2O. Monika used to send e-mails to him mainly [email protected] or [email protected] or sometimes from email ID createdin the name of the firms.

F.No. S33- 2312017 ADIN (A&A)

ma k.china@outlook. com ) on 27th March 2017. He had given printouts of thosesheets to Sri Navneet Kumar to instruct the Shed Officers accordingly. He hadalready submitted the printouts of the same documents from his mail account.

10.2.3. Voluntary statement of Md. Nasir Uddin, was further recorded on23.O6.2OL7 when he reiterated his previous statement and fufther stated inter aliathat: -

1O.2.3.1. He and Aloke Ghosh used to take delivery orders from Airlines in respectof consignments handled by M/s Sadguru Forwarders Pvt Ltd.

1O.2.3,2. As per instruction of Shri Navneet Kumar, DC of Customs, he handledthe impot consignments of the firms represented by Smt Monika.

10.2.3,4, Shri Navneet Kumar, the then DC of Customs, ACC Kolkata also toldthat along the AWBS, Invoices, Packing lists, the rough examination sheets would beforwarded to his mail Id '[email protected]' and he had to file challan on thebasis of that. Shri Navneet Kumar further told him that before filing the Bills of Entryeach set of documents need to be shown to him (Navneet Kumar). Accordingly, heshowed each and every set of documents to Shri Navneet Kumar which he receivedin his mail Id. Shri Navneet Kumar after verifying those documents asked him to fileBills of Entry which he had already stated before.

10.2.3.5. He used to contact Shri Navneet Kumar in his mobile number9830050950 and sometime 9163941885.

10.2.4. Voluntary statement of Shri Aloke Ghosh, was further recorded underSection 108 of Customs Act, 1962, on 06.O7.2017 when he relterated his previousstatement and further stated inter alia that:-

LO.2.4.1, Their clearance work at Air Cargo Complex was handled by Md. NasirUddin and he (Md. Nasir Uddin) used to negotlate with the importers.

LO,2.4.2. The stamp of M/s Sadguru Forwarders Pvt Ltd was lent out to him formonetary consideration of which he (Aloke Ghosh) and Shrl Sukhendu Maity werepa rty to it.

LO.2.4.3. Md. Nasir Uddin can only say whether KYC and Authorlzation of all theimporters were obtained. He enquired verbally with Md. Nasir Uddin regarding thesame and he (Md. Nasir Uddin) told that it was obtained.

LO.2.4.4. All the Bills of Entry were filed at CMC, ACC Kolkata. During filing of Billsof Entry or taking delivery of goods neither the CMC people nor Customs everchecked KYC or Authorization letter.

LO.2,4.5. He (Aloke Ghosh) used to sign the check list and look after the deliveryof goods. The import consignments were dellvered to different parties as instructedby Md Nasir Uddin.

LO.2.4,6, As instructed by Md. Nasir Uddin the imports of Delhi based importers,the goods were delivered mostly to two person namely Shri Santosh and Shri Jaydev.

SCN: DRI/ KZU/CF/INT-7,/ Pt. Sri Ram/464O dtd 4.72.77 Page 16 of 145

10.2.3.3. He never met the Proprietor, Director or Paftner of any firm representedby Smt Monika.

1O,2.5. Voluntary statement of f4d. Nasir06.07.2017 when he stated inter alia that:-

F.No. S33- 2312017 AD]N (A&A)

Uddin, was further recordedon

10.2,5.1, During filing of Bills of Entry or at any other point till delivery of 9oods,the CMC people or the Customs at ACC Kolkata never checked or took copies of KYCor Authorization for imports.

10.2,6. Voluntary statement of Shri Aloke Ghosh, was further recorded on79.O7.2077 when he stated. lnter-alia, that all related works right from assessment,noting, location, appraisement etc., were being done by Md. Nasir Uddin. He (NaslrUddin) handed over the gate pass for completion of all formalities by Customs and he(Aloke Ghosh) cleared the goods from Airport area only.

LO.2,7. Voluntary statement of Md. Nasir Uddin, was further recorded on19.O7.20-1,7 when he inter alia stated that:-

LO.2.7,L. He admltted that he did not have any authority to work for M/s SadguruForwarder Pvt Ltd though he was working with the said firm from January, 2017.

LO.2.7.2, All works related to clearance job was done by him by using the stampand seal of Customs Broker, M/s Sadguru Forwarder Pvt Ltd, which he knew wasillegal. Shri Aloke Ghosh of M/s Sadguru Forwarder Pvt Ltd used to sign on papersonly.

10.2,7.3, The fact of using the stamp and seal of M/s Sadguru Forwarder Pvt Ltdby Md Nasir Uddin for clearance of import consignments of different parties wasknown to Shri Sukhendu Maity, authorised signatory of M/s Sadguru Forwarder PvtLtd.

tO.2,7.4, He was compelled in importing the mis-declared items by differentimporters as Navneet Kumar, Deputy Commissioner of Customs directed him (Md.Nasir Uddin) to do so.

10.2.8.1, They had procured the clearance jobs of different importers from Md.Nasir Uddin but did not verify antecedents, identity of their clients and functioning oftheir clients at their declared address by using authentic sources in terms ofRegulation 11(n) of Customs Brokers Licensing Regulation 2013.

10.2.8.2. They filed Bills of Entry on the basis of KYC of the importers anddocuments provided by Md. Nasir Uddin.

10.2.8.3. They did rely not only on Md. Nasir Uddin but also on Shri NavneetKumar, Deputy Commissioner of Customs who assured them and told to clear theconsignments of Md. Nasir Uddin's client and for it they would not face any problem'

1(J.2,7.5. Though he was compelled to do the clearance job of mis-declared itemsas per direction of Shri Navneet Kumar, he (Md Nasir Uddin) received money for it.

10.2.8. Voluntary statement of Shri Aloke Ghosh, was further recorded on25.07.2017 when he reiterated his previous statements dated 08.06.2OL7,06.07.2017 and 19.07.2017 and further stated inter alia that:-

LO.2,8.4. They raised charge on an average of Rs. 1500/- for clearance perconsignment at ACC Kolkata. Out of which Rs 500/- was given to Shri SukhenduMaity and the rest amount of Rs. 1000/- was kept by him (Aloke Ghosh).

..'...SCN DRI/ KzU /cF/ INT-75/ Pt. Sri Ram/464O dtd 4.72.77 Page 17 of 145

F.No. 533 2312017 ADJN (A&A)

10.2.8.5. Ivld. Nasir Uddin gave him Rs 1500/- for small consignment like 1 to 10packages and for other consignment he gave him (Aioke Ghosh) Rs 2000/-

10.2.a.6. In the last three months up untill 25.A7.2017, they had handled morethan 300 consignments imported by the clients of Md. Nasir Uddin at ACC Kolkata forwhich Nasir paid him(Aloke Ghosh) Rs 2,00,000/-

LO,2,A.7. He was never present during examination of consignment by Customswhich were procured by Md. Nasir Uddin. He was specifically instructed by Md. NasirUddin for the same who told him that his presence was not required.

10.2.8.9. He came to know from Md. Nasir Uddin that many jobs were procuredthrough one Sajal Das who was associated with M/s Indo Foreign Agency. He wasalso not aware whether Shri Sajal Das was present during examination or not.

10.2.8,10. He only assisted Md. Nasir Uddin during delivery of the consignments.

LO.2.9. Voluntary statement of Md. Nasir Uddin,7.9.2OL7 when he categorically stated, inter-alia, that;

was further recorded on

10.2.9.3. He was introduced with Perwaiz Ansari, Pappu and Alam Perwaiz by ShriNavneet Kumar, DC. In respect of Monlka, Navneet Kumar gave him Monika's mobilenumber and instructed him to clear all her consignments. He further reiterated thatfor all the imports of firms under control of Perwaiz Ansari , Pappu. Alam Perwaiz andMonika, DC Navneet Kumar used to instruct Appraiser Vikki Kumar and EO

Pranabananda Bala to check only those packages which was contained no mis-declared goods and the examination were done accordingly. Many suchconsignments were given manual out of charge by Shri Vikki Kumar at per thedirection of Shri Navneet Kumar by giving writing instruction on the body of the EDIBills of Entry.

10.2.9.4, He further added that he was handpicked by Shri Navneet Kumar toclear such mis-declared consignments. Navneet Kumar also monitored those importsand used to take day to day report from him. The payments were received from

SCN: DRI/ KZU /CF/INT-7,/ Pt. Sri Ram/464O dtd 4.72,77 PaBe 18 of145 '"

10.2.8.8. He did not know why Shri Pranabananda Bala, EO stated that he used tobe present during examination of goods.

1O.2.9.L. Mr. Parwaiz Ansari was associated with two importing firm namely (1)Sharma Sales Corporation and (2) Biswas Enterprise and Ms. Monika was assoclatedwith (1) Yash International, (2) S. R. Solution, (3) Wish Sales Corporation (4)Raghav International (5) Raghav International, (6) S. S. Overseas, (7) ArcturusSystems Pvt. Ltd., (8) Pasific Enterprises, (9) Surya International, (10) Tapas Halder,(11) Syndicate Trading, (13) Siddhi Trading Company and (14) Lavish Enterprises;Mr. Mandeep was associated with Ambey Telecom; Mr. Gullu was associated withLotus Impex; Mr. Pappu was associated with Jash-Insha Exports Pvt. Ltd.; Mr. AlamPerwaiz was associated with Sony Trading Company; Mr. Kishan daga was associatedwith Kamal Impex and Narendra Inpex and Mr. Badshah was associated with Sri RamTraders.

1O.2.9.2. He also reiterated that certaln Departmental offlcers namely ShriNavneet Kumar, DC, Shri Pranabananda Bala, EO and Shri Vikki Kumar, Appraiserposted at ACC Kolkata were involved with the mis-declared imports made by theaforesaid firms as he has already stated in his previous statements.

F.No. S33- 2312017 ADIN (A&A)

either Santosh or Jay deb. So far his knowledge the goods were sent to Howrahstation by trucks for further transport by trains. He further stated that the Bills ofEntry No. 9959884 dated 05.06.2017 of Biswas Enterprises and 99488O4 dated03.06.2017 of Sri Ram Trader (the consignments of which examined later by DRIand found mis-declared good like cigarettes and shoes, respectively) were assessedby Group and then he brought these two Bills of Entry to DC's room for finalassessment at about 17.00 Hrs on 05.06.2017 as the declared value was more thanl lakh but he could not meet DC.

10.2.9.5, Query was raised by the DC on these Bills of Entry most probablyafter DRI's intervention on O5.O6,2O17. Regarding the Bill of Entry No. 994A7ABdated 03.06.2017 of Sri Ram Traders (in which DRI found branded watches andmobiles), the Bills of Entry was finally assessed by the DC on 03.06.2017 andexamined on 05.06.2017. He named another person named Arnab Sinha of NAFLogistics, Freight Forwarder, who was also involved in the imports of Sri Ram Traders.

10.2.9.6. He also stated that in respect of import of Lotus Impex (India) andAmbey Telecom, he received payments from M/ s Nir mala Bala Trading & Co, thefirm of Sajal Das who introduced him to Gullu and Mandeep for the two firms. Thesaid Sajal Das also introduced him to said Badsha @ Sahansah Mallick ofKhidderpore who had imported goods by using IEC of Sri Ram Traders.

1O.2.10. Voluntary statement of Sri Sukhendu Maity, authorised signatory of theCustoms Broker M/s Sadguru Forwarders Pvt. Ltd. was recorded on 27.06.L7 whereinhe inter alia stated that Sri Aloke Ghosh who is G card holder of SadguruForwarders Pvt. Ltd looked after all the import clearance at ACC Kolkata onbehalf of the Customs Broker. Aloke Ghosh procured jobs for clearance of theconsignments of different importers mainly from Nasir. Aloke Ghosh used to repofthim day to day basis. Aloke Ghosh used to take KYC and authorisation fromthe importers and keep with him (Aloke). He used to sign on the Annexurerequired for flling of BE. He(Sukhendu) did not know any importer who had importedthrough ACC Kolkata under Customs Broker license of Sadguru Forwarders Pvt. Ltd.Aloke Ghosh told him that he procured the jobs from Nasir and Saial whowere the men of DC Navneet Kumar.

1O.2.11. Further, three Summons were issued to said Sukhendu Maity but he didnot turn up. However, Death certificate of Sukendu Maity was received by the officefrom his family from where it could be seen that Sukendu Maity expired on07.tL.2017.

11. As per the statement of Md. Nasir Uddin, one Ms. Monika was sending him theimport documents and instruction for examination, in respect of the consignmentsimported in the name of different importers of Delhi and Kolkata, by e-mails.Intelligence developed further suggested that she (Monika) was an employee of oneMumbai based person, Mayur Mehta who had three-four Customs broking firmsincluding M/s Shreenathji Clearing & Forwarding Pvt. Ltd. and M/s MenegesClearing & Forwarding Pvt, Ltd. Intelligence also suggested that this MayurMehta played pivotal role in this massive smuggling made through ACC,Kolkata.

L2, Accordingly, under DRI Kolkata's letter dated 30.06.2017, DRI Mumbai ZonalUnit, Mumbai was requested to enquire with the said Mayur Mehta and Monika. On04.07.2017, the officers of DRI Mumbai visited the premises of both Mayur Mehtaand Monika, (whose name was found to be Ms. Swati Vora). However, neither MayurMehta nor Monika alias Swati Vora was available at their respective addresses.

SCN: DRI/ KZU/CF/ INT-75/ Pt, Sri Ram/464O dtd 4.72.77 Page 19 of145

F.No. 533- 2312017 ADJN (A&A)

12,1. Voluntary statement of one Shri Rahul Bhimaji Phaphale, employee of 1.4/s

Menezes Clearing & Forwarding Pvt. Ltd., (in which lvlr. Mayur Mehta was a Director)was recorded on 04.O7.201,7 wherein, he sald, inter alia, that:

L2.L.t. He was employed with M/s Menezes Clearing Forwarding Pvt. Ltd for theprevious 4-5 months;

12.1,3. Mayur Mehta was the Director of M/s Menezes Clearing Forwarding Pvt.Ltd;

L2.L.4. There were three employees in M/s Menezes Clearing Forwarding Pvt.Ltd i.e. Ms. Monika Vora, Shri Umed Singh and he himself;

12.1.5. Both Monika and he looked the office work, whereas, Umed Singhlooked after the clearance at cargo;

12,L.6. Their firm was into clearance of import goods from Air Cargo ComplexSahar and most of the clearances pertain to moblle accessories.

12.L.7. The office mail was looked after by Monika and she used to sendand receive mail on the direction of Mayur Mehta;

13. Summons dated 25.O7.2017, 11.08.2017 and 21.09.2017 under Section 108of the Customs Act, 1962 was issued to sald Shri Mayur Mehta with the direction toappear before DRI Kolkata on 03.08.2017, 77.O8.2077 and 05.10.2017. However, onall the occasions, Mayur Mehta expressed his inability to appear before the DRIofficer stating health reasons.

13.1. Voluntary statement of Shri Mayur Mehta, Managing Director of M/ s Om TransFreight Cargo Private Limited, M/s Menezes Clearing and forwarding Private Limitedand Director, M/s Shreenathji Clearing & Forwarders Private Limlted could be finallyrecorded on 22.10.2017, when he was apprehended by DRI, Gandhidham in relatlonto a case booked by them in respect of one mis-declared import consignmentthrough Mundra Port. In the said voluntary statement, recorded under Section 108 ofthe Customs Act, 1962, he, stated, inter-alia, that:

13.1.1. Though he do not have any office at Kolkata, he had controlled importconsignments of several importers of Delhi and Noida through Air Cargo Complex,NSCBI Airport, Kolkata.

13.1.2. The import work of the above firms were handled by one Nasir Uddln byusing the stamp of one Customs Broker namely Sadguru Forwarders Pvt. Ltd,Kolkata ;

13.1.3, He employed two persons named Santosh and Joydeb for takingdelivery of the goods after out of charge and sending the goods to the importer /user of the IEC and also for making payment to Nasir Uddin; The impofters whoseimport consignments were handled by him through ACC, Kolkata by using the licenseof Sadguru Forwarders Pvt. Ltd, used to import goods through ACC, Delhi, whichwere handled by his own Customs Broker firms but as during March, 2017 clearance

SCN: DRI/ KZU / CF/INT-7'/ Pt. Sri Ram/464O dtd 4,72.77 Page 20 of 145

12.1.2. Office of M/s Menezes Clearing Forwarding Pvt. Ltd was at Room No. 16,Mohammad Hasan Building, Sutar Pakhadi, near Sahar Air Cargo Complex.Previously, it was the office of Shreenathji Clearing & Forwarding Pvt.Ltd.

i l'l'1+o\

'l'*d4i.-; 4 E -

-i...":st*^e\.': '

F.No.533 2312017 ADJN (A&A)

tiirough ACC, Delhi became problematic due to strict vigil of Customs Department, heplanned to shift to some other port and had chosen Kolkata as the then DeputyCommissioner, Air Cargo Complex, Kolkata (Navneet Kumar) was known to him;

13.1.4, The Deputy Commissioner (Navneet Kumar) instructed him to importmis-declared goods through Air Cargo Complex, Kolkata and had introduced him withone Sajal Das for helping in clearance of such misdeclared goods;

13.1.5. Sajal Das introduced him to said Nasir Uddin and told him that NasirUddin will assist him in clearance of such misdeclared goods by using the license ofSadguru Forwarders Pvt. Ltd.;

13.1,6, It was also planned that he would be sending the original packing listsand invoices to Nasir Uddin, indicating the packets which should be opened forexamination, then Nasir Uddin would give it to the said Deputy Commissioner ofCustoms (Navneet Kumar) who would in turn instruct his subordinates to open thosepackets only during examination; One of his trusted employee, named Ms. SwatiVora allas Monika, who was also a Director of M/s Om Trans Cargo Freight Pvt. Ltd,used to send the original documents indicating the packets which should be openedfor examination to Nasir Uddin by emall from his office and Nasir used to supplythose documents to the said Deputy Commissioner (Navneet Kumar) and as per his(DC's) instruction only those packets marked as to be opened for examination wereopened by the EO, Appraiser of ACC Kolkata;

t3.L.7. He had bribed the said Deputy Commissioner with heavyamounts, for clearance of the mis-declared consignments;

13.1.8. Monika used to send the mails mainly from the email [email protected] and sometimes from different emails created in the names ofthe impofters;

13.1.9. After clearance of the goods, Nasir Uddin used to handover them toSantosh and Joydeb who also used to make him the payment which he used to sendto them by cash. Santosh and Joydeb also used to send the goods to differentpersons who had used the IEC of the said importers;

13.1.10. During June,2OL7 after DRI raid at ACC, Kolkata, he instructedNasir not to file any further bill of entry in respect of the cargo lying thereand stopped sending him further documents;

SCN: DRI/ KZU/CF/INT-75/ Pt. Sri Ram/464O dtd 4.72.77 Page 21 of 145

13.1.11. He admitted that the import consignments contained misdectared goods and the goods were also undervalued to evade duty;

13.1.12, He also stated that the imports made through ACC, Kolkata by theabovementioned firms were of different persons of Mumbal to whom he had providedthe IECS for their import but he could not recall their names, they were basicallygeneral traders of Musafirkhana Market and City Centre Market of Mumbai;

13.1.13. The IEC and their KYC documents were provided by one Vaibhav ofRajlnder Nagar, Karol Bagh, Delhi whose mobile number he had deleted after KolkataACC case;

13.1.14. He had handled another mis-declared consignments of one M/s' KashiImpex, imported through Kolkata Sea Port, which was also seized by DRI Kolkata. d!

F.No. S33- 2312017 ADJN (A&A)

He gave his mobile numbers as 9821710875 & 9619684111.13.1.15

13.1,16. Shri Mayur l4ehta was arrested by DRI, Gandhidham in relation to thecase of misdeclared import made through Mundra Port. Thereafter, the news of deathof Mayur Mehta in Ahmedabad Civil Hospital was received, whlle he was in JudicialCustody.

L4. Summons dated 25.O7.2017 and 26.70.2017 under Section 108 of theCustoms Act, 1962 were issued to Ms. Monika Vora @ Swati Vora directing her toappear at the office of DRI, Kolkata on 03.08.2017 and O6.17.2017 respectively.

14.1. Ms. Monika Vora, however, never attended DRI office in response to thesummons issued to her. In response to the summons dated 26.10.2017, fvls. Vora,vide her letter received on 07.11.2017, inter alia submitted that she used to send e-mail and whatsapp messages to Md. Nasir Uddin, regarding clearance of importconsignments, as per the instructions of Mayur lYehta. She also requested toconsider the letter sent by her as her statement in response to summons issued toher under Section 108 of the Customs Act, 1962.

14,2. As it appeared that Ms. Swati Vora @ Monika was deliberately keeping himselfaway from the course of investigation, complaint under Section 174 of the IndianPenal Code was lodged against her in the jurisdictional Court for non-appearanceagainst the Summons issued under Section 108 of the Customs Act, 1962.

15. The name of Shri Sajal Das surfaced during the course of investigation fromthe statements of different related persons as detailed above. As such, Shri Sajal Das,was summoned under Section 108 of the Customs Act, 1962 for explaining his role inthe instant fraud and his voluntary statement was recorded on 23.10.2017 and24.1O.2077 , where he identified himself to be the proprietor of M/s K.C. Das & Co, a

Customs Broker and Partner of Indo-Friends Agency, another Customs Broker,operating in Kolkata Airport and Kolkata Port. Further he inter alia stated that:

15.1. He knew Nasir Uddin as he (Nasir Uddin) used to work in his firms earlier

15.2. Nasir Uddin left their company in December 2016 and thereafter he introducedNasir Uddin with some importers /persons intending to bring goods through theairport at Kolkata.

15.3. The persons he introduced Nasir with Included one Mayur Mehta.

15.4. He himself was introduced to Mayur lt4ehta by the Deputy Commissioner ShriNavneet Kumar who asked him to clear some import consignments of Shri Mehta;

15.5. He had a meeting with Mayur Mehta in March 2017 in Hotel 02, VIP Road,Kolkata and Shri Das came to know that the consignments of Shri Mehta wouldcontain misdeclared goods and therefore he did not handle the same but he gave thework of clearance of such consignments to Md. Nasir Uddin.

15.6. However, from the study of the e-mail account of Sajal Das, it was seen thatthe import documents of two other offending firms namely M/ s. Lotus Impex andM/s. Ambey Telecom were initially received at the e-mail of one of his firm. M/s. IndoForeign Agency. In this regard, may be observed that the import consignments ofthe M/s. Lotus Impex and M/s. Ambey Telecom were also intercepted by DRI,Kolkata which on examination were found to be grossly misdeclared and for whlchseparate Show Cause Notices have been issued.

SCN: DRI/ KZU/CF/ INT-75/ Pt. sri Ram/464o dtd 4.72.77 Page 22 of L45

F.No. S33- 2312017 ADJN (A&A)

16. On enquiry with Mayur lvlehta, it was gathered that his Customs Broking firm,M/s Dabke Clearing & Forwarding Pvt. Ltd has an office in Kolkata near Airport 2112

No. Gate near 'Sabji' Market and his employees Santosh Mishra and loydev Das sitthere.

16,1. Further, subscriber details of the mobile number of Santosh obtained from theservice provider mention his address at Usashi Apartment, Ground Floor, 381/1Motilal Colony, 2 no. Airport Gate, Kolkata - 700081. Accordingly, officers of DRIvisited the said address on 01.11.2017. However, the office of said Dabke Clearing &Forwarding Pvt. Ltd was found locked. On enquiry with the neighbours, it wasgathered that the office was closed for the previous three months and nobody couldprovide the present whereabouts of Santosh Mishra and Joydeb Das.

16.2. Summons dated 22.1t.2ot7 under Section 108 of the Customs Act, 1962 weresent to Shri Santosh Mishra and Shri Joydev Das for their appearance on 27.11.2077but they did not turn up.

L7. Cancellation of License:

17.1. The Customs Broker License No. S-116 (PAN No. AAGCS7156L) of M/sSadguru Forwarders Pvt. Ltd was ordered to be suspended by the Commissloner ofCustoms (Airport & Administration) Custom House, Kolkata under CB Order No.07 /2017 dated . 07.O8.2017, with immediate effect until furthers under Rule 19(1) ofCustoms Broker Licensing Regulation , 2013, for their complete violation of theregulations laid down in the regulations, ibid.

18. INVOLVEMENT OF DEPARTMENTAL OFFICERS AND THEIR STATEMENTS:

18.1. The names of the following officers surfaced during the course of investigation,who were found to be involved in clearance of all such misdeclared consignments asdiscussed in Para 1 and also in the instant case of M/s Sri Ram Traders.

Shri Navneet Kumar, Deputy Commisioner, ACC, Kolkata.Shri Vikki Kumar, Appraiser, ACC, Kolkata.Shri Pranabananda Bala, Examining Officer, Kolkata,

19. Voluntary Statement of Shri Vikki Kumar, Appraiser of Customs posted at ACC,Kolkata, who was reported to have examined most of the mis-declared importconsignments of different importers and given out of charge which were handled byMd. Nasir Uddin under license of M/s Sadguru Forwarders Pvt. Ltd., was recorded on06.06.2017 under Section 108 of the Customs Act, 1962, wherein Shri Vikkl statedinter alia that: -

19.1. From 18.06.2016 to 30.09.2016, he worked as Examiner at ACC Kolkata, afterwhich he was working as Appraiser there;

'CN: DRI/ KZU/CF/INT-7,/ Pt. Sri Ram/464O dtd 4.72.77

As such enquiry was initiated to ascertain their roles in such massive fraud ofmisdeclared im ports.18.2. By DRI Kolkata letter dated 06.06.2017, Commissioner of Customs (Airport &Administration), Custom House, Kolkata was intimated the detention and seizure ofconsignments by DRI Kolkata. The list of consignments required to be examinedwere also forwarded. In the above letter, it was also intimated that preliminaryinvestigation indicated involvement of some departmental officers.

otl:"":;il'+ir'

,EN1

Page 23 of 145

F.No. s33 2312017 ADJN {A&A)19.2. He was looking after assessment related work in Bill of Entry in import Shed;

19.3. As per prevalent practice fo lowed at ACC Koikata, in the case of RtvlS (RiskManagement System) Blli of Entry, CHA used to submit Bill of Entry to the ExaminingOfficer who would check the lvlAwB (Master Airway Bill) and HAWB (House Airway Bill)of the concerned Bill of Entry. If MAWB and HAWB Nos. were found in order, the Billof Entry is presented before the Appraiser who checks the classification andcorrectness of notification benefit. If all the above parameters are found in order, Outof Charge is given in the system. In respect of Group assessed Bill of Entry, the ordergiven by the group is followed and after finding the goods as per description, Out ofCharge is given in the system only after submission of reports by the examiningofficer in the system;

19.4. In some instances where m is-decla rations were found, the Bill of Entry wasreturned back to Group with remarks;

19.5. Regarding manual out of charge, for any Bill of Entry, he only looked after theorder of the Deputy Commissioner (Import Shed). But he had no idea whether theCommissioner had given any order for manual out of charge for the said Bills of Entrywhich is mandatory requirement.

19.6. A register for manual out of charge was kept in the Import Shed and there areso many Bills of Entry mentioned in the register. On the previous day, manual out ofcharge was given for 10 Bills of Entry and within 3-4 days, all these Bills of Entrywould be updated in the EDI system.

L9.7, In the last 2 days, manual out of charge was given by him in respect of 4 Billsof Entry handled by the Customs Broker M/ s Sadguru Forwarders Pvt. Ltd. with thepermission of DC Import Shed. Apart from these 4 Bills of Entry, no other Bills ofEntry of pertaining to M/ s Sadguru Forwarders Pvt. Ltd was cleared by him in thelast 2 days.

19.8. He did not know the main person of Sadguru Forwarders Pvt. Ltd. One Nasirused to represent the Customs Broking firm.

20, Voluntary statement of Shri Pranabananda Bala, Examining Officer of Customsposted at ACC, Kolkata, who was reported to have examined most of the mis-declared import consignments of different importers which were handled by Md.Nasir Uddin under license of M/s Sadguru Forwarders Pvt. Ltd., was recorded on06.06.2077 and 07.06.2017 under Section 108 of the Customs Act, 1962, whereinShri Bala stated Inter alia that;

2O.1. From March 2016 to Feb 2017 he had been attached to ACC Appraising Unit,ACC Kolkata and since Feb 2077 he had been working in ACC Import Shed as EO;

2O.2. As per allocation, his duty was to examine goods those were presented to himand to report to Shed Appraiser for OOC (Out of Charge);

SCN: DRI/ KZU/CF/INT-75 / Pt. Sri Ram/464O dtd 4.72.77 Page 24 of L45