Opportunities for Impact Investment in Coastal and Water ...

Upload

khangminh22Category

view

4download

0

Investment Opportunities in the Rwandan Energy Sector

TRAIDE Rwanda

Evelien Lambooij, Thijs Rutgers, Emily ter Steeg and Marie Fidele Umutoniwase Ndahimana

May 2020

ContentsFACT SHEET RWANDAN ENERGY SECTOR 3BUSINESS OPPORTUNITIES 4Abbreviations 5

1. INTRODUCTION 5Rwandancontext 5Rwandanenergysector 6

2. STAKEHOLDERS AND ENABLING ENVIRONMENT 8NationalElectrificationPlan 8Publicsector 9IndependentPowerProducers 9Consumers 9

3. MAJOR TRENDS IN ON-GRID ELECTRIFICATION 11Hydroelectricpower 11Thermalpower 12Methanegas 12Peat 13Solar 13Energyimports 14Transmissionofenergy 14Distributionofenergy 14Fundingmechanisms 14Gridconnectionfees 15

4. OPPORTUNITIES IN ON-GRID ELECTRIFICATION 165. MAJOR TRENDS IN OFF-GRID ELECTRIFICATION 17SolarHomeSystems 17Mini-grids 19

6. OPPORTUNITIES IN OFF-GRID ELECTRIFICATION 21SolarHomeSystems 21Mini-grids 22

7. MAJOR TRENDS IN CLEAN COOKING 238. OPPORTUNITIES IN CLEAN COOKING 27ANNEXE 1 28ANNEXE 2 29REFERENCES 30

Fact sheet Rwandan energy sector

ACCESS TO ENERGY

CAPACITY

INEFFICIENT COOKING SOLUTIONS

INSTALLED CAPACITY

ENERGY CONSUMPTION

38% access to a grid connection line

/ aimed 52%

14% connected to an off-grid line1

1HeadofInfrastructureSectionLénaïcGeorgelin,2020;WhenapplyingIEAstandards,thispercentageis49.1.2ThesepercentagesarelowerwhentakingintoaccounttheWorldBankstandardthatelectricityshouldbeavailableforatleastfourhoursduringthedayandonehouratnight.Applyingthesestandards,only26.8percentwasconnectedin2020.3MinInfra,2018;REG,2019.4REG,2019.5USAID,2019;RDB,2017.6REG,2019.7Inefficientfuelsforcookingarewood,charcoal,coalandkerosene(CleanCookingAlliance,n.d.);MinInfra:BiomassStrategy,2019.8Extensiveresearchwasconductedforthe‘RwandaBeyondConnections’reportbasedonthemulti-tierframework(WorldBankincooperationwithAfDBandUN)tostudyelectricityconsumption,affordabilityandwillingnesstopayin2017.9WorldBank,2018.

governmental aim by

20242020

202020192010

2023-24includes a reserve margin of 15%

aim for 20247 42% 2020 98%

Rural 9.9 kWh

2000 RWF/month~ 2.15 USD

4700 RWF/month~ 5.05 USD9

Urban8 29.2 kWh

Average 20.8 kWh/month

2015 … 2017 2018 … 2020 … 2024

72.7 MW

218 MW

556 MW5

224.6 MW + 19.95 MW4

24% 32% 34.5% 38%2

11% 14%3

0%

48%

52%

2015 … … 2018 … 2020 … 2024

12.9 million

13.9 million(3.7 m households)

import fromDemocratic Republic of the Congo and Uganda6

methane gas

diesel peathydro solar

/ aimed 48%

101.

07

MW

45%27%14% 5.5 7% 1.5

60

.64

MW

31.

44

MW

12.3

5 M

W

15.7

2 M

W

3.3

7 M

W

Investment Opportunities in the Rwandan Energy Sector 4

Business opportunitiesON-GRID ELECTRIFICATION

• Rwandan government has awarded nine large-scale (>5MW) projects

andtwelvesmall-scale(<5MW)projectstoincreasetheMWgeneration

capacity inRwanda.Twolarge-scaleprojectsareregionalprojects, in-

volvingotherEast-Africancountries.

• Atthemoment,therearenoopentenders.Suppliersmightbeableto

provideservicesorinputsforprojectssuchasequipment,consultancies

andtraining.

• There areover seventeenprojects ongoing aiming toupgradeandex-

pandthetransmissionlinenetwork.Severaloftheseprojectsstillrequire

funding.Opportunitiesexistinrealisingtheinfrastructuredevelopment,

providingequipment,technicalsupport,projectsdesignandtrainingof

technicians.

OFF-GRID ELECTRIFICATION

Solar Home Systems

Product development

• ExploreopportunitiestocreateSolarHomeSystemsthatcanbeshared

bymultiplehouseholdsintermsofdesignandbusinessmodel.In2016,

55.5percentof theRwandanpopulationwas livingbelow thepoverty

rateearning57–59USDpermonth.Meanwhile,thepricerangefora

medium-sizeSolarHomeSystemsoldonthelocalmarketwas50–100USD.

Most households donot have themeans to purchase their own Solar

HomeSystem.

• DevelopstrongerSolarHomeSystemproducts.Therearesafety issues

withaffordableSolarHomeSystemkitsonthemarket:strongerequip-

mentandwiresareneededtoimprovethequalityofsystems.

Local production

• ExploreopportunitiestoassembleorproduceSolarHomeSystemkits

locallyandobtain investment incentives.MostSolarHomeSystemkits

are sourced fromChina, but one company is currently investigating

optionsforlocalproduction.

Financial model

• Benefit fromfinancial supportprovided toSolarHomeSystemcompa-

nies and consumers. The Scaling up Renewable Energy Program fund

andUbudehesubsidieswillbelaunchedsoonprovidingfundstoreach

low-incomehouseholds.

Mini-grids

Product development

• Benefit from falling internationalmarketpricesof solarPVpanels. Im-

provedcost-efficiencythankstoreducedcostsofequipmentgenerates

opportunities.

Financial model

• Tapintoblendedfinancetofundmini-griddevelopmentengagingdonors,

publicandprivateactors.Financial support forSHScompanieswillbe-

come available via the Scaling Up Renewable Energy Program fund,

whichisexpectedtobelaunchedin2021.Theprogramwillfundamaxi-

mumof37percentoftotalfinancingcosts.

Clean cooking

Product development

• Developaffordable,safeproductsforlow-incomehouseholdsfocusingon

tier0,1,2and3ImprovedCookingStoves.Forexample,companiescan

addinsulationtothestovetoincreaseheatefficiency.

Local production

• Investigatethepossibilitytoproducepelletsandbriquetteslocally,tore-

duceusagecostsoftier4–5stoves.Thegovernmentiswillingtofacilitate

accesstorawmaterialsforfactories(e.g.providingforestconcessionsto

pelletsmakers).

Awareness

• Contextualisesalesstrategiesandawarenesscampaignstolocalvalues.

Cookingpracticesarelinkedtostrongculturalandbehaviouralvaluesin

Rwanda.Consequently,it isdifficulttoconvincepeopletochangetheir

behaviourinbothurbanandruralareas.

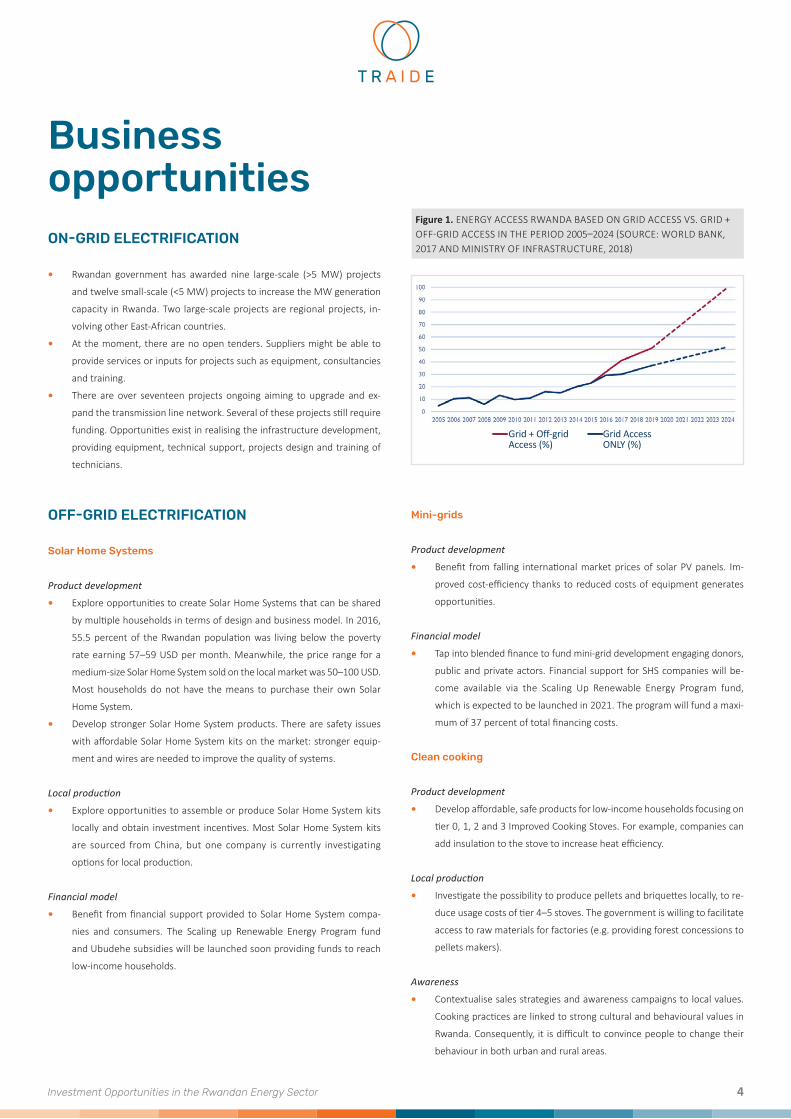

Figure 1.ENERGYACCESSRWANDABASEDONGRIDACCESSVS.GRID+OFF-GRIDACCESSINTHEPERIOD2005–2024(SOURCE:WORLDBANK,2017ANDMINISTRYOFINFRASTRUCTURE,2018)

Grid + Off-grid Access (%)

Grid AccessONLY (%)

Investment Opportunities in the Rwandan Energy Sector 5

1. IntroductionThis report will explore investment opportunities for Dutch and other

local or foreign businesses in the energy sector. Sustainable Development

Goal (SDG) 7: ‘Ensure access to affordable, reliable, sustainable and

modern energy for all’ is a top priority for the Rwandan government. The

Rwandan government aims to reach universal access to electricity for

the population by 2024. This agenda offers opportunities for the private

sector. Rwanda is moving through a phase of transition. The country

seeks to develop equitable relationships with other countries moving

from aid to trade. This report seeks to evaluate investment opportuni-

ties along the aid and trade spectrum: some of these business models

can be market-driven whilst others will require subsidies. Many energy

projects depend on external funding, and low-income rural households

often need funding mechanisms in order to afford the basic electricity

services offered by private energy businesses. Therefore, close collab-

oration between public and private stakeholders is very important.

RWANDAN CONTEXT

Rwanda is one of the smallest, most densely populated countries on the

Africancontinent.Around12.5millionpeopleliveinanareaof26,338square

kilometres.10EightypercentoftheRwandanpopulationlivesinremote,rural

areas.Therefore,itisdifficultandexpensivetoconnectthemtothenational

grid.Also,purchasingpoweroftheRwandanpopulationremainslow.In2016,

55.5percentof theRwandanpopulationwas livingbelowthepovertyrate

earning 57–59 USD per month. Meanwhile, the price range for a medi-

um-sizeSolarHomeSystem(SHS)soldonthelocalmarketwas50–100USD.

ABBREVIATIONS

ADF AfricanDevelopmentFundAfDB AfricanDevelopmentBankDRC DemocraticRepublicofCongoEARP EnergyAccessRoll-outProgrammeEDCL EnergyDevelopmentCorporationLimitedESSP EnergySectorStrategicPlanEU EuropeanUnionEUCL EnergyUtilityCorporationLimitedGACC GlobalAllianceforCleanCookstovesGDP GrossDomesticProductICS ImprovedCookstoveIEC InternationalElectrotechnicalCommissionIEA InternationalEnergyAgencyIPP IndependentPowerProducerJICA JapanInternationalCooperationAgencyKV KilovoltKW KilowattKWh KilowatthourLCPDP LeastCostPowerDevelopmentPlanLPG LiquefiedPetroleumGasLV LowVoltageMinEcoFin MinistryofFinanceandEconomicPlanningMinInfra MinistryofInfrastructureRwandaMoMo MobileMoneyMV MediumVoltageMW MegawattNELSAP NileEquatorialLakesSubsidiaryActionProgramNEP NationalElectrificationPlanPAYG PayAsYouGoPV PhotovoltaicRBF Results-BasedFinancingREG RwandaEnergyGroupRES RuralElectrificationStrategyRURA RwandaUtilitiesRegulatoryAuthorityRWF RwandanFrancSACCO SavingsandCreditCooperativeOrganizationSDG SustainableDevelopmentGoalSHS SolarHomeSystemSLS SolarLightingSystemSREP ScalingUpRenewableEnergyProgramUSD UnitedStatesDollarW WattWHO WorldHealthOrganizationWTP WillingnesstoPay

10Kooetal.:RwandaBeyondBorders,2018.

Investment Opportunities in the Rwandan Energy Sector 6

The Rwandan Gross Domestic Product (GDP) has experienced an average

growth rate of 7.5 percent since 2000. In 2019, economic growth even

exceededtenpercent.Priortotheglobalpandemic,growthratesofapproxi-

matelyeightpercentwereprojecteduntil2022.11Disruptionsofinternational

tradeandtravelarelikelytosuppressgrowthrates.Moreover,publicinvest-

ments supporting the expansion of (energy) infrastructure such as power

plantshavebeenamajordriverofgrowth.12Stableenergysupplycansupport

industrydevelopmentandsmallbusinesses.Atthemoment,72percentof

productiveusersinRwandahasaccesstoenergy.13Consideringrecentdevelop-

ments,delaysintheexecutionofenergygenerationprojectscanbeexpected.

RWANDAN ENERGY SECTOR

In 2020, the RwandanMinistry of Infrastructure (MinInfra) estimates that

52.2percentoftheRwandanpopulationhasaccesstoenergy.38percentofthe

Rwandanpopulationhasaccessviaagridconnectionandfourteenpercentis

connectedtoanoff-gridline.14Thispercentagemightbeslightlylowerwhen

applyingthestandardsoftheInternationalEnergyAgency(IEA)accordingto

which49percentoftheRwandanpopulationhadaccesstobasicelectricity

in 2019.15 The Rwandan government aims to reach universal access for the

populationtoelectricityby2024.Atthemoment,consumerelectricitydemand

is rather low because most households still use biomass for cooking, and

keroseneforlights.Around98percentofthetotalRwandanpopulationuses

biomassascookingfuel,whichmakesthehealthburdenofindoorairpollution

exposureoneofthelargestintheworld.16Thegovernmentaimstoreducethe

numberhouseholdsusingbiomassforcookingfrom98to42percentby2024.

The Ministry of Infrastructure (MinInfra) has set ambitious targets in the

Energy Sector Strategic Plan (ESSP) for 2018/2019–2023/2024.17 It distin-

guished between three subsectors: electricity, biomass and petroleum.18

Whereas, electricity and biomass are prioritised, petroleum is not. All

petroleum (including LPG) is imported from neighbouring countries and

so far, there is no evidence Rwanda has its own source. Rwanda’s ESSP

main target is reaching universal access to energy by 2024. Approximately

52 percent of energy generation should come from renewable energy

sources. The projected division between on-grid and off-grid access is 52

percent versus 48percent. Figure 4 shows that on-grid targets for the year

2018/19weremet.However,targetswerenotmetforoff-gridaccess,which

is fourteen percent at the moment instead of the projected 23 percent.

The main challenge is to reach low-income households in remote areas.

Figure 2.ACCESSTOELECTRICITYTOTALPOPULATION(SOURCE:POWERAFRICA,2019)

Figure 3.ENERGYCONSUMPTIONBYCONSUMERSINRWANDA(2016)

BIOMASS 85%

PETROLEUM 13%

ELECTRICITY 2%

11MinInfra:ESSP,2018.12AfricanDevelopmentBankGroup:AfricaEconomicOutlook,2020;WorldBank2020.13Productiveusersutiliseenergyforactivitiesthatenhanceincomeandwelfare.Examplesofproductiveusersarehealthandeducationfacilities,publicinfrastructure,andindustries(MinInfra:ESSP,2018).14HeadofInfrastructureSectionLénaïcGeorgelin,2020.15IEA(2019,p.36)definesaccesstoenergyforhouseholdswhen‘thehouseholdhasreliableandaffordableaccesstoelectricity(andcleancookingfacilities),whichisenoughtosupplyabasicbundleofenergyservices,andwiththelevelofservicecapableofgrowingovertime.Basicelectricityservicesaredefinedasowningasetofseverallightbulbs,phonecharging,aradioandpotentiallyafanortelevision.16IEA,2019.17MinInfra:ESSP,2018.18MinInfra:ESSP,2018.

Investment Opportunities in the Rwandan Energy Sector 7

In2020,Rwandahasan installedon-gridenergycapacityof224.6mega-

watt(MW)plusan installedoff-gridcapacityof19.95MW(mostly from

SHS).19 By 2023/24, the combined on-grid and off-grid capacity should

reach 556 MW, which includes a reserve margin of fifteen percent.20

The Rwandan on-grid generation capacity has tripled since 2010.

The current installed capacity of 224.6 megawatt comes from five

energy sources: 101 MW installed hydroelectric capacity, 60 MW

capacity from diesel resources, 31 MW from methane gas resources,

15.5 MW from peat resources and 12.5 MW from solar resources.

An additional 3.5 megawatt is imported from DRC and Uganda.21

Installed off-grid capacity is much lower than grid capacity. Off-grid elec-

tricity inRwanda is generated through SHS andmini-grids. The latter type

generates energy through solar PV or hydropower. In 2018, there were

27 companies distributing SHS and nine companies installing mini-grids.

Overall,theinstalledmini-grids(bothhydroandsolar)haveatotalcapacity

of250kilowatt (KW).22 The installed capacityof SHS,basedonanaverage

of 50 Watt (W) SHS is 12.7 MW. This is based on numbers from 2019.

Most investment opportunities for the private sector seem to exist in the

off-grid electrification. The Rwandan government is investing in on-grid

projects to raise the electrification rate. In remote, rural areas, it is too

expensive to establish grid connections and hence, innovative solutions

are required. The government has called upon the private sector to help

provide energy access for all Rwandan residents and businesses.23 Busi-

nesses can develop technologies and business models suited for these

challenging target groups in the electricity and biomass subsector.

Figure 4.PLANNEDCHANGESINON-ANDOFF-GRIDCONNECTIONS2018–2024(SOURCE:ESSP,2017)

%

%

%

0102030405060708090

100

0102030405060708090

100

0102030405060708090

100

New on-grid connectionsand share of on-grid access

2018/19

163,914

283,507

1.5

2018/19

2019/20

148,201

220,262

1.8

2019/20

2020/21

160,466

271,266

2.3

2020/21

2021/22

173,624

255,706

2.7

2021/22

2022/23

187,472

274,286

3.2

2022/23

2023/24

202,734

293,938

3.7

2023/24

New off-grid connectionsand share of off-grid access

Households connected (million) and share (%)

224.6 MW

101.07 MW 60.64 MW 31.44 MW 15.72 12.35

3.37DRC & Uganda

19REG,2019.20RDB,2017;USAID,2019.21REG,2019.22REG,2019.23MinInfra:ESSP,2018.24ThewebsiteofREG(2020)statesthe‘availablecapacity’(ratherthantheinstalledcapacity)iscurrently:88.41MWhydro(39%),43.07MWthermal(diesel)(19%),56.68MWmethanegas(25%),24.94MWimport(11%),4.53MWsolar(2%),9,07MWpeat(4%).ThedataregardinginstalledcapacitywascollectedduringaninterviewwithREG.

INSTALLED CAPACITY24

Investment Opportunities in the Rwandan Energy Sector 8

2. Stakeholders and enabling environment Three types of stakeholders can be distinguished in the energy sector,

namely:publicsector,independentpowerproducers(IPPs)andconsumers.

On-grid projects are generally large-scale investments managed by the

government(incollaborationwithaforeignIPP)andfundedthroughloans.

Theseprojectsincludetheconstructionofnewplantsaswellastheupgrading

of existingplants and transmission lines.Off-grid projects tend to be small-

scaleandarefrequentlyaid-basedimplementedbyIPPsinrural,remoteareas.

Please reviewAnnexe1 foranoverviewofcategorizeddonors foroff-grid,

on-grid and clean cooking. Please review Annexe 2 for an overview

of development organisations supporting energy projects in Rwanda.

NATIONAL ELECTRIFICATION PLAN

Thedivisionofgridandoff-gridconnectionsinRwandaisstrictlyregulated

by theNational Electrification Plan (NEP). TheNEP determines in a highly

detailed manner where grid connection lines have been and should be

installed.ThePlanshowsgrid linesarealreadypresentorplannedinmost

areas. By contrast, off-grid areas are scattered; mini-grid areas are also

scarcebecause thenumberofpermits is limited. In ‘gridextensionzones,’

investorsmust refrain from the instalment of off-grid connections.Hence,

the NEP clarifies in which areas IPPs can and in which areas they cannot

target potential customers. The NEP only distinguishes between grid and

off-gridareas.Hence, the typeofoff-grid source, amini-gridor SHS,does

notmatter.25 Thismeans thatoff-gridenergy suppliers ‘share’ theseareas.

25PersonalcommunicationGIZ,2020.26REG,2019.27REG,2019.

Figure 5.NATIONALELECTRIFICATIONPLAN2018

LEGENDUmuwalimu SACCO

Existing and ongoing MV

NEP Category

Crossed by MV

Grid Extension

Off-grid

Administratives

Waterbodies

National Park

District boundary

Sector boundary

20

19C

ON

NE

CT

ED

HO

US

EH

OL

DS

Southern Province26,27 31% + 16%

District of Kigali 65% + 2.7%

Investment Opportunities in the Rwandan Energy Sector 9

PUBLIC SECTOR

ThepublicsectoractorsaretheMinistryofFinanceandEconomicPlanning

(MinEcoFin)andMinInfra;policymakersshapingtheenablingenvironment.

MinEcoFin allocates the budget for energy investments and operations.

MinInfradevelopsenergypoliciesandtargets,whichmustbealignedwith

theSDGs.Subsequently,projectsareexecutedbytheRwandaEnergyGroup

(REG). REG is the national utility company in Rwanda and owned by the

government.REG is divided into twodepartments: EnergyUtilityCorpora-

tion Limited (EUCL) and Energy Development Corporation Limited (EDCL).

EUCLisresponsiblefortheoperationalisationandmaintenanceofgridconnec-

tion lines in Rwanda. They generate, transmit, and distribute energy to

customers.EDCLisinchargeofpublicinvestmentsinnewenergygeneration

projects. EDCL is themain contact forprivateenergy investors thatwant to

operateinthefieldofenergy,bothon-grid/off-gridandcleancooking.Rwanda

UtilitiesRegulatoryAuthority(RURA)setsthetariffsforenergypricesinRwanda.

Furthermore,EDCLdevelops theEnergyAccessRoll-outProgramme (EARP),

inwhichtheexpansionofaccesstoelectricityinRwandaisplanned.TheEARP

isfundedbytheRwandangovernmentanddevelopmentpartnerslikeAfrican

DevelopmentBank(AfDB)andtheEuropeanUnion(EU).Thereareadditional

non-governmentalfundssuppliedbygrantsorloansfromindependentdonors.28

INDEPENDENT POWER PRODUCERS

IPPsareofcrucialimportancetotheRwandangovernmentinhelpingto

achieveits2024goals.Thereareon-gridandoff-gridproducers.Thereare

only a couple of on-grid IPPs; foreign companies facilitating large-scale

grid investments. IPPshavesupportedthedevelopmentofthemethane

gasgenerationfacilityatLakeKivuaswellaslargesolarandpeatgeneration

sites.Bycontrast,off-gridelectrificationisdoneviaseveralsmallerprojects

scattered throughout the country by a variety of companies. Off-grid

IPPs aremostly involved in renewable energy projects: solar and hydro

power. There are also several IPPs involved in the clean cooking sector.

CONSUMERS

ConsumergroupsinRwandaarehighlydiverseintermsofconsumption

rates.Thisisthereasonwhytherearefixedelectricitytariffsfordifferent

consumergroups.Adistinctionismadebetweenresidential,non-residen-

tial(publicinstitutions,officesandhospitals)andindustrialconsumers.A

secondcategorisationismadewithinthethreeconsumergroupsonthe

basisofmonthlyconsumptionrates.Majordifferencesexistbetweenthe

charged tariffs for the low-income, low-demand households versus the

high-income,high-demandhouseholds.Moreover,small industrialusers

pay ahigherprice than large industrial users; businesses receivemajor

discountsonenergytariffsasaninvestmentincentive.29In2016,house-

holdsaccountedfor82percentoftotalenergyconsumptioninRwanda.

Figure 6.OPERATIONALFRAMEWORKENERGYSECTORRWANDA

Figure 7.ELECTRICITYTARIFFSFORDIFFERENTCONSUMERGROUPSIN2018–19AND2020(PRICEPERkWhinRWF)(SOURCE:REG,2020)

ECONOMIC CLUSTER

MINECOFINMinistry of Economics and Finance

MININFRAMinistry of Infrastructure

RURARwanda Utilities

Regulatory Agency

REGRwanda Energy Group

EUCLEnergy Utility

Corporation Limited

IPPsPrivate sector power

suppliers

CONSUM-ERS

EDCLEnergy Development Corporation Limited

BudgetTransferstoREGforinvestmentandoperations

Payments(Capacity+EnergyCharges)

Paymentviabilling

RegulatedbyRURA

Assets(Genertation,T&D)

Electricity Electricity

Small<22.000 kWh/year

INDUSTRIAL

NON-RESIDENTIAL

RESIDENTIAL

0–100 kWh

110134

87103

8094

204227

222225

8989

182212

210249

2018–19 2020

0–15 kWh

Medium22.000–660.000 kWh/year

Large>660.000 kWh/year

>100 kWh

15–50 kWh

>50 kWh

28MinInfra,2018.29Thesepricesarebasedonindustrialuserswithasmartmeter.Withoutasmartmeter,aflatrateischargedwhichincreasescostsperkWhwithapproximatelyfifteenpercent,2020.

Investment Opportunities in the Rwandan Energy Sector 10

Categorisation of residential consumers is based on their energy consump-

tion rates as well as the national social stratification system: ‘Ubudehe

categories.’ Ubudehe means ‘collective action and mutual support to solve

problems within a community.’ In the tier system, Rwandans are catego-

risedon thebasisof their socioeconomic status;one’s categorydetermines

the levelof supportprovidedby thegovernment.32Thereare fourUbudehe

categories; the first category includes the poorest people in society while

the fourth category is for the wealthiest members of society. Electricity

consumption rates are linked to the Ubudehe category: people in tier

four have the highest consumption rates (�load’) and use most appliances.

Table 1.LOADLEVELS,INDICATIVEELECTRICAPPLIANCESANDASSOCIATED

CAPACITYTIERS(SOURCE:RWANDABEYONDCONNECTIONS,2018)

Loadlevel IndicativeelectricappliancesCapacitytiertipicallyneeded

topowertheload

3–49 WTask lighting, phone charging, radio

50–199 WMultipoint general lighting, television, computer, printer, fan

200–799 WAir cooler, refrigerator, freezer, food processor, water pump, rice cooker

800–1999 WWashing machine, iron, hair dryer, toaster, microwave

2000 Wor more

Air conditioner, space heater, vacuum cleaner, water heater, electric cookstove

Average20.8 kWh/month30

URBAN29.2 kWh/month

RURAL9.9 kWh/month

2000 RWF~ 2.15 USD 4700 RWF

~ 5.05 USD31

Very low load

Highload

Low load

Very high load

Medium load

TIER 1

TIER 4

TIER 2

TIER 5

TIER 3

30Forthe‘RwandaBeyondConnections’reportbasedonthemulti-tierframework(WorldBankincooperationwithAfDBandUN),extensiveresearchwasdoneonelectricityconsumption,affordabilityandwillingnesstopayin2017.31WorldBank,2018.32GovernmentofRwanda,n.d.33LocalAdministrativeEntitiesDevelopmentAgency,2020.

1,902,800people

489,700households

People with no means to own or rent homes of their own and can hardly put food on the table.

4,721,000people

1,198,600households

People who have part time small jobs and either own cheap houses or are able to pay rent.

5,410,200people

1,187,700households

People who do not need help from the government for survival. They include farmers, professionals, and business owners.

152,700people

66,400households

People deemed to be rich such as government officials from the level of director upwards, and large business owners.

THE FOUR UBUDEHE CATEGORIES33

12 3 4

ENERGY CONSUMPTION

Investment Opportunities in the Rwandan Energy Sector 11

3. Major trends in on-grid electrifi-cation In 2020, Rwanda has an installed on-grid energy capacity of 224.6MW.34

Rwandan on-grid energy capacity has tripled since 2010. 52.5 percent

comes from renewable energy sources. The government expects on-grid

energy demand to peak around 2024, reaching 282–376 MW.35 Around

this time, the government expect on-grid capacity to be around 290MW

(52percentof thetotalcapacityof560MW). In2019,REGdevelopedthe

Least Cost Power Development Plan (LCPDP), which defines the genera-

tion extensionplans for 2019–2025. There are ongoing projects forwhich

construction has started.Most projects are still in the pipeline and some

projects are on hold because the funding phase has not been completed.

HYDROELECTRIC POWER

The total current installed capacity of all hydroelectric power plants in

Rwanda is 98.5 MW. About 45 percent of on-grid energy in Rwanda is

generatedbyhydroelectricpower.36Therearefive largeoperationalpower

plantswithatotalcapacityofaround73MW.Thelargepowerplantsarenot

workingonfullcapacityduetoseveralreasonssuchasweatherconditions

influencingwaterlevels.Thelargehydropowerplantsaregeneratingpower

from river runs and lakes, and their details are visible in themap below:

HYDROELECTRIC POWER

Figure 8.ON-GRIDGENERATIONMIXRWANDA2019(SOURCE:REG,2019)

Figure 9.INSTALLEDCAPACITYNATIONALGRID2009–2017(SOURCE:MININFRA,2018)

0

50

100

150

200

250

201720162015201420132012201120102009

MW

86 96 101112

131

164 164192

218

HYDROPOWER 45%

DIESEL 27%

METHANE 14%

PEAT 7%

SOLAR 5.5%

IMPORT 1.5%

Mukungwa I Power Station (Lake Ruhondo, Northern Province)

Coordinates:CM93+8XNyakinama,RwandaInstalledcapacity:12MWOperationalcapacity:6MWDateofinstallation:1982MAXOP

Ntakura Power Station (Lake Burera, Northern Province)

Coordinates:GQF2+34Ruhondo,RwandaInstalledcapacity:11.5MWOperationalcapacity:2.6MWDateofinstallation:1959MAXOP

Nyabarongo I Power Station (Nyabarongo River, Southern Province)

Coordinates:2J6M+G7Bulinga,RwandaInstalledcapacity:28MWOperationalcapacity:13.5MWDateofinstallation:2014MAXOP

Ruzizi II Power Plant (Ruzizi river, border Rwanda-DRC)

Coordinates:FVRG+73Bukavu,DemocraticRepublicoftheCongoInstalledcapacityforRwanda:12MW(43.8MWtotal)Operationalcapacity:10.7MWDateofinstallation:2017MAXOP

Rukarara Hydroelectric Power Station Coordinates:GHJ3+M8Kabacuzi,RwandaInstalledcapacity:9.5MWOperationalcapacity:3.8MWDateofinstallation:2011MAXOP

34REG,2019.35MinInfra,2018.36MinInfra,2018.

Investment Opportunities in the Rwandan Energy Sector 12

TotalRwandanpotential forhydropowerhasbeenestimatedat400MW.

Thedomesticpotentialis250MWandthereisanadditionalregionalpotential

of 150MWwhen the use of shared water resources is optimised. In the

coming five years, full domestic capacity of 250 MW should be realised

following thedevelopmentof newandmoreefficienthydroelectric power

plants. These projects will raise hydropower generation by 173 percent.

In the LCPDP, five large hydroelectric power plant projects arementioned

to be developed with a total MW capacity of 137.5 MW: Nyabarongo II

(43.5MW),RuziziIII(48.33MW),GiciyeIII(7.2MW),RukararaVI(6.7MW),

Rusumo(26.7MW)andBihongore(5.4MW).37,38Thefirstfourprojectsare

extensionsofcurrent installedplants.Additionally,31MWwillbe installed

through eighteen smaller and micro hydro projects; of which 7 MW will

be installed by IPPs in 2020.39Moreover, the LCPDP states existing power

hydro-plantswillremainoperational.However,thereisnoindicationinthe

planwhetherthegovernment isplanningto improvetheircapacityornot.

THERMAL POWER

Thermalpoweraccountsfor27percentoftotalenergycapacityinRwanda.40

Diesel is themainsourceused tomeetdemandduringpeakhours.Diesel

is relatively expensive because it is imported and inefficient,whichmakes

the generation of electricity costly. Industrial users are charged slightly

higher prices during peak hours. Improved affordability is expected when

extra supply is provided during peak hours following the completion of

new hydro and peat projects (rather than diesel). There are five thermal

powerplantsusingdiesel. The two largestplants are Jabana (phase1and2)

andSO-Energy,whicharebothsituatedinthedistrictofKigali.41Theyhave

an installed capacity of 27.8 and 30 MW respectively. No new projects

will be developed in the future. The Rwandan government is focusing

on renewable energy and moving away from diesel-generated power.

METHANE GAS

Rwanda has a unique source of energy: Lake Kivu where methane gas is

extractedtogenerateenergy.LakeKivuissituatedbetweenRwandaandthe

DemocraticRepublicofCongo(DRC)andconsideredasharedenergysource.

There is no other lake in theworld that containsmethane gas in the same

proportions. The high levels of methane are caused by the surrounding

active volcanic region. The total lake contains 60 billion m3 of methane

and it is estimated that a total of 700MW of electricity can be generated

over a period of 55 years.42 The total potential for Rwanda is 350 MW.

At the moment, there is one power plant on Lake Kivu located in the

Rwandan part of the lake. Kivuwatt is owned by a British company called

Contour Global and has been operational since 2015. The plant produces

26 MW over a period of 25 years, supplying the national grid of Rwanda.

The plant is running at full capacity. The construction of two additional

plants is planned raising total capacity of Kivuwatt to 75 MW.43 This

project is still in the pipeline. A second project is under construction at

Lake Kivu. Symbion, an American-based energy company, is constructing

a plant with a generation capacity of 56 MW over a period of 25 years.44

37REG,2019.38Twolargeplants,RusumoandRuziziIII,areregionalprojectsandthenumberofMWinbracketsisthecapacityassignedtoRwanda.39REG,2019.40REG,2019.41REG,2019.42DLAPiperAfrica,n.d.43ContourGlobal,n.d.44Symbion,n.d.

Investment Opportunities in the Rwandan Energy Sector 13

PEAT

Seven percent of energy is generated using peat. The first peat power

plant in Rwanda was completed in 2017; it was a pilot project and the

first of its kind in Africa. The plant is located in Gishoma, South-West

Rwanda and generates 15 MW electricity supplying the national grid.

A second, larger plant with a capacity of 72 MW is currently under

construction. The new power plant is located in Gisagara, Southern

Province and owned by Turkish Mining and Electricity company Hakan.

SOLAR

Only5.5percentofon-gridelectricityinRwandaisgeneratedbysolarpower.

Theinstalledcapacityforthegenerationofsolarpowerislow.Therearethree

powerplants:Jali(0.25MW),GigaWatt(8.5MW)andNashoSolarPP(3.3MW).

Thetotalinstalledcapacityisaround12MW.However,capacityonlyreaches

twentypercentonaverage,sincetherearenoenergystoragefacilities.Most

energy is needed during evening peak hours when there is no sunlight.

However,duetothelackofstoragesurplusenergycollectedduringthedayis

lost.Thegovernment-ownedNashoplantisasolar-poweredirrigationproject.

The largest plant, GigaWatt is running at the lowest capacity of 14 percent.

REG has announced the development of a new solar plant including

a storage facility, generating 30 MW of electricity. At the moment,

feasibility studies are being conducted. Moreover, REG acknowl-

edges the high potential of solar PV in Rwanda. Nonetheless, the focus

areas of the Rwandan government are hydro, methane and peat,

which can be explained by the short lifespan of solar infrastructure.

SOLAR POWER

PEAT POWER

Rwamagana Solar Power Station (GigaWatt)

Coordinates:X9FG+HVCollineNawe,RwandaInstalledcapacity:8.5MWOperationalcapacity:1.19MWDateofinstallation:2013MAXOP

Jali Solar Energy Plant Coordinates:4288+6GJali,Kigali,RwandaInstalledcapacity:0.25MWOperationalcapacity:0.04MWDateofinstallation:2007

MAXOP

Gishoma Peat to Power Plant (Western Province)

Coordinates:9WJP+RCGishoma,RwandaInstalledcapacity:15MWOperationalcapacity:14.25MWDateofinstallation:2017MAXOP

Hakan Peat to Power Plant (Southern Province)

Coordinates:GXG3+GXMuyaga,RwandaInstalledcapacity:72MWOperationalcapacity:68.4MWDateofinstallation:2020(planned)MAXOP

Nasho Solar PP

Coordinates:WP3R+9XMurundi,RwandaInstalledcapacity:3.3MWOperationalcapacity:0.66MWDateofinstallation:2017MAXOP

Investment Opportunities in the Rwandan Energy Sector 14

ENERGY IMPORTS

Energy imports are very small with 1.6 percent of the on-grid electricity

being imported fromUgandaandDRC.452MWofelectricity is importedvia

the Kawanda-Birembo High Voltage Power Transmission Line. This project

is part of the Nile Equatorial Lakes Subsidiary Action Program (NELSAP) of

East-African countries. The power line starts in Kawanda, Uganda and ends

inGasabodistrictinKigali.46ThisprojectisfinancedbyAfDBandJapanInter-

nationalCooperationAgency(JICA).3.5MWelectricity is importedfromthe

Ruzizi I power plant in DRC. This plant can generate 30 MW of electricity

andhasbeenoperational since1957.Theaimof theRwandangovernment

istophaseoutimportsfromDRC.Rwandadoesnotseektoincreaseenergy

importsinthefuturewiththeexceptionoftheregionalprojectsoftheNELSAP.

TRANSMISSION OF ENERGY

The transmission network transports generated electricity from the main

source to sub-stations, after which electricity is distributed to end-users.

ExistingtransmissionlinesinRwandaaremainly110kilovolt(kV)and220kV

andnewtransmissionlineswillsupportthesamevoltage.Between2010and

2017, the lengthof transmission lines inRwanda increased from462km to

744km.Moreover,therearesixteenplannedprojectstofurtherexpandthe

transmissionnetwork,forwhichfundinghasalreadybeensecured.Addition-

ally,therearetwentyprojectsinthepipeline,forwhichfundinghasnotbeen

secured. Theseprojects supportexpansionof transmission lines throughout

the entire country but the Kigali ring has been prioritised since 2016.

Transmission and distribution lines are not fully efficient: in 2018, capacity

losses were estimated to be around 22 percent. Goal is to reduce this to

fifteenpercentby2024.Tocompare:capacity losses intransmission lines in

theNetherlandswere4.8percentin2014,andglobalaverageis8.5percent.47

Annually,approximately22percentoftransmissionsarelost.Thefinancialcosts

arecurrentlyestimatedat28millionUSDandcan increase to102millionUSD

considering rapidly growing energy production and consumption rates.48

Losses are mainly caused by technical problems. Many transmission lines

consist of long medium voltage (MV) feeders, low voltage (LV) lines and

inefficient single-phase lines.49 Moreover, deficient planning results in

the incompatibility of lines or inefficient connections. Finally, poor work-

manship and old equipment are considered as major cause of technical

losses. Furthermore, there are also commercial losses resulting from faulty

accounting and record-keeping, theft and non-payment by customers.

Especially, non-payment by large customers causes major financial losses.

DISTRIBUTION OF ENERGY

Thewiringof theenergydistributionnetwork inRwanda is16,000km long,

of which 35 percent is covered by MV lines and 65 percent by LV lines.50

Currently, the distribution network has a suboptimal performance demon-

strated by the number of power outages each year. In 2016–2017, REG

customersfacedpoweroutagesfor36hoursonaverage.Theaimistoreduce

this number to fourteen hours by 2024.51 91.7 percent of grid-connected

householdsexperiencemorethanfourinterruptionsinelectricitysupplyeach

week.52Thisnumber includesbothurbanandruralareas,butoutagesseem

tooccurmoreoften inurbanareasbecauseof thegrid-connectiondensity.

The government has launched various projects to reduce power outages.

Several rehabilitation and expansion projects of the LV and MV networks

have started. 350 km of wiring will be added to the distribution network.

Thegovernmentisalsoupgradingsubstationslinkingtransmissionanddistri-

bution networks. Electricity connections for non-residential and industrial

users (public,commercialcentres, factories,hotelsandoffices)areprioritised

becausethemarginalcostsarerelativelylowincomparisontohouseholdsin

scattered,remoteareas.Moreover,residentialusersconsumealowamountof

electricity,whichreducestheincentivetotargetthisgroup.Thegovernment

aimstoconnectallproductiveusersby2022.Also,thedistrictsofHuyeand

Gisagarahaveahighprioritysinceaccesstoelectricityisverylowintheseareas.

FUNDING MECHANISMS

Thegovernmentmostly usesmixed fundingmechanismsblending govern-

ment, development partners and private investors resources to finance

transmission and distribution projects. The projects require large capital

investments, for which the government wants to involve development

partners and the private sector as well. Transmission projects are mainly

funded by the Rwandan government, AfDB and African Development

Fund (ADF). The biggest challenge is to mobilise funds for new trans-

mission projects. No funding has been secured for the 2020 projects

and this can result in severe delays; especially considering the impact

of the COVID-19 pandemic on economic growth around the world.

45REG,2019.46UETCL,2019.47WorldBank,2018.48MinInfra,2018.49MinInfra,2018.50REG,2019.51Thisnumberonlyconcernsofficiallyregisteredlong-lastingoutages.Additionally,manyRwandansexperience(short)outagesinrainyperiods.52RwandaBeyondConnections,WorldBank,2018.

Investment Opportunities in the Rwandan Energy Sector 15

GRID CONNECTION FEES

Consumption rates of both urban and rural households are insufficient

to publicly fund the cost of a grid connection. An average monthly

electricity consumption between 130–140 kWh is needed to break-

even.53 However, these high connection fees are also a major obstacle

for consumers. At themoment, thewillingness to pay (WTP) of uncon-

nected households is low, especially in rural areas (see figure below).

In 2017, connection fees were roughly 56,000 RWF (nearly 59 USD).

48 percent of customerswere notwilling to pay because the costs are

simply too high; connections fees are higher for consumers located

further away from the grid. The Rwandan government acknowledges

that the fees are a barrier to the target to quickly expand grid-access.

ELECTRIFIED HOUSEHOLDS

ELECTRICITY SERVICE

CONNECTION TO THE GRID:

ELECTRICITY USAGE:

AVERAGE MONTHLY CONSUMPTION IS 20.8 KWH

URBAN29.2 kWh/month

URBAN77.4%

RURAL9.9 kWh/month

81.3% of electrified households have

at least 8 HOURS of electricity supply a day,

at least 3 HOURS in the evening

49.6% receive electricity

23 HOURS a day, 7 DAYS a week

66.8% very low–load appliances

20.9% face VOLTAGE ISSUES(such as low or fluctuating voltage)

91.7%

more than FOUR electricity

DISRUPTIONS a week

RURAL15.6%

48.3%

2.4%

34.8%

14.4%

54.7%

36.5%

2.4% 2.0% 1.6% 2.8%

Figure 10.WILLINGNESSTOPAYFORAGRIDCONNECTIONINCREASESWHENPAYMENTISSPREADOVERTIME(SOURCE:RWANDABEYONDCONNECTIONS,2018)

Figure 11.OVERHALFOFUNCONNECTEDHOUSEHOLDSARENOTCONNECTEDTOTHEGRIDBECAUSEOFHIGHCONNECTIONCOST(SOURCE:RWANDABEYONDCONNECTIONS,2018)

willingtopay56,000RWFupfront

Connectioncostistooexpensive

Gridistoofar

Rent/landlord'sdecisionMonthlyfeeisexpensive

Other

Applicationsubmitted,waitingforconnection

willingtopay28,000RWFupfront

notwillingtopayatgiventerms

willingtopay56,000RWF(15,000–41,000over24months)

VOLT

53RuralElectrificationStrategy,MinInfra,2016.

Investment Opportunities in the Rwandan Energy Sector 16

4. Opportunities in on-grid electri-ficationInthepastyears,on-gridelectrificationhasbeenthemainfocusinRwanda

whereas the off-grid and clean cooking sector are still in the early stages

of development. Consequently, the on-grid sector has matured, energy

supply isplentifuland investmentopportunitiesare limited:manyprojects

are planned or ongoing. The installed capacity of MW will provide an

energy surplus following the completion of multiple large-scale national

and regional projects. Rwanda follows the regional trend of oversupply.

At this point, the government is not approving new projects nor signing

new contracts. The main challenge is the financing of the planned (and

ongoing) hydro and peat projects, which are at risk of being delayed.

Thereareopportunities in termsof improvingand layingout transmission

lines.REGisworkingontheimprovementoftransmissionlinesbutisinneed

ofinvestorsand/orinternationaldonorstoexpanditsoperations.Therefore,

opportunities exist related to infrastructure development and equipment.

Also, opportunities exist with regard to technical support, projects design

andtrainingoftechnicians.TheRwandangovernmenthascurrentlysixteen

transmission projects ongoing, which are partly funded by AfDB, EU and

theGermanNationalDevelopmentBank KfW.54 Transmissionprojectswith

anapproximatevalueof50millionareinthepipelineandrequirefunding.

Large-scale grid projects

• Atthemoment,therearenoopentenders.Suppliersmightbeableto

provideservicesorinputsforprojectssuchasequipment,consultancies

andtraining.Rwandangovernmenthasawardedninelarge-scale(>5MW)

projects and twelve small-scale (<5MW)projects to increase theMW

generation capacity in Rwanda. Two large-scale projects are regional

projectscollaboratingwithotherEast-Africancountries.

Transmission lines

• Thereareoverseventeenprojectsongoingaimingtoupgradeandexpand

the transmission line network. Several of these projects still require

funding.Opportunitiesexistinrealizingtheinfrastructuredevelopment,

providingequipment,technicalsupport,projectsdesignandtrainingof

technicians.

• Transmission network requires general improvement.MV and LV lines

needtobeshortenedtoreduceinefficiencyandlosses.

Substations

• Mostoperationalsubstationsareoutdatedandcausebadconnections.

Thenumberofoutages (which currently runat 36hours a year) can

bereducedthroughtheupgradingofsubstationsandimprovinglinkages

withthetransmissionnetwork.

• In remote areaswithpoor grid connections, productiveusers andor

public institutions could serve as substations. This would allow for

connectingcurrentlyoff-gridhouseholdsandimprovetheconnectedness

ofalreadyon-gridhouseholds.

Smart Meters

• Non-paymentratesofcustomersareratherhigh.Anopportunityliesinthe

distributionofsmartmeterstoavoidnon-paymentbylarge(r)customers.

• Accountingandrecord-keepingareaburdensometaskandtheprocesses

arepronetomistakes.Smartmeterscanreducefinancialerrorsresulting

frommiscalculations.

Awareness

• 6.5percentofelectricitygenerationislostduetocommerciallosses.

A large share of these losses is caused by illegally tapping electricity

fromthenationalnet.Companiescancollaboratewiththegovernment

toraiseawarenessontherisksofenergytheft. Illegallytappingenergy

canbeextremelydangerous,especiallywhenelectricityisdrainedfrom

MVorHVlines.

54Forthedistributionprojects,1,5milionUSDisprovidedbyMinEcoFin(Rwanda),73millionUSDbyAfDB,3.4millionbytheWorldBank,11millionbyEnabel.About46.4millionUSDstillneedstoberaised.

Investment Opportunities in the Rwandan Energy Sector 17

5. Major trends in off-grid electrifi-cationThe off-grid sector in Rwanda is developing but progress has not been

made as fast as in the on-grid sector. The off-grid sector should target

rural areas because of the low connection rates and high connec-

tion fees. Moreover, off-grid electrification is supposed to target

households rather than productive users. Only productive users located

800 meters or further from a grid infrastructure can be connected

to an off-grid source. The assigned areas for off-grid expansion are

visible in the NEP, which defines the target areas for off-grid sources.

Moreover, the Rural Electrification Strategy (RES) and NEP have

delegated the responsibility for off-grid development to IPPs.

The RES extensively describes the role of the private sector as

a key player and the possibilities to obtain financial support

from the government. The RES is divided into four programmes:

• Establishmentofamechanismtoallowlow-incomehouseholdstoac-

cessmodernenergyservicesthroughbasicsolarsystems;

• Establishmentofarisk-mitigationfacilityfortheprivatesectortomake

suresolarproductsareavailableonanaffordabletariffforthetarget

group;

• Developmentofmini-gridsbytheprivatesectorwithastrictoverviewof

thegovernment,whoidentifiessitesforthegrids,anddevelopmentof

financialframeworks;

• GovernmentcontinuestofocusonEARP.

After the launch of the RES and NEP, there was an impressive increase

in households, mainly rural, being connected to off-grid sources. This

rapid increase was mostly realised through SHS and to a lesser extent

by the more recent development of mini-grids. The government recog-

nises the high costs of off-grid electrification remain problem since most

target groups are low-income households with low consumption rates.

Looking at the existing policies and future plans, main focus is on the

development of SHS and more specifically, stand-alone solar systems.

SOLAR HOME SYSTEMS

The climate in Rwanda is suitable for SHS with slight seasonal variation:

daily solar irradiation ranges from 4 kWh/m2 in the north to 5.4 kWh/m2

in the south of the country.56 The Eastern and Southern Province have

the highest potential for solar power. There are different types of SHS

ranging from Solar Lighting System (SLS) powering two or more light

bulbs and have a phone charging capability, to SHS powering two or

more light bulbs and appliances such as a television, iron, microwave,

or refrigerator.57 Most Rwandans with an off-grid electricity connection

use a stand-alone SHS; there is no connection to the grid whatsoever.

CONNECTION TO AN OFF-GRID SOURCE55

BEFORE 20150%

201811%

201914%

55MinInfra,2018;REG,2019.56Get.Invest,n.d.57RwandaBeyondConnections,2018.

Investment Opportunities in the Rwandan Energy Sector 18

Businesses looking to enter the Rwandan market for SHS, should

follow strict governmental guidelines. All SHS on the Rwandan market

are required to meet certain minimum standards. Businesses need to

make sure their SHS product meets these criteria, which define ‘basic

access to energy.’ Otherwise, their product does not enable Rwanda

to achieve SDG 7. Systems which do not meet these standards cannot

be imported. A few examples of requirements are specified below:

• Quality of the system: systemsneed a proof of conformity recognized

under the International Electrotechnical Commission (IEC) Conformity

Assessmentand/orLightingGlobal;

• Technicalspecificationoflamps58,solarPVpanels59,andbatteries60;

• Warranty:productsbelowtier1(basicSLS)requireatleastone-yearwar-

ranty,tier1hasaminimumoftwo-yearwarranty(basicSHS),andtier2

andabovehasaminimumofthree-yearwarranty(moreadvancedSHS);

• Agreementbetweenpurchaserandsupplier:itneedstocoverresponsi-

bilitiesofbothparties,resolution/complainthandling,aftersalesservices

andatimeline.

The private sector has introduced innovative businessmodels to improve

financialaccessofhouseholdstoSHS.Servicemodelsseektoremovehigh

upfront costs for customers. In 2016, 55.5 percent of the Rwandan popu-

lation was living below the poverty rate earning 57–59 USD per month.

Meanwhile, the price range for amedium-size SHSwas 50–100USD. The

mainbusinessmodel isPayAsYouGo (PAYG): thismodality isused for96

percent of off-grid SHS sales.61 PAYG requires customers to make daily or

weekly instalment payments (usually) through Mobile Money (MoMo).

The SHS company has the ability to disable the system if the required

amount has not been paid.62 The PAYG system is designed to mitigate

risks associated with giving loans to customers with no credit history;

the prepaid system takes away the risk of non-payment of high costs.63

Nonetheless, it seems difficult to keep default rates and non-payment

low when households with lower and irregular incomes are reached.64

At the moment, SHS are distributed by both local and foreign private

sector investors.65 Many SHS companies are from Europe and North

America. Most SHS kits are produced in China. A Dutch company, NOTS,

is planning on moving assembly activities and subsequently, produc-

tion of SHS to Rwanda.66 Often these companies have received grants or

lenient loans from development organisations, larger private companies

or universities. Furthermore, the Rwandan government is developing

two financial schemes to raise household access to SHS: a subsidy

scheme targeting consumers and a support scheme targeting producers.

The SHS subsidy scheme for consumers is based on the Ubudehe cate-

gories. It targets households in tier 1, 2 and 3; no subsidies are provided

tohouseholds intier4and5.Most supportwill beavailable for themost

affordable SHS products developed for households in the lowest tier. The

supportplanswereannouncedin2019buthavenotbeenimplementedyet.

In addition to the subsidy scheme for consumers, the government

has developed financial support system for investors (IPPs) called the

Scaling up Renewable Energy Program (SREP) fund. This programme

has not yet been launched. It will offer the following ways of support67:

• Companies have access to riskmitigation facilities for SHSboughtby

householdsandproductiveusersinUbudehetiers2,3and4.68

• CompaniesinvestinginSHScanacquireloanstoinvestintheirSHSbusiness.

• HouseholdsinUbudehetiers2,3and4cangetaloanfromtheSavings

andCreditCooperatives(SACCO)tobuyaSHS.Loansarealreadybeing

provided.69

Figure 12.SOLARLIGHTINGPRODUCTSALESBYPAYMENTMODALITY(SOURCE:ENDEV,2018)

PAYGO 96%

UPFRONT SALES 4%

Figure 13.PLANNEDTARGETEDSUBSIDIESTOINCREASETHEAFFORD-ABILITYOFSOLARHOMESYSTEMS(SOURCE:MININFRA,2019)

UBUDEHE 3

UBUDEHE 2

UBUDEHE 180–90%

55–65%

30–40%

Range of subsidy level

58LED,>120lumens,2Wpowerconsumptionand>20,000lifetimehours.59CrystallineorPolySi,12/24/48Vandminimum12-WattPeak.60Deepcycle,maintenancefree,storagecapacityof60Whanddepthofdischargeof80percent.61EnDev,2018.62PowerAfrica,2019.63PowerAfrica,2019.64EnDev,2018.65ThefollowingSHScompaniesareactiveinRwanda:AptechAfrica(UG),Ared(IT/RW),Azuri(UK),BBOXX(UK),DASSYEnterprise(RW),DavisandShirtliff(RW),GreatLakesEnergy(RW),Ignite(UK/US),Mobisol(DE),Munyax(BE),NOTSsolarlamps(NL),RENERG(DE),ServeandSmileLTD(RW)andZola(US).66NOTS,2020.67MinInfra,2019.68Facilitieswillbe(partly)fundedbytheSREP.SREPhasatotalbudgetof50millionUSDfundassignedtoruralelectricityaccessexpansion.69ItisexpectedhouseholdsinUbudehetier2and3willnolongerneedloansoncethesubsidyschemeisintroduced.HouseholdsinUbudehetier4cannotmakeuseofthesubsidyschemeandcancontinuetoaccessloans.

Investment Opportunities in the Rwandan Energy Sector 19

An upcomingway by companies to finance off-grid electrification projects

is international crowdfunding. In this way, companies raise the initial

funds required to produce a high number of SHS systems, which can be

donatedtolowincomehouseholds.Thistrendhasbeenvisiblethroughout

East Africa. In 2018, 19 USDmillion of funding for SHS in East Africawas

supplied through crowdfunding, compared to 2.5 USD million in 2017.70

The main issues that arise with SHS are the limited purchasing power,

customers’ lack of understanding of the credit system, remaining uncer-

taintyamongthepopulationwithregardtothepotentialconstructionofgrid

connections, and increasing competition enabling customers to switch to

cheaper alternatives.71 These issuesmake it difficult for companies in SHS

tobecomeprofitable.ThefirstSHScompaniesenteredtheRwandanmarket

in 2014 and only recently in 2019–2020, some managed to break even.

MINI-GRIDS

There are three types of mini-grids: solar power, hydropower and

diesel. The latter is the least popular because of the limited supply of

diesel in remote areas, high operational costs and fossil fuel emissions.

Therefore, theRwandan government encourages private sector investors

to develop hydro and solar mini-grids. Mini-grids are considered a

potential source of energy for households and businesses located in

the most remote areas. These consumers are highly unlikely to get a

grid connection. Companies needed to wait for the finalisation of the

NEP, in which the zones for mini-grid development were determined.

Nowadays, mini-grid permits are still limited and expensive.72 It is obliga-

tory for companies to do extensive market research to assess potential

customers’ electricity demand prior to the installment of a mini-grid.

Themarketofmini-gridsupplyinRwandaisstillintheearlystagesofdevel-

opment. Thereare currently six companiesoperating inRwanda (Table2).

Mini-grid development requires a high initial investment and seemsmore

financially challenging in comparison to SHS in Rwanda. Installment and

material costs are high, whilst energy consumption rates and number of

customersare low.Thepriceof amini-gridproducingone kW range from

4,000–7,000 USD (including installment and transportation) and costs

per customer range from 250–650 USD.73 Some companies manage to

reduce costs per consumer connecting more households to a mini-grid;

MeshPower has connected on average 35 households to one mini-grid.

Table 2.MINI-GRIDCOMPANIESOPERATINGINRWANDA(SOURCE:ENDEV,2018)

Company Technology Location SizeNo of households connected

Grant support Headquarter locations

Neseltec Solar Kirehedistrict 30kW 183 EEP Rwanda

ECOS Hydro Muhangadistrict 11kW 303 EnDev Rwanda

RENERG Solar Nyamashekedistrict 30kW 121 USADF Germany

MeshPower SolarMultipleinBugeseraandNgomadistricts

1kWeach,57sites

2,046 EEP&EnDev USA

MeshPower Solar Bugeseradistrict 4kWAC/DC 78 None USA

Absolute Energy Solar Gatsibodistrict 50kW 505 EnDev UK

ARC Power Solar Nyamata,Bugeseradistrict 20kW 200RenewableEnergyPerformancePlatform(REPP)

UK/Rwanda

ARC Power Solar Nyamata,Bugeseradistrict 40kW 290RenewableEnergyPerformancePlatform(REPP)

UK/Rwanda

70PowerAfrica,2019.71EnDev,2018.72RURA,2015.73EnDev,2018.Thisnumberisbasedonanaveragemonthlyconsumptionof1kWhperruralhouseholdinRwanda.

Investment Opportunities in the Rwandan Energy Sector 20

Nonetheless, it seems unlikely mini-grid electricity will be affordable for

low-income households in the absence of government subsidy schemes

or other (donor) financing systems. The two main mechanisms used to

finance mini-grid development in Rwanda are grants and debt financing.

Most companies finance their operations through grants, which cover

40-70 percent of the investment costs. Grants are a type of results-

based financing (RBF) creating an initial risk for mini-grid developers.

Furthermore,theRwandangovernmenthasdesignedasubsidyandfinancial

support system formini-grids in the RES. The systemwould provide risk

mitigationfacilitiesformini-gridinvestors,targetinglow-incomehouseholds

andproductiveusers.74Companieswillhavethepossibilitytoacquireloans

toinvestintheirmini-gridbusiness.Whenamini-gridprojectisunsuccessful,

the government shares the risk of failure with private investors (IPPs).75

For example, amini-grid projectmight fail due to environmental reasons:

the source of a mini-hydro source can run dry following changing rain

patterns.Thissubsidyandfinancialsupportsystemhasyettobelaunched.

Solar mini-grids and nano-grids are ‘standalone’ energy distribution

networks powered by solar panels. Standalone means they are not

connected to the national grid.76 A major advantage of solar mini-grid

systems is the flexibility: they can be installed anywhere with suffi-

cient solar potential. The greatest disadvantage is the short lifespan of

solar panels, which need to be replaced approximately every ten years.

Currently, there are six sites with solarmini-grids and 57 sites with nano

mini-grids.77 In total, these mini-grids connect 3,726 households. 1 kW

nano-grid systems can supply an average of 35 households. Full potential

of 1 kW per hour (kWh) can be reached under optimal circumstances.

Hydro mini-grids or pico-hydro78 grids are powered by a source of water

withasufficient,constantflowofwater.Atthemoment,thereisoneopera-

tionalhydromini-gridinRwandaconnecting303households.Theadvantage

of hydromini-grids is the long life-span and lowmaintenance. The disad-

vantages are the dependence on high material costs, logistics and water

(rainfall). The latter disadvantage is most problematic: climate change

seems to result in shorter, more intense intervals of rainfall in Rwanda.

74MinInfra,2019.75Facilitieswillbe(partly)fundedbytheScalingUpRenewableEnergyPrograminLowIncomeCountries(SREP).SREPhasatotalbudgetof50millionUSDfundassignedtoruralelectricityaccessexpansion.76Nano-gridscangenerate1kWorless,andmini-gridsgenerateabove1kWelectricity.77All57nano-gridsweredevelopedbyMeshPower.78Pico-hydrogridsarethosemini-gridswithapoweroflessthan5kW.

Investment Opportunities in the Rwandan Energy Sector 21

6. Opportunities in off-grid electri-ficationThere aremajormarket opportunities in off-grid electrification in Rwanda

considering the urgent need to connect a high number of remote house-

holds: so far only fourteen percent of the Rwandan population has been

connectedtoanoff-gridsource,meaninganother34percent(approximately

1.2million households) still need to be connected by 2024. Furthermore,

the government has put the private sector in the driving seat to realise

quick expansion. Nonetheless, it remains a challenge to provide low-in-

come households in remote, rural areas with access to energy. Themain

issues hampering the rapid distribution of SHS andmini-grids are the low

purchasing power and energy consumption rates of Rwandan customers.

Eventual returns on investment remain unclear. Some SHS companies

have managed to break-even after 5–6 years of operations in Rwanda.

Allmini-grid companies are still dependent on loans and grants.However,

there are planned and ongoing government and donor programmes to

provide low-income households with access to energy via SHS or mini-

grids. Off-grid electrification is a domain of aid and trade solutions.

Innovative concepts are needed taking a multi-stakeholder approach

engaging the private sector, government and development organizations.

SOLAR HOME SYSTEMS

Product development

• In2016,55.5percentoftheRwandanpopulationwas livingbelowthe

povertyrateearning57-59USDpermonth.Meanwhile,thepricerange

foramedium-sizeSHSsoldonthelocalmarketwas50–100USD.

ͷ Improvethecost-efficiencyofSHSproductsandespecially,reduce

operatingexpensestoincreaseaffordability.

• MosthouseholdsareunabletoaffordtheirownSHS,buttheymightbe

abletoshareone.

ͷ ExploreopportunitiestocreateSHSthatcanbesharedbymultiple

householdsintermsofdesignandbusinessmodel.

• Thereareproductiveusers(suchasshopsandsmallfactories)whocan

purchasehigherelectricitygeneratingSHSkits.Theseuserscouldserve

asahostandprovidesurroundinghouseholdswithelectricityservices.

ͷ Identifyunconnectedproductiveusers,whocouldbecomehosts

forsurroundinghouseholds.

Local production

• MostSHSkitsarecurrentlybeingsourcedfromChina.Onecompanyis

investigating the option to set up a local assembly or production line.

Preferencefor ‘madeinRwanda’productscanprovidecompanieswith

accesstoinvestmentincentives.

ͷ ExploreopportunitiestoassembleorproduceSHSkitslocally.

• TherearesafetyissueswithaffordableSHSkitsonthemarket:stronger

equipmentandwiresareneededtoimprovethequalityofsystems.

ͷ DevelopstrongerSHSproductsfocusingonwiring.

Electricity Storage

• Mosthouseholdsdonothaveaccess toenergystorage facilities,while

energyconsumptionratespeakatnight.

ͷ Explorewaystoimprovestoragecapacityandtoenablethesharing

ofstoragecapacityamongneighborsorproductiveusersnearby.

Investment Opportunities in the Rwandan Energy Sector 22

Payment method

• WTPforSHSincreaseswhenhouseholdsareallowedtopayininstallments.

ͷ UseinnovativebusinessmodelsbasedonaPAYGsystemorprovide

micro-loanstohouseholds.

• Customerloyaltyislimited,whichresultsinhightransactioncosts.

ͷ Improvecontractsandcustomerrelationstoavoidcustomersfrom

switchingtocompetitorswithoutnotice.

Financial model

• Householdsareunable topay theactualpriceofSHSand thegovern-

menthaslimitedoptionsofsupport.Start-upandoperationalcostscan

potentially be coveredbydonors, private investors, universities. These

actorshaveprovedareliablesourceofincomeforothercompanies.

ͷ Tapintoalternativefinancialflowstosupportthebusinessmodel.

• Crowdfunding is an upcoming financing source, which has recently

gainedpopularity.Companiesraisetheinitialfundsrequiredtoproduce

ahighnumberofSHSsystems,whicharesubsequentlydonatedtolow

incomehouseholds.

ͷ Launchacrowdfundinginitiativetoscaleupabusiness.

• SREPfundandUbudehesubsidieswillbelaunchedsoonprovidingfunds

toreachlow-incomehouseholds.

ͷ Benefit from financial support provided to SHS companies and

consumers.

MINI-GRIDS

Product development

• InternationalmarketpricesofsolarPVpanelsarefalling.Opportunities

inthemini-gridsectoraregrowingforcompaniesthatmanagetoreduce

theirproductioncosts.

ͷ Improvecost-efficiencythankstoreducedcostsofinputs.

• Developpartnershipstrategiesbetweencompaniestolowerthecostof

mini-griddevelopment.

Production and installation

• Productioncostsformini-gridsarecurrentlyveryhigh.

ͷ Exploreopportunities for producing kits andmini-grids locally to

reducecosts.

• Installationandmaintenancecostscanbereduced followingthe in-

creasingavailabilityofskilledtechniciansinRwanda.

ͷ Providetrainingtoincreasethenumberofqualifiedtechnicians.

Payment method

• Themostsuitablepaymentmethodsforhouseholdsconnectedtoamini-

gridarePAYGandpaymentsininstallments.

ͷ Introduceflexibletariffsthatallowcustomerstoswitchtohigher

orlowertariffswhenevernecessarytoreducenon-paymentrates.

Financial model

• Financingofmini-gridswilllikelyrequireblendedpublic,donorandpri-

vatefunds.Closecollaborationwithgovernmentinstitutionsanddonors

isneededtodesignsuitableblendedfinancemechanismsandmitigate

investment risks. The Rwandan government iswilling to guarantee for

around50percentoftheinvestmentincaseoffailure.

ͷ Tapintoblendedfinancetofundmini-griddevelopmentengaging

donors,publicandprivateactors.

• Today’s competitivemarketmakes it difficult to generate investments.

Hence,itisnecessarytolookintoalternativefinancingmechanisms.

ͷ Usecrowdfundingtoraisethefinanceforthemini-grid.

• Mosthouseholdscannotaffordthehighenergyprices.Financialsupport

forSHScompanieswillbecomeavailableviatheSREPfund(expected

in2021)andcanreducecostsforhouseholds.SREPwillfundamaximum

of37percentoftotalfinancingcosts.

ͷ Benefit frompublicfinancial supportprovided toSHScompanies

andconsumers.

Investment Opportunities in the Rwandan Energy Sector 23

7. Major trends in clean cookingSDG7 ‘access to affordable, reliable, sustainable and modern energy’ also

includes access to clean cooking facilities. The transition to clean cooking

is important because traditional cooking has a severe negative impact on

thenaturalenvironmentandpublichealth.Traditionalcookingrequiresthe

use of biomass,mostly firewood and charcoal, of which the sourcing is a

majorcauseofdeforestation.79Also,biomass isahighlypollutingand inef-

ficient energy source causingup to 25percent of black carbon emissions.

Moreover,traditionalstovescausehouseholdairpollutionandposesecurity

risks;especiallyforwomenwhopreparethefamilymeals.Cookingfacilities

are qualified as ‘clean’ on the basis ofWorld Health Organization (WHO)

standardsforhouseholdairpollutionlevelsbasedontheemissionlevelsof

particulatematterandcarbonmonoxide.Availableoptionsforcleancooking

includeelectricity,gas,ethanol, solarandhighperformingbiomassstoves.

Traditionally, Rwandans only used wood as their cooking fuel. Between

1990 and 2005, the use of wood was 60 percent.80 Moreover, Rwandans

consume a high amount of beans,which have a long cooking time. There

isstill littleawarenesswithregardtothehealthproblemscausedbytradi-

tionalcookingpractices.Nowadays,eventhoughalternatives likeLiquefied

Petroleum Gas (LPG) are available on the market, people still prefer to

use wood because of tradition. This is especially the case in rural areas.

At thismoment,98percentof theRwandanpopulationstillusesbiomass for

cooking:wood,charcoalanddung.8191percentofhouseholdsstillrelyonthe

most inefficient type of biomass: firewood, which households collect every

day for 40-80 minutes. On average, households consume around 1.8 tons

offirewoodperyear.82Thetotalvalueofwoodusedforcooking isdifficult to

measurebecauseitisgatheredratherthanbought.80percentoftheRwandan

populationusescharcoalascookingfuel.Themarketofcharcoal(about150.000

tons)accountsfortwopercentofGDP,withatotalvalueof50millionUSD.83The

Rwandangovernmentaimstoreducenumberofhouseholdsdependentontradi-

tionalcookingtechnologiesbyfiftypercentby2024.84Furthermore,MinInfrahas

developedtheBiomassEnergyStrategytoreducetheamountofbiomassused

inRwanda.Thestrategyfocusesontheimprovedmanagementofwoodbiomass

resources, promotion of alternative fuels and efficiency of biomass usage.

79InRwanda,deforestationcauseserosion,landslidesandfloods.80NationalTreeFoundation,n.d.81FAO,2019.82FAO,2019.83GlobalAllianceforCleanCookstovesRwandaMarketAssessmentSectorMapping,2012.84MinInfra,2018.

Figure 14.CHANGESINBIOMASSUSEANDALTERNATIVEFUELACCESS2018–2024(ESSP,2017)

0

20

40

60

80

100

500000

1000000

1500000

2000000

2500000

100000

200000

300000

400000

2018/19 2019/20 2020/21 2021/22 2022/23 2023/24

2018/19 2019/20 2020/21 2021/22 2022/23 2023/24

Householdsusing firewood

Householdsusing alterna-tive fuels

Householdsmoved offfirewood

Investment Opportunities in the Rwandan Energy Sector 24

TherearemanytypesofImprovedCookstoves(ICS)ofvaryingqualityinterms

ofhealthandsafetystandards.TheGlobalAllianceforCleanCookstoves(GACC)

hasdefinedtiers(0-5)torankthequalityofstovesbasedontheWHOguide-

lines. Tier0 stovesareof the lowestquality includingfirewood stoves. Tier5

stovesarethehighestqualityincludingLPG,solarandelectricstoves.Improved

biomasscookingstovesbelongintier4:onlytier5stovesareconsideredclean

onthebasisofWHOguidelines.Nonetheless,tier4stovescanbeusedastran-

sitionalsolutionsbeingmuchsaferthantraditionalstoves.85Thereplacementof

biomasswithalternativecleancookingfuels(LPGandelectricity)isusuallytoo

expensiveforthelow-incomegroups.Only6.5percentoftheRwandanpopu-

lationcurrentlyusesdifferent typesofstovesmixingbiomassandclean fuels.

In Kenya, the uptake of ICS has beenmuch faster (Figure 16). This increase

can be explained by the fact that Kenya is a LPG-producing country, which

makes LPG distribution cheaper and widely available. Moreover, the usage

ofPay-As-You-Goand smartmeters for LPG is widespread,whichmakes this

fuelmoreaffordable for low-incomegroups.Kenyaalsohasmultiple factories

where ICS are being produced. Also, there is an ICS testing centre in Kenya

where official certificates are obtained for produced cookstoves. Rwandan

producers have to send stoves to Kenya for testing to obtain certification.

Figure 16.ACCESSTOCLEANFUELSANDTECHNOLOGIESFORCOOKING(%OFPOPULATION)(SOURCE:WORLDBANK,2019)

Figure 15.SEGMENTATIONOFANNUALCHARCOALMARKETVALUEIN2008(MILLIONUSD)

Retail6.6 million USD

Transport19.7 million USD

Remains in rural areas26.3 million USD

85GACC,2019.

Above: Firewood-based ICS from BURN Kuniokoa (Kenya, USA) on the left; Charcoal-based ICS from Ecozoom (Kenya, USA) on the right.Below: Charcoal-based ICS from GGS (Geni Green Solutions, Rwanda)

Investment Opportunities in the Rwandan Energy Sector 25

ATTRIBUTES TIER 0 TIER 1 TIER 2 TIER 3 TIER 4 TIER 5

COOKING EXPOSURE

Emission: Fuel Firewood,dung,twigs,leaves,ricehusks,processedbiomasspelletsorbriquette,charcoal,kerosene

Biogas,ethanol,highqualityprocessedbio-masspelletsorbriquettes

Electricity,solar,LPG

Emission: Stove design

Three-stonefire,tripod,flatmudring,traditionalcharcoalstove

ConventionaloroldgenerationICS

ICS+chimney,rocketstoveorICS+insulation

Rocketstovewithhighinsulationorwithchimney,ad-vancedinsulationcharcoalstoves

Rocketstovewithchimney(wellsealed),rocketstovegasifier,advancedsecondaryaircharcoalstove,forcedair

Ventilation: Volume of kitchen

Lessthan5m3 Morethan5m3 Morethan10m3 Morethan20m3 Morethan40m3 Openair

Ventilation: Structure

Noopeningexceptforthedoor

1windowMorethan1window

Significantopenings(largeopeningsbeloworaboveheightofthedoor)

Verandaorahoodisusedtoextractthesmoke

Openair

Ventilation level Bad Average Good

Contact time

Morethan7.5hours

Lessthan7.5hours

Lessthan6hoursLessthan4.5hours

Lessthan3hoursLessthan1.5hours

Bad Average Good

COOKSTOVE EFFICIENCY

ISO's voluntary performance targets (TBC)

Lessthan10% Morethan10% Morethan20% Morethan30% Morethan40% Morethan50%

CONVENIENCE

Fuel acquisition (through collec-tion or purchase) and preparation time (hours per week)

Morethan7hours Lessthan7hours Lessthan3hoursLessthan1.5hours

Lessthan0.5hour

Stove preparation time (minutes per meal)

Morethan15minutesLessthan15minutes

Lessthan10minutes

Lessthan5minutes

Lessthan2minutes

SAFETY OF PRIMARY COOKSTOVE

Seriousaccidentsoverthepast12monthsNoseriousaccidentsoverthepastyear

AFFORDABILITY Levelizedcostofcookingsolution(fuel)morethan5%ofhouseholdincomeLevelizedcostofcookingsolution(fuel)lessthan5%ofhouseholdincome

FUEL AVAILABILITY Primaryfuelavailablelessthan80%oftheyear

Primaryfuelisreadilyavailable80%oftheyear

Primaryfuelisreadilyavailablethroughouttheyear

Figure 17.MULTI-TIERFRAMEWORKFORICSANDCLEANCOOKINGALTERNATIVES(SOURCE:RWANDABEYONDCONNECTIONS,2018)

Investment Opportunities in the Rwandan Energy Sector 26

Table 3.TIERPERFORMANCETARGETSFORCOOKSTOVES(SOURCE:GACC,N.D.)

TierThermal Efficiency

(%)

Carbon Monoxide Emissions

(gram/megajoule delivered)

Fine Particu-late Matter Emissions

(milligram/megajoule delivered)

Safety(score)

Durability(score)

5 ≥ 50 ≤ 3.0 ≤ 5 ≥ 95 < 10

4 ≥ 40 ≤ 4.4 ≤ 62 ≥ 86 < 15

3 ≥ 30 ≤ 7.2 ≤ 218 ≥ 77 < 20

2 ≥ 20 ≤ 11.5 ≤ 481 ≥ 68 < 25

1 ≥ 10 ≤ 18.3 ≤ 1031 ≥ 60 < 35

0 < 10 > 18.3 > 1031 < 60 > 35

Rwanda already has a group of ICS suppliers.86 The government works with

several supplierswhose product quality ranges from tier 1 to 5.87 Businesses

arerequiredtopresentacertificatestatingthequalityofthestoves.88Themain

targetof thegovernment is to reduce thenumberofhouseholdsusing tradi-

tionalcookingstoveswhilstraisingthenumberofhouseholdsusinganimproved

biomasscookstove.Improvedbiomasscookstovesaremoreenergyefficientand

producinglessemissions.Thegovernmentappealstotheprivatesectorforthe

distributionof ICS recognising themajor role of businesses to reachbiomass

reductiontargets.TheobjectiveofRwandaistodistribute300,000ICSperyear.

Themainissueforthedistributionistheaffordabilityofthestoves.Businesses

shouldcarefullyconsidertheaffordabilityoftheirproduct(stove)andcooking

fuel.Householdsspendingthemosttimecollectingcookingfuelsaweek(around

130minutes)aremostwillingtopayforabiomass-basedimprovedcookstove.89

However, households are only able to spend approximately 3,000 RWF

(3.20USD).90Moreover,companiesneedtodevelopalternativebusinessmodels

or acquire external financial support because most households are unable/

unwilling topayupfront. Thereare severaloptions: installmentpaymentsare

themost common.Companieshavealsoexperimentedwithfixedpurchasing

agreementsofinputs;pelletsorbriquettes.CompaniessellingICSusingpellets

orbriquetteswill likelyneedtosetupafactorytoproducethesethemselves.

Consideringthesechallenges,thedistributionofICSwillrequireclosecollaboration

betweenthegovernment,developmentpartnersandprivatesector.Theobjective

oftheRwandangovernmentistodistribute300,000ICSperyear.Itappealsto

theprivatesectorforthedistributionofICSrecognisingthemajorroleofbusi-

nessestoreachitsbiomassreductiontargets.Hence,thegovernmentislooking

intooptionstoprovide(financial)supporttocustomersand/orsuppliers.Future

supportwill likelybeprovidedonthebasisofthetargetgroupandassociated

Ubudehecategories.Also,thegovernmentdesignsincentivesforthosecompanies

willingtoproducelocallyorthatarewillingtomoveitsheadquarterstoRwanda.

Table 4.NUMBEROFINCREASEINICSEACHYEAR(2017/18ISBASEYEAR)(SOURCE:MININFRA,2018)

Year ICS

2017/18 1,839,684ICSdisseminated

2018/19 137,219ICSdisseminated

2019/20 293,191ICSdisseminated

2020/21 315,490ICSdisseminated

2021/22 339,127ICSdisseminated

2022/23 364,112ICSdisseminated

2023/24 390,544ICSdisseminated

86Twocompanies,IgniteandGeniGreenSolutions,areoperatinginRwanda(anduntilrecentlyInyenyeri).Thereareseveralothercompanies,whicharestillintheir‘initiation’phase.87Nofurtherinformationonthesesuppliersisavailablewhenwritingthisreport.However,twoinvestors,GGSandSNVwereinterviewed.SNVisaDutchNGOexploringopportunitiesintheICSsector.GeniGreenSolutionsisaKigali-basedcompanysellingtier1–2ICSespeciallyinGasabodistrictinKigali,witharound6000customersatthemoment.88LocallyproducedstovesneedtobetransportedtoKenyasincethisisthenearestplacefortestingthequalityofstovesandacquiringacertificate.89Surveyincluded45householdslivinginKigali.90RwandaBeyondConnections,WorldBank,2017.

Investment Opportunities in the Rwandan Energy Sector 27

8. Opportunities in clean cooking

Product development

• ManyICScompaniestargettheuppermarketsegment,whilst,low-income

householdsareunabletoaffordtier4and5stoves.Amarketentrywith

analternative,improvedtier0–3cookingstoveprovidesalargercon-

sumerbase.Thesestovescanofferatransitionalsolution.

ͷ Developnewaffordableproductsforlow-incomehouseholds.

ͷ Upgradeexistingproductswithinsulationtoincreaseheatefficiency.

ͷ Sellsecond-handproducts.

• ExistingICSarestillproducedathighcostperunit.Themostcost-efficient

productscancountonthehighestsubsidiesfromtheRwandangovernment.

ͷ Attempt to reduceproductioncostsusingsecond-handmaterials

andfocusingonhighvolumesproducinginbulk.

• Companiescanfocusonsellinglessefficientstoves(WHOtier1–3).

Alternative cooking fuels

• Availabilityofpelletsandbriquettesislimited,andthesefuelsaresome-