OPPORTUNITIES FOR INVESTMENT IN RETAIL SECTOR IN EMERGING ECONOMIES

21

OPPORTUNITIES FOR INVESTMENT IN RETAIL SECTOR IN EMERGING ECONOMIES Ashish Deshpande Sufiyan Sarguroh MMS MMS [email protected] [email protected] 9769138482 7208850965 Sydenham Institute of Management Studies, Research and Entrepreneurship Education (SIMSREE), Churchgate

Transcript of OPPORTUNITIES FOR INVESTMENT IN RETAIL SECTOR IN EMERGING ECONOMIES

OPPORTUNITIES FOR INVESTMENT IN RETAIL SECTOR IN EMERGING ECONOMIES

Ashish Deshpande Sufiyan Sarguroh

MMS MMS [email protected] [email protected] 9769138482 7208850965

Sydenham Institute of Management Studies, Research and Entrepreneurship Education

(SIMSREE), Churchgate

Abstract:

This paper presents the investment opportunities in the retail sector in the emerging

economies through retrospective tracking of their past experiences and opportunities in the

future. The paper analyses the reforms and trends that drove growth in the emerging

nations' retail markets and the ones that need to be embraced to sustain and accelerate the

growth in the future. The focus of the paper would be the BRICS economies with a brief

outlook of other economies like Singapore, Indonesia inter alia.

Allowance of foreign investment in the retail sector boosted its volume tremendously in

Russia and China and triggered a development of sorts that led to flourishing of foreign as

well as local players in the same, providing impetus to the rise in the retail market volume.

Brazil developed its retail market by taming inflation and making credit easily available.

South Africa improved its distribution networks efficiently causing an improved supply chain

management and also cashed in on its demography by catering to the needs of its

predominantly young population. Indian retail sector thrives mainly on the unorganized

sector with organized sector forming a minor chunk of about 8%.

The paper analyses how investment in technology, infrastructure and appropriate reforms

can fuel the growth of retail market. With abundant opportunities in the virtual world,

adopting ecommerce or getting into online retailing, coupled with lowering of transaction

costs for the same, will make room for higher profitability and a wider consumer base.

Investments in the hypermarkets and supermarkets have provided boost in retail sales in

the past and still have potential to do the same, with cut throat competition in this sector

for acquiring the crème de la crème of real estate. Development of cold chains is the need

of the hour in India to prevent food wastage. A sound transportation infrastructure has the

capability to transform the retail scenario of nations like India and Brazil by improving its

supply chain management. A good transportation network simultaneously results in up

gradation of nation’s infrastructure, gives an impetus to the automobile industry and has

similar positive implications for many parallel industries. Strategic investments in

development of the SMEs can yield the retailers an assured supply coupled with significant

margins.

Policy decisions too can be a major game changer in this field. Allowance of FDI is expected

to get in retailing giants across the world to invest in here which can translate into

expansion of the organized retailing in India, which yields benefits for the farmers,

consumers and SMEs. Improved taxation, such as implementing GST, reduces the pecuniary

burden on the businesses. Cutting down on unnecessary bureaucracy, which is high in

nations like India and Russia, can result in transparent and smoother operations.

This paper will focus on the aforesaid aspects through a qualitative and quantitative analysis

of the same, backed by primary and secondary research.

Executive summary:

The paper deals with the retail scenario of the five emerging economies – Brazil, Russia,

India, China, and South Africa. The retail sector transition experienced by these nations has

been phenomenal with high potential present for further growth. Each of the economies

has had certain strong practices and some weaknesses prevalent. By focusing on its

strength, reducing weaknesses, learning from other successful retailers and adopting as

early as possible to the modern practices, the retail sector of these nations can develop to

the optimal extent at a time when opportunity availability for market expansion is

abundant.

MOTIVATION

The retail sector has been one of the most lucrative sectors in all the nations and more so in

the emerging ones.To understand the cause of this growth and analyze the requirements

needed to further this rapid growth,a case by case analysis of each country has been made

below.

INDIA

RETAIL SECTOR – TRANSITION FROM PAST TO PRESENT

Before 1997, India’s retail sector rested only on the mom and pop stores. Foreign

investment saw the light of the day in 1997 when Indian government permitted FDI up to

100% in cash and carry stores through government approval route, which was converted

into automatic route in 2006. 2006 also saw 51% FDI in single brand retail getting allowed in

India, which ultimately escalated to 100% in 2012 and with multi brand retail sector also

being allowed up to 51%. Despite these reforms the investment hasn’t been as expected

owing to the opposition from some state governments and local bodies. FDI in retail is

expected to improve the organized retail scenario of India which has started gaining a far

firmer foothold in India, though, it just accounts for approximately 8% of the total USD 518

bn market.

CURRENT POSITION OF THE RETAIL MARKET

The retail market of India sizes to USD 518bn with the modern retail being approximately

USD 41 bn with food and grocery sector leading the total market share and apparel sector

leading the organized market share.

0

10

20

30

40

50

60

Foo

d &

gro

cery

app

arel

Mo

bile

& t

elec

om

Foo

d s

ervi

ces

Jew

elle

ry

Co

nsu

mer

…

ph

arm

acy

oth

ers

Total retail share(%)

Organized retail share(%)

Source: India Retail Report 2013, Images Group, through Deloitte report “Indian Retail Market – Opening more doors”, dated Jan 2013. By 2015, the Indian retail market is expected to reach USD 869bn (18% growth rate), whereas

the modern retail will comprise of 10.2% of the total market equaling approximately USD 88bn

(29.7% growth rate).

MAJOR TRENDS DRIVING CHANGE:

- Rapid urbanization & rising disposable incomes

- Rise in online purchases, hence Scope for e-tailing

- Fast growing organized retail sector

- More investment planned in infrastructure sector, hence smoother logistical

operations

CHALLENGES

- Lack of clarity in government policies

- Opposition to foreign investments from various state politicians and local bodies

- Poor infrastructure in terms of bad roads, poorly developed ports, lack of proper

irrigation facilities etc.

- Expensive retail space

- Sorry state of the back end retail infrastructure (especially for food and grocery)

AREAS TO BE FOCUSSED ON

- Clear cut policies related to FDI in retail with an aim to develop a win-win situation for

all stakeholders

- Development of modern retail formats, while ensuring beneficial measures for SMEs

and farmers are in place, and at the same time keeping healthy the small retailers

- Developing quality retail space at affordable rates

- Developing the roads, ports and also improving the cold storage facilities

- Developing online retailing , if required getting FDI in the same

RUSSIA

RETAIL SECTOR – TRANSITION FROM PAST TO PRESENT

From just the state run retail shops during Soviet days to starting of McDonalds in 1990 to

spreading of foreign chains in late 1990s post Vladimir Putin’s accession to power, Russia

has seen a tremendous maturation of retail sector. This has been supplemented by

consistent economic growth of the nation, fuelled by the high prices of oil and gas exports

causing rise in the income of the Russian middle class. This rise in the consumer spending

power caused flourishing of the retail sector till 2009, when the recession caused a major

dip in the growth rate of economy which affected retail and also in the first half of 2010

when a severe drought struck Russia wherein food scarcity caused had its effect on the

Russian retail. In both the cases the government took proactive measures such as offering

of loan to retailers and keeping the business environment active through sale of the

government land to private parties. This strengthened the consumer confidence causing the

economy to bounce back and getting retail sector to the tune of USD 654bn by 2011-12.

CURRENT POSITION OF THE RETAIL MARKET

The retail market by the end of the FY 2011 was worth USD 654 bn out of which food retail

was worth USD 311bn. The rest part, i.e., the non-food retail has a major contribution from

apparel sector. The apparel retail contributes approximately USD 37.06bn in 2011 whereas

the consumer electronics market is to the tune of USD 28bn.

Figures in USD bn Source: http://www.ey.com/Publication/vwLUAssets/Retail-survey-RU-2011/$FILE/Retail-survey-RU-2011.pdf http://www.russiaretail.com/Russian_Retail_Data.shtml; PMR report “Retail in Russia 2013 – Regional focus. Market analysis and development

0

50

100

150

200

250

300

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Russia Food retail

Russia Non- Food retail

forecasts for 2013-2015”

The annual retail trade growth in Russia from 2009 (when recession struck there) to 2011

has been approximately 15.3%. In 2011, organized retail in Russia contributed

approximately 53% of its total revenue whereas the unorganized one did 47%. (Source:

Euromonitor, through Mckinsey report).

MAJOR TRENDS DRIVING CHANGE

- Host of M&A activities with foreign players keen on investing in the Russian retail

market

- Rising middle class and growing disposable incomes of people in Russia

- Incremental trends in the modern retailing format

- Level playing field for local as well as foreign retailers

CHALENGES

- Poor infrastructure, especially roads, affecting logistics of transportation causing

delayed supply of goods.

- Incapability of the third party logistics provider to cater to the transportation

requirement at a national level since they cover only limited area.

- Poor labor productivity owing to low sales per sq meter per employee

- Relative Poor operations practices of the modern stores

- Bureaucracy issues causing delayed development of real estate utilized for retail

purpose , hence resulting in low quality retail space per employee

- Financially weak retailers (post 2009 fiasco)

AREAS TO BE FOCUSSED ON:

- Infrastructure improvement ( which is expected to happen owing to the fact that

Russia is hosting 2018 soccer world cup)

- Operational improvement in retail stores – computerization and online retail

development, optimum staffing at stores, improved distribution centers

- Increasing access to quality retail space by avoiding delayed regulatory clearances

- Furthering modern retail and enhancing foreign investments for better technology &

practices

- Finding ways of strengthening the weaker players

CHINA

RETAIL SECTOR – TRANSITION FROM PAST TO PRESENT

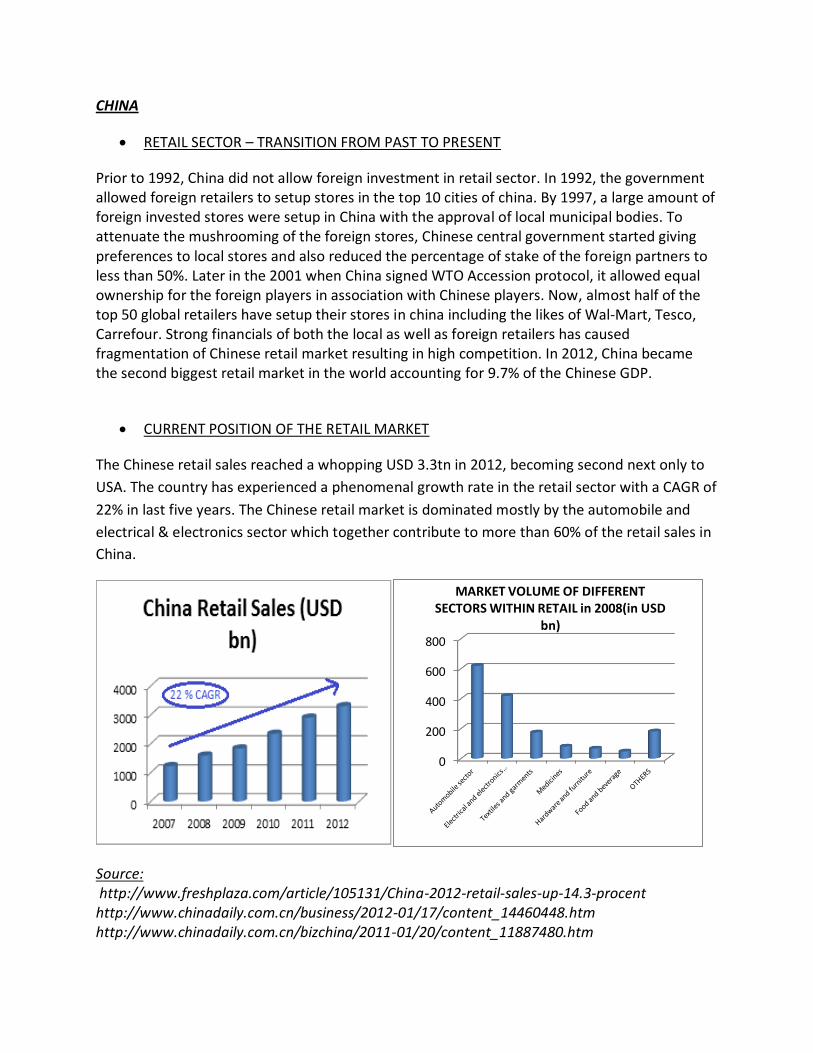

Prior to 1992, China did not allow foreign investment in retail sector. In 1992, the government allowed foreign retailers to setup stores in the top 10 cities of china. By 1997, a large amount of foreign invested stores were setup in China with the approval of local municipal bodies. To attenuate the mushrooming of the foreign stores, Chinese central government started giving preferences to local stores and also reduced the percentage of stake of the foreign partners to less than 50%. Later in the 2001 when China signed WTO Accession protocol, it allowed equal ownership for the foreign players in association with Chinese players. Now, almost half of the top 50 global retailers have setup their stores in china including the likes of Wal-Mart, Tesco, Carrefour. Strong financials of both the local as well as foreign retailers has caused fragmentation of Chinese retail market resulting in high competition. In 2012, China became the second biggest retail market in the world accounting for 9.7% of the Chinese GDP.

CURRENT POSITION OF THE RETAIL MARKET

The Chinese retail sales reached a whopping USD 3.3tn in 2012, becoming second next only to

USA. The country has experienced a phenomenal growth rate in the retail sector with a CAGR of

22% in last five years. The Chinese retail market is dominated mostly by the automobile and

electrical & electronics sector which together contribute to more than 60% of the retail sales in

China.

Source: http://www.freshplaza.com/article/105131/China-2012-retail-sales-up-14.3-procent http://www.chinadaily.com.cn/business/2012-01/17/content_14460448.htm http://www.chinadaily.com.cn/bizchina/2011-01/20/content_11887480.htm

0

200

400

600

800

MARKET VOLUME OF DIFFERENT SECTORS WITHIN RETAIL in 2008(in USD

bn)

http://www.mydeckercapital.com/Documents/20110130%20MDC%20China%20Retail%20Sector%20-%20Macro%20Trends.pdf

By 2011, approximately 68% of the Chinese retail sales were from the organized retail, which

has penetrated considerably there. (Source: Euromonitor, through Mckinsey report)

MAJOR TRENDS DRIVING CHANGE

- Fast growing economy, rising middle class coupled with their rising incomes and rapid

urbanization. Also rise in the wealthy population of China, resulting in indulgence

for luxury goods there.

- Online retailing, which is growing a fast pace (67% over the previous year in 2012,

approx. USD 213bn)

- Liberalized norms for FDI in retail sector resulting in considerable investment from top

retailers worldwide in China, without affecting the local players

- Fast growing modern retail sector

CHALLENGES

- Highly fragmented retail sector with the market leader occupying very low market

share and little difference in the market shares of the competitors

- Less brand loyalty among consumers

- Extremely high real estate rates

- Partiality prevalent with local players at an advantage over foreign players

AREAS TO BE FOCUSSED ON

- Providing level playing field to foreign retailers to take advantage of the cutting edge

technologies and operational practices they bring with them

- Real estate cost to be compensated for by choosing to lease the land

- Online retailing should be taken forward to ease the shopping experience for

consumers

- Consolidation of the retail players to ensure that the cutthroat competition doesn’t

result in an unhealthy business environment

- Non-core operations could be outsourced to increase focus on core operations

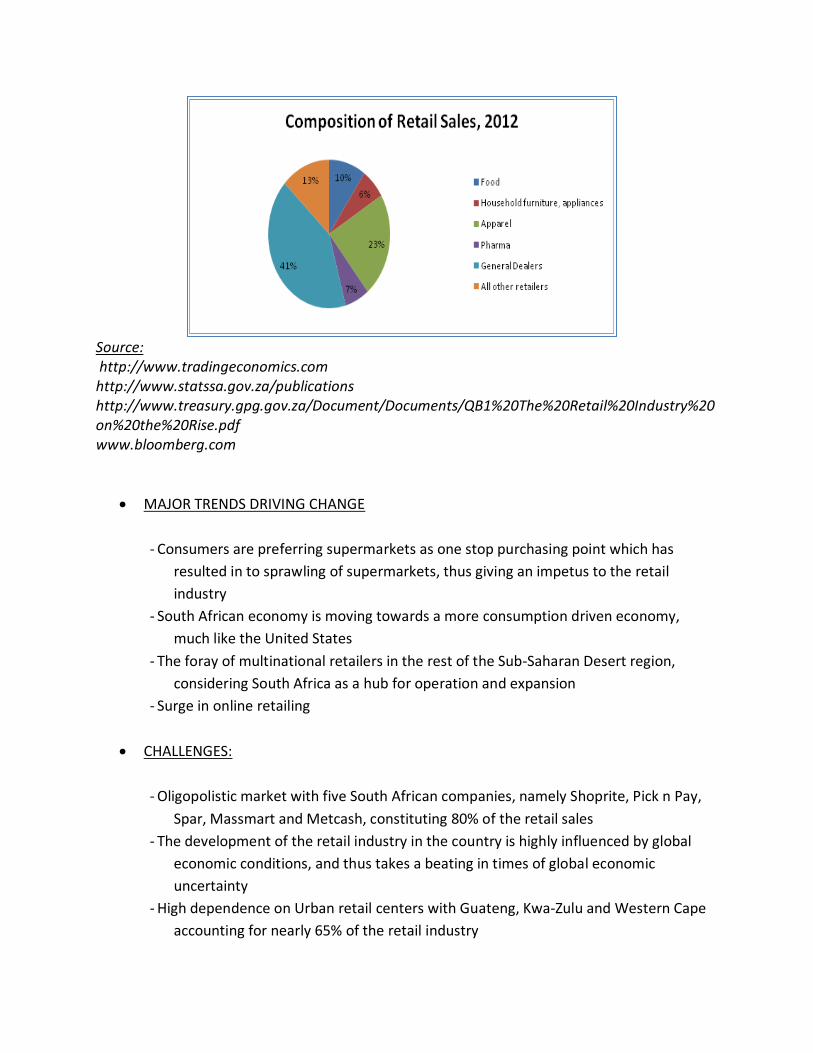

SOUTH AFRICA:

RETAIL SECTOR – TRANSITION FROM PAST TO PRESENT

South Africa was predominantly a mining and manufacturing nation. However, post 1990s, as the South African economy propelled, leading to development in infrastructure and industry, consumers with disposable income were available. Thus began the drift of the South African economy towards a consumer driven economy, which fuelled the growth of retail in South Africa. The increase in retail developments can be explained by the urban sprawl which led to increased retail sales. The retail industry has benefited through efficient logistics nationwide. Shopping centre development has shifted from being concentrated in inner-cities to suburbs and townships. Rapid construction of high-density housing in the surrounds of major urban areas has led to the demand for and increased developments of retail centers in these residential areas.

Current position of the retail market:

The retail industry grew by a CAGR of 2.3% in the past five years sizing USD 55.6bn in 2012, according to the Bureau of Market Research (BMR), out of which food sales comprised of 30%. The online retail sales have increased by 29% on an average annually. The organized sector accounts for almost 67% of the total retail market. BMR forecasts a 3-4% real growth rate for formal retail sales in the coming years. As of 2012, the wholesale and retail trade sector contributes 14% to the South African economy.

Source: http://www.tradingeconomics.com http://www.statssa.gov.za/publications http://www.treasury.gpg.gov.za/Document/Documents/QB1%20The%20Retail%20Industry%20on%20the%20Rise.pdf www.bloomberg.com

MAJOR TRENDS DRIVING CHANGE

- Consumers are preferring supermarkets as one stop purchasing point which has

resulted in to sprawling of supermarkets, thus giving an impetus to the retail

industry

- South African economy is moving towards a more consumption driven economy,

much like the United States

- The foray of multinational retailers in the rest of the Sub-Saharan Desert region,

considering South Africa as a hub for operation and expansion

- Surge in online retailing

CHALLENGES:

- Oligopolistic market with five South African companies, namely Shoprite, Pick n Pay,

Spar, Massmart and Metcash, constituting 80% of the retail sales

- The development of the retail industry in the country is highly influenced by global

economic conditions, and thus takes a beating in times of global economic

uncertainty

- High dependence on Urban retail centers with Guateng, Kwa-Zulu and Western Cape

accounting for nearly 65% of the retail industry

- Threat of retailers focusing on newer markets such as Nigeria

AREAS TO BE FOCUSSED ON:

- Focus on retailing in townships and rural areas, targeting communities in the lower

income groups

- Given the fact that Organized Retail constitutes almost 67% of the total retail market,

internationalization of retail must follow

- Entry of top retail giants by M&A activity as seen in May 2011, with Wal-Mart

purchasing 51% of Massmart, so as to bring in technology, capital etc.

- Transforming itself in to a hub for retail operations in the entire sub-Saharan region

BRAZIL:

RETAIL SECTOR – TRANSITION FROM PAST TO PRESENT

Before 1990, the Brazilian populace was characterized by extremes of wealth and abject poverty with no middle class prevailing. The economy was mired by extraordinarily high inflation which hampered the retail activity in the nation. However, introduction of the new currency, the Brazilian Real in the mid 1990s helped tame down inflation and bring stability to the economy. With the help of welfare schemes and generous pay hikes, the middle class grew, accounting for nearly 60% of the total population today, as compared to 38% in 2001 which is also the driving force behind the retail industry. The country’s demographics too have favored a growth of the retail industry with about 80% of the Brazilian population of 190 million living in urban areas. Also, the opening up of the credit market too favored the growth of the retail sector in Brazil. According to a 2011 McKinsey Quarterly Report, 60% people in Brazil use credit, as compared to 30% in India, 24% in Russia and 13% in China.

Current position of the retail market:

Since 2011 to date, it has been ranked 1 in the Global Retail Development Index by A.T.

Kearney. The Brazilian retail market is estimated to be worth USD 230 bn in 2012, driven mostly

by domestic demand. The retail sector has expanded in line with the GDP growth in Brazil.

Source: http://www.tradingeconomics.com http://www.thomaswhite.com/global-perspectives/retail-sector-in-brazil-riding-the-wave-of-middle-class-growth-and-consumer-credit-boom/ www.bloomberg.com Since majority of the population (80%) lives in urban areas, the organized retail in Brazil as a

percentage of the retail industry has grown considerably well, accounting for 36% share of the

total sales.

MAJOR TRENDS DRIVING CHANGE: - The credit market in Brazil has been a boon for the retail industry, and most of the

retailers are cashing in on the credit-readiness of the consumers

- Majority of the population lives in the urban areas, hence scope to expand the

organized sector retail beyond the existing 36%

- Policies favoring M&A have been proliferated since 2011, offering a lucrative scope in

the fast growing Brazilian retail market

CHALLENGES: - Unpredictable inflation has always been an underlying problem with Brazil

- Poor infrastructure also hinders the retailing process

- Corruption and Bureaucratic red tape have hampered the development of retail

sector

- Many analysts are alarmed over Brazil’s rapid credit growth, fearing that a bubble may

be brewing

AREAS TO BE FOCUSSED ON: - There is scope for M&A activity, which will certainly give a push to the retail sector in

Brazil, getting in foreign investments.

- The upcoming Soccer World Cup 2014 and Summer Olympics 2016 scheduled in Brazil

have given a push to the infrastructure development in Brazil, which would in turn

help all sectors, including Retail.

GENERAL REFORMS TO BE ADOPTED WITH THEIR BENEFITS

1. Effective crisis resolving policies

In the event of crisis, Governments of nations should step in with financial support for those firms which may in bad form at that particular time but have the potential to bounce back. One such example is Russian government’s decision of providing loan to key retail players during 2009 recession (USD 255mn loan to X5 retail group and USD 91mn to Magnit),which helped turn the tides for these companies. Also during the 2010 drought crisis Russian government saved the scenario by selling the state owned assets worth USD 32bn, thus changing the existing perception of the investors of low business activity in Russia. By formulating such policies governments can improve the business sentiment on a shorter as well as longer term. 2. Developing the infrastructure:

A lot of operational efficiency results from the fact that country doesn’t have up to the mark infrastructure. Poor roads cause delay in deliveries, lack of proper irrigation facilities cause inadequate yield, lack of transportation facilities or providers result in high costs for transportation of goods. Countries like India where the back end infrastructure such as cold storages is insufficient face issues of food wastage. South Africa is one of the classic examples of how change in infrastructure can result in improved economic activity with its retail space increasing from 5.6 million square meters of land in 2002 to 18.4 million square meters in 2010. 3. Foreign investment:

Globalization being the major driver in the economic activity worldwide, the retail sector in emerging economies can benefit tremendously from allowance of foreign investment. China retail sector experienced an upward change with advent of foreign players in the sector. Russia’s development also was a result of the same reason. Foreign investment also played a main role in modernizing the retail sector of South Africa and Brazil to a larger extent. India has now allowed FDI up to 51%. This is expected to provide rise in the modern retail formats, which in turn is expected to benefit farmers, SMEs, increase employment whilst increasing the sales of the sector. 4. Online retail:

With the virtual world gaining significance in all walks of life, retail sector too has no option but to adopt online retailing to benefit in the modern times. Adopting online retail has already caused tremendous hike in sales for some nations. One of Russia’s major electronics retailers MVideo has its online sales contributing approximately 2.5% of its total revenue in 2011 and 3.5% in 2012. Its brick-and-mortar stores averaged revenue of USD 20mn per

store whereas its online stores had it to the tune of USD 136mn. Due to saturation the brick-and-mortar stores are experiencing a growth of approximately 8%, whereas the online stores are experiencing it to the level of 57%. 5. Getting a balanced market:

The business environment should be balanced in the sense that there should neither be too much of competition resulting in market fragmentation nor should there be oligopolistic practices resulting in few players dominating the scenario leaving less room for others to enter. China faces the problem of market fragmentation wherein severe competitions, to the extent that top 5 retailers command only 11% of Chinese market share. Such high competition could result in players adopting unhealthy practices such as extremely very low pricing, which ultimately reduces company’s margins. Similarly South Africa has the issue of oligopoly which makes only 4-5 players dominate the market dynamics there. Whereas oligopoly can be tackled through shrewd policies, the fragmentation issue can be solved through merging multiple players. One of the examples here is Russian retail giant X5’s acquisition of Kopeika retail which did the job of saving a financially weak company at the same time improving the market share of the other. 6. Geographical expansion:

Most of the businesses focus on targeting the tier-1 cities when they enter business, be it local or foreign nations. These markets do offer a good market size but at the same time they bring with them high competition and overheads, thus lesser profits. To have a sustainable hold on the market a player needs to tap those markets which are lesser known but have strong business potential which is basically tier -2 cities. This offers them an early mover advantage and hence higher market share there with lower overheads and higher margins. 7. Making available attractive financing options:

One such option is availability of easy credit that has played a vital role in developing the retail market of Brazil. But such options should be evaluated well before implementing as these are also high risk options. To avoid contingencies care should be taken to make such options as risk free as possible, which could be done by taking measures such as verifying financial profile before offering credit, ensuring shorter payment periods, getting caution deposits in advance etc. 8. Keeping scope for strategic tie-ups or mergers & acquisitions:

To ensure a sustainable market share, players should try to avail the benefits of others in the same market that are not competing with each other’s. This helps them in complementing each other with their strengths and also makes them less susceptible to loss of market shares in the event of entry of another big player. As per the information given by one of the employees of a major Indian firm in the furniture market, this strategy has helped them counter competition from other international competitors. Also M&A activity has benefits in terms of improved economic activity, an example being PepsiCo’s acquisition of local dairy products company Wimm-Bil-Dann, with which it expects a 3 fold growth in its sales. 9. Innovative business models: Companies should focus on developing innovative models that help in market share expansion without much high cost investment. One such example is catering to maximum area of city without opening a brick-and-mortar store but by just opening a kiosk wherein a customer can place his order and collect it. The pickup point model of Ahold, a Netherlands based food retailer, has pickup points, comprising of a counter and a parking space, at different locations of a city, wherein one has to come to just collect the order he has placed online, by punching the order code at the counter and parking his vehicle at the designated slot where an employee would come and drop the customer’s deliverables in his vehicle. This helped Ahold expand their reach and also resulted in convenient shopping for customers.

CONCLUSION: With high growth potential prevalent in BRICS retail market, the countries need to reconsider its existing strategies to embrace growth in the best possible way. Brazil, Russia, China and South Africa have their retail markets orgainized to a great extent, whereas India has just begun to venture there. The countries having a developed organized retail should focus on increasing its presence whereas other, like India, should optimally accommodate the growth that the organized sector is experiencing. Also firms should take up their challenges and make them opportunities though following the most ultimate retail practices across the world. By adopting such measures retail sector can manage to rake in exceptional fortunes ahead!

References:

www.articles.economictimes.indiatimes.com/2013-08-07/news/41167918_1_indian-fmcg-consumer-confidence-consumer-awareness

“A brief report on Retail sector in India”, Aug. 2012, by Corporate Catalyst India

“The Indian Kaleidoscope – Emerging trends in Retail”, Sept.,2012 by Price Waterhouse Coopers

“ Indian Retail Market – Opening more doors”, dated Jan 2013, by Deloitte India

BRIC Spotlight – Retail Sector in China, June 2011 by Thomas White International

Alejandro Diaz, Max Magni, and Felix Poh,” From Oxcart to Wal-mart”, Oct. 2012, McKinsey Quarterly

2012 Global Retail Development Index – Full Report, A.T.Kearney

China Retail Sector – Macro Trends, Jan.2011, by My Decker Capital

China Power of retailing 2011, Deloitte

http://www.china.org.cn/business/2013-07/05/content_29331612.htm

BRIC Spotlight Consumer goods sector in Russia: Winds of change, Jan 2011, Thomas White International

Evgeny Kornilov,” Leadership In Russian Food Retail”,Sept.,2008

Global Agricultural information network report, “Russia retail markets steady on”,Sept.,2012

“Retail in Russia 2013 – Regional focus. Market analysis and development forecasts for 2013-2015”, PMR Market Insight

http://www.cgcsa.co.za

Kearney, A.T. 2011. Retail Global Expansion-Global Retail Development Index, Johannesburg; accessed athttp://www.atkearney.co.za/

http://www.wrseta.org.za/

The Retail Industry on the Rise in South Africa; accessed at http://www.treasury.gpg.gov.za/Document/Documents/QB1%20The%20Retail%20Industry%20on%20the%20Rise.pdf

Retail Sector in Brazil, Thomas White International; accessed at http://www.thomaswhite.com/global-perspectives/retail-sector-in-brazil-riding-the-wave-of-middle-class-growth-and-consumer-credit-boom/

www.bloomberg.com

www.tradingecomics.com