Investment and Control Decisions in Foreign Markets: Evidence from Service Industries

18

Investment and Control Decisions in Foreign Markets: Evidence from Service Industries Jose Pla-Barber, Esther Sanchez-Peinado and Anoop Madhok 1 Department of Management ‘Juan Jose Renau Piqueras’, University of Valencia, Avda de los Naranjos, s/n 46022 Valencia, Spain, and 1 Schulich School of Business, York University, Toronto, Ontario M3J 1P3, Canada Corresponding author email: [email protected] We empirically investigate the entry mode choice in the service sector. In contrast to current models, we propose a model for choice of entry mode that breaks down the decision into two levels of analysis: first, at the more macro level, the choice of the degree of commitment is influenced mainly by country-related variables; second, at the more micro level, the choice of the degree of control is addressed by firm-related variables. Based on a sample of 328 foreign market entries, our study contributes to the literature of entry mode in two ways: first, by showing the explanatory capacity of the hierarchical model in the analysis of entry mode choice in the service sector; and second, through identifying and analysing the moderating role of two important contingencies in this decision – capital intensity and degree of customization. Moreover, the study advances our knowledge of some of the particularities in the internationalization of service firms. Introduction The annals of business history report that, for every successful market entry, about four entries fail (Horn, Lovallo and Viguerie, 2005). Inexperienced start-ups suffer from some of these disappoint- ments, but so do many sophisticated corporations. Therefore, the choice of entry mode 1 constitutes one of the most critical decisions for international strategy success. It affects all the future decisions and operations of the firm in the new market. The importance of this choice is also reflected in the considerable amount of research undertaken in this field of study (e.g. Agarwal and Ramaswami, 1992; Anderson and Gatignon, 1986; Brouthers, 2002; Brouthers, Brouthers and Werner, 2000, 2008b; Herrmann and Datta, 2006; Hill, Hwang and Kim, 1990; Luo, 2001; Madhok, 1997, 1998). However, there is still room for further contribution to entry mode research. Although previous studies have shed light on various factors underlying entry mode choice, including both macro-level (country risk, cultural distance, market potential) and micro-level (marketing intensity, nature of knowhow, strategy, experience etc.) variables, the overall understanding of how managers make entry mode selection decisions and what is the underlying decision heuristic as yet remains somewhat unclear. Traditionally, previous research explains the choice of entry mode from either a sequential or a comparative perspective (e.g. Agarwal and Ramaswami, 1992; Brouthers and Brouthers, The authors acknowledge financial support from the Ministry of Education and Science of Spain (research project SEC 2003/06466). 1 An ‘entry mode’ is the way of operating in foreign markets by internationalizing firms. Overall they can be classified as contractual (franchising, licensing, manage- ment contracts etc.), exporting (direct or indirect) or investment modes (greenfield, acquisitions and joint ventures). These modes of entry may be differentiated according to the level of resource commitment and control. British Journal of Management, Vol. 21, 736–753 (2010) DOI: 10.1111/j.1467-8551.2010.00698.x r 2010 British Academy of Management. Published by Blackwell Publishing Ltd, 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA, 02148, USA.

Transcript of Investment and Control Decisions in Foreign Markets: Evidence from Service Industries

Investment and Control Decisionsin Foreign Markets: Evidence from

Service Industries

Jose Pla-Barber, Esther Sanchez-Peinado and Anoop Madhok1

Department of Management ‘Juan Jose Renau Piqueras’, University of Valencia, Avda de los Naranjos, s/n46022 Valencia, Spain, and 1Schulich School of Business, York University, Toronto, Ontario M3J 1P3, Canada

Corresponding author email: [email protected]

We empirically investigate the entry mode choice in the service sector. In contrast tocurrent models, we propose a model for choice of entry mode that breaks down

the decision into two levels of analysis: first, at the more macro level, the choice of

the degree of commitment is influenced mainly by country-related variables; second, at

the more micro level, the choice of the degree of control is addressed by firm-relatedvariables. Based on a sample of 328 foreign market entries, our study contributes to the

literature of entry mode in two ways: first, by showing the explanatory capacity of the

hierarchical model in the analysis of entry mode choice in the service sector; and second,

through identifying and analysing the moderating role of two important contingencies inthis decision – capital intensity and degree of customization. Moreover, the study

advances our knowledge of some of the particularities in the internationalization of

service firms.

Introduction

The annals of business history report that, for everysuccessful market entry, about four entries fail(Horn, Lovallo and Viguerie, 2005). Inexperiencedstart-ups suffer from some of these disappoint-ments, but so do many sophisticated corporations.Therefore, the choice of entry mode1 constitutesone of the most critical decisions for internationalstrategy success. It affects all the future decisionsand operations of the firm in the new market. The

importance of this choice is also reflected in theconsiderable amount of research undertaken in thisfield of study (e.g. Agarwal and Ramaswami, 1992;Anderson and Gatignon, 1986; Brouthers, 2002;Brouthers, Brouthers and Werner, 2000, 2008b;Herrmann and Datta, 2006; Hill, Hwang and Kim,1990; Luo, 2001; Madhok, 1997, 1998). However,there is still room for further contribution to entrymode research. Although previous studies haveshed light on various factors underlying entry modechoice, including both macro-level (country risk,cultural distance, market potential) and micro-level(marketing intensity, nature of knowhow, strategy,experience etc.) variables, the overall understandingof how managers make entry mode selectiondecisions and what is the underlying decisionheuristic as yet remains somewhat unclear.Traditionally, previous research explains the

choice of entry mode from either a sequential ora comparative perspective (e.g. Agarwal andRamaswami, 1992; Brouthers and Brouthers,

The authors acknowledge financial support from theMinistry of Education and Science of Spain (researchproject SEC 2003/06466).1An ‘entry mode’ is the way of operating in foreignmarkets by internationalizing firms. Overall they can beclassified as contractual (franchising, licensing, manage-ment contracts etc.), exporting (direct or indirect) orinvestment modes (greenfield, acquisitions and jointventures). These modes of entry may be differentiatedaccording to the level of resource commitment and control.

British Journal of Management, Vol. 21, 736–753 (2010)DOI: 10.1111/j.1467-8551.2010.00698.x

r 2010 British Academy of Management. Published by Blackwell Publishing Ltd, 9600 Garsington Road, OxfordOX4 2DQ, UK and 350 Main Street, Malden, MA, 02148, USA.

2003; Contractor and Kundu, 1998). From thesequential perspective, the process of adoptingmodes of entry into foreign markets is defined asa continuum of increasing degrees of resourcecommitment, risk exposure, control and profitpotential as firms acquire greater knowledge andexperience in international business. Studies thatadopt this perspective normally use ordinalregressions to estimate the effect that selectedfactors have on entry mode choice. In contrast,the comparative model analyses multiple entrymodes holding one of these as a baseline againstwhich other modes are compared. Generally, amultinomial logit regression is used to estimatethe effect of a group of factors on the probabilityof choosing a particular entry mode over another(or others).Despite this difference, however, both appro-

aches consider all entry modes simultaneouslyand all factors as being equally relevant at thesame time in determining the most suitable entrymode. The broad argument is that modes entail-ing greater commitment of resources face greaterrisks, and consequently firms favour modes offer-ing more control to compensate for such risk(Anderson and Gatignon, 1986). In other words,commitment and control go hand-in-hand, withcontrol typically being assessed through theextent of equity (e.g. Gatignon and Anderson,1988). Since ownership is accompanied by decis-ion rights, more internalized modes such aswholly owned subsidiaries are understood tooffer a greater level of control over decisionmaking than non-equity modes.Our study is distinctive in two ways: (i) in

contrast to prior research, it proposes a two-stepmodel of the market entry decision that distin-guishes between decisions regarding extent ofcommitment (equity versus non-equity) anddecisions regarding extent of control (sharedversus full control); and (ii) it extends the modelmore specifically to the service sector. As entrydecisions are so complex, managers would becognitively constrained to consider all the relevantvariables simultaneously. One way to managesuch complexity would be to prioritize by firstconsidering only a few key variables, and subse-quently consider other variables. In other words,managers structure their decision through a two-step hierarchical process, where a number ofcriteria are exclusive to each stage. We observedthis tendency in our initial interviews with

managers. We refer to this as the two-step orhierarchical model since the entry mode choice isbroken down into two decisions: first, at the moremacro level, the choice of the degree of commit-ment is influenced mainly by country-relatedvariables; subsequently, at the more micro level,the choice of the degree of control is addressed byfirm-related variables.In a recent and noteworthy contribution, Pan

and Tse (2000) proposed a similar model for theentry mode choice. They contended that theforemost issue is that of the choice of equityversus non-equity, this being a key strategicvariable since it has direct implications for theextent of commitment and the associated scale ofentry. Thus, decisions on the degree of commit-ment and control are adopted at differentmoments. Nevertheless, although Pan and Tse(2000) test the effect of a set of country andindustry factors on the choice regarding degree ofcommitment (e.g. equity versus non-equity modes),they do not empirically analyse the influence offirm-specific factors that impact the choice regard-ing the degree of control (shared versus full-controlmodes). Our study assesses the complete model,empirically analysing both macro-level (country)and micro-level (firm) variables. We posit, and ourresults confirm, that firms and their managers firstdecide on equity or non-equity based modes, afterwhich they make a decision on which specific modewithin equity and non-equity to consider further.In the latter decision, firm-specific characteristicsand the degree of control play a vital role.Generally speaking, empirical research on

entry mode has resulted in mixed findings,especially with regard to the influence of envir-onmental uncertainties. Some studies show thatwhen firms face higher levels of risk and greatercultural distance, they tend to choose methodswith a low degree of commitment/control inorder to maintain flexibility (Chang and Rosenz-weigh, 2001; Chen and Hu, 2002; Kim andHwang, 1992; Mutinelli and Piscitello, 1998).However, other studies have identified just theopposite relationship (Erramilli, Agarwal andDev, 2002; Madhok, 1998). For example, Mad-hok (1998) found that differences in capabilitiesand embeddedness in very different routines dueto a high sociocultural distance may result inperceived qualitative losses in transfer of kno-whow, which weakens its rent-generating poten-tial. Therefore, firms prefer to maintain the

Investment and Control Decisions in Foreign Markets 737

r 2010 British Academy of Management.

knowhow within their own boundaries throughsubsidiaries.In our opinion, such mixed and consistent

results may be because of the underlying supposi-tion of a coincidence between control andcommitment and thus a conflation of the twoconcepts, where there is a tendency to assumethat decisions regarding the degree of commit-ment abroad and decisions regarding the degreeof control are simultaneously adopted. Thisassumption is questionable, however, since thereare numerous mechanisms to exercise controleven without a dominant equity stake and onecan be present without the other (Friedmann andBeguin, 1971; Geringer and Hebert, 1989).According to these authors, numerous mechan-isms exist for exercising control even without adominant equity stake (e.g. veto rights, boardrepresentation, staffing key positions, specialtechnological or management service agreements,possession of critical resources such as technol-ogy etc). Conversely, even though one may havea dominant equity stake, with the associatedresource commitment, this does not necessarilytranslate into dominant control. For instance,many firms express frustration that in spite ofhaving a majority stake in their operations inChina, they have much less influence over thelocal operations than they had anticipated or feltdesirable (Dhanaraj and Beamish, 2004; Geringerand Hebert, 1989; Li, Zhang and Jing, 2008;Mjoen and Tallman, 1997), especially sincepolicies and decisions can be differently inter-preted and improperly enforced. The prominentunravelling of the Danone–Wahaha joint venturein China is just one recent example. In fact, oneof the main problems in many internationalequity joint ventures is the weak control overday-to-day management, quality and physicalassets (Contractor and Kundu, 1998).This separation of ownership and control

frequently occurs in service industries (Brown,Dev and Zho, 2003) and calls for a moresophisticated perspective on foreign market entrymode decisions. For many services, direct foreigninvestment does not imply a large investment ofresources in the host country, because it does notrequire sizeable investments in plants, machinery,buildings and other physical assets; in fact, afirm’s presence may be a single office (Erramilliand D’Souza, 1995). In such case, macro-levelvariables could be less important for these firms.

Here, the key question is not how to choosethe degree of commitment but how to choose thedegree of control for organizing their operationsin the foreign market.Moreover, there is an increasing recognition

that service firms may gain control throughnon-equity methods, with it being possible for aservice firm to exercise a degree of control thatis unrelated to its equity participation (Erramilliand Rao, 1993). In many services, capital-intensiveassets (such as real estate) can be separated fromknowledge-based or managerial expertise-relatedskills. Hence, control can be equally well achievedthrough interfirm cooperation in non-equity agree-ments such as franchising or management servicecontracts (Contractor and Kundu, 1998). In thistype of agreement, the foreign operation is run asif the property were part of the multinational firm.Even without ownership, control over codifiedstrategic assets (brands, technological systems etc.)and tacit expertise (trained personnel, routines,quality control etc.) remains with the multina-tional firm. Although equity is undoubtedly amajor means of control, there need not be a one-to-one mapping of the two since there are othermeans of control that may not be fully reflected inequity ownership. Therefore, factors influencingthe desire for control may differ from those relatedto considerations of commitment.The contribution of our study is twofold. First,

by separating out decisions regarding commit-ment and control, it becomes possible to identifyand distinguish which factors impact each ofthese respectively. We argue, and our resultssupport our argument, that different factors arerelevant for commitment and for control. Entrymode research may be confounding the analysisby not making this crucial distinction andlumping everything together. Second, our studyapplies the model to the service sector. Despitethe importance of the service sector in worldmarkets and the growth of foreign investmentsin this area during the last decade, the researchon services in an international context is stilllimited in comparison with research focused onthe manufacturing sector. Although there aresome important studies that have analysed entrymode choice in the service context (Agarwal andRamaswami, 1992; Anand and Delios, 1997;Contractor and Kundu, 1998; among others),they have been based on specific service sectorssuch as banking, advertising, hotels etc. Our

738 J. Pla-Barber, E. Sanchez-Peinado and A. Madhok

r 2010 British Academy of Management.

study analyses the entry mode choice in severalindustries across the service sector, spanning bothbusiness and consumer services. Moreover, noneof these prior studies in the service sector haveapplied the two-stage approach which, we be-lieve, provides the scope for a deeper under-standing of the entry mode choice. In doing so,we also identify and analyse the moderating roleof two important contingencies in this decision:capital intensity and degree of customization.The remainder of the paper is organized as

follows. The next section provides the theoreticalbackground and the hypotheses. Here, we brieflyreview relevant aspects of transaction cost theoryand discuss the role played by capital intensityand degree of customization as moderators.We also present our model and hypotheseson entry mode determinants in service firms. Inthe subsequent section, we elaborate on themethods and the major results. The resultssupport our hypotheses. We conclude by pointingout the contributions of this study.

Background

A large number of theories have been used toexplain the entry mode choice, such as transac-tion cost theory, the resource-based view, institu-tional theory and the eclectic framework(Dunning, 1988). However, despite several lim-itations (see Brouthers, Brouthers and Werner,2008a), transaction cost theory has served as thepredominant perspective for theorizing on entrymode choice and, accordingly, transaction-cost-related variables have been recognized as majordeterminants of entry mode choice (Zhao, Luoand Suh, 2004). Moreover, several studies havedemonstrated that transaction cost theory logicprovides a normatively superior method ofmaking this important strategic choice2 (e.g.Brouthers and Nakos, 2004; Brouthers,Brouthers and Werner, 2003). Transaction costtheory analyses which entry mode minimizes thetransaction cost associated with the exploitationof an existing competitive advantage in a foreignmarket. If transaction costs are low, a rational

firm will prefer the transaction to be governed bythe market (or non-equity modes). However, iftransaction costs are too high, the firm will preferan equity mode (Anderson and Gatignon, 1986;Williamson, 1975).In the international business literature, envir-

onmental uncertainties (host-country-related de-terminants) and behavioural uncertainties (firm-related determinants) have been commonly ana-lysed as the core attributes of a transaction andthe primary determinants of cost efficiency of agovernance choice (Zhao, Luo and Suh, 2004).Environmental uncertainty refers to the inabilityof an organization to predict future events. Itoften stems from the volatile nature of theeconomic and political conditions of the hostcountry and the peculiarities, and thus lack ofknowledge, of the local customs and culture(Miller, 1993). Proxies frequently used in measur-ing this type of uncertainty include marketpotential, country risk and cultural distance. Incontrast, behavioural uncertainty refers to therisk posed by the opportunistic behaviour of apotential partner. Such behaviour, and stepstaken to protect against it, can adversely impactthe efficient conduct of the relationship (Miller,1993).

Service characteristics: capital intensity andcustomization

As stated earlier, our study analyses the servicesector. A recent claim in the literature (Brouthersand Brouthers, 2003; Zhao, Luo and Suh, 2004)suggests that transaction cost theory may beequally applicable to manufacturing and servicefirms but that industry effects moderate the re-lationships between transaction costs and modechoice. In this context, two characteristics havebeen recognized by researchers as moderators ofthe different responses in the internationalizationprocess between service and manufacturing firms:the level of capital intensity and the degree ofcustomization (Brouthers and Brouthers, 2003;Erramilli and Rao, 1993).First, the level of capital intensity is different in

manufacturing and service sectors. Manufactur-ing frequently requires large commitments forplants and equipment. However, the level ofcapital intensity varies among different serviceswithin the service sector. Some service firms arepeople intensive (e.g. consulting, legal services,

2Although a detailed review of alternative theoreticalperspectives is beyond the purpose of this paper, weintroduce some control variables related to thesetheories in the Methods section.

Investment and Control Decisions in Foreign Markets 739

r 2010 British Academy of Management.

accounting, advertising) and thus high commit-ment entry modes such as wholly owned sub-sidiaries involve relatively low expense (Erramilliand Rao, 1993). Given similar risk perceptions,these service firms will respond quite differentlyfrom manufacturing firms because differences inswitching costs allow service firms to relocateactivities more easily if conditions become toovolatile. On the other hand, some service firmsare capital intensive (e.g. telecommunications,energy, airlines, hotels) and they are more likelyto show investment patterns similar to themanufacturing sector. The establishment of anew subsidiary abroad entails large fixed invest-ments and hence firms will prefer flexibility (lowresource commitment modes) to enter intocountries with adverse environmental conditions.Second, customization is a learning relation-

ship between the organization and its customersthat results in delivering products or services indirect response to a particular customer’s needsand preferences over time (Tsou, Ching andChen, 2007). Customization requires a highdegree of personal contact, which implies con-siderable judgement, discretion and situationaladaptation during service delivery. Customiza-tion occasions greater variety in service provi-sion. Since the uncertainty inherent to thisvariability makes it harder to control the output

of service organizations, the provider of acustomized service is probably inclined to keepoperations in-house (Safizadeh, Field and Ritz-man, 2008). At the same time, the inability ofthe consumer to evaluate the quality of mostcustomized services prior to consumption en-hances the importance of reputation and pro-prietary knowledge as key factors of success.Consequently, customization will intensify a firm’sdesire to protect valuable and specific assets.In our paper, we explore the impact of these

industry moderating effects. We argue that capitalintensity will have a greater influence on thedecision about the amount of resources committedabroad whereas the degree of customization willcondition the degree of control the firm wishes toexercise over the international operation.

Hypotheses

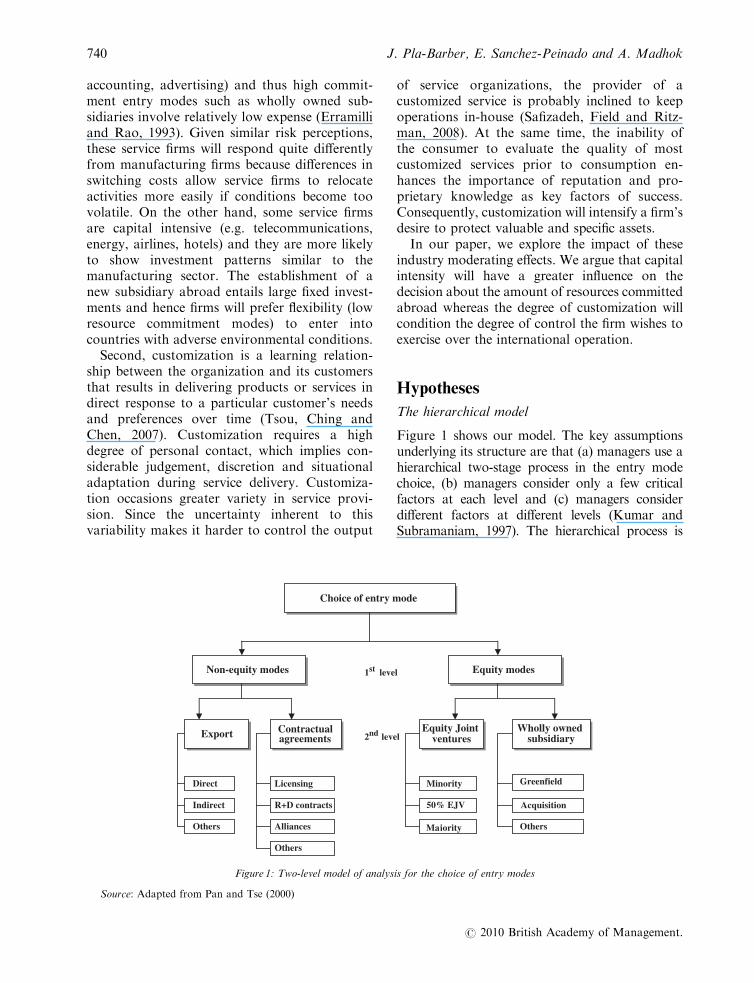

The hierarchical model

Figure 1 shows our model. The key assumptionsunderlying its structure are that (a) managers use ahierarchical two-stage process in the entry modechoice, (b) managers consider only a few criticalfactors at each level and (c) managers considerdifferent factors at different levels (Kumar andSubramaniam, 1997). The hierarchical process is

2nd level

Choice of entry mode

Equity modes Non-equity modes

Export Contractualagreements

Direct

Indirect

Others

Licensing

R+D contracts

Alliances

Others

Equity Joint ventures

Wholly owned subsidiary

Minority

50% EJV

Majority

Greenfield

Acquisition

Others

1st level

Figure 1: Two-level model of analysis for the choice of entry modes

Source: Adapted from Pan and Tse (2000)

740 J. Pla-Barber, E. Sanchez-Peinado and A. Madhok

r 2010 British Academy of Management.

suitable for the entry mode decision because itprovides a more precise picture of which factorsaffect the choice of entry modes and at what level.Moreover, for managers, the hierarchical model canbe useful to handle the information overload andthe complexity of the choice (Pan and Tse, 2000).

Environmental uncertainties and capital intensity

The first level of analysis is between equity andnon-equity entry modes. Here, the key issueswhen making a decision on entry mode aremainly those that refer to the environmentaluncertainties surrounding the target country,such as country risk, cultural differences orpotential for growth (Zhao, Luo and Suh,2004). According to transaction cost theory,environmental conditions (market-specific uncer-tainty) will influence the commitment of re-sources and the strategic flexibility that the firmseeks to maintain in the international market inorder to confront unforeseen changes in theenvironment (Brouthers and Brouthers, 2003;Pan and Tse, 2000). Resource commitmentinvolves the dedication of resources to specificuses that are either fixed or difficult to reallocatewithout considerable cost. Large resource commit-ments associated with equity modes create poten-tial exit barriers as firms become unwilling toabsorb the losses of sunk investments whenrevenues fail to materialize as planned. Incontrast, non-equity modes provide firms greaterflexibility, which is desirable in changing orunstable environments in order to speed upadaptation to changing conditions. Therefore, incountries with high environmental uncertainty,firms would be better off selecting non-equityinvestment modes. However, as we argue below,this relationship between equity/non-equity modesand environmental conditions will be moderatedby the level of capital intensity of the serviceinvolved in the international operation. As capitalintensity represents the relative magnitude of fixedinvestment, increasing capital intensity signifiesrising resource commitments and escalating costof internalization (Erramilli and Rao, 1993).

Market potential

Countries characterized by a high market poten-tial can absorb additional productive capacityand therefore provide opportunities for compa-

nies to achieve economies of scale and efficiencyin their activities (Brouthers, 2002). However, instatic markets, firms are reluctant to undertakelarge resource commitments as potential sales arenot high enough to absorb a large investment(Agarwal and Ramaswami, 1992; Erramilli,1992). This relationship is evident in capital-intensive service firms (e.g. telecommunications,energy, airlines, hotels) in which the establish-ment of a new operation abroad entails largefixed investments. Nevertheless, some types ofservices may not show this pattern. For knowl-edge-intensive firms, direct foreign investmentdoes not imply a large investment of resources inthe host country, as it does not require sizeablephysical investments. These firms compete on thebasis of proprietary knowledge and idiosyncraticinformation. Accordingly, market potential couldbe less important for them than for capital-intensive ones. Therefore:

H1: The positive relationship between marketpotential and service firms’ propensity forequity entry modes will become stronger withincreasing capital intensity.

Cultural distance

One major source of uncertainty is culturaldistance. Perceptions of significant culturaldistance between the country of origin andthe target country have been found to supportthe use of modes involving smaller resourcecommitments. In general, information acquisi-tion costs can be expected to increase with theincreasing cultural distance (Gatignon and An-derson, 1988; Johanson and Vahlne, 1977, Kogutand Singh, 1988).As cultural distance increases, there is a danger

that the transfer of firm knowledge to localpartners may be imperfect since local institutions,norms and routines differ (Fladmoe-Lindquistand Jacque, 1995; Madhok, 1998). The provis-ion of knowledge-intensive services requiressubstantial investments in human resources,since such services depend on the skills, talentand knowledge necessary to satisfy the needs andexpectations of the consumers (Erramilli andRao, 1993). In such circumstances, even thoughlocal adaptations may be required, knowledge-intensive firms would need to incur considerableinvestments to transfer management systems, to

Investment and Control Decisions in Foreign Markets 741

r 2010 British Academy of Management.

train local employees in the firm’s knowhow andto ensure that the quality of the service providedis not compromised. Such high levels of resourcecommitments would make it more likely thatequity ownership is maintained over the transfer.The provision of capital-intensive service firms,

on the other hand, relies relatively less on peoplethan in the case of knowledge-intensive servicefirms and is therefore less affected by the culturaldifferences between countries. As a result, thedesire to share large investments with a localpartner to lower the cost of acquiring informa-tion often overrides the desire for equity modes.Therefore:

H2: The inverse relationship between culturaldistance and service firms’ propensity forequity entry modes will become stronger withincreasing capital intensity.

Host country risk

Host country risk reflects uncertainty abouteconomic and political conditions and governmentpolicies that are deemed to be critical to thesurvival and profitability of a firm’s operations inthat country (Agarwal and Ramaswami, 1992). Byreducing resource commitment in risky environ-ments, firms minimize their financial exposure incases where they can be adversely affected orforced to cease their activity by unforeseen events(Hill, Hwang and Kim, 1990). On this premise, itwould be preferable for service firms to use non-equity modes rather than investments that involvecomplete ownership because the amount ofinvested funds is usually lower and the flexibilityin terms of abandoning the market is greater.Indeed, in some service sectors such as restaurantsand hotels, management contracts and franchisesallow the firm to exert a higher degree of controlover the foreign operation without the need totake on the risk of investment. In addition,payment through royalties linked to sales reducesthe risk significantly, since sales remain morestable than profits in unstable environments(Contractor and Kundu, 1998).Moreover, the participation of capital-intensive

service firms in international markets requiresconsiderable investments in plants, machinery,buildings and other physical assets. Given this,these service firms prefer to hold a flexible positionin countries with high levels of political and

economic instability and to share the investmentrisk with local partners by adopting non-equitymodes that minimize their resource commitments.Therefore,

H3: The inverse relationship between countryrisk and service firms’ propensity for equityentry modes will become stronger with increas-ing capital intensity.

Behavioural uncertainties and degree ofcustomization

The second level of analysis is between full-control and shared control modes. Here, the keyissues when making a decision on entry modeare mainly those that refer to the behaviouraluncertainties surrounding the operation due tothe potential opportunism of a partner. Undertransaction cost theory assumptions, the riskof undesired dissemination of a firm’s specificadvantage or proprietary asset is an importantsource of transaction costs. Due to the need toprotect against potential self-interested behaviourof other actors, under the assumption of oppor-tunism, it would be more efficient to conduct thetransaction within the firm in the presence of hightransaction costs rather than through arm’s-length exchange (Madhok, 1998). In such situa-tions, a firm would prefer to enter a marketthrough full-control modes.Hence, variables considered in the second level

of analysis will determine the level of control afirm wishes to exercise over the operation. Controlreflects the ability of the firm to influence thedecisions within the organization in order toimprove its competitive position and maximizereturns on firm-specific assets (Agarwal andRamaswami, 1992; Contractor and Kundu,1998). The type of service will also moderate therelationship between proprietary assets (e.g. com-mercial assets, knowhow) and the desire forcontrol. As we will argue below, the intimatecontact between producer and customer duringthe process of service delivery and the involvementof the customer in the production of the serviceinstigates the need for greater control (Capar andKotabe, 2003). Therefore, the degree of customi-zation would strengthen the probability of choos-ing full-control modes, since the consequences ofopportunistic behaviour would be too high.

742 J. Pla-Barber, E. Sanchez-Peinado and A. Madhok

r 2010 British Academy of Management.

Marketing intensity

Brand name, reputation, commercial skills or thefirm’s ability in sales are key specific assets forinternational firms. These assets are especiallyvulnerable to problems related to divulging ormisuse of information by third parties. Branddevelopment and sales knowhow is establishedover many years and is rooted in a firm’s culture,systems and routines. Given that the process ofcreation and maintenance of product differentia-tion requires time, the undesired dissemination ofsuch commercial capabilities to third partiescould become the subject of possible misuse andcould damage a firm’s reputation and prestige.Commercial assets such as brand name, reputa-

tion or commercial skills are even more importantif firms are offering customized services. Sincethese services are adapted to the needs andexpectations of the consumers, reputation forquality becomes particularly important becauseof the inability of the consumer to evaluate thequality of most service offerings prior to con-sumption (Bateson, 1992). As a result, a consumerrelies on the reputation of the firm as an indicatorof quality. Consequently, reputation is likely to bea key success factor for most service businesses(Ekeledo and Sivakumar, 2004). The less control afirm exercises, the more exposed it will be topossible opportunistic behaviour by its partner,who can compromise on quality while free-ridingon reputation, and the more salient will be thesignificance of such behaviour. Therefore, weexpect that customization of services will enhancethe positive relationship between marketing in-tensity and the use of full-control modes.

H4: The positive relationship between market-ing intensity and service firms’ propensity forfull-control entry modes will become strongerwith increasing degree of customization.

Tacit knowhow

The nature of the knowhow being transferred is amajor determinant of foreign entry decisions.Knowledge is often tacit in nature, embodiednot only in technological blueprints but also in thehuman capital of the firm and in informaloperating procedures or routines. When theknowhow necessary to sell a service is tacit, it ismore likely to be transferred within the firm than

in the market because firms are more efficientvehicles for knowhow transfer (Hill, Hwang andKim, 1990; Kogut and Zander, 1992; Madhok,1996). The difficulties and costs involved intransferring tacit knowhow provide incentives forfirms to use high control modes of foreign entry tofacilitate the intra-organizational transfer of tacitknowhow by relying on human capital, drawingon organizational memory, and using existingorganizational routines to structure and effectuatethe transfer (Hill, Hwang and Kim, 1990).The tacit nature of knowhow takes on even

greater significance in the context of customizedservices, where the degree of interaction betweenproducer and consumer is very high. Theperformance of employees who deal directly withcustomers is important for the maintenance of afirm’s standards and the extent of customersatisfaction. In this context, individual experiencein the application of knowledge to a particularproblem as well as the speed of responsivenessconstitutes a source of competitive advantage(Malhotra, 2003). Not only is this knowhowhighly idiosyncratic and largely tacit but it is alsoclosely intertwined with the customer experience.Thus, for services with a high degree of customi-zation, the firm would not want to take anychances with local partners, which would increasethe propensity to use full-control modes. Hence,

H5: The positive relationship between tacitknowhow and service firms’ propensity for full-control entry modes will become stronger withincreasing degree of customization.

Methods

Sample

We test the above hypotheses using an interna-tional database compiled by Dun and Bradstreet(for 2002) that provides information on Spanishcompanies with international activities in the year2002. The population consisted of 660 multi-national service firms and 1500 service firms withexports higher than 25% of sales. Consequently,the total population was 2160 cases. The surveyinstrument consisted of an extensive mailquestionnaire which was pre-tested by severalacademics specialized in international manage-ment and the service sector, ensuring the facevalidity of the instrument. Moreover, to confirm

Investment and Control Decisions in Foreign Markets 743

r 2010 British Academy of Management.

the convergent and discriminant validity of themeasures, a pre-test was conducted throughpersonal interviews with executives responsiblefor international operations of service firms (notincluded in the sample).We sent out 2160 questionnaires. The ques-

tionnaire was mailed to senior-level managerswho were most likely to be involved in theinternationalization process, including CEOs ordirectors in charge of international operations.Each respondent was asked to provide data on upto two foreign market entry decisions in whichhe/she was involved or had enough informationabout to answer. Each firm was contacted bytelephone to encourage managers to participatein the study. Finally, a reminder letter was sent tonon-respondents with a copy of the question-naire. Data were collected between October 2002and February 2003, with the final number ofobservations obtained for the study being 328entries from 170 firms (12% response rate).Entries consisted of 152 exports, 36 cooperationagreements, 33 joint ventures, 27 total acquisi-tions and 80 greenfield subsidiaries.Some of the main characteristics of the sample

used for this study are shown in Table 1.Questionnaires were analysed using the time

trend procedure proposed by Armstrong andOverton (1977). First, we sampled non-respon-dents and asked them ten questions contained inthe original questionnaire. No significant differ-ences were found between the respondent andnon-respondent samples on these questions.Second, in our paper, the midpoint of the datacollection period (October 2002 until February2003) was used as the cutoff point for distinguish-ing between early and late respondents: 62% ofthe responses were from early respondents andthe remaining 38% were from late respondents.

To ensure that the early respondents and laterespondents did not systematically differ, thesetwo groups were compared on their demographicdata, including foreign sales, foreign assets,number of employees, number of countries interms of exports, number of countries in terms ofsubsidiaries, international experience in exportsand international experience in investments. Weused independent sample t-tests to check forequality of means. The analysis indicated nosignificant differences in the variables of interestbetween early and late respondents.Additionally, responding firms were compared

to a random sample of 50 non-respondentsregarding size (sales volume) and experience (yearssince foundation). No significant differences werefound (po0.05), providing no evidence for non-response bias. Finally, variables from the surveyresponses were cross-checked against companyreports and published data, where possible. A highdegree of correspondence between published dataand survey responses was found, supporting theveracity of the survey responses.

Variables

Dependent variables. As the model includes twolevels of analysis, two dependent variables wereintroduced. At the first level (equity/non equity),we used a dummy variable coded 1 for equitymodes (joint ventures, partial and total acquisi-tions, greenfield subsidiaries) and 0 for non-equitymodes (exports and cooperation agreements).At the second level, firms should choose between

full or shared control, under the condition thatforeign direct investment took place. Therefore, theentry mode is captured by a dummy variable whichtakes the value 1 for full-control modes (greenfieldsubsidiaries and total acquisitions) and 0 for shared

Table 1. Characteristics of the sample

Characteristics of the firms Mean Standard deviation Median Minimum Maximum

% foreign salesa 2.29 1.052 2 1 4

Assets abroada 1.24 0.658 1 1 4

Number of countries exported to 13.91 16.687 8.50 0 106

Number of countries with affiliated companies 2.33 3.586 1 0 25

Experience in exports (number of years) 14.71 16.672 10 0 123

Investment experience (number of years) 7.05 11.622 3 0 102

N5 328 entries.aIn intervals of 1 to 4: value 1, o25%; value 2, 25%–50%; value 3, 50%–75%; value 4, o75%.

744 J. Pla-Barber, E. Sanchez-Peinado and A. Madhok

r 2010 British Academy of Management.

control (joint ventures). Much of the literaturefocused on international business has classifiedthose variables as a dichotomous variable (e.g.Chen and Hennart, 2002; Erramilli and Rao, 1993;Gatignon and Anderson, 1988; Hennart, 1991;Hennart and Reddy, 1997; Madhok, 1998; Makinoand Neupert, 2000; Mutinelli and Piscitello, 1998).

Independent variables: environmental uncer-tainties. Environmental uncertainties includedmarket potential, cultural distance and hostcountry risk. Following Brouthers (2002), marketpotential was measured using the manager’sperception of the potential for growth offeredby the target country on a five-point Likert-typescale (1, none; 5, high). Cultural distance wascalculated according to the composite index usedby Kogut and Singh (1988). This index measuresthe deviation along each of the four culturaldimensions identified by Hofstede (1980) (un-certainty avoidance, individuality, power distanceand masculinity–femininity) from the score ofa given focal country (in our case Spain) foreach target country. Country risk was derivedfrom the host country risk index published inEuromoney the year before each entry (see, forexample, Brouthers, Brouthers and Werner,2008b; Delios and Beamish, 1999). This publica-tion presents annual ratings of countries basedon composite measures of both political andeconomic risks. The index varies from 0 to 100:the value 0 represents instability of political andeconomic conditions, while the value 100 repre-sents stability of such conditions. The variablewas reverse coded, so high values indicate highcountry risk.

Independent variables: behavioural uncertain-ties. Following Kim and Hwang (1992), mar-keting intensity was measured with a three-itemscale based on managers’ perceptions (1, verylow; 5, very high) about (i) firm reputation withrespect to design and quality; (ii) internationalrecognition of brand name; (iii) advertisinginvestment (Cronbach’s alpha5 0.74). Tacit kno-whow was measured with a four-item scalederived from Kim and Hwang (1992) andErramilli, Agarwal and Dev (2002). It was basedon managers’ perceptions (1, very low; 5, veryhigh) about (a) the difficulty in transferringcapabilities and knowledge; (b) the difficulty in

assessing the proper price of the service; (c) thedifficulty in copying the skills and knowledge;and (d) the difficulty in understanding theknowhow (Cronbach’s alpha5 0.83).

Independent variables: characteristics of servi-ces. Capital intensity comprised two items thatcapture the degree to which the service isprovided by machines and the degree to whichthe service is provided by people (1, very low; 5,very high). This measure has been used byErramilli and Rao (1993) and Erramilli andD’Souza (1995). The people-intensive serviceitem was reverse coded and then we constructedan index with both items (Cronbach’s al-pha5 0.84). Therefore, high values indicate morecapital-intensive services. Following Erramilliand Rao (1993), degree of customization containstwo items that represent the degree to which firmsoffer different services adapted to customers’preferences or they offer similar services tocustomers (1, very low; 5, very high). This lastitem was reverse coded and then we constructedan index with both items (Cronbach’s al-pha5 0.76). A high value of the index representsmore customized services.

Control variables. A number of other determi-nants found to be related to mode choice inprevious research were included. Firm size andexperience can influence the entry mode choice.First, we asked managers to indicate the firm’ssales volume for the year of entry to capture thesize of the firm.3 Larger firms simply have moreresources than do smaller firms and therefore canuse more integrated modes. Second, firms withmore international experience develop organiza-tional capabilities that enable them to makegreater commitments to a foreign investment(Johanson and Vahlne, 1977). In our analysis weused the standardized value of the number of

3Size is a categorical variable that takes three values: 1,small firms; 2, medium firms; 3, large firms. We askedmanagers to indicate the firm’s sales volume for the yearof entry. The difficulty in remembering the exact salesvolume led us to ask this question in terms of intervals,following European Union Commission recommenda-tions: a sales volume lower than 7 million euros (small),between 7 million and 40 million euros (medium), higherthan 40 million euros (large). Results are interpretedwith reference to the last interval.

Investment and Control Decisions in Foreign Markets 745

r 2010 British Academy of Management.

years abroad. Finally, recent studies establish theimportance of global strategic considerations indetermining the degree of foreign channel inte-gration (Aulakh and Kotabe, 1997; Harzing,2002). Hill, Hwang and Kim (1990) suggest theuse of methods with a low level of control byfirms developing a multi-domestic strategy inorder to facilitate adaptation to local conditions.However, firms with a global strategy prefermethods with a high level of control due to thenecessity of tight coordination, possible synergyeffects and transfers of assets between units. Afour-item measure was derived from Harzing(2002). Respondents were asked to assess thefollowing statements (1, strongly disagree; 5,strongly agree): (a) the firm’s desire to achieveeconomies of scale by concentrating the impor-tant activities in a limited number of locations;(b) competitive position is defined in worldwideterms and markets are closely linked and inter-connected; (c) each subsidiary competes ona domestic level as markets are too different(reverse); (d) the firm responds to nationaldifferences by adapting products to the localmarket (reverse). We constructed a compositeindex with these items (Cronbach’s alpha5 0.69).High values indicate global strategic approaches.

Regression model and results

The model proposed in this study breaks downthe entry mode choice into two decisions:investment (equity) and control. As there alwaysexists the possibility to not invest in the market,a simple probit or logit estimation would lead toa sample selection bias. Therefore, we have to testthe entry mode decision under the condition thatan investment has been undertaken. Hence, weuse the Van de Ven and Van Praag (1981) pro-bit application of the Heckman (1979) selectionbias correction procedure. We first estimate aninvestment decision equation where a firmi decides to invest in country j.

investij ¼1 if invest�ij > 00 otherwise

�

where

invest�ij ¼ g0 þXEUb1 þXBUb2 þXCIb3þXCIXEUb4 þXDCb5þXDCXBUb6 þ uij

The dependent variable takes the value 1 if firmi has invested in country j, and zero if a firmhas not undertaken foreign direct investment incountry j. Environmental uncertainty explana-tory variables (XEU), behavioural uncertaintyvariables (XBU), service characteristics (capitalintensity (XCI) and degree of customization(XDC)) and their interactions with environmentaland behavioural uncertainty variables are in-cluded in the model.The second decision describes the choice

between full control (wholly owned subsidiaries)and shared control (joint ventures), conditionalon foreign direct investment taking place.

controlij ¼1 if control�ij > 0 and invest�ij > 0

0 if control�ij � 0 and invest�ij > 0

(

where

control�ij ¼ d0 þXEUa1 þXBUa2

þXCIa3 þXCIXEUa4 þXDCa5þXDCXBUa6 þ nij

Assuming that uij and nij are normal variableswith zero means and a correlation coefficient of r,through the computer package LIMDEP, weestimate these equations simultaneously by max-imum likelihood. The errors are corrected for acorrelation between observations for the samedestination country.The number of observations in the investment

decision is equal to the number of entries in thesample. In the second decision equation, the numberof observations is equal to the total number offoreign direct investments in the sample. All theindependent and control variables were entered intothe two equations in order to test whether managersconsider only a few critical factors at each level orwhether all variables are equally evaluated by themat each level.Prior to running the statistical analyses, the

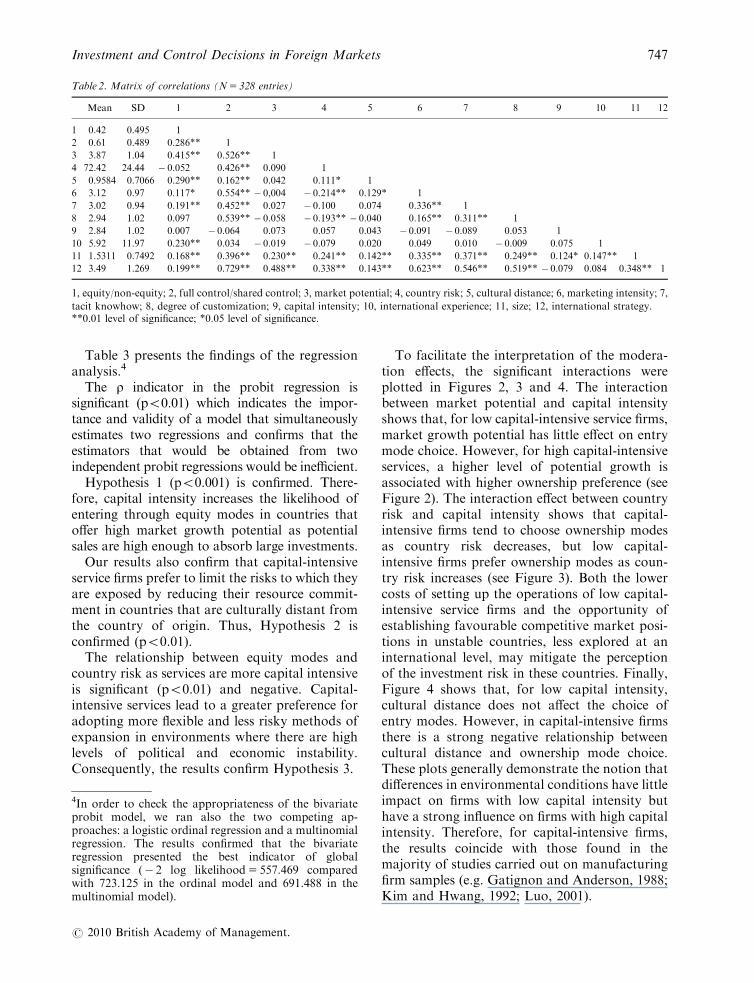

correlation matrix was examined (see Table 2).Most of the correlations among the variables aresmall. Further, the variance inflation factor (VIF)reveals that most of these are close to 1. The largestVIF value is 2.521, which is well below the cut-off at10 (Hair et al., 1999). Since the regression equationincluded both the individual predictors and thecross-product terms, multicollinearity was a con-cern. Mean-centred data were used to minimize thispotential effect.

746 J. Pla-Barber, E. Sanchez-Peinado and A. Madhok

r 2010 British Academy of Management.

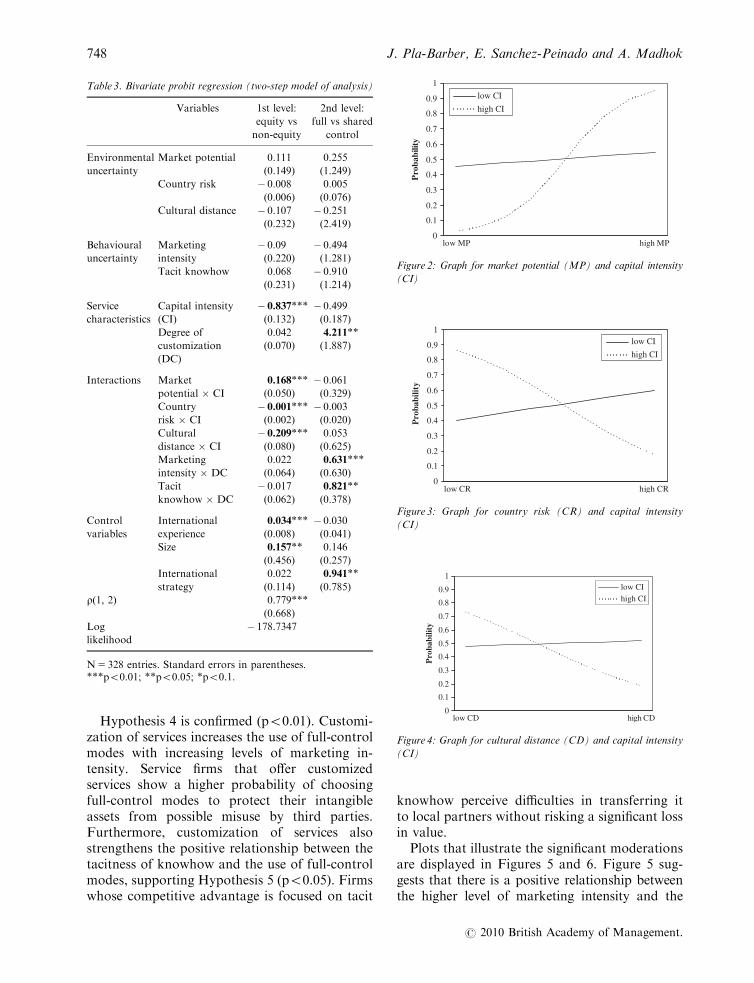

Table 3 presents the findings of the regressionanalysis.4

The r indicator in the probit regression issignificant (po0.01) which indicates the impor-tance and validity of a model that simultaneouslyestimates two regressions and confirms that theestimators that would be obtained from twoindependent probit regressions would be inefficient.Hypothesis 1 (po0.001) is confirmed. There-

fore, capital intensity increases the likelihood ofentering through equity modes in countries thatoffer high market growth potential as potentialsales are high enough to absorb large investments.Our results also confirm that capital-intensive

service firms prefer to limit the risks to which theyare exposed by reducing their resource commit-ment in countries that are culturally distant fromthe country of origin. Thus, Hypothesis 2 isconfirmed (po0.01).The relationship between equity modes and

country risk as services are more capital intensiveis significant (po0.01) and negative. Capital-intensive services lead to a greater preference foradopting more flexible and less risky methods ofexpansion in environments where there are highlevels of political and economic instability.Consequently, the results confirm Hypothesis 3.

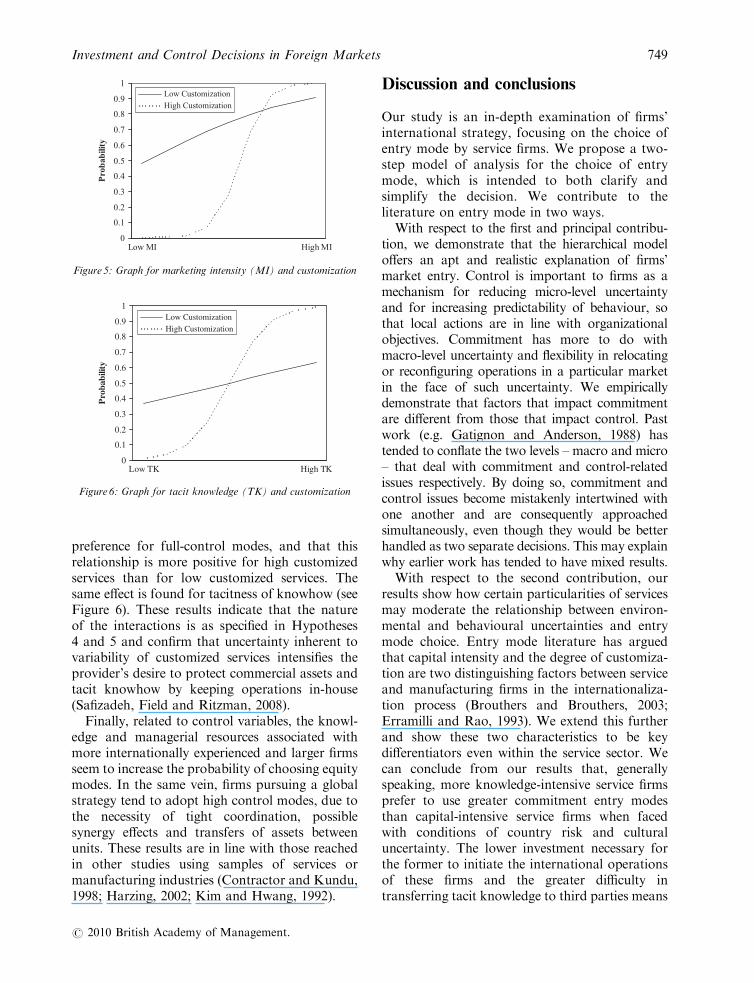

To facilitate the interpretation of the modera-tion effects, the significant interactions wereplotted in Figures 2, 3 and 4. The interactionbetween market potential and capital intensityshows that, for low capital-intensive service firms,market growth potential has little effect on entrymode choice. However, for high capital-intensiveservices, a higher level of potential growth isassociated with higher ownership preference (seeFigure 2). The interaction effect between countryrisk and capital intensity shows that capital-intensive firms tend to choose ownership modesas country risk decreases, but low capital-intensive firms prefer ownership modes as coun-try risk increases (see Figure 3). Both the lowercosts of setting up the operations of low capital-intensive service firms and the opportunity ofestablishing favourable competitive market posi-tions in unstable countries, less explored at aninternational level, may mitigate the perceptionof the investment risk in these countries. Finally,Figure 4 shows that, for low capital intensity,cultural distance does not affect the choice ofentry modes. However, in capital-intensive firmsthere is a strong negative relationship betweencultural distance and ownership mode choice.These plots generally demonstrate the notion thatdifferences in environmental conditions have littleimpact on firms with low capital intensity buthave a strong influence on firms with high capitalintensity. Therefore, for capital-intensive firms,the results coincide with those found in themajority of studies carried out on manufacturingfirm samples (e.g. Gatignon and Anderson, 1988;Kim and Hwang, 1992; Luo, 2001).

Table 2. Matrix of correlations (N5 328 entries)

Mean SD 1 2 3 4 5 6 7 8 9 10 11 12

1 0.42 0.495 1

2 0.61 0.489 0.286** 1

3 3.87 1.04 0.415** 0.526** 1

4 72.42 24.44 � 0.052 0.426** 0.090 1

5 0.9584 0.7066 0.290** 0.162** 0.042 0.111* 1

6 3.12 0.97 0.117* 0.554** � 0,004 � 0.214** 0.129* 1

7 3.02 0.94 0.191** 0.452** 0.027 � 0.100 0.074 0.336** 1

8 2.94 1.02 0.097 0.539** � 0.058 � 0.193** � 0.040 0.165** 0.311** 1

9 2.84 1.02 0.007 � 0.064 0.073 0.057 0.043 � 0.091 � 0.089 0.053 1

10 5.92 11.97 0.230** 0.034 � 0.019 � 0.079 0.020 0.049 0.010 � 0.009 0.075 1

11 1.5311 0.7492 0.168** 0.396** 0.230** 0.241** 0.142** 0.335** 0.371** 0.249** 0.124* 0.147** 1

12 3.49 1.269 0.199** 0.729** 0.488** 0.338** 0.143** 0.623** 0.546** 0.519** � 0.079 0.084 0.348** 1

1, equity/non-equity; 2, full control/shared control; 3, market potential; 4, country risk; 5, cultural distance; 6, marketing intensity; 7,

tacit knowhow; 8, degree of customization; 9, capital intensity; 10, international experience; 11, size; 12, international strategy.**0.01 level of significance; *0.05 level of significance.

4In order to check the appropriateness of the bivariateprobit model, we ran also the two competing ap-proaches: a logistic ordinal regression and a multinomialregression. The results confirmed that the bivariateregression presented the best indicator of globalsignificance (� 2 log likelihood5 557.469 comparedwith 723.125 in the ordinal model and 691.488 in themultinomial model).

Investment and Control Decisions in Foreign Markets 747

r 2010 British Academy of Management.

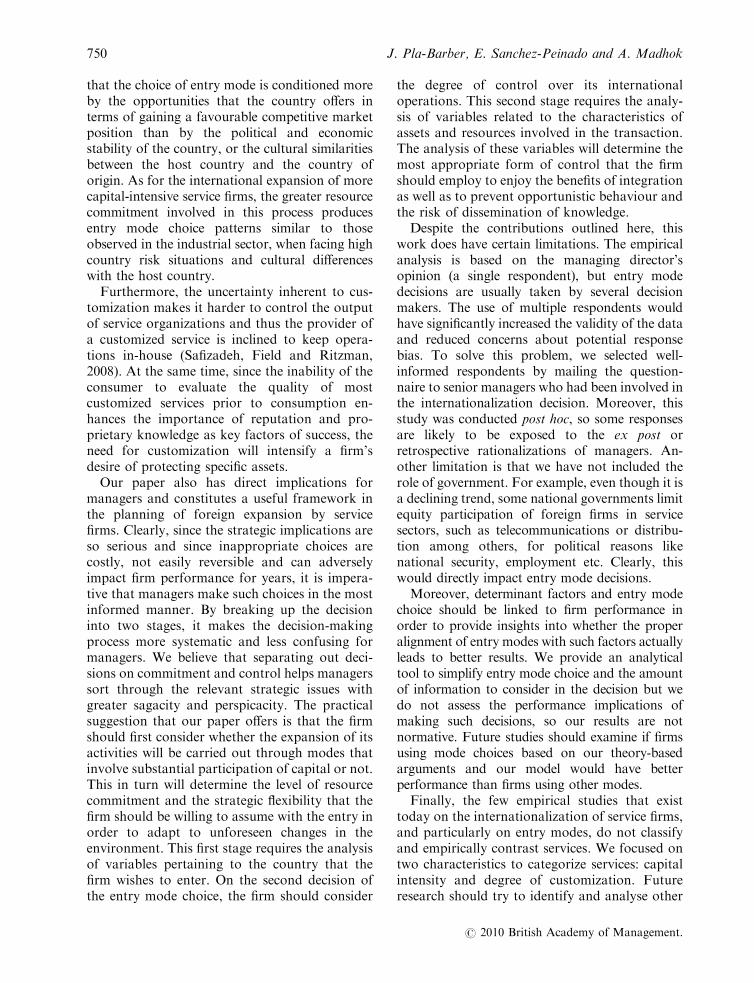

Hypothesis 4 is confirmed (po0.01). Customi-zation of services increases the use of full-controlmodes with increasing levels of marketing in-tensity. Service firms that offer customizedservices show a higher probability of choosingfull-control modes to protect their intangibleassets from possible misuse by third parties.Furthermore, customization of services alsostrengthens the positive relationship between thetacitness of knowhow and the use of full-controlmodes, supporting Hypothesis 5 (po0.05). Firmswhose competitive advantage is focused on tacit

knowhow perceive difficulties in transferring itto local partners without risking a significant lossin value.Plots that illustrate the significant moderations

are displayed in Figures 5 and 6. Figure 5 sug-gests that there is a positive relationship betweenthe higher level of marketing intensity and the

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

PMhgihPMwol

Pro

babi

lity

low CI

high CI

Figure 2: Graph for market potential (MP) and capital intensity

(CI)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

RC hgihRC wol

Pro

babi

lity

low CI

high CI

Figure 3: Graph for country risk (CR) and capital intensity

(CI)

Table 3. Bivariate probit regression (two-step model of analysis)

Variables 1st level:

equity vs

non-equity

2nd level:

full vs shared

control

Environmental

uncertainty

Market potential 0.111 0.255

(0.149) (1.249)

Country risk � 0.008 0.005

(0.006) (0.076)

Cultural distance � 0.107 � 0.251

(0.232) (2.419)

Behavioural Marketing � 0.09 � 0.494

uncertainty intensity (0.220) (1.281)

Tacit knowhow 0.068 � 0.910

(0.231) (1.214)

Service Capital intensity � 0.837*** � 0.499

characteristics (CI) (0.132) (0.187)

Degree of 0.042 4.211**

customization

(DC)

(0.070) (1.887)

Interactions Market 0.168*** � 0.061

potential � CI (0.050) (0.329)

Country � 0.001*** � 0.003

risk � CI (0.002) (0.020)

Cultural � 0.209*** 0.053

distance � CI (0.080) (0.625)

Marketing 0.022 0.631***

intensity � DC (0.064) (0.630)

Tacit � 0.017 0.821**

knowhow � DC (0.062) (0.378)

Control

variables

International 0.034*** � 0.030

experience (0.008) (0.041)

Size 0.157** 0.146

(0.456) (0.257)

International 0.022 0.941**

strategy (0.114) (0.785)

r(1, 2) 0.779***

(0.668)

Log

likelihood

� 178.7347

N5 328 entries. Standard errors in parentheses.***po0.01; **po0.05; *po0.1.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

DC hgihDCwol

Pro

babi

lity

low CIhigh CI

Figure 4: Graph for cultural distance (CD) and capital intensity

(CI)

748 J. Pla-Barber, E. Sanchez-Peinado and A. Madhok

r 2010 British Academy of Management.

preference for full-control modes, and that thisrelationship is more positive for high customizedservices than for low customized services. Thesame effect is found for tacitness of knowhow (seeFigure 6). These results indicate that the natureof the interactions is as specified in Hypotheses4 and 5 and confirm that uncertainty inherent tovariability of customized services intensifies theprovider’s desire to protect commercial assets andtacit knowhow by keeping operations in-house(Safizadeh, Field and Ritzman, 2008).Finally, related to control variables, the knowl-

edge and managerial resources associated withmore internationally experienced and larger firmsseem to increase the probability of choosing equitymodes. In the same vein, firms pursuing a globalstrategy tend to adopt high control modes, due tothe necessity of tight coordination, possiblesynergy effects and transfers of assets betweenunits. These results are in line with those reachedin other studies using samples of services ormanufacturing industries (Contractor and Kundu,1998; Harzing, 2002; Kim and Hwang, 1992).

Discussion and conclusions

Our study is an in-depth examination of firms’international strategy, focusing on the choice ofentry mode by service firms. We propose a two-step model of analysis for the choice of entrymode, which is intended to both clarify andsimplify the decision. We contribute to theliterature on entry mode in two ways.With respect to the first and principal contribu-

tion, we demonstrate that the hierarchical modeloffers an apt and realistic explanation of firms’market entry. Control is important to firms as amechanism for reducing micro-level uncertaintyand for increasing predictability of behaviour, sothat local actions are in line with organizationalobjectives. Commitment has more to do withmacro-level uncertainty and flexibility in relocatingor reconfiguring operations in a particular marketin the face of such uncertainty. We empiricallydemonstrate that factors that impact commitmentare different from those that impact control. Pastwork (e.g. Gatignon and Anderson, 1988) hastended to conflate the two levels – macro and micro– that deal with commitment and control-relatedissues respectively. By doing so, commitment andcontrol issues become mistakenly intertwined withone another and are consequently approachedsimultaneously, even though they would be betterhandled as two separate decisions. This may explainwhy earlier work has tended to have mixed results.With respect to the second contribution, our

results show how certain particularities of servicesmay moderate the relationship between environ-mental and behavioural uncertainties and entrymode choice. Entry mode literature has arguedthat capital intensity and the degree of customiza-tion are two distinguishing factors between serviceand manufacturing firms in the internationaliza-tion process (Brouthers and Brouthers, 2003;Erramilli and Rao, 1993). We extend this furtherand show these two characteristics to be keydifferentiators even within the service sector. Wecan conclude from our results that, generallyspeaking, more knowledge-intensive service firmsprefer to use greater commitment entry modesthan capital-intensive service firms when facedwith conditions of country risk and culturaluncertainty. The lower investment necessary forthe former to initiate the international operationsof these firms and the greater difficulty intransferring tacit knowledge to third parties means

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

IM hgiHIM woL

Probability

Low CustomizationHigh Customization

Figure 5: Graph for marketing intensity (MI) and customization

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

KThgiHKTwoL

Pro

babi

lity

Low Customization

High Customization

Figure 6: Graph for tacit knowledge (TK) and customization

Investment and Control Decisions in Foreign Markets 749

r 2010 British Academy of Management.

that the choice of entry mode is conditioned moreby the opportunities that the country offers interms of gaining a favourable competitive marketposition than by the political and economicstability of the country, or the cultural similaritiesbetween the host country and the country oforigin. As for the international expansion of morecapital-intensive service firms, the greater resourcecommitment involved in this process producesentry mode choice patterns similar to thoseobserved in the industrial sector, when facing highcountry risk situations and cultural differenceswith the host country.Furthermore, the uncertainty inherent to cus-

tomization makes it harder to control the outputof service organizations and thus the provider ofa customized service is inclined to keep opera-tions in-house (Safizadeh, Field and Ritzman,2008). At the same time, since the inability of theconsumer to evaluate the quality of mostcustomized services prior to consumption en-hances the importance of reputation and pro-prietary knowledge as key factors of success, theneed for customization will intensify a firm’sdesire of protecting specific assets.Our paper also has direct implications for

managers and constitutes a useful framework inthe planning of foreign expansion by servicefirms. Clearly, since the strategic implications areso serious and since inappropriate choices arecostly, not easily reversible and can adverselyimpact firm performance for years, it is impera-tive that managers make such choices in the mostinformed manner. By breaking up the decisioninto two stages, it makes the decision-makingprocess more systematic and less confusing formanagers. We believe that separating out deci-sions on commitment and control helps managerssort through the relevant strategic issues withgreater sagacity and perspicacity. The practicalsuggestion that our paper offers is that the firmshould first consider whether the expansion of itsactivities will be carried out through modes thatinvolve substantial participation of capital or not.This in turn will determine the level of resourcecommitment and the strategic flexibility that thefirm should be willing to assume with the entry inorder to adapt to unforeseen changes in theenvironment. This first stage requires the analysisof variables pertaining to the country that thefirm wishes to enter. On the second decision ofthe entry mode choice, the firm should consider

the degree of control over its internationaloperations. This second stage requires the analy-sis of variables related to the characteristics ofassets and resources involved in the transaction.The analysis of these variables will determine themost appropriate form of control that the firmshould employ to enjoy the benefits of integrationas well as to prevent opportunistic behaviour andthe risk of dissemination of knowledge.Despite the contributions outlined here, this

work does have certain limitations. The empiricalanalysis is based on the managing director’sopinion (a single respondent), but entry modedecisions are usually taken by several decisionmakers. The use of multiple respondents wouldhave significantly increased the validity of the dataand reduced concerns about potential responsebias. To solve this problem, we selected well-informed respondents by mailing the question-naire to senior managers who had been involved inthe internationalization decision. Moreover, thisstudy was conducted post hoc, so some responsesare likely to be exposed to the ex post orretrospective rationalizations of managers. An-other limitation is that we have not included therole of government. For example, even though it isa declining trend, some national governments limitequity participation of foreign firms in servicesectors, such as telecommunications or distribu-tion among others, for political reasons likenational security, employment etc. Clearly, thiswould directly impact entry mode decisions.Moreover, determinant factors and entry mode

choice should be linked to firm performance inorder to provide insights into whether the properalignment of entry modes with such factors actuallyleads to better results. We provide an analyticaltool to simplify entry mode choice and the amountof information to consider in the decision but wedo not assess the performance implications ofmaking such decisions, so our results are notnormative. Future studies should examine if firmsusing mode choices based on our theory-basedarguments and our model would have betterperformance than firms using other modes.Finally, the few empirical studies that exist

today on the internationalization of service firms,and particularly on entry modes, do not classifyand empirically contrast services. We focused ontwo characteristics to categorize services: capitalintensity and degree of customization. Futureresearch should try to identify and analyse other

750 J. Pla-Barber, E. Sanchez-Peinado and A. Madhok

r 2010 British Academy of Management.

factors that would enable a more refined classi-fication of services, which may enable betterinterpretation of patterns of behaviour in thissector, one which, despite being among the mostdynamic in developed economies, has receivedrelatively scarce attention from researchers

References

Agarwal, S. and S. N. Ramaswami (1992). ‘Choice of foreign

market entry mode: impact of ownership, location and

internalization factors’, Journal of International Business

Studies, 23, pp. 1–27.

Anand, J. and A. Delios (1997). ‘Location specificity and the

transferability of downstream assets to foreign subsidiaries’,

Journal of International Business Studies, 28, pp. 579–603.

Anderson, E. and H. Gatignon (1986). ‘Modes of foreign entry:

a transaction cost analysis and propositions’, Journal of

International Business Studies, 17, pp. 1–26.

Armstrong, J. S. and T. Overton (1977). ‘Estimating non-

response bias in mail surveys’, Journal of Marketing

Research, 14, pp. 396–402.

Aulakh, P. S. and M. Kotabe (1997). ‘Antecedents and perfor-

mance implications of channel integration in foreign markets’,

Journal of International Business Studies, 28, pp. 145–175.

Bateson, J. E. G. (1992). Managing Services Marketing, 2nd

edn. Fort Worth, TX: Dryden Press.

Brouthers, K. D. (2002). ‘Institutional, cultural and transaction

cost influences on entry mode choice and performance’,

Journal of International Business Studies, 33, pp. 203–221.

Brouthers, K. D. and L. E. Brouthers (2003). ‘Why service and

manufacturing entry mode choices differ: the influence of

transaction cost factors, risk and trust’, Journal of Manage-

ment Studies, 40, pp. 1179–1204.

Brouthers, K. D. and G. Nakos (2004). ‘SME entry mode

choice and performance: a transaction cost perspective’,

Entrepreneurship: Theory and Practice, 28, pp. 229–247.

Brouthers, L. E., K. D. Brouthers and S. Werner (2000).

‘Perceived environmental uncertainty, entry mode choice and

satisfaction with EC-MNC performance’, British Journal of

Management, 11, pp. 183–195.

Brouthers, K.D, L. E. Brouthers and S. Werner (2003). ‘Transac-

tion cost-enhanced entry mode choices and firm performance’,

Strategic Management Journal, 24, pp. 1239–1248.

Brouthers, K. D., L. E. Brouthers and S. Werner (2008a). ‘Real

options, international entry mode choice and performance’,

Journal of Management Studies, 45, pp. 936–960.

Brouthers, K. D., L. E. Brouthers and S. Werner (2008b).

‘Resource-based advantages in an international context’,

Journal of Management, 34, pp. 189–217.

Brown, J. R., C. S. Dev and Z. Zho (2003). ‘Broadening the

foreign market entry mode decision: separating ownership

and control’, Journal of International Business Studies, 34, pp.

473–488.

Capar, N. and M. Kotabe (2003). ‘The relationship between

international diversification and performance in service

firms’, Journal of International Business Studies, 34, pp.

345–355.

Chang, S. J. and P. M. Rosenzweigh (2001). ‘The choice of

entry mode in sequential foreign direct investment’, Strategic

Management Journal, 22, pp. 747–776.

Chen, S.-F. S. and J.-F. Hennart (2002). ‘Japanese investors’

choice of joint ventures versus wholly-owned subsidiaries in

the US: the role of market barriers and firm capabilities’,

Journal of International Business Studies, 33, pp. 1–18.

Chen, H. and M. Hu (2002). ‘An analysis of determinants of

entry mode and its impact on performance’, International

Business Review, 11, pp. 193–210.

Contractor, F. J. and S. K. Kundu (1998). ‘Modal choice in a

world of alliances: analyzing organizational forms in the

international hotel sector’, Journal of International Business

Studies, 29, pp. 325–358.

Delios, A. and P. W. Beamish (1999). ‘Ownership strategy

of Japanese firms: transactional, institutional and experi-

ence influences’, Strategic Management Journal, 20, pp. 915–

933.

Dhanaraj, C. and P. W. Beamish (2004). ‘Effect of equity

ownership on the survival of international joint ventures’,

Strategic Management Journal, 25, pp. 295–305.

Dunning, J. H. (1988). ‘The eclectic paradigm of international

production: a restatement and some possible extensions’,

Journal of International Business Studies, 19, pp. 1–32.

Ekeledo, I. and K. Sivakumar (2004). ‘International market

entry mode strategies of manufacturing firms and service

firms. A resource-based perspective’, International Marketing

Review, 21, pp. 68–101.

Erramilli, M. K. (1992). ‘Influence of some external and

internal environmental factors on foreign market entry mode

choice in service firms’, Journal of Business Research, 25, pp.

263–276.

Erramilli, M. K. and D. E. D’Souza (1995). ‘Uncertainty and

foreign direct investment: the role of moderators’, Interna-

tional Marketing Review, 12, pp. 47–60.

Erramilli, M. K. and C. P. Rao (1993). ‘Service firms’

international entry-mode choice: a modified transaction-cost

analysis approach’, Journal of Marketing, 57, pp. 19–38.

Erramilli, M. K., S. Agarwal and C. S. Dev (2002). ‘Choice

between non-equity entry modes: an organizational capabil-

ity perspective’, Journal of International Business Studies, 33,

pp. 223–242.

Fladmoe-Lindquist, K. and L. L. Jacque (1995). ‘Control

modes in international service operations: the propensity to

franchise’, Management Science, 41, pp. 1238–1249.

Friedmann, W. G. and J. P. Beguin (1971). Joint International

Business Ventures in Developing Countries. New York: Columbia

University Press.

Gatignon, H. and E. Anderson (1988). ‘The multinational

corporation’s degree of control over foreign subsidiaries: an

empirical test of a transaction cost explanation’, Journal of

Law, Economics, and Organization, 4, pp. 305–336.

Geringer, M. and L. Hebert (1989). ‘Control and performance

of international joint ventures’, Journal of International

Business Studies, 20, pp. 235–254.

Hair, J., R. Anderson, R. Tatham and W. Black (1999).

Multivariate Data Analysis. Madrid: Prentice Hall Iberica.

Harzing, A. W. (2002). ‘Acquisitions vs greenfield investments:

international strategy and management of entry modes’,

Strategic Management Journal, 23, pp. 211–227.

Heckman, J. (1979). ‘Sample selection bias as a specification

error’, Econometrica, 47, pp. 153–161.

Investment and Control Decisions in Foreign Markets 751

r 2010 British Academy of Management.

Hennart, J.-F. (1991). ‘The transaction costs theory of

joint ventures: an empirical study of Japanese subsidi-

aries in the United States’, Management Science, 37, pp.

483–497.

Hennart, J.-F. and S. Reddy (1997). ‘The choice between

mergers/acquisitions and joint ventures: the case of Japanese

investors in the United States’, Strategic Management

Journal, 18, pp. 1–12.

Herrmann, P. and D. K. Datta (2006). ‘CEO experiences:

effects on the choice of FDI entry mode’, Journal of

Management Studies, 43, pp. 755–778.

Hill, C. W. L., P. Hwang and W. C. Kim (1990). ‘An eclectic

theory of the choice of international entry mode’, Strategic

Management Journal, 11, pp. 117–128.

Hofstede, G. (1980). Cultures Consequence: International

Differences in Work-related Values. Beverly Hills, CA: Sage.

Horn, J. T., D. Lovallo and P. Viguerie (2005). ‘Beating the

odds in market entry’, McKinsey Quarterly, 4, pp. 35–45.

Johanson, J. and J. E. Vahlne (1977). ‘The internationalization

process of the firm: a model of knowledge development and

increasing foreign market commitments’, Journal of Interna-

tional Business Studies, 8, pp. 23–32.

Kim, W. C. and P. Hwang (1992). ‘Global strategy and

multinationals’ entry mode choice’, Journal of International

Business Studies, 23, pp. 29–53.

Kogut, B. and H. Singh (1988). ‘The effect of national culture

on the choice of entry mode’, Journal of International

Business Studies, 19, pp. 411–432.

Kogut, B. and U. Zander (1992). ‘Knowledge of the firm,

combinative capabilities, and the replication of technology’,

Organization Science, 3, pp. 383–397.

Kumar, V. and V. Subramaniam (1997). ‘A contingency

framework for the mode of entry decision’, Journal of World

Business, 32, pp. 53–72.

Li, M., Y. Zhang and R. Jing (2008). ‘Does ownership and culture

matter to joint venture success?’, International Management

Review, 4, pp. 88–100.

Luo, Y. (2001). ‘Determinants of entry in an emerging

economy: a multilevel approach’, Journal of Management

Studies, 38, pp. 443–472.

Madhok, A. (1996). ‘The organization of economic activity:

transaction costs, firm capabilities, and the nature of

governance’, Organization Science, 7, pp. 577–590.

Madhok, A. (1997). ‘Cost, value and foreign market entry

mode: the transactions and the firm’, Strategic Management

Journal, 18, pp. 39–61.

Madhok, A. (1998). ‘The nature of multinational firm bound-

aries: transaction costs, firm capabilities and foreign market

entry mode’, International Business Review, 7, pp. 259–290.

Makino, S. and K. E. Neupert (2000). ‘National culture,

transaction costs, and the choice between joint venture and

wholly owned subsidiary’, Journal of International Business

Studies, 31, pp. 705–713.

Malhotra, N. (2003). ‘The nature of knowledge and the entry

mode decision’, Organization Studies, 24, pp. 935–959.

Miller, K. D. (1993). ‘Industry and country effects on managers’

perceptions of environmental uncertainties’, Journal of

International Business Studies, 24, pp. 693–714.

Mjoen, H. and S. Tallman (1997). ‘Control and performance in

international joint ventures’, Organization Science, 8, pp.

257–274.

Mutinelli, M. and L. Piscitello (1998). ‘The entry mode choice

of MNEs: an evolutionary approach’, Research Policy, 27,

pp. 491–506.

Pan, Y. and D. K. Tse (2000). ‘The hierarchical model of

market entry modes’, Journal of International Business

Studies, 31, pp. 535–554.

Safizadeh, M. H., J. M. Field and L. P. Ritzman (2008). ‘Sourcing

practices and boundaries of the firm in the financial services

industry’, Strategic Management Journal, 29, pp. 79–91.

Tsou, H. T., R. K. H. Ching and J. S. Chen (2007).

‘Performance effects of IT capability and customer service:

the moderating role of service process innovation’, 2007

IEEE Conference Proceedings, International Conference on

Wireless Communications, Networking and Mobile Comput-

ing, WiCom 2007, New York: IEEE Press.

Van de Ven, W. P. M. M. and B. M. S. Van Praag (1981). ‘The

demand for deductibles in private health insurance: a probit