Integrating Social and Political Risk Into Management ...

49

MANAGEMENT STRATEGY MEASUREMENT Integrating Social and Political Risk Into Management Decision-Making By Tamara Bekefi and Marc J. Epstein Published by: MANAGEMENT ACCOUNTING GUIDELINE

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Integrating Social and Political Risk Into Management ...

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

Integrating Socialand Political RiskInto ManagementDecision-Making

By

Tamara Bekefi andMarc J. Epstein

Published by:

MANAGEMENT ACCOUNTING GUIDELINE

NOTICE TO READERS

The material contained in the Management Accounting Guideline Integrating Social and Political Risk Into Management Decision-Making is designed to provide illustrative information with respect to the subject matter covered. It does not establish standardsor preferred practices. This material has not been considered or acted upon by any senior technical committees or the board ofdirectors of either the AICPA or the Society of Management Accountants of Canada and does not represent an official opinion orposition of either the AICPA or the Society of Management Accountants of Canada.

S T R A T E G Y

M E A S U R E M E N T

Integrating Socialand Political RiskInto ManagementDecision-Making

By

Tamara BekefiHarvard UniversityandMarc J. EpsteinRice University

MANAGEMENT ACCOUNTING GUIDELINE

Published by The Society of Management Accountants of Canadaand The American Institute of Certified Public Accountants

M A N A G E M E N T

Copyright © 2006 by the Society of Management Accountants of Canada (CMA-Canada).All rights reserved.Reproduced by AICPA by arrangement with CMA-Canada.

All rights reserved. For information about the procedure for requesting permission to make copies of any part of this work,please visit www.copyright.com or call (978) 750-8400.

1 2 3 4 5 6 7 8 9 0 PP 0 9 8 7 6

ISBN 0-87051-656-6

INTRODUCTION

The corporate risk landscape has shiftedsignificantly in recent years. Larger andmore varied risks than ever previouslythought have been seen in companiesand countries who had believed theywere immune from those risks. Rapidlyincreasing globalization poses a commonchallenge—how to integrate the socialand political risks of governmentinstability, political corruption, businesscorruption, child labor practices, anti-corporate sentiment, terrorism,environmental pollution, and others, intomanagement decisions. To date, no

adequate methodology for integratingthese issues into risk management hasbeen found.

Developing and implementing anappropriate model for decision-makingand measurement of social and political risks is critical for improvingorganizational performance by moreeffectively (a) anticipating, evaluating,preparing for, and mitigating risks,and (b) managing alternatives.Toeffectively manage risk and improve the resource allocation process, risksmust be measured and integrated into ROI calculations.

INTEGRATING SOCIAL AND POLITICALRISK INTO MANAGEMENT

DECISION-MAKING

CONTENTS EXECUTIVE SUMMARY

Today risks are both larger and morevaried than ever previously thought.Theyare far broader and have been seen incompanies and countries that thoughtthey were shielded.With globalizationincreasing rapidly, a common challenge ishow to integrate social and political risksof political instability, political corruption,business corruption, child labor practices,anti-corporate sentiment, terrorism,environmental pollution, and so forthinto management decisions.

This publication building on the modeldeveloped in the Management AccountingGuideline “Identifying,Measuring, andManaging Organizational Risk forImproved Performance” provides thetools, techniques, and specificity neededto aid managers to more effectivelyintegrate social and political risks intotheir decision making processes.

INTRODUCTION 5BACKGROUND 6CURRENT PRACTICES IN

IDENTIFYING AND MEASURING SOCIAL AND POLITICAL RISK 8

INTEGRATING SOCIAL AND POLITICAL RISKS INTO GENERAL RISK MANAGEMENT 10• RISK IDENTIFICATION 12• ASSESSING AND MEASURING

SOCIAL AND POLITICAL RISK 24• MANAGE AND MONITOR

POLITICAL AND SOCIAL RISK 32• COMMUNICATING SOCIAL

AND POLITICAL RISK 39CONCLUSION 41APPENDIX 1:REAL AND PERCEIVED RISK 44APPENDIX 2: POLITICAL RISK

CONSULTING FIRMS AND THEIR OFFERINGS 46

Page

S T R A T E G Y

5

6

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

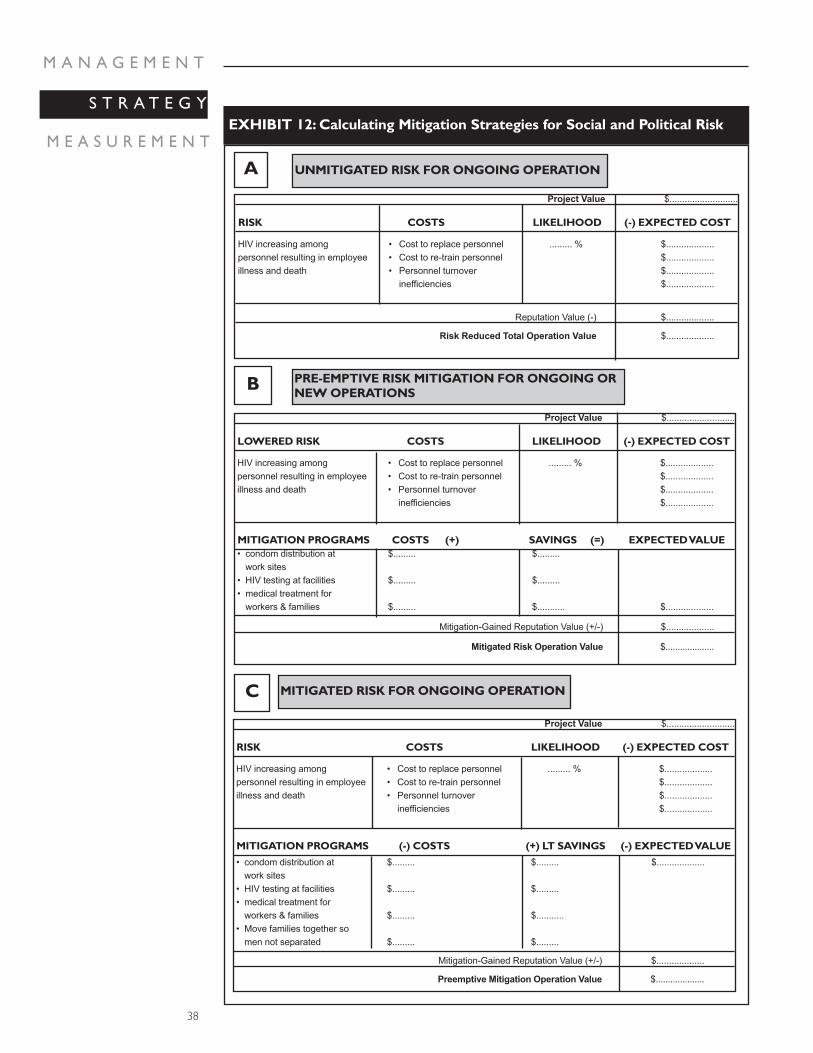

These calculations can be applied to day-to-dayoperational decisions and capital investmentplanning, such as choices about plant location.Robust decisions under both circumstances arepredicated on sound identification of risks, theirassessment, and their mitigation and avoidance.We know, for example, that a wide array ofpolitical and social issues in both the developedand developing world can often cause a majorimpact on profits in an organization’s homecountry.These risks affect all types oforganizations, including for-profit, non-profit,global, domestic, and large and small enterprises.

Generally, risk can be described as any event oraction that will adversely affect an organization’sability to achieve its business objectives andsuccessfully execute its strategies. Risk relates tothe probability that exposure to a hazard willhave negative consequences. Social risk relatesto the potential impact of, for example, disease,damage to the environment, infringement of therights of indigenous peoples, and challenges bystakeholders due to negative perceptions ofbusiness practices—all of which can jeopardizea company’s value. Political risk can generally beunderstood as execution of political power thatthreatens a company’s value.The distinctionbetween social and political risk is, however,often blurred, and different sectors in variedlocations can be affected differently by eitherkind of risk.

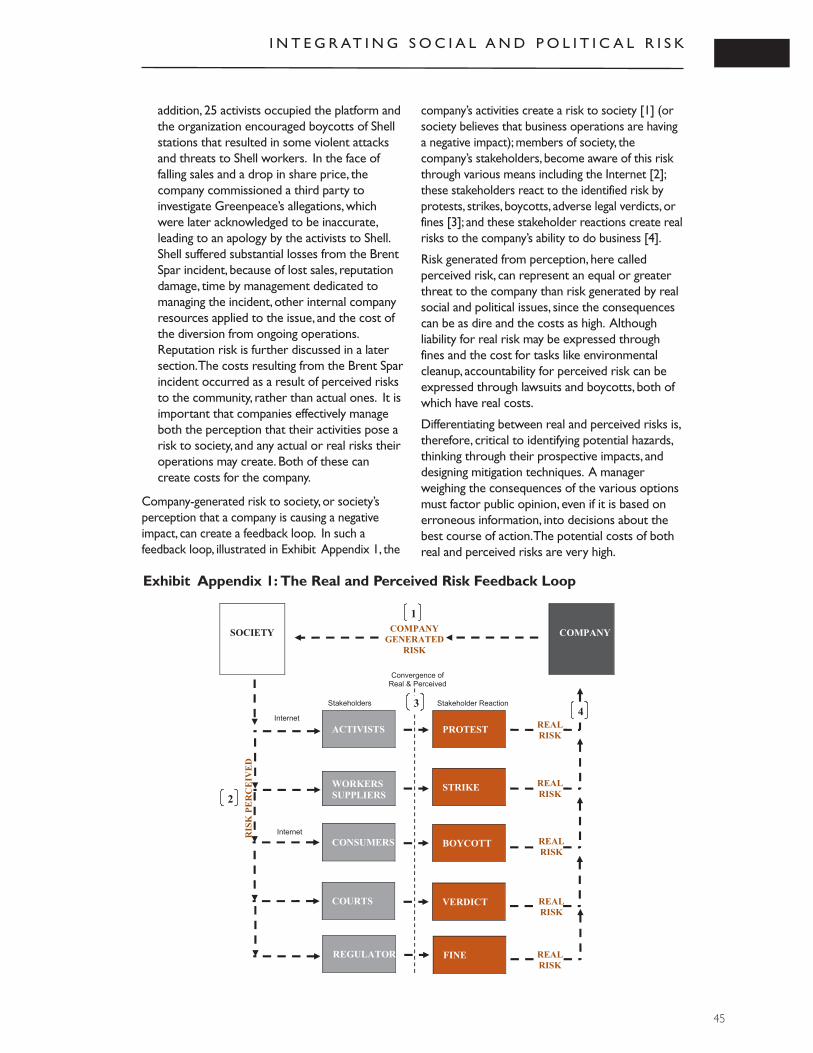

Societal perceptions of the connectionsbetween a company and particular social andpolitical risks can cause enormous costs tocompanies, regardless of the company’s directinvolvement in the issue. Whether society isreacting to a real or perceived risk, it may takeaction, including consumer boycotts, leading toloss of sales or increased regulation thatnegatively affect a company,whether by (a)increasing its costs, or (b) prejudicing itsachievement of business objectives or its abilityto carry out its strategies. [Note that I havebrought in language similar to that used in definingrisk earlier.].Thus,managing these types of risksis critical,whether they are real or perceived.(For further discussion of real and perceivedrisks, see Appendix 1.)

Public perception of companies has proven tobe an important component of risk. Researchfollowing anti-World Trade Organizationprotests in Seattle showed that investors drovedown the market capitalization of companieswithout a reputation for corporateresponsibility on average by $378 million per

company, but did not penalize firms reputed tobe socially responsible. (Schneitz and Epstein,2004). This demonstrates the significant positivefinancial impact of a reputation for managingsocial and political risks well.

[The now deleted sentence doesn’t identify who is concerned. I altered the second sentence.]Companies must more clearly recognize theimportance of (a) integrating a broader set ofrisks into management decisions, and (b)developing expertise in measuring the impact ofsocial and political issues on financialperformance.This clearer recognition requiresmanagers to include measurement of social andpolitical risks in ROI calculations. Currently,companies that do consider these issues oftenrelegate them to a footnote in the reporting ofinvestment decision and do not include them incalculating ROI.That effectively gives a zerovaluation to risks that can negatively affectcorporate earnings, shareholder value, andbrand value.

Some businesses are prone to social andpolitical risk because of the location of theirfacilities, their product and customercharacteristics, the nature of their employmentrelationships, or industry characteristics, etc.Well-known examples include Nike,Wal-Mart,and Shell, as well as the notorious social risksassociated with industries like mining, footwear,apparel, toys, and chemicals. Also, varying socialand political risks, and degrees of risk, affectcompanies located in specific countries orregions of the world. More globally, devastatingterrorism attacks such as September 11, 2001have dramatically increased risk, resulting notonly in a terrible impact on individuals andgovernment, but also an overwhelming impacton businesses.Corporations hoping to properlymanage risk require more analysis, evaluation,preparation,mitigation, and response planning.

This Guideline, aimed at CEOs,CFOs, and othertop managers, provides a model for identifyingand measuring social and political risk, andincluding these risks in ROI calculations, tocreate a more robust enterprise riskmanagement (ERM) system. This modelingforms one small part of ERM, simply by includingpreviously ignored risks.

BACKGROUND

In a recent Management Accounting Guideline(“Identifying,Measuring, and ManagingOrganizational Risk for Improved

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

7

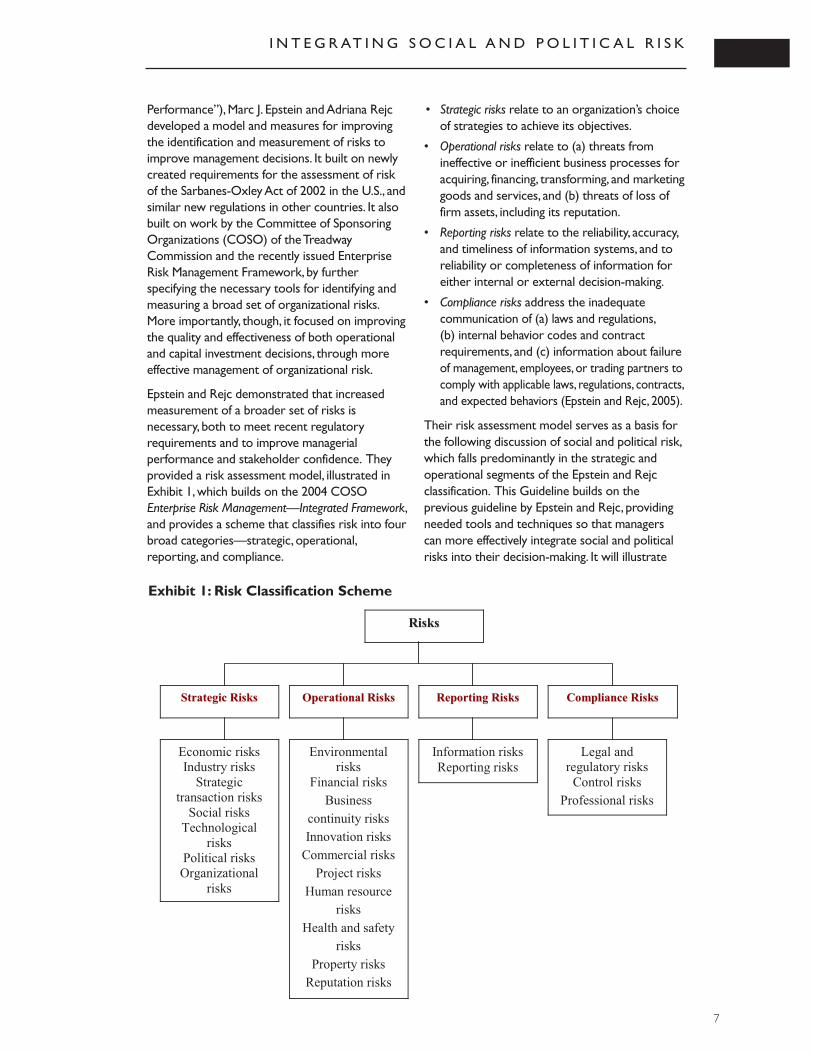

Performance”),Marc J. Epstein and Adriana Rejcdeveloped a model and measures for improvingthe identification and measurement of risks toimprove management decisions. It built on newlycreated requirements for the assessment of riskof the Sarbanes-Oxley Act of 2002 in the U.S., andsimilar new regulations in other countries. It alsobuilt on work by the Committee of SponsoringOrganizations (COSO) of the TreadwayCommission and the recently issued EnterpriseRisk Management Framework, by furtherspecifying the necessary tools for identifying andmeasuring a broad set of organizational risks.More importantly, though, it focused on improvingthe quality and effectiveness of both operationaland capital investment decisions, through moreeffective management of organizational risk.

Epstein and Rejc demonstrated that increasedmeasurement of a broader set of risks isnecessary, both to meet recent regulatoryrequirements and to improve managerialperformance and stakeholder confidence. Theyprovided a risk assessment model, illustrated inExhibit 1,which builds on the 2004 COSOEnterprise Risk Management—Integrated Framework,and provides a scheme that classifies risk into fourbroad categories—strategic, operational,reporting, and compliance.

• Strategic risks relate to an organization’s choiceof strategies to achieve its objectives.

• Operational risks relate to (a) threats fromineffective or inefficient business processes foracquiring, financing, transforming, and marketinggoods and services, and (b) threats of loss offirm assets, including its reputation.

• Reporting risks relate to the reliability, accuracy,and timeliness of information systems, and toreliability or completeness of information foreither internal or external decision-making.

• Compliance risks address the inadequatecommunication of (a) laws and regulations,(b) internal behavior codes and contractrequirements, and (c) information about failureof management, employees, or trading partners tocomply with applicable laws, regulations, contracts,and expected behaviors (Epstein and Rejc, 2005).

Their risk assessment model serves as a basis forthe following discussion of social and political risk,which falls predominantly in the strategic andoperational segments of the Epstein and Rejcclassification. This Guideline builds on theprevious guideline by Epstein and Rejc, providingneeded tools and techniques so that managerscan more effectively integrate social and politicalrisks into their decision-making. It will illustrate

Exhibit 1: Risk Classification Scheme

OOppeerraattiioonnaall RRiisskkss SSttrraatteeggiicc RRiisskkss RReeppoorrttiinngg RRiisskkss

Economic risks Industry risks

Strategic transaction risks

Social risks Technological

risks Political risks Organizational

risks

Environmental risks

Financial risks

Business

continuity risks

Innovation risks

Commercial risks

Project risks

Human resource

risks

Health and safety

risks

Property risks

Reputation risks

Information risks Reporting risks

CCoommpplliiaannccee RRiisskkss

Legal and regulatory risks

Control risks

Professional risks

RRiisskkss

8

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

why it is important for companies to understandsocial and political risk, and how to measure itfor more effective risk management.

Although identifying and classifying risks arecritical first steps, it is essential to managementpractices that their impacts on the firm bemeasured.The previous guideline emphasizesthe importance of assessing risks, both interms of their cost if they materialize, and thebenefits flowing from appropriate riskresponse.Of particular relevance tounderstanding,measuring, and managing socialand political risk is the capability to quantifytheir potential impacts.

We build on the previous guideline by describinghow companies can more effectively integratesocial and political risks into operational andcapital investment decisions, including how toidentify and measure them.The enhanced model also provides specific guidance thatpermits ROI calculations to include a formal and explicit assessment of these risks.Thisassessment will improve resource allocationdecisions and risk management, both of whichare the responsibility of senior corporatemanagers and boards of directors.

CURRENT PRACTICES IN IDENTIFYING AND MEASURINGSOCIAL AND POLITICAL RISK

Companies face complex political and socialchallenges.They are wide-ranging and havedifferent impacts on organizations, depending onsector, geographic location, and type ofoperation. Further, consideration of risk issubstantively different if a company is consideringopening a new venture or tackling challenges toexisting operations. Previously, corporate riskwas more narrowly focused on internal financialcontrols and corporate frauds.Now, identifying,measuring and seeking preventive or mitigationstrategies to address social and political issueshave become crucial to firms functioning invarious countries.All companies are struggling tomake business decisions that integrate financialinformation with insight into social and politicalconcerns that can seriously affect their projectsand bottom lines. Integration of social andpolitical risks into the financial equation has,however, remained a challenge.

Qualitative Approaches

Techniques to evaluate and communicatepolitical risk have been emerging since the mid-

1970s,when multinational firms, particularly inthe extractives and banking industries, built in-house teams employing political scientists andformer CIA and U.S. State Departmentpersonnel.These teams looked at riskassessment qualitatively, producing detailed localbriefings that outlined challenges in variouslocations.While providing sound insight intopolitical instability and risks, these local briefingsdid not capture the cost of risk, because theyfailed to connect the issues to the business orexplain their potential negative impact. For thisreason, the briefings did not enable executivedecision-makers to integrate these insights intobusiness assessments. In fact, importantinformation contained within those briefings wassometimes relegated to a footnote in thedecision-making process.

Quantitative Approach

From the qualitative model emerged efforts toquantify political risk, to make it more relevantto corporate management.To accomplish this,various methods were developed.

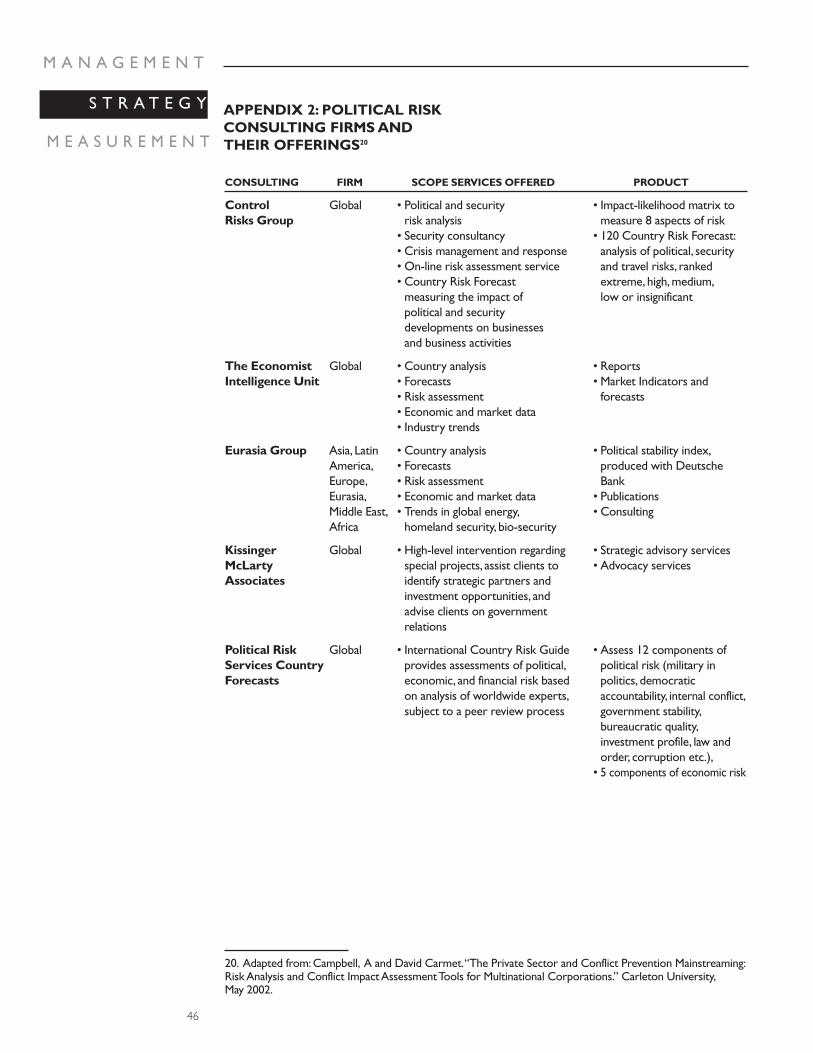

• Scorecards: Indicators of potential politicaland social risks, such as judiciaryindependence, corruption, and governmentturnover,were evaluated and assigned anumerical score. For example, a governmentviewed as highly corrupt could be assigned a10 in a possible scale of 1-10.Then, dependingon the methodology, the scores from theseindicators were aggregated or the statisticswere analyzed to generate a final measurethat reflected the political risk of a country.An indicator listing that looks specifically atcorruption,Transparency International, ranksthe world’s countries on the basis ofperceived levels of corruption. Anotherpolitical risk consulting firm divides itsindicators into four subcategories—government, society, security, and theeconomy—first calculating ratings for eachsubject, then aggregating them to create anational stability rating that can range from‘failed states’ to ‘maximum stability’. Suchscoring is helpful, because it enables acomparison between countries. It falls short,however, of being directly useful to businessdecision-making, because the risks are notconverted into monetary terms. (SeeAppendix 2 for a listing of companies thatprovide such data).

• Statistical analysis: Probability analysisrequires risk personnel to identify probable

issues and quantify them. Staff considers eachrisk and assigns a rating of high,medium,orlow, and expected values, as well as acorresponding probability for an occurrence, allprobabilities associated with a single riskequaling one.The data is then loaded into aspreadsheet application, such as Crystal Ball,which uses Monte Carlo simulations.CrystalBall is an analytical tool that automaticallygenerates equations to capture uncertainty,such as the cost of a coup to the company. Ituses the Monte Carlo simulation model,whichmimics the random chance of casino games,generating values for variables that have aknown range of values, but an uncertain valuefor a particular time or event. Hundreds oreven thousands of simulations can be run in amatter of minutes, and forecasts are generatedfor each point in the pre-determined range(high,medium, low) of risk.The results showproject managers either the most sensitiveissues on which to concentrate—sensitivityanalysis—or a cumulative probability curveindicating the potential economic performanceof a project—based on a pre-constructeddecision tree that indicates key decisions anduncertainties.Although this methodologyinvolves quantification and the consideration ofpotential risk impacts, the outputs of thesecalculations,which include charts, graphs, anddynamic models, cannot be integrated intofinancial evaluations.This is because they donot generate an ROI number, a political/socialrisk beta, or any monetary results that can beincluded into financial calculations.

• Scenario-based methods: Risk mapping is one method popular with corporations.Thismethod plots the expected frequency, severityand degree of exposure of various risks on agraph,with probable frequency on thehorizontal axis and expected severity on thevertical axis. (Birbeck, 1999).Calculations aremade according to the following formula:

Exposure = (event) x (hypotheticallikelihood) x (hypothetical consequence)

The benefit of such modeling is that it allowsmeasurement of various types of risk,andenables managers to visualize where to allocateresources for risk management. In addition,mapping is a valuable communication tool,providing a comprehensible visual review ofexposures, though they are not usually expressedin monetary terms.For this reason,mapping ascurrently practiced does not provide a link to thefinancial statement,or to the ROI calculation that

is critical for comparisons between possibleproject options. With some modification,including assignment of monetary values to thehypothetical consequences,however,axis pointson such a risk map could correlate to financialdata and be integrated into ROI calculations.

• Adjusted Discount Rate & Cost of Capital:One method of integrating social and politicalrisks issues into financial modeling is theinclusion of social and political risk in a discountrate or cost of capital calculation that flows intocash flow calculations.This can be done bycreating a social discount rate that employs theweighted average cost of capital (WACC) andthe traditional capital asset pricing model(CAPM).This is done in three steps:

1. calculate the cost of equity;

2. develop the risk-free rate (RF) by assigningthe long-term government bond rate;

3. develop a risk-adjusted “beta”, based on thedifference between the return earned byinvestors in an industry and the averagereturn earned by investors in the market asa whole.

When dealing with markets that may exhibithallmarks of social and political risk, this adjustedWACC accounts for social and political factors.

However, this method is difficult to implement.Todate, the calculations for a risk-adjusted beta haverelied largely on the standard country risk ratingsmethodology generated by political risk consultingfirms (see Appendix 2 for more detail on thesefirms). Although useful as a theoretical methodology,such point-based risk ratings as the basis for betacalculations are too broad to achieve the neededobjectives.These ratings are neither industry-,project-, nor company-specific, though social andpolitical risks affect companies and their reputationsdifferently, even if they operate in the same country.To be really useful as a basis for a social/political riskbeta, the country risk ratings generated by politicalrisk assessment firms require customization toparticular companies, locations, and projects.

We therefore propose another method toquantify social and political risk for inclusion infinancial calculations, one that includes integratingthe costs and probabilities of each social andpolitical risk, and calculating an expected value.

Observations

In a recent survey of risk management executives,more than 60% of respondents anticipated acontinuation of “significant external risk” in the

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

9

10

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

next five years, based on recent historical events(The Conference Board and Mercer OliverWyman). According to a McKinsey global surveyof business executives,

• Only 3% of the 4,238 executives whoresponded to a poll reported that theircompanies were doing a good job ofanticipating risk.

• 46% of respondents said they have“substantial room for improvement.”

This growing recognition of the need to betterintegrate insight into how social and politicalissues may affect the firm necessitates anadequate methodology to quantify these issuesin a way that supports effective managementdecision-making.

Given the lack of such a methodology to date,most companies largely make capital investmentdecisions and operational choices with aprimary focus on financial risk, as it is mostnarrowly defined. As a result, they fail to make a more comprehensive calculation that couldsubstantially affect decision-making andcorporate financial performance. Currently,there is a tendency to separately treat financialrisk,which has traditionally been measured, andsocial and political risk,which has historicallybeen analyzed qualitatively, and now morerecently quantitatively, to produce weighted riskindicators and maps. In cases where theseissues have been considered, they have oftenbeen relegated to an addendum to theinvestment decisions process and are notincluded in the calculation of ROI.This places azero dollar value on potential risks that candamage profits. As a result, operational andother decisions are often based on quantifiedfinancial factors, simply for methodologicalreasons, leaving key issues,which may havedramatically negative impacts on ROI,unaccounted for.

Many components of risk must be included in acomprehensive risk assessment. Althoughmeasuring some of them is only possiblethrough estimating rather than exactcalculation, all risks can be quantified to someextent. If they are not then included in financial

calculations, the company will ofteninadequately integrate these risks intomanagement decisions and simply gamble thatthey will not emerge.Discussing theimportance of these risks and their potentialimpact is not intended to inhibit investments.Rather, including these risks in calculations aims at creating more informed decisions.The very act of deciding on a number (or arange) to include in calculations means thatdecision-makers are discussing these issues and their importance.There is, however, adanger of declining to invest because hurdlerates were not met due to inclusion of socialand political risks,without senior managementever being aware of it.Therefore, it is critical to share the thinking and decisions made inassigning risk values.This is discussed more fully in a later section.

Further,without fully understanding some of thecomplex risks facing the business, (a) decision-makers may not include pre-emptive measuresinto project planning and execution, and (b)opportunities for growth and profit from day-to-day operations may be lost.

INTEGRATING SOCIAL ANDPOLITICAL RISKS INTO GENERALRISK MANAGEMENT

To manage risk effectively requires:

• comprehending the socio-political andcorporate environments that might affect risk;

• identifying risks;

• evaluating and measuring their potential effects;

• identifying and analyzing possible solutions;

• adopting the most appropriate riskmanagement actions;

• communicating results; and

• monitoring evolving risks.

In this section,we build on and modify the RiskManagement Process model provided in the2005 Management Accounting Guideline1

(Exhibit 2), by including social and political risk,and offering additional tools and techniques toenable companies to integrate these new risksinto management decisions.

1. Epstein,Marc J. and Adriana Rejc Buhovac. Identifying,Measuring, and Managing Organizational Risk for ImprovedPerformance. Risk Management Accounting Guideline.CMA Canada and AICPA. 2005.

I. RISK IDENTIFICATION Complex social and political issues often affectcompany operations. Identifying risks that canaffect company value as the first step inmeasuring and managing political and social risk is therefore important.

Social Risk

Many social issues can affect a company doingbusiness nationally and internationally,whether indeveloping or developed countries. Someindustries are more prone to these risks than areothers. For example, businesses with biginstallations like factories, ports,mines, andrefineries can lead to dissatisfaction and unrest in a local population when:

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

11

Exhibit 2: Risk Management Process

Event Identification

Risk Assessment

Accept Risk

Control Activities

Is Risk/Reward

Acceptable?

Avoid Risk Can Risk Be Mitigated?

Information &

Communication

Monitoring

Quantify

Magnitude

Assess

Probability Quantify Impact Cost/Benefit

Analysis

Priority/

Rank

Yes No

No Yes

Reduce Risk Transfer Risk Share Risk

Risk

Resp

onse

1

2

3

4

5

6

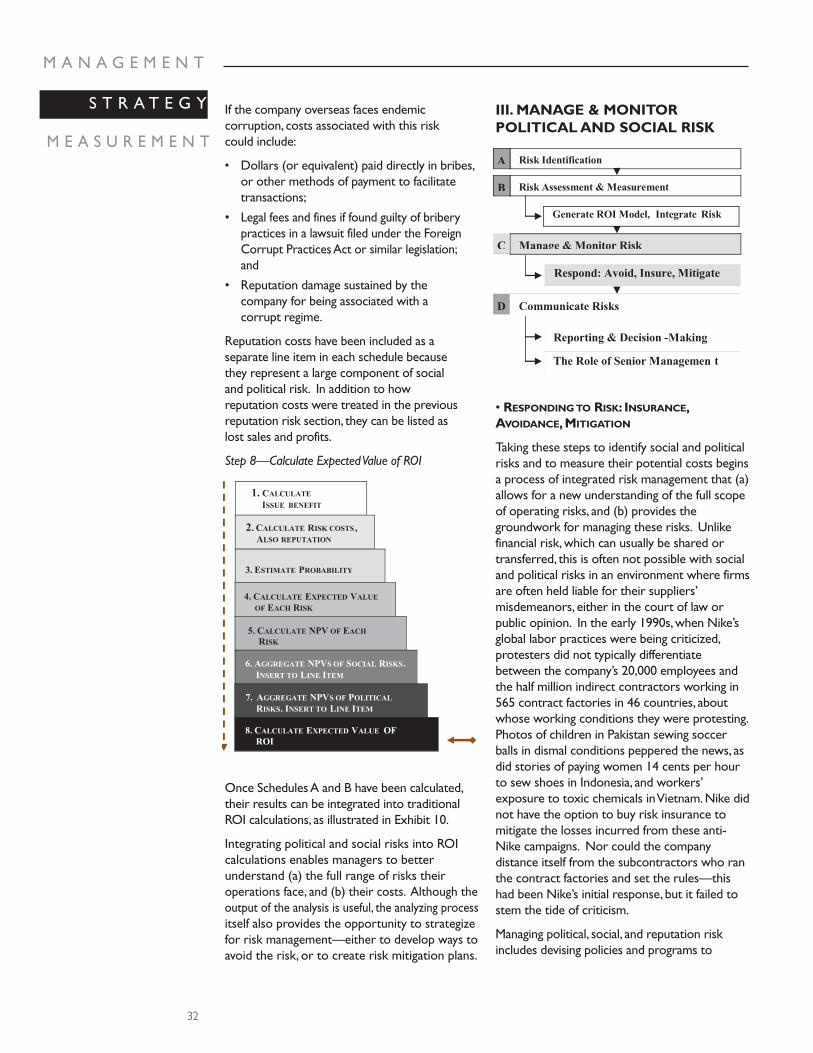

Generate ROI Model, Integrate Risk

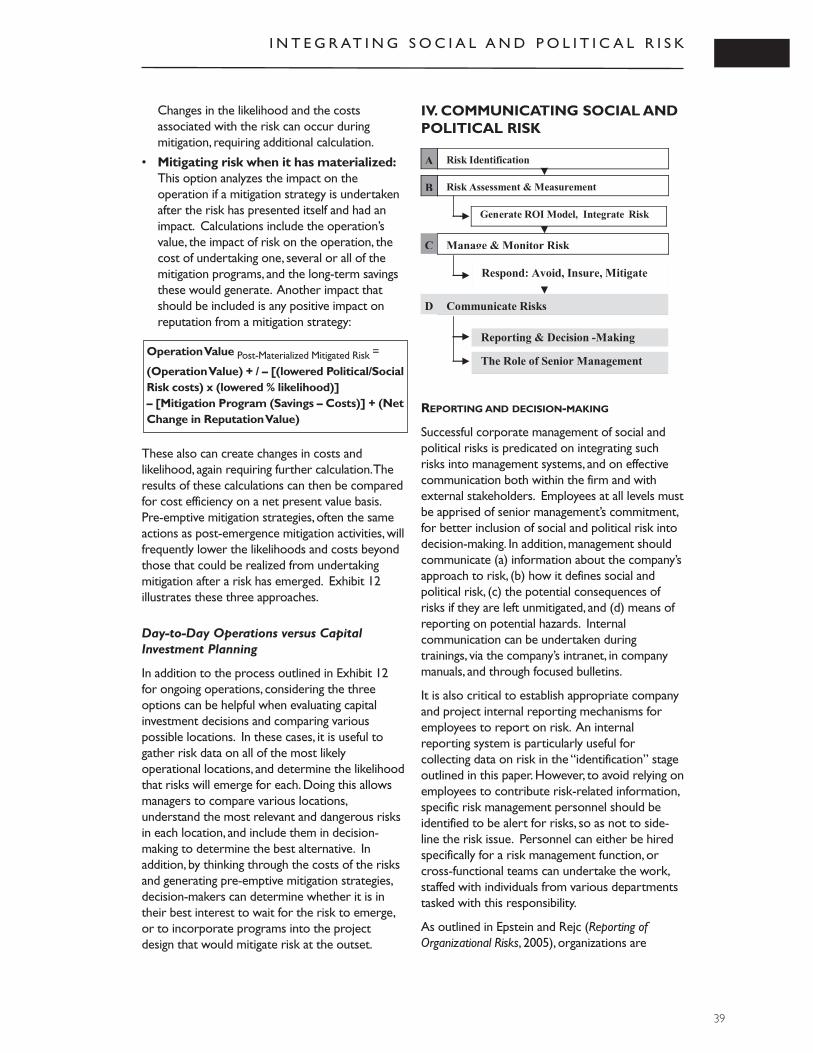

Manage & Monitor RiskC

Respond: Avoid, Insure, Mitigate

Communicate Risks D

Reporting & Decision -Making

The Role of Senior Management

Risk Identification

Risk Assessment & Measurement

A

B

12

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

In Exhibit 3,we illustrate how companies caninclude social and political risk into overall riskmanagement. We include the detailed steps and

analysis necessary to identify and assess politicaland social risk in a manner that is relevant tofinancial decision-making.

Exhibit 3: Social and Political Risk Integration Model

Generate ROI Model and Integrate Risk

Manage & Monitor Political & Social Risk C

Respond to Risk: Avoid, Insure, Mitigate

Communicating Social and Political Risks D

Reporting & Decision-Making

The Role of Senior Management

Social & Political Risk Identification

Social & Political Risk Assessment and Measurement

A

B

2. Pan, Esther.“Small Window for Peace in Papua,” Council on Foreign Relations. April 19, 2006.http://www.cfr.org/publication/10484/small_window_for_peace_in_papua.html

3. Seelye,Katharine Q.“Indonesia:Mining Company Notes U.S. Review of Payments to Indonesian Military,” TheNew York Times. January 19th, 2006.

• there is the perception that localexpectations are not being met;

• the surrounding area is being polluted; or

• business is undertaken in a region of generalpolitical unrest,where the military isprotecting a site and using its presence toharass the local population for reasonsunrelated to the business.The local populationcan sometimes associate the company withthese practices, and begin to target it as aproxy for the government or the military.

The experience of US-based Freeport McMoran,which owns a large gold and copper mine inPapua, Indonesia, is a case in point. The companylost approximately $48 million and 20% of itsshare price2 due to clashes with the populationssurrounding the Freeport mine. Tension hadalready mounted in the region because of a

December, 2005 New York Times report thatFreeport,which employs 180,000 people and isone of Indonesia’s largest taxpayers, had paidIndonesian military and police officers close to$20 million between 1998 and 2004, leading toan investigation by the U.S. government andprotests by the local population.3

Further ill-will brewed when poor residents nearthe Freeport mine,with few economicopportunities, began prospecting for gold in thewaste rock from the company’s operations.Citing possible health concerns from exposureto this material, the company moved to prohibitprospecting, positioning private security guardsaround the mine,who allegedly had authority toshoot at prospectors.The local community,however,was suspicious of the cited healthreasons, as it already perceived that a largeforeign company was making huge profits from

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

13

use of its land. Impoverished local residentsbelieved that they were being unjustly preventedfrom sharing, even marginally, in the big company’swealth. In reaction, the community began proteststhat closed the mine for four days—at anapproximate cost of $12 million a day.

Nigeria presents another example of risks that canemerge on the arrival of a large company to arelatively isolated or under-developed area.Thearrival of petroleum companies createdunintended consequences when a sudden influx ofpeople,mostly unskilled, began looking for work atthe oil installation.When no jobs were available,some turned to violent behavior.A number ofunemployed Nigerian youths began attacking oilpipelines, taking personnel hostage, and in onecase, seizing an offshore oil rig, demanding thatthey be given jobs.4

A further potential unintended long-termconsequence of new operations is the focus of thelocal economy exclusively on one industry over along period of time, resulting in dependence onone company, operation, or industry sector.Whenthe company leaves or the industry is no longerviable, the surrounding area is usually economicallydevastated, creating a potential backlash againstthe company by local populations.This hashappened frequently in company towns in the U.S.and abroad, in industries ranging from steel millingto coal mining. For example,Detroit,Michigan sawa tremendous dip in its standard of living when theautomotive industry became less competitive.Some industries are less prone to these risks, butit is critical that companies that must or choose toremain in one location for the long-term,understand and mitigate these risks. In many cases,mitigation calls for both an effective communityrelations strategy, as well as an exit strategy thatdeals with both environmental and economicissues to diminish negative consequences.Riskmitigation is discussed in a later section.

Health, safety, and environmental issues affect allcompanies. Recently, debate has begun onregulating emissions at major U.S. ports. This would create additional unexpected costs for both freight companies and importers andexporters of goods from places like the Ports of Los Angeles and Long Beach.

Companies working internationally face oftencostly worker and community health issues for avariety of reasons, including lack of adequatemedical care in certain regions of the world.HIVinfection has become a particular risk forcompanies in the extractive and transportationsectors, both heavily male-dominated,whereoperations attract increased prostitution. Thisincreased level of HIV infection of workers canquickly lead to sickness and eventual death. Leftunchecked, this trend will expose companies thathave trained workers and rely on their skills forproduction to additional costs. Road accidents, akiller that will eclipse both AIDS and war by 2020according to the World Health Organization, alsorepresent a tremendous cost to companies relianton long-haul trucking. 80% of total road deathsoccur in developing countries, often resulting fromovercrowded vehicles and an unsafe mix ofanimals, people and vehicles on the road.Statistically, companies that rely on roads in theseparts of the world will be exposed to loss of theirdrivers or cargo due to unsafe road conditions.Some companies try to mitigate this risk bytraining their own staff and contract drivers, aswell as working with other companies andmultilateral organizations to address road safety.5

Using labor forces—like children and forcedlabor—that certain societies considerunacceptable can put companies at risk. In someareas of the world it is customary that childrenwork, and this is one of the better optionsavailable to them.However, use of child labor hasled to product boycotts by customers opposed tothe practice and terrible publicity. The use offorced labor, a practice that has been exposed inthe supply chain of some companies, can alsocreate great problems, even if the company did not directly employ this labor. In 1996, activistsand Burmese villagers filed a lawsuit against Unocal under the Alien Tort Claims Act (ATCA).The ATCA grants to a U.S. federal courtjurisdiction over a claim,when a non-U.S. citizenor alien sues for a tort committed in violation of aUnited States treaty or other international law. Inthis ATCA case,Unocal was accused of (a)complicity in the Burmese military’s use of forcedlabor to build the Yadana pipeline, of which Unocalwas a junior partner, and (b) allowing Burmese

4.“Nigerian oil fuels Delta conflict,” BBC, January 16, 2006.

5. Bekefi,Tamara. The Global Road Safety Partnership and Lessons in Multisectoral Collaboration:Corporate SocialResponsibility Initiative,Kennedy School of Government,Report # 1—August 2005.

14

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

troops guarding the project to rape,murder, andenslave villagers.The company denied any part inthese human rights abuses, but settled the suitfor an undisclosed amount of money in 2004.6

All of these social issues emerged as risks tocompanies, and some risks took companies bysurprise and came at a great cost.The largest ofthese costs, lost sales and profits, often resultsfrom damage to reputation.Other risks thatpresent a potential monetary liability seempoised on the horizon.One example is climatechange,which may present a potential futuremonetary liability. Although there is still debateon climate change and liability is not a certainty,its likelihood warrants some companies toconsider it by factoring it into decision-making.

Political Risk

Generally, political risk can be understood asexecution of political power in a way thatthreatens a company’s value.Two types ofpolitical risk are relevant to companies doingbusiness internationally: industry- or firm-specific political risk and country-specificpolitical risk.On the one hand mass anti-government protests, then,may not pose apolitical risk to a firm if they do not affect (a) government policies towards business, or (b) the firm’s current or future operations orvalue.On the other hand, changes in the legalframework governing contracts could have asignificant negative impact on the company.Industry- and firm-specific political risk isexperienced by one industry or firm, such asthreats by Bolivia’s President Evo Morales tonationalize the country’s oil and gas sector.Companies including Brazil’s Petrobras andSpain’s Repsol YPF have invested $3.5 billion into

developing Bolivia’s natural gas fields, thesecond-largest natural gas reserves in SouthAmerica.7 Morales’ threats have recently beentranslated into specific actions against foreignenergy companies, beginning with (a) forcedaudits of their financial documentation, and (b)the demand to renegotiate concessionagreements and revenue-sharing from gas fielddevelopment to give the government a majoritystake within six months.

Sector-, provincial-, and country-specific politicalrisk is spread more widely. These risks caninclude a civil war, drastic changes in foreigncurrency rules, or sweeping changes to the taxcode. These types of risks can be generateddirectly from the host country government, oremerge from an unstable social situation withinthe country. Regardless of the source, acompany attempting to understand potentialpolitical risk must recognize the differencebetween (a) political issues that can affectcorporate performance, and (b) dramaticsituations that have no financial impact on thecompany. In addition, companies shouldunderstand the potential reputation damage,and associated costs, related to political risk.

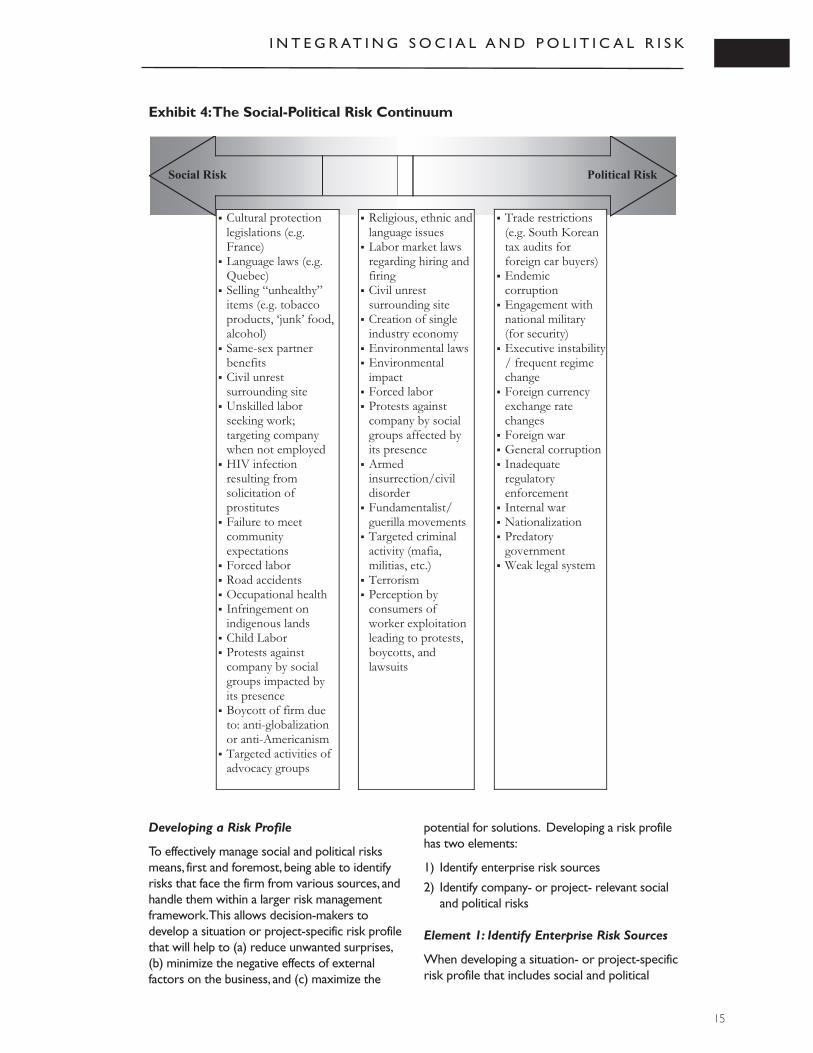

The distinction between social and political risks isoften blurred.We consider these issues to fallalong a continuum, as illustrated in Exhibit 4.Thesubjects in Exhibit 4 are only some of the mostcritical social and political risks facing globalcompanies today. Although the Exhibit does nottry to list all risks, the wide variety of risks itincludes provides a sample of relevant issues facingcompanies. Each organization should generate itsown list of social and political risks, based on theirrelevance to its business(es) and the businessenvironments in which it/they operate(s).

6.David Baker.“Purchase of Unocal by Chevron Deal puts new sources of gas and crude in the right places forEast Bay oil giant,” San Francisco Chronicle.Tuesday, April 5, 2005.

7.The Economist,December 2005.

Developing a Risk Profile

To effectively manage social and political risksmeans, first and foremost, being able to identifyrisks that face the firm from various sources, andhandle them within a larger risk managementframework.This allows decision-makers todevelop a situation or project-specific risk profilethat will help to (a) reduce unwanted surprises,(b) minimize the negative effects of externalfactors on the business, and (c) maximize the

potential for solutions. Developing a risk profilehas two elements:

1) Identify enterprise risk sources

2) Identify company- or project- relevant socialand political risks

Element 1: Identify Enterprise Risk Sources

When developing a situation- or project-specificrisk profile that includes social and political

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

15

Exhibit 4:The Social-Political Risk Continuum

Political Risk Social Risk

� Religious, ethnic and language issues � Labor market laws

regarding hiring and firing � Civil unrest

surrounding site � Creation of single

industry economy � Environmental laws � Environmental

impact � Forced labor � Protests against

company by social groups affected by its presence � Armed

insurrection/civil disorder � Fundamentalist/

guerilla movements � Targeted criminal

activity (mafia, militias, etc.) � Terrorism � Perception by

consumers of worker exploitation leading to protests, boycotts, and lawsuits

� Cultural protection legislations (e.g. France) � Language laws (e.g.

Quebec) � Selling “unhealthy”

items (e.g. tobacco products, ‘junk’ food, alcohol) � Same-sex partner

benefits � Civil unrest

surrounding site � Unskilled labor

seeking work; targeting company when not employed � HIV infection

resulting from solicitation of prostitutes � Failure to meet

community expectations � Forced labor � Road accidents � Occupational health � Infringement on

indigenous lands � Child Labor � Protests against

company by social groups impacted by its presence � Boycott of firm due

to: anti-globalization or anti-Americanism � Targeted activities of

advocacy groups

� Trade restrictions (e.g. South Korean tax audits for foreign car buyers) � Endemic

corruption � Engagement with

national military (for security) � Executive instability

/ frequent regime change � Foreign currency

exchange rate changes � Foreign war � General corruption � Inadequate

regulatory enforcement � Internal war � Nationalization � Predatory

government � Weak legal system

16

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

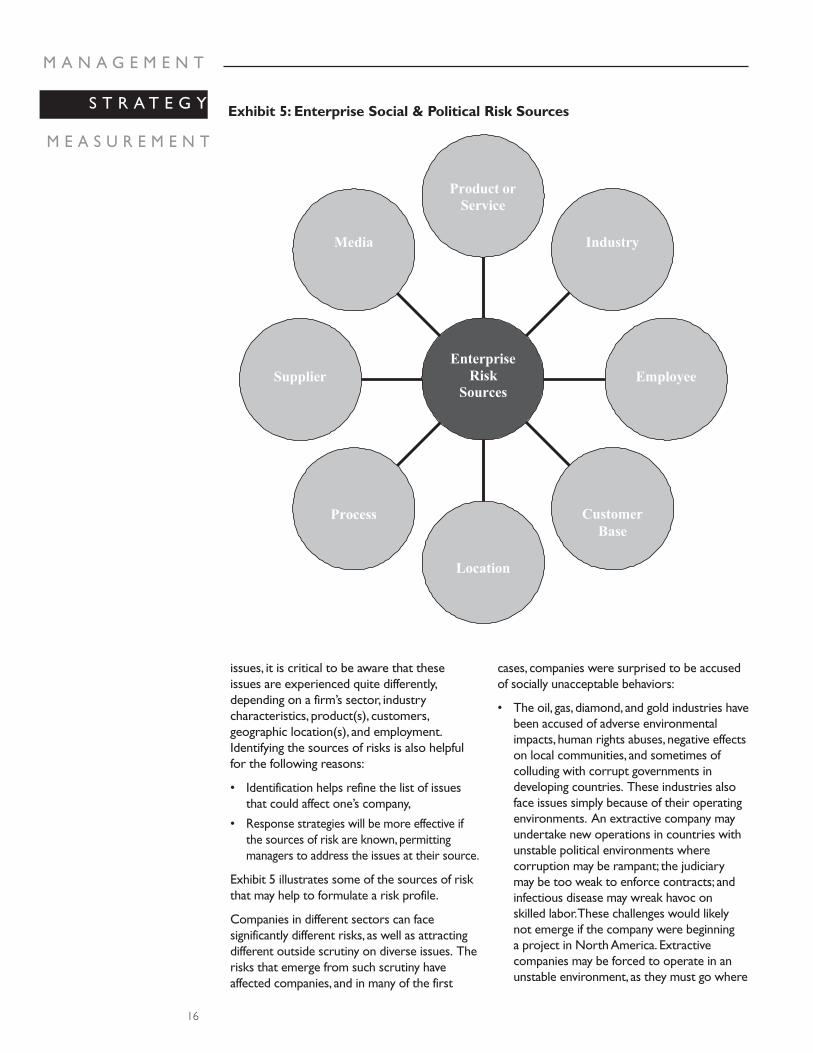

issues, it is critical to be aware that these issues are experienced quite differently,depending on a firm’s sector, industrycharacteristics, product(s), customers,geographic location(s), and employment.Identifying the sources of risks is also helpfulfor the following reasons:

• Identification helps refine the list of issuesthat could affect one’s company,

• Response strategies will be more effective ifthe sources of risk are known, permittingmanagers to address the issues at their source.

Exhibit 5 illustrates some of the sources of riskthat may help to formulate a risk profile.

Companies in different sectors can facesignificantly different risks, as well as attractingdifferent outside scrutiny on diverse issues. Therisks that emerge from such scrutiny haveaffected companies, and in many of the first

cases, companies were surprised to be accusedof socially unacceptable behaviors:

• The oil, gas, diamond, and gold industries havebeen accused of adverse environmentalimpacts, human rights abuses, negative effectson local communities, and sometimes ofcolluding with corrupt governments indeveloping countries. These industries alsoface issues simply because of their operatingenvironments. An extractive company mayundertake new operations in countries withunstable political environments wherecorruption may be rampant; the judiciary may be too weak to enforce contracts; andinfectious disease may wreak havoc on skilled labor.These challenges would likelynot emerge if the company were beginning a project in North America. Extractivecompanies may be forced to operate in anunstable environment, as they must go where

Exhibit 5: Enterprise Social & Political Risk Sources

Media

Supplier

Process

Location

Customer

Base

Employee

Industry

Product or

Service

Enterprise

Risk

Sources

the product is found. Companies in othersectors are often not so limited.Companieshaving or choosing to operate in higher riskenvironments must identify these risks as afirst step in evaluating and managing them.DeBeers,which operates in regions where theincidence of HIV/AIDS is the highest in theworld, calculates that 10% of its employeeswere likely infected with HIV and that aprogram to treat its infected employees wouldcost the company US$1,200-US$3,500 perworker annually for 10-14 years.DeBeersconsidered this a cost-effective approachcompared to its other two choices: (a) thecost of losing HIV-infected workers to AIDS-related illness and death requiring the hiringand training of new workers, or (b) the costand inefficiency of hiring and training threeworkers for each job, to prepare for AIDS-related losses. DeBeers is currentlyimplementing an HIV/AIDS employeeeducation and treatment program.8

• Footwear and clothing production have beenassociated with low wages, child labor, andunfair working conditions. Companies withmanufacturing operations in developingcountries, and thus faced with non-Westernlabor practices in areas such as wages,overtime, and child labor, find that thesepractices are often scrutinized by the media orthe companies’ customers both of whom aresensitive to these practices.

■ Nike was accused of employing children asyoung as ten years old in Cambodia andPakistan to produce sneakers, clothing, andfootballs, leading to consumer boycotts.These consumers did not differentiatebetween the company and its subcontractors.

■ In 1997,Kathy Lee Gifford’s clothing linecame under attack when the news mediabroke a story alleging that the televisionstar’s clothing line was being manufacturedby Honduran women and girls as young as12,who were working in dreadful conditions.

■ In September 2005, a class action lawsuit wasfiled against Wal-Mart on behalf of workersin Bangladesh, Swaziland, Indonesia,China,

and Nicaragua. The lawsuit alleged that theworld’s largest retailer had failed to monitorworking conditions in its supply chain, andthat its demand for low prices forcessuppliers to enforce sweatshop conditions.

• A computer chip manufacturer might strugglewith stakeholder reactions to chemical use andits impacts on the local environment. Thesebusiness-to-business industries are oftenaffected less by damage to reputation relatedto social and political issues than arecompanies in other sectors.

• Telecommunications firms may face negativereactions by its customers over use of theirpersonal information and records of their useof the telephone or Internet. Refusing toshare such information, however,may presentother risks. Recently, news has emerged thatthe U.S.National Security Agency (NSA) hasbeen secretly collecting the telephone recordsof millions of Americans by agreement withAT&T,Verizon, and BellSouth. When QWEST, afourth company, declined to participate, theNSA threatened negative consequence ingovernment dealings for failure to cooperate.9

• Prescription drugs and their producers havebeen linked to developing countries’ lack ofaccess to essential medicines.HIV/AIDS drugproducers were boycotted because they wouldnot lower product prices in South Africa.

• Food and beverage companies have beenassociated with the obesity epidemic;McDonald’s has been accused of encouragingobesity through marketing its products.

The obesity-related lawsuit against McDonald’swas revived in January 2005, and has led to moregeneral changes in both production andmarketing practices of the food industry.McDonald’s began to offer salads and fruits inaddition to the traditional hamburgers andFrench fries, and PepsiCo’s Frito-Lay snack unitreplaced trans-fats with corn oil in its products ata cost of $57 million, and began producingreduced-fat Lay’s potato chips and Cheetos.10 Thethreat of legal liability could reach as far as localsupermarkets and convenience stores, sincerecent studies have found that products in stores

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

17

8.Global Business Coalition on HIV/AIDS <www.businessfightsaids.org>

9.Cauley, Lesley.“NSA has massive database of Americans’ phone calls.” USA Today May 11, 2006.

10.“Food Giants Scramble to Avoid Lawsuits.” The Agribusiness Examiner, August 30, 2004.http://www.organicconsumers.org/school/obesitylawsuits083004.cfm

18

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

located in the poor neighborhoods of NorthAmerica offer more convenience (junk) foodand few fresh fruits, and hardly any vegetables.11

Some convenience store chains like 7-Eleven areresponding by offering organic and healthiersnacks to consumers.

Companies beginning to identify social andpolitical risks that may affect them or theirproducts must understand the setting for theirbusinesses, and how that setting might generaterisks. This process need not necessarily becostly and time-consuming, though the degree ofinvestment in risk identification would likelydepend on the size and importance of thecompany or project.

Risk may emerge simply from:

• Operating Location: Locating a plant inMyanmar,where a totalitarian militarygovernment is known to encourage the useof forced labor,will likely pose more risksthan doing business in Singapore,where thisis not a common practice. Likewise, opening apub near a school may generate protestsfrom the local community.

• Reaction of society or a group of peopleaffected by,or who believe they will beaffected by, business activities: In Peru’sCajamarca region,Newmont Mining has beengrappling with the local community’sdissatisfaction and its sometimes violentreactions.This is based in part on changes inthe community since the arrival of the mine,such as rising housing prices and inflation. Itis also based on the perception that miningoperations have contaminated and siphonedoff local water supplies, and are negativelyaffecting human health, farming yields, andfishing.The matter is further complicated byinvolvement of activist groups,who are usingthe Internet to spread information, in somecases destabilizing relations between thecompany and the community. Local distrust isat such a high level that when NewmontMining began exploration of a nearbymountain as a potential site for furthermining activities, rioting began and thecompany abandoned its expansion.

• An employee base that is deemedunacceptable to society:Wal-Mart recentlysettled a lawsuit brought by the U.S.Department of Labor for $135,540, for 24

violations of employing teenagers and allowingworkers to operate hazardous equipment.12

Although the amount of the settlement maybe insignificant to the company, the negativeimpact on its reputation is reverberatingthrough the company.

The new power of communications technologyto spread information quickly and efficiently,withlittle oversight,means that companies have to beeven more aware of their social and politicalrisks to avoid targeting by activists.This isdiscussed further in Appendix 1:Real vs.Perceived Risk.

Exhibit 6 outlines some of the social and politicalrisks generated by product, sector, customer,geographic location, employee base, and industrycharacteristics, as well as examples of industriesaffected by these issues. Risk can be divided into:(a) risks to society that could createdissatisfaction, and (b) other issues that couldnegatively affect the company, thereby posingrisk to the company. Analyzing thecharacteristics of these two kinds of risk, aidscompanies in understanding their potentialimpacts on the company or project, a criticalfirst step in developing a risk profile andestimating the effect on profitability.

A comprehensive risk identification process willascertain risk variables that may apply to one’scompany. Additionally, identifying the issues towhich stakeholders may be sensitive (if theywere to discover companies engaged in them) isimportant, since the financial effects ofstakeholder reactions can be significant andeasily spiral out of control.

Element 2: Identify Company- or Project-Relevant Social and Political Risks

Next in critical importance after identifyinggeneral enterprise risk sources and issues(Element 1) is identifying company- or project-relevant social and political risks.These can vary,depending on specifics such as location within acountry, and can be more nuanced than thosepreviously identified.The discussion of riskmanagement often focuses on financial issues, tothe exclusion of other similarly important matters.

Although the CEO and the board are theultimate risk managers in the company,employees in many parts of a company can

11. “Where You Live Affects What You Eat.” NAASO, The Obesity Society. http://www.naaso.org/news/20041118.asp

12.“Wal-Mart settles child labor cases.Company denies charges but agrees to pay penalty.” Associated Press,February 12, 2005.

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

19

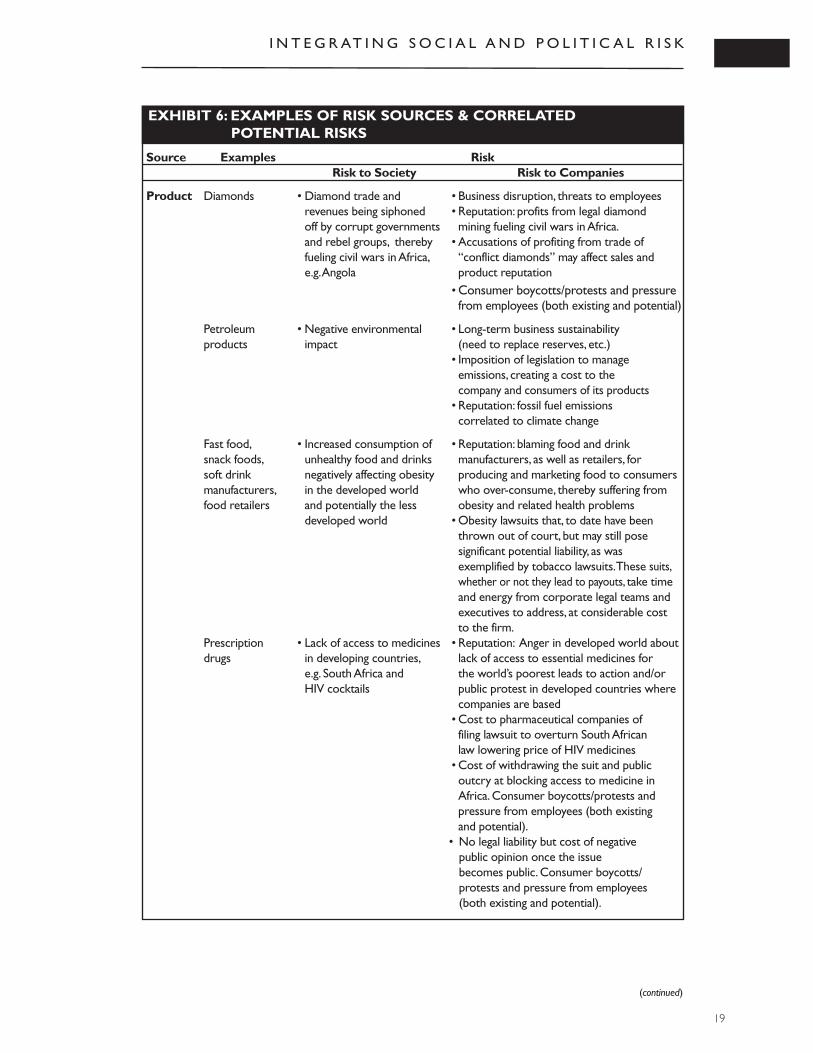

EXHIBIT 6: EXAMPLES OF RISK SOURCES & CORRELATED POTENTIAL RISKS

Source Examples RiskRisk to Society Risk to Companies

Product Diamonds • Diamond trade and • Business disruption, threats to employeesrevenues being siphoned • Reputation: profits from legal diamondoff by corrupt governments mining fueling civil wars in Africa.and rebel groups, thereby • Accusations of profiting from trade offueling civil wars in Africa, “conflict diamonds” may affect sales and e.g.Angola product reputation

• Consumer boycotts/protests and pressurefrom employees (both existing and potential)

Petroleum • Negative environmental • Long-term business sustainability products impact (need to replace reserves, etc.)

• Imposition of legislation to manage emissions, creating a cost to the company and consumers of its products

• Reputation: fossil fuel emissions correlated to climate change

Fast food, • Increased consumption of • Reputation: blaming food and drinksnack foods, unhealthy food and drinks manufacturers, as well as retailers, for soft drink negatively affecting obesity producing and marketing food to consumersmanufacturers, in the developed world who over-consume, thereby suffering from food retailers and potentially the less obesity and related health problems

developed world • Obesity lawsuits that, to date have beenthrown out of court, but may still posesignificant potential liability, as wasexemplified by tobacco lawsuits.These suits,whether or not they lead to payouts, take time and energy from corporate legal teams and executives to address, at considerable cost to the firm.

Prescription • Lack of access to medicines • Reputation: Anger in developed world aboutdrugs in developing countries, lack of access to essential medicines for

e.g. South Africa and the world’s poorest leads to action and/orHIV cocktails public protest in developed countries where

companies are based• Cost to pharmaceutical companies of filing lawsuit to overturn South African law lowering price of HIV medicines

• Cost of withdrawing the suit and public outcry at blocking access to medicine in Africa.Consumer boycotts/protests and pressure from employees (both existing and potential).

• No legal liability but cost of negative public opinion once the issue becomes public.Consumer boycotts/protests and pressure from employees(both existing and potential).

(continued)

20

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N TSource Examples Risk

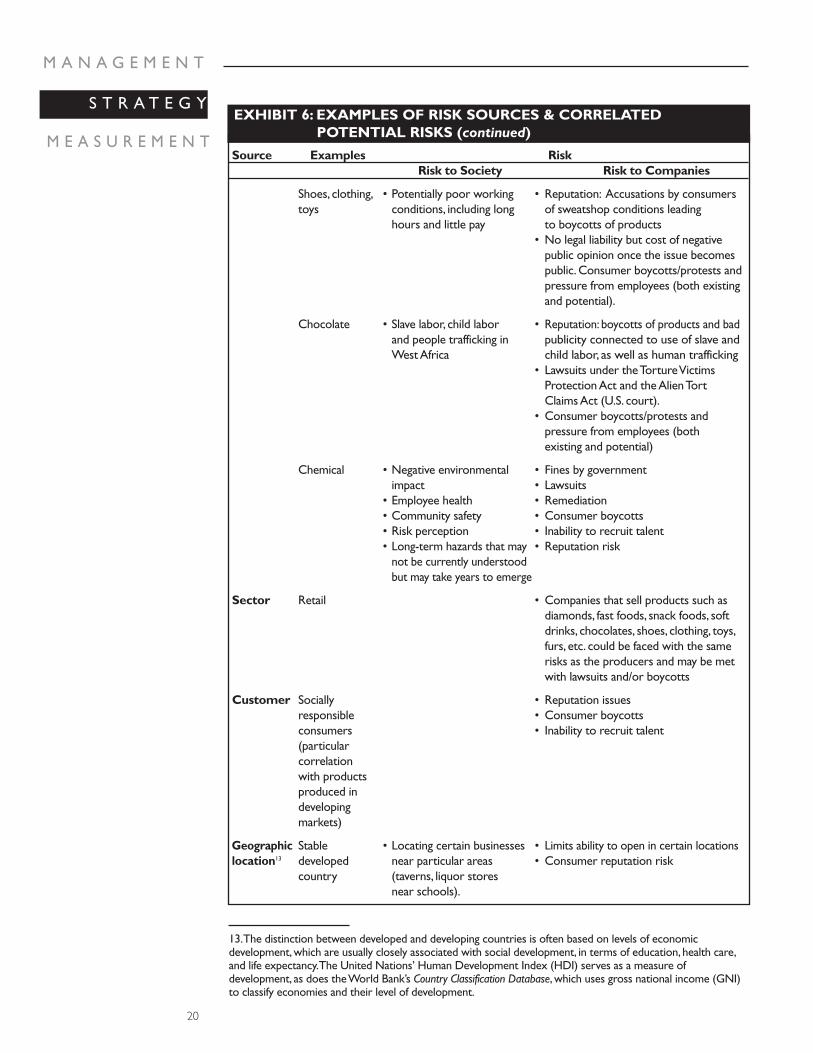

Risk to Society Risk to Companies

Shoes, clothing, • Potentially poor working • Reputation: Accusations by consumerstoys conditions, including long of sweatshop conditions leading

hours and little pay to boycotts of products• No legal liability but cost of negative

public opinion once the issue becomes public.Consumer boycotts/protests and pressure from employees (both existing and potential).

Chocolate • Slave labor, child labor • Reputation: boycotts of products and badand people trafficking in publicity connected to use of slave andWest Africa child labor, as well as human trafficking

• Lawsuits under the Torture Victims Protection Act and the Alien Tort Claims Act (U.S. court).

• Consumer boycotts/protests and pressure from employees (both existing and potential)

Chemical • Negative environmental • Fines by governmentimpact • Lawsuits

• Employee health • Remediation• Community safety • Consumer boycotts• Risk perception • Inability to recruit talent• Long-term hazards that may • Reputation risk

not be currently understoodbut may take years to emerge

Sector Retail • Companies that sell products such as diamonds, fast foods, snack foods, soft drinks, chocolates, shoes, clothing, toys,furs, etc. could be faced with the same risks as the producers and may be met with lawsuits and/or boycotts

Customer Socially • Reputation issuesresponsible • Consumer boycottsconsumers • Inability to recruit talent(particular correlation with products produced in developing markets)

Geographic Stable • Locating certain businesses • Limits ability to open in certain locationslocation13 developed near particular areas • Consumer reputation risk

country (taverns, liquor stores near schools).

EXHIBIT 6: EXAMPLES OF RISK SOURCES & CORRELATED POTENTIAL RISKS (continued)

13.The distinction between developed and developing countries is often based on levels of economicdevelopment,which are usually closely associated with social development, in terms of education, health care,and life expectancy.The United Nations’ Human Development Index (HDI) serves as a measure ofdevelopment, as does the World Bank’s Country Classification Database,which uses gross national income (GNI)to classify economies and their level of development.

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

21

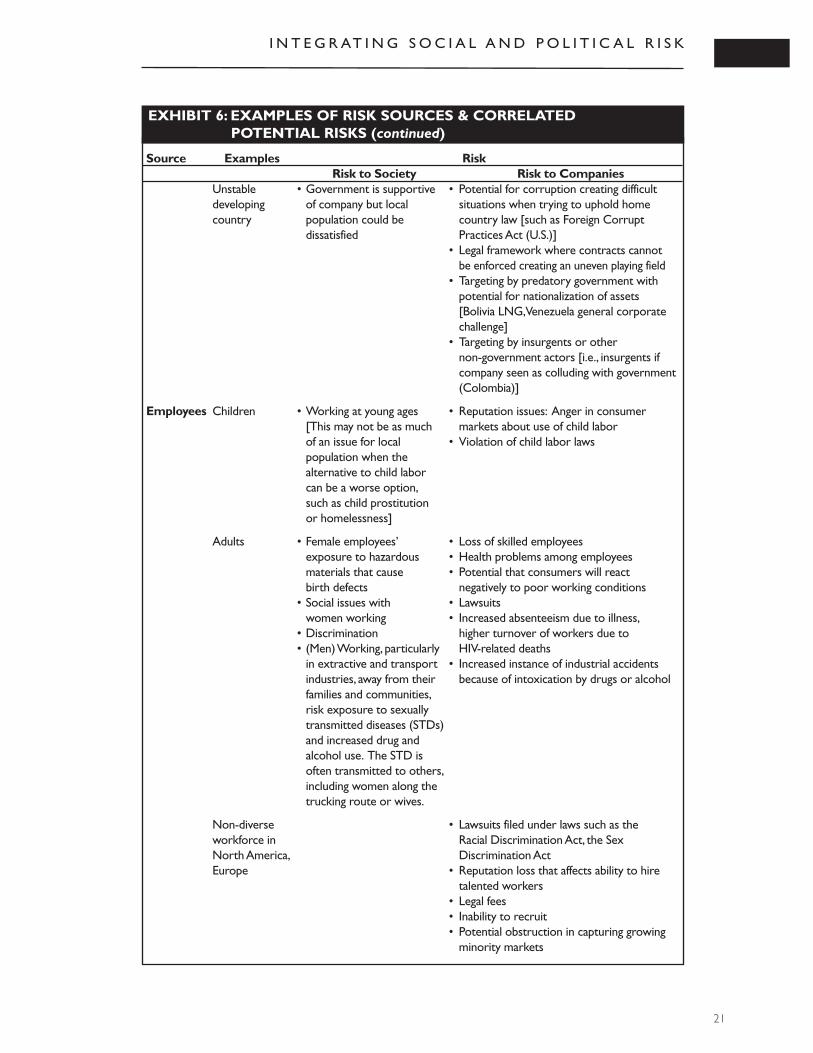

Source Examples RiskRisk to Society Risk to Companies

Unstable • Government is supportive • Potential for corruption creating difficultdeveloping of company but local situations when trying to uphold homecountry population could be country law [such as Foreign Corrupt

dissatisfied Practices Act (U.S.)]• Legal framework where contracts cannot

be enforced creating an uneven playing field• Targeting by predatory government with

potential for nationalization of assets [Bolivia LNG,Venezuela general corporate challenge]

• Targeting by insurgents or other non-government actors [i.e., insurgents if company seen as colluding with government (Colombia)]

Employees Children • Working at young ages • Reputation issues: Anger in consumer[This may not be as much markets about use of child laborof an issue for local • Violation of child labor lawspopulation when the alternative to child labor can be a worse option,such as child prostitution or homelessness]

Adults • Female employees’ • Loss of skilled employeesexposure to hazardous • Health problems among employeesmaterials that cause • Potential that consumers will reactbirth defects negatively to poor working conditions

• Social issues with • Lawsuitswomen working • Increased absenteeism due to illness,

• Discrimination higher turnover of workers due to• (Men) Working, particularly HIV-related deaths

in extractive and transport • Increased instance of industrial accidentsindustries, away from their because of intoxication by drugs or alcoholfamilies and communities,risk exposure to sexually transmitted diseases (STDs) and increased drug and alcohol use. The STD is often transmitted to others,including women along the trucking route or wives.

Non-diverse • Lawsuits filed under laws such as theworkforce in Racial Discrimination Act, the Sex North America, Discrimination ActEurope • Reputation loss that affects ability to hire

talented workers• Legal fees• Inability to recruit• Potential obstruction in capturing growing

minority markets

EXHIBIT 6: EXAMPLES OF RISK SOURCES & CORRELATED POTENTIAL RISKS (continued)

22

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

integrate risk management into their jobs.Financial risk is usually managed in a specific andestablished manner.On the other hand, theintensification of social and political risks oftenrequires an integrated risk management processacross a firm, to adequately identify emergingissues. Personnel who can become aware of riskat an early stage include a line manager at a plantin a developing country. That manager may beaware of negative community reactions to thecorporation through discussions amongworkers, or from personnel in public affairs wholearn of negative government attitudes to thefirm while lobbying. These first signals can heraldmuch larger issues if left ignored.

To anticipate social and political risks, personnelmust be aware of what constitutes risk to thefirm, and understand how to identify these risks.Identification is a two-step scanning process:

1) Generate a risk profile for the corporation(Element 1) that can include some of theissues illustrated in Exhibit 4. A variety ofrisks can materialize from factors such assector, industry characteristics, product,customers, geographic location, andemployment. A risk profile is simply a list ofrisks generated from these contextual issues.

2) Generate a risk catalogue for thecorporation (Element 2): risks can be specificto a particular project or location. Forexample, a new shoe manufacturing plant inBolivia will face different risks than an existingrefining facility in Oman. A risk catalogue issimply a more specific list of ‘red flag’ issues,developed from the general risk profile, thatare connected to a certain project or location.

Existing Operations vs. New Investments

Evaluating and responding to risks is significantlydifferent for existing operations than for newinvestments. Ongoing operations are oftendifficult or costly to uproot if a major riskmaterializes. In some cases, such as extractive orother materials-based operations that bring acompany to a particular location and require largeinitial investment, the risk would have to beimminent, or have the potential to exactenormous consequences, to warrant movingoperations or withdrawing.When ongoingoperations face social and political risks, they mustfind ways of minimizing their impact,whilemaximizing their potential for continuingoperations.The same applies to changes tooperations that generate risk. However,when

new investments are considered, companies canevaluate a variety of locations and compare theirrisk impacts. In addition, evaluating risk for newoperations can present opportunities for pre-emptive mitigation and management of unavoidablerisks. That is not possible in ongoing operations.Risk mitigation is discussed in a later section.

Reputation Risk

For most firms, reputation is a large issue, andintangible assets such as brand can account forover 60% of a company’s market value.Reputation damage from issues such as negativepublicity and costly litigation can create a loss ofrevenue, a decline in customers, or the exit of keyemployees. (Argenti; 2005) Negative perceptionsabout a corporation can emerge from the socialand political issues it deals with, and put thecompany’s reputation at risk. Although a goodreputation can have potentially positive outcomes,such as (a) enhanced access to capital markets,and (b) the ability to attract investors and betteremployees, and charge premium prices, theconverse can also be true. Reputation issuesarising from social and political risk can negativelyaffect the organization as much as the risksthemselves, and can account for some of thelargest costs—lost sales and profits. As acomponent of social and political risks a companyfaces, reputation risk also needs to be managed.

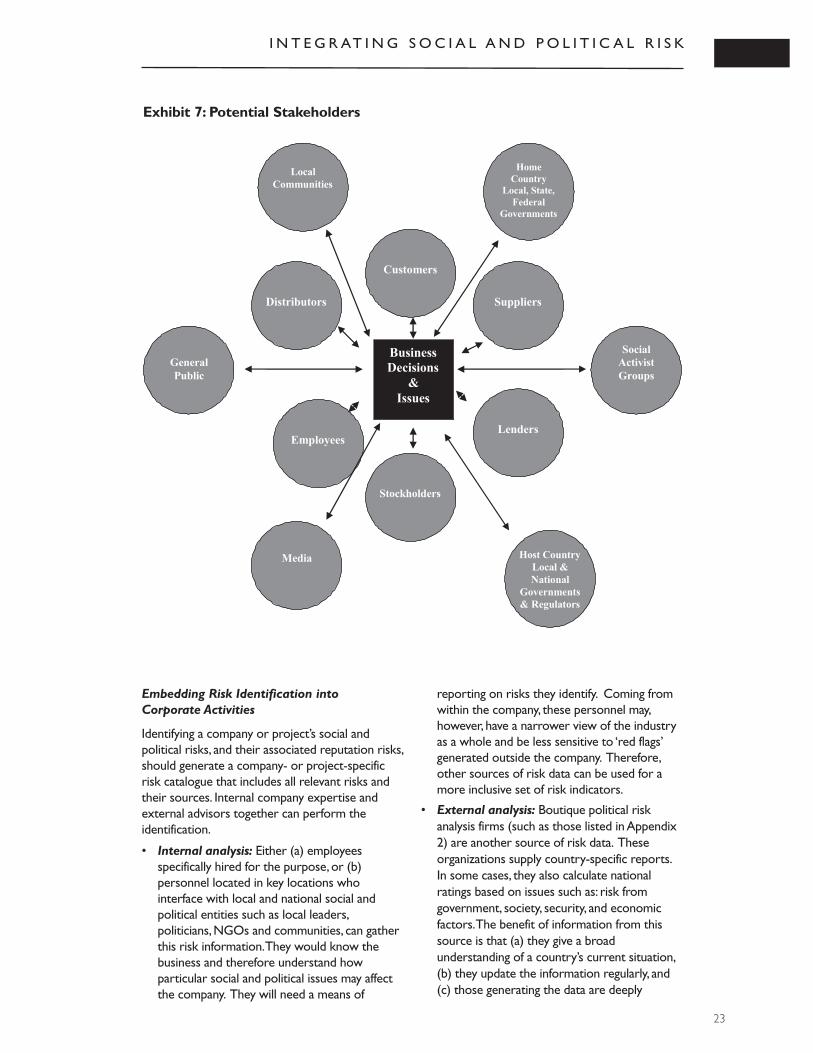

Increased consumer interest, instantaneouscommunication via the Internet, and professionalactivist organizations have generated newchallenges for companies trying to managereputation risk. They must identify thestakeholders that may be affected by, or mayhave an impact on, a particular issue. Exhibit 7illustrates stakeholders that may be involved.

Evaluating a firm’s stakeholders and thereputation risks they may generate is animportant part of creating the corporate riskprofile. Identifying these reputation risks followsthe same steps used in identifying political andsocial risk. Identifying the stakeholder group thatis the source of this reputation risk is also criticalto creating mitigation strategies. Riskidentification does not have to be a long andcostly process—even a few people spending afew hours discussing and identifying risks, andassigning probability values to them, can producehelpful, if not precise, results.This is better thanno risk deliberation at all.More thoroughdeliberations can be expected when moremoney is at stake.

Embedding Risk Identification into Corporate Activities

Identifying a company or project’s social andpolitical risks, and their associated reputation risks,should generate a company- or project-specificrisk catalogue that includes all relevant risks andtheir sources. Internal company expertise andexternal advisors together can perform theidentification.

• Internal analysis: Either (a) employeesspecifically hired for the purpose, or (b)personnel located in key locations whointerface with local and national social andpolitical entities such as local leaders,politicians,NGOs and communities, can gatherthis risk information.They would know thebusiness and therefore understand howparticular social and political issues may affectthe company. They will need a means of

reporting on risks they identify. Coming fromwithin the company, these personnel may,however, have a narrower view of the industryas a whole and be less sensitive to ‘red flags’generated outside the company. Therefore,other sources of risk data can be used for amore inclusive set of risk indicators.

• External analysis: Boutique political riskanalysis firms (such as those listed in Appendix2) are another source of risk data. Theseorganizations supply country-specific reports.In some cases, they also calculate nationalratings based on issues such as: risk fromgovernment, society, security, and economicfactors.The benefit of information from thissource is that (a) they give a broadunderstanding of a country’s current situation,(b) they update the information regularly, and(c) those generating the data are deeply

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

23

Exhibit 7: Potential Stakeholders

Employees

Business

Decisions

&

Issues

Stockholders

Lenders

Suppliers

Customers

Distributors

Local

Communities

Home

Country

Local, State,

Federal

Governments

& R l t

Social

Activist

Groups

Host Country

Local &

National

Governments

& Regulators

Media

General

Public

24

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

knowledgeable about the regions they cover.In addition, the country risk ratings simplifythe process of comparing countries. This isparticularly useful when beginning newoperations and trying to decide where tolocate them.One limitation of the productsthese firms generate is that they are usuallyneither industry- nor region- specific. This issignificant, since what could be lethal to oneindustry located in one part of a certaincountry could pose no threat whatsoever toanother. In addition, these firms’ products arenot monetized so as to be useful ininvestment decision-making.

• Stakeholder scanning: Stakeholders such assuppliers, consumers, and surroundingcommunities are sources of data on social and political risk. Information can be gathered from surveys, interviews, communitymeetings, and market perception studies, aswell as hiring local advisors. The drawback of these methods, particularly in countrieswhere new operations are being established,is that undertaking the study could reinforceexisting expectations of stakeholders that the company will find hard to meet. Inaddition, engaging stakeholders can sometimesembroil the company in local politics inunanticipated ways. For these reasons, acompany wanting this information would bewise to seek assistance from a third party, orhire personnel trained in conducting social impact assessments.

It is possible, and likely most useful, to combineelements of all of the above methods. Forinstance, a company could assign general riskoversight to several people within thecompany,while also enlisting personnel in thefield and training them to be aware of ‘red flags’indicating potential problems. Boutiquepolitical risk firms could supplement thiscountry information at various stages ofoperations, and a social impact assessmentcould be undertaken periodically within theproject life-cycle by a lending agency, a thirdparty, or specifically hired personnel.Thisprocess should not, however, become all-consuming. Instead, companies should adopt amethodology for gathering and reportinginformation that is appropriate to the companyand the project. Section IV further discussesreporting and decision-making.

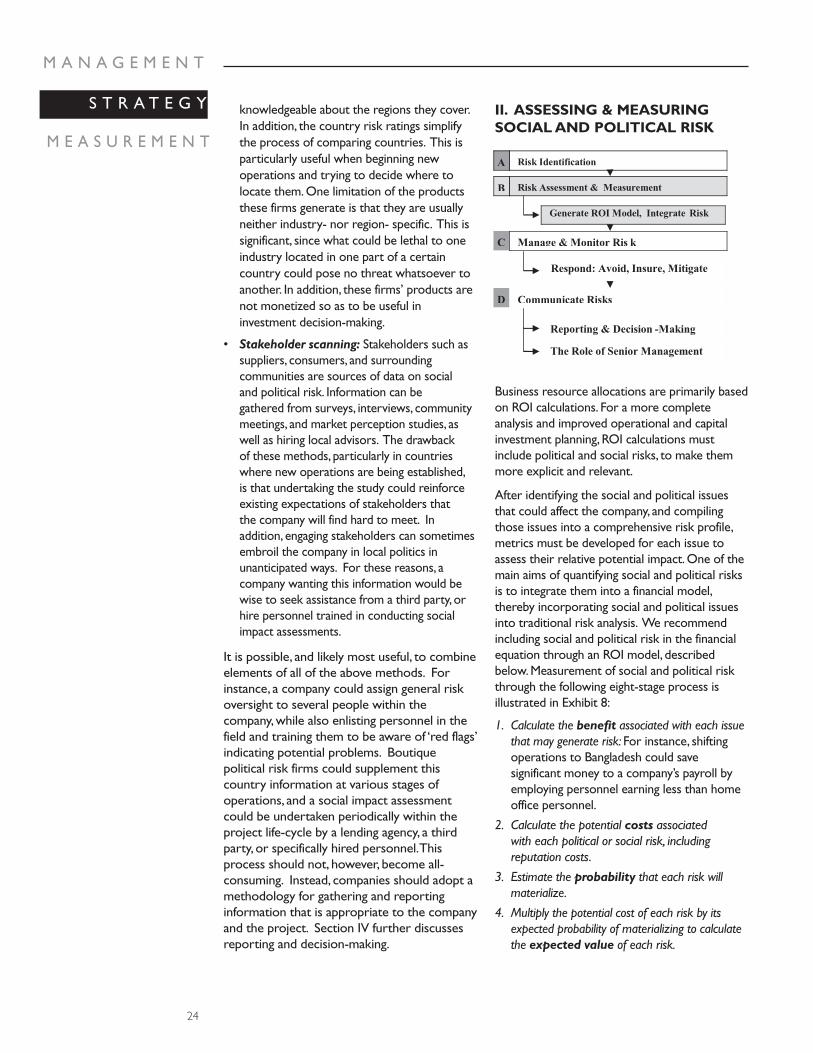

II. ASSESSING & MEASURINGSOCIAL AND POLITICAL RISK

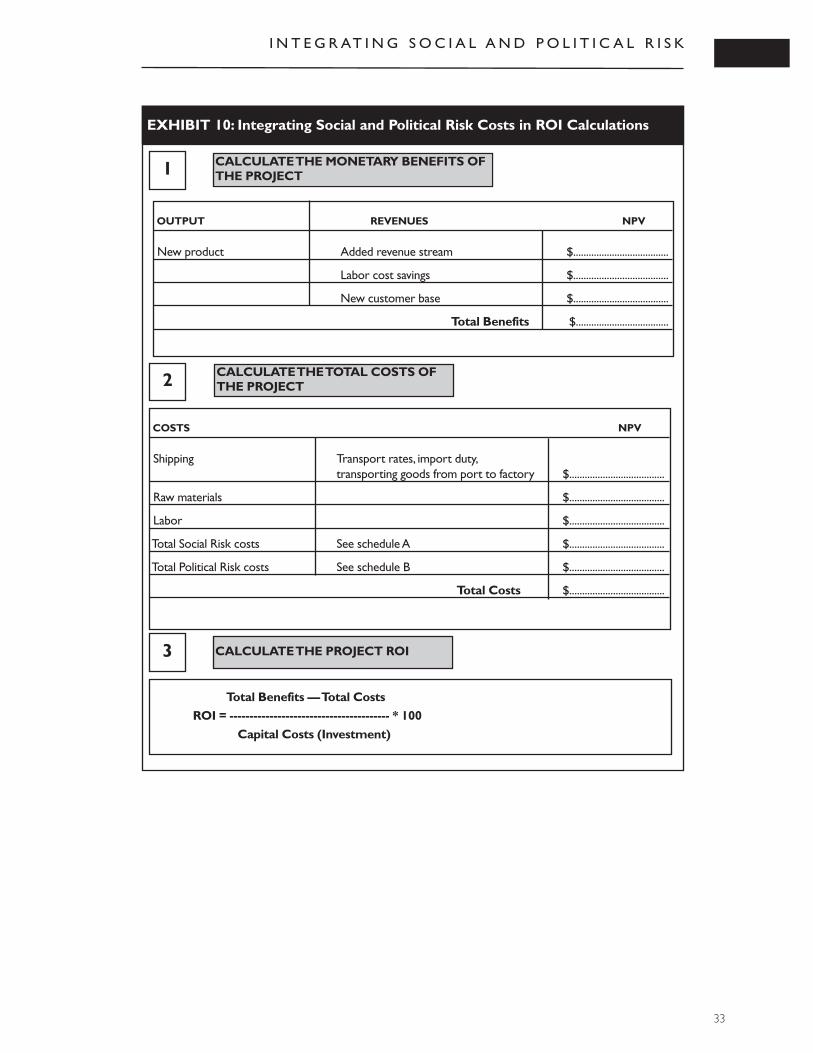

Business resource allocations are primarily basedon ROI calculations. For a more completeanalysis and improved operational and capitalinvestment planning, ROI calculations mustinclude political and social risks, to make themmore explicit and relevant.

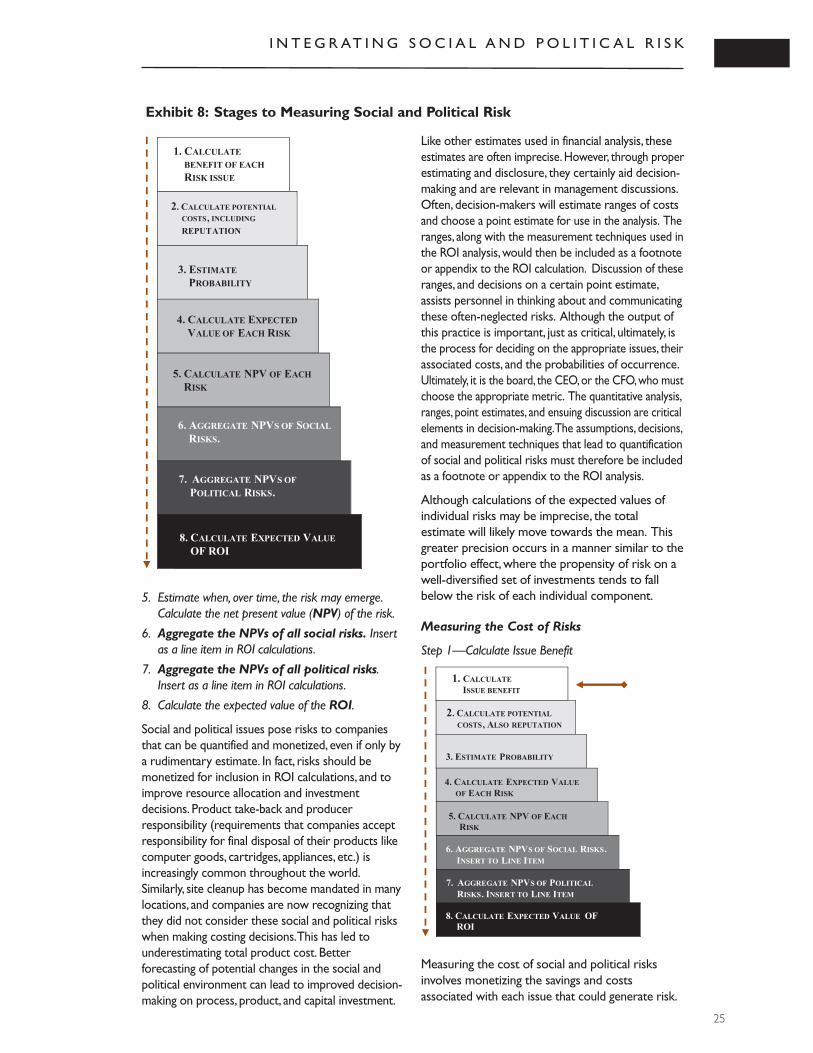

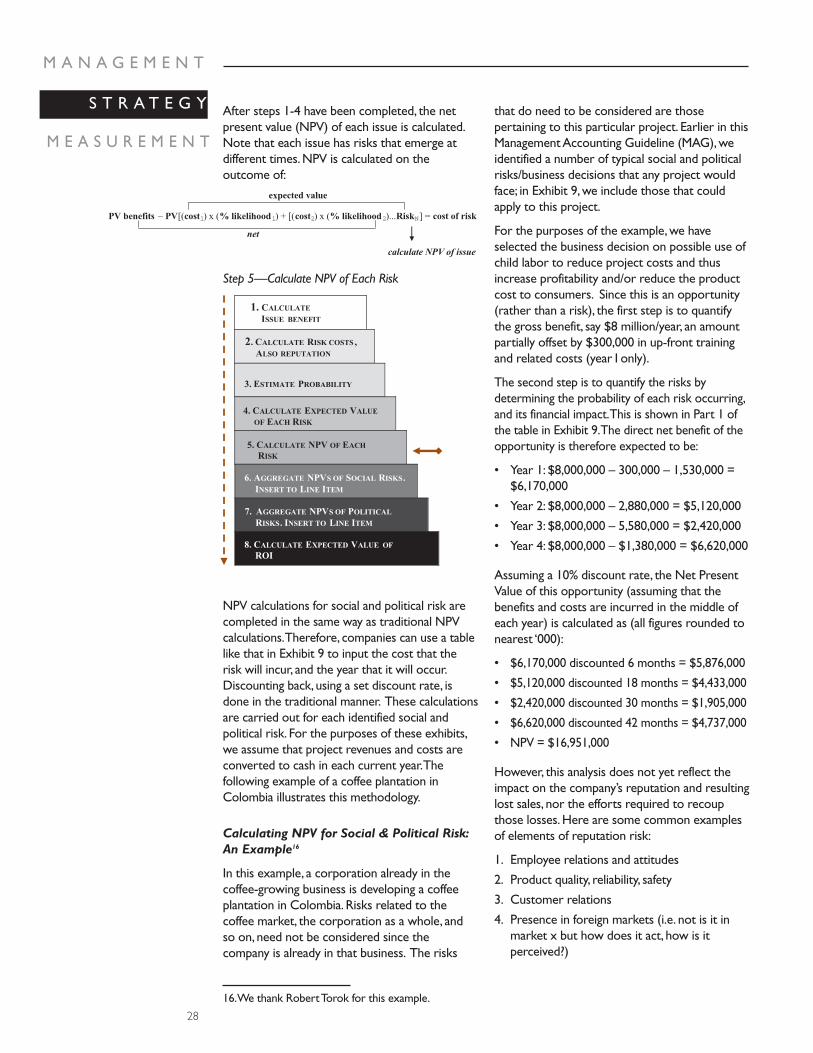

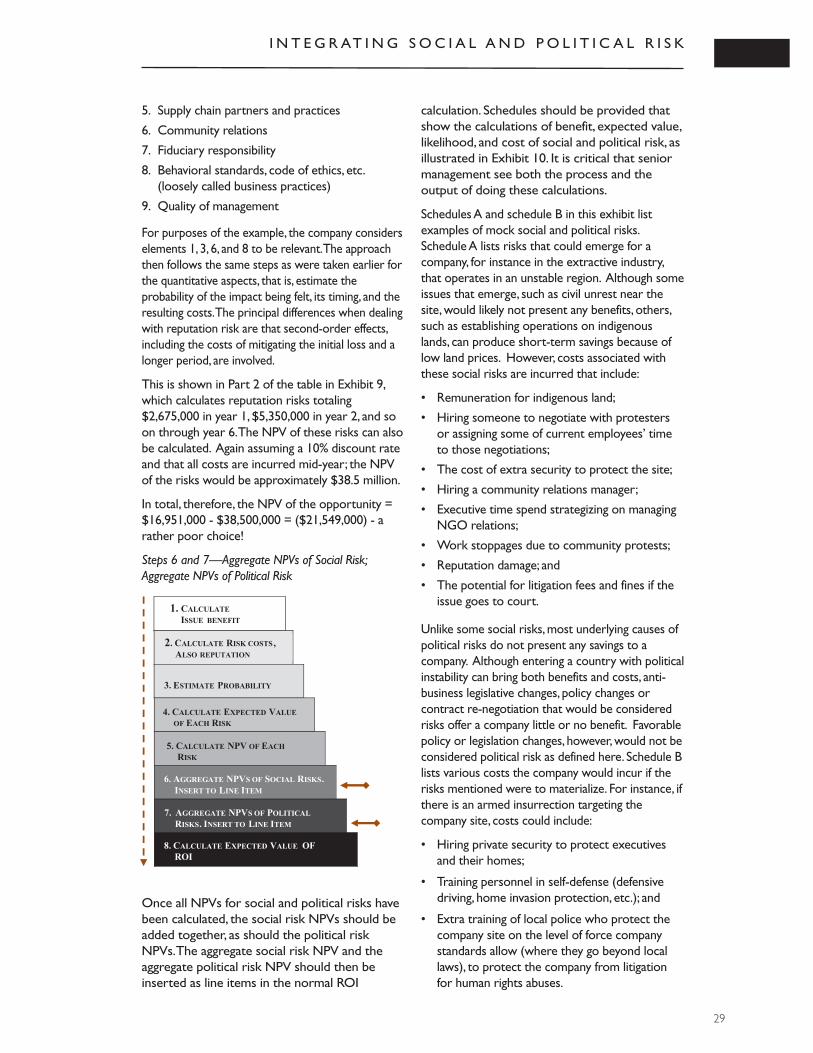

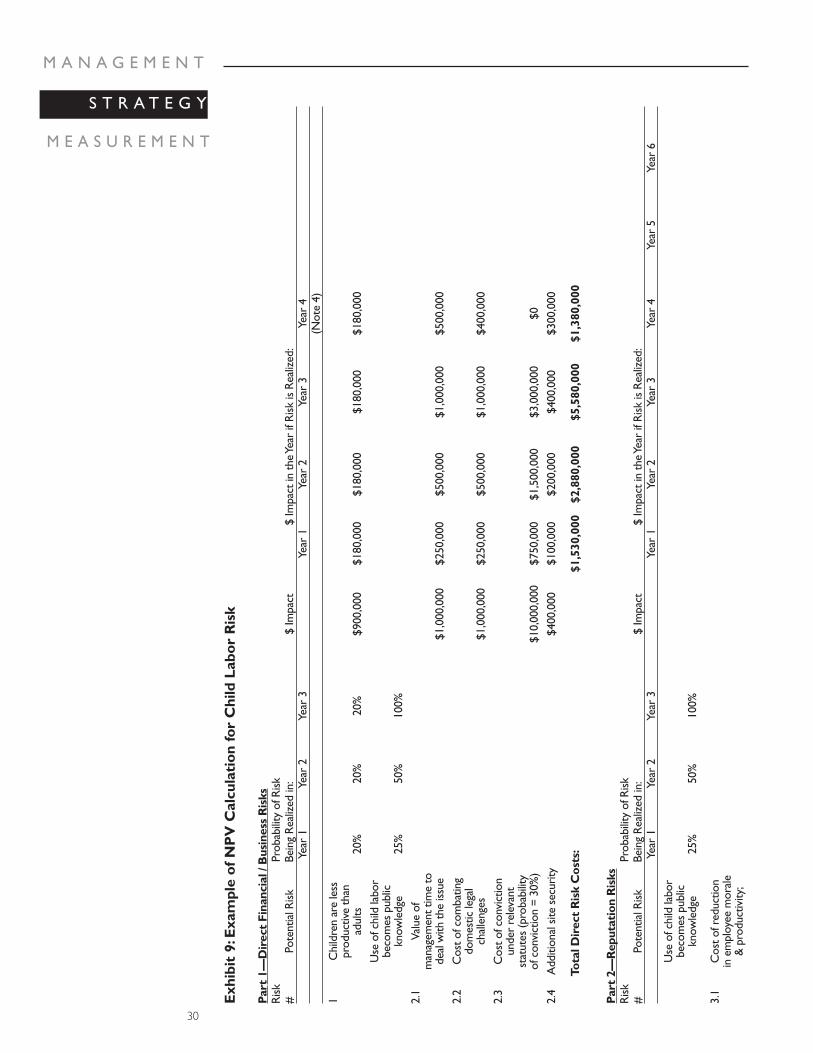

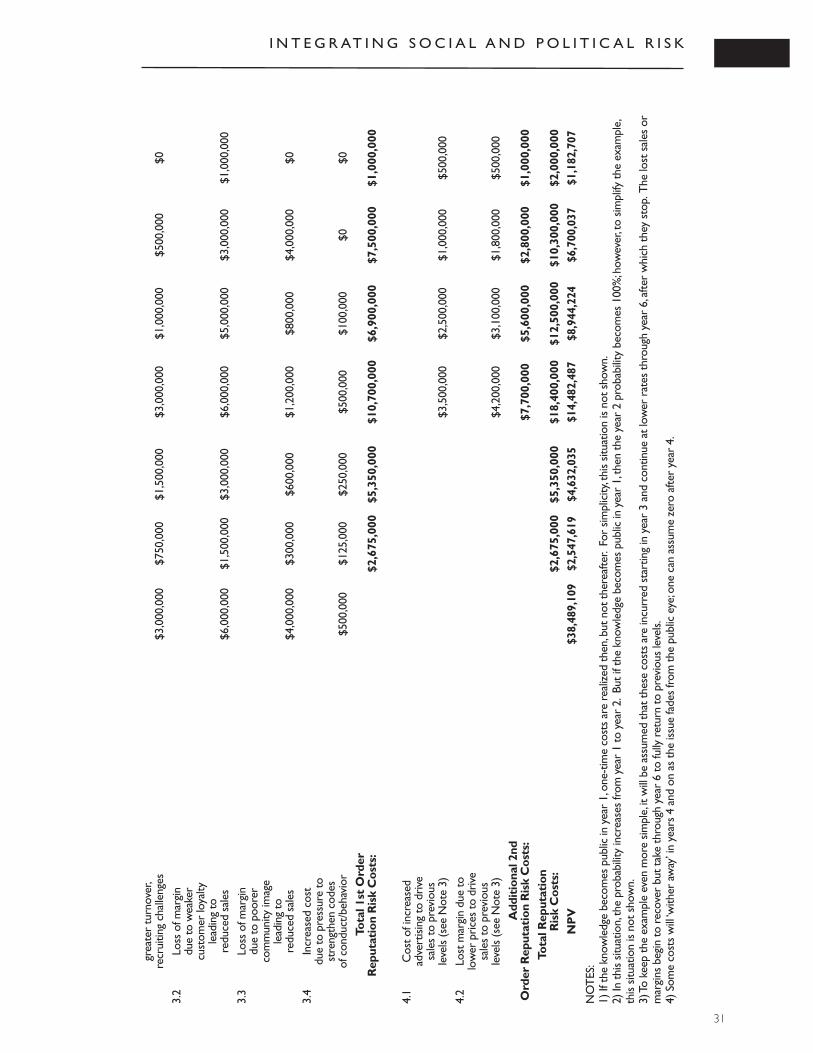

After identifying the social and political issuesthat could affect the company, and compilingthose issues into a comprehensive risk profile,metrics must be developed for each issue toassess their relative potential impact.One of themain aims of quantifying social and political risksis to integrate them into a financial model,thereby incorporating social and political issuesinto traditional risk analysis. We recommendincluding social and political risk in the financialequation through an ROI model, describedbelow.Measurement of social and political riskthrough the following eight-stage process isillustrated in Exhibit 8:

1. Calculate the benefit associated with each issuethat may generate risk:For instance, shiftingoperations to Bangladesh could savesignificant money to a company’s payroll byemploying personnel earning less than homeoffice personnel.

2. Calculate the potential costs associated with each political or social risk, including reputation costs.

3. Estimate the probability that each risk willmaterialize.

4. Multiply the potential cost of each risk by itsexpected probability of materializing to calculatethe expected value of each risk.

Generate ROI Model, Integrate Risk

Manage & Monitor Ris k C

Respond: Avoid, Insure, Mitigate

Communicate RisksD

Reporting & Decision -Making

The Role of Senior Management

Risk Identification

Risk Assessment & Measurement

A

B

5. Estimate when, over time, the risk may emerge.Calculate the net present value (NPV) of the risk.

6. Aggregate the NPVs of all social risks. Insertas a line item in ROI calculations.

7. Aggregate the NPVs of all political risks.Insert as a line item in ROI calculations.

8. Calculate the expected value of the ROI.

Social and political issues pose risks to companiesthat can be quantified and monetized, even if only bya rudimentary estimate. In fact, risks should bemonetized for inclusion in ROI calculations, and toimprove resource allocation and investmentdecisions. Product take-back and producerresponsibility (requirements that companies acceptresponsibility for final disposal of their products likecomputer goods, cartridges, appliances, etc.) isincreasingly common throughout the world.Similarly, site cleanup has become mandated in manylocations, and companies are now recognizing thatthey did not consider these social and political riskswhen making costing decisions.This has led tounderestimating total product cost. Betterforecasting of potential changes in the social andpolitical environment can lead to improved decision-making on process, product, and capital investment.

Like other estimates used in financial analysis, theseestimates are often imprecise.However, through properestimating and disclosure, they certainly aid decision-making and are relevant in management discussions.Often, decision-makers will estimate ranges of costsand choose a point estimate for use in the analysis. Theranges, along with the measurement techniques used inthe ROI analysis,would then be included as a footnoteor appendix to the ROI calculation. Discussion of theseranges, and decisions on a certain point estimate,assists personnel in thinking about and communicatingthese often-neglected risks. Although the output ofthis practice is important, just as critical, ultimately, isthe process for deciding on the appropriate issues, theirassociated costs, and the probabilities of occurrence.Ultimately, it is the board, the CEO,or the CFO,who mustchoose the appropriate metric. The quantitative analysis,ranges, point estimates, and ensuing discussion are criticalelements in decision-making.The assumptions, decisions,and measurement techniques that lead to quantificationof social and political risks must therefore be includedas a footnote or appendix to the ROI analysis.

Although calculations of the expected values ofindividual risks may be imprecise, the totalestimate will likely move towards the mean. Thisgreater precision occurs in a manner similar to theportfolio effect,where the propensity of risk on awell-diversified set of investments tends to fallbelow the risk of each individual component.

Measuring the Cost of Risks

Step 1—Calculate Issue Benefit

Measuring the cost of social and political risksinvolves monetizing the savings and costsassociated with each issue that could generate risk.

I N T E G R AT I N G S O C I A L A N D P O L I T I C A L R I S K

25

Exhibit 8: Stages to Measuring Social and Political Risk

1. CALCULATE

BENEFIT OF EACH

RISK ISSUE

2. CALCULATE POTENTIAL

COSTS, INCLUDING

REPUTATION

3. ESTIMATE

PROBABILITY

4. CALCULATE EXPECTED

VALUE OF EACH RISK

5. CALCULATE NPV OF EACH

RISK

6. AGGREGATE NPVS OF SOCIAL

RISKS.

7. AGGREGATE NPVS OF

POLITICAL RISKS.

8. CALCULATE EXPECTED VALUE

OF ROI

1. CALCULATE

ISSUE BENEFIT

2. CALCULATE POTENTIAL

COSTS, ALSO REPUTATION

3. ESTIMATE PROBABILITY

4. CALCULATE EXPECTED VALUE

OF EACH RISK

5. CALCULATE NPV OF EACH

RISK

6. AGGREGATE NPVS OF SOCIAL RISKS.

INSERT TO LINE ITEM

7. AGGREGATE NPVS OF POLITICAL

RISKS. INSERT TO LINE ITEM

8. CALCULATE EXPECTED VALUE OF

ROI

26

M A N A G E M E N T

S T R A T E G Y

M E A S U R E M E N T

For example,when corporations are consideringoperating in a region where child labor is thenorm, they may contemplate following this norm.In considering this option, the savings from usingchildren would be calculated by measuring thedifference in the wage rates between paying anadult and a child.The savings of using child laborwould represent the issue benefit,which isgenerally assigned a positive value.

Although some industries like clothing and shoemanufacturing have been seriously damaged by theuse of child labor, and have therefore attempted tostop the practice, others like the chocolateindustry did not consider this a risk.Childrenworking as cocoa bean pickers were employed inthe supply chain. Chocolate and candymanufacturers largely ignored the issue, untilnewspapers began publishing stories of kidnappingsand forced child labor on cocoa plantations inWest Africa. If the company considered thisoutcome, it should calculate each potential costassociated with employing this labor force, and thepublic discovering it.These costs could include:

• Lost sales and other reputation impacts(measuring reputation is addressed in a later section);

• Managing a consumer boycott by hiring apublic relations firm, creating a newadvertising campaign, hiring a stakeholderrelations manager, communicating internallywith employees, and senior management’stime devoted to dealing with the issues;

• Diminished brand value; and

• Negative impact on recruiting potential hires.

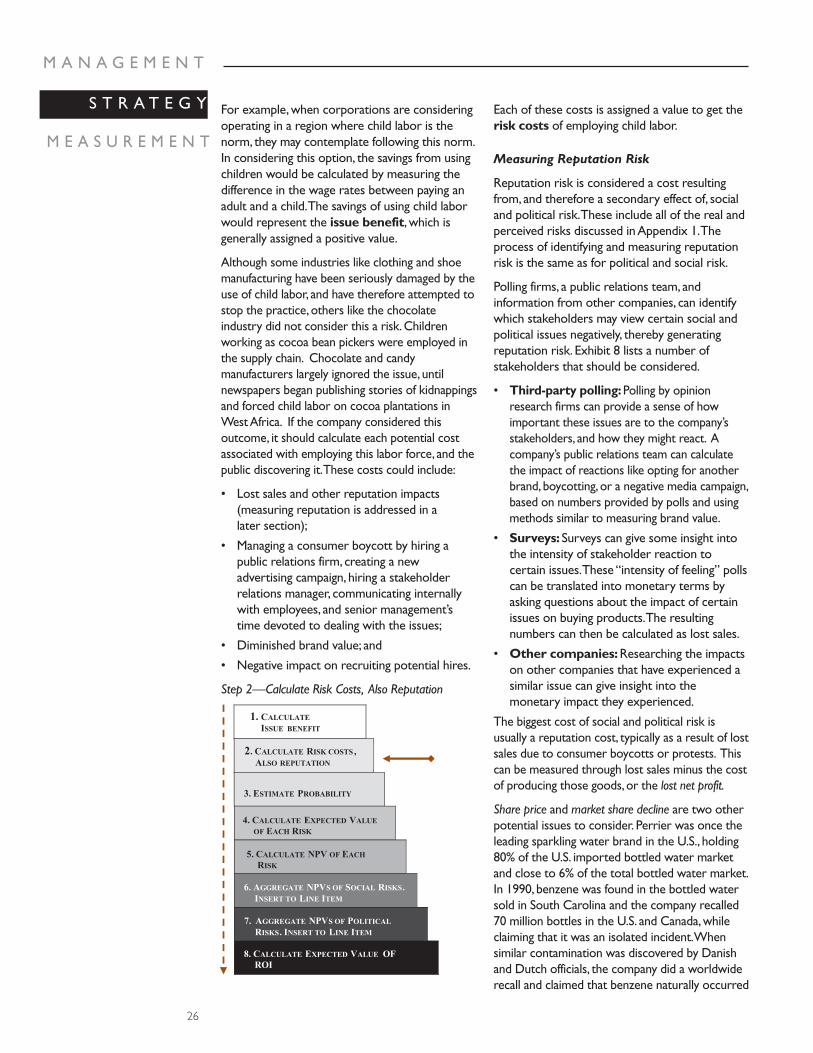

Step 2—Calculate Risk Costs, Also Reputation

Each of these costs is assigned a value to get therisk costs of employing child labor.

Measuring Reputation Risk

Reputation risk is considered a cost resultingfrom, and therefore a secondary effect of, socialand political risk.These include all of the real andperceived risks discussed in Appendix 1.Theprocess of identifying and measuring reputationrisk is the same as for political and social risk.

Polling firms, a public relations team, andinformation from other companies, can identifywhich stakeholders may view certain social andpolitical issues negatively, thereby generatingreputation risk. Exhibit 8 lists a number ofstakeholders that should be considered.

• Third-party polling:Polling by opinionresearch firms can provide a sense of howimportant these issues are to the company’sstakeholders, and how they might react. Acompany’s public relations team can calculatethe impact of reactions like opting for anotherbrand, boycotting, or a negative media campaign,based on numbers provided by polls and usingmethods similar to measuring brand value.

• Surveys:Surveys can give some insight intothe intensity of stakeholder reaction tocertain issues.These “intensity of feeling” pollscan be translated into monetary terms byasking questions about the impact of certainissues on buying products.The resultingnumbers can then be calculated as lost sales.

• Other companies:Researching the impactson other companies that have experienced asimilar issue can give insight into themonetary impact they experienced.

The biggest cost of social and political risk isusually a reputation cost, typically as a result of lostsales due to consumer boycotts or protests. Thiscan be measured through lost sales minus the costof producing those goods, or the lost net profit.

Share price and market share decline are two otherpotential issues to consider. Perrier was once theleading sparkling water brand in the U.S., holding80% of the U.S. imported bottled water marketand close to 6% of the total bottled water market.In 1990, benzene was found in the bottled watersold in South Carolina and the company recalled70 million bottles in the U.S. and Canada,whileclaiming that it was an isolated incident.Whensimilar contamination was discovered by Danishand Dutch officials, the company did a worldwiderecall and claimed that benzene naturally occurred

1. CALCULATE

ISSUE BENEFIT

2. CALCULATE RISK COSTS ,

ALSO REPUTATION

3. ESTIMATE PROBABILITY

4. CALCULATE EXPECTED VALUE

OF EACH RISK

5. CALCULATE NPV OF EACH

RISK

6. AGGREGATE NPVS OF SOCIAL RISKS.

INSERT TO LINE ITEM

7. AGGREGATE NPVS OF POLITICAL

RISKS. INSERT TO LINE ITEM

8. CALCULATE EXPECTED VALUE OF

ROI