INFORMATION MEMORANDUM - CMA Publications

272

In respect of the offer to the public and listing of Kenya Shillings six billion (Kes.6,000,000,000) senior unsecured fixed rate notes and senior unsecured equity linked notes 14 May 2015 INFORMATION MEMORANDUM 2015

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of INFORMATION MEMORANDUM - CMA Publications

In respect of the offer to the public and listing of Kenya Shillings six billion

(Kes.6,000,000,000) senior unsecured fixed rate notes and senior

unsecured equity linked notes

14 May 2015

INFORMATION MEMORANDUM

2015

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

ii

Serial Number:

Champions of Governance the second time round...We always strive to adhere to the highest corporate governance practices and consistent focus on improving our reporting systems both as a financial company and listed firm hence success in winning these awards.

www.centum.co.ke

Information Memorandum i

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

Centum Investment Company Limited

Incorporated in Kenya under the Companies Act (Chapter 486, Laws of Kenya) (Registration Number C.8/67)

Information Memorandum in respect of the offer to the public and listing of Kenya Shillings six billion (Kes.6,000,000,000) senior unsecured fixed rate notes

and senior unsecured equity linked notes

14 May 2015

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

ii

1. IMPORTANT NOTICES AND STATEMENTS 1

2. EXECUTIVE SUMMARY 4

3. DEFINITIONS AND ABBREVIATIONS 11

3.1 DEFINITIONS 11

3.2 ABBREVIATIONS 15

4. SUMMARY OF CORPORATE INFORMATION 17

5. ADVISERS TO THE ISSUER ON THE NOTE ISSUE 19

6. TIMETABLE 21

7. SUMMARY OF THE OFFER 22

7.1 SUMMARY OF THE PROPOSED NOTES 22

8. USE OF PROCEEDS 28

8.1 FINANCIAL SERVICES 29

8.2 ENERGY 30

8.3 REAL ESTATE 31

8.4 OFFER RELATED EXPENSES 31

9. ABOUT THE ISSUER 32

9.1 COMPANY OVERVIEW 32

9.2 VISION, MISSION AND STRATEGY 32

9.3 BUSINESS MODEL 33

9.4 TRACK RECORD 34

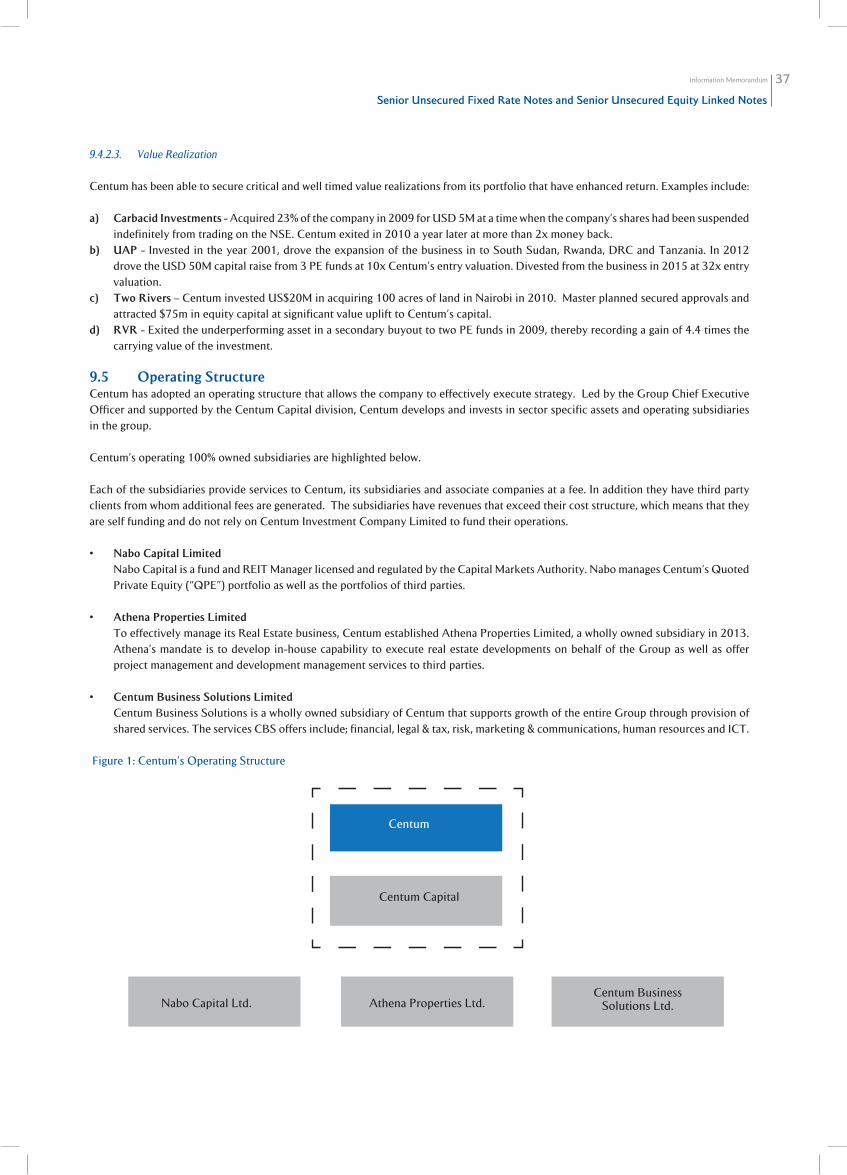

9.5 OPERATING STRUCTURE 37

9.6 CENTUM’S PORTFOLIO AND SECTOR FOCUS 38

9.6.1 Financial Services (FS) Sector 38

9.6.2 FMCG Sector 39

9.6.3 Energy Sector 40

9.6.4 Real Estate Sector 42

9.6.5 Education and Healthcare Sector 49

9.6.6 Agriculture Sector 49

9.6.7 Quoted Private Equity (“QPE”) Portfolio 49

9.6.8 Other Portfolio 50

9.7 DIVIDEND POLICY 50

9.8 PRINCIPAL SHAREHOLDERS 50

9.9 SHAREHOLDING BY DIRECTORS 51

9.10 DISTRIBUTION OF SHAREHOLDING 51

9.11 EMPLOYEES 51

10. TERMS AND CONDITIONS OF THE NOTES 52

11. KEY INVESTMENT CONSIDERATIONS 62

11.1 BUSINESS MODEL 62

11.2 TRACK RECORD OF CONSISTENT PERFORMANCE AND LONG TERM GROWTH 63

Contents

Information Memorandum iii

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

11.3 UNUTILISED DEBT CARRYING CAPACITY 64

11.4 STRONG CASH FLOWS 65

11.5 A WELL-DIVERSIFIED INVESTMENT PORTFOLIO 65

11.6 STRONG CORPORATE GOVERNANCE 66

11.7 STRONG BRAND NAME 67

12. ECONOMIC OVERVIEW 68

12.1 KENYA MACRO - ECONOMIC OVERVIEW 68

12.2 UGANDA MACRO - ECONOMIC OVERVIEW 70

13. INDUSTRY OVERVIEW 73

13.1 POWER SECTOR 73

13.1.1 Overview of the East African Power Sector 73

13.1.2 Power Sector in Kenya 73

13.2 FAST MOVING CONSUMER GOODS (FMCG) SECTOR 78

13.2.1 About FMCG 78

13.2.2 Key Drivers of FMCG in Africa 78

13.3 FINANCIAL SERVICES SECTOR 82

13.3.1 Kenya Banking Sector Overview 82

13.3.2 Industry Performance 82

13.3.3 Challenges 83

13.3.4 Opportunities 83

13.3.5 Overview of Kenya Insurance Industry 84

13.3.6 Industry Performance 84

13.3.7 Kenya Insurance Market Outlook 84

13.3.8 Performance Overview 85

13.4 RECENT PRIVATE EQUITY TRANSACTIONS IN EAST AFRICA 85

13.5 THE ASSET MANAGEMENT INDUSTRY 86

13.5.1 Traditional Asset Managers 86

13.5.2 Pension Industry 86

13.5.3 Individual Retirement Benefits Schemes and Service Providers 87

13.6 REAL ESTATE INDUSTRY IN AFRICA 88

13.7 REAL ESTATE INDUSTRY IN KENYA 89

13.7.1 Property Market Segment 89

13.8 REAL ESTATE INDUSTRY IN UGANDA 90

13.8.1 Property Market Segment 90

13.8.2 Retail market 90

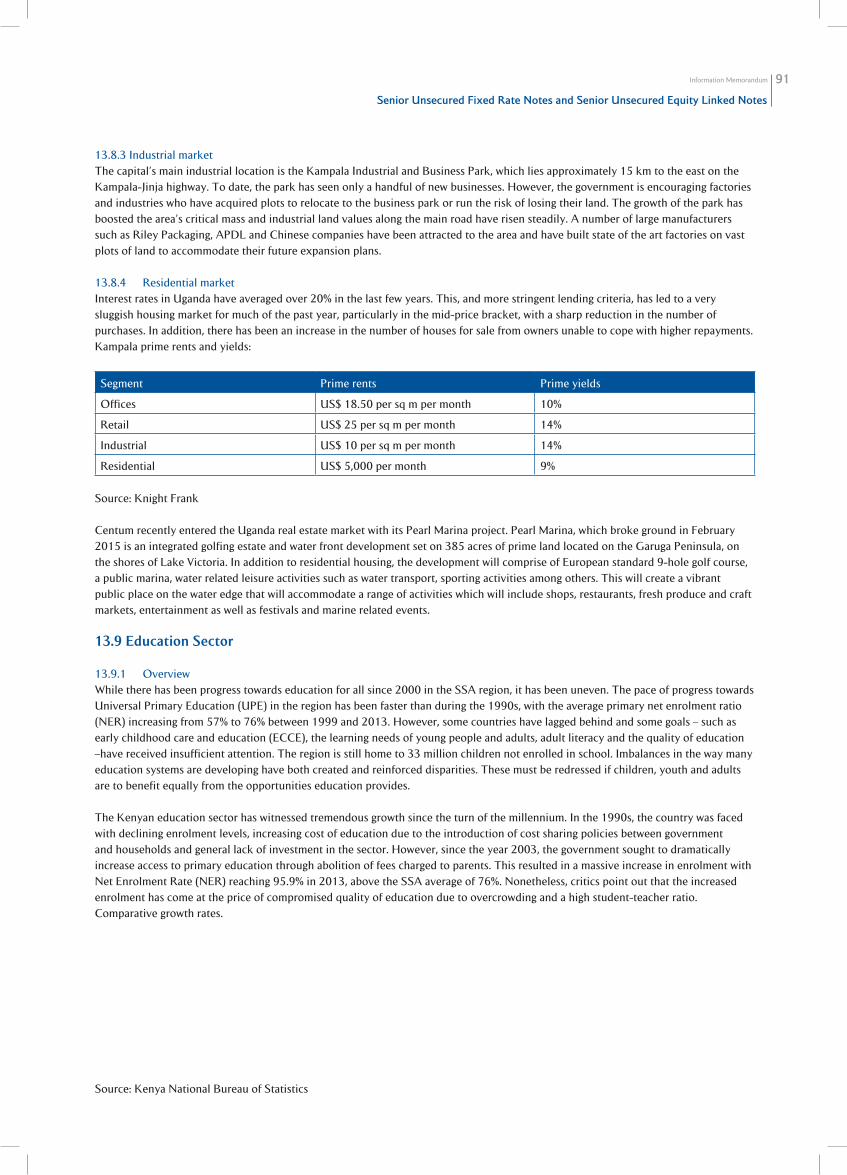

13.8.3 Industrial market 91

13.8.4 Residential market 91

13.9 EDUCATION SECTOR 91

13.9.1 Overview 91

13.9.2 Key Drivers for Growth of the Education Sector in Kenya 91

13.9.3 Rising disposable income 93

13.10 HEALTHCARE SECTOR 93

13.10.1 Healthcare in Africa 93

13.10.2 Healthcare in Kenya 93

13.10.3 Pharmaceutical 94

13.10.4 Private Healthcare Sector in Kenya 94

13.11 INFORMATION AND COMMUNICATIONS TECHNOLOGY(ICT) SECTOR 95

13.11.1 Industry Overview 95

13.11.2 Kenya ICT Sector 95

13.11.3 Opportunities in ICT 96

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

iv

13.12 AGRICULTURAL SECTOR OVERVIEW 96

13.12.1 Agriculture in Africa 96

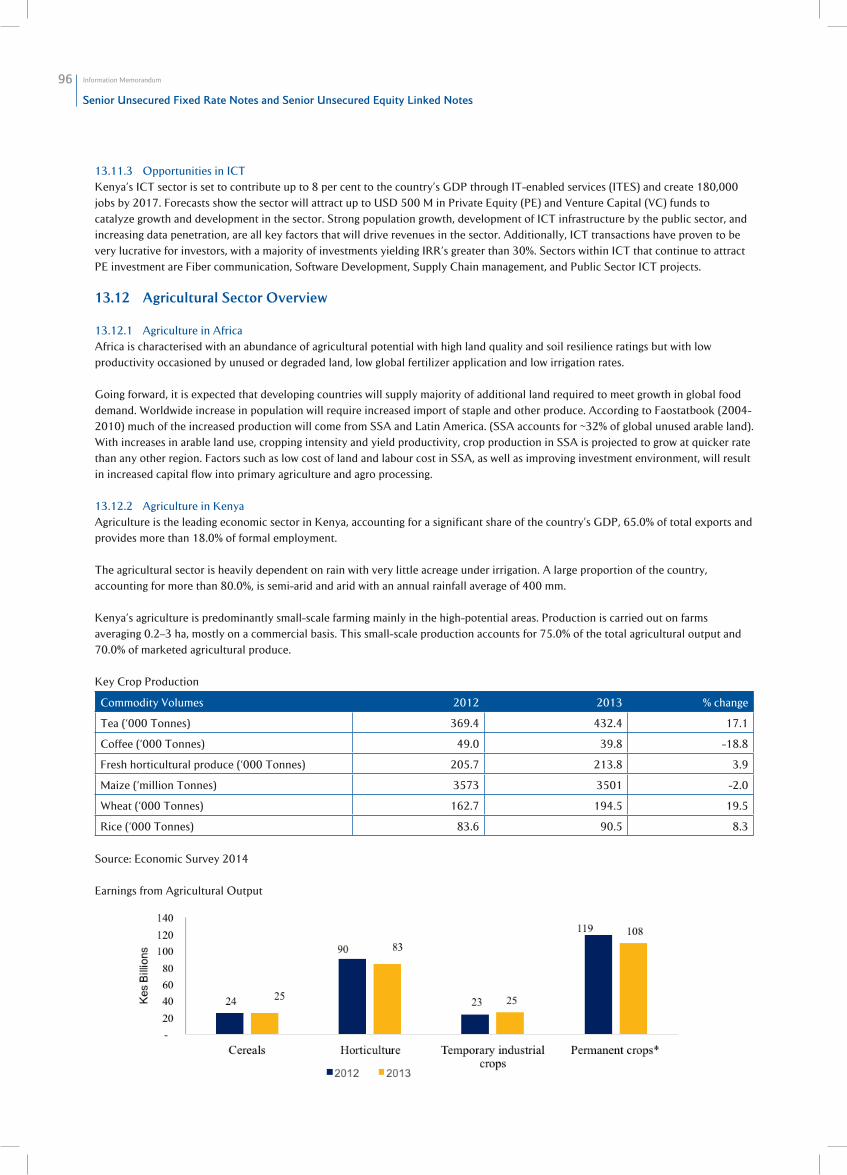

13.12.2 Agriculture in Kenya 97

13.12.3 Factors Driving Agriculture Business in Kenya 97

13.12.4 Opportunities 97

13.12.5 Challenges 97

13.12.6 Technology 97

14. SUMMARY OF FINANCIAL INFORMATION AND OTHER SELECTED DATA 98

14.1 AUDITORS 98

14.2 COMPANY STATEMENT OF COMPREHENSIVE INCOME 98

14.3 CONSOLIDATED STATEMENT OF FINANCIAL POSITION 99

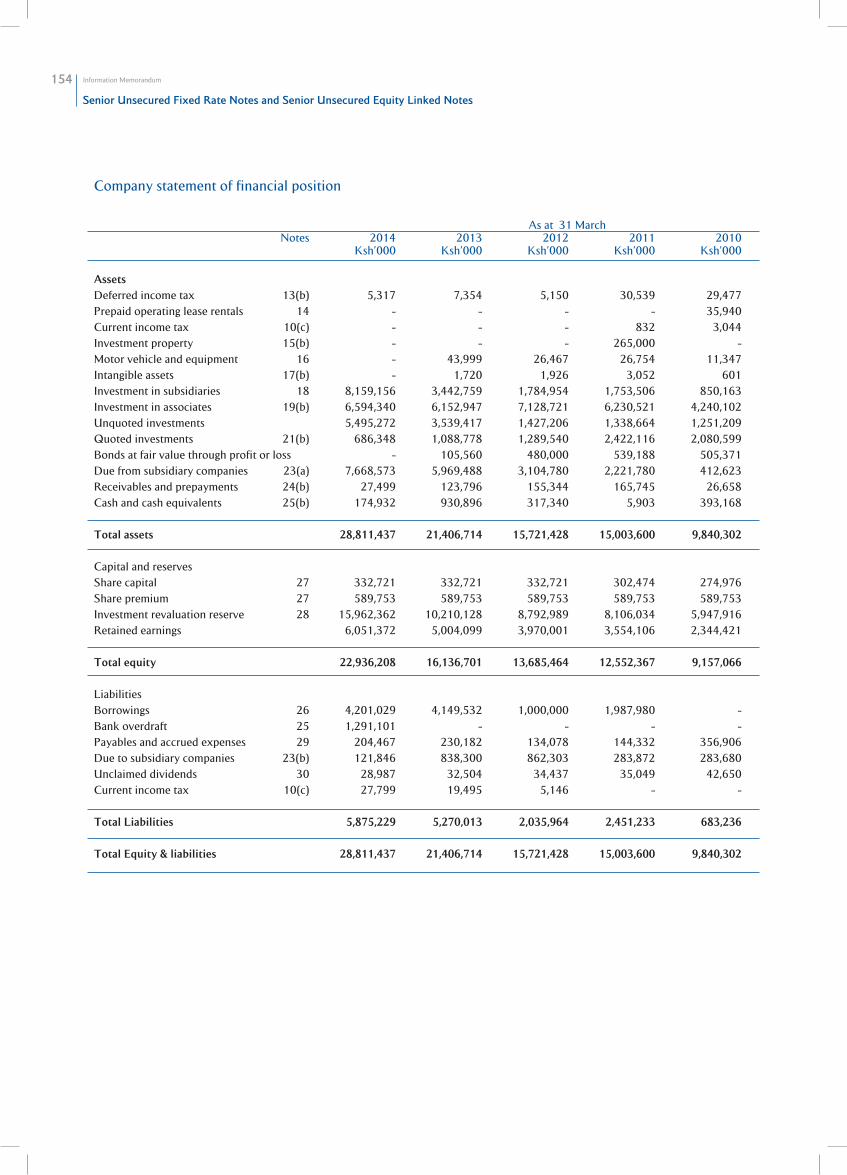

14.4 COMPANY STATEMENT OF FINANCIAL POSITION 100

14.5 STATEMENT OF CASH FLOWS (INTERNALLY GENERATED FUNDS) 101

14.6 COMPANY STATEMENT OF TOTAL RETURN 102

14.7 PROFORMA FINANCIAL INFORMATION 103

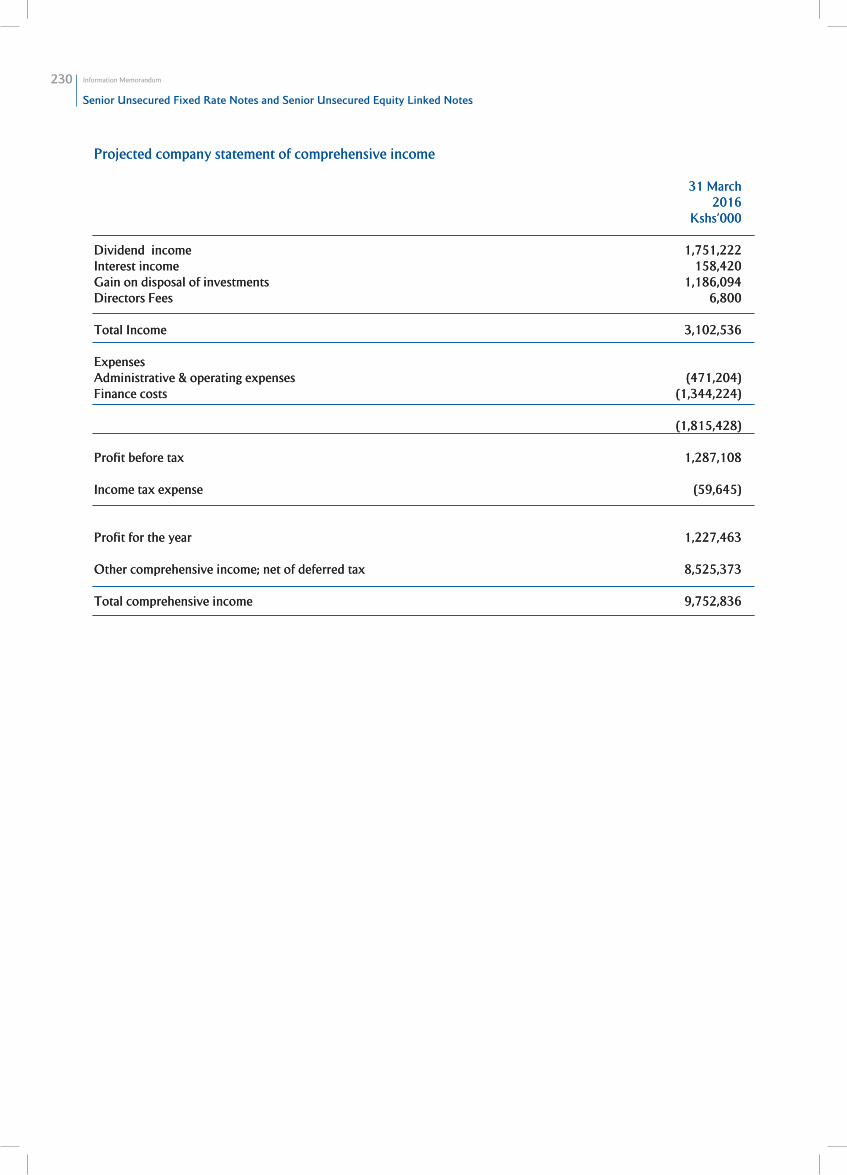

14.7.1 Projected consolidated statement of comprehensive income 103

14.7.2 Projected company statement of comprehensive income 104

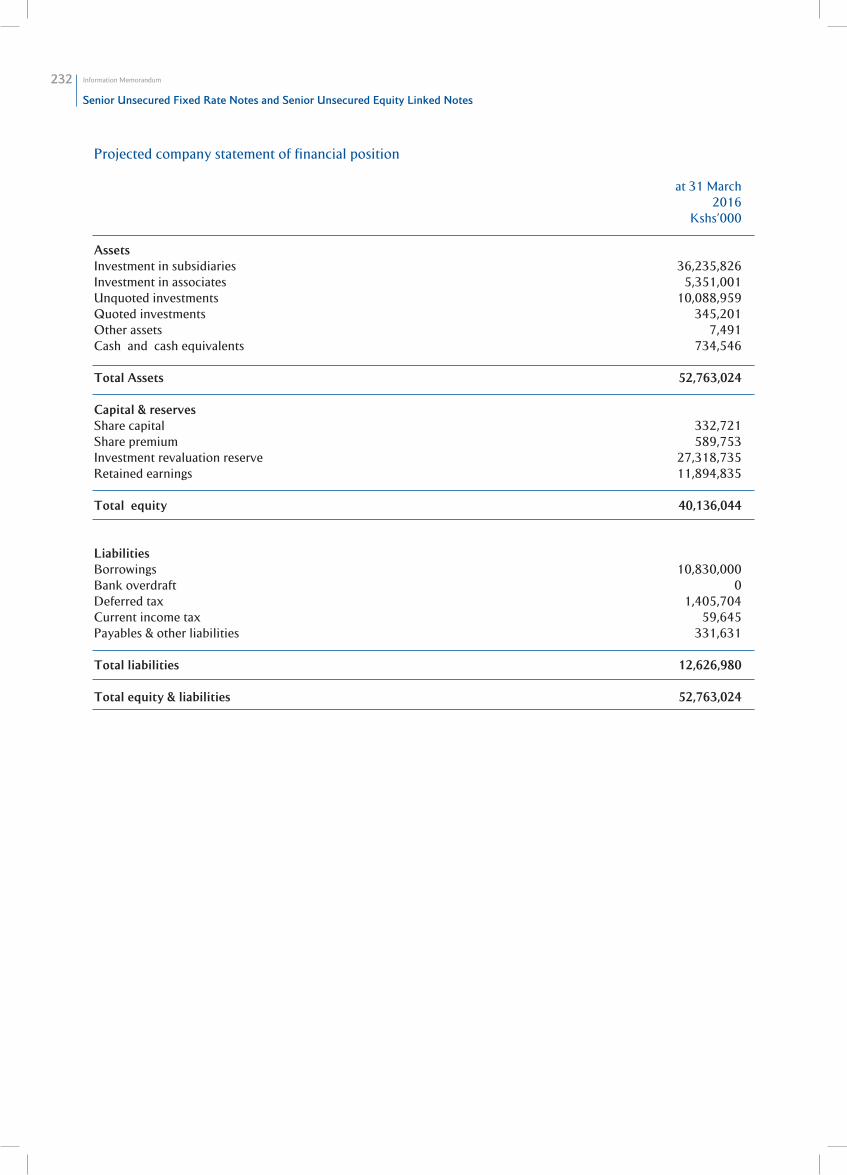

14.7.3 Projected consolidated statement of financial position 105

14.7.4 Projected company statement of financial position 106

15. RISK FACTORS AND MITIGATION MEASURES 108

15.1 INVESTMENT RISKS 108

15.1.1 Investment Decisions 108

15.2 INVESTMENT PERFORMANCE 108

15.3 INVESTMENT CONCENTRATION 108

15.4 INVESTMENT VALUATIONS AND EXIT OPPORTUNITIES 108

15.5 FINANCIAL RISKS 109

15.5.1 Liquidity risks 109

15.5.2 Interest rate risk 109

15.5.3 Inflation risk 109

15.5.4 Foreign Exchange Risk 109

15.5.5 Credit Risk 109

15.5.6 Commodity Risk 110

15.6 OPERATIONAL RISKS 110

15.7 EXTERNAL RISKS 110

15.8 REPUTATIONAL RISK 110

15.9 PROJECT RISK 110

15.10 EXECUTION RISK 111

15.11 FINANCE RISK 111

15.12 MARKET RISK 111

16. CORPORATE GOVERNANCE 112

17. LEGAL AND CORPORATE INFORMATION 121

17.1 NAME, PLACE AND DATE OF REGISTRATION 121

17.2 CAPITAL STRUCTURE 121

17.3 VOTING RIGHTS AND CONTROL 121

17.4 LISTING 121

17.5 ISSUES OF SHARES IN THE THREE YEARS IMMEDIATELY PRECEDING

THE DATE OF THIS INFORMATION MEMORANDUM 121

17.6 PRINCIPAL OBJECTS (AS CONTAINED IN THE MEMORANDUM OF ASSOCIATION) 121

17.7 PROVISIONS OF THE ARTICLES RELATING TO BORROWING 122

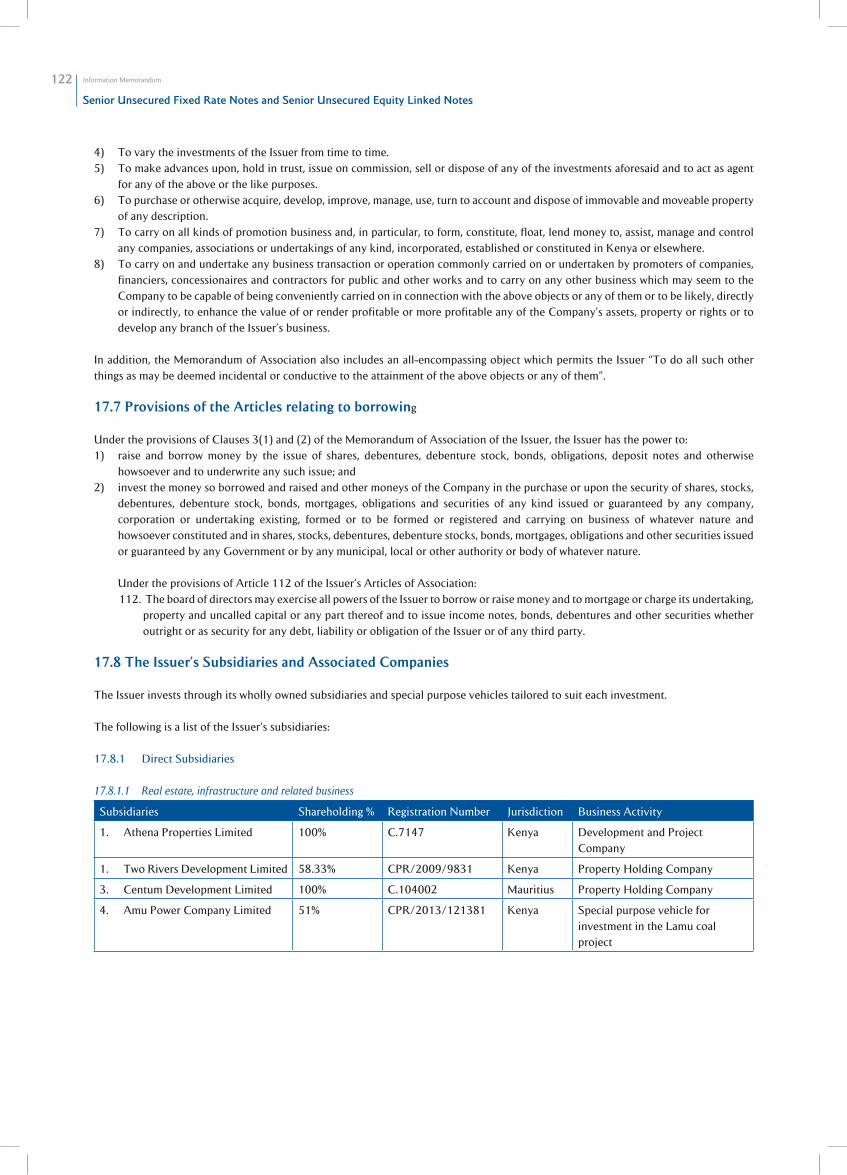

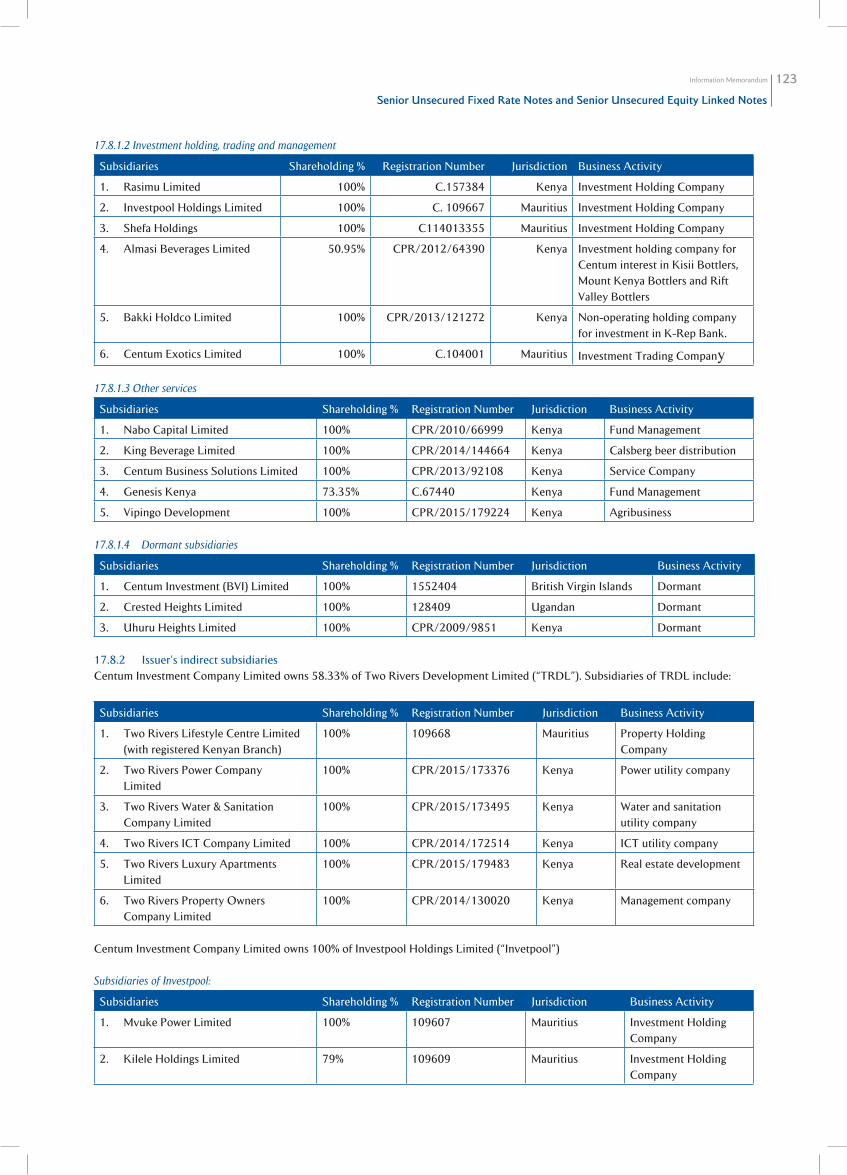

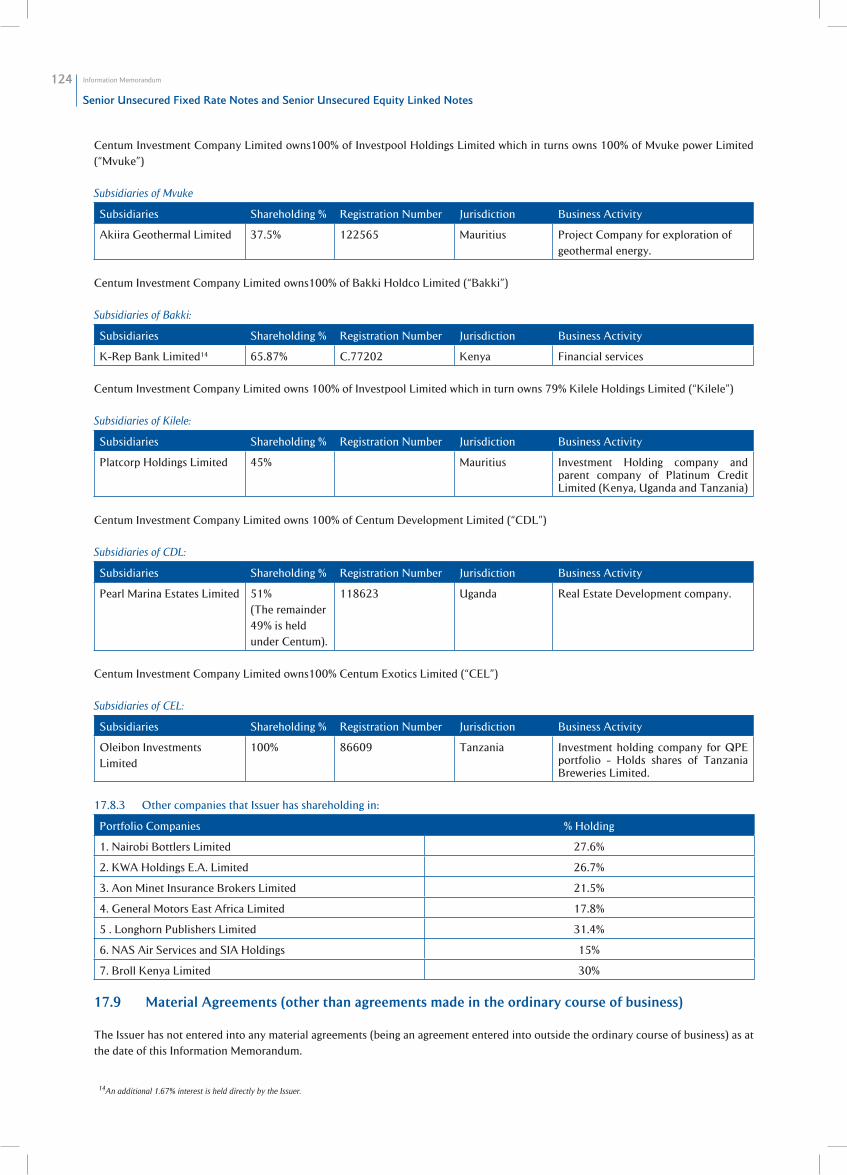

17.8 THE ISSUER’S SUBSIDIARIES AND ASSOCIATED COMPANIES 122

Information Memorandum v

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

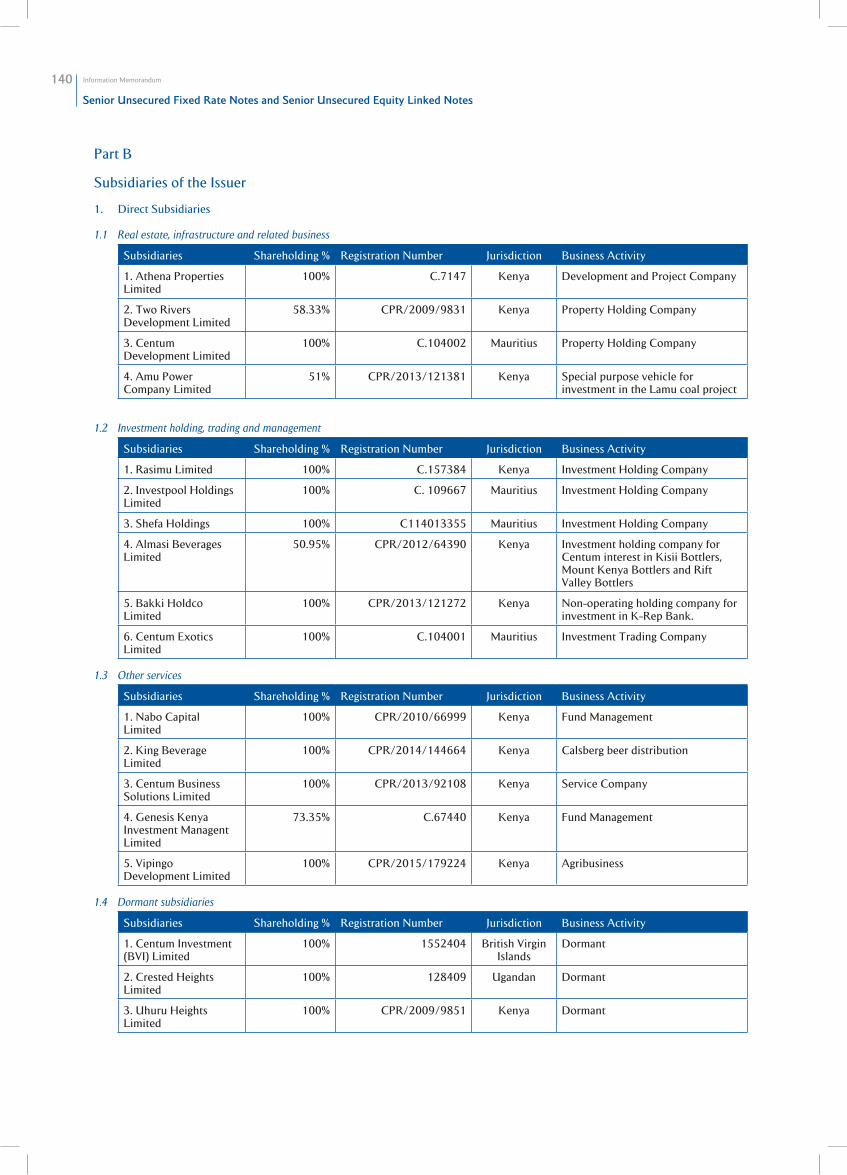

17.8.1 Direct Subsidiaries 122

17.8.2 Issuer’s indirect subsidiaries 122

17.8.3 Other companies that Issuer has shareholding in: 124

17.9 MATERIAL AGREEMENTS

(OTHER THAN AGREEMENTS MADE IN THE ORDINARY COURSE OF BUSINESS) 124

17.10 ONEROUS COVENANTS AND DEFAULT 125

17.11 RELATED PARTY AGREEMENTS (LOAN AGREEMENTS WITH SUBSIDIARIES, ETC

WITH DETAILS ON AMOUNTS, PURPOSE, INTEREST RATES, ETC) 125

17.12 LOAN/FINANCE AGREEMENTS 125

17.12.1 Senior Unsecured Fixed Rate Notes and Senior Equity Linked Notes 125

17.12.2 Facilities from Co-operative Bank of Kenya Limited 126

17.12.3 Facility from FirstRand Bank Limited 126

17.13 RELEVANT SUBSIDIARY LOAN/FINANCE AGREEMENTS 127

17.14 LOANS TO DIRECTORS AND SENIOR MANAGEMENT 127

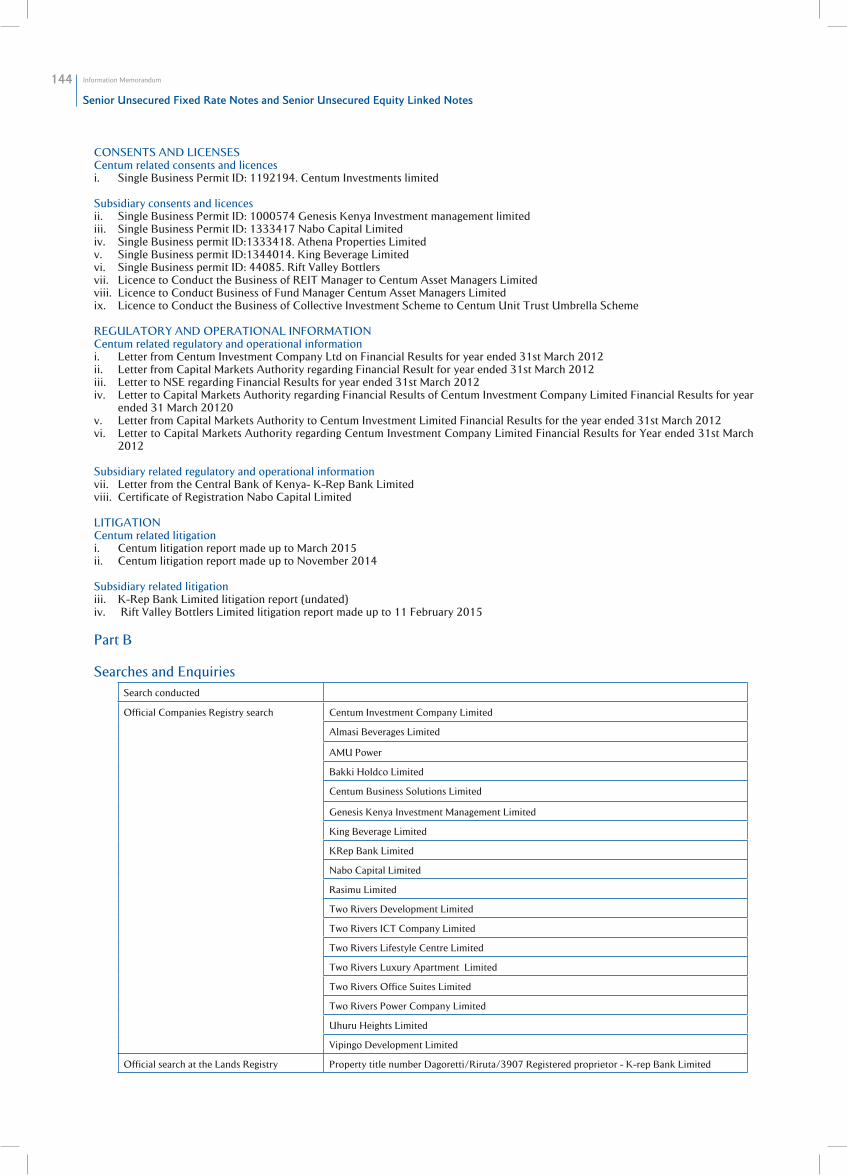

17.15 LICENSES AND PERMITS 127

17.15.1 The Issuer 127

17.15.2 Subsidiaries 127

17.16 PROPERTY AND INFORMATION ON VENDORS ON MATERIALS

ASSETS ACQUIRED IN THE LAST THREE YEARS 127

17.17 PROVISIONS OF THE ARTICLES WITH RESPECT TO DIRECTORS 128

17.18 MATERIAL LITIGATION 128

17.19 OTHER DISCLOSURES 129

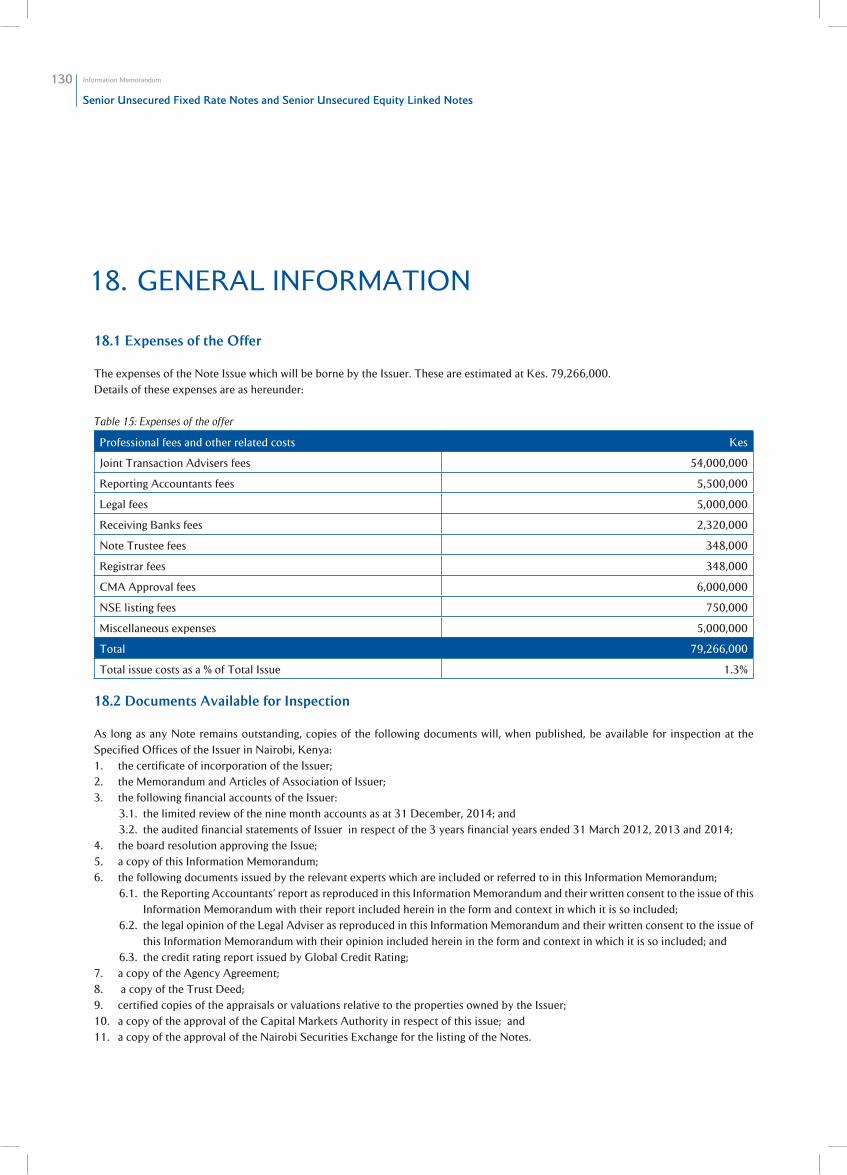

18. GENERAL INFORMATION 130

18.1 EXPENSES OF THE OFFER 130

18.2 DOCUMENTS AVAILABLE FOR INSPECTION 130

18.3 MINIMUM SUBSCRIPTION LEVEL 131

18.4 APPLICATION PROCEDURE 131

18.5 TRADING OF THE NOTES 131

18.6 CHANGES IN SENIOR MANAGEMENT 131

18.7 INTERRUPTIONS IN GROUP’S BUSINESS 131

18.8 MATERIAL CHANGES 131

18.9 DIRECTORS STATEMENT AS TO LIQUIDITY REQUIREMENT 131

18.10 DIRECTORS’ DECLARATION 131

19. FREQUENTLY ASKED QUESTIONS ON EQUITY LINKED NOTES 132

20. APPENDIX 135

20.1 LEGAL OPINION 135

20.2 REPORTING ACCOUNTANTS REPORT 147

20.3 FORM OF LETTER OF UNDERTAKING FOR REQUESTED ALLOCATION 258

20.4 FORM OF THE NOTE APPLICATION FORM 259

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

vi

Joint Transaction Advisers

Placing Agents and Joint Sponsoring Stock-brokers

Receiving Banks

Reporting Accountants

Fiscal Agent and Registrar

Legal Advisers

Note Trustee

Information Memorandum 1

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

1. IMPORTANT NOTICES AND STATEMENTS

The Note Issue:This information memorandum is issued by Centum in compliance with the requirements of the Companies Act and a copy of this

Information Memorandum together with the documents required under section 43(1) of the Companies Act have been delivered to the

Registrar of Companies at the State Law Office for registration.

This Information Memorandum has been prepared in compliance with the Capital Markets Act and the Public Offer Regulations in

connection with the offer to the public and listing on the fixed income market segment (“FISMS”) of the Nairobi Securities Exchange

Limited (“NSE”) of Kenya Shillings six billion (Kes.6,000,000,000) senior unsecured fixed rate notes and senior unsecured equity linked

(the “Notes”).

ApprovalsThe CMA has approved the public offering and listing of the Notes on the FISMS of the NSE.

As a matter of policy, the CMA assumes no responsibility for the correctness of any statements or opinions made or reports contained

in this Information Memorandum. Approval of the Note Issue and/or listing is not to be taken as an indication of the merits of Notes or

the Issuer.

The NSE has authorised the Issuer to list the Notes on the FISMS. The Notes have not been and will not be registered or issued under any

jurisdiction outside Kenya. The NSE assumes no responsibility for the correctness of any of the statements made or opinions or reports

expressed or referred to in this Information Memorandum. Admission to the FISMS of the NSE is not to be taken as an indication of the

merits of the Notes or the Issuer.

The Notes will be issued in book entry form as a dematerialized security under section 24 of the Central Depositories Act. The sale or

transfer of Notes by Noteholders will be subject to the rules of the NSE, and where applicable, the CDSC Rules, the Terms and Conditions

of the Notes and the provisions of the Agency Agreement. The register for the Notes will be the record of depositors maintained by the

Central Depository and Settlement Corporation (“CDSC”) in accordance with the Central Depositories Act.

There are currently no restrictions on the sale or transfer of Notes under Kenyan law. In particular, there are no restrictions on the sale

or transfer of Notes by or to non-residents of Kenya.

ResponsibilityThe Directors whose names appear on page 17 of this Information Memorandum accept responsibility for the information contained in

this Information Memorandum. To the best of their knowledge and belief (having taken all reasonable care to ensure that such is the case)

the information contained in this Information Memorandum is in accordance with the facts and does not omit anything likely to affect the

import of such information. The Directors, having made all reasonable enquiries, confirm that this Information Memorandum contains

or incorporates all information which is material in the context of the Note Issue, that the information contained or incorporated in this

Information Memorandum is true and accurate in all material respects and is not misleading in any material respect, that the opinions

and the intentions expressed in this document are honestly held and that there are no other factual omissions which would make this

document, or any such information or expression of any such opinions or intentions, misleading in any material respect and that all

proper enquiries have been made to verify the foregoing.

Important NoticesThe Joint Lead Transaction Advisers and the other advisers to the Issue have relied on the information provided by the Issuer and

the Issuer’s professional advisers and have not verified the information contained in this Information Memorandum. Accordingly, the

Joint Lead Transaction Advisers and the other Advisers to the Issue make no representations as to the accuracy or completeness of the

information contained in this Information Memorandum. The Joint Lead Transaction Advisers and the other agents and advisers to the

Issue do not accept any liability or responsibility in relation to information contained in this Information Memorandum.

Neither this Information Memorandum nor any other information supplied in connection with the Notes is intended to provide the

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

2

complete basis of any credit or other evaluation, nor should it be considered as a recommendation by the Joint Lead Transaction

Advisers or the other agents or advisers to the Issue that any recipient of this Information Memorandum or any other information

supplied in connection with this Note Issue should subscribe for or purchase the Notes. Each investor contemplating subscribing for or

purchasing the Notes should make their own independent investigation of the financial condition and affairs, and its own appraisal of

the creditworthiness of the Issuer. Investors are advised to consult their professional advisers before making an investment decision. The

attention of prospective investors is drawn to the Risk Factors set out in Section 15 of this Information Memorandum.

The delivery of this Information Memorandum does not at any time imply that the information contained herein concerning the Issuer is

correct at any time subsequent to the date hereof or that any other information supplied in connection with the Notes is correct as of any

time subsequent to the date indicated in the document containing the same.

No person has been authorized to give any information or make any representation other than those contained in this Information

Memorandum and if given or made, such information or representation should not be relied upon as having been authorized by or on

behalf of the Issuer, the Joint Lead Transaction Advisers or the other advisers and Agents to the Note Issue.

Selling RestrictionsThe Notes may not be offered or sold, directly or indirectly, and neither this document nor any other supplemental Information

Memorandum or any prospectus, form of application, advertisement, other offering material or other information relating to the Issuer or

the Notes may be issued, distributed or published in any jurisdiction, other than Kenya.

The distribution of this Information Memorandum and the offer for subscription or sale of the Notes may be restricted by law in certain

jurisdictions. Persons into whose possession this Information Memorandum or any Notes may come must first inform him or herself

about and observe any such restrictions.

Supplemental Information MemorandumThe Issuer will, for so long as any Note remains outstanding and listed on any exchange, publish a supplement to the Information

Memorandum where there has been:

(a) a material adverse change in the condition (financial or otherwise) of the Issuer; or

(b) any modification of the terms of the Note Issue which would then make the Information Memorandum inaccurate or misleading.

The Issuer shall seek the prior approval of the CMA in connection with any amendment or supplement to this Information Memorandum

and the Issuer shall, in addition, supply to the Joint Lead Transaction Advisers and other Agents and the CMA such number of copies of

such supplement to this Information Memorandum as the Joint Lead Transaction Advisers and other advisers and agents and the CMA

may reasonably require or as may be required to be provided by law. If the terms of the Issue are modified or amended in a manner

which would make this Information Memorandum, as supplemented, inaccurate or misleading, a new Information Memorandum will be

prepared by the Issuer after seeking the approval of the CMA and the NSE.

Forward Looking StatementsSome statements in this Information Memorandum may be deemed to be “forward-looking statements”. Forward-looking statements

include statements concerning the Issuer’s plans, objectives, goals, strategies and future operations and performance and the assumptions

underlying these forward-looking statements.

When used in this Information Memorandum, the words “anticipates”, “estimates”, “believes”, “intends” “plans”, “may”, “will”, “should”

and any similar expressions are used to identify forward-looking statements. The Issuer has based these forward-looking statements on the

current view of its Board of Directors with respect to future events and financial performance. These views reflect the best judgement of

the Issuer’s Board of Directors but involve uncertainties and are subject to certain risks the occurrence of which could cause actual results

to differ materially from those predicted in the Issuer’s forward-looking statements and from past results, performance or achievements.

Although the Issuer believes that the estimates and the projections reflected in its forward-looking statements are reasonable, if one or

more of the risks or uncertainties materialise or occur, including those which the Issuer has identified in this Information Memorandum,

or if any of the Issuer’s underlying assumptions prove to be incomplete or incorrect, the Issuer’s actual results of operations may vary

from those expected, estimated or projected.

These forward-looking statements apply only as at the date of this Information Memorandum. Without prejudice to any requirements

under Applicable Laws and regulations, the Issuer expressly disclaims any obligations or undertaking to disseminate after the date of

this Information Memorandum any updates or revisions to any forward-looking statements contained herein to reflect any change in its

expectations with regard thereto or any change in events, conditions or circumstances on which any forward-looking statement is based.

A prospective purchaser of the Notes should not place undue reliance on these forward-looking statements.

Information Memorandum 3

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

RoundingSome numerical figures included in this Information Memorandum have been subject to rounding adjustments. Accordingly, numerical

figures shown as totals in certain figures may not be an arithmetic aggregation of the figures that preceded them.

The Issuer will provide, free of charge, to each person to whom a copy of the Information Memorandum has been delivered, upon request

of such person, a copy of any of the documents deemed to be incorporated herein by reference, unless such documents have been

modified or superseded.

Requests for such documents should be directed to:

Centum Investment Company Limited

5th Floor

International House

Mama Ngina Street

P.O. Box 10518-00100 Nairobi GPO

For the kind attention of the Company Secretary.

The information may also be obtained from the Issuer’s website: www.centum.co.ke.

Legal Adviser’s Opinion In compliance with disclosure requirement under disclosure F.08 of the Public Offer Regulations, Coulson Harney, the Legal Advisers,

have given and not withdrawn their written consent to the inclusion in this Information Memorandum of their Legal Opinion (attached

as Appendix 20.1), in the form and context in which the Legal Opinion appears and the references to their names, and have authorised

the contents of the said Legal Opinion.

Reporting Accountants’ Opinion In compliance with disclosure requirement under disclosure F.08 of the Public Offer Regulations, PricewaterhouseCoopers, the Reporting

Accountants, have given and not withdrawn their written consent to the inclusion in this Information Memorandum of their statements

(attached as Appendix 20.2), in the form and context in which their statements appear and the references to their names, and have

authorised the contents of the said statements.

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

4

2. EXECUTIVE SUMMARY

Centum is one of East Africa’s largest1 quoted investment companies with total assets of Kes.36.8 billion as at 31 December 2014

and managing an additional Kes.140 billion of third party funds, through its fund management subsidiaries, Genesis Kenya Investment

Management Limited and Nabo Capital Limited.

Centum’s vision is “To be Africa’s foremost investment channel”

Centum works towards this vision by playing the role of a creator of investment grade opportunities. Within the strategy period 2014/19,

Centum will focus its development activities in eight key sectors: (i) financial services, (ii) fast moving consumer goods (“FMCG”), (iii)

real estate (iv) power (v) agriculture, (vi) education, (vii) healthcare and (viii) information communication technology (“ICT”). The

decision to focus on these sectors was informed by the size of the market, growth potential and our ability to develop and build Centum’s

capabilities in the development of investment grade assets.

Within the sectors, we look to develop opportunities of scale and attract third party investors to participate in high quality investment

grade opportunities. By way of illustration, Centum has successfully executed this strategy in the development of its Two Rivers real

estate project, which has attracted Kes.6.75 billion of equity capital and an additional Kes.7.2 billion of debt capital.

Focus on the eight sectors as highlighted below is a key theme of our 2014/19 strategy. Other themes for the strategy period are

highlighted below.

• Deliveryofmarketbeatingreturns.Inthisregardwehavesetanannualizedreturntargetof35%overthestrategyperiod

• ScaleupoftheGroupbygrowingCentum’stotalassetvaluetoKes120Billionby2019andtotalAssetsundermanagement(AUMs)

to Kes 720 Billion

• BuildingtheCentumbrandbydeliveringtopromisethroughpeoplehencedevelopingteamswithsectorexpertise

• Managementofoperatingcostsatbelow2%oftotalassets

In the following sections of the executive summary, we highlight four (4) key points:

(1) Our track record of delivery.

(2) The current Kes.6 billion issue of debt will be a component of the funding to be applied to the development of proprietary

opportunities that are in the deal pipeline that we have created;

(3) Centum has an unutilized debt carrying capacity: and

(4) Centum has strong cash flows to service the current and new debt.

2.1. Track record of delivery

2.1.1. A review of performance against our 2009/14 strategic targets.

During the strategy period 2009/14, we defined our business as an investment channel that sought to provide investors access to an

otherwise inaccessible, quality and diversified portfolio of investments. To this end we focused on five strategic objectives.

i. To deliver a return on shareholder funds consistently above market returns. Prior to this time Centum’s returns were strongly

correlated to the NSE;

ii. To scale up assets under management with a target of Kes 30 Billion by 2014 from Kes 6 Billion in 2009.

iii. ToincreaseourgeographicalfootprinttotherestofAfricawithatargetofatleast50%oftheportfoliooutsideKenya;

iv. To enhance Centum’s brand by developing processes, systems, controls and human capital to ensure the company would consistently

deliver to its promises;

v. Tomaintainportfoliocostsatbelow2.5%ofassetsundermanagement.

1Nairobi Securities Exchange Limited Market Capitalisation stock data

Information Memorandum 5

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

Our performance against the above objectives is highlighted below.

i. Delivery of market beating returns

Wehaveoverthelast5years(the2009-2014strategyperiod)deliveredanaveragereturnof33%perannum.Thisperformance

representeda19%outperformancetotheNSE20ShareIndexanda19%outperformanceagainsttotheMCSIFrontierMarket

index.

ThetablesbelowhighlighttheperformanceofCentumagainsttheMCSIFrontierMarketindexinUnitedStatesDollars(USD):

The table below highlights the performance of Centum against the NSE 20 share index in Kenya Shillings (KES):

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

6

The table below highlights Centum’s book value against the Market Capitalisation.

ii. Growth in assets under management

Centum’s portfolio grew by Kes. 27.8 Billion from Kes. 9 Billion in March 2010 to Kes. 36.8 Billion in December 2014. Total assets

under management stood at Kes 177 Billion in December 2014 representing a 19.5 times growth since March 2010.

iii. Geographical and asset class diversification

Duringthestrategyperiod2009/14,thediversificationtargetwastohave50%oftheportfoliooutsideofKenya.Weprogressively

increasedourexposureoutsideofKenyafromlessthan1%asatMarch2010to19%asatMarch2014.Inlinewithourmissionof

providingaccesstoinaccessibleportfolio,ourexposuretoprivateequityandrealestateincreasedfrom59%to83%atthecloseof

that period.

iv. Brand at Centum is defined as consistent delivery to promise. Throughout the 2009/14 strategy period we built capacity in the

organization through the recruitment of competent and experienced team members as well as through leadership development. As

a result of the strong team, we were able to deliver over and above our ambitious strategy targets.

v. Thecosttoassetratio(excludingthirdpartyfunds)wasmaintainedbelow2.3%withinthe2009/14strategyperiod.

Information Memorandum 7

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

2.1.2. Our track record in developing investment grade assets and realizing value at significantly higher multiples

Over the last six years, Centum has had a lot of success in developing investment-grade opportunities and realizing significant return

at expanded multiples on its initial investment. Some examples are highlighted below:

Investment

Stages

Description

Deal Sourcing Centum has developed an extensive network of relationships within the region. This has enabled identification

of high-value early stage opportunities and high-potential acquisitions which have delivered significant growth

in Centum’s NAV. Examples of such investments are:

a) Amu Power – A Gulf Energy/Centum Consortium that won the award of tender to construct a 1,050MW

coal-fired power plant in Lamu, Kenya.

b) Akiira One Geothermal – Centum is part of the consortium developing Sub-Saharan Africa’s first

independent geothermal development, which when complete is expected to generate 140MW.

c) Two Rivers – A 100 acres development in Nairobi, acquired in 2010.

d) KRepBank–Acquisitionof65.7%shareholdingintheBankin2014.

e) PlatCorp –Acquisition of 35% shareholding in PlatCorpHoldings in 2012. PlatCorpHoldings is the

holdingcompanyofPlatinumCreditKenya,PlatinumCreditUgandaandPlatinumCreditTanzania.

f) GenesisKenya–Acquisitionof73.35%shareholdinginKenya’ssecondlargest2 fund manager in 2013.

Value Addition Through active execution of value creation strategies, Centum has improved the underlying performance of its

portfolio companies, which has resulted in an increase in profit attributable to Centum.

Value

Realization

Centum has been able to secure critical and well timed value realizations from its portfolio that have enhanced

return.

a) CarbacidInvestments-Acquired23%ofthecompanyin2009forUSD5Matatimewhenthecompany’s

shares had been suspended indefinitely from trading on the NSE. Centum exited in 2010 a year later at

more than 2x money back.

b) UAP-Investedintheyear2001,drovetheexpansionofthebusinessintoSouthSudan,Rwanda,DRC

andTanzania.In2012drovetheUSD50Mcapitalraisefrom3PEfundsat10xCentum’sentryvaluation.

Divested from the business in 2015 at 32x entry valuation.

c) TwoRivers–CentuminvestedUS$20Minacquiring100acresoflandinNairobiin2010.Masterplanned

securedapprovalsandattracted$75minequitycapitalatsignificantvalueuplifttoCentum’scapital.

d) RVR - Exited the underperforming asset in a secondary buyout to two PE funds in 2009, thereby recording

a gain of 4.4 times the carrying value of the investment.

2Retirement Benefits Authority Industry Performance Report, December 2013 to June 2015, published on 31 March 2015

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

8

2.2. The Kes. 6,000,000,000 issue of debt will be a component of the funding applied to develop proprietary opportunities

Centum has developed a pipeline of attractive investment opportunities in the energy, financial services, real estate and agriculture

sectors. The table below highlights the deal pipeline.

Table 1: Deal Pipeline

Sector Target Companies Nature of

Investment

Description Deal value

(Kes. M)

Financial Services K-Rep Bank Limited Equity

investment*

Acquisition of majority shareholding of

K-Rep Bank and additional investment in

the Bank to increase its core capital so as

to enable the Bank to increase its ability to

attract deposits as well as increase its loans

and advances.

3,600

Energy (i) Akiira One Geothermal

Limited

(ii) Amu Power Limited

Equity

investment

Finance Centum’s equity investment in

Centum’s current opportunities in the

energy sector.

2,100

Real Estate Pearl Marina Estates Limited Equity

investment

The construction of Phase 1 of the Pearl

Marina Development commenced in March

2015. Phase 1 is estimated to cost Kes

2.75Bn. Centum intends on funding this

with60%debtand40%equity.Therefore,

the equity investment at phase 1 is Kes

1.1Bn.

1,100

Real Estate Vipingo Development

Limited

Equity

Investment

Centum is in the process of acquiring

9,646 acres of land in Vipingo at a price

of Kes. 180,000 per acre and Vipingo

Estates Limited, a subsidiary of Rea

Vipingo Plantations Limited, which

owns approximately 900 acres of land at

approximately Kes. 340 Mn.

2,100

Quoted private

equity

Centum Exotics Equity

Investment

Increase the proportion of listed

investments held by Centum.

2,000

Total 10,900

In line with Centum’s capital structure, these opportunities will be financed through a mix of internally generated funds (dividend

and interest income, as well as realizations of existing investments) and debt. This is highlighted in the table below.

Sources of funding Amount (Kes. M)

Internally generated funds (dividends, interest and investment realisations ) 4,978

Debt 5,922

Total 10,900

The debt component of funding will be through the issuance of Kenya Shillings six billion (Kes.6, 000,000,000) senior unsecured

fixed rate notes and senior unsecured equity linked notes.

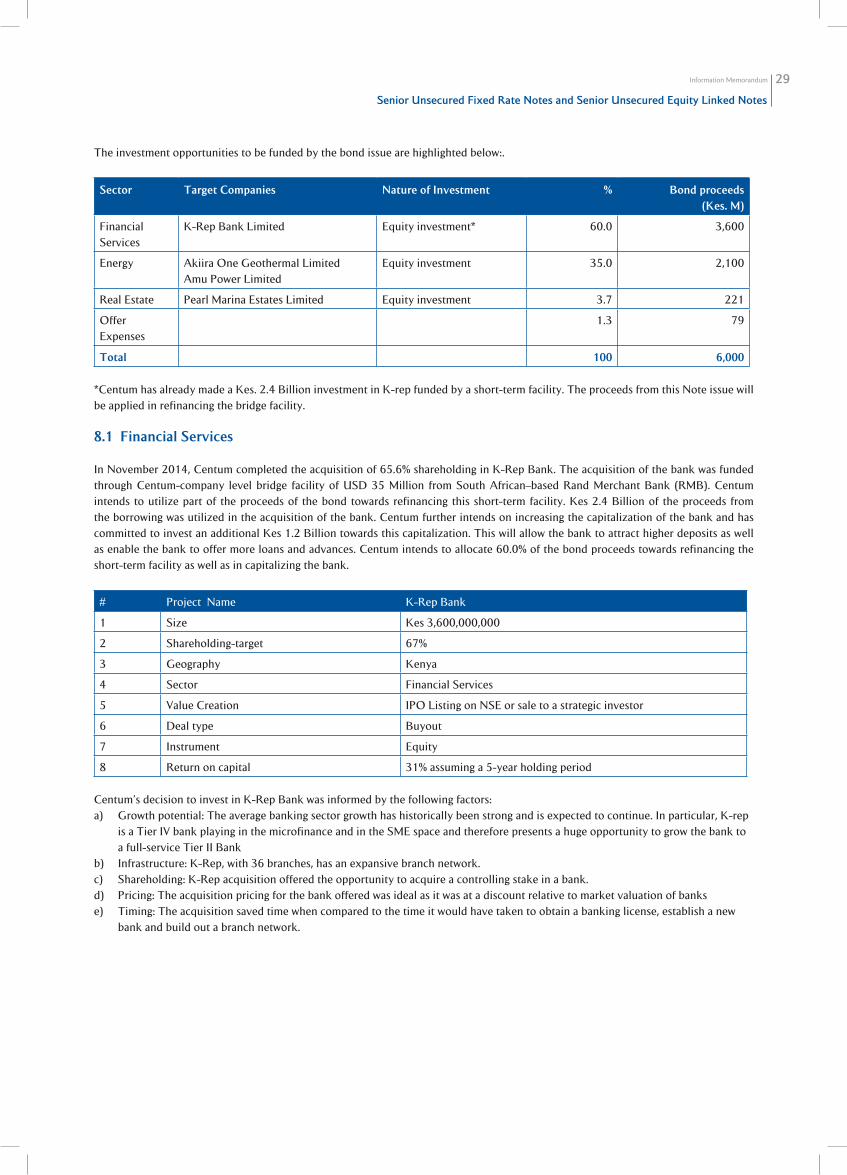

The investment opportunities to be funded by the bond issue are highlighted below:

Sector Target Companies Nature of Investment % Bond proceeds

(Kes. M)

Financial Services K-Rep Bank Limited Equity investment* 60.0 3,600

Energy Akiira One Geothermal Limited

Amu Power Limited

Equity investment 35.0 2,100

Real Estate Pearl Marina Estates Limited Equity investment 3.7 221

Offer Expenses 1.3 79

Total 100 6,000

*Centum has already made a Kes. 2,355,000,000 investment in K-rep funded by a short-term facility. The proceeds from this Note

issue will be applied in refinancing the short-term facility.

Information Memorandum 9

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

A. Financial services

Centumcompletedtheacquisitionof65.6%shareholdinginK-RepBankinNovember2014.Theacquisitionwasfundedthrough

abridgefacilityofUSD35Mn.Centumintendstoutilizepartoftheproceedsofthebondtowardsrefinancingthisshort-term

facility Centum further intends on increasing the capitalization of the bank and has committed to invest an additional Kes 1.2 Billion

towards this capitalization. This will allow the bank to attract higher deposits as well as enable the bank to offer more loans and

advances.

B. Energy

Centum has identified two opportunities in the energy sector.

i. Akiira One Geothermal

Akiira One Geothermal, founded in 2012, is the first private sector Greenfield geothermal private development in SSA. Centum

owns37.5%oftheequityintheprojectcompanythatisprospectingforgeothermalandwhencomplete,itwillgenerate70MW

of geothermal electricity with this being the first phase of the planned total 140MW.

ii. Amu Power

Amu Power is Special Purpose Vehicle (SPV) set up by the consortium that was awarded the tender to construct a 1050 MW

coal-fired power plant in Lamu County, Kenya. Centum is the lead project equity sponsor in the consortium.

C. Real Estate

PearlMarinaEstatesLimited(Uganda)owns385acresofprimelandsituatedbetweenEntebbeInternationalAirportandKampala

with 4km of lake frontage. The vision of Pearl Marina is to develop a premium world-class water front destination recognized in East

Africa and beyond.

Centum has commenced on Phase 1 construction of 102 villas, a gatehouse and supporting infrastructure for the Pearl Marina

project.Phase1isestimatedtocostKes.2.75Bn,whichwillbefunded40%byequityand60%bydebt.

Outcome of development of the proprietary opportunities in the pipeline

With these opportunities to be funded by the issue of additional debt, which are in addition to existing opportunities and current

investmentsthatarefundedfrominternallygeneratedfunds,Centum’sNAVissettogrowatbetween30%to35%p.a.inthecurrent

strategy period (2014-2019) and see Centum’s NAV grow to Kes.120 billion by the close of the period.

2.3. Unutilizeddebtcarryingcapacity

Centumhasarelativelylowlevelofgearing,withdebttoshareholderfundsratioat15%asat31March2015asshownbelow:

Kes. M 2010 2011 2012 2013 2014 2015

Net Debt (Total debt less cash) - 1,988 678 2,647 4,649 3,763

Gearing 16% 5% 20% 23% 15%

WiththecurrentdebtissueofKes.6billionbeingfullysubscribed,thelevelofgearingwillincreaseto31%,whichisstillrelatively

lowandwithinCentum’sexistingdebtcovenantsofaceilinggearingratioof50%.

The level of gearing at Centum excludes debt at the subsidiary company level. At subsidiary level, project specific funding at no

recourse to Centum is procured. Therefore, the value at risk for Centum in relation to the debt at subsidiary levels is limited to the

extent of Centum’s equity investment in the respective subsidiary.

2.4. Strong cash flows to service the current and new debt

Centum has strong cash flows from dividend, interest and exits from its portfolio of assets. The table below highlights the cash

generated from operations over the last six years. With our dual focus on cash return and investment value appreciation, Centum is

set to maintain healthy cash flows into the future.

Kes. M 2010 2011 2012 2013 2014 Dec 2014

Operating inflows 1,722 2,349 6,619 2,547 4,146 4,112

Operating outflows (199) (305) (309) (380) (463) (565)

Cash from Operations 1,523 2,044 6,310 2,167 3,683 3,547

Interest paid 44 148 230 344 660 391

Debt service coverage 34.61 13.81 27.43 6.30 5.58 9.07

Aminimalaverageof14%ofourcashinflowsgoestowardsservicingofoperatingexpensesatCentumInvestmentCompanyLimited.

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

10

To better manage our cost structure, we have created operational subsidiaries in the following lines of business:

Business line Operational Subsidiary

Real estate - development management and project management Athena Properties Limited

Fund management of quoted securities Nabo Capital Limited

Shared Services (Finance, HR, ICT, Legal, Company Secretarial, Tax, Risk, Marketing

& Communications)

Centum Business Solutions Limited

Each of the operating subsidiaries provides services to Centum, its subsidiaries and associates companies at a fee. In addition, they have

third party clients from whom additional fees are generated. Each of the subsidiaries have revenues that exceed their cost structure,

which means that they do not add to the cost structure of Centum but rather each make a contribution to the bottom line of Centum as

they are run as separate businesses.

This therefore means that the bulk of cashflows generated from operations by Centum are available to service additional debt as well as

repay our current Kes 4.2 Bn bond in 2017.

Over the period, Centum has maintained debt service coverage way above the bond covenant of 1.5 times.

Centum is rated for credit quality by the Global Credit Rating Company (GCR). Centum received an initial rating of A- in 2012. Its

current rating is A for both short term and long term credit quality, well above the minimum investment grade rating.

Forecast debt service capacity

Given current cash flows from operations and an assumption of no growth, Centum will still be in a position to adequately service the

additional Kes.6 billion debt. This is illustrated below.

Assuming that cash from operations is at the focused Kes 3.2 Bn and an additional annual debt service of approximately Kes 800 million

from the bond raise, the debt service coverage will be 2.0 times which is within the bond covenant target.

Kes. M 2015E 2016E

Cash from Operations 8,352 2,706

Interest paid 730 1,344

Debt service coverage 11.44 2.01

Minimum debt service coverage ratio 1.5 1.5

CONCLUSION

We invite you to partner with Centum in this exciting journey of developing local institutions of scale that will attract foreign and local

investors searching for investment-grade assets in this region and will further serve to deepen our capital markets.

Information Memorandum 11

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

3. DEFINITIONS AND ABBREVIATIONS

Subject Definition

Agency Agreement the agreement dated 14 May 2015 between the Issuer and the Fiscal Agent in relation to

the Notes

Agents the Note Trustee, Registrar and Fiscal Agent or any one of the them and includes any

successor agents appointed by the Issuer from time to time in accordance with the Agency

Agreement

Applicable Laws any laws or regulations (including any foreign exchange rules or regulations) of any

governmental or other regulatory authority which may govern the Issue, the Conditions

of the Notes and the Notes issued there under in accordance with which the same are to

be construed

Basis Point or BPS unitthatisequaltoonehundredthofonepercent(1%of1/100)

Business Day a day (other than a Saturday or Sunday or public holiday) when banks in Nairobi are open

for ordinary business

Capital Markets Act Capital Markets Act (Chapter 485A of the Laws of Kenya)

Capital Markets Authority or CMA the Capital Markets Authority set up pursuant to the provisions of Capital Markets Act

Centum Centum Investment Company Limited

Company Centum Investment Company Limited

CD Act Central Depositories Act (Act 4 of 2000)

CDS means the central depository system maintained by the CDSC

CDSC means the Central Depository and Settlement Corporation Limited established under

the CD Act

CDSC Account means an account opened and maintained with a Central Depository in accordance with

the CD Act and the rules and regulations issued thereunder;

CDSC Rules means the operational and procedural rules issued or to be issued by the CDSC with

respect to operation of CDS Accounts and trading in immobilised securities;

Companies Act the Companies Act (Chapter 486 of the Laws of Kenya)

Commencement Date the date upon which the Notes are issued

Conditions the terms and conditions in relation to the Note as set out Trust Deed and Section 7.1 of

this Information Memorandum

Cross-Default any one of the circumstances described in Condition iii(d).

Directors the Directors of the Issuer, whose names appear in Section 4 of this Information

Memorandum.

Due Date inrelationtoanyUnpaidAmount,thedateonwhichthatUnpaidAmountfellduefor

payment (if a scheduled or accelerated payment of interest) or repayment (if a scheduled

or accelerated repayment of principal) by Centum in accordance with the terms of the

Conditions or the Agency Agreement.

Enforcement Notice a notice issued by the Note Trustee to the Issuer pursuant to Section 10 (Terms and

Conditions) Condition 13.2 (Acceleration) declaring all amounts payable under the Notes

to be immediately due and repayable; and demanding that the Issuer immediately repay

the outstanding principal amount of the Notes (together with all accrued interest thereon)

3.1 Definitions

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

12

Subject Definition

Event of Default any one of the circumstances described in Section (Terms and Conditions) Condition 13.1

(Events of Default).

Extraordinary Resolution has the meaning set out in Section 10 (Terms and Conditions) Condition 16 (Meeting of

Noteholders)

Fair Value It is the amount at which the asset could be bought or sold in a current transaction between

willing parties, or transferred to an equivalent party, other than in a liquidation sale

Final Due Amount the amount due and owing from Centum under each of the Notes as determined by the

Agent on or after the Maturity Date

Final Net Asset Value the Net Asset Value, in Kenya Shillings, of Centum as reported in Centum’s Company

Statement of Financial Position as at 31st March 2020, subject to adjustments for

secondary issue of shares during the tenor of the Notes

Fiscal Agent the institution initially appointed by the Issuer pursuant to the conditions of the Agency

Agreement

Holders the Noteholders and/or the Variable Return Holders (as the case may be)

Independent Director a director who:

i. has not been employed by Centum in an executive capacity within the last five years;

ii. is not associated to an adviser or consultant to the Company or a member of

Centum’s senior management or a significant customer or supplier of Centum or

with a not-for-profit entity that receives significant contributions from Centum; or

within the last five years, has not had any business relationship with Centum (other

than service as a director) for which Centum has been required to make disclosure;

iii. has no personal service contract(s) with Centum, or a member of Centum’s senior

management;

iv. is not employed by a public listed company at which an executive officer of Centum

serves as a director;

v. is not a member of the immediate family of any person described above; or

vi. has not had any of the relationships described above with any affiliate of Centum.

Information Memorandum this Information Memorandum dated 14 May 2015

Initial Net Asset Value the Net Asset Value, in Kenya Shillings, of Centum as reported in Centum’s Statement of

Financial Position as at 31 December 2014

Insolvency Event (a) The completion of the winding-up or liquidation of Centum with it ceasing to exist;

or

(b) Any of the following which has the effect of permanently preventing the payment

or repayment by Centum of all of its liabilities under the Notes and the Agency

Agreement:

i. a war, revolution, riot or other similar event in Kenya;

ii. an earthquake, volcanic eruption, tidal wave or other act of God; or,

iii. action taken by the GoK to intervene in the business of Centum

Interest the amount of interest payable in respect of each Principal Amount of the Notes as

determined in accordance with Condition 6 (Interest) of Section 10(Terms and Conditions)

Interest Payment Date the dates which interest is payable as Condition 6 (Interest) of 10 (Terms and Conditions)

Interest Rate means13%fortheSeniorUnsecuredFixedRateNoteand12.5%fortheSeniorUnsecured

Equity Linked Note

Issue the total sums raised from the Notes

Issue and Paying Agent the Fiscal Agent

Issue Price the price at which the Notes are issued by the Issuer (being, at the election of the Issuer, at

par or at a discount to, or premium over their nominal amount as specified)

Issuer Centum Investment Company Limited

Joint Lead Arrangers or Joint Lead

Transaction Advisers

Equity Investment Bank Limited, Dyer & Blair Investment Bank Limited

Kenya The Republic of Kenya and “Kenyan” shall be construed accordingly

Information Memorandum 13

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

Subject Definition

Kes or Shilling Kenya Shillings being the lawful currency of the Republic of Kenya

Late Payment Rate InterestRateplusamarginof2.0%perannum

Liabilities or Liability any loss, damage, cost, charge, claim, demand, expense, judgment, action, proceeding or

other liability whatsoever (including, without limitation, in respect of taxes, duties, levies,

imposts and other charges) and including any value added tax or similar tax charged or

chargeable in respect thereof and legal fees and expenses on a full indemnity basis

Maturity Date 8 June 2020

Month a period from and including a particular day in a calendar month to and excluding the

numerically corresponding day in the next calendar month, except that:

(a) (subject to paragraph (c) below) if the numerically corresponding day is not a

Business Day, that period shall end on the next Business Day in that calendar month

in which that period is to end if there is one, or if there is not, on the immediately

preceding Business Day;

(b) if there is no numerically corresponding day in the calendar month in which that

period is to end, that period shall end on the last Business Day in that calendar

month; and

(c) if an Interest Period begins on the last Business Day of a calendar month, that

Interest Period shall end on the last Business Day in the calendar month in which

that Interest Period is to end

NAV Net Asset Value calculated as total assets of a company less all its liabilities including loan capital and preference shares, divided by the number of outstanding shares.

NAVUpside difference between the Initial Net Asset Value and the Final Net Asset Value

Note Documents the Trust Deed and the Agency Agreement

Note Issue means the issue by the Company of medium term notes denominated in Kenya Shillings in an aggregate amount of up to Kenya Shillings six billion (Kes.6,000,000,000).

Note Trustee the person appointed to act as such in relation to the Note in pursuant to the Agency Agreement

Noteholder a person in whose name a Note is registered in the relevant Register as at the relevant date or, in the case of joint holders, the first-named thereof

Notes KenyaShillingssixbillion(Kes.6,000,000,000)13%SeniorUnsecuredFixedRateNotesand12.5%SeniorUnsecuredEquityLinkedNotesissuedpursuanttothis InformationMemorandum and the Agency Agreement.

Principal Amount the nominal amount of each Note credited in the CDSC Account in respect of that Note

Public Offer Regulations Capital Markets (Securities) (Public Offers, Listing and Disclosures) Regulations, 2002

Record Date in the case of payments of Interest or Principal, 1700 hrs Nairobi time 15 calendar days before the relevant date for payment or such other date as may be agreed between the Trustee (on behalf of the Noteholders), Centum and the relevant Agents

Redemption Price Payment at the Maturity Date for the ELN

Register means the respective official records of Noteholders and the Variable Return Holders in the CDS as maintained by the CDSC pursuant to section 25 of the CD Act;

Registrar the person appointed by the Issuer or acting as registrar pursuant to the Conditions and the Agency Agreement

Repay, Redeem and Pay shall each include both the others and cognate expressions shall be construed accordingly

Security a mortgage, charge, pledge, lien or other security interest securing any obligation of any person or any other agreement or arrangement having a similar effect

Senior Unsecured Equity Linked

Note

a Note which is issued pursuant to the Agency Agreement and this Information Memorandum whose return comprises Interest and a variable return based on the NAV UpsideasprovidedinCondition7(Computation of Variable Return) of Section 10 (Terms and Conditions)

SeniorUnsecuredFixedRateNote a Note which is issued pursuant to the Agency Agreement and this Information Memorandum whose return comprises of Interest to be calculated and paid on a fixed rate basis

Shareholder Funds a firm's total assets minus its total liabilities

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

14

Subject Definition

Specified Office in relation to any Note Agent, either the office identified with its name in the Conditions or any other office notified to any relevant parties pursuant to the Agents agreement with the Issuer

Strategy Period Either of Centum’s strategy periods between years 2009-2014 and 2014-2019

Subsidiary in respect of any person, company or corporation, any other person, company or corporation who is controlled, directly or indirectly, by the first-mentioned person, company or corporation or more than half the issued share capital of which is beneficially owned, directly or indirectly, by the first-mentioned person, company or corporation. or which is a subsidiary of another subsidiary of the first-mentioned person, company or corporation and, for these purposes, a company or corporation shall be treated as being controlled by another person, company or corporation if that other company or corporation is able to direct its affairs and/or to control the composition of its board of directors or equivalent body

Successor in relation to the Agents, such other or further person, as may from time to time be appointed as an Agent

Tax any tax, levy, impost, duty or other charge or withholding of a similar nature (including any penalty or interest payable in connection with any failure to pay or any delay in paying any of the same)

Total Assets Centum’s portfolio of investments

Trust Deed the trust deed dated 14 May 2015 between Issuer and Ropat Trust Company Limited in relation to the Notes

UnpaidAmount that part of:(a) a scheduled payment of Interest under the Notes; or(b) a scheduled repayment of Principal under the Notes; or(c) a scheduled repayment of the Variable Return; or(d) any repayment of Principal by way of early redemption; or(e) the outstanding Principal Amount of the Notes (together with all interest thereon)

or outstanding Variable Return following delivery of an Enforcement Notice in accordance with the Agency Agreement, which, in each case, is not paid by Centum to the Fiscal Agent in accordance with the Agency Agreement by the applicable Due Date

US$orUSDorDollarsor$ UnitedStatesofAmericadollarsbeingthelawfulcurrencyoftheUnitedStatesofAmerica

Variable Return the variable return in relation to the equity linked component of the ELN as provided in Condition 7(Computation of Variable Return) of Section 10 (Terms and Conditions)

Variable Return Holder a person in whose name a Variable Return is registered in the relevant Register as at the relevant date or, in the case of joint holders, the first-named thereof

Written Resolution a resolution in writing signed by or on behalf of holders of Notes who for the time being are entitled to receive notice of a meeting in accordance with the provisions of the Trust Deed and who together hold not less than three-quarters in value of the principal amount of the Notes then outstanding whether contained in one document or several documents in like form, each signed by or on behalf of one

Information Memorandum 15

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

Subject Definition

AUM AssetsUnderManagementwhichincludetotalassetsandthirdpartyfunds

BA Bachelors of Arts

Bcom Bachelors of Commerce

BSc Bachelors of Science

Bn or bn Billion

CAIA Chartered Alternative Investment Analyst

CAGR Compounded Annual Growth Rate

CBK Central Bank of Kenya

CFA Chartered financial Analyst

CIMA Chartered Institute of Public Finance and Accountancy

CMA Capital Markets Authority

CDS Central Depository System

CFA Chartered Financial Analyst

COD Commercial Operating Date

CPA (K) Certified Public Accountant of Kenya

CPS (K) Certified Public Secretary of Kenya

CIMA Chartered Institute of Management Accountants

EFT Electronic Funds Transfer

ELN SeniorUnsecuredEquityLinkedNote

FCCA Fellow of the Association of Chartered Certified Accountants

FMCG Fast moving consumer goods

FISM Fixed Income Securities Market Segment

FRN SeniorUnsecuredFixedRateNote

FTE Full time employee

GDP Gross Domestic Product

GoK Government of Kenya

ICDC Industrial Commercial Development Corporation

ICT Information and communications technology

IFRS international accounting standards within the meaning of the IAS Regulations 1606/2002

ICPAK Institute of Certified Public Accountants of Kenya

IMF International Monetary Fund

IRR Internal Rate of Return

JSD Doctor of Juridical Science

KenGen Kenya Electric Generating Company Limited

Km Kilometre

KPLC Kenya Power and Lighting Company Limited

LLB Bachelor of Laws

LLM Master of Laws

MA Master of Arts

MBA Master Business Administration

Mn Million

MW Megawatts

NAV Net Asset Value calculated as total assets of a company less all its liabilities including loan

capital and preference shares, divided by the number of outstanding shares.

3.2 Abbreviations

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

16

Subject Definition

NAVUpside difference between the Initial Net Asset Value and the Final Net Asset Value

NSE Nairobi Securities Exchange Limited

PE Private Equity

PPP Public Private Partnership

PS Permanent Secretary

PhD Doctor of Philosophy

QPE Quoted Private Equity

RE&I Real Estate and Infrastructure

REIT Real Estate Investment Trust

RTGS Real Time Gross Settlement

sq ft Square feet

SQM or sq m Square metres

SSA Sub Sahara Africa

USA UnitedStatesofAmerica

USE UgandanSecuritiesExchangeLimited

Information Memorandum 17

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

4. SUMMARY OF CORPORATE INFORMATION

Name of Issuer: Centum Investment Company Limited

Registration Number C8/67

Registered Office and Head Office International House

Mama Ngina Street

P. O. Box 10518 – 00100

Nairobi, Kenya

Tel: +254 (20) 2286000

Fax: +254 (20) 2223223

Mobile: +254 722 205339

Contact Persons James Mworia

Group Chief Executive Officer

Email: [email protected]

Risper Mukoto

Managing Director; Centum Business Solutions Limited

Email: [email protected]

Fred Murimi

Corporate Affairs Director & Company Secretary

Email: [email protected]

BOARD OF DIRECTORS OF THE COMPANY

Name Position Address

James Muguiyi Chairman

Non Executive Director

P.O. Box 10518, 00100 Nairobi, Kenya

Dr. James McFie Deputy Chairman

Independent Director

P.O. Box 10518, 00100 Nairobi, Kenya

James Mworia Chief Executive Officer

Executive Director

P.O. Box 10518, 00100 Nairobi, Kenya

Christopher Kirubi Non Executive Director P.O. Box 10518, 00100 Nairobi, Kenya

Peter Kimurwa Non Executive Director

(Alternate Director representing ICDC)

P.O. Box 10518, 00100 Nairobi, Kenya

Laila Macharia Independent Director P.O. Box 10518, 00100 Nairobi, Kenya

Margaret Byama Non Executive Director

(Alternate Director representing the PS Ministry of EA

Affairs, Commerce & Tourism)

P.O. Box 10518, 00100 Nairobi, Kenya

Imtiaz Khan Independent Director P.O. Box 10518, 00100 Nairobi, Kenya

Henry Njoroge Independent Director P.O. Box 10518, 00100 Nairobi, Kenya

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

18

OTHER CORPORATE INFORMATION

Secretary Fred Murimi

Company Secretary/ Corporate Affairs Director

International House

Mama Ngina Street

P.O. Box 10518-00100

Nairobi, Kenya

Legal Advisers Coulson Harney

5th Floor, ICEA Lion Centre

West Wing

Riverside Park

Chiromo Road

P.O. Box 10643-00100

Nairobi, Kenya

Auditor PricewaterhouseCoopers

PwC Tower

Waiyaki Way/Chiromo Road

Westlands

P. O. Box 43963-00100

Nairobi, Kenya

Registrars Custody and Registrars Services Limited

6th Floor, Bruce House

Standard Street

P.O. Box 8484-00100

Nairobi, Kenya

Bankers Co-operative Bank of Kenya Limited

Co-operative Bank House

Haile Selassie Avenue

P.O. Box 48231–00100

Nairobi, Kenya

Commercial Bank of Africa Limited

International House

Mama Ngina Street

P.O. Box 30437–00100

Nairobi, Kenya

Information Memorandum 19

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

Equity Investment Bank Limited

6th Floor, Equity Centre

Hospital Road

Upperhill.

P.O. Box 75104-00200

Nairobi, Kenya

Tel:+254 719 056 501

Fax: 020-2737276

Contact Person: Irungu Nyakera

Email: [email protected]

Dyer & Blair Investment Bank Limited

10th Floor, Pension Towers

Loita Street

P.O. Box 45396-00100

Nairobi, Kenya

Tel:+254 20 3240104

Fax: 020 3240 114

Contact Person: Paul M. Nyaga

Email: [email protected]

Equity Investment Bank Limited

6th Floor, Equity Centre

Hospital Road

Upperhill.

P.O. Box 75104-00200

Nairobi, Kenya

Tel:+254 719 056 501

Fax: 020-2737276

Contact Person: Irungu Nyakera

Email: [email protected]

Dyer & Blair Investment Bank Limited

10th Floor, Pension Towers

Loita Street

P.O. Box 45396-00100

Nairobi, Kenya

Tel:+254 20 3240104

Fax: 020 3240 114

Contact Person: Paul M. Nyaga

Email: [email protected]

K-Rep Bank Limited

K-Rep Center

Wood Avenue,

Kilimani

P.O. Box 25363-00603 Nairobi, Nairobi

Tel: : +254 20 3906000/1-7

Contact Person: Judy Githae

Email: [email protected]

Co-operative Bank of Kenya Limited

Co-operative House

Haile Selassie

P.O. Box 48231 - 00100

Nairobi, Kenya

Tel: +254 20 3276000

Fax : +254 20 219831

Contact Person: Jacqualine Waithaka

Email: [email protected]

PricewaterhouseCoopers Limited

PwC Tower

Waiyaki Way/Chiromo Road

Westlands

P. O. Box 43963-00100

Nairobi, Kenya

Tel: +254 20 2855525

Fax: +254 20 2855001

Contact: Richard Njoroge

Email: [email protected]

Coulson Harney

5th Floor, ICEA Lion Centre, West Wing

Riverside Park

Chiromo Road

P.O. Box 10643-00100

Nairobi, Kenya

Tel: +254 20 289 9000

Fax: +254 20 2899100

Contact: Kamami Christine Mweti

Email: [email protected]

5. ADVISERS TO THE ISSUER ON THE NOTE ISSUE

Placing Agents and Joint Sponsoring Stock-brokers

Receiving Banks

Reporting Accountant Legal Adviser

Joint Lead Transaction Advisers

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

20

Custody and Registrars Services Limited

6th Floor, Bruce House

Standard Street

P.O. Box 8484-00100

Nairobi, Kenya

Tel : +254 20 2230518

Fax: +254 20 2211773

Contact Person: Kerry-Anne Makatiani

Email: [email protected]

Ropat Trust Company Limited

Kenya Re Towers, off Ragati Road

P.O. Box 1243, 00100

Nairobi, Kenya

Tel: +254 20 2723322

Fax: +254 20 2723474

Contact Person: Patrick Gacheru

Email: [email protected]

Fiscal Agent and Registrar Note Trustee

Information Memorandum 21

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

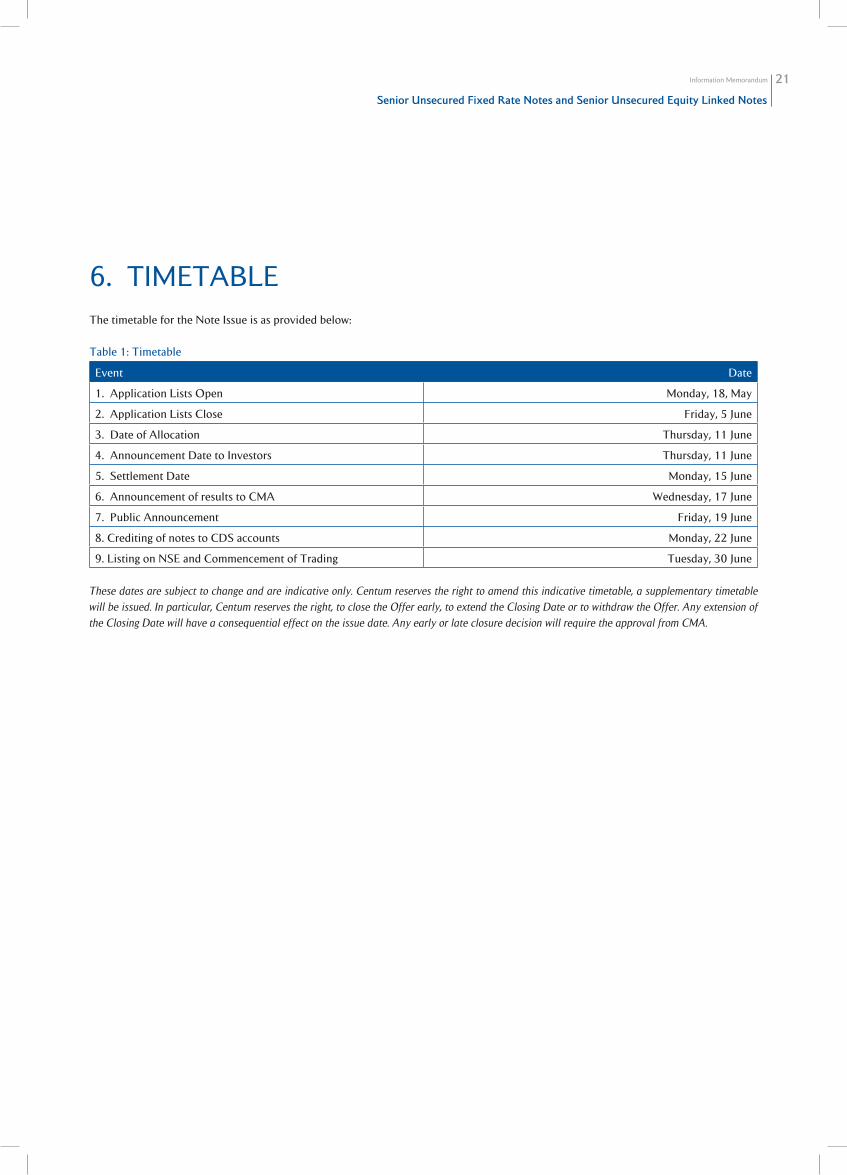

6. TIMETABLEThe timetable for the Note Issue is as provided below:

Table 1: Timetable

Event Date

1. Application Lists Open Monday, 18, May

2. Application Lists Close Friday, 5 June

3. Date of Allocation Thursday, 11 June

4. Announcement Date to Investors Thursday, 11 June

5. Settlement Date Monday, 15 June

6. Announcement of results to CMA Wednesday, 17 June

7. Public Announcement Friday, 19 June

8. Crediting of notes to CDS accounts Monday, 22 June

9. Listing on NSE and Commencement of Trading Tuesday, 30 June

These dates are subject to change and are indicative only. Centum reserves the right to amend this indicative timetable, a supplementary timetable

will be issued. In particular, Centum reserves the right, to close the Offer early, to extend the Closing Date or to withdraw the Offer. Any extension of

the Closing Date will have a consequential effect on the issue date. Any early or late closure decision will require the approval from CMA.

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

22

7. SUMMARY OF THE OFFER

7.1 Summary of the Proposed Notes

The following summary does not purport to be complete and is taken from, and is qualified in its entirety by, the remainder of this

Information Memorandum. Words and expressions defined in “Description of the Notes” below shall have the same meanings in this

summary of the offering.

Table 2: Summary of the Note

1. Issuer Centum Investment Company Limited.

2. Joint Lead Transaction Advisers Dyer & Blair Investment Bank Limited

Equity Investment Bank Limited

3. Joint Sponsoring Stock Brokers

and Placing Agents

Dyer & Blair Investment Bank Limited

Equity Investment Bank Limited

4. Registrar/Fiscal Agent Custody and Registrars Services Limited

5. Note Trustee Ropat Trust Company Limited

6. Legal Adviser Coulson Harney

7. Reporting Accountant PricewaterhouseCoopers

8. Receiving Banks Co-operative Bank of Kenya Limited

K-Rep Bank Limited

9. Issue Description Up toKenyaShillings sixbillion (Kes.6,000,000,000) comprisingSeniorUnsecuredFixed

Rate Notes and Senior Unsecured Equity Linked Notes both due 8 June 2020 and the

subsequent listing of the Notes on the FISM of the NSE.

TheSeniorUnsecuredFixedRateNotesareissuedwithafixedinterestrateof13%.

TheSeniorUnsecuredEquityLinkedNotesaremadeupoftwocomponents:

a) afixedratebondof12.5%(the“12.5%Coupon”);and

b) an equity linked component (the “Variable Return”), the value of which will be determined

by the growth of the Issuer’s NAV upto a maximum of twenty five per cent (25%)

appreciationoftheInitialNAVandwhichwillearnthecouponholdersuptoten(10%)

ofthePrincipalAmountifthemaximumtwentyfivepercent(25%)NAVappreciationis

achieved.

The Variable Return will be issued and traded as units. It will be issued in the ratio of 1:1 with

respect to the Equity Linked Notes.

The Variable Return will be detachable and transferable at the option of the Noteholder in

accordance with the Conditions.

The Variable Return does not constitute a Note and its holder shall therefore not be deemed

to be a Noteholder by mere holding of the Variable Return.

10. Issuance in Series TheIssuerwillissueSeniorUnsecuredFixedRateNotesinoneseriesandSeniorUnsecured

Equity Linked Notes in another series. Within each series, the Issuer may issue Notes subject

to terms identical to those series Notes.

11. StatusofSeniorUnsecured

Fixed Rate Notes

TheSeniorUnsecuredFixedRateNotesconstituteSenior,unsubordinated,unsecuredand

unconditional obligations of the Issuer ranking paripassu among themselves and with all its

other present and future unsecured obligations (other than any secured debt obligations and

those preferred by mandatory provisions of law).

Information Memorandum 23

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

12. StatusofSeniorUnsecured

Equity Linked Notes

The SeniorUnsecured Equity LinkedNotes constitute Senior unsubordinated, unsecured,

direct, and unconditional obligations of the Issuer ranking paripassu among themselves and

with all its other present and future unsecured obligations (other than any secured debt

obligations and those preferred by mandatory provisions of law).

13. Allotment of Notes A maximum of Kes 6,000,000,000 (six billion, Kenya Shillings) in Notes will be made

available for subscription.

The Issuer and the Joint Lead Arrangers will determine the allotment of Notes at their sole

discretion. Of particular note however is that FRN applications will be given preference over

ELN applications.

Centum reserves the right, whether the Issue is over-subscribed or not, to reject any

application in whole or in part and may therefore allot less than the amount applied for.

In the event that the total number of Notes subscribed for by applicants is equal to or less

than the Issue Amount, all subscriptions will be allocated in full as per the number of Notes

applied for by applicants.

Successful applicants will be notified by the Placing Agent of the amount allotted to them no

later than the date and time specified in Section 6 (Timetable).

14. Currency The Notes will be denominated in Kenya Shillings (“Kes”).

15. Issue Price The Notes will be issued on a fully paid basis at par.

16. Tenor Five years.

17. Purpose The proceeds of the Notes will be used for investments in the following sectors:

• Financialservices;

• Energy;

• RealEstate.

18. SeniorUnsecuredNotesFixed

Interest Rate

13.0%perannumpayablesemi-annuallyinarrearson100%ofeachspecifieddenomination

of the principal amount.

19. SeniorUnsecuredEquity

Linked Notes Fixed Interest

Rate

12.5%perannumpayablesemi-annuallyinarrearson100%ofeachspecifieddenomination

of principal amount.

20. Late Payment Interest Rate Theinterestrateplus2%perannum.

21. Cross Default Cross-default: any present or future indebtedness of Centum in connection with

moneys borrowed or raised exceeding in aggregate Kenya Shillings five hundred million

(Kes.500,000,000/=) (or its equivalent):

i) Is not satisfied when due, or at the end of any originally applicable grace period; or

ii) Becomes prematurely payable following delivery of an Enforcement Notice by the Note

Trustee to Centum, as the case may be, as a result of a default by Centum except to

the extent in any instance that the existence or enforceability of the relevant obligation

is being disputed in good faith by it by appropriate proceedings; or

iii) Any encumbrance over any assets of Centum or any Subsidiary of Centum becomes

enforceable.

22. Interest Payment Frequency Semi-annually in arrears.

23. Day Count Fraction Actual/364

24. Interest Commencement Date The Interest payment commencement date shall be six (6) months after the Settlement Date

25. Interest Periods Each period commencing on (and including) an interest payment date (or the interest

commencement date) and ending on (but excluding) the next, or first, interest payment date

(as the case may be).

26. Minimum success level 50%oftheaggregateissueamountfortheIssue

27. Final Maturity • ThefinalmaturityoftheSeniorUnsecuredFixedRateNoteswillbefive(5)yearsafter

the Settlement Date

• ThefinalmaturityoftheEquityLinkedNoteswillbefive(5)yearsaftertheSettlement

Date

Information Memorandum

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

24

28. Redemption and Purchase Condition 9 (Redemption and purchase).

Redemption at Maturity

Unlesspreviouslyredeemedorpurchasedandcancelledasspecifiedbelow,eachNotewill

be redeemed by the Issuer at its Final Due Amount on the Maturity Date.

Redemption at the option of the Issuer

The Issuer may upon giving not less than thirty (30) and not more than sixty (60) days’

prior notice in writing to the Noteholders and the Trustee in accordance with condition 15

(Notices)toredeemallorsomeoftheSeniorUnsecuredFixedRateNotesoutstanding;

The Early Redemption Notice shall specify the date on which the redemptions is to be

effected which date shall be an Interest Repayment or Principal Repayment Day; then and

upon expiration of such notice, the Issuer shall redeem such Notes.

IftheIssuerredeemsonlysomeoftheSeniorUnsecuredFixedRateNotes,thepartial

redemption shall be of an aggregate principal amount of not less than Kenya Shillings one

billion (Kes 1,000,000,000) and integral multiple of Kenya Shillings one hundred million

(Kes 100,000,000).

SeniorUnsecuredFixedRateNotesmayonlyberedeemedafterthethirdanniversaryof

theirissuanceandatapremiumof1%(onepercent).

SeniorUnsecuredEquityLinkedNoteswillbeeligibleforearlyredemption,inwhich

case the Final NAV will be calculated based on the Issuer’s latest publicly issued financial

statements, being either half year accounts or full year accounts as the case may be.

Purchases

The Issuer may at any time purchase Notes at any price in the open market or otherwise,

subject to any approvals required from the CMA or the NSE or to any other restrictions

under applicable law. In the event of the Issuer purchasing Notes, such Notes may be held

or resold, or at the discretion of the Issuer, cancelled. All Notes which are redeemed or

purchased by or on behalf of the Issuer may be cancelled by giving notice to that effect to the

Registrar, the Fiscal Agent and the CDSC

29. Form of the Notes The Notes will be registered in the CDS Account of each Noteholder held with the CDSC in

accordance with the CD Act.

30. Denomination of the Notes The Notes will be issued in denominations of Kes 100,000 and integral multiples of Kes

100,000 in excess thereof, subject to a minimum subscription amount of Kes 1,000,000.

31. Security The Notes shall be unsecured.

32. Payment All amounts payable by the Issuer in respect of each Note or Variable Return (as the case

may be) shall be paid by EFT or RTGS transferred to the account of the Holder as set forth in

the relevant Register maintained by the Registrar, made available to the Holders or a person

nominated by the Holder and sent to the registered address of the Holder or such person.

33. Compliance The placement and transfer of the Notes shall comply with the following:

• therequirementsoftheCompaniesActwithrespecttoissuanceandsubscription;

• therequirementsoftheCMAwithrespecttoissuanceandsubscription;

• therequirementsoftheCMAandNSEwithrespecttothelistingoftheNotesonthe

NSE;

• theCMAandNSEreportingrequirementsfromtimetotime;and

• anyotherapplicableprovisionsofthelawinKenyarelatingtocompaniesanddebt

capital markets that is in existence or that may be passed before the issue of the Notes

or during the pendency of the issue of the Notes.

Information Memorandum 25

Senior Unsecured Fixed Rate Notes and Senior Unsecured Equity Linked Notes

34. Events of default Condition 13 (Events of Default)

Other than as a result of a Force Majeure Event, each of the events set out below is an Event

of Default:

(a) Non-payment: Centum fails to pay any amount due in respect of all the Notes or some

of the Notes or the Variable Return on the Due Date for payment and such default

continues for a period of seven (7) Business Days unless;

(i) the failure to pay is caused by administrative or technical error;

(ii) payment is made within three (3) Business Days thereafter; or

(iii) the failure to pay is in order to comply with any Applicable Laws or order of any

court of competent jurisdiction or in case of doubt as to the validity or applicability

of any such law, regulation or order, in accordance with advice as to such validity

or acceptability given at any time during such period by independent advisers

acceptable to the Fiscal Agent; or

(b) Breach of other obligations: Centum defaults in the performance or observance of any

of its other covenants and obligations under the Note Documents and (except where

such default is incapable of remedy) such default continues for a period of thirty (30)

Business Days following service of a notice by the Note Trustee requiring the same to

be remedied; or

(c) Misrepresentation: any representation, warranty or statement made or repeated in, or

in connection with the Agency Agreement or in any accounts, certificate, statement,

opinion or the Information Memorandum delivered by or on behalf of Centum or in

connection with the Notes or the Note Documents is incorrect to a material extent

when made or deemed to be repeated; or

(d) Cross-default: any present or future indebtedness of Centum in connection with

moneys borrowed or raised exceeding in aggregate Kenya Shillings five hundred million

(Kes.500,000,000/=) (or its equivalent):

(i) is not satisfied when due, or at the end of any originally applicable grace period; or

(ii) becomes prematurely payable following delivery of an Enforcement Notice by the

Note Trustee to Centum, as the case may be, as a result of a default by Centum

except to the extent in any instance that the existence or enforceability of the

relevant obligation is being disputed in good faith by it by appropriate proceedings;

or

(iii) any encumbrance over any assets of Centum or any Subsidiary of Centum

becomes enforceable; or

(e) Insolvency: an Insolvency Event occurs in respect of Centum; or

(f) Winding up: a petition is presented or an application is made (which is not challenged

by Centum within thirty (30) days of such petition or application) in respect of or any

order is made or a resolution is passed for or any notice is issued to convene a meeting

for the purpose of passing such resolution for the winding up or dissolution of Centum;

or

(g) Compositions: Centum stops payment or becomes unable to pay its debts within the

meaning of Section 220 of the Companies Act or any steps are taken with a view to

proposing, under any enactment or otherwise, any kind of composition, scheme of

arrangement, compromise or arrangement involving Centum and its creditors generally,