Indirect Taxes — Looking Back and Looking Ahead - assets ...

39

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Indirect Taxes — Looking Back and Looking Ahead - assets ...

2© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Lachlan WolfersGlobal Head of Indirect Taxes

KPMG International

P: +852 2685 7791

Lennert JanssenSenior Manager

KPMG in China

P: +852 2847 5084

3© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

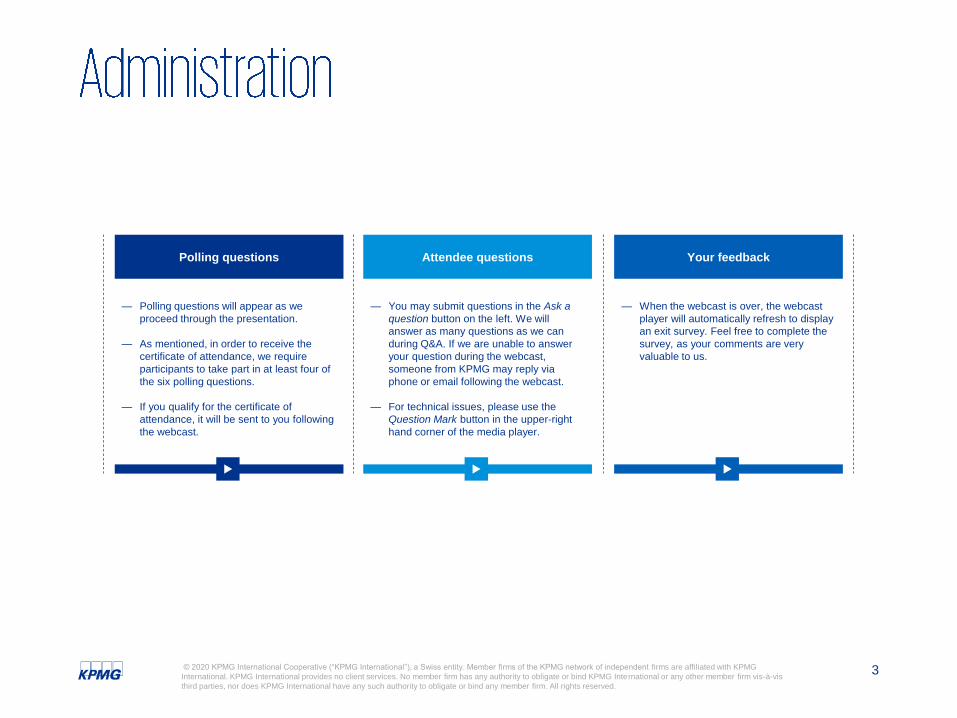

Polling questions Your feedbackAttendee questions

— When the webcast is over, the webcast

player will automatically refresh to display

an exit survey. Feel free to complete the

survey, as your comments are very

valuable to us.

— You may submit questions in the Ask a

question button on the left. We will

answer as many questions as we can

during Q&A. If we are unable to answer

your question during the webcast,

someone from KPMG may reply via

phone or email following the webcast.

— For technical issues, please use the

Question Mark button in the upper-right

hand corner of the media player.

— Polling questions will appear as we

proceed through the presentation.

— As mentioned, in order to receive the

certificate of attendance, we require

participants to take part in at least four of

the six polling questions.

— If you qualify for the certificate of

attendance, it will be sent to you following

the webcast.

4© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

4© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

AgendaLooking back 5 years ago

Looking ahead 5 years

Questions

6© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Indirect tax will be charged at the place of

consumption

2013–2014–2015

There will be a Customs Duty regime for

services

XXX

7© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Every country has a VAT regime

2020

Proliferation of new and old indirect taxes that

you will own

XXX

8© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Indirect tax rates accelerate dramatically

2020

We know where you are! “Use and Enjoyment”

provisions are here to stay!

12 MONTHS

9© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

From paper to dataNo more periodic returns — tax will be settled

in real-time

10© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Big data will close the VAT gapThe tax transparency debate will shift to

indirect taxes

11© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Data quality and analysis will be the new audit

battlegroundYou won’t control all your own data anymore

12© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Your data will become very interesting to othersIndirect tax legislation will be written with data

analytics in mind

13© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

You will be redundant by 2020!

15© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Consumption taxes will

dominate

Growth of government

regulated invoicing

systems

VAT refunds will

largely end

VAT will be applied to

financial services

VAT returns will die

Tax professionals to be

transformed

VAT will more closely

resemble sales tax

Tax professionals

disintermediated by tax

authorities

Simplifications will reduce

the risk of fraud

VAT compliance =

technology outsourcing

16© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

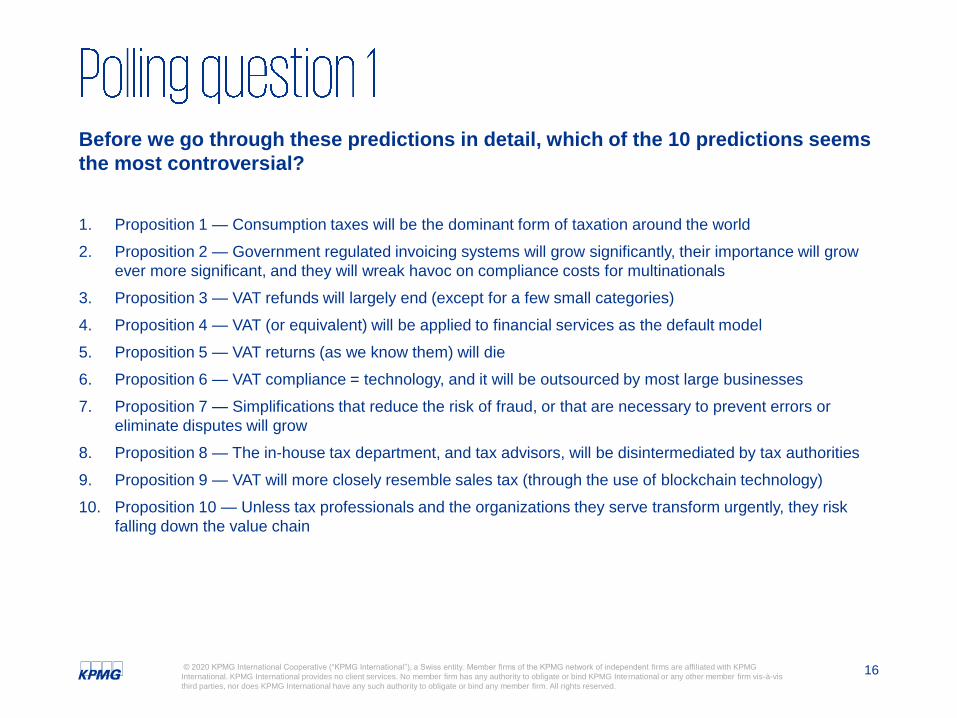

Before we go through these predictions in detail, which of the 10 predictions seems

the most controversial?

1. Proposition 1 — Consumption taxes will be the dominant form of taxation around the world

2. Proposition 2 — Government regulated invoicing systems will grow significantly, their importance will grow

ever more significant, and they will wreak havoc on compliance costs for multinationals

3. Proposition 3 — VAT refunds will largely end (except for a few small categories)

4. Proposition 4 — VAT (or equivalent) will be applied to financial services as the default model

5. Proposition 5 — VAT returns (as we know them) will die

6. Proposition 6 — VAT compliance = technology, and it will be outsourced by most large businesses

7. Proposition 7 — Simplifications that reduce the risk of fraud, or that are necessary to prevent errors or

eliminate disputes will grow

8. Proposition 8 — The in-house tax department, and tax advisors, will be disintermediated by tax authorities

9. Proposition 9 — VAT will more closely resemble sales tax (through the use of blockchain technology)

10. Proposition 10 — Unless tax professionals and the organizations they serve transform urgently, they risk

falling down the value chain

17© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Corporate and

personal taxes

Consumption-

based Taxes

Total Tax Revenue

Tax in place of value creation, or place of

consumption?

Which has greater alignment with business interests?

Digital services taxes

Increase in environmentally oriented

consumption-based taxes

1977 1978 1979 1980 2017 2018 2019 2020+

1977Adoption of VAT

by 25 countries

2018Corporate tax

rate of 26.5%

2019Adoption of VAT

by 168 countries

1980Corporate tax

rate of 46.6%

18© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Increase in compliance costs for multinational companies

— Slightly different forms, unique software & hardware requirements in

different countries

— Benefits of centralization of compliance will be lost

— Need for business to use interface solutions with their own ERP

solutions

— Duplication of invoices, ring-fencing, reconciliation

Currently variations of same

theme adopted in China,

Brazil, Taiwan, Indonesia,

Korea, India, Vietnam,

Portugal (amongst others)

Real time reporting

— Government gets transaction

level data on a real time basis

— Carries out D&A or

reconciliation with VAT return

information

Regulated invoicing systems

— Government interposed in the

invoicing process

— The system is used to

determine the VAT liability

Machine to

machine invoicing?

19© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Tax authorities TaxpayerVAT Refunds

Recent developments in VAT refunds

— Carousel and missing trader fraud — increased scrutiny and time required to process refunds from tax authorities

— Tax authorities increasingly imposing tax audits as a precondition to refunds

— Or refunds set-off against other tax obligations before being paid

— Disallowing VAT refunds to foreign businesses unless the principle of reciprocity is followed

— Tourist VAT refund schemes seem to be diminishing

— Countries expanding scope of zero rating reduces need for foreign businesses to claim refunds (Russia, Indonesia, Cambodia, China)

Businesses are increasingly reluctant to claim VAT refunds by amending prior returns

Countries such as France,

Italy, Costa Rica reducing need

for refunds for exporters &

zero-rated suppliers?

Limitations on refunds?

E.g. time periods

20© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

The starting point

Only specific services are exempt.

Broadly where there is:

— a change in legal/financial situation between

parties (payments, securities transactions, credit

card processing etc.);

— operation of a bank account; or

— financial intermediation.

Then the services may qualify for VAT exemption.

Is the service exempt?

Next stage is to drill down into the detail.

It is critical to really understand what the

service is and what it does.

For example: SDC, Bookit, DPAS and Card

Point.

Does it include the provision of taxable or

exempt elements?

What does the customer really want?

Is any element ancillary or a better means

of enjoying another element?

Tax authority challenges

Tax Authorities focus on restrictive

interpretation and seek to restrict

exemption by looking at the technical detail

of what/how the services are supplied

(Nordea).

They also seek to “taint” exempt elements

in bundled supplies (single vs multiple

supply).

For example: technology build services

swamping exempt functionality.

In particular, project management, IT build

and licensing.

Nature of the services

The legal and commercial/economic

realities need to be aligned and it is critical

not to mischaracterize what is actually

being done.

For example: the difference between IT

build/licensing vs. providing exempt

functionality.

21© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Key issues impacting on VAT exemption

Terms of contracts

Contractual recitals and details of the services will be critical.

Reality

Marketing materials and the way the services are positioned publically will be relevant.

Commercial documents

Exchange(s) of correspondence internally and between parties.

Fee structures

Clarity of fees structures which may give indication to HMRC of tax treatment.

Global contracts

May give rise to place of supply issues or use and enjoyment issues, depending on

detail and structure.

Billing arrangements

VAT and wider tax impact of Hub vs Regional vs Country-to-country billing to be considered.

22© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Past/current

Same service

Withdraw

from ATM

Credit card surcharge,

or payment

processing fee

Future

VAT will be applied to FS with 3 major

exceptions:

Personal loan products

Trading of derivatives and

other financial instruments

Where substitutes for VAT

are in place (e.g IPT (EU),

Education Tax (Korea), SBT

(Thailand)

Source: The Guardian, 18 June 2019

23© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Do you believe that VAT will be applied to most financial services by 2025 in your

jurisdiction?

A) Yes

B) No

24© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

India

Brazil

Europe

Inevitable consequence of several factors

Electronic invoicing through government regulated

invoicing systems

The need to carry out data matching or verification of

purchase invoicing through government regulated

invoicing systems

Real-time reporting of transaction level data (e.g.

Spain, Hungary, SAF-T)

Short and medium term

— VAT returns will be pre-filled for taxpayers (e.g. India)

— Reconciliation exercise to check the accuracy of the

returns, and to perform adjustments required

Long term

— The actual filing of VAT returns to be rendered

completely redundant — blockchain technology & POS

collection

25© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Challenges facing in-house tax departments

— Data management problems

— Unable to fully comply with tax laws because of

system limitations

Deploy technology tools

Tax compliance will be outsourced by most

large businesses

— Comes down to simple economics

— Requires significant up-front investment cost if

built by the organization for their own needs

The use of

multiple systems

Reconciling the

data/making manual

adjustments

Extracting data from

multiple systems

The continuation of

historical practices

Data

management

problems

26© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

27© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Motor vehicle usage

costs

Mobile phone costs

for employees for

business use

Meal costs and

entertainment-related

costs for employees

Digitalization — impact

of systematized

processes

Judgment and

resources to verify the

correctness of these

credit claims

Deny credits outright

OR

Provide an

automatically

determined credit

amount or

percentage

Applicable to partial exemption/

apportionment such as in financial

services? (e.g Singapore)

Are current approaches or

methodologies for calculating input tax

credits relevant in an era of

digitalization?

28© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Deal electronically with business

— Publish extensive information to

help businesses comply — self-

help

— Chatbots and similar programs can

provide 24/7 support

Tax authority dealing directly with

business

1

Data flowing directly

— Government regulated invoicing or

real time reporting allow

government to obtain transaction

level data automatically

— Data and analytics testing

Tax authority having the data

2

Use of tax authority technology

— Government can mandate use of

technology tools by all taxpayers

— Technology tools generally

enhance compliance

— ROI need only be $1

Tax authority controls your

systems

3

Development in tax authorities’ practices

29© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Extract from the Explanatory Memorandum to Australia’s GST Act

21st century taxation system?

Sells timber for $220

(including $20 GST)

Buys timber for $220

Makes and sells table

for $440

(including $40 GST)

Buys table for $440

Sells table for $550

(including $50 GST)

Buys table for $550

Commissioner

Timber merchantFurniture

manufacturerFurniture retailer Consumer

$20 GST

$20 input tax

credit

$40 GST

$40 input tax

credit

$50 GST

30© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Is multiplicity of obligations in VAT systems still able to prevent fraud and ensure VAT is

properly accounted for?

— Imposing collection

obligations on online

platforms (e.g. Australia

& post-Wayfair)

— Overcomes fundamental

limitations in traditional

VAT collection methods

for non-resident

— Use of intermediaries as

principal in accounting

for VAT

— Application to domestic

transactions?

— Critics failed to take into

account the impact of

technology

developments — create

greater security and

validity in the transaction

lifecycle

— B2B highly publicized

fraud examples —

precious metals, trading

of carbon permits

Special rules or exceptions

are increasingly being used

to combat fraud

Examples:

— Domestic reverse

charge

— VAT withholding on

property (Australia)

— B2B zero rated land

supplies (New Zealand)

— B2B transactions —

supplier not to remit and

recipient not to claim —

digital certification

— B2C — fundamentally

transforms the VAT

collection process with

greater transparency

and security

— Connect taxpayers, tax

authorities,

intermediaries and even

banks

Growth of e-commerce

platforms

Michael Gove proposal —

replace UK’s VAT with sales

tax system

Special rules to combat

fraud

Use of blockchain or

distributed ledger

technology

31© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Do you believe that VAT will resemble a retail sales tax by 2030 in your jurisdiction?

A) Yes

B) No

32© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

We can’t get the data

The quality of our data is poor

Inordinate amount of time scrubbing and

reconciling data

Significant manual adjustments — all done in

Excel

Data is spread across multiple systems,

which do not speak to each other

The tax authorities believe we have the data

at the ready, in the form in which they want it

Current data problems Future Transformation

Easier to teach a tax professional about IT,

or to teach an IT professional about Tax?

33© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

In your experience, is it easier to:

A) Teach a Tax professional about IT

B) Teach a IT professional about Tax

34© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

What other prediction(s) have we missed?

35© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Now that we have gone through the 10 future predictions, choose the most accurate

statement of your belief:

A) I agree with all of the predictions

B) I agree with most of the predictions

C) I disagree with many of the predictions

D) I disagree with all of the predictions

37© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG

International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis

third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Lachlan WolfersGlobal Head of Indirect Taxes

KPMG International

P: +852 2685 7791

Lennert JanssenSenior Manager

KPMG in China

P: +852 2847 5084

© 2020 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG

network of independent firms are affiliated with KPMG International. KPMG International provides no client

services. No member firm has any authority to obligate or bind KPMG International or any other member firm

vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member

firm. All rights reserved.

The information contained herein is of a general nature and is not intended to address the circumstances of any

particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no

guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in

the future. No one should act on such information without appropriate professional advice after a thorough

examination of the particular situation.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

home.kpmg/socialmedia