Indian Fiscal Scenario: When will the domestic growth pick-up

164

www.plindia.com | www.majorgainz.com October to December 2013 India Strategy & Quarterly Report Indian Fiscal Scenario: When will the domestic growth pick-up

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Indian Fiscal Scenario: When will the domestic growth pick-up

www.plindia.com | www.majorgainz.com

October to December 2013

India Strategy & Quarterly Report

Indian Fiscal Scenario: When will the domestic growth pick-up

Oct-Dec 2013 Earnings Preview

January 09, 2014 2

THIS PAGE IS INTENTIONALLY LEFT BLANK

Oct-Dec 2013 Earnings Preview

January 09, 2014 3

Contents Page No.

India Strategy ..................................................................................... 5

Agri Products & Chemcials ............................................................... 25

Automobiles ..................................................................................... 36

Auto Ancillary ................................................................................... 45

Banks ................................................................................................ 51

Capital Goods ................................................................................... 72

Cement ............................................................................................. 86

Consumer ......................................................................................... 92

Information Technology ................................................................. 105

Metals & Mining ............................................................................ 117

Pharmaceuticals ............................................................................. 128

Power ............................................................................................. 139

Others ............................................................................................ 150

Annexure ........................................................................................ 152

(All prices as on January 08, 2014)

Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Please refer to important disclosures and disclaimers at the end of the report

Oct-Dec 2013 Earnings Preview

January 09, 2014 4

THIS PAGE IS INTENTIONALLY LEFT BLANK

Oct-Dec 2013 Earnings Preview

January 09, 2014 5

R Sreesankar [email protected] +91-22-6632 2214

India Strategy

Indian Fiscal Scenario: When will the domestic growth pick‐up?

Q3 FY14 PL’s Coverage Universe Earnings Preview

The revenue growth for all the companies in the PL Universe is estimated at 12.3% YoY and the EBITDA is expected to lead the topline growth at 15.9% YoY. Information Technology, Pharmaceuticals, Power, Auto and Auto Ancillary are the sectors leading the expansion in margins.

Sector‐wise growth and margin expectations – Q3FY14 PL estimates

Revenue (%) PAT (%) EBITDA Margin (bps)

YoY QoQ YoY QoQ YoY QoQ

Agri Products & Chemicals 5.1 (8.2) 20.1 (9.7) 113 8

Automobiles 13.6 4.0 40.5 (9.1) 163 (130)

Auto Ancillary 11.4 3.3 40.1 (2.3) 248 25

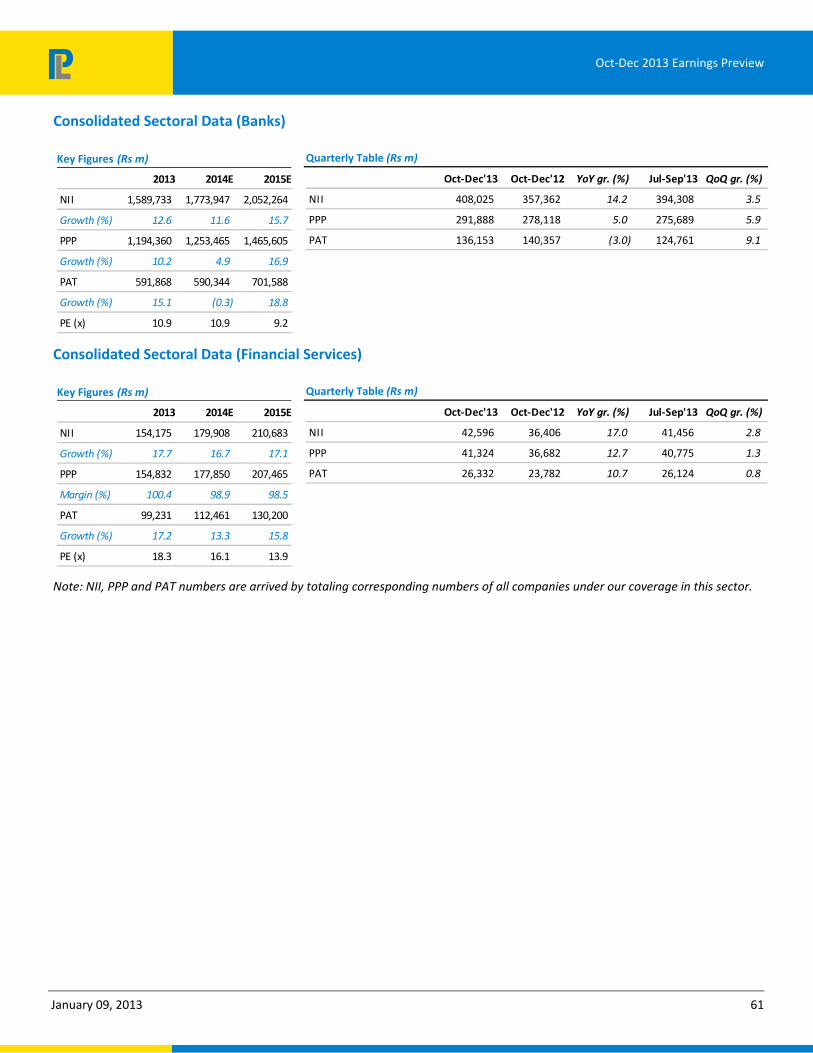

Banks 14.2 3.5 (3.0) 9.1

Capital Goods 2.0 7.5 (13.9) 18.9 (162) 139

Cement (3.4) 5.7 (30.6) 32.7 (238) 133

Consumer Staples 10.3 7.7 11.5 7.7 48 (27)

Financial Services 17.0 2.8 10.7 0.8

Information Tech. 24.7 2.4 27.4 2.8 195 35

Metals 13.9 2.5 29.4 30.3 190 236

Pharma 20.5 2.9 38.8 (12.1) 253 (18)

Power 4.5 2.0 5.4 (4.3) 74 (106)

Others 17.5 0.2 4.3 (9.8) (302) (339)

PL Universe 12.3 3.3 14.4 6.1 74 38

Source: Company Data, PL Research *EBITDA Margins are excluding BFSI

In our report dated December 9, 2014, we have recommended a portfolio with a defensive bias and we continue with the same defensive bias now as well. Our portfolio preference continue to be with IT, FMCG and Healthcare being the favoured ones. We have added both L&T and Crompton Greaves (buy on declines on December 9, 2013 report) in our top picks following the sharp price corrections and also reflecting the view that we have. We still continue see political stability as the main catalyst for a kickstart in dometsic growth and till the time we see a clarity, we expect to see the domestic growth stutter and hence a defensive stance.

Oct-Dec 2013 Earnings Preview

January 09, 2014 6

The small and mid cap stocks have been having a good run for the last few weeks. This has been mainly on the back of fictional news rather than factual news flow. On a 12 month basis, The BSE small cap index fell 12.8% against a gain of 1.6% in the BSE 100 index. However, we believe that some of the stocks in the small mid cap sector looks attarctive and warrants a closer look.

We estimate a stronger growth of 16.9% in FY15. While we expect 1QFY15 to be muted on account of parliament elections, the major growth is expected to come from the remaining three quarters. This growth is expected to be spread across the sectors excluding cement, which we feel may take time to recover as the surplus supply keeps the cement prices subdued.

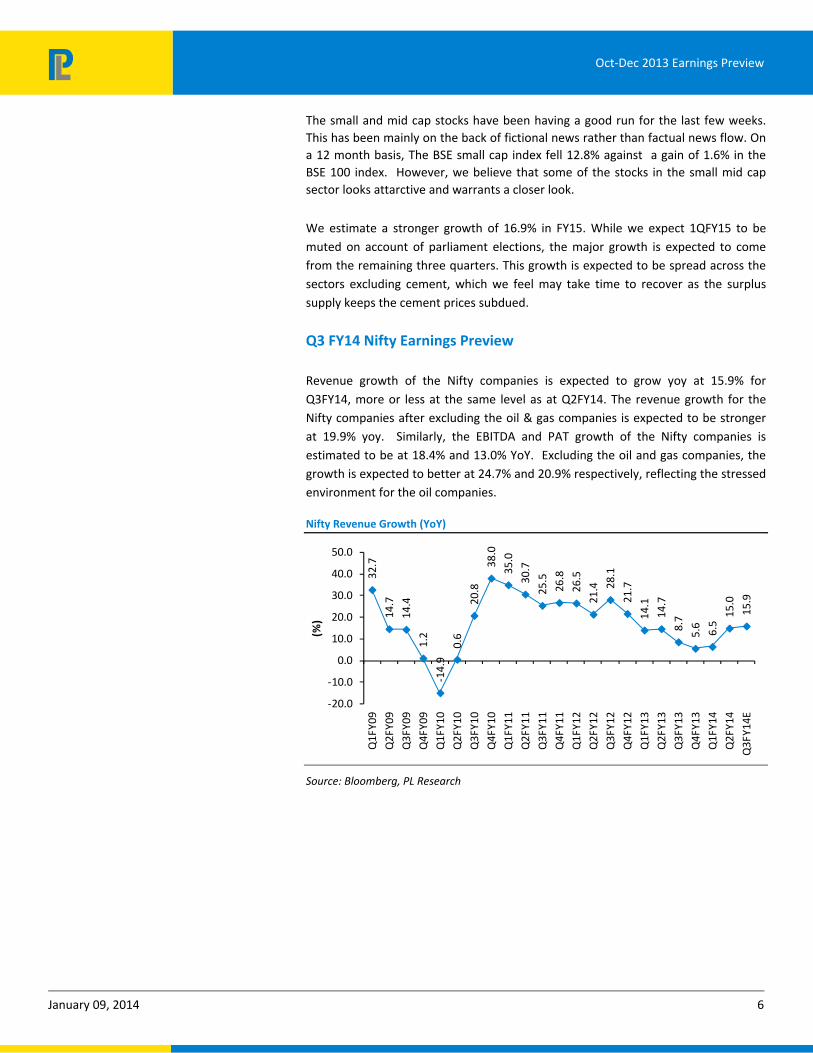

Q3 FY14 Nifty Earnings Preview

Revenue growth of the Nifty companies is expected to grow yoy at 15.9% for Q3FY14, more or less at the same level as at Q2FY14. The revenue growth for the Nifty companies after excluding the oil & gas companies is expected to be stronger at 19.9% yoy. Similarly, the EBITDA and PAT growth of the Nifty companies is estimated to be at 18.4% and 13.0% YoY. Excluding the oil and gas companies, the growth is expected to better at 24.7% and 20.9% respectively, reflecting the stressed environment for the oil companies.

Nifty Revenue Growth (YoY)

32.7

14.7

14.4

1.2

-14.

90.

620

.838

.035

.030

.725

.526

.826

.521

.4 28.1

21.7

14.1

14.7

8.7

5.6

6.5

15.0

15.9

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

Q1F

Y09

Q2F

Y09

Q3F

Y09

Q4F

Y09

Q1F

Y10

Q2F

Y10

Q3F

Y10

Q4F

Y10

Q1F

Y11

Q2F

Y11

Q3F

Y11

Q4F

Y11

Q1F

Y12

Q2F

Y12

Q3F

Y12

Q4F

Y12

Q1F

Y13

Q2F

Y13

Q3F

Y13

Q4F

Y13

Q1F

Y14

Q2F

Y14

Q3F

Y14E

(%)

Source: Bloomberg, PL Research

Oct-Dec 2013 Earnings Preview

January 09, 2014 7

Nifty EBITDA Growth (YoY)

35.4

18.3

1.9

12.6

-7.7

2.0

20.4 23

.9 31.9 40

.430

.727

.415

.56.

7 10.9 14

.85.

513

.35.

25.

4 11.7

8.7

18.4

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

Q1F

Y09

Q2F

Y09

Q3F

Y09

Q4F

Y09

Q1F

Y10

Q2F

Y10

Q3F

Y10

Q4F

Y10

Q1F

Y11

Q2F

Y11

Q3F

Y11

Q4F

Y11

Q1F

Y12

Q2F

Y12

Q3F

Y12

Q4F

Y12

Q1F

Y13

Q2F

Y13

Q3F

Y13

Q4F

Y13

Q1F

Y14

Q2F

Y14

Q3F

Y14E

(%)

Source: Bloomberg, PL Research

Nifty PAT Growth (YoY)

12.6

5.0

1.7

15.2

-12.

1

-18.

0

2.5

15.9

29.6

59.1

42.0

30.6

10.5

2.6 10

.4 21.0

2.7

26.5

3.2

1.8 11

.9

0.9

13.0

-30.0-20.0-10.0

0.010.020.030.040.050.060.070.0

Q1F

Y09

Q2F

Y09

Q3F

Y09

Q4F

Y09

Q1F

Y10

Q2F

Y10

Q3F

Y10

Q4F

Y10

Q1F

Y11

Q2F

Y11

Q3F

Y11

Q4F

Y11

Q1F

Y12

Q2F

Y12

Q3F

Y12

Q4F

Y12

Q1F

Y13

Q2F

Y13

Q3F

Y13

Q4F

Y13

Q1F

Y14

Q2F

Y14

Q3F

Y14E

(%)

Source: PL Research

Domestic economy

In the last six months, the trade deficit has been brought under US$10bn a month. While India’s exports have been hovering around the US$24.6bn levels in Nov 13, the non oil, non gold/silver imports have declined to yearly low of US$19.8 bn. While this has helped to arrest the trade deficit to a sub US$10bn level in Nov 13, any improvements in the domestic economy could result in further increase in the trade deficit numbers. Various measures implemented has resulted in the reduction of the current account deficit to US$5.1bn

Oct-Dec 2013 Earnings Preview

January 09, 2014 8

Trade Deficit

(US$ m) May'13 Jun'13 Jul'13 Aug'13 Sep'13 Oct'13 Nov'13 YTD

Exports 23,969 23,593 25,834 26,182 27,679 27,270 24,613 203,990

Imports 44,673 35,901 38,103 36,715 34,440 37,820 33,833 303,892

‐ Oil 15,060 12,730 12,731 15,095 13,197 15,131 12,965 111,059

‐ Gold & Silver 8,383 2,388 2,972 1,004 803 1,300 1,050 25,314

‐ Non Oil Non Gold/Silver 21,230 20,783 22,400 20,616 20,440 21,390 19,818 167,158

Trade Deficit (20,704) (12,308) (12,268) (10,534) (6,760) (10,550) (9,220) (99,902)

Source: RBI, PL Research

India’s Balance of Payments

(US$ m) Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 YoY QoQ

1. Current Account (16,932) (20,976) (31,857) (18,078) (21,772) (5,153) ‐75% ‐76%

Goods and Services (28,868) (31,465) (41,732) (28,676) (33,616) (14,934) ‐53% ‐56%

Goods (43,849) (47,793) (58,378) (45,635) (50,484) (33,305) ‐30% ‐34%

Services 14,982 16,328 16,645 16,960 16,868 18,372 13% 9%

Primary Income (4,889) (5,581) (5,800) (5,185) (4,830) (6,322) 13% 31%

Secondary Income 16,825 16,070 15,675 15,783 16,675 16,103 0% ‐3%

2. Capital Account (218) (248) 22 150 767 (65) ‐74% ‐108%

3. Financial Account 16,070 20,999 30,754 17,626 20,076 5,028 ‐76% ‐75%

Net errors and omissions 1,080 226 1,081 302 929 190 ‐16% ‐79%

Source: RBI, PL Research

Capital Accounts & Finance Account

(US$ m) Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 YoY QoQ

Net FDI 8,159 2,106 5,733 6,495 6,889 ‐16% 6%

Net FII (Equity+Debt) 7,718 9,781 11,314 (225) (6,602) ‐186% NA

Net Overseas borrowings by Banks 2,645 2,592 (6,366) 4,783 (6,634) ‐351% ‐239%

Net ECBs (321) (160) 38 427 180 ‐156% ‐58%

Net Short term credit to India 4,133 7,678 4,468 2,451 (1,862) ‐145% ‐176%

NRI Deposits 2,846 2,651 2,794 5,497 8,340 193% 52%

Net inflows under Capital & Finance account 20,745 31,470 20,549 20,514 (5,375) ‐126% ‐126%

Source: RBI, PL Research

As we enter the New Year 2014, there is nothing in the ground that brings cheer to the economy. The demand growth seems to be subsiding, indicated by the falling price in cement across the regions, lacklustre demand in steel, aluminium, automobiles etc. We expect the first quarter of CY 2014 to be faced with head winds on the domestic front and no significant changes are expected in the near term. While the immediate worry on the CAD front seems to have been addressed, containing the fiscal deficit seems to be a challenge especially on account of lower than expected revenue mobilizations. The desire to keep the fiscal deficit at less than 4.8% of GDP could result in lower plan expenditure. In our view, this could even lead to a weak quarter performance for the domestic focused companies.

Oct-Dec 2013 Earnings Preview

January 09, 2014 9

Trends in Tax Receipts

Tax Revenue (Rs bn) Upto

Nov'12 Upto

Nov'13 % YoY

Budget Est (FY14)

% to total Budget Est.

Corporate Tax 1,630 1,817 11% 4,195 43%

Income Tax 1,053 1,269 21% 2,476 51%

Customs 1,048 1,100 5% 1,873 59%

Union Excise Duties 941 883 ‐6% 1,976 45%

Service Tax 715 839 17% 1,801 47%

Other Tax 57 63 9% 37 169%

Gross Tax Revenue 5,445 5,970 10% 12,359 48%

Surcharges 23 26 11% 48 54%

Assignment to states 1,725 1,983 15% 3,470 57%

Net Tax Revenue 3,696 3,962 7% 8,841 45%

Source: Controller General of Accounts – Ministry of Finance, PL Research

Trends in Disinvestment, Sale of Minority Stakes and Telecom Auction Proceeds

(Rs bn) Upto

Nov'13 Budget Est

(FY14) % to total Budget Est.

Divestment of Govt Holding in Equity 15.89 400 4%

Sale of shares in non-government companies or SUUTI 0 158 0%

Telecom proceeds from spectrum auction 0 200 0%

Source: Controller General of Accounts – Ministry of Finance, PL Research

Trends in Subsidy Expenditure

(Rs bn) Upto

Nov'12 Upto

Nov'13 % YoY

Budget Est (FY14)

% to total Budget Est.

Non-Plan Expenditure 6243 7302 17% 11100 66%

-Dept. of Fertilizers 552 530 ‐4% 660 80%

-Dept. of Food & PDS 726 853 17% 908 94%

-Dept. of Petroleum & Gas 403 549 36% 651 84%

Source: Controller General of Accounts – Ministry of Finance, PL Research

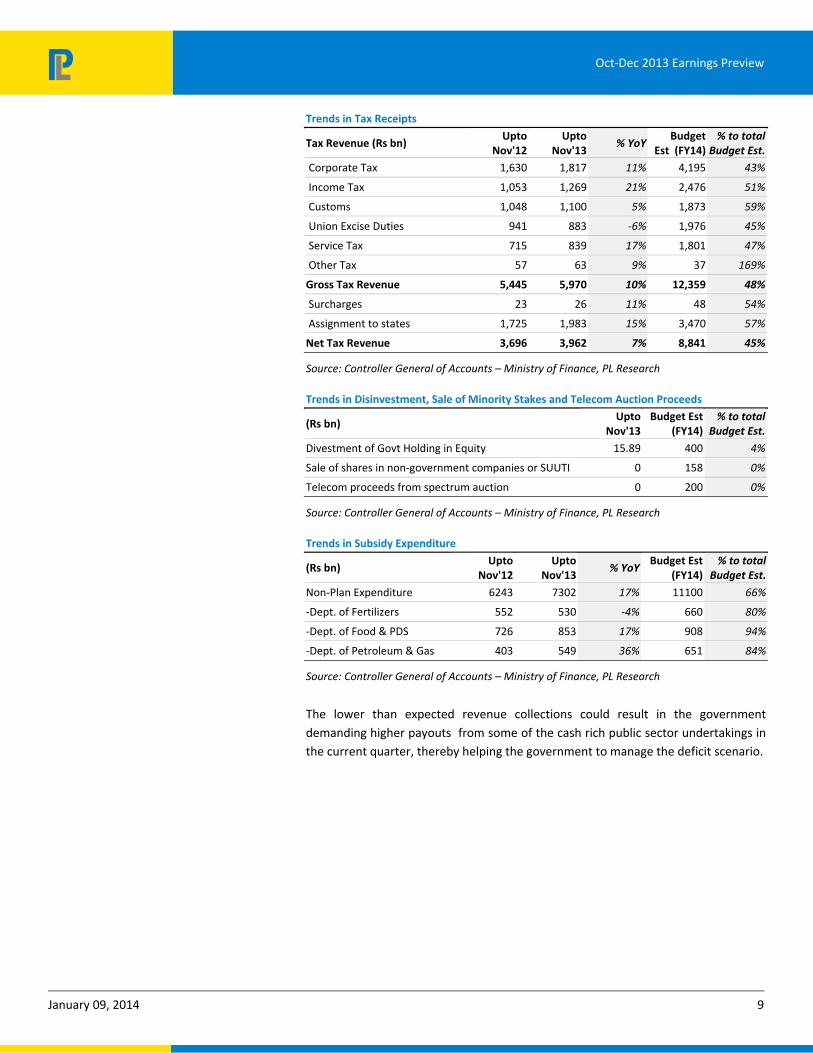

The lower than expected revenue collections could result in the government demanding higher payouts from some of the cash rich public sector undertakings in the current quarter, thereby helping the government to manage the deficit scenario.

Oct-Dec 2013 Earnings Preview

January 09, 2014 10

Inflation, will it start to recede?

Inflation has been on an elevated level for the last six months at both the WPI and the CPI levels. While the WPI was up 7.52%, the component of Food inflation is up 19.93% yoy. In the same period, while the CPI was up at 11.2%, the food inflation too was high at 14.5%. The high levels of inflation have been one of the reasons for the elevated interest rates. On the CPI front, Food constitutes 49% of the weightage and within food articles, vegetables constitute only 5.4%. Though, of late, we have seen a correction in the prices of vegetables, we do not believe that this will be sufficient to result reversal of the elevated inflation levels as all other food components have seen an increase. Hence we continue to believe that the short term interest rates are likely to remain at elevated levels.

WPI Inflation

7.31

%

7.31

%

7.28

%

5.65

%

4.77

%

4.58

% 5.16

% 5.85

%

6.99

%

7.05

%

7.00

%

7.52

%

4.0%4.5%5.0%5.5%6.0%6.5%7.0%7.5%8.0%

Dec

12

Jan

13

Feb

13

Mar

13

Apr

13

May

13

Jun

13

Jul 1

3

Aug

13

Sep

13

Oct

13

Nov

13

Source: Ministry of Commerce & Industry

Food Article

10.6

9%

12.1

7%

11.9

5%

8.63

%

6.08

% 8.25

% 10.2

7% 12.2

9%

19.1

7%

18.4

0%

18.1

9%

19.9

3%

4%6%8%

10%12%14%16%18%20%22%

Dec

12

Jan

13

Feb

13

Mar

…

Apr

13

May

…

Jun

13

Jul 1

3

Aug

…

Sep

13

Oct

13

Nov

…

Source: Ministry of Commerce & Industry

CPI Inflation

10.610.8 10.9

10.4

9.4 9.3

9.99.6 9.5

9.810.2

11.2

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

Dec

-12

Jan-

13

Feb-

13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-

13

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Source: CSO

Oct-Dec 2013 Earnings Preview

January 09, 2014 11

CPI Index Basket Weights

Sub group/group Rural Urban Combined (Rural+Urban)

Cereals and products 19.1 8.7 14.6

Pulses and products 3.3 1.9 2.7

Milk and milk products 8.6 6.6 7.7

Oils and fats 4.7 2.9 3.9

Egg, fish and meat 3.4 2.3 2.9

Vegetables 6.6 4.0 5.4

Fruits 1.9 1.9 1.9

Sugar etc 2.4 1.3 1.9

Condiments and spices 2.1 1.2 1.7

Non- alcoholic beverages 2.0 2.0 2.0

Prepared meals etc 2.6 3.2 2.8

Pan, tobacco and Intoxicants 2.7 1.4 2.1

Food, beverages and tobacco 59.3 37.2 49.7

Fuel and light 10.4 8.4 9.5

Clothing and bedding 4.6 3.3 4.1

Footwear 0.8 0.6 0.7

Clothing, bedding and footwear 5.4 3.9 4.7

Housing 22.5 9.8

Education 2.7 4.2 3.4

Medical care 6.7 4.3 5.7

Recreation and amusement 1.0 2.0 1.4

Transport and communication 5.8 9.8 7.6

Personal care and effects 3.1 2.7 2.9

Household requisites 4.5 3.9 4.3

Others 1.1 1.0 1.1

Miscellaneous 24.9 28.0 26.3

All Groups 100 100 100

Source: CSO

Global economy, beginning to come out of the trough

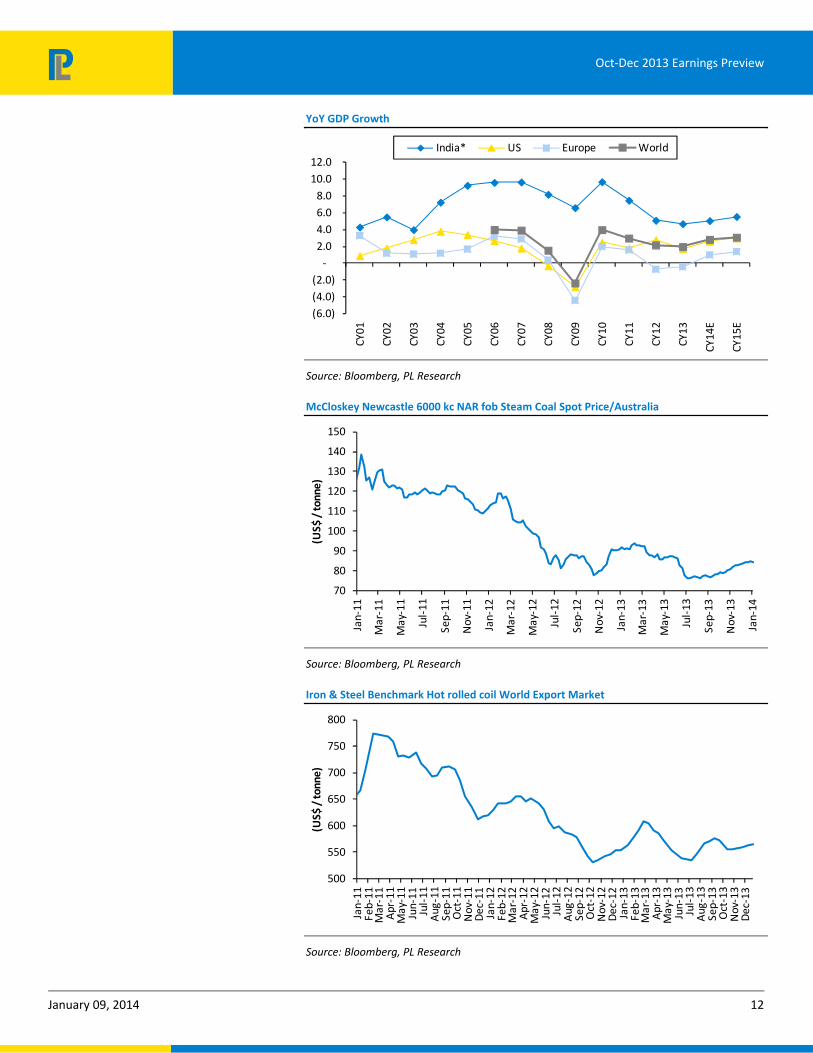

All through 2004-2008, the booming period in Indian economy, apart from the thrust on infrastructure, the Indian economy had the benefit of a strong global economy acting as a tail wind. Both the Euro zone and USA had a strong growth resulting in a boom period for the commodities. These changed during the financial crisis in 2008 and the economies across the globe have been facing challenging times. After long periods of low prices, we believe that the commodity prices have begun to bottom out and with the economic growth seen in both the Eurozone and USA, we have also started to see a recovery in various global commodities. We believe that improving Eurpoean and US economies should result in improvement in global trade, which is already reflected in the firm up in the Baltic Freight Indices (BFI).

Oct-Dec 2013 Earnings Preview

January 09, 2014 12

YoY GDP Growth

(6.0)(4.0)(2.0)

-2.0 4.0 6.0 8.0

10.0 12.0

CY01

CY02

CY03

CY04

CY05

CY06

CY07

CY08

CY09

CY10

CY11

CY12

CY13

CY14

E

CY15

E

India* US Europe World

Source: Bloomberg, PL Research

McCloskey Newcastle 6000 kc NAR fob Steam Coal Spot Price/Australia

70

80

90

100

110

120

130

140

150

Jan-

11

Mar

-11

May

-11

Jul-

11

Sep-

11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-

12

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-

13

Sep-

13

Nov

-13

Jan-

14

(US$ / tonne)

Source: Bloomberg, PL Research

Iron & Steel Benchmark Hot rolled coil World Export Market

500

550

600

650

700

750

800

Jan-

11Fe

b-11

Mar

-11

Apr

-11

May

-11

Jun-

11Ju

l-11

Aug

-11

Sep-

11O

ct-1

1N

ov-1

1D

ec-1

1Ja

n-12

Feb-

12M

ar-1

2A

pr-1

2M

ay-1

2Ju

n-12

Jul-

12A

ug-1

2Se

p-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13Fe

b-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug

-13

Sep-

13O

ct-1

3N

ov-1

3D

ec-1

3

(US$ / tonne)

Source: Bloomberg, PL Research

Oct-Dec 2013 Earnings Preview

January 09, 2014 13

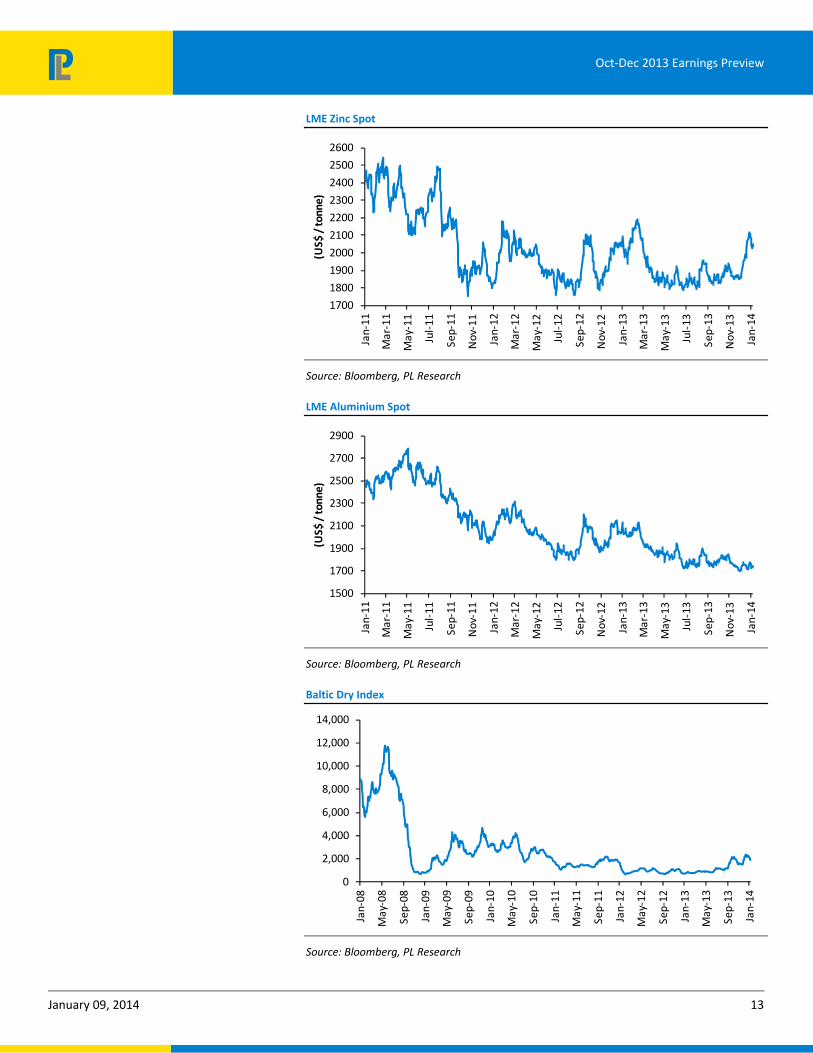

LME Zinc Spot

1700

1800

1900

2000

2100

2200

2300

2400

2500

2600

Jan-

11

Mar

-11

May

-11

Jul-

11

Sep-

11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-

12

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-

13

Sep-

13

Nov

-13

Jan-

14

(US$ / tonne)

Source: Bloomberg, PL Research

LME Aluminium Spot

1500

1700

1900

2100

2300

2500

2700

2900

Jan-

11

Mar

-11

May

-11

Jul-

11

Sep-

11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-

12

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-

13

Sep-

13

Nov

-13

Jan-

14

(US$ / tonne)

Source: Bloomberg, PL Research

Baltic Dry Index

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

Source: Bloomberg, PL Research

Oct-Dec 2013 Earnings Preview

January 09, 2014 14

Baltic Dirty Tanker Index

0

500

1,000

1,500

2,000

2,500

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

Source: Bloomberg, PL Research

Baltic Clean Tanker Index

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

Source: Company Data, PL Research

Where to invest in 2014?

Though the first quarter of CY 2014 does not offer any optimism in terms of growth for the economy, it looks like that the improvement in Eurozone and USA should benefit some sectors and some companies specifically. In our view, the obvious beneficiaries seem to be the IT sector which should see a better improvement in traction with fresh IT spending. The players in the health care sector with a focus on US is likely to be more in demand and beneficiaries of global trade, shipping could turn out to be the game changers for the first half of CY 2014.

Oct-Dec 2013 Earnings Preview

January 09, 2014 15

Where do we see Nifty at the end of 2014: In our report dated 08 December 2013, we have given our estimates of the trading range for the Nifty between 5950-6500 levels for the current quarter. While we are yet to see any improvements in the domestic front, the global scenario has started to improve and this could considerably change the outlook for at least some of the sectors which have a direct impact on global trade. However, with the political uncertainty continuing to be a dampener, we estimate the market remaining range bound between 5800-6500 till the political uncertainty is sorted out.

India: FII/DII Equity Flows

(200.00)

(100.00)

-

100.00

200.00

300.00

Jan-

12Fe

b-12

Mar

-12

Apr

-12

May

-12

Jun-

12Ju

l-12

Aug

-12

Sep-

12O

ct-1

2N

ov-1

2D

ec-1

2Ja

n-13

Feb-

13M

ar-1

3A

pr-1

3M

ay-1

3Ju

n-13

Jul-

13A

ug-1

3Se

p-13

Oct

-13

Nov

-13

Dec

-13

DII Net Cash Market FII Net Cash Market

CY12 ‐ Total FII buying Rs1,293.2bn against DII net

selling at Rs-568.9bn

YTD CY13

FII Rs1125.39bnDII Rs-734.64bn

Source: Bloomberg, PL Research

Oct-Dec 2013 Earnings Preview

January 09, 2014 16

Global Equity Markets Performance

Month‐on‐Month

5.4 3.5 3.2 2.8 2.5 1.8 1.3

0.5

(1.0) (1.1) (1.3)(3.1)

(8.6)(10.0)(8.0)(6.0)(4.0)(2.0)

-2.0 4.0 6.0 8.0

Japa

n

Ger

man

y

USA

FTSE

Aus

tral

ia

S&P

Rus

sia

Indo

nesi

a

Bra

zil

S.Ko

rea

Indi

a

Hon

g Ko

ng

Chin

a

(%)

Source: Bloomberg, PL Research

Calendar Year‐to‐date

(1.0)(0.7)

(0.3) (0.2)

(0.7) (0.6)

(2.4)

(1.7)(2.1)

(2.6)

(2.1)

(1.3)

(3.4)(4.0)

(3.5)

(3.0)

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

-

Japa

n

Ger

man

y

USA

FTSE

Aus

tral

ia

S&P

Rus

sia

Indo

nesi

a

Bra

zil

S.Ko

rea

Indi

a

Hon

g Ko

ng

Chin

a

(%)

Source: Bloomberg, PL Research

Year‐on‐Year

53.4

23.3 24.0

11.3 13.3

26.1

(0.4) (4.5)

(17.5)

(2.0)

5.0

(0.5)(10.2)

(30.0)(20.0)(10.0)

-10.0 20.0 30.0 40.0 50.0 60.0

Japa

n

Ger

man

y

USA

FTSE

Aus

tral

ia

S&P

Rus

sia

Indo

nesi

a

Bra

zil

S.Ko

rea

Indi

a

Hon

g Ko

ng

Chin

a

(%)

Source: Bloomberg, PL Research

The strong pay roll numbers and the

optimism in the economies have resulted in

a better performance for the developed

markets. Lower domestic growth in China

have been a concern

Developed markets continue with the out

performance on subdued inflation and

improving economic strength.

Oct-Dec 2013 Earnings Preview

January 09, 2014 17

Indian Equities – Sector Performance

Month‐on‐Month

7.7 7.0

2.7 2.1

(0.5) (1.2) (1.2)(3.4)

(5.3) (5.5) (5.7)(8.0)(6.0)(4.0)(2.0)

-2.0 4.0 6.0 8.0

10.0

(%)

Source: Bloomberg, PL Research

Calendar Year‐to‐date

(0.1)

2.2

(2.2)

(0.7) (0.7) (0.9)

(3.7)(4.5)

(5.1)

(2.9)

(5.4)(6.0)(5.0)(4.0)(3.0)(2.0)(1.0)

-1.0 2.0 3.0

(%)

Source: Bloomberg, PL Research

Year‐on‐Year

56.9

22.7

(36.4)

10.8

(24.8)

4.3

(15.0)(4.7) (10.3) (13.7) (21.0)

(60.0)(40.0)(20.0)

-20.0 40.0 60.0 80.0

(%)

Source: Bloomberg, PL Research

Capital goods corrected sharply on account

of a bleak domestic outlook for the next

quarter. Defensives continue with the out

performance.

Capital Goods and Power under‐perform

due to concerns on stalled investment

cycle. Depreciating rupee & gathering

strength in the US economy help propel IT

as the best performing sector. Defensives

like Healthcare & FMCG too outperform

Oct-Dec 2013 Earnings Preview

January 09, 2014 18

India: Market cap‐wise Performance

Month‐on‐Month

6.9

4.8

0.1

(0.9)(2.0)

(1.0)

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

BSESMCAP Index BSEMDCAP Index BSE500 Index BSE100 Index

(%)

Source: Bloomberg, PL Research

Calendar Year‐to‐date

1.6

(0.1)

(1.6)(2.0)

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

-

0.5

1.0

1.5

2.0

BSESMCAP Index BSEMDCAP Index BSE500 Index BSE100 Index

(%)

Source: Bloomberg, PL Research

Year‐on‐Year

(12.8)

(8.7)

(0.4)

1.9

(14.0)

(12.0)

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

BSESMCAP Index BSEMDCAP Index BSE500 Index BSE100 Index

(%)

Source: Bloomberg, PL Research

Small‐Caps out perform mid caps which in‐

turn outperform Large‐Caps

Large Caps post low‐single digit positive

returns whereas Small Caps lose 12.8%

over the last year

Oct-Dec 2013 Earnings Preview

January 09, 2014 19

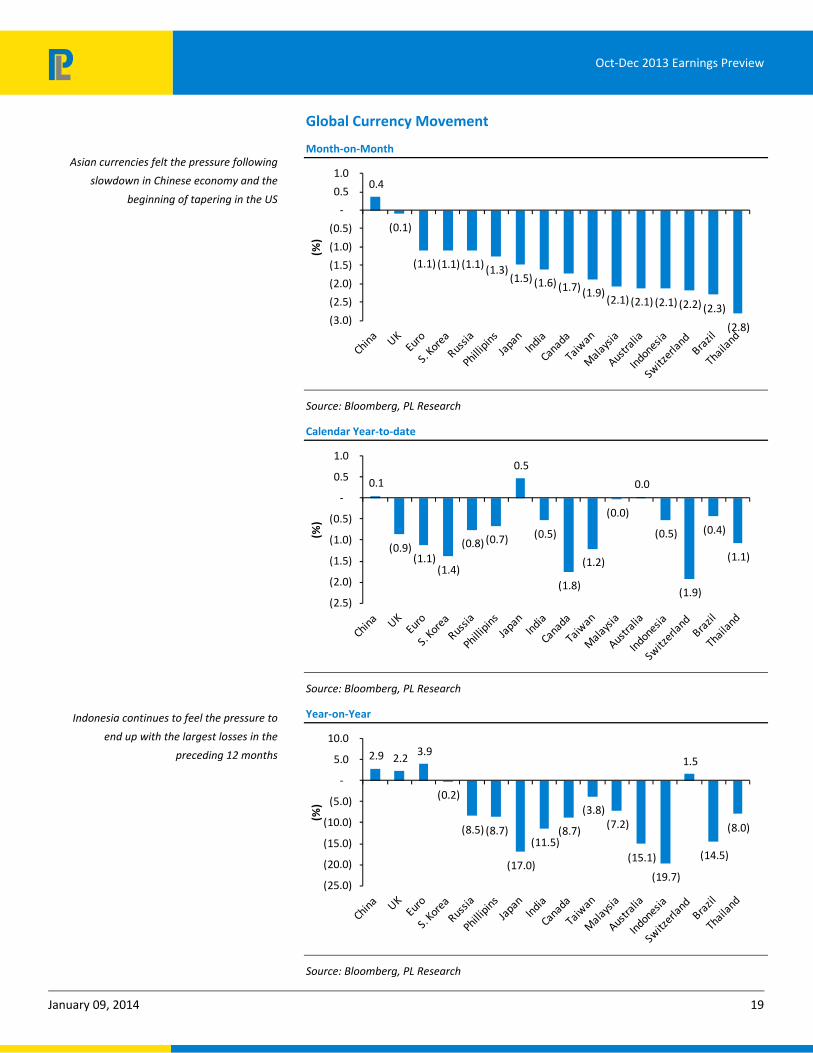

Global Currency Movement

Month‐on‐Month

0.4

(0.1)

(1.1) (1.1) (1.1) (1.3)(1.5) (1.6) (1.7) (1.9)

(2.1) (2.1) (2.1) (2.2) (2.3)

(2.8)(3.0)

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

-

0.5

1.0

(%)

Source: Bloomberg, PL Research

Calendar Year‐to‐date

0.1

(0.9)(1.1)

(1.4)

(0.8) (0.7)

0.5

(0.5)

(1.8)

(1.2)

(0.0)

0.0

(0.5)

(1.9)

(0.4)

(1.1)

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

-

0.5

1.0

(%)

Source: Bloomberg, PL Research

Year‐on‐Year

2.9 2.2 3.9

(0.2)

(8.5) (8.7)

(17.0)

(11.5)(8.7)

(3.8)(7.2)

(15.1)

(19.7)

1.5

(14.5)

(8.0)

(25.0)

(20.0)

(15.0)

(10.0)

(5.0)

-

5.0

10.0

(%)

Source: Bloomberg, PL Research

Asian currencies felt the pressure following

slowdown in Chinese economy and the

beginning of tapering in the US

Indonesia continues to feel the pressure to

end up with the largest losses in the

preceding 12 months

Oct-Dec 2013 Earnings Preview

January 09, 2014 20

Global Agricultural Commodities

Performance of Global Agricultural Commodities

60

70

80

90

100

110

120

130

Jan-

13

Feb-

13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-

13

Aug

-13

Sep-

13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Rice Wheat Corn Soya Plam Oil Sugar

Source: Bloomberg, PL Research

Month‐on‐Month Performance

(1.6) (1.7)

(2.8) (3.0)(3.4)

(7.0)(8.0)

(7.0)

(6.0)

(5.0)

(4.0)

(3.0)

(2.0)

(1.0)

-

Rice Corn Soya Palm Oil Sugar Wheat

(%)

Source: Bloomberg, PL Research

Wheat prices declined during Dec’13 due to

expectation of bumper wheat crop next

year which could keep prices under check

Sugar prices declined on strong harvest in

Brazil which added to the surplus supply

globally

Soyabean prices dropped due to

expectation of favourable weather

boosting crop prospects

Corn prices declined due to jump in corn

stocks and expectation of good production

Oct-Dec 2013 Earnings Preview

January 09, 2014 21

Global Industrial Commodities

Month‐on‐Month

8.9

3.4 2.9

1.1 0.2

(1.8)

(4.0)(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

8.0

10.0

Zinc Copper Lead Thermal Coal

Aluminium Nickel Brent crude

(%)

Source: Bloomberg, PL Research

Calendar Year‐to‐date

(1.7)

(0.2)

(2.9)

(0.4)

(0.9)

(2.7)

(3.3)(3.5)

(3.0)

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

-

Zinc Copper Lead Thermal Coal

Aluminium Nickel Brent crude

(%)

Source: Bloomberg, PL Research

Year‐on‐Year

3.3

(8.4)(7.1) (8.1)

(14.3)

(21.5)

(4.4)

(25.0)

(20.0)

(15.0)

(10.0)

(5.0)

-

5.0

Zinc Copper Lead Thermal Coal

Aluminium Nickel Brent crude

(%)

Source: Bloomberg, PL Research

Base metal prices (except Aluminium)

remained strong on account of supply

issues. Crude weakened due to high base

effect and elevated inventory

Oct-Dec 2013 Earnings Preview

January 09, 2014 22

NIFTY: Earnings growth and valuations

We estimate the free float EPS of the Nifty companies in FY14 and FY15 at Rs400.6 and Rs468.4 respectively, reflecting a growth of 7.3% and 16.9% respectively. IT (30.2% and 19.7%), Pharma (25.7%and 11.8%), Auto (19.0% and 23.3%), FMCG (14.0% and 19.9%) and Metals (17.5% and 13.0%) is expected to lead the way, while the laggards are expected to be Cement, engineering & Power and Oil & Gas.

Nifty trades at a PER of 15.4x FY14 and 13.2x FY15 earnings. The last ten year average of Nifty was at 14.6x and the Nifty at 13.8x trades at discount to the last ten year average.

Historically, the MSCI India index has always traded at a premium to MSCI Asia. The last ten years average premium has been around 24% and currently the index trades at a 19% premium, indicating a de rating of the market due to the continued problems affecting the domestic economy.

While our fundamental view has not changed from what we had in December, we believe that the global economy is beginning to show improvements and it is likely that stocks related to global trade could see better time ahead, while we continue to believe that the domestic focused companies will be under pressure.

Our portfolio preference continue to have a defensive bias while we have added Larsen & Toubro and Crompton Greaves to our top picks to reflect the change in our thought process.

Nifty 1‐yr forward PE

13.8

5.0

10.0

15.0

20.0

25.0

30.0

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Average14.6

Source: Bloomberg, PL Research

MSCI India Premium to MSCI Asia (Ex‐Japan)

19%

-30%-20%-10%

0%10%20%30%40%50%60%

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

10 year Avg.24%

Source: Bloomberg, PL Research

Oct-Dec 2013 Earnings Preview

January 09, 2014 23

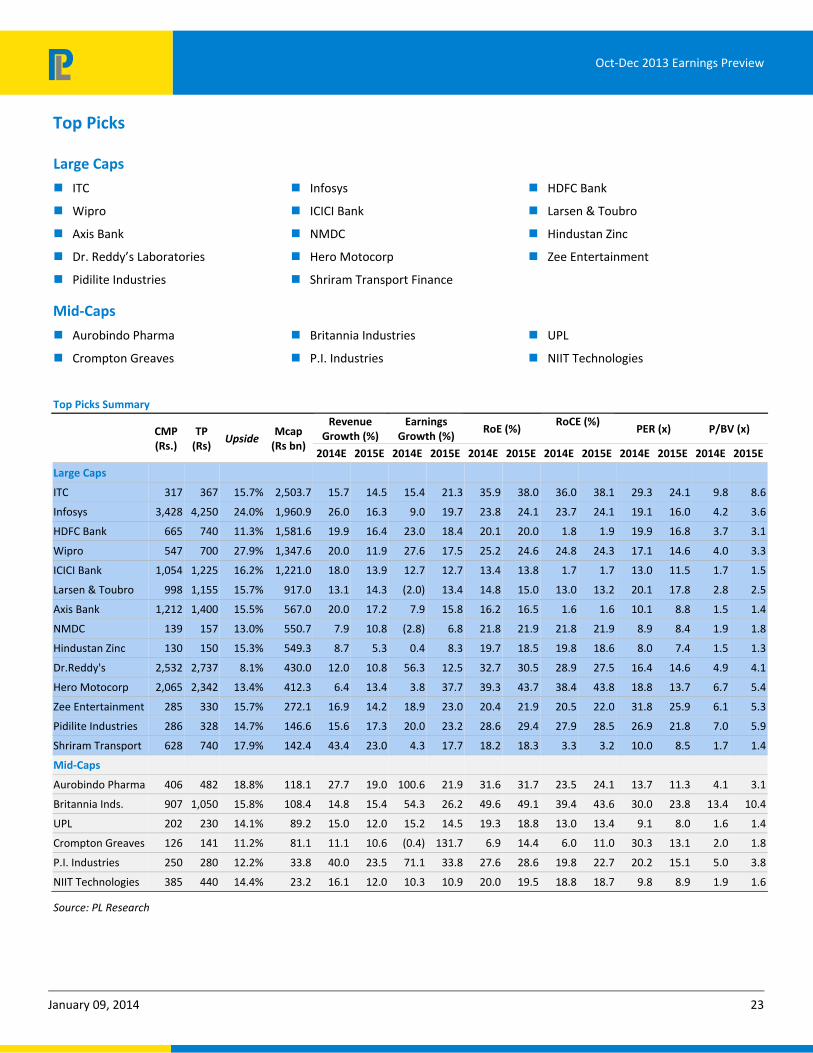

Top Picks

Large Caps

ITC Infosys HDFC Bank

Wipro ICICI Bank Larsen & Toubro

Axis Bank NMDC Hindustan Zinc

Dr. Reddy’s Laboratories Hero Motocorp Zee Entertainment

Pidilite Industries Shriram Transport Finance

Mid‐Caps

Aurobindo Pharma Britannia Industries UPL

Crompton Greaves P.I. Industries NIIT Technologies

Top Picks Summary

CMP (Rs.)

TP (Rs)

Upside Mcap (Rs bn)

Revenue Growth (%)

Earnings Growth (%)

RoE (%) RoCE (%)

PER (x) P/BV (x)

2014E 2015E 2014E 2015E 2014E 2015E 2014E 2015E 2014E 2015E 2014E 2015E

Large Caps

ITC 317 367 15.7% 2,503.7 15.7 14.5 15.4 21.3 35.9 38.0 36.0 38.1 29.3 24.1 9.8 8.6

Infosys 3,428 4,250 24.0% 1,960.9 26.0 16.3 9.0 19.7 23.8 24.1 23.7 24.1 19.1 16.0 4.2 3.6

HDFC Bank 665 740 11.3% 1,581.6 19.9 16.4 23.0 18.4 20.1 20.0 1.8 1.9 19.9 16.8 3.7 3.1

Wipro 547 700 27.9% 1,347.6 20.0 11.9 27.6 17.5 25.2 24.6 24.8 24.3 17.1 14.6 4.0 3.3

ICICI Bank 1,054 1,225 16.2% 1,221.0 18.0 13.9 12.7 12.7 13.4 13.8 1.7 1.7 13.0 11.5 1.7 1.5

Larsen & Toubro 998 1,155 15.7% 917.0 13.1 14.3 (2.0) 13.4 14.8 15.0 13.0 13.2 20.1 17.8 2.8 2.5

Axis Bank 1,212 1,400 15.5% 567.0 20.0 17.2 7.9 15.8 16.2 16.5 1.6 1.6 10.1 8.8 1.5 1.4

NMDC 139 157 13.0% 550.7 7.9 10.8 (2.8) 6.8 21.8 21.9 21.8 21.9 8.9 8.4 1.9 1.8

Hindustan Zinc 130 150 15.3% 549.3 8.7 5.3 0.4 8.3 19.7 18.5 19.8 18.6 8.0 7.4 1.5 1.3

Dr.Reddy's 2,532 2,737 8.1% 430.0 12.0 10.8 56.3 12.5 32.7 30.5 28.9 27.5 16.4 14.6 4.9 4.1

Hero Motocorp 2,065 2,342 13.4% 412.3 6.4 13.4 3.8 37.7 39.3 43.7 38.4 43.8 18.8 13.7 6.7 5.4

Zee Entertainment 285 330 15.7% 272.1 16.9 14.2 18.9 23.0 20.4 21.9 20.5 22.0 31.8 25.9 6.1 5.3

Pidilite Industries 286 328 14.7% 146.6 15.6 17.3 20.0 23.2 28.6 29.4 27.9 28.5 26.9 21.8 7.0 5.9

Shriram Transport 628 740 17.9% 142.4 43.4 23.0 4.3 17.7 18.2 18.3 3.3 3.2 10.0 8.5 1.7 1.4

Mid‐Caps

Aurobindo Pharma 406 482 18.8% 118.1 27.7 19.0 100.6 21.9 31.6 31.7 23.5 24.1 13.7 11.3 4.1 3.1

Britannia Inds. 907 1,050 15.8% 108.4 14.8 15.4 54.3 26.2 49.6 49.1 39.4 43.6 30.0 23.8 13.4 10.4

UPL 202 230 14.1% 89.2 15.0 12.0 15.2 14.5 19.3 18.8 13.0 13.4 9.1 8.0 1.6 1.4

Crompton Greaves 126 141 11.2% 81.1 11.1 10.6 (0.4) 131.7 6.9 14.4 6.0 11.0 30.3 13.1 2.0 1.8

P.I. Industries 250 280 12.2% 33.8 40.0 23.5 71.1 33.8 27.6 28.6 19.8 22.7 20.2 15.1 5.0 3.8

NIIT Technologies 385 440 14.4% 23.2 16.1 12.0 10.3 10.9 20.0 19.5 18.8 18.7 9.8 8.9 1.9 1.6

Source: PL Research

Oct-Dec 2013 Earnings Preview

January 09, 2014 24

Nifty Valuation

Source: Company Data, Bloomberg, PL Research

Note: Telecom Nos. is Bloomberg Consensus / Sector Weightages are updated as on December 31, 2013

For Detailed Break‐up of Company & Sector wise please refer Page No. 152‐160

Weight‐

age (%)FY12 FY13 FY14E FY15E

Weight‐

age (%)FY12 FY13 FY14E FY15E

Banking & Fin. 26.3% Cement 2.9%

PER (x) 14.6 12.7 12.5 10.6 PER (x) 19.2 14.8 16.7 16.2 PAT Growth (%) 26.8 15.1 1.0 18.2 PAT Growth (%) 10.1 29.6 (11.2) 3.2

Technology 16.8% Telecom 1.9%

PER (x) 33.0 26.6 20.5 17.1 PER (x) 31.2 58.4 35.3 20.9 PAT Growth (%) 16.9 23.7 30.2 19.7 PAT Growth (%) (29.6) (46.6) 65.4 68.7

Oil & Gas 11.7% Real Estate 0.4%

PER (x) 10.4 10.1 9.6 8.4 PER (x) 23.5 37.9 28.7 20.3 PAT Growth (%) 13.6 3.9 4.9 13.6 PAT Growth (%) (20.5) (37.8) 32.1 41.4

FMCG 11.6% Nifty as on Jan 8 6,175

PER (x) 43.1 35.4 31.1 25.9 PAT Growth (%) 35.5 21.8 14.0 19.9 EPS (Rs) ‐ Free Float 365.9 373.4 400.6 468.4

Growth (%) 9.7 2.1 7.3 16.9

Auto 9.0% PER (x) 16.9 16.5 15.4 13.2

PER (x) 13.9 14.9 12.6 10.2 PAT Growth (%) 23.1 (6.8) 19.0 23.3 EPS (Rs) ‐ Free Float

Nifty Cons. 365.9 373.4 403.6 474.8

Eng. & Power 8.2% Var. (PLe v/s Cons.) (%) ‐ ‐ (0.7) (1.4)

PER (x) 12.8 12.3 13.0 11.7 PAT Growth (%) 7.2 3.8 (5.1) 11.1

Sensex as on Jan 8 20,729

Pharma 6.1%

PER (x) 32.0 27.5 21.9 19.6 EPS (Rs) ‐ Free Float 1,188.5 1,173.4 1,243.6 1,463.5

PAT Growth (%) 44.3 16.3 25.7 11.8 Growth (%) 8.8 (1.3) 6.0 17.7

PER (x) 17.4 17.7 16.7 14.2

Metals 5.2%

PER (x) 11.1 11.4 9.7 8.6 Sensex Cons. 1,188.5 1,173.4 1,253.2 1,483.1

PAT Growth (%) 1.2 (2.1) 17.5 13.0 Var. (PLe v/s Cons.) (%) ‐ ‐ (0.8) (1.3)

January 09, 2014 25

Oct-Dec 2013 Earnings Preview

Balwindar Singh [email protected] +91-22-6632 2239

Top picks

PI Industries

UPL

Agri Products & Chemicals On an aggregate basis, we expect our universe to report sales growth of 5.1%

YoY with EBITDA margin improvement of 113bps YoY. For Q3, we expect aggregate PAT to increase by 20.1% YoY.

Complex Fertilisers‐ Inventory normalizes; company level sales growth picks

up: Good monsoons this year have led to significant uptick in consumption of complex fertilizers. However, as system was flushed with excess inventory of 3-4m mt, company level sales growth remained elusive in H1. Post the good monsoons, inventory has normalized in the system and company level sales growth seems to be getting back on track.

Decline in global fertilizer prices makes risk‐reward attractive for importers: As we have been highlighting earlier that imports can pick up due to a decline in global fertilizer prices, Nov’13 witnessed imported complex fertilisers volumes increasing by 17.5% YoY. Imported DAP volumes increased by 7.6% YoY even on a higher base of 556,000mt last year. Our interaction with industry points to the fact that FY15E is likely to witness increase in imported volumes.

Higher discounts being offered on DAP as costs come down: Decline in global phosphoric acid and ammonia prices have led to a reduction in global fertilizer prices. This have led to reduction in cost of production for domestic players too. Our channel checks suggests that companies are passing on the benefits of lower raw material costs through increase in discounts.

Delay in subsidy remains a key overhang on sector: Though government has recently sanctioned special banking arrangements of Rs100bn for clearing the subsidy over dues, the amount sanctioned is substantially lower than the requirement. We expect subsidy delays to continue as govt. is itself strapped with finances.

Global urea prices remain weak; IPP profitability impacted: Global urea prices continue to remain weak due to demand-supply mismatch. Though urea prices have recovered from the lows of $280/mt witnessed in Nov’13, they are currently quoting at $315/mt which is still a decline of 20% YoY. At this price point, IPP-linked production is not viable.

Urea subsidy to increase in the event of gas price hike: Gas price hikes, which is likely to be implemented from April 1, 2014 is likely to increase subsidy by ~Rs90-95bn. With every increase of $1/mmbtu in gas prices, the production cost would increase by Rs1,384/mt resulting into increase in costs by Rs24.5bn for 18m mt of urea produced by gas in India. Hence, increase in gas prices by $4/mmbtu would result into increase in subsidy by ~Rs90-95bn. We also do not rule out the possibility of a modest increase in urea prices which will somewhat lower the subsidy burden of govt.

January 09, 2014 26

Oct-Dec 2013 Earnings Preview

Agrochemicals‐ Rabi expected to be strong: Our channel checks suggests that rabi has witnessed strong growth in volume terms driven by robust rabi sowing patterns, increase in MSPs, upbeat sentiments etc. Companies including Dhanuka, PI Industries, UPL have been aggressive in placements resulting into impressive volume growth.

Companies have increased prices to offset the impact of rupee depreciation: Though costs have gone up by ~10-15% due to the depreciation of rupee, industry was not able to pass on the total impact of price hikes during the Kharif season. We estimate that the industry took price increases of 5-6% during the Kharif season. During the current Rabi season, companies have taken further price hikes to pass on increased costs.

Prefer agrochemicals over fertilisers in the near term: Though we are positive on the fertiliser space from a medium/long term point of view, in the near-term we prefer agrochemicals over fertilisers due to industry challenges and lack of any high conviction idea. Subsidies are likely to be delayed as govt. is strapped with its finances and this being an election year, budgetary allocation, going ahead, will be a constraint. Resumption of trading is another worrisome factor. Comparatively, agrochemicals companies are well-placed.

PI Industries and United Phosphorus are our top picks: PI Industries (launch of new molecules in domestic business to garner increasing market share, strong momentum in custom synthesis business, healthy order book, increase in margins due to increasing share of custom synthesis), & United Phosphorus (earnings growth combined with improvement in return ratios, gradual improvement in balance sheet, attractive valuation upside) are our top picks.

January 09, 2014 27

Oct-Dec 2013 Earnings Preview

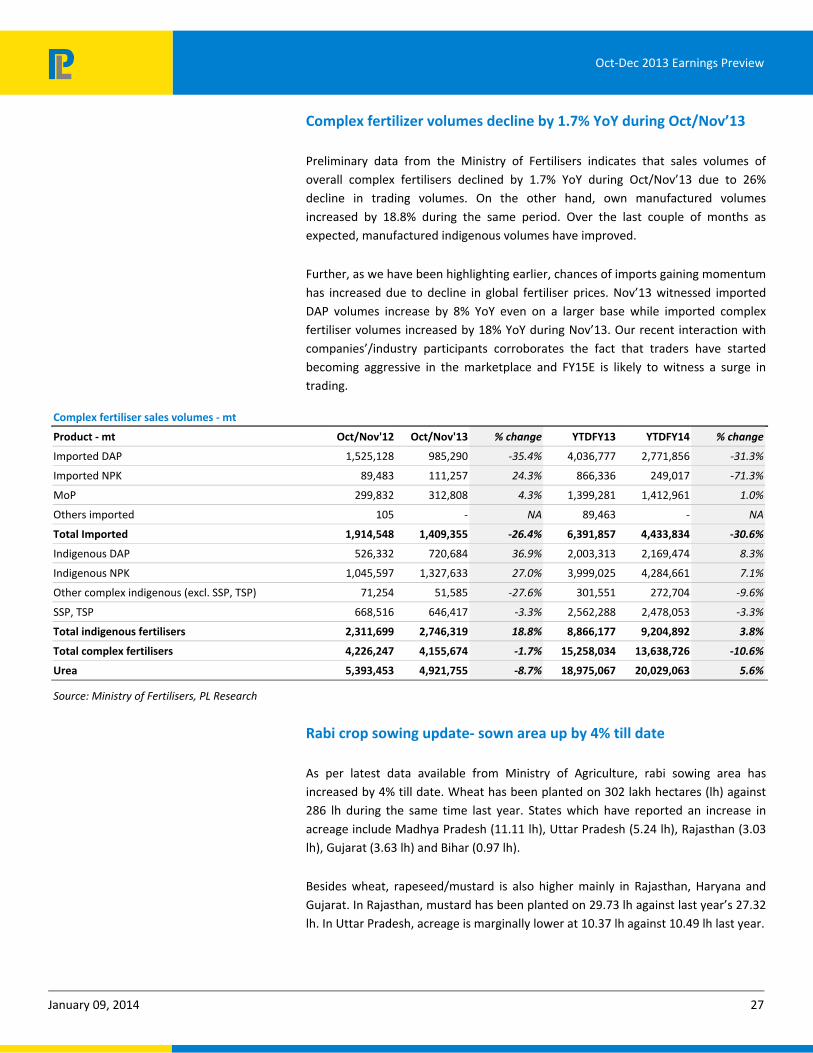

Complex fertilizer volumes decline by 1.7% YoY during Oct/Nov’13

Preliminary data from the Ministry of Fertilisers indicates that sales volumes of overall complex fertilisers declined by 1.7% YoY during Oct/Nov’13 due to 26% decline in trading volumes. On the other hand, own manufactured volumes increased by 18.8% during the same period. Over the last couple of months as expected, manufactured indigenous volumes have improved.

Further, as we have been highlighting earlier, chances of imports gaining momentum has increased due to decline in global fertiliser prices. Nov’13 witnessed imported DAP volumes increase by 8% YoY even on a larger base while imported complex fertiliser volumes increased by 18% YoY during Nov’13. Our recent interaction with companies’/industry participants corroborates the fact that traders have started becoming aggressive in the marketplace and FY15E is likely to witness a surge in trading.

Complex fertiliser sales volumes ‐ mt

Product ‐ mt Oct/Nov'12 Oct/Nov'13 % change YTDFY13 YTDFY14 % change

Imported DAP 1,525,128 985,290 ‐35.4% 4,036,777 2,771,856 ‐31.3%

Imported NPK 89,483 111,257 24.3% 866,336 249,017 ‐71.3%

MoP 299,832 312,808 4.3% 1,399,281 1,412,961 1.0%

Others imported 105 - NA 89,463 - NA

Total Imported 1,914,548 1,409,355 ‐26.4% 6,391,857 4,433,834 ‐30.6%

Indigenous DAP 526,332 720,684 36.9% 2,003,313 2,169,474 8.3%

Indigenous NPK 1,045,597 1,327,633 27.0% 3,999,025 4,284,661 7.1%

Other complex indigenous (excl. SSP, TSP) 71,254 51,585 ‐27.6% 301,551 272,704 ‐9.6%

SSP, TSP 668,516 646,417 ‐3.3% 2,562,288 2,478,053 ‐3.3%

Total indigenous fertilisers 2,311,699 2,746,319 18.8% 8,866,177 9,204,892 3.8%

Total complex fertilisers 4,226,247 4,155,674 ‐1.7% 15,258,034 13,638,726 ‐10.6%

Urea 5,393,453 4,921,755 ‐8.7% 18,975,067 20,029,063 5.6%

Source: Ministry of Fertilisers, PL Research

Rabi crop sowing update‐ sown area up by 4% till date

As per latest data available from Ministry of Agriculture, rabi sowing area has increased by 4% till date. Wheat has been planted on 302 lakh hectares (lh) against 286 lh during the same time last year. States which have reported an increase in acreage include Madhya Pradesh (11.11 lh), Uttar Pradesh (5.24 lh), Rajasthan (3.03 lh), Gujarat (3.63 lh) and Bihar (0.97 lh).

Besides wheat, rapeseed/mustard is also higher mainly in Rajasthan, Haryana and Gujarat. In Rajasthan, mustard has been planted on 29.73 lh against last year’s 27.32 lh. In Uttar Pradesh, acreage is marginally lower at 10.37 lh against 10.49 lh last year.

January 09, 2014 28

Oct-Dec 2013 Earnings Preview

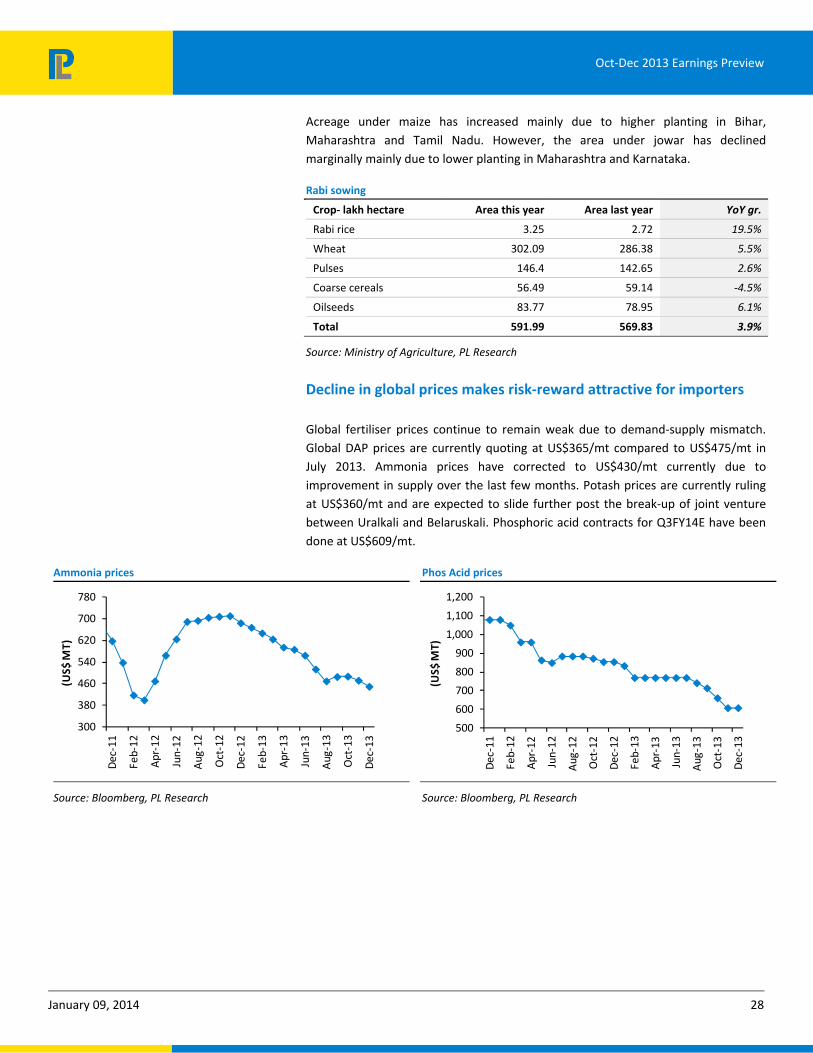

Acreage under maize has increased mainly due to higher planting in Bihar, Maharashtra and Tamil Nadu. However, the area under jowar has declined marginally mainly due to lower planting in Maharashtra and Karnataka.

Rabi sowing

Crop‐ lakh hectare Area this year Area last year YoY gr.

Rabi rice 3.25 2.72 19.5%

Wheat 302.09 286.38 5.5%

Pulses 146.4 142.65 2.6%

Coarse cereals 56.49 59.14 ‐4.5%

Oilseeds 83.77 78.95 6.1%

Total 591.99 569.83 3.9%

Source: Ministry of Agriculture, PL Research

Decline in global prices makes risk‐reward attractive for importers

Global fertiliser prices continue to remain weak due to demand-supply mismatch. Global DAP prices are currently quoting at US$365/mt compared to US$475/mt in July 2013. Ammonia prices have corrected to US$430/mt currently due to improvement in supply over the last few months. Potash prices are currently ruling at US$360/mt and are expected to slide further post the break-up of joint venture between Uralkali and Belaruskali. Phosphoric acid contracts for Q3FY14E have been done at US$609/mt.

Ammonia prices

300

380

460

540

620

700

780

Dec

-11

Feb-

12

Apr

-12

Jun-

12

Aug

-12

Oct

-12

Dec

-12

Feb-

13

Apr

-13

Jun-

13

Aug

-13

Oct

-13

Dec

-13

(US$

MT)

Source: Bloomberg, PL Research

Phos Acid prices

500

600

700

800

900

1,000

1,100

1,200

Dec

-11

Feb-

12

Apr

-12

Jun-

12

Aug

-12

Oct

-12

Dec

-12

Feb-

13

Apr

-13

Jun-

13

Aug

-13

Oct

-13

Dec

-13

(US$

MT)

Source: Bloomberg, PL Research

January 09, 2014 29

Oct-Dec 2013 Earnings Preview

Rock Phospate prices

507090

110130150170190210

Dec

-11

Feb-

12

Apr

-12

Jun-

12

Aug

-12

Oct

-12

Dec

-12

Feb-

13

Apr

-13

Jun-

13

Aug

-13

Oct

-13

Dec

-13

Source: Bloomberg, PL Research

Potash prices

350380410440470500530560590

Dec

-11

Feb-

12

Apr

-12

Jun-

12

Aug

-12

Oct

-12

Dec

-12

Feb-

13

Apr

-13

Jun-

13

Aug

-13

Oct

-13

Dec

-13

(US$

MT)

Source: Bloomberg, PL Research

Global DAP prices

300350400450500550600650700

Dec

-11

Feb-

12

Apr

-12

Jun-

12

Aug

-12

Oct

-12

Dec

-12

Feb-

13

Apr

-13

Jun-

13

Aug

-13

Oct

-13

Dec

-13

(US$ MT)

Source: Bloomberg, PL Research

Urea prices

250

320

390

460

530

600

670

740

Dec

-11

Feb-

12

Apr

-12

Jun-

12

Aug

-12

Oct

-12

Dec

-12

Feb-

13

Apr

-13

Jun-

13

Aug

-13

Oct

-13

Dec

-13

(US$

/ M

T)

Source: Bloomberg, PL Research

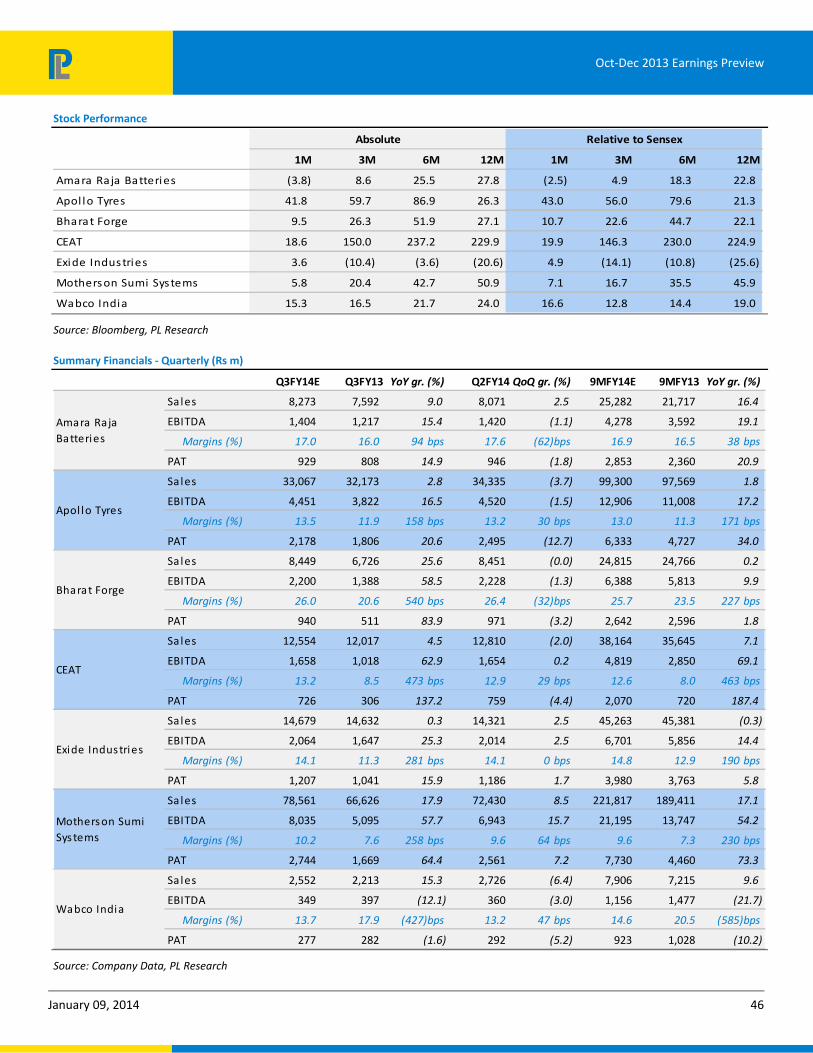

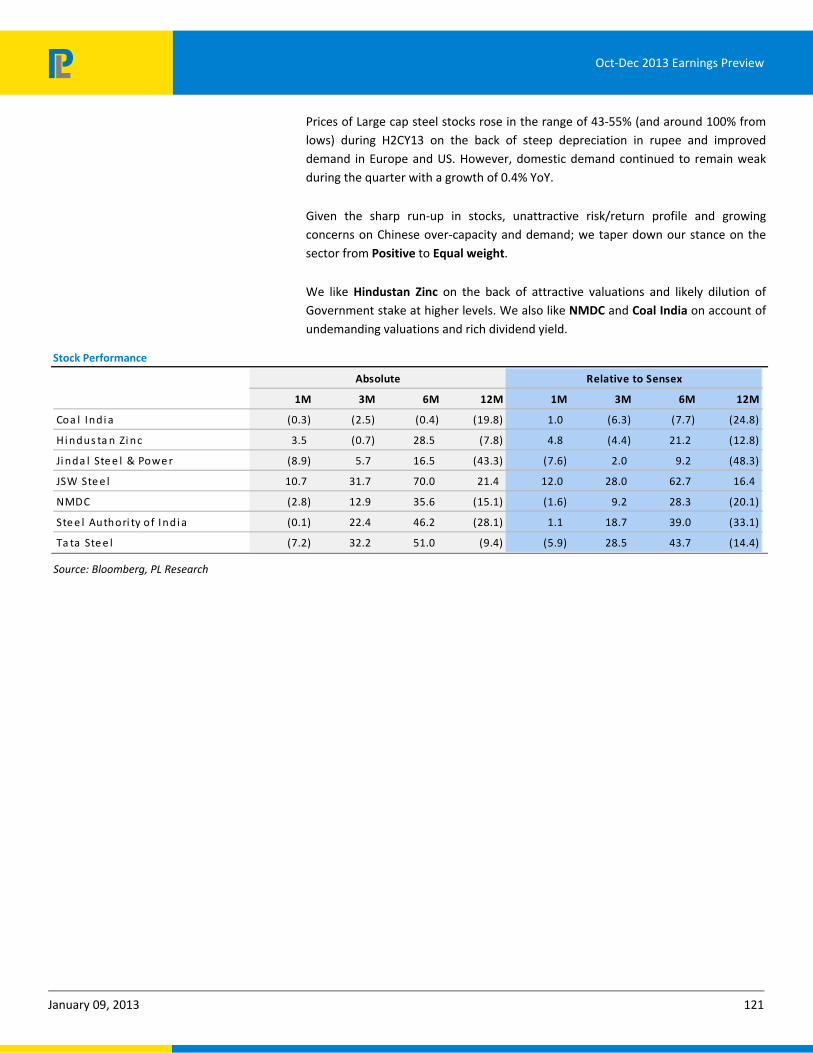

Stock Performance

1M 3M 6M 12M 1M 3M 6M 12M

Chambal Ferti l i zers & Chemica ls 4.3 9.5 7.0 (43.5) 5.6 5.7 (0.3) (48.5)

Coromandel International 9.4 9.1 36.9 (7.1) 10.6 5.4 29.6 (12.1)

Deepak Ferti l i sers & Petrochemica ls Corporation (1.0) (6.3) 8.8 (19.6) 0.3 (10.0) 1.5 (24.6)

Dhanuka Agri tech 14.1 42.5 42.6 48.1 15.4 38.7 35.4 43.1

Gujarat State Ferti l i sers & Chemicals (6.9) 0.8 (13.2) (25.7) (5.7) (3.0) (20.5) (30.7)

P.I . Industries 11.5 64.0 84.3 93.8 12.8 60.3 77.1 88.8

Ra l l i s India 2.3 18.4 28.2 18.9 3.6 14.7 21.0 13.9

Tata Chemica ls (0.6) 11.4 (2.2) (28.2) 0.7 7.7 (9.4) (33.2)

UPL 18.9 34.5 48.4 46.5 20.2 30.8 41.1 41.5

Absolute Relative to Sensex

Source: Bloomberg, PL Research

January 09, 2014 30

Oct-Dec 2013 Earnings Preview

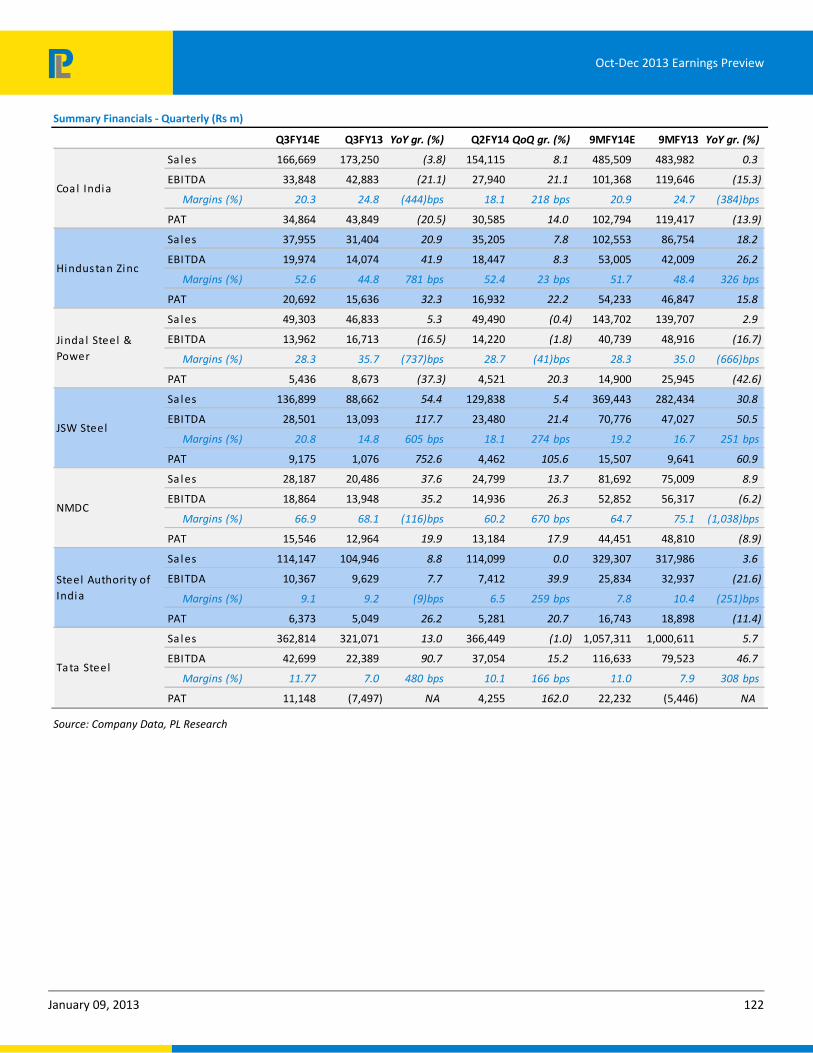

Summary Financials ‐ Quarterly (Rs m)

Q3FY14E Q3FY13 YoY gr. (%) Q2FY14 QoQ gr. (%) 9MFY14E 9MFY13 YoY gr. (%)

Sales 21,239 20,885 1.7 24,903 (14.7) 63,038 57,937 8.8

EBITDA 1,940 2,105 (7.8) 1,946 (0.3) 5,405 5,972 (9.5)

Margins (%) 9.1 10.1 (94)bps 7.8 132 bps 8.6 10.3 (173)bps

PAT 741 961 (22.9) 775 (4.4) 1,974 2,668 (26.0)

Sales 24,575 24,245 1.4 32,154 (23.6) 75,357 68,468 10.1

EBITDA 2,350 1,284 83.1 2,976 (21.0) 6,375 5,766 10.6

Margins (%) 9.6 5.3 427 bps 9.3 31 bps 8.5 8.4 4 bps

PAT 1,208 684 76.6 1,727 (30.1) 3,106 3,367 (7.7)

Sales 8,612 6,234 38.2 9,901 (13.0) 25,938 19,508 33.0

EBITDA 1,006 696 44.6 1,059 (5.0) 3,032 2,521 20.3

Margins (%) 11.7 11.2 52 bps 10.7 99 bps 11.7 12.9 (123)bps

PAT 523 316 65.1 454 15.0 1,479 1,228 20.5

Sales 1,649 1,397 18.0 2,534 (34.9) 5,845 4,541 28.7

EBITDA 231 158 45.7 437 (47.2) 919 622 47.8

Margins (%) 14.0 11.3 266 bps 17.2 (325)bps 15.7 13.7 203 bps

PAT 162 117 38.6 321 (49.5) 656 466 40.8

Sales 12,956 16,728 (22.6) 14,180 (8.6) 37,316 45,007 (17.1)

EBITDA 1,852 1,742 6.3 1,809 2.4 4,854 6,142 (21.0)

Margins (%) 14.3 10.4 388 bps 12.8 154 bps 13.0 13.6 (64)bps

PAT 1,226 991 23.7 1,298 (5.5) 3,127 4,223 (26.0)

Sales 3,548 2,826 25.6 4,628 (23.3) 12,236 8,202 49.2

EBITDA 575 453 26.9 921 (37.6) 2,285 1,383 65.3

Margins (%) 16.2 16.0 17 bps 19.9 (370)bps 18.7 16.9 181 bps

PAT 333 233 43.1 579 (42.4) 1,363 772 76.6

Sales 3,883 3,425 13.4 6,024 (35.5) 14,026 11,733 19.5

EBITDA 540 466 15.8 1,216 (55.6) 2,309 1,849 24.9

Margins (%) 13.9 13.6 29 bps 20.2 (628)bps 16.5 15.8 70 bps

PAT 302 247 22.4 821 (63.2) 1,455 1,052 38.3

Sales 45,276 41,968 7.9 43,440 4.2 121,831 114,147 6.7

EBITDA 5,536 5,362 3.3 5,743 (3.6) 15,394 16,475 (6.6)

Margins (%) 12.2 12.8 (55)bps 13.2 (99)bps 12.6 14.4 (180)bps

PAT 1,855 1,749 6.1 1,574 17.9 4,616 5,639 (18.1)

Sales 26,163 22,956 14.0 23,316 12.2 74,037 63,658 16.3

EBITDA 4,788 4,042 18.4 4,259 12.4 13,613 11,167 21.9

Margins (%) 18.3 17.6 69 bps 18.3 3 bps 18.4 17.5 84 bps

PAT 2,098 1,735 20.9 1,805 16.2 6,439 5,192 24.0

UPL

Ral l i s India

Tata Chemica ls

P.I. Industries

Chambal Ferti l i zers & Chemica ls

Coromandel International

Deepak Ferti l i sers & Petrochemica ls Corporation

Dhanuka Agri tech

Gujarat State Ferti l i sers & Chemica ls

Source: Company Data, PL Research

January 09, 2014 31

Oct-Dec 2013 Earnings Preview

Consolidated Sectoral Data

Quarterly Table (Rs m)

Oct‐Dec'13 Oct‐Dec'12 YoY gr. (%) Jul‐Sep'13 QoQ gr. (%)

Net Sa les 147,900 140,663 5.1 161,080 (8.2)

EBITDA 18,818 16,308 15.4 20,366 (7.6)

Margin (%) 12.7 11.6 113 bps 12.6 8 bps

PAT (Excl . Ex Items) 8,449 7,033 20.1 9,354 (9.7)

Note: Revenue, EBITDA and PAT numbers are arrived by totaling corresponding numbers of all companies under our coverage in this

sector.

We expect Chambal to report urea revenue growth of 11.2% YoY to Rs11.4bn, driven primarily by pricing increase (due to increase in weighted average gas prices). Urea volumes are likely to decline by 6% YoY to 542,720mt. Trading revenues are expected to decline by 12% YoY to Rs8.1bn due to lower fertiliser prices. Fertiliser trading volumes are expected to increase by 5.0% YoY. We expect urea to report EBIT margins of 11.0% (-250bps YoY/40 bps QoQ), while trading margins are expected at 4.6% (-380bps YoY/200bps QoQ). Shipping business profitability is likely to remain under pressure. Quarterly Table (Rs m)

Y/e MarchQ3

FY14E

Q3

FY13

YoY gr.

(%)

Q2

FY14

9M

FY14E

9M

FY13

YoY gr.

(%)

Net Sa les 21,239 20,885 1.7 24,903 63,038 57,937 8.8

EBITDA 1,940 2,105 (7.8) 1,946 5,405 5,972 (9.5)

Margin (%) 9.1 10.1 (94)bps 7.8 9 10 (173)bps

Reported PAT 741 961 (22.9) 942 2,813 2,827 (0.5)

PAT (Excl . Ex Items ) 741 961 (22.9) 775 1,974 2,668 (26.0)

Operating Metrics

Revenue Gr. (%)

Urea 11.2 26.8 (1,557)bps 33.5 21.1 24.1 (300)bps

Trading (11.6) 15.8 NA (21.5) (16.4) 56.6 (7,300)bps

EBIT margins (%)

Urea 11.0 13.5 (251)bps 10.6 11.6 12.9 (130)bps

Key Figures (Rs m)

2013 2014E 2015E

Net Sa les 531,228 569,571 619,712

Growth (%) 8.1 7.2 8.8

EBITDA 66,990 72,447 82,856

Margin (%) 12.6 12.7 13.4

PAT 31,421 33,042 39,876

Growth (%) (16.3) 5.2 20.7

PE (x) 11.2 10.7 8.8

Chambal Fertilisers

Rating Accumulate

Price (Rs ) 40

Target Pri ce (Rs ) 48

M/Cap (Rs bn) 16.6

Shares o/s (m) 416.2

Key Figures (Rs m)

Y/e March FY13 FY14E FY15E

Net Sa les 82,020 77,855 82,647

EBITDA 6,842 6,704 7,455

Margin (%) 8.3 8.6 9.0

PAT 2,266 2,272 2,721

EPS (Rs ) 5.4 5.5 6.5

Growth (%) (24.4) 0.3 19.8

RoE (%) 12.8 11.8 13.1

PE (x) 7.3 7.3 6.1

P / BV (x) 0.9 0.8 0.8

EV / E (x) 9.2 7.9 6.8

January 09, 2014 32

Oct-Dec 2013 Earnings Preview

We expect Coromandel’s (excl. Liberty) manufactured volumes to increase by 40% YoY, while trading volumes are likely to decline by 85% YoY. Coromandel continues to substitute manufacturing over trading. Non-subsidy business is likely to remain strong and we expect revenue growth of 20% YoY. Resultant, total revenues are expected to increase by 1.4% YoY. EBITDA margins are likely to improve by 430bps YoY to 9.6%. We have modeled for EBITDA margins/mt of Rs2,300. Company is likely to report PAT of Rs1.2bn, 77% YoY with EPS of Rs4.3.

Quarterly Table (Rs m)

Y/e MarchQ3

FY14E

Q3

FY13

YoY gr.

(%)

Q2

FY14

9M

FY14E

9M

FY13

YoY gr.

(%)

Net Sa les 24,575 24,245 1.4 32,154 75,357 68,468 10.1

EBITDA 2,350 1,284 83.1 2,976 6,375 5,766 10.6

Margin (%) 9.6 5.3 427 bps 9.3 8 8 4 bps

Reported PAT 1,208 684 76.6 1,601 3,023 4,204 (28.1)

PAT (Excl . Ex Items ) 1,208 684 76.6 1,727 3,106 3,367 (7.7)

Complex fertiliser Volumes‐mt

Trading 18,507 123,380 (85.0) 71,336 107,494 156,059 (31.1)

755,414 1,058,055 984,877 7.4 Manufactured - excl . Liberty

639,793 456,995 40.0

We expect chemicals to report revenue growth of 30% YoY driven primarily by higher chemical volumes. On the fertiliser side, manufactured revenues are likely to increase by 91% YoY driven by higher volumes. We expect manufactured fertiliser volumes to double YoY. Trading revenues are expected to increase by 31% YoY. Chemicals margins are expected to improve 250bps QoQ due to softening of raw materials prices. However, Deepak has initiated a Voluntary Retirement Scheme (VRS) recently. On account of this, it is likely to take a one-time hit of Rs100m during the quarter (we have not incorporated this as it is a one-off item).

Quarterly Table (Rs m)

Y/e MarchQ3

FY14E

Q3

FY13

YoY gr.

(%)

Q2

FY14

9M

FY14E

9M

FY13

YoY gr.

(%)

Net Sa les 8,612 6,234 38.2 9,901 25,938 19,508 33.0

EBITDA 1,006 696 44.6 1,059 3,032 2,521 20.3

Margin (%) 11.7 11.2 52 bps 10.7 12 13 (123)bps

Reported PAT 523 316 65.1 454 1,404 1,178 19.2

PAT (Excl . Ex Items ) 523 316 65.1 454 1,479 1,228 20.5

Sales volumes‐ mt

TAN 76,733 54,037 42.0 73,327 136,100 116,013 17.3

Nitric Acid 31,881 29,795 7.0 34,669 59,114 65,228 (9.4)

IPA 23,824 23,130 3.0 18,426 39,196 35,791 9.5

Manufactured ferti l i s 69,992 34,996 100.0 73,337 125,694 80,727 55.7

Coromandel International

Rating Accumulate

Price (Rs ) 246

Target Pri ce (Rs ) 230

M/Cap (Rs bn) 69.5

Shares o/s (m) 282.6

Key Figures (Rs m)

Y/e March FY13 FY14E FY15E

Net Sa les 89,249 101,397 111,494

EBITDA 6,591 8,146 9,765

Margin (%) 7.4 8.0 8.8

PAT 3,469 3,970 5,246

EPS (Rs ) 12.3 14.0 18.5

Growth (%) (44.3) 14.4 32.0

RoE (%) 15.1 17.4 20.9

PE (x) 20.0 17.5 13.3

P / BV (x) 3.2 2.9 2.6

EV / E (x) 14.2 11.0 8.9

Deepak Fertilisers

Rating Accumulate

Price (Rs ) 103

Target Pri ce (Rs ) 130

M/Cap (Rs bn) 9.1

Shares o/s (m) 88.2

Key Figures (Rs m)

Y/e March FY13 FY14E FY15E

Net Sa les 26,101 30,577 32,806

EBITDA 3,221 3,780 4,363

Margin (%) 12.3 12.4 13.3

PAT 1,519 1,912 2,277

EPS (Rs ) 17.2 21.7 25.8

Growth (%) (35.4) 25.9 19.1

RoE (%) 12.0 13.9 15.0

PE (x) 6.0 4.8 4.0

P / BV (x) 0.7 0.6 0.6

EV / E (x) 5.7 5.0 4.2

January 09, 2014 33

Oct-Dec 2013 Earnings Preview

We expect Dhanuka to report revenue growth of 18.0% YoY. Our channel checks suggest that Q3 has been pretty strong for Dhanuka and it is likely to report robust topline growth. New launches are also expected to gain momentum over the course of FY14E. We expect Dhanuka to report EBITDA of Rs231m, 46% YoY with margins of 14.0%. The company is likely to report PAT of Rs162m, 39% YoY.

Quarterly Table (Rs m)

Y/e MarchQ3

FY14E

Q3

FY13

YoY gr.

(%)

Q2

FY14

9M

FY14E

9M

FY13

YoY gr.

(%)

Net Sa les 1,649 1,397 18.0 2,534 5,845 4,541 28.7

EBITDA 231 158 45.7 437 919 622 47.8

Margin (%) 14.0 11.3 266 bps 17.2 16 14 203 bps

Reported PAT 162 117 38.6 321 656 466 40.8

PAT (Excl . Ex Items ) 162 117 38.6 321 656 466 40.8

We expect fertiliser revenues to decline by 40% YoY to Rs7.6bn due to lower complex fertiliser trading this year. Chemicals revenues are expected to increase by 15.0% YoY . Caprolactam-benzene spreads remained weak during the quarter though they were stable at ~$1,100/mt. We expect company to report PAT of Rs1.3bn, 24% YoY with EPS of Rs3.1.

Quarterly Table (Rs m)

Y/e MarchQ3

FY14E

Q3

FY13

YoY gr.

(%)

Q2

FY14

9M

FY14E

9M

FY13

YoY gr.

(%)

Net Sa les 12,956 16,728 (22.6) 14,180 37,316 45,007 (17.1)

EBITDA 1,852 1,742 6.3 1,809 4,854 6,142 (21.0)

Margin (%) 14.3 10.4 388 bps 12.8 13 14 (64)bps

Reported PAT 1,226 1,370 (10.5) 1,013 2,295 4,602 (50.1)

PAT (Excl . Ex Items ) 1,226 991 23.7 1,298 3,127 4,223 (26.0)

Operating Metrics

Revenues (Rs m)

Ferti l i ser 7,601 12,638 (39.9) 8,454 11,675 18,150 (35.7)

Chemica ls 5,355 4,656 15.0 5,726 10,661 10,128 5.3

EBIT Margin (%)

Ferti l i ser 8.0 8.8 (83)bps 7.2 10.4 8.7 170 bps

Chemica ls 18.0 9.2 876 bps 16.1 12.7 24.2 (1,150)bps

Dhanuka Agritech

Rating BUY

Price (Rs ) 189

Target Pri ce (Rs ) 220

M/Cap (Rs bn) 9.5

Shares o/s (m) 50.0

Key Figures (Rs m)

Y/e March FY13 FY14E FY15E

Net Sa les 5,869 7,286 8,452

EBITDA 865 1,151 1,369

Margin (%) 14.7 15.8 16.2

PAT 644 818 977

EPS (Rs ) 12.9 16.4 19.5

Growth (%) 12.8 26.9 19.4

RoE (%) 27.0 27.7 26.7

PE (x) 14.7 11.6 9.7

P / BV (x) 3.6 2.9 2.3

EV / E (x) 11.3 8.5 7.0

GSFC

Rating Accumulate

Price (Rs ) 54

Target Pri ce (Rs ) 60

M/Cap (Rs bn) 21.4

Shares o/s (m) 398.5

Key Figures (Rs m)

Y/e March FY13 FY14E FY15E

Net Sa les 61,967 54,957 58,220

EBITDA 7,813 7,023 8,091

Margin (%) 12.6 12.8 13.9

PAT 5,187 4,455 5,206

EPS (Rs ) 13.0 11.2 13.1

Growth (%) (32.3) (14.1) 16.8

RoE (%) 13.9 10.8 11.5

PE (x) 4.1 4.8 4.1

P / BV (x) 0.5 0.5 0.5

EV / E (x) 4.5 4.1 3.2

January 09, 2014 34

Oct-Dec 2013 Earnings Preview

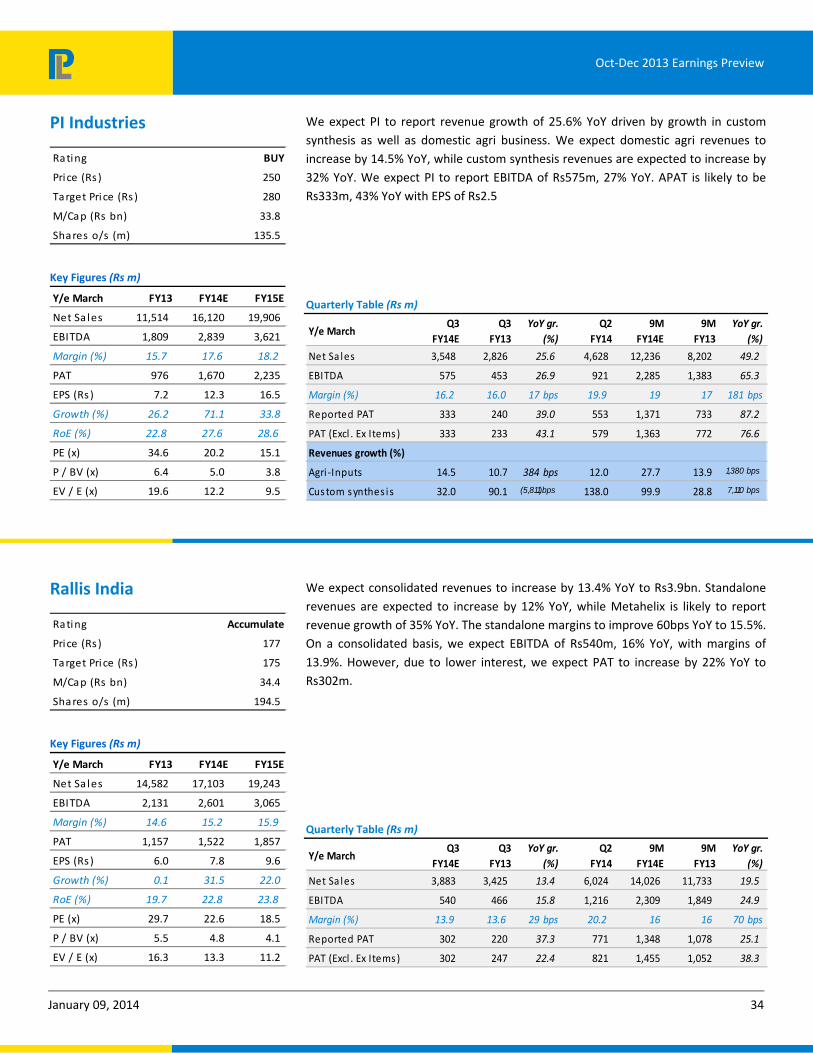

We expect PI to report revenue growth of 25.6% YoY driven by growth in custom synthesis as well as domestic agri business. We expect domestic agri revenues to increase by 14.5% YoY, while custom synthesis revenues are expected to increase by 32% YoY. We expect PI to report EBITDA of Rs575m, 27% YoY. APAT is likely to be Rs333m, 43% YoY with EPS of Rs2.5

Quarterly Table (Rs m)

Y/e MarchQ3

FY14E

Q3

FY13

YoY gr.

(%)

Q2

FY14

9M

FY14E

9M

FY13

YoY gr.

(%)

Net Sa les 3,548 2,826 25.6 4,628 12,236 8,202 49.2

EBITDA 575 453 26.9 921 2,285 1,383 65.3

Margin (%) 16.2 16.0 17 bps 19.9 19 17 181 bps

Reported PAT 333 240 39.0 553 1,371 733 87.2

PAT (Excl . Ex Items ) 333 233 43.1 579 1,363 772 76.6

Revenues growth (%)

Agri -Inputs 14.5 10.7 384 bps 12.0 27.7 13.9 1,380 bps

Cus tom synthes is 32.0 90.1 (5,811)bps 138.0 99.9 28.8 7,110 bps

We expect consolidated revenues to increase by 13.4% YoY to Rs3.9bn. Standalone revenues are expected to increase by 12% YoY, while Metahelix is likely to report revenue growth of 35% YoY. The standalone margins to improve 60bps YoY to 15.5%. On a consolidated basis, we expect EBITDA of Rs540m, 16% YoY, with margins of 13.9%. However, due to lower interest, we expect PAT to increase by 22% YoY to Rs302m.

Quarterly Table (Rs m)

Y/e MarchQ3

FY14E

Q3

FY13

YoY gr.

(%)

Q2

FY14

9M

FY14E

9M

FY13

YoY gr.

(%)

Net Sa les 3,883 3,425 13.4 6,024 14,026 11,733 19.5

EBITDA 540 466 15.8 1,216 2,309 1,849 24.9

Margin (%) 13.9 13.6 29 bps 20.2 16 16 70 bps

Reported PAT 302 220 37.3 771 1,348 1,078 25.1

PAT (Excl . Ex Items ) 302 247 22.4 821 1,455 1,052 38.3

PI Industries

Rating BUY

Price (Rs ) 250

Target Pri ce (Rs ) 280

M/Cap (Rs bn) 33.8

Shares o/s (m) 135.5

Key Figures (Rs m)

Y/e March FY13 FY14E FY15E

Net Sa les 11,514 16,120 19,906

EBITDA 1,809 2,839 3,621

Margin (%) 15.7 17.6 18.2

PAT 976 1,670 2,235

EPS (Rs ) 7.2 12.3 16.5

Growth (%) 26.2 71.1 33.8

RoE (%) 22.8 27.6 28.6

PE (x) 34.6 20.2 15.1

P / BV (x) 6.4 5.0 3.8

EV / E (x) 19.6 12.2 9.5

Rallis India

Rating Accumulate

Price (Rs ) 177

Target Pri ce (Rs ) 175

M/Cap (Rs bn) 34.4

Shares o/s (m) 194.5

Key Figures (Rs m)

Y/e March FY13 FY14E FY15E

Net Sa les 14,582 17,103 19,243

EBITDA 2,131 2,601 3,065

Margin (%) 14.6 15.2 15.9

PAT 1,157 1,522 1,857

EPS (Rs ) 6.0 7.8 9.6

Growth (%) 0.1 31.5 22.0

RoE (%) 19.7 22.8 23.8

PE (x) 29.7 22.6 18.5

P / BV (x) 5.5 4.8 4.1

EV / E (x) 16.3 13.3 11.2

January 09, 2014 35

Oct-Dec 2013 Earnings Preview

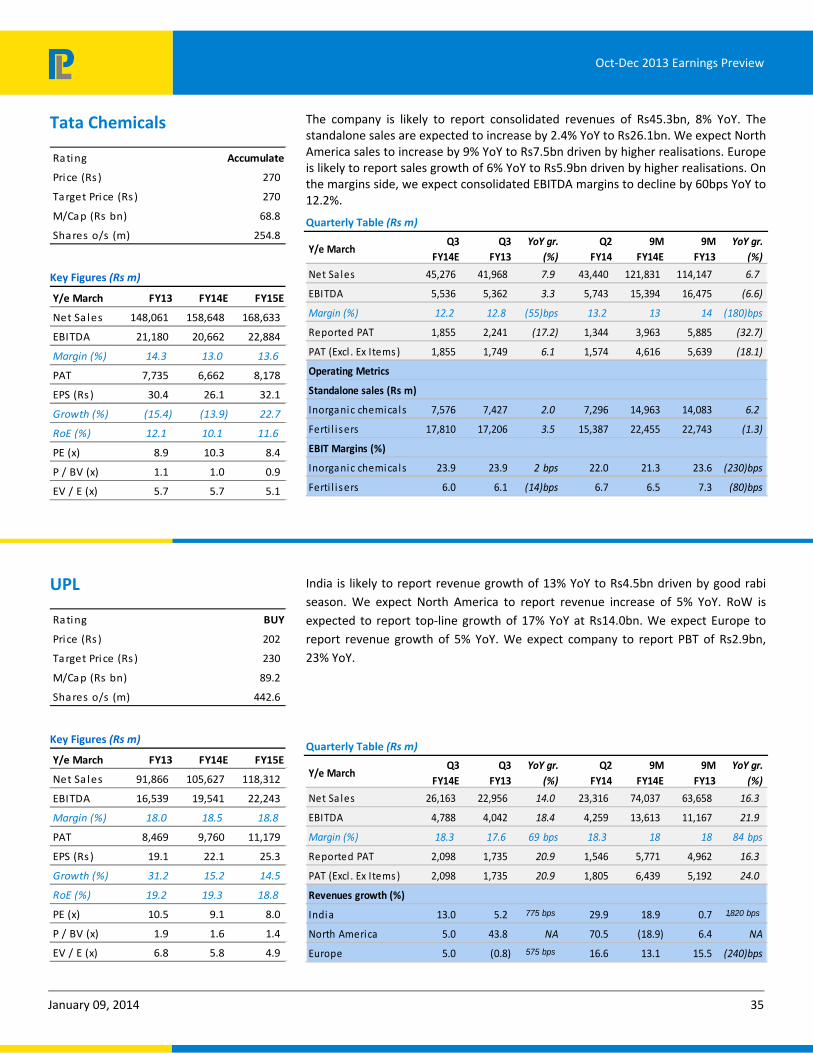

The company is likely to report consolidated revenues of Rs45.3bn, 8% YoY. The standalone sales are expected to increase by 2.4% YoY to Rs26.1bn. We expect North America sales to increase by 9% YoY to Rs7.5bn driven by higher realisations. Europe is likely to report sales growth of 6% YoY to Rs5.9bn driven by higher realisations. On the margins side, we expect consolidated EBITDA margins to decline by 60bps YoY to 12.2%.

Quarterly Table (Rs m)

Y/e MarchQ3

FY14E

Q3

FY13

YoY gr.

(%)

Q2

FY14

9M

FY14E

9M

FY13

YoY gr.

(%)

Net Sa les 45,276 41,968 7.9 43,440 121,831 114,147 6.7

EBITDA 5,536 5,362 3.3 5,743 15,394 16,475 (6.6)

Margin (%) 12.2 12.8 (55)bps 13.2 13 14 (180)bps

Reported PAT 1,855 2,241 (17.2) 1,344 3,963 5,885 (32.7)

PAT (Excl . Ex Items ) 1,855 1,749 6.1 1,574 4,616 5,639 (18.1)

Operating Metrics

Standalone sales (Rs m)

Inorganic chemicals 7,576 7,427 2.0 7,296 14,963 14,083 6.2

Ferti l i sers 17,810 17,206 3.5 15,387 22,455 22,743 (1.3)

EBIT Margins (%)

Inorganic chemicals 23.9 23.9 2 bps 22.0 21.3 23.6 (230)bps

Ferti l i sers 6.0 6.1 (14)bps 6.7 6.5 7.3 (80)bps

India is likely to report revenue growth of 13% YoY to Rs4.5bn driven by good rabi season. We expect North America to report revenue increase of 5% YoY. RoW is expected to report top-line growth of 17% YoY at Rs14.0bn. We expect Europe to report revenue growth of 5% YoY. We expect company to report PBT of Rs2.9bn, 23% YoY.

Quarterly Table (Rs m)

Y/e MarchQ3

FY14E

Q3

FY13

YoY gr.

(%)

Q2

FY14

9M

FY14E

9M

FY13

YoY gr.

(%)

Net Sa les 26,163 22,956 14.0 23,316 74,037 63,658 16.3

EBITDA 4,788 4,042 18.4 4,259 13,613 11,167 21.9

Margin (%) 18.3 17.6 69 bps 18.3 18 18 84 bps

Reported PAT 2,098 1,735 20.9 1,546 5,771 4,962 16.3

PAT (Excl . Ex Items ) 2,098 1,735 20.9 1,805 6,439 5,192 24.0

Revenues growth (%)

India 13.0 5.2 775 bps 29.9 18.9 0.7 1,820 bps

North America 5.0 43.8 NA 70.5 (18.9) 6.4 NA

Europe 5.0 (0.8) 575 bps 16.6 13.1 15.5 (240)bps

Tata Chemicals

Rating Accumulate

Price (Rs ) 270

Target Pri ce (Rs ) 270

M/Cap (Rs bn) 68.8

Shares o/s (m) 254.8

Key Figures (Rs m)

Y/e March FY13 FY14E FY15E

Net Sa les 148,061 158,648 168,633

EBITDA 21,180 20,662 22,884

Margin (%) 14.3 13.0 13.6

PAT 7,735 6,662 8,178

EPS (Rs ) 30.4 26.1 32.1

Growth (%) (15.4) (13.9) 22.7

RoE (%) 12.1 10.1 11.6

PE (x) 8.9 10.3 8.4

P / BV (x) 1.1 1.0 0.9

EV / E (x) 5.7 5.7 5.1

UPL

Rating BUY

Price (Rs ) 202

Target Pri ce (Rs ) 230

M/Cap (Rs bn) 89.2

Shares o/s (m) 442.6

Key Figures (Rs m)

Y/e March FY13 FY14E FY15E

Net Sa les 91,866 105,627 118,312

EBITDA 16,539 19,541 22,243

Margin (%) 18.0 18.5 18.8

PAT 8,469 9,760 11,179

EPS (Rs ) 19.1 22.1 25.3

Growth (%) 31.2 15.2 14.5

RoE (%) 19.2 19.3 18.8

PE (x) 10.5 9.1 8.0

P / BV (x) 1.9 1.6 1.4

EV / E (x) 6.8 5.8 4.9

January 09, 2013 36

Oct-Dec 2013 Earnings Preview

Surjit Arora [email protected] +91-22-6632 2235

Top picks

Hero Motocorp

Automobiles Domestic two‐wheeler grew by ~7.0% YoY: On account of higher fuel prices, general inflation and slowdown in the economy, the domestic two-wheeler segment growth was tepid at 7.0% YoY in volume terms during the quarter. Hero Motocorp (HMCL) is likely to grow at a faster clip of 6.9% on account of strong 20%+ growth in the scooter segment. On the other hand, Bajaj Auto (BJA) registered de-growth of ~24.0% YoY on account of slowdown in demand and increased competition from HMSI. HMSI continues to clock impressive volumes with a growth of ~29.2% YoY for the quarter led by increased capacity in the motorcycles segment.

Recovery in two-wheeler industry demand is likely, given the good monsoon, coupled with possible increase in government spending ahead of 2014 national elections. We expect 12-13% CAGR in scooter volumes for the next two years. We expect two-wheeler volumes to grow at ~7% CAGR, mainly led by 12.2% CAGR in scooter volumes and 6.0% CAGR in motorcycle volumes over FY13-FY15E period. Scooter share in the last three years has increased from 15% to 21% of two-wheeler volumes mainly driven by (a) growing acceptability of gearless scooters, particularly by women, (b) rising urbanization and increasing proportion of working women.

Going by the current trend of rising rural incomes with higher yields and minimum support prices, the outlook on two-wheelers is positive. Low penetration level, lack of adequate mode public transport and rising per capita income in rural India would lead to long-term healthy volume of two-wheelers. With rural economy accounting for 40-45% of the sales for two-wheelers, we expect good times ahead for two-wheeler manufacturers.

Quarterly trend in two‐wheeler segment sales

Particulars Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14E

Two-Wheelers 3,597,592 3,420,937 3,490,677 3,526,294 3,848,000

QoQ Growth (%) 10.4% ‐4.9% 2.0% 1.0% 9.1%

Source: SIAM Data, PL Research

Two‐wheeler segment sales

Q3FY14E Q3FY13 YoY gr. (%)

Domestic Two‐wheelers 3,848,000 3,597,592 7.0

Hero Motocorp 1,680,940 1,573,145 6.9

Bajaj Auto 523,759 687,351 (23.8)

HMSI 977,000 644,737 51.5

Source: SIAM Data, PL Research

January 09, 2013 37

Oct-Dec 2013 Earnings Preview

Higher interest rates, increased fuel prices were negated by lower base of MSIL leading to a 4.7% de‐growth in the passenger vehicle (Cars +UVs) segment:

Quarterly trend in passenger car segment sales

Particulars Q3FY13 Q4FY13 Q1FY14 Q2FY14E Q3FY14E

Passenger Cars 618,825 664,439 607,469 540,498 590,000

QoQ Growth (%) 11.0% 6.3% ‐8.6% ‐11.0% 8.8%

Source: SIAM Data, PL Research

Consumer sentiment has been impacted negatively on account of higher prices of cars (Excise duty + Registration Tax) and higher fuel prices. Demand for petrol cars has weakened YTD which is evident from the high inventory levels for petrol cars and higher discounts on the same. It is unlikely that this scenario will improve in the coming months.

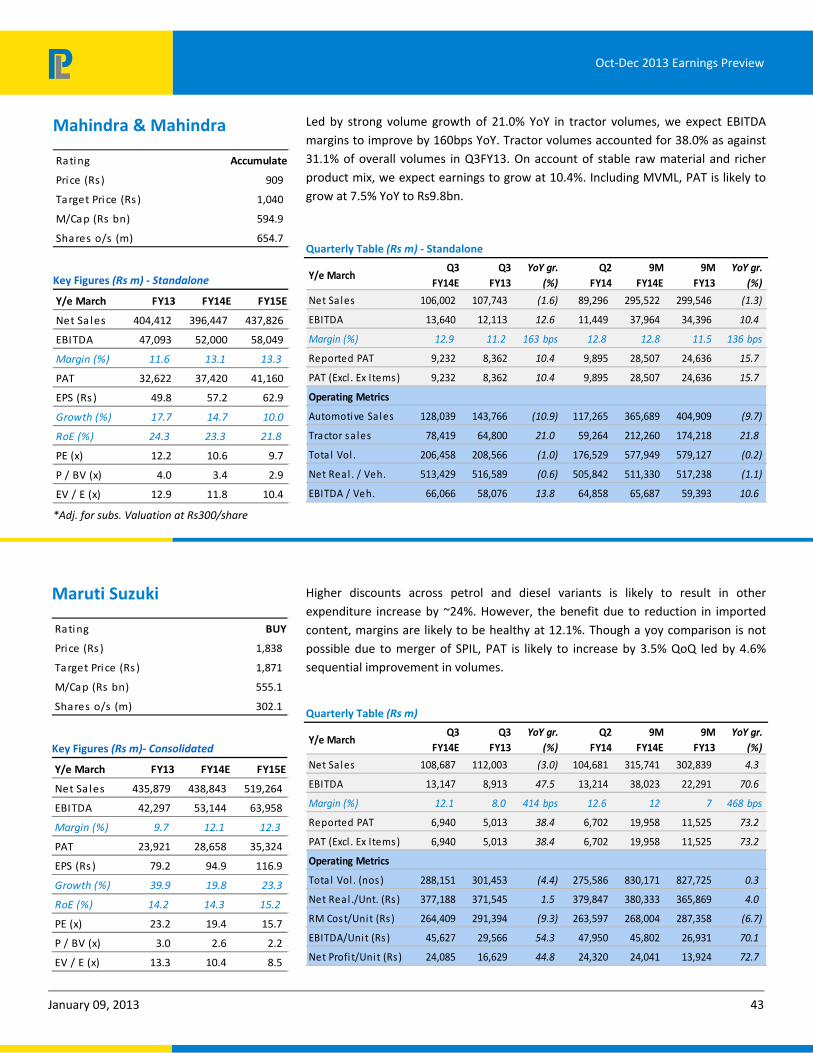

At the same time, given the current slowdown in the economy, the diesel car demand is also fading with a de-growth during the quarter, with the diesel cars of Maruti Suzuki (MSIL) are now available off the shelf and carry discounts on them.

M&M is facing the brunt of a slowdown in UV space coupled with intense competition especially from Ford ‘EcoSport’. M&M continued its steep decline in the Passenger vehicle segment with a de-growth of 24.4% for the quarter.

We believe the recovery is still some time away and the decline in volumes for the industry is likely to continue in the near term (at least for the next 4-6 months).

Passenger Vehicle (Car + UV) segment sales

Q3FY14E Q3FY13 YoY gr. (%)

Domestic Passenger Vehicle 590,000 618,825 (4.7)

Maruti Suzuki 242,066 243,619 (0.6)

Hyundai 100,702 97,071 3.7

M&M 56,131 74,297 (24.4)

Tata Motors 33,781 53,335 (36.7)

Ford 25,300 20,038 26.2

Source: SIAM Data, PL Research

Medium & Heavy Commercial Vehicles (M&HCV) sales decline by 30.8% YoY on account of lower freight rates and slowdown in economic activity

Quarterly trend in M&HCV segment sales

Particulars Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14E

M&HCVs 57,539 70,184 55,945 49,552 39,784

QoQ Growth (%) ‐22.9% 21.9% ‐20.3% ‐11.4% ‐19.7%

Source: SIAM Data, PL Research

January 09, 2013 38

Oct-Dec 2013 Earnings Preview

Truck rentals remain stable on trunk routes on account of a) lesser availability of truck fleet due to disruption caused by heavy rains and floods in several states during Aug 2013 and b) improved cargo availability on account of arrival of fruits and vegetables in APMCs.

Despite record discounts on sales and subvention to auto financers, M&HCV goods segment reported a sharp decline of ~38.0% YoY mainly on account of low cargo offering across segments and negative sentiments on the ground level. We maintain our negative view on the Trucking industry (M&HCV segment) for the next 4-6 months.

YTD M&HCV segment sales

Q3FY14E Q3FY13 YoY gr. (%)

Domestic M&HCV 39,784 57,539 (30.8)

Tata Motors 22,417 31,482 (28.8)

Ashok Leyland 10,698 14,681 (27.1)

Source: SIAM Data, PL Research

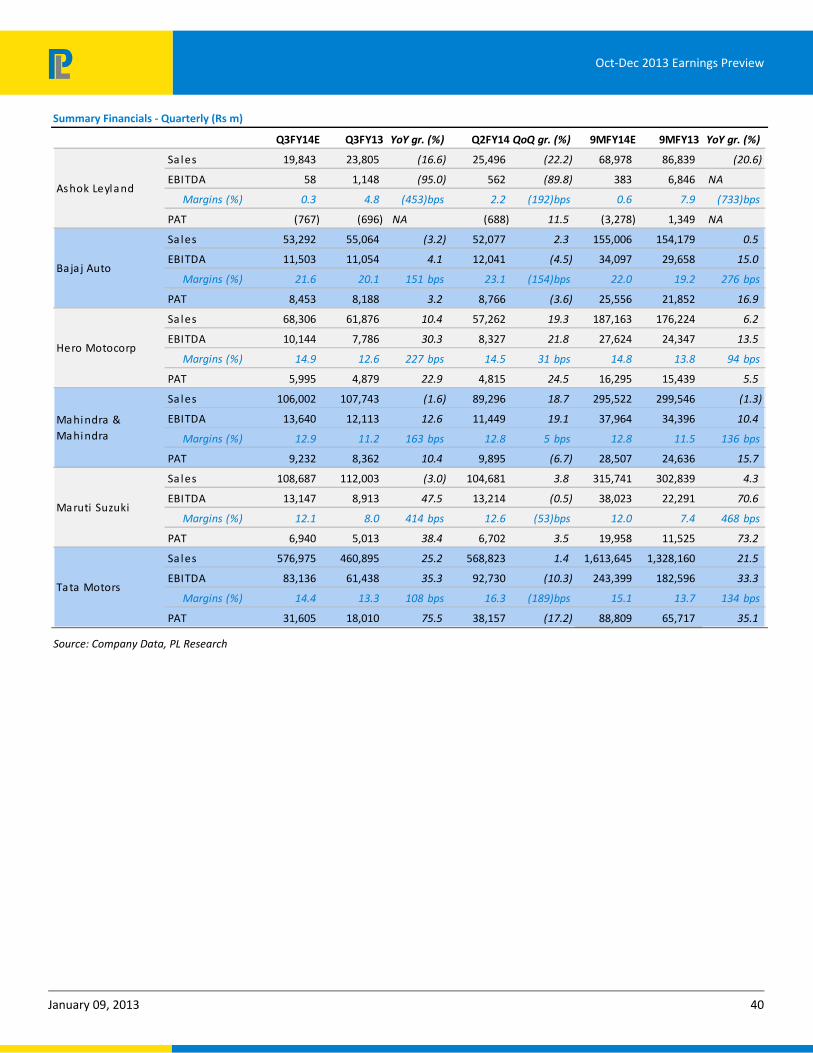

Auto companies under our coverage are likely to post a 13.5% YoY top-line growth mainly led by volume growth and price increases.

Auto Companies ‐ Raw Material Index

94.0

96.0

98.0

100.0

102.0

104.0

106.0

108.0

Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14E

Source: PL Research

We have built a raw material index giving different weightage to different commodities. We have assigned highest weightage to Steel (45%), followed by Aluminium (20%) and Plastics/Polymers (15%). Our raw material index declined by ~3.0% QoQ. Major raw materials have declined by 4-5% in the last few months. On account of stable raw material, coupled with cost-cutting efforts by companies and price increases, we expect EBITDA margins to improve by 160bps YoY for the quarter.

January 09, 2013 39

Oct-Dec 2013 Earnings Preview

Our universe – Volume numbers

Company Q3FY14E YoY gr (%) QoQ gr (%)

Ashok Leyland 18,453 (18.6) (20.2)

Bajaj Auto 993,690 (11.9) 3.4

Hero Motocorp 1,680,940 6.9 18.7

M&M 206,458 (1.0) 17.0

Maruti Suzuki 288,151 (4.4) 4.6

Tata Motors 130,337 (36.1) (14.3)

Tata Motors JLR 103,431 9.1 1.5

Source: Company Data, PL Research

PAT for the coverage universe is likely to grow by 40.5%, led by 75.5% growth for TTMT and a 38.4% growth for MSIL (not comparable due to merger with Suzuki Powertrain), for the quarter. Exc. TTMT, the PAT for the coverage universe is likely to grow by 16.0%.

Hero Motocorp: We believe that with the interest rate inching up and robust rural economy, two-wheeler stocks are likely to outperform over the next one year. Three key factors leading to our stance are a) Strong rural economy led by good monsoon and increase in MSPs b) Export potential - Indian firms are better placed compared to Chinese counterparts on currency and labour cost front 3) Valuation attractive at ~13.7x 1yr fwd P/E, given the strong 18% earnings CAGR, coupled with strong balance sheet and better corporate governance. We maintain ‘Accumulate’ rating with a TP of Rs2,352.

Stock Performance

1M 3M 6M 12M 1M 3M 6M 12M

As hok Le yl a nd 12.3 16.2 (1.9) (31.6) 13.6 12.5 (9.2) (36.6)

Ba ja j Auto (1.6) (9.3) 3.0 (12.7) (0.4) (13.1) (4.3) (17.7)

He ro Motocorp (1.5) 2.2 24.9 9.8 (0.2) (1.5) 17.6 4.8

Ma hi ndra & Ma hi ndra (3.9) 5.3 (4.1) (5.1) (2.6) 1.5 (11.3) (10.1)

Ma ruti Suzuki 8.0 30.6 18.5 16.7 9.3 26.9 11.2 11.7

Ta ta Motors (5.3) 5.6 28.6 17.9 (4.0) 1.9 21.4 12.9

Absolute Relative to Sensex

Source: Bloomberg, PL Research

January 09, 2013 40