India: Appraisal of Second Foodgrain Storage Project - World ...

175

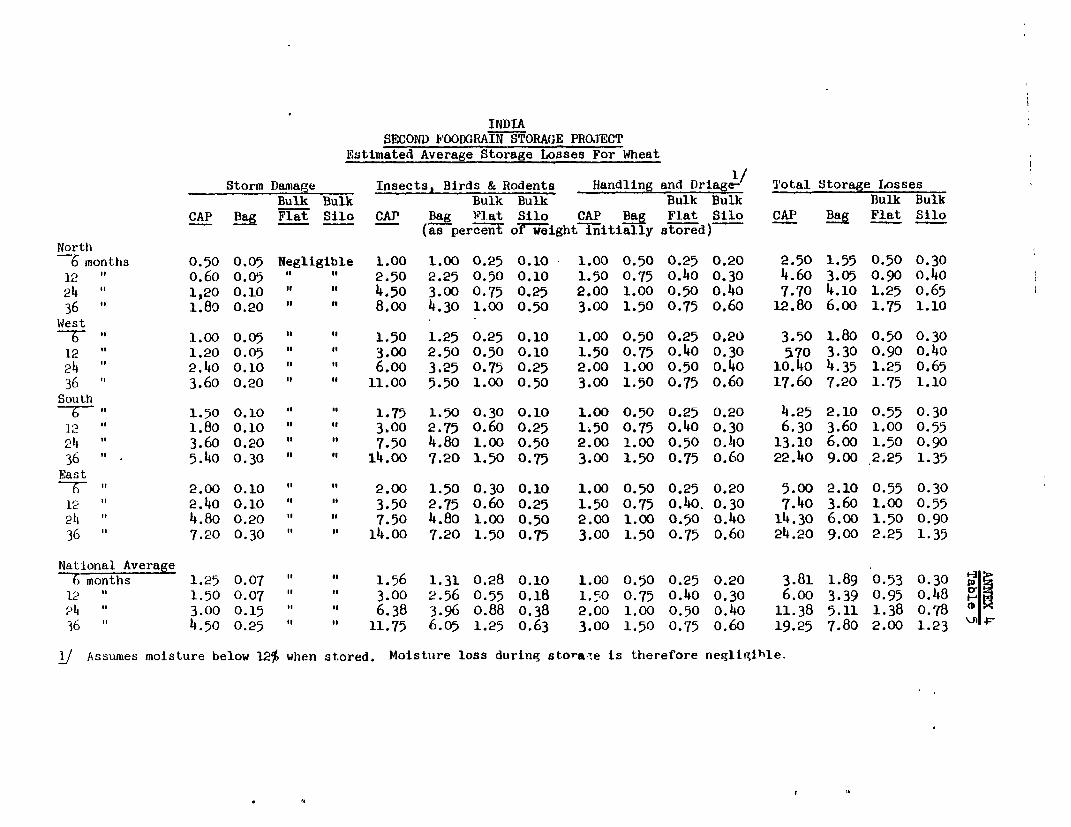

FILE COPY Report No.1643a-IN India: Appraisal of Second Foodgrain Storage Project November3, 1977 South Asia Projects Department AgricultureD Division FOR OFFICIAL USE ONLY Document of the World Bank This cocument hasa restricted distributionarJ maybe used by recipients in: i Ehe Performance of their official duties. 1's contentsmaynot utnerv&ise be disclcsed without World Hank authurization Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

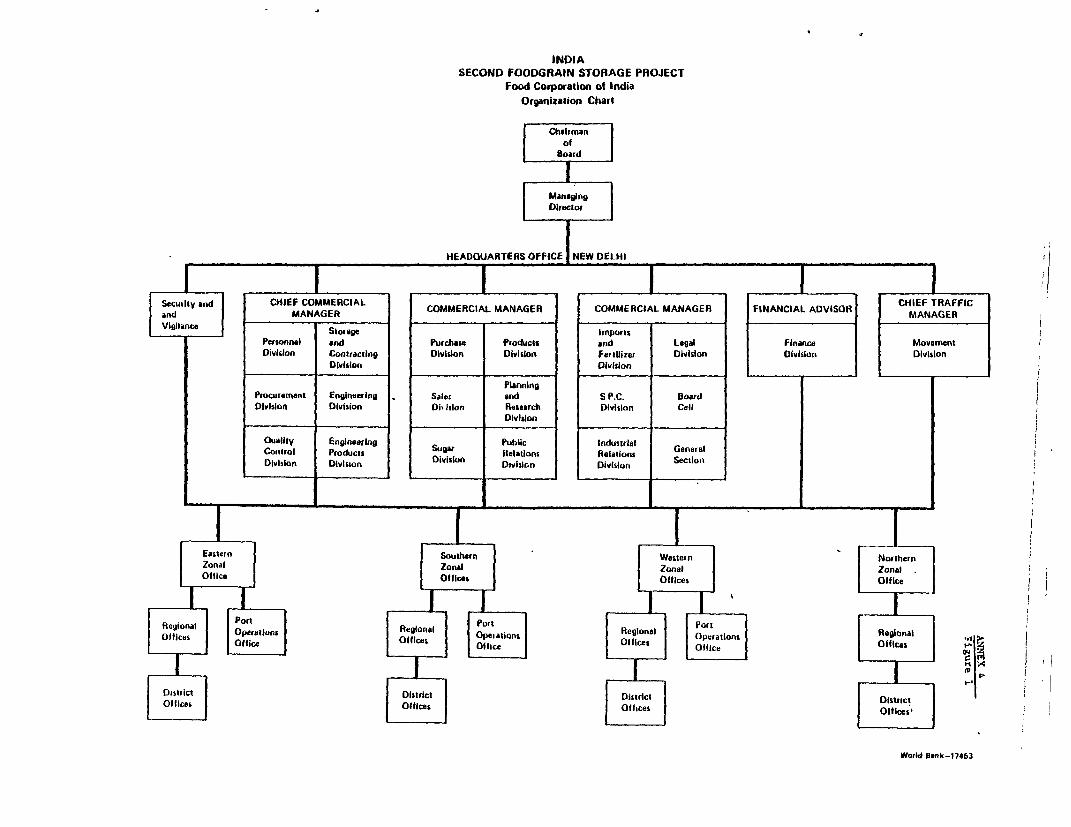

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of India: Appraisal of Second Foodgrain Storage Project - World ...

FILE COPYReport No. 1643a-IN

India: Appraisal of Second FoodgrainStorage Project

November 3, 1977

South Asia Projects DepartmentAgriculture D DivisionFOR OFFICIAL USE ONLY

Document of the World Bank

This cocument has a restricted distribution arJ may be used by recipientsin: i Ehe Performance of their official duties. 1's contents may not

utnerv&ise be disclcsed without World Hank authurization

Pub

lic D

iscl

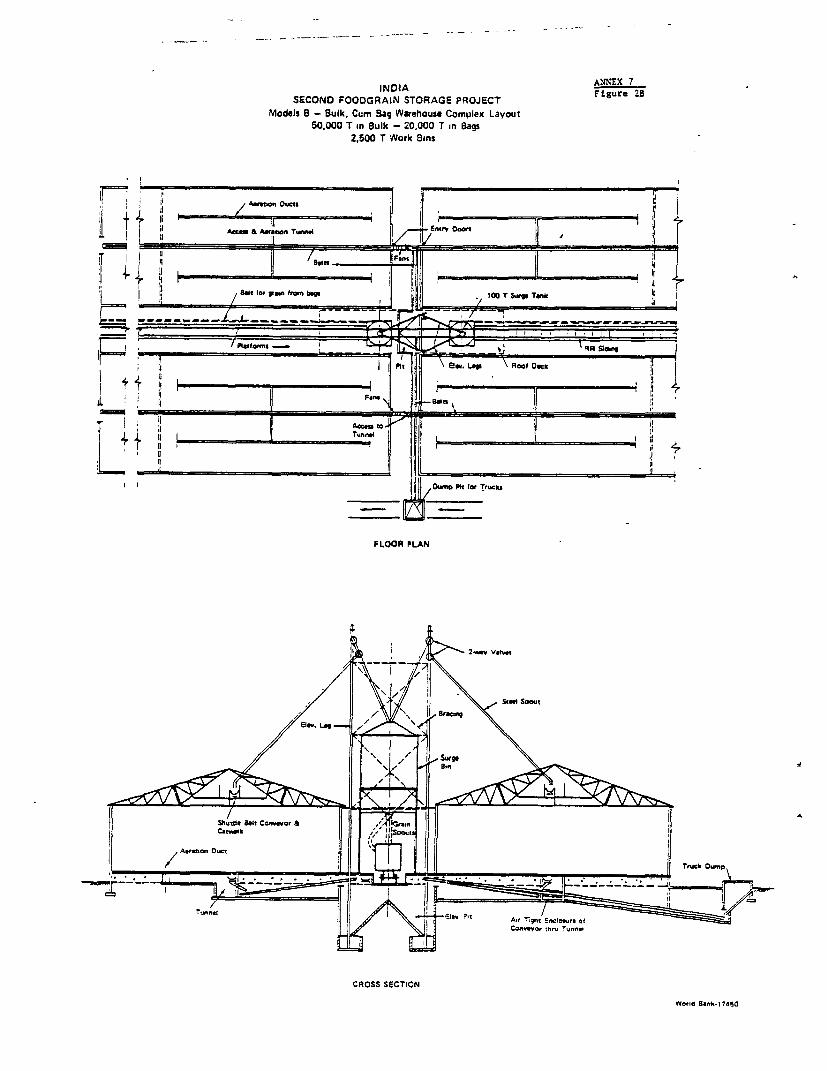

osur

e A

utho

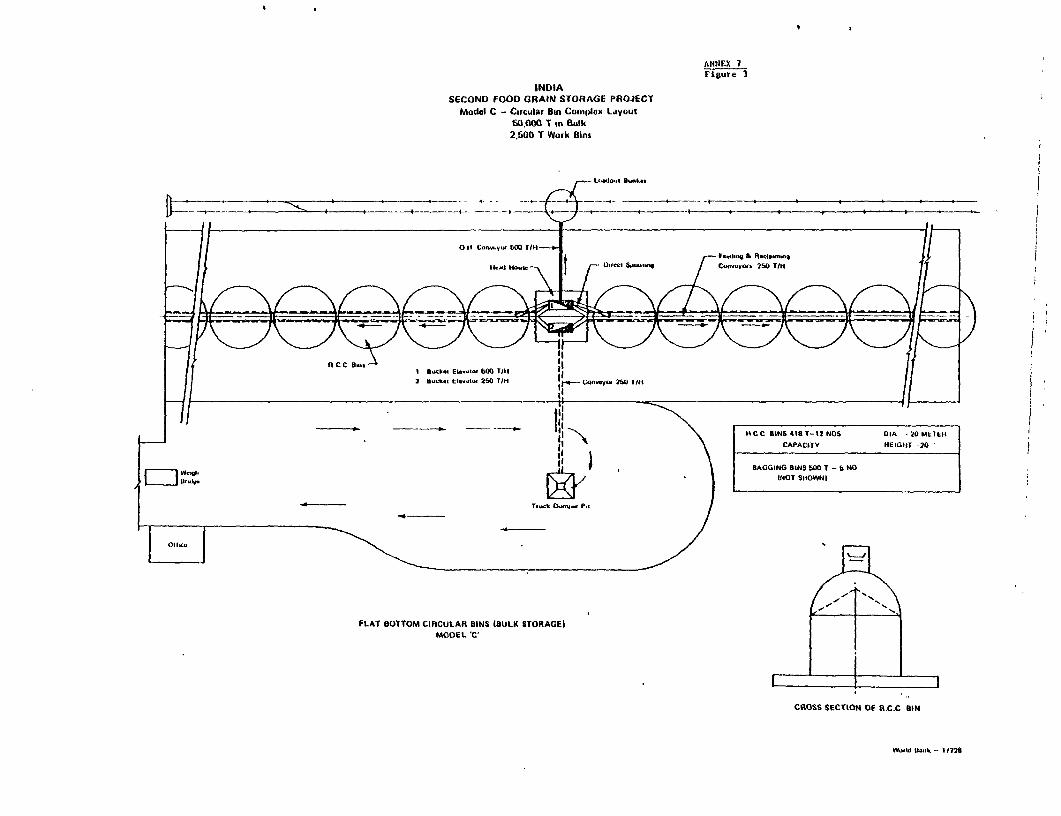

rized

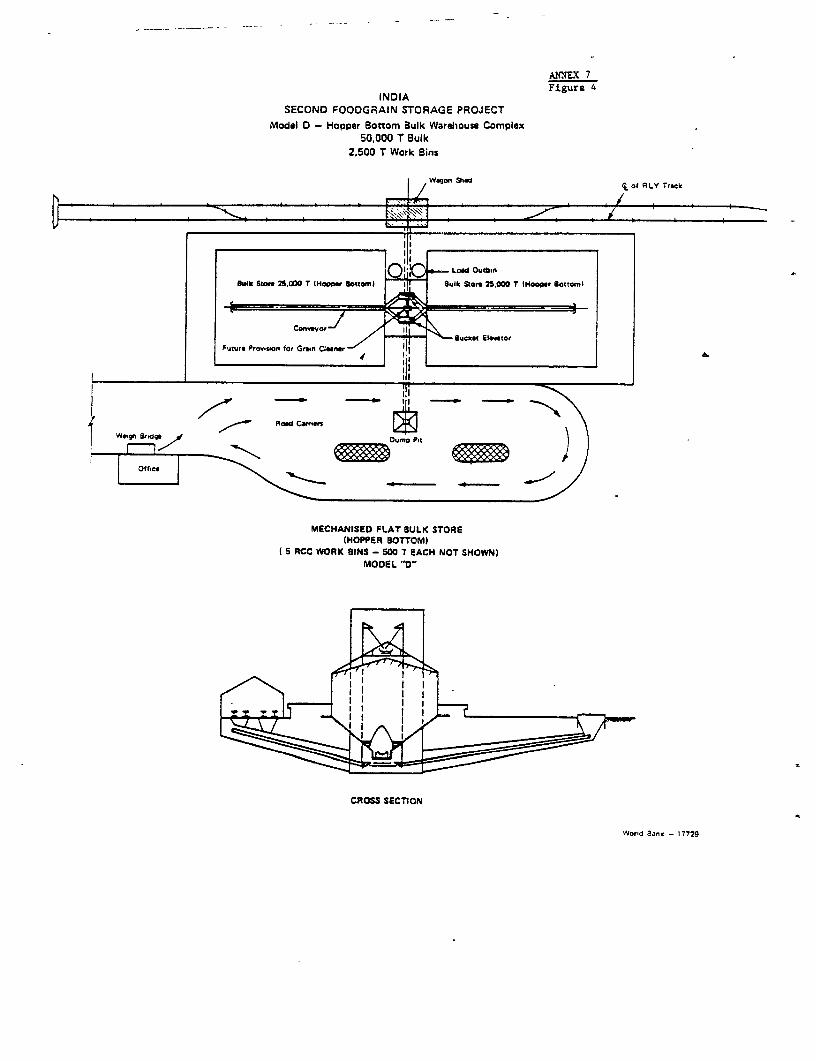

Pub

lic D

iscl

osur

e A

utho

rized

Pub

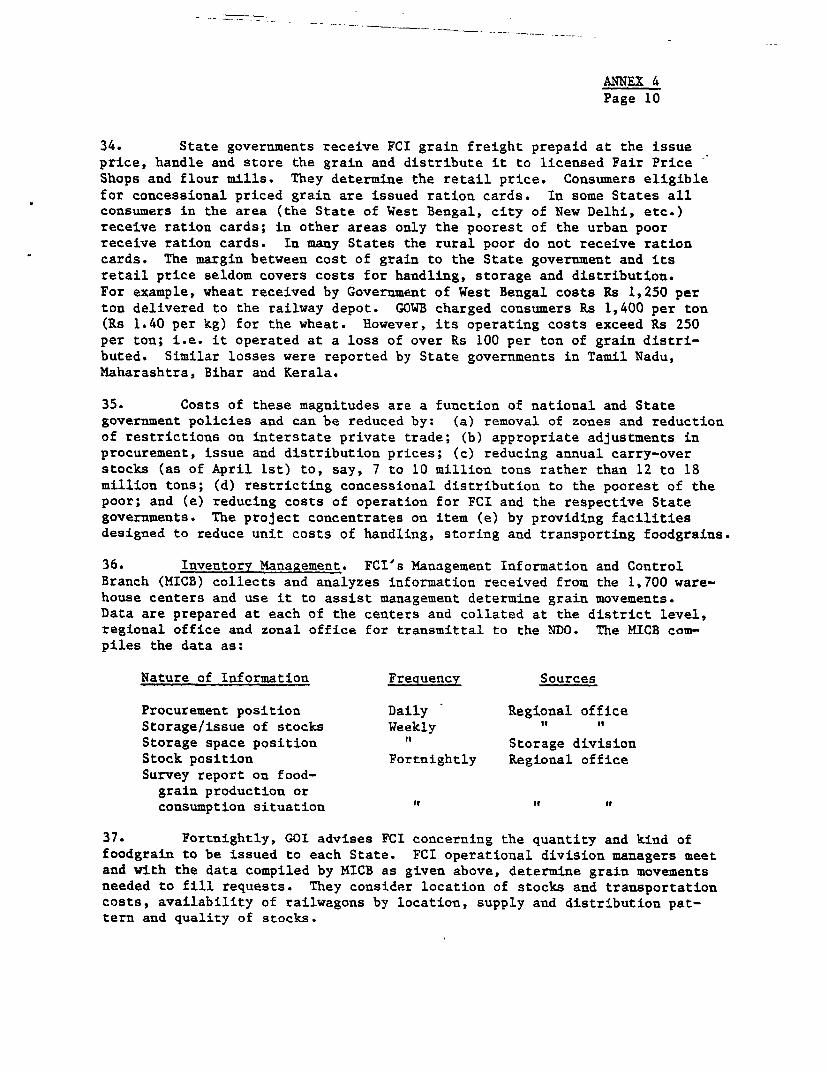

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCy EQUIVALENTS

US$1.00 = Rupees (Rs) 8.7Rs 1.00 = US$0.11Rs 1 million = US$114.286

WEIGHTS AND MEASURES (METRIC SYSTEM)

1 metric ton = 1,000 kilograms (kg)1 grain bag = About 100 kg Wheat

- About 57 kg PaddyAbout 75 kg Rice

ABBREVIATIONS

ASCI - Administrative Staff College of India, HyderabadCAP - Cover and plinth (bagged grain placed on brick

plinth and covered with polyethylene sheets)CSS - Central Storage CommitteeCWC - Central Warehousing CorporationFCI - Food Corporation o' IndiaGOI - Government of IndiaIR - Indian RailwaysMICB - Management Information and Control Branch - of FCIPID - Project Implementation Division - of FCI

Indian Fiscal Year

April 1 - March 31

FOR OanUCL UQ ONLY

INDIA

SECOND FOODGRAIN STORAGE PROJECT

Table of Contents

Pala No.

SUMMARY AND CONCLUSIONS . ...................... ....... i - iii.

A. General *......*.... *******t*e.*****

B. Background ........... c

tI. FOODG.AINS IT INDIA .................................... 2

III. FOOD CORPORATION OF INDIA .'............................ 6

A. General *..*o ......... . ......*............ IB. Analysis of Operations ........ ................... . 7C. Review of Wheat Storage Project (Credit 267-lN) ... 9

IV. THE PROJECT ................................ ..... ***so 9

A. General *................. 9B. Detailed Features ........ * ... .*............ 10C. Iupleeutatiou Schedule............................ 14 -

D. Cost Estimates ........... . ....................... 14E. Proposed Financing ...................... 16Fe Procurement ............. 16Go Disbursement ........ **.**e ..*..17

V. O GANIZATION AND MANAGEMENT ............. ............ ... 18

A. General .................................... *.... 18B. Project Implementation Divlsios ................... 18C. Accoumets and Audit .................o.................. 20D. Youitoring and Evaluation ........ . .......-.... 20

VI. ECONOMIC BENEFITS AND JUSTIFICATION *........o.*oo*%.o 21

VII. RECOMMENDATIONS ...... ....... .o ........ ooo ...... 22

l Tbi document hae a tricted dwuUte am v wed by Po, Go igk the pwrmace0f thei ocal dutio Iu contents my s oehui be eni wihw Werd dsk B"*ihoinion.

Table of Contents (Cont'd)

ANNEXES

1. Review of First Wheat Storage Prolect (Cr. 267-IN)

2. Foodgrain Production, Consumption and Prolections

A. Gross Foodgrain ProductionB. Projections of Foodgrain ProductionC. Foodgrain ConsumptionD. Projection of Foodgrain Consumption

3. Government FoodRrain Policies and Practices

A. ObjectivesB. Instruments of Foodgrain PolicyC. Government Programs of Procurement, Distribution and

ImportsD. Buffer Stock Operations

4. The Food Corporation of India

A. BackgrountdB. Organization and ManagementC. FunctionsD. Financial ManagementE. TrainingF. Analysis of FCI OperationsC. Construction and Maintenance of Storage Facilities

5. Foodgrain Resources and Needs

A. Without the ProjectB. With the Project

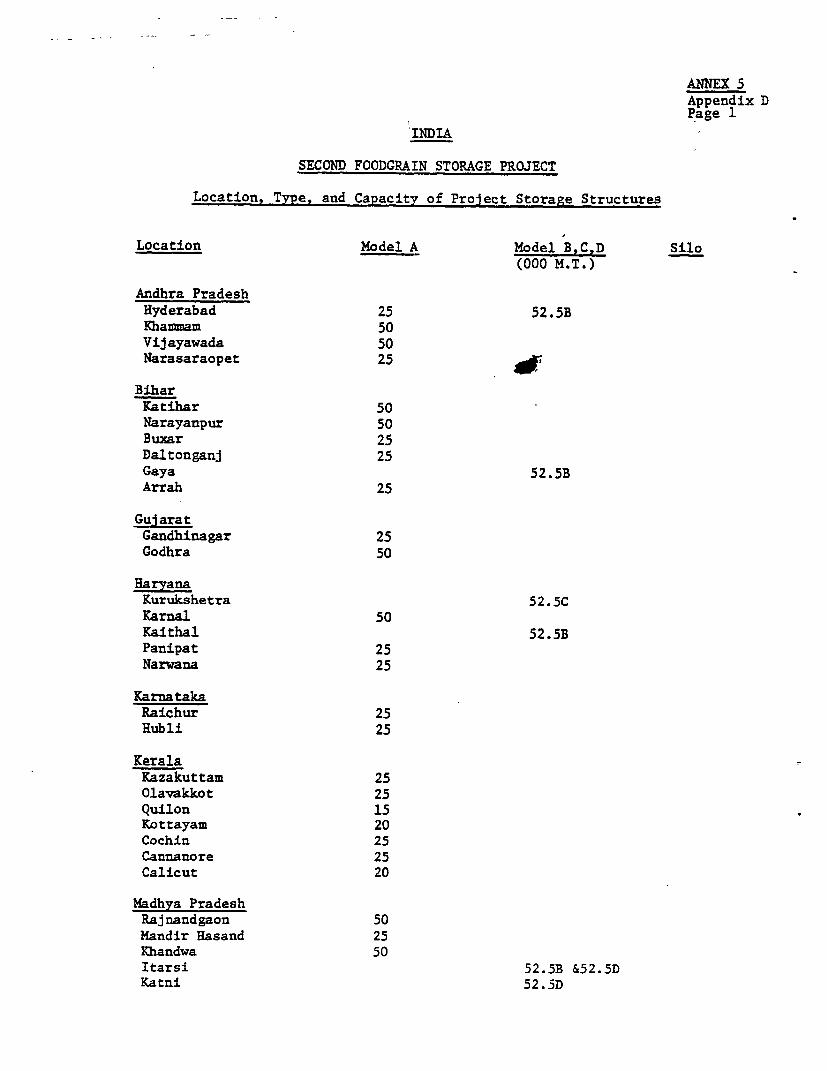

Appendix A - Location and Type of Existing Grain Storage WarehousesOwned by FCI

Appendix B - Criteria for Site Selection and Type of Storage

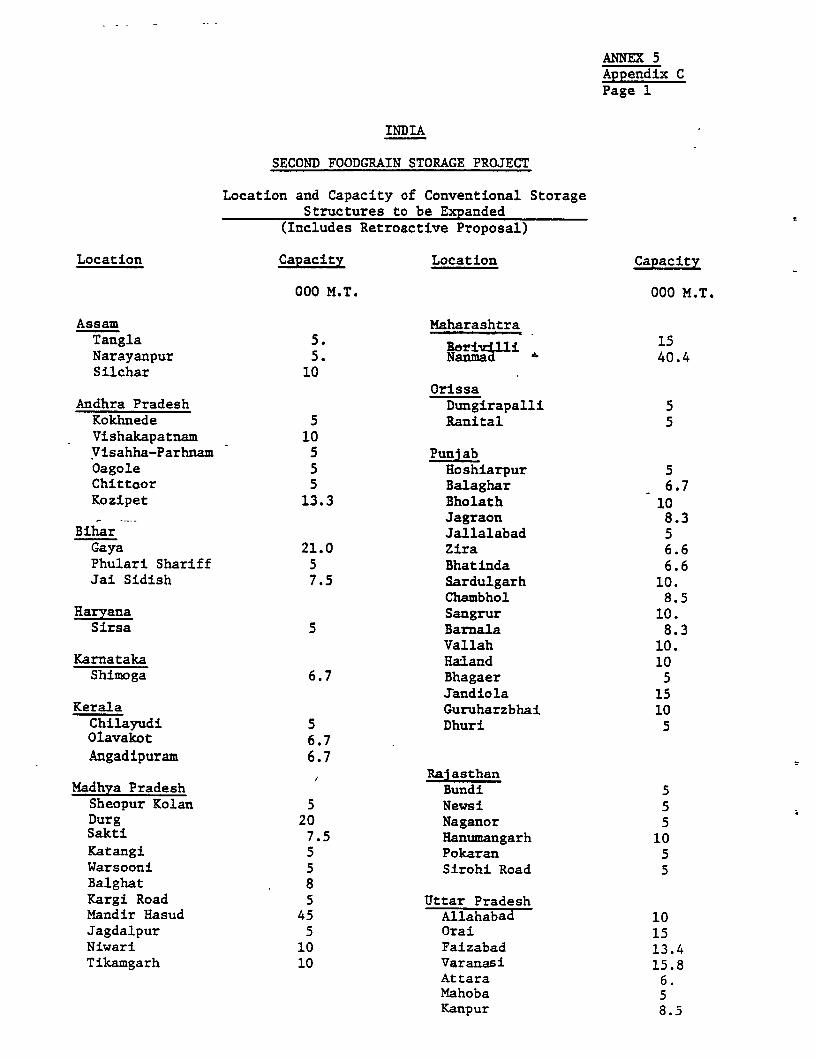

Appendix C - Location and Capacity of Conventional StorageStructures to be Expanded

Appendix D - Locations, Type and Storage Capacity of Storage Structuresto be Constructed

6. Resources for Transporting Foodgrains

Table of Contents (Cont'd)

7. Description and Specifications for Grain Storage Warehousesand Model Complexes

A. GeneralB. Specifications for Model A Warehouse ComplexC. Specifications for Model B Warehouse ComplexD. Specifications for Model C Circular BinsE. Specifications for Model D Hopper Bottom Flat Bulk WarehouseF. Specifications for Port SilosG. Relative Merits of Each Type of Model Warehouse ComplexH. Rural Grain Procurement Centers

Figure 1 - Model A Warehouse Complex LayoutFigure 2 - Model B Warehouse Complex LayoutFigure 3 - Model C Circular Bin Complex LayoutFigure 4 - Model D Warehouse Complex Layout

8. ProJect Organization and Management

A. GeneralB. Project Implementation DivisiouC. ProcurementD. Accounts and AuditsE. Monitoring and Evaluation

9. Estimated Prolect Costs

10. Project Implementation Schedule

11. Estimated Disbursement Schedule

12. Economic and Financial Analysis

A. GeneralB. Economic AnalysisC. Economic Rate of ReturnD. Financial Rate of Return

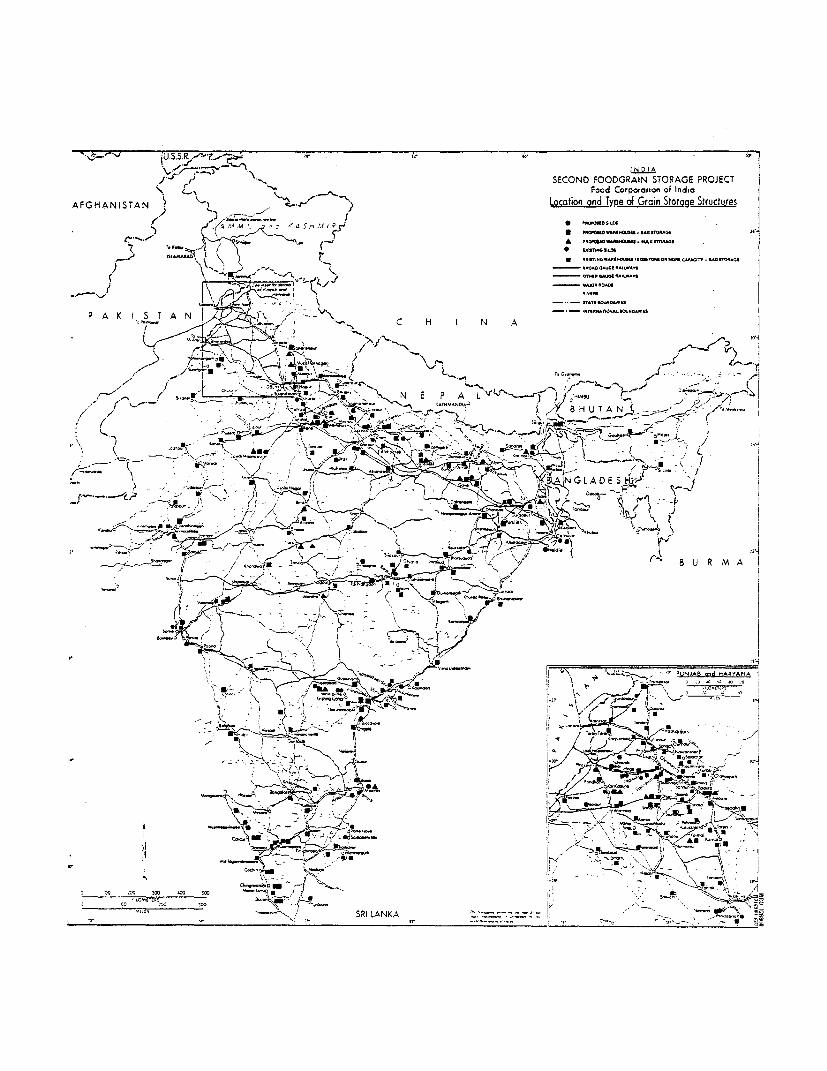

IBRD Map 12880 - Showing Location of Existing and Proposed Storage Sites

INDIA

SECOND FOODGRAIN STORAGE PROJECT

SUMMARY AND CONCLUSIONS

i. Agriculture, the largest sector in the Indian economy, accountsfor over 40% of GNP and about 70% of total employment. Foodgrains, partic-ularly cereals, are the most important crops grown, accounting for about 75%of total cultivated area. Foodgrain production increased at 2.3% annuallyfrom 1953/54 to 1975/76, about the same rate as population increase. Food-grain imports have taken place all these years to meet shortfalls in domesticsupply even though self-sufficiency has been a major economic goal of thegovernment since independence in 1947. Since the mid-1960's foodgrain pro-duction has increased at the higher rate of 2.8% per annum, resulting mainlyfrom the successful green revolution in wheat. It appears that this higherrate can be maintained or even increased, given the continuing extension ofirrigation and use of the new seed-fertilizer technology. Although importsmay continue through the 1980s, self-sufficiency can be attained gradually.The weather remains the main determinant of the annual fluctuations in food-grain production.. Recently, favourable monsoons have led to good harvestsin 1975-76 and 1976-77 and to record foodgrain stock levels (reported at 20.7million tons in July 1977).

ii. India's foodgrain policy has three major objectives: (a) self-sufficiency in production; (b) price stability; and (c) equitable foodgraindistribution. Food pclicy is the responsibility of both the Central andState governments. In 1964-65, the Government of India (GOI) establishedthe Food Corporation of India (FCI) to serve as the agency responsible forimplementing national food procurement and distribution programs. Instrumentsof policy have included the use of food zones to regulate inter-district andinterstate trade; support, procurement and issue price regulations; procure-ment, storage and distribution of seasonal and buffer stocks; imports offoodgrains and rationing of public sector procured supplies to eligible con-sumers at concessional prices. Foodgrain prices have been regulated to (i)ensure reasonable prices to producers; (ii) procure a sizeable portion ofmarketed foodgrains on behalf of GOI and State governments; (iii) releasefoodgrains through the public distribution system in order to protect lowincome groups; (iv) minimize seasonal and interregional price variations,and (v) build up sizeable buffer stocks to protect consumers from widevariations in production caused by irregular and untimely monsoons.

iii. FCI operates with a Board of twelve government appointed Directorsunder the general direction of the Ministry of Food and Agriculture. A re-gular staff of about 60,000 are engaged in procuring foodgrains at over 2,500market centers and operating warehouses at 1,700 locations throughout India.In recent years, FCI has procured annually 3.0 to 10.0 million tons, or 10 to35% of foodgrains marketed, in addition to handling grain imports of 3.5 to7.5 millicn tons per annum. FCI's distribution of grains at concessionalprices has ranged from 8.0 million tons to 14.0 million tons per annum.

- ii,-

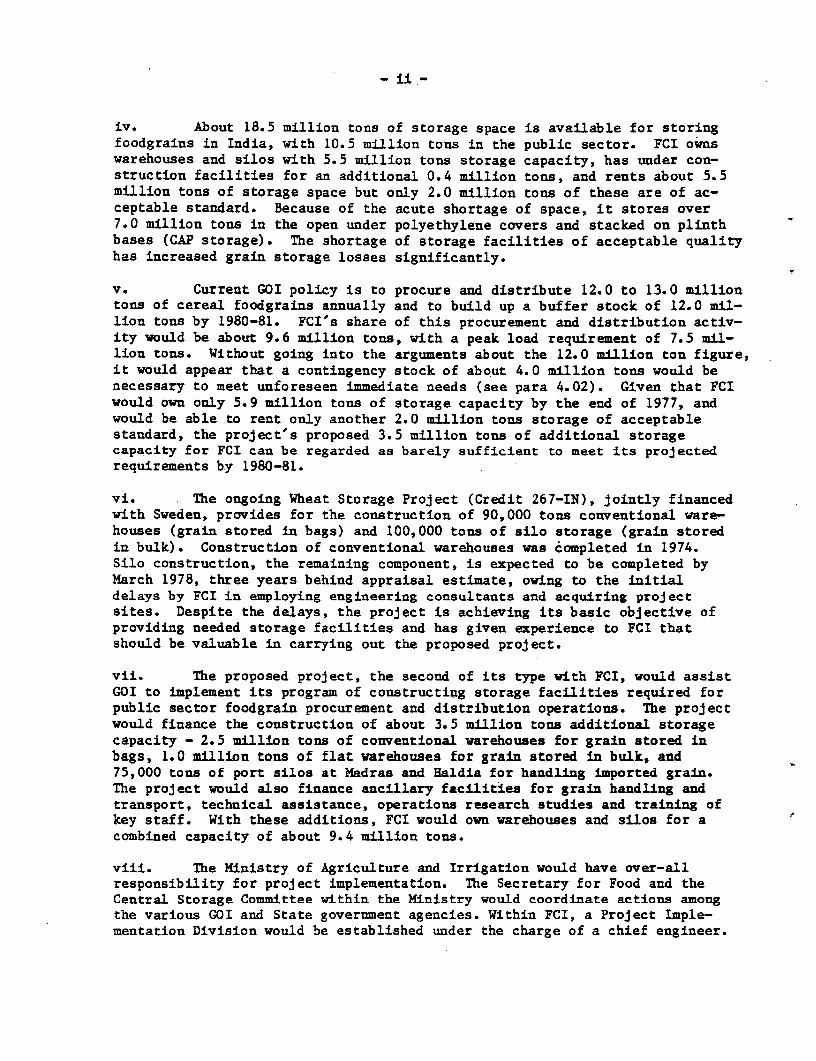

iv. About 18.5 million tons of storage space is available for storingfoodgrains in India, with 10.5 million tons in the public sector. FCI ownswarehouses and silos with 5.5 million tons storage capacity, has under con-struction facilities for an additional 0.4 million tons, and rents about 5.5million tons of storage space but only 2.0 million tons of these are of ac-ceptable standard. Because of the acute shortage of space, it stores over7.0 million tons in the open under polyethylene covers and stacked on plinthbases (CAP storage). The shortage of storage facilities of acceptable qualityhas increased grain storage losses significantly.

v. Current GOI policy is to procure and distribute 12.0 to 13.0 milliontons of cereal foodgrains annually and to build up a buffer stock of 12.0 mil-lion tons by 1980-81. FCI's share of this procurement and distribution activ-ity would be about 9.6 million tons, with a peak load requirement of 7.5 mil-lion tons. Without going into the arguments about the 12.0 million ton figure,it would appear that a contingency stock of about 4.0 million tons would benecessary to meet unforeseen immediate needs (see para 4.02). Given that FCIwould own only 5.9 million tons of storage capacity by the end of 1977, andwould be able to rent only another 2.0 million tons storage of acceptablestandard, the project's proposed 3.5 million tons of additional storagecapacity for FCI can be regarded as barely sufficient to meet its projectedrequirements by 1980-81.

vi. The ongoing Wheat Storage Project (Credit 267-IN), jointly financedwith Sweden, provides for the construction of 90,000 tons conventional ware-houses (grain stored in bags) and 100,000 tons of silo storage (grain storedin bulk). Construction of conventional warehouses was completed in 1974.Silo construction, the remaining component, is expected to be completed byMarch 1978, three years behind appraisal estimate, owing to the initialdelays by FCI in employing engineering consultants and acquiring projectsites. Despite the delays, the project is achieving its basic objective ofproviding needed storage facilities and has given experience to FCI thatshould be valuable in carrying out the proposed project.

vii. The proposed project, the second of its type with FCI, would assistGOI to implement its program of constructing storage facilities required forpublic sector foodgrain procurement and distribution operations. The projectwould finance the construction of about 3.5 million tons additional storagecapacity - 2.5 million tons of conventional warehouses for grain stored inbags, 1.0 million tons of flat warehouses for grain stored in bulk, and75,000 tons of port silos at Madras and Baldia for handling imported grain.The project would also finance ancillary facilities for grain handling andtransport, technical assistance, operations research studies and training ofkey staff. With these additions, FCI would own warehouses and silos for acombined capacity of about 9.4 million tons.

viii. The Ministry of Agriculture and Irrigation would have over-allresponsibility for project implementation. The Secretary for Food and theCentral Storage Committee within the Ministry would coordinate actions amongthe various GOI and State government agencies. Within FCI, a Project Imple-mentation Division would be established under the charge of a chief engineer.

- iii -

FCI's engineering sections would be strengthened and would be assisted byengineering consultants, including 60 man-months of internationally recruitedgrain storage engineers.

ix. Project costs over a four and a half year disbursement period areestimated at US$215.5 million, including US$16.1 million in foreign exchangecost. Storage facilities would require US$156.7 million, auxiliary itemsUS$17.9 million, and contingencies US$40.9 million.

x. The proposed IDA Credit of US$107.0 million would cover 50% ofproject costs, net of taxes and duties (estimated to be about US$2.0 million).This is equivalent to the foreign exchange cost plus about 42% of local costs.GOI would be the borrower and would use US$2.4 million of the Credit to pur-chase railwagon equipment, to be owned and operated by Indian Railways. GOIwould onlend the remaining US$104.6 million Credit proceeds to FCI at an annualinterest of 10.5%, to be repaid in not more than 20 years including 4 years'grace for principal and with 0.25% interest rebate for timely repayment.GOI would finance the remaining US$108.5 million project cost in the form ofequity investment in FCI.

xi. Civil works contracts for the two port silos (US$8.1 million) andthe bulk warehouse complexes (US$24.5 million) would be awarded on the basisof international competitive bidding. Civil works contracts for bag warehousecomplexes (US$75.5 million) and rural procurement centers (US$0.9 million)would be procured through competitive bidding following national and statewideadvertising. For railway sidings (US$18.4 million), civil works contractswould be with the Indian Railways since the work is highly specializedand requires close coordination with the existing railway system. Orders formajor equipment items would be bulked into orders of US$100,000 or more audtendered for internationl competitive bidding. Equipments not lending them-selves to bulking and/or which cost less than US$100,000 when bulked would beprocured by nationally advertised tender while prudent shopping would be usedfor items costing less than US$10,000. Vehicles would be procured on thebasis of nationally advertised competitive bidding from suppliers who wouldbe able to provide spare parts and maintenance services. Equipment costs,including vehicles, are estimated at US$33.2 million.

xii. At full development, savings from the reduction in operating costsand grain storage losses would be about US$57.0 million annually. The projectwould enable GOI to implement its national foodgrain policies more efficiently,thus benefiting farmers with marketable cereal grains, and consumers throughmore stable foodgrain supplies and prices. The estimated economic rates ofreturn are about 19% for the warehouse component, about 24% for the port silos,and about 20% for the entire project investment.

xiii. The project is suitable for an IDA Credit of US$107.0 million.

INDIA

SECOND FOODGRAIN STORAGE PROJECT

I. INTRODUCTION

A. General

1.01 The Government of India (GOI) has requested IDA assistance for theexpansion of foodgrain storage and handling facilities to be owned and oper-ated by the Food Corporation of India (FCI). The proposed project would bethe Bank Group's second foodgrain storage project in India. The first, theongoing Wheat Storage Project (Credit 267-IN), financed jointly with theKingdom of Sweden, provided for 90,000 tons of conventional bag storage and100,000 tons of silo storage and is expected to be completed in FY78 (Annex 1).The proposed project would provide additional storage for about 3.5 milliontons of foodgrains.

1.02 The project was prepared by a GOI committee which included represen-tatives from the Ministries of Agriculture and Irrigation, Railways and Financeand from the Planning Commission, FCI and the Central Warehousing Corporation(CWC). This report is based on the findings of an appraisal mission comprisingMessrs. Dorris D. Brown and Kok Peng Teh (IDA), and H.J. Barre, F.E. Bender andT.G. Burke (Consultants), who visited India in February/March 1977.

B. Background

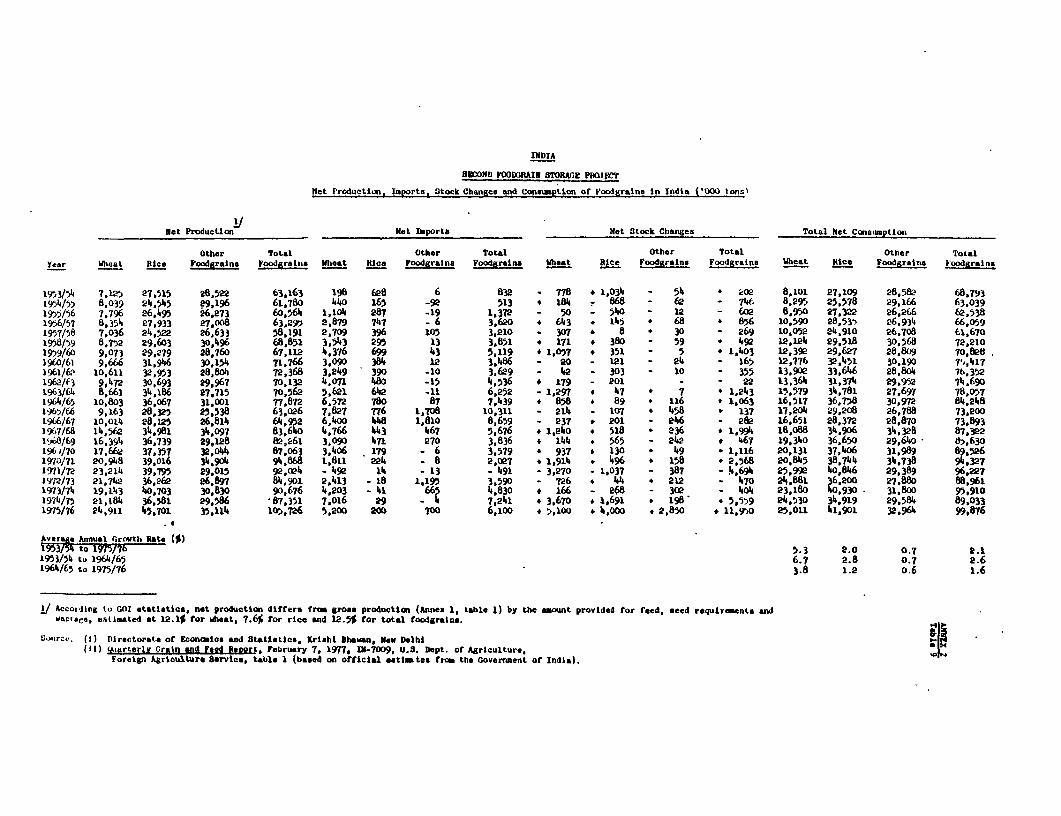

1.03 The General Economq. India's population of over 600 million isgrowing at an annual rate of 2.3%. National income grew in real terms atabout 3.7% per annum between 1950-51 and 1975-76 and per capita GNP reachedUS$150 in 1975-76. Per capita consumption.of cereal grains averaged 133 kgduring the 1950's, increased to 144 kg during the 1960's and is expected toexceed 150 kg by 1980-85. Since 1950, annual per capita availability of cerealgrains has varied from 119 kg to 154 kg. GOI has imported cereal grains,ranging from 2 to 16% of net consumption all these years, to provide for basicnutritional requirements and maintain reasonable prices.

1.04 Although nationaL income has increased, there has been only a minorimprovement in the living standards of the urban and rural poor, who make upabout one-third of the population. During years of low grain production,prices increase rapidly, beyond the means of low-income families. Duringsevere famines, masses of people suffer malnutrition. To alleviate thissituation, GOI and the respective State governments established ad hoc systemsof price ceilings at the primary market and consumer levels in the 1950s andearly 1960s, attempted various types of procurement from surplus areas fortransfer to controlled distribution areas, and established foodgrain zones to

-2-

control interstate or inter-district grain shipments. Foodgrains were alsoimported to relieve scarcity conditions. As public involvement in the food-grain sector increased, GOI established FCI in 1964 to operate a public sectorfoodgrain procurement and distribution program designed to stabilize consumerprices and assure an equitable distribution of the national foodgrain supply.

1.05 The Agricultural Sector. Agriculture's share of net domestic pro-duct ranges from 40 to 49%, about 2-1/2 times greater than the industrialsector. Foodgrain production, particularly rice and wheat, dominates theagricultural sector and is the dominant focus of India's agricultural devel-opment policy. About 75% of total cropped area is devoted to foodgrains.Likewise, about 75% of labor, fertilizer and irrigation utilized inagriculture is for foodgrain production.

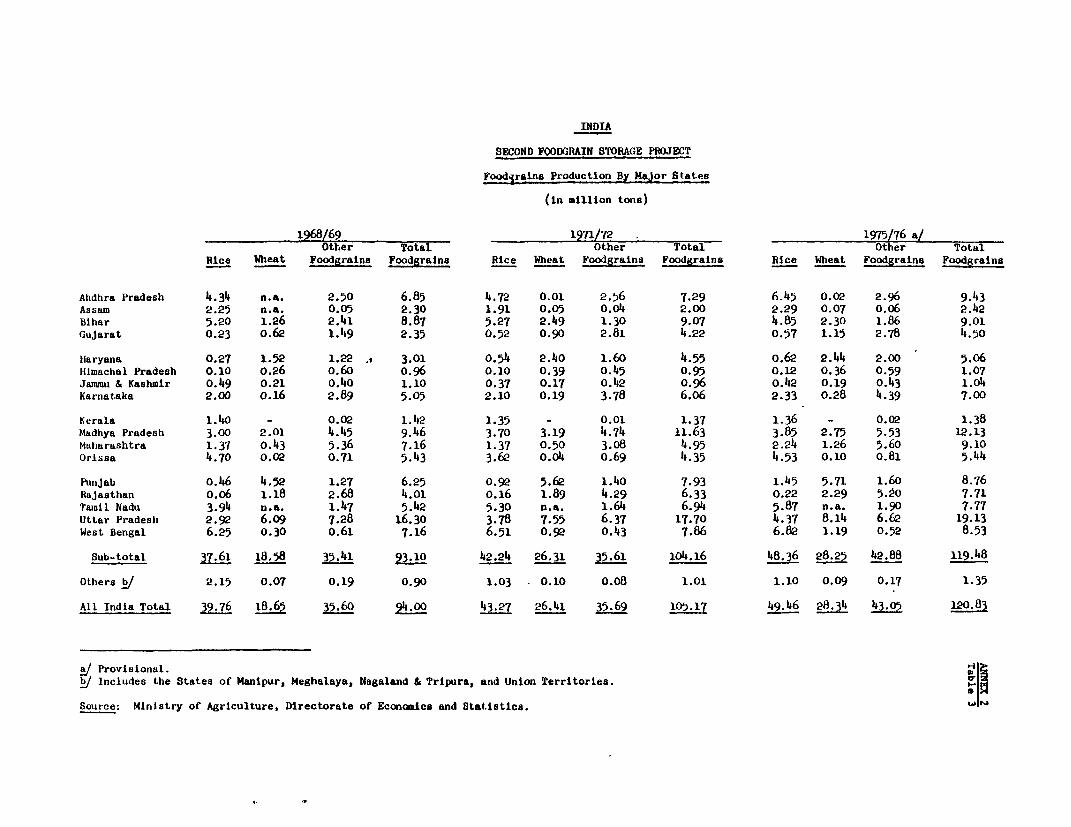

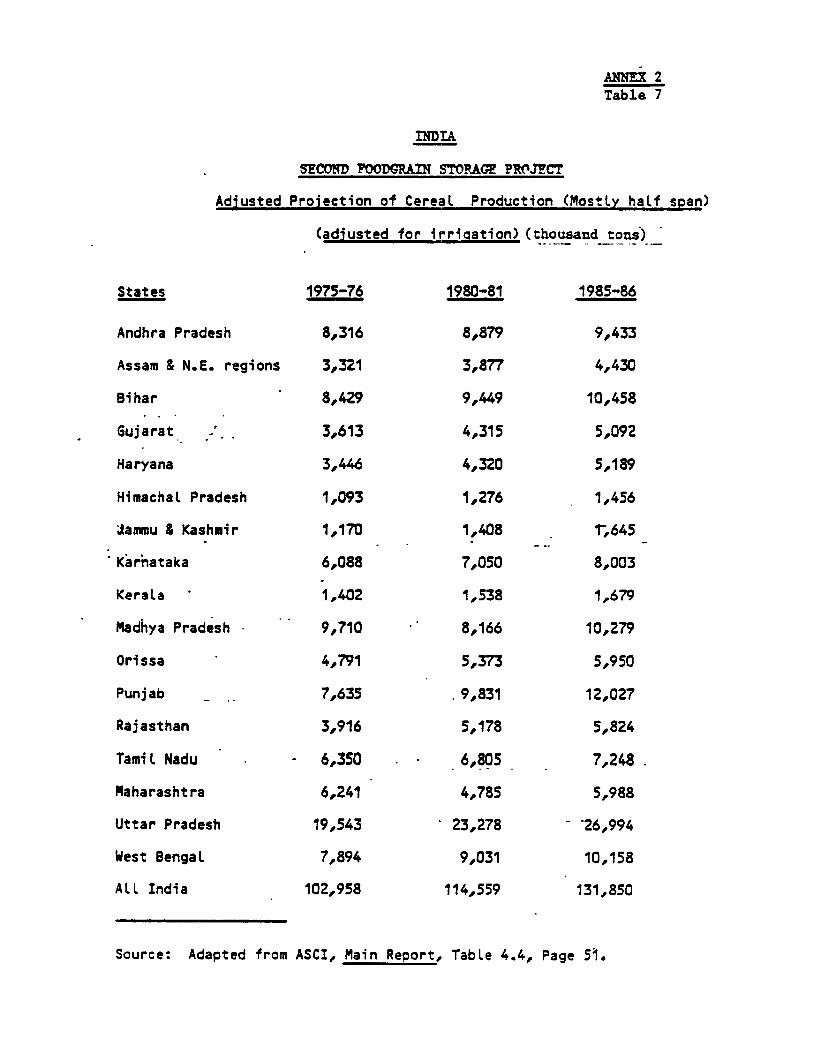

1.06 A basic problem of the economy is the low annual growth rate inagricultural production, especially foodgrains, which has merely kept pacewith the 2.3% rate of population increase. However, with near ideal rainfallconditions, foodgrain production increased more rapidly in 1975-76 and 1976-77,providing a growth rate of 2.8% per annum. Most of the increase has been inwheat production although rice production also increased substantially in1975-76 (Annex 2).

II. FOODGRAINS IN INDIA

2.01 Production Characteristics. Over 80% of India's foodgrain pro-duction, i.e. cereals and pulses, is concentrated in 10 of the larger States.About 67% of the rice production is concentrated in A.P., Bihar, Orissa, TamilNadu, U.P. and West Bengal and over 80% of the wheat is produced in Bihar,Haryana, M.P., Punjab, Rajasthan and U.P. In recent years wheat and riceproduction has increased most rapidly in the northern and eastern Stateswhere the combination of new varieties and added irrigation and fertilizershas been highly profitable for farmers.

2.02 A major characteristic of foodgrain production in India is its widefluctuations from trend, due mostly to the time and amount of monsoon rainsreceived. Variations of 15 to 20% from trend have been experienced about onceevery 5 years (See Annex 2, Figure 1). With production expanding at 2.3% to2.8% per annum, a poor crop-year means famine conditions for millions of peopleunless foodgrains are held over from the good crop-years as buffer stocks orimported and distributed in the famine areas. Other major factors influencingincreased production include the introduction of more responsive varieties,use of more fertilizers and expansion of area irrigated.

2.03 Marketing Practices. Only 30% to 35% of foodgrains produced entercommercial marketing channels; about 65Z of production is consumed by theproducer families or used for feed and seed in the villages. About 38% ofwheat and 30% of the rice crop are marketed. Typically, farmers operatingless than 1 ha of irrigated land or 2.5 ha unirrigated land market very little,

-3-

if any, grain of their own production. Indeed, they may have to buy foodgrainfor family requirements. Price incentive programs benefit only those farmerswho market foodgrains.

2.04 Typically, in Punjab and Haryana, wheat is harvested in April,threshed and delivered to a Regulated Market Yard in bulk form for sale inApril, May or June. At the market yard the wheat is displayed, auctioned,cleaned, bagged, weighed and delivered to the buyer under the supervision ofgovernment market regulatory agents. A 1% charge against sales value coverscosts of operating the regulated market system. In other States, where aRegulated Market Act has not been enacted, buyers usually negotiate for thewheat with each farmer and take delivery from the threshing floor or as agreed.Paddy marketing practices are similar to wheat except that in some areas onlypolished rice is marketed. In these cases the paddy is milled and the ricebagged before delivery.

2.05 Storage Practices and Losses. Farmers usually store grains re-served for family consumption in traditional grain bins or gunny bags. Food-grain merchants store their grains in bags in their own warehouses and ricemills or in space rented from the Central and State Warehousing Corporations.They may buy grain from the farmer and have him store it until needed. Co-operatives store grain only on account for the State government or the FoodCorporation of India (FCI) or for their own current sales.

2.06 Storage losses depend on the moisture content and the type ofgrain stored, type of storage, duration of storage, location and storagemanagement. Immediately after threshing, wheat has 10% to 12% moisture andcan be stored successfully. Paddy usually contains excessive moisture andcannot be stored successfully without drying to below 14% moisture. Forwheat, losses under CAP storage are estimated to range from 3.8% for 6 monthsstorage to 19% for 36 months. For bag storage in-conventional warehouses, therange is 1.9% for 6 months to 7.8% for 36 months, while for bulk storage insimilar warehouses, the range is 0.5% for 6 months to 2.0% for 36 months.Losses are minimal in the low rainfall and low humidity regions of northernIndia and high in the high rainfall, high humidity regions of eastern andsouthern India. Finally, the regularity and quality of fumigration of grainsand maintenance of storage facilities determine losses from insects, rodentsand birds.

2.07 StoraRe Resources. In 1975/76, India's warehouse storage capacitysuitable for grain was estimated to be about 18.48 million tons, withA0.48million tons in the public sector and 8.0 million tons in the private sector.These figures have remained generally unchanged in early 1977. A matrix ofgrain storage use and ownership for 1975/76 is shown as follows:

-4-

Grain StoraRe Use (owned and hired)Private-

Grain Storage Ownership FCI CWC SG SWC Co-op Sector- Total_ - __- million tons

Food Corporation of India (FCI) 5.47 - - - - - 5.47Central Warehousing Corp. (CWC) 0.88 0.36 - - - - 1.24State Govt. (SG) 0.71 0.02 1.11 - - - 1.84State Warehousing Corp. (SWC) 0.85 - - 0.05 - - 0.90Cooperatives - - - - 1.03 - 1.03Private Sector 1.30 0.34 1.20 0.88 0.82 3.46 8.00

Total 9.21 0.72 2.31 0.93 1.85 3.46 18.48

2.08 FCI owns warehouses and silos with about 5.5 million tons storagecapacity and has under construction 100,000 tons of silo type storage and about300,000 tons of conventional warehouses for bag storage. When these are com-pleted FCI will ovn about 5.9 illlion tons of storage capacity. In addition,FCI rented 3.7 million tons in 1975/76, which increased to about 5.5 milliontons in March 1977. Of this 5.5 million tons, only 2.0 million tons can beconsidered of acceptable standard in a normal situation; the other 3.5 milliontons is hired only because of present storage shortage. Another 7.0 milliontons of FCI grain stocks are now stored in the open under polyethylene coversand stacked on plinth bases (CAP). The project would replace CAP and rentedstorage with safer bag or bulk conventional warehouse storage. When theproject is completed in 1981, FCI would own about 9.4 million tons of accept-able quality grain storage space. Other than FCI, there are five main cate-gories of entities which together own grain storage of about 13.0 milliontons: CWC which owns 1.24 million tons of storage, leases most of it to FCI;State governments have 1.8 million tons, most of which they require for theirown grain storage; SWCs have 0.9 million tons and virtually all are leased toFCI; Cooperatives own 1.0 million tons which are inadequate for their ownrequirements; and the private sector owns 8.0 million tons, much of which issub-standard for storing grains. It is projected that Cooperatives would add

--about 1.0 million tons by 1980/81 to meet their own requirements and theprivate sector would construct another 1.0 million tons, most of which wouldreplace existing dilapidated warehouses. Thus, there is no major grain storageconstruction program projected by entities other than FCI itself for the nextseveral years which might raise questions about the appropriateness of thescale of construction program proposed for the project.

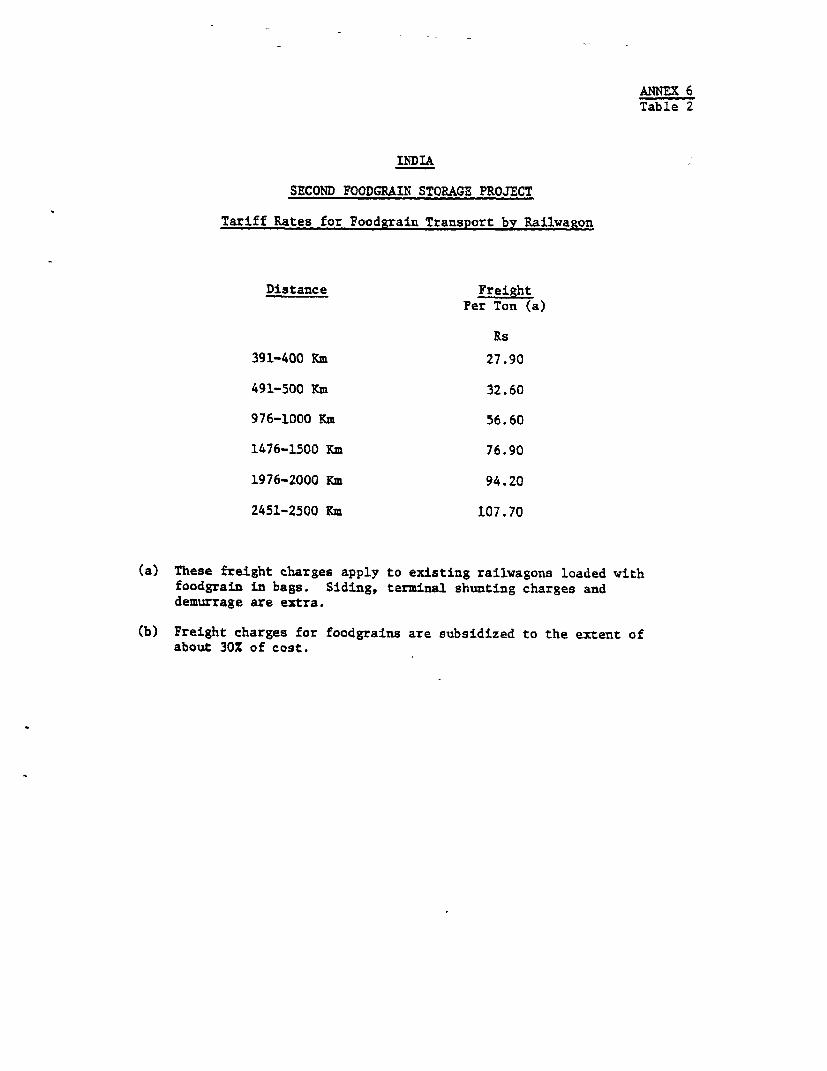

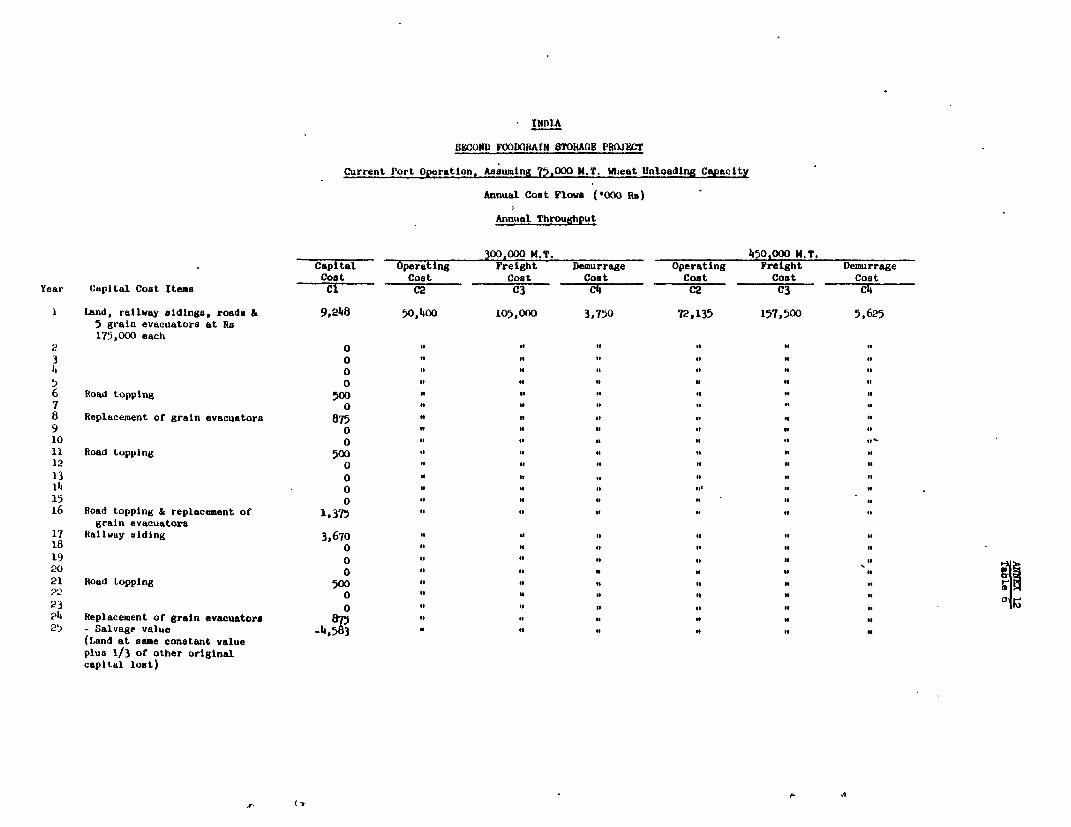

2.09 Transportation Resources and Practices. Most foodgrains transportedmore than 150 km from the primary market center move by railwagon. The IndianRailways (IR), a public sector agency, owns and operates the nation's 60,000km railway system. IR transports between 200 and 250 million tons of goodsannually. Foodgrain freight has varied from 14.0 to 16.0 million tons peryear in recent years, and mostly in unit trains carrying only grain. Theaverage haul distance is 920 kilometers. Details of the railway network aregiven in Annex 6 and shown on IBRD Map 12880.

2.10 Whilst foodgrain transport has a high priority in obtaining rail-wagon space, a number of constraints operate to increase the transportationcosts of shippers such as FCI. First, the maximum gross train load capacityis about 4,500 tons because of the type of hook or coupling used between rail-wagons. Train length is limited to 600 meters in most switch yards. Movementis slow as round trip time varies between 12 and 15 days per 1,000 km distance.The grain must be carried in gunny bags due to lack of grain-tight railwagondoors and bulk loading and unloading equipment. A shift to the transportationof wheat in bulk and larger capacity unit trains would reduce shippers' costs.

2.11 Foodgrain movement by truck is generally limited to distances ofless than 150 km but occasionally up to 300 km. Most truck transportationis from a primary procurement market yard or port to a nearby warehouse andfrom the warehouse to a railwagon or nearby consumer market. Transportationby truck is of bagged grains.

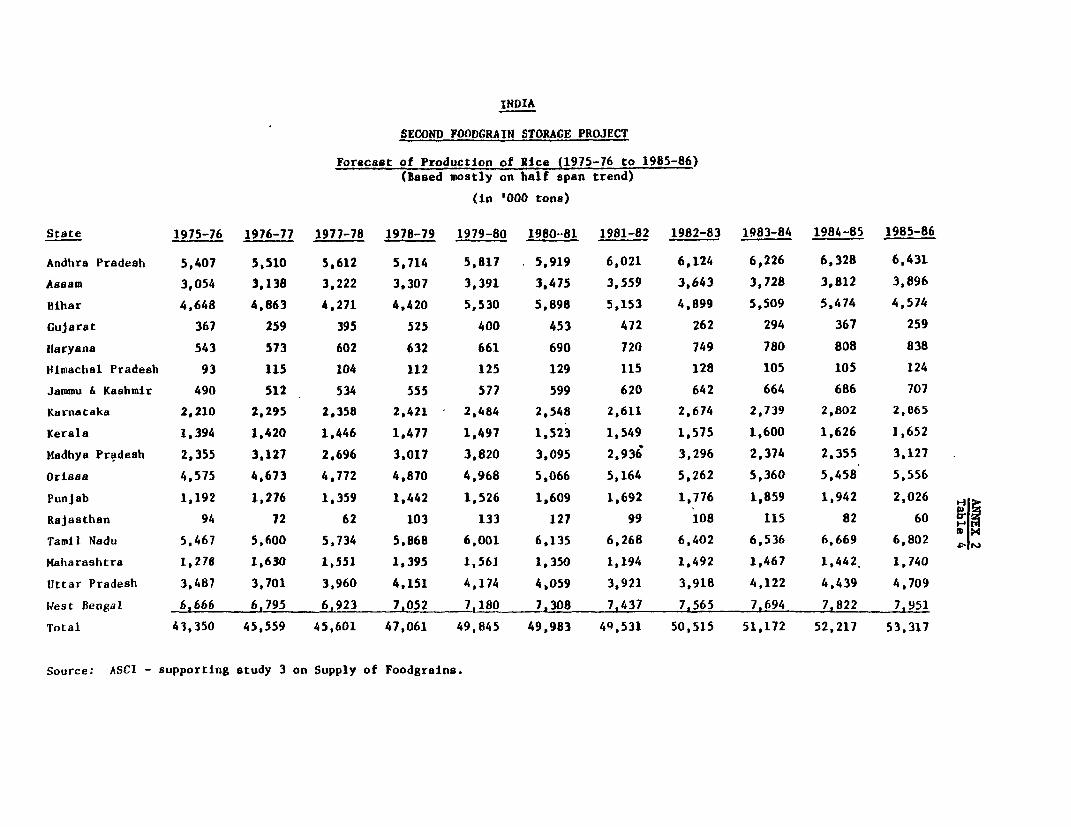

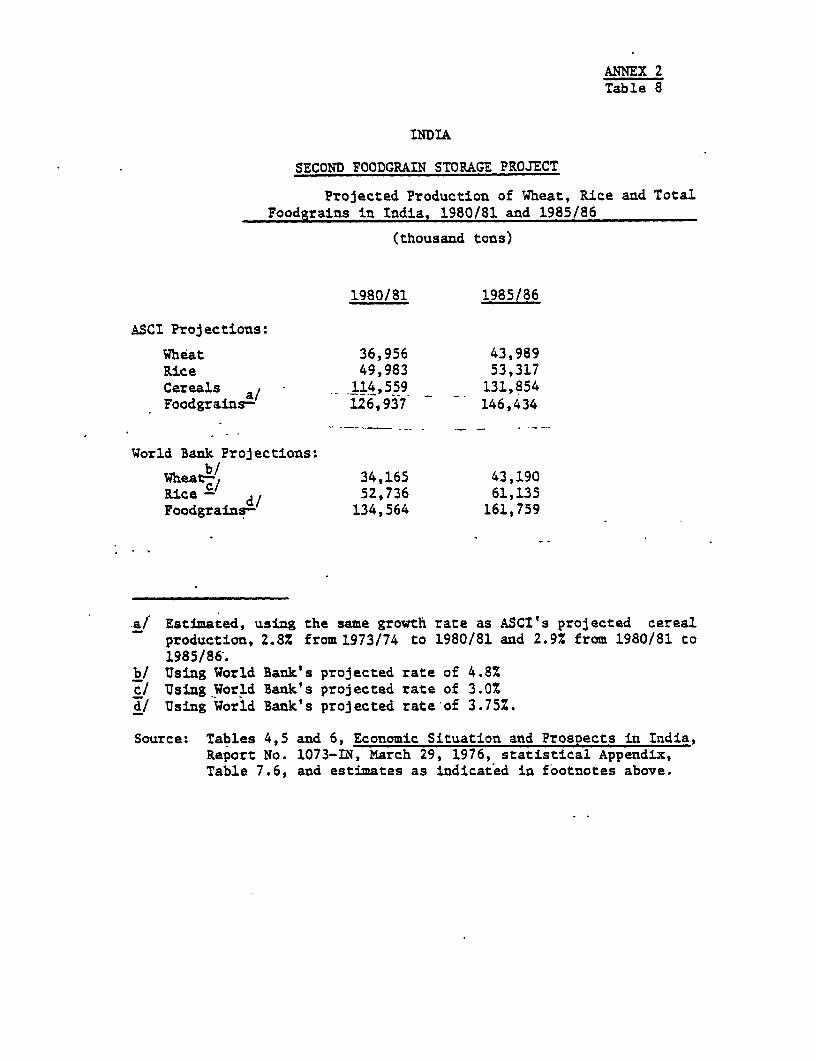

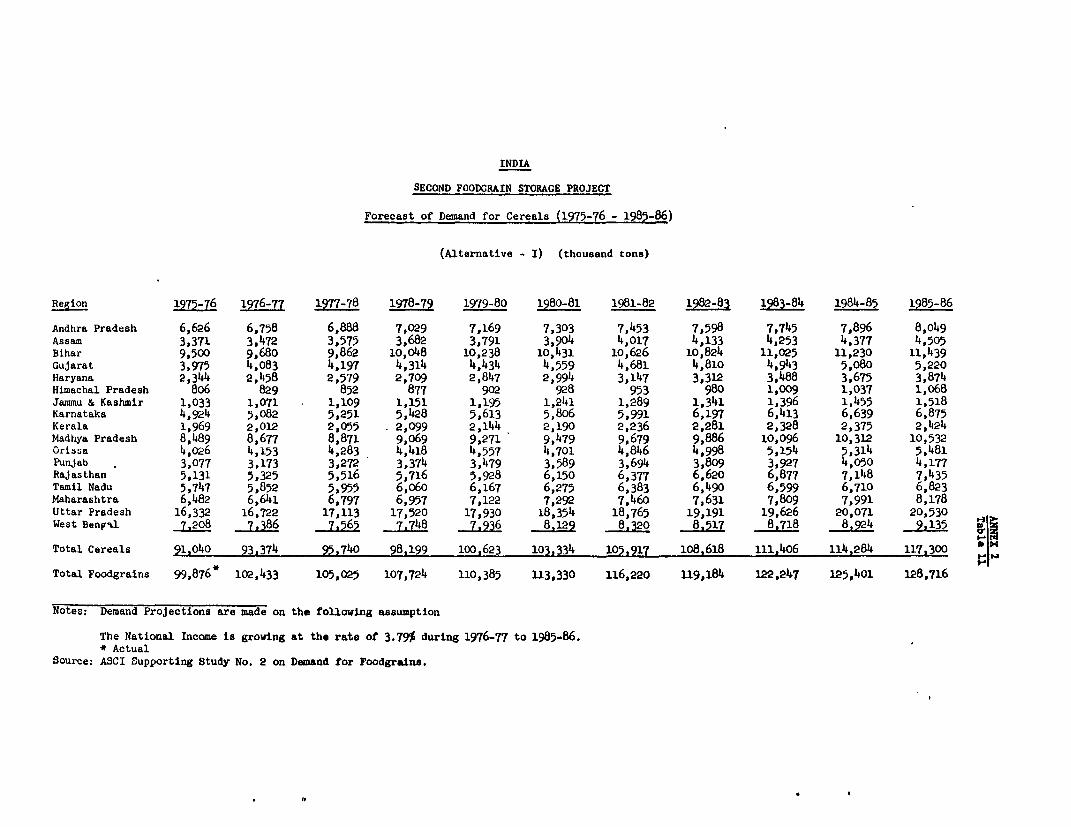

2.12 Consumer Demand and Proiections. Per capita foodgrain consumptionhas been about 145 kg and is expected to increase to over 150 kg by 1985.Production has ranged from about 84S to 98% of consumption, with the gapsupplied from imports, mostly of wheat. Projections (Annex 2, Table 14)indicate a relatively higher rate of growth of foodgrain production than ofconsumption, thus reducing the current 3.0 million ton annual import require-ment to about 0.6 million by 1985-86. Current production at 115.0 to 120.0million tons per year is expected to expand to about 145.0 million tons by1985-86. With currently available storage resources fully utilized (Annex 5),additional storage capacity would be needed to protect the expected incrementin foodgrain production and safeguard consumers from wide seasonal and annualvariations in supplies and prices.

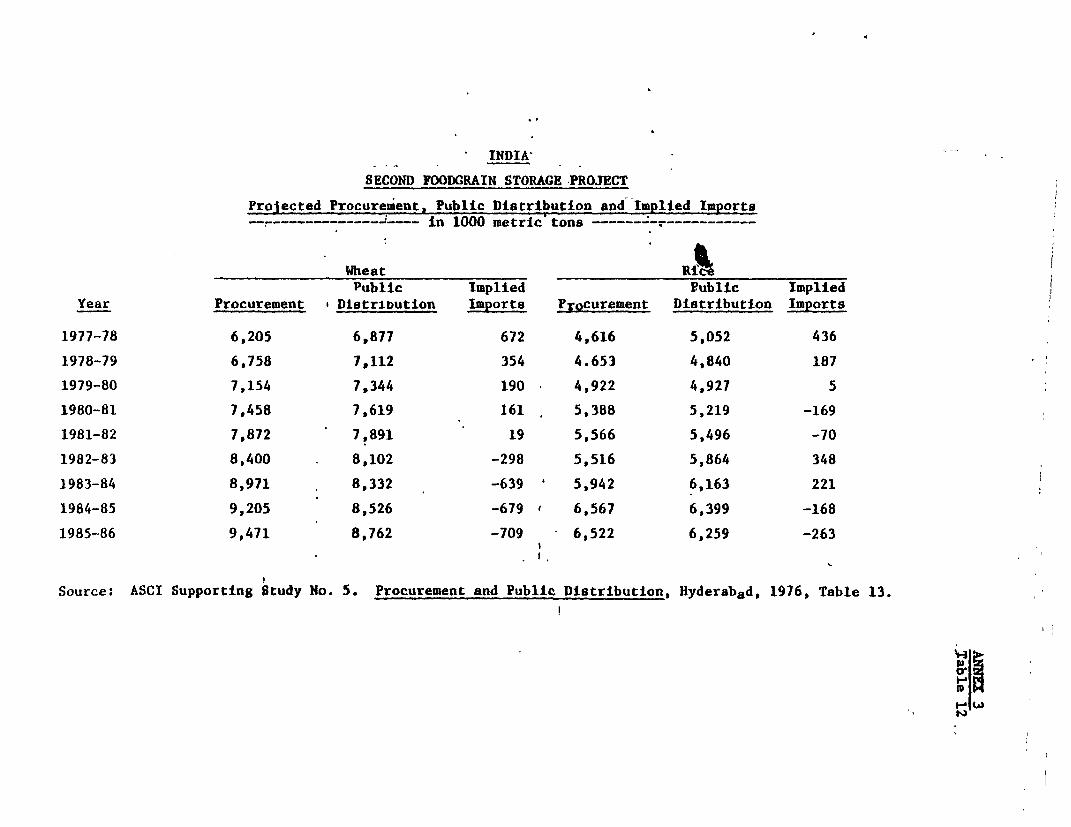

2.13 Foodgrain Policies and Practices. GOI foodgrain policy has threemajor objectives: (a) self-sufficiency in production; (b) price stability;and (c) an equitable foodgrain distribution to low income consumers. Throughthe annually announced procurement price (which usually functions as the sup-port price as well), backed by a readiness to purchase any amount of grainat that price, it is intended to assure foodgrain producers of a stable,reasonably attractive price in order to encourage increases in foodgrain pro-duction, leading to self-sufficiency. The production effect of the procure-ment price depends on the price elasticity of supply and whether the pricecovers the cost of production. A recent Bank-sponsored study has shown thatwheat and paddy production in India is quite price responsive. 1/ This priceresponsiveness of supply is thought to be more pronounced where the technologyof high yielding varieties is involved because its success depends cruciallyon the provision of associated outlays, which the farmers would be reluctantor unable to incur unless assured of attractive prices for their produce. TheBank-sponsored study also showed that, broadly speaking, the procurement priceduring the past decade did cover the cost of production. The present procure-ment price of Rs 1,100 per ton for wheat appears to provide an adequate incen-tive for increasing production; this may not be the case for paddy, whose

1/ Raj Krishna and G.S. Ray Chandhuri, "'Some Aspects of Wheat PricePolicy in India", and "Some Aspects of Rice Price Policy in India",(mimeographed), University of Delhi, Delhi, India, January 1977.

-6-

procurement price is Rs 740 per ton. Market prices have more often been aboveprocurement prices so that, until April 1977, food zones were used, in whichgrain surplus areas were cordoned off to restrict private grain trade, in orderto facilitate government procurement. The government distribution of domesticand imported grains at concessional prices is intended to safeguard the in-terests of low income consumers. Although the ration cards entitling theirholders to government distributed foodgrain are issued to all those living inthe urban areas regardless of their income, it appears that the location ofthe Fair Price Shops, the queues, the limits on quantities available, and thelower quality of publicly distributed grain effectively ration it to lowerincome groups. Following the foodgrain shortages of 1973 and 1974, the govern-ment decided on the policy of building up 12.0 million tons of buffer stocks.This policy is under review, the situation having changed completely; twosuccessive good harvests in subsequent years have resulted in foodgrain stocklevels being report 1 d at 20.7 million tons in July 1977.

2.14 Both Central and State governments are involved in establishingand implementing food policy. GOI's Agricultural Prices Commission issuesfoodgrain policy papers every year recommending procurement prices andtargets for consideration by the Minister of Agriculture and other cabinetmembers. A meeting is then held of Chief Ministers and other State officersto discuss and agree upon policy recommended by GOI for the coming season.Implementation, in the form of grain procurement and distribution, is carriedout in each State by the departments of Civil Supply or FCI or both. FCI,in addition, stores the grains it procures and arranges transportation ofgrains procured from surplus States and imported grains for distribution indeficit States. About 80% of public procurement of wheat and rice is handledby FCI (India's foodgrain policies and practices are detailed and evaluatedin Annex 3).

III. FOOD CORPORATION OF INDIA

A. General

3.01 FCI was established in 1964-65 by GOI to implement more effectivelyits national food policies. It is required to undertake the purchase, storage,transport, distribution and sale of foodgrains and other foods as decided byGOI. In recent years, FCI has procured annually 3.0 to 10.0 million tons offoodgrains (about 1OZ to 352 of the total marketed by farmers) and importedanother 3.5 to 7.5 million tons. The volume procured generally varies withproduction and the relative differential between procurement and market priceswhile the volume imported has tended to be highest during and after droughtyears.

3.02 Management. Under the general direction of the Ministry of Foodand Agriculture, FCI operates with a Board of twelve Directors appointed byGOI. The Board selects an Executive Committee from its members, including theChairman and Managing Director who are responsible for day-to-day managementand operations.

-7 -

3.03 Staff. A staff of about 60,000 on a regular basis operate 4 zonaloffices, 19 regional offices, 140 district offices and 5 port offices. Food-grains are procured at over 2,500 market centers and stored in warehouses at1,700 locations. Details are given in Annex 5 and IBRD Map 12880.

3.04 Financial Management. FCI's financial and accounting systems arecentrally controlled from its headquarters. The general books of account(ledgers, cash books and journals) and annual financial statements, includingprofit and loss account and balance sheets, are prepared in accordance withcommercial principles. Detailed records are maintained at the zonal, regionaland port offices. Periodical returns are furnished from these offices to theheadquarters where the budgets, cost accounts and other financial statementsare consolidated. FCI's finance department is adequately staffed and includesfive specialized divisions - budget and cost control, accounting, finance,internal audit and physical verification. Independent audits of FCI's annualaccounts are carried out jointly by two firms of chartered accountants. Inaddition there are several other firms of chartered accountants functioningas independent auditors of FCI's regional offices. Supplementary audits arealso performed by the Comptroller and Auditor General. Accounts for 1976/77have been audited and passed by the Board.

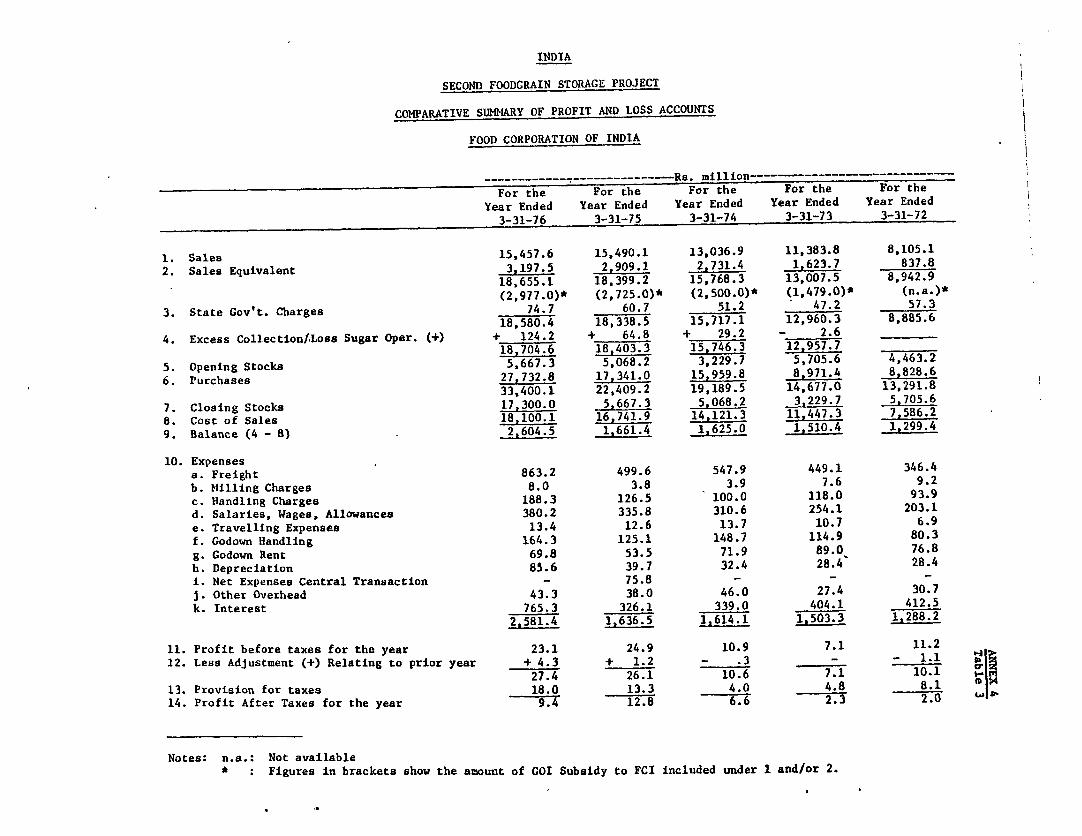

3.05 Operating funds are made available in the form of GOI owned equitycapital, GOI loans, commercial bank loans and overdrafts, depreciation reservesand GOI deficit budget allocations. Assets currently in excess of Rs 21,000million (US$2,400 million) are held mostly in the form of foodgrain inven-tories. Details are given in Annex 4, Tables 2 and 3.

B. Analysis of Operations

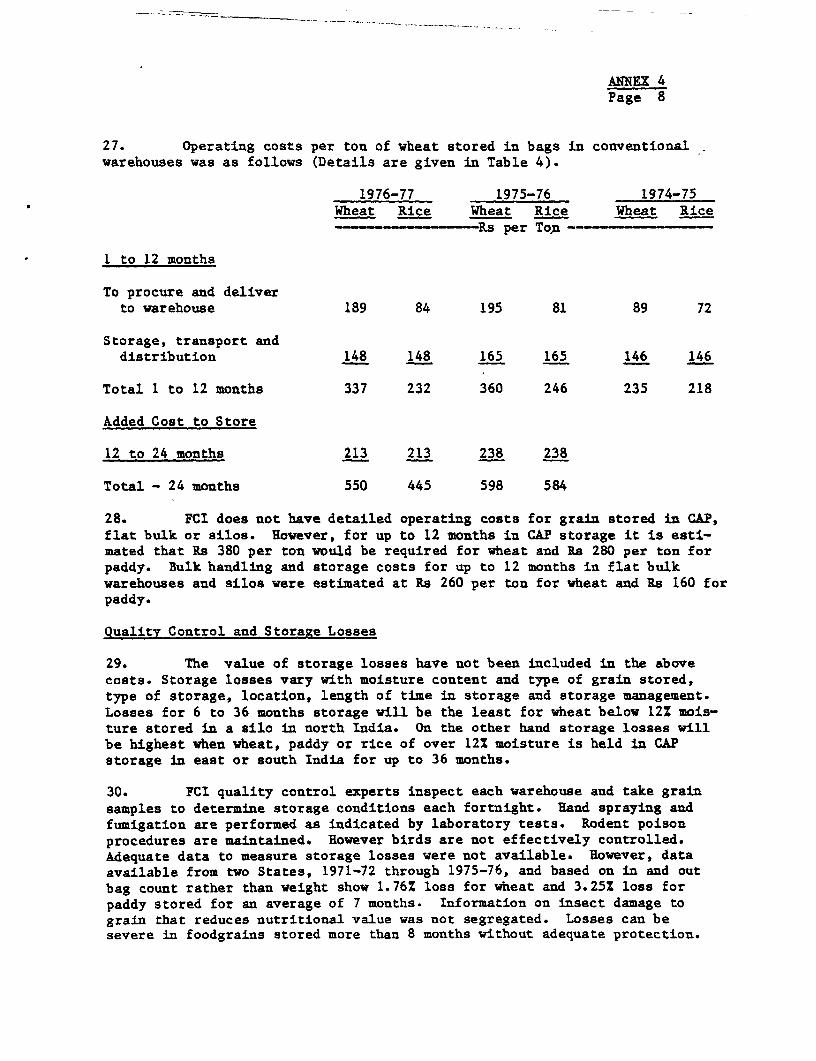

3.06 Costs and deficit financing. FCI, as a large, national publicsector business organization, is constrained by GOI policy from operatingprofitably. GOI determines both domestic procurement and issue prices offoodgrains marketed by FCI. Procurement prices are set at levels to assurefoodgrain producers of a stable and reasonably attractive price; issueprices are concessional, intended to benefit low income consumers. Becauseof these overriding policy requirements, PCI has never been managed as aprofit oriented institution, but has instead played an important role inprice stabilization and in ensuring some degree of equity in the provisionof foodgrains. For example, in 1976-77, the procurement price for wheat wasRs 1,050 per metric ton and the issue price was Rs 1,250 per metric ton, adifference of Rs 200 per metric ton. But PCI's operating costs 1/ alone, forwheat stored in bags in a conventional warehouse up to 12 months, was Rs 337per ton. If the length of storage increases to 24 months, the operating costsbecome Rs 550 per ton. Thus, GOI has had to grant an annual subsidy to FCI

1/ i.e., excluding depreciation, operating costs are defined here toinclude cost of procurement (excluding procurement price) and deliveryto storage, cost of storage and cost of delivery to State governmentsfor distribution.

- 8 -

which, in 1976-77 (a year of very high stocks), amounted to Rs 4,500 million(US$514.3 m..Llion). FCI's deficit financing is inevitable, given GOI's -policyobjectives, and is not an indicator, one way or another, of efficiency. Infact, it may be argued that FCI, in helping to fulfill GOI's food policy,generates social benefits which are not reflected in its financial statements,and the subsidy may be regarded as the price GOI is willing to pay for thesebenefits.

3.07 Inventory Management. FCI's Management Information and ControlBranch (MICB) collects and analyzes information received from the 1,700 ware-house centers and uses it to assist management in determining grain movements.Monthly, GOI advises FCI on the quantity and kind of foodgrain to be issuedto each State. FCI's operational division managers meet and, with the datacompiled by MICB, determine grain movements needed to fill requests. Time-liness and accuractv f information appear to be satisfactory but there aredelays in receivide data from the field. Movement planning becomes morecomplex as the grain volume and number of locations involved increase. Acomputerized scheduling program could be useful in helping FCI's inventorymanagement.

3.08 Quality Control. Stocks received for storage are analyzed by FCI'squality control staff to determine moisture content and insect infestation.Fortnightly, stocks are re-examined to determine grain condition and presenceof insects. Fumigation is undertaken if stocks show signs of infestation.Prophylactic treatment is given to prevent cross infestation. Rodent poisonprocedures are maintained. However, birds are not effectively controlled.Training sessions are frequently held for the quality control staff at alllevels to exchange experiences in storing grain and to disseminate new infor-mation. Within the resources available, FCI has done a fine job in qualitycontrol, especially given the present large stocks and in particular, thosein open CAP which require intensive care.

3.09 Construction and Maintenance of Grain Storage Structures. FCIhas two divisions dealing with the construction and maintenance of grainstorage structures. Each division is under the charge of a Senior ManagingEngineer. One division, with a staff of 787 engineers and draftsmen, isresponsible for designing and constructing new conventional bag storage ware-houses and maintaining existing ones. It also hires engineering servicesof the grain storage division of the Central Public Works Department (CPWD)to design and supervise a part of the new construction. The other division,with a professional staff of 246, is responsible for the design, constructionand maintenance of bulk grain storage facilities. It engages engineeringconsultants to assist in the design, in tender documentation and evaluation,and supervision of new construction. In the construction of new warehouses,civil works and electrical and mechanical equipment contracts are usuallyprocured by nationally advertised tenders.

- 9 -

C. Review of Wheat Storage Project (Credit 267-IN)

3.10 The ongoing Wheat Storage Project, costing US$15.9 million, and -

financed jointly with Sweden, originally consisted of 200,000 tons silostorage and 100,000 tons of conventional warehouses for storing grain inbags, training silo personnel and a study of India's foodgrain storage anddistribution. Credit agreement was signed in August 1971 but credit effec-tiveness was delayed until November 1972 due to the difficulties FCI and GOIhad in engaging engineering consultants to assist in the design and construc-tion of silos using the slip form method which was new to Indian contractors.Land acquisition was more time-consuming than anticipated during appraisalbecause, for some of the sites selected, land acquisition proved to belegally difficult while for other sites, the locations were found to be un-suitable with regard to grain receipt and distribution, and transport facil-ities. Implementation was further delayed by the time required by FCI andthe engineering consultants to prepare and execute documentation for civilworks and equipment, and the requirement that the contract for coustructionof the silos should be bulked and on a turn-key basis. This procurementprocedure was not practical and was subsequently abandoned.

3.11 The conventional warehouses were completed by 1974 and have storedfoodgrains since then. The India foodgrain distribution study was completedby October, 1976 and provided valuable information for this appraisal report.The silos are still under construction but are expected to be completed andused for wheat storage by April, 1978, and the training of silo personnel isunderway. Despite the frustrating delays, the project is achieving its basicobjective of providing needed grain storage facilities. The experieucesgained, particularly in procurement and land acquisition, should stand FCIin good stead in implementing the proposed project.

IV. TEE PROJECT

A. General

4.01 The project would assist GOI in carrying out its program of construc-ting storage facilities required for foodgrain procurement and distributionoperations and improving foodgrain handling practices including bulk handlingactivities planned for implementation during the next four and half yearsbeginning July 1977. The project would comprise: (i) construction of 3.5million tons of foodgrain storage consisting of 2.5 million tons bag, 1 mil-lion tons bulk, and 75,000 tons port silos for grain loading and unloading;(ii) ancillary facilities for grain handling and transport; and (iii) tech-nical assistance for project implementation; operations research; and trainingof management and key technical staff. With project completion in 1981, FCIwould have storage of its own of about 9.4 million tons of foodgrains - 7.7million tons in bags and 1.7 million tons in bulk. The proposed facilitieswould be used for storage of wheat, paddy, rice and other foodgrains.

- 10 -

4.02 From 1980/81 onwards, annual public procurement and distributionof wheat and rice is expected to be about 12.0 million tons and more (seeAnnex 3, Table 12). Since its share of this activity is expected to beabout 80%, FCI would be handling 9.6 million tons by 1980/81. The peakstorage requirement, occuring in June (see Annex 3, Table 13), for this 9.6million tons would be 6.0 million tons. (Procurement would be concentratedduring the harvest months while the off-take would be more evenly distributed).>At any given peak, there would be some storage facilities that cannot be fullyloaded because they are located in pockets of poor harvest or are temporarilyinaccessible or because there is imperfect substitution between wheat and ppaddy storage. Taking these factors into account, it is estimated that atpeak, the storage facilities on average would be only 80% loaded, so that7.5 million tons of storage capacity would be necessary to handle FCI'sprojected June peak of 6.0 million tons. The above calculations assume noyear-to-year fluctuations in procurement and demand on the public distribu-tion system. In fact, fluctuations do occur in such a way that procurementis high when offtake from the public distribution system is low, resultingin rapid stock buildup, as occurred in 1975/76 when peak stocks rose to 18.0million tons. Rapid stock drawdown can occur when procurement is low at thesame time demand is high, and maintaining supplies to vulnerable groups thenrequires iarger than normal quantities of grain. GOI's policy is to buildthe capacity to hold 12.0 million tons of grain in addition to those neededfor normal operations purpose; FCI's requirement would then be about 20.0million tons. With this project FCI would own 9.4 million tons of capacityby 1980/81. FCI would continue to make use of storage space rented fromother public and private entities; but only about 2.0 million tons of the5.5 million tons currently rented is of acceptable statdard; the substandardremainder is being hired because it is better than open, CAP storage. After1980/81, FCI will have access to 11.4 million tons of secure storage capacity,about 4 million tons above that needed simply for operations in a normal yearbut 8.0 million tons less than needed to fulfill GOI's buffer stocking goals.Stock accumulations above 11.4 million tons will have to be accommodated insubstandard rented storage or CAP storage. After the current building programis completed, the GOI will have the opportunity to decide upon another trancheof FCI's expansion program, either reaffirming current goals for Government-owned storage or altering these goals in response to changed policies.

B. Detailed Features

ProJect Area

4.03 The 3.5 million tons of storage would be constructed in the Statesof Andhra Pradesh, Assam, Bihar, Gujarat, Haryana, Jammu and Kashmir, Karnataka,Kerala, Maharashtra, Madhya Pradesh, Orissa, Punjab, Rajasthan, Tamil Nadu,Uttar Pradesh and West Bengal at the critical grain procurement and distribu-tion centers. Criteria for selecting each location (town), site and type ofstorage structure have included: (i) existing and projected procurement and

distribution; (ii) type, capacity and location of existing grain storage facil-ities in relation to existing and projected procurement/distribution at theproposed sites; (iii) transportation facilities serving the locale; and (iv)climatic conditions (which determine duration of storage). Locations arelisted in Annex 5, Appendices C & D. Proposed locations are shown on IBRD Map12880. All sites would have road and rail access. Civil works would includewarehouses, office buildings, on-site road improvements and connecting railsidings. The two silo units would be constructed only at port side and wouldbe equipped to receive, store and handle imported grain. During negotiations,the proposed locations and type of storage complexes to be built were agreedwith GOI and FCI. Since land acquisition for all project sites would be alengthy process (as evidenced by the first storage project), to enable theproject to get underway without delay, yet ensuring GOI's and FCI's commit-ment to it, it was made a condition of Board presentation that land wouldhave been acquired for 28 or more project sites. During negotiations, GOIprovided evidence that 50 project sites had been acquired, so the conditionwas easily met.

Storage Buildings

4.04 The project would finance construction of the following:

unit Number of TotalModel Type Capacity Units Capacity

(000 tons) (000 tons)

A Bag 5 to 50 119 2,500.0B Bulk (or Bag) 52.5 11 577.5c Bulk 52.5 4 210.0D Bulk 52.5 3 157.5D Bulk 55.0 1 55.0Port Silo Bulk 50.0 1 50.0Port Silo Bulk 25.0 1 25.0RuralProcurement Centers 6

Total 146 3,575.0

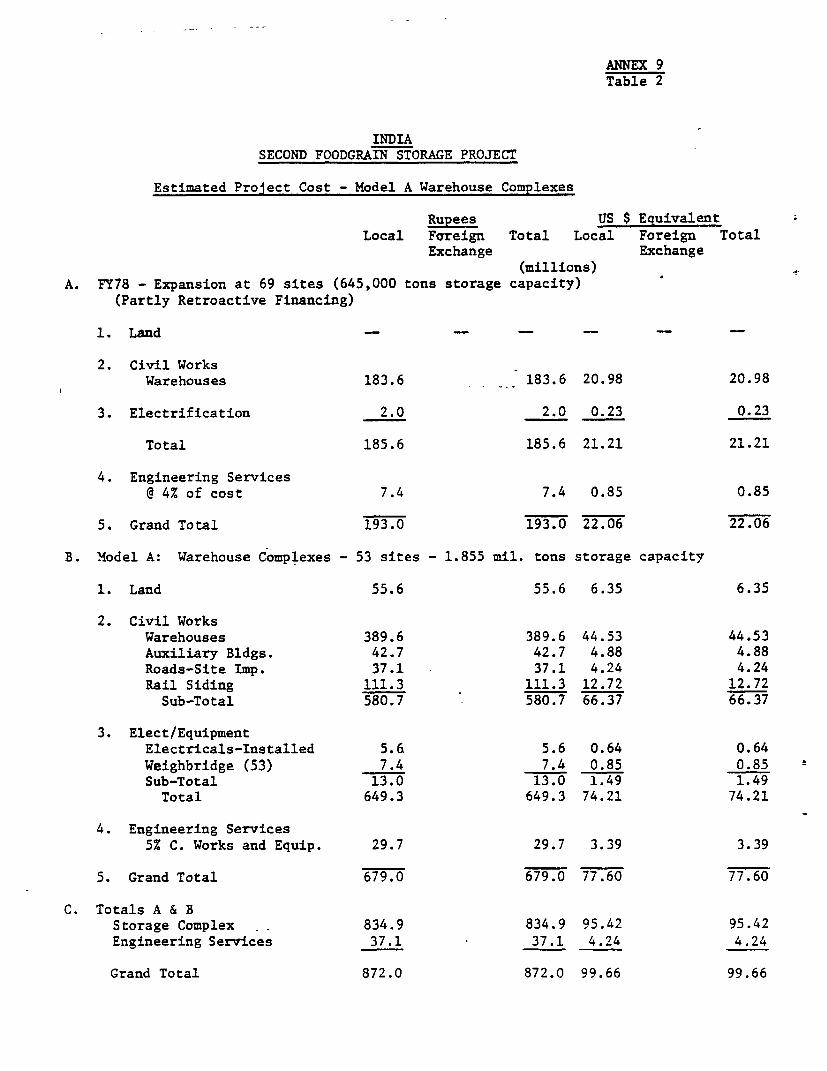

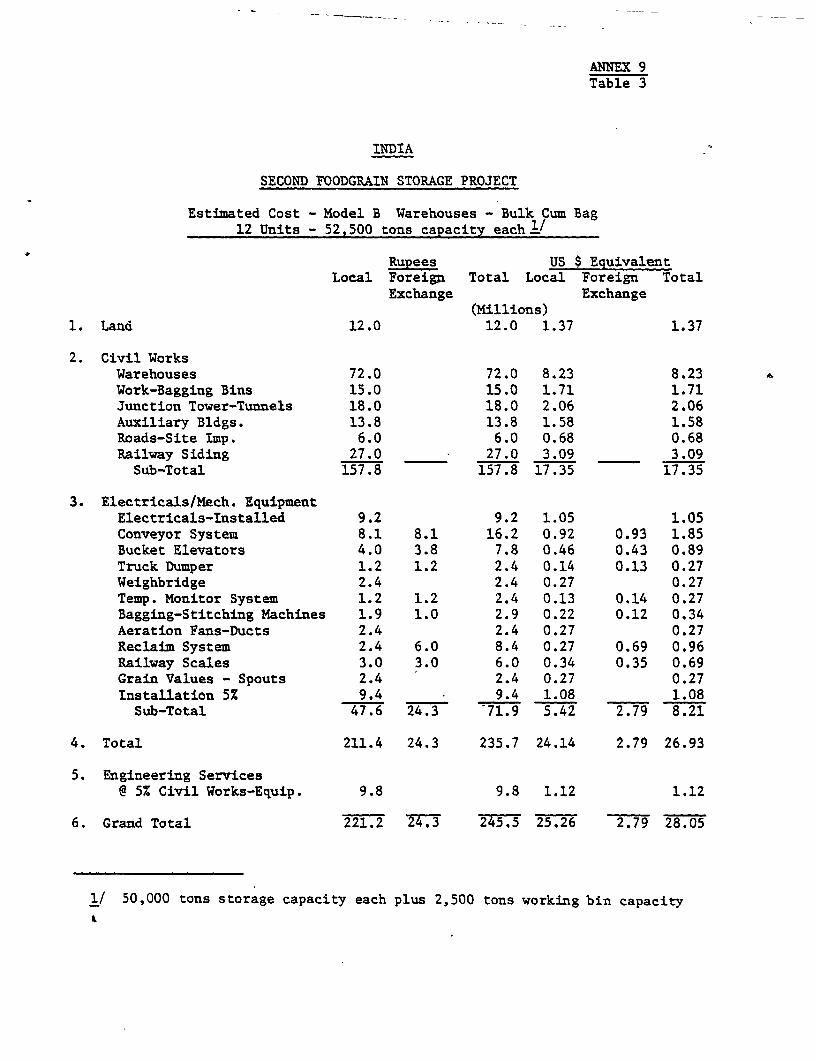

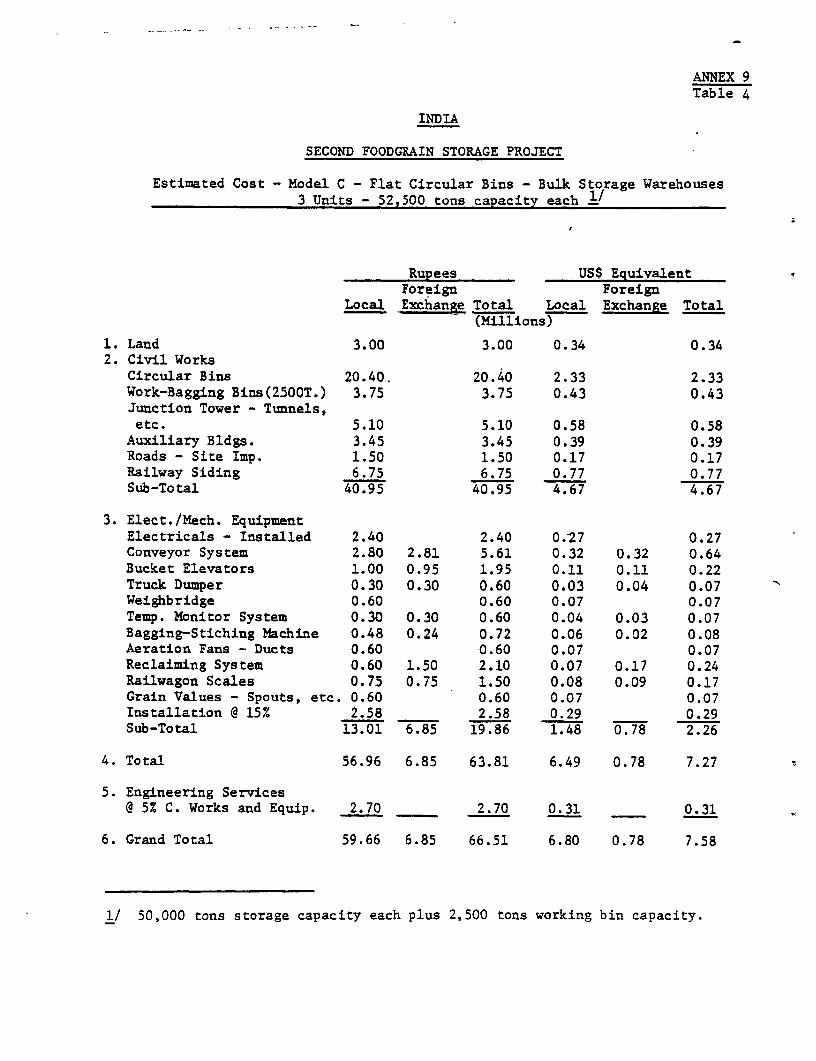

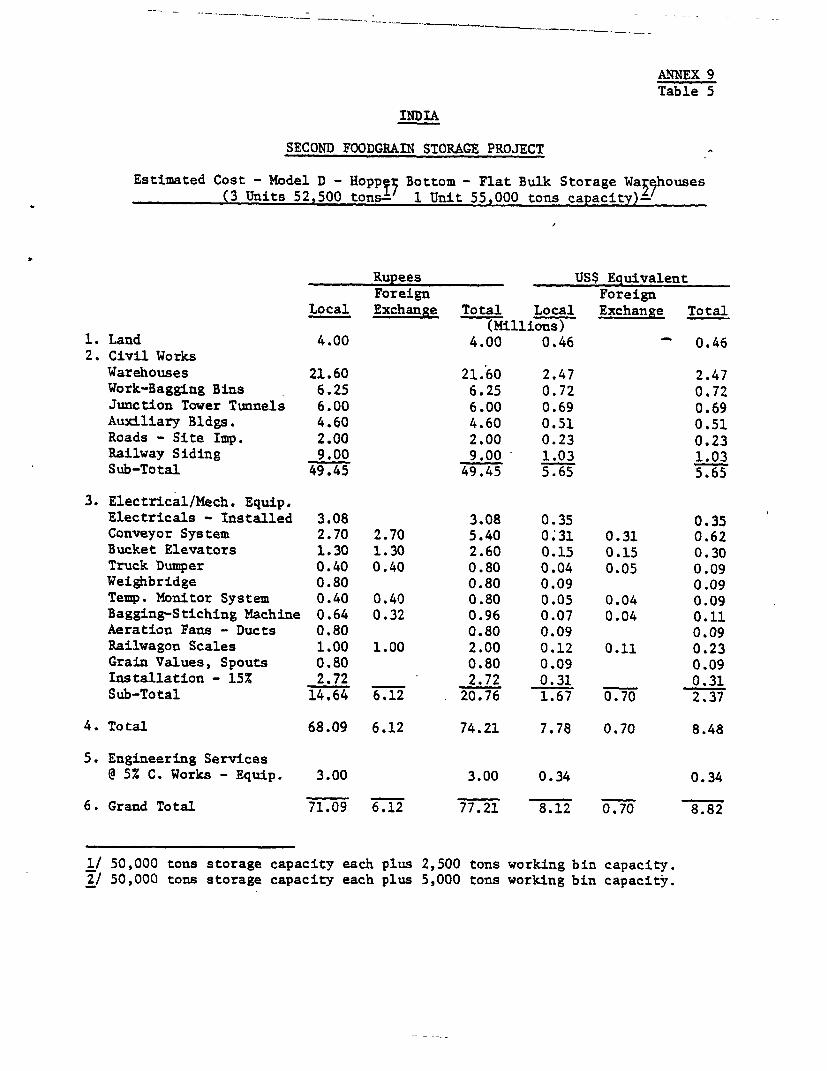

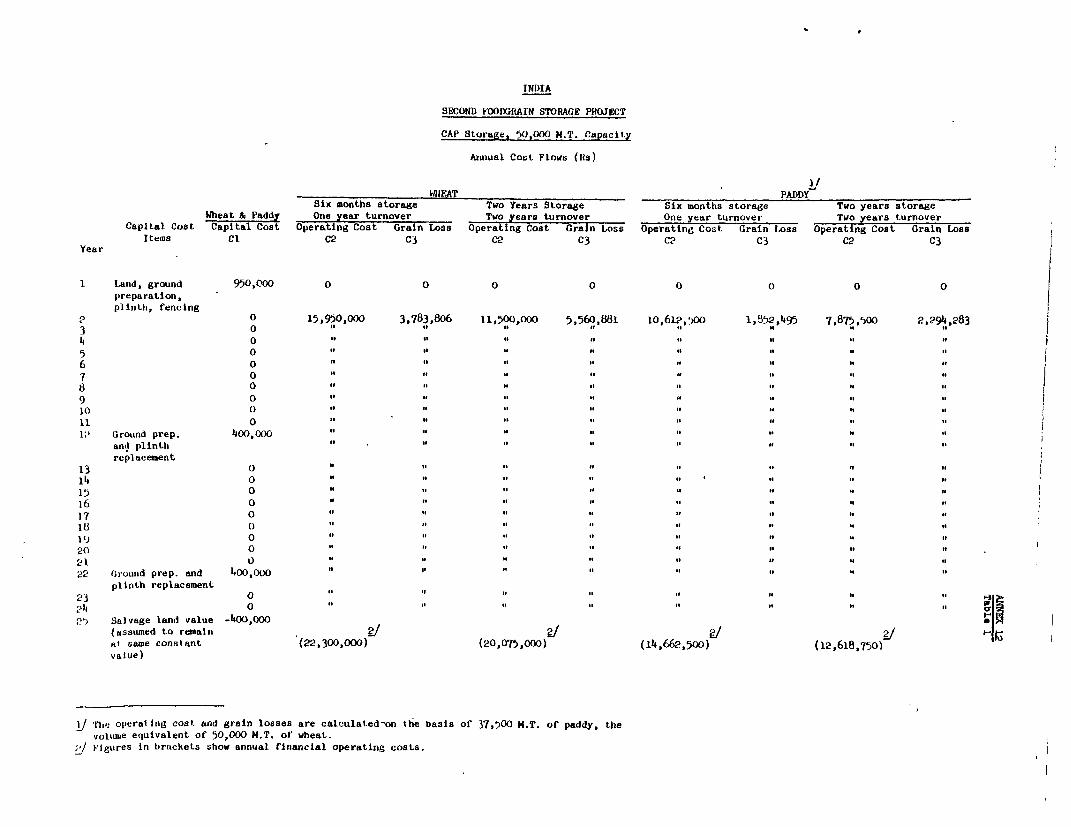

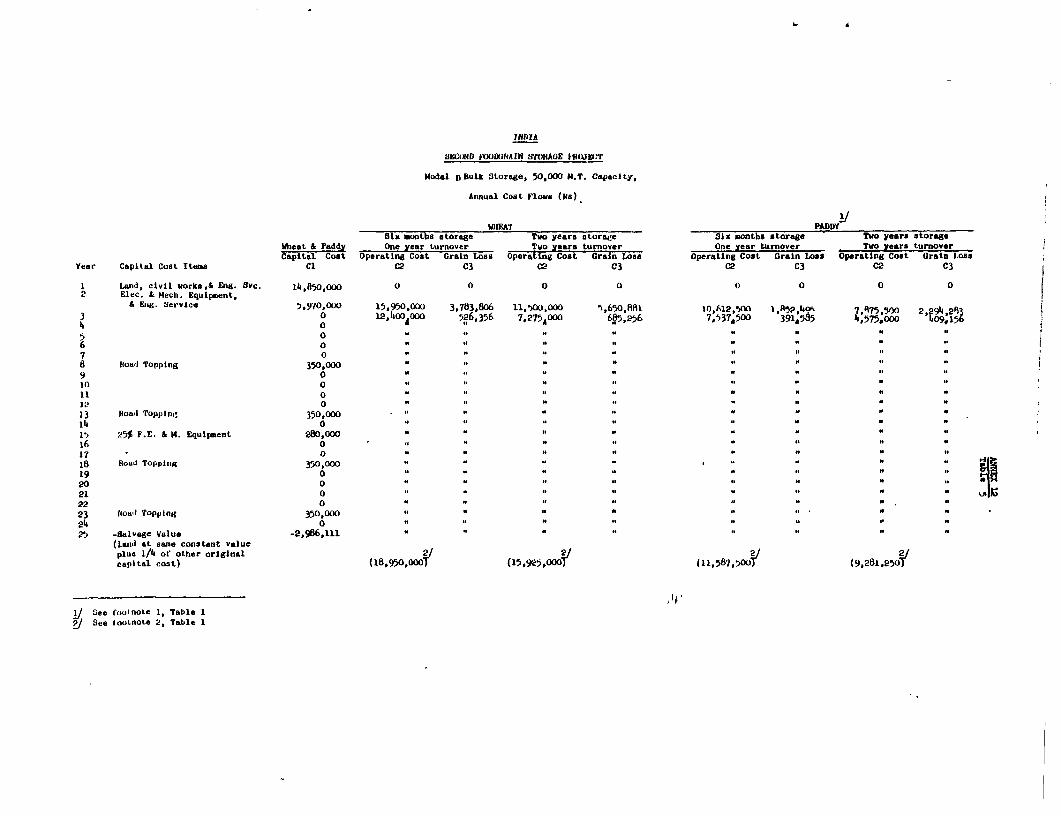

Designs and specifications are detailed in Annex 7. Detailed cost estimatesfor each type of storage complex are given in Annex 9, Tables 1 to 7.

4.05 Models A and B warehouses would be of identical dimensions: 21.8 mwidth, 127.6 m length and 6.35 m height from floor to eaves. Model A is theFCI conventional warehouse constructed with reinforced concrete columns, cur-tain brick and mortar walls and concrete floor. It would have a rated staticstorage capacity of 5,000 tons wheat in gunny bags and would be built in com-plexes ranging from 5,000 to 50,000 tons. The Model B warehouse would be con-structed with reinforced concrete floors and walls. Each building would in-clude tunnel and aeration ducts used for grain handling, aeration, drying andfumigation. A grain conveying system, work bins and bagging machines would be

- 12 -

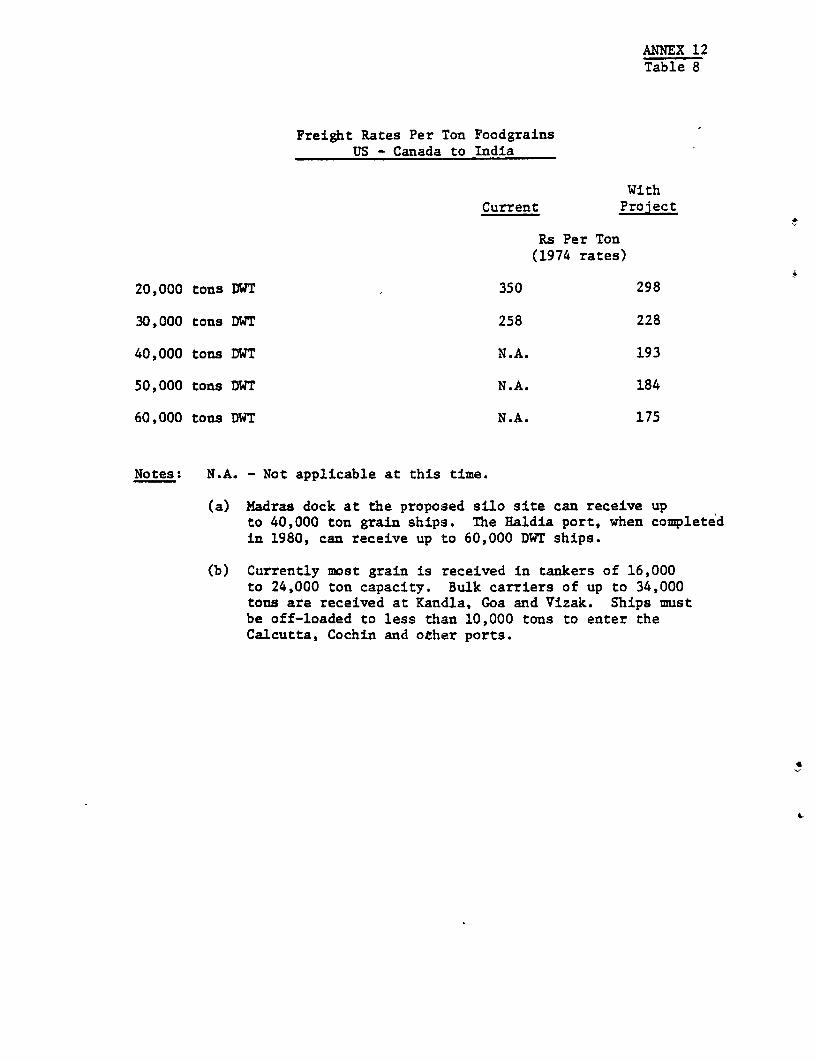

added. Bulk-head type doors facilitate grain storage in bulk or bag. Eachwarehouse would have a static storage capacity of 12,500 tons wheat in bulk or5,000 tons in gunny bags. Model B would be built in a complex of 52,500 tonscapacity including 2,500 tons of work bin space. The Model C circular binswould store only bulk grain. Each complex would have a capacity of 52,500tons, including 2,500 tons of work bin space. This model would be designedfor locations where groundwater conditions prevent construction of tunnels andelevator pits at depths of over 5 m. The entire structure would be of rein-forced concrete. An aeration system and conveying equipment would be provided.The Model D hopper-bottom warehouse would handle and store bulk grain. Itwould be constructed in complexes which store 52,500 tons of wheat, including2,500 tons of work bins. Port silos would be constructed at Haldia and Madras,where grain imports have ranged from 250,000 to over 1.0 million tons annually.The slip form or other superior method of construction would be used, sincethis method is less costly, results in stronger walls and has a lower likeli-hood of leaks. The costs of a complex of 50,000 tons of wheat storage capacityare estimated to be Rs 18.4 million for Model A, Rs 20.5 million for Model B,Rs 22.2 milliion for Model C and Rs 19.0 million for Model D.

Project Warehouse Configuration

4.06 Although the estimated investment costs of a standard 50,000 tonscomplex are higher for Models B, C and D than Model A, the operating costand grain losses of these bulk warehouses would be lower (Annex 4, Tables 5and 6, and Annex 9, Table 11), and their estimated economic rates of returnhigher. The project warehouse configuration, however, consists predominantlyof Model A for the following three principal considerations: (i) flat bulkstorage would not be suitable at most of the project sites because the match-ing bulk transportation and handling facilities would not be available forsome time; (ii) many of the project depots would have throughputs not largeenough to warrant bulk handling; and (iii) flat bulk storage is still rela-tively untried in India and should be regarded as a pilot development.

Rural Grain Procurement Centers

4.07 The project would finance two large and four small grain procure-ment centers, equipped with facilities for-mechanical handling of the procuredgrain (including temporary storage in some cases), and portable grain handlingequipment (cost US$1.7 million), for about fifty primary grain markets in thestates of Punjab, Haryana, Uttar Pradesh, Andhra Pradesh and Tamil Nadu.Under existing practice, most farmers deliver their grain (wheat) in bulk tothe primary market where the grain is placed in a heap on the market floor,priced, cleaned, bagged, weighed, purchased by FCI (or other buyers) and thendelivered to the warehouse. The facilities to be provided by the proposedprocurement centers would eliminate the need for bagging; the grain would beprocured in bulk and transferred to the center. Alternatively, the grain maybe delivered directly by the farmer to the procurement center, bypassingthe primary market. At the procurement center, the grain would be graded,weighed, and conveyed into elevated steel hopper bins where it is kept until

- 13 -

trucks transport it to a larger warehouse for storage or to the railways forshipment to points of distribution. It is estimated that these centers wouldreduce FCI's handling and transport costs by about Rs 33 per ton of grain(see Annex 9, Table 7).

Grain Transport Equipment

4.08 Trucks equipped to transport grain in bulk would be provided toFCI for delivery to storage facilities or from storage to flour mills. Papergrain door retainers for existing modified railwagons and new special grainrailwagons would be provided to transport grain by rail in unit trains fromexisting storage facilities and those to be financed under the project.Details are given in Annex 6 and in Annex 9, Table 8.

Technical Assistance

4.09 FCI engineers and contractors have had considerable experience inthe constructiou of the Model A warehouse complex, having built it at morethan 1,500 locations. The layout, design and auxiliary units have been stan-dardized and are acceptable to IDA. Nevertheless, FCI would need the assis-tance of hired engineering services to construct 2.5 million tons of suchstorage within four years. Hence, the grain storage engineering services ofCWC and the Central Public Works Department (CPWD) would be engaged to assistin the preparation of designs and tender documents and supervision of con-struction. FCI engineers and Indian engineering services have had limitedexperience in the design and construction of flat bulk grain storage ware-houses and silos. Domestic consultants and 60 man months of internationallyrecruited consultants would therefore be engaged to assist FCI prepare layoutplans, designs, tender documents, bid evaluations and to supervise construc-tion for the Models B, C and D complexes and port silos. During negotiations,assurances were obtained that GOI and FCI would engage engineering servicesand consultants, under arrangements and terms acceptable to IDA, not laterthan March 31, 1978.

Designs Development and Operations Research

4.10 The project would provide Rs 4.0 million (US$457,000) for FCI tostrengthen its Planning and Research Unit and develop designs for specialrailway wagons and modification to existing railway wagons, and conduct ope-rations research studies to ascertain comparative costs of receiving, hand-ling, storing and transporting grain in bag and bulk. These studies wouldreview relative costs and benefits of the different classes of warehouses -Models A, B, C and D warehouse complexes as well as CAP storage - when usedin different centers 1/ and for varying periods of storage. Similarly,alternative transport facilities and usage would be evaluated. Bag transportwould be compared with bulk transport using conventional trucks, specialgrain trucks, paper grain retention doors on railwagons and hopperbottom

1/ at (i) primary procurement centers; (ii) intermediate storage centers;(iii) urban distribution centers.

- 14 -

grain wagons. Such studies would be financed to obtain much more detailedinformation concerning the costs and benefits of the system of bulk handling,storage and transportation of grain (which would be provided under the projectas a pilot scheme), as compared to existing bag system, in order that the useof existing storage facilities may be optimized, and the planning and designof future storage projects be made more effective. Assurance was obtainedfrom GOI that plans acceptable to IDA would be prepared for carrying out suchoperations research studies by December 31, 1978.

4.11 Training. FCI would need additional staff, trained in grain hand-ling including bulk transportation, quality control and accounting to managethe new grain storage complexes. The project would provide Rs 3.5 million(US$400,000) for both domestic and overseas training of experts for thesepurposes (Annex 9, Table 9). During negotiations, agreement was obtainedfrom GOI and FCI that plans for training acceptable to IDA would be preparedby June 30, 1978.

C. Implementation Schedule

4.12 Implementation of the project is expected to take four and a halfyears, starting July 1, 1977 (with retroactive financing - see para. 4.15).Expenditures for each of the fiscal years are estimated as follows (Rs mil-lion): FY78 - 240.0; FY79 - 220.0; FY80 - 600.0; FY81 - 575.0; FY82 (6 months)- 251.0. The detailed time implementation schedule for the various projectcomponents is given in Annex 10.

D. Cost Estimates

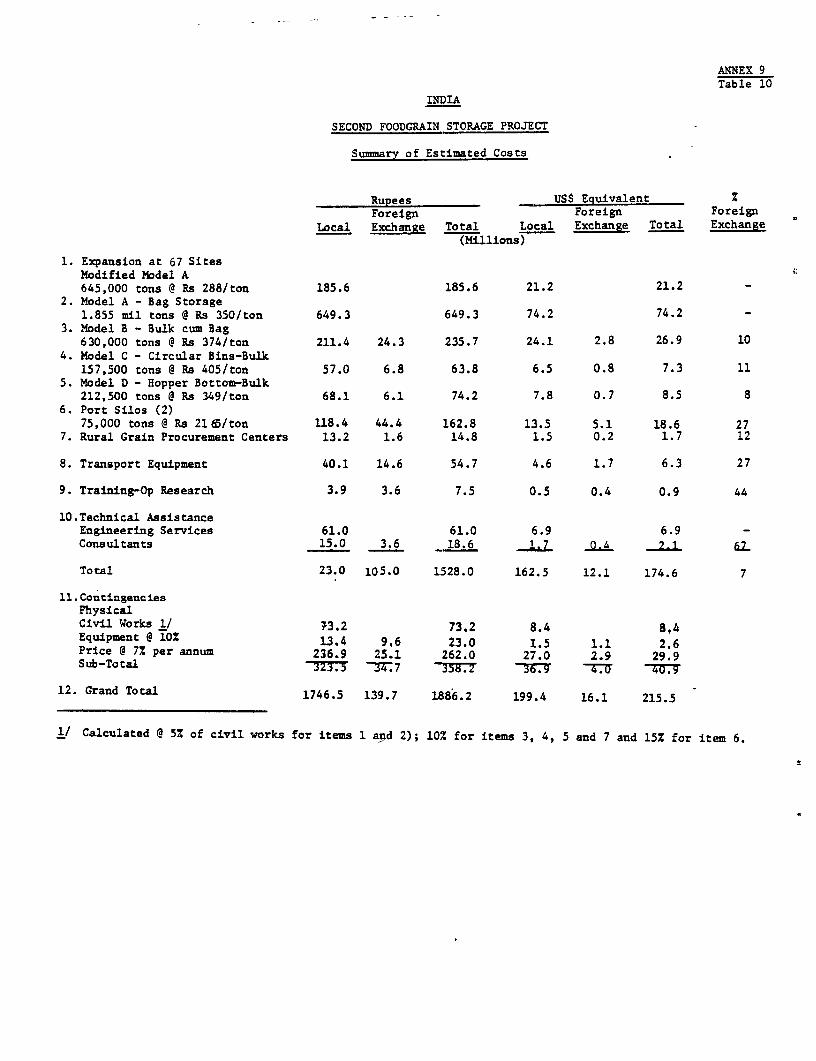

4.13 Total cost of the project, including that of land acquisition andcontingencies, is estimated at Rs 1,886 million (US$215.5 million). Theforeign exchange component of Rs 139.7 million (US$16.1 million) representsabout 7% of total costs and includes grain handling equipment, expatriateengineering services and training not available in India. Costs are basedon contract rates competitively awarded in mid-1977 for similar items. Phy-sical contingencies for civil works have been calculated at 5% for Model A,10Z for Models B, C and D and 15% for port silos. Physical contingencies forequipment have been calculated at 10% for all models and port silos. Pricecontingencies have been provided for at 7% per annum. Taxes and duties areestimated to be about US$2.0 million for the whole project. The followingtable presents a summary of the cost estimates:

- 15 -

Rupees US$ Equivalent %Foreign Foreign Foreign

Local Exchange Total Local Exchange Total Exchange- _ -(Millions)-

1. Expansion at67 Sites Modified.Model A - 645,000tons @ Rs 288/ton 185.6 - 185.6 21.2 - 21.2 -

2. Model A - BagStorage 1.855 mil.tons @ Rs 350/ton 649.3 - 649.3 74.2 - 74.2 -

3. Model B - 630,000tons @ Rs 374/ton 211.4 24.3 235.7 24.1 2.8 26.9 10

4. Model C - Cir-cular Bins 157,500tons @ Rs 405/ton 57.0 6.8 63.8 6.5 0.8 7.3 11

5. Model D - HopperBottom 212,500 tons@ Rs 349/ton 68.1 6.1 74.2 7.8 0.7 8.5 8

6. Port Silos (2)75,000 tons @Rs 2,165/ton 118.4 44.4 162.8 13.5 5.1 18.6 27

7. Rural Procure-ment Centers 13.2 1.6 14.8 1.5 0.2 1.7 12

8. TransportEquipment 40.1 14.6 54.7 4.6 1.7 6.3 27

9. Training-OpResearch 3.9 3.6 7.5 0.5 0.4 0.9 44

10. TechnicalAssistance:EngineeringServices 61.0 - 61.0 6.9 - 6.9 -

Consultants 15.0 3.6 18.6 1.7 0.4 2.1 19

Total 1, 423.0 105.0 1,528.0 162.5 12.1 174.6 7

11. Contingencies:Physical -a) C. Works 73.2 - 73.2 8.4 - 8.4

b) Equipment @ 10% 13.4 9.6 23.0 1.5 1.1 2.6Price - 7% per

annum 236.9 25.1 262.0 27.0 2.9 29.9

Sub-Total 323.5 34.7 358.2 36.9 4.0 40.9

12. Grand Total 1,746.5 139.7 1,886.2 199.4 16.1 215.5

- 16 -

E. Proposed Financing

4.14 It is proposed that IDA provide US$107.0 million (Rs 936.0 million)to finance 50% of the project cost, net of taxes and duties. IDA credit wouldbe to GOI and GOI would use US$2.4 million of the credit to purchase railwagonequipment, to be owned and operated by Indian Railways. GOI would on-lend theremaining US$104.6 million credit proceeds to FCI for a term not exceeding 20years, including a four year grace, at an annual interest of 10.5%, with a0.25% interest rebate for timely repayment. The remaining US$108.5 millionproject cost would be provided by GOI as GOI equity in FCI. The 10.5% interestrate, with 0.25% rebate is the standard formula that GOI uses for loans tosimilar public sector undertakings at the present time. GOI would pay in itsequity contribution in annual installments in equivalent of US$15.0 millionfor FY78, US$20.0 million for FY79, US$36.5 million for FY80, US$25.0 millionfor FY81, and US$12.0 million for FY82.

4.15 In 1976-77, to alleviate the sudden acute shortage of grain storagespace resulting from a good monsoon harvest, FCI began construction of 900,000tons of additional warehouse capacity, estimated to cost Rs 259.0 million(US$29.6 million). At that time, preparation of the proposed Second FoodgrainStorage Project was already close to completion, and the 900,000 tons capacityof warehouse construction was included in the proposal. However, GOI felt thatit had to act quickly to meet urgent storage needs rather than wait for theproject to be appraised and approved. By July 1, 1977, about Rs 73.5 million(US$8.4 million) of construction cost had been expended or tendered. Theremaining Rs 185.5 million (US$21.2 million) would be tendered after July 1,1977, and it is proposed to include this under the project in the light ofthe exceptional circumstances described above. It is proposed that expendi-tures made prior to credit signing against awards be made eligible for retro-active financing up to a maximumvof US$5.0 million, on the basis of standard50% financing formula for India.

F. Procurement 1/

4.16 All procurement, including employment of consultants, would be inaccordance with Bank guidelines. In all international competitive bidding,domestic bidders would be given a 7.5% preference on civil works. A 15%preference on equipment, based on the c.i.f price of each item or the actualtariff applicable, whichever is lower, would be granted to the domesticbidders. FCI would prequalify all domestic and foreign bidders for civilworks.

1/ Procurement costs are given inclusive of engineering services but exclu-sive of contingency provisions.

-17-

4.17 Civil Works for Bulk Storage Facilities: All civil works contractsfor bulk storage facilities (US$24.5 million) and the two port silos (US$8.1million) would be awarded on the basis of international competitive bidding.To the extent practical, these contracts would be bulked.

4.18 Civil Works for Conventional Storage Facilities and RuralProcurement Centers: Although in the aggregate the total cost of the bagstorage facilities would be very large (US$75.5 million), international com-petitive bidding would not be suitable because the construction sites wouldbe scattered across the country, the value of each contract relatively small,and Indian contractors are considered highly competitive. Civil works con-tracts for these facilities, therefore, together with those for rural procure-ment centers (US$0.9 million) would be awarded on the basis of competitivebidding advertised nationally and statewide under procedures satisfactory toIDA. Tenders would be in packages of three or more contracts, except instates with few storage facilities to be constructed. Contractors would beable to bid for any one contract individually or for a combination of con-tracts or for the entire lot.

4.19 Civil Works for Railway Sidings: Civil works contracts for railwaysidings (US$18.4 million) are highly specialized, and need to be coordinatedclosely with the existing railway system. Competitive bidding would not beappropriate, and civil works contracts for each location would be awardedby FCI (giving regard to economy and efficiency) to Indian Railways uaderprocedures satisfactory to IDA.

4.20 Malor Equipment Items: Procurement of weighbridges, temperatureindicator systems, aeration fans and ducts, railway scales, passenger ele-vators and railwagon movers for all sites, and material handling systems(grain conveyors, bucket elevators, truck dumpers, grain reclaimers, grainvalves, spouts) for all sites would be on the basis of international com-petitive bidding. To the extent practical, these equipment would be bulked.The special railwagons and paper grain door retainers would be packagedseparately and also awarded on the basis of international competitive bidding.

4.21 Miscellaneous Equipment Items: Miscellaneous items not lendingthemselves to bulking or expected to cost less than US$100,000 when bulkedwould be procured by tenders advertised nationally, and prudent shopping wouldbe used for items which individually or when bulked cost less than US$10,000.

4.22 Trucks. The 50 grain trucks would be procured on the basis ofnationally advertised competitive bidding from suppliers able to providespare parts and maintenance services. (Equipment costs, including trucks,are estimated to be about US$33.2 million).

G. Disbursement

4.23 The Credit would be disbursed against eligible expenditures asfollows: (i) 40% of civil works (US$59.0 million); (ii) for equipment

- 18 -

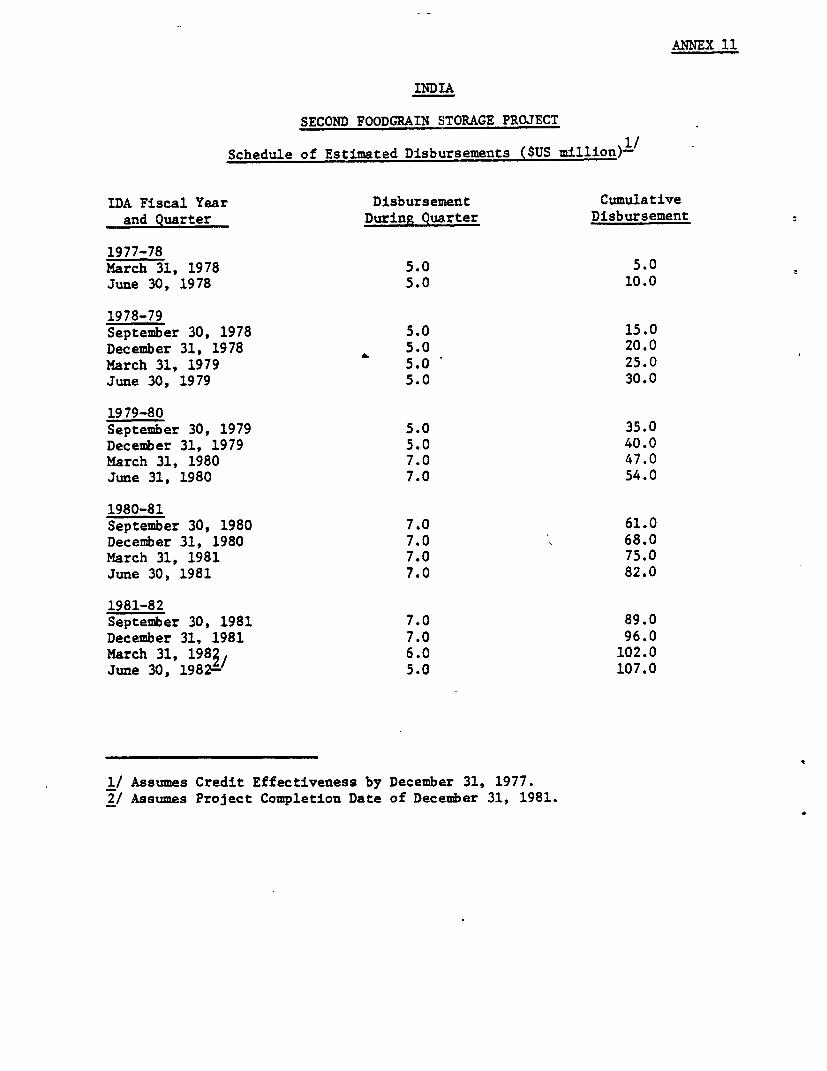

(US$38.0 million), 100% of foreign expenditures or 100% of local expenditures(ex-factory), for orders awarded under ICB or 50% of other locally procuredorders; and (iii) 100% of expenditures for engineering consultant services,training, designs development, and operations research (US$10.0 million).Expenditures incurred on the project after July 1, 1977, but prior to Creditsigning would be eligible for disbursement up to a limit of US$5.0 millionequivalent provided procurement procedures employed are determined by IDA ashaving been satisfactory. Disbursements would be made against appropriatedocumentation and would be exclusive of land. The estimated disbursementschedule is given in Annex 11.

V. ORGANIZATION AND MANAGEMENT

A. General

5.01 The Ministry of Agriculture and Irrigation would have overallresponsibility for the project. Within the Ministry, the Secretary for Foodand the Central Storage Committee (CSC) would be responsible for achievingcoordination of action among the various agencies within GOI and between GOIand the respective State governments. FCI would be responsible for imple-menting the project.

B. Prolect Implementation Division

5.02 FCI would establish a Project Implementation Division (PID), underthe direction of the Managing Director, which would be responsible fordetailed execution of the project. PID would be under the charge of a chiefengineer with at least 10 years experience of grain storage construction. Itwould have three sections: (i) Conventional Storage Section, to be respon-sible for the construction of all Model A bag warehouses; (ii) Bulk StorageSection, to be responsible for the construction of all Models B, C and D bulkwarehouses, port silos and rural procurement centers; and (iii) Finance andAdministration section, to be responsible for the accounts and audits, per-sonnel and legal matters of the project. The chief engineer would also super-vise the preparation and conduct of the designs development, operationsresearch and training programs.

- 19 -

5.03 The current staffing of the two existing engineering sections andthat proposed for PID are smmarized below:

No. of PersonsProject

Present Addition Total

Chief of PID 1 1Consultants 60 man-months

Conventional Storage SectionSenior Engineering Manager 1 - IEngineering Manager - I IJoint Engineering Manager 11 7 18Other Professional Staff 775 261 1,036Supporting Staff 280 708 988

Subtotal 1,067 2,044

Bulk Storage SectionEngineering Manager 1 1 2Joint Engineering Manager 2 16 18Other Professional Staff 61 380 441Supporting Staff 30 221 251

Subtotal 94 618 712

Finance and Administration SectionFinance Manager - 1 1Joint Manager 2 4 6Other Professional Staff 45 148 193Supporting Staff 550 936 1,486

Subtotal 597 1,089 1,686

Grand Total 1,758 2,685 4.443

Qualifications for the professional engineering and finance staff range fromthe equivalent of a graduate or Master's Degree and 5 or more years of ex-perience in their relevant fields to a Diploma and 1 or 2 years' experience(details on pattern and qualifications of staffing are shown in Annex 8,Appendix A).

5.04 The Conventional Storage Section of PID would not be adequatelystaffed to execute the construction of 2.5 million tons of Model A warehousesand to maintain existing ones. FCI would therefore enter into engineeringservice contracts with the grain storage engineering sections of CWC andCPWD for assistance in preparing designs and tender documents, evaluatingbids and supervising construction. Nonetheless, PID would be completelyin charge of the construction of about 1.5 million tons at 67 sites in 10states.

- 20 -

5.05 The establishment of PID, and posting of the chief engineer and thethree Managers of the Sections, under arrangements terms and staff qualifica-tions acceptable to IDA, would be a condition of credit effectiveness. Duringnegotiations, assurances were obtained that terms and conditions of the CWCand CPWD engineering service arrangements would be acceptable to IDA.

5.06 The implementation plan is shown in Annex 10. GOI and FCI haveprepared full details of the plan, which was finalized and agreed uponduring negotiations.

C. Accounts and Audits

5.07 FCI would maintain separate accounts for expenditures under thisproject. The annual budgets and accounts prepared by FCI should distinguishproject activities from its other operations. FCI'seannual accounts wouldbe audited by independent auditors acceptable to IDA. Assurances wereobtained from GOI and FCI on these actions. Assurances were also obtainedthat copies of these documents would be submitted to IDA as follows:

Annual budgets not later than one month prior to thebeginning of FCI's financial year;

Quarterly progress reports within one month of theclose of each quarter; and

Audited final accounts of the project within four monthsof the close of FCI's financial year.

D. Monitoring and Evaluation

5.08 On the basis of the detailed project implementation plan, the Chiefof PID (or, preferably, an assistant in charge of monitoring and reportingto him) would monitor and compare actual project progress with that planned.Problems could then be identified or foreseen, evaluated and action takento solve them to avoid slippage. IDA, through the receipt of a quarterlyprogress report from PID (on land acquisition, tendering, bid awards, pro-curement, disbursement, construction, training etc.) and periodic supervisionmissions, would help to ensure the adequacy of the monitoring and evaluationbeing carried out and to solve the problems that occur. During negotiations,assurances were obtained that FCI would establish a monitoring and evaluationsystem for the project by June 30, 1978.

5.09 The operations research studies described in para 4.10, to befinanced under the project, would constitute an em-post evaluation of therelative costs and benefits of the various types of warehouses, and moregenerally, of the system of bulk handling, storage and transportation ofgrain. This would help in the planning and design of future projects inIndia.

- 21 -

VI. ECONOMIC BENEFITS AND JUSTIFICATION

6.01 Without the warehouse storage component, FCI procured foodgrain wouldhave to be stored in the open, under cover and plinth (CAP), and grain storagelosses would be extensive. The economic benefit of the warehouse componentwould therefore be the reduction in grain storage losses and in the significantsavings on operating costs. The reduction in grain storage losses would havethe benefit of a saving on grain imports and therefore on foreign exchange.lowever, grain trade will continue and the port silo component of the projectis provided to reduce the cost of handling such grain.

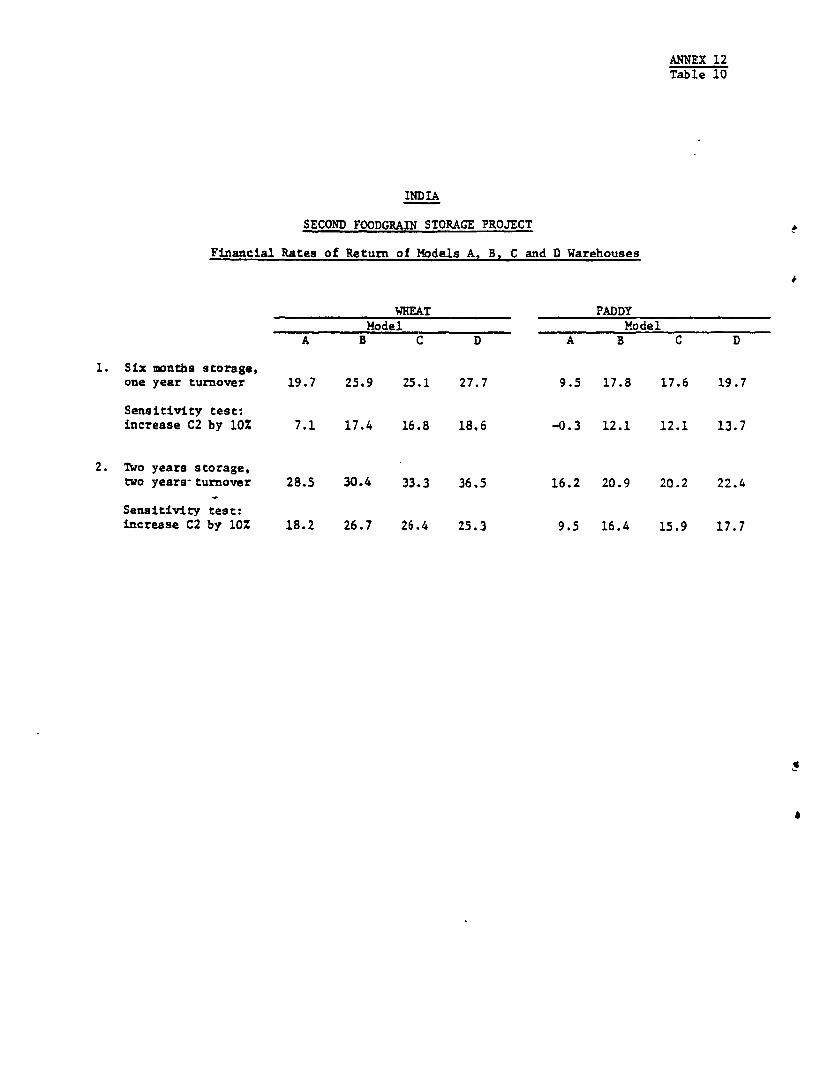

6.02 Project facilities would enable FCI to reduce storage losses by180,000 tons of wheat and paddy per year valued at about Rs 200 million(US$22.9 million) and to save on operating cost by about Rs 300 million(US$34.3 million). The estimated economic rate of return is about 20% forthe entire project investment; it is about 19% for the warehouse componentand 24% for the port silos (see Annex 12 for underlying assumptions andanalytic procedures). The rates of return on wheat and paddy storage forthe various project components based on duration of storage are given below:

Wheat PaddyModel Model Model Model Model Model Model Model

A B C D A B C D

1. 6 Months in Storage 19.7 25.9 25.8 28.4 9.5 17.8 17.6 19.7Sensitivity test:

I turnover per year(i) Increase capital

Cost - 15% 16.8 22.7 22.6 25.0 7.8 15.4 15.2 17.1(ii) Increase Oper.

Cost - 10% 11.1 20.1 20.2 22.4 2.9 14.0 14.0 15.7(iii) Increase grain

Loss - 10% 18.6 24.6 25.3 27.8 9.0 17.5 17.3 19.4

2. 24 Months in Storage 29.1 34.3 33.6 36.7 16.1 20.9 20.0 22.3Sensitivity test:

(i) Increase capitalCost - 15% 25.1 30.3 29.6 32.5 13.7 18.1 17.4 19.4

(ii) Increase Oper.Cost - 10% 23.8 30.8 30.1 33.0 12.3 18.5 17.8 19.8

(iii) Increase grainLoss - 10% 27.7 33.5 32.3 35.8 13.4 20.6 19.7 21.9

6.03 As can be seen, the bulk storage warehouses (Models B, C and D) havehigher rates of return than bag warehouses (Model A). Additional benefitswould arise from the resulting greater effectiveness of GOI's food procurementand distribution operations, which would induce increased grain production,enhance the welfare of producers and improve the real income of low incomeconsumers.

- 22 -

Project Risks

6.04 The major risk is the possibility of excess storage capacity,-dueto low procurement and low imports. It is, however, unlikely that the FoodCorporation's operational storage capacity would be much underutilized fora prolonged period because the circumstances leading to stock depletion -harvest shortfalls, high market prices, low public procurement and rapidofftake of grain - also would lead to increased imports as the GOI triesto maintain or increase levels of Governmental distribution of grain. Thechances that the relatively small capacity to hold contingency stocks wouldnot be used as planned are remote since weather induced fluctuations inharvest size, price, and therefore in GOI procurement and distribution arelikely to continue.

VII. RECOMMENDATIONS

7.01 During negotiations, IDA obtained assurances from GOI and FCIon the following:

(a) procurement would be in accordance with procedures statedin paras 4.16 and 4.22;

(b) IDA would be informed on at least a quarterly basis ofprogress in project execution (para 5.07);

(c) accounting and auditing procedures would be as set out inpara 5.07;

(d) a plan for developing designs and conducting operationsresearch by December 31, 1978 (para 4.10) and for stafftraining by June 30, 1978 (para 4.11), acceptable to IDA,would be prepared (para 5.08);

(e) a monitoring and evaluation system for the project would beestablished by June 30, 1978; and

(f) the employment of engineering services and consultantsunder arrangements and terms acceptable to IDA, byMarch 31, 1978 (para 4.09).

7.02 As a condition of Credit effectiveness, GOI and FCI would haveestablished the PID together with the posting of the chief engineerand the heads of the three sections (para 5.05).

7.03 With the above assurances, the proposed project is suitable for anIDA Credit of US$107.0 million to GOI.

ANNEX 1Page 1

INDIA

SECOND FOODGRAIN STORAGE PROJECT

Review of First Wheat Storage Project (Cr-267-IN)

1. The project, costing US$15.9 million, and financed jointly withSweden, originally consisted of: (a) constructing and equipping ten silosof 20,000 tons each and ten bag storage units of 10,000 tons each to providea total capacity of 300,000 tons; (b) training silo personnel; and (c) a studyof India's foodgrain storage and distribution. The project was intended tohelp meet urgent storage needs resulting from rapid increases in wheat pro-duction in Northern India in the late 1960's and to provide the basis fordeveloping a more effective nationwide system of grain storage and distri-bution.

2. The Food Corporation of India (FCI) was responsible for implement-ing the bulk of the project - construction and operation of storage facili-ties and training of silo personnel. The Credit agreement was signed inAugust 1971, but did not become effective until November 1972. Numerousfurther delays occurred after credit effectiveness, so that the project isnot expected to be completed until mid-1978, three years behind the appraisalestimate. Reasons for the delays both before and after credit effectivenessare discussed below in relation to implementation of project components.Despite the frustrating delays, the project is achieving its basic objectiveof providing needed grain storage facilities. The experiences gained, par-ticularly in procurement and land acquisition, should stand FCI in good steadin implementing the proposed project.

Silo Construction

3. The Credit Agreement provided, as one of the conditions of effec-tiveness, for the appointment by FCI of an engineering consultant acceptableto IDA, for the design and supervision of silo construction using the slipform method. This appointment took a long time because of FCI's unfamiliar-ity with IDA's procedure for the appointment of consultants, and FCI'sinternal administrative procedures. In accordance with IDA's procedure, PCIhad invited offers from three approved consulting firms to give particularsonly of their qualifications and experience. On this basis, one firm wasselected, and negotiations with this firm began. When the negotiations be-came prolonged as a result of difficulty in reaching an acceptable price,PCI called for offers with price quotations from the second and third firms,explaining that the offers would not be open until negotiations with the firstfirm had failed. This was considered by IDA to be a breach of procedure andaccordingly, FCI was requested to re-open negotiations with the first firm.

ANNEX 1Page 2

Negotiations continued to proceed slowly and were complicated by the involve-ment of negotiating and reviewing committees and administrative clearanceprocedures within FCI and the Food Department. It was not until nine monthslater that agreement was reached with the firm on November 10, 1972. TheCredit was declared effective four days later.

4. The Credit Agreement also required FCI to acquire all the 20 siloand godown sites as a condition of effectiveness. Difficulties were en-countered in the acquisition of these sites. In the end, when only one silosite remained to be acquired, and when agreement with the consultant hadbeen reached, IDA waived the site acquisition requirement.

5. Initial implementation difficulties encountered included a lackof knowledge of the silo component requirements by FCI's key engineeringstaff owing to lack of access to the project appraisal report and documents.This was quickly remedied. Next and more importantly, the Joint FinancingAgreement stipulated a single-bid requirement for all ten silos and anotherfor all ten godowns. Implicit was the assumption that the civil engineer-ing design and construction would be identical. Preliminary site surveys,however, showed varying soil conditions between sites, requiring individualfoundation designs, entailing in turn different bin heights and diameters toensure economic construction. In addition, several of the proposed silo siteswere found to be unsuitable because of inability to acquire land, bad sitelocation with regard to receiving and distributing grains, and unavailabilityof railway sidings and usable access roads. FCI therefore requested waivingof the requirements for a single bid for 10 silo units in favor of multipleinvitation to bid for construction of those silos whose sites were suitableand foundation designs completed. The request was agreed to by IDA in January1974.

6. During the delays caused by the above problems, costs, particu-larly for silo constructiou, escalated and the project was reappraised inearly 1975. The number of silos were reduced to keep costs at the originalappraisal estimates. As revised, the project finances the constructionof nine 10,000 ton flat storage godowns, five 20,000 ton silos (at Khurja,Lucknow, Moga, Jagraon and Modi Gobingarh), four bulk grain handlingfacilities, staff training and an All-India Grain Storage Study.