IMPORTANT NOTICE NOT FOR DISTRIBUTION TO ANY U.S. ...

279

IMPORTANT NOTICE NOT FOR DISTRIBUTION TO ANY U.S. PERSON OR TO ANY PERSON OR ADDRESS IN THE U.S. IMPORTANT: You must read the following before continuing. The following applies to the prospectus (the prospectus) following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the prospectus. In accessing the prospectus, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY THE SECURITIES OF THE ISSUER IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE SECURITIES ACT), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE U.S. OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THE FOLLOWING PROSPECTUS MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. PERSON OR TO ANY U.S. ADDRESS. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. This prospectus has been delivered to you on the basis that you are a person into whose possession this prospectus may be lawfully delivered in accordance with the laws of the jurisdiction in which you are located. By accessing the prospectus, you shall be deemed to have confirmed and represented to us that (a) you have understood and agree to the terms set out herein, (b) you consent to delivery of the prospectus by electronic transmission, (c) you are not a U.S. Person (within the meaning of Regulation S under the Securities Act) or acting for the account or benefit of a U.S. Person and the electronic mail address that you have given to us and to which this e-mail has been delivered is not located in the United States, its territories and possessions (including Puerto Rico, the U.S. Virgin Islands, Guam, American Samoa, Wake Island and the Northern Mariana Islands) or the District of Columbia and (d) if you are a person in the United Kingdom, then you are a person who (i) has professional experience in matters relating to investments or (ii) is a high net worth entity falling within Article 49(2)(a) to (d) of the Financial Services and Markets Act (Financial Promotion) Order 2005. This prospectus has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission and consequently none of TCHG Capital plc or TradeRisks Limited nor any person who controls any of them nor any director, officer, employee nor agent of any of them or affiliate of any such person accepts any liability or responsibility whatsoever in respect of any difference between the prospectus distributed to you in electronic format and the hard copy version available to you on request from TradeRisks Limited.

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of IMPORTANT NOTICE NOT FOR DISTRIBUTION TO ANY U.S. ...

IMPORTANT NOTICE

NOT FOR DISTRIBUTION TO ANY U.S. PERSON OR TO ANY PERSON OR ADDRESS IN THE U.S.

IMPORTANT: You must read the following before continuing. The following applies to the prospectus (the prospectus) following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the prospectus. In accessing the prospectus, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access.

NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY THE SECURITIES OF THE ISSUER IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE SECURITIES ACT), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE U.S. OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS.

THE FOLLOWING PROSPECTUS MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND IN PARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. PERSON OR TO ANY U.S. ADDRESS. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS.

This prospectus has been delivered to you on the basis that you are a person into whose possession this prospectus may be lawfully delivered in accordance with the laws of the jurisdiction in which you are located. By accessing the prospectus, you shall be deemed to have confirmed and represented to us that (a) you have understood and agree to the terms set out herein, (b) you consent to delivery of the prospectus by electronic transmission, (c) you are not a U.S. Person (within the meaning of Regulation S under the Securities Act) or acting for the account or benefit of a U.S. Person and the electronic mail address that you have given to us and to which this e-mail has been delivered is not located in the United States, its territories and possessions (including Puerto Rico, the U.S. Virgin Islands, Guam, American Samoa, Wake Island and the Northern Mariana Islands) or the District of Columbia and (d) if you are a person in the United Kingdom, then you are a person who (i) has professional experience in matters relating to investments or (ii) is a high net worth entity falling within Article 49(2)(a) to (d) of the Financial Services and Markets Act (Financial Promotion) Order 2005.

This prospectus has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission and consequently none of TCHG Capital plc or TradeRisks Limited nor any person who controls any of them nor any director, officer, employee nor agent of any of them or affiliate of any such person accepts any liability or responsibility whatsoever in respect of any difference between the prospectus distributed to you in electronic format and the hard copy version available to you on request from TradeRisks Limited.

Preliminary Prospectus dated 26 June, 2014 Subject to completion and amendment

TCHG CAPITAL PLC (Incorporated in England and Wales with limited liability under the Companies Act 2006, registered number 8971695)

£80,000,000 4.665 per cent. Secured Bonds due 2045 Issue Price: 100 per cent. payable in full on the Issue Date

The £80,000,000 4.665 per cent. Secured Bonds due 2045 (the Bonds) are to be issued by TCHG Capital plc (the Issuer) on 3rd July, 2014 (the Issue Date).

Application has been made to the Financial Conduct Authority in its capacity as competent authority (the UK Listing Authority) for the Bonds to be admitted to the Official List of the UK Listing Authority and to the London Stock Exchange plc (the London Stock Exchange) for the Bonds to be admitted to trading on the London Stock Exchange's regulated market. The London Stock Exchange's regulated market is a regulated market for the purposes of Directive 2004/39/EC (the Markets in Financial Instruments Directive). An investment in the Bonds involves certain risks. For a discussion of these risks see Risk Factors.

Subject as set out below, the net proceeds from the issue of the Bonds will be advanced by the Issuer to Town and Country Housing Group (the Original Borrower) pursuant to a loan agreement made between the Issuer and the Original Borrower to be dated on or around the Issue Date (the Original Loan Agreement) to be applied in accordance with the Original Borrower's constitution. The Aggregate Funded Commitment (being, on the Issue Date, the amount of the Original Borrower's Original Commitment (as defined below)) may be drawn in one or more drawings, each in a nominal amount up to an amount which corresponds to the sum of (a) the Minimum Value of the Initial Properties (as defined below) and (b) the Minimum Value of any Additional Properties (as defined below) which have been charged in favour of the Issuer and the Security Trustee (the Additional Properties) less the nominal amount of all previous drawings in respect of the Aggregate Funded Commitment (subject, in the case of each Borrower (as defined below), to the maximum of its respective Commitment (as defined below)).

For so long as (1) insufficient security has been granted (or procured to be granted) by the Borrowers in favour of the Issuer and the Security Trustee to permit the drawing of the Aggregate Funded Commitment in full or (2) the Borrowers have not otherwise drawn any part of the Aggregate Funded Commitments, the amount of the Aggregate Funded Commitment that remains undrawn shall be retained in a charged account (the Initial Cash Security Account) of the Issuer in accordance with the terms of the Account Agreement (and may be invested in Permitted Investments (as defined below)) (the Retained Proceeds, which will include any prepayments under a Loan Agreement which are not applied in or towards redemption of the Bonds). Any Retained Proceeds and any Further Proceeds (being any net issue proceeds from a further issue of Bonds pursuant to Condition 19 (Further Issues)), to the extent that Properties of a corresponding value have been charged in favour of the Issuer, may be advanced at a later date pursuant to the Original Loan Agreement or an Additional Loan Agreement (as defined below) to the Original Borrower and/or any other Additional Borrower (being a person which (a) is a charity, (b) is a Registered Provider of Social Housing, (c) is a member of the Group (such requirements in (a), (b) and (c) being the Borrower Minimum Requirements) and (d) is a borrower under the Original Loan Agreement or under an additional loan agreement between the Issuer (as lender), the Additional Borrower and the Security Trustee where all the liabilities of such Additional Borrower are secured by the Security Agreements (as defined below) (each an Additional Loan Agreement and, together with the Original Loan Agreement, the Loan Agreements and each a Loan Agreement)).

As described in Condition 7 (Interest), interest on each Bond is payable semi-annually in arrear on 3rd July and 3rd January in each year (each an Interest Payment Date) on its Outstanding Principal Amount (as defined below), commencing on 3rd January, 2015, at the rate of 4.665 per cent. per annum in respect of the period from (and including) the Issue Date to (but excluding) the Maturity Date. Payments of principal of, and interest on, the Bonds will be made without withholding or deduction on account of United Kingdom taxes unless required by law. In the event that any such withholding or deduction is so required, the Issuer may opt to gross up payments due to the Bondholders in respect thereof as described in Condition 10 (Taxation).

Unless previously redeemed, or purchased and cancelled, the Bonds will be redeemed at their Outstanding Principal Amount in 20 equal instalments of £50 per £1,000 in original nominal amount on each Interest Payment Date from, and including, 3rd January, 2036 to, and including 3rd July, 2045 (the Maturity Date) (each such date an Instalment Redemption Date). The Bonds may be redeemed at any time prior to the Maturity Date, in whole or in part, as the case may be, upon the optional prepayment by a Borrower of its loan (each a Loan) in whole or in part or the Loan otherwise becoming repayable in whole or in part in accordance with the terms of the Loan Agreement at the higher of their Outstanding Principal Amount and an amount calculated by reference to the sum of (1) the yield on the relevant outstanding UK Government benchmark conventional gilt having the nearest average maturity to that of the Bonds and (2) 0.20 per cent., together with accrued interest (or, in respect of a prepayment of a Loan following an event of default thereunder, at their Outstanding Principal Amount, together with accrued interest). The Bonds will also be redeemed (a) at their Outstanding Principal Amount, plus accrued interest, in an aggregate Outstanding Principal Amount equal to the nominal amount outstanding of the relevant Loan in the event of a mandatory prepayment of a Loan following a Borrower ceasing to satisfy each of the Borrower Minimum Requirements (other than if such Borrower complies with the Borrower Minimum Requirements within 180 days) or a Loan becoming repayable as a result of a Borrower Default (as defined in each Loan Agreement) or (b) at their Outstanding Principal Amount, plus accrued interest, in full in the event of any withholding or deduction on account of United Kingdom taxes being required and the Issuer not opting to pay (or having so opted to pay notifying the Bond Trustee (as defined below) of its intention to cease to pay) additional amounts in respect of such withholding or deduction.

The Original Borrower has been assigned a credit rating of "AA-", and it is expected that the Bonds will be rated "AA-", by Standard & Poor’s Credit Market Services Group Limited (S&P). A rating is not a recommendation to buy, sell or hold securities and may be subject to revision, suspension or withdrawal at any time by the assigning rating organisation. S&P is established in the European Union and is registered under Regulation (EC) No. 1060/2009 (as amended). As such S&P is included in the list of credit rating agencies published by the European Securities and Markets Authority on its website in accordance with such Regulation.

The Bonds will be issued in denominations of £100,000 and integral multiples of £1,000 in excess thereof.

The Bonds will be initially represented by a temporary global bond (a Temporary Global Bond) without principal receipts or interest coupons and which will be deposited on or about 3rd July, 2014 (the Closing Date) with a common safekeeper for Euroclear Bank S.A./N.V. (Euroclear) and Clearstream Banking, société anonyme (Clearstream, Luxembourg). On or after 12 August, 2014 (the Exchange Date), upon certification as to non-U.S. beneficial ownership, interests in the Temporary Global Bond will be exchangeable for interests in a permanent global bond without principal receipts or interest coupons (the Permanent Global Bond and, together with the Temporary Global Bond, the Global Bonds). Interests in a Permanent Global Bond will be exchangeable for definitive Bonds only in certain limited circumstances. See Form of the Bonds and Summary of Provisions relating to the Bonds while in Global Form.

The Issuer shall also be at liberty from time to time with the prior consent of the Bondholders, granted by way of Extraordinary Resolution, and of the Original Borrower to create and issue further bonds having terms and conditions (and backed by the same assets) the same as the Bonds or the same in all respects save for the amount and date of the first payment of interest thereon and so that the same shall be consolidated and form a single series with the outstanding Bonds. See Condition 19 (Further Issues).

Arranger and Dealer

TradeRisks Limited

The date of this Prospectus is 1st July, 2014.

I-A7.4.2

I-LR2.2.1(1)

I-A7.4.3

I-LR2.2.7(1)

I-A13.4.2

I-A13.4.5

I-A13.4.5

I-A13.4.9

I-A13.4.13 I-LR2.2.9(1)

I-LR2.2.10(2)(a)

A-A13.2

I-A13.5.1

I-A7.3.1

I-LR2.2.2(3)

A-A9.3.1

G-A6.1

I-A8.2.2.7

I-A8.3.3

I-A8.3.4.4

I-A13.4.8

I-A13.7.5

I-A8.1.1

I-LR2.2.4(1)

I-A13.4.14

I-A8.2.4

Thi

s P

reli

min

ary

Pro

spec

tus

is s

ubje

ct t

o co

mpl

etio

n an

d am

endm

ent

wit

hout

not

ice.

Thi

s P

reli

min

ary

Pro

spec

tus

does

not

con

stit

ute

an o

ffer

to

sell

or

the

soli

cita

tion

of

an o

ffer

to

buy

any

secu

riti

es o

f th

e Is

suer

. It

is

an a

dver

tise

men

t an

d do

es n

ot c

ompr

ise

a pr

ospe

ctus

for

the

purp

oses

of

Dir

ecti

ve 2

003/

71/E

C a

nd/o

r P

art

VI

of t

he F

inan

cial

Ser

vice

s an

d M

arke

ts A

ct 2

000

of t

he U

nite

d K

ingd

om o

r ot

herw

ise.

The

def

init

ive

term

s of

the

tra

nsac

tion

s de

scri

bed

here

in w

ill

be d

escr

ibed

in

the

fina

l ve

rsio

n of

thi

s P

rosp

ectu

s. I

nves

tors

sho

uld

not

subs

crib

e fo

ran

y se

curi

ties

ref

erre

d to

her

ein

exce

pt o

n th

e ba

sis

of in

form

atio

n co

ntai

ned

in th

e fi

nal f

orm

of

the

Pro

spec

tus.

Whe

n av

aila

ble,

the

fina

l Pro

spec

tus

wil

l be

mad

e av

aila

ble

to th

e pu

blic

in a

ccor

danc

e w

ith

Dir

ecti

ve 2

003/

71/E

C a

nd/o

r P

art V

I of

the

Fina

ncia

l Ser

vice

s an

d M

arke

ts A

ct20

00 a

nd in

vest

ors

may

obt

ain

a co

py f

rom

the

link

set

out

in th

e R

NS

ann

ounc

emen

t whi

ch c

orre

spon

ds to

the

Issu

er's

info

rmat

ion

page

on

the

web

site

of

the

Lon

don

Sto

ck E

xcha

nge.

2

This Prospectus comprises a prospectus for the purposes of Directive 2003/71/EC (the Prospectus Directive).

The Issuer accepts responsibility for the information contained in this Prospectus. To the best of the knowledge of the Issuer (having taken all reasonable care to ensure that such is the case) the information contained in this Prospectus is in accordance with the facts and does not omit anything likely to affect the import of such information.

The Original Borrower accepts responsibility for the information relating to it under the heading Factors which may affect the Borrowers' ability to fulfil their obligations under the Loan Agreements in the section Risk Factors, the information under the heading Guarantee and Indemnity in the sections Overview and Description of the Loan Agreements and the information relating to it contained under the headings Material or Significant Change and Litigation in the section General Information and, to the best of its knowledge (having taken all reasonable care to ensure that such is the case), such information is in accordance with the facts and does not omit anything likely to affect the import of such information.

The Original Borrower also accepts responsibility for the information under the heading The Original Borrower in the section Description of the Original Borrower and the Group and the financial statements relating to the Original Borrower in Appendix 1 - Financial Statements of the Original Borrower and for the information contained in this Prospectus relating to the security created by it pursuant to its Security Agreements (as defined below) under the heading Underlying Security in the section Overview, under the heading Considerations relating to the Issuer Security and the Underlying Security in the section Risk Factors and in the section Description of the Issuer Security, the Security Agreements and the Security Trust Deed and, to the best of its knowledge (having taken all reasonable care to ensure that such is the case), such information is in accordance with the facts and does not omit anything likely to affect the import of such information.

Savills Advisory Services Limited (the Valuer) accepts responsibility for the information contained in the section Valuation Report and in Appendix 2 - Valuation Report and, to the best of its knowledge (having taken all reasonable care to ensure that such is the case), such information is in accordance with the facts and does not omit anything likely to affect the import of such information. The figures and data:

(a) referred to in paragraphs 1.8 and 9.4 of the Valuation Report were obtained from the Volume 26, No. 4 edition of Social Housing published in April 2014,

(b) referred to in paragraph 8.1 of the Valuation Report were obtained from the May 2014 edition of the HCA Monthly Housing Market Bulletin published by the Homes and Communities Agency,

(c) referred to in the section entitled "The Nationwide House Price Index May 2014 reported" in Appendix 5 of the Valuation Report were obtained from the May 2014 edition of the Nationwide House Price Index published by Nationwide Building Society, and

(d) referred to in the section entitled "Savills Residential Property Focus Bulletin Q2 2014 reported the following" in Appendix 5 of the Valuation Report were obtained from the Q2 2014 edition of the Savills Residential Property Focus Bulletin published by Savills plc.

The Valuer confirms that such figures and data have been accurately reproduced and that, as far as the Valuer is aware and is able to ascertain from information published by Social Housing, the Homes and Communities Agency, Nationwide Building Society and Savills plc, no facts have been omitted which would render the reproduced figures and data inaccurate or misleading. For the avoidance of doubt, with the exception of the information contained in the section Valuation Report and in Appendix 2 - Valuation Report, the Valuer does not accept any responsibility in relation to the information contained in this Prospectus or any other

I-A13.1.1

I-A13.1.2

A-A9.1.1

A-A9.1.2

I-A7.1.1

I-A7.1.2

I-A13.1.1

I-A13.1.2

A-A9.1.1

A-A9.1.2

I-A7.1.1

I-A7.1.2

I-A13.1.1

I-A13.1.2

A-A9.1.1

A-A9.1.2

I-A7.1.1

I-A7.1.2

I-A13.1.1

I-A13.1.2

A-A9.1.1

A-A9.1.2

I-A7.1.1

I-A7.1.2

I-A7.9.2

A-A9.13.2

I-A13.7.4

3

information provided by the Issuer or the Original Borrower connection with the issue of the Bonds.

Save for the Issuer, the Original Borrower and (solely in respect of the section Valuation Report and in Appendix 2 - Valuation Report) the Valuer, no other person has independently verified any information contained herein. No representation, warranty or undertaking, express or implied, is made and no responsibility or liability is accepted by TradeRisks Limited in its role as arranger (the Arranger) or in its role as dealer (the Dealer) or Prudential Trustee Company Limited (the Bond Trustee) as to the accuracy or completeness of the information contained in this Prospectus or any other information provided by the Issuer or the Original Borrower in connection with the offering of the Bonds. None of the Arranger, the Dealer and the Bond Trustee accepts any liability in relation to the information contained in this Prospectus or any other information provided by the Issuer in connection with the issue of the Bonds.

No person is or has been authorised by the Issuer, the Arranger, the Dealer or the Bond Trustee to give any information or to make any representation not contained in or not consistent with this Prospectus or any other information supplied in connection with the offering of the Bonds and, if given or made, such information or representation must not be relied upon as having been authorised by the Issuer, the Arranger, the Dealer or the Bond Trustee.

To the fullest extent permitted by law, none of the Arranger, the Dealer and the Bond Trustee accepts any responsibility for the contents of this Prospectus or for any other statement made or purported to be made by it or on its behalf in connection with the Issuer, the Original Borrower or the issue and offering of the Bonds. Each of the Arranger, the Dealer and the Bond Trustee accordingly disclaims all and any liability whether arising in tort or contract or otherwise (save as referred to above) which it might otherwise have in respect of this Prospectus or any such statement.

Neither this Prospectus nor any other information supplied in connection with the Bonds should be considered as a recommendation by the Issuer, the Arranger, the Dealer or the Bond Trustee that any recipient of this Prospectus or any other information supplied in connection with the Bonds should purchase any Bonds. Each investor contemplating purchasing any Bonds should make its own independent investigation of the financial condition and affairs, and its own appraisal of the creditworthiness, of the Issuer and the Original Borrower. Neither this Prospectus nor any other information supplied in connection with the offering of the Bonds constitutes an offer or invitation by or on behalf of the Issuer, the Arranger, the Dealer or the Bond Trustee to any person to subscribe for or to purchase the Bonds.

Neither the delivery of this Prospectus nor the offering, sale or delivery of the Bonds shall in any circumstances imply that the information contained herein concerning the Issuer or the Original Borrower is correct at any time subsequent to the date hereof or that any other information supplied in connection with the offering of the Bonds is correct as of any time subsequent to the date indicated in the document containing the same. The Arranger, the Dealer and the Bond Trustee expressly do not undertake to review the financial condition or affairs of the Issuer or the Original Borrower during the life of the Bonds or to advise any investor in the Bonds of any information coming to their attention.

The Bonds have not been and will not be registered under the United States Securities Act of 1933, as amended (the Securities Act) and are subject to U.S. tax law requirements. Subject to certain exceptions, the Bonds may not be offered, sold or delivered within the United States or to, or for the account or benefit of, U.S. persons (see Purchase and Sale).

This Prospectus does not constitute an offer to sell or the solicitation of an offer to buy any Bonds in any jurisdiction to any person to whom it is unlawful to make the offer or solicitation in such jurisdiction. The distribution of this Prospectus and the offer or sale of Bonds may be restricted by law in certain jurisdictions. The Issuer, the Arranger, the Dealer and the Bond Trustee do not represent that this Prospectus may be lawfully distributed, or that the Bonds may

4

be lawfully offered or sold, in compliance with any applicable registration or other requirements in any such jurisdiction, or pursuant to an exemption available thereunder, or assume any responsibility for facilitating any such distribution or offering. In particular, no action has been taken by the Issuer, the Arranger, the Dealer or the Bond Trustee which is intended to permit a public offering of the Bonds or the distribution of this Prospectus in any jurisdiction where action for that purpose is required. Accordingly, no Bonds may be offered or sold, directly or indirectly, and neither this Prospectus nor any advertisement or other offering material may be distributed or published in any jurisdiction, except under circumstances that will result in compliance with any applicable laws and regulations. Persons into whose possession this Prospectus or any Bonds may come must inform themselves about, and observe, any such restrictions on the distribution of this Prospectus and the offering and sale of Bonds. In particular, there are restrictions on the distribution of this Prospectus and the offer or sale of Bonds in the United States and the United Kingdom (see Purchase and Sale).

Prospective purchasers of Bonds should ensure that they understand the nature of the Bonds and the extent of their exposure to risk, that they have sufficient knowledge, experience and access to professional advisers to make their own legal, tax, accounting and financial evaluation of the merits and the risks of investment in the Bonds and that they consider the suitability of the Bonds as an investment in light of their own circumstances and financial condition.

All references in this Prospectus to Sterling and £ refer to pounds sterling.

5

CONTENTS

OVERVIEW.......................................................................................6 Structure diagram of the transaction..........................................6 Issuer ..........................................................................................6 Description of the Bonds ...........................................................6 Issue Price ..................................................................................7 Use of Proceeds .........................................................................7 Form of Bonds ...........................................................................7 Interest........................................................................................7 Instalment Redemption..............................................................7 Early Redemption ......................................................................7 Early Redemption for Tax Reasons...........................................8 Mandatory Early Redemption ...................................................8 Purchase .....................................................................................9 Events of Default .......................................................................9 Issuer Security............................................................................9 Initial Cash Security Account..................................................10 Ongoing Cash Security Account .............................................10 Permitted Investments .............................................................11 Account Agreement and Custody Agreement.........................12 Guarantee and Indemnity.........................................................12 Underlying Security.................................................................13 Addition, substitution and release of Charged Properties .......14 Enforcement of the Underlying Security and the Issuer

Security..............................................................................17 Priorities of Payments..............................................................17 Status of the Bonds ..................................................................19 Covenants.................................................................................19 Taxation ...................................................................................19 Meetings of Bondholders.........................................................19 Risk Factors .............................................................................19 Listing and admission to trading .............................................20 Ratings .....................................................................................20 Arranger ...................................................................................20 Dealer .......................................................................................20 Principal Paying Agent ............................................................20 Account Bank ..........................................................................20 Custodian .................................................................................20 Bond Trustee............................................................................20 Security Trustee .......................................................................20 Original Borrower....................................................................20 Borrowers.................................................................................20 Eligible Group Member...........................................................20 Corporate Services Provider ....................................................21 Selling Restrictions ..................................................................21 Governing Law ........................................................................21

RISK FACTORS...............................................................................22 Factors which may affect the Issuer's ability to fulfil its

obligations under the Bonds..............................................22 Factors which may affect the Borrowers' ability to fulfil

their obligations under the Loan Agreements ...................22 Factors which are material for the purpose of assessing the

market risks associated with the Bonds ............................30 Risks Relating to the Security of the Bonds............................33 Risks Relating to the Market Generally ..................................35

FORM OF THE BONDS AND SUMMARY OF PROVISIONS

RELATING TO THE BONDS WHILE IN GLOBAL FORM................36 Form of the Bonds ...................................................................36 Summary of Provisions relating to the Bonds while in

Global Form.......................................................................37 USE OF PROCEEDS .........................................................................39 DESCRIPTION OF THE LOAN AGREEMENTS...................................40

Facility .....................................................................................40 Purpose.....................................................................................42 Interest......................................................................................42 Commitment Fee......................................................................42 Repayment, Purchase and Prepayment....................................43 Warranties and Covenants .......................................................44 Guarantee and Indemnity.........................................................45 Asset Cover Test ......................................................................45 Substitution and Release of Charged Properties and

Statutory Disposals............................................................46 Valuations ................................................................................48 Loan Events of Default and Enforcement ...............................48 Taxes ........................................................................................51

Governing Law........................................................................ 51 DESCRIPTION OF THE ISSUER SECURITY, THE SECURITY

AGREEMENTS AND THE SECURITY TRUST DEED .................... 52 Security framework................................................................. 52 Security Agreements ............................................................... 54 Security Trust Deeds............................................................... 55 Enforcement of security and application of proceeds ............ 56

DESCRIPTION OF THE ACCOUNT AGREEMENT AND THE

CUSTODY AGREEMENT ........................................................... 58 Account Agreement ................................................................ 58 Custody Agreement................................................................. 60

DESCRIPTION OF THE CORPORATE SERVICES AGREEMENT......... 62 Corporate Services Provider ................................................... 62 Corporate Services Agreement ............................................... 62

TERMS AND CONDITIONS OF THE BONDS..................................... 63 1. Definitions ........................................................................ 63 2. Form, Denomination and Title ......................................... 68 3. Status................................................................................. 69 4. Security ............................................................................. 69 5. Order of payments ............................................................ 69 6. Covenants.......................................................................... 70 7. Interest .............................................................................. 71 8. Payments ........................................................................... 72 9. Redemption and Purchase ................................................ 73 10. Taxation ............................................................................ 76 11. Prescription ....................................................................... 76 12. Events of Default and Enforcement ................................. 77 13. Replacement of Bonds, Receipts, Coupons and Talons... 78 14. Exchange of Talons .......................................................... 79 15. Notices .............................................................................. 79 16. Substitution ....................................................................... 79 17. Meetings of Bondholders, modification and waiver ........ 79 18. Indemnification and protection of the Bond Trustee

and Bond Trustee contracting with the Issuer .................. 81 19. Further Issues.................................................................... 81 20. Contracts (Rights of Third Parties) Act 1999................... 82 21. Governing law .................................................................. 82 22. Submission to Jurisdiction................................................ 82

DESCRIPTION OF THE ISSUER........................................................ 83 Incorporation and Status ......................................................... 83 Principal Activities.................................................................. 83 Directors .................................................................................. 83 Share Capital and Major Shareholders ................................... 84 Operations ............................................................................... 84

DESCRIPTION OF THE ORIGINAL BORROWER AND THE GROUP ... 85 The Group ............................................................................... 85 The Original Borrower............................................................ 86 Financial Statements of the Original Borrower ...................... 88

VALUATION REPORT .................................................................... 89 Summary of valuations ........................................................... 89

TAXATION..................................................................................... 90 United Kingdom Taxation ...................................................... 90 The Proposed Financial Transactions Tax.............................. 92

PURCHASE AND SALE ................................................................... 93 GENERAL INFORMATION .............................................................. 94

Authorisation........................................................................... 94 Listing of Bonds...................................................................... 94 Documents Available.............................................................. 94 Clearing Systems..................................................................... 94 Characteristics of underlying assets........................................ 94 Material or Significant Change............................................... 95 Litigation ................................................................................. 95 Auditors................................................................................... 95 Post-issuance information ....................................................... 95 Arranger and the Dealer transacting with the Issuer or the

Borrowers.......................................................................... 95 Yield ........................................................................................ 96

GLOSSARY .................................................................................... 97 APPENDIX 1 - FINANCIAL STATEMENTS OF THE ORIGINAL

BORROWER.............................................................................. 99 APPENDIX 2 - VALUATION REPORT............................................ 100

6

OVERVIEW

The following overview does not purport to be complete and is taken from, and is qualified in its entirety by, the remainder of this Prospectus.

This overview must be read as an introduction to this Prospectus and any decision to invest in the Bonds should be based on a consideration of this Prospectus as a whole.

Words and expressions defined in Form of the Bonds and Summary of Provisions relating to the Bonds while in Global Form, Terms and Conditions of the Bonds and Description of the Loan Agreements shall have the same meanings in this overview.

Structure diagram of the transaction

Note: On the Issue Date, the Original Borrower will be the only Borrower. However, Additional Borrowers and/or Additional Eligible Group Members may accede to the structure at a future date.

Issuer TCHG Capital plc

Description of the Bonds £80,000,000 4.665 per cent. Secured Bonds due 2045 (the Bonds), to be issued by the Issuer on 3rd July, 2014 (the Issue Date).

The Bonds will be issued in denominations of £100,000 and integral multiples of £1,000 in excess thereof.

I-A8.3.1

I-A8.3.1

I-A8.3.2

I-A7.5.2

I-A7.4.2

I-LR2.2.7(1)

I-A13.4.1

I-A13.4.2

I-A13.4.5 I-A13.4.13

Bondholders

Loan Agreement(s)

Issuer TCHG Capital plc

Bond Trustee Prudential Trustee Company Limited

Additional Borrower(s)

Security Trustee Prudential Trustee Company Limited

Eligible Group Member

Bond Trust Deed

Security Trust Deeds and Security Agreements

Benefit of Issuer Security

Benefit of Underlying Security

Bonds

Cashflows

Security

Original Borrower 1 Town and Country Housing

Group

7

Issue Price 100 per cent.

Use of Proceeds Subject as described in Initial Cash Security Account below, the net proceeds of the issue of the Bonds will be on-lent by the Issuer to the Original Borrower or (to the extent that the Original Borrower hasreduced the Original Commitment) to an Additional Borrower to beapplied in accordance with the constitution of the relevant OriginalBorrower or Additional Borrower, as the case may be.

The Issuer may from time to time invest the funds held in the InitialCash Security Account and the Ongoing Cash Security Account inPermitted Investments (as defined below) until such time as suchfunds are on-lent, or returned, to the relevant Borrower pursuant to the relevant Loan Agreement.

Form of Bonds The Bonds will be issued in bearer form as described in Form of the Bonds and Summary of Provisions relating to the Bonds while inGlobal Form.

Interest Each Bond will bear interest on its Outstanding Principal Amountfrom (and including) 3rd July, 2014, payable semi-annually in arrear on 3rd July and 3rd January in each year subject to adjustment in accordance with Condition 8.5 (Payment Day) (each, an Interest Payment Date) at the rate of 4.665 per cent. per annum in respect of the period from (and including) the Issue Date to (but excluding) theMaturity Date.

Instalment Redemption Unless previously redeemed or purchased and cancelled in accordance with Condition 9 (Redemption and Purchase), the Bonds will be redeemed in 20 equal instalments on each Interest Payment Date from, and including, 3rd January, 2036 to, and including, 3rd July, 2045 (the Maturity Date).

Early Redemption Subject as described in Mandatory Early Redemption below theBonds may be redeemed at any time prior to the Maturity Date, in each case in whole or in part, as the case may be, if:

(1) a Borrower elects to prepay its Loan in whole or in part priorto the repayment date specified in the relevant LoanAgreement and cancels an amount of the Commitment equal to all or any part of the prepaid amount (and no replacementCommitment is put in place with another Borrower); or

(2) the relevant Loan otherwise becomes repayable in whole orin part prior to the repayment date specified in the relevantLoan Agreement (other than as a result of the Bondsbecoming due and repayable including, for the avoidance ofdoubt, as a result of a repayment pursuant to Clause 5.6 (Mandatory Prepayment – Change of status) of the relevant Loan Agreement),

the Issuer shall redeem the Bonds in whole or, in respect of a prepayment in part, in an aggregate Outstanding Principal Amountequal to (in the case of (1) above) the relevant nominal amount of theCommitment cancelled and not replaced or (in the case of (2) above)the nominal amount of the relevant Loan to be repaid on the datewhich is two Business Days after that on which payment is made by

I-A8.1.1

I-A13.3

I-A13.4.4

I-A13.4.8

I-A13.4.9

I-A13.4.9

8

the relevant Borrower under the relevant Loan Agreement (the Loan Prepayment Date).

Redemption of the Bonds pursuant to Condition 9.2 shall be made at the higher of the following:

(a) their Outstanding Principal Amount (or, in the case of a partialredemption, the relevant proportion of their Outstanding PrincipalAmount calculated in accordance with Condition 9.5 (Notice of Early Redemption and Partial Redemptions)); and

(b) the amount (as calculated by a financial adviser nominated by the Issuer and approved by the Bond Trustee (the Nominated Financial Adviser) and reported in writing to the Issuer and the Bond Trustee) which is equal to the amount under (a) abovemultiplied by the price (expressed as a percentage and calculatedby the Nominated Financial Adviser) (rounded to three decimalplaces (0.0005 being rounded upwards)) at which the GrossRedemption Yield on the Bonds (if the Bonds were to remainoutstanding until their original maturity) on the DeterminationDate would be equal to the sum of (i) the Gross RedemptionYield at 3:00 pm (London time) on the Determination Date of theBenchmark Gilt and (ii) 0.20 per cent.,

together with any interest accrued up to (but excluding) the Loan Prepayment Date.

See Condition 9.2 (Early Redemption) and Condition 9.5 (Notice of Early Redemption and Partial Redemptions).

Early Redemption for Tax Reasons

The Issuer shall redeem the Bonds in whole, but not in part, at theirOutstanding Principal Amount, together with any interest accrued, if, as a result of any actual or proposed change in tax law, the Issuerdetermines that it would be required to make a withholding ordeduction on account of tax in respect of payments to be made by it inrespect of the Bonds and the Issuer does not opt to pay additional amounts pursuant to Condition 10.2 (No obligation to pay additional amounts) or, having so opted, notifies the Bond Trustee of itsintention to cease paying such additional amounts.

Mandatory Early Redemption

The Bonds shall be redeemed in an aggregate Outstanding PrincipalAmount equal to the nominal amount of the relevant Loan upon themandatory prepayment of a Loan following the relevant Borrower ceasing to satisfy each of the Borrower Minimum Requirements (otherthan if such Borrower complies with the Borrower MinimumRequirements within 180 days), plus accrued interest.

In addition, if a Loan becomes repayable as a result of a Borrower Default the Bonds shall be redeemed in an aggregate OutstandingPrincipal Amount equal to the nominal amount of the relevant Loan,plus accrued interest.

A Borrower Default includes non-payment, breach of other obligations, cross-acceleration, winding-up, cessation of business, insolvency, unlawfulness and breach of the Asset Cover Test set out inClause 14 (Borrower Default) of the Original Loan Agreement (or as will be set out in the corresponding clause of each Additional Loan Agreement) and described further in Description of the Loan

I-A13.4.9

I-A13.4.9

9

Agreements – Loan Events of Default and Enforcement.

See Condition 9.4 (Mandatory Early Redemption).

Purchase The Issuer, any Borrower and any other member of the Group maypurchase Bonds at any time in the open market or otherwise at anyprice.

Any Bonds so purchased by a Borrower or any other member of theGroup may be surrendered to the Issuer for cancellation inconsideration for an amount equal to the Outstanding PrincipalAmount of the Bonds being surrendered being deemed to be prepaid under the Loan Agreement specified by such Borrower or othermember of the Group or, to the extent that the relevant Loan is notthen outstanding, an amount of the Undrawn Commitment (as definedbelow) in respect of such Loan Agreement equal to the Outstanding Principal Amount of the Bonds surrendered being deemed to becancelled.

Events of Default Following an Event of Default, the Bond Trustee may, and if sorequested by the holders of at least one-fourth in Outstanding Principal Amount of the Bonds then outstanding shall (subject to it being secured and/or indemnified and/or pre-funded to its satisfaction and, upon certain events, the Bond Trustee having certified to theIssuer that such event is, in its opinion, materially prejudicial to theinterests of the Bondholders), give notice to the Issuer and the Bondsshall become immediately due and repayable.

The Events of Default include, inter alia, non-payment of any principal and interest due in respect of the Bonds, failure of the Issuerto perform or observe any of its other obligations under the Conditionsand the Bond Trust Deed, insolvency, unlawfulness and acceleration,or non-payment, in respect of other indebtedness in an aggregateamount equal to or in excess of £10,000,000 (or its equivalent).

Upon the Bonds becoming repayable prior to the Maturity Date (otherthan as a result of a prepayment or termination of a Loan Agreement),each Borrower is required to prepay its Loan in full together withaccrued interest and commitment fee to and including the date of redemption. Each Borrower is also required to pay to the Issuer,within three Business Days of demand, its pro rata share of the Issuer's reasonable costs, expenses and liabilities throughout the life ofthe Bonds.

Issuer Security The Issuer's obligations in respect of the Bonds are secured pursuantto the Bond Trust Deed in favour of the Bond Trustee for the benefitof itself and the Bondholders and the other Secured Parties by thefollowing (the Issuer Security):

(a) an assignment by way of security of the Issuer's rights, title andinterest arising under each Loan Agreement, the SecurityAgreements, the Security Trust Deed, the Agency Agreement, theAccount Agreement and the Custody Agreement, in each case tothe extent they relate to the Bonds;

(b) a charge by way of first fixed charge over all moneys and/orsecurities from time to time standing to the credit of theTransaction Account, the Ongoing Cash Security Account, the

I-A8.3.3

10

Initial Cash Security Account and the Custody Account and all debts represented thereby;

(c) a charge by way of first fixed charge over all sums held fromtime to time by the Paying Agents for the payment of principal orinterest in respect of the Bonds; and

(d) a first floating charge over all of the Issuer's property, assets, rights and revenues (whether or not the subject of fixed securityas aforesaid).

Initial Cash Security Account

For so long as (a) insufficient security has been granted (or procuredto be granted) by the Borrowers in favour of the Issuer to permit the drawing of the Aggregate Funded Commitment in full or (b) theBorrowers have not otherwise drawn any part of the AggregateFunded Commitment, the amount of the Aggregate FundedCommitment that remains undrawn shall be retained in a charged account (the Initial Cash Security Account) of the Issuer (and may be invested in Permitted Investments) in accordance with the terms ofthe Account Agreement and the Custody Agreement (the Retained Proceeds, which will include any prepayments under a LoanAgreement which are not applied in or towards redemption of theBonds).

Any Retained Proceeds may be advanced to one or more Borrowers ata later date pursuant to the relevant Loan Agreement to the extent that Properties of a corresponding value have been charged in favour ofthe Issuer.

Funds standing to the credit of the Initial Cash Security Account may:(a) be held on deposit, in which case it shall accrue interest at the rate (which may be positive, negative or zero) notified from time to timeby the Account Bank to the Issuer pursuant to the Account Agreementor (b) be invested in Permitted Investments in accordance with theCustody Agreement. See Permitted Investments below.

Pursuant to the Loan Agreements, each Borrower shall pay, on eachLoan Payment Date, to the Issuer a commitment fee in respect of itsUndrawn Commitment during the relevant Loan Interest Period in anamount equal to its pro rata share of (a) the aggregate of the interest payable by the Issuer under the Bonds on the following InterestPayment Date less (b) the aggregate amount of interest received fromthe Borrowers under the Loan Agreements on such Loan Payment Date and the interest otherwise received by the Issuer in respect of theRetained Proceeds during that period (including, but not limited to,any income received in respect of any Permitted Investments in whichany Retained Proceeds are, for the time being, invested).

See Description of the Loan Agreements below.

Ongoing Cash Security Account

Pursuant to the Loan Agreements, each Borrower is (or will be)required to procure that the specified Asset Cover Test is complied with (see Description of the Loan Agreements below). In the event that the value of any Charged Property is insufficient to maintaincompliance with the relevant Asset Cover Test, the Borrowers may deposit moneys into the Ongoing Cash Security Account. Such

I-A8.3.4.4

I-A8.3.4.4

11

moneys will be charged in favour of the Bond Trustee pursuant to theterms of the Bond Trust Deed.

Funds standing to the credit of the Ongoing Cash Security Accountmay: (a) be held on deposit, in which case it shall accrue interest at the standard rate (which may be positive, negative or zero) set by theCustodian in its deposit terms and conditions, as may be issued by itfrom time to time pursuant to the Custody Agreement or (b) beinvested in Permitted Investments in accordance with the CustodyAgreement. See Permitted Investments below.

Moneys standing to the credit of the Ongoing Cash Security Accountmay be withdrawn (a) to be applied in the acquisition of Property to be charged in favour of the Security Trustee for the benefit of theIssuer or (b) to the extent that the relevant Asset Cover Test would notbe breached immediately after such withdrawal.

Permitted Investments Permitted Investments shall consist of:

(a) triple-A rated money market funds,

(b) direct obligations of the United Kingdom or of any agency orinstrumentality of the United Kingdom which are guaranteed bythe United Kingdom,

(c) demand and time deposits in, certificates of deposit of and bankers' acceptances issued by any depositary institution or trustcompany with a maturity of no more than 360 days subject to,inter alia, such debt obligation having a long term debt creditrating of not less than "AA" from S&P and "Aa2" from Moody's Investors Service Limited (Moody's) or a short term debt or issuer (as applicable) credit rating of not less than "A-1" from S&P and "P-1" from Moody's (or, in each case, any other equivalent rating given by a credit rating agency registered under the CRA Regulation (an Equivalent Rating)),

(d) securities bearing interest or sold at a discount to the face amountthereof issued by any corporation having a long term credit ratingof not less than "AA" from S&P and "Aa2" from Moody's (or an Equivalent Rating), and/or

(e) commercial paper or other short-term obligations which, inter alia, have a short term credit rating of not less than "A-1" from S&P and "P-1" from Moody's (or an Equivalent Rating),

provided that, in the case of (b) to (e) above, such investment shall be an investment which is an obligation of the United Kingdom or acompany incorporated in the United Kingdom, and in all cases, suchinvestment shall be an investment (i) the maturity of which is no later than the Maturity Date and (ii) which is denominated in Sterling.

In the event that any Permitted Investments are sold to fund a drawingby a Borrower pursuant to a Loan Agreement and such sale results ina loss realised by the Issuer, such drawing to be made by the Issuer to such Borrower pursuant to such Loan Agreement shall be advanced ata discount in an amount equal to the Actual Advance Amount (asdefined in each Loan Agreement).

In the event that any Permitted Investments are sold to fund anadvance to a Borrower pursuant to a Loan Agreement and such sale

I-A8.3.4.4

12

results in a gain realised by the Issuer (such gain, the Permitted Investment Profit), the Issuer shall advance monies to such Borrower at the nominal amount requested and shall make a gift aid payment to a charitable member of the Group (a Charitable Group Member) in an amount equal to the Permitted Investment Profit.

Immediately prior to the end of each accounting period, to the extent that the Issuer would otherwise be required to recognise a profit fortax purposes in respect of its Permitted Investments as a result of themovement in the fair value recognised in its accounts of suchPermitted Investments for that accounting period, the Issuer shall sell Permitted Investments in an aggregate amount equal to theAccounting Profit (as defined in each Loan Agreement) and shall, inthe same accounting period, make a gift aid payment to any CharitableGroup Member in an amount equal to the Accounting Profit.

See Description of the Loan Agreements – Facility.

Account Agreement and Custody Agreement

The Issuer has appointed The Bank of New York Mellon, London Branch as its Account Bank and its Custodian pursuant to the AccountAgreement and the Custody Agreement, respectively.

Pursuant to the Account Agreement, the Account Bank shall maintain three accounts for the Issuer in respect of the Bonds: the TransactionAccount, the Initial Cash Security Account and the Ongoing CashSecurity Account. Pursuant to the Account Agreement and the BondTrust Deed, the Issuer has entered into certain covenants in respect of the monies which may be credited to and debited from each Account.

Pursuant to the Custody Agreement, the Custodian shall, subject toreceipt of such documents as it may require, open the CustodyAccount (consisting of the Ongoing Cash Security Custody Sub-Account, the Initial Cash Security Custody Sub-Account, the Ongoing Cash Security Cash Sub-Account and the Initial Cash Security Cash Sub-Account). The Issuer has authorised the Custodian to makepayments and delivery out of the Custody Account only for the purpose of any acquisition or sale of Permitted Investments or as setout therein.

See Description of the Account Agreement and the CustodyAgreement below.

Guarantee and Indemnity Pursuant to the Loan Agreement, the Original Borrower has (and eachAdditional Borrower will have) irrevocably and unconditionally:

(a) guaranteed to the Issuer the punctual performance by each otherBorrower of all such Borrowers' obligations under, inter alia, their respective Loan Agreements, the Security Trust Deed (ifapplicable) and their respective Security Agreements (ifapplicable), other than each other Borrower's obligations to repayprincipal and any Prepayment Premium thereon pursuant to their respective Loan Agreements (such amounts being, theGuaranteed Interest and Fee Amounts);

(b) undertaken with the Issuer that, whenever any other Borrowerdoes not pay any Guaranteed Interest and Fee Amounts when due under its respective Loan Agreement, the Security Trust Deed orits respective Security Agreement(s), it must, immediately on

I-A8.3.3

I-A8.3.8

I-A8.3.4.4

G-A6.2

G-A6.2

13

demand by the Security Trustee and/or the Issuer, pay theGuaranteed Interest and Fee Amounts as is if it were the principal obligor;

(c) undertaken with the Issuer that, to the extent that the proceeds ofthe enforcement of the Underlying Security are insufficient tosatisfy the Borrowers' obligations under their respective LoanAgreements in full (the shortfall being, the Guaranteed Principal Amount), it must, immediately on demand by the Security Trustee and/or the Issuer, pay the Guaranteed PrincipalAmount as if it were the principal obligor; and

(d) agreed to indemnify the Issuer immediately on demand against any loss or liability suffered by the Issuer if any obligationguaranteed by it is or becomes illegal or invalid.

Underlying Security Pursuant to a Security Trust Deed originally dated 6 November 2000(and having been amended and restated on 1 March 2005 and 19August 2008) between, inter alios, the Original Borrower and the Security Trustee (as amended from time to time, the Original Borrower Security Trust Deed) a security trust was established pursuant to which the Security Trustee holds for the benefit ofdesignated beneficiaries security created by the Original Borrowerfrom time to time in favour of the Security Trustee. On the IssueDate, the Issuer has been designated as a beneficiary under the Original Borrower Security Trust Deed.

The Original Borrower has entered into Fixed Charges and MortgageDeeds (the Original Security Agreements), in each case substantially in the form set out in the Security Trust Deed, pursuant to which theOriginal Borrower has created the following security in favour of theSecurity Trustee for the benefit of itself and the Beneficiaries (asdefined in the Security Trust Deed):

(a) a charge by way of first legal mortgage of all the Original Borrower's right, title and interest from time to time in the InitialProperties;

(b) an assignment of the following, in each case as held by theOriginal Borrower:

(1) the personal agreements and covenants (still subsisting and capable of being enforced) entered into by tenants, lessees,licensees or other parties under letting and tenancydocuments in respect of the Initial Properties and relatedsecurity and rights; and

(2) all agreements, now or from time to time entered into or to be entered into to enable the charging of the Security Assetsand for the sale, letting or other disposal or realisation of thewhole or any part of the Initial Properties and including anydevelopment agreements, contracts or warranties in relation to the Initial Properties the benefit of which is or will bevested in the Original Borrower (so far as such areassignable); and

(c) a first fixed charge over the benefit of the Insurances and thebenefit of all present and future licences, consents and

I-A8.3.3

G-A6.1

G-A6.2

14

authorisations (statutory or otherwise) held in connection with theSecurity Assets.

Following the accession of the Issuer as a Beneficiary and theallocation of the Initial Properties to the Issuer pursuant to the securityTrust Deed the Security Trustee shall hold the above security on trust for itself and the Issuer as security for Borrowers' liabilities under theLoan Agreements (the Original Borrower Secured Liabilities).

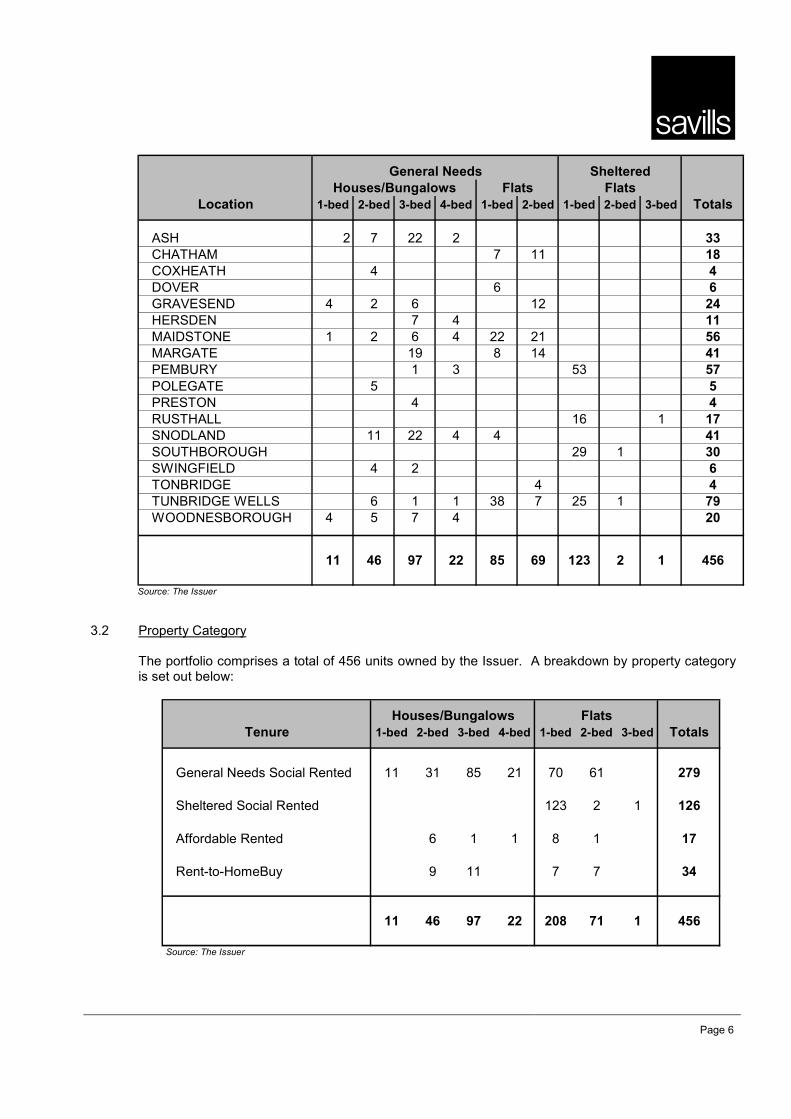

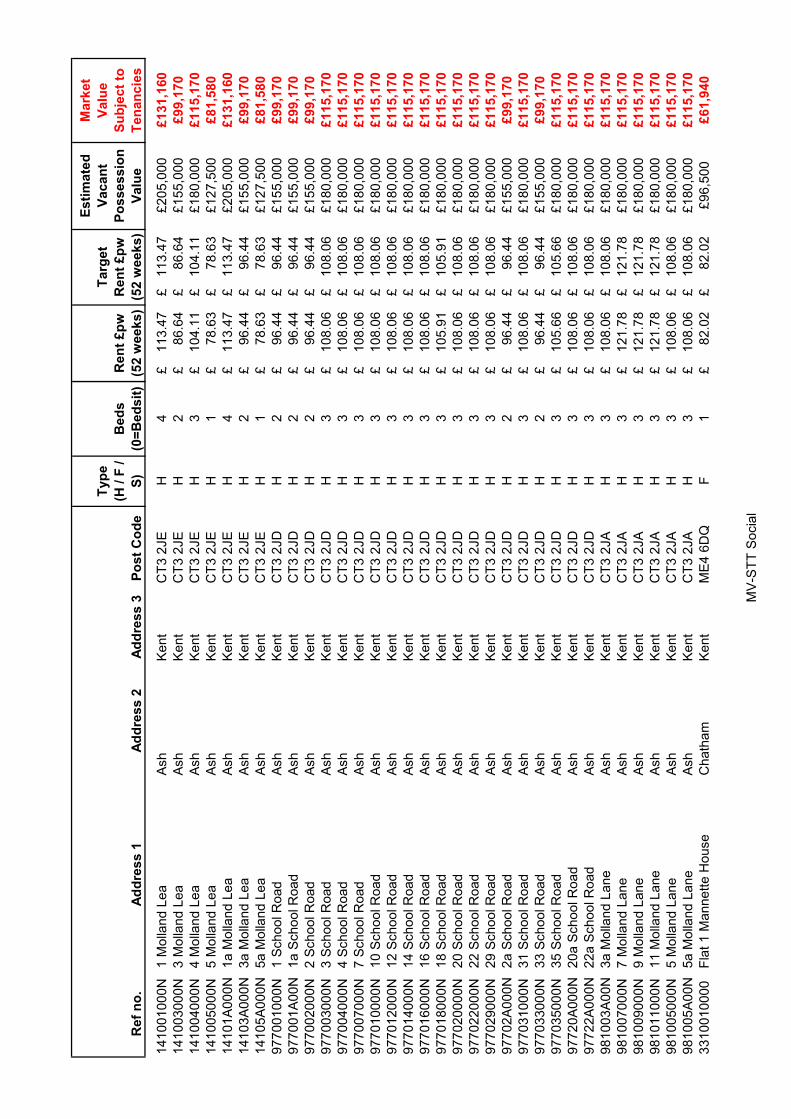

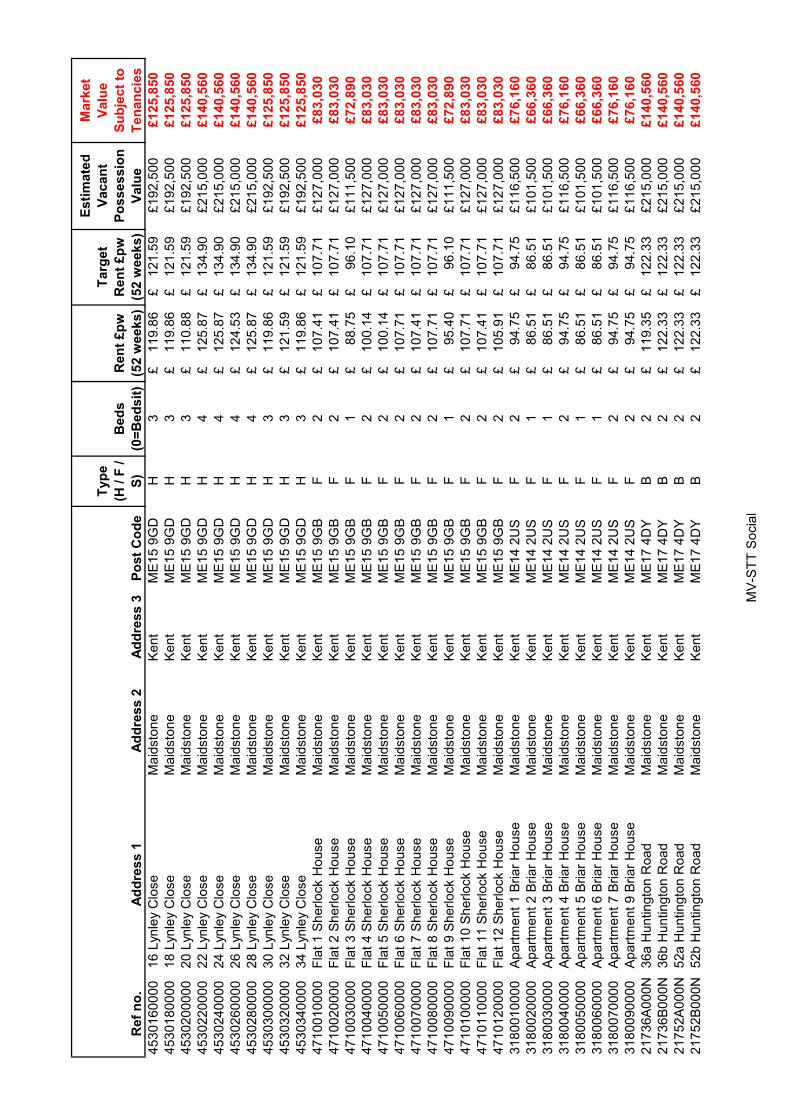

See Valuation Report for further information in relation to the Initial Properties, being residential properties of a type and nature that areusually owned by Registered Providers of Social Housing.

The Issuer and Security Trustee may from time to time agree to another Borrower or Eligible Group Member acceding to the OriginalBorrower Security Trust Deed or entering into one or more othersecurity trust deeds (each an Additional Security Trust Deed and, together with the Original Borrower Security Trust Deed, the Security Trust Deeds and each a Security Trust Deed) which establish a security trust similar to the Original Borrower Security Trust Deed, ineach case with the effect that security created by such Borrower orEligible Group Member from time to time in favour of the SecurityTrustee is held by the Security Trustee on trust for the benefit of theIssuer.

From time to time a Borrower or an Eligible Group Member may enter into one or more additional security agreements in favour of theSecurity Trustee (each an Additional Security Agreement and, together with each Original Security Agreement, the Security Agreements) in accordance with the terms of a Security Trust Deedpursuant to which (1) such Borrower provides security in respect of its liabilities under the relevant Loan Agreement or (2) such EligibleGroup Member provides security in respect of one or more Borrowers' liabilities under one or more Loan Agreements, in each case includingfixed charges, legal mortgages and assignments having substantiallythe same nature and effect in relation to the relevant ChargedProperties as the fixed charges, legal mortgages and assignments created by the Original Borrower in relation to the Initial Propertiesunder the Original Security Agreements.

The security subsisting from time to time under the SecurityAgreements and Security Trust Deeds and held by the Security Trustee on trust for the Issuer constitutes the Underlying Security.

The Issuer has secured its rights, title and interest in respect of theUnderlying Security in favour of the Bond Trustee pursuant to the Bond Trust Deed.

See Description of the Issuer Security, the Security Agreements andthe Security Trust Deed below.

Addition, substitution and release of Charged Properties

Pursuant to each Security Trust Deed, on or prior to entering into a Security Agreement in respect of any Property for the benefit of theIssuer, the relevant Borrower or Eligible Group Member must, inrespect of such security, provide the conditions precedent documentsspecified therein. In addition, pursuant to the Loan Agreements, therelevant Borrower or Eligible Group Member must provide acompleted Additional Property Certificate confirming that, inter alia,

I-A8.2.2.9

15

the proposed Charged Properties are residential properties of a type and nature that are usually owned by Registered Providers of SocialHousing, Full Valuation Reports in respect of each such Property anda Certificate of Title in respect of each tranche of Properties charged.

At the request and expense of a Borrower or an Eligible Group Member, the Security Trustee shall (subject to receiving an amendedSecurity Certificate from the Borrowers and the Issuer in accordancewith the Security Trust Deed) release from the relevant SecurityDocuments (and/or reallocate, if applicable) such of the Properties forming part of the Issuer's Designated Security and substitute such ofthe Properties as may be selected by such Borrower or Eligible GroupMember, provided that such Borrower or Eligible Group Membersatisfies the conditions precedent specified in the Loan Agreements in relation to the Substitute Properties. Such conditions precedentinclude, inter alia, a completed Substitute Property Certificate certifying, inter alia, that the relevant Substitute Property is a residential property of a type and nature that is usually owned byRegistered Providers of Social Housing, that, immediately followingsuch release (and/or reallocation, if applicable) and substitution, theAsset Cover Test will not be breached as a result of the substitution of the relevant Charged Properties and that no Event of Default orPotential Event of Default has occurred and is continuing, andprovision of a Full Valuation Report in respect of each SubstituteProperty and a Certificate of Title in respect of the Substitute Properties.

At the request and expense of a Borrower or an Eligible GroupMember, the Security Trustee shall release (subject to receiving anamended Security Certificate from the Borrowers and the Issuer inaccordance with the Security Trust Deed) from the relevant Security Documents (and/or reallocate, if applicable) such Charged Propertiesas may be selected by such Borrower or Eligible Group Memberprovided that such Borrower or Eligible Group Member delivers to theIssuer and the Security Trustee a completed Property Release Certificate (as defined in each Loan Agreement), certifying that,immediately following such release (and/or reallocation, ifapplicable), the Asset Cover Test will not be breached as a result ofthe release (and/or reallocation, if applicable) of such part of the security and that no Event of Default or Potential Event of Default hasoccurred and is continuing.

Notwithstanding the above, where any disposal is a Statutory Disposala Borrower or an Eligible Group Member shall have the right to withdraw such Property from the Issuer's Designated Security. In suchcircumstances such Borrower or Eligible Group Member is obliged todeliver (or procure the delivery), as soon as reasonably practicableafter it has received notice of such Statutory Disposal, a completed Statutory Disposal Certificate to the Issuer and the Security Trusteeconfirming that the relevant withdrawal relates to a Statutory Disposaland, if the Statutory Disposal would result in a breach of the Asset Cover Test, confirming that it shall procure that additional Propertiesare charged pursuant to a Security Trust Deed and/or moneys aredeposited into the Ongoing Cash Security Account, in accordancewith the Loan Agreements, such that any breach of the Asset Cover Test will be cured.

16

Statutory Disposal means a Shared Ownership Sale, the exercise of a Right-to-Buy, a Social HomeBuy disposal or any other disposal of aProperty (where such disposal is not part of a transaction involving the simultaneous disposal of more than one Property or Unit) where it isrequired that some or all of the relevant disposal proceeds be creditedto the disposal proceeds fund (as defined in section 177 of theHousing and Regeneration Act) of a Borrower or any Eligible Group Member.

Shared Ownership Sale means the disposal of the whole or any interest in a Unit of residential accommodation by the relevantBorrower or Eligible Group Member (or of the retained interest of the relevant Borrower or Eligible Group Member in any Unit ofresidential accommodation) which, immediately before the disposal,was comprised in a Shared Ownership Property (where such disposalis not part of a transaction involving the simultaneous disposal of more than one Unit or Property).

Shared Ownership Property means any Properties acquired by a Borrower or Eligible Group Member then being occupied on sharedownership terms or in respect of which such Borrower or Eligible Group Member grants a lease on shared ownership terms so that suchBorrower or Eligible Group Member holds, or is intending to holdupon disposal on shared ownership terms, less than 100 per cent. ofthe beneficial (or heritable) interest in that Property and the purchaser of the balance of that beneficial (or heritable) interest has the right toacquire a further portion of such Borrower's or Eligible GroupMember's retained beneficial (or heritable) interest.

Right-to-Buy mean the right of a tenant of a Property:

(A) to buy that property from the relevant Borrower or EligibleGroup Member under section 180 of the Housing andRegeneration Act or under Part V of the Housing Act 1985 (orany similar right replacing those rights) or under any contract conferring such a right and including, without limitation, suchrights preserved notwithstanding any previous transfers of thatproperty to such Borrower or Eligible Group Member from anylocal authority;

(B) to acquire an interest in that property from the relevant Borrower or Eligible Group Member by means of a shared-ownership lease where the terms of any such lease comply with the regulatoryrequirements of the Regulator or have been approved by theLender; or

(C) to buy or acquire an interest in that property from the relevant Borrower or Eligible Group Member under any voluntary schemeapproved by the Lender.

Social HomeBuy has the meaning given to it in the Local Authorities (Capital Finance and Accounting) (Amendment) (England) Regulations 2006.

17

Unit means, at any time, a Charged Property or part thereof in relationto which there is or, when let, there would be, a separate rentalcontract entered into with a Borrower or an Eligible Group Member.

Enforcement of the Underlying Security and the Issuer Security

Following a Borrower Default, the Issuer may declare the UnderlyingSecurity immediately enforceable and/or declare the relevant Loanimmediately repayable. Pursuant to the Security Trust Deed, theSecurity Trustee shall only be required to take action to enforce orprotect the security in respect of the Loan Agreements if so instructedby the Issuer (and then only if it has been indemnified and/or securedto its satisfaction).

The Issuer has assigned its rights under, inter alia, the Security Agreements and the Security Trust Deeds, and, pursuant toCondition 6.3, has covenanted not to take any action or direct theSecurity Trustee to take any action pursuant thereto except with the prior consent of the Bond Trustee. The Bond Trustee may seek theconsent of the Bondholders in accordance with the Bond Trust Deedprior to giving any such consent.

In enforcing the Issuer Security (including the Issuer's rights, title and interests in the Security Agreements and the Security Trust Deedsinsofar as they relate to the Bonds) the Bond Trustee may act in itsdiscretion. It is, however, required to take action, pursuant toCondition 12.2, where so directed by the requisite majority of theBondholders provided, however, that it is secured and/or indemnifiedand/or pre-funded to its satisfaction.

See Description of the Issuer Security, the Security Agreements andthe Security Trust Deed below.

Priorities of Payments Prior to the enforcement of the Issuer Security, the Issuer shall applythe monies standing to the credit of the Transaction Account on eachInterest Payment Date and such other dates on which a payment is due in respect of the Bonds in the following order of priority (thePre-enforcement Priority of Payments):

(a) first, in payment of any taxes due and owing by the Issuer to any taxing authority (insofar as they relate to the Bonds);

(b) second, in payment of any unpaid fees, costs, charges, indemnitypayments (if any), expenses and liabilities incurred by or due tothe Bond Trustee (including remuneration payable to it and any Appointee) in carrying out its functions under the TransactionDocuments;

(c) third, in payment of any unpaid fees, expenses and liabilities(including indemnity payments, if any, due from the Issuer) ofthe Issuer owing to the Corporate Services Provider under the Corporate Services Agreement, the Paying Agents under theAgency Agreement, the Account Bank under the AccountAgreement and the Custodian under the Custody Agreement on apro rata and pari passu basis;

(d) fourth, in payment of any other unpaid fees, expenses and liabilities of the Issuer (in so far as they relate to the Bonds) on apro rata and pari passu basis;

I-A8.3.4.6

18

(e) fifth, in payment, on a pro rata and pari passu basis, to the Bondholders of any interest due and payable in respect of theBonds;

(f) sixth, in payment, on a pro rata and pari passu basis, to the Bondholders of any principal due and payable in respect of theBonds;

(g) seventh, in payment, on a pro rata and pari passu basis, to the Borrowers of any amounts due and payable under the terms of theLoan Agreements; and

(h) eighth, in payment of any Permitted Investment Profit orAccounting Profit, as the case may be, to any Charitable GroupMember.

Following the enforcement of the Issuer Security, all monies standingto the credit of the Transaction Account, the Ongoing Cash Security Account and the Initial Cash Security Account and the net proceeds ofenforcement of the Issuer Security shall be applied in the followingorder of priority (the Post-enforcement Priority of Payments):

(a) first, in payment or satisfaction of any unpaid fees, costs, charges,indemnity payments (if any), expenses and liabilities incurred byor due to the Bond Trustee, any Appointee or any receiver inpreparing and executing the trusts and/or in carrying out their respective functions under the Transaction Documents (includingthe costs of realising any Issuer Security and the Bond Trustee'sand such receiver's remuneration);

(b) second, in payment of all amounts owing to the CorporateServices Provider under the Corporate Services Agreement, the Paying Agents under the Agency Agreement, the Account Bankunder the Account Agreement and the Custodian under theCustody Agreement on a pro rata and pari passu basis;

(c) third, in payment, on a pro rata and pari passu basis, to the Bondholders of any interest due and payable in respect of theBonds;