Idaho Fiscal Sourcebook 2010 Edition

342

Idaho Fiscal Sourcebook 2010 Edition Legislative Services Office Budget & Policy Analysis

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Idaho Fiscal Sourcebook 2010 Edition

Idaho Fiscal

Sourcebook

2010 Edition

Legislative Services Office Budget & Policy Analysis

Mike Nugent Manager

Cathy Holland-Smith Manager

Don Berg Manager

Glenn Harris Manager

Research & Legislation Budget & Policy Analysis Legislative Audits Network Administration [email protected] [email protected] [email protected] [email protected]

Legislative Services Office Serving the Idaho State Legislature

Jeff Youtz State Capitol Director P.O. Box 83720

November 2010 Boise, ID 83720-0054

208-334-2475; Fax 334-2454

www.legislature.idaho.gov

How to Use this Book The Idaho Fiscal Sourcebook, 2010 Edition details the sources and uses of funds for state agencies. It includes those funds specifically appropriated by the Legislature and those funds that are continuously appropriated or limited only by revenues as provided by statute. It is compiled by legislative staff and acts as a companion to two other publications, the Legislative Budget Book, the primary reference document used by the Joint Senate Finance – House Appropriations Committee (JFAC) to set the Idaho State Budget, and the Legislative Fiscal Report, the comprehensive record of budget decisions made by the JFAC. This publication organizes each state department that has spending authority for the listed funds into six broad functional areas: 1) Education, 2) Health and Human Services, 3) Public Safety, 4) Natural Resources, 5) Economic Development, and 6) General Government. Some departments are then divided into divisions or agencies for budgeting purposes. The relevant funds are next, sorted within three fund categories (general, dedicated, and federal) then by the accounting code number. The State Controller’s Accounting Identification Code Structure is summarized on page vii. A description of the fund sources and fund uses then follows. The Statewide Accounting and Reporting System (STARS) budget unit and agency code follow on the next line as a cross-reference to the accounting system. The term "(Cont)" found after certain budget units signifies a continuous appropriation. Each budget unit representing a fixed appropriation has a corresponding program in the Legislative Fiscal Report. The next line lists five fiscal years of actual expenditures from the stated fund for that budget unit. The state's fiscal year (FY) begins July 1 and ends June 30. These unaudited numbers, derived from STARS, are the sum of the cash expenditures and the encumbrances for each respective fiscal year.

(Continued)

ii

The agency's fiscal officer or legislative budget and policy analyst provided the descriptions of fund sources and uses. Provisions of the Idaho Code are cited throughout to provide a legal reference to the sources and uses of state funds. The title, chapter and section numbers are placed in parentheses following the statement that refers to or summarizes the relevant Idaho Code provision. For example, "(§67-3516)" inserted in the description of a source of funds indicates that further information about that fund source may be found in Title 67, Chapter 35, Section 16 of the Idaho Code. Locating fund sources and uses depends on what you want to know. If you want to know what funds are used by a certain agency, go to the Table of Contents on pages iii through vi to find the functional area, agency, and page number. If you want to know which agencies use a particular fund, turn to the Index by Fund Name on pages 323 through 332 to find those agencies and their page numbers. If you only know the fund number, turn to Crosswalk by Fund Number on pages 319 through 321 to find the name of the fund, and then turn to Index by Fund Name to find the page numbers.

Finally, we’ve included an Appendix: Laws Governing the State Budget on pages 303 through 317. This appendix contains the sections of Idaho State Constitution and Idaho Code that pertain to the responsibilities of the Legislature and the Governor in the establishment and execution of the state budget. This publication is named after the Idaho Fiscal Sourcebook published in four editions from 1971 to 1974 by the University of Idaho, Bureau of Public Affairs Research. The Idaho Fiscal Sourcebook, 2010 Edition represents a snapshot in time and should be considered as part of an on-going project. Each edition incorporates changes as funds or budget units are added, combined, or deleted or as names are changed or descriptions improved.

For more information contact:

Legislative Services Office Budget & Policy Analysis

Room C305, State Capitol Boise, ID 83720 (208) 334-3531

or visit our website at

http://www.legislature.idaho.gov/budget/publications.htm

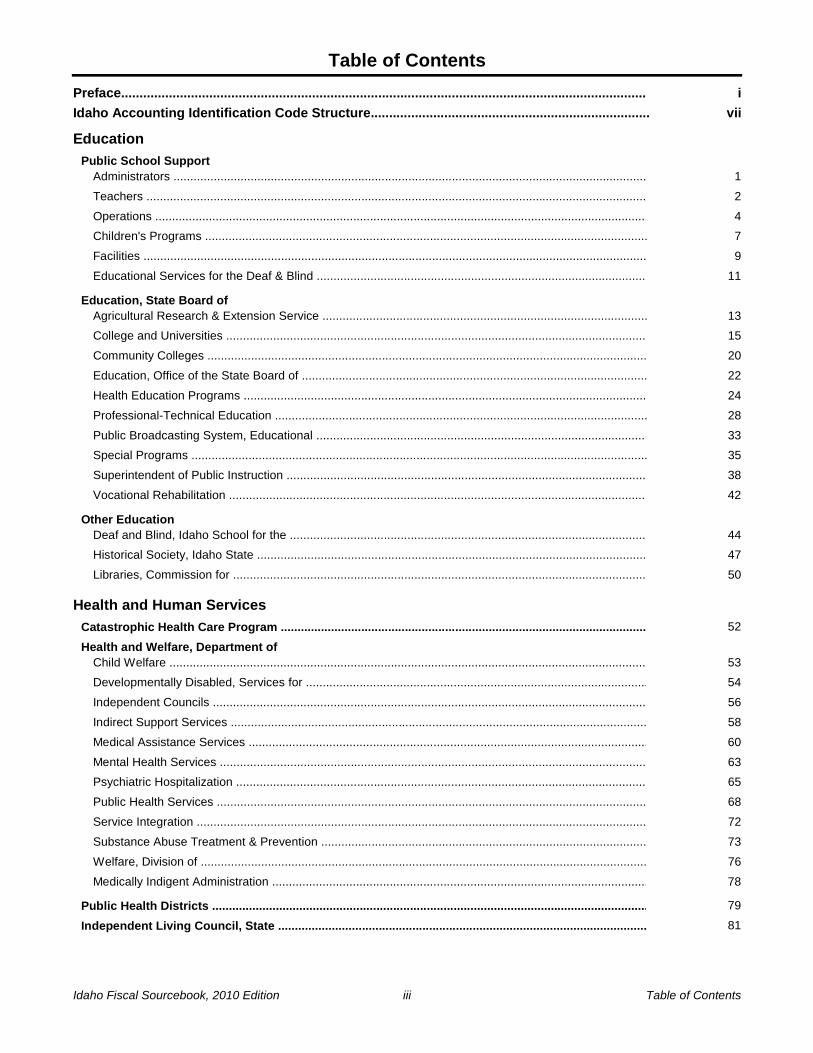

Table of Contents

Preface............................................................................................................................................... i

Idaho Accounting Identification Code Structure............................................................................ vii

Education

Public School SupportAdministrators ............................................................................................................................................. 1

Teachers ..................................................................................................................................................... 2

Operations ................................................................................................................................................... 4

Children's Programs .................................................................................................................................... 7

Facilities ...................................................................................................................................................... 9

Educational Services for the Deaf & Blind .................................................................................................. 11

Education, State Board ofAgricultural Research & Extension Service ................................................................................................. 13

College and Universities ............................................................................................................................. 15

Community Colleges ................................................................................................................................... 20

Education, Office of the State Board of ....................................................................................................... 22

Health Education Programs ........................................................................................................................ 24

Professional-Technical Education ............................................................................................................... 28

Public Broadcasting System, Educational .................................................................................................. 33

Special Programs ........................................................................................................................................ 35

Superintendent of Public Instruction ........................................................................................................... 38

Vocational Rehabilitation ............................................................................................................................. 42

Other EducationDeaf and Blind, Idaho School for the .......................................................................................................... 44

Historical Society, Idaho State .................................................................................................................... 47

Libraries, Commission for ........................................................................................................................... 50

Health and Human Services

52Catastrophic Health Care Program .............................................................................................................

Health and Welfare, Department ofChild Welfare ............................................................................................................................................... 53

Developmentally Disabled, Services for ...................................................................................................... 54

Independent Councils ................................................................................................................................. 56

Indirect Support Services ............................................................................................................................ 58

Medical Assistance Services ....................................................................................................................... 60

Mental Health Services ............................................................................................................................... 63

Psychiatric Hospitalization .......................................................................................................................... 65

Public Health Services ................................................................................................................................ 68

Service Integration ...................................................................................................................................... 72

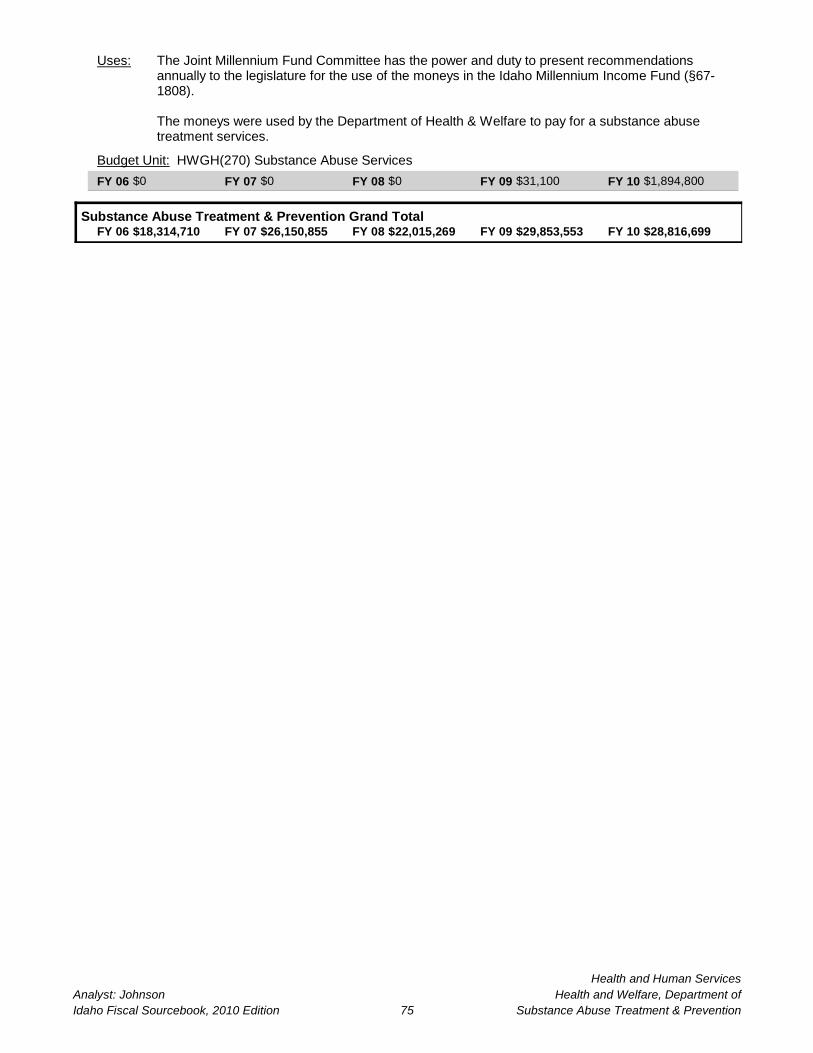

Substance Abuse Treatment & Prevention ................................................................................................. 73

Welfare, Division of ..................................................................................................................................... 76

Medically Indigent Administration ................................................................................................................ 78

79Public Health Districts ..................................................................................................................................

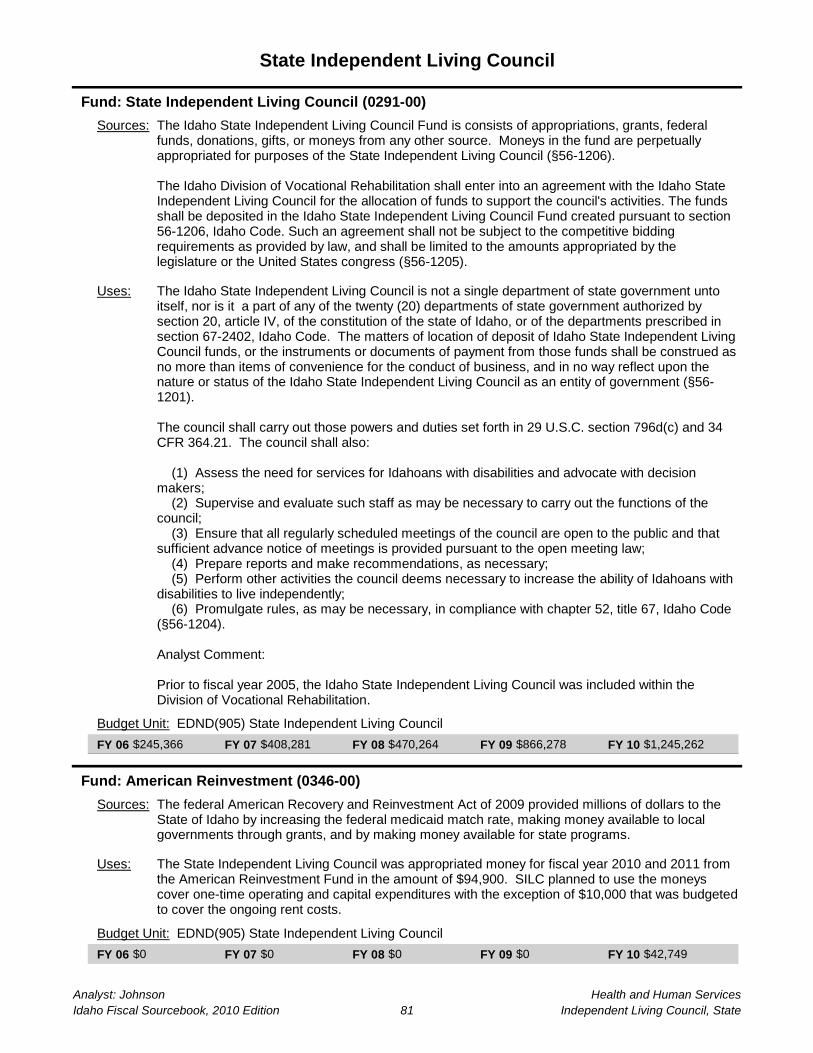

81Independent Living Council, State ..............................................................................................................

iii Table of ContentsIdaho Fiscal Sourcebook, 2010 Edition

Public Safety

Correction, Department ofManagement Services ................................................................................................................................. 83

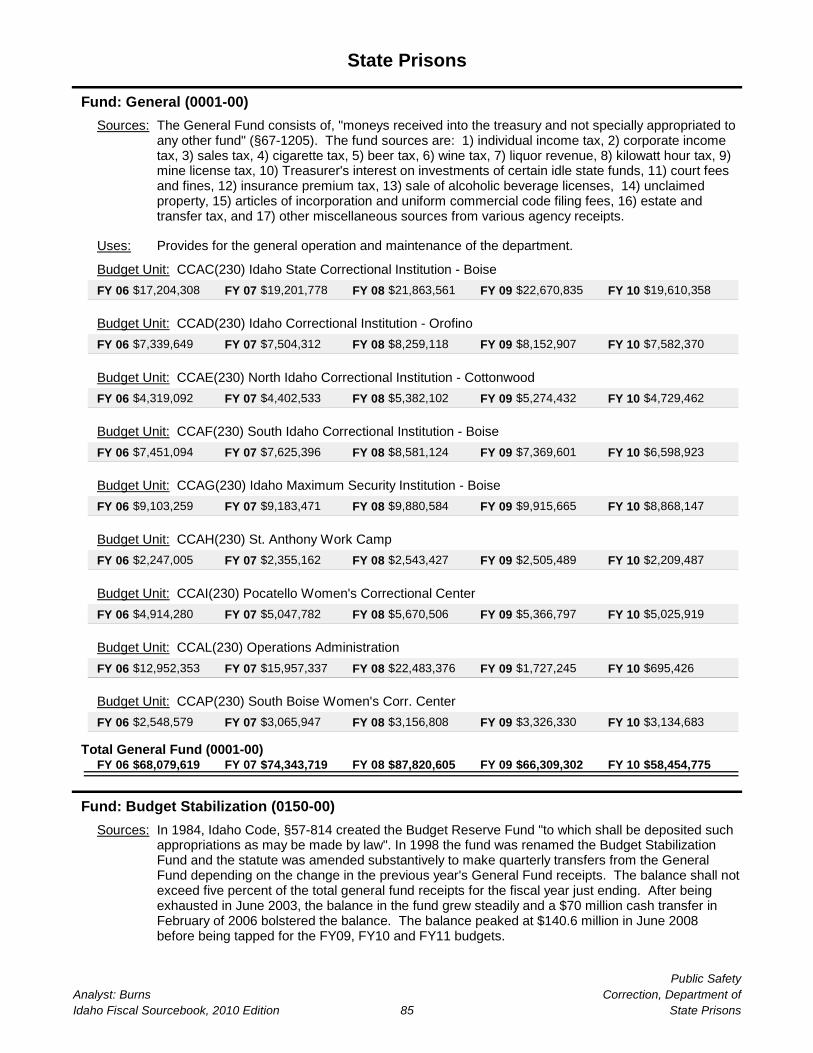

State Prisons ............................................................................................................................................... 85

Private Prisons ............................................................................................................................................ 90

County & Out-of-State Placement ............................................................................................................... 91

Correctional Alternative Placement ............................................................................................................. 92

Community Corrections ............................................................................................................................... 93

Education & Treatment ................................................................................................................................ 96

Medical Services ......................................................................................................................................... 98

Pardons & Parole, Commission .................................................................................................................. 99

Correctional Industries ................................................................................................................................ 100

101Judicial Branch .............................................................................................................................................

106Juvenile Corrections, Department of ..........................................................................................................

Police, Idaho StateBrand Inspection ......................................................................................................................................... 109

Police, Division of Idaho State .................................................................................................................... 110

POST Academy ........................................................................................................................................... 120

Racing Commission .................................................................................................................................... 122

Natural Resources

124Environmental Quality, Department of ........................................................................................................

130Fish and Game, Department of ....................................................................................................................

Land, Board of CommissionersInvestment Board, Endowment Fund .......................................................................................................... 134

Lands, Department of .................................................................................................................................. 135

Parks and Recreation, Department ofParks and Recreation, Department of ......................................................................................................... 142

Lava Hot Springs Foundation ...................................................................................................................... 148

149Water Resources, Department of ................................................................................................................

Economic Development

Agriculture, Department ofAgriculture, Department of .......................................................................................................................... 155

Soil and Water Conservation Commission ................................................................................................. 169

171Commerce, Department of ...........................................................................................................................

176Finance, Department of ................................................................................................................................

177Industrial Commission .................................................................................................................................

180Insurance, Department of .............................................................................................................................

183Labor, Department of ....................................................................................................................................

189Public Utilities Commission .........................................................................................................................

iv Table of ContentsIdaho Fiscal Sourcebook, 2010 Edition

Economic Development

Self-Governing AgenciesBuilding Safety, Division of .......................................................................................................................... 190

Hispanic Affairs, Commission on ................................................................................................................ 196

Board of Examiners ..................................................................................................................................... 198

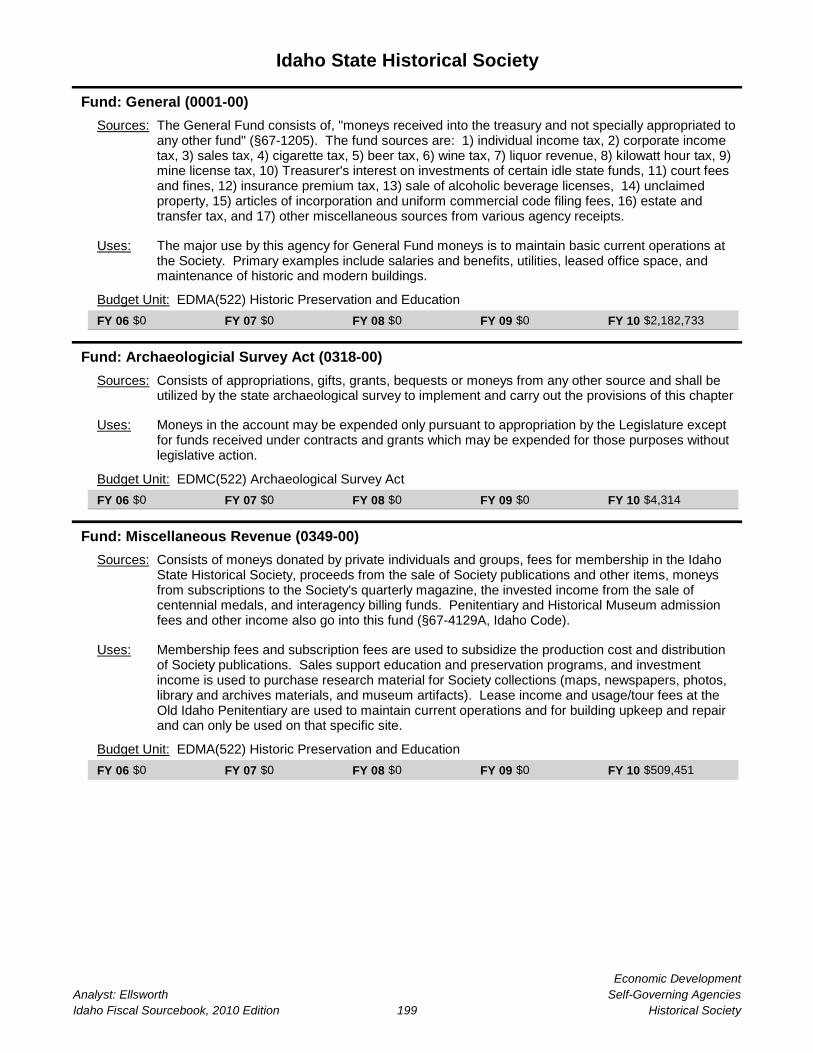

Historical Society ......................................................................................................................................... 199

Libraries, Commission for ........................................................................................................................... 202

Lottery, State ............................................................................................................................................... 204

Medical Boards ............................................................................................................................................ 205

Regulatory Boards ....................................................................................................................................... 210

State Appellate Public Defender ................................................................................................................. 214

Veterans Services, Division of .................................................................................................................... 215

Transportation Department, IdahoTransportation Services .............................................................................................................................. 217

Planning ...................................................................................................................................................... 223

Motor Vehicles ............................................................................................................................................. 224

Highway Operations .................................................................................................................................... 226

Contract Construction & Right-of-Way Acquisition ..................................................................................... 228

General Government

Administration, Department ofAdministration, Department of ..................................................................................................................... 230

Permanent Building Fund ............................................................................................................................ 237

Capitol Commission .................................................................................................................................... 240

241Attorney General ...........................................................................................................................................

244Controller, State ............................................................................................................................................

Governor, Office of theAging, Commission on ................................................................................................................................ 246

Arts, Commission on the ............................................................................................................................. 248

Blind and Visually Impaired, Commission for the ........................................................................................ 250

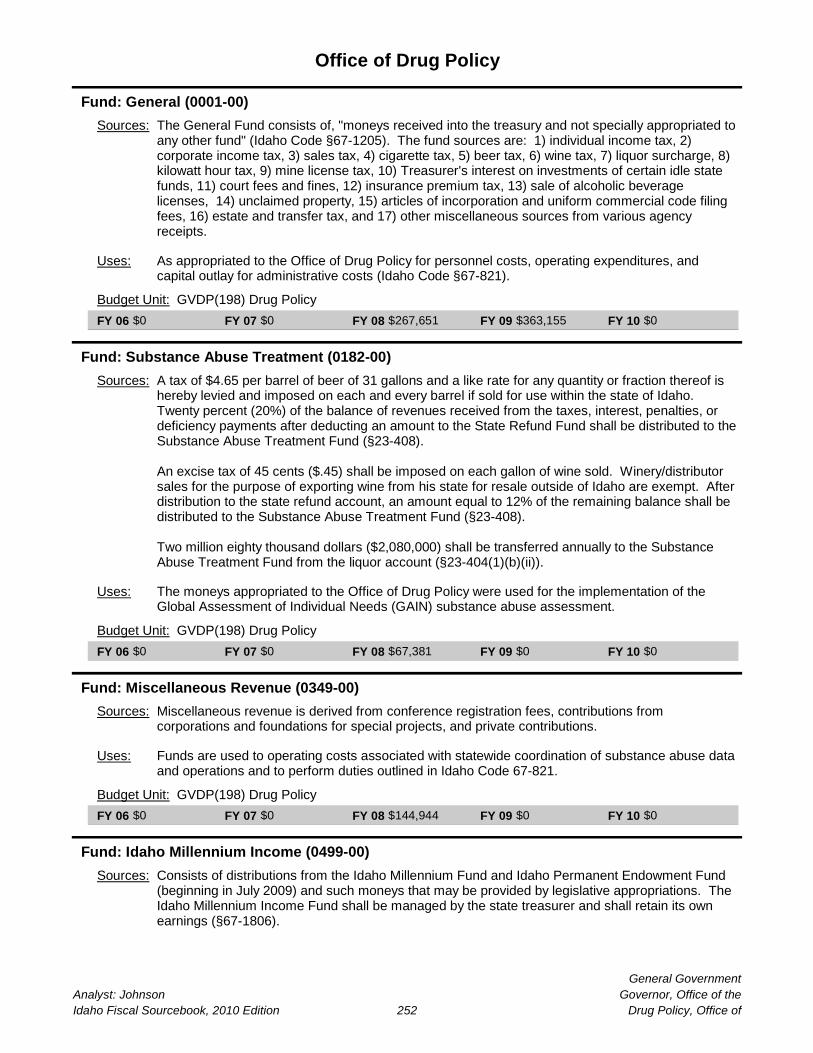

Drug Policy, Office of ................................................................................................................................... 252

Energy Resources, Office of ....................................................................................................................... 254

Financial Management, Division of ............................................................................................................. 256

Governor, Executive Office of the ............................................................................................................... 257

Human Resources, Division of .................................................................................................................... 260

Human Rights Commission ......................................................................................................................... 261

Liquor Division, State .................................................................................................................................. 262

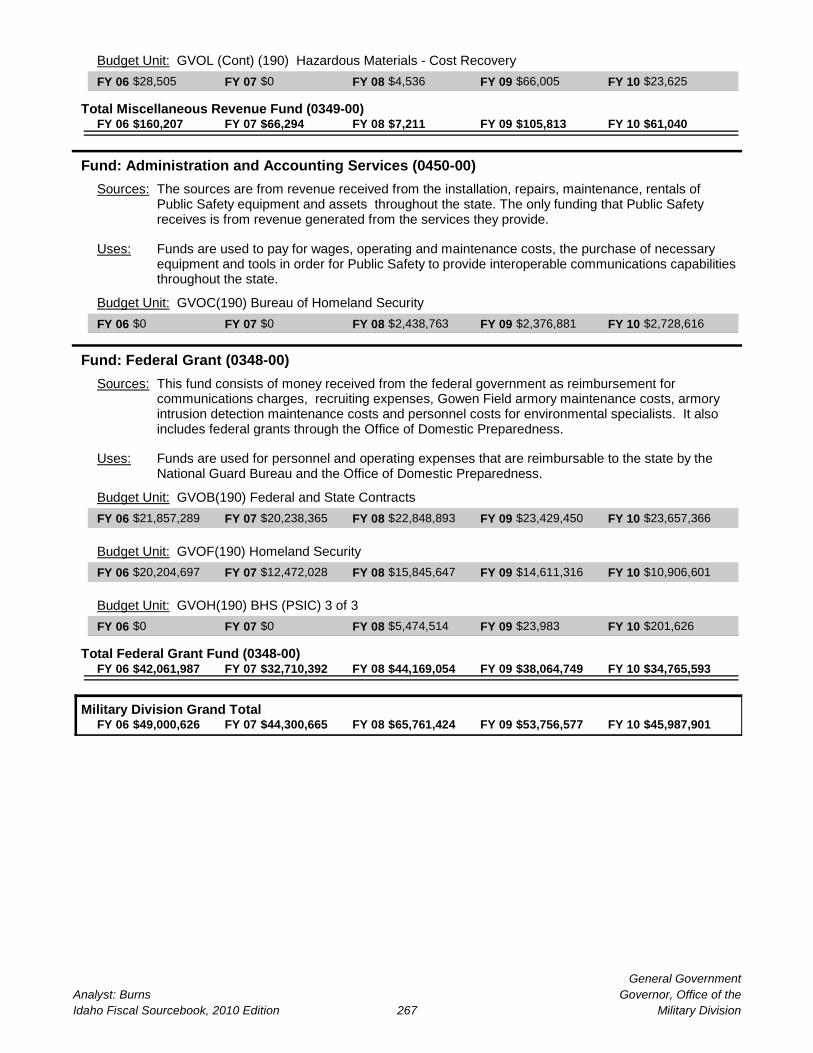

Military Division ........................................................................................................................................... 264

Public Employee Retirement System .......................................................................................................... 268

Species Conservation, Office of .................................................................................................................. 270

Women's Commission ................................................................................................................................ 271

Insurance Fund, State ................................................................................................................................. 272

v Table of ContentsIdaho Fiscal Sourcebook, 2010 Edition

General Government

Legislative BranchLegislature ................................................................................................................................................... 274

Legislative Services Office .......................................................................................................................... 276

Legislative Technology ................................................................................................................................ 278

Performance Evaluations, Office of ............................................................................................................. 279

Redistricting Commission ............................................................................................................................ 280

Capitol Renovation & Restoration ............................................................................................................... 281

282Lieutenant Governor .....................................................................................................................................

Revenue and Taxation, Department ofTax Appeals, Board of ................................................................................................................................. 283

Tax Commission, State ............................................................................................................................... 284

292Secretary of State ..........................................................................................................................................

Treasurer, StateTreasurer, State .......................................................................................................................................... 295

Idaho Millennium Fund ................................................................................................................................ 298

299Control Agencies ..........................................................................................................................................

Appendix: Laws Governing the State Budget............................................................................... 303

Index by Fund Name.........................................................................................................................

319Crosswalk by Fund Number............................................................................................................

323

vi Table of ContentsIdaho Fiscal Sourcebook, 2010 Edition

Idaho Fiscal Sourcebook, 2010 Edition vii Accounting Identification Code Structure

IDAHO ACCOUNTING IDENTIFICATION CODE STRUCTURE The State Controller has the responsibility for maintaining a statewide accounting system which reflects generally accepted government accounting principles as developed by the governmental accounting standards board (§67-1021). The State Controller established the Idaho Accounting Identification Code Structure and organized the following Fund Groups, Fund Types, and Account Groups:

Governmental 0001 - 0399 General 0001

to account for all financial resources except those required to be accounted for in another fund.

Special 0009 - 0349 to account for the proceeds of specific revenue sources (other than expendable trusts or for major capital projects) that are legally restricted to expenditures for specified purposes.

Capital Projects 0350 - 0374 to account for financial resources to be used for the acquisition or construction of major capital facilities (other than those financed by proprietary funds and trust funds).

Debt Service 0375 - 0399 to account for the accumulation of resources for, and the payment of, general long-term debt principal and interest.

Proprietary 0400 - 0480 Enterprise 0400 - 0425

to account for operations (a) that are financed and operated in a manner similar to private business enterprises - where the intent of the governing body is that the costs (expenses, including depreciation) of providing goods or services to the general public on a continuing basis be financed or recovered primarily through user charges; or (b) where the governing body has decided that periodic determination of revenues earned, expenses incurred, or net income is appropriate for capital maintenance, public policy, management control, accountability, or other purposes.

Internal Service 0426 - 0480 to account for the financing of goods or services provided by one department or agency to other departments or agencies of the governmental unit, or to other governmental units, on a cost-reimbursement basis.

Fiduciary 0481 - 0649 to account for assets held by a governmental unit in a trustee capacity or as an agent for individuals, private organizations, other governmental units, or other funds.

Expendable Trust 0481 - 0525 Non-expendable Trusts 0526 - 0549 Pension Trusts 0550 - 0574 Agency and Clearing 0575 - 0649 College and Universities 0650 - 0699 Account Groups 0700 - 0749

account groups are not funds, they do not reflect expendable financial resources during the current accounting period, but are used to account for fixed assets and long-term debt.

General Fixed Assets 0700 - 0724 General Long-term Debt 0725 -0749 Rotary Fund 0800 – 0999

a revolving expense account created within an agency's fund structure to expedite disbursements. It is authorized under section 67-2019, Idaho Code.

Administrators

Fund: American Reinvestment (0346-00)

Sources: This fund receives federal moneys exclusively from the American Recovery and Reinvestment Act of 2009 (ARRA), Public Law 111-5, passed during the first session of the 111th Congress.

Uses: According to the various titles of ARRA, moneys are to be used for job preservation and creation, education, infrastructure investment, energy efficiency and science, assistance to the unemployed, and State and local fiscal stabilization.

$0 $0 $0 $0 $5,234,400FY 06 FY 07 FY 09FY 08 FY 10

EDPA(170) AdministrationBudget Unit:

Fund: Public School Income (0481-01)

Sources: According to §33-903, Idaho Code, the sources of moneys to the Public School Income Fund include :(a) Moneys from the public school earnings reserve fund and other sources the Legislature deems appropriate;(b) Proceeds of all state taxes levied for public school purposes;(c) Federal government grants for public school purposes when other disposition is not specified by law;(d) Ninety percent (90%) of any moneys received by any department of state government from the federal government from sales, royalties, bonuses or rentals of oil, gas or mineral lands;(e) Legislative appropriations in support of the public schools and other moneys required by law.

Also, earnings on the investment of moneys in the fund remain in the fund.

The majority of moneys in the Public School Income Fund include transfers from the General Fund pursuant to the annual appropriation for public schools and dedicated revenues as provided by statute. The General Fund consists of 1) individual income tax, 2) corporate income tax, 3) sales tax, 4) cigarette tax, 5) beer tax, 6) wine tax, 7) liquor revenue, 8) kilowatt hour tax, 9) mine license tax, 10) Treasurer's interest on investments of certain idle state funds, 11) court fees and fines, 12) insurance premium tax, 13) sale of alcoholic beverage licenses, 14) unclaimed property, 15) articles of incorporation and uniform commercial code filing fees, 16) estate and transfer tax, and 17) other miscellaneous sources from various agency receipts.

Also included are dedicated moneys such as permanent endowment fund earnings (§33-902A, Idaho Code), liquor funds, pari-mutuel racing receipts, car company taxes, fines and forfeitures, federal oil, gas, or mineral royalties, State Treasurer's interest earnings, and miscellaneous fees.

Uses: Funds in this account are appropriated for purposes as designated by the appropriation bills for public schools (§33-903, Idaho Code). Uses include the public school foundation program, unemployment insurance, social security taxes, and for any special programs or projects. Payments to school districts are made each fiscal year in five installments - August (30%), October (30%), November (20%), February (10%), and May (10%) (§33-1009, Idaho Code). Beginning in FY 2004, the legislature broke out the appropriation for Public School Support into five divisions for budgeting purposes as follows: Administrators, Teachers, Operations, Children's Programs, and Facilities. The Idaho Educational Services for the Deaf and the Blind (formerly Idaho School for the Deaf and the Blind) was added as the sixth division of the Public School Support program in FY 2010.

$70,159,632 $79,701,000 $82,423,375 $85,308,222 $76,295,802FY 06 FY 07 FY 09FY 08 FY 10

EDPA(170) AdministrationBudget Unit:

$70,159,632 $79,701,000 $82,423,375 $85,308,222 $81,530,202Administrators Grand Total

FY 06 FY 07 FY 08 FY 09 FY 10

Administrators

EducationPublic School SupportAnalyst: Headlee

1Idaho Fiscal Sourcebook, 2010 Edition

Teachers

Fund: American Reinvestment (0346-00)

Sources: This fund receives federal moneys exclusively from the American Recovery and Reinvestment Act of 2009 (ARRA), Public Law 111-5, passed during the first session of the 111th Congress.

Uses: According to the various titles of ARRA, moneys are to be used for job preservation and creation, education, infrastructure investment, energy efficiency and science, assistance to the unemployed, and State and local fiscal stabilization.

$0 $0 $0 $0 $29,956,500FY 06 FY 07 FY 09FY 08 FY 10

EDPT(170) TeachersBudget Unit:

Fund: Public School Income (0481-01)

Sources: According to §33-903, Idaho Code, the sources of moneys to the Public School Income Fund include :(a) Moneys from the public school earnings reserve fund and other sources the Legislature deems appropriate;(b) Proceeds of all state taxes levied for public school purposes;(c) Federal government grants for public school purposes when other disposition is not specified by law;(d) Ninety percent (90%) of any moneys received by any department of state government from the federal government from sales, royalties, bonuses or rentals of oil, gas or mineral lands;(e) Legislative appropriations in support of the public schools and other moneys required by law.

Also, earnings on the investment of moneys in the fund remain in the fund.

The majority of moneys in the Public School Income Fund include transfers from the General Fund pursuant to the annual appropriation for public schools and dedicated revenues as provided by statute. The General Fund consists of 1) individual income tax, 2) corporate income tax, 3) sales tax, 4) cigarette tax, 5) beer tax, 6) wine tax, 7) liquor revenue, 8) kilowatt hour tax, 9) mine license tax, 10) Treasurer's interest on investments of certain idle state funds, 11) court fees and fines, 12) insurance premium tax, 13) sale of alcoholic beverage licenses, 14) unclaimed property, 15) articles of incorporation and uniform commercial code filing fees, 16) estate and transfer tax, and 17) other miscellaneous sources from various agency receipts.

Also included are dedicated moneys such as permanent endowment fund earnings (§33-902A, Idaho Code), liquor funds, pari-mutuel racing receipts, car company taxes, fines and forfeitures, federal oil, gas, or mineral royalties, State Treasurer's interest earnings, and miscellaneous fees.

Uses: Funds in this account are appropriated for purposes as designated by the appropriation bills for public schools (§33-903, Idaho Code). Uses include the public school foundation program, unemployment insurance, social security taxes, and for any special programs or projects. Payments to school districts are made each fiscal year in five installments - August (30%), October (30%), November (20%), February (10%), and May (10%) (§33-1009, Idaho Code). Beginning in FY 2004, the legislature broke out the appropriation for Public School Support into five divisions for budgeting purposes as follows: Administrators, Teachers, Operations, Children's Programs, and Facilities. The Idaho Educational Services for the Deaf and the Blind (formerly Idaho School for the Deaf and the Blind) was added as the sixth division of the Public School Support program in FY 2010.

$598,260,868 $684,864,900 $718,279,709 $743,082,799 $688,495,998FY 06 FY 07 FY 09FY 08 FY 10

EDPT(170) TeachersBudget Unit:

Teachers

EducationPublic School SupportAnalyst: Headlee

2Idaho Fiscal Sourcebook, 2010 Edition

Fund: School Restructuring Research and Development (0481-50)

Sources: A portion of the General Fund appropriation for public schools. All enhancements for the public school support budget are expended from this fund/detail (excluding the technology and substance abuse enhancements).

Uses: Funds are used to facilitate the enhancement programs detailed in the public school support budget. Examples would be the LEP program, the G/T program, the reading initiative, etc.

$500,000 $500,000 $1,000,000 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDPT(170) TeachersBudget Unit:

Fund: Federal Grant (0348-00)

Sources: The primary sources of revenue in this fund include grants from federal agencies, which may include moneys from the American Recovery and Reinvestment Act of 2009 (ARRA), Public Law 111-5. The fund may also receive grant and contract revenue from other state agencies, private foundations, and corporations.

Uses: Uses include the portion of the grants that are attributable to the division of the Public Schools Support budget in which it is housed.

$13,674,827 $12,621,912 $14,599,363 $13,259,371 $11,515,952FY 06 FY 07 FY 09FY 08 FY 10

EDPT(170) TeachersBudget Unit:

$612,435,695 $697,986,812 $733,879,072 $756,342,171 $729,968,450Teachers Grand Total

FY 06 FY 07 FY 08 FY 09 FY 10

Teachers

EducationPublic School SupportAnalyst: Headlee

3Idaho Fiscal Sourcebook, 2010 Edition

Operations

Fund: School District Building (0315-03)

Sources: The School District Building Account shall have paid into it such appropriations or revenues as may be provided by law (§33-905(1), Idaho Code), a percentage of the net income from State Lottery sales according to §67-7434, Idaho Code, and interest earned on the investment of moneys in the Public Schools Facilities Cooperative Fund (§33-909(10), Idaho Code). Due to amendments in H275, 2009 Session, the annual distribution from the State Lottery sales to the School District Building Account will be flat at $17 million. This provision will sunset on September 30, 2014, at which time the distribution will return to 50% of the Lottery's net income.

Uses: Typical uses are for maintenance and improvement of school sites, however, in fiscal years 2010 and 2011, notwithstanding language was used in the appropriations bills to move these moneys from the Facilities Division into the Operations Division of the public school support program to be used as discretionary funding.

$0 $0 $0 $0 $17,270,500FY 06 FY 07 FY 09FY 08 FY 10

EDPP(170) Public Schools OperationsBudget Unit:

Fund: American Reinvestment (0346-00)

Sources: This fund receives federal moneys exclusively from the American Recovery and Reinvestment Act of 2009 (ARRA), Public Law 111-5, passed during the first session of the 111th Congress.

Uses: These moneys have been applied to the discretionary funds per support unit to be spent at the discretion of the school districts.

$0 $0 $0 $0 $144,057,900FY 06 FY 07 FY 09FY 08 FY 10

EDPP(170) Public Schools OperationsBudget Unit:

Fund: Public School Income (0481-01)

Sources: According to §33-903, Idaho Code, the sources of moneys to the Public School Income Fund include :(a) Moneys from the public school earnings reserve fund and other sources the Legislature deems appropriate;(b) Proceeds of all state taxes levied for public school purposes;(c) Federal government grants for public school purposes when other disposition is not specified by law;(d) Ninety percent (90%) of any moneys received by any department of state government from the federal government from sales, royalties, bonuses or rentals of oil, gas or mineral lands;(e) Legislative appropriations in support of the public schools and other moneys required by law.

Also, earnings on the investment of moneys in the fund remain in the fund.

The majority of moneys in the Public School Income Fund include transfers from the General Fund pursuant to the annual appropriation for public schools and dedicated revenues as provided by statute. The General Fund consists of 1) individual income tax, 2) corporate income tax, 3) sales tax, 4) cigarette tax, 5) beer tax, 6) wine tax, 7) liquor revenue, 8) kilowatt hour tax, 9) mine license tax, 10) Treasurer's interest on investments of certain idle state funds, 11) court fees and fines, 12) insurance premium tax, 13) sale of alcoholic beverage licenses, 14) unclaimed property, 15) articles of incorporation and uniform commercial code filing fees, 16) estate and transfer tax, and 17) other miscellaneous sources from various agency receipts.

Also included are dedicated moneys such as permanent endowment fund earnings (§33-902A, Idaho Code), liquor funds, pari-mutuel racing receipts, car company taxes, fines and forfeitures, federal oil, gas, or mineral royalties, State Treasurer's interest earnings, and miscellaneous fees.

Operations

EducationPublic School SupportAnalyst: Headlee

4Idaho Fiscal Sourcebook, 2010 Edition

Uses: Funds in this account are appropriated for purposes as designated by the appropriation bills for public schools (§33-903, Idaho Code). Uses include the public school foundation program, unemployment insurance, social security taxes, and for any special programs or projects. Payments to school districts are made each fiscal year in five installments - August (30%), October (30%), November (20%), February (10%), and May (10%) (§33-1009, Idaho Code). Beginning in FY 2004, the legislature broke out the appropriation for Public School Support into five divisions for budgeting purposes as follows: Administrators, Teachers, Operations, Children's Programs, and Facilities. The Idaho Educational Services for the Deaf and the Blind (formerly Idaho School for the Deaf and the Blind) was added as the sixth division of the Public School Support program in FY 2010.

$330,297,000 $526,832,600 $551,011,794 $569,823,624 $404,366,622FY 06 FY 07 FY 09FY 08 FY 10

EDPO(170) Public Schools OperationsBudget Unit:

$9,364,032 $6,400,597 $0 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDPS (Cont) (170) Public School Stabilization FundBudget Unit:

$339,661,032 $533,233,197 $551,011,794 $569,823,624 $404,366,622Total Public School Income Fund (0481-01)

FY 06 FY 07 FY 08 FY 09 FY 10

Fund: Public School Technology (0481-53)

Sources: Moneys in this fund originate from the General Fund appropriation for public schools. The amount of the technology funds are designated as a specific amount of the total public school appropriation through legislative intent in the annual appropriation bill. The authority for this program is found in the public school technology grant program established in §33-4804, Idaho Code.

Uses: Funds are used by schools to provide Idaho classrooms with the equipment and resources necessary to integrate information-age technology with instruction and to further connect those classrooms with external telecommunications services.

$9,150,000 $9,147,366 $9,150,100 $9,149,987 $9,150,000FY 06 FY 07 FY 09FY 08 FY 10

EDPO(170) Public Schools OperationsBudget Unit:

Fund: Public Education Stabilization (0481-55)

Sources: Sources include the transfer of any excess funds in the public school budget that result from the net overestimation of certain variable factors, such as support unit growth, and any moneys appropriated to the fund by the Legislature (§33-907; §33-1018, §33-1018A, §33-1018B, Idaho Code).

Uses: Continuously appropriated for the purposes of making up for any shortfall in the amount of discretionary funding available per support unit, as stated in the appropriation for the Division of Operations (§33-1018, Idaho Code). The fund may also be used by the Board of Examiners to pay for the Public Schools' proportional share of any General Fund budget holdback. The Legislature may also appropriate moneys from the fund to make up for declining endowment distribution, for state matching funds for the School District Building Account, or for other purposes as stated in appropriation bills (§33-1018; §33-1018A, §33-1018B, Idaho Code).

Additionally, any accumulated balance in the fund that is in excess of 8.344% of the current year's appropriation shall be transferred to the Bond Levy Equalization Fund (§33-907, Idaho Code).

$0 $0 $2,215,820 $1,043,645 $4,831,844FY 06 FY 07 FY 09FY 08 FY 10

EDPS (Cont) (170) Public School Stabilization FundBudget Unit:

Operations

EducationPublic School SupportAnalyst: Headlee

5Idaho Fiscal Sourcebook, 2010 Edition

Fund: Federal Grant (0348-00)

Sources: The primary sources of revenue in this fund include grants from federal agencies, which may include moneys from the American Recovery and Reinvestment Act of 2009 (ARRA), Public Law 111-5. The fund may also receive grant and contract revenue from other state agencies, private foundations, and corporations.

Uses: Uses include the portion of the grants that are attributable to the division of the Public Schools Support budget in which it is housed.

$5,947,476 $4,001,546 $4,430,307 $4,334,865 $4,008,717FY 06 FY 07 FY 09FY 08 FY 10

EDPO(170) Public Schools OperationsBudget Unit:

$354,758,508 $546,382,109 $566,808,020 $584,352,120 $583,685,583Operations Grand Total

FY 06 FY 07 FY 08 FY 09 FY 10

Operations

EducationPublic School SupportAnalyst: Headlee

6Idaho Fiscal Sourcebook, 2010 Edition

Children's Programs

Fund: Public School Income (0481-01)

Sources: According to §33-903, Idaho Code, the sources of moneys to the Public School Income Fund include :(a) Moneys from the public school earnings reserve fund and other sources the Legislature deems appropriate;(b) Proceeds of all state taxes levied for public school purposes;(c) Federal government grants for public school purposes when other disposition is not specified by law;(d) Ninety percent (90%) of any moneys received by any department of state government from the federal government from sales, royalties, bonuses or rentals of oil, gas or mineral lands;(e) Legislative appropriations in support of the public schools and other moneys required by law.

Also, earnings on the investment of moneys in the fund remain in the fund.

The majority of moneys in the Public School Income Fund include transfers from the General Fund pursuant to the annual appropriation for public schools and dedicated revenues as provided by statute. The General Fund consists of 1) individual income tax, 2) corporate income tax, 3) sales tax, 4) cigarette tax, 5) beer tax, 6) wine tax, 7) liquor revenue, 8) kilowatt hour tax, 9) mine license tax, 10) Treasurer's interest on investments of certain idle state funds, 11) court fees and fines, 12) insurance premium tax, 13) sale of alcoholic beverage licenses, 14) unclaimed property, 15) articles of incorporation and uniform commercial code filing fees, 16) estate and transfer tax, and 17) other miscellaneous sources from various agency receipts.

Also included are dedicated moneys such as permanent endowment fund earnings (§33-902A, Idaho Code), liquor funds, pari-mutuel racing receipts, car company taxes, fines and forfeitures, federal oil, gas, or mineral royalties, State Treasurer's interest earnings, and miscellaneous fees.

Uses: Funds in this account are appropriated for purposes as designated by the appropriation bills for public schools (§33-903, Idaho Code). Uses include the public school foundation program, unemployment insurance, social security taxes, and for any special programs or projects. Payments to school districts are made each fiscal year in five installments - August (30%), October (30%), November (20%), February (10%), and May (10%) (§33-1009, Idaho Code). Beginning in FY 2004, the legislature broke out the appropriation for Public School Support into five divisions for budgeting purposes as follows: Administrators, Teachers, Operations, Children's Programs, and Facilities. The Idaho Educational Services for the Deaf and the Blind (formerly Idaho School for the Deaf and the Blind) was added as the sixth division of the Public School Support program in FY 2010.

$4,950,000 $6,985,000 $12,064,533 $29,773,000 $32,194,279FY 06 FY 07 FY 09FY 08 FY 10

EDPC(170) Children's ProgramsBudget Unit:

Fund: School Restructuring Research and Development (0481-50)

Sources: A portion of the General Fund appropriation for public schools. All enhancements for the public school support budget are expended from this fund/detail (excluding the technology and substance abuse enhancements).

Uses: Funds are used to facilitate the enhancement programs detailed in the public school support budget. Examples would be the LEP program, the G/T program, the reading initiative, etc.

$7,859,940 $8,840,000 $8,840,000 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDPC(170) Children's ProgramsBudget Unit:

Children's Programs

EducationPublic School SupportAnalyst: Headlee

7Idaho Fiscal Sourcebook, 2010 Edition

Fund: Cigarette, Tobacco and Lottery Income Taxes (0481-54)

Sources: Sources of revenue include:

1) a 5.1746 cent sales tax on the wholesale price per pack of 20 cigarettes imposed by §63-2506, Idaho Code; 2) fifty-percent (50%) of the five-percent (5%) tax levied on all tobacco products by §63-2552A, Idaho Code; and 3) through annual appropriation bill language, income taxes on Idaho Lottery winnings (§67-7439, Idaho Code).

Uses: Funds are to be utilized to facilitate and provide substance abuse programs in the public school system.

$4,698,033 $5,492,296 $6,978,223 $6,940,079 $5,532,872FY 06 FY 07 FY 09FY 08 FY 10

EDPC(170) Children's ProgramsBudget Unit:

Fund: Idaho Digital Learning Academy (0481-56)

Sources: The amount of funding is determined by formula outlined in §33-1020, Idaho Code, and then appropriated by the Legislature through the Public School Support program.

Uses: To support the "infrastructure" of the Idaho Digital Learning Academy (§33-5508, Idaho Code).

$900,000 $1,100,000 $3,237,896 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDPC(170) Children's ProgramsBudget Unit:

Fund: Federal Grant (0348-00)

Sources: The primary sources of revenue in this fund include grants from federal agencies, which may include moneys from the American Recovery and Reinvestment Act of 2009 (ARRA), Public Law 111-5. The fund may also receive grant and contract revenue from other state agencies, private foundations, and corporations.

Uses: Uses include the portion of the grants that are attributable to the division of the Public Schools Support budget in which it is housed.

$162,352,293 $161,499,712 $173,978,134 $178,187,798 $204,583,328FY 06 FY 07 FY 09FY 08 FY 10

EDPC(170) Children's ProgramsBudget Unit:

$180,760,267 $183,917,008 $205,098,785 $214,900,876 $242,310,479Children's Programs Grand Total

FY 06 FY 07 FY 08 FY 09 FY 10

Children's Programs

EducationPublic School SupportAnalyst: Headlee

8Idaho Fiscal Sourcebook, 2010 Edition

Facilities

Fund: General (0001-00)

Sources: The General Fund consists of, "moneys received into the treasury and not specially appropriated to any other fund" (§67-1205). The fund sources are: 1) individual income tax, 2) corporate income tax, 3) sales tax, 4) cigarette tax, 5) beer tax, 6) wine tax, 7) liquor surcharge, 8) kilowatt hour tax, 9) mine license tax, 10) Treasurer's interest on investments of certain idle state funds, 11) court fees and fines, 12) insurance premium tax, 13) sale of alcoholic beverage licenses, 14) unclaimed property, 15) articles of incorporation and uniform commercial code filing fees, 16) estate and transfer tax, and 17) other miscellaneous sources from various agency receipts.

Uses: As appropriated.

$0 $4,500,000 $1,249,842 $1,899,910 $0FY 06 FY 07 FY 09FY 08 FY 10

EDPF(170) FacilitiesBudget Unit:

Fund: Bond Levy Equalization (0315-02)

Sources: Moneys are made available through appropriations (§33-906A, Idaho Code), distribution of moneys collected pursuant to §63-2520; in certain circumstances Lottery funds (§67-7434, Idaho Code); and as appropriated from the School District Building Account (§33-905, Idaho Code).

Uses: To subsidize the interest-cost portion of school bonds passed after September 15, 2002. Subsidies range from 10% to 100% of interest costs, depending on the relative wealth and economic vitality of each school district. (§33-906 and §33-906B, Idaho Code).

$3,704,555 $0 $0 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDPF(170) FacilitiesBudget Unit:

$0 $6,595,309 $11,200,000 $16,500,000 $16,605,281FY 06 FY 07 FY 09FY 08 FY 10

EDPM (Cont) (170) Facilities - Bond Levy EqualizationBudget Unit:

$3,704,555 $6,595,309 $11,200,000 $16,500,000 $16,605,281Total Bond Levy Equalization Fund (0315-02)

FY 06 FY 07 FY 08 FY 09 FY 10

Fund: School District Building (0315-03)

Sources: The School District Building Account shall have paid into it such appropriations or revenues as may be provided by law (§33-905(1), Idaho Code), a percentage of the net income from State Lottery sales according to §67-7434, Idaho Code, and interest earned on the investment of moneys in the Public Schools Facilities Cooperative Fund (§33-909(10), Idaho Code). Due to amendments in H275, 2009 Session, the annual distribution from the State Lottery sales to the School District Building Account will be flat at $17 million. This provision will sunset on September 30, 2014, at which time the distribution will return to 50% of the Lottery's net income.

Facilities

EducationPublic School SupportAnalyst: Headlee

9Idaho Fiscal Sourcebook, 2010 Edition

Uses: According to §33-905(2), Idaho Code, moneys in the account are to be distributed to all Idaho school districts on the basis of average daily attendance.

According to §33-905(3), Idaho Code, moneys in the account are to be used for those purposes stated in §33-1019(3), Idaho Code, which are:

". . . shall be used exclusively for the maintenance and repair of school buildings or any serious or imminent safety hazard on the property of said school buildings as identified pursuant to chapter 80, title 39, Idaho Code, and shall be utilized, first, to abate serious or imminent safety hazards, as identified pursuant to chapter 80, title 39, Idaho Code. Unexpended moneys in a school district's school building maintenance allocation shall be carried over from year to year and shall remain allocated for the purposes specified in this subsection (3)."

Any payments from the school district building account received by a school district in excess of the state match requirements of 33-1019, may be used for the purposes stated in §33-1102, Idaho Code, which are:

a.) to acquire, purchase, or improve a school site; b.) to build a schoolhouse or other building; c.) to demolish or remove school buildings; d.) to add to, remodel, or repair any existing building; e.) to furnish and equip buildings, including all lighting, heating, ventilation and sanitation; and f.) to purchase school buses;

At the state level, any excess moneys not needed to meet these provisions of 33-1019 are to be deposited into the Public Education Stabilization Fund.

$8,922,500 $11,627,591 $20,070,263 $18,353,517 $0FY 06 FY 07 FY 09FY 08 FY 10

EDPF(170) FacilitiesBudget Unit:

Fund: Facilities Cooperative (0315-06)

Sources: The fund shall contain such moneys as may be directed pursuant to appropriation. To date, there has been a single appropriation of $25 million to this fund.

Uses: Moneys in the fund shall be used exclusively to finance the public school facilities cooperative funding program and are continuously appropriated. Moneys in the fund shall be invested by the state treasurer and interest earned on the investments shall be credited to the school district building account (§ 33-909(10), Idaho Code).

$0 $0 $0 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDPM (Cont) (170) Facilities - Bond Levy EqualizationBudget Unit:

$12,627,055 $22,722,900 $32,520,105 $36,753,427 $16,605,281Facilities Grand Total

FY 06 FY 07 FY 08 FY 09 FY 10

Facilities

EducationPublic School SupportAnalyst: Headlee

10Idaho Fiscal Sourcebook, 2010 Edition

Educational Services for the Deaf & Blind

Fund: General (0001-00)

Sources: The General Fund consists of, "moneys received into the treasury and not specially appropriated to any other fund" (§67-1205). The fund sources are: 1) individual income tax, 2) corporate income tax, 3) sales tax, 4) cigarette tax, 5) beer tax, 6) wine tax, 7) liquor surcharge, 8) kilowatt hour tax, 9) mine license tax, 10) Treasurer's interest on investments of certain idle state funds, 11) court fees and fines, 12) insurance premium tax, 13) sale of alcoholic beverage licenses, 14) unclaimed property, 15) articles of incorporation and uniform commercial code filing fees, 16) estate and transfer tax, and 17) other miscellaneous sources from various agency receipts.

Uses: As appropriated. Historically, approximately 95% of the annual appropriation to the School for the Deaf and the Blind has been comprised of General Fund moneys.

$0 $0 $0 $0 $4,674,453FY 06 FY 07 FY 09FY 08 FY 10

EDDA(502) Campus ProgramsBudget Unit:

$0 $0 $0 $0 $2,593,982FY 06 FY 07 FY 09FY 08 FY 10

EDDC(502) Outreach ProgramsBudget Unit:

$0 $0 $0 $0 $7,268,435Total General Fund (0001-00)

FY 06 FY 07 FY 08 FY 09 FY 10

Fund: ISDB Contingency Reserve (0315-01)

Sources: Established pursuant to §33-3414, Idaho Code. This Fund includes unspent appropriations deposited by the board of trustees. The fund balance may not exceed 5% of the total General Fund appropriation to the Idaho Eduational Services for the Deaf and the Blind.

Uses: Disbursements from this continuously appropriated fund may be made as the board of trustees determines necessary for contingencies that may arise.

$0 $0 $0 $0 $361,441FY 06 FY 07 FY 09FY 08 FY 10

EDDB (Cont) (502) General Fund Contingency ReserveBudget Unit:

Fund: Miscellaneous Revenue (0349-00)

Sources: Moneys in this fund come from a variety of sources including rental income receipts, out-of-state tuition, donations received from individuals, organizations, and foundations.

Uses: Moneys in this fund are subject to appropriation and are typically used for the general operating budget, to pay utilities and for other maintenance expenses at the campus in Gooding. Moneys from donations are expended per the directions of the donors. If a use is not specified, donated moneys are used to support "students in need" at the campus, but not for general operating budget.

$0 $0 $0 $0 $197,630FY 06 FY 07 FY 09FY 08 FY 10

EDDA(502) Campus ProgramsBudget Unit:

Fund: School for the Deaf and the Blind (Endowment) (0481-22)

Sources: This fund consists of all moneys distributed from the Charitable Institutions Fund according to §66-1106, Idaho Code, of which 1/30 is directed to the School for the Deaf and the Blind (also known as Idaho Educational Services for the Deaf and the Blind).

Uses: Moneys from this fund are to be used for maintenance and expenses at the School for the Deaf and the Blind (campus facilities) according to §66-1107, Idaho Code.

Educational Services for the Deaf & Blind

EducationPublic School SupportAnalyst: Headlee

11Idaho Fiscal Sourcebook, 2010 Edition

$0 $0 $0 $0 $134,800FY 06 FY 07 FY 09FY 08 FY 10

EDDA(502) Campus ProgramsBudget Unit:

Fund: Federal Grant (0348-00)

Sources: The primary sources of revenue in this fund include grants from federal agencies, which may include moneys from the American Recovery and Reinvestment Act of 2009 (ARRA), Public Law 111-5. Federal grant moneys for the Idaho Educational Services for the Deaf and the Blind originate from a variety of federal programs, but primarily from those programs administered by the Idaho State Department of Education.

Uses: Moneys expended in this fund according to federal guidelines, which are to improve comprehensive educational programs for deaf/hard of hearing and/or blind/visually-impaired students at the Gooding campus as well as other locations.

$0 $0 $0 $0 $268,227FY 06 FY 07 FY 09FY 08 FY 10

EDDA(502) Campus ProgramsBudget Unit:

$0 $0 $0 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDDC(502) Outreach ProgramsBudget Unit:

$0 $0 $0 $0 $268,227Total Federal Grant Fund (0348-00)

FY 06 FY 07 FY 08 FY 09 FY 10

$0 $0 $0 $0 $8,230,532Educational Services for the Deaf & Blind Grand Total

FY 06 FY 07 FY 08 FY 09 FY 10

Educational Services for the Deaf & Blind

EducationPublic School SupportAnalyst: Headlee

12Idaho Fiscal Sourcebook, 2010 Edition

Agricultural Research & Extension Service

Fund: General (0001-00)

Sources: The General Fund consists of, "moneys received into the treasury and not specially appropriated to any other fund" per §67-1205, Idaho Code. The revenue sources are: 1) individual income tax, 2) corporate income tax, 3) sales tax, 4) cigarette tax, 5) beer tax, 6) wine tax, 7) liquor revenue, 8) kilowatt hour tax, 9) mine license tax, 10) Treasurer's interest on investments of certain idle state funds, 11) court fees and fines, 12) insurance premium tax, 13) sale of alcoholic beverage licenses, 14) unclaimed property, 15) articles of incorporation and uniform commercial code filing fees, 16) estate and transfer tax, and 17) other miscellaneous sources from various agency receipts.

Uses: General Fund moneys provide base support for agricultural research and extension programming, and provides leverage to generate additional grant and contract funding for ongoing program needs as well as new program redirections. The Cooperative Extension Service has offices in 42 of Idaho's 44 counties (all except Boise and Lewis counties) that are staffed by those who are specially trained to work with agriculture, families, youth and communities.

$25,479,485 $26,129,000 $22,719,577 $27,002,088 $23,054,000FY 06 FY 07 FY 09FY 08 FY 10

EDHA(514) Agricultural Research and Extension ServiceBudget Unit:

Fund: Economic Recovery Reserve (0150-01)

Sources: Moneys in the fund are from cigarette taxes (deposits made pursuant to §63-2520(5), Idaho Code) and interest earnings from the investment of idle moneys in the fund. Although not specified in law, it also includes transfers from the general fund or other funds as approved by the Legislature.

Uses: The fund was created for the purpose of meeting general fund revenue shortfalls, meeting expenses incurred as the result of a major disaster declared by the governor, or for providing one-time tax relief payments to the citizens of Idaho. It has been used for 27th pay period in FY 2006, one-time replacement equipment costs, economic development projects, and other line-items as approved by the Legislature. (§67-3520, Idaho Code)

$802,800 $90,000 $0 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDHA(514) Agricultural Research and Extension ServiceBudget Unit:

Fund: Miscellaneous Revenue (0349-00)

Sources: Miscellaneous revenue is generated primarily from Agricultural Research and Extension Service (ARES) farming operations, and to a lesser extent, conferences, publications, and other research and extension/education activities.

Uses: Miscellaneous revenues are used to support the overall operations of the College of Agriculture and the operations of the ten off-campus Research & Extension Centers.

NOTE: This fund is shown for informational purposes only and is not controlled in the Statewide Accounting and Reporting System (STARS).

$0 $0 $0 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDHA(514) Agricultural Research and Extension ServiceBudget Unit:

Fund: Equine Education (0660-05)

Sources: Equine Education funds come from the Idaho State Racing Commission. They are a portion of the "handle" generated by pari-mutuel horse racing wagering in the state in accordance with §54-2513(B)(4)(c), Idaho Code and §57-818, Idaho Code .

Uses: This dedicated fund is used by the veterinary science program specifically to enhance and forward the work conducted at the Northwest Equine Reproduction Laboratory.

Agricultural Research & Extension Service

EducationEducation, State Board ofAnalyst: Headlee

13Idaho Fiscal Sourcebook, 2010 Edition

$26,133 $37,154 $38,629 $18,596 $5,208FY 06 FY 07 FY 09FY 08 FY 10

EDHA(514) Agricultural Research and Extension ServiceBudget Unit:

Fund: Federal Grant (0348-00)

Sources: The Agricultural Research and Extension Service (ARES) receives federal funds consisting of Hatch Formula Funds, Hatch Regional Research Funds, Smith-Lever Formula Funds and Farm Safety Funds. These federal funds are allocated by formula through the U.S. Department of Agriculture. See §33-2813, Idaho Code. See also, §33-2902, Idaho Code, for Idaho's assent to the Hatch Act.

Uses: The federal funds received by ARES are used to support research activity that addresses problems that are relevant to Idaho's agriculture. Research support uses include faculty and support personnel salaries and benefits, travel, operational, and equipment funds.

Regional Research funds are specifically used to support research activity in which two or more state agricultural experiment stations are cooperating to solve problems that concern the agriculture of more than one state. Research support uses include faculty and support personnel salaries and benefits, travel, operational, and equipment funds.

Smith-Lever formula funds are allocated to the State Cooperative Extension Services in order to aid in the dissemination of useful and practical information on subjects relating to agriculture, uses of solar energy with respect to agriculture, and home economics. Funds are distributed primarily on the basis of farm and rural population, and to some extent on the basis of special problems and needs. Uses of these formula funds consists of agricultural extension work which includes the development of instruction and practical demonstrations of existing or improved technologies in agriculture, uses of solar energy with respect to agriculture, home economics, and subjects relating to persons not attending or resident in colleges in the communities of the state. Extension support uses include faculty and support personnel salaries and benefits, travel, operational, and equipment funds used in carrying out authorized objectives in accordance with the Annual Plan of Work.

Farm Safety funds are allocated under Smith-Lever 3(d) which provides for funds in addition to Smith-Lever formula funding. Funds appropriated under this section are earmarked for specific purposes and must be used for these purposes if accepted by the state. In accordance with policy guidelines, Farm Safety funds are used to support agricultural extension work consisting of the development of practical applications of research knowledge and giving of instruction and practical demonstrations of existing or improved practices or technologies in agricultural safety, worker safety, accident analysis, agricultural machinery management, chemical application, and alternative energy sources. Extension support uses include faculty and support personnel salaries and benefits, travel, operational, and equipment funds in carrying out farm safety extension objectives as outlined in Annual Plan of Work.

NOTE: This fund is shown for informational purposes only and is not controlled in the Statewide Accounting and Reporting System (STARS).

$0 $0 $0 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDHA(514) Agricultural Research and Extension ServiceBudget Unit:

$26,308,418 $26,256,154 $22,758,206 $27,020,684 $23,059,208Agricultural Research & Extension Service Grand Total

FY 06 FY 07 FY 08 FY 09 FY 10

Agricultural Research & Extension Service

EducationEducation, State Board ofAnalyst: Headlee

14Idaho Fiscal Sourcebook, 2010 Edition

College and Universities

Fund: General (0001-00)

Sources: Idaho's four 4-year college and universities, the University of Idaho, Boise State University, Idaho State University and Lewis-Clark State College, form a statewide higher education system. Most of the appropriated funding they receive comes from the General Fund. The General Fund consists of, "moneys received into the treasury and not specially appropriated to any other fund" (§67-1205, Idaho Code). The fund sources are: 1) individual income tax, 2) corporate income tax, 3) sales tax, 4) cigarette tax, 5) beer tax, 6) wine tax, 7) liquor revenue, 8) kilowatt hour tax, 9) mine license tax, 10) Treasurer's interest on investments of certain idle state funds, 11) court fees and fines, 12) insurance premium tax, 13) sale of alcoholic beverage licenses, 14) unclaimed property, 15) articles of incorporation and uniform commercial code filing fees, 16) estate and transfer tax, and 17) other miscellaneous sources from various agency receipts.

Uses: The 4-year college and universities use their General Fund appropriation to support and maintain the instruction, research and public service functions of the university, including related institutional support, operation and maintenance activities.

$72,111,400 $75,673,600 $81,906,600 $83,827,000 $72,897,600FY 06 FY 07 FY 09FY 08 FY 10

EDGA(512) College & Universities: BOISE STATE UNIVERSITYBudget Unit:

$63,925,700 $65,967,200 $73,383,100 $72,973,400 $61,144,400FY 06 FY 07 FY 09FY 08 FY 10

EDGB(513) College & Universities: IDAHO STATE UNIVERSITYBudget Unit:

$86,185,468 $89,414,800 $94,842,300 $94,165,700 $77,402,400FY 06 FY 07 FY 09FY 08 FY 10

EDGC(514) College & Universities: UNIVERSITY OF IDAHOBudget Unit:

$11,778,700 $12,580,800 $14,009,200 $15,364,700 $12,572,000FY 06 FY 07 FY 09FY 08 FY 10

EDGD(511) College & Universities: LEWIS-CLARK STATE COLLEGEBudget Unit:

$74,946 $79,896 $69,191 $103,937 $54,849FY 06 FY 07 FY 09FY 08 FY 10

EDGE(501) College & Universities: EDUCATION BOARD OFFICEBudget Unit:

$234,076,214 $243,716,296 $264,210,391 $266,434,737 $224,071,249Total General Fund (0001-00)

FY 06 FY 07 FY 08 FY 09 FY 10

Fund: Economic Recovery Reserve (0150-01)

Sources: Moneys in the fund are from cigarette taxes (deposits made pursuant to §63-2520, Idaho Code) and interest earnings from the investment of idle moneys in the fund. Although not specified in law, it also includes transfers from the General Fund or other funds as approved by the Legislature.

Uses: The fund was created for the purpose of meeting General Fund revenue shortfalls, meeting expenses incurred as the result of a major disaster declared by the governor, or for providing one-time tax relief payments to the citizens of Idaho. It has been used for 27th pay period in FY 2006, one-time replacement equipment costs, and other line-items as approved by the Legislature (§67-3520, Idaho Code).

$1,228,000 $1,135,552 $619,848 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDGA(512) College & Universities: BOISE STATE UNIVERSITYBudget Unit:

$1,598,700 $1,162,000 $0 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDGC(514) College & Universities: UNIVERSITY OF IDAHOBudget Unit:

College and Universities

EducationEducation, State Board ofAnalyst: Headlee

15Idaho Fiscal Sourcebook, 2010 Edition

$280,400 $126,700 $0 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDGG(511) Lewis-Clark State CollegeBudget Unit:

$1,140,800 $1,390,108 $251,892 $0 $0FY 06 FY 07 FY 09FY 08 FY 10

EDGH(513) Idaho State UniversityBudget Unit:

$4,247,900 $3,814,360 $871,740 $0 $0Total Economic Recovery Reserve Fund (0150-01)

FY 06 FY 07 FY 08 FY 09 FY 10

Fund: American Reinvestment (0346-00)

Sources: This fund receives federal moneys exclusively from the American Recovery and Reinvestment Act of 2009 (ARRA), Public Law 111-5, passed during the first session of the 111th Congress.

Uses: According to Title 14 of ARRA, moneys are to be used for education and general expenditures, and in such a way to mitigate the need to raise tuition and fees for in-State student, or for modernization, renovation, or repair of institution of higher education facilities that are primarily used for instruction, research, or student housing.

$0 $0 $0 $0 $4,100,404FY 06 FY 07 FY 09FY 08 FY 10

EDGA(512) College & Universities: BOISE STATE UNIVERSITYBudget Unit:

$0 $0 $0 $0 $3,442,165FY 06 FY 07 FY 09FY 08 FY 10

EDGB(513) College & Universities: IDAHO STATE UNIVERSITYBudget Unit:

$0 $0 $0 $0 $5,329,056FY 06 FY 07 FY 09FY 08 FY 10

EDGC(514) College & Universities: UNIVERSITY OF IDAHOBudget Unit:

$0 $0 $0 $0 $887,300FY 06 FY 07 FY 09FY 08 FY 10

EDGD(511) College & Universities: LEWIS-CLARK STATE COLLEGEBudget Unit:

$0 $0 $0 $0 $13,758,924Total American Reinvestment Fund (0346-00)

FY 06 FY 07 FY 08 FY 09 FY 10

Fund: Agricultural College Endowment Income (0481-02)

Sources: The University of Idaho is the beneficiary of the Agricultural College Endowment Fund (§33-2913 and §33-2914, Idaho Code). This fund receives income from the sale of land on contract, timber sales, land rentals, cottage site rentals, grazing rentals and mineral rentals from lands granted to the State of Idaho by Congress for the support and maintenance of the agricultural college at the University of Idaho.

Uses: Section 33-2914, Idaho Code, directs that these funds be used for the support and maintenance of the agricultural college at the University of Idaho.

$0 $661,200 $725,000 $794,000 $850,800FY 06 FY 07 FY 09FY 08 FY 10

EDGC(514) College & Universities: UNIVERSITY OF IDAHOBudget Unit:

College and Universities

EducationEducation, State Board ofAnalyst: Headlee

16Idaho Fiscal Sourcebook, 2010 Edition

Fund: Charitable Institutions Endowment Income (0481-03)

Sources: Idaho State University is a beneficiary of the Charitable Institutions Endowment Fund created in §66-1103, Idaho Code. Moneys in the fund are generated from the following:

(a) Proceeds from the sale of lands granted to the state of Idaho for charitable, educational, penal and reformatory institutions by the Idaho Admission Bill, 26 Stat. L. 215, ch. 656, and lands granted in lieu thereof;(b) Proceeds of royalties from the extraction of minerals on charitable institutions endowment lands owned by the state;(c) Moneys allocated from the charitable institutions earnings reserve fund.

Section 66-1105, Idaho Code, creates the charitable institutions fund that is credited for all the above revenue and §66-1106, Idaho Code, transfers the funds in the charitable institutions fund to "the following designated funds in the following proportions:"

Idaho State University - 4/15 State Juvenile Corrections Institutions- 4/15 State Hospital North - 4/15 Division of Veteran's - 5/30 School for Deaf and Blind - 1/30

Uses: Section 66-1107, Idaho Code, specifies that these funds be used for the "support or maintenance" of the institutions listed above.

$0 $629,700 $688,500 $753,600 $790,400FY 06 FY 07 FY 09FY 08 FY 10

EDGB(513) College & Universities: IDAHO STATE UNIVERSITYBudget Unit:

Fund: Normal School Endowment Income (0481-04)

Sources: According to §33-3301B, Idaho Code, the fund shall consist of all moneys distributed from the normal school earnings reserve fund and from other sources as the Legislature deems appropriate. Additionally, pursuant to §33-3301A, Idaho Code, moneys in the normal school earnings reserve fund originate from:

(a) All earnings of the normal school permanent endowment fund;(b) Proceeds of the sale of timber growing on normal school endowment lands;(c) Proceeds of leases of normal school endowment lands;(d) Proceeds of interest upon deferred payments on normal school endowment lands or timber on those lands; and(e) All other proceeds received from the use of normal school endowment lands and not otherwise designated for deposit in the normal school permanent endowment fund.

Idaho State University (§33-3304, Idaho Code) and Lewis-Clark State College (§33-3302, Idaho Code) are the beneficiaries of the Normal School Endowment Fund.

Uses: Section 33-3304, Idaho Code, provides: "Fifty percent (50%) of all the moneys that now are in or which may hereafter accrue to the normal school income fund are hereby appropriated and set apart for the support and maintenance of the department of education at Idaho State University . . ."

Section 33-3302, Idaho Code, provides: "Fifty percent (50%) of all moneys that now are in or whichmay hereafter accrue to the normal school income fund are perpetually appropriated and set apart for the support and maintenance of the Lewis-Clark State College, . . ."

$1,602,800 $1,057,800 $1,155,000 $1,267,100 $1,330,900FY 06 FY 07 FY 09FY 08 FY 10

EDGB(513) College & Universities: IDAHO STATE UNIVERSITYBudget Unit:

College and Universities

EducationEducation, State Board ofAnalyst: Headlee

17Idaho Fiscal Sourcebook, 2010 Edition

$1,613,003 $1,016,429 $1,171,743 $1,294,525 $1,330,700FY 06 FY 07 FY 09FY 08 FY 10

EDGD(511) College & Universities: LEWIS-CLARK STATE COLLEGEBudget Unit:

$3,215,803 $2,074,229 $2,326,743 $2,561,625 $2,661,600Total Normal School Endowment Income Fund (0481-04)

FY 06 FY 07 FY 08 FY 09 FY 10

Fund: Scientific School Endowment Income (0481-06)

Sources: The University of Idaho is the beneficiary of the Scientific School Endowment Fund (§33-2911 and §33-2912, Idaho Code). This fund receives the income from the sale of land on contract, timber sales, land rentals, cottage site rentals, grazing rentals and mineral rentals from lands granted to the State of Idaho by Congress for the support and maintenance of a scientific college or department at the University of Idaho.

Uses: Section 33-2912, Idaho Code, directs that these funds be used for the support and maintenance of a scientific college or department at the University of Idaho.

$2,848,500 $2,375,800 $2,138,000 $2,332,300 $2,984,400FY 06 FY 07 FY 09FY 08 FY 10

EDGC(514) College & Universities: UNIVERSITY OF IDAHOBudget Unit:

Fund: University Endowment Income (0481-08)

Sources: The University of Idaho is the beneficiary of the University Permanent Endowment Fund (§33-2909 and §33-2910, Idaho Code). This fund receives the income from the sale of land on contract, timber sales, land rentals, cottage site rentals, grazing rentals and mineral rentals from lands granted to the State of Idaho by Congress for the support and maintenance of the university.

Uses: Section 33-2910, Idaho Code, directs that these funds be set apart for the support and maintenance of the University of Idaho.

$3,465,500 $1,822,600 $1,990,000 $2,181,000 $2,329,200FY 06 FY 07 FY 09FY 08 FY 10

EDGC(514) College & Universities: UNIVERSITY OF IDAHOBudget Unit:

Fund: Unrestricted (0650-00)

Sources: Unrestricted Funds are student tuition and fees collected by BSU, ISU, LCSC, and UI (beginning in FY 2012). In addition to tuition, all students are charged a variety of fees, where applicable, including: part-time fees, graduate fees, professional fees (e.g. law, medicine, pharmacy, architecture, etc.), course overload fees, summer session fees, in-service teacher fees, Western Undergraduate Exchange (WUE) fees, employee/spouse fees and senior citizen fees. Traditionally, interest earned on tuition and fees was deposited into the General Fund, however, beginning in FY 2012, interest earned from appropriated tuition and fees will be deposited to the newly created Higher Education Stabilization fund (H544, 2010 Session).

Uses: BSU, ISU, LCSC, and UI (beginning in FY 2012) can expend tuition and fees without restriction in the performance of the primary objectives of the institution, e.g. for instruction, research, extension, and public service, and for programs that support those functions. The expenditure detail for the University of Idaho is not included below. Unlike BSU, ISU and LCSC, the constitutional status of the UI allows it to retain, manage and expend all student fees directly rather than depositing those moneys with the State Treasurer and expending them through the State Controller.